tomra capital markets day presentation - cision

TRANSCRIPT

TOMRA Capital Markets Day Presentation

Oslo, Norway

May 20th, 2011

2

“A tiny blue and green oasis of life in a cold universe.” – David Suzuki

3

TRANSFORMATION

The world population and standard of living is increasing dramatically

4

World resources are under unprecedented pressure

5

Resource productivity must increase to ensure sustainable development

6

TRANSFORMATION

7

At TOMRA we have always thought this way. From inventing the world’s first reverse vending machine in 1972 to providing the most innovative sensor-based sorting systems today.

8

TOMRA is transforming how we obtain our resources…

9

Our sorters can increase recovery of valuable minerals by up to 25%

Our sorters can reduce water consumption with 3-4 cubic meters per ton ore

Our sorters can reduce energy consumption in mining by 15%

10

TOMRA is transforming how we use our resources…

11

More than 30 per cent of fruits and vegetables grown for North American consumers are discarded before they reach grocery store shelves because of cosmetic imperfections*

One of our optical sorters can individually analyze millions of potatoes, tomatoes etc. per day and quality sort each and every one to maximize efficient use of the produce

Our steam peelers increase the yield of a potato with up to 20% compared to mechanical peeling

12

TOMRA is transforming how we reuse our resources…

13

30 billion used beverage containers are every year captured by our reverse vending machines

Our optical waste sorter can analyze and sort a football stadium covered with waste in less than 15 minutes

450 000 tons of metal is recovered every year by our metal recycling machines

Our vertical balers enable daily savings of 45,000 transport movements, 700,000 liters of fuel and up to 50% of customers’ waste handling costs

14* According to MAF Roda

TOMRA creates transformative sensor-based solutions for optimal resource productivity

15

Today we are seeing more opportunities for transformative solutions than ever before.

16

Deposits into refunds…

17

Waste into wealth…

18

19

Source into resource…

Purpose into profits…

20

Profits into progress…

21

TOMRA is showing that we can move past the false choice between the earth and the economy

22

This is the resource revolution

23

TOMRA is leading it

24

TOMRA Collection Technology

25

24

1

2823

9

76 2

30

29

22

14

0 0 0 0

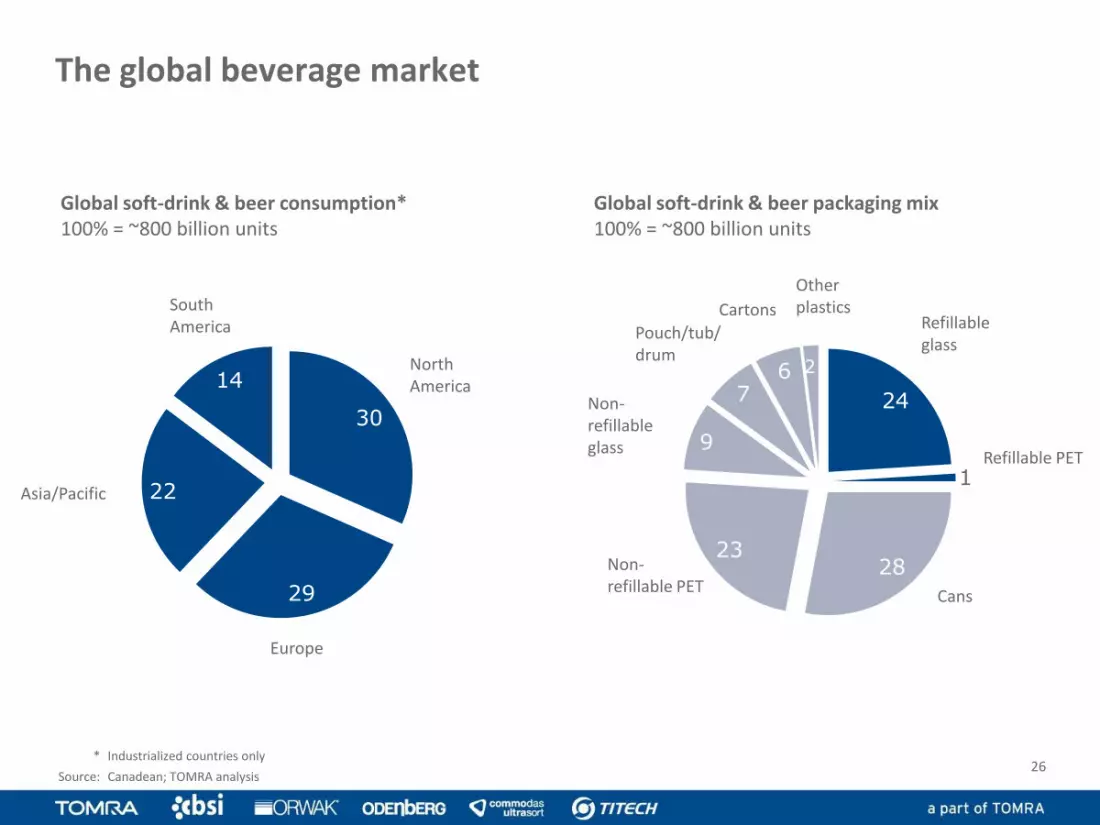

The global beverage market

Global soft-drink & beer consumption*100% = ~800 billion units

North America

Asia/Pacific

Europe

South America

Global soft-drink & beer packaging mix100% = ~800 billion units

Refillable glass

Non-refillable PET

Refillable PET

Cans

Non-refillable glass

Pouch/tub/ drum

Cartons

Other plastics

* Industrialized countries only

Source: Canadean; TOMRA analysis26

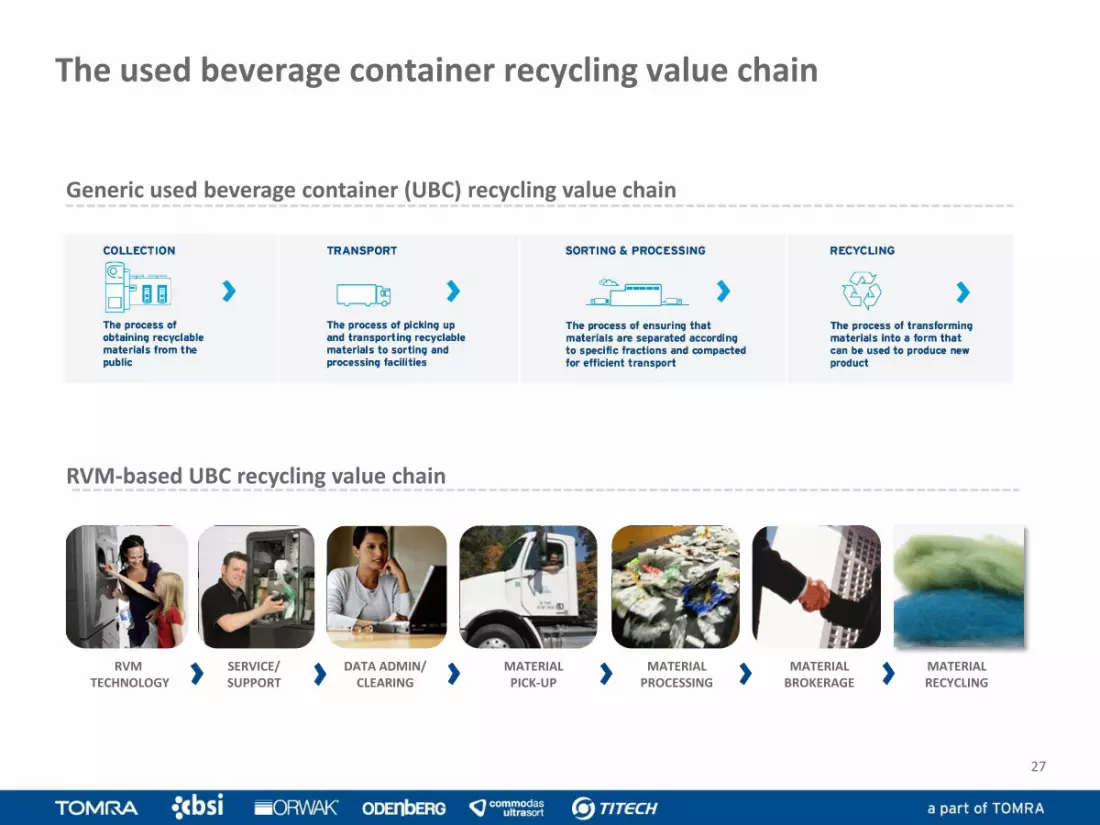

RVM TECHNOLOGY

SERVICE/SUPPORT

DATA ADMIN/CLEARING

MATERIALPICK-UP

MATERIALBROKERAGE

MATERIALPROCESSING

MATERIALRECYCLING

The used beverage container recycling value chain

Generic used beverage container (UBC) recycling value chain

RVM-based UBC recycling value chain

27

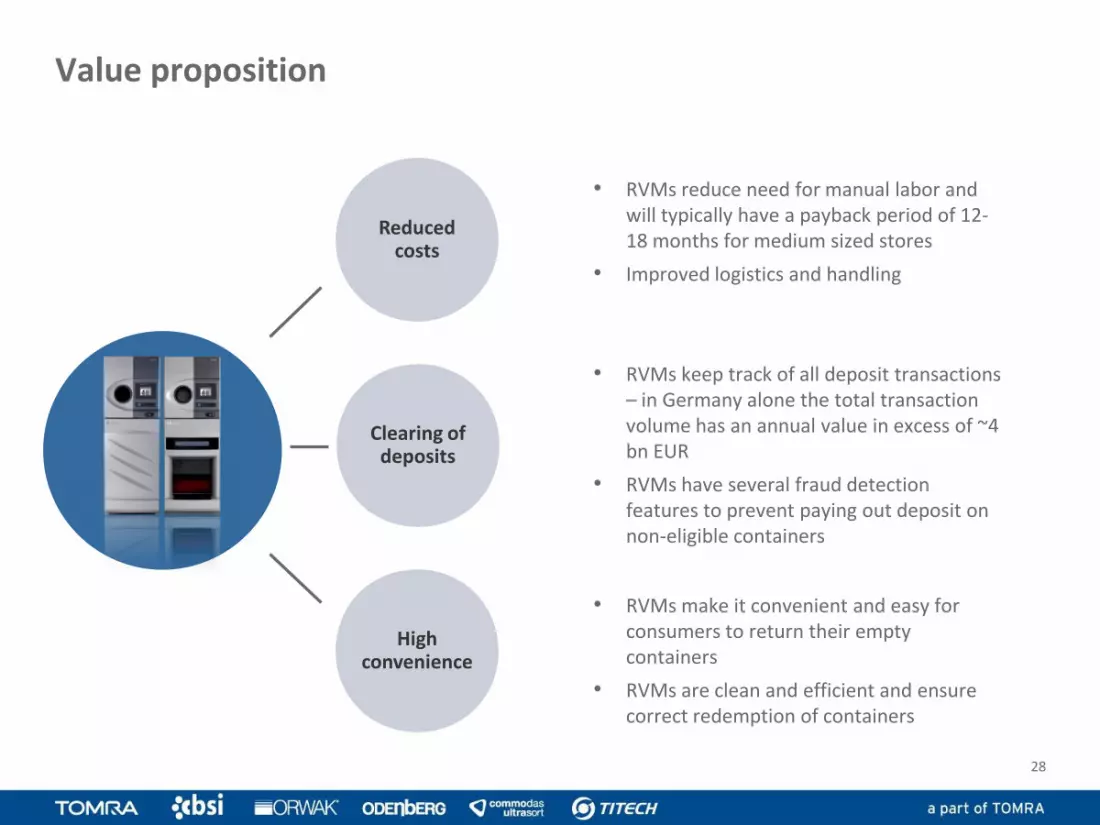

Value proposition

• RVMs reduce need for manual labor and will typically have a payback period of 12-18 months for medium sized stores

• Improved logistics and handling

• RVMs keep track of all deposit transactions – in Germany alone the total transaction volume has an annual value in excess of ~4 bn EUR

• RVMs have several fraud detection features to prevent paying out deposit on non-eligible containers

• RVMs make it convenient and easy for consumers to return their empty containers

• RVMs are clean and efficient and ensure correct redemption of containers

Reduced costs

Clearing of deposits

High convenience

28

• Non-refillables account for 75% of all containers sold and are popular due to simplified distribution/manufacturing and consumer marketing aspects

• Some markets have MANDATORY deposit systems to ensure proper collection of containers

• RVMs are used to make these systems more effective and efficient

• In markets without deposit there might still be a need to organize collection of empty containers, either to support overall recycling targets/ambitions or to demonstrate corporate social responsibility

• Although the rationale for using RVMs varies from market to market, RVMs can in general be used to facilitate the collection process

Other incentive-based markets(non-deposit)

Mandatory (non-refillable)deposit markets

• Refillable containers account for ~25% of all containers sold and have traditionally been used by local and regional breweries outside NA

• Refillable containers are typically part of a VOLUNTARY deposit system to incentivize consumers to return containers for reuse

• RVMs are used to make this system more effective and efficient

Voluntary (refillable) deposit markets

Market segments and business models

1

2

3

29

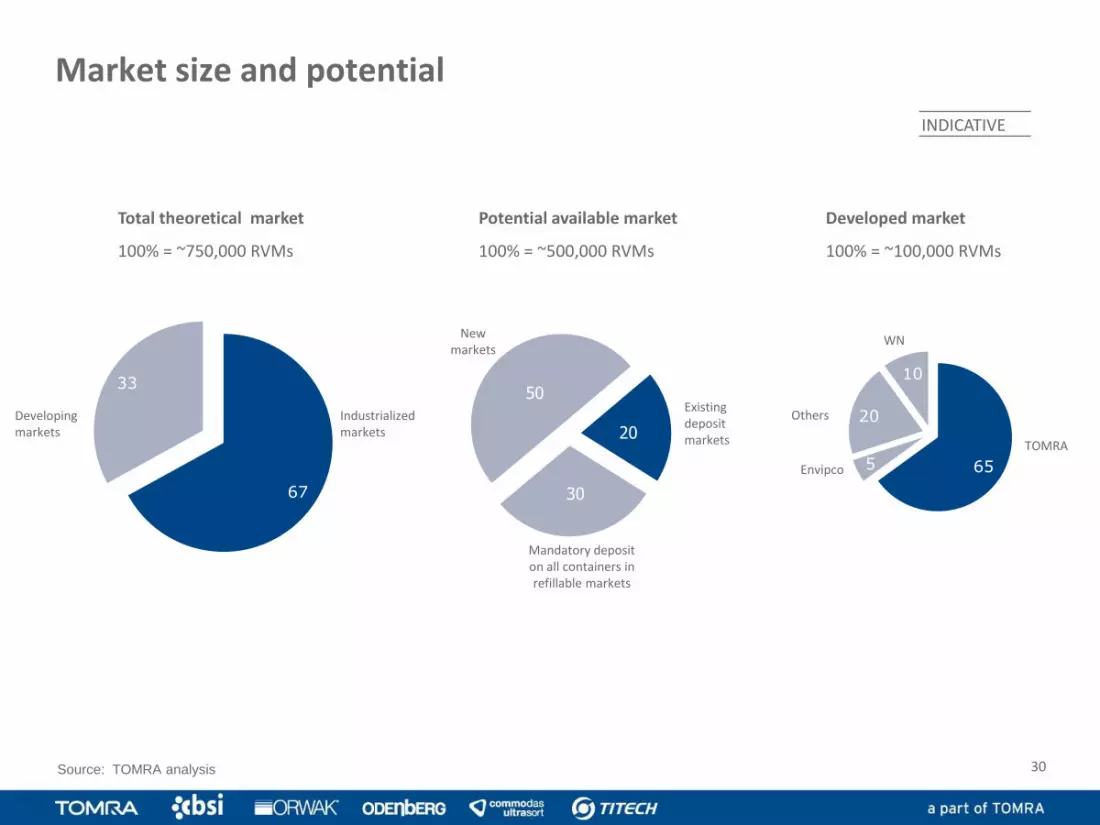

New markets

Mandatory deposit on all containers in refillable markets

Total theoretical market

100% = ~750,000 RVMs

Others

Envipco

TOMRA

WN

Developed market

100% = ~100,000 RVMs

Potential available market

100% = ~500,000 RVMs

Developing markets

Industrialized markets

Existing deposit markets

INDICATIVE

Market size and potential

Source: TOMRA analysis

67

33

0 0

655

20

10

30

20

30

50

* Trautwein has ~20,000 small RVMs installed in corporate cantinas, factories etc.

Source: TOMRA analysis

Current global installed base of RVMs in deposit markets

South America: ~1,000

Nordic: ~20,000

Germany: ~30,000 / 45,000*

North America: ~19,000

Other Europe: ~20,000

Japan: ~500

All deposit (7)

Non-refillable

Refillable

ESTIMATES

31

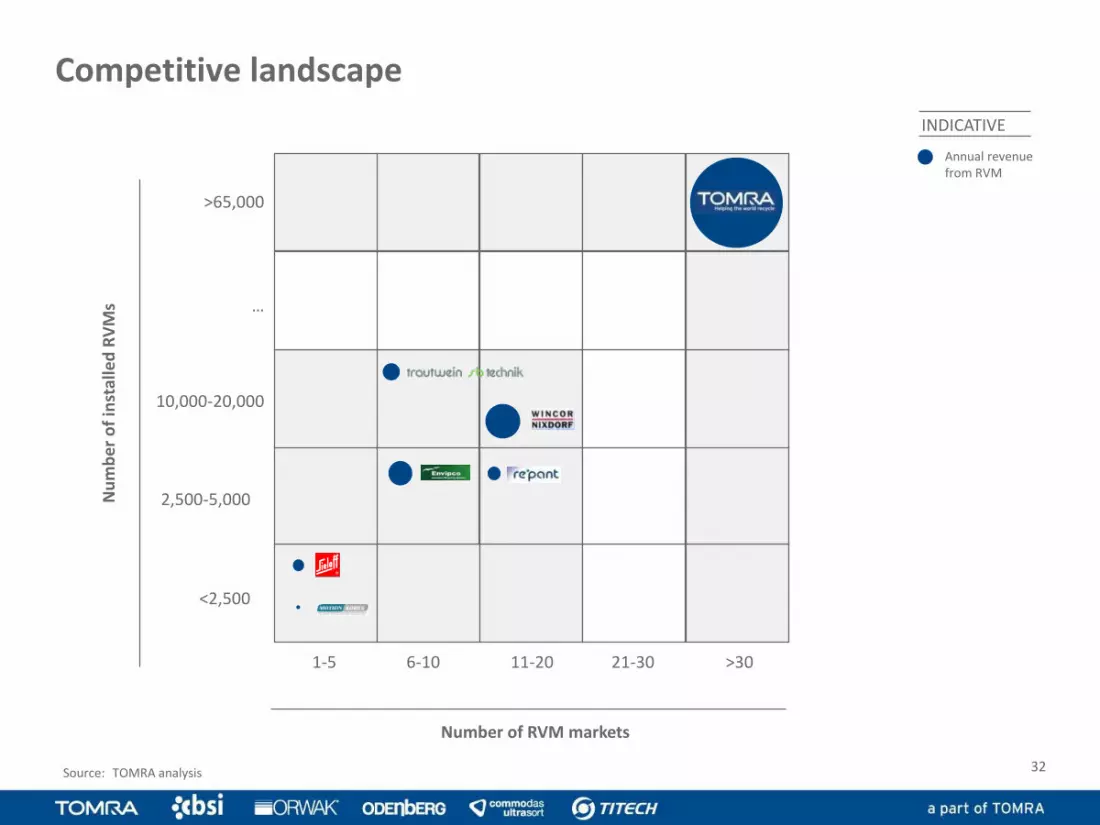

Annual revenue from RVM

INDICATIVE

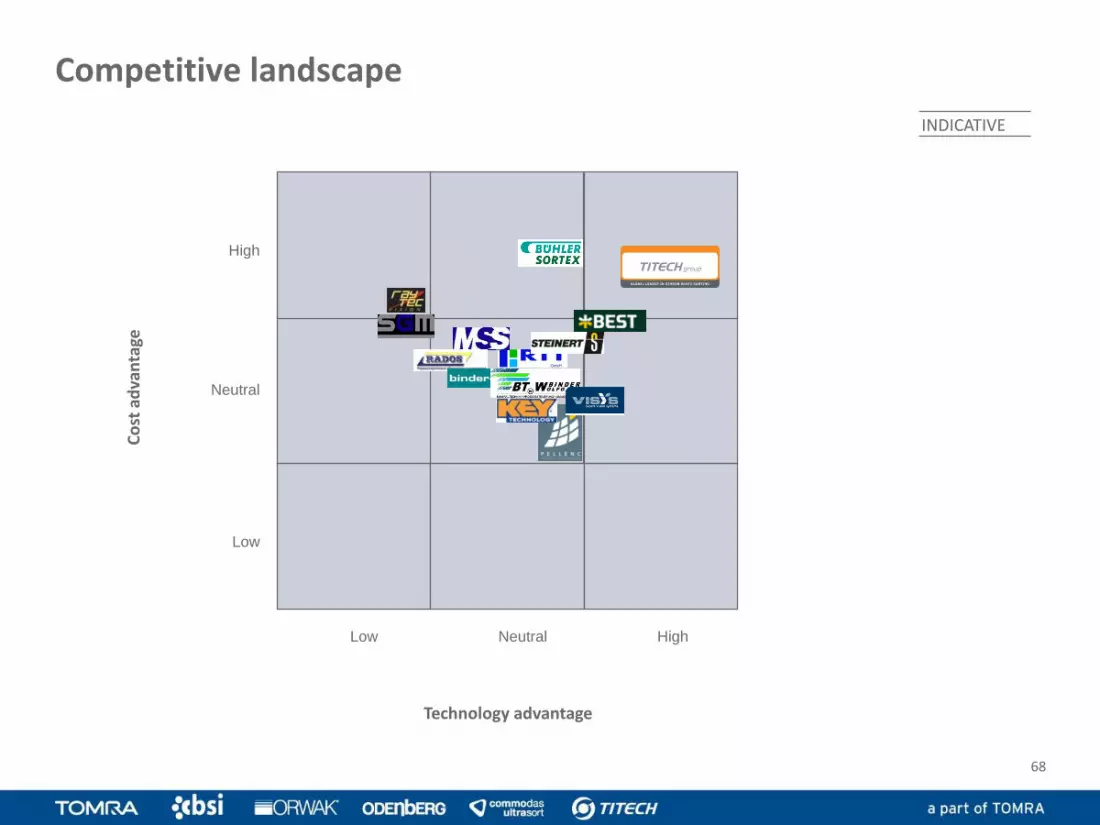

Competitive landscape

Source: TOMRA analysis

1-5 11-20

Nu

mb

ero

fin

stal

led

RV

Ms

Number of RVM markets

<2,500

6-10

2,500-5,000

10,000-20,000

>65,000

>3021-30

…

32

Protect and defendexisting business

Spur growth in existing markets

Succeed in new markets

• Cost leadership

• Increased differentiation

• Accelerated machine replacement

• Incremental revenue streams on installed base

• New segments/channels

• New deposit markets

• Viable non-deposit business models

Our strategy

33

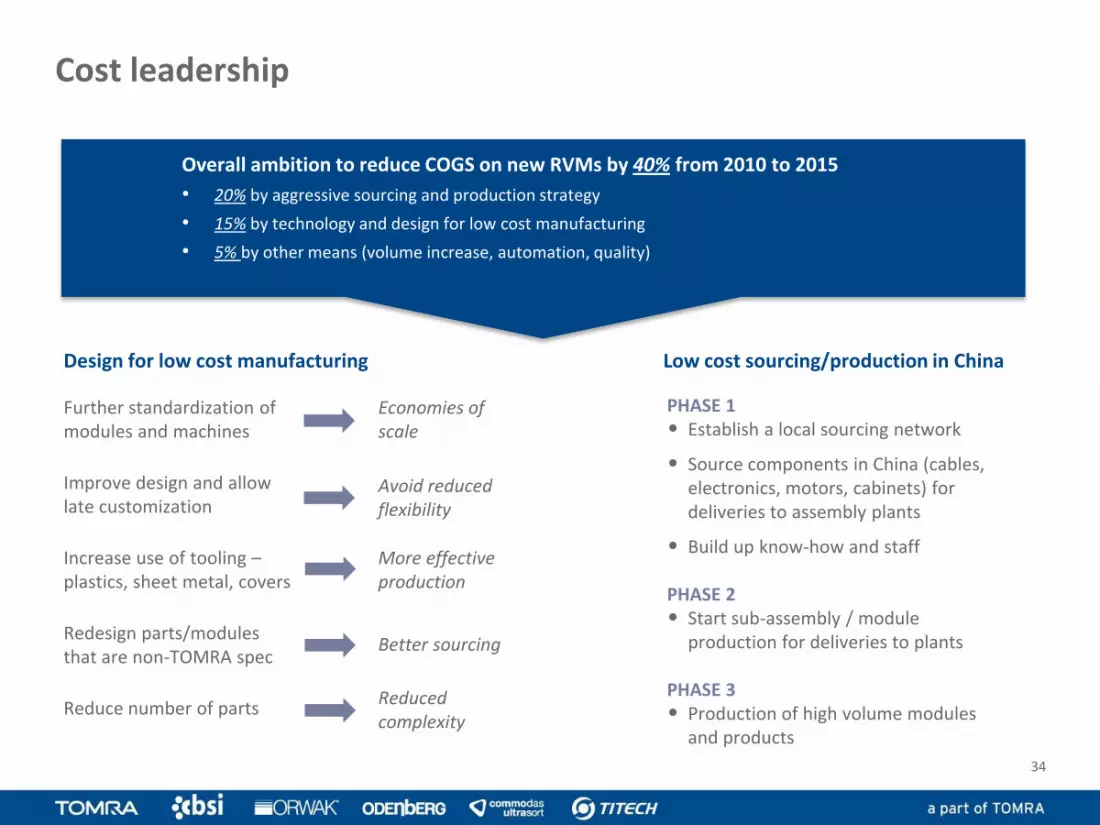

Cost leadership

Overall ambition to reduce COGS on new RVMs by 40% from 2010 to 2015

• 20% by aggressive sourcing and production strategy

• 15% by technology and design for low cost manufacturing

• 5% by other means (volume increase, automation, quality)

Further standardization of modules and machines

Improve design and allow late customization

Increase use of tooling –plastics, sheet metal, covers

Redesign parts/modules that are non-TOMRA spec

Reduce number of parts

PHASE 1• Establish a local sourcing network

• Source components in China (cables, electronics, motors, cabinets) for deliveries to assembly plants

• Build up know-how and staff

PHASE 2• Start sub-assembly / module

production for deliveries to plants

PHASE 3• Production of high volume modules

and products

Economies of scale

Avoid reduced flexibility

More effective production

Better sourcing

Reduced complexity

Design for low cost manufacturing Low cost sourcing/production in China

34

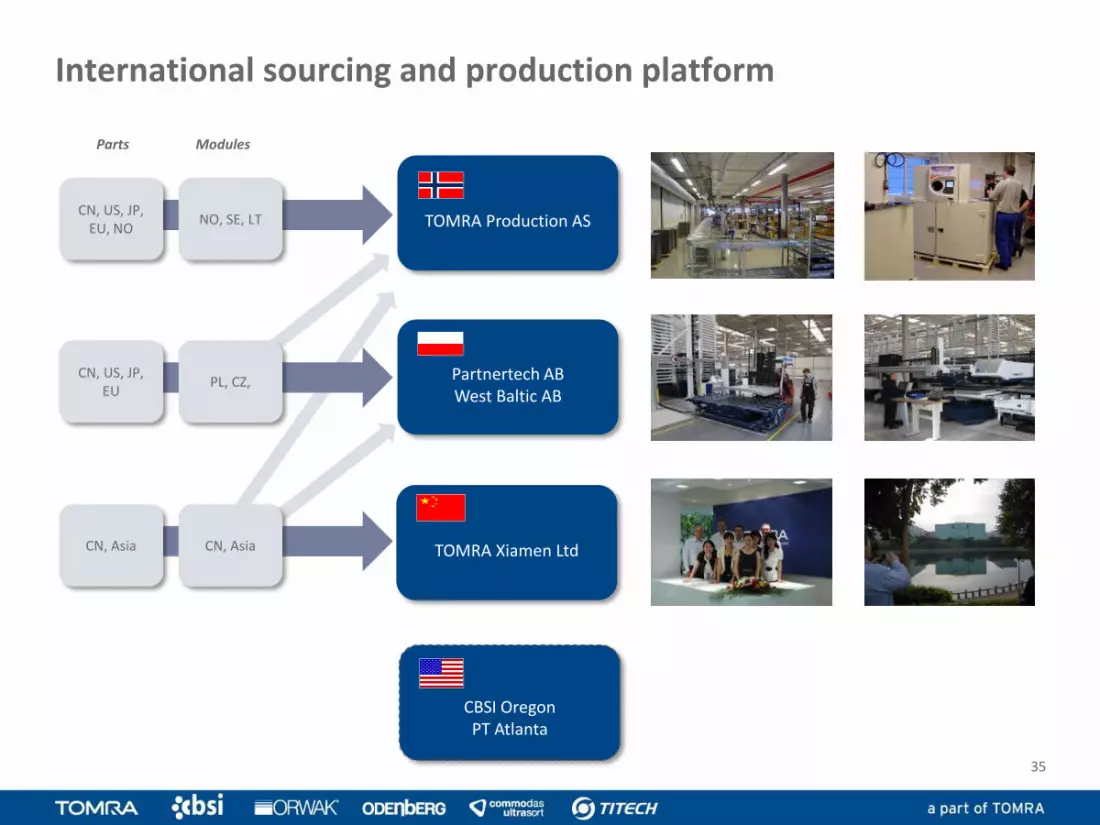

International sourcing and production platform

TOMRA Production AS

Parts Modules

Partnertech ABWest Baltic AB

TOMRA Xiamen Ltd

NO, SE, LT

PL, CZ,

CN, Asia

CN, US, JP, EU, NO

CN, US, JP, EU

CN, Asia

35

CBSI OregonPT Atlanta

Increase differentiation by fulfilling stakeholder needs

“Appealing”Quick & convenient

RewardingI contribute

“In charge” Intuitive

Easy and CleanI contribute

“Compliant”Useful tool

Easily integrated

“In control”Predictable

Marketing channelEfficient

RETAIL CHAIN MGMT

IT MGMT

STAFF/PERSONNEL

USER/CONSUMER

“Unattractive”Annoying

FilthySlow

“Hassle”Unpredictable

Dirty

“Awkward”Proprietary Protective

“Complicated”Unpredictable

Expensive

Past Future

36

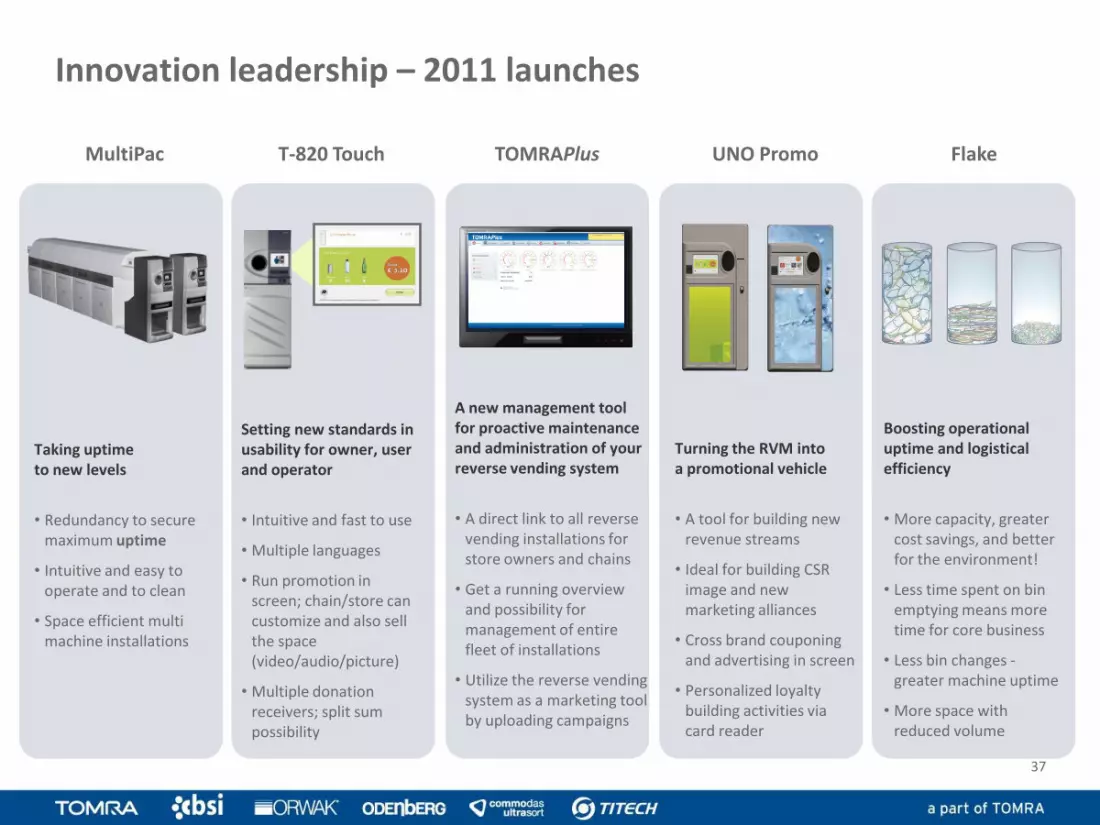

Innovation leadership – 2011 launches

MultiPac T-820 Touch TOMRAPlus UNO Promo

Taking uptime to new levels

• Redundancy to secure maximum uptime

• Intuitive and easy to operate and to clean

• Space efficient multi machine installations

Setting new standards in usability for owner, user and operator

• Intuitive and fast to use

• Multiple languages

• Run promotion in screen; chain/store can customize and also sell the space (video/audio/picture)

• Multiple donation receivers; split sum possibility

Turning the RVM into a promotional vehicle

• A tool for building new revenue streams

• Ideal for building CSR image and new marketing alliances

• Cross brand couponing and advertising in screen

• Personalized loyalty building activities via card reader

A new management tool for proactive maintenance and administration of your reverse vending system

• A direct link to all reverse vending installations for store owners and chains

• Get a running overview and possibility for management of entire fleet of installations

• Utilize the reverse vending system as a marketing tool by uploading campaigns

Flake

Boosting operational uptime and logistical efficiency

• More capacity, greater cost savings, and better for the environment!

• Less time spent on bin emptying means more time for core business

• Less bin changes -greater machine uptime

• More space with reduced volume

37

RVM product portfolio

38

New markets

39

North America Europe/Other

UK: 20,000-25,000 RVMs fully penetrated

Australia:

4,000-5,000 RVMsfully penetrated

Spain:

15,000-20,000 RVMsfully penetrated

Proposed expansion/amendments

Industry Funded Repeal Campaign

CDL campaign

INDICATIVE

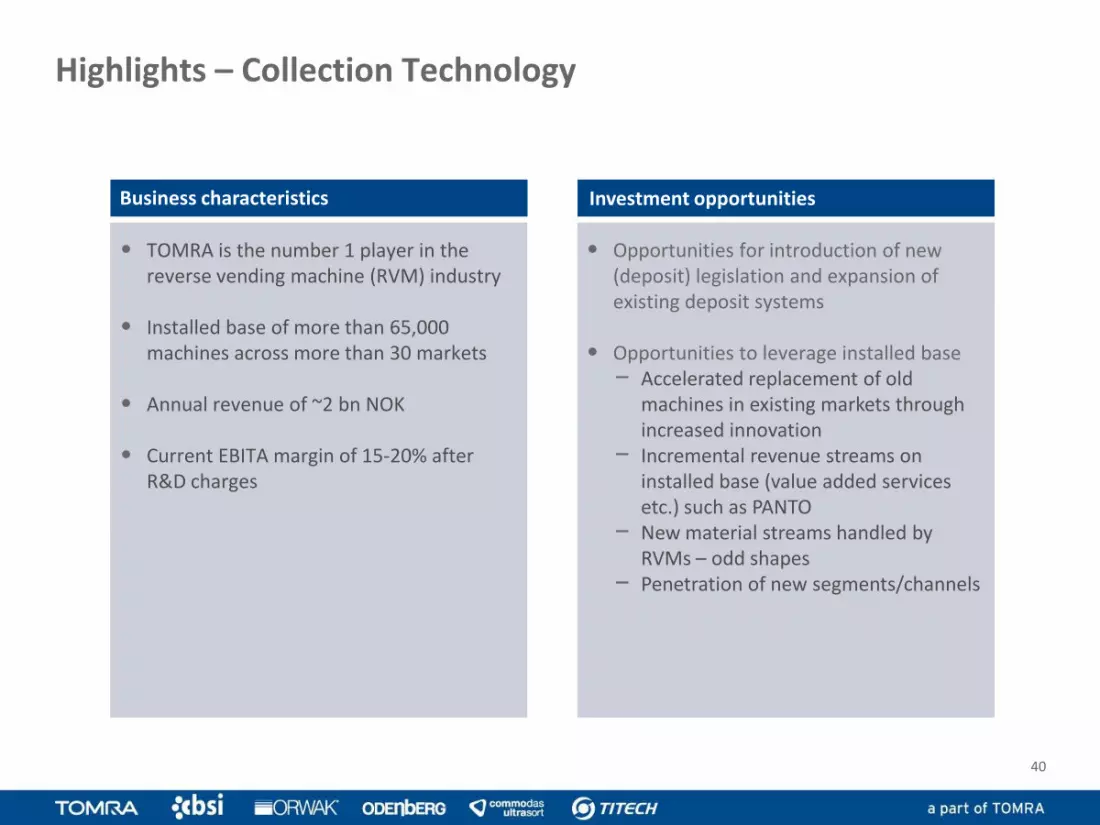

Highlights – Collection Technology

• TOMRA is the number 1 player in the reverse vending machine (RVM) industry

• Installed base of more than 65,000 machines across more than 30 markets

• Annual revenue of ~2 bn NOK

• Current EBITA margin of 15-20% after R&D charges

• Opportunities for introduction of new (deposit) legislation and expansion of existing deposit systems

• Opportunities to leverage installed base– Accelerated replacement of old

machines in existing markets through increased innovation

– Incremental revenue streams on installed base (value added services etc.) such as PANTO

– New material streams handled by RVMs – odd shapes

– Penetration of new segments/channels

Business characteristics Investment opportunities

40

TOMRA Sorting Technology

41

Cutting-edge technology for industries where automated sorting and processing are key for value creation

GLOBAL LEADER IN SENSOR BASED SORTING

42

• High-tech sensors are utilized

to identify objects on a

conveyor belt

• High speed processing of

information: material, shape,

size, color, defect, damage

and location of objects

• Precise sorting by air jets or

mechanical fingers

Our core technology: the eyes and brains of sorting and processing

43

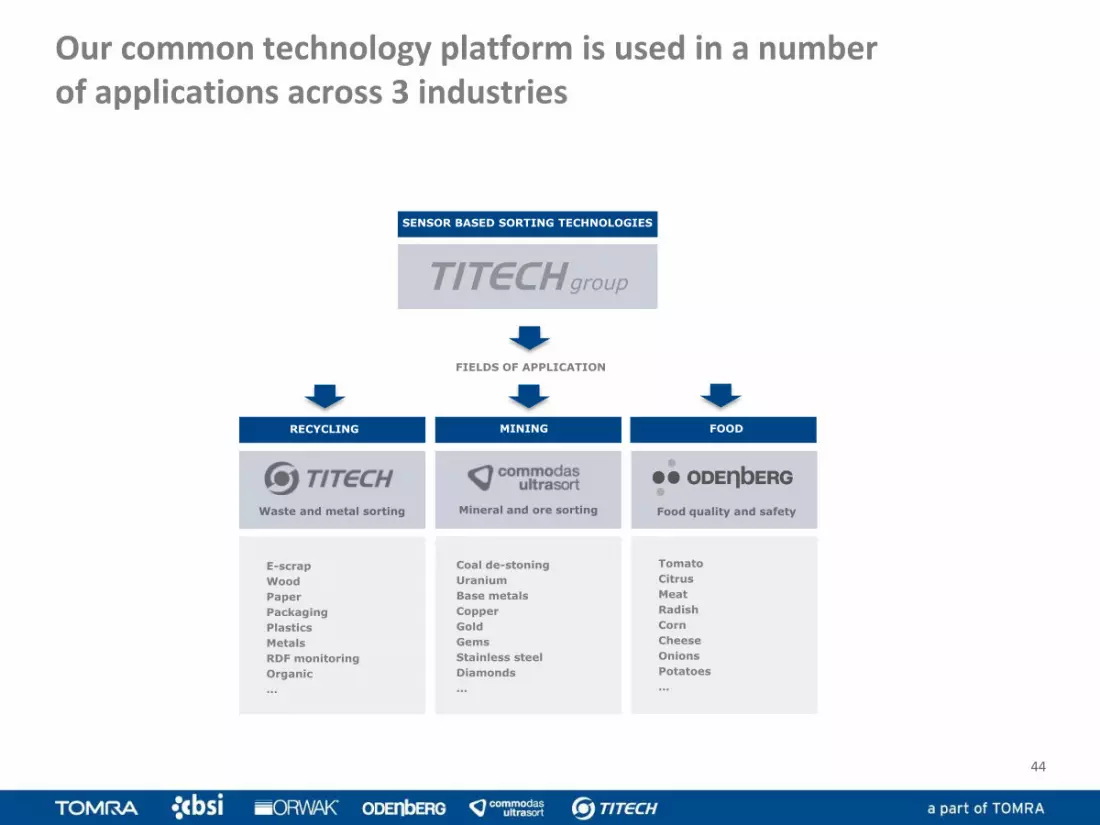

Our common technology platform is used in a numberof applications across 3 industries

44

SENSOR BASED SORTING TECHNOLOGIES

FIELDS OF APPLICATION

RECYCLING

Waste and metal sorting

E-scrap

Wood

Paper

Packaging

Plastics

Metals

RDF monitoring

Organic

…

MINING

Mineral and ore sorting Food quality and safety

Coal de-stoning

Uranium

Base metals

Copper

Gold

Gems

Stainless steel

Diamonds

…

FOOD

Tomato

Citrus

Meat

Radish

Corn

Cheese

Onions

Potatoes

…

RECYCLING MINING FOOD

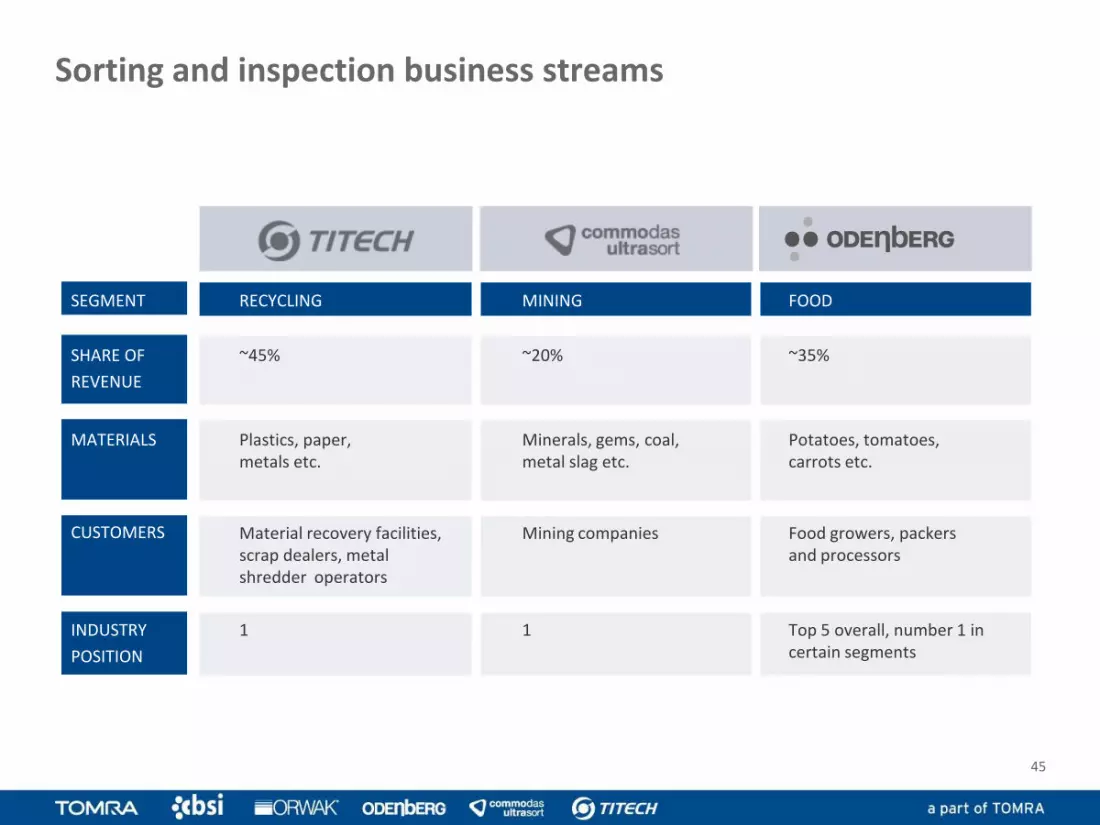

Sorting and inspection business streams

SEGMENT

SHARE OF

REVENUE

MATERIALS

CUSTOMERS

INDUSTRY

POSITION

1 1 Top 5 overall, number 1 in certain segments

~45%

Plastics, paper, metals etc.

Material recovery facilities, scrap dealers, metal shredder operators

~20%

Minerals, gems, coal, metal slag etc.

Mining companies

~35%

Potatoes, tomatoes, carrots etc.

Food growers, packers and processors

45

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

• Revenue growth, organic plus inorganic, of nearly 40% per year from 2004-10

• Technology base and segment/application knowledge expanded both through acquisitions and in-house ventures

• Growth driven by

− Favorable changes in regulatory framework (DSD, WEEE, ELV, etc)

− Price increases in food, commodities & landfill costs

− Strong sales and service network

− Technology leadership

− Higher quality and food safety demands

TITECH Visionsort AS established

CommoDas acquired

Ultrasort acquired

QVision AS established

>100

Strong revenue growth since inception in 1996

Revenue development and key milestones for TITECH GroupEUR million

Real Vision Systems acquired

TITECH acquired by TOMRA

14.5

0.5

Odenberg acquired

46

RECYCLING

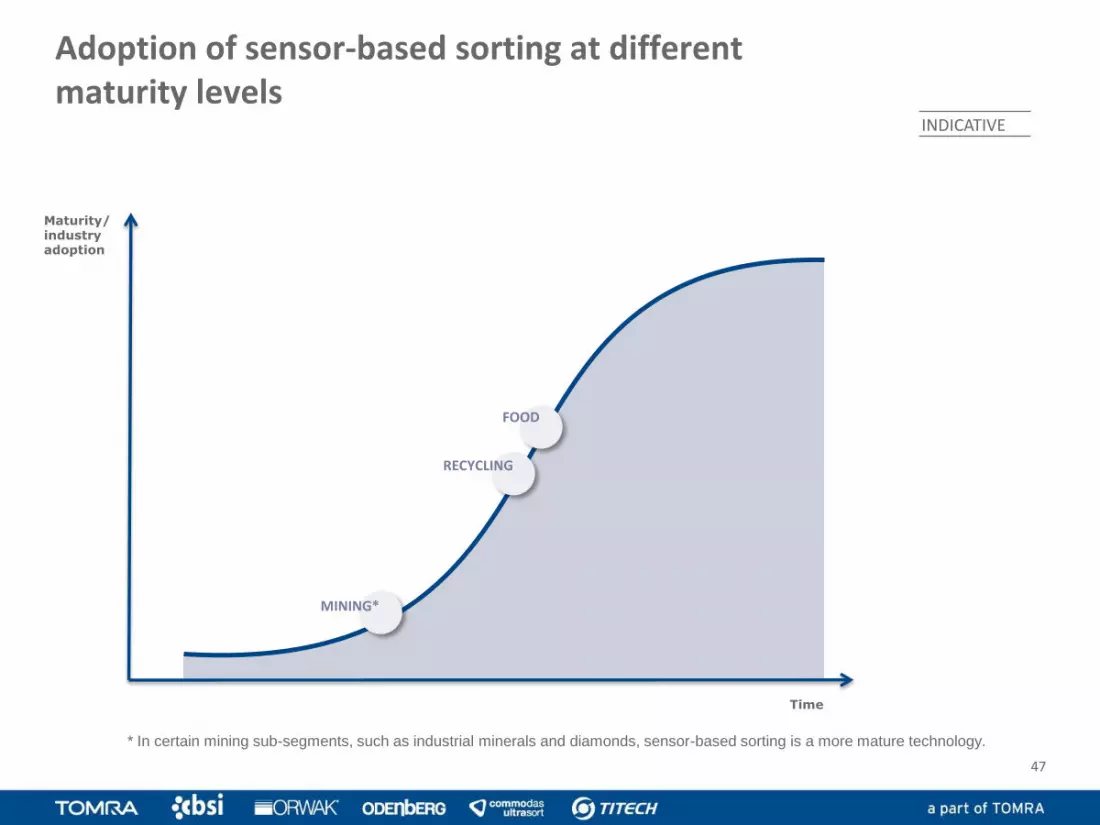

Adoption of sensor-based sorting at different maturity levels

Maturity/ industry adoption

Time

* In certain mining sub-segments, such as industrial minerals and diamonds, sensor-based sorting is a more mature technology.

FOOD

MINING*

47

INDICATIVE

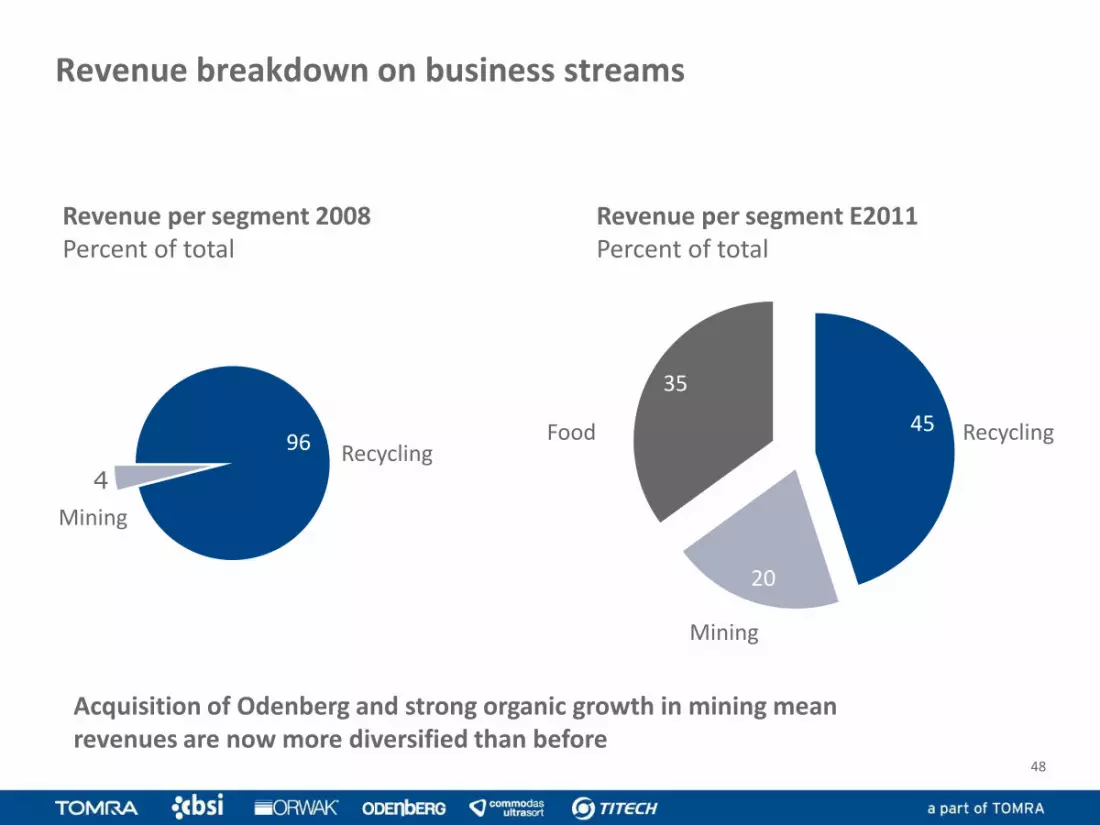

Revenue breakdown on business streams

Acquisition of Odenberg and strong organic growth in mining meanrevenues are now more diversified than before

Revenue per segment 2008Percent of total

Recycling

Mining

96

4

Revenue per segment E2011Percent of total

Food Recycling45

20

35

0

Mining

48

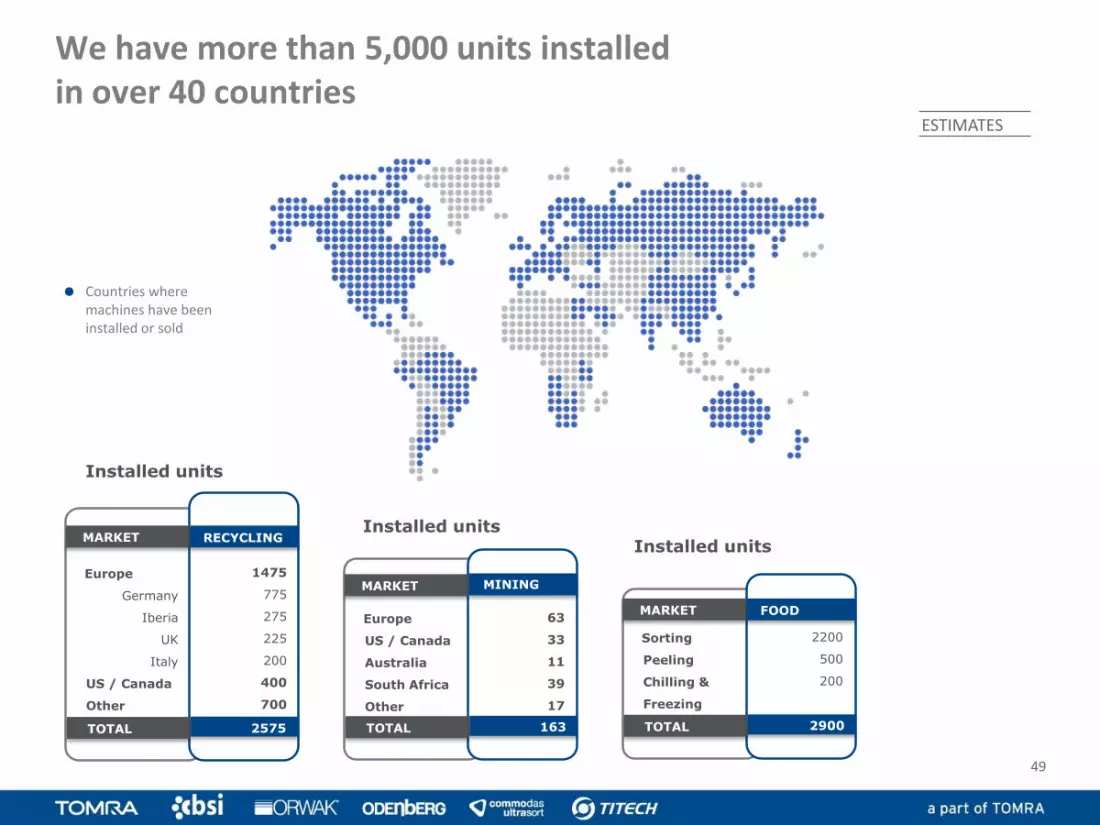

Countries where machines have been installed or sold

We have more than 5,000 units installed in over 40 countries

Europe

Germany

Iberia

UK

Italy

US / Canada

Other

Installed units

MARKET

TOTAL

RECYCLING

2575

1475

775

275

225

200

400

700

Europe

US / Canada

Australia

South Africa

Other

Installed units

MARKET

TOTAL

MINING

63

33

11

39

17

163

Sorting

Peeling

Chilling &

Freezing

Installed units

MARKET

TOTAL

2200

500

200

2900

FOOD

49

ESTIMATES

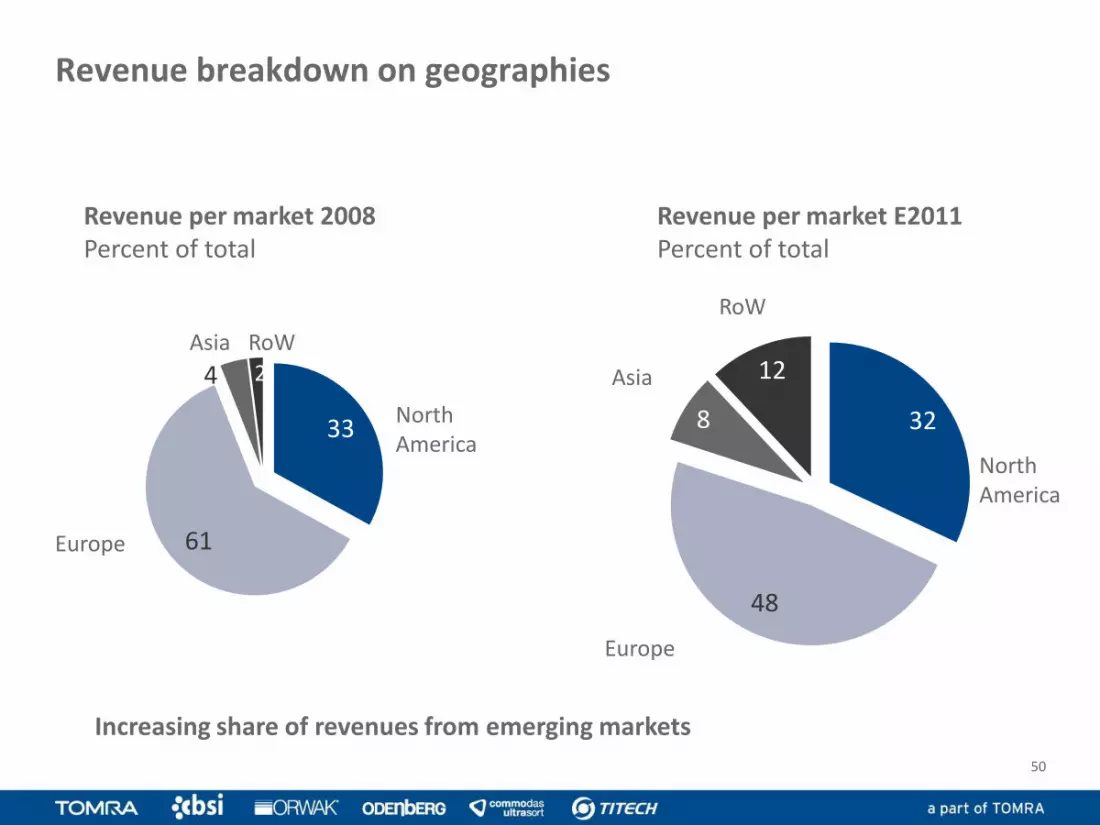

Revenue breakdown on geographies

Increasing share of revenues from emerging markets

Revenue per market 2008Percent of total

North America

Europe

33

61

4 2

Asia RoW

North America

Europe

32

48

8

12Asia

RoW

Revenue per market E2011Percent of total

50

Total annual market size for different sensor-based sorting segments

EUR million

Market size and potential

ESTIMATES

Source: TOMRA analysis

~500-550

~850-900

50 90407020

60

400

650

2010 2015

Food

Mining

Metal

Waste

51

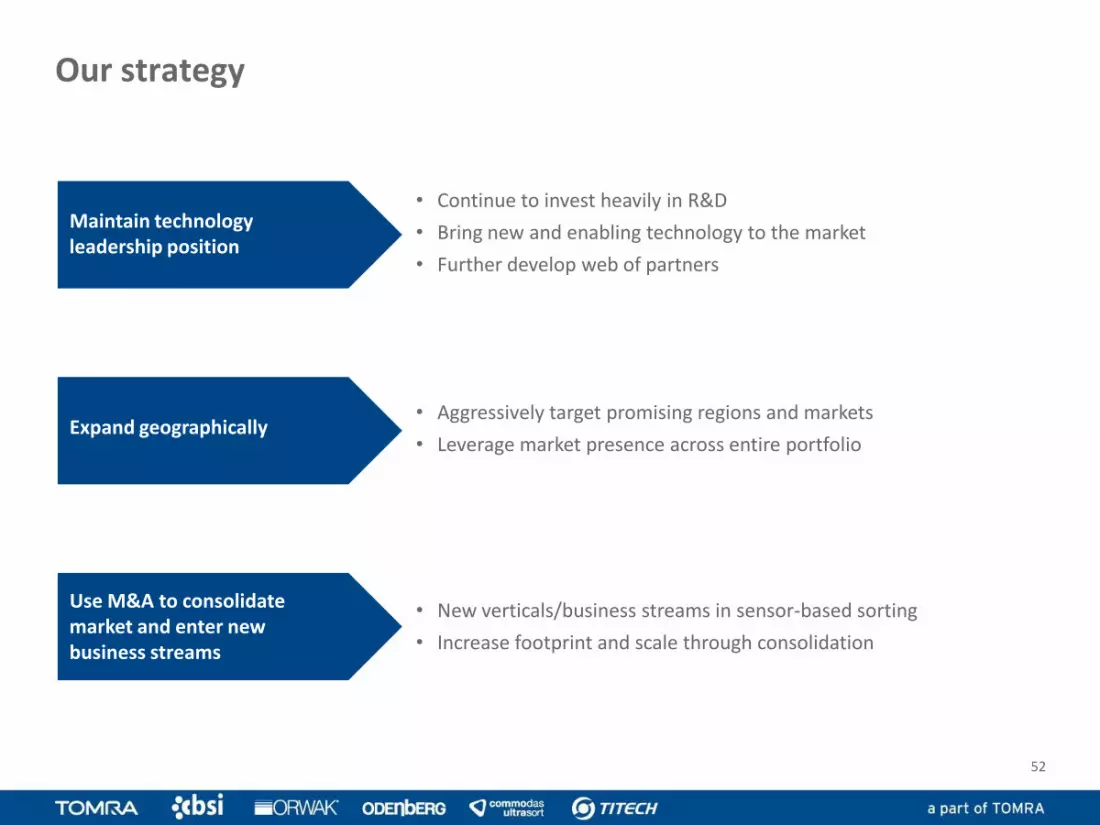

Maintain technology leadership position

Expand geographically

Use M&A to consolidate market and enter new business streams

• Continue to invest heavily in R&D

• Bring new and enabling technology to the market

• Further develop web of partners

• Aggressively target promising regions and markets

• Leverage market presence across entire portfolio

• New verticals/business streams in sensor-based sorting

• Increase footprint and scale through consolidation

Our strategy

52

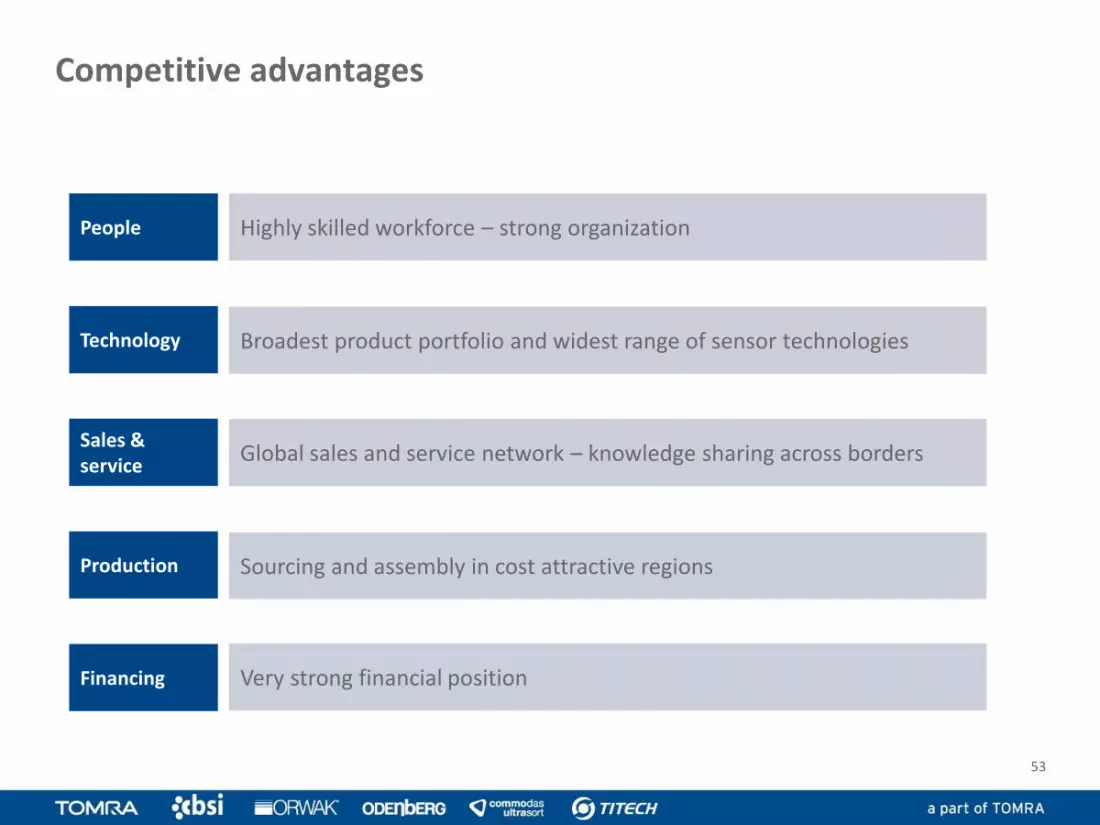

Competitive advantages

Highly skilled workforce – strong organizationPeople

Broadest product portfolio and widest range of sensor technologiesTechnology

Sales & service

Production

Financing Very strong financial position

Sourcing and assembly in cost attractive regions

Global sales and service network – knowledge sharing across borders

53

• World leader in sensor-based sorting

• Focused on recycling, mining and food -number 1 in waste and mining and a key player in food

• Installed base of ~5,000 optical sorters and 500 peelers across 45 markets

• Total 2010 revenue of more than 100 MEUR

• Strong value propositions and attractive ROI for customers based on reduction of operational costs and/or increased quality/output of material stream

• Expansion into new segments (new verticals/industries) and new geographies

• Potential for increased scale benefits and rapid growth through industry consolidation

Business characteristics Investment opportunities

Highlights – Sensor Based Sorting

54

55

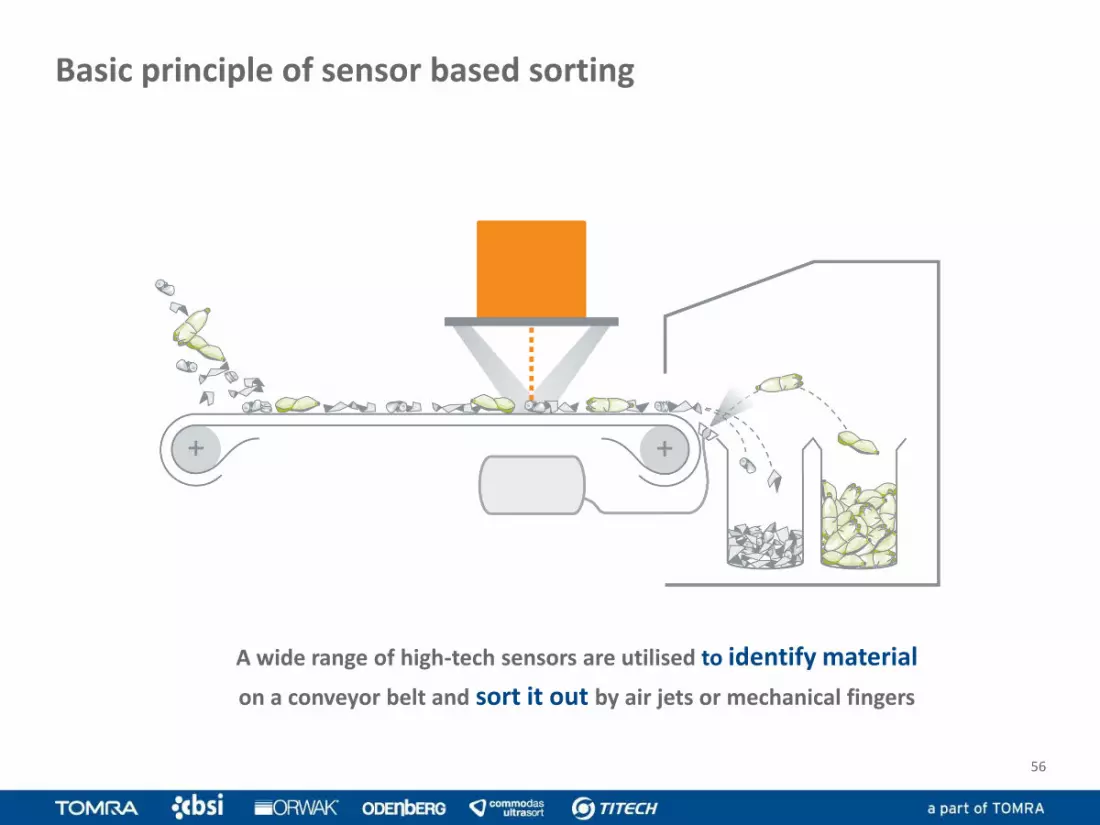

Technology overview

A wide range of high-tech sensors are utilised to identify material

on a conveyor belt and sort it out by air jets or mechanical fingers

Basic principle of sensor based sorting

56

Sensor/Technology

Material Property Segment

RM (Radiometric) Natural Gamma Radiation Mining

XRT (X-ray transmission) Atomic Density Recycling, Mining, Food

XRF X ray fluorescence (Elemental Spectroscopy)

Recycling, Mining

COLOR (CCD Color Camera) VIS (Visual Spectrometry)

Reflection, Absorption, Transmission

Recycling, Mining, Food

PM (Photometric) Monochromatic Reflection /Absorption of Laser Light

Mining

NIR / MIR (Near/MediumInfrared Spectrometry)

Reflection, Absorption (Molecular Spectroscopy)

Recycling, Mining, Food

LIBS Laser induced breakdown spectroscopy

Recycling, Mining

EM (Electro-Magnetic sensor)

Conductivity,permeability

Recycling, Mining, Food

10-12

10-11

10-10

10-9

10-8

10-7

10-6

10-5

10-4

10-3

10-2

10-1

101

102

103

104

Ultraviolett (UV)

Visible light (VIS)

Near Infrared (NIR)

Microwaves

X-ray

Gamma-radiation

Alternating current(AC)

Radio waves

[m]

Infrarot (IR)

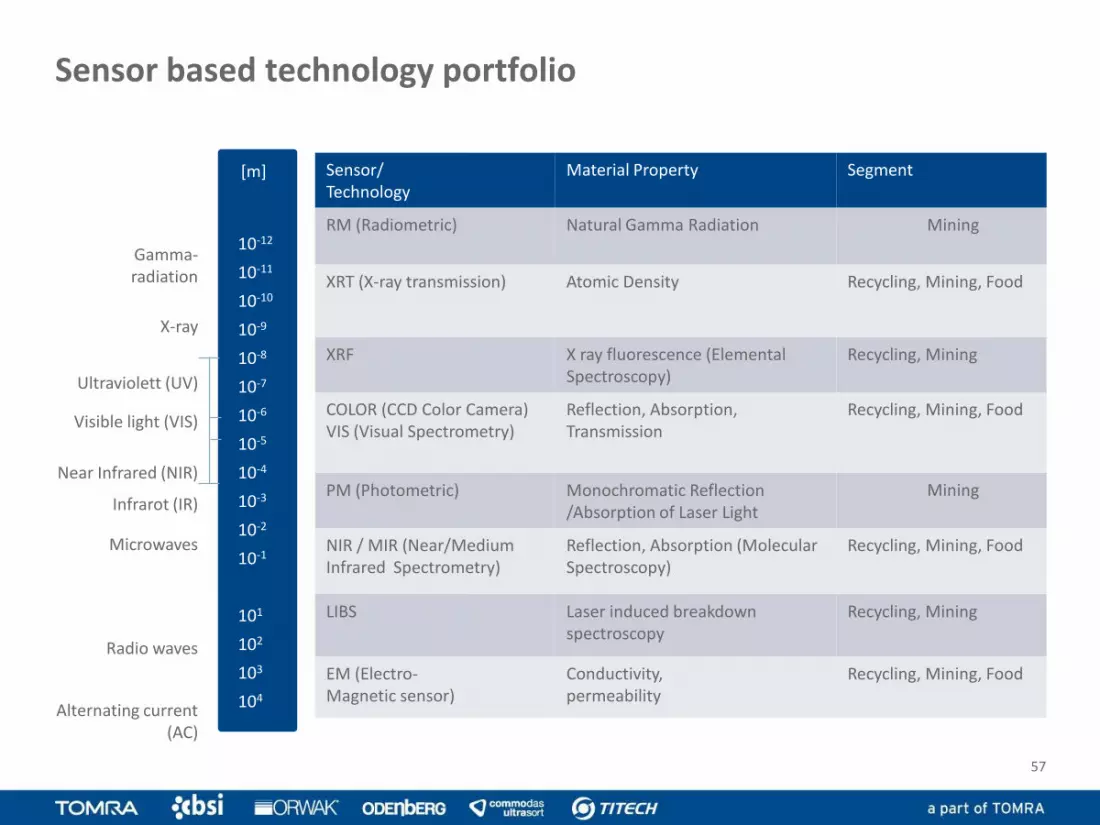

Sensor based technology portfolio

57

• Multitude of applications with each individual product

• Application development mainly in software

• Sorting products based on common core sorting components

• Different mechanical and electrical design but common core components

• Sensors

• Electronics

• Software

• Ejection modules

Technology pyramid

58

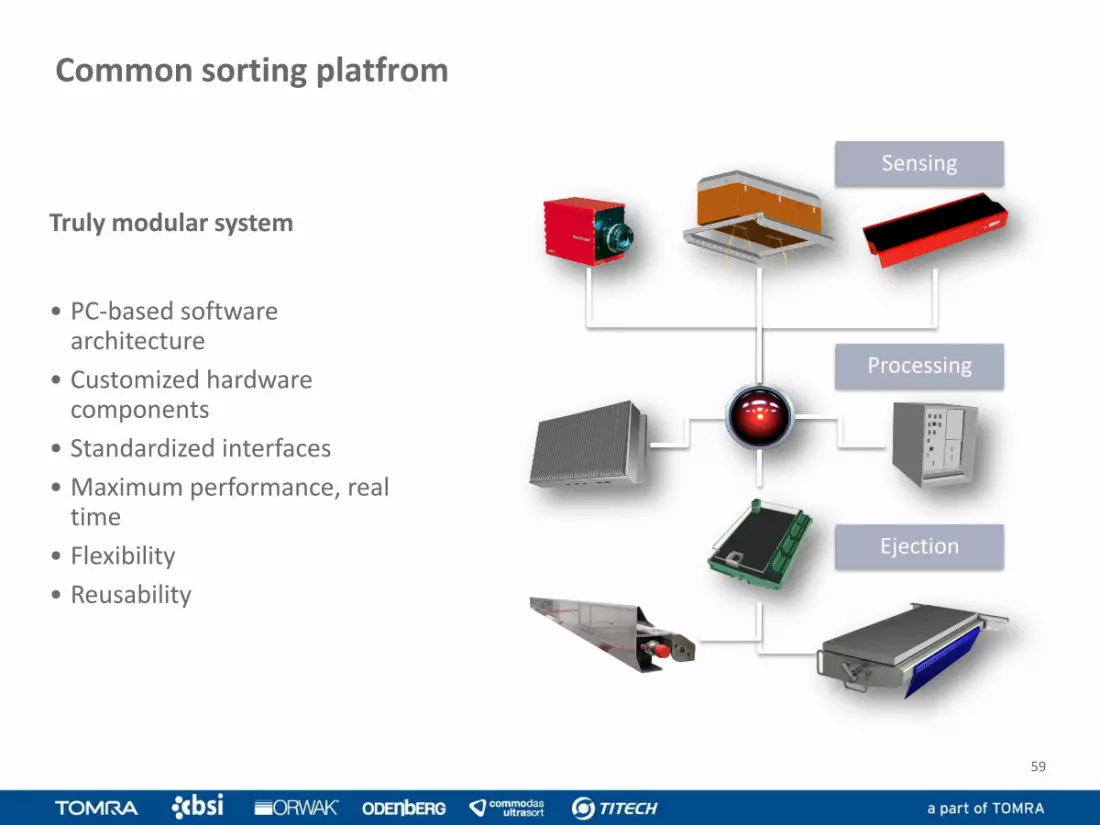

Common sorting platfrom

59

Processing

Sensing

Ejection

• PC-based software architecture

• Customized hardware components

• Standardized interfaces

• Maximum performance, real time

• Flexibility

• Reusability

Truly modular system

Product families recycling

TITECH finderTITECH autosort

• Extremely flexible belt sorters

• +6..-300mm covered by three models

• Sensors NIR, VIS and EM

• Sophisticated belt sorters

• +8..-120mm covered by three models

• Sensors XRT, XRF and EM

TITECH x-tract

• Simple and robust belt sorters

• +8..-150mm covered by two models

• Sensors EM and NIR

• Sorting of small materials using NIR

• +2..-20mm covered

• Sensors NIR, VIS, RGB and EM

TITECH autosort flake TITECH combisense

• Sophisticated belts sorters

• +2..-120mm covered by two models

• Sensors RGB and EM

60

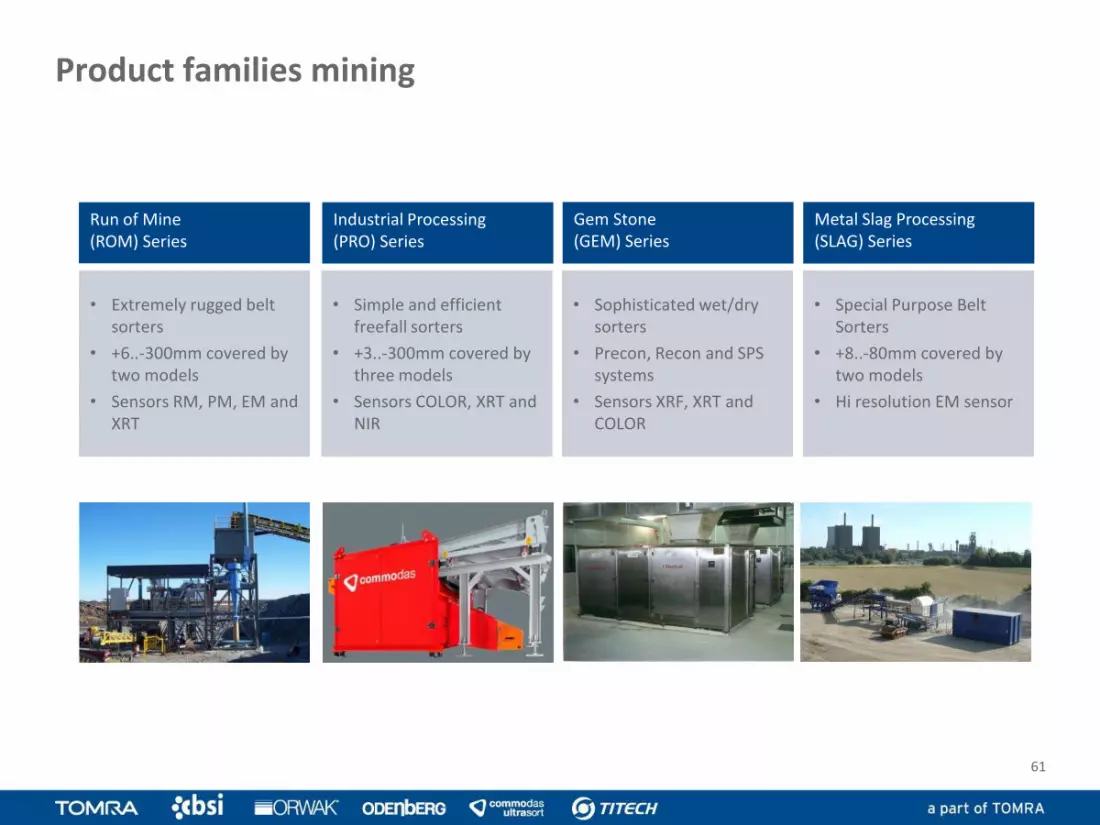

Industrial Processing (PRO) Series

Run of Mine(ROM) Series

• Extremely rugged belt sorters

• +6..-300mm covered by two models

• Sensors RM, PM, EM and XRT

• Sophisticated wet/dry sorters

• Precon, Recon and SPS systems

• Sensors XRF, XRT and COLOR

Gem Stone (GEM) Series

• Simple and efficient freefall sorters

• +3..-300mm covered by three models

• Sensors COLOR, XRT and NIR

• Special Purpose Belt Sorters

• +8..-80mm covered by two models

• Hi resolution EM sensor

Metal Slag Processing (SLAG) Series

Product families mining

61

Product families food

62

Sorting Solutions

Sentinel, NFM, Iris, Alpha

Sorting Solutions

Halo, Titan II, Iris II

• Premium Sorter range

• Enhanced accuracy

• Superior size, shape, aspect sort

• Sensors NIR, VIS

• Least cost formulation

• Yield process control

• Eliminate “out of spec” claims

• Transflection

Process Analytics

Q-Vision, Peel Scanner2

• Simple and robust sorters

• Low maintenance

• Easy to use

• High Efficiency

• Sensors NIR, VIS

• Assured Product Quality

• Energy Efficiency

• Productions Advantages

• VRT

Chilling & Freezing

Pallet-link, RT Systems

Peeling Solutions

Peelers, Deskinners, Washers, lines

• Most advanced Steam peeler in the market

• Increased Yield

• Increased Efficiency

• Energy Savings

Our common technology platform is used in a numberof applications across 3 industries

63

SENSOR BASED SORTING TECHNOLOGIES

FIELDS OF APPLICATION

RECYCLING

Waste and metal sorting

E-scrap

Wood

Paper

Packaging

Plastics

Metals

RDF monitoring

Organic

MINING

Mineral and ore sorting Food quality and safety

Coal de-stoning

Uranium

Base metals

Copper

Gold

Gems

Stainless steel

Diamonds

FOOD

Tomato

Citrus

Meat

Radish

Corn

Cheese

Onions

Potatoes

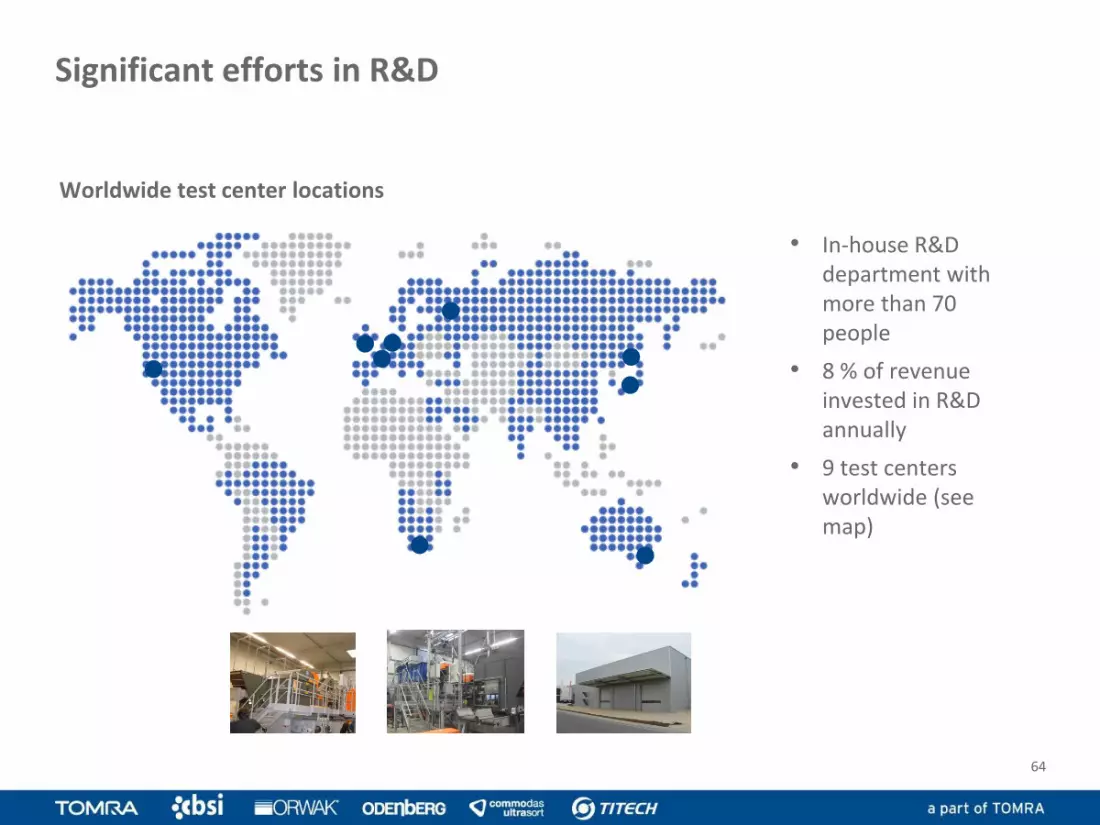

Significant efforts in R&D

• In-house R&D department withmore than 70 people

• 8 % of revenueinvested in R&D annually

• 9 test centersworldwide (seemap)

64

Worldwide test center locations

2011 2012 2013

Horizon 1Short term projects“Extend and defend our core business”

2014

Horizon 3Long term projects“Develop breakthrough applications”

Horizon 2Medium term projects“Develop our current technology and sorting capabilities”

• Higher resolution/more wavelengths

• XRF

• NIR for food

• Cost savings

• ME-XRT

• MIR

• Thermal Imaging

• LIBS

• Terahertz Spectroscopy

• Long-term segments

Substantial R&D efforts to sustain the competitive edge

65

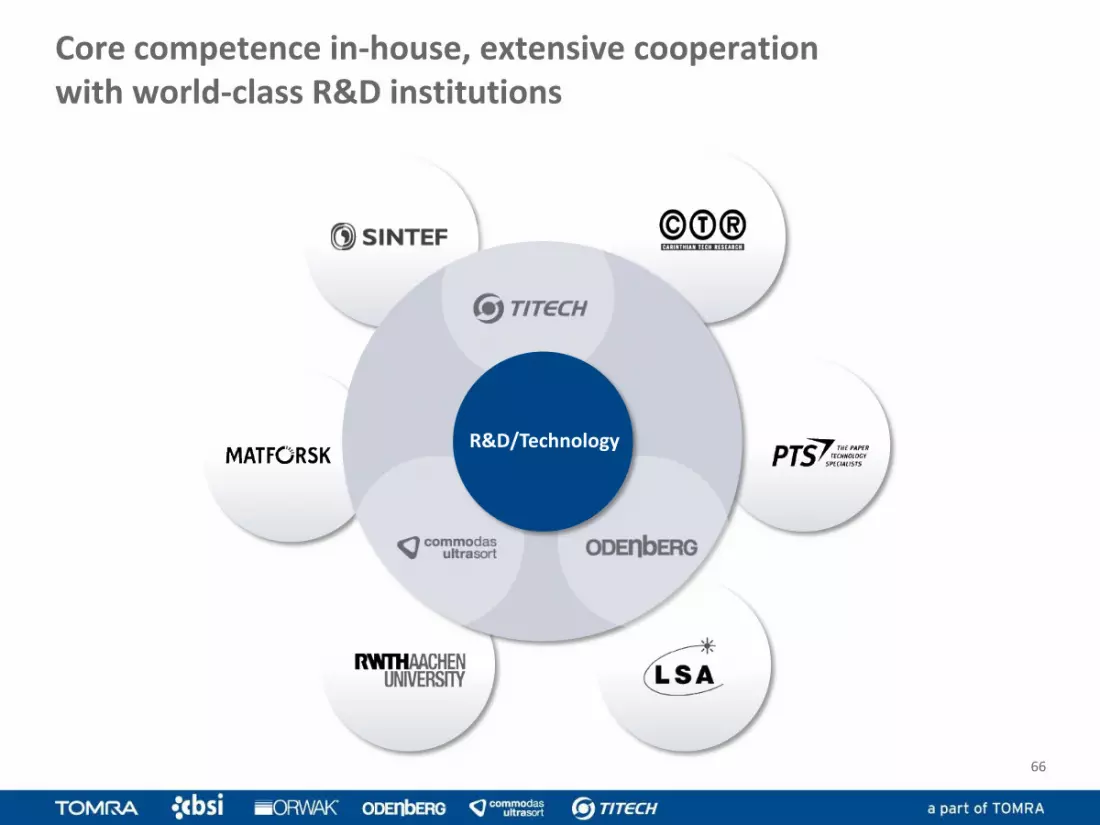

Core competence in-house, extensive cooperation with world-class R&D institutions

66

R&D/Technology

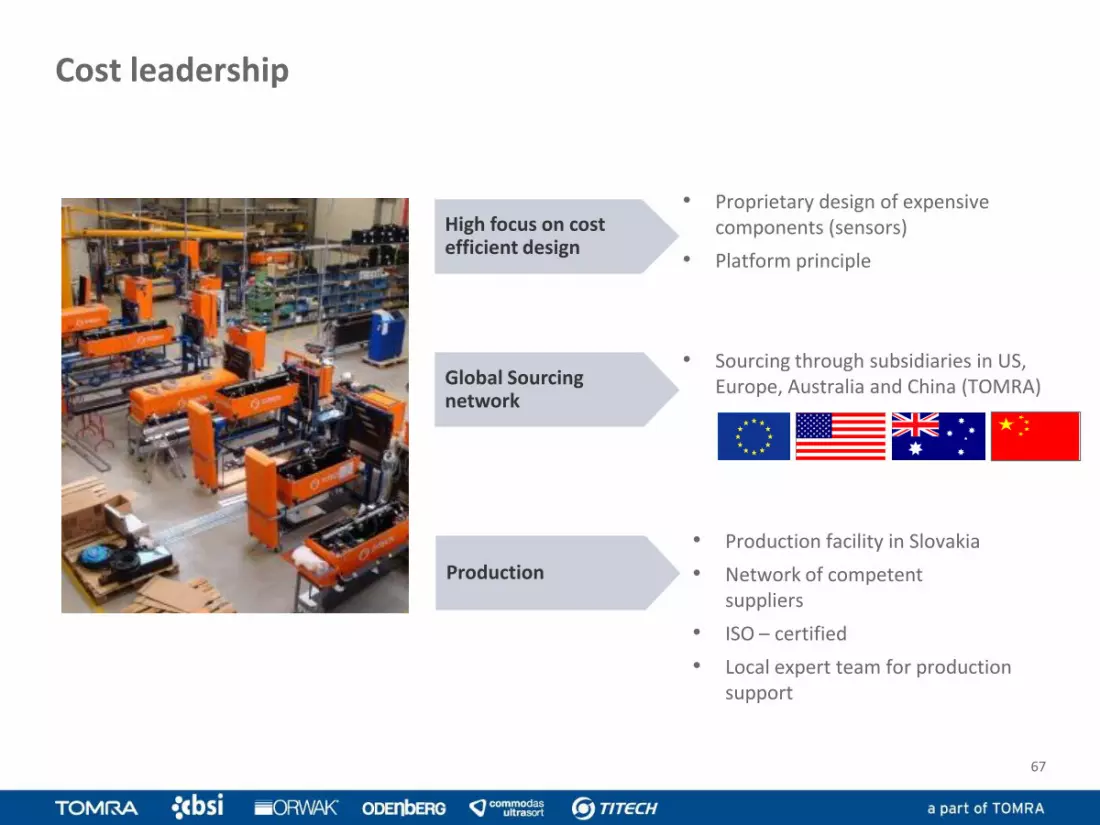

Cost leadership

• Production facility in Slovakia

• Network of competent suppliers

• ISO – certified

• Local expert team for production support

• Sourcing through subsidiaries in US, Europe, Australia and China (TOMRA)

• Proprietary design of expensive components (sensors)

• Platform principle

High focus on cost efficient design

Global Sourcing network

Production

67

Competitive landscape

68

INDICATIVE

Neutral

Low High

Co

st a

dva

nta

ge

Technology advantage

Low

Neutral

High

TITECH – Transforming efficiency and quality in recycling

69

Input stream

News print

Pre-sorting

Screen

Mixed paper

Ballistic

Containers

Container sorting(manual or optical)

PE Colored

PE natural

Tin

PET

Alu

Baler

The concept of a Material Recovery Facility (MRF)

70

71

Manual sorting

71

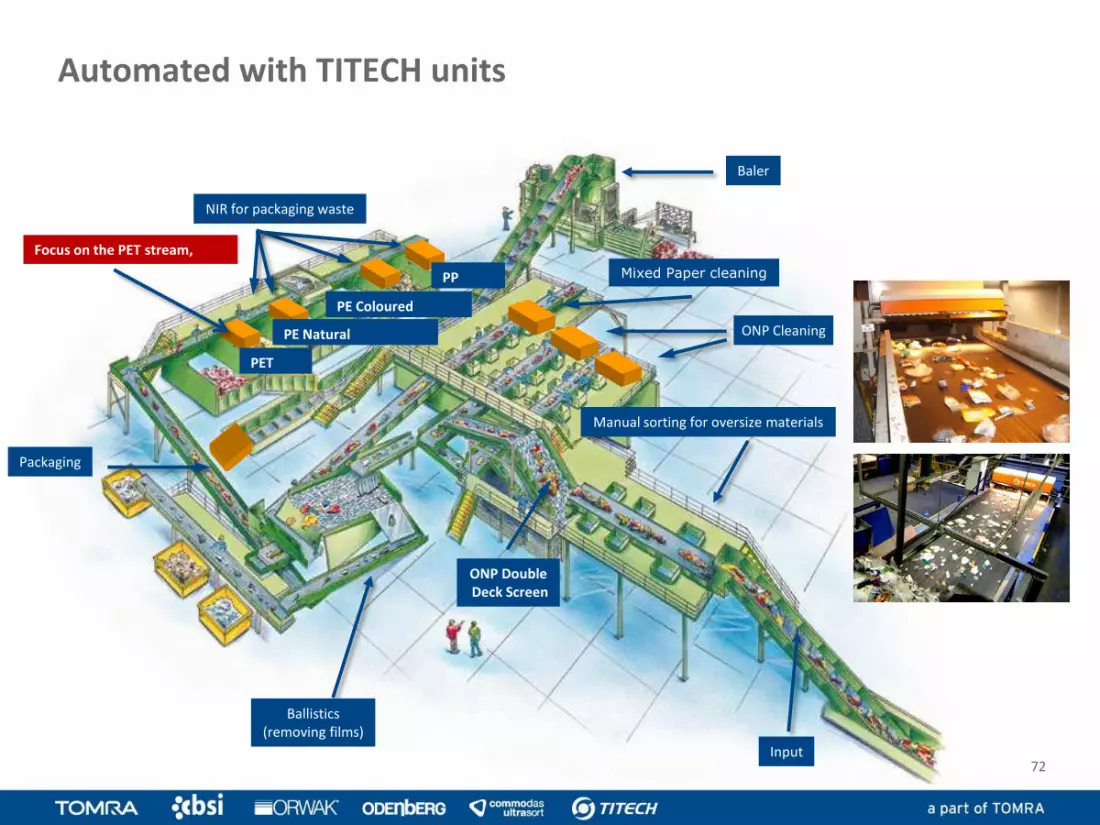

Automated with TITECH units

PET

PE Natural

PE Coloured

PP

ONP DoubleDeck Screen

Input

Manual sorting for oversize materials

ONP Cleaning

Mixed Paper cleaning

Ballistics(removing films)

Packaging

NIR for packaging waste

Baler

Focus on the PET stream,

72

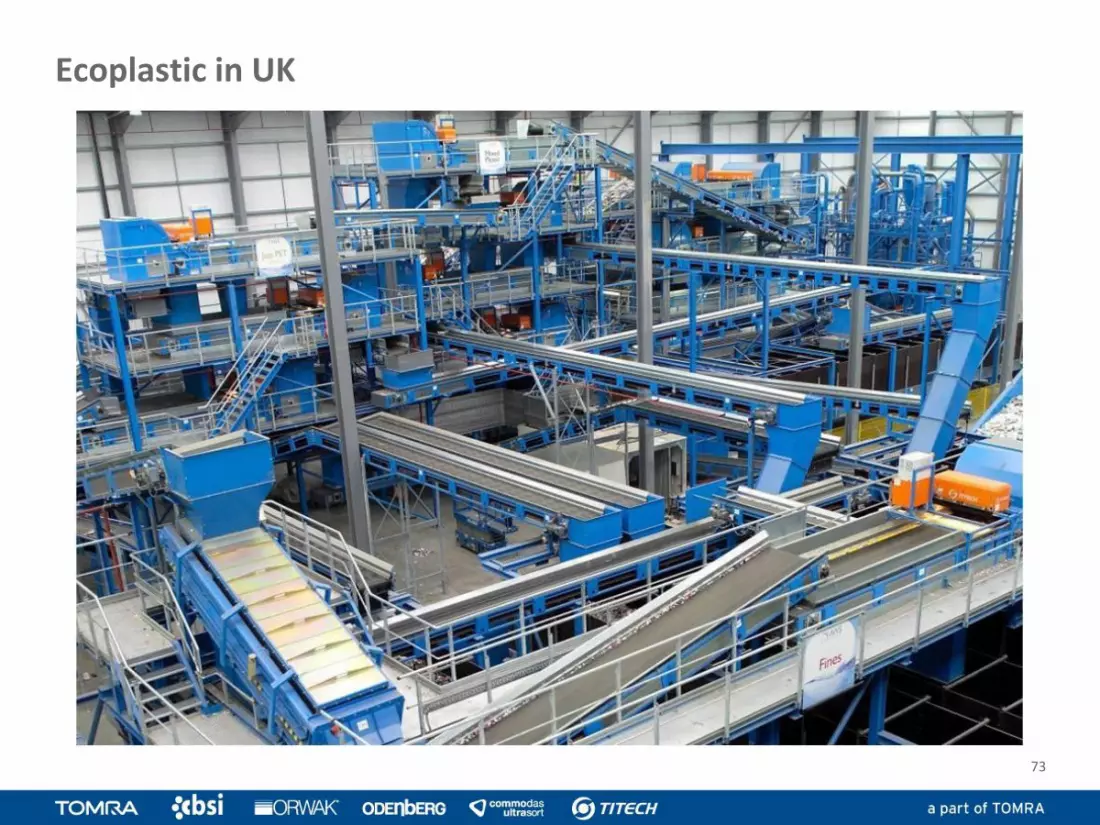

Ecoplastic in UK

73

• Bottle to bottle principle (highest quality level)Re-granulate for beverage bottle production

• Packaging film (highest quality level) Single layer film, suitable for use in food

• Packaging film (lower quality)3 layer film, middle layer is made from recycling PET, outside layer from virgin material, film is suitable for use in food

• Fiber industry (lower quality)PET flakes for fiber production, used for textile, filter, carpets, etc.

• Other use (lowest quality)Flake for fiber production, used for straps, etc.

74

Aim is to produce various grades of PET flakes

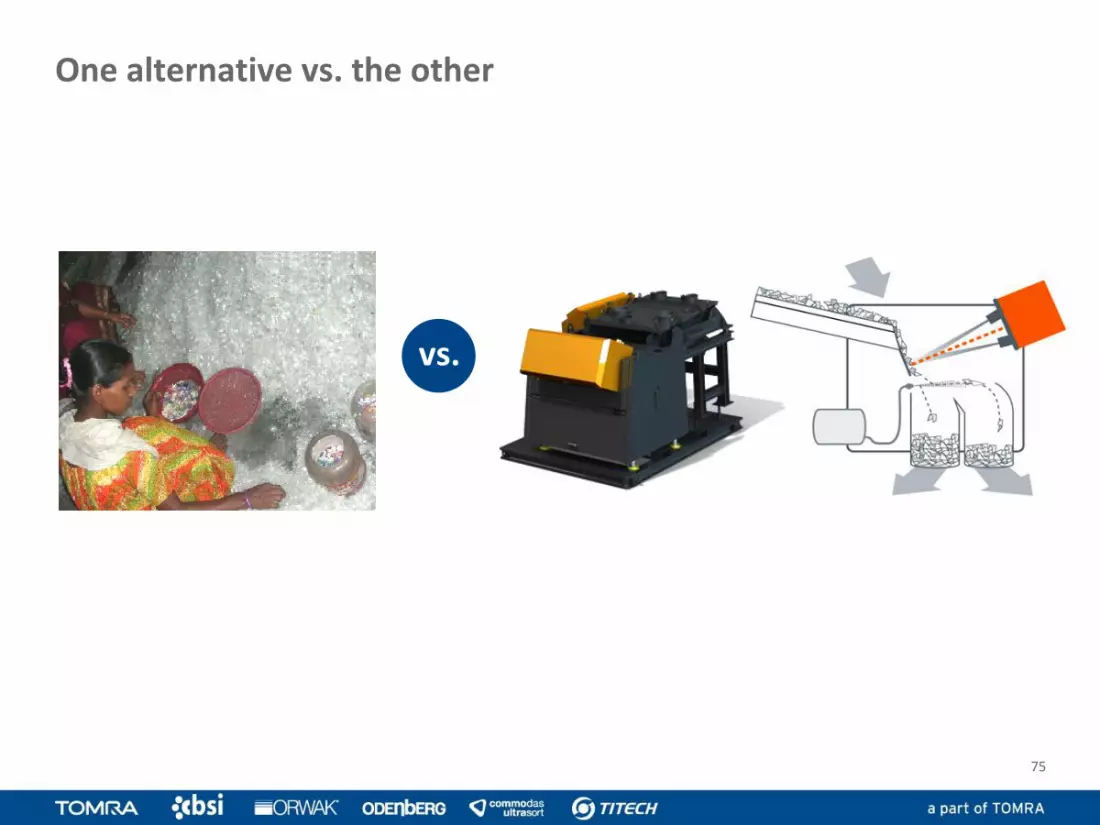

vs.

One alternative vs. the other

75

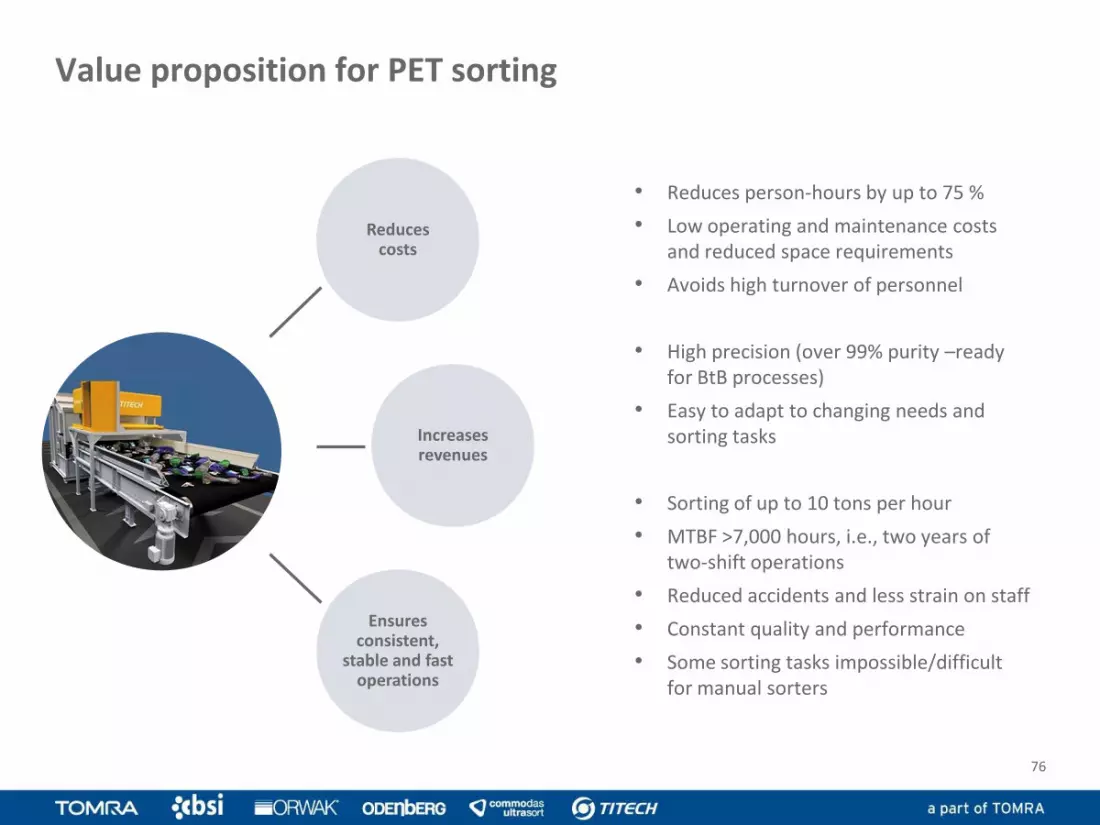

Value proposition for PET sorting

Reducescosts

Increasesrevenues

Ensures consistent,

stable and fast operations

• Reduces person-hours by up to 75 %

• Low operating and maintenance costs and reduced space requirements

• Avoids high turnover of personnel

• High precision (over 99% purity –ready for BtB processes)

• Easy to adapt to changing needs and sorting tasks

• Sorting of up to 10 tons per hour

• MTBF >7,000 hours, i.e., two years of two-shift operations

• Reduced accidents and less strain on staff

• Constant quality and performance

• Some sorting tasks impossible/difficult for manual sorters

76

Market segments in recycling

Waste recycling Metal recycling

PackagingSorting

Commercial & Industrial Wate Sorting

Construction & demolition WasteSorting

Single Stream Recycling

Paper Sorting

Mixed MunicipalSolid WasteSorting

RefuseDerived Fuel

Pre-sortedMaterial Sorting

End of Life VehiclesScrap Sorting

Electronic Scrap Sorting

Non-FerrousMetals Sorting

Ash Sorting

WireRecovery

77

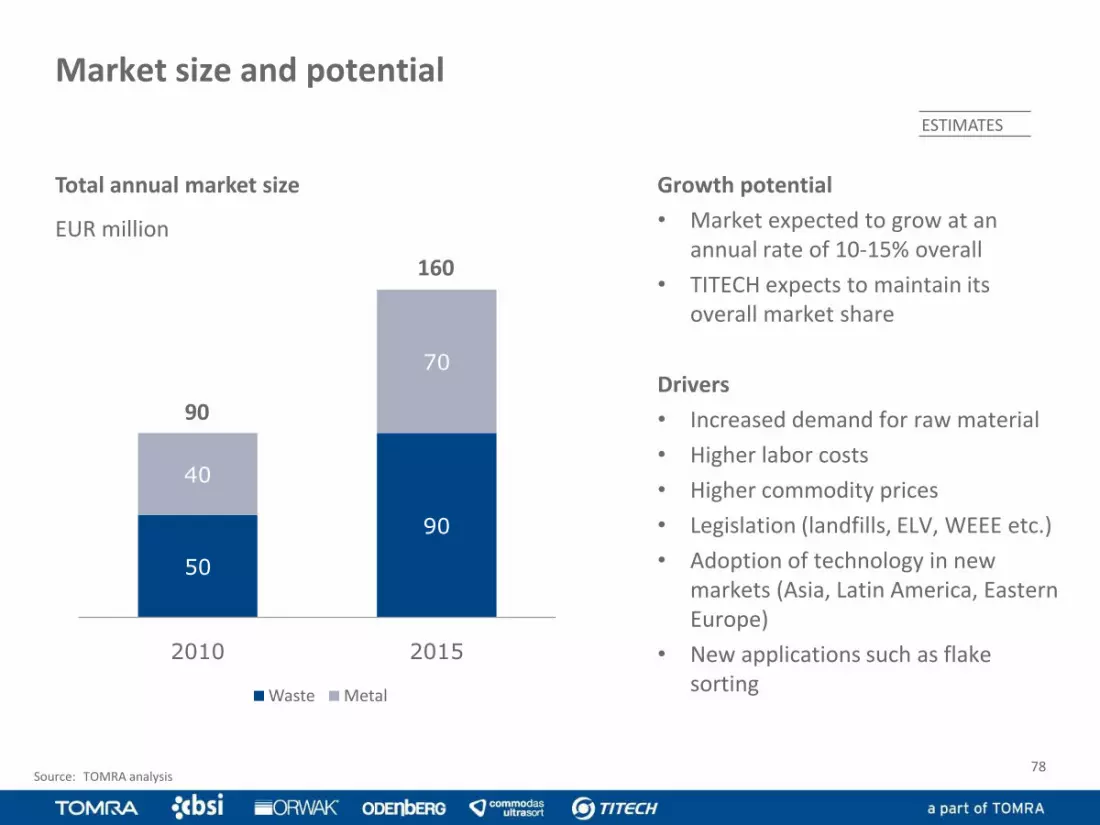

Total annual market size

EUR million

Growth potential

• Market expected to grow at an annual rate of 10-15% overall

• TITECH expects to maintain its overall market share

Drivers

• Increased demand for raw material

• Higher labor costs

• Higher commodity prices

• Legislation (landfills, ELV, WEEE etc.)

• Adoption of technology in new markets (Asia, Latin America, Eastern Europe)

• New applications such as flake sorting

Market size and potential

90

160

Source: TOMRA analysis

50

90

40

70

2010 2015

Waste Metal

78

ESTIMATES

• TITECH pioneered optical sorting of waste and is the number 1 player in this industry

• Serves all key market segments such as recycling of plastics, paper, metals etc.

• Installed base of more than 2,500 units

• Strong sales and service network

• Unrivalled technology platform

• Growing business, historically the annual growth rate has been in excess of 20%

• Favorable macro drivers– Increasing waste volumes– More ambitious recycling targets and

programs– Labor costs continue to increase– Attractive commodity prices

• Continued strong organic growth driven by geographical expansion and new sorting applications– Asia, Middle East and South America

are growing markets– Demand for more advanced sorting

solutions as markets become more sophisticated and experienced with sensor based sorting

Highlights - TITECH

Business characteristics Investment opportunities

79

Commodas Ultrasort –Finding mindful solutions

80

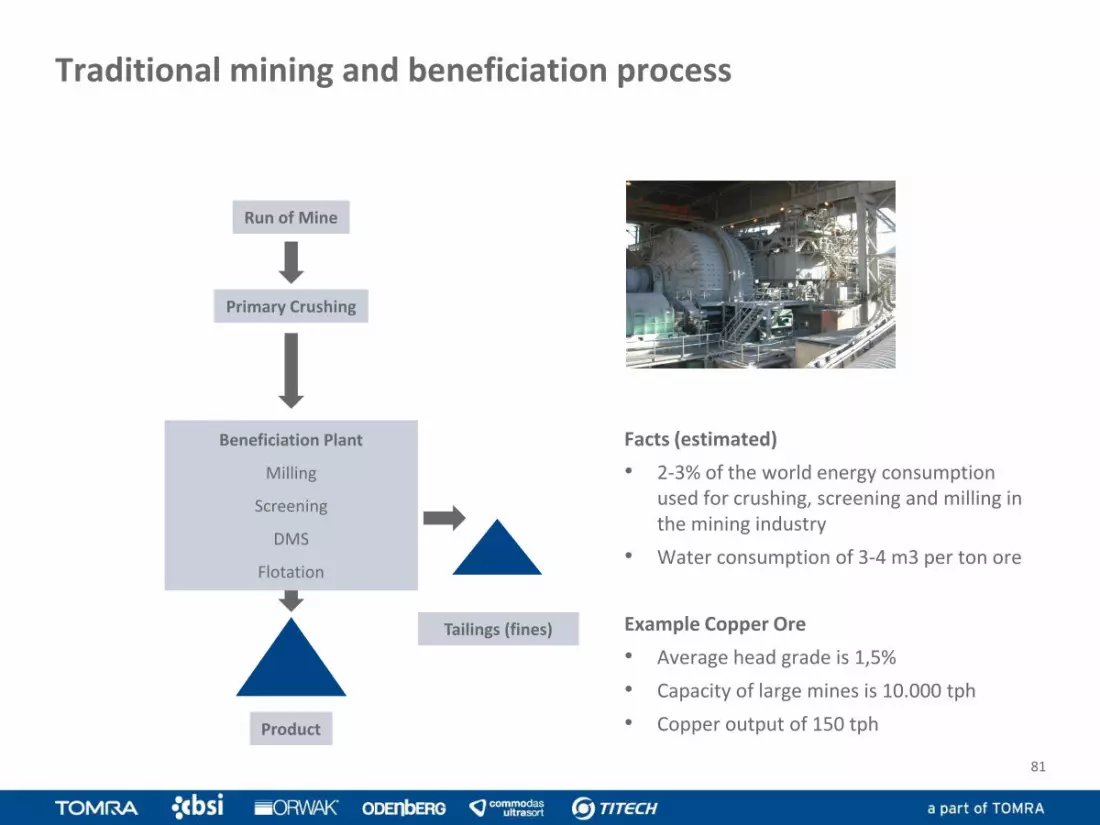

Traditional mining and beneficiation process

Tailings (fines)

Product

Primary Crushing

Run of Mine

Beneficiation Plant

Milling

Screening

DMS

Flotation

Facts (estimated)

• 2-3% of the world energy consumption used for crushing, screening and milling in the mining industry

• Water consumption of 3-4 m3 per ton ore

Example Copper Ore

• Average head grade is 1,5%

• Capacity of large mines is 10.000 tph

• Copper output of 150 tph

81

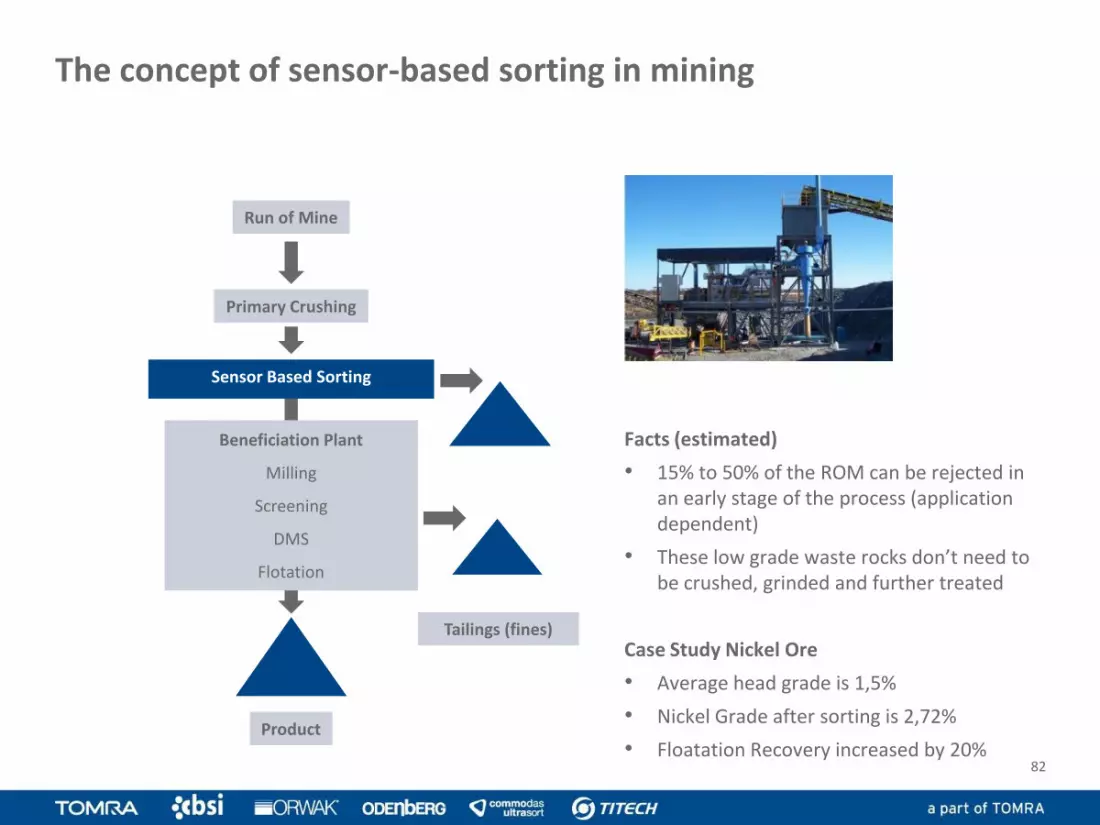

The concept of sensor-based sorting in mining

Tailings (fines)

Product

Primary Crushing

Run of Mine

Sensor Based Sorting

Beneficiation Plant

Milling

Screening

DMS

Flotation

Facts (estimated)

• 15% to 50% of the ROM can be rejected in an early stage of the process (application dependent)

• These low grade waste rocks don’t need to be crushed, grinded and further treated

Case Study Nickel Ore

• Average head grade is 1,5%

• Nickel Grade after sorting is 2,72%

• Floatation Recovery increased by 20%82

Value proposition

Increased access to resources

Cost savings

Environ-mental

benefits

• Lower head grade can be processed

• Better utilization of existing deposits

• Old dumps turn into resources

• Significant capacity increase of the traditional beneficiation plant

• Energy costs savings

• Less wear and tear and chemicals costs

• Better carbon footprint

• Reduction of acid mine drainage

• Less pollution

83

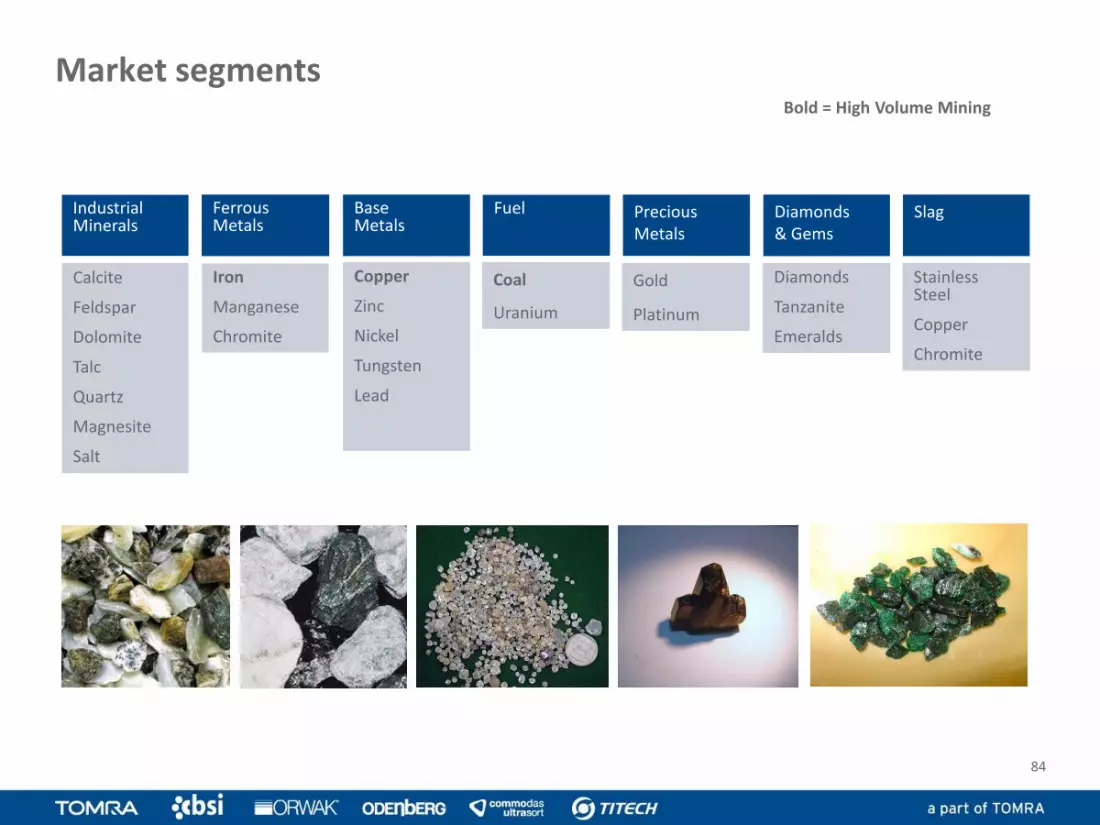

PreciousMetals

IndustrialMinerals

Calcite

Feldspar

Dolomite

Talc

Quartz

Magnesite

Salt

Diamonds

Tanzanite

Emeralds

Diamonds& Gems

Gold

Platinum

BaseMetals

Iron

Manganese

Chromite

FerrousMetals

Copper

Zinc

Nickel

Tungsten

Lead

Fuel

Coal

Uranium

StainlessSteel

Copper

Chromite

Slag

Bold = High Volume Mining

Market segments

84

Market size and potential

Total annual market size

EUR million Growth Potential• Market expected to grow at an

annual rate of around 20-30% overall

• Commodas Ultrasort expects to maintain its overall market share

Drivers• Increasing demand for

commodities from emerging markets

• Increased pressure on costs but high/increasing energy and water costs

Source: TOMRA analysis

20

60

2010 2015

85

ESTIMATES

• CommoDas UltraSort is the number 1 player in sensor-based sorting of mining materials

• Covers all key industry segments such as minerals, metals, gemstones etc.

• ~160 units installed worldwide

• Rapidly growing business

• Increasing demand for commodities from emerging markets

• Increased pressure on costs but high/increasing energy and water costs

• Tougher environmental regulations

• Lower head grade

Business characteristics Investment opportunities

Highlights - Commodas Ultrasort

86

Odenberg – Securing quality, efficiency, and productivity

87

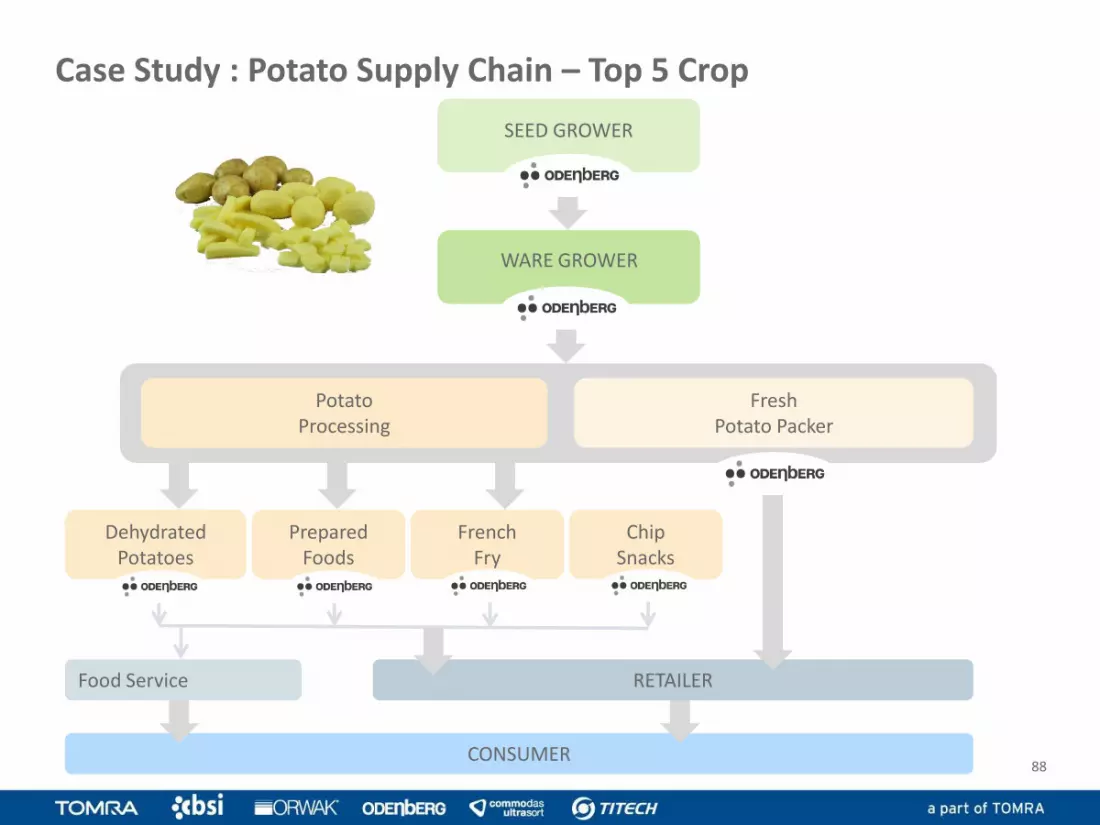

CONSUMER88

SEED GROWER

WARE GROWER

Potato Processing

Fresh Potato Packer

PreparedFoods

FrenchFry

Dehydrated Potatoes

RETAILER

Case Study : Potato Supply Chain – Top 5 Crop

ChipSnacks

Food Service

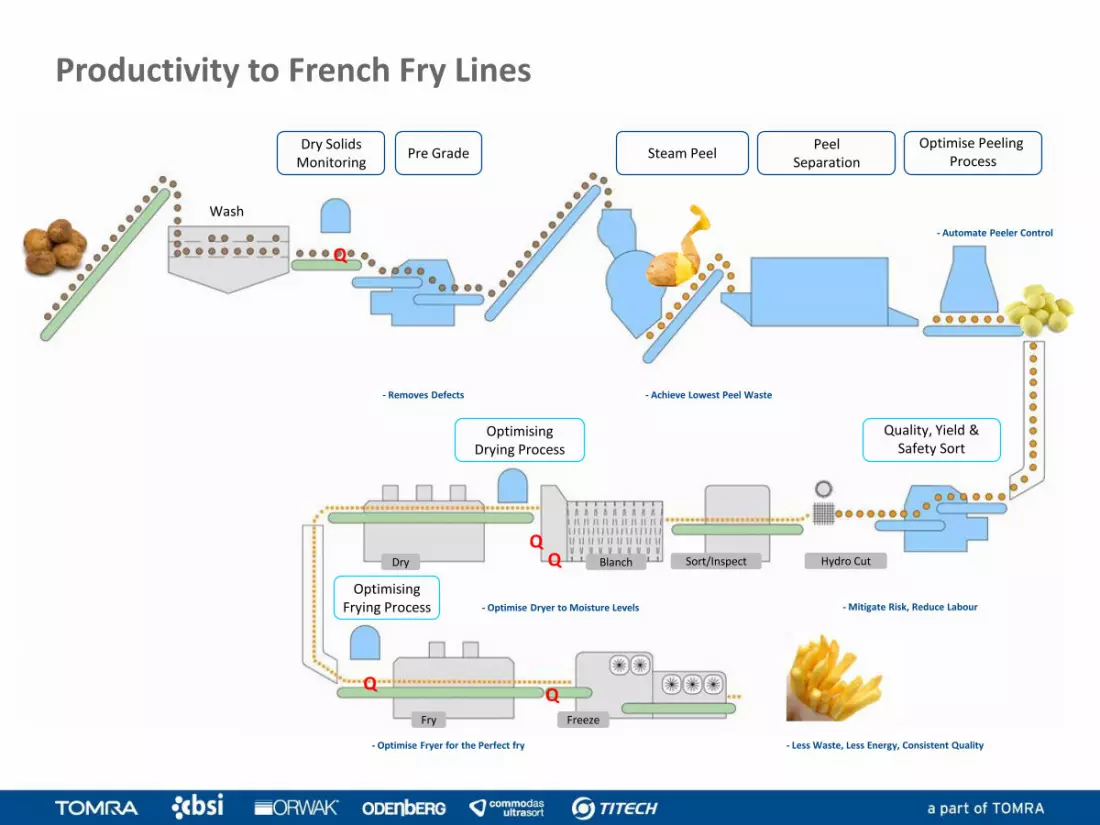

Dry SolidsMonitoring

Wash

Dry Blanch Sort/Inspect Hydro Cut

Fry Freeze

Q

Pre Grade Steam PeelPeel

Separation

Optimise Peeling Process

Quality, Yield &Safety Sort

OptimisingDrying Process

OptimisingFrying Process

- Removes Defects - Achieve Lowest Peel Waste

- Automate Peeler Control

- Mitigate Risk, Reduce Labour- Optimise Dryer to Moisture Levels

- Optimise Fryer for the Perfect fry - Less Waste, Less Energy, Consistent Quality

Productivity to French Fry Lines

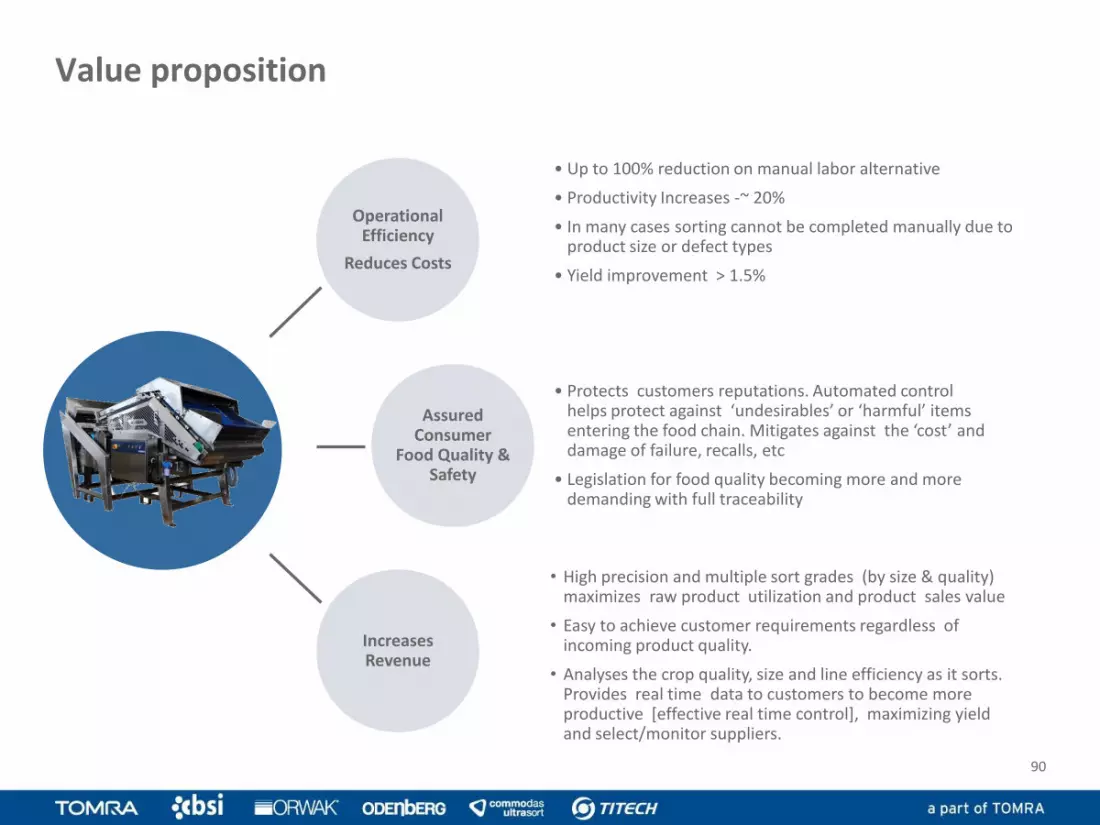

Value proposition

90

Operational Efficiency

Reduces Costs

Assured Consumer

Food Quality & Safety

Increases Revenue

• Up to 100% reduction on manual labor alternative

• Productivity Increases -~ 20%

• In many cases sorting cannot be completed manually due to product size or defect types

• Yield improvement > 1.5%

• Protects customers reputations. Automated control helps protect against ‘undesirables’ or ‘harmful’ items entering the food chain. Mitigates against the ‘cost’ and damage of failure, recalls, etc

• Legislation for food quality becoming more and more demanding with full traceability

• High precision and multiple sort grades (by size & quality) maximizes raw product utilization and product sales value

• Easy to achieve customer requirements regardless of incoming product quality.

• Analyses the crop quality, size and line efficiency as it sorts. Provides real time data to customers to become more productive [effective real time control], maximizing yield and select/monitor suppliers.

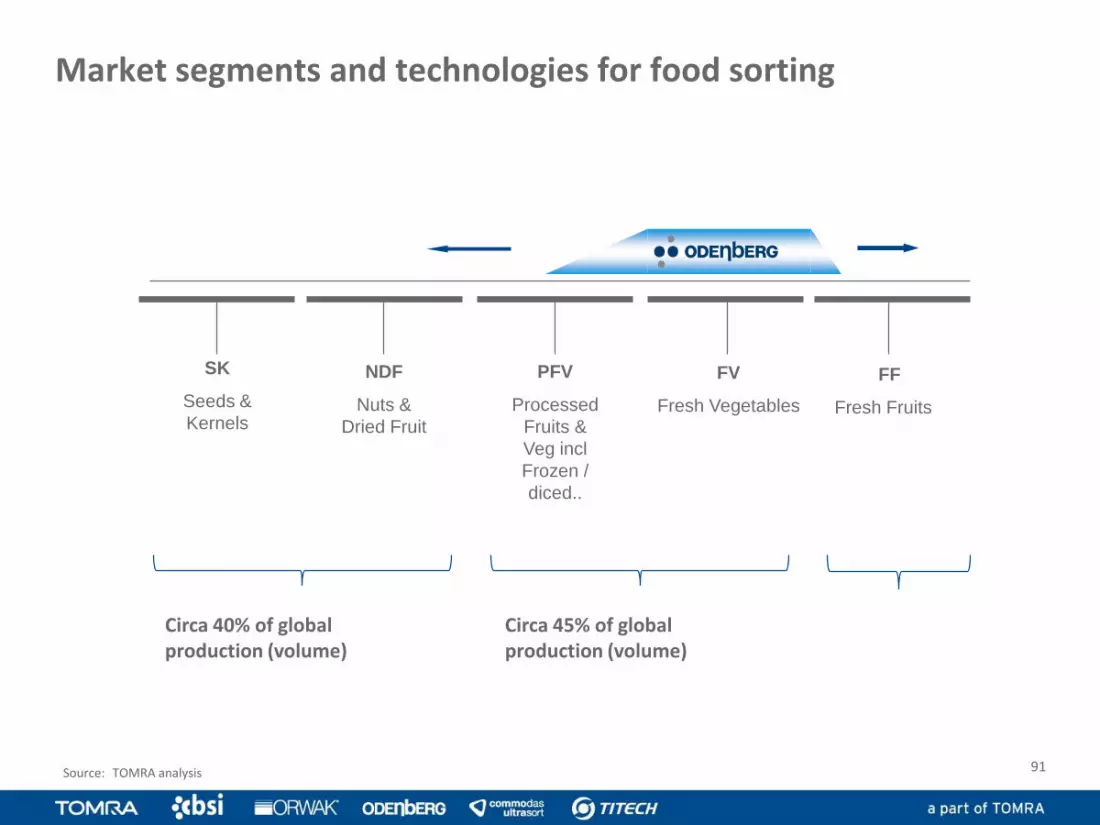

Market segments and technologies for food sorting

Source: TOMRA analysis 91

SK

Seeds &

Kernels

PFV

Processed

Fruits &

Veg incl

Frozen /

diced..

FF

Fresh Fruits

FV

Fresh Vegetables

NDF

Nuts &

Dried Fruit

Circa 45% of global production (volume)

Circa 40% of global production (volume)

Market segments

VEGETABLES

FRUIT MEAT DAIRY

92

• Productivity, Consumer Quality & Safety

– Sort & Grade of fruits and vegetables sorted by shape, color, defect, blemish, damage, size & removal of foreign objects

– Peel / Skin removal on Potatoes, Carrots, Beets, Peppers

– Freezing & Chilling Systems to reliably & safely freeze meats, soups & sauces

– Process Analytics to measure meat and potato constituents (fat, water, sugar, etc)

• Key segments include:

– Potatoes (From field to store, fresh & processed, whole, peeled & cut)

– Tomatoes (In Field and Processing Plants whole, peeled & cut/diced)

– Whole vegetables and fruits– Cut and diced fruits and vegetables– Dried fruits – Ground Meat

•Active in five continents and 30 markets

•Odenberg provides sorting solutions for

–Growers – harvester mounted tomato and potato sorters

– Packers – sorting of many different types of fruit and vegetables by color, size, shape, defect, blemish, damage or foreign objects

– Processors – sorting of processed potatoes (french fries, chips), fruits and vegetables

•6 of the 10 largest, global food companies are Odenberg customers.

•30% of workforce dedicated to sales and support (~50 employees)

Customer base

93

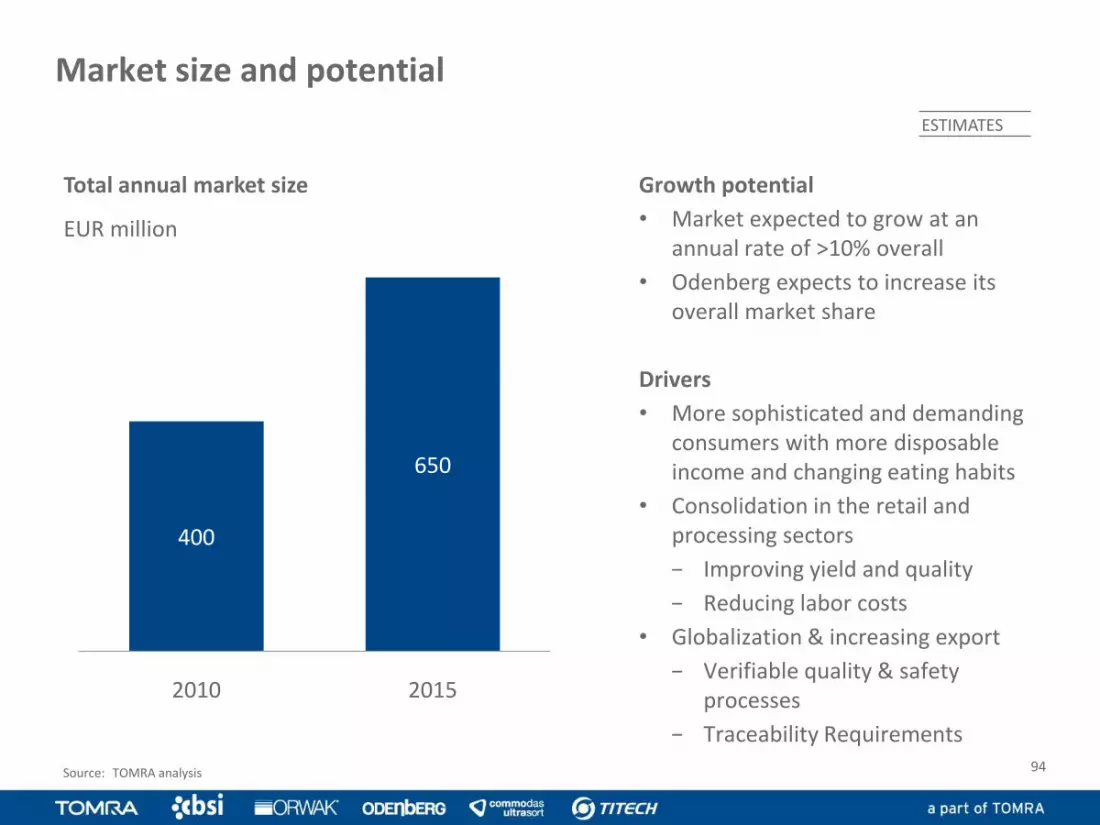

Market size and potential

Total annual market size

EUR million

400

650

2010 2015

Growth potential

• Market expected to grow at an annual rate of >10% overall

• Odenberg expects to increase its overall market share

Drivers

• More sophisticated and demanding consumers with more disposable income and changing eating habits

• Consolidation in the retail and processing sectors

− Improving yield and quality

− Reducing labor costs

• Globalization & increasing export

− Verifiable quality & safety processes

− Traceability Requirements

Source: TOMRA analysis 94

ESTIMATES

New product innovations increase Odenberg’s addressable market

95

NFM Color SorterField Sorter

Alpha Color & Defect

Process Spec

SentinelGross Sort – Major

Color, Defect & Safety

New HaloHigh Resolution Sort For whole fruits and vegetables –Color,

Defect, Size, Shape & Safety

New Titan IIHigh Capacity Quality Sort - Color,

Defect & Safety.

Price & Functionality

New Iris IIHigh Resolution Sort

Small Produce Color,

Defect, Size, Shape & Safety

2011 Releases

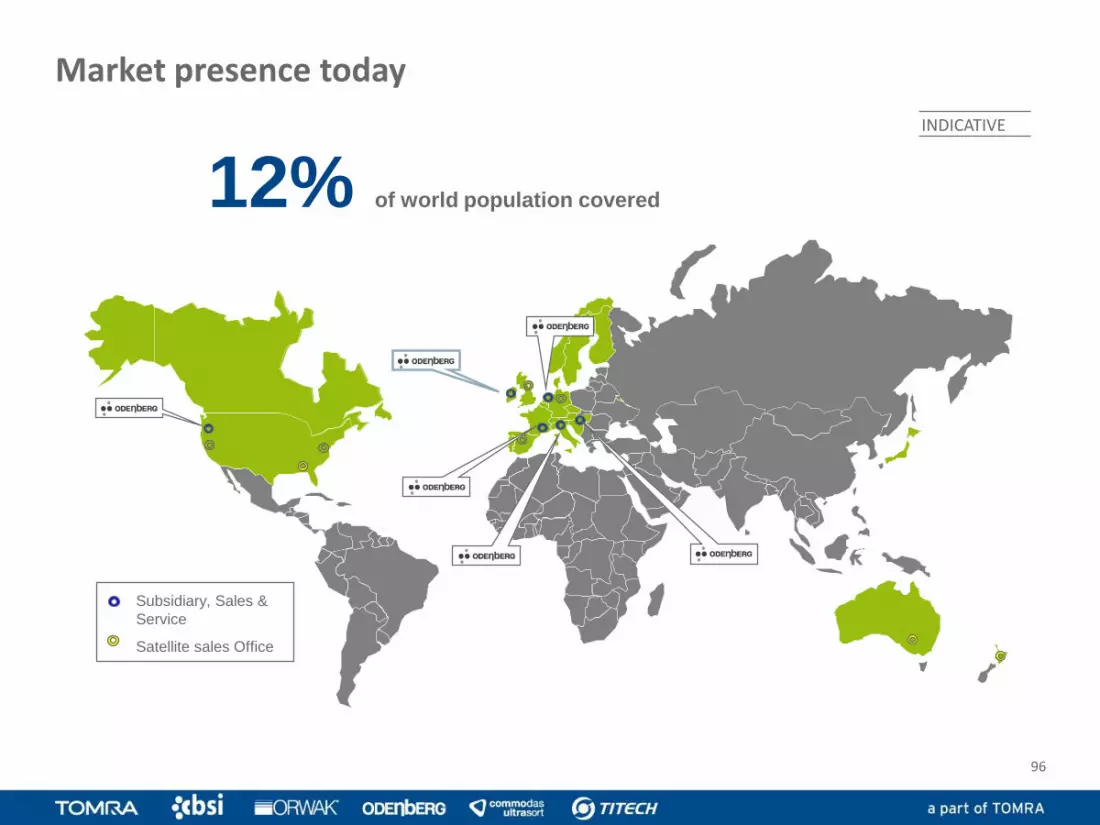

12% of world population covered

Market presence today

96

Subsidiary, Sales &

Service

Satellite sales Office

INDICATIVE

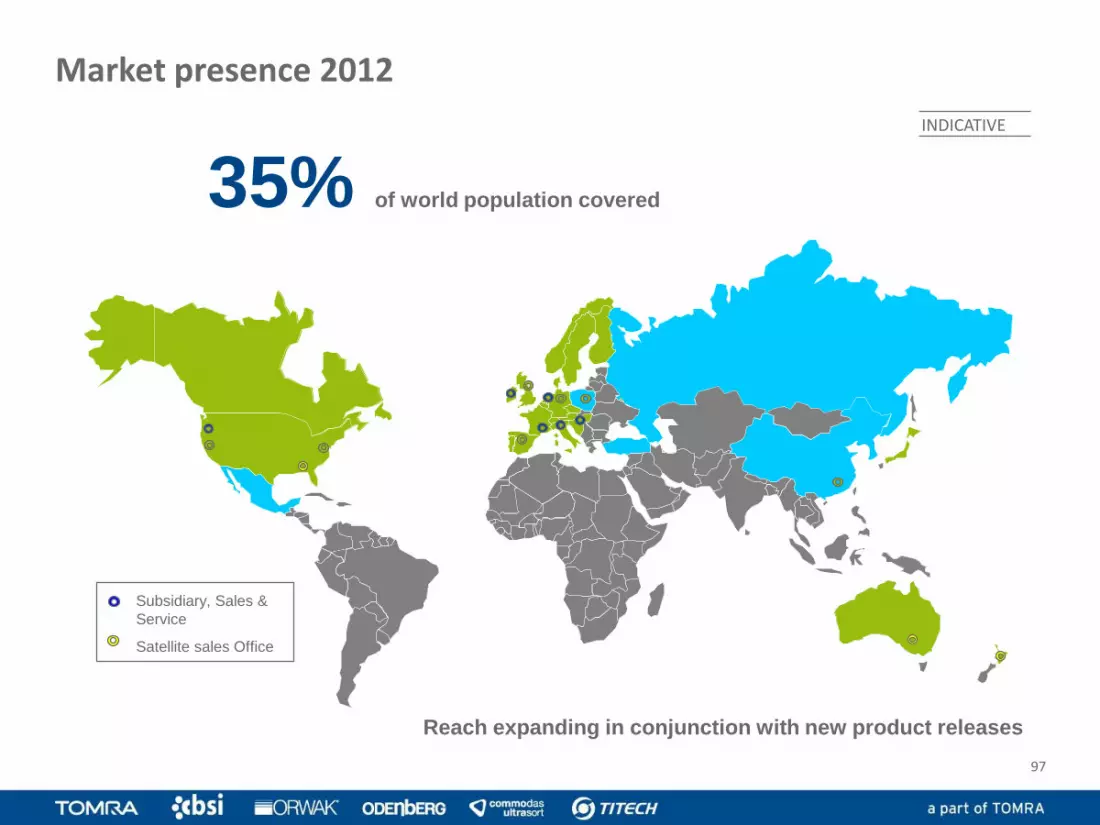

35% of world population covered

Market presence 2012

97

Subsidiary, Sales &

Service

Satellite sales Office

Reach expanding in conjunction with new product releases

INDICATIVE

56% of world population covered

Market presence 2013

98

Subsidiary, Sales &

Service

Satellite sales Office

Reach expanding in conjunction with new product releases

INDICATIVE

• Top 5 player in optical sorting and processing solutions for food.

• #1 in sorting of potatoes, tomatoes & peaches and # 1 in steam peeling of potatoes

• Diversified both geographically and by customer type

• Proven & loyal partner to some of worlds top food companies

• Installed base of ~2,200 optical sorters and ~500 steam peelers

• Rapidly growing business, revenue doubled from 2005 to 2010

Business characteristics Investment opportunities

Highlights - Odenberg

• Increasing global consumption of food

• Growing middle class population (70 million per year) with increasing demands for food quality, in particular from BRIC countries

• Relentless industry focus on reducing costs through automation and improved quality control

• Stricter rules and regulations regarding food safety [farm to fork]

• Huge liability issues for food manufacturers if products are defect or contaminated

99

Financial performance and targets

100

Collection Technology - Segment financials

101

Gross and EBITA margin developmentPercent

Revenue developmentNOK million

0

500

1000

1500

2000

2500

2007 2008 2009 2010

Q1 Q2 Q3 Q4 Full year

4345 46

48

16 16

2119

0

5

10

15

20

25

30

35

40

45

50

2007 2008 2009 2010

GM EBITA

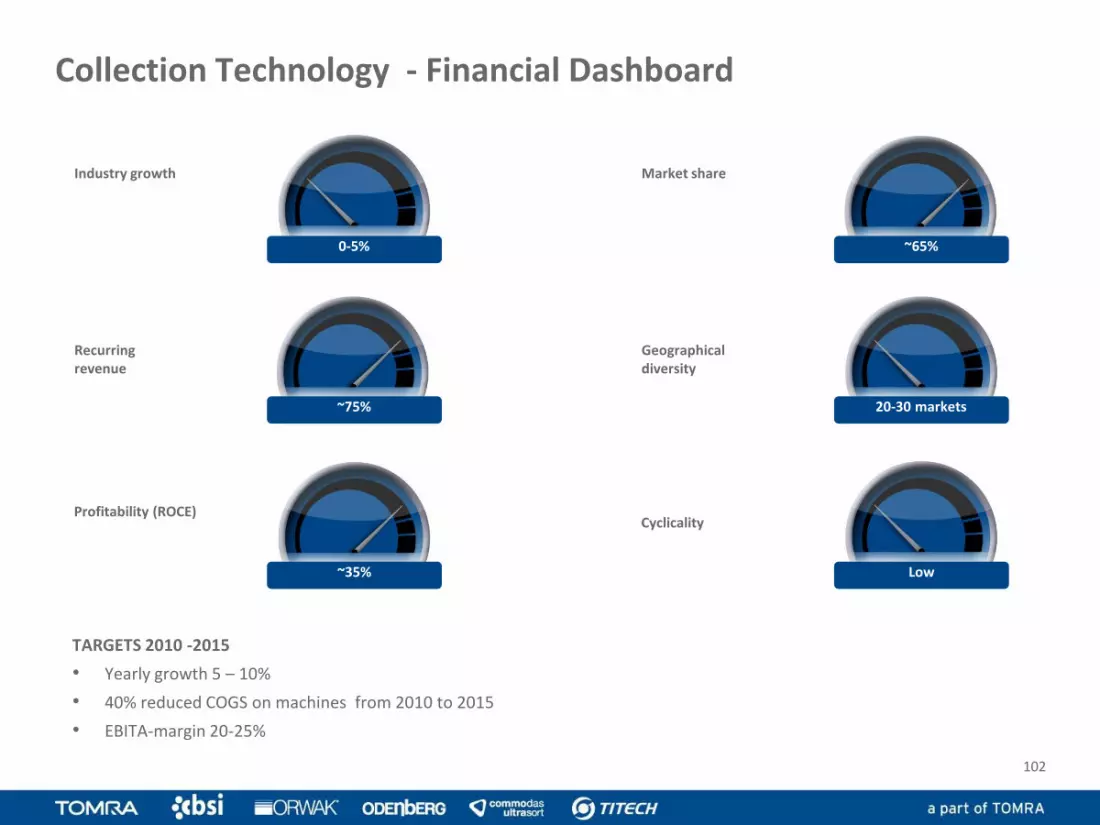

Collection Technology - Financial Dashboard

102

~75%

~35%

Industry growth

Profitability (ROCE)

Recurringrevenue

Dashboard

20-30 markets

~65%

Low

Market share

Geographicaldiversity

Cyclicality

0-5%

TARGETS 2010 -2015

• Yearly growth 5 – 10%

• 40% reduced COGS on machines from 2010 to 2015

• EBITA-margin 20-25%

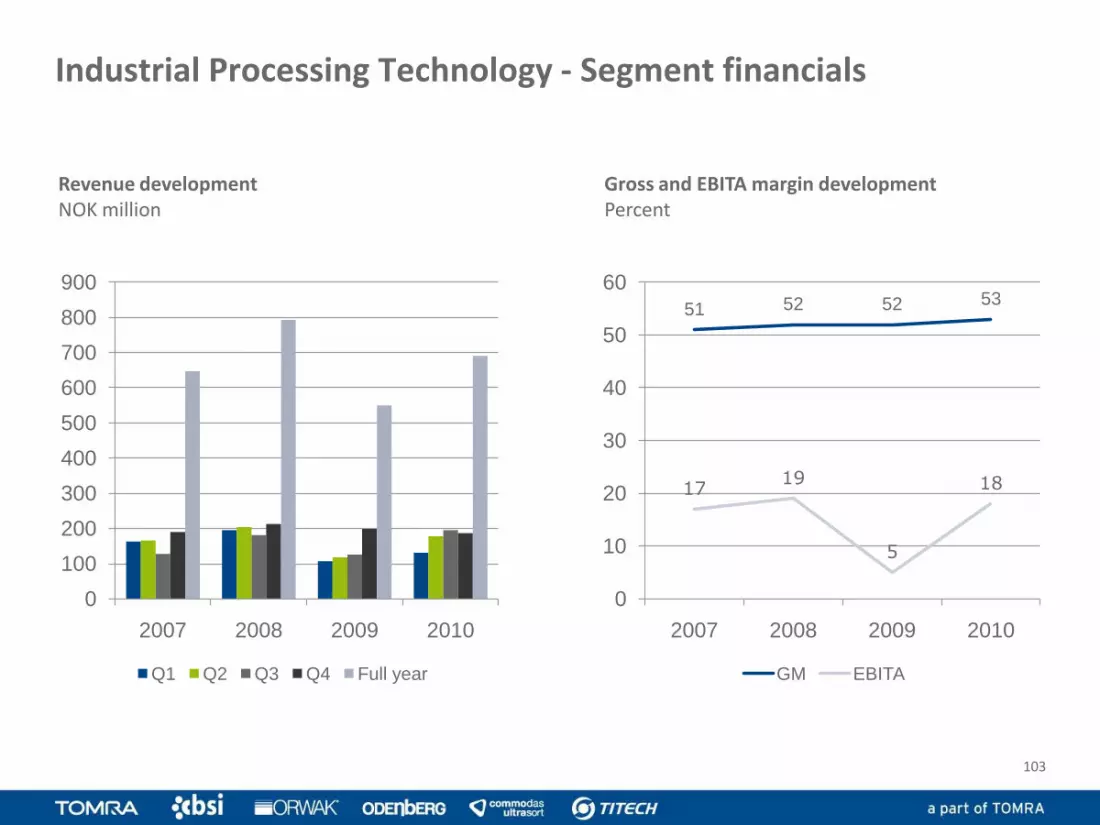

Industrial Processing Technology - Segment financials

103

Gross and EBITA margin developmentPercent

Revenue developmentNOK million

0

100

200

300

400

500

600

700

800

900

2007 2008 2009 2010

Q1 Q2 Q3 Q4 Full year

51 52 52 53

1719

5

18

0

10

20

30

40

50

60

2007 2008 2009 2010

GM EBITA

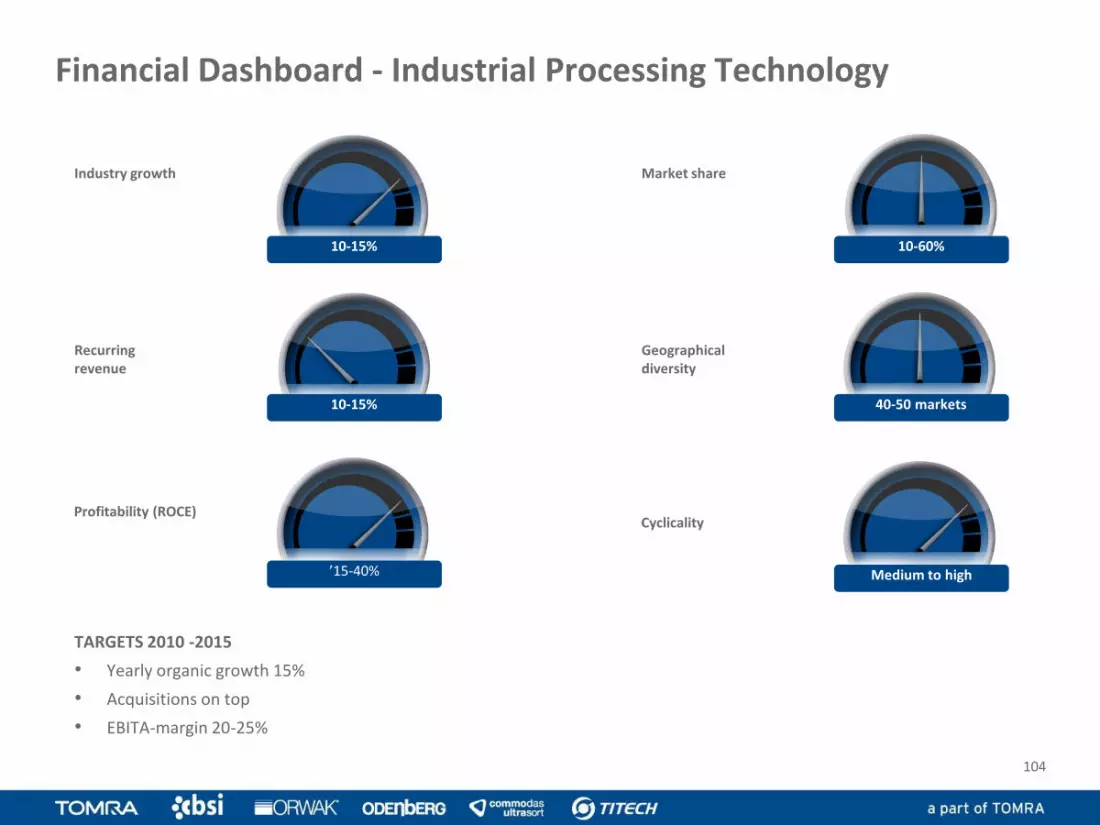

Financial Dashboard - Industrial Processing Technology

104

10-15%

’15-40%

Industry growth

Profitability (ROCE)

Recurringrevenue

Dashboard

40-50 markets

10-60%

Medium to high

Market share

Geographicaldiversity

10-15%

TARGETS 2010 -2015

• Yearly organic growth 15%

• Acquisitions on top

• EBITA-margin 20-25%

Cyclicality

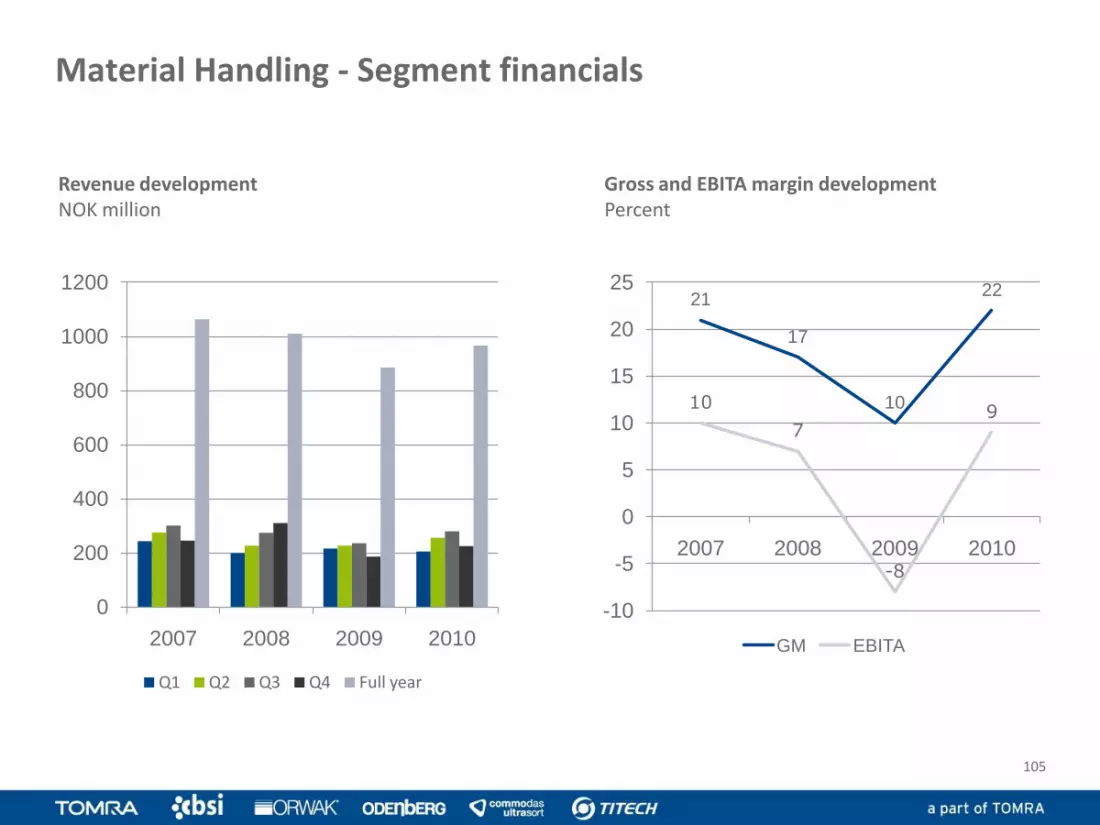

Material Handling - Segment financials

105

Gross and EBITA margin developmentPercent

Revenue developmentNOK million

0

200

400

600

800

1000

1200

2007 2008 2009 2010

Q1 Q2 Q3 Q4 Full year

21

17

10

22

10

7

-8

9

-10

-5

0

5

10

15

20

25

2007 2008 2009 2010

GM EBITA

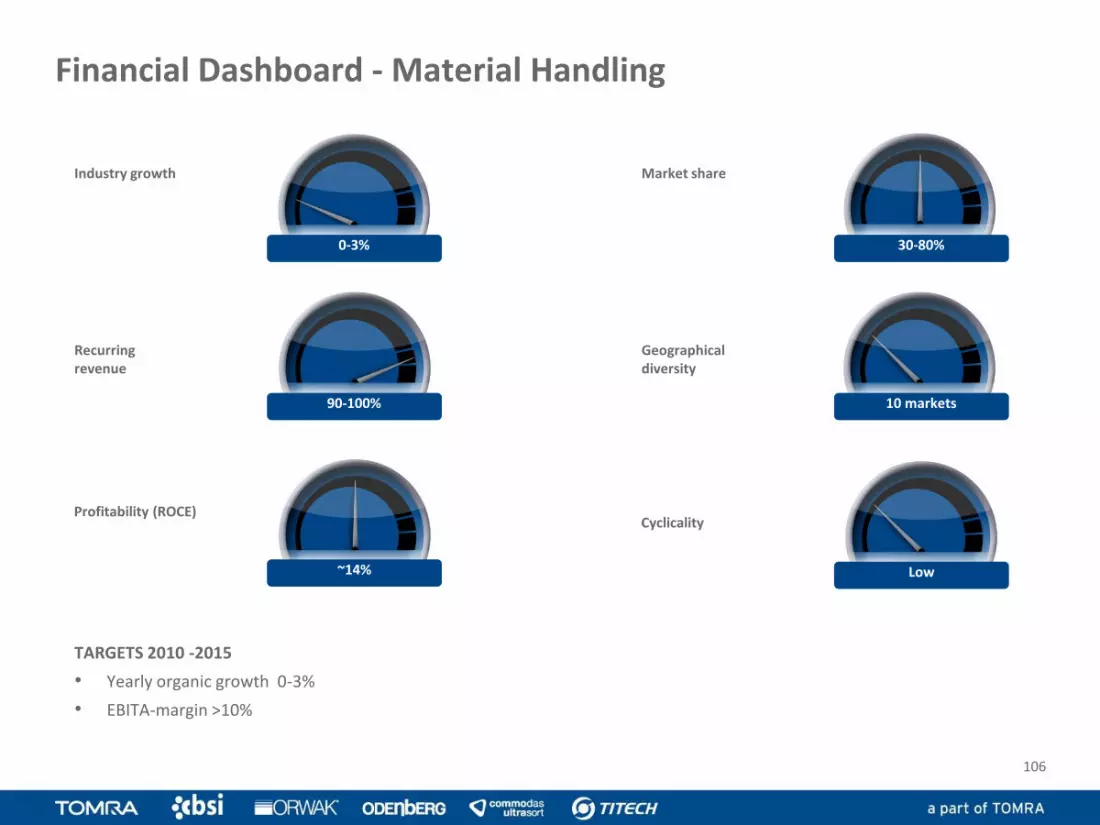

Financial Dashboard - Material Handling

106

90-100%

~14%

Industry growth

Profitability (ROCE)

Recurringrevenue

Dashboard

10 markets

30-80%

Market share

Geographicaldiversity

0-3%

TARGETS 2010 -2015

• Yearly organic growth 0-3%

• EBITA-margin >10%

Low

Cyclicality

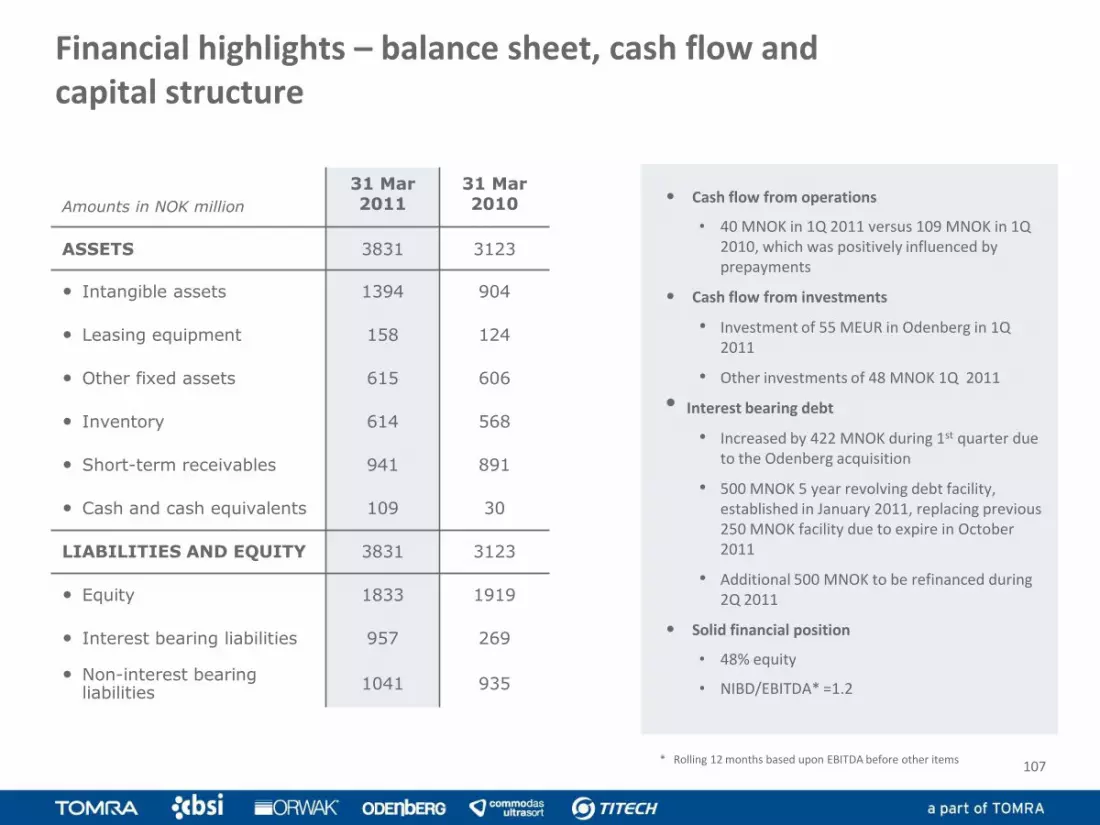

• Cash flow from operations

• 40 MNOK in 1Q 2011 versus 109 MNOK in 1Q 2010, which was positively influenced by prepayments

• Cash flow from investments

• Investment of 55 MEUR in Odenberg in 1Q 2011

• Other investments of 48 MNOK 1Q 2011

• Interest bearing debt

• Increased by 422 MNOK during 1st quarter due to the Odenberg acquisition

• 500 MNOK 5 year revolving debt facility, established in January 2011, replacing previous 250 MNOK facility due to expire in October 2011

• Additional 500 MNOK to be refinanced during 2Q 2011

• Solid financial position

• 48% equity

• NIBD/EBITDA* =1.2

Amounts in NOK million

31 Mar 2011

31 Mar 2010

ASSETS 3831 3123

• Intangible assets 1394 904

• Leasing equipment 158 124

• Other fixed assets 615 606

• Inventory 614 568

• Short-term receivables 941 891

• Cash and cash equivalents 109 30

LIABILITIES AND EQUITY 3831 3123

• Equity 1833 1919

• Interest bearing liabilities 957 269

• Non-interest bearing liabilities

1041 935

* Rolling 12 months based upon EBITDA before other items

Financial highlights – balance sheet, cash flow and capital structure

107

TOMRA creates transformative sensor-based solutions for optimal resource productivity

108

Today we are seeing more opportunities for transformative solutions than ever before.

109

Deposits into refunds…

110

Waste into wealth…

111

112

Source into resource…

Purpose into profits…

113

Profits into progress…

114

TOMRA is showing that we can move past the false choice between the earth and the economy

115

This is the resource revolution

116

TOMRA is leading it

117