three essays in venture capital - research explorer

TRANSCRIPT

Three Essays in Venture Capital

A thesis submitted to the University of Manchester for the degree of

Doctor of Philosophy

in the Faculty of Humanities

June 2015

Fan Wang

Manchester Business School

2

CONTENTS

Abstract ............................................................................................................................. 6

Declaration ........................................................................................................................ 7

Copyright Statement ......................................................................................................... 8

Dedication ......................................................................................................................... 9

Acknowledgements ......................................................................................................... 10

Chapter 1

Introduction

1.1 Motivation ................................................................................................................ 11

1.2 Thesis structure ......................................................................................................... 18

References ....................................................................................................................... 19

Chapter 2

Syndicated Venture Capital Investments: What's in it for

Local Venture Capitalists?

Abstract ........................................................................................................................... 21

2.1 Introduction ............................................................................................................... 22

2.2 Literature and hypothesis development .................................................................... 25

2.2.1 Theoretical framework ....................................................................................... 25

2.2.2 Syndicate experience .......................................................................................... 30

2.2.3 Syndicate experience and investment selection .................................................. 31

2.2.4 Syndicate experience and investment performance ............................................ 33

2.3. Data and methodology ............................................................................................. 34

2.3.1 Data and sample ................................................................................................. 34

3

2.3.2 Dependent variables ........................................................................................... 37

2.3.3 Explanatory variables ........................................................................................ 38

2.3.4 Control variables ................................................................................................ 39

2.3.5 Estimation models .............................................................................................. 40

2.4 Analysis ..................................................................................................................... 44

2.4.1 Local VC firms’ foreign syndicate experience ................................................... 44

2.4.3 Univariate analysis of selection and performance ............................................. 45

2.4.2 Local VC firms with foreign syndicate experience ............................................. 47

2.4.4 Investment selection ........................................................................................... 49

2.4.5 Investment performance ..................................................................................... 50

2.4.6 Robustness check ................................................................................................ 51

2.5 Conclusion ................................................................................................................ 53

References ....................................................................................................................... 55

Appendix ......................................................................................................................... 73

Chapter 3

Do Venture Capital Firms Benefit as Boards of Directors in

Mature Public Companies?

Abstract ........................................................................................................................... 74

3.1 Introduction ............................................................................................................... 75

3.2 Literature review and hypothesis development ........................................................ 77

3.2.1 VC characteristics and directorships ................................................................. 77

3.2.2 Directorships and VC fundraising ..................................................................... 79

3.2.3 Directorships and investment performance ....................................................... 81

3.3 Data and methodology .............................................................................................. 82

3.3.1 Data and sample ................................................................................................. 82

4

3.3.2 Dependent variables ........................................................................................... 85

3.3.3 Determinants of VC directorship ....................................................................... 86

3.3.4 Estimation models .............................................................................................. 88

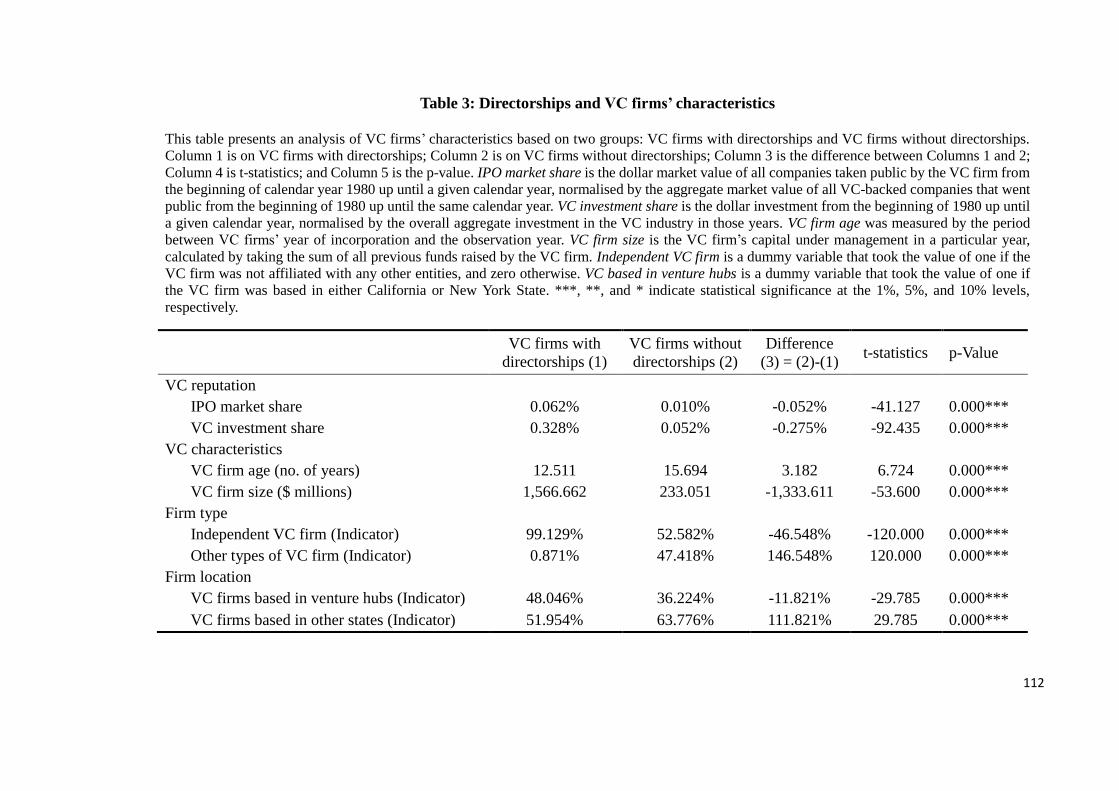

3.4 Analysis ..................................................................................................................... 93

3.4.1. Directorship and VC firm characteristics ......................................................... 93

3.4.1.1 Univariate analysis ................................................................................................. 93

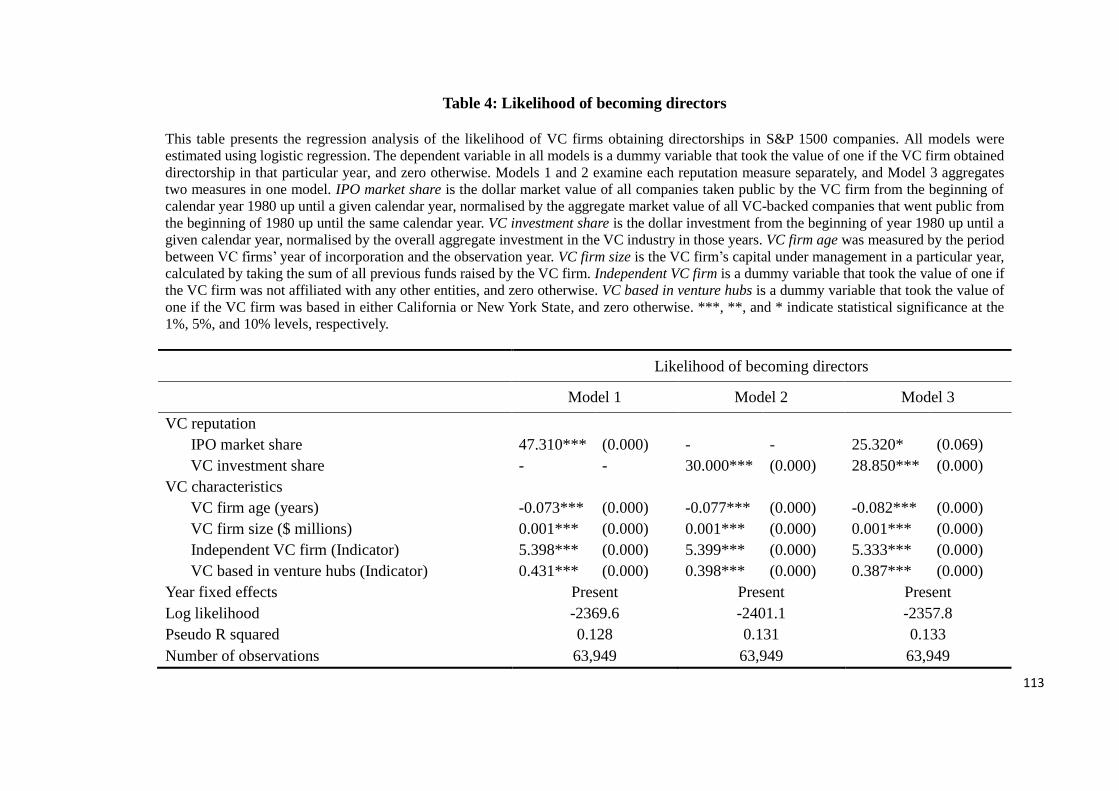

3.4.1.2 Multivariate analysis............................................................................................... 94

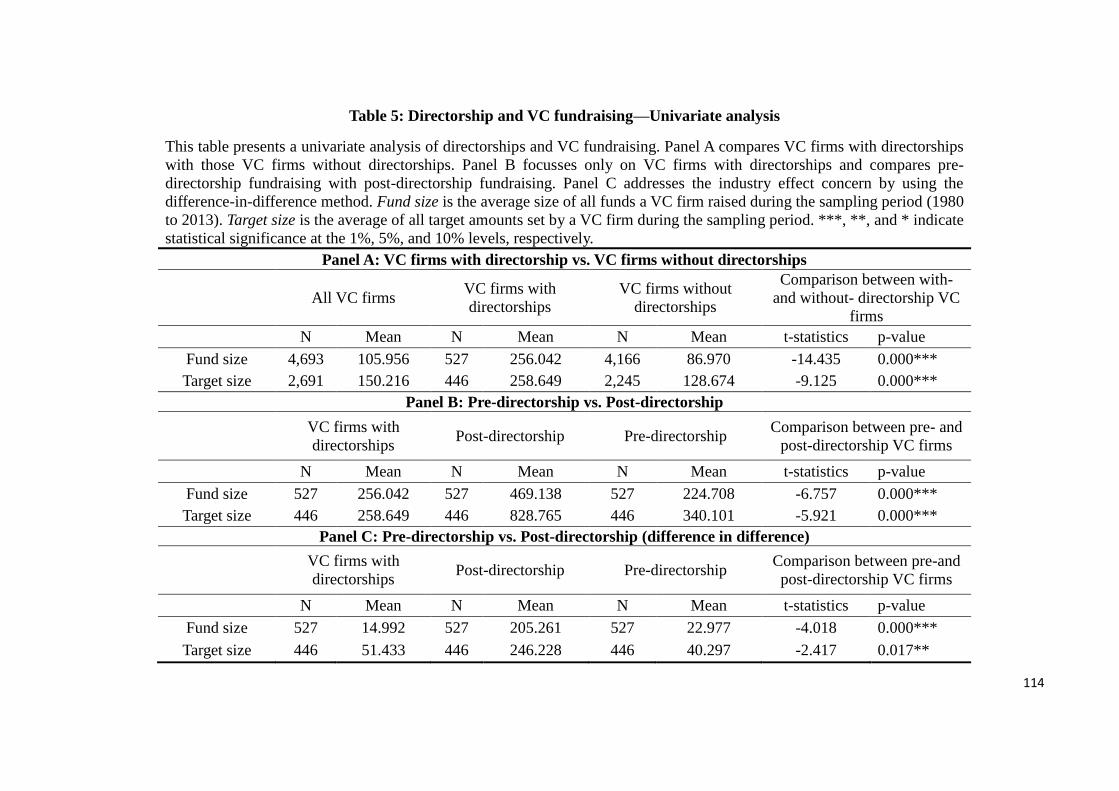

3.4.2 Directorship and fundraising ............................................................................. 96

3.4.2.1 Univariate analysis ................................................................................................. 98

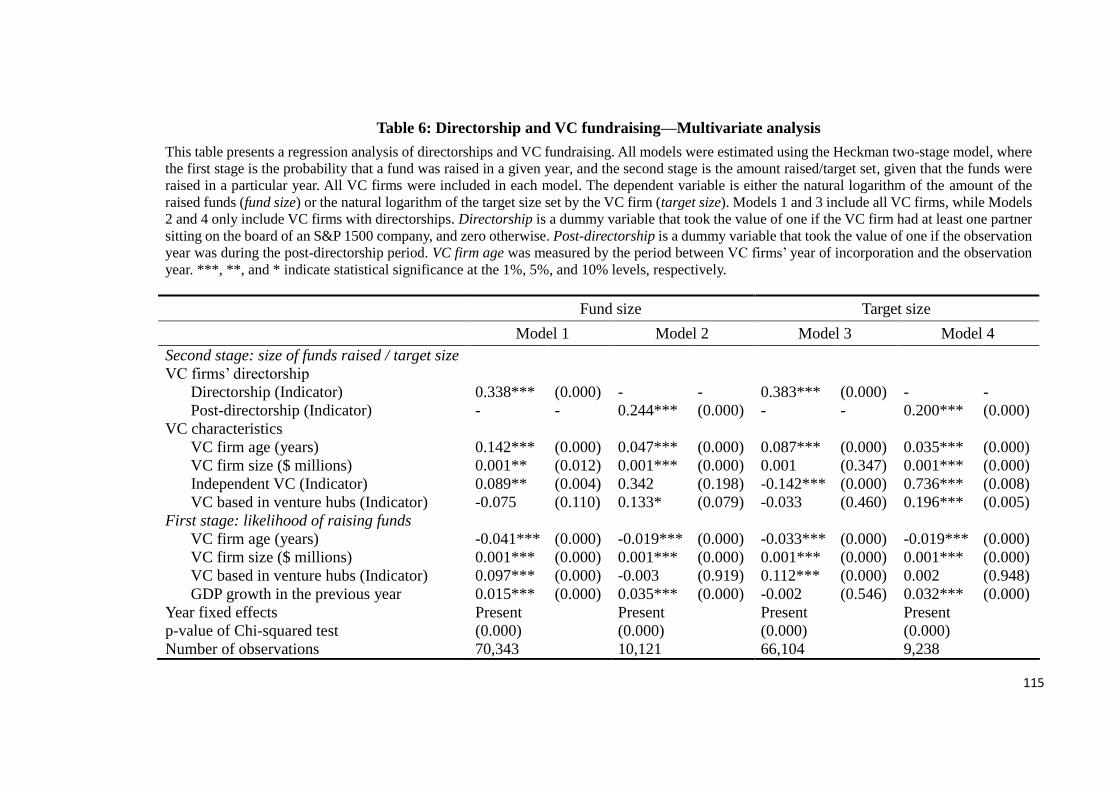

3.4.2.2 Multivariate analysis............................................................................................... 99

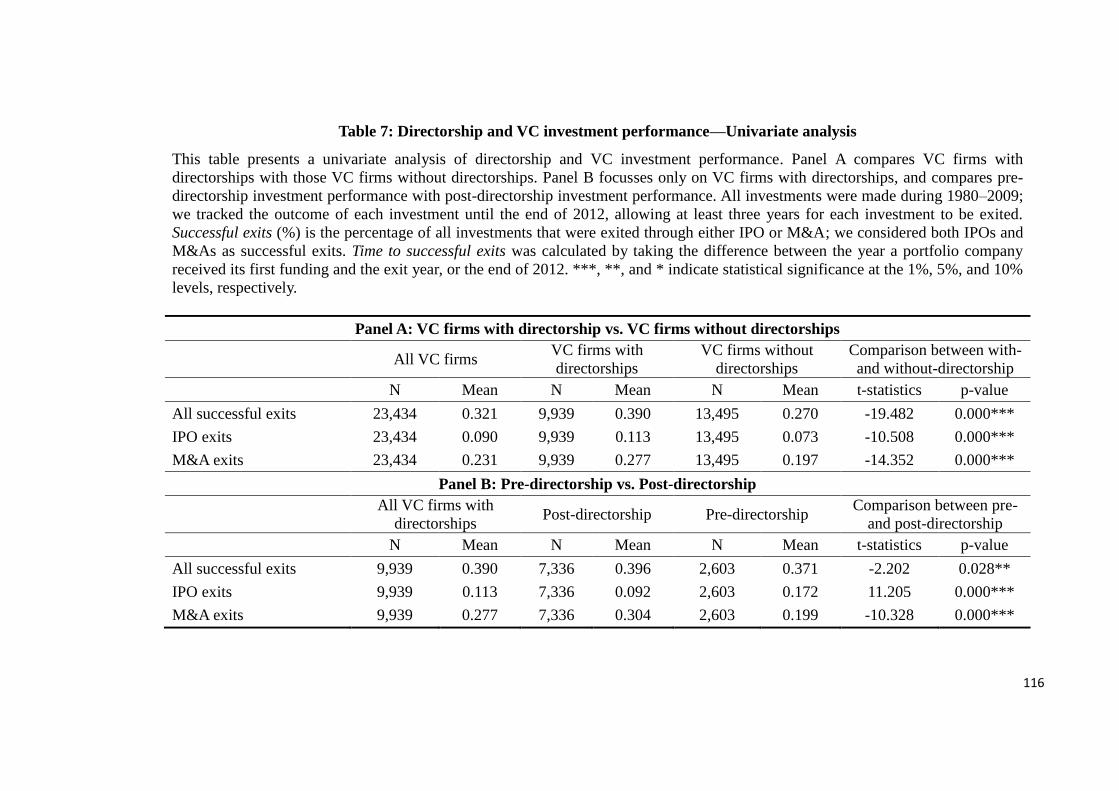

3.4.3 Directorship and investment performance ....................................................... 101

3.4.3.1 Univariate analysis ............................................................................................... 101

3.4.3.2 Multivariate analysis............................................................................................. 102

3.5 Conclusion .............................................................................................................. 104

References ..................................................................................................................... 107

Appendix ....................................................................................................................... 120

Chapter 4

Dead Investors: What do we Know about the Failure of

Venture Capital Firms?

Abstract ......................................................................................................................... 122

4.1 Introduction ............................................................................................................. 123

4.2 Literature and hypothesis development .................................................................. 125

4.2.1 VC activities and failure of VC firms ............................................................... 126

4.2.1.1 Fundraising ........................................................................................................... 126

4.2.1.2 Investment ............................................................................................................. 128

5

4.2.1.3 Exits ....................................................................................................................... 129

4.2.2 VC characteristics and failure of VC firms ...................................................... 131

4.2.2.1 VC firm location .................................................................................................... 132

4.2.2.2 VC firm year of incorporation .............................................................................. 133

4.3 Data and methodology ............................................................................................ 134

4.3.1 Data and sample ............................................................................................... 134

4.3.2 Identifying failed VC firms ............................................................................... 135

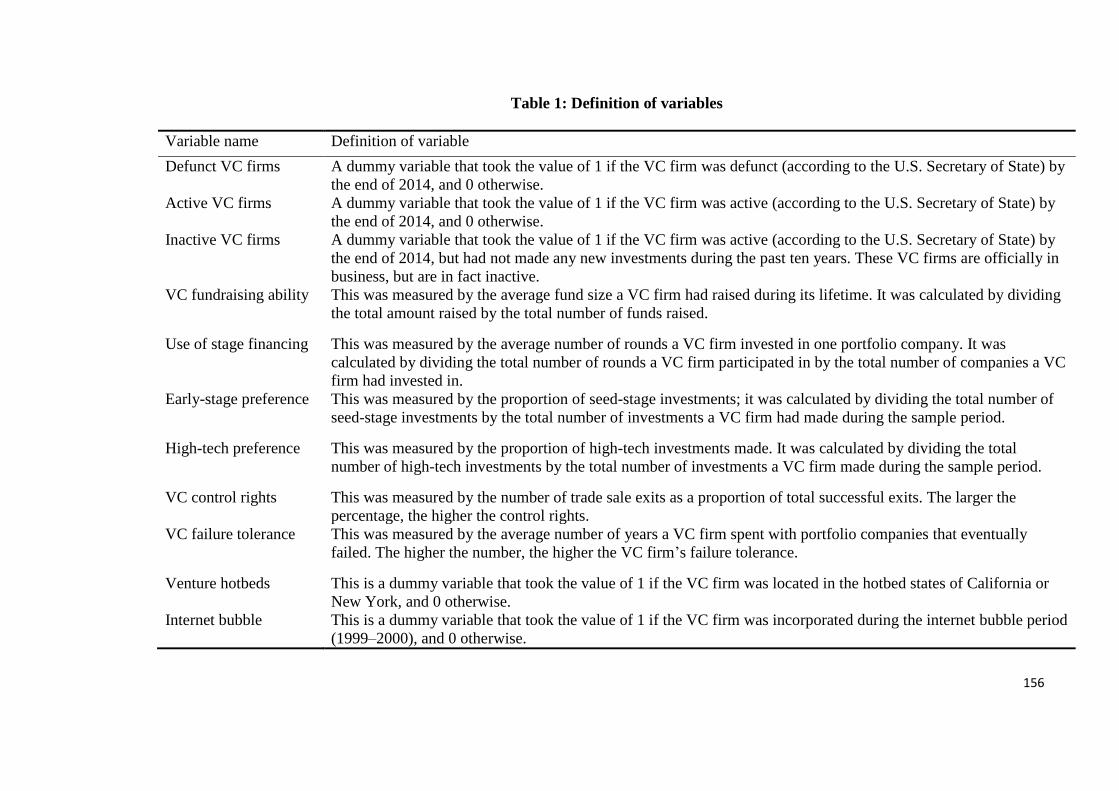

4.3.3 Dependent variables ......................................................................................... 136

4.3.4 Explanatory variables ...................................................................................... 137

4.3.5 Estimation model .............................................................................................. 139

4.4 Analysis and results ................................................................................................ 141

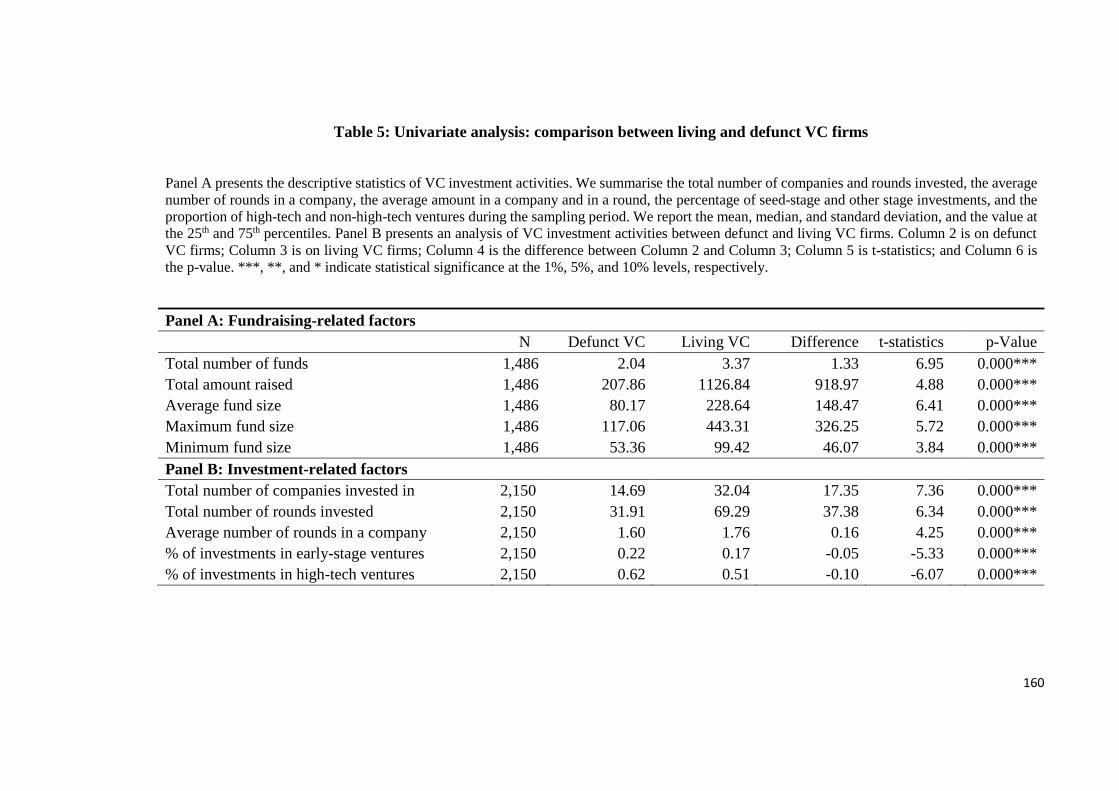

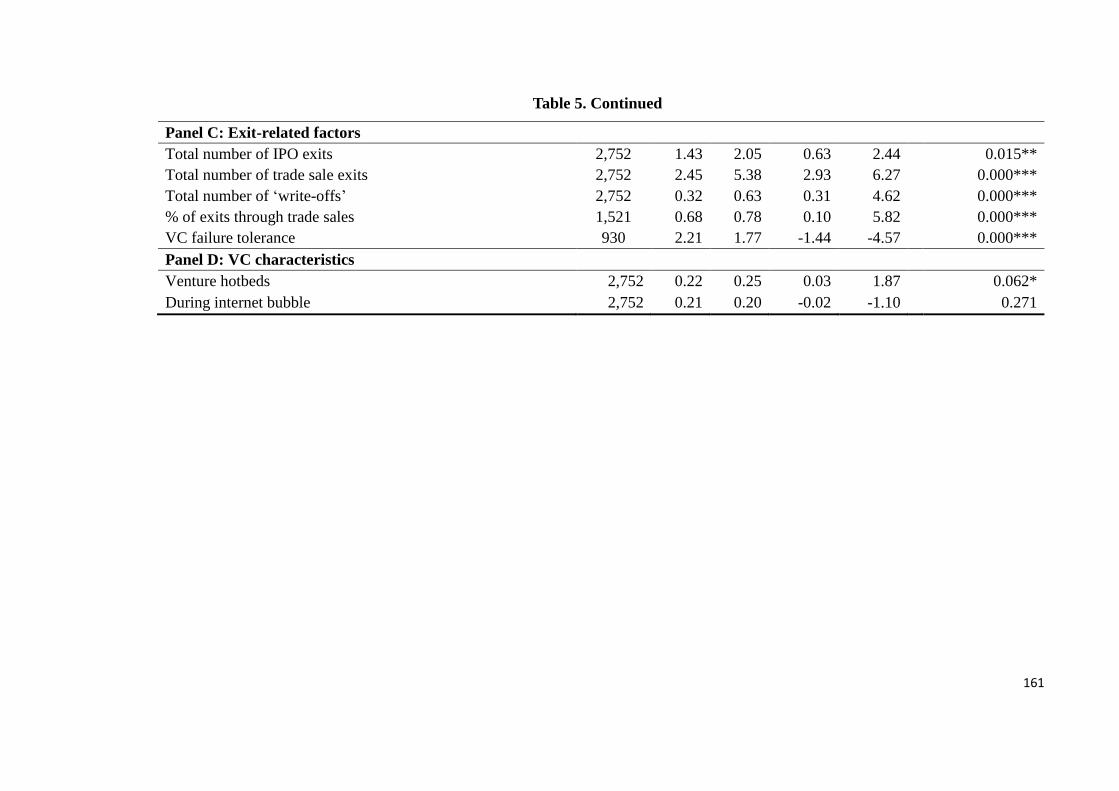

4.4.1 Summary statistics ............................................................................................ 141

4.4.2 Univariate analysis ........................................................................................... 144

4.4.3 VC firm failure .................................................................................................. 147

4.5 Conclusion .............................................................................................................. 151

References ..................................................................................................................... 153

Chapter 5

Conclusion

5.1 Summary and suggestions for future research ........................................................ 165

5.2. Implications for market practitioners and policy makers ....................................... 170

References ..................................................................................................................... 172

This thesis contains 43,070 words, including title page, tables, appendices, and footnotes.

6

Abstract The University of Manchester

Fan Wang

Doctor of Philosophy (Ph.D.)

Three Essays in Venture Capital

June 2015

This thesis examines various issues related to venture capital (VC) firms. The thesis

consists of three essays that try to answer the following questions: Do local VC firms

benefit from their syndication experience with foreign partners? Do VC firms benefit

from their directorships in mature public companies? What do we know about the failure

of VC firms?

The first essay examines the benefits of cross-border syndication to ‘local’ (in the context

of the first essay, Asian) VC firms. The main finding is that, post-syndication, local VC

firms invest more in the high-tech industry than they did pre-syndication. I interpret this

as a result of enhanced knowledge and confidence in assessing and taking on rather risky

investments. Further, local VC firms have a higher likelihood of successful exits from

their portfolio companies post-syndication. I interpret these results as being benefits to

local VC firms that they derive from syndicating with their foreign partners. Overall, my

results indicate that there are tangible benefits for local VC firms from syndicating with

international VC partners. These benefits are more pronounced when the foreign partners

are from North America or Europe.

The second essay examines the benefits to venture capital firms through their

directorships in mature public companies. I investigate the benefits to venture capital

firms in terms of fundraising and investment performance. First, my empirical results

show that venture capital firms raise more funds and set higher fund-raising targets during

the post-directorship period. Second, I show that venture capital firms are more likely to

exit successfully from their investments post-appointment as a board of director in an

S&P 1500 company. Overall, my results indicate that being on the board of mature public

companies brings tangible benefits to venture capital firms.

The third essay examines the failure of VC firms. Based on a sample of 2,752 VC firms

in the United States established between 1980 and 2004, the study finds that almost one-

third of VC firms in the sample had gone out of business by the end of 2014. I then

investigate the causal factors of VC firm failure. Specifically, I examine VC

characteristics (location and year of incorporation) and factors related to VC activities

(fundraising, investments, and exits). The empirical results show that VC firms with a

higher level of failure tolerance and risk appetite are more likely to fail, whereas VC firms

with better fundraising abilities and stronger control rights are less likely to do so.

7

Declaration

I, Fan Wang, declare that no portion of the work referred to in this thesis has been

submitted in support of an application for another degree or qualification of this or any

other institute of learning.

8

Copyright Statement

i. The author of this thesis (including any appendices and/or schedules to this thesis)

owns certain copyright or related rights in it (the ‘Copyright’), and he has given

the University of Manchester certain rights to use such Copyright, including for

administrative purposes.

ii. Copies of this thesis, either in full or in extracts, and whether in hard or electronic

copy, may be made only in accordance with the Copyright, Designs and Patents

Act 1988 (as amended) and regulations issued under it or, where appropriate, in

according with licensing agreements which the University has entered into from

time to time. This page must be part of any such copies made.

iii. The ownership of certain Copyright, patents, designs, trademarks, and other

intellectual property (the ‘Intellectual Property’) and any reproductions of

copyright works in the thesis, for example graphs and tables (‘Reproductions’),

which may be described in this thesis, may not be owned by the author and may

be owned by third parties. Such Intellectual Property Rights and Reproductions

cannot and must not be made available for use without the prior written permission

of the owner(s) of the relevant Intellectual Property Rights and/or Reproductions.

iv. Further information on the conditions under which disclosure, publication, and

commercialisation of this thesis, the Copyright and any Intellectual Property

Rights, and/or Reproductions described in it may take place is available in the

University IP Policy (see http://documents.manchester.ac.uk/

DocuInfo.aspx?DocID=487), in any relevant Thesis restriction declarations

deposited in the University Library, the University’s Library’s regulations (see

http://www.manchester.ac.uk/library/aboutus/regulations), and in the University’s

policy on Presentation of Theses.

9

Dedication

This thesis is dedicated to Yong Wang, my father.

10

Acknowledgements

I would like to acknowledge all those who supervised, supported, encouraged, or

accompanied me along this journey. First and foremost, I am very grateful to my

supervisors, Professor Arif Khurshed and Dr Abdul Mohamed, who gave me the

opportunity and freedom to conduct my research in the area of my interest. Their

continuous encouragement and guidance motivated me through the Ph.D. programme.

I would like to thank my Ph.D. examiners Dr Susanne Espenlaub and Professor Neslihan

Ozkan for their valuable comments and feedback during my viva. I would also like to

thank other committee members, university staff, and colleagues, Dr Konstantinos

Stathopoulos, Professor Stuart Hyde, Dr Maria Marchica, Dr Ning Gao, Professor

Norman Strong, Dr George Christodoulakis, Professor Ser-Huang Poon, Professor

Richard Stapleton, Dr Edward Lee, Dr Marie Dutordoir, Dr Roberto Mura, and Dr

Abdulkadir Mohamed. My sincere thanks also go to Professor Arif Khurshed, who gave

me the opportunity to assist teach at Manchester Business School.

In addition, I would like to thank all my friends in Manchester—Zhe Wen, Hanpeng Xiao,

Baochao Gao, Qinye Lu, Jingya Wang, Caiwei Ye, and Ye Su—all of whom provided me

with unforgettable memories.

In addition, I would like to thank the U.S. Financial Management Association and IPAG

Business School, who invited me to present my research findings. I would also like to

thank the participants of the 2014 FMA Annual Meeting and my discussant Jonathan A.

Daigle, who provided me with valuable comments and feedback.

I want to give my special thanks to my parents, Yong Wang and Yun Hu, for their undying

love and unconditional support, and for encouraging me to chase my dreams with courage.

Finally, I owe a heartfelt thanks to Yinting Wu for accompanying me on this journey.

11

Chapter 1

Introduction

1.1 Motivation

The venture capital market has experienced rapid growth during the past three decades.

The total amount of VC investments increased from only $610 million in 1980 to over

$30 billion in 2010.1 As the market has grown, a number of new trends have emerged.

According to Chemmanur and Fulghieri (2014), two of the most important trends that

have affected the industry are globalisation and the changing role of VC firms.

Specifically, VC firms have been actively expanding their activities internationally, and

have shifted from their traditional role as capital providers in small private companies to

innovation facilitators in large mature companies. Following these trends, a number of

recent studies have examined related issues such as cross-border VC investment (e.g.,

Dai, Jo, and Kassicieh, 2011); VC failure tolerance and corporate innovation (e.g., Tian

and Wang, 2014); and VCs’ role in mature companies (e.g., Celikyurt, Sevillir, and

Shivdasani, 2012). These studies, however, have exclusively focussed on the capital

receivers (i.e. portfolio companies that received VC financing) but have ignored how the

VC firms could have been affected by the new trends. My thesis, which consists of three

essays, separately examines three newly emerging issues in the global VC market, with a

focus on capital providers, i.e. VC firms. Specifically, the thesis explores the following

three research questions: (1) do local VC firms benefit from their syndication experience

with foreign VC firms? (2) do VC firms benefit from their directorship status in mature

public companies? and (3) what do we know about the failure of VC firms? These essays

1 Based on data on the U.S. market, published by PricewaterhouseCoopers’ Moneytree report.

12

provide new perspectives on existing VC studies, and have opened up new areas for future

research.

The focus of the first essay is on cross-border VC investments; it examines whether local

VC firms benefit from their partnership with foreign VC firms within the context of the

Asian VC market. Cross-border investments by VC firms have grown rapidly during the

past two decades (Aizenman and Kendall, 2012; Dai et al., 2012). In particular, VC firms

from developed economies such as the United States and Europe have expanded their

activities internationally, with a focus on Asian countries, due to the rapid growth of

entrepreneurial activities and the rise of investment opportunities (Deloitte, 2007). At the

same time, many Asian countries have taken steps to remove major obstacles and

impediments to foreign investors, which has created favourable legal and regulatory

environments for foreign VCs to conduct their business. Following this emerging trend,

several recent studies have examined various aspects of cross-border VC investments,

mainly from the perspective of foreign investors (e.g., Dai et al., 2012; Wang and Wang,

2012; Humphery-Jenner and Suchard, 2013). These studies have provided empirical

evidence that syndication or joint ventures with local VC firms is an effective way for

foreign VC firms to alleviate information asymmetry and enhance investment

performance. Whether such partnerships also benefit local VC firms, however, remains

unexplored, thus leaving a gap in the VC literature. I postulate that such collaborations

between local and foreign VC firms should be mutually beneficial: if foreign VC firms

benefit from forming partnerships with local VC firms in the form of lower levels of

information asymmetry, there should also be accrued benefits to local VC firms. Because

the Asian VC market is relatively less developed than that of the Western economies, the

arrival of U.S. and European VC firms has not only brought capital but also learning

13

opportunities to local VC firms. The potential benefits could include better contract

design, knowledge on advising and nurturing entrepreneurs, knowledge of monitoring

portfolio companies, and the ability to take them to successful exits (Dai et al., 2012).

Using a sample of 3,309 investments from 1996 to 2009 in Asia, I examine the potential

benefits to local VC firms through their syndicate experience with foreign VC firms.2 I

examine benefits from two aspects: changes in local VC firms’ investment behaviours,

and successful exits from portfolio companies. I find that local VC firms that have

invested heavily in non-tech portfolio companies increase their exposure to high-tech

industries (especially the information technology and telecommunication sectors)

significantly post-syndication. This switch from traditional industries to high-tech

ventures suggests that during their collaborations, local VC firms have acquired

knowledge and expertise from their foreign partners, which are mostly firms that are

experienced with assessing high-tech ventures. In terms of investment performance, I find

that local VC firms with foreign syndicate experience tend to have a higher likelihood of

successful exits than local VC firms without any foreign exposure. Overall, the results

suggest that partnerships between local and foreign VC firms are mutually beneficial.

Syndicate experience with foreign VC firms increases local VC firms’ exposure to high-

tech industries, and enhances their ability to take portfolio companies to successful exits.

This essay makes several contributions to the existing literature on VC investments. First,

my study complements previous research (Dai et al., 2012; Wang and Wang, 2012;

Humphery-Jenner and Suchard, 2013) on cross-border VC investments by examining the

2 The sample covers the following countries: China, Hong Kong (treated separately from China for the

purposes of this study), India, Indonesia, Japan, Malaysia, Pakistan, The Philippines, Singapore, South

Korea, Taiwan, Thailand, and Vietnam.

14

value of cross-border syndication from the perspective of local VC firms. It is the first

study to provide empirical evidence that collaborations between local and foreign VC

investors are mutually beneficial. Second, this study contributes to the literature on VC

syndication. In addition to the risk-sharing (Lockett and Wright, 2001) and resource-

based motives (Hopp and Rieder, 2011), the study’s findings suggest that learning is also

an important motive for VC firms to form syndication. Third, this study contributes to

studies on strategic alliances (Dodgson, 1993; Inkpen and Crossan, 1995; Lane and

Lubatkin, 1998) by providing some of the first empirical evidence of organisational

learning within the context of venture capital markets.

My second essay examines whether VC firms benefit as boards of directors in mature

public companies. Although previous studies have long recognised the role of VC firms

as capital providers and monitors of small and young companies, a recent study by

Celikyurt et al. (2012) brought VC firms’ role in mature public companies to the attention

of academics. In their study, Celikyurt and colleagues documented that 30.5 percent of

Standard & Poor (S&P) 1500 companies had directors with a VC background before

joining the board. While they found that the presence of VC directors improves corporate

innovation (as measured by number of patents produced and citations of patents), their

study is only from the perspective of portfolio companies (i.e. S&P 1500 companies). The

question of whether VC firms benefit from their directorship status in these companies

remains unexplored. It seems to be costly for VC firms to have partners on the boards of

mature public companies, considering the time and effort they need to dedicate to those

companies, and the potential for distraction from their primary responsibilities at their

VC firms. As ‘smart’ players in the financial market, however, I posit that VC firms make

such decisions based on the fact that they derive substantial benefits related to their board

15

appointments. The potential benefits include credibility, visibility, enhanced networks and

reputation, and detailed knowledge of R&D at large public companies (Celikyurt, 2012),

all of which in return may benefit VC firms’ activities such as fundraising and investment

performance.

I hand-collected data on VC directors by following Celikyurt et al. (2012). The final

sample consists of 1,359 unique VC directors, working in 700 different VC firms. I also

collected data on fundraising, investments, and exits from VentureXpert. I examined

potential benefits to VC firms from two aspects: fundraising and investment performance.

First, I found that VC firms with directorships raised a significantly larger amount than

VC firms without directorships. To address the concern of the selection effect, I compared

fundraising performance during the pre-appointment and post-appointment periods and

found consistent results. I also addressed the concern of industry trend effects by using

the difference-in-difference method, and yet the results remained qualitatively the same.

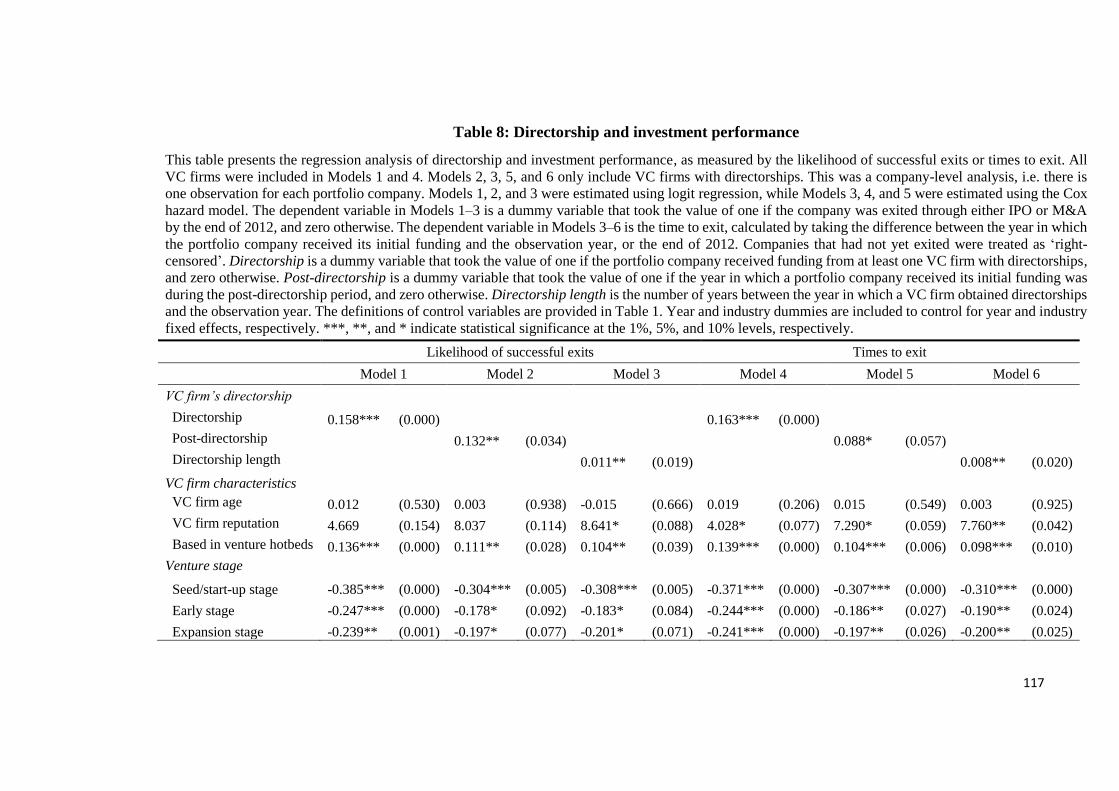

Second, in terms of investment performance, the results show that VC firms with

directorships tend to have a higher likelihood of successful exits than those without

directorships. Overall, these results suggest that directorships in mature public companies

do provide benefits to VC firms in terms of fundraising and investment performance. I

interpret this as a result of credibility, enhanced networks, and knowledge and expertise

acquired through having directorships in mature public companies.

This study contributes to the emerging literature on VC firms’ changing roles. It is the

first to study VC firms’ roles in mature public companies from the perspective of VC

firms. My findings complement the study by Celikyurt et al. (2012) by providing

empirical evidence of the benefits that accrue to VC firms through directorships in mature

16

public companies. Second, this study adds to the literature on VC fundraising (Gompers

and Lerner, 1998; Gompers, 1996; Jeng and Wells, 2000; Mayer et al., 2004). The results

suggest that, in addition to VC ‘grandstanding’ (Gompers, 1996) (i.e. quickly taking

portfolio companies public), VC firms can also enhance their reputation through

directorships in large public companies, which then improves their ability and prospects

for raising new funds. Third, this study provides empirical evidence of VC firms’ role as

knowledge intermediaries. A number of recent studies (e.g., González-Uribe, 2013; Dessi

and Yin, 2014) show that VC investors can communicate valuable knowledge to

entrepreneurs and among portfolio companies. The results of this study suggest that VC

firms can transfer knowledge and expertise gained in mature public companies to their

small private portfolio companies, and therefore improve their likelihood of successful

exits.

The third essay examines the failure of VC firms. Although previous studies have

extensively examined the survival of VC-backed firms (e.g., Ruhnka et al., 1992; Kaplan

and Stromberg, 2003 and 2004; Cumming, Fleming, and Schwienbacher 2005; Nahata,

2008), the survival of the capital providers (i.e. VC firms) remains relatively unknown.

In recent years, a number of articles in major VC-related media have brought the issue of

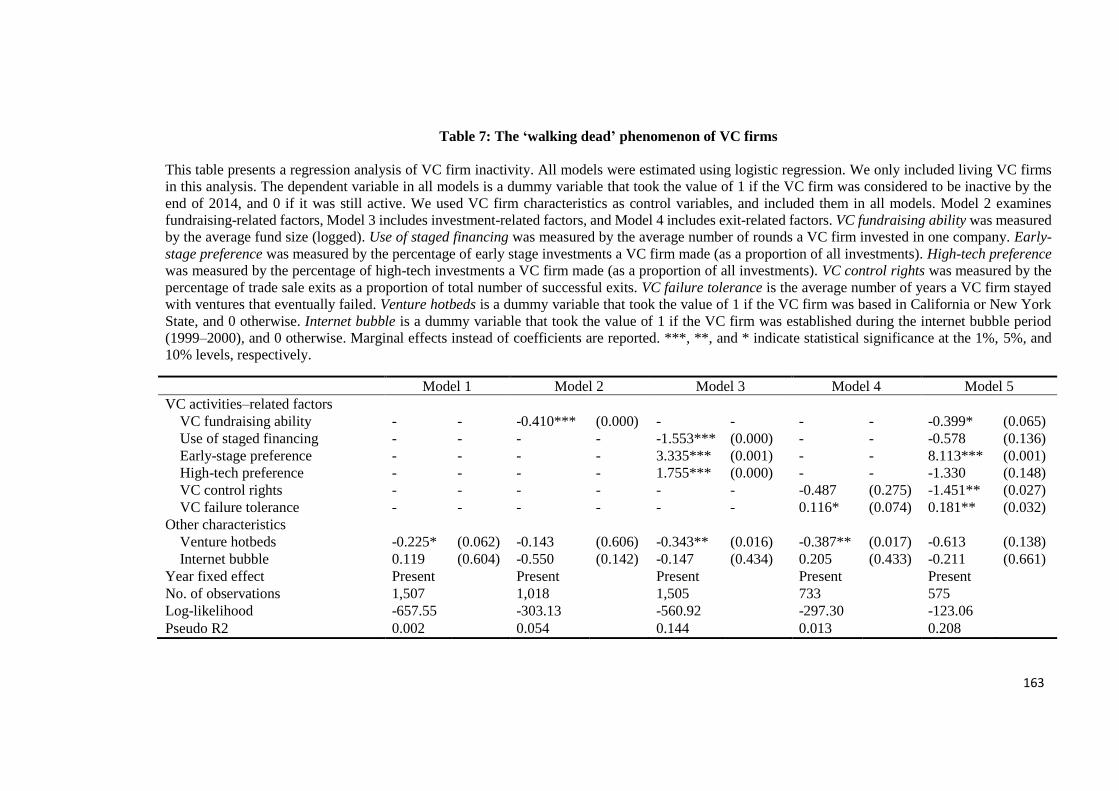

VC firm failure to the attention of researchers. These articles have tried to identify a list

of ‘walking dead’ VC firms—those that are officially in business but have not made any

new investments during the past ten years—although the reasons behind such inactivity

remain unexplored. My study aims to complete the picture by examining the broader issue

of VC firm failure, which incorporates both ‘walking dead’ as well as ‘dead’ VC firms.

This issue of VC firm failure is at least as important as the failure of VC-backed firms,

since the survival of capital providers directly influences entrepreneurial firms.

17

Understanding the failure of VC firms enables both investors and investees to make better

investment decisions, and therefore benefits the development of entrepreneurship.

I hand-collected on VC firm status from the office of the U.S. Secretary of State rather

than from VentureXpert due to better data quality in the former. The final sample consists

of 2,752 independent VC firms in the United States established between 1980 and 2004.

The results show that almost one-third of VC firms had failed by the end of 2014, which

is a surprisingly large proportion. This suggests that the high failure rate not only applies

to VC-backed companies, but also to VC firms themselves. I then examine the casual

factors of VC firm failure from two aspects: VC activities–related factors and VC

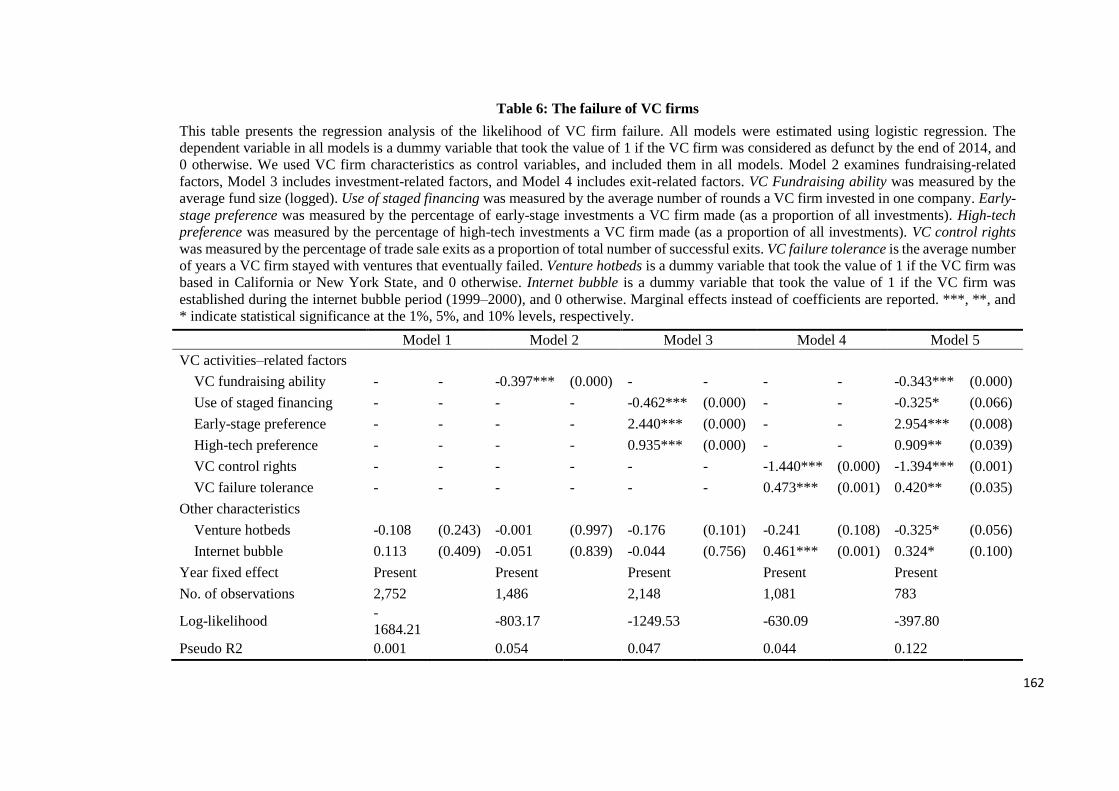

characteristics. Specifically, I examine fundraising ability, investment preference (risk

appetite), control rights, failure tolerance, location, and year of incorporation. I model the

likelihood of failure and inactivity with logit regressions. The results show that VC firms

with a higher level of failure tolerance and risk appetite are more likely to fail, while VC

firms with better fundraising abilities and control rights over entrepreneurs are less likely

to fail. Overall, my results suggest that VC firms fail mainly due to internal factors (such

as their attitude towards risk and tolerance for failure) rather than external factors (such

as the entrepreneurial and economic environment).

This study is the first to examine the failure of VC firms. These findings complement

previous studies by providing original, broad evidence of VC firm failure. My study

extends the recently discussed phenomena by providing a more comprehensive and

detailed analysis of both ‘dead’ and ‘walking dead’ VC firms. In addition, my study adds

to the literature on VC failure tolerance (e.g., Tian and Wang, 2014; Chemmanur,

Loutskina, and Tian, 2014). The study provides the first empirical evidence of the effects

18

of failure tolerance on VC firms.

1.2 Thesis structure

The structure of this thesis follows the format accepted by the Manchester Accounting

and Finance Group, Manchester Business School. All chapters are incorporated into a

format suitable for submission and publication in peer-reviewed academic journals. The

chapters in this thesis are self-contained; each has a separate literature review, answers

unique and original questions, and uses different datasets. The tables, figures, equations,

footnotes, and appendices are independent, and are numbered from the beginning of each

chapter. Page numbers, titles, and subtitles have sequential order throughout the thesis.

This thesis is structured as follows. Chapter 1 includes the introduction; Chapter 2

examines the benefits of cross-border syndication to local VC firms; Chapter 3 studies

the benefits of directorships in mature public companies to VC firms; Chapter 4 examines

the failure of VC firms; and Chapter 5 provides a conclusion. From Chapter 2 to Chapter

4, I use the third person (we) instead of the first (I), because these chapters are working

papers co-authored with my supervisors.

19

References

Aizenman, J., and Kendall, J. 2012. The internationalization of venture capital. Journal

of Economic Studies 39, 488-511.

Celikyurt, U., Sevilir, M., and Shivdasani, A. 2014. Venture capitalists on boards of

mature public firms. Review of Financial Studies 27, 56-101.

Chemmanur, J. T., and Fulghieri, P. 2014. Entrepreneurial finance and innovation: An

introduction and agenda for future research, Review of Financial Studies 27, 1-19.

Chemmanur, J. T., Loutskina, E., and Tian, X. 2014. Corporate venture capital, value

creation, and innovation. Review of Financial Studies 27, 2434-2473.

Cumming, D., Fleming, G., and Schwienbacher, A. 2006. Legality and VC exits.

Journal of Corporate Finance 12, 214-245.

Dai, N., Jo, H., and Kassicieh, S. 2012. Cross-border venture capital investments in Asia:

Selection and exit performance. Journal of Business Venturing 27, 666-684.

Deloitte, 2007. Global trends in venture capital 2007 survey. Available:

https://www.deloitte.com/assets/Dcom-Canada/Local%20Assets/Documents/ca_

en_TMT_VC_2007survey_dec2007 (1).pdf. [7 August 2012]

Dessi, R., and Yin, N. 2014. Venture capital and knowledge transfer. Working paper.

Dodgson, M. 1993. Learning, trust, and technological collaboration. Human Relations

46, 77-95.

Gompers, P. 1996. Grandstanding in the venture capital industry. Journal of Financial

Economics, 42, 133-156.

Gompers, P., Lerner, J., Blair, M., and Hellmann, T. 1998. What drives venture capital

fundraising? Brookings Paper on Economic Activity. Microeconomics, 149-204.

González-Uribe, J. 2013. Venture capital and the diffusion of knowledge. Working

paper.

Hopp, C., and Rieder, F. 2011. What drives venture capital syndication? Applied

Economics 43, 3089-3102.

Humphery-Jenner, M., and Suchard, J. A. 2013. Foreign VCs and venture success:

Evidence from China. Journal of Corporate Finance 21, 16-35.

Inkpen, A. C., and Crossan, M. M. 1995. Believing is seeing: Joint ventures and

organization learning. Journal of Management Studies 32, 595-618.

Jeng, L. A., and Wells, P. C. 2000. The determinants of venture capital fundraising:

Evidence across countries. Journal of Corporate Finance 6, 241-289.

20

Kaplan, S., and Stromberg, P. 2003. Financial contracting theory meets the real word:

An empirical analysis of venture capital contracts. Review of Economic Studies 70,

281-315.

Kaplan, S., and Stromberg, P. 2004. Characteristics, contracts, and actions: Evidence

from venture capitalist analyses. Journal of Finance 59: 2177-2210.

Lane, P. J., and Lubatkin, M. 1998. Relative absorptive capacity and inter-organisational

learning. Strategic Management Journal 19, 461-77.

Lockett, A., and Wright, M. 2001. The syndication of venture capital investments.

Omega 29, 375-390.

Mayer, C., Schoors, K., and Yafeh, Y. 2004. Sources of funds and investment activities

of venture capital funds: Evidence from Germany, Israel, Japan and the U.K.

Journal of Corporate Finance 11, 586-608.

Nahata, R. 2008. Venture capital reputation and investment performance. Journal of

Financial Economics 90, 127-151.

Ruhnka, J., Feldman, H., and Dean, T. 1992. The ‘living dead’ phenomenon in venture

capital investments. Journal of Business Venturing 7, 137-155.

Tian, X., and Wang, T. 2014. Tolerance for failure and corporate innovation. Review of

Financial Studies 27, 211-255.

Wang, L., and Wang, S., 2012. Cross-border venture capital performance: Evidence

from China. Pan-Basin Finance Journal 19, 71-79.

21

Chapter 2

Syndicated Venture Capital Investments: What’s in it for

Local Venture Capitalists?

Abstract

This paper examines the benefits of cross-border syndications to local venture capital (VC)

firms. Post-syndication, we find that local VC firms invest more in the high-tech industry

than they did pre-syndication. We interpret this as a result of an enhanced knowledge and

confidence in assessing and taking on rather risky investments. Further, local VC firms

have a higher likelihood of a successful exit from their portfolio companies post-

syndication. We interpret these results as being benefits to local VC firms that are derived

from syndicating with their foreign partners. Overall, our results indicate that there are

tangible benefits for local VC firms from syndicating with international VC partners.

These benefits are more pronounced when the foreign partners are from North America

or Europe.

22

2.1 Introduction

Cross-border venture capital (VC) investment has been a growing trend in recent years

(Aizenman and Kendall, 2012; Dai et al., 2012). Several recent studies have examined

various aspects of cross-border VC investment from the perspective of foreign VC

investors (Dai et al., 2012; Wang and Wang, 2012; Humphery-Jenner and Suchard, 2013).

These studies have concluded both theoretically and empirically that syndication or joint

venture with local VC firms is an effective way for foreign VC firms to alleviate

information asymmetry and to enhance their investment performance. The benefits of

collaboration between local and foreign VC firms from the perspective of local VC firms,

however, has not been analysed, thus leaving a gap in the VC literature. If foreign VC

firms benefit from collaboration with local VC firms (i.e. there is a lower level of

information asymmetry), there should also be accrued benefits to local VC firms. The

potential benefits could include taking the firms to successful exits; better contract design;

and increased knowledge on advising and nurturing entrepreneurs and monitoring

portfolio companies (Dai et al., 2012). This paper contributes to the literature by

examining the benefits to local VC firms from syndicating with foreign VC firms,

focussing on their investment behaviour post-syndication and the likelihood of successful

exits from their portfolio companies.

VC firms are actively expanding their operations internationally, particularly in Asian

countries (Deloitte, 2007). For example, many U.S. and European VC firms have moved

to Asia due to growth and the rise of investment opportunities in the region.3 Generally,

3 For instance, New Enterprise Associates (NEA), the world’s largest U.S. VC firm, recently announced a

move to China, while Kleiner, Perkins, Caufield, & Byers (a Silicon Valley–based VC firm) has re-

23

VC firms require their portfolio companies to be in a country with favourable laws and

regulations. Many Asian countries have opened their economies by taking steps to

remove major obstacles and impediments to foreign VC investment. Foreign VC firms

not only bring capital; they also provide an opportunity for local VC firms to form

syndicates with them.

This study examines the benefits for local VC firms that syndicate with foreign VC firms

in Asia, using a sample of 3,966 investment rounds in 3,309 portfolio companies from

1996 to 2009. We measured the benefits to local VC firms through successful exits from

their portfolio companies and changes in their investment behaviours. We focussed on

portfolio companies that were based in China, Hong Kong (treated separately from China

for the purposes of this study), India, Indonesia, Japan, Malaysia, Pakistan, The

Philippines, Singapore, South Korea, Taiwan, Thailand, and Vietnam. We defined a VC

firm as ‘local’ if it was based in the country of the portfolio company, and ‘foreign’ if it

was headquartered in a country other than the country where its portfolio company exists.

Our empirical results show changes in the local venture capitalists’ investment behaviour

post-syndication with foreign venture capitalists. Local VC firms that had invested in

non-tech portfolio firms had a tendency, post-syndication, to invest heavily in high-tech

portfolio companies with foreign VC firms. We found that post-syndication, local VC

firms’ investments were clustered in the information technology (IT) and

telecommunication sectors. These sectors require enhanced expertise and knowledge in

assessing successful investments. A switch from non-tech to the high-tech sector is

established its headquarters in India. (See https://www.gsb.stanford.edu/news/bmag/sbsm0805/feature-

vcasia.html): ‘3i Group invests 10 percent of their capital in Asia’. (See the annual report 2014 at

http://www.3i.com/investor-relations/results-reports/reports?set_disclaimer=true.)

24

attributable to the skills and expertise that local VC firms master during their syndication

with foreign VC firms. In order to investigate if the changes in local venture capitalists’

investment behaviour is due to syndication with foreign VC firms (and not because of

other factors such as industry trends), we used a control sample of local VC firms that did

not syndicate with foreign VC firms throughout our sample period. Our results show that

the matched control sample tended to invest more in the non-tech than in the high-tech

industry during our sample period.

In terms of investment performance, although we found that syndicate experience with

foreign VC firms increases the likelihood of a successful exit for local VC firms, this

evidence was more pronounced in local VC firms that syndicated with European or North

American VC firms than was the case with VC entities from other Asian countries. When

comparing the pre- and post-syndication periods, we found that the likelihood of

successful exits increased significantly post-syndication. These results were robust when

compared to a control sample of local VC firms that had no syndication with foreign VC

firms.

Overall, our results suggest that local VC firms learn from their foreign VC partners. This

learning experience gives them the expertise and the confidence to invest in rather risky

industries such as the high-tech industry. In addition, local VC firms see an enhancement

in the performance of their investments in terms of successful exits. These findings allow

us to provide a more complete picture of the benefits of syndication between local and

foreign VC firms from the perspective of the local VC firm.

The remainder of this paper is organised as follows: in Section 2 we provide a discussion

25

of the theoretical framework and testable hypotheses of our study. Section 3 outlines our

data and methodology. In Section 4 we present our results, and Section 5 concludes the

paper.

2.2 Literature and hypothesis development

2.2.1 Theoretical framework

VC syndication has always been one of the most enduring characteristics of the VC

industry (Tykvová and Schertler, 2011; Meuleman and Wright, 2011). ‘Syndication’ may

be broadly defined as two or more venture capital firms that co-invest in a portfolio

company and share a joint pay-off. More broadly, syndication between VC firms is

essentially a form of inter-firm alliance (Wright and Lockett, 2003). Various reasons and

motives have been proposed to explain firms’ incentives to form alliances (joint ventures),

including risk reduction, economies of scale, access to markets, and the pursuit of

legitimacy (e.g., Hennart, 1988; Kogut, 1998).

Hennart (1988) examined the motivation to form joint ventures by focussing on the

perspective of transaction costs. He investigated two types of equity joint ventures (JVs):

‘scale’ JVs and ‘link’ JVs. While ‘scale’ joint ventures are formed when all the parents

take similar moves, such as vertical integration, horizontal expansion, or entering into a

new market, in ‘link’ joint ventures, parents take different moves. Hennart argues that

firms make joint venture decisions based on both the general market environment and the

potential transaction costs. He also contends that the minimisation of transaction costs is

26

not the sole reason behind joint ventures. Following Hennart (1988), Kogut (1988)

examined the motivation to enter JVs by comparing the transaction cost perspective and

the strategic behaviour perspective. The former predicts that firms form joint ventures to

minimise transaction costs, while the latter predicts that firms choose joint venture

partners to improve competitive positioning of the parties. Kogut argues that the primary

differences in the implications of these two perspectives are the motives to cooperate, and

the choice of partners. While these earlier studies have examined joint ventures in a broad

way, outlining the general motives behind joint ventures, they have not focussed on VC

firms.

Another branch of studies has focussed on VC firms specifically, examining the motives

for VC firms to form alliances (i.e. to make syndicated investments). Various studies in

the literature on VC syndication have documented that syndicates are usually formed to

share risk (the risk-sharing perspective), or to gain access to valuable resources (the

resource-based perspective). The risk-sharing perspective views syndication as a means

of diversifying risk without sacrificing the returns (e.g., Lockett and Wright, 2001). From

this perspective, information asymmetries and adverse selection problems could be

mitigated through syndication, because joint decision-making among VC firms enhances

the accuracy of the assessment and provides increased ‘deal flows’ (discussed below) at

the pre-investment stage. For instance, Lerner (1994) examined the rationale for the

syndication of VC investments. By using a sample of 271 U.S. biotechnology firms, he

found that VC firms use syndication to resolve or to exploit informational uncertainties.

Specifically, he found that experienced VC firms only syndicate first-round investments

to VC firms with a similar level of experience. In later rounds, however, experienced VC

firms syndicate with both their peers and with less experienced VC firms. This result

27

suggests that VC firms use syndication to mitigate information asymmetries in early-stage

investments where there is a greater level of uncertainty. On the other hand, the resource-

based perspective suggests that syndication is a way of sharing resources among

participating VC firms (e.g., Hopp and Rieder, 2011). This perspective suggests that

different information and heterogeneous skills brought by various VC firms could

enhance the post-investment performance of the portfolio companies (e.g., Ferrary, 2010).

In addition to the traditional risk-sharing and resource-based perspective, another

important motive for VC firms to form syndicates is ‘deal flow’. Given that VC

investment has a relatively high failure rate, VC firms need to be in a position where they

can select from a wide supply of deals so that they can increase the likelihood of

encountering high-quality ventures. This is especially the case during times when there is

more capital available than is required by entrepreneurial firms. Syndication provides a

good platform for VC firms to share networks, contacts, and the knowledge of potential

investment opportunities, and therefore may increase future deal flow for VC firms.

Several empirical studies have examined the motives for VC syndication. An earlier study

by Bygrave (1987) examined syndicated VC investments from the perspective of

networking. Based on a sample of 464 VC firms and 1,501 portfolio companies in the

United States, Bygrave found that the sharing of information is more important than the

spreading of financial risk as a reason to form syndicates. That is to say, syndication

between VC firms in the United States is mostly driven by the resource-based motive

rather than the risk-sharing motive. Bygrave also controlled for the size of these VC firms,

and yet found consistent results. Studies in other developed economies, however, have

not yielded consistent results. For instance, Lockett and Wright (2001) examined different

28

motives for the syndication of VC investments. By surveying a sample of 60 VC firms

based in the United Kingdom, they found that overall the risk-sharing motive provides a

strong explanation. But for early stage investments, they found the resource-based motive

to be much more important. Their results suggest that VC firms hold heterogeneous

attitudes towards syndication. VC firms that are involved in early-stage transactions tend

to use more syndication, and consider the sharing of resources as their primary motive.

Among all the studies on motives to form alliances or joint ventures, the studies of Grant

(1996), Hamel (1991), and Khanna et al., (1998) in particular have documented that

organisational learning is another very important motive. Their studies suggest that firms

form alliances in order to form a platform for organisational learning, which provides

access to the knowledge of their partners. Through the experience of mutual

interdependence, problem-solving, and observation of alliances’ activities and outcomes,

participating firms are able to learn from their partners (Inkpen, 1998). Inkpen (1998)

found that the formation of an alliance is an acknowledgement that the alliance partner

has useful knowledge that can be used by the alliance partner to enhance its own strategy

and operations. This type of knowledge is valuable to the partner firm, even outside the

specific terms of the alliance agreement. Alliances between firms provide a better

platform for organisational learning than other contexts, thus resulting in risk reduction

(Powell, 1987). A number of empirical studies (Dodgson, 1993; Inkpen and Crossan,

1995; Lane and Lubatkin, 1998) have also addressed the importance of alliances in the

learning process.

The formation of alliances, partnerships, and/or syndicates between local and foreign VC

firms could also be attributed to the learning motive. From the perspective of foreign VC

29

firms, the inclusion of a local partner that is geographically close to the investee company,

and has superior knowledge of the local market, technology, and legal environments, as

well as having linguistic skills and valuable contacts, may help to reduce the level of

information asymmetry caused by cultural differences and geographical distance (Mäkelä

and Maula 2006, 2008). In other words, foreign VC firms learn from the knowledge and

experience provided by local VC firms, thus mitigating information asymmetry and

leading to better performance (Humphery-Jenner and Suchard, 2013; Dai et al., 2012).

On the other hand, from the perspective of local VC firms, forming partnerships with

foreign VC firms allows local VC firms to access heterogeneous knowledge and skills

and provides them with opportunities to learn from their foreign partners. The learning

opportunities for the local VC firms stem from the fact that the venture capital industry

in Asia is still rather young and underdeveloped (Dai et al., 2012). The number of local

VC firms is small; firms often operate on a small scale and are unlikely to provide value-

adding advice to their portfolio companies (Bruton and Manigart, 2005).

Foreign VC firms, on the other hand, especially VC firms from North America and

Europe, have relatively rich experience developed in their home countries, and are able

to provide a larger amount of capital and better networks (Dai et al., 2012). Through such

collaboration, local VC firms are able to access foreign VC firms’ rich experience and

expertise, and acquire better knowledge on how to advise and nurture entrepreneurial

firms and exit their portfolio successfully. The need to syndicate with foreign VC firms

from the perspective of local VC firms might arguably be due to mutual benefits between

local and foreign VC firms.

30

2.2.2 Syndicate experience

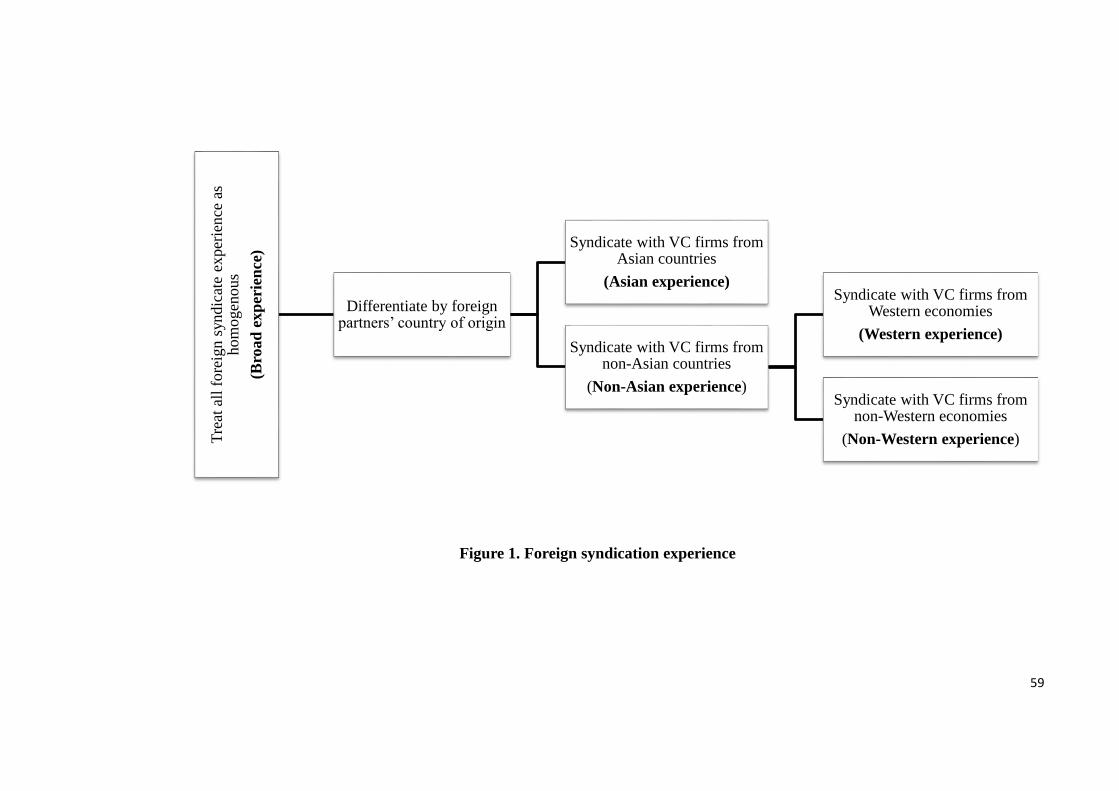

Although our analysis of syndicate experience starts with the assumption that the

experience of all foreign syndicates is homogenous (see Figure 1), knowledge and

expertise, which both add value to the local VC, may vary significantly based on the

region or country of the VC firms.

A large body of strategic management literature (Inkpen, 1998; Inkpen and Crossan, 1995)

has pointed out factors such as learning objectives, leadership commitment, and cultural

alignment as important determinants in knowledge acquisition. The idea of ‘cultural

alignment’ posits that the effectiveness of knowledge acquisition might be improved as a

result of a lower level of cultural differences (i.e. higher cultural alignment). Within the

context of cross-border VC syndication, local VC firms’ learning effectiveness might be

subject to cultural distance between local and foreign VC firms. In other words, the

cultural alignment among Asian countries is higher, and the syndicate might provide a

better platform for organisational learning and could lead to effective knowledge

acquisition. Hence, in our analysis we differentiated broad foreign syndicate experience

based on foreign partners’ country of origin. Specifically, we divided the broad experience

into ‘Asian experience’ (syndicate experience with non-local Asian VC firms) and ‘non-

Asian experience’ (syndicate experience with non-local, non-Asian VC firms). We then

further classified the non-Asian experience category into ‘Western experience’ (syndicate

experience with VC firms from Western economies, specifically North America and

Europe) and ‘non-Western experience’ (syndicate experience with VC firms from non-

Western economies). Despite the high cultural and institutional distance between local

31

and non-Asian foreign countries, the learning effectiveness of syndication might be

significant. Provided the fact that Asian VC firms are less experienced and less developed

than those from Western economies (Dai et al., 2012), the level of knowledge and

expertise brought by Western VC firms might be significantly valuable to local VC firms.

In other words, the richness of the skills and experience to some extent could mitigate the

obstacles caused by cultural misalignment, and therefore could lead to effective

knowledge acquisition.

Overall, the effectiveness of this knowledge transfer in Asian countries might be high due

to a higher level of cultural alignment. In addition, the effectiveness might be high in the

syndicates between Asian and Western countries due to the superior knowledge and skills

of Western VC firms. Therefore, in our analysis we focussed on three types of foreign

syndicate experience: broad experience, Asian experience, and Western experience.

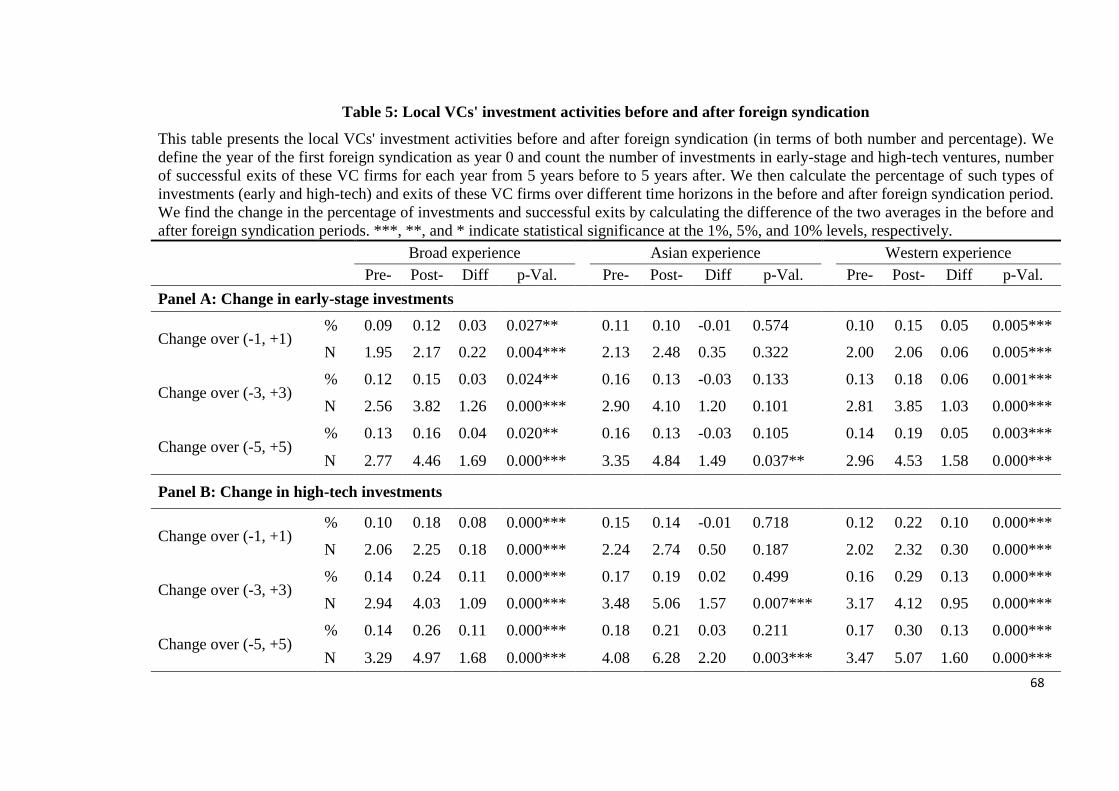

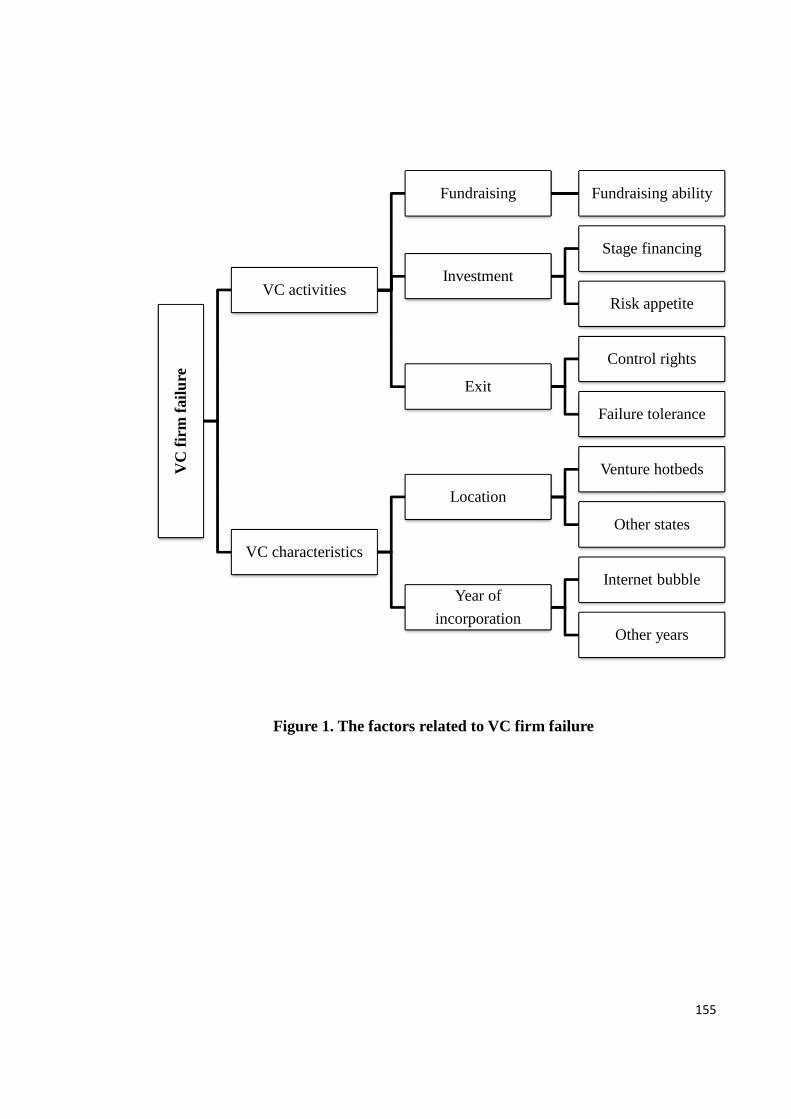

[INSERT FIGURE 1 HERE]

2.2.3 Syndicate experience and investment selection

As discussed above, local VC firms may learn from their foreign partners during their

collaboration, and use the knowledge in their follow-up investments. In other words, the

syndicate experience may influence local VC firms’ future investment behaviour. For

instance, investment selection and focus might change drastically due to foreign syndicate

exposure. Foreign VC firms, especially from Western economies, are more experienced

in investing in early-stage high-tech ventures. According to Cumming and Dai (2010),

32

64.3 percent of VC investments in the United States between 1980 and 2009 invested in

the IT sector (with 18 percent in the medical sector and the remaining 18 percent in other

sectors). Asian VC firms, on the other hand, tend to invest more in traditional industries

and expansion-stage ventures. As Dai et al. (2012) documented, about 30 percent of VC

investments in Asia between 1996 and 2006 were in non-technology industries, and 54

percent were in expansion-stage ventures. As such, Asian VC firms were less experienced

and less likely to invest in high-tech industries or early-stage ventures. By working side-

by-side with foreign VC firms that had extensive experience and knowledge of investing

in early-stage and high-tech industries, local VC firms could learn from their foreign

partners and acquire the necessary skills in selecting promising deals. On the other hand,

from the resource-based point of view, local VC firms with foreign syndicate experience

are likely to be more knowledgeable and experienced than their peers. They are thus likely

to make riskier (but potentially more lucrative) investments in early-stage or high-tech

ventures.

Ultimately, local VC firms are likely to use knowledge gained via syndication in their

follow-up investments to make appropriate investment decisions, not only in high-tech

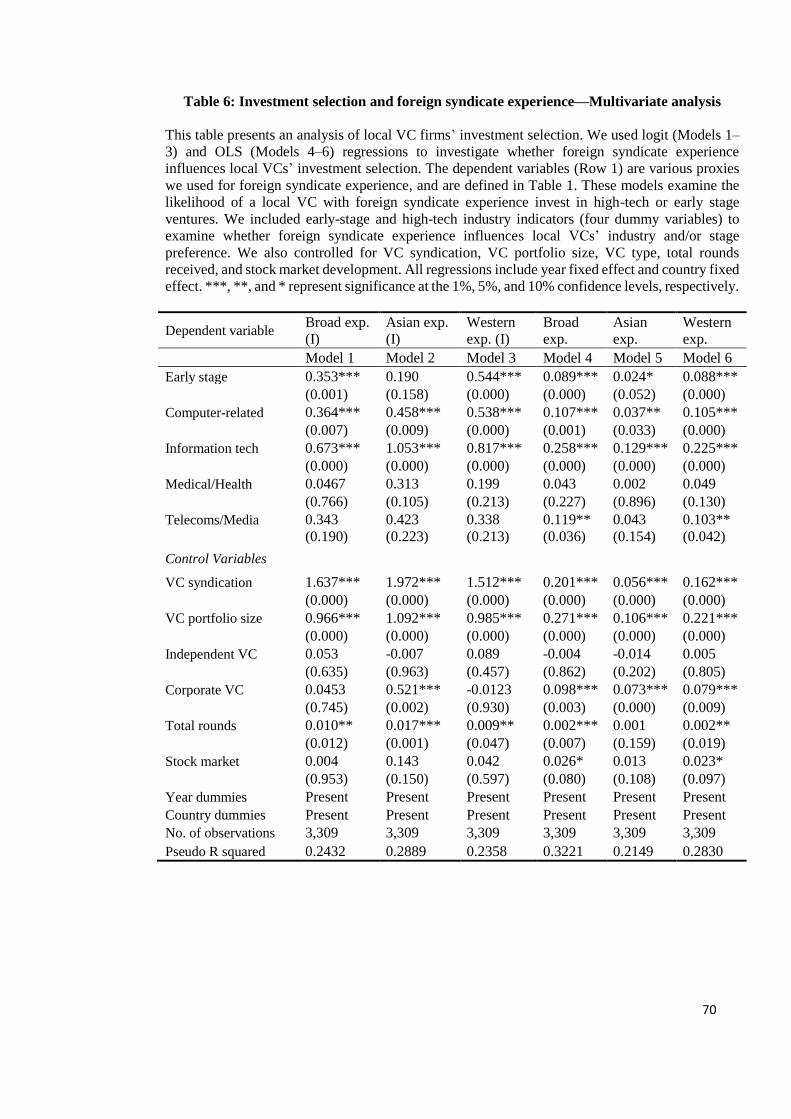

industries but also in early-stage investments. We therefore hypothesise that local VC

firms that syndicate with foreign VC firms are more likely to invest in high-tech and

early-stage financing rounds. We tested our hypothesis on different types of syndicate

experience. As is the case with ‘broad’ experience, Asian and Western experiences both

provide a platform for organisational learning, where local VC firms acquire knowledge

and skills from their foreign partners. Both types of experience may influence local VC

firm investment behaviour. The effect of syndicate experience might be comparable,

however, given that the focus is on the knowledge and skills of investing in high-tech and

33

early-stage ventures. We formulate the following hypothesis:

Hypothesis 1: Local VC firms with foreign syndication experience are more likely to

invest in high-technology industries and early-stage ventures.

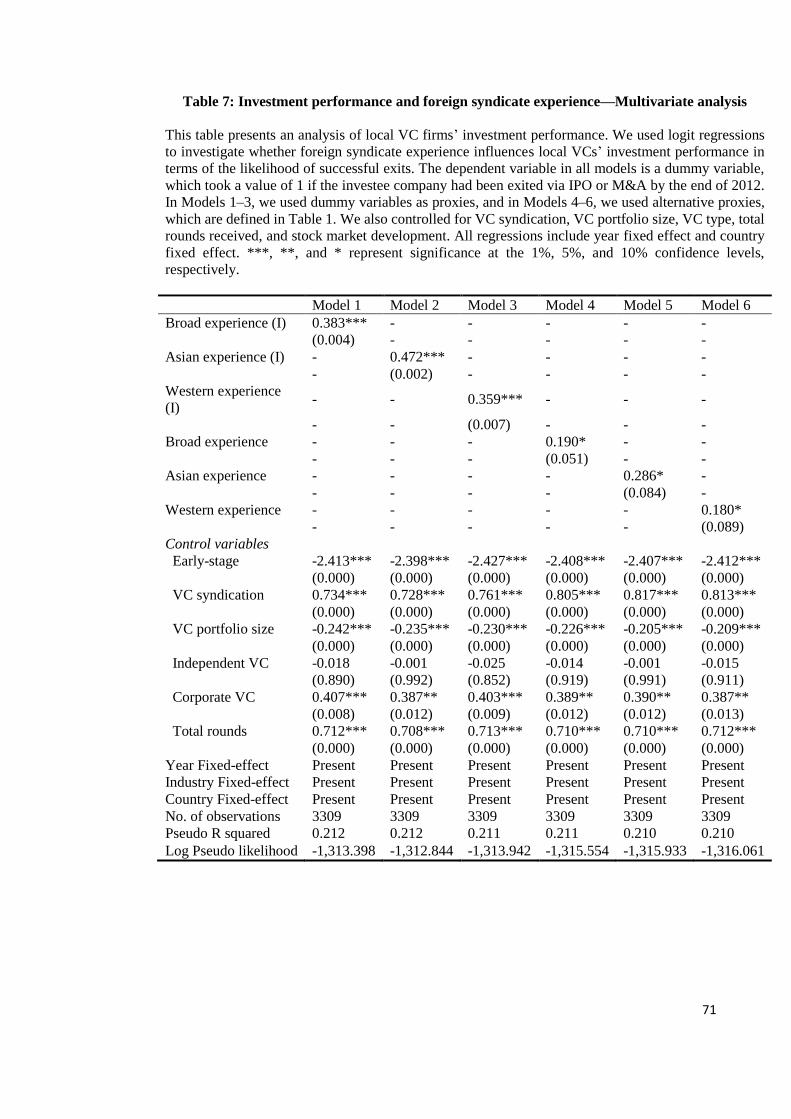

2.2.4 Syndicate experience and investment performance

In the previous section, we posited that syndicate experience with foreign VC firms would

influence local VC firms in their investment selection. Various studies, including those

by Cumming and Johan (2008) and Giot and Schwienbacher (2007), have examined VC

exits in different contexts. While some studies (Cumming and Johan, 2008; Elisabete,

Cesaltina, and Mohamed, 2008) have reported that the characteristics of VC firms and

investee companies affect the exits, others (Cumming, Fleming, and Schwienbacher, 2006;

Cumming and MacIntosh, 2003) have found that better economic conditions and legal

environments increase the likelihood of exits. In addition, VC syndication (Megginson

and Weiss, 1991; Lerner, 1994; Giot and Schwienbacher, 2007), geographical distance,

and cultural disparity (Cumming and Dai, 2010) also influence a VC firm’s exit in cross-

border investments. Recent studies on Asian VC markets (Dai et al., 2012; Wang and

Wang, 2012; Humphery-Jenner and Suchard, 2013) have found supportive evidence that

a joint venture or a partnership between foreign and local VC firms leads to better

investment performance for foreign VC firms.

If local VC firms gain experience via syndication with foreign partners, their investment

performance is likely to improve as compared to their investments prior to foreign

34

syndication. Therefore, we hypothesise that a local VC firm’s syndicate experience with

foreign VC firms increases the likelihood of a successful exit. We tested the following

related hypothesis:

Hypothesis 2: Post-syndication, the likelihood of a successful exit for a local VC firm will

be higher than in the pre-syndication period.

2.3. Data and methodology

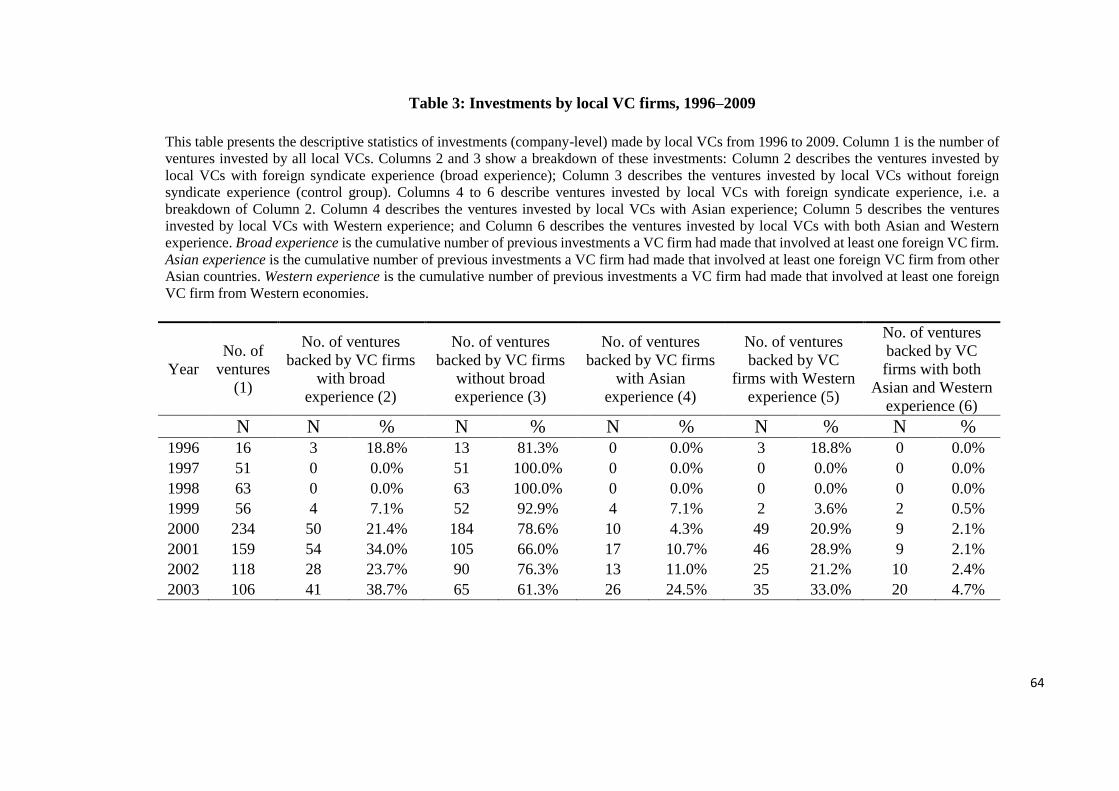

2.3.1 Data and sample

We collected venture capital investment and exit data from the Asia Venture Capital

Journal (AVCJ) database. This database provides better coverage for Asian deals than

VentureXpert (see Brander, Du, and Hellmann, 2014).4

We constructed our sample as follows: we collected all available venture capital

investment in the AVCJ database, which included 11,748 VC investments made by both

foreign and local VC firms from 1990 to 2013. We included investments that received

initial funding between 1996 and 2009, because the globalisation of venture capital only

started to quicken its pace starting in the mid-1990s (Iriyama, Li, and Madhavan, 2010).

We then tracked the outcome of each investment until the end of 2012, and allowed for at

least three years to observe an exit for an investment made in 2009 (Gompers and Lerner,

2000; Hochberg et al., 2007; Nahata, 2008). We included in our sample all portfolio

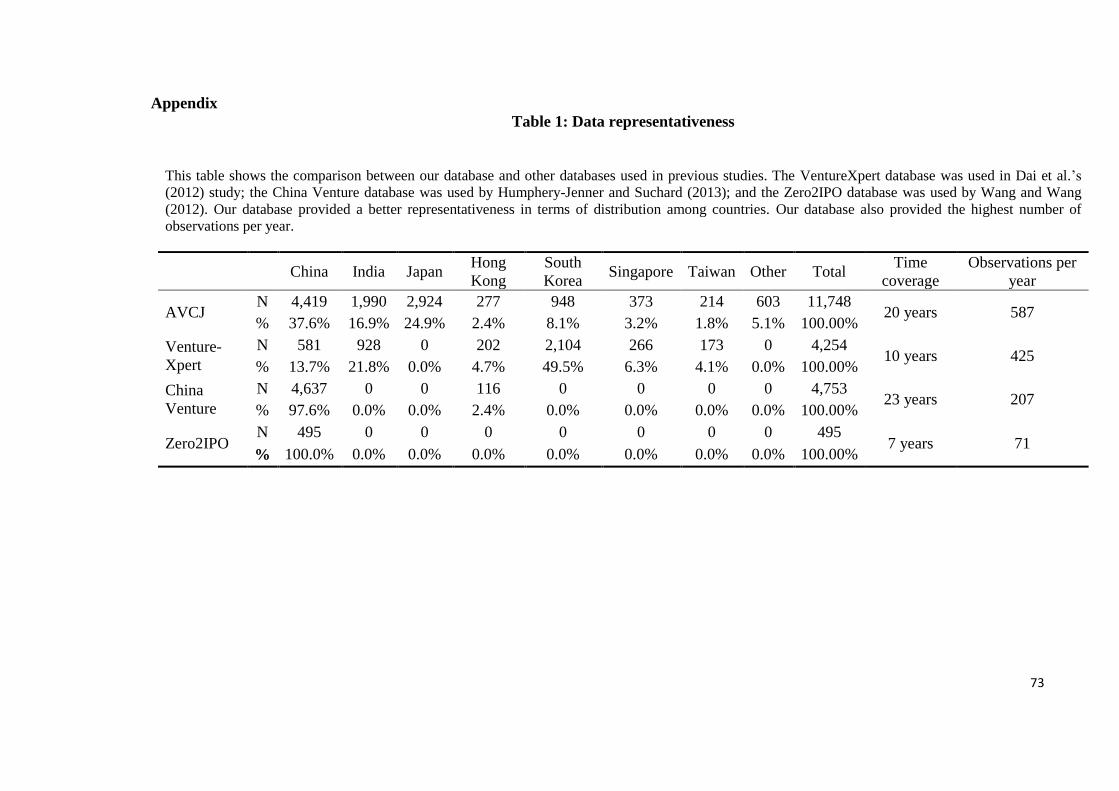

4 See Table 1 in the Appendix for a comparison of data representativeness between AVCJ and other

databases, including VentureXpert.

35

companies that had received local VC funding. In order to be included in the sample, we

required that exit date, investment size, and region of the VC firms was available. This

filtration led to a final sample of 3,309 investments in portfolio companies from the period

1996 through 2009. Our final sample includes VC investments in the following countries:

China, Hong Kong (treated as separate from China for the purposes of this study), India,

Indonesia, Japan, Malaysia, Pakistan, The Philippines, Singapore, South Korea, Taiwan,

Thailand, and Vietnam.

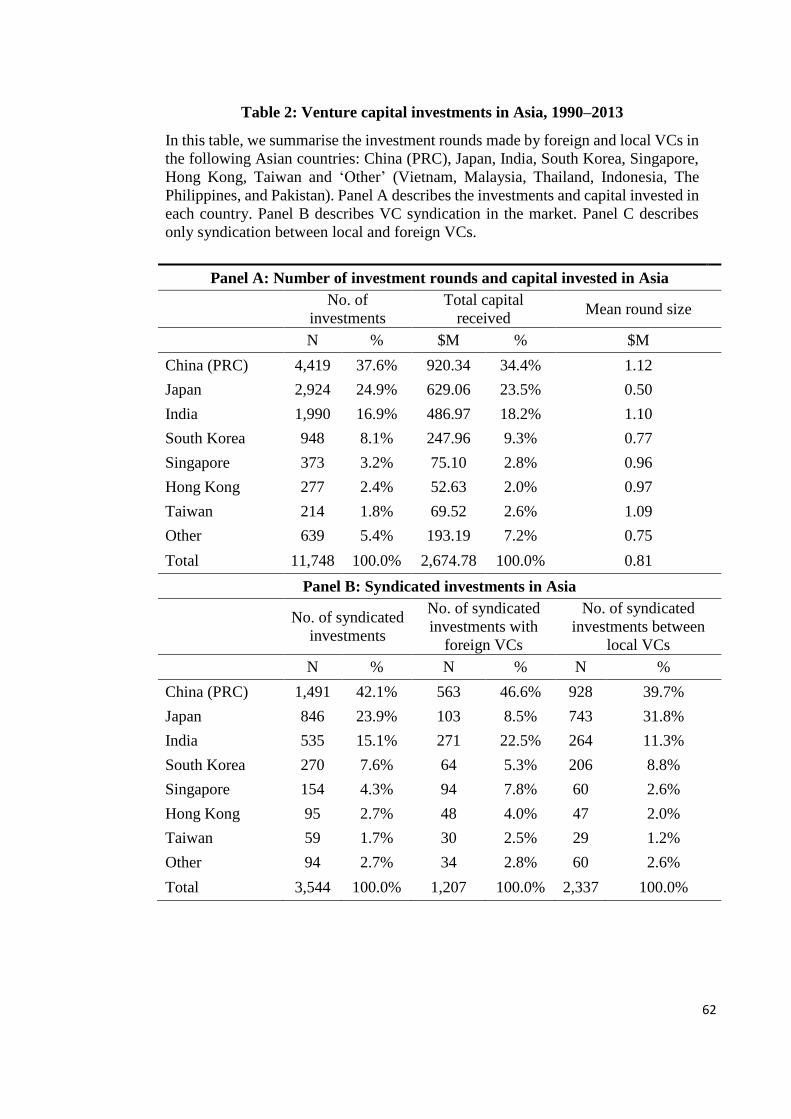

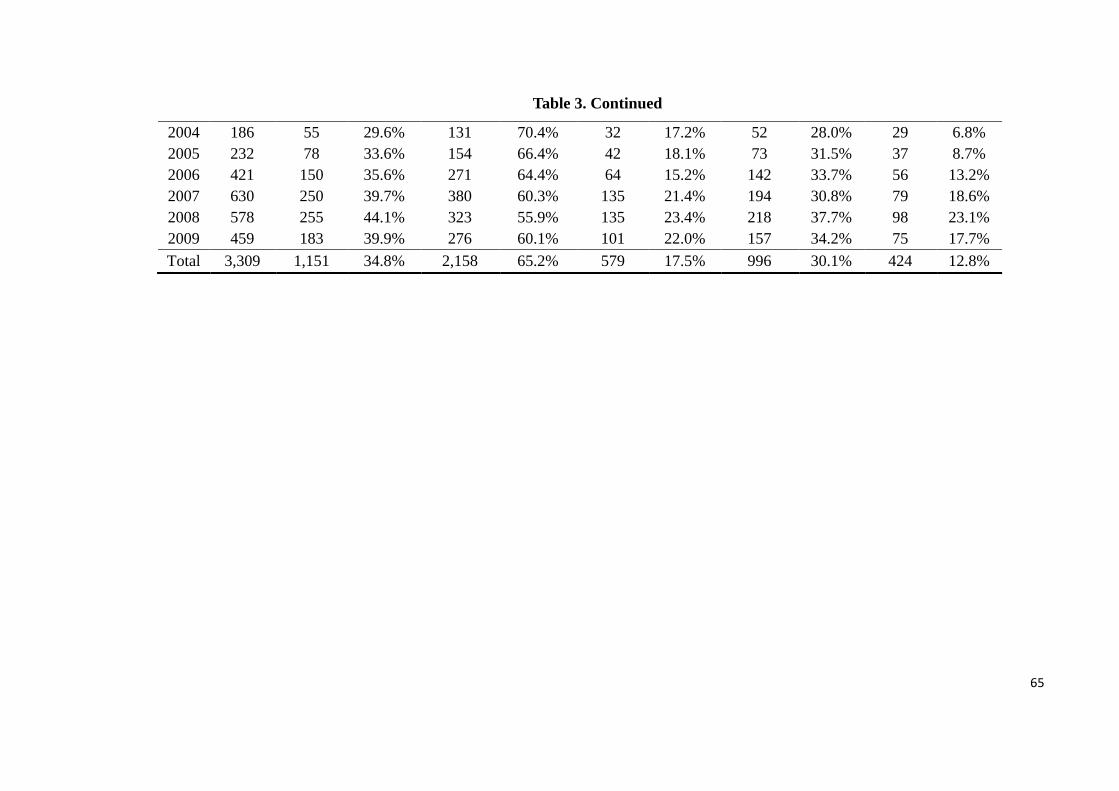

Table 2 presents the descriptive statistics of the Asian VC market from 1990 to 2013.5

Panel A of the table shows that China attracted 37.6 percent of all investments in Asia

during this period, followed by Japan (24.9 percent) and India (16.9 percent). This

indicates that developing countries such as China and India were the most popular

investment destinations, while traditional developed countries such as Japan still

remained economically significant. In terms of total capital invested in Asia, China

received $920 million in total from 1990 to 2013, while Japan and India received in total

$629 million and $487 million, respectively. It is clear from the table that most of the VC

capital during this period was invested in emerging economies, specifically China and

India. China and India attracted more than half of the total capital invested in Asia. Panel

B provides a summary of syndication in the Asian market. The results show that

syndicated investments only accounted for approximately 30 percent (3,544/11,748) in

Asia, while the remaining 70 percent (8,204/11,748) were non-syndicated investments.

This is quite different from other developed economies, where syndicated investments

5 This table is based on all investment rounds made in Asia from 1990 to 2013. We started with this initial

sample of 11,748 rounds of investments and constructed our proxies for syndicate experience from this

sample. In order to provide a more comprehensive picture of the VC market in Asia, we provide the

descriptive statistics of the initial sample first, followed by our sample of 3,309 in Table 3.

36

usually account for a large proportion. In terms of syndication with foreign VC firm, 34.1

percent (1,207/3,544) were syndicated with foreign firms during this period, while the

remaining were syndications among local VC firms. This result shows that the majority

of syndicated investments in Asia are made by local VC firms, and that collaboration

between local and foreign VC firms is not a very common phenomenon.

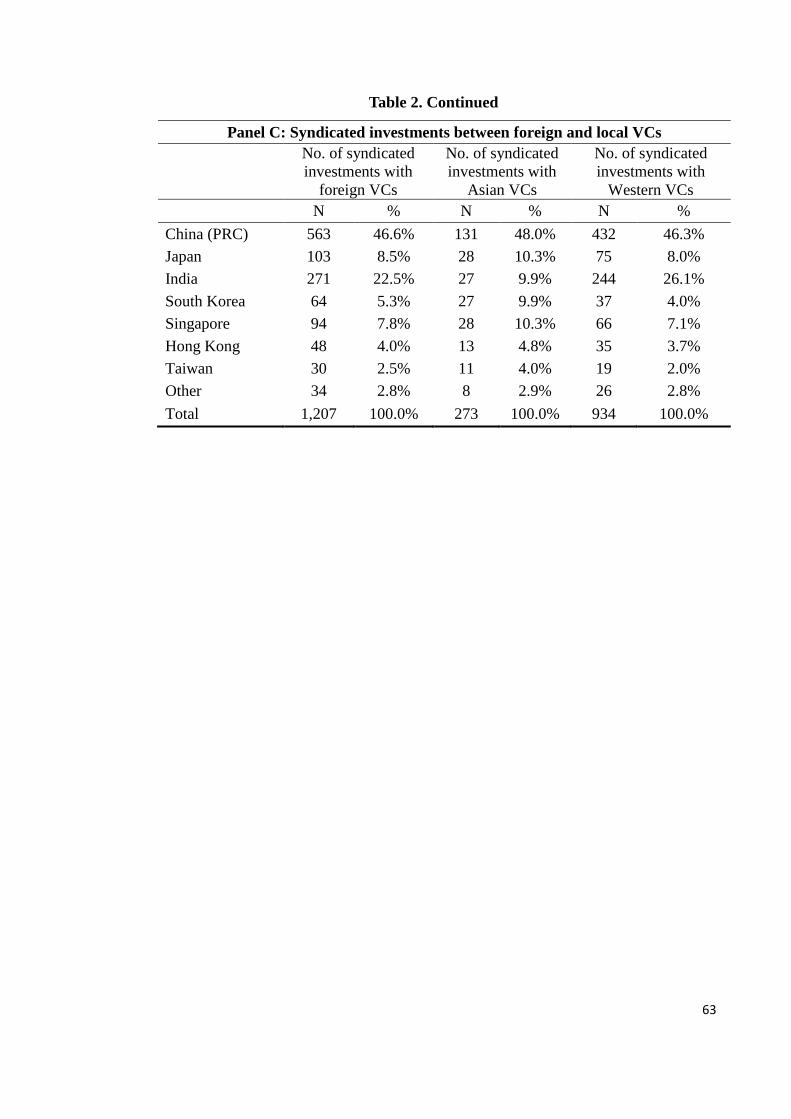

Panel C of the table further examines syndicated investments made by both local and

foreign VC firms. As shown in the table, syndication with Western VC firms is more

common than syndication with foreign Asian VC firms (934 vs. 273). This result suggests

that there is a tendency for local VC firms to syndicate with Western (European and North

American) VC firms as compared to VC firms from other Asian counties. Among all the

countries in our sample, we found that most of the collaboration between local and foreign

VC firms took place in China and India, while in developed economies such as Japan and

South Korea, syndicated investments with foreign VC firms only accounted for a very

small proportion. The explanation could be that developed economies have their own VC

market; their local VC firms are relatively mature and are able to provide sufficient capital

to local entrepreneurial firms. Emerging economies, on the other hand, have less

developed VC markets and require more capital than local VC firms can provide in order

to sustain their fast-growing entrepreneurial activities.

Overall, our results indicate that syndication is less common in the Asian VC market as

compared to Western countries, especially North America, where more than half of the

investments were syndicated during the period of this study (Nahata, 2008). Syndication

with foreign (both Asian and Western) investors accounts for 34 percent, while

syndication with local firms accounts for 66 percent. China and India appear to be the

37

most attractive destinations for Western VC firms.

[INSERT TABLE 2 HERE]

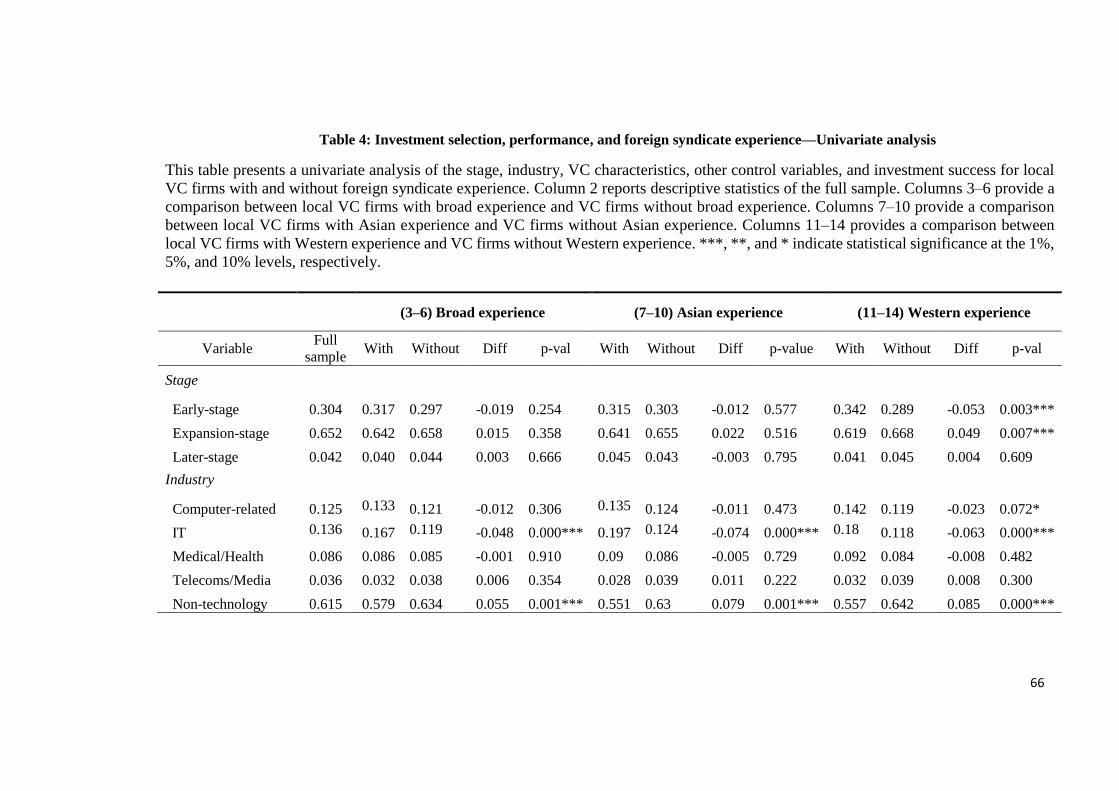

2.3.2 Dependent variables

We used two sets of dependent variables in our analysis of investment selection. In

Models 1–3 of Table 6, we used dummy variables to indicate whether an investment was

made by local VC firms with foreign syndicate experience (‘Broad’, ‘Asian’, and

‘Western’). This took the value of one if the investment was made by a local VC with

foreign syndicate experience, and zero otherwise. We also used the actual number of

foreign syndicate experience as dependent variables in Models 4–6 of Table 6.

The dependent variable in our analysis of investment performance was a dummy that took

the value of one if the investee company was exited through an initial public offering

(IPO) or mergers and acquisitions (M&A) by the end of 2012, and zero otherwise. We

considered exits via both the IPO and M&A routes as successful exits, since VC firms

generate returns primarily by exiting successfully through these two routes (Triantis,

2001). Several recent studies of VC firms have used this measure of VC investment

success (see Bottazzi et al., 2008; Cumming and Dai, 2010; Dai et al., 2012; Nahata, 2008;

Zarutskie, 2010).

38

2.3.3 Explanatory variables

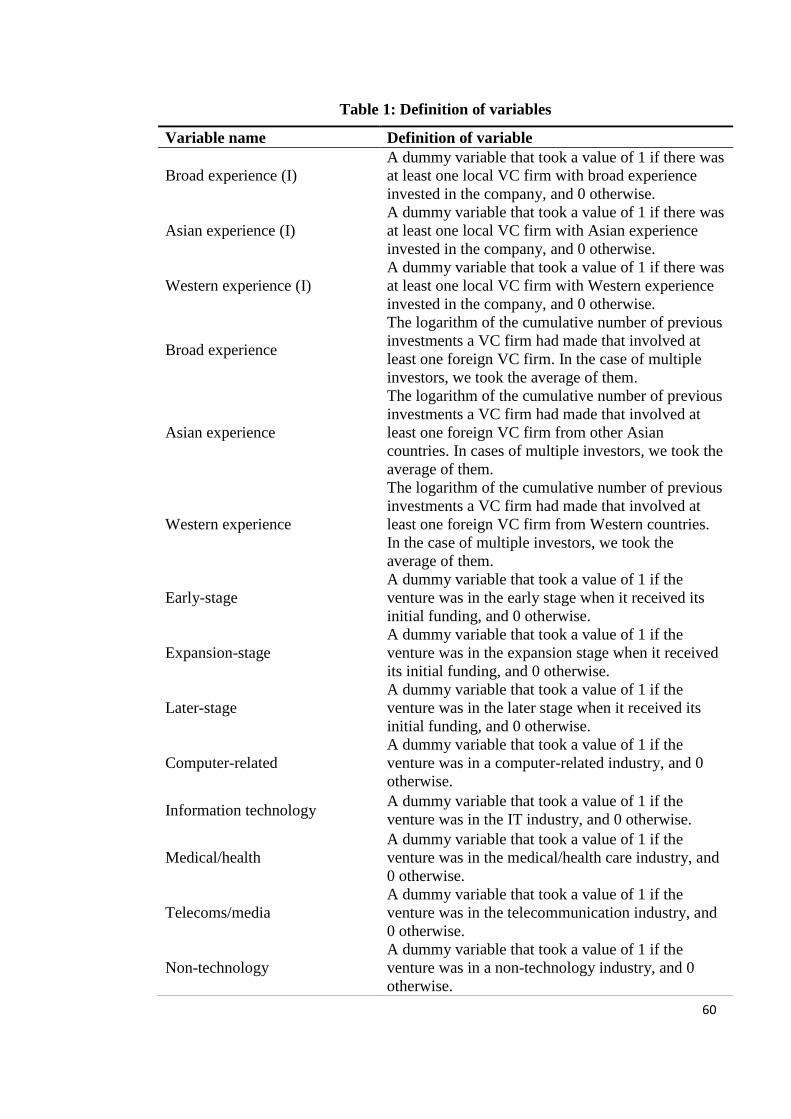

Broad experience

We measured ‘broad experience’ as the cumulative number of investments made by a

local VC in the past that included foreign VC firms. We classified any previously

syndicated investment with a non-local VC firm as a ‘broad’ experience. In the case of

multiple investors, we took the average of this variable; we also took the logarithm of this

variable in our analysis. Broad experience (I) is a dummy variable that took the value of

1 if there was at least one broad experience, and 0 otherwise.

Asian experience

We measured ‘Asian experience’ as the cumulative amount of investments made by a

local VC in the past, but involving only foreign Asian VC firms. We only classified

syndicated investments with non-local Asian VC firms as an Asian experience. In the

event of multiple investors, we took the average of this variable; we also took the

logarithm of this variable in our analysis. Asian experience (I) is a dummy variable, which

took the value of 1 if there was at least one broad experience, and 0 otherwise.

Western experience

We measured ‘Western experience’ as the cumulative amount of investment by a local

VC in the past that involved only Western VC firms (i.e. VC firms from North America

or Europe). We only considered syndicated investments between non-local and Western

39

VC firms as a Western experience. In the case of multiple investors, we took the average

of this variable; we also took the logarithm of this variable in our analysis. Western

experience (I) is a dummy variable, which took the value of 1 if there was at least one

broad experience, and 0 otherwise.

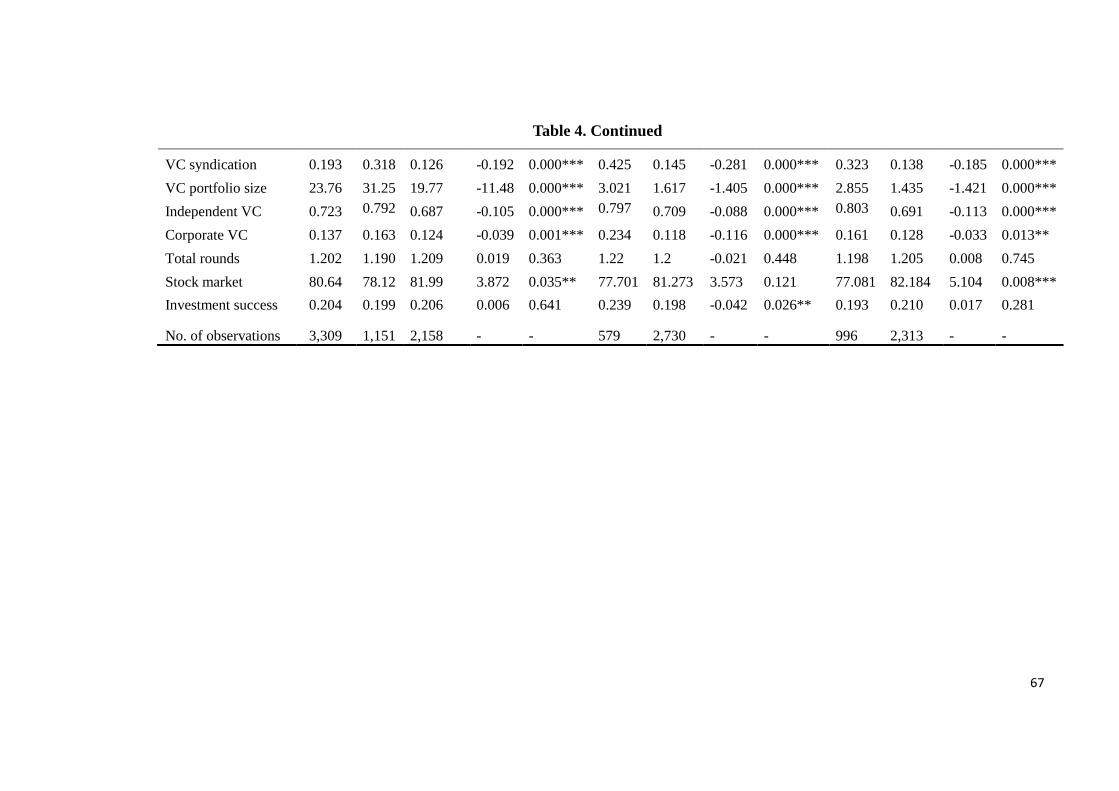

2.3.4 Control variables

Selection and performance are influenced by VC and portfolio company characteristics.

We included several variables to control for VC characteristics, investee companies, and

the country of the VC firms. VC syndication is important and can systematically reduce

the level of uncertainty. Megginson and Weiss (1991) and Lerner (1994) found that VC

syndication is positively related to the likelihood of IPO exits. Giot and Schwienbacher

(2007) found that the larger the size of VC syndication, the shorter the time to exit a

portfolio company. Similarly, recent studies on the Asian and Chinese markets (Dai et al.,

2012; Wang and Wang, 2012; Humphery-Jenner and Suchard, 2013) provided evidence

on VC syndication for investment performance. We therefore included a dummy variable

that took the value of one if the deal involved more than one VC firm. We also controlled

for VC portfolio size, since previous studies by Cumming (2006) found that portfolio size

is negatively related to the likelihood of a successful exit. We also included VC-type

dummies to indicate different types of VC firms.

We controlled for venture-related characteristics. We included dummy variables that

indicated financing stages (venture’s stage). Specifically, we included early-stage,

expansion-stage, and later-stage dummies in our analysis. We included these variables

40

because previous studies have suggested that early-stage ventures are risky and have a

high failure risk (Cochrane, 2005). The levels of information asymmetry and uncertainty

are higher at the early stage than at the later stage (Dai et al., 2012). In addition, we also

accounted for venture industry–specific fixed effects by including industry dummies in

our estimations.

The time-varying variables, related to the country of the VC firms, were included to

capture the effect of selection and investment performance. Stock market development

measures the level of stock market development in the country of a portfolio company.

This was measured as the average of stock market capitalisation, scaled by gross domestic

product (GDP). Previous studies in the United States (such as the study by Black and

Gilson, 1998) have shown that a well-developed market is extremely important to the

development of the VC industry, as it provides a viable exit mechanism for both investors

and entrepreneurs. Stock market development is undoubtedly important in the context of

cross-border investments, since VC firms are more likely to exit successfully the higher

the level of stock market development (Hazarika et al., 2010; Jeng and Wells, 2000). We

also included total rounds received in our study to control for investment size. In addition,

we included venture-nation dummies and year dummies to control for VC country fixed

effects and unobservable temporal effects.

2.3.5 Estimation models

Logit model

We used a logit model to estimate selection and investment performance (at the company

41

level). Since the dependent variables in both analyses were binary in nature, we applied

a logit model (Greene, 2002). The basic function of the non-linear model is described as:

�̂�𝑖 = 𝑒𝑢/(1 + 𝑒𝑢) (1)

In Table 6 (Models 1–3), �̂�𝑖 is the probability that the investment is made by a local VC

firm with at least one foreign syndicate experience (any type) for the ith investment; �̂�𝑖

equals 1 if the VC firm had at least one foreign syndicate experience, and 0 otherwise.

The analytical form of the logit model is as follows:

𝐿𝑖𝑘𝑒𝑙𝑖ℎ𝑜𝑜𝑑 𝑜𝑓 𝑖𝑛𝑣𝑒𝑠𝑡𝑚𝑒𝑛𝑡 𝑖𝑛 𝑒𝑎𝑟𝑙𝑦 𝑠𝑡𝑎𝑔𝑒 𝑜𝑟 ℎ𝑖𝑔ℎ 𝑡𝑒𝑐ℎ 𝑣𝑒𝑛𝑡𝑢𝑟𝑒𝑠

= 𝑓(𝛼 + 𝛽1𝐸𝑎𝑟𝑙𝑦 𝑠𝑡𝑎𝑔𝑒 + 𝛽2𝐶𝑜𝑚𝑝𝑢𝑡𝑒𝑟 𝑟𝑒𝑙𝑎𝑡𝑒𝑑

+ 𝛽3𝐼𝑛𝑓𝑜𝑟𝑚𝑎𝑡𝑖𝑜𝑛 𝑡𝑒𝑐ℎ𝑛𝑜𝑙𝑜𝑔𝑦 + 𝛽4𝑀𝑒𝑑𝑖𝑐𝑎𝑙 𝑎𝑛𝑑 𝐻𝑒𝑎𝑙𝑡ℎ 𝑐𝑎𝑟𝑒

+ 𝛽5𝐶𝑜𝑚𝑚𝑢𝑛𝑖𝑐𝑎𝑡𝑖𝑜𝑛 𝑎𝑛𝑑 𝑚𝑒𝑑𝑖𝑎 + 𝛽6𝑉𝐶 𝑠𝑦𝑛𝑑𝑖𝑐𝑎𝑡𝑖𝑜𝑛

+ 𝛽7𝑉𝐶 𝑝𝑜𝑟𝑡𝑓𝑜𝑙𝑖𝑜 𝑠𝑖𝑧𝑒 + 𝛽8𝐼𝑛𝑑𝑒𝑝𝑒𝑛𝑑𝑒𝑛𝑡 𝑉𝐶 + 𝛽9𝐶𝑜𝑟𝑝𝑜𝑟𝑎𝑡𝑒 𝑉𝐶

+ 𝛽10𝑇𝑜𝑡𝑎𝑙 𝑟𝑜𝑢𝑛𝑑𝑠 𝑟𝑒𝑐𝑒𝑖𝑣𝑒𝑑 + +𝛽11𝑌𝑒𝑎𝑟 𝑑𝑢𝑚𝑚𝑖𝑒𝑠

+ 𝛽12𝐶𝑜𝑢𝑛𝑡𝑟𝑦 𝑑𝑢𝑚𝑚𝑖𝑒𝑠)

(2)

Where early stage is a dummy variable that took the value of one if the portfolio company

was in the early stage when it received its funding, and zero otherwise. Computer related,

information technology, medical and health care, and communication and media are

dummy variables that indicate the venture’s industry. VC syndication is a dummy variable

that took the value of one if the investment was made by more than one VC firm, and

zero otherwise. VC portfolio size is the number of companies that the VC firm held in its

42

current portfolio; independent VC is a dummy variable that took the value of one if the

VC firm was not affiliated with corporations, financial institutions, or governments, and

zero otherwise. Corporate VC is a dummy that took the value of one if the VC firm was

affiliated with a corporation, and zero otherwise. Total rounds received is the total number

of rounds a portfolio company had received since the first-round investment. Year

dummies and country dummies are sets of dummy variables that indicate the year of

investment and VC firms’ country of origin, respectively.

In Table 7 (Models 1–9), �̂�𝑖 is the estimated probability of a successful exit for the ith

investment; �̂�𝑖 equals 1 if the deal was successfully exited by the end of 2012, and equals

0 otherwise. The analytical form of the logit model is as follows:

𝐿𝑖𝑘𝑒𝑙𝑖ℎ𝑜𝑜𝑑 𝑜𝑓 𝑠𝑢𝑐𝑐𝑒𝑠𝑠𝑓𝑢𝑙 𝑒𝑥𝑖𝑡𝑠

= 𝑓(𝛼 + 𝛽1𝐹𝑜𝑟𝑒𝑖𝑔𝑛 𝑆𝑦𝑛𝑑𝑖𝑐𝑎𝑡𝑒 𝐸𝑥𝑝𝑒𝑟𝑖𝑒𝑛𝑐𝑒 + 𝛽2𝐸𝑎𝑟𝑙𝑦 𝑠𝑡𝑎𝑔𝑒

+ 𝛽3𝑉𝐶 𝑠𝑦𝑛𝑑𝑖𝑐𝑎𝑡𝑖𝑜𝑛 + 𝛽4𝑉𝐶 𝑝𝑜𝑟𝑡𝑓𝑜𝑙𝑖𝑜 𝑠𝑖𝑧𝑒 + 𝛽5𝐼𝑛𝑑𝑒𝑝𝑒𝑛𝑑𝑒𝑛𝑡 𝑉𝐶

+ 𝛽6𝐶𝑜𝑟𝑝𝑜𝑟𝑎𝑡𝑒 𝑉𝐶 + 𝛽7𝑇𝑜𝑡𝑎𝑙 𝑟𝑜𝑢𝑛𝑑𝑠 𝑟𝑒𝑐𝑒𝑖𝑣𝑒𝑑 + 𝛽8𝑌𝑒𝑎𝑟 𝑑𝑢𝑚𝑚𝑖𝑒𝑠

+ 𝛽9𝐼𝑛𝑑𝑢𝑠𝑡𝑟𝑦 𝑑𝑢𝑚𝑚𝑖𝑒𝑠 + 𝛽10𝐶𝑜𝑢𝑛𝑡𝑟𝑦 𝑑𝑢𝑚𝑚𝑖𝑒𝑠)

(3)

Where foreign syndicate experience indicates whether the local VC firm had foreign

syndicate experience (dummy variables that indicate Broad, Asian, and Western

experience) or the actual number of foreign syndicate experience (the number of

syndicated investments with foreign VC firms). Early stage is a dummy variable that took

the value of one if the portfolio company was in early stage when it received its funding,

and zero otherwise. VC syndication is a dummy variable that took the value of one if the

43

investment was made by more than one VC firm, and zero otherwise. VC portfolio size is

the number of companies that the VC firm held in its current portfolio. Independent VC

is a dummy variable that took the value of one if the VC firm was not affiliated with

corporations, financial institutions, or governments, and zero otherwise. Corporate VC is

a dummy that took the value of one if the VC firm was affiliated with a corporation, and

zero otherwise. Total rounds received is the total number of rounds a portfolio company

had received since the first-round investment. Industry dummies are dummy variables that

indicate the portfolio company’s industry, including computer-related, information

technology, medical and health care, and communication and media. Year dummies and

country dummies are sets of dummy variables that indicate the year of investment and the

VC firms’ country of origin, respectively.

In equation (1), u is the normal linear regression model, which is:

𝑢 = 𝛼 + 𝛽1𝑋1 + 𝛽2𝑋2 + ⋯ + 𝛽𝑡𝑋𝑡 (4)

Where 𝛼 is the constant and 𝛽1 to 𝛽𝑡 are coefficients of independent variables 𝑋1

to 𝑋𝑡. The log transformation of the logistic model is given by:

𝑙𝑛[�̂�𝑖/(1 − �̂�𝑖)] = 𝛼 + 𝛽1𝑋1 + 𝛽2𝑋2 + ⋯ + 𝛽𝑡𝑋𝑡 (5)

The parameters were estimated through the maximum likelihood method. To test the

statistical significance of the predictor variable, we used the Wald test. Pseudo 𝑅2 was

used to measure the goodness fit of the model; pseudo 𝑅2 is similar to 𝑅2 in the