the publishing market in germany

TRANSCRIPT

The Publishing Market in Germany

Summer School School of Information Management Nanjing University Svenja Hagenhoff Institute for the Study of the Book Epublishing and Digital Markets Group August 2012

Svenja Hagenhoff short CV

● 2011 – Present: Professor for E-Publishing and Digital Markets at Friedrich-Alexander University Erlangen-Nuremberg, Germany

● 2011 - 2012: Lecturer for Media Management at University of Applied Sciences St. Pölten, Sankt Pölten, Austria

● 2010 - 2011: Head of the Institute of Media Economics at University of Applied Sciences St. Pölten, Sankt Pölten, Austria

● 2009 - 2010: Lecturer for Information Systems at Welfenakademie Braunschweig, Braunschweig, Germany

● 2007 – 2007: Lecturer für E-Commerce at International School of New Media at the University of Lübeck, Lübeck, Germany

● 2006 – 2006: Guest Researcher at UCLA Anderson School of Management, Los Angeles, California, United States

● 2004 – 2005: Interims Professor of Information Systems at Universität Hildesheim - University of Hildesheim, Hildesheim, Germany

● 2004 – 2004: Lecturer for Information Systems at Universität Hildesheim - University of Hildesheim, Hildesheim, Germany

● 2002 – 2010: Assistant Professor in Application Systems and E-Business at Georg-August University, Göttingen, Germany

● 2002 – 2010: Head of the Research Group "Internet Economics" at Georg-August University, Göttingen, Germany

● 1997 – 2001: Lecturer for Information at Leibniz-Akademie Hannover, Hanover, Germany

● 1997 – 2002: Research Assistant at Georg-August Universität, Göttingen, Germany

● 1992 – 1997: Studying Business Administration and Information Systems at Georg-August University Göttingen, Germany

2

Outline

● Media Market in General

● Markets for Specific Types of Media

● E-Publishing and Paid Digital Content

● Regulatory Aspects

● Innovative Business Models

● Results of a Survey: Crossmedia Publishing

3

Media Market in General

● Structure

● Revenues

● Media Usage

4

costs

revenue

Structure of the German media market

5

media markets

markets for non-electronic

media (print)

Markets for elektronic media

newspaper markets

magazine markets

book markets

Movie markets

TV markets

Radio markets

Music markets

Video and computer game markets

Internet markets

recipients

advertisement

procurement

Similar to: Wirtz, B.: Medien- und Internetmanagement, Wiesbaden 2006.

Out of home markets

Media Market in General

● Structure

● Revenues

● Media Usage

6

Different kinds of revenues

7

0% 20% 40% 60% 80% 100%

Free newspaper

Free-TV

Newspaper

Scientific magazine

Pay-TV

Book

Recipient‘s revenues Advertising revenues

Part of total revenues

Data from PricewaterhouseCoopers: German Entertainment and Media Outlook: 2011-2015. Frankfurt 2012

Revenue trend total (advertisement & recipients)

8

14970

15949

15988

14484

15239

15718

16300

16799

17322

17800

33100

33603

34054

34880

35046

35397

35907

36714

37410

38048

-1.00

0.00

1.00

2.00

3.00

4.00

5.00

6.00

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

delta

in %

Reve

nue

in m

illio

n Eu

ro

Recipient revenues (million Euro)

Advertising revenues (million Euro)

delta in %

2012-2015 estimated

Data from PricewaterhouseCoopers: German Entertainment and Media Outlook: 2011-2015. Frankfurt 2012

Revenue trend total (print & electronic)

9

22,397

23,456

24,165

24,712

25,529

26,187

27,082

28,142

29,160

30,115

25,673

26,096

25,877

24,652

24,756

24,928

25,134

25,371

25,572

25,733

-2

-1

0

1

2

3

4

5

6

7

0

10,000

20,000

30,000

40,000

50,000

60,000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

delta

in %

Reve

nues

in m

illio

n Eu

ro

Revenue Print (in million Euro)

Revenue electronic (in million Euro)

delta in %

2012-2015 estimated

Data from PricewaterhouseCoopers: German Entertainment and Media Outlook: 2011-2015. Frankfurt 2012

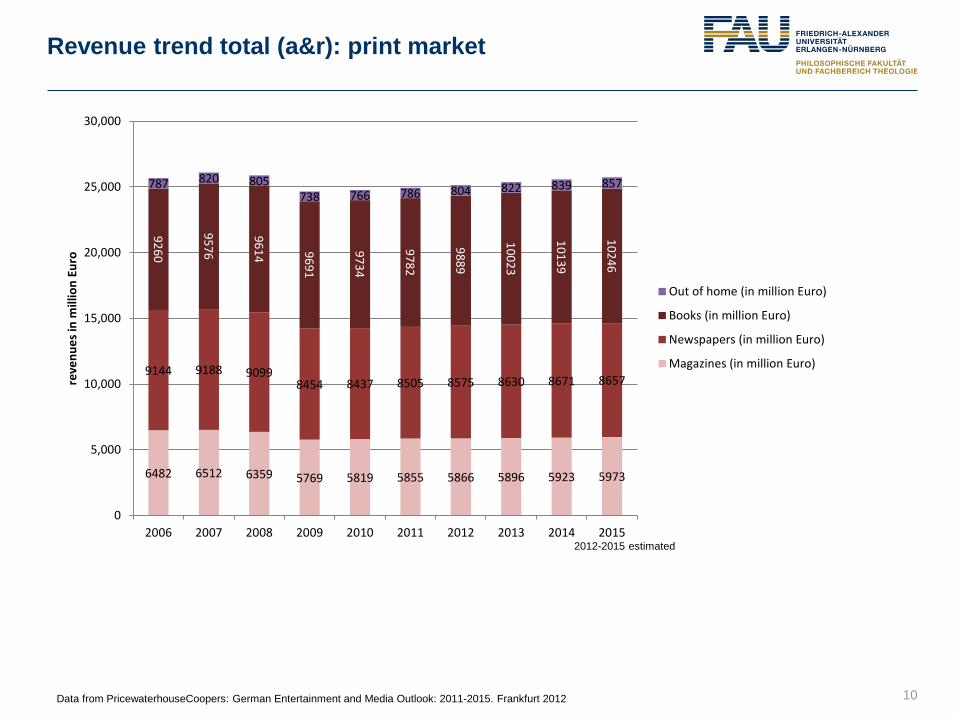

Revenue trend total (a&r): print market

10

2012-2015 estimated

6482 6512 6359 5769 5819 5855 5866 5896 5923 5973

9144 9188 9099 8454 8437 8505 8575 8630 8671 8657

9260

9576

9614

9691

9734

9782

9889

10023

10139

10246

787 820 805 738 766 786 804 822 839 857

0

5,000

10,000

15,000

20,000

25,000

30,000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

reve

nues

in m

illio

n Eu

ro

Out of home (in million Euro)

Books (in million Euro)

Newspapers (in million Euro)

Magazines (in million Euro)

Data from PricewaterhouseCoopers: German Entertainment and Media Outlook: 2011-2015. Frankfurt 2012

Revenue trend total (a&r): electronic market

11 PricewaterhouseCoopers: German Entertainment and Media Outlook: 2011-2015. Frankfurt 2012

2012-2015 estimated

6482

6512

6359

5769

5819

5855

5866

5896

5923

5973

11854

11885

11910

11981

12485

12720

13061

13365

13603

13790

1705 1652 1623 1575 1489 1422 1373 1345 1332 1330

3322

3393

3365

3448

3442

3426

3404

3491

3512

3520

1762

2521

3019

3216

3610

4023

4490

4989

5493

5968 1347 1639

1891 1863 1913

1984 2074 2191 2329

2494

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

reve

nues

in m

illio

n Eu

ro

Videogames (in million Euro)

Online advertisement (in million Euro)

Radio (in million Euro)

Music (in million Euro)

TV (million Euro)

Movies (in million Euro)

Revenue trend advertising: total

12

6,578

7,454

7,820

7,583

8,311

8,794

9,435

10,005

10,618

11,176

8,392

8,495

8,168

6,901

6,928

6,924

6,865

6,794

6,704

6,624

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Revenue Print (in million Euro)

Revenue electronic (in million Euro)

Data from PricewaterhouseCoopers: German Entertainment and Media Outlook: 2011-2015. Frankfurt 2012

2012-2015 estimated

Revenue trend advertising: print market

13

2812

2838

2724

2261

2306

2323

2305

2288

2255

2230

4793

4837

4639 3902

3856

3815

3756

3684

3610

3537

787

820 805

738

766

786

804

822

839

857

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Out of home (in million Euro)

Newspapers (in million Euro)

Magazines (in million Euro)

Data from PricewaterhouseCoopers: German Entertainment and Media Outlook: 2011-2015. Frankfurt 2012

2012-2015 estimated

Revenue trend advertising: electronic market

14

4114

4156

4036

3640

3954

4000

4150

4200

4280

4350

680

743

720 678

692

705

719

732

753

761

1762

2521

3019

3216

3610

4023

4490

4989

5493

5968

22 34

45 49 55

66 76

84 92

97

0

2,000

4,000

6,000

8,000

10,000

12,000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Videogames (in million Euro)

Online advertisement (in million Euro)

Radio (in million Euro)

TV (million Euro)

Data from PricewaterhouseCoopers: German Entertainment and Media Outlook: 2011-2015. Frankfurt 2012

2012-2015 estimated

Revenue trend recipients: print market

15

3670

3674

3635

3508

3513

3532

3561

3608

3668

3743

4351

4351

4460

4552

4581

4690

4819

4946

5061

5120

9260

9576

9614

9691

9734

9782

9880

10023

10139

10246

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Books (in million Euro)

Newspapers (in million Euro)

Magazines (in million Euro)

Data from PricewaterhouseCoopers: German Entertainment and Media Outlook: 2011-2015. Frankfurt 2012

2012-2015 estimated

Revenue trend recipients: electronic market

16

2407

2366

2357

2629

2590

2612

2680

2761

2891

3013

7740

7729

7874

8341

8531

8720

8911

9165

9323

9440

1705

1652

1623

1575

1489

1422

1373

1345

1332

1330

2642

2650

2645

2770

2750

2721

2685

2759

2759

2759

1325

1605

1846

1814

1858

1918

1998

2107

2237

2397

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Videogames (in million Euro)

Radio (in million Euro)

Music (in million Euro)

TV (million Euro)

Movies (in million Euro)

Data from PricewaterhouseCoopers: German Entertainment and Media Outlook: 2011-2015. Frankfurt 2012

2012-2015 estimated

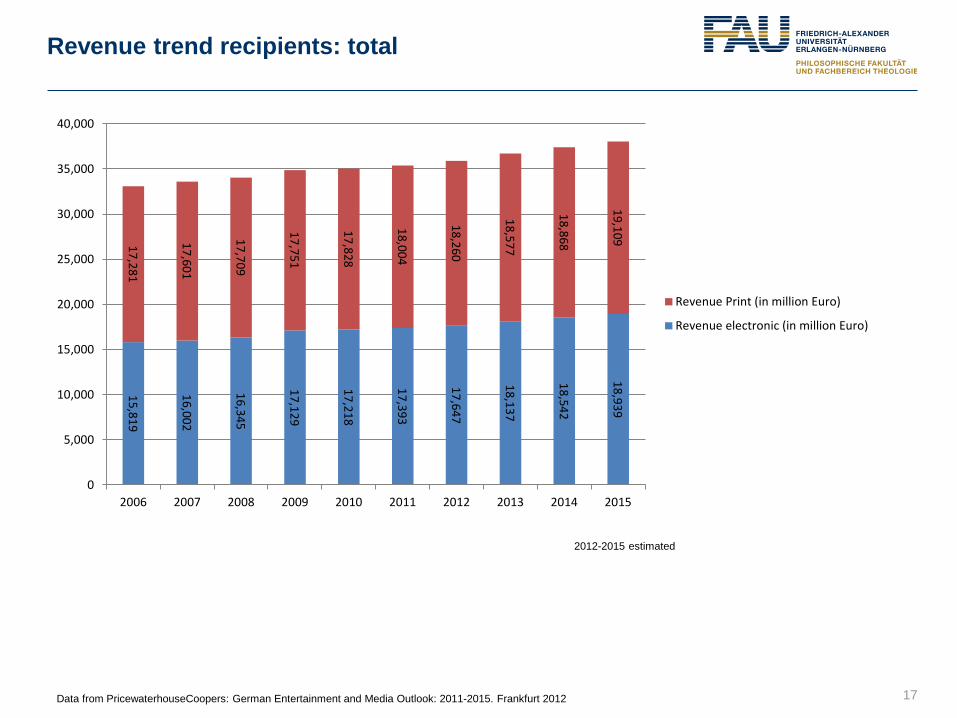

Revenue trend recipients: total

17

15,819

16,002

16,345

17,129

17,218

17,393

17,647

18,137

18,542

18,939

17,281

17,601

17,709

17,751

17,828

18,004

18,260

18,577

18,868

19,109

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Revenue Print (in million Euro)

Revenue electronic (in million Euro)

Data from PricewaterhouseCoopers: German Entertainment and Media Outlook: 2011-2015. Frankfurt 2012

2012-2015 estimated

Economic growth and revenue trends

18

Growth media industry Economic growth nominal

grow

th in

%

Data from PricewaterhouseCoopers: German Entertainment and Media Outlook: 2011-2015. Frankfurt 2012

2012-2015 estimated

Media Market in General

● Structure

● Revenues

● Media Usage

19

Media use in Germany

20 Data from: Verbraucher Analyse Klassik Märkte III 2011, Axel Springer AG, Bauer Media Group

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Listening to audiobooks

Playing video / computer games

Reading books

Reading magazines

Using internet

Reading newspaper

Watching television

strongly like

like

dislike

strongly dislike

Media use 2011 in minutes per day

21

TV Radio Newspaper Audio Book

Average 14-19 years 20-29 years 30-49 years ≥ 50 years

PricewaterhouseCoopers: German Entertainment and Media Outlook: 2011-2015. Frankfurt 2012

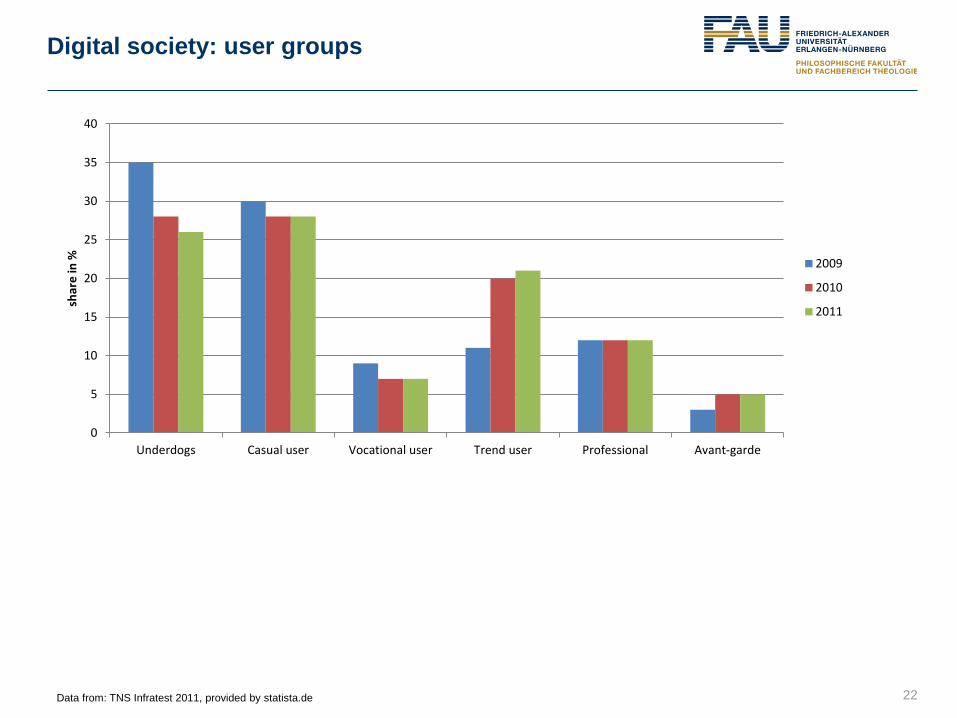

Digital society: user groups

22

0

5

10

15

20

25

30

35

40

Underdogs Casual user Vocational user Trend user Professional Avant-garde

shar

e in

%

2009

2010

2011

Data from: TNS Infratest 2011, provided by statista.de

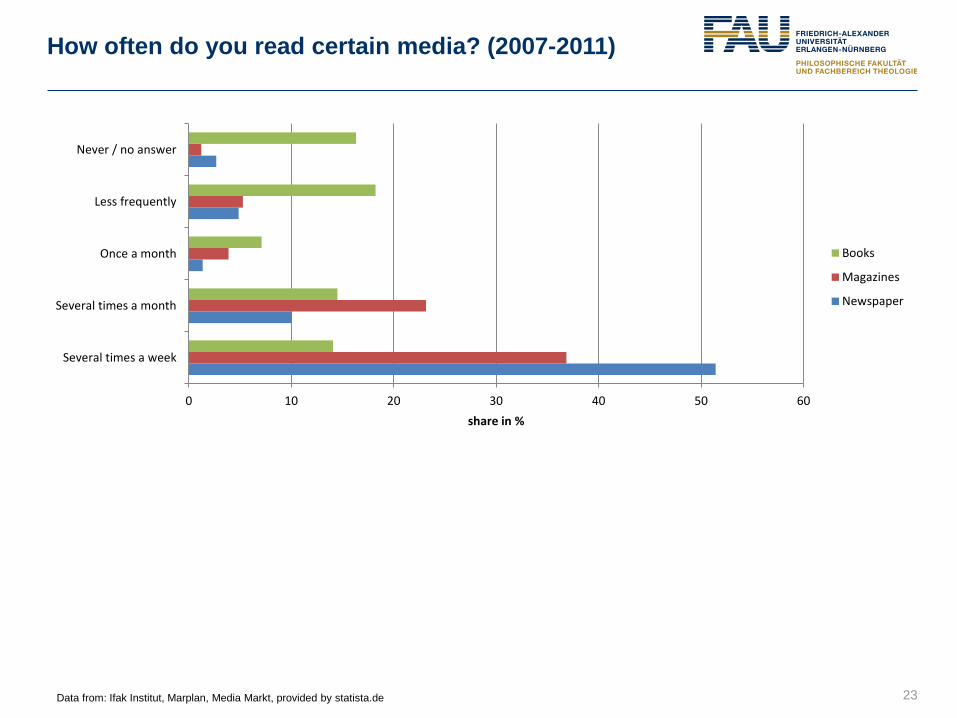

How often do you read certain media? (2007-2011)

23

0 10 20 30 40 50 60

Several times a week

Several times a month

Once a month

Less frequently

Never / no answer

share in %

Books

Magazines

Newspaper

Data from: Ifak Institut, Marplan, Media Markt, provided by statista.de

Book reading in Germany (2011)

24

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

60–69 yrs.

50–59 yrs.

40–49 yrs.

30–39 yrs.

20–29 yrs.

14–19 yrs.

strongly like

like

dislike

strongly dislike

Data from: Verbraucher Analyse Klassik Märkte III 2011, Axel Springer AG, Bauer Media Group

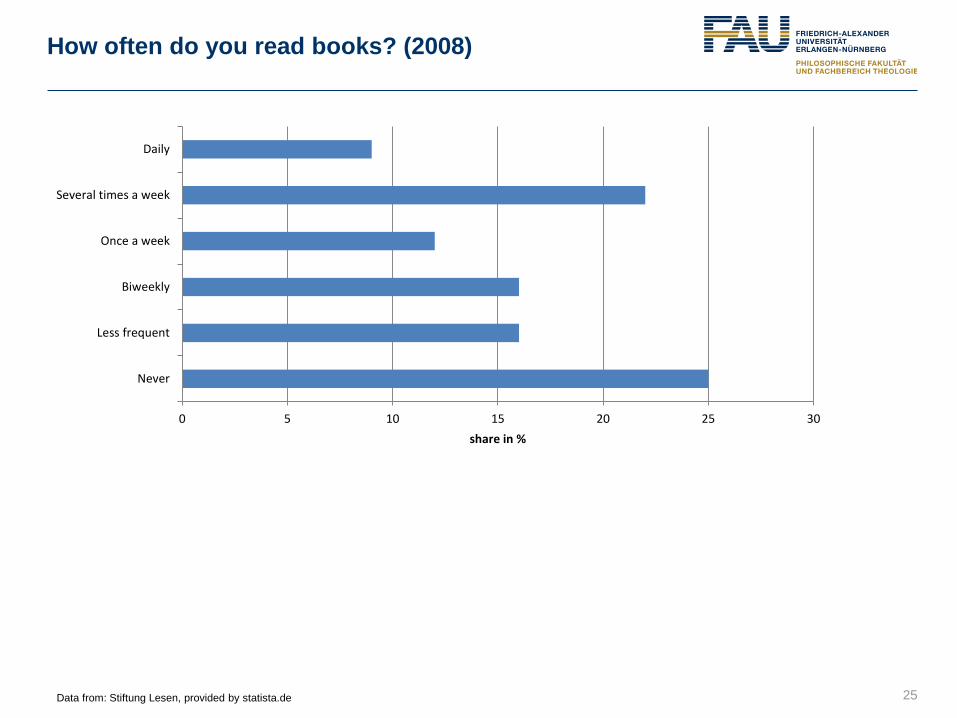

How often do you read books? (2008)

25

0 5 10 15 20 25 30

Never

Less frequent

Biweekly

Once a week

Several times a week

Daily

share in %

Data from: Stiftung Lesen, provided by statista.de

When do you read books? (2008)

26 Data from: TNS Emnid, provided by statista.de

0 10 20 30 40 50 60 70 80 90

Leisure time

Holidays

Before going to bed

On my way to work

Other opportunities

Never

I do not know

share in %

female

male

How many books do you have at home? (2008)

27

57

23

12

6

0

10

20

30

40

50

60

less than 50 50 to 100 100 to 250 more than 250

In %

Data from: German Publishers and Book Sellers Association, provided by statista.de

Outline

● Media Market in General

● Markets for Specific Types of Media

● E-Publishing and Paid Digital Content

● Regulatory Aspects

● Innovative Business Models

● Results of a Survey: Crossmedia Publishing

28

Markets for Specific Types of Media

● TV and Radio Markets

● Newspaper Markets

● Magazine Markets

● Book Markets

29

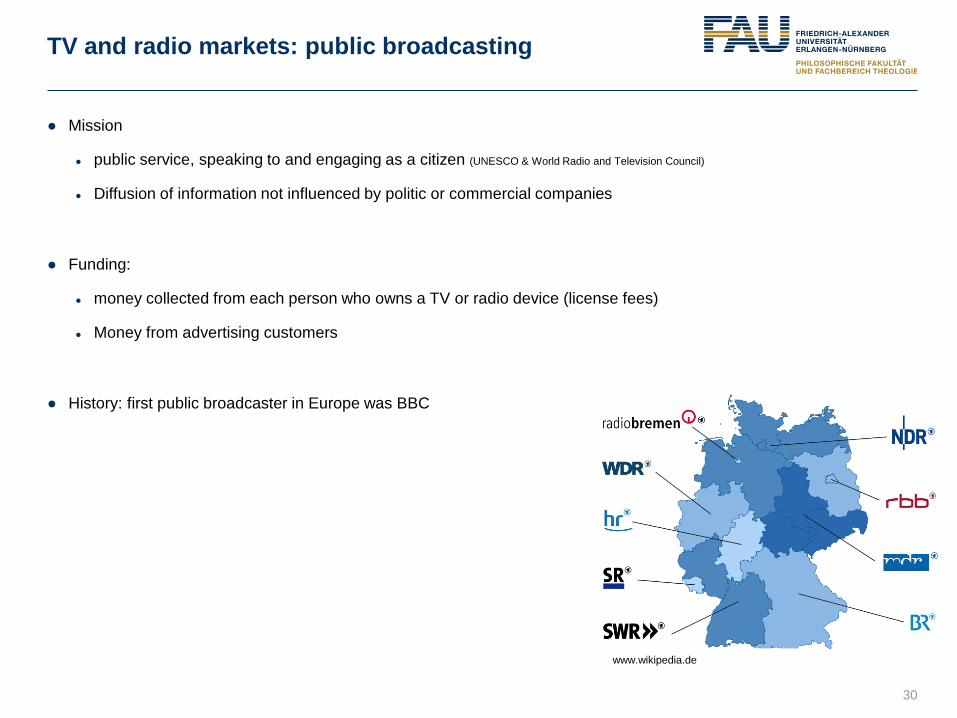

TV and radio markets: public broadcasting

30

● Mission

● public service, speaking to and engaging as a citizen (UNESCO & World Radio and Television Council)

● Diffusion of information not influenced by politic or commercial companies

● Funding:

● money collected from each person who owns a TV or radio device (license fees)

● Money from advertising customers

● History: first public broadcaster in Europe was BBC

www.wikipedia.de

TV and radio markets: private broadcasting

31

● Mission:

● Very different concepts

● often specialized programs (e.g. only sports, only movies,…)

● Funding:

● Money from advertising customers

● Pay TV

● History: beginning of 1980ies deregulation of the broadcasting market in Europe started

Markets for Specific Types of Media

● TV and Radio Markets

● Newspaper Markets

● Magazine Markets

● Book Markets

32

Revenue trend newspaper market

33 Data from PricewaterhouseCoopers: German Entertainment and Media Outlook: 2011-2015. Frankfurt 2012

4793

4837

4639

3902

3856

3815

3756

3684

3610

3537

96 126 155

162 186 215 245 270 299 331

4261

4261

4373 4470

4473

4568

4671

4747

4800

4823

0 0 0 0 22 37.2 63.2 115.5 174.6 209.3

90 90 87 82 86 85 84 84 86 88

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

10000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Supplements

Recipients digital

Recipients print

Advertisement digital

Advertisement print

2012-2015 estimated

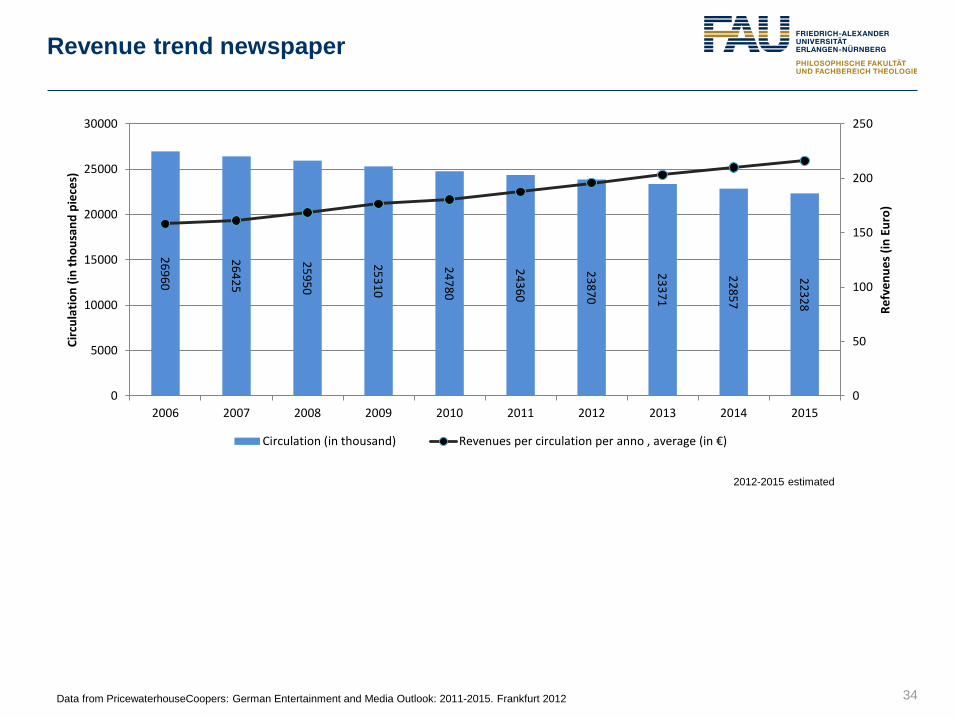

Revenue trend newspaper

34

26960

26425

25950

25310

24780

24360

23870

23371

22857

22328

0

50

100

150

200

250

0

5000

10000

15000

20000

25000

30000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Refv

enue

s (in

Eur

o)

Circ

ulat

ion

(in th

ousa

nd p

iece

s)

Circulation (in thousand) Revenues per circulation per anno , average (in €)

Data from PricewaterhouseCoopers: German Entertainment and Media Outlook: 2011-2015. Frankfurt 2012

2012-2015 estimated

Regularly readers of newspapers

35

40

45

50

55

60

65

70

75

80

85

90

2005 2006 2007 2008 2009 2010

part

of p

erso

ns in

%

14-19

20-29

30-39

40-49

50-59

60-69

>69

Total (in %)

Data from PricewaterhouseCoopers: German Entertainment and Media Outlook: 2011-2015. Frankfurt 2012

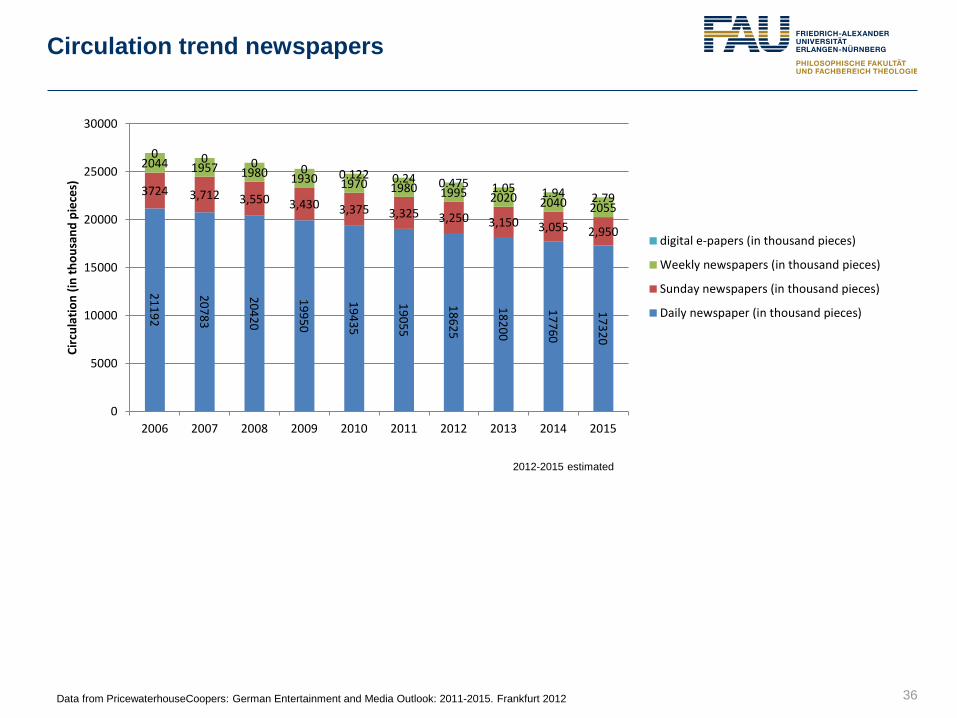

Circulation trend newspapers

36

21192

20783

20420

19950

19435

19055

18625

18200

17760

17320

3724 3,712 3,550 3,430 3,375 3,325 3,250 3,150 3,055 2,950

2044 1957 1980 1930 1970 1980 1995 2020 2040 2055

0 0 0 0 0.122 0.24 0.475 1.05 1.94 2.79

0

5000

10000

15000

20000

25000

30000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Circ

ulat

ion

(in th

ousa

nd p

iece

s)

digital e-papers (in thousand pieces)

Weekly newspapers (in thousand pieces)

Sunday newspapers (in thousand pieces)

Daily newspaper (in thousand pieces)

Data from PricewaterhouseCoopers: German Entertainment and Media Outlook: 2011-2015. Frankfurt 2012

2012-2015 estimated

Revenue trend (recipients) digital newspapers

37

122 240

475

1050

1940

2790

0

20

40

60

80

100

120

140

160

180

200

0

500

1000

1500

2000

2500

3000

2010 2011 2012 2013 2014 2015

Reve

nues

per

circ

ulat

ion

(in m

illio

n €)

Circ

ulat

ion

(in th

ousa

nd p

iece

s)

Circulation (in thousand pieces)

Revenues per circulation per anno, average (in million €)

Data from PricewaterhouseCoopers: German Entertainment and Media Outlook: 2011-2015. Frankfurt 2012

2012-2015 estimated

Markets for Specific Types of Media

● TV and Radio Markets

● Newspaper Markets

● Magazine Markets

● Book Markets

38

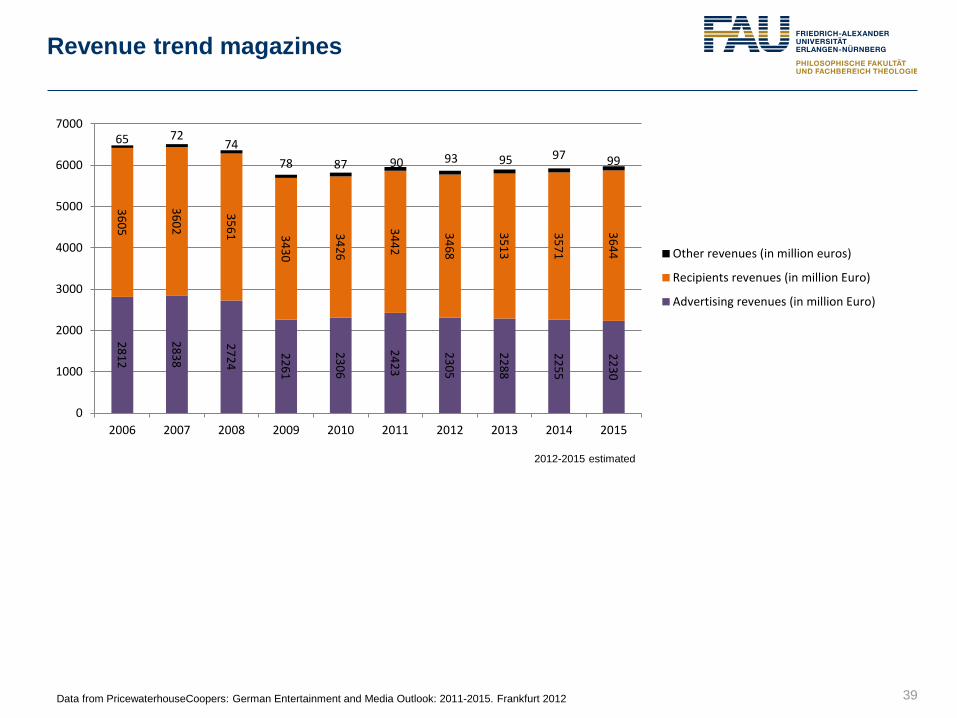

Revenue trend magazines

39 Data from PricewaterhouseCoopers: German Entertainment and Media Outlook: 2011-2015. Frankfurt 2012

2812

2838

2724

2261

2306

2423

2305

2288

2255

2230

3605

3602

3561 3430

3426

3442

3468

3513

3571

3644

65 72 74

78 87 90 93 95 97 99

0

1000

2000

3000

4000

5000

6000

7000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Other revenues (in million euros)

Recipients revenues (in million Euro)

Advertising revenues (in million Euro)

2012-2015 estimated

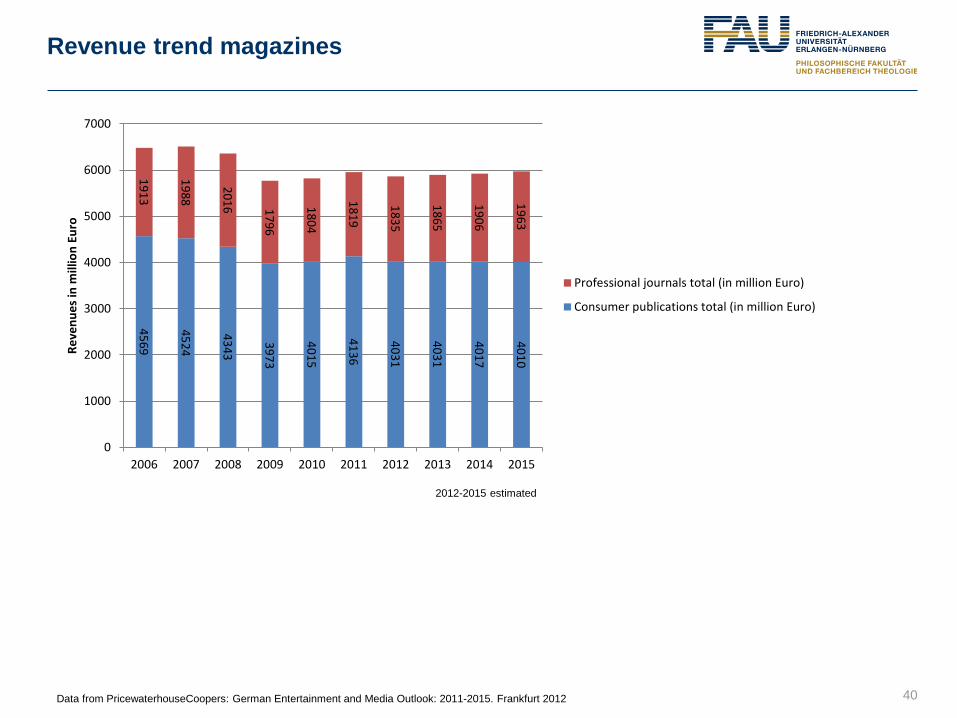

Revenue trend magazines

40 Data from PricewaterhouseCoopers: German Entertainment and Media Outlook: 2011-2015. Frankfurt 2012

4569

4524

4343

3973

4015

4136

4031

4031

4017

4010

1913

1988

2016 1796

1804

1819

1835

1865

1906

1963 0

1000

2000

3000

4000

5000

6000

7000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Reve

nues

in m

illio

n Eu

ro

Professional journals total (in million Euro)

Consumer publications total (in million Euro)

2012-2015 estimated

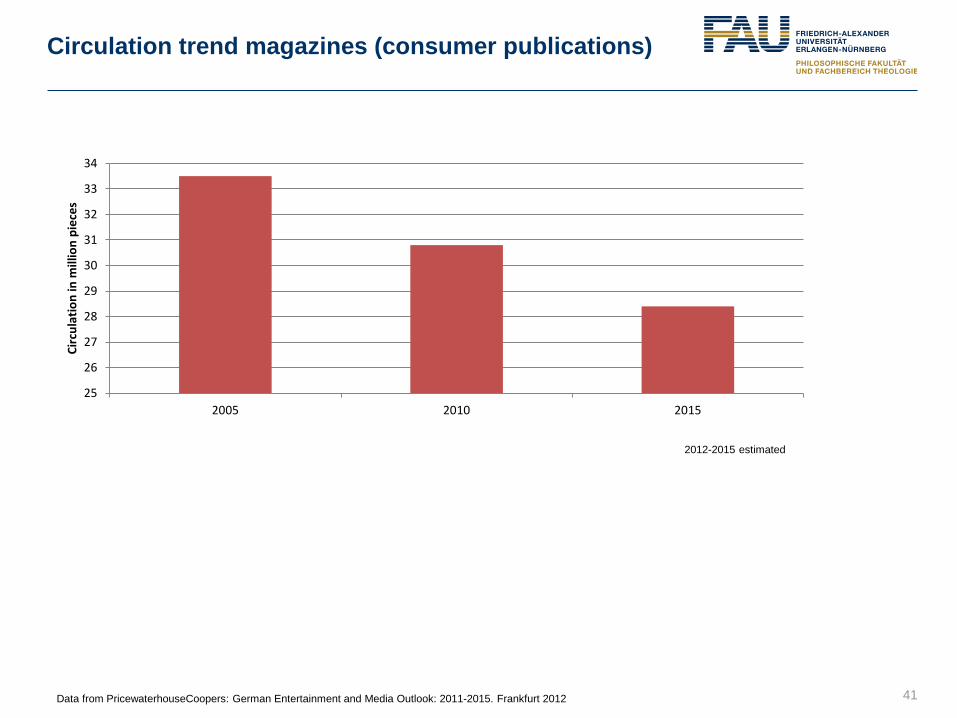

Circulation trend magazines (consumer publications)

41 Data from PricewaterhouseCoopers: German Entertainment and Media Outlook: 2011-2015. Frankfurt 2012

25

26

27

28

29

30

31

32

33

34

2005 2010 2015

Circ

ulat

ion

in m

illio

n pi

eces

2012-2015 estimated

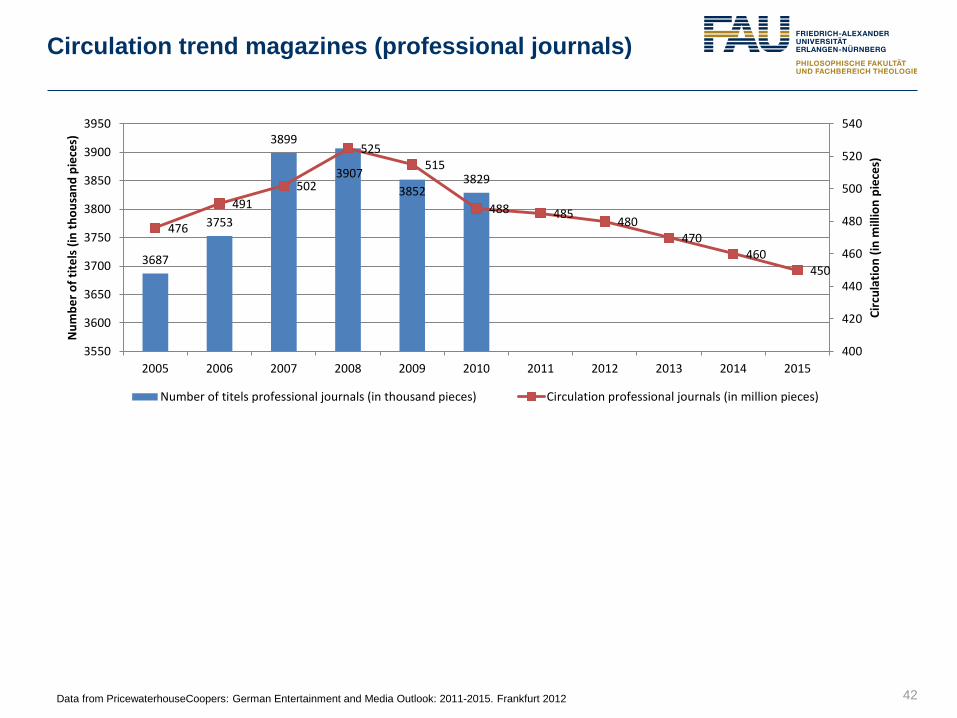

Circulation trend magazines (professional journals)

42 Data from PricewaterhouseCoopers: German Entertainment and Media Outlook: 2011-2015. Frankfurt 2012

3687

3753

3899

3907 3852

3829

476

491 502

525 515

488 485 480 470

460 450

400

420

440

460

480

500

520

540

3550

3600

3650

3700

3750

3800

3850

3900

3950

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Circ

ulat

ion

(in m

illio

n pi

eces

)

Num

ber o

f tite

ls (i

n th

ousa

nd p

iece

s)

Number of titels professional journals (in thousand pieces) Circulation professional journals (in million pieces)

Markets for Specific Types of Media

● TV and Radio Markets

● Newspaper Markets

● Magazine Markets

● Book Markets

43

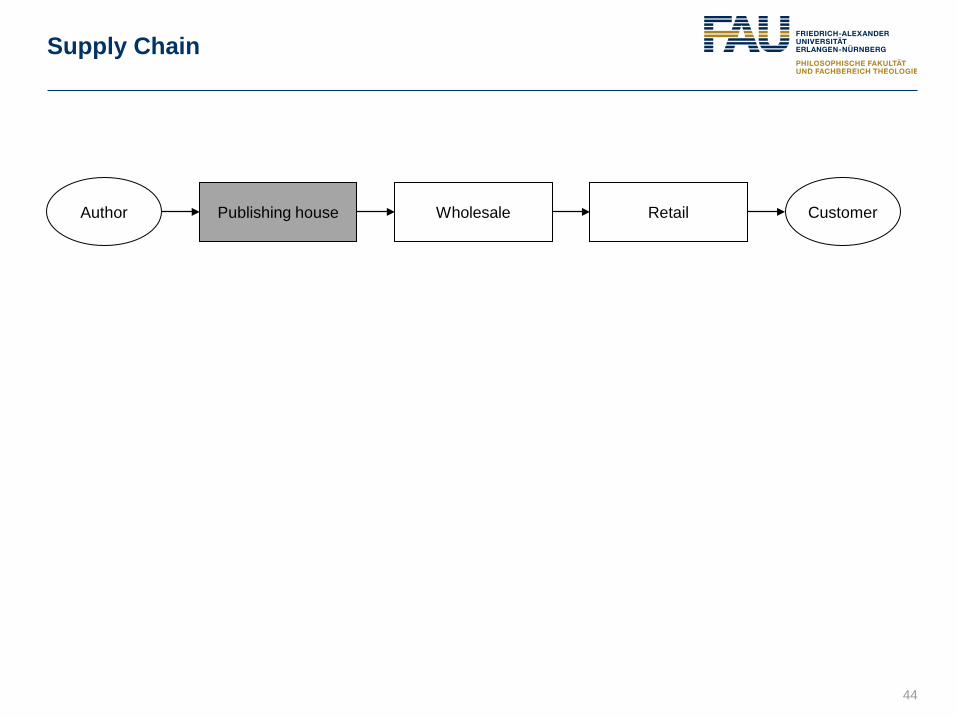

Supply Chain

44

Publishing house Wholesale Retail Customer Author

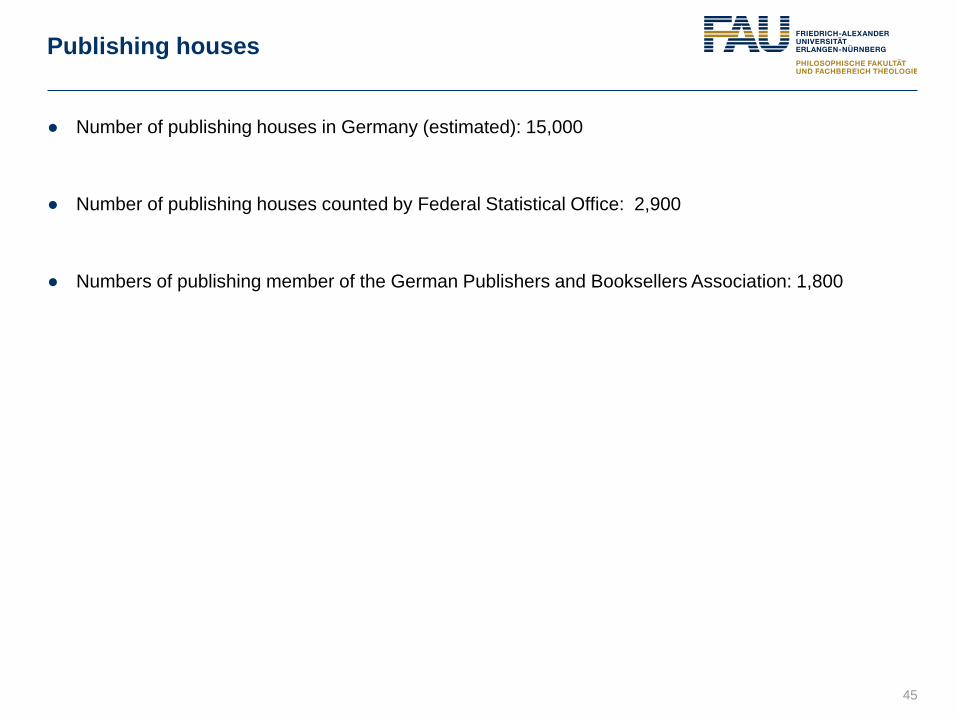

Publishing houses

● Number of publishing houses in Germany (estimated): 15,000

● Number of publishing houses counted by Federal Statistical Office: 2,900

● Numbers of publishing member of the German Publishers and Booksellers Association: 1,800

45

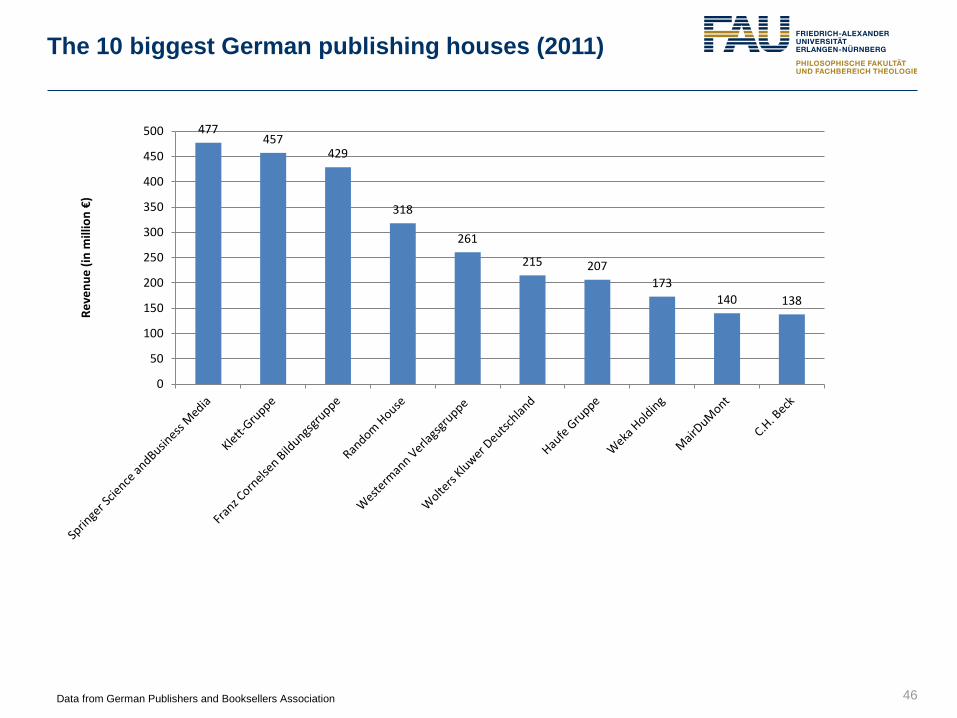

The 10 biggest German publishing houses (2011)

46 Data from German Publishers and Booksellers Association

477 457

429

318

261

215 207 173

140 138

0

50

100

150

200

250

300

350

400

450

500

Reve

nue

(in m

illio

n €)

New book titles trend

47

59,916 61,538

74,074 78,082

81,177 86,084

83,381 81,793 84,351

82,048

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Num

bre

of n

ew ti

tles

Data from German Publishers and Booksellers Association

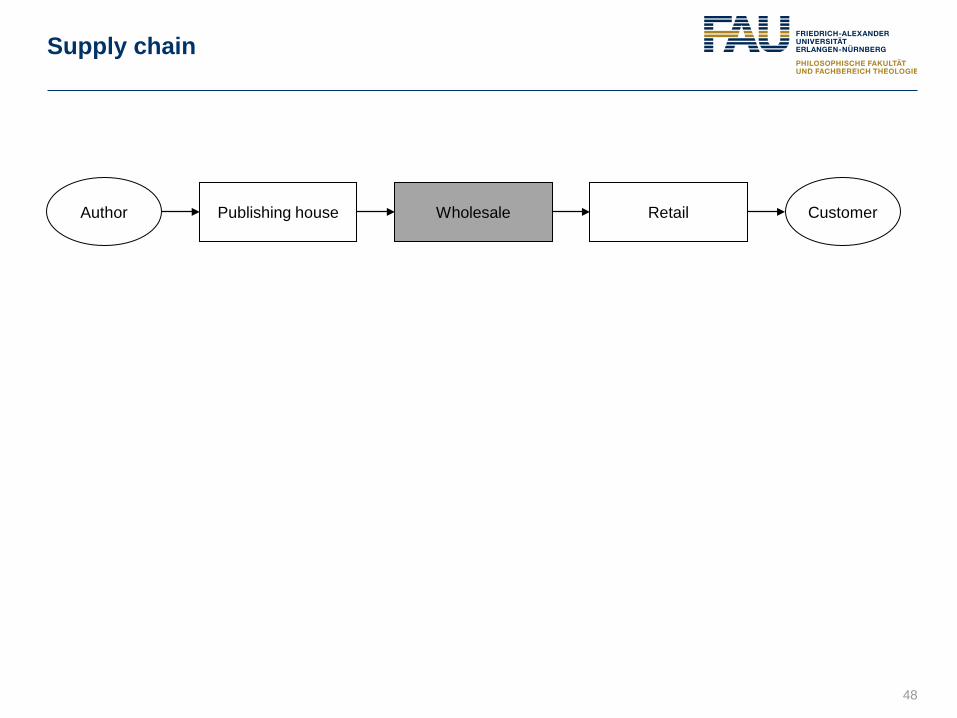

Supply chain

48

Publishing house Wholesale Retail Customer Author

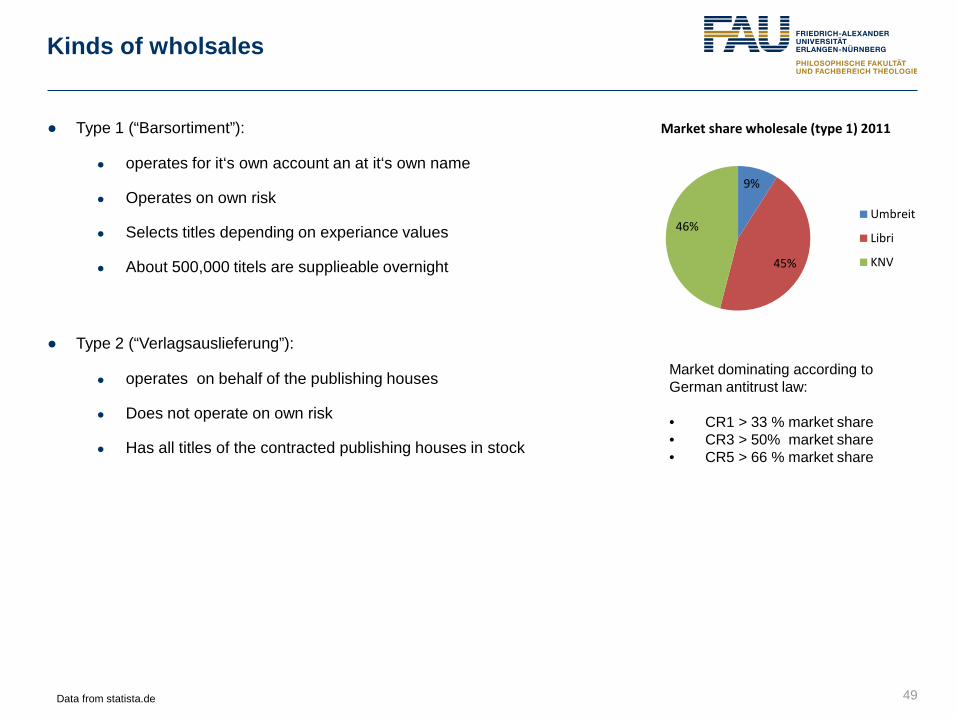

Kinds of wholsales

● Type 1 (“Barsortiment”):

● operates for it‘s own account an at it‘s own name

● Operates on own risk

● Selects titles depending on experiance values

● About 500,000 titels are supplieable overnight

● Type 2 (“Verlagsauslieferung”):

● operates on behalf of the publishing houses

● Does not operate on own risk

● Has all titles of the contracted publishing houses in stock

49

9%

45%

46%

Market share wholesale (type 1) 2011

Umbreit

Libri

KNV

Market dominating according to German antitrust law: • CR1 > 33 % market share • CR3 > 50% market share • CR5 > 66 % market share

Data from statista.de

Supply chain

50

Publishing house Wholesale Retail Customer Author

Kinds of retail

51

● Retail bookshops

● Department stores

● Catalogue selling

● Antiquarian bookshops

● Special bookshops

● Book shops in railway stations

● Book clubs

● Secondary markets

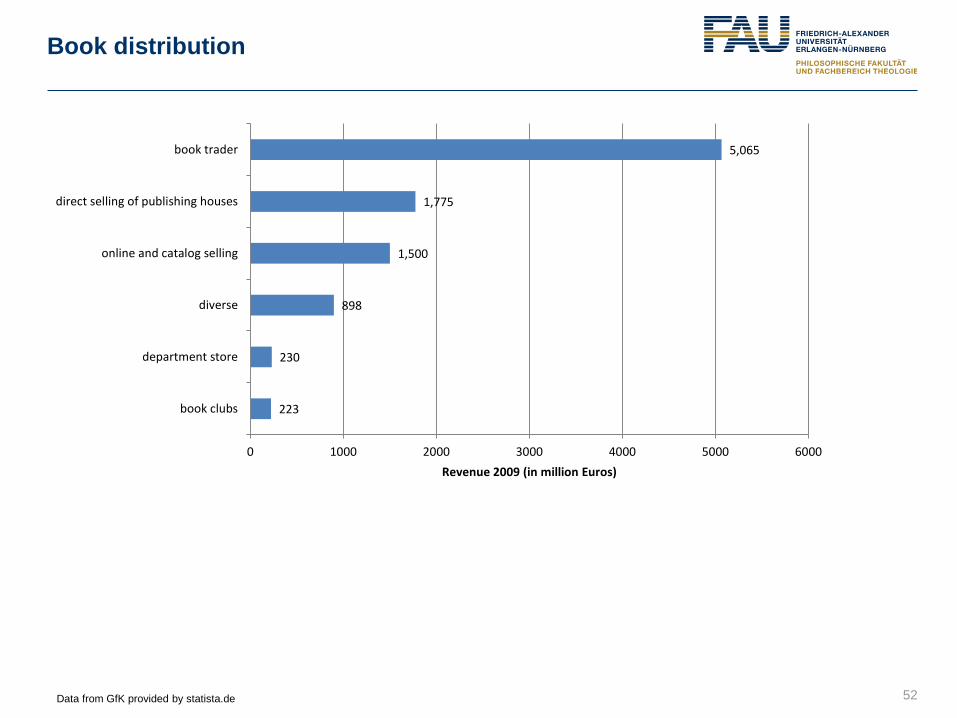

Book distribution

52

223

230

898

1,500

1,775

5,065

book clubs

department store

diverse

online and catalog selling

direct selling of publishing houses

book trader

0 1000 2000 3000 4000 5000 6000Revenue 2009 (in million Euros)

Data from GfK provided by statista.de

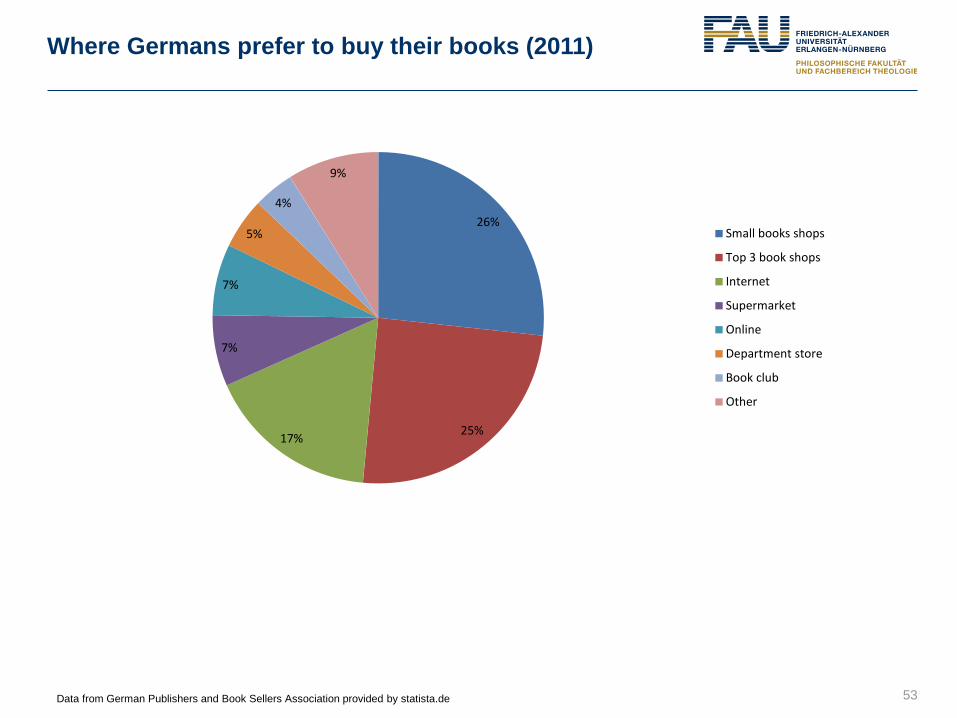

Where Germans prefer to buy their books (2011)

53

26%

25% 17%

7%

7%

5%

4%

9%

Small books shops

Top 3 book shops

Internet

Supermarket

Online

Department store

Book club

Other

Data from German Publishers and Book Sellers Association provided by statista.de

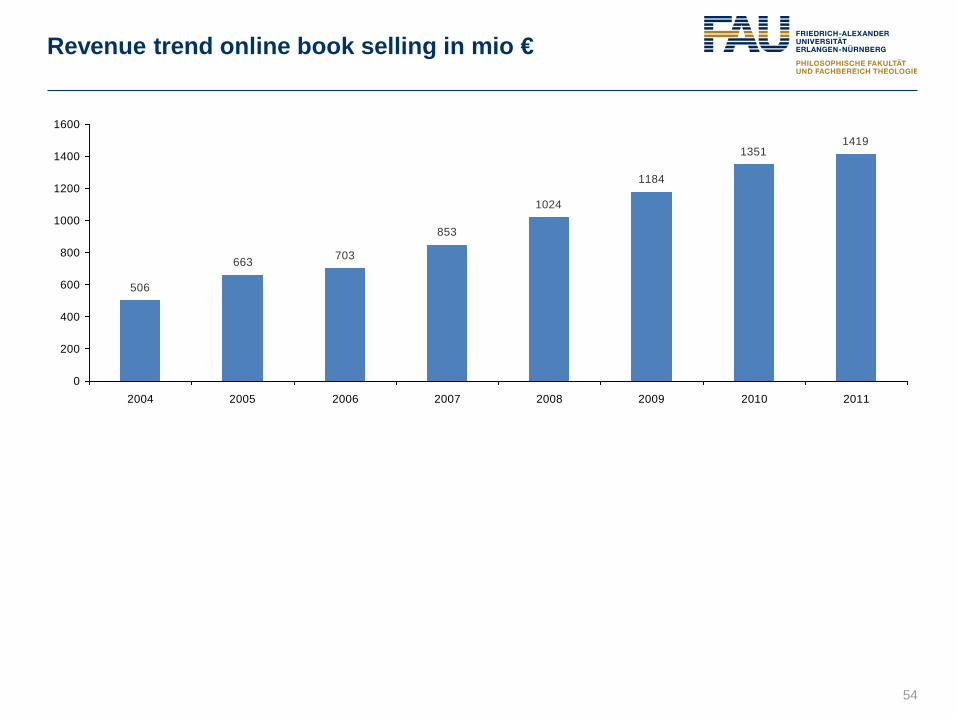

Revenue trend online book selling in mio €

54

663 703

853

1024

1184

13511419

506

0

200

400

600

800

1000

1200

1400

1600

2004 2005 2006 2007 2008 2009 2010 2011

Retail bookshops

55

● Kind of shops

● General assortment (wide assortment)

● Specialized assortment (deep assortment: scientific books, special interests)

● Trends (general assortment shops)

● Step 1: large area bookshops

● Step 2: downsizing as well as non-book assortments (toys, paper, cookies,…)

223 230

898

1,500

1,775

5,065

Revenues 2009 (in million Euros)

book clubs

department store

diverse

online and catalog selling

direct selling of publishing houses

book trader

Retail bookshops

56 Photos: Svenja Hagenhoff, August 8th, 2012; Bookshop Rupprecht, Erlangen, Germany

Retail bookshops

57 Photos: Svenja Hagenhoff, August 8th, 2012; Bookshop Thalia Palm & Enke, Erlangen, Germany

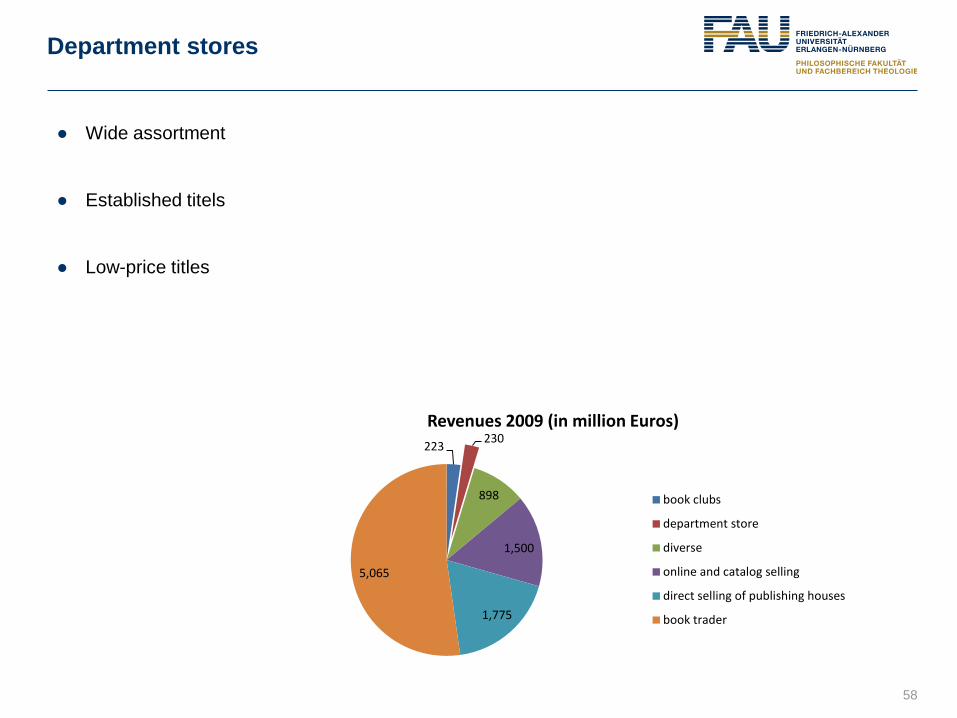

Department stores

58

223 230

898

1,500

1,775

5,065

Revenues 2009 (in million Euros)

book clubs

department store

diverse

online and catalog selling

direct selling of publishing houses

book trader

● Wide assortment

● Established titels

● Low-price titles

Department stores

59 Photos: Svenja Hagenhoff, August 8th, 2012; Department store Galeria Kaufhof, Erlangen, Germany

Online trading

60

223 230

898

1,500

1,775

5,065

Revenues 2009 (in million Euros)

book clubs

department store

diverse

online and catalog selling

direct selling of publishing houses

book trader

● Electronic market places

● Online warehouses, e.g. amazon

● All kinds of goods

● E.g. amazon.de, otto.de

● Online book stores

● Only books

● E.g. libreka.de, buecher.de

● Online book stores of traditional book stores

● E.g. Thalia.de, rupprecht.de, hugendubel.de

● Digital marketplaces for ebooks (only digital goods), e.g. iTunes, PagePlace, textunes

Online warehouses

61

Online bookshops

62

Online book stores of traditional book stores

63

Digital market places

64

iTunes from Apple PagePlace from T-Online

Textunes

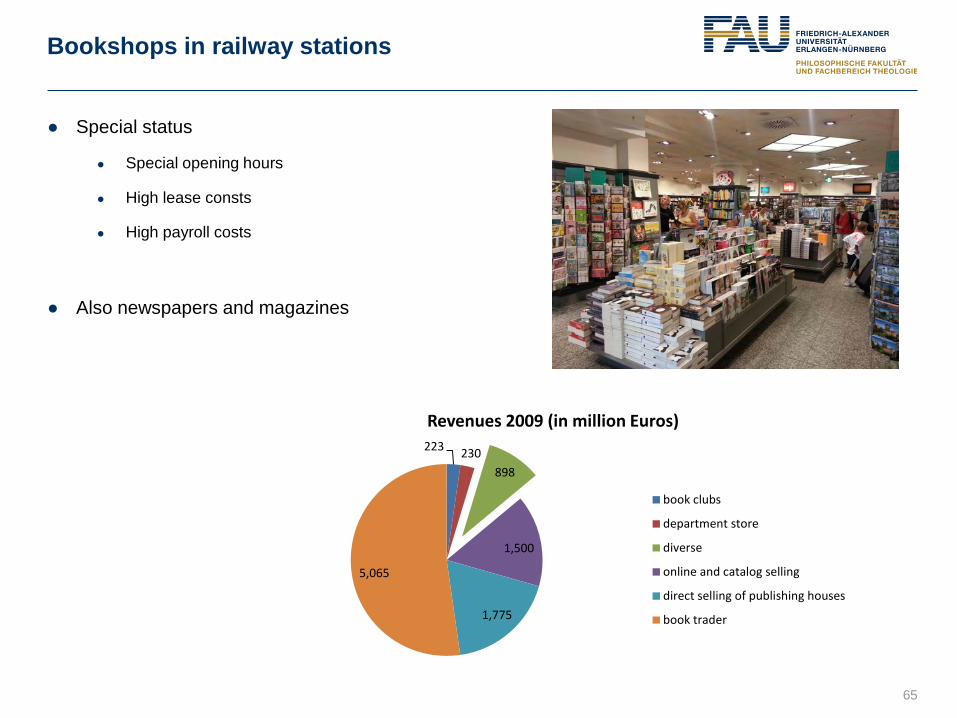

Bookshops in railway stations

65

● Special status

● Special opening hours

● High lease consts

● High payroll costs

● Also newspapers and magazines

223 230 898

1,500

1,775

5,065

Revenues 2009 (in million Euros)

book clubs

department store

diverse

online and catalog selling

direct selling of publishing houses

book trader

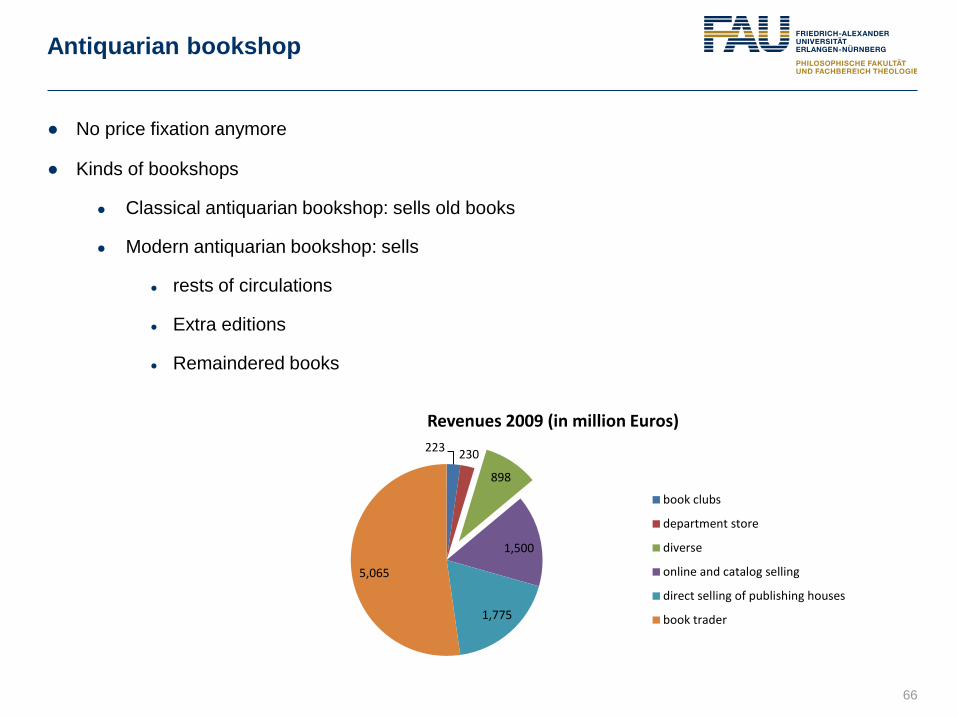

Antiquarian bookshop

66

● No price fixation anymore

● Kinds of bookshops

● Classical antiquarian bookshop: sells old books

● Modern antiquarian bookshop: sells

● rests of circulations

● Extra editions

● Remaindered books

223 230

898

1,500

1,775

5,065

Revenues 2009 (in million Euros)

book clubs

department store

diverse

online and catalog selling

direct selling of publishing houses

book trader

Secondary markets

67 Photos: Svenja Hagenhoff, August 8th, 2012; drugstore Müller, Erlangen, Germany

Books as additional assortment in supermarkets, drugstores etc.

223 230

898

1,500

1,775

5,065

Revenues 2009 (in million Euros)

book clubs

department store

diverse

online and catalog selling

direct selling of publishing houses

book trader

Book clubs

68 Photos: Svenja Hagenhoff, August 8th, 2012; drugstore Müller, Erlangen, Germany

● Subscription model

● Customer

● needs to be member of the club

● Has to buy at least a certain number of books per time

223

230

898

1,500

1,775

5,065

Revenues 2009 (in million Euros)

book clubs

department store

diverse

online and catalog selling

direct selling of publishing houses

book trader

Book revenues: trade groups (2011, in %)

69 Data from PricewaterhouseCoopers: German Entertainment and Media Outlook: 2011-2015. Frankfurt 2012

34

16 14

10

9

6

5 5 3

Fiction books

Children and youth books

Advice booklets

Non-fiction books

School and learning

Travel

Natural Sciences, Medicine, Computer Sciences

Humanities, Arts, Music

Social Sciences, Economics, Law

Revenue trend book market

70

9,067 9,076 9,159

9,260

9,576 9,614 9,691 9,734 9,782

9,889 10,023

10,139 10,246

8,400

8,600

8,800

9,000

9,200

9,400

9,600

9,800

10,000

10,200

10,400

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Reve

nues

in m

illio

n Eu

ro

Data from PricewaterhouseCoopers: German Entertainment and Media Outlook: 2011-2015. Frankfurt 2012

2012-2015 estimated

The biggest German book traders 2009

71

910

743

170 165 88 85 74 72

0

100

200

300

400

500

600

700

800

900

1,000

Revenues in million Euro (total 2,300 million Euro)

Data from PricewaterhouseCoopers: German Entertainment and Media Outlook: 2011-2015. Frankfurt 2012

72

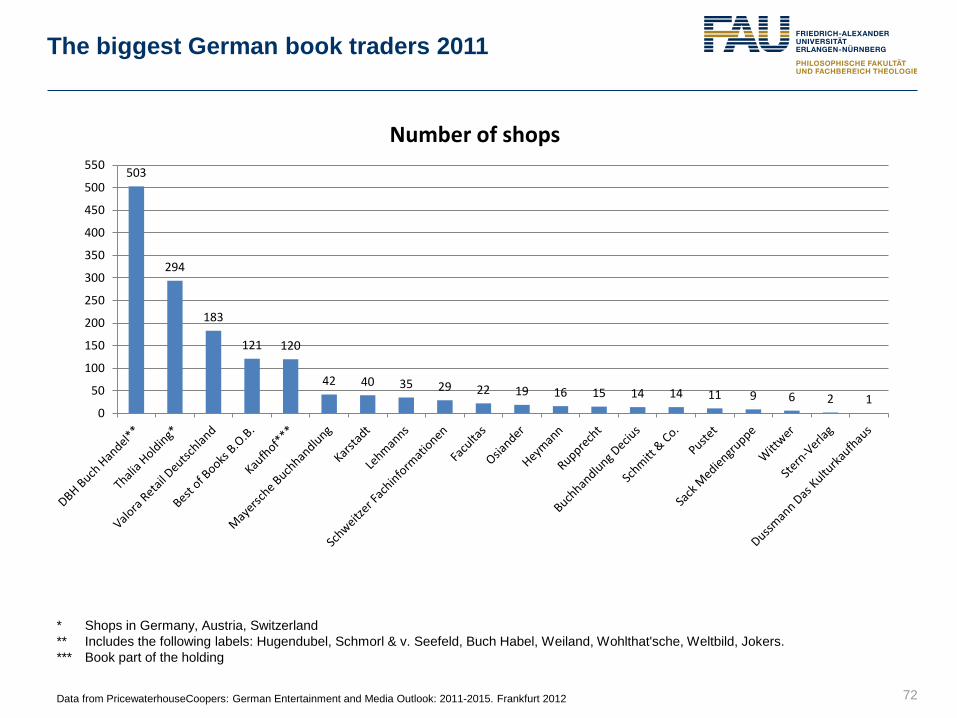

* Shops in Germany, Austria, Switzerland ** Includes the following labels: Hugendubel, Schmorl & v. Seefeld, Buch Habel, Weiland, Wohlthat'sche, Weltbild, Jokers. *** Book part of the holding

503

294

183

121 120

42 40 35 29 22 19 16 15 14 14 11 9 6 2 1 0

50

100

150

200

250

300

350

400

450

500

550

Number of shops

The biggest German book traders 2011

Data from PricewaterhouseCoopers: German Entertainment and Media Outlook: 2011-2015. Frankfurt 2012

Revenue trend books

73

4,195

4,388

4,507

4,797

4,779

4,867

4,974

5,086

5,185

5,278

2,778

2,126

2,144

2,060

2,015

2,000

2,015

2,025

2,032

2,037

2,287

3,062

2,963

2,834

2,940

2,915

2,900

2,912

2,922

2,931

0

2000

4000

6000

8000

10000

12000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Revenue non-fiction books print (in million €)

Revenue school and lecture books (in million €)

Revenue fiction books total (in million €)

Data from PricewaterhouseCoopers: German Entertainment and Media Outlook: 2011-2015. Frankfurt 2012

Outline

● Media Market in General

● Markets for Specific Types of Media

● E-Publishing and Paid Digital Content

● Regulatory Aspects

● Innovative Business Models

● Results of a Survey: Crossmedia Publishing

74

E-Publishing and Paid Digital Content

● Market Data E-Publishing

● Reader‘s behaviour

● Publishing Houses‘ behaviour

● Paid Digital Content and Services as a Challenge

75

Ebook market 2011

76

Values Revenues in million € 38

Revenue trend (basis: 2010) in % 77

Sold ebooks in million 4.70

Ebook share of sales of total revenues in % 1

Data from statista.de

Ebook revenues fictional books

77

Revenues in Millionen Euro (data 2012-2015 estimated)

21

67

137

216

287

355

30

50

100

150

200

250

300

350

400

2009 2010 2011 2012 2013 2014 2015

Data PwC, German Entertainment and Media Outlook: 2011-2015

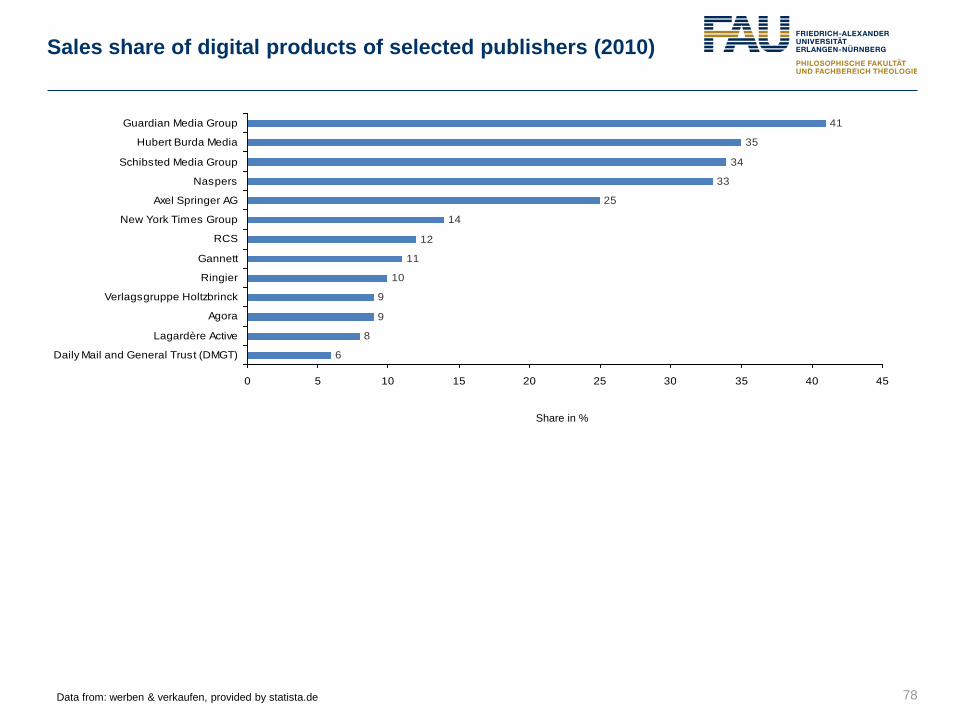

Sales share of digital products of selected publishers (2010)

78 Data from: werben & verkaufen, provided by statista.de

6

8

9

9

10

11

12

14

25

33

34

35

41

0 5 10 15 20 25 30 35 40 45

Daily Mail and General Trust (DMGT)

Lagardère Active

Agora

Verlagsgruppe Holtzbrinck

Ringier

Gannett

RCS

New York Times Group

Axel Springer AG

Naspers

Schibsted Media Group

Hubert Burda Media

Guardian Media Group

Share in %

E-Book devices

79

Kindle 4 Oyo 2 SONY PRS T1 Kobo Reade Touch

TouchMe iPad Samsung Galaxy

Date of appearance

2011 2011 2011 2011 2011 2011 2011

Manufacturer Amazon Thalia / Medion Sony Kobo Thalia/Smartscreens

Apple Samsung

Disitribution Online via Amazon

Thalia Booktrader Diverse shops Diverse shops Thalia booktrader Diverse shops Diverse shops

File transfer WIFI, PC WIFI, PC WIFI, PC WIFI, PC PC

WIWI, 3G, PC WIWI, 3G, PC

File formats AZW, TXT, PDF, unprotected MOBI, PRC, HTML, DOC

EPUB, PDF, TXT, HTML

EPUB, PDF, TXT, HTML

EPUB, PDF, MOBI, PDF, TXT, HTML, RTF, CBZ, CBR

ePub, PDF, Mobi, HTML, TXT, PDB, RTF, LRC, FB2, TVT, MPG, AVI

via Apps every format possible

via Apps every format possible

Shopping facilities

Amazon kindle store

via WIFI at Thalia.de and via PC at every independent

via WIFI at the Sony e-book store and via PC at every independent

at the Kobo e-book store and at every independent

via WIFI at Thalia.de and via PC at every independent

Every online bookstore

Every online bookstore

Operation 10 physical buttons

Touchscreen, 4 physical Buttons

Touchscreen and 5 physical buttons

Touchscreen and 5 physical buttons

Touchscreen and 4 physical buttons

Touchscreen and 3 physical buttons

Touchscreen and 3 physical buttons

Additional functions

MP3 player MP3 player MP3 player

MP3 Player MP3 player, camera, videos

MP3 player, camera, videos

Price in Euro 99 139 149 139 60 500 - 800 460-630

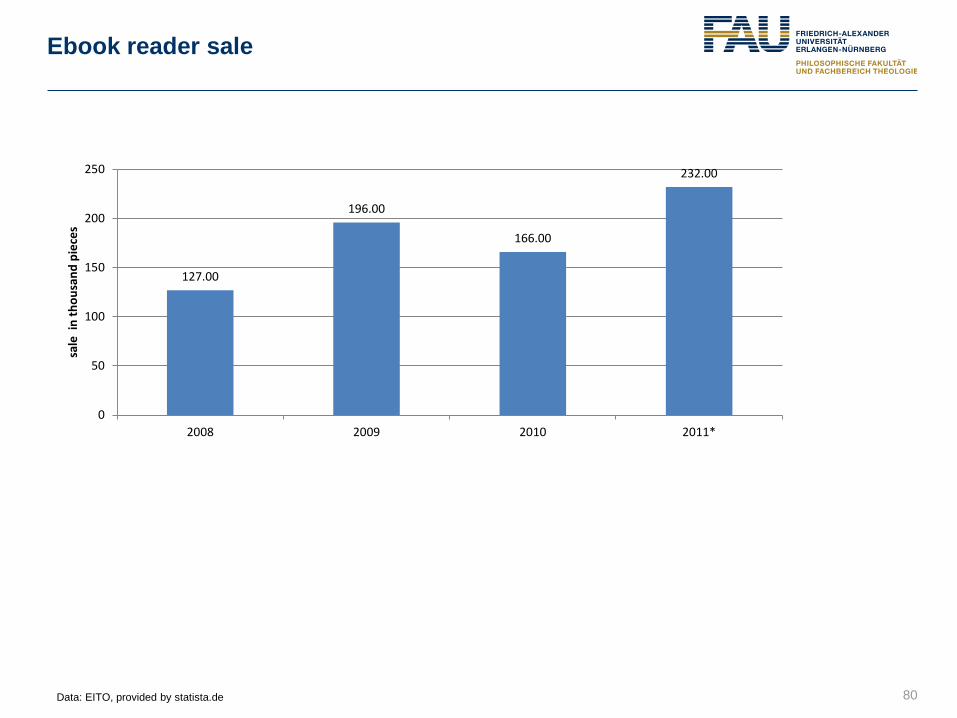

Ebook reader sale

80

127.00

196.00

166.00

232.00

0

50

100

150

200

250

2008 2009 2010 2011*

sale

in

thou

sand

pie

ces

Data: EITO, provided by statista.de

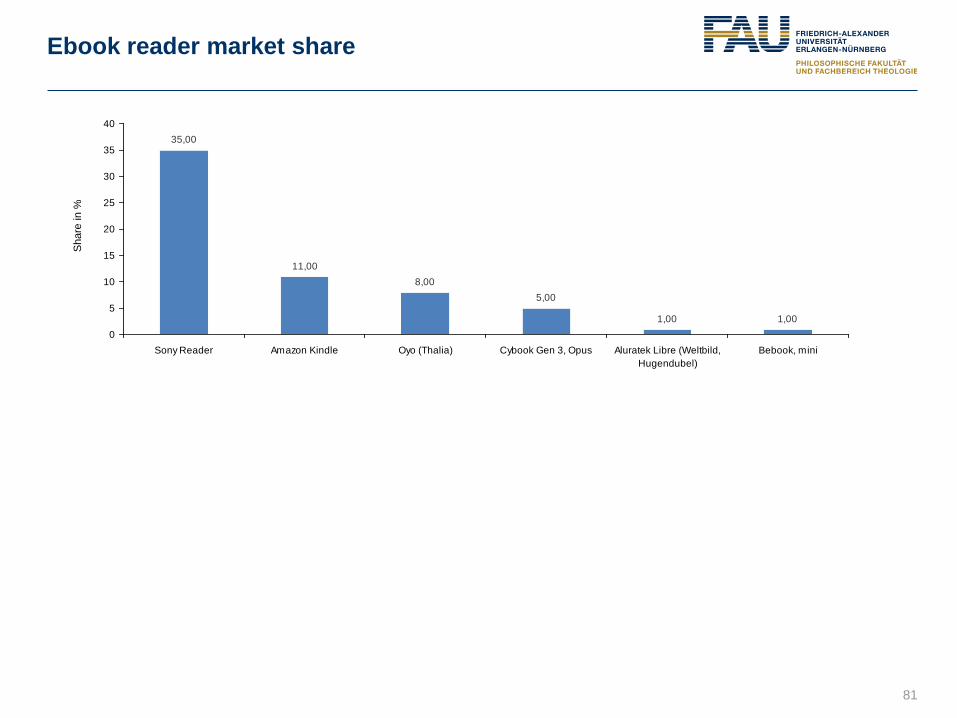

Ebook reader market share

81

11,008,00

5,00

1,00 1,00

35,00

0

5

10

15

20

25

30

35

40

Sony Reader Amazon Kindle Oyo (Thalia) Cybook Gen 3, Opus Aluratek Libre (Weltbild,Hugendubel)

Bebook, mini

Sha

re in

%

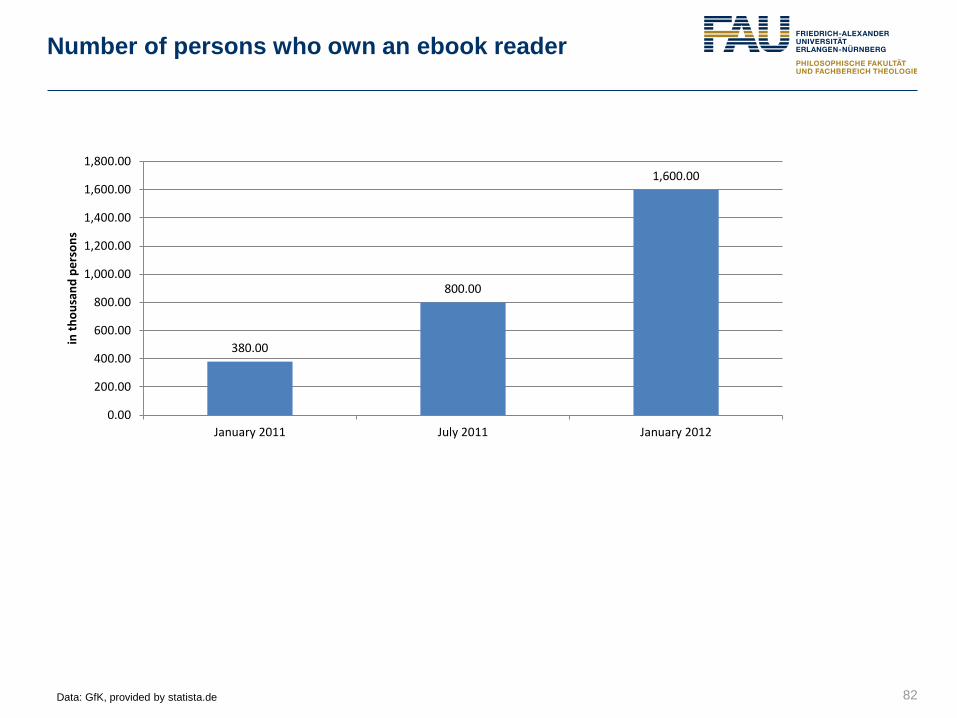

Number of persons who own an ebook reader

82 Data: GfK, provided by statista.de

380.00

800.00

1,600.00

0.00

200.00

400.00

600.00

800.00

1,000.00

1,200.00

1,400.00

1,600.00

1,800.00

January 2011 July 2011 January 2012

in th

ousa

nd p

erso

ns

Willingness to pay for an ebook reader (2011)

83

1%

3%

11%

22%

41%

22%

0% 5% 10% 15% 20% 25% 30% 35% 40% 45%

more than €300

€200–€300

€150–€200

€100–€150

€50–€100

up to €50

Data from: GfK Media*Scope

Average price of an ebook reader: 135 €

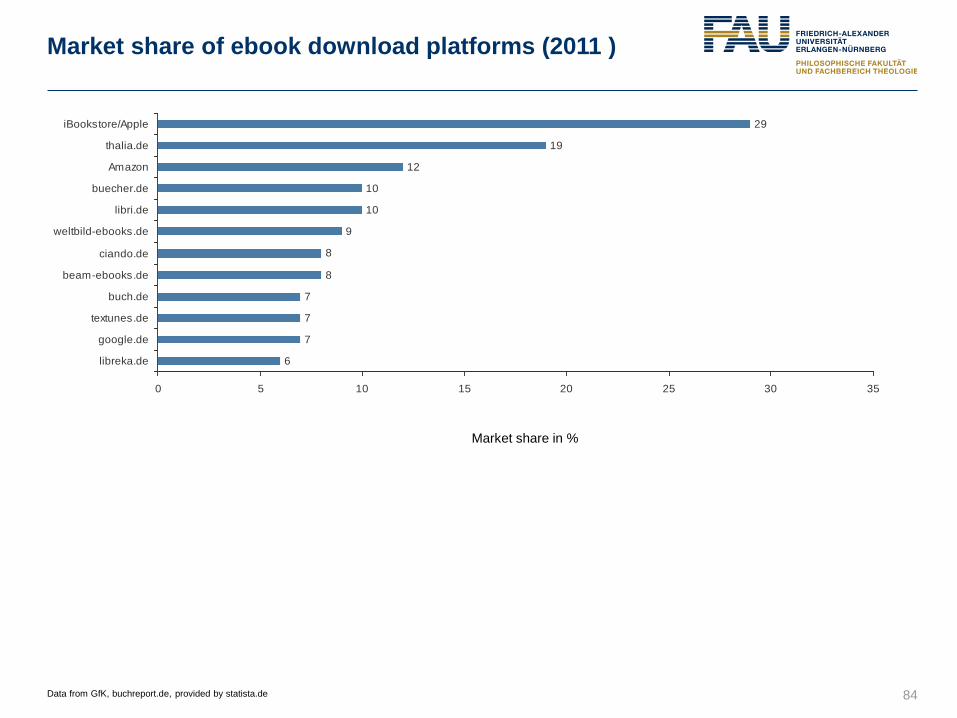

Market share of ebook download platforms (2011 )

84

Market share in %

6

7

7

7

8

8

9

10

10

12

19

29

0 5 10 15 20 25 30 35

libreka.de

google.de

textunes.de

buch.de

beam-ebooks.de

ciando.de

weltbild-ebooks.de

libri.de

buecher.de

Amazon

thalia.de

iBookstore/Apple

Data from GfK, buchreport.de, provided by statista.de

E-Publishing and Paid Digital Content

● Market Data E-Publishing

● Reader‘s behaviour

● Publishing Houses‘ behaviour

● Paid Digital Content and Services as a Challenge

85

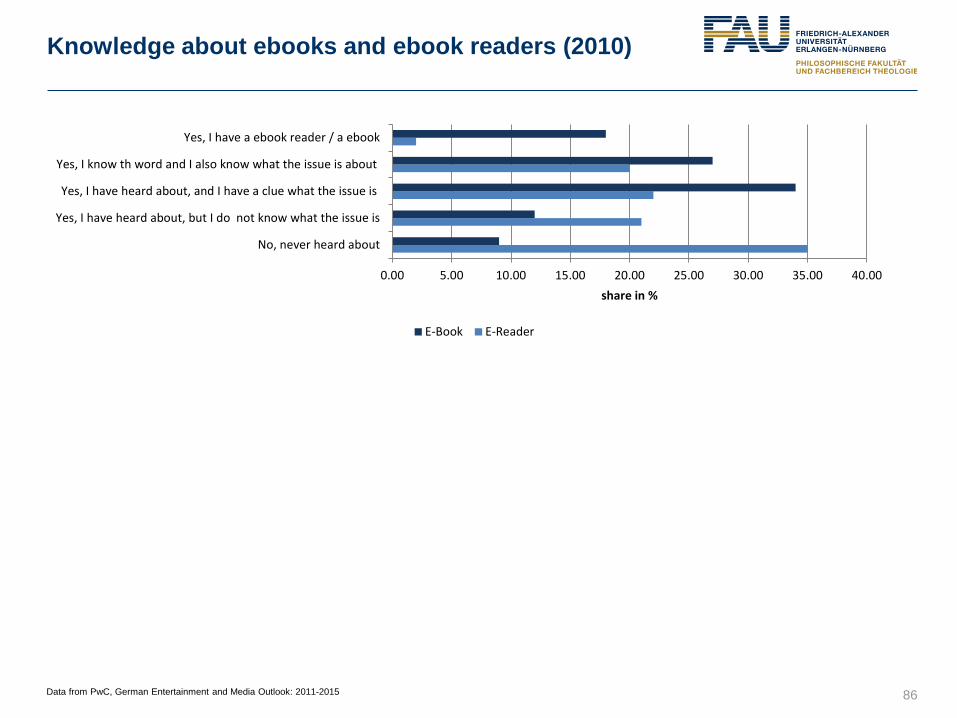

Knowledge about ebooks and ebook readers (2010)

86

0.00 5.00 10.00 15.00 20.00 25.00 30.00 35.00 40.00

No, never heard about

Yes, I have heard about, but I do not know what the issue is

Yes, I have heard about, and I have a clue what the issue is

Yes, I know th word and I also know what the issue is about

Yes, I have a ebook reader / a ebook

share in %

E-Book E-Reader

Data from PwC, German Entertainment and Media Outlook: 2011-2015

Printed books or ebooks buying behaviour (2012)

87

0.00 5.00 10.00 15.00 20.00 25.00 30.00 35.00 40.00 45.00 50.00

I only buy printed books

I usually buy printed books

I buy printed books as well as ebooks

I do not / I seldom buy books in general

I usually buy ebooks

no answer

I only buy ebooks

Share in %

Data from German Publishers and Book Sellers Association , Markt mit Perspektiven - Das E-Book in Deutschland 2011, provided by statista.de

Agreement to statements

88

0 10 20 30 40 50 60 70 80 90 100

I like it having books at home in my shelf

I love printed books. Electronic devices have nothing on thereading experiance

I prefer to invest in printed books

I do not want to read from displays

I think that reading from screens is not good for the eyes (even ifit is flickerfree)

E-Books are ecofriendly because thy save paper

E-books can be sold cheaper than the printed book

I can solve my space problems with ebooks

E-Books are modern and thy will be the new way of reading

Share in % of all asked persons

2009

2010

2011

2012

Data from GfK Panel Services Deutschland (Media*Scope Buch), provided by statista.de

For what purpose do you use your tablet? (2011)

89 Data from: PWC, provided by statista.de

0 10 20 30 40 50 60 70 80 90 100

Search engines

News of the day

using the internet without a specific intention

Watching videos

Using social networks

Onlinebanking

Playing games

Blogging

Using the telephone

share in %

Frequency of usage of digital magazines on iPads

90

0 5 10 15 20 25 30 35 40

Many times a week

Daily / nearly daily

Once a week

Many times a month

Once a month

I never used a digital magzine on my ipad

share in%

Data from: Kirchner + Robrecht; pangea labs, provided by statista.de

Mobile applications: usage (2011)

91 Data from: IP Deutschland, provided by statista.de

0 10 20 30 40 50 60 70 80

News

Weather

Games

Entertainment

Social media

Music

Search engines

Sport

Personal information (e.g. photos)

Price check

Books and education

Travel

share in %

Arguments against ebook reader (2010)

92

0

10

20

30

40

50

60

Too expensive Dependency(energy)

Haptic: no bookto hold in the

hand

Cannot place itinto the

bookshelf

Do not want tohave moreelectronic

devices

Not enoughebook choice

Too complicated None of thementioned

aspects above

shar

e in

%

Data from: Gesellschaft für innovative Marktforschung mbH, provided by statista.de

E-Publishing and Paid Digital Content

● Market Data E-Publishing

● Reader‘s behaviour

● Publishing Houses‘ behaviour

● Paid Digital Content as a Challenge

93

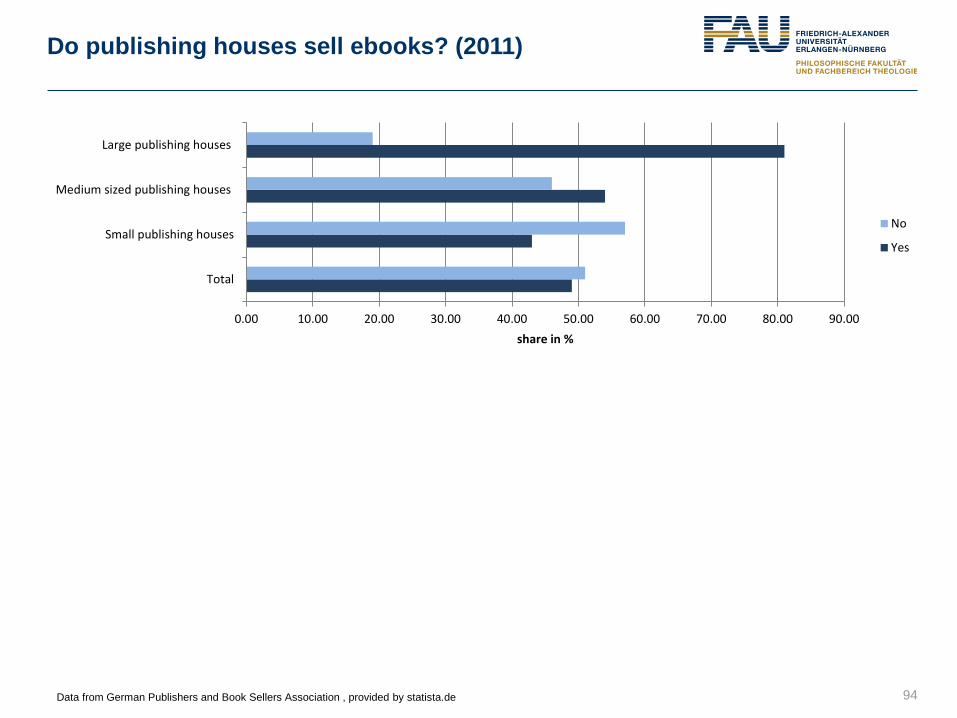

Do publishing houses sell ebooks? (2011)

94

0.00 10.00 20.00 30.00 40.00 50.00 60.00 70.00 80.00 90.00

Total

Small publishing houses

Medium sized publishing houses

Large publishing houses

share in %

No

Yes

Data from German Publishers and Book Sellers Association , provided by statista.de

Challenges concerning launching ebooks in your publishing house (2011)

95 Data from German Publishers and Book Sellers Association, provided by statista.de

0 5 10 15 20 25 30

Organisational structure and culture

Missing standards in formats

Missing acceptance by customers

Piracy

Missing know-how

Ebook reader too expensive

Missing budget

Fixed price agreements

share in %

Ebook investments in publishing houses (2010)

96 Data from German Publishers and Book Sellers Association , provided by statista.de

0.00

10.00

20.00

30.00

40.00

50.00

60.00

70.00

80.00

90.00

100.00

Total Small publishinghouses

medium sizedpublishing houses

Large publishinghouses

Shar

ein

%

Yes

No, but we will within the next 2 years

No, and we neither want

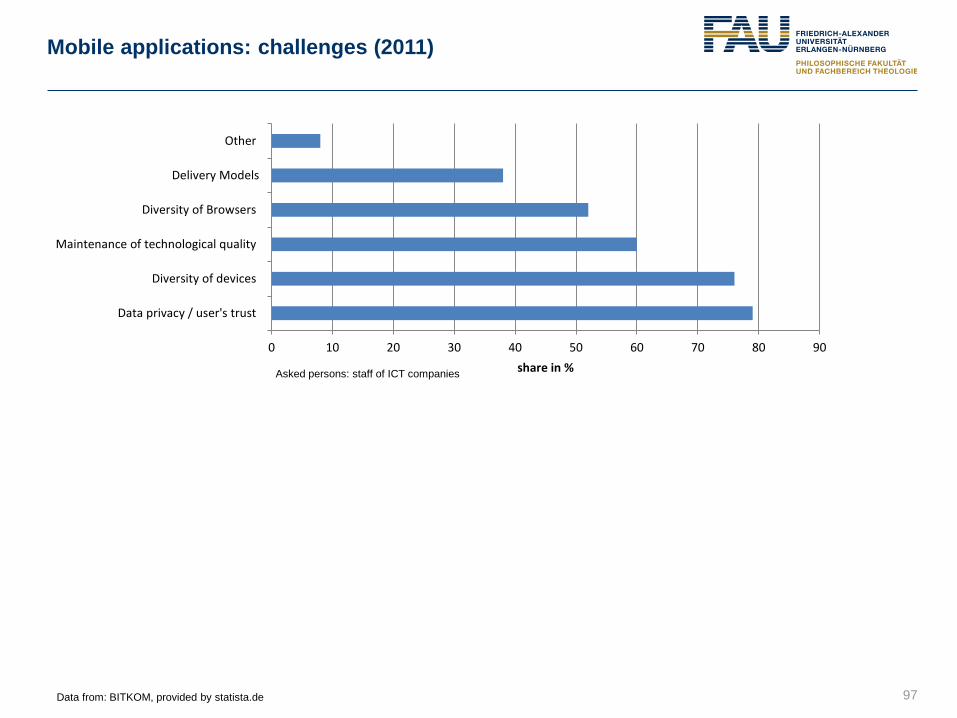

Mobile applications: challenges (2011)

97 Data from: BITKOM, provided by statista.de

0 10 20 30 40 50 60 70 80 90

Data privacy / user's trust

Diversity of devices

Maintenance of technological quality

Diversity of Browsers

Delivery Models

Other

share in % Asked persons: staff of ICT companies

E-Publishing and Paid Digital Content

● Market Data E-Publishing

● Reader‘s behaviour

● Publishing Houses‘ behaviour

● Paid Digital Content and Services as a Challenge

98

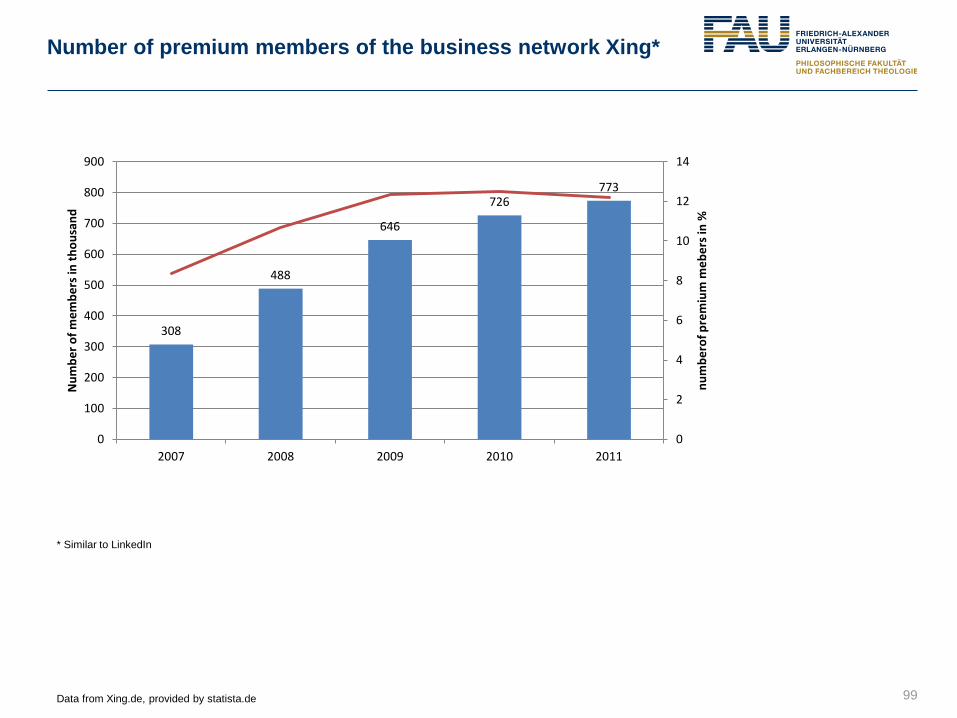

Number of premium members of the business network Xing*

99

308

488

646

726 773

0

2

4

6

8

10

12

14

0

100

200

300

400

500

600

700

800

900

2007 2008 2009 2010 2011

num

bero

f pre

miu

m m

eber

s in

%

Num

ber o

f mem

bers

in th

ousa

nd

Data from Xing.de, provided by statista.de

* Similar to LinkedIn

Paid content on www.test.de

100

860,000

815,000

770,000 756,000

0.00

0.50

1.00

1.50

2.00

2.50

700,000

720,000

740,000

760,000

780,000

800,000

820,000

840,000

860,000

880,000

2007 2008 2009 2010

reve

nue

usag

e

Usage of charged content Revenue by usage of charged content in million €

“Stiftung Warentest (www.test.de) is a German consumer organisation and foundation involved in investigating and comparing goods and services in an unbiased way” (wikipedia.de)

Data from Stiftung Warentest, provided by statista.de

What people think about paid online content (2009)

101 Data from GfK, provided by statista.de

05

101520253035404550

All content should befree, but I would accept

advertisement

All content should befree, and there should

not be anyadvertisement as well

I would pay for content,but I do not want

advertisement

I would pay for content,and I also acceptadvertisement

None of thesestatements matches to

my opinion

shar

ein

%

Germany

Europe

Agreement to statements

102

0 10 20 30 40 50 60 70 80 90

Newspaper and magazine ipad apps are good for an exceptionalmultimedia experience

I think I would read more newspapers and magazines as appsthan as printed product (only reader of charged digital papers

were asked)

Reading newspapers or magaines is more fun than readingprinted products

share in %

Data from Axel Springer, provided by statista.de

Barriers concerning paying for online content

103

0 10 20 30 40 50 60 70 80

Costs too highNo acceptance in society

Technical challengesMissing standards

Problems with data privacyMissing innovation culture

Inadequate educationToo less investment in infrastructure

Too less investments by companiesInvestments are hampered by regulatory parameters

Missing interdisciplinarityLong product life cycles

Public investments in R&D are too smallSkilled worker shortage

share in %

Data from TNS Infratest, provided by statista.de

Outline

● Media Market in General

● Markets for Specific Types of Media

● E-Publishing and Paid Digital Content

● Regulatory Aspects

● Innovative Business Models

● Results of a Survey: Crossmedia Publishing

104

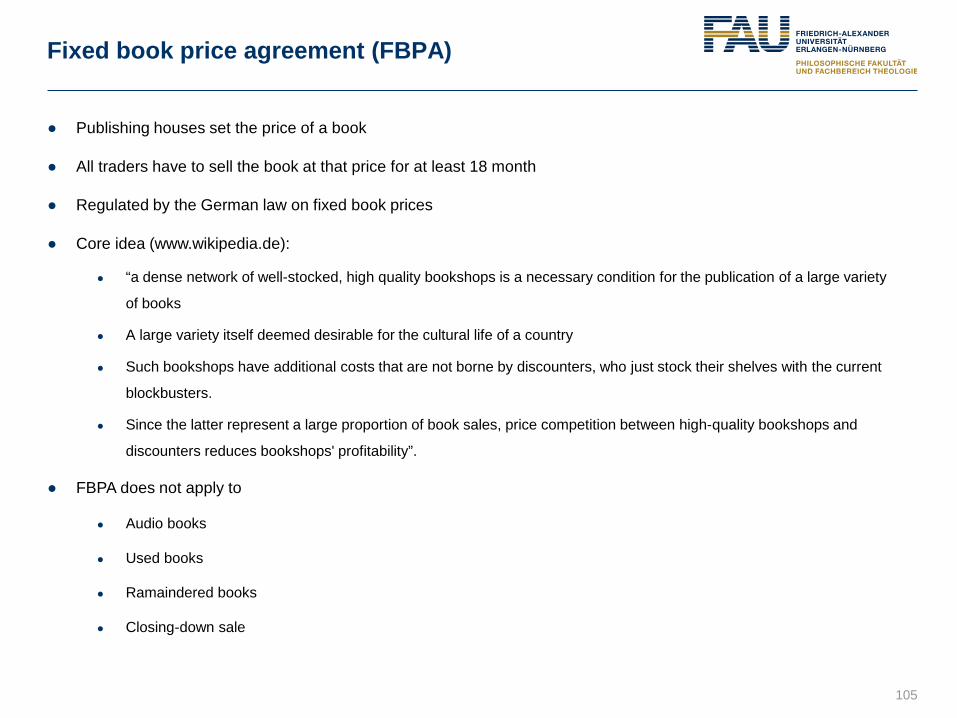

Fixed book price agreement (FBPA)

● Publishing houses set the price of a book

● All traders have to sell the book at that price for at least 18 month

● Regulated by the German law on fixed book prices

● Core idea (www.wikipedia.de):

● “a dense network of well-stocked, high quality bookshops is a necessary condition for the publication of a large variety

of books

● A large variety itself deemed desirable for the cultural life of a country

● Such bookshops have additional costs that are not borne by discounters, who just stock their shelves with the current

blockbusters.

● Since the latter represent a large proportion of book sales, price competition between high-quality bookshops and

discounters reduces bookshops' profitability”.

● FBPA does not apply to

● Audio books

● Used books

● Ramaindered books

● Closing-down sale

105

Sales tax in Europe (selected countries)

106

Country Sales tax % Reduced sales tax % Sales tax for e-books % FBPA Duration FP

Germany 19 7 19 Law 18 month

Austria 20 10 20 Law 24 month

Switzerland 8 2.5 7 Free prices -

U.K 20 0 20 Law 24 month

Denmark 25 25 25 Free prices -

Sweden 25 6 25 No -

Netherlands 19 6 19 Law 12 month

Spain 18 4 18 Law 24 month

France 19.6 7 7 Law 24 month

Luxemburg 15 3 3 Law

Data from German Publishers and Booksellers Association

Outline

● Media Market in General

● Markets for Specific Types of Media

● E-Publishing and Paid Digital Content

● Regulatory Aspects

● Innovative Business Models

● Results of a Survey: Crossmedia Publishing

107

E-Publishing and Paid Digital Content

● Ebook cards

● Epubli

● Skoobe

● Paper C

108

Idea

● www.ebookcards.de

● Voucher for giving away an ebook

● Revenue remains at traditional book store

Customers view

110

Buy a ebook card Go to the website

www.ebookcard.de

Enter the code

(or scan the QR with

your mobile)

Enter your mailadress

and download the

ebook

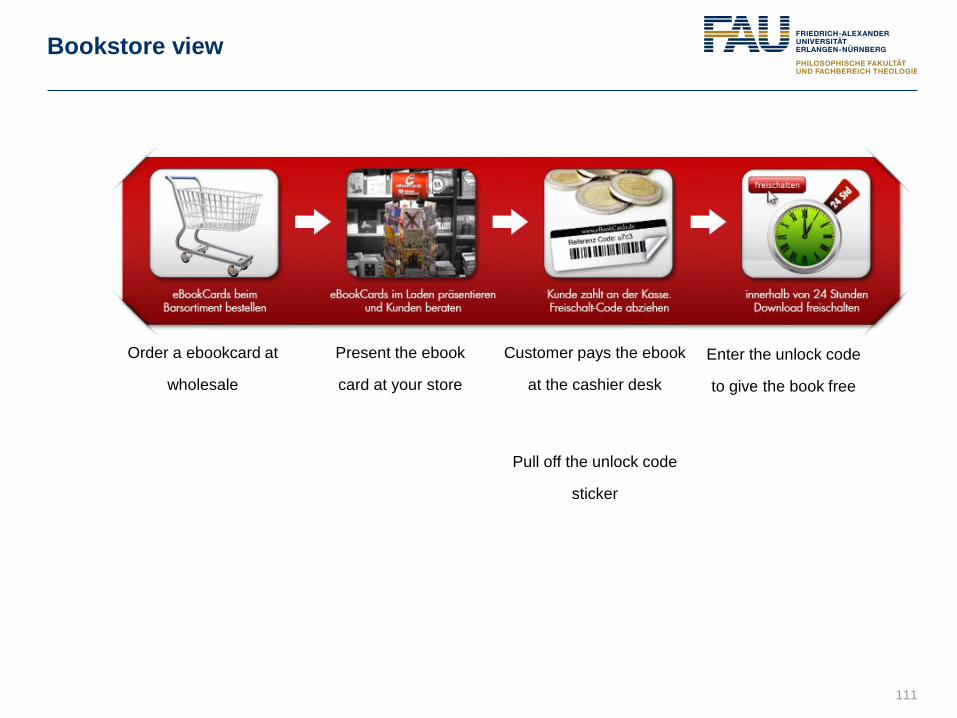

Bookstore view

111

Order a ebookcard at

wholesale

Present the ebook

card at your store

Customer pays the ebook

at the cashier desk

Pull off the unlock code

sticker

Enter the unlock code

to give the book free

E-Publishing and Paid Digital Content

● Ebook cards

● Epubli

● Skoobe

● Paper C

112

Idea

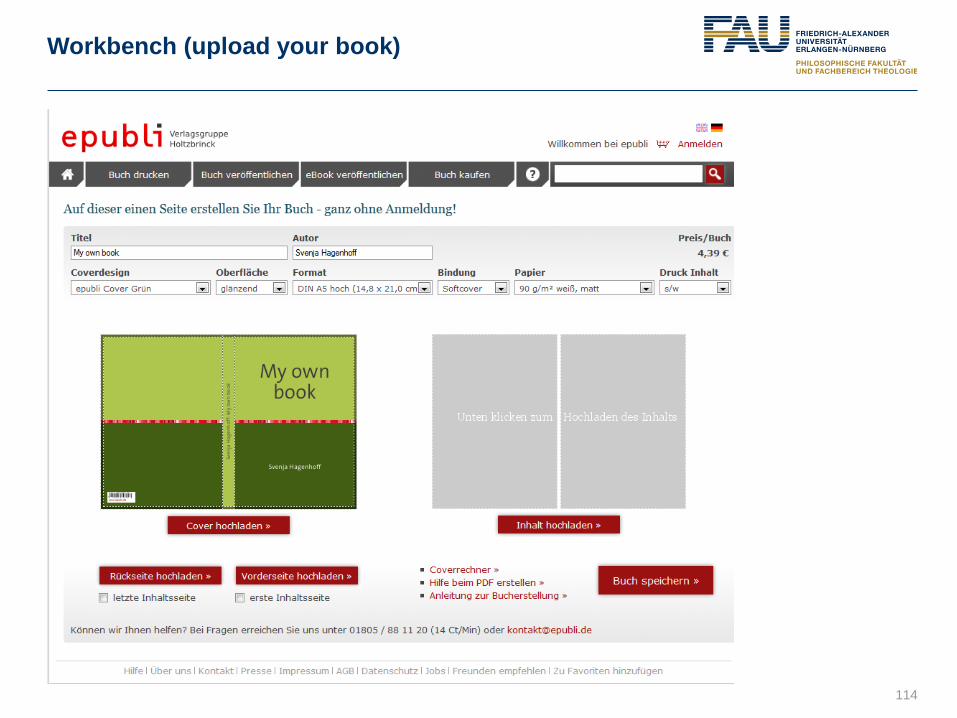

113

● www.epubli.de

● Self publishing platform

● Company of the publishing group Holtzbrinck

● Reactions of established publishing houses

● None (silence)

● Badmouthing (it cannot work, it only produces bad or trivial titles)

Workbench (upload your book)

114

Calculate your royalty

115

E-Publishing and Paid Digital Content

● Ebook cards

● Epubli

● Skoobe

● Paper C

116

Idea

● www.skoobe.de

● Digital store for ebooks

● Flat rate revenue model

● Customer pays 9.99 Euro a month

● Customer can borrow 5 books concurrently

● Customer pays for access to the books and not for possession

● Each book can be used offline for 30 days

● The private library will be synchronized to all devices

117

Library

118

E-Publishing and Paid Digital Content

● Ebook cards

● Epubli

● Skoobe

● Paper C

119

Idea

● www.paperc.de

● Online platform for textbooks

● Price model: Freemium

● Reading is free

● Additional features are priced (e.g. 10 cents per page for printing, tagging, etc.)

● Contains about 15.000 E-Books from 90 national and international publishing houses

120

Homepage

121

A book

122

Outline

● Media Market in General

● Markets for Specific Types of Media

● E-Publishing and Paid Digital Content

● Regulatory Aspects

● Innovative Business Models

● Results of a Survey: Crossmedia Publishing

123

Survey setting

• Topic: crossmedia publishing in specialist publishing houses

• Aim of the survey: to find out about the state of the art of crossmedia publishing

• Questions:

• Do publishers crossmedia publishing?

• How do they do it?

• Are there different degrees of maturity depending on kinds of products or size of the publishing house

• What are the most challenges in crossmedia publishing

• Survey was conducted spring to autumn 2011

• Methodology:

• Qualitative survey: interviews with 13 experts from 13 publishing houses

• Quantitative survey: written questionnaires (441 publishing houses)

• Response rate 17 % (73 datasets)

Characeristics of the sample

Very small companies: < 10 employees, small companies: < 50 employees, medium size companies <250 employees

Very small companies: ≤ 2 Mio. €, small companies: ≤ 10 Mio. €, medium size companies ≤ 50 Mio. €

Size of the publishing house (number of employees) (n=73, failure quota 0.00 %)

Data absolute

Size of the publishing house (revenue) (n=73, failure quota 8.22 %)

Data absolute

Very small companies

Small companies

Medium size companies

Large companies

Not assignable

Very small companies

Small companies

Medium size companies

Large companies

What is your primary source of revenue? (n=73, failure quota 26.03 %)

Data absolute

Professionals (B2B)

Laypersons

Scientific customer

Other

Books (print & electronic)

Magazines (print & electronic)

Loos-leaf collections (print & electronic)

Other

The biggest part of your revenue do come from which kind of customers? (n=73, failure quota 8.22 %)

Data absolute

Kinds of products

126

56

69

8 18

9

25

6

01020304050607080

Books Magazines Newspapers Loose-leafcollections

calendars Newsletter other

num

ber o

f ans

wer

s

Which kinds of products do you produce (print)? (n = 73, failure quota: 0,00 %)

26 25

5

32

17

28

50

17 21

50

10 4

0102030405060

num

ber o

f ans

wer

s Which kinds of products do you produce (electronic)?

(n = 73, failure quota 5,48 %)

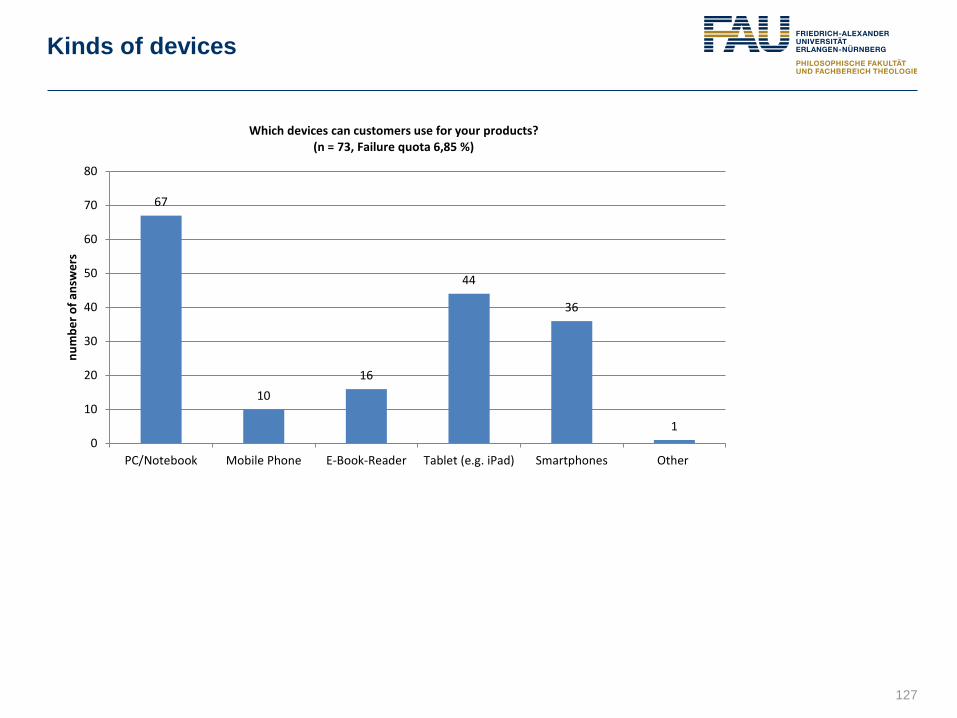

Kinds of devices

127

67

10 16

44

36

1 0

10

20

30

40

50

60

70

80

PC/Notebook Mobile Phone E-Book-Reader Tablet (e.g. iPad) Smartphones Other

num

ber o

f ans

wer

s

Which devices can customers use for your products? (n = 73, Failure quota 6,85 %)

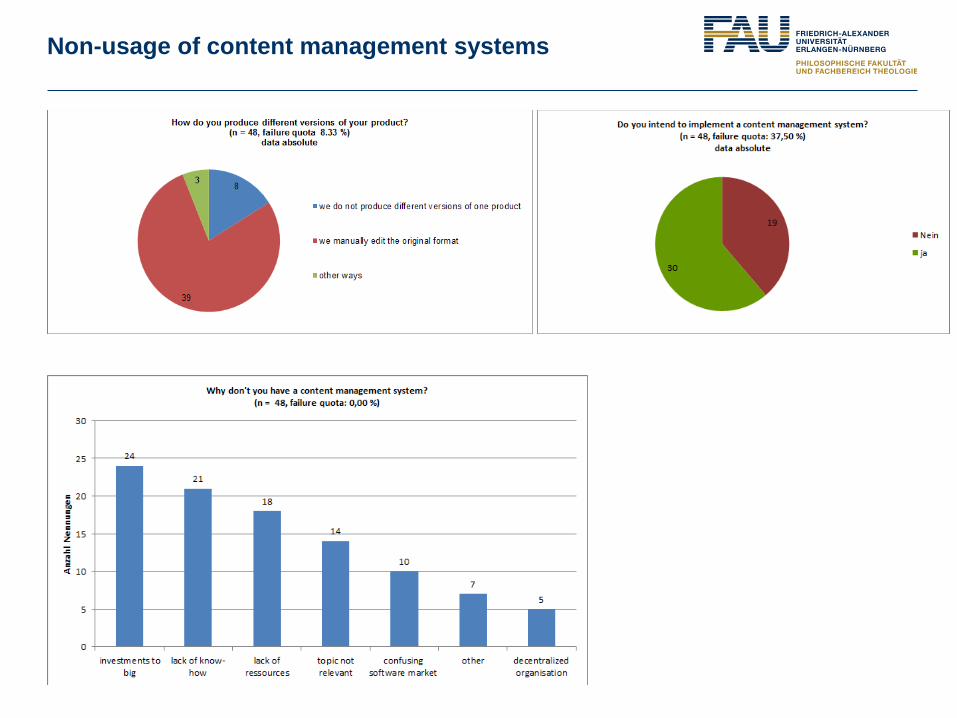

Usage of content management systems (1)

25

48

Do you have a content management system in your publishing house?

(n = 73, failure quota 0,00 %) data absolute

yes

no 1 1 1

4

2 2 2

3

2

0

1

2

3

4

5

2000 2002 2004 2005 2006 2008 2009 2010 2011

num

ber o

f ans

wer

s

When did you start using the software? (n=18, FQ: 28,00 %)

Usage of content management systems (2)

Non-usage of content management systems

The biggest challenge in crossmedia publishing is…

0: I cannot estimate 1: I do not agree 2: I do rather not agree 3: I do rather agree 4: I do agree

1

6

3

1

0

2

2

4

17

28

47

24

34

49

49

27

54

37

23

48

39

21

21

42

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

still thinking in print (n=72, FQ: 1,37 %)

technical aspects (n=73, FQ: 2,74 %)

legal aspects (n=73, FQ: 0,00 %)

lacking of proceeds (=73, FQ: 0,00 %)

characteristics of the product der Produkte (n=73, FQ:0,00 %)

consequences for organisation are not assessable (n=73,FQ: 0,00 %)

consequences for organisation are not controllable(n=72, FQ: 1,37 %)

big investments (n=73, FQ: 0,00 %)

Agreement to the statement: the biggest challenge in crossmedia publishing is ... (Scale normalized, values absolute)

Abstention

negative statement

postitive statement