the future of the guangdong-hong kong-macao greater bay

TRANSCRIPT

GBA Background Document

© Copyright 2022 Foundation, 2019. 1

The Future of the Guangdong-Hong Kong-Macao

Greater Bay Area

Background Document

2022 Foundation

January 2019

GBA Background Document

© Copyright 2022 Foundation, 2019. 2

Contents

0. This Document ................................................................................................................................ 6

1. Introduction .................................................................................................................................... 7

An Economic Region ........................................................................................................................... 8

2. The Region .................................................................................................................................... 11

Historical Background ....................................................................................................................... 11

Regional Economic Profile ................................................................................................................ 12

Linkages and Interactions in the Region ........................................................................................... 15

Trade in Goods .............................................................................................................................. 15

Cargo Flows ................................................................................................................................... 18

Trade in Services ........................................................................................................................... 22

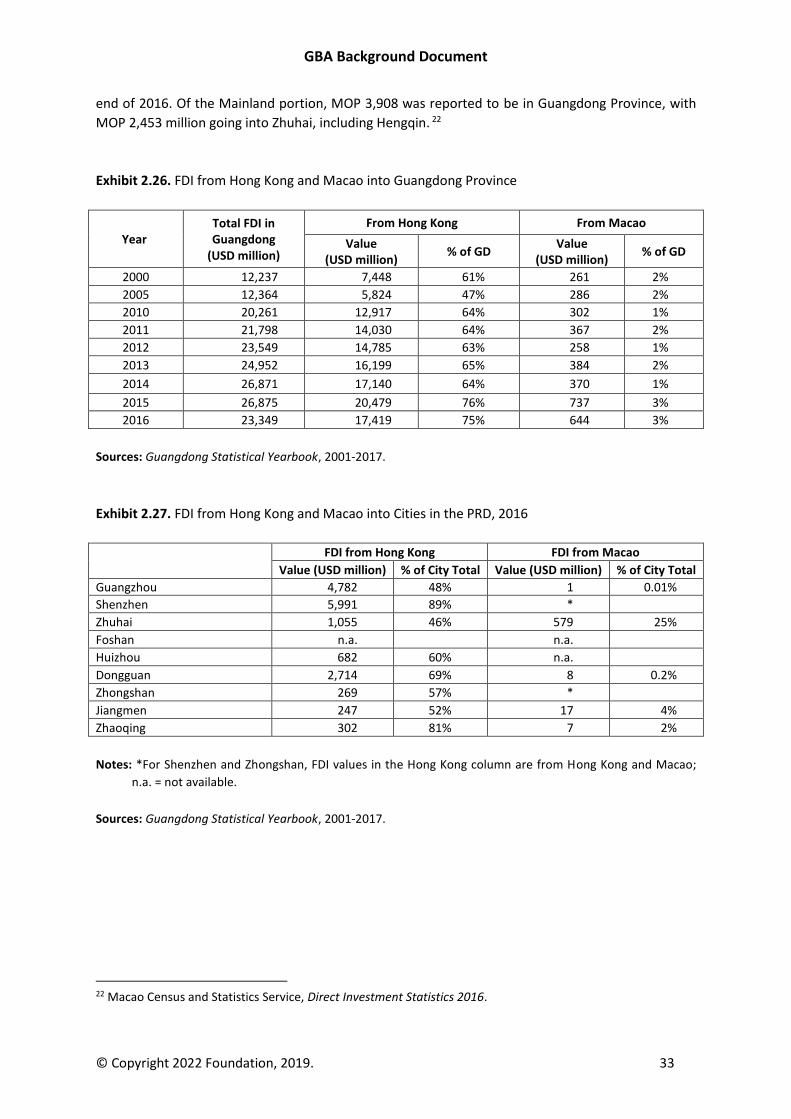

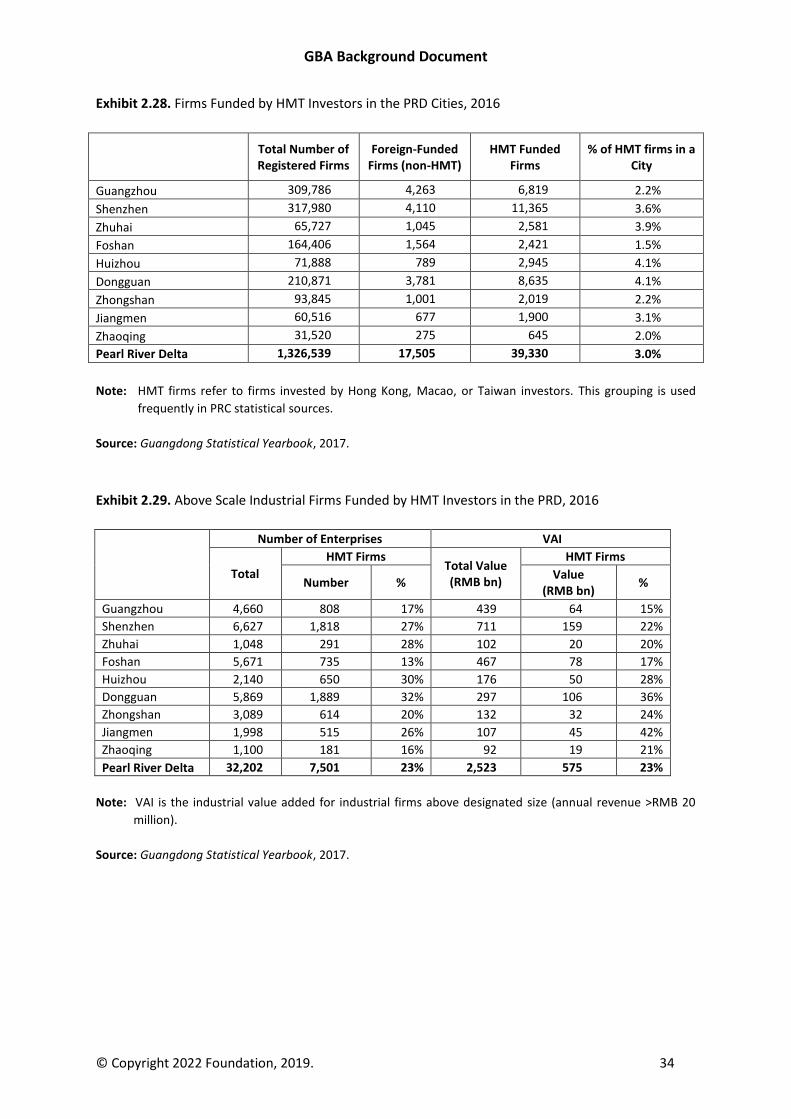

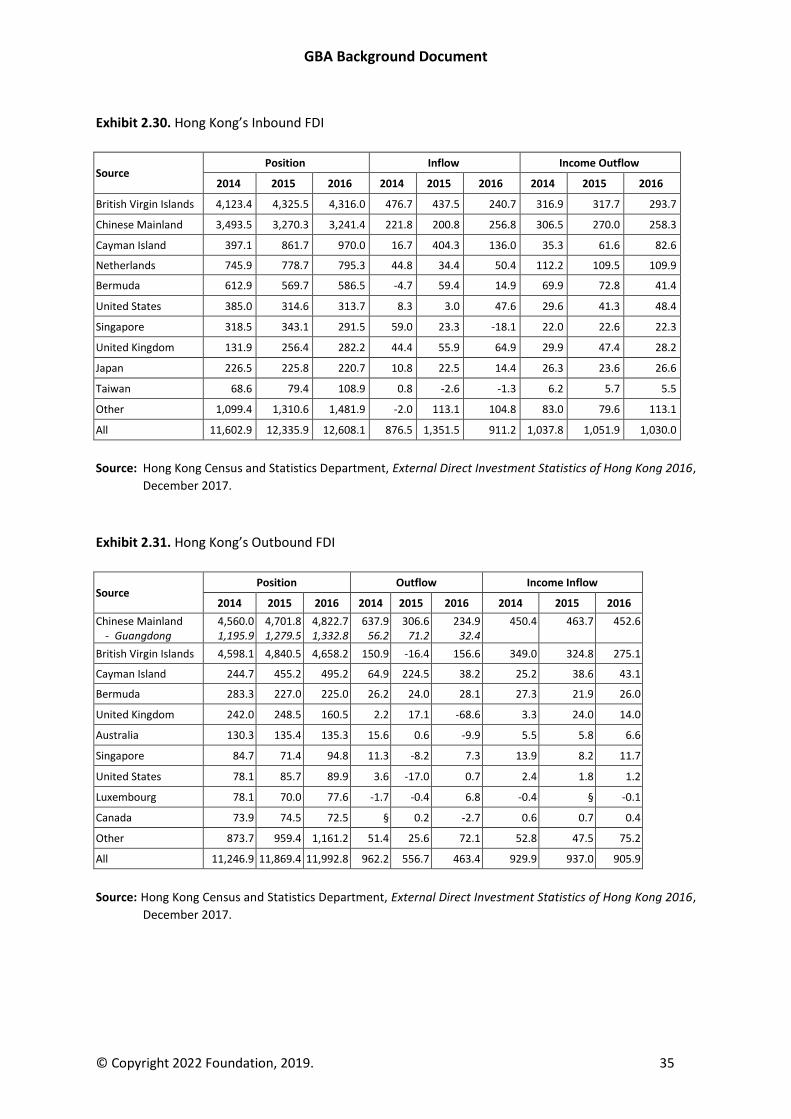

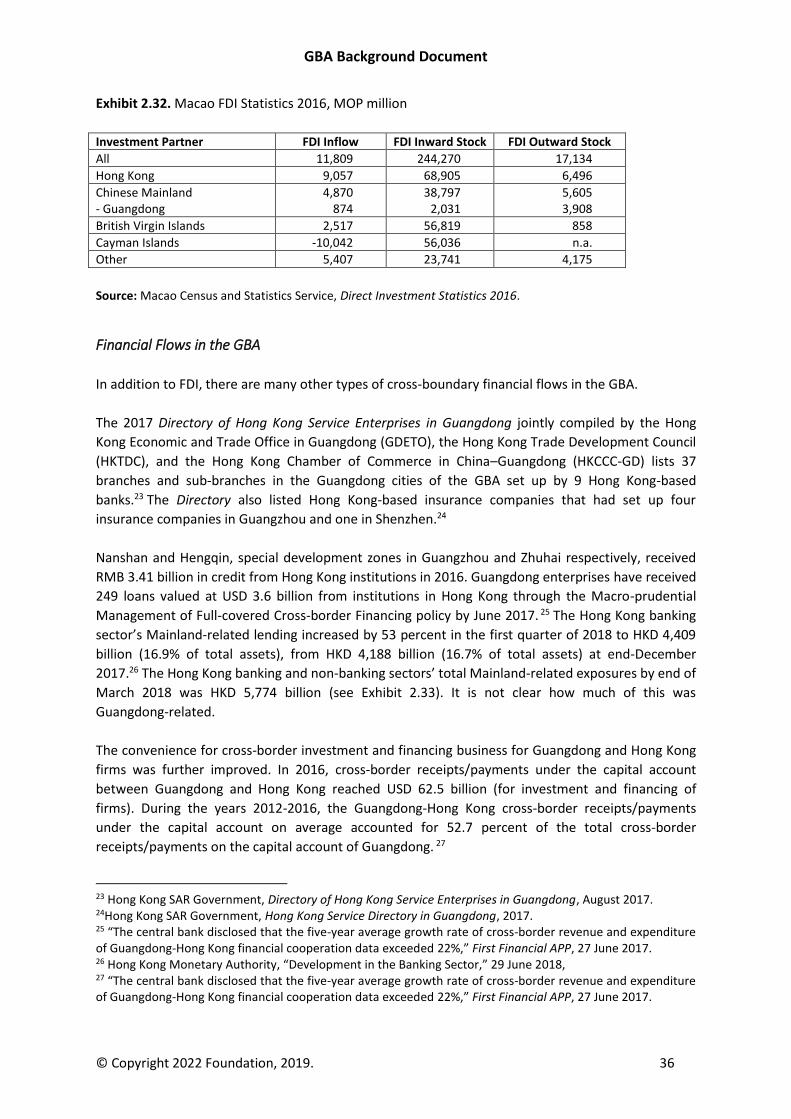

“Foreign Investment” .................................................................................................................... 31

Financial Flows in the GBA ............................................................................................................ 36

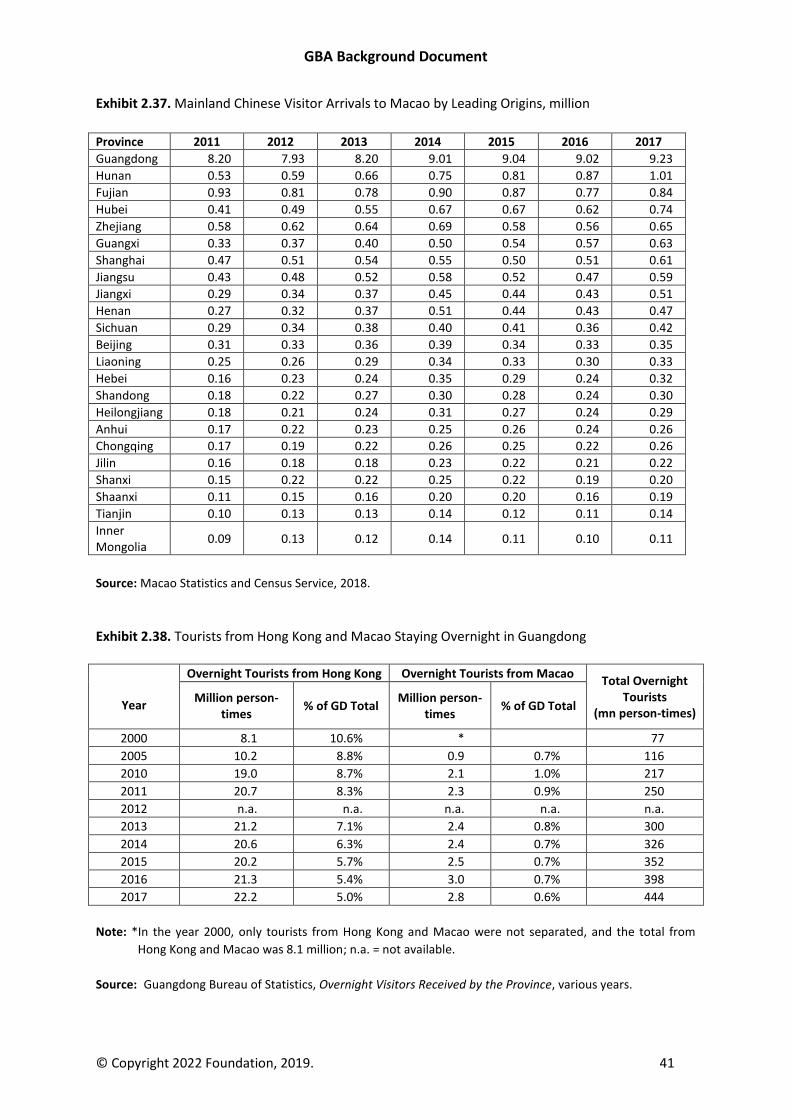

Visitor Flows in the GBA ................................................................................................................ 38

Education Links in the GBA ........................................................................................................... 42

Cultural and Creative Exchange .................................................................................................... 45

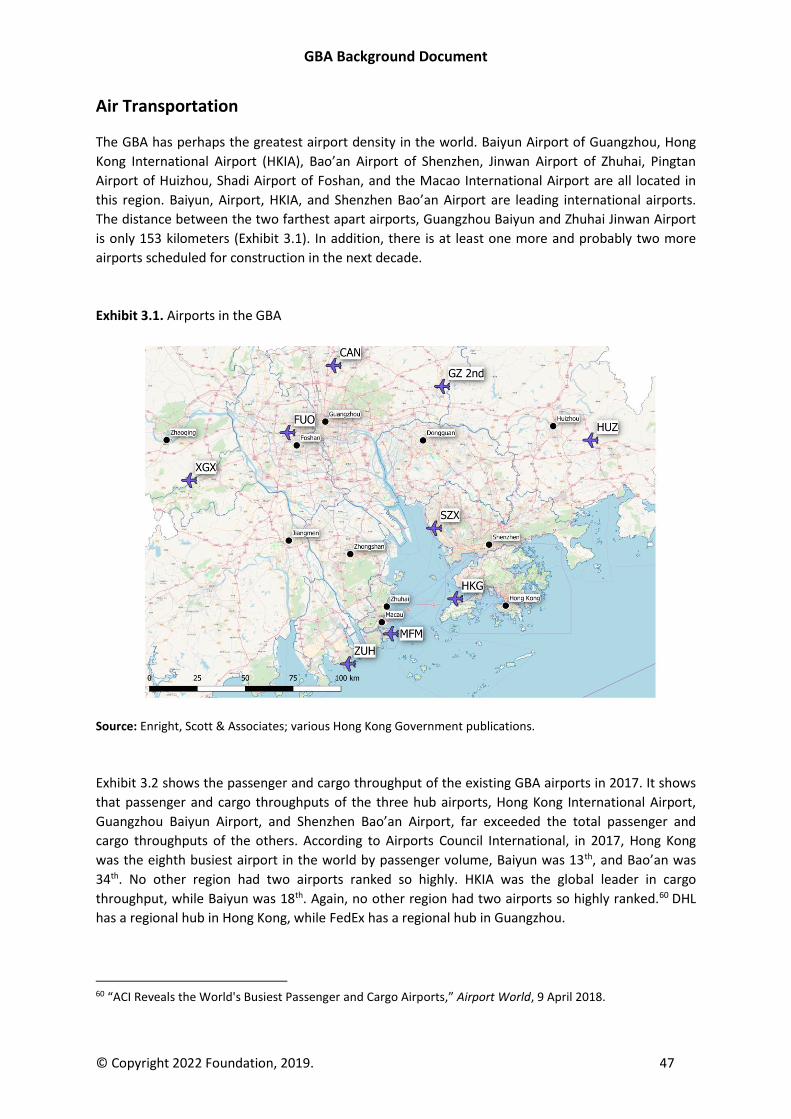

3. The GBA’s Transportation Connectivity ........................................................................................ 46

Air Transportation ............................................................................................................................. 47

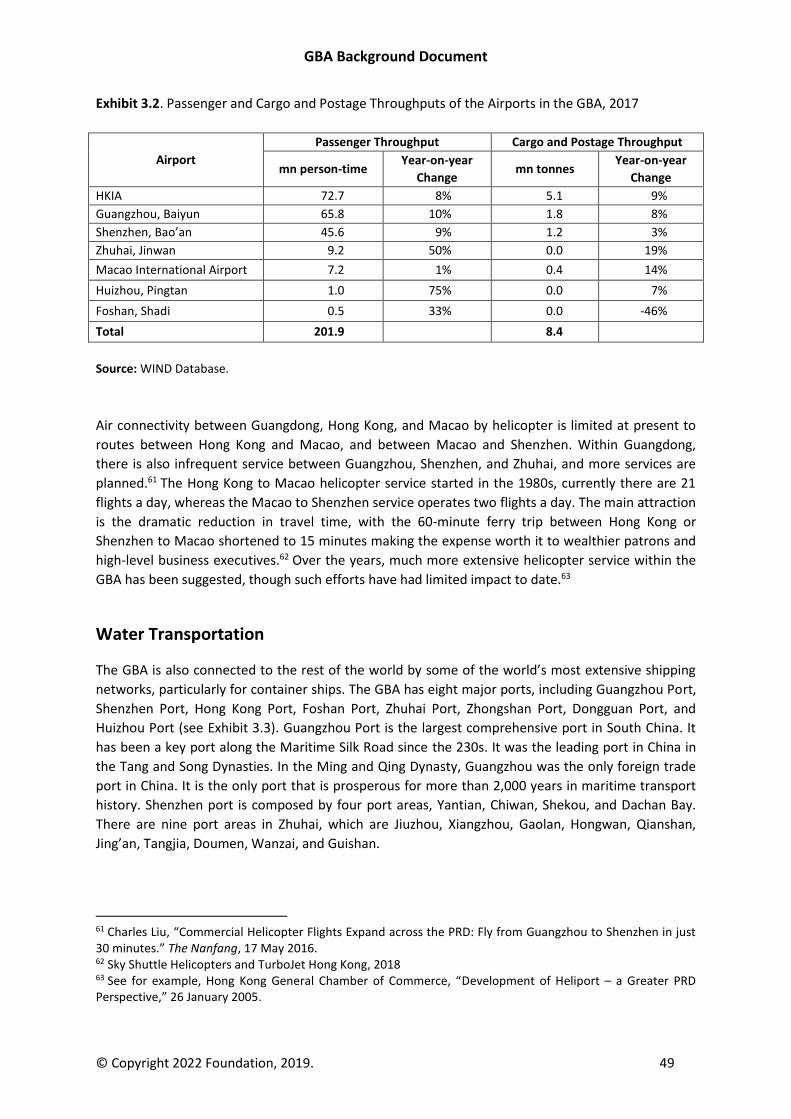

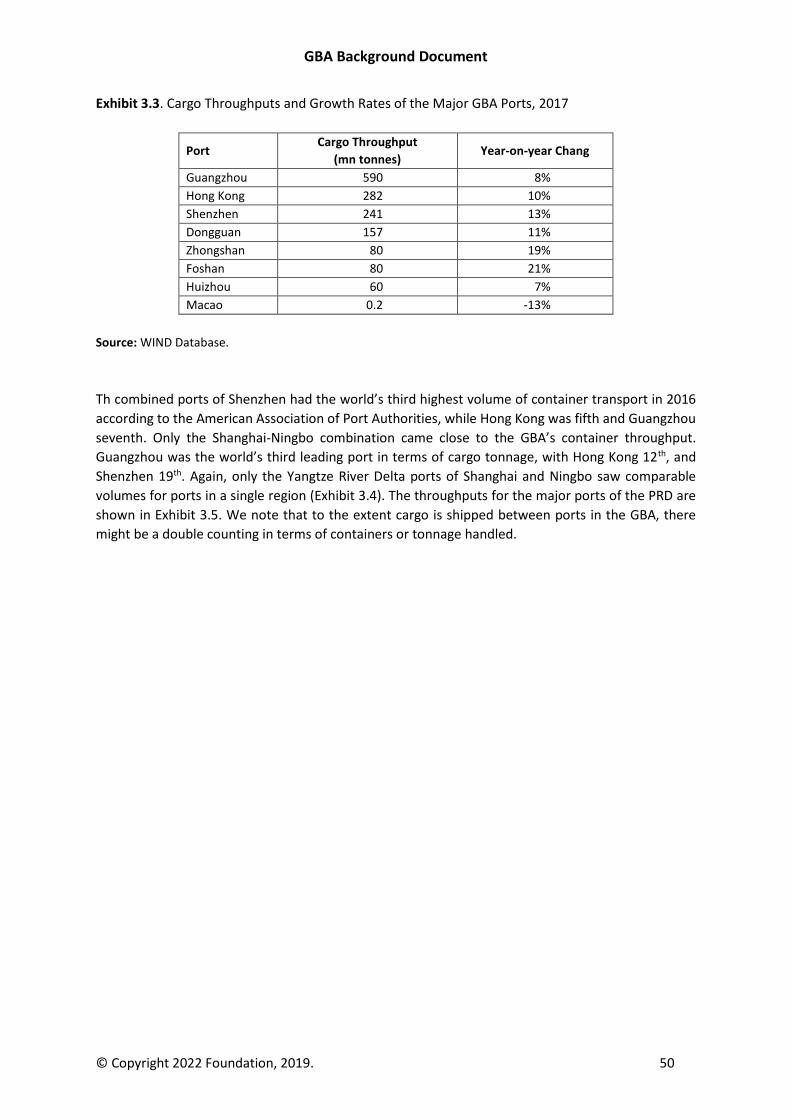

Water Transportation ....................................................................................................................... 49

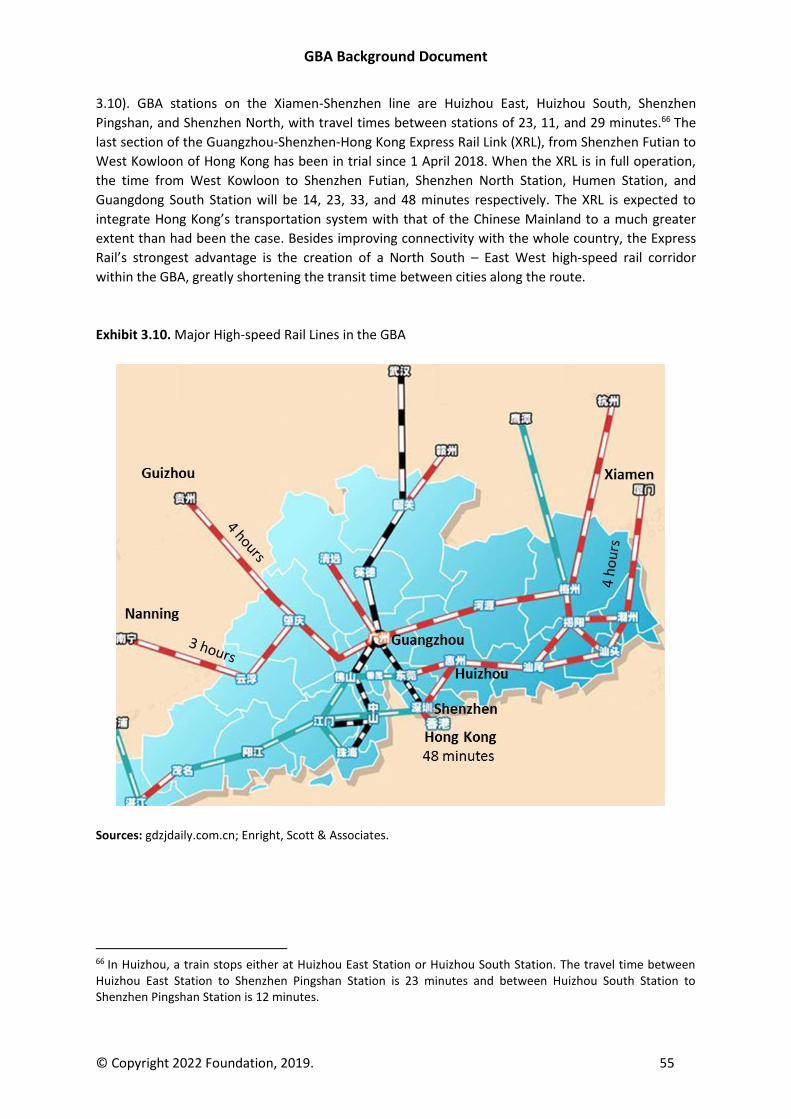

High-speed Rail ................................................................................................................................. 53

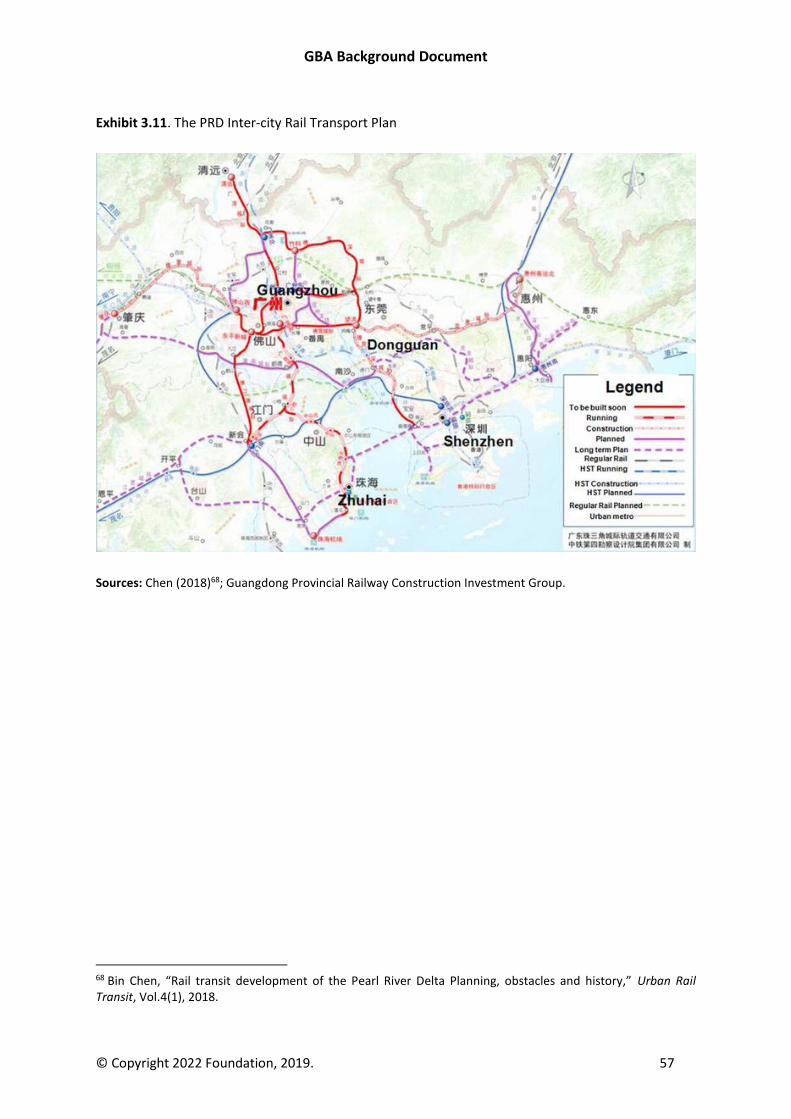

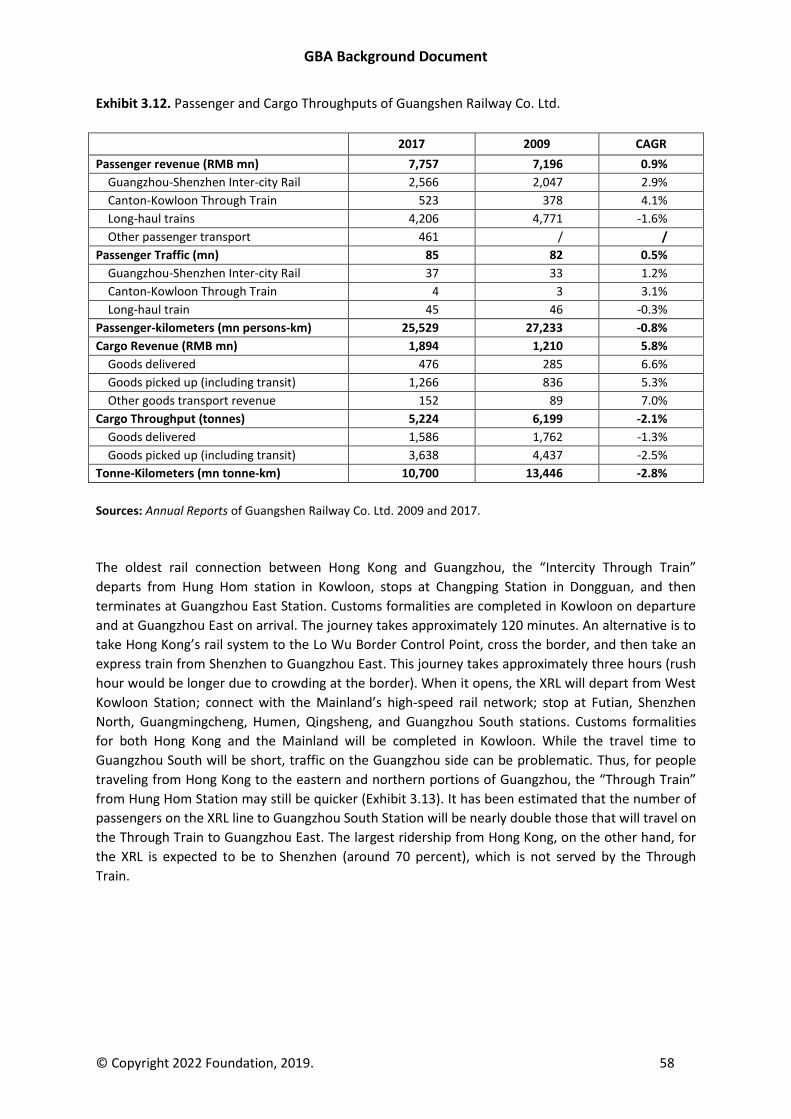

Inter-city Rail ..................................................................................................................................... 56

Metro Systems .................................................................................................................................. 60

Road Transport ................................................................................................................................. 60

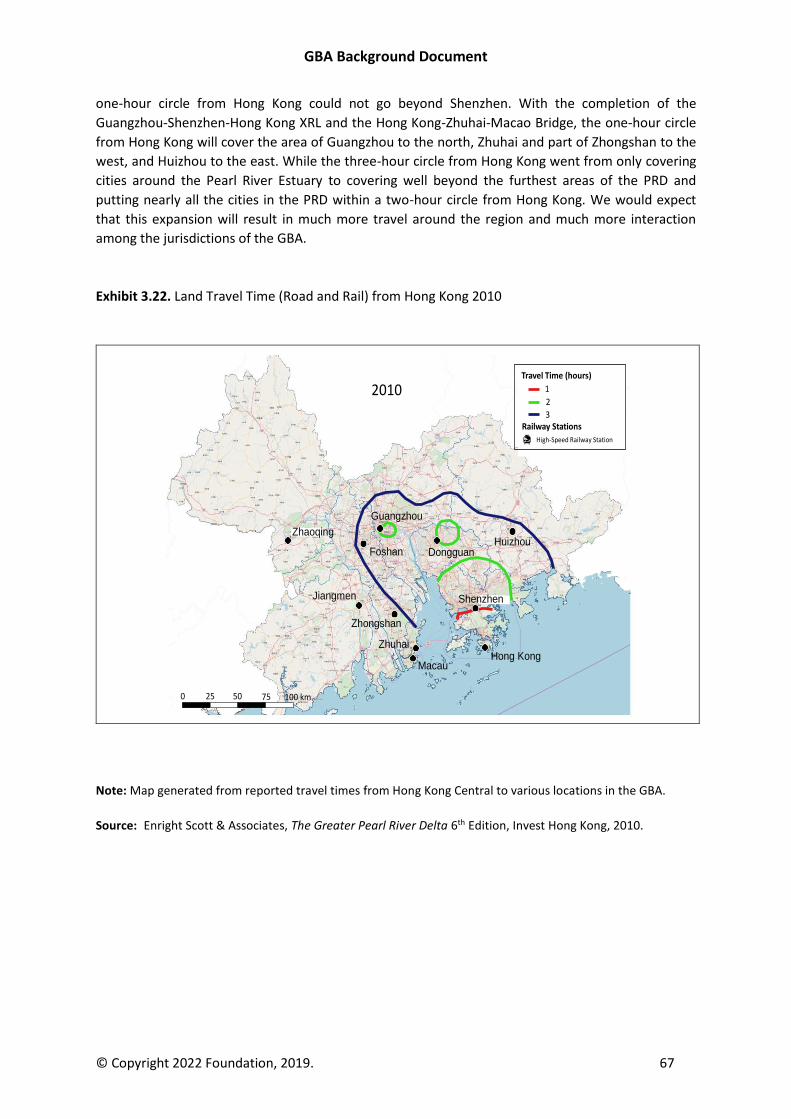

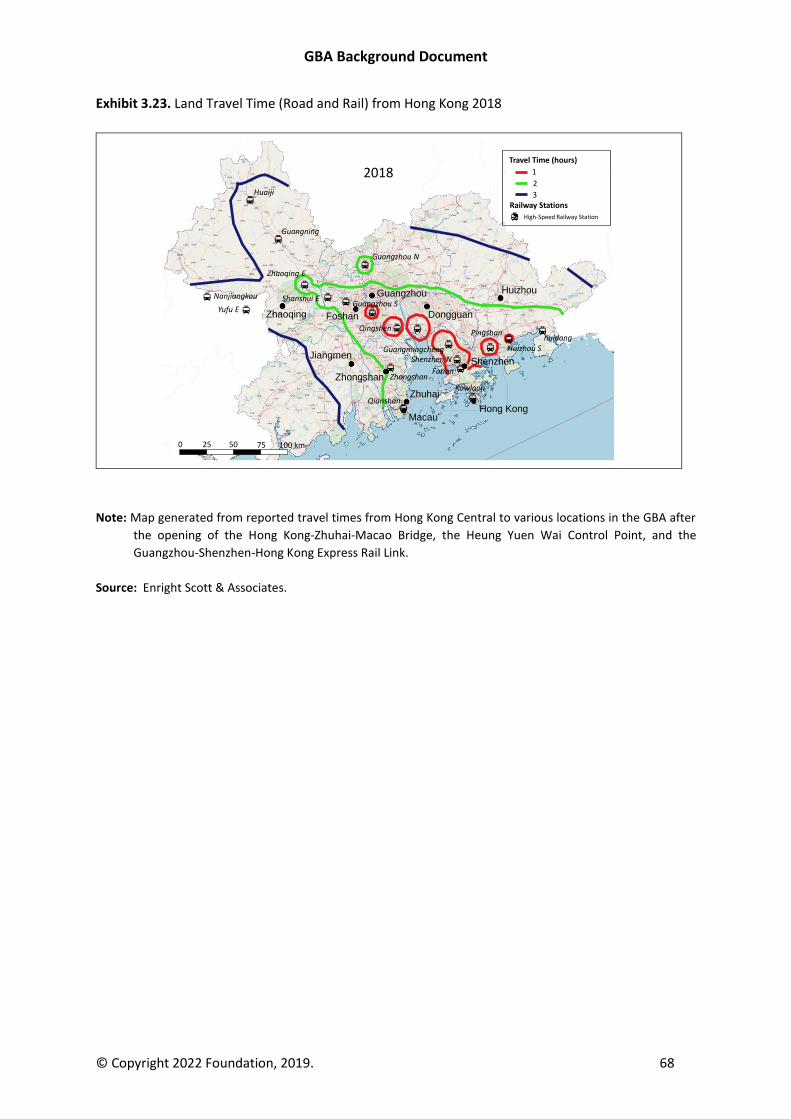

Transport Connectivity in the GBA ................................................................................................... 66

4. Boundary Crossing ........................................................................................................................ 69

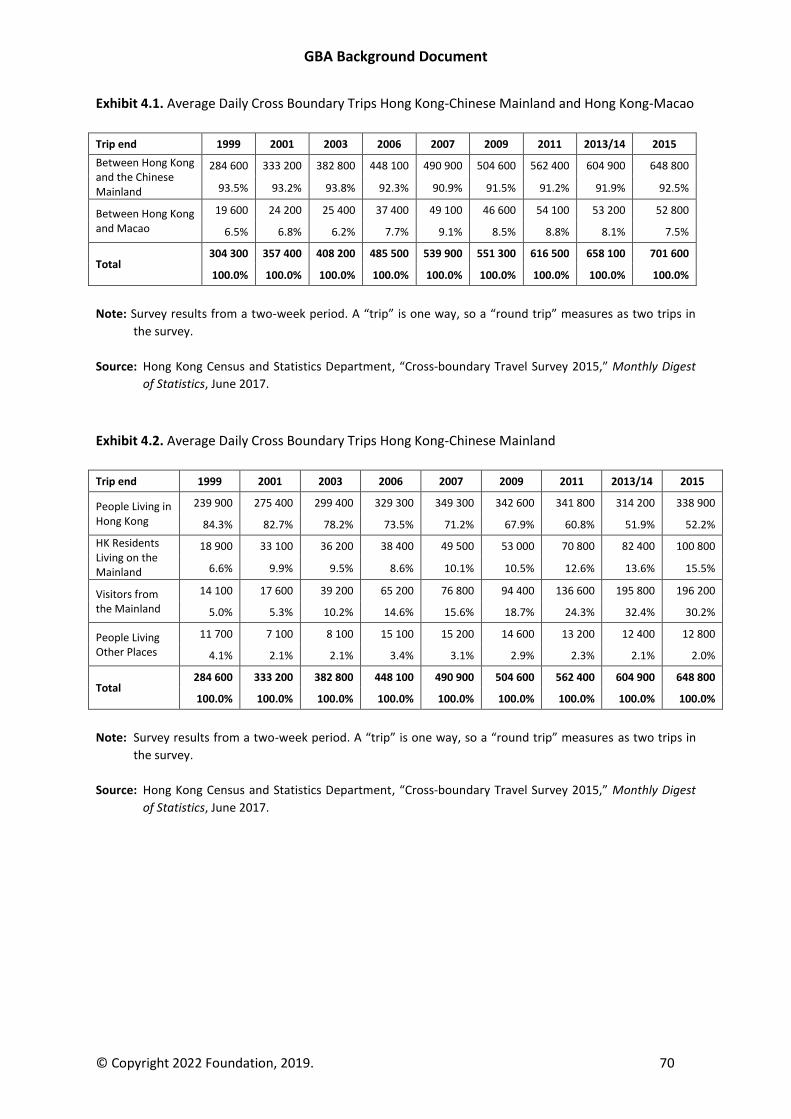

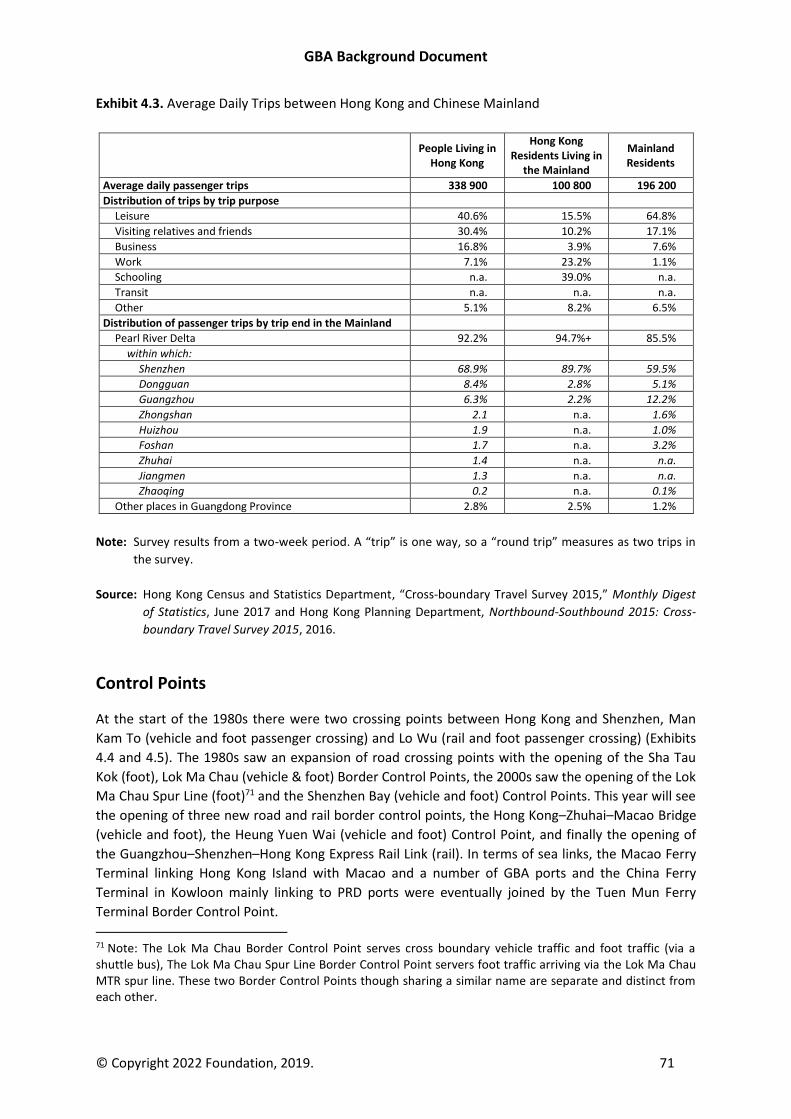

Cross Boundary Trips ........................................................................................................................ 69

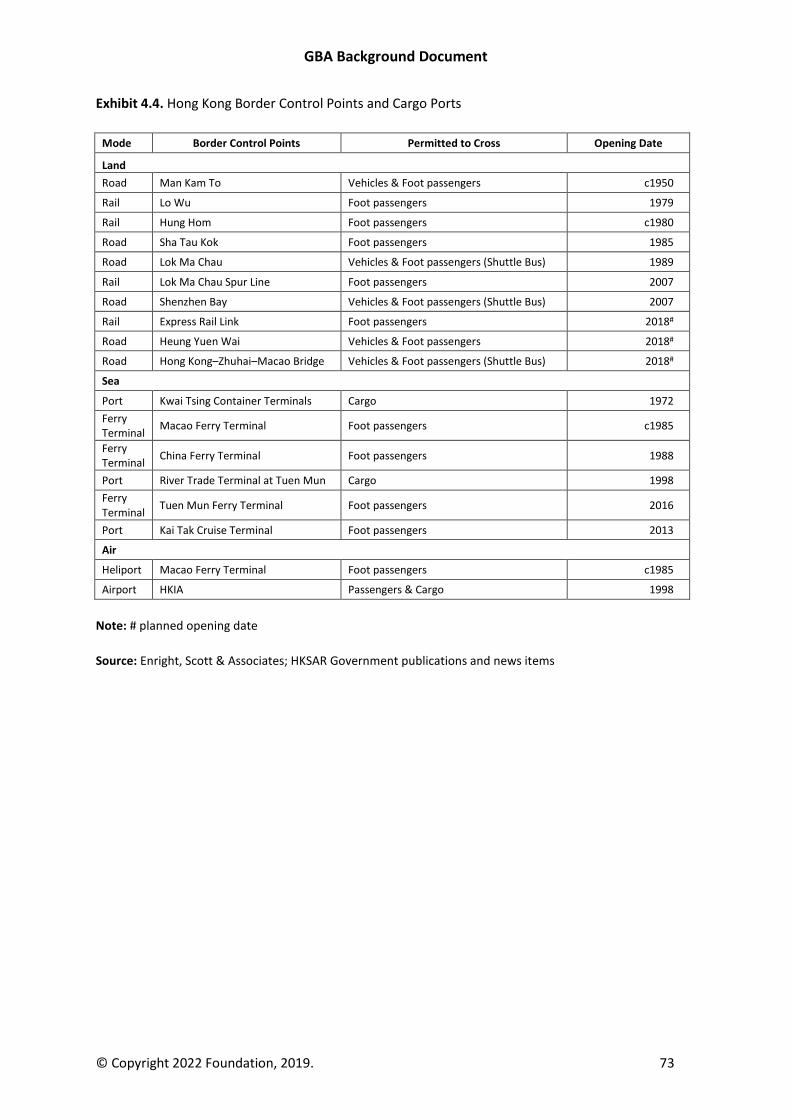

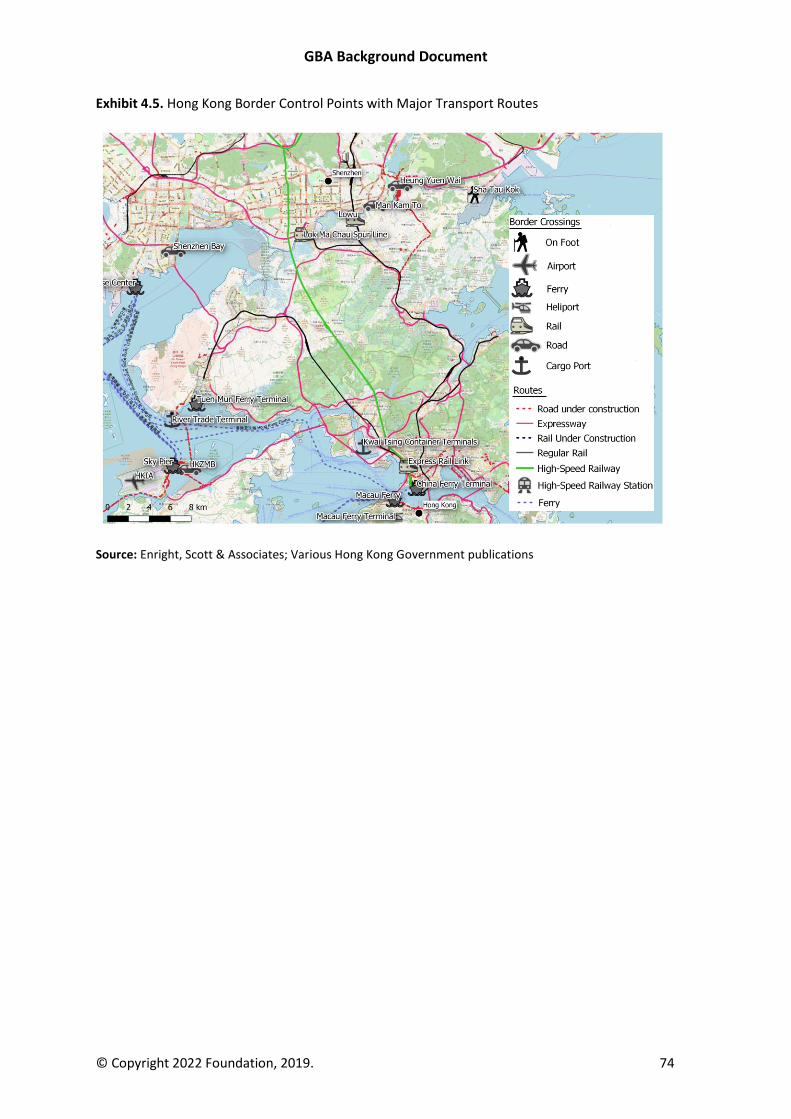

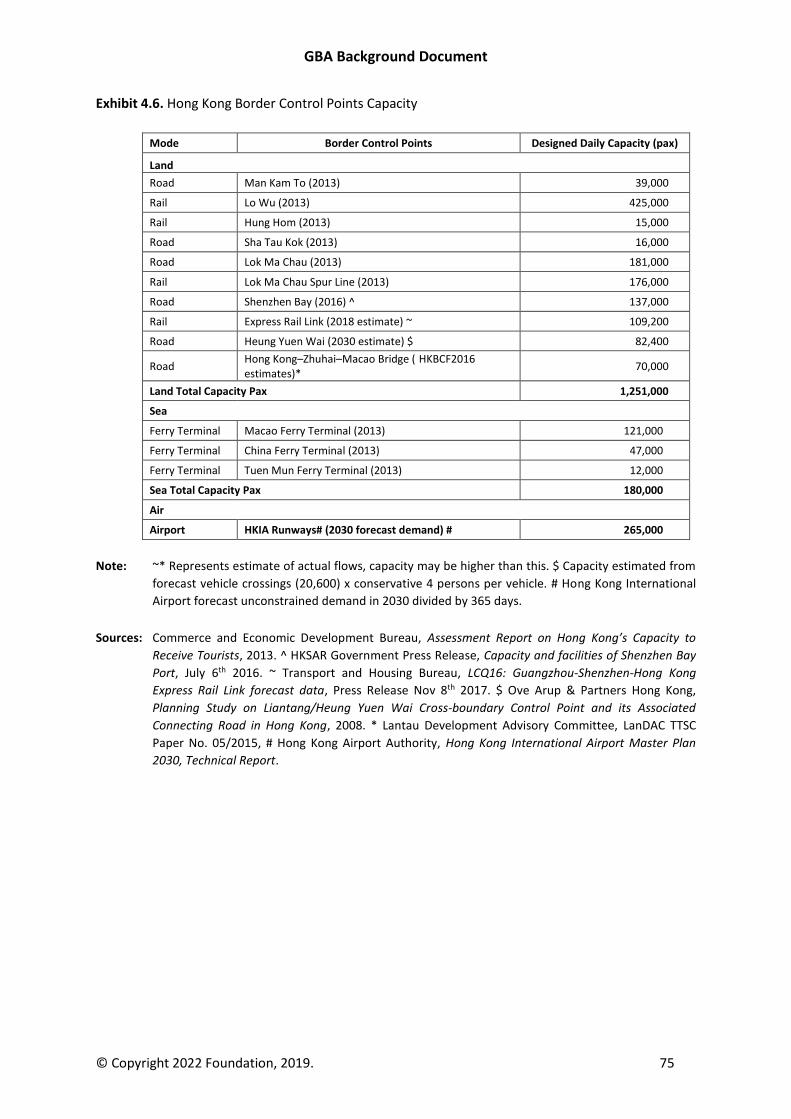

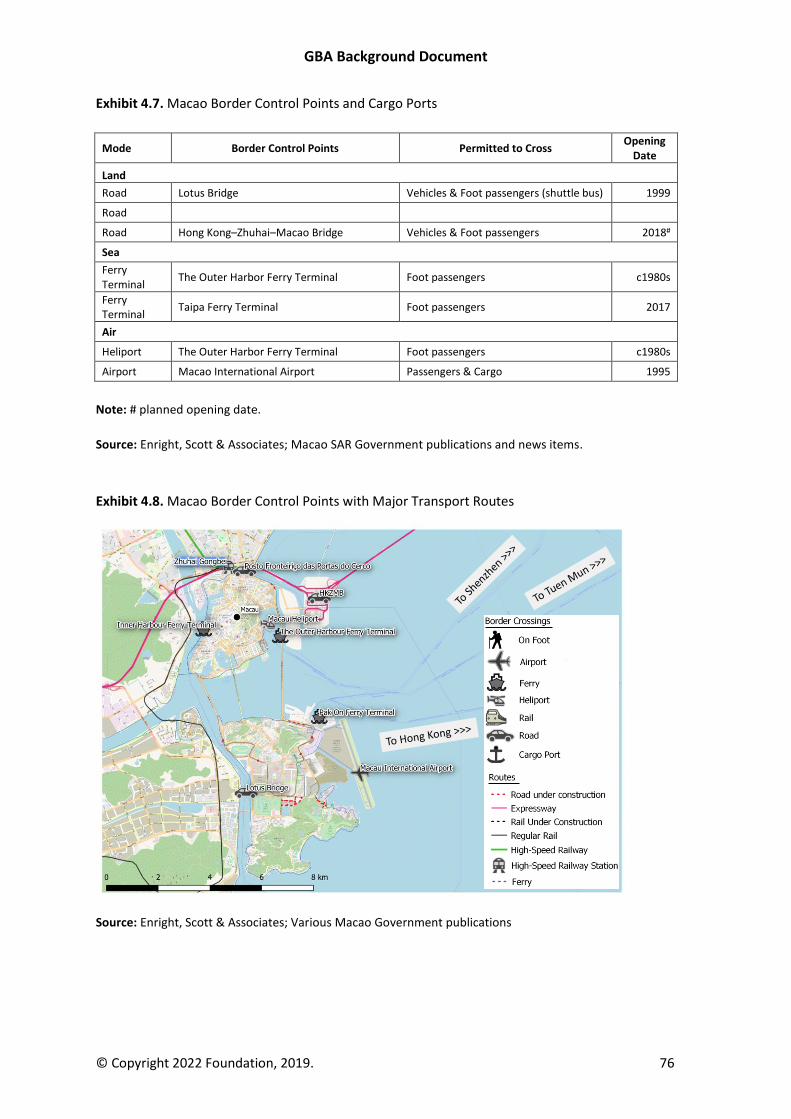

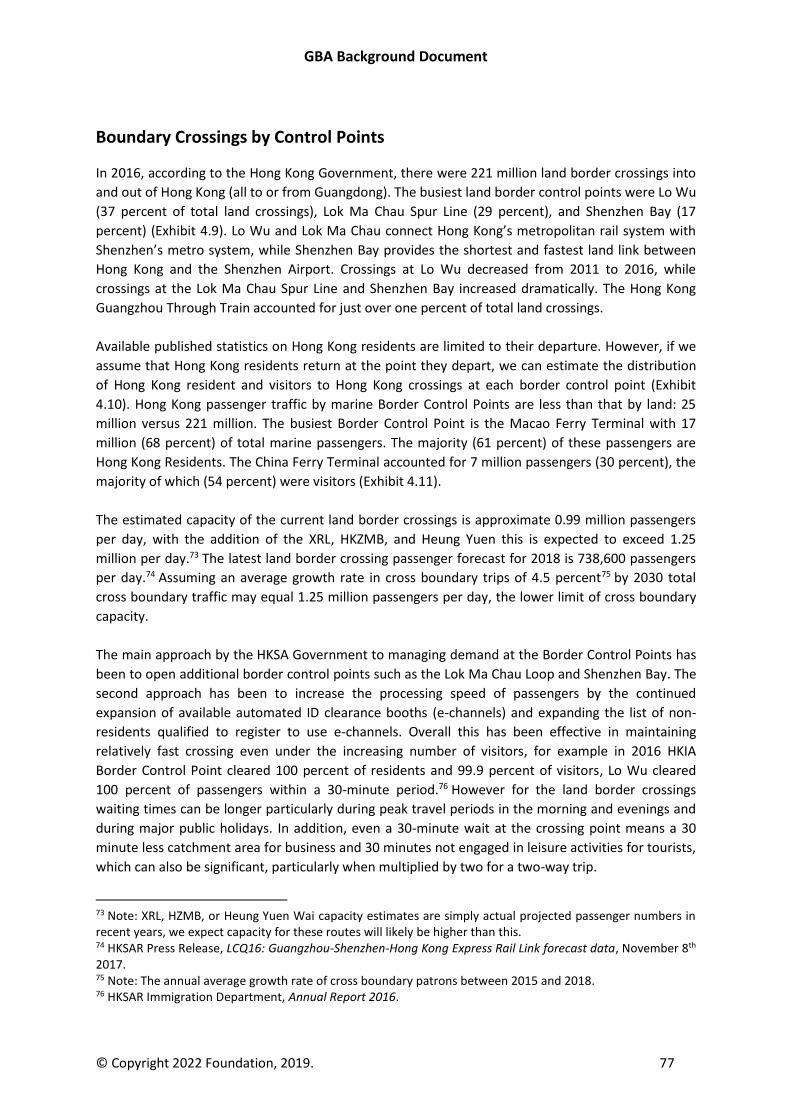

Control Points ................................................................................................................................... 71

Boundary Crossings by Control Points .............................................................................................. 77

Border Crossing Points in the GBA .................................................................................................... 80

5. Human Mobility in the Greater Bay Area ..................................................................................... 82

Guangdong Province ......................................................................................................................... 82

Work Permits, Residence, and Social Security: People from the Chinese Mainland .................... 82

Work Permits, Residence, and Social Security: Hong Kong and Macao Residents ....................... 84

Short-Term Business and Tourist Visas ......................................................................................... 87

Ability to Buy Property .................................................................................................................. 88

Hong Kong and Macao ...................................................................................................................... 91

GBA Background Document

© Copyright 2022 Foundation, 2019. 3

Work Permits, Residence, and Social Security .............................................................................. 91

Short Term Business and Tourist Visas into Hong Kong and Macao ............................................ 94

Ability to Purchase Property in Hong Kong and Macao ................................................................ 96

Human Mobility in the GBA .............................................................................................................. 97

6. Initiatives, Programs, Plans, and Policies Related to GBA Cooperation and Development.......... 99

Plans Specific to the GBA .................................................................................................................. 99

The GBA Initiative ......................................................................................................................... 99

Prior GBA Plans ............................................................................................................................... 100

Plans Related to the GBA ................................................................................................................ 102

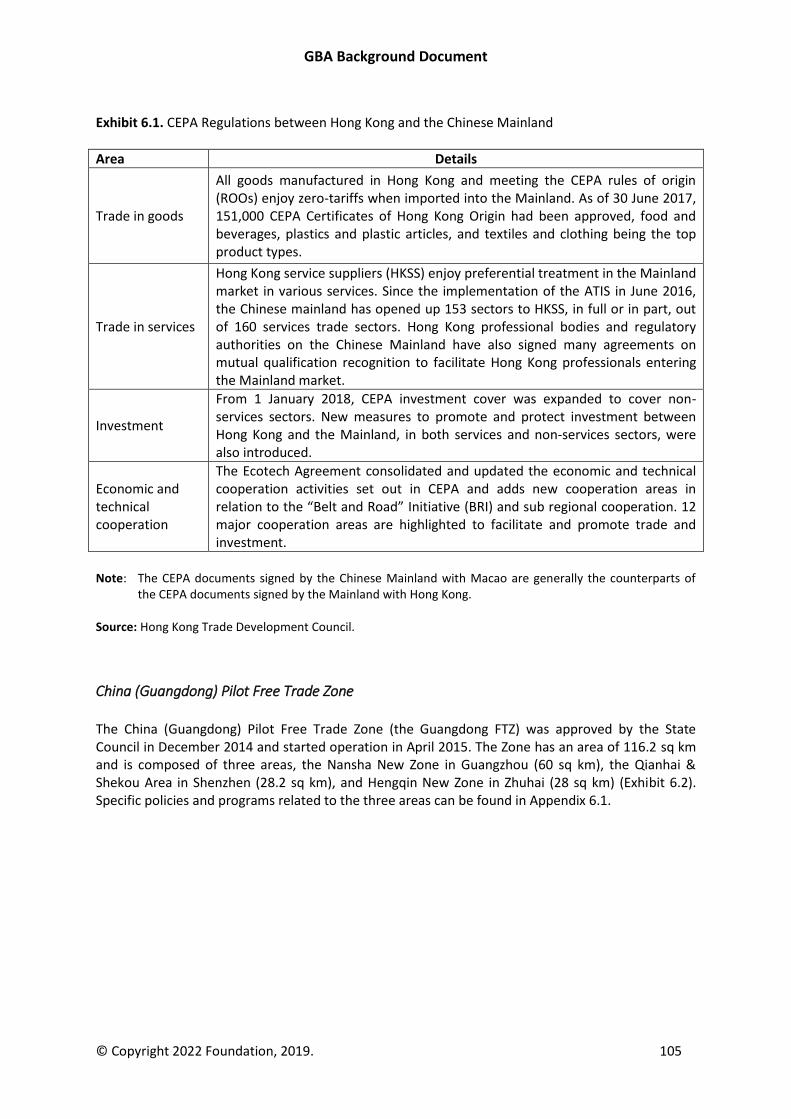

CEPA ............................................................................................................................................ 102

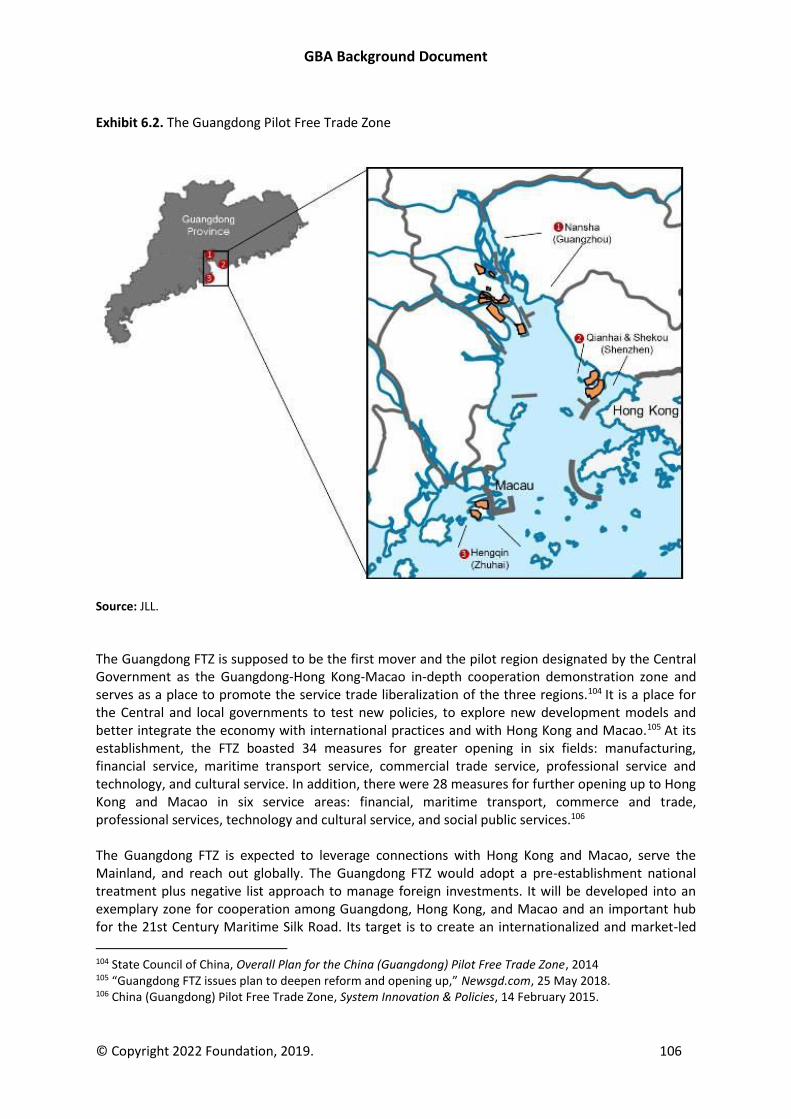

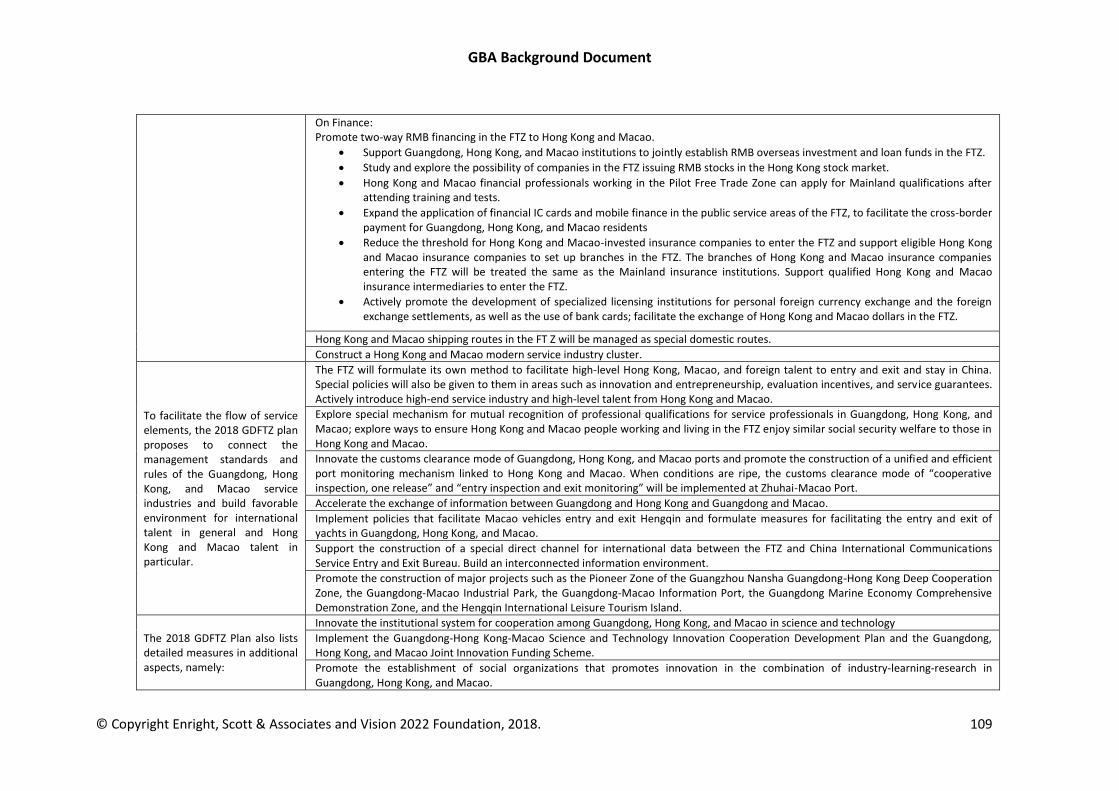

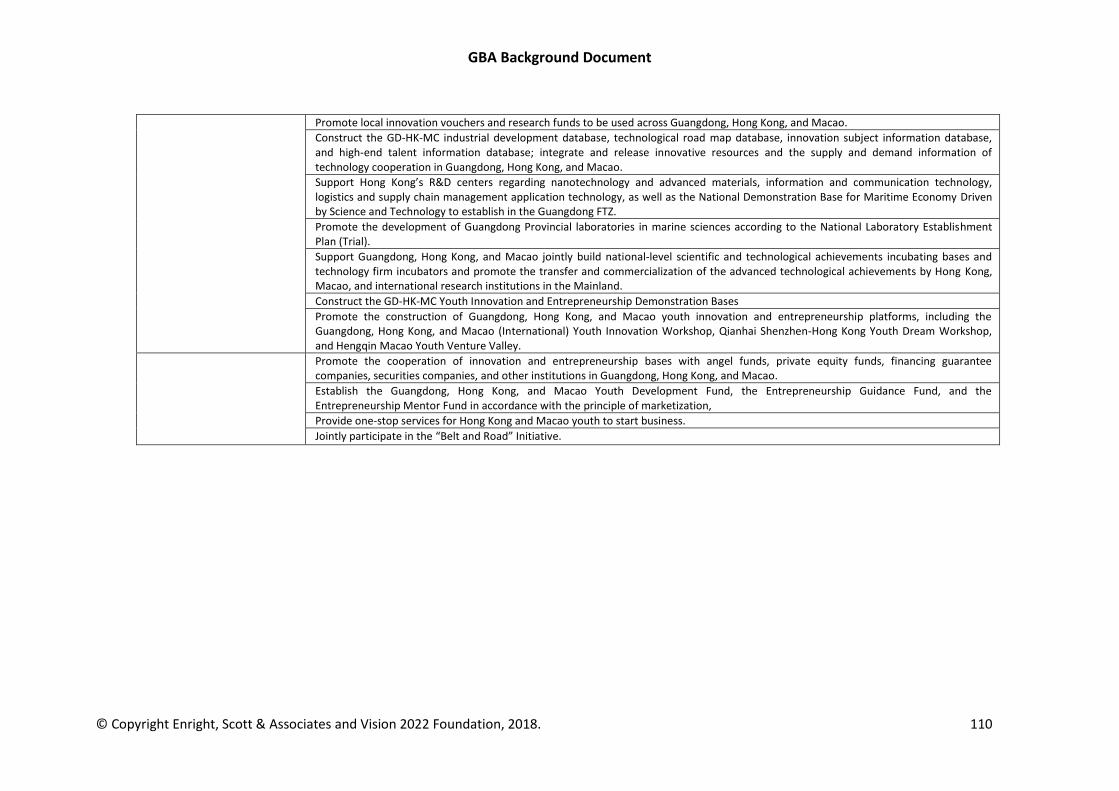

China (Guangdong) Pilot Free Trade Zone .................................................................................. 105

Framework Agreement on Guangdong’s Cooperation with Hong Kong and Macao ................. 111

The Thirteenth Five Year Program for the National Economy and Social Development of Guangdong .................................................................................................................................. 112

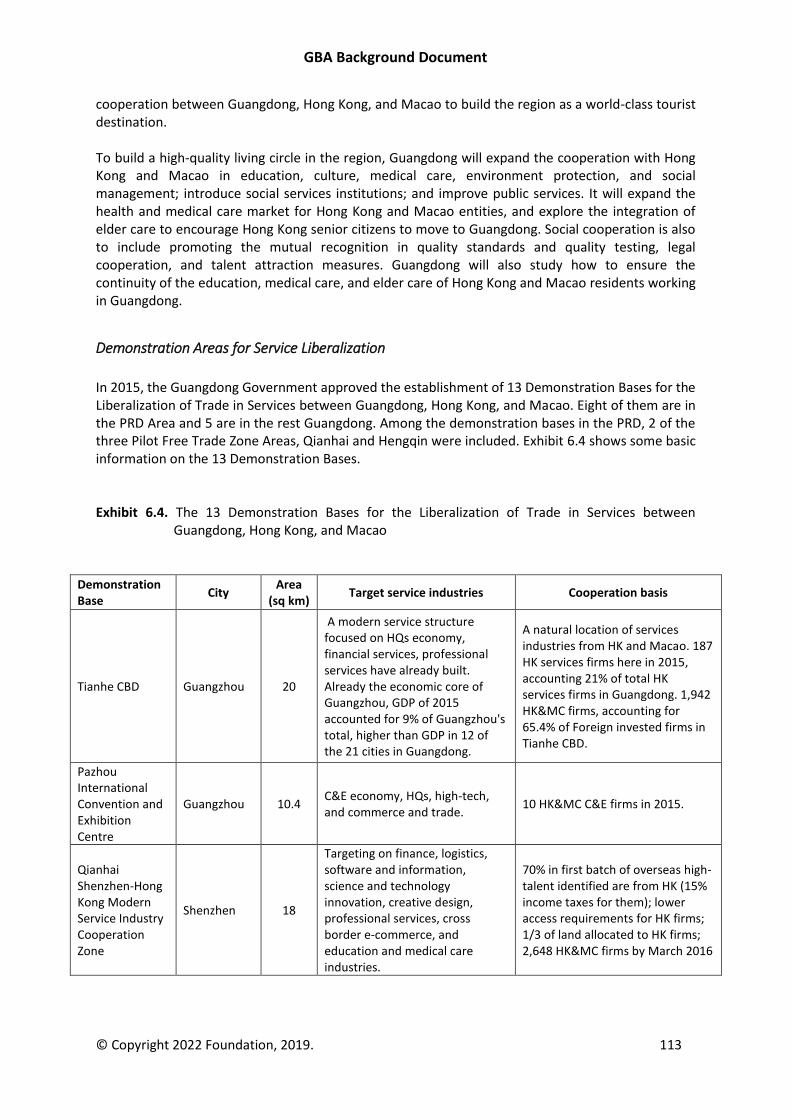

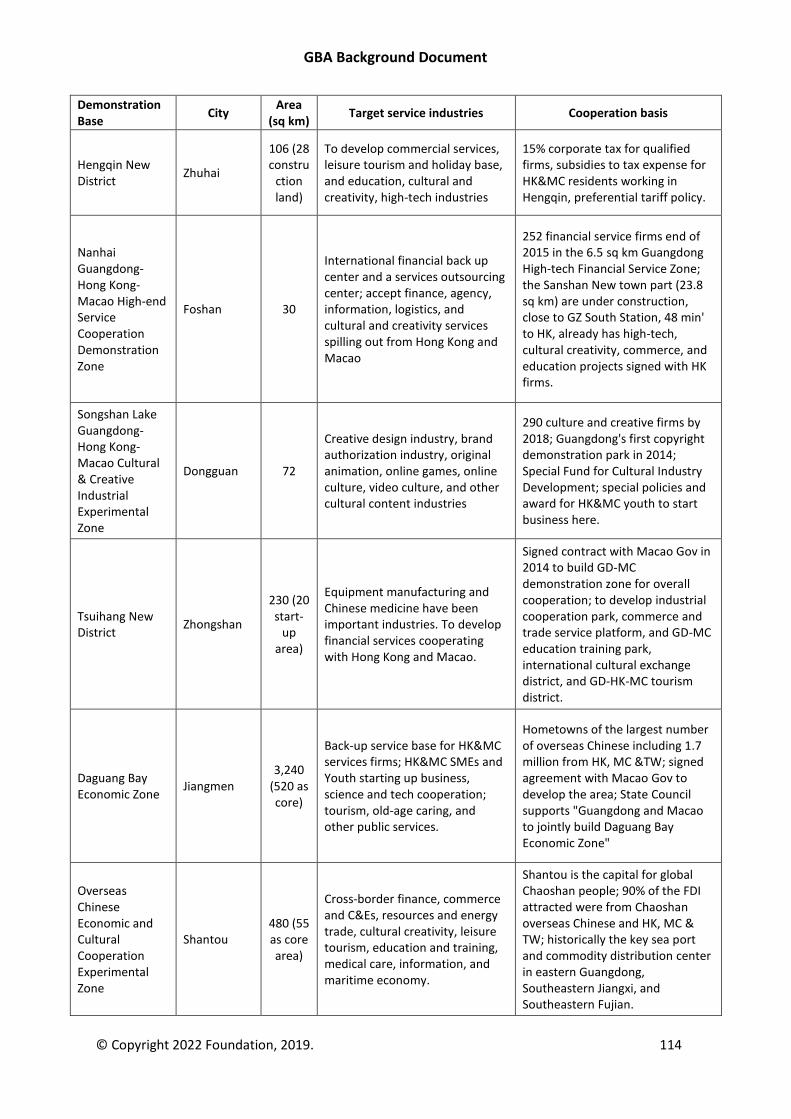

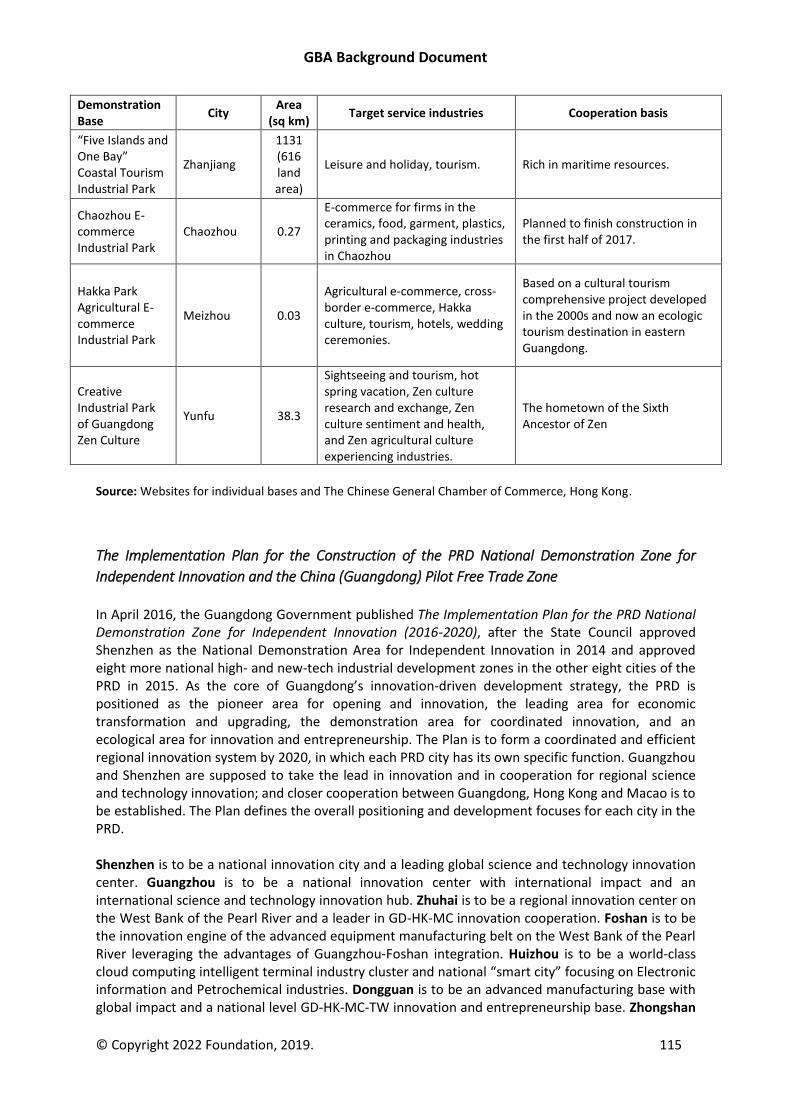

Demonstration Areas for Service Liberalization ......................................................................... 113

The Implementation Plan for the Construction of the PRD National Demonstration Zone for Independent Innovation and the China (Guangdong) Pilot Free Trade Zone ............................ 115

The Plan for Guangzhou-Shenzhen Scientific Technology and Innovation Corridor .................. 117

Hong Kong Programs for Cooperation in the GBA .......................................................................... 117

Macao Programs for Cooperation in the GBA ................................................................................ 119

Appendix 6.1. Specific Areas for GBA Cooperation under the GFTZ .............................................. 120

Nansha Area ................................................................................................................................ 120

Qianhai and Shekou Area ............................................................................................................ 121

Hengqin Area .............................................................................................................................. 122

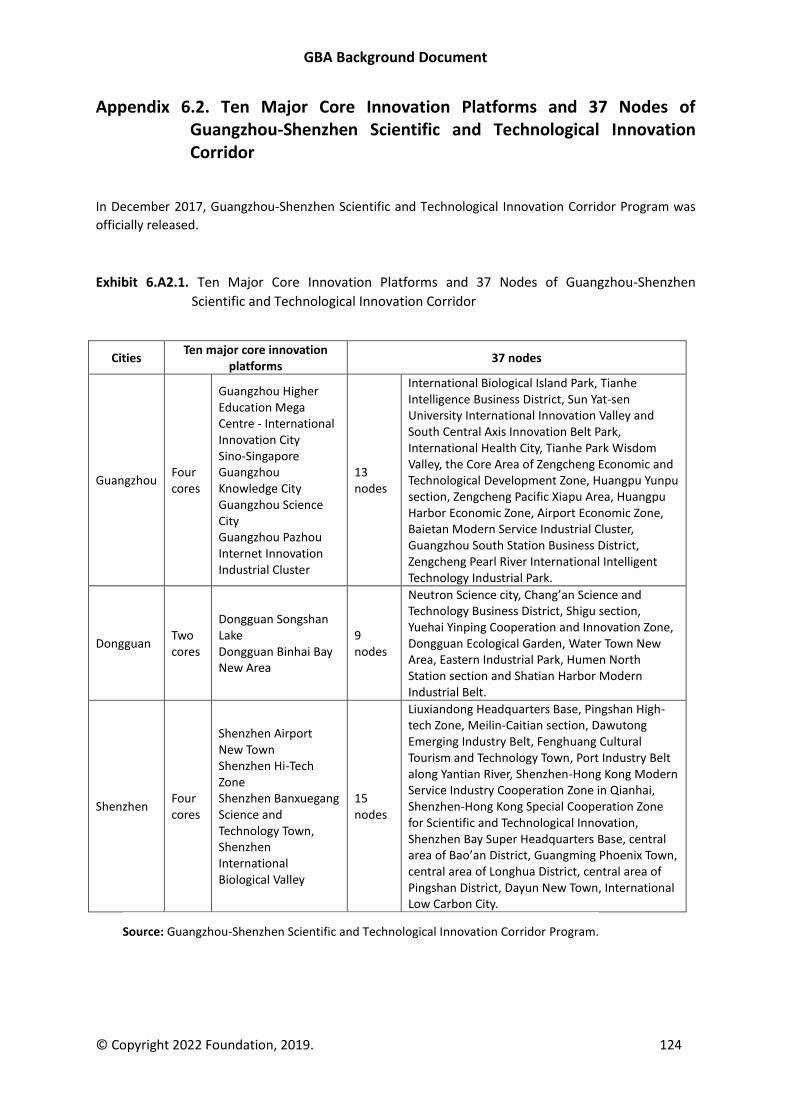

Appendix 6.2. Ten Major Core Innovation Platforms and 37 Nodes of Guangzhou-Shenzhen Scientific and Technological Innovation Corridor ........................................................................... 124

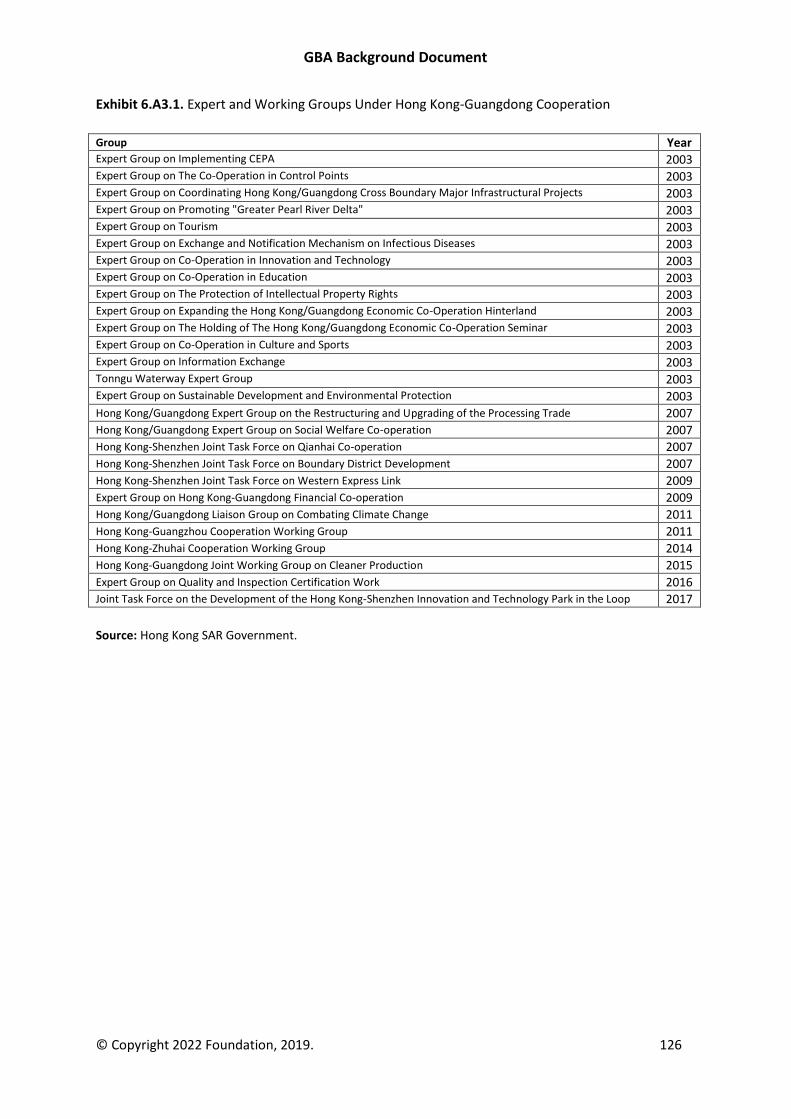

Appendix 6.3. Examples of Inter-Governmental Interaction in the GBA ........................................ 125

7. Economic Circles in the PRD........................................................................................................ 127

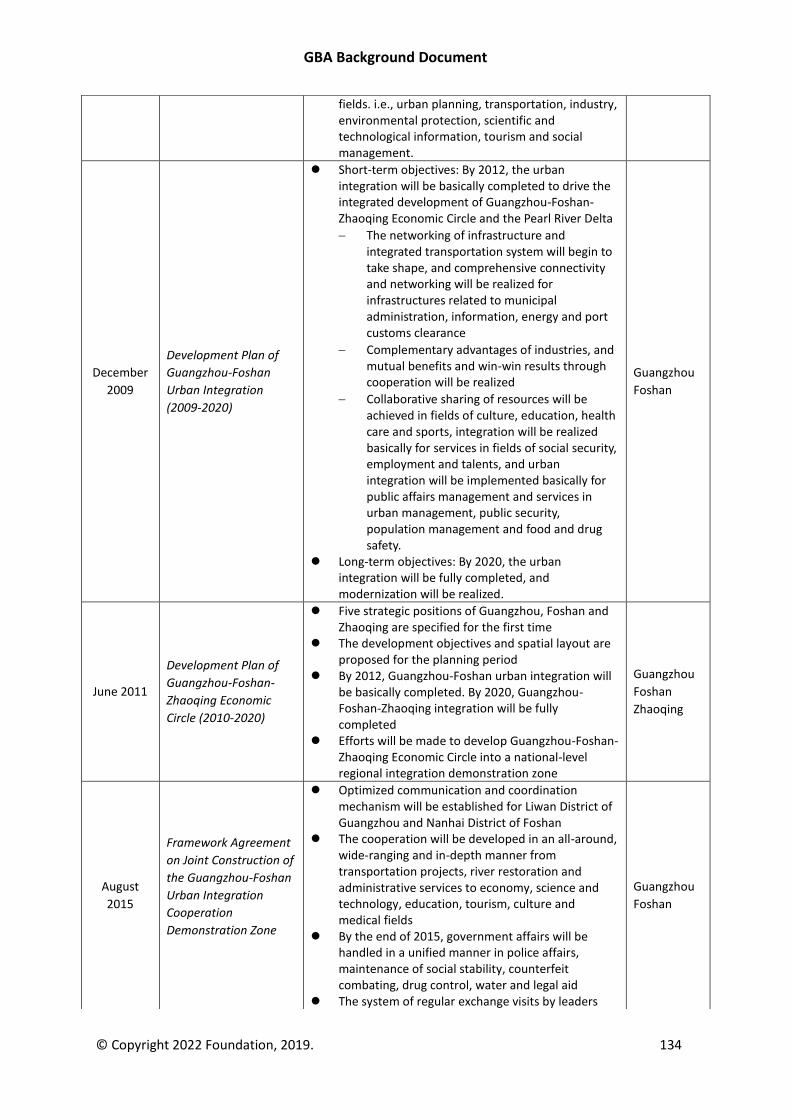

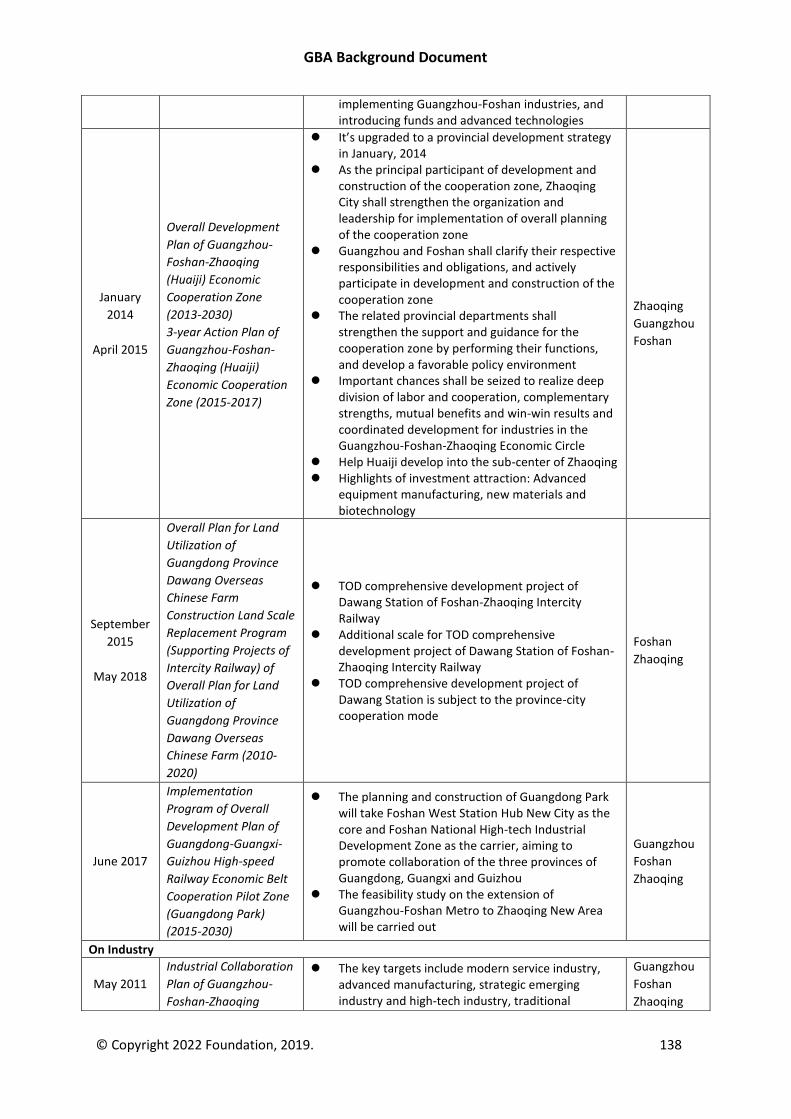

Guangzhou-Foshan-Zhaoqing Integration ...................................................................................... 127

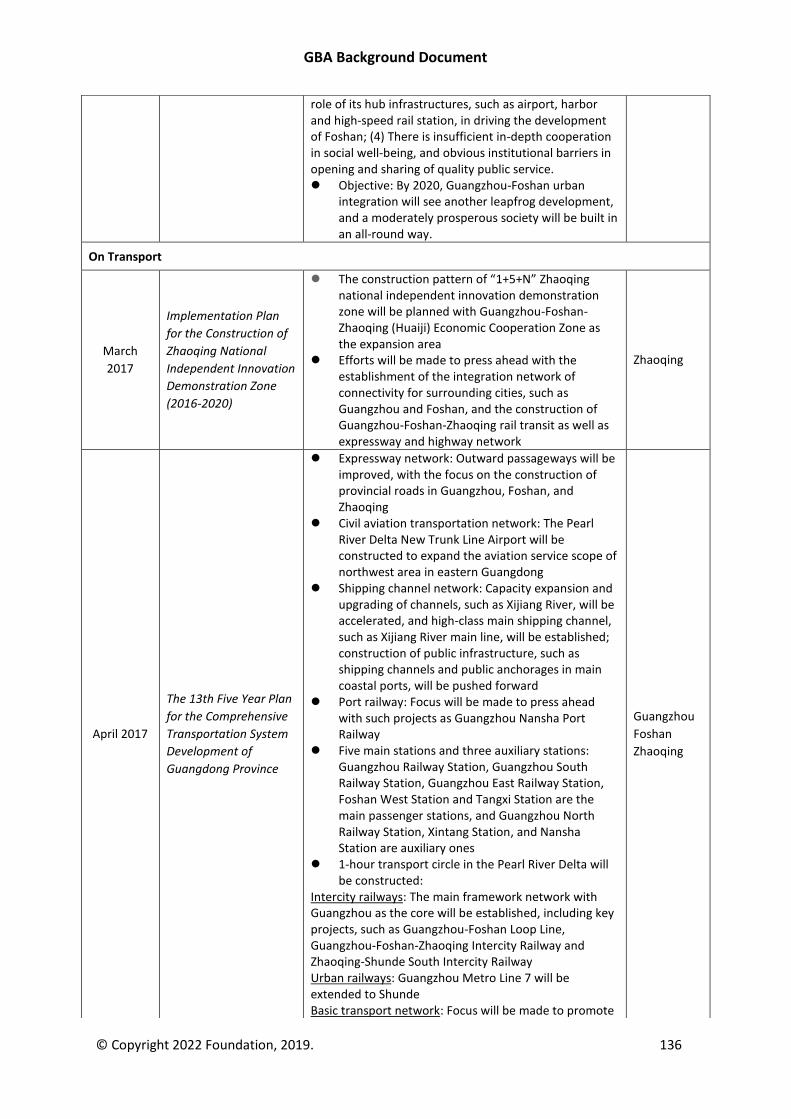

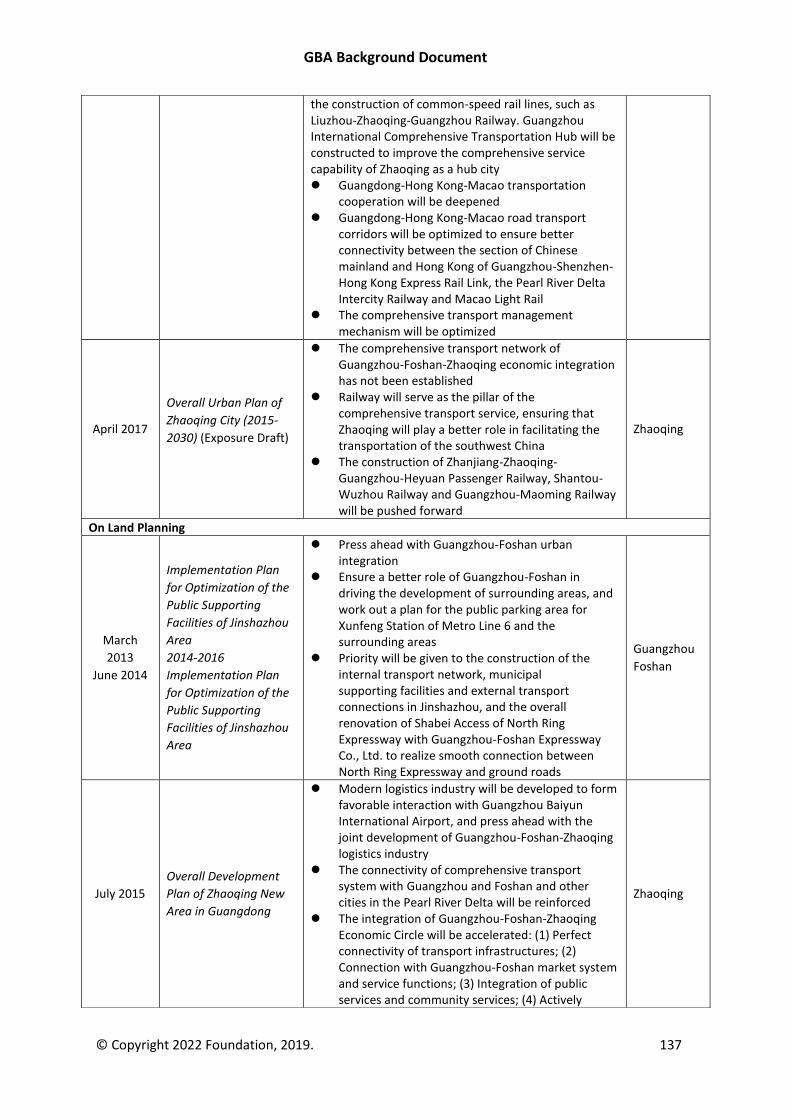

Transport Integration .................................................................................................................. 127

Land Planning Integration ........................................................................................................... 129

Economic Planning Integration ................................................................................................... 129

Integration of Public Services...................................................................................................... 129

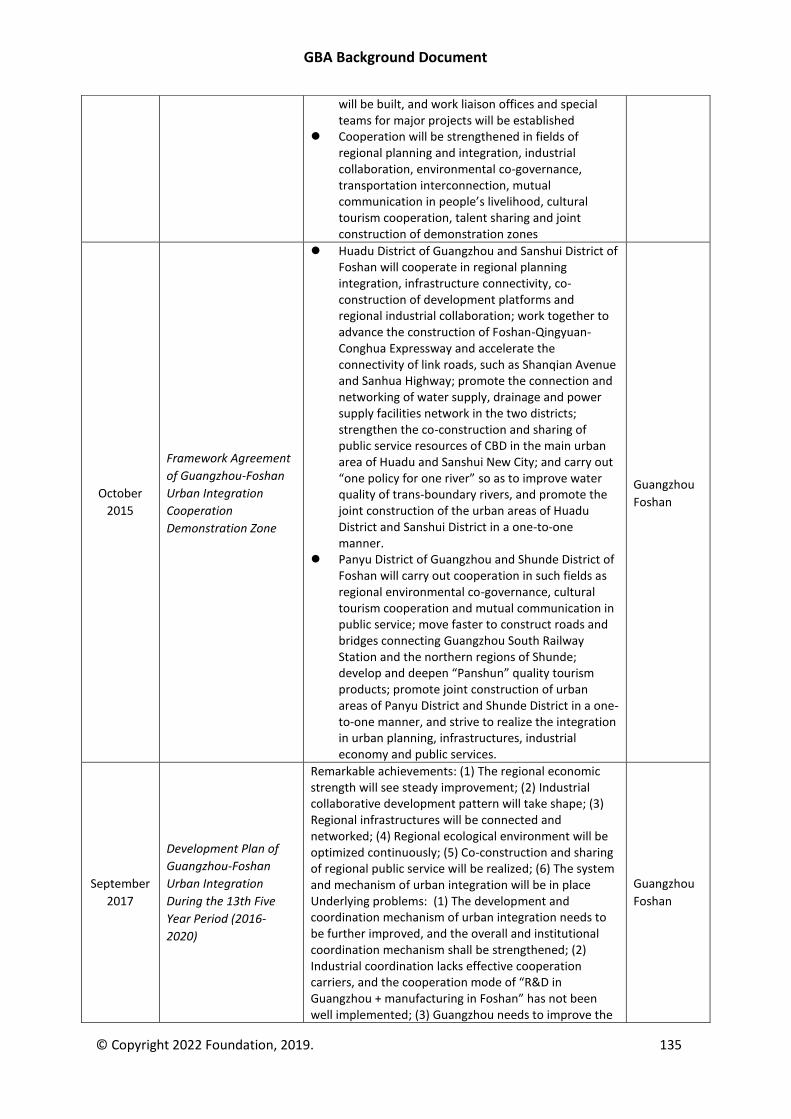

Further plans for integration ...................................................................................................... 132

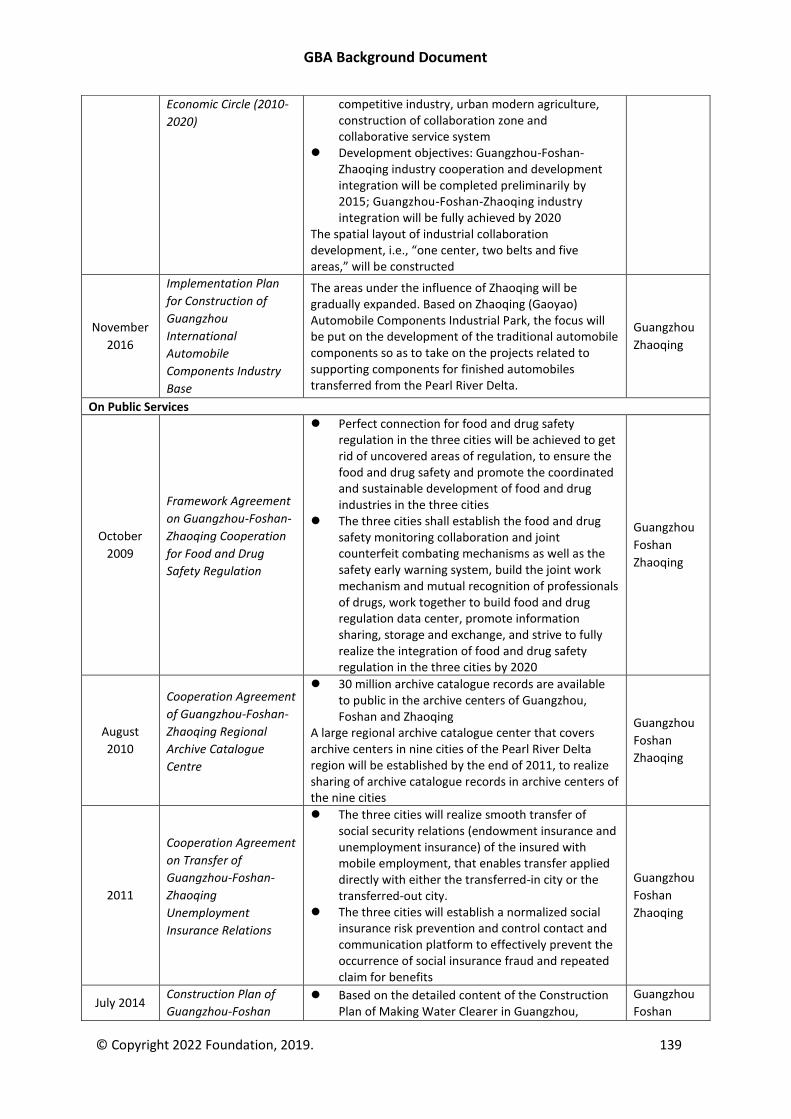

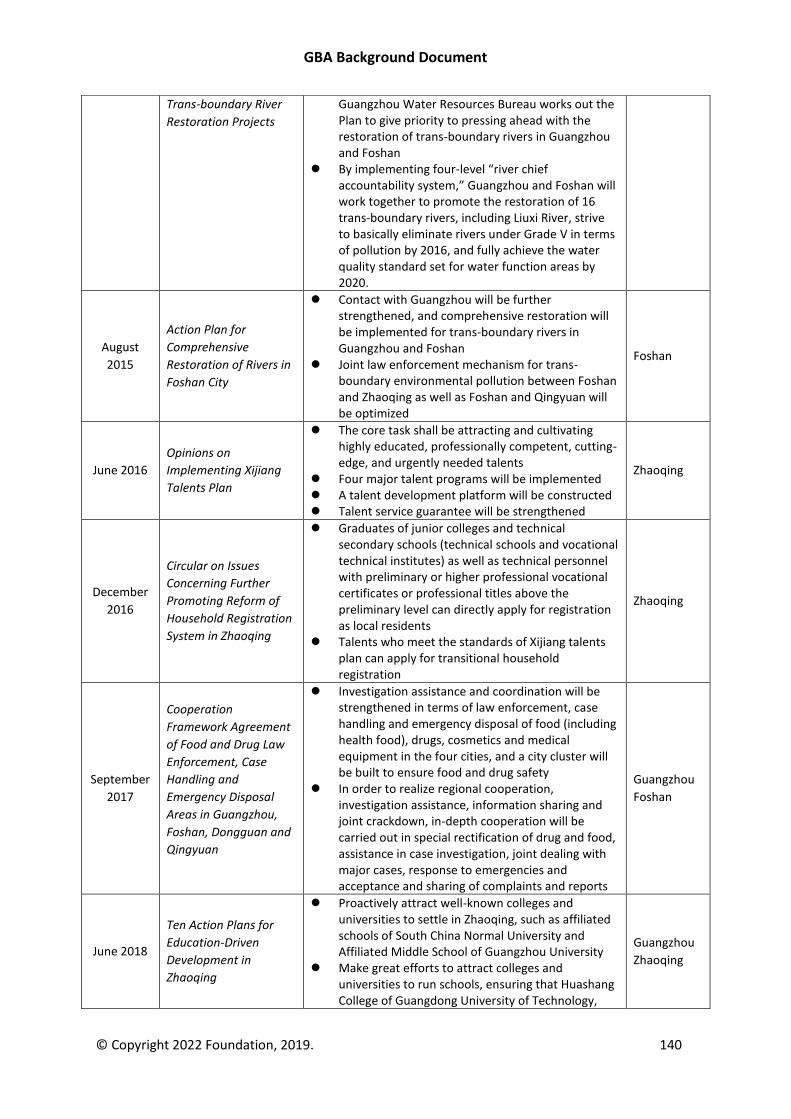

Appendix 7.1. Agreements and Policies on Guangzhou-Foshan-Zhaoqing Integration ................ 133

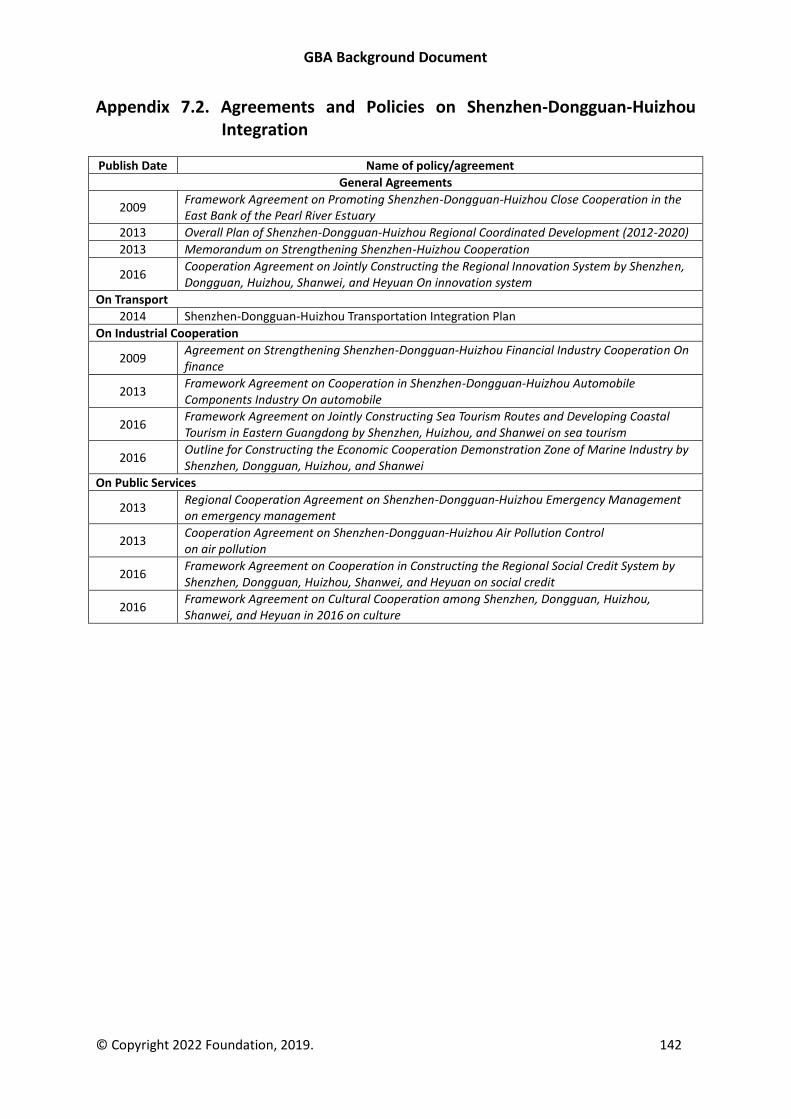

Appendix 7.2. Agreements and Policies on Shenzhen-Dongguan-Huizhou Integration ................. 142

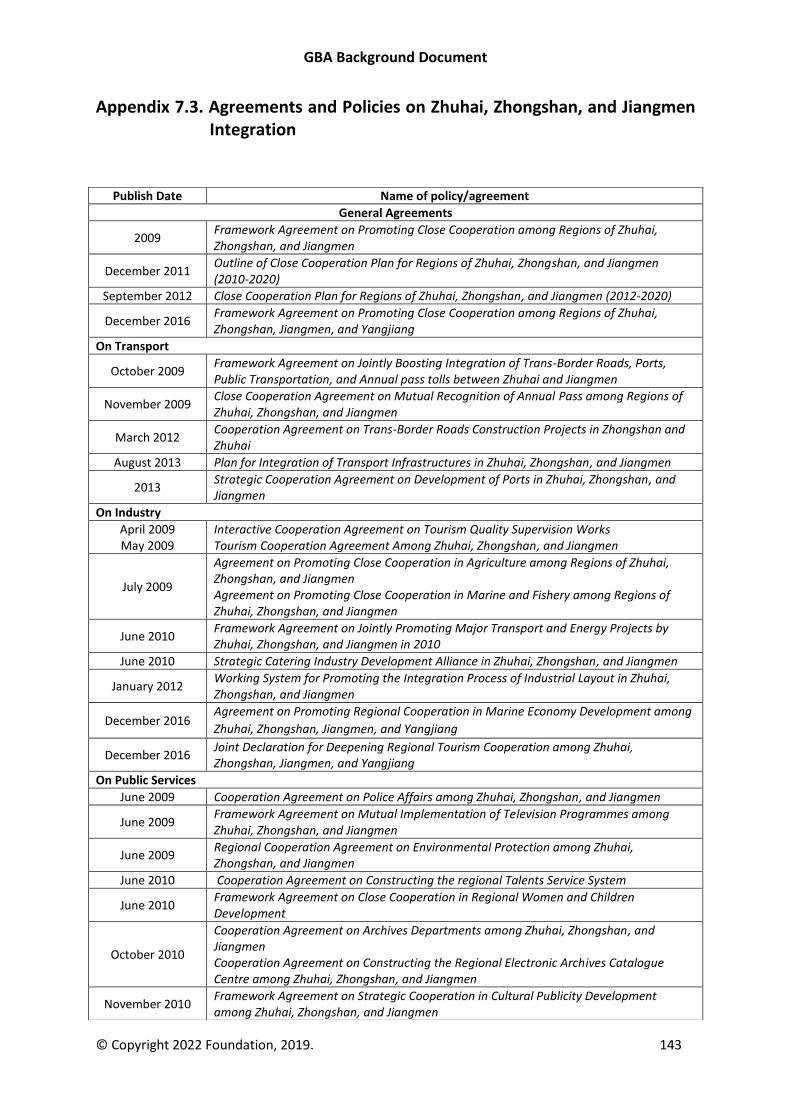

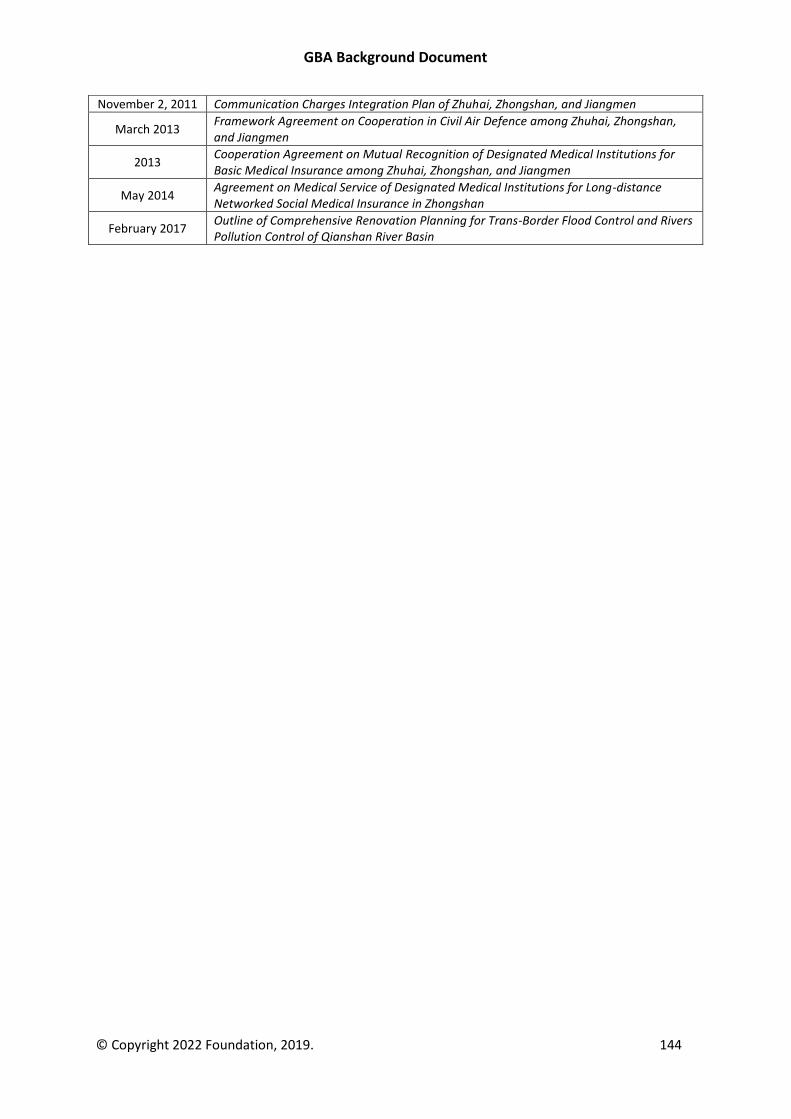

Appendix 7.3. Agreements and Policies on Zhuhai, Zhongshan, and Jiangmen Integration .......... 143

8. The Jurisdictions of the GBA ....................................................................................................... 145

GBA Background Document

© Copyright 2022 Foundation, 2019. 4

Guangzhou ...................................................................................................................................... 145

Development Plans ..................................................................................................................... 145

Plan for Cooperation with Hong Kong and Macao ..................................................................... 146

Positioning................................................................................................................................... 146

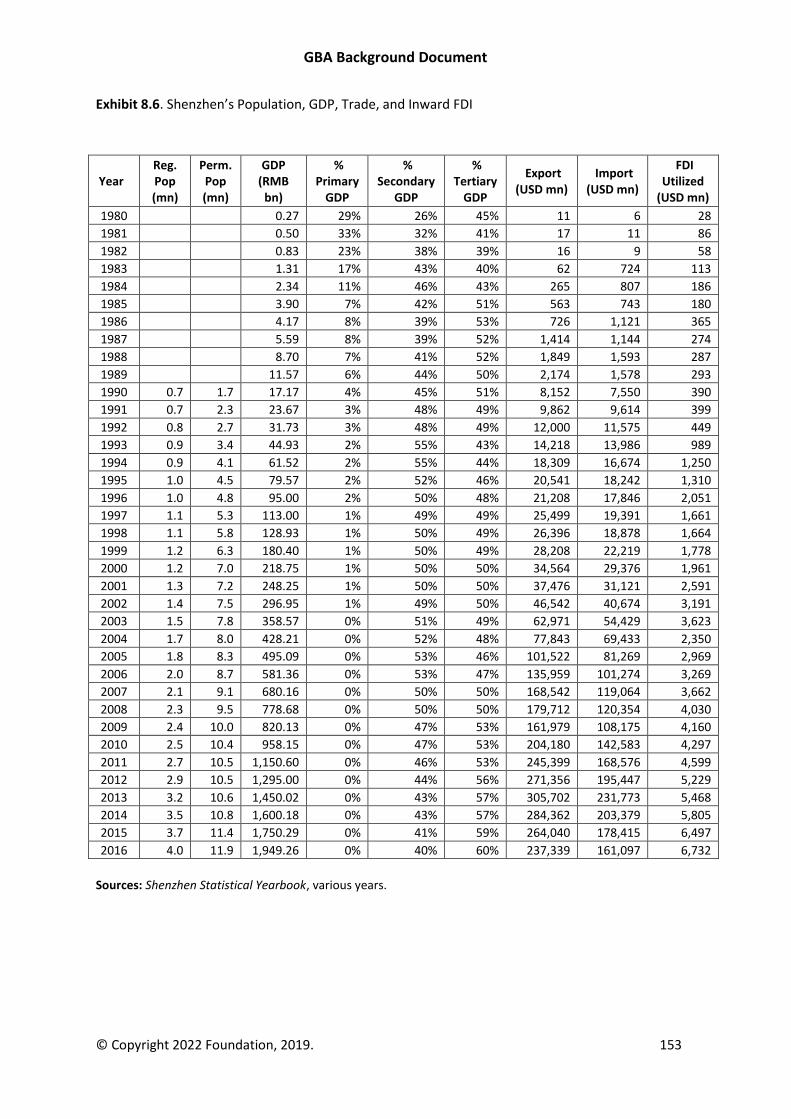

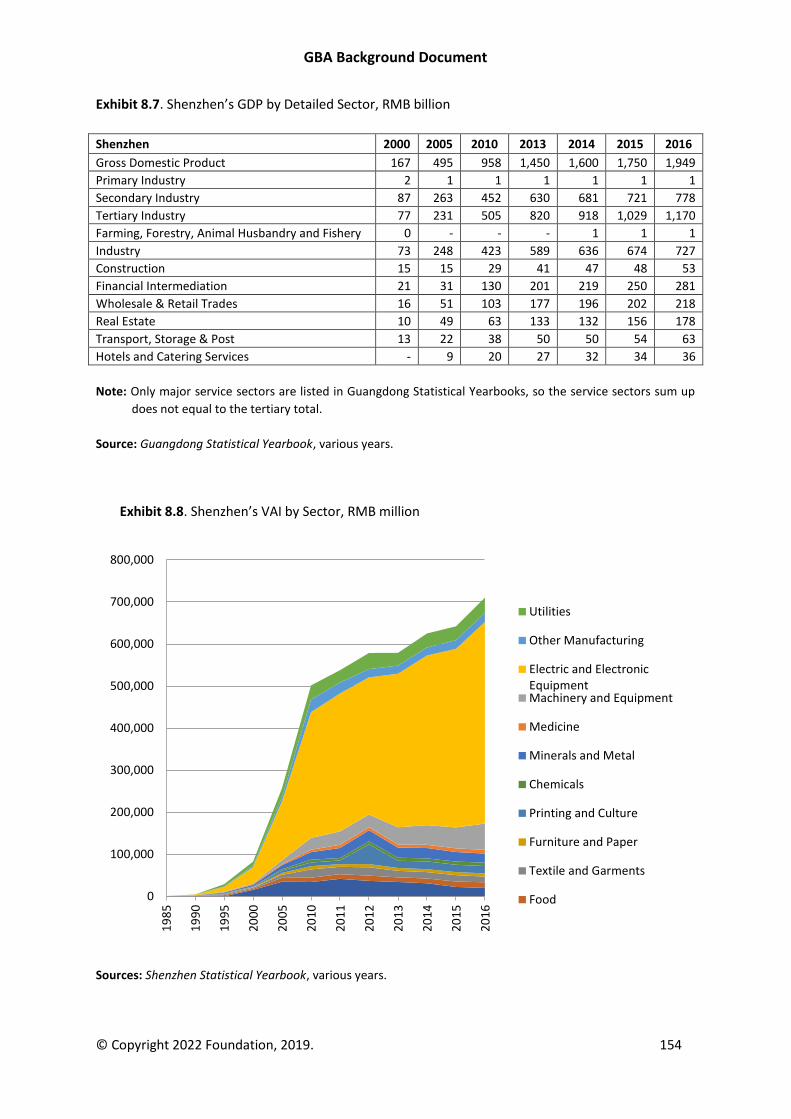

Shenzhen ......................................................................................................................................... 150

Development Plans ..................................................................................................................... 150

Plan for Cooperation with Hong Kong and Macao ..................................................................... 151

Positioning................................................................................................................................... 151

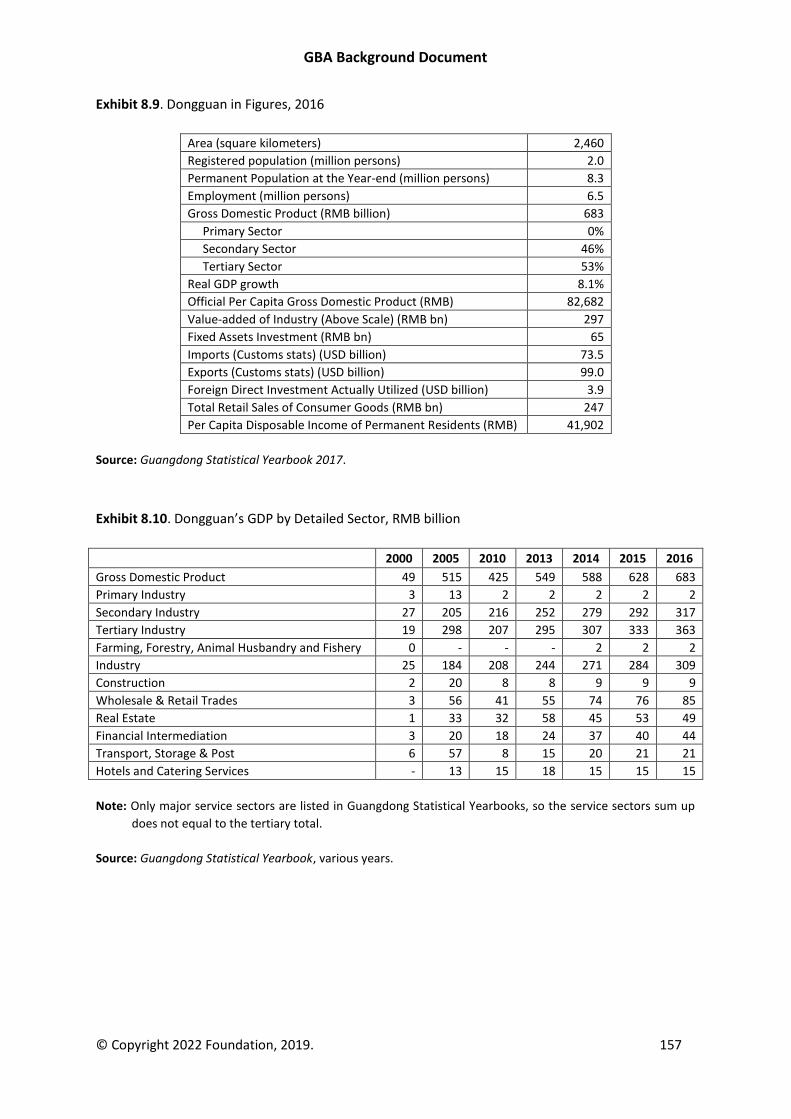

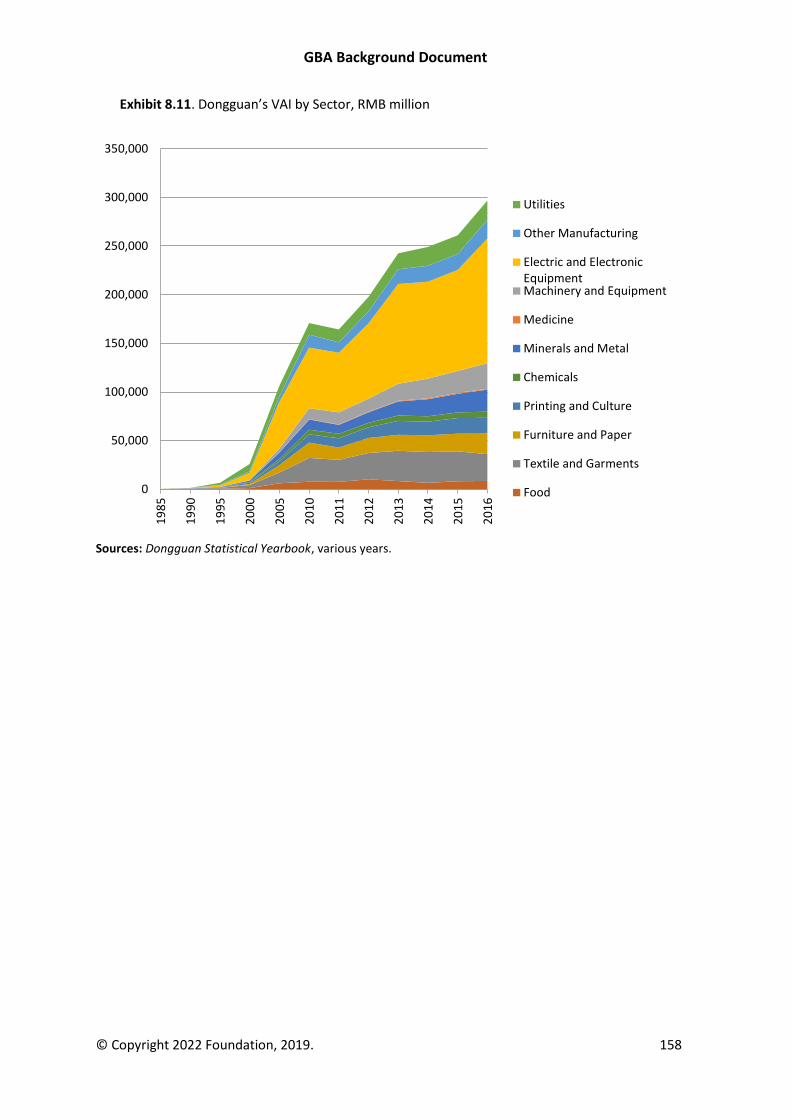

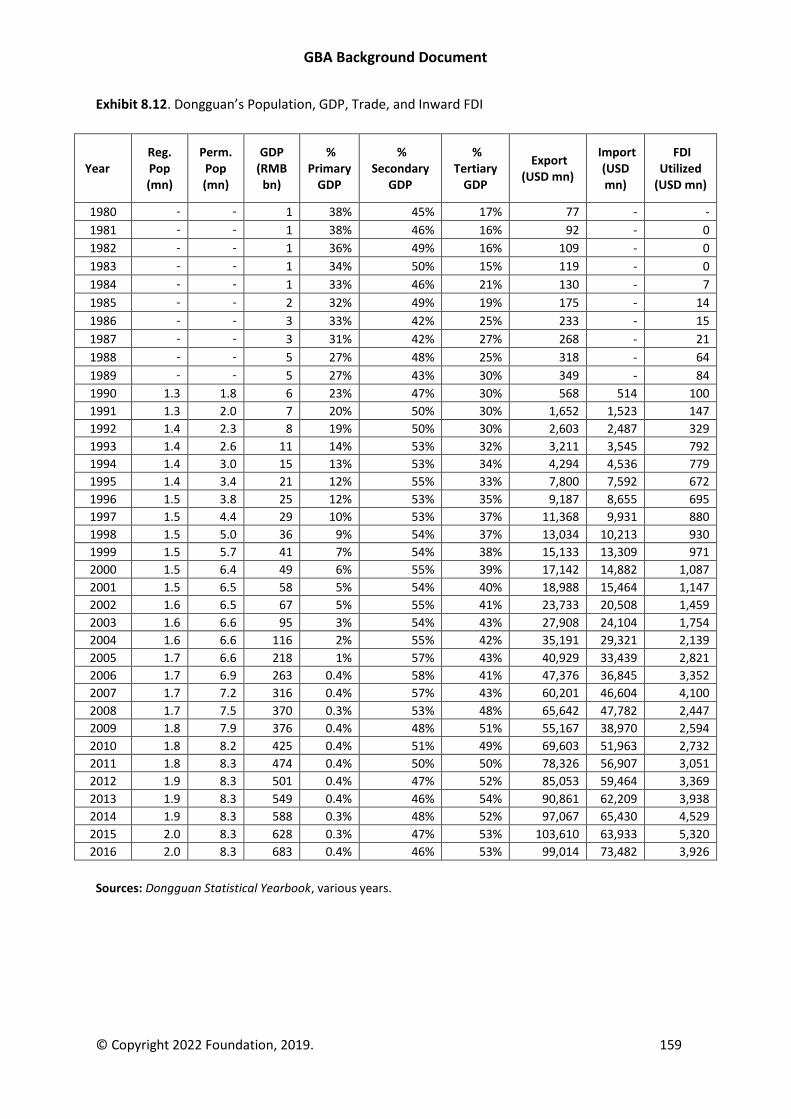

Dongguan ........................................................................................................................................ 155

Development Plans ..................................................................................................................... 155

Plan for Cooperation with Hong Kong and Macao ..................................................................... 156

Positioning................................................................................................................................... 156

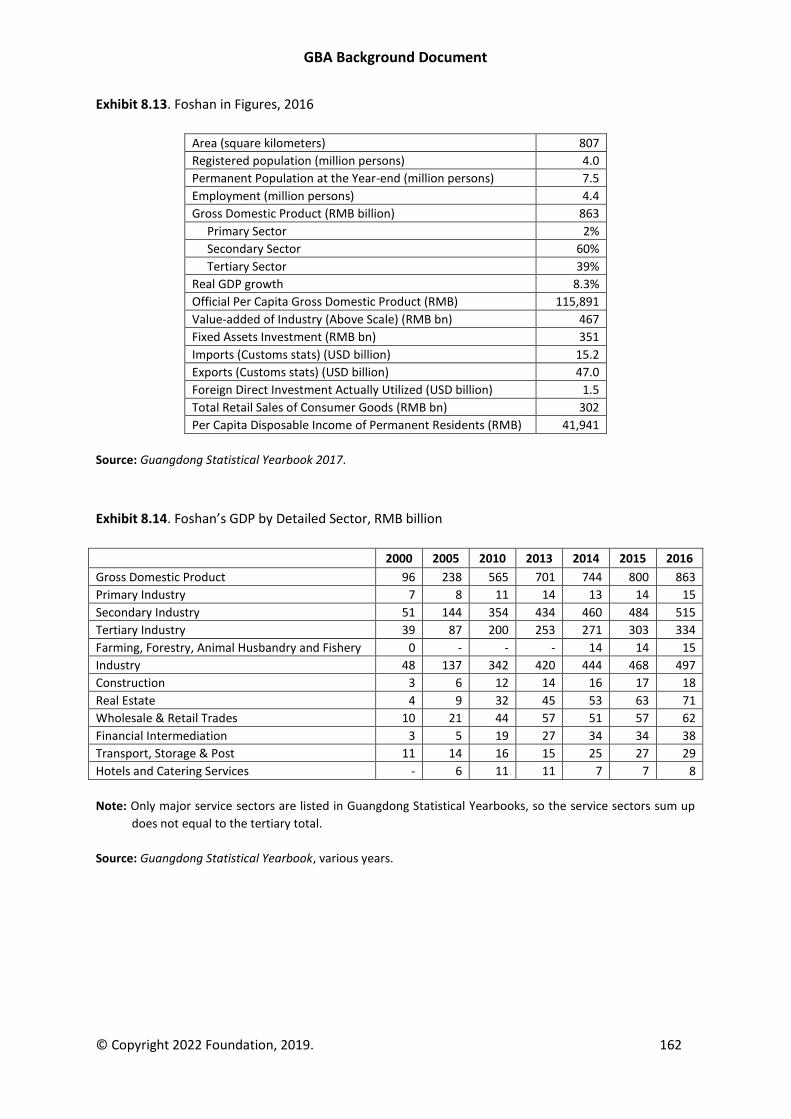

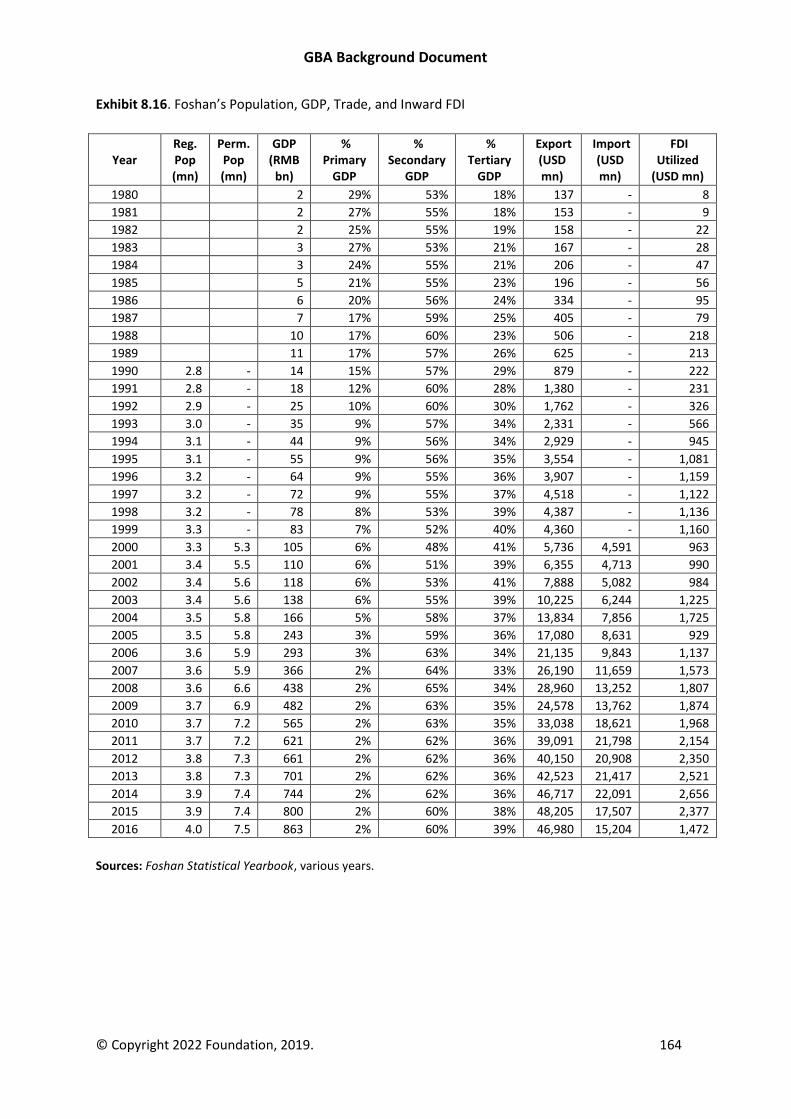

Foshan ............................................................................................................................................. 160

Development Plans ..................................................................................................................... 160

Plan for Cooperation with Hong Kong and Macao ..................................................................... 161

Positioning................................................................................................................................... 161

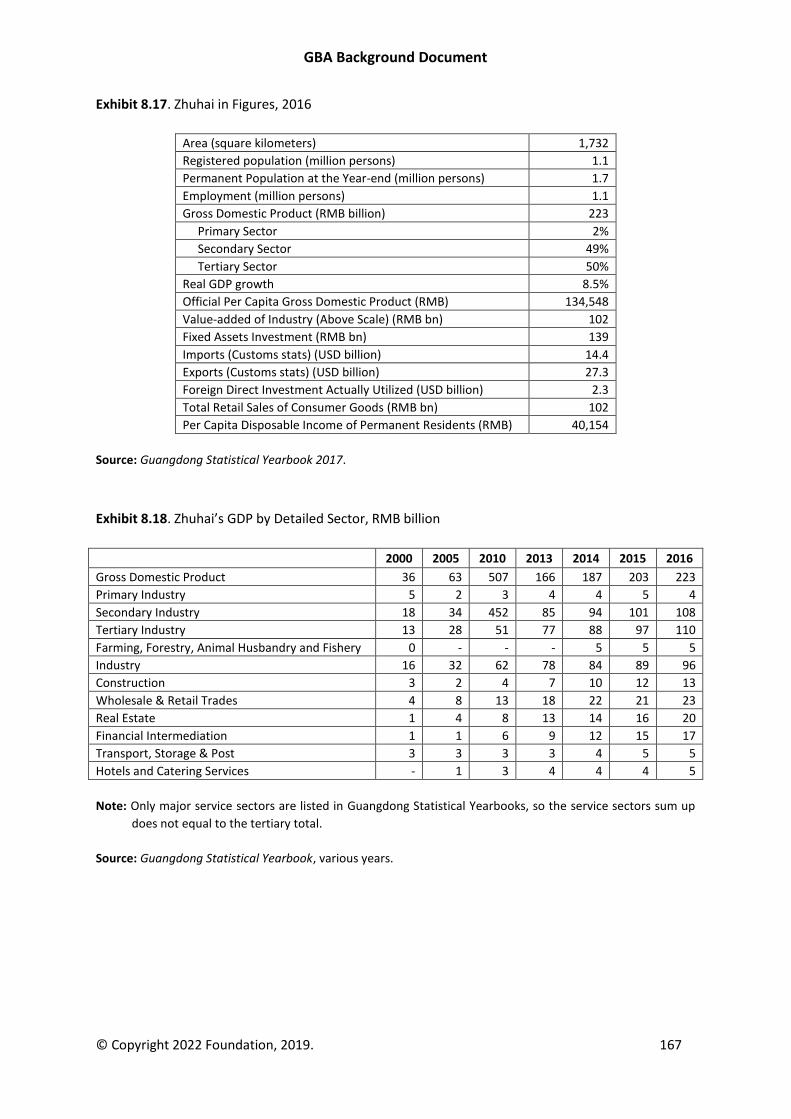

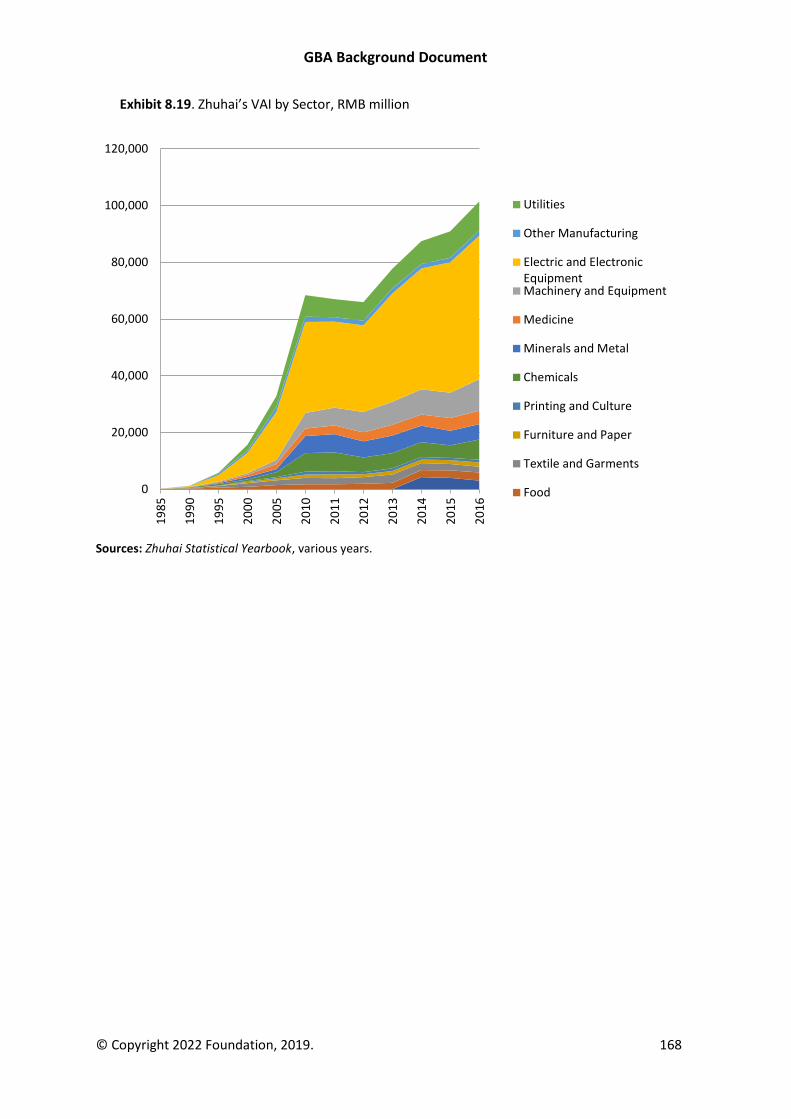

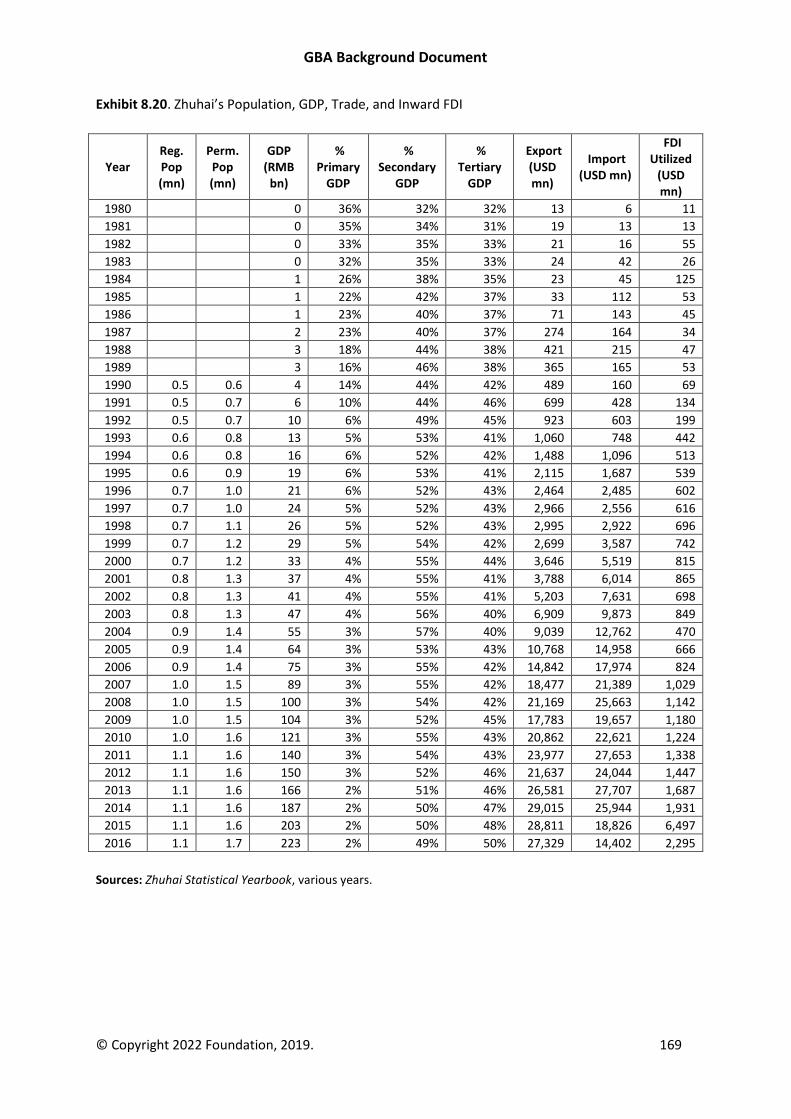

Zhuhai ............................................................................................................................................. 165

Development Plans ..................................................................................................................... 165

Plan for Cooperation with Hong Kong and Macao ..................................................................... 165

Positioning................................................................................................................................... 166

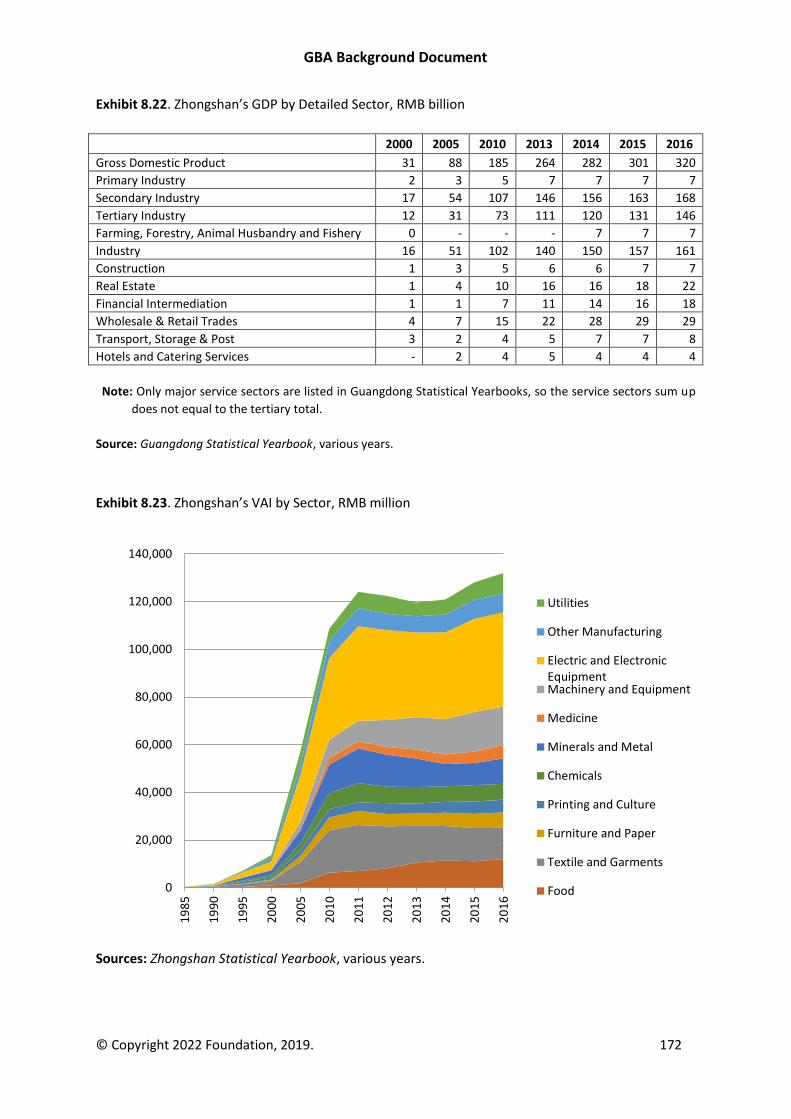

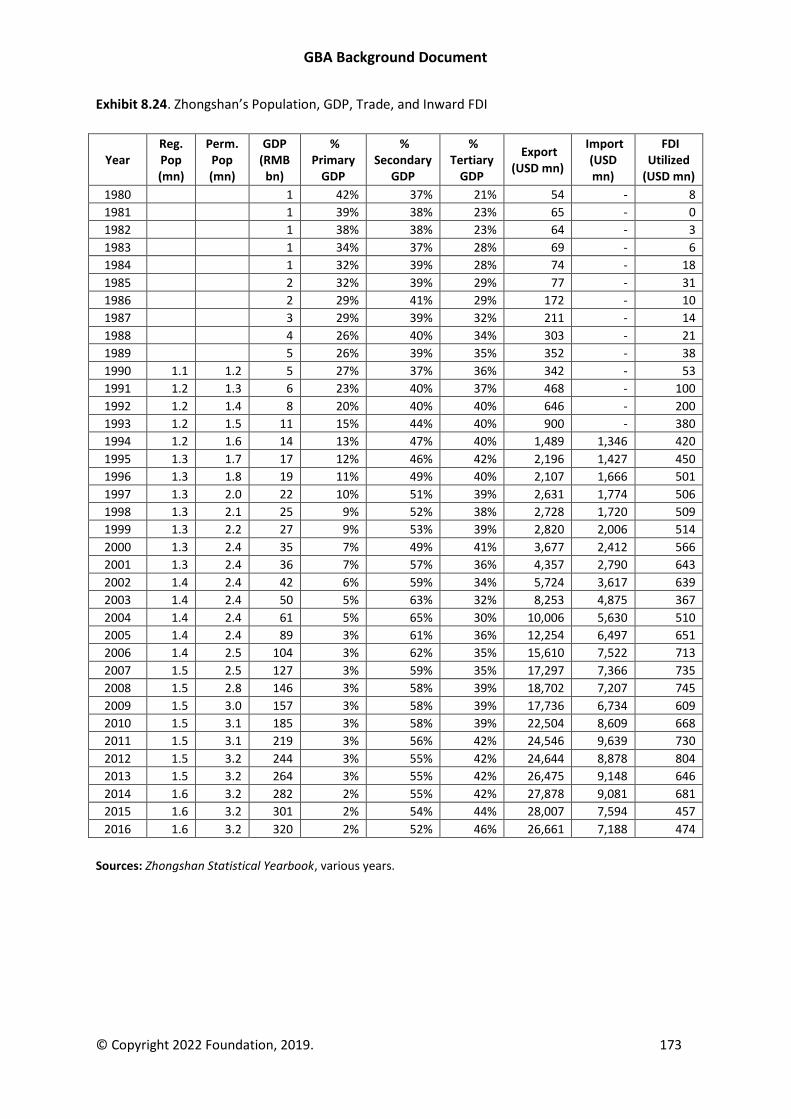

Zhongshan ....................................................................................................................................... 170

Development Plans ..................................................................................................................... 170

Plan for Cooperation with Hong Kong and Macao ..................................................................... 170

Positioning................................................................................................................................... 170

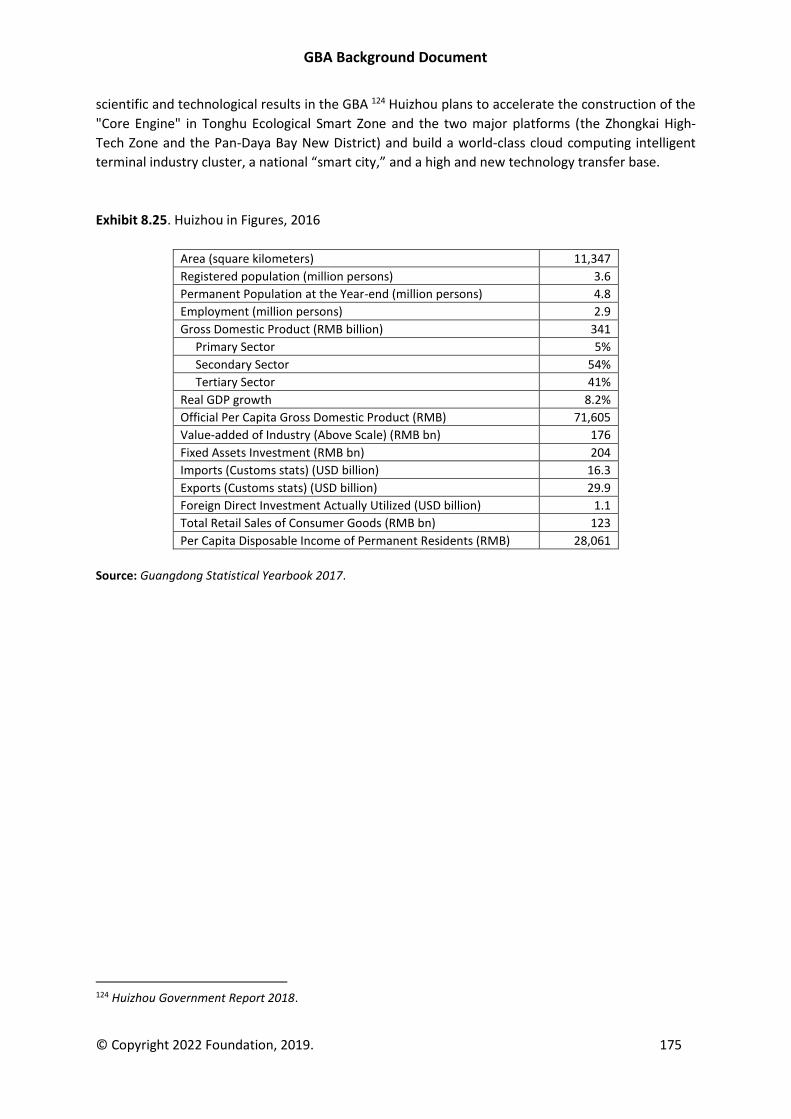

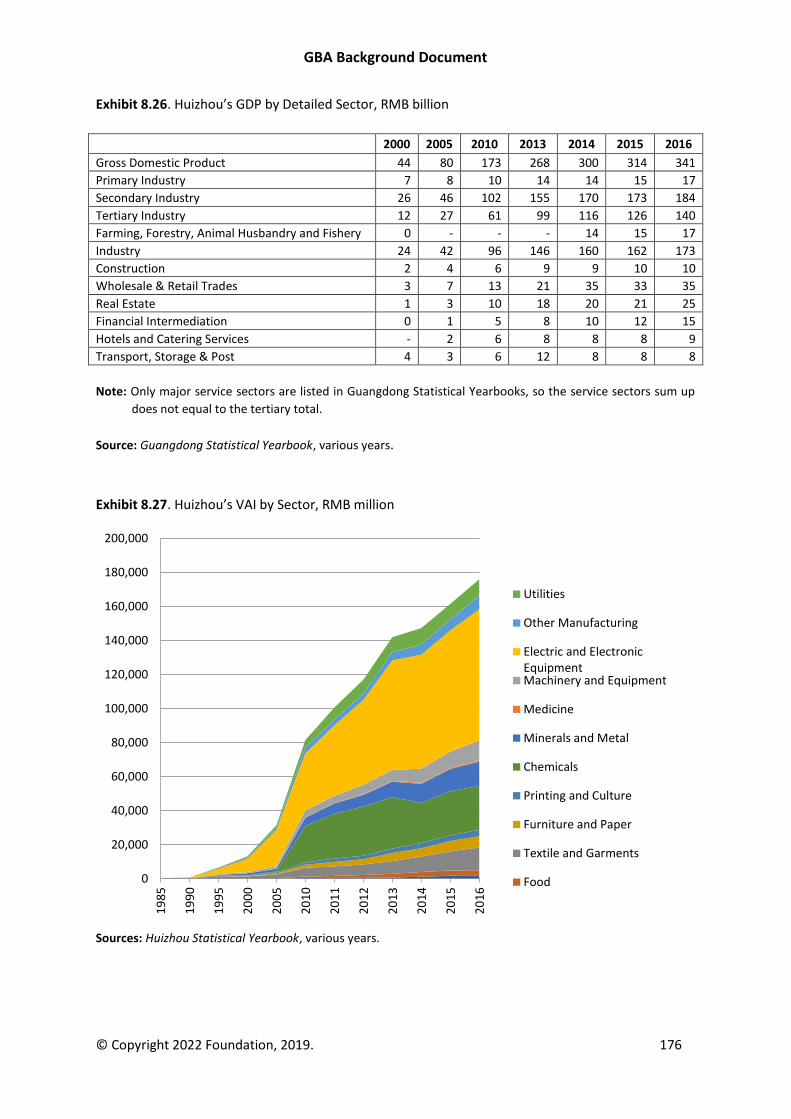

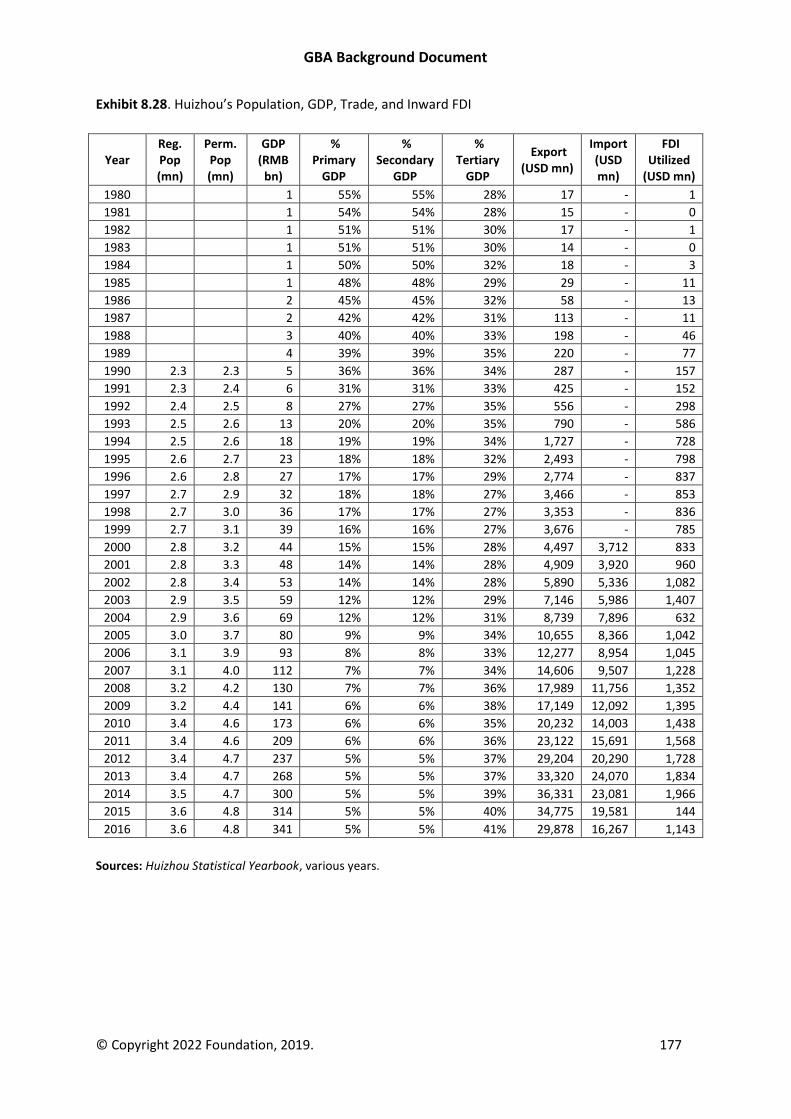

Huizhou ........................................................................................................................................... 174

Development Plans ..................................................................................................................... 174

Plan for Cooperation with Hong Kong and Macao ..................................................................... 174

Positioning................................................................................................................................... 174

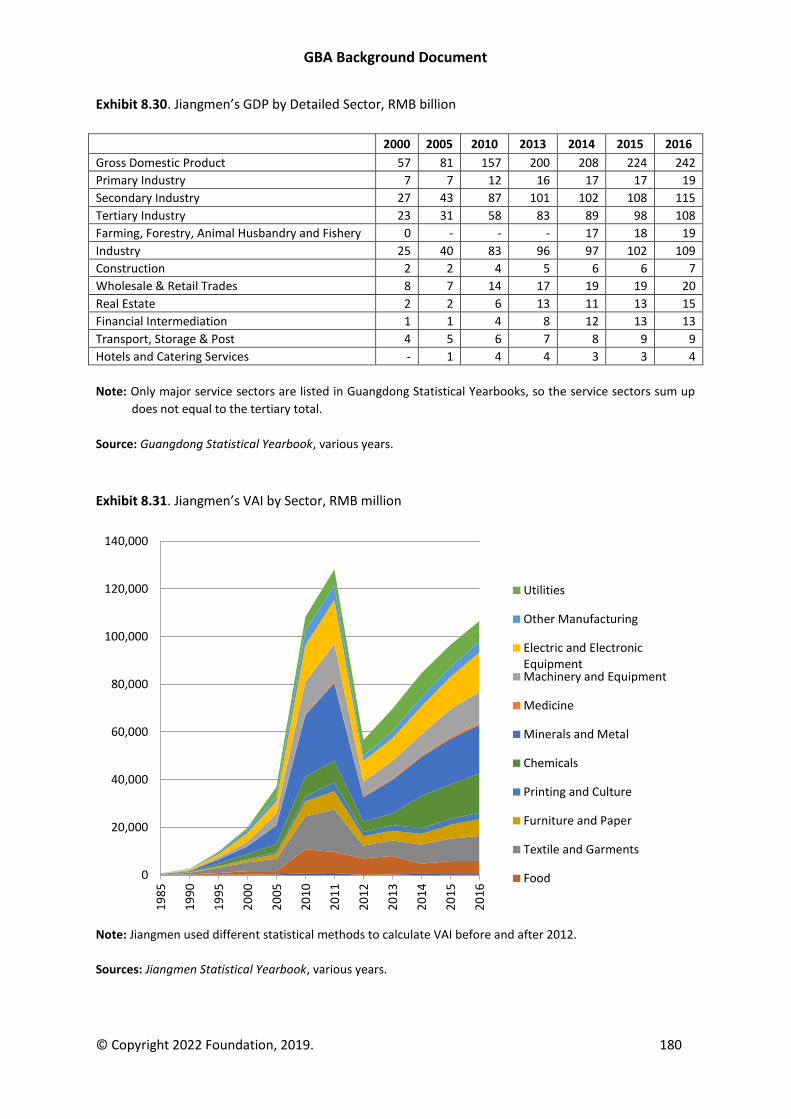

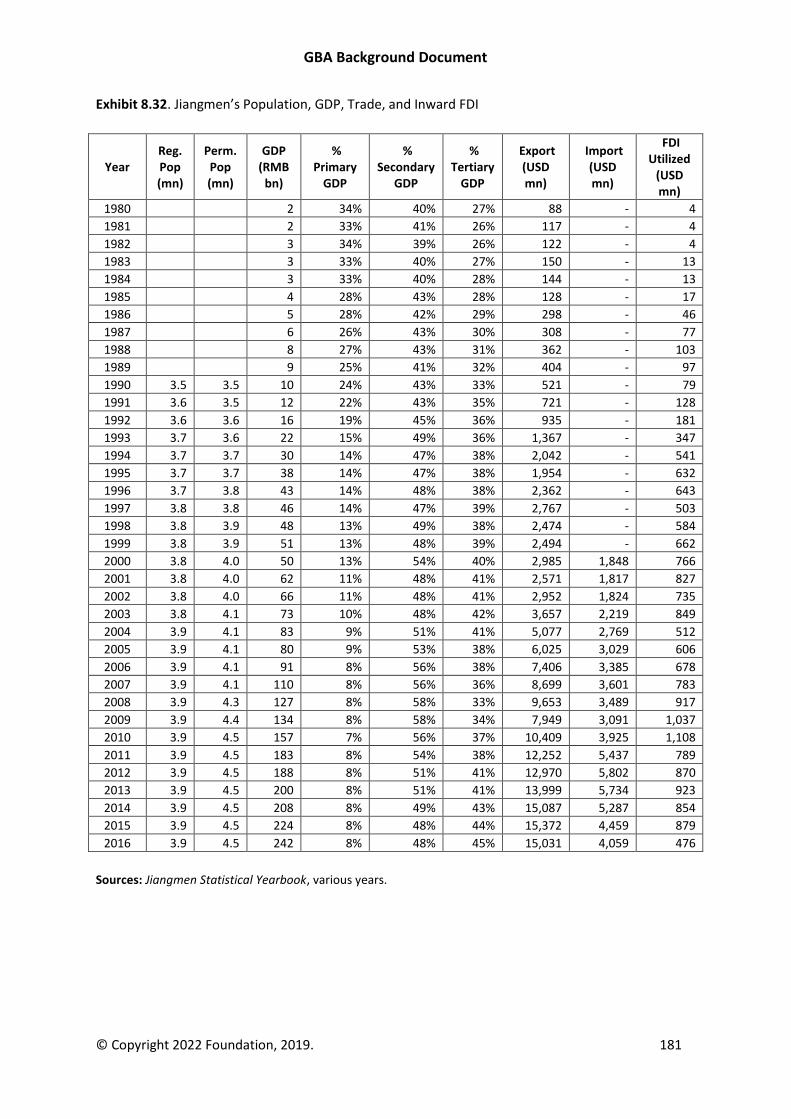

Jiangmen ......................................................................................................................................... 178

Development Plans ..................................................................................................................... 178

Plan for Cooperation with Hong Kong and Macao ..................................................................... 178

Positioning................................................................................................................................... 179

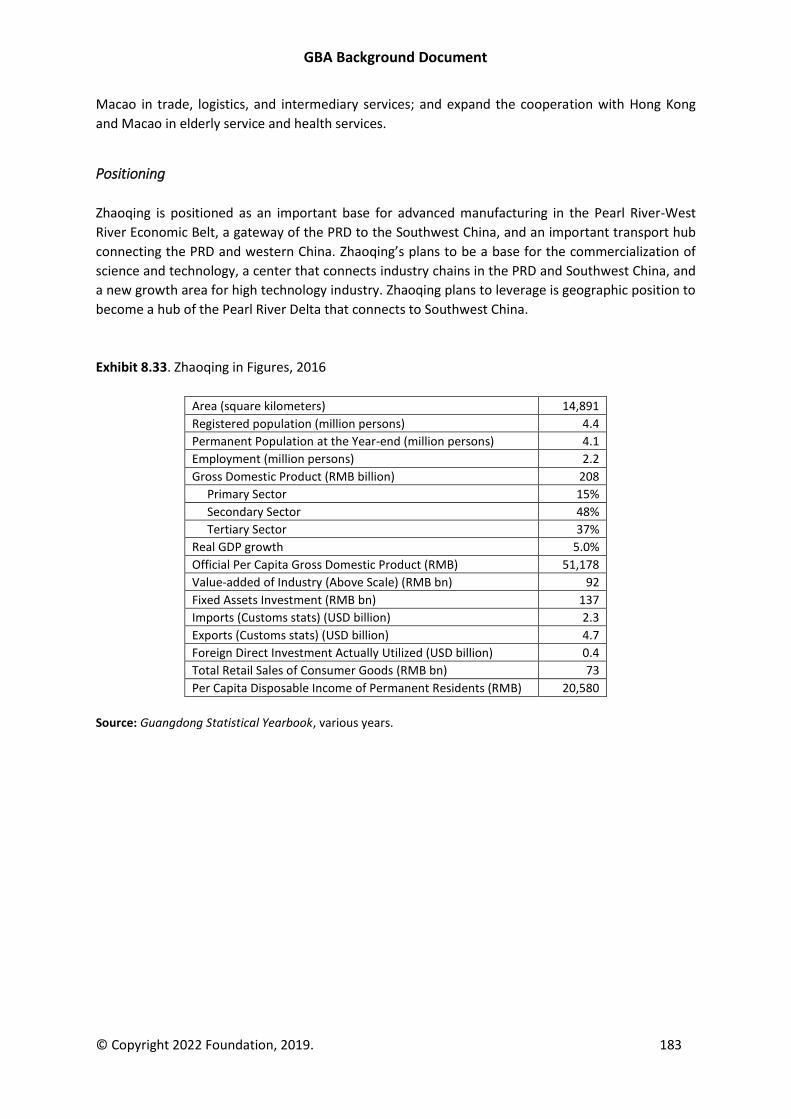

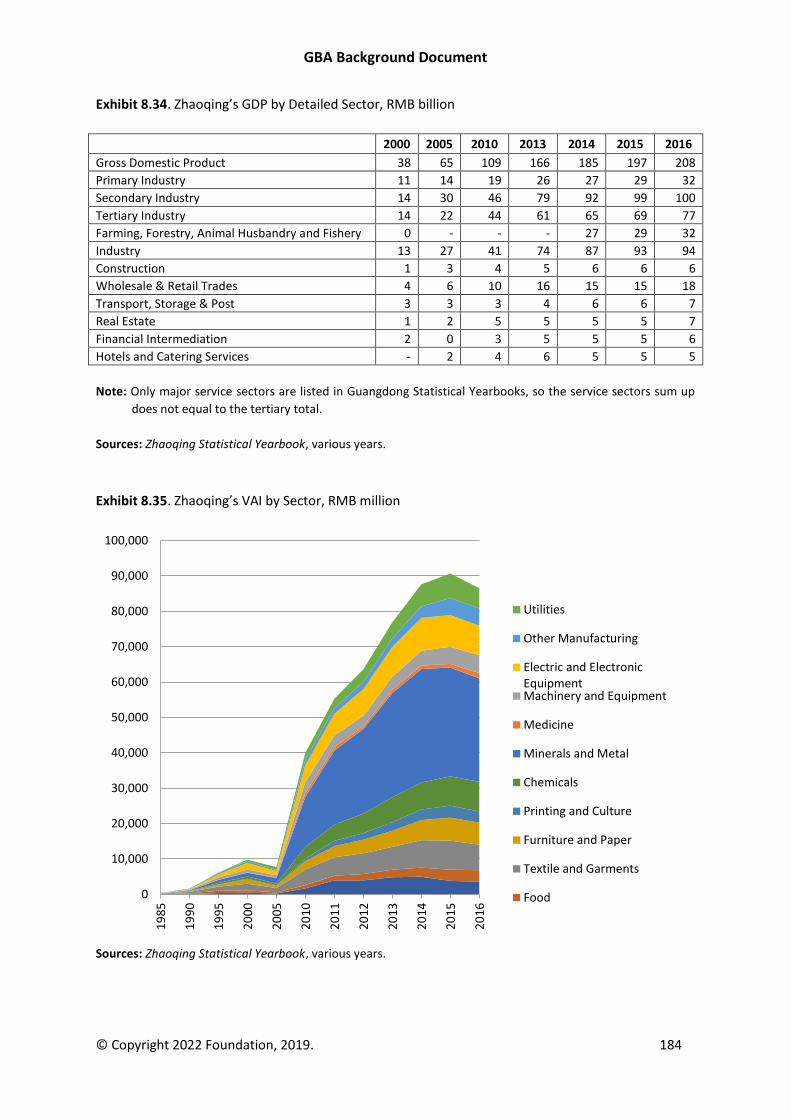

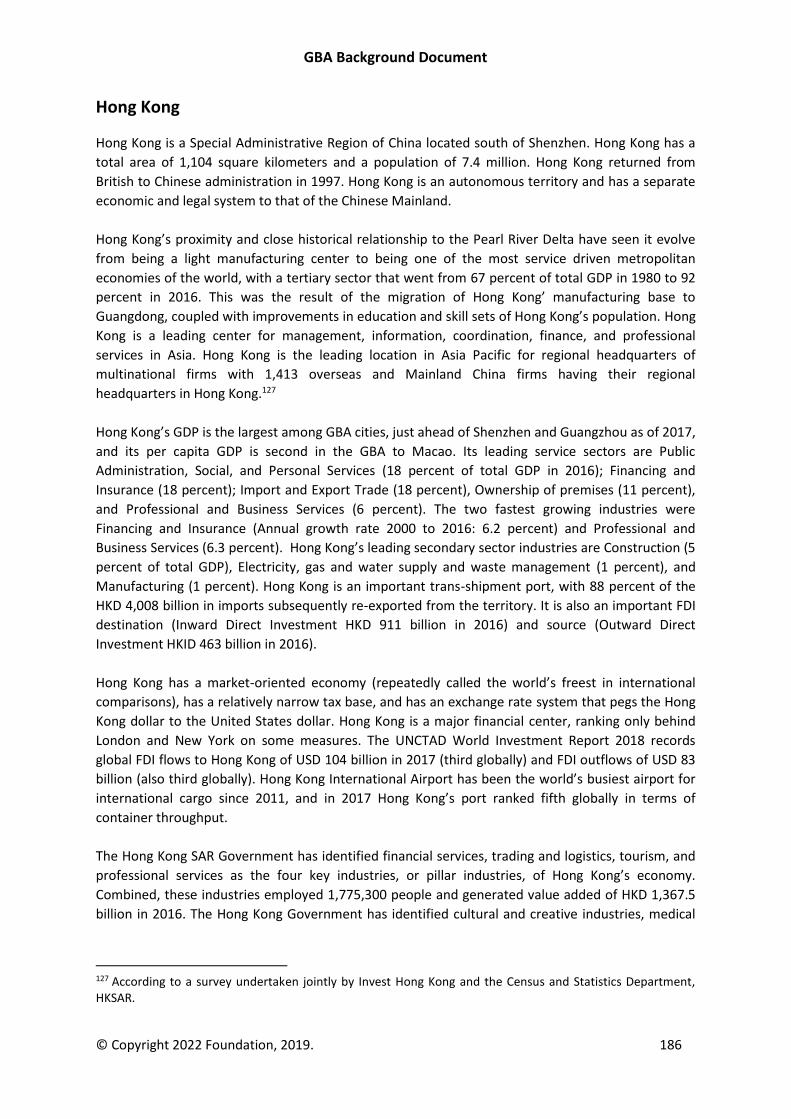

Zhaoqing ......................................................................................................................................... 182

Development Plans ..................................................................................................................... 182

Plan for Cooperation with Hong Kong and Macao ..................................................................... 182

Positioning................................................................................................................................... 183

Hong Kong ....................................................................................................................................... 186

Development Plans ..................................................................................................................... 187

GBA Background Document

© Copyright 2022 Foundation, 2019. 5

Positioning................................................................................................................................... 187

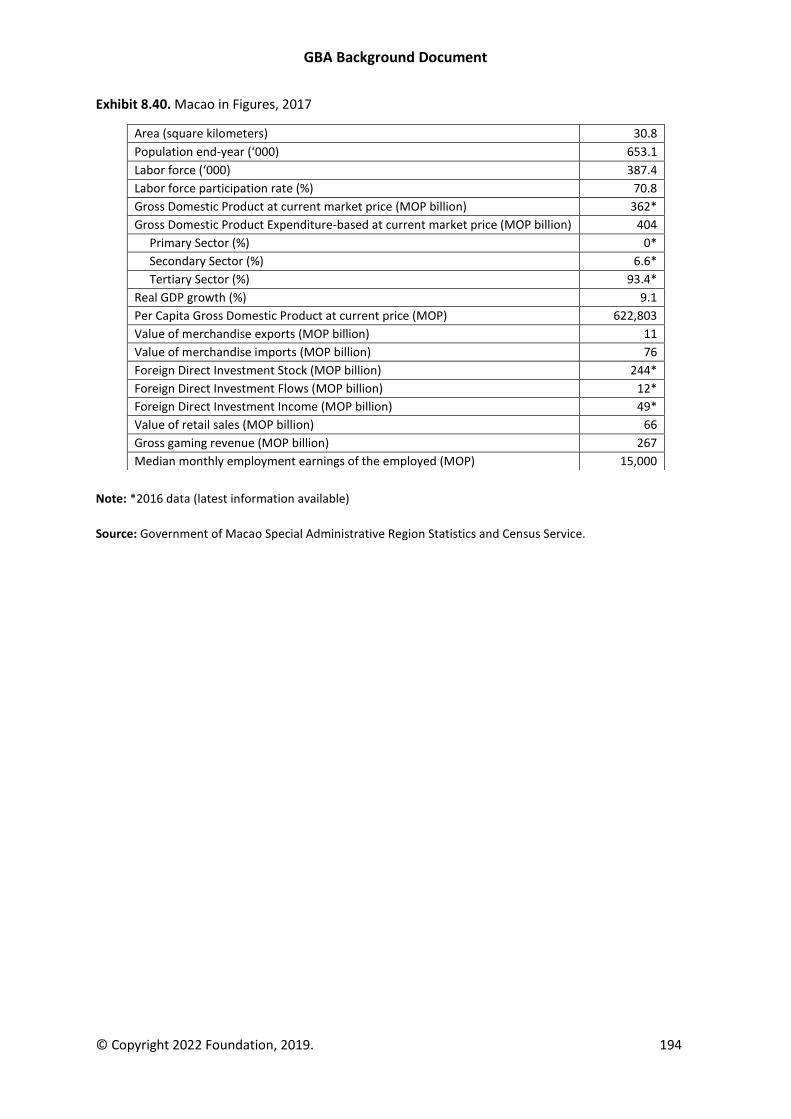

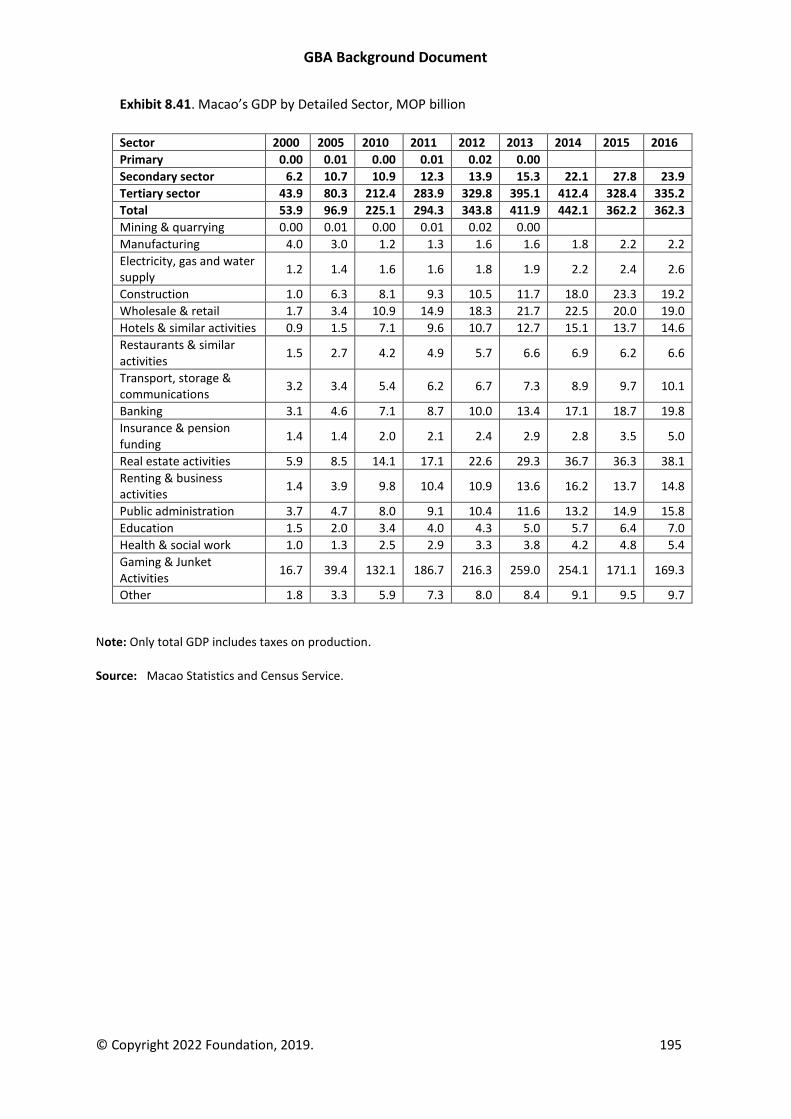

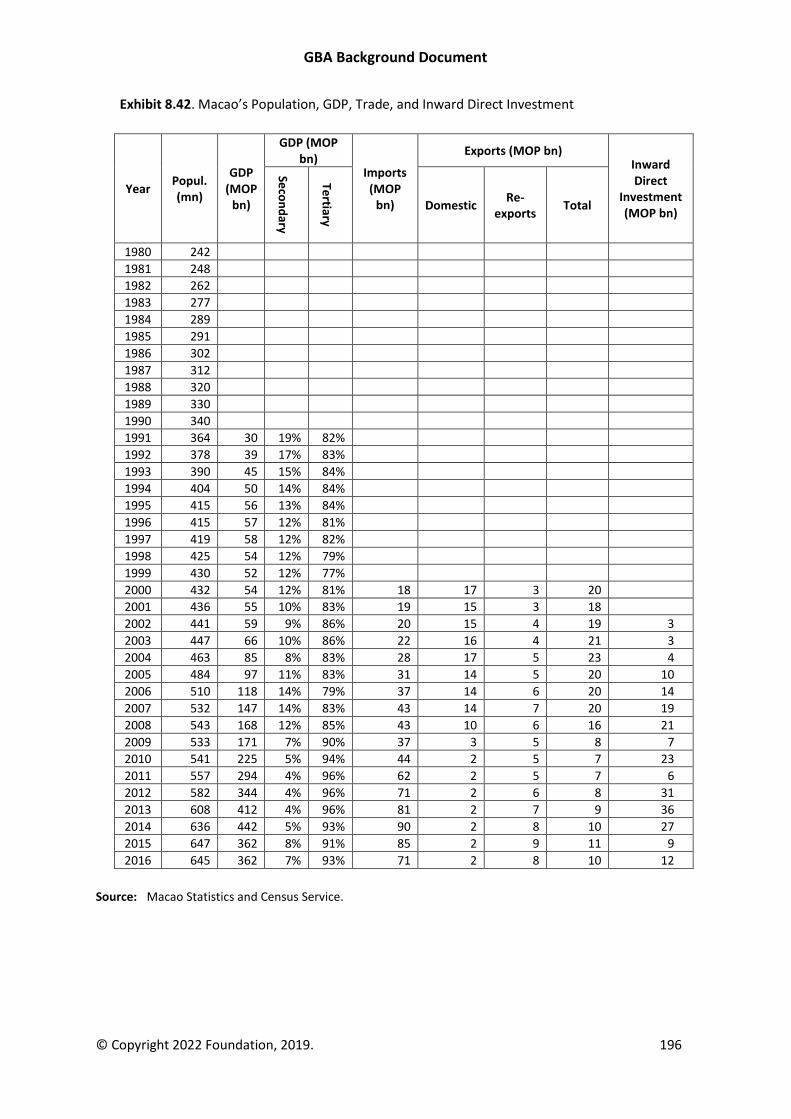

Macao ............................................................................................................................................. 192

Development Plans ..................................................................................................................... 192

Positioning................................................................................................................................... 193

9. 9. A Selection of Reports and Surveys on the GBA ..................................................................... 197

10. Background on the European Union ........................................................................................... 202

The EU Integration Process: Milestones ......................................................................................... 202

Free Movement of Goods ........................................................................................................... 202

Free Movement of Services ........................................................................................................ 203

Free Movement of the Workforce .............................................................................................. 204

Free Movement of Capital .......................................................................................................... 204

Common Competition Law (including prohibition to subsidize at the member-state level) ..... 205

The Legislative Process in the EU .................................................................................................... 205

EU Competences and Relations with Member States .................................................................... 206

The Source and Distribution of Competences in the European Union ....................................... 206

Exclusive Competence ................................................................................................................ 207

Shared Competence .................................................................................................................... 207

Supporting Competence ............................................................................................................. 208

Decision-making in the EU .......................................................................................................... 209

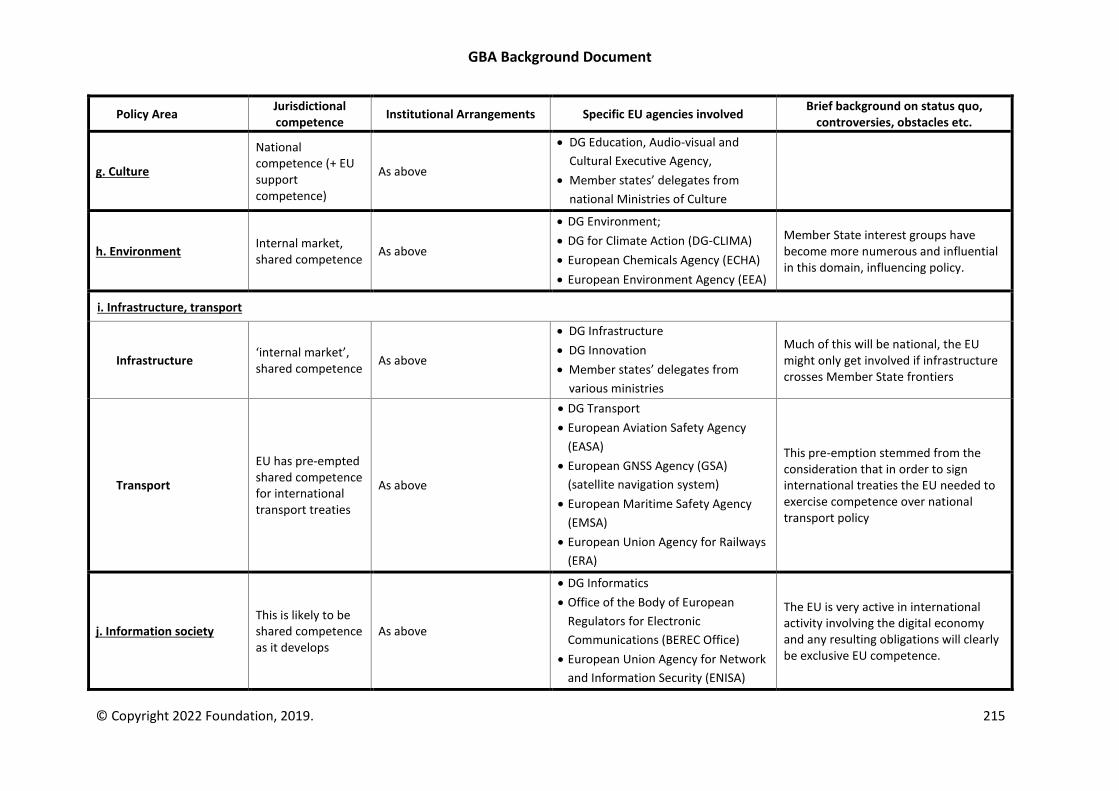

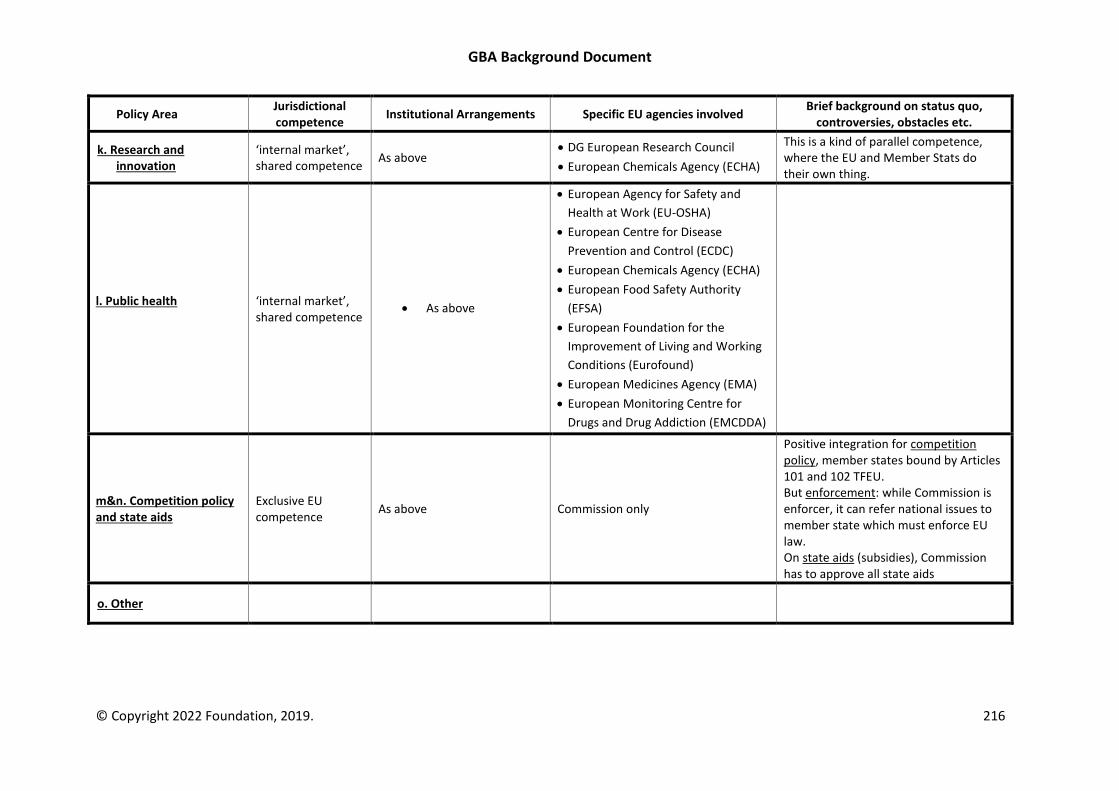

Competence by Topic: the EU “Competence Matrix” ................................................................ 210

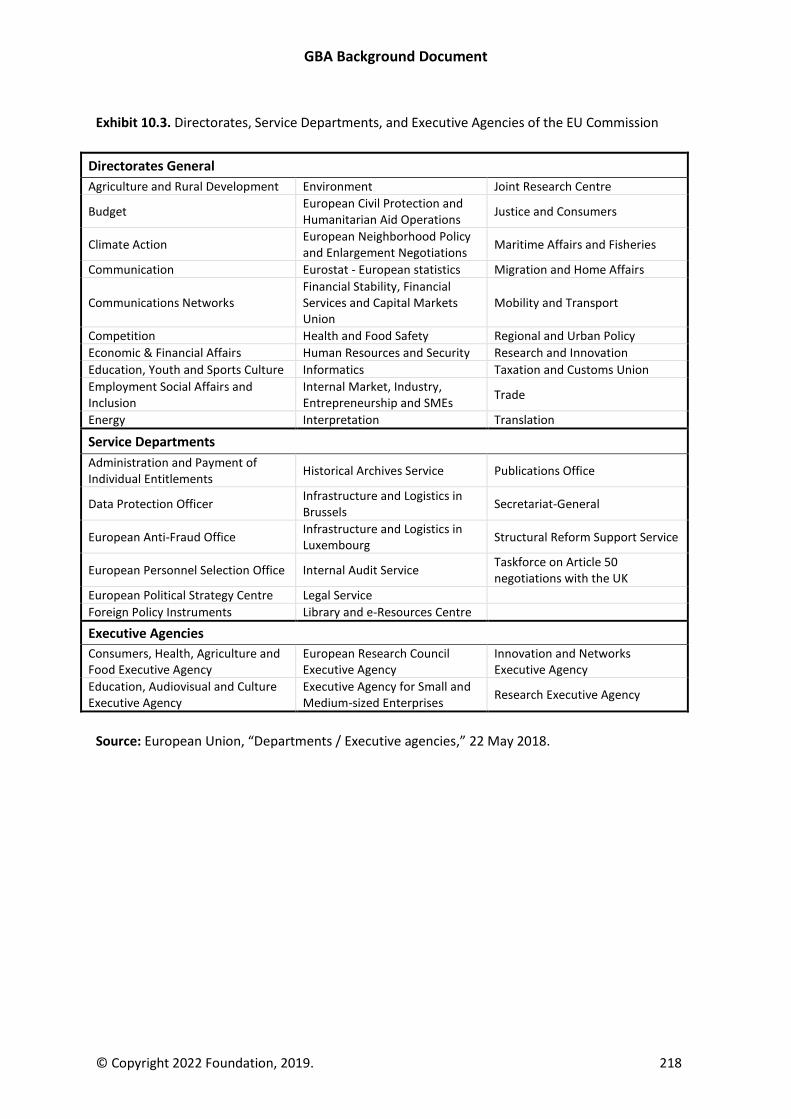

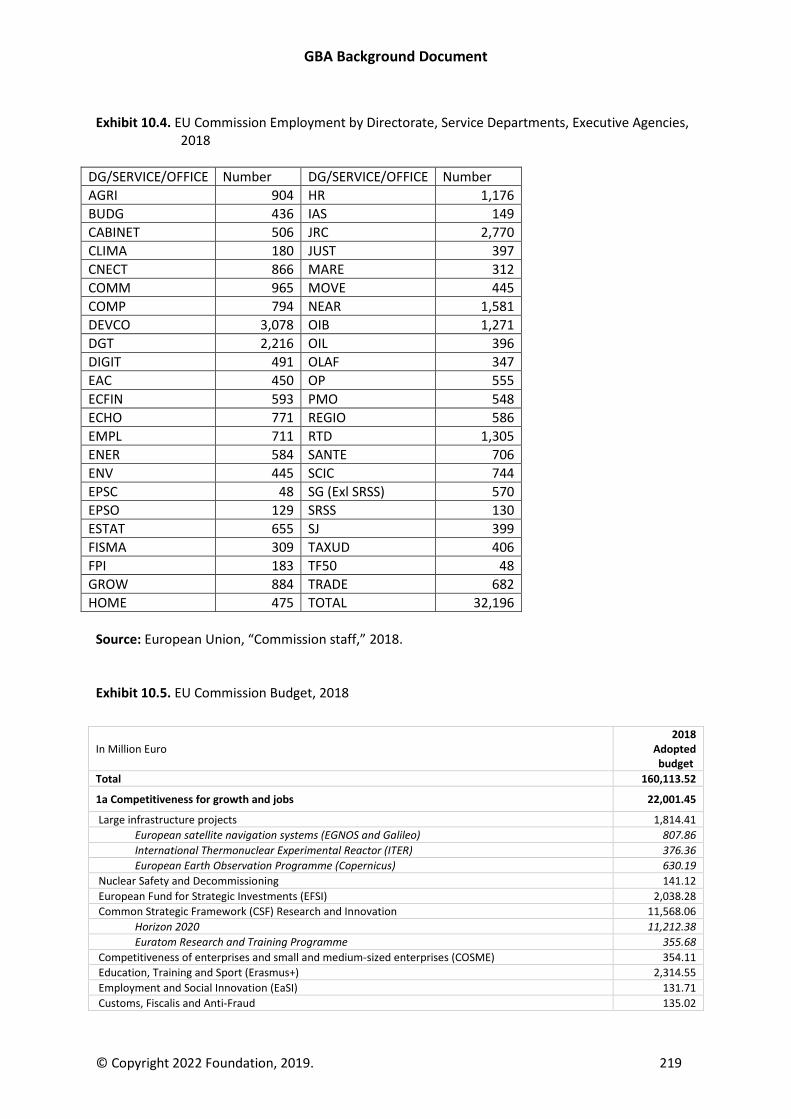

EU Organization .............................................................................................................................. 217

GBA Background Document

© Copyright 2022 Foundation, 2019. 6

0. This Document

This document is the Background Document for “The Future of the Guangdong-Hong Kong-Macao

Greater Bay Area” Project. It compiles information on the Greater Bay Area (GBA), its jurisdictions,

and programs and policies that may affect the future of the GBA. Given the complex nature of the

region (9 cities or prefectures in Guangdong Province and two Special Administrative Regions in

three customs zones); the multiple governments involved (Central Government of the People’s

Republic of China, Provincial Government of Guangdong, Hong Kong SAR Government, Macao SAR

Government, and the governments of the 9 cities of the Guangdong portion of the GBA); and the

multiple laws, regulations, agreements, programs, policies, and initiatives that influence the GBA,

establishing the fact base is an important undertaking.

This Document is one of the outputs from a six-month investigation into the Greater Bay Area of

Southern China undertaken under the auspices of the 2022 Foundation.

This Document has been prepared by a team at Hong Kong-based consultancy Enright, Scott &

Associates (ESA) under the direction of Professor Michael J. Enright, with substantial input from

Professor Feng Xiaoyun (of Guangzhou's Jinan University), Professor Patrick Low (of the Asia Global

Institute and University of Hong Kong), Professor Petros Mavroidis (of Columbia University and

University of Neuchâtel); and a team at the Fung Business Intelligence Centre including Chang Ka-

Mun, Denise Cheung WY, and Chan Kaiyip.

The goal has been to pull together information on the region to be used by researchers, analysts,

and others, as well as to provide background for the Main Report and Executive Summary for the

Project. These documents provide analysis, implications, and suggestions to enhance the economic

development of the GBA region.

GBA Background Document

© Copyright 2022 Foundation, 2019. 7

1. Introduction

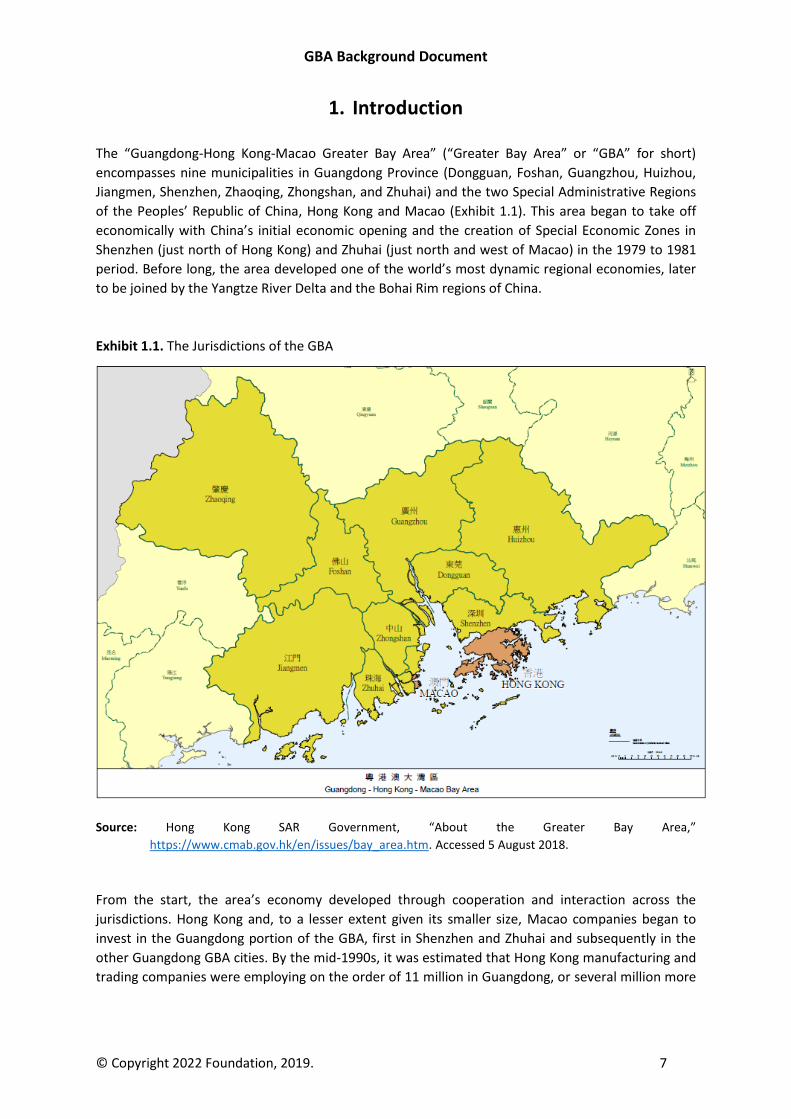

The “Guangdong-Hong Kong-Macao Greater Bay Area” (“Greater Bay Area” or “GBA” for short)

encompasses nine municipalities in Guangdong Province (Dongguan, Foshan, Guangzhou, Huizhou,

Jiangmen, Shenzhen, Zhaoqing, Zhongshan, and Zhuhai) and the two Special Administrative Regions

of the Peoples’ Republic of China, Hong Kong and Macao (Exhibit 1.1). This area began to take off

economically with China’s initial economic opening and the creation of Special Economic Zones in

Shenzhen (just north of Hong Kong) and Zhuhai (just north and west of Macao) in the 1979 to 1981

period. Before long, the area developed one of the world’s most dynamic regional economies, later

to be joined by the Yangtze River Delta and the Bohai Rim regions of China.

Exhibit 1.1. The Jurisdictions of the GBA

Source: Hong Kong SAR Government, “About the Greater Bay Area,”

https://www.cmab.gov.hk/en/issues/bay_area.htm. Accessed 5 August 2018.

From the start, the area’s economy developed through cooperation and interaction across the

jurisdictions. Hong Kong and, to a lesser extent given its smaller size, Macao companies began to

invest in the Guangdong portion of the GBA, first in Shenzhen and Zhuhai and subsequently in the

other Guangdong GBA cities. By the mid-1990s, it was estimated that Hong Kong manufacturing and

trading companies were employing on the order of 11 million in Guangdong, or several million more

GBA Background Document

© Copyright 2022 Foundation, 2019. 8

than the total population of Hong Kong.1 Hong Kong companies were also leaders in investing in and

managing the toll roads, ports, and power plants that helped provide the hard industrial

infrastructure for parts of the GBA as well as the hotels, office buildings, and facilities that helped

provide the soft industrial infrastructure.2

Guangdong became a leader in China’s reform process and an attractive location for talented

individuals from all over China. In the process, the province’s population increased from 52.3 million

in 1980 to 70.5 million in 1997 to 111.7 million in 2017. The “Pearl River Delta Economic Zone”

jurisdictions of Dongguan, Foshan, Guangzhou, Huizhou, Jiangmen, Shenzhen, Zhaoqing, Zhongshan,

and Zhuhai (but particularly Shenzhen, Dongguan, Guangzhou, and Foshan in the eastern and central

Pearl River Delta) saw wave upon wave of economic development, which included simple assembly

and basic infrastructure, followed by multi-stage processing, component production, and logistics;

followed by more advanced industries, support services, research and development, and complex

infrastructure; followed by advanced manufacturing, indigenous innovation, high-tech development,

and medium to high-end services.

Hong Kong’s economy benefitted enormously from China’s opening; its GDP grew at a real rate of

6.3 percent per year from 1980 to 1997. Despite the Asian Financial Crisis, the Global Financial Crisis,

and other international economic downturns, Hong Kong’s GDP grew at a real rate of 3.4 percent per

year from 1997 to 2017. The Hong Kong economy, which had already shifted from a manufacturing

economy to a services economy by 1997 (services 85.2 percent3 of GDP) continued the trend and by

2016 services accounted for 92.2 percent4 of Hong Kong’s GDP, with financial services, professional

services, trade-related services, and tourism accounting for 56.6 percent of GDP. 5

The Macao economy, which had been dominated by tourism related to the gaming industry along

with light manufacturing, took off with the ending of the gaming monopoly and the opening of

facilities of new competitors in 2004. Macao’s economy grew at a rate of 8.9 percent per year from

1999 to 2004, 13.2 percent per year from 2004 to 2010, and 6.6 percent per year from 2010 to 2017.

By 2016, the tourism and gaming sector accounted for 61.1 percent6 of GDP.

An Economic Region

The idea of the Greater Bay Area as an integrated economic region with greater cooperation from a

planning standpoint started to take root after the return of Hong Kong and Macao to Chinese

1 Michael J. Enright, Edith E. Scott, and David Dodwell, The Hong Kong Advantage (Hong Kong: Oxford University Press, 1997). 2 Michael J. Enright, Chang Ka-Mun, Edith E. Scott, and Zhu Wenhui, Hong Kong and the Pearl River Delta: The Economic Interaction (Hong Kong: The 2022 Foundation, 2003). 3 Hong Kong Census and Statistics Department, “GDP by economic activity (b) Percentage contribution to GDP at current prices, 1980-1998,” Gross Domestic Product 1961 to 1999, March 2000. 4 Hong Kong Census and Statistics Department, “Gross Domestic Product (GDP) by Major Economic Activity - Percentage Contribution to GDP at Basic Current Prices,” Accessed August 2018. 5 Hong Kong Census and Statistics Department, “Value added of the Four Key Industries, Feature Article: The Four Key Industries and Other Selected Industries in the Hong Kong Economy,” Hong Kong Monthly Digest of Statistics, May 2018. 6 Statistics and Census Service of the Government of Macao Special Administrative Region, Macao’s Tourism Satellite Account, 2018.

GBA Background Document

© Copyright 2022 Foundation, 2019. 9

administration in 1997 and 1999 respectively. For example, when the 2022 Foundation released its

report, Hong Kong and the Pearl River Delta: The Economic Interaction7 in February 2003, the search

term “The Greater Pearl River Delta,” the name that was being promoted for the area as an

integrated economic region at the time, registered 175 “hits” in a Google search. By the end of 2005,

when a book from the project, Regional Powerhouse: The Greater Pearl River Delta and the Rise of

China,8 was published, the number of hits was 15,600 and by May 2010, when the 6th edition of

Invest Hong Kong’s The Greater Pearl River Delta9 by some of the same authors was published, the

number was 1,450,000.

In the meanwhile, Hong Kong and Macao both have CEPAs, or Closer Economic Partnership

Arrangements, with the Chinese Mainland that were signed in June and October of 2003

respectively. By 2018, there had been 10 supplements to each of the CEPA arrangements as well as

agreements on trade in services. Hong Kong and Macao, which have been two of the world’s most

open economies, signed their own CEPA in October 2017. The dominant business interaction and

integration that the various rounds of CEPA negotiations have facilitated have taken place within the

GBA.

There have been clear benefits to the economic interaction and integration that has taken place

between Guangdong, Hong Kong, and Macao. Hong Kong was a critical source of investment and

access to the rest of the world for Guangdong-based manufacturing facilities in the early days of

China’s economic opening, and still plays an important role as investor and connector to this day.

Guangdong provided the manufacturing base that allowed Hong Kong to become a leading trading

economy and Guangdong still provides a vast production base and market for Hong Kong firms, as it

has progressed on its own as well. The vast majority of the tourists that drive Macao’s economy

once came from Hong Kong and now come from Guangdong. The economic interaction within the

GBA transformed the region from an economic backwater to one of the world’s most dynamic and

important economic regions.

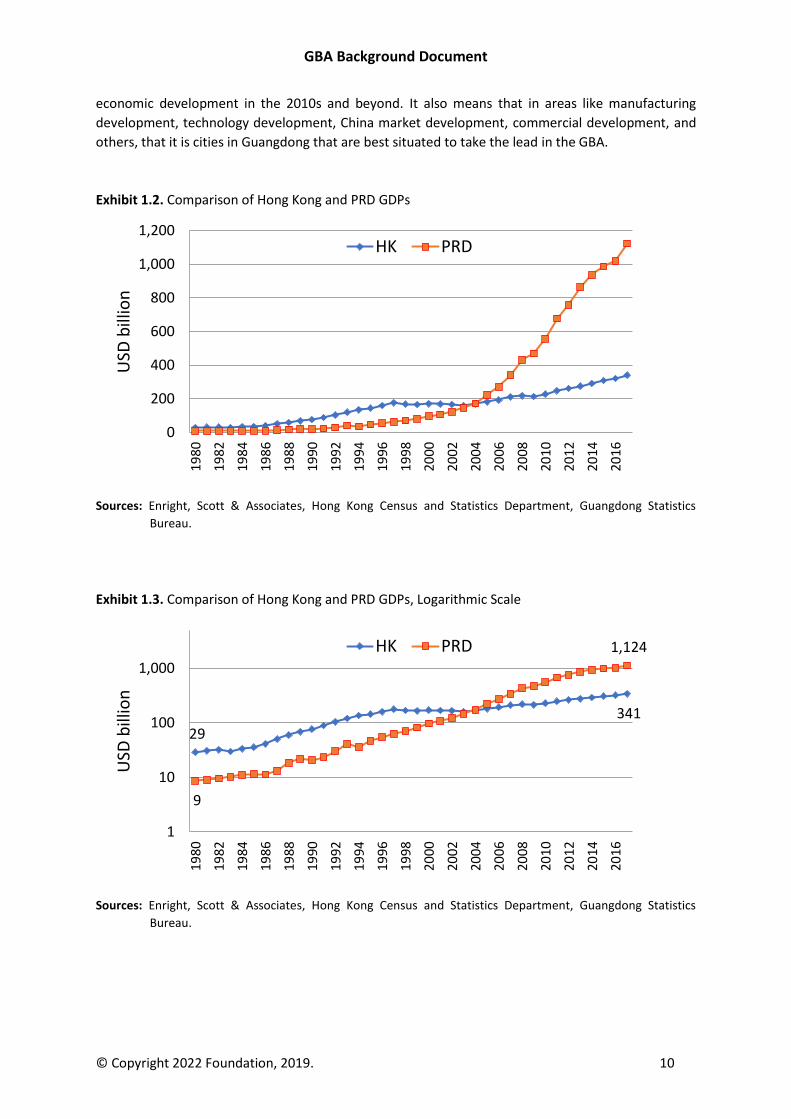

Hong Kong, which was once the leading economic player in the GBA, has seen its relative importance

diminish with the rise of the economies of jurisdictions in Guangdong Province. In 1980, near the

beginning of China’s opening, Hong Kong’s GDP was three times that of the nine Pearl River Delta

cities of Guangdong. At the time of the return of Hong Kong to Chinese administration in 1997, Hong

Kong’s GDP was still nearly three times that of the PRD cities. By 2017, the tables had been turned,

and the PRD cities’ economy was nearly three times the size of Hong Kong’s (Exhibits 1.2 and 1.3, the

logarithmic scale in the latter is to show the values in the early period more clearly).

This was not due to poor planning or poor performance on the part of Hong Kong, but rather to the

fact that Guangdong’s economy, unleashed by China’s opening and facilitated by Hong Kong and

Macao, grew so rapidly. This means that Hong Kong’s regional role, which was to lead the region’s

economic development in the 1980s and 1990s, needs to evolve to one that supports the region’s

7 Michael J. Enright, Chang Ka-Mun, Edith E. Scott, and Zhu Wenhui, Hong Kong and the Pearl River Delta: The Economic Interaction (Hong Kong: The 2022 Foundation, 2003). 8 Michael J. Enright, Edith E. Scott, and Chang Ka-Mun, Regional Powerhouse: The Greater Pearl River Delta and the Rise of China (New York and Singapore: Wiley, 2005). 9 Michael J. Enright, Edith E. Scott, and Richard M. Petty, The Greater Pearl River Delta 6th edition (Hong Kong: Invest Hong Kong, 2010).

GBA Background Document

© Copyright 2022 Foundation, 2019. 10

economic development in the 2010s and beyond. It also means that in areas like manufacturing

development, technology development, China market development, commercial development, and

others, that it is cities in Guangdong that are best situated to take the lead in the GBA.

Exhibit 1.2. Comparison of Hong Kong and PRD GDPs

Sources: Enright, Scott & Associates, Hong Kong Census and Statistics, Guangdong Statistical Bureau

Sources: Enright, Scott & Associates, Hong Kong Census and Statistics Department, Guangdong Statistics

Bureau.

Exhibit 1.3. Comparison of Hong Kong and PRD GDPs, Logarithmic Scale

Sources: Enright, Scott & Associates, Hong Kong Census and Statistics, Guangdong Statistical Bureau

Sources: Enright, Scott & Associates, Hong Kong Census and Statistics Department, Guangdong Statistics

Bureau.

29

341

9

1,124

1

10

100

1,000

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

200

4

200

6

2008

2010

2012

2014

2016

USD

bill

ion

HK PRD

0

200

400

600

800

1,000

1,200

19

80

19

82

19

84

19

86

19

88

19

90

19

92

19

94

19

96

19

98

20

00

20

02

200

4

200

6

20

08

20

10

20

12

20

14

20

16

USD

bill

ion

HK PRD

GBA Background Document

© Copyright 2022 Foundation, 2019. 11

2. The Region

The Greater Bay Area consists of nine cities of Guangdong Province, which account for around 30

percent of the land mass of Guangdong Province, plus the Special Administrative Regions of Hong

Kong and Macao. It is located in the Pearl River Delta along the South China coast.

Historical Background

Guangdong was first incorporated into the Chinese empire in 222 BCE, when the first emperor of the

Qin dynasty, conquered the area. In 111 BCE Chinese domination was extended to the whole of

what is now Guangdong. Over the next centuries Guangdong became more integrated into China

and by the 1100s Guangzhou had become a major transit point for international trade and a city

with a population of hundreds of thousands. By the 17th century Guangdong became a source of

emigration, first to other parts of China and then to other parts of the world. When China closed

itself off from the rest of the world, Guangzhou became the leading conduit for foreign trade. After

the founding of the People’s Republic of China, Guangdong retained its leading role in trade, but

otherwise was economically behind the Eastern and Northeastern coasts of China. With the advent

of China’s economic reform and opening program in 1979-1981, Guangdong took a leadership role in

reform and opening, a role it retains to today, and emerged as one of the most economically

dynamic provinces of China.

The British took control over Hong Kong Island and the Kowloon Peninsula in the 1840s as a result of

the Opium Wars. Subsequently a lease was signed that gave the British control over the more

extensive New Territories adjacent to Kowloon. China never acknowledged the legitimacy of foreign

administration over Hong Kong and Macao and when the 99-year lease on the New Territories (over

80 percent of the Hong Kong land mass) came up for expiry, China indicated its desire to reassume

administration. This was achieved based on the Joint Declaration of the Government of the United

Kingdom of Great Britain and Northern Ireland and the Government of the People's Republic of China

on the Question of Hong Kong, signed in December 1984, and The Basic Law of the Hong Kong

Special Administrative Region, which was adopted on 4 April 1990 by the National People's Congress

of the PRC and came into effect on 1 July 1997.

Macao’s colonial history was much longer than that of Hong Kong. Macao is reported to have been

established by one Jorge Alvarez, a Portuguese explorer in the mid-1550s as one of the first trading

ports in the Far East. After initial success, increased competition from other foreign powers in the

region, the opening up of further Chinese ports to foreign trade, and trade restrictions applied by

Chinese leaders, the colony saw a decline in its wealth and influence. The granting of a gaming

monopoly in 1962 brought investment that helped build a tourism industry to supplement Macao’s

trading and light manufacturing. In the 1970s, the Portuguese Government decided to dis-invest

itself of all its colonial possessions. This coincided with China’s desire to reassert administration over

its territory. Discussions between the Portugal and Chinese leaders resulted in the signing of the

Joint Declaration of the Government of the People's Republic of China and the Government of the

Portuguese Republic on the Question of Macao, in March 1987 and The Basic Law of the Macao

Special Administrative Region of the People's Republic of China, which was adopted by the National

People's Congress of the PRC on 31 March 1993 and came into effect on 20 December 1999.

GBA Background Document

© Copyright 2022 Foundation, 2019. 12

Regional Economic Profile

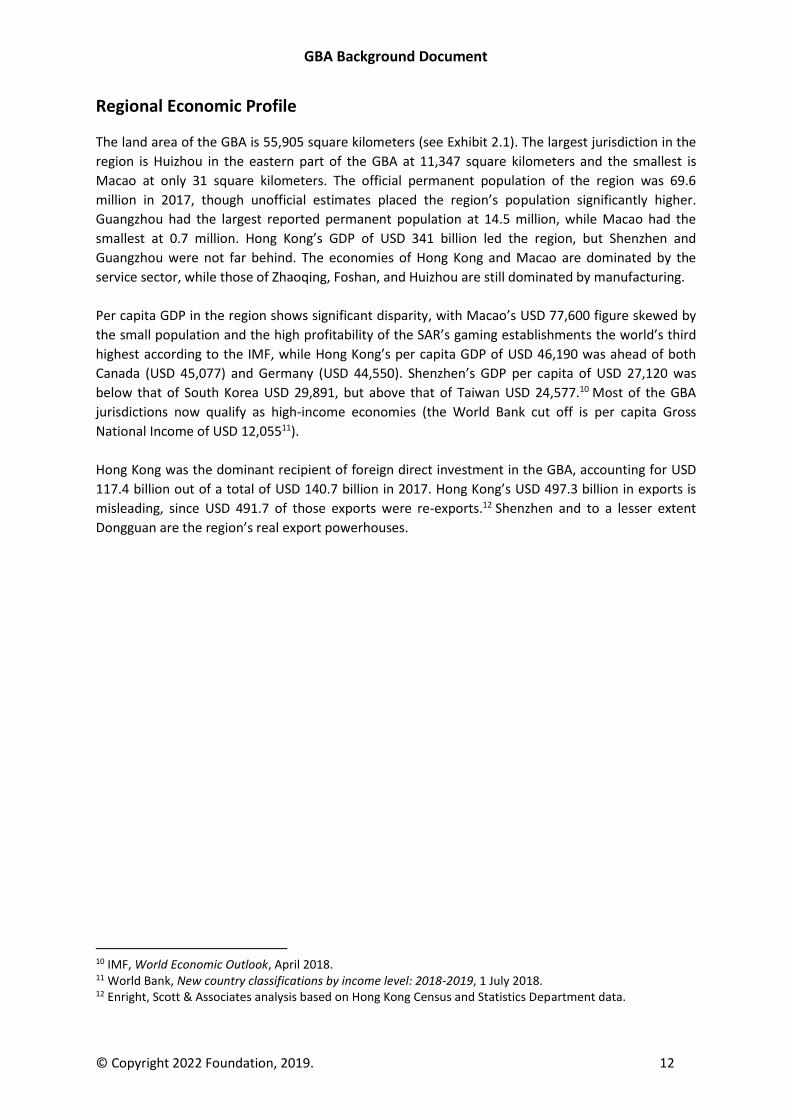

The land area of the GBA is 55,905 square kilometers (see Exhibit 2.1). The largest jurisdiction in the

region is Huizhou in the eastern part of the GBA at 11,347 square kilometers and the smallest is

Macao at only 31 square kilometers. The official permanent population of the region was 69.6

million in 2017, though unofficial estimates placed the region’s population significantly higher.

Guangzhou had the largest reported permanent population at 14.5 million, while Macao had the

smallest at 0.7 million. Hong Kong’s GDP of USD 341 billion led the region, but Shenzhen and

Guangzhou were not far behind. The economies of Hong Kong and Macao are dominated by the

service sector, while those of Zhaoqing, Foshan, and Huizhou are still dominated by manufacturing.

Per capita GDP in the region shows significant disparity, with Macao’s USD 77,600 figure skewed by

the small population and the high profitability of the SAR’s gaming establishments the world’s third

highest according to the IMF, while Hong Kong’s per capita GDP of USD 46,190 was ahead of both

Canada (USD 45,077) and Germany (USD 44,550). Shenzhen’s GDP per capita of USD 27,120 was

below that of South Korea USD 29,891, but above that of Taiwan USD 24,577.10 Most of the GBA

jurisdictions now qualify as high-income economies (the World Bank cut off is per capita Gross

National Income of USD 12,05511).

Hong Kong was the dominant recipient of foreign direct investment in the GBA, accounting for USD

117.4 billion out of a total of USD 140.7 billion in 2017. Hong Kong’s USD 497.3 billion in exports is

misleading, since USD 491.7 of those exports were re-exports.12 Shenzhen and to a lesser extent

Dongguan are the region’s real export powerhouses.

10 IMF, World Economic Outlook, April 2018. 11 World Bank, New country classifications by income level: 2018-2019, 1 July 2018. 12 Enright, Scott & Associates analysis based on Hong Kong Census and Statistics Department data.

GBA Background Document

© Copyright 2022 Foundation, 2019. 13

Exhibit 2.1. Major Economic Indicators of GBA, 2017

City Land Area

(sq km) Population

(mn)

GDP

(USD bn)

Per-capita GDP (USD)

GDP share of tertiary

industry (%)

Exports (USD bn)

Utilized FDI (USD

bn) 2

GBA 55,906 69.6 1,513.4 21,750 65.6 1,090.2 140.7

Hong Kong1 1,106 7.4 341.4 46,190 92.2 497.3 117.4

Macao1 31 0.7 50.4 77,600 93.4 1.4 1.5

Guangzhou 7,249 14.5 318.2 22,320 70.9 85.7 6.3

Shenzhen 1,997 12.5 332.0 27,120 58.6 244.6 7.4

Foshan 3,798 7.7 141.3 18,450 40.1 46.7 1.6

Dongguan 2,460 8.3 112.2 13,530 52.3 104.0 1.7

Huizhou 11,347 4.8 56.7 11,880 40.7 33.0 1.1

Zhongshan 1,784 3.3 51.1 15,750 47.8 30.4 0.5

Jiangmen 9,505 4.6 39.8 8,740 44.7 15.9 0.5

Zhuhai 1,736 1.8 38.0 22,100 48.0 27.9 2.4

Zhaoqing 14,891 4.1 32.6 7,940 38.3 3.3 0.2

Notes: 1GDP shares of tertiary industry for Hong Kong and Macao are 2016 figures. 22017 average exchange

rates for USD 1 are HKD 7.794, RMB 6.759, MOP 8.026; Hong Kong exports include re-exports of

goods sourced from or destined for the Chinese Mainland, mostly the PRD Area.

Source: Hong Kong Trade Development Council, Statistics of the Guangdong-Hong Kong-Macao Bay Area, 22 June 2018.

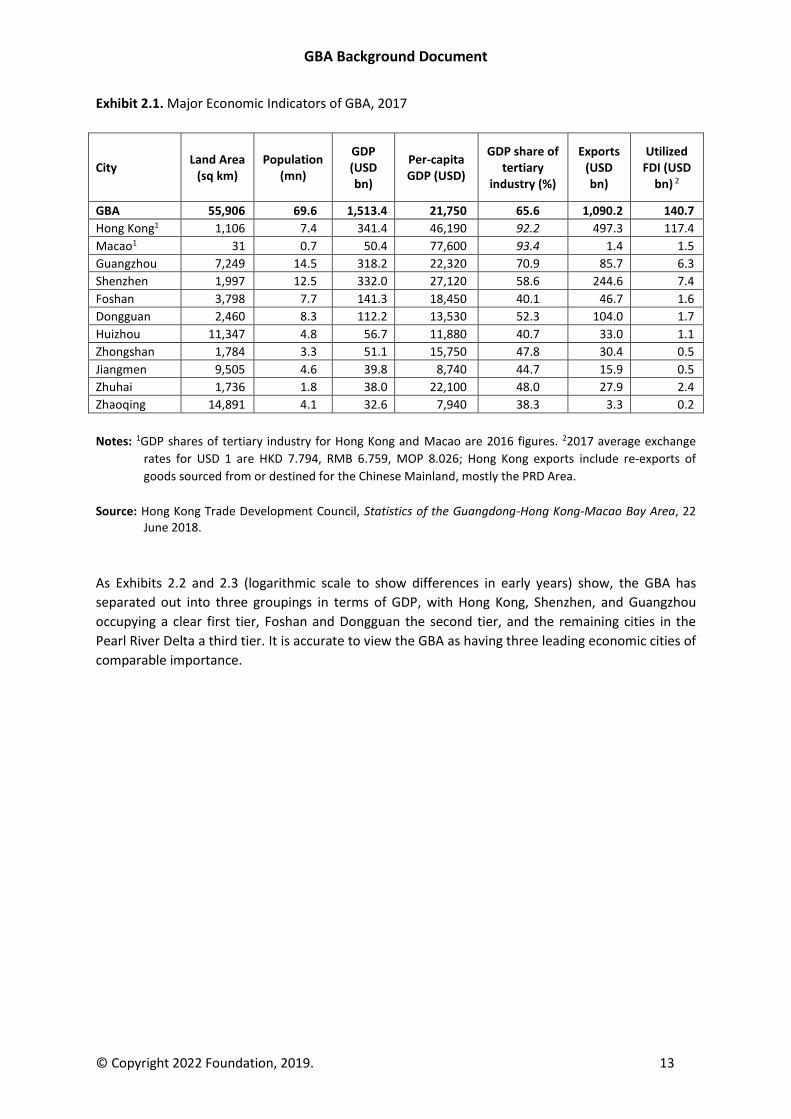

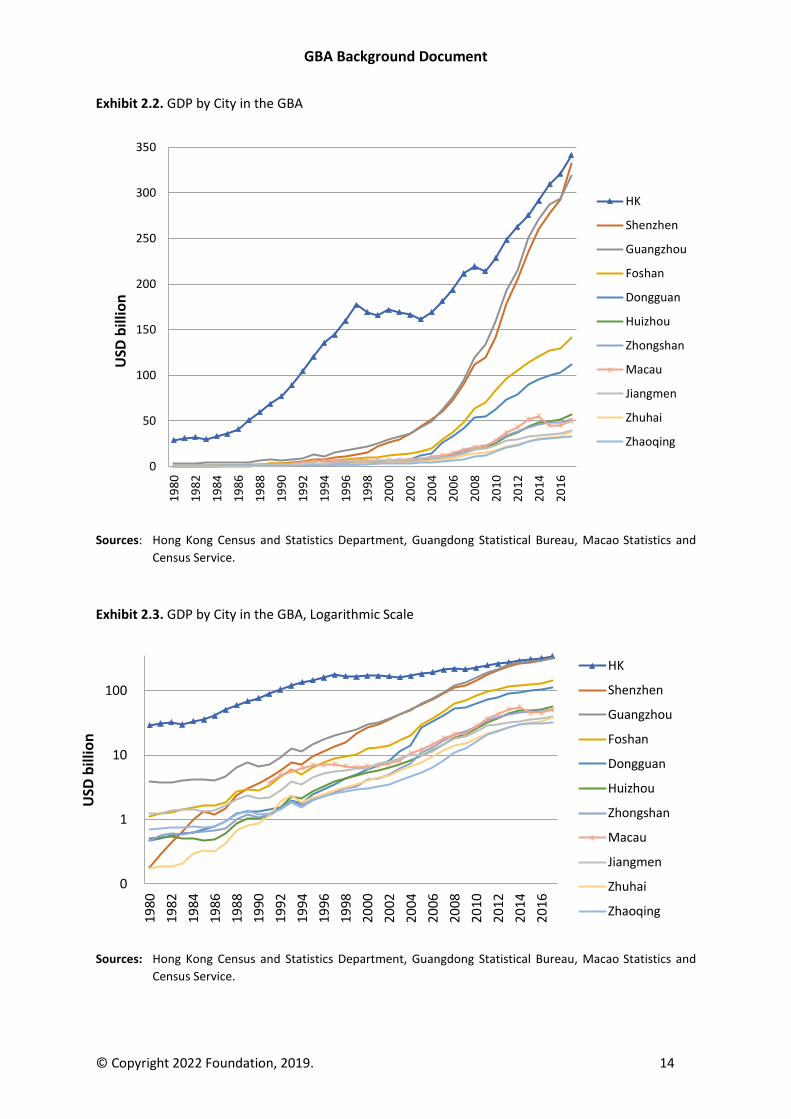

As Exhibits 2.2 and 2.3 (logarithmic scale to show differences in early years) show, the GBA has

separated out into three groupings in terms of GDP, with Hong Kong, Shenzhen, and Guangzhou

occupying a clear first tier, Foshan and Dongguan the second tier, and the remaining cities in the

Pearl River Delta a third tier. It is accurate to view the GBA as having three leading economic cities of

comparable importance.

GBA Background Document

© Copyright 2022 Foundation, 2019. 14

Exhibit 2.2. GDP by City in the GBA

Sources: Hong Kong Census and Statistics Department, Guangdong Statistical Bureau, Macao Statistics and

Census Service.

Exhibit 2.3. GDP by City in the GBA, Logarithmic Scale

Sources: Hong Kong Census and Statistics Department, Guangdong Statistical Bureau, Macao Statistics and

Census Service.

0

50

100

150

200

250

300

350

19

80

19

82

19

84

19

86

19

88

19

90

19

92

19

94

19

96

19

98

20

00

20

02

20

04

20

06

20

08

20

10

20

12

20

14

20

16

USD

bill

ion

HK

Shenzhen

Guangzhou

Foshan

Dongguan

Huizhou

Zhongshan

Macau

Jiangmen

Zhuhai

Zhaoqing

0

1

10

100

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

USD

bill

ion

HK

Shenzhen

Guangzhou

Foshan

Dongguan

Huizhou

Zhongshan

Macau

Jiangmen

Zhuhai

Zhaoqing

GBA Background Document

© Copyright 2022 Foundation, 2019. 15

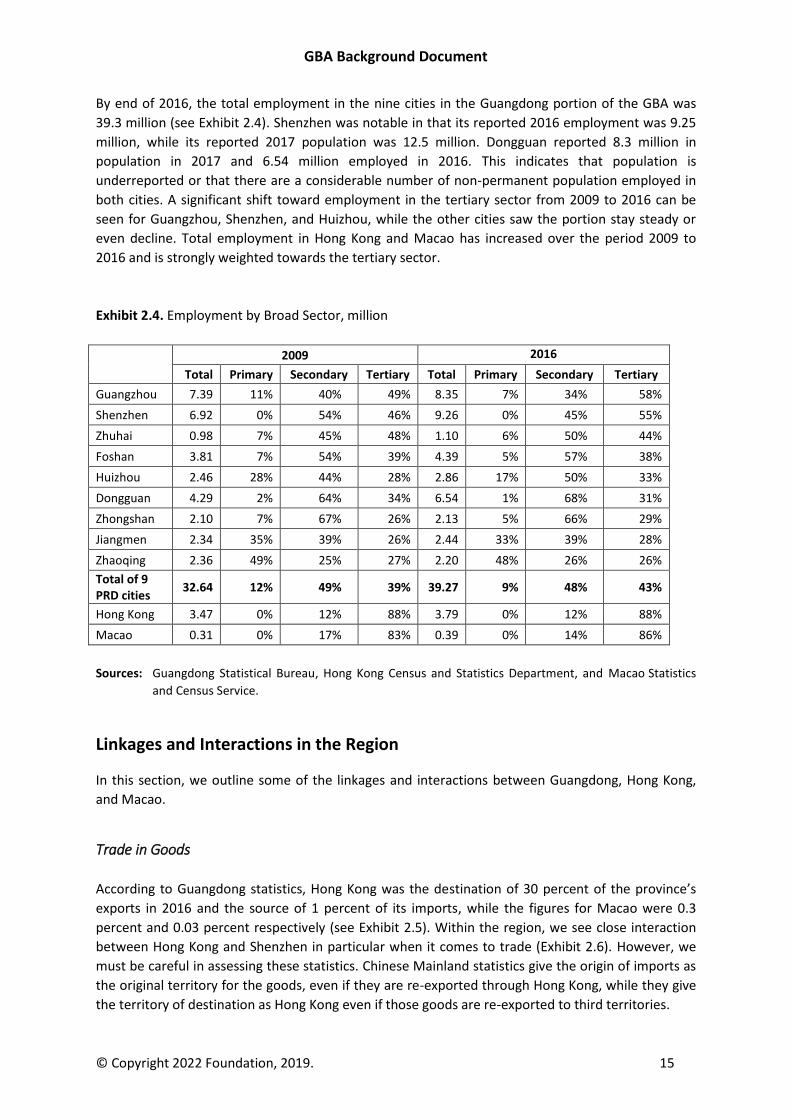

By end of 2016, the total employment in the nine cities in the Guangdong portion of the GBA was

39.3 million (see Exhibit 2.4). Shenzhen was notable in that its reported 2016 employment was 9.25

million, while its reported 2017 population was 12.5 million. Dongguan reported 8.3 million in

population in 2017 and 6.54 million employed in 2016. This indicates that population is

underreported or that there are a considerable number of non-permanent population employed in

both cities. A significant shift toward employment in the tertiary sector from 2009 to 2016 can be

seen for Guangzhou, Shenzhen, and Huizhou, while the other cities saw the portion stay steady or

even decline. Total employment in Hong Kong and Macao has increased over the period 2009 to

2016 and is strongly weighted towards the tertiary sector.

Exhibit 2.4. Employment by Broad Sector, million

2009 2016

Total Primary Secondary Tertiary Total Primary Secondary Tertiary

Guangzhou 7.39 11% 40% 49% 8.35 7% 34% 58%

Shenzhen 6.92 0% 54% 46% 9.26 0% 45% 55%

Zhuhai 0.98 7% 45% 48% 1.10 6% 50% 44%

Foshan 3.81 7% 54% 39% 4.39 5% 57% 38%

Huizhou 2.46 28% 44% 28% 2.86 17% 50% 33%

Dongguan 4.29 2% 64% 34% 6.54 1% 68% 31%

Zhongshan 2.10 7% 67% 26% 2.13 5% 66% 29%

Jiangmen 2.34 35% 39% 26% 2.44 33% 39% 28%

Zhaoqing 2.36 49% 25% 27% 2.20 48% 26% 26%

Total of 9 PRD cities

32.64 12% 49% 39% 39.27 9% 48% 43%

Hong Kong 3.47 0% 12% 88% 3.79 0% 12% 88%

Macao 0.31 0% 17% 83% 0.39 0% 14% 86%

Sources: Guangdong Statistical Bureau, Hong Kong Census and Statistics Department, and Macao Statistics

and Census Service.

Linkages and Interactions in the Region

In this section, we outline some of the linkages and interactions between Guangdong, Hong Kong,

and Macao.

Trade in Goods

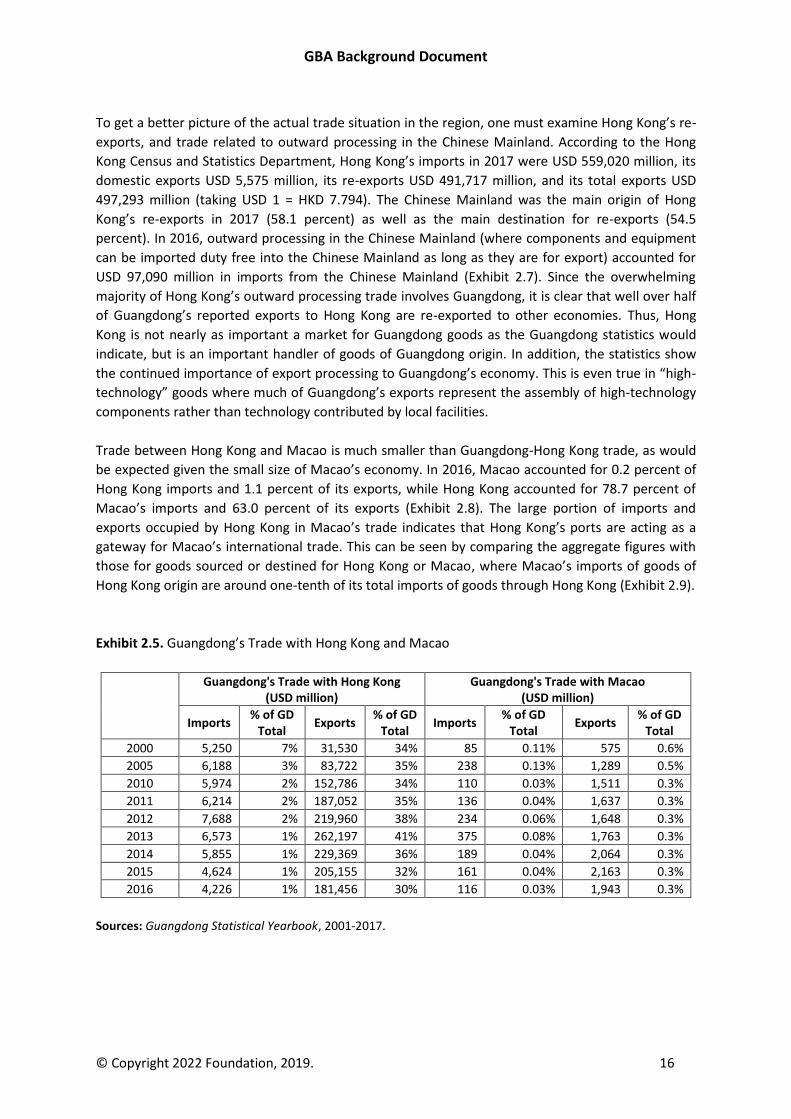

According to Guangdong statistics, Hong Kong was the destination of 30 percent of the province’s

exports in 2016 and the source of 1 percent of its imports, while the figures for Macao were 0.3

percent and 0.03 percent respectively (see Exhibit 2.5). Within the region, we see close interaction

between Hong Kong and Shenzhen in particular when it comes to trade (Exhibit 2.6). However, we

must be careful in assessing these statistics. Chinese Mainland statistics give the origin of imports as

the original territory for the goods, even if they are re-exported through Hong Kong, while they give

the territory of destination as Hong Kong even if those goods are re-exported to third territories.

GBA Background Document

© Copyright 2022 Foundation, 2019. 16

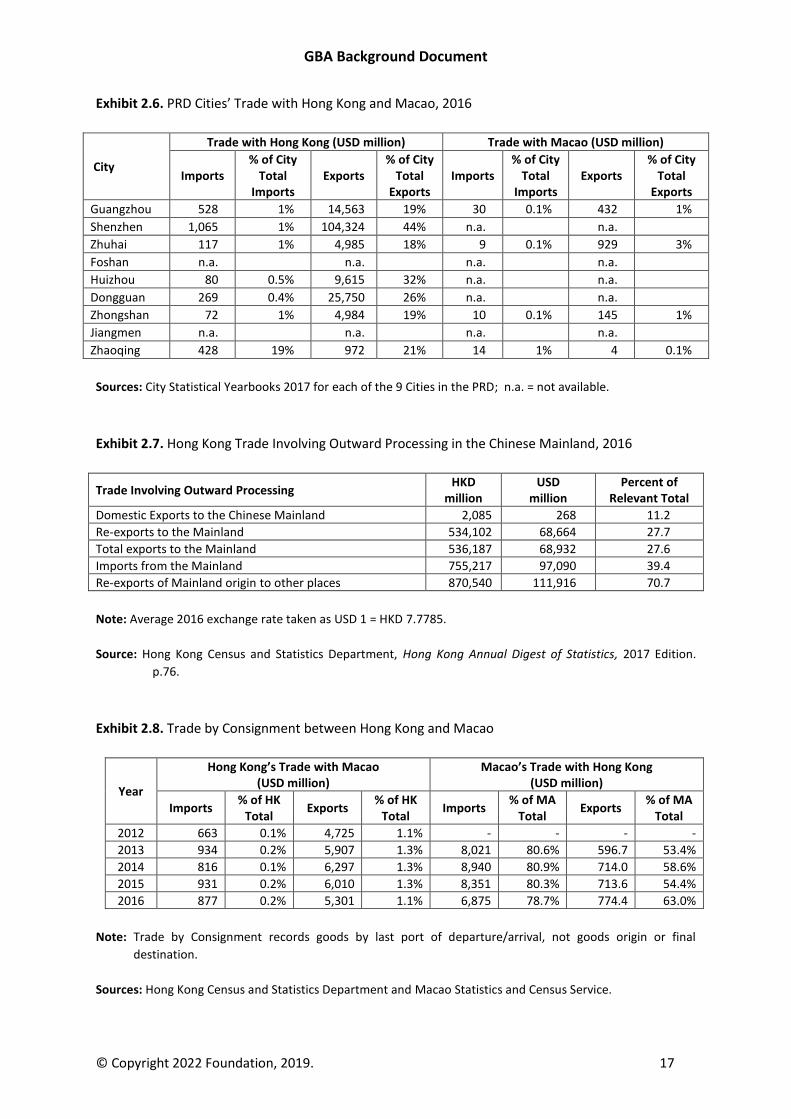

To get a better picture of the actual trade situation in the region, one must examine Hong Kong’s re-

exports, and trade related to outward processing in the Chinese Mainland. According to the Hong

Kong Census and Statistics Department, Hong Kong’s imports in 2017 were USD 559,020 million, its

domestic exports USD 5,575 million, its re-exports USD 491,717 million, and its total exports USD

497,293 million (taking USD 1 = HKD 7.794). The Chinese Mainland was the main origin of Hong

Kong’s re-exports in 2017 (58.1 percent) as well as the main destination for re-exports (54.5

percent). In 2016, outward processing in the Chinese Mainland (where components and equipment

can be imported duty free into the Chinese Mainland as long as they are for export) accounted for

USD 97,090 million in imports from the Chinese Mainland (Exhibit 2.7). Since the overwhelming

majority of Hong Kong’s outward processing trade involves Guangdong, it is clear that well over half

of Guangdong’s reported exports to Hong Kong are re-exported to other economies. Thus, Hong

Kong is not nearly as important a market for Guangdong goods as the Guangdong statistics would

indicate, but is an important handler of goods of Guangdong origin. In addition, the statistics show

the continued importance of export processing to Guangdong’s economy. This is even true in “high-

technology” goods where much of Guangdong’s exports represent the assembly of high-technology

components rather than technology contributed by local facilities.

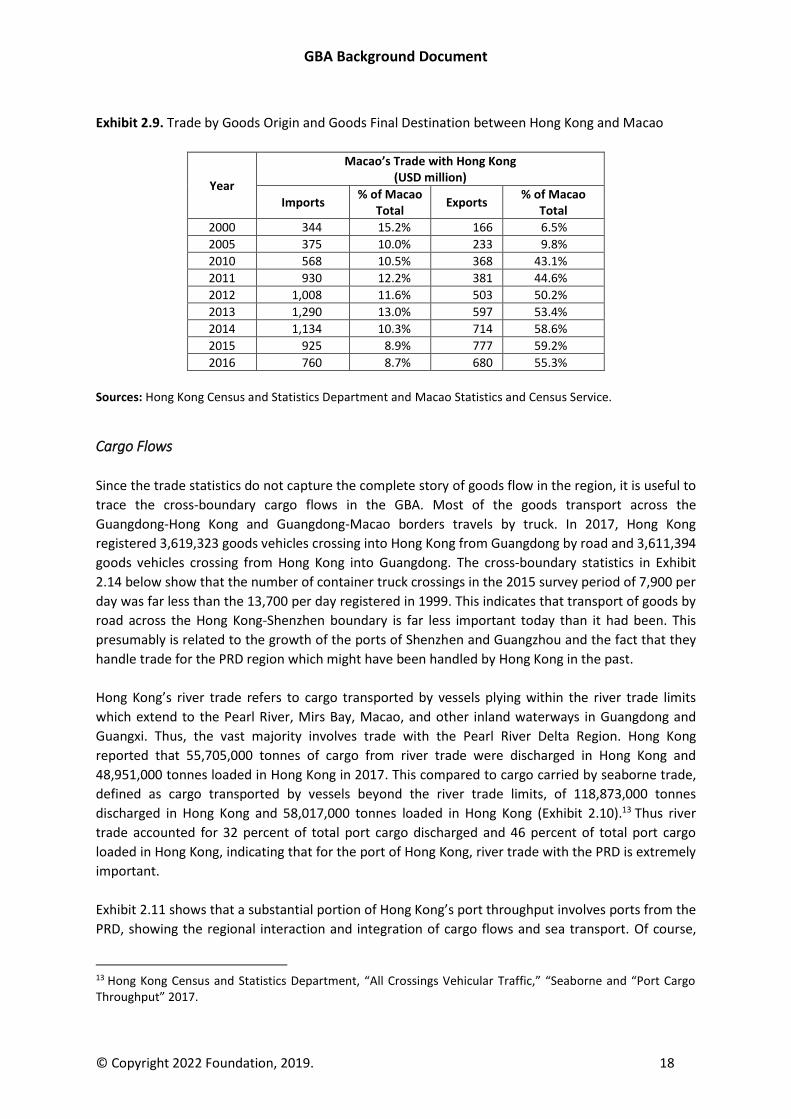

Trade between Hong Kong and Macao is much smaller than Guangdong-Hong Kong trade, as would

be expected given the small size of Macao’s economy. In 2016, Macao accounted for 0.2 percent of

Hong Kong imports and 1.1 percent of its exports, while Hong Kong accounted for 78.7 percent of

Macao’s imports and 63.0 percent of its exports (Exhibit 2.8). The large portion of imports and

exports occupied by Hong Kong in Macao’s trade indicates that Hong Kong’s ports are acting as a

gateway for Macao’s international trade. This can be seen by comparing the aggregate figures with

those for goods sourced or destined for Hong Kong or Macao, where Macao’s imports of goods of

Hong Kong origin are around one-tenth of its total imports of goods through Hong Kong (Exhibit 2.9).

Exhibit 2.5. Guangdong’s Trade with Hong Kong and Macao

Guangdong's Trade with Hong Kong (USD million)

Guangdong's Trade with Macao (USD million)

Imports % of GD

Total Exports

% of GD Total

Imports % of GD

Total Exports

% of GD Total

2000 5,250 7% 31,530 34% 85 0.11% 575 0.6%

2005 6,188 3% 83,722 35% 238 0.13% 1,289 0.5%

2010 5,974 2% 152,786 34% 110 0.03% 1,511 0.3%

2011 6,214 2% 187,052 35% 136 0.04% 1,637 0.3%

2012 7,688 2% 219,960 38% 234 0.06% 1,648 0.3%

2013 6,573 1% 262,197 41% 375 0.08% 1,763 0.3%

2014 5,855 1% 229,369 36% 189 0.04% 2,064 0.3%

2015 4,624 1% 205,155 32% 161 0.04% 2,163 0.3%

2016 4,226 1% 181,456 30% 116 0.03% 1,943 0.3%

Sources: Guangdong Statistical Yearbook, 2001-2017.

GBA Background Document

© Copyright 2022 Foundation, 2019. 17

Exhibit 2.6. PRD Cities’ Trade with Hong Kong and Macao, 2016

City

Trade with Hong Kong (USD million) Trade with Macao (USD million)

Imports % of City

Total Imports

Exports % of City

Total Exports

Imports % of City

Total Imports

Exports % of City

Total Exports

Guangzhou 528 1% 14,563 19% 30 0.1% 432 1%

Shenzhen 1,065 1% 104,324 44% n.a. n.a.

Zhuhai 117 1% 4,985 18% 9 0.1% 929 3%

Foshan n.a. n.a. n.a. n.a.

Huizhou 80 0.5% 9,615 32% n.a. n.a.

Dongguan 269 0.4% 25,750 26% n.a. n.a.

Zhongshan 72 1% 4,984 19% 10 0.1% 145 1%

Jiangmen n.a. n.a. n.a. n.a.

Zhaoqing 428 19% 972 21% 14 1% 4 0.1%

Sources: City Statistical Yearbooks 2017 for each of the 9 Cities in the PRD; n.a. = not available.

Exhibit 2.7. Hong Kong Trade Involving Outward Processing in the Chinese Mainland, 2016

Trade Involving Outward Processing HKD

million USD

million Percent of

Relevant Total

Domestic Exports to the Chinese Mainland 2,085 268 11.2

Re-exports to the Mainland 534,102 68,664 27.7

Total exports to the Mainland 536,187 68,932 27.6

Imports from the Mainland 755,217 97,090 39.4

Re-exports of Mainland origin to other places 870,540 111,916 70.7

Note: Average 2016 exchange rate taken as USD 1 = HKD 7.7785.

Source: Hong Kong Census and Statistics Department, Hong Kong Annual Digest of Statistics, 2017 Edition.

p.76.

Exhibit 2.8. Trade by Consignment between Hong Kong and Macao

Year

Hong Kong’s Trade with Macao (USD million)

Macao’s Trade with Hong Kong (USD million)

Imports % of HK

Total Exports

% of HK Total

Imports % of MA

Total Exports

% of MA Total

2012 663 0.1% 4,725 1.1% - - - -

2013 934 0.2% 5,907 1.3% 8,021 80.6% 596.7 53.4%

2014 816 0.1% 6,297 1.3% 8,940 80.9% 714.0 58.6%

2015 931 0.2% 6,010 1.3% 8,351 80.3% 713.6 54.4%

2016 877 0.2% 5,301 1.1% 6,875 78.7% 774.4 63.0%

Note: Trade by Consignment records goods by last port of departure/arrival, not goods origin or final

destination.

Sources: Hong Kong Census and Statistics Department and Macao Statistics and Census Service.

GBA Background Document

© Copyright 2022 Foundation, 2019. 18

Exhibit 2.9. Trade by Goods Origin and Goods Final Destination between Hong Kong and Macao

Year

Macao’s Trade with Hong Kong (USD million)

Imports % of Macao

Total Exports

% of Macao Total

2000 344 15.2% 166 6.5%

2005 375 10.0% 233 9.8%

2010 568 10.5% 368 43.1%

2011 930 12.2% 381 44.6%

2012 1,008 11.6% 503 50.2%

2013 1,290 13.0% 597 53.4%

2014 1,134 10.3% 714 58.6%

2015 925 8.9% 777 59.2%

2016 760 8.7% 680 55.3%

Sources: Hong Kong Census and Statistics Department and Macao Statistics and Census Service.

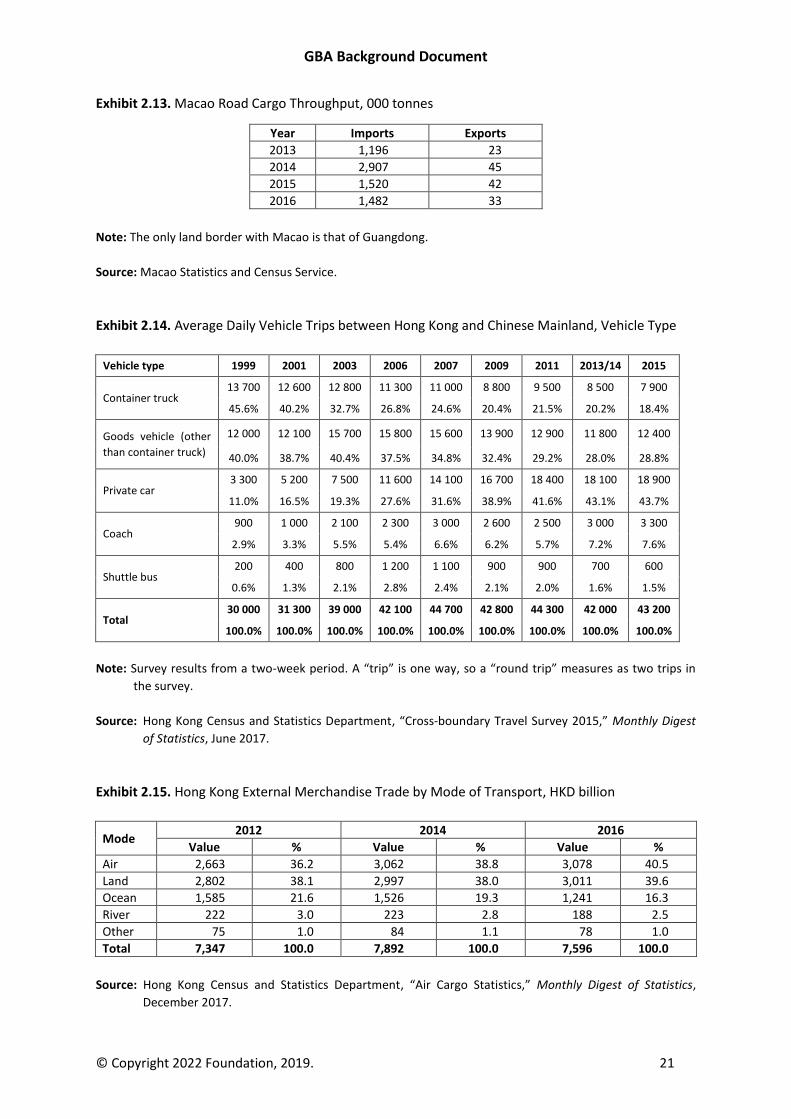

Cargo Flows

Since the trade statistics do not capture the complete story of goods flow in the region, it is useful to

trace the cross-boundary cargo flows in the GBA. Most of the goods transport across the

Guangdong-Hong Kong and Guangdong-Macao borders travels by truck. In 2017, Hong Kong

registered 3,619,323 goods vehicles crossing into Hong Kong from Guangdong by road and 3,611,394

goods vehicles crossing from Hong Kong into Guangdong. The cross-boundary statistics in Exhibit

2.14 below show that the number of container truck crossings in the 2015 survey period of 7,900 per

day was far less than the 13,700 per day registered in 1999. This indicates that transport of goods by

road across the Hong Kong-Shenzhen boundary is far less important today than it had been. This

presumably is related to the growth of the ports of Shenzhen and Guangzhou and the fact that they

handle trade for the PRD region which might have been handled by Hong Kong in the past.

Hong Kong’s river trade refers to cargo transported by vessels plying within the river trade limits

which extend to the Pearl River, Mirs Bay, Macao, and other inland waterways in Guangdong and

Guangxi. Thus, the vast majority involves trade with the Pearl River Delta Region. Hong Kong

reported that 55,705,000 tonnes of cargo from river trade were discharged in Hong Kong and

48,951,000 tonnes loaded in Hong Kong in 2017. This compared to cargo carried by seaborne trade,

defined as cargo transported by vessels beyond the river trade limits, of 118,873,000 tonnes

discharged in Hong Kong and 58,017,000 tonnes loaded in Hong Kong (Exhibit 2.10).13 Thus river

trade accounted for 32 percent of total port cargo discharged and 46 percent of total port cargo

loaded in Hong Kong, indicating that for the port of Hong Kong, river trade with the PRD is extremely

important.

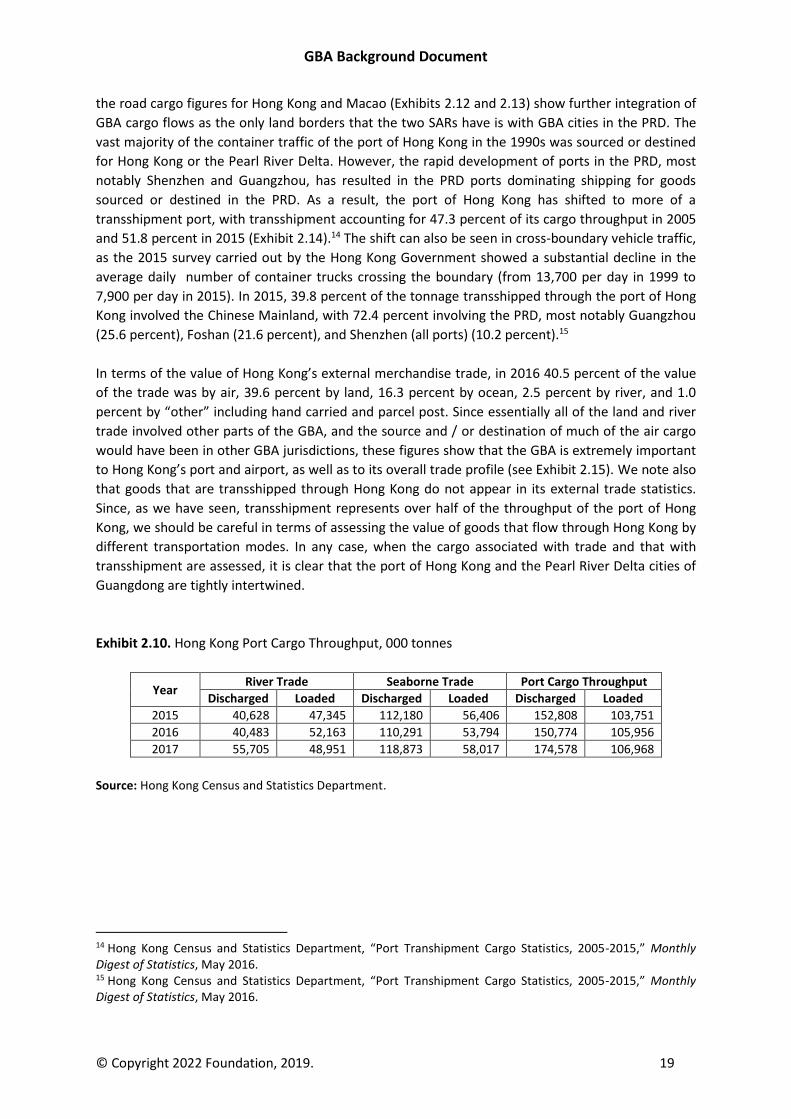

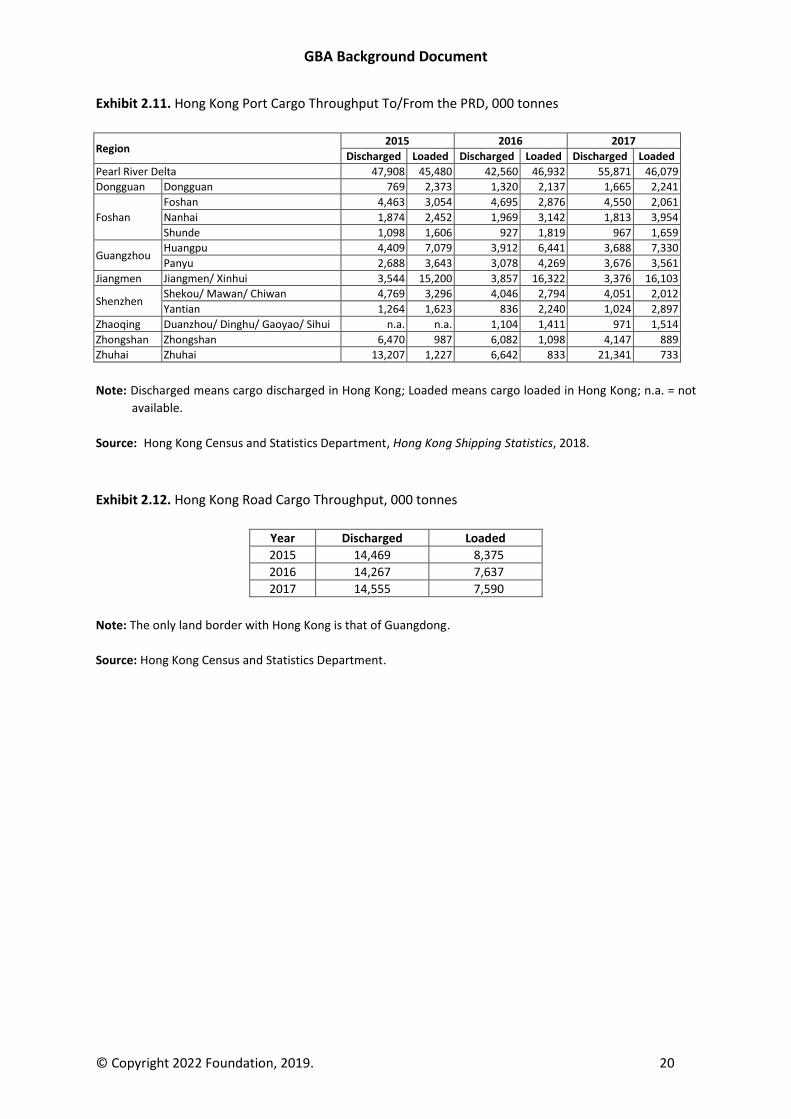

Exhibit 2.11 shows that a substantial portion of Hong Kong’s port throughput involves ports from the

PRD, showing the regional interaction and integration of cargo flows and sea transport. Of course,

13 Hong Kong Census and Statistics Department, “All Crossings Vehicular Traffic,” “Seaborne and “Port Cargo Throughput” 2017.

GBA Background Document

© Copyright 2022 Foundation, 2019. 19

the road cargo figures for Hong Kong and Macao (Exhibits 2.12 and 2.13) show further integration of

GBA cargo flows as the only land borders that the two SARs have is with GBA cities in the PRD. The

vast majority of the container traffic of the port of Hong Kong in the 1990s was sourced or destined

for Hong Kong or the Pearl River Delta. However, the rapid development of ports in the PRD, most

notably Shenzhen and Guangzhou, has resulted in the PRD ports dominating shipping for goods

sourced or destined in the PRD. As a result, the port of Hong Kong has shifted to more of a

transshipment port, with transshipment accounting for 47.3 percent of its cargo throughput in 2005

and 51.8 percent in 2015 (Exhibit 2.14).14 The shift can also be seen in cross-boundary vehicle traffic,

as the 2015 survey carried out by the Hong Kong Government showed a substantial decline in the

average daily number of container trucks crossing the boundary (from 13,700 per day in 1999 to

7,900 per day in 2015). In 2015, 39.8 percent of the tonnage transshipped through the port of Hong

Kong involved the Chinese Mainland, with 72.4 percent involving the PRD, most notably Guangzhou

(25.6 percent), Foshan (21.6 percent), and Shenzhen (all ports) (10.2 percent).15

In terms of the value of Hong Kong’s external merchandise trade, in 2016 40.5 percent of the value

of the trade was by air, 39.6 percent by land, 16.3 percent by ocean, 2.5 percent by river, and 1.0

percent by “other” including hand carried and parcel post. Since essentially all of the land and river

trade involved other parts of the GBA, and the source and / or destination of much of the air cargo

would have been in other GBA jurisdictions, these figures show that the GBA is extremely important

to Hong Kong’s port and airport, as well as to its overall trade profile (see Exhibit 2.15). We note also

that goods that are transshipped through Hong Kong do not appear in its external trade statistics.

Since, as we have seen, transshipment represents over half of the throughput of the port of Hong

Kong, we should be careful in terms of assessing the value of goods that flow through Hong Kong by

different transportation modes. In any case, when the cargo associated with trade and that with

transshipment are assessed, it is clear that the port of Hong Kong and the Pearl River Delta cities of

Guangdong are tightly intertwined.

Exhibit 2.10. Hong Kong Port Cargo Throughput, 000 tonnes

Year River Trade Seaborne Trade Port Cargo Throughput

Discharged Loaded Discharged Loaded Discharged Loaded

2015 40,628 47,345 112,180 56,406 152,808 103,751

2016 40,483 52,163 110,291 53,794 150,774 105,956

2017 55,705 48,951 118,873 58,017 174,578 106,968

Source: Hong Kong Census and Statistics Department.

14 Hong Kong Census and Statistics Department, “Port Transhipment Cargo Statistics, 2005-2015,” Monthly Digest of Statistics, May 2016. 15 Hong Kong Census and Statistics Department, “Port Transhipment Cargo Statistics, 2005-2015,” Monthly Digest of Statistics, May 2016.

GBA Background Document

© Copyright 2022 Foundation, 2019. 20

Exhibit 2.11. Hong Kong Port Cargo Throughput To/From the PRD, 000 tonnes

Region 2015 2016 2017

Discharged Loaded Discharged Loaded Discharged Loaded

Pearl River Delta 47,908 45,480 42,560 46,932 55,871 46,079

Dongguan Dongguan 769 2,373 1,320 2,137 1,665 2,241

Foshan

Foshan 4,463 3,054 4,695 2,876 4,550 2,061

Nanhai 1,874 2,452 1,969 3,142 1,813 3,954

Shunde 1,098 1,606 927 1,819 967 1,659

Guangzhou Huangpu 4,409 7,079 3,912 6,441 3,688 7,330

Panyu 2,688 3,643 3,078 4,269 3,676 3,561

Jiangmen Jiangmen/ Xinhui 3,544 15,200 3,857 16,322 3,376 16,103

Shenzhen Shekou/ Mawan/ Chiwan 4,769 3,296 4,046 2,794 4,051 2,012

Yantian 1,264 1,623 836 2,240 1,024 2,897

Zhaoqing Duanzhou/ Dinghu/ Gaoyao/ Sihui n.a. n.a. 1,104 1,411 971 1,514

Zhongshan Zhongshan 6,470 987 6,082 1,098 4,147 889

Zhuhai Zhuhai 13,207 1,227 6,642 833 21,341 733

Note: Discharged means cargo discharged in Hong Kong; Loaded means cargo loaded in Hong Kong; n.a. = not

available.

Source: Hong Kong Census and Statistics Department, Hong Kong Shipping Statistics, 2018.

Exhibit 2.12. Hong Kong Road Cargo Throughput, 000 tonnes

Year Discharged Loaded

2015 14,469 8,375

2016 14,267 7,637

2017 14,555 7,590

Note: The only land border with Hong Kong is that of Guangdong.

Source: Hong Kong Census and Statistics Department.

GBA Background Document

© Copyright 2022 Foundation, 2019. 21

Exhibit 2.13. Macao Road Cargo Throughput, 000 tonnes

Year Imports Exports

2013 1,196 23

2014 2,907 45

2015 1,520 42

2016 1,482 33

Note: The only land border with Macao is that of Guangdong.

Source: Macao Statistics and Census Service.

Exhibit 2.14. Average Daily Vehicle Trips between Hong Kong and Chinese Mainland, Vehicle Type

Vehicle type 1999 2001 2003 2006 2007 2009 2011 2013/14 2015

Container truck 13 700 12 600 12 800 11 300 11 000 8 800 9 500 8 500 7 900

45.6% 40.2% 32.7% 26.8% 24.6% 20.4% 21.5% 20.2% 18.4%

Goods vehicle (other

than container truck)

12 000 12 100 15 700 15 800 15 600 13 900 12 900 11 800 12 400

40.0% 38.7% 40.4% 37.5% 34.8% 32.4% 29.2% 28.0% 28.8%

Private car 3 300 5 200 7 500 11 600 14 100 16 700 18 400 18 100 18 900

11.0% 16.5% 19.3% 27.6% 31.6% 38.9% 41.6% 43.1% 43.7%

Coach 900 1 000 2 100 2 300 3 000 2 600 2 500 3 000 3 300

2.9% 3.3% 5.5% 5.4% 6.6% 6.2% 5.7% 7.2% 7.6%

Shuttle bus 200 400 800 1 200 1 100 900 900 700 600

0.6% 1.3% 2.1% 2.8% 2.4% 2.1% 2.0% 1.6% 1.5%

Total 30 000 31 300 39 000 42 100 44 700 42 800 44 300 42 000 43 200

100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0% 100.0%

Note: Survey results from a two-week period. A “trip” is one way, so a “round trip” measures as two trips in

the survey.

Source: Hong Kong Census and Statistics Department, “Cross-boundary Travel Survey 2015,” Monthly Digest

of Statistics, June 2017.

Exhibit 2.15. Hong Kong External Merchandise Trade by Mode of Transport, HKD billion

Mode 2012 2014 2016

Value % Value % Value %

Air 2,663 36.2 3,062 38.8 3,078 40.5

Land 2,802 38.1 2,997 38.0 3,011 39.6

Ocean 1,585 21.6 1,526 19.3 1,241 16.3

River 222 3.0 223 2.8 188 2.5

Other 75 1.0 84 1.1 78 1.0

Total 7,347 100.0 7,892 100.0 7,596 100.0

Source: Hong Kong Census and Statistics Department, “Air Cargo Statistics,” Monthly Digest of Statistics,

December 2017.

GBA Background Document

© Copyright 2022 Foundation, 2019. 22

Trade in Services

There is more limited data on trade in services in the GBA. While China has established a good

reporting system for trade in services statistics, statistics on trade in services at the provincial and

city level are not officially published at present. We collected data from various sources for the trade

in services of Guangdong, in an attempt to identify the general patterns. Exhibit 2.16 shows the

trade in service in Guangdong from 2010 to 2016, its position in China, and some patchy data for

Guangdong’s trade in services with Hong Kong. Guangdong’s trade in services increased with an

annual average rate of 20.2 percent from 2010 to 2016, reached USD 145 billion in 2016, and

decreased to USD 124 billion in 2017. In 2017, Guangdong’s trade in services ranked the third in

China, after Shanghai (USD 151 billion) and Beijing (USD 143 billion).16

Exhibit 2.16 also shows that, Guangdong’s trade in services with Hong Kong (imports and exports)

increased from USD 28 billion in 2010 to USD 56 billion in 2015, an average annual growth rate of

14.8 percent. Trade in services between Guangdong and Hong Kong accounted for 42 percent of

Guangdong’s total trade in services in that year, showing the importance of Hong Kong in

Guangdong’s services trade. It is expected that Guangdong’s trade in services will reach over USD

200 billion in 2020, of which half of the value will be with Hong Kong.17

Data on Guangdong’s trade in services by category is not published, but trade in services by major

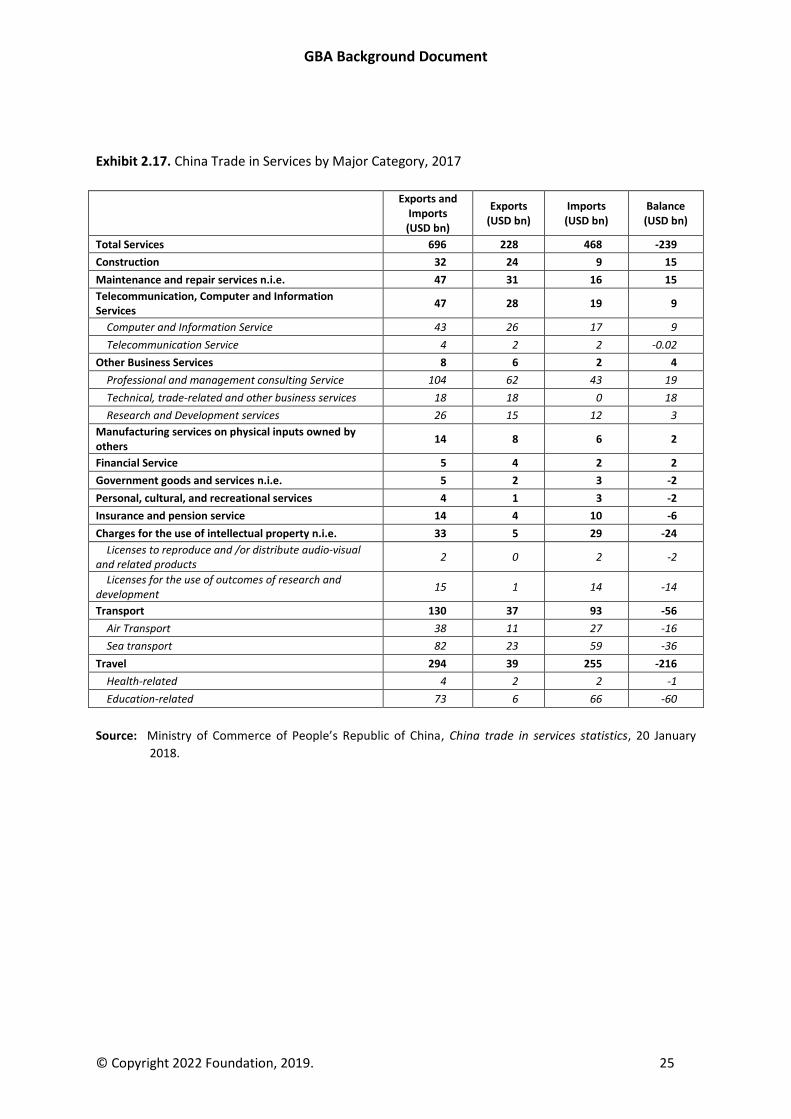

category is available for China as a whole. Exhibit 2.17 shows China’s trade in services by major

sector in 2017, ranking in descending order by trade balance (exports exceeding imports). It shows

that China runs large surpluses in trade in Construction; Maintenance and repair services; and

Telecommunication, computer, and information services. It runs large deficits in Travel; Transport;

and Charges for the use of intellectual property. Since 2015, the Ministry of Commerce of the

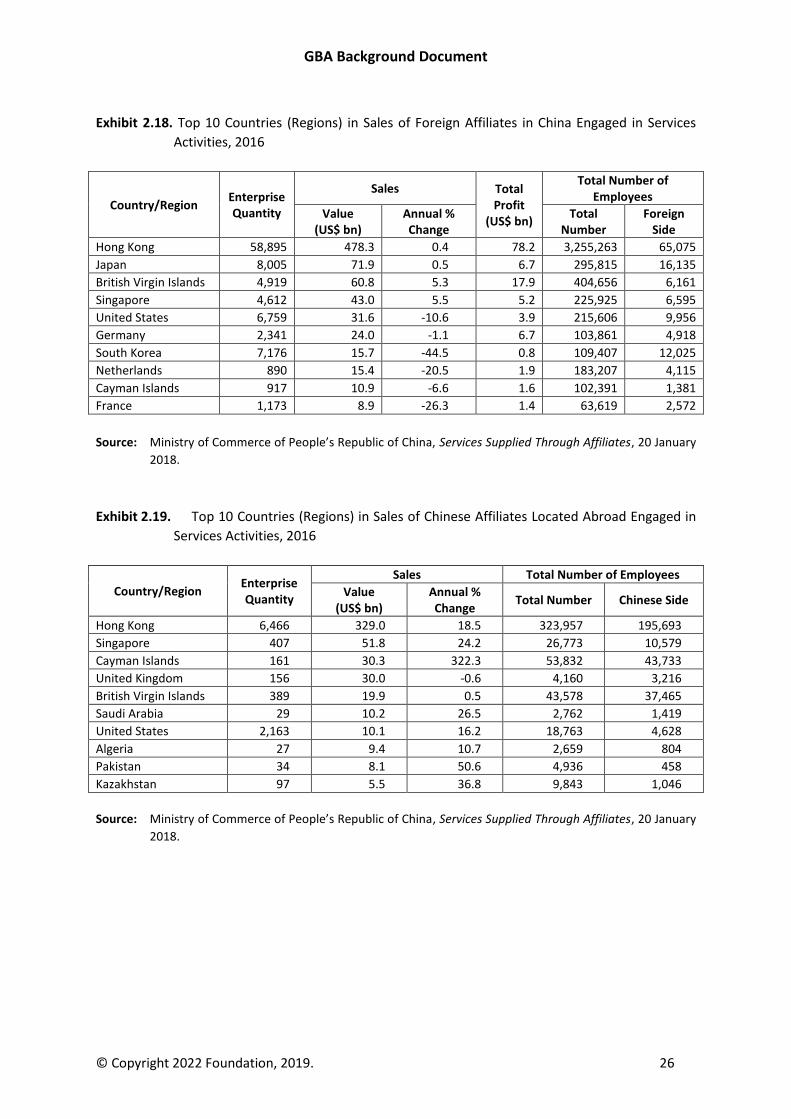

People’s Republic of China has also published the statistics on foreign service affiliates located in

China and Chinese service affiliates located abroad. As shown by Exhibits 2.18 and 2.19, Hong Kong

ranked first both as the source region of the foreign service affiliates in China and the destination of

Chinese service affiliation in terms of sales, and the number of firms as well. This shows the

importance of the interaction of Hong Kong and the Chinese Mainland in services sectors.

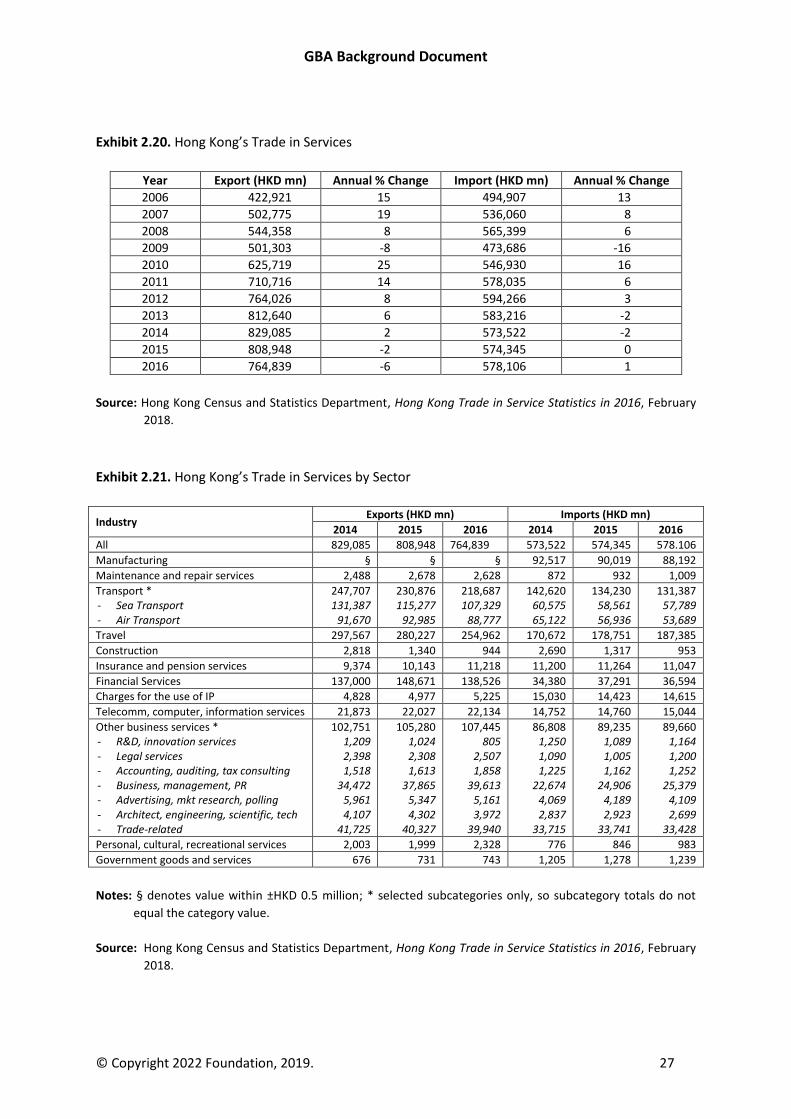

For Hong Kong, there is data available for its total trade in services as well as its trade in services

with the Chinese Mainland (Exhibits 2.20, 2.21, and 2.22). This does not break out services trade

with Guangdong Province. However, when we match up the Guangdong data with the Hong Kong

data for the year 2015, then Guangdong’s trade in services with Hong Kong in 2015 accounted for 82

percent of Hong Kong’s service trade with the Chinese Mainland in that year.18 Thus Guangdong

represents the bulk of Hong Kong’s trade in services with the Chinese Mainland.

16 Ministry of Commerce of PRC, MOFCOM Department of Trade in Services and Commercial Services on the operation of service trade in 2017. 17 “Guangdong service trade expected to reach 1 trillion, Half of it with Hong Kong,” Taikungpao, 30 August

2017 (“粤服贸进出口上望万亿港佔半”). 18 Hong Kong’s services imports and exports with the Chinese Mainland was HKD 532,443 million (USD 68.7billion, USD 1=7.752 in 2015). Hong Kong trade in services data from Hong Kong Census and Statistics Bureau.

GBA Background Document

© Copyright 2022 Foundation, 2019. 23

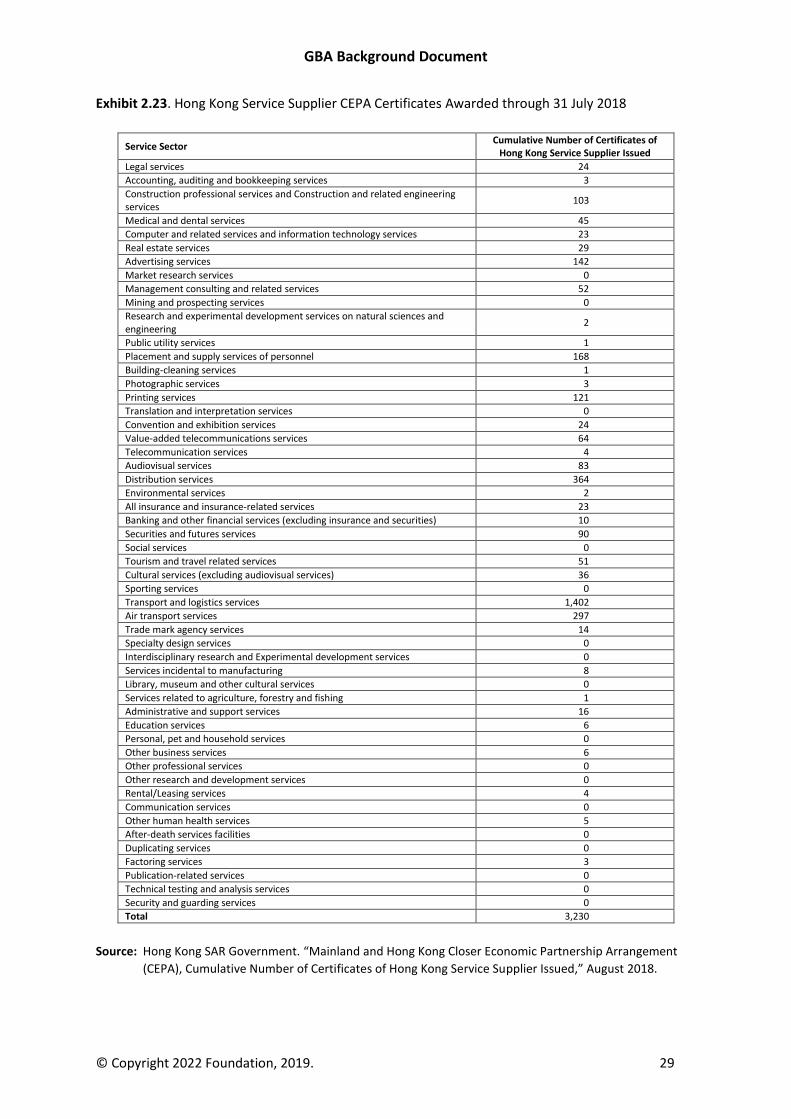

The same is probably true of the Hong Kong service providers that have received certificates

allowing them to operate in the Chinese Mainland under CEPA (Exhibit 2.23). The Exhibit shows that

3,230 Hong Kong companies had received CEPA certification to operate in the Chinese Mainland as

of 31 July 2018. While this is for the Mainland as a whole, most of the companies are likely to be

operating in the Guangdong portion of the GBA. The largest number was in Transport and logistics

services (1,402), followed by Distribution services (364), Air transport services (297), and Placement

and supply services of personnel (168).

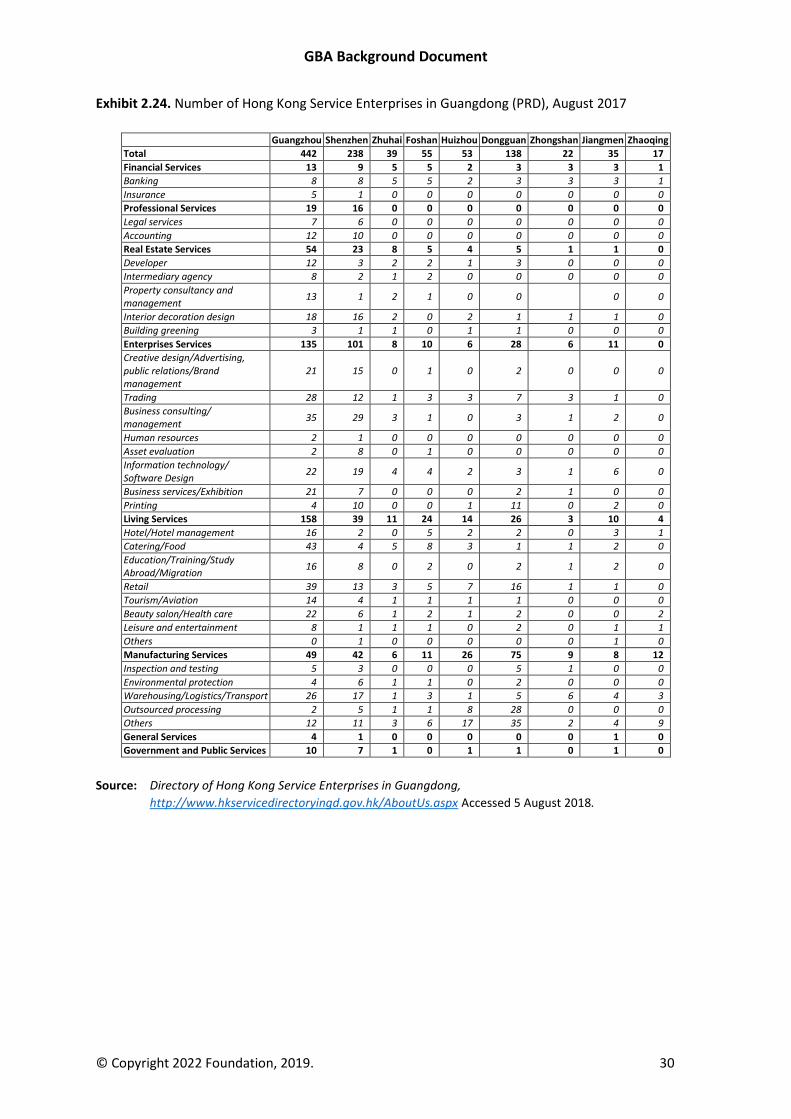

Exhibit 2.24 shows that the vast majority of the Hong Kong service companies identifiably active in

the PRD have set up in the Shenzhen-Dongguan-Guangzhou corridor. This is likely due to the

combination of market size of these cities plus their proximity to Hong Kong. It will be interesting to

see whether the opening of the Hong Kong-Zhuhai-Macao Bridge (HZMB), the connection of Hong

Kong to the XRL high-speed rail line, and the opening of additional border crossings and transport

routes within the PRD that have set up in the PRD cities will influence this distribution. One would

assume that with easier connectivity that there will be a significant diversification of company

locations, though they will still be drawn to the largest markets.

When we think about how Hong Kong service providers might contribute more to the GBA a good

place to start is to determine in which sectors Hong Kong has comparative advantages and then in

which of these sectors are those advantages not being leveraged as much as they might be. Exhibit

2.21 shows the service sectors in which Hong Kong has comparative advantages (as measured by

trade surpluses or exports exceeding imports). Hong Kong runs large surpluses in trade in

Transportation services, Travel services, and Financial services. It runs a significant trade surplus in

Other business services (mostly Business, management, and public relations; and Trade-related

services) and Telecommunications, computer, and information services. Hong Kong runs a sizable

trade deficit in Charges for use of IP; a slight deficit in R&D and innovation services; and a modest

trade surplus in Architectural, engineering, scientific, and technical services; but this latter surplus is

likely more to do with architectural and engineering related to building and infrastructure than to

scientific and other technical pursuits.

The strong indication is that Hong Kong has comparative advantages in Transportation services;

Travel services; Financial services; Business, management, and public relations; Trade-related

services; and Telecommunications, computer, and information services. These are the service

sectors in which it is most likely to make a positive contribution to the GBA. Considering the

breakdown of trade in services of the Chinese Mainland, it did indicate that the Mainland and Hong

Kong, and to a lesser extent, Guangdong and Hong Kong are complementary at least in Transport

services, Travel services, and Telecommunication, computer, and information services. On the other

hand, both China and Hong Kong have deficits in Charges for the use of intellectual property

services. As Hong Kong has comparative disadvantages in services related to IP, R&D, and

innovation services, it may be less likely to make a positive contribution to the GBA in these areas.

The bulk of Hong Kong’s service exports to the Chinese Mainland (over two-thirds) have been in

travel, with transport accounting for nearly another 20 percent in 2016. The third leading category

was “Other Business Services,” which includes professional services among others (Exhibit 2.22).

Comparing Exhibits 2.21 and 2.22, Hong Kong is apparently leveraging its advantages in

Transportation and Travel services when it comes to business in the Chinese Mainland and may be

leveraging advantages in Financial services, though this is difficult to tell since much of the fees,

commissions, and interest rates on loans are measured indirectly (as part of Financial Intermediation

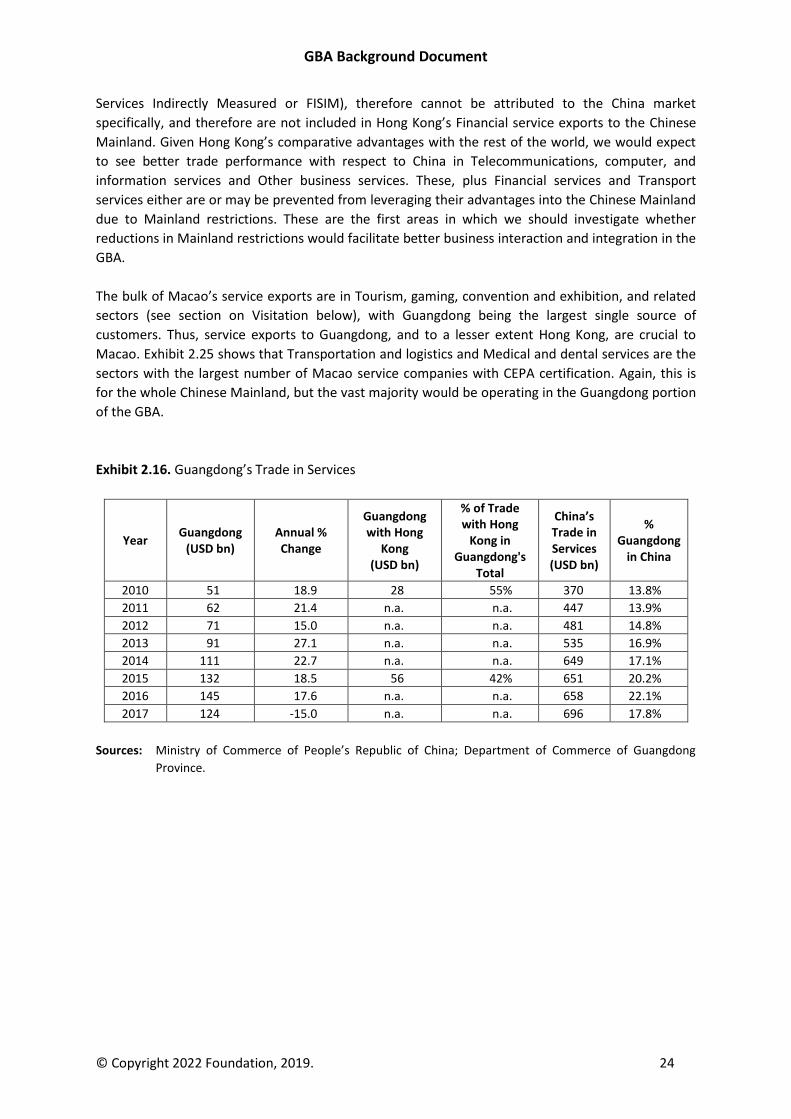

GBA Background Document

© Copyright 2022 Foundation, 2019. 24

Services Indirectly Measured or FISIM), therefore cannot be attributed to the China market

specifically, and therefore are not included in Hong Kong’s Financial service exports to the Chinese

Mainland. Given Hong Kong’s comparative advantages with the rest of the world, we would expect

to see better trade performance with respect to China in Telecommunications, computer, and

information services and Other business services. These, plus Financial services and Transport

services either are or may be prevented from leveraging their advantages into the Chinese Mainland

due to Mainland restrictions. These are the first areas in which we should investigate whether

reductions in Mainland restrictions would facilitate better business interaction and integration in the

GBA.

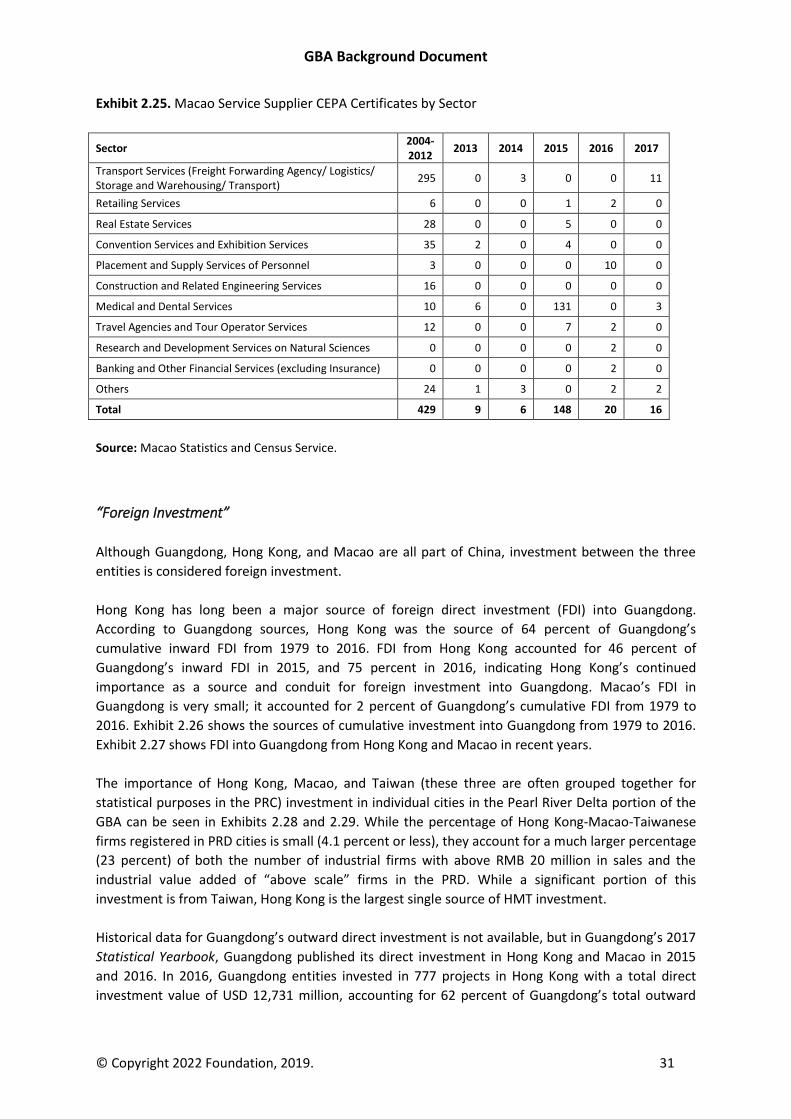

The bulk of Macao’s service exports are in Tourism, gaming, convention and exhibition, and related

sectors (see section on Visitation below), with Guangdong being the largest single source of

customers. Thus, service exports to Guangdong, and to a lesser extent Hong Kong, are crucial to

Macao. Exhibit 2.25 shows that Transportation and logistics and Medical and dental services are the

sectors with the largest number of Macao service companies with CEPA certification. Again, this is

for the whole Chinese Mainland, but the vast majority would be operating in the Guangdong portion

of the GBA.

Exhibit 2.16. Guangdong’s Trade in Services

Year Guangdong

(USD bn) Annual % Change

Guangdong with Hong

Kong (USD bn)

% of Trade with Hong

Kong in Guangdong's

Total

China’s Trade in Services (USD bn)

% Guangdong

in China

2010 51 18.9 28 55% 370 13.8%

2011 62 21.4 n.a. n.a. 447 13.9%

2012 71 15.0 n.a. n.a. 481 14.8%

2013 91 27.1 n.a. n.a. 535 16.9%

2014 111 22.7 n.a. n.a. 649 17.1%

2015 132 18.5 56 42% 651 20.2%

2016 145 17.6 n.a. n.a. 658 22.1%

2017 124 -15.0 n.a. n.a. 696 17.8%

Sources: Ministry of Commerce of People’s Republic of China; Department of Commerce of Guangdong

Province.

GBA Background Document

© Copyright 2022 Foundation, 2019. 25

Exhibit 2.17. China Trade in Services by Major Category, 2017

Exports and

Imports (USD bn)

Exports (USD bn)

Imports (USD bn)

Balance (USD bn)

Total Services 696 228 468 -239

Construction 32 24 9 15

Maintenance and repair services n.i.e. 47 31 16 15

Telecommunication, Computer and Information Services

47 28 19 9

Computer and Information Service 43 26 17 9

Telecommunication Service 4 2 2 -0.02

Other Business Services 8 6 2 4

Professional and management consulting Service 104 62 43 19

Technical, trade-related and other business services 18 18 0 18

Research and Development services 26 15 12 3

Manufacturing services on physical inputs owned by others

14 8 6 2

Financial Service 5 4 2 2

Government goods and services n.i.e. 5 2 3 -2

Personal, cultural, and recreational services 4 1 3 -2

Insurance and pension service 14 4 10 -6

Charges for the use of intellectual property n.i.e. 33 5 29 -24

Licenses to reproduce and /or distribute audio-visual and related products

2 0 2 -2

Licenses for the use of outcomes of research and development

15 1 14 -14

Transport 130 37 93 -56

Air Transport 38 11 27 -16

Sea transport 82 23 59 -36

Travel 294 39 255 -216

Health-related 4 2 2 -1

Education-related 73 6 66 -60

Source: Ministry of Commerce of People’s Republic of China, China trade in services statistics, 20 January

2018.

GBA Background Document

© Copyright 2022 Foundation, 2019. 26

Exhibit 2.18. Top 10 Countries (Regions) in Sales of Foreign Affiliates in China Engaged in Services

Activities, 2016

Country/Region Enterprise Quantity

Sales Total Profit

(US$ bn)

Total Number of Employees

Value (US$ bn)

Annual % Change

Total Number

Foreign Side

Hong Kong 58,895 478.3 0.4 78.2 3,255,263 65,075

Japan 8,005 71.9 0.5 6.7 295,815 16,135

British Virgin Islands 4,919 60.8 5.3 17.9 404,656 6,161

Singapore 4,612 43.0 5.5 5.2 225,925 6,595

United States 6,759 31.6 -10.6 3.9 215,606 9,956

Germany 2,341 24.0 -1.1 6.7 103,861 4,918

South Korea 7,176 15.7 -44.5 0.8 109,407 12,025

Netherlands 890 15.4 -20.5 1.9 183,207 4,115

Cayman Islands 917 10.9 -6.6 1.6 102,391 1,381

France 1,173 8.9 -26.3 1.4 63,619 2,572

Source: Ministry of Commerce of People’s Republic of China, Services Supplied Through Affiliates, 20 January

2018.

Exhibit 2.19. Top 10 Countries (Regions) in Sales of Chinese Affiliates Located Abroad Engaged in

Services Activities, 2016

Country/Region Enterprise Quantity

Sales Total Number of Employees

Value (US$ bn)

Annual % Change

Total Number Chinese Side

Hong Kong 6,466 329.0 18.5 323,957 195,693

Singapore 407 51.8 24.2 26,773 10,579

Cayman Islands 161 30.3 322.3 53,832 43,733

United Kingdom 156 30.0 -0.6 4,160 3,216

British Virgin Islands 389 19.9 0.5 43,578 37,465

Saudi Arabia 29 10.2 26.5 2,762 1,419

United States 2,163 10.1 16.2 18,763 4,628

Algeria 27 9.4 10.7 2,659 804

Pakistan 34 8.1 50.6 4,936 458

Kazakhstan 97 5.5 36.8 9,843 1,046

Source: Ministry of Commerce of People’s Republic of China, Services Supplied Through Affiliates, 20 January

2018.

GBA Background Document

© Copyright 2022 Foundation, 2019. 27

Exhibit 2.20. Hong Kong’s Trade in Services

Year Export (HKD mn) Annual % Change Import (HKD mn) Annual % Change

2006 422,921 15 494,907 13

2007 502,775 19 536,060 8

2008 544,358 8 565,399 6

2009 501,303 -8 473,686 -16

2010 625,719 25 546,930 16

2011 710,716 14 578,035 6

2012 764,026 8 594,266 3

2013 812,640 6 583,216 -2

2014 829,085 2 573,522 -2

2015 808,948 -2 574,345 0

2016 764,839 -6 578,106 1

Source: Hong Kong Census and Statistics Department, Hong Kong Trade in Service Statistics in 2016, February

2018.

Exhibit 2.21. Hong Kong’s Trade in Services by Sector

Industry Exports (HKD mn) Imports (HKD mn)

2014 2015 2016 2014 2015 2016

All 829,085 808,948 764,839 573,522 574,345 578.106

Manufacturing § § § 92,517 90,019 88,192

Maintenance and repair services 2,488 2,678 2,628 872 932 1,009

Transport * - Sea Transport - Air Transport

247,707 131,387

91,670

230,876 115,277

92,985

218,687 107,329

88,777

142,620 60,575 65,122

134,230 58,561 56,936

131,387 57,789 53,689

Travel 297,567 280,227 254,962 170,672 178,751 187,385

Construction 2,818 1,340 944 2,690 1,317 953

Insurance and pension services 9,374 10,143 11,218 11,200 11,264 11,047

Financial Services 137,000 148,671 138,526 34,380 37,291 36,594

Charges for the use of IP 4,828 4,977 5,225 15,030 14,423 14,615

Telecomm, computer, information services 21,873 22,027 22,134 14,752 14,760 15,044

Other business services * - R&D, innovation services - Legal services - Accounting, auditing, tax consulting - Business, management, PR - Advertising, mkt research, polling - Architect, engineering, scientific, tech - Trade-related

102,751 1,209 2,398 1,518

34,472 5,961 4,107

41,725

105,280 1,024 2,308 1,613

37,865 5,347 4,302

40,327

107,445 805

2,507 1,858

39,613 5,161 3,972

39,940

86,808 1,250 1,090 1,225

22,674 4,069 2,837

33,715

89,235 1,089 1,005 1,162

24,906 4,189 2,923

33,741

89,660 1,164 1,200 1,252

25,379 4,109 2,699

33,428

Personal, cultural, recreational services 2,003 1,999 2,328 776 846 983

Government goods and services 676 731 743 1,205 1,278 1,239

Notes: § denotes value within ±HKD 0.5 million; * selected subcategories only, so subcategory totals do not

equal the category value.

Source: Hong Kong Census and Statistics Department, Hong Kong Trade in Service Statistics in 2016, February

2018.

GBA Background Document

© Copyright 2022 Foundation, 2019. 28

Exhibit 2.22. Hong Kong’s Trade in Services with the Chinese Mainland

Industry Exports (HKD mn) Imports (HKD mn)

2014 2015 2016 2014 2015 2016

All 321,650 310,792 296,363 216,521 221,651 220,991

Manufacturing § § § 92,517 90,019 88,192

Maintenance and repair services 397 411 435 238 245 198

Transport 49,447 48,196 57,593 29,567 30,143 29,353

Travel 234,408 221,485 197,846 51,232 55,155 56,686

Construction *** *** *** *** *** ***

Insurance and pension services 3,628 4,166 4,961 3,807 4,490 4,468

Financial Services 6,938 9,377 8,311 2,424 3,677 3,599

Charges for the use of IP 1,425 1,608 1,774 817 868 834

Telecommunications, computer, and information services

6,294 6,465 6,152 4,734 4,523 4,632

Other business services 17,402 17,586 17,860 30,624 31,787 32,209

Personal, cultural, and recreational services

*** *** *** 66 103 178

Government goods and services *** *** *** *** *** ***

Notes: § denotes value within ±HKD 0.5 million, *** denotes figures not released, financial intermediation

services indirectly measured (FISIM) cannot be attributed to a geography and are not included in this

Exhibit.

Source: Hong Kong Census and Statistics Department, Hong Kong Trade in Service Statistics in 2016, February

2018.

GBA Background Document

© Copyright 2022 Foundation, 2019. 29

Exhibit 2.23. Hong Kong Service Supplier CEPA Certificates Awarded through 31 July 2018

Service Sector Cumulative Number of Certificates of

Hong Kong Service Supplier Issued

Legal services 24

Accounting, auditing and bookkeeping services 3

Construction professional services and Construction and related engineering services

103

Medical and dental services 45

Computer and related services and information technology services 23

Real estate services 29

Advertising services 142

Market research services 0

Management consulting and related services 52

Mining and prospecting services 0

Research and experimental development services on natural sciences and engineering

2

Public utility services 1

Placement and supply services of personnel 168

Building-cleaning services 1

Photographic services 3

Printing services 121

Translation and interpretation services 0

Convention and exhibition services 24

Value-added telecommunications services 64

Telecommunication services 4

Audiovisual services 83

Distribution services 364

Environmental services 2

All insurance and insurance-related services 23

Banking and other financial services (excluding insurance and securities) 10

Securities and futures services 90

Social services 0

Tourism and travel related services 51