the effect of bank debt downgrades on stock prices of other banks

TRANSCRIPT

Financial The EFA

Eastern Fiance Review Association

The Financial Review 36 (2001) 139-156

The Effect of Bank Debt Downgrades on Stock Prices of Other Banks

Robert Schweitzer

Samuel H. Szewczyk

Raj Varma*

University of Delaware

Drexel University

University of Delaware

Abstract

We find that debt downgrades of money center banks elicit negative stock price responses in nondowngraded money center banks. Stock prices of larger regional banks also react to these downgrades. Although downgrades of regional banks evoke negative stock price responses for regional banks in the same geographic region, the importance of geographic region as a factor determining the extent of intra-industry reactions has diminished since 1989. Our results indicate that the merger and expansion activities triggered by interstate banking have blurred differences between regional and money center banks as interstate banking activity has moved towards nationwide banking

Keywords: contagion effects, debt ratings, intra-industry effects, interstate banking, rating changes

JEL Classification: G2 1

'Corresponding author: University of Delaware, Department of Finance, Newark, DE 19716, USA; Phone: (302) 831-1786; Fax: (302) 831-3061; E-mail: [email protected]

Financial support for this project was provided by grants from the Bennett S. LeBow College of Business at Drexel University and from the University of Delaware. In addition, we also acknowledge helpful comments from Harold Black, George Tsetsekos, Breck Robinson, Michael Gombola, and especially Don Puglisi on earlier versions of this paper.

139

140 R. Schweitzer, S. H. Szewczyk and, R. Varm/The Financial Review 36 (2001) 139-156

1. Introduction

Much empirical research focuses on intra-industry effects in the banking indus- try, especially those triggered by releases of negative information.’ Papers that study large bank failures, such as Aharony and Swary (1983, 1996), Peavy and Hempel (1988), Karafiath and Glascock (1989), and Dickinson, Peterson, and Christiansen (1991) argue that banks share clienteles, and so news relevant to the value of one bank’s loan portfolio might also be relevant for others. Other intra-industry studies such as those by Docking, Hirschey, and Jones (1997) and Slovin, Sushka, and Polonchek (1992, 1999) build on the idea that bank managers have private informa- tion about portfolio values, which may be signaled by their actions.

In this study, we expand on the notion that debt-rating agencies also possess private information about banks, and that this information is signaled by rating- changes. We know from recent research by Billet, Garfinkel, and O’Neal (1998) and Schweitzer, Szewczyk, and Varma (1992) that stock prices of banks react negatively when rating agencies downgrade of their debt. We investigate the extent to which unfavorable information released by such downgrades spill over beyond the stock price of the downgraded banks to affect the share values of other banks. We analyze stock price responses for both downgraded and nondowngraded banks and evaluate the magnitude, significance, and direction of the intra-industry effects.

Our study provides insights on the nature of the information conveyed in a rating change, Our work shows whether a rating change conveys new information on the value of the bank’s loan portfolio and is therefore relevant to the portfolio values of other banks, or whether some other sort of firm-specific information is conveyed which might allow competitive effects to dominate the stock price reaction, such as information on the bank’s growth opportunities.

Our results help clarify the extent to which releases of unfavorable information about a particular bank produce intra-industry effects in the banking industry. Most empirical studies find no evidence of industry-wide contagion effects in which negative information about a particular bank has resulted in negative revisions in the stock prices of all banks in general. Instead, when intra-industry effects do exist, the spillover tends to be narrower in scope and confined to specific sets of similar banks. Several characteristics, including asset size, geographic region, and loan portfolio composition have been used to define the specific set of banks, but there is no consensus on the relative importance of these characteristics. Therefore, the precise characteristics that define the specific set of banks experiencing the spillover remain unclear.

’ The enduring significance of contagion effects is reflected in the following remarks made by Edward Kelly, Federal Reserve Board Governor, at the 1997 Seminar on Bank Soundness and Monetary Policy in a World of Global Capital Markets: “Banks remain quite special in their susceptibility to runs and in the severe consequences that large-scale banking panic would involve today. Balancing the need for a banking ‘safety net’ to defuse potential bank runs with the need to create the right incentives for banks in assessing and assuming risk is one of the most difficult challenges we face as central bankers.”

R. Schweitzer, S. H. Szewczyk and, R. Varma/The Financial Review 36 (2001) 139-156 141

In our tests, as in previous research, we distinguish between money center and regional banks. We define money center banks as large banks with domestic and international operations, and regional banks as smaller banks with domestic opera- tions within a given region. Thus, our investigation sheds light on the role of asset size in intra-industry effects. We also divide the regional banks in our sample into regional areas to obtain insights into the role of geographic location in intra-industry effects.

We provide evidence on the effect of interstate banking on intra-industry effects in the banking industry. The evolution of interstate banking is changing the competitive environment in which banks operate. A key element that is driving this evolution and effecting changes in the competitive environment is the reworking of state regulations that deal with interstate acquisitions. Traditionally mergers that crossed state lines were not permitted, but in the 1980’s a number of states relaxed boundary restrictions and interstate banking rapidly expanded. By 1989, interstate banking was widely adopted and the ensuing merger activity created super regional bankdgiant banks. We test how the dismantling of interstate barriers has influenced the role of asset size and geographic region in determining intra-industry effects.

Our results indicate that stock prices of nondowngraded money center banks respond to announcements of downgrades of other money center banks by dropping a statistically significant amount. We find that stock prices of some regional banks also react to these downgrades. We report that since 1989, downgrades of money center banks have a more pronounced intra-industry effect on the share prices of larger regional banks. We also find that announcements of downgrades of regional banks are associated with statistically significant stock price responses only for nondowngraded regional banks in the same geographic region as a downgraded bank. However, since 1989, geographic region has diminished as a factor determining intra-industry responses to downgrades of regional banks. Our results provide some support for the contention that interstate banking resulted in greater similarities between the financial attributes of money center and regional banks and that the information inferred from downgrades pertains to common problems facing a specific subset of banks defined by asset size.

Our work has regulatory implications. Many economists believe that large banks such as money center banks are disproportionately important to the health of the banking industry. Regulators are particularly concerned with the potential for a widespread loss of public confidence in the soundness and safety of banks that could be triggered by the release of negative information about a particular money center bank. Such releases of information would be a concern if money center banks are associated with irrational contagion effects, i.e., when negative information about a money center bank rapidly impacts other banks regardless of whether the negative inference is warranted or not. The limited spillover effects we find for debt down- grades of money center banks indicate that the market is discriminating in how it applies information inferred from these downgrades. The absence of industry-wide contagion effects implies that the market applies the inferred information rationally,

142 R. Schweitzer, S. H. Szewczyk and, R. Varrna/The Financial Review 36 (2001) 139-156

and that the information is relevant to common problems facing a specific set of banks.

The paper is organized as follows. In Section 2, we discuss testable hypotheses on the intra-industry effects of rating downgrades on nondowngraded banks. Section 3 describes the data and methods we use to measure stock price responses to rating changes. Section 4 presents results. Section 5 presents a summary and conclusion.

2. The information content of downgrades of bank debt

Since the 1970s, the major bond rating agencies have been assigning quality ratings to the debt issues of banks. Rating agencies gather information that enables them to assess the probability of default by the bank, then quantify their assessment by assigning a rating to the debt. A change in rating reflects that the rating agency has significantly reassessed the bank’s probability of default. If rating changes are in fact informative events, then systematic revisions in stock prices should follow announcements of debt rating changes.

Recent research by Billet, Garfinkel and O’Neal(l998) and Schweitzer, Szewc- zyk, and Varma (1992) show that banks’ stock prices react negatively when rating agencies downgrade bank debt. This evidence indicates that rating agencies perform a valuable monitoring service. Downgrades of bank debt provide timely new informa- tion that leads to an unfavorable reassessment of the bank in the capital market.

What is not clear is the extent to which information conveyed by a rating change affects share prices of nondowngraded banks. If the information in the rating change is strictly firm specific and therefore not relevant to other banks, only the share price of the downgraded bank should be affected. We develop the irrelevance effect hypothesis, which states that:

HI: The information contained in the downgrade is not relevant to other banks. Therefore, bank downgrades provide no new information about rival or other banks.

However, the information in the rating change can have a wider impact on stock prices. Two types of intra-industry effects may occur. We base the competitive effect on the assumption that the announcement of a downgrade will lead to an increase in the demand for the services of nondowngraded rival bank.* According to the competitive effect, nondowngraded banks will benefit from the difficulties of downgraded banks. If so, a downgrade announcement should lead to positive stock price responses for nondowngraded rival banks. Therefore, the competitive effect hypothesis states that:

H2: Problems at a specific bank will lead to a preference for nondowngraded rival banks.

Schweitzer, Szewczyk and Varma (2000) use similar arguments to show that downgrades of money center banks elicit negative revisions in EPS forecast revisions for nondowngraded money center banks.

R. Schweitzer, S. H. Szewczyk and, R. Varma/The Financial Review 36 (2001) 139-156 143

On the other hand, we base information and contagion effects on the assumption that the problems underlying a downgrading are also common to nondowngraded banks. Studies such as Docking, Hirschey (1997) and Slovin, Sushka, and Polonchek (1992) suggest that bank managers have private information about portfolio values, and that this information may be signaled by their actions. Rating agencies might also possess private information about banks, and this information is signaled by ratings changes. Holthausen and Leftwich (1986) note that “the rating process usually includes discussions with management, visits to company premises, and forecasts of income statement and balance sheet data provided by management.’ ’ They suggest that rating agencies gain access to private information about the rated firm through the rating process. Consequently, rating changes may convey private information uncovered by the rating agency to outside investors.

Information and contagion effects imply that problems at a specific bank have negative consequences for market values of other banks. The assumption underlying the information effect is that difficulties at a downgraded bank are symptomatic of problems at a specific subset of banks. If the difficulties underlying a bank are symptomatic of difficulties at rival banks, the information effect predicts that when a downgrade is announced, there will be negative stock price responses for nondown- graded rival banks. Therefore, the information effect hypothesis states that:

H3: Problems in a specific bank indicate problems in rival banks. Unlike the information effect, the contagion effect assumes that the difficulties

underlying a bank are symptomatic of difficulties of all other banks. Therefore, the contagion effect predicts negative stock price responses for all banks, rivals as well as non-rivals, in response to bank debt downgrades. This view on the informativeness of bond ratings suggests the contagion effect hypothesis concerning the effect of rating changes on nondowngraded banks.

H4: Problems in a specific bank indicate problems in the entire banking industry. The distinction between contagion effects (i.e., stock price reactions across the

entire banking industry) and information effects (i.e., reactions across a narrowly defined group of banks) is more than a matter of degree. To regulators of the banking industry, a contagion effect is an indiscriminate, irrational, and reflexive application of negative information about a particular bank to other banks, even if the application is not warranted. Seen in this light, regulators are obviously concerned by contagion. On the other hand, an information effect is a discriminate and rational application of information about a particular bank to other similar banks. If we find reactions only within narrowly defined groups of banks, it would indicate that the market discriminates in how it applies information from bank debt downgrades.

3. Data and methods

We obtain an initial sample of all bank holding companies (BHCs) whose debt was downgraded between 1977 and 1998 from lists supplied by Standard and Poor’s

144 R. Schweitzer, S. H. Szewczyk and, R. VarmdThe Financial Review 36 (2001) 139-156

(S&P) Corporation. We exclude rating changes if the BHC’s common stock was not listed on the New York Stock Exchange (NYSE) or the American Stock Exchange (ASE) at the time of the change, sufficient stock price data were not available on the Daily Returns File of the Center for Research in Security Prices (CRSP) database during the period surrounding the rating change, and, to avoid problems associated with clustered events, downgrades of other BHCs occurred within one trading day of the announcement date. After imposing these selection criteria, our final sample comprises 92 announcements of rating downgrades made by S&P for BHCs. There are 39 downgrades for 12 different money center banks. The remaining 53 down- grades are for 21 different regional banks. The sample of 12 downgraded money center banks include Bank of Boston Corp., BankAmerica Corp., Chase Manhattan Corp., Chemical Banking Corp., Citicorp, Continental Bank Corp., First Chicago Corp., First Interstate Bancorp, Manufacturers Hanover Corp., Mellon Bank Corp., Security Pacific Corp., New Wells Fargo & Co. The sample of 21 downgraded regional banks include Amsouth Bancorporation, Banc One Corp., Bank New York Inc., Barnett Banks Inc., Equimark Corp., First Bank Systems Inc., First Boston Inc., First City Bancorporation Tx Inc, First Fidelity Bancorporation, First Repub- licbank Corp, Interfirst Corp., Keycorp, M Corp, National Westminster Bk Plc, Norstar Bancorp Inc., Norwest Corp., Seafirst Corp., Signet Banking Corp., South- east Banking Corp., Texas American Bancshares Inc., Texas Commerce Bancshares Inc. Table 1 reports descriptive statistics for the sample banks.

We use event-study methodology to examine stock price responses to rating change announcements made by S&P. The abnormal return (ARit) for bank i on day t is the deviation of bank i’s realized return (Ri,) from an expected return generated by the market model.

(1) n

AR;, = R,, (& + p; R,,,,)

The coefficients in equation (1) are the OLS estimates of bank i’s market model parameters. We obtain these results from an estimation period of 140 consecutive

Table 1

Descriptive statistics for downgraded money center and regional banks This table presents descriptive statistics for 39 downgrades of money center banks and 53 downgrades of regional banks. The banks were downgraded by Standard and Poor’s between 1977 and 1998.

Money center banks Regional Banks

Market value of equity ($ millions) Mean 2465.4 Median 2280.3

Mean 83083.4 Median 72266.0

Asset size ($ millions)

763.3 516.8

27743.5 18589.3

R. Schweitzer, S. H. Szewczyk and, R. Vama/The Financial Review 36 (2001) 139456 145

trading days beginning 200 trading days prior to the announcement date. Our empiri- cal testing procedure requires at least 50 returns during the estimation period. We use the CRSP Equally Weighted Index to measure the market return over day t (Rmt).

We measure abnormal performance over individual trading days and over specified intervals of trading days in event time. We define the announcement date (day 0 in event time) as the earlier of the day prior to the date on which the downgrade was reported in the Wall Street Journal Index; the press release date supplied by S&P; and the date on which a news story about the downgrade appeared on the Dow Jones News/Retrieval Service. Our testing procedure requires no missing returns during the announcement period. For a sample of N securities, we calculate the average abnormal return (AAR) over an interval beginning on day TI and ending day T2 as:

To control for heteroskedasticity, we base our test statistics on standardized abnormal returns (SARs). The SAR for security i on day t is:

where:

In equation (4), Vi is the residual variance of bank i’s market model regression, ED is the total number of days in the regression’s estimation period, and R, is the average market return over the estimation period.

We calculate the average standardized abnormal return (ASAR) from day T 1 to day T2 by:

To test the hypothesis that the ASAR over day TI to T2 is equal to zero, we compute the following z-statistic:

146 R. Schweitzer, S. H. Szewczyk and, R. V a m / T h e Financial Review 36 (2001) 139-156

The z-statistic in equation (6) is distributed unit normal under the null hypothesis. We also perform Wilcoxcon signed rank tests to test the null hypothesis that the percentage of abnormal returns that have negative/positive signs is 50%.

To determine the intra-industry effects of the downgrades, we examine the share price reaction of nondowngraded money center and regional banks. In the event tests we perform on these banks, we modify the procedure outlined above. For each downgrade, we construct an equally weighted industry portfolio of non- downgraded banks and perform event tests on the returns to the industry portfolios.

To construct the industry portfolios, we develop industry lists using all NYSE and AMEX listed bank holding companies that have returns on the CRSP database over the study’s time frame. Using the lists of money center banks in Docking, Hirschey, and Jones (1997) and Slovin, Sushka, and Polonchek (1992), we identify 17 money center banks. We classify the other 66 banks as regional banks. We further classify the regional banks geographically, using a classification scheme similar to the one used by Docking, Hirschey, and Jones (1997) who closely follow the scheme used by the American Banker. The state in which the bank is headquar- tered determines its geographic region classification. The states and number of banks in each region are as follows:

New England: Mid-Atlantic: Midwest:

Southeast Southwest Mountain Pacific

CT, ME, MA, NH, RI, VT (3 banks) DE, DC, MD, NJ, MY, PA (19 banks) IA, IL, IN, KS, KY, MI, MN, MO, NE, ND, OH, SD, WI ( 10 banks) AL, AR, FL, GA, MS, NC, SC, TN, VA, WV (13 banks) CO, LA, NM, OK, TX, UT (10 banks) AZ, ID, MT, NV, WY (2 banks) AK, CA, HI, OR, WA (9 banks)

The tests using nondowngraded bank portfolios aggregate between 433 and 1520 individual returns. Given the number of individual returns and the wide distribu- tion of downgrades over a number of years, we assume that, in the process of calculating both bank portfolio returns and average abnormal returns for the total sample, unsystematic firm specific events unrelated to the downgrades are effectively diversified. To test for robustness, we perform the event tests using the value- weighted index in the market model and again using the market-adjusted model for estimating expected returns. The results are qualitatively similar to those reported. We also examine alternative event windows. However, the traditional two-day window best captured systematic abnormal performance.

4. Results

4.1 Analysis of downgrades of money center banks Table 2 shows stock price responses to 39 downgrades of money center banks.

The table presents average abnormal returns (AARs) for downgraded money center

R. Schweitzer, S. H. Szewczyk and, R. Varma/The Financial Review 36 (2001) 139-156 147

Table 2

Abnormal returns for downgraded money center banks and industry portfolios of nondowngraded money center banks and nondowngraded regional banks This table presents two-day average abnormal returns at the announcement of 39 downgrades of money center banks by S&P over the period 1977-1998. We base the z-statistic on standardized abnormal returns. The statistics test the null hypothesis that the two-day average abnormal return equals zero. Percent negative is the percentage of abnormal returns that have negative values. We use the Wilcoxon signed ranks test to test the null hypothesis that the proportion of negative two-day abnormal returns equals 0.5.

Two-day Z- Percent Abnormal statistic negative

return

Downgraded money center banks

Industry portfolios of nondowngraded money center banks

Industry portfolios of nondowngraded regional banks for 17 downgrades of money center banks, 1977-1988

Industry portfolios of nondowngraded regional banks for 22 downgrades of money center banks, 1989-1998

-2.85% -6.12*** 71.8***

-0.56 -2.77*** 61.5**

-0.28 -1.61 70.6*

-0.44 -2.09** 68.2*

*** Indicates statistical significance at the 0.01 level. ** Indicates statistical significance at the 0.05 level. * Indicates statistical significance at the 0.10 level.

banks as well as industry portfolios of nondowngraded money center and regional banks. For downgraded money center banks, the two-day AAR over event days 0 and 1 is -2.85% with an associated z-statistic of -6.72, indicating statistical signifi- cance at the 0.01 level. The proportion of downgrade observations with negative abnormal returns is 71.8%. The Wilcoxon signed rank test, which we use to test whether the proportion of announcement period negative abnormal returns is signifi- cantly different from 50%, indicates significance at the 0.01 level. These results agree with those of Billet, Garfinkel, and O’Neal(l998) and Schweitzer, Szewczyk, and Varma (1992) for downgrades of bank debt.

The average abnormal return for the industry portfolios of nondowngraded rival money center banks is -0.56% with a z-statistic of -2.77. The proportion of observations with negative announcement period abnormal returns is 6 1.5%, which is significantly different from 50% at the 0.05 level. Clearly money center banks downgrades elicit negative intra-industry responses in nondowngraded rival money center banks.

Average abnormal returns are negative for both downgraded money center banks and industry portfolios of nondowngraded rival money center banks. This

148 R. Schweitzer, S. H. Szewczyk and, R. V a m / T h e Financial Review 36 (2001) 139-156

supports the information effect rather than the competitive effect hypothesis, which predicts a positive response for the rival money center banks. However, we cannot strictly conclude from a comparison of two sample means that the individually matched downgraded bankdindustry portfolios have the same or opposite directional reactions to the downgrade. Therefore, we followed the method used in Szewczyk (1992) and conducted correlation tests between the matched abnormal returns for downgraded money center banks and the industry portfolios to determine whether the intra-industry effect results from a competitive or an information effect. We find a significant positive correlation between downgraded and nondowngraded rival money center banks. The Pearson correlation coefficient for the abnormal returns of downgraded and nondowngraded rival money center banks is 0.43 1 with an associated p-value of 0.01. The results support the information effect hypothesis, under which the market interprets problems at a specific money center bank as being symptomatic of problems at other money center banks as well.

Interstate banking provides opportunities for bank holding companies to in- crease the size and scope of their operations, especially through out-of-state acquisi- tions and mergers, and to geographically diversify risk. Therefore, interstate banking can blur the differences between some regional banks and money center banks in such a way that they could be classified as rivals. To examine the influence of interstate banking on the intra-industry response to downgrades of money center banks, we divide our sample into two subperiods, 1977 to 1988 and 1989 to 1998, and conduct event tests on industry portfolios of nondowngraded regional banks. Seventeen of the money center downgrades occurred in the earlier period, twenty- two in the later period.

Prior to 1982, interstate banking was still prohibited in every state except Maine, which allowed interstate banking in 1975. Most state legislatures passed their interstate banking laws between 1982 and 1988. By 1989, interstate banking had been widely adopted and the merger activity that ensued created the super regional banks/giant banks that have evolved. By the beginning of 1989, all the regional banks on our industry list are headquartered in states allowing interstate banking. The percentages of sample regional banks in states allowing interstate banking by year are: 1982, 15%; 1983, 17%; 1984, 21%; 1985,44%; 1986, 68%; 1987,98%; 1988, 100%.

If the evolutionary dynamics set off by interstate banking blurred differences between money center and regional banks, we should see a wider industry reaction in the 1989 to 1998 period, as the changes wrought by these dynamics become evident. Table 2 shows that industry portfolios of regional banks in the 1989 to 1998 period have a negative average abnormal return of -0.44%, which is statistically significant at the 0.05 level (z-statistic = -2.09). On the other hand, the average abnormal return to the industry portfolios of regional banks in the 1982 to 1988 period (-0.28%) is not statistically significant at the 0.05 level (z-statistic = -1.61).

Next, we investigate the relation between the asset size of regional banks and their stock response to downgrades of money center banks. The results in Table 2

R. Schweitzer, S. H. Szewczyk and, R. Varma/The Financial Review 36 (2001) 139-156 149

suggest that regional banks, through interstate banking, evolve to the point where some can be classified as rivals to money center banks. These regional banks are likely to be large in asset size. Therefore, we would expect to find a relation between the asset size of nondowngraded regional banks and their stock response to downgrades of money center banks, especially in the 1989 to 1998 period. Moreover, such a relation would be consistent with the information effect hypothesis. We calculate announcement period abnormal returns for each regional bank in the sample. We estimate the following regression model for the 1977-1988 period and the 1989- 1998 period:

(7) ARi = bo + bl DSIZEj + bz RSIZEi + b3 MOODYSj

where:

ARi = two-day announcement period abnormal return for regional bank i at the announcement of the downgrade of money center bank j

DSIZEj log of the asset size of money center bank j at the beginning of the downgrade year reported in COMPUSTAT

RSIZEi = log of the asset size of regional bank i at the beginning of the downgrade year reported in COMPUSTAT

MOODYSj = dummy variable set equal to one if, in the year of the down- grade, money center bank j’s downgrade by S&P is preceded by a similar rating change by Moody’s, and zero otherwise

=

Downgrades of larger money center banks could elicit stronger intra-industry responses among rivals. Therefore, we predict a negative coefficient for DSIZE. To the extent that larger regional banks are closer rivals for money center banks, we predict a negative coefficient for RSIZE. If a previous downgrade by Moody’s leads the market to anticipate a similar action by S&P, then we predict a positive coefficient for MOODYS. On the other hand, if the market interprets the downgrade by S&P as a confirmation of the assessment contained in an earlier downgrade by Moody’s, then we predict a negative coefficient for MOODYS. The results of the regression for the 1977 to 1988 period are (t-statistics are in parentheses):

ARi = 3.421 - 0.337 DSIZEj + 0.020 RSIZEi - 0.644 MOODYSj (8) (1.11) (-1.26) (0.17) (- 1.49)

The results of the regression for the 1989 to 1998 period are:

ARi = 1.123 + 0.036 DSIZEj - 0.176 RSIZEi - 0.557 MOODYSj (9) (0.47) (0.17) (-1.74) (-1.43)

The coefficients for DSIZE and RSIZE are not statistically significant in the regression estimated for the 1977 to 1988 period. In the regression for 1989 to

150 R. Schweifzer, S. H. Szewczyk and, R. Varma/The Financial Review 36 (2001) 139-156

1998, the coefficient for RSIZE is negative, as predicted by the information effect hypothesis, and significant at the 0.1 level in a one-tailed test. The coefficient for MOODYS is not statistically significant in both regressions.

4.2 Analysis of downgrades of regional banks

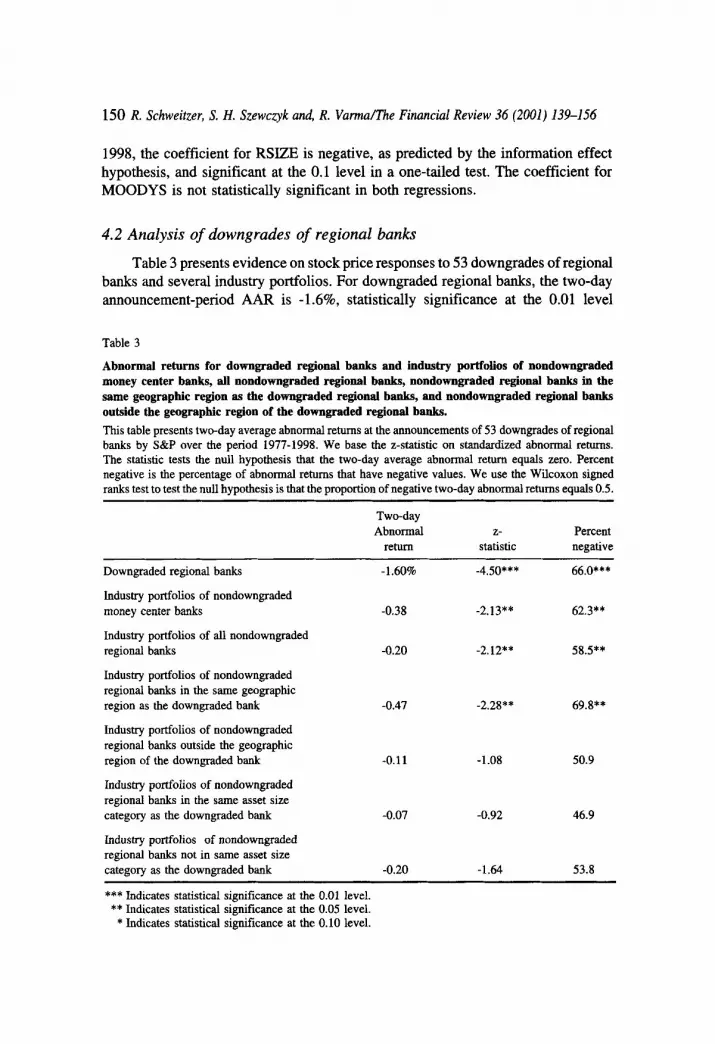

Table 3 presents evidence on stock price responses to 53 downgrades of regional banks and several industry portfolios. For downgraded regional banks, the two-day announcement-period AAR is -1.6%, statistically significance at the 0.01 level

Table 3

Abnormal returns for downgraded regional banks and industry portfolios of nondowngraded money center banks, all nondowngraded regional banks, nondowngraded regional banks in the same geographic region as the downgraded regional banks, and nondowngraded regional banks outside the geographic region of the downgraded regional banks. This table presents two-day average abnormal returns at the announcements of 53 downgrades of regional banks by S&P over the period 1977-1998. We base the z-statistic on standardized abnormal returns. The statistic tests the null hypothesis that the two-day average abnormal retum equals zero. Percent negative is the percentage of abnormal returns that have negative values. We use the Wilcoxon signed ranks test to test the null hypothesis is that the proportion of negative two-day abnormal returns equals 0.5.

Two-day Abnormal Z- Percent

retum statistic negative

Downgraded regional banks -1.60% -4.50* * * 66.0***

Industry portfolios of nondowngraded money center banks -0.38 -2.13** 62.3**

Industry portfolios of all nondowngraded regional banks -0.20 -2.12** 58.5**

Industry portfolios of nondowngraded regional banks in the same geographic region as the downgraded bank -0.47 -2.28** 69.8**

Industry portfolios of nondowngraded regional banks outside the geographic region of the downgraded bank -0.11 -1.08 50.9

Industry portfolios of nondowngraded regional banks in the same asset size category as the downgraded bank -0.07 -0.92 46.9

Industry portfolios of nondowngraded regional banks not in same asset size category as the downgraded bank -0.20 -1.64 53.8

*** Indicates statistical significance at the 0.01 level. ** Indicates statistical significance at the 0.05 level. * Indicates statistical significance at the 0.10 level.

R. Schweitzer, S. H. Szewczyk and, R. Vanna/The Financial Review 36 (2001) 139-156 151

(z-statistic of -4.5). The proportion of downgrade observations recording negative abnormal returns is 66%. The Wilcoxon signed rank test indicates significance at the 0.05 level. We observe a significant negative average abnormal return, -0.38%, in the nondowngraded money center bank industry portfolios (z-statistic of -2.13). The Wilcoxon signed rank test indicates that the percentage of industry portfolios with negative abnormal returns (62.3%) is significantly different from 50% at the 0.05 level. This finding supports the belief that interstate banking has narrowed differences in the size, scope, and nature of operations between some of the regional banks that engage in interstate banking and the money center banks. However, the evidence is not strong because the Pearson conelation coefficient in Table 4 is not statistically significant.

We also find significant abnormal returns for nondowngraded regional banks. Perhaps the information inferred from downgrades of regional banks is more relevant to the assessment of banks in the same geographic region as the downgraded bank. This could be true even with interstate banking if most banks have not yet expanded their out-of-state operations significantly beyond their larger geographic regions.

We construct separate industry portfolios for regional banks that operate in the same geographic region as the downgraded bank, and regional banks operating outside the geographic region. As described previously, we classify banks into seven

Table 4

Pearson correlation tests between downgraded regional banks and nondowngraded money center banks and nondowngraded regional banks. This table presents results of Pearson Correlation tests between abnormal returns for 53 downgraded regional banks and abnormal returns for industry portfolios of nondowngraded money center banks, all nondowngraded regional banks, nondowngraded regional banks in the same geographic region, and nondowngraded regional banks outside the geographic region. The p-values are in parentheses. Standard and Poor's announced downgrades of the 53 regional banks over the period 1977-1998.

Downgraded regional banks

Nondowngraded money center banks

Nondowngraded regional banks

Nondowngaded regional banks in same geographic region

Nondowngraded regional banks outside geographic region

Nondowngraded regional banks in same asset size category

0.115 (0.41)

0.070 (0.61)

0.367 (0.01)

(0.62)

0.264 (0.07)

-0.070

Nondowngraded regional banks not in same asset size category -0.078 (0.58)

152 R. Schweitzer, S. H. Szewczyk and, R. Varma/The Financial Review 36 (2001) 139-156

geographic regions: New England, Mid-Atlantic, Midwest, Southeast, Southwest, Mountain, and Pacific.

We find there is a geographic impact for downgrades of regional banks. The AAR for the industry portfolios of nondowngraded regional banks in the same region as the downgraded regional bank is -0.47% with a z-statistic of -2.28. The proportion of observations with negative announcement period abnormal returns is 69.8%, which is significantly different from 50% at the 0.05 level. We do not observe statistically significant intra-industry effects for regional banks outside the geographic region of the downgraded regional bank.

These results do not support the existence of a competitive effect. Instead the evidence indicates there is an information effect. However, the evidence is not strong. The difference in the average abnormal returns for same region industry portfolios and out of region industry portfolios is not statistically significant (t= -1).

We also examine the relation between asset size and the stock price response of nondowngraded regional banks to downgrades of other regional banks. Since regional banks differ substantially in size, the intra-industry reactions might be more pronounced when the nondowngraded regional banks are similar in asset size to the downgraded bank.

We construct separate industry portfolios for regional banks that are similar in asset size to the downgraded bank and for regional banks that are not. For each year in the study’s time frame, we rank the NYSElASE listed bank holding companies on our industry lists by their asset size and divided them into asset size quartiles. We classify nondowngraded regional banks that are in the same asset size quartile as the downgraded bank in the downgrade year as “in the same asset size category as the downgraded bank.” We classify nondowngraded regional banks that are not in the same asset size quartile as the downgraded bank are as “not in the same asset size category as the downgraded bank.”

Table 4 shows that we find no evidence that industry responses are stronger when downgraded and nondowngraded regional banks are similar in asset size. The AAR for industry portfolios of nondowngraded regional banks in the same asset size category as the downgraded bank is not statistically different from zero.

To assess over time the influence of geographic region and similarity in asset size over, we calculate announcement period abnormal returns for each nondown- graded regional bank in the sample. We estimate the following regression model for the 1977-1988 period and the 1989-1998 period

ARi = bo + bl DSIZEj + b2 SIZECATi + b4 GEOi + b5 MOODYSj (10)

where:

ARi = two-day announcement period abnormal return for regional bank i at the announcement of the downgrade of regional bank j

R. Schweitzer, S. H. Szewczyk and, R. Varma/The Financial Review 36 (2001) 139-156 153

DSIZEj =

SIZECATi =

log of the asset size of regional j at the beginning of the downgrade year reported in COMPUSTAT dummy variable set to one if regional bank i is in the same asset size category as downgraded regional bank j, and zero otherwise dummy variable set to one if regional bank i is headquartered in the same geographic region as downgraded regional bank j, and zero otherwise dummy variable set equal to one if, in the year of the down- grade, regional bank j’s downgrade by S&P is preceded by a similar rating change by Moody’s, and zero otherwise

GEO, =

MOODYSj =

Downgrades of larger regional banks could elicit stronger intra-industry re- sponses among rivals. Therefore, we predict a negative coefficient for DSIZE. To the extent that regional banks of similar asset size are closer rivals, we predict a negative coefficient for SIZECAT. To the extent that regional banks headquartered in the same geographic region are closer rivals, we predict a negative coefficient for GEO. If a previous downgrade by Moody’s leads the market to anticipate a similar action by S&P, then we predict a positive coefficient for MOODYS. But if the market interprets the downgrade by S&P as a confirmation of the assessment contained in an earlier downgrade by Moody’s, then we predict a negative coefficient for MOODYS.

The results of the regression for the 1977-1988 period are (t-statistics are in parentheses):

ARi = -1.455 + 0.138 DSIZEj + 0.259 SIZECATi-0.540 GEOi-0.417 MOODYSj (1 1) (-0.75) (0.14) (0.26) (-1.93) (-1.04)

The results of the regression for the 1989-1998 period are (t-statistics are in parentheses):

ARi = -1.135-0.108 DSIZEj-0.414 SIZECATi-0.021 GE0,-2.40 MOODYSj (12) (0.50) (-0.49) (-0.69) (-0.03) (-2.39)

In both time period regressions, the coefficients for DSIZE and SIZECAT are not significantly different from zero. The coefficient for GEO is negative and statistically significant at the 0.01 level for the 1977-1988 time period, and negative but statistically insignificant in the 1989-1998 period. These results suggest that the importance of geographic region in determining the bounds of intra-industry information transfers diminishes as interstate banking activity moves outside of larger geographic regions and towards nationwide banking. We note that the coefficient for MOODYS is negative and significant for 1989-1998 and insignificant in the earlier

154 R. Schweitzer, S. H. Szewczyk a d , R. Varma/llre Financial Review 36 (2001) 139-156

period. Perhaps, due to the dynamic changes occurring in the banking industry, the market values a confirmation provided by a similar downgrade issued by a competing rating agency of an earlier negative assessment.

5. Summary and conclusion

Our results show that announcements of bank debt downgrades are associated with statistically significant negative stock price responses for downgraded money center and regional banks. Stock prices of nondowngraded money center banks also drop by a statistically significant amount in response to announcements of downgrades of money center banks.

We report significantly negative reactions in the stock prices of nondowngraded regional banks for downgrades of money center banks made since 1989. For these downgrades, we find a significant inverse relation between the asset size of the regional banks and their stock price reaction, where larger regional banks are associ- ated with more negative abnormal returns. We find no statistically significant stock price response for nondowngraded regional banks to money center bank downgrades made before 1989.

The statistically significant intra-industry effect that we find for downgrades of money center banks in the stock prices of rival money center banks shows that the market infers new information regarding common factors underlying money center bank values. Our findings for nondowngraded regional banks suggest that since the spread of interstate banking, the intra-industry impact of money center bank downgrades has widened to include regional banks. However, our evidence does not support the existence of any industry-wide contagion effects associated with bad news at a money center bank.

Two findings indicate that the market applies private information released by rating agencies in a discriminatory, and therefore rational, manner. The first finding is the insignificant stock price reaction by regional banks to money center bank downgrades made before 1989. The second finding is the relation between the asset size of the regional bank and its stock price response to downgrades made since 1989. Collectively, the evidence on stock price responses of nondowngraded regional banks to downgrades of money center banks provides supports the contention that interstate banking has resulted in greater similarities between the financial attributes of money center banks and regional banks.

For downgrades of regional banks, we find that the stock prices of nondown- graded regional banks in the same geographic region as a downgraded bank drop by a statistically significant amount. However, stock prices of nondowngraded regional banks outside the geographic region of a downgraded bank do not react significantly to their downgrades. The negative response of nondowngraded regional banks in the same geographic region as the downgraded bank and the significant positive correlation between the abnormal returns indicate that the inferred informa- tion pertains to common problems facing the banks rather than changes in competitive

R. Schweitzer, S. H. Szewczyk and, R. Varma/The Financial Review 36 (2001) 139-156 155

positions. These results support the belief that there are strong similarities between the financial attributes of regional banks operating in the same geographic region. However, subsequent regression analysis indicates that since 1989, the importance of geographic region as a factor determining the extent of intra-industry reactions has diminished as interstate banking activity moved increasingly outside of larger geographic regions and towards nationwide banking.

References

Aharony, J. and I. Swary, 1996,.Additional evidence on the information-based contagion effects of bank failures, Journal of Banking and Finance 20, 57-69.

Aharony, J. and I. Swary, 1983. Contagion effects of bank failures: Evidence from capital markets, Journal of Business 56, 305-322.

Billett, M.A., J.A. GarFinkel and E.S. O’Neal, 1998. The cost of market versus regulatory discipline in banking, Journal of Financial Economics 48, 333-358.

Dickinson,A., D. Peterson and W. Christiansen, 1991. An empirical investigation into the failure of First Republic Bank: Is there a contagion effect?, Financial Review 26, 303-318.

Docking, D.S., M. Hirschey, and E. Jones, 1997. Information and contagion effects of bank loan-loss reserve announcements, Journal of Financial Economics 43, 219-239.

Holthausen, R. and R. Leftwich, 1986. The effect of bond rating changes on common stock prices, Journal of Financial Economics 17, 57-89.

Karafiath, I. and J. Glascock, 1989. Intra-Industry effects of a regulatory shift: Capital market evidence from Penn Square, Financial Review 24, 123-134.

Peavy, J. and G. Hempel, 1988. The Penn Square Bank failure: Effect on commercial bank security returns- A note, Journal of Banking and Finance 12, 141-150.

Schweitzer, R., S. Szewczyk, and R. Varma, 1992. Bond rating agencies and their role in bank market discipline, Journal of Financial Services Research 6, 249-263.

Schweitzer, R., S. Szewczyk, and R. Varma, 2000. Too big to downgrade: The response of financial analysts to bond downgrades of money center banks, Managerial Finance 26, 31-41.

Slovin, M.B., M.E. Sushka, and J.A. Polonchek, 1992. Information externalities of seasoned equity issues: Differences between banks and industrial f m s , Joumul of Financial Economics 32.87-101.

Slovin, M.B., M.E. Sushka, and J.A. Polonchek, 1999. An analysis of contagion and competitive effects at commercial banks, Journal of Financial Economics 54, 197-225.

Szewczyk, S.H., 1992. The intra-industry transfer of information inferred from announcements of corpo- rate security offerings, Journal of Finance 47, 1935-1941.