take control - opuscapita

TRANSCRIPT

TAKE CONTROLIn-house bank at the core of proactive cash management

The headaches of multinational cash management

5 STEPS TO VISIBILITY

AND CONTROL

5 KEY BENEFITS OF IN-HOUSE

BANKING

PAGE 2 | IN-HOUSE BANK AT THE CORE OF PROACTIVE CASH MANAGEMENT

Contents INTRODUCTION: GROUP TREASURY TAKES CONTROL ..................................................................3

THE HEADACHES OF MULTINATIONAL CASH MANAGEMENT ..................................................4

5 STEPS TO VISIBILITY AND CONTROL ....................................................................................................7

5 KEY BENEFITS OF IN-HOUSE BANKING ........................................................................................... 15

SUMMARY: QUESTIONS TO ASK YOURSELF ...................................................................................... 19

PAGE 3 | IN-HOUSE BANK AT THE CORE OF PROACTIVE CASH MANAGEMENT

In today’s fast-moving global business environment, corporate treasurers and cash managers feel the pressure to deliver high-level financial support to the business. Operational excellence is not enough: corporate management also expects finance leaders to provide them with a constant flow of relevant, real-time information and insight. Well-oiled financial processes have become increasingly important in deciding the success of an organization.

“Treasurers and cash managers in international corporations need to maintain both visibility and a firm grip on the company-wide cash flows and working capital.”

The group treasury needs to be able to steer financial processes efficiently to enhance business operations and sup-port needed investments. To this end, treasurers and cash managers in inter-national corporations need to maintain both visibility and a firm grip on the company-wide cash flows and working capital. Factors such as uncertainty in the economic and political landscape

and currency volatility highlight the importance of comprehensive, infalli-ble, group-level risk management.

In this whitepaper, we outline the ben-efits of a modern in-house bank solu-tion as the basis for transparent group- level cash management. We discuss the challenges that treasurers in inter-national organizations face, and review

the situations where establishing an in-house bank is a good solution. We also provide step-by-step instructions for increasing harmonization and deep-ening centralization with an in-house bank solution to give the group trea-sury the ability to truly control cash and working capital.

CHAPTER 1

INTRODUCTION Group treasury takes control

PAGE 4 | IN-HOUSE BANK AT THE CORE OF PROACTIVE CASH MANAGEMENT

CHAPTER 2

THE HEADACHES OF MULTINATIONAL CASH MANAGEMENTDespite the many advances in centralizing financial processes, many cash managers and group treasurers in multinational corporations are still struggling with inadequate visibility of group-level cash and exposures.

CAUSES OF SUB-OPTIMAL CASH MANAGEMENTThe causes of sub-optimal cash man-agement are varied. Maybe the organi-zation has grown through mergers, re-sulting in a variety of payment systems and processes in different countries and subsidiaries. Maybe there is a decentral-ized business model where locally oper-ated units use different systems leading to work-arounds like weekly spread-sheet reports to the group treasury.

The amount of trading and invoicing be-tween subsidiaries may be considerable, while the processes around these internal transactions may be disparate – leading to inefficient handling. Or, maybe the group treasury has visibility over most of the in-coming and outflowing cash, but simply lacks the proper tools to control it and make it truly available for profitable use.

POOR VISIBILITY INTO BANK ACCOUNTSIn practice, a frequent source of head-

aches at group treasuries is poor visi-bility into bank accounts. In a complex operating environment of multiple subsidiaries and business units in mul-tiple countries and dozens of banks, it’s often the case that no one has a com-prehensive overview of all the bank ac-counts and types of transactions they are used for, let alone an up-to-date view of the balance on each account.

In such an environment, transparency and cash forecasting are often hindered further by the myriad of different bank-ing, ERP, and financial management systems. Administering the bank ac-counts and managing the bank proxies alone is tedious, and takes time away from performing value adding treasury services.

DECENTRALIZED CASHAnother common pain point is decen-tralized cash, and insufficient means to collect it. Treasury, who is in charge of making the most out of the working

capital on a group level, is time and time again faced with the imbalance. On the one hand are subsidiaries which hoard cash in their local bank accounts without submitting it to the treasury. This leaves the treasury powerless to mitigate the risk of cash being kept in a bad bank. On the other hand are subsidiaries who negotiate loans with their local banks without the oversight of the group treasury. These decentral-ized loans don’t leverage the potential economies of scale for more attractive rates.

CURRENCY EXCHANGE FEESSiloed actions in the subsidiaries easily lead to unnecessary costs and banking fees. FX translation is a good example. When subsidiaries operate in violation of financial policy best practices and pay FX invoices from their local curren-cy bank accounts, the cost of currency exchange can cause severe leaks in the treasury’s operational budget.

Is in-house banking

a good fit?

PAGE 5 | IN-HOUSE BANK AT THE CORE OF PROACTIVE CASH MANAGEMENT

PAGE 6 | IN-HOUSE BANK AT THE CORE OF PROACTIVE CASH MANAGEMENT

The more banking relationships your organization has, the more your organization can save on the transaction and management costs with an in-house bank.

NUMBER OF BANKING

RELATIONSHIPS

The higher the volume of internal invoices, the more your organization can benefit from decreasing bank transaction fees or fees from FX deals with an in-house bank.

INTERNAL TRANSACTION

VOLUMES

The higher the number of subsidiaries, the more value your organization can gainfrom an in-house bank, and the greater the improvements in visibility over cash.

NUMBER OF SUBSIDIARIES OR ENTITIES

The more loans your subsidiaries take out locally to run their operations and projects, the more cost-efficiency an in-house bank can bring your organization by enabling the distribution of cash for operations centrally.

SUBSIDIARY LOANS

THINGS TO CONSIDER WHEN DECIDING WHETHER AN IN-HOUSE BANK IS RIGHT FOR YOU

PAGE 7 | IN-HOUSE BANK AT THE CORE OF PROACTIVE CASH MANAGEMENT

CHAPTER 3

Well-run treasuries in large and mid-sized corporations have already embarked on the journey towards deeper centralization of cash management processes.

5 STEPS TO VISIBILITY AND CONTROL

How to build an in-house bank

Figure 1. The step-by-step approach to centralizing cash and finance processes with a modern in-house bank.

PAGE 8 | IN-HOUSE BANK AT THE CORE OF PROACTIVE CASH MANAGEMENT

01

02

03

04

05

Managing corporate bank account structure

Visibility to daily balance on company and subsidiary level, reduced number

of banking partners.

Harmonized and automated internal pay-ment processes, lower costs from avoiding

value date losses and transaction fees.

Centralized, controlled and cost-efficient external payment process,

increased safety and fraud prevention.

Improved working capital management, increased indepence of banks,

maximized cost efficiency.

Effective internal financing, decreased need for external loans.

5 STEPS TO VISIBILITY AND CONTROL

WITH AN IN-HOUSE BANK

Streamlining internal payments

Establishing Payments on-behalf-of (POBO)

Establishing Collections on-behalf-of (COBO)

Centralizing control over financing

Their goal is real-time visibility over cash. An in-house bank gives the group treasury the widest set of tools for managing working capital efficiently, increasing visibility and control of the cash flow processes, and strengthen-ing payment security and risk manage-ment. The solution can feature different levels of harmonization depending on how deep of an integration between

the group and the subsidiaries is de-sired, and depending on which func-tions the treasury wants to control.

The implementation of an in-house bank structure does not have to be done all at once. In fact, the full central-ization of cash and finance processes is best built step-by-step [as illustrated in Figure 1].

PAGE 9 | IN-HOUSE BANK AT THE CORE OF PROACTIVE CASH MANAGEMENT

“Ultimately, a group treasury can even reach a single-source-of-contact structure where the

local units only communicate with the treasury, and the treasury is the only entity

with direct connections to external banks.”

A good way to start the centralization ex-ercise is to collect all the account balance information from all the group compa-nies in one place. International compa-nies tend to have many country-specific or bank-specific account structures in use. Typically, the cash is centralized at a group level with zero balance accounts: at the end of each banking day, a sweep occurs and the cash balances of the units’ bank accounts are transferred to the parent company’s account. The chal-lenge with these cash pool structures is that the subsidiaries’ real balances be-come blurry in the process.

With an in-house bank, the manage-ment of the group’s balances hap-pens in a similar, but internal, account structure. The sweep/top transactions of the zero-balance accounts can be automated so that the transfers are allocated correctly to the subsidiaries’ internal accounts. This allows visibility of the up-to-date company or unit-spe-cific balance. In addition, sweep/top transactions from several external bank accounts can be allocated to a single internal account. As a result, the struc-ture enables a single, daily balance per subsidiary.

Creating an in-house bank to man-age the corporate account structure can replace a multitude of external bank accounts, making it possible to reduce the number of banking part-ners at a corporate level. Ultimately, a group treasury can even reach a single-source-of-contact structure where the local units only communicate with the treasury, and the treasury is the only entity with direct connections to exter-nal banks.

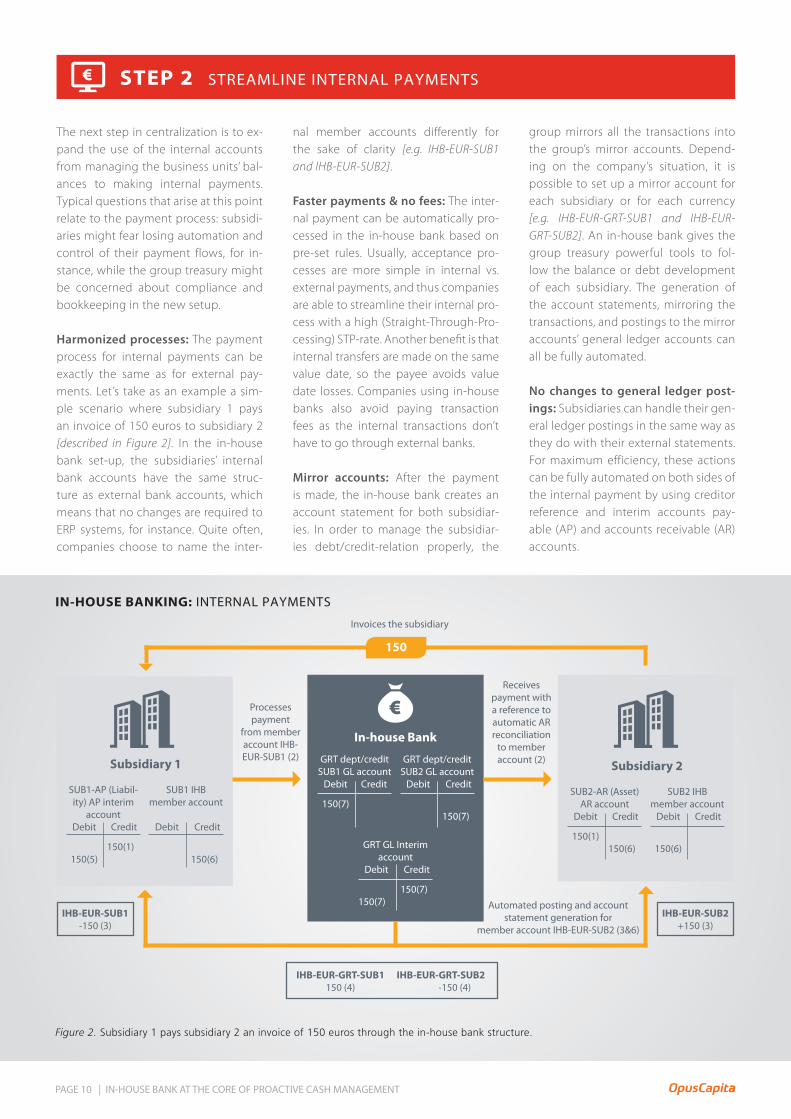

STEP 1 MANAGE CORPORATE BANK ACCOUNT STRUCTURE

The next step in centralization is to ex-pand the use of the internal accounts from managing the business units’ bal-ances to making internal payments. Typical questions that arise at this point relate to the payment process: subsidi-aries might fear losing automation and control of their payment flows, for in-stance, while the group treasury might be concerned about compliance and bookkeeping in the new setup.

Harmonized processes: The payment process for internal payments can be exactly the same as for external pay-ments. Let’s take as an example a sim-ple scenario where subsidiary 1 pays an invoice of 150 euros to subsidiary 2 [described in Figure 2]. In the in-house bank set-up, the subsidiaries’ internal bank accounts have the same struc-ture as external bank accounts, which means that no changes are required to ERP systems, for instance. Quite often, companies choose to name the inter-

nal member accounts differently for the sake of clarity [e.g. IHB-EUR-SUB1 and IHB-EUR-SUB2].

Faster payments & no fees: The inter-nal payment can be automatically pro-cessed in the in-house bank based on pre-set rules. Usually, acceptance pro-cesses are more simple in internal vs. external payments, and thus companies are able to streamline their internal pro-cess with a high (Straight-Through-Pro-cessing) STP-rate. Another benefit is that internal transfers are made on the same value date, so the payee avoids value date losses. Companies using in-house banks also avoid paying transaction fees as the internal transactions don’t have to go through external banks.

Mirror accounts: After the payment is made, the in-house bank creates an account statement for both subsidiar-ies. In order to manage the subsidiar-ies debt/credit-relation properly, the

group mirrors all the transactions into the group’s mirror accounts. Depend-ing on the company’s situation, it is possible to set up a mirror account for each subsidiary or for each currency [e.g. IHB-EUR-GRT-SUB1 and IHB-EUR-GRT-SUB2]. An in-house bank gives the group treasury powerful tools to fol-low the balance or debt development of each subsidiary. The generation of the account statements, mirroring the transactions, and postings to the mirror accounts’ general ledger accounts can all be fully automated.

No changes to general ledger post-ings: Subsidiaries can handle their gen-eral ledger postings in the same way as they do with their external statements. For maximum efficiency, these actions can be fully automated on both sides of the internal payment by using creditor reference and interim accounts pay-able (AP) and accounts receivable (AR) accounts.

PAGE 10 | IN-HOUSE BANK AT THE CORE OF PROACTIVE CASH MANAGEMENT

Figure 2. Subsidiary 1 pays subsidiary 2 an invoice of 150 euros through the in-house bank structure.

IN-HOUSE BANKING: INTERNAL PAYMENTS

In-house Bank

Subsidiary 2Subsidiary 1 GRT dept/creditSUB1 GL account Debit Credit

150(7)SUB2-AR (Asset)

AR account Debit Credit

150(1) 150(6)

SUB1-AP (Liabil-ity) AP interim

account Debit Credit

150(1) 150(5)

SUB2 IHB member account Debit Credit

150(6)

SUB1 IHB member account

Debit Credit

150(6)

GRT GL Interim account

Debit Credit

150(7)150(7)

GRT dept/creditSUB2 GL account Debit Credit

150(7)

150

Invoices the subsidiary

Receives payment with a reference to automatic AR reconciliation

to member account (2)

Processes payment

from member account IHB-EUR-SUB1 (2)

Automated posting and account statement generation for

member account IHB-EUR-SUB2 (3&6)

IHB-EUR-SUB2+150 (3)

IHB-EUR-SUB1-150 (3)

IHB-EUR-GRT-SUB1 IHB-EUR-GRT-SUB2 150 (4) -150 (4)

STEP 2 STREAMLINE INTERNAL PAYMENTS

PAGE 11 | IN-HOUSE BANK AT THE CORE OF PROACTIVE CASH MANAGEMENT

The next step to centralization is to ex-tend the in-house bank functionalities to external payments. Payments on-be-half-of (POBO) will deepen the integra-tion. They reduce the need for external accounts from the subsidiaries as all the external payments can be directed through the parent company’s account.

In the POBO model, the subsidiaries process the payment data in their sys-tems according to internally harmo-nized processes, and the group trea-sury decides on the most cost-efficient payment method and banking connec-tion. The group treasury is able to cen-tralize cash outflows, which significant-ly enhances the safety of and control over the payment process.

Let’s take a situation where a subsidiary receives an invoice of 300 euros from an external creditor [illustrated in the Figure 3]. After the invoice is processed, the subsidiary uses its internal account

[e.g. IHB-EUR-SUB1] to initiate the pay-ment. In in-house-bank settings, there are rules set by companies or currencies (or both) to automate the selection of the external account from which the pay-ment will be paid. If the currency of the payment differs from account currency, FX is managed inside the in-house bank. The information about the ultimate debt-or on the transaction data is maintained so that the external creditor will be able to see the actual payment originator and also any additional data on the payment.

Once the account statements for the group’s external bank account are re-ceived, the transactions are automatical-ly allocated in the in-house bank to the appropriate internal member accounts, and mirrored into in-house-bank mirror accounts to maintain subsidiary debt. The transactions in the in-house bank account are posted for bookkeeping just as account statement transactions from external bank accounts.

“The group treasury is able to centralize cash outflows, which significantly enhances the safety of and control over the payment process.”

STEP 3 TAKE ADVANTAGE OF PAYMENTS ON-BEHALF-OF (POBO)

Figure 3. In the POBO (payments on-behalf-of) model, a subsidiary receives an invoice, which gets paid from the group’s external bank account.

IN-HOUSE BANKING: PAYMENTS ON-BEHALF-OF (POBO)

Creditor

In-house Bank

Banks

Subsidiary GRT dept/creditSUB1 GL account Debit Credit

300(9)

SUB1-AP (Liabil-ity) AP interim

account Debit Credit

300(1) 300(7)

SUB1 IHB member account

Debit Credit

300(7)

GRT bank account GL account

Debit Credit

300(8)

GRT GL interimaccount

Debit Credit

300(8) 300(9)

300

Invoices the subsidiary

Member account switched to group’s

external bank account (3)

Processes payment

from member account IHB-EUR-SUB1 (2)

Account statement delivered for the external bank account

FIXX1234567890XX (4)

Automated allocation and posting from group’s bank account to

member account IHB-EUR-SUB1 (5&7)IHB-EUR-SUB1

-300 (5)

FIXX1234567890XX-300 (4)

IHB-EUR-GRT-SUB1300 (6)

PAGE 12 | IN-HOUSE BANK AT THE CORE OF PROACTIVE CASH MANAGEMENT

PAGE 13 | IN-HOUSE BANK AT THE CORE OF PROACTIVE CASH MANAGEMENT

Collection on-behalf-of (COBO) makes it possible for the group to reach the high-est level of independence from banks and maximize cost efficiency. Payments arriving to subsidiaries can be received through the group’s external bank ac-count if there is a way to identify which subsidiary actually owns the cash arriv-ing in the group’s account.

Let’s look at an example: In the COBO model, the subsidiary sends out an in-voice of 500 euros to their customer, who settles the payment to the group’s external bank account [as illustrated in figure 4]. In the in-house bank, the pay-ment transaction is visible in the ex-ternal bank account statement, and is automatically allocated to the original collector’s member account.

In countries where the payment dis-cipline is high, and the use of creditor

reference is the norm, COBO becomes as simple as setting up POBO. Another easy way to arrange COBO is to set up a virtual bank account structure with the external bank. In this case, the transac-tions are all routed to the top account owned by the group treasury, and the subsidiaries’ virtual bank account num-bers are used to allocate the cash ap-propriately in the in-house bank.

The centralized collection of receivables is usually the most challenging part of in-house bank implementation. The lack of good uniform practices for the remittance information on the incom-ing transactions makes it difficult to re-liably identify the original creditor and reconcile the incoming transactions. Global standards have been established for the creditor reference, but they are not widely used except in the Nordics. In the USA, lock box files are commonly

used to simplify collection. Alternative-ly, you can build your own identification mechanics. New intelligent automation technologies such as machine learning will provide new ways to automate rec-onciliation of incoming cash in interna-tional corporations.

Centralizing the collection of receiv-ables at a group level can have a for-midable impact on the working capital management of the entire organiza-tion. In most cases, it is wise to set up at least external collection accounts with zero balance structure for the sub-sidiaries. These accounts can be either owned and maintained by the group treasury – in which case all the account statement transactions are allocated to the right subsidiary – or they can be owned by the subsidiaries themselves, with agreed daily or weekly sweeps to the group treasury account.

STEP 4 REACH FURTHER WITH COLLECTION ON-BEHALF-OF (COBO)

IN-HOUSE BANKING: COLLECTIONS ON-BEHALF-OF (COBO)

Figure 4. In the COBO (Collection on-behalf-of) model, when a subsidiary sends an invoice, it gets paid to the group’s external bank account.

In-house Bank

Banks

Subsidiary GRT dept/creditSUB1 GL account Debit Credit

300(9)

SUB1-AR (rec) AR interim account

Debit Credit

500(1) 500(7)

SUB1 IHB member account Debit Credit

500(7) GRT bank account

GL account Debit Credit

500(8)

GRT GL interimaccount

Debit Credit

500(8) 500(9)

500

Subsidiary sends an invoice

Account statement delivered for the external bank account

FIXX1234567890XX (4)

Payment to GRT’sExternal account

Automated allocation and posting from group’s bank account to

member account IHB-EUR-SUB1 (5&7)IHB-EUR-SUB1

+500 (5)

FIXX1234567890XX+500 (4)

IHB-EUR-GRT-SUB1-500 (6)

Debtor

PAGE 14 | IN-HOUSE BANK AT THE CORE OF PROACTIVE CASH MANAGEMENT

An in-house bank also provides effec-tive tools for internal financing. For in-stance, short-term financing needs can easily be covered by internal account balances and credit limits. An in-house bank simplifies the otherwise complex process of lending and depositing cash between parent company and its sub-sidiaries – no more arranging and man-aging loan agreements for each debt.

When the margins, interest rates, and credit limits have been agreed on in the in-house bank account contract, there is no need to create separate loan agreements. Nowadays, organizations are subject to manifold transfer pricing

regulations to ensure profits are treat-ed using fair tax principles. An in-house bank brings transparency and automa-tion to contracts, and helps to docu-ment and control the rules of transfer pricing.

Management of internal financing in the in-house bank also eases book-keeping procedures and speeds up the month-end reconciliation activ-ities. Calculating interest is a basic functionality of an in-house bank, and it eliminates the need to process the accumulated interest for each internal short-term loan. Instead, the interest is simply calculated and booked to the

internal account at the end of each month. Centralizing internal financing with an in-house bank provides an easy way to document the processes for regulatory compliance.

From a group perspective, the in-house bank setup provides visibility of the aggregated cash of the entire organi-zation, eliminating the all too common situation where one subsidiary is forced to use its account credit limits while an-other subsidiary has surplus cash lying idle in its account. An in-house bank decreases the need for lending, as the net cash of the whole group can be used for payments and investments.

“An in-house bank decreases the need for lending, as the net cash of the whole group can be used for payments and investments. ”

“Centralizing the collection of receivables at a group level can have a formidable impact on the working capital management of the entire organization. ”

STEP 5 BENEFIT OF INTERNAL FINANCING

PAGE 15 | IN-HOUSE BANK AT THE CORE OF PROACTIVE CASH MANAGEMENT

CHAPTER 4

Setting up an in-house bank has both operational and strategic benefits. In today’s complex business environment, the strategic benefits that are gained from centralized management of cash flows, giving a full transparency and visibility over group-level liquidity, are starting to overtake the operational benefits that result from cost and process efficiency.

KEY BENEFITS OF IN-HOUSE BANKING

Engage inproactive cash

management

THE EFFECT OF CENTRALIZING CASH FLOWS

Figure 5. An example of the effect of centralizing cash flows on working capital. The illustration describes a company making EUR 300 million in revenue, “as is” and “improved”. The figures are based on several OpusCapita customer cases.

PAGE 16 | IN-HOUSE BANK AT THE CORE OF PROACTIVE CASH MANAGEMENT

PREVENT PAYMENT MISUSE: Fraud prevention is high on the agenda of many group treasurers as international cybercriminals are increasingly targeting the payment processes of companies. Centralization of outgoing payments and harmonization of all related process helps to prevent payment misuse, and

gives the group treasury the right van-tage point to keep a close eye on the actual cash outflows of the organization.

LOWER RISKS: The in-house bank structure can replace a myriad of exter-nal bank accounts and banking connec-tions, even up to the point where there

is no local access to external banks. The risks related to data security and han-dling of payment files are mitigated when treasury is in control. The auto-mated internal payment management adds to the security, as does the internal compliance enforced through a unified payment processes.

AS IS IMPROVED

Unit UnitUnit UnitUnit UnitUnit Unit

GROUP 1GROUP 1

Working capital EUR 30 million (10% of revenue)

Working capital EUR 3 million (1% of revenue)

Group Treasury

nn Decentralized corporate structurenn Plenty of subsidiariesnn Local cash managementnn Local business processesnn The lack of integration

leads to suboptimization

nn Centralized cash managementnn Full visibility and control

of all cash flows in all subsidiariesnn Option to optimize the

working capitalnn The freed working capital

creates the opportunity to invest

€Xm €Xm €Xm €Xm

Investment

Group Treasury

Report and forecast once a week (spreadsheet)

€Xm €Xm €Xm €Xm

MORE EFFICIENT CASH FLOWS: A well set-up in-house bank will improve the efficiency of both internal and ex-ternal cash flows. This, in turn, will en-able optimal liquidity management and better cash forecasting. Reliable cash forecasts are a powerful tool for group treasuries who are looking to get the most out of their working capital.

BETTER BUSINESS DECISION-MAK-ING: With the in-house bank structures for concentrating external payments

and internal financing, the treasury has the control needed to make the most of the group’s cash assets. Clear visi-bility of cash flows supports not only financial but also business operations and decision-making. Having direct in-put from each subsidiary in the group allows the management to evaluate the performance of each unit individ-ually, and to adjust development initia-tives or budgeting accordingly.

FREE UP WORKING CAPITAL: Cor-

porations are usually surprised when they realize how much cash is trapped in local functions and bank accounts in a decentralized financial and corporate structure. Our experience has shown that by increasing visibility and con-trol, the share of working capital tied to operations can be reduced from 10% to approximately 1% of net sales [as illustrated in figure 5]. The liquidity the company needs for investments may have been hiding in the non-transpar-ent processes all along.

BENEFIT #1 GAIN VISIBILITY AND CONTROL OVER CASH

BENEFIT #2 DETECT AND PREVENT FRAUD

PAGE 17 | IN-HOUSE BANK AT THE CORE OF PROACTIVE CASH MANAGEMENT

INDEPENDENCE: With in-house bank services available to subsidiaries, the group treasury can choose a few key banking partners to provide the need-ed external financial services. As the structure is maintained by the treasury, the group is free to change banks if they want to. If the solution is built in a modern multi-banking environment – utilizing for instance integrated single-point-of-entry solution to the SWIFT Network – the company is, technically, independent of banks.

LEVERAGE: When banking relation-ship management is centralized to the treasury, it will add to its negotiation

power. The aggregated payment vol-umes and currency balances improve the corporation’s bargaining position over the pricing with the commercial banks. On the other hand, even short-term investments of assets can be ne-gotiated profitably using economies of scale.

COST REDUCTION: In addition, mak-ing extensive use of the on-behalf-of functionalities and internal payment structure of the in-house bank, exter-nal banking costs can be reduced con-siderably, and, furthermore, value day losses can be avoided.

Centralizing cash management in the group treasury opens up the possibili-ty to further boost and streamline the cash flow processes with automation.

AUTOMATE WORKFLOWS & INTEREST CALCULATIONS: For instance, replac-ing subsidiaries’ multiple external bank accounts with an internal account structure tailored to the group’s needs allows for fully automated cash flows between subsidiaries, decreasing the

work involved in internal payment management. If the subsidiaries short-term financing needs are covered with credit limits within the in-house bank, interest calculations can also be auto-mated, and the management of trans-fer pricing documentation, for instance, can be substantially simplified.

FREE UP STAFF TO DO MORE VALUE- ADDING WORK: With an in-house bank, all the posting and bookkeep-

ing for the subsidiaries’ in-house bank accounts can be automated. Even in a multi-ERP and multi-bank environ-ment, the group treasury can automate balance reporting for up-to-date infor-mation. Removing manual steps from the financial processes not only speeds up the month-end activities and frees up the human resources for more val-ue-adding tasks, but also helps to avoid unwanted mistakes that are laborious to correct.

“If the subsidiaries short-term financing needs are covered with credit limits within the in-house bank, interest calculations can also be automated ”

BENEFIT #3 STREAMLINE WITH AUTOMATION

BENEFIT #4 INCREASE INDEPENDENCY FROM BANKS

THE BENEFITS OF IN-HOUSE BANKING

Figure 6. The features and benefits of a modern in-house bank set-up.

PAGE 18 | IN-HOUSE BANK AT THE CORE OF PROACTIVE CASH MANAGEMENT

HEDGE FX RISK EFFICIENTLY: With efficient and reliable cash forecasts, the group treasury can also take responsi-bility for currency risk management. A clear overview of the company’s for-eign exchange exposure and currency position enables group treasury to take the necessary actions to hedge the FX risk at a group level. The in-house

bank accounts can be multi-currency accounts. This eliminates the need for separate currency accounts in the sub-sidiaries. Internal multi-currency pay-ments also means savings in currency exchange costs.

REMOVE OVERLAPPING WORK: The group-level oversight removes over-

lapping work as the currency risk man-agement for a single currency might have been previously done in several subsidiaries. In addition, group trea-suries with the aggregated transaction volumes are usually in a better position to negotiate with banks over the hedg-ing prices than the individual subsidi-aries are.

Features Benefits

SWIFT-ready cloud solution powered by thousands of bank connections and ERP format integrations

Zero Balance Accounts

Automated Balance

Reconciliation

Interest Calculation

Internal Financing

On-Behalf-Of POBO/COBO

Internal & External

Payments

Visibility over both internal and external cash flows

Centralized control over financing, investments, FX risk and hedging

Harmonized payment process for internal, external and on-behalf-of payments

Automated bookkeeping and month end process activities

Lower costs from reduced number of external banking partners and transaction volumes

BENEFIT #5 IMPROVE CURRENCY RISK MANAGEMENT

PAGE 19 | IN-HOUSE BANK AT THE CORE OF PROACTIVE CASH MANAGEMENT

CHAPTER 5

For a long time, doing more with less has been a key driver for group treasurers and cash managers. Their focus has been on examining and optimizing corporations’ financial processes. In the coming years, international corporations’ finance organizations will need to tackle the challenge of supporting the company operations and growth strategy, while bringing increasingly insightful in-depth information and forecasts to the table. All this with ever shrinking budgets, and limited resources.

SUMMARY Questions to ask yourself

PAGE 20 | IN-HOUSE BANK AT THE CORE OF PROACTIVE CASH MANAGEMENT

“The difference between a company that is at the median level – in terms of cash and working capital management – and a top performer can be surprisingly large. This difference may even decide the future success of the companies.”

Questions to ask

Given these challenges, the difference between a company that is at the me-dian level – in terms of cash and work-ing capital management – and a top performer can be surprisingly large.

This difference may even decide the fu-ture success of the companies.

To secure a place among the successful companies, the group treasury should

first take a comprehensive look at the organization’s finance, risk and cash man-agement, and payments processes.

What are the effects of the existing structure on the overall financial performance of the corporation?

How are the financing needs of the subsidiaries met? What happens to the cash surplus of the units in different countries?

Who is in charge of preventing fraud and cybercrime, and eliminating FX risk?

Do the subsidiaries/units actually need relationships with local banks?

Are internal and external payment processes harmonized? Are they cost-efficient?

And, most importantly, what is needed to have the level of visibility and control that are needed to optimize working capital and achieve a new level of cash management?

Contact us to discuss your organization’s situation, and to find out how OpusCapita'scash management solutions can help you to take the next steps. www.opuscapita.com/contact-sales

Learn more about proactive cash management at www.opuscapita.com/solutions/cash-management

JAAKKO KILPINEN has over 15 years of experience in corporate cash management and has deep expertise in cash forecasting, netting, and in-house banking. Jaakko has previously held e.g. a position as Group Treasurer in a publicly listed Finnish company.

Currently Jaakko works as a Solution Manager at OpusCapita.

CONTAC T [email protected]

JUKKA SALLINEN is a cash management domain expert with a strong hands on background from international and complex payment factory and SWIFT projects. Previously Jukka has been working in various R&D roles, focusing on bank and ERP integrations and security topics.

Currently Jukka is the Head of Cash Management at OpusCapita.

CONTAC T [email protected]

Writers

OpusCapita helps organizations sell, buy and pay more effectively by providing them with extended purchase-to-pay and cash management solutions. With €100 Billion in

payments processed annually by over 800 customers across more than 100 countries, we have created a global ecosystem where buyers, suppliers, banks and other parties

connect, transact and grow. Our secure, cloud-based solution enables Treasury and Finance professionals to harmonize global processes, centralize Treasury management, and

reduce complexity. This brings full visibility to cash positions while reducing the risk of fraud. To learn more about how proactive cash management can help your company,

please visit www.opuscapita.com/solutions/cash-management

Founded in 1984, OpusCapita is headquartered in Helsinki, Finland.