spillovers from china - quarterly bulletin - bank of england

TRANSCRIPT

Quarterly Bulletin2018 Q2

© Bank of England 2018ISSN 2399-4568

Topical articleFrom the Middle Kingdom to the United Kingdom: spillovers from China

Topical articles Spillovers from China 1

From the Middle Kingdom to the United Kingdom: spillovers from ChinaBy Robert Gilhooly, Jen Han, Simon Lloyd, Niamh Reynolds and David Young of the Bank’s International Directorate.(1)

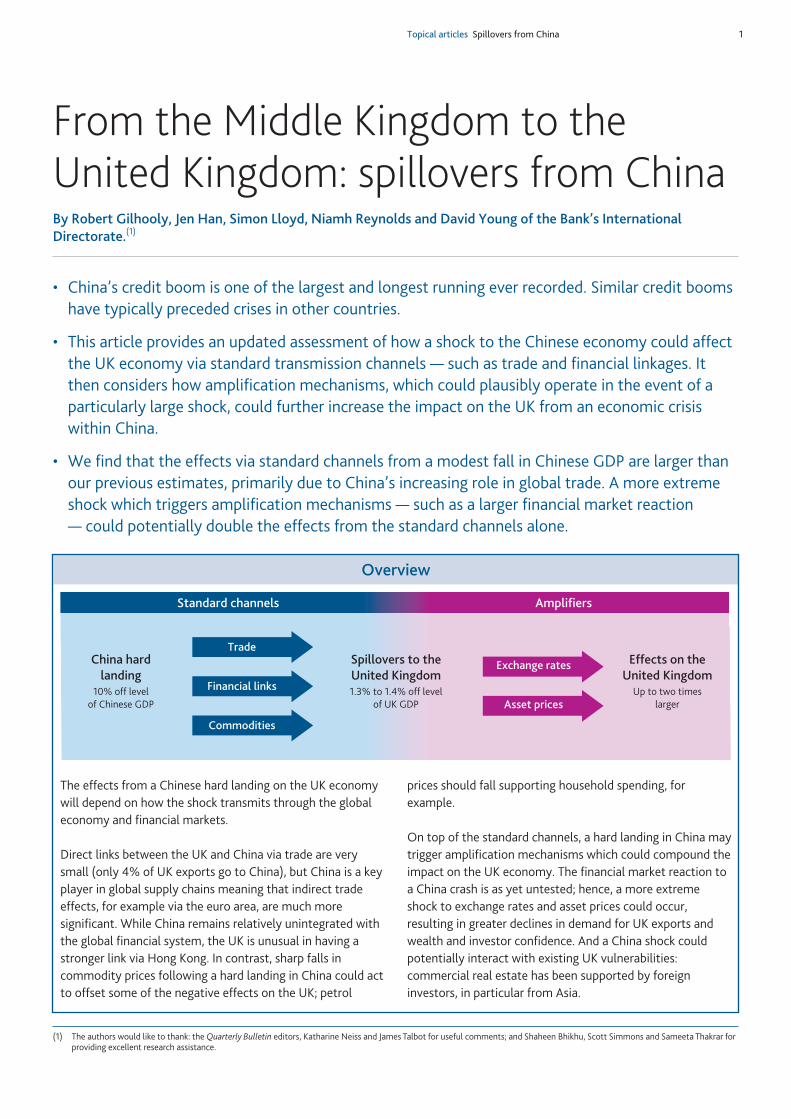

• China’screditboomisoneofthelargestandlongestrunningeverrecorded.Similarcreditboomshavetypicallyprecededcrisesinothercountries.

• ThisarticleprovidesanupdatedassessmentofhowashocktotheChineseeconomycouldaffecttheUKeconomyviastandardtransmissionchannels—suchastradeandfinanciallinkages.Itthenconsidershowamplificationmechanisms,whichcouldplausiblyoperateintheeventofaparticularlylargeshock,couldfurtherincreasetheimpactontheUKfromaneconomiccrisiswithinChina.

• WefindthattheeffectsviastandardchannelsfromamodestfallinChineseGDParelargerthanourpreviousestimates,primarilyduetoChina’sincreasingroleinglobaltrade.Amoreextremeshockwhichtriggersamplificationmechanisms—suchasalargerfinancialmarketreaction—couldpotentiallydoubletheeffectsfromthestandardchannelsalone.

Overview

TheeffectsfromaChinesehardlandingontheUKeconomywilldependonhowtheshocktransmitsthroughtheglobaleconomyandfinancialmarkets.

DirectlinksbetweentheUKandChinaviatradeareverysmall(only4%ofUKexportsgotoChina),butChinaisakeyplayeringlobalsupplychainsmeaningthatindirecttradeeffects,forexampleviatheeuroarea,aremuchmoresignificant.WhileChinaremainsrelativelyunintegratedwiththeglobalfinancialsystem,theUKisunusualinhavingastrongerlinkviaHongKong.Incontrast,sharpfallsincommoditypricesfollowingahardlandinginChinacouldacttooffsetsomeofthenegativeeffectsontheUK;petrol

pricesshouldfallsupportinghouseholdspending,forexample.

Ontopofthestandardchannels,ahardlandinginChinamaytriggeramplificationmechanismswhichcouldcompoundtheimpactontheUKeconomy.ThefinancialmarketreactiontoaChinacrashisasyetuntested;hence,amoreextremeshocktoexchangeratesandassetpricescouldoccur,resultingingreaterdeclinesindemandforUKexportsandwealthandinvestorconfidence.AndaChinashockcouldpotentiallyinteractwithexistingUKvulnerabilities:commercialrealestatehasbeensupportedbyforeigninvestors,inparticularfromAsia.

(1) Theauthorswouldliketothank:theQuarterly Bulletineditors,KatharineNeissandJamesTalbotforusefulcomments;andShaheenBhikhu,ScottSimmonsandSameetaThakrarforprovidingexcellentresearchassistance.

AmplifiersStandard channels

Trade

Financial links

Commodities

China hardlanding

10% off levelof Chinese GDP

Up to two timeslargerAsset prices

Exchange rates Effects on theUnited Kingdom

1.3% to 1.4% off levelof UK GDP

Spillovers to theUnited Kingdom

Quarterly Bulletin 2018 Q2 2

Introduction

China’seconomicgrowthandintegrationintotheglobaleconomyhasbeenparticularlyrapid.Chinaaccountedforjust2%ofglobalGDPin1990,butnowmakesup15%ofglobalGDP(in2017USdollarterms).FollowingaccessiontotheWorldTradeOrganisation(WTO)in2001,Chinahasbecometheworld’slargestexporterofgoods.AndChinaisamajorproducerandconsumerofcommodities.

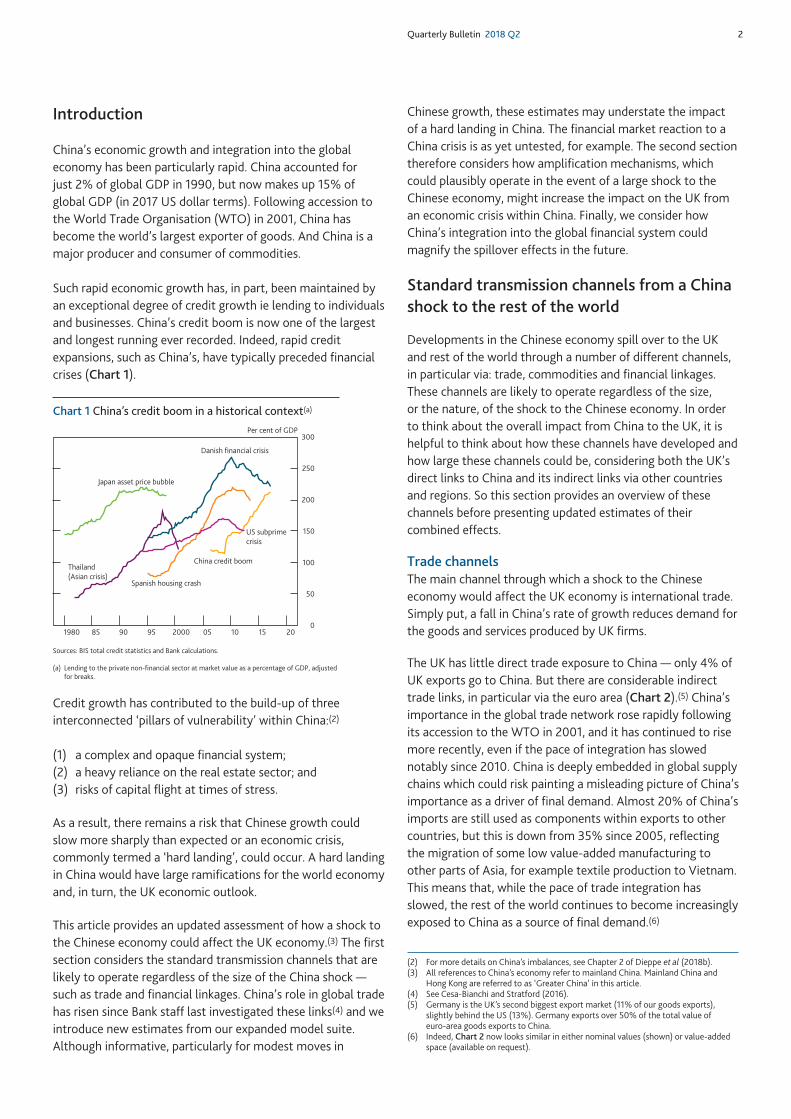

Suchrapideconomicgrowthhas,inpart,beenmaintainedbyanexceptionaldegreeofcreditgrowthielendingtoindividualsandbusinesses.China’screditboomisnowoneofthelargestandlongestrunningeverrecorded.Indeed,rapidcreditexpansions,suchasChina’s,havetypicallyprecededfinancialcrises(Chart 1).

Creditgrowthhascontributedtothebuild-upofthreeinterconnected‘pillarsofvulnerability’withinChina:(2)

(1) acomplexandopaquefinancialsystem;(2) aheavyrelianceontherealestatesector;and(3) risksofcapitalflightattimesofstress.

Asaresult,thereremainsariskthatChinesegrowthcouldslowmoresharplythanexpectedoraneconomiccrisis,commonlytermeda‘hardlanding’,couldoccur.AhardlandinginChinawouldhavelargeramificationsfortheworldeconomyand,inturn,theUKeconomicoutlook.

ThisarticleprovidesanupdatedassessmentofhowashocktotheChineseeconomycouldaffecttheUKeconomy.(3)ThefirstsectionconsidersthestandardtransmissionchannelsthatarelikelytooperateregardlessofthesizeoftheChinashock—suchastradeandfinanciallinkages.China’sroleinglobaltradehasrisensinceBankstafflastinvestigatedtheselinks(4)andweintroducenewestimatesfromourexpandedmodelsuite.Althoughinformative,particularlyformodestmovesin

Chinesegrowth,theseestimatesmayunderstatetheimpactofahardlandinginChina.ThefinancialmarketreactiontoaChinacrisisisasyetuntested,forexample.Thesecondsectionthereforeconsidershowamplificationmechanisms,whichcouldplausiblyoperateintheeventofalargeshocktotheChineseeconomy,mightincreasetheimpactontheUKfromaneconomiccrisiswithinChina.Finally,weconsiderhowChina’sintegrationintotheglobalfinancialsystemcouldmagnifythespillovereffectsinthefuture.

Standard transmission channels from a China shock to the rest of the world

DevelopmentsintheChineseeconomyspillovertotheUKandrestoftheworldthroughanumberofdifferentchannels,inparticularvia:trade,commoditiesandfinanciallinkages.Thesechannelsarelikelytooperateregardlessofthesize,orthenature,oftheshocktotheChineseeconomy.InordertothinkabouttheoverallimpactfromChinatotheUK,itishelpfultothinkabouthowthesechannelshavedevelopedandhowlargethesechannelscouldbe,consideringboththeUK’sdirectlinkstoChinaanditsindirectlinksviaothercountriesandregions.Sothissectionprovidesanoverviewofthesechannelsbeforepresentingupdatedestimatesoftheircombinedeffects.

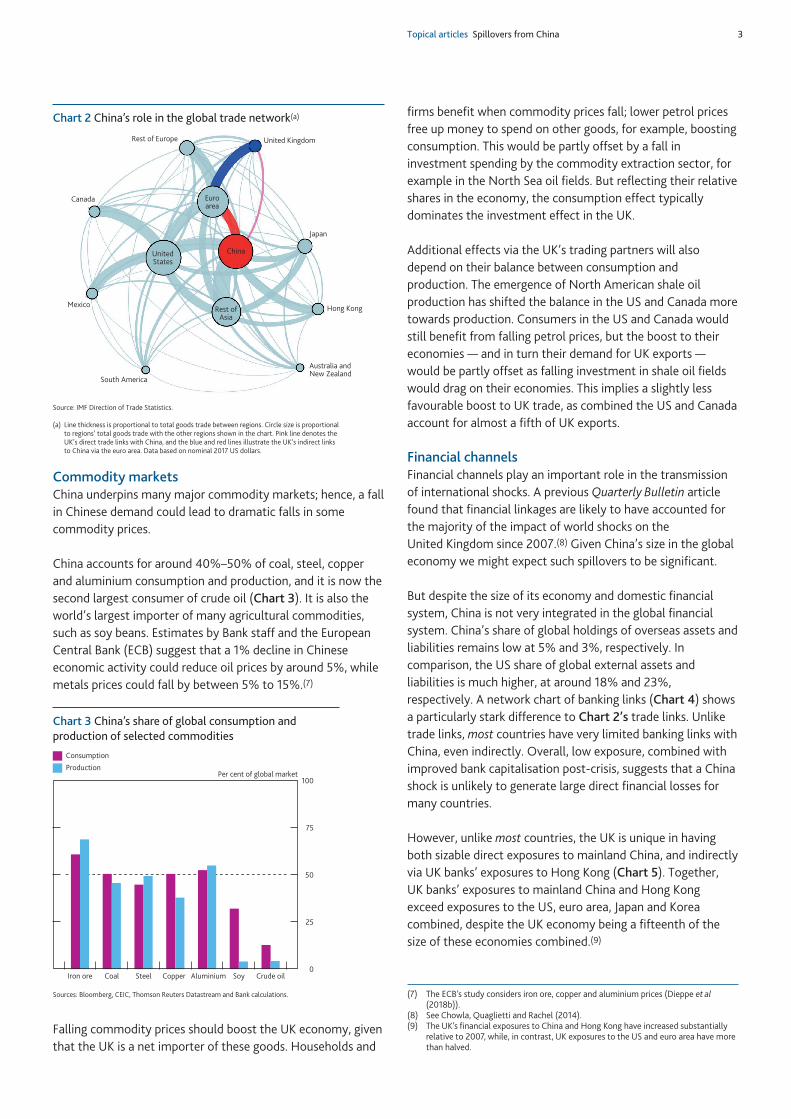

Trade channelsThemainchannelthroughwhichashocktotheChineseeconomywouldaffecttheUKeconomyisinternationaltrade.Simplyput,afallinChina’srateofgrowthreducesdemandforthegoodsandservicesproducedbyUKfirms.

TheUKhaslittledirecttradeexposuretoChina—only4%ofUKexportsgotoChina.Butthereareconsiderableindirecttradelinks,inparticularviatheeuroarea(Chart 2).(5)China’simportanceintheglobaltradenetworkroserapidlyfollowingitsaccessiontotheWTOin2001,andithascontinuedtorisemorerecently,evenifthepaceofintegrationhasslowednotablysince2010.ChinaisdeeplyembeddedinglobalsupplychainswhichcouldriskpaintingamisleadingpictureofChina’simportanceasadriveroffinaldemand.Almost20%ofChina’simportsarestillusedascomponentswithinexportstoothercountries,butthisisdownfrom35%since2005,reflectingthemigrationofsomelowvalue-addedmanufacturingtootherpartsofAsia,forexampletextileproductiontoVietnam.Thismeansthat,whilethepaceoftradeintegrationhasslowed,therestoftheworldcontinuestobecomeincreasinglyexposedtoChinaasasourceoffinaldemand.(6)

0

50

100

150

200

250

300

1980 85 90 95 2000 05 10 15 20

Per cent of GDP

Japan asset price bubble

Danish financial crisis

China credit boom

US subprimecrisis

Spanish housing crash

Thailand(Asian crisis)

Chart 1 China’s credit boom in a historical context(a)

Sources:BIStotalcreditstatisticsandBankcalculations.

(a) Lendingtotheprivatenon-financialsectoratmarketvalueasapercentageofGDP,adjustedforbreaks.

(2) FormoredetailsonChina’simbalances,seeChapter2ofDieppeet al(2018b).(3) AllreferencestoChina’seconomyrefertomainlandChina.MainlandChinaand

HongKongarereferredtoas‘GreaterChina’inthisarticle.(4) SeeCesa-BianchiandStratford(2016).(5) GermanyistheUK’ssecondbiggestexportmarket(11%ofourgoodsexports),

slightlybehindtheUS(13%).Germanyexportsover50%ofthetotalvalueofeuro-areagoodsexportstoChina.

(6) Indeed,Chart 2nowlookssimilarineithernominalvalues(shown)orvalue-addedspace(availableonrequest).

Topical articles Spillovers from China 3

Commodity marketsChinaunderpinsmanymajorcommoditymarkets;hence,afallinChinesedemandcouldleadtodramaticfallsinsomecommodityprices.

Chinaaccountsforaround40%–50%ofcoal,steel,copperandaluminiumconsumptionandproduction,anditisnowthesecondlargestconsumerofcrudeoil(Chart 3).Itisalsotheworld’slargestimporterofmanyagriculturalcommodities,suchassoybeans.EstimatesbyBankstaffandtheEuropeanCentralBank(ECB)suggestthata1%declineinChineseeconomicactivitycouldreduceoilpricesbyaround5%,whilemetalspricescouldfallbybetween5%to15%.(7)

FallingcommoditypricesshouldboosttheUKeconomy,giventhattheUKisanetimporterofthesegoods.Householdsand

firmsbenefitwhencommoditypricesfall;lowerpetrolpricesfreeupmoneytospendonothergoods,forexample,boostingconsumption.Thiswouldbepartlyoffsetbyafallininvestmentspendingbythecommodityextractionsector,forexampleintheNorthSeaoilfields.Butreflectingtheirrelativesharesintheeconomy,theconsumptioneffecttypicallydominatestheinvestmenteffectintheUK.

AdditionaleffectsviatheUK’stradingpartnerswillalsodependontheirbalancebetweenconsumptionandproduction.TheemergenceofNorthAmericanshaleoilproductionhasshiftedthebalanceintheUSandCanadamoretowardsproduction.ConsumersintheUSandCanadawouldstillbenefitfromfallingpetrolprices,buttheboosttotheireconomies—andinturntheirdemandforUKexports—wouldbepartlyoffsetasfallinginvestmentinshaleoilfieldswoulddragontheireconomies.ThisimpliesaslightlylessfavourableboosttoUKtrade,ascombinedtheUSandCanadaaccountforalmostafifthofUKexports.

Financial channelsFinancialchannelsplayanimportantroleinthetransmissionofinternationalshocks.ApreviousQuarterly BulletinarticlefoundthatfinanciallinkagesarelikelytohaveaccountedforthemajorityoftheimpactofworldshocksontheUnitedKingdomsince2007.(8)GivenChina’ssizeintheglobaleconomywemightexpectsuchspilloverstobesignificant.

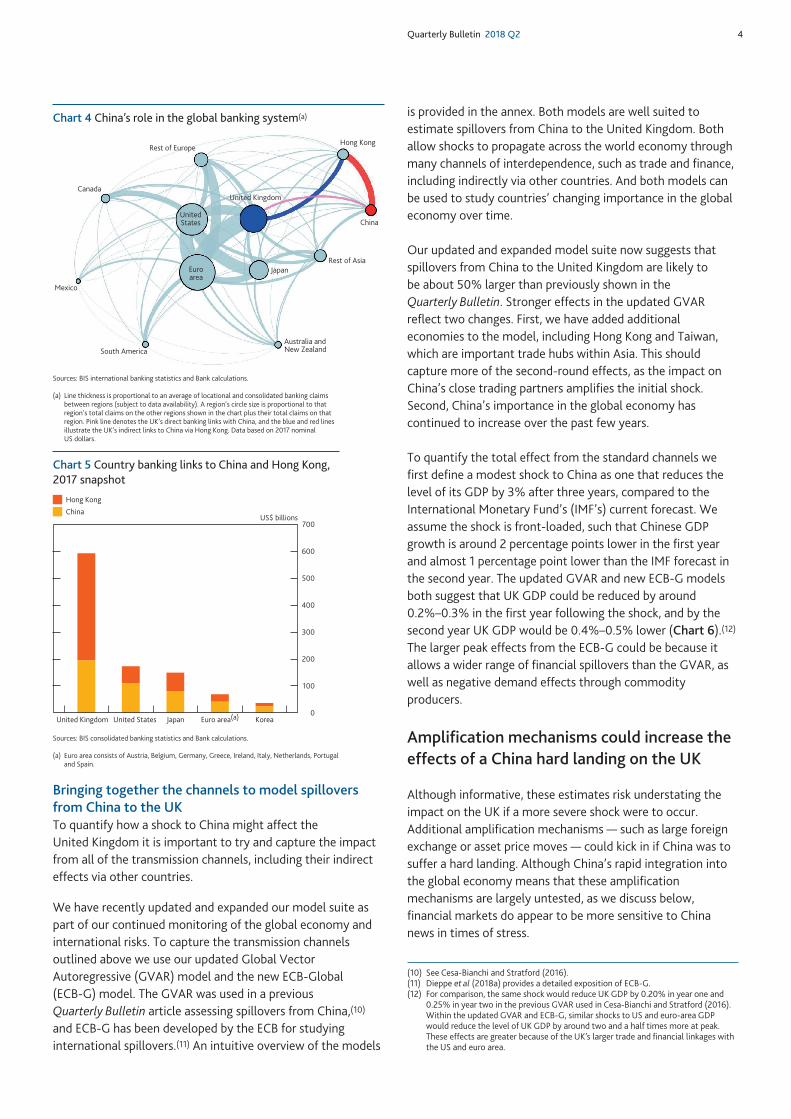

Butdespitethesizeofitseconomyanddomesticfinancialsystem,Chinaisnotveryintegratedintheglobalfinancialsystem.China’sshareofglobalholdingsofoverseasassetsandliabilitiesremainslowat5%and3%,respectively.Incomparison,theUSshareofglobalexternalassetsandliabilitiesismuchhigher,ataround18%and23%,respectively.Anetworkchartofbankinglinks(Chart 4)showsaparticularlystarkdifferencetoChart 2’stradelinks.Unliketradelinks,mostcountrieshaveverylimitedbankinglinkswithChina,evenindirectly.Overall,lowexposure,combinedwithimprovedbankcapitalisationpost-crisis,suggeststhataChinashockisunlikelytogeneratelargedirectfinanciallossesformanycountries.

However,unlikemostcountries,theUKisuniqueinhavingbothsizabledirectexposurestomainlandChina,andindirectlyviaUKbanks’exposurestoHongKong(Chart 5).Together,UKbanks’exposurestomainlandChinaandHongKongexceedexposurestotheUS,euroarea,JapanandKoreacombined,despitetheUKeconomybeingafifteenthofthesizeoftheseeconomiescombined.(9)

Rest of Europe United Kingdom

ChinaUnitedStates

Rest ofAsia

Australia andNew Zealand

Hong Kong

Japan

Canada

Mexico

South America

Euroarea

Chart 2 China’s role in the global trade network(a)

Source:IMFDirectionofTradeStatistics.

(a) Linethicknessisproportionaltototalgoodstradebetweenregions.Circlesizeisproportionaltoregions’totalgoodstradewiththeotherregionsshowninthechart.PinklinedenotestheUK’sdirecttradelinkswithChina,andtheblueandredlinesillustratetheUK’sindirectlinkstoChinaviatheeuroarea.Databasedonnominal2017USdollars.

(7) TheECB’sstudyconsidersironore,copperandaluminiumprices(Dieppeet al(2018b)).

(8) SeeChowla,QuagliettiandRachel(2014).(9) TheUK’sfinancialexposurestoChinaandHongKonghaveincreasedsubstantially

relativeto2007,while,incontrast,UKexposurestotheUSandeuroareahavemorethanhalved.

0

25

50

75

100

Iron ore Coal Steel Copper Aluminium Soy Crude oil

Per cent of global marketProduction

Consumption

Chart 3 China’s share of global consumption and production of selected commodities

Sources:Bloomberg,CEIC,ThomsonReutersDatastreamandBankcalculations.

Quarterly Bulletin 2018 Q2 4

Bringing together the channels to model spillovers from China to the UKToquantifyhowashocktoChinamightaffecttheUnitedKingdomitisimportanttotryandcapturetheimpactfromallofthetransmissionchannels,includingtheirindirecteffectsviaothercountries.

Wehaverecentlyupdatedandexpandedourmodelsuiteaspartofourcontinuedmonitoringoftheglobaleconomyandinternationalrisks.TocapturethetransmissionchannelsoutlinedaboveweuseourupdatedGlobalVectorAutoregressive(GVAR)modelandthenewECB-Global(ECB-G)model.TheGVARwasusedinapreviousQuarterly BulletinarticleassessingspilloversfromChina,(10)andECB-GhasbeendevelopedbytheECBforstudyinginternationalspillovers.(11)Anintuitiveoverviewofthemodels

isprovidedintheannex.BothmodelsarewellsuitedtoestimatespilloversfromChinatotheUnitedKingdom.Bothallowshockstopropagateacrosstheworldeconomythroughmanychannelsofinterdependence,suchastradeandfinance,includingindirectlyviaothercountries.Andbothmodelscanbeusedtostudycountries’changingimportanceintheglobaleconomyovertime.

OurupdatedandexpandedmodelsuitenowsuggeststhatspilloversfromChinatotheUnitedKingdomarelikelytobeabout50%largerthanpreviouslyshownintheQuarterly Bulletin.StrongereffectsintheupdatedGVARreflecttwochanges.First,wehaveaddedadditionaleconomiestothemodel,includingHongKongandTaiwan,whichareimportanttradehubswithinAsia.Thisshouldcapturemoreofthesecond-roundeffects,astheimpactonChina’sclosetradingpartnersamplifiestheinitialshock.Second,China’simportanceintheglobaleconomyhascontinuedtoincreaseoverthepastfewyears.

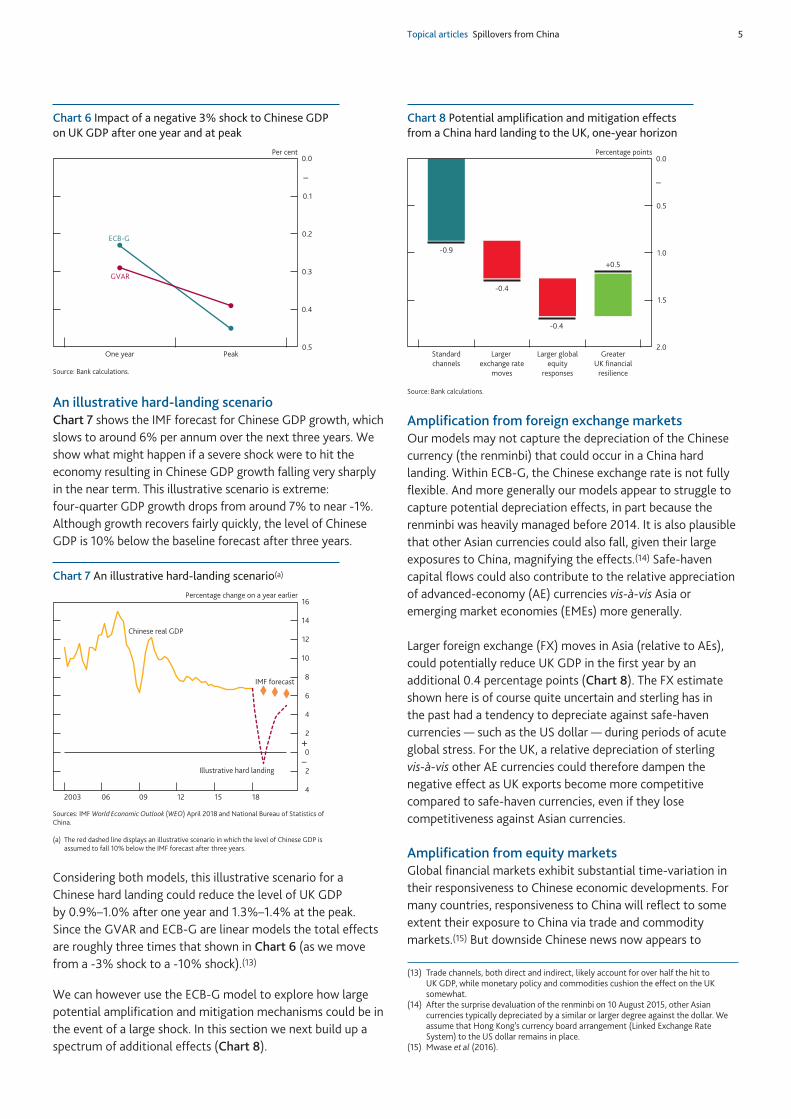

ToquantifythetotaleffectfromthestandardchannelswefirstdefineamodestshocktoChinaasonethatreducesthelevelofitsGDPby3%afterthreeyears,comparedtotheInternationalMonetaryFund’s(IMF’s)currentforecast.Weassumetheshockisfront-loaded,suchthatChineseGDPgrowthisaround2percentagepointslowerinthefirstyearandalmost1percentagepointlowerthantheIMFforecastinthesecondyear.TheupdatedGVARandnewECB-GmodelsbothsuggestthatUKGDPcouldbereducedbyaround0.2%–0.3%inthefirstyearfollowingtheshock,andbythesecondyearUKGDPwouldbe0.4%–0.5%lower(Chart 6).(12)ThelargerpeakeffectsfromtheECB-GcouldbebecauseitallowsawiderrangeoffinancialspilloversthantheGVAR,aswellasnegativedemandeffectsthroughcommodityproducers.

Amplification mechanisms could increase the effects of a China hard landing on the UK

Althoughinformative,theseestimatesriskunderstatingtheimpactontheUKifamoresevereshockweretooccur.Additionalamplificationmechanisms—suchaslargeforeignexchangeorassetpricemoves—couldkickinifChinawastosufferahardlanding.AlthoughChina’srapidintegrationintotheglobaleconomymeansthattheseamplificationmechanismsarelargelyuntested,aswediscussbelow,financialmarketsdoappeartobemoresensitivetoChinanewsintimesofstress.

UnitedStates

Rest of EuropeHong Kong

China

Rest of AsiaJapanEuro

areaMexico

CanadaUnited Kingdom

Australia andNew Zealand South America

Chart 4 China’s role in the global banking system(a)

Sources:BISinternationalbankingstatisticsandBankcalculations.

(a) Linethicknessisproportionaltoanaverageoflocationalandconsolidatedbankingclaimsbetweenregions(subjecttodataavailability).Aregion’scirclesizeisproportionaltothatregion’stotalclaimsontheotherregionsshowninthechartplustheirtotalclaimsonthatregion.PinklinedenotestheUK’sdirectbankinglinkswithChina,andtheblueandredlinesillustratetheUK’sindirectlinkstoChinaviaHongKong.Databasedon2017nominalUSdollars.

0

100

200

300

400

500

600

700

United Kingdom United States Japan Euro area(a) Korea

US$ billions

Hong Kong

China

Chart 5 Country banking links to China and Hong Kong, 2017 snapshot

Sources:BISconsolidatedbankingstatisticsandBankcalculations.

(a) EuroareaconsistsofAustria,Belgium,Germany,Greece,Ireland,Italy,Netherlands,PortugalandSpain.

(10) SeeCesa-BianchiandStratford(2016).(11) Dieppeet al(2018a)providesadetailedexpositionofECB-G.(12) Forcomparison,thesameshockwouldreduceUKGDPby0.20%inyearoneand

0.25%inyeartwointhepreviousGVARusedinCesa-BianchiandStratford(2016).WithintheupdatedGVARandECB-G,similarshockstoUSandeuro-areaGDPwouldreducethelevelofUKGDPbyaroundtwoandahalftimesmoreatpeak.TheseeffectsaregreaterbecauseoftheUK’slargertradeandfinanciallinkageswiththeUSandeuroarea.

Topical articles Spillovers from China 5

An illustrative hard-landing scenarioChart 7showstheIMFforecastforChineseGDPgrowth,whichslowstoaround6%perannumoverthenextthreeyears.WeshowwhatmighthappenifasevereshockweretohittheeconomyresultinginChineseGDPgrowthfallingverysharplyinthenearterm.Thisillustrativescenarioisextreme:four-quarterGDPgrowthdropsfromaround7%tonear-1%.Althoughgrowthrecoversfairlyquickly,thelevelofChineseGDPis10%belowthebaselineforecastafterthreeyears.

Consideringbothmodels,thisillustrativescenarioforaChinesehardlandingcouldreducethelevelofUKGDPby0.9%–1.0%afteroneyearand1.3%–1.4%atthepeak.SincetheGVARandECB-GarelinearmodelsthetotaleffectsareroughlythreetimesthatshowninChart 6(aswemovefroma-3%shocktoa-10%shock).(13)

WecanhoweverusetheECB-Gmodeltoexplorehowlargepotentialamplificationandmitigationmechanismscouldbeintheeventofalargeshock.Inthissectionwenextbuildupaspectrumofadditionaleffects(Chart 8).

Amplification from foreign exchange marketsOurmodelsmaynotcapturethedepreciationoftheChinesecurrency(therenminbi)thatcouldoccurinaChinahardlanding.WithinECB-G,theChineseexchangerateisnotfullyflexible.Andmoregenerallyourmodelsappeartostruggletocapturepotentialdepreciationeffects,inpartbecausetherenminbiwasheavilymanagedbefore2014.ItisalsoplausiblethatotherAsiancurrenciescouldalsofall,giventheirlargeexposurestoChina,magnifyingtheeffects.(14)Safe-havencapitalflowscouldalsocontributetotherelativeappreciationofadvanced-economy(AE)currenciesvis-à-visAsiaoremergingmarketeconomies(EMEs)moregenerally.

Largerforeignexchange(FX)movesinAsia(relativetoAEs),couldpotentiallyreduceUKGDPinthefirstyearbyanadditional0.4percentagepoints(Chart 8).TheFXestimateshownhereisofcoursequiteuncertainandsterlinghasinthepasthadatendencytodepreciateagainstsafe-havencurrencies—suchastheUSdollar—duringperiodsofacuteglobalstress.FortheUK,arelativedepreciationofsterlingvis-à-visotherAEcurrenciescouldthereforedampenthenegativeeffectasUKexportsbecomemorecompetitivecomparedtosafe-havencurrencies,eveniftheylosecompetitivenessagainstAsiancurrencies.

Amplification from equity markets Globalfinancialmarketsexhibitsubstantialtime-variationintheirresponsivenesstoChineseeconomicdevelopments.Formanycountries,responsivenesstoChinawillreflecttosomeextenttheirexposuretoChinaviatradeandcommoditymarkets.(15)ButdownsideChinesenewsnowappearsto

(13) Tradechannels,bothdirectandindirect,likelyaccountforoverhalfthehittoUKGDP,whilemonetarypolicyandcommoditiescushiontheeffectontheUKsomewhat.

(14) Afterthesurprisedevaluationoftherenminbion10August2015,otherAsiancurrenciestypicallydepreciatedbyasimilarorlargerdegreeagainstthedollar.WeassumethatHongKong’scurrencyboardarrangement(LinkedExchangeRateSystem)totheUSdollarremainsinplace.

(15) Mwaseet al(2016).

0.5

0.4

0.3

0.2

0.1

0.0Per cent

One year Peak

–

GVAR

ECB-G

Chart 6 Impact of a negative 3% shock to Chinese GDP on UK GDP after one year and at peak

Source:Bankcalculations.

4

2

0

2

4

6

8

10

12

14

16

2003 06 09 12 15 18

Chinese real GDP

IMF forecast

Percentage change on a year earlier

Illustrative hard landing

+

–

Chart 7 An illustrative hard-landing scenario(a)

Sources:IMFWorld Economic Outlook (WEO)April2018 andNationalBureauofStatisticsofChina.

(a) ThereddashedlinedisplaysanillustrativescenarioinwhichthelevelofChineseGDPisassumedtofall10%belowtheIMFforecastafterthreeyears.

2.0

1.5

1.0

0.5

0.0

Standardchannels

Larger exchange rate

moves

Larger globalequity

responses

GreaterUK financial

resilience

Percentage points

–

-0.9

-0.4

-0.4

+0.5

Chart 8 Potential amplification and mitigation effects from a China hard landing to the UK, one-year horizon

Source:Bankcalculations.

Quarterly Bulletin 2018 Q2 6

mattermorethanitdidpreviously.Forexample,on24August2015(knownasChina’s‘BlackMonday’)Chineseequitiesfellbyover8%,erasinggainsfortheyear.Thestockmarketcollapsespilledovertoequitymarketselsewheretoo,withAEandEMEindicesfallingby4%–5%ontheday(Chart 9)—thisisconsiderablymorethantheaveragereactiontolargestockmarketmovesinChina,shownbytheredbars.Andonthesameday,theVIX—ameasureoffinancialmarketuncertainty—surgedsomuchthatquotationsweresuspendedintheearlytradingsession.Ifweaddinalargerequityshocktoourmodels—inasimilarveintoChina’s‘BlackMonday’—thiscouldknockafurther0.4percentagepointsoffUKGDP.Hence,thecombinedeffectfrommoreadversefinancialmarketmovescouldnearlydoubletheeffectofaChinahardlandingontheUK(Chart 8).

Mitigation from a more robust UK banking sector Post-crisisregulatoryreformmaymitigatesomeofthenegativeeffectsontheUKeconomy.Simplyput,morerobustbanksintheUKshouldabsorbsomeofthenegativeeffectsbeforetheyreachhouseholdsandfirms.

WeillustratethisinECB-GbyassumingthataddedUKbankresiliencecouldlimittheextenttowhichhigherriskpremiainfinancialmarketsarepassedontointerestratesfacingborrowers.(16)Thiscouldmitigatearound0.5percentagepointsoftheshocktotheUKeconomy.Andtotheextentthatbanksgloballyarealsosignificantlymorerobustthanthepre-crisisperiod,thiswouldalsofurtherdampentheshocktotheUKbyreducingthenegativeeffectscomingfromtheUK’smaintradingpartners.

Risks from Chinese investment in UK real estate Finally,whilemostoftheeffectsfromaChinahardlandingcomeindirectlyviabroadmacrofinancialeffects,thereisonedirectchannelthatposesariskwhichwedonotmodel:investmentfromChinainUKproperty.

EstimatesofChineseinvestmentinUKpropertyaresomewhatuncertain,butitappearsthatinvestmentfromAsiahasrisennotablysince2010andaccountedforover40%ofLondoncommercialrealestatepurchasesin2017,upfromonly6%in2010.(17)AndasflaggedintheFinancial Stability Report,Londoncommercialrealestatevaluationslookstretched.

Overall,itisnotclearwhattheimplicationsofaChinahardlandingwouldbe:investmentscouldbeliquidated,butcapitalflightfromChinatotheUKmayalsoactasasupport,furtherbuoyingmarkets.

China’s integration into the global financial system will raise spillover effects in the future

Asdiscussedearlier,China’sfinancialintegrationhaslaggedwellbehindChina’sintegrationintotheglobaleconomy(Chart 10).OnereasonforthisisthatChina’scapitalaccount—whichreflectscross-borderflowsofinvestment—hasbeenveryrestricted.Forinstance,althoughforeigndirectinvestmentinflowshavebeengraduallyliberalisedsincethelate1970s,tightrestrictionsonportfolioandbankingflowshavepersisteduntilveryrecently.Andalthoughithasbecomemoreopenovertime,restrictionsonChina’scapitalaccountremainhighrelativetootherG20countries.

Impact of liberalisation — an illustrative scenarioOverthepastfewyearstheChineseauthoritieshavegraduallytakenanumberofmeasurestofurtheropenupthecapitalaccount.Althoughprogressslowedin2016inresponsetocapitaloutflowpressures,Chineseauthoritiesmaintaintheircommitmenttofurthercapitalaccountliberalisationinthefuture.

ApreviousQuarterly BulletinexploredthepotentialimpactoffullfinancialliberalisationinChinaontheglobalfinancialsystem,(18)whichwilldependonthespeedandscaleofcapitalaccountopening,andonthefuturesizeandcompositionofChina’sexternalbalancesheet.(19)Underaplausiblescenario

40 30 20 10 –

–

0

VIX (inverted,top axis)

AE equityindex

EME equityindex

ShanghaiComposite

10 5 0

One-day per cent change

One-day per cent change

Chinese ‘Black Monday’

Average for large stock market falls

Chart 9 Equity market and VIX moves around large Chinese stock market events(a)

Sources:Bloomberg,ThomsonReutersDatastreamandBankcalculations.

(a) AlargeChinesestockmarketeventisdefinedasadateonwhichtheShanghaiCompositefellbymorethan5%andwasassociatedwithChinesenews(foralistofdates,seeArslanalpet al(2016)).AEequityindexisanaverageofFTSE100,S&P500andEuroStoxx50.EMEequityindexisMSCI.

(16) Wemodelthisbystoppingrisingprivatesectorriskpremiafrombeingpassedontoborrowers—areasonablystrict,buttractable,modellingassumption.ThiscouldalsobeachievedbytheBankofEnglandusingaTermFundingScheme,whichprovidesfundingtobanksandbuildingsocietiesatratesclosetoBankRate—itisdesignedtoencouragethemtoreflectcutsinBankRateintheinterestratesfacedbyhouseholdsandbusinesses.

(17) Wong(2017),usingavarietyofsources,showsthatmorethan10%ofChineseforeignresidentialrealestateinvestmenttypicallyendsupintheUK—worthabout£7billionin2015.

(18) SeeHooley(2013).(19) ThecompositionofChina’sexternalbalancesheetismuchmoreheavilyweightedto

foreigndirectinvestmentontheliabilitiessideandofficialforeignexchangereservesontheassetsidecomparedtoothermajoreconomies.

Topical articles Spillovers from China 7

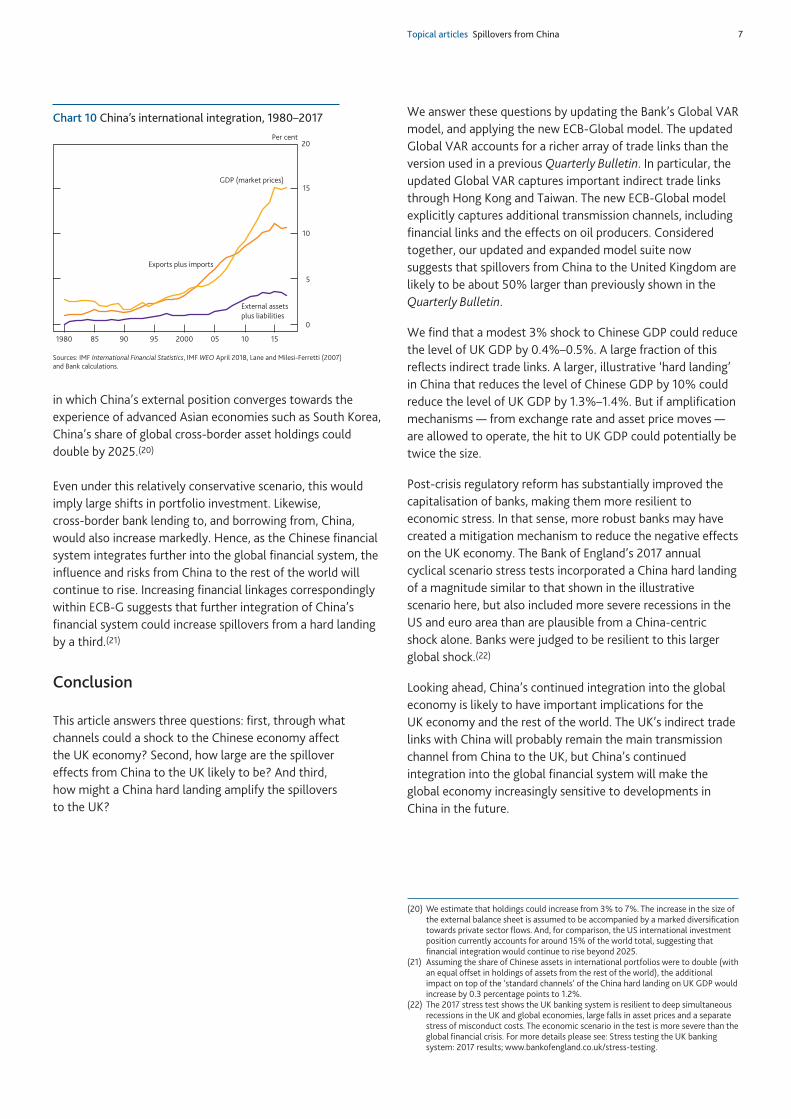

inwhichChina’sexternalpositionconvergestowardstheexperienceofadvancedAsianeconomiessuchasSouthKorea,China’sshareofglobalcross-borderassetholdingscoulddoubleby2025.(20)

Evenunderthisrelativelyconservativescenario,thiswouldimplylargeshiftsinportfolioinvestment.Likewise,cross-borderbanklendingto,andborrowingfrom,China,wouldalsoincreasemarkedly.Hence,astheChinesefinancialsystemintegratesfurtherintotheglobalfinancialsystem,theinfluenceandrisksfromChinatotherestoftheworldwillcontinuetorise.IncreasingfinanciallinkagescorrespondinglywithinECB-GsuggeststhatfurtherintegrationofChina’sfinancialsystemcouldincreasespilloversfromahardlandingbyathird.(21)

Conclusion

Thisarticleanswersthreequestions:first,throughwhatchannelscouldashocktotheChineseeconomyaffecttheUKeconomy?Second,howlargearethespillovereffectsfromChinatotheUKlikelytobe?Andthird,howmightaChinahardlandingamplifythespilloverstotheUK?

WeanswerthesequestionsbyupdatingtheBank’sGlobalVARmodel,andapplyingthenewECB-Globalmodel.TheupdatedGlobalVARaccountsforaricherarrayoftradelinksthantheversionusedinapreviousQuarterly Bulletin.Inparticular,theupdatedGlobalVARcapturesimportantindirecttradelinksthroughHongKongandTaiwan.ThenewECB-Globalmodelexplicitlycapturesadditionaltransmissionchannels,includingfinanciallinksandtheeffectsonoilproducers.Consideredtogether,ourupdatedandexpandedmodelsuitenowsuggeststhatspilloversfromChinatotheUnitedKingdomarelikelytobeabout50%largerthanpreviouslyshownintheQuarterly Bulletin.

Wefindthatamodest3%shocktoChineseGDPcouldreducethelevelofUKGDPby0.4%–0.5%.Alargefractionofthisreflectsindirecttradelinks.Alarger,illustrative‘hardlanding’inChinathatreducesthelevelofChineseGDPby10%couldreducethelevelofUKGDPby1.3%–1.4%.Butifamplificationmechanisms—fromexchangerateandassetpricemoves—areallowedtooperate,thehittoUKGDPcouldpotentiallybetwicethesize.

Post-crisisregulatoryreformhassubstantiallyimprovedthecapitalisationofbanks,makingthemmoreresilienttoeconomicstress.Inthatsense,morerobustbanksmayhavecreatedamitigationmechanismtoreducethenegativeeffectsontheUKeconomy.TheBankofEngland’s2017annualcyclicalscenariostresstestsincorporatedaChinahardlandingofamagnitudesimilartothatshownintheillustrativescenariohere,butalsoincludedmoresevererecessionsintheUSandeuroareathanareplausiblefromaChina-centricshockalone.Bankswerejudgedtoberesilienttothislargerglobalshock.(22)

Lookingahead,China’scontinuedintegrationintotheglobaleconomyislikelytohaveimportantimplicationsfortheUKeconomyandtherestoftheworld.TheUK’sindirecttradelinkswithChinawillprobablyremainthemaintransmissionchannelfromChinatotheUK,butChina’scontinuedintegrationintotheglobalfinancialsystemwillmaketheglobaleconomyincreasinglysensitivetodevelopmentsinChinainthefuture.

0

5

10

20

15

1980 85 90 95 2000 05 10 15

Exports plus imports

GDP (market prices)

External assetsplus liabilities

Per cent

Chart 10 China’s international integration, 1980–2017

Sources:IMFInternational Financial Statistics,IMFWEOApril2018,LaneandMilesi-Ferretti(2007)andBankcalculations.

(20)Weestimatethatholdingscouldincreasefrom3%to7%.Theincreaseinthesizeoftheexternalbalancesheetisassumedtobeaccompaniedbyamarkeddiversificationtowardsprivatesectorflows.And,forcomparison,theUSinternationalinvestmentpositioncurrentlyaccountsforaround15%oftheworldtotal,suggestingthatfinancialintegrationwouldcontinuetorisebeyond2025.

(21) AssumingtheshareofChineseassetsininternationalportfoliosweretodouble(withanequaloffsetinholdingsofassetsfromtherestoftheworld),theadditionalimpactontopofthe‘standardchannels’oftheChinahardlandingonUKGDPwouldincreaseby0.3percentagepointsto1.2%.

(22) The2017stresstestshowstheUKbankingsystemisresilienttodeepsimultaneousrecessionsintheUKandglobaleconomies,largefallsinassetpricesandaseparatestressofmisconductcosts.Theeconomicscenariointhetestismoreseverethantheglobalfinancialcrisis.Formoredetailspleasesee:StresstestingtheUKbankingsystem:2017results;www.bankofengland.co.uk/stress-testing.

Quarterly Bulletin 2018 Q2 8

AnnexA quick overview of the models

The Global VAR(GVAR)isanempiricalmodelestimatedwithhistoricaldata.Itshouldcapturetheaveragespilloversfromshocksthathavebeenseeninthepast.Themodelallowsshockstopropagateacrosstheworldthroughmanychannels,includingdirectandindirectspilloversthroughtradeaswellassomeassetandcommoditypricelinks.

ApreviousQuarterly BulletinarticledescribedGVARestimatesofthespilloversfromChinatotheUKeconomy.ThatarticlealsoincludesamoredetaileddiscussionoftheadvantagesanddisadvantagesoftheGVARmodellingapproach.Themodelisestimatedintwosteps.First,individualmodelsarebuiltforalargenumberofeconomies.Inthesemodels,anumberofkeydomesticvariables—realGDP,inflation,equityprices,interestratesandtheexchangerate—areallaffectedbyeachother,aswellasbyinternationalvariablesliketheoilprice,worldGDPandworldinflation.Second,individualcountrymodelsarelinkedwithinternationalvariablestocreateaglobalmodelfortheworldeconomy.

The ECB-Global(ECB-G)modelisarichmulti-countrymodelfortheeuroarea,theUS,theUK,Japan,China,oil-producingeconomies,andtherestoftheworld.LiketheGVAR,shocks

canpropagateacrosstheworldthroughdirectandindirecttradechannelsinECB-G.Inaddition,ECB-Gincludesmoredetailedcross-countryfinanciallinksthantheGVAR.

WithinECB-G,coredomesticmacroeconomicvariables,likeinflationandGDP,aredeterminedbywell-knownstructuralrelationshipsthatunderpinaggregatedemandandaggregatesupplyineacheconomy.Tradeflowsarealsoaccountedforusingdataoncountries’bilateraltradeflows.Asaconsequence,areductioninoneregion’sGDP(egChina)canspillovertotheUKthroughboththedirecttradinglinksbetweenChinaandtheUK,andindirecttradinglinksthroughthirdcountries(egtradebetweenChinaandtheeuroareaand,inturn,tradebetweentheeuroareaandUK).

Themodelcoreisenrichedbyequationswhichcapture,amongotherthings,therelationshipsbetweenfinancialriskpremiaandthestateoftheeconomy.Theriskpremiaaremodelledtoreplicaterealisticrelationshipsbetweenassetpricesandthestateoftheeconomy.Forinstance,financialriskpremiaareassumedtoincreasewheneconomicactivitywithinacountryfalls.Reflectinginternationalfinanciallinks,changesinfinancialriskpremiainoneregion(egChina)canspillovertotheUKwithinthemodel.Aswiththetradelinks,financialspilloverscanbedirectorindirectandaredeterminedbyregions’internationalfinancialexposures.

Topical articles Spillovers from China 9

References

Arslanalp, S, Liao, W, Piao, S and Seneviratne, D (2016),‘China’sgrowinginfluenceonAsianfinancialmarkets’,IMF Working Paper WP/16/173,August.

Cesa-Bianchi, A and Stratford, K (2016),‘HowcouldashocktogrowthinChinaaffectgrowthintheUnitedKingdom?’,Bank of England Quarterly Bulletin,2016Q1;www.bankofengland.co.uk/quarterly-bulletin/2016/q1/how-could-a-shock-to-growth-in-china-affect-growth-in-the-united-kingdom.

Chowla, S, Quaglietti, L and Rachel, Ł (2014),‘HowhaveworldshocksaffectedtheUKeconomy?’,Bank of England Quarterly Bulletin,2014Q2;www.bankofengland.co.uk/quarterly-bulletin/2014/q2/how-have-world-shocks-affected-the-uk-economy.

Dieppe, A, Georgiadis, G, Ricci, M, Van Robays, I and Van Roye, B (2018a),‘ECB-Global:IntroducingtheECB’sglobalmacroeconomicmodelforspilloveranalysis’,Economic Modelling,inpress.

Dieppe, A, Gilhooly, R, Han, J, Korhonen, I and Lodge, D (2018b),‘ThetransitionofChinatosustainablegrowth—implicationsfortheglobaleconomyandtheeuroarea’,European Central Bank Occasional PaperNo. 206,January;www.ecb.europa.eu/pub/pdf/scpops/ecb.op206.en.pdf.

Hooley, J (2013),‘BringingdowntheGreatWall?GlobalimplicationsofcapitalaccountliberalisationinChina’,Bank of England Quarterly Bulletin,2013Q4;www.bankofengland.co.uk/quarterly-bulletin/2013/q4/bringing-down-the-great-wall-global-implications-of-capital-account-liberalisation-in-china.

Lane, P and Milesi-Ferretti, G (2007),‘TheexternalwealthofnationsmarkII:revisedandextendedestimatesofforeignassetsandliabilities,1970–2004’,Journal of International Economics, Vol.73,November,pages223–50.

Mwase, N, N’Diaye, P, Oura, H, Ricka, F, Svirydzenka, K and Zhang, Y (2016),‘SpilloversfromChina:financialchannels’,Spillover Notes No. 5,InternationalMonetaryFund.

Wong, A (2017),‘China’scurrentaccount:externalrebalancingorcapitalflight?’,International Finance Discussion Papers No. 1208,BoardofGovernorsoftheFederalReserveSystem,June.