sovereign bond ratings and neoliberalism in latin america

TRANSCRIPT

Sovereign Bond Ratings and Neoliberalismin Latin America

GLEN BIGLAISER

Texas Tech University

KARL DEROUEN, Jr.

The University of Alabama

The importance of credit rating agencies (CRAs) in rating sovereignbonds has grown as developing countries increasingly issue bonds toattract foreign capital. Although in their methodologies CRAs claim thatthe initiation of neoliberal reforms influences bond ratings, given thesecrecy surrounding ratings, it is unclear what impact reforms actuallyhave on CRAs. Controlling for macroeconomic and political determi-nants, we use statistical analyses, as well as recent qualitative evidence,for some 16 Latin American countries from 1992 to 2003 to assess theeffects of economic reforms on CRA decisions. We find that amongneoliberal policies only trade liberalization positively and consistentlyimpacts bond ratings. The relative ease of implementation along withthe credible commitment to maintain trade policies help explain higherbond ratings. The results also show that inflation and bond defaultsnegatively affect CRA assessments. The findings provide reasons foroptimism. Many economic policies, often politically difficult to imple-ment, do not lead to higher ratings. Others that are relatively easy toimplement do. Policy makers in Latin American countries have moreoptions to lessen political tensions, lower the cost of capital, and increaseits availability for investment and growth than previously predicted.

The past 40 years have witnessed a change in how Latin American countries ac-quire foreign capital. Unlike the 1960s when aid programs such as the Alliance forProgress provided assistance, and the 1970s when commercial banks, flush withpetrodollars, lent aggressively to developing countries, the 1980s to today haveseen a reliance on the International Monetary Fund (IMF), other internationalagencies, and private capital sources (Sinclair 2003).

Among private capital sources, sovereign bonds, debt securities issued bygovernment ministries, are increasing in popularity in Latin America. From 1994to 2000, for example, the stock of outstanding debt securities issued abroad rosefrom $24 billion to $58 billion for Mexico, and from $13 billion to $76 billionfor Argentina (Vaaler, Schrage, and Block 2005:66). To assess the default risk

Authors’ note: The authors are indebted to Paul Vaaler who not only shared data but also provided extensivecomments on an earlier draft. We also thank Candace Archer, Marshall Garland, Nate Jensen, Layna Mosley, Andy

Sobel, Mike Tomz, Jeff Wooldridge, Joe Young, and the anonymous reviewers at ISQ. We also greatly acknowledgethe generosity of the bond raters for giving us insights on the ratings process.

r 2007 International Studies Association.Published by Blackwell Publishing, 350 Main Street, Malden, MA 02148, USA, and 9600 Garsington Road, Oxford OX4 2DQ, UK.

International Studies Quarterly (2007) 51, 121–138

associated with such bonds, investors look to major credit rating agencies (CRAs)such as Moody’s Investor Services (Moody’s) and Standard & Poor’s Ratings Service(S&P). Their letter-grade risk ratings on specific sovereign bonds and the govern-ments that issue them are directly linked to bond pricing, likelihood of default, andoverall attractiveness to private investors. CRAs have emerged as key intermedi-aries between investors and recipients of foreign capital (Block and Vaaler2004:918) and are nothing less than the guardians of the gates of capital to emerg-ing markets (Sinclair 2005).

The importance and controversies surrounding CRAs have grown. As Cantorand Packer (1996b), Larraın, Reisen, and von Maltzan (1997), and Kaminsky andSchmukler (2002) note, changes in sovereign ratings have important short-termeffects on market-determined credit spreads for many developing countries; higherspreads raise the cost of acquiring capital by sovereign issuers (Vaaler, Schrage, andBlock 2005:12).1 Many studies also document the potential negative effects of sov-ereign bond rating agencies on stability in emerging financial markets (Cantor andPacker 1996a; Kaminsky and Schmukler 2002; King and Sinclair 2003;Reisen 2003). Portfolio investors, in particular, may cause potential investment in-stability for developing countries. Unlike foreign direct investment (FDI), whereinvestors pursue more long-term economic strategies, portfolio investors, attractedby higher risk-adjusted returns based on CRA evaluations, may undermine long-term development (Mosley 2003:110–111). The increasing role played by CRAs isat odds with the secrecy surrounding how bond ratings are determined. The rat-ings secrecy is disconcerting to investors, policy makers, and industry insiders es-pecially when CRA ‘‘experts’’ error during crucial times, such as in the Asian,Russian, and Latin American financial crises of 1997–1998.2

Much of the determinants of bond ratings literature posits economic explan-ations including inflation, current account balance, total external debt, GrossDomestic Product (GDP) per capita, GDP growth rate, and bond default (Cantor andPacker 1996b; Eichengreen and Mody 1998; Nogues and Grandes 2001; Afonso2003; Rowland and Torres 2004), and political factors based on political institutionsand regime type (Block and Vaaler 2004; Vaaler and Schrage 2004; Vaaler Schrageand Block 2005).3 The literature tends not to stress economic policy choice. Despitesupport for market-oriented policies in the financial community not only by theIMF and ‘‘Washington Consensus’’4 but also by bond rating services in their pub-lished methodologies and in interviews, the effects of neoliberal reforms5 on bondratings have received limited inquiry. With the exception of trade openness, mostmarket reforms are not assessed (Min 1998; Rowland and Torres 2004; Rowland2005). In addition, not all reforms are necessarily equal for CRAs. Policies includingprivatization and tax reform may be politically difficult to implement and havedifferent effects on bond ratings versus trade liberalization, domestic financial re-form, and unobstructed international capital flows that face fewer veto players.What effect do neoliberal reforms have on bond ratings?

1 The spread between the yield of an emerging market sovereign issue and a U.S. Treasury of comparablematurity relates to the higher yield that investors demand to tolerate the greater default risk that the emergingmarket issue carries over a U.S. Treasury (Rowland 2005:4–8).

2 See Ferri, Liu, and Stiglitz (1999) and Karacadag and Samuels (1999) about CRA failures during the Asiancrisis. For a rich account of crisis-induced turbulence caused by CRAs, see Vaaler and McNamara (2004:691).

3 Sinclair (2005) provides a compelling explanation based on what he calls ‘‘mental frameworks.’’ Sinclair sug-gests that CRAs have certain preconceived models of what constitutes appropriate policies on the part of borrowers,and these may not necessarily be correlated with the economic performance of the real economy. Data limitationsprevent us from statistically testing the mental frameworks argument.

4 See Williamson (1990), who coined the phrase ‘‘Washington Consensus,’’ for details on the policies supposedlyfavored by international financial institutions.

5 Neoliberal is a term popularized in the 1970s and 1980s to describe free market economics. The most commonpolicies associated with neoliberalism are: domestic financial and international capital liberalization, trade and taxreform, and privatization. For a review of ideas identified with neoliberalism, see Friedman (1975).

Sovereign Bond Ratings and Neoliberalism in Latin America122

This research tests existing theories to determine whether all forms of economicliberalization implemented in Latin America since the 1990s are assessed similarlyby CRAs. Latin America’s need to attract foreign capital and its implementation ofreforms before most other developing countries make it an ideal region for com-parison. We provide an analysis of CRA bond ratings that includes three groupsof independent variables: (a) economic reforms; (b) macroeconomic outcomes; and(c) political factors. Controlling for macroeconomic and political factors, we testwhether bond ratings form important constraints on economic reform. Using thesovereign bond ratings from the two largest CRAs Moody’s and S&P,6 we analyzethe following kinds of economic reforms implemented across Latin Americancountries in the 1990s: tax, trade, and financial reform, privatization, and capitalmarket liberalization.

Using panel data as well as qualitative evidence for 16 Latin American countries7

from 1992 to 2003, this study shows that most economic reforms do not signif-icantly affect sovereign bond ratings. Building on sovereign spread work byRowland (2005), Rowland and Torres (2004), and Min (1998), we find that tradereform positively affects bond ratings. Congruent with Buthe and Milner (2005),who argue that membership in trade agreements attract FDI, we suggest that therecent advance of trade associations and their support for trade reform also im-proves bond ratings. Since the early 1990s, Latin American countries have joined orstrengthened regional trading blocs. Membership in trade associations supportsmore credible commitments to CRAs about the country’s maintenance of neoliberalpolicies because these international commitments are costly to renege on. Unlikedomestic financial reform and capital liberalization that are relatively easy to initiateand reverse, and tax reform and privatization that are difficult to implement be-cause of veto players, membership in trade associations provide a credible com-mitment to CRAs that the country is serious about trade openness.

In contrast to other economic reforms that are initiated unilaterally, trade in-volves relationships among countries, which supports a credible commitmentamong parties. Interdependence among trade partners has a stickiness that oftenextends beyond the initial agreement. Regional trade associations can also facilitatethe resolution of conflicts between members and ‘‘reduce the cost of enforcingcontracts [and] encourage their creation’’ (Russett and Oneal 2001:163–164). Easilyenforceable contracts and conflict resolution channels enhance investment stabilityand are likely to impress CRAs.

In addition, beneficiaries from freer trade are likely to mobilize to sustain open-market policies.8 Although Olson (1965) contends that because the benefits of tradeopening are diffuse and the costs concentrated, protectionists will have greatercapacity to influence politician decisions, Latin America’s crises in the 1980s tied tothree decades of market closure generated backing for an export orientation. Asmany Latin American governments initiated trade reform more than a decade ago,export-oriented businesses are maturing and can lobby officials to maintain freertrade.9 Freer trade policies also led to the collapse of many uncompetitive busi-nesses, resulting in fewer protectionist groups to lobby politicians. While tradepolicy reversals are always possible, the increasing winners from freer trade anddecline of losers may help sustain trade liberalization.

6 We considered using the sovereign bond ratings from a third CRA, Fitch Services. Fitch has risen quickly basedon its merger with other CRAs between 1997 and 2000. However, much of our data includes 1992–2000, a timewhen Fitch acquired International Bank Credit Analysis, followed by Duff & Phelps Credit Rating Company, andthen Thomson Bank Watch. There is too much missing data to make meaningful assessments on Fitch.

7 The countries in this study are: Argentina, Bolivia, Brazil, Chile, Colombia, Costa Rica, the Dominican Re-public, Ecuador, El Salvador, Guatemala, Jamaica, Mexico, Paraguay, Peru, Uruguay, and Venezuela.

8 Thanks to Marshall Garland for noting the mobilization of local trade winners.9 See Markusen and Venables (1999), Markusen (1995), and Rhee (1990) who show that trade beneficiaries are

able to mobilize themselves.

GLEN BIGLAISER AND KARL DEROUEN, JR. 123

Complementing Afonso (2003), Block and Vaaler (2004), Cantor and Packer(1996b), Vaaler and McNamara (2004), and Vaaler, Schrage, and Block (2006),inflation and bond default decrease sovereign ratings. Other economic and politicalfactors appear to have less consistent impact on CRA assessments.

Our findings hold important implications for the relationship between bondratings investment and structural reform. First, our research shows the relevance oftrade relative to other economic reforms for improving bond ratings. Mobilizationby freer trade winners and membership in trade associations suggest commitmentsthat enhance policy credibility with CRAs. Trade is also expected to strengtheneconomies, increasing the likelihood of bond repayment, an issue bond ratersraised (Moody’s 2005; S&P 2005). Second, the results provide reasons for opti-mismFthe fact that most economic reforms are not necessary for enhancing bondratings suggests that painful policies drawing heated debate in Latin America maynot be critical for attracting capital. Of course, Latin American countries must notignore the inflationary effects of their policy choices. But if we accept Sinclair’s(2005) claim that CRAs are the guardians of capital, the results suggest that strictpolicy constraints imposed on emerging markets because of globalization (Robinson1996; Gill 1997; Mosley 2003) are looser than predicted. Developing countries havemore economic policy options that could lessen political tensions, lower the cost ofcapital, and increase its availability for investment and growth.

In the first section, we discuss the possible determinants of bond ratings, identifyingthe hypotheses we test in our empirical analysis. Issues of model specification arepresented in the second section. The results are presented in the third section. Thefourth section interprets and discusses the results. The final section concludes the paper.

The Determinants of Bond Ratings

CRAs have a long history dating back to the 1850s. Started in the United States toprovide private information for the American financial markets, their importancehas ebbed and flowed based on the availability of alternative capital sources. Ratingsissuers developed between the 1907 financial crisis and the 1912 Pujo hearings(King and Sinclair 2003:348). While many CRAs have come and gone over theyears, two rating services dominate the bond rating business: Moody’s and S&P.

The relevance of CRAs as key intermediaries in financial markets has grownrecently because of massive increases in sovereign bond issues. Based on WorldBank (2004) data for the developing world, annual bond issues purchased by for-eign investors rose from about $1 trillion in the 1970s to 4 trillion in the 1980s, tonearly $50 trillion in 1996, leveling off at $30 trillion by the turn of the century. Theexplosion of bond sales has led Sinclair (2005) to argue that the CRAs and theirauthoritative source of judgment are the ‘‘second superpowers,’’ dwarfed only byU.S. superpower status.

Historically, CRAs have played a less critical role in the developing world butthat of course has changed. Before the 1980s, most credit ratings assessed largecompanies from the United States or other OECD nations or the sovereign debtfor developed countries. Since the 1980s, capital market changes have madedeveloping countries important actors in the sovereign bond market. From the1940s–1970s, nationalism and protectionism impacted borrower and lender rela-tionships in Latin America. Fueled by the dependency theory, which claimedinferior terms between the developed and developing world, Latin Americancountries opposed foreign investment in areas that offered high profits, such asnatural resources and infrastructure.10 These countries preferred to promote do-mestic firms through import-substituting industrialization (ISI). ISI brought early

10 Negative perceptions of foreign investors also drew less interest from the international community, whoworried about asset expropriation.

Sovereign Bond Ratings and Neoliberalism in Latin America124

success, as Latin American countries averaged annual growth rates of over 5%between 1945 and 1972 (Thorp 1998:15). ISI’s early triumph dampened interest inissuing bonds to obtain foreign capital.

Cold War politics in the 1960s also provided foreign resources to Latin Americangovernments, reducing the need for sovereign bond issues. As part of the U.S.’sAlliance for Progress, a program intended to provide $100 billion in grants, loans,and investment to the Western Hemisphere to fuel economic growth and democracyagainst the potential Soviet alternative, Latin America received few incentives to issuebonds. Petrodollars of the 1970s also offered ample capital sources. Despite themonetary drain produced by uncompetitive ISI policies,11 abundant variable-rateloans from international financial organizations and commercial banks more thancompensated for the capital shortages. Fighting the effects of inflation, centralbankers in developed countries raised their prime rates to curb domestic purchases.Higher prime rates led to exorbitant interest rates on Latin America’s loans, caus-ing debt crisis and capital flight in the 1980s (Toral 2001:61).12 With limited capitalstocks, Latin American countries pursued new capital sources, such as sovereignbond issues. The question is how could Latin American governments obtain highbond ratings from CRAs to attract investors and keep capital costs down?

CRAs provide sovereign ratings methodology profiles about how bond ratingsare determined. Standard and Poor’s (2004:3) formula uses broad categories, in-cluding political risk, income and economic structure, economic growth prospects,fiscal flexibility, general government debt burden, offshore and contingent liabil-ities, monetary flexibility, external liquidity, public-sector external debt burden,and private-sector external debt burden, with many subcategories. Moody’s (1995)uses fairly similar measures; however, specific details about how the categories andsubcategories are weighted and determined are proprietary information.

Given the lack of transparency, developing countries are never sure about whichpolicies will enhance their bond ratings. Despite no specific sovereign bond ratingmechanism, neoliberal reforms are among CRA policy goals. Standard and Poor’s(2004:3) states that, ‘‘Prosperity, diversity, and degree to which [the] economy ismarket-oriented’’ affects their ratings. In interviews, bond raters at Moody’s (2005)and S&P (2005) also mentioned the importance of economic reforms. In addition,economic crises under ISI and pressure from international financial institutionsencouraged many Latin American policy makers to initiate neoliberal policiesfavored by financial markets. After nearly 20 years of economic liberalization, inpart, to attract foreign investment, the effects of reforms on bond ratings is stillreceiving minimal attention in the bond rating literature.13

There are five main neoliberal policies that are expected to enhance sovereignbond ratings: domestic and international capital liberalization, trade and taxreform, and privatization. Domestic financial reform involves banking measuresthat help lower interest rates and attract foreign investors. International capitalliberalization is also an incentive for foreign investors and is expected to improvebond ratings. The flexibility to move capital freely offers profit opportunities andreduces investor risk (Ramirez 2001). Trade reform (e.g., lower tariffs) is alsoexpected to raise bond ratings. As the post-World War II era shows, countries thatare more integrated in the world market generally reap great economic rewards viaenhanced development and per capita GDP. Indeed, bond ratings are highest forexport-oriented developed countries. Similarly, tax reform increases bond ratings.Policies that improve tax collection efficiency, install the maximum marginal tax rateon corporate and personal incomes, and institute value added taxes raise revenue,

11 For the negative consequences of ISI, see Baer (1972), Edwards (1995:117–123), and Hirschman (1968).12 For sources on the debt crisis, see Frieden (1991) and Stallings and Kaufman (1989).13 In contrast, the implementation of reforms to draw in foreign capital obtains serious inquiry in the foreign

direct investment literature (Birch 1991; Pastor 1992; Amirahmadi and Wu 1994; Baer and Miles 2001).

GLEN BIGLAISER AND KARL DEROUEN, JR. 125

increasing the likelihood for debt repayment (Root and Ahmed 1978; Amirahmadiand Wu 1994). Lastly, privatization suggests a commitment to the private over thepublic sector. The sale of state-owned enterprises (SOEs) provides revenue streamsand may allow the removal of loss-making assets from the books, making thecountry more attractive to CRAs (Biglaiser and Brown 2003).

The more common bond rating determinants are lumped into two categories:macroeconomic and political factors. Among the macroeconomic factors are infla-tion, current account balance, total external debt/GDP, GDP per capita, GDPgrowth rate, and bond default (see Cantor and Packer 1996b; Eichengreen andMody 1998; Nogues and Grandes 2001; Afonso 2003; Rowland 2005).14 Theexpectation is that bond ratings are positively correlated with good economic news.Countries experiencing low levels of inflation, debt, and bond defaults are betterrisks for prospective investors. Similarly, developing countries with high GDP percapita, growth rates, and current account balances provide profit opportunitieswithin the country, which limit default risks.

Political conditions such as the ‘‘democratic advantage’’ are also relevant in thebond ratings literature. According to Schultz and Weingast (2003), democraticcountries present more credible commitments to repay debts without reschedulingor defaulting. Constraints on liberal governments, such as electoral accountability,provide the populace with a means to punish sovereigns, thus compelling govern-ments to comply with their debt obligations.15 Democracies are charged lower riskpremium spreads, comparable to a higher bond rating from CRAs. In contrast,Saiegh (2005) empirically shows that, unlike developed countries, developingcountries are more likely to reschedule their debts. He argues that there is littledifference in the interest rates paid by democratic and authoritarian countries inthe developing world.

Other political factors including the role of the IMF, the president’s ideology,election cycles, and honeymoon effects are also assessed in the bond literature(Block and Vaaler 2004; Vaaler and Schrage 2004). IMF agreements are expectedto improve bond ratings as IMF loan recipients are required to initiate economicreforms. The IMF also distributes capital, which may foster economic development.Presidential ideology also affects bond ratings. Leftist executives presumably op-pose economic reforms because these policies lead to job losses and price hikes thatweigh most heavily on their constituents.16 Election cycles may influence CRA as-sessments. Presidents in election years are expected to ignore budgetary and fiscalconstraints in order to win reelection, a common element in many Latin Americancountries that recently instituted constitutional changes that permit multiple terms.In contrast, newly elected officials experience a honeymoon period. Having earneda popular mandate and with a longer time horizon, political leaders have morefreedom to implement economic reforms.17 CRAs raters are expected to lowerbond ratings in election years and raise ratings following elections.

This study develops three hypotheses to explain the determinants of bondratings in Latin America. The first hypothesis claims a positive relationship betweenthe introduction of economic reforms and bond ratings. Privatization, tradeopening, tax reform, and domestic and international financial liberalization are

14 Bond currency denomination is another possible macroeconomic factor. Bonds denominated in local cur-rency instead of U.S. dollars or other foreign currencies are presumed riskier to foreign investor because ofcurrency devaluation. Data limitations prevent us from assessing bond denominations. However, factors such asinflation or current account deficit that are likely to induce devaluation are included in the models.

15 There are many Latin American cases where the domestic population will not punish incumbents who default

on external debt. Argentine President Nestor Kirchner is the latest executive to blame external debt crises oncreditors to increase popular support.

16 See Johnson and Crisp (2003), who argue that political ideology, as conditioned by the institutional context,affects economic policy choice.

17 See Biglaiser and Brown (2003) for a discussion of the honeymoon hypothesis.

Sovereign Bond Ratings and Neoliberalism in Latin America126

anticipated to promote economic recovery and raise bond ratings. The secondhypothesis contends that political factors account for bond ratings. Democracy, inparticular, raises CRA bond rating assessments. The third hypothesis posits thatmacroeconomic policies are the driving force for bond ratings. Differences ininflation, economic development, bond default, and other domestic economicfactors are responsible for CRA evaluations.

Research Design

We gathered data for 16 Latin American countries on an annual basis from 1992 to2003. These years are useful for comparison since market-oriented reforms pene-trated nearly all Latin American countries during this time. The unbalanced data(i.e., not all the countries are rated by the two agencies during the entire 11 years)are comprehensive.

Dependent Variables

We use the annual bond ratings from S&P and Moody’sFthe largest bond raters inthe world and most often used in Latin America during the past decade. Similar toother recent sovereign bond rating research including Afonso (2003), Block andVaaler (2004:925), and Vaaler, Schrage, and Block (2006), we convert the publishedagency sovereign rating lettering system into ordinal values measured on a17-point (0–16) scale, with 16 as the highest bond rating (‘‘AAA’’) and zero as thelowest (‘‘C’’). We collect bond rating data using Bloomberg International (2005)on-line sources, which provides information for changes in ratings for each bondagency. In cases where a bond rating changes in a particular year, we consider therating that the country held for the majority of the 12-month period.

Independent Variables

Economic ReformsFMorley, Machado, and Pettinato (1999 [updated to 2003]) assessthe dynamics of economic reform. The authors evaluate five economic reforms:(1) commercial index (a measure of trade liberalization based on tariff policy); (2)financial reform index (a measure of domestic financial reform in the bankingindustry); (3) capital account liberalization index (a measure of international financialliberalization); (4) privatization index (a measure of the size of the state sector in theeconomy); and (5) tax reform index (a measure of tax efficiency and governmentregulation).18 Morley, Machado, and Pettinato (1999) record the value for eachindex on a scale between zero and one, with zero corresponding to the worstobservation for any country and any year among the period and countries in theLatin American study. A score of one is the most reformed or free from governmentinterference of the countries and years in the entire sample. The normalizationprocedure measures each country’s performance relative to the most liberalizedcountry in the region during the entire period of the study. We lag the economicreform variables because it takes time to implement reforms. Moreover, bondratings are not likely to change with simply the government’s announcement of itsintention to initiate reforms.

Political FactorsFThe determinants of the bond ratings literature complement re-gime-type research. Some contend that developing countries under authoritarian ruleenhance political stability, an important factor for bond rating agencies(Huntington 1968; Oneal 1994). Others connect democratic rule with investorconfidence, prompting improved bond ratings (Jensen 2003; Li and Resnick 2003).

18 Specific details about each reform measure are available in Morley, Machado, and Pettinato (1999).

GLEN BIGLAISER AND KARL DEROUEN, JR. 127

Democracies are also better able to make credible commitments to repay their debts(Schultz and Weingast 2003). Alternatively, Saiegh (2005) argues that there is littledifference between the interest rates paid by democracies and authoritariangovernments in developing countries. We control for regime using the laggedpolity2 variable contained within the Polity IV data (Marshall and Jaggers 2002).Polity2 provides a continuous measure of democracy on a 21-point scale from � 10to 10 (10 is the most ‘‘democratic’’ score).

Based on Vaaler and Schrage (2004) and Block and Vaaler (2004), we also testpolitical factors including IMF influence, presidential ideology, election cycles, andhoneymoon periods to control for domestic political effects on bond ratings. Weassess IMF structural adjustment programs (http://www.imf.org/external/np/tre/tad/extarr1.cfm) using a dummy variable coded 1 if a country operated under a stand-by program and 0 if not. Presidential ideology (from Beck et al. 2002) is coded 1 if aleftist president was in charge and 0 if not. Election cycles are coded as 1 during theelection period and 0 in nonelection years. Honeymoon effect counts how long theexecutive held power. All the political variables are lagged a year.

Total External Debt and Current Account BalanceFTotal external debt and currentaccount balance are expected to affect bond ratings. High external debt is likely tocorrespond to a higher risk of debt default and thus a lower bond rating. Similarly,current account deficit increases bond default risk for developing countries. Bothtotal external debt (as a percent of GDP, converted to constant 1995 U.S.$ millions,lagged) and current account balance (lagged) are taken from World Bank (2004).19

GDP Growth Rates and GDP Per CapitaFPositive GDP growth rates and GDP percapita are macroeconomic variables that are often used to explain bond ratings.The expectation is that countries with higher growth rates and more wealth arebetter risks for investors. In both cases, higher growth and income are supposed tolessen debt burdens over time, lowering the long-term risk of sovereign bonds(Cantor and Packer 1996b:39). Both GDP growth rates (lagged) and GDP percapita (lagged) are obtained from the World Bank (2004).

InflationFHigh inflation is a common problem for Latin American countries. Inves-tors are wary of extreme political instability and potential bond default, given theconsequences of inflation. This study uses the lagged consumer price index(CPI), the most frequently used indicator of inflation, to operationalize themacroeconomic indicator. Estimates of inflation are obtained from the World Bank(2004).

Bond DefaultFA history of bond default is a blueprint of a country’s probabilityto default in the future. As Argentina learned in its recent negotiations withbondholders, reputation affects CRA assessments. Countries that default regularlygain a high-risk credit reputation (cf. Cantor and Packer 1996b). Following Blockand Vaaler (2004:925), we measure default history using a 0–1 indicator (1 ifdefault; 0 if no default), indicating that the sovereign has defaulted on its long-termforeign currency denominated debt in the last 5 years (lagged a year). Defaulthistory is based on evidence at Standard and Poor’s (2004).

Summary statistics for the variables are presented in Table 1.

19 See Vaaler and Schrage (2004), Block and Vaaler (2004), and Vaaler, Schrage, and Block (2006), who also useWorld Development Indicators for economic measures.

Sovereign Bond Ratings and Neoliberalism in Latin America128

Method

A long history of bond rating estimation from Horrigan (1966) to Cantor andPacker (1996a, 1996b) and Vaaler and McNamara (2004) have used OLS. Thisapproach has the advantage of simplicity and ease in interpretation of effects. Onthe other hand, OLS estimates of the standard errors in a panel setting may beproblematic because of panel heteroskedasticity or spatial correlation of the errorsthat leads to inconsistent standard errors. Beck and Katz (1995) suggest usingpanel-corrected standard errors (PCSE) to deal with the former problem. Thisalternative estimation approach has been employed in various other political–economic analyses (see Jensen 2003; Li and Resnick 2003; Biglaiser and DeRouen2006). The PCSE method assumes ‘‘the disturbances are heteroskedastic andcontemporaneously correlated across panels’’ (StataCorp 2003:150). This type ofcorrelation would be expected if, for example, interest rates, recession or oil priceshad a similar effect on all panels (countries). In the case of serial correlation ofthe errors, the Wooldridge test (Drukker 2003) indicates the presence of AR(1)in our models. Stata’s PCSE program employs Prais–Winsten regression in the

TABLE 1. Summary Statistics

Variable Observed Mean SD Minimum Maximum

Moody’sBond rating 133 4.180451 2.551988 0 9Trade reform 133 0.9377963 0.0270923 0.8112959 0.9978791Financial reform 133 0.782716 0.1643583 0.5364308 0.9876156Privatization 127 0.7986653 0.1877783 0.1432927 1Tax reform 133 0.5805916 0.0998359 0.1186177 0.7736412Capital opening 133 0.8510428 0.1157079 0.48 1Polity (Democracy) 125 7.6 2.225222 0 10Election year 125 0.232 0.4238076 0 1Honeymoon 125 3.536 2.270228 1 10President’s ideology 124 0.2822581 0.4519242 0 1IMF agreement 124 0.4596774 0.5003932 0 1Inflation 125 170.0392 156.5154 0.0129808 1,022.401Current account balance 124 � 2.568732 3.839382 � 14.22086 12.63721GDP growth 125 2.343222 3.908493 � 10.89448 12.66971GDP per Capita 125 3,616.058 1,955.649 933.8787 8,685.504Bond default 133 0.2030075 0.4037588 0 1External debt/GDP 117 0.3945228 0.1451298 0.18904221 0.129269

S&PBond rating 142 4.514085 2.477519 0 11Trade reform 142 0.9415874 0.0240344 0.8786718 0.9978791Financial reform 142 0.7873715 0.162292 0.5364308 0.9876156Privatization 137 0.8056366 0.1793056 0.1432927 1Tax reform 142 0.5870538 0.0985983 0.1186177 0.7736412Capital opening 142 0.8497998 0.1082285 0.53 1Polity (Democracy) 133 7.56391 2.064686 0 10Election year 134 0.2164179 0.4133476 0 1Honeymoon 134 3.492537 2.293326 1 10President’s ideology 133 0.2406015 0.4290648 0 1IMF agreement 133 0.443609 0.4986882 0 1Inflation 134 166.002 150.8112 2.76845 1,022.401Current account balance 133 � 2.4868 3.603607 � 14.22086 12.63721GDP growth 134 2.707314 3.964061 � 10.89448 12.27793GDP per Capita 134 3,532.304 1,906.76 933.8787 8,685.504Bond default 142 0.1830986 0.3881164 0 1External debt/GDP 129 0.4038407 0.1658139 0.1962219 1.219388

GLEN BIGLAISER AND KARL DEROUEN, JR. 129

presence of first order autoregression. The Hausman test indicates that fixed effectsare not an issue in either model. We report findings for two separate models, onefor each CRA.

Results

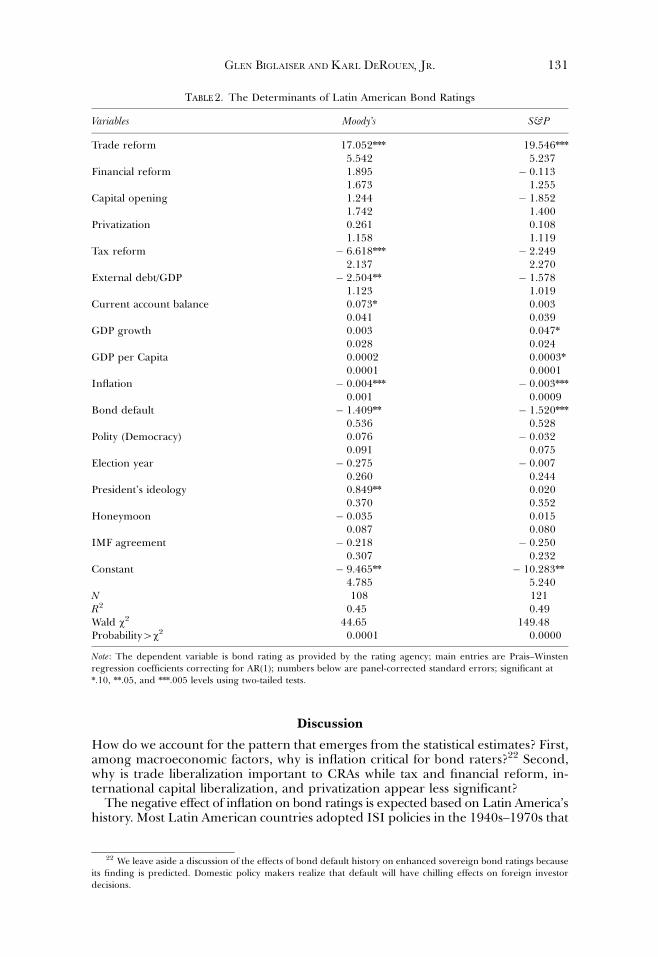

The two models account for a respectable amount of variation in bond ratingsacross Latin America (see Table 2). The three most obvious findings are that lowinflation, fewer bond defaults, and more trade openness promote higher bondratings for Moody’s and S&P.20 The other reforms have no consistent impact. Whiletax reform surprisingly appears to have a significant negative effect on Moody’sbond ratings, its effect is also negative but not significant for S&P. Similarly,economic determinants including economic growth and GDP per capita are allsignificant and the coefficients are in the expected direction in the S&P model, butthose determinants are not significant in the Moody’s model. By the same token,external debt (as a percent of GDP) and current account balance are significant forMoody’s but appear less important for S&P’s bond raters. Interestingly, amongthe political variables only president’s ideology is significant and just for Moody’s.Regime type, IMF programs, election cycle, and honeymoon effect are apparentlynot the most important factors weighed by Moody’s and S&P when rating sovereignbonds in Latin America.

The results are also backed by qualitative work. In lengthy phone interviews weconducted with analysts at Moody’s (2005) and S&P (2005) to learn aboutthe methods they use to determine ratings, most said that while political factorsare considered, it is generally related to the effect on debt repayment. No con-sensus existed among the analysts about the ideal political institutions to raisesovereign ratings.

The estimates in Table 2 can be used to perform simulations of interest. We carryout such simulations and the results are reported in Table 3. First, we tookthe average rating from each sample. Although the samples differ, the two averagesare remarkably similar ranging from 4.18 (Moody’s) to 4.51 (S&P). We then ran thetwo models with each variable set at its mean.21 As expected, the predicted ratingsin these baseline models are exceptionally close to the actual data averages. Next wecreated a ‘‘best-case’’ scenario using variables from the two equations in Table 2(external debt/GDP, GDP/Capita and inflation) with positive coefficients at their90th percentile and those with negative signs at their 10th percentile. The worst-case predictions are based on the opposite simulation. Bond default was set to1 (best case) or 0 (worst case). Here, differences across the predicted ratingsemerge. The Moody’s ratings generate a wide range going from the best case (5.96)to the worst case (2.31). S&P’s sample ranges from 6.30 to 3.85. How do theseratings stand up in comparison to the actual data? Chile has by far the best ratingsin the sample (using both agencies) with an average of 9.5. Chile’s inflation rateis lower than that of the sample mean and its trade openness is above average.Ecuador, on the other hand, has an average rating of just 0.62 for the years wecover. The country suffered staggering inflation, defaulted on some bonds, and hada below average trade openness measure.

The keys to obtaining a higher bond rating are to control inflation, reducedefault risk, and liberalize trade. Our findings also suggest that external debt isimportant. The implementation of other liberal reforms does not consistently en-hance bond ratings in Latin America. Political factors appear to have limited effecton bond ratings.

20 See Mosley (2003) who also finds that bond default and inflation affect emerging market ratings.21 The percentile and average figures for each variable are based on all available data for each agency.

Sovereign Bond Ratings and Neoliberalism in Latin America130

Discussion

How do we account for the pattern that emerges from the statistical estimates? First,among macroeconomic factors, why is inflation critical for bond raters?22 Second,why is trade liberalization important to CRAs while tax and financial reform, in-ternational capital liberalization, and privatization appear less significant?

The negative effect of inflation on bond ratings is expected based on Latin America’shistory. Most Latin American countries adopted ISI policies in the 1940s–1970s that

TABLE 2. The Determinants of Latin American Bond Ratings

Variables Moody’s S&P

Trade reform 17.052nnn 19.546nnn

5.542 5.237Financial reform 1.895 � 0.113

1.673 1.255Capital opening 1.244 � 1.852

1.742 1.400Privatization 0.261 0.108

1.158 1.119Tax reform � 6.618nnn � 2.249

2.137 2.270External debt/GDP � 2.504nn � 1.578

1.123 1.019Current account balance 0.073n 0.003

0.041 0.039GDP growth 0.003 0.047n

0.028 0.024GDP per Capita 0.0002 0.0003n

0.0001 0.0001Inflation � 0.004nnn � 0.003nnn

0.001 0.0009Bond default � 1.409nn � 1.520nnn

0.536 0.528Polity (Democracy) 0.076 � 0.032

0.091 0.075Election year � 0.275 � 0.007

0.260 0.244President’s ideology 0.849nn 0.020

0.370 0.352Honeymoon � 0.035 0.015

0.087 0.080IMF agreement � 0.218 � 0.250

0.307 0.232Constant � 9.465nn � 10.283nn

4.785 5.240N 108 121R2 0.45 0.49Wald w2 44.65 149.48Probability4w2 0.0001 0.0000

Note: The dependent variable is bond rating as provided by the rating agency; main entries are Prais–Winstenregression coefficients correcting for AR(1); numbers below are panel-corrected standard errors; significant atn.10, nn.05, and nnn.005 levels using two-tailed tests.

22 We leave aside a discussion of the effects of bond default history on enhanced sovereign bond ratings becauseits finding is predicted. Domestic policy makers realize that default will have chilling effects on foreign investordecisions.

GLEN BIGLAISER AND KARL DEROUEN, JR. 131

contributed to inflation. In an effort to protect uncompetitive domestic industries,governments imposed high tariffs on finished goods from abroad, forcingdomestic consumers to buy overpriced goods (Edwards 1995:117–123). Overpricedgoods as well as spending to maintain politicians’ survival goals, stimulated high (andeven hyper) inflation in Latin America in the 1980s and early 1990s (World Bank2004). A common response to inflation involved printing more money, which ex-acerbated price conditions. Under inflationary pressures, bond default and debtrepayment received low priority, stirring CRA unease (Frieden 1991).

Political instability produced by inflation also raises CRA concerns (Cantor andPacker 1996b:39). Inflation metes out significant punishment for nearly everyone,wealthy as well as poor (Rodrik 1994; Weyland 2004). However, the effects ofinflation are often felt most strongly by the largest portion of the electorate, low andfixed income voters, furthering poverty and political frustration (De Soto 2000;Armijo and Faucher 2002). Differences in the effects of inflation also aggravateincome distribution, particularly between union workers whose contracts maycontain cost of living adjustments and the working poor in the informal sectorwhose wages are not adjusted. Inflation’s chilling effects on increased poverty andincome disparities breed political instability, which prompts fear of bond default.

The importance of trade liberalization compared to other economic reformsfor CRAs makes sense based on the ability to implement and commit to tradereform. A concern expressed by interviewees is whether the country will implementthe economic reforms it proposes. Not all economic reforms are the same; somereforms receive more opposition than others do. Privatization and tax reformface many veto players that may slow down or collapse the process. Not only mustthe executive support the reforms, but backing from the legislature, from stateemployees (in the case of privatization), from powerful interest groups, and othershinder deep reforms. The fact that political leaders can use state enterprises asforms of patronage, delivering individual benefits to government officials, cadres ofthe ruling party, and their closest allies, also hampers privatization (Biglaiser andBrown 2003). Tax reform similarly draws close scrutiny as the richest 10% ofhouseholds in Latin America are still not taxed effectively (cf. Mahon 2004:5). Thedifficulty in initiating privatization and tax policies based on many veto players mayexplain their limited impact on sovereign bond ratings.

Ironically, the ease by which domestic financial reform and capital liberalization areinitiated and reversed suggests why CRAs take such reforms less seriously. Domesticbank sector reforms (e.g., control of borrowing and lending rates and the reserves todeposits ratio at banks) or capital liberalization are executive decisions with centralbank input that have fewer veto players to slow the reform’s initiation. Althoughcapital liberalization can raise controversy, the quick pace by which these reforms aremodified may explain why bond raters place less emphasis in their assessment.

TABLE 3. Marginal Effects

CRA and Simulation Predicted Rating

Moody (actual average ¼ 4.18)Baseline 4.48Best case 5.96Worst case 2.31

S&P (actual average ¼ 4.51)Baseline 4.64Best case 6.30Worst case 3.85

Note: Based on models in Table 2; baseline simulation ¼ all variables set to mean; best-case simulation: inflation,debt, GDP/capita set to 10th or 90th percentile, depending on sign and bond default set to 0; worst-case simulation:same variables set to 10th or 90th percentile, depending on sign and bond default set to 1.

Sovereign Bond Ratings and Neoliberalism in Latin America132

In contrast, trade reform is both relatively less difficult to initiate and challengingto overturn, garnering it more significance with CRAs. Unlike privatization and taxreform that generate societal hostility, changes in the world economy have madeLatin Americans recognize the value of trade for development. Although Olson(1965) claims that because the costs to losers from trade opening are concentratedand benefits diffuse protectionists will have greater capacity to mobilize and influ-ence politician decisions, many studies show that trade winners are able to mobilize(Rhee 1990; Markusen 1995; Markusen and Venables 1999). Latin America’s ISIcrisis fueled a break with protectionism and the advance of an export-orientedmodel (Boeker 1993). After more than 10 years of lowered tariffs, businesses thatbenefit from freer trade should lobby officials to sustain trade reform. Freer tradepolicies also led to the collapse of many uncompetitive businesses previously nur-tured by high tariffs, reducing the number of groups seeking protection. Whilereversals on trade policy are possible, the winners from freer trade are capable ofmobilizing, helping to sustain trade liberalization.

Latin America’s export orientation is also cemented through its strong regionaltrade associations. Complementing Buthe and Milner (2005), who contend thatmembership in trade agreements shows a credible commitment to maintain openmarkets that attract foreign investment, the same logic also applies to improvingbond ratings. According to Buthe and Milner (2005:12), bilateral investment treat-ies create a stable and credible policy environment for FDI ‘‘because reneging onsuch commitments made internationally is more costly than simply changing policyat home.’’ Governments that sign trade agreements usually do so with the under-standing that they are opening their markets to all of the agreement’s members.For a country to renege on the terms of the trade association might be very costly asother countries punish the country through lost access to important markets. As aresult, trade association members credibly demonstrate a commitment to free-tradepolicies, bolstering their position with CRAs. Moreover, trade interdependence hasa stickiness that often extends beyond the initial agreement. Similarly, internationalorganizations that focus on development often facilitate transparent and effectivegovernment practices among members (Russett and Oneal 2001:168) that are likelyto affect CRA scoring.

Latin America’s initial trade agreements date back to the late 1960s with thecreation of the Caribbean Free Trade Association in 1968, which 5 years laterevolved into the Caribbean Community and Common Market (CARICOM), com-prising 15 member states and five associate members.23 The Andean Pact, consist-ing of Bolivia, Colombia, Ecuador, Peru, and Venezuela, was formed in 1969, andcreated a full free-trade zone in 199324 and a free-trade area with the SouthernCommon Market (MERCOSUR) in 1998. The MERCOSUR was developed in 1991with Argentina, Brazil, Paraguay, and Uruguay as members, and Bolivia and Chileas associate members. The North American Free Trade Agreement (NAFTA) wentinto effect in 1994. Trade has grown immensely inside these trade associations, withBrazil increasing exports with other MERCOSUR members by nearly fourfoldbetween 1991 and 2004; Venezuela by nearly fourfold with Andean members;Trinidad and Tobago by sixfold with CARICOM members; and Mexico by almostfivefold with its northern neighbors (USAID 2004).

Trade index data from Morley, Machado, and Pettinato (1999) show that tradeopenness grew after the creation of trade associations. Among the MERCOSURmembers, trade openness expanded in 1992, the year after the signing of theagreement, by 2.2% in Argentina, 6.3% in Brazil, 3.4% in Paraguay, and 3.5% inUruguay. If we compare the trade openness figures among Andean Pact members

23 A free-trade zone dates back to 1960 with the Latin American Free Trade Association. However, members inthe recent trade associations are more tightly linked together.

24 Peru did not join the free-trade zone in 1993.

GLEN BIGLAISER AND KARL DEROUEN, JR. 133

from the year the Pact was created in 196925 to 1993 when a full free-trade zoneemerged, the degree of openness is huge. Trade openness increased by 37.4% inBolivia, 49.7% in Colombia, 22.4% in Ecuador, 80.6% in Peru, and 87.4% in Vene-zuela. Similar trade openness findings are found for CARICOM members, too.26

The data also reflect that cumulative years of membership in trade associations arepositively correlated with trade reform. If we code the first year of association mem-bership as 1, the second as 2, and so on, this variable is positively correlated with thedegree of trade liberalization in the Moody’s and S&P samples.27 The dramatic tradeincrease and trade openness not only between members but also with other asso-ciations reinforces the trade commitment and helps explain why CRAs treat com-merce more importantly than other economic reforms for bond ratings.

Conclusion

CRA sovereign bond assessments are gaining in importance with the growing cap-ital needs of developing countries. As international financial institutions recom-mend the implementation of economic reforms to attract foreign capital, it isnoteworthy that few studies examine the effects of different economic reforms onbond ratings. We tested the relative strength of five economic reforms on bondassessments while controlling for macroeconomic and political variables. Otherthan inflation and history of bond default, most macroeconomic and political fac-tors did not significantly affect bond ratings. Building on Afonso (2003), Cantor andPacker (1996b), Vaaler and McNamara (2004), Block and Vaaler (2004), and Vaaler,Schrage, and Block (2006), the negative correlation between inflation, history ofbond defaults, and bond ratings are expected.

More interestingly, our results indicate that among economic reforms, only tradeliberalization is correlated with bond ratings. In a finding consistent with Rowland(2005), Rowland and Torres (2004), and Min (1998), trade reform positively affectsbond ratings. The results suggest that bond ratings appear unfazed by most eco-nomic reforms including privatization, and tax, financial, and international capitalliberalization. Unlike domestic financial reform and capital liberalization that areeasily implemented and reversed, and privatization and tax reform that are hard toreverse but challenging to implement, trade liberalization is both relatively popularand difficult to overturn. The economic blight of three protectionist decades inLatin America started the initial push toward an export orientation. Entering intotrade associations cemented the commitment to freer trade. Complementing Butheand Milner’s (2005) work on FDI, membership in trade associations provide acredible commitment to CRAs that the country is serious about sustaining tradeliberalization based on the costs of reneging on its trade partners. Unlike othereconomic reforms that are often initiated unilaterally, trade involves relationshipsamong different countries that support a credible commitment among partners.Interviewees at CRAs claimed that they wanted proof that the country would im-plement the proposed economic reforms. PTAs and previous crises related to pro-tectionism provide CRAs with some evidence that trade reforms will be sustained.

25 We used 1970 in place of 1969 because the dataset begins in 1970.26 Mexico and its membership in NAFTA may be an exception to increased trade openness only because of the

economic crisis it experienced in late 1994, the initial year that NAFTA went into effect. However, by 1996, tradeopenness again expanded.

27 We wanted to test the effect of preferential trade agreements (PTAs) in our models but there are serious

complications. First, since all the cases are PTA members since 1992 we could not test the effect of PTA membershipon bond ratings because there is no variation in the variable. We also considered using the number of PTAs that eachcountry joined; however, we would then have to address weighting problems. It makes little sense for smallernations that have multiple PTAs with each other to have greater impact relative to Mexico’s NAFTA membershipthat involves substantial trade but only with the United States and Canada.

Sovereign Bond Ratings and Neoliberalism in Latin America134

Despite the minimal effect most economic reforms have on sovereign bond rat-ings, we perceive this finding positively. If we accept Sinclair’s (2005) claim thatCRAs are the new guardians of capital, the results have wide-ranging implicationson policy in the developing world. In contrast to Mosley (2003) who argues thatpolicy choices in emerging markets are highly constrained by strong and broadfinancial market influence, the fact that most economic reforms are apparently notessential for achieving higher bond ratings suggests that developing countries mayhave more policy options than previously predicted. The need to please pro-marketconstituents and international lenders at the expense of other domestic interestgroups appears overstated.

In the broadest terms, this paper speaks to globalization and domination debates.Robinson (1996) and Gill (1997), for example, argue that the spread of globali-zation and neoliberalism helps to perpetuate domination by developed countriesagainst the developing world. The expectation is that neoliberalism narrows dra-matically and fundamentally the options developing countries have for how theyintegrate into the global economy. Our results suggest that developing countrieshave much greater policy leeway. Over the past 15 years, nearly all Latin Americancountries have adopted some economic reforms with the hope of attracting foreigncapital. Pressures are building against neoliberal reforms. The finding that mosteconomic reforms are not important for bond ratings may lessen the division be-tween proponents and opponents of market-oriented policies. Countries must stillrecognize the effects of their policy on inflation. But privatization, tax reform, anddomestic financial and capital liberalization may not be critical for reducing pricepressures. The economic policy toolbox for developing countries is more open thanthe literature predicts.

References

AFONSO, ANTONIO. (2003) Understanding the Determinants of Sovereign Debt Ratings: Evidence forthe Two Leading Agencies. Journal of Economics and Finance 27:56–74.

AMIRAHMADI, HOOSHANG, AND WEIPANG WU. (1994) Foreign Direct Investment in DevelopingCountries. Journal of Developing Areas 26:167–190.

ARMIJO, LESLIE, AND PHILIPPE FAUCHER. (2002) We Have a Consensus: Explaining Political Support forMarket Reforms in Latin America. Latin American Politics and Society 44:1–51.

BAER, WERNER. (1972) Import Substitution and Liberalization in Latin America. Latin AmericanResearch Review 7:95–122.

BAER, WERNER, AND WILLIAM R. MILES, EDS. (2001) Foreign Direct Investment in Latin America: ItsChanging Nature at the Turn of the Century. Binghamton: International Business Press.

BECK, NATHANIEL, AND JONATHAN N. KATZ. (1995) What to Do (and Not to Do) with Time-SeriesCross-Section Data. American Political Science Review 89:634–647.

BECK, THORSTEN, GEORGE CLARKE, ALBERTO GROFF, PHILIP KEEFER, AND PATRICK WALSH. (2002) NewTools and New Tests in Comparative Political Economy: The Database of Political Institutions. Washington,DC: World Bank.

BIGLAISER, GLEN, AND DAVID BROWN. (2003) The Determinants of Privatization in Latin America.Political Research Quarterly 56:73–85.

BIGLAISER, GLEN, AND KARL DEROUEN JR. (2006) Economic Reforms and Inflows of Foreign DirectInvestment in Latin America. Latin American Research Review 41:51–75.

BIRCH, MELISSA H. (1991) Changing Patterns of Foreign Investment in Latin America. Latin AmericanBusiness Review 31:141–158.

BLOCK, STEVEN A., AND PAUL M. VAALER. (2004) The Price of Democracy: Sovereign Risk Ratings,Bond Spreads and Political Business Cycles in Developing Countries. Journal of InternationalMoney Finance 23:917–946.

BLOOMBERG. (2005) International Bond Series: Bloomberg On-line Data Services. New York: BloombergInternational.

BOEKER, PAUL H. (1993) Latin America’s Turnaround: Privatization, Foreign Investment, and Growth. SanFrancisco: International Center for Economic Growth: Institute of the Americas: ICS Press.

BUTHE, TIM, AND HELEN V. MILNER. (2005) The Politics of Foreign Direct Investment into DevelopingCountries: Increasing FDI through Policy Commitment via Trade Agreements and Investment

GLEN BIGLAISER AND KARL DEROUEN, JR. 135

Treaties? Paper prepared for The Political Economy of Multinational Corporations and ForeignDirect Investment, Washington University, St. Louis, MO, June 3–4.

CANTOR, RICHARD, AND FRANK PACKER. (1996a) Sovereign Risk Assessment and Agency Credit Ratings.European Financial Management 2:247–256.

CANTOR, RICHARD, AND FRANK PACKER. (1996b) Determinants and Impacts of Sovereign CreditRatings. Foreign Reserve Bank of New York Economic Policy Review, October: 37–52.

DE SOTO, HERNANDO. (2000) The Mystery of Capitalism: Why Capitalism Triumphs in the West and FailsEverywhere Else. New York: Basic Books.

DRUKKER, DAVID M. (2003) Testing for Serial Correlation in Linear Panel-Data Models. Stata Journal3:168–177.

EDWARDS, SEBASTIAN. (1995) Crisis and Reform in Latin America: From Despair to Hope. New York: OxfordUniversity Press.

EICHENGREEN, BARRY, AND ASHOKA MODY. (1998) What Explains Changing Spreads on Emerging-Market Debt: Fundamentals or Market Sentiment? Cambridge, MA: Working paper no. 6408,National Bureau of Economic Research.

FERRI, G, L. LIU, AND J. STIGLITZ. (1999) The Procyclical Role of Rating Agencies: Evidence from theEast Asian Crisis. Economic Notes 28:335–355.

FRIEDEN, JEFFRY A. (1991) Debt, Development, and Democracy: Modern Political Economy in Latin America.Princeton: Princeton University Press.

FRIEDMAN, MILTON. (1975) An Economist’s Protest. Glenridge: T. Horton.GILL, STEPHEN. (1997) Global Structural Change and Multilateralism. In Globalization, Democratization,

and Multilateralism, edited by S. Gill. New York: St Martin’s Press.HIRSCHMAN, ALBERT O. (1968) The Political Economy of Import-Substitution Industrialization in Latin

America. Quarterly Journal of Economics 82:1–32.HORRIGAN, JAMES O. (1966) The Determination of Long-Term Credit Standing with Financial Ratios.

Journal of Accounting Research 4:44–62.HUNTINGTON, SAMUEL P. (1968) Political Order in Changing Societies. New Haven: Yale University Press.JENSEN, NATHAN M. (2003) Democratic Governance and Multinational Corporations: Political Regimes

and Inflows of Foreign Direct Investment. International Organization 57:587–616.JOHNSON, GREGG B., AND BRIAN F. CRISP. (2003) Mandates, Powers, and Policies. American Journal of

Political Science 47:127–141.KAMINSKY, GRACIELA, AND SERGIO L. SCHMUKLER. (2002) Emerging Market Instability: Do Sovereign

Ratings Affect Country Risk and Stock Returns? The World Bank Economic Review 16:171–195.

KARACADAG, CEM, AND BARBARA SAMUELS. (1999) In Search of the Market Failure in the Asian Crisis.Fletcher Forum World Affairs 23:131–144.

KING, MICHAEL R., AND TIMOTHY J. SINCLAIR. (2003) Private Actors and Public Policy: A Requiem forthe New Basel Capital Accord. International Political Science Review 24:345–362.

LARRAIN, GUILLERMO, HELMUT REISEN, AND JULIA VON MALTZAN. (1997) Emerging Market Risk andSovereign Credit Ratings. Working paper 124. OECD Development Centre, Paris. Available athttp://www.oecd.org/dataoecd/38/42/1922778.pdf.

LI, QUAN, AND ADAM RESNICK. (2003) Reversal of Fortunes: Democratic Institutions and Foreign DirectInvestment Inflows to Developing Countries. International Organization 57:175–211.

MAHON, JAMES E. JR. (2004) Causes of Tax Reform in Latin America, 1977–1995. Latin AmericanResearch Review 39:3–30.

MARKUSEN, JAMES R. (1995) The Boundaries of Multinational Enterprises and the Theory ofInternational Trade. The Journal of Economic Perspectives 9:169–189.

MARKUSEN, JAMES R., AND ANTHONY J. VENABLES. (1999) Foreign Direct Investment as a Catalyst forIndustrial Development. European Economic Review 43:335–356.

MARSHALL, MONTY G., AND KEITH JAGGERS. (2002) Polity IV Project: Political Regime Characteristics andTransitions, 1800–2000. College Park: University of Maryland. Available at http://www.cidcm.umd.edu/inscr/polity/.

MIN, HONG. (1998) Determinants of Emerging Market Bond Spread: Do Economic FundamentalsMatter? World Bank Research Working Paper, Washington, DC: World Bank. Available at http://econ.worldbank.org/docs/640.pdf.

MOODY’S. (1995) Sovereign Risk: Bank Deposits vs. Bonds. New York: Global Credit Research, Moody’sInvestors Service.

MOODY’S. (2005) Phone Interview on December 14 with a Moody’s Bond-Rating Analyst.MOSLEY, LAYNA. (2003) Global Capital and National Governments. Cambridge: Cambridge University

Press.

Sovereign Bond Ratings and Neoliberalism in Latin America136

MORLEY, SAMUEL A., MACHADO ROBERTO, AND STEFANO PETTINATO. (1999) Indexes of Structural Reform inLatin America. Santiago: ECLAC.

NOGUES, JULIO, AND MARTIN GRANDES. (2001) Country Risk: Economic Policy, Contagion Effect orPolitical Noise? Journal of Applied Economics 4:125–162.

OLSON, MANCUR. (1965) The Logic of Collective Action: Public Goods and the Theory of Groups. Cambridge,MA: Harvard University Press.

ONEAL, JOHN. (1994) The Affinity of Foreign Investors for Authoritarian Regimes. Political ResearchQuarterly 47:565–589.

PASTOR, MANUEL JR. (1992) Inversion Privada y el ‘Efecto Arrastre’de la Deuda Externa en AmericaLatina. El Triemestre Economico 59:107–151.

RAMIREZ, MIGUEL D. (2001) Foreign Direct Investment in Mexico and Chile: A Critical Appraisal. InForeign Direct Investment in Latin America: Its Changing Nature at the Turn of the Century, edited byW. Baer and W. R. Miles. Binghamton: International Business Press.

REISEN, HELMUT. (2003) Ratings Since the Asian crisis. Working Paper no. 214. Paris: OECDDevelopment Centre. Available at http://www.oecd.org/dataoecd/22/8/1934625.pdf.

RHEE, YUNG WHEE. (1990) The Catalyst Model of Development: Lessons from Bangladesh’s Successwith Garment Exports. World Development 18:33–46.

ROBINSON, WILLIAM I. (1996) Promoting Polyarchy: Globalization, US Intervention, and Hegemony.Cambridge: Cambridge University Press.

RODRIK, DANI. (1994) The Rush to Free Trade in the Developing World: Why So Late? Why Now? Willit Last? In Voting for Reform: Democracy, Political Liberalization, and Economic Adjustment, edited byS. Haggard and S. B. Webb. New York: Oxford.

ROOT, FRANKLIN, AND AHMED A. AHMED. (1978) The Influence of Policy Instruments on ManufacturingDirect Foreign Investment in Developing Countries. Journal of International Business Studies 9:81–94.

ROWLAND, PETER. (2005) Determinants of Spread, Credit Ratings and Creditworthiness for Emerging MarketSovereign Debt: A Follow-Up Study Using Pooled Data Analysis. Bogota: Borradores de Economıa,Banco de la Republica. Available at http://www.banrep.gov.co/docum/ftp/borra296.pdf.

ROWLAND, PETER, AND JOSE L. TORRES. (2004) Determinants of Spread and Creditworthiness for EmergingMarket Sovereign Debt: A Panel Data Study. Bogota: Borradores de Economıa, Banco de la Republica.

RUSSETT, BRUCE, AND JOHN ONEAL. (2001) Triangulating Peace. New York: Norton.S&P. (2005) Phone Interviews on December 12 with Two S&P Bond-Rating Analysts.SAIEGH, SEBASTIAN M. (2005) Do Countries Have a ‘Democratic Advantage’? Political Institutions,

Multilateral Agencies, and Sovereign Borrowing. Comparative Political Studies 38:366–387.SCHULTZ, KENNETH, AND BARRY WEINGAST. (2003) The Democratic Advantage. International Organization

57:3–42.SINCLAIR, TIMOTHY J. (2003) Global Monitor: Bond Rating Agencies. New Political Economy 8:147–161.SINCLAIR, TIMOTHY J. (2005) The New Masters of Capital: American Bond Rating Agencies and the Politics of

Creditworthiness. Ithaca: Cornell University Press.STALLINGS, BARBARA, AND ROBERT R. KAUFMAN. (1989) Debt and Democracy in the 1980s: The Latin

American Experience. In Debt and Democracy in Latin America, edited by B. Stallings andR. R. Kaufman. Boulder: Westview Press.

STANDARD AND POOR’S. (2004) Sovereign Credit Ratings: A Primer. New York: Ratings Direct, Standard &Poor’s. Available at http://www2.standardandpoors.com/spf/pdf/fixedincome/Sovereign%20Defaults%20Set%20to%20Fall%20Again%20in%202005%20(9.28.2004).pdf.

STATACORP. (2003) Stata Statistical Software: Release 8.0. College Station: Stata Corporation.THORP, ROSEMARY. (1998) Progress, Poverty and Exclusion: An Economic History of Latin America in the 20th

Century. Washington, DC: Inter-American Development Bank.TORAL, PABLO. (2001) The Reconquest of the New World: Multinational Enterprises and Spain’s Direct

Investment in Latin America. Burlington: Ashgate.USAID. (2004) Latin America and the Caribbean: Selected Economic and Social Data, 2004. Washington,

DC. Available at http://qesdb.cdie.org/lac/index.html.VAALER, PAUL M., AND BURKHARD N. SCHRAGE. (2004) Privatizing Firms and Residual State Influence

on Financial Performance. Working paper.VAALER, PAUL M., AND GERRY MCNAMARA. (2004) Crisis and Competition in Expert Organizational

Decision Making: Credit Rating Agencies and their Response to Turbulence in EmergingEconomies. Organization Science 15:687–703.

VAALER, PAUL M., BURKHARD N. SCHRAGE, AND STEVEN A. BLOCK. (2005) Counting the Investor Vote:Political Business Cycle Effects on Sovereign Bond Spreads in Developing Countries. Journal ofInternational Business Studies 36:62–88.

GLEN BIGLAISER AND KARL DEROUEN, JR. 137

VAALER, PAUL M., BURKHARD N. SCHRAGE, AND STEVEN A. BLOCK. (2006) Elections, Opportunism,Partisanship and Sovereign Ratings in Developing Countries. Review of Development Economics10:154–170.

WEYLAND, KURT. (2004) The Politics of Market Reform in Fragile Democracies: Argentina, Brazil, Peru, andVenezuela. Princeton: Princeton University Press.

WILLIAMSON, JOHN. (1990) The Progress of Policy Reform in Latin America. Washington, DC: Institute forInternational Economics.

WORLD BANK. (2004) World Development Indicators. Washington, DC.

Sovereign Bond Ratings and Neoliberalism in Latin America138