socio-economic implications of gi registration for agricultural

TRANSCRIPT

Vol-1: Analysis of country-wide survey results of 75 products

An out put from project funded by United Nations Conference on

Trade and Development, New Delhi

Authors

S.K. Soam

&

R. Kalpana Sastry

National Academy of Agricultural Research Management, Rajendranagar, Hyderabad- 500 407

Socio-economic implications of GI registration for agricultural and non-

agricultural commodities/ products in India

Copyright© 2008 : National Academy of Agricultural Research Management,

Hyderabad and United Nations Conference on Trade and Development, New Delhi.

Authors : Dr S.K. Soam, Senior Scientist, NAARM and Dr R. Kalpana Sastry, Principal Scientist, NAARM.

Cover design : Shri P. Namdev, Technical Officer, NAARM.

Correspondence : National Academy of Agricultural Research Management (NAARM), Rajendranagar, Hyderabad- 500 407, India

Citation : S.K. Soam and R. Kalpana Sastry (2008). Socio-economic implications of GI registration for agricultural and non-agricultural commodities/ products in India: Volume-1: Analysis of country-wide survey results of 75 products. NAARM, Hyderabad.

First printed : 2008, 503 p+

Published by : Director National Academy of Agricultural Research Management (NAARM), Rajendranagar, Hyderabad- 500 407, India.

Printed at : NAARM, Hyderabad, India.

Acknowledgements

The development of this study owes much to the encouragement and support provided by the

education division of Indian Council of Agricultural Research (ICAR). We are indebted to Dr S. Prakash

Tiwari, DDG (Edn), ICAR for his approval, encouragement and wholehearted support to the project. We

express our grateful thanks to Dr S. M. Ilyas, Director, NAARM for his over all supervision and technical

guidance to the project. Dr Ilyas as an expert on technical and IPR matters provided his invaluable

guidance and unstinted support to this research study.

We express our profound thanks to Dr R.K. Samanta, formerly Acting Director, NAARM and

Joint Director (Trg), NAARM, who provided all kinds of technical guidance and administrative support.

The project team is also grateful to Dr N.H. Rao, Joint Director, NAARM and Dr T. Balaguru, HoD

(ARSMP) for their time-to-time interaction and overall supervision of the project progress. The special

thanks are due to Mr Suresh Kumar, CAO, NAARM, Mr V. S. Subramanian, FAO, NAARM, Mr Subodh

Kumar, Executive Counselor, APTDC, Hyderabad and Mr V.K. Unni, Associate Professor, NALSAR, who

in capacity of members of ‘Policy Backstopping Group’ contributed lot to the project.

Mr Abhijit Das, Senior Trade Officer, UNCTAD and Ms Rashmi Banga, consultant, UNCTAD

and Mr Sanjay Kumar, Formerly Director at Ministry of Commerce deserves special mention because of

their technical guidance through out the conceiving of project, data collection, analysis and interpretation.

We are also thankful to Mr Abhay Mishra, Managing Director, Fintec-Genesis, who as another partner of

the UNCTAD study project contributed at several milestone phases to the project.

The large data collection work may not have possible without active support of ‘Data Facilitators’

and ‘Data Enumerators’ affiliated to several Agricultural Universities, ICAR research institutes and other

organizations. The project team is highly thankful to them. Ms Delphine Marrie-VIVIEN, visiting

researcher at National Law School, Bangalore deserves special thanks for writing one of the chapters.

Thanks are due to facilitators of case studies namely Dr P. Nayak, of textile committee, Dr SS Chandel of

HP government, Mr Vijayan of KSIC, Mr Ramakrishna, SISI and Mr Muzaffar Kalle Bhai of Chanderi.

The Project Assistant, Ms H.B. Rashmi was the core of the project, the investigators do not have

words to thank her for her extraordinary contribution to the project. We acknowledge help from Dr

Jaganadham Challa, Principal Scientist, NAARM, who supported the project in most difficult times of data

analysis. The team is thankful to the analysis assistance provided by Ms Sneha and Ms Praveena. The

Administrative, Finance and Technical personals of the Academy contributed immensely for the success of

all small and big activities of the project. We thank Mr P.P. Brahmaji, AAO, Mr Y. Shanker Rao, AAO, Mr

C. Bagaiha, Ms Vijya Lakshmi, Mr P.G. Kohad, Mr M. Sridhar, Mrs Jhansi Laxmi, Mr P. Srinivas, Mr

Shekhar Reddy, Mr P. Namdev and other staff at the Academy.

NAARM, Hyderabad

April, 2008

S.K. Soam

R. Kalpana Sastry

Content

Chapter/ Annex no. Chapter/ Annex title Page no.

Volume-1

Executive Summary i-xii

Instructions for Readers xiii-xv Chapter-1 Introduction, Background and Scope of Work 01-07

Chapter-2 Listing, Ranking and Synopsis of GI Suitable Products 08-22

Chapter-3 Approach and Methodology 23-29

Chapter-4 Socio-economic Profile of Producers 30-47

Chapter-5 Analytical Profile of Agricultural Products and Producers: opinion survey of producers

48-80

Chapter-6 Analytical Profile of Non-Agricultural Products and Producers: opinion survey of producers

81-110

Chapter-7 Analytical Profile of Products Involving Indigenous Knowledge: opinion of stakeholders

111-142

Chapter-8 Analytical Profile of Registered GI Products: opinion of stakeholders

143-170

Chapter-9 Opinion, Knowledge, Role and Suggestions of Institutional Stakeholders about Agricultural and Non-Agricultural Products

171-204

Chapter-10 Opinion, Knowledge and Suggestions of Consumers about Agricultural and Non-Agricultural Products

205-213

Chapter-11 Opinion, Knowledge and Suggestions of Traders about Agricultural and Non-Agricultural Products

214-234

Chapter-12 Case Studies of Few Registered Products 235-278

Chapter-13 Geographical Indications in India: The legal framework, its implementation and Issues for the future

279-318

Chapter-14 Action Framework: Facts & Recommendations 319-337

Bibliography Annexure

Annexure-IV Socio-economic profile of producers 338-345

Annexure-V Analytical profile of agricultural products and producers 346-366

Annexure-VI Analytical profile of non-agricultural products and producers

367-393

Annexure-VII Analytical profile of products involving indigenous knowledge: opinion of stakeholders

394-404

Annexure-VIII Analytical profile of registered GI products: opinion of

stakeholders 405-416

Annexure-IX Opinion, knowledge, role and suggestions of institutional stakeholders about agric. and non-agricultural products

417-445

Annexure-X Opinion and knowledge of consumers about agricultural and non-agricultural products

446-454

Annexure-XI Opinion, knowledge and Suggestions of traders about agricultural and non-agricultural products

455-471

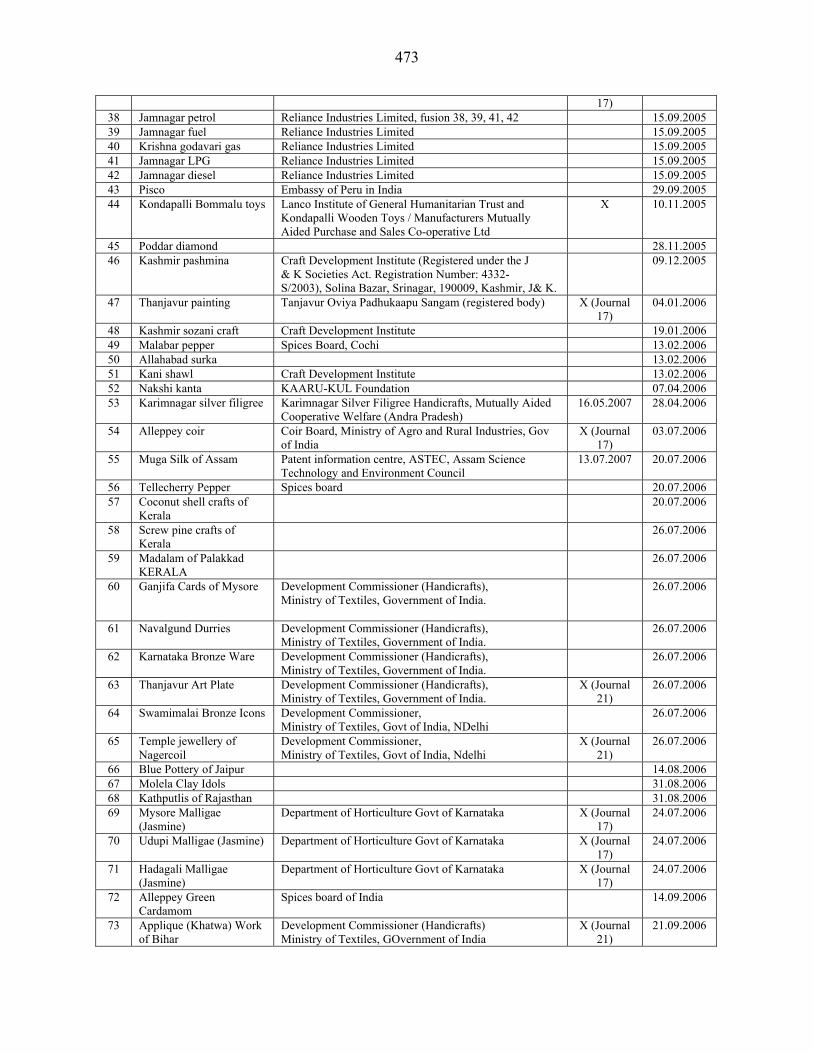

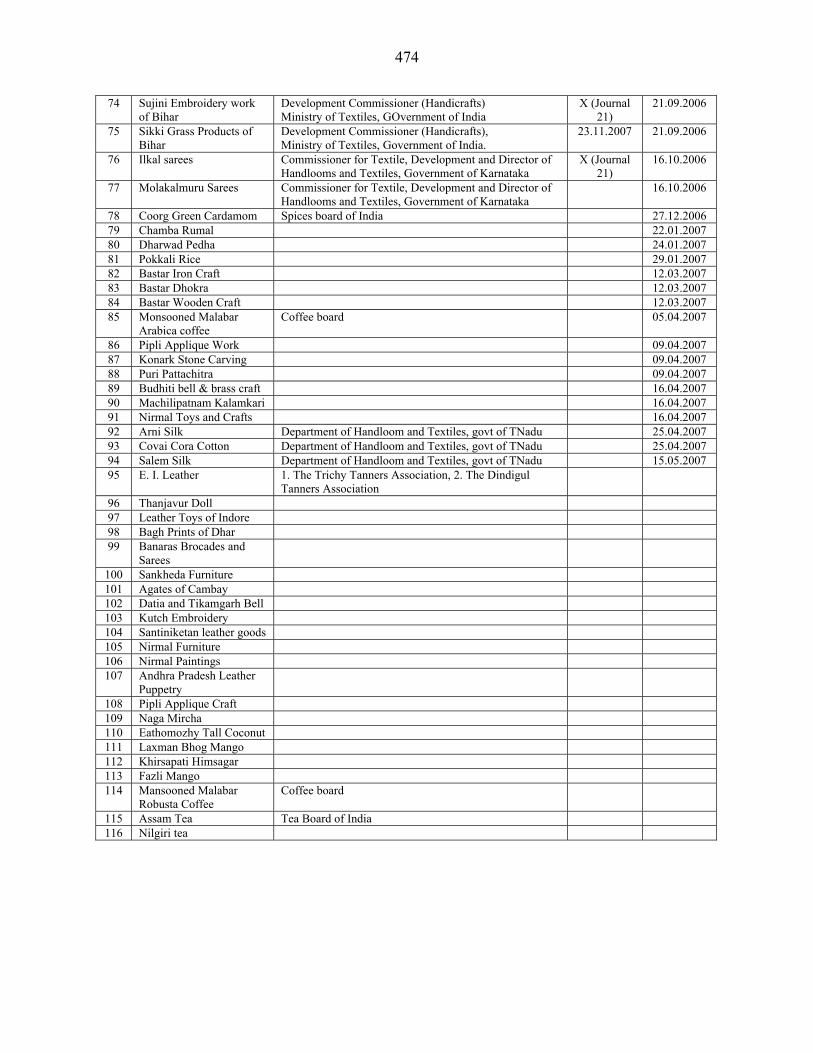

Annexure-XIII List of applied and registered GIs in India 472-474

Action framework: Facts as per agricultural GI types 475-489 Annexure-XIV

Action framework: Facts as per non-agricultural GI types 490-503

Volume-2

Annexure-XV Product profile of agricultural products: Stakeholders survey

1-24

Annexure-XVI Product profile of non-agric. products: Stakeholders survey

25-52

Annexure-XVII Product profile of agricultural products: Literature survey 53-109

Annexure-XVIII Product profile of non-agric. products: Literature survey 110-229

Annexure-XIX List of identified potential GI products 230-245

Annexure-XX List of the facilitators of the study 246-255

Survey questionnaires used in the study: Household survey- schedule-2

256-258

Survey questionnaires used in the study: Socio economic survey of agricultural products involving producers- schedule-3.1

259-269

Survey questionnaires used in the study: Socio economic survey of non-agricultural products involving producers- schedule-3.2

270-281

Survey questionnaires used in the study: Socio economic survey of agricultural and non-agricultural products involving institutional stakeholders- schedule-4

282-306

Annexure-XXI

Survey questionnaires used in the study: Socio economic survey of agricultural and non-agricultural products involving consumers and traders- schedule-5

307-311

Executive Summary

Objectives and scope of study

Following were the objectives of the study:

To explore, using specific examples, how geographical indications (GIs) as a

form of intellectual property impact the market opportunities

Analyze how the grant of GIs could impact the lives and livelihoods of those

producing (directly or indirectly) the products that have been/ could be protected

To understand whether geographical indications provides an extra competitive

advantage to people associated with the protected product under GI.

The terms of reference of the study included the identification of specific products in

different classes, both agricultural and non-agricultural, from three different regions, of

the country where GI protection play / can play a determining role in enhancing the value

of the product in the domestic/export market. Overall, at least 25 products must be

identified in each of the three regions, which may be suitable for GI registration. The

major items of observations in the study are:

1. Legal & policy structure of GI protection

2. Listing, classification, and ranking of GI products

3. Critical analysis of the producers

4. Critical analysis of marketing scenario and future strategies

a. Product profile

b. Production profile and strategies

c. Market profile and strategies

d. Pricing policies

e. Distribution networks

f. Livelihood systems of producers

ii

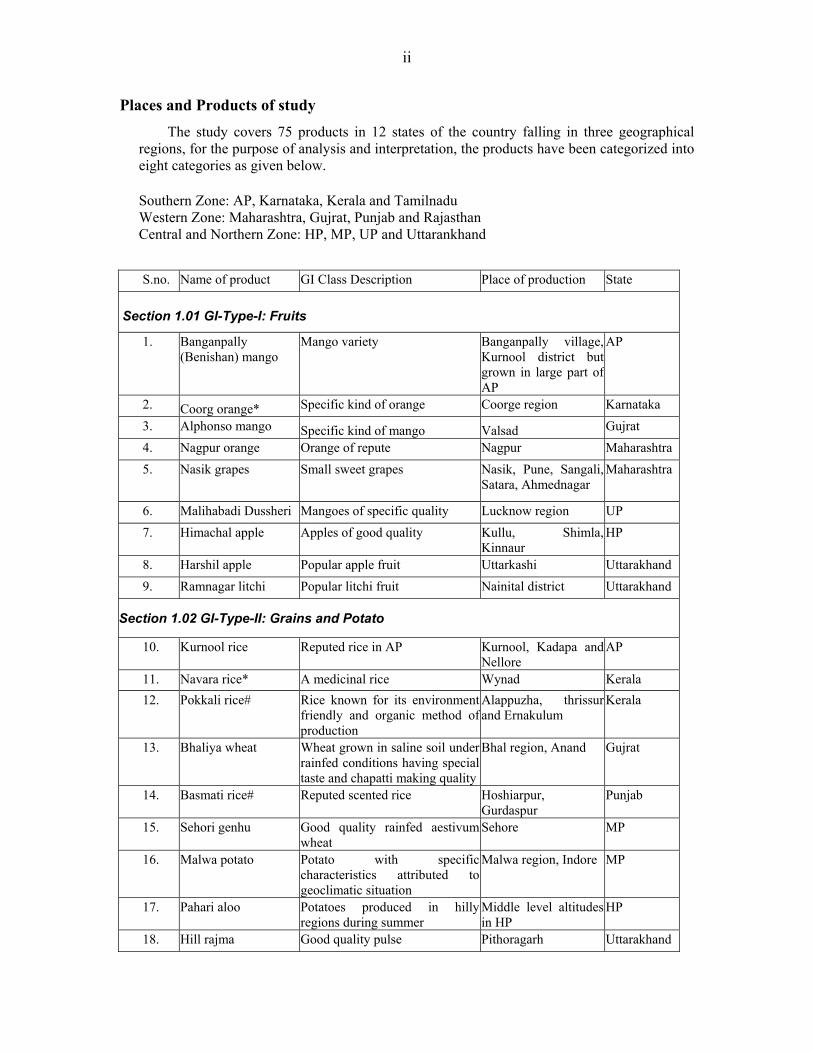

Places and Products of study

The study covers 75 products in 12 states of the country falling in three geographical regions, for the purpose of analysis and interpretation, the products have been categorized into eight categories as given below.

Southern Zone: AP, Karnataka, Kerala and Tamilnadu Western Zone: Maharashtra, Gujrat, Punjab and Rajasthan Central and Northern Zone: HP, MP, UP and Uttarankhand

S.no. Name of product GI Class Description Place of production State

Section 1.01 GI-Type-I: Fruits

1. Banganpally (Benishan) mango

Mango variety Banganpally village, Kurnool district but grown in large part of AP

AP

2. Coorg orange* Specific kind of orange Coorge region Karnataka 3. Alphonso mango Specific kind of mango Valsad Gujrat 4. Nagpur orange Orange of repute Nagpur Maharashtra 5. Nasik grapes Small sweet grapes Nasik, Pune, Sangali,

Satara, Ahmednagar Maharashtra

6. Malihabadi Dussheri Mangoes of specific quality Lucknow region UP 7. Himachal apple Apples of good quality Kullu, Shimla,

Kinnaur HP

8. Harshil apple Popular apple fruit Uttarkashi Uttarakhand 9. Ramnagar litchi Popular litchi fruit Nainital district Uttarakhand

Section 1.02 GI-Type-II: Grains and Potato

10. Kurnool rice Reputed rice in AP Kurnool, Kadapa and Nellore

AP

11. Navara rice* A medicinal rice Wynad Kerala 12. Pokkali rice# Rice known for its environment

friendly and organic method of production

Alappuzha, thrissur and Ernakulum

Kerala

13. Bhaliya wheat Wheat grown in saline soil under rainfed conditions having special taste and chapatti making quality

Bhal region, Anand Gujrat

14. Basmati rice# Reputed scented rice Hoshiarpur, Gurdaspur

Punjab

15. Sehori genhu Good quality rainfed aestivum wheat

Sehore MP

16. Malwa potato Potato with specific characteristics attributed to geoclimatic situation

Malwa region, Indore MP

17. Pahari aloo Potatoes produced in hilly regions during summer

Middle level altitudes in HP

HP

18. Hill rajma Good quality pulse Pithoragarh Uttarakhand

iii

Section 1.03 GI-Type-III: Plantation and spices

19. Guntur chilli (karam) Pungent and dark red colored chillies

Guntur AP

20. Coorg coffee Reputed coffee Coorge region Karnataka 21. Wayanadan tea Tea leaves Wayanad Kerala 22. Telichery black

pepper# Dried black pepper Telichery, Kannur

district Kerala

23. Alleppy cardamom# Good quality cardamom Alleppy Kerala 24. Nilgiri tea# Good quality tea Nilgiri ranges Tamilnadu 25. Dungarpur zinger Zinger of high quality Dungarpur Rajasthan 26. Amleta & Mahadev

garlic Good quality local garlic Mandsaur, Neemach MP

27. Kumbhraj dhania Coriander of good flavour and good oil content

Guna, Rajgarh, Neemach, Mandsaur

MP

28. Fenugreek (Methi) Good quality bold seeded fenugreek or methi

Jaora, Ratlam, Neemach

MP

29. Mahoba paan Betel leaf Mahoba UP 30. Kangra tea* Tea of repute Kangra district and

other areas of HP HP

GI-Type-IV: Unexploited indigenous products

31. Nannari sharbat A black color medicinal drink made from roots of a creeper wild plant known as 'sugandhapalu'.

Kadapa AP

32. Kokam fruit juice

Juice of Garcinia known to reduce weight

Western ghats Karnataka

33. Buraansh juice Juice made from red flowers of Buraansh tree (pink flower are known to be poisonous)

Hilly districts of Uttaranchal

Uttarakhand

GI-Type-V: Confectionery

34. Tirunelveli halwa A sweet food product Tirunelveli district Tamilnadu 35. Dodha A milk based sweet product

famous in Punjab and Haryana Muktsar, Ludhiana, Amritsar, Moga districts, originated from katkapura

Punjab

36. Bikaneri bhujia A salted snack material called 'namkeen'

Bikaner Rajasthan

37. Bikaneri rasgolla Sweet product Bikaner Rajasthan 38. Agra petha Sweet made of ash gourd Agra UP 39. Bal mithai Sweet chocolate blocks with

cover of post seeds Almora Uttarakhand

GI-Type-VI: Handicrafts

40. Kondapalli bommalu*

Wooden Toys Kondapalli, Krishna district

AP

iv

41. Chennapatana toys* Colored wooden toys Mandya, Bangalore rural

Karnataka

42. Thanjavur plate#

Painted plate used as souvinir Thanjavur Tamilnadu

43. Kolhapuri chappal Leather shoes and slippers Kolhapur Maharashtra 44. Warli paintings Traditional cloth painting by the

tribal people Thane Maharashtra

45. Panjabi jooti Special kind of footwear with embroidary on it for men and women, also known as khusa and kadi jooti

Patiala, Muktsar and other places

Punjab

GI-Type-VII: Manufactured products with organized trade

46. Hyderabad pearls Pearls of repute Hyderabad AP 47. Mysore sandal soap* Cosmatics Mysore Karnataka 48. Nilgiri oil Good quality non-edible oil Nilgiri ranges Tamilnadu 49. Sivakasi patakha Fire crackers Sivakasi,

Virudhunagar district Tamilnadu

50. Coimbatore wet grinder*

Machine used for making paste of cereal/pulses for prperation of south Indian dishes

Coimbatore Tamilnadu

51. Harambha thresher Wheat thresher Rampura phool district Bhatinda, Ludhiana, Faridkot and Moga

Punjab

52. Makrana marble Stone as building material Rajasthan Rajasthan 53. Jaipur blue pottery # Pottery and souvinirs made of

porcelain Jaipur Rajasthan

54. Ferozabad chundia and glassware

Specific design and process for making glass bangles (Chudia) and cut glass items

Ferozabad UP

55. Moradabad brass material

Utensils and decorative articles of brass

Moradabad UP

56. Saharanpur furniture Specific design of furniture made of 'Sisso'

Saharanpur UP

57. Khurja pottery China clay pottery Khurja, Bulandshahar district

UP

Section 1.04 GI-Type-VIII: Textiles

58. Gadwal saree Women wear in cotton, silk with pure silk border

Gadwal, Mahaboobnagar district

AP

59. Srikalahasti kalamkari*

Free hand printing on cloth with natural dyes

Chittoor AP

60. Mysore silk* Reputed silk clothing including Mysore Karnataka

v

saree 61. Kancheepuram silk*

Famous silk sarees Kancheepuram Tamilnadu

62. Bandhani saree

Sarees made from binding method and block printing with herbal dyes

Jamnagar, Ahemdabad

Gujrat

63. Patola saree

Double ikat known for design dyeing and weaving

Patan, Rajkot

Gujrat

64. Kutch embroidery# Specific embroidery with fabric designs and mirror on cloth, various decorative articles and on houses

Kutch Gujrat

65. Paithani saree Specific saree style prepared at Yewala

Paithan, Nasik district, Aurangabad

Maharashtra

66. Solapuri chadar* Bedsheets/ cover sheets Solapur Maharashtra 67. Phulkari# Specific Kind of embroidery on

women wear Patiala and adjacent areas

Punjab

68. Ludhiana hosiery

Cotton based undergarments and woolen material

Ludhiana

Punjab

69. Jaipuri rajai#

Light in weight quilt made of cotton

Jaipur Rajasthan

70. Sanganeri print A particular print for bedsheets Jaipur Rajasthan

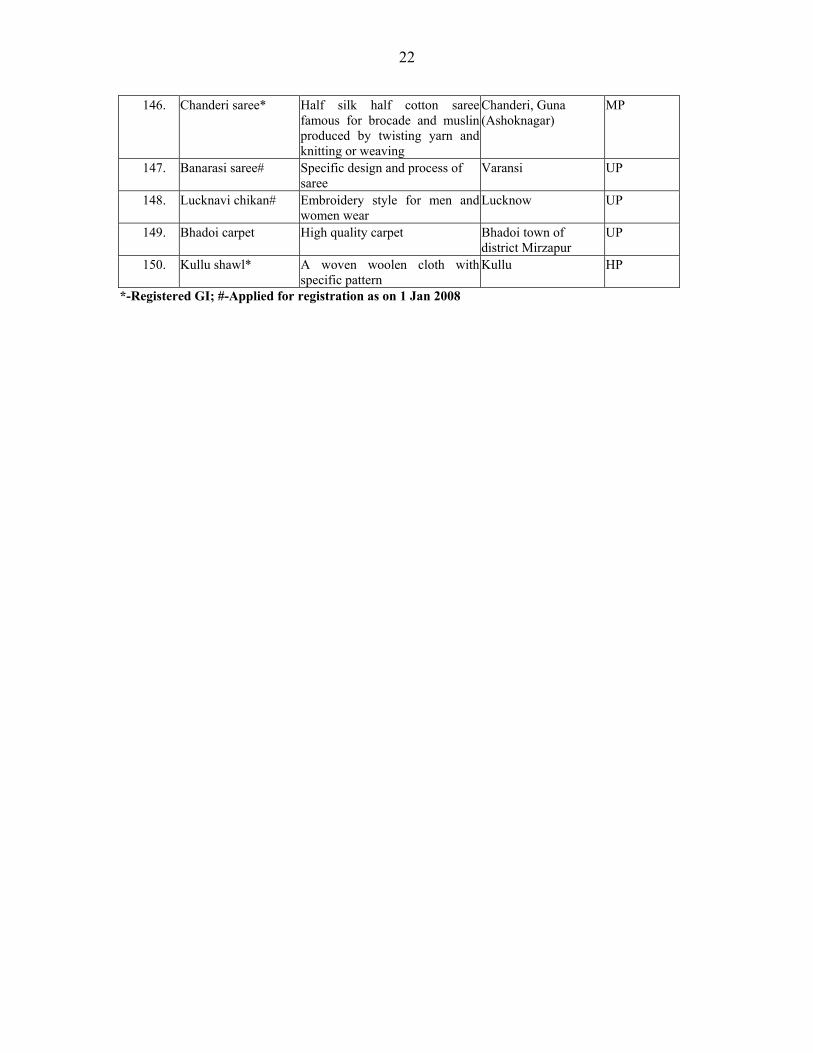

71. Chanderi saree*

Half silk half cotton saree famous for brocade and muslin produced by twisting yarn and knitting or weaving

Chanderi, Guna (Ashoknagar)

MP

72. Banarasi saree# Specific design and process of saree

Varansi UP

73. Lucknavi chikan# Embroidery style for men and women wear

Lucknow UP

74. Bhadoi carpet High quality carpet Bhadoi town of district Mirzapur

UP

75. Kullu shawl* A woven woolen cloth with specific pattern

Kullu HP

*-Registered GI; #-Applied for registration as on 1 Jan 2008

Data collection and respondents for the survey

For the study, 1865 respondents were surveyed, therefore the interview schedules

so designed were administered to 28 persons for each product in the following fashion:

1. Ten producers on appropriate schedule. For agricultural product it is schedule 2

and schedule 3.1. For non-agricultural product it is schedule 2 and schedule 3.2.

2. Eight different institutional stakeholders on schedule 4

3. Five different consumers on schedule 5

4. Five different retailing traders on schedule 5

vi

The data collection process included arrangements of ‘Facilitators’ in various states

for each product for data collection administration and data is collected by the

‘Enumerators’. The data was collected from 45 villages and 60 district towns in 12 states.

Background of the producers

The producers of agricultural and non-agricultural products are mainly engaged in

their respective enterprise only, it is their main livelihood. About 7-8% respondents in

agricultural and non-agricultural products engaged in other subsidiary enterprise also.

The producers mainly belong to either other backward classes (OBCs) or communities

other than Scheduled Castes (SCs) or Scheduled Tribes (STs). The trend is almost same

for agricultural and non-agricultural enterprises.

Only 15.3% of total respondents provided any detail of their income, it has been

observed that respondents were not much willing to share information on income, asset

and expenditure etc., and this tendency was more prevalent in the non-agricultural

producers. About 62% of the total producers were below Rs. 50,000/- annual income,

10% between 50,000 to 100,000 and 28% beyond 100,000. The income-expenditure-asset

analysis was therefore, done for the following three groups.

• Category A: Respondents of annual income up to Rs 50,000/-

• Category B: Respondents of annual income > 50,000/- to 200,000/-

• Category C: respondents of annual income of >200,000/-

Highlight of opinion survey of agricultural producers

• Mostly the producers are engaged in production only. Some do the trading also

but providing training is mostly not in their agenda.

• In almost all cases, the head of family is also head of enterprise and in no case the

non-family members was principal operator.

• Skill acquisition through formal training is less than 3%.

• The number of engaged skilled women workers is almost double of the engaged

skilled men workers.

• The producers surveyed are mainly producers of product in question but they do

not allot the whole land for the product only. But producers of more than 50% of

vii

the product put their 60% or more land under the cultivation of product, therefore,

the product is main livelihood for them.

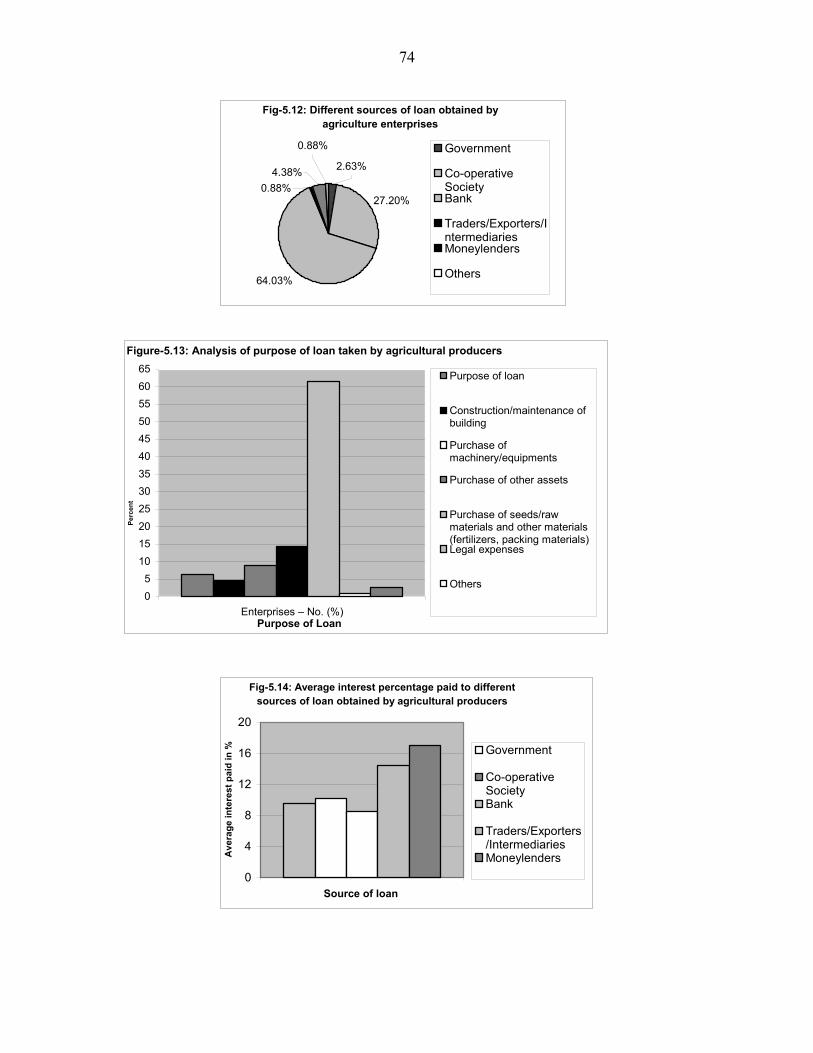

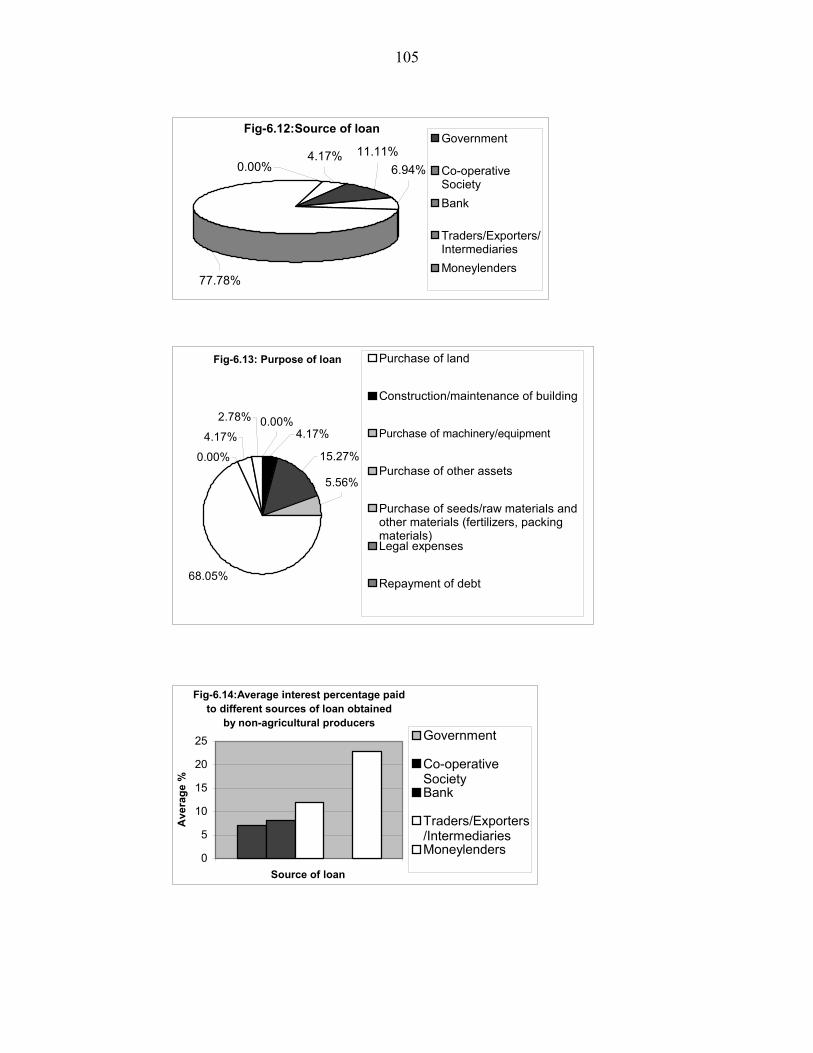

• About 53 percent of the producers have actually taken the loans, which is less

than Rs. 50,000, the loan is mostly taken for purchase of inputs.

• Only in 30 per cent respondents inform about pucca packing otherwise mostly it

is either no packing or raw packing.

• In 28 per cent cases no grading, in rest of the cases the grading is done but mostly

its is based on physical traits.

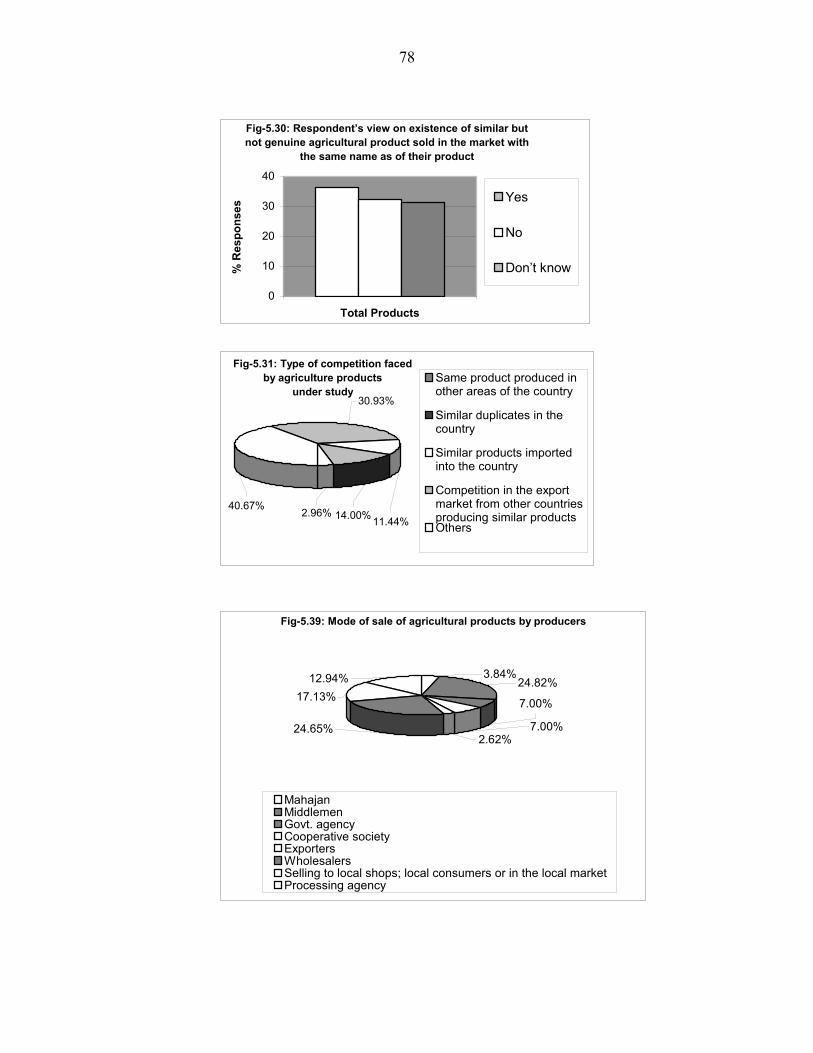

• In 14% cases only, it is either sale to government agency or cooperative society.

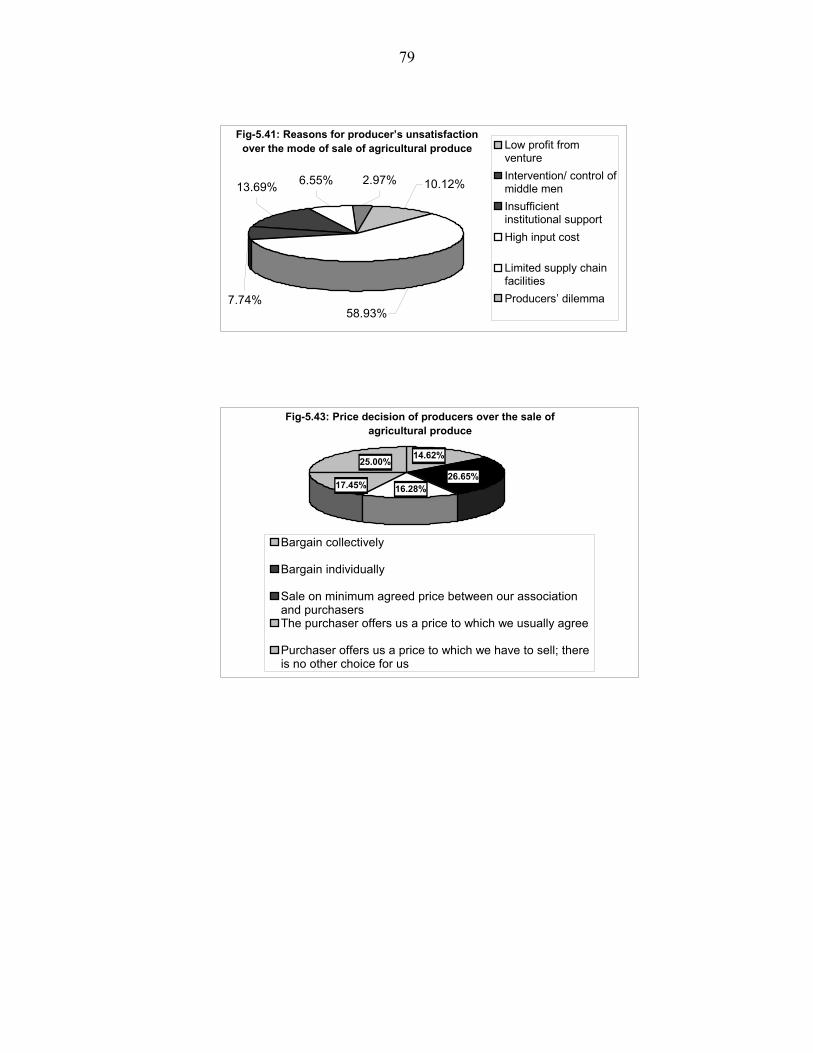

• The prices of product for sale are mostly decided either through individual

bargain or purchaser offer a price to which producers had to agree and there is no

other choice.

• The most important constraints in production are hindrances from

agronomic/natural factors, market insecurity leading to low profitability, labour

scarcity and low marketing infrastructure.

• In case of 75% of enterprises, the inspection and quality control is either by

producers themselves at production level on field and harvesting level or there is

no inspection and quality control.

• Technical standards are very weak, as observed from following responses from

the producers;

o Whether production is as per technical guidelines of government? About

74% respondents say ‘no’.

o Whether production is as per technical guidelines of any NGO? 92%

respondents say ‘no’

o Whether production is as per technical guidelines of producers

association? About 74% respondents say ‘no’.

• As post registration expectation, more than 70% wish higher unit price and

market expansion. About 42% producers expect 5-10% premium over prevailing

cost.

• About 58% producers feel that earning from enterprise is average.

viii

• On increasing the production, margin of profit and marketing needs, the producers

have given diverse views as per the GI type, but many of them are hopeful for

betterment, if timely availability of resources is assured to them.

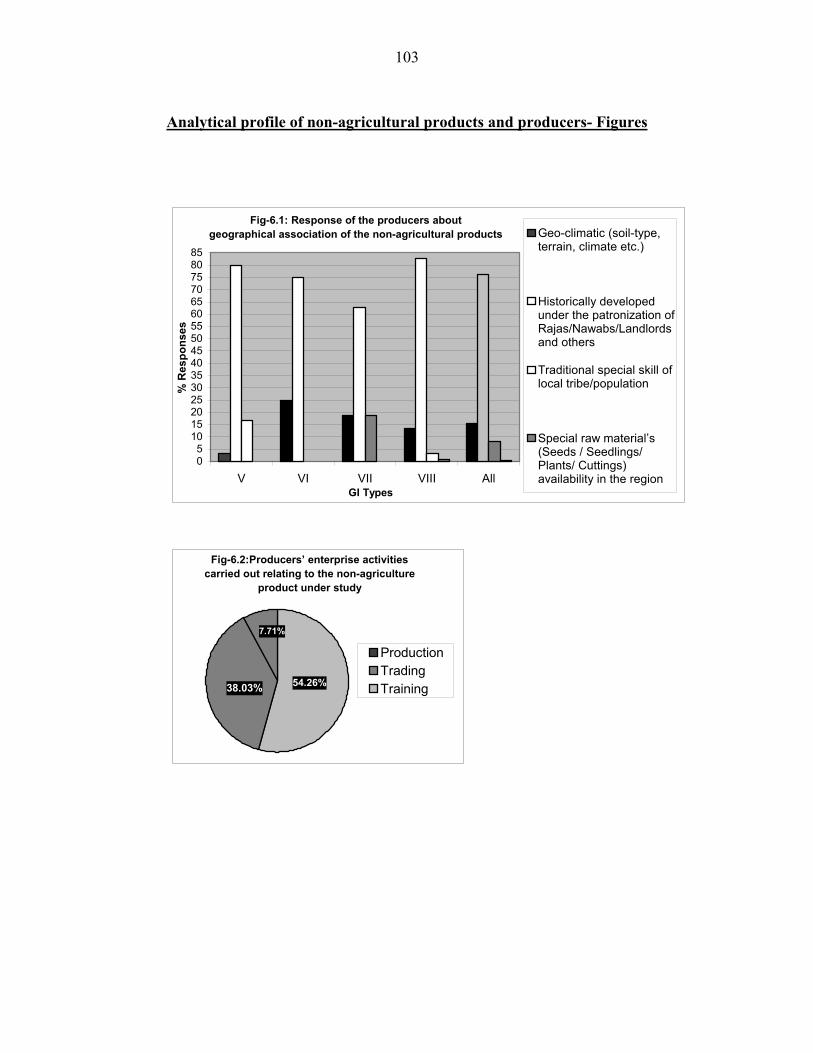

Highlight of opinion survey of non-agricultural producers

• Nearly 54 percent of the producers are engaged in production only while 38

percent are also engaged in trading. More than 45 percent of enterprises are either

part of family enterprise or of sole ownership. An important point also emerging

is that most enterprises in all group types are main activity for the owners with no

other means of business. In almost all cases, the head of family is also head of

enterprise (89 per cent) and only 8 per cent enterprises are owned by other

members of households.

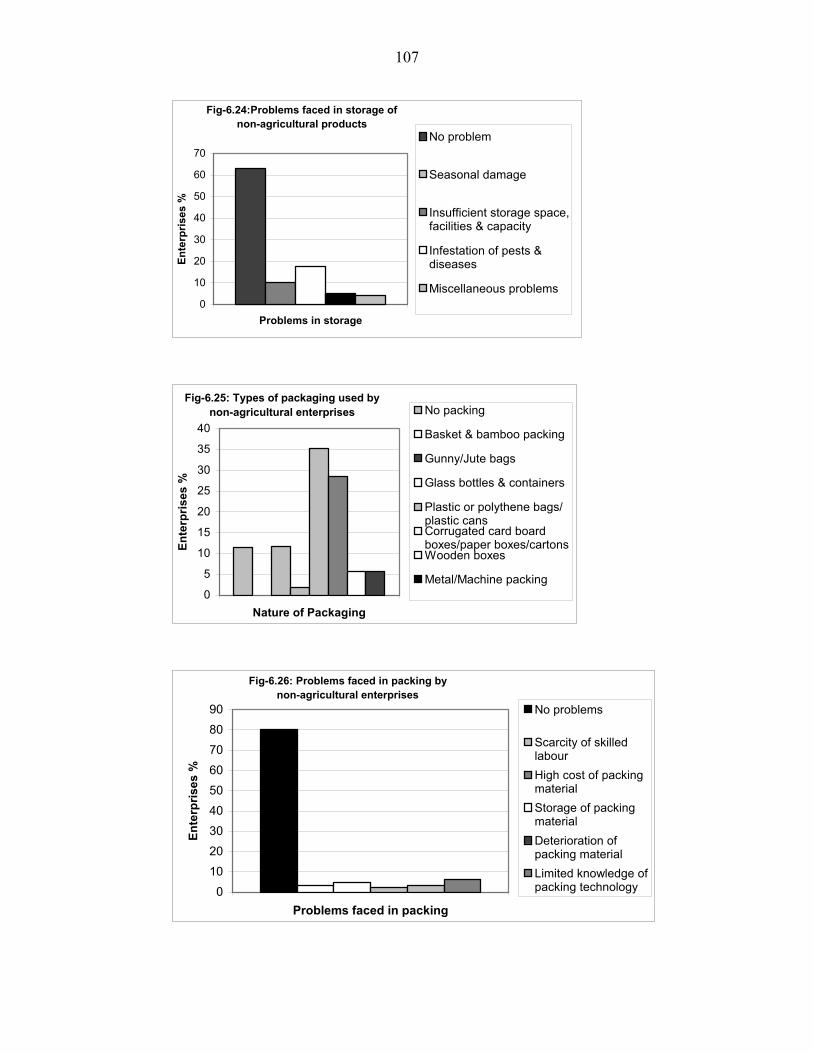

• Nearly 40 per cent of the respondents informed about no measures for storage.

Among the remaining types of storage mechanisms asked, most respondents (26

per cent) used raw packing in a bulk manner or wrapping in cloth or plastic

sheets. Forty eight per cent of respondents responded that grading of products on

traits for maintaining the quality of the products. Grading in rest of the cases is

done based on other parameters like physical traits (26%).

• Various modes of sales are there, with nearly 32 per cent respondents report direct

sales, but mostly it is to local shops followed by wholesalers.

• Only 22% respondents say that they bargain collectively.

• The most important constraints in production are hindrances from high

competition, finance, difficulty in getting inputs, scarcity of skilled workers, and

insecure markets.

• While 35 per cent do not adhere to inspection, 48 percent maintain quality

through inspection at production level at workshop and 12.9 per cent at

processing and grading level.

• About 90% of producers say that the technical guidelines from their forefathers

are ones followed by them.

• Competition- 38% believe that these are same product but produced elsewhere in

the country. The threat perceived from competition from similar products

imported in the country is fairly high (40% producers believe so).

ix

• About 56% of producers are not members of any formal or informal group.

Highlights of opinion survey of institutional stakeholders

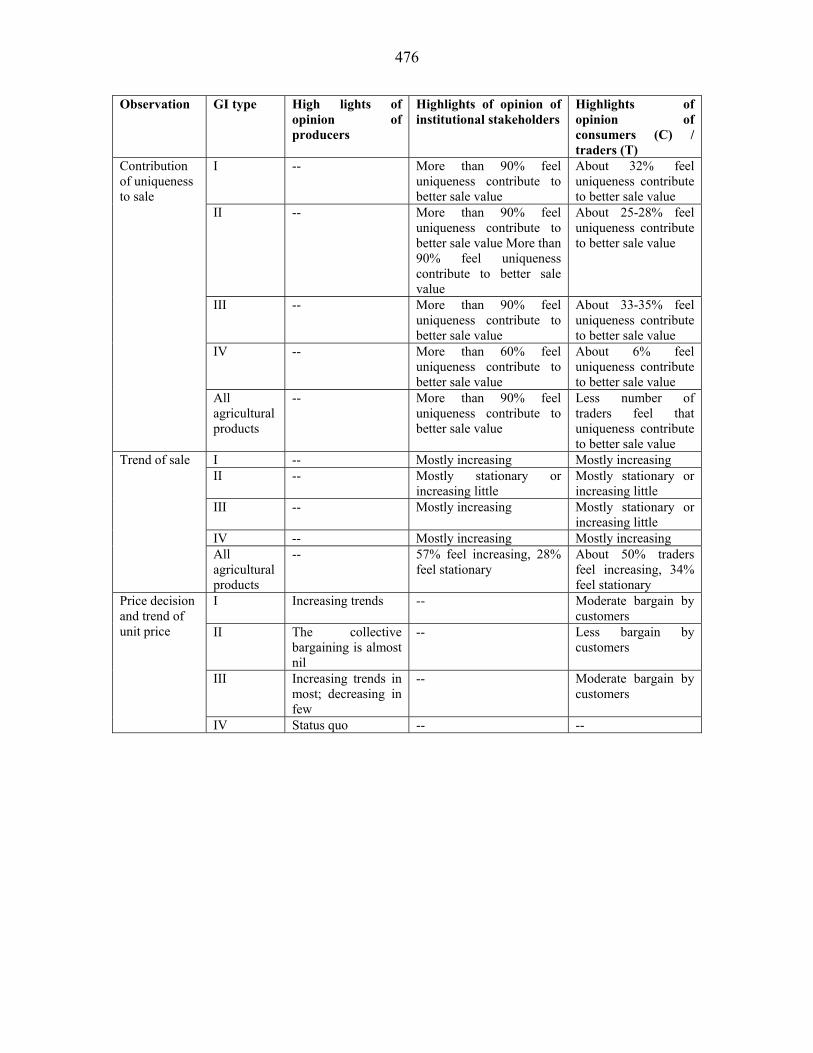

• In the opinion of institutional stakeholders, the agricultural products’ sale is

mostly confined to the region where their origin is claimed.

• Most respondents, 57% in agric and 62% in non-agric products believe that sale is

increasing.

• Stakeholders give their opinion about price increment in supply chain for

agricultural products and non-agricultural products. They feel that in the supply

chain, the intermediate stakeholders earn more than the producer.

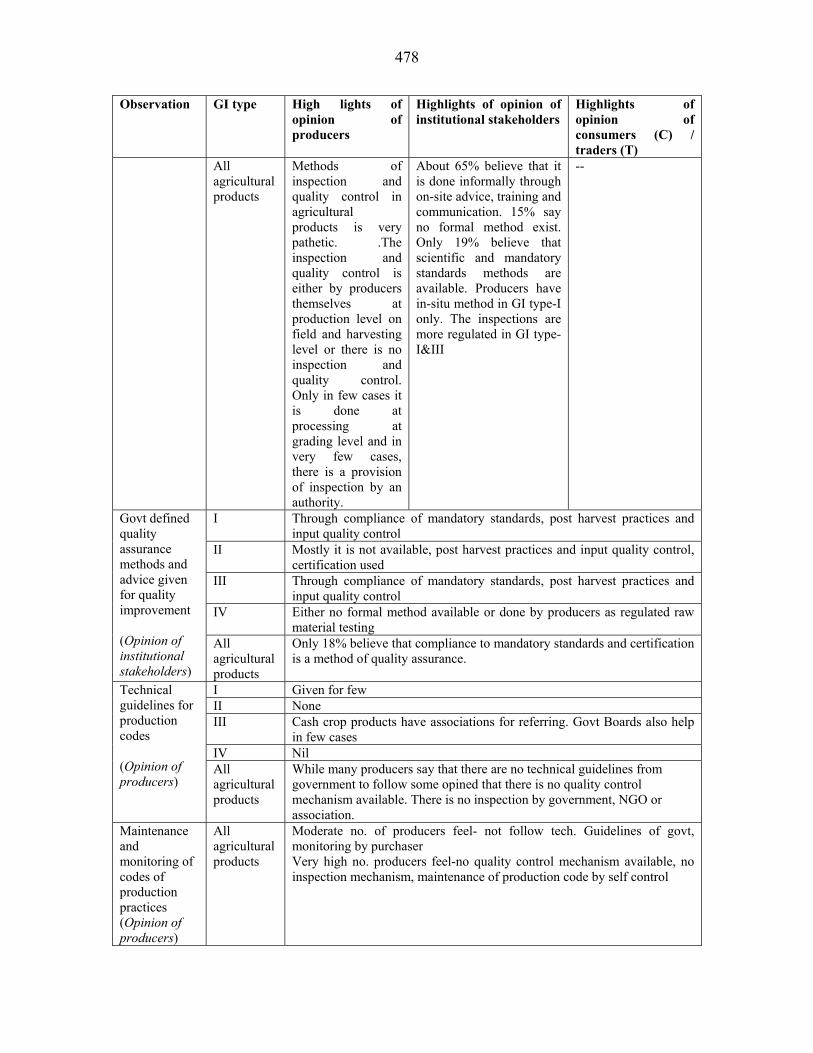

• Inspection method: In agricultural products around 45% feel that on-site advice

and inspection is the most prevalent method of quality control. In case of non-

agricultural products 19% respondents clearly believe that there are no formal

methods.

• Quality assurance: The main form of government-defined method of quality

assurance in agriculture is regulating post harvest practices and production

practices along with input supply. In non-agricultural products, majority believes

that producers regulated raw material testing is the most prevailing method.

• Major source of competition is same product produced in other areas of country.

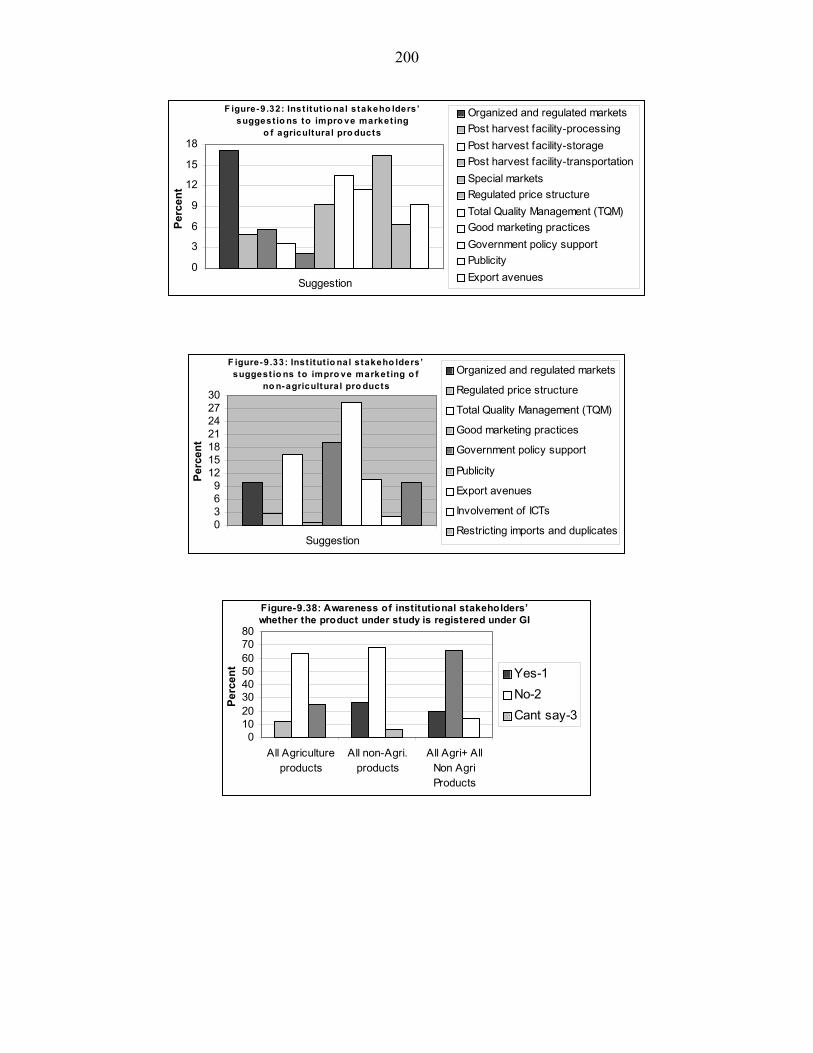

• Awareness of institutional stakeholders about community patent that is GI was

very low. In agriculture only 19% respondents knew it, while in non-agricultural

products 40% respondents knew it.

• The respondents have given various suggestions to improve the marketing of

products. The top three suggestions in agricultural products are – organized and

regulated market, government policy support and TQM, while the top three

suggestions in non-agricultural products are – publicity, government policy

support and TQM.

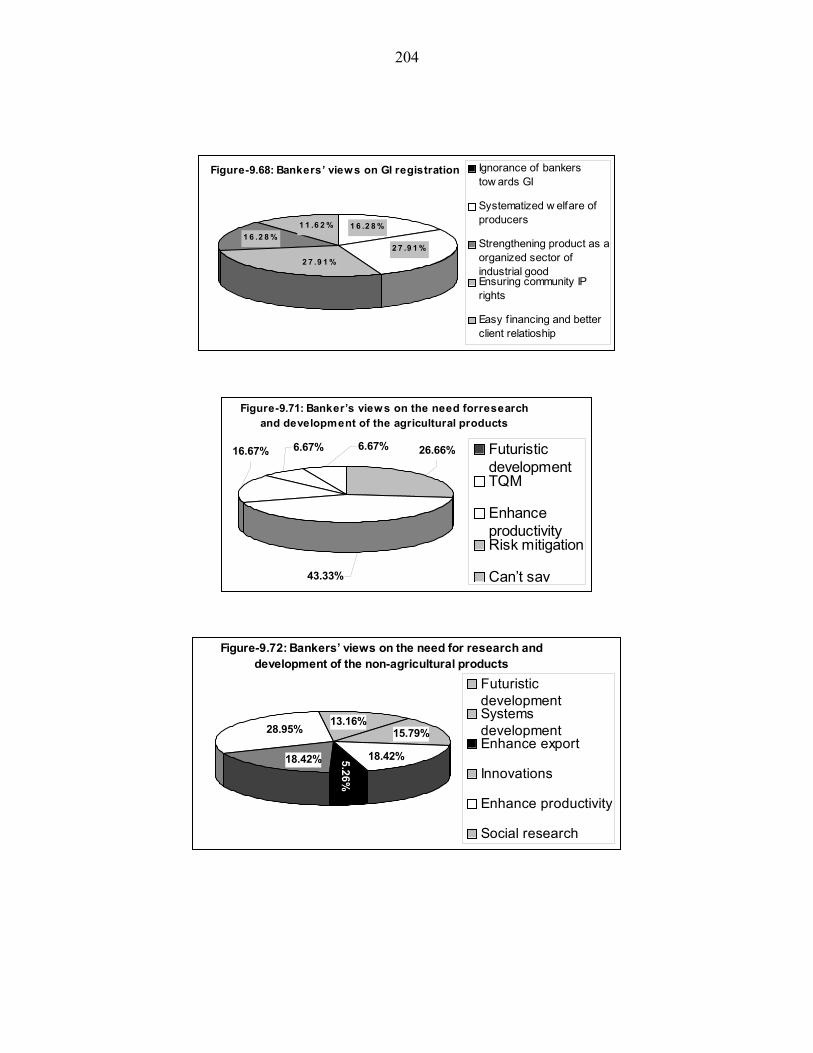

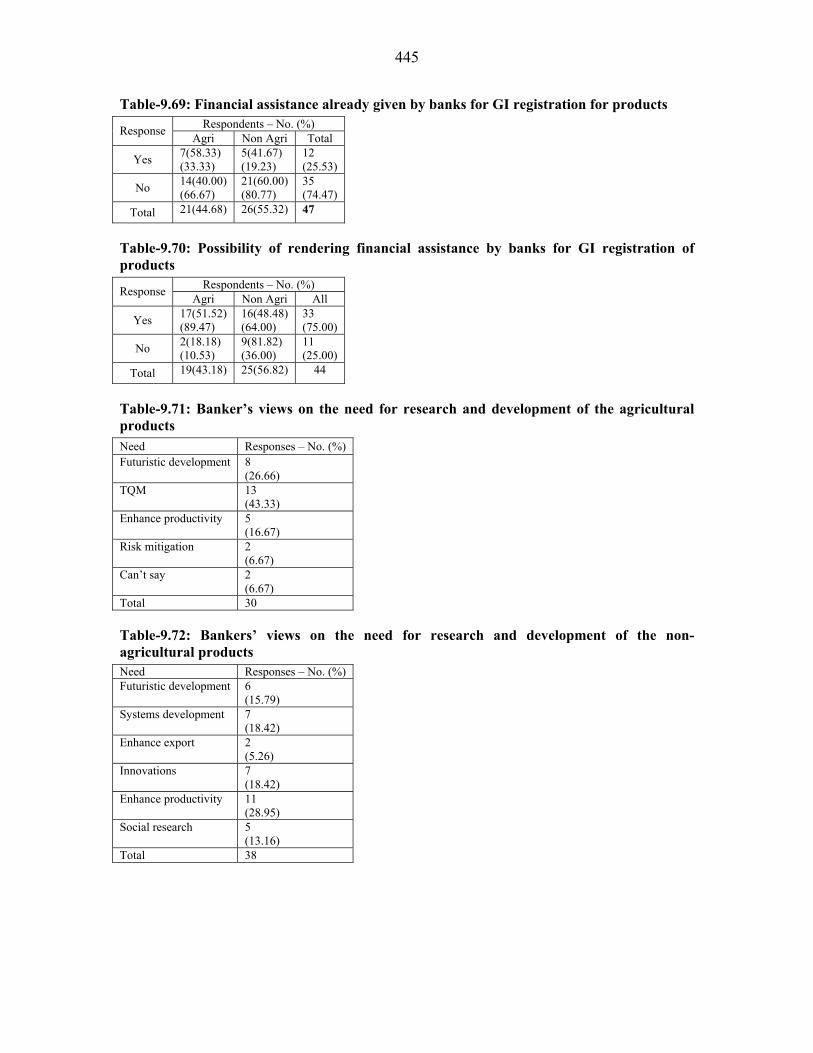

• The bankers also have suggested the areas of research. In agricultural products,

the top priority is TQM followed by futuristic development and enhancement of

productivity. While in non-agricultural products, the top area suggested is

x

enhancing productivity, followed by innovations and systems development with

equal emphasis.

• The major observations from institutional stakeholders analysis is;

- There is no specific department dealing with GI registration.

- There is no systematically arranged fixed responsibility along with target to

anyone.

- Mostly the GI registration have been done by the own knowledge gained by the

top brass/any dynamic individual of a department or subsidiary organizations

from training or elsewhere and out of their personal interest and involvement, the

registration could be done.

- In non-agricultural production, the responsibility has been taken by several

agencies of central or state government (e.g. textile committee, handicraft

development corporations, etc.). But this could not happen in case of agricultural

products except few products, where central government boards have taken

initiative.

- To avoid any future problems, it is strongly suggested that only government

supported departments and organizations should be allowed to retain the

ownership of a GI, and not any private organization because in very few cases

only a single organization represents the interest of larger group of society. The

small NGOs or any organization created by few persons does not necessarily

represent the interest of a larger group of society. Highlights of opinion survey of consumers

• Around 80% consumers in all GI types believe that product quality will become

standard and grading will improve after registration. While comparing agricultural

and non-agricultural product, it seems that impact would be more in case of

agricultural products.

• At the time of purchase a product, whether consumers are sure that product is

genuine? About 87% consumers in agricultural products and 96% in non-

agricultural products are sure about it. It means the confidence in agri-products is

little less. 51% consumers in agricultural product and 77% in non-agricultural

products make some efforts to ensure purchase of guanine products.

xi

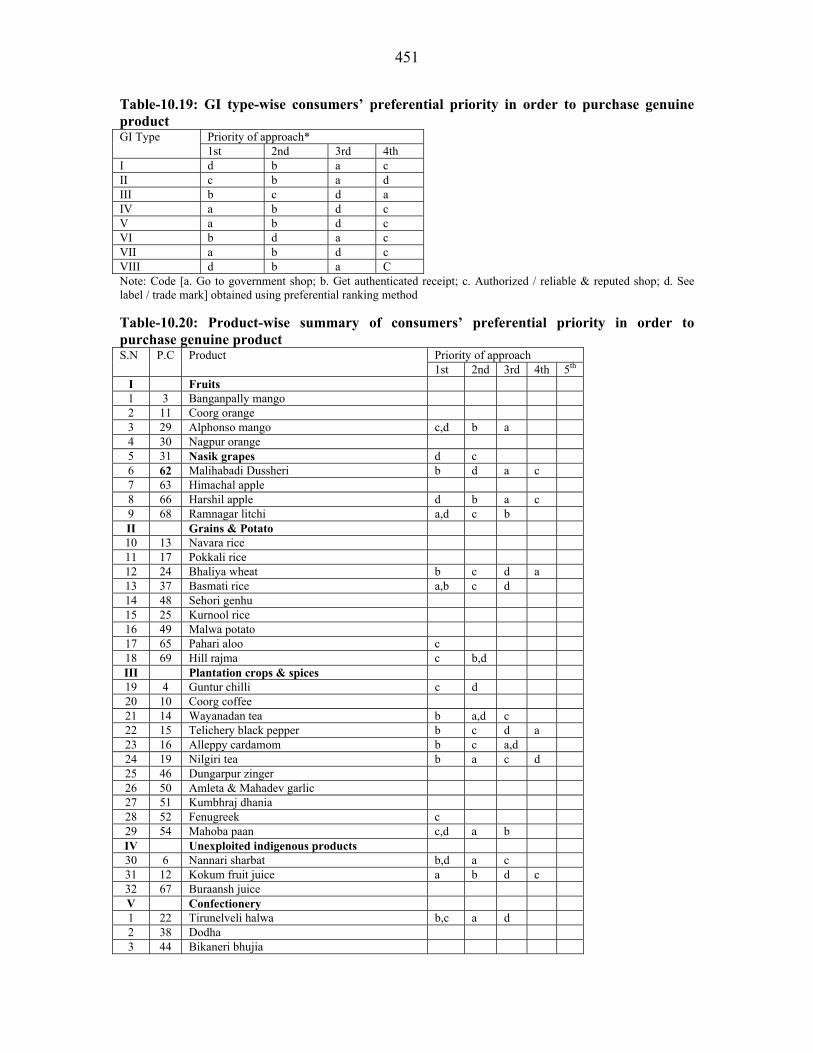

• To ensure genuine product, the most reliable method for consumers is ‘going to

authorized/ reliable / reputed shop’ followed by looking for a label or trademark

in agricultural products and taking authentic receipt in case of no-agric. products.

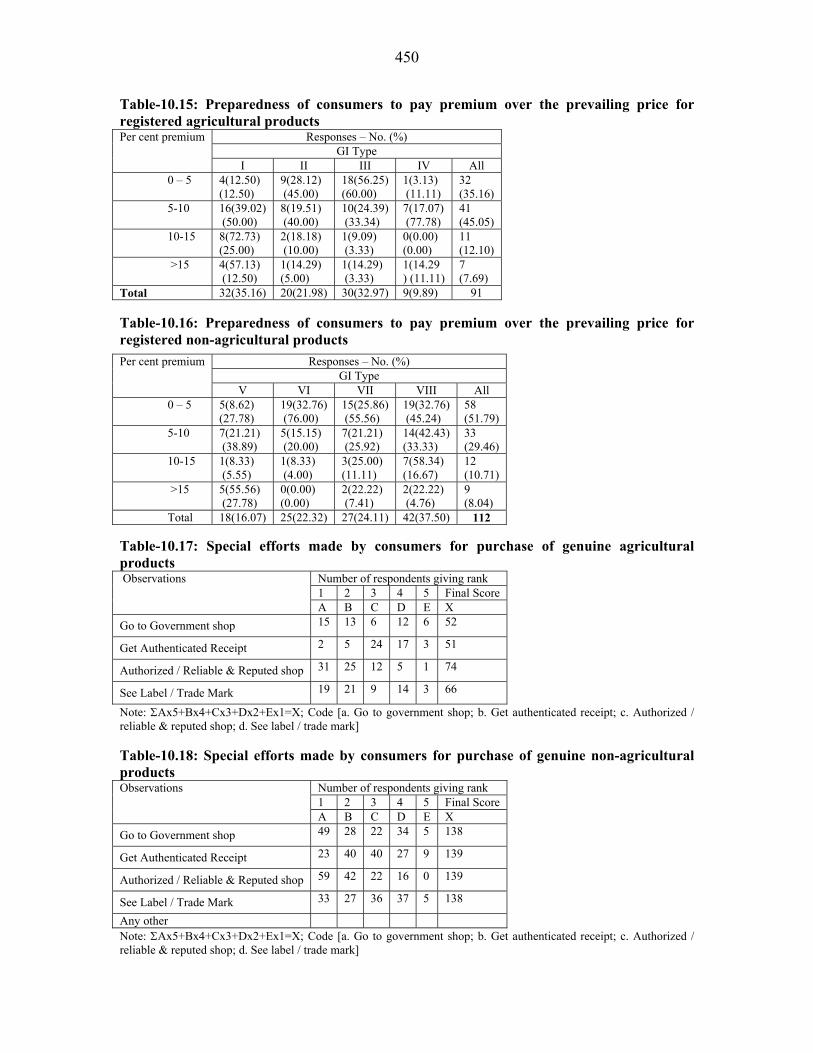

• Depending on type of GI, 40-70% consumers favour registration. As post

registration effect, 85% consumers in agricultural products and 61% in non-

agricultural products are willing to pay higher. But how much premium over the

prevailing price? In agricultural products, most agree for 5 - 10%, in case of non-

agricultural products, most agree for 0 - 5.

• Most consumers consider that unique quality; reputation, traditionality and other

characteristics are attributed to geographical origin.

• Suggestions for increasing sale;

o In agricultural products- standardize the quality followed by easy assured

availability, more publicity and reasonable price and the last suggestion is

to make innovative changes keeping the traditional base.

o In non-agricultural products- standardization of quality, reasonable price

and innovative changes are most important.

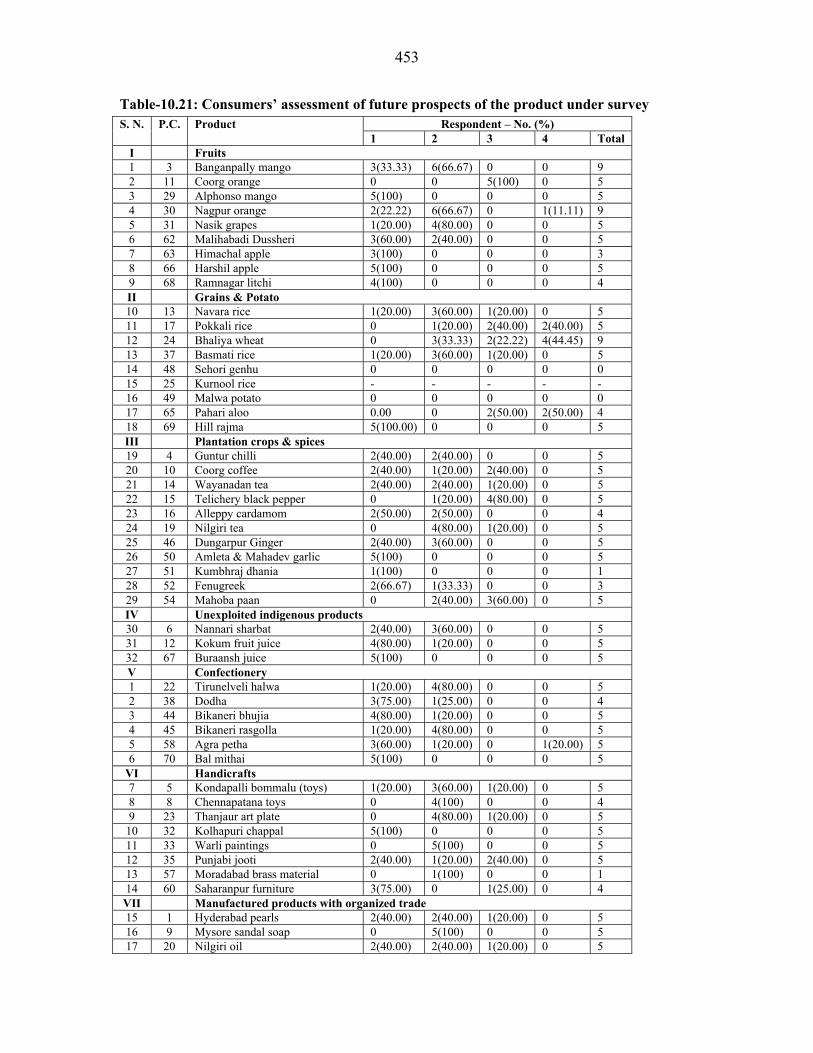

• Consumers gave ranked suggestion for the future prospects of the product.

Products where future is either stationery or not bight are - Coorg orange, Pokkali

rice, Bhaliya wheat, Pahari aloo, Coorg coffee, Telicherry, Black pepper,

Mahoba pan, Punjabi jooti, Harambha thresher, Patola saree and Bhadoi carpe.

Highlights of opinion survey of traders

• The modes of purchase by the traders have direct impact on the price

decision-making system of the producers. In non-agricultural products, the

direct purchase is more prevalent than agricultural products.

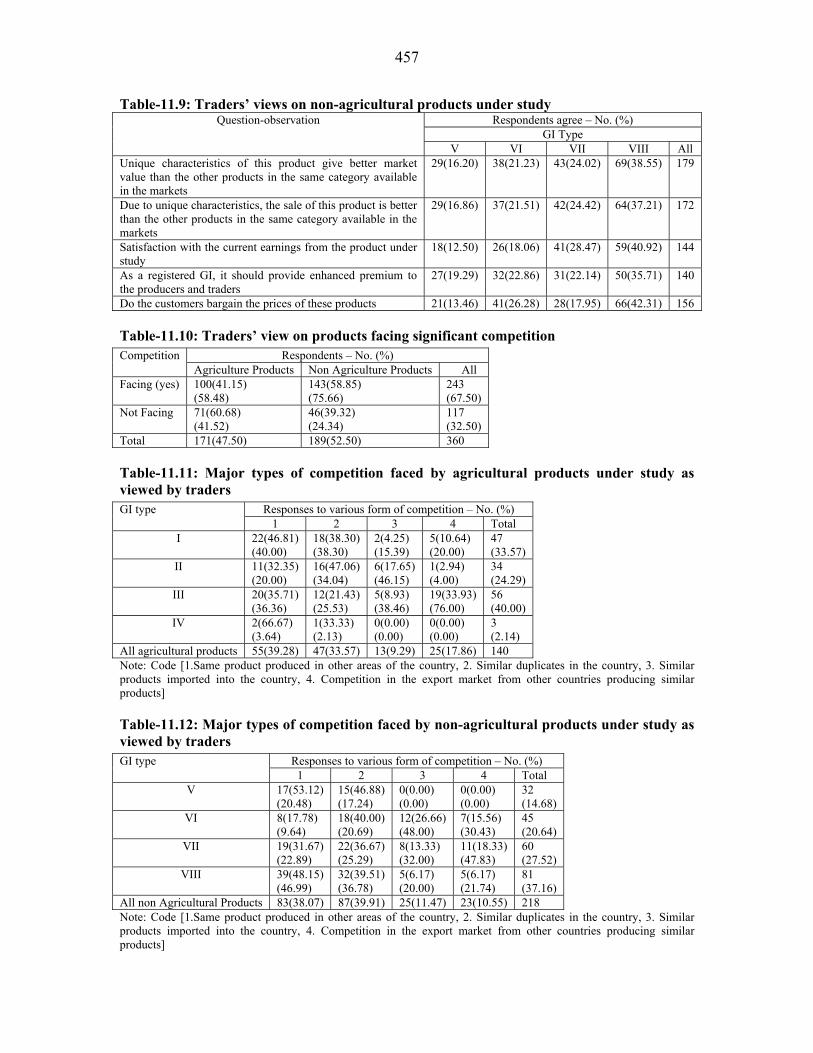

• Depending upon type of GI, 20-30% traders feel that unique characteristics of

the product give better market value.

• In general about half of traders feel that sale is increasing significantly.

• In the price decision between trader and consumer bargaining is main process

to arrive on a win-win situation for both. In agricultural products, the main

bargaining is in GI type I, III and II in that order, in GI type IV no bargaining.

xii

In non-agricultural products, the main bargaining is in GI type VIII, followed

by VI, VII and V.

• In the products high quality production practices and also inputs is the major

concern.

• For non-agricultural products most traders’ view duplicates are available but

half of them believe that these are of inferior quality.

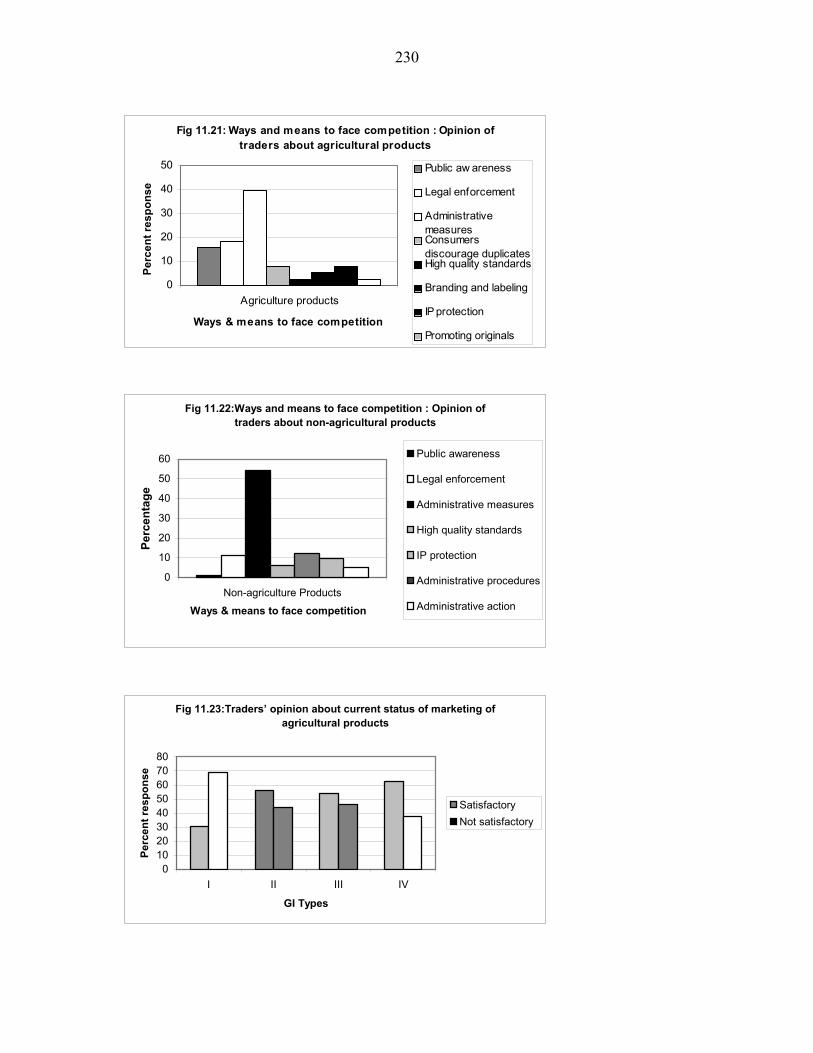

• About 67% percent traders feel that products are facing competition in their

items. Among these about 59 percent are for non-agricultural products

• Methods to face competition: In agricultural products, the most important

suggested method is introduction of quality control and inspection

mechanism. In non-agricultural products, the suggested methods are little

different than agricultural products. The most important method here is

improvement through design and development followed by equally important

‘improvement in marketing methods’ and ‘intensive publicity’.

• Traders gave their ranked opinion for trade suitability of the product.

• As post registration activity, the traders want increase over prevailing cost

price for agriculture 10% or less and for non-agric. products between 10-15%.

They wish to have enhanced premium over selling price, in case of both

agricultural and non-agricultural products, most traders expect enhancement

of 15% or below.

• Not many traders are satisfied with their earnings from sale of agricultural and

non-agric. GI product.

• Traders gave their opinion about future prospects of the product. For

improving the economic viability and future prospects of the product, the

traders have suggested various constructive measures. In case of agriculture,

the major suggestions are improvement at production level, quality

standardization, maintenance and assurance, good marketing practices and

publicity of the product. For non-agricultural products, the top priority is same

as in agricultural products i.e. production level improvements, it follows the

government support and then equally important quality management and good

marketing practices

xiii

Instructions for Readers Chapters and Annexes

The complete analysis and information has been presented in two volumes, the vol-2 does

not contain any chapter, and it contains seven annexure only, which is only

supportive/additional material for information. The volume-1 is the major analytical

component, which contains the major body text and associated annexure. In the vol-1,

there are 14 chapters and 10 annexure, chapters 4 to11 are the major analytical chapters.

The additional matter (mainly data tables) of a chapter are presented in the annexure;

therefore the number given to the annexure is same as the number given to a chapter, if

any chapter (e.g. chapters 1,2,3 &12) does not have any annexure, these numbers (in

roman) would be missing from the list of Annexure. All the data tables are in the

annexure and number of the table start with the number of the concerned chapter e.g.

tables in Annex-IV, which is for chapter-4 will start from table-4.1 and this annexure

contains 29 tables, therefore the last table is table-4.29, the same pattern is followed for

all other annexure. The figures (graphs), wherever available are included at the end of the

text of each chapter and figure no. in each chapter is the same as the table no. in the

respective annexure from where the material for figure (graph) has been taken e.g. Figure

no. 4.1 in chapter-4 has been taken from table 4.1 in Annexure-IV. If readers are

interested in more details they can refer the particular table.

Footnote Each chapter has its own footnotes with their numbers limited to that chapter only

Chapter content

For the major analytical chapters i.e. chapter 4 to 11, a uniform pattern of paragraph has

been adopted. Each chapter has either all or selected few major heads/subheads of the

paragraph as given below in the table:

xiv

Paragraph number

Paragraph description

1. Socio-economic profile of producers 1.1 Livelihood and social groups 1.2 Household particulars 1.3 Housing particulars 1.4 Household income, expenditure and assets 1.5 Welfare indicators 2. Product description 2.1 Nature and geographical association 2.2 Unique characteristics 2.3 Specialty of production process 2.4 History of production- in region and by individual 3. Enterprise and operations 3.1 Ownership and activities 3.2 Activities-seasonality 3.3 Resources- persons engaged and equity issues 3.4 Resources- persons engaged in organizations 3.5 Resources skill & training 3.6 Resources- physical particulars of land (agric)/ inventory of fixed assets (non-agric) 3.7 Resources- loans 3.8 Resources- raw material 3.9 Quantity and value of production 4. Marketing operations 4.1 Storage methods and problems 4.2 Packing methods and problems 4.3 Grading methods 4.4 Mode of sale and satisfaction level 4.5 Mode of purchase by traders 4.6 Spectrum of region-wise sale of product 4.7 Contribution of uniqueness to sale 4.8 Trend of sale 4.9 Price decision and trend of unit price 4.10 Price increments in supply chain 4.11 Constraints in production and marketing 5. Inspection, quality control & quality assurance 5.1 Inspection, quality control at various stages of production 5.2 Govt defined quality assurance methods and advice given for quality improvement 5.3 Technical guidelines for production codes 5.4 Maintenance and monitoring of codes of production practices 5.5 Traders’ view to maintain product quality 6. Perceived changes after registration 6.1 Presumed results of non-registration 6.2 Expected changes after registration- on market 6.3 Expected changes after registration- enhanced premium as expected by producers

and traders 6.4 Expected changes after registration- livelihoods & overall socio-economic

conditions 6.5 Expected changes after registration- consumers’ expectations 6.6 Visualized benefits at time of GI registration Other changes 7. Perceived impact on market 7.1 Duplicates and similar products 7.2 Consumers’ efforts to purchase genuine product

xv

Paragraph number

Paragraph description

7.3 Competition- types and sources 7.4 Import of similar product and difference between imported and domestic product 7.5 Import of the products 7.6 Export and trade option of the products 8. Observed impacts after registration 8.1 Observed changes after registration- on market 8.2 Observed changes after registration- livelihoods & overall socio-economic

conditions 8.3 Observed changes after registration- enhanced premium felt by producers 8.4 Other observed changes 9. Willingness to pay 9.1 Willingness for registration and payment thereof 9.2 Money paid by producers for registration 9.3 Willingness to pay for expected enhanced premium 10. Suggestions on policy implications 10.1 Production characteristics 10.2 Production constraints 10.3 Earnings and income 10.4 Financial and infrastructure needs- for increasing production 10.5 Awareness of producers and stakeholders about GI 10.6 Role of agencies in development and strengthening of producers’ associations 10.7 Other interventions- market expansion strategies 10.8 Future prospects of the product 10.9 Constructive measures to make production viable and improve future prospects 10.10 Status of marketing and suggestions for improvement 10.11 Suggestions for improvement to increase sale 10.12 Scientific endeavors in product development 10.13 Endeavors by depts. and agencies responsible or concerned with GI registration 10.14 Endeavors by financial institutions 11. Legal and administrative aspects 11.1 Current level of protection, drawback, enforcement problems 11.2 Problems and bottlenecks related to acquisition and maintenance of GI 11.3 Identification of beneficiaries

Chapter 1

Introduction, Background and Scope of Work

Introduction

The geographical locations either due to geo-climatic features or due to specially

attained skills by the local people impart special characteristics and therefore reputation

to some agricultural (Fruits& vegetables, spices, cereals, and non-agricultural products

(such as sweets, textiles, handicraft & artifact, manufactured products & machines etc.),

which has reputation due to its belongingness to that particular place. In compliance with

Agreement on Trade Related Aspects of Intellectual Property Rights (TRIPS). The

intellectual worth of the geographical indications was established in India by The

Geographical Indications of Goods (Registration and Protection) Act 1999, which came

into force from 15th September 2003.

The definition of GI in GI Act is in accordance with Art 22.1 of TRIPS; in

addition the goods have been categorized into agricultural, natural, manufactures,

handicraft or industrial goods including foodstuff (Section 2.1.f), these goods as per

international classification are classified into 34 classes as given in the fourth schedule;

definition of producers is available in Section 2.1.k. TRIPS does not provide procedural

requirements for protection of GI, therefore GI Act has its own but TRIPS compliant

provisions for the application of registration for GI (Section 7.2) and authorized users

(Section 7.3). Application for registration of GI must fulfill certain requirements as given

in Section 11.2, the requirement of inspection body as asked in GI application form no.

GI-1 is not given under this section of GI Act but it is covered by Section 11.2.f, which

states ‘such other particulars as may be prescribed’’. The applicants have to provide

address of principal place of business in India, and address for service in India (Rule 16

& 17). In case, applicant does not have principal place of business, then address of

2

residence in India for Indian citizens (Rule 3.iii) and for foreign applicant from

convention countries, the address of residence must be given (Rule 15.3). With respect to

registration of GI and authorized user, the GI Act does not discriminate between Indian

citizens and foreigners, except few provisions such as 1. Pursuant to Art 24.9 of TRIPS,

Section 9.f of GI Act prohibits registration of those GI, which are not protected in their

country, 2. Under Rule 24.1 of GI Act, foreigners from convention countries have to

produce a certificate from registry or competent authority of GI office of that country.

Objectives of the study

Purpose of the study was to development of recommendation domain for the

effective and efficient geographical indications portfolios for sustainable rural livelihood

systems. Following were the objectives of the study:

To explore, using specific examples, how geographical indications (GIs) as a

form of intellectual property impact the market opportunities

Analyze how the grant of GIs could impact the lives and livelihoods of those

producing (directly or indirectly) the products that have been/ could be protected

To understand whether geographical indications provides an extra competitive

advantage to people associated with the protected product under GI.

The purpose, objectives and terms of reference given by the UNCTAD are

transformed into a mission statement of the proposed study as given hereunder,

“Comprehensive understanding of GIs with respect to their availability & suitability,

ranked priority, and existing and suggested scenario of associated stakeholders’ situation

such as- socio economic conditions, knowledge system and livelihood systems of

producers; marketing opportunities and competitive edge with regard to domestic and

foreign trade; and legal, administrative and policy framework of GI protection system in

India”

3

Scope of the study

The terms of reference of the study include the following:

i. To evaluate the legal and policy structure for the protection of GIs in India,

including the customary/common law protection, post GI Act protection and

enforcement problems.

ii. To identify specific products in different classes, both agricultural and non-

agricultural, from four different regions of the country where GI protection play /

can play a determining role in enhancing the value of the product in the

domestic/export market. Overall, at least 25 products must be identified in each of

the three regions, which may be suitable for GI registration.

iii. In respect of each of the product identified in a region, to highlight the product

profile, e.g. market, both domestic and export, value of the product, number of

people dependent on the product, nature of the product, special features of the

product etc. and how GI registration could have an impact on market

opportunities and enhance competitiveness of the product concerned.

iv. In respect of each of the product identified in a region, to highlight the socio-

economic condition of the community involved in the production and trade of the

product.

v. In respect of each of the product identified in a region, to analyze how the grant of

GIs could impact the lives and livelihoods of those producing (directly or

indirectly) the product.

vi. On the basis of objective criteria, to rank the products identified in a particular

region for their suitability for GI registration. Some of the objective criteria which

could be used for ranking include association of the product with geographical

name, restriction of production to specific geographical limits, distinct

characteristics of the product, contribution of natural factors like geo-climatic

factors to distinct product characteristics, contribution of local skills to distinct

product characteristics, potential for international trade.

4

vii. To assess the state of awareness about protecting GIs among producers and

suggest ways to enhance the awareness.

viii. To explore how GI protection can be exploited to protect traditional knowledge,

with reference to two or three products.

ix. To evaluate the quality control and inspection mechanisms existing in GI products

and suggest means for improving the same.

x. To identify the major bottlenecks in the acquisition and maintenance of a GI in

India.

xi. To explore the role(s) which state agencies/producer networks can play in the

acquisition and maintenance of a GI.

Items of observation

5. Legal & policy structure of GI protection

a. GI Enforcement procedures and bottlenecks in acquisition and

maintenance of GI

b. Critical study of registered GI

c. Identification of stakeholders for future GI portfolio development

6. Listing, classification, and ranking of GI products on the basis of following

criteria

a. Nature of product

b. Specific characteristics of the product

c. Specific characteristic as potential GI

d. Distribution of production area

e. Association of the product with geographical name

f. Restriction of production to specific geographical limits

g. Distinct characteristics of the product

h. Contribution of natural factors like geo-climatic factors to distinct product

characteristics

i. Contribution of local skills to distinct product characteristics

5

j. Potential for international trade

7. Critical analysis of the producers

a. Socio-economic conditions- Number of producers, do they belong to

certain community, do they have any association, district and

taluka/mandal/block of production, is it produced in another state, socio-

economic background of the producers

b. Knowledge system- Awareness level about GI, existing mechanism,

provisions for knowledge system development

c. Existing Livelihood systems, and likely to be changed after registered GI

d. Existing quality control and inspection mechanisms, provisions for its

development and strengthening

8. Critical analysis of marketing scenario and future strategies

a. Product profile

i. Product differentiation

ii. Uniqueness & Reputation

iii. Measures for building up collective reputation

iv. Protection against the dilution of an indication

b. Production profile and strategies

i. Quality control and inspection mechanisms (existing, proposed &

suggestion to improve)

ii. Codes of good production practices vis-à-vis technical regulations

and production standards

iii. Permissible changes

c. Market profile and strategies

i. Agencies/networks for acquisition and maintenance of GI

ii. Competitive edge as registered GI

iii. Marketing approaches- Advertising and publicity, Consumer

perceptions, Market spying to avoid free riding and loss to

6

reputation, lawful acquirement of GI, Packaging methods and

practices

iv. IP protection forms- Firm label, collective label, Certification

Trademark (CTM)

d. Pricing policies

i. Collective bargaining, individual firm bargaining, minimum agreed

price

e. Distribution networks

i. Wholesalers, retailers, exporters, direct selling, specialized outlets,

local markets, supermarkets

f. Livelihood systems of producers

i. Expected shift in present livelihood

ii. Expected growth in income generation of producer through

registered GI

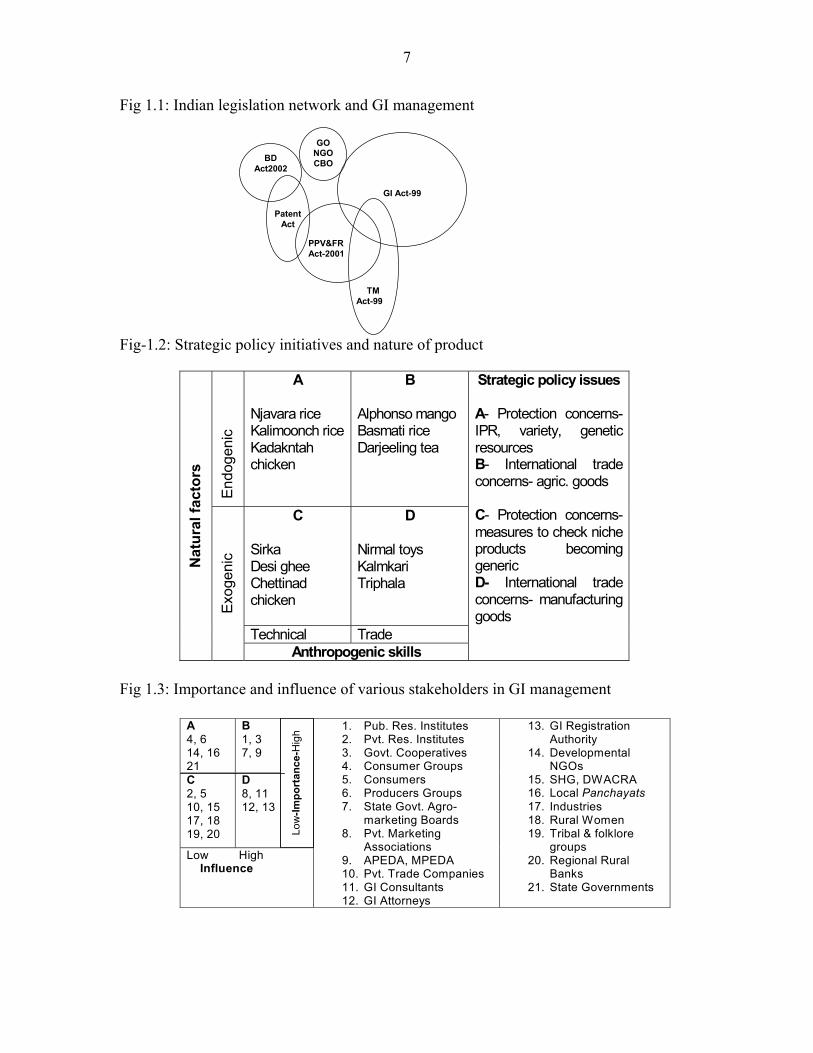

Strategic policy initiatives

The strategic policy initiatives to be identified in terms of action framework, on

the basis of mainly following sub-components1:

1. Interactions of various legal provisions (Biological diversity Act, patent Act,

Protection of Plant Variety and Farmers Rights Act, Trademark Act; and role

players such as government, non-government or community based organizations-

see fig 1.1

2. Contribution of natural factors/ anthropogenic factors in product development and

trade potential- see fig 1.2

3. Stakeholder management- see fig 1.3

1 For detailed analysis see Soam et al. (2007).

7

Fig 1.1: Indian legislation network and GI management

Fig-1.2: Strategic policy initiatives and nature of product

Fig 1.3: Importance and influence of various stakeholders in GI management

Endo

geni

c

A Njavara rice Kalimoonch rice Kadakntah chicken

B Alphonso mango Basmati rice Darjeeling tea

C Sirka Desi ghee Chettinad chicken

D Nirmal toys Kalmkari Triphala

Technical Trade

Nat

ural

fact

ors

Exog

enic

Anthropogenic skills

Strategic policy issues A- Protection concerns- IPR, variety, genetic resources B- International trade concerns- agric. goods C- Protection concerns- measures to check niche products becoming generic D- International trade concerns- manufacturing goods

GI Act-99

GONGOCBO

TM Act-99

PPV&FR Act-2001

BD Act2002

Patent Act

A 4, 6 14, 16 21

B 1, 3 7, 9

C 2, 5 10, 15 17, 18 19, 20

D 8, 11 12, 13

Low High Influence

1. Pub. Res. Institutes 2. Pvt. Res. Institutes 3. Govt. Cooperatives 4. Consumer Groups 5. Consumers 6. Producers Groups 7. State Govt. Agro-

marketing Boards 8. Pvt. Marketing

Associations 9. APEDA, MPEDA 10. Pvt. Trade Companies 11. GI Consultants 12. GI Attorneys

13. GI Registration Authority

14. Developmental NGOs

15. SHG, DWACRA 16. Local Panchayats 17. Industries 18. Rural Women 19. Tribal & folklore

groups 20. Regional Rural

Banks 21. State Governments

Low

-Impo

rtan

ce-H

igh

8

Chapter 2

Listing, Ranking and Synopsis of GI Suitable Products

For the selection of the product for the study, the following general process was

adopted

Identification of GI suitable agricultural and non-agricultural products in twelve

states of the country

Preliminary screening of the products for the preferential ranking

Preferential ranking for final selection of 75 products

The complete process in detail is described below:

1. Process of selection of the products

STEP-1

Identification of the products, about 629 products identified in 12 states (enclosed

as Annexure-XIX).

STEP-2

Screening of the products on the basis of secondary information available with

respect to their worthiness about eligibility as a GI and also feasible role in creating

socio-economic impact on the society. About 160 products short-listed for making final

selection, rest are rejected for consideration in the present study.

9

STEP-3

The products are selected finally on the basis of the preferential ranking method2.

About 150 persons participated in this exercise; the persons from the state ‘A’ gave rating

for the products from state ‘A’. Each participant was asked to rate the product on scale of

0-2 with respect each of the attribute from A to H. Later through computational analysis

as given in table-2.1, the weighted scores were assigned to each product. The score is

directly proportional to the desirability of the product for the study. Generally products

from top ranks have been selected with few exceptions as given in the justification for

selection of the products.

Table-2.1: A model of preferential ranking matrix used in selecting the products

Rating (ri) of attributes with respect to G.I.; no=0, medium = 1, high = 2 Attributes* and their weight# (in parenthesis- wi) Weighted

score

Product name

A (3)

B (1)

C (2)

D (4)

E (2)

F (3)

G (3)

H (4) ∑ riwi.

Rank

1 1 - - - - - - n n

* Attributes rated on the scale of 0-2 for each product A. Production restricted to geographical limits B. Unique product characteristics C. Product reputation D. Contribution of natural factors (geo-climatic) for specific

characteristics E. Contribution human (local skills) factors for specific

characteristics F. Domestic trade potential G. International trade potential H. As registered GI, the role in socio-economic upliftment of the

producers

# Weight of attributes (wi) 1- Reasonable importance 2- Moderate importance 3- High importance 4- Very high importance

2 Methodology suggested by Soam, 2005

10

2. Preferentially ranked GI suitable products- state-wise in various zones

Southern zone

Product

GI class code

GI class description Weighted Score

Ranking

Andhra Pradesh

Hyderabad pearls 14 Jewellery 39.75 1 Gadwal saree 24 Saree 38.75 2 Kalamkari art* 24,25 Textile products, clothing 37.50 3 Banganpally (Benishan) mango 31 Fruits / propagating material 35.50 4 Guntur chilli 31 Spices and condiments 33.75 5 Kondapalli Bommalu* 28 Toys 33.25 6 Nirmal paintings 16 Traditional painting 31.50 7 Hyderabad gun metal 6 Metal souvenirs 30.00 8 Tandur bluestone 19 Building material 28.75 9 Kurnool/Nellore /Molagolukulu rice

30 Rice Grains 25.50 10

Arku coffee 30 Coffee 24.00 11 Ponduru khadi3 24,25 Textile, Clothing 23.50 12 Kakinada kaja 30 Confectionary 22.25 13 Attrepuram tandra/Alamanda mango jelly/ pulp

29 Mango jelly 21.50 14

KP Onion 31 Vegetables 17.00 15 Nannari sharbat4 32 Fruit drink 14.00 16 Chitti mythylu 30 Rice grains 12.25 17 Pochampalli Ikat*5 Ranking was not done as its established GI, which is 1st product

registered GI product in the class of 24 and 25

3 It has unique process of khadi making, the cloths are of very high quality, usually worn by the wealthy people. Khadi Village Industry Commission (KVIC) is doing efforts for export of this product, while the weavers are poor. Complete information is available on various websites on net. 4 High amount of traditional knowledge is involved. The fruit drink is known to have several medicinal properties 5 Its first product registered as GI in the class of 24 and 25, trade value is established.

11

Tamilnadu

Kancheepuram silk* 24 Saree 38.86 1 Nilgiri tea 30 Tea 37.33 2 Nilgiri oil 3 Essential oil 36.38 3 Sivakasi patakha 13 Fireworks 34.86 4 Tirunelveli halwa 30 Confectionary 29.43 5 Thanjaur plate 16 Traditional souvenirs 29.33 6 Dindigul lock 6 Metal hardware 29.00 7 Virupakshi banana 31 Fruits 28.95 8 Thanjaur doll 28 Toys 28.14 9 Salem steel 14 Metal alloy 26.57 10 Oothukkuli butter 29 Milk &milk products 26.29 11 Chetinad Chicken 29 Meat recipe 19.14 12 Melur plough 7 Agricultural implement 17.38 13 Coimbatore Wet grinder*6 Ranking was not done as it is 1st product registered in class 7

Karnataka Mysore silk* 24 Textile goods 41.25 1 Chennapatana toys* 28 Toys 38.5 2 Mysore sandal soap* 3 Soap 37 3 Dharwar peda 29 Milk & milk products 36.5 4 Coorge coffee 30 Coffee/ propagating material 35.5 5 Mysore agarbatti* 3 Perfumery 35 6 Coorge orange* 31 Fruits 33 7 Mannakulnur saree 24 Saree 32.75 8 Coorge honey 30 Honey 32.5 9 Nanjanogod rasabale* 31 Fruits 32.25 10 Mysore mallige 31 Flowers/ 3 essential oil 31.5 11 Mysore rosewood* 20 Furniture 30 12 Ilkal sarees 24 Saree 28.75 13 Bidri craft* 6 Metal souvenirs 28.25 14 Mysore pak 30 Confectionary 26 15 Kokam fruit juice7 32 Fruit drink 23.25 16

Kerala

Njvara rice 30 Rice grain/31 seeds 34.8 1 Aranmula hand mirror*8 20 Mirror 34.6 2 6 First product registered in its class 7 High amount of traditional knowledge, the fruit drink is claimed to have lot of medicinal properties, the juice is famous through out the western coast. On internet lot of information is available about this fruit drink. The research paper published in current science about its antioxidant properties is also available. 8 Already registered product, made by very limited households, socio-economic impact on larger population is not very high

12

Wayanadan tea 30 Tea 32.2 3 Payyannur sacred ring9 14 Jewellery 31 4 Telichery black pepper 30 Spices and condiments 30.6 5 Alleppey cardamom 30 Spices and condiments 28.6 6 Pokkali rice 30 Rice grain/31 seeds 28.4 7

Jeerakshala / Gandhakshala rice 30 Rice grain/5- dietetic substances

27 8

Alleppy ginger 30 Spices and condiments 26 9 Alleppey turmeric 30 Spices and condiments 25.6 10 * Registered GI product at the time of preferential ranking done in March, 2007

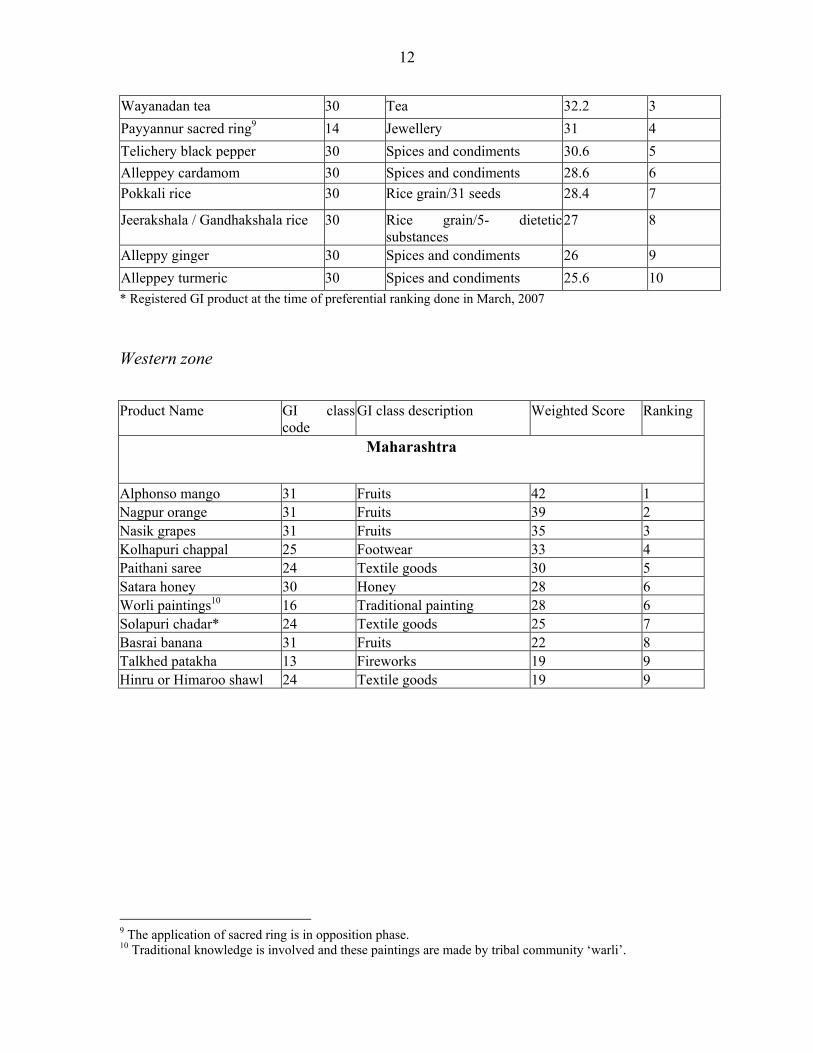

Western zone

Product Name

GI class code

GI class description

Weighted Score

Ranking

Maharashtra

Alphonso mango 31 Fruits 42 1 Nagpur orange 31 Fruits 39 2 Nasik grapes 31 Fruits 35 3 Kolhapuri chappal 25 Footwear 33 4 Paithani saree 24 Textile goods 30 5 Satara honey 30 Honey 28 6 Worli paintings10 16 Traditional painting 28 6 Solapuri chadar* 24 Textile goods 25 7 Basrai banana 31 Fruits 22 8 Talkhed patakha 13 Fireworks 19 9 Hinru or Himaroo shawl 24 Textile goods 19 9

9 The application of sacred ring is in opposition phase. 10 Traditional knowledge is involved and these paintings are made by tribal community ‘warli’.

13

Product Name

GI class code

GI class description

Weighted Score

Ranking

Punjab Punjabi jooti 25 Foot wear 36.00 1 Phulkari 26 Embroidery 36.00 1

Basmati rice 30 Rice grain 35.25 2 Dodha 29 Milk &milk products 35.00 3 Ruri marka11 33 Alcoholic beverages 34.00 4 Patiala shahi salwar 24 Textile goods 33.00 5 Pranda 25 Clothing 32.50 6 Laung 14 Jewellary 32.00 7 Harambha thresher12 7 Agricultural implement 31.50 8 Dhol 15 Musical instrument 31.00 9 Tumbi 15 Musical instrument 30.75 10 Wheat straw combine 7 Agricultural implement 29.00 11 Sandook 21 Household container of

wood 27.75 12

Ludhiana hosiery13 24,25 Clothing Rajasthan

Jaipuri rajai 24 Textile goods 28.33 1 Makrana marble 19 Building material 28.00 2

Sanganeri print 16 Print blocks/ 24 textile goods, 25 clothing 27.00 3

Bikaneri bhujia 30 Confectionary 26.00 4 Kota stone 19 Building material 24.00 5 Bikaneri rasgolla 29 Milk &milk products 22.67 6 Keshar kisturi/Jagmohan/ Mehansar special14 33 Alcoholic beverages 16.00 7 Dungarpur zinger

30

Spices and condiments/ 31 propagating material

14.00

8

Kota doria*15 24 Saree/ 25 clothings 12.67 9 Mavadi 33 Alcoholic beverage 11.00 10

11 Locally brewed liquor, high indigenous knowledge is involved, but it is brewed illegally, it would be difficult to collect data of illegal producers hence not considered for selection. 12 Punjab is famous for agricultural machinery, and it’s a fit product in its class 13 Geographical link to be established because it’s a large industry and large no. of persons depend on it 14 Locally brewed liquor since the time of raja maharajs, high indigenous knowledge is involved, but now these liquor are brewed by the state government factory ‘Ganganagar Suger Mills’. 15 This is the first product from Rajasthan, which has been registered.

14

Product Name

GI class code

GI class description

Weighted Score

Ranking

Ajrak printing 16 Printing block/ 24 textile goods, 25 clothing 7.67 11

Bandhani 24 Saree 6.00 12 Jaipur patang16 Kite Not ranked - Jaipur blue pottery17 Clay pottery Not ranked -

Gujrat18

Bhaliya wheat 31 Wheat grains Not ranked - Kesar mango 31 Fruit Not ranked - Bandhani saree 24 Textile product Not ranked - Patola saree 24 Textile product Not ranked - Kutch embroidery 26 Embroidery Not ranked - * Registered GI product at the time of preferential ranking done in March, 2007

Central and northern zone

Product Name

GI class code

GI class description

Weighted Score

Ranking

Himachal Pradesh

Himachal apple 31 Fruits 38.5 1 Kangra tea19* 30 Tea 31.5 2 Kullu shawl* 24 Textile goods 31 3 Pahari Aloo 31 Vegetables 28.5 4

Kangra painting 16 Traditional painting 24.5 5

Chamba juti 25 Footwear 24.5 5 Himachali honey 30 Honey 15 6

Himachali turmeric 30

Spices

15

6

Himachali zinger 30 Spices 13.5 7 Himachali topi 25 Head gear 12.5 8

16 It was not ranked, in Jaipur it is large industry involving hundreds of small households. The socio-economic impact would be tremendous as a GI. If geographical origin to be established 17 It was not ranked, in Jaipur it is large industry providing good employment 18 Formally preferential ranking has not been done for this state, the products are selected on the basis of feedback received from knowledgeable persons through email and personal telephonic conversations. 19 First agricultural product registered by the scientific institution

15

Product Name

GI class code

GI class description

Weighted Score

Ranking

Uttarakhand

Dehradooni Basmati 30 Rice grain 34.46 1 Ramnagar litchi 31 Fruits 32.50 2 Buraansh juice 32 Fruit drink 33.33 3 Rajma 31 Pulses 32.17 4 Bal Mithai 30 Confectionery 31.17 5 Ganga water/ natural mineral water20 32 Mineral water 31.17 5 Harshil apples 31 Fruits 28.00 6 Chakrata adrak 30 Spices 24.83 7 Beninag tea 30 Tea 23.50 8 Kalibhat- Kali Soybean 31 Pulse grain 21.67 9 Gahat (horse gram) 31 Pulse grain 17.67 10

Uttar Pradesh

Banarasi saree 24 Saree 36.91 1

Mahoba paan 31 Horticultural product 34.46 2

Ferozabad chundia and glassware 21 Glassware 34.43 3 Lucknavi chikan 26 Embroidery 34.17 4

Moradabad brass material

6

Metal souvinirs, mirror frames, picture frames/ 21 utensils, 28 toys, 34Ash trey

33.34

5

Agra petha 30 Confectionary 33.23 6 Kanpur leather21 18 Leather articles 31.97 7 Aligarh locks 6 Metal hardware 31.89 8 Mathura ka peda

29

Milk &milk products

31.29

9

Agra Shoes 25 Footwear 27.69 10 Bhadoi carpet22 27 Carpet 27.07 11

20 It may be good GI product only if significant number of producers of natural mineral water exist 21 It may be selected only after in-depth analysis for establishing uniqueness and geographical link 22 National Human Rights Commission made a special study during 2004 with respect to child labour involved in this industry and later took some corrective measures to address the problem

16

* Registered GI product at the time of preferential ranking done in March, 2007

4. List of the finally selected products

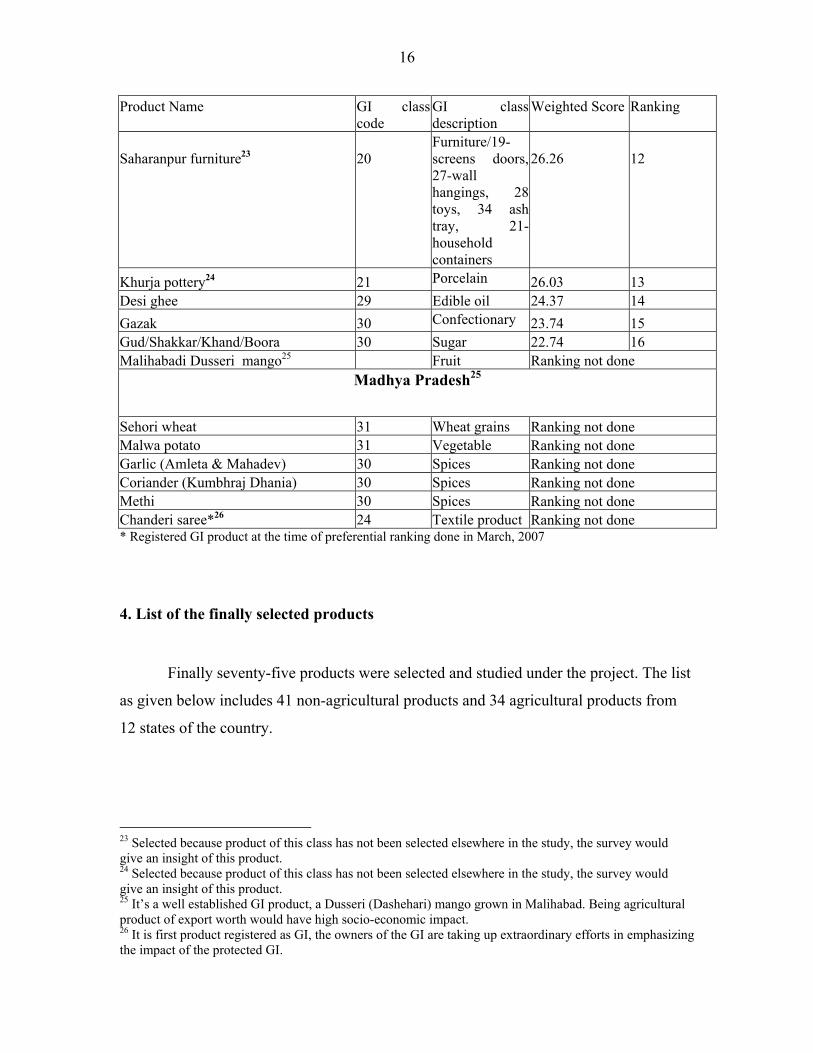

Finally seventy-five products were selected and studied under the project. The list

as given below includes 41 non-agricultural products and 34 agricultural products from

12 states of the country.

23 Selected because product of this class has not been selected elsewhere in the study, the survey would give an insight of this product. 24 Selected because product of this class has not been selected elsewhere in the study, the survey would give an insight of this product. 25 It’s a well established GI product, a Dusseri (Dashehari) mango grown in Malihabad. Being agricultural product of export worth would have high socio-economic impact. 26 It is first product registered as GI, the owners of the GI are taking up extraordinary efforts in emphasizing the impact of the protected GI.

Product Name

GI class code

GI class description

Weighted Score

Ranking

Saharanpur furniture23

20

Furniture/19-screens doors, 27-wall hangings, 28 toys, 34 ash tray, 21-household containers

26.26

12

Khurja pottery24 21 Porcelain 26.03 13 Desi ghee 29 Edible oil 24.37 14 Gazak 30 Confectionary 23.74 15 Gud/Shakkar/Khand/Boora 30 Sugar 22.74 16 Malihabadi Dusseri mango25 Fruit Ranking not done

Madhya Pradesh25

Sehori wheat 31 Wheat grains Ranking not done Malwa potato 31 Vegetable Ranking not done Garlic (Amleta & Mahadev) 30 Spices Ranking not done Coriander (Kumbhraj Dhania) 30 Spices Ranking not done Methi 30 Spices Ranking not done Chanderi saree*26 24 Textile product Ranking not done

17

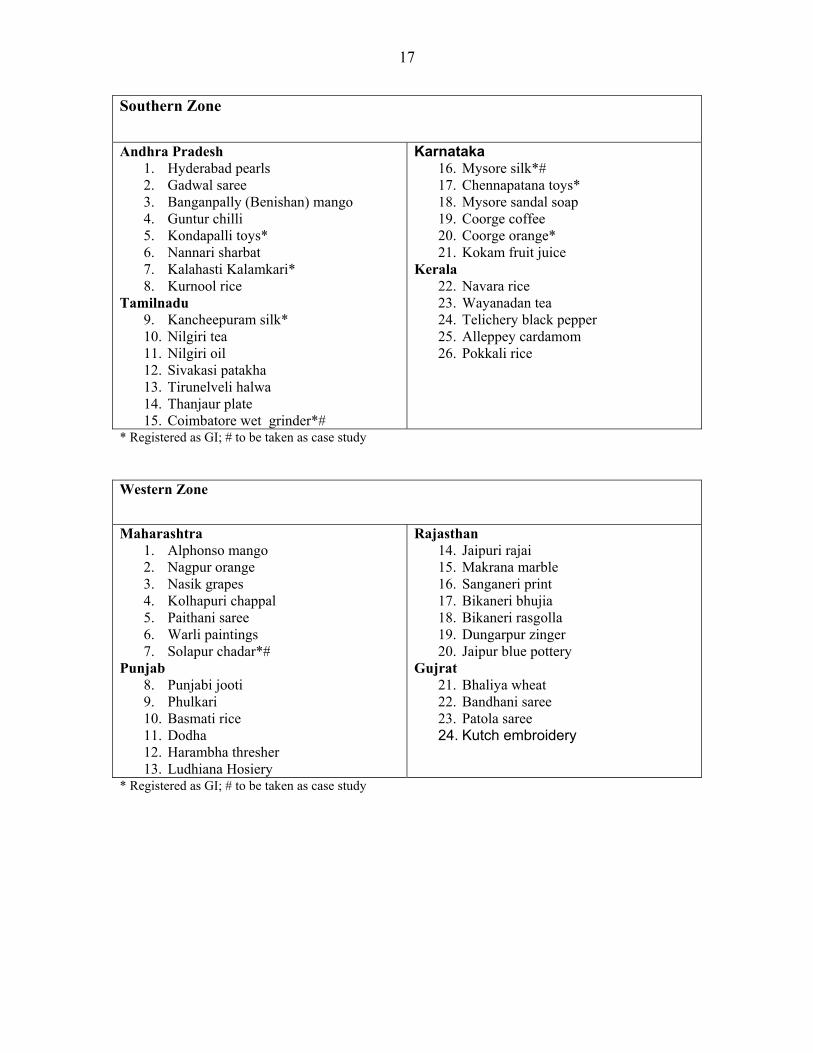

Southern Zone

Andhra Pradesh

1. Hyderabad pearls 2. Gadwal saree 3. Banganpally (Benishan) mango 4. Guntur chilli 5. Kondapalli toys* 6. Nannari sharbat 7. Kalahasti Kalamkari* 8. Kurnool rice

Tamilnadu 9. Kancheepuram silk* 10. Nilgiri tea 11. Nilgiri oil 12. Sivakasi patakha 13. Tirunelveli halwa 14. Thanjaur plate 15. Coimbatore wet grinder*#

Karnataka 16. Mysore silk*# 17. Chennapatana toys* 18. Mysore sandal soap 19. Coorge coffee 20. Coorge orange* 21. Kokam fruit juice

Kerala 22. Navara rice 23. Wayanadan tea 24. Telichery black pepper 25. Alleppey cardamom 26. Pokkali rice

* Registered as GI; # to be taken as case study

Western Zone

Maharashtra

1. Alphonso mango 2. Nagpur orange 3. Nasik grapes 4. Kolhapuri chappal 5. Paithani saree 6. Warli paintings 7. Solapur chadar*#

Punjab 8. Punjabi jooti 9. Phulkari 10. Basmati rice 11. Dodha 12. Harambha thresher 13. Ludhiana Hosiery

Rajasthan 14. Jaipuri rajai 15. Makrana marble 16. Sanganeri print 17. Bikaneri bhujia 18. Bikaneri rasgolla 19. Dungarpur zinger 20. Jaipur blue pottery

Gujrat 21. Bhaliya wheat 22. Bandhani saree 23. Patola saree 24. Kutch embroidery

* Registered as GI; # to be taken as case study

18

Central & Northern Zone

Himachal Pradesh

1. Himachal apple 2. Kangra tea*# 3. Kullu shawl* 4. Pahadi Aloo

Uttaranchal 5. Harshil Apple 6. Buraansh juice 7. Ramnagar litchi 8. Rajma 9. Bal Mithai

Madhya Pradesh 10. Sehori wheat 11. Malwa potato 12. Garlic (Amleta & Mahadev) 13. Coriander (Kumbhraj Dhania) 14. Methi 15. Chanderi saree*#

Uttar Pradesh 16. Banarasi saree 17. Mahoba paan 18. Ferozabad chundia and glassware 19. Lucknavi chikan 20. Moradabad brass material 21. Agra petha 22. Bhadoi carpet 23. Saharanpur furniture 24. Khurja pottery 25. Malihabadi dussehri mango

* Registered as GI; # to be taken as case study

5. Synopsis of the products selected for study

Among the study of 75 products, 34 are agricultural products and 41 are non-

agricultural products. Out of the total 75 products, 13 products are registered (10 non-

agricultural and 03 are agricultural) and 12 products (07 non-agricultural and 05

agricultural) have been applied. The synopses of all the products under study have been

given below. These products have been classified into eight GI type groups.

S.no. Name of product GI Class Description Place of production State GI-Type-I: Fruits

76. Banganpally (Benishan) mango

Mango variety Banganpally village, Kurnool district but grown in large part of AP

AP

77. Coorg orange* Specific kind of orange Coorge region Karnataka 78. Alphonso mango Specific kind of mango Valsad Gujrat 79. Nagpur orange Orange of repute Nagpur Maharashtra 80. Nasik grapes Small sweet grapes Nasik, Pune, Sangali,

Satara, Ahmednagar Maharashtra

19

81. Malihabadi Dussheri Mangoes of specific quality Lucknow region UP 82. Himachal apple Apples of good quality Kullu, Shimla,

Kinnaur HP

83. Harshil apple Popular apple fruit Uttarkashi Uttarakhand 84. Ramnagar litchi Popular litchi fruit Nainital district Uttarakhand

GI-Type-II: Grains and Potato

85. Kurnool rice Reputed rice in AP Kurnool, Kadapa and Nellore

AP

86. Navara rice* A medicinal rice Wynad Kerala

87. Pokkali rice# Rice known for its environment friendly and organic method of production

Alappuzha, thrissur and Ernakulum

Kerala

88. Bhaliya wheat Wheat grown in saline soil under rainfed conditions having special taste and chapatti making quality

Bhal region, Anand Gujrat

89. Basmati rice# Reputed scented rice

Hoshiarpur, Gurdaspur

Punjab

90. Sehori genhu Good quality rainfed aestivum wheat

Sehore MP

91. Malwa potato Potato with specific characteristics attributed to geoclimatic situation

Malwa region, Indore MP

92. Pahari aloo Potatoes produced in hilly regions during summer

Middle level altitudes in HP

HP

93. Hill rajma Good quality pulse Pithoragarh Uttarakhand GI-Type-III: Plantation and spices

94. Guntur chilli (karam) Pungent and dark red colored chillies

Guntur AP

95. Coorg coffee Reputed coffee Coorge region Karnataka 96. Wayanadan tea Tea leaves Wayanad Kerala 97. Telichery black

pepper# Dried black pepper Telichery, Kannur

district Kerala

98. Alleppy cardamom# Good quality cardamom Alleppy Kerala

99. Nilgiri tea# Good quality tea Nilgiri ranges Tamilnadu 100. Dungarpur zinger Zinger of high quality Dungarpur Rajasthan 101. Amleta & Mahadev

garlic Good quality local garlic Mandsaur, Neemach MP

102. Kumbhraj dhania Coriander of good flavour and good oil content

Guna, Rajgarh, Neemach, Mandsaur

MP

103. Fenugreek (Methi) Good quality bold seeded fenugreek or methi

Jaora, Ratlam, Neemach

MP

104. Mahoba paan Betel leaf Mahoba UP 105. Kangra tea* Tea of repute Kangra district and

other areas of HP HP

20

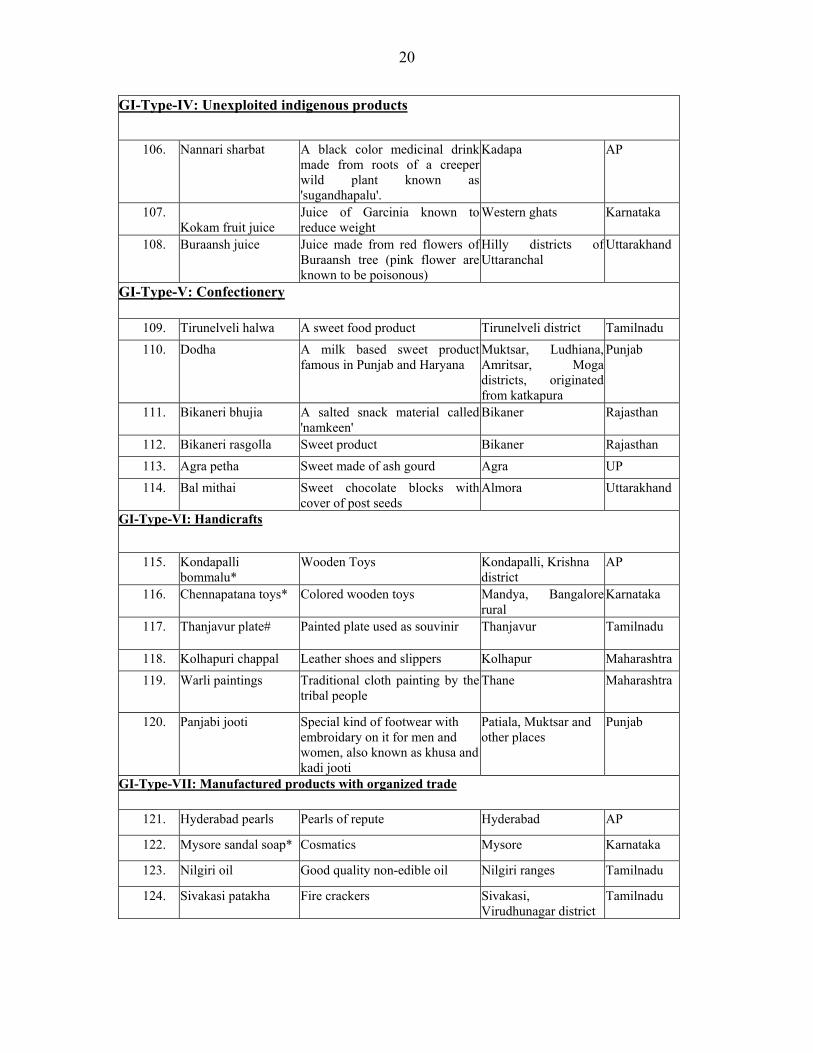

GI-Type-IV: Unexploited indigenous products

106. Nannari sharbat A black color medicinal drink

made from roots of a creeper wild plant known as 'sugandhapalu'.

Kadapa AP

107. Kokam fruit juice

Juice of Garcinia known to reduce weight

Western ghats Karnataka

108. Buraansh juice Juice made from red flowers of Buraansh tree (pink flower are known to be poisonous)

Hilly districts of Uttaranchal

Uttarakhand

GI-Type-V: Confectionery

109. Tirunelveli halwa A sweet food product Tirunelveli district Tamilnadu 110. Dodha A milk based sweet product

famous in Punjab and Haryana Muktsar, Ludhiana, Amritsar, Moga districts, originated from katkapura

Punjab

111. Bikaneri bhujia A salted snack material called 'namkeen'

Bikaner Rajasthan

112. Bikaneri rasgolla Sweet product Bikaner Rajasthan 113. Agra petha Sweet made of ash gourd Agra UP 114. Bal mithai Sweet chocolate blocks with

cover of post seeds Almora Uttarakhand

GI-Type-VI: Handicrafts

115. Kondapalli

bommalu* Wooden Toys Kondapalli, Krishna

district AP

116. Chennapatana toys* Colored wooden toys Mandya, Bangalore rural

Karnataka

117. Thanjavur plate#

Painted plate used as souvinir Thanjavur Tamilnadu

118. Kolhapuri chappal Leather shoes and slippers Kolhapur Maharashtra 119. Warli paintings Traditional cloth painting by the

tribal people Thane Maharashtra

120. Panjabi jooti Special kind of footwear with embroidary on it for men and women, also known as khusa and kadi jooti

Patiala, Muktsar and other places

Punjab

GI-Type-VII: Manufactured products with organized trade

121. Hyderabad pearls Pearls of repute Hyderabad AP

122. Mysore sandal soap* Cosmatics Mysore Karnataka

123. Nilgiri oil Good quality non-edible oil Nilgiri ranges Tamilnadu

124. Sivakasi patakha Fire crackers Sivakasi, Virudhunagar district

Tamilnadu

21

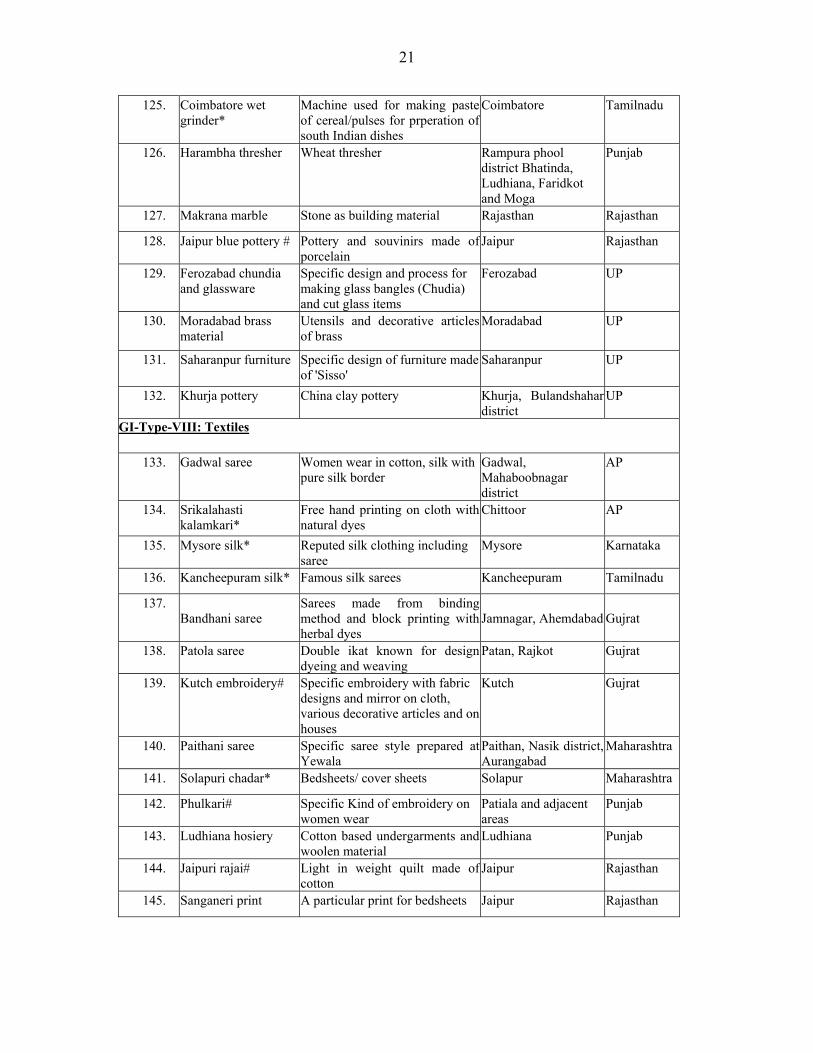

125. Coimbatore wet grinder*

Machine used for making paste of cereal/pulses for prperation of south Indian dishes

Coimbatore Tamilnadu

126. Harambha thresher Wheat thresher Rampura phool district Bhatinda, Ludhiana, Faridkot and Moga

Punjab

127. Makrana marble Stone as building material Rajasthan Rajasthan

128. Jaipur blue pottery # Pottery and souvinirs made of porcelain

Jaipur Rajasthan

129. Ferozabad chundia and glassware

Specific design and process for making glass bangles (Chudia) and cut glass items

Ferozabad UP

130. Moradabad brass material

Utensils and decorative articles of brass

Moradabad UP

131. Saharanpur furniture Specific design of furniture made of 'Sisso'

Saharanpur UP

132. Khurja pottery China clay pottery Khurja, Bulandshahar district

UP

GI-Type-VIII: Textiles

133. Gadwal saree Women wear in cotton, silk with pure silk border

Gadwal, Mahaboobnagar district

AP

134. Srikalahasti kalamkari*

Free hand printing on cloth with natural dyes

Chittoor AP

135. Mysore silk* Reputed silk clothing including saree

Mysore Karnataka

136. Kancheepuram silk* Famous silk sarees Kancheepuram Tamilnadu

137. Bandhani saree

Sarees made from binding method and block printing with herbal dyes

Jamnagar, Ahemdabad

Gujrat

138. Patola saree

Double ikat known for design dyeing and weaving

Patan, Rajkot

Gujrat

139. Kutch embroidery# Specific embroidery with fabric designs and mirror on cloth, various decorative articles and on houses

Kutch Gujrat

140. Paithani saree Specific saree style prepared at Yewala

Paithan, Nasik district, Aurangabad

Maharashtra

141. Solapuri chadar* Bedsheets/ cover sheets Solapur Maharashtra

142. Phulkari# Specific Kind of embroidery on women wear

Patiala and adjacent areas

Punjab

143. Ludhiana hosiery

Cotton based undergarments and woolen material

Ludhiana

Punjab

144. Jaipuri rajai#

Light in weight quilt made of cotton

Jaipur Rajasthan

145. Sanganeri print A particular print for bedsheets Jaipur Rajasthan

22

146. Chanderi saree*

Half silk half cotton saree famous for brocade and muslin produced by twisting yarn and knitting or weaving

Chanderi, Guna (Ashoknagar)

MP

147. Banarasi saree# Specific design and process of saree

Varansi UP

148. Lucknavi chikan# Embroidery style for men and women wear

Lucknow UP

149. Bhadoi carpet High quality carpet Bhadoi town of district Mirzapur

UP

150. Kullu shawl* A woven woolen cloth with specific pattern

Kullu HP

*-Registered GI; #-Applied for registration as on 1 Jan 2008

23

Chapter 3 Approach and Methodology

The study of 75 products include 33 agricultural products and 42 non-agricultural

products. The detailed socio-economic survey was done for 70 products that include 32

agricultural and 38 non-agricultural products. Five products were studied through case

study method. Theses five products are- Coimbatore wet grinder, Mysore silk, Solapur

chaddar, Chanderi saree and Kangra tea.

1. Data collection methodology

Objectives and instruments of socio-economic survey

The objectives of the socio-economic survey were to collect information from

producers, institutional stakeholders, consumers and traders. Several data collection

instruments (interview schedules) were designed for the purpose; a brief description is

given below (schedules enclosed as Annex-XXI):

Schedule no. Purpose of schedule Schedule 1.1 Listing of Households Schedule 1.2 Listing of Non-household establishments and institutions Schedule 2 Household socio-economic survey and enterprise particulars Schedule 3.1 Household enterprise or non – household establishment survey on activities

relating to production of agricultural products under study Schedule 3.2 Household enterprise or Non-household establishment survey on activities

relating to production of Non-agricultural products under study Schedule 4 Survey on G.I. information/ activities related to products under study of: Govt.

Depts. / Agencies including G.I. specific offices; Apex Bodies/ Marketing Boards and similar institutions; NGOs/ SHGs/ Primary Cooperative Societies etc.; Producer’s Association; Scientific & Research Institutions, Knowledgeable Persons; and Banks and Financial Institutions

Schedule 5 Special survey of consumers, local shop-keepers in market complexes, stall holders in exhibition/fairs etc.

24

Respondents for the socio-economic survey

The interview schedules so designed were to be administered to 28 persons for

each product in the following fashion:

5. Ten producers on appropriate schedule. For agricultural product it is schedule 2

and schedule 3.1. For non-agricultural product it is schedule 2 and schedule 3.2.

6. Eight different institutional stakeholders on schedule 4

7. Five different consumers on schedule 5

8. Five different retailing traders on schedule 5

It can therefore be said that for 70 products, 1960 respondents were planned to be

interviewed in 12 states of the country. But finally 1865 were interviewed as given in the

table below:

Respondents Number Producers 691 Institutional stakeholders 429 Consumers 370 Traders 375 Total 1865

Case study of selected products

Five products are studied through case study method, the justification for case

study is also given. The salient features of the cases are also given.

S.No. Product-state Justification for study through case study method 1. Coimbatore wet grinder-

Tamilnadu It’s a first product as RGI in its class 7, the study will give directions for the future applicants in machines