shale gas and oil in international trade

TRANSCRIPT

Shale Gas And Oil In International Trade

Dr Gary K. Busch

The increased production of oil and gas from the fracturing of shale

formations has been one of the most potent influences in

international relations. It has empowered the economy of the U.S. by

lowering the domestic price of petroleum products and changed the

U.S. industry from an importer to an exporter of petroleum products

in a very short period. It has been the engine for growth in a range

of industries associated with “fracking” and has produced feedstocks

for new chemical, fertiliser and plastics industries. Moreover it

has permitted to U.S. to re-evaluate its stance on its former

dependence on foreign oil producing countries and allowed it to

develop the use of energy as a weapon against its enemies.

Until recently the search for oil and gas reserves has been a very

expensive process of drilling at ever-decreasing depths to find

pools oil trapped below the surface of the earth or seabed. The

exploration for oil and gas has been the search for pockets of oil

and gas trapped below the earth’s surface and drilling a pipe down

to open a passageway for that oil and gas to rise to the surface

where it could be loaded aboard giant tankers, pumped into oil or

gas pipelines, or refrigerated into liquefied natural gas or

liquefied petroleum. The technology concentrated on producing

equipment which could go ever deeper below the surface to reach

these oil and gas pockets. Gradually a substantial part of current

oil recovery has been from deep sea wells.

However, there are other deposits of oil and gas which are not part

of subterranean pools of oil or gas. There are a number of

formations which are "continuous" oil accumulations; i.e. the oil

resource is dispersed throughout a geologic formation rather than

existing as discrete, localized occurrence. There is a substantial

amount of oil and gas trapped in shale below a hard crust of rock

not very far below the surface. In recent years there has been the

development of a technology which can access these shale oil

deposits and deliver the entrapped oil and gas to the surface. These

technologies include “horizontal oil well drilling” and “hydraulic

fractioning or “fracking”. “The first new technology was horizontal

drilling, which allowed one vertical well to tap widely into a whole

layer of oil or gas. The second is hydraulic fracturing, or

"fracking," which involved pumping mixtures of water and chemicals

into shale rock. This high-pressure injection of water and chemicals

breaks up the shale and releases the oil and gas that had been

trapped in the rock. Most fracking is on dry land and do not require

deep sea wells or pumping stations.

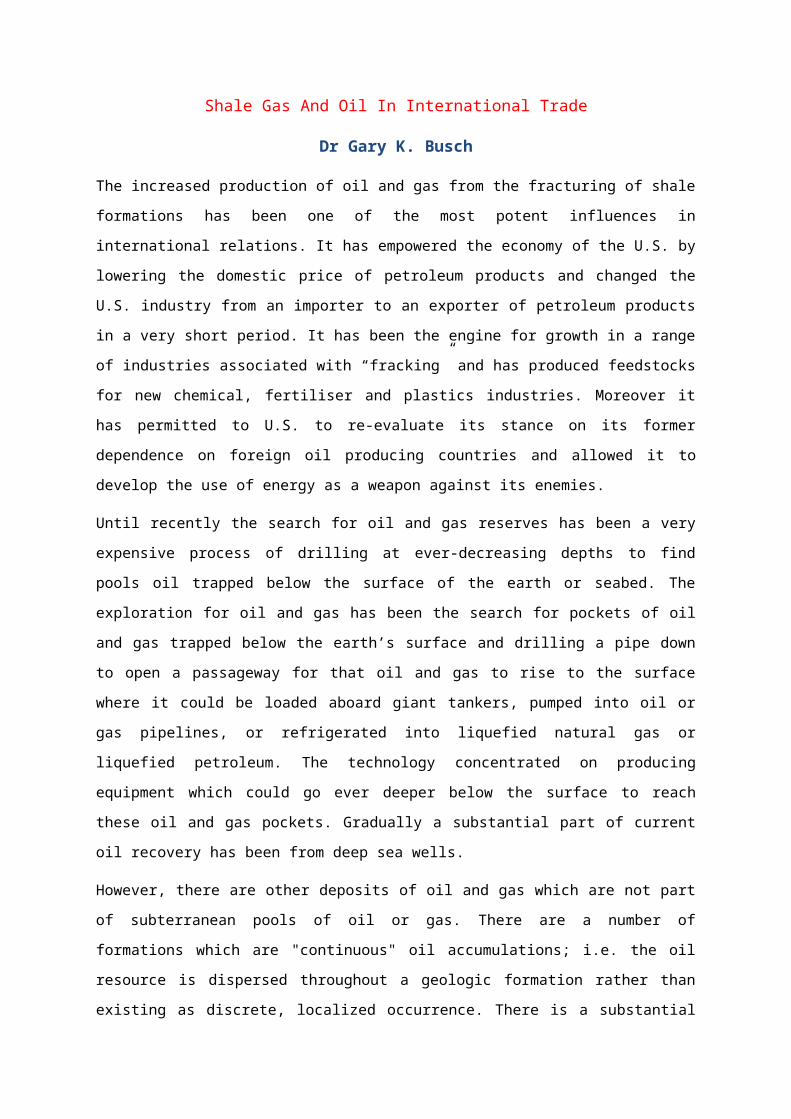

There have been massive finds of “continuous” formations of oil and

gas in the continental U.S.

Within a short period of time the US became virtually self-sufficient in oil and natural gas. Rather than build the planned LNGreceiving trains for the import of gas, the U.S. has begun to buildliquefaction plants and trains for the export of natural gas to therest of the world. U.S. energy costs have shrunken dramatically andremain stable. This availability of lower cost gas is creating manynew jobs and attracting industry investments into North America fromacross the globe as energy costs are reduced and feed stocks of avariety of petrochemical derivatives are dramatically lessexpensive. In September, 2012 a large Egyptian construction companyannounced that it would build a new nitrogen fertilizer productionplant in southeast Iowa to supply customers in the U.S. Corn Belt;it said the $1.4 billion plant would be “the first world-scale,natural gas-based fertilizer plant built in the United States innearly 25 years” and would reduce U.S. dependence on importedfertilizers. Royal Dutch Shell announced plans for a $2 billionpetrochemical plant northwest of Pittsburgh, where it can usenatural gas supplies from the state’s enormous Marcellus shaleformation. Many German companies are moving their plants to accessthe U.S. shale gas opportunities.

Several transport industries are switching from petroleum and dieselto gas, both for savings and for reducing the carbon burden on theenvironment. The use of generating clean energy using gas willgreatly reduce the emission of carbon dioxide. It can also improvethe efficiencies of renewable energy sources as a back-up to solarand wind-power stations which stop or slow down when the wind dropsand the sun sets. These developments have already had a major effecton world trade and development.

By 2020, the U.S. is expected to produce more gas than it needs. Theoil and gas companies are making ready more than fifteen new exportshipping terminals, sufficient to export a full third of currentdomestic LNG consumption around the world. More than a half-milliongas wells are operating in the U.S., a 50% increase since 2000,according to the Energy Information Administration In 2000, shalegas was 2 per cent of the U.S. natural gas supply; by 2012, it was37 per cent. EIA says the U.S. has 300 trillion cubic feet of gas inproven reserves and potentially ten times that amount in unprovenreserves, much of which is in shale deposits. By comparison, theU.S. currently consumes about 25 trillion cubic feet of natural gasannually. If current trends continue, EIA estimates, the U.S. willbe producing more gas than it consumes within the next seven years.

Indeed, the U.S. reserves of shale gas are probably a grossunderestimate. Oil companies have found that there are vast

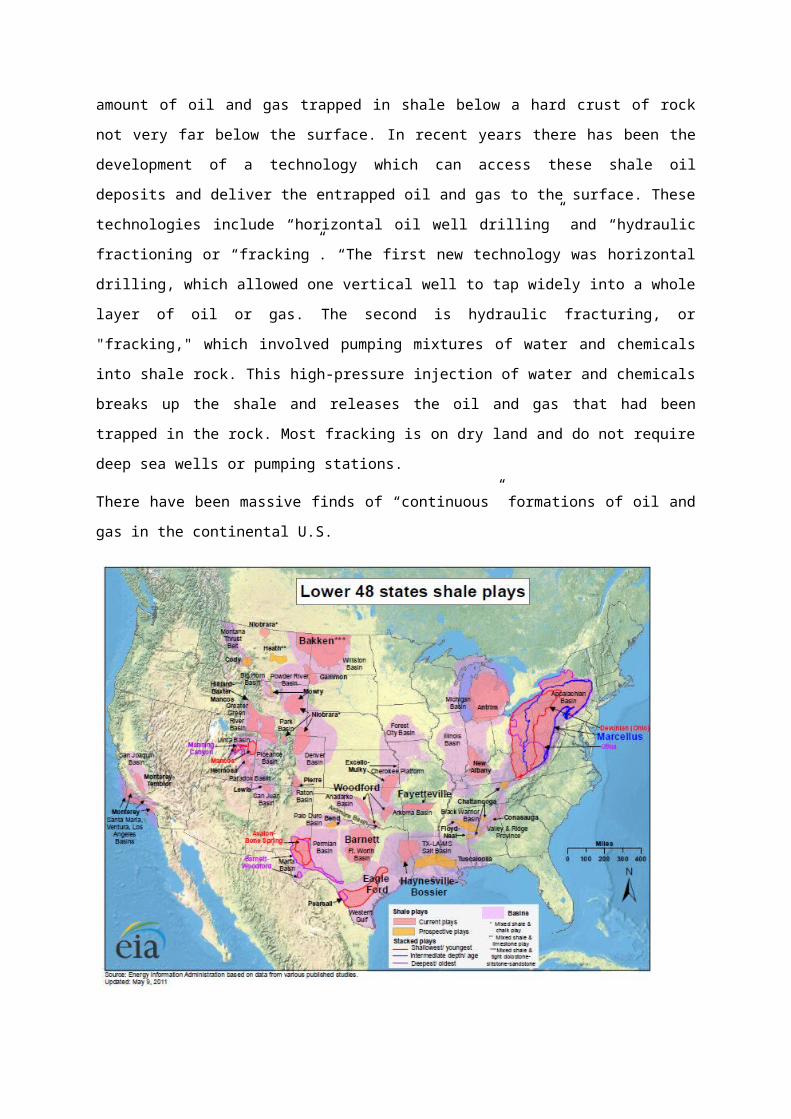

entrapped gas reserves underneath the current shale gas formations.The Utica Gas play lies beneath the huge Marcellus field. TheMarcellus Shale captured public attention when leasing and drillingactivities began pumping billions of dollars into local economies in2004.

Now, just a few years later, the Marcellus Shale is being developedinto one of the world's largest natural gas fields. However, whatgeologists have found shows that the Marcellus is only the firststep in a sequence of natural gas plays. The second step is startingin the Utica Shale which is found below the Marcellus Shale find.

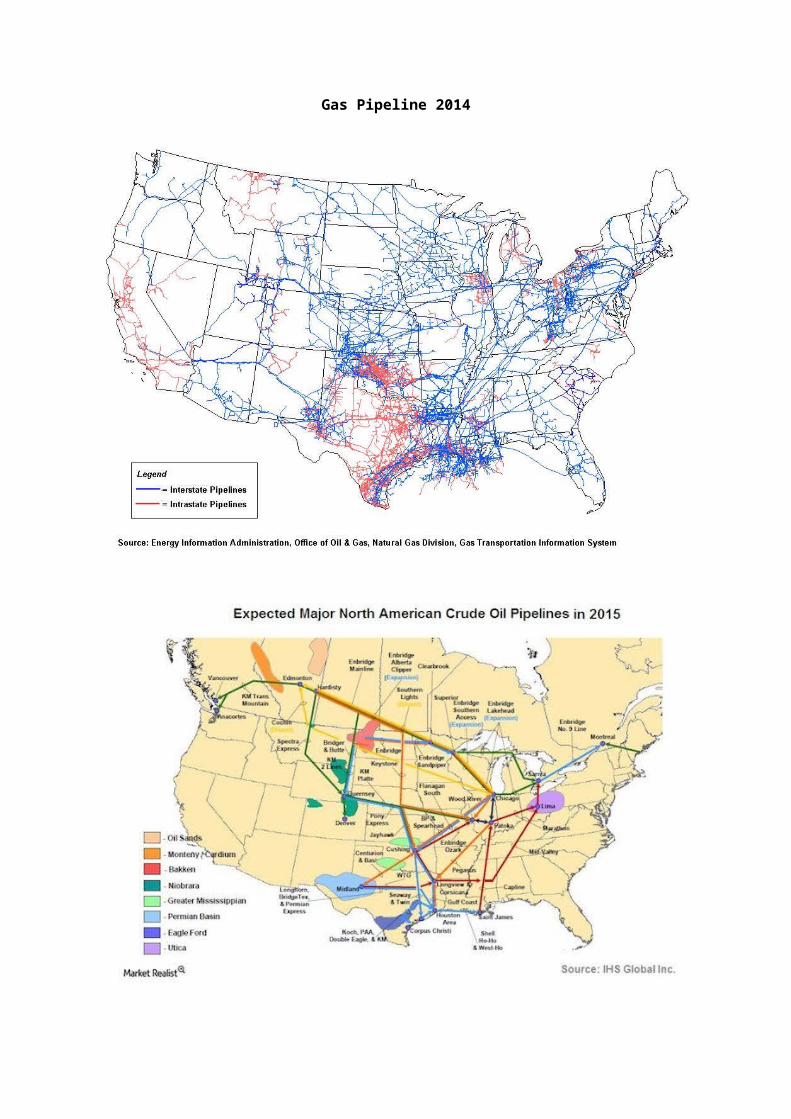

One of the reasons that shale gas and oil development proceeded so

quickly in the U.S. was that there already existed a well-developed

interstate gas and oil pipeline systems which could move the gas

into the national network grid.

Gas Pipeline 2014

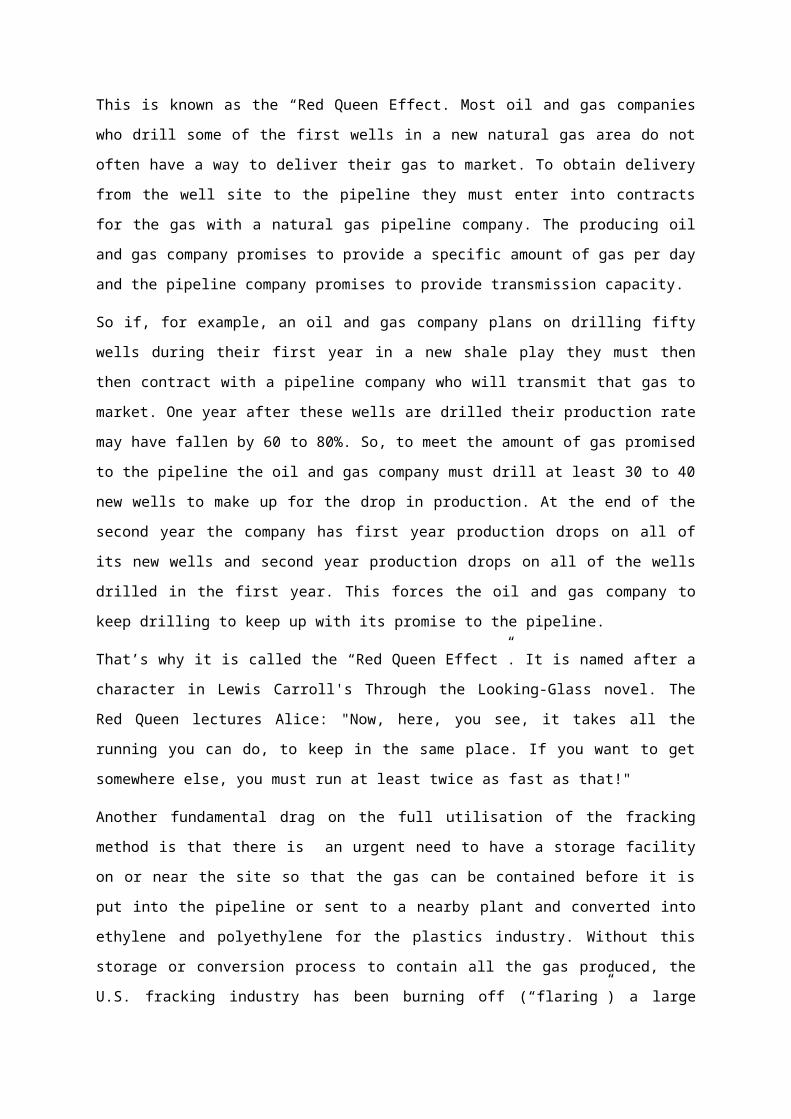

While growth in the U.S. fracking business is very positive there

are some unusual characteristics of this form of extraction which

acts as a constraint on its expansion. These wells yield a high

volume of product immediately after drilling but the yields decline

rapidly during the first year and then more slowly over time.

When a new well is drilled it penetrates a rock unit with abundant

gas, sometimes under pressure. These new wells can yield at a very

high rate, but over time - as gas escapes from the well - the

pressure in the formation goes down and the result is a well with a

lower rate of yield

Most lower yield wells produce one to two million cubic feet per day

in the first month. Many wells yield between three and five million

cubic feet per day, but gigantic wells could produce as much as

twenty million cubic feet per day. The more the well yields in the

first month the more valuable it generally will be over time. A

typical well might yield as much as half of its gas in the first

five years of production. Wells might then continue to produce for a

total of twenty to thirty years but at lower and lower production

rates. So it is necessary to keep drilling new wells to keep up the

production levels on the acreage available,

Year InitialProduction

ClosingProduction

Decline fromPrevious Year

Annual Royalties $4/mcfGas 12.5% Share

First 2.0 Mmcf/d 0.70 Mmcf/d 68% $207,605Second 0.70 Mmcf/d 0.36 Mmcf/d 41% $82,037

Third 0.36 Mmcf/d 0.25 Mmcf/d 27% $53,327Forth 0.25 Mmcf/d 0.19 Mmcf/d 24% $38,966Fifth 0.19 Mmcf/d 0.15 Mmcf/d 19% $29,536Sixth 0.15 Mmcf/d 0.12 Mmcf/d 18% $23,428TABLE: Production decline statistics from a hypothetical natural gas well in shale with horizontal drilling and hydraulic fracturing..

This is known as the “Red Queen Effect. Most oil and gas companies

who drill some of the first wells in a new natural gas area do not

often have a way to deliver their gas to market. To obtain delivery

from the well site to the pipeline they must enter into contracts

for the gas with a natural gas pipeline company. The producing oil

and gas company promises to provide a specific amount of gas per day

and the pipeline company promises to provide transmission capacity.

So if, for example, an oil and gas company plans on drilling fifty

wells during their first year in a new shale play they must then

then contract with a pipeline company who will transmit that gas to

market. One year after these wells are drilled their production rate

may have fallen by 60 to 80%. So, to meet the amount of gas promised

to the pipeline the oil and gas company must drill at least 30 to 40

new wells to make up for the drop in production. At the end of the

second year the company has first year production drops on all of

its new wells and second year production drops on all of the wells

drilled in the first year. This forces the oil and gas company to

keep drilling to keep up with its promise to the pipeline.

That’s why it is called the “Red Queen Effect”. It is named after a

character in Lewis Carroll's Through the Looking-Glass novel. The

Red Queen lectures Alice: "Now, here, you see, it takes all the

running you can do, to keep in the same place. If you want to get

somewhere else, you must run at least twice as fast as that!"

Another fundamental drag on the full utilisation of the fracking

method is that there is an urgent need to have a storage facility

on or near the site so that the gas can be contained before it is

put into the pipeline or sent to a nearby plant and converted into

ethylene and polyethylene for the plastics industry. Without this

storage or conversion process to contain all the gas produced, the

U.S. fracking industry has been burning off (“flaring”) a large

percentage of its production before it ever reaches the pipeline. In

August 2014 the North Dakota Industrial Commission announced that

the August capture percentage was 73 percent with increased daily

volume of gas flared from July to August of 23.5 million cubic feet

per day. Before the improvements the historical high flared percent

was 36 percent in September, 2011. As the retention and intermediate

storage capacity increases the decline in well output is compensated

for by reduced flaring. Once these storage facilities are built they

can be used for the replacement wells without extra as they come on

stream.

In the early days of horizontal drilling and hydraulic fracturing of

shale it was customary practice to allow the well to produce at full

capacity as soon as it was placed on line. This produced rapid

income for the company and helped generate enough funds to build

intermediate storage facilities to reduce flaring. Recent

experiments suggest that throttling the production of a new well

might result in a longer productive lifetime for the well and a

greater total recovery of gas. The theory behind this is that rapid

initial production allows the pore spaces in the shale to deflate

unevenly. Pores near the well collapse first as the gas rapidly

moves to the well and that causes more distant gas to be trapped

within the formation. Slowing the production rate allows the pores

to deflate more evenly and allows an orderly, more efficient and

more complete gas recovery. (see Geology.com. Production and RoyaltyDeclines in a Natural Gas Well Over Time 11/13

The other constraint on the fracking industry is the need for large

and reliable supplies of water. The U.S. is generally well-supplied

with water in most of the areas in which shale extraction takes

place. However, this growth of fracking sites has added to the

general burden on water supplies and is having a negative impact on

farming a human consumption. That is because there are not

sufficient systems in place to clean and reuse the water. It is

wasteful to take good water out of the system when the water-

chemical mixtures used from fracking can relatively easily be

remediated and recycled, using electronic separators or algae

installations to clean and restore the water used. As in most

technologies each further step generates another technology which

fills the needs. The growth of a water recycling process is becoming

an industry on its own and many people are also looking into re-

working existing wells to reclaim the gas not yet removed; much as

stripper wells did for the oil industry.

The impact of this process of fracking oil and gas shale on the

world market has been very strong. The price to the consumer of

shale gas and oil has diminished. It has become more economical to

use this gas as a fuel in trucks, buses and trains, reducing

transport costs for many industries. Singapore has just built a

facility to refuel marine vessels with gas in a whole new bunkering

industry. There is a mass market for cheap energy and the U.S. is

preparing to export gas as well as oil to international markets.

This is a very important development; not only as a revenue-earner

for U.S. suppliers, but also as a method of keeping prices low in

the U.S... If the U.S. doesn’t export its oil and gas the

consequences can be severe. If the U.S. market for shale oil and gas

cannot absorb the full supply then it becomes uneconomic for

producers to keep drilling new wells. However the Red Queen Effect

demands that new wells be drilled. Without these new wells the rapid

fall-off of supply from existing wells will soon make it too

expensive to keep up with new drilling in the face of a diminished

demand and prices will rise. If the U.S. producers can export the

shale oil and gas then the unit price of newly drilled and renewed

oil and gas supplies remains under less domestic pressure for higher

prices.

The political consequences are equally serendipitous. As the Russian

supplies of oil to Europe diminish, either through sanctions,

political pressure or Russian programs of self-injury, there needs

to be a reliable source of substitute energy to make up the

shortfalls Where it used to be economic for gas to be frozen and

shipped as LNG from export trains on specialised freezing vessels to

receiving regasification plants technology has introduced several

important improvements. By freezing gas the volume of the gas

shipped is reduced 600 times in its liquid form. This is an

expensive process; refrigerated ships are expensive and

regasification plants are expensive. Now there are specialised

vessels which compress gas, as opposed to freezing it; when the

pressure is reduced the gas flows through a pipeline. This means

that the receiving country or port doesn’t need such an expensive

cryogenic infrastructure as LNG. It can use compressed gas through a

pipeline flange.

Equally, the vessels needed to carry this gas do not have be

contracted for twenty-five years to a specific project as is true in

most LNG agreements. Ordinary ships can be fitted out to carry

compressed gas. This means that the journey from producer to

consumer does not require vessels moving vast distances under

ballast (without cargo). For example, an LG vessel loads at Woodside

in Australia and delivers its cargo to Louisiana and then sails back

thousands of miles empty to Australia. That is a crazy waste of

money. By removing the need for cryogenics these vessels can deliver

the cargo from one country and then pick up a cargo nearby for

transport to a different buyer. This allows natural gas to be

handled as a spot trade rather than a contracted voyage with long

periods of ballast. There are a number of floating production,

storage and offloading (FPSO) vessels being moored in the world’s

ports to receive gas cargos and which are linked to pipelines. This

will free up vessels, ports and obviate the need for cryogenic

systems.

This is just the beginning of the international spot and contract

business of natural gas and, with foresight, the restrictions on

U.S. exports will be lifted in their entirety soon..