s corporations - center for agricultural law and taxation

TRANSCRIPT

9/8/2015

1

S Corporations

Kristy MaitreTax SpecialistCenter for Agricultural Law and TaxationSeptember 9, 2015

S Corporations

• Elect to pass corporate income, losses, deductions, and credits through to their shareholder via personal tax returns

• Tax is assessed at the individual income tax rates

• Avoid double taxation on the corporate income

• S corporations are responsible for tax on certain built‐in gains and passive income at the entity level – will not be discussed in today’s presentation

Qualifying for S Corporation Status

• Be a domestic corporation• Have only allowable shareholders

– May be individuals– Certain trusts, and estates and– May not be partnerships, corporations or non‐resident alien shareholders

– Every shareholder must be a US citizen or US resident

• Have no more than 100 shareholders• Have only one class of stock• Not be an ineligible corporation (i.e. certain financial

institutions, insurance companies, and domestic international sales corporations)

9/8/2015

2

Form 2553

• The corporation must submit Form 2553 Election by a Small Business Corporation signed by all the shareholders

When To Make the Election

• Complete and file Form 2553:

– No more than two months and 15 days after the beginning of the tax year the election is to take effect, or

– At any time during the tax year preceding the tax year it is to take effect

When To Make the Election

• For this purpose, the 2‐month period begins on the day of the month the tax year begins and ends with the close of the day before the numerically corresponding day of the second calendar month following that month

• If there is no corresponding day, use the close of the last day of the calendar month

9/8/2015

3

Example 1 ‐ No Prior Tax Year

• A calendar year small business corporation begins its first tax year on January 7

• The 2‐month period ends March 6 and 15 days after that is March 21

• To be an S corporation beginning with its first tax year, the corporation must file Form 2553 during the period that begins January 7 and ends March 21

• Because the corporation had no prior tax year, an election made before January 7 will not be valid

Example 2 ‐ Prior Tax Year

• A calendar year small business corporation has been filing Form 1120 as a C corporation but wishes to make an S election for its next tax year beginning January 1

• The 2‐month period ends February 28 (29 in leap years) and 15 days after that is March 15

• To be an S corporation beginning with its next tax year, the corporation must file Form 2553 during the period that begins the first day (January 1) of its last year as a C corporation and ends March 15th of the year it wishes to be an S corporation

• Because the corporation had a prior tax year, it can make the election at any time during that prior tax year

Example 3 ‐ Tax Year Less than 2 1/2 Months

• A calendar year small business corporation begins its first tax year on November 8

• The 2‐month period ends January 7 and 15 days after ‐ that is January 22

• To be an S corporation beginning with its short tax year, the corporation must file Form 2553 during the period that begins November 8 and ends January 22

• Because the corporation had no prior tax year, an election made before November 8 will not be valid

9/8/2015

4

Rev. Proc. 2013‐30

• When filing Form 2553 for a late S corporation election, the corporation (entity) must write in the top margin of the first page of Form 2553 “FILED PURSUANT TO REV. PROC. 2013‐30.”

• Also, if the late election is made by attaching Form 2553 to Form 1120S, the corporation (entity) must write in the top margin of the first page of Form 1120S “INCLUDES LATE ELECTION(S) FILED PURSUANT TO REV. PROC. 2013‐30.”

Relief for a Late S Corporation Election Filed by a Corporation

• A late election to be an S corporation generally is effective for the tax year following the tax year beginning on the date entered on line E of Form 2553

• However, relief for a late election may be available if the corporation can show that the failure to file on time was due to reasonable cause

• To request relief for a late election, a corporation that meets the following requirements can explain the reasonable cause in the designated space on page 1 of Form 2553

Page 1 of Form 2553

9/8/2015

5

Relief for Late Elections

• 1. The corporation intended to be classified as an S corporation as of the date entered on line E of Form 2553

• 2. The corporation fails to qualify as an S corporation on the effective date entered on line E of Form 2553 solely because Form 2553 was not filed by the due date

• 3. The corporation has reasonable cause for its failure to timely file Form 2553 and has acted diligently to correct the mistake upon discovery of its failure to timely file Form 2553;

• 4. Form 2553 will be filed within 3 years and 75 days of the date entered on line E of Form 2553;

Relief for Late Elections

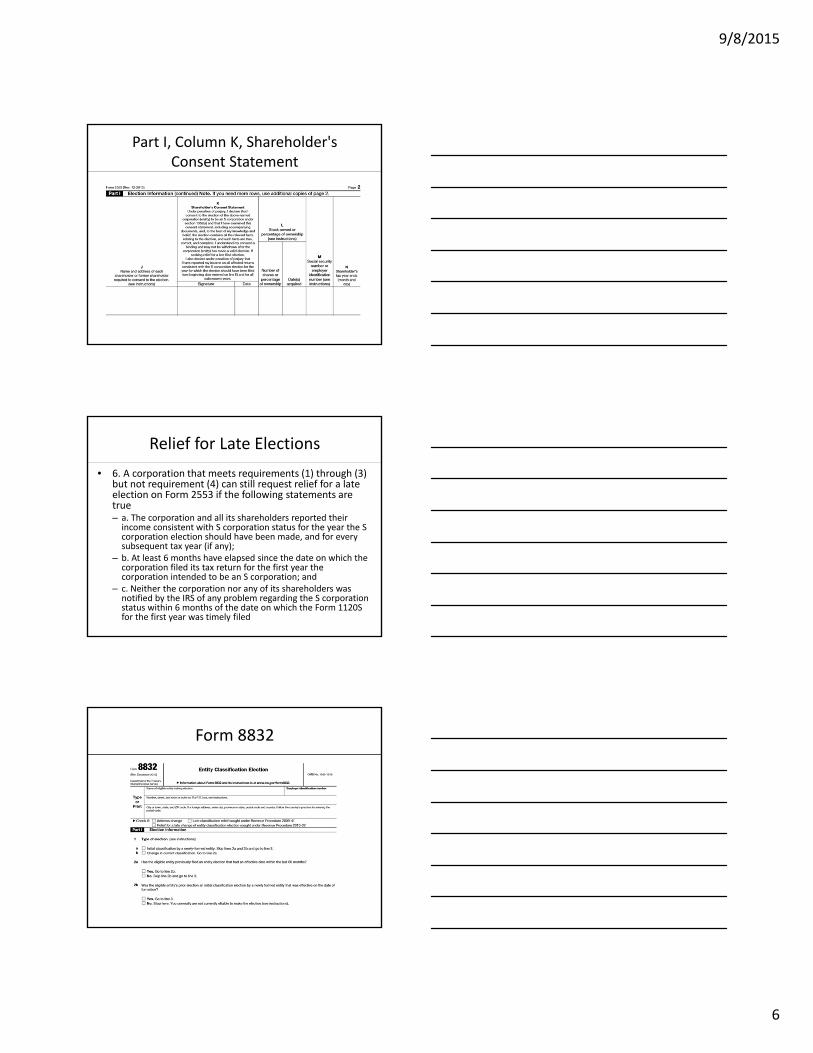

• 5. A corporation that meets requirements (1) through (4) must also be able to provide statements from all shareholders who were shareholders during the period between the date entered on line E of Form 2553 and the date the completed Form 2553 is filed stating that they have reported their income on all affected returns consistent with the S corporation election for the year the election should have been made and all subsequent years

• Completion of Form 2553, Part I, column K, Shareholder's Consent Statement (or similar document attached to Form 2553), will meet this requirement;

Form 2553

9/8/2015

6

Part I, Column K, Shareholder's Consent Statement

Relief for Late Elections

• 6. A corporation that meets requirements (1) through (3) but not requirement (4) can still request relief for a late election on Form 2553 if the following statements are true– a. The corporation and all its shareholders reported their income consistent with S corporation status for the year the S corporation election should have been made, and for every subsequent tax year (if any);

– b. At least 6 months have elapsed since the date on which the corporation filed its tax return for the first year the corporation intended to be an S corporation; and

– c. Neither the corporation nor any of its shareholders was notified by the IRS of any problem regarding the S corporation status within 6 months of the date on which the Form 1120S for the first year was timely filed

Form 8832

9/8/2015

7

Form 8832

Form 8832Electing to be classified as an S corporation

• An eligible entity that timely files Form 2553 to elect classification as an S corporation and meets all other requirements to qualify as an S corporation is deemed to have made an election under Regulations section 301.7701‐3(c)(v) to be classified as an association taxable as a corporation

Relief for Late Elections

• To request relief for a late election when the above requirements are not met, the corporation generally must request a private letter ruling and pay a user fee in accordance with Rev. Proc. 2014‐1, 2014‐1 I.R.B. 1 (or its successor)

9/8/2015

8

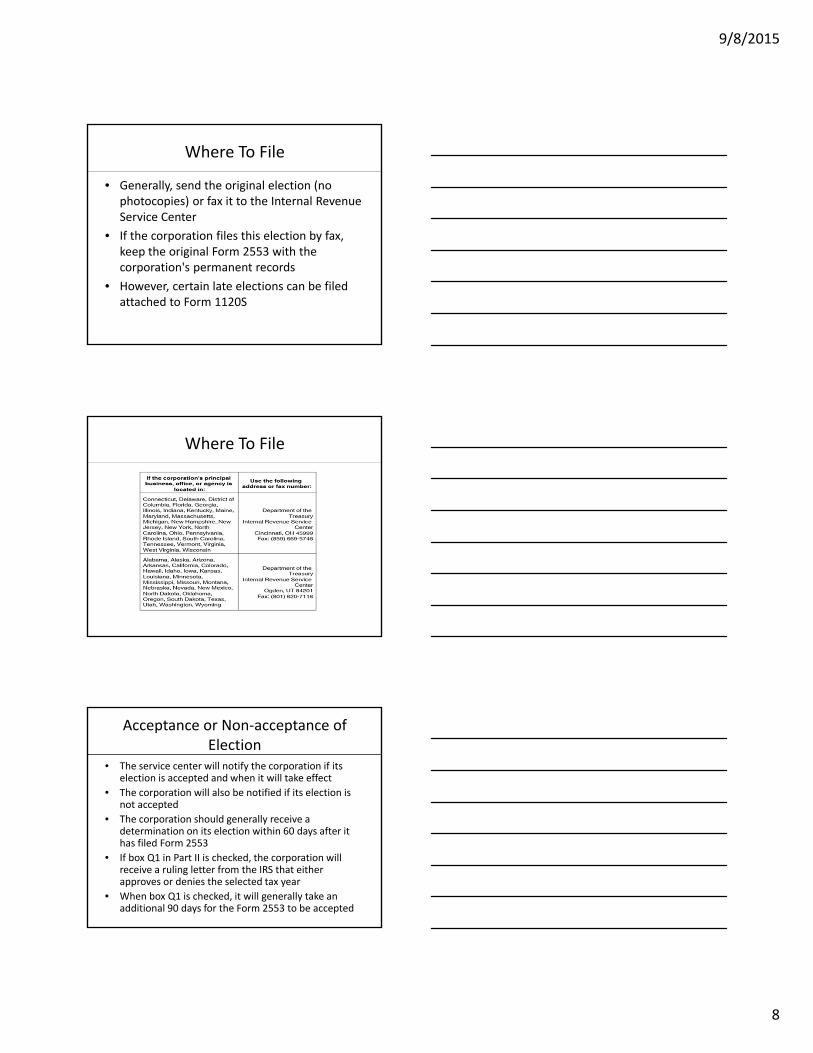

Where To File

• Generally, send the original election (no photocopies) or fax it to the Internal Revenue Service Center

• If the corporation files this election by fax, keep the original Form 2553 with the corporation's permanent records

• However, certain late elections can be filed attached to Form 1120S

Where To File

Acceptance or Non‐acceptance of Election

• The service center will notify the corporation if its election is accepted and when it will take effect

• The corporation will also be notified if its election is not accepted

• The corporation should generally receive a determination on its election within 60 days after it has filed Form 2553

• If box Q1 in Part II is checked, the corporation will receive a ruling letter from the IRS that either approves or denies the selected tax year

• When box Q1 is checked, it will generally take an additional 90 days for the Form 2553 to be accepted

9/8/2015

9

Q1 in Part II

Acceptance or Non‐acceptance of Election

• Care should be exercised to ensure that the IRS receives the election

• If the corporation is not notified of acceptance or non‐acceptance of its election within 2 months of the date of filing (date faxed or mailed), or within 5 months if box Q1 is checked, take follow‐up action by calling 1‐800‐829‐4933

Acceptance or Non‐acceptance of Election

• If the IRS questions whether Form 2553 was filed, an acceptable proof of filing is:– A certified or registered mail receipt (timely postmarked) from the U.S. Postal Service, or its equivalent from a designated private delivery service (Notice 2004‐83, 2004‐52 I.R.B. 1030)

– Form 2553 with an accepted stamp;

– Form 2553 with a stamped IRS received date; or

– An IRS letter stating that Form 2553 has been accepted

9/8/2015

10

End of Election

• Once the election is made, it stays in effect until it is terminated or revoked

• IRS consent generally is required for another election by the corporation (or a successor corporation) on Form 2553 for any tax year before the 5th tax year after the first tax year in which the termination or revocation took effect

• Regulations §1.1362‐5

S Corporations Advantages

• Pass‐through Taxation ‐ An S corporation is a pass‐through entity for federal (and most state) income tax purposes – taxed at shareholder level

• Ease of Conversion ‐ An S corporation can be converted to a C corporation

• Easier accounting rules ‐ S Corporations without inventory can opt to use the cash method of accounting, which is generally much simpler than the accrual method

S Corporations Advantages

• Tax Savings ‐Wages of the S Corp shareholder who is an employee are subject to employment tax– The remaining income is paid to the owner as a "distribution," which is taxed at a lower rate, if at all

• Perpetual Life ‐ An S Corporation designation also allows a business to have an independent life, separate from its shareholders– If a shareholder leaves the company, or sells his or her shares, the S Corporation can continue doing business relatively undisturbed

– Maintaining the business as a distinct corporate entity defines clear lines between the shareholders and the business that improve the protection of the shareholders

9/8/2015

11

S Corporations Advantages

• Protection from liability – The owner of an S Corporation personal assets are separate from the business’s assets and are protected against judgments that occur against the business entity

• Generally must operate on a calendar year

• No corporate income tax

• 100 limit, family is treated as one shareholder

S Corporations Advantages

• Straightforward transfer of ownership ‐ Interests in an S corporation can be freely transferred without triggering adverse tax consequences– The S corporation does not need to make adjustments to property basis or comply with complicated accounting rules when an ownership interest is transferred

• Heightened credibility ‐ Operating as an S corporation may help a new business establish credibility with potential customers, employees, vendors and partners because they see the owners have made a formal commitment to their business

S Corporations Advantages

• Favorable charitable contribution rules –separately stated item flows through

• If active participant profits are not subject to NIIT

• Retirement funding

• Minimize the risk of hobby loss issue

• FICA only applies to wages not distributions

9/8/2015

12

Disadvantages of an S Corporation

• Accounting Records – more precise recordkeeping is required

• Tax Preparation fees often are higher

• Extra Banking & Legal Costs

• Ownership Restrictions

• Extra Costs to Start and Stop

• The exclusion for up to 100% of the gain on the sale of "qualified small business stock" under §1202 does not apply to the sale of stock in an S corporation (expired end of 2014)

Disadvantages of an S Corporation

• Stricter Operational Processes ‐ As a separate structure, S corps require scheduled director and shareholder meetings, minutes from those meetings, adoption and updates to by‐laws, stock transfers and records maintenance– In addition, like a C Corporation, S Corporations are required to file a number of official state and federal documents

– Shareholder restrictions ‐ shareholders will be taxed for any income the company has, even if they did not receive any portion of that income

– S Corporations are only allowed to issue one class of stock, which may discourage some investors

Disadvantages of an S Corporation

• Who is responsible for keeping track of stock basis?

• Profits are taxed even when not distributed

• §179 limitations could be an issue if multiple entities are owned and §179 is passed through and not useable ‐ lost

9/8/2015

13

Disadvantages of an S Corporation

• No fringe benefits for 2% shareholders

• K‐1 reporting

• Once basis reaches zero, losses cannot be deducted

Disadvantages of an S Corporation

• Shareholder Compensation Requirements ‐ A shareholder must receive reasonable compensation

• The IRS takes notice of shareholder like low salary/high distribution combinations, and may reclassify the distributions as wages

• You could pay a higher employment tax because of an audit with these results

• Salary requirements: The Internal Revenue Service requires all officers and owners of an S Corporation to make a salary, even if the company is not yet making a profit– This could be problematic for new businesses struggling to make

payroll– A “reasonable salary” is what a person with the appropriate skills

needed for the position would be paid on the free market – www.salary.com is a good resource

Disadvantages of an S Corporation

• Closer IRS scrutiny ‐ Amounts distributed to a shareholder can be dividends or salary

– The IRS scrutinizes these payments and can re‐characterized payments as

• Distributions may be re‐characterized as wages, which subjects the corporation to employment taxes

9/8/2015

14

Wages vs. Distributions

• Corporate officers are specifically included within the definition of employee for FICA (Federal Insurance Contributions Act), FUTA (Federal Unemployment Tax Act) and federal income tax withholding under the Internal Revenue Code

• When corporate officers perform services for the corporation, and receive or are entitled to receive payments, their compensation is generally considered wages

• Subchapter S corporations should treat payments for services to officers as wages and not as distributions of cash and property or loans to shareholders

Wages

• S corporations should not attempt to avoid paying employment taxes by having their officers treat their compensation as cash distributions, payments of personal expenses, and/or loans rather than as wages

Who’s an Employee of the Corporation?

• Generally, an officer of a corporation is an employee of the corporation

• The fact that an officer is also a shareholder does not change the requirement that payments to the corporate officer be treated as wages

• Courts have consistently held that S corporation officer/shareholders who provide more than minor services to their corporation and receive or are entitled to receive payment are employees whose compensation is subject to federal employment taxes

• The Treasury Regulations provide an exception for an officer of a corporation who does not perform any services or performs only minor services and who neither receives nor is entitled to receive, directly or indirectly, any remuneration– Such an officer would not be considered an employee

9/8/2015

15

What's a Reasonable Salary?

• The instructions to the Form 1120S, U.S. Income Tax Return for an S Corporation, state– "Distributions and other payments by an S corporation to a corporate officer must be treated as wages to the extent the amounts are reasonable compensation for services rendered to the corporation"

• There are no specific guidelines for reasonable compensation in the Code or the Regulations

• The various courts that have ruled on this issue have based their determinations on the facts and circumstances of each case

Factors Considered by the Courts in Determining Reasonable Compensation

• Training and experience

• Duties and responsibilities

• Time and effort devoted to the business

• Dividend history

• Payments to non‐shareholder employees

• Timing and manner of paying bonuses to key people

• What comparable businesses pay for similar services

• Compensation agreements

• The use of a formula to determine compensation

Reminder ‐ IRS stated:

• An S Corporation must pay reasonable compensation (subject to employment taxes) to shareholder‐employee(s) in return for the services that the employee provides to the corporation, before a non‐wage distributions may be made to that shareholder‐employee

• This issue has been identified as an area of non‐compliance and will receive greater scrutiny in the foreseeable future

9/8/2015

16

Distributions/Dividends

• How Are S Corporation Distributions Taxed?

• Regular corporations, pay dividends which are taxed

• But S corporations pay distributions

• In general the distributions paid by an S corporation to the S corporation shareholders are not taxable to the shareholders depending on basis issues

Distributions

• S corporation’s makes distributions of profits to shareholders• As a disregarded entity, an S corporation must allocate profits and

losses to shareholders every year so the amounts can be taxed at the individual level

• These amounts must be allocated every year for tax purposes, but the S corporation is not required to actually distribute the profits

• S corporation shareholders can end up paying taxes on profits in a year when they do not necessarily receive those profits in hand

• The only way an S corporation would have traditional dividends to pay out is if it has a leftover retained earnings account from when it was taxed as a C corporation, before it made the subchapter S election

Distributions

• Whether an S corporation calls shareholder payments distributions or dividends, the decision regarding whether to pay out profits to shareholders is made by the board of directors

9/8/2015

17

Shareholder Loss Limitations

• There are three shareholder loss limitations:– Stock and Debt Basis Limitations– At Risk Limitations– Passive Activity Loss Limitations

• Each limitation must be met, and in the order presented, before a shareholder is allowed to claim a flow‐through loss

• The fact that a shareholder receives a K‐1 reflecting a loss does not mean that the shareholder is automatically entitled to claim the loss

S Corporation Shareholders are Required to Compute Both Stock and Debt Basis

• The amount of a shareholder's stock and debt basis in the S corporation is very important

• Unlike a C corporation, each year a shareholder's stock and/or debt basis of an S corporation increases or decreases based upon the S corporation's operations

• The S corporation will issue a shareholder a Schedule K‐1• It is important to understand that the K‐1 reflects the S

corporation's items of income, loss and deduction that are allocated to the shareholder for the year

• The K‐1 shows the amount of non‐dividend distribution the shareholder receives; it does not state the taxable amount of a distribution

S Corporation Shareholders are Required to Compute Both Stock and Debt Basis

• The taxable amount of a distribution is contingent on the shareholder's stock basis

• It is not the corporation's responsibility to track a shareholder's stock and debt basis but rather it is the shareholder's responsibility

• If a shareholder receives a non‐dividend distribution from an S corporation, the distribution is tax‐free to the extent it does not exceed the shareholder's stock basis

• Debt basis is not considered when determining the taxability of a distribution

9/8/2015

18

Loss or Deduction Flow‐Through Items

• If a shareholder is allocated an item of S corporation loss or deduction, the shareholder must first have adequate stock and/or debt basis to claim that loss and/or deduction item

• In addition, it is important to remember that, even when the shareholder has adequate stock and/or debt basis to claim the S corporation loss or deduction item, the shareholder must also consider the at‐risk and passive activity loss limitations and therefore may not be able to claim the loss and/or deduction item

Importance of Stock Basis

• It is important that a shareholder know his/her stock basis when:– The S corporation allocates a loss and/or deduction item to the

shareholder– In order for the shareholder to claim a loss, they need to demonstrate

they have adequate stock and/or debt basis

• The S corporation makes a non‐dividend distribution to the shareholder– In order for the shareholder to determine whether or not the

distribution is non‐taxable they need to demonstrate they have adequate stock basis

• The shareholder disposes of their stock– As with any asset when the asset is sold or disposed of, basis needs to

be established in order to reflect the proper gain or loss on the disposition

• Since shareholder stock basis in an S Corporation changes every year, it must be computed every year

Computing Stock Basis

• In computing stock basis, the shareholder starts with their initial capital contribution to the S corporation or the initial cost of the stock they purchased

• That amount is then increased and/or decreased based on the flow‐through amounts from the S corporation

• An income item will increase stock basis while a loss, deduction, or distribution will decrease stock basis

9/8/2015

19

Distributions

• The order in which stock basis is increased or decreased is important

• Because both the taxability of a distribution and the deductibility of a loss are dependent on stock basis, there is an ordering rule in computing stock basis

• Stock basis is adjusted annually, as of the last day of the S corporation year, in the following order:– Increased for income items and excess depletion;– Decreased for distributions;– Decreased for non‐deductible, non‐capital expenses and depletion; and

– Decreased for items of loss and deduction

Distributions

• When determining the taxability of a distribution, the shareholder looks solely to his/her stock basis (debt basis is not considered)

• For loss and deduction items, which exceed a shareholder's stock basis, the shareholder is allowed to deduct the excess up to the shareholder's basis in loans personally made to the S corporation

• Debt basis is computed similarly to stock basis but there are some differences– If a shareholder has S corporation loss and deduction items in

excess of stock basis and those losses and deductions are claimed based on debt basis, the debt basis of the shareholder will be reduced by the claimed losses and deductions

– If an S corporation repays reduced basis debt to the shareholder, part or all of the repayment is taxable to the shareholder

Important Things You Should Know

• A distribution in excess of stock basis is taxed as a capital gain on the shareholder's personal return– It is a long‐term capital gain (LTCG) if the S corporation stock has been

held for longer than one year

• Non‐deductible expenses reduce a shareholder's stock and/or debt basis before loss and deduction items– If non‐deductible expenses exceed stock and/or debt basis, they are

not suspended and carried forward

• If the current year has different types of loss and deduction items, which exceed stock and/or debt basis, the allowable loss and deduction items must be allocated pro rata based on the amount of the particular loss and deduction items

• A shareholder is not allowed to claim loss and deduction items in excess of stock and/or debt basis– Loss and deduction items not allowable in the current year are

suspended due to basis limitations and are carried over to the subsequent year

9/8/2015

20

Important Things You Should Know

• Suspended losses and deductions due to basis limitations retain their character in subsequent years– Any suspended loss or deduction items in excess of stock and/or debt basis are carried

forward indefinitely

• In determining current year allowable losses, current year loss and deduction items are combined with the suspended loss and deduction items carried over from the prior year, though the current year and suspended items should be separately stated on the Form 1040 Schedule E or other appropriate schedule on the return

• A shareholder is only allowed debt basis to the extent he or she has personally lent money to the S corporation– A loan guarantee is not sufficient to allow the shareholder debt basis

• If a shareholder contends he or she has contributed or loaned substantial funds to the S corporation, consideration should be given to whether the shareholder had the financial means to make the contribution or loan

• Part or all of the repayment of a reduced basis debt is taxable to the shareholder• If a shareholder sells their stock, suspended losses due to basis limitations are

lost– Any gain on the sale of the stock does not increase the shareholder's stock basis.

S Corporation Taxes

• Excess Net Passive Income Tax §1375

• Built‐In Gains Tax (BIG) §1374

• Inventory – FIFO vs LIFO §1363

• Investment Credit Recapture

• Avoid Accumulated Earnings Tax

Filing Date

9/8/2015

21

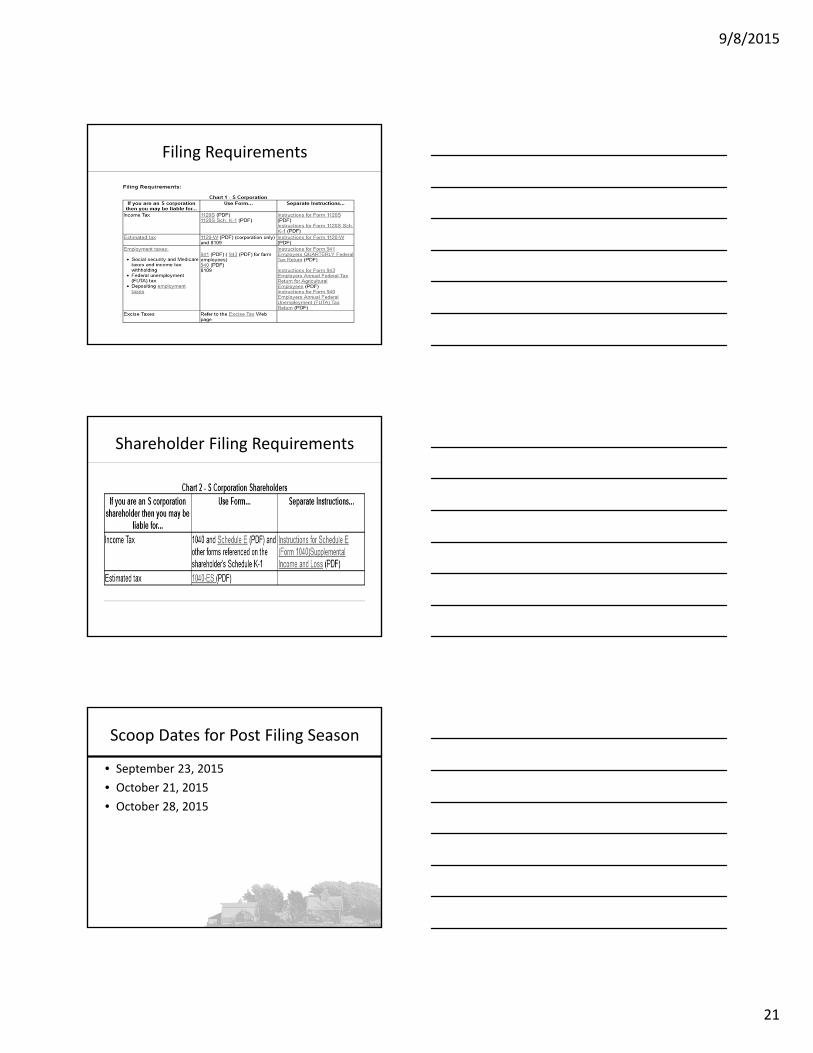

Filing Requirements

Shareholder Filing Requirements

Scoop Dates for Post Filing Season

• September 23, 2015

• October 21, 2015

• October 28, 2015

9/8/2015

22

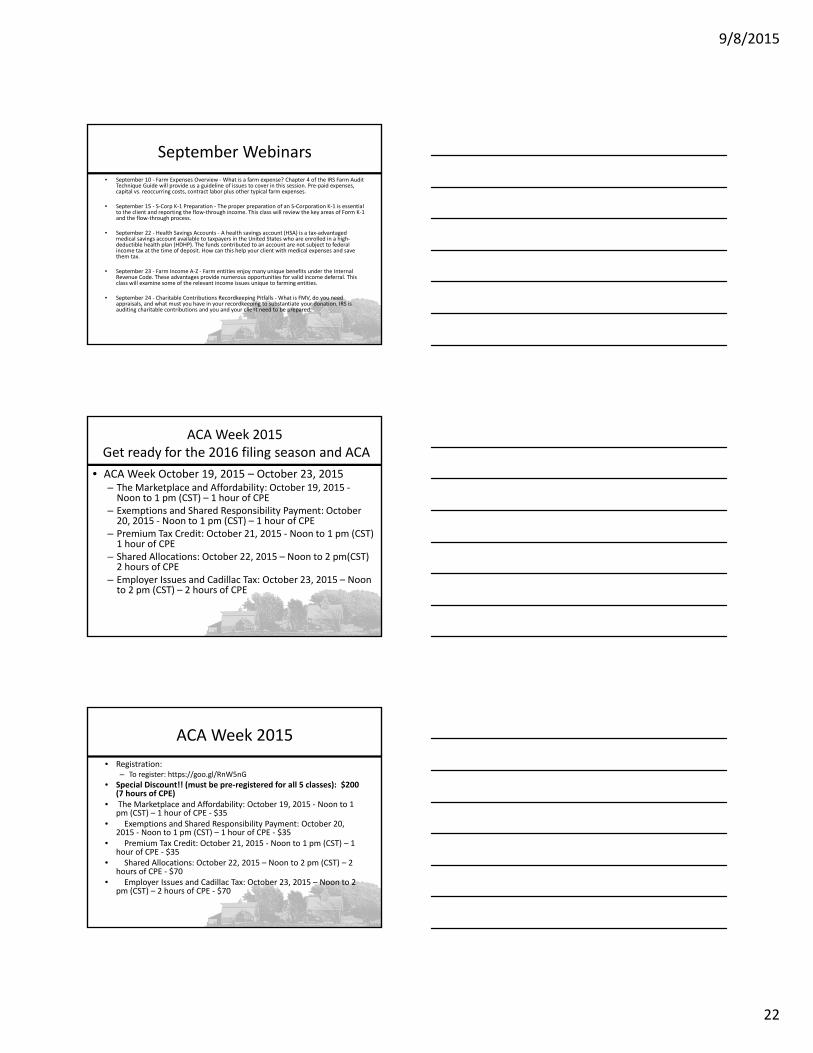

September Webinars

• September 10 ‐ Farm Expenses Overview ‐What is a farm expense? Chapter 4 of the IRS Farm Audit Technique Guide will provide us a guideline of issues to cover in this session. Pre‐paid expenses, capital vs. reoccurring costs, contract labor plus other typical farm expenses.

• September 15 ‐ S‐Corp K‐1 Preparation ‐ The proper preparation of an S‐Corporation K‐1 is essential to the client and reporting the flow‐through income. This class will review the key areas of Form K‐1 and the flow‐through process.

• September 22 ‐ Health Savings Accounts ‐ A health savings account (HSA) is a tax‐advantaged medical savings account available to taxpayers in the United States who are enrolled in a high‐deductible health plan (HDHP). The funds contributed to an account are not subject to federal income tax at the time of deposit. How can this help your client with medical expenses and save them tax.

• September 23 ‐ Farm Income A‐Z ‐ Farm entities enjoy many unique benefits under the Internal Revenue Code. These advantages provide numerous opportunities for valid income deferral. This class will examine some of the relevant income issues unique to farming entities.

• September 24 ‐ Charitable Contributions Recordkeeping Pitfalls ‐What is FMV, do you need appraisals, and what must you have in your recordkeeping to substantiate your donation. IRS is auditing charitable contributions and you and your client need to be prepared.

ACA Week 2015Get ready for the 2016 filing season and ACA

• ACA Week October 19, 2015 – October 23, 2015– The Marketplace and Affordability: October 19, 2015 ‐Noon to 1 pm (CST) – 1 hour of CPE

– Exemptions and Shared Responsibility Payment: October 20, 2015 ‐ Noon to 1 pm (CST) – 1 hour of CPE

– Premium Tax Credit: October 21, 2015 ‐ Noon to 1 pm (CST) 1 hour of CPE

– Shared Allocations: October 22, 2015 – Noon to 2 pm(CST) 2 hours of CPE

– Employer Issues and Cadillac Tax: October 23, 2015 – Noon to 2 pm (CST) – 2 hours of CPE

ACA Week 2015

• Registration: – To register: https://goo.gl/RnW5nG

• Special Discount!! (must be pre‐registered for all 5 classes): $200 (7 hours of CPE)

• The Marketplace and Affordability: October 19, 2015 ‐ Noon to 1 pm (CST) – 1 hour of CPE ‐ $35

• Exemptions and Shared Responsibility Payment: October 20, 2015 ‐ Noon to 1 pm (CST) – 1 hour of CPE ‐ $35

• Premium Tax Credit: October 21, 2015 ‐ Noon to 1 pm (CST) – 1 hour of CPE ‐ $35

• Shared Allocations: October 22, 2015 – Noon to 2 pm (CST) – 2 hours of CPE ‐ $70

• Employer Issues and Cadillac Tax: October 23, 2015 – Noon to 2 pm (CST) – 2 hours of CPE ‐ $70

9/8/2015

23

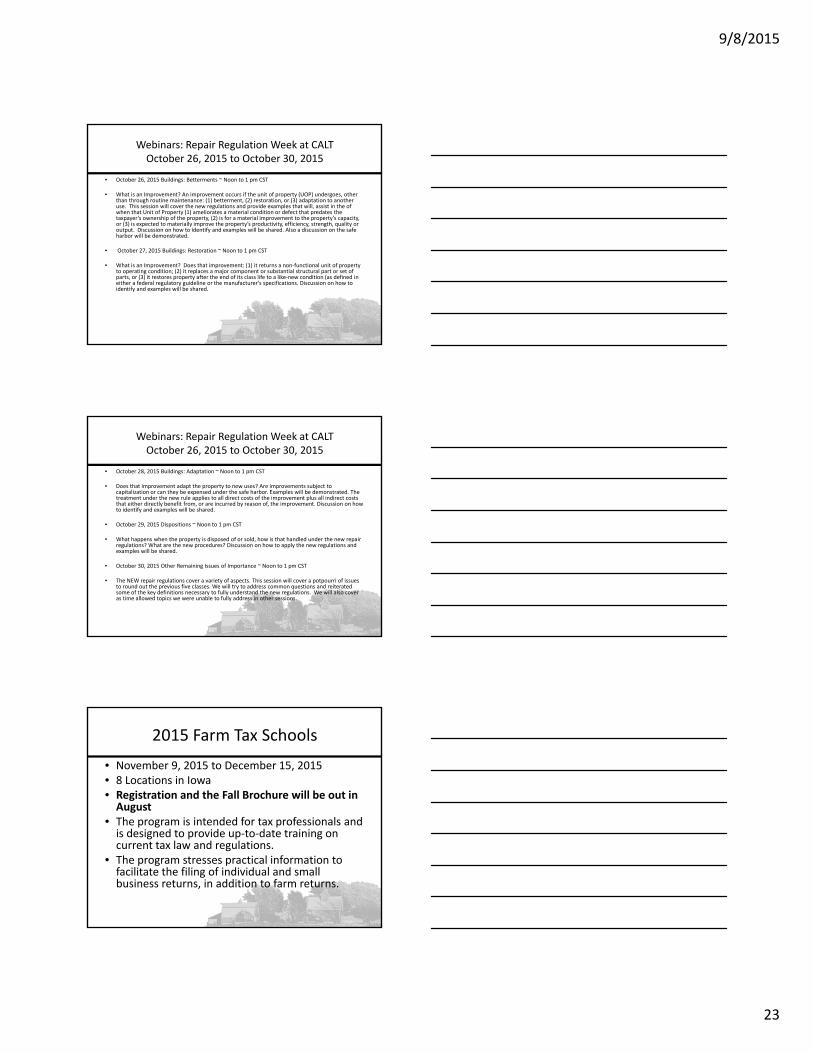

Webinars: Repair Regulation Week at CALTOctober 26, 2015 to October 30, 2015

• October 26, 2015 Buildings: Betterments ~ Noon to 1 pm CST

• What is an Improvement? An improvement occurs if the unit of property (UOP) undergoes, other than through routine maintenance: (1) betterment, (2) restoration, or (3) adaptation to another use. This session will cover the new regulations and provide examples that will, assist in the of when that Unit of Property (1) ameliorates a material condition or defect that predates the taxpayer’s ownership of the property, (2) is for a material improvement to the property’s capacity, or (3) is expected to materially improve the property’s productivity, efficiency, strength, quality or output. Discussion on how to identify and examples will be shared. Also a discussion on the safe harbor will be demonstrated.

• October 27, 2015 Buildings: Restoration ~ Noon to 1 pm CST

• What is an Improvement? Does that improvement: (1) it returns a non‐functional unit of property to operating condition; (2) it replaces a major component or substantial structural part or set of parts, or (3) it restores property after the end of its class life to a like‐new condition (as defined in either a federal regulatory guideline or the manufacturer’s specifications. Discussion on how to identify and examples will be shared.

Webinars: Repair Regulation Week at CALTOctober 26, 2015 to October 30, 2015

• October 28, 2015 Buildings: Adaptation ~ Noon to 1 pm CST

• Does that improvement adapt the property to new uses? Are improvements subject to capitalization or can they be expensed under the safe harbor. Examples will be demonstrated. The treatment under the new rule applies to all direct costs of the improvement plus all indirect costs that either directly benefit from, or are incurred by reason of, the improvement. Discussion on how to identify and examples will be shared.

• October 29, 2015 Dispositions ~ Noon to 1 pm CST

• What happens when the property is disposed of or sold, how is that handled under the new repair regulations? What are the new procedures? Discussion on how to apply the new regulations and examples will be shared.

• October 30, 2015 Other Remaining Issues of Importance ~ Noon to 1 pm CST

• The NEW repair regulations cover a variety of aspects. This session will cover a potpourri of issues to round out the previous five classes. We will try to address common questions and reiterated some of the key definitions necessary to fully understand the new regulations. We will also cover as time allowed topics we were unable to fully address in other sessions.

2015 Farm Tax Schools

• November 9, 2015 to December 15, 2015 • 8 Locations in Iowa• Registration and the Fall Brochure will be out in August

• The program is intended for tax professionals and is designed to provide up‐to‐date training on current tax law and regulations.

• The program stresses practical information to facilitate the filing of individual and small business returns, in addition to farm returns.

9/8/2015

24

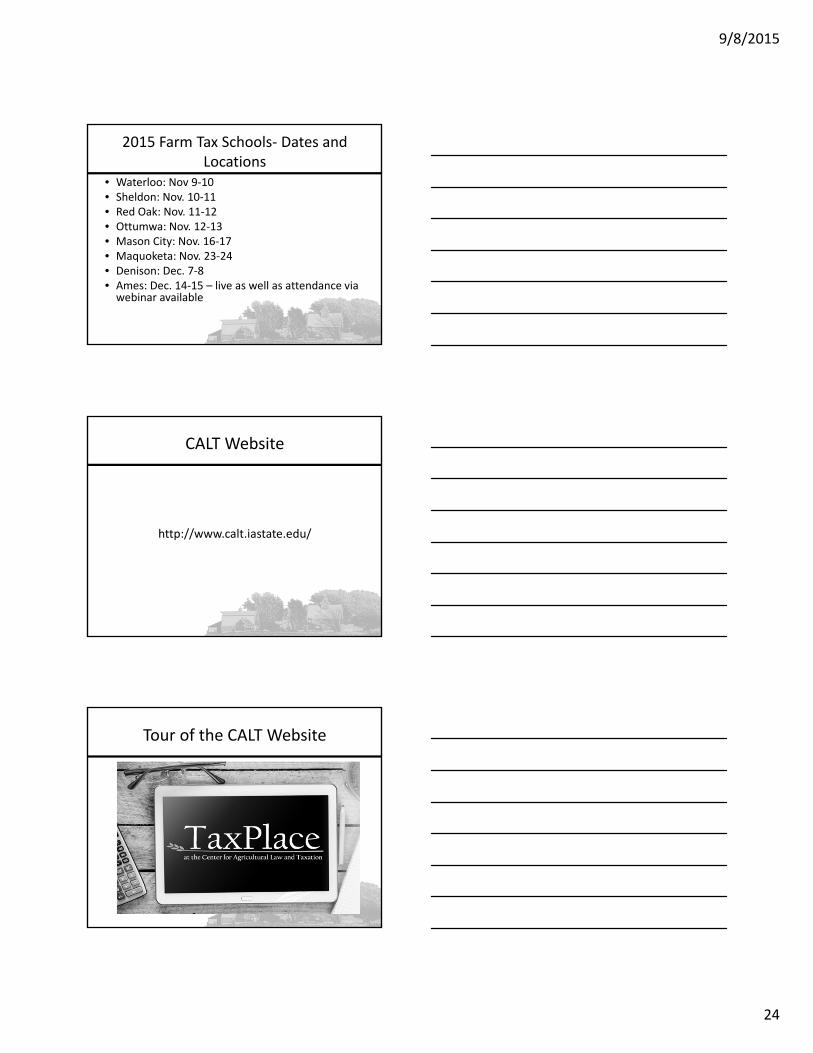

2015 Farm Tax Schools‐ Dates and Locations

• Waterloo: Nov 9‐10• Sheldon: Nov. 10‐11• Red Oak: Nov. 11‐12• Ottumwa: Nov. 12‐13• Mason City: Nov. 16‐17• Maquoketa: Nov. 23‐24• Denison: Dec. 7‐8• Ames: Dec. 14‐15 – live as well as attendance via webinar available

CALT Website

http://www.calt.iastate.edu/

Tour of the CALT Website

9/8/2015

25

CALT Staff

Roger A. McEowenCALT Director and is a Leonard Dolezal Professor in Agricultural LawEmail: [email protected]: (515) 294‐4076Fax: (515) 294‐0700

Kristine A. TidgrenStaff AttorneyE‐mail: [email protected]: (515) 294‐6365Fax: (515) 294‐0700

CALT Staff

Kristy S. MaitreTax SpecialistE‐mail: [email protected]: (515) 296‐3810Fax: (515) 294‐0700

Tiffany KayserProgram AdministratorEmail: [email protected]: (515) 294‐5217Fax: (515) 294‐0700