pre-feasibility study report (picoco iii housing development project

TRANSCRIPT

2013

Pre-Feasibility Study Report

(PICOCO III HOUSING DEVELOPMENT PROJECT)

At Boane, Matola District, Maputo, Mozambique

Prepared by

Indala Consulting Services (Pty) Ltd The Avenues North, Birch

6 Mellis Road

Rivonia,

Sandton,

2128

Pre-Feasibility Study Report – PICOCO III HOUSING DEVELOPMENT

EXECUTIVE SUMMARY

This report elaborates the technical, market and financial feasibility of implementing a housing

development project in the greater Matola Municipal area, Boane District, close to the city of

Maputo, Mozambique. Prior to the presentation of site specific details it also includes some general

information about the demographics and economic highlights of Mozambique as background

information on the project.

According to the mobilized funding for the project, potential capacity of the allocated land (271ha) is

around 4000 housing units, stand-alone houses and apartments included. Capacity projected to be

utilized in the first phase of the project is around 1000 housing units.

The agreement between the Fundo para o Fomento Habitacao and Imbani Projects (Pty) Ltd to

develop the Boane district using the latest construction technology from South African will retain up

to 60% of professionals considering relocating from Mozambique due to accommodation challenges.

The total cost of the project in the initial stage will be US$133 391 940, the subsequent phases will

be funded from sales and rental proceeds. The Net Present Value (NPV) and the Internal Rate of

Return (IRR) is estimated at US$11 018 000 and 53% respectively. It was FFH’s wish that the

project be a minimal profit project.

The growth of the Mozambican economy has brought about need for industrial, light industrial and

warehousing space. The general growth of the population over available infrastructure has increased

the demand for space to rent and buy.

The technical, financial and market feasibility of this project is satisfactory and it can be

recommended as a very good investment opportunity.

Pre-Feasibility Study Report – PICOCO III HOUSING DEVELOPMENT

TABLE OF CONTENTS

i) COVER PAGE

ii) EXECUTIVE SUMMARY

iii) TABLE OF CONTENTS

1 GENERAL INFORMATION

1.1 MOZAMBICAN DEMOGRAPHICS

1.2 MOZAMBICAN ECONOMIC PERFOMANCE HIGHLIGHTS

1.3 HOUSING PARASTATAL & MANDATE

1.4 PICOCO III HOUSING DEVELOPMENT PROJECT OVERVIEW

2.0 SITE INFORMATION

2.1 LOCATION

2.2 ACCESS

3.0 TECHNICAL ANALYSIS

3.1 SITE LOCATION

3.2 HOUSING TYPOLOGIES

3.2.1 UNIT TYPE 90A

3.2.2 UNIT TYPE 90B

3.2.3 UNIT TYPE 110A

3.2.4 UNIT TYPE 11B

3.2.5 UNIT TYPE 130A

3.2.6 UNIT TYPE 130B

3.2.7 UNIT TYPE 150A

3.2.8 UNIT TYPE T2B

3.2.9 UNIT TYPE T3B

3.2.10 UNIT TYPE T2C

3.2.11 UNIT TYPE T3C

3.2.12 UNIT TYPE T4

4.0 REAL ESTATE MARKET ANALYSIS

Pre-Feasibility Study Report – PICOCO III HOUSING DEVELOPMENT

4.1 MARKET OVERVIEW

4.2 MARKET TRENDS AND PROSPECTS

4.3 MARKET SEGMENTATION

4.3.1 END-USER SEGMENTATION

4.3.1.1 HOUSING

4.3.1.2 OFFICE

4.3.1.3 RETAIL

4.3.1.4 WAREHOUSING/ LOGISTICS/ INDUSTRIAL

4.3.2 RENT/SALE SEGMENTATION

4.3.3.0 OTHER RELEVANT VARIABLES

4.3.3.1 BUSINESS CYCLES

4.3.3.2 INVESTMENT/ EXIT STRATEGY

4.3.3.3 LOCAL INTELLIGENCE

5.0 FINANCIAL ANALYSIS

5.1 PROJECT COSTS

5.1.1 CAPITAL EXPENDITURE

5.1.2 OPERATIONAL EXPENDITURE

5.1.3 AGGREGATE COSTS

5.2 HOUSING UNITS STATISTICAL MODELING

5.2.1 UNIT COST AND SALES PRICES

5.2.2 ASSOCIATE AREAS AND COSTS

5.3 ECONOMICS OF THE PROJECT

6 CONCLUSION

Pre-Feasibility Study Report – PICOCO III HOUSING DEVELOPMENT

1 General Information

1.1 Mozambican Demographics

The total population in Mozambique was last recorded at 25.2 million people in 2012 from 7.7

million in 1960, changing 229 percent during the last 50 years. Population in Mozambique is

reported by the World Bank. From 1960 until 2012, Mozambique Population averaged 14.3 Million

reaching an all-time high of 25.2 Million in December of 2012 and a record low of 7.7 Million in

December of 1960. The population of Mozambique represents 0.35 percent of the world´s total

population which arguably means that one person in every 291 people on the planet is a resident of

Mozambique.

Source: www.tradingeconomics.com

Of the 25.2 million Mozambicans, the populace aged between 0 and 14 years constitute 44.1%,

52.6% of the population is between 15 and 64 years of age , while those above 65 years of age only

constitute 3.3%. This thus shows that more than half the population is the economically productive

stereotype and thus ought to be catered for accommodation wise individually and dually (married) .

Since the end of the colonial era in 1975 up until the end of the Mozambican civil war in 1992, the

country had negative growth economically but has since emerged to become one of the world’s

fastest growing economies to date. With a Gross Domestic Product of US$14.59 billion and 7.4%

Growth rate as well as a controlled inflation of 1.1%, Mozambique has been growing in

competitiveness over the past several years.

0

5

10

15

20

25

30

Mozambican Population (Millions)

Mozambican Population(Millions)

Pre-Feasibility Study Report – PICOCO III HOUSING DEVELOPMENT

1.2 Mozambican Economical performance highlights:

• Strong economic performance over the past 15 years; in a 16 year period,

Mozambique’s GDP grew at an average annual rate of 8% registered the highest growth in all

non-oil sub-Saharan Africa economies (EIU, August 2010);

• Macroeconomic stability resulting from a series of structural reforms, and a substantial flow

of foreign aid and large investment projects from abroad, means that Mozambique is

considered one of the fastest growing economies in the world in the last decade, prospected to

be one of the 3 fastest growing economies over the next years;

Mozambique’s economic growth to exceed 7% in 2012, boosted by strong public and private

sector investment, easing of monetary policy and continued growth of the agricultural sector

(the largest economic sector);

In 2011, the MZN was among the top performing currencies in the world, boosted by strong

FDI inflows, tight monetary conditions and the implementation of a new foreign exchange law.

Aluminium makes up above 50% of Mozambique’s total exports and is an important

FX earner for the country;

• Large mining projects (particularly coal and natural gas) provide a key pillar for growth, and

foreign direct investment is expected to remain strong;

Pre-Feasibility Study Report – PICOCO III HOUSING DEVELOPMENT

• Throughout 2011 a number of companies drilling for gas and oil in the Rovuma

basin (Northern Mozambique) have consistently reported significant findings of large natural

gas reserves, making this area one of the greatest gas fields to be unveiled over the last

decade and putting Mozambique in the world map of gas;

• A number of key investments in the energy sector (thermo and hydro-electric generation as

well as in energy transportation) should create the conditions for further growth in other

sectors such as industry, potentially inducing further economic growth;

• Large investments in infrastructure (rail, airports and ports) connected to the main sectors

driving DFI are expected to have a strong impact in other areas of the economy, including

tourism, agriculture and agro-industry, improving logistics and more generally the viability of

investment projects.

Pre-Feasibility Study Report – PICOCO III HOUSING DEVELOPMENT

Despite this positive growth, Mozambique still has inadequate infrastructure mostly in the housing

sector. To this effect, one would expect that as an individual grows and they start working, that they

would move out of their parents’ house and rent an apartment. For most Mozambicans this notion is

not true as they continue to live with their parents due to unavailability of housing stock. The lack of

adequate supply of housing stock forces the rental rates upwards. Rentals in the Maputo CBD are

currently tagged at approximately US$4,000 for a two bedroom 70m² apartments. A similar type of

apartment can be purchased for an equivalent of up to US$300,000.

Below is a typical urban settlement in Mozambique.

Source: African Development Bank Group website –Urban Settlement

Pre-Feasibility Study Report – PICOCO III HOUSING DEVELOPMENT

1.3 Housing Parastatal and Mandate

As far as accommodation is concerned the “Fundo para o Fomento de Habitacao” (FFH, the Housing

Promotion Fund) which was created in 1995 by the decree n ֯ 24/95 has been limited by the

inadequate allocation of funding from the Ministry of Finance. FFH’s mandate being

(i) Conducting studies and research in the housing sector

(ii) Providing land with associated infrastructure such as roads, bulk water

and electricity supply

(iii) Procuring funding to develop housing projects

In the recent past, the FFH mandate has been expanded to include, inter alia, facilitation of

mechanisms to attract local and foreign financing schemes for government housing programs as well

as establishment of partnerships with developers and funders to achieve this aim. With these

activities, it was anticipated that the FFH will be able to fund its operation in the long-run without

relying on allocation from the Ministry of Finance.

1.4 Picoco III Housing Development Project Overview

The proposed housing development will be the largest residential undertaking of its kind in the

history of Mozambique. It will comprise residential units, shopping facilities, light industrial and

business parks, a healthcare facility, petrol station, public amenities such as schools, a police station,

fire station as well as a clubhouse with various recreational and sporting facilities and restaurants.

The development will feature comprehensive high quality infrastructure such as paved roads, street

lighting, fiber-optic cable for both telecommunication and television, gas reticulation and grey water

systems for irrigation. Incorporated also will be lifestyle elements comprising state-of-the-art

security with controlled access to ensure the safety of resident families and their guests.

The housing units on offer will range from 50m², one bedroom apartments, to a standard two

bedroom apartment, a variety of three and four bedroom apartments to three bedroom townhouses

and a double-storey four bedroom stand-alone house type. The architecture of the units will be

contemporary, spacious and, indicative of refined opulent urban living.

Developed as a modern and affordable lifestyle estate, Picoco III will have a strong emphasis on

“green” living and residents will be encouraged to reduce their carbon footprint where possible.

Pre-Feasibility Study Report – PICOCO III HOUSING DEVELOPMENT

Picoco III will set the benchmark for mixed use residential developments in Mozambique and in

every instance the development will provide the end-user a valuable asset of lasting quality and

integrity.

2 Site Information

2.1 Location

Picoco III housing development will be located 30km west of the city of Maputo, in the Boane

District of the Maputo Province.

Source: Google maps website; an aerial view of the location of Picoco III Housing Development

project

2.2 Access

The construction of a 5km road to link the Boane District to Belo Horizonte will be the main

accessibility tool. Belo Horizonte then links Picoco III to every other major location and will be fully

refundable by the Mozambican government upon completion. To this effect the development will

also offer shuttle bus facilities on regular intervals between Picoco III and the Maputo CBD, Matola

and the airport. The shuttle buses would be to offer alternative transport facilities to people who do

not want to travel to work in their own cars as well as provide transport to students who prefer going

to schools in the Maputo CBD or Matola areas.

Pre-Feasibility Study Report – PICOCO III HOUSING DEVELOPMENT

3 Technical analyses

3.1 Site Selection

The location was provided by the Fundo para o Fomento de Habitaciao (FFH) as all land in

Mozambique is owned by the government. This therefore elaborates the fact that this land was

pegged for such a development in the Maputo expansion master plan. Imbani Projects in its

agreement with FFH are required to perform the construction process, engineering, and architectural

designs for the project and post-construction management (facilities management).

This site was chosen as it is the best location for a commuter town where workers can commute to

work around the Maputo province conveniently.

3.2 Housing typologies

A comparison on each of the unit types to assess the unit cost structure as compared to the quantity

of each typology rolled out in phase 1 is laid out below.

3.2.1 Unit type 90A

90A unit type housing unit is a three bedroom stand-alone house of (92m²) ninety-two square

meters. If 100 of these are initially rolled out, each of them will cost US$126,149. However, if the

second option of rolling out 208 housing units under this typology is adopted then the unit cost will

be US$123,368. The selling price of each of these 90A unit type housing units will be US$126,960.

Pre-Feasibility Study Report – PICOCO III HOUSING DEVELOPMENT

3.2.2 Unit Type 90B

90B unit type housing unit is a three bedroom stand-alone house of (89m²) eighty-nine square

meters. If Picoco III rolls out 200 in Phase 1 construction then each units will cost US$113,081. On

the other hand, if an initial 417 units are constructed then the unit price drops to US$110,587. The

selling price of each of these 90B unit type housing units will be US$122,820. This stand-alone type

of housing unit is ideal for a small family.

Pre-Feasibility Study Report – PICOCO III HOUSING DEVELOPMENT

3.2.3 Unit Type 110A

Unit type 110A has a floor area of 109m², also is three bedroomed, a stand-alone and is ideal for a

family setup. Given option 1 of constructing 60 Unit type 110A housing units in the first phase of

the project the unit cost of one such housing unit is estimated to be around US$135,931. However,

where 125 units are rolled out the per unit cost drops to US$132,935. The selling price is pegged at

US$152,600.

Pre-Feasibility Study Report – PICOCO III HOUSING DEVELOPMENT

3.2.4 Unit Type 110B

Unit type 110B has a floor area of 112m², also is three bedroomed, a stand-alone and is ideal for a

family setup. Where 60 Unit type 110B housing units are constructed in the first phase of the project,

the unit cost of one such housing unit is estimated to be around US$145,870. Alternatively the

construction of 125 units drops the cost per unit to US$142,654. These will be sold for US$156,800.

Pre-Feasibility Study Report – PICOCO III HOUSING DEVELOPMENT

3.2.5 Unit Type 130A

Unit type 130A has a floor area of 130m², also is three bedroomed, a stand-alone and is ideal for a

family setup. The construction of only 20 Unit type 130A housing units will cost US$171,069 per

unit. On the other hand, the increase in initial supply to 42 brings down the unit cost to US$167,297.

They will be sold for US$188,500. Apart from the other above mentioned stand-alone housing units,

the 130A now has a double garage and a study thus more accommodative.

Pre-Feasibility Study Report – PICOCO III HOUSING DEVELOPMENT

3.2.6 Unit Type 130B

Unit type 130B has a floor area of 137m², is three bedroomed, stand-alone and is ideal for a family

setup. The roll out of 20 Unit type 130B housing units attracts a unit cost of US$169,973, whereas,

42 of these will bring the cost per unit to US$166,226 They will be priced at US$191,400.

Pre-Feasibility Study Report – PICOCO III HOUSING DEVELOPMENT

3.2.7 Unit Type 150A

This is a four bedroom double storey stand-alone housing unit with a lettable space of 150m². If the

first phase of the project rolls out 20 units of this typology unit cost will be US$187,581. If the

second option however, of 42 is adopted then unit cost is brought down to US$183,445. Selling price

is US$217,500.

Pre-Feasibility Study Report – PICOCO III HOUSING DEVELOPMENT

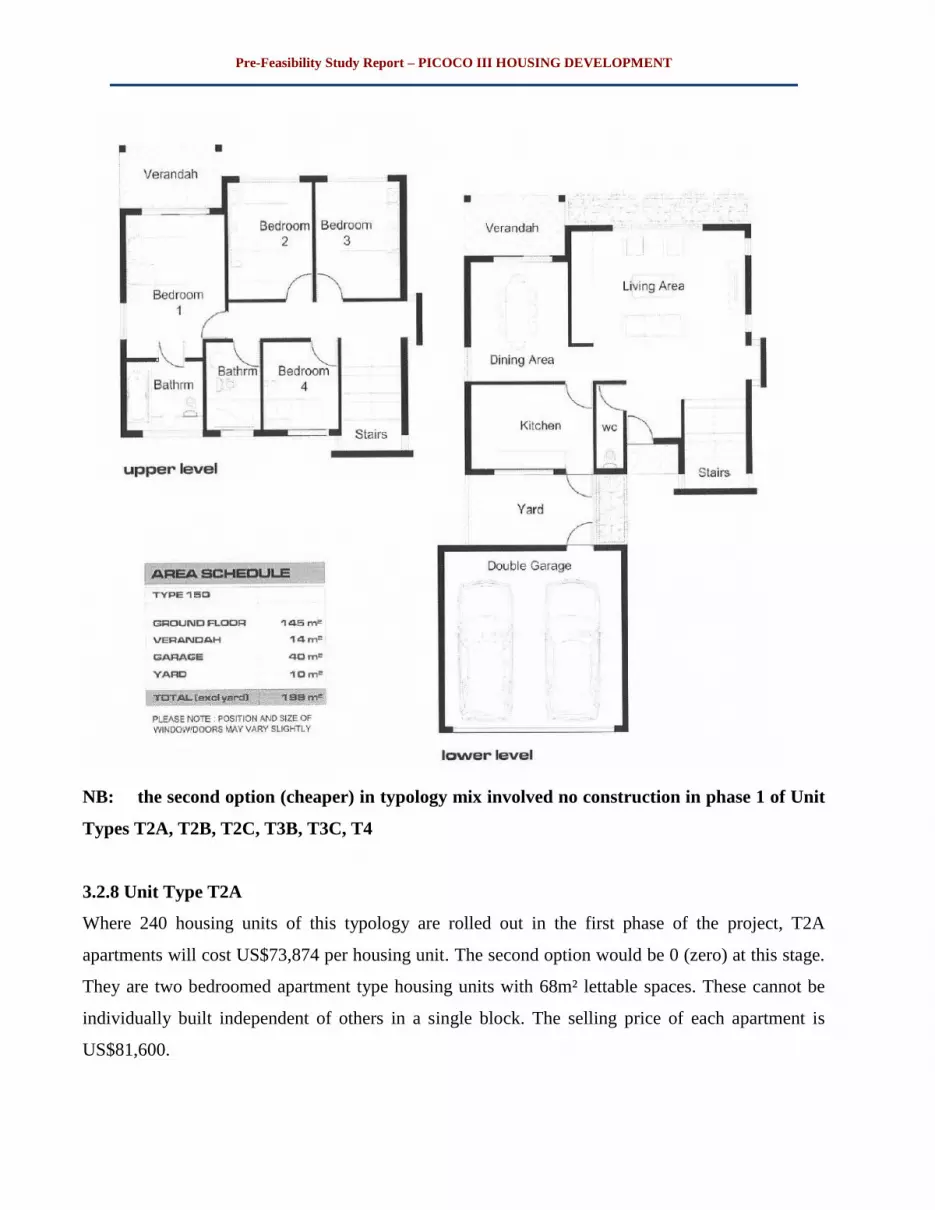

NB: the second option (cheaper) in typology mix involved no construction in phase 1 of Unit

Types T2A, T2B, T2C, T3B, T3C, T4

3.2.8 Unit Type T2A

Where 240 housing units of this typology are rolled out in the first phase of the project, T2A

apartments will cost US$73,874 per housing unit. The second option would be 0 (zero) at this stage.

They are two bedroomed apartment type housing units with 68m² lettable spaces. These cannot be

individually built independent of others in a single block. The selling price of each apartment is

US$81,600.

Pre-Feasibility Study Report – PICOCO III HOUSING DEVELOPMENT

3.2.9 Unit Type T2B

The unit type T2B is a two bedroom flat with 88 m² at an estimated cost of US$101,420 and to be

sold for US$105,600. The number of units projected to be constructed is 40 units. The second option

would obviously be zero units initially again for this one as mentioned above.

3.2.10 Unit type T3B

These differ from the T2B in that they have 3 bedrooms as opposed to the two above. They have a

102m² lettable space and 40 units of these are going to be constructed in the first phase. The

estimated cost per unit type apartment will be US$111,437 and to be sold US$132,600.

3.2.11 Unit Type T2C

The T2C unit type apartment has two bedrooms and has 77m² with an estimated cost per apartment

of US$85,143 to be sold at US$92,400. The first phase has an estimated 80 units.

3.2.12 Unit Type T3C

The T3C unit type apartment has three bedrooms and has 97m² with an estimated cost per apartment

of US$110,185 and to be sold at US$126,100. The first phase will involve the construction of an 80

units.

3.2.13 Unit Type T4

The T4 apartment is a two bedroom flat with 108m² at an estimated cost of US$113,941 and to be

sold for US$140,400. The projected number of units to be constructed is 40 units.

4. Real Estate Market Analysis

4.1 Market Overview

A real estate market study for the Maputo, Tete, Chimoio and Nampula markets is a presentation to

provide a first inside view of the Mozambican Real Estate sector for potential investors. It is not

intended to be an in-depth analysis as it is still at pre-feasibility level. As such the general format is

qualitative rather than quantitative.

Indala took particular care in sustaining its assumptions used in financial modeling and

advisory work on its clients investment projects based on quantifiable and observable data,

Pre-Feasibility Study Report – PICOCO III HOUSING DEVELOPMENT

including measuring exposure to relevant risk factors /uncertainty.

While still obviously unstructured and lacking the systematic data collection to precisely

monitor the sector evolution, particularly relevant to forecast trends and guideline

investments, the Real Estate sector in Mozambique is most definitely gaining

momentum and real high-return investment opportunities do exist. Equally, significant

risk factors deterring main-stream investors to firmly enter the market do persist and they

should not be overlooked.

4.2 Market trends and prospects

The real-estate environment is characterized by strong growing demand and high rates of

consumption specially residential space (as well as other products such as office or retail), seen by

the low share of vacant space and rental rates that keep growing at 15% p.a. and easily doubling over

the past couple of years in the fastest growing areas and within the relevant segments.

Private sector offer as focused on the higher income segments of the market with lower

segments generally resourcing to own-construction to access new housing;

With demand largely outstripping supply, current real estate market conditions are very

favorable for green-field real-estate developments;

Given the long-term nature of the investments fuelling Mozambican economic growth, it is

reasonable to assume that the real estate market will not get to close saturation for the next 5-10

years particularly in the regions where most large investments are to take place;

With a growing influx of FDI, there is a major supply shortage of high end homes and grade A office

space ,that are targeted primarily at the international market and investor community;

The current stock of quality housing is experiencing a huge pressure from expatriates for 3-4

bedroom, hence supply of houses for this segment strong. Grade A office rental space will remain

difficult to find because of the scale of the offerings and the tendency to offer space to buy rather

than to let.

A major obstacle for the development of real estate assets is the difficulty in accessing financing; the

inexistence of adequate financial instruments (such as fluid/structured capital markets or dedicated

Pre-Feasibility Study Report – PICOCO III HOUSING DEVELOPMENT

investment funds) determines that most funding relies on debt from commercial banks which, given

the low level of own capital by promoters and relatively high interest rates, seriously limit the

financial capability to develop real estate projects;

Despite the strong signs of a booming – as much as sustained – market, the prevailing high- risk

perception of Mozambique as an investment destination and the general lack of reliable data on the

market adds on to deterring main-stream foreign investors to enter it;

Short track-record of local promoters and uncertainty on exit strategies further determine the

relatively low investment pace on the supply side to accommodate the soaring demand for real

estate products;

Still, demand is strong and prospective returns on real estate projects are extremely attractive.

Fast growth is also fuelling competition among contractors and suppliers of building materials

which combined with increasing scale is pushing down building costs and extending margins for

developers;

The development of the real estate sector is also contributing to the improvement of local

capabilities in all aspects of project implementation/management, from conceptualization and

planning to actual building and market placement, be it in direct technical areas or in its financial

structuring and backing-up; despite this trend, the Mozambican market significantly lags behind

mature markets in experience and expertise;

While overall presenting firm growth indicators, the market is rather thin and overshooting supply is

a risk; off-take agreements from key buyers/tenants, differentiation factors, added- value propositions

are strategies that minimize such risks; good local intelligence is key;

The market demand is generally geared towards rental-type of products as for the greatest part

demand is based on the large investment projects (mining, gas,…) which do not want to add real

estate assets to their core, high-capital intensive investments and/or those expat workers who will rent

before buying property.

Pre-Feasibility Study Report – PICOCO III HOUSING DEVELOPMENT

Housing

Office

Retail

Warehousing

Logistics

Industrial

Real

Estate

Built-to-

rent Build-

to-sell

4.3 Market Segmentation

Basic Segmentation Vectors

End User Rental/Sale

4.3.1 End-User Segmentation

4.3.1.1 Housing

The surge of demand in the housing segment of the market is grounded in

four main trends:

i. Substantial and growing FDI fluxes and the technical and management staff

associated with these investments, directly by the investor companies or their suppliers;

ii. Growing middle-class of Mozambican citizens with increasing purchasing power

and wider access to credit;

iii. General high growth rate of the population with a relatively stable stock of built

houses over the previous decades;

iv. Private investors applying excess wealth in real estate assets.

Given the fast growing in demand and prices, housing is also a central priority in

Pre-Feasibility Study Report – PICOCO III HOUSING DEVELOPMENT

governmental policy. Since most new supply of housing by the private sector is focused on

the higher end of the market, the government has stepped in to encourage solutions to lower

income segments. Such policies concurrently aim at controlling urban development in a

sustainable fashion.

The sub-segmentation of the housing market is crucial when defining the real estate

investment profile and correctly position it in the market. Different positioning strategies

may be equally valid depending on the particular supply and demand trends in particular

areas.

4.3.1.2 Office

Demand for office space is primarily originated by the large corporations directly involved in the

anchor investment projects but is then replicated by the numerous business opportunities they

encompass.

Primary suppliers to these projects are rapidly positioning themselves in

Mozambique driving up demand for office space, including service

providers (ranging from technical consultancy practices to legal advisory,

IT, banking and insurance, within a much vaster array), equipment,

materials and consumer goods sellers as well as manufacturers.

The magnitude of the investments underway are continuous and increasingly pulling a wide range of

SMEs into the Mozambican economy, all demanding for suitable premises from where they can

operate their businesses.

Given the long-term nature of the underlying primary large investments, it is predictable that the

trend is also of durable nature. The dispersion of the large investments along the various pivotal

points where they are settling in makes the trend widespread even in regions where formal economic

activity has been sparse or nearly inexistent.

The increase in demand is not only in the office space (size) itself but also in its sophistication

with service and quality aspects gradually gaining relevance.

4.3.1.3 Retail

The economic growth brings along changes in consumer needs and

habits. The prevailing traditional retail landscape is gradually giving way to

new commercial areas where modern retail is increasingly gaining

Pre-Feasibility Study Report – PICOCO III HOUSING DEVELOPMENT

relevance. In most urban areas larger operators, with particular relevance for South African retail

chains, are opening new shops as anchor tenants of malls and shopping centers.

The general growth trend of the economy, as far as retail is concerned, is further speeded up by the

increasing numbers of people entering the formal employment market, away from agriculture into

extractive, processing and services industries. With average disposable income on the rise there is a

growing demand for consumer goods and retail is booming, particularly in its modern formats.

Adding to this the expat community is also expanding bringing with them the consumption needs and

habits as much as the purchasing power.

Retail is on the rise as much as the demand for space specifically conceived for it, particularly in the

key geographic areas where economic expansion is strongly felt. The retail chains, keen to expand

in this market, offer the possibility of conceiving real estate retail areas together with their future

tenants, diminishing the investments risks. They are generally ready to enter long-term contracts

which diminish uncertainty over future cash flows from investments in retail parks, malls or other

formats.

4.3.1.4 Warehousing/ Logistics/ Industrial

The need for premises to handle the fluxes of physical goods, processing and logistics, is a

pressing need arising from the economic growth, particularly critical as the large investments depend

on these to materialize. The stakes are high and the ball is rolling. The

large investments are being made in remote and rural areas where little

infrastructure exist.

The urban areas that will serve as the logistical basis are not equipped to

match the challenge and the need for warehousing space is enormous,

even more so in the hubs around ports and rail. From simple storage of commodities in large

quantities (such as coal), to cold storage facilities, warehousing of goods, parts and equipment, there

is a large and growing unsatisfied demand.

The existing infrastructure is just a marginal part of what will be when mining, gas and other

investments reach full scale operations. The gap is wide and offers numerous investment

opportunities, in terms of space/premises required as well as the management and handling

Pre-Feasibility Study Report – PICOCO III HOUSING DEVELOPMENT

expertise.

From single warehouses to large multimodal logistic platforms, a number of projects are currently

taking shape and will require adequate funding.

4.3.2 Rent/ Sale Segmentation

A central segmentation criterion, with a significant impact on the return profile of a real estate

investment is its market positioning in terms of a rental or a sale product. The general trend

observable in Mozambique is that the bulk of the market is on the

rental side. Most demand is originated by the large anchor

investments which prefer to rent/outsource what is not within their

core businesses, not to add complexity to their management

challenges and to limit initial capital expenditures.

The critical consequence is that most real estate products should be conceived taking this factor into

consideration. If highly geared, the financial charges may eat up a considerable part of the returns

and if not properly financed (adequate time span) they may actually not survive to see the light of

day. On the other hand, the rents are increasing sharply and may yield much higher returns for an

investor with a longer term perspective.

Coincidently, while build-to-sell products face slow market acceptance and penetration, build- to-rent

are in sharp contrast facing an unmet demand willing to pay substantial premiums for not having the

initial capital outflow associated with the purchase.

Pre-Feasibility Study Report – PICOCO III HOUSING DEVELOPMENT

4.3.3.0 Other Relevant Variables

4.3.3.1 Business Life-Cycle

Unlike more mature real estate markets, Mozambique is rather unstructured although going through

rapid and profound changes. Most projects are in their early stages and being developed in a

somewhat amateur form.

They generally struggle to raise adequate funding and are based in little or no

previous research, lacking the necessary analytical basis on their planning stage.

Projects are built based on the general assumption that the demand will rapidly

absorb whatever is offered. While to some extent that has been the reality, such loose approach will

most probably lead to a number of investment flops, and if not so drastic, most investments will be

far from achieving their potential returns with sub-optimal options being taken.

Existing projects in search for finance and equity partners exist in all major segments, be it

geographically, by product type and size.

A strategy for entering the Mozambican market should take into consideration that most projects will

be presented as green-field and require additional effort to improve them up to being best options.

Such a strategy at this stage makes good business sense although may deter less flexible players from

entering.

Pre-Feasibility Study Report – PICOCO III HOUSING DEVELOPMENT

For an investor, particularly of a more financial nature, this means that entering the project in early

stages and contributing to its design and financial planning phases may bring additional gains.

Generally most existing projects an investor may consider to participate in still require some effort in

their various components. It does not mean they are not good investment proposals, it just means

that the prospective investor may see advantages in entering at an earlier stage and not expect to

be presented with “ready-to-invest” propositions. Such approach may encompass a significant

up-side not to mention being in itself a clear risk-mitigation strategy.

Pre-Feasibility Study Report – PICOCO III HOUSING DEVELOPMENT

Traditional Exit Alternatives

Exit

Investment

Second Stage

Investors

Structured

Markets

Investment Funds

Individuals

End Market

5 10 20 40 80 150 300 600

1000

Scale

Project scale somewhat reflects the development stage of the market. Scale/size of projects is quite

diverse ranging from stand-alone buildings to large urbanizations up to one billion USD investment

schedule. The most common projects are worth up to one hundred million USD (investment size).

4.3.3.2 Investment/ Exit Strategy

The simple perception that the

market is booming is not enough

to enter it as what an outsider will

see is a blurred picture of a

changing reality which in financial

terms is equivalent to high perceived

risk. Since for its own nature real

estate investments require significant

up-front capital commitments, this

risk translates into limited funding

available.

The financing of real estate projects is further limited by the fact that the

bulk of the market is on the rental side. While returns are high, the

profile changes dramatically in terms of the time span they occur. In

addition to facing an undefined investment environment, the investor is

asked to wait for long-term prospective returns. It all adds up to deter investors.

Corporates

Individuals

Pre-Feasibility Study Report – PICOCO III HOUSING DEVELOPMENT

There is a great deal of space for further structuring the projects, by creating innovative project-

finance type of solutions to ensure viability and mitigate high perceived risks. For investors willing

to make the effort, the market offers potentially high returns. The traditional resource to commercial

banks debt as the primary source of finance should give way to other possibilities, from equity to

hybrid financing instruments for it is not enough, adequate and local banks exposure to real estate, in

a context of limited capital, seriously hinders their appetite for additional financing the sector.

A serious concern for someone investing in green-field projects is the options to exit the investment.

Thus far the projects have been pretty much developed with the end market (end users) as the

prospective off-takers of the investment.

Yet, with the development of the market and the growing interest it is generating, additional options

are becoming viable, particularly with the formation and entrance of real estate dedicated funds with

a longer term approach, willing to keep the assets in their portfolios as a source of a steady income

stream.

The trend is quite tangible with an increasing number of different funds of different origins

and sizes enquiring on potential investment targets.

As the sector evolves the spectrum of exit strategies will become wider benefiting those who took

the risk in its early stages.

4.3.3.3 Local Intelligence

In a fast changing sector with a short track record, information is scarce.

Statistics and research is poor which difficult the ability of assessing

market potential and risks, identify opportunities and form a clear

strategy. While good investment opportunities exist, thus far most

players in the market have taken an ad-hoc opportunistic approach and

new entrants struggle to gain an up-front vision of the market as a whole

from which to decide on whether and where to invest. The short lived and fast moving environment

makes it is even more difficult to grasp trends and envision the future, key to decide on positioning

investments and products. In such a context what is being projected and under licensing is more

relevant than what can be observed or the data gathered on it, particularly important to understand

Pre-Feasibility Study Report – PICOCO III HOUSING DEVELOPMENT

the supply side of the industry. Understanding the dynamics of this fast evolving environment is not

only fundamental, it requires creative research approaches to get the relevant information and some

additional effort to access it.

While technical capabilities for the development of projects have been gained by the association of

local promoters to outside experts (such as architects or designers) information gathering still needs

to be done locally, requiring physical presence to understand the market context, access/filter the

investment opportunities, and structure them in a format an investor can understand in order to

evaluate as potential investment targets.

5 Financial Analysis

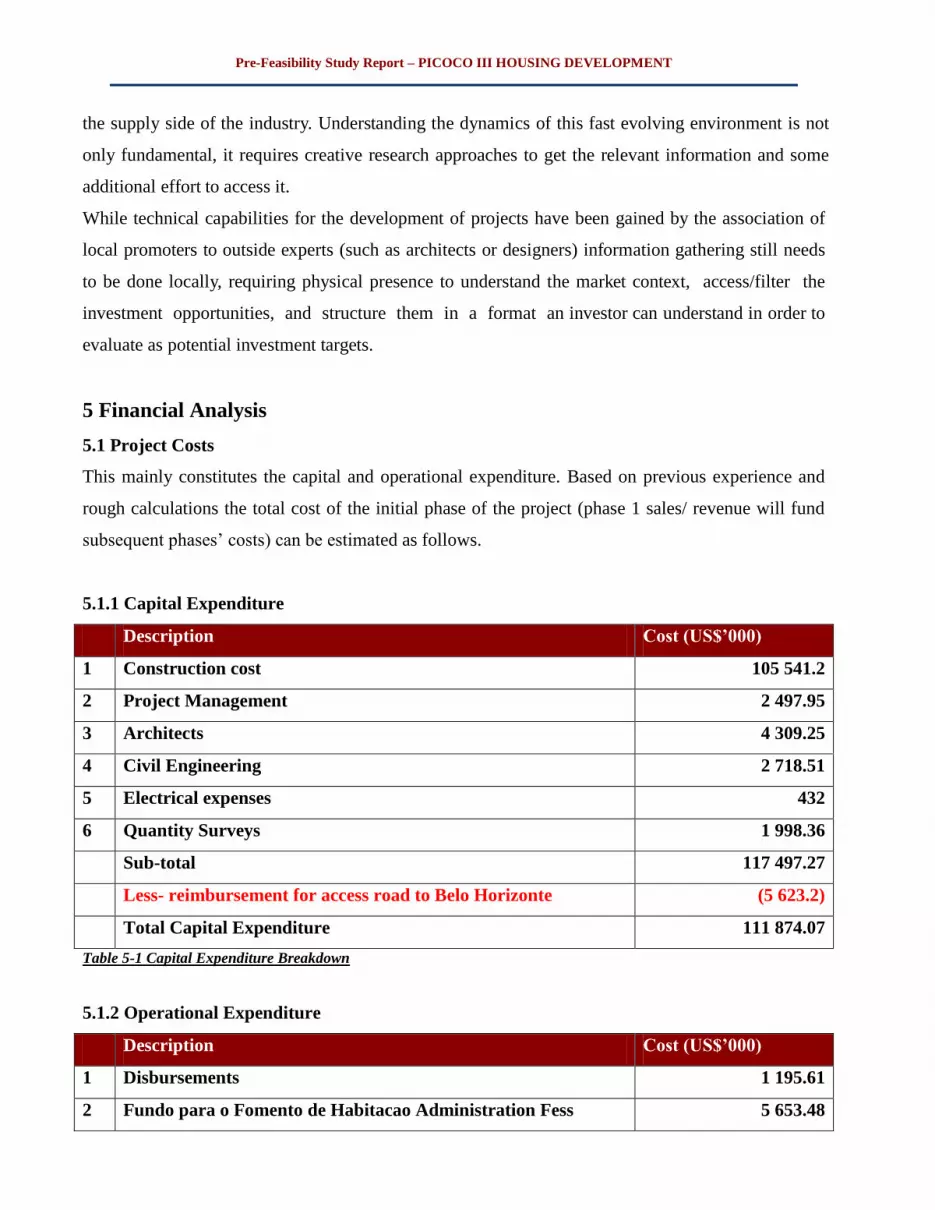

5.1 Project Costs

This mainly constitutes the capital and operational expenditure. Based on previous experience and

rough calculations the total cost of the initial phase of the project (phase 1 sales/ revenue will fund

subsequent phases’ costs) can be estimated as follows.

5.1.1 Capital Expenditure

Description Cost (US$’000)

1 Construction cost 105 541.2

2 Project Management 2 497.95

3 Architects 4 309.25

4 Civil Engineering 2 718.51

5 Electrical expenses 432

6 Quantity Surveys 1 998.36

Sub-total 117 497.27

Less- reimbursement for access road to Belo Horizonte (5 623.2)

Total Capital Expenditure 111 874.07

Table 5-1 Capital Expenditure Breakdown

5.1.2 Operational Expenditure

Description Cost (US$’000)

1 Disbursements 1 195.61

2 Fundo para o Fomento de Habitacao Administration Fess 5 653.48

Pre-Feasibility Study Report – PICOCO III HOUSING DEVELOPMENT

3 Developers’ Fees 3 392.09

4 Marketing Cost 1 130.7

5 Insurance Cost 2 261.39

6 Legal Cost 2 261.39

Total Operational Expenditure 15 894.67

Table 5-2 Operational Expenditure Breakdown

5.1.3 Aggregated Costs

Description Cost (US$’000)

1 Capital Expenditure 117 497.27

2 Operational Expenditure 15 894.67

Aggregated Expenditure 133 391.94

Table 5-2 Aggregated Expenditure

Pre-Feasibility Study Report – PICOCO III HOUSING DEVELOPMENT

5.2 Housing Units Modeling

5.2.1 Unit Costs and Sales Prices

Unit Type No. of Units Living area

m²

Unit cost

US$

Unit cost

US$ per m²

Total Costs

US$

Sales Price

US$ per m²

Unit Sales

Price US$

Total Sales

US$

House 90A 208 92 123 368 1 341 25 701 707 1 380 126 960 26 450 000

House 90B 417 89 110 587 1 243 46 078 123 1 380 122 820 51 175 000

House 110A 125 109 132 935 1 220 16 616 823 1 400 152 600 19 075 000

House 110B 125 112 142 654 1 274 17 831 755 1 400 156 800 19 600 000

House 130A 42 130 167 297 1 287 6 970 711 1 450 188 500 7 854 167

House 130B 42 132 166 226 1 259 6 926 068 1 450 191 400 7 975 000

House 150A 42 145 183 445 1 265 7 643 547 1 500 217 500 9 062 500

Total Houses

Avg House

1000 127 768 735

127 769

141 191 667

141 192

Apart. A 0 68 72 245 1 062 0 1 200 81 600 0

Apart. B2 0 88 99 184 1 127 0 1 200 105 600 0

Apart. B3 0 102 108 980 1 068 0 1 300 132 600 0

Apart. C2 0 77 83 266 1 081 0 1 200 92 400 0

Apart. C3 0 97 107 756 1 111 0 1 300 126 100 0

Apart. D 0 108 111 429 1 032 0 1 300 140 400 0

Total Apart.

Avg Apart.

0 0

90 056

0

103 818

Table 5-4: Unit Costs and Sales Prices

Pre-Feasibility Study Report – PICOCO III HOUSING DEVELOPMENT

Page 35 of 35

5.2.2 Housing Unit Area and Costs Allocations

Table 5-4 Housing area breakdowns and cost allocation

Unit Type No. of Units

Per stand

No. of

stands

No. of

Units

Stand Size

(land) m²

Roads + Parking

Per unit m²

Access roads per

unit m²

Total roads

area m²

Combined

area m²

House 90A 1 100 208 500 100 100 41 667 91 667

House 90B 1 200 417 500 100 100 83 333 183 333

House 110A 1 60 125 500 100 100 25 000 55 000

House 110B 1 60 125 500 100 100 25 000 55 000

House 130A 1 20 42 500 100 100 8 333 18 333

House 130B 1 20 42 500 100 100 8 333 18 333

House 150A 1 20 42 500 100 100 8 333 18 333

Apart. A 4 60 0 500 60 60 0 0

Apart. B2 4 10 0 500 60 60 0 0

Apart. B3 4 10 0 500 60 60 0 0

Apart. C2 4 20 0 500 60 60 0 0

Apart. C3 4 20 0 500 60 60 0 0

Apart. D 4 10 0 500 60 60 0 0

Total 610 100 200 000 440 000

Pre-Feasibility Study Report – PICOCO III HOUSING DEVELOPMENT

Page 35 of 35

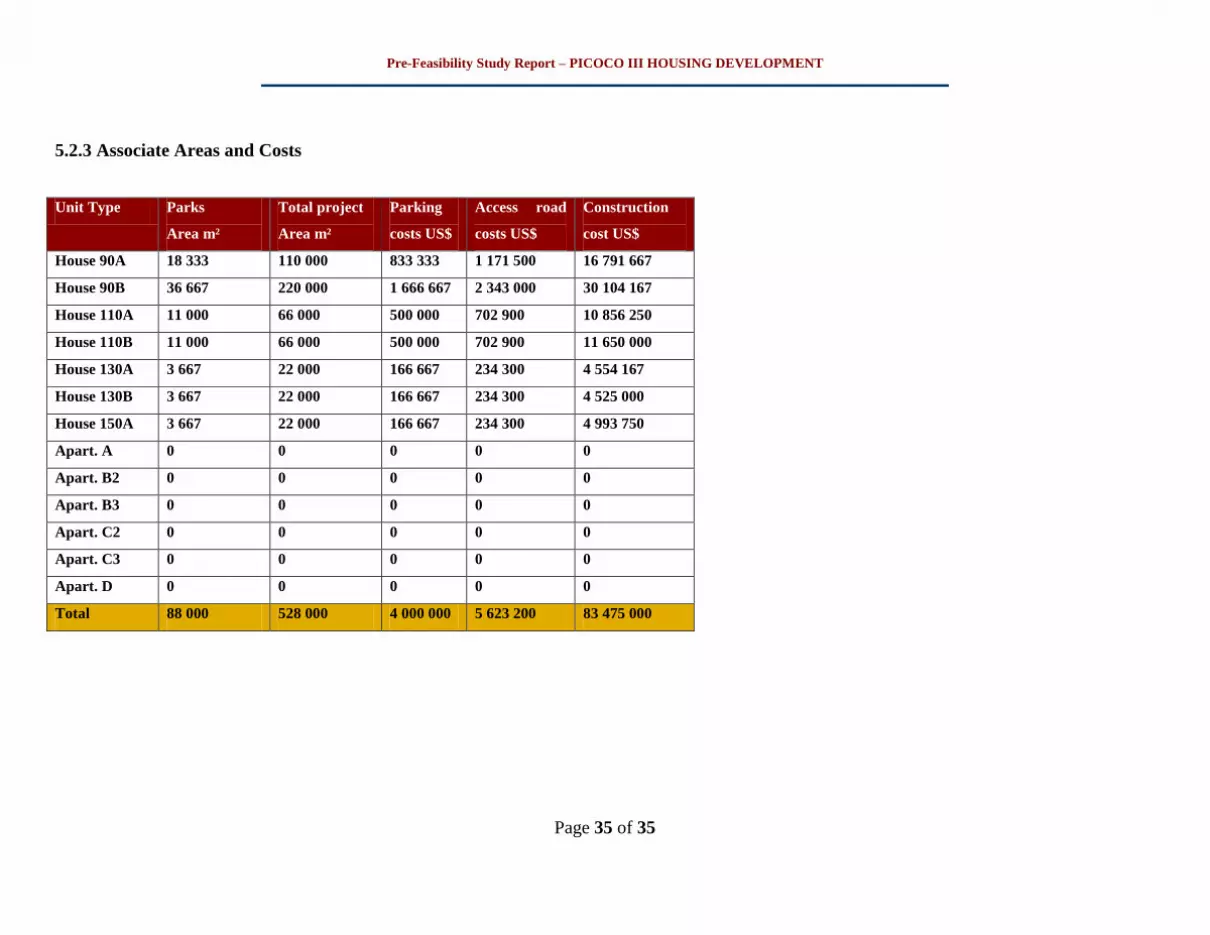

5.2.3 Associate Areas and Costs

Unit Type Parks

Area m²

Total project

Area m²

Parking

costs US$

Access road

costs US$

Construction

cost US$

House 90A 18 333 110 000 833 333 1 171 500 16 791 667

House 90B 36 667 220 000 1 666 667 2 343 000 30 104 167

House 110A 11 000 66 000 500 000 702 900 10 856 250

House 110B 11 000 66 000 500 000 702 900 11 650 000

House 130A 3 667 22 000 166 667 234 300 4 554 167

House 130B 3 667 22 000 166 667 234 300 4 525 000

House 150A 3 667 22 000 166 667 234 300 4 993 750

Apart. A 0 0 0 0 0

Apart. B2 0 0 0 0 0

Apart. B3 0 0 0 0 0

Apart. C2 0 0 0 0 0

Apart. C3 0 0 0 0 0

Apart. D 0 0 0 0 0

Total 88 000 528 000 4 000 000 5 623 200 83 475 000

Pre-Feasibility Study Report – PICOCO III HOUSING DEVELOPMENT

Page 35 of 35

Table 5-4 (continued)

5.3 Economics of the Project

Financial analysis has been done based on the above figures and the following assumptions;

Cumulative Preference shares/ Mezzanine Loans from Old Mutual Investment Group South

Africa overally worth up to US$11,924,000 raised in a revolving nature in the first 4 years of

the project with a 30 month tenure at 6% p. a and a grace period of months.

Shelter Afrique will contribute 48 month 7% per anum once off US$10million loan with a

grace period of 18 months.

Other sources yet to be confirmed total US$12,2million

All the phases of the project are to be complete 5 years after project commencement date.

The planning discount rate for the project funds is 10%

Considering the above the Net Present Value will be US$11 018 000 and the Internal Rate of

Return at 53%.

6 Conclusion

According to the technical, market and financial feasibility studies, this is a very economical housing

project.

As far as the report is concerned a brief summary of the study are included in the main text in order

to emphasize the most important facts only. Any Detailed information is given as annexures.