past, present and future of mobile payments research: a literature review

TRANSCRIPT

Available online at www.sciencedirect.com

www.elsevier.com/locate/ecra

Electronic Commerce Research and Applications 7 (2008) 165–181

Past, present and future of mobile payments research:A literature review

Tomi Dahlberg a, Niina Mallat a, Jan Ondrus b,*, Agnieszka Zmijewska c

a Helsinki School of Economics, P.O. Box 1210, 00101 Helsinki, Finlandb Ecole des HEC, University of Lausanne, Internef, 1015 Dorigny, Switzerland

c University of Technology, Sydney, 235 Jones Street, Broadway NSW 2007, Australia

Received 16 September 2006; received in revised form 3 February 2007; accepted 4 February 2007Available online 9 February 2007

Abstract

The mobile payment services markets are currently under transition with a history of numerous tried and failed solutions, and a futureof promising but yet uncertain possibilities with potential new technology innovations. At this point of the development, we take a lookat the current state of the mobile payment services market from a literature review perspective. We review prior literature on mobilepayments, analyze the various factors that impact mobile payment services markets, and suggest directions for future research in thisstill emerging field. To facilitate the analysis of literature, we propose a framework of four contingency and five competitive force factors,and organize the mobile payment research under the proposed framework. Consumer perspective of mobile payments as well as technicalsecurity and trust are best covered by contemporary research. The impacts of social and cultural factors on mobile payments, as well ascomparisons between mobile and traditional payment services are entirely uninvestigated issues. Most of the factors outlined by theframework have been addressed by exploratory and early phase studies.� 2007 Elsevier B.V. All rights reserved.

Keywords: Mobile payments (m-payments); Literature review; Future research

1. Introduction

Mobile phones have transformed telephony profoundly.They are equipped with functionalities which surpass tele-phony needs, and which inspire the development ofvalue-added mobile services, the use of mobile phones asaccess devices, and mobile commerce in general. The num-ber of mobile phones in use far exceeds any other technicaldevices that could be used to market, sell, produce, or deli-ver products and services to consumers. These develop-ments open lucrative opportunities to merchants andservice providers.

Purchased products and services have to be paid for. Ini-tially, fixed-line telephony billing systems were modified to

1567-4223/$ - see front matter � 2007 Elsevier B.V. All rights reserved.

doi:10.1016/j.elerap.2007.02.001

* Corresponding author. Tel.: +41 21 692 3414; fax: +41 21 692 3405.E-mail addresses: [email protected] (T. Dahlberg), Niina.Mal-

[email protected] (N. Mallat), [email protected] (J. Ondrus), [email protected](A. Zmijewska).

charge mobile telephony. Later, mobile telephony billingsystems were introduced, and used also to charge variousmobile services when such services emerged. Yet, paymentsbased on billing systems have several limitations. Theseinclude comparatively high payment transaction fees, mer-chant and service provider complaints about unfair reve-nue sharing, and the necessity to provision services tobilling systems [66,80]. In some areas, such as the EuropeanUnion, credited payment services to third parties require a(limited) credit institution license. The lack of suitable pay-ment instruments has for a long time been regarded as afactor that hampers the development of mobile commerce.

Mobile payments are payments for goods, services, andbills with a mobile device (such as a mobile phone,smart-phone, or personal digital assistant (PDA)) by tak-ing advantage of wireless and other communication tech-nologies. Mobile devices can be used in a variety ofpayment scenarios, such as payment for digital content(e.g., ring tones, logos, news, music, or games), tickets,

166 T. Dahlberg et al. / Electronic Commerce Research and Applications 7 (2008) 165–181

parking fees and transport fares, or to access electronicpayment services to pay bills and invoices. Payments forphysical goods are also possible, both at vending and tick-eting machines, and at manned point-of-sale (POS)terminals.

A mobile payment is carried out with a mobile paymentinstrument such a mobile credit card or a mobile wallet. Inaddition to pure mobile payment instruments, most elec-tronic and many physical payment instruments have beenmobilized. Furthermore, mobile payments, as all otherpayments, fall broadly into two categories: payments fordaily purchases, and payments of bills (credited payments).For purchases, mobile payments complement or competewith cash, cheques, credit cards, and debit cards. For bills,mobile payments typically provide access to account-basedpayment instruments such as money transfers, Internetbanking payments, direct debit assignments, or electronicinvoice acceptance.

In the early 2000s, mobile payment services became ahot topic and remained so even after the burst of the Inter-net hype. Hundreds of mobile payment services, includingaccess to electronic payments and Internet banking, wereintroduced all over the world. Strikingly many of theseefforts failed. For example, most, if not all, of the dozensof mobile payment services available in EU countries andlisted in the ePSO database in 2002 [5] have been discontin-ued. To facilitate the development of better mobile pay-ment services, it is important to understand the lessons ofthis history by learning what previous studies have discov-ered about mobile payments and about the mobile pay-ment services markets, as well as what issues haveremained unanswered.

The aim of this paper is to summarize findings from pastmobile payments research, and to suggest promising direc-tions for future research. There are a number of factorsthat highlight the significance and usefulness of such a lit-erature review. Firstly, the field has seen a growing numberof publications, yet a thorough review of existing work ismissing. The lack of published literature reviews impedesthe progress in the field; review articles are critical tostrengthening an area as a field of study [88]. Secondly,research so far seems fragmented, and lacks a roadmapor an agenda. Reviewing existing literature not only leadsto a better understanding of the state of the research inthe field, but it also discerns patterns in the developmentof the field itself. Finally, a synthesis of existing findingsallows researchers not to repeat similar work, and discoverimportant gaps. In other words, it closes areas where aplethora of research already exists, and at the same timeuncovers those areas where research is lacking [88].

Another contribution of this literature review is the pro-posed theoretical framework, around which the review isorganized. Webster and Watson [88] recommend that thebest reviews need to be conceptually structured, and basedon a guiding theory. Our framework provides a guidingstructure that allows us to effectively accumulate knowl-edge, and to interpret previous findings. Because the frame-

work itself aims to explain relevant factors in the mobilepayment services market, basing the literature review onthe framework ensures that the review is comprehensiveand holistic, and reveals research gaps that could otherwisebe overlooked. The framework not only helps to explainthe existing body of knowledge on each factor of the frame-work, but, more importantly, it also provides an overviewof the mobile payment services market, illustrating how thevarious perspectives and research findings fit together aspart of the big picture.

2. Framework for the literature review

The framework used for the review of literature appliestwo guiding theories. They are the five forces model devel-oped by Porter [68], and the generic contingency theory,which emerged from the work of Lawrence and Lorch[41], Perrow [67], and Thompson [81]. The framework isused to classify past research, to analyze research findingsof classified studies, and to propose meaningful researchquestions for future research for each factor.

The prime actors in the mobile payment services marketare mobile payment service providers and their customers.Various parties assuming these roles in the market includeconsumers, merchants, financial institutions and telecomoperators. Additional parties, typically vendors of hand-sets, software, networks and other technologies may alsobe involved. The power and the interests of these partiesimpact how technologies and other resources are orches-trated into mobile payment services, and how these servicesare offered to and used by the market. Moreover, mobilepayment services compete for the attention of customersand other parties against physical and electronic paymentservices. Mobile payment services are a natural choice topay for mobile services. Yet, to succeed, mobile paymentservices may have to offer added value and be availablefor other relevant payment environments as well.

Porter’s [68] competitive factors strategy model, or thefive forces model, describes both the key role of a mobilepayment service provider, and other market factors. Themodel applies insights from industrial organization theoryto analyze the competitive environment on the level ofbusiness units [3], and relates the average profitability ofthe participants in an industry to competitive forces [30].The basic proposition is that organizational performancemainly depends on the industry structure. According toPearce and Robinson [65] and Johnson [29], the strengthsof Porter’s model are that it provides one simple approachto analyze industry structure, identify and determine theattractiveness of an industry, reveal insights on profitabil-ity, inform important decisions about whether to leave orenter industries or sectors, and develop strategic optionsto improve relative performance in the industry or influ-ence relative position in the industry. As one of the mostinfluential management tools for strategic industry analysis[3], the model has been applied by numerous practitionersand academics [30]. The above arguments suggest that the

Changes in Legal, Regulatory, and Standardization

Environment

Changes in TechnologicalEnvironment

Changes in Social/Cultural Environment

Changes in Commerce

Environment

ConsumerPower

MOBILE PAYMENTSERVICE

Competition between m-payment service

providers

MerchantPower

TraditionalPaymentServices

NewE-paymentServices

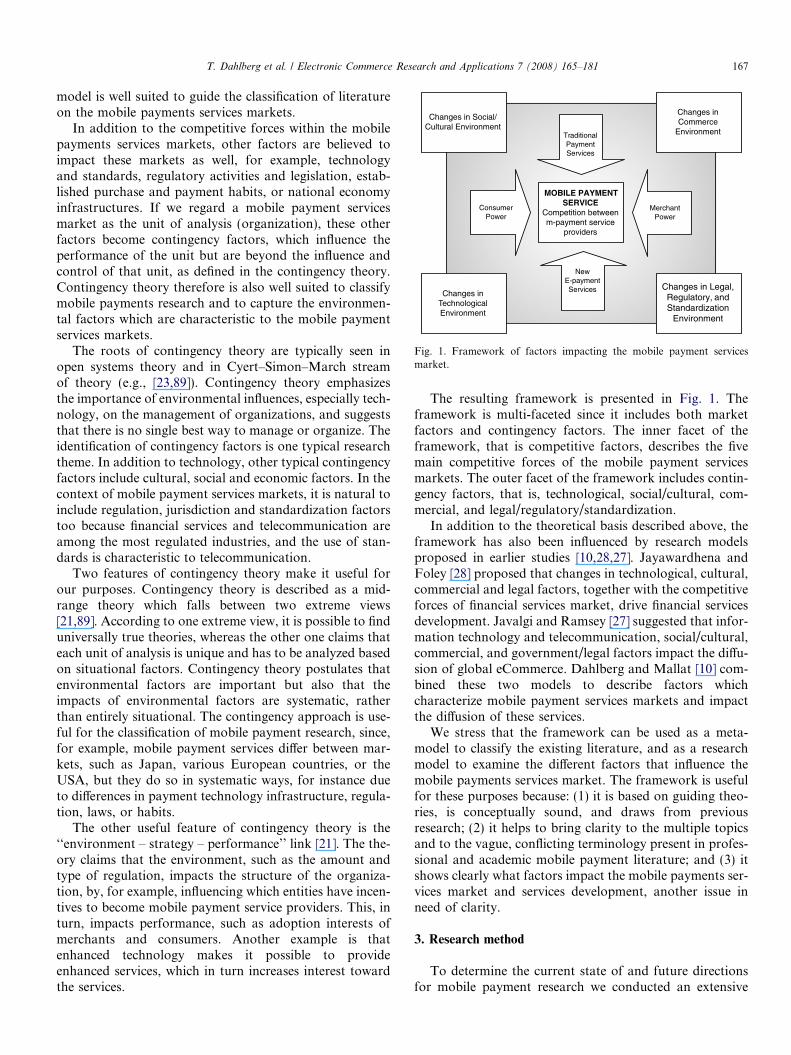

Fig. 1. Framework of factors impacting the mobile payment servicesmarket.

T. Dahlberg et al. / Electronic Commerce Research and Applications 7 (2008) 165–181 167

model is well suited to guide the classification of literatureon the mobile payments services markets.

In addition to the competitive forces within the mobilepayments services markets, other factors are believed toimpact these markets as well, for example, technologyand standards, regulatory activities and legislation, estab-lished purchase and payment habits, or national economyinfrastructures. If we regard a mobile payment servicesmarket as the unit of analysis (organization), these otherfactors become contingency factors, which influence theperformance of the unit but are beyond the influence andcontrol of that unit, as defined in the contingency theory.Contingency theory therefore is also well suited to classifymobile payments research and to capture the environmen-tal factors which are characteristic to the mobile paymentservices markets.

The roots of contingency theory are typically seen inopen systems theory and in Cyert–Simon–March streamof theory (e.g., [23,89]). Contingency theory emphasizesthe importance of environmental influences, especially tech-nology, on the management of organizations, and suggeststhat there is no single best way to manage or organize. Theidentification of contingency factors is one typical researchtheme. In addition to technology, other typical contingencyfactors include cultural, social and economic factors. In thecontext of mobile payment services markets, it is natural toinclude regulation, jurisdiction and standardization factorstoo because financial services and telecommunication areamong the most regulated industries, and the use of stan-dards is characteristic to telecommunication.

Two features of contingency theory make it useful forour purposes. Contingency theory is described as a mid-range theory which falls between two extreme views[21,89]. According to one extreme view, it is possible to finduniversally true theories, whereas the other one claims thateach unit of analysis is unique and has to be analyzed basedon situational factors. Contingency theory postulates thatenvironmental factors are important but also that theimpacts of environmental factors are systematic, ratherthan entirely situational. The contingency approach is use-ful for the classification of mobile payment research, since,for example, mobile payment services differ between mar-kets, such as Japan, various European countries, or theUSA, but they do so in systematic ways, for instance dueto differences in payment technology infrastructure, regula-tion, laws, or habits.

The other useful feature of contingency theory is the‘‘environment – strategy – performance’’ link [21]. The the-ory claims that the environment, such as the amount andtype of regulation, impacts the structure of the organiza-tion, by, for example, influencing which entities have incen-tives to become mobile payment service providers. This, inturn, impacts performance, such as adoption interests ofmerchants and consumers. Another example is thatenhanced technology makes it possible to provideenhanced services, which in turn increases interest towardthe services.

The resulting framework is presented in Fig. 1. Theframework is multi-faceted since it includes both marketfactors and contingency factors. The inner facet of theframework, that is competitive factors, describes the fivemain competitive forces of the mobile payment servicesmarkets. The outer facet of the framework includes contin-gency factors, that is, technological, social/cultural, com-mercial, and legal/regulatory/standardization.

In addition to the theoretical basis described above, theframework has also been influenced by research modelsproposed in earlier studies [10,28,27]. Jayawardhena andFoley [28] proposed that changes in technological, cultural,commercial and legal factors, together with the competitiveforces of financial services market, drive financial servicesdevelopment. Javalgi and Ramsey [27] suggested that infor-mation technology and telecommunication, social/cultural,commercial, and government/legal factors impact the diffu-sion of global eCommerce. Dahlberg and Mallat [10] com-bined these two models to describe factors whichcharacterize mobile payment services markets and impactthe diffusion of these services.

We stress that the framework can be used as a meta-model to classify the existing literature, and as a researchmodel to examine the different factors that influence themobile payments services market. The framework is usefulfor these purposes because: (1) it is based on guiding theo-ries, is conceptually sound, and draws from previousresearch; (2) it helps to bring clarity to the multiple topicsand to the vague, conflicting terminology present in profes-sional and academic mobile payment literature; and (3) itshows clearly what factors impact the mobile payments ser-vices market and services development, another issue inneed of clarity.

3. Research method

To determine the current state of and future directionsfor mobile payment research we conducted an extensive

Table 1Conferences included in the literature search

Conferences by topics

Information Systems

International Conference on Information Systems, ICISHawaii International Conference on System Sciences, HICSSAmericas Conference on Information Systems, AMCISEuropean Conference on Information Systems, ECISPacific Asia Conference on Information Systems, PACISAustralasian Conference on Information Systems, ACISIEEE Conference proceedings

Electronic Commerce

Bled Electronic Commerce Conference, BLEDInternational Conference on Electronic Commerce, ICECInternational Conference on Electronic Business, ICEBIADIS International Conference on E-CommerceIADIS International Conference on WWW/Internet

Mobile Commerce

International Conference on Mobile Business, ICMB (previouslymBusiness)

Mobility Roundtable

168 T. Dahlberg et al. / Electronic Commerce Research and Applications 7 (2008) 165–181

literature review. The first phase of the review was to deter-mine the review scope and relevant source material. Sincemobile payments are an interdisciplinary topic similar toelectronic and mobile business, relevant articles are pub-lished in a wide variety of journals. Furthermore, mobilepayment research is still an emerging research area andmost of the contemporary research is published in confer-ence proceedings. Therefore, we included both academicjournal papers from various disciplines and also conferenceproceedings in our search. Despite a potentially lower qual-ity of the conference proceedings, they are informative forcharting the current research topics in this rapidly pro-gressing area of research, and for identifying gaps to becovered by future research. We also expect that the bestconference papers will evolve to journal articles and thusserve as leading indicators for the focus of future journalpublications. Book chapters were excluded from the searchas they are not peer reviewed.

We started the literature search with a wide systematicscan of online academic journal and conference databases.The following databases were searched:

� ProQuest Direct� EBSCO Business Source Premier� ScienceDirect� IEEE Xplore� ACM Digital Library� AIS eLibrary� M-lit online bibliographical database dedicated to

mobile business literature� Google Scholar for academic conference papers

From the papers identified we also went backwards byreviewing other work of the authors as well as citationsin the papers [88]. Search was based on the descriptors‘‘mobile payments’’, ‘‘m-payments’’, and ‘‘wireless pay-ments’’ that were to be found in the title or abstract ofthe paper. We excluded papers where mobile paymentswere just a minor section of a research on mobile com-merce or e-payments.

To ensure the quality of the conference papers wefocused our search on a few established conferences in thefields of IS, electronic commerce and mobile business thatare listed in Table 1. Not all of the selected conferenceshad published papers about mobile payments. The IEEEproceedings include various conferences that were searchedthrough the IEEE Xplore. Some of the papers published inthe IEEE proceedings were highly technical, addressingmostly engineering and computer science topics, and werethus excluded from the review. The selected conferences uti-lize a selective peer review process, with the exception of theMobility Roundtable conference, which was included dueto its high relevance and since recent and ongoing researchis presented there. The search resulted in 73 papers, whichwere published between 1999 and August 2006.

In the second phase of the review we classified thepapers into the nine categories according to our frame-

work. The classification proceeded as follows. Tworesearchers independently reviewed the title, abstract anddiscussion/conclusions sections of the paper and deter-mined its main topic, for example, consumers. Theresearchers then classified the paper to the correspondingfactor within the framework. The two classifications weresubsequently compared and, in case of differing results, athird researcher repeated the classification. The most com-mon factor was then selected. Some publications focusedon several factors, but not on any in detail, which calledfor a new classification of ‘multiple categories’ papers. Sev-eral other papers presented market overviews [11,19,53,84],summarizing the state of mobile payments, its challenges orpotentials – such papers were classified as ‘overviews’. Twoof the papers focused in detail on two factors and relation-ships between them, so they were included in both catego-ries [83,91].

Next, we analyzed methodologies used. We first classi-fied each research to ‘empirical’ and ‘conceptual’ and thendivided the ‘empirical’ further to ‘qualitative’, ‘quantita-tive’ and ‘design research’. Most technical papers proposedconceptual constructs but some mainly described technolo-gies, therefore we divided conceptual studies into proposedconstructions and descriptions. The reader should notethat all studies regarding the technology factor that wereclassified as ‘empirical’ evaluated the proposedconstruction.

4. Results of the analysis

4.1. Descriptive findings

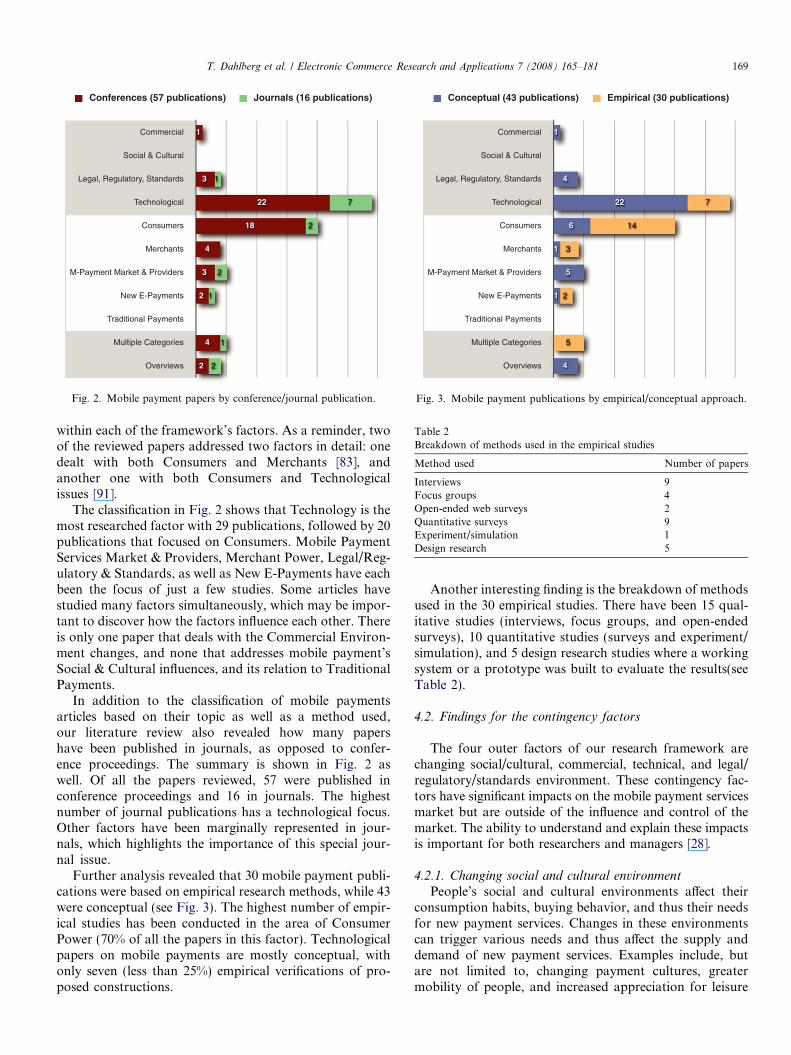

As the previous section explained, our literature searchfollowed established procedures and criteria that endedup in the classification of 73 mobile payment publications.Fig. 2 reveals a number of papers that address topics

Conceptual (43 publications) Empirical (30 publications)

Overviews

Multiple Categories

Traditional Payments

New E-Payments

M-Payment Market & Providers

Merchants

Consumers

Technological

Legal, Regulatory, Standards

Social & Cultural

Commercial

7

14

3

2

5

1

4

22

6

1

5

1

4

Fig. 3. Mobile payment publications by empirical/conceptual approach.

Conferences (57 publications) Journals (16 publications)

Overviews

Multiple Categories

Traditional Payments

New E-Payments

M-Payment Market & Providers

Merchants

Consumers

Technological

Legal, Regulatory, Standards

Social & Cultural

Commercial

1

7

2

2

1

1

2

1

3

22

18

4

3

2

4

2

Fig. 2. Mobile payment papers by conference/journal publication.

T. Dahlberg et al. / Electronic Commerce Research and Applications 7 (2008) 165–181 169

Table 2Breakdown of methods used in the empirical studies

Method used Number of papers

Interviews 9Focus groups 4Open-ended web surveys 2Quantitative surveys 9Experiment/simulation 1Design research 5

within each of the framework’s factors. As a reminder, twoof the reviewed papers addressed two factors in detail: onedealt with both Consumers and Merchants [83], andanother one with both Consumers and Technologicalissues [91].

The classification in Fig. 2 shows that Technology is themost researched factor with 29 publications, followed by 20publications that focused on Consumers. Mobile PaymentServices Market & Providers, Merchant Power, Legal/Reg-ulatory & Standards, as well as New E-Payments have eachbeen the focus of just a few studies. Some articles havestudied many factors simultaneously, which may be impor-tant to discover how the factors influence each other. Thereis only one paper that deals with the Commercial Environ-ment changes, and none that addresses mobile payment’sSocial & Cultural influences, and its relation to TraditionalPayments.

In addition to the classification of mobile paymentsarticles based on their topic as well as a method used,our literature review also revealed how many papershave been published in journals, as opposed to confer-ence proceedings. The summary is shown in Fig. 2 aswell. Of all the papers reviewed, 57 were published inconference proceedings and 16 in journals. The highestnumber of journal publications has a technological focus.Other factors have been marginally represented in jour-nals, which highlights the importance of this special jour-nal issue.

Further analysis revealed that 30 mobile payment publi-cations were based on empirical research methods, while 43were conceptual (see Fig. 3). The highest number of empir-ical studies has been conducted in the area of ConsumerPower (70% of all the papers in this factor). Technologicalpapers on mobile payments are mostly conceptual, withonly seven (less than 25%) empirical verifications of pro-posed constructions.

Another interesting finding is the breakdown of methodsused in the 30 empirical studies. There have been 15 qual-itative studies (interviews, focus groups, and open-endedsurveys), 10 quantitative studies (surveys and experiment/simulation), and 5 design research studies where a workingsystem or a prototype was built to evaluate the results(seeTable 2).

4.2. Findings for the contingency factors

The four outer factors of our research framework arechanging social/cultural, commercial, technical, and legal/regulatory/standards environment. These contingency fac-tors have significant impacts on the mobile payment servicesmarket but are outside of the influence and control of themarket. The ability to understand and explain these impactsis important for both researchers and managers [28].

4.2.1. Changing social and cultural environment

People’s social and cultural environments affect theirconsumption habits, buying behavior, and thus their needsfor new payment services. Changes in these environmentscan trigger various needs and thus affect the supply anddemand of new payment services. Examples include, butare not limited to, changing payment cultures, greatermobility of people, and increased appreciation for leisure

170 T. Dahlberg et al. / Electronic Commerce Research and Applications 7 (2008) 165–181

time. Mobile payment research on these factors wasexpected to compare the characteristics of various socialand cultural environments, and to examine which charac-teristics affect the development and success of mobile pay-ments services markets.

We did not identify any academic papers that wouldhave investigated the effects of social and cultural changeson the demand and development of mobile payment ser-vices. Relevant research reports and studies within relatedfields (other payment services or wireless communication)have identified specific social and cultural issues that maybe important to mobile payment studies. These include dis-tinguishable payment cultures in various countries, indus-try strengths, electronic banking readiness of consumers,strong mobile phone inclination of certain nations [2]; cul-tural similarity and adoption timing [77]; demographicsand lifestyle characteristics, or cultural differences in devel-oped and developing countries [50]. Since we found nostudies on mobile payments that would have addressedsuch issues, it is especially important for future researchto study how the social and cultural factors influencemobile payments services markets. We propose the follow-ing research questions for future research:

RESEARCH QUESTION 1.1: What are the cultural and lifestyledifferences between countries that affect the demand formobile payment services?Research on mobile commerce has discussed the impactof lifestyle and cultural differences on the formation ofmobile commerce market and on the adoption of mobileservices. These studies have enhanced knowledge onmobile commerce adoption and also questioned somecommon but ambiguous conceptions such as the posi-tive impact of commuting on the use of mobile services[76]. Influential lifestyle and cultural factors should becharted in the context of mobile payment services aswell. A specific part of the overall culture and lifestyleof the society is that of the payment culture. To addressthis issue we propose:RESEARCH QUESTION 1.2: How do the characteristics of dif-ferent payment cultures and systems between countriesimpact the development and success of mobile paymentservices markets?International banking statistics (e.g., The Bank of Inter-national Settlements or European Central Bank) demon-strate that different payment cultures exist, for example,the cash-centric culture of Japan, the account/giro-centriccultures of Germany and Scandinavia, and the wide useof cheques in the USA and France [2]. It is importantfor future mobile payments research to recognize thesedifferences and to examine how they impact mobile pay-ment services. A unique opportunity for cultural studieswithin the Euro currency countries of the EU is open dur-ing the time that payments are harmonized into the SingleEuro Payment Area (SEPA) in these countries. Empiricalmulti-cultural comparisons are suggested as a suitableapproach for research questions 1.1 and 1.2.

4.2.2. Changing commercial environment

Changes in the commercial environment include thedevelopment of the Internet and mobile networks intocommercial channels, as well as increasing automationand self-service orientation of payment services. Otheraspects of this factor include the structure and developmentof financial, telecommunication and ICT infrastructuresand markets within the studied environments. Changes inthe commercial environment may trigger the developmentof new or enhanced mobile payment services. We expectedthat mobile payments research in this factor had looked athow market structures, business practices and infrastruc-tures have changed, and how these changes influence thedevelopment and success of mobile payments.

The literature search provided only one paper address-ing this factor. Hampe et al. [24] discuss the foundationsof mobile electronic commerce and analyze those charac-teristics of mobile telephony that offer potential for mobiletelecommunication service providers to take a greater rolein retail payments. The authors suggest that increasingintegration of mobile telecommunication and electroniccommerce, and the growing use of ubiquitous mobile com-puting will enhance the role of telecommunication compa-nies as payment service providers.

Research on this factor is clearly underrepresented.Thus, there is a need for rigorous research on how commer-cial environments impact the development and success ofmobile payment services. We propose the followingresearch questions for future research:

RESEARCH QUESTION 2: What is the impact of the financialservices market structures on the development and suc-cess of mobile payment services markets?The structures of financial services markets within variouscountries may support or inhibit the development ofmobile payment services. In bank-centric financial sys-tems most entities have bank account, payment transac-tions are typically transfers between accounts, andbanks have a strong mediator role. In market-centricfinancial systems, the proportion of bearer-held instru-ments (issued and traded through capital markets) isimportant, cash and cheques could be used frequentlyfor payments, and banks have a less dominant role. Itis important for mobile payments research to understandhow different financial systems and also how the degree ofelectronification of financial services influences mobilepayment services markets.RESEARCH QUESTION 3: What is the impact of the telecom-munication infrastructure on the development and suc-cess of mobile payment services markets?Differences in information and telecommunication infra-structures between countries may guide the developmentof payment services. Japan, for example, is characterizedby a strong mobile telecommunication infrastructure anda relatively weaker fixed-line Internet infrastructure. Themobile on-line payment services may, for that reason, finda strong basis for their development. In the US, on the

T. Dahlberg et al. / Electronic Commerce Research and Applications 7 (2008) 165–181 171

other hand, fixed-line Internet infrastructure has beenprevailing and Internet-based payment systems, such asPayPal or iTunes are actively developed [4].RESEARCH QUESTION 4: How do the telecommunicationmarket structures in a given country impact the organi-zation of the respective mobile payment services marketsand the developers of the mobile payment services?The impact of telecommunication market structures canbe examined by comparing, for example, the conse-quences of NTT Docomo’s dominant position in Japanto those of more open telecommunication markets inthe US and especially in Europe. While different telecom-munication market structures have been analyzed in thecontext of mobile telecommunication market in general,similar studies should be conducted in the context ofmobile payment services. Expert interviews and compar-ative case studies are suggested as a suitable approach forsolving research questions 2–4.

4.2.3. Changing technological environment

Technological environment consists of wireless andother related technologies which are used to develop andproduce mobile payment services. Some of these technolo-gies develop slowly, such as mobile network technology ortransaction protocols. Some other technologies have veryshort development cycles, such as mobile handsets andtheir components. Continuous development of technolo-gies facilitates more reliable, user friendly, versatile, andfunctionally rich mobile payment services.

Research on technologies was expected to analyze thestrengths and limitations of various technologies and topropose new technological advancements to improvemobile payment services and remove identified technicallimitations. Research was also expected to evaluate theimplementability of proposed technologies, as well as toachieve expected technical and technology enabledimprovements with prototypes, pilots and with evalua-tions of implemented payment services. Studies wereexpected to apply constructive approaches and to verifythe proposed construction with evaluative empiricalevidence.

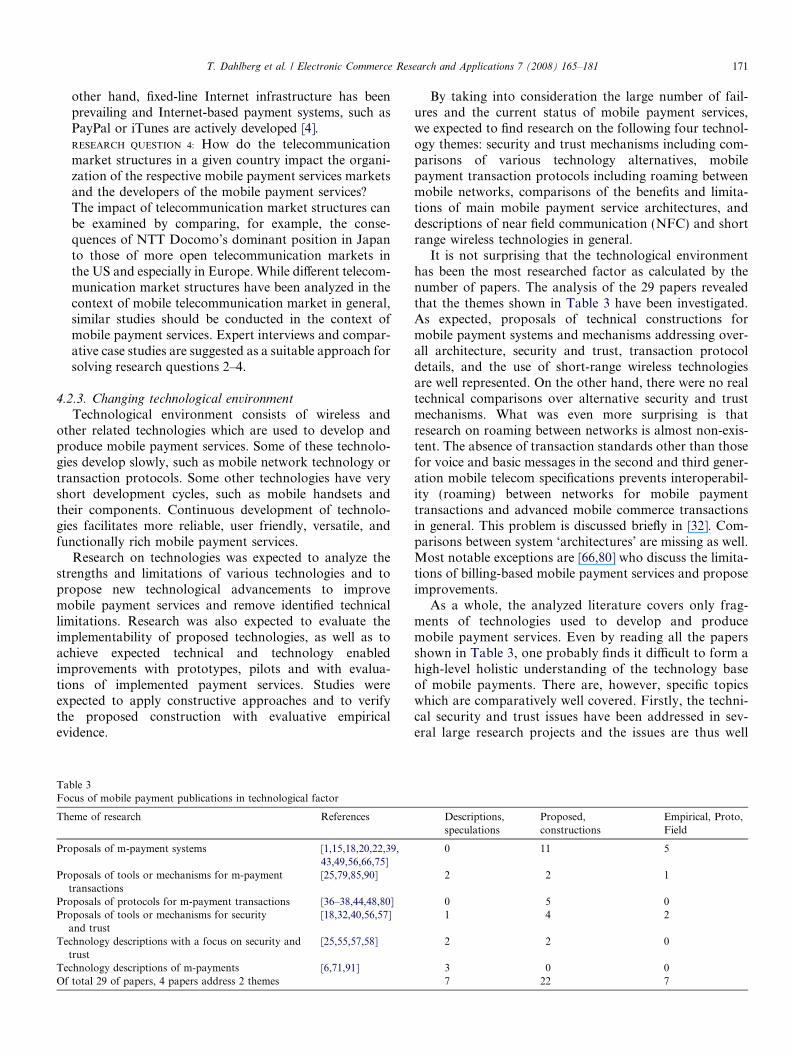

Table 3Focus of mobile payment publications in technological factor

Theme of research References

Proposals of m-payment systems [1,15,18,20,22,39,43,49,56,66,75]

Proposals of tools or mechanisms for m-paymenttransactions

[25,79,85,90]

Proposals of protocols for m-payment transactions [36–38,44,48,80]Proposals of tools or mechanisms for security

and trust[18,32,40,56,57]

Technology descriptions with a focus on security andtrust

[25,55,57,58]

Technology descriptions of m-payments [6,71,91]Of total 29 of papers, 4 papers address 2 themes

By taking into consideration the large number of fail-ures and the current status of mobile payment services,we expected to find research on the following four technol-ogy themes: security and trust mechanisms including com-parisons of various technology alternatives, mobilepayment transaction protocols including roaming betweenmobile networks, comparisons of the benefits and limita-tions of main mobile payment service architectures, anddescriptions of near field communication (NFC) and shortrange wireless technologies in general.

It is not surprising that the technological environmenthas been the most researched factor as calculated by thenumber of papers. The analysis of the 29 papers revealedthat the themes shown in Table 3 have been investigated.As expected, proposals of technical constructions formobile payment systems and mechanisms addressing over-all architecture, security and trust, transaction protocoldetails, and the use of short-range wireless technologiesare well represented. On the other hand, there were no realtechnical comparisons over alternative security and trustmechanisms. What was even more surprising is thatresearch on roaming between networks is almost non-exis-tent. The absence of transaction standards other than thosefor voice and basic messages in the second and third gener-ation mobile telecom specifications prevents interoperabil-ity (roaming) between networks for mobile paymenttransactions and advanced mobile commerce transactionsin general. This problem is discussed briefly in [32]. Com-parisons between system ‘architectures’ are missing as well.Most notable exceptions are [66,80] who discuss the limita-tions of billing-based mobile payment services and proposeimprovements.

As a whole, the analyzed literature covers only frag-ments of technologies used to develop and producemobile payment services. Even by reading all the papersshown in Table 3, one probably finds it difficult to form ahigh-level holistic understanding of the technology baseof mobile payments. There are, however, specific topicswhich are comparatively well covered. Firstly, the techni-cal security and trust issues have been addressed in sev-eral large research projects and the issues are thus well

Descriptions,speculations

Proposed,constructions

Empirical, Proto,Field

0 11 5

2 2 1

0 5 01 4 2

2 2 0

3 0 07 22 7

172 T. Dahlberg et al. / Electronic Commerce Research and Applications 7 (2008) 165–181

understood (e.g., [32,57,58]). Secondly, several recentpapers address the use of NFC and short-range wirelesstechnologies such as Bluetooth, Infrared, radio frequencyidentification (RFID) (e.g., [6,71,91]). The mentionedpapers, however, mainly list and describe these technolo-gies and their layers. Thirdly, authentication andaccountability in secure electronic transaction (SET)environments used, for example, in the connection ofVisa credit cards have been covered. Kungpisdan et al.[36–38] describe in detail how accountability disputescan be resolved with their logic protocol and how theirsymmetric key protocol can be used to improve transac-tion security as compared to those of SET and iPK. DiP-ietro et al. [18] explain an authentication scheme forfinancial transactions in SET environments. The SETstandard preceded the current EMV (Eurocard, Master-card, Visa) standard.

In only seven papers, constructions proposed were alsoevaluated empirically. In six cases evaluation was donewith (laboratory) prototypes [20,32,39,56,66,85] and inone case [49] with a field experiment. Thus, evaluationsof implemented mobile payment systems or services havenot been conducted.

We conclude that despite the large number of papers,many issues in the technology environment have notbeen investigated thoroughly and some issues seem tobe poorly understood. Academics investigating mobilepayment services need to have a more profoundunderstanding of the underlying technology to guaranteethat their studies provide contributions. Based on theanalysis, we offer three research questions for futureresearch:

RESEARCH QUESTION 5: What are the technological andtechnology-related strengths and limitations of the maintechnology ‘architectures’?Current mobile payment services typically apply one ofthe following technology architectures: (1) mobile bill-ing systems (mobile network elements/billing and/orseparate billing software), (2) stored value account sys-tems (e.g., wallets) usually with light authentication(e.g., SIM-card, intelligent network subscriber register,and/or mobile handset identifications), where handsetscan use short range wireless technologies (e.g., to com-municate with vending machines), (3) account basedsystems with strong authentication needed to commitlarge value payments (e.g., EMV services based onthe 4D secure model and the use of wireless PKI forauthentication), and (4) use of mobile handsets toaccess electronic payment services (e.g., payment withan Internet banking service), often with proprietarystrong authentication (e.g., credentials issued by a bankto its customers). There is a clear need for studieswhich systematically describe the technical compositionof main architecture alternatives, and compare typicaluse situations, strengths and limitations of each archi-tecture for providing mobile payment services. The

wide variety of mobile payment pilots, service launchesand the numerous failures of past efforts motivate thisresearch. Research could also help the positioning ofproposed constructions, and assist in separating case-specific idiosyncratic features from generic concepts.Such understanding could be used to plan, validateand describe the context of research on other mobilepayment issues. Solving this research question couldstart with a literature review which would capture thecharacteristics of the main ‘architectures’, analyse theiruse areas, strengths and limitations, as well as list mainmobile payment service providers. Case studies, expertinterviews, and surveys among mobile payment serviceproviders could then verify and complement the find-ings of literature reviews.RESEARCH QUESTION 6: What security and trust mecha-nisms fit various types of mobile payment services?The centricity of security and trust in mobile paymentservices is the motivator for this research question. Thereis a trade-off between security and, for example, ease ofuse. It is not clear whether we have too little or too muchsecurity in various types of mobile payment services.This issue could also be investigated from legal andbehavioral perspectives since trust is both a technicaland a social phenomenon. Exploration of this researchquestion could start with user and expert interviews,continue with case studies followed by design researchand comparative field studies.RESEARCH QUESTION 7: Can standardized transaction pro-tocols and interoperability mechanisms help to solve theroaming problem between networks to facilitate mobilecommerce and payment transactions?This urgent research question has been addressed bynumerous practitioners, so far with limited success.This difficult issue seems well suited for academicresearch; it has been able to successfully solve other dif-ficult technological problems, related to the architec-ture of relational databases, programming languages,Internet and data communication. The proposals ofacademics – often backed by visionary practitioners –have opened up developments of practical technologi-cal tools and services. The best way to solve thisresearch question is probably to use theoretical deduc-tion and to test the theoretical constructions with logi-cal, conceptual testing.

4.2.4. Changing legal, regulatory, and standardization

environment

Changes in the legal, regulatory and standardizationenvironment deal with evolving jurisdiction, regulationsand other norms with requirements to comply. These con-tingency items may trigger needs for new or enhanced pay-ment services, and drive or hinder the development ofmobile payments. Mobile payments research on this factorwas expected to examine the impact of regulation, legisla-tion and standardization on the development and successof mobile payment services markets.

T. Dahlberg et al. / Electronic Commerce Research and Applications 7 (2008) 165–181 173

Cross-border mobile transactions can be complex due toa complicated web of law and regulations [72]. Previousstudies on the regulation of international mobile paymentservices suggest that unifying regulation and legal frame-works such as the EU directives in the European Commis-sion may reduce complexity and support the developmentof international mobile payment services [33,72]. Karnous-kos and Vilmos [33] present the secure mobile payment ser-vice (SEMOPS) initiative as an example of an internationalmobile payment project that aims to respond to the chal-lenges presented to an international mobile paymentservice.

The process of standardization for mobile payments hasbeen another focus of the prior mobile payment research[33,45,46]. The cited studies identify various organizationsthat aim to standardize and develop mobile payment ser-vices but also note that none of these organizations has adominant role in standardization and that there are differ-ences in the requirements and in the preferences they set forstandards [33,45]. Currently, the mobile payment servicesmarket is at a pre-standardization phase where no collec-tive standards have been achieved and where various indus-tries and consortia, most notably the financial andtelecommunication industries, compete to form the domi-nant standard [45]. Some studies which have looked atthe mobile payment services market from the point of viewof multiple actors have discussed the standardization ofmobile payments and emphasized the need for a technolog-ical and organizational consensus between the players inthe industry [62–64].

The current research on legislation and standardizationof mobile payments provides an informative description onthe complexities and problems surrounding these topics.Yet, there are no good solutions to solve these legislationand standardization issues. We thus propose the followingresearch questions for future research:

RESEARCH QUESTION 8.1: How much and what kind oflegislation is needed to support mobile payment serviceswithin specific countries and markets, and also interna-tionally?Legislation concerning mobile payments, such as thee-money directive in the EU, is only currently beingformulated. Important questions for future researchinclude the role and the extent of regulation needed toprovide a viable, fair and secure environment for variousparties in the mobile payment services market.RESEARCH QUESTION 8.2: What regulatory bodies shouldhave the authority to regulate mobile payment serviceswithin countries and internationally?Previous studies have emphasized the need to unify lawsand regulation to facilitate the development of interna-tional mobile payment services. It may be complicated,however, to determine the responsibilities and divisionof work between the national and international legisla-tive bodies. Future research should therefore addressthis question and examine the most optimal mechanisms

and bodies for regulating international mobile paymentservices.RESEARCH QUESTION 9: How should effective standardiza-tion be formed for mobile payments and by whom?Prior studies which have emphasized the need for com-mon standards for advancing the mobile payment ser-vices markets [62–64] motivate this research question.Prior studies have also detected that the current stateand the outlook of the standardization process formobile payments is problematic [45,46]. Future researchcould therefore try to determine critical parties neededto support common standards and make suggestionsfor effective forums and mechanisms through whichstandards can be advanced more effectively. Researchapproaches suitable to address research questions 8.1–9include expert interviews and case studies, augmentedwith legal analysis.

4.3. Findings for competitive factors

The five inner factors of our framework are consumerpower, merchant power, traditional payment services (bar-riers to entry), new e-payment services (substitutes), andmobile payment service providers. These competitive fac-tors drive the developments of mobile payment servicesmarkets and determine market structures.

4.3.1. Consumer power

Consumers place demands on mobile payment servicesand drive their success by adopting and using specific ser-vices. Information systems research has developed andapplied various technology acceptance [16] and diffusionmodels [73]; it was expected that research had exploredthe suitability of such models in mobile payments context,and possibly modified them to suit the specific characteris-tics of this context. We also expected to find studies whichinvestigate consumer attitudes towards paying with mobiledevices and examine which characteristics of the new pay-ment services drive or inhibit the adoption. Consumersmay be willing to accept the non-fulfillment of some crite-ria, but reject services based on specific weaknesses. Thus,we expected to detect empirical research where the criteriawould have been rated on their importance in order toreveal which of the indicators mattered most to consumers.On the other hand, we also expected to find qualitativestudies which would supplement quantitative findings withmore in-depth explanations of consumers’ attitudes andexpectations. Such consumer-centric research would ensurethat payment service providers, when implementing theirservices, will fulfill the real needs of consumers, not justthe assumed ones.

Method-wise we expected to find case studies, surveys ordesign research where potential users had indicated whatproblems other methods of payments have, and what theirpayment habits, preferences and behaviors are. We alsoexpected to find investigations on existing users and theirdaily use of mobile payment services. The existing users

Table 5The constructs used to study consumer adoption

Constructs References

Attractiveness of alternative (–) [51]Cost (–) [34,51,52,69,83,94,95]Convenience [8,14,17,69]Context [52]Compatibility [7,8,14,42,51,52]Ease of use [7,8,13,14,12,17,34,51,52,83,94,95]Expressiveness [95]Mobility [52,95]Network externalities [51]Observability [7]Privacy [8,17]Risk (–) [8,51,52,83]Security [8,17,69,94]Social influence [14,34,42,52]Speed of transaction [8,14,17]System quality [34,42]Technology anxiety (–) [42]Trialability [7]Trust [14,12,51,52,94,95]Usefulness [7,8,13,12,17,34,52,94,95]

174 T. Dahlberg et al. / Electronic Commerce Research and Applications 7 (2008) 165–181

could provide insights grounded in their first-hand experi-ence, and such studies might also have revealed findingswhich differ from projected views and expectations of bothmobile payment service providers and non-users.

The analysis of mobile payments consumer researchrevealed that most of the studies did indeed investigateadoption factors (see Table 4). This is not surprising sincetechnology adoption is a popular topic in information sys-tems research. It seems especially important in an emergingarea such as mobile payments.

As also expected, adoption/acceptance research ofteninvolved traditional acceptance models. The research wasmostly based on the technology acceptance model (TAM)[16] and diffusion of innovations model [73]. The analysedstudies often used the models as the base of their research,investigating whether the models’ theoretical constructs arealso likely to influence the intention to use, and the actualuse of a mobile payment service (e.g., [7,8,13,14,34]), orexamining whether consumers are ready to adopt mobilepayments based on the assumed factors [17]. Some studiesproposed additional factors that are considered specific tothe mobile payment environment, such as cost[34,51,52,69,83,95], network externalities [51], trust andsecurity [13,12] or mobility [52,95]. Table 5 summarizesthe various acceptance factors proposed. The factors initalics and with a minus sign are the ones that would neg-atively affect adoption, such as high perceived risk of usinga procedure. The especially important adoption factors formobile payment services seem to be ease of use, trust andsecurity, usefulness, cost, and compatibility (see Table 5for the authors of the studies).

Further analysis revealed that a number of consumeradoption studies did include users who already had experi-ence with mobile payments [14,51]. These participantscould comment on their concrete experience with mobilepayment services.

As shown in Table 4, there have also been attempts tocategorize mobile payment services. Classification of ser-vices may help researchers in this still emerging field whereconfusing initiatives take place. A consumer-centric viewmeans that studies had focused on characteristics that mat-ter to consumers, which may help adoption studies [93].Properties used to classify mobile payment services haveincluded, for example, registration requirements, value ofpayment, and cost of transactions [93]. Another classifica-tion included Internet payment services, POS mobile pay-ments, payment for mobile commerce services, and

Table 4Focus of mobile payment publications in consumer factor

Theme of research References

Consumer adoption/acceptance [7,8,12–14,17,34,42,552,69,70,83,95]

Classification and analysis of m-payment solutionswith a consumer-centric view

[47,82,93,94]

Consumer value perceptions [10]

person-to-person mobile payments [82]. In another classifi-cation study [47], security items that mattered most to con-sumers were confidentiality and encryption.

As can be seen in Table 4, the methodologies used tostudy the consumer factor are balanced between quantita-tive and qualitative approaches. Researchers conductedsurveys for quantitative data, and mostly focus groupsfor qualitative data. This has ensured that a number of per-spectives have been covered. A few papers were conceptualas they presented models and frameworks but did not val-idate them empirically.

To sum up, in order to launch mobile payment servicesthat will be adopted by consumers, it is crucial to understanduser adoption factors. This is a relatively well explored issuewith both quantitative and qualitative studies. The findingsinclude the direct experience of actual users. The adoptionfactors can be further explored to discover more specific rec-ommendations that can be applied by mobile payment ser-vice providers. What seems still to be missing as well isresearch that would explore the extent to which consumersshould have an influence on the development of these ser-vices. Research questions offered for future research are:

RESEARCH QUESTION 10: What are specific needs of con-sumers regarding the adoption factors established inexisting research?

Empiricalqualitative

Empiricalquantitative

Conceptual speculativecommentary

1, 4 7 4

1 1 2

1

Table 6Focus of mobile payment publications in merchant factor

Theme of research References Empiricalqualitativeinterviews

Conceptualspeculativecommentary

Merchants adoption/acceptance

[54,78,83] 3 0

Mobile payment POSarchitecture formerchants

[60] 0 1

T. Dahlberg et al. / Electronic Commerce Research and Applications 7 (2008) 165–181 175

To advance consumer adoption research, each adoptionfactor should be investigated in more detail. Cost, forexample, was identified as an important adoption factor.Research should find out what will be an acceptable costto consumers, in various payment scenarios and for var-ious products and services. Similarly, usefulness hasbeen confirmed as an important adoption factor. Fur-ther research should reveal what consumers mean whenthey think of ‘‘usefulness’’ in the context of mobile pay-ment services. Qualitative studies using interviews orfocus groups would help to reveal further details aboutthe adoption factors identified in the previous research.RESEARCH QUESTION 11: How should consumers beinvolved in the development of mobile payment services?Consumer influence on the development of new mobilepayment services most likely contributes to their success.The consumer power needs to be understood in order tobuild mobile payment services that consumers will use.However, consumers do not necessarily have a directinfluence on service providers at an early stage of servicedevelopment, and with limited consumer influence, therisks of solutions failure may increase. A possibleresearch approach could be conducting case studies ofexisting initiatives and learning from them how consum-ers can be successfully involved in such projects, andidentifying mistakes that should be avoided in thefuture.

4.3.2. Merchant power

Similar to consumers, merchants are adopters of pay-ment solutions. Merchants create the market for financialinstitutions and other mobile payment service providersby accepting payments with mobile payment instruments(acquirer role) or even by issuing them (issuer role). Theiractive participation in promoting a payment service is cru-cial to consolidate a large number of points of acceptance.Research was expected to look into the role of the mer-chants in terms of adoption and market developmentactions. Adoption factors were expected to be studied witha focus on understanding how to design mobile paymentservices for merchants. In terms of market development,we expected to identify studies on merchants’ participationto network externalities creation.

Surprisingly, we identified only four papers focusingexclusively on merchants. Three of them uncovered thevarious barriers to the merchant adoption [54,83,78].Researchers found barriers such as high costs (transactionfees), complexity (ease of use), lack of relative advantage,low compatibility, and the interdependence between con-sumers and merchants at an early stage of development.One of the papers proposed an original POS architecturefor effective payment processes and consumer loyaltyenhancement [60].

In terms of methodologies, it was surprising to us thatmerchant adoption had not been studied with quantitativedata and surveys, as had been the case in consumer adop-tion research. Quantitative studies are needed to add to

the existing qualitative results and contribute to a betterunderstanding of merchant adoption factors. The analysisresults for the merchant factor literature are shown inTable 6.

The number and diversity of publications is disappoint-ing compared to the number of consumer studies. We pro-pose the following research questions for future research:

RESEARCH QUESTION 12: How to involve merchants in thedesign and development of mobile payment services?The participation of merchants in the design and devel-opment of mobile payments services is crucial. There isa need to better understand what roles merchantsshould have in the development process. Many failuresof payment services may be explained by the lack ofinvolvement of merchants during the early stages ofdesign. Researchers need to discover how the activeparticipation of merchants should be organized inorder to maximize the chance of success. Design scienceresearch seems useful for addressing this researchquestion.RESEARCH QUESTION 13: How should merchants redesigntheir business processes to realize potential value fromthe mobile payment technology?Previous studies suggest that incompatibility of mobilepayments with existing business was one of the mainbarriers to merchant adoption [54]. Future researchtherefore needs to investigate the role of process redesignin the use of mobile payment services and thus enhance-ment of existing businesses.RESEARCH QUESTION 14.1: What are the appropriate incen-tives to attract merchants to an existing mobile paymentservices network?Merchants need incentives to adopt mobile payments.At the same time, the participation of the merchants isthe key in securing a high number of acceptance pointsfor mobile payment instruments. A more profoundunderstanding and analysis of merchants expectationsand incentives is thus needed.RESEARCH QUESTION 14.2: How can merchants effectivelyenhance network externalities of an existing mobile pay-ment service?Future research needs to explore how merchants canbest attract customers and other merchants to an exist-ing mobile payment services network. Case studiesappear useful for addressing research questions 13 and

176 T. Dahlberg et al. / Electronic Commerce Research and Applications 7 (2008) 165–181

14. Research is helpful to uncover patterns related to themerchants’ role and also the ‘‘chicken- and-egg’’dilemma.

4.3.3. The traditional payment services

International banking statistics (e.g., The Bank ofInternational Settlements or European Central Bank)show that popular payment instruments used for the pay-ments of daily purchases include cash, cheques, debit andcredit cards [2]. The development of mobile commerceestablishes the basic demand for mobile payment services.If mobile payments diffuse, then the use of some tradi-tional payment services has to decrease at least propor-tionally. Mobile payment instruments may threaten theposition of current payment instruments and new partiesmay enter the payment services markets (e.g., mobile net-work operators). New features of mobile technology suchas contact-less payment schemes may make some tradi-tional instruments disappear (e.g., contactless magneticcards). It is, however, also possible that mobile phonesare just a new access channel for current card andaccount-based payment services. Thus, we expected tofind research which had compared traditional and mobilepayment services, and also research on which propertiesmobile payments should be able to offer in order toreplace traditional payment services.

None of the found articles focused solely on the compar-ison between traditional and mobile payment services. Fourmultiple categories papers written by Ondrus and Pigneurtackle the confrontation between traditional and mobiletechnologies [61–64]. Their findings indicate that cards werestill preferred to phones for payments in Switzerland froman industry point of view. Moreover, their results suggestthat mobile payments are more likely to become a comple-ment for existing payment instruments at the early stages ofdevelopment. Similarly Dahlberg and Oorni [14] report thatin Finland mobile payment instruments are marginally usedto pay for both daily purchases (as compared to five otherpayment instruments) and for invoices (as compared tofour other payment instruments). We propose the followingresearch questions for future research:

RESEARCH QUESTION 15: What features of traditional pay-ment services could slow down the proliferation ofmobile payment services?If consumers are satisfied with traditional paymentinstruments, as the study of [14] implies, then futureresearch should clarify what specific factors hinder thediffusion of mobile payment services. Mobile paymentservices may need to offer valuable properties that tradi-tional payment services do not have, and at the sametime include the most valuable properties of the servicesreplaced.RESEARCH QUESTION 16: What are the dynamics betweenmobile and traditional payment services?Mobile payment services may complement or substitutetraditional payment services. Researchers should investi-

gate which payment instruments are used in various pay-ment scenarios to improve knowledge about paymenthabits and their changes. The ability to discover inwhich scenarios traditional payment services are notappropriate will provide hints about where and whenmobile payment services should be used. Consumerand merchant surveys, as well as payment service pro-vider interviews seem appropriate approaches to tackleresearch questions 15 and 16.

4.3.4. New electronic payment services

When electronic commerce created need for electronicpayment services, financial institutions brought to marketsnew services extending traditional card and account-basedpayment instruments, and introduced Internet banking/payments, e-invoices, and e-direct debit/credit assignmentsfor bill and invoice payments. A few new intermediariessuch as PayPal, Peppercoin and Paystone seem to have suc-ceeded in fulfilling some of the needs of online merchantsand consumers; apparently credit card-based services werenot adapted fast enough or appeared vulnerable to fraudand identification theft. Thus, a new generation of paymentservice providers were able to emerge to complement, andsometimes compete with, existing service providers. Weexpected to find research which compared e-payment ser-vices with mobile payment services. These studies wereexpected to focus on the underlying differences betweenthe two payment methods and their applicability for spe-cific payment scenarios.

We found only four papers that had addressed this factor.As a reminder, we only reviewed articles which comparedmobile and e-payment services. Chou et al. [9] evaluated var-ious payment technology alternatives using technological,economic, and social factors. The results showed that pay-ments charged to the telecom bill were the least preferredalternative. Jaring et al. [26] analyzed various micropaymentmethods and discussed their current status in Finland.

Salut and Galuszewska [74] described the impact of e-payment solutions on the banking industry. We identifieda lack of depth in comparisons between e-payment andm-payment services; therefore, we propose the followingresearch questions to address this issue in the future.

RESEARCH QUESTION 17: What features of new e-paymentservices threat the proliferation of mobile payment ser-vices?Electronic and mobile payment services differ in numer-ous ways. Each service must embed unique propertieswhich make it superior for certain payment scenarios.There is a need to investigate how electronic and mobilepayment services compete.RESEARCH QUESTION 18: What are the dynamics betweenmobile payments and new e-payment services?The complementarity and substitutability of electronicand mobile payments merits research as well. By solvingresearch questions 17 and 18, it becomes possible tounderstand for which situations electronic and mobile

T. Dahlberg et al. / Electronic Commerce Research and Applications 7 (2008) 165–181 177

payments are most appropriate. Expert and focus groupinterviews, as well as surveys seem useful researchapproaches.

4.3.5. m-Payment market and providers

At the time of writing, it was still uncertain whether andwhen large-scale adoption and use of mobile paymentswould happen. Financial institutions, mobile operators,and incumbent mobile payment service providers try tounderstand this issue. They launch isolated initiatives tomeet to specific market needs. The business value of mobilepayment services and the roles of the players in the mobilepayments service markets are unclear. One scenario is thatthe current payment service providers will be able to keepcontrol over the payment process and mobile networkoperators will create the new channel by providing mobilenetwork infrastructure. At the other extreme, some incum-bents have launched mobile payment services where finan-cial institutions and mobile operators are used only asvendors with limited roles. In addition, some merchantshave taken an active role and become payment service pro-viders (e.g., public transportation operators). These devel-opments could become a threat to financial institutionsespecially, unless they respond to these developments. Weexpected to find research on mobile payment servicesindustry rivalry and on the capabilities or lack of capabil-ities of various players.

We have identified five papers that focused exclusivelyon this factor, and, additionally, several ‘‘Multiple Catego-ries’’ papers provided important insights. Some researchershave conducted analysis on current mobile payment ser-vices and their characteristics [31,35]. This helps to comparethe features of mobile payment services. In order to investi-gate the roles and ambitions of various actors, some studieshave exposed the strengths and weaknesses of selected pay-ment service providers [87,92]. Vilmos and Karnouskosdescribed the SEMOPS project that intended to give birthto a European standard for mobile payment architectures[86]. To justify their proposed architecture, they discussedthe current market requirements and explained how SEM-OPS could be deployed in such an environment.

Using a higher level of abstraction, Ondrus et al. [59]claimed that a more complete analysis of the mobile pay-ment services market should take into account various inter-related perspectives such as the market (value propositions

Table 7Focus of mobile payment publications in m-payment market & providers fact

Theme of research References Empirical qinterviews

Analysis of existing m-payment solutions andcharacteristics

[31,35] 0

Framework to analyze the actors and theirvalue proposition

[59,61,63,64] 3

Analysis of strengths and weaknesses of theactors

[87,92] 0

Proposition of a mobile payment system [86] 0

and customers segments), the actors and their agendas.Following this proposal, Ondrus and Pigneur adopted amulti-actor multi-criteria approach in order to analyzethe market from multiple perspectives [61,63]. One aspectof their research was the evaluation of a merchant’s rolein a situation where the merchant disrupted a market bybecoming a payment service provider. They also found thatretailers have a preference for self-operated payment ser-vices. This might be a signal that merchants are temptedto launch their own services (at least in Switzerland), assome of them already do to a certain extent in other coun-tries (e.g., IKEA and public transport operators). The anal-ysis of past studies is shown in Table 7. Four researchquestions for future studies are outlined.

RESEARCH QUESTION 19: What are the optimal roles of dif-ferent players in the mobile payment value chain?The organization of the mobile payment services valuechain has a significant role in the development of mobilepayment services. As long as the roles of key players areunclear, mobile payment services will proceed at a slowpace. Alternative value chain models with benefits anddrawbacks for each player could be analyzed with eco-nomic modelling and design research, and be backedby interviews and expert panels. These approaches arealso applicable to research questions 20 and 21.RESEARCH QUESTION 20: How should inter-firm coopera-tion in the mobile payment services markets be orga-nized? Is ‘‘cooperation’’ possible?Studies carried out in different parts of the world havecome to the same conclusions about the need for coop-eration between various players to create sustainablemarkets for mobile payment services. A critical questionfor future research is to examine how this type of ‘‘coo-petition’’ can be achieved and what incentives areneeded to secure collaboration between players.RESEARCH QUESTION 21: What are the competitive impactsof mobile payment services operated by merchants?As merchants could become mobile payment serviceproviders, research should investigate the competitiveconsequences of such cases. Large retailers with highbusiness transaction volume could threaten financialinstitutions’ payment service business. An interestingexample from Hong Kong is the Octopus service. Onepossible scenario is that financial institutions will abandon

or

ualitative Empirical quantitativesurvey

Conceptual speculativecommentary

0 2

0 1

1 1

0 1

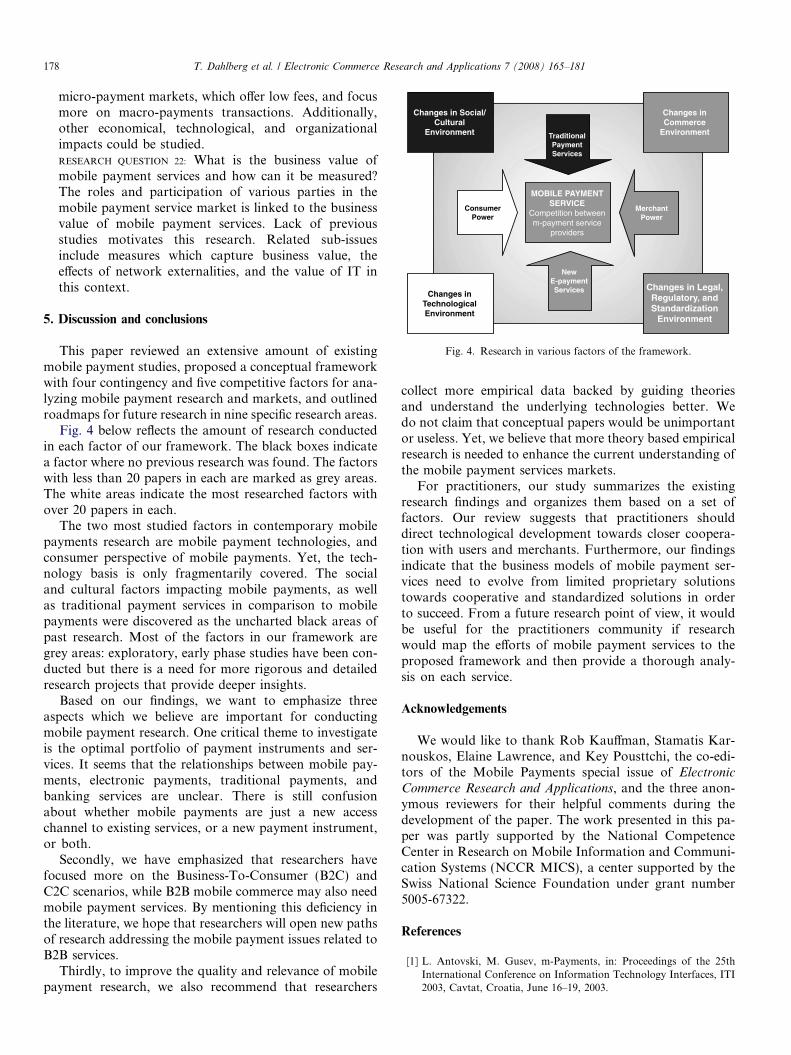

Changes in Legal, Regulatory, and Standardization

Environment

Changes in TechnologicalEnvironment

Changes in Social/Cultural

Environment

Changes in Commerce

Environment

ConsumerPower

MOBILE PAYMENTSERVICE

Competition between m-payment service

providers

MerchantPower

TraditionalPaymentServices

NewE-paymentServices

Fig. 4. Research in various factors of the framework.

178 T. Dahlberg et al. / Electronic Commerce Research and Applications 7 (2008) 165–181

micro-payment markets, which offer low fees, and focusmore on macro-payments transactions. Additionally,other economical, technological, and organizationalimpacts could be studied.RESEARCH QUESTION 22: What is the business value ofmobile payment services and how can it be measured?The roles and participation of various parties in themobile payment service market is linked to the businessvalue of mobile payment services. Lack of previousstudies motivates this research. Related sub-issuesinclude measures which capture business value, theeffects of network externalities, and the value of IT inthis context.

5. Discussion and conclusions

This paper reviewed an extensive amount of existingmobile payment studies, proposed a conceptual frameworkwith four contingency and five competitive factors for ana-lyzing mobile payment research and markets, and outlinedroadmaps for future research in nine specific research areas.

Fig. 4 below reflects the amount of research conductedin each factor of our framework. The black boxes indicatea factor where no previous research was found. The factorswith less than 20 papers in each are marked as grey areas.The white areas indicate the most researched factors withover 20 papers in each.

The two most studied factors in contemporary mobilepayments research are mobile payment technologies, andconsumer perspective of mobile payments. Yet, the tech-nology basis is only fragmentarily covered. The socialand cultural factors impacting mobile payments, as wellas traditional payment services in comparison to mobilepayments were discovered as the uncharted black areas ofpast research. Most of the factors in our framework aregrey areas: exploratory, early phase studies have been con-ducted but there is a need for more rigorous and detailedresearch projects that provide deeper insights.

Based on our findings, we want to emphasize threeaspects which we believe are important for conductingmobile payment research. One critical theme to investigateis the optimal portfolio of payment instruments and ser-vices. It seems that the relationships between mobile pay-ments, electronic payments, traditional payments, andbanking services are unclear. There is still confusionabout whether mobile payments are just a new accesschannel to existing services, or a new payment instrument,or both.

Secondly, we have emphasized that researchers havefocused more on the Business-To-Consumer (B2C) andC2C scenarios, while B2B mobile commerce may also needmobile payment services. By mentioning this deficiency inthe literature, we hope that researchers will open new pathsof research addressing the mobile payment issues related toB2B services.

Thirdly, to improve the quality and relevance of mobilepayment research, we also recommend that researchers

collect more empirical data backed by guiding theoriesand understand the underlying technologies better. Wedo not claim that conceptual papers would be unimportantor useless. Yet, we believe that more theory based empiricalresearch is needed to enhance the current understanding ofthe mobile payment services markets.

For practitioners, our study summarizes the existingresearch findings and organizes them based on a set offactors. Our review suggests that practitioners shoulddirect technological development towards closer coopera-tion with users and merchants. Furthermore, our findingsindicate that the business models of mobile payment ser-vices need to evolve from limited proprietary solutionstowards cooperative and standardized solutions in orderto succeed. From a future research point of view, it wouldbe useful for the practitioners community if researchwould map the efforts of mobile payment services to theproposed framework and then provide a thorough analy-sis on each service.

Acknowledgements

We would like to thank Rob Kauffman, Stamatis Kar-nouskos, Elaine Lawrence, and Key Pousttchi, the co-edi-tors of the Mobile Payments special issue of Electronic

Commerce Research and Applications, and the three anon-ymous reviewers for their helpful comments during thedevelopment of the paper. The work presented in this pa-per was partly supported by the National CompetenceCenter in Research on Mobile Information and Communi-cation Systems (NCCR MICS), a center supported by theSwiss National Science Foundation under grant number5005-67322.

References

[1] L. Antovski, M. Gusev, m-Payments, in: Proceedings of the 25thInternational Conference on Information Technology Interfaces, ITI2003, Cavtat, Croatia, June 16–19, 2003.

T. Dahlberg et al. / Electronic Commerce Research and Applications 7 (2008) 165–181 179

[2] K. Bohle, M. Krueger, Payment culture matters – a comparative eu-us perspective on Internet payments, Technical report, BackgroundPaper No. 4, Electronic Payment Systems Observatory (ePSO), EUR19936 EN, Seville, Spain, 2001.

[3] E. Breedveld, B. Meijboom, A. de Roo, Labour supply in the homecare industry: a case study in a Dutch region, Health Policy 76 (2)(2006) 144–155.

[4] M. Bruno-Britz, Is the end of cash at hand, Bank Systems &Technology 42 (10) (2005) 24–29.

[5] G. Carat, epayment systems database – trends and analysis, Technicalreport, Background Paper No. 9, Electronic Payment SystemsObservatory (ePSO), EUR 20264 EN, Seville, Spain, 2002.

[6] J.J. Chen, C. Adams, Short-range wireless technologies with mobilepayments systems, Proceedings of the Sixth International Conferenceon Electronic Commerce (ICEC), Delft, The Netherlands, October25–27ACM International Conference Proceeding Series, vol. 60,ACM Press, New York, NY, USA, 2004.

[7] J.J. Chen, C. Adams, User acceptance of mobile payments: atheoretical model for mobile payments, in: Proceedings of the FifthInternational Conference on Electronic Business (ICEB), HongKong, December 5–9, 2005.

[8] L.-D. Chen, A theoretical model of consumer acceptance of mpay-ment, in: N. Romano Jr. (Ed.), Proceedings of the 12th AmericasConference on Information Systems (AMCIS), Acapulco, Mexico,August 4–6, Association for Information Systems, Atlanta (GA),2006.

[9] Y. Chou, C.-W. Lee, J. Chung, Understanding m-commerce paymentsystems through the analytic hierarchy process, Journal of BusinessResearch 57 (2004) 1423–1430.

[10] T. Dahlberg, N. Mallat, Mobile payment service development –managerial implications of consumer value perceptions, in: S. Wrycza(Ed.), Proceedings of the 10th European Conference on InformationSystems (ECIS), Gdansk, Poland, June 6–8, 2002.

[11] T. Dahlberg, N. Mallat, J. Ondrus, A. Zmijewska, Mobile paymentmarket and research – past, present and future, in: Presentation atHelsinki Mobility Roundtable, Helsinki, Finland, June 1–2, 2006.

[12] T. Dahlberg, N. Mallat, A. Oorni, Consumer acceptance of mobilepayment solutions – ease of use, usefulness and trust, in: Proceedingsof the Second International Conference on Mobile Business (ICMB),Vienna, Austria, June 23–24, 2003.

[13] T. Dahlberg, N. Mallat, A. Oorni, Trust enhanced technologyacceptance model – consumer acceptance of mobile paymentsolutions, in: Presentation at Stockholm Mobility Roundtable,Stockholm, Sweden, May 22–23, 2003.

[14] T. Dahlberg, A. Oorni, Understanding changes in consumer paymenthabits – do mobile payments attract consumers? in: Presentation atHelsinki Mobility Roundtable, Helsinki, Finland, June 1–2,2006.

[15] M. Das, A. Saxena, V. Gulati, A security framework for mobile-to-mobile payment network, in: IEEE International Conference onPersonal Wireless Communications (ICPWC), New Delhi, India,January 23–25, 2005.

[16] F.D. Davis, Perceived usefulness, perceived ease of use, and useracceptance of information technology, MIS Quarterly 13 (3) (1989)319–340.

[17] S.G. Dewan, L.-D. Chen, Mobile payment adoption in the USA: across-industry, cross-platform solution, Journal of Information Pri-vacy & Security 1 (2) (2005) 4–28.

[18] R. Di Pietro, G. Me, M.A. Strangio, A two-factor mobile authen-tication scheme for secure financial transactions, in: Proceedings ofthe Fourth International Conference on Mobile Business (ICMB),Sydney, Australia, July 11–13, 2005.

[19] M.S. Ding, J.F. Hampe, Reconsidering the challenges of mpayments:a roadmap to plotting the potential of the future mcommerce market,in: Proceedings of the 16th Bled eCommerce Conference, Bled,Slovenia, June 9–11, 2003.