oa and mk breaking the law

TRANSCRIPT

BREAKING THE LAWHardening Soft Law in the Basel

Committee

Omar Ahmad and Michael Koehler

A h m a d & K o e h l e r B r e a k i n g t h e L a wP a g e |1

Table of Contents

1. The Role of the Basel Committee

2. Logic of the Legal Barrier to

A. Regimes

B. Rational Choice

C. Path Dependence

D. Political Economy

3. Strategy Options

A. Harder Law

B. Restructuring of Soft Law

4. Optimal Strategy

5. Implementation

6. Bibliography

A h m a d & K o e h l e r B r e a k i n g t h e L a wP a g e |2

1. The Role of Basel

Past attempts by the Bank for International Settlements

(BIS) to coordinate international financial regulation (IFR) have

been difficult. Simmons argues that rule development for

financial regulation “has tended to involve small numbers of

national regulators or supervisors, working briefly but

intensively on relatively narrow issues, and producing nonbinding

agreements.”1 Verdier agrees with Simmons by characterizing the

international financial regulation as a system of decentralized

transnational regulatory networks (TRNs) functioning through

mostly “soft law”.2

The BIS is one such international financial network. Its

mission is to provide monetary and financial stability by

coordinating the actions of its membership of 60 central banks. 1 Beth A. Simmons, (2001), “The International Politics of Harmonization: The Case of Capital Market Regulation”, International Organization vol. 55, no. 3, 592.2 Pierre-Hugues Verdier, “The Political Economy of International Financial Regulation”, Indiana Law Journal Vol. 88, 1405.

A h m a d & K o e h l e r B r e a k i n g t h e L a wP a g e |3

The BIS also acts as a bank to its member central banks,

providing consultation and actually extending temporary credits

to central banks.3 The BIS functions through a series of

subcommittees specializing in specific areas of financial

regulation.

The Basel Committee on Banking Supervision (BCBS),

originally comprised of G-10 member central bankers, sets

standards for banking regulation with the purpose of increasing

financial stability.4 The BCBS plays an essential role, because

coordinated capital regulation “provides a buffer against bank

losses, protecting creditors in the event a bank nonetheless

fails, and creating a disincentive to excessive risk taking or

shirking by bank owners and managers.”5 The most useful

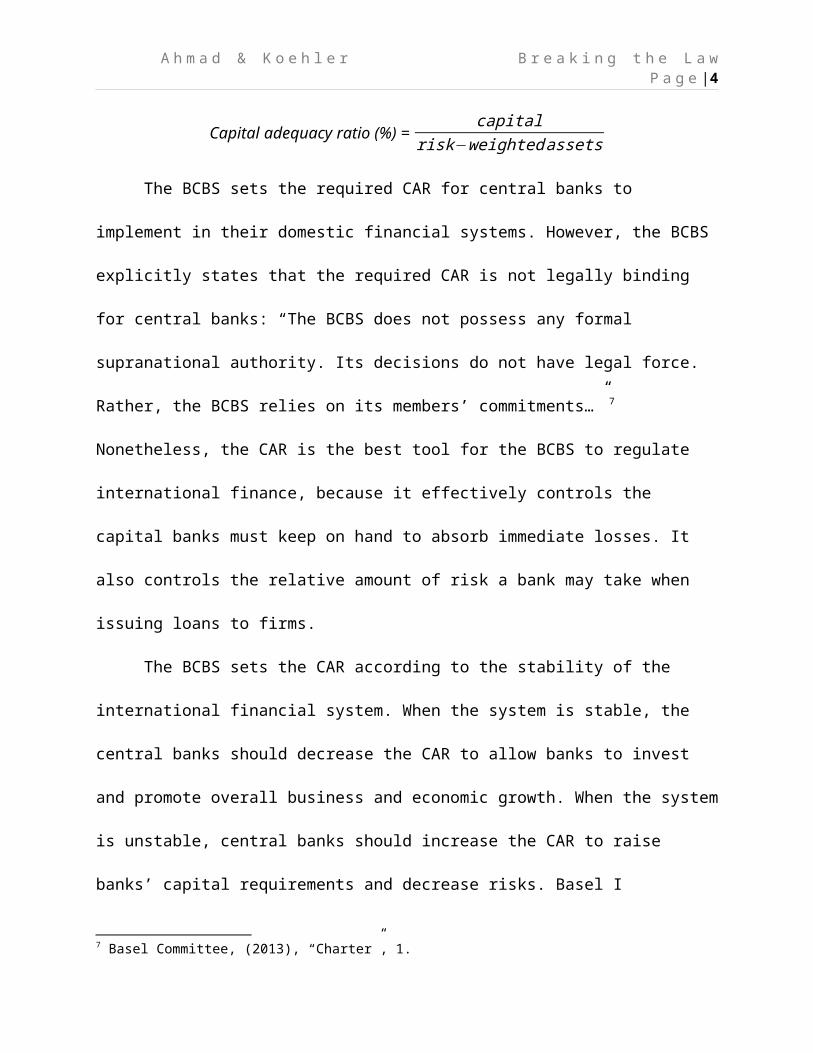

regulatory practice the BCBS uses is the capital adequacy ratio

(CAR) 6:

3 Bank for International Settlements, “BIS Mission Statement”, retrieved from http://www.bis.org/about/mission.htm. 4 Basel Committee on Banking Supervision, (2013), “Charter”, retrieved from www.bis.org/bcbs/charter.pdf, 1.5 Daniel K. Tarullo, (2008), Banking on Basel: The Future of International Financial Regulation, (Washington, Dc: Peterson Institute for International Economics), 16.6 Basel Committee on Banking Supervision, (2011), “Basel III: A Global Regulatory Framework for More Resilient Banks and Banking Systems”, retrieved from www.bis.org/publ/bcbs189.pdf, 12.

A h m a d & K o e h l e r B r e a k i n g t h e L a wP a g e |4

Capital adequacy ratio (%) = capital

risk−weightedassets

The BCBS sets the required CAR for central banks to

implement in their domestic financial systems. However, the BCBS

explicitly states that the required CAR is not legally binding

for central banks: “The BCBS does not possess any formal

supranational authority. Its decisions do not have legal force.

Rather, the BCBS relies on its members’ commitments…” 7

Nonetheless, the CAR is the best tool for the BCBS to regulate

international finance, because it effectively controls the

capital banks must keep on hand to absorb immediate losses. It

also controls the relative amount of risk a bank may take when

issuing loans to firms.

The BCBS sets the CAR according to the stability of the

international financial system. When the system is stable, the

central banks should decrease the CAR to allow banks to invest

and promote overall business and economic growth. When the system

is unstable, central banks should increase the CAR to raise

banks’ capital requirements and decrease risks. Basel I

7 Basel Committee, (2013), “Charter”, 1.

A h m a d & K o e h l e r B r e a k i n g t h e L a wP a g e |5

(CAR=8%)8, Basel II (specifically targeted types of risk)9, and

Basel III (set required Tier 1 capital at 6.0%)10 were subsequent

amendments to the components of the CAR to stabilize the

financial system. Unfortunately, all three were post facto

reactions to dramatic shocks to the system: Basel I following the

Latin American financial crisis in the late 1980s, Basel II

following the terrorist attacks of September 11, and Basel III

following the global financial crisis of 2007-2008. The

increasing frequency and severity of international financial

crises expose a legal barrier to the effectiveness of the BIS,

because the rules specified by the BCBS as a regime are not

obligatory for central banks. This follows Iida’s definition of

“legal effectiveness”.11

We argue that the problem facing the BCBS is that it fails

to prevent crises of capital adequacy, because it can neither

prevent nor punish noncompliance of central banks to its capital 8 Basel Committee on Banking Supervision, (1988), “International Convergence of Capital Measurement and Capital Standards”, retrieved from www.bis.org/publ/bcbs04a.pdf, 11. 9 Basel Committee on Banking Supervision, (2005), “International Convergence of Capital Measurement and Capital Standards: A Revised Framework”, retrieved from www.bis.org/publ/bcbs118.pdf, 12-5.10 Basel Committee, (2011), “Basel III”, 12-3.11 Keisuke Iida, (2004), “Is WTO Dispute Settlement Effective?”, Global Governance vol. 10, 208.

A h m a d & K o e h l e r B r e a k i n g t h e L a wP a g e |6

adequacy requirements (CARs). This represents a legal barrier to

the effectiveness of the BCBS, because its institutionalized soft

law (lack of obligation and delegation) fails to manage the

increased intensity and frequency of crises of capital adequacy.

We will proceed by explaining how the logic of relevant

theories of international organization support our assertion of

the legal barrier to effectiveness. We will also use these

theories to suggest two realistically and theoretically grounded

strategies for the BCBS to overcome the barrier: 1) a hardening

of soft law, and 2) a restructuring of the current soft law. We

will argue that hardening soft law is the optimal strategy for

the BCBS, because the current legal apparatus does not stabilize

today’s complex and immense international financial system. At

the end, we will suggest methods for implementing obligation and

delegation.

2. Logic of the Legal Barrier to Effectiveness

Four relevant theories (regimes, rational choice, path

dependence, and political economy) of international organization

A h m a d & K o e h l e r B r e a k i n g t h e L a wP a g e |7

explain why the legal barrier to effectiveness causes the BCBS to

fail to prevent financial crises.

A. Regimes

Simmons argues that in a situation where there are

significant negative externalities and high incentives for

smaller actors to emulate the larger one, market harmonization

will occur with institutional assistance.12 Today, the high

interdependence of private international banks creates high

negative externalities. “The globalization of banking increases

the possibility that any weak bank involved in the increasingly

dense network of interbank relations potentially can transmit

weakness throughout the international banking system.”13 High

costs incurred by the failure of a highly interconnected bank

motivate central banks to seek financial stability. This

represents a “dilemma of common aversion”, because all central

banks share a common interest in avoiding the high costs of

financial instability. Dilemmas of common aversion simply require

12 Simmons, “The International Politics of Harmonization”, 598. 13 Simmons, “The International Politics of Harmonization”, 601.

A h m a d & K o e h l e r B r e a k i n g t h e L a wP a g e |8

actors to coordinate policies in order to overcome a common

problem.14

The BCBS seeks to facilitate this process by forming a

coordination regime around which central banks’ financial

regulation expectations converge.15 According to Keohane, an

international regime is a set of implicit or explicit principles,

norms, rules, and decision making procedures around which actors’

expectations converge. Regimes solve common problems by

facilitating cooperation between actors, but the regimes do not

impinge on the self-interests of the actors.16 The BCBS is

therefore a regime.

Simmons argues that the success of the BCBS in the

implementation of Basel I came from banks’ desire to avoid

reputation costs associated with defection from the CAR.

Borrowers view banks which do not implement the BCBS’ CARs as

unstable or risky. Here, the negative perception of defection

14 Arthur Stein, “Coordination and Collaboration: Regimes in an Anarchic World”, International Organization Vol. 36, No. 2, 309-12.15 Stephen D. Krasner, (1982) “Structural Causes and Regime Consequences: Regimes as Intervening Variables”, International Organization vol. 36, no. 2, 185.16 Robert O. Keohane, (1984), “Cooperation and International Regimes”, in After Hegemony: Cooperation and Discord in the World Political Economy (Princeton: Princeton University Press), 57-64.

A h m a d & K o e h l e r B r e a k i n g t h e L a wP a g e |9

from the dominant regime causes banks to harmonize their CARs to

remain competitive.17 Therefore, the CAR implementation of Basel

I was relatively successful at coordinating central bank policy.

However, the BCBS fails to effectively coordinate the

actions of central banks to prevent international financial

crises, because the soft law regime allows the interests of

private banks to influence the decisions of central banks,

causing some central banks to defect. Private banks, as profit

maximizers, desire to remain competitive in the financial market.

If the BCBS imposes a higher CAR on a central bank, which

compromises a private bank’s ability to issue a loan, the private

bank will pressure the central bank not to accept the BCBS’ CAR.

Pressure from the financial industry often causes central banks

to refuse losing any of their independent decision-making ability

to the BCBS. This situation represents a defection, not because

the central banks disagree on the problem, but rather central

banks disagree on which policy best solves the problem.18 Hence,

central banks are careful not to give any obligation or

17 Simmons, “International Politics of Harmonization”, 602. 18 Stein, “Coordination”, 319.

A h m a d & K o e h l e r B r e a k i n g t h e L a wP a g e |10

enforcement power to the BCBS, because they may disagree on the

chosen CAR. Regime theorists would argue that this is the reason

the BCBS maintains a regime of soft law where there is weak

obligation to adopt the recommended CAR, and no delegated

enforcement mechanism exists to punish cheating or defection.

Soft law creates a legal barrier to effectiveness for the BCBS.

B. Rational Choice

Rational choice theorists explain that states rationally

design international agreements to pursue their self-interests

and achieve joint gains.19 They argue that cooperation is

necessary in issue areas requiring collective action to provide

public goods, like international financial stability. Bargaining

is the method by which states cooperate to provide financial

stability.20 According to Brummer, “most of the sources of

international financial law are informal, intergovernmental

institutions that set agendas and standards for the global

regulatory committee.”21 Koremenos, Lipson, and Snidal state that

19 Verdier, “Political Economy”, 1423.20 Robert O. Keohane, (1986), “Rational-Choice and Functional Explanations”, in After Hegemony: Cooperation and Discord in the World Political Economy (Princeton: Princeton University Press), 69-70. 21 Chris Brummer, (2010), “Why Soft Law Dominates International Finance – And Not Trade”, Journal of International Economic Law vol. 13, no. 3, 627.

A h m a d & K o e h l e r B r e a k i n g t h e L a wP a g e |11

institutions are “rational, negotiated responses to the problems

international actors face.”22 When the central banks of the G-10

members drafted the charter of the BCBS in 1974, they protected

the independent decision-making ability of the central banks by

intentionally omitting any obligation, allowing a higher degree

of flexibility.23 Brummer argues that central banks prefer soft

law, because “the absence of any formal obligation enables a

cheap exit from commitments, and by extension permits opportunism

when it suits a country.”24

Rational choice theorists argue that the BCBS fails to

effectively prevent the occurrence of international financial

crises, because the previously effective design of the BCBS does

not adapt well to changes in the external environment. Even

though soft law allows the BCBS a higher degree of flexibility

than hard law, it has been unable to sufficiently adapt and

regulate the rapid expansion of international capital markets in

the past three decades. In 1960, only ten US banks held overseas

22 Barbara Koremenos, Charles Lipson, and Duncan Snidal, (2001), “The RationalDesign of International Institutions”, International Organization vol. 55, no. 4, 768.23 Basel Committee, “Charter”, 1.24 Brummer, (2010), “Why Soft Law”, 630.

A h m a d & K o e h l e r B r e a k i n g t h e L a wP a g e |12

branches. In 1977, more than 100 had overseas branches. In 2007,

global financial assets accounted for 343% of world GDP. In 2010,

international finance institutions traded $4 trillion daily.

According to Verdier, this increase in international banking

activity sprouts from increases in technology and capital market

developments in the last three decades. There are more

opportunities for banks to invest globally. Indeed, those which

fail to expand globally may be less competitive. 25

Soft law cannot adequately adapt to this increase in scope

of the enforcement problem facing the BCBS, because soft law

allows private banks to sway the interests of central bankers.

There are increasingly higher incentives for banks to lend

internationally, meaning it will be more difficult for central

banks to implement higher CARs.26 With increased incentives to

issue risky loans, the BCBS will be less able agree to mutually

acceptable CARs which stabilize the international financial

system. Increased obligations and enforcement mechanisms would

decrease this incentive for private banks to make risky loans and

25 Verdier, “Political Economy”, 1414-5.26 Koremenos, “The Rational Design”, 776.

A h m a d & K o e h l e r B r e a k i n g t h e L a wP a g e |13

create a more stable system.27 Therefore, rationalists agree that

soft law in the BCBS creates a legal barrier to effectiveness in

preventing financial crises.

C. Path Dependence

Path dependence scholars disagree with the basic assumption

made by rational choice theorists that central banks rationally

design agreements to achieve joint gains. They argue that the use

of soft law in IFR does not necessarily maximize gains for all

parties involved. According to Fioretos, institutional decisions

originally made during the formation of an organization

effectively constrain its future evolution. In this way, the

trajectory of an organization toward its goal is not linear nor

constant. Policy options in the present depend on decisions made

in the past, because radical change to existing agreements incurs

high costs.28 Therefore, organizations tend to resist radical

changes to existing procedures and rules. Instead, Fioretos

posits that states engage in a process called institutional

27 Kenneth W. Abbott, Robert O. Keohane, Andrew Moravcsik, Anne-Marie Slaughter, and Duncan Snidal, “The Concept of Legalization”, International Organization vol. 54, no. 3, 401. 28 Fioretos, Orfeo, “Historical Institutionalism in International Relations”, International Organization Vol. 5, Iss. 2, 379.

A h m a d & K o e h l e r B r e a k i n g t h e L a wP a g e |14

layering, where states solve problems by creating new, more

focused organizations within existing arrangements.29 Verdier

explains that the existing design of an institution may not be

optimal if the actors initially designed the institution to

suffice a short-term goal. In this way, the design of an

institution may only be temporarily rational but become

irrational when the external circumstances change.

Path dependence theorists would argue that the framers at

Bretton Woods did not believe private international finance

needed regulation, because the amount of internationally traded

capital at the time was negligible. Therefore, they did not

develop any legalized form of international financial regulation

like they did with international trade (see GATT and WTO). When

the Bretton Woods system ended and international banking greatly

expanded, central banks regulated international finance with

mostly ad hoc agreements negotiated through TRNs. This informal

network, which utilizes the flexibility of soft law to address

immediate problems with short-term arrangements, worked when the

29 Ibid., 389.

A h m a d & K o e h l e r B r e a k i n g t h e L a wP a g e |15

number of actors involved in the negotiations was relatively

small.30

However, today, there are an increasingly vast amount of

internationally active banks, meaning that the nature of the

problem facing the BCBS is more difficult today. According to

Koremenos, there is an inverse relationship between the number of

actors and the flexibility of an agreement.31 Path dependency

theory, therefore, agrees that the current soft law of the BCBS

creates a legal barrier to effectiveness in the prevention of

financial crises. Soft law and the informal system of TRNs worked

when the degree of international banking was relatively low,

however, the increased amount of internationally traded capital

and number of international banks require a change in the current

laws of the BCBS to meet these challenges.

D. Political Economy

Political economy theory posits that international

agreements are outcomes of negotiations between influential

actors. Verdier identifies three main actors in international

30 Verdier, “Political Economy”, 1421. 31 Koremenos, “The Rational Design”, 794.

A h m a d & K o e h l e r B r e a k i n g t h e L a wP a g e |16

financial regulation: central banks, the financial industry, and

great powers. Legislative bodies typically delegate national

financial regulation powers to their central banks, because

learning and understanding the complicated international

financial system requires a high degree of time and effort. This

delegation may cause a principal-agent problem, because oversight

of central bank activity tends to be reactive. Legislatures

rarely review the actions of a central bank unless a dramatic

event prompts them to do so.32 Financial crises occur cyclically,

because domestic audiences demand higher stability only when the

system is unstable, and the financial industry demands lower

constraints when the system is stable allowing them to take more

risks. This indicates that central banks only balance the demands

of their constituents, rather than actively creating a more

stable international financial system in an effort to avoid

legislative review.33 The agent (central banks) does not achieve

the goals assigned by the principal (legislatures).

32 Verdier, “Political Economy”, 1427-9.33 John Ferejohn and Charles Shipan, (1990) “Congressional Influence on Bureaucracy”, Journal of Law, Economics, and Organization vol. 6, 1-5.

A h m a d & K o e h l e r B r e a k i n g t h e L a wP a g e |17

Political economy theorists argue that the BCBS fails to

prevent financial crises, because soft law allows central banks

too much independent decision-making ability. The actions of

central banks reflect the interests of the most influential

groups. Therefore, the only check on a central bank is the

principal legislature. However, because the legislature delegate

a high degree of independent decision-making ability to central

banks, there is little oversight or review of their actions.

Coupled with the inability of the BCBS to enact neither

obligatory nor enforceable requirements, actions of central banks

depend almost exclusively on the influences of the public and

domestic banks.34 Thus, the BCBS fails to prevent international

financial crises, because soft law allows domestic audiences and

the private banking industry to influence the actions of central

banks and potentially destabilize the international finance

system. In this way, the BCBS faces a legal barrier to

effectiveness.

3. Strategy Options

34 Verdier, “Political Economy”, 1427-32.

A h m a d & K o e h l e r B r e a k i n g t h e L a wP a g e |18

The recurrence of international financial crises and the

failure of the BCBS to effectively prevent or mitigate their

effects indicate that the BCBS fails to regulate the current

international system. All four theoretical explanations support

our assertion that the current system of soft law is a legal

barrier to effectiveness.

Therefore, we will weigh the costs and benefits of two

possible strategies which target the legal apparatus of the BCBS

to more effectively prevent the occurrence of international

financial crises.

A. Hardening of Soft Law

The first strategy option for the BCBS to overcome its legal

barrier to effectiveness is

move toward harder law. Abbott et al. classify three components

of hard law: obligation, precision, and delegation.35 The

recommendations and requirements of the BCBS currently hold a

high level of precision. However, relatively higher levels of

obligation and delegation would enable the BCBS to more

effectively regulate international capital markets. The mission

35 Abbott, “The Concept of Legalization”, 401.

A h m a d & K o e h l e r B r e a k i n g t h e L a wP a g e |19

of the BCBS is to facilitate international financial stability,

and a hardening of the soft law would enable it to more

effectively accomplish this mission.

Legal obligation would benefit the BCBS, because its

authority would invoke internationally accepted rules and

procedures of international legal discourse. Legal obligation

entails a responsibility by those who sign an agreement to follow

that agreement. In this way, the organization holds those parties

which break the legal obligation or do not abide by its mandates

legally accountable, meaning they will be subject to some sort of

legal sanctioning procedure. Therefore, parties who enter into

legally obligatory agreements acknowledge that accepting will

restrict their strategic options.36 This means that those who

enter into agreements are able to make credible commitments. The

international community views the actions of those who legally

commit to agreements as credible, because they acknowledge that

reneging on that agreement incurs a reprimand.37 Therefore, legal

36 Abbott, “Concept of Legalization”, 408-10.37 Kenneth W. Abbott and Duncan Snidal, (2000) “Hard and Soft Law in International Governance”, International Organization vol. 54, no. 3, 426-9.

A h m a d & K o e h l e r B r e a k i n g t h e L a wP a g e |20

obligation leads to greater international financial stability

through credible commitments.

In the case of the BCBS, those central banks which did not

ratify the BCBS CAR would not be able to credibly commit as much

as those central banks that did. This means that the

international community would not trust the stability of the

financial industry in countries whose central banks failed to

ratify the BCBS CAR. Central banks would realize that the loss in

credibility via non-ratification would reduce the domestic

financial industry’s ability to compete, and the central bank

would be more likely to harmonize its capital regulation with the

BCBS CAR requirements.38

Legal obligation would also provide a mechanism to overcome

the problem of volatile of central bank influences raised by the

political economy theorists. Legal obligation would decrease the

ability of the domestic financial industry to influence the

actions of the central banks. Private banks as profit maximizers

seek to increase their competitiveness in the international

financial capital market. One way for them to increase

38 Simmons, “International Politics of Harmonization”, 602.

A h m a d & K o e h l e r B r e a k i n g t h e L a wP a g e |21

competitiveness is to lobby their central bank to allow for a

lower CAR than other central banks. With a lower CAR, the bank

can then issue more loans increasing their future profits through

accrued interests and investment. If the BCBS CAR requirements

were legally obligatory, then the potentially risky influences of

the domestic private banks could only increase the central bank’s

CAR, rather than decrease, creating an even more stable financial

system.

Delegation of legal enforcement to the BCBS would also

enable it to more effectively achieve its mission of

international financial stability. According to Abbott et al.,

delegation of authority to third parties allows them to

interpret, implement, and apply rules made by the organization.39

Higher degrees of delegation allow organizations to govern the

actions of decision makers and legitimize its rules. When

organizations have binding regulations in rule making and

implementation of rules, those governed by the organization are

more likely to implement the rules and not break them.40

39 Abbott, “Concept of Legalization”, 401. 40 Ibid., 416-7

A h m a d & K o e h l e r B r e a k i n g t h e L a wP a g e |22

Legal delegation would allow the BCBS to monitor and enforce

the implementation of its CAR requirements in domestic

legislation. If central banks failed to effectively implement the

requirements, then the BCBS could begin a legal discourse

sanctioning the central bank. This sanction could come in the

form of legislative review of the central bank. Legislatures, as

principals, have the ability to limit the actions of central

banks, as agents, and reorder central bank preferences to more

effectively regulate finance through the use of BCBS CAR

requirements.41 Central banks would therefore work with the BCBS

to implement the CAR requirements under the stated timeline to

avoid legislative oversight. Thus, legal delegation would enable

the BCBS to more effectively regulate and stabilize international

capital markets through the use of sanctions and legislative

review.

Despite the benefits of hard law, higher degrees of

obligation and delegation would also incur costs on the BCBS.

Restrictions on independent decision making and sovereignty

resulting from higher levels of obligation, increase the

41 Verdier, “Political Economy”, 1428.

A h m a d & K o e h l e r B r e a k i n g t h e L a wP a g e |23

ratification and bargaining costs, because actors are cautious to

restrict their behavior when uncertainty about the future is

high. In other words, the time needed to decide the appropriate

CAR increases when rules are obligatory. This increased time may

exacerbate emergency financial situations. Also, when uncertainty

is high, like the volatile financial market, actors resist

reducing their flexibility.42 The financial industry will lobby

central banks to resist implementing any hard law mandates from

the BCBS, because banks do not want to limit their ability to

issue loans and make profits.43 The financial industry will also

influence the public to pressure central banks to refrain from

hard law, because a higher CAR would restrict the banks’ ability

to issue loans causing a short-term economic slump.44

These are serious problems facing the argument for harder law in

the BCBS. However, we argue that the long-term benefits from the

increased capacity of the BCBS to provide the public good of

42 Koremenos, “The Rational Design”, 793-4. 43 Verdier, “Political Economy”, 1431-4.44 Basel Committee on Banking Supervision, (2010) “Assessing the MacroeconomicImpact of the Transition to Stronger Capital and Liquidity Requirements”, retrieved from http://www.bis.org/publ/othp12.htm, 9.

A h m a d & K o e h l e r B r e a k i n g t h e L a wP a g e |24

international financial stability outweigh the short term

bargaining and economic costs.

B. Restructuring of Soft Law

The second potential strategy to address the legal barrier

to effectiveness is “soft law” reform. Brummer argues that

contrary to hard financial law, smaller reforms “can amplify the

compliance pull of international regulations by improving the

institutional support system promoting monitoring and information

sharing.”45 There are more effective ways to modify current

financial regulatory standards to match the environment in the

post Financial Crisis era. Strategic reforms to increase

transparency are an effective alternative strategy to addressing

the legal barrier.

The lack of coordination is the central pillar supporting a

soft law reform strategy. Information sharing and assurance

issues are two types of coordination problems that appear in the

current international financial regulatory system. Financial

institutions do not always share information effectively,

45 Chris Brummer, (2011), “How International Financial Law Works (And How It Doesn’t)”, Georgetown Law Journal vol. 99, 312.

A h m a d & K o e h l e r B r e a k i n g t h e L a wP a g e |25

creating asymmetrical information dilemmas. Central banks must

assure that they will follow the recommended CARs in order to

achieve the optimal effects. Information and trust are the

hurdles to coordination, and the institutions that currently

exist mitigate these effects.46

Currently, financial regulation is profoundly institutional.

The BCBS is an institution because it has rules about scope and

membership, but it fails to institutionalize coordination. In

order for IFR coordination to work, some level of compliance

needs to exist. Brummer states that “The extent of compliance

depends on significant coordinating mechanisms to ensure adequate

monitoring and information sharing.”47 The aim of soft law

reforms should then be to improve monitoring and information

sharing.

The benefit of soft law is its nonobligatory nature. Members

need to ratify hard law, which imposes a sovereignty cost. “The

potential for inferior outcomes, loss of authority, and

diminution of sovereignty makes states reluctant to accept hard

46 Brummer, “Financial Law”, 269.47 Brummer, “Financial Law”, 316.

A h m a d & K o e h l e r B r e a k i n g t h e L a wP a g e |26

legalizations – especially when it includes significant levels of

delegation.”48 The uncertain nature of the financial system would

deters central banks from entering legal commitments. Instead,

they enter into nonbinding agreements. Soft law manages

uncertainty, by using arrangements that are precise but

nonbinding.

Soft law reform focusing on monitoring and information

sharing is not without its drawbacks. One drawback is that there

is still a problem of institutional credibility. Since the CAR is

voluntary, the BCBS, as an institution, loses a significant

amount of credibility, because its recommendations are still not

enforceable. “A country does not, for example, necessarily have

to follow in lockstep with the approaches of international

regulatory leaders, even where it is a client state of

international financial institutions.”49 The BCBS would still

lack some legitimacy since central banks do not have to follow

CARs, despite the creation of monitoring and information sharing

48 Abbott & Snidal, “Hard and Soft Law”, 437.49 Brummer, “Financial Law”, 324.

A h m a d & K o e h l e r B r e a k i n g t h e L a wP a g e |27

mechanisms. The use of soft law still does not guarantee

compliance.

Another drawback to the creation of new soft law mechanisms

are the effects it will have on already existing costs. Soft law

is preferred when members want to keep costs low. “However, where

more monitoring is employed, the instruments will implicitly be

made harder because defection will be made more visible and, by

extension, more costly.” 50 In this case, contracting costs would

increase and would lead to a smaller number of agreements made.

4. Optimal Strategy

After weighing the costs and benefits of each strategy, we

argue that Strategy A – Hardening of Soft Law is the best option

to maximize the legal effectiveness of the BCBS in preventing

financial crises and stabilizing international capital markets.

Though harder law is more difficult than soft law to implement,

the obligatory commitments and delegation would enable the BCBS

to more effectively regulate the currently volatile international

financial system and provide the public good of financial

stability.

50 Brummer, “Financial Law”, 322.

A h m a d & K o e h l e r B r e a k i n g t h e L a wP a g e |28

Indeed, Abbott and Snidal recommend harder legal commitments

when the benefits of cooperation are great, but the potential for

opportunistic costs are high.51 This clearly applies to the

situation facing the BCBS. The BCBS used soft law effectively to

achieve international financial stability when the number of

international banks and the amount of internationally traded

capital were low.52 However, in the last 30 years, technological

advancements and market developments allowed the expansion of

these variables and created a more complex system with a high

level of opportunism for private international banks.53 To

regulate the complicated financial system, the BCBS must legalize

obligation and delegation to increase the incentives for central

banks to follow CAR requirements and ensure sanctioning to those

who break their commitments and destabilize the system.54

Our argument is that the vast and complicated modern

international capital market creates more opportunities for

private international banks to engage in risky behavior and

destabilize the international financial system. Therefore, the 51 Abbott, “Hard and Soft Law”, 429.52 Koremenos, “The Rational Design”, 793-5.53 Verdier, “Political Economy”, 1405.54 Abbott, “Concept of Legalization”, 401.

A h m a d & K o e h l e r B r e a k i n g t h e L a wP a g e |29

BCBS must adopt harder law via more obligatory requirements and

delegate enforcement to more effectively manage this system and

prevent financial instability.

5. Implementation

The BCBS need to implement obligation and delegation. As

previously stated, the BCBS already has a high level of precision

with the CAR requirements. Therefore, we propose a hardening of

the two soft dimensions. Increased obligation requires a

redrafting of Article 1, Section 3 of the BCBS Charter. Legal

delegation requires the adoption of an enforcement mechanism in

the BCBS.

Article 1, Section 3 of the BCBS Charter states “the BCBS

does not possess any formal supranational authority. Its

decisions do not have legal force.”55 Implementing obligation

requires a shift toward pacta sunt servunda. The law must clearly

state obligation to the BCBS requirements. “The fundamental

international legal principle of pacta sunt servunda means that the

rules and commitments contained in legalized international

agreements are regarded as obligatory, subject to various

55 Basel Committee, “Charter”, 1.

A h m a d & K o e h l e r B r e a k i n g t h e L a wP a g e |30

defenses or exceptions, and not to be disregarded as preferences

change.”56

Implementation of delegation must include rule

implementation and enforcement to the BCBS. Abbott et al. refer

to delegation as to “the extent to which states and other actors

delegate authority to designated third parties – including

courts, arbitrators, and administrative organizations – to

implement agreements.”57 To punish those who break the legalized

CARs, the BCBS must be able to punish those who break the rules.

If central banks violate the CARs set by the BCBS, the

punishment would be legislative overview. Verdier finds that “the

primary concern of (national) regulators is to avoid legislative

intervention.”58 Additional regulative legislature is believed to

create market inefficiency, so financial institutions avoid

costly review and possible loss of decision making ability.

Therefore, if financial firms still choose to not comply,

national legislatures will have the right to intervene and

reprimand defection. Cooperation between the BCBS and national

56 Abbott, “Concept of Legalization”, 409.57 Abbott, “Concept of Legalization”, 415.58 Verdier, “Political Economy”, 1429.

A h m a d & K o e h l e r B r e a k i n g t h e L a wP a g e |31

legislative bodies can mitigate the effects of the principle-

agent problem by the sharing of information and proposing of

appropriate penalties to actors in noncompliance. This is a

challenging task to accomplish. The BCBS demands that financial

firms be subject to international oversight. Firms also “resist

standards whose domestic implementation would require legislation

and prefer less ambitious ones that they can implement under

their existing authority.”59 Central banks need to realize that

the benefits of strong financial regulation outweigh the costs of

an unconstrained financial system.

Financial firms, even if they adhere to the CAR, could still

face potential failure. This is not reflective of the CAR, but of

exogenous variables, over which the BCBS has no control. A

bailout should be used on a financial firm that faces exogenous

problems in order to prevent a financial crisis. The funds for

the bailout would come from the BIS’ own reserves. Each member of

the BIS already has to deposit a premium to the BIS, so funds are

available. In this sense, the BIS is the lender of last resort to

central banks.

59 Verdier, “Political Economy”, 1431.

A h m a d & K o e h l e r B r e a k i n g t h e L a wP a g e |32

Delegation also implies the creation of rule implementation

mechanisms. We do not argue that the CAR should be a certain

percentage. We argue that whatever the CAR is, it should be

obligatory and enforceable. Expert research and debate will

determine the optimal CAR. The BCBS charter will include a method

to vote in proposed CARs. We recommend that a proposed CAR

require two-thirds vote from the central bank members of the

BCBS. Hard law makes agreements more difficult to achieve, so

unanimous votes would be infrequent. A two-thirds vote still

holds a majority and would result in high number of agreeable

commitments.

6. Bibliography

Abbott, Kenneth W. and Duncan Snidal. (2000). “Hard and Soft Law

in International Governance”. International Organization Vol. 54,

No. 3, 421-456.

A h m a d & K o e h l e r B r e a k i n g t h e L a wP a g e |33

Abbott, Kenneth W., Robert O. Keohane, Andrew Moravcsik, Anne-

Marie Slaughter, and Duncan Snidal. (2000). “The Concept of

Legalization”. International Organization Vol. 54, No. 3, 401-418.

Bank for International Settlements. “BIS Mission Statement”.

Retrieved from www.bis.org/about/mission.htm.

Basel Committee on Banking Supervision. (1988). “International

Convergence of Capital Measurement and Capital Standards”.

Retrieved from www.bis.org/publ/bcbs04a.pdf.

Basel Committee on Banking Supervision. (2005). “International

Convergence of Capital Measurement and Capital Standards: A

Revised Framework”. Retrieved from

www.bis.org/publ/bcbs118.pdf.

Basel Committee on Banking Supervision. (2010). “Assessing the

Macroeconomic Impact of the Transition to Stronger Capital

and Liquidity Requirements”. Retrieved from

http://www.bis.org/publ/othp12.htm.

Basel Committee on Banking Supervision. (2011). “Basel III: A

Global Regulatory Framework for More Resilient Banks and

A h m a d & K o e h l e r B r e a k i n g t h e L a wP a g e |34

Banking Systems”. Retrieved from

www.bis.org/publ/bcbs189.pdf.

Basel Committee on Banking Supervision. (2013). “Charter”.

Retrieved from www.bis.org/bcbs/charter.pdf.

Brummer, Chris. (2010). “Why Soft Law Dominates International

Finance – And Not Trade”. Journal of International Economic Law Vol.

13, No. 3, 623-643.

Ferejohn, John and Charles Shipan. (1990). “Congressional

Influence on Bureaucracy”. Journal of Law, Economics, and

Organization Vol. 6, Special Issue, 1-20.

Fioretos, Orfeo. (2011). “Historical Institutionalism in

International Relations”. International Organization Vol. 65, Iss.

2, 367-399.

Iida, Keisuke. (2004). “Is WTO Dispute Settlement Effective?”.

Global Governance Vol. 10, 207-225.

Kapstein, Ethan B. (1989). “Resolving the Regulator’s Dilemma:

International Coordination of Banking Regulations”.

International Organization Vol. 43, No. 2, 323-347.

A h m a d & K o e h l e r B r e a k i n g t h e L a wP a g e |35

Keohane, Robert O. (1984). After Hegemony: Cooperation and Discord in the

World Political Economy (Princeton: Princeton University Press).

Koremenos, Barbara, Charles Lipson, and Duncan Snidal. (2001).

“The Rational Design of International Institutions”.

International Organization Vol. 55, No. 4, 761-799.

Krasner, Stephen D. (1982). “Structural Causes and Regime

Consequences: Regimes as Intervening Variables”. International

Organization Vol. 36, No. 2, 185-205.

Simmons, Beth A. (2001). “The International Politics of

Harmonization: The Case of Capital Market Regulation”.

International Organization Vol. 55, No. 3, 589-620.

Stein, Arthur. (1982). “Coordination and Collaboration: Regimes

in an Anarchic World”. International Organization, Vol. 36, No. 2,

299-324.

Tarullo, Daniel K. (2008). Baking on Basel: The Future of International

Financial Regulation, (Washington: Peterson Institute for

International Economics).

A h m a d & K o e h l e r B r e a k i n g t h e L a wP a g e |36

Verdier, Pierre-Hugues. (2013). “Political Economy of

International Financial Regulation”. Indiana Law Journal Vol.

88, 1405-1476.