nairobi securities exchange esg disclosures

TRANSCRIPT

NairobiSecurities

Exchange ESGDisclosures

Guidance Manual

NOVEMBER2021

ACKNOWLEDGEMENTThe Nairobi Securities Exchange would like to thank the Global Reporting Initiative (GRI),

the Swedish International Development Cooperation Agency (SIDA), the African Securities Exchanges Association (ASEA) and Seven Levers LLP, for their technical and financial support

in the development of this ESG Disclosures Guidance Manual.

ESG Disclosures Guidance Manual | November 20213

Foreword

Interest by investors and other stakeholders in Environmental, Social and Governance (“ESG”) matters has surged with the modern investor in the capital markets being more discerning and demanding more disclosure from companies. Stakeholders are increasingly looking for more comprehensive information from companies – and not just around financial performance, but also on governance and societal issues. The COVID-19 pandemic, global environmental and social crises, the transition to renewables and the renewed focus on human rights has intensified the need and drive for ESG integration by corporates.

As ESG issues become more prominent in the global economy, there is an increasing uptake of various forms of ESG reporting by corporates. This is aimed at disclosing to stakeholders how ESG issues are managed within the organisation. The Nairobi Securities Exchange (NSE) believes that ESG reporting provides a framework through which investors, owners of capital and the public at large can have a more comprehensive view of the company’s activities and performance, beyond its financial numbers.

By issuing these guidelines, the NSE aims at improving and standardizing ESG information reported by listed companies in Kenya. These guidelines provide a granular, tactical approach to ESG reporting that meets international standards on ESG reporting. Further guidance has been provided on how listed companies can integrate ESG considerations into their organisations, helping capture significant opportunities for stakeholders while managing critical business risks.

Consistent application of these guidelines will help improve the capital markets in Kenya by providing information that investors are now demanding to facilitate decision making and capital allocation. This is a key objective of the capital markets.

The NSE would like to appreciate the role played by African Securities Exchanges Association (ASEA) in this project and in enhancing the integration of ESG issues and disclosure within capital markets in Africa. Further, the NSE would like to appreciate the Global Reporting Initiative (GRI) and the Swedish International Development Cooperation Agency (SIDA) for providing sponsorship for this initiative. The GRI Standards are the most widely used framework for sustainability/ESG reporting. We also acknowledge the contribution by Seven Levers LLP in the design and development of these ESG Disclosure Guidelines.

Geoffrey O. Odundo Chief Executive Officer Nairobi Securities Exchange

ESG Disclosures Guidance Manual | November 20214

Transparency on the impacts of a business is essential for continuous improvement as well as for stakeholder relationships. Without transparency, there is no trust – and without trust, markets do not function efficiently, and institutions lose their legitimacy. That is why the practice of sustainability reporting has been steadily growing over the past two decades, with GRI leading the way by providing the world’s most widely adopted standards for sustainability impacts: the GRI Standards.

Governments, stock exchanges, market regulators, investors, civil society and other stakeholders are demanding more and better information on the sustainability impacts of businesses. GRI recognizes the importance of aligning corporate sustainability reporting with the information needs of these stakeholders, providing decision-useful data to direct capital towards sustainable business practices.

Regulatory changes that make environmental, social and governance (ESG) disclosure a mandatory requirement are on the rise. Firstly, the new corporate sustainability reporting standards being developed by the EU, which GRI is helping to co-construct, will contribute to the global convergence of reporting. Secondly, the IFRS Trustees have set out an intention to develop enterprise value standards, so that financial reporting is inclusive of the risks and opportunities presented by a company’s sustainability performance.

What global trends such as these signify is the importance of providing robust guidance to companies on how to effectively disclose their sustainability impacts, as enabled by the GRI Standards. We therefore commend the Nairobi Securities Exchange (NSE) for producing this new ESG guide, which will help Kenyan companies to be accountable for their impacts while increasing their competitiveness in the global marketplace.

GRI appreciates the opportunity to collaborate on this publication with the NSE and the African Securities Exchanges Association, and we acknowledge the support of the Swedish International Development Cooperation Agency. We look forward to continuing to work together in support of a sustainable future.

Peter Paul van de Wijs Chief External Affairs Officer Global Reporting Initiative (GRI)

Foreword � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 3

Abbreviations and Definitions of Terms � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 7

List of acronyms and abbreviations � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 7

Definitions of terms � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 7

Getting Started � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 8

Introduction � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 8

ESG Disclosures Guidance Manual � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 8

ESG and Investments � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 9

Expected Benefits For Listed Companies � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 9

Implementation Timelines � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 10

Primary References � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 10

Key steps in the ESG reporting process � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 13

Overview � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 13

Detailed description of the key steps � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 14

Step 1: Governance over ESG integration and reporting � � � � � � � � � � � � � � � � � � � � � � � 14

What is the role of the Board? � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 14

What is the role the Chief Executive Officer? � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 15

What is the role of the Sustainability Manager? � � � � � � � � � � � � � � � � � � � � � � � � � � � 15

1� Recruit ESG champions from across the organisation � � � � � � � � � � � � � � � � � � 15

2� Operationalise the management committee on ESG � � � � � � � � � � � � � � � � � � � 16

3� Gather and familiarise the reporting team with the ESG reporting requirements and resources � � � � � � � � � � � � � � � � � � � � � � � � 16

4� Raise awareness � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 16

5� Develop a project management plan � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 17

6� Conduct kick-off meetings � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 17

Step 2: Situational analysis and stakeholder engagement � � � � � � � � � � � � � � � � � � � � � � 17

Step 3: Materiality analysis � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 22

GRI guidance on identifying material topics � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 23

Additional guidance on materiality analysis � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 24

Step 4: Value creation � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 25

Opportunity assessment � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 25

Risk assessment � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 26

Performance disclosure � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 26

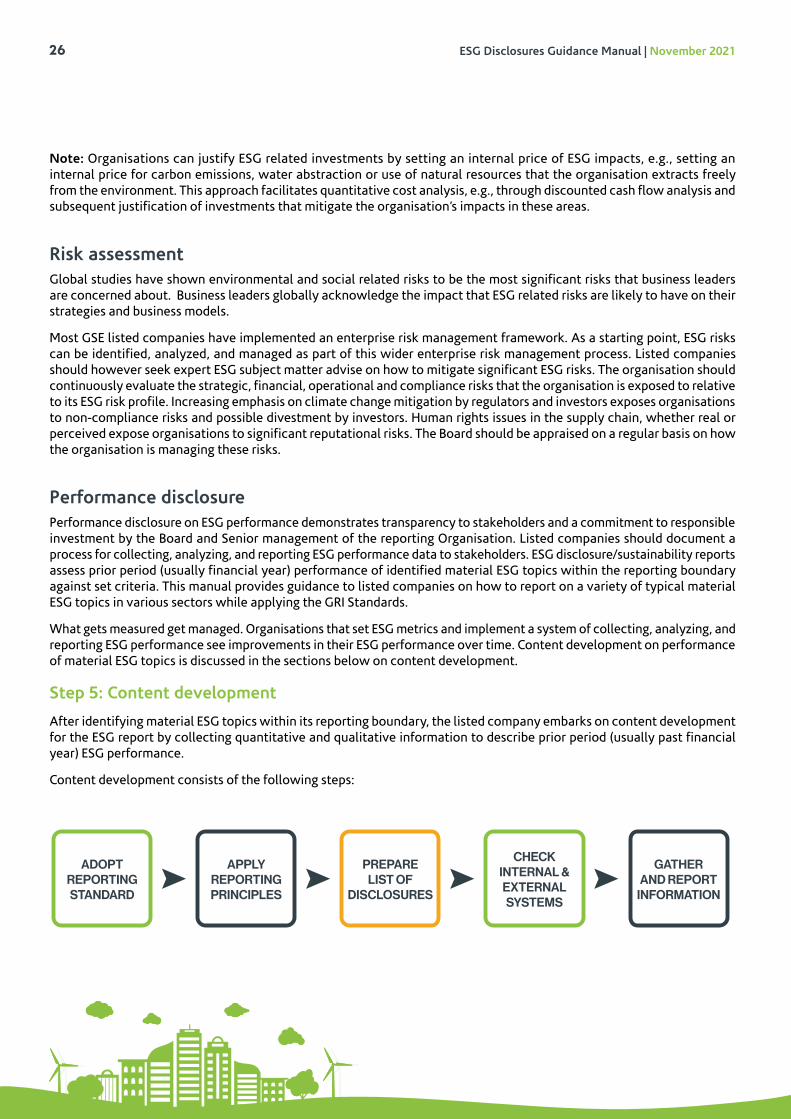

Step 5: Content development � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 26

Adopt reporting standard � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 27

Apply reporting principles � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 27

CONTENTS

Prepare list of disclosures � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 27

Mandatory ESG Disclosures � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 27

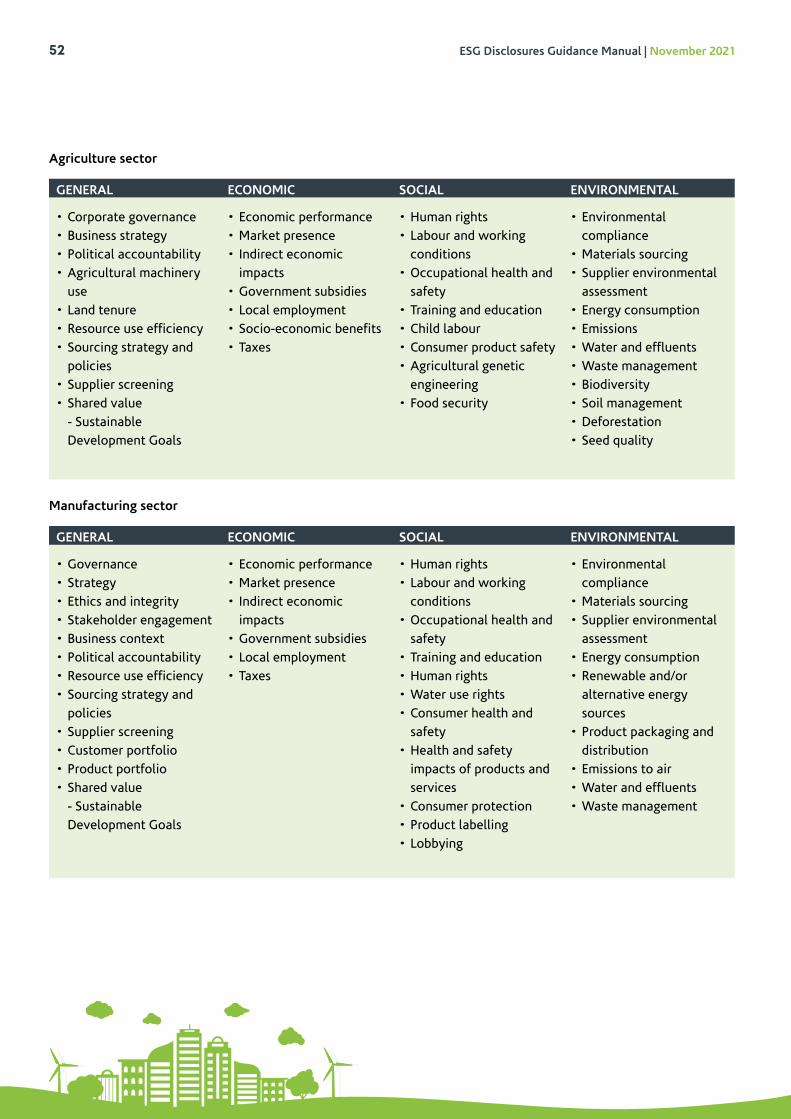

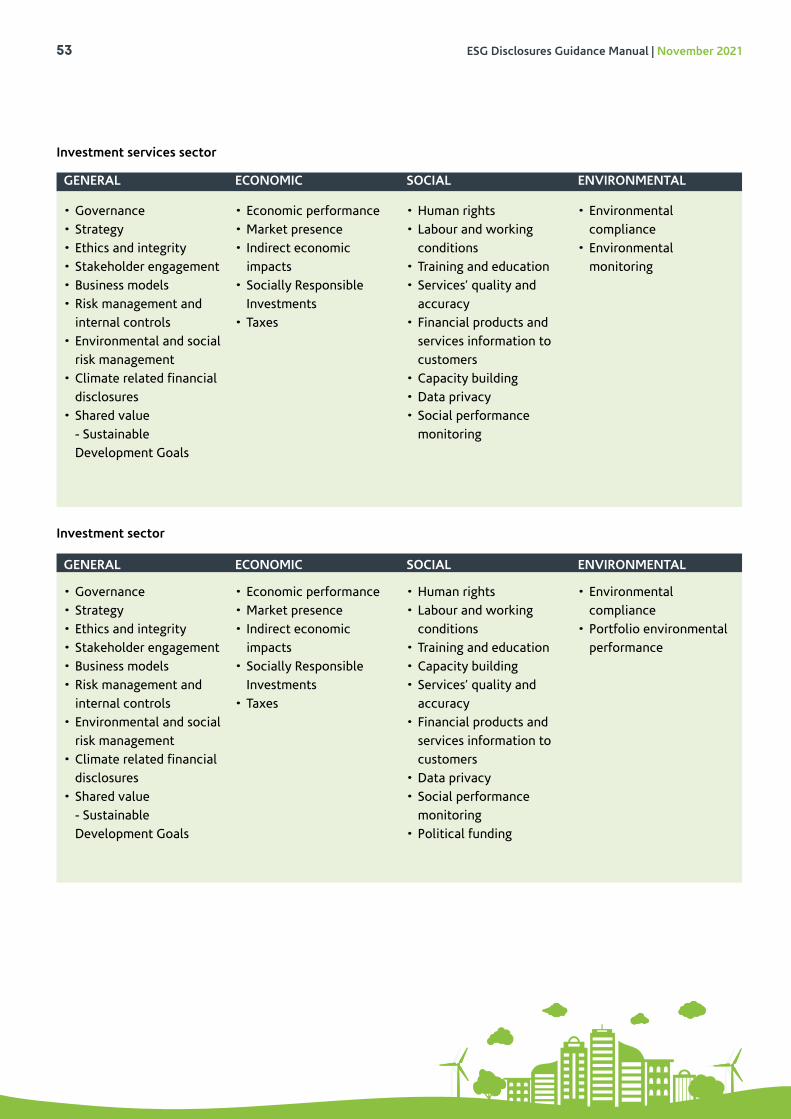

Sector Specific ESG Disclosures � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 28

Check internal and external data systems � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 29

Gather and report information � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 29

Examples of content on mandatory ESG topics � � � � � � � � � � � � � � � � � � � � � � � � � � � � 30

Step 6: Assurance and internal controls � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 31

External assurance � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 31

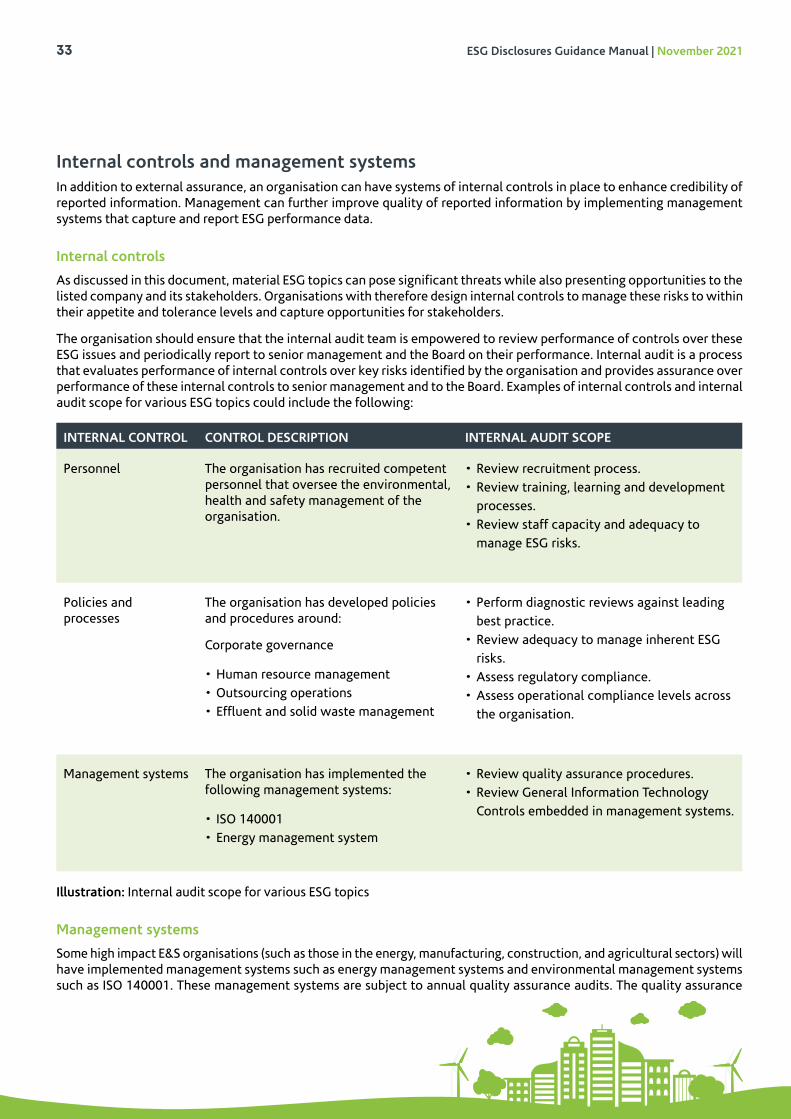

Internal controls and management systems � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 33

Internal controls � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 33

Management systems � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 33

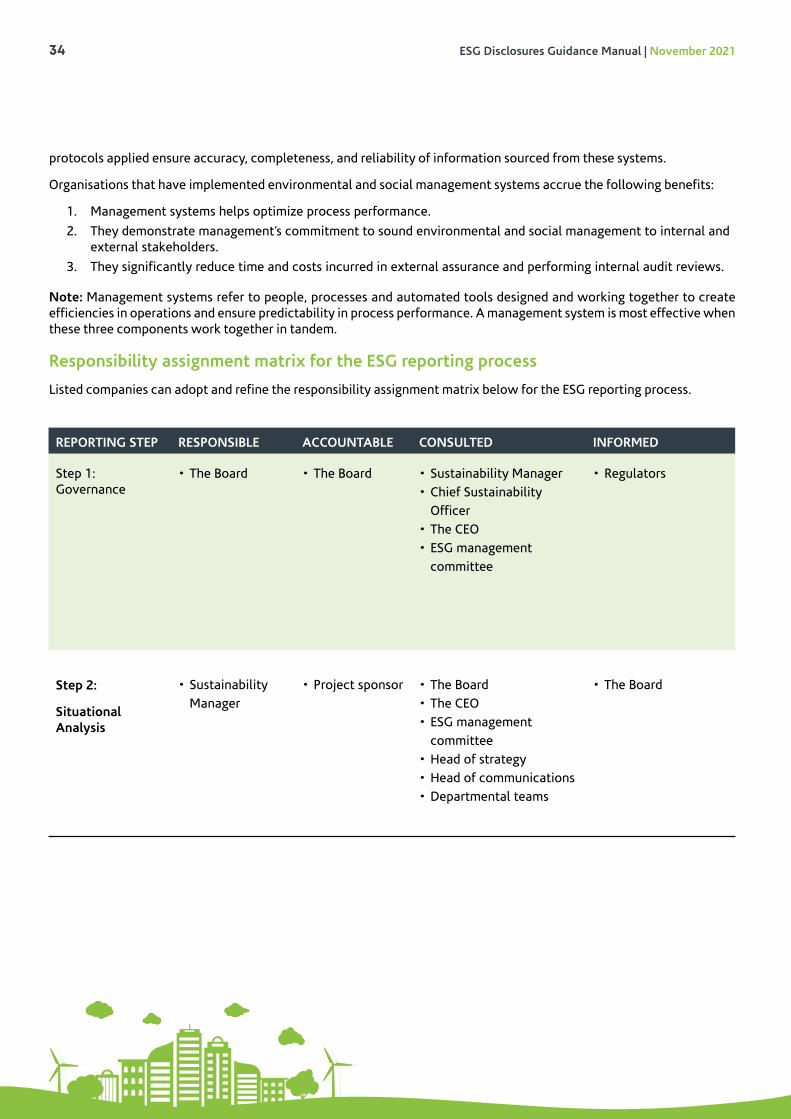

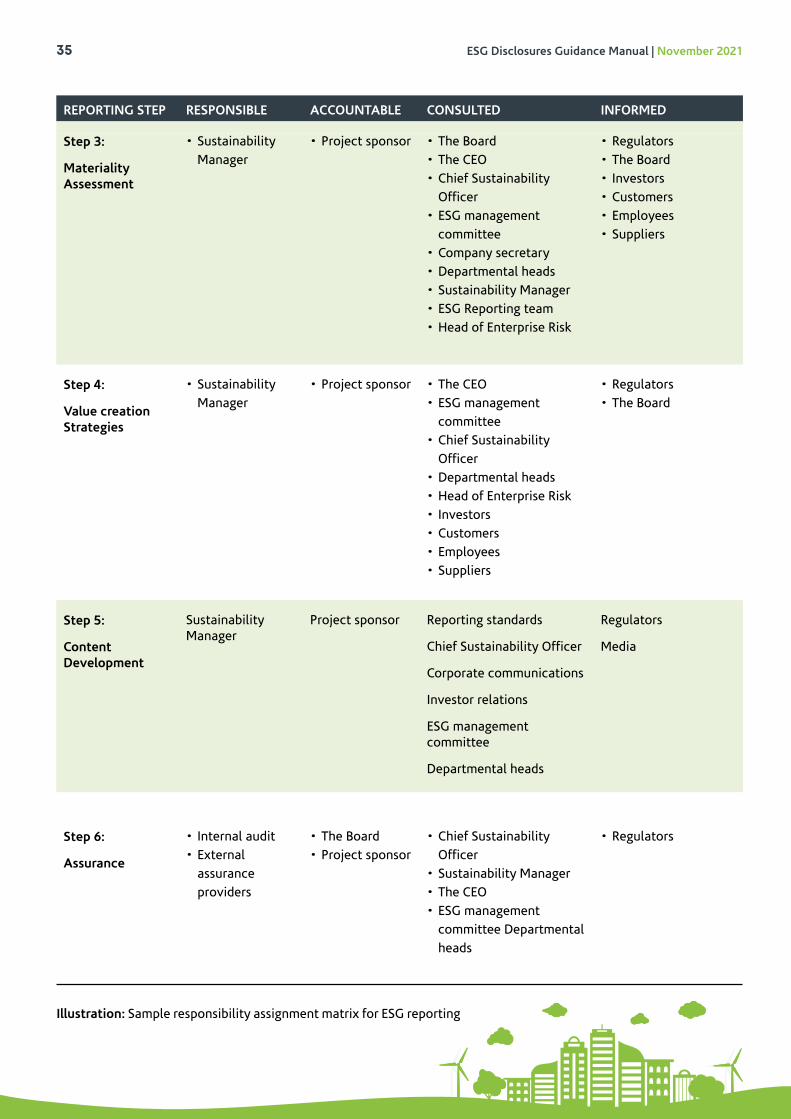

Responsibility assignment matrix for the ESG reporting process � � � � � � � � � � � � � � � � 34

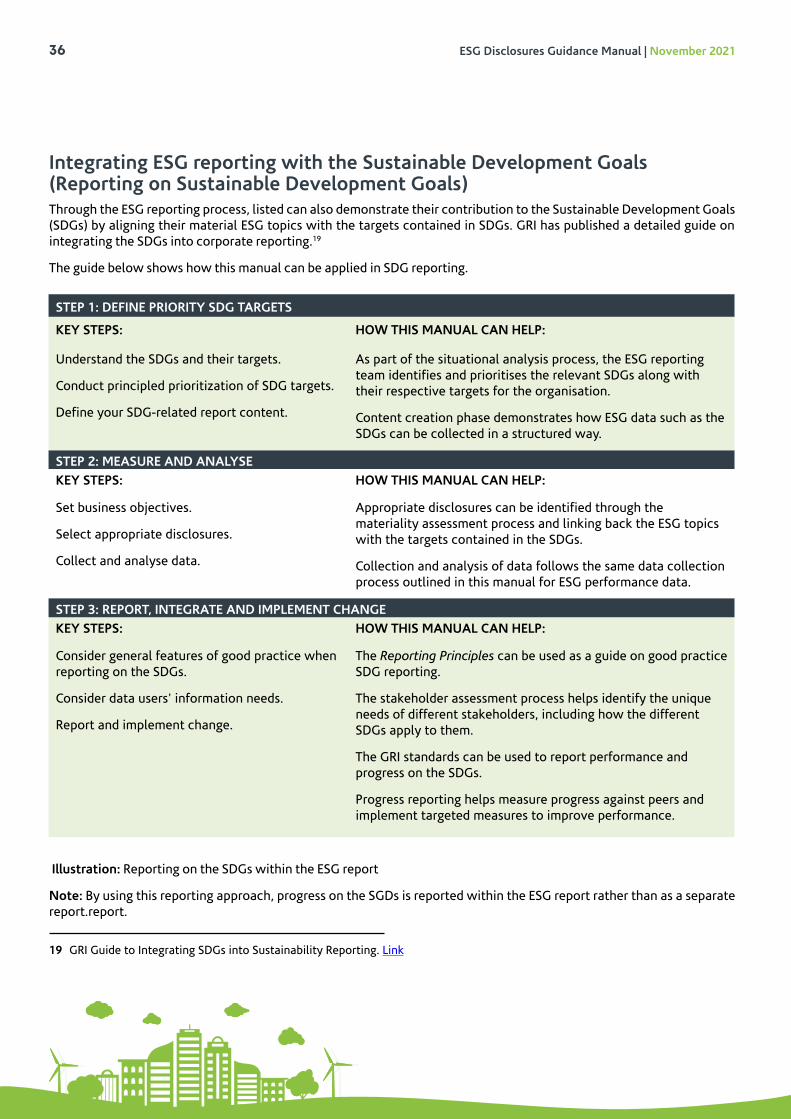

Integrating ESG reporting with the Sustainable Development Goals (Reporting on Sustainable Development Goals) � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 36

Publishing your ESG report � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 37

ESG reporting requirements from other organisations � � � � � � � � � � � � � � � � � � � � � � � � � � � 37

The Capital Markets Authority � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 38

Investor groups � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 38

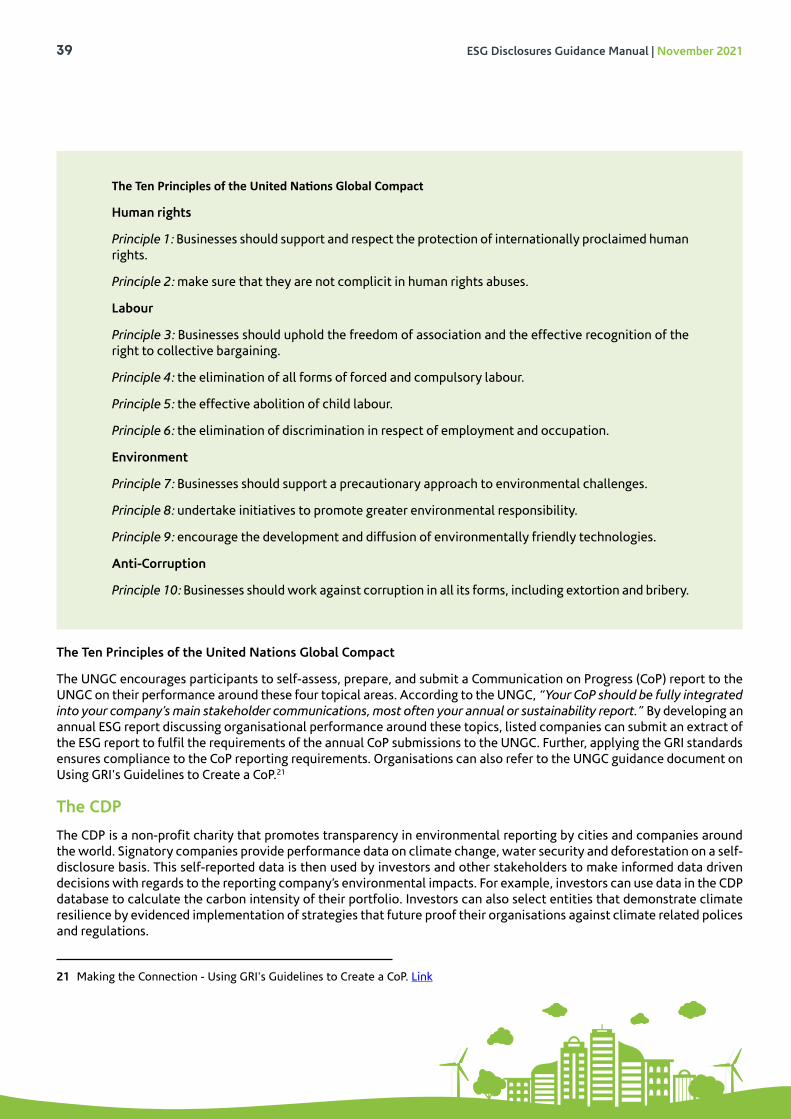

United Nations Global Compact � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 38

The CDP � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 39

Industry level reporting � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 40

Annexes � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 41

Annex 1: Sample outline framework for an ESG report � � � � � � � � � � � � � � � � � � � � � � � � 41

Introduction � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 41

Strategic Outlook, Governance and Ethics � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 41

Reporting boundary and approach to ESG reporting � � � � � � � � � � � � � � � � � � � � � � � � 41

Stakeholder engagement � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 41

Materiality analysis and ESG Impact � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 41

Assurance Statement � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 42

Annex 2: Data collection template (Quantitative and qualitative data) � � � � � � � � � � 43

Annex 3: Sample materiality assessment scoring model � � � � � � � � � � � � � � � � � � � � � � � 45

Annex 4: Stakeholder engagement strategies � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 46

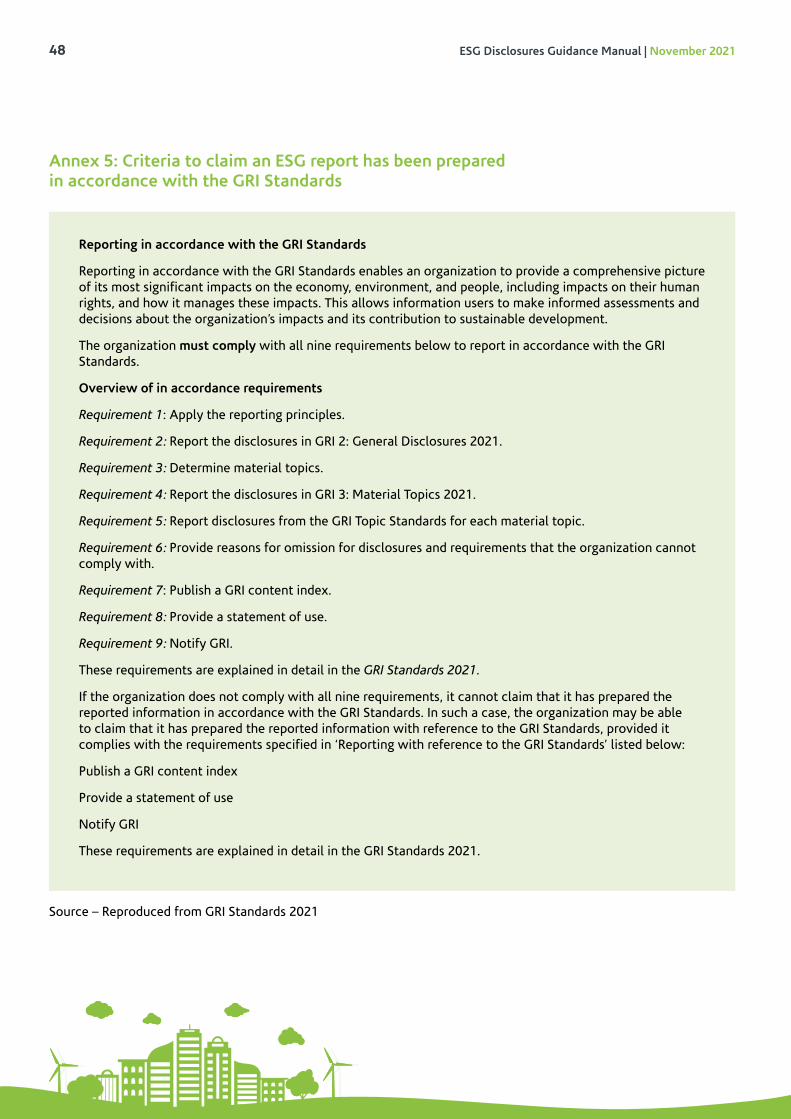

Annex 5: Criteria to claim an ESG report has been prepared in accordance with the GRI Standards � � � � � � � � � � � � � � � � � � � � � � � � � � � � � � 48

Annex 6: Sector specific ESG topics for NSE Listed Companies � � � � � � � � � � � � � � � � � 49

ESG Disclosures Guidance Manual | November 20217

Abbreviations and Definitions of Terms

List of acronyms and abbreviations

ABBREVIATION MEANING

CMA Capital Markets Authority

CoP Communication on Progress

DFI Development Finance Institution

ESG Environmental, Social and Governance

E&S Environmental and Social

ESMS Environmental and Social Management System

EMEA Europe, the Middle East, and Africa

GHG Greenhouse Gases

GRI Global Reporting Initiative

ISO International Organisation for Standardization

IFC International Finance Corporation

NEMA National Environmental Management Authority (Kenya)

NSE Nairobi Securities Exchange

SDG Sustainable Development Goals

SIDA Swedish International Development Cooperation Agency

SWOT Strengths, Weaknesses, Threats and Opportunities

UNGC United Nations Global Compact

Definitions of terms

TERM MEANING

CMA CodeThe Code of Corporate Governance Practices for Issuers of Securities to the Public issued by the Capital Markets Authority in 2015.

ESG Reporting

An organisation’s practice of reporting publicly on its economic, environmental, and/or social impacts, and hence its contributions – positive or negative – towards the goal of sustainable development. Also commonly referred to as sustainability reporting or non-financial reporting.

GRI Standards The Global Reporting Initiatives (GRI) Sustainability Reporting Standards, 2018.

Materiality assessmentThe process of prioritizing ESG topics for reporting and based on the assessed needs of different stakeholders.

Responsible investmentThe practice of capital allocation that considers the wider environmental and societal impact of the investment in addition to financial returns

Sustainable Development Goals

The Sustainable Development Goals (SDGs), also known as the Global Goals, were adopted by the United Nations in 2015 as a universal call to action to end poverty, protect the planet, and ensure that by 2030 all people enjoy peace and prosperity.

Value creationRefers to creating (and preserving) financial and societal value for stakeholders by developing strategies that manage material ESG risks and capture related opportunities.

ESG Disclosures Guidance Manual | November 20218

GETTING STARTED

Introduction

1 Global Reporting Initiative Standards 2021. Link2 UNPRI, 2018. Financial performance of ESG integration in US investing. Link3 S&P Global Market Intelligence - ESG funds beat out S&P 500 in 1st year of COVID-19. Link4 The Time has Come - The KPMG Survey on Sustainability Reporting 2020. Link

Global trends in assessment of corporate performance indicate a shift in focus from a one-dimensional view focusing on just financial performance to a more wholistic view on both financial and non-financial performance. To facilitate this assessment, organisations are required to disclose both financial and non-financial performance metrics to an increasingly diverse set of stakeholders. These stakeholders include - among others - investors, regulators, and customers keen to understand the wider economic, social, and environmental impacts the organisation has on society while in pursuit of shareholder value.

According to GRI, Sustainability Reporting is an Organisation’s practice of reporting publicly on its economic, environmental, and/or social impacts, and hence its contributions – positive or negative – towards the goal of sustainable development. Through this process, an Organisation identifies its significant impacts on the economy, the environment, and/or society and discloses them in accordance with a globally accepted standard.1

There is consensus that embedding ESG into organisational strategy, operations and performance management generates significant value to stakeholders and builds organisational resilience. Further, there is a growing body of evidence that good ESG performance is positively correlated with higher returns and financial performance. (2) (3) ESG integration is further enhanced and demonstrated through transparency in ESG performance disclosures to stakeholders.

ESG Disclosures Guidance ManualEngagement with listed companies in Kenya indicates a general awareness of ESG issues and corporate sustainability. There is however a need for sustained capacity building on how organisations can integrate ESG into their strategies and ultimately, how to report ESG performance in a consistent, transparent and principle-based approach that meets stakeholder expectations.

The focus of this document therefore is to illustrate and guide how listed companies in Kenya and other organisations interested in ESG reporting can collect, analyse, and publicly disclose important ESG information using an approach that meets international standards on sustainability reporting. This document can also act a guide on how to progressively integrate ESG in strategy, operations, and performance management.

To help reduce uncertainties on which framework or standards to apply, this manual recommends the adoption of the GRI Standards as the common framework for ESG reporting by listed companies in Kenya. According to a 2020 Global Survey on Sustainability reporting conducted by KPMG, the GRI Standards are the most widely used framework for sustainability reporting.4 Listed companies on the NSE that already report publicly on ESG performance have chosen the GRI standards as their preferred framework for ESG Reporting. Refer to Annex 5 for criteria to claim a report has been prepared in accordance with the GRI Standards.

A common set of ESG metrics has also been proposed for reporting by all listed companies. This is intended to help facilitate comparability of ESG performance of listed companies in Kenya – and especially where the common reporting framework has been adopted. Over time, and with improved maturity on ESG disclosures, stakeholders will be able to correlate financial performance with specific ESG indicators such diversity and air emissions, as well as compare the ESG performance of organisations reporting within the same sector. A responsible investment index is planned by the Nairobi Securities Exchange (NSE) in future.

ESG Disclosures Guidance Manual | November 20219

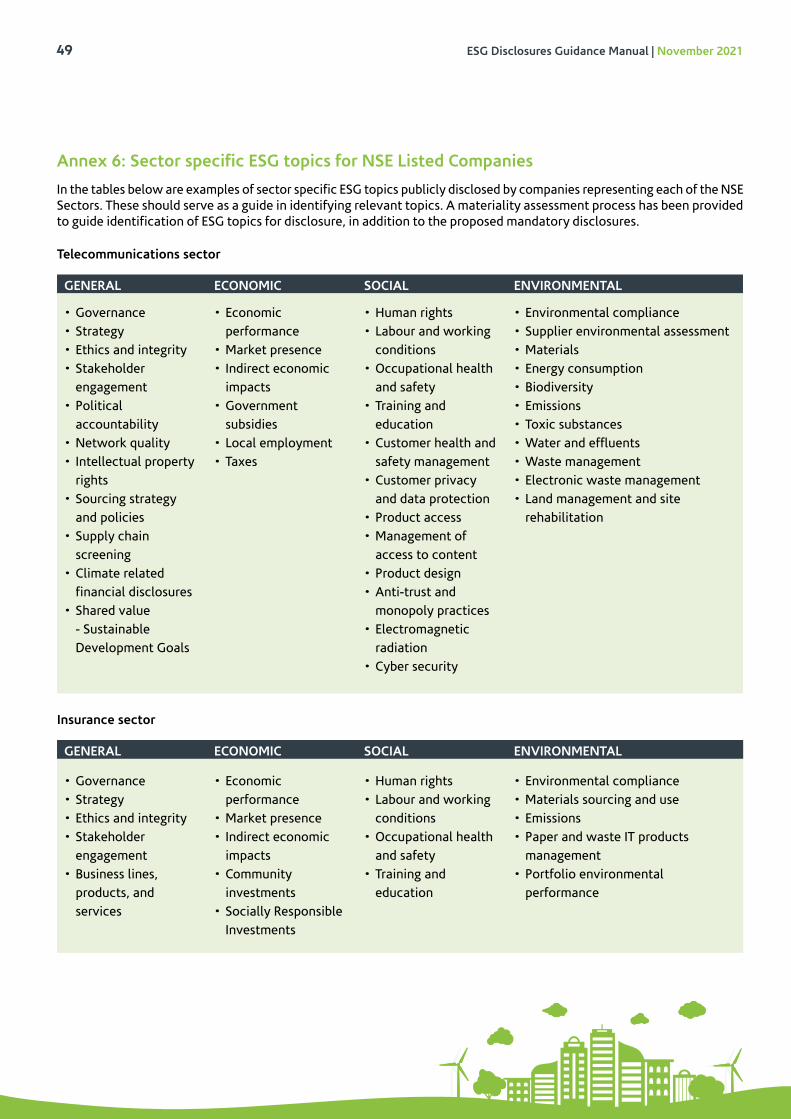

Examples of sector specific ESG disclosures have also been provided for reference by listed companies in Annex 6 of this manual.

Applying this document should also assist listed companies comply with reporting requirements for other organisations such as the CDP and UNGC. This manual also includes a guide on how to meet corporate governance reporting requirements contained in the CMA code.5

ESG and InvestmentsApplying ESG criteria in investment selection has gained momentum in recent years. This is a trend that is expected to continue. Along with national policies and directives, ESG considerations in investments has probably been the most important driving force for ESG integration and disclosure in capital markets. According to a survey done by IHS Markit,6 the top ESG metrics commonly sought by investors are:

• Presence of an overarching ESG policy.

• Assignment of ESG management responsibility.

• Corporate code of ethics

• Presence of litigation.

• People diversity.

• Net employee composition.

• Environmental policy.

• Estimation of carbon footprint.

• Data and cybersecurity incidents.

• Health and safety events.

According to a 2020 global survey by FTSE Russell,7 Sustainable Investment is now firmly part of the mainstream, with 81% of EMEA asset owners expressing interest in applying ESG considerations in investment criteria.

Expected Benefits For Listed Companies1. Transparency in ESG disclosures helps in building integrity and trust in the capital markets thus enhancing

competitiveness to attract investment to the capital markets. Adoption and promotion of ESG reporting by the NSE will enhance trust and integrity of the capital markets in Kenya by providing valuable information that is of increasing importance to investors, thus contributing to more efficient capital allocation. Some of the expected benefits of integrating and disclosing ESG performance by listed companies in Kenya include:

2. Investors can assess and preferentially invest in issuers that demonstrate better ESG linked financial performance, resulting in more efficient capital allocation.

3. Organisations that demonstrate responsible investment practices can access new sources of capital from sustainability conscious investors such as Development Finance Institutions (DFIs) and Private Equity firms.

4. A wholistic view of corporate value facilitates product innovation by enabling consideration and management of the embodied environmental and social impacts of products and services.

5. Measuring and reporting ESG performance enables organisations embed circularity in their operating models and achieve operational efficiencies by optimizing energy and raw costs in production.

5 The Code of Corporate Governance Practices for Issuers of Securities to the Public, 2015. Link6 IHS Markit - Top 10 ESG Metrics for Private Equity. Link7 Smart Sustainability: 2020 global survey findings from asset owners. Link

ESG Disclosures Guidance Manual | November 202110

6. Organisations that demonstrate additionality of ESG integration into their supply chains, production systems and service delivery can benefit from preferential access to new markets.

7. The ESG value creation framework helps organisations proactively address non-financial but critical environmental and social risks, thereby preserving and creating long term value for stakeholders.

8. ESG integration enhances regulatory compliance and helps anticipate the impact of future ESG related regulations and policies.

9. Organisations are perceived as responsible corporate citizens and achieve brand value enhancement by systematically identifying and responding to stakeholder needs and expectations.

Implementation TimelinesListed companies on the NSE are to report publicly on their ESG performance at least annually. The steps outlined in this ESG Disclosures Guidance Manual are expected to guide such reporting.

This manual is also available as a public good for other organisations that would be interested in ESG reporting.

Listed companies will have a grace period of one year from the issuance of these guidelines to interact and familiarize themselves with the ESG reporting steps contained in these guidelines. Thereafter, listed companies will be expected to include a sustainability/ESG report in their annual integrated reports containing - at minimum - the mandatory ESG disclosures discussed in Chapter 6 of this manual.

Issuers can also choose to publish a separate ESG/sustainability report.

Primary ReferencesThis document should be read and applied together with the following documents as primary references. Additional references are provided as footnotes in this document.

1. The Code of Corporate Governance Practices for Issuers of Securities to the Public, 2015 (Capital Markets Authority).

2. The Global Reporting Initiatives (GRI) Sustainability Reporting Standards.ESG reporting principles

ESG Disclosures Guidance Manual | November 202111

To ensure quality of reported information, ESG reports should abide by a set of reporting principles. Quality information enables information users to make sound assessments of the organisation’s impacts and aids in decision making.

Reporting Principles: Source – Reproduced from GRI Standards 20218

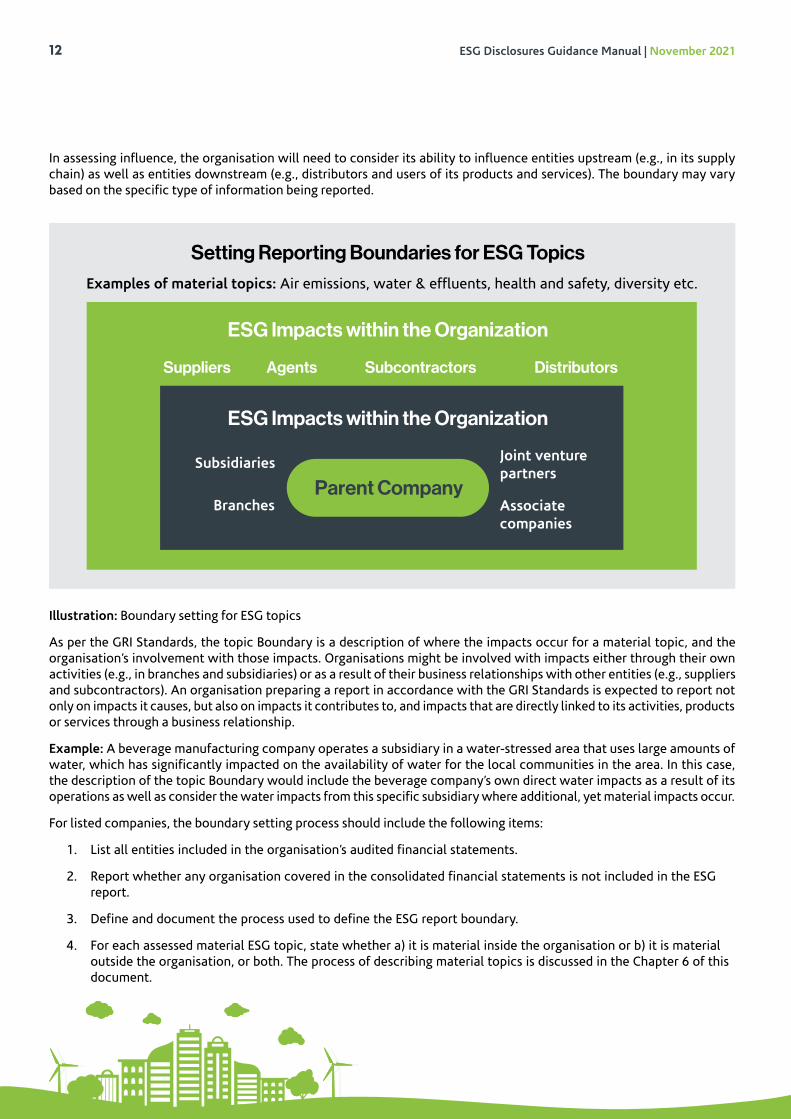

ESG REPORTING BOUNDARYIn accordance with the GRI Standards, ‘Boundary’ refers to the range of entities (e.g., subsidiaries, joint ventures, sub-contractors, etc.) whose performance is represented by the ESG disclosures report. Unless otherwise stated in the ESG report, the reporting boundary for the listed companies should at minimum include the financial reporting boundary. This is emphasized since investors and other stakeholders are interested in linkages between information publicly disclosed in annual financial reports and the listed company’s wider ESG impacts.

In setting the boundary for its report, an organisation must consider the range of entities over which it exercises control (often referred to as the ‘organisational boundary’, and usually linked to definitions used in financial reporting) and over which it exercises influence (often called the ‘operational boundary’).

8 GRI Standards 2021 - Link

The GRI Reporting Principles

The GRI has proposed a set of reporting principles to guide organizations in ensuring the quality and proper presentation of the reported information. The organization is required to apply the reporting principles to be able to claim that it has prepared information in accordance with the GRI Standards.

These principles are summarised below:

Accuracy - The organization shall report information that is factually correct and sufficiently detailed to enable the assessment of the organization’s impacts.

Balance - The organization shall report information in an unbiased way and provide a fair representation of the organization’s negative and positive impacts.

Clarity - The organization shall present information in a way that is accessible and understandable.

Comparability - The organization shall select, compile, and report information in a consistent manner, to enable the analysis of changes in the organization’s impacts over time and an analysis of these impacts relative to other organizations.

Completeness - The organization shall provide sufficient information to enable the assessment of the organization’s impacts during the reporting period.

Sustainability context - The organization shall report information about its impacts in the wider context of sustainable development.

Timeliness - The organization shall report information on a regular schedule and make it available in time for information users to make decisions.

Verifiability - The organization shall gather, record, compile, and analyze information in a way that the information can be examined to establish its quality.

For detailed guidance on how to apply the reporting principles, listed companies should refer to the GRI Standards 2021.

ESG Disclosures Guidance Manual | November 202112

In assessing influence, the organisation will need to consider its ability to influence entities upstream (e.g., in its supply chain) as well as entities downstream (e.g., distributors and users of its products and services). The boundary may vary based on the specific type of information being reported.

Illustration: Boundary setting for ESG topics

As per the GRI Standards, the topic Boundary is a description of where the impacts occur for a material topic, and the organisation’s involvement with those impacts. Organisations might be involved with impacts either through their own activities (e.g., in branches and subsidiaries) or as a result of their business relationships with other entities (e.g., suppliers and subcontractors). An organisation preparing a report in accordance with the GRI Standards is expected to report not only on impacts it causes, but also on impacts it contributes to, and impacts that are directly linked to its activities, products or services through a business relationship.

Example: A beverage manufacturing company operates a subsidiary in a water-stressed area that uses large amounts of water, which has significantly impacted on the availability of water for the local communities in the area. In this case, the description of the topic Boundary would include the beverage company’s own direct water impacts as a result of its operations as well as consider the water impacts from this specific subsidiary where additional, yet material impacts occur.

For listed companies, the boundary setting process should include the following items:

1. List all entities included in the organisation’s audited financial statements.

2. Report whether any organisation covered in the consolidated financial statements is not included in the ESG report.

3. Define and document the process used to define the ESG report boundary.

4. For each assessed material ESG topic, state whether a) it is material inside the organisation or b) it is material outside the organisation, or both. The process of describing material topics is discussed in the Chapter 6 of this document.

Setting Reporting Boundaries for ESG TopicsExamples of material topics: Air emissions, water & effluents, health and safety, diversity etc.

ESG Impacts within the Organization

ESG Impacts within the Organization

Suppliers Agents Subcontractors Distributors

Joint venture partners

Parent CompanyAssociate companies

Branches

Subsidiaries

ESG Disclosures Guidance Manual | November 202113

KEY STEPS IN THE ESG REPORTING PROCESS

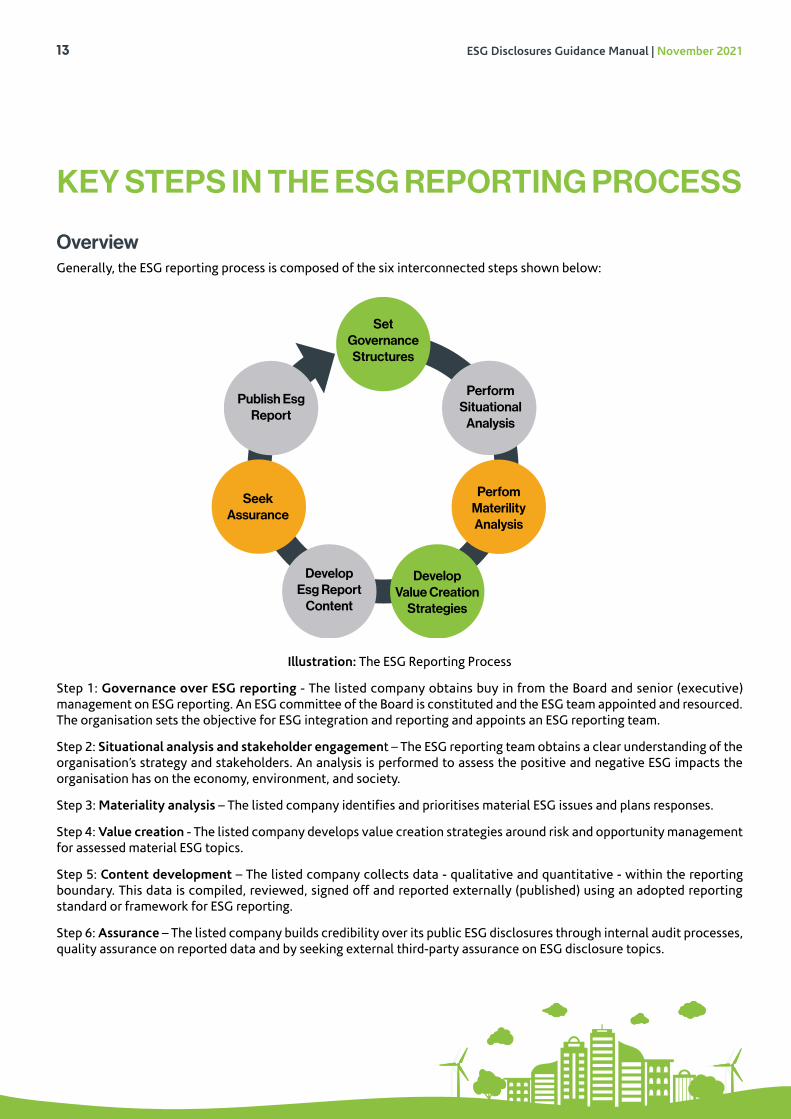

OverviewGenerally, the ESG reporting process is composed of the six interconnected steps shown below:

Illustration: The ESG Reporting Process

Step 1: Governance over ESG reporting - The listed company obtains buy in from the Board and senior (executive) management on ESG reporting. An ESG committee of the Board is constituted and the ESG team appointed and resourced. The organisation sets the objective for ESG integration and reporting and appoints an ESG reporting team.

Step 2: Situational analysis and stakeholder engagement – The ESG reporting team obtains a clear understanding of the organisation’s strategy and stakeholders. An analysis is performed to assess the positive and negative ESG impacts the organisation has on the economy, environment, and society.

Step 3: Materiality analysis – The listed company identifies and prioritises material ESG issues and plans responses.

Step 4: Value creation - The listed company develops value creation strategies around risk and opportunity management for assessed material ESG topics.

Step 5: Content development – The listed company collects data - qualitative and quantitative - within the reporting boundary. This data is compiled, reviewed, signed off and reported externally (published) using an adopted reporting standard or framework for ESG reporting.

Step 6: Assurance – The listed company builds credibility over its public ESG disclosures through internal audit processes, quality assurance on reported data and by seeking external third-party assurance on ESG disclosure topics.

Set Governance

Structures

Perform Situational

Analysis

Publish EsgReport

Perfom Materility Analysis

Seek Assurance

Develop Value Creation

Strategies

Develop Esg Report

Content

ESG Disclosures Guidance Manual | November 202114

Step 7: Publish ESG report – The listed company publishes its final ESG report on its website, social media, and/or avails printed copies to stakeholders. Publishing the ESG report is covered in more detail in Chapter 8 of this document.

The ESG reporting process delivers an annual ESG report. Since the intended deliverable is clearly defined, the ESG reporting process is best projectized, i.e., implemented within a project management framework.

Detailed description of the key steps

Step 1: Governance over ESG integration and reporting

Sustainability integration into business strategies is a core component of good corporate governance practices. ESG issues pose significant business continuity and long-term viability risks for the organisation. They also present significant opportunities for shareholder value creation. It is the responsibility of the Board and senior management to ensure that a process exists to identify, assess and manage ESG related risks and opportunities in the organisation. The Board retains overall accountability for ESG performance and disclosure to stakeholders.holders.

What is the role of the Board?The Board, on behalf of shareholders and other stakeholders is expected to ensure that the long-term sustainability of the organisation is assured and is demonstrated through senior management’s decisions on operational aspects of the business. The Board holds the CEO and senior management to account on corporate sustainability performance as a fiduciary responsibility to stakeholders.

Policy enablers on the expected role of the Board in corporate sustainability in Kenya include:

1. The Kenya Companies Act requires company directors to review environmental, social and community issues that my affect the future development, performance, and position of the company.9

2. The Code of Corporate Governance Practices for Issuers of Securities to the Public, 2015 requires companies to put in place environmental, social and governance (ESG) frameworks and proposes public disclosure of ESG performance in annual reports.

3. The Mwongozo Code of Governance for State Corporations requires the Board to ensure that the strategy of the organisation is aligned to the long-term goals of the organisation on sustainability so as not to compromise the ability of future generations to meet their own needs. The Board should also monitor the organisation’s performance and ensure sustainability.10

To facilitate integration of ESG into strategy, operations and performance management, the Boards of listed companies will form a committee of the Board that oversees sustainability matters in the organisation, including the ESG reporting process. Where a separate committee might not be feasible, the sustainability committee could sit within the strategy committee of the board – but with clear ESG related terms of reference. The board can consider additional guidance on the composition and functions of a sustainability committee from the Social and Ethics committee requirements for South African Companies. (11)(12)

The Board will also task the CEO to appoint and resource a focal point for sustainability within the organisation, otherwise referred to in this document as the Sustainability Manager. Some organisations have set up the role/function of a Chief Sustainability Officer/ Sustainability Director.13

9 The Companies Act, 2017 of Kenya – Section 655 on Directors reports. Link10 Mwongozo – The Code of Governance for State Corporations. Chapter 1 on Board of Directors. Link11 The Social and Ethics Committee - Section 72 of the Companies Act, 2008 of South Africa. Link12 The Social and Ethics Committee Handbook – A Guidebook for South African Companies. Link 13 The Chief sustainability Officer: Organizational strategist and futurist. Link

ESG Disclosures Guidance Manual | November 202115

What is the role the Chief Executive Officer?The CEO provides sponsorship for the ESG reporting process, key of which is appointing and resourcing the Sustainability Manager for the organisation. The Sustainability Manager is responsible for tactically leading the ESG reporting process. Ideally, this person is also the Head of Sustainability and is part of the senior management in the organisation.

To ensure ESG integration in the organisation, the CEO should:

1. Routinely engage with internal and external stakeholders to assess needs and address concerns.

2. Assess materiality of ESG topics in the context of the business and its stakeholders.

3. Set policies and directives to guide management of material ESG issues.

4. Design ESG metrics and evaluate these as part of routine organisational performance management.

5. Ensure a capacity building plan is in place to create awareness of current and emerging ESG topics and build competencies in ESG management.

6. Foster and embed a sustainability culture within the organisation by:

7. Appointing and sufficiently resourcing the Sustainability Manager

8. Developing and approving an annual ESG implementation plan for the organisation.

9. Demonstrating consideration of ESG factors in strategic decision making, e.g., in market entry, product design and recruitment decisions.

10. Disclosing ESG performance to stakeholders on an annual basis.

Chair the management committee on ESG. This committee should be composed of the CEO, the Sustainability Manager and heads of department from across the organisation.

What is the role of the Sustainability Manager?The Sustainability Manager is the focal point and primary contact for the ESG reporting exercise. The Sustainability Manager owns the reporting process, scope and timelines and is responsible for communicating progress to the executive team and to the CEO/project sponsor.

To kickstart the ESG reporting process, the Sustainability Manager should:

1� Recruit ESG champions from across the organisation

ESG reporting is a multidisciplinary undertaking. The Sustainability Manager should work with senior management to identify ESG champions from across the organisation. Ideally, every department should be represented by a person with decision making ability. This person can delegate tactical responsibilities such as data collection to a member of their department. They however retain full accountability for information related to their department.

ESG Disclosures Guidance Manual | November 202116

2� Operationalise the management committee on ESG

The Sustainability manager is responsible for the operations of the management committee on ESG. This committee is chaired by the CEO and its membership is drawn from heads of department from across the organisation. Ideally, this committee should sit quarterly to discuss ESG related objectives, milestones and the ESG reporting process. The roles of the management committee on ESG should include:

1. Setting the organisational ESG strategy in liaison with the Board and the CEO.

2. Ensuring the development of enabling polices and guidelines across the organisation to facilitate implementation of the ESG strategy.

3. Assessing how current ESG issues are likely to impact organisational performance, including monitoring ESG metrics and taking appropriate decisions.

4. Monitoring and reviewing the impact to the organisation of current trends, regulations and international standards on ESG.

5. Engagement with other management committees to discuss cross cutting themes such as human rights and identification of ESG risks and opportunities.

6. Making recommendations to the Board on ESG matters, including resourcing, ESG investments, and performance management.

7. Acting as a gate point in the ESG reporting process.

The Sustainability Manager will be responsible for coordinating the activities of the management committee on ESG.

3� Gather and familiarise the reporting team with the ESG reporting requirements and resources

The Sustainability Manager should ensure that the reporting team has a clear understanding of the ESG reporting process. The ESG reporting team should obtain and familiarise themselves with the following documents that form the basis of and provide guidance on sustainability reporting:

1. Organisational strategy document.

2. Stakeholder engagement guidelines (can be obtained from communications and investor relations teams).

3. The CMA Code.

4. The GRI Standards.

5. ESG Disclosure Guidance Manual for Listed Entities in Kenya (this document).

4� Raise awareness

The Sustainability Manager and project sponsor (CEO) should work towards obtaining sufficient buy-in from the executive team and the Board on the ESG reporting process.

The ESG reporting team is tasked with raising awareness in their own areas of operation on the business and societal case for ESG integration and reporting. They are also responsible for working with the departmental heads to implement any initiatives and recommendations that are generated from the ESG reporting process.

While various forms of ESG reporting could be mandated by policy and regulations, the best approach in seeking buy-in is to develop a quantified business case for ESG integration in the organisation.

ESG Disclosures Guidance Manual | November 202117

5� Develop a project management plan

The Sustainability Manager should develop a project management plan that culminates in a published ESG report. The project management plan should contain:

1. The business and societal case for ESG integration and reporting.

2. The ESG reporting process.

3. The ESG reporting team (internal and external).

4. The reporting boundary and scope of material issues for reporting.

5. The standard and framework identified for reporting – in this case, the standard should be the GRI Standards.

6. Project timelines – should be same as financial reporting timelines for reporting companies.

7. Internal and external stakeholders that will be engaged in the reporting process.

8. Communication plan.

9. Budget allocation.

10. Key measures of success.

11. Project review – an analysis of outcomes, lessons learnt and planning for the next reporting cycle.

6� Conduct kick-off meetings

The Sustainability Manager should facilitate kick-off meetings with internal and external stakeholders. The objective of the kick-off meeting is to familiarise stakeholders with the project management plan, important milestones in the ESG reporting process and to assign roles and responsibilities. External consultants and other identified external stakeholders e.g., publishing houses can be invited into the kick-off meetings. The Sustainability Manager will also use this opportunity to clarify any issues and set out expectations of all stakeholders involved in the reporting process.

Step 2: Situational analysis and stakeholder engagement

Situational analysis is a process by which an organisation’s internal and external environment is analysed in order to evaluate its current and potential capabilities to build stakeholder value. In the ESG reporting context, a situational analysis is performed to achieve the following:

1. An understanding of the organisation’s strategy.

2. An understanding of the organisation’s internal and external stakeholders and their respective needs or expectations of the organisation.

3. An assessment of the value that ESG integration brings (potentially) to the organisation.

The ESG reporting team should work with the organisational strategy team to understand the key strategic priorities of the business. The team should obtain a good enough understanding of the financial ambition, key products and markets and the business & operating model of the listed company.

SDGs progress reporting: As part of the situational analysis, the ESG reporting team can work with senior management and departmental heads to prioritise the most relevant Sustainable Development Goals (SDGs) for the organisation. A key emphasis of the SGDs is creating shared value (value to the business and to society) within the organisation’s own core operations. The reporting process illustrated in this manual can be used to report progress on the SDGs within the ESG report. The GRI has developed a practical guide14 on how to report on the SDGs.

ESG reports target at a wider set of stakeholders compared to financial reporting. Stakeholder analysis, prioritization and engagement is therefore a critical step in the ESG reporting process to ensure that the ESG report meets the needs of these diverse sets of stakeholders.

14 Integrating the SDGs into Corporate Reporting: A Practical Guide. Link

ESG Disclosures Guidance Manual | November 202118

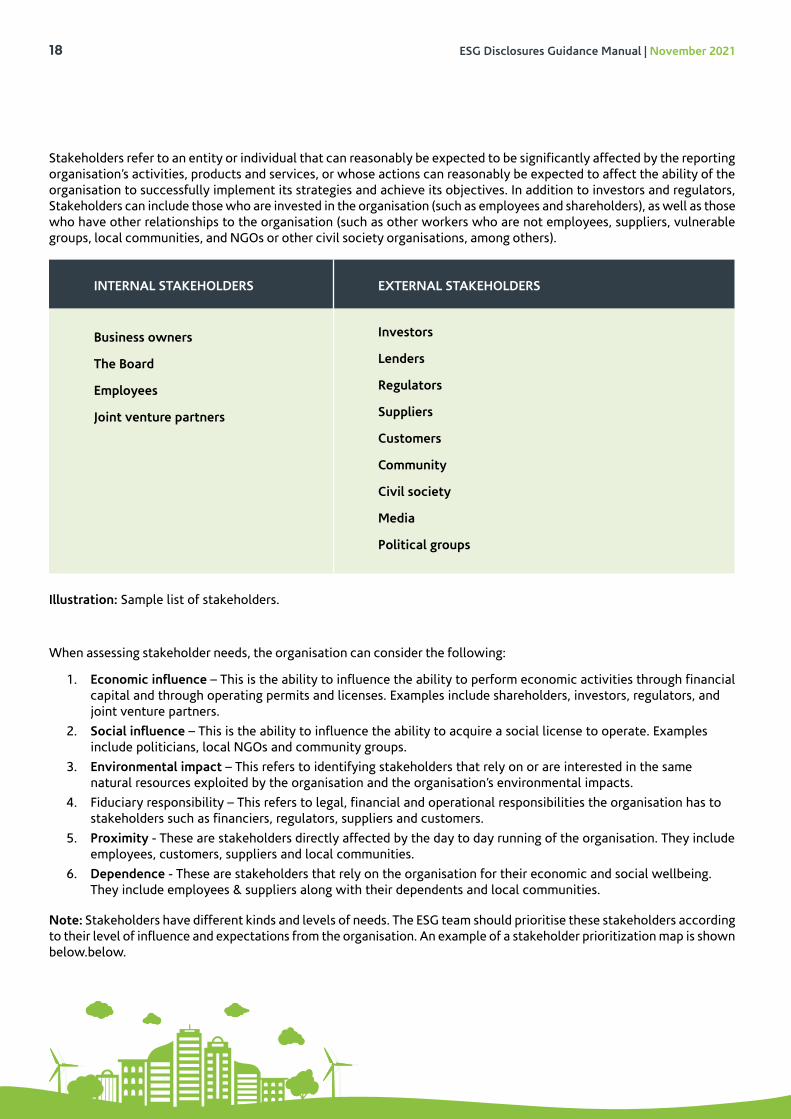

Stakeholders refer to an entity or individual that can reasonably be expected to be significantly affected by the reporting organisation’s activities, products and services, or whose actions can reasonably be expected to affect the ability of the organisation to successfully implement its strategies and achieve its objectives. In addition to investors and regulators, Stakeholders can include those who are invested in the organisation (such as employees and shareholders), as well as those who have other relationships to the organisation (such as other workers who are not employees, suppliers, vulnerable groups, local communities, and NGOs or other civil society organisations, among others).

Illustration: Sample list of stakeholders.

When assessing stakeholder needs, the organisation can consider the following:

1. Economic influence – This is the ability to influence the ability to perform economic activities through financial capital and through operating permits and licenses. Examples include shareholders, investors, regulators, and joint venture partners.

2. Social influence – This is the ability to influence the ability to acquire a social license to operate. Examples include politicians, local NGOs and community groups.

3. Environmental impact – This refers to identifying stakeholders that rely on or are interested in the same natural resources exploited by the organisation and the organisation’s environmental impacts.

4. Fiduciary responsibility – This refers to legal, financial and operational responsibilities the organisation has to stakeholders such as financiers, regulators, suppliers and customers.

5. Proximity - These are stakeholders directly affected by the day to day running of the organisation. They include employees, customers, suppliers and local communities.

6. Dependence - These are stakeholders that rely on the organisation for their economic and social wellbeing. They include employees & suppliers along with their dependents and local communities.

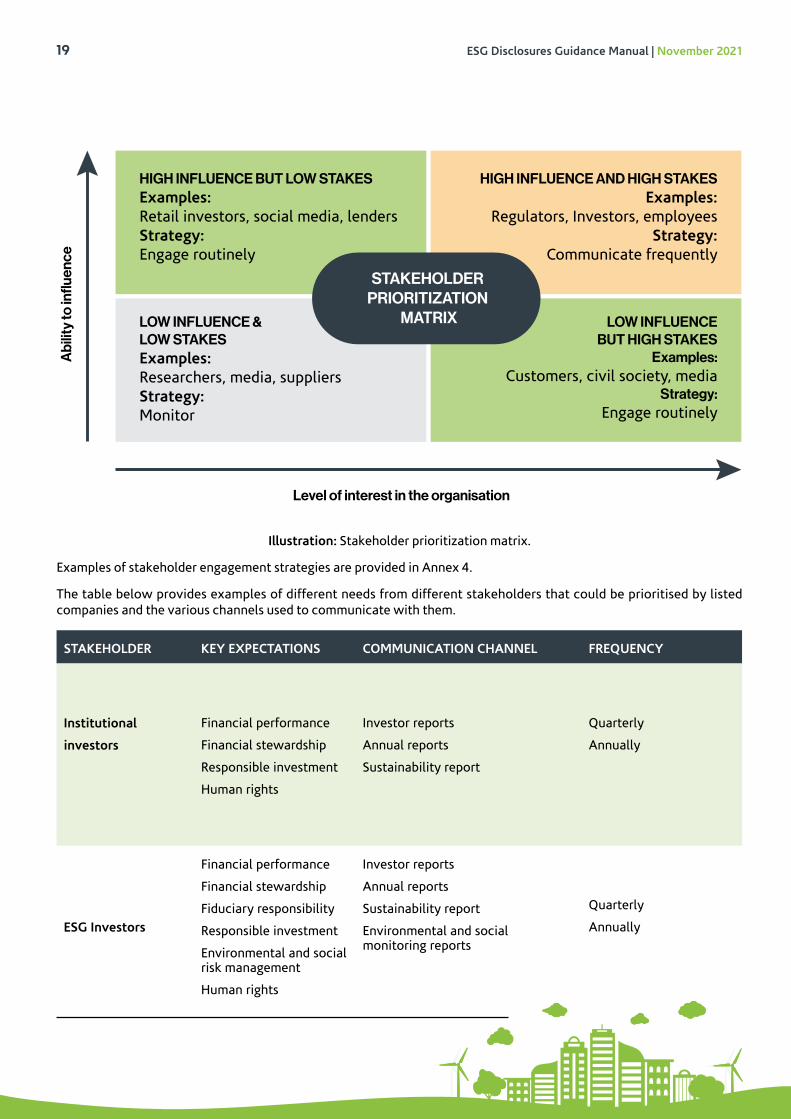

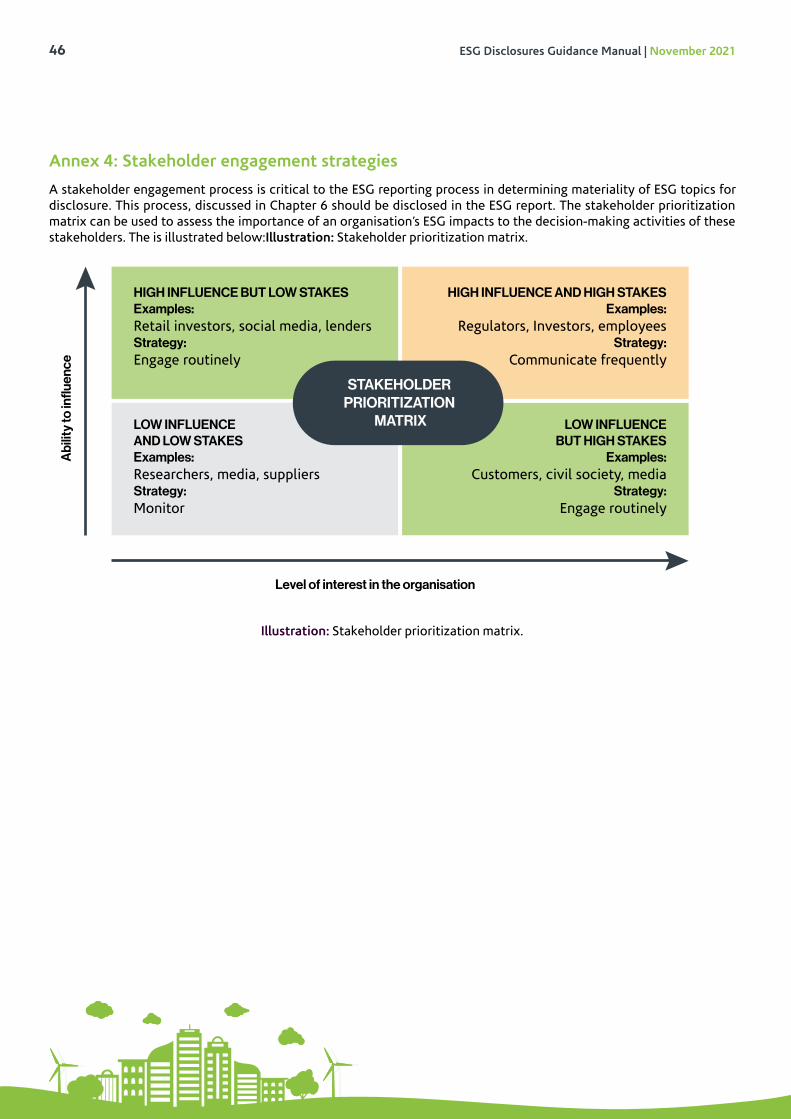

Note: Stakeholders have different kinds and levels of needs. The ESG team should prioritise these stakeholders according to their level of influence and expectations from the organisation. An example of a stakeholder prioritization map is shown below.below.

INTERNAL STAKEHOLDERS EXTERNAL STAKEHOLDERS

Business owners

The Board

Employees

Joint venture partners

Investors

Lenders

Regulators

Suppliers

Customers

Community

Civil society

Media

Political groups

ESG Disclosures Guidance Manual | November 202119

Illustration: Stakeholder prioritization matrix.

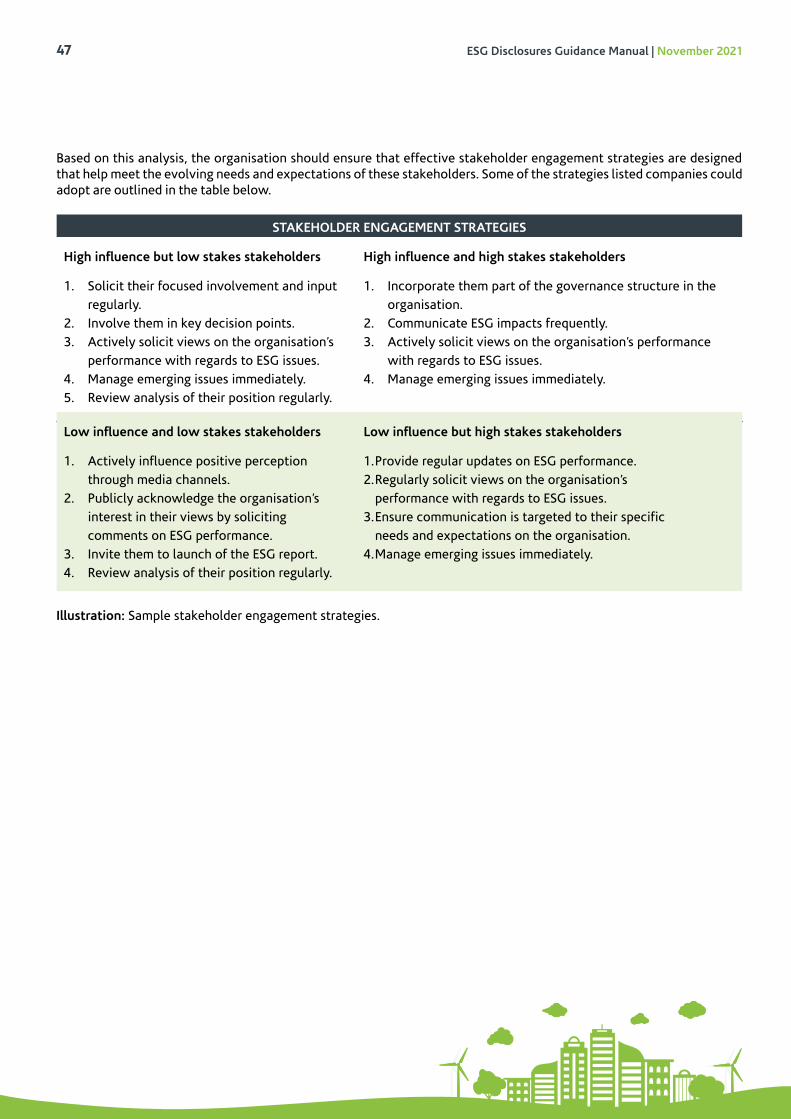

Examples of stakeholder engagement strategies are provided in Annex 4.

The table below provides examples of different needs from different stakeholders that could be prioritised by listed companies and the various channels used to communicate with them.

HIGH INFLUENCE BUT LOW STAKESExamples: Retail investors, social media, lendersStrategy: Engage routinely

HIGH INFLUENCE AND HIGH STAKESExamples:

Regulators, Investors, employeesStrategy:

Communicate frequently

LOW INFLUENCE &LOW STAKESExamples: Researchers, media, suppliersStrategy: Monitor

LOW INFLUENCE BUT HIGH STAKES

Examples: Customers, civil society, media

Strategy: Engage routinely

STAKEHOLDER PRIORITIZATION

MATRIX

Abi

lity

to in

fluen

ce

Level of interest in the organisation

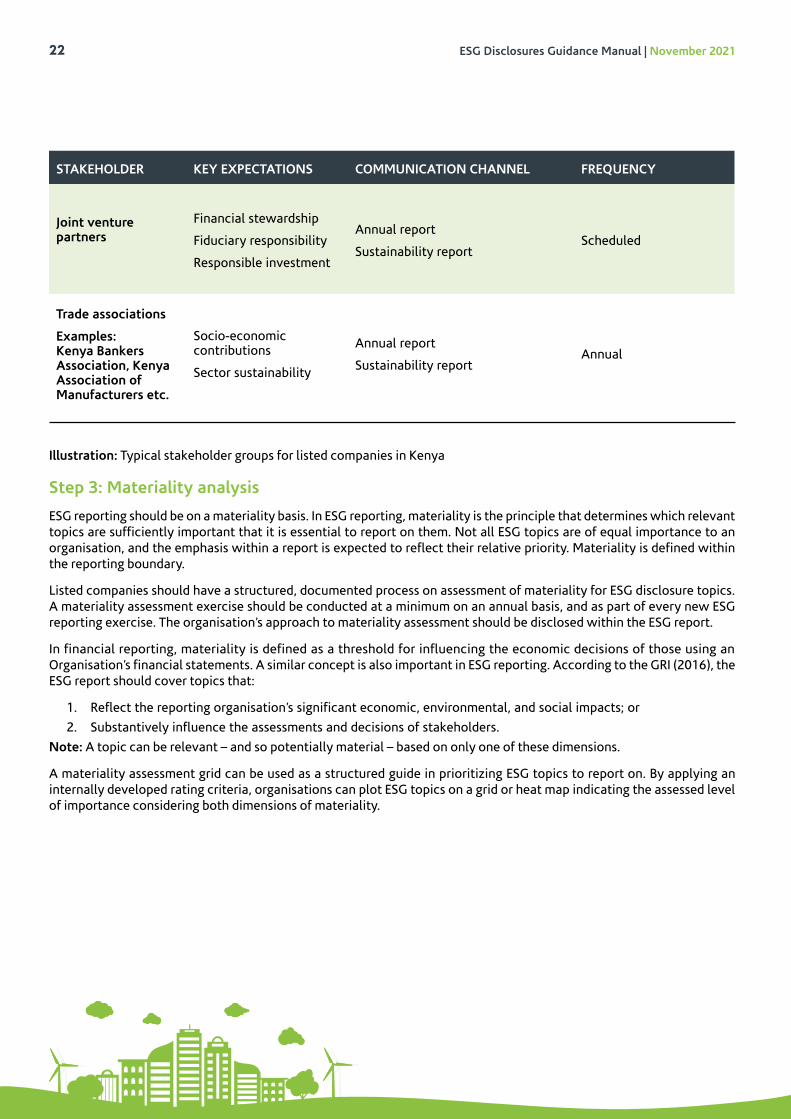

STAKEHOLDER KEY EXPECTATIONS COMMUNICATION CHANNEL FREQUENCY

Institutional

investors

Financial performance

Financial stewardship

Responsible investment

Human rights

Investor reports

Annual reports

Sustainability report

Quarterly

Annually

ESG Investors

Financial performance

Financial stewardship

Fiduciary responsibility

Responsible investment

Environmental and social risk management

Human rights

Investor reports

Annual reports

Sustainability report

Environmental and social monitoring reports

Quarterly

Annually

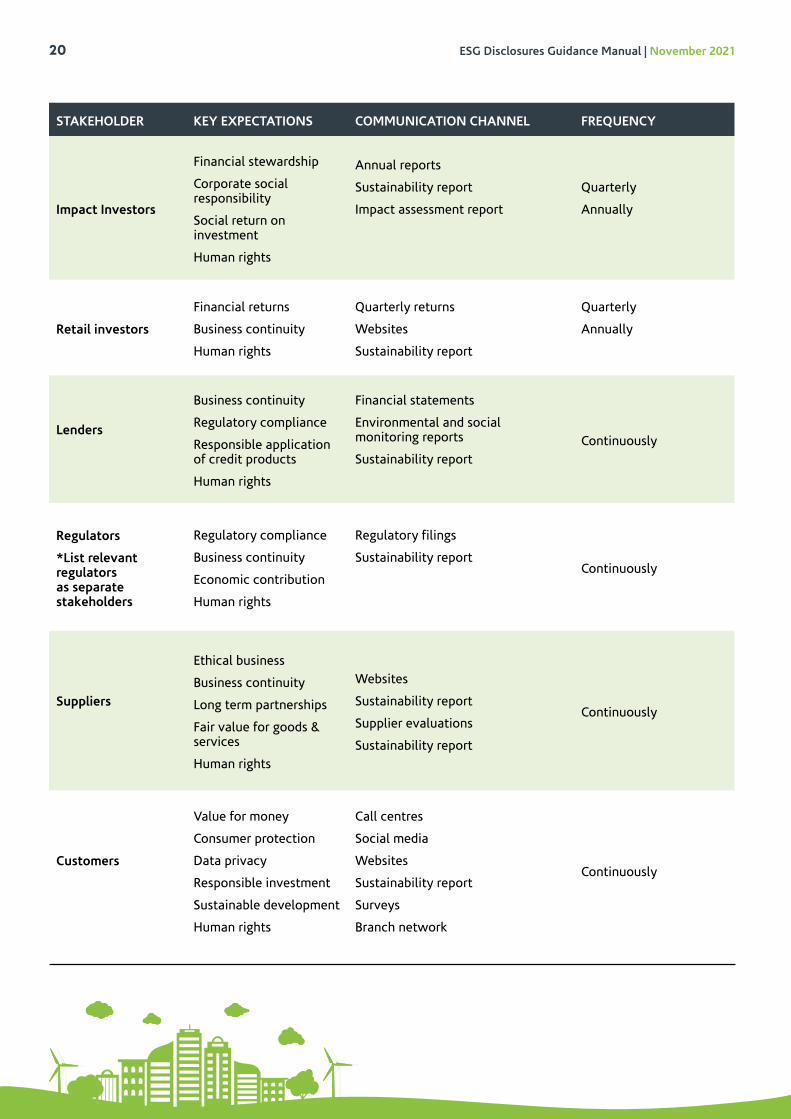

ESG Disclosures Guidance Manual | November 202120

STAKEHOLDER KEY EXPECTATIONS COMMUNICATION CHANNEL FREQUENCY

Impact Investors

Financial stewardship

Corporate social responsibility

Social return on investment

Human rights

Annual reports

Sustainability report

Impact assessment report

Quarterly

Annually

Retail investors

Financial returns

Business continuity

Human rights

Quarterly returns

Websites

Sustainability report

Quarterly

Annually

Lenders

Business continuity

Regulatory compliance

Responsible application of credit products

Human rights

Financial statements

Environmental and social monitoring reports

Sustainability reportContinuously

Regulators

*List relevant regulators as separate stakeholders

Regulatory compliance

Business continuity

Economic contribution

Human rights

Regulatory filings

Sustainability reportContinuously

Suppliers

Ethical business

Business continuity

Long term partnerships

Fair value for goods & services

Human rights

Websites

Sustainability report

Supplier evaluations

Sustainability report

Continuously

Customers

Value for money

Consumer protection

Data privacy

Responsible investment

Sustainable development

Human rights

Call centres

Social media

Websites

Sustainability report

Surveys

Branch network

Continuously

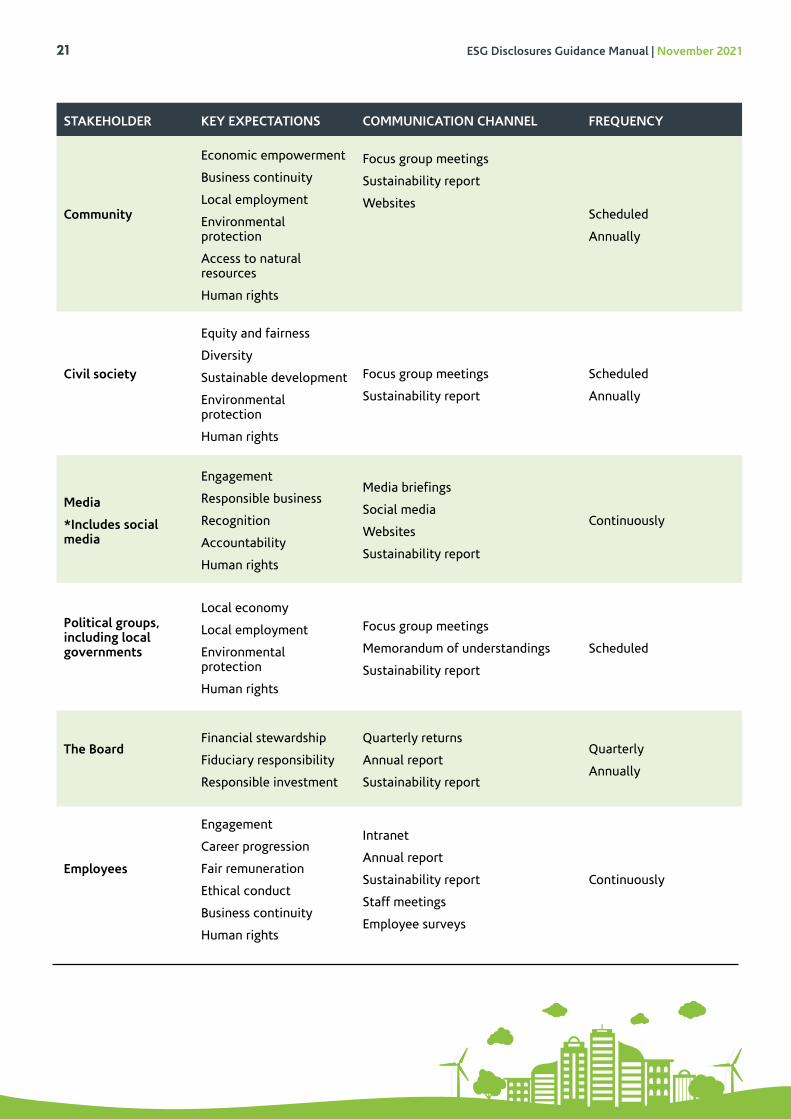

ESG Disclosures Guidance Manual | November 202121

STAKEHOLDER KEY EXPECTATIONS COMMUNICATION CHANNEL FREQUENCY

Community

Economic empowerment

Business continuity

Local employment

Environmental protection

Access to natural resources

Human rights

Focus group meetings

Sustainability report

WebsitesScheduled

Annually

Civil society

Equity and fairness

Diversity

Sustainable development

Environmental protection

Human rights

Focus group meetings

Sustainability report

Scheduled

Annually

Media

*Includes social media

Engagement

Responsible business

Recognition

Accountability

Human rights

Media briefings

Social media

Websites

Sustainability report

Continuously

Political groups, including local governments

Local economy

Local employment

Environmental protection

Human rights

Focus group meetings

Memorandum of understandings

Sustainability report

Scheduled

The BoardFinancial stewardship

Fiduciary responsibility

Responsible investment

Quarterly returns

Annual report

Sustainability report

Quarterly

Annually

Employees

Engagement

Career progression

Fair remuneration

Ethical conduct

Business continuity

Human rights

Intranet

Annual report

Sustainability report

Staff meetings

Employee surveys

Continuously

ESG Disclosures Guidance Manual | November 202122

Illustration: Typical stakeholder groups for listed companies in Kenya

Step 3: Materiality analysis

ESG reporting should be on a materiality basis. In ESG reporting, materiality is the principle that determines which relevant topics are sufficiently important that it is essential to report on them. Not all ESG topics are of equal importance to an organisation, and the emphasis within a report is expected to reflect their relative priority. Materiality is defined within the reporting boundary.

Listed companies should have a structured, documented process on assessment of materiality for ESG disclosure topics. A materiality assessment exercise should be conducted at a minimum on an annual basis, and as part of every new ESG reporting exercise. The organisation’s approach to materiality assessment should be disclosed within the ESG report.

In financial reporting, materiality is defined as a threshold for influencing the economic decisions of those using an Organisation’s financial statements. A similar concept is also important in ESG reporting. According to the GRI (2016), the ESG report should cover topics that:

1. Reflect the reporting organisation’s significant economic, environmental, and social impacts; or

2. Substantively influence the assessments and decisions of stakeholders.

Note: A topic can be relevant – and so potentially material – based on only one of these dimensions.

A materiality assessment grid can be used as a structured guide in prioritizing ESG topics to report on. By applying an internally developed rating criteria, organisations can plot ESG topics on a grid or heat map indicating the assessed level of importance considering both dimensions of materiality.

STAKEHOLDER KEY EXPECTATIONS COMMUNICATION CHANNEL FREQUENCY

Joint venture partners

Financial stewardship

Fiduciary responsibility

Responsible investment

Annual report

Sustainability reportScheduled

Trade associations

Examples: Kenya Bankers Association, Kenya Association of Manufacturers etc�

Socio-economic contributions

Sector sustainability

Annual report

Sustainability reportAnnual

ESG Disclosures Guidance Manual | November 202123

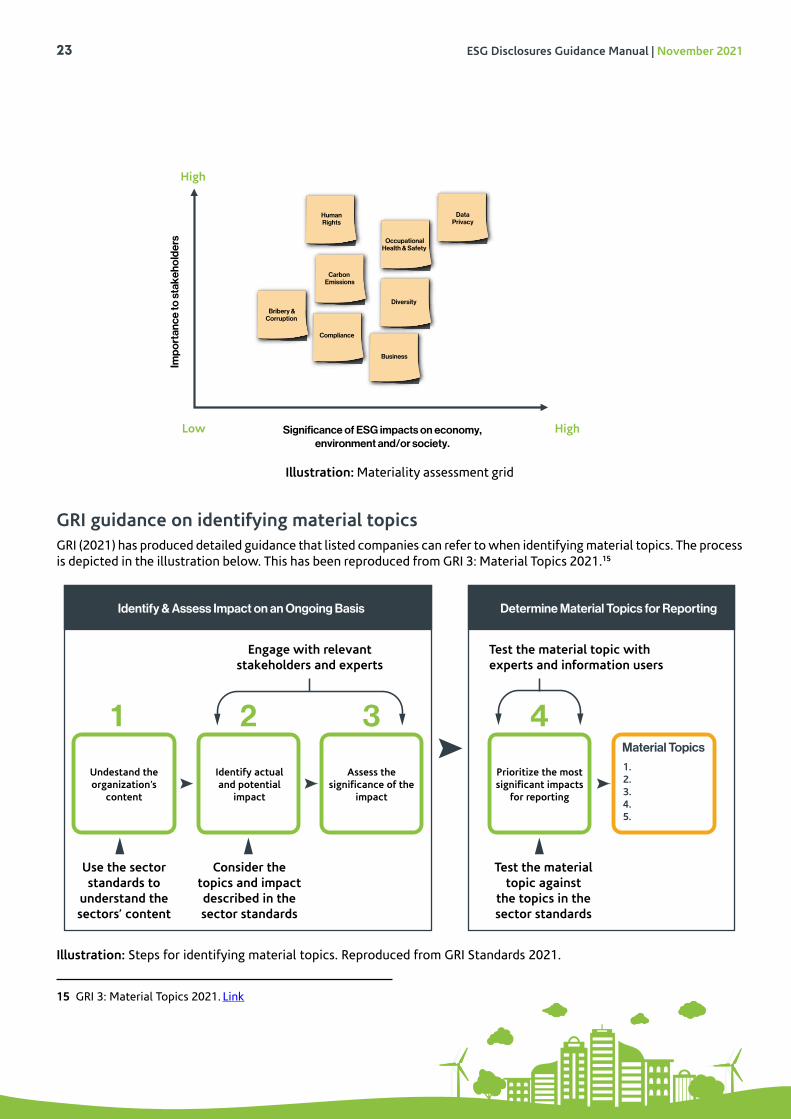

Illustration: Materiality assessment grid

GRI guidance on identifying material topicsGRI (2021) has produced detailed guidance that listed companies can refer to when identifying material topics. The process is depicted in the illustration below. This has been reproduced from GRI 3: Material Topics 2021.15

Illustration: Steps for identifying material topics. Reproduced from GRI Standards 2021.

15 GRI 3: Material Topics 2021. Link

Low

con�nuity

Impo

rtan

ce to

sta

keho

lder

s

Significance of ESG impacts on economy,environment and/or society.

High

High

HumanRights

OccupationalHealth & Safety

Bribery & Corruption

Diversity

Compliance

DataPrivacy

Business

Carbon Emissions

Identify & Assess Impact on an Ongoing Basis

Engage with relevantstakeholders and experts

Test the material topic withexperts and information users

Test the material topic against

the topics in the sector standards

Use the sector standards to

understand the sectors’ content

Consider the topics and impact described in the sector standards

Determine Material Topics for Reporting

1 2 3 4Material Topics

1.2.3.4.5.

Undestand theorganization’s

content

Identify actual and potential

impact

Assess the significance of the

impact

Prioritize the mostsignificant impacts

for reporting

ESG Disclosures Guidance Manual | November 202124

The approach applied for each step will vary according to the specific circumstances of the organisation, such as its business model; sector; geographic, cultural and legal operating context; ownership structure; and the nature of its impacts. Given these specific circumstances, the steps should be systematic, documented, replicable, and used consistently in each reporting period. The organisation should document any changes in its approach together with the rationale for those changes and their implications.

The organisation’s highest governance body should oversee the process and review and approve the material topics.

Detailed guidance on the GRI materiality assessment process can be obtained in the GRI Standards 2021.

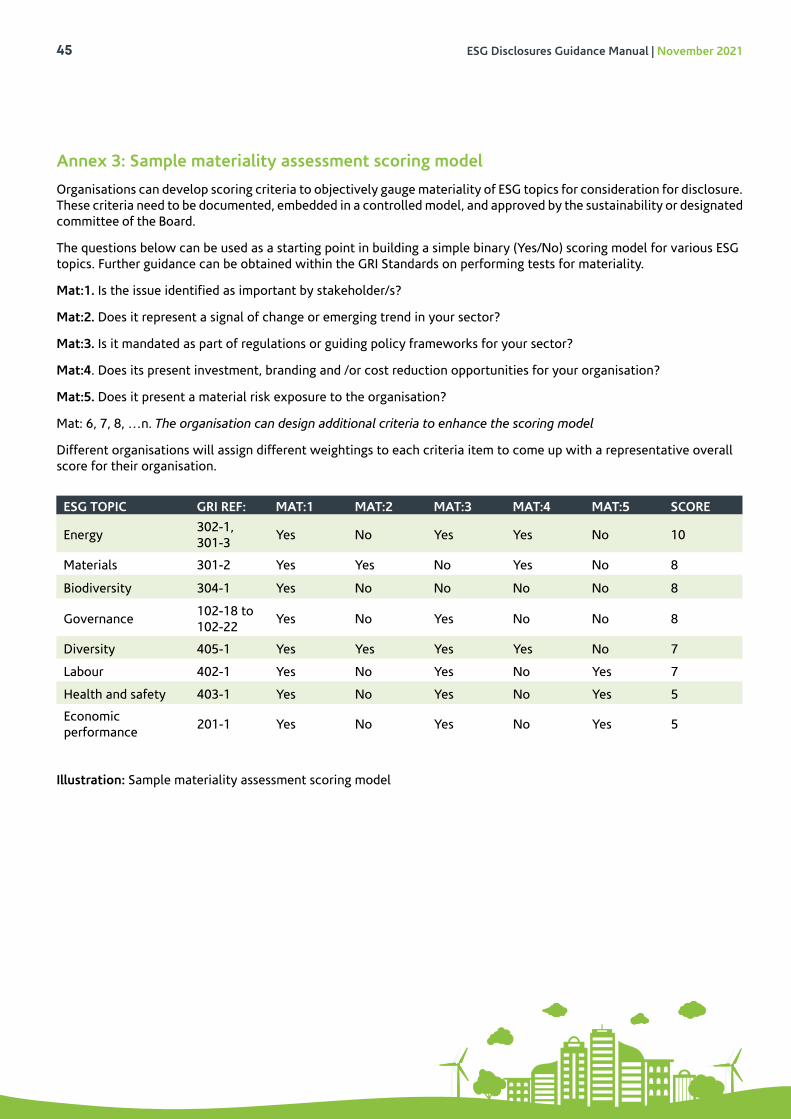

A sample materiality assessment scoring model has been provided for reference in Annex 3.

Additional guidance on materiality analysisMandatory ESG disclosures have been proposed for NSE listed companies to help achieve comparability and to facilitate compliance with the CMA Code, relevant international treaties, ESG standards and local regulations. These will be discussed in step 5 on content development.

Further, the CMA Code provides examples of topics that the Boards of listed companies should treat as material. Material information as per the CMA code means any information that may affect the price of an issuer’s securities or influence investment decisions. Listed firms are advised to refer to the Code when selecting material topics for disclosure.

The SDGs can also help in the identification of material topics and or impact. By aligning organisational objectives with the SDGs, organisations can identify significant impact areas that affect their contribution to the SDGs.

Recent discussions around assessment of materiality in ESG reporting has introduced the concept of double-materiality. As proposed by the European Commission (European Commission, 2019) in Guidelines on Non-financial Reporting, double-materiality refers to assessing materiality from two perspectives:

1. The extent necessary for an understanding of the company’s development, performance and position” and “in the broad sense of affecting the value of the company”; and

2. Environmental and social impact of the company’s activities on a broad range of stakeholders.

The concept also implies the need to assess the interconnectivity of the two.

GRI commissioned a white paper that investigated how double-materiality is implemented in ESG reporting, and the benefits and challenges of doing so.16 Key findings in the paper include:

1. The identification of financially materiality issues are incomplete if companies do not first assess their impacts on sustainable development.

2. Reporting material sustainable development issues can enhance financial performance, improve stakeholder engagement and enable more robust disclosure.

3. Focusing on the impacts of organisations on people and planet, rather than financial materiality, increases engagement with the Sustainable Development Goals.

Listed companies are therefore encouraged to assess impact of ESG issues to their organisations (such as climate change and human rights) in addition to their organisations own ESG impacts to society (such as material resource use and emissions) when determining material ESG impacts for disclosure.

16 The double-materiality concept. Application and issues. Link

ESG Disclosures Guidance Manual | November 202125

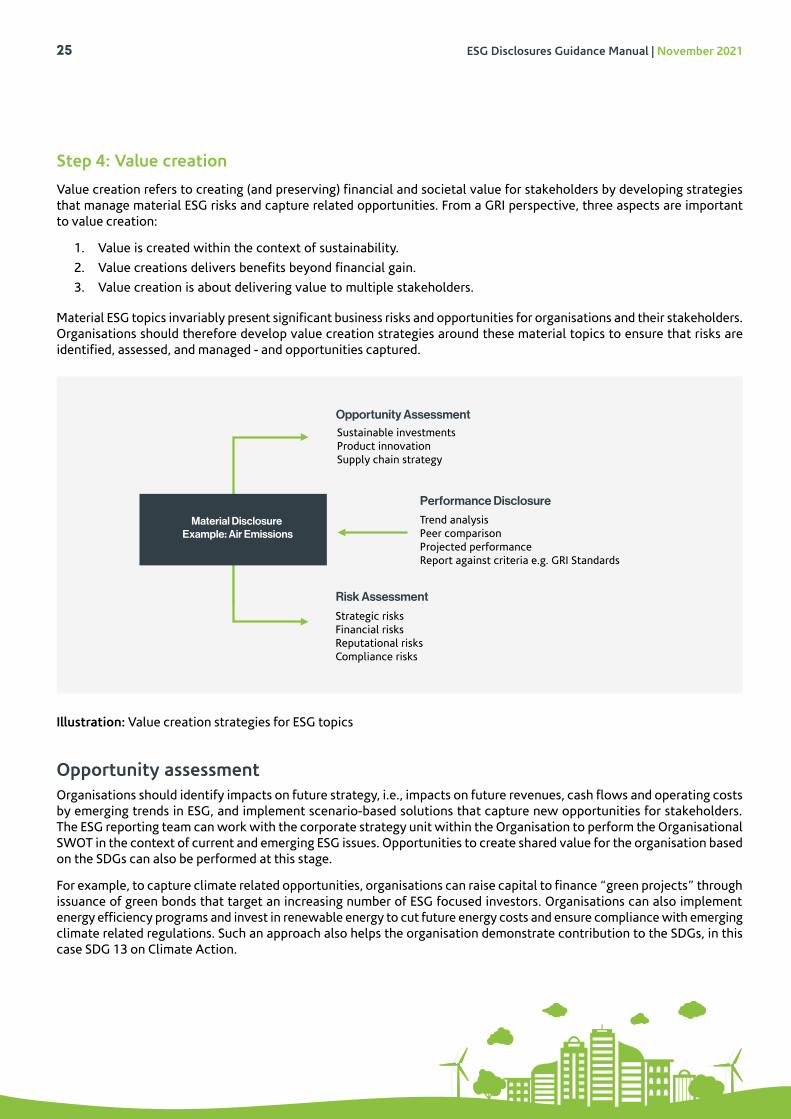

Step 4: Value creation

Value creation refers to creating (and preserving) financial and societal value for stakeholders by developing strategies that manage material ESG risks and capture related opportunities. From a GRI perspective, three aspects are important to value creation:

1. Value is created within the context of sustainability.

2. Value creations delivers benefits beyond financial gain.

3. Value creation is about delivering value to multiple stakeholders.

Material ESG topics invariably present significant business risks and opportunities for organisations and their stakeholders. Organisations should therefore develop value creation strategies around these material topics to ensure that risks are identified, assessed, and managed - and opportunities captured.

Illustration: Value creation strategies for ESG topics

Opportunity assessmentOrganisations should identify impacts on future strategy, i.e., impacts on future revenues, cash flows and operating costs by emerging trends in ESG, and implement scenario-based solutions that capture new opportunities for stakeholders. The ESG reporting team can work with the corporate strategy unit within the Organisation to perform the Organisational SWOT in the context of current and emerging ESG issues. Opportunities to create shared value for the organisation based on the SDGs can also be performed at this stage.

For example, to capture climate related opportunities, organisations can raise capital to finance “green projects” through issuance of green bonds that target an increasing number of ESG focused investors. Organisations can also implement energy efficiency programs and invest in renewable energy to cut future energy costs and ensure compliance with emerging climate related regulations. Such an approach also helps the organisation demonstrate contribution to the SDGs, in this case SDG 13 on Climate Action.

Performance Disclosure

Trend analysisPeer comparisonProjected performanceReport against criteria e.g. GRI Standards

Risk Assessment

Strategic risksFinancial risksReputational risksCompliance risks

Opportunity Assessment

Sustainable investmentsProduct innovationSupply chain strategy

Material Disclosure Example: Air Emissions

ESG Disclosures Guidance Manual | November 202126

Note: Organisations can justify ESG related investments by setting an internal price of ESG impacts, e.g., setting an internal price for carbon emissions, water abstraction or use of natural resources that the organisation extracts freely from the environment. This approach facilitates quantitative cost analysis, e.g., through discounted cash flow analysis and subsequent justification of investments that mitigate the organisation’s impacts in these areas.

Risk assessmentGlobal studies have shown environmental and social related risks to be the most significant risks that business leaders are concerned about. Business leaders globally acknowledge the impact that ESG related risks are likely to have on their strategies and business models.

Most GSE listed companies have implemented an enterprise risk management framework. As a starting point, ESG risks can be identified, analyzed, and managed as part of this wider enterprise risk management process. Listed companies should however seek expert ESG subject matter advise on how to mitigate significant ESG risks. The organisation should continuously evaluate the strategic, financial, operational and compliance risks that the organisation is exposed to relative to its ESG risk profile. Increasing emphasis on climate change mitigation by regulators and investors exposes organisations to non-compliance risks and possible divestment by investors. Human rights issues in the supply chain, whether real or perceived expose organisations to significant reputational risks. The Board should be appraised on a regular basis on how the organisation is managing these risks.

Performance disclosurePerformance disclosure on ESG performance demonstrates transparency to stakeholders and a commitment to responsible investment by the Board and Senior management of the reporting Organisation. Listed companies should document a process for collecting, analyzing, and reporting ESG performance data to stakeholders. ESG disclosure/sustainability reports assess prior period (usually financial year) performance of identified material ESG topics within the reporting boundary against set criteria. This manual provides guidance to listed companies on how to report on a variety of typical material ESG topics in various sectors while applying the GRI Standards.

What gets measured get managed. Organisations that set ESG metrics and implement a system of collecting, analyzing, and reporting ESG performance see improvements in their ESG performance over time. Content development on performance of material ESG topics is discussed in the sections below on content development.

Step 5: Content development

After identifying material ESG topics within its reporting boundary, the listed company embarks on content development for the ESG report by collecting quantitative and qualitative information to describe prior period (usually past financial year) ESG performance.

Content development consists of the following steps:

ADOPT REPORTING STANDARD

APPLY REPORTING PRINCIPLES

PREPARE LIST OF

DISCLOSURES

CHECK INTERNAL & EXTERNAL SYSTEMS

GATHER AND REPORT

INFORMATION

ESG Disclosures Guidance Manual | November 202127

Adopt reporting standard – The GRI Standards have been recommended as the standard for ESG reporting by listed companies in Kenya. The GRI Standards are the most widely used standards for ESG reporting globally.

Apply reporting principles – All ESG performance data should be checked against the reporting principles discussed in Chapter 4 of this manual.

Prepare a list of identified material topics to report on – These are composed of the issues identified from the materiality assessment and the mandatory disclosures (proposed) for listed companies.

Check internal and external systems – the ESG reporting team should identify and validate sources of internal and external ESG performance data.

Gather and report information – All quantitative and qualitative information should be sourced from verifiable sources with checks and balances to ensure accuracy and completeness. Internally sourced information should be signed off by respective heads of department before it is processed for ESG reporting. Information obtained from external sources should be clearly referenced and linked back to the source.

Note: For an entity to claim that their ESG report has been prepared in accordance with the GRI Standards, the ESG report must comply with the Reporting Principles and the reporting criteria outlined in the Annex 5.

The content development steps are described in detail in the sections below:

Adopt reporting standardThe GRI Standards have been recommended as the framework for ESG reporting for listed companies in Kenya. The GRI standards are the most comprehensive and widely used standards for ESG and sustainability reporting globally and have been the standard of choice for listed companies in Kenya that already publish sustainability reports.

The GRI Standards create a common language for organisations to report on their sustainability impacts in a consistent and credible way. This enhances comparability and enables transparency and accountability by listed companies.

Apply reporting principlesGRI has developed Reporting Principles for ensuring quality of the reporting process and information. These are discussed in Chapter 4. Listed companies should use these as their point of reference when gathering information for reporting as when as when writing the report. Listed companies should apply the tests under each principle each ESG disclosure topic and overall report content. A data collection template that can help listed companies apply these principles is provided in Annex 2.

Note: Where the GRI standards are adopted as suitable reporting criteria, external assurance methodologies place an emphasis on application of the reporting principles in the disclosed ESG information. It is therefore important that the listed company can demonstrate application of these principles before seeking assurance services on any ESG subject matter.

Prepare list of disclosuresThe list of ESG topics for disclosure will at minimum consist of the proposed mandatory ESG disclosures. Additional topics for disclosure can be identified through the materiality assessment exercise.

Mandatory ESG Disclosures

To promote compliance with existing policies and achieve comparability of ESG reports prepared by listed companies in Kenya, all listed companies will report on the following ESG topics:

ESG Disclosures Guidance Manual | November 202128

In reporting against the mandatory ESG disclosures, listed companies should refer to the following documents that define these proposed mandatory disclosures in the Kenyan context:

1. The CMA Code (for minimum requirements on governance disclosures)

2. The GRI Standards (all indicators in the table above are described in detail within the GRI Standards)

3. IFC Performance Standards on Environmental and Social Sustainability

4. UN Guiding Principles on Business and Human Rights

5. Prevailing environmental regulations in Kenya (Refer to the NEMA - Kenya website for updates on environmental regulations in Kenya)

6. Kenya’s National Climate Change Action Plan

7. Occupational Safety and Health Act (Kenya)

8. Consumer Protection Act (Kenya)

9. Data Protection Act (Kenya)

Note 1: The mandatory ESG disclosures above represent the ESG topics that must be disclosed by listed companies in Kenya. This should however not restrict a listed company’s initiative in reporting on additional ESG topics. A materiality assessment process has been provided to guide identification of additional ESG topics for disclosure.

Note 2: As part of the situational analysis process, the regulations that a listed companies are subject to are identified and their requirements analysed. Where some of the proposed mandatory disclosures have not been explicitly defined by local regulations, e.g., diversity and training & education, the listed companies can use the materiality assessment approach to identify and prioritise the various sub-components of these proposed mandatory disclosures for reporting. These components are provided within the GRI Standards for reference.

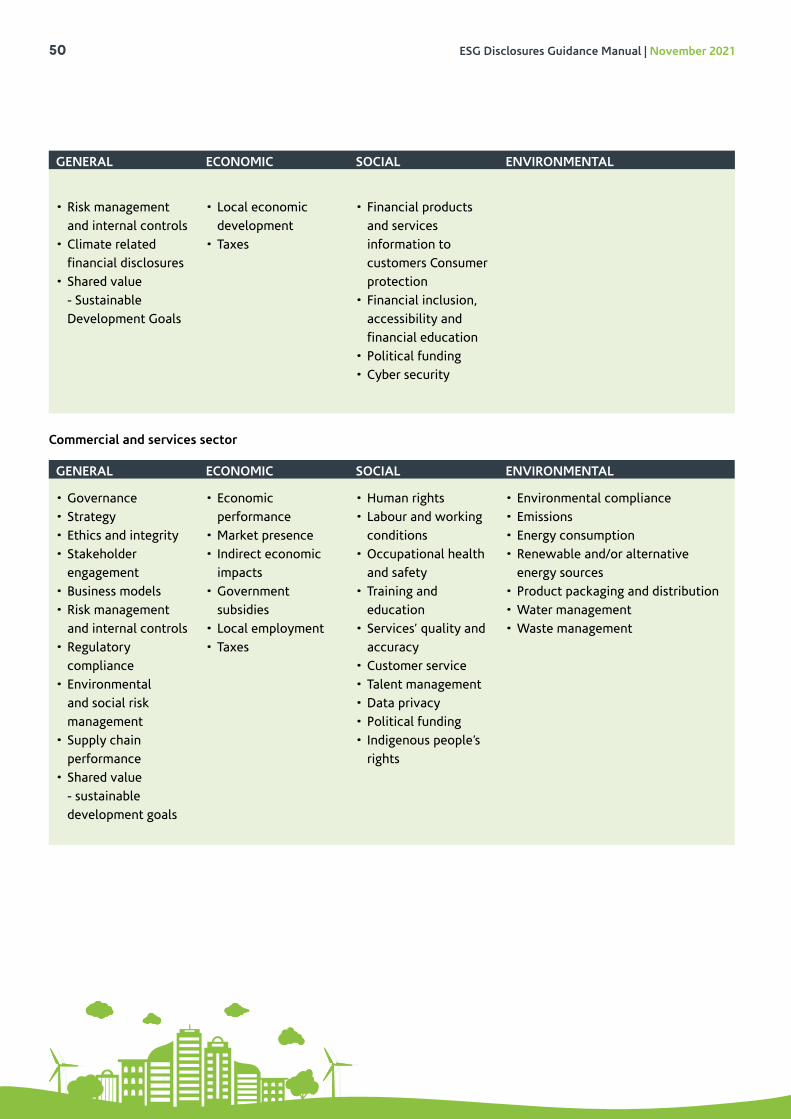

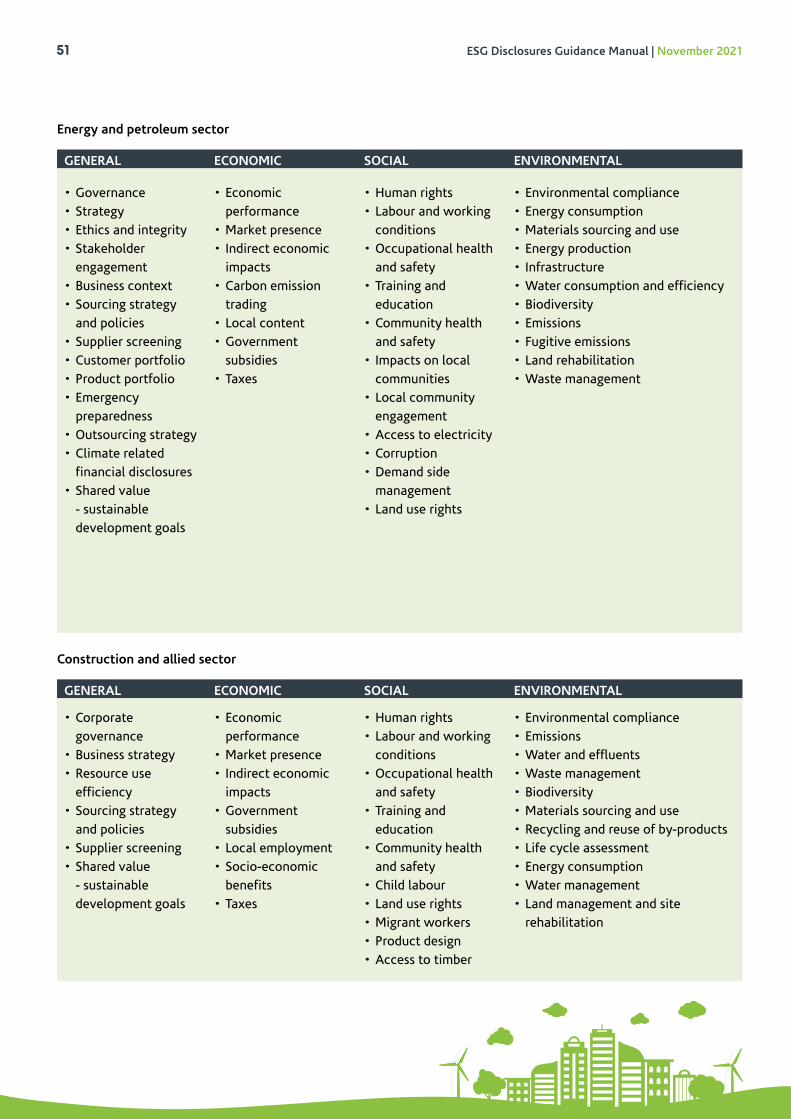

Sector Specific ESG Disclosures

Different sectors will have different types and levels of ESG impacts, positive and negative, to the economy, environment and to society.

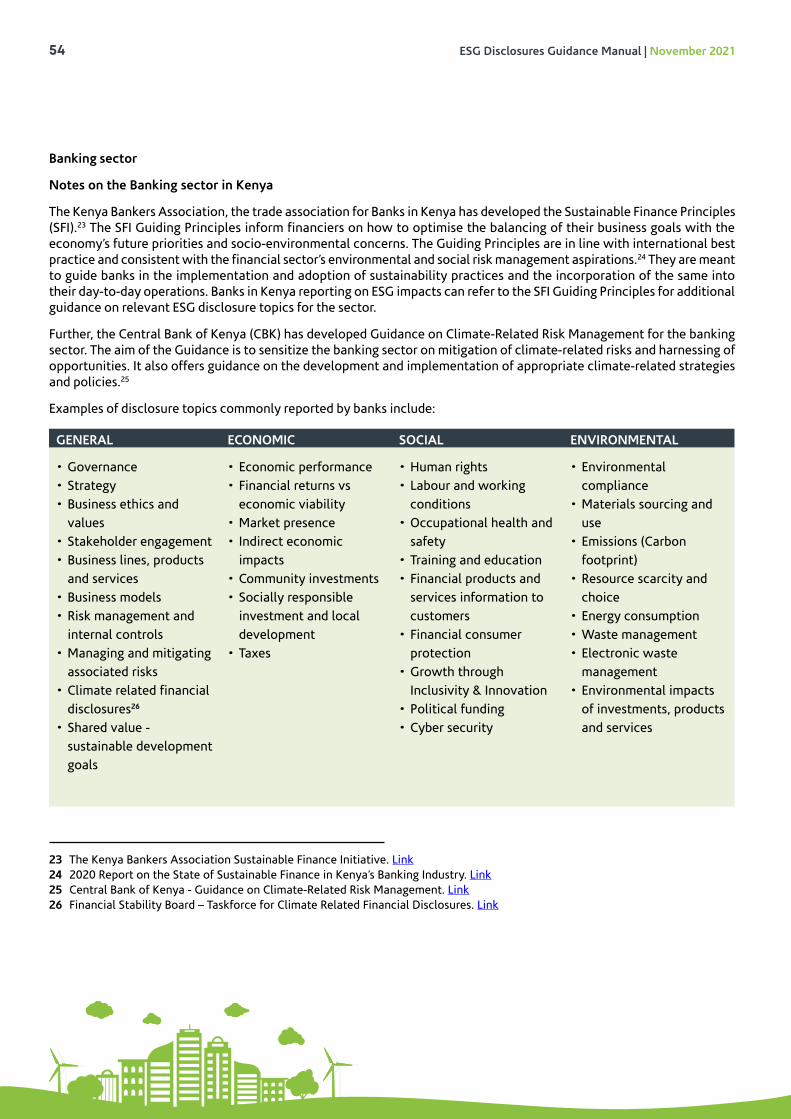

The guidance on materiality assessment provided in this document should be used to facilitate identification of these unique but material sector specific ESG issues. Examples of the most reported ESG topics for NSE listed companies, by sector, are provided in the Annex 6.

GENERAL ECONOMIC SOCIAL ENVIRONMENTAL

Governance

Environmental and social risk management

Stakeholder engagement

Regulatory compliance

Supply chain screening

Economic performance

Taxes

Anti-corruption

Human rights

Labour and working conditions

Occupational health and safety

Training and education

Diversity and equal opportunity

Consumer protection

Data privacy

Environmental compliance

Emissions (Carbon footprint assessment)

ESG Disclosures Guidance Manual | November 202129

Listed companies are also encouraged to report progress and contribution to the Sustainable Development Goals (SDGs). The identified material ESG disclosures can be linked with the specific targets for the prioritised SDGs and progress reported using the approach presented in this manual. Listed companies are also encouraged to report progress and contribution to the Sustainable Development Goals (SDGs). The identified material ESG disclosures can be linked with the specific targets for the prioritised SDGs and progress reported using the approach presented in this manual.

Check internal and external data systemsOnce the list of ESG disclosure topics and reporting standard (the GRI Standards) have been selected, the organisation is now ready to collect performance data on the ESG topics.

Information on ESG performance data should be reliable, accurate and complete for the disclosure being reported on.

Internal data systems generate internal ESG performance data such as employee demographic data, water consumption and energy consumption. To ensure accuracy and completeness of data sourced from internal systems, such systems should ideally be composed of:

1. Standardised operating procedures that outline how data is generated, collected, and processed.

2. Trained personnel responsible to collecting and recording the performance data.

3. Auditable management systems that are subject to annual quality assurance reviews.

Information can also be sourced from external sources. The sources will be informed by the reporting boundary and the choice of material ESG topics. Examples of information sourced externally include industry statistics, general population data and economic performance data. Before external data is used for reporting, the organisation must ensure the following:

1. An internal system exists to check that such information is reliable, accurate and complete.

2. The external data enables comparability between listed companies.

The external data is available and relevant within the ESG reporting period.

Gather and report informationQualitative and quantitative information is sourced from internal and external sources to describe organisational ESG performance. Listed companies should describe the management approach for each material topic along with the specific disclosures. Management approach is discussed in detail under GRI 103.17 The ESG reporting team should ensure the following when collecting, monitoring, and reporting ESG information:

1. Determine a schedule of when information on each ESG disclosure is received and is available for measurement and validation. Some data might be available on a weekly or a monthly basis. Externally sourced data could only be available annually.

2. Allocate responsibilities within the reporting team on who collects and monitors different kinds of ESG data. For example, a team could be tasked with collection and monitoring of environmental and energy performance data, while another could be tasked with collection of relevant external data such as industry statistics.

3. Ensure that information collected from various units or departments within the organisation is signed off by the respective heads of department.

4. All information should be clearly referenced and stored in a central location. The Sustainability Manager should ensure that all information used in the ESG report can be reconciled with source data.

5. Prepare the detailed management approach for each material ESG topic reported along with the specific disclosures.

17 GRI 103: Management Approach. Link

ESG Disclosures Guidance Manual | November 202130

6. Ensure there is a consistent, systematic method of communicating progress on ESG performance internally (e.g., to the Board and Project Sponsor) and externally through a published ESG report. Publishing the ESG report is discussed in Chapter 8.

To help consolidate and report on the identified material topics in a balanced and using a principle-based approach, listed companies should refer to the GRI Standards introduced earlier in this document. The GRI Standards provide a comprehensive set of standards for reporting publicly on a wide set ESG disclosures – including those proposed as mandatory disclosures for listed companies.

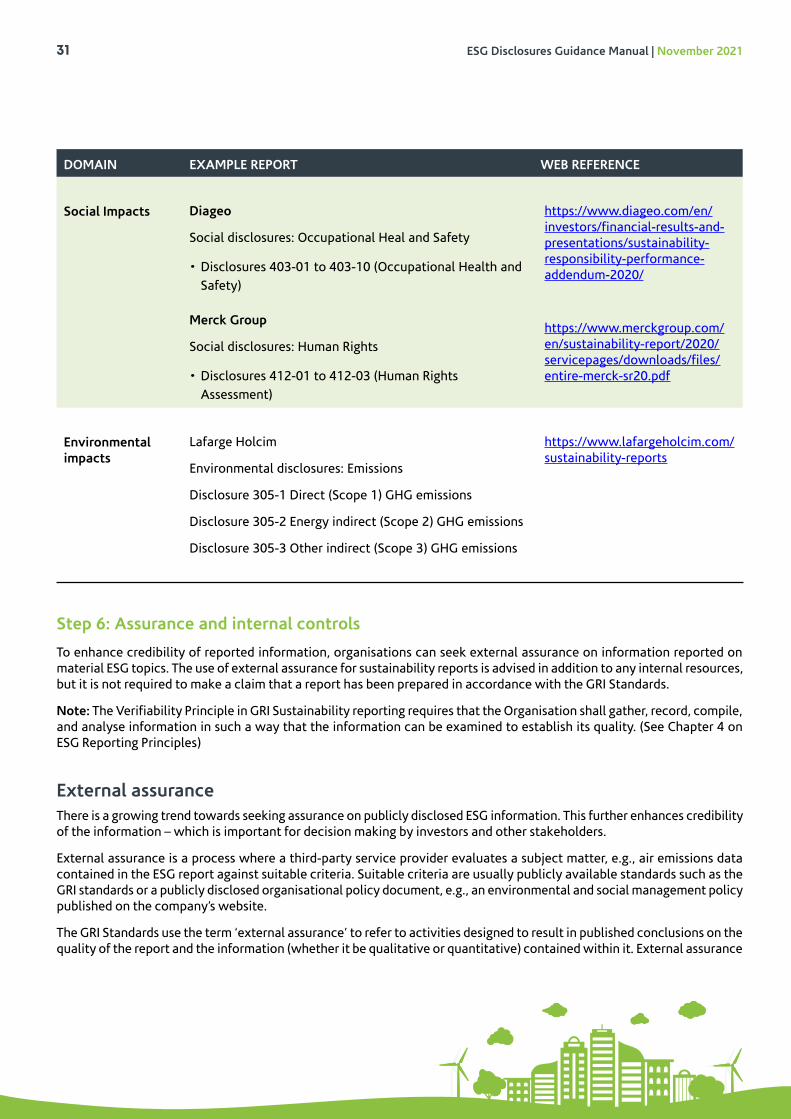

Examples of content on mandatory ESG topicsThe reports published by the organisations listed below contain practical examples on how to report on a variety of ESG topics while applying the GRI Standards.

DOMAIN EXAMPLE REPORT WEB REFERENCE

General

Disclosures

Kenya Commercial BankGeneral disclosures: Governance

• Disclosures 102-19 to 102-39 (Governance).

https://kcbgroup.com/wp-content/uploads/2021/05/KCB-SUSTAINABILITY-REPORT-2020.pdf

Economic impacts Safaricom PLC

• Economic disclosures: Economic Impacts, Anticorruption• Disclosure 201 : Management Approach: Economic

Performance• Disclosure 201-1: Direct economic value generated and

distributed• Disclosure 201-2: Financial implications and other risks

and opportunities due to climate change• Disclosure 201-3: Defined benefit plan obligations

and other retirement plans• Disclosure 205: Management Approach: Anti-corruption• Disclosure 205-1: Operations assessed for risks related

to corruption• Disclosure 205-2: Communication and training about

anti-corruption policies and procedures• Disclosure 205-3: Confirmed incidents of corruption and

actions taken

https://www.safaricom.co.ke/sustainabilityreport_2020/our-business/

ESG Disclosures Guidance Manual | November 202131

Step 6: Assurance and internal controls

To enhance credibility of reported information, organisations can seek external assurance on information reported on material ESG topics. The use of external assurance for sustainability reports is advised in addition to any internal resources, but it is not required to make a claim that a report has been prepared in accordance with the GRI Standards.

Note: The Verifiability Principle in GRI Sustainability reporting requires that the Organisation shall gather, record, compile, and analyse information in such a way that the information can be examined to establish its quality. (See Chapter 4 on ESG Reporting Principles)

External assuranceThere is a growing trend towards seeking assurance on publicly disclosed ESG information. This further enhances credibility of the information – which is important for decision making by investors and other stakeholders.