monetary policy and stock market movements in turkey

TRANSCRIPT

School of Economics and Finance

Queen Mary University of London

MONETARY POLICY AND STOCK MARKET MOVEMENTS IN TURKEY

Izzet Onur SERAKIBI

Email Address

M.Sc. in Business Finance

August,2013

I.TABLE OF CONTENTS:I.TABLE OF CONTENTS:.............................................2

II.ABSTRACT:.....................................................4

1-INTRODUCTION:..................................................4

2.A BRIEF REVIEW OF THE LITERATURE ON THE MONETARY POLICY AND ASSET PRİCE RELATIONS:...........................................6

2.1.The Taylor Rule:.............................................7

2.1.1. Specification of the Taylor Rule:.........................9

2.1.1.1. Estimation Data:........................................9

2.1.1.2. A Brief Information About Turkish Stock Market:.........9

2.1.1.2.1. The Credit Outlook of Turkey as an Investment Criteria:................................................................10

2.1.1.3.The Standart Taylor Rule:...............................10

2.1.1.4.The Augmented Taylor Rule:..............................11

2.1.1.5. Forward Looking Models and Generalized Method of Moments:................................................................11

2.1.2. Estimation of the Taylor Rule:..........................12

2.1.2.1. Graphical Inspection of the Data:......................12

2.1.2.2. Standart Taylor Rule with Ordinary Least-Squares Method:...............................................................14

2.1.2.3. The Wald Test:.........................................15

2

2.1.2.4.Visual Impression Regarding the Model:..................16

2.1.2.5.Chow Breakpoint Test:...................................16

2.1.2.6. Estimating The Augmented Taylor Rule:..................17

2.1.2.6.1.Ordinary Least-Squares Analysis (ATR):................17

2.1.2.6.2. Diagnostic- Normality Test:..........................18

2.1.2.6.3. Diagnostic- Heteroskedasticity Test:.................19

2.1.2.6.4. Diagnostic- Breusch-Godfrey Serial Correlation LM Test:................................................................19

2.1.2.6.5. Ordinary Least Squares Method (Newey-West Option):. . .19

2.1.2.6.6. Generalized Method of Moments(GMM) Estimator:........21

3.CONCLUSION:...................................................22

REFERENCES......................................................24

3

II.ABSTRACT:

In this dissertation, we investigate the hypothesis that

monetary policy responds to movements in asset prices.In the study

the arguments in favor and against the above hypothesis will be

studied, the empirical framework will be discussed and the

hypothesis will be tested. In the investigation, we adopt the

Taylor rule as the empirical framework and used its standard and

augmented versions in order to reach a conclusion.In this study,

we will especially explore that whether the stock market movements

play a crucial role in shaping monetary policy either directly or

indirectly in Turkey between the years 1997 and 2012.

4

1-INTRODUCTION:

Turkish economy showed an outstanding performance between the

years of 1997 and 2012.During the period, the inflation rate

dropped to %6.16 from %85 and parallel to the inflation rate

interest rate dropped almost %60 while GDP rose almost %4 annually

in average. Additionally BIST100, the stock market value of Turkey

rose almost 60% in 2012 and reached the 80.000 index level while

it was only at 1.613 index level at 1997.

The objective of this investigation is to test the hypothesis

that monetary policy responds to movements in asset prices. In

this study, we will try to prove that there is a significant

correlation between monetary policy and asset pricing.Policy rules

of central bank of Turkey and reflections of those decisions in

the stock market between the period of 1997 and 2012 will be the

main investigation subject of this study.

According to Bernanke and Mihov (1998) the process by which

the central banks control the money supply in order to keep the

interest rate at certain levels for promoting economic growth and

price stability is called monetary policy.The need to the central

banks in providing a stable economic outlook has increased during

the last years. So as a policy maker, central banks should

struggle with inflation as well as they should prevent the markets

from the financial crisis.

5

Bernanke (2000) also claims that inflation is no longer a

great issue to concern about since the world’s leading central

banks have been very successful at keeping it under control over

the past twenty years. Nowadays an apparent increase in financial

instability and increased volatility of asset prices seem to be

the next battles facing central banks.

According to Mishkin (2012) mismanagement of financial

liberalization and asset-price booms and busts can trigger

financial crises which usually results in failures of major

financial institutions and increased uncertainty in the financial

markets.When investor psychology affects the assets prices such

as equity shares and real estate above their fundamental economic

values, the rise of asset prices called as an asset-price bubble.

Those bubbles in asset prices are often driven by credit booms

which are usually supported by the policies of the central banks.

Allen and Gale (2000) argue that the recent financial crises

which was caused by the bubble of asset prices is resulted with

widespread defaults of some leading financial institutions. The

money borrowed from banks for asset investment is always

attractive for investors who plan to default on the loan rather

than making safe but small amounts of profit in their investments.

At the times of financial fragility, the risk appetite of the

investors in both the real and financial sectors investments can

lead the asset prices to very high levels and cause crisis due to

the insufficient positive credit expansion.

6

There have been two major asset bubble crisis in 1929 and 1980

at the last century.Both of them caused protracted recessions and

deflation.According to Bordo and Jeanne (2002) The policy makers

have a perennial interest in the relation of monetary policy and

asset price movements since it is essential to decide whether

trying to prevent the results of an asset market collapse before

it turns to a financial crisis or whether it was more effective to

react the asset prices after financial markets completely went

down.

Bean (2004) claims that in the aftermath of the recent crisis

caused by asset price bubbles in Japan and U.S. the most popular

debate between central bankers and academic circles was the role

of the asset prices in the setting of monetary policy. Views of

Gilchrist and Leahy (2002) remind the following period of

increased volatility in asset prices in Japan and US.Then most of

the economists had called for central banks to respond to asset

price volatility against to large swings in growth rates.

2.A BRIEF REVIEW OF THE LITERATURE ON THE MONETARY POLICY AND ASSET PRİCE RELATIONS:

The role of asset price movements in shaping monetary policy

can be explained by two opposite view in the literature. Some

economist such as Bernanke and Gertler (2001) and Vickers (1999)

claim that there is no need to believe in asset price volatility

as a key determinant for setting monetary policy but on the other

hand, Cecchetti, Genberg and Wadhwani (2002) believe volatility in

7

asset prices can help central banks when shaping monetary policy

by providing more information.

According to Bernanke and Gertler (2001) the appropriate

position of asset prices in the monetary policy has been witnessed

to many debates. The question of whether central banks should

respond to volatility in asset prices or not can be answered by

the inflation-targeting approach. According to this view

volatility in asset prices may affect the monetary policy if only

the expected inflation rate is affected negatively from those

movements. For instance, a bubble in asset prices can increas the

aggregate demand by increasing consumers wealth and affect the

inflation negatively.Furthermore, once the effects of asset prices

in the general price level have been accounted for central banks

should not response the changes in the asset prices anymore. This

is a crucial point in monetary policy because this kind of

attempts to influence asset prices can affect the investors

psychology and lead the markets unpredictable future.

According to Cecchetti et al. (2002), it is possible to

improve macroeconomic performance by reacting to asset price

misalignments systematically. Just by setting policy rates with an

eye toward particularly in misalignments and generally in asset

prices can help to smooth output and inflation fluctuations.

Distortions in investment and consumption created by asset price

bubbles can cause excessive increases followed by severe falls

in both inflation and GDP. To raise interest rates when asset

prices rise above the expected levels and to lower them modestly

8

when asset prices fall below the reasonable levels will help

central banks to offset the impact on inflation and output gap of

these bubbles. The important outcome of this kind of monetary

policy is to show the markets that central banks can take the

necessary measurement in this way. The probability of bubbles in

equity prices might be reduced and a contribution to greater

macroeconomic stability would also be provided by this method.

Bernanke and Gertler (2001), claim whether the volatility in

asset prices is the result of bubbles or technological shocks, an

aggressive inflation-targeting policy stabilizes output and

inflation. In their opinion the study of Cecchetti et al. ignores

the fact of shocks other than bubble shocks and the probabilistic

nature of the bubble. Their theory lies on the assumption of a

bubble shock which lasts precisely five periods. Also, the

knowledge of the central banks about the reasons and the bursting

moment of the bubbles are both highly unlikely conditions. A

panic-driven financial instability that could affect the economy

negatively can be reduced and macroeconomic stability can be

sustained by inflation targeting monetary policy. In the end, they

conclude for plausible parameter values the central banks should

not respond to asset prices.

On the other hand, Cecchetti et al.(2002) claims that the

underlying sources of shocks to the economy determines the

relationship between fluctuations in asset prices on the one hand,

and output and inflation on the other. So they suggest that

monetary authority should not interfere to all changes in asset

9

prices mechanically and in the same way. Since the private sector

might possess more information about equilibrium valuations of

asset prices, it would be possible to react anything from asset

price fluctuations that can help to shape monetary policy.

Cecchetti et al. (2002) also claims that not all asset price

changes, but the asset price instability should be identified and

responded in an inflation-targeting strategy. That means stock

market value should be included in the information sets in order

to be processed by the central bank just as well as the output

gap. The problem of to differentiate the asset price movements

and to realize whether they are justified by underlying

fundamentals or not is the main challenge of the policymakers.

2.1.The Taylor Rule:

As a major tool of monetary policy central banks should

change the interest rate in order to provide macro economic

stability first and then keep the employment in maximum

levels.Taylor rule which was proposed by world renowned monetary

economist John B. Taylor and named after him can help central

banks with the question of how much would it be the optimum

interest rate. Taylor principle is a different aspect of taylor

rule and stipulates that the nominal interest rate should be raise

more than the increase in the inflation rate.

According to Castro (2008) to set up the interest rate past

or current values of inflation and output gap is a commonly used

method by central banks.In its very original form, the main

10

objectives of the Taylor rule are providing the price stability

and keeping the economy moving towards maximum employment.In order

to keep the general price level stable Taylor rule simply

recommends that when the inflation rate is exceeded the target

level central banks should rise the interest rate above the level

of the stabilizing rate and when it is below the target level

interest rate should be decreased to the levels below the

target.In order to accomplish the second objective of the Taylor

rule it is suggested that the interest rate should be determined

above the stabilizing rate when real GDP is above the target. If

real GDP is below the potential real GDP Taylor, recommends that

the interest rate should be reduced below the stabilizing rate.

According to Taylor (1993) conducive monetary policy requires

to put equal weights on the impact of inflation and GDP since

putting more weight on the inflation gap could be a sign of more

aggressive policy to target inflation by the central banks.

Godhart and Hofmann (2000) believe that the question of how

asset price volatility should be considered in principle for

objectives of monetary policy is subject to a consensus among

leading economists.An inflation target which can also be defined

as achieving price stability is the primary objective of the

central banks while inflation is a price index which consist of

current goods and services but excludes assets prices directly.

11

Frait and Komarek (2006) point out that asset price

developments are usually taken into account when refining monetary

policy, even if central banks formally targets price stability.

The reason for this approach lies on the fact that asset price

movements, especially physical assets, can impact on CPI inflation

by tempting the people to invest in those assets.Once people

starts buying those assets the production of the assets rises as

well as the demand for the raw materials and this cycle triggers

the CPI inflation.

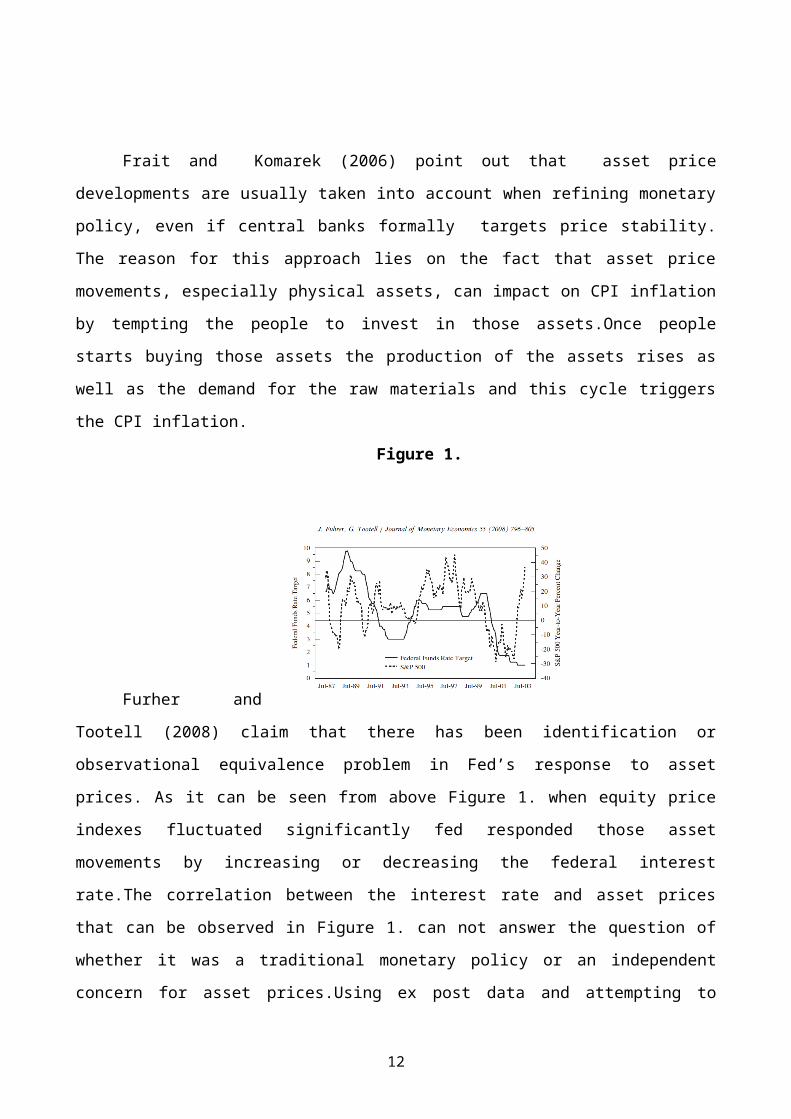

Figure 1.

Furher and

Tootell (2008) claim that there has been identification or

observational equivalence problem in Fed’s response to asset

prices. As it can be seen from above Figure 1. when equity price

indexes fluctuated significantly fed responded those asset

movements by increasing or decreasing the federal interest

rate.The correlation between the interest rate and asset prices

that can be observed in Figure 1. can not answer the question of

whether it was a traditional monetary policy or an independent

concern for asset prices.Using ex post data and attempting to

12

identify the effects of asset prices on monetary policy may have a

misleading impact.

2.1.1. Specification of the Taylor Rule:

Many scholars all around the world highly interested and used

the Taylor rule in the past years.Since it can provide an answer

to how to set monetary policy by a simple method in this study,

“the Taylor rule” will be the econometric framework that is going

to be used in the analysis.

2.1.1.1. Estimation Data:

As we mentioned above in this study, the Taylor rule will be

used as the estimation framework as well as some of the Turkish

economic data ranging from 1997:1Q to 2012:4Q., will be used as

the estimation data.In the study we will apply RGDP, which is the

Turkish real GDP, CPI, which is the consumer price index of Turkey

, interest is the interest rate, set by the Central Bank of Turkey

and BIST100 which is the stock market value of Turkey to our

model to estimate the Taylor rule.

The data which we need to carry out our study including GDP,

CPI, Interest Rates and BIST100 index of Turkey were extracted

from International Monetary Fund International Financial

Statistics via UK Data Service international macrodata.

2.1.1.2. A Brief Information About Turkish Stock Market:

First time in Turkish history on January 3, 1986 stock trading

started at the Cağaloğlu building of Istanbul Stock Exchange

13

(IMKB) with a number of 80 listed companies.On October,1992 IMKB

was accepted to The World Federation of Exchanges as a full

member. The legal framework of Turkish capital markets, consist of

Capital Markets Law (CML) and Turkish Commercial Code.The more

detailed regulations are manifested as Communiqués of Capital

Markets Board and Regulations of Stock Exchange. In order to

harmonize the Turkish capital markets regulation with the EU

acquis, the Capital Markets Law No. 6362 was enacted by the

Turkish law maker.With that amendment in Capital Markets Law

Turkish government also aimed to liberalize the activity of

running organized markets and re-brand IMKB as Borsa Istanbul

(BIST).After the recent changes in the Capital Markets Law Borsa

Istanbul is now subject to private law as a joint-stock company.

Borsa Istanbul (2013).

By the end of 2012, the number of the traded companies on BIST

reached to 404 while it was 258 at 1997. Under the name of Borsa

Istanbul, two major national indices are existed. SERPAM (2013).

Those are BIST30 and BIST100.BIST30 is consisted of 30 large

companies by the value of outstanding shares traded in the stock

market. Financial institutions and a couple of leading holding

companies are examples of firm types of the BIST30.BIST100 is the

major index of Borsa Istanbul.It is consisted of BIST30 and the

following largest industrial companies by the value of outstanding

shares traded in the stock market. Usually BIST30 companies have

higher beta value than BIST100 companies and BIST30 index also

considered as a more reliable indicator about the general trend of

the markets.

14

2.1.1.2.1. The Credit Outlook of Turkey as an Investment Criteria:

By the august of 2013, the long-term foreign-currency credit

rating of Turkey was confirmed as BB+ by S&P, BBB- by Fitch and

Baa3 by Moody’s. Moody’s and Fitch already upgraded Turkey’s

foreign-currency sovereign credit rating to the investment

grade.Another foreign-currency sovereign credit rating upgrade is

expected by S&P which will lift the general credit outlook of

Turkey to the investment grade in foreign-currency.

2.1.1.3.The Standart Taylor Rule:

The Taylor rule which formulates the linear relation between

inflation ,GDP and the interest rate was established by John B.

Taylor in 1993.At this point of the study, the very first step of

our econometric analysis consists of estimating the standard

Taylor rule (STR) as it is given below as equation (1).

According to Taylor (1993), in the above formula

represents the log of the interest rate(the federal funds rate), c

represents the constant, represents the actual annual inflation

rate, represents the desired inflation rate, represents the

log of GDP and is the potential GDP. We will assume that “

” in order to keep the analysis simple.

15

2.1.1.4.The Augmented Taylor Rule:

Among the monetary policy makers two opposite views emerged

regarding how to set a well refined monetary policy. According to

the first view monetary authority should not respond to movements

in asset prices and wait for to see the progress in the economic

data such as the inflation rate. On the other hand, stock market

movements could help to predict the future fluctuations in the

monetary markets and the augmented Taylor rule which is employed

by monetary authorities would be the best econometric framework

for this purpose.

The second step of the econometric analysis will be estimating

the augmented Taylor rule. In the 1main literature, asset price

volatility suppose to bring more information to the central banks

and by doing so it could affect the decisions of the monetary

authority.According to Castro (2008) a financial conditions index

containing data from stock market movements can be included in the

standard Taylor rule to have an augmented version of it. In order

to test this possibility, we should include in equation the

variable, which measures the stock market value. If we start our

estimation for the equation by using only one lag of “s” and

reached the conclusion of that s(-1) is statically significant, we

can estimate the model again with using more lags until we meet, a

non significant lagged regressor. The augmented version of Taylor

rule is given below as equation (2).

16

2.1.1.5. Forward Looking Models and Generalized Method of Moments:

As John Maynard Keynes (1923) once said that we might have

been too late if we would have waited until a price movement was

actually very close before taking some measurements. This words

reflect the importance of the forward-looking models in monetary

policy. When private economic actors change their economic

behavior in a particular economic subject some variables such as

long-term interest rates may be changed. According to Kamada and

Muto (2000) this mechanism of expectation formation is generally

called as rational expectations models while the models that

integrated with such expectations regardless current and past

information are called as forward looking models. Mavroeidis

(2004) points out that since they based on micro-foundations and

built on rational expectations, generalized method of moments

(GMM) methods have become popular for estimating forward-looking

models.

The third step of the econometric analysis will be estimating

our model by GMM. This is a general estimation method which is

derived from the method of moment. It is developed by Lars Peter

Hansen in 1982. Many other estimators can be considered as special

cases of generalized method of moments. It can allow economic

models to be specified without making unwanted assumptions. It is

consistent and asymptotically normal. In order to produce

estimates of the unknown parameters of the model it combines

17

observed data with the information extracted from orthogonality

conditions. Hansen (2007) also points out that it can be used when

maximum likelihood estimation is not applicable and the parameter

of interest is finite-dimensional. Its properties of taking

account of both sampling and estimation error and being

constructed without specifying the full data generating process

made generalized method of moments a widely used estimator.

2.1.2. Estimation of the Taylor Rule:

The main purpose of this exercise is to test whether the

stock market movements play a crucial role in shaping monetary

policy either directly or indirectly.

2.1.2.1. Graphical Inspection of the Data:

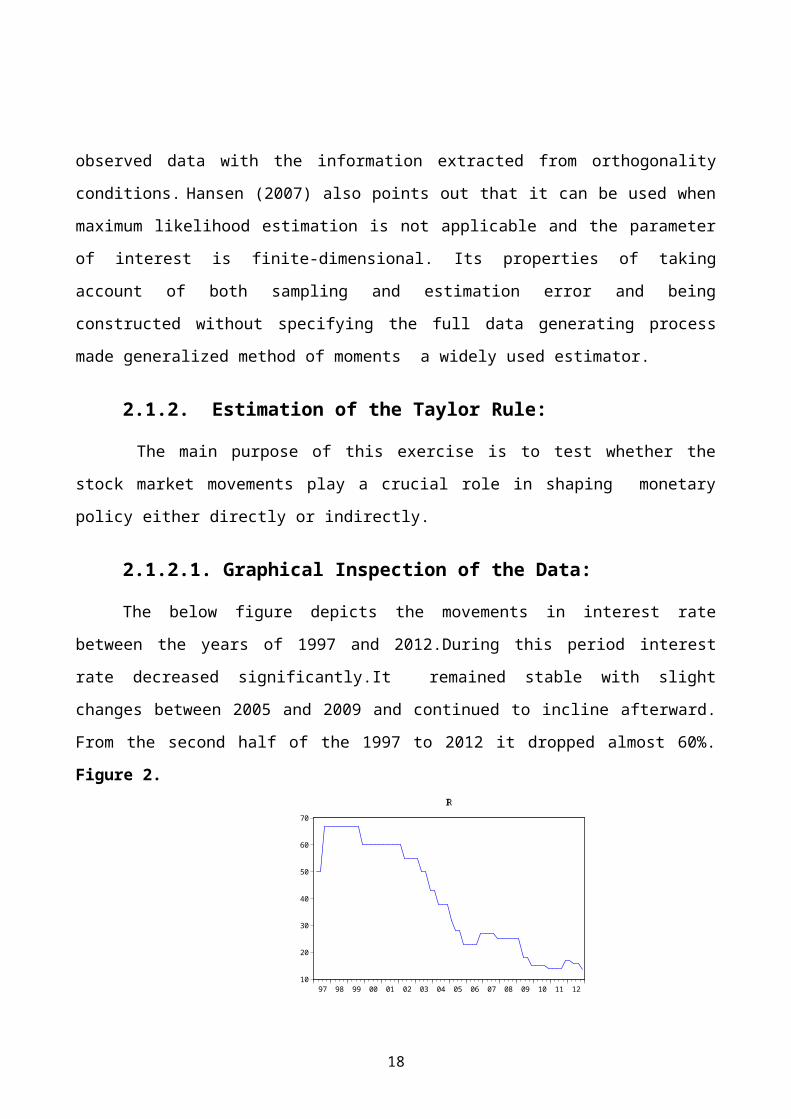

The below figure depicts the movements in interest rate

between the years of 1997 and 2012.During this period interest

rate decreased significantly.It remained stable with slight

changes between 2005 and 2009 and continued to incline afterward.

From the second half of the 1997 to 2012 it dropped almost 60%.

Figure 2.

10

20

30

40

50

60

70

97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12

IR

18

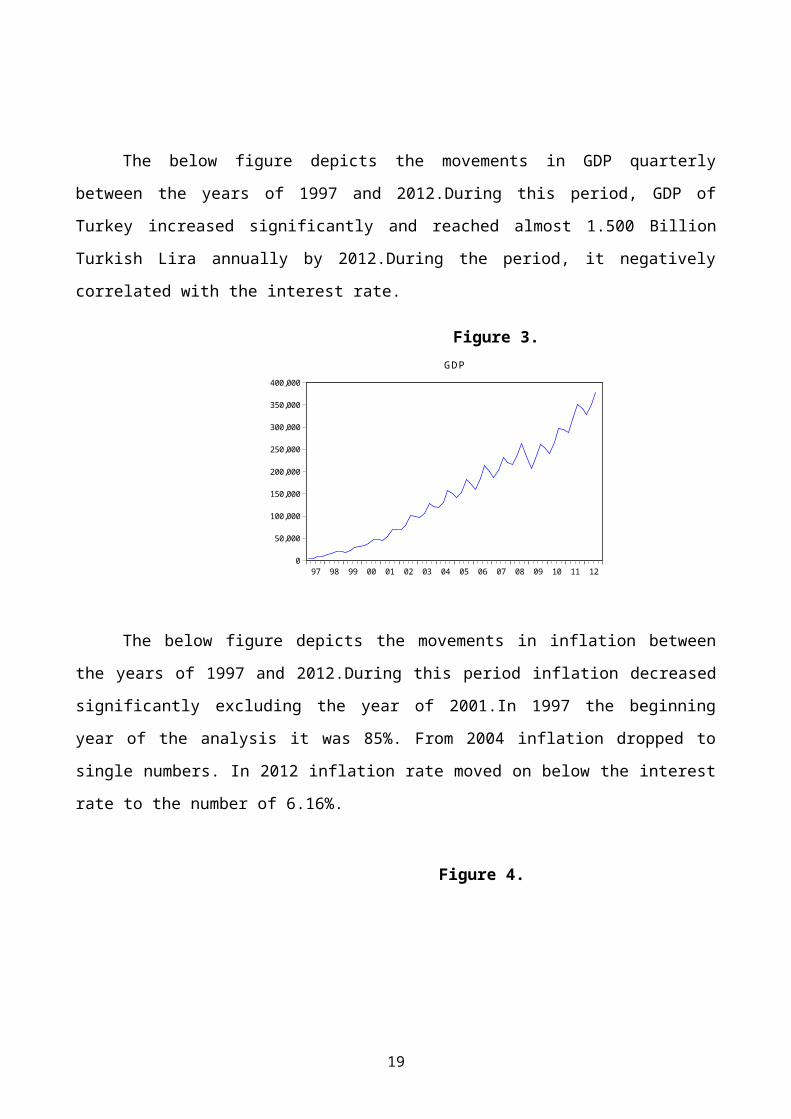

The below figure depicts the movements in GDP quarterly

between the years of 1997 and 2012.During this period, GDP of

Turkey increased significantly and reached almost 1.500 Billion

Turkish Lira annually by 2012.During the period, it negatively

correlated with the interest rate.

Figure 3.

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12

GDP

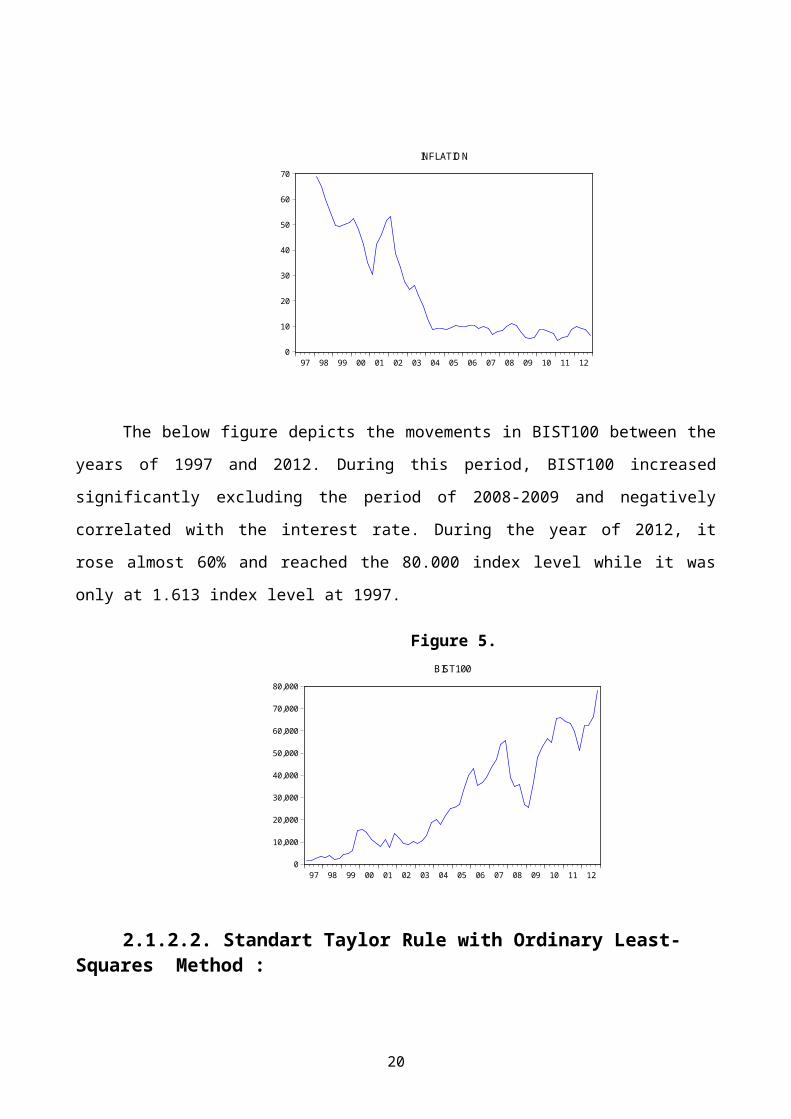

The below figure depicts the movements in inflation between

the years of 1997 and 2012.During this period inflation decreased

significantly excluding the year of 2001.In 1997 the beginning

year of the analysis it was 85%. From 2004 inflation dropped to

single numbers. In 2012 inflation rate moved on below the interest

rate to the number of 6.16%.

Figure 4.

19

0

10

20

30

40

50

60

70

97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12

INFLATIO N

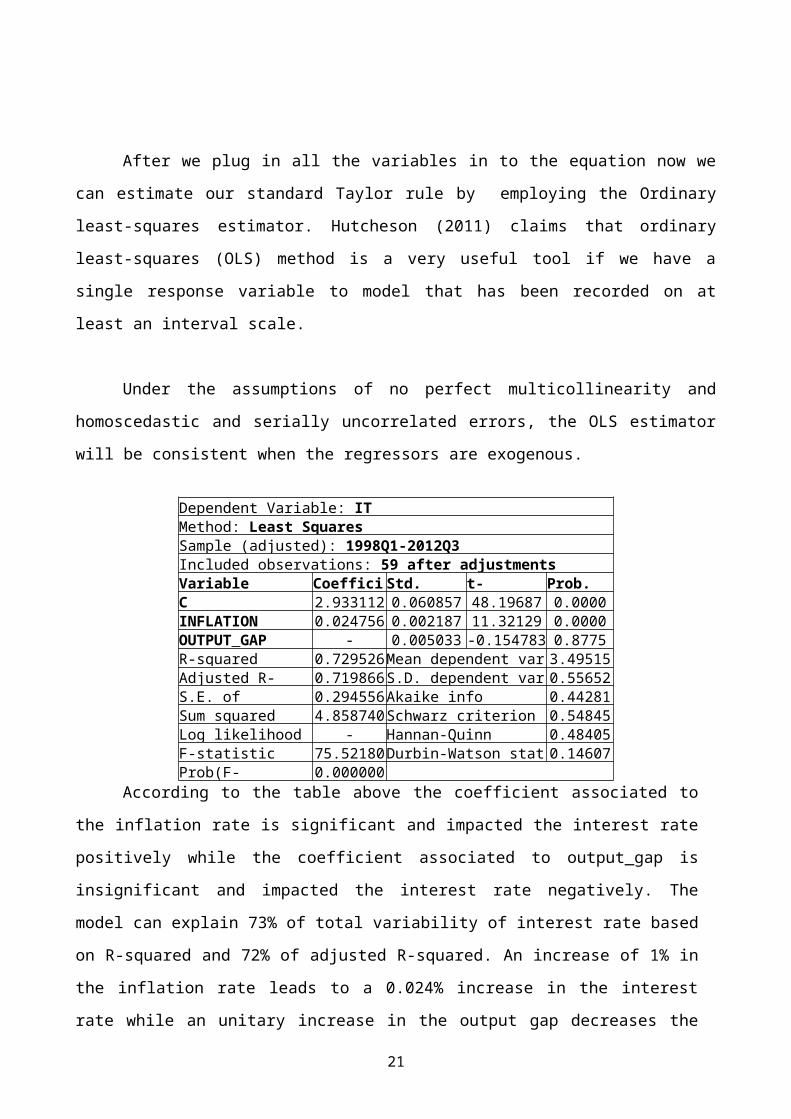

The below figure depicts the movements in BIST100 between the

years of 1997 and 2012. During this period, BIST100 increased

significantly excluding the period of 2008-2009 and negatively

correlated with the interest rate. During the year of 2012, it

rose almost 60% and reached the 80.000 index level while it was

only at 1.613 index level at 1997.

Figure 5.

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12

BIST100

2.1.2.2. Standart Taylor Rule with Ordinary Least-Squares Method :

20

After we plug in all the variables in to the equation now we

can estimate our standard Taylor rule by employing the Ordinary

least-squares estimator. Hutcheson (2011) claims that ordinary

least-squares (OLS) method is a very useful tool if we have a

single response variable to model that has been recorded on at

least an interval scale.

Under the assumptions of no perfect multicollinearity and

homoscedastic and serially uncorrelated errors, the OLS estimator

will be consistent when the regressors are exogenous.

Dependent Variable: ITMethod: Least SquaresSample (adjusted): 1998Q1-2012Q3Included observations: 59 after adjustmentsVariable Coeffici Std. t- Prob.C 2.933112 0.060857 48.19687 0.0000INFLATION 0.024756 0.002187 11.32129 0.0000OUTPUT_GAP - 0.005033 -0.154783 0.8775R-squared 0.729526Mean dependent var 3.49515Adjusted R- 0.719866S.D. dependent var 0.55652S.E. of 0.294556Akaike info 0.44281Sum squared 4.858740Schwarz criterion 0.54845Log likelihood - Hannan-Quinn 0.48405F-statistic 75.52180Durbin-Watson stat 0.14607Prob(F- 0.000000

According to the table above the coefficient associated to

the inflation rate is significant and impacted the interest rate

positively while the coefficient associated to output_gap is

insignificant and impacted the interest rate negatively. The

model can explain 73% of total variability of interest rate based

on R-squared and 72% of adjusted R-squared. An increase of 1% in

the inflation rate leads to a 0.024% increase in the interest

rate while an unitary increase in the output gap decreases the

21

interest rate by -0.000779%. In the model, the constant is

positive and indicates that when the output_gap and inflation are

zero, the stabilizing interest rate would be at the rate of

2.933112.The probability of F-statistic is zero which is a value

that support the correctness of the model and shows that our

regressors are jointly different from zero.According to this

argument the null hypothesis can be rejected.The final conclusion

of the OLS test points out that there might be a serial

correlation problem in the model since the DW statistic is more

than 10%.

2.1.2.3. The Wald Test:

Engle (1984) points out that in order to test the

aforementioned restriction, we need to set a Wald test which is

based upon Wald’s elegant analysis upon asymptotic approximation

to the T and F tests in econometrics.

According to Taylor (1993) output gap and the inflation own an

equal weight in shaping monetary policy.In order to do that both

second and third coefficient should be set equal to 50% The

Central Banks that adopts a more severe inflation targeting

policy should put more weight on inflation compared to the output

gap.According to that argument when we set the restriction as

all the coefficients are equal to 50%.The variations in the

dependent variable can not be explained by the independent

variables.

22

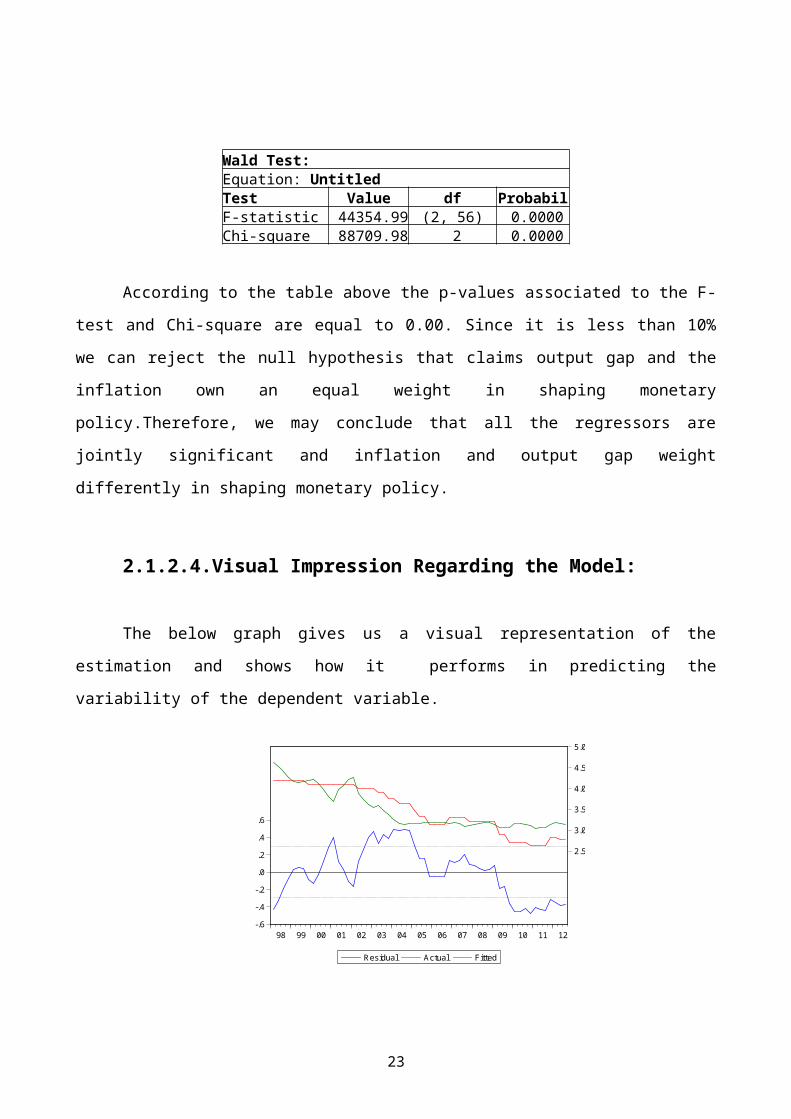

Wald Test:Equation: UntitledTest Value df ProbabilF-statistic 44354.99 (2, 56) 0.0000Chi-square 88709.98 2 0.0000

According to the table above the p-values associated to the F-

test and Chi-square are equal to 0.00. Since it is less than 10%

we can reject the null hypothesis that claims output gap and the

inflation own an equal weight in shaping monetary

policy.Therefore, we may conclude that all the regressors are

jointly significant and inflation and output gap weight

differently in shaping monetary policy.

2.1.2.4.Visual Impression Regarding the Model:

The below graph gives us a visual representation of the

estimation and shows how it performs in predicting the

variability of the dependent variable.

-.6

-.4

-.2

.0

.2

.4

.6

2.5

3.0

3.5

4.0

4.5

5.0

98 99 00 01 02 03 04 05 06 07 08 09 10 11 12

Residual Actual Fitted

23

The above model consistently underestimates the actual

interest rate from 1998 to 2009 while it overestimates it from

2009 onwards. Since the residual do not seem to be i.i.d. , we can

conclude the regression model misses something.

2.1.2.5.Chow Breakpoint Test:

On the basis of the visual representation of the estimation, a

possibility of omitted variables problem may rise. At this point

of the study, the presence of some shocks that can affect the

stability of the relationship under investigation will be checked

by chow breakpoint test.

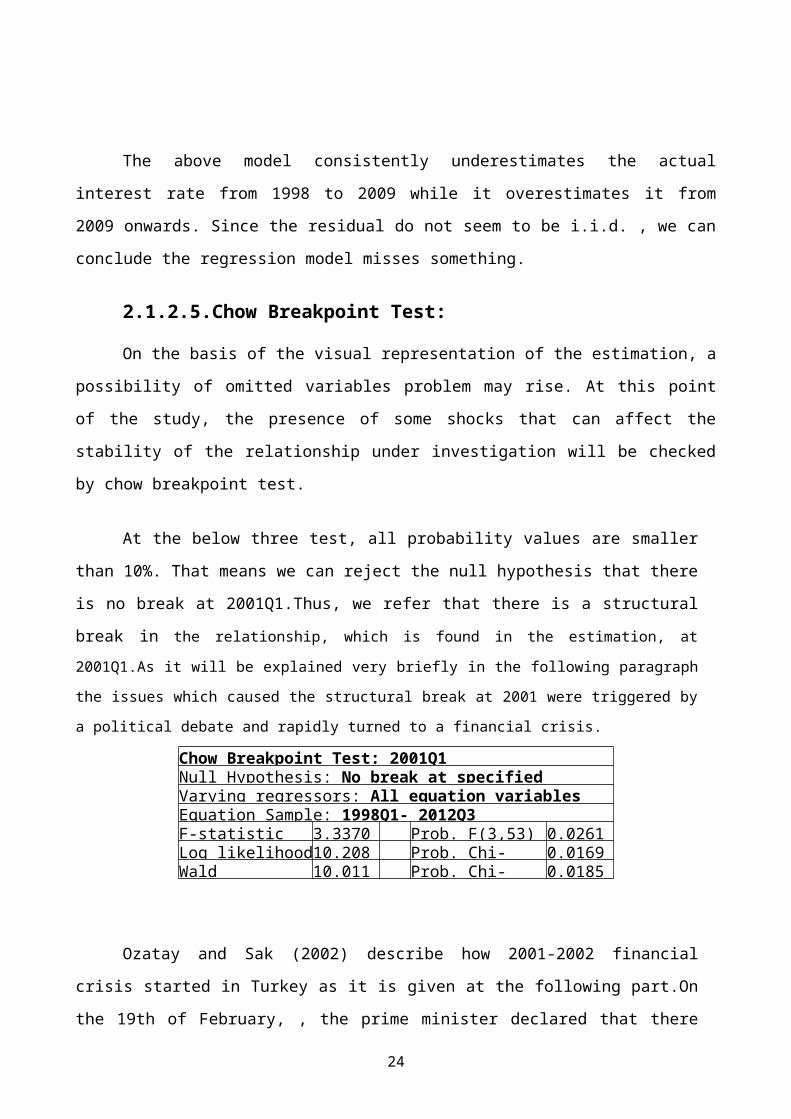

At the below three test, all probability values are smaller

than 10%. That means we can reject the null hypothesis that there

is no break at 2001Q1.Thus, we refer that there is a structural

break in the relationship, which is found in the estimation, at

2001Q1.As it will be explained very briefly in the following paragraph

the issues which caused the structural break at 2001 were triggered by

a political debate and rapidly turned to a financial crisis.

Chow Breakpoint Test: 2001Q1 Null Hypothesis: No break at specified Varying regressors: All equation variablesEquation Sample: 1998Q1- 2012Q3F-statistic 3.3370 Prob. F(3,53) 0.0261Log likelihood10.208 Prob. Chi- 0.0169Wald 10.011 Prob. Chi- 0.0185

Ozatay and Sak (2002) describe how 2001-2002 financial

crisis started in Turkey as it is given at the following part.On

the 19th of February, , the prime minister declared that there

24

was political conflict between him and the President soon after

he left the National Security Council meeting.After this

announcement the over-night rate increased to 2058% on the

following day and 4019% on the 21th of February.The banking

sector rushed to foreign currency. Since the US markets were closed

at that specific date, the Central Bank could not satisfy the foreign

currency demand of the banking sector.After the announcement about the

country was switching to a freely floating exchange rate system the

dollar rate jumped almost 40%.

2.1.2.6. Estimating The Augmented Taylor Rule:

As we mentioned before on chapter 2.1.1.4. according to

Castro (2008) a financial conditions index containing data from

the stock market movements can be included in the standard Taylor

rule to have an augmented version of it by including in equation

the variable “s” which measures the stock market value.The

augmented version of Taylor rule (ATR) is given below as equation

(2).

2.1.2.6.1.Ordinary Least-Squares Analysis (ATR):

In order to explain the variability of dependent variable

better we included the stock market value in the model.At the

table given below the coefficient associated to s(-1) which

25

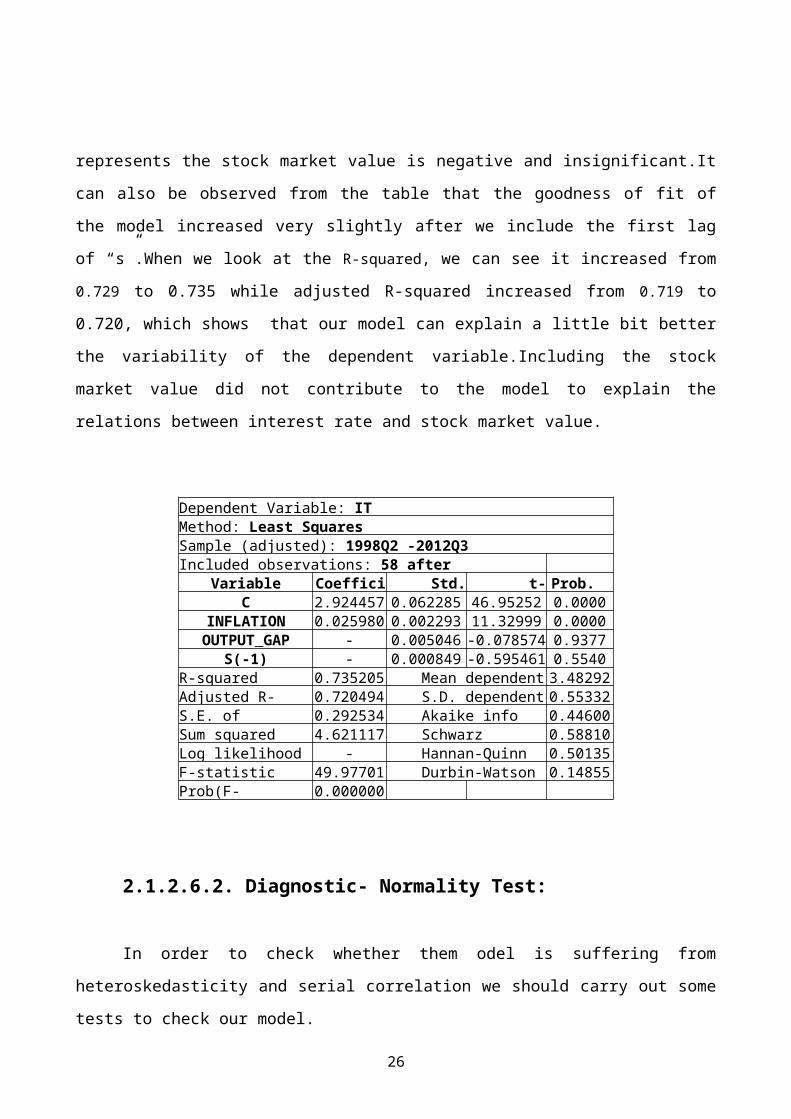

represents the stock market value is negative and insignificant.It

can also be observed from the table that the goodness of fit of

the model increased very slightly after we include the first lag

of “s”.When we look at the R-squared, we can see it increased from

0.729 to 0.735 while adjusted R-squared increased from 0.719 to

0.720, which shows that our model can explain a little bit better

the variability of the dependent variable.Including the stock

market value did not contribute to the model to explain the

relations between interest rate and stock market value.

Dependent Variable: ITMethod: Least SquaresSample (adjusted): 1998Q2 -2012Q3Included observations: 58 after

Variable Coeffici Std. t- Prob. C 2.924457 0.062285 46.95252 0.0000

INFLATION 0.025980 0.002293 11.32999 0.0000OUTPUT_GAP - 0.005046 -0.078574 0.9377

S(-1) - 0.000849 -0.595461 0.5540R-squared 0.735205 Mean dependent 3.48292Adjusted R- 0.720494 S.D. dependent 0.55332S.E. of 0.292534 Akaike info 0.44600Sum squared 4.621117 Schwarz 0.58810Log likelihood - Hannan-Quinn 0.50135F-statistic 49.97701 Durbin-Watson 0.14855Prob(F- 0.000000

2.1.2.6.2. Diagnostic- Normality Test:

In order to check whether them odel is suffering from

heteroskedasticity and serial correlation we should carry out some

tests to check our model.

26

0

1

2

3

4

5

6

-0.4 -0.2 0.0 0.2 0.4

Series: ResidualsSample 1998Q3 2012Q3Observations 57

Mean 3.17e-16Median 0.003373Maximum 0.529819Minimum -0.462369Std. Dev. 0.279457Skewness 0.113068Kurtosis 2.172355

Jarque-Bera 1.748319Probability 0.417213

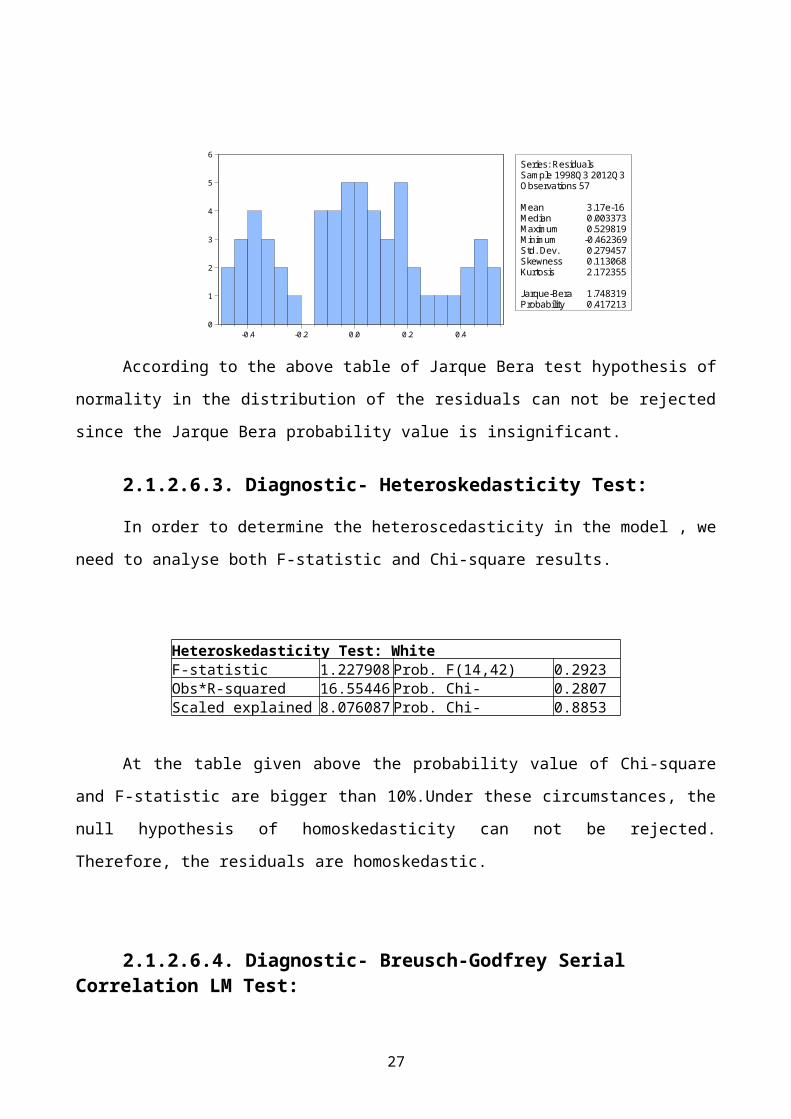

According to the above table of Jarque Bera test hypothesis of

normality in the distribution of the residuals can not be rejected

since the Jarque Bera probability value is insignificant.

2.1.2.6.3. Diagnostic- Heteroskedasticity Test:

In order to determine the heteroscedasticity in the model , we

need to analyse both F-statistic and Chi-square results.

Heteroskedasticity Test: WhiteF-statistic 1.227908 Prob. F(14,42) 0.2923Obs*R-squared 16.55446 Prob. Chi- 0.2807Scaled explained 8.076087 Prob. Chi- 0.8853

At the table given above the probability value of Chi-square

and F-statistic are bigger than 10%.Under these circumstances, the

null hypothesis of homoskedasticity can not be rejected.

Therefore, the residuals are homoskedastic.

2.1.2.6.4. Diagnostic- Breusch-Godfrey Serial Correlation LM Test:

27

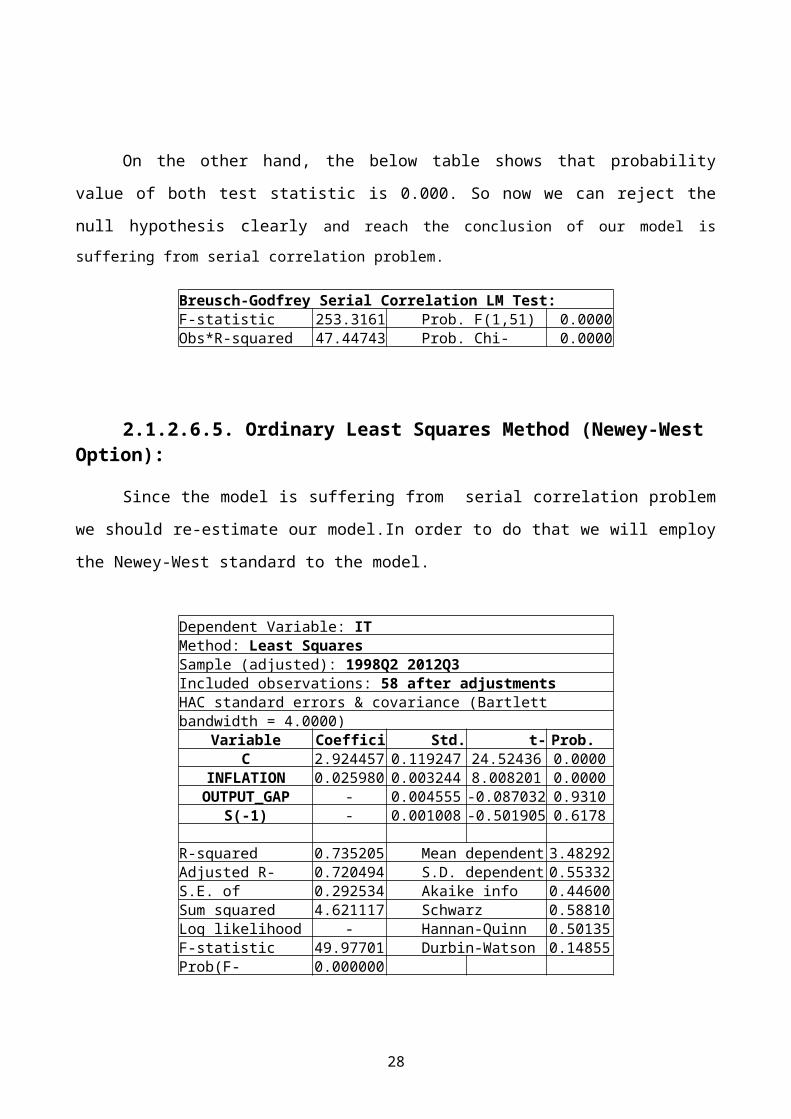

On the other hand, the below table shows that probability

value of both test statistic is 0.000. So now we can reject the

null hypothesis clearly and reach the conclusion of our model issuffering from serial correlation problem.

Breusch-Godfrey Serial Correlation LM Test:F-statistic 253.3161 Prob. F(1,51) 0.0000Obs*R-squared 47.44743 Prob. Chi- 0.0000

2.1.2.6.5. Ordinary Least Squares Method (Newey-West Option):

Since the model is suffering from serial correlation problem

we should re-estimate our model.In order to do that we will employ

the Newey-West standard to the model.

Dependent Variable: ITMethod: Least SquaresSample (adjusted): 1998Q2 2012Q3Included observations: 58 after adjustmentsHAC standard errors & covariance (Bartlett bandwidth = 4.0000)

Variable Coeffici Std. t- Prob. C 2.924457 0.119247 24.52436 0.0000

INFLATION 0.025980 0.003244 8.008201 0.0000OUTPUT_GAP - 0.004555 -0.087032 0.9310

S(-1) - 0.001008 -0.501905 0.6178

R-squared 0.735205 Mean dependent 3.48292Adjusted R- 0.720494 S.D. dependent 0.55332S.E. of 0.292534 Akaike info 0.44600Sum squared 4.621117 Schwarz 0.58810Log likelihood - Hannan-Quinn 0.50135F-statistic 49.97701 Durbin-Watson 0.14855Prob(F- 0.000000

28

In order to correct the estimation, the Newey-West standard

errors were employed to the model.At the table, the results of

this correction can be seen. Under the projection of new results,

both stock market value and output_gap are negative and

insignificant.

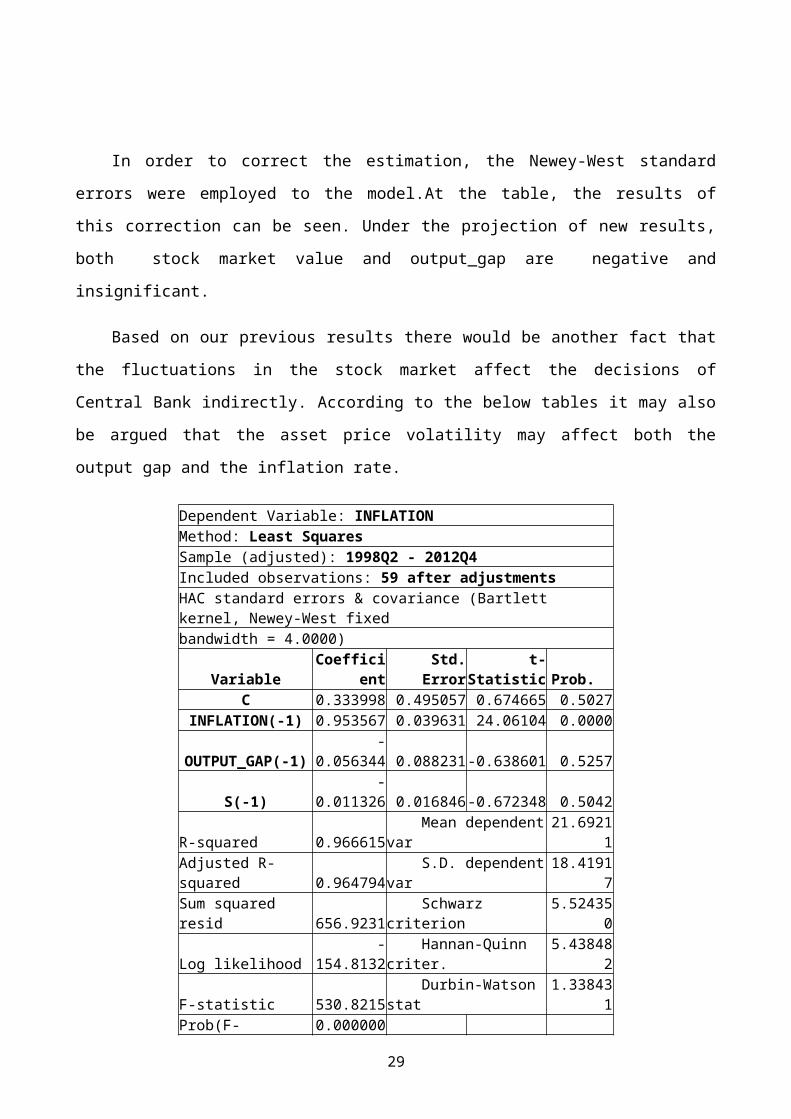

Based on our previous results there would be another fact that

the fluctuations in the stock market affect the decisions of

Central Bank indirectly. According to the below tables it may also

be argued that the asset price volatility may affect both the

output gap and the inflation rate.

Dependent Variable: INFLATIONMethod: Least SquaresSample (adjusted): 1998Q2 - 2012Q4Included observations: 59 after adjustmentsHAC standard errors & covariance (Bartlett kernel, Newey-West fixedbandwidth = 4.0000)

VariableCoeffici

entStd.

Errort-

Statistic Prob. C 0.333998 0.495057 0.674665 0.5027

INFLATION(-1) 0.953567 0.039631 24.06104 0.0000

OUTPUT_GAP(-1)-

0.056344 0.088231-0.638601 0.5257

S(-1)-

0.011326 0.016846-0.672348 0.5042

R-squared 0.966615 Mean dependentvar

21.69211

Adjusted R-squared 0.964794

S.D. dependentvar

18.41917

Sum squared resid 656.9231

Schwarz criterion

5.524350

Log likelihood-

154.8132 Hannan-Quinn criter.

5.438482

F-statistic 530.8215 Durbin-Watson stat

1.338431

Prob(F- 0.000000

29

statistic)

At the above table inflation is added to the model as a

dependent variable.The results show that the probability value of

the stock market index is negative and insignificant. On the other

hand at the below table output_gap is added to the model as a

dependent variable and the results show that the probability value

of the stock market index is positive but still insignificant.

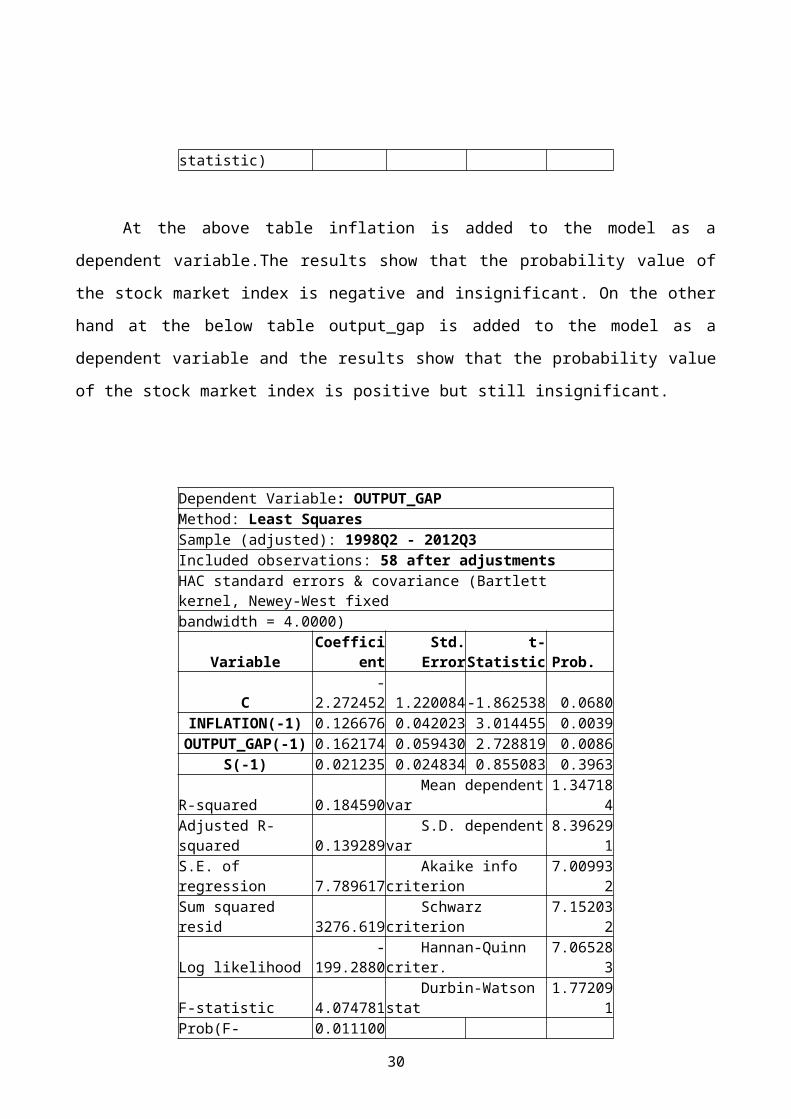

Dependent Variable: OUTPUT_GAPMethod: Least SquaresSample (adjusted): 1998Q2 - 2012Q3Included observations: 58 after adjustmentsHAC standard errors & covariance (Bartlett kernel, Newey-West fixedbandwidth = 4.0000)

VariableCoeffici

entStd.

Errort-

Statistic Prob.

C-

2.272452 1.220084-1.862538 0.0680INFLATION(-1) 0.126676 0.042023 3.014455 0.0039OUTPUT_GAP(-1) 0.162174 0.059430 2.728819 0.0086

S(-1) 0.021235 0.024834 0.855083 0.3963

R-squared 0.184590 Mean dependentvar

1.347184

Adjusted R-squared 0.139289

S.D. dependentvar

8.396291

S.E. of regression 7.789617

Akaike info criterion

7.009932

Sum squared resid 3276.619

Schwarz criterion

7.152032

Log likelihood-

199.2880 Hannan-Quinn criter.

7.065283

F-statistic 4.074781 Durbin-Watson stat

1.772091

Prob(F- 0.011100

30

statistic)

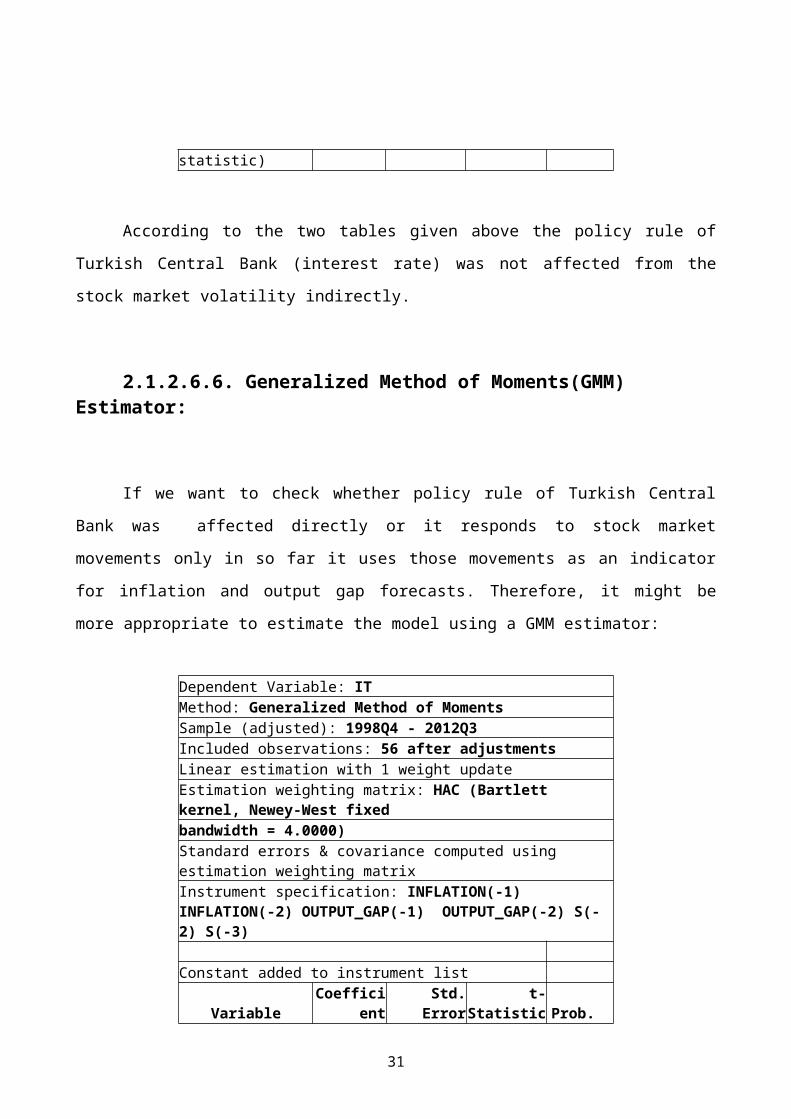

According to the two tables given above the policy rule of

Turkish Central Bank (interest rate) was not affected from the

stock market volatility indirectly.

2.1.2.6.6. Generalized Method of Moments(GMM) Estimator:

If we want to check whether policy rule of Turkish Central

Bank was affected directly or it responds to stock market

movements only in so far it uses those movements as an indicator

for inflation and output gap forecasts. Therefore, it might be

more appropriate to estimate the model using a GMM estimator:

Dependent Variable: ITMethod: Generalized Method of MomentsSample (adjusted): 1998Q4 - 2012Q3Included observations: 56 after adjustmentsLinear estimation with 1 weight updateEstimation weighting matrix: HAC (Bartlett kernel, Newey-West fixedbandwidth = 4.0000)Standard errors & covariance computed using estimation weighting matrixInstrument specification: INFLATION(-1) INFLATION(-2) OUTPUT_GAP(-1) OUTPUT_GAP(-2) S(-2) S(-3)

Constant added to instrument list

VariableCoeffici

entStd.

Errort-

Statistic Prob.

31

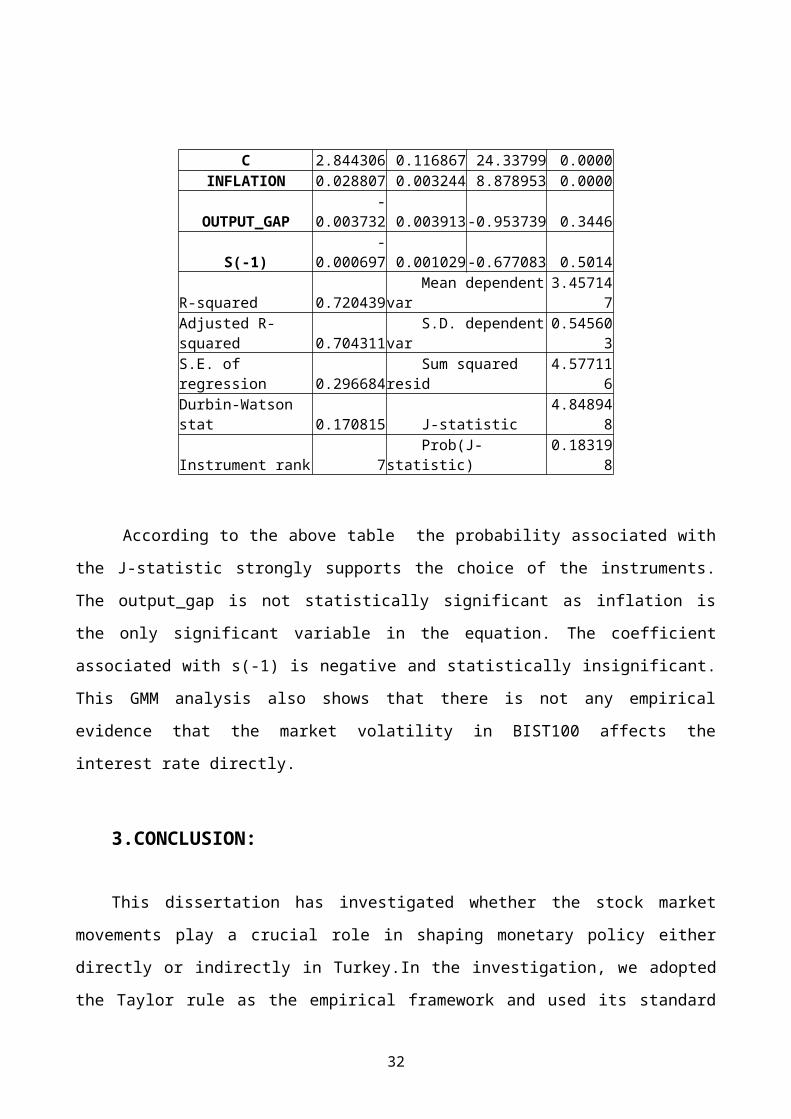

C 2.844306 0.116867 24.33799 0.0000INFLATION 0.028807 0.003244 8.878953 0.0000

OUTPUT_GAP-

0.003732 0.003913-0.953739 0.3446

S(-1)-

0.000697 0.001029-0.677083 0.5014

R-squared 0.720439 Mean dependentvar

3.457147

Adjusted R-squared 0.704311

S.D. dependentvar

0.545603

S.E. of regression 0.296684

Sum squared resid

4.577116

Durbin-Watson stat 0.170815 J-statistic

4.848948

Instrument rank 7 Prob(J-statistic)

0.183198

According to the above table the probability associated with

the J-statistic strongly supports the choice of the instruments.

The output_gap is not statistically significant as inflation is

the only significant variable in the equation. The coefficient

associated with s(-1) is negative and statistically insignificant.

This GMM analysis also shows that there is not any empirical

evidence that the market volatility in BIST100 affects the

interest rate directly.

3.CONCLUSION:

This dissertation has investigated whether the stock market

movements play a crucial role in shaping monetary policy either

directly or indirectly in Turkey.In the investigation, we adopted

the Taylor rule as the empirical framework and used its standard

32

and augmented versions in order to reach a conclusion. Right from

the beginning at every stage of the investigation all the tests

results we obtained show that the stock market movements do not

play a crucial role in shaping monetary policy neither directly

nor indirectly in Turkey.

As we mentioned before at previous chapters of our

investigation Turkish economy showed an outstanding performance

between the years of 1997 and 2012.During the period, the

inflation rate dropped to %6.16 from %85 and parallel to the

inflation rate interest rate dropped almost %60 while GDP rose

almost %4 annually in average. Additionally BIST100, the stock

market value of Turkey rose almost 60% in 2012 and reached the

80.000 index level while it was only at 1.613 index level at 1997.

All those macro economic data of Turkey given above and our

test results together show that during our investigation period,

Turkish Central Bank’s policy rule was to achieve and maintain

price stability which is also its primary objective that was given

by the law.The Central Bank of Turkey aimed to achieve and

maintain price stability at the first place while it was also

supporting a sustainable growth and increased employment instead

of supporting the stock market. At the end of the investigation,

we can claim that there is not any empirical evidence that

supports the hypothesis of the stock market movements play a

crucial role in shaping monetary policy directly or indirectly in

Turkey.

33

REFERENCES

Allen, F. and D. Gale (2000), “Bubbles and Crises”, The Economic

Journal, 110, pp. 236-55.

Taylor, John B., (1993). “Discretion Versus Policy Rules in

Practice", Carnegie-Rochester Conference Series on Public Policy 39,pp.195-214

34

Bernanke, B. S. , Mihov, I., (1998). ‘‘Measuring Monetary

Policy’’, The Quarterly Journal of Economics, Vol. 113, No. 3., pp.869-

902.

Bernanke, B. S. , Gertler, M. (2000). “Monetary Policy And Asset

Price Volatility” NBER Working Paper, No. 7559.

Bernanke, B. S. and Gertler, M. (2001). “Should central banks

respond to movements in asset prices?”, American Economic Review,

91(2), pp. 253-257.

Bean, C.R., (2004). “Asset Prices, Financial Instability and

Monetary Policy”, The American Economic Review,Vol. 94, No. 2, pp. 14-18

Bordo, M.D., Jeanne, O. (2002). “Boom-Busts In Asset Prices,

Economic Instability And Monetary Policy” NBER Working Paper, No. 8966

Borsa İstanbul, (2013). Corporate, (online). Available at

http://borsaistanbul.com/en/corporate/about-borsa-istanbul/about-

us, (accesed) 04.08.2013

Castro, V.M.A. (2008) “Are Central Banks following a linear or

nonlinear (augmented) Taylor rule?”, “Working Paper”, University of

Warwick, Department of Economics, Coventry.

35

Cecchetti, S., Genberg, H. and Wadhwani, S. (2002). “Asset Prices

In a Flexible Inflation Targetting Framework”, NBER Working Paper No.

8970.

Engle, R. F. ,(1984).”Wald, Likelihood Ratio, and Lagrange

Multiplier Tests in Econometrics”, Handbook of Econometrics, Volume II,

pp.776-825

Frait, J., Komarek, L., (2006). “Monetary Policy and Asset

Prices,What Role for Central Banks in New EU Member States”,

Warwick Economic Research Papers, No.738

Generalized Method of Moments Estimation, Hansen, L.P., (2007).

(online). Available at http://home.uchicago.edu/.../ Generalized

Method Of Moments (accesed) 02.08.2013

Gilchrist, S., Leahy, J.V., (2002). “Monetary Policy and Asset

Price”, Journal of Monetary Economics,No.49, pp.75-97

Godhart, C., Hofmann, B., (2000). “Do Asset Prices Help to Predict

Consumer Price Index”, The Manchester School Supplement, No.1463-6786,

pp.122-140

Hutcheson, G. D. (2011). “Ordinary Least-Squares Regression”, The

SAGE Dictionary of Quantitative Management Research, Pp.224-228

36

Koichiro Kamada, K. , Muto, I. (2000). “Forward-looking Models

and Monetary Policy in Japan”, Research and Statistic Department, Bank of

Japan, April 2000

Keynes, J. M., (1923). “A tract on monetary reform”, London: Macmillan.

Mavroeidis, S., (2004). “Weak identification of forward-looking

models in monetary economics” Discussion Paper: 2004/06, Department of

Quantitative Economics, University of Amsterdam

Mishkin, F.S. (2012).“The Economics of Money, Banking and Financial Markets”

Global Edition 10. edition, Pearson Education Limited,Harlow,UK

Ozatay, F. , G. Sak (2002). “The 2000-2001 Financial Crisis in

Turkey”, Paper presented at the Currency Crisis Conference of the Brookings

Institution, May 2002, Washington, D.C

SERPAM , (2013). “Türkiye Sermaye Piyasası 2012 Yılı Raporu”,

University of Istanbul SERPAM Research Papers.

37