management research review article information: users who downloaded this article also downloaded:...

TRANSCRIPT

Management Research ReviewClient satisfaction in Indian banks: an empirical studyAayushi Gupta Santosh Dev

Article information:To cite this document:Aayushi Gupta Santosh Dev, (2012),"Client satisfaction in Indian banks: an empirical study", ManagementResearch Review, Vol. 35 Iss 7 pp. 617 - 636Permanent link to this document:http://dx.doi.org/10.1108/01409171211238839

Downloaded on: 30 September 2014, At: 03:56 (PT)References: this document contains references to 88 other documents.To copy this document: [email protected] fulltext of this document has been downloaded 1342 times since 2012*

Users who downloaded this article also downloaded:Terrence Levesque, Gordon H.G. McDougall, (1996),"Determinants of customer satisfaction in retailbanking", International Journal of Bank Marketing, Vol. 14 Iss 7 pp. 12-20Koushiki Choudhury, (2013),"Service quality and customers’ purchase intentions: an empirical studyof the Indian banking sector", International Journal of Bank Marketing, Vol. 31 Iss 7 pp. 529-543 http://dx.doi.org/10.1108/IJBM-02-2013-0009Hayat Muhammad Awan, Khuram Shahzad Bukhari, Anam Iqbal, (2011),"Service quality and customersatisfaction in the banking sector: A comparative study of conventional and Islamic banks in Pakistan",Journal of Islamic Marketing, Vol. 2 Iss 3 pp. 203-224

Access to this document was granted through an Emerald subscription provided by 527677 []

For AuthorsIf you would like to write for this, or any other Emerald publication, then please use our Emerald forAuthors service information about how to choose which publication to write for and submission guidelinesare available for all. Please visit www.emeraldinsight.com/authors for more information.

About Emerald www.emeraldinsight.comEmerald is a global publisher linking research and practice to the benefit of society. The companymanages a portfolio of more than 290 journals and over 2,350 books and book series volumes, as well asproviding an extensive range of online products and additional customer resources and services.

Emerald is both COUNTER 4 and TRANSFER compliant. The organization is a partner of the Committeeon Publication Ethics (COPE) and also works with Portico and the LOCKSS initiative for digital archivepreservation.

*Related content and download information correct at time of download.

Dow

nloa

ded

by J

AY

PEE

IN

STIT

UT

E O

F IN

FOR

MA

TIO

N T

EC

HN

OL

OG

Y U

NIV

ER

SIT

Y N

OID

A A

t 03:

56 3

0 Se

ptem

ber

2014

(PT

)

Client satisfaction in Indianbanks: an empirical study

Aayushi Gupta and Santosh DevHumanities and Social Sciences Department,

Jaypee Institute of Information Technology, Noida, India

Abstract

Purpose – The purpose of this paper is to identify the factors impacting customer satisfaction inIndian banks and analyze their effects the level of customer satisfaction through a regression analysis.The primary contribution of this study is the analysis and resulting insights on the critical factorsimpacting client satisfaction within the Indian retail banking sector.

Design/methodology/approach – A 28 item questionnaire was prepared based on literature reviewand discussions with current customers of Indian banks. The questionnaire was then sent out to currentcustomers of 13 retail banks in India. In total, 420 completed questionnaires were received, out of which400 were found to have been accurately and completely answered. The 28-item instrument has beenempirically tested for unidimensionality, reliability and validity using Cronbach alpha and exploratoryfactor analysis.

Findings – A factor analysis suggests that there are five factors driving customer satisfaction: “servicequality”, “ambience/hygiene”, “client participation/involvement”, “accessibility” and “financial”.Subsequent multiple regression analysis revealed that “service quality”, “ambience and hygiene”, and“client participation and involvement” in that order are the most important factors impacting clientsatisfaction.

Practical implications – The identified dimensions are expected to bring clarity to the issue ofcustomer satisfaction in retail banking, to aid retail bankers in improving specific parameters of servicein order to increase overall customer satisfaction. This would help the management of the banks tocreate strategies and action plans to retain their current customers and to attract new customers.

Originality/value – The results from the current study are crucial because previous studies haveproduced scales that bear a resemblance to SERVQUAL, a generic measure of service quality, whichmay not be solely adequate to assess the perceived quality of service in the Indian banking sector. Incontrast, the present study captured customers’ satisfaction levels in a 28-item questionnaire exclusivelydesigned, keeping in mind the unique nature of the Indian banking sector.

Keywords India, Banks, Customer satisfaction, Customer service management

Paper type Research paper

1. IntroductionThere is no denying the fact that India’s economic growth has been accelerated by theexpansion of the banking system. The Indian banking industry has registeredspectacular growth during the past decade. Banking is a service industry and delivers itsservices across the counter to the ultimate customer. If a satisfied customer has potentialto influence and bring in 100 new customers, a dissatisfied customer can potentiallyinfluence 1,000 customers (Sangwan, 2009). A satisfied customer is the best ambassadorand salesman for a retail bank.

The banking industry in India has undergone sea change post independence.More recently, liberalisation, the opening up of the economy in the 1990s and thegovernment’s decision to privatise banks by reduction in state ownership culminated inthe banking reforms based on the recommendations of the Narasimham committee.

The current issue and full text archive of this journal is available at

www.emeraldinsight.com/2040-8269.htm

Clientsatisfaction

617

Management Research ReviewVol. 35 No. 7, 2012

pp. 617-636q Emerald Group Publishing Limited

2040-8269DOI 10.1108/01409171211238839

Dow

nloa

ded

by J

AY

PEE

IN

STIT

UT

E O

F IN

FOR

MA

TIO

N T

EC

HN

OL

OG

Y U

NIV

ER

SIT

Y N

OID

A A

t 03:

56 3

0 Se

ptem

ber

2014

(PT

)

Like any other financial services, the banking industry, too, is facing a market that ischanging rapidly. New technologies are being introduced and there is always a fear ofeconomic uncertainties. Fierce competition, more demanding customers and thechanging climate have presented an unparalleled set of challenges (Lovelock, 2001).This has led the Indian banking industry to experience difficult times. In such testingtimes of mature and acute competitive pressures, it is very urgent and important thatbanks are able to retain a loyal base of clients. To attain this and to improve their marketand profit positions, banks in India have to formulate their strategies and policiestowards increasing customer satisfaction levels.

Banking institutions across the globe have recognized the importance of customersatisfaction and of developing and maintaining enduring relationship with theircustomers as two crucial parameters leading to increased business profits. At the sametime, several banking institutions are experiencing increasing level of retail customerdissatisfaction. Research suggests that customer dissatisfaction is still the major reasonof bank customers’ switch to other banks (Manrai and Manrai, 2007). This dissatisfactioncould be because of a variety of reasons (access, services, products, prices, image,personnel skills, treatment, credibility, responsiveness, waiting time, location,technology, and store appearance).

Therefore, the present study aims to identify the factors impacting customersatisfaction in Indian banks and investigate the effects of these factors on the level ofsatisfaction of banking customers.

2. Literature reviewCustomer satisfaction is one of the important outcomes of marketing activity (Oliver,1980; Surprenant and Churchill, 1982; Spreng et al., 1996; Mick and Fournier, 1999).It serves to link processes culminating purchase and consumption with post purchasephenomena such as attitude change, repeat purchase, and brand loyalty (Surprenant andChurchill, 1982). This opinion has been supported by Jamal and Naser (2003) and Mishra(2009). Customer satisfaction is generally described as fully meeting their expectationand is the feeling or attitude of a customer towards a product or service after it has beenused (Oliver, 1980). Likewise, many researchers (Oliver, 1981; Brady and Robertson,2001) conceptualize customer satisfaction as an individual’s feeling of pleasure ordisappointment resulting from comparing a product’s perceived performance(or outcome) in relation to his or her expectations.

Customer satisfaction has been considered the essence of success in today’s highlycompetitive banking industry. Prabhakaran and Satya (2003) mentioned that thecustomer is the king. Heskett et al. (1997) argued that profit and growth are stimulatedprimarily by customer loyalty. Ndubisi (2005), Gee et al. (2008) and Pfeifer (2005) pointedout that the cost of serving a loyal customer is five or six times less than a new customer.Several researchers including Tariq and Moussaoui (2009), Han et al. (2008) and Ehigie(2006) found that loyalty is a direct outcome of customer satisfaction. Generallyspeaking, if the customers are satisfied with the provided goods or services, theprobability that they use the services again increases (East, 1997). Also, satisfiedcustomers will most probably talk enthusiastically about their buying or the use of aparticular service; this will lead to positive advertising (File and Prince, 1992; Richens,1983). On the other hand, dissatisfied customers will most probably switch to a differentbrand; this will lead to negative advertising (Nasserzadeh et al., 2008). The significance

MRR35,7

618

Dow

nloa

ded

by J

AY

PEE

IN

STIT

UT

E O

F IN

FOR

MA

TIO

N T

EC

HN

OL

OG

Y U

NIV

ER

SIT

Y N

OID

A A

t 03:

56 3

0 Se

ptem

ber

2014

(PT

)

of satisfying and keeping a customer in establishing strategies for a market andcustomer oriented organization cannot be ignored (Kohli and Jaworski, 1990).

Most of the researchers found that service quality is the antecedent of customersatisfaction (Bedi, 2010; Kassim and Abdullah, 2010; Kumar et al., 2010; Yee et al., 2010;Kumar et al., 2009; Naeem and Saif, 2009; Balaji, 2009; Parasuraman et al., 1988). Qualitycustomer service and satisfaction are recognized as the most important factors for bankcustomer acquisition and retention (Jamal, 2004; Armstrong and Seng, 2000; Lassar et al.,2000). Service quality is considered as one of the critical success factors that influence thecompetitiveness of an organization. A bank can differentiate itself from competitors byproviding high quality service. Service quality is one of the most attractive areas forresearchers over the last decade in the retail banking sector (Avkiran, 1994; Stafford,1996; Johnston and Jeffrey, 1996; Angur et al., 1999; Lassar et al., 2000; Bahia and Nantel,2000; Sureshchandar et al., 2002; Gounaris et al., 2003; Choudhury, 2008).

Gronroos (1994) defined service as:

A service is a process consisting of a series of more or less intangible activities that normally,but not necessarily always, take place in interactions between the customer and serviceemployees and/or physical resources or goods and/or systems of the service provider, whichare provided as solutions to customer problems.

Services have unique characteristics that distinguish them from the physical goods(Zeithaml and Bitner, 1996). Services are often characterized by intangibility,inseparability, heterogeneity, and perishability (Lovelock, 2001). The importance of theabove characterizations is that using them for evaluation before, while, and after using aparticular service by the customers is often very hard (Legg and Baker, 1996). Because ofthe quality of being intangible, understanding how the customers would evaluate thequality of the organization’s services is often very hard (Zeithaml and Bitner, 1996). Inaddition, the services are real time, i.e. they are used by the customers as soon as offered.They cannot be stored and quality passed like physical goods. Therefore, any bad servicewill most probably be experienced by a customer, which results in customer’sdissatisfaction while using the service (East, 1997).

The foundations of service quality may be viewed from widely accepted perspectivesof the SERVQUAL model. SERVQUAL offers five dimensions of service quality to beevaluated in any service setting; reliability, responsiveness, assurance, empathy, andtangibles (Parasuraman et al., 1988), and it has been widely used in practice in its originaland modified form (Levesque and McDougall, 1996). Over the past two decades, a varietyof SERVQUAL-related studies has been undertaken within the banking industry(Avkiran, 1994; Bahia and Nantel, 2000). A review of current literature identified threecategories of SERVQUAL-related studies (Guo et al., 2008). First, replication studies haveassessed the applicability of the SERVQUAL model to the retailing banking industry.Blanchard and Galloway (1994) interviewed both 439 current account customers and39 bank staff in the UK, concluding that the bank staff sample confirmed the gapsapproach, providing some support for the application of SERVQUAL within UK retailbanking. Newman (1996) presented an empirical study of major quality improvementinitiatives undertaken by two British banks. SERVQUAL was administered firstto a bank’s 500 customers and 1,350 customers of its main competitors, and second to84,000 bank customers. Newman reported that both banks were able to report animprovement in service quality and fresh evidence was provided in favour of theSERVQUAL model.

Clientsatisfaction

619

Dow

nloa

ded

by J

AY

PEE

IN

STIT

UT

E O

F IN

FOR

MA

TIO

N T

EC

HN

OL

OG

Y U

NIV

ER

SIT

Y N

OID

A A

t 03:

56 3

0 Se

ptem

ber

2014

(PT

)

Second, comparative studies between SERVQUAL and other service quality modelshave been undertaken in the banking service sector. Cronin and Taylor (1992) comparedSERVQUAL with three competing models (i.e. SERVPERF, an importance-weightedversion of the SERVQUAL scale and an importance-weighted version of the SERVPERFscale), by surveying 660 customers of banking, pest control, dry cleaning and fast food inthe USA. The study yielded a unidimensional model of service quality. Furthermore,Cronin and Taylor (1992) found that the performance-based SERVPERF scale is a moreappropriate means of measuring the service quality construct. Angur et al. (1999)undertook a replication study of Cronin and Taylor (1992) comparative analysis in India.Using a sample of 143 retail banking customers, their findings contradict Cronin andTaylor (1992), reporting that SERVQUAL provides more diagnostic information thanSERVPERF, with the caveat that the five dimensions do not seem to be completelyapplicable to the specific service setting. Cui et al. (2003) also undertook a replicationstudy of Cronin and Taylor (1992) in South Korea, sampling 153 retail banking customers.Cui et al.’s results suggest that both SERVQUAL and SERVPERF are multidimensionalmeasures, but lack construct validity. In addition, Lassar et al. (2000) administratedSERVQUAL along with the technical/functional quality model to 65 international privatebanking customers in an effort to empirically compare their ability to predict levels ofcustomer satisfaction. They reported that the technical/functional quality model was asuperior predictor of customer satisfaction compared to SERVQUAL (Lassar et al., 2000).

Third, researchers have developed niche models which could outperform SERVQUALin specific banking service contexts. Avkiran (1994) created his inventory of retail bankingservice attributes by surveying 791 retail banking customers in Australia, proposing ascale called BANKSERV with 17 items across four discriminating dimensions: staffconduct, credibility, communication, and access to teller services. Bahia and Nantel (2000)developed a specific new scale for perceived service quality in retail banking in their studyperformed in Canada. This bank service quality (BSQ) model was an extension of theoriginal ten dimensions of the model of Parasuraman incorporating additional items suchas courtesy, price, and access. Bahia and Nantel (2000) mentioned that in subsequentreplications, primary qualitative research with bank customers should be a priority. BSQcomprised 31 items, with six dimensions labelled: effectiveness and assurance, access,price, tangibles, services portfolio, and reliability (Bahia and Nantel, 2000). In comparingBSQ with SERVQUAL, Bahia and Nantel (2000) argued that the main advantage of BSQ forbanks is related to its content validity. For example, the services portfolio dimension andthe price dimension of BSQ are absent from SERVQUAL (Petridou et al., 2007). The mainlimitation of BSQ lies in the fact that the scale construction is entirely based on “expert”opinions and published literature. Guo et al. (2008) created Chinese Banking Service Quality(CBSQ) measurement instrument; constructs were utilised from the generic service qualityliterature, Chinese business culture and through interviews with 18 financial managers.CBSQ was administered to 259 corporate customers in China. Exploratory andconfirmatory factor analyses were used to assist data reduction, test hypothesised models,and refine scales. Factor analysis identified that service quality in Chinese corporatebanking is measured by a nested model, consisting of two higher-order constructs (i.e.functional quality and technical quality) and four lower-order dimensions (i.e. reliability,human capital, technology, and communication). Kumar et al. (2010) developed modifiedSERVQUAL model consisting of four critical factors (dimensions) as detected by factoranalysis: tangibility, reliability, competence, and convenience. There study aimed to find

MRR35,7

620

Dow

nloa

ded

by J

AY

PEE

IN

STIT

UT

E O

F IN

FOR

MA

TIO

N T

EC

HN

OL

OG

Y U

NIV

ER

SIT

Y N

OID

A A

t 03:

56 3

0 Se

ptem

ber

2014

(PT

)

the differences in the service quality (if any) between two types of banks, namelyconventional and Islamic, from different parts of Malaysia using a sample of 308 bankcustomers. The results revealed that the expectations on competence and convenience aresignificantly different between conventional banks and Islamic banks, whereas theperceptions on tangibility and convenience are found to be significantly different betweenthese two types of banks. In India, Choudhury (2008) explored the dimensions of customerperceived service quality in the context of the Indian retail banking industry. Theseparameters were used in the context of four of the largest banks in India to identify theunderlying dimensions of service quality, using factor analysis. The study suggested thatcustomers distinguish four dimensions of service quality in the case of the retail bankingindustry in India, namely, attitude, competence, tangibles, and convenience.

Though, the SERVQUAL model has been the major generic model used to measure andmanage service quality across different service settings and various culturalbackgrounds, a number of theoretical and empirical criticisms of the measurementmodel have been pointed out. (Buttle, 1996; Van Dyke et al., 1997, 1999; Ladhari, 2008).More significantly, the universality of its five dimensions across different types of serviceshad been questioned in a number of subsequent studies (Babakus and Mangold, 1989;Carman, 1990; Finn and Lamb, 1991; Fick and Ritchie, 1991; Babakus and Boller, 1992).Moreover, these five dimensions are not sufficiently generic. Also, there has been anargument that a simple revision of the SERVQUAL items is not enough for measuringservice quality across different service settings. As a result, Ladhari (2008, p. 68) statedthat “It has been suggested that industry-specific measures of service quality might bemore appropriate than a single generic scale”. This argument was supported byDabholkar et al. (1996, p. 14) who stated that “It appears that a measure of service qualityacross industries is not feasible; therefore, future research on service quality shouldinvolve the development of industry-specific measures of service quality”. Manyresearchers including Van Dyke et al. (1997, 1999) and Ladhari (2008) recognized a numberof conceptual and empirical criticisms of SERVQUAL. First, they argued that the use ofgap scores is not the right method because of the lack of the support in literature toconsumers evaluating service quality in terms of perception-minus-expectation. Theystated that it has been recommended that service quality is more precisely and correctlyevaluated by measuring only perceptions of quality. On the other hand, they mentionedthat the concept expectation is not well defined and can be interpreted from differentperspectives; as a result, the operationalisation of SERVQUAL may have differentinterpretations as well. In addition, they pointed out that previous research suggestedusing perception-only scores rather than gap scores for the overall assessment of servicequality. Another major criticism of SERVQUAL model is that there is high degree of intercorrelation among the various dimensions (Gilmore, 2003) leading to multicollinearity. Inthe presence of interdependency of the factors, the multiple regression analysis maybecome unstable.

One of the major conclusions that can be drawn from the literature review is that nosimple generalization of relative importance of determinants of service quality ispossible. Thus, it must be noted that the importance of determinants of quality forcustomers would vary across different service types. This could be expected becausedifferent services are structured and delivered in different contexts and providersconsciously position them at different levels of variables of concern (Emari et al., 2011).In summary, a wide range of service quality measurement studies exist in a range of

Clientsatisfaction

621

Dow

nloa

ded

by J

AY

PEE

IN

STIT

UT

E O

F IN

FOR

MA

TIO

N T

EC

HN

OL

OG

Y U

NIV

ER

SIT

Y N

OID

A A

t 03:

56 3

0 Se

ptem

ber

2014

(PT

)

cultural contexts. Results suggest that the applicability of service quality models isheavily influenced by the cultural and service setting.

3. Research problemThe Indian banks studied here are passing through a fiercely competitive landscape.With banks losing 8 percent of their clients every year (Storbacka, 2000), literature thusfar encouraged the authors to bring sharper clarity to the issue of customer satisfactionin Indian retail banking, its determinants and relative influence. This would aid retailbankers in improving specific service parameters in order to increase overall customersatisfaction. This would help the management of the banks to develop strategies andaction plans to retain their present customers and to attract new clients for their banks.

The objectives of the present study are as follows:

(1) to identify the determinants of customer satisfaction in retail banking in India;and

(2) to assess the level of influence of these determinants on overall customersatisfaction in retail banking in India.

Based on the above objectives, a hypothesis has been framed which is presented below:

H1. The customer satisfaction determinants impact the satisfaction levels of thebank customers.

3.1 Research methodologyA systematic and coherent approach has been adopted for the research study. First, theobjectives of the study were chalked out on the basis of focus group discussion andexhaustive literature review. Based on literature review, items were identified to assess thesatisfaction level of Indian bank customers. Apart from the items from the SERVQUALmodel (in a modified form), additional items of accessibility and price as suggested byBahia and Nantel (2000) were taken. These items were then discussed with 30 bankcustomers. The customers felt that their involvement in the bank also plays a major role inthe satisfaction level and hence two more items were incorporated – “the bank takesregular feedback from the clients in order to improve its service” and “the bank implementsthe good suggestions given by the clients”. Based on the discussions with the clients in thepilot study and in-depth literature review, an exhaustive list of 28 items was identified asshown in Table I. The list is all-inclusive as these items were meticulously drawn out afterthrough interviews and comprehensive literature review. Based on these 28 items,a questionnaire was prepared. For identifying the satisfaction factors, the respondentswere asked to rate their bank on these 28 items. All the items were put on a five-point likertscale ranging from strongly disagree to strongly agree. The questionnaire was tested on30 respondents. The questionnaire was considered reliable as the Cronbach’s a came outas 0.989. The questionnaire also captured the personal characteristics of the respondent viz.age, gender, qualification and income, etc.

For the data collection, the questionnaire was administered to customers of 13 banksin India. Seven of these banks were public sector banks namely, State Bank of India(SBI), Bank of Baroda, Canara Bank, Indian Overseas Bank, Orient Bank of Commerce,Punjab National Bank (PNB), and United Bank of India. Other six were private sectorbanks namely, Housing Development Finance Corporation (HDFC), Industrial Credit

MRR35,7

622

Dow

nloa

ded

by J

AY

PEE

IN

STIT

UT

E O

F IN

FOR

MA

TIO

N T

EC

HN

OL

OG

Y U

NIV

ER

SIT

Y N

OID

A A

t 03:

56 3

0 Se

ptem

ber

2014

(PT

)

and Investment Corporation of India (ICICI), Industrial Development Bank of India(IDBI), Nainital Bank, Axis Bank, and Royal Bank of Scotland. Seven public sector bankswere chosen as they have the largest network of branches in India. ICICI, HDFC,and IDBI were selected because they are the first private banks to introduce“intelligent” banking in India. These banks show a strong retail presence and provide acomprehensive range of information to the customer. They have started takinginitiatives to satisfy customers and provide quality added services.

The questionnaire was administered to faculty members teaching in variouscolleges and their family members. The questionnaire was sent online to various collegesin India. Total of 420 questionnaires were received out of which 400 were found to becompletely and accurately filled, the rest 20 were discarded due to incompleteinformation. Statistical package for the social sciences (SPSS) version 17.0 was used forthe statistical analyses.

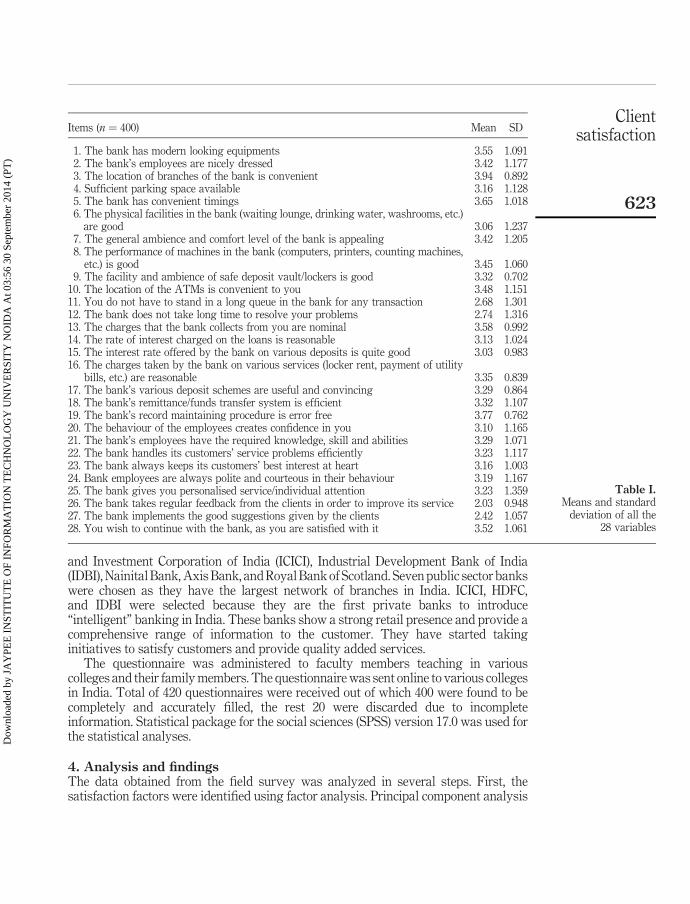

4. Analysis and findingsThe data obtained from the field survey was analyzed in several steps. First, thesatisfaction factors were identified using factor analysis. Principal component analysis

Items (n ¼ 400) Mean SD

1. The bank has modern looking equipments 3.55 1.0912. The bank’s employees are nicely dressed 3.42 1.1773. The location of branches of the bank is convenient 3.94 0.8924. Sufficient parking space available 3.16 1.1285. The bank has convenient timings 3.65 1.0186. The physical facilities in the bank (waiting lounge, drinking water, washrooms, etc.)

are good 3.06 1.2377. The general ambience and comfort level of the bank is appealing 3.42 1.2058. The performance of machines in the bank (computers, printers, counting machines,

etc.) is good 3.45 1.0609. The facility and ambience of safe deposit vault/lockers is good 3.32 0.702

10. The location of the ATMs is convenient to you 3.48 1.15111. You do not have to stand in a long queue in the bank for any transaction 2.68 1.30112. The bank does not take long time to resolve your problems 2.74 1.31613. The charges that the bank collects from you are nominal 3.58 0.99214. The rate of interest charged on the loans is reasonable 3.13 1.02415. The interest rate offered by the bank on various deposits is quite good 3.03 0.98316. The charges taken by the bank on various services (locker rent, payment of utility

bills, etc.) are reasonable 3.35 0.83917. The bank’s various deposit schemes are useful and convincing 3.29 0.86418. The bank’s remittance/funds transfer system is efficient 3.32 1.10719. The bank’s record maintaining procedure is error free 3.77 0.76220. The behaviour of the employees creates confidence in you 3.10 1.16521. The bank’s employees have the required knowledge, skill and abilities 3.29 1.07122. The bank handles its customers’ service problems efficiently 3.23 1.11723. The bank always keeps its customers’ best interest at heart 3.16 1.00324. Bank employees are always polite and courteous in their behaviour 3.19 1.16725. The bank gives you personalised service/individual attention 3.23 1.35926. The bank takes regular feedback from the clients in order to improve its service 2.03 0.94827. The bank implements the good suggestions given by the clients 2.42 1.05728. You wish to continue with the bank, as you are satisfied with it 3.52 1.061

Table I.Means and standard

deviation of all the28 variables

Clientsatisfaction

623

Dow

nloa

ded

by J

AY

PEE

IN

STIT

UT

E O

F IN

FOR

MA

TIO

N T

EC

HN

OL

OG

Y U

NIV

ER

SIT

Y N

OID

A A

t 03:

56 3

0 Se

ptem

ber

2014

(PT

)

(PCA) was used as the method of extraction and varimax was used as the rotationmethod. Second, correlation and regression analysis were conducted to determine theeffect of these factors on the satisfaction level of the customers.

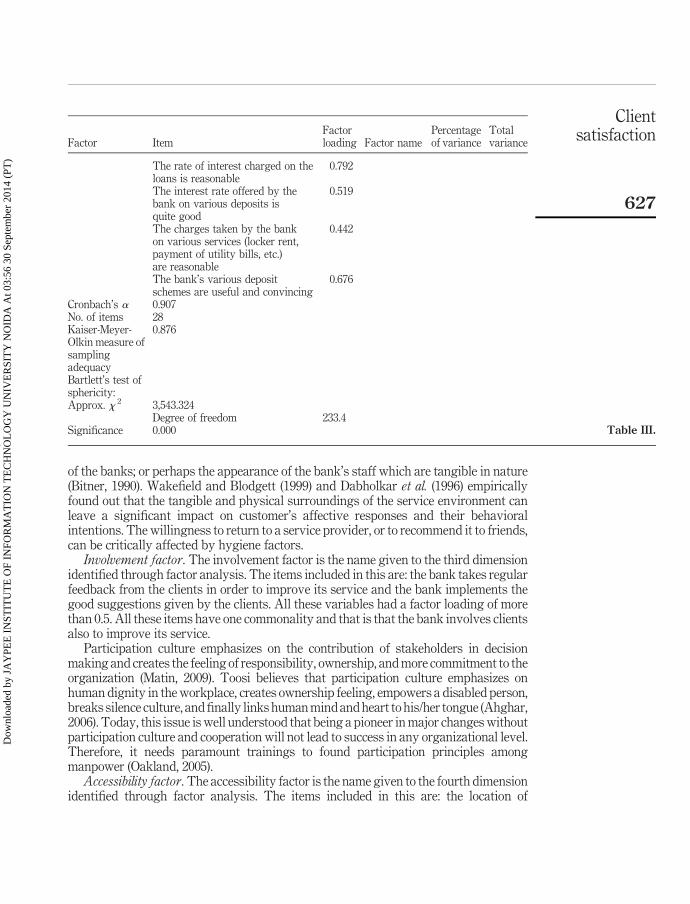

To test the validity of the instrument, Cronbach’s a and Kaiser-Meyer-Olkin (KMO)measure of adequacy tests were computed. Cronbach’s a was calculated to measure theinternal consistency and reliability of the instrument. The Cronbach’s a came as 0.907 asshown in Table III, thus the instrument was considered reliable for the study. The KMOmeasure of sampling adequacy is a statistical tool that indicates the proportion of variancein the variables that might be caused by underlying factors. High values (close to 1.0)generally indicate that a factor analysis may be useful with the data. If the value is less than0.70, the results of the factor analysis probably will not be very useful. As shown in Table III,the KMO value for the instrument was 0.876, which is acceptable as a good value (Rubin andBabbie, 2002). Similarly, Bartlett’s test of sphericity tests the hypothesis that the correlationmatrix is an identity matrix, which would indicate that the variables are unrelated andtherefore unsuitable for structure detection. Small values (less than 0.05) of the significancelevel indicate that a factor analysis may be useful with the data. The Bartlett’s test showed asignificant level and hence the instrument was accepted for further study.

The analysis below presents the profile of the respondents, followed by identificationof factors using factor analysis and finally ending with the regression model.

4.1 Descriptive analysis and personal profile of the respondentsThe means and standard deviations were calculated for all the 28 items and have beenshown in Table I. The demographic profile of the clients can be seen in Table II. Out ofthe 400 respondents, who filled the questionnaire, 52 percent were clients of publicsector banks and 48 percent were of private sector banks. As the respondents weremainly faculty members and their family members, there are very high proportions of“postgraduates and above” (71 percent) and persons with a “service” occupation(74 percent) in the data as can be seen from Table II.

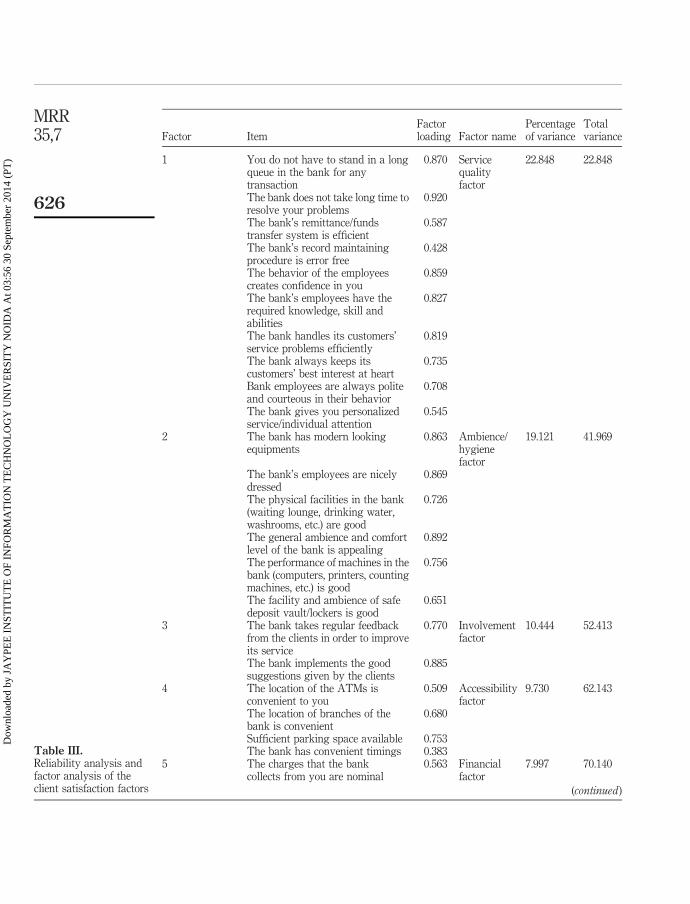

4.2 Identification of satisfaction factorsSince the satisfaction variables were large in number and were inter-related, factor analysiswas done to extract the factors affecting the satisfaction of clients. PCA was the method ofextraction. Varimax was the rotation method. As per the Kaiser (1960) criterion, onlyfactors with eigenvalues greater than one were retained. Five factors in the initial solutionhave eigenvalues greater than one. Together, they accounted for almost 70 percent of thevariability in the original variables, which can be regarded as well beyond sufficient.

After extracting the eigen values, rotation of principal components was done throughvarimax rotation. After the number of extracted factors was decided upon, the next stepwas to interpret the factors by identifying which factors were associated with theoriginal variables. The five factors extracted for further study are shown in Table III.These five factors that were extracted have been referred as the satisfaction dimensionsin further analysis. Table III is followed by the explanation of all these five dimensions.

Service quality factor. The service quality factor is the name given to the firstdimension identified through factor analysis. As can be seen from Table III, all the itemsunder this factor have one commonality, good quality service. All these items in totalityencompass the SERVQUAL dimensions (empathy, responsiveness, assurance, andreliability) except for tangibility.

MRR35,7

624

Dow

nloa

ded

by J

AY

PEE

IN

STIT

UT

E O

F IN

FOR

MA

TIO

N T

EC

HN

OL

OG

Y U

NIV

ER

SIT

Y N

OID

A A

t 03:

56 3

0 Se

ptem

ber

2014

(PT

)

A trusted organizational culture is necessary because customers are the surviving forcefor any organization and there is no alternative for good service to customers. Successfulorganizations breed good relations and good services to customers and finally,customers’ loyalty (Stanley, 2007). A bank’s human resources play a significant role inattracting and maintaining its customers (Mylonakis, 2009).

The importance of service quality in customer satisfaction has been time and againreiterated by many researchers (Bedi, 2010; Kassim and Abdullah, 2010; Kumar et al.,2010; Yee et al., 2010; Kumar et al., 2009; Naeem and Saif, 2009; Balaji, 2009;Parasuraman et al., 1988). A survey by KPMG (2010) of the Nigerian banking industryrevealed speedy transaction processing as the key expectation of customers in retailbanking.

Ambience and hygiene factor. The ambience and hygiene factor is the name given tothe second dimension identified through factor analysis. The items included in this canbe seen from Table III. All these variables had a factor loading of more than 0.5. All theseitems have one commonality and that is the ambience and hygiene factors of a bank andit is similar to the tangibility dimension of SERVQUAL.

Due to the intangible nature of services that the banks offer, it is often difficult forcustomers to comprehend services and they tend to make influences on the basis of thephysical facilities like equipments, machines and their performance; premises

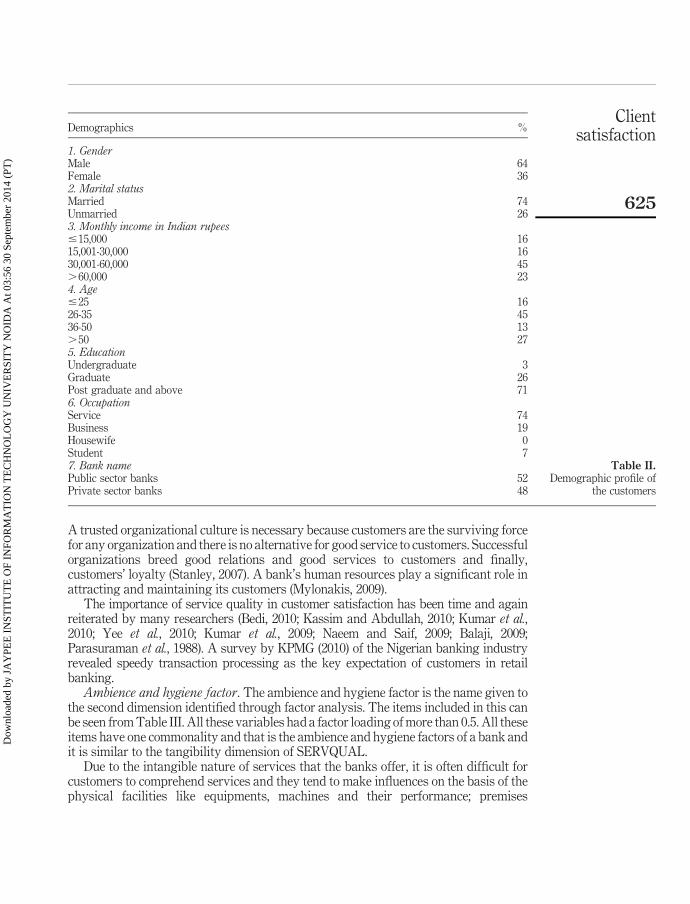

Demographics %

1. GenderMale 64Female 362. Marital statusMarried 74Unmarried 263. Monthly income in Indian rupees#15,000 1615,001-30,000 1630,001-60,000 45.60,000 234. Age#25 1626-35 4536-50 13.50 275. EducationUndergraduate 3Graduate 26Post graduate and above 716. OccupationService 74Business 19Housewife 0Student 77. Bank namePublic sector banks 52Private sector banks 48

Table II.Demographic profile of

the customers

Clientsatisfaction

625

Dow

nloa

ded

by J

AY

PEE

IN

STIT

UT

E O

F IN

FOR

MA

TIO

N T

EC

HN

OL

OG

Y U

NIV

ER

SIT

Y N

OID

A A

t 03:

56 3

0 Se

ptem

ber

2014

(PT

)

Factor ItemFactorloading Factor name

Percentageof variance

Totalvariance

1 You do not have to stand in a longqueue in the bank for anytransaction

0.870 Servicequalityfactor

22.848 22.848

The bank does not take long time toresolve your problems

0.920

The bank’s remittance/fundstransfer system is efficient

0.587

The bank’s record maintainingprocedure is error free

0.428

The behavior of the employeescreates confidence in you

0.859

The bank’s employees have therequired knowledge, skill andabilities

0.827

The bank handles its customers’service problems efficiently

0.819

The bank always keeps itscustomers’ best interest at heart

0.735

Bank employees are always politeand courteous in their behavior

0.708

The bank gives you personalizedservice/individual attention

0.545

2 The bank has modern lookingequipments

0.863 Ambience/hygienefactor

19.121 41.969

The bank’s employees are nicelydressed

0.869

The physical facilities in the bank(waiting lounge, drinking water,washrooms, etc.) are good

0.726

The general ambience and comfortlevel of the bank is appealing

0.892

The performance of machines in thebank (computers, printers, countingmachines, etc.) is good

0.756

The facility and ambience of safedeposit vault/lockers is good

0.651

3 The bank takes regular feedbackfrom the clients in order to improveits service

0.770 Involvementfactor

10.444 52.413

The bank implements the goodsuggestions given by the clients

0.885

4 The location of the ATMs isconvenient to you

0.509 Accessibilityfactor

9.730 62.143

The location of branches of thebank is convenient

0.680

Sufficient parking space available 0.753The bank has convenient timings 0.383

5 The charges that the bankcollects from you are nominal

0.563 Financialfactor

7.997 70.140

(continued )

Table III.Reliability analysis andfactor analysis of theclient satisfaction factors

MRR35,7

626

Dow

nloa

ded

by J

AY

PEE

IN

STIT

UT

E O

F IN

FOR

MA

TIO

N T

EC

HN

OL

OG

Y U

NIV

ER

SIT

Y N

OID

A A

t 03:

56 3

0 Se

ptem

ber

2014

(PT

)

of the banks; or perhaps the appearance of the bank’s staff which are tangible in nature(Bitner, 1990). Wakefield and Blodgett (1999) and Dabholkar et al. (1996) empiricallyfound out that the tangible and physical surroundings of the service environment canleave a significant impact on customer’s affective responses and their behavioralintentions. The willingness to return to a service provider, or to recommend it to friends,can be critically affected by hygiene factors.

Involvement factor. The involvement factor is the name given to the third dimensionidentified through factor analysis. The items included in this are: the bank takes regularfeedback from the clients in order to improve its service and the bank implements thegood suggestions given by the clients. All these variables had a factor loading of morethan 0.5. All these items have one commonality and that is that the bank involves clientsalso to improve its service.

Participation culture emphasizes on the contribution of stakeholders in decisionmaking and creates the feeling of responsibility, ownership, and more commitment to theorganization (Matin, 2009). Toosi believes that participation culture emphasizes onhuman dignity in the workplace, creates ownership feeling, empowers a disabled person,breaks silence culture, and finally links human mind and heart to his/her tongue (Ahghar,2006). Today, this issue is well understood that being a pioneer in major changes withoutparticipation culture and cooperation will not lead to success in any organizational level.Therefore, it needs paramount trainings to found participation principles amongmanpower (Oakland, 2005).

Accessibility factor. The accessibility factor is the name given to the fourth dimensionidentified through factor analysis. The items included in this are: the location of

Factor ItemFactorloading Factor name

Percentageof variance

Totalvariance

The rate of interest charged on theloans is reasonable

0.792

The interest rate offered by thebank on various deposits isquite good

0.519

The charges taken by the bankon various services (locker rent,payment of utility bills, etc.)are reasonable

0.442

The bank’s various depositschemes are useful and convincing

0.676

Cronbach’s a 0.907No. of items 28Kaiser-Meyer-Olkin measure ofsamplingadequacy

0.876

Bartlett’s test ofsphericity:Approx. x 2 3,543.324

Degree of freedom 233.4Significance 0.000 Table III.

Clientsatisfaction

627

Dow

nloa

ded

by J

AY

PEE

IN

STIT

UT

E O

F IN

FOR

MA

TIO

N T

EC

HN

OL

OG

Y U

NIV

ER

SIT

Y N

OID

A A

t 03:

56 3

0 Se

ptem

ber

2014

(PT

)

branches of the bank is convenient, the location of the ATMs is convenient, sufficientparking space is available, and the bank has convenient timings. All these items haveone commonality and that is the accessibility factors of the bank.

Bahia and Nantel (2000), McKechnie (1992) and Thwaites and Vere (1995), are of theopinion that access/convenience is a dominant criterion both for subsequent satisfactionand selection of institution. Howcroft (1991) has argued that some consumers havepositive attitudes towards ATMs based on dominant perceptions of convenience/accessibility/ease of use. The benefits of convenience and accessibility are enabling factorsthat make it easy for the customer to do business with the bank. The bank’s ability todeliver these benefits on a continuing basis to its existing customers will probably impacton customer satisfaction (Jamal and Naser, 2002; Mittal, 1999; Levesque and McDougall,1996). Large number of branches and ATMs at various locations make the bank moreapproachable to the customers. ATM near to the residence or office enables them towithdraw cash not only in a secure environment but also gives them easy access to fundswhenever required. KPMG (2010) survey of the Nigerian banking industry found ATMservices as the second most key expectation of customers in retail banking.

Financial factor. Financial factor is the name given to the fifth dimension identifiedthrough factor analysis. As can be seen from Table III, Factor five consisted of itemsrelated to the pricing policy of the banks. All these items have one commonality and thatis the financial factors associated with the monetary transactions facilitated by thebanks and the interest/charges levied/offered by the bank.

Bahia and Nantel (2000) in his research emphasized the importance of price inassessing the bank’s service quality. Parasuraman et al. (1994), match the point thatservice satisfaction and satisfaction with price were essentials in the overall satisfactionmeasurement. Reidenbach (1995) argued that customer value is a more viable factor thancustomer satisfaction because it includes not only the usual benefits that most banksfocus on but also a consideration of the price that the customer pays. Customer value is adynamic that must be managed.

On the basis of the factor identified, the initial hypothesis was further subdivided intofive different hypotheses which are as follows:

H1a. The service quality factor affects the satisfaction levels of the bank customers.

H1b. The ambience/hygiene factor affects the satisfaction levels of the bank customers.

H1c. The involvement factor affects the satisfaction levels of the bank customers.

H1d. The accessibility factor affects the satisfaction levels of the bank customers.

H1e. The financial factor affects the satisfaction levels of the bank customers.

The next step involved conducting a regression analysis to validate the above hypotheses.

4.3 Correlations and regression model for assessing the level of influence of thedeterminants of customer satisfaction on overall customer satisfaction in retail bankingin IndiaIn order to assess the relation between the determinants of customer satisfaction asidentified by factor analysis with the overall customer satisfaction level,correlations were computed. The independent variables were the five customersatisfaction dimensions, namely service quality, ambience and hygiene, involvement,

MRR35,7

628

Dow

nloa

ded

by J

AY

PEE

IN

STIT

UT

E O

F IN

FOR

MA

TIO

N T

EC

HN

OL

OG

Y U

NIV

ER

SIT

Y N

OID

A A

t 03:

56 3

0 Se

ptem

ber

2014

(PT

)

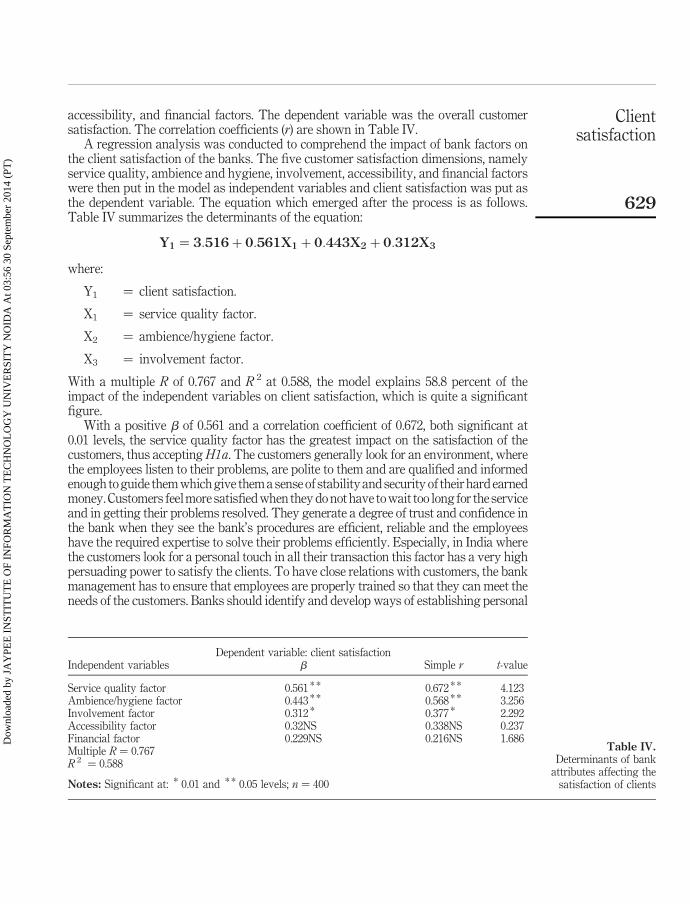

accessibility, and financial factors. The dependent variable was the overall customersatisfaction. The correlation coefficients (r) are shown in Table IV.

A regression analysis was conducted to comprehend the impact of bank factors onthe client satisfaction of the banks. The five customer satisfaction dimensions, namelyservice quality, ambience and hygiene, involvement, accessibility, and financial factorswere then put in the model as independent variables and client satisfaction was put asthe dependent variable. The equation which emerged after the process is as follows.Table IV summarizes the determinants of the equation:

Y1 ¼ 3:516þ 0:561X1 þ 0:443X2 þ 0:312X3

where:

Y1 ¼ client satisfaction.

X1 ¼ service quality factor.

X2 ¼ ambience/hygiene factor.

X3 ¼ involvement factor.

With a multiple R of 0.767 and R 2 at 0.588, the model explains 58.8 percent of theimpact of the independent variables on client satisfaction, which is quite a significantfigure.

With a positive b of 0.561 and a correlation coefficient of 0.672, both significant at0.01 levels, the service quality factor has the greatest impact on the satisfaction of thecustomers, thus accepting H1a. The customers generally look for an environment, wherethe employees listen to their problems, are polite to them and are qualified and informedenough to guide them which give them a sense of stability and security of their hard earnedmoney. Customers feel more satisfied when they do not have to wait too long for the serviceand in getting their problems resolved. They generate a degree of trust and confidence inthe bank when they see the bank’s procedures are efficient, reliable and the employeeshave the required expertise to solve their problems efficiently. Especially, in India wherethe customers look for a personal touch in all their transaction this factor has a very highpersuading power to satisfy the clients. To have close relations with customers, the bankmanagement has to ensure that employees are properly trained so that they can meet theneeds of the customers. Banks should identify and develop ways of establishing personal

Dependent variable: client satisfactionIndependent variables b Simple r t-value

Service quality factor 0.561 * * 0.672 * * 4.123Ambience/hygiene factor 0.443 * * 0.568 * * 3.256Involvement factor 0.312 * 0.377 * 2.292Accessibility factor 0.32NS 0.338NS 0.237Financial factor 0.229NS 0.216NS 1.686Multiple R ¼ 0.767R 2 ¼ 0.588

Notes: Significant at: * 0.01 and * * 0.05 levels; n ¼ 400

Table IV.Determinants of bank

attributes affecting thesatisfaction of clients

Clientsatisfaction

629

Dow

nloa

ded

by J

AY

PEE

IN

STIT

UT

E O

F IN

FOR

MA

TIO

N T

EC

HN

OL

OG

Y U

NIV

ER

SIT

Y N

OID

A A

t 03:

56 3

0 Se

ptem

ber

2014

(PT

)

relationship, nurturing security and a sense of belonging and sharing of personal advice orsupport as this will help them retain customers for a lifetime.

The second most influencing factor is the ambience factors with ab-value of 0.443 anda correlation coefficient of 0.568. Thus, H1b is also accepted. The customers are happy ifthe bank is clean, hygienic. The performance of computers and other equipments alsohave a high impact on the customers as the clients are generally busy and they want theirwork one as soon as possible. So when they visit the bank and the server is down, they arehighly dissatisfied; not just as their work has been hampered but they have wasted theirmoney, energy and time in getting to the bank.

The third factor influencing highly to the satisfaction level of the customers is theinvolvement factors with a b of 0.312. So the H1c is also accepted. The involvementfactor includes items like implementation of the suggestions/feedback given by clients inthe bank. Participation culture gives a sense of belonging to customers which in turnincrease their satisfaction levels. The banks should give more attention to the issues oforganization culture and customer involvement because that, in customer’s view, is verynecessary. According to customers, an evolved organization is one that thinks abouthis/her opinion and meets his/her ideas ( Jelodari, 2006).

The other two factors, namely accessibility factors and financial factors are notshowing a significant influence on the satisfaction of the employees. So theH1d andH1eare rejected. This might be due to the reason that as the Indian banks are regulated byRBI, individual banks do not have much say on the interest/deposit rates and generallyall banks offer almost the same standard interest/deposit rates. Moreover, almost all thebanks have large number of branches and ATMs at strategic locations; therefore,accessibility is now seen as a necessity rather than as a satisfaction factor to the clients.

5. ConclusionThis research aimed to test the viability of the proposed hypothesis that client satisfaction,a dependent variable, depends on service quality, ambience/hygiene, involvement,accessibility, and financial factors of the bank. As per the findings, client satisfactiondepends on service quality, ambience, and hygiene in the bank, client participation andinvolvement. Proximity of the bank and the financial factors of the bank do not have muchinfluence on the satisfaction level of the customers.

As compared to the SERVQUAL model where there are five different dimensionsempathy, responsiveness, assurance and reliability and tangibility which affectsatisfaction of the clients, the present study suggests that the dimensions of theSERVQUAL are inter-related and only two factors encompass all the five dimensions ofSERVQUAL. The first factor “service quality” identified in the present study, and whichhas a positive b-value of 0.561 with client satisfaction, includes all items of theSERVQUAL’s four dimensions namely empathy, responsiveness, assurance, andreliability. The second factor, i.e. the ambience and hygiene factor with a positiveb of 0.443 with client satisfaction, is the same as the tangibility dimension ofSERVQUAL. The third factor identified in the study is the involvement factor, with apositive b-value of 0.312; this factor also has a high influence on the satisfaction level ofthe customers in the Indian banks. This factor, as per the literature studied, has not beentaken into account in the existing models for measuring service quality in banks. Thefourth and the fifth factors, i.e. the accessibility and the financial factors as identified bythe factor analysis, were the same as the additional factors identified in the BSQ model.

MRR35,7

630

Dow

nloa

ded

by J

AY

PEE

IN

STIT

UT

E O

F IN

FOR

MA

TIO

N T

EC

HN

OL

OG

Y U

NIV

ER

SIT

Y N

OID

A A

t 03:

56 3

0 Se

ptem

ber

2014

(PT

)

Both these factors are non-significant at the 0.05 level in the regression analysis,thus suggesting that the incorporation of these two factors does not have any significantimpact on the satisfaction levels of the Indian bank clientage.

5.1 Managerial implicationsThe findings of this study confirm the observations of earlier studies done in the area ofbanking industry. Regression models establish the criteria that improvement in servicequality in banking industry increase the customer satisfaction. Services given tocustomers in the banks directly and significantly affect perceived service value which isthe final antecedent to customer satisfaction in banking (Gil et al., 2007). The higherthe (perceived) service quality, the more satisfied and loyal the customers are(Petruzzellis et al., 2006). In the current competitive scenario, with little or no distinctionin the product offerings, it is the quality of service (0.561b-value as shown in the result ofthe study) that can differentiate one bank from another. The banks need to focus on thequality of the services they are rendering to clients. Ioanna (2002) proposed that productdifferentiation is impossible in a competitive environment like the banking industry.Banks all over the place are delivering the identical products. Bank prices are fixed anddriven by the marketplace. Therefore, bank management tends to distinguish itscompany from competitors through service quality. Service quality is an imperativefactor impacting customers’ satisfaction level in the banking industry. In banking,quality is a multi-variable idea, which includes differing types of convenience,reliability, services portfolio, and critically, the staff delivering the service.

The study aimed to establish that ambience and hygiene factors in the banks result inmaking customers happy and satisfied. Customers carry impressions about theservices on the basis of the ambience and hygiene factors of the bank (Bitner, 1990).Dabholkar et al. (1996) reported similar findings that the tangibles aspects do influencecustomers’ satisfaction. The results indicate that ambience or the tangible factors alsoplay an important role in making a particular bank different from another. In the modernera and especially when the life has become so stressful, the clients in the banks expect arelaxing environment where they can feel comfortable and have all the facilities which arespected citizen of any nation has the right to have.

At last but not the least, there can be no better opportunity for any bank than toimprove the client satisfaction by taking feedback and suggestions by its customersand implement them if they are valuable and enjoy a win-win situation. The currentresearch contributes towards understanding relationship between clients’ participationand their satisfaction. Clients’ participation in the form of taking their feedback andimplementing then create a strong bonding between the banks and their clients. This is inline with empirical findings reported earlier. The findings of this study imply that banksshould ensure that customer feel comfortable and safe, both physically and mentally,in the banks. Banks will be in danger of disintermediation if they do not develop relationsand satisfy the customers (Jham and Mohd, 2009).

5.2 Limitations and future researchThe research gauges the effect of the determinants of customer satisfaction on overallcustomer satisfaction in retail banking in India. However, the study is limited on fewgrounds. First, the sample of the study consists only from 13 banks, i.e. seven publicsector banks and six private sector banks. It is also important to note that the study

Clientsatisfaction

631

Dow

nloa

ded

by J

AY

PEE

IN

STIT

UT

E O

F IN

FOR

MA

TIO

N T

EC

HN

OL

OG

Y U

NIV

ER

SIT

Y N

OID

A A

t 03:

56 3

0 Se

ptem

ber

2014

(PT

)

is limited to a sample size of 400 customers residing and having bank accounts in themetropolitan cities of India. Therefore, the scope of the study is limited to the sample sizeand the number of banks.

References

Ahghar, G. (2006), “Studying the role of schools’ organizational culture in job tiresome ofteachers in Tehran secondary schools”, Pedagol Q, Vol. 86, pp. 93-123.

Angur, M.G., Nataraajan, R. and Jahera, J.S. (1999), “Service quality in the banking industry:an assessment in a developing economy”, International Journal of Bank Marketing, Vol. 17No. 3, pp. 116-23.

Armstrong, R.W. and Seng, T.B. (2000), “Corporate-customer satisfaction in the bankingindustry of Singapore”, International Journal of Bank Marketing, Vol. 18 No. 3, pp. 97-111.

Avkiran, K.N. (1994), “Developing an instrument to measure customer service quality in branchbanking”, The International Journal of Bank Marketing, Vol. 12 No. 6, pp. 10-19.

Babakus, E. and Boller, G.W. (1992), “An empirical assessment of the SERVQUAL scale”,Journal of Business Research, Vol. 24, pp. 253-68.

Bahia, K. and Nantel, J. (2000), “A reliable and valid measurement scale for the perceived servicequality of banks”, The International Journal of Bank Marketing, Vol. 18 No. 2, p. 84.

Balaji, M. (2009), “Customer satisfaction with Indian mobile services”, IUP Journal ofManagement Research, Vol. 8 No. 10, pp. 52-62.

Bedi, M. (2010), “An integrated framework for service quality, customer satisfaction andbehavioural responses in Indian banking industry: a comparison of public and privatesector banks”, Journal of Services Research, Vol. 10 No. 1, pp. 157-72.

Bitner, M.J. (1990), “Evaluating service encounters: the effects of physical surroundings andemployee responses”, Journal of Marketing, Vol. 54, pp. 69-82.

Blanchard, R. and Galloway, R. (1994), “Quality in retail banking”, International Journal ofService Industry Management, Vol. 54, pp. 5-23.

Brady, M.K. and Robertson, C.J. (2001), “Searching for a consensus on the antecedent role ofservice quality and satisfaction: an exploratory cross-national study”, Journal of BusinessResearch, Vol. 51 No. 1, pp. 53-60.

Buttle, F. (1996), “SERVQUAL: review, critique, research agenda”, European Journal ofMarketing, Vol. 30 No. 1, pp. 8-32.

Carman, J.M. (1990), “Consumer perceptions of service quality: an assessment of the SERVQUALdimensions”, Journal of Retailing, Vol. 66, pp. 33-5.

Choudhury, K. (2008), “Service quality: insights from the Indian banking scenario”,Australasian Marketing Journal, Vol. 16 No. 1, pp. 48-61.

Cronin, J. Jr and Taylor, S.A. (1992), “Measuring service quality: a reexamination and extension”,Journal of Marketing Research, Vol. 56, July, pp. 55-68.

Cui, C.C., Lewis, B.R. and Park, W. (2003), “Service quality measurement in the banking sector inSouth Korea”, International Journal of Bank Marketing, Vol. 21 No. 4, pp. 191-201.

Dabholkar, P.A., Thorpe, D.I. and Rentz, J.O. (1996), “A measure of service quality for retailstores: scale development and validation”, Journal of the Academy of Marketing Science,Vol. 24, pp. 3-16.

East, R. (1997), Consumer Behavior: Advances and Applications in Marketing, Prentice-Hall,London.

MRR35,7

632

Dow

nloa

ded

by J

AY

PEE

IN

STIT

UT

E O

F IN

FOR

MA

TIO

N T

EC

HN

OL

OG

Y U

NIV

ER

SIT

Y N

OID

A A

t 03:

56 3

0 Se

ptem

ber

2014

(PT

)

Ehigie, B.O. (2006), “Correlates of customer loyalty to their banks: a case study in Nigeria”,International Journal of Bank Marketing, Vol. 24 No. 7, pp. 494-508.

Emari, H., Iranzadeh, S. and Bakhshayesh, S. (2011), “Determining the dimensions of servicequality in banking industry: examining the Gronroos’s model in Iran”, Trends in AppliedSciences Research, Vol. 6, pp. 57-64.

Fick, G.R. and Ritchie, J.R.B. (1991), “Measuring service quality in the travel and tourismindustry”, Journal of Travel Research, Vol. 30 No. 2, pp. 2-9.

File, K.M. and Prince, R.A. (1992), “Positive word-of-mouse: customer satisfaction and buyerbehavior”, International Journal of Bank Marketing, Vol. 15 No. 1, pp. 25-39.

Finn, D.W. and Lamb, C.W. (1991), “An evaluation of the SERVQUAL scales in a retailingsetting”, in Solomon, R.H. (Ed.), Advances in Consumer Research, Association of ConsumerResearch, Provo, UT.

Gee, R., Coates, G. and Nicholson, M. (2008), “Understanding and profitably managing customerloyalty”, Marketing Intelligence & Planning, Vol. 26 No. 4, pp. 359-74.

Gil, I., Berenguer, G. and Cervera, A. (2007), “The roles of service encounters, service value,and job satisfaction in achieving customer satisfaction in business relationships”,Industrial Marketing Management, Vol. 37 No. 8, pp. 921-39.

Gilmore, A. (2003), Services, Marketing and Management, Sage, London.

Gounaris, S.P., Stathakopoulos, V. and Athanassopoulos, A.D. (2003), “Antecedents to perceivedservice quality: an exploratory study in the banking industry”, The International Journalof Bank Marketing, Vol. 21 Nos 4/5, pp. 168-90.

Gronroos, C. (1994), “Quo vadis, marketing? Towards a relationship marketing paradigm”,Journal of Marketing Management, Vol. 10, pp. 347-60.

Guo, X., Duff, A. and Hair, M. (2008), “Service quality measurement in the Chinese corporatebanking market”, International Journal of Bank Marketing, Vol. 26 No. 5, pp. 305-27.

Han, X., Kwortnik, R. and Wang, C. (2008), “Service loyalty: an integrated model andexamination across service contexts”, Journal of Service Research, Vol. 11 No. 1, pp. 22-42.

Heskett, J.L., Sasser, W.E. and Schlesinger, L.A. (1997), The Service Profit Chain, The Free Press,New York, NY.

Howcroft, B. (1991), “Customer service in selected branches of a UK clearing bank: a pilot study”,The Service-Manufacturing Divide: Synergies and Dilemmas, Proceedings of the ServiceIndustries Management Research Unit Conference.

Ioanna, P.D. (2002), “The role of employee development in customer relations: the case ofUK retail banks”, Corporate Communication, Vol. 7 No. 1, pp. 62-77.

Jamal, A. (2004), “Retail banking and customer behaviour: a study of self concept, satisfactionand technology usage”, International Review of Retailing, Distribution and ConsumerResearch, Vol. 14 No. 3, pp. 357-79.

Jamal, A. and Naser, K. (2002), “Customer satisfaction and retail banking: an assessment of someof the key antecedents of customer satisfaction in retail banking”, International Journal ofBank Marketing, Vol. 20 No. 4, pp. 146-60.

Jamal, A. and Naser, K. (2003), “Factors influencing customer satisfaction in the retail bankingsector in Pakistan”, International Journal of Commerce &Management, Vol. 13 No. 2, p. 29.

Jelodari, M.B. (2006), Organizational Excellence, 2nd ed., Industrial Studies and Training Center,Tehran.

Jham, V. and Mohd, K. (2009), “Customer satisfaction and its impact on performance in banks:a proposed model”, South Asian Journal of Management, Vol. 16 No. 2, pp. 109-26.

Clientsatisfaction

633

Dow

nloa

ded

by J

AY

PEE

IN

STIT

UT

E O

F IN

FOR

MA

TIO

N T

EC

HN

OL

OG

Y U

NIV

ER

SIT

Y N

OID

A A

t 03:

56 3

0 Se

ptem

ber

2014

(PT

)

Johnston, W.J. and Jeffrey, E.L. (1996), “Organizational buying behaviour: toward an integrativeframework”, Journal of Business Research, Vol. 35 No. 1, pp. 1-15.

Kaiser, H.F. (1960), “The application of electronic computers to factor analysis”, Educational andPsychological Measurement, Vol. 20, pp. 41-151.

Kassim, N. and Abdullah, N.A. (2010), “The effect of perceived service quality dimensions oncustomer satisfaction, trust, and loyalty in e-commerce settings: a cross cultural analysis”,Asia Pacific Journal of Marketing and Logistics, Vol. 22 No. 3, pp. 351-71.

Kohli, A.K. and Jaworski, B.J. (1990), “Market orientation: the construct, research propositions,and managerial implications”, Journal of Marketing, Vol. 54, pp. 20-35.

KPMG, Banking Survey (2010), Banking Industry Preserving Customer Confidence and Trust ina Rapidly Changing Industry, Customer Satisfaction Survey, KPMG, Nigeria.

Kumar, M., Kee, F.T. and Charles, V. (2010), “Comparative evaluation of critical factors indelivering service quality of banks: an application of dominance analysis in modifiedSERVQUAL model”, International Journal of Quality & Reliability Management, Vol. 27No. 3, pp. 351-77.

Kumar, M., Kee, F.T. and Manshor, A.T. (2009), “Determining the relative importance of criticalfactors in delivering service quality of banks: an application of dominance analysis inSERVQUAL model”, Managing Service Quality, Vol. 19 No. 2, pp. 211-28.

Ladhari, R. (2008), “Alternative measure of service quality: a review”, Journal of ManagingService Quality, Vol. 18 No. 1, pp. 65-86.

Lassar, W.M., Manolis, C. and Winsor, R.D. (2000), “Service quality perspectives and satisfactionin private banking”, The Journal of Services Marketing, Vol. 14 No. 3, pp. 244-71.

Legg, D. and Baker, J. (1996), “Advertising strategies for service firms”, in Lovelock, C.H. (Ed.),Services Marketing, Prentice-Hall, Englewood Cliffs, NJ.

Levesque, T. and McDougall, G.H.G. (1996), “Determinants of customer satisfaction in retailbanking”, International Journal of Bank Marketing, Vol. 14 No. 7, pp. 12-20.

Lovelock, C. (2001), “Loyalty in private retail banking: an empirical study”, IUP Journal ofManagement Research, Vol. 9 No. 4, pp. 21-38.

McKechnie, S. (1992), “Customer buying behaviour in financial services: an overview”,International Journal of Bank Marketing, Vol. 10 No. 5, pp. 4-12.

Manrai, L.A. and Manrai, A.K. (2007), “A field study of customers’ switching behaviour for bankservices”, Journal of Retailing and Consumer Services, Vol. 14, pp. 208-15.

Matin, H.Z. (2009), “Designing a competent organizational culture model for customer orientedcompanies”, African Journal of Business Management, Vol. 3, pp. 281-93.

Mick, D. and Fournier, S. (1999), “Rediscovering satisfaction”, Journal of Marketing, Vol. 63 No. 4.

Mishra, A.A. (2009), “A study on customer satisfaction in Indian retail banking”, IUP Journal ofManagement Research, Vol. 8 No. 11, pp. 45-61.

Mittal, B. (1999), “The advertising of services: meeting the challenge of intangibility”, Journal ofService Research, Vol. 2 No. 1, pp. 98-116.

Mylonakis, J. (2009), “Bank satisfaction factors and loyalty: a survey of the Greek bankcustomers”, Innovative Marketing, Vol. 5 No. 1, pp. 16-25.

Naeem, H. and Saif, I. (2009), “Service quality and its impact on customer satisfaction:an empirical evidence from the Pakistani banking sector”, The International Business andEconomics Research Journal, Vol. 8 No. 12, p. 99.

MRR35,7

634

Dow

nloa

ded

by J

AY

PEE

IN

STIT

UT

E O

F IN

FOR

MA

TIO

N T

EC

HN

OL

OG

Y U

NIV

ER

SIT

Y N

OID

A A

t 03:

56 3

0 Se

ptem

ber

2014

(PT

)

Nasserzadeh, S.M.R., Jafarzadeh, M.H., Mansouri, T. and Sohrabi, B. (2008),“Customer satisfaction fuzzy cognitive map in banking industry”, Communications ofthe IBIMA, Vol. 2, pp. 151-62.

Ndubisi, N. (2005), “Customer loyalty and antecedents: a relational marketing approach”,Proceedings of the Allied Academies International Conference, Academy of MarketingStudies, Vol. 10 No. 2, pp. 49-54.

Newman, K. (1996), “Promoting service quality in British retail banking: the experience of twoBritish clearing banks”, International Journal of Bank Marketing, Vol. 14 No. 6, pp. 1-9.

Oakland, J.S. (2005), Organizational Prevalence Excellence, 1st ed., Rasa Cultural Institute,Banglore, (translated by Alvandi M.).

Oliver, R.L. (1980), “A cognitive model of the antecedents and consequences of satisfactiondecisions”, Journal of Marketing Research, Vol. 17 No. 4, p. 460.

Oliver, R.L. (1981), “Measurement and evaluation of satisfaction processes in retail settings”,Journal of Retailing, Vol. 57 No. 3, pp. 25-48.

Parasuraman, A., Berry, L.L. and Zeithaml, V.A. (1988), “SERVQUAL: a multiple-item scale formeasuring consumer perceptions of service quality”, Journal of Retailing, Vol. 64 No. 1,p. 12.

Petruzzellis, L., D’Uggento, A.M. and Romanazzi, S. (2006), “Student satisfaction and quality ofservice in Italian universities”, Managing Service Quality, Vol. 16 No. 4, pp. 349-64.

Pfeifer, P. (2005), “The optimal ratio of acquisition and retention costs”, Journal of Targeting,Measurement and Analysis for Marketing, Vol. 13 No. 2, pp. 179-88.

Prabhakaran, S. and Satya, S. (2003), “An insight into service attributes in banking sector”,Journal of Services Research, Vol. 3 No. 1, pp. 157-69.

Reidenbach, R.E. (1995), Value-Driven Bank: Strategies for Total Market Satisfaction, Irwin,Burr Ridge, IL.

Richens, M.L. (1983), “Negative word-of-mouth by dissatisfied consumers: a pilot study”,Journal of Marketing, Vol. 47, p. 69.

Rubin, A. and Babbie, E. (2002), Research Methods for Social Work, Cole Publishing,Pacific Grove, CA.

Sangwan, D.S. (2009), Human Resource Management in Banks, National Publishing House,New Delhi.

Spreng, R.A., Mackenzie, S.B. and Olshavsky, R.W. (1996), “A re-examination of thedeterminants of consumer satisfaction”, Journal of Marketing, Vol. 60 No. 3, p. 15.

Stafford, M.R. (1996), “Demographic discriminators of service quality in the banking industry”,The Journal of Services Marketing, Vol. 10 No. 4, p. 6.

Stanley, T.L. (2007), “Generate a positive corporate culture”, Super Vision, Vol. 68 No. 9, pp. 5-7.

Storbacka, K. (2000), “Customer profitability: analysis and design issues”, in Sheth, J. andParvatiyar, A. (Eds), Handbook of Relationship Marketing, Sage, Thousand Oaks, CA.

Sureshchandar, G.S., Rajendran, C. and Anantharaman, R.N. (2002), “Determinants ofcustomer-perceived service quality: a confirmatory factor analysis approach”,The Journal of Services Marketing, Vol. 16 No. 1, pp. 9-34.

Surprenant, C. and Churchill, G. (1982), “An investigation into the determinants of customersatisfaction”, Journal of Marketing Research, Vol. 19 No. 4, p. 491.

Tariq, A.N. and Moussaoui, N. (2009), “The main antecedents of customer loyalty in Moroccanbanking industry”, International Journal of Business andManagement Science, Vol. 2 No. 2,pp. 101-15.

Clientsatisfaction

635

Dow

nloa

ded

by J

AY

PEE

IN

STIT

UT

E O

F IN

FOR

MA

TIO

N T

EC

HN

OL

OG

Y U

NIV

ER

SIT

Y N

OID

A A

t 03:

56 3

0 Se

ptem

ber

2014

(PT

)

Thwaites, D. and Vere, L. (1995), “Bank selection criteria – student perspective”, Journal ofMarketing Management, Vol. 11, pp. 133-49.

Van Dyke, T.P., Kappelman, L.A. and Prybutok, V.R. (1997), “Measuring information systemsservice quality: concerns on the use of the SERVQUAL questionnaire”, MIS Quarterly,Vol. 21 No. 2, pp. 195-208.

Van Dyke, T.P., Prybutok, V.R. and Kappelman, L.A. (1999), “Cautions on the use of SERVQUALmeasure to assess the quality of information systems services”, Decision Sciences, Vol. 30No. 3, p. 15.

Wakefield, K. and Blodgett, J. (1999), “Customer response to intangible and tangible servicefactors”, Psychology & Marketing, Vol. 16 No. 1, pp. 51-68.

Yee, R., Yeung, A. and Cheng, T. (2010), “An empirical study of employee loyalty, service qualityand firm performance in the service industry”, International Journal of ProductionEconomics, Vol. 124 No. 1, p. 109.

Zeithaml, V.A. and Bitner, M.J. (1996), Services Marketing, International edition, McGraw-Hill,London.

Further reading

Babakus, E., Pedric, D. and Richardson, A. (1995), “Assessing perceived quality in industrialservice settings: measure development and application”, Journal of Business-to-BusinessMarketing, Vol. 2 No. 3, pp. 47-67.

Kumar, S.A., Mani, B.T., Mahalingam, S. and Vanjikovan, M. (2010), “Influence of service qualityon attitudinal loyalty in private retail banking: an empirical study”, IUP Journal ofManagement Research, Vol. 9 No. 4, pp. 21-38.

Narasimham Committee Report (1997), available at: www.indianembassy.org/enews/apr98.pdf

Corresponding authorAayushi Gupta can be contacted at: [email protected]

MRR35,7

636

To purchase reprints of this article please e-mail: [email protected] visit our web site for further details: www.emeraldinsight.com/reprints

Dow

nloa

ded

by J

AY

PEE

IN

STIT

UT

E O

F IN

FOR

MA

TIO

N T

EC

HN

OL

OG

Y U

NIV

ER

SIT

Y N

OID

A A

t 03:

56 3

0 Se

ptem

ber

2014

(PT

)

This article has been cited by:

1. Alessio Ishizaka, Nam Hoang Nguyen. 2013. Calibrated fuzzy AHP for current bank account selection.Expert Systems with Applications 40:9, 3775-3783. [CrossRef]

Dow

nloa

ded

by J

AY

PEE

IN

STIT

UT

E O

F IN

FOR

MA

TIO

N T

EC

HN

OL

OG

Y U

NIV

ER

SIT

Y N

OID

A A

t 03:

56 3

0 Se

ptem

ber

2014

(PT

)