main body

TRANSCRIPT

Corporate Financial Reporting Practices

Introduction

A financial statement or financial report is a formal

record of the financial activities of a business person,

company, business house or any other entity. A financial

report is often referred to as an account, although the

term financial statement is also used, particularly by

the accountants. For large corporations, these statements

are often complex and may include an extensive set of

notes to the financial statements and explanation of

financial policies and management discussion and

analysis. The notes typically describe each item on the

balance sheet, income statement and cash flow statement

in further detail. Notes to financial statements are

considered an integral part of the financial statements.

Purpose of financial reports by business entities is to

provide information about the financial position,

performance and changes in financial position of an

enterprise that is useful to a wide range of users in

making economic decisions. Financial statements should be

A Comparative Study Between MNC & Local Organization Page 1

Corporate Financial Reporting Practices

understandable, relevant, reliable and comparable.

Reported assets, liabilities, equity, income and expenses

are directly related to an organization’s financial

position. Financial statements or reports are intended to

be understandable by readers who have a reasonable

knowledge of business and economic activities and

accounting and who are willing to study the information

diligently.

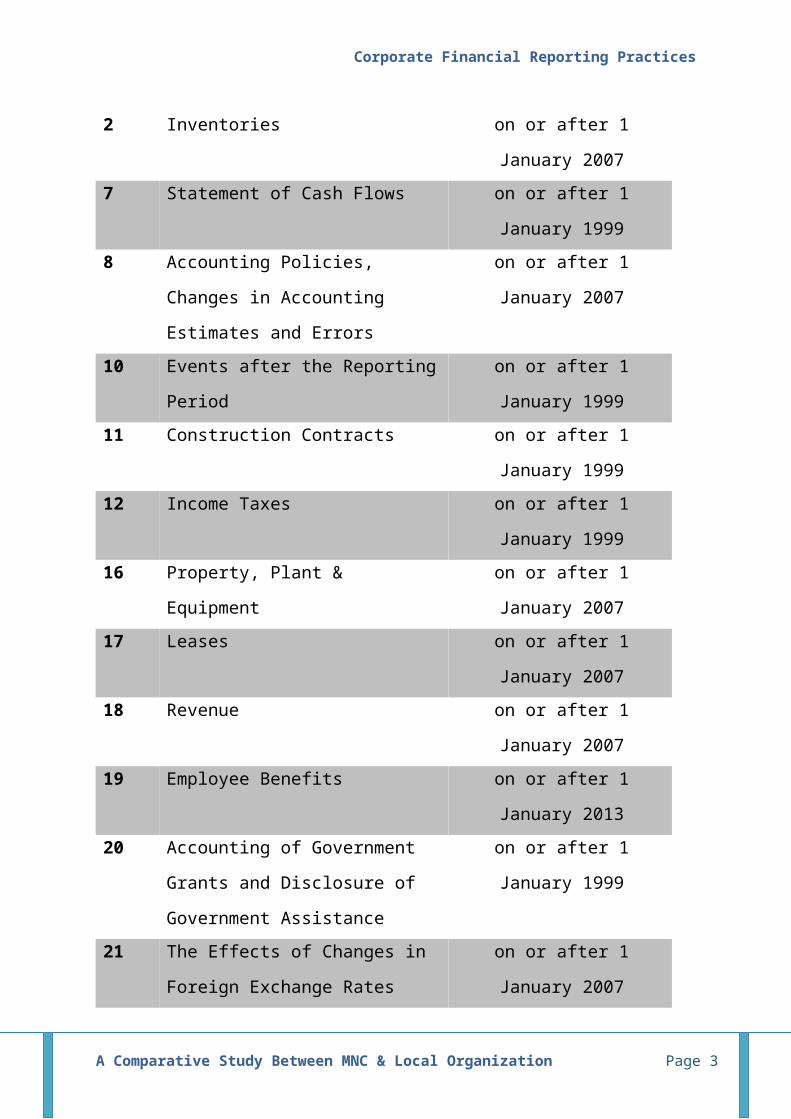

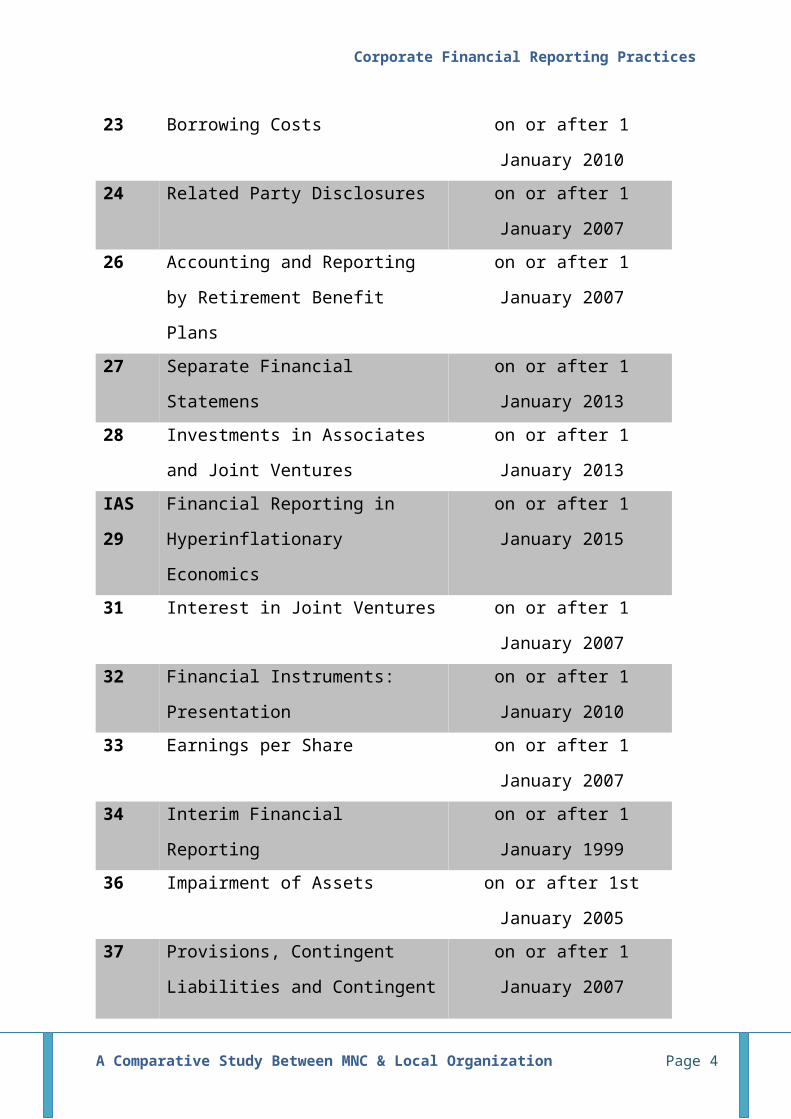

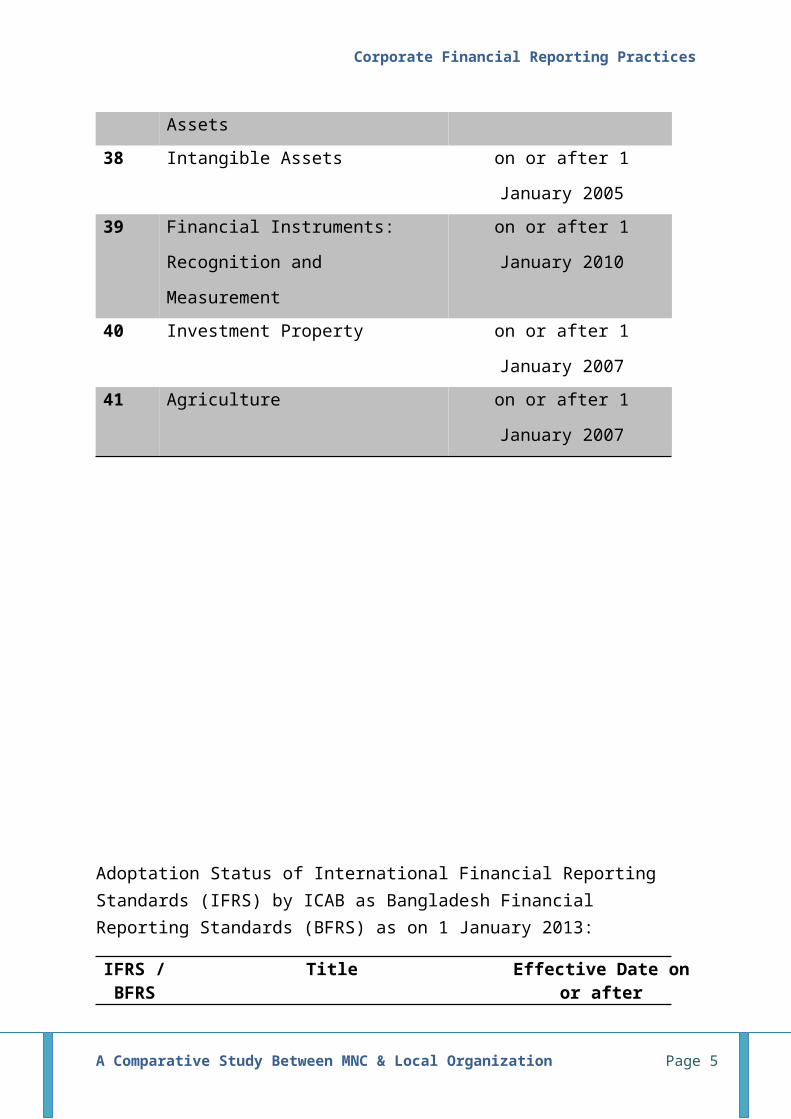

Current Status of Bangladesh Accounting Standards(BAS) and Bangladesh Financial Reporting Framework

Adoptation Status of International Accounting Standards (IASs) by ICAB as Bangladesh Accounting Standards (BAS) as on 1 January 2013:

BAS

No.

BAS Title BAS Effective Date

1 Presentation of Financial

Statements

on or after 1

January 2010

A Comparative Study Between MNC & Local Organization Page 2

Corporate Financial Reporting Practices

2 Inventories on or after 1

January 20077 Statement of Cash Flows on or after 1

January 19998 Accounting Policies,

Changes in Accounting

Estimates and Errors

on or after 1

January 2007

10 Events after the Reporting

Period

on or after 1

January 199911 Construction Contracts on or after 1

January 199912 Income Taxes on or after 1

January 199916 Property, Plant &

Equipment

on or after 1

January 200717 Leases on or after 1

January 200718 Revenue on or after 1

January 200719 Employee Benefits on or after 1

January 201320 Accounting of Government

Grants and Disclosure of

Government Assistance

on or after 1

January 1999

21 The Effects of Changes in

Foreign Exchange Rates

on or after 1

January 2007

A Comparative Study Between MNC & Local Organization Page 3

Corporate Financial Reporting Practices

23 Borrowing Costs on or after 1

January 201024 Related Party Disclosures on or after 1

January 200726 Accounting and Reporting

by Retirement Benefit

Plans

on or after 1

January 2007

27 Separate Financial

Statemens

on or after 1

January 201328 Investments in Associates

and Joint Ventures

on or after 1

January 2013IAS

29

Financial Reporting in

Hyperinflationary

Economics

on or after 1

January 2015

31 Interest in Joint Ventures on or after 1

January 200732 Financial Instruments:

Presentation

on or after 1

January 201033 Earnings per Share on or after 1

January 200734 Interim Financial

Reporting

on or after 1

January 199936 Impairment of Assets on or after 1st

January 200537 Provisions, Contingent

Liabilities and Contingent

on or after 1

January 2007

A Comparative Study Between MNC & Local Organization Page 4

Corporate Financial Reporting Practices

Assets38 Intangible Assets on or after 1

January 200539 Financial Instruments:

Recognition and

Measurement

on or after 1

January 2010

40 Investment Property on or after 1

January 200741 Agriculture on or after 1

January 2007

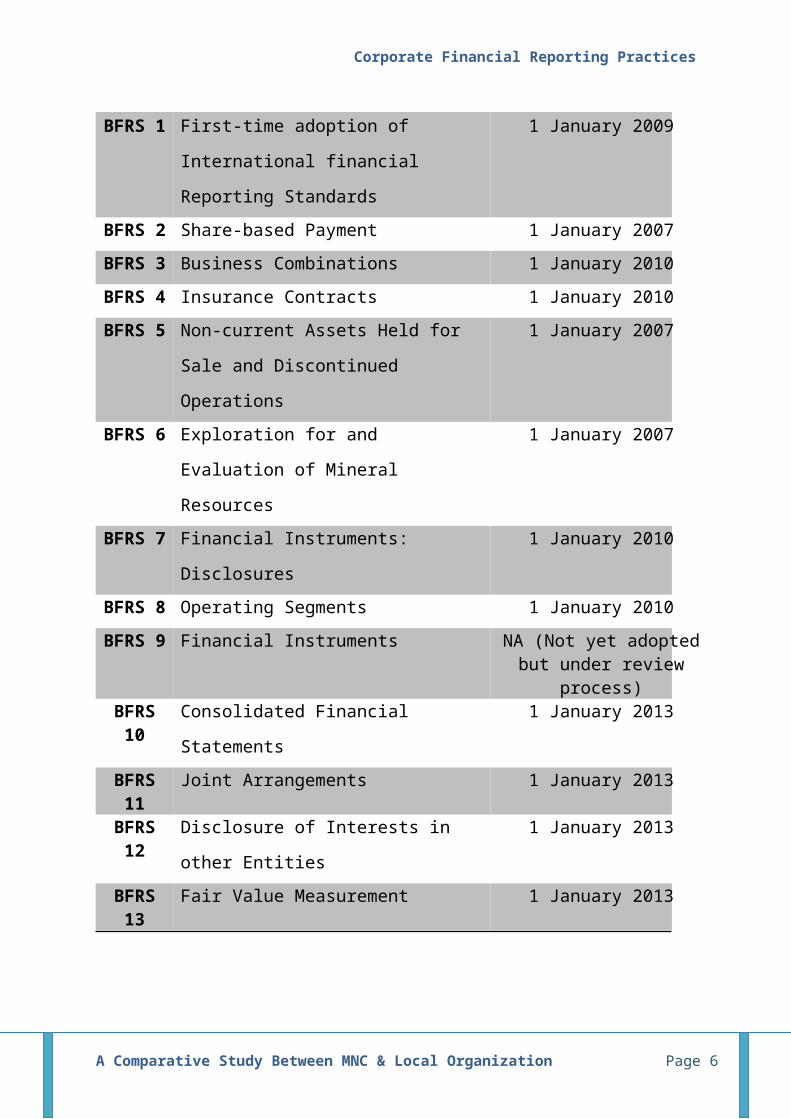

Adoptation Status of International Financial Reporting Standards (IFRS) by ICAB as Bangladesh Financial Reporting Standards (BFRS) as on 1 January 2013:

IFRS /BFRS

Title Effective Date onor after

A Comparative Study Between MNC & Local Organization Page 5

Corporate Financial Reporting Practices

BFRS 1 First-time adoption of

International financial

Reporting Standards

1 January 2009

BFRS 2 Share-based Payment 1 January 2007BFRS 3 Business Combinations 1 January 2010BFRS 4 Insurance Contracts 1 January 2010BFRS 5 Non-current Assets Held for

Sale and Discontinued

Operations

1 January 2007

BFRS 6 Exploration for and

Evaluation of Mineral

Resources

1 January 2007

BFRS 7 Financial Instruments:

Disclosures

1 January 2010

BFRS 8 Operating Segments 1 January 2010BFRS 9 Financial Instruments NA (Not yet adopted

but under reviewprocess)

BFRS10

Consolidated Financial

Statements

1 January 2013

BFRS11

Joint Arrangements 1 January 2013

BFRS12

Disclosure of Interests in

other Entities

1 January 2013

BFRS13

Fair Value Measurement 1 January 2013

A Comparative Study Between MNC & Local Organization Page 6

Corporate Financial Reporting Practices

Corporate Financial Reporting Practices in

Bangladesh

It is an old cliché that ‘Financial Reporting’ (FR)

provides useful information to a wide range of users in

making their economic decisions. Nonetheless, the term,

FR, is being uttered too often by the people in

economic game. Following the Enrorn, WorldCom, Sunbeam,

Parmalat, Global Crossing, Halliburton, Nicor Energy

and many other cases of real life corporate accounting

scandals 1which preceded the ongoing global recession2

—originated in 2007 in the USA partly from a creative

accounting and reporting of notorious sub-prime

mortgages known as derivatives— and the recent Stock

Market Crash in Bangladesh, market regulators and

various users of corporate financial information are

now clamoring for quality financial reporting after

being badly hurt by the devastating effect of the

financial disasters. Bangladesh Stock Market plunge

A Comparative Study Between MNC & Local Organization Page 7

Corporate Financial Reporting Practices

particularly has caused bewildering financial loss and

embarrassed people from all walks of life including the

government. Financial reporting is blamed in those

instances as there are ostensible claims that the

reported financial information could have saved the

damage to some extent, though not entirely. The cited

cases are classic examples of Corporate Crime or White-

collar Crime which in its own right entails several

misdeeds perpetrated by educated people with

responsible duties in business organizations. And at

times financial reporting can be instrumental in

committing such a crime as we can now vouch from these

remarkable scams where FR had been compromised abusing

the loopholes of the financial reporting regulations.

“Financial Reporting”, that underpins accountability, is

a process to provide information about the financial

position, financial performance, and cash flows of an

entity through a set of general purpose financial

statements that is useful to a wide range of users to

make a diversity of investment, credit, and other

decisions including tax assessment. Users, the buyer of

the information in the reported financial statements,

need to know the status of the business as a result of

its past performances to expect and predict current or

future capacity of the entity. They at varying degrees

A Comparative Study Between MNC & Local Organization Page 8

Corporate Financial Reporting Practices

hinge upon the information that the concerned

organization supplies to allure them. Therefore, it is of

paramount importance that the information be useful and

attributive of qualitative characteristics.

Considering the information need in the market and its

role in economic activities, the International Accounting

Standard Committee (IASC), the predecessor of the

International Accounting Standard Board (IASB) of which

the Institute of Chartered Accountants of Bangladesh

(ICAB) is a member has issued a Framework explaining the

purpose of a set of general purpose financial statements,

and the concepts that underlie the preparation and

presentation of financial statements for external users.

In addition to the Framework and BFRS, the local

regulators like the Registrar of Joint Stock Companies

and Firms, the Securities and Exchange Commission, NGO

Affairs Bureau, Bangladesh Bank etc. can prescribe

industry specific formats of presentation of financial

statements. Thus an applicable Financial Reporting

Framework emanates from local statute, international

standards. The range of regulatory activities typically

includes setting minimum standards and requirements for

corporate reporting, requiring submission of the

financial reports to the oversight body for its review,

making regular inspections, and investigating and

A Comparative Study Between MNC & Local Organization Page 9

Corporate Financial Reporting Practices

prosecuting misconduct by the corporate entities for

breaching and abusing reporting framework. Therefore,

strongly active Financial Reporting Regulations can

encourage and compel standardized financial reporting

within applicable framework.

A Comparative Study between MNC & Local

Organization

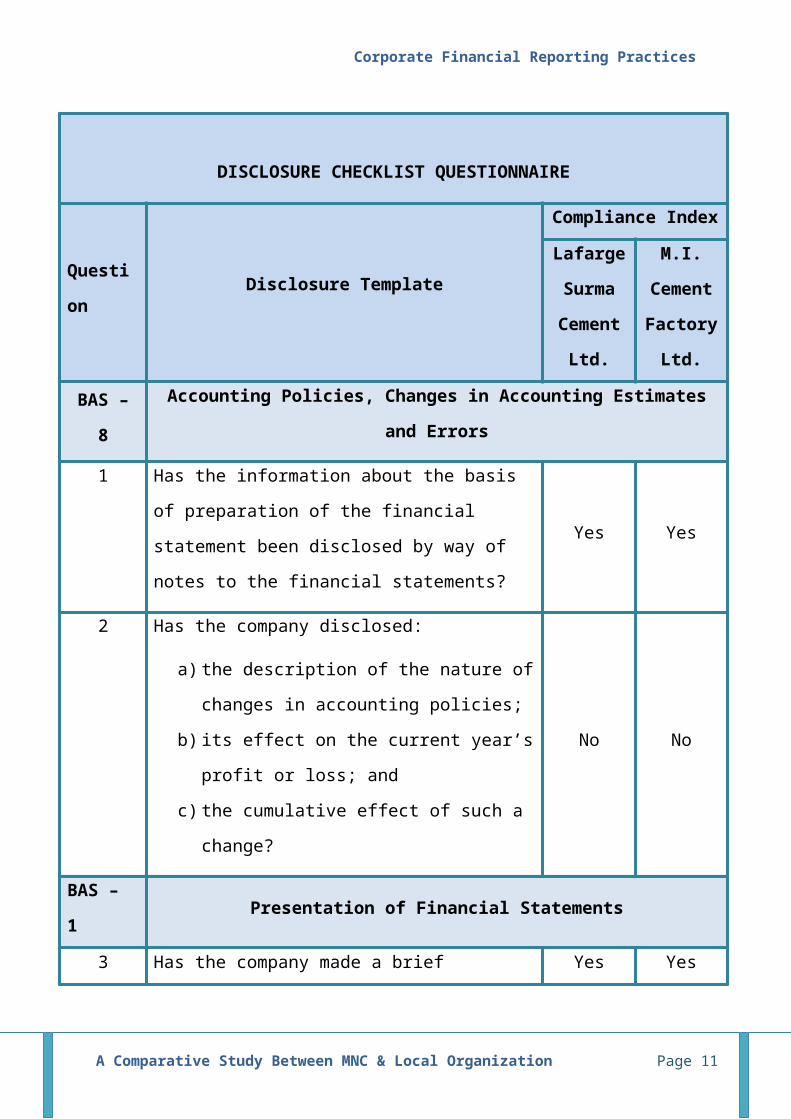

To Compare Corporate Financial Reporting Practices

between MNC and Local Organization a Disclosure Checklist

Questionnaire by comparing two companies i.e. operating

in Bangladesh in which Lafarge Surma Cement Limited is a

MNC and M.I. Cement Factory Limited is a local

organization is given below:

A Comparative Study Between MNC & Local Organization Page 10

Corporate Financial Reporting Practices

DISCLOSURE CHECKLIST QUESTIONNAIRE

Questi

onDisclosure Template

Compliance Index

Lafarge

Surma

Cement

Ltd.

M.I.

Cement

Factory

Ltd.

BAS –

8

Accounting Policies, Changes in Accounting Estimates

and Errors

1 Has the information about the basis

of preparation of the financial

statement been disclosed by way of

notes to the financial statements?

Yes Yes

2 Has the company disclosed:

a) the description of the nature of

changes in accounting policies;

b) its effect on the current year’s

profit or loss; and

c) the cumulative effect of such a

change?

No No

BAS –

1Presentation of Financial Statements

3 Has the company made a brief Yes Yes

A Comparative Study Between MNC & Local Organization Page 11

Corporate Financial Reporting Practices

description of activities?

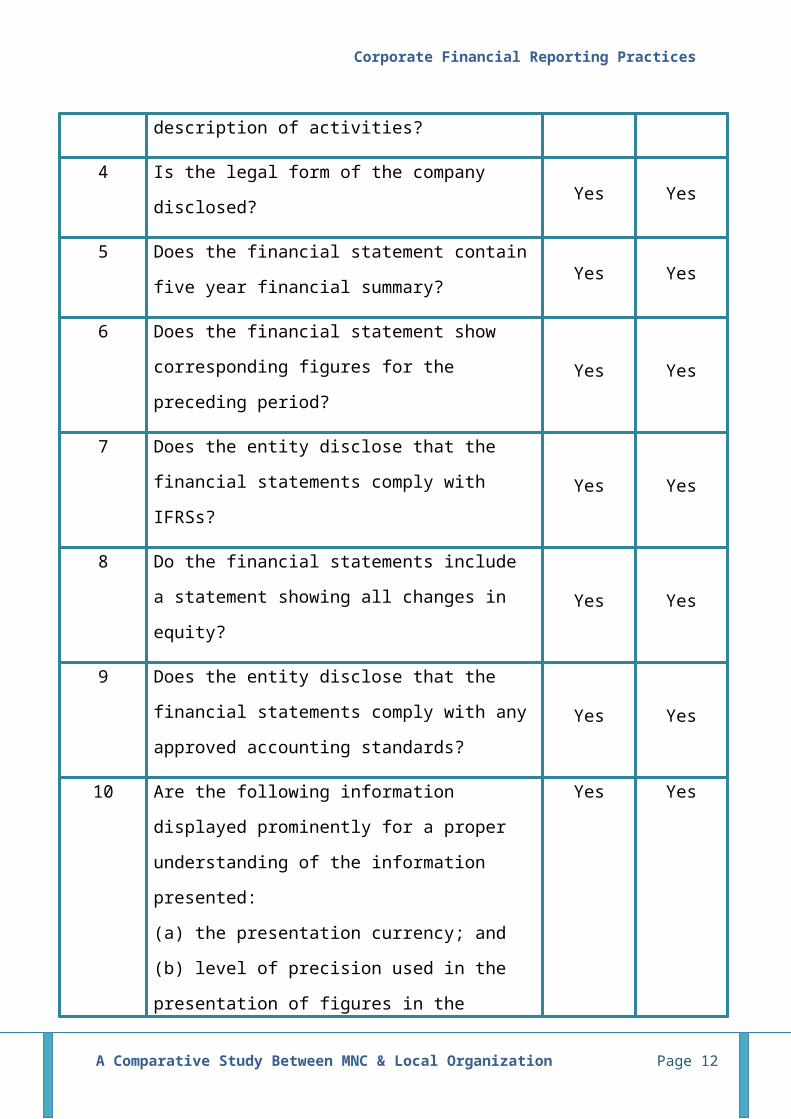

4 Is the legal form of the company

disclosed? Yes Yes

5 Does the financial statement contain

five year financial summary? Yes Yes

6 Does the financial statement show

corresponding figures for the

preceding period?Yes Yes

7 Does the entity disclose that the

financial statements comply with

IFRSs?Yes Yes

8 Do the financial statements include

a statement showing all changes in

equity?Yes Yes

9 Does the entity disclose that the

financial statements comply with any

approved accounting standards?Yes Yes

10 Are the following information

displayed prominently for a proper

understanding of the information

presented:

(a) the presentation currency; and

(b) level of precision used in the

presentation of figures in the

Yes Yes

A Comparative Study Between MNC & Local Organization Page 12

Corporate Financial Reporting Practices

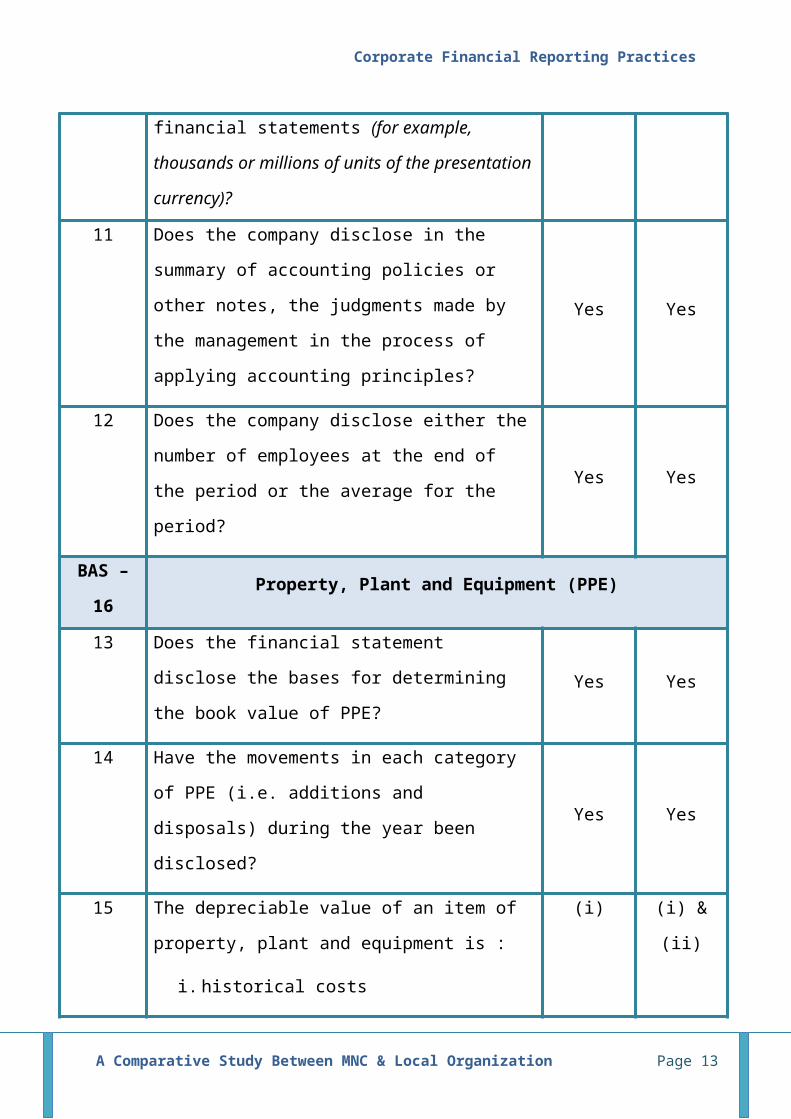

financial statements (for example,

thousands or millions of units of the presentation

currency)?

11 Does the company disclose in the

summary of accounting policies or

other notes, the judgments made by

the management in the process of

applying accounting principles?

Yes Yes

12 Does the company disclose either the

number of employees at the end of

the period or the average for the

period?

Yes Yes

BAS –

16Property, Plant and Equipment (PPE)

13 Does the financial statement

disclose the bases for determining

the book value of PPE?Yes Yes

14 Have the movements in each category

of PPE (i.e. additions and

disposals) during the year been

disclosed?

Yes Yes

15 The depreciable value of an item of

property, plant and equipment is :

i. historical costs

(i) (i) &

(ii)

A Comparative Study Between MNC & Local Organization Page 13

Corporate Financial Reporting Practices

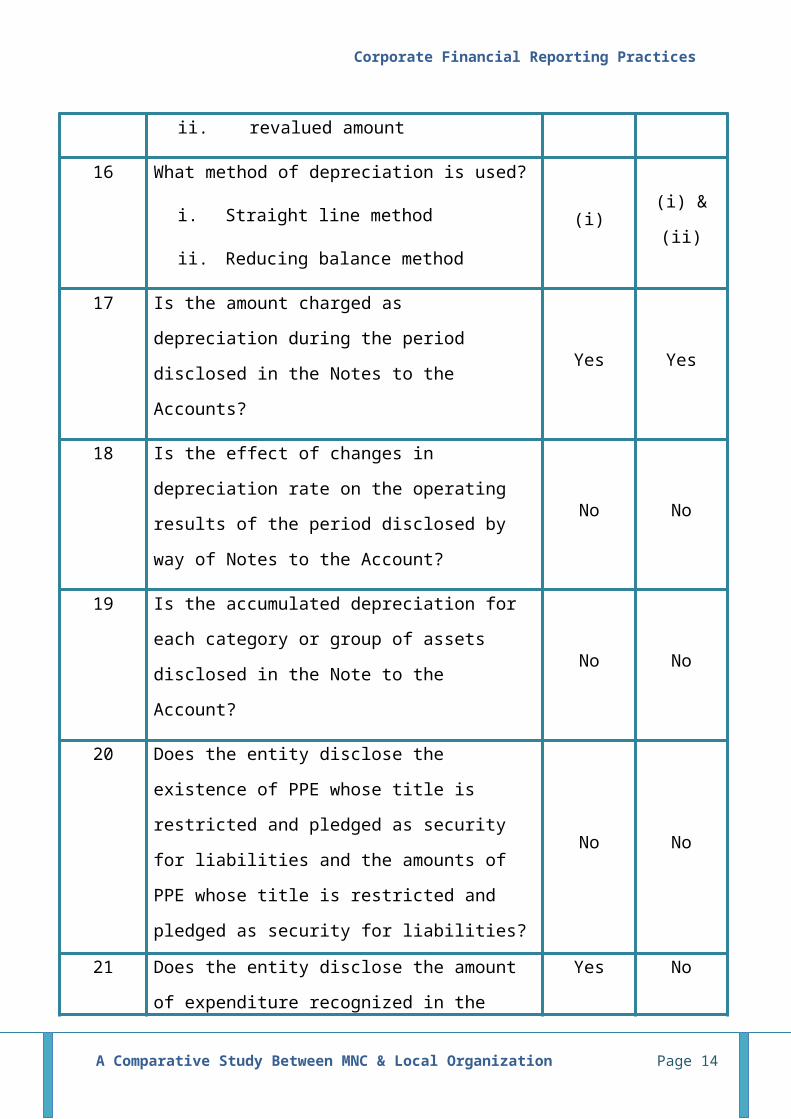

ii. revalued amount

16 What method of depreciation is used?

i. Straight line method

ii. Reducing balance method

(i)(i) &

(ii)

17 Is the amount charged as

depreciation during the period

disclosed in the Notes to the

Accounts?

Yes Yes

18 Is the effect of changes in

depreciation rate on the operating

results of the period disclosed by

way of Notes to the Account?

No No

19 Is the accumulated depreciation for

each category or group of assets

disclosed in the Note to the

Account?

No No

20 Does the entity disclose the

existence of PPE whose title is

restricted and pledged as security

for liabilities and the amounts of

PPE whose title is restricted and

pledged as security for liabilities?

No No

21 Does the entity disclose the amount

of expenditure recognized in the

Yes No

A Comparative Study Between MNC & Local Organization Page 14

Corporate Financial Reporting Practices

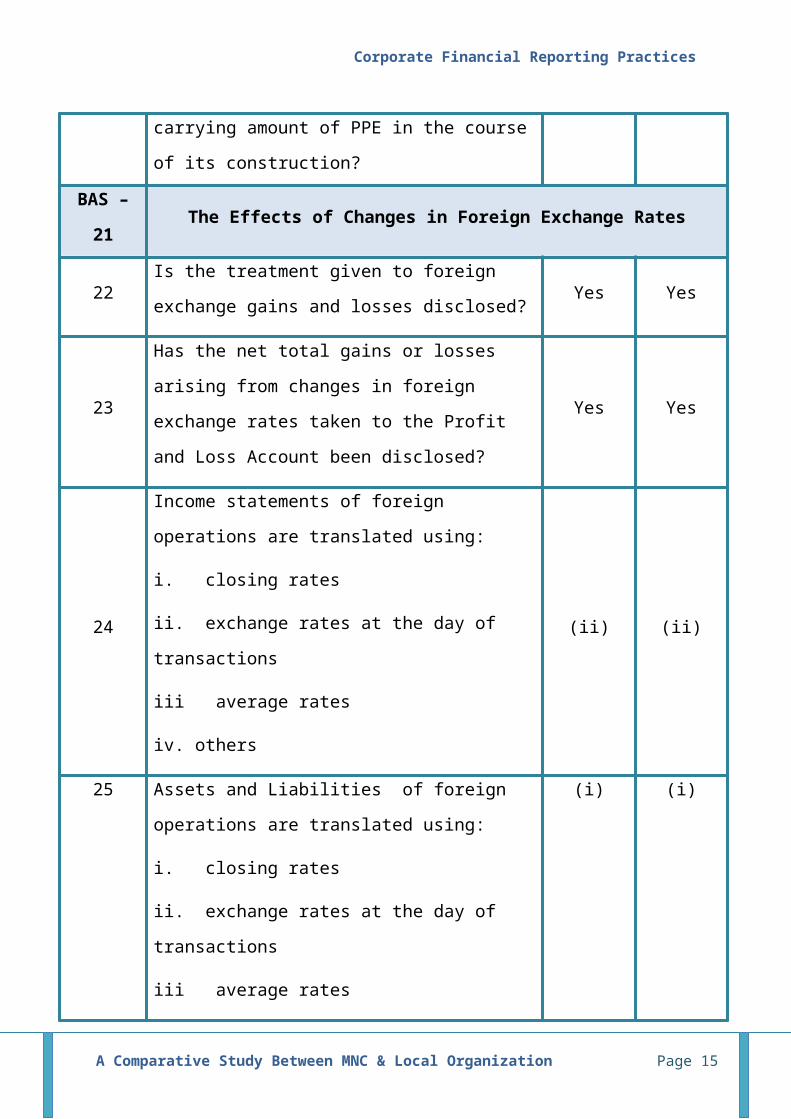

carrying amount of PPE in the course

of its construction?

BAS –

21The Effects of Changes in Foreign Exchange Rates

22Is the treatment given to foreign

exchange gains and losses disclosed? Yes Yes

23

Has the net total gains or losses

arising from changes in foreign

exchange rates taken to the Profit

and Loss Account been disclosed?

Yes Yes

24

Income statements of foreign

operations are translated using:

i. closing rates

ii. exchange rates at the day of

transactions

iii average rates

iv. others

(ii) (ii)

25 Assets and Liabilities of foreign

operations are translated using:

i. closing rates

ii. exchange rates at the day of

transactions

iii average rates

(i) (i)

A Comparative Study Between MNC & Local Organization Page 15

Corporate Financial Reporting Practices

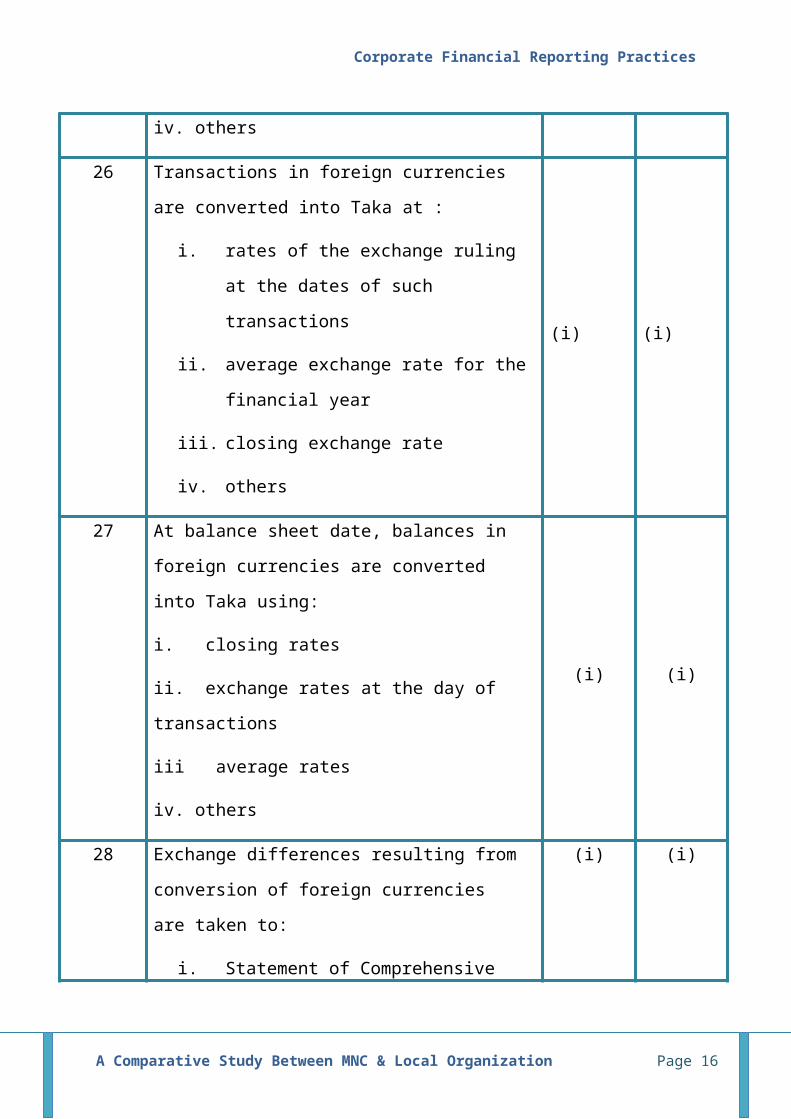

iv. others

26 Transactions in foreign currencies

are converted into Taka at :

i. rates of the exchange ruling

at the dates of such

transactions

ii. average exchange rate for the

financial year

iii. closing exchange rate

iv. others

(i) (i)

27 At balance sheet date, balances in

foreign currencies are converted

into Taka using:

i. closing rates

ii. exchange rates at the day of

transactions

iii average rates

iv. others

(i) (i)

28 Exchange differences resulting from

conversion of foreign currencies

are taken to:

i. Statement of Comprehensive

(i) (i)

A Comparative Study Between MNC & Local Organization Page 16

Corporate Financial Reporting Practices

Income

ii. Reserves

iii. Others

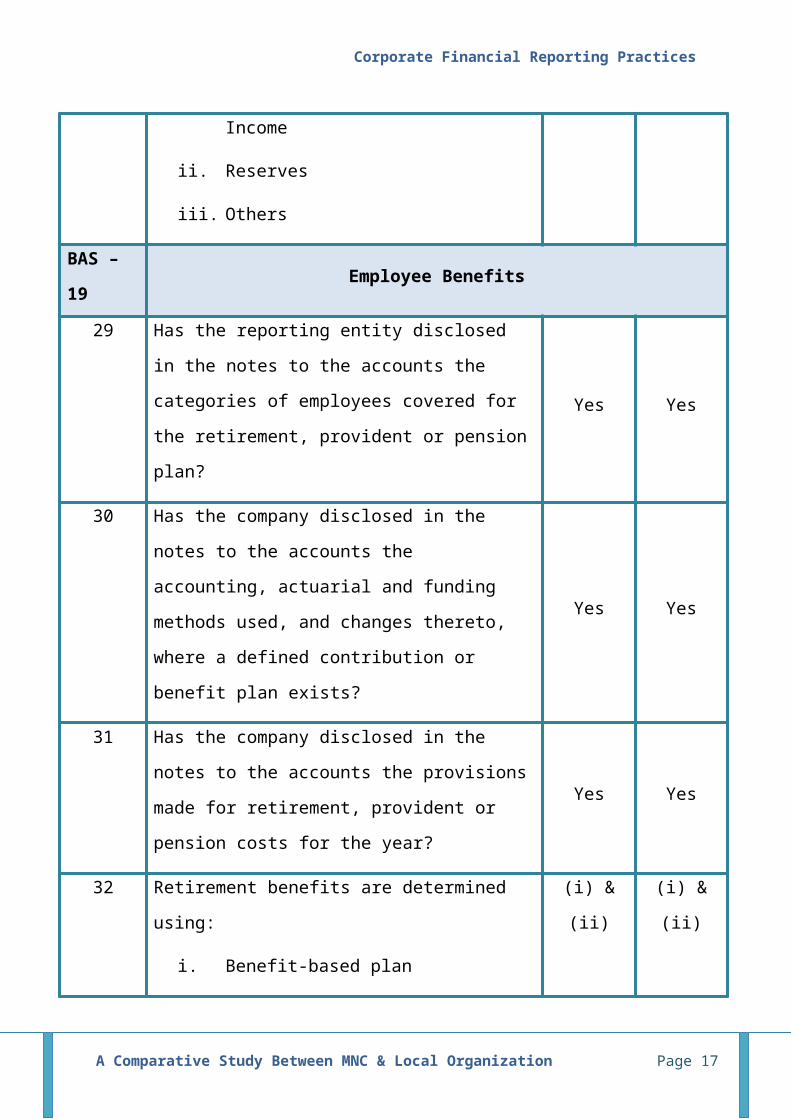

BAS –

19Employee Benefits

29 Has the reporting entity disclosed

in the notes to the accounts the

categories of employees covered for

the retirement, provident or pension

plan?

Yes Yes

30 Has the company disclosed in the

notes to the accounts the

accounting, actuarial and funding

methods used, and changes thereto,

where a defined contribution or

benefit plan exists?

Yes Yes

31 Has the company disclosed in the

notes to the accounts the provisions

made for retirement, provident or

pension costs for the year?

Yes Yes

32 Retirement benefits are determined

using:

i. Benefit-based plan

(i) &

(ii)

(i) &

(ii)

A Comparative Study Between MNC & Local Organization Page 17

Corporate Financial Reporting Practices

ii. Contribution-based plan

iii. Others – unfunded

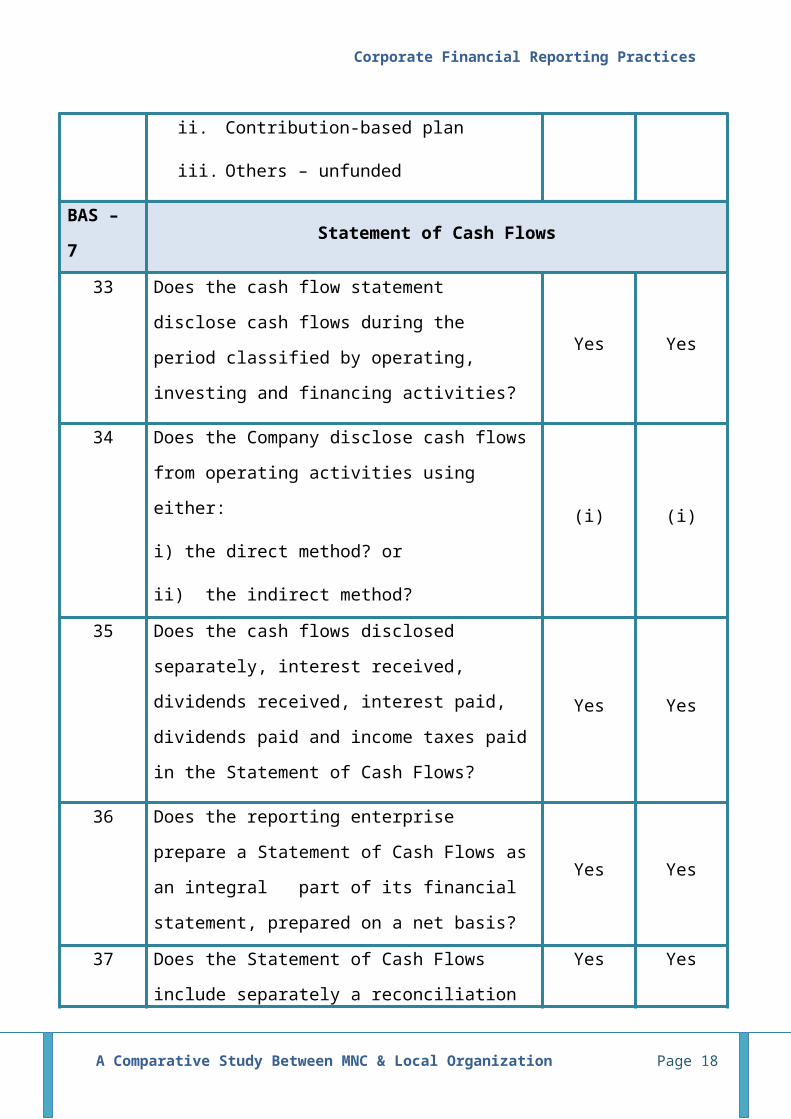

BAS –

7Statement of Cash Flows

33 Does the cash flow statement

disclose cash flows during the

period classified by operating,

investing and financing activities?

Yes Yes

34 Does the Company disclose cash flows

from operating activities using

either:

i) the direct method? or

ii) the indirect method?

(i) (i)

35 Does the cash flows disclosed

separately, interest received,

dividends received, interest paid,

dividends paid and income taxes paid

in the Statement of Cash Flows?

Yes Yes

36 Does the reporting enterprise

prepare a Statement of Cash Flows as

an integral part of its financial

statement, prepared on a net basis?

Yes Yes

37 Does the Statement of Cash Flows

include separately a reconciliation

Yes Yes

A Comparative Study Between MNC & Local Organization Page 18

Corporate Financial Reporting Practices

of the increase and decrease in cash

and cash equivalents during the

reporting period with opening and

closing balances?

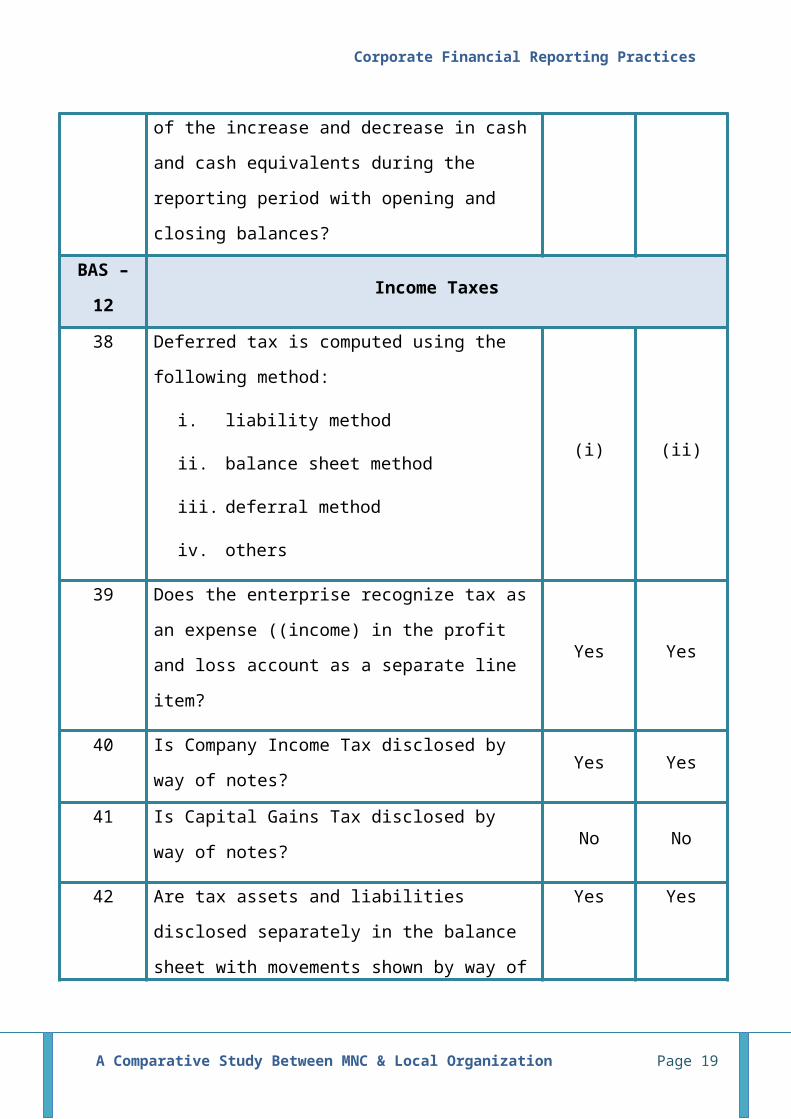

BAS –

12Income Taxes

38 Deferred tax is computed using the

following method:

i. liability method

ii. balance sheet method

iii. deferral method

iv. others

(i) (ii)

39 Does the enterprise recognize tax as

an expense ((income) in the profit

and loss account as a separate line

item?

Yes Yes

40 Is Company Income Tax disclosed by

way of notes?Yes Yes

41 Is Capital Gains Tax disclosed by

way of notes? No No

42 Are tax assets and liabilities

disclosed separately in the balance

sheet with movements shown by way of

Yes Yes

A Comparative Study Between MNC & Local Organization Page 19

Corporate Financial Reporting Practices

notes?

a. Current Taxes

b. Deferred Taxes

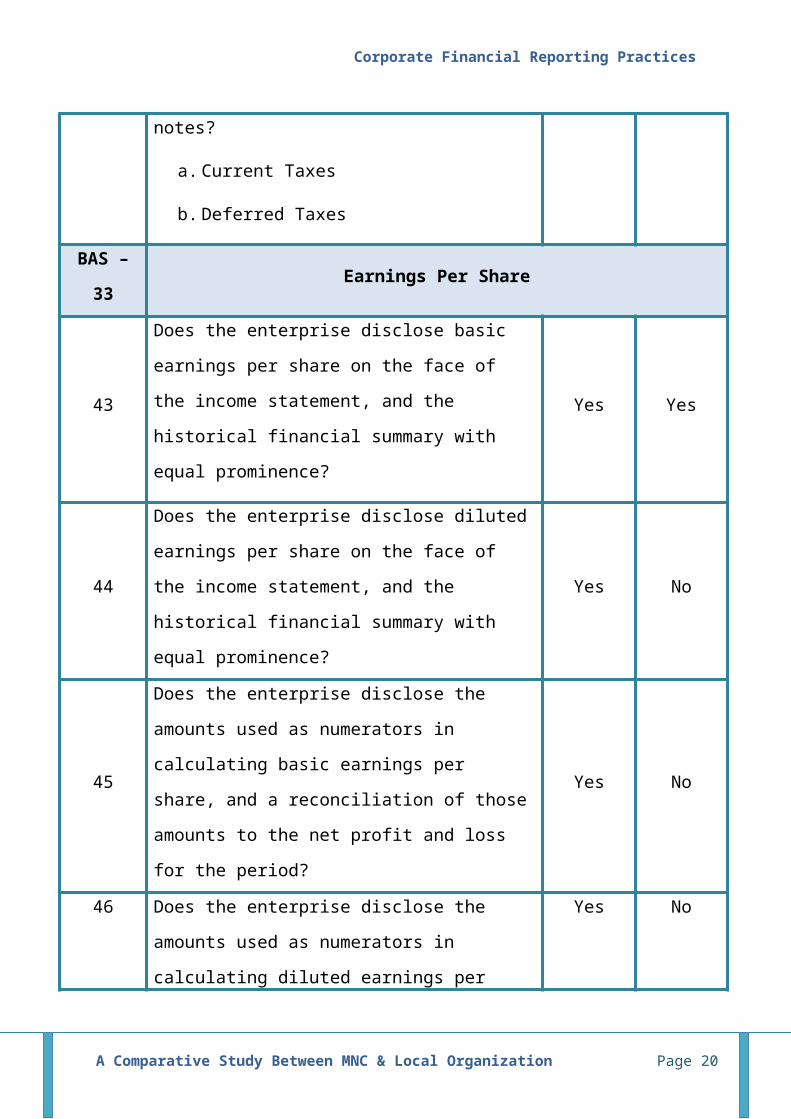

BAS –

33Earnings Per Share

43

Does the enterprise disclose basic

earnings per share on the face of

the income statement, and the

historical financial summary with

equal prominence?

Yes Yes

44

Does the enterprise disclose diluted

earnings per share on the face of

the income statement, and the

historical financial summary with

equal prominence?

Yes No

45

Does the enterprise disclose the

amounts used as numerators in

calculating basic earnings per

share, and a reconciliation of those

amounts to the net profit and loss

for the period?

Yes No

46 Does the enterprise disclose the

amounts used as numerators in

calculating diluted earnings per

Yes No

A Comparative Study Between MNC & Local Organization Page 20

Corporate Financial Reporting Practices

share, and a reconciliation of those

amounts to the net profit and loss

for the period?

47

Does the enterprise disclose any

changes in the number of shares used

to compute earnings per share?

Yes Yes

BAS –

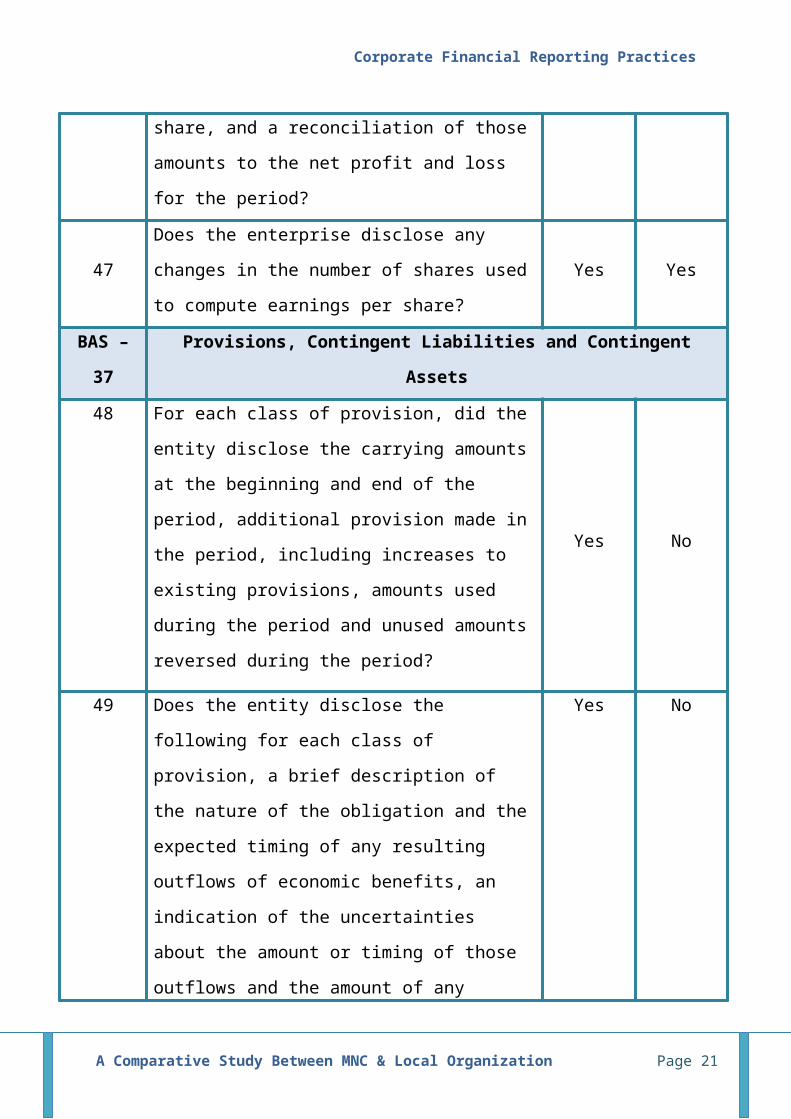

37

Provisions, Contingent Liabilities and Contingent

Assets

48 For each class of provision, did the

entity disclose the carrying amounts

at the beginning and end of the

period, additional provision made in

the period, including increases to

existing provisions, amounts used

during the period and unused amounts

reversed during the period?

Yes No

49 Does the entity disclose the

following for each class of

provision, a brief description of

the nature of the obligation and the

expected timing of any resulting

outflows of economic benefits, an

indication of the uncertainties

about the amount or timing of those

outflows and the amount of any

Yes No

A Comparative Study Between MNC & Local Organization Page 21

Corporate Financial Reporting Practices

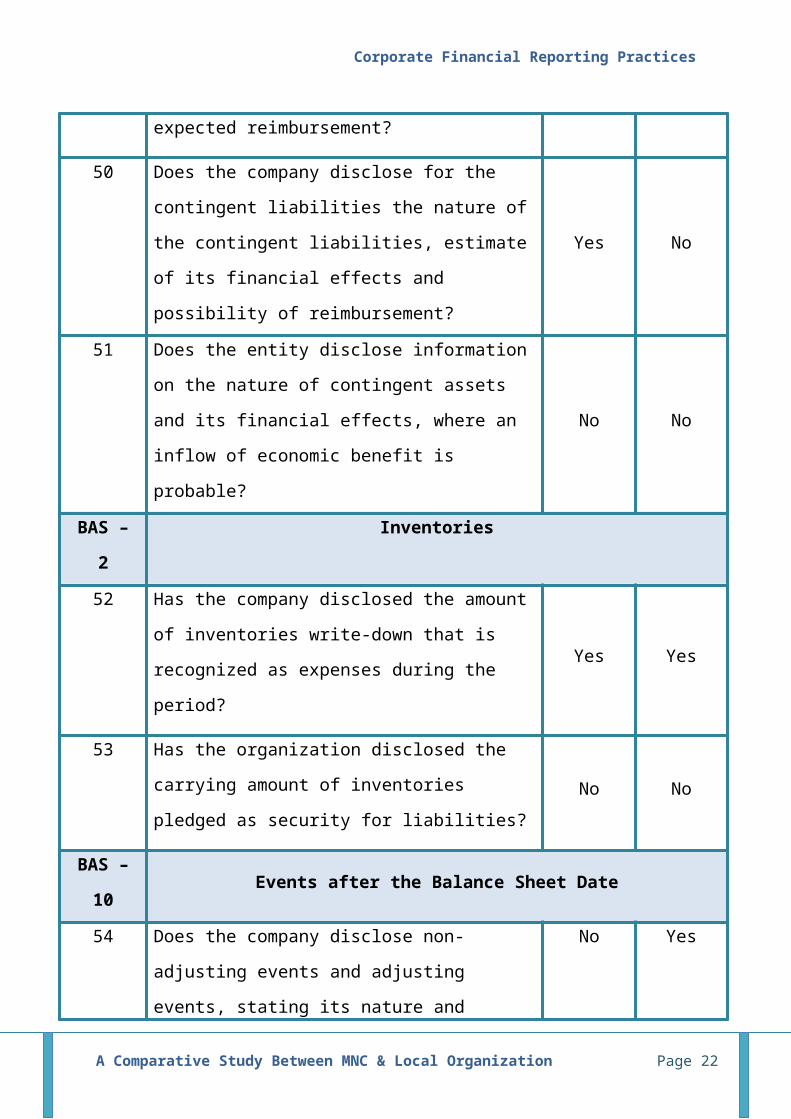

expected reimbursement?

50 Does the company disclose for the

contingent liabilities the nature of

the contingent liabilities, estimate

of its financial effects and

possibility of reimbursement?

Yes No

51 Does the entity disclose information

on the nature of contingent assets

and its financial effects, where an

inflow of economic benefit is

probable?

No No

BAS –

2

Inventories

52 Has the company disclosed the amount

of inventories write-down that is

recognized as expenses during the

period?

Yes Yes

53 Has the organization disclosed the

carrying amount of inventories

pledged as security for liabilities?No No

BAS –

10Events after the Balance Sheet Date

54 Does the company disclose non-

adjusting events and adjusting

events, stating its nature and

No Yes

A Comparative Study Between MNC & Local Organization Page 22

Corporate Financial Reporting Practices

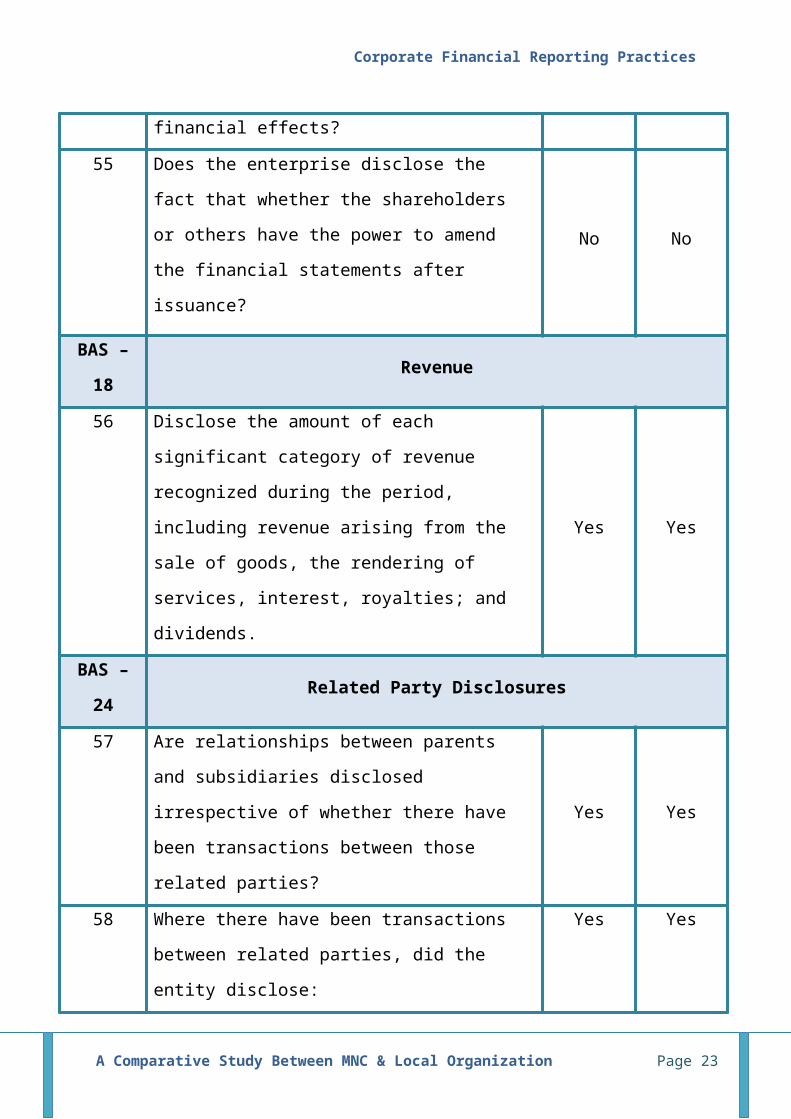

financial effects?

55 Does the enterprise disclose the

fact that whether the shareholders

or others have the power to amend

the financial statements after

issuance?

No No

BAS –

18Revenue

56 Disclose the amount of each

significant category of revenue

recognized during the period,

including revenue arising from the

sale of goods, the rendering of

services, interest, royalties; and

dividends.

Yes Yes

BAS –

24Related Party Disclosures

57 Are relationships between parents

and subsidiaries disclosed

irrespective of whether there have

been transactions between those

related parties?

Yes Yes

58 Where there have been transactions

between related parties, did the

entity disclose:

Yes Yes

A Comparative Study Between MNC & Local Organization Page 23

Corporate Financial Reporting Practices

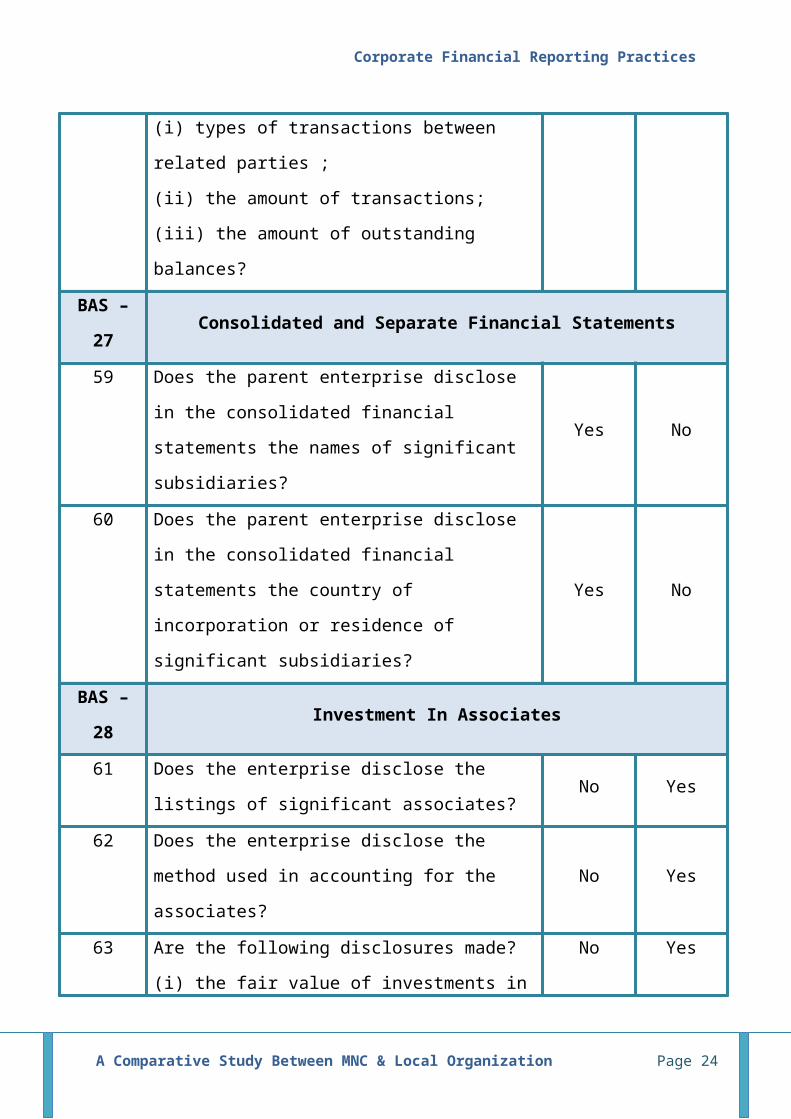

(i) types of transactions between

related parties ;

(ii) the amount of transactions;

(iii) the amount of outstanding

balances?

BAS –

27Consolidated and Separate Financial Statements

59 Does the parent enterprise disclose

in the consolidated financial

statements the names of significant

subsidiaries?

Yes No

60 Does the parent enterprise disclose

in the consolidated financial

statements the country of

incorporation or residence of

significant subsidiaries?

Yes No

BAS –

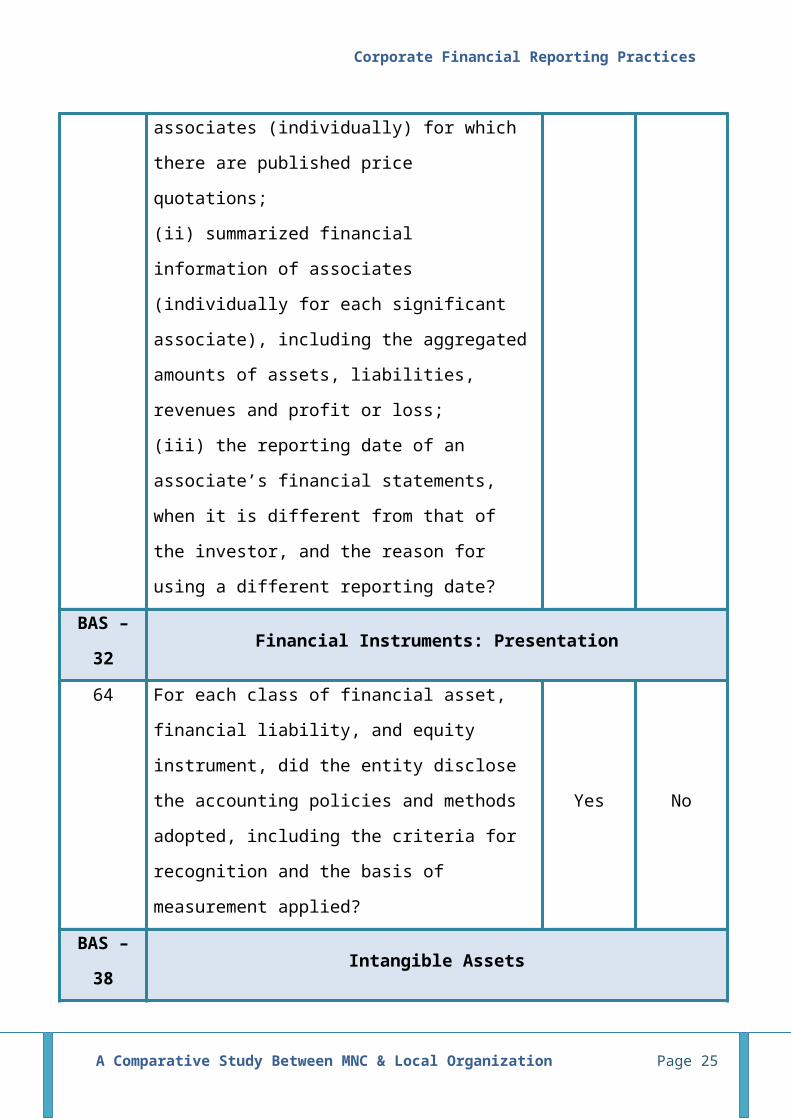

28Investment In Associates

61 Does the enterprise disclose the

listings of significant associates?No Yes

62 Does the enterprise disclose the

method used in accounting for the

associates?

No Yes

63 Are the following disclosures made?

(i) the fair value of investments in

No Yes

A Comparative Study Between MNC & Local Organization Page 24

Corporate Financial Reporting Practices

associates (individually) for which

there are published price

quotations;

(ii) summarized financial

information of associates

(individually for each significant

associate), including the aggregated

amounts of assets, liabilities,

revenues and profit or loss;

(iii) the reporting date of an

associate’s financial statements,

when it is different from that of

the investor, and the reason for

using a different reporting date?

BAS –

32Financial Instruments: Presentation

64 For each class of financial asset,

financial liability, and equity

instrument, did the entity disclose

the accounting policies and methods

adopted, including the criteria for

recognition and the basis of

measurement applied?

Yes No

BAS –

38Intangible Assets

A Comparative Study Between MNC & Local Organization Page 25

Corporate Financial Reporting Practices

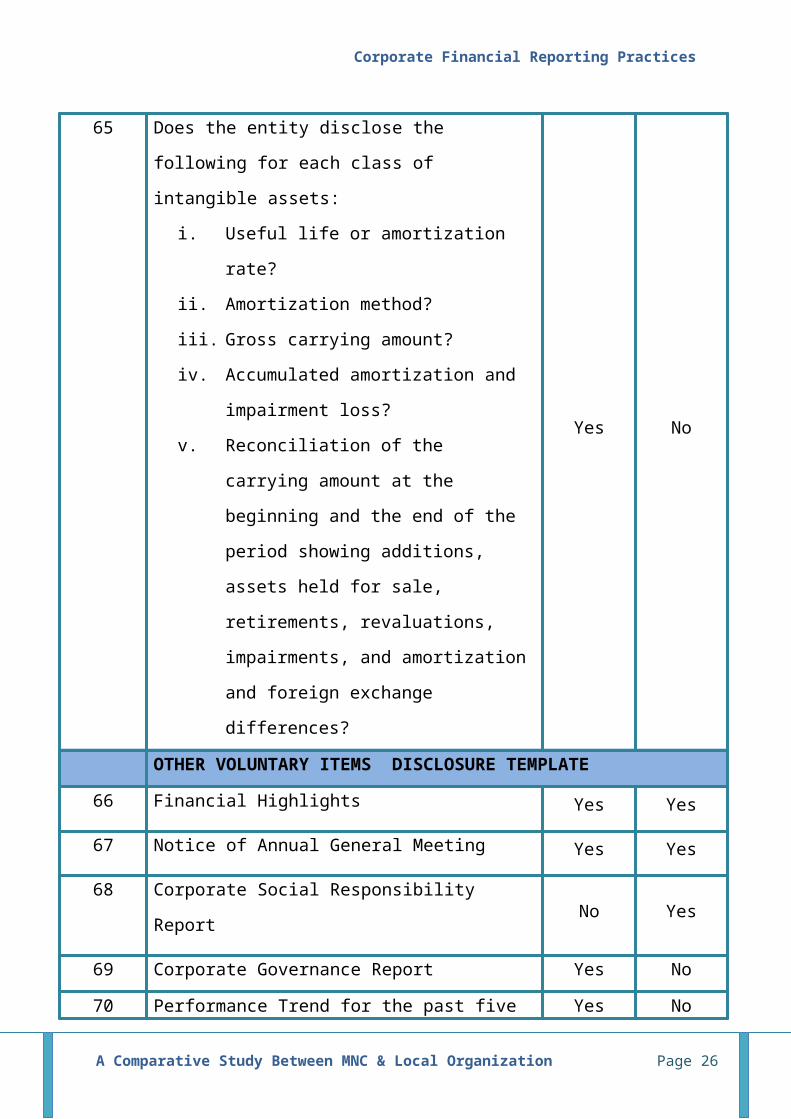

65 Does the entity disclose the

following for each class of

intangible assets:

i. Useful life or amortization

rate?

ii. Amortization method?

iii. Gross carrying amount?

iv. Accumulated amortization and

impairment loss?

v. Reconciliation of the

carrying amount at the

beginning and the end of the

period showing additions,

assets held for sale,

retirements, revaluations,

impairments, and amortization

and foreign exchange

differences?

Yes No

OTHER VOLUNTARY ITEMS DISCLOSURE TEMPLATE

66 Financial Highlights Yes Yes

67 Notice of Annual General Meeting Yes Yes

68 Corporate Social Responsibility

Report No Yes

69 Corporate Governance Report Yes No

70 Performance Trend for the past five Yes No

A Comparative Study Between MNC & Local Organization Page 26

Corporate Financial Reporting Practices

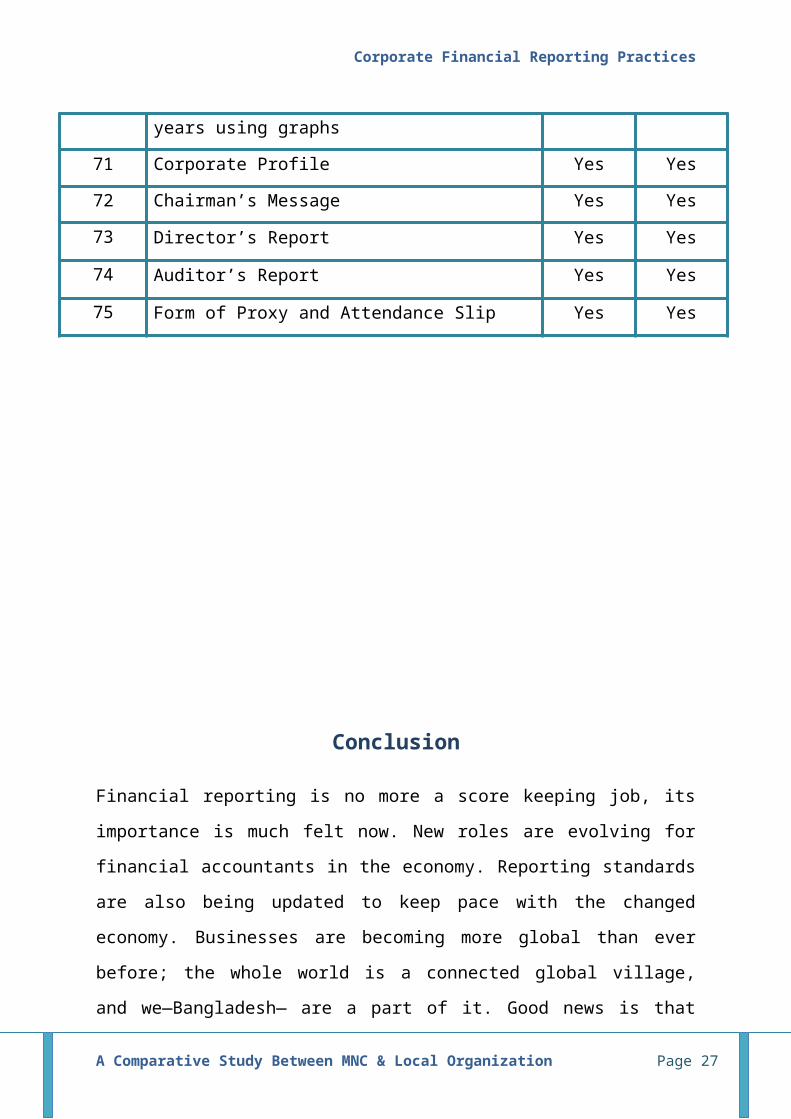

years using graphs

71 Corporate Profile Yes Yes

72 Chairman’s Message Yes Yes

73 Director’s Report Yes Yes

74 Auditor’s Report Yes Yes

75 Form of Proxy and Attendance Slip Yes Yes

Conclusion

Financial reporting is no more a score keeping job, its

importance is much felt now. New roles are evolving for

financial accountants in the economy. Reporting standards

are also being updated to keep pace with the changed

economy. Businesses are becoming more global than ever

before; the whole world is a connected global village,

and we—Bangladesh— are a part of it. Good news is that

A Comparative Study Between MNC & Local Organization Page 27

Corporate Financial Reporting Practices

Bangladesh is moving forward, albeit the ongoing global

economic turmoil, to join the league of the “Middle

Income Countries” in tandem with the target to achieve

Millennium Development Goal within the shortest possible

time. These targets have been manifested in global forum;

investors from both the developed and the developing

countries find interest in Bangladesh for its growth

potential. They are calling for globalized standards

under the auspices of the development partners—bilateral

and multilateral— and international organizations. In

time, if not sooner, the demand for standardized

reporting of financial information will be at its peak.

A Comparative Study Between MNC & Local Organization Page 28