lost in translation - mckinsey

TRANSCRIPT

Consumer Packaged Goods

Lost in translationThe challenge of global channel and customer management

Lessons from Europe, Latin America, and the United States

March 2014

CONTENTS

Lost in translation: The challenge of global channel and customer management

Introduction 1

The Customer and Channel Management Survey 2

Five global customer-management imperatives 3

1. Identify pockets of growth and align resources against them 3 Case study: Reaching the Hispanic population through ZIP-code segmentation 3

2. Overinvest in collaborative relationships with most important customers 4 Case study: Codeveloping new beverage products 5

3. Use deep insights and analytics to realize greater returns from pricing and promotion activities 5 Case study: Analyzing returns on beverage promotions 5

4. Translate distinctive consumer insights into in-store advantages 6 Case study: Mining data to inform pricing of nutritional products 6

5. Increase sales using optimized route-to-market models 6 Case study: Mapping the retail-outlet landscape in Brazil 7

Building global customer-management excellence 8

1

INTRODUCTIONAlthough consumer-packaged-goods (CPG) companies worldwide have faced obstacles to growth over the past few years, some of them are faring much better than their competitors. According to our latest global research—in which we surveyed 141 of the world’s leading CPG manufacturers—companies with best-in-class capabilities in customer and channel management are delivering superior performance, growing net sales three to six percentage points faster than relevant peers. Furthermore, these outperformers are achieving almost double the return on their trade investment. This disparity in performance exists in each of three regions we studied—Europe, Latin America, and the United States (see sidebar, The Customer and Channel Management survey).

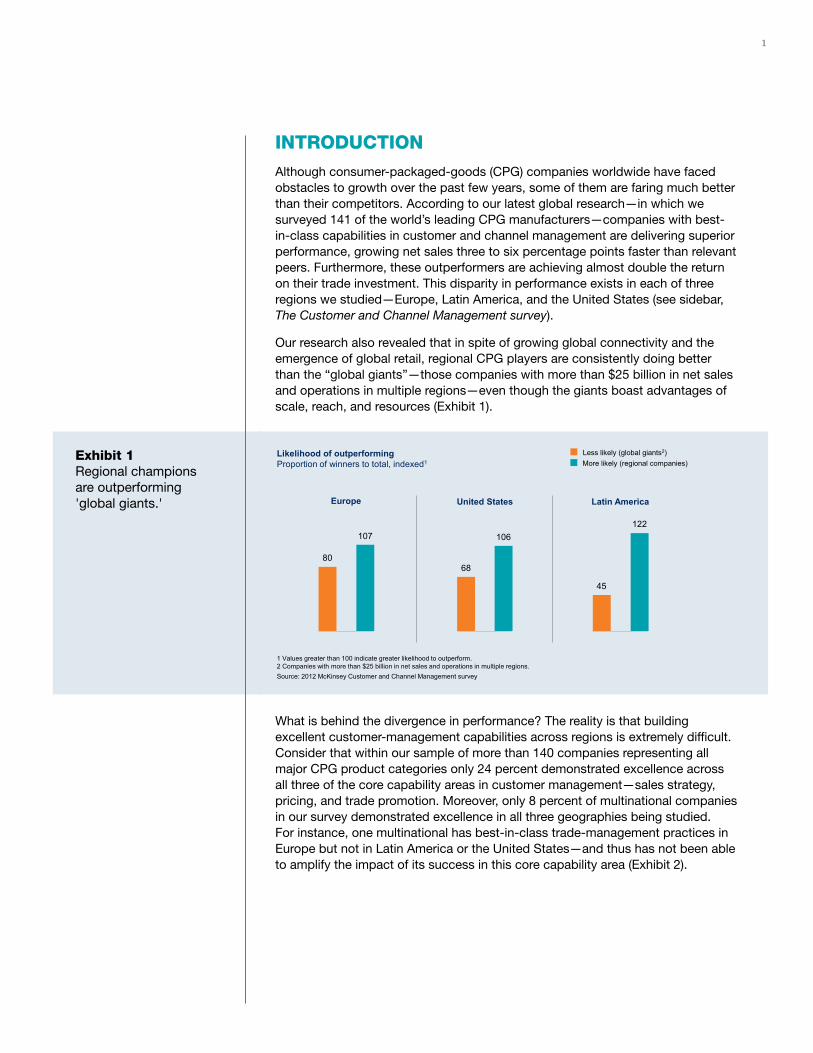

Our research also revealed that in spite of growing global connectivity and the emergence of global retail, regional CPG players are consistently doing better than the “global giants”—those companies with more than $25 billion in net sales and operations in multiple regions—even though the giants boast advantages of scale, reach, and resources (Exhibit 1).

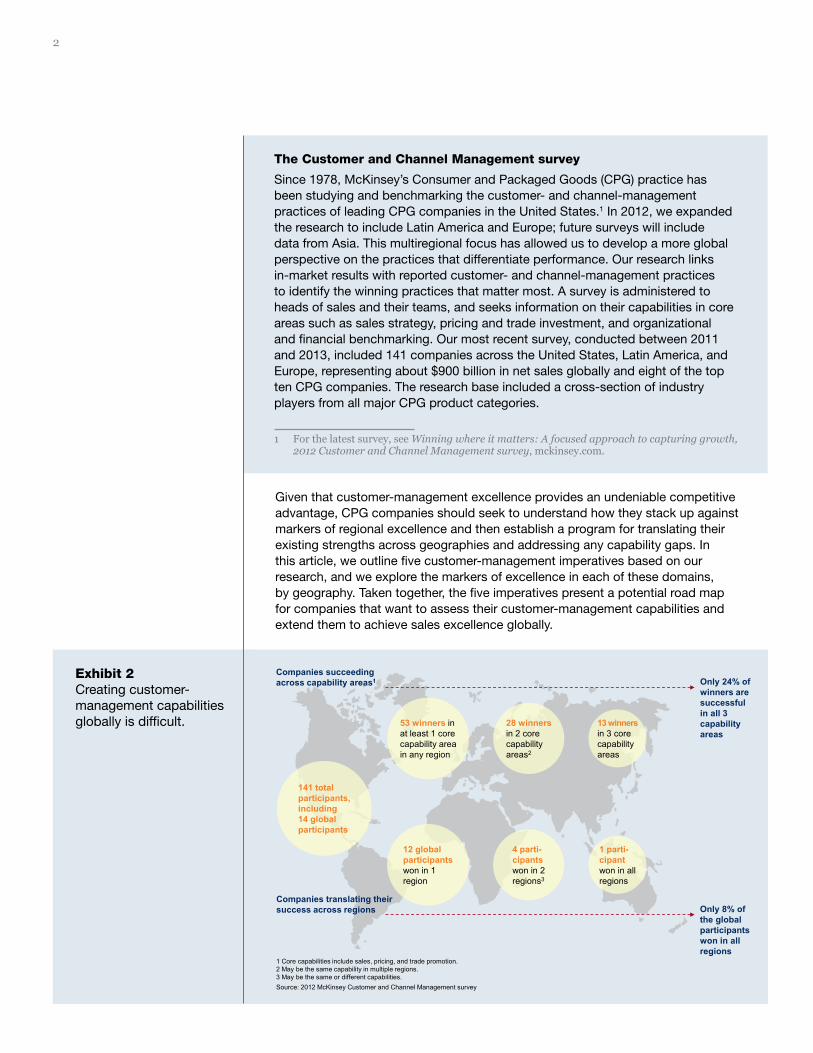

What is behind the divergence in performance? The reality is that building excellent customer-management capabilities across regions is extremely difficult. Consider that within our sample of more than 140 companies representing all major CPG product categories only 24 percent demonstrated excellence across all three of the core capability areas in customer management—sales strategy, pricing, and trade promotion. Moreover, only 8 percent of multinational companies in our survey demonstrated excellence in all three geographies being studied. For instance, one multinational has best-in-class trade-management practices in Europe but not in Latin America or the United States—and thus has not been able to amplify the impact of its success in this core capability area (Exhibit 2).

Exhibit 1Regional champions are outperforming 'global giants.'

1 Values greater than 100 indicate greater likelihood to outperform.2 Companies with more than $25 billion in net sales and operations in multiple regions.Source: 2012 McKinsey Customer and Channel Management survey

Exhibit 1 Regional champions are outperforming ‘global giants.’

Less likely (global giants2)More likely (regional companies)

Likelihood of outperformingProportion of winners to total, indexed1

Latin America

122

45

Europe

107

80

United States

106

68

2

Given that customer-management excellence provides an undeniable competitive advantage, CPG companies should seek to understand how they stack up against markers of regional excellence and then establish a program for translating their existing strengths across geographies and addressing any capability gaps. In this article, we outline five customer-management imperatives based on our research, and we explore the markers of excellence in each of these domains, by geography. Taken together, the five imperatives present a potential road map for companies that want to assess their customer-management capabilities and extend them to achieve sales excellence globally.

The Customer and Channel Management survey

Since 1978, McKinsey’s Consumer and Packaged Goods (CPG) practice has been studying and benchmarking the customer- and channel-management practices of leading CPG companies in the United States.1 In 2012, we expanded the research to include Latin America and Europe; future surveys will include data from Asia. This multiregional focus has allowed us to develop a more global perspective on the practices that differentiate performance. Our research links in-market results with reported customer- and channel-management practices to identify the winning practices that matter most. A survey is administered to heads of sales and their teams, and seeks information on their capabilities in core areas such as sales strategy, pricing and trade investment, and organizational and financial benchmarking. Our most recent survey, conducted between 2011 and 2013, included 141 companies across the United States, Latin America, and Europe, representing about $900 billion in net sales globally and eight of the top ten CPG companies. The research base included a cross-section of industry players from all major CPG product categories.

1 For the latest survey, see Winning where it matters: A focused approach to capturing growth, 2012 Customer and Channel Management survey, mckinsey.com.

Exhibit 2Creating customer-management capabilities globally is difficult.

Exhibit 2 Creating customer-management capabilities globally is difficult.

1 Core capabilities include sales, pricing, and trade promotion. 2 May be the same capability in multiple regions.3 May be the same or different capabilities. Source: 2012 McKinsey Customer and Channel Management survey

Companies succeeding across capability areas1

Companies translating their success across regions

Only 24% of winners are successful in all 3 capability areas

Only 8% of the global participants won in all regions

53 winners in at least 1 core capability area in any region

141 total participants, including 14 global participants

28 winnersin 2 core capability areas2

13 winnersin 3 core capability areas

12 global participants won in 1 region

4 parti-cipantswon in 2 regions3

1 parti-cipantwon in all regions

Consumer Packaged Goods (Americas)Lost in translation: The challenge of global channel and customer management 3

FIVE GLOBAL CUSTOMER-MANAGEMENT IMPERATIVESOur research points to several important capabilities displayed by outperforming CPG companies, each of which addresses the core elements of customer and channel management.

1. Identify pockets of growth and align resources against them.Compared with their category peers, the outperformers in our research allocate a disproportionate amount of their resources to high-growth channels, customers, and geographies. For instance, convenience is one of the fastest-growing channels in Europe, and the most successful CPG companies in Europe are investing more of their trade dollars (11 percent of net sales) in the convenience channel than their category peers are (7 percent). Meanwhile, dollar stores and drug stores are the fastest-growing channels for consumables in the United States, and the outperforming US companies in our study allocate 15 to 25 percent more full-time staff to the account teams handling these channels than relevant peers do.

Outperformers use this resource-allocation strategy for high-growth local regions as well: in Latin America, for example, outperforming companies are 2.5 times more likely than category peers to skew their trade investments to capture growth opportunities in specific zones or provinces. And outperformers in the United States are directing their investments in sales coverage and in-store merchandising toward micromarkets that are densely populated with attractive, high-growth consumer segments.

Case study: Reaching the Hispanic population through ZIP–code segmentation

A snack-food manufacturer in the United States has realized growth, in part because of its decisions to overinvest in and tailor its go-to-market strategies to Hispanic shoppers. The company identifies certain postal-code areas as attractive based on the percentage of people of Hispanic origin living there. It then identifies the highest-potential streets within those ZIP codes by visiting neighborhoods and noting the location of Hispanic-themed stores. In the highest-density Hispanic areas, the company has invested more in local advertising and in-store merchandising materials. Based on the percentage of Hispanics in an area, the snacks manufacturer customizes its merchandising (providing retailers with more in-store signs and posters in Spanish), product assortment (incorporating different flavors and brands, or limiting its assortment to focus on more successful SKUs), and sales-force profile (employing Spanish-speaking sales agents to improve relationships with store operators). This tailored strategy is just one factor, but the company’s overall sales are growing at around 30 percent annually.

4

Outperformers also invest time and resources in customizing account plans—not only for large, high-priority trade customers but also for high-potential independent stores in fragmented retail markets. Outperforming CPG companies in Latin America, for instance, are 60 percent more likely than relevant peers to consider “future growth potential” as a criterion when segmenting retail outlets—even though outlet-level projections demand more sophisticated analytical models and require field sales teams to collect data from every point of sale (Exhibit 3).

2. Overinvest in collaborative relationships with most important customers.Outperforming CPG companies collaborate with high-priority customers more broadly than category peers do. Top European companies, for instance, engage with customers to jointly strategize on an average of seven topics, including product assortment, promotion, merchandising, and innovation. By contrast, category peers typically focus on only three to five such topics. Successful CPG companies in the United States are almost twice as likely as category peers to share new product concepts with top retail partners at least 12 months prior to launch. In doing so, they generate strong retailer support (by way of broader distribution, prioritized shelf placement, and preferential merchandising) and, in some cases, a more compelling product (Exhibit 4).

Exhibit 3Latin American outperformers segment independent retail outlets based on growth potential.

Last Modified 2/27/2014 5:07 PM

Eastern Standard Time

Printed 1/22/2014 12:20 PM Eastern Standard Tim

e

Exhibit 3 Latin American outperformers segment independent retail outlets based on growth potential.

Criteria used to segment independent retail outlets % of companies

OthersOutperformers

Connection to previously identified and prioritized pockets of growth

Future growth potential

88

25

36

55

Source: 2012 McKinsey Customer and Channel Management survey

Exhibit 4US outperformers consistently share and 'sell in' new-product ideas early.

Timing of communication/sell-in of new concepts prior to product launch% of US consumer-packaged-goods companies

Exhibit 4 US outperformers consistently share and ‘sell in’ new-product ideas early.

18–24 months

Source: 2012 McKinsey Customer and Channel Management survey

0–12 months

100

60

54

20

12–18 months

40

36

20

Share

9

60

Sell-in

OthersOutperformers

Consumer Packaged Goods (Americas)Lost in translation: The challenge of global channel and customer management 5

Additionally, outperforming CPG companies invest a greater percentage of their key account-team resources in customer-facing functional expertise. Outperformers in Latin America, for instance, dedicate 66 percent of their key account resources to core disciplines such as trade marketing, shopper marketing, and category management, and the remaining 34 percent to noncore functions such as finance and administration. By contrast, category peers dedicate only 48 percent to core functions.

3. Use deep insights and analytics to realize greater returns from pricing and promotion activities.The outperforming companies in our research consistently use revenue-management and trade-promotion optimization tools to improve their pricing and promotion results, as well as their return on trade investment. Successful CPG companies in the United States and Latin America, for instance, are 40 percent more likely than category peers to use or build such tools. Our research also indicates that outperforming companies in the United States are 4.5 times more likely than category peers to conduct trade-performance reviews at least monthly. And the outperformers are increasingly incorporating advanced analytics, including analysis of loyalty- and shopper-card data, into their assessments of trade promotion effectiveness.

Case study: Codeveloping new beverage products

A spirits manufacturer in the United States worked with one of its key retail partners to codevelop new products for new consumer segments. The manufacturer shared product concepts with the retailer early in their development, and it mined the retailer’s data on shoppers to provide direction on package design, product assortment, and merchandising. The manufacturer’s analysis of the data revealed that several flavors were underrepresented within its lines—flavors that would appeal to some of the customer’s priority-shopper segments and differentiate the manufacturer’s brand. The collaborative nature of the initiative built excitement and support within the customer’s buying and merchandising organization. The manufacturer and customer co-designed product-launch plans that included preferential placement in stores and strong promotional support.

Case study: Analyzing returns on beverage promotions

A leading global beverage manufacturer, with complex offerings in several large, highly promoted categories, sought to improve its return on trade investment. Its product and sales data were dispersed across multiple internal and external databases, and the company’s process and metrics for analyzing trade investments had been inconsistent. To address these issues, the manufacturer rolled out a suite of robust technologies. On the back end, disparate types of data—for instance, shipment data, shopper card data, and information about pricing and promotional context—were automatically collected weekly from more than ten independent sources. The company also used analytics software to better plan its promotions; it devised an advanced program for assessing the various factors affecting the results of critical promotional events. It was then able to develop a new, data-driven promotional strategy. Early results show that the company is on track to realize a 10 to 15 percent improvement on total trade investment dollars through the use of these technologies.

6

4. Translate distinctive consumer insights into in-store advantages.Compared with category peers, high-performing CPG companies across all three geographies are regularly collecting unique shopper insights and applying them more broadly. Outperformers in the United States, for instance, are 50 percent more likely than category peers to experiment with in-store shopper interaction tools and technologies for collecting behavioral data. These companies are using the insights they glean to inform their in-store marketing, promotion, and assortment strategies, and innovating accordingly.

Similarly, winning CPG companies in Europe are 50 percent more likely than category peers to use shopper data to better understand product interactions and to shape trade-promotion strategy and tactics. Outperforming companies in Latin America are applying shopper insights across both modern and traditional trade activities; armed with these data, they are establishing format- and trade-specific execution standards. Leaders in outperforming CPG companies in Latin America were ten times more likely than category peers to credit shopper insights as being critical to winning in-store activation.

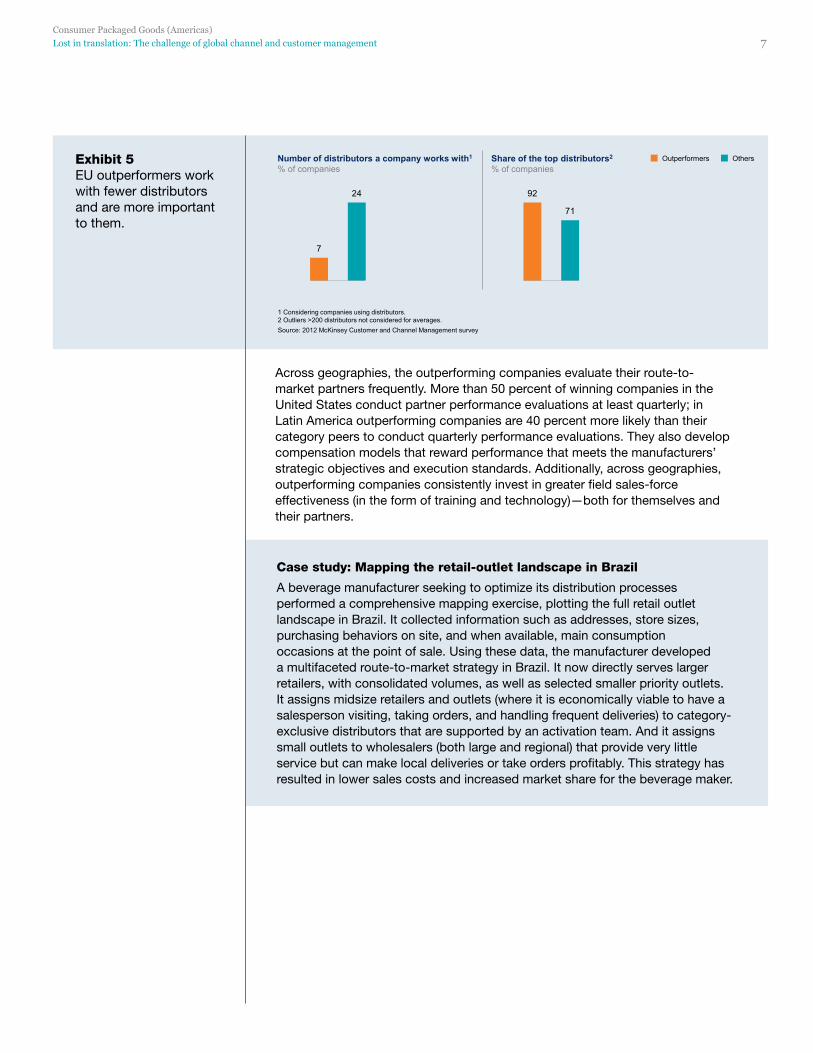

5. Increase sales using optimized route-to-market models.Outperforming companies have a disciplined process for optimizing their route-to-market models based on economics and strategic priorities. In Latin America, 90 percent of outperforming companies review their route-to-market strategies—across direct store delivery, wholesalers, and distributors—at least annually. The outperformers in our research also tend to have fewer, deeper third-party relationships. Outperformers in Europe, for instance, work with three times fewer distributors than their category peers, but build collaborative, trust-based relationships with them (Exhibit 5).

Case study: Mining data to inform pricing of nutritional products

For a number of years, a nutritional products company had believed it competed primarily with private-label makers. Through its use of an advanced category-management tool, however, the company gained certain insights that prompted it to make some changes in strategy. The company’s category analysis revealed that consumers shopped by need (for a vitamin supplement, for instance, or a meal replacement) rather than by ingredients or price, as was previously believed. And the company’s products mostly competed with other national brands, not private label, the tool showed. Based on these insights, the company refocused its pricing and shelving strategies to be “needs based.” It simultaneously increased its prices after several years of no increases, and reduced its promotions targeted at combating private-label companies. Within one year, the company turned around a long-term decline in sales of about 4 percent; sales expanded by 6 percent.

Consumer Packaged Goods (Americas)Lost in translation: The challenge of global channel and customer management 7

Across geographies, the outperforming companies evaluate their route-to-market partners frequently. More than 50 percent of winning companies in the United States conduct partner performance evaluations at least quarterly; in Latin America outperforming companies are 40 percent more likely than their category peers to conduct quarterly performance evaluations. They also develop compensation models that reward performance that meets the manufacturers’ strategic objectives and execution standards. Additionally, across geographies, outperforming companies consistently invest in greater field sales-force effectiveness (in the form of training and technology)—both for themselves and their partners.

Exhibit 5EU outperformers work with fewer distributors and are more important to them.

Exhibit 5 EU outperformers carefully select the best distributors to become true partners.

1 Considering companies using distributors.2 Outliers >200 distributors not considered for averages. Source: 2012 McKinsey Customer and Channel Management survey

Share of the top distributors2

% of companiesNumber of distributors a company works with1

% of companies

24

7

71

92

OthersOutperformers

Case study: Mapping the retail-outlet landscape in Brazil

A beverage manufacturer seeking to optimize its distribution processes performed a comprehensive mapping exercise, plotting the full retail outlet landscape in Brazil. It collected information such as addresses, store sizes, purchasing behaviors on site, and when available, main consumption occasions at the point of sale. Using these data, the manufacturer developed a multifaceted route-to-market strategy in Brazil. It now directly serves larger retailers, with consolidated volumes, as well as selected smaller priority outlets. It assigns midsize retailers and outlets (where it is economically viable to have a salesperson visiting, taking orders, and handling frequent deliveries) to category-exclusive distributors that are supported by an activation team. And it assigns small outlets to wholesalers (both large and regional) that provide very little service but can make local deliveries or take orders profitably. This strategy has resulted in lower sales costs and increased market share for the beverage maker.

8

BUILDING GLOBAL CUSTOMER-MANAGEMENT EXCELLENCEAs our findings suggest, a small set of CPG companies is capturing the advantages of global customer-management excellence; a much larger group is wrestling with the challenges of how to do so. There are multiple approaches leading companies are taking to achieve customer-management excellence worldwide:

Capitalizing on a strong global commercial function. A global sales organization sets the capability-building agenda and marshals the resources (talent and budgets) and influence (performance evaluations and compensation schemes) to deliver results.

Establishing strong regional accountability. Excellence is built within a market or region; best practices are shared formally and informally by a well-networked organization.

Establishing centers of excellence as well as local accountability. The capability-building agenda is created through regional consensus and collaboration. A lean global sales infrastructure develops enabling processes and tools and facilitates the sharing of best practices across regions.

The key is selecting the optimal capability-building model for your organization. Important considerations include the company's overall operating model and culture, the degree to which sales talent is distributed across regions, and the amount of overlap in customer-management priorities across regions. We advise leaders to:

• Know where you stand. Build a fact-based perspective of your commercial capabilities across geographies.

• Pick your battles. Prioritize your market-level capabilities based on the potential effects of your activities, and the size of the prize; factor in both your company’s starting point in the market and the local dynamics of the market.

• Play to your strengths. Conduct an honest assessment of your company’s operating model and your sales organization’s culture and composition. Consider what that assessment implies about the "right" capability-building approach.

• Manage for impact. Invest in and establish processes for creating transparency across your global operations; this includes instituting a performance-management program that measures outcomes and facilitates the sharing of best practices.

Kicking off a global capability effort is easier said than done. Our research findings show that faster-than-average growth and higher returns on commercial investment are both functions of best-in-class customer- and channel-management capabilities. The time for CPG companies to build global capabilities in these areas is now.

Consumer Packaged Goods (Americas)Lost in translation: The challenge of global channel and customer management 9

We have developed a set of diagnostics and tools that can help companies in their efforts to build global capabilities, and that can deliver short- and long-term impact. For more about the survey and our findings, or to discuss how to build a custom roadmap to customer and channel excellence, please contact:

Kari Alldredge, master expert, Consumer/Packaged Goods Practice, Minneapolis ([email protected])

Carlos Angrisano, principal, São Paulo ([email protected])

Brandon Brown, consultant, Dallas ([email protected])

Putney Cloos, senior expert, Consumer/Packaged Good Practice, New Jersey ([email protected])

Cristina Del Molino, expert, Consumer/Packaged Goods Practice, London ([email protected])

Alejandro Diaz, director, Dallas ([email protected])

Ryan LaMontagne, specialist, New Jersey ([email protected])

Contact for distribution: Kari Alldredge Phone: +1 (612) 371-3188 E-mail: [email protected]

Consumer Packaged Goods (Americas)March 2014 Designed by Global Editorial Services Copyright © McKinsey & Company