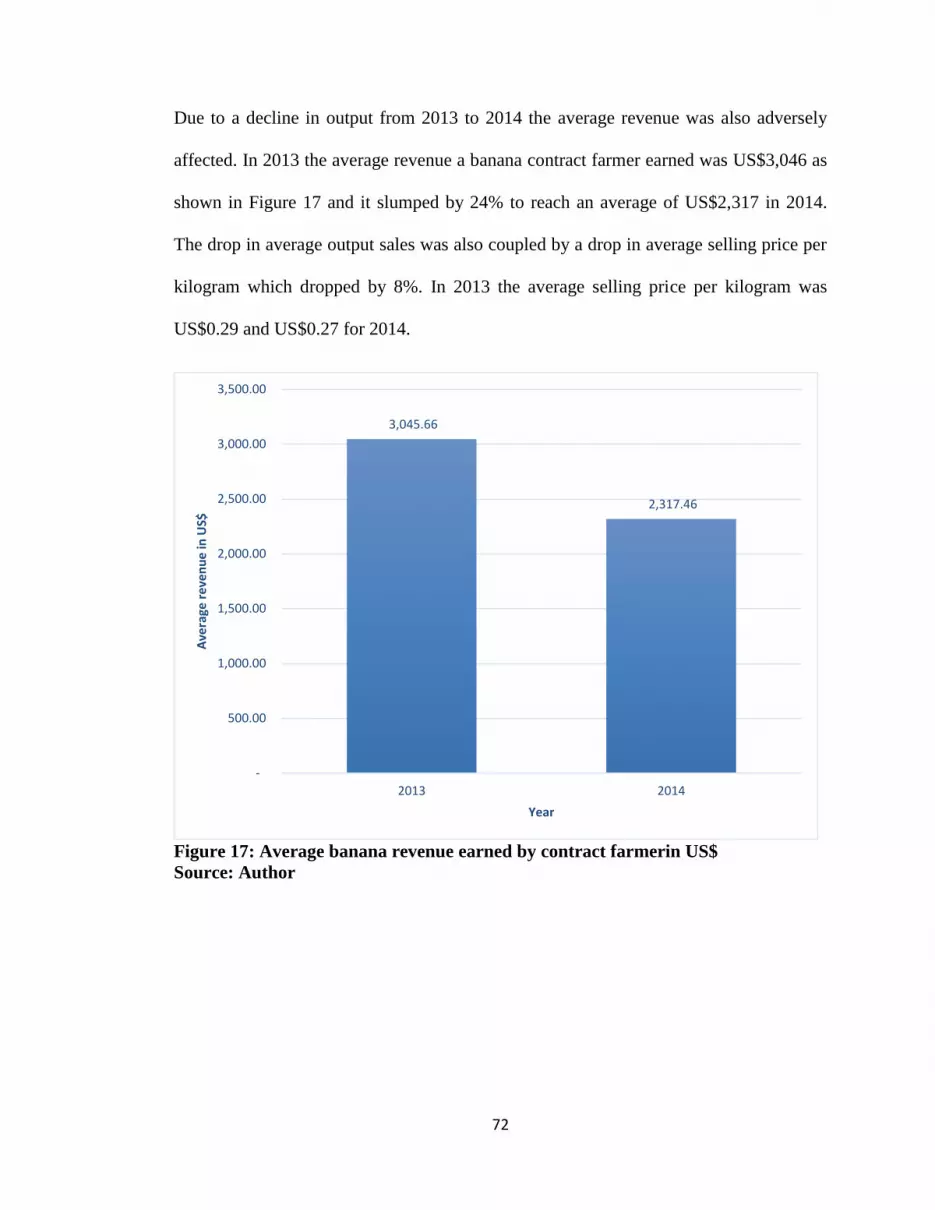

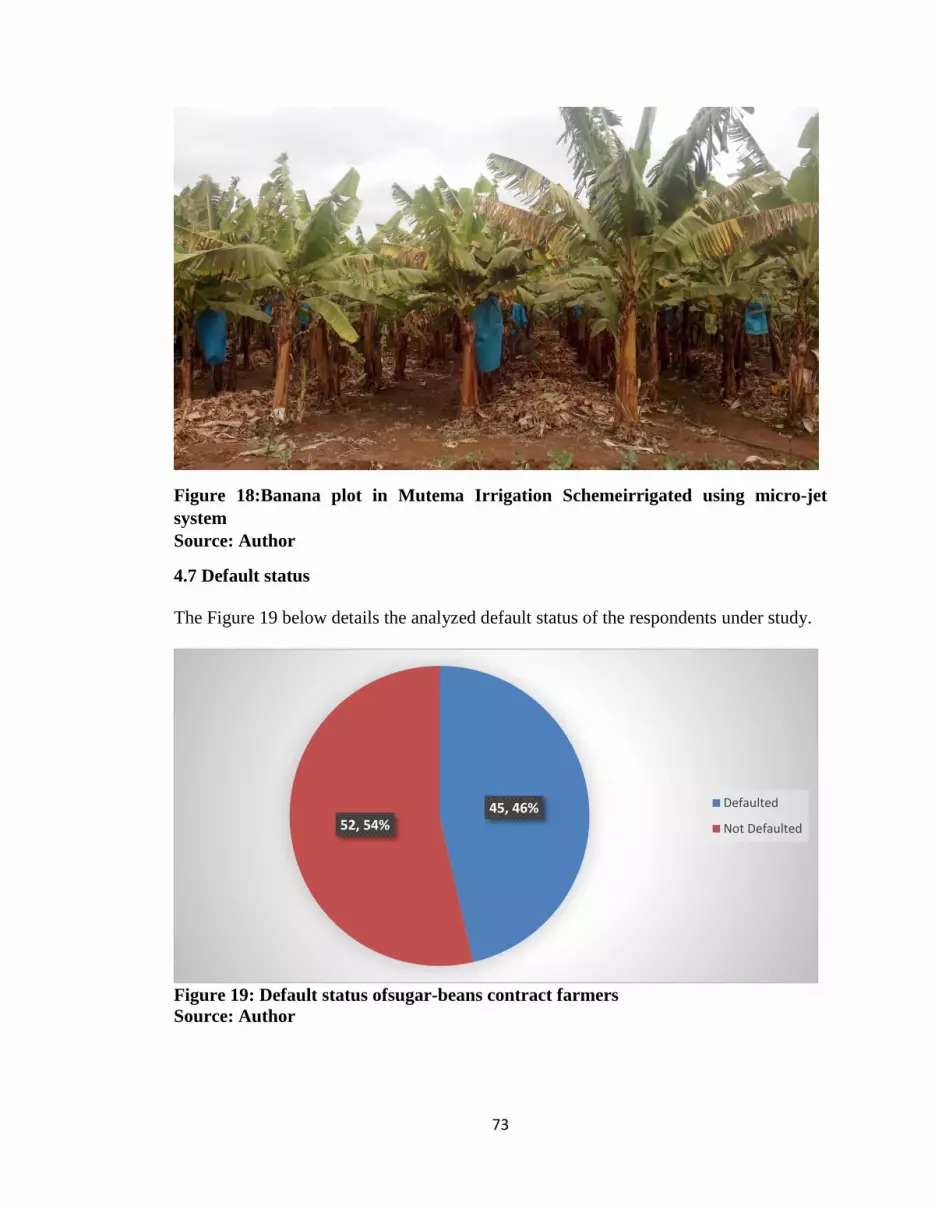

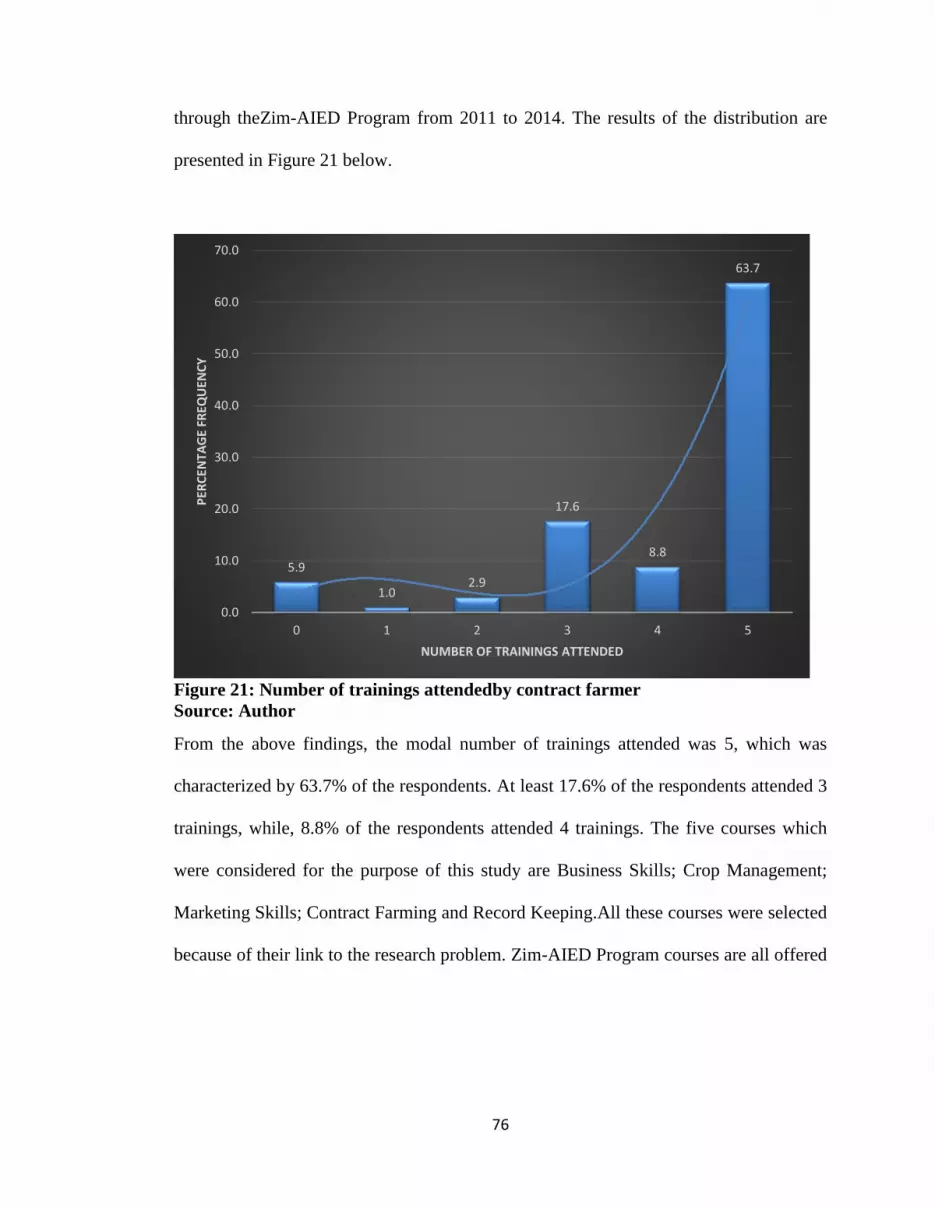

loan repayment under sugar beans and banana contract farming in irrigation schemes in chipinge...

TRANSCRIPT

i

A comparative assessment of factors influencing loan repayment under

contract farming for sugar-beans and bananas in Mutema and Chibuwe-

Musikavanhu irrigation schemes in Chipinge district.

A DISSERTATION SUBMITTED

IN PARTIAL FULFILMENT OF THE REQUIREMENTS FOR THE

DEGREE OF MASTER OF SCIENCEAGRIBUSINESS

BY

THOMAS TSAHA

FACULTY OF AGRICULTURE AND NATURAL RESOURCES

AFRICA UNIVERSITY

2015

ii

ABSTRACT

Contract farming offers finance and creates reliable market linkages for farmers as

well as supply of raw-materials to agro-processors. The contract farming

relationship is dependent on loan repayment by contracted farmers. Therefore the

main objective of this study was to find the factors influencing loan repayment

under contract farming. A total of 134 questionnaires were administered through

face-to-face interviews for sugar-beans and banana contract farmers, structured

schedules for sugar-beans contractors and unstructured interviews. The study was

conducted inirrigation schemes in Chipinge District, located in the south-eastern

part of Manicaland Province.One-Way ANOVA and Decision Tree Analysis were

concurrently used to ascertain the primary predictors that influence loan

repayment and out of ten independent variables only four variables were

statistically significant (p≤0.05) to influence loan repayment for sugar-beans

contracts. These are age of contract farmer, number of trainings attended,

household size and output. Multivariate Approach was also used to determine the

linear regression model for the study and only two predictors were found to be

statistically significant in influencing loan repayment. These are number of

trainings attended and age of contract farmer. The loans issued were concessionary

in nature.The contractors did not request for collateral from contract farmers. Two-

tier screening mechanism was found to be a mitigation measure to minimize loan

defaults, whereby all farmers in need of contract loans are vetted by their

Irrigation Management Committee and then by Agriculture Extension officers.

Reducing of funding and group lending were the other mitigation measures found

to reducethe default rate. Insuring of risks associated with agriculture activities

should be designed to minimize exposure of parties in contract farming. Group

lending and training of farmers are recommended as ways to enhance contract

farmers’ capacity to repay their loans and ensure sustainability of the contract

farming arrangement.

iii

DECLARATION

I, Thomas Tsaha, (Student ID: 991119), declare that the work contained in this

dissertation is my own original work, where other people’s work has been used it

is properly acknowledged and referenced in accordance with departmental

requirements. I have not used work previously produced by me or another person

for degree purposes at this university or any other university.

_______________________________ ________________________

Student’s name: Thomas Tsaha Date

_______________________________ ________________________

Supervisor: Mrs M. Mrema Date

iv

COPYRIGHT

No part of this thesis shall be reproduced, stored or duplicated in any retrieval system or

transmitted in any form or by any means for scholarly purposes without prior written

permission of the author or Africa University on behalf of the author.

v

ACKNOWLEDGEMENTS

This research study was achieved through the assistance of many organizations

and persons who are acknowledged here: -

The Faculty of Agriculture and Natural Resources at Africa University and

theirrespective staff who provided me with initial guidance to undertake research

in Chipinge District. Special mention goes to my supervisor MrsMrema I am very

grateful for your assistance, patience and guidance in the entire research process

and Dr L. Dube who gave the initial insight of undertaking the research process.

The support given by Mr Kennedy Zimunya and his fellow colleagues working for

Fintrac Inc. Zimbabwe among them Mr Mark Benzon, Gift Chidoko and

GodknowsMasunda and many others who contributed in various ways to the

information required for this researchis greatly appreciated.

I am grateful to the Agritex Officers in Chipinge District. Special mention goes to

Mr. Chagwesha, Mr.Pondo, Mr.Chitekuteku and Mr. D. Mlambo and their team.

In Mutema Irrigation Scheme I thank Ms.Mayakayaka andMr.Mutocho.

I thank Mr. Gary Ngara for assistingin the statistical analysis process of the

research.

My appreciationalso goes to my fellow classmatesat Africa University for keeping

Last but not least, my sincere gratitude to my familywhose unwavering support is

beyond words to describe I thank you.

And to all, who in one way or the other contributed to my study, may God richly

bless you.

vi

DEDICATION

To my familyI dedicate this study,especially Daniel, my father, for the unwavering

support and inspiration to forge against odds.

vii

TABLE OFCONTENTS

ABSTRACT .................................................................................................................................... i

DECLARATION ......................................................................................................................... iii

COPYRIGHT ............................................................................................................................... iv

ACKNOWLEDGEMENTS ......................................................................................................... v

DEDICATION ............................................................................................................................. vi

TABLE OF CONTENTS ........................................................................................................... vii

LIST OF TABLES ........................................................................................................................ x

LIST OF FIGURES ..................................................................................................................... xi

APPENDICES ............................................................................................................................ xiii

CHAPTER ONE: INTRODUCTION .........................................................................................1

1.1 Background .........................................................................................................................1

1.2 Statement of the problem ...................................................................................................3

1.3 Justification for the study ...................................................................................................4

1.4 Research objectives .............................................................................................................6

Overall Objective ..................................................................................................................6

Specific Aims .........................................................................................................................7

1.5 Research questions ..............................................................................................................7

1.6 Ethical considerations .........................................................................................................7

1.7 Limitations and delimitation for the study .......................................................................8

1.8 Scope of the study ...............................................................................................................9

1.9 Significance and value of the study ................................................................................ 10

CHAPTER TWO: LITERATURE REVIEW ......................................................................... 13

2.1 Contract farming arrangements in Zimbabwe ............................................................. 13

2.2 Contract farming models ................................................................................................ 15

2.3 Sources of finance for farmers ........................................................................................ 16

2.4 Key enablers for access to finance and loan repayment performance ........................ 22

2.5 Factors influencing loan repayment performance ........................................................ 25

Demographic factors .......................................................................................................... 25

Agronomic factors .............................................................................................................. 28

Financial factors ................................................................................................................. 30

Socio-economic factors ...................................................................................................... 33

Political factors ................................................................................................................... 34

viii

2.6 Types of loans and their conditions ................................................................................ 36

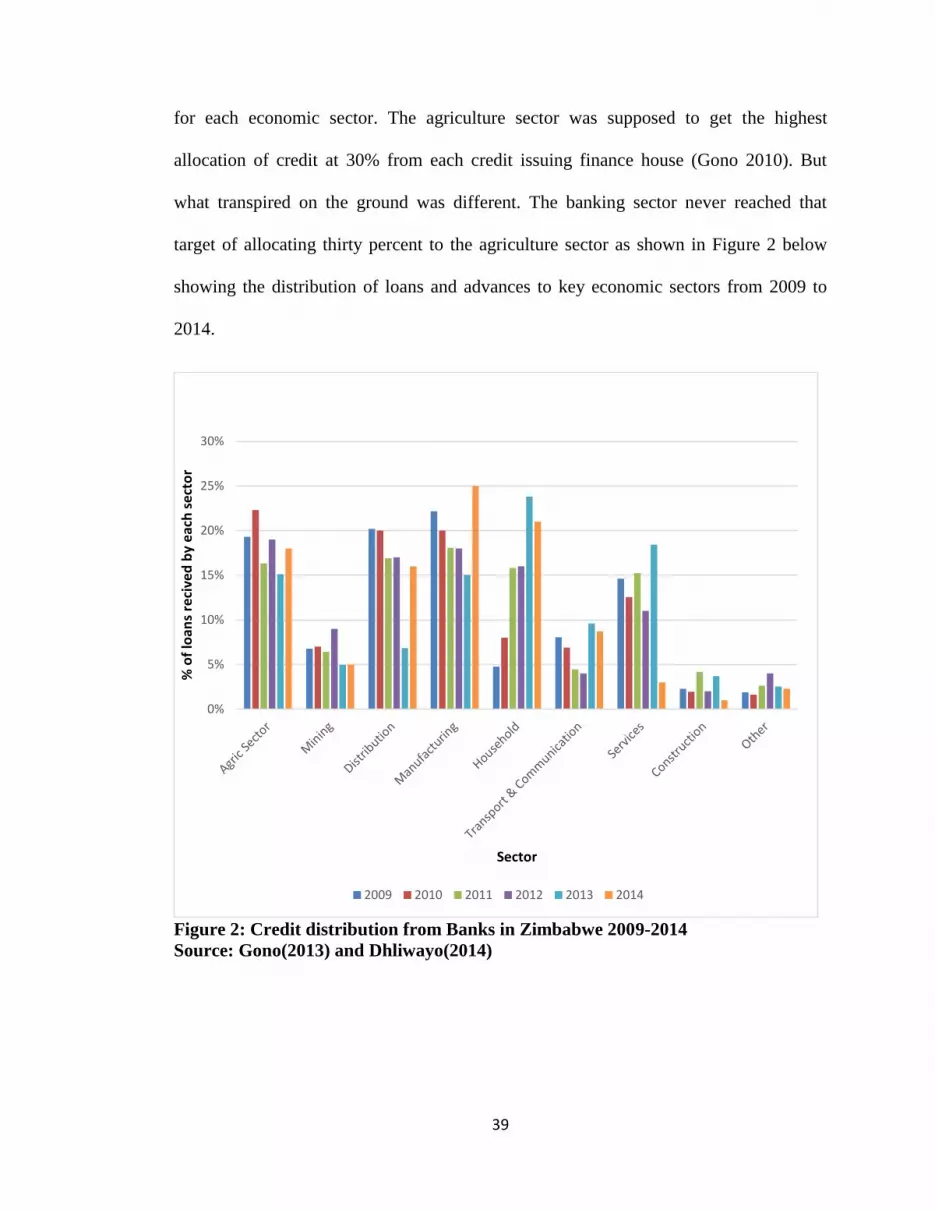

Zimbabwe context .............................................................................................................. 38

2.7 Mitigation measures to avert loan defaulting ................................................................ 42

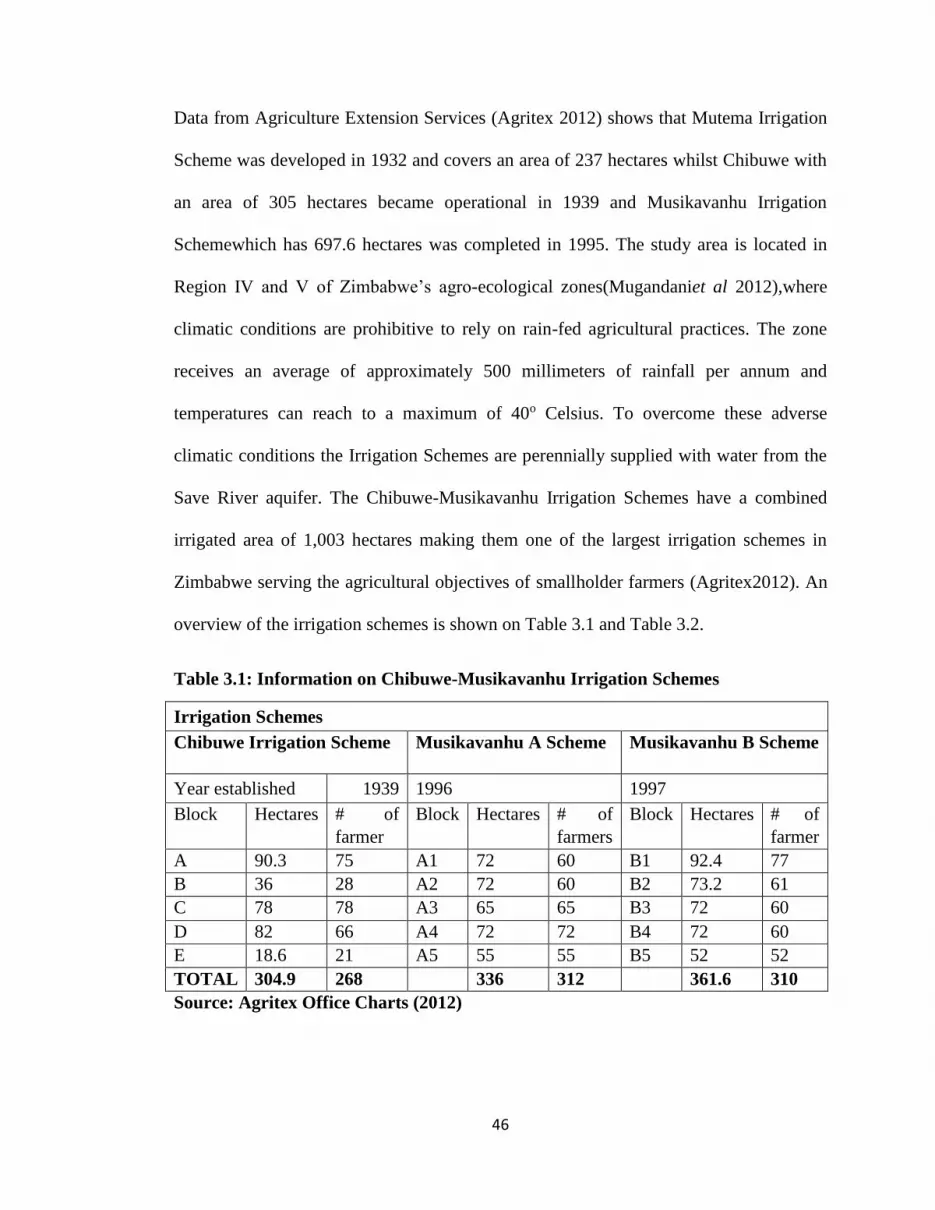

CHAPTER THREE: METHODOLOGY ................................................................................ 44

3.1 Research design ................................................................................................................ 44

3.2 Area of study .................................................................................................................... 44

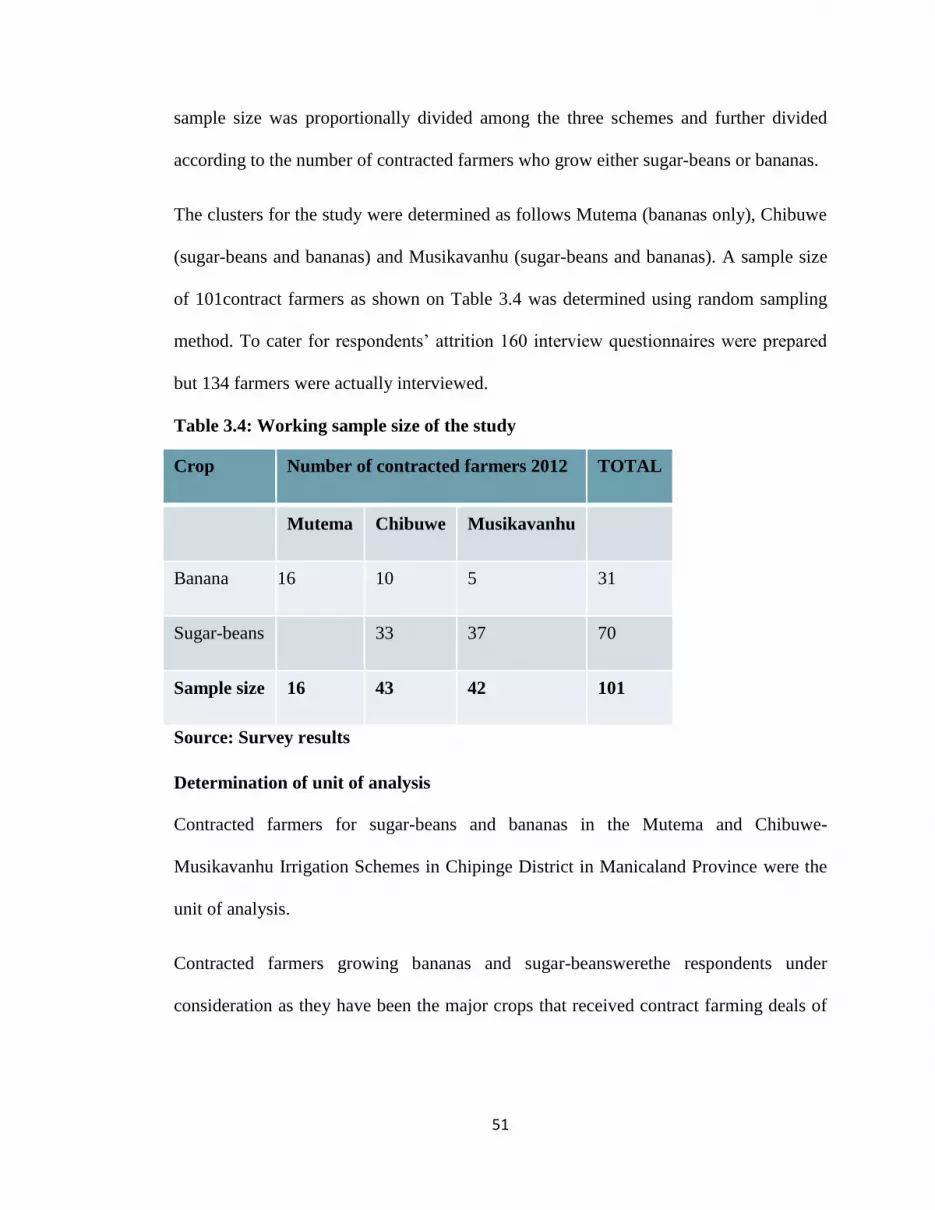

3.3 Study population and sampling technique .................................................................... 48

The Sample and the Sampling Techniques ...................................................................... 49

Determination of the study’s sample size ......................................................................... 50

Determination of unit of analysis ...................................................................................... 51

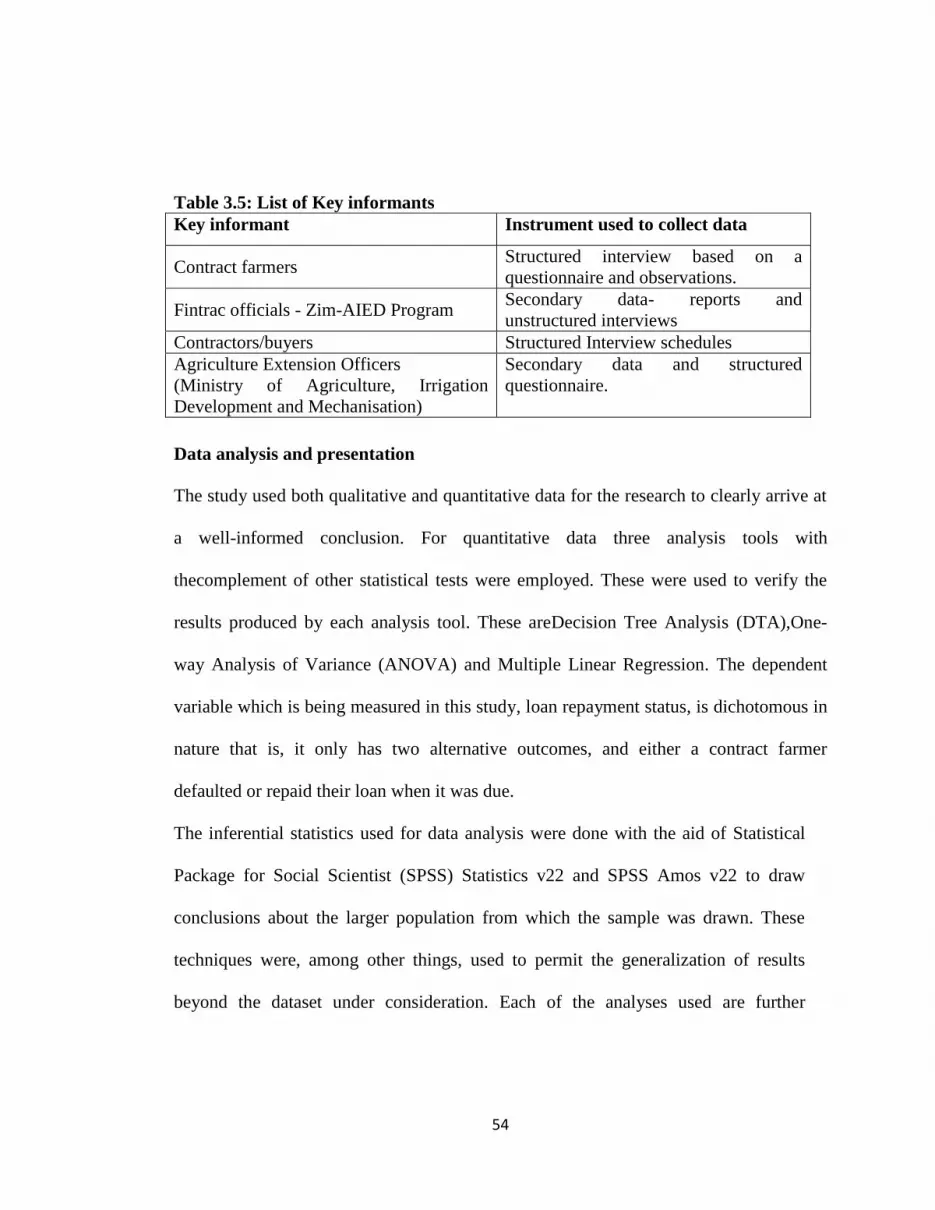

3.4 Data collection .................................................................................................................. 52

Research instruments used for the study ......................................................................... 53

Data analysis and presentation ......................................................................................... 54

CHAPTER FOUR: RESULTS AND DISCUSSION .............................................................. 58

4.1 Response rate of the respondents in the study .............................................................. 58

4.3 Reliability analysis results ............................................................................................... 59

4.4 Demographic results of the study ................................................................................... 59

Gender distribution of contract farmers ......................................................................... 59

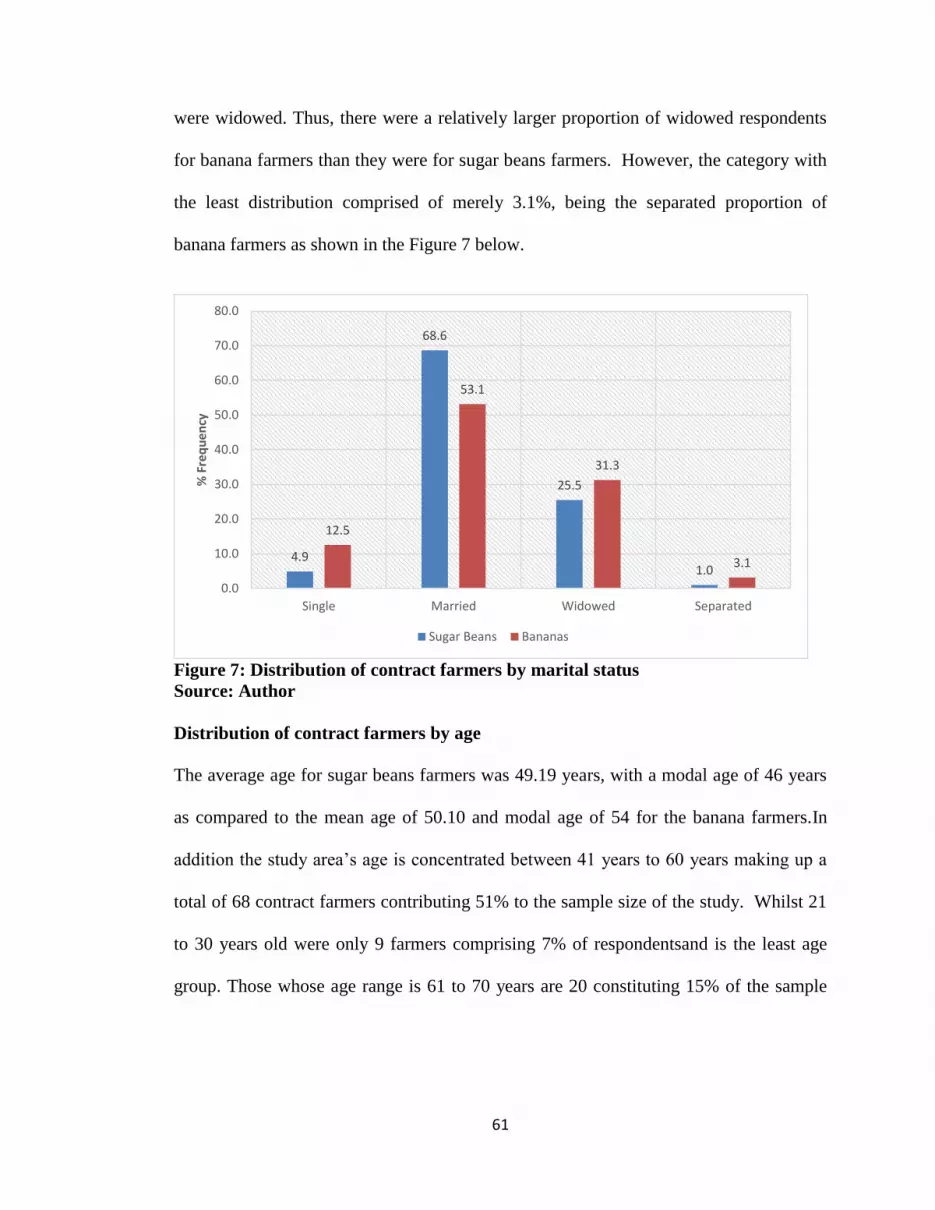

Distribution of contract farmers by marital status ......................................................... 60

Distribution of contract farmers by age ........................................................................... 61

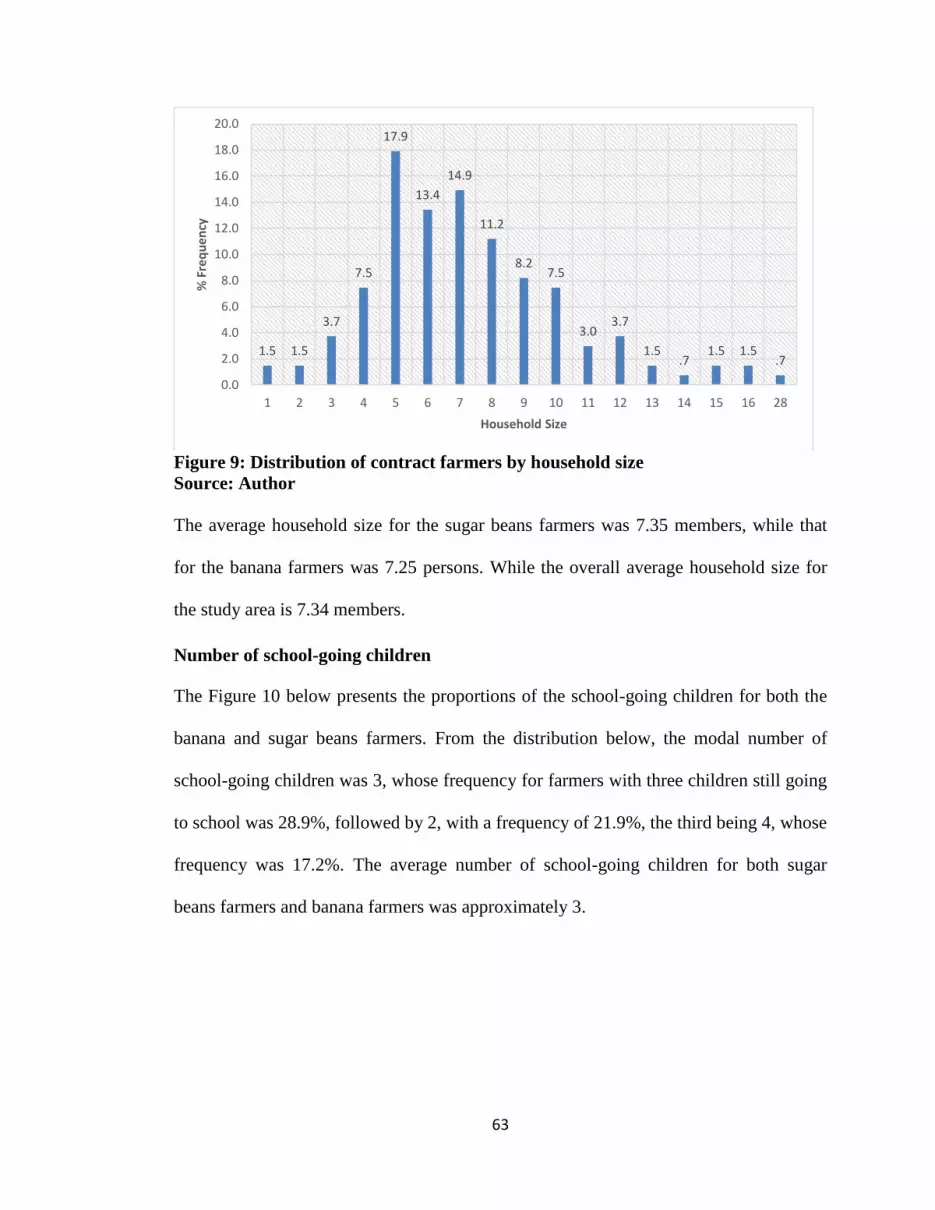

Distribution of contract farmers by household size ........................................................ 62

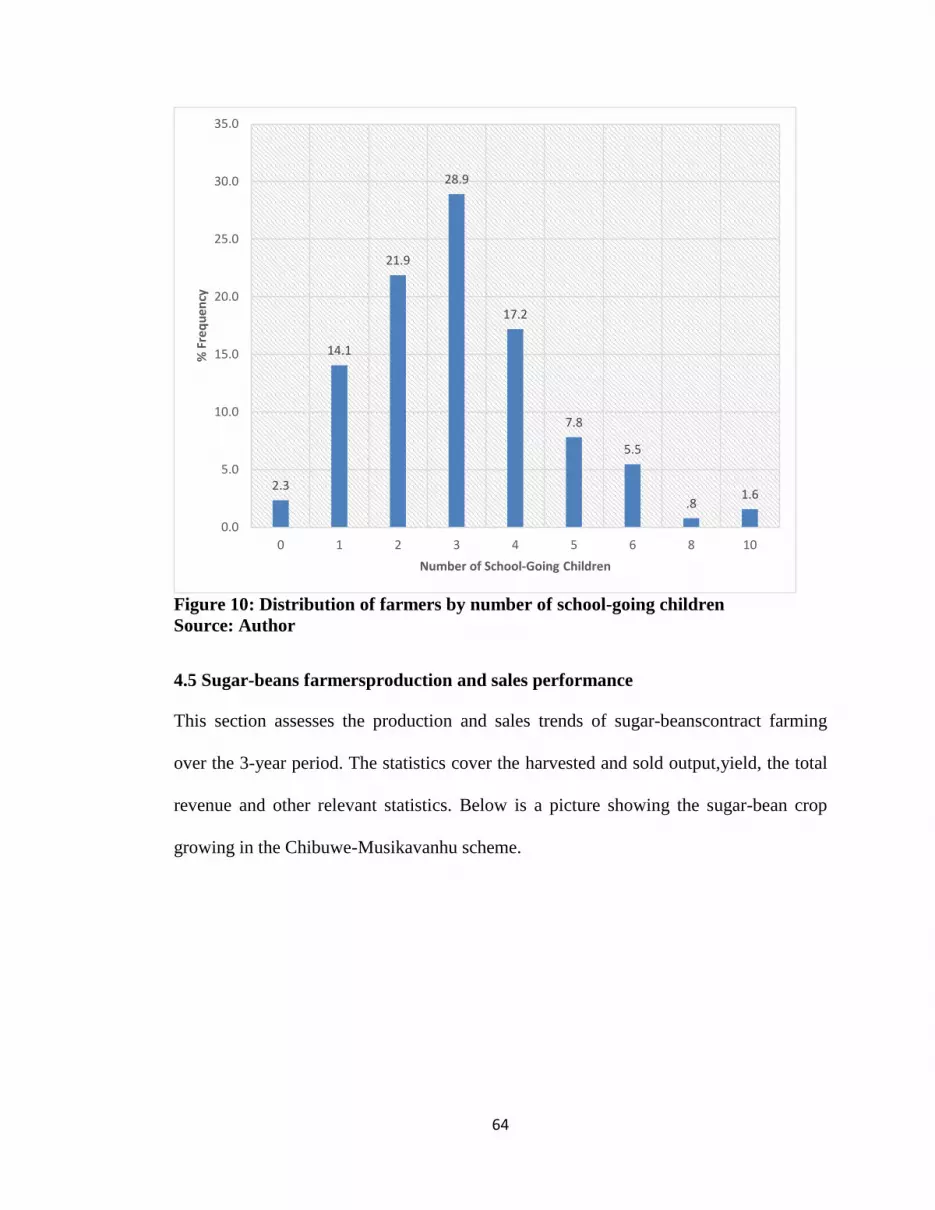

Number of school-going children ..................................................................................... 63

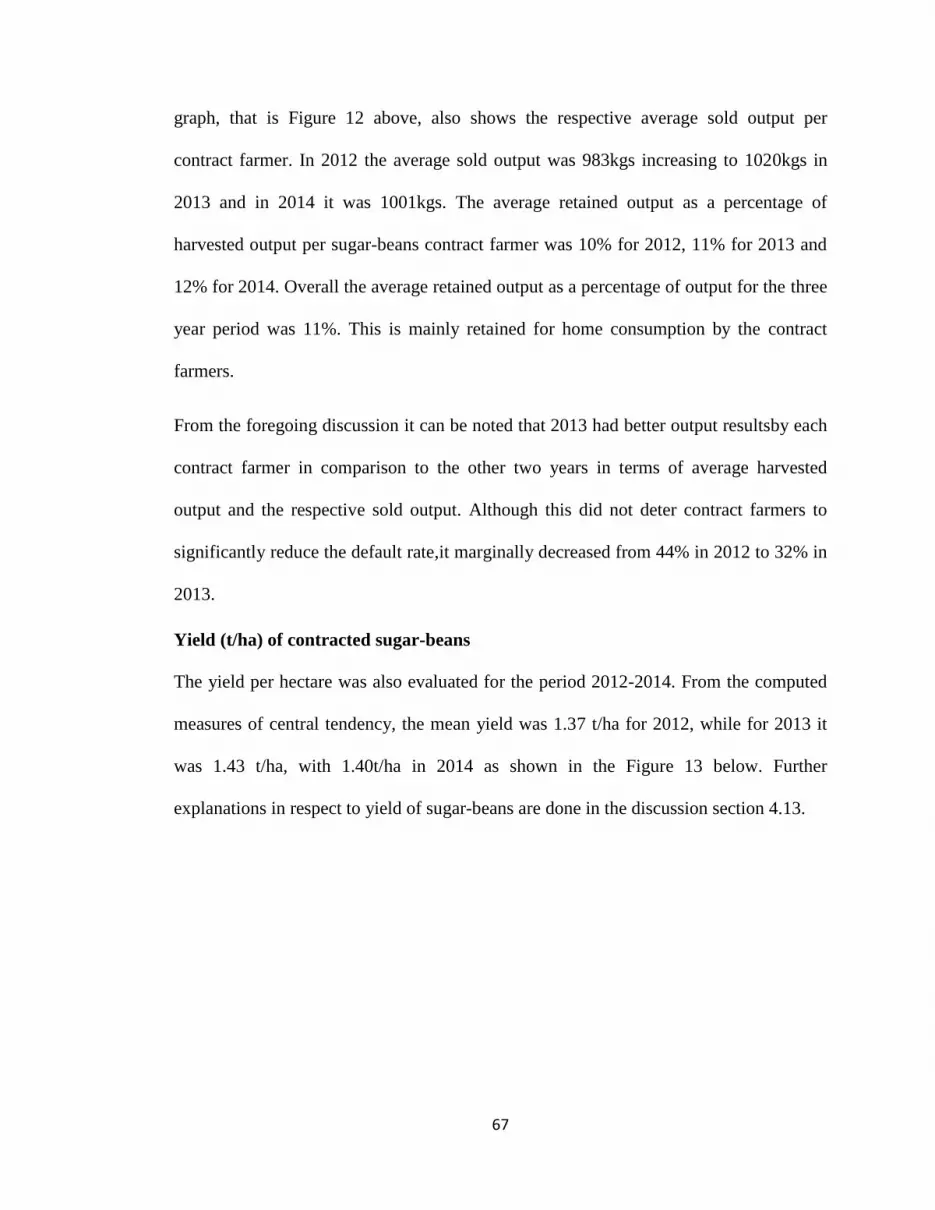

4.5 Sugar-beans farmers production and sales performance ............................................ 64

Sugar-beans harvested, sold and retained output in kilograms (kgs) ........................... 65

Yield (t/ha) of contracted sugar-beans ............................................................................. 67

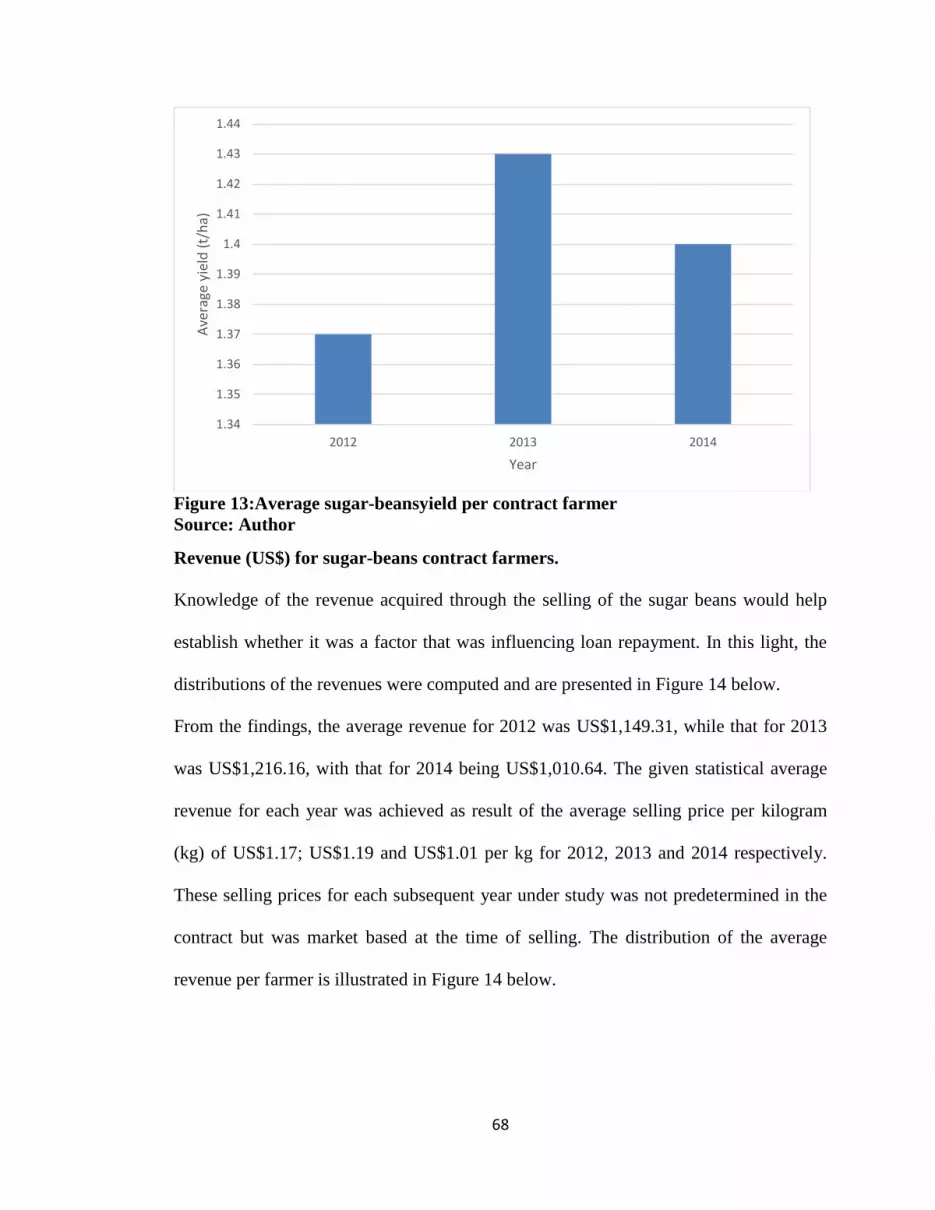

Revenue (US$) for sugar-beans contract farmers. .......................................................... 68

4.6 Banana farmers production and sales performance ..................................................... 69

4.7 Default status .................................................................................................................... 73

4.8 Farming characteristics ................................................................................................... 74

Source of labor for all contract farmers .......................................................................... 74

Number of trainings attended by contract farmer ......................................................... 75

Number of Agritex Officer’s visit per week .................................................................... 77

4.9 Factors influencing loan repayment for sugar-beans contract .................................... 78

ix

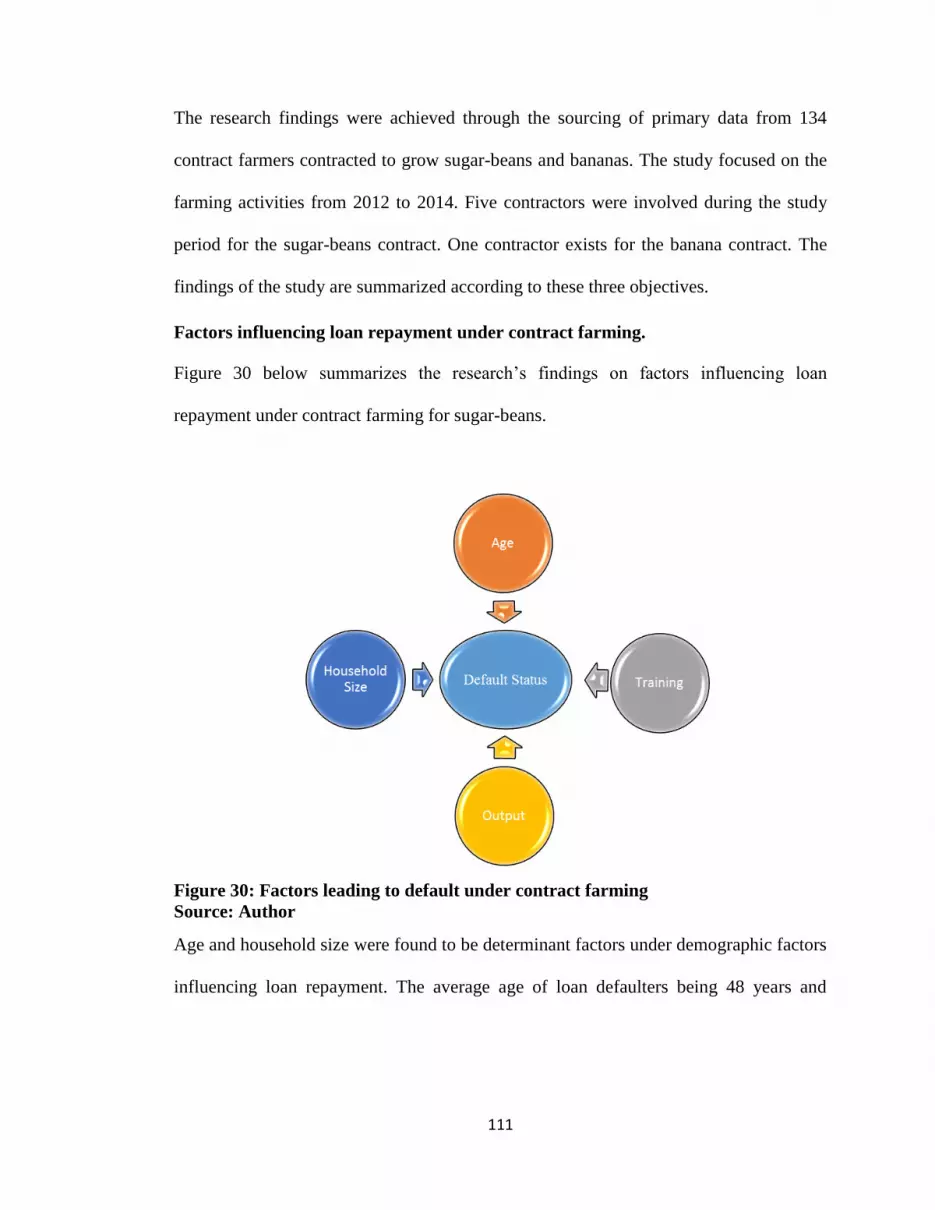

Age as a factor influencing loan repayment .................................................................... 80

Household size as a Factor influencing loan repayment for sugar-beans ..................... 81

Number of trainings attended by farmer as a factor influencing loan repayment ...... 83

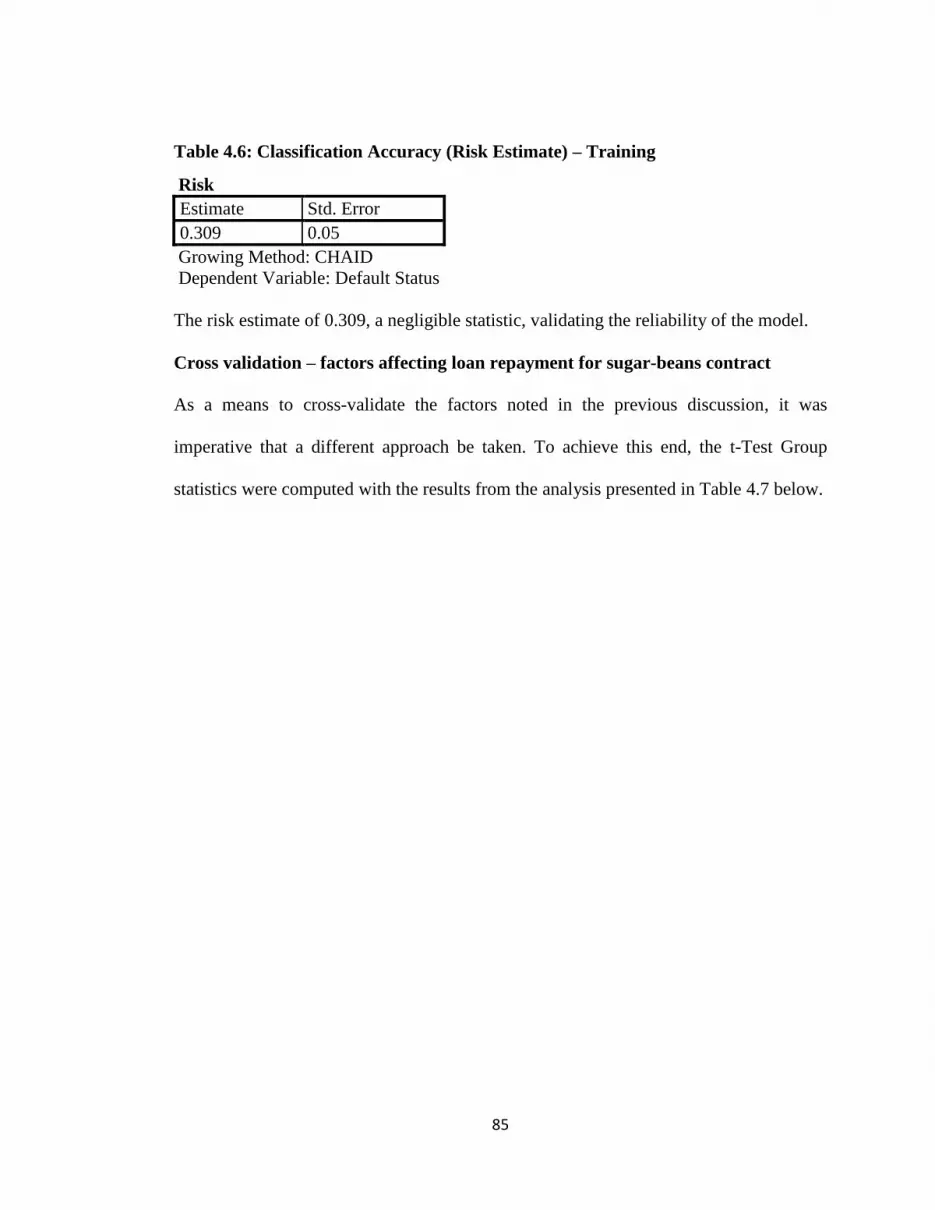

Cross validation – factors affecting loan repayment for sugar-beans contract............ 85

4.10 Determinants of loan default – Output ........................................................................ 87

4.11 Linear regression model for the study ......................................................................... 91

4.12 Types and conditions of loans issued under contract farming in study area ........... 95

4.13 Mitigation measures to reduce default risk by farmers ............................................. 99

4.14Discussion of the research findings ............................................................................. 101

Gender............................................................................................................................... 102

Marital status ................................................................................................................... 102

Age of contract farmer .................................................................................................... 103

Household size of contract farmer and source of labor ................................................ 104

Number of school-going children ................................................................................... 105

Output, yield and revenue for sugar-beans contract .................................................... 106

Number of trainings attended by contract farmer ....................................................... 107

Number of Agritex Officer’s visits per week ................................................................. 108

Banana contract farming loan repayment performance .............................................. 109

CHAPTER 5: SUMMARY, CONCLUSION AND RECOMMENDATIONS ................... 110

5.1 Summary of the study .................................................................................................... 110

Factors influencing loan repayment under contract farming. ..................................... 111

Type and the conditions of loans offered to farmers under contract farming. .......... 112

Mitigation measures to avert defaults among contract farmers. ................................. 113

5.2 Conclusion ...................................................................................................................... 114

5.3 Recommendations .......................................................................................................... 116

REFERENCES......................................................................................................................... 120

APPENDICES .......................................................................................................................... 127

x

LIST OF TABLES

Table 2.1: Contract farming players in Zimbabwe 13

Table 2.2: Contract farming models and characteristics 15

Table 2.3: Informal sources of finance and their characteristics 17

Table 3.1: Information on Chibuwe-Musikavanhu Irrigation Schemes 45

Table 3.2: Important information relating to the Irrigation Schemes 46

Table 3.3: Population size of the study 48

Table 3.4: Working sample size of the study 50

Table 3.5: List of Key informants 53

Table 3.6: Independent variables investigated for the study 55

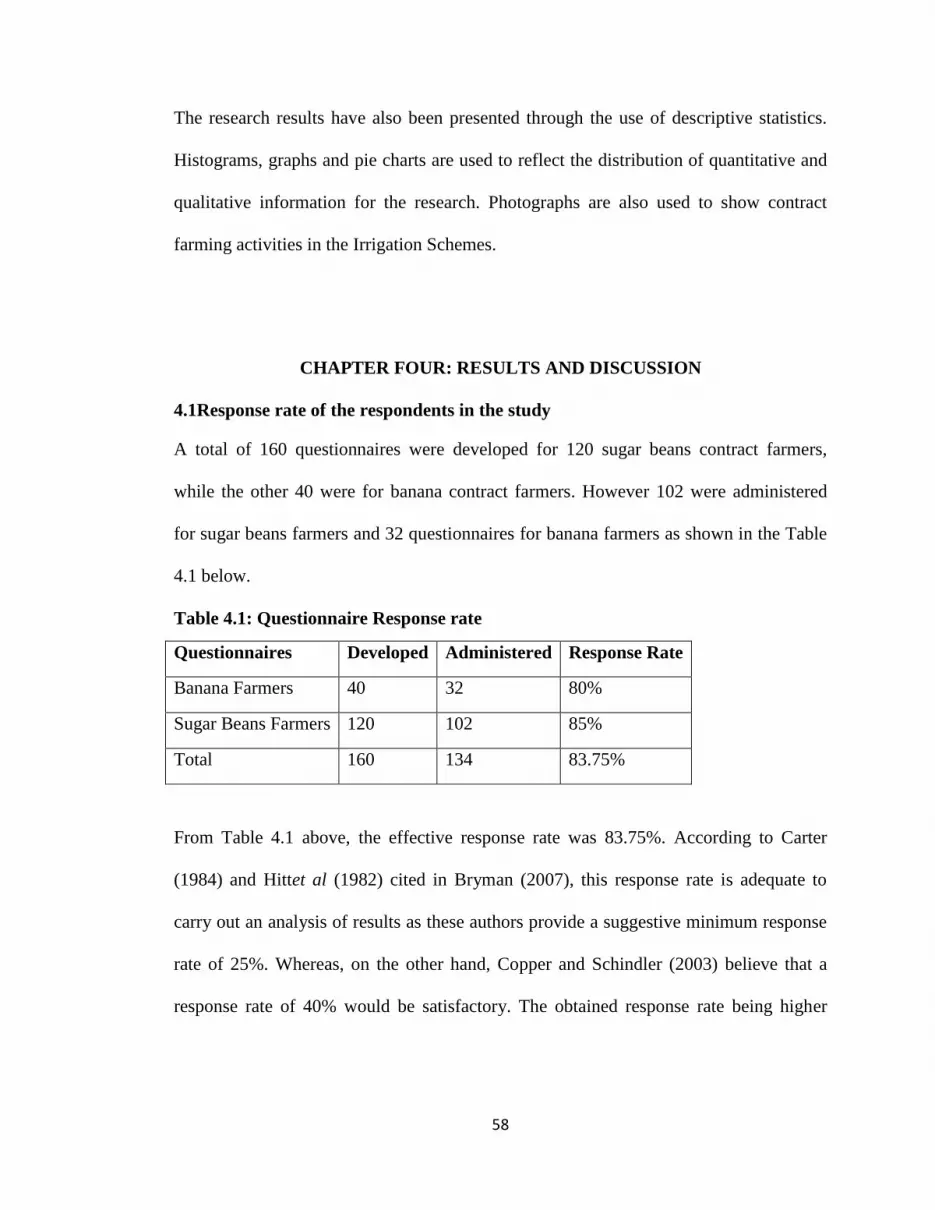

Table 4.1: Questionnaire Response rate 57

Table 4.2 Reliability Analysis of research questionnaire 58

Table 4.3: ANOVA Analysis – Eight independent variables 78

Table 4.4: Classification Accuracy (Risk Estimate) – Age and Default Status 80

Table 4.5: Classification Accuracy (Risk Estimate) – household size 81

Table 4.6: Classification Accuracy (Risk Estimate) – Training 84

Table 4.7: t-Test Group Statisticsfor independent variables 85

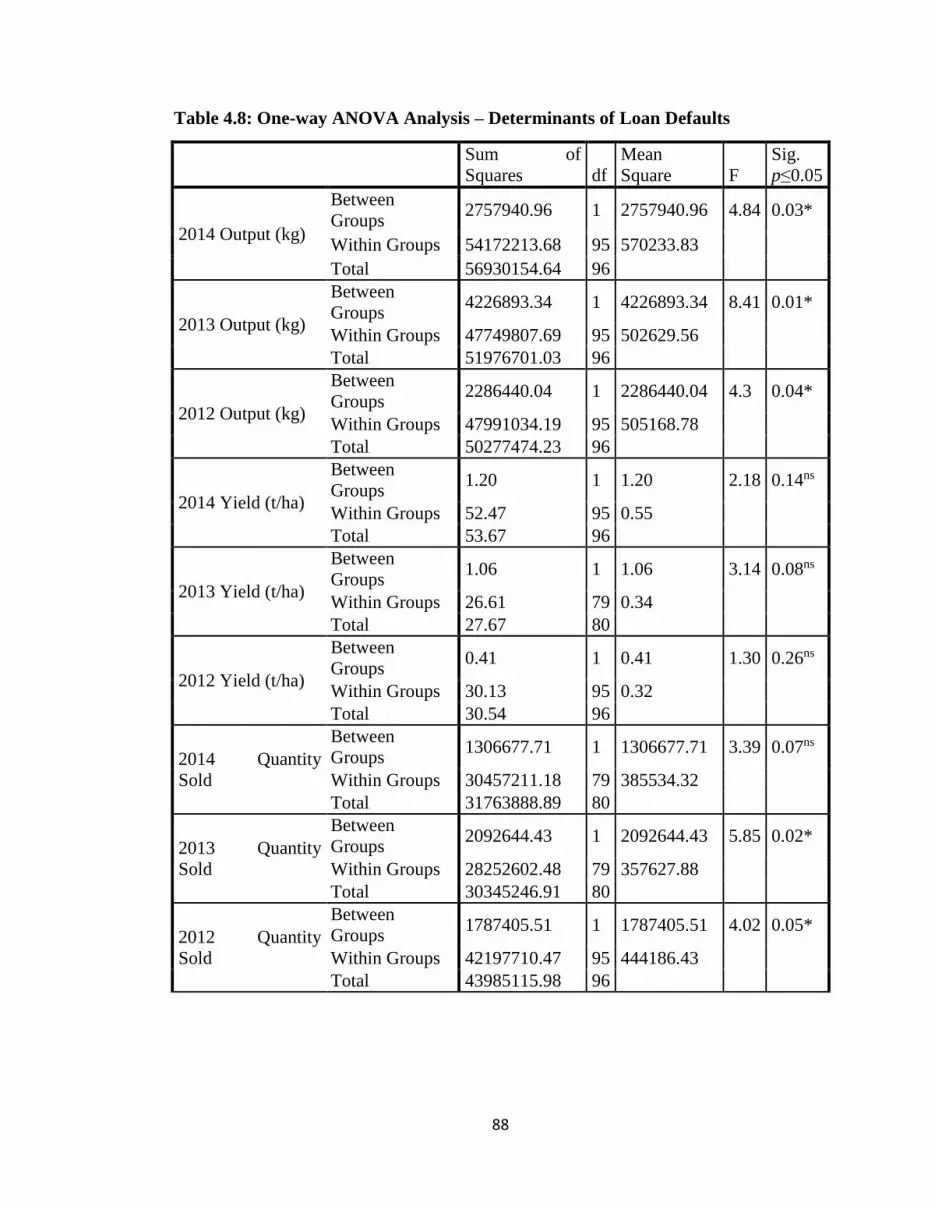

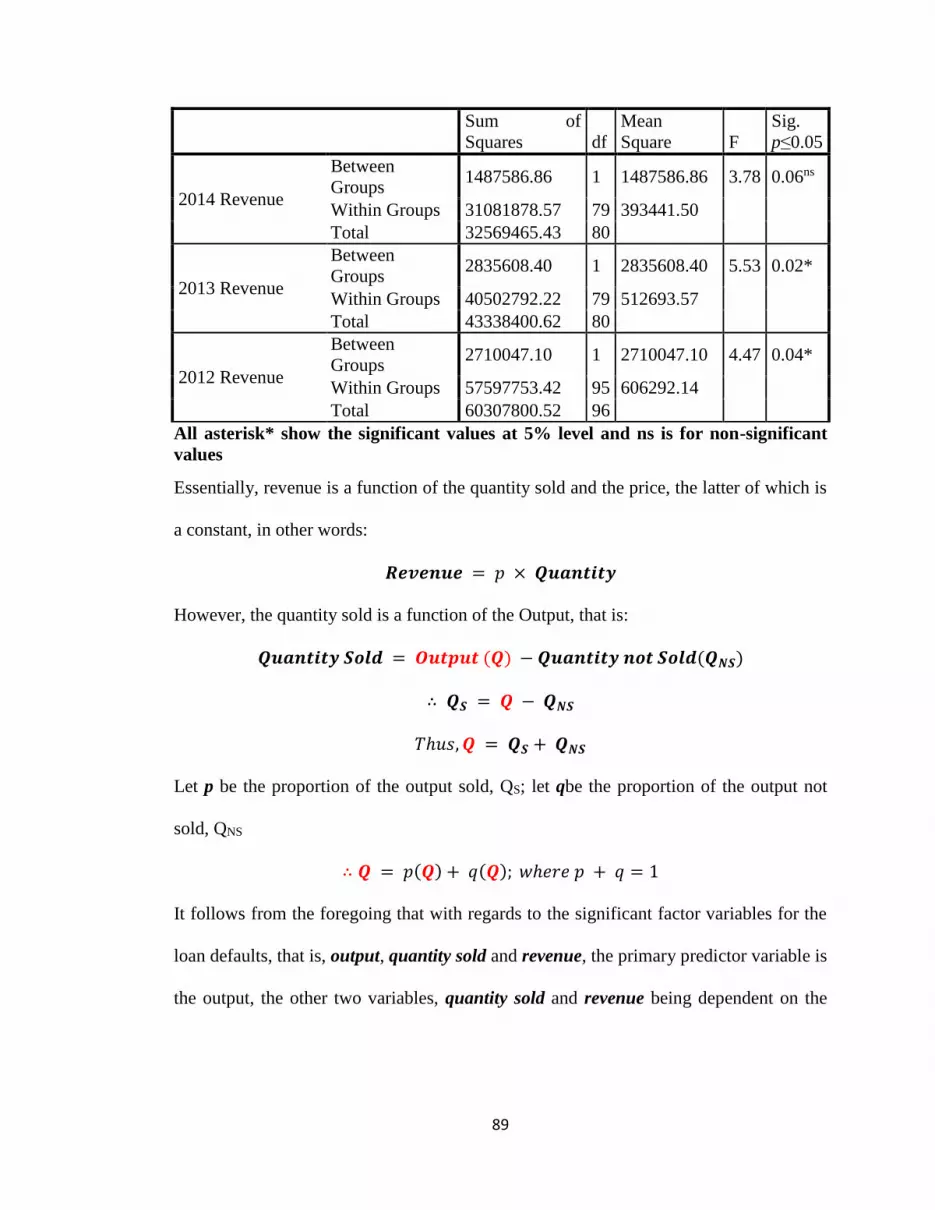

Table 4.8: ANOVA Analysis – Determinants of Loan Defaults 87

Table 4.9: Group Statistics – Output levels of sugar-beans in kilograms 89

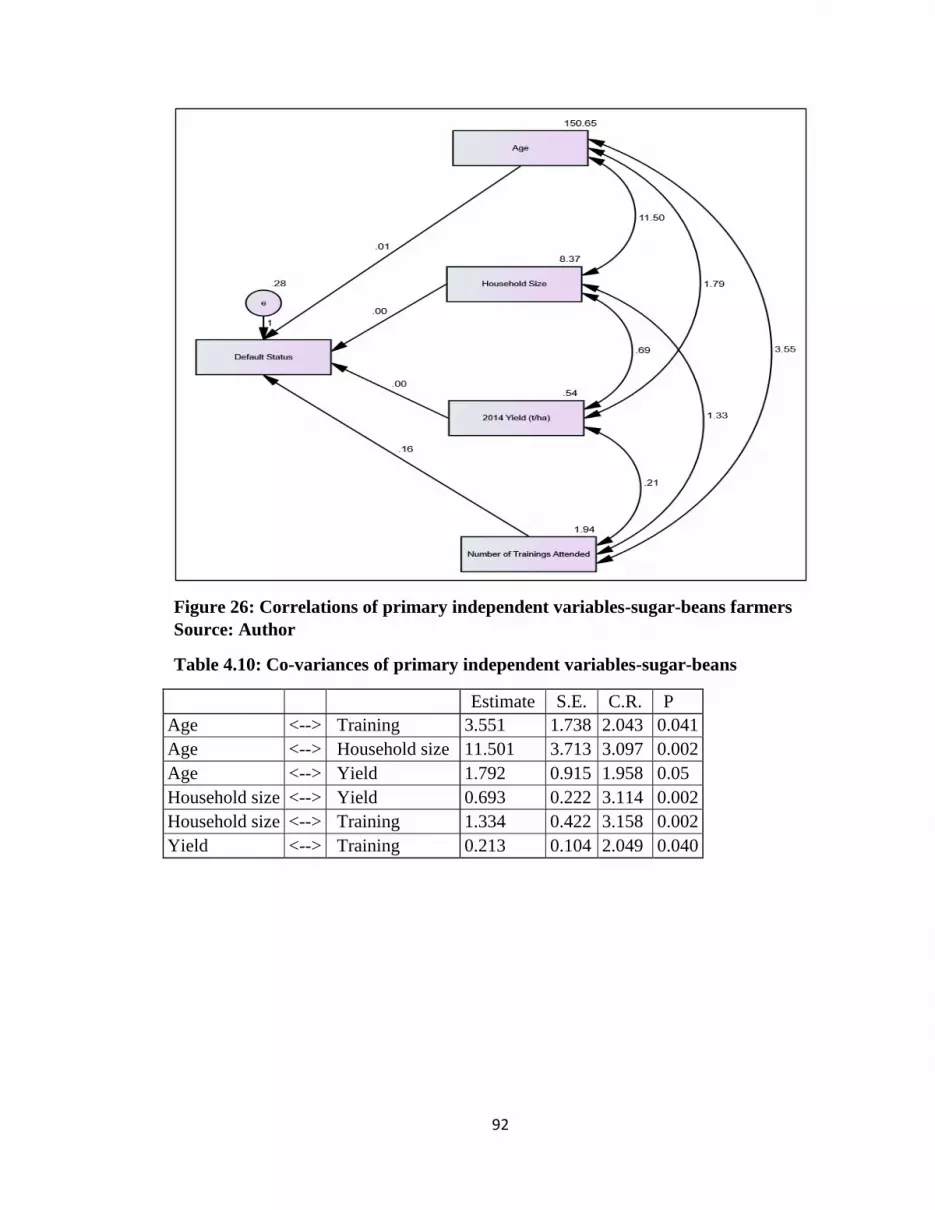

Table 4.10: Co-variances of primary independent variables 91

Table 4.11 Regression model summary for sugar-beans contract farmers 92

Table 4.12: Regression weights for independent variables 93

Table 4.13: Regression coefficients of four primary independent variables 93

xi

LIST OF FIGURES

Figure 1: Symbiotic relationship under contract farming 2

Figure 2: Credit distribution from Banks in Zimbabwe 2009-2014 38

Figure 3: Loans from commercial banks in Zimbabwe to Agriculture sector 39

Figure 4: Musikavanhu Constituency location of Irrigation Schemes in

ManicalandProvince 44

Figure 5: FAO irrigation statistics 2013 46

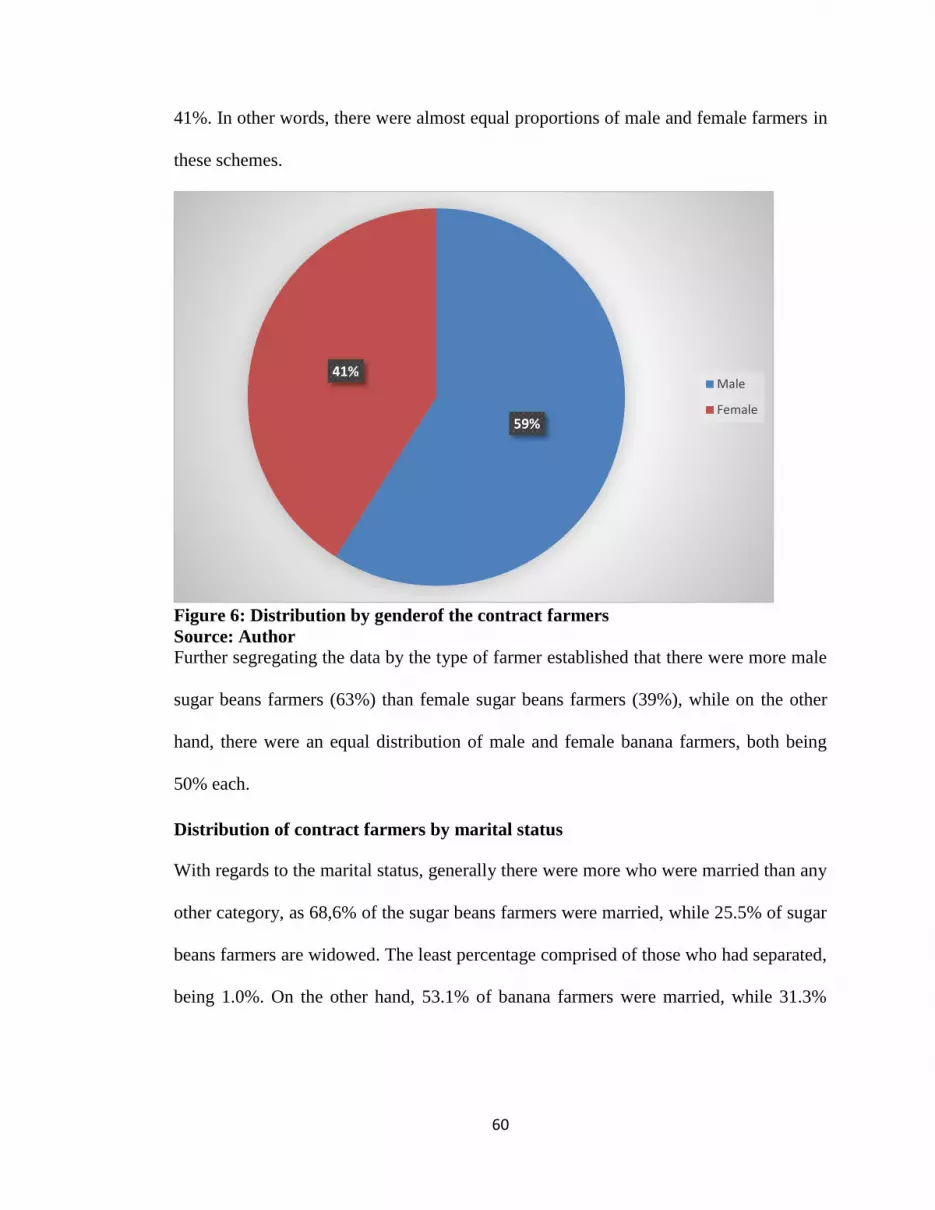

Figure 6: Distribution by gender of the contract farmers 59

Figure 7: Distribution of contract farmers by marital status 60

Figure 8: Age distribution of contract farmers for sugar-beans and bananas 61

Figure 9: Distribution of contract farmers by household size 62

Figure 10: Distribution of farmers by number of school-going children 63

Figure 11: Sugar-beans plot in Chibuwe-Musikavanhu under flood irrigation

system 64

Figure 12: Consolidated graph showing average output for sugar-beans 65

Figure 13: Average sugar-beans yield per contract farmer 67

Figure14: Average sugar-beans revenue (US$) distribution per contact farmer 68

Figure 15: Average banana sales (kgs) per contract farmer 69

Figure 16: Average banana yield (t/ha) achieved by contract farmer 70

Figure 17: Average banana revenue earned by contract farmer in US$ 71

Figure 18: Banana plot in Mutema Irrigation Scheme irrigated using

micro-jet system 72

Figure 19: Default status of sugar-beans contract farmers 72

Figure 20: Source of labor for all contract farmers 74

xii

Figure 21: Number of trainings attended by contract farmer 75

Figure 22: Number of Agritexofficer’s visits/week 76

Figure 23: Decision Tree Analysis – age and default status 79

Figure 24: Decision Tree Analysis – household size 82

Figure 25: Decision Tree Analysis – Number of trainings attended by

contract farmer 83

Figure 26: Correlations of primary independent variables-sugar-beans farmers 91

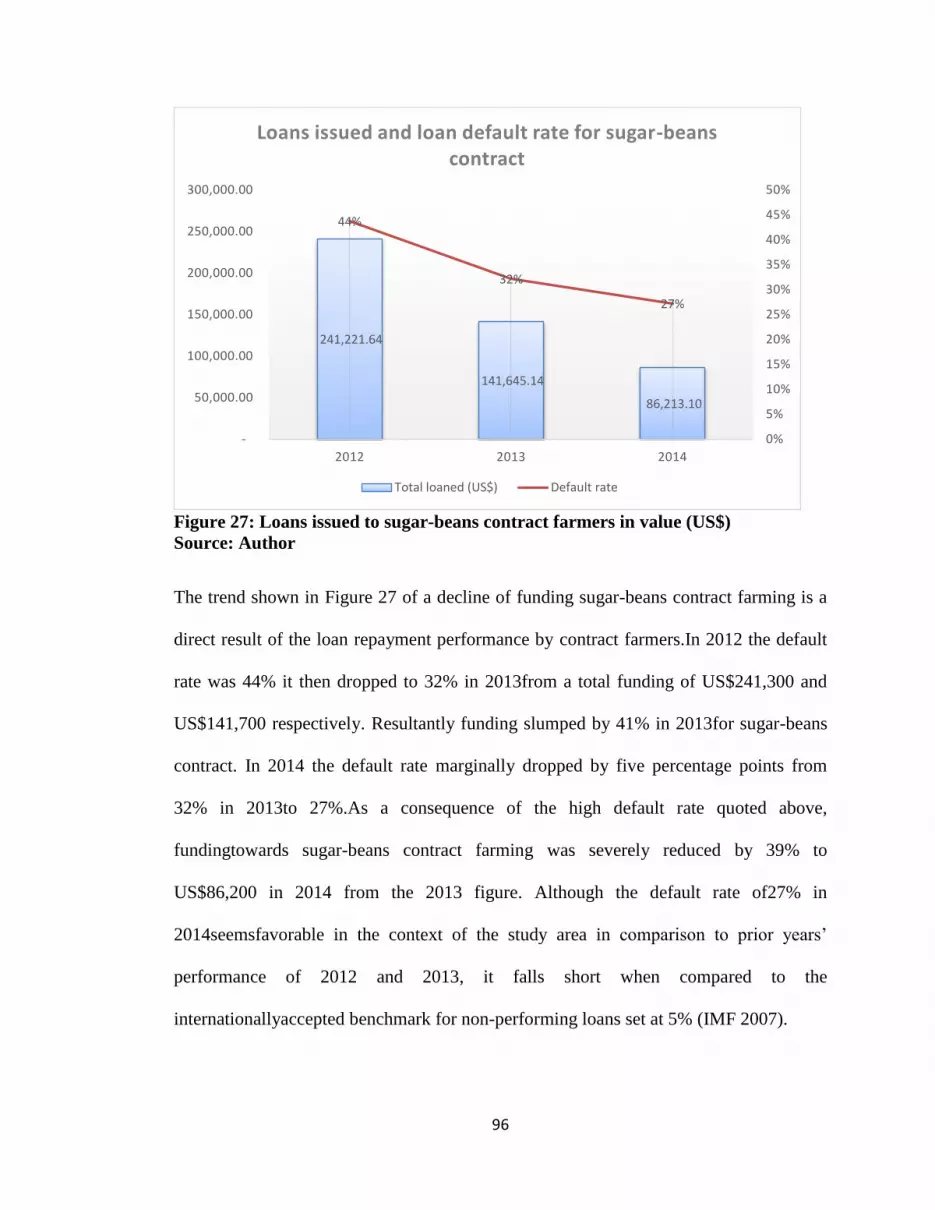

Figure 27: Loans issued to sugar-beans contract farmers in value (US$) 95

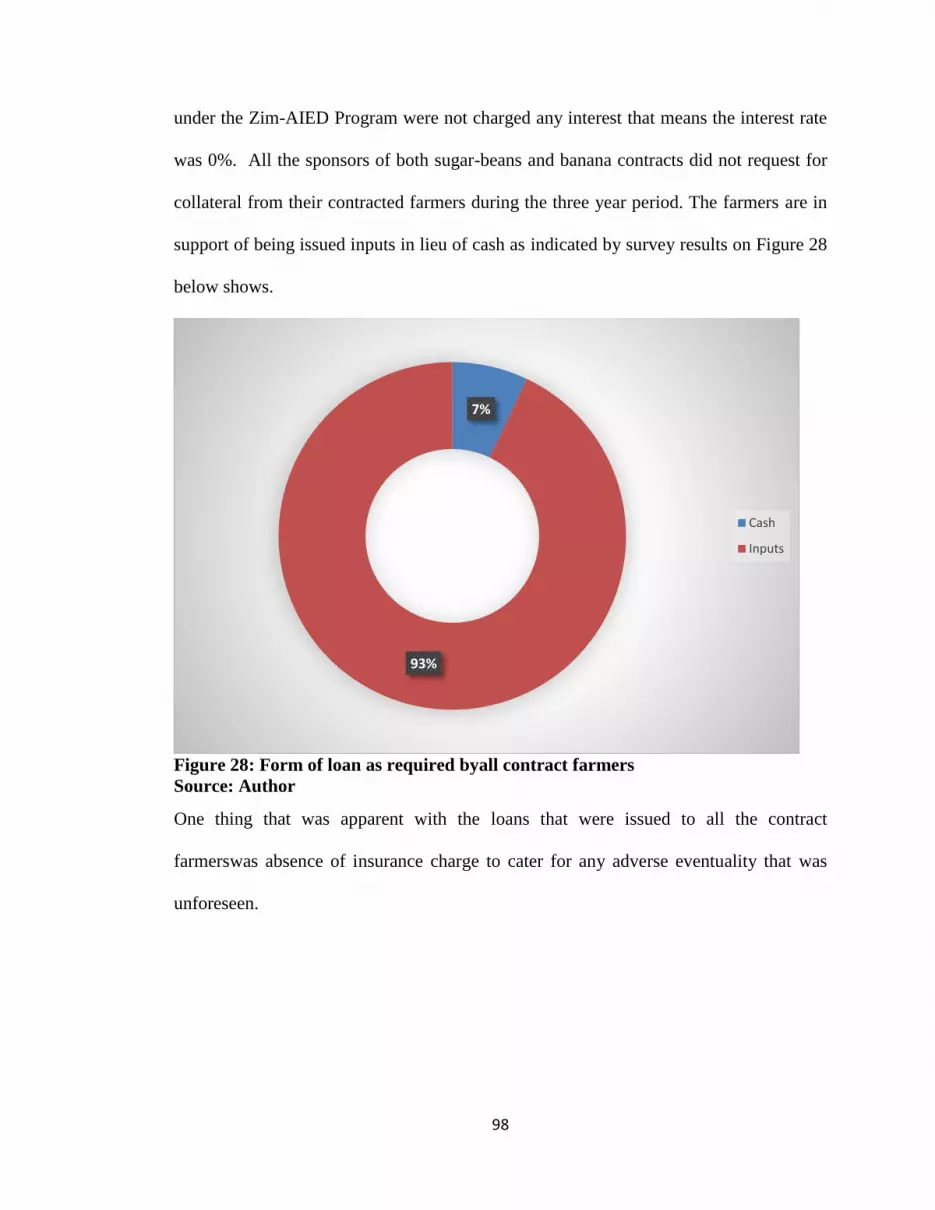

Figure 28: Form of loanas required by all contract farmers 97

Figure 29: Zim-AIED and Agritex officials witness handover of inputs to farmers 98

Figure 30: Factors leading to default under contract farming 110

xiii

APPENDICES

Appendix 1: ANOVA Analysis – Determinants of Loan Defaults ...................................................... 126

Appendix 2: Banana contract farmers questionnaire ........................................................................... 127

Appendix 3: Sugar-beans contract farmers questionnaire ................................................................... 130

Appendix 4: Assessment of Sugar-beans Contract Performance for 2012-2014 by

Agritex Officers ................................................................................................................................... 133

Appendix 5: Sugar-beans Loan performance schedule by contractor from 2012 to

2014……………………………………………………………………………………133

1

CHAPTER ONE: INTRODUCTION

1.1 Background

With the introduction of the multi-currency regime a set of new challenges emerged in

the Zimbabwe financial landscape. The first being liquidity constraints to service the

dire need of credit in the economy in order to revive all socio-economic sectors

including agriculture which had virtually collapsed (Gono 2010). These major monetary

changes in February 2009 (Kramarenko, Engtrom, Verdieret al2010) also brought in

new paradigms in the financial markets and credit access systems in Zimbabwe. This

had a direct impact on the agricultural financing models in Zimbabwe.

One model that had always existed and that crossed over in the new monetary

dispensation was the offering of loans to contract farmers by major agro-commodity

buyers. These arrangements are done directly between the contract farmer and the

respective agro-commodity buyer. An intermediary can also be nominated by the agro-

commodity dealer especially a commercial bank to provide finance for inputs to the

contract farmer on behalf of the agro-commodity dealer.

The financing of agricultural production through contract farming has brought a good

fortune to both smallholder and commercial farmers and provided agro-processors with

the required raw materials. Thus farmers and agro-processors create a binding business

relationship which can only be sustained when each of the parties stick to their

obligations as stipulated in the contract. This has the tendency to perpetuate the funding

cycle in the agriculture sector of any country.

2

As previously stated, an intermediary player may exist in contract farming arrangements.

The intermediary party is mainly a finance house which might bea commercial bank,

micro-finance institution, informal credit scheme and agricultural development bank

among many others. They come in handy to provide with requisite finance for

agricultural production allowing for a tripartite business relationship to work as long as

there are manageable risks. This conventional contract farming relationship can be

summarized in Figure 1 below.

Figure 1: Symbiotic relationship under contract farming

Source: Author

In view of the business relationship brought about by contract farming it has to be noted

that challenges arise to manage and sustain the relationship. The asymmetric and

disruptive pattern around contract farming on Figure 1 symbolizes the strains the

Agro-processor/buyer

Farmer

Finance House

Access to Market

Access to raw produce

Access to finance

Access to market for financial

services

Contract Farming

3

tripartite relationship can experience if contractual obligations are not honored by

anyone of the parties to the contract. The disruptive pattern is also indicative of the

business risks that accrue to honest parties to the arrangement.

The major dilemma being faced by the economic players in the contract farming

arrangement arise from the fact that some farmers successfully honor their contractual

obligations whilst others default in repaying loans accessed under the same contract

arrangement. It is the interest of this research to identify factors that influence farmers to

repay loans under contract farming. It tries to find the answers to why other farmers fail

to perform (default) as expected, when other farmers are successful in repaying their

loans, bearing in mind that all the farmers are assured of a ready market for their

produce.

1.2 Statement of the problem

Zimbabwe has been riddled with a burden of non-performing loans since the inception

of the multi-currency regime in 2009 (Gono 2013). Non repayment of loans is also

pervasive in the agriculture sector through contract farming mechanism. The non-

performance of loans has adversely affected the relationship among contract farming

parties. Assessment of the factors that influence farmers who access their financing

through the contract farming arrangement have to be determined as way to sustain this

agribusiness model.

4

1.3 Justification for the study

The reality of non-performing loans in Zimbabwe has been heralded by the monetary

authorities in their monetary policy statements since the commencement of the multiple

currency regime in 2009. In a recent announcement for the 2013 Monetary Policy

Statement, the rate of non-performing loans stood at 15.92% as at December 2013 from

as low as 1.80% in 2009 surging to 4.24% in December 2010; 8.21% in December 2011

and 11.59% in December 2012 for loans issued by commercial banks (Dhliwayo 2014).

This has had an adverse effect on provision of loans to the agriculture sector which

received the lion’s share of loans and advances in 2012 at 19% (Gono 2013) of all loans

issued by banks that year but it dropped to 15.12% in 2013 (Dhliwayo 2014). Sao Tome

e’Principe, a Central African island nation, is also steeped in this precarious state of non-

performing loans at a rate of 20% as of 2013 (Synge and Van-Valen2014). Yet

according to the United Nations country report on Zimbabwe for 2013,states that

agriculture is still the single largest source of employment for the economy of Zimbabwe

with over 65% of the working population directly or indirectly employed in agriculture

related operations.

The scourge of non-performing loans was not only limited to the conventional financial

services sector but also affected loan arrangements done under the contract farming

model. This has been noted from recent headlines in the print media.

In a newspaper publication in November 2013 titled ‘Zimbabwe Contract Farming at

Crossroads’.The newspaper article noted that Amalgamated Industrial Corporation

Africa Limited (AICO) now called Cottco announced that it had suspended contracting

5

farmers to grow soya beans after it lost more than US$1 million through side-marketing.

This was quoted from a statement by the Chief Executive Officer of the Zimbabwe

Stock Exchange listed agro-industrial conglomerate in September 2013. Under the same

report, DuPont Pioneer a seed manufacturing entity had suspended its maize seed

contract farming arrangements after farmers had failed to repay their loans (Muza 2013).

This then raises questions within the agricultural sector, chief among them, “is contract

farming a viable arrangement in engaging farmers in the face of loan repayment

defaults?” This might also see the dearth of contract farming mechanisms in Zimbabwe

if answers are not proffered to mitigate defaulting by contract farmers in repaying their

loans.

On the contrary contract farming has had a fair share of its successes. This has been

acknowledged by Will (2013) that the adoption of contract farming model has been on

the increase. In the report, Will (2013) noted that in the United States of America (USA)

agricultural production coming from contract farming rose from 12% in 1969 to 36% in

2004. The same report also highlights that 75% of poultry production in Brazil comes

from contract farming. In Gezira,that is Central Sudan, small scale farmers were

contracted to grow cotton and it has been hailed as a success as espoused by Eaton and

Shepherd (2001).In another study conducted by Natural Resource Institute in 2001, ithas

shown that the issuing of loans through the contract farming model has worked in

Uganda for sugar-beans production which was initiated by The Agricultural

Development Corporation (ADC) (Kindness and Gordon 2001).

6

In addition to these success stories of contract farming Olam International stands out as

beneficiary a of this agribusiness model in Africa. Olam International is a Singapore

based agribusiness entity. It operates one of the most successful contract farming

schemes in Africa. In an interview in African Business magazine of August-September

2013, Sunny Verghese, the agribusiness entity’s Chief Executive, notes that the

company through the nucleus model contracted ten thousand small holder farmers

growing different crops in various regions of Africa. This makes it the largest out grower

scheme and most successful contract farming arrangement in Africa. This has seen the

company grow from Africa to be one of the largest global agribusiness players(Versi and

Verghese2013). This shows that contract farming has been and is a success. What

remains to be answeredis to identify the factors leadingfarmers to successfully

honortheir contract farming obligations through repaying their dues whether in kind or

in cash.

1.4 Research objectives

Overall Objective

To identify factors influencing loan repayment (success or default) under contract

farming.

7

Specific Aims

To identify factors that lead farmers to successfully repay loans or default

repayment under contract farming.

To find out the type and the conditions of loans offered to farmers under contract

farming.

To identify the mitigation measures available to contractors to recover unpaid

loans from defaulting contract farmers.

1.5 Research questions

What are the factors influencing loan repayment under contract farming?

What type of loans and the conditions under which they were disbursed to

farmers under contract farming?

What mitigation measures exist for contractors to recover unpaid loans?

1.6 Ethical considerations

The research was conducted through the consideration of the following ethical

principles:

Right to confidentiality: The data is confidentially kept to avoid conflict with contract

farmers the key respondents in the survey. Relevant sources of literature that have been

accessed from various key informants is safely stored and has not been used for any

other purpose than to meet the academic objective of this research.

Right to Informed Consent: the researcher sought informed consent from each of the

participating parties in the research without coercing or inducing undue pressure on key

8

informants. The researcher ensured that explanation was given to parties concerned prior

to accessing information,of why the research is being undertaken.

Right to anonymity: No names have been used for data analysis and in reporting of the

research findings.

Right to privacy: whatever it is the participants deem to be private information and

cannot be accessed by the researcher then the researcher was bound not to further seek

such information.

Adherence to copyright laws: Relevant sources of literature that have been cited in this

researchhave been referenced accordingly. This has been done not to infringe copyright

laws.

1.7 Limitations and delimitation for the study

Time constraint:The research has been time constrained to fully evaluate all the

information gathered and to have more farmers and other crops to be taken on board in

the research. In order to effectively manage the timelines for the research only two

crops, sugar-beans and bananas, have been considered.

Furthermore accessingkey respondents was difficult as they were tied to their scheduled

scheme and community events. The researcher had to ask for a schedule of dates of

Scheme meetings and then plan accordingly to meet key respondents. This was done in

collaboration with Irrigation Management Committee leadership,government’s

Agriculture Extension (Agritex) Officers and Zim-AIED officials.

9

Financial constraint: A research requires financial input that necessitates for the

seamless flow of personnel to execute the research plan within the required time without

restraint. Due to limited financial resources, the research objectives have been narrowed

down to three. The research plan was streamlined in accordance with the available

financial resources.

Lack of control on key respondents and informants: The researcher had no direct control

on key respondents and informants as the researcher was independent of the work

processes ofresearch subjects in the study area. The key informants had their own

pressing schedules to attend to and could not give the researcher enough attention to get

essential data for the research. The researcher had to use negotiating skills and build

relationships to have access to key resource persons and have access to confidential

information. The researcherhad an introductory letter from the Faculty of Agriculture

and Natural Resources as a tool to access key informants. This gave key informants

confidence towork with the researcher. The introductory letter was stating the intention

of the research and status of the researcher.

1.8 Scope of the study

The study was undertaken in Manicaland Province in the south-eastern part of

Zimbabwe. It focused onfarmers who have been assisted by Zimbabwe Agricultural

Income and Employment Development Program (Zim-AIED) in various ways to

increase their yields and have access to market and finance through contract farming.

The program is being implemented by Fintrac Incorporation on behalf of the United

10

States Agency for International Development (USAID) under Feed the Future Program

in Zimbabwe.

The research has been narrowed down to focus on contract farmers who have benefited

from market linkages and finance arrangements organized through the Zim-AIED

Program. The farmers operate in Chibuwe-Musikavanhu and Mutema Irrigation

Schemes in Chipinge District. The major crops which the farmers have grown under

contract farming are sugar-beans and bananas. In addition to contractors who came into

the Irrigation Schemes through the Zim-AIED Program, the study has also considered

other contractors who were active in the Irrigation Schemes prior to commencement of

the Zim-AIED Program. For sugar-beansfive contractors have been active from 2012 to

2014, which is theperiod of study for the research. For bananas there is only one

contractor who was introduced by the Zim-AIED Program to the Schemes and it was the

first time farmers in the Irrigation Schemes have grown bananas on a commercial basis.

1.9 Significance and value of the study

The study is significant in that major research on contract farming which has been

undertaken in Zimbabwe has mostly focused on contract farming performance on two

major crops tobacco and cotton. A gap exists in other contracted crops such as paprika,

Africa Bird’s Eye chilli, sugar-beans and bananas just to mention a few. This research is

significant as it has diverted from looking at contract farming as a market linkage

mechanism but also as a source of funding for farmers. The research investigated

unconventional crops grown under contract farming and these crops, sugar-beans and

bananas, are not even listed on the contracted crops checklist of the state regulatory body

11

in Zimbabwe for marketing agricultural produce the Agriculture Marketing Authority

(AMA).

There are quite a number of stakeholders who will benefit from this research among

them farmers, policymakers, sponsors of contract farming, non-governmental

organizations, players in the business of issuing loans (banks, informal credit providers

and microfinance institutions) and other researchers.

Farmers: Farmers need to be aware of the consequences that accrue from failure to

service their loans to other farmers and this research will act to bridge the gap by

providing the research results to them.

Policymakers: These include government agriculture institutions, non-governmental

organizations involved in agriculture value chain financing, academia and farmer

organizations such as Zimbabwe Farmers Union; Commercial Farmers Union and

Zimbabwe Commercial Farmers Union. The research will create awareness to these

stakeholders on current trends in contract farmers’ performance in servicing their loans

and act as a checkpoint on the relevance of contract-farming agreements and the

respective business dynamics with this agriculturemarket model. This will also help in

policy development that is relevant to the needs of farmer’s loan arrangements and

providers of loans and contract farming agents.

Financiers of smallholder farmers - companies who provide the platform for contract

farming need to have understanding of the current issues that are transpiring in the field.

It is the purpose of this research to offer such knowledge to industrial players and

financiers alike, so that they decide on an informed basis and avoid blind spotswhen they

12

are deciding to engage smallholder farmers in contract farming and issuing them with

loans.

13

CHAPTER TWO: LITERATURE REVIEW

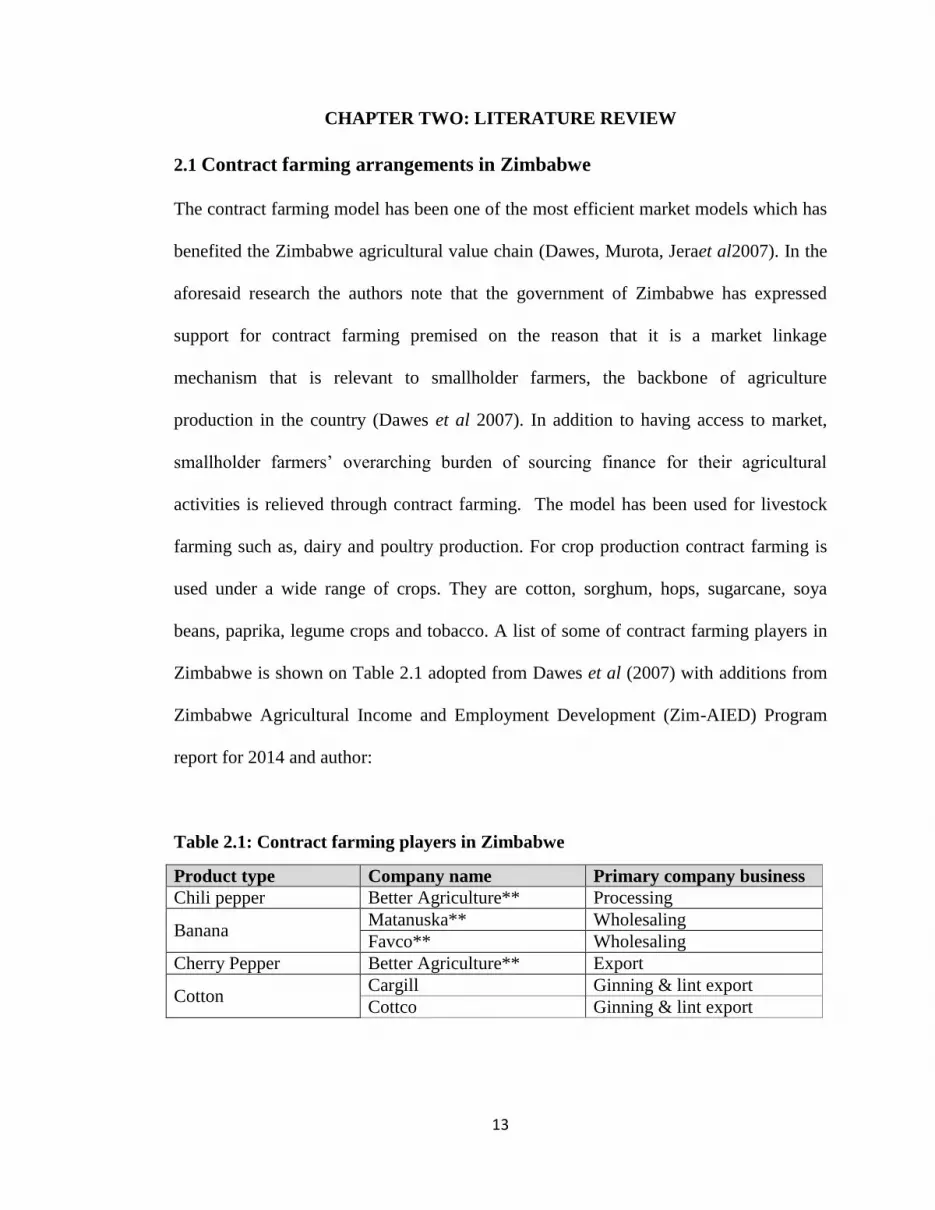

2.1 Contract farming arrangements in Zimbabwe

The contract farming model has been one of the most efficient market models which has

benefited the Zimbabwe agricultural value chain (Dawes, Murota, Jeraet al2007). In the

aforesaid research the authors note that the government of Zimbabwe has expressed

support for contract farming premised on the reason that it is a market linkage

mechanism that is relevant to smallholder farmers, the backbone of agriculture

production in the country (Dawes et al 2007). In addition to having access to market,

smallholder farmers’ overarching burden of sourcing finance for their agricultural

activities is relieved through contract farming. The model has been used for livestock

farming such as, dairy and poultry production. For crop production contract farming is

used under a wide range of crops. They are cotton, sorghum, hops, sugarcane, soya

beans, paprika, legume crops and tobacco. A list of some of contract farming players in

Zimbabwe is shown on Table 2.1 adopted from Dawes et al (2007) with additions from

Zimbabwe Agricultural Income and Employment Development (Zim-AIED) Program

report for 2014 and author:

Table 2.1: Contract farming players in Zimbabwe

Product type Company name Primary company business

Chili pepper Better Agriculture** Processing

Banana Matanuska** Wholesaling

Favco** Wholesaling

Cherry Pepper Better Agriculture** Export

Cotton Cargill Ginning & lint export

Cottco Ginning & lint export

14

Olam International* Ginning & lint export

Quton Seed sales

Legume crops

Grain Marketing Board Wholesaling

Olivine Canning

Reapers Wholesale

Ostriches and chickens

Ostrindo Poultry processing

Irvine’s* Chickens processing

Hy-veld Oleoresin extraction

Seed crops

AgriSeeds Seed sales

ARDA Seeds Seed sales

SeedCo Seed sales

Du Pont Pioneer* Seed sales

Sorghum Delta Brewing

Sugar cane TongaatHulets Zimbabwe* Sugar manufacture

Green Fuel* Ethanol manufacture

Sweet potatoes SimFresh International** Wholesale

Tobacco

Northern Tobacco Processing and export

Tribac Processing and export

Tian-ze* Processing and export

Zimbabwe Leaf Tobacco Processing and export

Vegetables and/or fruit

Cairns Canning

Favco Wholesaling

Honeywood Canning

Wholesale Fruiterers Wholesaling

Selby Enterprises Processing and export

Source:Dawes et al (2007); *Author (2014); **Fintrac Inc. Zimbabwe (2014).

According to the Food and Agricultural Organisation of the United Nations, contract

farming is defined, as an agricultural production system carried out according to an

agreement between a buyer and farmers, which establishes conditions for the production

and marketing of a farm product or products (Pultrone, da Silva and Shepherd 2012). It

has also been defined as forward agreements specifying the obligations of farmers and

buyers as partners in business (Will 2013). The intent is that the buyer will make

provision of efficient extension services and appropriate inputs (Shepherd 2012).

Pultroneet al (2012) asserts that contract farming should include the provision of product

15

quality standards and land preparation services. Additionally, timely distribution of

inputs; collection of produce and payment of farmers, are some of the factors that will

sustain the contract agreement on the part of the buyer and enhance loan repayments on

time by farmers (Dawes et al 2007). This arrangement minimizes risks of default of loan

repayments if it is properly executed between the parties involved.

2.2 Contract farming models

Five business models under contract farming have been identified by Eaton and

Shepherd (2001). These are centralized model; the nucleus estate model; multipartite

model; informal model and the intermediary model. Each of these has its inherent

advantages and disadvantages either to the farmer or to the buyer. The model to be used

depends on the farm product, resources of the sponsors and the relational dynamics

between buyer and farmer (Will 2013). The multipartite model has been noted to have a

desirable success rate in a research done by

StichtingNederlandseVrijwilligers(SNV)Netherlands Development Organisation

translated as Foundation of Netherlands Volunteers in 2007 in Zimbabwe (Dawes et al

2007).

In order to bring out a thorough understanding of these models Table 2.2 shows a brief

description of each model as outlined by Eaton and Shepherd (2001).

Table 2.2: Contract farming models and characteristics

Model Characteristics

Centralized

model

Involves a centralized processor and/or packer buying from a

large number of small farmers.

Is used for tree crops, annual crops, poultry and dairy. Products

16

often require a high degree of processing, such as tea or

vegetables for canning or freezing.

Is vertically coordinated, with quota allocation and tightquality

control.

Sponsor involvement varies from minimal to extremely involved

depending with produce sensitive.

Nucleus estate

model

It is a variation of the centralized model.

The sponsor manages a central estate or plantation.

The central estate is usually used to guarantee throughput for the

processing plant but is sometimes used only for research or

breeding purposes.

Is often used with resettlement or transmigration schemes.

Involves a significant provision of material and management

inputs.

Multipartite

model

This model describes contract conditions when more than one

organization jointly participates to contract the farmer.

Involves statutory bodies.

Separate organizations may be responsible for credit provision,

production, and management, processing and marketing.

Informal model

Is characterized by individual entrepreneurs or small companies.

Involves informal production contracts, usually on a seasonal

basis.

Often requires government support services such as research and

extension.

Involves greater risk of extra-contractual marketing.

Intermediary

model

Involves sponsor in subcontracting linkages with farmers to

intermediaries.

There is a danger that the sponsor loses control of productionand

quality as well as prices received by farmers.

Source: Eaton and Shepherd (2001)

2.3 Sources of finance for farmers

Globally farmers have a wide array of options to finance their farming activities and

Zimbabwean farmers are no exception. The sources of finance vary from informal

finance schemes to formal finance houses. In between there are other funding

mechanisms and this is where sponsors of contract farming fall into and these are what

17

Klein, Meyer, Hanniget al(1999) term as interlinked credit arrangements providers.

These sources of finance, but not all of them, are ultimately the source of loans that can

and are advanced to farmers either in terms of cash or kind as noted by Kohansal and

Mansoori (2008) in their study in Iran. Giehler (1999) mentions that loans to farmers are

financed by various sources which include but not limited to the following; farmers

household savings, capital markets, equity, fiscal allocations, monetary policy

authorities financing interventions and international borrowing. In addition to these

sources of finance Muchati (2015) mentions that contract farming isa funding

mechanism that farmers accessto finance their agriculture activities.

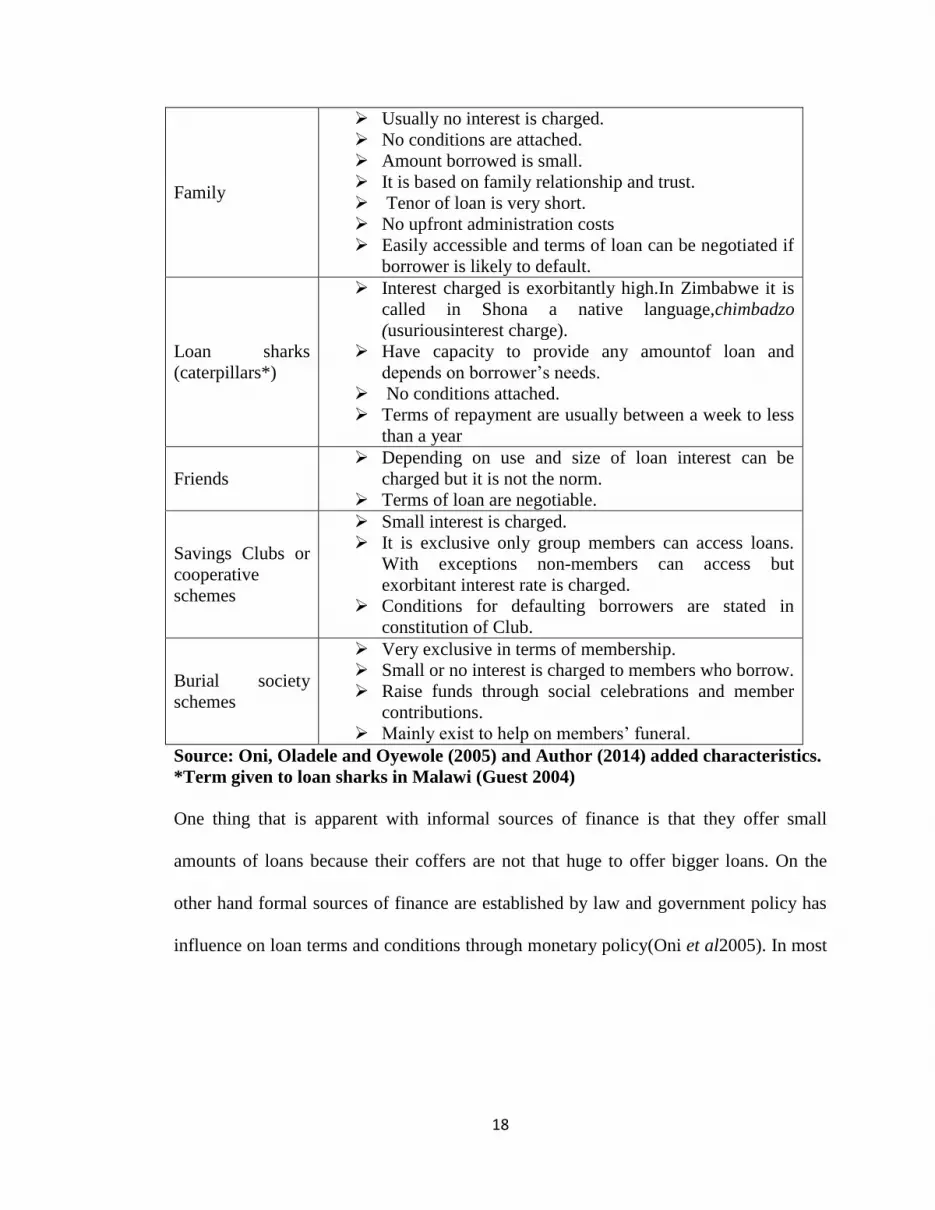

Informal sources of finance are described as unregulated sources of finance that are

arranged without any formalities and strict conditions on performance. The players in

the informal credit system are not registered with any regulatory authority and the

transactions are usually based on social relationships and trust between members of the

community (Giehler 1999). One thing that makes informal finance sources to thrive is

there proximity to clients. They are very prevalent in rural economic systems and poor

societies whose bankability status is viewed with skepticism by conventional banking

system. Table 2.3 shows a list of some informal sources of finance and their respective

characteristics.

Table 2.3: Informal sources of finance and their characteristics

Source Characteristics

18

Family

Usually no interest is charged.

No conditions are attached.

Amount borrowed is small.

It is based on family relationship and trust.

Tenor of loan is very short.

No upfront administration costs

Easily accessible and terms of loan can be negotiated if

borrower is likely to default.

Loan sharks

(caterpillars*)

Interest charged is exorbitantly high.In Zimbabwe it is

called in Shona a native language,chimbadzo

(usuriousinterest charge).

Have capacity to provide any amountof loan and

depends on borrower’s needs.

No conditions attached.

Terms of repayment are usually between a week to less

than a year

Friends

Depending on use and size of loan interest can be

charged but it is not the norm.

Terms of loan are negotiable.

Savings Clubs or

cooperative

schemes

Small interest is charged.

It is exclusive only group members can access loans.

With exceptions non-members can access but

exorbitant interest rate is charged.

Conditions for defaulting borrowers are stated in

constitution of Club.

Burial society

schemes

Very exclusive in terms of membership.

Small or no interest is charged to members who borrow.

Raise funds through social celebrations and member

contributions.

Mainly exist to help on members’ funeral.

Source: Oni, Oladele and Oyewole (2005) and Author (2014) added characteristics.

*Term given to loan sharks in Malawi (Guest 2004)

One thing that is apparent with informal sources of finance is that they offer small

amounts of loans because their coffers are not that huge to offer bigger loans. On the

other hand formal sources of finance are established by law and government policy has

influence on loan terms and conditions through monetary policy(Oni et al2005). In most

19

countriesformal sources of finance’s operations are either monitored by central or

reserve bank authorities.

In Zimbabwe, according to Kramarenko et al (2010), the rise of informal finance

schemes came to being during persistent economic difficulties experienced during

the,‘lost decade’ of 1999 to 2009. Dhliwayo (2014) further alludes to this fact when

presenting the 2013 Monetary Policy Statement. The statement noted that a major source

of finance for Zimbabweans has been money coming through informal channels from

the Diaspora but bemoaned that the funds are usually used for consumptive purposes

rather than productive endeavors to stimulate economic growth. Meaning that even

agriculture, one of Zimbabwe’s key productive sectors, was not benefiting from this

informal source of finance. Whereas in Nigeria, Adebayo and Adeola (2008) reported

that agricultural production undertaken by smallholder farmers relied on loans from

informal sources mainly from unregistered cooperatives.

One key element of accessing finance in the form of loan arrangements, whether it is

cash or kind, is that the funds carry a cost of borrowing charged to the borrower by the

issuer of loan, called interest. Due to the prohibitive lending rates averaging 22% in

2012 and following a similar pattern in 2013 as noted by Gono (2013) and Dhliwayo

(2014) in their annual monetary policy statements, most farmers in Zimbabwe have been

deterred to borrow from conventional banks. This has also been exacerbated by the short

term nature of loans being offered by commercial banks in Zimbabwe. Because of these

20

adverse conditions, most farmers have shunned this all too familiar source of finance for

their farming activities.

In an article by Cox (2014) in Spore Magazineit highlighted the issue of high interest

charged for agricultural loans issued to farmers in Ghana.The farmers are charged

exorbitant rates of 25% to 40% per annum. To worsen the situation of farmers only 6%

of commercial lending in Ghana has been earmarked for the agriculture sector (Cox

2014). Truly this gives a reason for the existence of informal sources of finance. World

Bank (2008) summed it by saying, “agriculture continues to be a fundamental instrument

for sustainable development and poverty reduction yet, financial constraints in

agriculture remain pervasive, and they are costly and inequitably distributed, severely

limiting smallholders’ ability to compete” in various lucrative agricultural value chains.

These adverse conditions did not shut other avenues of financing for farmers that are

available to the Zimbabwean agricultural sector because of its pivotal role in the

economy. Apart from accessing loans for agricultural production from conventional

banking system with their punitive conditions on the borrower, farmers have also

accessed loans through contract farming arrangements by accessing inputs, technical

expertise and land preparation from buyers of their commodities. It has proved to be a

familiar arrangement with buyers of major cash crops in Zimbabwe as shown on Table

2.1. Therefore contract farming becomes a recognizable loan arrangement mechanism in

agricultural production in Zimbabwe to assist farmers with inputs, ready markets for

their crops and many other benefits organized by the buyers. Contract farming can

21

therefore be classified as either a formal or informal source of finance depending on how

it has been crafted by the sponsors.

In addition to loan arrangements advanced by agro-commodity buyers another source of

funding has emerged to the convenience of farmers. In recent years the donor

community has remodeled their aid mechanisms moving away from issuing handouts to

offering pro-business development solutions to their recipient communities. One such

arrangement has been financial intervention through issue of loans to smallholder

farmers and ensuring that farmers are trained so that they operate their farming activities

as profit making ventures. This ensures that farmers produce for their food security

needs, have reliable income streams to meet other pressing financial needs in the home

and operate their farming activities as businesses (Fintrac 2014). Zimbabwe has

benefited from the presence of these not-for-profit organizations such as SNV

Netherlands, Development Alternatives Incorporation (DAI Inc.) and Fintrac

Incorporation a United States Agency for International Development (USAID)

agribusiness contractor among many others. These have offered financial reprieve to

many farmers and the non-governmental organizations are offering these funds not as

free handouts but as loans. Farmers are required to payback once they sale their produce.

This has added to the portfolio of loan arrangements available to farmers. The

arrangement has not been spurred from the dismal performance of loan repayments

foregoing in the Zimbabwe economy.

22

2.4 Key enablers for access to finance and loan repayment performance

To ensure viability of loans issued under contract farming there are key enablers that are

expected for all the parties concerned to do their role in the arrangement with

transparency. Viability in this instance is measured by either success in repayment of

loan or default in repaying loans.

A critical component that necessitates factor mobility such as capital in the form loans

for farmers is the institutional environment. These institutions constitute the legal and

administrative systems within which individuals, enterprises and governments function

and interact properly to create wealth as outlined in The Global Competitiveness Report

2013-14 (Schwab and Sala-i-Martin 2013). The report further states that the quality of

institutions has a bearing on productivity of major sectors of the economy key among

them the agriculture sector. These include quality of political governance institutions,

enforcement of the rule of law, respect for property rights, proper management of public

finance and transparency in reporting by private enterprises (Schwab and Sala-i-

Martin2013).

Apart from institutional environment, the report enlists eleven other key enablers for

productivity but only seven are mentioned here because of their direct link to agriculture

finance. These are infrastructure (roads, dams and telecommunication), macroeconomic

environment (fiscal and monetary issues), higher education and training, goods market

efficiency and financial market development. All these key enablers are very critical in

agriculture production especially for smallholder farmers’ finance and market needs.

23

These are necessary for smallholder farmers who have been deemed to be too risk to

provide loans and un-bankable (Klein et al 1999). Concurrently smallholder farmers are

very much in need of the State as a conduit to advocate for their financial inclusion.

They also need the state to create an enabling environment so that they have access to

the mainstream economy through access to markets offering competitive prices for their

produce. More so for contract farming arrangements, which need enforcement through

the provision of a viable legal framework. To sum it Fan, Voegele and Pandya-Lorch

(2010) wrote that, “An enabling policy environment and legal framework, enforcement

of rules and regulations, and a supportive rural infrastructure all contribute to making

access to finance a reality” for smallholder farmers.

Miller and Jones (2010) mention that lenders should look at five key areas to assess

borrowers prior to issuing them with loans. These have been termed as the five Cs of

loan assessments. Character, capacity, capital, collateral and conditions constitute the

five Cs that lenders have to use to assess borrowers. These are key enablers on the part

of lenders and can also be appliedby sponsors of contract farming. Among these five Cs

the major one which formal finance houses mostly put as a key requirement to issue

their funds is the need for collateral. The need for collateral always excludes smallholder

farmers, from access to financial services such as loans, whose assets such as indigenous

livestock and huts have low economic value and they are not easily tradable on the open

market. Another setback is that most financially deprived rural farmers do not have

tenure of land in which they practice their farming activities. The land is State owned. In

some regions land is communally or customary owned but it will be under the auspice of

24

traditional leaders to determine its exchangeability on the open market. This leaves most

smallholder farmers with few “dead assets” (De Soto 2000) to use as collateral.

Moreover one key explanation to Africa’s incessant poverty is that most of its populace

are unable to turn their assets into liquid capital as noted by Guest (2004) in his book

The Shackled Continent. This then leads most Africans to be starved of capital which is

a key factor of production and the lifeblood of capitalism (Guest 2004). This is very

profound especially when farmers need loans to finance their activities and lenders insist

on collateral. In the same script Guest cites De Soto (2000), a Peruvian economist who

noted that the value of rural land, where Africans plough and graze their livestock, is

worth USD390 billion. The valuation was done in 2000. This is a huge sum of money if

farmers’ land was formally registered and owned (Guest 2004).

The issue of land security still remains one of Africa’s unresolved colonial legacy. After

fourteen years nothing much has changed since De Soto (2000) published his work in

2000. African countries stand to benefit by effecting this necessary change. The change

is effective with this in mind that the USD390 billion, the estimate value for rural land,

is still a huge sum of money today even without adjusting for the time value of money.

If this process of giving land entitlement to smallholder farmers is pragmatically pursued

it would unlock value to the benefit of all African economies. And the term dead capital

will cease to exist in agriculture finance vocabulary.

25

2.5 Factors influencing loan repayment performance

Factors that influence farmers to either repay their loans or default are as varied as the

farming systems that farmers undertake to earn their livelihood.These are analyzed and

reviewed by looking at five factors. These are demographic, agronomic,financial,socio-

economic and political.

Demographic factors

Demographic structure of any nation contributes either positively or negatively to the

performance of an economy and its effects are even more pronounced in agriculture

based economies especially in most African economies.

The United Nations Country Analysis Report for Zimbabwe (2010) shows that seventy

percent of Zimbabwe’s population relies on agriculture production for food, employment

and income. It is also a major foreign exchange earner contributing 40% to export

receipts and 60% of raw materials required in the manufacturing sector coming directly

from the agriculture sector (UN Country Report, 2010). Thus a great proportion of the

economically active age group of between 20 to 65 years is directly or indirectly

dependent on agriculture. As of 2012, Zimbabwe’s population stood at 13 million

comprising 48% male and 52% female (ZimStat 2013).

Age is defined as the amount of time a person has lived from the date of birth to the

current date of existence, measured in years (Merriam –Webster 2015). The age of the

farmer has been found to have an effect in loan repayment by many researchers.

Research in Iran by Kohansaland Mansoori(2008) made a conclusion that age was

26

negatively related to loan repayment performance among farmers in Khorasan-Rasavi

Province. The researchers came to thisconclusion by sampling 175 farmers and using the

logit model to analyze their data. On the other hand studies in Ghana and Nigeria show

different results to Kohansal’s study in Iran. Wongnaaand Awunyo-Vitor(2013) in Sene

Districtand Awunyo-Vitor (2012) in BrongAhafo Region inGhana noted that age of

farmers was positively related to loan repayment performance. The study by

Wongnaaand Awunyo-Vitor(2013) was based on surveys conducted on one hundred

yam farmers and probit regression model was used to analyze factors influencing loan

repayment performance by farmers. This was also related to research findings in other

studies carried out in Ogun State of Nigeria key among them Ayandaand Ogunsekan

(2012) and Oni et al (2005). For the study done by Oni et al (2005) age was the

dominant factor affecting loan repayment performance compared to other eleven

independent variables.

In Zimbabwe through a government initiated empowerment loan facility, popularly

known as Kurera-Ukondla Youth Fund, provided by Old Mutual Zimbabwe to the tune

of USD10 million earmarked to benefit the youth had a default rate of over 60%

(Zhangazha 2014). This then labelled the age group between 18 to 35 years as loan

defaulters in the Zimbabwean context. The loan limit that was supposed to be accessible

to each youth initiated project was USD5 thousand. Yet it is on record that some youths

accessed USD300 thousand as individuals, sixty times more than the prescribed limit.

The statistics did not make further breakdown to category of activity – that is sector

specific loan repayment performance, which had the most non-performing loans.

27

Information is currently lacking on the availability of the factors that contributed to this

dismal failure of the Youth Fund apart from age.

Household size, gender and marital status are the other variables that have influence in

loan repayment performance under demographic factors. Gender for the purpose of this

study means male and female. Household size is defined as the number of people under

the care of the farmer. Udoh (2008) in AkwaIbom State in Nigeria came to a conclusion

that household size was statistically significant to loan performance and noted that those

farmers with a large household size are likely to default than those with smaller

household sizes. Whilst a study by Wongnaaand Awunyo-Vitor (2013) concluded that

household size was not clear. It was ambiguous in their findings. In the same study,

gender and marriage were known to have a negative effect on yam farmers’ loan

repayment abilities.

In relation to genderUdoh (2008) notes that male beneficiaries had higher tendencies to

default than females. The research noted that the multiplicity of responsibilities of men

as breadwinners, which may require them to divert the proceeds from their farms to

offset domestic financial commitments rather than fulfilling their loan obligations might

have contributed to defaulting. This was also confirmed by a study in Vietnam by Duy

(2013). The study made an observation that women are generally good borrowers. The

reason being that they are likely not to spend on non-productive expenses such as social

pleasures like alcohol.In this study, Duy (2013) employed three analysis models. The

determinants of repayment performance of borrowers were analyzed using the double

28

hurdle approach and an instrumental variable probit model while scheduled repayment

performance was analyzed by a Tobit model. The same sentiments that women perform

better that men in loan repayment is shared by Kleinet al (1999) in their booktitled

Better Practices in Agricultural Lending.

Agronomic factors

The list of agronomic factors includes but is not limited to type of crops grown and the

respective variety, type of soil where crops are grown, access to extension services and

training, good agricultural practices such as crop rotation and conservation farming, use

and application of fertilizers and crop protection chemicals.

Gates and Gates (2015) put an emphasis on the need for agricultural extension services.

They assert that many farmers would not be productive if they have no access to

agricultural extension services. The report noted that agricultural extension is the

process by which farmers get information — what seeds to plant, how to rotate crops to

protect their soil, how to get the best prices on the market. Furthermore, traditionally

agriculture extension services require highly trained agricultural experts who know the

best crops grow in every region of they operate in (Gates and Gates 2015). This sets

agriculture extension services as a key factor that contributes positively to loan

repayment. This is a special requisite under contract farming as farmers need the help of

contract farming sponsor’s extension workers to fully operationalize the contract in

relationship to agronomic issues. This includes expected yield, quality of output and

29

standards that have to be adhered to in terms of application of crop chemicals and post-

harvest management of the output (Dawes et al2007 and Will 2013).

Roslanand Karim (2009) concurs that training in credit management and good

agricultural practices reduces loan repayment default among microcredit beneficiaries in

Malaysia. On the contrary the study showed that farmers who did not undergo any form

of training defaulted in repaying their loans. The study did not specify the courses that

farmers undertook, it just generically mentions training in good agricultural practices

which in essence covers many issues some of them not related to loan repayment

performance or contract farming. Similarly a study in Ghana byAwunyo-Vitor(2012)

came to the same results that the larger the loan amount and the longer the repayment

period as well as access to training are more likely to reduce loan repayment default.

Althoughthe study did not give the actual length of time spent on training farmers and

when the training was conducted, that is prior to loans issued or after farmers had

received their loans, the study still validates training as a factor influencing loan

repayment. The data collected for the research in Ghana came from a survey of 374

farmers in five districts whilst the probit model was used to analyze the data.

In Zimbabwe a study carried out by SNV Netherlands in 2007 noted that farmers with

very low yields will not often be able to repay their input loans jeopardizing the contract

agreement. This was experienced by Olivine Industries with their contract arrangement

for missy navy beans with Hama Mavhaire farmers in Chirimuhanzu in Midlands

Province. The company suspended the arrangement in the 2006/07 season (Dawes et al

30

2007).The study could not show the number of hours spent per day training farmers on

good agricultural practices by Olivine Industries in order for contract farmers to produce

the expected yield. Perhaps this could have been the missing link in averting the mishap

of terminating the contract arrangement and failure by farmers to repay their loans for

inputs received.

A related factor to extension services and training is regular visits either by loan issuer

or contract farming sponsor. In the same study undertaken by Dawes et al (2007) it

noted that contracting companies who regularly visited their contract farmers had low

contract defaults than those contractors who never visited at all. The issue of resources

and distance to where contract farmers are located might be a deterring factor for

contractors to regularly follow up on their contract farmers. This leaves them with one

alternative. In the case of Zimbabwe the exercise can be done by Agritex officers, where

each district ward has one or more officers depending on productivity of region, to

conduct the regular visits on behalf of the contract farming sponsors or providers of

loans.

Financial factors

The key determinants of loan repayment performance to be considered under financial

factors are:

Loan size measured as the amount of loan issued to farmer in monetary value though

it might be in kind that is inputs and other services.

31

Interest on loan measured by the interest rate per annum or per month charged by

lender.

Tenor of loan measured as the time of repaying the loan as stipulated by lender.

Upfront costs: these are total application costs including administrative charges.

Collateral issues: this is usually requested by formal lenders and collateral is usually

an asset with a value that the lender can dispose after borrower has defaulted.

Post-harvest price: this is the price of farmers’ commodity on the open market. It is

usually affected by demand and supply factors of the commodity in question and is

measured as price per kilogram or price per ton for most agriculture products.

Profit earned from farming venture this is determined by calculating the gross

margin by using monetary values.

Off-farm income is any amount in monetary value that the farmerearns from other

activities besides farming.

Repayment frequency measured as number of times the loan is repaid it might be

weekly, monthly (instalments) or a terminal loan (principal amount and interest are

fully paid at the end of loan tenor).

These are generally the financial factors that influence farmers when they either default

or successfully repay their loans. These are major determinants that each farmer has to

take cognizance of prior to tying themselves to a debt provider. And the need for

financial prudence is highly valuable as this will determine whether the farmer will be

able to repay or not.

32

With reference to the same research carried out Iran in 2008 the researchersfound out

that loan interest rate is the most important factor affecting the repayment of agricultural

loans (Kohansaland Mansoori2008). It also made a conclusion that farmer’s experience,

income received; loan size and collateral value have positive effect on farmer’s loan

repayment.This was also confirmed in a research done in Nigeria in 2011. It noted that

farmers were unable to repay their loans due to high interest rate. In addition to the high

interest rate factor, the other factors contributing to loan repayment default was delayed

farm output due to late rainfall and weak recovery efforts by the officials of the Bank of

Agriculture (Ayandaand Ogunsekan 2012). The researchers used multi-staged sampling

method to survey 120 respondents with the descriptive and Pearson Moment Correlation

Statistics being employed for data analysis.

In a research done in India byDeiningerand Liu (2010), though not for loans issued

under contract farming, its findings are worth noting as it focused on factors influencing

loan repayment. First the researchers, Deininger,a World Bank economist, and Liu from

the International Food Policy Research Instituterevealed that high installment frequency

enhance loan repayment performance. This, they said, is in line with the notion that

frequent small repayments will inhibit loan repayment default for households who have

little access to credit. Data for this study was collected from a survey of 299 village

organizations with a mandate of issuing loans to their members. Secondly the study

came to the conclusion that the probability of loan repayment increases with the size of

the group with an optimum number of fourteen group members. Beyond a group with

fourteen members the results showed that the probability for a group to repay decreases.

33

This is a necessary consideration when seeking guidance on group formation with the

intention of provision of loans to groups. The results did not specify the composition of

the age groups that defaulted and that repaid. Lastly their research indicated that the

probability to default increased with the length of time a group has been in existence up

to approximately five years. The opposite is true that the lesser the years a group has

been in existence the better the repayment performance.

Hamza (2007) asserts that the level of livelihood diversification with the relative

importance of off-farm income of farm households seems to be important for credit

repayment by both poor and non-poor households with the view that if farm activities

fail to raise income to repay loans other sources of income can be a source of funds to

liquidate the loan burden.

Socio-economic factors

Education is a necessary tool to improve the livelihood of most poor people. It helps in

the process of decision making and for farmers it is essential in that they have an

understanding of the consequences of the decisions they undertake especially in relation

to loan repayment. Education is therefore a socio-economic factor that has an influence

on loan repayment. It is generally agreed among researchers (Duy 2013; Awunyo-Vitor

2012 and Heney 2000) on loan repayment performance that the higher the education

attained or completed by a farmer the better is their loan repayment performance holding

other factors constant.

34

Apart from education another relevant socio-economic factor that affects loan repayment

performance is size of landholding where farmers practice farming and in what form the

landholding exists.

According to research done in Ghana the results showed that educational level, number

of years of farming experience, profit gained from loan, age of farmer, supervisory visits

to farmers and access to off-farm income have positive effects on yam farmers’ ability to

repay the loans given to them by financial institutions (Awunyo-Vitor 2012). A rise in

each of these factors enhanced yam farmers’ loan repayment abilities.Those with a

higher level of education fared better in servicing their loans than their peers whose

educational level was deemed low. In the same vain,in Vietnam, Duy (2013) found that

farmers grouped according to their educational level fared better in terms of their loan

repayment status.

Another factor for consideration leading to loan repayment default is expenditure on

traditional social ceremonies which include weddings, funerals and circumcision rites.

These results emerged from a study carried out in two regions of Ethiopia. Those small

scale farmers who were recipients of agricultural loan inputs who encountered a

traditional social ceremony, prior to the loan falling due, were likely to default in

repaying their loans (Bekele, Kassa and Demeke2004).

Political factors

Political factors are the issuesto do with governance of group schemes and affiliation of

individual farmers to farmer organizations. For most irrigation schemes they have

35

irrigation management committees (IMCs). These affiliations act as confluences for key

information for most farmers as some have capacity to organize loans for farmers,

encourage group buying for inputs to cut transactions costs and organize market

linkages. All these then, affects the conduct of farmers when it comes to loan repayment.

If farmers are loyal and know they accrue benefits from the leadership governing their

group or scheme they usually will not default as a way to protect the group or scheme

from bad publicity and perpetuate its existence (Deininger and Liu 2010).This is equally

the same with members who are affiliated to a farmer organization. Unfortunately this is

based on farmer’s perception and it cannot easily be measured because human

perception is complex.

In Zimbabwe there are various farmer organizations that advocate for farmers. There is

Commercial Farmers Union (CFU), Zimbabwe Commercial Farmers Union (ZCFU) and

Zimbabwe Farmers Union (ZFU). These are the major ones. Not much information is

available on the effectiveness of these organizations’ role to ensure that their members

repay their loans.