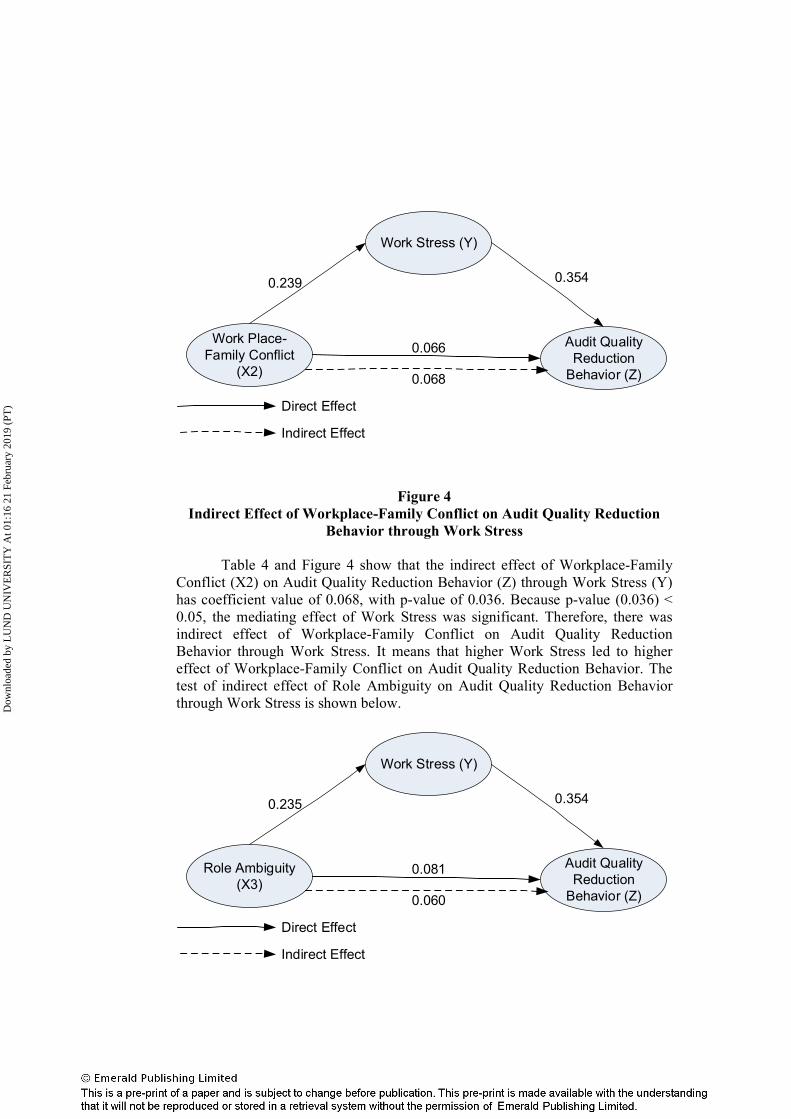

lampiran.pdf - universitas multimedia nusantara

TRANSCRIPT

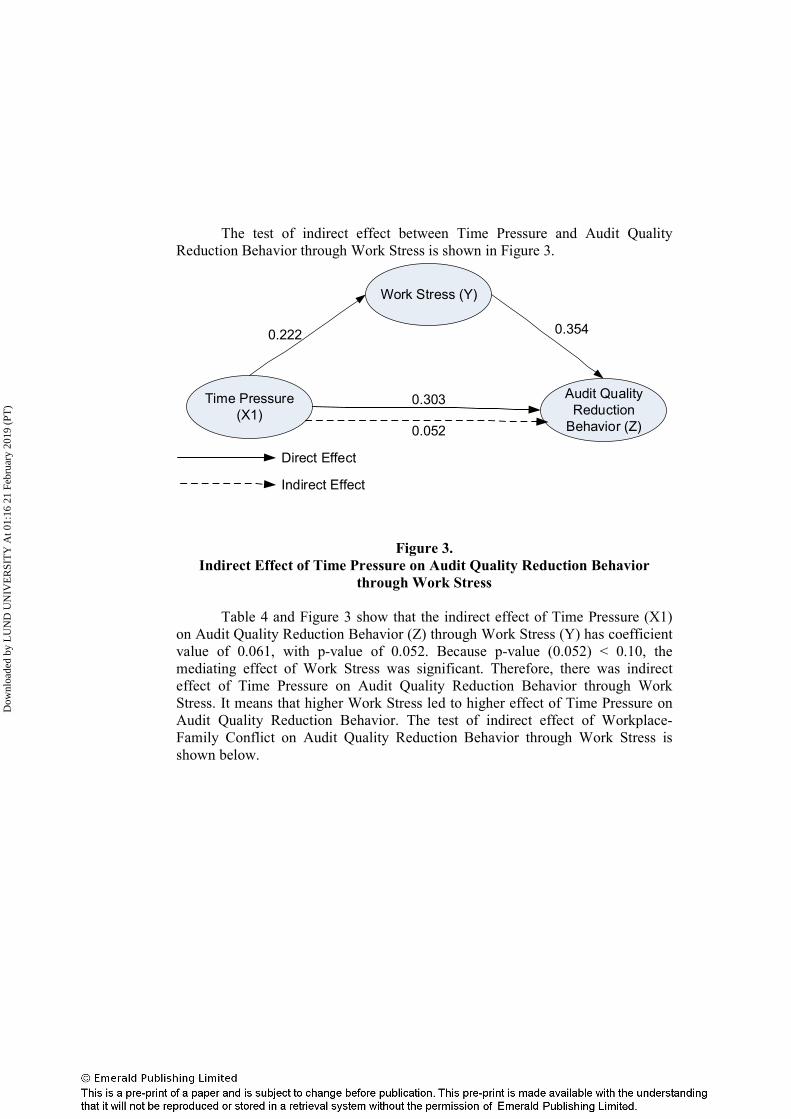

157

LAMPIRAN

Data Uji Validitas dan Reliabilitas Pre-Test

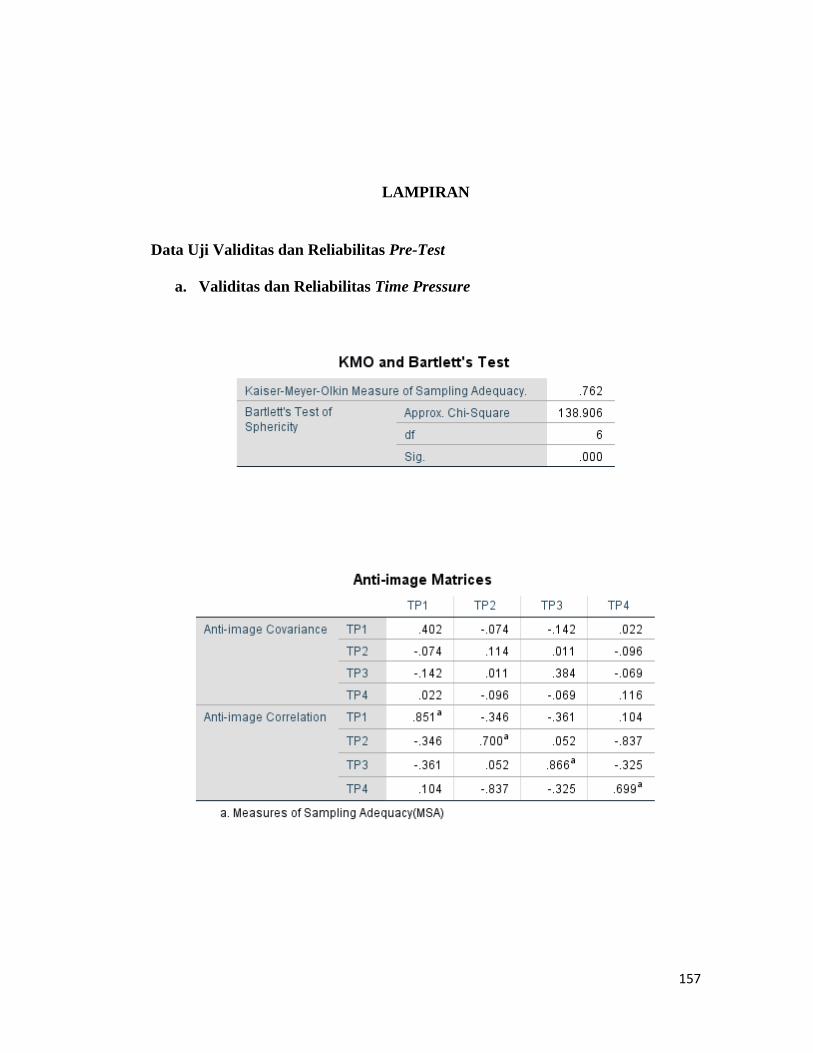

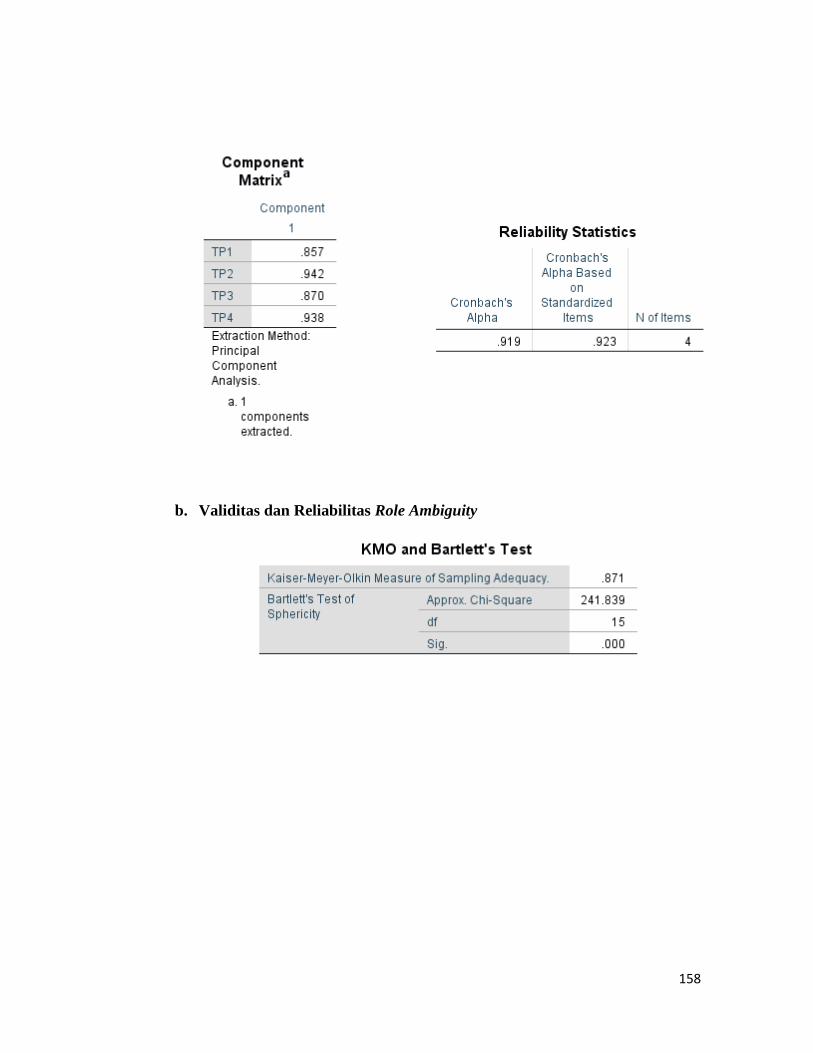

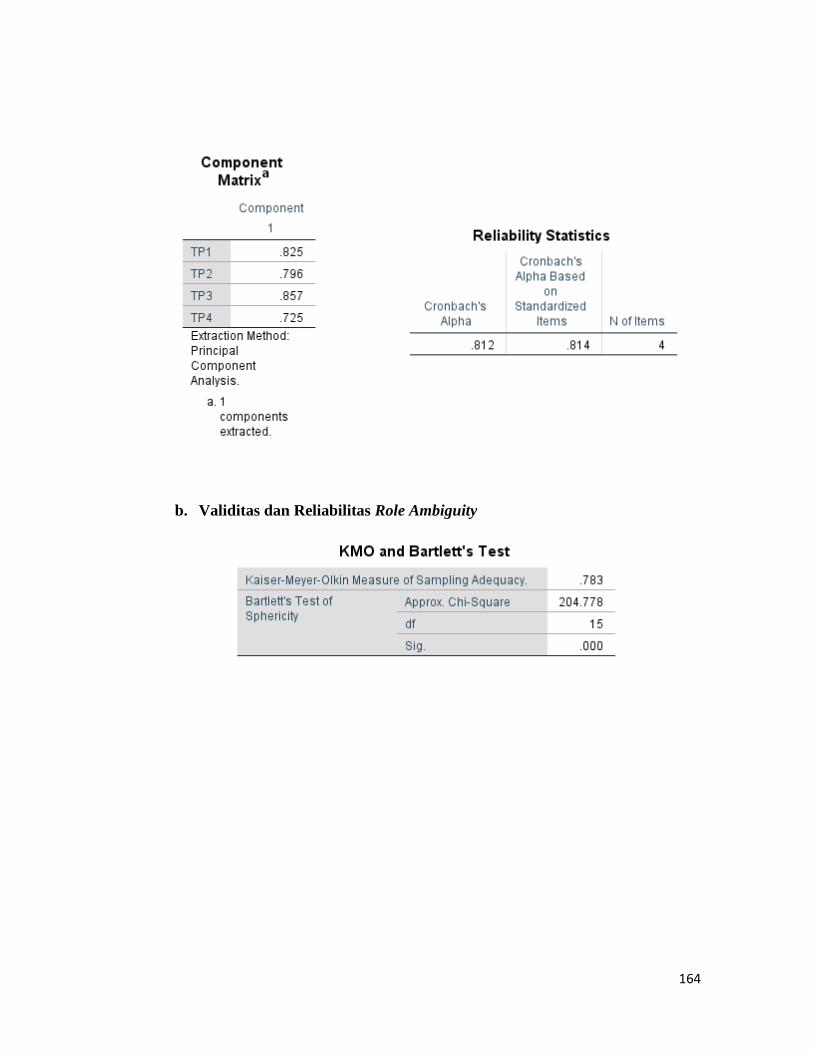

a. Validitas dan Reliabilitas Time Pressure

158

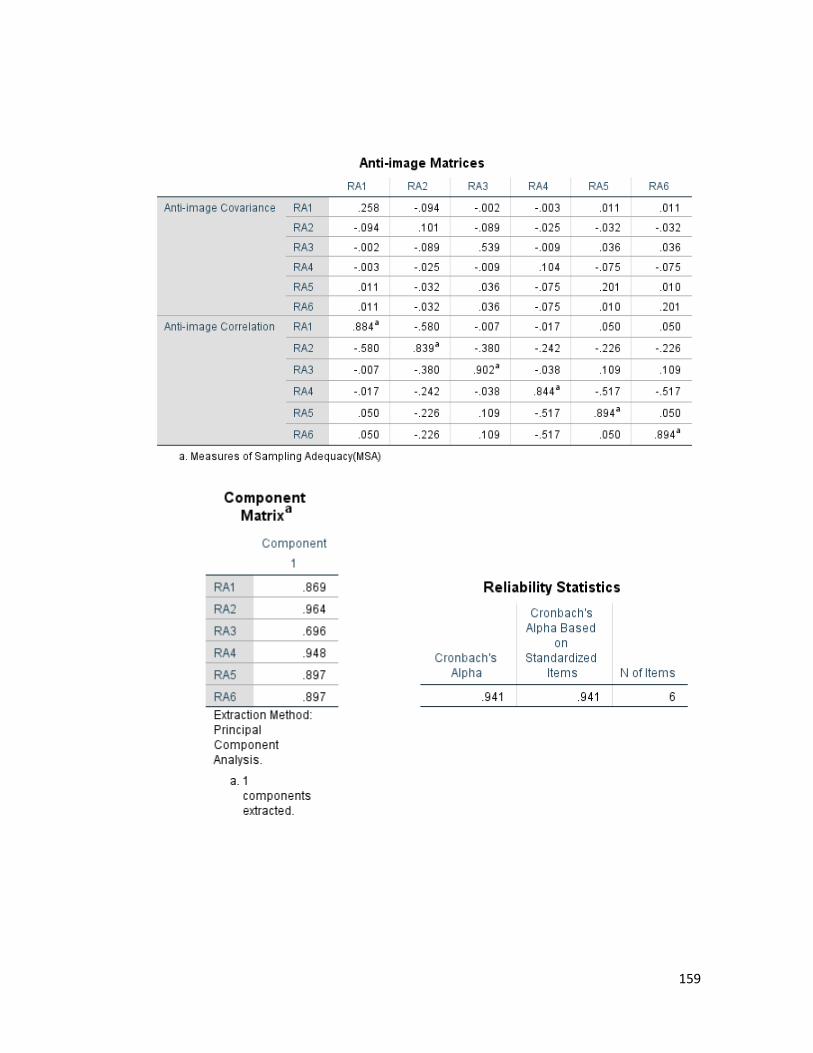

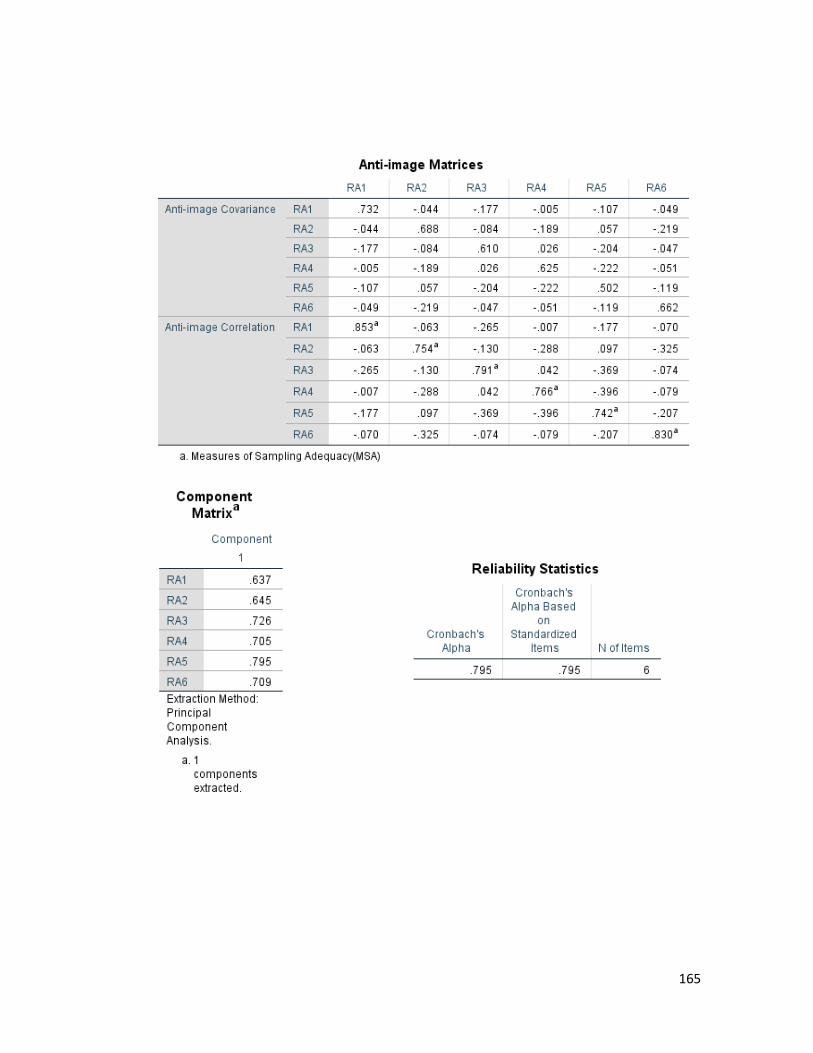

b. Validitas dan Reliabilitas Role Ambiguity

159

160

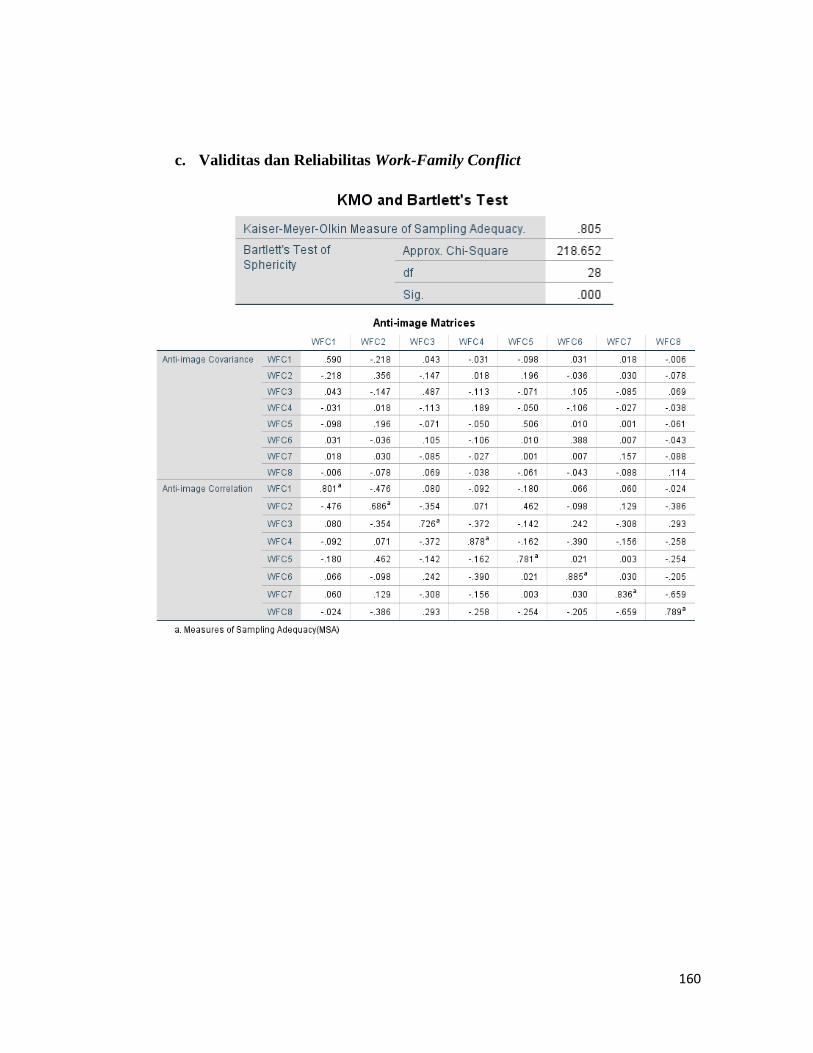

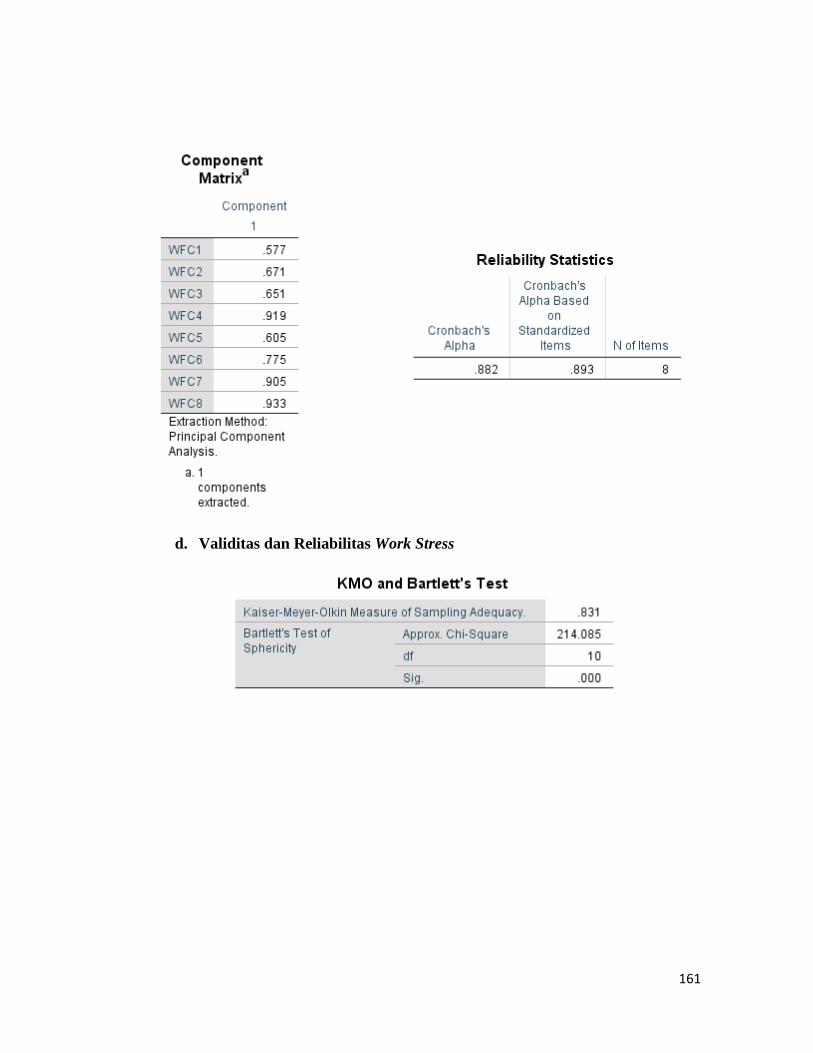

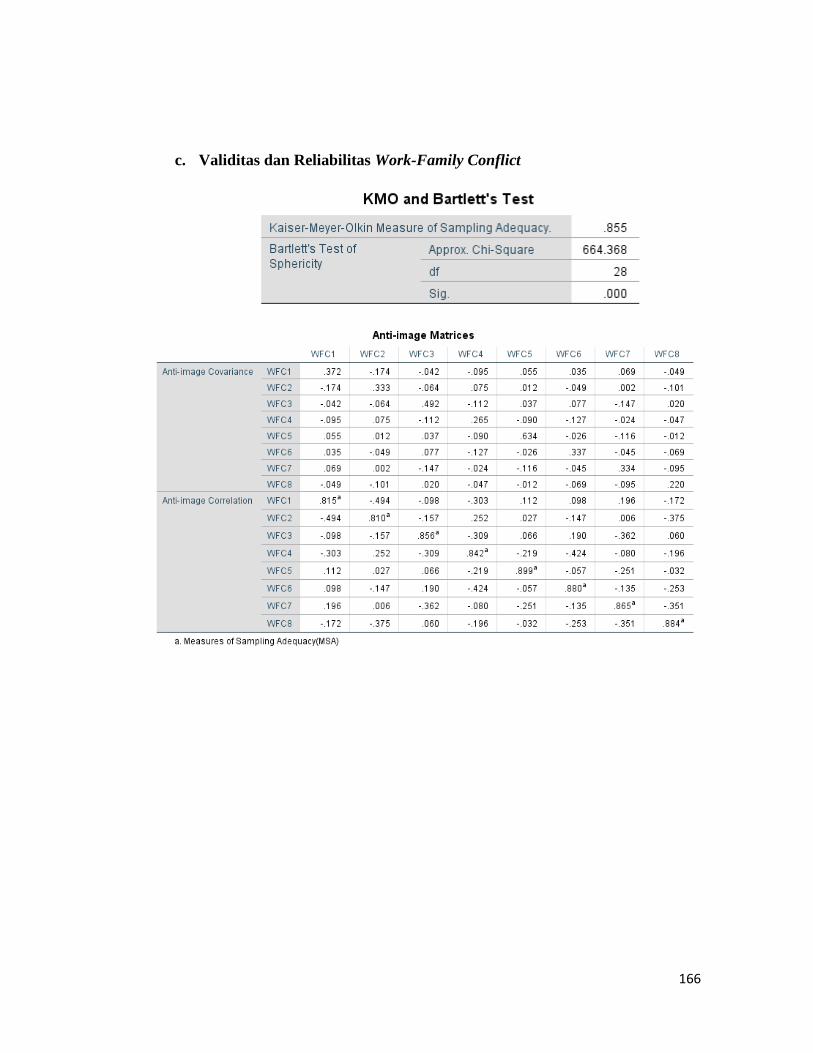

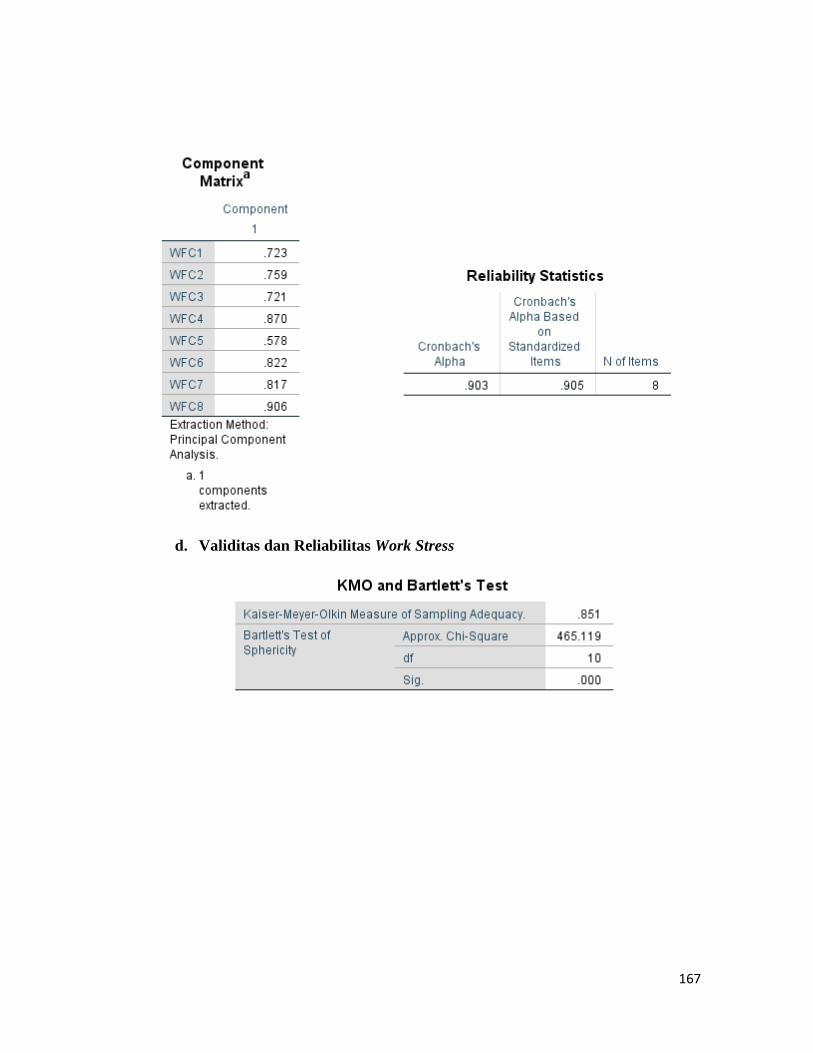

c. Validitas dan Reliabilitas Work-Family Conflict

161

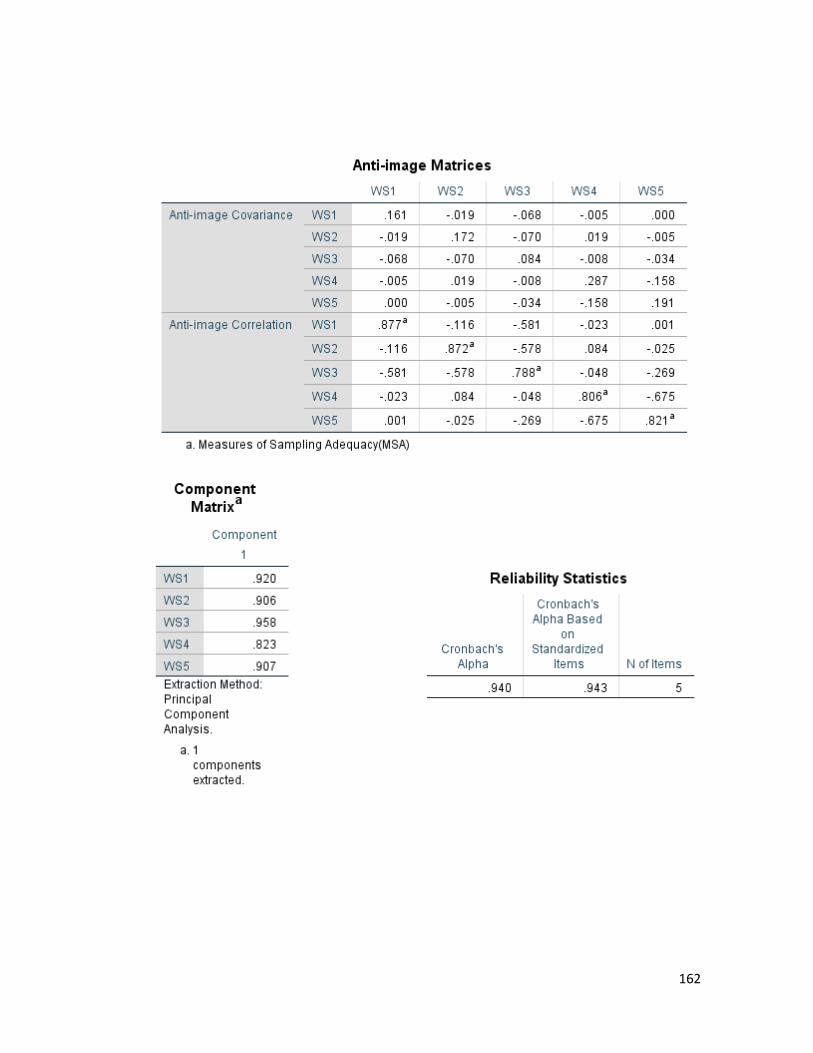

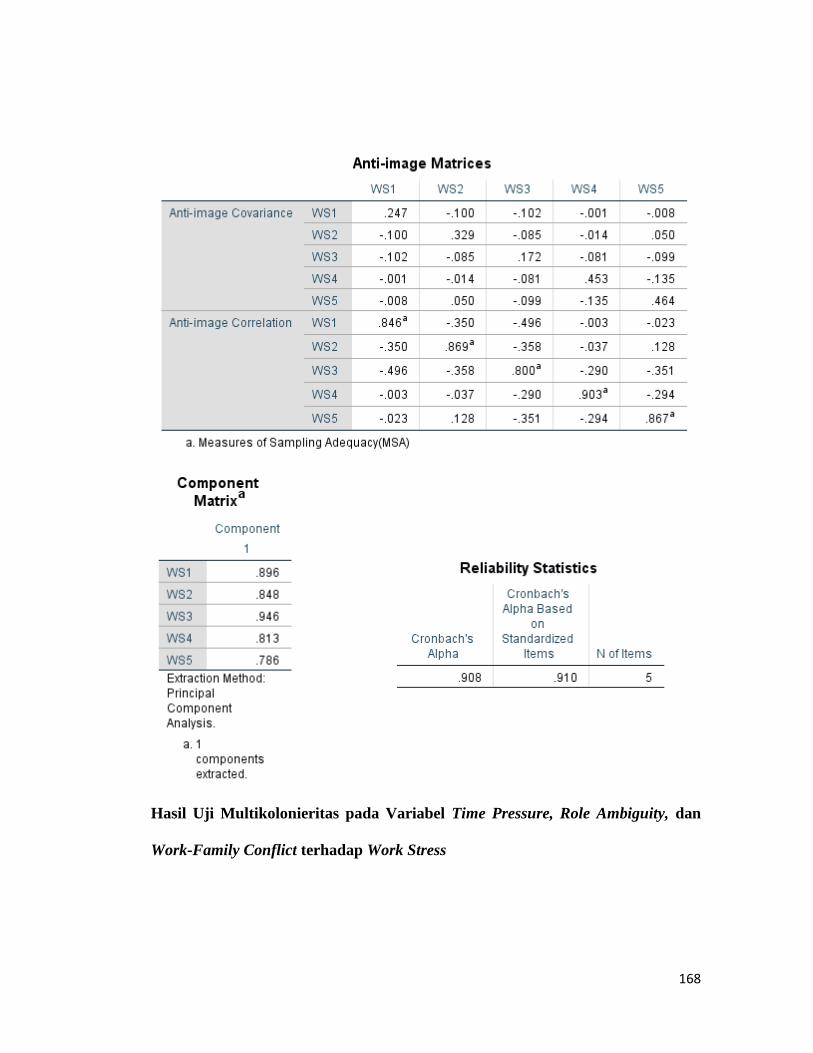

d. Validitas dan Reliabilitas Work Stress

162

163

Data Uji Validitas dan Reliabilitas Main-Test

a. Validitas dan Reliabilitas Time Pressure

164

b. Validitas dan Reliabilitas Role Ambiguity

165

166

c. Validitas dan Reliabilitas Work-Family Conflict

167

d. Validitas dan Reliabilitas Work Stress

168

Hasil Uji Multikolonieritas pada Variabel Time Pressure, Role Ambiguity, dan

Work-Family Conflict terhadap Work Stress

169

Hasil Uji Heterokedastisitas pada Variabel Time Pressure, Role Ambiguity, dan

Work-Family Conflict terhadap Work Stress

170

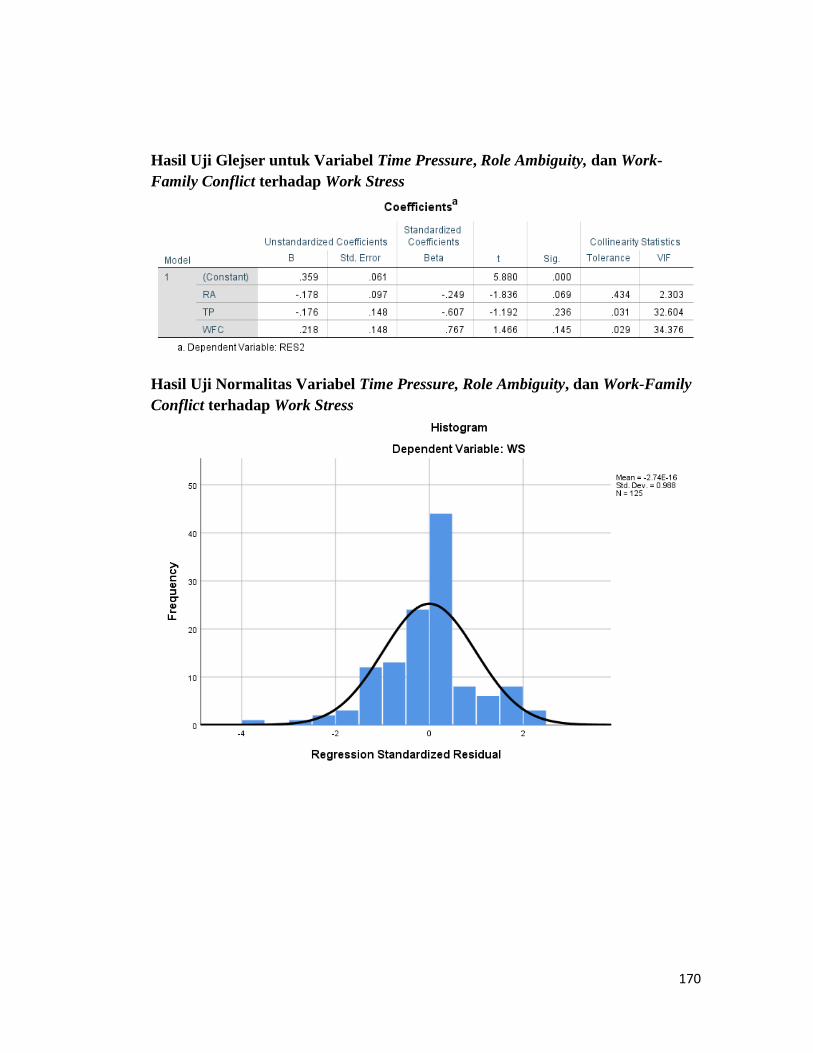

Hasil Uji Glejser untuk Variabel Time Pressure, Role Ambiguity, dan Work-

Family Conflict terhadap Work Stress

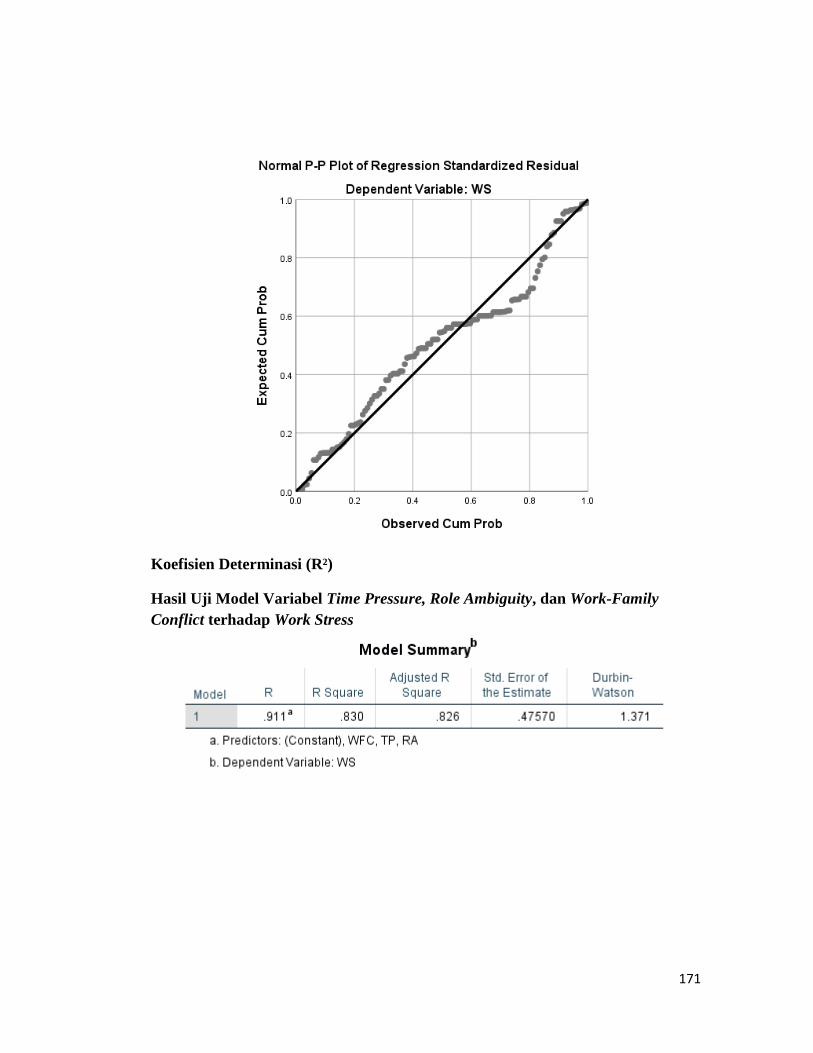

Hasil Uji Normalitas Variabel Time Pressure, Role Ambiguity, dan Work-Family

Conflict terhadap Work Stress

171

Koefisien Determinasi (R²)

Hasil Uji Model Variabel Time Pressure, Role Ambiguity, dan Work-Family

Conflict terhadap Work Stress

172

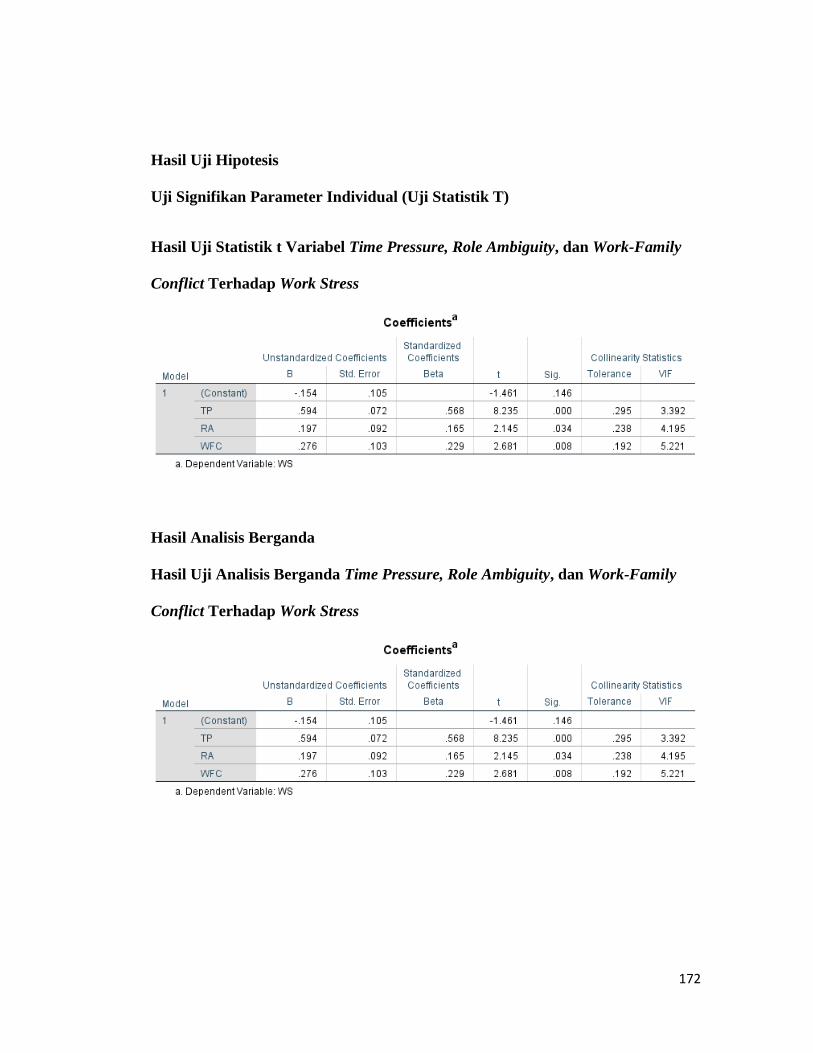

Hasil Uji Hipotesis

Uji Signifikan Parameter Individual (Uji Statistik T)

Hasil Uji Statistik t Variabel Time Pressure, Role Ambiguity, dan Work-Family

Conflict Terhadap Work Stress

Hasil Analisis Berganda

Hasil Uji Analisis Berganda Time Pressure, Role Ambiguity, dan Work-Family

Conflict Terhadap Work Stress

173

Data Kuisioner Excel Main-Test

a. Time Pressure

TP1 TP2 TP3 TP4 TTP

3 3 3 3 12

5 3 3 3 14

5 3 3 3 14

5 3 3 1 12

2 2 2 1 7

5 1 4 1 11

4 3 3 3 13

3 3 2 2 10

4 1 3 1 9

2 2 2 1 7

2 5 2 2 11

1 2 1 1 5

1 1 1 1 4

2 2 2 2 8

1 2 2 2 7

2 2 2 2 8

1 2 2 2 7

2 2 2 2 8

2 1 1 1 5

1 1 1 5 8

2 4 4 1 11

1 1 1 1 4

1 1 1 5 8

1 1 1 5 8

1 4 1 1 7

1 1 1 1 4

1 2 1 1 5

5 4 4 4 17

1 1 1 5 8

1 1 1 1 4

1 1 1 1 4

1 1 1 1 4

1 1 1 1 4

174

3 4 3 3 13

1 3 1 5 10

1 1 4 1 7

5 5 4 4 18

3 4 3 3 13

4 4 4 4 16

1 1 1 1 4

1 1 1 1 4

2 2 2 2 8

1 2 1 1 5

1 1 1 1 4

2 2 2 5 11

1 2 2 2 7

2 2 2 2 8

1 2 2 2 7

2 2 2 2 8

2 1 1 1 5

5 1 1 4 11

4 4 4 4 16

1 1 1 1 4

1 1 1 1 4

1 5 1 1 8

1 1 1 1 4

1 1 1 1 4

1 2 1 1 5

5 4 4 4 17

1 1 1 1 4

1 1 1 1 4

1 1 1 1 4

1 1 1 1 4

1 1 5 4 11

3 4 3 1 11

4 3 1 1 9

1 1 1 1 4

5 5 4 4 18

3 4 3 3 13

4 4 4 4 16

1 1 1 1 4

175

1 1 1 1 4

2 2 2 2 8

1 2 1 1 5

1 1 1 4 7

2 2 2 2 8

1 2 2 2 7

2 2 2 2 8

1 2 2 2 7

2 2 2 2 8

2 1 1 1 5

1 5 1 1 8

4 4 4 4 16

1 1 1 1 4

1 1 1 1 4

1 1 1 4 7

1 1 1 4 7

1 1 1 1 4

1 2 1 1 5

5 4 4 4 17

4 1 1 1 7

1 1 1 1 4

1 1 1 1 4

1 1 5 4 11

1 1 1 1 4

3 4 3 3 13

1 3 1 1 6

1 1 1 1 4

5 5 4 4 18

3 4 3 3 13

4 4 4 4 16

1 1 1 1 4

1 1 1 4 7

2 2 2 2 8

1 2 1 1 5

1 1 1 1 4

2 2 2 2 8

1 2 2 2 7

2 2 2 2 8

176

1 2 2 2 7

5 4 2 2 13

4 2 5 5 16

2 5 4 4 15

3 1 2 2 8

3 5 5 5 18

2 3 4 4 13

1 2 2 2 7

4 1 5 1 11

1 2 3 3 9

4 5 2 2 13

5 4 5 5 19

2 5 5 5 17

4 4 4 4 16

5 2 2 5 14

4 5 1 4 14

b. Role Ambiguity

RA1 RA2 RA3 RA4 RA5 RA6 TRA

2 3 3 3 3 3 17

2 3 2 3 3 3 16

2 3 2 2 3 3 15

1 1 1 1 3 1 8

1 1 1 1 1 1 6

1 1 1 1 1 1 6

1 1 2 2 2 2 10

2 2 2 2 2 2 12

1 2 1 2 2 1 9

1 1 1 1 1 1 6

4 1 4 2 5 1 17

5 1 5 1 5 1 18

4 1 4 1 1 1 12

2 2 4 2 2 2 14

1 2 2 2 1 2 10

1 4 1 1 2 2 11

2 2 1 1 1 2 9

177

2 2 2 1 3 2 12

5 1 2 2 2 1 13

2 1 1 1 1 1 7

4 4 1 4 4 4 21

1 1 1 1 1 1 6

5 1 1 1 1 1 10

1 1 1 1 1 1 6

1 1 1 1 1 1 6

4 1 1 1 1 1 9

1 1 1 1 1 1 6

4 2 5 1 5 4 21

1 1 1 1 1 1 6

1 1 1 1 2 1 7

4 1 1 1 1 1 9

1 4 1 1 1 1 9

1 1 1 1 1 1 6

2 2 4 4 3 4 19

2 3 1 2 1 3 12

1 1 1 1 1 1 6

5 5 5 4 5 5 29

2 3 2 3 3 4 17

4 4 4 4 4 4 24

2 2 1 1 1 1 8

2 1 1 1 1 1 7

2 1 2 2 2 5 14

1 1 2 1 1 4 10

4 1 1 1 4 4 15

2 2 1 2 4 5 16

1 2 2 2 1 2 10

1 4 1 1 2 2 11

2 5 1 1 1 2 12

2 2 2 1 2 2 11

5 1 4 2 2 1 15

2 1 1 3 1 1 9

4 4 4 4 4 4 24

1 1 1 1 1 1 6

5 1 1 1 1 1 10

1 1 1 1 1 1 6

178

1 1 1 1 1 1 6

2 1 1 3 4 1 12

1 1 1 4 5 2 14

4 2 5 4 5 1 21

1 1 1 1 1 1 6

1 1 1 1 1 1 6

1 1 1 1 1 1 6

1 1 1 1 1 1 6

1 1 1 1 1 1 6

2 2 1 4 3 4 16

2 3 1 2 1 3 12

1 1 1 5 1 1 10

5 2 5 2 5 5 24

2 3 2 3 3 4 17

4 4 4 2 4 1 19

2 2 1 1 1 1 8

2 1 1 1 2 1 8

5 1 2 2 2 2 14

1 1 2 1 1 2 8

1 1 1 1 1 1 6

2 2 1 2 2 2 11

1 2 2 2 1 2 10

1 2 4 1 2 2 12

2 2 1 1 1 2 9

2 2 2 1 2 2 11

5 1 2 2 1 1 12

2 5 1 1 1 1 11

4 4 4 4 2 4 22

1 1 1 1 1 1 6

5 1 1 1 1 1 10

1 1 1 1 1 1 6

1 1 1 1 1 2 7

4 1 1 1 1 4 12

1 1 1 1 1 2 7

4 2 5 4 5 4 24

1 1 4 1 1 1 9

4 1 5 1 1 1 13

1 1 1 4 1 1 9

179

1 4 1 5 1 1 13

1 1 1 1 1 1 6

2 2 4 4 3 4 19

2 3 1 2 1 3 12

1 1 1 1 1 1 6

5 5 5 4 5 5 29

2 3 2 3 3 4 17

4 4 4 4 1 4 21

2 2 1 1 1 1 8

2 1 1 1 1 1 7

2 4 5 2 2 2 17

1 1 2 1 1 5 11

1 1 1 1 1 1 6

2 2 1 2 2 2 11

1 2 2 2 1 2 10

1 2 1 4 2 2 12

2 2 1 1 1 2 9

1 2 1 5 5 4 18

4 5 2 4 4 2 21

5 4 3 2 2 5 21

4 2 2 3 1 4 16

5 5 1 3 3 5 22

4 4 4 5 2 3 22

2 5 1 4 1 2 15

5 4 2 5 4 1 21

1 2 5 5 4 2 19

2 5 5 2 4 5 23

3 1 2 5 5 1 17

2 3 3 1 2 5 16

5 3 2 3 2 4 19

4 2 5 2 5 2 20

1 5 4 1 1 1 13

180

c. Work-Family Conflict

WFC1 WFC2 WFC3 WFC4 WFC5 WFC6 WFC7 WFC8 TWFC

3 3 3 3 3 3 3 3 24

2 2 2 2 3 3 3 2 19

2 3 2 4 3 2 3 2 21

5 5 3 1 1 3 1 5 24

1 1 2 2 2 2 2 1 13

1 2 1 1 4 4 4 3 20

2 2 3 2 2 2 2 1 16

2 2 2 2 2 2 2 2 16

1 2 2 3 2 2 1 1 14

1 2 2 2 2 2 1 1 13

1 2 4 2 2 1 2 2 16

2 2 5 2 1 1 2 1 16

1 2 4 1 1 1 1 1 12

2 2 2 1 2 2 1 2 14

1 2 2 1 1 2 2 2 13

2 1 2 1 1 2 1 1 11

1 1 2 2 2 2 1 1 12

2 2 2 1 2 2 2 1 14

2 1 4 2 5 1 2 2 19

2 2 1 2 2 1 1 1 12

2 2 4 4 4 4 4 4 28

1 1 1 1 1 1 1 1 8

1 1 1 1 5 1 1 1 12

1 1 1 1 1 1 1 1 8

1 1 1 1 1 1 1 1 8

1 1 1 1 4 1 1 1 11

1 1 1 1 1 1 1 1 8

2 2 4 3 4 2 5 4 26

1 1 2 1 1 1 1 1 9

1 1 1 1 1 1 1 1 8

1 1 1 1 1 1 1 1 8

1 1 1 1 1 1 1 1 8

1 1 1 1 1 1 1 1 8

3 3 2 3 2 2 4 4 23

2 2 2 2 2 3 1 2 16

181

1 1 1 1 1 1 1 1 8

1 2 4 4 5 5 5 4 30

3 4 3 3 2 3 2 3 23

2 2 4 4 4 4 4 4 28

1 1 2 2 2 2 1 1 12

2 1 1 1 2 1 1 1 10

1 2 4 2 2 1 2 2 16

2 2 5 2 1 1 2 1 16

1 2 4 1 1 1 1 1 12

2 2 2 1 2 2 1 2 14

1 2 2 1 1 2 2 2 13

2 1 2 1 1 2 1 1 11

1 1 2 2 2 2 1 1 12

2 2 2 1 2 2 2 1 14

2 1 4 2 5 1 2 2 19

2 2 1 2 2 1 1 1 12

2 2 4 4 4 4 4 4 28

1 1 1 1 1 1 1 1 8

1 1 1 1 5 1 1 1 12

1 1 1 1 1 1 1 1 8

1 1 1 1 1 1 1 1 8

1 1 1 1 4 1 1 1 11

1 1 1 1 1 1 1 1 8

2 2 4 3 4 2 5 4 26

1 1 2 1 1 1 1 1 9

1 1 1 1 1 1 1 1 8

1 1 1 1 1 1 1 1 8

1 1 1 1 1 1 1 1 8

1 1 1 1 1 1 1 1 8

3 3 2 3 2 2 4 4 23

2 2 2 2 2 3 1 2 16

1 1 1 1 1 1 1 1 8

1 2 4 4 5 5 5 4 30

3 4 3 3 2 3 2 3 23

2 2 4 4 4 4 4 4 28

1 1 2 2 2 2 1 1 12

2 1 1 1 2 1 1 1 10

1 2 4 2 2 1 2 2 16

182

2 2 5 2 1 1 2 1 16

1 2 4 1 1 1 1 1 12

2 2 2 1 2 2 1 2 14

1 2 2 1 1 2 2 2 13

2 1 2 1 1 2 1 1 11

1 1 2 2 2 2 1 1 12

2 2 2 1 2 2 2 1 14

2 1 4 2 5 1 2 2 19

2 2 1 2 2 1 1 1 12

2 2 4 4 4 4 4 4 28

1 1 1 1 1 1 1 1 8

1 1 1 1 5 1 1 1 12

1 1 1 1 1 1 1 1 8

1 1 1 1 1 1 1 1 8

1 1 1 1 4 1 1 1 11

1 1 1 1 1 1 1 1 8

2 2 4 3 4 2 5 4 26

1 1 2 1 1 1 1 1 9

1 1 1 1 1 1 1 1 8

1 1 1 1 1 1 1 1 8

1 1 1 1 1 1 1 1 8

1 1 1 1 1 1 1 1 8

3 3 2 3 2 2 4 4 23

2 2 2 2 2 3 1 2 16

1 1 1 1 1 1 1 1 8

1 2 4 4 5 5 5 4 30

3 4 3 3 2 3 2 3 23

2 2 4 4 4 4 4 4 28

1 1 2 2 2 2 1 1 12

2 1 1 1 2 1 1 1 10

1 2 4 2 2 1 2 2 16

2 2 5 2 1 1 2 1 16

1 2 4 1 1 1 1 1 12

2 2 2 1 2 2 1 2 14

1 2 2 1 1 2 2 2 13

2 1 2 1 1 2 1 1 11

1 1 2 2 2 2 1 1 12

5 4 3 4 1 2 1 5 25

183

4 2 2 5 2 5 2 4 26

5 3 5 4 5 4 3 2 31

4 2 4 5 4 2 2 3 26

2 5 2 2 5 5 5 3 29

5 4 5 5 4 4 4 5 36

3 2 3 4 2 5 1 4 24

2 5 2 3 5 4 2 5 28

5 4 5 2 1 2 5 5 29

4 2 4 5 2 5 5 2 29

5 5 4 4 3 4 2 5 32

4 4 5 2 2 3 3 4 27

2 2 2 5 5 3 2 3 24

3 3 5 4 4 2 5 2 28

2 2 5 5 1 5 4 5 29

d. Work Stress

WS1 WS2 WS3 WS4 WS5 TWS

3 3 3 3 3 15

2 3 3 3 2 13

2 2 2 2 3 11

1 1 1 1 1 5

1 1 1 1 1 5

1 1 3 1 3 9

1 2 2 3 3 11

1 1 1 1 1 5

1 1 1 1 1 5

1 1 1 1 1 5

2 2 2 2 2 10

1 2 1 1 1 6

1 1 1 1 1 5

2 2 2 2 2 10

1 2 2 2 2 9

2 2 2 2 5 13

1 2 2 2 2 9

2 2 2 2 2 10

2 1 1 1 1 6

184

1 1 1 5 1 9

4 4 4 4 4 20

1 1 1 1 1 5

1 1 1 5 5 13

1 1 1 5 1 9

1 1 1 1 1 5

1 1 1 1 4 8

1 2 1 1 1 6

5 4 4 4 4 21

1 1 1 5 5 13

1 1 1 1 1 5

1 1 1 1 1 5

1 1 1 1 1 5

1 1 1 1 4 8

3 4 3 3 3 16

1 3 1 5 1 11

1 1 1 1 1 5

5 5 4 4 4 22

3 4 3 3 3 16

4 4 4 4 4 20

1 1 1 1 1 5

1 1 1 1 5 9

2 2 2 2 2 10

1 2 1 1 1 6

1 1 1 1 1 5

2 2 2 2 2 10

1 2 2 2 2 9

2 2 2 2 2 10

1 2 2 2 2 9

2 2 2 2 2 10

2 1 1 1 1 6

1 1 1 4 1 8

4 4 4 4 4 20

1 1 1 1 1 5

1 1 1 1 1 5

1 1 1 1 1 5

1 1 1 1 4 8

1 1 1 1 1 5

185

1 2 1 1 1 6

5 4 4 4 4 21

1 1 1 1 1 5

1 1 1 1 1 5

1 1 1 1 4 8

1 1 1 1 1 5

1 1 1 4 1 8

3 4 3 3 3 16

1 3 1 1 1 7

1 1 1 1 4 8

5 5 4 4 4 22

3 4 3 3 3 16

4 4 4 4 4 20

1 1 1 1 1 5

1 1 1 1 1 5

2 2 2 2 2 10

1 2 1 1 1 6

1 1 1 4 1 8

2 2 2 2 2 10

1 2 2 2 2 9

2 2 2 2 2 10

1 2 2 2 2 9

2 2 2 2 2 10

2 1 1 1 1 6

1 1 1 1 1 5

4 4 4 4 4 20

1 1 1 1 1 5

1 1 1 1 1 5

1 1 1 4 5 12

1 1 1 4 5 12

1 1 1 1 1 5

1 2 1 1 1 6

5 4 4 4 4 21

1 1 1 1 1 5

1 1 1 1 1 5

1 1 1 1 1 5

1 1 1 1 1 5

1 1 1 1 1 5

186

3 4 3 3 3 16

1 3 1 1 1 7

1 1 1 1 5 9

5 5 4 4 4 22

3 4 3 3 3 16

4 4 4 4 4 20

1 1 1 1 1 5

1 1 1 4 1 8

2 2 2 2 2 10

1 2 1 1 1 6

1 1 1 1 1 5

2 2 2 2 2 10

1 2 2 2 2 9

2 2 2 2 2 10

1 2 2 2 2 9

5 4 2 2 2 15

4 2 5 5 5 21

2 5 4 4 4 19

3 4 2 2 2 13

3 5 5 5 5 23

2 3 4 4 4 17

1 2 2 2 2 9

4 1 5 5 5 20

4 2 3 3 3 15

4 5 2 2 2 15

5 4 5 5 5 24

2 5 5 5 5 22

4 4 4 4 4 20

5 2 5 5 5 22

4 5 4 4 4 21

187

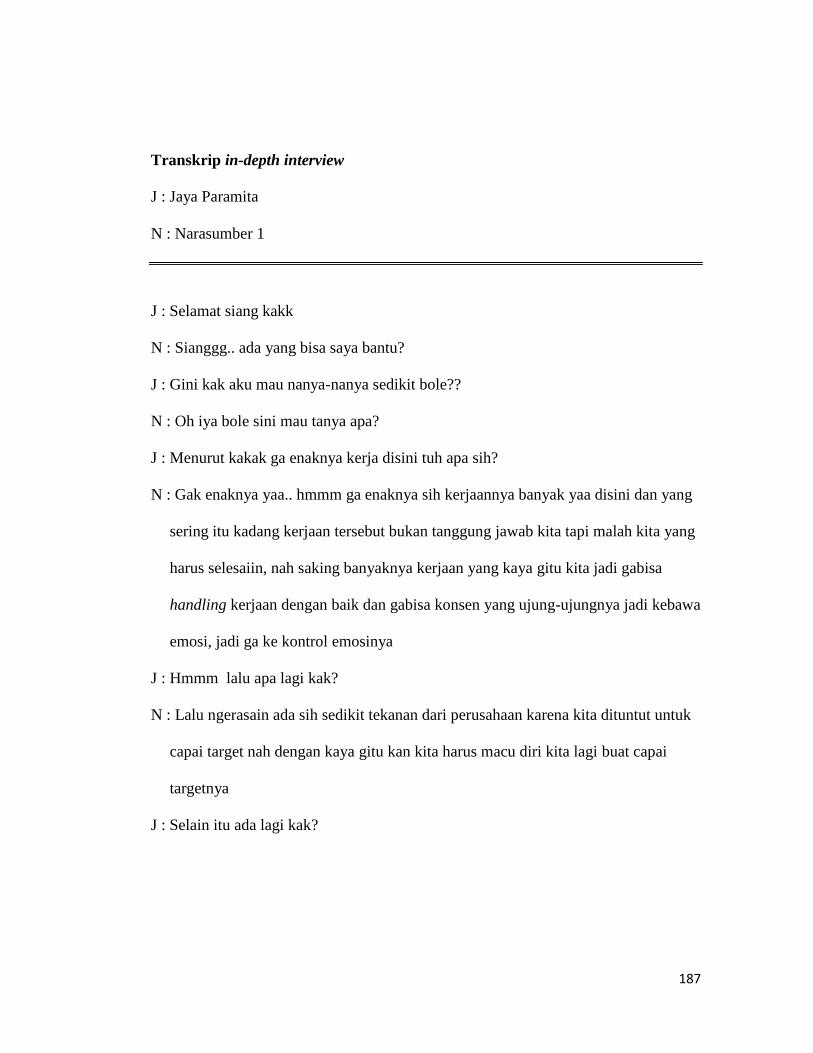

Transkrip in-depth interview

J : Jaya Paramita

N : Narasumber 1

J : Selamat siang kakk

N : Sianggg.. ada yang bisa saya bantu?

J : Gini kak aku mau nanya-nanya sedikit bole??

N : Oh iya bole sini mau tanya apa?

J : Menurut kakak ga enaknya kerja disini tuh apa sih?

N : Gak enaknya yaa.. hmmm ga enaknya sih kerjaannya banyak yaa disini dan yang

sering itu kadang kerjaan tersebut bukan tanggung jawab kita tapi malah kita yang

harus selesaiin, nah saking banyaknya kerjaan yang kaya gitu kita jadi gabisa

handling kerjaan dengan baik dan gabisa konsen yang ujung-ujungnya jadi kebawa

emosi, jadi ga ke kontrol emosinya

J : Hmmm lalu apa lagi kak?

N : Lalu ngerasain ada sih sedikit tekanan dari perusahaan karena kita dituntut untuk

capai target nah dengan kaya gitu kan kita harus macu diri kita lagi buat capai

targetnya

J : Selain itu ada lagi kak?

188

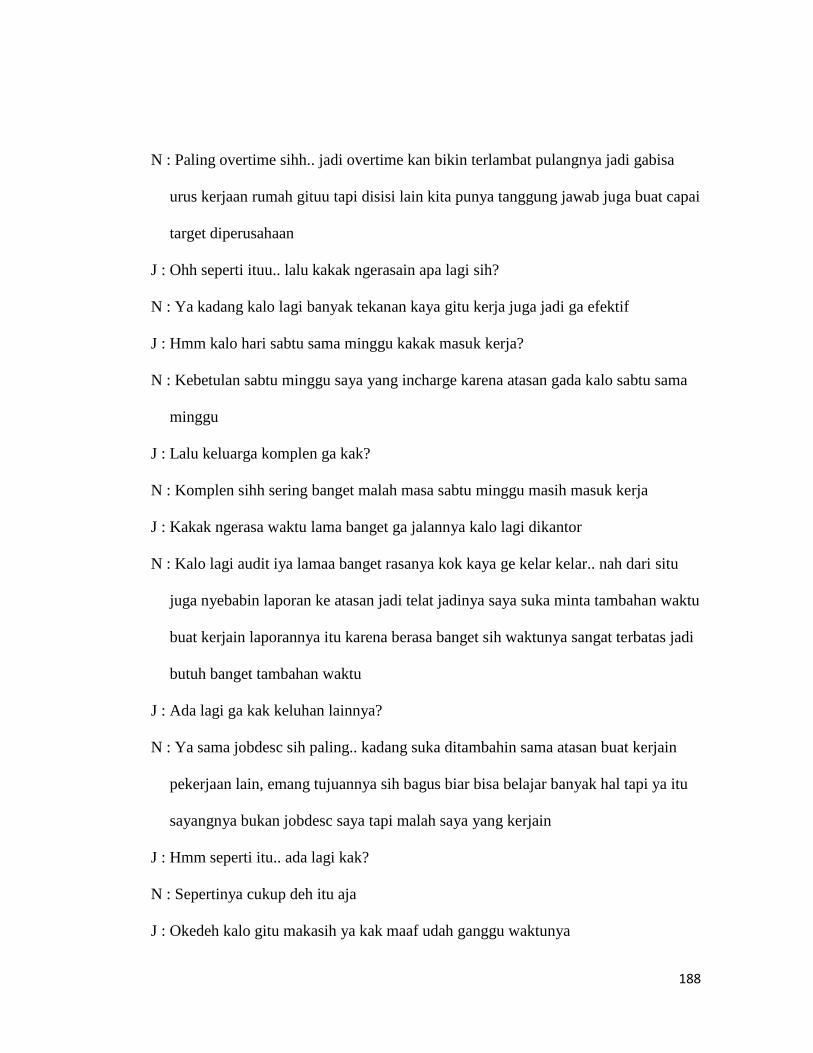

N : Paling overtime sihh.. jadi overtime kan bikin terlambat pulangnya jadi gabisa

urus kerjaan rumah gituu tapi disisi lain kita punya tanggung jawab juga buat capai

target diperusahaan

J : Ohh seperti ituu.. lalu kakak ngerasain apa lagi sih?

N : Ya kadang kalo lagi banyak tekanan kaya gitu kerja juga jadi ga efektif

J : Hmm kalo hari sabtu sama minggu kakak masuk kerja?

N : Kebetulan sabtu minggu saya yang incharge karena atasan gada kalo sabtu sama

minggu

J : Lalu keluarga komplen ga kak?

N : Komplen sihh sering banget malah masa sabtu minggu masih masuk kerja

J : Kakak ngerasa waktu lama banget ga jalannya kalo lagi dikantor

N : Kalo lagi audit iya lamaa banget rasanya kok kaya ge kelar kelar.. nah dari situ

juga nyebabin laporan ke atasan jadi telat jadinya saya suka minta tambahan waktu

buat kerjain laporannya itu karena berasa banget sih waktunya sangat terbatas jadi

butuh banget tambahan waktu

J : Ada lagi ga kak keluhan lainnya?

N : Ya sama jobdesc sih paling.. kadang suka ditambahin sama atasan buat kerjain

pekerjaan lain, emang tujuannya sih bagus biar bisa belajar banyak hal tapi ya itu

sayangnya bukan jobdesc saya tapi malah saya yang kerjain

J : Hmm seperti itu.. ada lagi kak?

N : Sepertinya cukup deh itu aja

J : Okedeh kalo gitu makasih ya kak maaf udah ganggu waktunya

189

N : Iya gapapa jayy.. sama-sama yaa

Transkrip in-depth interview

J : Jaya Paramita

N : Narasumber 2

J : Selamat siang kak, kak bole minta waktunya sebentar gak buat nanya-nanya ??

hehehe

N : Siangg.. bole kokk, mau tanya apa?

J : Oke kakk jadi gini aku mau tanya ga enaknya kerja disini tuh apa sih kalo menurut

kak?

N : Disini ga enaknya itu kerjaannya banyak banget jadi gabisa ke handle semua.. jadi

gabisa konsen juga, gabisa kontrol emosi juga.. tekanan dari atas juga lumayan gitu

jadi imbasnya ya gitu emosilah

J : Lalu menurut kakak pemimpin disini itu bagaimana? Membantu kakak dalam

mengerjakan pekerjaan tidak?

N : Kalo pemimpin sih disini membantu banget, walau udah setingkat executive chef

juga dia masih tetep masak masih turun tangan

J : Lalu kakak masuk hari apa aja?

N : Saya libur pokoknya kalo ga hari selasa berarti rabu

J : Berarti sabtu minggu masuk?

190

N : Masukkk

J : Nah kalo sabtu minggu gitu masuk keluarga komplen ga kak?

N : Komplen lahh.. jadi ya gimana ya namanya kita punya keluarga haduhh

dampaknya jadi kerjaan keganggu gara-gara keluarga juga, terus kerjaan dirumah

juga jadi ga kepegang maksudnya kaya gimana yaa.. ya jadi kurang aja waktu buat

sama istri

J : Ohh jadi keganggu ya

N : Iya keganggu

J : Hmmm oke okee.. lalu tadi diatas kan kakak ada bilang kita harus bisa pegang

semua kerjaan, nah itu kalo dari kakak sendiri gimana?

N : Namanya tangan ini kan cuma dua sedangkan kerjaan banyak ya jadinya ga

efektif aja sihh.. kalo ditempat saya yang dulu kan biasanya dimasing-masing section

ada orangnya masing-masing tersendiri jadi kalo ngomongin soal rating dan masakan

ya pastinya maksimal karena udah ada spesialisnya masing-masing karena gitu ya

saya kerjanya juga jadi lebih maksimal. Terus karena harus ngerjain semua, saya juga

jadi ngerasa atasan gabisa menilai peforma saya

J : Loh kenapa seperti itu kak??

N : Ya pokoknya jadi bingung baru beresin yang ini udah diajarin yang lainnya lagi,

kadang yang ini aja belom kelarrr.. gitulah

J : Hmm okedeh sekian pertanyaan dari aku kakk.. terima kasih ya buat waktu dan

kesempatannya

N : Oke jay.. iya sama-sama

191

Transkrip in-depth interview

J : Jaya Paramita

N : Narasumber 3

J : Selamat siang kakk

N : Iya siangg

J : Kak.. bole minta waktunya ga buat nanya nanya sedikit

N : Iya bole kok mau nanya apa?

J : Jadi aku mau nanya ga enaknya kerja disini menurut kakak itu apa sih?

N : Ga enaknya yaa.. hmmm kalo lagi shift malam sendiri kerjanya hehehe

J : Oh gituu lalu ada lagi ga kakk?

N : Ya ga enaknya kalo lagi ada masalah banyak dan gabisa diselesaikan sendiri tapi

malah saya masuk shift yang lagi sendiri

J : Disini tuh menurut kakak tugasnya banyak ga sihh

N : Iya banyakk

J : Nah dampak buat kakak itu gimana?

N : Yang jelas jadi keteteran

J : Ohh keteteran.. selain itu ada apa lagi kak?

N : Jadi gabisa ke kontrol sih emosinya, ya pusing

J : Ada lagi kak?

N : Ya jadi gabisa konsentrasi juga karena banyak.. jadi ambyarr hehehe

192

J : Lalu ada lagi?

N : Udah itu aja sih

J : Dari pekerjaan yang banyak itu, kakak masih sempat tidak bagi waktu untuk

pekerjaan dan diri sendiri?

N : Jadi gabisa urus pekerjaan rumah sih jadinya

J : Oh karena saking banyaknya pekerjaan ya kak

N: Iyaa betul

J :Lalu ada lagi ga kak dampaknya?

N : Jadi keganggu urusan keluarga jadinya

J : Selain itu ada lagi ga kak?

N : Kerjaan jadi keganggu gara-gara urusan keluarga

J : Ohh berarti kebalikannya ya kak kalo kakak pilih keluarga kerjaan jadi terganggu

dan kalo kakak pilih kerjaan, keluarga jadi ke ganggu

N : Kendala lainnya juga kerja jadi ga efektif karena kerjaannya sendiri sudah banyak

dan kadang sering diburu-buru jadi ga rapih dan ga sesuai aja sama apa yang

diharapkan

J : Ada lagi ga kak?

N : Terus atasan kita juga jadi gabisa nilai kinerja saya dengan adil dan fair

J : Karena?

N : Karena pekerjaan yang diberikan terlalu banyak lalu selalu diburu-buru dan harus

selesai dalam sekian waktu dan cepat serta menjadi ga fokus dalam 1 pekerjaan saja

193

J : Oke kak itu saja pertanyaan dari aku.. makasih ya buat waktu dan kesempatan

bertanyanya

N : Iya sama-sama

Transkrip in-depth interview

J : Jaya Paramita

N : Narasumber 4

J : Selamat siang bapakk.. pak saya mau tanya – tanya sedikit bolehh?

N : Iya boleh silahkan

J : Oke baik pakk terimakasih.. jadi saya mau bertanya, ga enaknya kerja di Novotel

itu apa sih pak?

N : Ohh oke baik.. ga enaknya kerja disini itu saya gabisa handling pekerjaan dengan

baik

J : Ohh kalau boleh tahu itu karena apa ya pak?

N : Ya hmm karena saking banyaknya pekerjaan yang diberikan dari perusahaan

sehingga saya tidak bisa meng-handle-nya dengan baik selain itu juga karena hal

tersebut saya menjadi tidak bisa kontrol emosi saya.. tidak konsen jugaa lalu saya

juga merasakan ada tekanan dari perusahaan yang kuat

J : Ohh seperti itu ya pakk.. pekerjaan disini banyak

194

N : Iya lalu pekerjaan disini juga jadinya mengganggu waktu keluarga saya dirumah

karena saya harus menyelesaikan pekerjaan yang ada disini

J : Ohh seperti itu ya pakk.. lalu ada lagi tidak pak keluhan pekerjaan disini?

N : Ya itu tadi dekk.. karena saya harus mengerjakan pekerjaan disini waktu untuk

mengurus pekerjaan rumah tangga juga jadi tidak ada

J : Lalu apalagi pak hambatannya?

N : Hmm ya sebaliknya dekk.. kalo saya lebih pilih waktu untuk keluarga pekerjaan

disini jadinya terganggu karena harus urus keluarga juga kan terus sedangkan disini

kerjaannya banyak.

J : Ohh oke seperti itu ya pakk.. ada lagi pak?

N : Lalu tanggung jawabnya itu jadi ga jelas pas saya bekerja karena saking

banyaknya pekerjaan karena ketidakjelasannya itu saya juga bekerja menjadi tidak

efektif.. terus saya merasa atasan saya juga jadi gabisa menilai kinerja saya dengan

baik karena ketidakjelasan tanggungjawab itu dan saking banyaknya pekerjaan yang

diberikan jadi atasan juga gabisa membedakan mana yang bawahan dan mana yang

atasan karena saking serabutannya pekerjaan yang diberikan

J : Ohh seperti itu ya pakk.. lalu ada lagi tidak pak kendala-kendala yang ada ?

N : Ya kalau disini sih ya gimana yahh kalo menurut saya sih banyak toleransi dari

pribadi masing-masing gitu ya karena seperti saya contohnya kalau saya tidak

mengerjakannya sendiri tapi itu juga termasuk ke tanggungjawab saya ya jadinya mau

tidak mau menjadi pekerjaan saya juga akhir-akhirnya gitu jadi kita juga tidak

mengandalkan ke orang lain… tidak bisa seperti itu

195

J : Ohh baik seperti itu ya pakk

N : Iyaa

J : Ohh okedeh pak.. itu saja pertanyaan dari saya, terimakasih banyak ya pak buat

waktunya.. thank youu

N : Sama-samaa..

Transkrip in-depth interview

J : Jaya Paramita

N : Narasumber 5

J : Selamat sore pakk..

N : Iya selamat sore

J : Perkenalkan nama saya Jaya

N : Iya selamat sore Mas Jaya

J : Saya mau nanya pak.. dukanya kerja disini bagi bapak itu apa ya?

N : Hmm ini kan hotel ya mas yah.. jadi kalau hotel itu melayani tamu.. lalu melayani

orang liburan yang mungkin bahasanya bisa jadi kalau lagi ada event besar nih untuk

yang Muslim Lebaran terus untuk yang Non-Muslim berarti Natalan sometimes

gabisa libur gitu aja sih mas bedanya dari pekerjaan lainnya

J : Jadi dukanya itu seperti apa pak ?

196

N : Dukanya jadi gabisa pulang pas Lebaran ada.. gabisa pulang pas hari besar

kumpul sama keluarga seperti itu

J : Okehh

N : Tapi itu untuk pekerjaan hotel ya.. tidak hanyak Novotel tapi rata-rata hotel

seperti itu soalnya disaat tanggal merah hotel rame jadi kita gabisa libur

J : Okee.. lalu disini overtime ga sih pak untuk kerjanya ?

N : Overtime gimana nih ?

J : Overtime lebih dari jam kerja gitu pakk

N : Sebetulnya kalau untuk lebih dari 1 sampai 2 jam terserah sih itu mas sebutnya

overtime atau tidak karena kita jadwal jam 6 nih lalu baru pulang setengah 7 jam 7 itu

pandangan mas sih gimana

J : Tapi kalau dari bapak sendiri gimana ?

N : Ya kita sih tidak keberatan.. karena kan memang pekerjaannya belum selesai

karena itu kan tanggungjawab kita juga ya mas

J : Okeyy berarti tidak overtime ya bagi bapak ?

N : Hmm tidakk

J : Baik.. lalu bapak itu masuk kerja hari apa saja ?

N : Senin sampai jumat mas

J : Untuk sabtu minggu masuk tidak ?

N : Sometimes sih mas

J : Okeyy kalau pas sabtu minggu itu masuk.. keluarga, temen atau pacar itu komplen

ga sih pak ?

197

N : Ya tidak sih kan masih ada hari lainnya seperti misal masuk hari sabtu, hari

minggunya kan masih ada karena bahasanya gimana ya kan memang pekerjaan itu

kebutuhan juga kalau pekerjaan kita ga beres juga kan kita gabisa

J : Baikk.. lalu sekarang ini bapak masih bisa ga sih bagi waktu antara keluarga,

pekerjaan, dan untuk bapak sendiri ?

N : Ada, masih bisa

J : Oke pakk.. sekian pertanyaan dari saya, terimakasih pak buat waktunya.. thank

youu

Transkrip in-depth interview

J : Jaya Paramita

N : Narasumber 6

J : Selamat malam kakk..

N : Selamat malamm

J : Kak, aku mau nanya dongg.. dukanya kerja disini bagi kakak itu apa sih ?

N : Dukanya apa ya.. kalau dari departemen aku kaya susahnya pengadaan barang,

maintenance alat, manning.. tapi so far dibawa enjoy aja karena orang kerja pasti ada

sulitnya

J : Ohh okee lalu disini menurut kakak overtime ga sih kerjanya ?

198

N : Mostly iya.. untuk saya sendiri kalau diliat dari LOI itu 8 jam tapi saya bisa 12

jam kerja

J : Selanjutnya.. kakak kerja disini hari apa aja ?

N : Karena disini perbandingannya 5 : 2 jadi ga tentunya juga ya masuknya hari apa

aja tergantung operasional juga kalau lagi rame saya back-up buat yang lain gitu

pokoknya tergantung operasional

J : Sabtu minggu masuk ga kak ?

N : Tergantung operasional kalau memangnya saya harus masuk ya saya masuk

J : Nah kalau lagi masuk gitu pacar, suami, keluarga gitu suka komplen ga sih ?

N : Terkadang iya.. mereka sampai nanya memang kerjanya apa sih sampai segitu

lamanya, lalu apa saja sih yang dikerjakan itu aja sih

J : Nah tadi kan kakak ada bilang kerja sampai 12 jam, dari situ kakak ada waktu ga

sih buat diri kakak sendiri, buat temen, buat keluarga ?

N : Hmm paling kalau lagi pas libur aja sih tapi kalau lagi kerja mah gada waktu buat

diri sendiri

J : Jadi pas lagi kerja gada waktu yahh, tetapi kalau dari kakak pribadi itu hambatan

tidak sih bagi kakak ?

N : Secara pribadi iya, karena jadi kurang bersosialisasi tapi kalau untuk pekerjaan

karena ini hobi saya jadi saya menikmati

J : Baik kakk.. terakhir nihh waktu kakak kerja, kakak merasa waktu itu jalannya

cepat atau lambat ?

199

N : Cepat sih karena saya menikmati yang lama itu kalau lagi gada barang, alat-

alatnya rusak kan mesti nunggu maintenance dulu ya.. karena saya jadi tidak bisa

cepat mengerjakan sesuatu, kaya gitu sih

J : Oke deh kakk sekian itu saja pertanyaan dari aku.. terimakasih ya kakk

N : Iya sama-sama Jayaa, terima kasih juga selamat malamm

J : Selamat malamm

Transkrip in-depth interview

J : Jaya Paramita

N : Narasumber 7

J : Selamat malam kakk

N : Selamat malamm

J : Aku mau tanya dong kak, gak sukanya kerja di Novotel itu apa sih kak ?

N : Gak sukanya jam kerjanya gila sih disini

J : Jam kerjanya.. okee abis itu ?

N : Pressurenya lumayan besar

J : Pressure lumayan besar

N : Lalu kita itu tim, tim tapi kerjanya masih kaya berasa kerja sendiri sih

J : Ada lagi gak kakk ?

200

N : Tugasnya banyak banget, apalagi saya yang didepan, di-hostest juga, gliter juga,

cashier juga jadi waitress juga pokoknya semuanya saya karena di floor itu gada

staffnya, di floor itu kebanyakan black jacketnya seperti manager, supervisor,

sedangkan staffnya hanya saya sendiri per shift dan di floor itu hanya ada anak

trainee dan gabisa dong andelin anak trainee memberi tanggungjawab kalau misal ada

tamu datang pasti kan ujung-ujungnya saya juga

J : Hmmm jadi kerjaannya itu dicover sama kakak semua yaaa

N : Iyaaa.. belom lagi file-file yang harus ditandatangan sama misalnya GM sama

atasan kan jadi kebagi antara operation sama back office

J : Hmm okee.. lalu semangat ga kak kerja disini ?

N : Kalau lagi semangat, semangat banget, kalau lagi datang jenuhnya, lagi stress,

stress banget

J : Lebih sering yang mana ?

N : Lebih sering karena mungkin aku udah setahun kali ya 2 tahun jadi udah tau

banget yang ngerasain yang namanya proses kali yaa

J : Jadi kalau sekarang ?

N : Kalau sekarang sudah berkurang sih jadi legowo aja

J : Jadi intinya semangat apa ngga nih ?

N : Di semangat-semangatin saja hehe

J : Hayoo berarti tidak dong jawabannya, iya kan ?

N : Iya ngga.. stress tau

J : Stress.. oke mantapp, lalu kakak kerja dihari apa saja ?

201

N : Tidak menentu karena kan shifting paling ngga sih normalnya itu kerja 5 hari

dalam seminggu 2 harinya libur tapi kalau lagi karena kan kita staffnya limit jadi

menyesuaikan juga bisa jadi kita libur jadi seminggu kaya gitu, kalau lagi rame juga

eh jadi hanya sehari

J : Lalu.. berarti sabtu minggu bisa masuk nih kakk ?

N : Bisa

J : Nah kalau sabtu minggu lagi masuk itu seperti orang tua kakak, pacar kakak

mungkin, itu pada komplen gak sih kaya ih sabtu minggu bukannya libur masih aja

masuk kerja

N : Tidak sih kalau untuk orang tua dan pasangan juga sih karena mungkin sudah

mengerti kali ya karena kita kan kerja bukan kaya orang kerja kantoran tapi dibagian

operasional mungkin kalau ada yang komplen sih itu temen, temen yang lebih

komplen

J : Okehh.. selanjutnya suka tidak sama pekerjaan kakak saat ini ?

N : Suka.. ada tidak sukanya juga sih

J : Apa tuh kak tidak sukanya ?

N : Jobdesc disini terlalu banyak sehingga kita harus korbanin waktu.. waktu yang

jadi korbannya kalau misal tidak dikerjain makin lama makin molor

J : Nahh.. terkait sama waktu tadi tuh lalu sama pekerjaan yang banyak, jam kerja

yang gila, pressure yang lumayan besar, saat ini kakak masih bisa tidak bagi waktu

antara pekerjaan kakak, sama urusan pribadi kakak, sama keluarga kakak itu kira-kira

jadi hambatan ga gitu karena pekerjaan disini ?

202

N : Sebenernya hambatan, cuma pinter-pinter kitanya saja. Sebenernya yang paling

penting sih istirahat karena kurang banget buat istirahat karena aku aja masuk pagi

jam 6.. pulang kalau misalnya lagi rame banget bisa pulang jam 8.. bayangin aja itu

kerja lebih dari 12 jam. Bisa kalau ya luangin waktu buat keluarga paling seminggu

sekali, sama pacar juga seminggu sekali paling tidak

J : Tapi sebenernya hambatan ?

N : Hambatan.. tapi pinter-pinter kitanya nyari waktu aja sih

J : Hmm oke kak.. itu sekian pertanyaan dari aku terimakasih banyak yaa

N : Iyaa sama-samaa..

Transkrip in-depth interview

J : Jaya Paramita

N : Narasumber 8

J : Selamat sore pakk

N : Selamat sore..

J : Kalau menurut bapak sendiri, disini itu kerjanya overtime ga sih pak ?

N : Overtime.. ngga sih di sini sebenarnya wajib loyalitas cuma kadang-kadang saya

juga pulang cepat karena ada kebutuhan mendadak ada perencanaan keluarga gituu

J : Jadi menurut bapak sendiri itu jam kerjanya berlebihan atau tidak ?

N : Tidakk

203

J : Tidak yaa okee.. lalu bapak masuk kerja hari apa saja ?

N : Saya masuk di hari senin sampai rabu, kamis jumat libur

J : Sabtu minggu masuk tidak pak ?

N : Masukk.. karena kan saya dibagian maintenance ya jadinya kalau hari sabtu dan

minggu itu masuknya ke bagian operasional

J : Nah kalau sabtu minggu masuk gitu.. maaf nih sebelumnya bapak sudah

berkeluarga belum ?

N : Sudahh

J : Nah.. anak istri bapak itu pada komplen ga kan harusnya kalau sabtu minggu pada

jalan-jalan

N : Tidak sihh jangankan sabtu minggu pak, saya aja kalau tiap Lebaran ga pernah

dirumah karena ngikutin atasan kan udah kamu Lebaran masuk aja ya

J : Ohh okee.. nah bapak itu selama ini bisa ga sih ngebagi waktu buat sama keluarga,

diri sendiri, dan sama pekerjaan ?

N : Ya gimana ya.. saya tiap malam jumat udah pasti jalan-jalan tuh sama keluarga

sama malam sabtu itu saya jalan sama anak.. kalau siangnya sih saya istirahat

J : Berarti tidak ada hambatan ya pak di situ ?

N : Tidak ada hambatan.. ga sampe mengganggu inilah prioritas sendiri jadi sudah

memang menikmati dan keluarga juga mengerti

J : Hmm oke bapak itu saja pertanyaan dari saya

N : Iyaa

J : Terimakasih banyak ya pak

204

N : Sama-sama pak..

Transkrip in-depth interview

J : Jaya Paramita

N : Narasumber 9

J : Selamat siang pakk

N : Iya siang pak Jaya

J : Pak saya mau nanya dong pak.. dukanya kerja di Novotel itu apa sih ?

N : Sebenernya lebih banyak sukanya sih disini daripada dukanya.. karena disini

kekeluargaannya kental dan kita itu kerjanya teamwork jadi kalau ada masalah

apapun kita selesaikannya bareng-bareng

J : Hmm oke.. disini itu bapak sering overtime ga sih pak ?

N : Kalau untuk overtime sih udah pasti iya karena kita kan bagiannya emang di

engineering jadi itu waktu juga tidak harus jam 5 pulang teng gitu ga mungkin itu

pasti ada pekerjaan yang harus tetap urgent dan gabisa dihitung dengan waktu itu

kalau bagian engineering

J : Okee.. lalu disini banyak ga sih pak pekerjaannya ?

N : Kalau untuk pekerjaan disini sih banyak karena kan kita sudah punya project

masing-masing lalu monthly project jadi harus mencapai semuanya itu

205

J : Nah lalu dari banyaknya pekerjaan itu tadi, bapak masih bisa ga sih bagi waktu

sama keluarga, istri, pacar mungkin nah itu jadi kehambat ga sih pak gara-gara

overtime tadi ?

N : Hmm kebetulan.. disini kan di Novotel kalau kita lembur itu kan ga dibayar

itungannya tapi akan diberikan hari libur atau EO (Extra Off) nah extra off itu

biasanya bole diambil kapan saja sesuai dengan apa yang udah dicapai di lemburnya

itu kita diganti dengan extra off dan untuk waktu buat sama keluarga itu saya

manfaatin di hari libur saya 2 hari itu, itu bener-bener saya manfaatin hari liburnya

J : Berarti tidak ada hambatan ya pakk ?

N : Tidak ada pak.. jadi bener-bener saya kerja 5 hari 2 hari libur saya manfaatin buat

anak-anak sama isteri, ibaratnya meskipun dirumah ya kumpul aja gitu dirumah

walaupun ga jalan juga.. pinter-pinter kitalah atur-atur waktu di hari libur itu.

J : Bapak itu kerjanya dihari apa saja sih pak ?

N : Saya dihari senin, selasa, jumat, sabtu, minggu itu in-charge saya untuk bulan ini

selebihnya saya libur dan saya masuk pagi terus

J : Nah kan itu ada hari sabtu dan minggu masuk ya pakk.. anak isteri bapak itu

komplen ga sih pak kok hari libur bapak kerja ?

N : Ohh.. ngga sama sekali sih pak ga komplen karena emang udah tau, sebelum saya

menikah juga beliau sudah tahu jadi beliau sudah biasa menghadapi yang seperti itu

gitu.. sebelum nikah juga sudah tahu masuknya di hari sabtu minggu

J : Okedeh baik pakk.. terima kasih ya pakk

N : Oke dehh

206

Transkrip in-depth interview

J : Jaya Paramita

N : Narasumber 10

J : Selamat siang kakk

N : Sianggg

J : Kak.. aku mau tanya dong dukanya kerja di Novotel itu apa sih ?

N : Dukanya disini karena staffnya sedikit ya jadi ga terlalu banyak jadi orangnya itu-

itu aja terus misalnya kita kerja kan itu relatifnya relasi jadi kalau misalnya kita butuh

bantuan agak lama karena ya emang karyawannya terbatas

J : Nah kakak itu selama kerja disini masih bisa ga sih bagi waktunya buat sama

pacar, keluarga atau temen gitu ?

N : Masih bisa sihh.. bahkan sangat bisa ya tergantung orang sih di departemen

manapun sesibuk apapun kalau memangnya orang tersebut dapat bagi waktu

semuanya itu bisa sih di kendalikan

J : Nah kalau disini itu kakak berasa jalannya waktu lambat ga sih ?

N : Justru ini sebaliknya.. baru megang komputer tau-tau udah 3 jam saja terus

kerjaan baru disini-sini aja

J : Lalu disini overtime ga sih kak ?

N : Sebenarnya kalau dibilang overtime tidak juga sih karena kalau diliat dari

kasusnya jam 6 juga udah selesai terus kan saya paling males sama jam macet lalu

207

nunggu jam sholat.. jam sholat itu juga lumayan bentar sambil nunggu itu ya mending

overtime sambil nunggu macetnya selesai jadi harusnya bisa pulang jam 6 saya

pulang jam setengah 8 ya gapapa sih yang penting kerjaan selesai juga

J : Tetapi bukan dari karena pekerjaan ya pak ?

N : Tidak juga sih.. terkadang kalau dari pekerjaan paling hanya untuk beberapa

bulan saja misalnya di akhir bulan.. di beberapa hari itu pasti ada closingan nah itu

pasti ada overtime

J : Ohh seperti itu

N : Karena kan kalau di departemen saya sendiri ada yang namanya openning report

dan closing report nah di situ yang agak-agak makan waktu jadi di situ bisa overtime

J : Lalu kakak itu kerja dihari apa saja sih ?

N : Kalau kerja saya di hari senin sampai jumat tapi terkadang kalau memangnya lagi

closingan sabtu minggu bisa masuk karena kan kalau di akhir bulan itu kita gatau ya

jatuhnya di hari apa misalnya kalau 30 atau 31 nya di hari minggu nah karena kita

kerjanya berdasarkan period jadi mau gamau harus masuk

J : Nah misalnya itu tadi kakak masuk dihari sabtu dan minggu.. keluarga kakak,

pacar kakak itu kira-kira komplen ga sih kok hari sabtu minggu masih kerja sih ?

N : Kalau dibilang komplen mungkin semua yang udah berkeluarga pasti komplen

karena kan memang waktunya libur tapi masih aja kerja terus yang punya orang tua

juga pasti berpikiran ini kok kerja terus gada waktu buat keluarga, gada waktu buat

istirahat tapi ya memang tugasnya di bandingkan kita harus mengabaikan yasudah

kita kerjakan saja

208

J : Lalu, aku mau tanya pekerjaan kakak saat ini sesuai ga sih sama waktu kakak

apply dahulu ?

N : Berbeda sih.. banyak tugas tambahan aja di sini.. sebenernya working desc-nya itu

udah sesuai job desc-nya udah pas tapi karena Novotel gayanya minimalis jadinya 1

orang itu dituntut buat bisa multitasking

Transkrip in-depth interview

J : Jaya Paramita

N : Narasumber 11

J : Selamat siang kakk.. jadi aku mau nanya kak dukanya kerja disini itu apa sih

menurut kakak ?

N : Dukanyaa.. mungkin jam pulangnya aja kali ya

J : Ohh jam pulangnya kenapa tuh ya kak ?

N : Mungkin apa sih tuh namanya loyalitas tanpa batas kali ya kalau kata anak-anak

perhotelan itu

J : Lalu ada lagi ga kak ?

N : Ngga ada sih kayaknya

J : Terkait sama jam pulangnya nih kak, kerjaannya banyak ga sih kak disini ?

N : Kalau untuk aku ya ?

J : Iya

209

N : Kalau aku kan kerjanya dibawah sementara aku tuh kaya yang harus nungguin

semua orang pada turun, anak-anak sudah bubar, baru deh aku bubar gitu loh jadi aku

kaya disamain kaya supervisor

J : Nah dengan jam kerja yang seperti itu, kakak jadi ada waktu ga sih buat keluarga

kakak atau pacar gitu misalnya dan buat diri kakak sendiri itu ada ga sih ?

N : Masih ada sihh.. mungki karena aku single kali ya belum nikah

J : Kakak itu kerja disini hari apa aja ya ?

N : Senin, selasa, rabu, sabtu, minggu ?

J : Sabtu minggu.. nah kalau sabtu minggu itu tapi kakak masuk kerja, karena kakak

kan tadi masih single, mungkin hubungannya ke orang tua kali ya.. kakak masih

tinggal sama orang tua ?

N : Masih

J : Nah mungkin orang tua kakak tuh kaya suka nanya kok hari sabtu minggu masih

aja masuk kerja.. suka komplen ga ?

N : Ngga.. karena mama aku juga dari perhotelan jadi udah ngerti gitu

J : Dulu waktu pertama kali apply sesuai ga sama pekerjaan sekarang ini ?

N : Ngga.. karena dulu aku kan ngelamarnya jadi room attendant tapi di kasihnya OT

di sini ya alhamdullilah sih cuma aku kan harus belajar lagi gitu ya biar banyak ilmu

juga sih

J : Oke kak.. sekian itu saja pertanyaan dari aku terima kasih banyak yaa

N : Okee.. semangatt!!

210

Transkrip in-depth interview

J : Jaya Paramita

N : Narasumber 12

J : Selamat siang kakk

N : Iya siangg

J : Kak, mau tanya dong dukanya kerja di sini tuh apa sih ?

N : Dukanya ya paling kerjanya overtime aja sih sama kurang orang hehe

J : Dampak dari overtime sama kurang orang itu bagi kakak itu apa jadinya ?

N : Ya gimana ya kerjanya jadi harus bener-bener over dan manfaatin waktu banget

gabisa nyantai namanya kita gada orang terus kerjanya over, ya kalau misalnya

banyak orang juga mungkin kerjanya ga bakal over mungkin karena orangnya emang

kurang jadi kerjanya ya over

J : Lalu, dari kakak sendiri ada waktu ga sih buat diri sendiri, keluarga, dan pekerjaan

nah menyangkut overtime yang tadi tuh pekerjaan jadi banyak. Dari situ kakak ada

waktu ga sih buat urus keluarga buat urus diri sendiri

N : Ya pasti ada lah karena kan di sini kerjnya 5 hari kerja 2 hari off kalau memang

misalnya lagi emergency atau revenue lagi rame atau mungkin ada acara wedding

atau ada acara dadakan yang mungkin emang bener-bener harus masuk ya saya

masuk namun paling di ganti sama hari off jadi di undurin off-nya, yang penting bisa

211

manfaatin waktu aja sih, planning waktu biar kita nantinya juga kerjaan jadi ga

kendala, kerjaan dirumah juga jadi ga kendala

J : Berarti ga gitu ke hambat ya kak sama jam kerja disini ?

N : Ngga juga sih soalnya udah lama juga kerja didunia kuliner jadinya ya kaya gitu

konsekuensi orang kerja didunia kuliner

J : Hmm okee.. biasa kakak itu kerja di hari apa saja sih ?

N : Biasa senin sampai jumat

J : Sabtu minggu ?

N : Sabtu minggu libur.. tetapi kalau misal ada event sabtu masuk libur di pindah jadi

ke senin

J : Nah kalau misalnya sabtu minggu lagi masuk, keluarga kakak komplen ga sih ?

N : Ya nggalah.. kan udah lama mereka jadinya sudah mengerti juga

J : Oke kak.. itu saja pertanyaan dari saya.. thank you ya kak

N : Iya sama-sama

1/23/2020 Survey Penelitian

https://docs.google.com/forms/d/1LzgKkoQHz4GYOeZHnfsPVV3cE1ORzdeYQInDONaTv8Q/edit 1/7

Survey PenelitianResponden yang terhormat,

Saya Jaya Paramita, peneliti dari Universitas Multimedia Nusantara angkatan 2016 program studi Manajemen, saat ini saya sedang melakukan penelitian untuk tugas akhir saya.Saya berharap responden dapat menjawab semua pertanyaan-pertanyaan dengan jujur, sesuai dengan apa adanya.

Panduan pengisian :1. Pertanyaan yang diajukan dan jawaban-jawaban yang diterima adalah untuk tujuan penelitian.2. Isi dan pilihlah salah satu jawaban atas pertanyaan-pertanyaan yang diajukan dengan memberi tanda silang (X) pada setiap jawaban yang anda pilih dalam waktu kurang lebih 15 MENIT.3. Pastikan bahwa jawaban-jawaban yang anda berikan adalah jawaban yang jujur, apa adanya, dan sesuai kenyataan.

Jika Anda memiliki pertanyaan seputar kuisioner ini, Silahkan menghubungi saya di [email protected] atau [email protected] atau ke nomor 082288881870. Bagi responden terbaik akan mendapatkan GIFT berupa saldo gopay. Thank you :)

* Wajib

Identitas RespondenSemua jawaban anda akan saya jaga kerahasiaannya.

1. Email

2. Nomor Handphone

3. Department *Tandai satu oval saja.

Admin and General

Front Office

Engineering

FB Kitchen

FB Service

Finance

Fit and Spa

Talent and Culture

Housekeeping

Sales and Marketing

Security

1/23/2020 Survey Penelitian

https://docs.google.com/forms/d/1LzgKkoQHz4GYOeZHnfsPVV3cE1ORzdeYQInDONaTv8Q/edit 2/7

4. Gender *Tandai satu oval saja.

Male

Female

5. Umur di Tahun 2019 *Tandai satu oval saja.

16 - 20 Tahun

21 - 25 Tahun

26 - 30 Tahun

31 - 35 Tahun

36 - 40 Tahun

41 - 45 Tahun

> 45 Tahun

6. Lama Bekerja *Tandai satu oval saja.

0.5 - 1 Tahun

1 - 2 Tahun

3 - 4 Tahun

5 - 6 Tahun

7 - 8 Tahun

> 8 Tahun

7. Posisi Jabatan *Tandai satu oval saja.

Staff

Supervisor

Manager

Director

Yang lain:

8. Status Perkawinan *Tandai satu oval saja.

Menikah

Belum Menikah

Yang lain:

1/23/2020 Survey Penelitian

https://docs.google.com/forms/d/1LzgKkoQHz4GYOeZHnfsPVV3cE1ORzdeYQInDONaTv8Q/edit 3/7

9. Pendidikan Terakhir *Tandai satu oval saja.

SMA

D3

S1

S2

Yang lain:

Bagian 1Jawaban Anda akan saya jaga kerahasiaannya. 1 = "Sangat Tidak Setuju", 2 = "Tidak Setuju", 3 = "Netral", 4 = "Setuju", 5 = "Sangat Setuju"

10. Saya mempunyai waktu yang sangat terbatas untuk menyelesaikan pekerjaan saya *Tandai satu oval saja.

1 2 3 4 5

Sangat Tidak Setuju Sangat Setuju

11. Jumlah pekerjaan saya perlu dikurangi agar saya dapat menyelesaikan pekerjaan *Tandai satu oval saja.

1 2 3 4 5

Sangat Tidak Setuju Sangat Setuju

12. Saya meminta waktu tambahan untuk dapat menyelesaikan pekerjaan saya *Tandai satu oval saja.

1 2 3 4 5

Sangat Tidak Setuju Sangat Setuju

13. Saya tidak dapat menyelesaikan pekerjaan saya dengan tepat waktu *Tandai satu oval saja.

1 2 3 4 5

Sangat Tidak Setuju Sangat Setuju

Bagian 2Jawaban Anda akan saya jaga kerahasiaannya. 1 = "Sangat Tidak Setuju", 2 = "Tidak Setuju", 3 = "Netral", 4 = "Setuju", 5 = "Sangat Setuju"

1/23/2020 Survey Penelitian

https://docs.google.com/forms/d/1LzgKkoQHz4GYOeZHnfsPVV3cE1ORzdeYQInDONaTv8Q/edit 4/7

14. Tanggung jawab pekerjaan saya tidak jelas *Tandai satu oval saja.

1 2 3 4 5

Sangat Tidak Setuju Sangat Setuju

15. Saya tidak mengetahui informasi mengenai peluang promosi yang diberikan perusahaan *Tandai satu oval saja.

1 2 3 4 5

Sangat Tidak Setuju Sangat Setuju

16. Saya tidak dapat mengerjakan pekerjaan secara efektif *Tandai satu oval saja.

1 2 3 4 5

Sangat Tidak Setuju Sangat Setuju

17. Saya tidak mendapatkan informasi secara lengkap terkait bagaimana cara menyelesaikanpekerjaan saya *Tandai satu oval saja.

1 2 3 4 5

Sangat Tidak Setuju Sangat Setuju

18. Saya tidak mengetahui bagaimana cara atasan saya menilai kinerja saya *Tandai satu oval saja.

1 2 3 4 5

Sangat Tidak Setuju Sangat Setuju

19. Waktu untuk menyelesaikan pekerjaan saya tidak ditentukan dengan jelas *Tandai satu oval saja.

1 2 3 4 5

Sangat Tidak Setuju Sangat Setuju

Bagian 3Jawaban Anda akan saya jaga kerahasiaannya. 1 = "Sangat Tidak Setuju", 2 = "Tidak Setuju", 3 = "Netral", 4 = "Setuju", 5 = "Sangat Setuju"

1/23/2020 Survey Penelitian

https://docs.google.com/forms/d/1LzgKkoQHz4GYOeZHnfsPVV3cE1ORzdeYQInDONaTv8Q/edit 5/7

20. Jumlah pekerjaan saya saat ini mengganggu kehidupan pribadi saya *Tandai satu oval saja.

1 2 3 4 5

Sangat Tidak Setuju Sangat Setuju

21. Waktu kerja yang panjang membuat saya sulit memenuhi kewajiban sebagai anggota keluarga*Tandai satu oval saja.

1 2 3 4 5

Sangat Tidak Setuju Sangat Setuju

22. Terlalu banyak tuntutan pekerjaan dari perusahaan yang membuat saya tidak dapatmelakukan aktivitas pribadi dirumah *Tandai satu oval saja.

1 2 3 4 5

Sangat Tidak Setuju Sangat Setuju

23. Saya kelelahan dalam menyelesaikan pekerjaan saya *Tandai satu oval saja.

1 2 3 4 5

Sangat Tidak Setuju Sangat Setuju

24. Terdapat aktivitas dirumah yang berubah karena pekerjaan saya *Tandai satu oval saja.

1 2 3 4 5

Sangat Tidak Setuju Sangat Setuju

25. Terdapat ketidakselarasan antara permintaan waktu dari anggota keluarga dengan aktivitaskerja yang harus saya lakukan *Tandai satu oval saja.

1 2 3 4 5

Sangat Tidak Setuju Sangat Setuju

26. Saya menunda kegiatan ditempat kerja saya karena permintaan keluarga *Tandai satu oval saja.

1 2 3 4 5

Sangat Tidak Setuju Sangat Setuju

1/23/2020 Survey Penelitian

https://docs.google.com/forms/d/1LzgKkoQHz4GYOeZHnfsPVV3cE1ORzdeYQInDONaTv8Q/edit 6/7

Diberdayakan oleh

27. Konflik keluarga mempengaruhi kemampuan saya dalam bekerja di perusahaan *Tandai satu oval saja.

1 2 3 4 5

Sangat Tidak Setuju Sangat Setuju

Bagian 4Jawaban Anda akan saya jaga kerahasiaannya. 1 = "Sangat Tidak Setuju", 2 = "Tidak Setuju", 3 = "Netral", 4 = "Setuju", 5 = "Sangat Setuju"

28. Saya tidak mampu menangani pekerjaan yang diberikan kepada saya *Tandai satu oval saja.

1 2 3 4 5

Sangat Tidak Setuju Sangat Setuju

29. Saya merasa depresi karena beban pekerjaan yang ada *Tandai satu oval saja.

1 2 3 4 5

Sangat Tidak Setuju Sangat Setuju

30. Saya kesulitan dalam mengontrol emosi saya *Tandai satu oval saja.

1 2 3 4 5

Sangat Tidak Setuju Sangat Setuju

31. Saya kurang mampu berkonsentrasi saat bekerja *Tandai satu oval saja.

1 2 3 4 5

Sangat Tidak Setuju Sangat Setuju

32. Saya mendapat tekanan besar ditempat kerja *Tandai satu oval saja.

1 2 3 4 5

Sangat Tidak Setuju Sangat Setuju

International Journal of Law and ManagementMediating effect of work stress on the influence of time pressure, work-family conflict and roleambiguity on audit quality reduction behaviorAmir Amiruddin,

Article information:To cite this document:Amir Amiruddin, "Mediating effect of work stress on the influence of time pressure, work-family conflict and role ambiguity onaudit quality reduction behavior", International Journal of Law and Management, https://doi.org/10.1108/IJLMA-09-2017-0223Permanent link to this document:https://doi.org/10.1108/IJLMA-09-2017-0223

Downloaded on: 21 February 2019, At: 01:16 (PT)References: this document contains references to 0 other documents.To copy this document: [email protected]

Access to this document was granted through an Emerald subscription provided by emerald-srm:187893 []

For AuthorsIf you would like to write for this, or any other Emerald publication, then please use our Emerald for Authors serviceinformation about how to choose which publication to write for and submission guidelines are available for all. Pleasevisit www.emeraldinsight.com/authors for more information.

About Emerald www.emeraldinsight.comEmerald is a global publisher linking research and practice to the benefit of society. The company manages a portfolio ofmore than 290 journals and over 2,350 books and book series volumes, as well as providing an extensive range of onlineproducts and additional customer resources and services.

Emerald is both COUNTER 4 and TRANSFER compliant. The organization is a partner of the Committee on PublicationEthics (COPE) and also works with Portico and the LOCKSS initiative for digital archive preservation.

*Related content and download information correct at time of download.

Dow

nloa

ded

by L

UN

D U

NIV

ER

SIT

Y A

t 01:

16 2

1 Fe

brua

ry 2

019

(PT

)

The Effects Of Time Pressure, Work-Family Conflict And Role Ambiguity

On Work Stress And Its Effect On Audit Quality Reduction Behavior

Amiruddin, Gagaring Pagalung, Kartini and Arifuddin Department of Accounting, Universitas Hasanuddin, Makassar, Indonesia

Abstract:

Purpose - The purpose of this study is to investigate the relationships between time pressure,

workplace-family conflict, and role ambiguity and work stress, with audit quality reduction

behavior as a mediating variable. It means that the paper investigated the direct effects of (1) time

pressure, workplace-family conflict, and role ambiguity on audit quality reduction behavior, and

(2) time pressure, workplace-family conflict, role ambiguity, and audit quality reduction behavior

on work stress.

Design/methodology/approach - The population in this study was all auditors working in KAP

(Public Accounting Firms) in Indonesia. The Public Accounting Firms consisted of The Big-Four,

affiliated KAP (outside of Big-Four) and non-affiliated KAP. The sample selection in this study

was performed by purposive sampling method because it was based on the criteria set by the

researcher. The study used quantitative analysis with Structural Equation Modeling (SEM) to

analyze direct and indirect effects.

Findings - The research found that Time Pressure had positive and significant effect on Work

Stress, Time Pressure had positive and significant effect on Turnover Intention, Time Pressure had

positive and significant effect on Audit Quality Reduction Behavior. High Time Pressure impacted

high Work Stress, Turnover Intention, and Audit Quality Reduction Behavior.

Originality - The originality of this paper is in SEM model used by involving mediation variable

namely audit quality reduction behavior. No previous study investigates comprehensively the

relationship between time pressure, workplace-family conflict, and role ambiguity, and work

stress, with the audit quality reduction behavior as a mediating variable, especially in Public

Accounting Offices (KAP) in Indonesia.

Keywords: Work Stress, Time Pressure, Work-Family Conflict, Role Ambiguity

1. Introduction

Quality of audit is a warranty as the quality will be used to compare actual condition with expected condition. So that an audit report produced by auditor has high quality, the auditor must perform their work professionally and independently, comply with auditing standard, obtain competent and sufficient evidence and perform complete stages of audit procedure (Francis and Yu, 2009; Neri and Russo, 2014). High quality audit is audit which can improve the quality of information to be reliable.

Auditing is inseparable from behavior issue, e.g. possibility of an auditor to perform dysfunctional behavior, thus reducing the quality of an audit. Quality reduction in audit means deliberate reduction of quality in auditing by auditor (Coram and Woodliff, 2003). Malone and Roberts (1996) state that audit quality reduction behavior is an action taken by auditor when performing audit program which leads to reduced effectiveness of audit evidence which should be collected.

Work stress is often associated with audit profession. There have been many studies on the work stress of auditors, but they only discuss the effects on

Dow

nloa

ded

by L

UN

D U

NIV

ER

SIT

Y A

t 01:

16 2

1 Fe

brua

ry 2

019

(PT

)

performance (Chen et al., 2006), job satisfaction (Chen and Silverthorne 2008), turnover intention (Hsieh and Wang, 2012), and turnover of audit (Dalton et al., 1997). Previous studies on the effect of work stress on audit quality reduction behavior were performed by Robinson and Bennett (1995), Boyd et al. (2009) and Mohd Nor (2011), who find that work stress leads to auditor’s dysfunctional behavior.

Golparvar et al. (2012) find that work stress at low level has negative effect on audit quality reduction behavior, while work stress at high level has positive effect on audit quality reduction behavior. In another study, work stress causes job dissatisfaction and reduces work performance (Hayes and Weathington, 2007; Chen and Silverthone, 2008), leading to auditor’s dysfunctional behavior (Lawrence and Robinson, 2008; Paino et al., 2012). On the other hand, work stress is sometimes deliberately created to challenge someone to improve their work performance (Moore, 2000). Auditor who has stress at certain level may show better work performance in organization (Spector et al., 1988; Chen et al., 2006; Virtanen et al., 2009).

The results of researches on reduction of quality of edit by previous researchers are varied, so there should be further research. The present study is different from previous studies which research factor causing (antecedent) auditor’s work stress, e.g. time pressure, role conflict and role ambiguity, while the present study adds work-family conflict and locus of control which simultaneously affect reduction of quality of audit. Role ambiguity occurs due to lack of information or information which is not relayed. Role ambiguity is also caused by heavy work demands and uncertain supervision by superior which forces employee to guess and predict their own actions (Bamber et al., 1989).

Researches on role stress in KAP show similar evidence but they’re still contradictive, e.g. role conflict and role ambiguity have negative correlations with work satisfaction but positive correlations with turnover intention (Gregson, 1992). Moreover, role conflict has positive relation with work stress (Roberts et al., 1997) and positive and significant relation with audit quality reduction behavior (Mohd Nor, 2011). Someone who has role ambiguity tends to have reduced physical and psychological health. It leads to stress at work and turnover intention, as well as audit quality reduction behavior because the individual works ineffectively and doesn’t concentrate at work (Fogarty et al., 2000; Fisher, 2001; Viator, 2001 and Jones et al., 2010). Moreover, high role ambiguity may reduce one’s confidence in their ability to work effectively (Fisher, 2001; Viator, 2001). However, a study by Jannah et al. (2016) finds that role ambiguity doesn’t have any positive relation with turnover intention and Mohd Nor (2011) states that role ambiguity doesn’t have any significant relation with audit quality reduction behavior.

The results of researches on reduction of quality of edit by previous researchers are still varied, so there should be further research. The present study is different from previous studies which research factor causing (antecedent) auditor’s work stress, e.g. time pressure, role conflict and role ambiguity, while the present study added work-family conflict which was expected to also effect turnover intention as variables which simultaneously affected audit quality

Dow

nloa

ded

by L

UN

D U

NIV

ER

SIT

Y A

t 01:

16 2

1 Fe

brua

ry 2

019

(PT

)

reduction behavior. Audit quality reduction behavior in KAP has been the focus of many studies for a long period and in many countries, e.g. Australia (Coram and Woodliff, 2003), France (Herrbach, 2001), New Zealand (Cook and Kelly, 1991; Gundry and Liyanarachchi, 2007), United States (Alderman and Deitrick, 1982; Donnely et al., 2004; Kelley and Margheim, 1990; Malone and Roberts, 1996) and United Kingdom (Willett and Page, 1996). All researches show relatively high number in which auditors were involved in audit quality reduction behavior and prove that auditors tend to compromise effectiveness of audit and don’t completely perform audit program. For example, Coram and Woodliff (2003), Kelley and Margheim (1990), and Otley and Pierce (1996a) find that over 50% of auditors perform at least one practice of audit quality reduction throughout their careers.

Work-family conflict is the role demands of work and family which can’t align in several things. According to Greenhouse and Beutell (1985), work-family conflict is the amount of emerging pressure in performing one role so one has difficulty in fulfilling other role(s). This conflict will cause stress on an employee at work, so that the problem will eventually cause the employee to want to change job, as found by Netemeyer et al. (1996) and Boles et al. (1997). The finding mentions that work-family conflict has positive effect on turnover intention (Pasewark and Viator, 2006; Blomme et al., 2010). Similarly, higher conflict between work and family faced by an individual may affect their performance or, in auditing, may cause audit quality reduction behavior (Williams and Anderson, 1991; Lestari, 2015).

Based on the background above, the purpose of this study is to investigate the relationships between time pressure, workplace-family conflict, and role ambiguity and work stress, with audit quality reduction behavior as a mediating variable. It means that the paper investigated the direct effects of (1) time pressure, workplace-family conflict, and role ambiguity on audit quality reduction behavior, and (2) time pressure, workplace-family conflict, role ambiguity, and audit quality reduction behavior on work stress. The originality of this paper is in SEM model used by involving mediation variable namely audit quality reduction behavior.

Several previous study has investigated the partial relationship between each variables, such as (1) Time Pressure (X1) and Work Stress (Z) by Odio, M.A., et al., (2013), Herrington, J.D., et al., (1995), Moeller, C., et al., (2013), Baehler, K., et al., (2008), Thornton, P.J., (1996); (2) Workplace-Family Conflict (X2) and Work Stress (Z) by Huffman, A., et al., (2013), Kremer, I (2016), Ahmad, M.S., et al., (2011), Howard, W.G., et al., (2004), (3) Role Ambiguity (X3) and Work Stress (Z) by Conley, S., et al., (2000), Siegall, M., (2000), Elloy, D.F., et al., (2003), Conner, D.S., et al., (2005); (4) Time Pressure (X1) and Audit Quality Reduction Behavior (Z) by Svanberg, J., et al., (2013), Brown, V.L., et al., (2016), Salehi, M., et al., (2017), Yuen, D.C.Y., et al., (2013), Lee, H., (2012); (5) Workplace-Family Conflict (X2) and Audit Quality Reduction Behavior (Z) by Zgarni, I., et al., (2016), Karim, A.K.M.W., et al., (2013), Khan, A., et al., (2016)r, Koyuncu, M., et al., (2012). (6) Role Ambiguity (X3) and Audit Quality Reduction Behavior (Z) by Zgarni, I., et al., (2016), Alfraih, M.M., (2016), Peursem, K.A.V., (2005) , Alfraih, M.M., (2016), and (7) Work Stress (Z)

Dow

nloa

ded

by L

UN

D U

NIV

ER

SIT

Y A

t 01:

16 2

1 Fe

brua

ry 2

019

(PT

)

and Audit Quality Reduction Behavior (Z) by Carmona, P., et al., (2015), Brown, V.L., et al., (2016), Yuen, D.C.Y., et al., (2013), Larson, L.L., (2004). No previous study investigates comprehensively the relationship between time pressure, workplace-family conflict, and role ambiguity, and work stress, with the audit quality reduction behavior as a mediating variable, especially in Public Accounting Offices (KAP) in Indonesia.

The research results are expected to have theoretical and practical

contributions. Theoretically, the research result is expected to contribute some

insight on behavioral accounting literatures, especially in auditing related with

factors causing auditor’s work stress and audit quality reduction behavior and it’s

also expected to be used as a reference for future studies. Practically, the research

result is expected to benefit public accounting offices (KAP) in evaluating

policies to create conducive work environment and create an organizational

culture or climate which harmonizes professional expectations and demands to

reduce the stress faced by auditors in working and to mitigate the possibility of

auditor performing audit quality reduction. Moreover, there is increased demands

of users of financial statements on auditors’ professionalism to get quality audit

reports.

2. Literature Review

Work-Family Conflict. Work and family are two interrelated things and very important for everyone. It’s very difficult to combine them, especially if an individual has family of their own (Chiun Lo and Ramayah, 2011). Therefore, conflict will emerge when someone has to choose between two roles (roles in family and at work) so the individual must play multiple roles. In other words, conflict is relation between two parties or more when individual senses incompatibility between the existing condition and the expected condition. Generally, people think conflict should be avoided, but according to Fisher et al. (2001), conflict is useful in life and is a part of human existence. However, others state that conflict may inhibit team work, thus causing unethical behaviors to achieve objectives.

Work-family conflict is a conflict which happens due to role imbalance between responsibilities at home and at work (Greenhaus and Beutell, 1985; Boles, et al., 1997). The assumption is there are two demands at the same level but can’t be performed equally and potentially causes incompatibility of function and discomfort in both positions (Pasewark and Viator, 2006). This will cause work stress. Work-family conflict seems to affect several professions (Parasuraman and Simmers, 2001). Moreover, a profession which directly interacts with many clients easily causes conflict, and there is positive relation with turnover intention (Connor et al., 1999). Similarly, public accountant has contacts with many clients and is more vulnerable to the conflict (Pasewark and Viator, 2006). Work-family conflict impacts high turnover intention in some public accounting offices (KAP).

Dow

nloa

ded

by L

UN

D U

NIV

ER

SIT

Y A

t 01:

16 2

1 Fe

brua

ry 2

019

(PT

)

Companies are expected to pay more attention to their employees’ wellbeing by increasing their satisfaction so that the employees behave appropriately for the interests of the companies in the long term. Therefore, companies should prevent work-family conflict in their employees. The impacts of work-family conflict in employee are work stress, turnover intention and maybe audit quality reduction behavior. They occur to cover inability to solve the problem, i.e. inability to balance family and work roles, thus creating internal conflict.

Lu et al. (2008) reveal that work-family conflict has positive and significant effect on organizational commitment, while Zhao’s (2012) study shows that individual which has conflict between work and family will have ambiguity and it will cause reduced organizational commitment. Similarly, discomfort or work pressure will have positive effect.

Role Conflict and Role Ambiguity. Role conflict emerges due to two simultaneous different orders (Wolfe and Snoke, 1962). Moreover, role conflict happens if someone has opposing roles as an employee or a member of an organization which must obey all norms and regulations in effect and be loyal to organization, and as a professional member which must obey ethical codes and professional performance standard (Siegel and Marconi, 1989). Employees in KAP have standard work structure. If there is disturbance in coordination of work flow and information on task progress, role conflict will occur. In other words, role conflict is related to two opposing demands (Rizzo et al., 1970).

Role ambiguity happens when an employee receives inadequate information, unclear policy and direction, uncertain authority, task and relation with others to perform their work (Bamber et al., 1989; Jackson and Schuler, 1985; Senatra, 1980). Furthermore, role ambiguity includes work flow coordination, violation in chain of command, job description and adequacy of communication flow. Therefore, role ambiguity refers to time pressure in task due to lack of clarity or not understanding one’s proper role in organization (DeZoort and Lord, 1997).

Role ambiguity may happen in Public Accounting Offices (KAP) if they have changes in structures and personnel regulations which cause problems such as demand and pressure for better work (Ameen et al., 1995). The role ambiguity can be eliminated by predicting the result of response of a behavior and by clarity of behavioral requirements which may help guide behaviors (Rizzo et al., 1970).

Role conflict and role ambiguity have potential impacts. It may be caused by high pressure related to work, causing work stress and, even further, may increase turnover intention and audit quality reduction behavior (Fisher, 2001; Viator, 2001). In other words, role conflict affects performance or audit quality reduction behavior.

Role conflict and role ambiguity as stress triggers are well-documented in previous studies. These elements are found and affect work result and works related to an attitude (Rebelle and Michaels, 1990; Belias et al., 2015). For some decades, many studies reveal that accounting profession may be associated with role conflict and role ambiguity among public accountants (Senatra, 1980;

Dow

nloa

ded

by L

UN

D U

NIV

ER

SIT

Y A

t 01:

16 2

1 Fe

brua

ry 2

019

(PT

)

Bamber et al., 1989; Rebele and Michaels, 1990; Fisher, 2001; Sweeney and Summers, 2002).

In terms of work stress, Fogarty (1996) and Smith et al. (2007) find that role conflict and role ambiguity have positive and significant relations with work stress. In other words, an individual or auditor understands that high role conflict will make them have high work stress, so conducive environment is required for auditors to work in accordance with their capacity.

Senatra (1980) states that the implications of role conflict and role ambiguity in KAP may cause serious problems such as low quality of auditor’s performance. The result of Senatra’s (1980) study on role stress is role ambiguity has negative effect on job satisfaction, while role conflict doesn’t affect job satisfaction. It’s because role conflict is an intrinsic part of auditing, so role conflict is necessary to motivate auditor in working.

Rebele and Michaels (1990), as well as Fisher (2001) perform similar studies as Senatra (1980) on the regulation between role stress and auditor’s jobs satisfaction and performance. The analysis result is role conflict has no significant relation with auditor’s performance but role conflict and role ambiguity have positive and significant relations with auditor’s work stress. Meanwhile, according to Norman and Weir (2010), both conflicts, i.e. role conflict and role ambiguity, have negative relations with job satisfaction.

Audit Quality Reduction Behavior. Audit quality reduction behavior is defined as actions taken by auditor during auditing task which reduce the effectiveness of the collected audit evidence (Malone and Robert, 1996). Moreover, Herrbach (2001) defines audit quality reduction behavior as a bad consequence of audit procedure which reduces the level of evidence collected for audit, so the collected evidence isn’t reliable, incorrect or insufficient quantitatively or qualitatively.

Audit quality reduction behavior happens when auditor incorrectly performs audit procedure required to finish their tasks. Audit quality reduction behavior is a serious problem because this behavior won’t only give negative effect on individual auditor, but also threatens the validity of audit opinion, affecting overall company performance and economic decision of audit report user. Although quality reduction behavior doesn’t only lead KAP to release unqualified opinion, if audit work isn’t performed correctly, audit risk will increase (Coram and Woodliff, 2003), meaning the probability of company to release incorrect opinion is higher. It’s because auditor may reach conclusion which is considered sufficient but on the other hand there isn’t enough evidence collected during audit engagement.

Audit quality reduction may reduce public trust on accounting profession and reduce the credibility of public accountants for their audit results. Therefore, there should be prevention or effort to minimize audit quality reduction by coordinating and motivating public accountants as their role is massive in the business world.

Stress Theory. Stress is psychologically defined as something experienced by an individual when facing demand, obstacle and/or opportunity which has significant but uncertain result (Greenhaus and Parasuraman, 1987).

Dow

nloa

ded

by L

UN

D U

NIV

ER

SIT

Y A

t 01:

16 2

1 Fe

brua

ry 2

019

(PT

)

Moreover, recognizing symptoms in stress response and identifying stress are very important to reduce and avoid excessive stress. Based on this definition, stress consists of two main elements; stress source and implication of stress. Previous studies on stress usually use three different definitions of stress which are as stimulus, response or relation between stimulus and response (Weick, 1983; Beehr and Franz, 1987; Jex at al., 1992). Stimulus is external power or environmental situation which requires physical or psychological response from individual (Greenhaus and Parasuraman, 1987; Jex et al., 1992). Stimulus is also called causative factor of stress. A response (strain) is called effect of forces on individual (Jex et al., 1992) or stress symptom (Greenhaus and Parasuraman, 1987). In other words, response is implication of external or environmental event on individual.

The researchers who use this stress definition refer to interaction between environmental condition or event and individual response to the condition. Some researches use the output of response as the definition of stress (Greenhaus and Parasuraman, 1987). Stress has the potential to encourage or disrupt work, depending on its level. Excessive stress level may have negative impact on auditor’s work quality. Some factors influencing stress are work environment factors related to work condition, such as work conflict, time pressure, and role stress. Another factor which effects work stress is individual characteristic which is related with personality type and personal experience of an auditor (Newstrom and Davis, 1993).

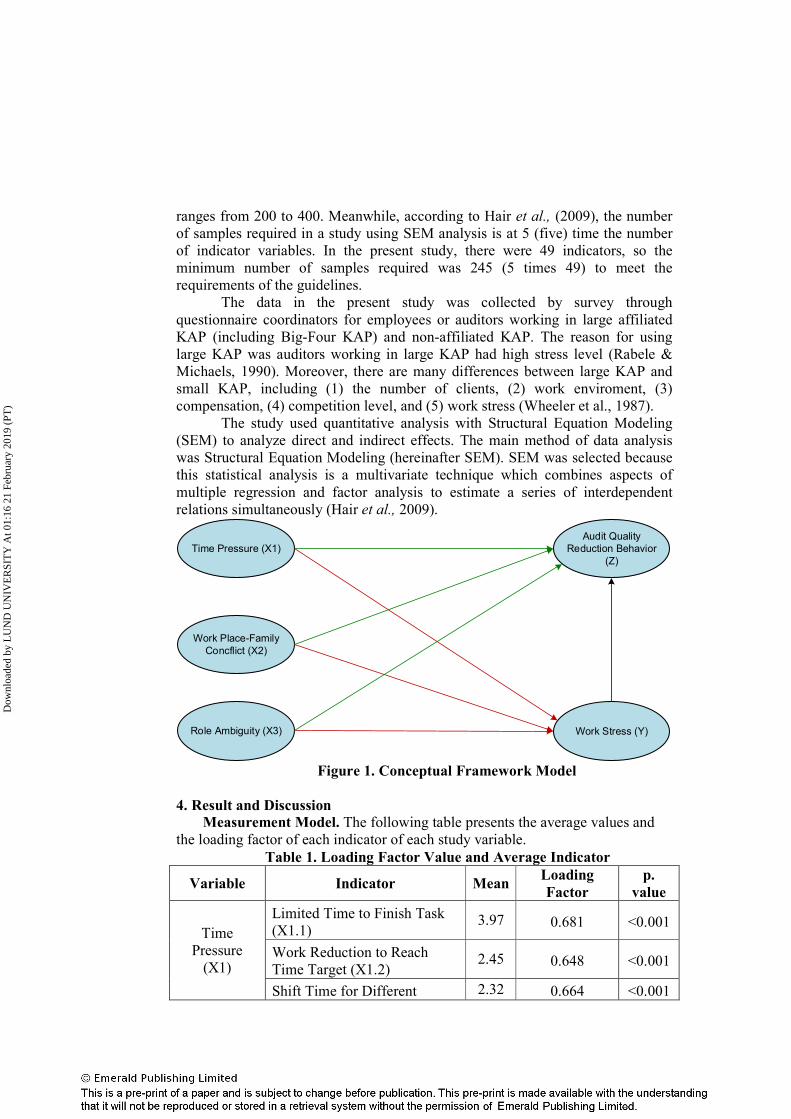

Conceptual framework and hypothesis building. The present study uses

the modified work stress model by Parker and Decotiis (1983) to examine the

effect of stress on audit quality reduction behavior. Moreover, the present study

focuses on the behavior of individual auditor and several variables which cause

stress. The present research study three fields, i.e. work characteristic,

characteristic of KAP and characteristic of individual explain the behaviors

among auditors. Some intra-organization stresses identified by Cooper and

Marshall (1976) are organized into two groups as work characteristic or

characteristic of company.

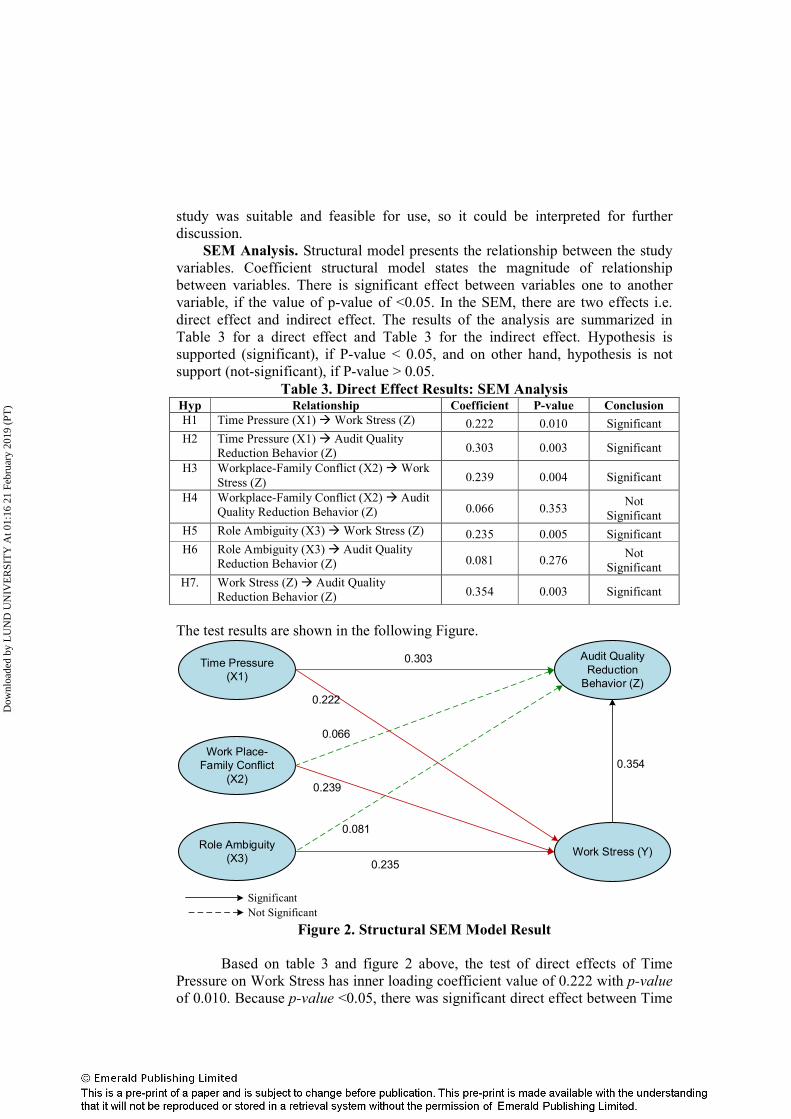

High time pressure in KAP may affect auditor’s behaviors (Otley and

Pierce, 1996a). Similarly, Kelly et al. (1999), reveal that time pressure is a

pressure on the deadline of audit which has been set to finish the audit on time, so

the time pressure will reduce the efficiency and effectiveness of audit, which may

increase auditor’s level of work stress (Lau and Buckland, 2001). In other words,

there is a positive relation between time pressure and work stress, and audit

quality reduction behavior. Based on the description, the following hypotheses

were formulated: H1: High time pressure will increase auditor’s work stress. H2: High time pressure will increase audit quality reduction behavior. Someone professional in their job sometimes has difficulty in balancing work and family demands, leading to internal stress and reducing work satisfaction Moreover, individual facing conflict between work and family will

Dow

nloa

ded

by L

UN

D U

NIV

ER

SIT

Y A

t 01:

16 2

1 Fe

brua

ry 2

019

(PT

)

have confusion and it will cause audit quality reduction behavior. The higher the experienced conflict, the higher the work stress and audit quality reduction behavior. Based on the description, the following hypotheses were formulated: H3 : High workplace-family conflict will increase auditor’s work stress. H4 : High workplace-family conflict will increase audit quality reduction

behavior. Someone who has role ambiguity tends to have reduced physical and

psychological health, as well as anxiety, and they will work less effectively than other individuals (Tang & Chang, 2010). The result of the study by Viator (2001) shows that role ambiguity has negative correlation with work achievement, or in other words, it has positive correlation with auditor quality reduction. Moreover, role ambiguity is also related with job stress. H5 : High role ambiguity will increase auditor’s work stress. H6 : High role ambiguity will increase audit quality reduction behavior. High work stress experienced by auditor may affect the auditor’s work achievement (Choo, 1995; Fisher, 2001; McDaniel, 1990; Rebele and Michaels, 1990). McDaniel (1990) reveals that auditor’s performance will lower significantly if there is pressure which causes the auditor to have work stress. Auditor is said to have high work stress if the work effectively and efficiently, i.e. finishing audit procedure correctly and collecting sufficient evidence and finishing on time (McDaniel, 1990). However, if auditor doesn’t performed audit procedure effectively and efficiently or there is negligence, it will affect audit quality. There is possibility that auditor performs audit quality reduction related with promotion to be performed by the head of KAP. H7 : High work stress will increase audit quality reduction behavior.

3. Methodology

The population in this study was all auditors working in KAP (Public Accounting Firms) in Indonesia. The Public Accounting Firms consisted of The Big-Four, affiliated KAP (outside of Big-Four) and non-affiliated KAP. The analysis units in this study were auditors at all levels of hierarchy of KAP organizations, i.e. junior auditor/staf, senior auditor, manager audit, and audit partner and those involved in implementing audit program on corporate financial statement audit performed by the KAP, who had minimum audit experience of 2 (two) years. The criteria were used because generally auditors who have at least 2 (two) years of work experience in KAP are given responsibility to perform audit program.

The sample selection in this study was performed by purposive sampling method because it was based on the criteria set by the researcher. Furthermore, random sample selection didn’t necessarily produce samples which represented auditors at all levels and types of KAP. The present study used the 2016directory of members of Indonesian Public Accountant Institute. Sample selection was determination of the size of the research samples. The determination of the number of samples was based on the size of the samples required by data analysis using structural equation model. According to Ghozali (2008), the number of samples required for maximum likelihood estimation by structural equation model

Dow

nloa

ded

by L

UN

D U

NIV

ER

SIT

Y A

t 01:

16 2

1 Fe

brua

ry 2

019

(PT