june 1995 - iaph

TRANSCRIPT

June 51995Vo1.40 No.

The main passenger terminal in Lisbon (Roeha do Conde de Obidos)

AUTHORITY OF THE PORT OF LISBON

Rua da Junqueira, 94 - 1349 Lisboa CodexTel.:3611024-Fax:3611019

A more rational use of the existing equip

ment and certain building, to say nothing of

improving the road and rail approaches to the

Port of Lisbon (which are expected to cost

some Esc.: 15 000 000 000$00) will make the

port more attractive commercially, thus

paving the way for additional recourse to its

services and, consequently, the offer of more

competitive charges for international

sea-going traffic.

A new passenger terminal is due to operate

throughout 1995 at Santa Apol6nia facilities,

while the existing Santa Apol6nia Container

Terminal (TCSA) is to 18 ha (app.) with a

1,300 m long wharf and draught of 8,5 m (app.)

We are adapting an existing warehouse at

Jardim do Tabaco to become the third

passenger terminal in Lisbon, besides Rocha

and Alcantara.

Rocha is the existing main terminal,

Aldintara has mixed functions and is used

solely when Rocha is fully occupied and there

are extra vessels in the port or if some vessels

have a deeper draught.

Jardim do Tabaco will provide a new terminal,

10 minutes away from the airport and in the

city center, in the vicinity of the most typical

quarter in town - Alfama - which was a former

Moorish area, near Lisbon's castle.

Third passenger terminal will be here, just in the City Center

IMPROVEMENT IN THE COMPETITIVITYAND EFFICIENCY 0F THEPORT OF LISBON

Ports & HarborsJune, 1995VoI. 40No. 5

Port arbors Published byThe IatematioDaI AssociatioD.ofPorts aDd HarborsNGO Consultative Status, United Nations(ECOSOC, UNCTAD; IMO, CCC, UNEP)Secretary General:Hiroshi KusakaHead OfJice:Kotohira-Kaikan Bldg., 2-8, Toranomon1-chome, Minato-ku, Tokyo 105, JapanTel: 81-3-3591-4261FaX: 81-3-3580-0364Telex: 22225t6IAPH JCable: "IAPHCENTRAL TOKYO"

IAPHOfficersPresident:

Carmen LunettaPort Director,·Port of MiamiU.SA.

First Vice-President:Robert CooperChief ExecutivePorts of Auckland Ltd.New Zealand

SecoDd Vice-President:Jean SmaggheInspector GeneralMinistry of Equipment,Transport and Tourism,FranceExecutive Vice-President,International Affairs ofAssociation of FrenchPorts (UPACCIM)

Third Vice-President:Oominic TaddeoPresident & Chief Executive OfficerPort of MontrealCanada

CoDfereace Vice-Presidents:Mic R. OinsmoreExecutive DirectorPort of SeattleU.SA.

John J. TerpstraExecutive DirectorPort of TacomaU.SA.

ContentsIAPH ANNOUNCEMENTS & NEWS

Board to Appoint Nominating Committee Members. Thailand RetractsCandidacy for Host of 1999 Meeting 3

IAPH Information Technology Award 1995 .4The IPD Fund Contribution Report 6Mr. Kondoh Represents IAPH at WCO Regional Meeting. Membership

Notes. IAPH African/European Members Meet in Paris 7OPEN FORUM

Special Report on Shipping Firms' Prospects ." 10INTERNATIONAL MARITIME INFORMATIONWORLD PORT NEWS

Anti-Drugs Alliance Between HMC&E and BPA • Regional Seminar onDrug Enforcement 20

International Standards Help Transport People, Goods • MarineIndustry '95 in Tianjin Sports Center • Electronic Commerce:A Giant Step Forward 22

Seaport Development Conference in London. New Publication 23The AmericasNorth Fraser Policy for Safe Transport of Goods 24Japan Remains Leading Market for US Exports,. Long Beach

No. 1 North America Container Port. Errol Bush ElectedChairman of AAPA 25

Home Depot's New Facility in Savannah. Louisiana, Panama Work onLong-range Plans. Port of Redwood City: Tonnage onRecord Pace 26

Africa/EuropeDirect Train Service Between Lille and Le Havre • Biggest Containership

Calls in at Le Havre. New Loading/Unloading System atGoteborg 27

World's Longest Quay Getting Even Longer. Dublin: Irish Record forFreight Throughput • KPA Signs Cooperation Pact With Hamburg ...28

New UK Independent Port Association Launched. Largest-everS. African Cargo: Immingham • Felixstowe: £3.5 MillionSystems Contract 29

PLA Head Re-affirms Commitment to Future 30London's Position as UK's Largest Port Intact 31Asia/OceaniaPort of Quingdao: Great Containerization Efforts. .. 31Kawasaki Contributing to Met Area Distribution • World Class Cement

Terminal at Jurong • Hong Kong Remains Busiest Container Port• Hong Kong: Anchorages, Fairways Rearranged 32

Yokohama: Its Diverse Activities and Vision 33Yokohama to Kobe: Requital After 72 Years .36

The Port ofNagoya'sMeiko West BridgeMain Span: 405mHeight: 38m

isfor Convenience.

one

1801

"$~'- laPORTOfNAGO'lA

NAGOYA PORT AUTHORITY8-21 Irifune 1-chome Minato-ku Nagoya 455 JAPAN

Tel: 81-52-654-7840 Fax:81-52-654-7995

IAPI1 ArlrlOUrlCEMErlTSArlDrlE~VS

Board to AppointNominatingComm. Members

In accordance with the requirements of the By-Laws, five committees are to be formed for each conference of our Association.Of the five conference committees, the members of theNominating Committee (which will prepare the nominations ofthe offices of President, First Vice-President, Second VicePresident and Third Vice-President for the next two-year term,and will present them to the Board) are to be appointed by theBoard, while those of the other four committees - the Credentials,Budget, Resolutions and Bills and Honorary MembershipCommittees - are to be appointed by the President from amongthe Association's eligible members whose registrations have beenconfirmed.

The Secretary General, upon consultation with the President,has prepared a list of the proposed Nominating Committee members and submitted it to the Board of Directors for their voting bycorrespondnce, setting the voting date for May 27, 1995.Furthermore, the memberhip of the other committees is to beappointed by President Lunetta prior to the June Conference. Theproposed membership of the Nominating Committee submittedfor Board's voting was as follows:

Proposed Membership of theNominating Committee

(The meeting is scheduled for 1700-1730, Saturday,June 10, 1995)

African/European Region:PJ. Keenan, Cork Harbour Commissioners, IrelandlM. Moulod, Port of Abidjan, Cote d'lvoireA. Graillot, Port of Le Havre, France

American RegionD.F. Bellefontaine, Port of Halifax; CanadaC. 1 Lunetta, Port of Miami, U.S.A. (as Chairman)C. M. Rowland, Canaveral Port Authority, U.S.A.

Asian Region:John Hayes, Maritime Services Board of New South Wales(Sydney), AustraliaH. Toshima, Ministry of Transport, JapanGoon Kok Loon, Port of Singapore Authority, Singapore

Thailand RetractsCandidacy for HostOf 1999 Meeting

The Secretary General has recently received a letter dated April24, 1995 from the Director General of the Port Authority ofThailand (PAT), confirming that the PAT has decided to withdraw its candidacy for the host of the 21 st IAPH Conference to beheld in the Asian Region in 1999. The PAT Director General Mr.Sunananta says, "We would not be in a situation to adequatelypresent the case for Thailand to host the 21 st World PortsConference in 1999 and have therefore decided not to proceedwith our candidacy. He further comments, "We believe that, inthe absence of Thailand, the three other candidate ports of Klang,Osaka and Yokohama can provide very acceptable venues for theConference which will illustrate the dynamic growth of the Asianregion."

In closing his letter, Mr. Sunananta says, "I regret having to takethis decision but you may rest assured the Port Authority ofThailand's representatives will be attending the 19th IAPHConference in Seattle. We will also be pleased to continue to support IAPH activities in the future."

Under the circumstances, the candidates for the host of the 21stIAPH Conference (as of April 26, 1995) are: Port of Osaka(Japan), Port Klang (Malaysis) and Port of Yokohama(Japan), asa result of the withdrawals of Kobe (in January 1995) and now thePort of Thailand (in April 1995).

IAPH REGISTRATION AS OF MAY 18, 1995TOTAL DELEGATES REGISTERED: 434TOTAL ACZCOMPANYING GUESTS REGISTERED: 170TOTAL NUMBER OF REGISTRANTS: 604

CONFERENCE HOTELThe Westin Hotel, Seattle: The Front Door To City. Seattle's grandentrance to the city's most inviting neighborhood, located in the centerof shopping and popular attractions. The Westin has panoramic viewsand deluxe amenities including a pool, spa, fitness center & 24-hourroom service. For dining, choose from the elegance of The Palm Court,NIKKO Japanese restaurant or Market Cafe. The Westin Hotel,Seattle. 1900 Fifth Avenue, Seattle, Wash. 98101. U.SATe/:(206)728-1000 Fax:(206)728·2259

PORTS AND HARBORS June, 1995 3

VIET PORTEX '95The 1st International· Exhibition for Portand Waterway Construction, ShipbuildingIndustr)', Offshore Technology and Transport

November 21-24, 1995

IAPH InfonnationTechnology Award 1995

To the call for papers for the IAPH Information TechnologyAward Scheme 1995, which was established last year at the initiative of the IAPH Trade Facilitation Committee chaired by Mr.David Jeffery (Port of London Authority) to recognize the outstanding application of information techonology in a port, by theclosing date set at 4 pm, Japan time, April 21, 1995, a total offour papers had been received from the following organizations.

List of Entrants to IAPH InformationTechnology Award 1995

1. Sundsvalls Hamn ABBox 805S-851 23 SundsvallSwedenFax: +4660 193507Attn: Mr. Owe Linton, President

Ho CHI MINH CITY, Vietnam

--------------------------------------------~

If you want to be kept posted right from the start aboutVIET PORTEX '95, just return this coupon. We will send youall the important information free of charge.

YES,I'd like to be kept up-ta-date on VIET PORTEX '95 4. Nagoya·Port Authority

8-21 Irifune l-chomeMinato-ku, Nagoya 455JapanAttn: Ms. Ooharu, Port Promotion

2. Empresa Nacional de Puertos S.A.Av. Guardia Chalaca SINCallao, PeruFax: (511) 4658158Attn: Mr. Juan R. Atkins

3. Puerto de SantanderCarlos Haya, 2339071 SantanderSpainFax: (42) 311312Attn: Mr. Ignacio Merino, Logistics Manager

visitor 0

First name

I am exhibitor 0

Surname

Company

The entry papers are being reviewed and screened by theSelection Committee, which is composed of the following individuals:

Adress

Country

VIET PORTEX '95Project Management

Hamburg Messe und Congress GmbHJungiusstraBe 13· D-20355 Hamburg

Federal Republic of GermanyTel.: +49 40/35 69 - 21 90/92

Fax: +49 40/35 69 - 21 87 . Tx: 21 2609 messe

David Jeffery, Chairman of the IAPH Trade FacilitationCommittee (London)John Hirst, Executive Director, The Association ofAustralian Ports and Marine Authorities, a member of the IAPHTrade Facilitation CommitteeUdo Mehlberg, Director of Technology & Research, Port ofTacoma, representing the host ports for the 19th World PortsConference of IAPHRinnosuke Kondoh, Deputy Secretargy General, representing theIAPH Head Office

The results of the Selection Committee's deliberations willbe announced by May 26, 1995. The presentation of the awardsto the successful applicants will be made during Working SessionNo.6, which is scheduled for the morning of Friday, June 16, .1995 dealing with Technical Committee Activities in the ''TradeAffairs" Group.

4 PORTS AND HARBORS June, 1995

TRADE OLD ROUTES FOR THE NEW WAY TO GO - POIn OF MIAMI.More and more shippers wqrldwide now recognizePort of Miami's unique adv~tages:

A ~trategic location as thenaturaI hub for trade betweenNorthiAmerica, Latin Americaand the Caribbean.

Th~ most service to and ;from Latin America and the~aribbean, with steadily ;growing traffic to and from ~urope.

Quick distribution of spipments from the FarEast and Europe throughOllt the Southeastern D.S.,with rapid "in transit" delivery to Latin Americaand the Caribbean.

The first port with complete capabilities to serve

. •...~

Panamax vessels once tley transit the Panama Canal.Computerized tern}inal operating systems to

provide real time cargo status, automated gates,bookings and release~ fully integrated with D.S.Customs and other fed$'al regulatory bodies.

Cohesive, ongoing~evelopment that recentlyadded 80 acres of spac~, 3 new RoRo berths, 1,000feet of additional container berth, and 4 moregantry container cranes~

For information on ~e world's new "Way To Go':write Port of Miami, (~015 North America Way,Miami, FL 33132, or:l .~call (305) 371-7678;.;1 n' PORTofFax (305) 347-4843.rl MIAMII PORT OF THE AMERICAS

I

The IPD Fund: Contribution Report

Contributions to The Special FundSince June 1992

(As of May 10, 1995)

100

300180200250500

570243500

150500

1,000860274

3,185

367200

1,000100500518

3,564250100

1001,000

500254

1,90550032

US$54,159

Deparment of Transport South Australia,Australia

Marine Department, Hong KongMaritime Services Board of New South Wales,

AustraliaMauritius Marine Authority, MauritiusMelbourne Authority, Port of, AustraliaMiri Port Authority, MalaysiaMontreal, Port of, CanadaNagoya Container Berth Co., Ltd., JapanNagoya Port Authority, JapanNanaimo Harbour Commission, CanadaNapier, Port of, Limited, New ZealandNew York & New Jersey, Port Authority

of, U.S.A.Niigata, Port of, (Niigata Prefecture), JapanOkubo, Mr. Kiichi, JapanOsaka, City of, JapanOsaka Port Terminal Development Corp.,

JapanPacific Consutants International, JapanPenta Ocean Construction Co., Ltd., JapanPoint Lisas Industrial Port Development Co. Ltd.,

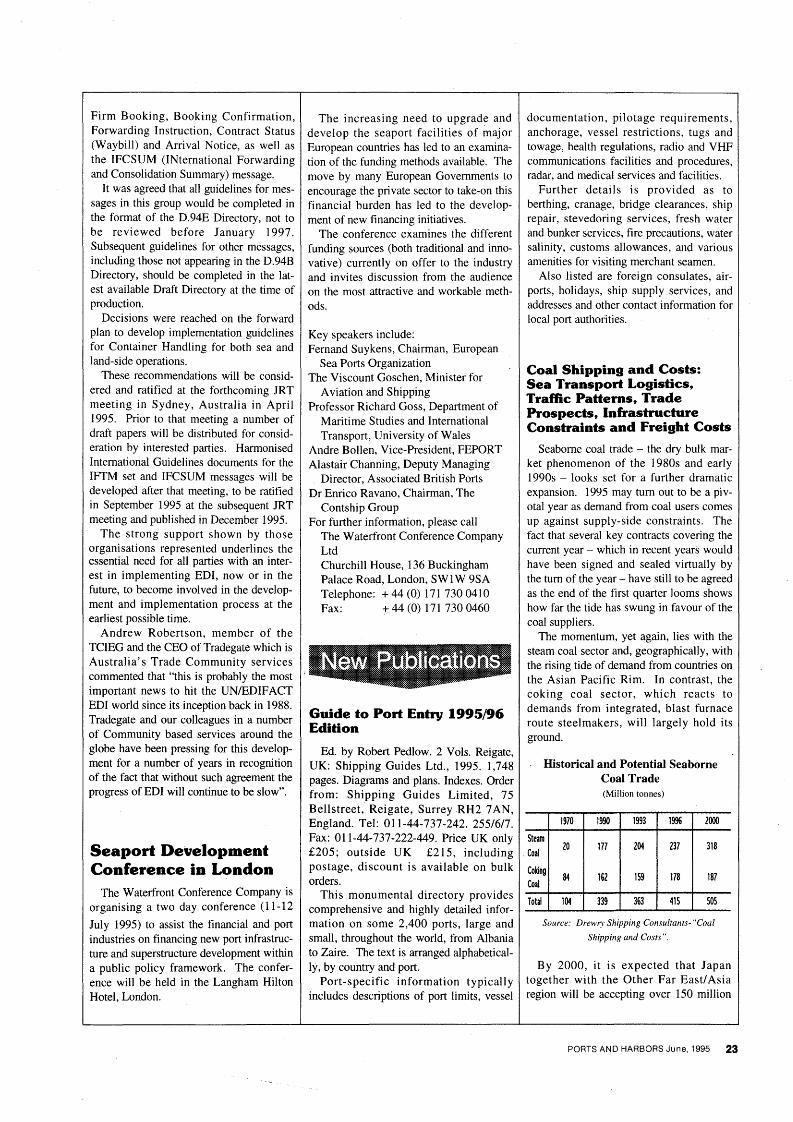

Trinidad*Primer Concurso Internacional de Memorias

Portuarias: Carlos Armero Sisto, Anuariode Puertos: Buenos Aires, Argentina

Public Port Corporation I, IndonesiaPusan East Container Terminal Co.Ltd., KoreaQubec, Port of, CanadaShipping Guides Limited, U.K.Solomon Islands Ports Authority, Solomon

IslandsSouth Carolina State Ports Authority, U.S.A.Tauranga, Port of, New ZealandToyama Prefecture, JapanUPACCIM (French Ports Association), FranceVancouver, Port of, CanadaYamaguchi Prefecture, JapanTotal:

Spreial Report on Shipping Fmns' Prospectscnntributed by 'Box Carriers' MagazineIn January this year, Box Carriers magazine which is pub

lished monthly by Tokyo News Service, Ltd., carried a specialreport of 'how leaders of the world's liner shipping firms viewtheir administations' prospects on the basis of interviews thepublisher conducted late last year. For the benefit of IAPH'sworldwide members, the publisher has made special arrangements for us to allow the reproduction of the report, whichoriginally appeared in the January 1995 issue of Box Carriersmagazine. It is with the deepest appreciation that we introducethis valuable report in the OPEN FORUM column of thisissue.

*Ist International- Contest of Port Annual Repprts sponsored bythe Yearbook of the Port of Buenos Aires (Editor, Mr. CarlosArmero Sisto)

493

259

267

350

4,000500100

1,000500

1,000200480

516500

1,702200

3,665924100

1,000

2501,000

2501,000

1001,000

3,0003,000

230

Amount(US$)

ABP (Associated British Ports), U.K.Abu Dhabi Seaport Authority (Mina Zayed)

Akatsuka, Dr. Yuzo, Univ. ofSaitma, JapanAkiyama, Mr. Toru, IAPH Secretary General

Emeritus, JapanAuckland, Ports of, Limited, New ZealandBarcelona, Puerto Autonomo de, SpainBintulu Port SDN BHD, MalaysiaCameroon National Ports Authority, CameroCayman Islands, Port Authority of, the

Cayman IslandsClydeport Ltd., U.K.Constanta Port Administration, RomaniaCopenhagen Authority, Port of, DenmarkCotonou, Port Autonome de, BeninCyprus Ports Authority, CyprusDelfzijVeemshaven, Port Authority of,

the Netherlandsde Vos, Dr. Fred, IAPH Life Supporting Member,

Canada 500Dubai Ports Authority, U.A.E. 500Dundee Port Authority, U.K. 250Empresa Nacional de Administracao dos Portos, E.P.,

Cabo Verde 250Fiji, Ports Authority of, Fiji 100Fraser River Harbour Commission, Canada 250Fremantle Port Authority, Australia 250Gambia Ports Authority, the Gambia 250Ghana Ports and Harbors Authority, Ghana 250Hakata, Port of, (Fukuoka City) Japan 1,705Halifax, Port of, Canada 250Helsingborg, Port of, Sweden 500Hiroshima Prefecture, Japan 523Irish Port Authorities Association, Ireland 1,000Japan Academic Society for Port Affairs,

the, JapanJapan Cargo Handling Mechanization

Association, JapanJapan Port and Harbor Association,

the, JapanJapanese Shipowners' Association,

the, JapanJohor Port Sdn. Bhd., MalaysiaKawasaki, City of, JapanKlang Port Authority, MalaysiaKobe, Port of, JapanKobe Port Terminal Corporation, JapanKorea Container Terminal Authority, KoreaKSC (Kuwait Oil Company), KuwaitKudo, Dr. Kazuo, Tokyo Denki University,

JapanLondon Authority, Port of, U.K.Maldives Ports Authority, MaldivesMarine and Harbours Agency of the

Contributors (in alphabetical order)Paid:

6 PORTS AND HARBORS June. 1995

Mr. Kondoh RepresentsIAPH at WOO Regional Meeting

lAP" African/EuropeanMembers Meet in Paris

The World Customs Organization (WCO), which is the working name for the CCC, held a regional meeting on drug enforcement in February 1995 in Tokyo. The seminar was attended byrepresentatives from all Asia and Pacific WCO MemberAdministrations, with the exception of Iran. Representing IAPH,Deputy Secretary Gneral Kondoh of the Head Office attended theseminar. Later in this issue (in its INTERNATIONAL MARITIME INFORMATION Column) we reproduce the report of thefive-day seminar prepared by the WCO's secretariat in Brusselswhich has been made available to this office through InternationalAffairs & Research Division, Japan's Customs & Tariff Bureau,Ministry of Finance, Kasumigaseki, Tokyo.

Following our brief report in the last issue on the regionalmeeting of IAPH AfricanlEuropean members in Paris, in this issuewe are featuring a more comprehensive report on the Paris meeting which was provided by Mr. Jean Smagghe, 2nd VicePresident of IAPH and Chairman of the meeting.

Meeting of IAPH Officialsfrom African/European Region

in the offices of UPACCIM(French Ports Association)

in Parison 14 and 15 March 1995

Tel:Fax:

2nd Vice-President, IAPHCyprus Ports AuthorityPort of HamburgPort of MiamiGuangzhouPort AuthorityPort of Le HavrePort of LimerickPort of Tema (Ghana Ports)Port of SeattlePort of Le HavrePort of Nantes-Saint-NazairePort of LondonIAPH Head OfficePort of TacomaPort of Le HavreEuropean Sea Ports Association(ESPO)Clydeport PlcKenya Ports AuthorityKenya Ports AuthorityPort of AbidjanCameroon National Ports AuthorityPuertos del Estado Espania (SpanishState Ports)Port of Nantes-Saint-NazaireUPACCIMUPACCIMPort of Le HavrePort of Le HavreIAPH European Rep (c/o BritishPorts Association)Port of BordeauxPort of RotterdamPort of DunkerqueDundee Port AuthorityPort of Goteborg

Mr. VallsMr. van der KIuitMr. VergobbiCapt. WatsonMr. Wennergren

Present:

Mr. Smagghe (Chairman)Mr. BayadaMr. BethMs. BoyntonMr. CaoMr. ColobyMr. DonnellyCdr DovloMr. FriedmanMr. GraillotMr. GuillemotMr. JefferyMr. KondohMr. KoonMr. LannouMrs. Le Garrec

1. In his welcoming address the Chairman referred to theslowness of the process of recovery from recession in the Regionand the consequent effects of this on port activity. In France inparticular, an additional difficulty is the feeling of uncertaintyassociated with the current Presidential election process. TheChairman then expressed pleasure at being able to greet the participants, a number of whom had travelled long distances to be

Mr. PateyMs. PernotteMr. PietriMr. PrevotMr. ScherrerMr. Smith

Mr. MatherMr. MkallaMr. KabugaMr. MoulodMr. MoussaMr. Palao

Av. Marina Mercante No. 2107 Piso, Veracruz, VER. 91700

Mailing Addressee: Mr. Herman L. DeutschMarketing Director52 (29) 32 131952 (29) 32 3040

Busan Container Terminal Operation Corporation[Regular] (Korea)Mailing Addressee: Mr. Lee, Hak Koo, President

Associate Member

Advisory Services on Ports and Marine Transport[Class A-3-3] (Australia)Address: 46 Martin Court, West Lakes, SA 5021Mailing Addressee: Mr. Robert Buchanan

Marine ConsultantTel: 61 8-499813Fax: 61 8-499813

Changes

Port of Reykjavik [Regular] (Iceland)Address: Harbour Building

Tryggvagata 17, ReykjavikMailing Addressee: Mr. Hannes Valdimarsson

Port DirectorTel: 354-552-8211Fax: 354-552-8990

Administracion Portuairia Integral de Veracruz S.A. de C.V.(Mexico)Address:

Membership Notes:New MembersTemporary Member

Port of Sundsvall AB (Sweden)Address: P.O. Box 805, S-851 23 SundsvallMailing Addressee: Mr. Owe Linton

Managing DirectorTel: +4660 193525Fax: +46 60 193507

PORTS AND HARBORS June, 1995 7

present as, for example, Mr. Kondoh from the IAPH Secretariat,Tokyo, as well as our African and American colleagues.

The Chairman took this opportunity to express his own personal grief and that of IAPH members to the IAPH Secretariat and itsstaff as well as to our colleagues at Kobe and Osaka, followingthe recent disaster that hit that area.

Mr. Kondoh expressed the thanks of IAPH Headquarters andgrateful appreciation for the many expressions of sympathy whichhad been received following the recent Kobe earthquake disaster.These were duly conveyed to the Port of Kobe.

2.. Ms. Boynton, on behalf of the President of IAPH, expressedMr. Lunetta's regrets for his unavoidable absence. He wished themeeting well in its deliberations. Mr. Mather, in his capacity asImmediate Past President, added his words of welcome and goodwill.

The Chairman said how pleased he was to see so manyAfrican ports represented. This was testimony to the vitality ofIAPH in the region: He also referred to his visit to the PMAWCA Conference in Gambia in October 1994, where about 200people participated.

3.. IAPH Membership in Europe/AfricaMr. Kondoh reported that, generally speaking, more interest

had been shown in IAPH activities and membership during thelast year (240 members from 82 countries). Participation in committee activities was also increasing.

Mr. Bayada, who during visits to various countries in theEastern Mediterranean area took every opportunity to promoteIAPH membership, was hopeful about the current situation. Heundertook to provide Mr. Kondoh with leads to follow up.· TheChairman thanked Mr. Bayada for his excellent work in areaswhich may sometimes be difficult.

Further reports were given by Mr. Wennergren for the Balticarea, Mr. Mkalla for the East African area and Mr. Dovlo for theWestern African area. Contacts in all areas were frequent but little more could be done at present because of the general economicmalaise.

The Chairman noted that, although the location of the midterm Conference 2000 was yet to be determined, such an event,which was likely to be held in the region would be very helpfulfor recruitment purposes..

4.. Links between IAPH, ESPO andthe European Union

The Chairman noted that a measure of the importance attachedto the link between IAPH and ESPO was the presence at themeeting of ESPO's Vice-Presidents and Secretary General.ESPO's President was unavoidably unable to be present but hadsent his apologies for his absence.

Mr. Jeffery, an ESPO Vice-President, explained that sinceESPO's inception in January 1993 with a membership comprisingthe ports of all EU and aspirant States, most attention had beengiven to keeping abreast of Directives, Recommendations and thelike issued by the European Commission and Parliament. ESPO,however, was now becoming more proactive - as, for example, inits development of a Ports Policy paper for presentation toParliament.

ESPO's participation in the Union's Maritime IndustriesForum enhanced contacts with port users and also general awareness of matters of common concern.

Mr. Palao, the other ESPO Vice-President, suggested that therecould be a lack of awareness of IAPH's aims and objectives onthe part of some Commission officials, which may be the fault ofthe Commission's inter-departmental communication systems.He thought it would be useful for IAPH to meet Commission officials to put matters right and, in particular, to make it clear thatIAPH's role was distinctly different from that of ESPO.

Mr. Palao's suggestion met with general approval and ESPO'sSecretary-General was asked to consider how such a meetingcould be arranged.

The Chairman said that a close working relationship existedbetween IAPH and ESPO, which was particularly important in thecontext of IAPH' s access to IMO. It was seen as very helpful tolink ESPO into discussion on IMO activities. In the same waymutual cooperation should exist between ESPO, the African PortAssociations and IAPH. Each of these organizations could beused to encourage action.

5.. Specific African Port ConcernsMr. Dovlo, speaking in his capacity as Chairman, the Port

Management Association of West and Central Africa (PMAWCA), expressed the area's hopes for increased cooperation andtechnical and financial assistance from the European Union andIAPH to deal with a range of problems. For instance, regionaldredging was of great concern because of costs. African portswere considering pooling policy resources in the region. Theseincluded the need to enhance transport management and information systems, the development of human resources and transportintegration.

A major problem had become much more apparent with rapidtechnology change, namely equipment and spare parts deficiencies.

Mr. Dovlo continued that consideration was also being givento the formation of an African Ports Association inclusive of thePorts Managements Associations of North, East, South and WestAfrica to speak with greater authority in relevant fora.

Mr. Mkalla, in his capacity as Chairman, Port ManagementAssociation of East and Southern Africa (PMAESA), noted thatPMAESA had faced reorganisational problems which had now all

From left: F. Palao (Madrid), A.J. Smith (London), R. Kondoh (Tokyo), J. Smagghe (Paris) and P. Prevot (Le Havre).

8 PORTS AND HARBORS June, 1995

but been overcome. A new Secretary General had been appointedto be based in Mombasa, Kenya.

The area's ports were experiencing dredging problems and difficulties with the restructuring of ports. In that latter regard aSeminar would be held in South Africa during November 1995.Arrangements had been made for a Regional Training Centrelocated in Mombasa to tackle port needs, including the exchangeof information between ports and pollution control. The area'sdifficulties were, of course, compounded by local wars andfamine.

Mr. Tchouta Moussa felt that IAPH should give more emphasis to African affairs and concerns and should be restructured forthat purpose. He continued that the bottom line was "What canIAPH do about all the stated problems, and took the view that thestarting point must be an in-depth discussion of them.

Mr. Moulod agreed with his African colleagues and added thatthe area's port managers should become actively involved inIAPH committees.

Mr. Lannou, supported by Mr. Bayada, said that the HumanResources Committee was aware of the problems expressed.Dealing with them in Committee however was subject to the disadvantage of the wide geographical spread of membership. Hewondered, as Chairman Jean Smagghe had suggested earlier,whether it would be feasible to secure the appointment of a VicePresident representing Africa in the Committee or even perhaps inIAPH. It was agreed that a first step would be to ask Mr. GoonKok Loon whether it would be appropriate to appoint a ViceChairman from Afric.a on his Human Resources Committeeand/or to organise meetings in Africa with the help of UNCTADand its TRAINMAR programme.

Mr. Kondoh urged all African members to become moreinvolved in IAPH's business activities.

6. Reports of the TechnicalCommittees' Activities

The Chairman noted with satisfaction the presence at the meet-ing of the Chairmen of the following Technical Committees:

Port Safety & EnvironmentMarine OperationsLegal ProtectionTrade FacilitationShip TrendsCombined Transport & Distribution

The respective Chairmen reported briefly on the more significant aspects of their Committees' activities and confirmed thatthey would be holding meetings on the occasion of the 19th IAPHConference in June 1995 in Seattle.

Mr. Mather drew the attention of Mr. Valls, Chairman,Committee on Legal Protection, to the increasing concern of portsand their officials at difficulties being put in their way by the public in demonstrating against the perceived right of ports to engagein lawful maritime trade. He instanced recent public demonstrations in the UK against the export of livestock through someports, which had resulted in public disorder and, in one case, theforced resignation of a Port's Chief Executive. He asked whetherthe Legal Protection Committee could consider and comment onthe rights and obligations of ports to engage in lawful trade. Mr.Valls agreed to include the matter on the Committee's agenda.

Mr. Kondoh reminded the Chairmen that their reports to the19th IAPH Conference were required for printing purposes by thefirst week of May and that, of course, the co-ordinating VicePresidents needed a copy of their reports before so that they couldsend their own introductions in time.

7. IAPH/IMO RelationshipsThe Chairman reported on developments following the forma-

tion of the IAPH/IMO Interface Group at the Exco meeting inCopenhagen in June 1994, being himself Chairman of that group. Fourwell-attended meetings had been held to date with TechnicalCommittee Chairmen invited to attend ex-officio. He said that theimportance of the subject matter dealt with was.in no doubt, given thecurrent propensity for States and/or Regional groupings such as theEuropean Union to legislate on the basis of IMO Resolutions andRecommendations.

The Group had submitted position papers to IMO on a range ofissues which were under current consideration. Others were planned orunder way.

Mr. Smith, in his capacity as IAPH's Liaison Officer with IMO,underlined the Chairman's remarks and the need for IAPH'sCommittees to establish reasoned, coherent port-related responses to anumber of matters under discussion at IMO. These responses could beused both by IAPH representatives at relevant IMO meetings and as anaide-memoire for IAPH members in their consultations with theirrespective Governments.

Mr. Smith then provided some examples of issues to be addressedby IAPH which would be discussed by forthcoming IMO meetingsduring 1995.

There was general agreement by the meeting as to the importance ofthe Group's activities and it was proposed that the Group could bemade more effective by the addition of one or two more people fromeach region. In that regard Mr. Palao proposed that an ESPO representative should be included, having regard to the strategic interest ofEuropean ports in IMO activities.

Mr. Palao's proposal was generally supported, together with hisemphasis on the need for cooperation and coordination between IAPHand ESPO. It was accepted, however, that ESPO necessarily reflecteda regional viewpoint. IAPH, on the other hand, needed to secure a balanced global port viewpoint.

To exemplify the situation, ESPO offered to provide IAPH with an'informed' paper on unwanted aquatic organisms in ballast water as acontribution to IAPH's consideration of the subject.

8. Oslo/Paris Commissions

Mr. Smith referred to the urgent need for European ports to assessthe extent to which it continues to be advantageous for IAPH to havemuch prized Observer Status with the Commissions or even, perhaps,whether it might be more appropriate for that Status to be transferred toESPO, being a body representative ofthe Region's ports.

He stressed, however, that Observer Status entailed commitments toensure that an adequate and expert input is made to the relevant workareas of the Commissions.

ESPO representatives agreed to consider the matter and inform Mr.Smith of their decision in due course.

9. Organisation of the SeaITacConference

Audio-visual presentations were made by Mr. Koon, Tacoma, andMr. Friedman, Seattle, on the various facets of the Conference programme.

The meeting made some proposals for amending some aspects ofthe pre-Conference Technical Committee arrangements and WorkingSessions Nos. I, 4 and 6.

Mr. Smagghe, in his capacity as Chairman of Working SessionNo.6, confirmed his acceptance of the proposed revisions. It was thenagreed that Mr. Kondoh would obtain the necessary confirmation fromthe Chairmen of Working Sessions Nos. I and 4 and inform theOrganizing Committee accordingly.

In' his closing remarks, the Chairman again thanked those presentfor their attendance and wished them safe return or onwardjourneys.

PORTS AND HARBORS June, 1995 9

OPErlFOAUMShipping Firms' Prospects

Acknowledgement by the IAPH Head Office: The article is reproduced from the January 1995 issue ofBox Carriers magazine through the special arrangements made by the publisher, Tokyo News Service, Ltd.This office expresses its deep apperciation and thanks to the publisher for the permission accorded to IAPHto publish this valuable report. .

Leaders of World's LinerShipping Firms Air ViewsThe international magazine Box Carriers interviewed the leaders of the

world's liner shipping firms at the end of 1994 about the prospects andisuesfacing them in the new year 1995.The following three questions were asked:1. Your prospects for cargo traffic on the world's major liner routes and liner

shipping markets in 1995.2. Issues the world's major liner operators are expected to address in 1995.3. Issues your firm is planning to address in the new year.

Given below are the opinions of the world's top carriers:

J. (George) HayashiPresidentChief Executive OfficerAmerican President Lines-1. Generally, the outlook for theglobal liner trade is extremelypositive for this year, and that'son top ofsubstantial growth during1994. We expect double-digit expansion in both the transpacifictrade, which is APL's traditionalmarket, and the Asia-Europe trade,which we will be entering inMarch.

Among the positive trends: first,the continued globalization ofsourcing and marketing, as 'companies seek to increase theircompetitiveness; second, theopening or further development

10 PORTS AND HARBORS June, 1995

of emerging markets such asChina, India, Vietnam, easternEurope, Mexico and other areasof Latin America, and - potentially - Cuba and North Korea;and third, the escalated dismantling of tariff and non-tariff barriersto trade through GATT andNAFTA, and the recent APECannouncements from Indonesia.All of this bodes well for globalmanufacturers and retailers, andfor the liner sector. But even aswe witness a strong growth in demand, there is concern that theinflux of new capacity may imbalance the supply ratio in ourindustry.-2. The problem of overcapacityin the liner sector seems to beperennial. The industry will againbe addressing the issue - alongwith related pricing questions as large new vessels come intoservice during 1995-96. In our owncase, much ofthe new tonnage willbe replacement capacity. Also, inthe case of the Asia-Europe trade,we have pledged initially to slot-

charter capacity rather than introduce new vessels of our own,so as 'not to contribute to a supplyimbalance by virtue of our entryinto the trade. The industry hasmade impressive strides in the useof alliances and rationalizationofvessel operations to mitigate thecapacity problem, while at thesame time improving service to thecustomer.

When people ask me why overcapacity is so prevalent in ourindustry, I like to explain that thedevelopment oflarge capital assetssuch as post-Panamax containerships must be undertaken for thelong term, in anticipation offuturetrade growth. These ships havelong economic lives, and vesselreplacement programs by theirvery size and nature cannot beprecisely timed to coincide withrare periods of demand imbalance.The opposite. of overcapacity, ofcourse, is a situation that is notdesirable to the customer community; an undertonnaged trade canresult in severe space constraintsand lack of service predictability.

Another issue some in the industry will grapple with in 1995(and beyond) is how to ensure anadequate return in a fiercelycompetitive, capital-intensive business - one in which the econmhicplaying field is not level. Witheconomic returns as low as theyare, it may seem surprising thatthe industry continues to reinvestcapital in the form ofnewbuildings,

new technologies and new marketsand services. In fact, some of thismassive investment occurs in partbecause many operators do nothave to pay equitably for capital,or to adhere to the same economicobjectives as those of us who mustgenerate a reasonable shareholderreturn. We compete every day withsuch companies.-3. APL has several goals that Imight share to help answer thisquestion. First, we'd like to workwith our alliance partners to develop additional areas for rationalization - beyond ship assets.These might include terminals andland-based operations, for example.

Second, we'd like to work withCongress and the U.S. administration to attempt to revitalizemaritime reform in 1995, andthereby preserve a U.S.-flag presence. Why? We think it's not onlyimportant as a matter of nationalsecurity, but also for commercialreasons; that it's not healthy forexporters and importers in theUnited States ---' the world's largesttrading nation - to rely solely onforeign shipping interests for theirtransportation needs.

Third, we have begun a programto re-engineer and simplify ourwork processes, with the objectiveof making it easier for our customers to do business with us. Weexpect to begin implementing someof these improved processes thisyear.

Olav K. RakkenesChairmanChief Executive Officer

Atlantic Container Line-The North Atlantic started outin 1994 with a situation of extremely heavy volumes in thewestbound direction, leading tovirtually full vessel utilization inthat trade leg. This was due to thestrong economic climate in NorthAmerica, as evidenced by strong

automobile sales and housingstarts. In the eastbound directionvessels were operating in the 60-70percent utilization range with theEuropean economies still comingout of recession.

By the end of 1994, both NorthAmerican and European economies were growing at a healthypace, so that eastbound volumeshad grown substantially closer tothose of westbound, putting several carriers in the pleasant position of being relatively full inboth directions.

The competitive climate has remained quite stable in 1994, despitethe comings and goings of severalnew carriers and increased capacity on the part of several existing operators. As a result, supplywas added to match increased demand without any major degreeof turmoil in the trade. 1995 willsee one new entry, Hanjin, but noother major changes are foreseenat this time.

The key question mark facingAtlantic liner operators in 1995 is

Chen ZhongbiaoPresident

COSCO Group.-1. 1994 has seen great changesin the world economy, trade andthe international shipping market.As far as the liner shipping marketsare concerned, the container carrying capacity has increased to acertain amount on three majoreast/west world liner routes. Apparently, it is more and more difficult for the liner operators tohandle their business because ofthe overcapacity growth whichresulted when a large amount ofnewbuildings entered the services.

Some routes have suffered forsome time from depressed marketconditions where the competitionis fierce; look at the fact that theliner operation of EACBen wastaken over in 1993 and" that CGMof France has withdrawn fromAsia/Europe service recently.

With the world economy recovering further in 1995 and the farreaching GATT agreement, theworld will see expansion of com-

how the regulatory agencies inWashington and Brussels willchange the rules of engagement.The economic environment bodesvery well for a balance of supplyand demand in 1995, with mostlines finally able to consider service enhancements. As an example,ACL will be adding a fifth weeklyservice to the trade as a result ofimproved rationalization with itsoperating partners. Yet that couldall change if the bureaucrats decide to rewrite the laws and changethe way conferences have operatedsince the beginning of containerization.

Of immediate concern is how theEuropean Commission will dealwith intermodal ratemaking, andhow they will rule on the TransAtlantic Conference Agreement.On the other side of the Atlanticare the issues of the future of theFederal Maritime Administrationand tariff filing. The outcomes ofthese two issues will determine thecourse of liner shipping for yearsto come.

mercial trade, which will boostglobal seaborne trade. World boxvolume growth of five percent isexpected in 1995. Transpacificcontainer trade has recorded310,000TEUs in the fist halfof1994,a 12 percent increase over the sameperiod of 1993. A greater growthof transpacific container trade isestimated with the recovery of theU.S. economy and continuance offast growth of the East Asianeconomy. Asia/Europe service willexperience expansion of containervolume as the exports from Chinaand NIEs continue to soar, although the Japanese import andexport volume will decrease somewhat.

However, we have to realize thatmany large containerships beingordered by liner operators willmake a notable impact on the worldliner market, which is not too optimistic for 1995, particularly ontranspacific and Asia/Europetrades where competition is set tobe fierce as large containerships(especially post-Panamax vessels)come into service.-2. In my opinion, there are twoissues they are expected to address.First, the supply and demand on

PORTS AND HARBORS June, 1995 11

extensive growth in China; however, with deployment of largersize vessels by major carriers andexpansion of joint services, competition for cargo procurementwill intensify.

In the Europe-Aisa route, withlarger than 4,000-TEU-class vessels being heavily integrated intothe market, overcapacity is a majorconcern. For the transatlanticroute, a positive increase in cargovolumes is also expected andTACA's efforts to stabilize theservice will foster the maintainingof a favorable market.-2. This year will continue to seeconstruction of larger vessels bythe world's major ocean carriers.Futhermore, these larger vesselspresumed to be deployed mainlyin the Europe-Asia lane, will produce overcapacity by the end ofthe year.

The increase of cooperative relationships between carriers isforseen for the reduction of costsand for the improvement ofservicequality. Thus, the super-consortiatrend will keep going, but the regulation of consoritia will betightened as the principles offree-competition in the maritimeindustry deepen.

Another major issue for themaritime industry this year willbe vessel safety and environmentalconcerns. As safe vessel management becomes an internationalstandard, ocean carriers will beexpected to secure ISO 9000 andISM Code certifications, and amplification of safety and environmental protectionism will be afactor causing an increase of everycarrier's cost base.-3. During this year, HanjinShipping will strengthen international competitiveness to continueits qualitative and quantitativeevolution into a total logisticscompany. The company will alsofocus on service expansion andglobalization of comp~ny management resources through development of new service markets.

In 1995, Hanjin Shipping willbegin new service in the transatlantic trade through a slot-charteragreement with the Tricon consortium. Hanjin's new transatlantic service will link North Europe and the U.S. East Coast by

1. IMF predicts that the worldeconomy will enter a productiveperiod with 3.6 percent expansionin 1995. With this growth, a strongincrease in trade movement is expected this year, but nations andeconomic regions will acceleratetheir efforts for economic leverage.

With the economic recovery ofmajor nations, higher international interest rates will be maintained as countries encourage apolicy of increasing interest ratesto alleviate the pressure on inflatiQn.

According to the various forecasts, the world's largest tradelane, the transpacific, will seecargo volume growth of more thansix percent with the economic recovery of the U.S. and Japan and

bly grow 10 percent and more,whereas Africa may only reach fivepercent.-2. The most important subjectall lines must address is the frontalattack on "cooperative agreements" among shipping lines by theEU Commission in Brussels, to asomewhat lesser extent by theFMC and certain circles in Congress as well as by groups ofshippers (NTLG in the U.S.) and"shippers councils" in Europe andsome Asian countries.

The most dangerous case is thealmost certain move of DG IV inBrussels to declare "intermodalauthority" for conferences illegal.It will endanger the whole systemwhich worked well for over ahundred years.-3. Like most major containercarriers, DSR-SENATOR willprepare itself for the future in thatit will join forces with other lineson most of the trade routes itserves. The aim is to improve service quality and to cut costs.

K.H. SagerChairmanof the Executive Board

DSR-SENATOR LINES-1. 1995 will be a year of consid-erable growth in world trade.Container traffic on the majoreast/west routes will grow at aboutat least eight percent.

North/south things will differ.Latin America's trade will proba-

major container liner routes; andsecond, the coordination and cooperation between major lineroperators.

Being China's leading maritimetransporter, COSCO's main taskis to provide transport service forChina's foreign trade. What I amthinking about is how to meet theneeds of China's growing foreignfrade through the rationalizationprogram of COSCO's fleet..-3. COSCO Group is a multi-na-tional enterprise engaged mainlyin shipping with diversificationof business. It will make efforts forfuture development both on landand at sea.

In 1995, COSCO will strengthenits shipping activities through therationalization of its fleet, improvement of management, appropriate training of seafarers toimprove their service capabilities,and the setting up step by step ofa global shipping network that canprovide its customers with betterand more prompt service.

Apart from shipping activities,COSCO is also getting involved infinance, tourism, air transport,real estate, port management,warehousing, industry,commer-cial trade, insurance and invest-ment, ect., as diversification ofbusiness is COSCO'spolicy . forfuture development.

1995 will be a new year forcontinuing expansion of the Sooho Choland-side industry for COSCO PresidentGroup. Taicang City, which is in Hanjin Shipping Co., Ltd.the vicinity of Shanghai, has beenchosen by COSCO as the land-side -base for future development. Weare looking forward to strengthening cooperation with foreign anddomestic friends to achieve mutualdevelopments.

12 PORTS AND HARBORS June, 1995

offering alternatives to customerswhile preventing undue competition and thus contributing to thestabilization of the trade lane.

In an effort to achieve a fairbalance between the container andbulk trades, Hanjin Shipping willreinforce its bulk fleet, includingLNG vessels, this year. But aboveall of these, our company will makeevery effort to provide servicewhich brings the utmost satisfaction to our customers. I sincerelywish for a prosperous year for allin our industry.

Isao ShintaniPresidentKawasaki Kisen Kaisha, Ltd.-Prospects for the world's majorliner rO\ltes may be summed up asfollows:

North America: Eastboundcargo traffic on the transpacificloute registered a stable growthof seven to eight percent in 1994centering on shipments from Chinaand ASEAN countries to NorthAmerica, under the impetus of theU.S. economic recovery. Regarding the outlook for 1995 and 1996,the growth pace is likely to calmdown owing to high interest ratesand a trend toward higher taxesin the U.S. Basically, however, theU.S. move toward expansion ofimports from Asia has taken firmroot, and a slow annual growthof at least five to six percent isexpected.

The westbound transpacifictrade posted double-digit growthrates in 1994 in stark contrast withstagnation in 1992 and 1993. Majorfactors that can be cited for thisinclude the rapid growth of theChinese economy, the strong yenand an investment boom inSoutheast Asia. As regards theoutlook for 1995 and 1996, thegrowth pace of westbound cargoseems likely to slow down partlybecause of China's tight-moneypolicy. But the purchasing powerstemming from the economic development of Asian countries willcontinue to improve, while the

U.S. will increase pressure forexpansion ofAsia nations' imports.Accordingly, an annual increaseof at least about five percent maybe expected.

As for the ship supply-demandrelationship, no major fleet expansion seems likely to take placein 1996, but no optimism is warranted as yet for 1996 and after.A large-ship building rush currentlyseen among shipping firmsis apparently intended mainly forthe European route. However,there is the possibility that someships will be shifted from the European to the North Americanroute. In that case, the supply-demand situation may ease in spiteof smooth cargo traffic.

Asia: After the end of the ColdWar, intra-Asia trade, as a "factoryof the world" and a "major consuming market," has shown remarkable growth, and in 1993, theintra-Asia cargo traffic reachedabout four million TEUs. Amongthe world's Big Three trade routes,the intra-Asia route ranks secondonly to transpacific trade. It is alsocharacteristic that the intra-Asiantrade has an inter-relationshipwith the transpacific trade.

According to conference statistics on cargo traffic to and fromJapan, an increase of about 12percent was seen in the first halfof 1994 compared with the sameperiod ofthe previous year. Despitethe sustained rise in the yen's exchange value, Japan's exports toother Asian nations continue briskpossibly because the shipment ofmaterials resulting from Japanesemakers' shifting their productionto these countries is gatheringadded momentum. As for China,which is now serving as a"locomotive" for pulling the intra-Asian trade ahead, a calming-down trend may be expectedfrom 1995 owing to the Chinesegovernment's tight-money policy,Hong Kong's reversion to China(1997) and other factors. Nevertheless, the intra-Asian trade isexpected to grow smoothly by fiveto 10 percent from 1995 to 1996.

Europe: The European economystarted to rebound in the secondhalf of last year, and an expansionary trend took root in Germany as well, following Britainand France. Along with these EUnations, the former socialist states

in eastern Europe have also startedto show stable economic growth.

This year, westward cargo trafficis likely to continue smooth growthcentering on daily necessities fromHong Kong, China and SoutheastAsia. Eastbound cargo traffic isalso expected to be brisk, supportedby the economic growth of theseAsian countries.

The problem lies in that thesuccessive commissioning of newlarge-sized vessels by variousshipping firms, which is expectedto start around this spring, willcause the growth of tonnage tooutpace that of cargo volume,which in turn will become a disturbing factor in the market. Inorder to avert the expected confusion, we intend to continue our

. efforts for cooperation transcending the frameworks of conferenceand non-conference lines.

As regards "K" Line's basicpolicy for management and business in 1995, the key phrase willbe "the strengthening of international competitiveness through athorough shift of operations toother countries and the reductionof costs." Under this policy, weare now implementing a sweeping"reengineering" plan with a viewto providing customers with satisfactory service and securingstable revenues even if the yenremains strong at the¥100 level.

Called the "K.R. ("K" Line Reengineering) Plan," this plan isbased on the following two concepts, and we are exerting company-wide efforts to achieve itsobjectives by the end of fiscal 1995.-1. In the liner division, whichis deeply affected by the strong yen,we will set up a structure capableof turning a profit through partialtransfer of business to othercountries, "slimming" of operations, reduction of ship-operationcosts, based on thorough application ofthe principle ofcompetition,and the strengthening of costcompetitiveness, involving the"K" Line group firms, by the timethe K.R. Plan comes to an end.-2. In order to further expand ourbusiness in the marine transportof raw materials and other cargoin bulk, automobiles and energysources, we will assign managerial

PORTS AND HARBORS June, 1995 13

progressive worldwide recovery inconsumer demand will translateinto increased shipping activity,and benefit shipping companies.

We are glad to note the steadyupturn in the American economy,which was also reflected by theU.S. Federal Reserve's concernson runaway growth and inflationrates. The carriers in the Transpacific Stabilization Agreement(TSA) have been successful instabilizing the trade and ensuringthat shippers are provided withadequate capacities at high servicelevels. We expect the transpacificcapacity to grow by only fourpercent to 7.5 percent between 1995and 1996 compared to a sevenpercent and 15 percent cargogrowth on the eastbound andwestbound sectors respectively.

The Far East-Europe trade isexpected to grow by about sixpercent next year against a capacity increase of about eightpercent. Contrary to fears of anovercapacity in this trade, we feelthat this incremental capacity willbe easily absorbed during the peakmonths. The German economy isexpected to recover fully by 1995and be able to lead the rest ofEurope. The advent of CentralEuropean economies will help tofurther boost the ovenill Europeaneconomy.-2. A general concern amongshipping carriers is the potentialscenario of an unmanageable capacity surplus in 1995 when allrecently-ordered newbuildings aredelivered. This concern is a littleoverstated, as these newbuildingdelIveries will be spread over threeyears from 1995 to 1997. Moreover,by 1996 about seven percent of theexisting TEU capacity of theworld's top carriers will be fromships over 25 years of age. Thiscapacity is likely to be scrappedand will dampen the net capacityincrease.

Nonetheless, an enduring problem that box carriers face is thatthe unitized capacity of box shipsis "lumpy" in nature. The container liner industry is more likelyto face a surge in capacity, ratherthan incremental increases, whencarriers replace smaller old tonnages with larger new ones. Carriers can moderate these high increases through space sharing

investment plans, the prime taskwill be to maximize the effect ofintegration with APL, Nedlloyd,OOCL and MISC, which links theBig Four shipping markets of theworld. As for the tramper, dedicated carrier and gas tanker divisions, we intend to tackle, withadded vigor, the task of ensuringsafe and stable transport of energyand other raw materials that support our country.

resources to these sectors on apriority basis to strengthen thesystem of securing stable revenue.

Masaharu IkutaPresidentMitsui O.S.K. Lines, Ltd.-Prospects for the world's linerroutes seems to remain as severeas at present, but the ship supply-demand situation will not beso bad as is generally said. Whenwe consider the economic devel- Lua Cheng Engopment ofAsia and progress in the Chief Executive OfficerEuropean economic recovery, it Neptune Orient Lines Ltd.is conceivable that the supply-de-mand situation will head toward -a large measure of equilibrium on 1. In the last forty years of theboth the Trans-Pacific and Euro- GATT-Bretton Woods era, thepean routes. world economy has grown faster

In short, all will depend on than in any other period in. ourwhether we can rectify the false, history. The establishment of theunjust conference/non-conference World Trade Organization thisrelationship, whicl\ still persists year will ensure that the successfuleven though the quality of service rules for the international ecohas been all but equalized, and also nomic game under the GATTon whether we can normalize the Bretton Woods trading systemcurrent freight rates which have. continues. The root of its positivefallen into confusion due to that impact will be gradually evidentrelationship. I hope that 1995 will from 1995 as nations strive to rebe made the year to start normal- duce or eliminate trade barriersization through concerted efforts and tariffs.of the Japanese shipping commu- 1995 looks a promising year.nity. Since last year, I have been Asia-Pacific economies in factcalling upon shipowners, through started building their foundationsuch forums as the Box Club, to for free and open trade when theshow good sense and voluntarily Asia-Pacific Economic Cooperrefrain from constructing new ation (APEC) agreed in 1994 to setvessels. I hope this appeal will be fixed deadlines to liberalize trade.heeded. Both Japan and Europe appear

As for the issues our firm intends to have emerged from their worstto address in 1995, the most im- recessions during 1994. The diffiportant is to bring to fruition our cult years following Germany's"MOL's Creative & Aggressive reunification seemed to be overRedesigning (MOCAR, 90's)" plan with the eastern part of Germanynow being pushed ahead. The aim now registering impressive growthis to strengthen our structure to rates. The U.S. economy appearsthe extent ofturning a stable profit to have peaked in 1994, but willeven if the yen's exchange value continueitsslowerbutsuregrowthto the dollar rises to ¥90, and to in 1995. The Asian newly indusestablish our system asa powerful trializing economies are expectedcomprehensive operator in the to continue doing well.remaining years of the 1990s with These favorable conditions canan eye to the 21st century. only benefit world trade and the

Regarding our· liner division, shipping industry is a direct benwhich has completed a series of eficiary of the world economy. A

14 PORTS A·ND HARBORS June, 1995

cooperations.It will be cruicial for carriers to

maintain a stable operating environment through responsible actions so that shippers can continueto enjoy the high level of servicethat is being provided.

We are also concerned about thelack of reality on the part of regulators in Europe. The recent objections to the Trans-AtlanticAgreement (TAA) and the Europe-Asia Trade Agreement(EATA) were not justifiable andwere not up with the times. Theobjections of the EuropeanCommission's (EC) CompetitionDirectorate (DG-4) to inland pricing, for example, do not take intoaccount that the shippers' requirements have evolved into onethat demands a comprehensivemultimodal service from shippingcarriers.

The provision for and thus thepricing of inland transportation'services by shipping carriers is nodifferent from the provision of limousine or hotel services by· someairlines. It is customer driven!Attempts by regulators to artificially delineate industries willcreate more confusion than helpconsumers.

In fact, today's ocean carriersshould more accurately be referredto as total transportation providers. The rationalization of oceanand land transportation by carriers or groups of carriers will leadto cost efficiencies that will ultimately benefit shippers.

The EC's unrealistic stand wasalso reflected in the final text ofthe proposed regulation on shipping partnerships which tried toregulate technical space-sharingpartnerships between carriers bycontrolling the size of their marketshares and size of the partnership.This attempt is an antithesis to thecarriers' attempts to minimizecosts by rationalizing their operations and improve on cost andservice efficiency to shippers.

There is a need to increase ourdialogue with regulators like theDG-4 and the Federal MaritimeCommission of the U.S. to putforward our views. Box carrierswill also have to impress on theseregulators that they should concentrate on more pressing issueslike the deregulation of cabotagetransportation, which will directlylead to better service levels and

lower costs to shippers. For example, consumers in Japan and theU.S. are unable to benefit fromcompetition that can be providedby the presence of efficient andlow-cost international carriers oncabotage trade lanes.-3. We will continue to be cus-tomer driven and will base ourstrategies on our customers' needs.We are also radically re-examiningour business theories as the needsof our custome"rs change. Certainoperating assumptions and customer requirements are either nolonger valid or adequate.

In the last three years, NOL hasenhanced its presence in Northand South Asia by taking advantage of the economic boom in theseareas. Our immediate task is toconsolidate our position so thatwe continue to be competitive tomeet challenges in the marketplace.

The NOL fleet has also undergone rapid expansion over the lasttwo years. Since 1992, we havetaken delivery of three 3,600-TEUcontainerships as well as six double-hull Aframax tankers. By 1996,NOL will take delivery of anotherthree double-hull Aframax tankersand six 4,400-TEU containerships.Preparatory work for their deployment will be part of our focus,keeping in mind that we seek toobtain the best possible returns forour shareholders for their investments.

Hiroshi Takahashi'Executive Vice-PresidentNippon Yusen KabushikiKaisha-As for cargo traffic on majorliner routes in 1995, a generallystrong trend may be expected onthe transpacific route. In 1994,cargo traffic from Japan suffereda drop of five to six percent in thefirst quarter from a year before,but recovered to the year-before

level in the second quarter.Briskness was also maintained inthe third and fourth quarters. 1995will see a firm trend. Cargo fromthe ANERA-controlled areasposted a remarkable increase of10 to 13 percent in 1994, comparedwith the previous year.

In 1995, a rise of seven to 10percent may be expected. I amrather optimistic about the shipsupply-demand situation on thetranspacific route as a whole.Westbound cargo traffic on thetranspacific route also showed asubstantial increase in 1994, witha brisk trend also anticipated for1995.

As regards the European route,cargo traffic from Japan to Europetended to be slow in 1994, but in1995, a slight increase may be expected. Cargo from Asia to Europeposted a gain of7.5 percent in 1994,with a further 10 percent rise likelyin 1995.

Among other routes, a more orless leveling-off tendency willprevail on the Middle Eastern,Australian, New Zealand and Latin American routes. By contrast,the intra-Asia trade will show arobust growth of seven to 10 percent.

A major issue confronting theworld's liner shipping firms is, after all, the stabilization of trade.It is necessary to establish mutualtrust through such open and fairdiscussion· forums as the TSA,WTSA, EATA and IADA. As regards policy issues, full attentionwill have to be paid to the trendsof the shipping policies of the U.S.and the EU.

In respect to U.S. shipping policies, moves are are being seenseeking a review of the whole aspect of the FMC, while in the EU,the EC Commission has workedout policies that ignore the established practice of internationalshipping with regard to consortiaand the setting by conferences ofintermodal freight rates. Strongopposition is therefore called foragainst such moves.

The issues facing NYK in 1995are to promote cooperation withthe world's major liner shippingfirms and stabilize trade, to enhance profitability in the linerdivision, and to cope with the ongoing rapid change in the international logistics structure.

PORTS AND HARBORS June, 1995 15

T.R. ChangChief OperatingOfficerOrient OverseasContainer Line-1. We are taking a moderate,optimistic view on market prospects on the world's major linerroutes in 1995. The outlook of theworld economy is positive. AsiaPacific and the USA will continueto be strong; Europe and Japanare on their way to recovery, andthe Uruguay round of GATT isexpected to become a reality. Thefavorable economic environmentwill give rise to buoyant liner tradegrowth in 1995.

However, at the same time, agreat deal ofcapacity will be addedon the major liner routes in thenext two years, particularly in theAsia/Europe trade. In spite of that,1995 will, on balance, still be ahealthy year for the liner shippingindustry.

2. How to maintain trade stability will be a common agenda forthe world's major liner operators.Improving operating efficiencywill also be a common goal for theliner operators. The benefits ofboth will eventually be shared byshippers.-3. Our company will continueto focus on customer service andthe quality of service. To achievethese goals, we have invested inbuilding six 4,960-TEU vessels forour transpacific and Asia/Europeservices as well as one 2,300-TEUice-class vessel for the St. Lawrence service. Complementing thenewbuildings will be a significantinjection of capital for newequipment. In addition to hardware, we will continue tostrengthen our software establishment.

People have always been regarded as one ofthe critical successfactors to our company. The de~

velopment and motivation of ourstaff is essential and we have developed various programs to realize this objective. Informationtechnology and system support is

16 PORTS AND HARBORS June, 1995

also an area where we will injectour resources. We will also continue our emphasis on logisticdevelopment in the PRC in 1995.

Our investments in both hardware and software are aimed toprovide quality service to meet ourcustomers' requirements. Therefore, of equal importance, we willcontinue with our quality assurance process, including obtainingISO 9002 accreditation for all ouroffices and vessel SEP certification. In 1994, our offices in theU.K., France, Germany, and theBenelux, as well as Hong Kong,were accredited and all the vesselsin our fleet achieved SEP certification.

John P.ClanceyPresidentChief Executive Officer

Sea-Land Service, Inc.

-I'll start with a brief update onproductivity and cost reductioninitiatives. Sea-Land has madesignificant progress. The companyachieved $138 million in cost reductions in 1992, added $124 million in cost reductions in 1993 andis on target to reach its goal of$112million in cost reductions for 1994.We expect comparable savings in1995, sufficient at least to offsetinflation.

These gains deliver importantbenefits to Sea-Land. They enhance our earnings, improve ourservice levels, and help us meetour customers' requirement thatwe be a low-cost carrier. This, inturn, improves our market positionand provides operating leverage.

Going forward, our process improvement teams (PITs) will leadthe way. For the last year, ninePITs have been focusing on howwe manage our core functions,from inventory practices and accounts receivables to equipmentmaintenance and safety initiatives. Efficiencies are being realized, services are being improved, and unnecessary costs and

activities are being taken out.Let me focus on the growth side

of our business. We believe thatthe prospects are positive. Cargovolume in all major trades this year- the Pacific, Atlantic, LatinAmerica and Asia-Europe - areup by about 10. percent overall.And over the next three years, weexpect these same trade lanes togrow by another seven to eightpercent each year. Clearly, container shipping is in a period ofsustained growth.

Pacific EastboundOur forecasts show that this

trade lane will finish the year up10.3 percent over last year. Takinga look at 1995 througb 1997, wepredict a compound annual average increase ofsix to seven percent.The continuing U.S. recovery willstimulate growth in the eastboundPacific trade, as will rising consumer confidence, and continuedstrong economies in SoutheastAsia, China and Hong Kong.

Pacific WestboundThis trade will be up by 12 per

cent in 1994 over 1993, and we seeit increasing at seven percent peryear for the next three years. Themarket really made a rebound in1994 and the directional balanceis improving with the reefer tradeleading the way - it's up 22 percentover the first half of 1993. We arealso seeing strong volume growthto China, Hong Kong, and Southeast Asia. A weaker dollar shouldcontinue to stimulate exports.

Atlantic EastboundFor 1994, we see the eastbound

transatlantic shipments up fivepercent, with increases of six percent per year through 1997. Theweaker dollar has helped to liftU.S. exports of commodities suchas chemicals, agricultural products, wood, reefer products, andkraftpaper. While Germany,France and Belgium are leadingthis growth, the United Kingdomcontinues to expand. Exports fromthe U.S. to the CIS are continuingto grow, up 186 percent since 1989.

Atlantic WestboundContinued growth in the U.S. is

helping to feed the transatlanticwestbound shipments of paper,chemicals, machinery, foodstuffsand metals. The strongest growth

rates are from the CIS to theU.S.,and from northern Europe to theU.S. With the improving healthof the European manufacturingsector, volumes in the Atlanticwestbound trade for 1994 were up14.4 percent and we see six percentgrowth for 1995-1997.

Americas NorthboundThe volume of shipments from

Latin America to North Americais up 6.1 percent this year, and weexpect volumes to be up anotherseven to eight percent per yearfrom 1995-1997. Contributing tothis growth of northbound cargois a rise in non-traditional exports,greater containerization of bulkcargos, strong growth in northbound cargo from Central. andSouth America and slightly lowergrowth from Puerto Rico and theCaribbean.

Americas SouthboundWe see volume in the south

bound Americas trade finishingthe year up 9.2 percent for 1994and another eight percent per yearin 1995-1997, although the southbound market is less certain dueto the political uncertainty andhigh inflation. The prospects, ofthis trade are promising and aredriven by free trade policies, investment deregulation and economic growth. Cargo growth isespecially strong in Central andSouth America and increased U.S.investment wiUboost U.S. exports.

Europe to Asia EastboundThis trade will be up 10 percent

in 1994 and, looking out over thenext three years, should grow another seven to eight percent. Themajor commodities shipped in thistrade are chemicals, reefer foodsand machinery. Eastbound volumes are building as Japan gradually rebounds - we see stronggrowth from Europe to SoutheastAsia and China.

Asia to Europe WestboundThe volume of cargo moving

westound from Asia to Europe willgrow about eight percent this yearand will continue with eight tonine percent growth through 1997,thanks in large part to the continued economic recovery in Europe. Westbound cargo will outpace eastbound growth, driven bya rising Asian investment in Eu-

rope and higher demand for Asianconsumer goods, including appliances and electronics, apparel anddry foods.

Supply/Demand:Favorable Picture

Market growth is only one sideof the equation. The other side iscapacity. A number of carriershave announced plans to build newships, and on the surface, thispresents the potential for signif-icant capacity additions. To seethe true impact of supply and demand, we need to look at thesenumbers by trade. In cases wheretrade grows at a faster pace thancapacity, the supply-demand picture will improve for carriers.Overall, we see a favorable picture.

Some examples: in the transpacific, we project annual tradegrowth at about 6.5 percent out to1997, and capacity growth at aboutsix percent. In the transatlantic,annual trade is forecast to growat better than five percent versusalmost flat capacity. In the Americas, trade growth is expected atseven to eight percent, versus anincrease in capacity of just fivepercent. The Asia to Europe tradewill rise by about eight percentwhile capacity will be up only fivepercent.

Asset OptimizationWe see opportunities to take part

in attractive market growth. Thesupply/demand ratio is favorablein most markets and the economicsdo not support continued ratepressure. In fact, this environmentmay allow for rate improvement.To capitalize on these opportunities, we will use what we feel isa unique competitive advantagethat gives us a better understanding of our business than anyoneelse in the industry.

We are developing an innovativeanalytical tool that enhances ourreturns by enabling us to betteruse our assets. This tool helps usbetter understand the total costs- including opportunity costs for each load of cargo we carry.We call this technology the Dynamic Yield Management System,or DYM$. DYM$ takes into consideration a range of importantinformation, including cargoforecasts, equipment availability,terminal capabilities, vessel deployments, cost structures and

rates, in evaluating the yield associated with a unit of cargo.

With DYM$, we are better positioned to manage our equipmentin a way that minimizes emptyrepositioning costs, reduce ourcosts with an enhanced knowledgeof the effect of each unit of incremental volume on our cost structure, provide additional opportunities for "back haul" cargo,increase out system reliability and,above all, capture the greates~

yield from every container loadthat we move.. Our next step will be to tie thesesystems together to optimize cargoflows on a global basis. We areconfident that DYM$ will addsignificantly to our bottom line.

Operational EfficienciesWe have also developed another

new technology that is beginningto deliver sustainable efficienciesin our core business. Our terminalsare the nerve centers of Sea-Land.How quickly we work -our ships,how efficiently we move containersthrough the ports - these are vitalindicators of how well we run ourbusiness.

We took a hard luok at how ourterminals function. Traditionally,each functional area - gate operations, yard operations, maintenance, and ship management has functioned as a separate epJ-,ity.A study showed the benefits oflinking the entire port operationto one system to achieve operatingefficiencies and speed the flow ofcargo to customers. In 1992, webegan developing the TerminalAutomation System, or TAS. Thissystem automates all major functions in the terminal, creates gate,yard, marine, and maintenanceefficiencies and reduces costswhile boosting productivity.

This is a key technology thatwe developed with AT&T and Microsoft. Workers in all areas update container information onhand-held radio units, which thenfeed the information to a mainframe computer that is accessibleto all parties. Everyone knows thecurrent location and status ofeachcontainer. Our pilot of TAS inCharleston, S.C. is running well.Trucker time has been cut by 20percent, our ships are beingworked more efficiently and ourlifts per hour are at record levels.\ The long·term benefits of TAS

PORTS AND HARBORS June, 1995 17

include significant cost reductionsthrough improved productivityand better freight delivery. Thenext step is to implement TAS atour Elizabeth, N.J., terminal, androll the system out at strategiclocations worldwide in 1995-1997.With DYM$ and TAS, Sea-Landhas technologies that enhance ourreturns, are unique to the industry,offer clear competitive advantagesand position us to capitalize onmarket growth opportunities.

T.H. ChenPresident

Yangming MarineTransport Corporation

-1. In macro aspect, it will be 6.7percent growth in global linershipping for 1994. This is certainlybetter than last year's 3.7 percentgrowth. We expect the that growthrate will be more than five percentfor 1995.

a) Far East-North Americatrade: With the help of the lastingrecovery of the U.S. economy, thecargo traffic will experience anoutstanding progress in botheastbound and westbound trade.According to our sources, eastbound trade will have seen 7.2percent growth in 1994, reaching3.9 million TEUs. And we expectthe growth rate can be 6.1 percentin 1995. As for westbound trade,the growth rate will be 14.4 percentand 8.2 percent for 1994 and 1995,reaching 2.4 and 2.7 million TEUsrespectively.

From the above prospectus ontraffic, all carriers will enrollbigger capacity vessels or plan todeploy new ordered vessels intothis trade to upgrade servicequality and to try to take a biggermarket share.

b) Far East-Europe trade:Over-tonnage pressure will stillbe there in this trade. Accordingto reports, utilizations were about66 percent and 80 percent for NorthEurope/Far East trade and FarEast/North Europe trade respec-

18 PORTS AND HARBORS June, 1995

tively in 1994 and are expected toremain the same or experience aslight improvement in 1995.

c) Far East-Mediterranean: ForMediterranean-Far East trade,utilizations were about 68 percentand 76 percent in 1994 for eastbound and westbound respectivelyand are expected to be 72 percentand 79 percent in 1995 respectively.

d) Intra-Asia trade: Intra-Asiantrade continued to be the largest,fastest growing liner trade in theworld in 1994, up 12 percent to 4.4million TEUs. We expect that theannual growth rate will be 10percent in 1995.-2.We believe you may summarizethese issues from the third question below upon receipt of responses from those operators youinvolved in this survey.

-3. For YML, the year of 1995will be one full of hope. YML willproceed continuously with a seriesof improvements to management,fleet, finance, etc., as well asstrengthen hardware to reach ourtarget. Following are major issuesworth addressing in 1995.

(a) Ship Orders: An order for theconstruction of five 3,604-TEUfull-container high-speed vesselshas been placed, all of which areexpected to be delivered by the endof December, 1995 (starting fromMay, 1995) and will then immediately join the main trade routesafter delivery.

In October 1994, YML successfully issued Overseas ConvertibleBonds (OCB) ofUS$160,000,000 forthe portion ofthe above order fund,through which YML has achieveda more positive position in respectto fund operation.

(b) Strategic Alliances: To upgrade our service quality and saveoperating fleet and costs, jointservice remains as one of the majorbusiness strategies for YML.YML's current joint operationsare for Far East/USEC servicewith HJS and Far East/Mediterranean service with CMA/NYK.In 1995, the above mentioned jointoperations will last continuously.In the future, YML is open to seekcooperation with any suitablepartners in any possible trades,even in terminal and other sides.