islamic valuation premium

TRANSCRIPT

Journal of Business Valuation andEconomic Loss Analysis

Manuscript 1095

The valuation premium of the common stocksof Islamic financial institutions

M. F. Omran, Nile University

©2011 Berkeley Electronic Press. All rights reserved.

The valuation premium of the common stocksof Islamic financial institutions

M. F. Omran

Abstract

The study examines the valuation premiums paid by investors for the common stocks ofIslamic financial institutions in the United Arab Emirates (UAE). The UAE stock markets, duringthe period 2001-2005, were dominated by financial institutions which counted for 58% of all listedstocks. The study employs the price to book and the price to sales valuation multiples. Valuationby price to book value is more relevant and accurate for financial firms due to the high liquidity oftheir assets. It is found that there is a strong clientele preference for Islamic stocks despite themodest financial performance achieved in comparison with other financial institutions andinsurance companies. The clientele preference in the UAE, measured by higher valuationpremium, is for Islamic financial institutions first followed by commercial banks and last bytraditional insurance companies and financial services companies.

KEYWORDS: Islamic Financial Institutions, Valuation, Clientele Preference

Author Notes: The author would like to thank Jim Hoffman and two anonymous referees for theirvery helpful comments and suggestions that led to a better presentation of the paper’s ideas. Anearlier draft of this paper was presented at the research symposium in business and economics,American University of Sharjah, February 11th, 2010 and the tenth Islamic countries conferenceon statistical sciences, Cairo, Egypt, December 20-23, 2009. The author would like to thank allparticipants for their useful feedbacks.

1. INTRODUCTION

The interest in Islamic finance has been growing for several years. The interesting

trend in the last few years is the growing interest of non-Muslims in Islamic

financial products and institutions. The interests of non Muslims is obviously not

due to religion but it is rooted in the fact that many of the high risk endeavors

taken by traditional financial institutions are not allowed at all under Islamic

finance. However, the variety of Islamic financial products failed to grow at the

same rate as the growth in interest in Islamic finance. The fact remains that there

are not many products that comply with Islamic laws that can absorb the massive

flow of funds. That could have an impact on profitability of Islamic financial

institutions since they have to accept deposits that they may not have use for.

There is very little written on how Islamic financial institutions perform in

comparison with traditional financial institutions.

Omran (2009) was the first study to examine the financial performance of

Islamic financial institutions compared with traditional financial institutions in the

United Arab Emirates. His results indicate that the return on equity of Islamic

financial institutions lagged behind the UAE stock markets for the period from

2001 to 2005. However, Islamic financial institutions price to earnings multiples

were the highest in the market despite of the poor financial performance. This can

only be attributed to the clientele effect of the UAE investors. They prefer to pay

a premium for their faith namely for the comfort of knowing that their money is in

full compliance with Islamic laws and regulations. The most probable reason for

the low return on equity is the lack of financial products that comply with Islamic

regulations. Therefore, most of the funds lie idle which in turn reduces the return

on equity. Return on equity has three drivers. The first is the net profit margin

which is net profit after taxes divided by sales. Sales in case of financial

institutions are revenues from loans and revenues from other services. The second

driver is assets turnover which is sales divided by total assets. High assets

turnover will certainly lead to higher return on equity. The last driver is the

financial leverage which is total assets divided by equity. It is the second driver

which is the problem in Islamic financial institutions. Total liabilities (and

therefore total assets) are not limited since no financial institution can refuse

deposits. However, the assets’ product mix available for Islamic financial

institutions is still limited which leads to a very low assets turnover and

subsequently lower return on equity. The limited mix of products is due mainly to

the insufficient academic research carried out on how to create innovative

products that comply with Islamic laws and can utilize the idle funds available to

Islamic financial institutions.

1

Omran: Valuation Premium

The objective of the current study is to determine if the results of Omran

(2009) remain valid if different measures of valuation multiples are used. In other

words, is the clientele effect still there if we use different measures of valuation

multiples? We also improve on Omran’s (2009) results by eliminating the

potential bias that could result from using some correlated accounting variables

on both sides of regression. Also, the bootstrapping method is used to drive the

empirical distributions of the extra valuation premiums’ estimates.

The study employs the price to book value and price to sales multiples

instead of the price to earnings multiple used in Omran (2009). The study

confirms the results of Omran (2009) that there is a strong clientele preference for

Islamic financial institutions in the UAE regardless of which measure of valuation

is adopted.

The study is divided into 5 sections with the introduction in the first

section. Section 2 discusses the composition and drivers of values for the price to

book value and price to sales multiples. Section 3 describes the data set. Section 4

examines the significance of the Islamic valuation premiums using the price to

book value and price to sales multiples. Section 5 concludes the study.

2. VALUATION MODELS

Common stocks valuation can mainly be done by one of two methods: discounted

cash flows and price multiples. The discounted cash flows method requires

forecasting future cash flows, dividends payout, growth in dividends, and

discount rates. It also requires the estimation of the growth periods in the case of

supernormal growth when a company is expected to grow at above average

growth rate before it reaches the constant growth stage. A fundamental price is

then reached by discounting all future dividends expected from the stock. Fund

managers may then use that fundamental price to compare it with market price in

order for them to reach a buy, hold, or sell decision. While theoretically sound,

empirically it is quite difficult to apply because of the many estimates of future

variables required. It is even a more difficult method to use in emerging and

developing economies because of unavailable data and lack of transparency. In

sharp contrast to developed economies, emerging markets do not have long

history of data which makes it difficult to compute historical cost of capital and

risk premiums. For example, estimation of historical betas, which are measures of

non diversifiable risk in common stocks, requires a relatively long time series

which are often not available in many emerging markets. Also, emerging stock

markets suffer from illiquidity which leads to stall prices and possible downside

bias in risk measures.

The price multiple approaches to valuation are much simpler and easier to

compute. The multiples relate the price to some fundamental values of the firm

such as earnings per share, book value of equity, sales per share, and cash flows

2

Submission to Journal of Business Valuation and Economic Loss Analysis

http://www.bepress.com/jbvela

per share. The multiples can be taken as a vote of confidence from the market in

case of high multiple and vice versa. It simply means that investors are valuing

the future prospects of the stock fundamentals so much that they are willing to

pay a higher multiple to buy it. The approach is cross sectional in nature since it

compares the price multiple of the company in a specific industry to that industry

average price multiple. For example, an average price to book value multiple of

3.43 for a particular Islamic bank means that investors are willing to pay a price

equivalent to 3.43 times the book value per share of that bank. The average price

to book value multiple along with its standard deviation can be used to judge if a

particular Islamic bank is significantly under or overvalued in comparison to its

peers. Significant deviations from the average should be explained by changes in

important economic variables. An overvalued bank in terms of price to book

value multiple compared with its peer’s average should be explained by some

economic variables such as higher potential growth due to new markets, specific

competitive advantage, or lower cost of capital that led investors to bidding up the

price of the bank’s stock.

The most widely used multiple is the price to earnings per share (PE)

multiple. The PE multiple is used by security analysts to identify mispriced stocks

in addition to corporate finance analysts who are interested in mergers or

acquisitions. However, the multiple suffers from accounting manipulation of

earnings and its ambiguity in case of companies with negative earnings. A

negative PE multiple is hard to explain. The situation becomes more critical in

case of an economy in recession or an economy slowing down as many more

companies can have negative earnings. Alternative multiples such as price to book

value (PBV) and price to sales (PS) can prove more valuable in general in case of

profits recession. They are also more relevant for financial institutions due to the

high liquidity of their assets. Lie and Lie (2002) found that PBV multiple

valuations seem to be more accurate for financial firms in the USA. Tseng and

Lee (2007) found that PS multiple is the most appropriate model for evaluating

financial firms in Taiwan’s commercial banking industry.

The price to book value multiple, PBV, for a stable firm that is growing at

a constant growth rate, g, can be derived as follows. Let P0 represent the common

stock price for a stable company that is growing at a constant growth rate, g, at

time zero. Gordon (1962) showed that the price, P0, is gK

DP

−= 1

0 , where D1 is the

expected dividends at time one, K is the common stockholders’ required rate of

return (cost of equity) and g is the constant growth rate. Since expected dividends

at time one are basically equal to the part of the expected net income that is going

to be distributed to common stockholders, the price, P0, becomes gK

bNIP

−

−=

)1(10

,

where NI1 is the net income per share expected at time one, (1-b) is the dividends

payout ratio, and b is the retention ratio. The formula can be divided further into

3

Omran: Valuation Premium

its principal components when NI1 is replaced by, BV0 multiplied by ROE1, where

BV0 is the book value at time zero and ROE1 is the return on equity expected at

time 1. The price, P0, becomesgK

bROEBVP

−

−=

)1)(( 100

. To reach at the price to book

value multiple, we divide both sides by BV0. The price to book value multiple,

PBV, isgK

bROE

BV

P

−

−=

)1)(( 1

0

0 . The PBV is an increasing function of return on equity and

the constant growth rate and a decreasing function of the retention ratio and the

required rate of return.

The above analysis assumes that the firm has reached maturity and that its

fundamentals can only grow at a constant rate. However, the analysis also applies

to companies experiencing supernormal growth in its early years although the

formulas have to be adjusted to take into account the extra future earnings for the

supernormal growth years. Since no company can keep growing at higher than

average economic growth forever, otherwise the company will be bigger than the

economy itself, the PBV of the supernormal growing company will be higher than

an equivalently priced stable company to take into account the present value of

future growth opportunities.

The most influential variable to affect the PBV multiple is the ROE. ROE

is an indicator of the firm’s overall performance because it provides an indication

of how well the company is creating value to its shareholders. The value of the

firm’s common stocks is determined by the relationship between the firm’s ROE

and its cost of equity, K. Those firms that are creating value by earning higher

returns on equity than their costs of equity will be rewarded by higher market

prices compared to their book values (PBV>1). Those firms that are expected to

just earn their costs of equity capital should be traded at equity prices that are

close to their book values (PBV=1). Those firms that are destroying value by

earning lower ROE than their costs of equity will be trading at lower equity prices

than their book values (PBV<1).

Industries with higher ROE compared with the equity cost of capital will

attract new entrants which will lead to an eventual reduction of the ROE to the

cost of equity capital in the long run. Companies with a competitive advantage

will be rewarded with higher ROE and consequently higher PBV multiples in the

short term. In the long term and with the new entrants into the market the ROE

will reverse towards the equity cost of capital and the value of the stock price will

reverse to the stable constant growth model.

The price to sales (PS) multiple for a stable firm that is growing at a

constant growth rate, g, can be derived as follows. Let P0 represent the common

stock price at time zero for a stable company that is growing at a constant growth

rate, g. The Gordon’s (1962) constant growth model stock price, P0, is gK

DP

−= 1

0 ,

where D1 is the expected dividends at time one, K is the common stockholders

4

Submission to Journal of Business Valuation and Economic Loss Analysis

http://www.bepress.com/jbvela

required rate of return (cost of equity) and g is the constant growth rate. Since the

dividends expected to be paid at time one are basically equal to the part of the net

income at time one that is going to be distributed to common stockholders, the

price becomes gK

bNIP

−

−=

)1(10

, where NI1 is the net income per share expected at time

one, (1-b) is the dividends payout ratio, and b is the retention ratio. The formula

can be divided further into its principal components when NI1 is replaced by, S1

multiplied by NPM1, where S1 is the company’s sales per share at time one and

NPM1 is net profit margin expected at time one. The price at time zero

becomesgK

bNPMSP

−

−=

)1)(( 110

. Since the company is stable and growing at a constant

growth g, S1 can be replaced by its components which are S0 multiplied by (1+g).

The price becomesgK

bNPMgSP

−

−+=

)1)()(1( 100 . To reach at the price to sales multiple, we

divide both sides by S0. The price to sales multiple, PS, isgK

bNPMg

S

P

−

−+=

)1)()(1( 1

0

0 . The

PS is an increasing function of net profit margin and the constant growth rate, and

a decreasing function of the retention ratio and the required rate of return (cost of

equity).

The above analysis assumes that the firm has reached maturity and that its

sales can only grow at a constant rate. However, the analysis also applies to

companies experiencing supernormal growth in sales in its early years although

the formulas have to be adjusted to take into account the extra future sales for the

supernormal growth years. Since no company can keep growing at higher than

average economic growth forever, the price of the company will eventually

reverse towards the stable growth price over time. In the short term, the PS of the

supernormal growing company will be higher than an equivalently priced stable

company to take into account the present value of future growth opportunities.

The most important driver for the PS multiple is the net profit margin,

NPM. A firm’s net profit margin shows the profitability of the company’s

operating activities. An analysis of NPM can indicate the efficiency of the firm’s

operating management. If we assume that the company is as efficient as its

industry in controlling its expenses, the NPM will then reflect the ability of the

firm to charge a premium on its products. Companies with superior products and

higher sales will achieve higher net profit margins due to their ability of dictating

prices. However, in a perfectly competitive environment, new entrants will be

attracted to those industries with higher net profit margins which will eventually

reduce net profit margins to their the long run equilibrium.

3. DATA

The study is a regression analysis of the panel data for the firms listed in the local

share directory in the United Arab Emirates (UAE) from 2001 to 2005. The local

share directory is published by the national bank of Abu Dhabi. The sample has

5

Omran: Valuation Premium

88 companies that are traded in at least one of the two major stock markets in the

UAE, the Abu Dhabi Stock Market or Dubai Financial Market. The sample

includes 8 financial services companies, 18 banks, 19 insurance companies, 6

Islamic financial institutions (3 banks and 3 insurance companies), and 37 non

financial firms in other sectors of the economy. The UAE stock market in the

period of study was dominated by financial institutions. There were 51 financial

firms among the 88 companies listed. The percentage of financial firms is 58% of

all listed companies. The pooled data approach is used in the study. There are 308

observations in the sample. The data are end of year values and pooled in time

series and cross section directions. For example, for each company in the sample

the end of year results are included and pooled with the rest of the companies in

the cross section sample. Since the study is covering a period of 4 years for 88

companies, one should expect 352 observations. However, some companies were

not listed during the whole sample period which led to the 308 observations

collected. Dummies will be added in next section to take into account different

intercepts per industry.

4. ISLAMIC VALUATION PREMIUM

The objective of the paper is to test for the existence of significant valuation

premiums in case of Islamic financial institutions in the UAE. Islamic and

traditional financial institutions count for 58% of all listed companies in the UAE.

Traditional financial institutions include commercial banks, insurance companies,

and finance companies that deal with mortgages and other credit related activities.

The analysis in this section is based on the price to book value (PBV) and price to

sales (PS) multiples.

The analysis in section 2 indicated that return on equity (ROE) is the most

influential value driver for the price to book value multiple (PBV). PBV is

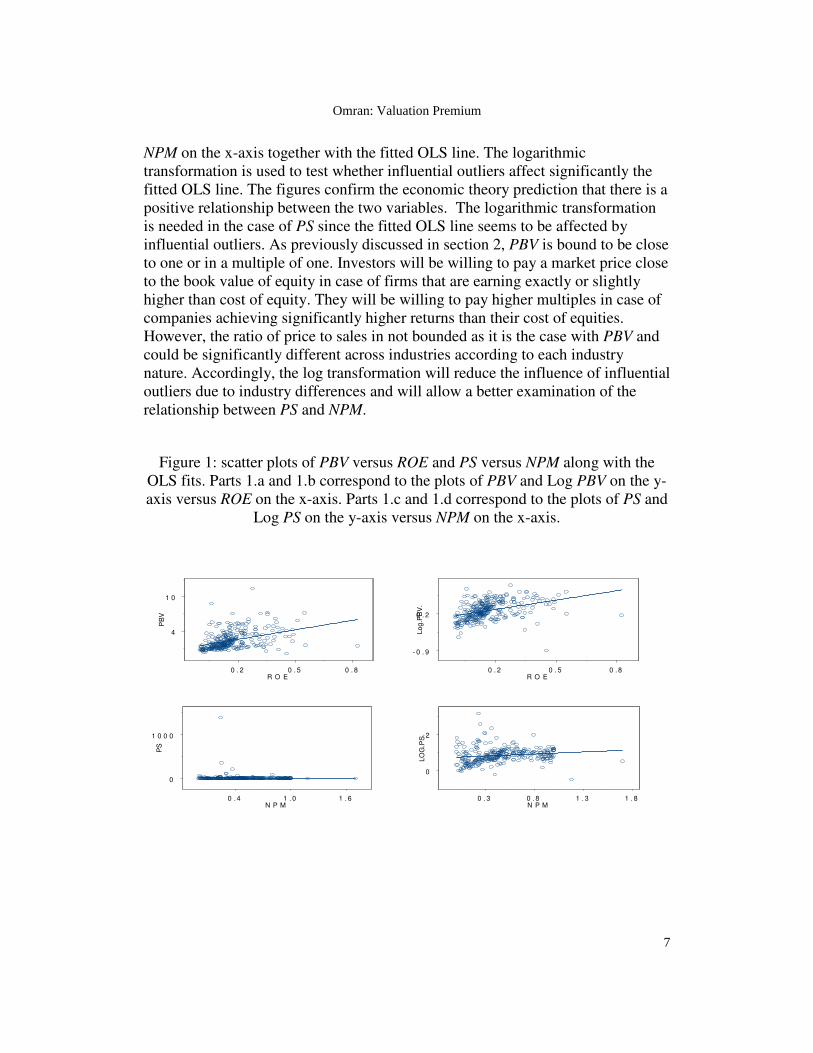

expected to be positively related to ROE. Figure 1.a shows the PBV on the y-axis

versus ROE on the x-axis together with the fitted ordinary least squares (OLS)

line. Figure 1.b has the logarithmic transformation of the PBV to the base ten on

the y-axis versus ROE on the x-axis together with the OLS line. The logarithmic

transformation is used to test whether influential outliers affect significantly the

fitted OLS line. The figures confirm the previously discussed economic theory

prediction that there is a positive relationship between the two variables. The

logarithmic transformation is not needed in the case of PBV since the fitted OLS

line seems not to be affected much by influential outliers.

The analysis in section 2 indicated that net profit (NPM) is the most

influential value driver for the price to sales multiple (PS). PS is expected to be

positively related to NPM. Figure 1.c shows the PS on the y-axis versus NPM on

the x-axis together with the fitted ordinary least squares (OLS) line. Figure 1.d

has the logarithmic transformation of the PS to the base ten on the y-axis versus

6

Submission to Journal of Business Valuation and Economic Loss Analysis

http://www.bepress.com/jbvela

NPM on the x-axis together with the fitted OLS line. The logarithmic

transformation is used to test whether influential outliers affect significantly the

fitted OLS line. The figures confirm the economic theory prediction that there is a

positive relationship between the two variables. The logarithmic transformation

is needed in the case of PS since the fitted OLS line seems to be affected by

influential outliers. As previously discussed in section 2, PBV is bound to be close

to one or in a multiple of one. Investors will be willing to pay a market price close

to the book value of equity in case of firms that are earning exactly or slightly

higher than cost of equity. They will be willing to pay higher multiples in case of

companies achieving significantly higher returns than their cost of equities.

However, the ratio of price to sales in not bounded as it is the case with PBV and

could be significantly different across industries according to each industry

nature. Accordingly, the log transformation will reduce the influence of influential

outliers due to industry differences and will allow a better examination of the

relationship between PS and NPM.

Figure 1: scatter plots of PBV versus ROE and PS versus NPM along with the

OLS fits. Parts 1.a and 1.b correspond to the plots of PBV and Log PBV on the y-

axis versus ROE on the x-axis. Parts 1.c and 1.d correspond to the plots of PS and

Log PS on the y-axis versus NPM on the x-axis.

0 . 2 0 . 5 0 . 8R O E

4

1 0

PB

V

0 . 2 0 . 5 0 . 8R O E

- 0 . 9

0 . 2

Lo

g.P

BV

.

0 . 4 1 . 0 1 . 6N P M

0

1 0 0 0

PS

0 . 3 0 . 8 1 . 3 1 . 8N P M

0

2

LO

G.P

S.

7

Omran: Valuation Premium

Table 1 summarizes the key variables of interest by industry for the period 2001-

2005. The table includes the number of firms in each category. The sample is

divided to five categories, financial services, banks, insurance, Islamic financial

institutions and non financial firms. The table has the average PBV, the average

logarithm to base ten of PS, average growth, average payout, average ROE and

average NPM.

Table 1: Average PBV and log(PS) by sectors along with averages for growth

rates, payouts, return on equity (ROE) and net profit margin (NPM) during the

period from 2001 to 2005.

No. PBV log(PS) Growth Payout ROE NPM

The Whole

Sample

88 2.42 0.85 39.88% 43.67% 16.45%

46.7%

Financial

Services

8

2.33 0.73 90.24% 23.85% 24.13%

56.4%

Banks 18 2.56 0.92 23.40% 33.63% 16.06% 41.5%

Insurance 19 1.66 0.94 33.94% 40.45% 17.68% 82.2%

Islamic 6 3.43 1.34 130.81% 43.21% 13.17% 38.9%

Non Financial 37 2.33 0.68 27.37% 57.46% 14.85% 25.8%

Islamic financial institutions has the highest average PBV of 3.43 followed by

banks at 2.56, financial services and non financial firms at 2.33, and insurance

companies at 1.66. Insurance companies seem to be the least valued sector in

terms of PBV multiples. The table shows that Islamic financial institutions have

1.01 more premium in PBV compared with the average PBV of the UAE stock

markets. Islamic financial institutions have demanded the highest premium

despite of the fact that they had achieved the lowest return on equity during the

period (13.17%). The highest ROE of 24.13% was achieved by financial services.

The growth in total assets of Islamic financial institutions averaged

130.81% during the period in contrast with an overall average of 39.88% for the

market. The huge growth in the assets of Islamic financial institutions is a clear

indication for the UAE clientele preference for companies closely following

Islamic laws despite of the fact that those companies achieved the lowest return

on equity compared with the rest of the companies in the market.

Islamic financial institutions have the highest average logarithm of PS of

1.34 followed by insurance companies at 0.94 and banks at 0.92. However,

Islamic financial institutions had underperformed other financial firms in the

sample when it came to NPM. They had the lowest NPM compared with other

financial institutions although their NPM was still higher than non financial

institutions. Insurance companies achieved the best NPM of all industries. Their

NPM stood at 82.2% compared with an overall NPM average of 46.7%. Islamic

financial institutions had the highest payout ratio among financial institutions.

8

Submission to Journal of Business Valuation and Economic Loss Analysis

http://www.bepress.com/jbvela

They distributed 43.21% of profits. However, their payout was lower than that of

the non financial institutions which was 57.46%.

The next step in the analysis is to test for the significance of the excess

premium for Islamic financial institutions once we have accounted for economic

drivers of value. To achieve that end, two regressions were run. The first

regression controls for the effects of known value drivers on the multiple of

interest. The second regression uses the residuals from the first regression to test

for the existence of significant premium for Islamic financial institutions. Since

58% of the firms included are financial firms, there is a need to account for the

different capital structures. It is expected that financial firms have much more

debts into their capital structure than non financial firms due to the nature of their

business. The average debt to equity ratios for the five categories in our sample

are 53.9% for financial services, 80.1% for banks, 25.5% for insurance, 67.7% for

Islamic financial institutions and 30.1% for non financial firms. The debt to equity

ratio for Islamic financial institutions is much lower than that of banks but still

much higher than that of financial services. A new variable defined as financial

risk is introduced as an independent variable in the second stage regression.

Financial risk (FRisk) is defined as )/(

)/(

II

iii

ED

EDFRisk = where Di/Ei stands for the debt

to equity for firm i and DI/EI stands for the average debt to equity ratio for that

industry (category). A negative relationship is expected between the financial risk

ratio and the valuation multiple of interest since higher financial risk will lead to

higher cost of equity which, as shown in section 2, will lead to lower valuation

multiples for either the PBV or PS. Equation 1 has the first stage regression

equation.

Equation 1

iiiii uPayoutGrValueDriveMultiple ++++= 3210 αααα

Where:

Multiplei: either the price to book value (PBV) or the log to base ten of the price to

sales (PS) for company i,

ValueDriveri : either the return on equity (ROE) in case of PBV multiple for

company i, or net profit margin (NPM) in case of the log(PS) multiple for

company i,

Gi: the growth rate in total assets from one year to the next for company i,

Payouti : the payout ratio for company i,

3210 ,,, αααα : OLS parameters’ estimates,

ui : the random error that is assumed to be normally distributed with zero mean

and constant variance.

9

Omran: Valuation Premium

Equation 1 models PBV multiple or the log(PS) multiple as a dependent variable.

The independent variables are either ROE in case of the PBV multiple or NPM in

case of the log(PS) multiple, growth (G), and payout ratio. The error terms (u) in

equation 1 are assumed to follow the normal distribution with a mean of zero and

constant variance. It is important to state that the objectives behind the first stage

regression are to control for the effects of the independent variables. The

dependent and independent variables on both sides of regression 1 are accounting

variables that are correlated with each other. However, while the accounting

variables correlation may bias the parameters’ estimates of the OLS of equation 1,

the residuals of the regression will still represent information independent from

the accounting variables controlled for by the regression line. The error terms (u)

are used as the dependent variable in the second stage regression. The

independent variables are financial risk, and four dummy variables to represent

financial services, banks, insurance and Islamic financial institutions. The

constant in the second stage regression represents non-financial firms. Financial

risk is used in the second stage regression rather than the first stage since it is a

ratio that is dependent on the firm and its industry. Therefore, it does not suffer

from the same correlation with other accounting variables as other independent

variables used in equation 1. The second stage regression is presented in equation

2.

Equation 2

iii eDIslamicDInsuranceDBanksDFServicesFRisku ++++++= 543210 ββββββ

Where:

ui: the residuals obtained from the first stage regression,

FRiski : the ratio of debt/equity for each company divided by the relevant industry

debt/equity ratio,

DFService: a dummy variable that takes a value of one for financial services such

as mortgages and credit firms, and zero otherwise,

DBanks: a dummy variable that takes a value of one for a bank, and zero

otherwise.

DInsurance: a dummy variable that takes a value of one for insurance companies,

and zero otherwise.

DIslamic: a dummy variable that takes a value of one for an Islamic financial

institution (whether it is a bank or insurance company), and zero otherwise.

543210 ,,,,, ββββββ : OLS parameters’ estimates,

ei : the random error that is assumed to be normally distributed with zero mean

and constant variance.

10

Submission to Journal of Business Valuation and Economic Loss Analysis

http://www.bepress.com/jbvela

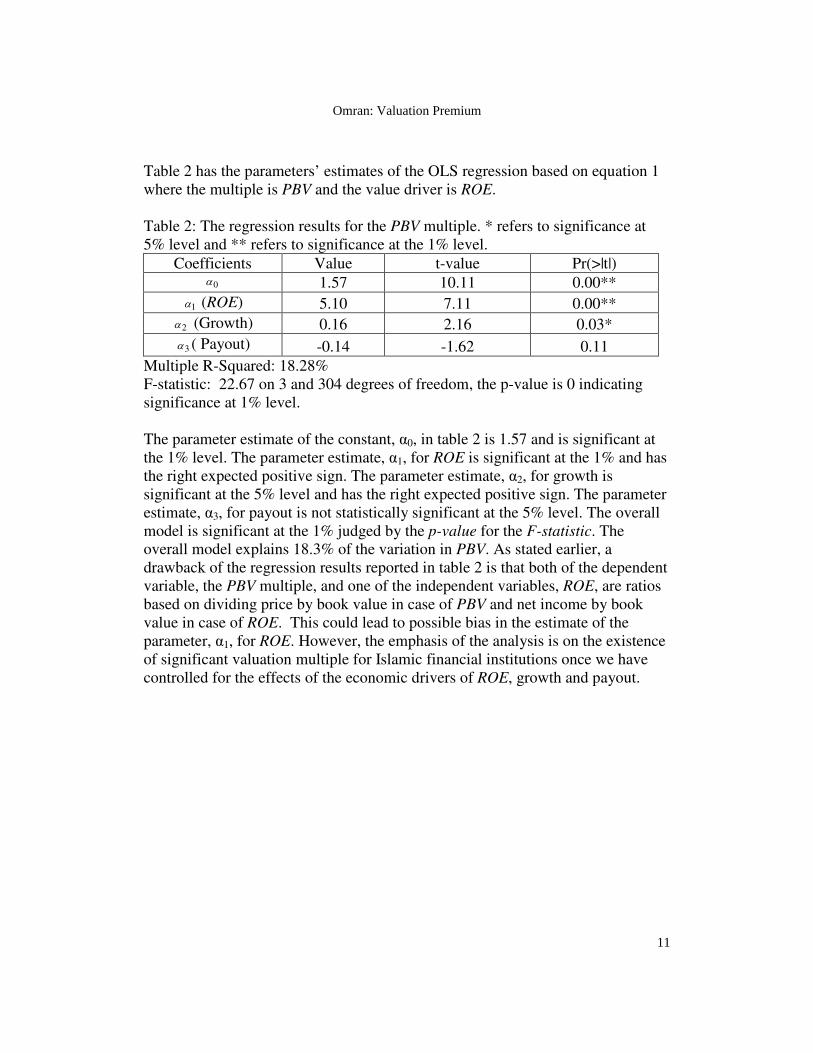

Table 2 has the parameters’ estimates of the OLS regression based on equation 1

where the multiple is PBV and the value driver is ROE.

Table 2: The regression results for the PBV multiple. * refers to significance at

5% level and ** refers to significance at the 1% level.

Coefficients Value t-value Pr(>|t|)

0α 1.57 10.11 0.00**

1α (ROE) 5.10 7.11 0.00**

2α (Growth) 0.16 2.16 0.03*

3α ( Payout) -0.14 -1.62 0.11

Multiple R-Squared: 18.28%

F-statistic: 22.67 on 3 and 304 degrees of freedom, the p-value is 0 indicating

significance at 1% level.

The parameter estimate of the constant, α0, in table 2 is 1.57 and is significant at

the 1% level. The parameter estimate, α1, for ROE is significant at the 1% and has

the right expected positive sign. The parameter estimate, α2, for growth is

significant at the 5% level and has the right expected positive sign. The parameter

estimate, α3, for payout is not statistically significant at the 5% level. The overall

model is significant at the 1% judged by the p-value for the F-statistic. The

overall model explains 18.3% of the variation in PBV. As stated earlier, a

drawback of the regression results reported in table 2 is that both of the dependent

variable, the PBV multiple, and one of the independent variables, ROE, are ratios

based on dividing price by book value in case of PBV and net income by book

value in case of ROE. This could lead to possible bias in the estimate of the

parameter, α1, for ROE. However, the emphasis of the analysis is on the existence

of significant valuation multiple for Islamic financial institutions once we have

controlled for the effects of the economic drivers of ROE, growth and payout.

11

Omran: Valuation Premium

Table 3: The regression results for the residuals of the PBV multiple. * refers to

significance at 5% level and ** refers to significance at the 1% level.

Coefficients Value t-value Pr(>|t|)

0β -0.21 -1.11 0.27

1β (Financial

Risk) 0.24 1.75 0.08

2β ( Financial

Services) -0.39 -1.31 0.19

3β ( Banks) 0.52 2.67 0.00**

4β ( Insurance) -0.84 -4.27 0.00**

5β ( Islamic) 1.01 3.21 0.00**

Multiple R-Squared: 16.55%

F-statistic: 11.98 on 5 and 302 degrees of freedom, the p-value is 0 indicating

significance at 1% level.

The parameter estimates of the second regression of the residuals from equation 1

where PBV is the multiple and the ROE is the value driver are reported in table 3.

The dependent variable in equation two are the residuals obtained from the first

stage regression. The parameter estimate of the constant, β0, is not statistically

significant which is expected since the residuals from the first stage regression

have an unconditional mean of zero. The parameter estimate, β1, for the financial

risk variable is not statistically significant at the 5% level. The parameter estimate

for the premium of the financial services, β2, is not statistically significant at the

5% level. The parameter estimates for the premium of banks, β3, and the premium

for the Islamic financial institutions, β5, are both positive and highly significant at

the 1%, indicating investors’ willingness to pay higher prices for the book values

of banks and Islamic financial institutions. However, the premium (1.01) for

Islamic financial institutions is almost double the premium (0.52) for banks. The

parameter estimate for the premium for insurance companies, β4, is negative and

highly significant at the 1% level indicating that investors are not willing to pay a

high premium for insurance companies. The result confirms with the averages

reported in table 1 where the insurance industry lagged behind all other

companies and traded at a PBV of 1.66. The issue requires some future

investigation since insurance companies have achieved a higher average ROE

(17.68%) than the average ROE (16.45%) for the 88 companies in the sample.

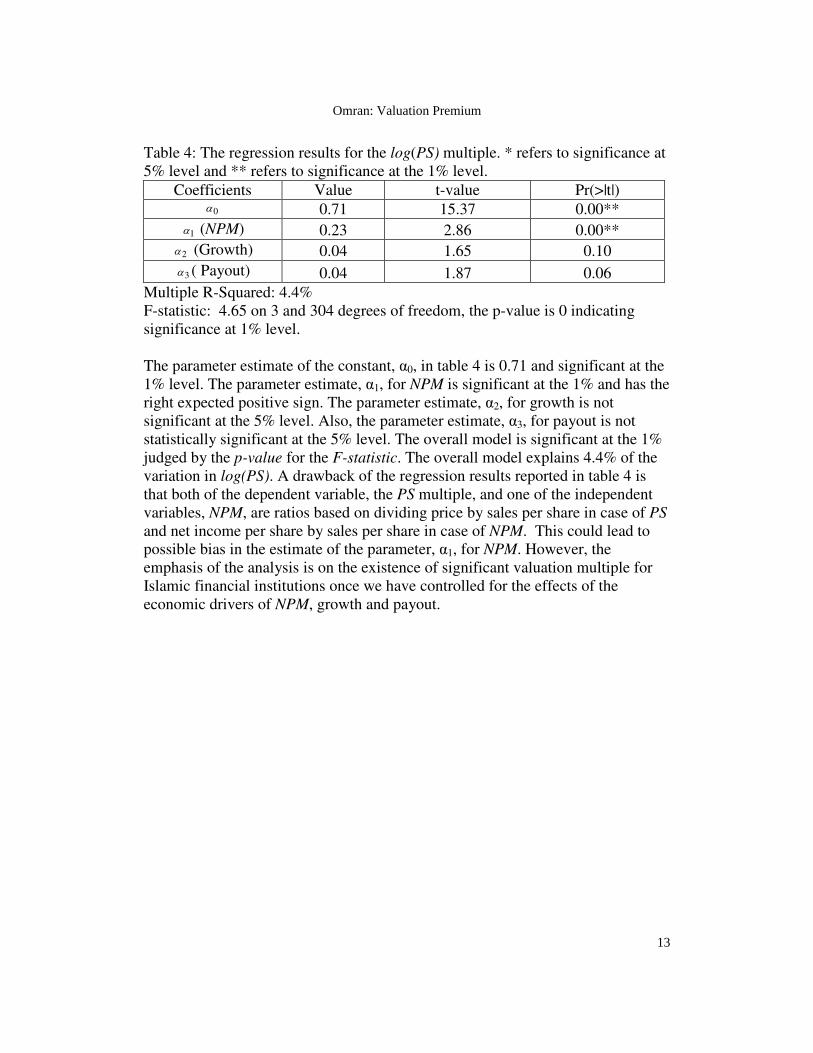

Table 4 reports the parameter estimates for equation 1 where the multiple

is the logarithm to base ten of the price to sales, log(PS) and the value driver is

NPM.

12

Submission to Journal of Business Valuation and Economic Loss Analysis

http://www.bepress.com/jbvela

Table 4: The regression results for the log(PS) multiple. * refers to significance at

5% level and ** refers to significance at the 1% level.

Coefficients Value t-value Pr(>|t|)

0α 0.71 15.37 0.00**

1α (NPM) 0.23 2.86 0.00**

2α (Growth) 0.04 1.65 0.10

3α ( Payout) 0.04 1.87 0.06

Multiple R-Squared: 4.4%

F-statistic: 4.65 on 3 and 304 degrees of freedom, the p-value is 0 indicating

significance at 1% level.

The parameter estimate of the constant, α0, in table 4 is 0.71 and significant at the

1% level. The parameter estimate, α1, for NPM is significant at the 1% and has the

right expected positive sign. The parameter estimate, α2, for growth is not

significant at the 5% level. Also, the parameter estimate, α3, for payout is not

statistically significant at the 5% level. The overall model is significant at the 1%

judged by the p-value for the F-statistic. The overall model explains 4.4% of the

variation in log(PS). A drawback of the regression results reported in table 4 is

that both of the dependent variable, the PS multiple, and one of the independent

variables, NPM, are ratios based on dividing price by sales per share in case of PS

and net income per share by sales per share in case of NPM. This could lead to

possible bias in the estimate of the parameter, α1, for NPM. However, the

emphasis of the analysis is on the existence of significant valuation multiple for

Islamic financial institutions once we have controlled for the effects of the

economic drivers of NPM, growth and payout.

13

Omran: Valuation Premium

Table 5: The regression results for the residuals of the log(PS) multiple. * refers

to significance at 5% level and ** refers to significance at the 1% level.

Coefficients Value t-value Pr(>|t|)

0β -0.04 -0.84 0.40

1β (Financial

Risk) -0.08 -2.16 0.03*

2β ( Financial

Services) -0.03 -0.36 0.72

3β ( Banks) 0.21 3.93 0.00**

4β ( Insurance) 0.14 2.45 0.01**

5β ( Islamic) 0.59 6.73 0.00**

Multiple R-Squared: 16.5%

F-statistic: 11.93 on 5 and 302 degrees of freedom, the p-value is 0 indicating

significance at 1% level.

The parameter estimates of the second regression of the residuals from equation 1

where log(PS) is the multiple and the NPM is the value driver are reported in

table 5. The dependent variable in equation 2 is the residuals obtained from the

first stage regression. The parameter estimate of the constant, β0, is not

statistically significant which is expected since the residuals from the first stage

regression have an unconditional mean of zero. The parameter estimate, β1, for

the financial risk variable is statistically significant at the 5% level and has the

right expected negative sign. As theoretically predicated, higher financial risk

depress the PS multiple. The parameter estimate for the premium of the financial

services, β2, is not statistically significant at the 5% level. The parameter

estimates for the premium of banks, β3, the premium for insurance companies, β4,

and the premium for the Islamic financial institutions, β5, are all positive and

highly significant at the 1%, indicating investors’ willingness to pay higher prices

for the sales per share of banks, insurance and Islamic financial institutions.

However, the premium (0.59) for Islamic financial institutions is almost three

times the premium (0.21) for banks and more than four times the premium (0.14)

for insurance companies. The overall model is significant at 1% level as judged

by the p-value for the F-statistic.

To check for the conformity of the residuals from regression 2 to the

normal distribution, figures 2 and 3 have the quantile to quantile (QQ) plots of the

residuals for the PBV and log(PS) multiples. The QQ plot is a two dimensional

plot with the observed data (the residuals from the second stage regression) on the

y-axis while the corresponding quantiles from the standardized normal

distribution are on the x-axis. In case of normality, the plotted points should be

14

Submission to Journal of Business Valuation and Economic Loss Analysis

http://www.bepress.com/jbvela

close to a straight imaginary line going from the lower left corner to the upper

right corner of the graph.

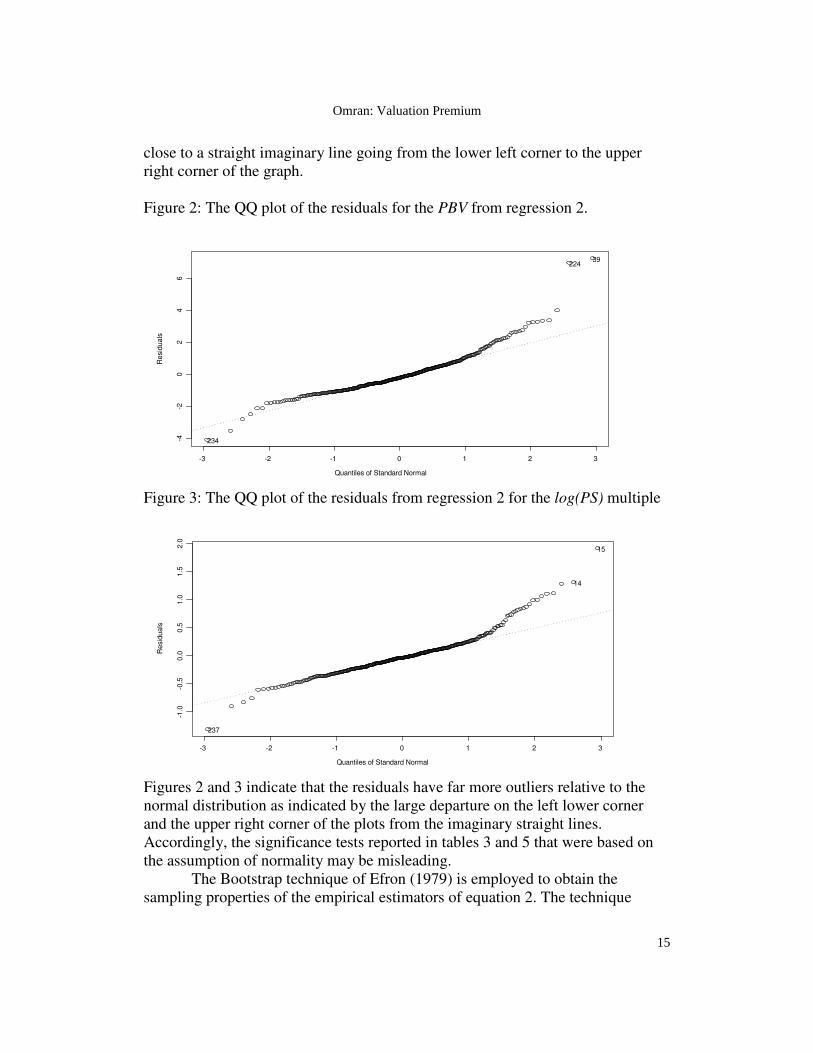

Figure 2: The QQ plot of the residuals for the PBV from regression 2.

Quantiles of Standard Normal

Re

sid

ua

ls

-3 -2 -1 0 1 2 3

-4-2

02

46

234

22439

Figure 3: The QQ plot of the residuals from regression 2 for the log(PS) multiple

Quantiles of Standard Normal

Re

sid

ua

ls

-3 -2 -1 0 1 2 3

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

237

14

15

Figures 2 and 3 indicate that the residuals have far more outliers relative to the

normal distribution as indicated by the large departure on the left lower corner

and the upper right corner of the plots from the imaginary straight lines.

Accordingly, the significance tests reported in tables 3 and 5 that were based on

the assumption of normality may be misleading.

The Bootstrap technique of Efron (1979) is employed to obtain the

sampling properties of the empirical estimators of equation 2. The technique

15

Omran: Valuation Premium

samples with replacement the observations used in equation 2 while keeping the

cross section information intact. The size of each resample is the same size of the

original data (308 observations). The regression parameters are then estimated for

each bootstrap attempt and the procedure is repeated 1000 times to obtain the

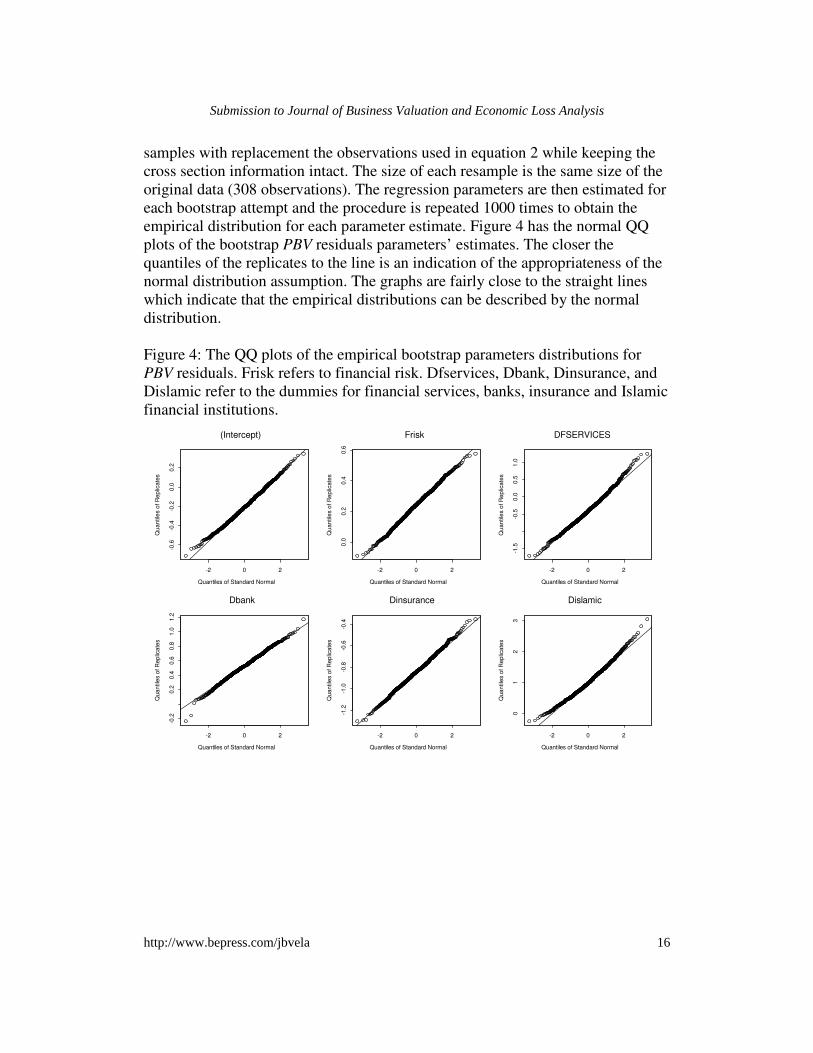

empirical distribution for each parameter estimate. Figure 4 has the normal QQ

plots of the bootstrap PBV residuals parameters’ estimates. The closer the

quantiles of the replicates to the line is an indication of the appropriateness of the

normal distribution assumption. The graphs are fairly close to the straight lines

which indicate that the empirical distributions can be described by the normal

distribution.

Figure 4: The QQ plots of the empirical bootstrap parameters distributions for

PBV residuals. Frisk refers to financial risk. Dfservices, Dbank, Dinsurance, and

Dislamic refer to the dummies for financial services, banks, insurance and Islamic

financial institutions.

Quantiles of Standard Normal

Qu

an

tile

s o

f R

ep

lica

tes

-2 0 2

-0.6

-0.4

-0.2

0.0

0.2

(Intercept)

Quantiles of Standard Normal

Qu

an

tile

s o

f R

ep

lica

tes

-2 0 2

0.0

0.2

0.4

0.6

Frisk

Quantiles of Standard Normal

Qu

an

tile

s o

f R

ep

lica

tes

-2 0 2

-1.5

-0.5

0.0

0.5

1.0

DFSERVICES

Quantiles of Standard Normal

Qu

an

tile

s o

f R

ep

lica

tes

-2 0 2

-0.2

0.2

0.4

0.6

0.8

1.0

1.2

Dbank

Quantiles of Standard Normal

Qu

an

tile

s o

f R

ep

lica

tes

-2 0 2

-1.2

-1.0

-0.8

-0.6

-0.4

Dinsurance

Quantiles of Standard Normal

Qu

an

tile

s o

f R

ep

lica

tes

-2 0 2

01

23

Dislamic

16

Submission to Journal of Business Valuation and Economic Loss Analysis

http://www.bepress.com/jbvela

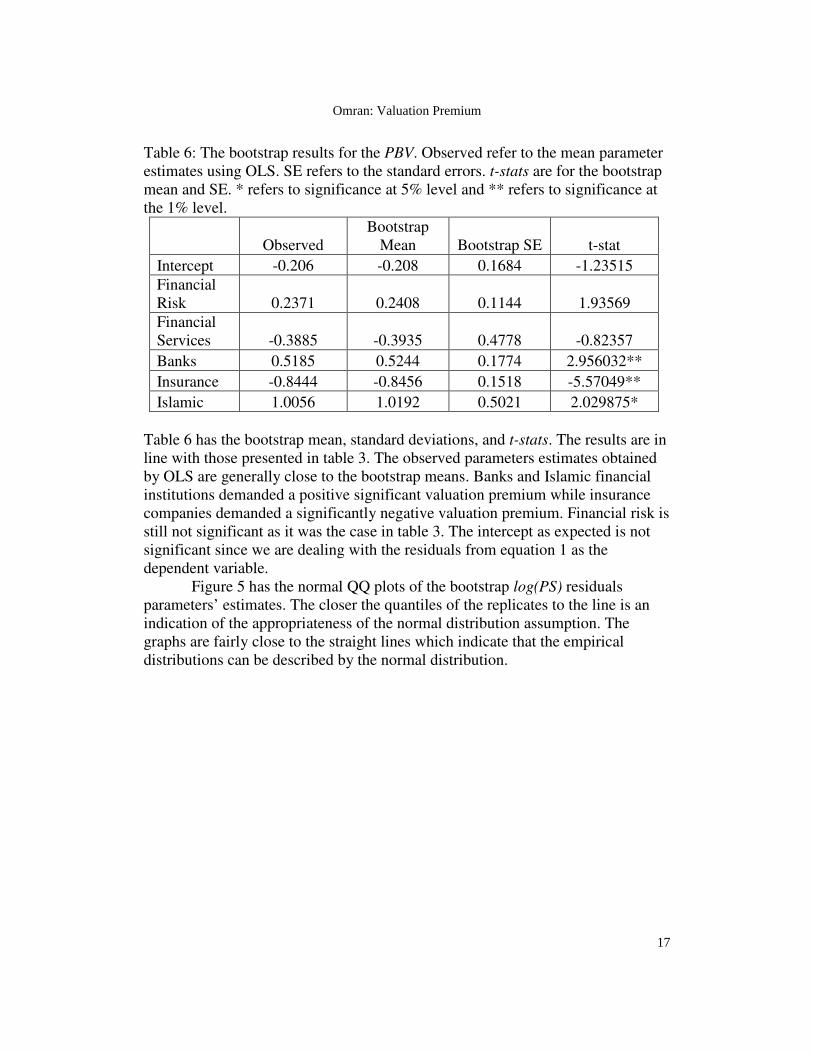

Table 6: The bootstrap results for the PBV. Observed refer to the mean parameter

estimates using OLS. SE refers to the standard errors. t-stats are for the bootstrap

mean and SE. * refers to significance at 5% level and ** refers to significance at

the 1% level.

Observed

Bootstrap

Mean Bootstrap SE t-stat

Intercept -0.206 -0.208 0.1684 -1.23515

Financial

Risk 0.2371 0.2408 0.1144 1.93569

Financial

Services -0.3885 -0.3935 0.4778 -0.82357

Banks 0.5185 0.5244 0.1774 2.956032**

Insurance -0.8444 -0.8456 0.1518 -5.57049**

Islamic 1.0056 1.0192 0.5021 2.029875*

Table 6 has the bootstrap mean, standard deviations, and t-stats. The results are in

line with those presented in table 3. The observed parameters estimates obtained

by OLS are generally close to the bootstrap means. Banks and Islamic financial

institutions demanded a positive significant valuation premium while insurance

companies demanded a significantly negative valuation premium. Financial risk is

still not significant as it was the case in table 3. The intercept as expected is not

significant since we are dealing with the residuals from equation 1 as the

dependent variable.

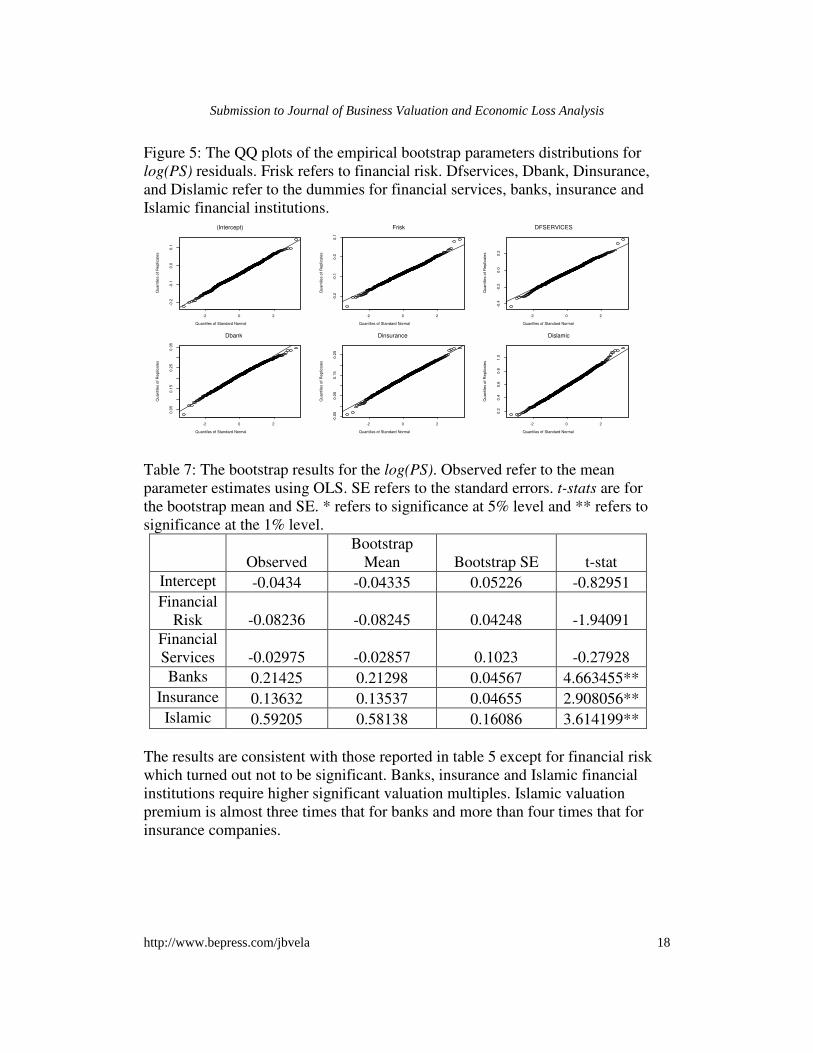

Figure 5 has the normal QQ plots of the bootstrap log(PS) residuals

parameters’ estimates. The closer the quantiles of the replicates to the line is an

indication of the appropriateness of the normal distribution assumption. The

graphs are fairly close to the straight lines which indicate that the empirical

distributions can be described by the normal distribution.

17

Omran: Valuation Premium

Figure 5: The QQ plots of the empirical bootstrap parameters distributions for

log(PS) residuals. Frisk refers to financial risk. Dfservices, Dbank, Dinsurance,

and Dislamic refer to the dummies for financial services, banks, insurance and

Islamic financial institutions.

Quantiles of Standard Normal

Qu

an

tile

s o

f R

ep

lica

tes

-2 0 2

-0.2

-0.1

0.0

0.1

(Intercept)

Quantiles of Standard NormalQ

ua

ntile

s o

f R

ep

lica

tes

-2 0 2

-0.2

-0.1

0.0

0.1

Frisk

Quantiles of Standard Normal

Qu

an

tile

s o

f R

ep

lica

tes

-2 0 2

-0.4

-0.2

0.0

0.2

DFSERVICES

Quantiles of Standard Normal

Qu

an

tile

s o

f R

ep

lica

tes

-2 0 2

0.0

50

.15

0.2

50

.35

Dbank

Quantiles of Standard Normal

Qu

an

tile

s o

f R

ep

lica

tes

-2 0 2

-0.0

50

.05

0.1

50

.25

Dinsurance

Quantiles of Standard Normal

Qu

an

tile

s o

f R

ep

lica

tes

-2 0 2

0.2

0.4

0.6

0.8

1.0

Dislamic

Table 7: The bootstrap results for the log(PS). Observed refer to the mean

parameter estimates using OLS. SE refers to the standard errors. t-stats are for

the bootstrap mean and SE. * refers to significance at 5% level and ** refers to

significance at the 1% level.

Observed

Bootstrap

Mean Bootstrap SE t-stat

Intercept -0.0434 -0.04335 0.05226 -0.82951

Financial

Risk -0.08236 -0.08245 0.04248 -1.94091

Financial

Services -0.02975 -0.02857 0.1023 -0.27928

Banks 0.21425 0.21298 0.04567 4.663455**

Insurance 0.13632 0.13537 0.04655 2.908056**

Islamic 0.59205 0.58138 0.16086 3.614199**

The results are consistent with those reported in table 5 except for financial risk

which turned out not to be significant. Banks, insurance and Islamic financial

institutions require higher significant valuation multiples. Islamic valuation

premium is almost three times that for banks and more than four times that for

insurance companies.

18

Submission to Journal of Business Valuation and Economic Loss Analysis

http://www.bepress.com/jbvela

5. COMMENTS AND CONCLUSION

This study examined if the Islamic clientele preference found by Omran (2009)

were specific to the valuation model used in his study. The study improved on

Omran (2009) by employing two different valuation multiples, removing possible

biases in the estimation process, and using bootstrapping to drive the empirical

distributions of the parameters’ estimates. The study found that the results of

Omran (2009) hold true regardless of the valuation model and other possible

shortcomings. Both of the price to book value PBV and price to sales PS multiples

show Islamic clientele preference for Islamic financial institutions regardless of

low profitability. It is recommended that a study is conducted on why investors in

the UAE have the least regard to the stocks of insurance companies compared to

other financial institutions. Traditional financial institutions such as commercial

banks and finance houses are prohibited because of fixed interest dealing which is

forbidden under Islamic laws (Riba, see Omran (2009)). Traditional insurance

companies are also strictly forbidden not only because of their fixed interest

dealings but also because they are considered a form of gambling (Maysir, see

Omran (2009)). It is not clear why investors would prefer to deal less with

insurance companies compared with commercial banks since both organizations

do not comply with Islamic laws. However, it is commonly believed in the

Islamic world that banks are less of an evil than insurance companies. Insurance

seems to somehow contradict with god willing. However, the author could not

find written literature on the reasons why Muslims tend to hold insurance in low

regard compared with commercial banks in general.

References

Efron, B. (1979), Bootstrapping methods: another look at the jackknife, Annals of

statistics, 7, 1-26.

Gordon, M. (1962), The investment, financing, and valuation of the corporation,

Homewood III, Richard D. Irwin.

Lie, E., and Lie H. (2002), Multiples used to estimate corporate value, Financial

Analysts Journal, 58, 2, 44-54.

Omran, M.F. (2009), Examining the effects of Islamic Beliefs and Teachings on

the Valuation of Financial Institutions in the United Arab Emirates, Review of

Middle East Economics and Finance, 5, 1, article 4.

Tseng, N. and Lee, Y. (2007), Equity valuation and forecasting capability: an

empirical analysis of Taiwan’s commercial banking industry, The Business

Review, 7, 2, 124-128

19

Omran: Valuation Premium