inventory management and financial

TRANSCRIPT

i

INVENTORY MANAGEMENT AND FINANCIAL PERFORMANCE IN

SUPPLY CHAIN INSTITUTIONS IN RWANDA

CASE STUDY OF MEDICAL PROCUREMENT AND PRODUCTION

DIVISION

DIANE TUGIRAMAHORO

MBA/3947/13

Research Project Submitted in Partial Fulfillment for the Award of a

Degree in Master of Business Administration (Finance and Accounting

Option) of Mount Kenya University

JULY 2015

ii

DECLARATION

This research study is my original work and has not been presented to any other institution.

No part of this research should be reproduced without the authors‟ consent or that of Mount

Kenya University.

Students Name: DIANE TUGIRAMAHORO

Sign ____________________ Date _____________

Declaration by the supervisor

This research has been submitted with our approval as The Mount Kenya University

Supervisor.

Name: RUSIBANA CLAUDE

Sign ____________________ Date _____________

iii

DEDICATION

I dedicate this research to my husband Jules RUTIKANGA and my parents Mr. Ignace

KALISA and Ms. Ezeulie MUKANGANGO who stood by side during the entire time that I

was undergoing my learning.

iv

ACKNOWLEDGEMENT

I would like to acknowledge the following people for their contribution towards my

education. I am very grateful to my family especially my husband for the outstanding support

they offered throughout my career. To RUSIBANA Claude, my supervisor, thank you for

sparing time and giving me good and professional ideas that enabled me to successfully

complete my project. Thank you for being so flexible amidst your busy schedule. Thank you

for your parental guidance and great contribution, I truly appreciate. To all my friends who

were always there for me spiritually, emotionally and socially, thanks pals. Lastly I

appreciate my colleagues the finance and accounting class especially those in the discussion

group, for being there for me in this journey and for all discussions held in the course of my

career.

v

ABSTRACT

Inventory is any idle resource that is held for future use whenever the input or the output of a

company is not used as available. Nowadays, the field of inventory is ignored by managers

of the company. This study focused on Inventory management and performance of the

company was conducted in Medical Procurement and Production Division (MPPD). The

general objective of this study was to assess the contribution of inventory management on

financial performance of supply institutions in Rwanda. Specific Objectives were to assess

the techniques used by Medical Procurement and Production Division during inventory

management; to examine the factors that affect Medical Procurement and Production

Division performance through inventory management and to establish the relationship

between inventory management and performance in Medical Procurement and Production

Division. The findings of this study should provide literature that is important for the

individuals, public and private institutions. This research was designed under case study;

secondary data were obtained from financial statements of MPPD. The target population of

this study was 128 employees of Medical Procurement and production Division, from this

target population, the research determines the sample size using Yamane formula, where n =

79.Primary data was gotten from the questionnaires administered to the respondents. This

study used both correlational and descriptive statistics to through SPSS program to analyze

data and profitability ratios to analyze level of performance of MPPD. Inventory

management techniques in MPPD have been discussed where, 83.8% respondents confirmed

that MPPD focused on inventory control techniques as a tool of its performance, 72.2%

perceived that MPPD focused on Economic Order Quantity technique during inventory

control, 83.3% of respondents perceived that MPPD focused on ABC control system during

inventory control and 97.3% respondents confirmed that MPPD also used VMI. The

researcher found that 86.1% respondents confirmed savings of tax revenue is among of the

factors that affect the performance of MPPD. The study also found that 73.6 % respondents

confirmed that availability of goods and services in MPPD influence its performance. Finally

73.6% respondents confirm that transfer from treasury influence the performance of MPPD.

The researcher used Pearson correlation coefficient and found a correlation of 0.893 (89.3

%); this implies there is strong and positive relationship between inventory control and

performance in MPPD. This study recommended that The MPPD should practice many

techniques of inventory management rather than ABC system and Economic Order Quantity

(EOQ), this is due to the fact that each technique carries its own different advantages which

would be beneficial to the company and it helps in cutting down some costs related with

inventory.

vi

TABLE OF CONTENTS

DECLARATION..................................................................................................................... ii

DEDICATION........................................................................................................................ iii

ABSTRACT ............................................................................................................................. v

TABLE OF CONTENTS ...................................................................................................... vi

LIST OF TABLES .................................................................................................................. x

LIST OF FIGURES .............................................................................................................. xii

LIST OF ACRONYMNS AND ABBREVIATIONS ........................................................ xiii

DEFINITION OF KEY TERMS ........................................................................................ xiv

CHAPTER ONE: INTRODUCTION ................................................................................... 1

1.0 Introduction ......................................................................................................................... 1

1.1 Background of the Study .................................................................................................... 1

1.2 Problem Statement .............................................................................................................. 3

1.3 Objectives of the Study ....................................................................................................... 4

1.3.1 General Objective ............................................................................................................ 4

1.3.2 Specific Objectives .......................................................................................................... 4

1.4 Research Questions ............................................................................................................. 5

1.5 Significance of the Study .................................................................................................... 5

1.6 Limitations of the Study...................................................................................................... 6

1.7 Scope of the Study .............................................................................................................. 6

vii

1.8 Organization of the Study ................................................................................................... 7

CHAPTER TWO: REVIEW OF RELATED LITERATURE ........................................... 8

2.0 Introduction ......................................................................................................................... 8

2.1 Theoretical Literature .......................................................................................................... 8

2.1.1 Inventory Management Overview ................................................................................... 8

2.1.2 Types of Inventory ......................................................................................................... 11

2.1.3 Inventory Management Approaches .............................................................................. 13

2.1.4 Factors Influencing Inventory Management .................................................................. 18

2.1.5 Overview of Organizational Performance ..................................................................... 21

2.1.6 Techniques of Organizational Performance Analysis .................................................... 22

2.1.7 Measurements of Organizational Performance .............................................................. 23

2.1.8 Inventory Management and Organizational Performance ............................................. 25

2.2 Empirical Literature .......................................................................................................... 26

2.3 Critical Review and Research Gap Identification ............................................................. 29

2.4 Theoretical Framework ..................................................................................................... 30

2.4.1 Theory of Constraints .................................................................................................... 30

2.4.2 Learning Curve Theory .................................................................................................. 31

2.5. Conceptual Framework .................................................................................................... 32

CHAPTER THREE: RESEARCH METHODOLOGY ................................................... 33

viii

3.0 Introduction ....................................................................................................................... 33

3.1 Research Design................................................................................................................ 33

3.2 Target Population .............................................................................................................. 33

3.3 Sample Design .................................................................................................................. 33

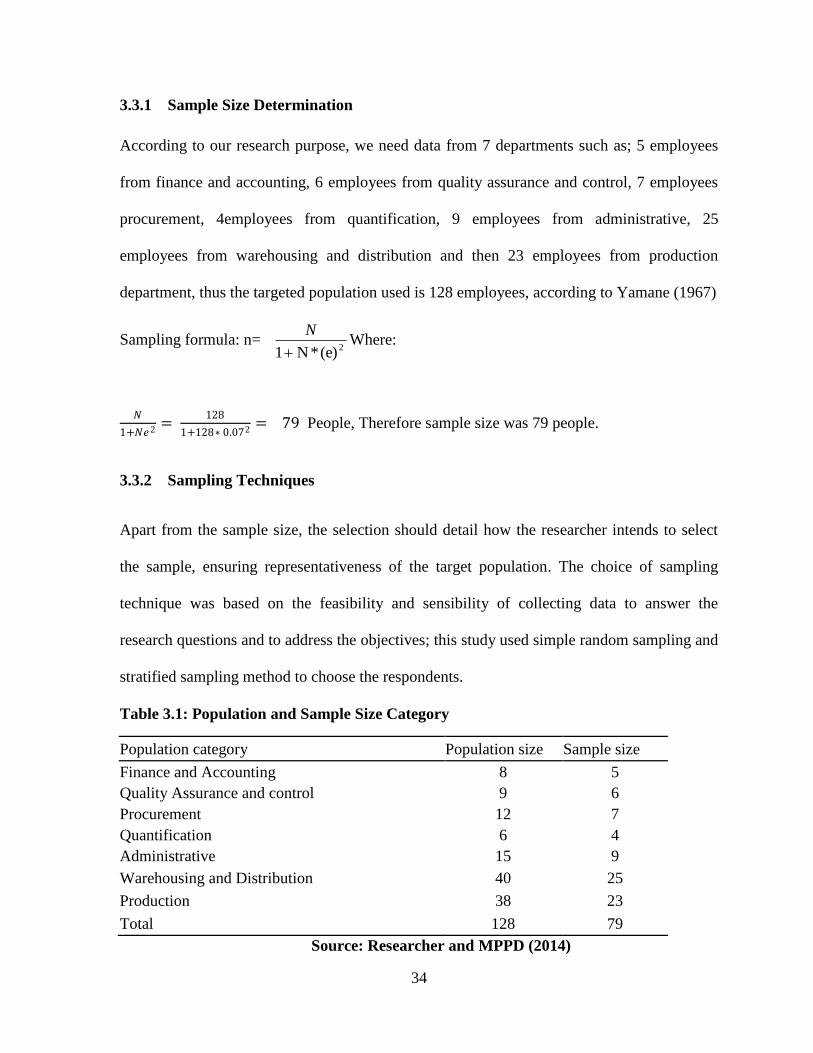

3.3.1 Sample Size Determination............................................................................................ 34

3.3.2 Sampling Techniques ..................................................................................................... 34

3.4 Data Collection Methods .................................................................................................. 35

3.4.1Data Collection Instrument ............................................................................................. 35

3.4.2 Administration of Data Collection Instrument .............................................................. 35

3.4.3 Reliability and Validity .................................................................................................. 36

3.5 Data Analysis Procedures ................................................................................................. 36

3.6 Ethical consideration ......................................................................................................... 37

CHAPTER FOUR: RESEARCH FINDINGS AND DISCUSSION ................................ 38

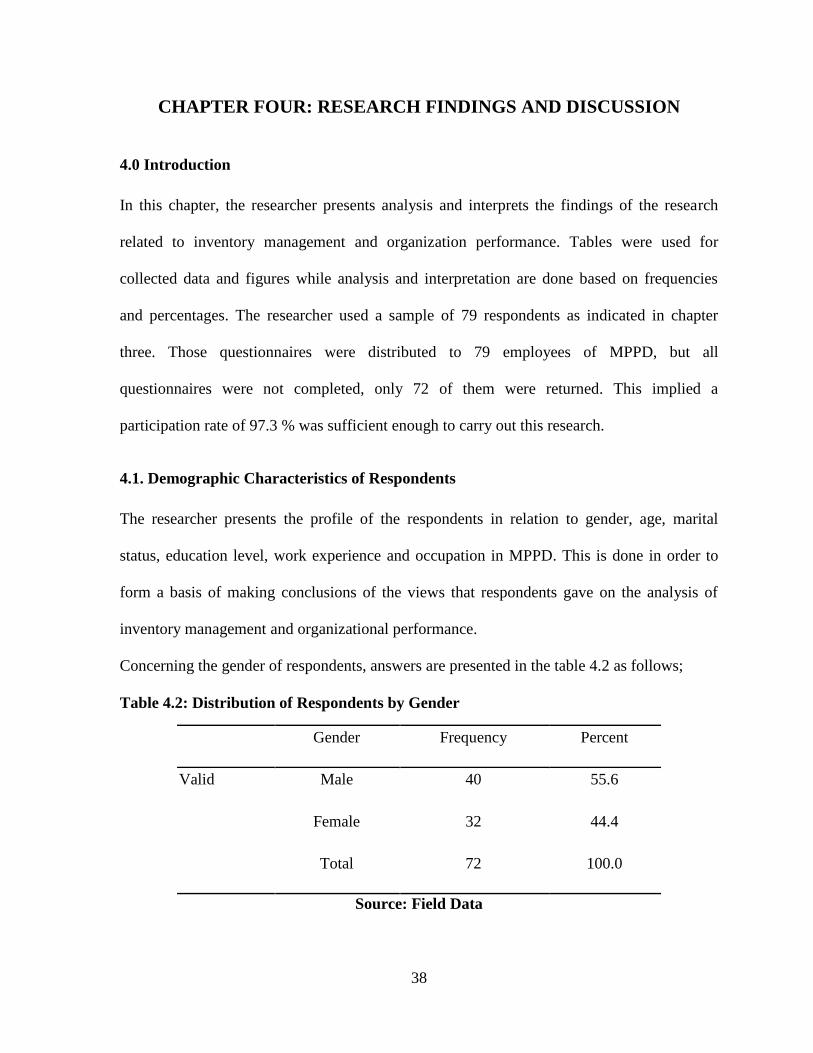

4.0 Introduction ....................................................................................................................... 38

4.1. Demographic Characteristics of Respondents ................................................................. 38

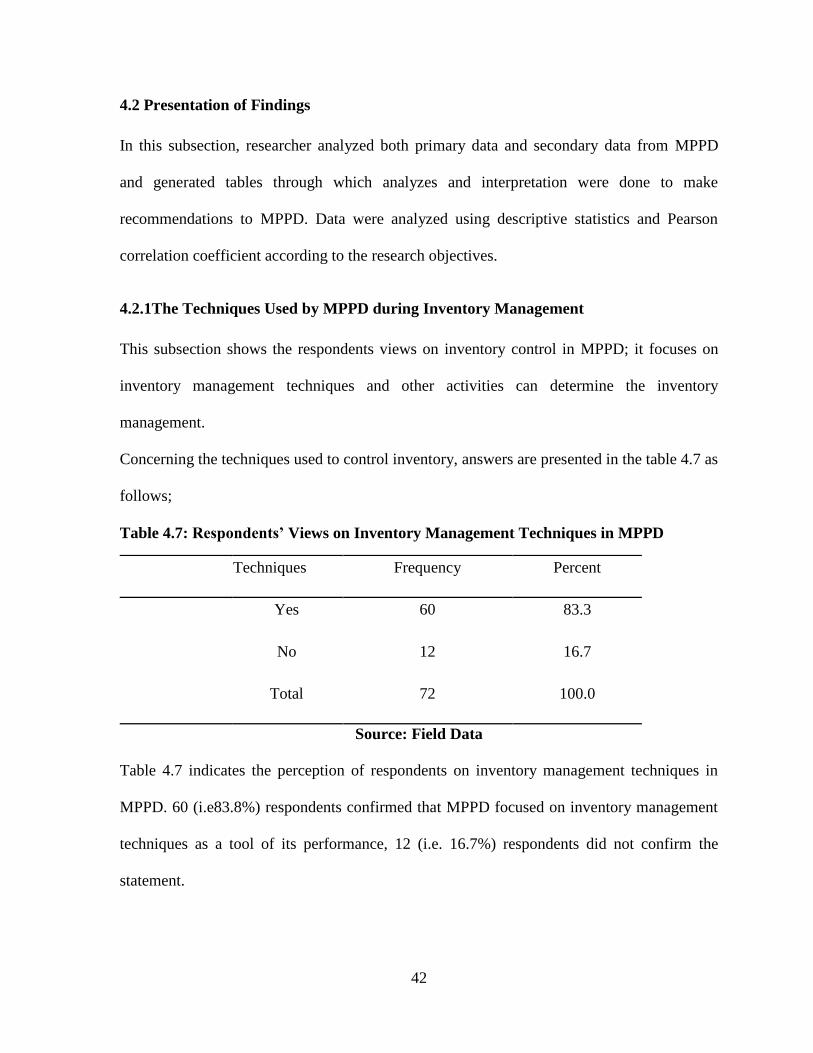

4.2 Presentation of Findings ................................................................................................... 42

4.2.1The Techniques Used by MPPD during Inventory Management ................................... 42

4.2.2 The Factors that Affect MPPD Performance through Inventory Management ............. 48

4.2.3 Correlation between Inventory Management and Performance in MPPD .................... 55

ix

CHAPTER FIVE: SUMMARY, CONCLUSIONS AND RECOMMENDATIONS ...... 58

5.0 Introduction ....................................................................................................................... 58

5.1 Summary of Findings ........................................................................................................ 58

5.1.1 The Inventory Control Techniques Used in MPPD ....................................................... 58

5.1.2 The Level of Performance of MPPD from 2010 – 2013 ............................................. 59

5.1.3 Relationship between Inventory Management Techniques and Organizational

Performance ............................................................................................................................ 59

5.2. Conclusion ....................................................................................................................... 60

5.3 Recommendations ............................................................................................................. 61

5.4 Suggestions for Further Study .......................................................................................... 61

REFERENCES ...................................................................................................................... 62

APPENDICES ....................................................................................................................... 65

AUTHORIZATION LETTER ............................................................................................ 66

BLANK QUESTIONNAIRE ............................................................................................... 69

x

LIST OF TABLES

Table 3.1: Population and Sample Size Category ................................................................... 34

Table 4.2: Distribution of Respondents by Gender ................................................................ 38

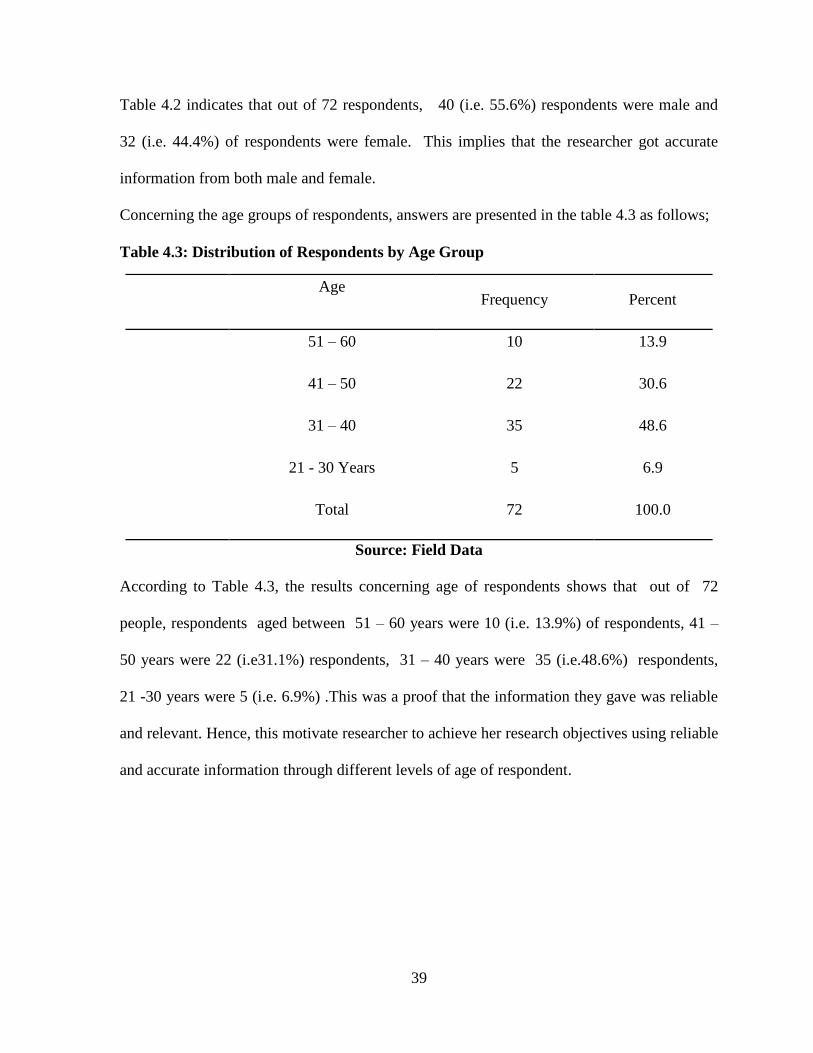

Table 4.3: Distribution of Respondents by Age Group .......................................................... 39

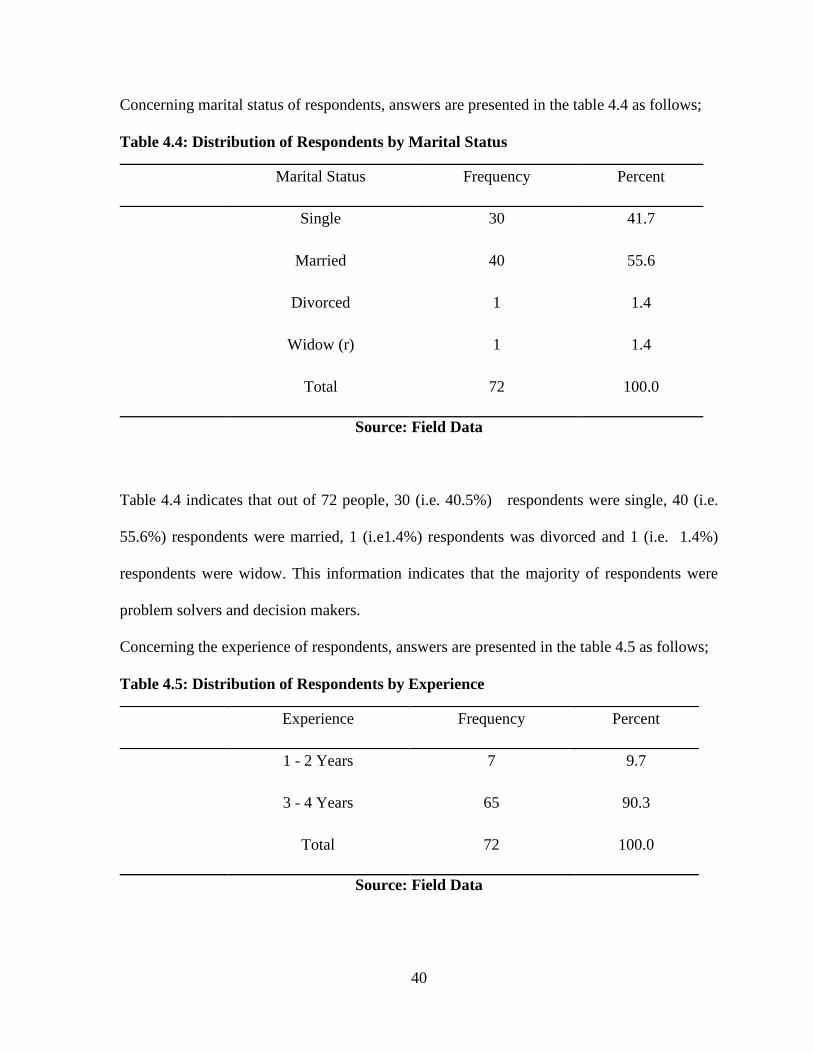

Table 4.4: Distribution of Respondents by Marital Status ...................................................... 40

Table 4.5: Distribution of Respondents by Experience .......................................................... 40

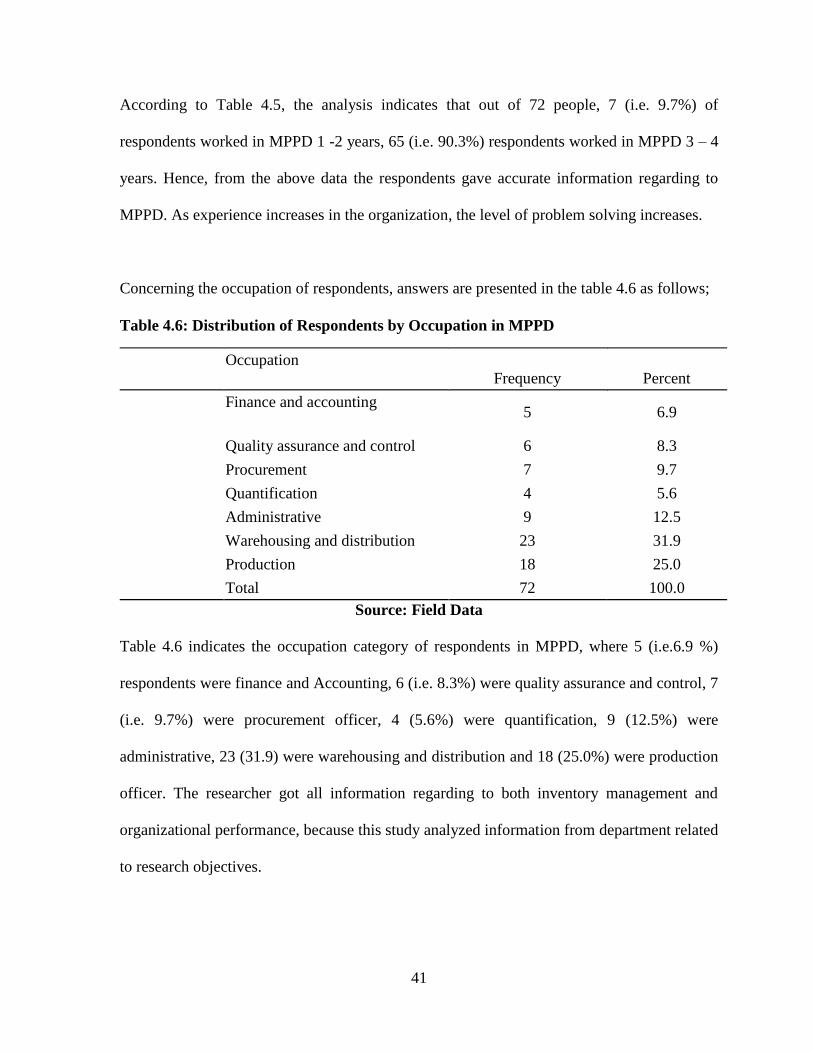

Table 4.6: Distribution of Respondents by Occupation in MPPD .......................................... 41

Table 4.7: Respondents‟ Views on Inventory Management Techniques in MPPD ............... 42

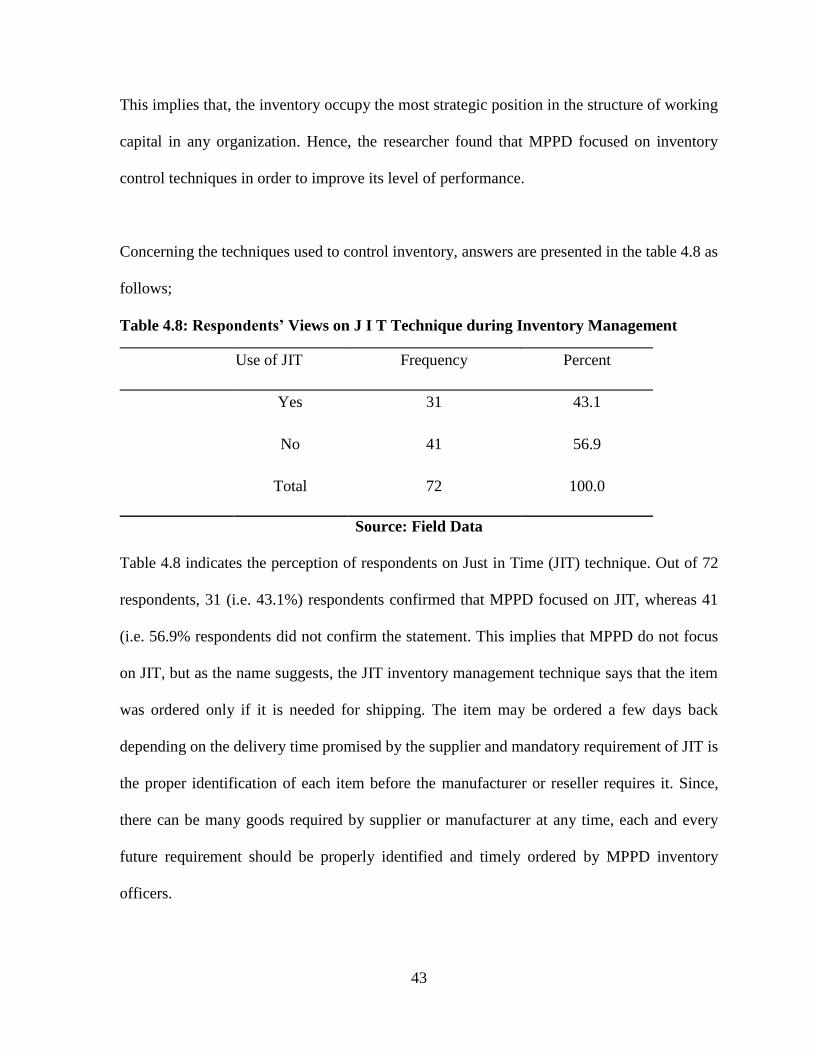

Table 4.8: Respondents‟ Views on J I T Technique during Inventory Management ............. 43

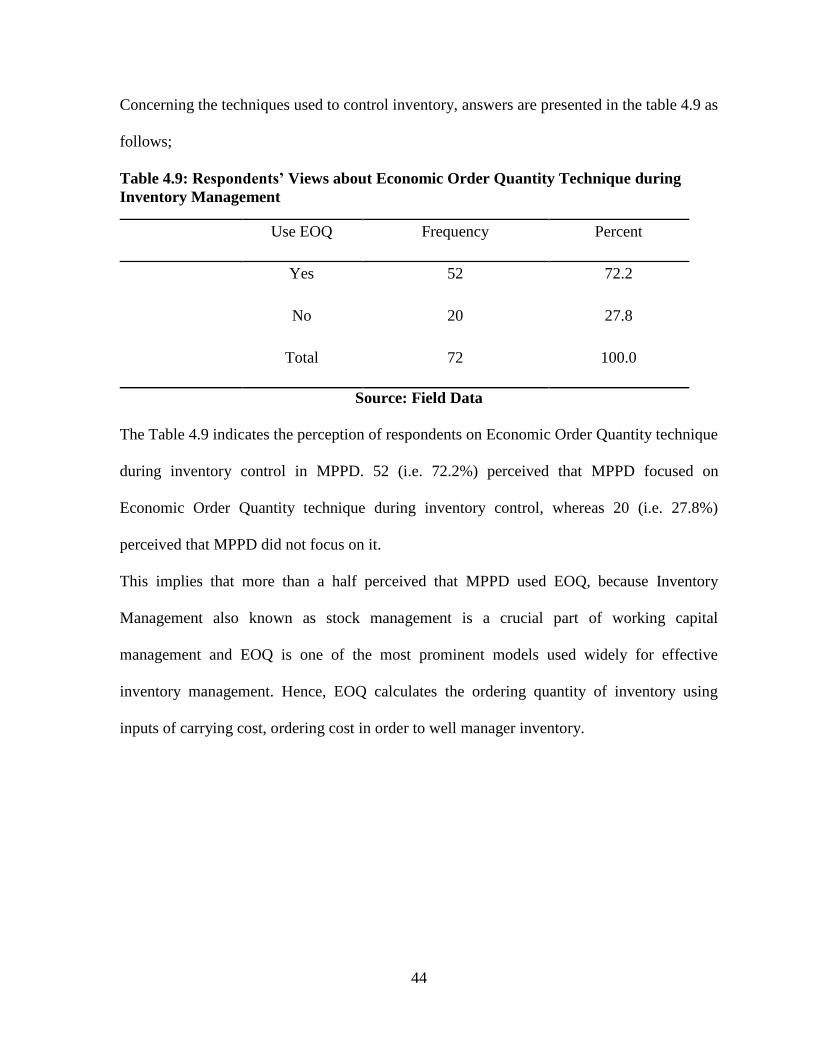

Table 4.9: Respondents‟ Views about Economic Order Quantity Technique during Inventory

Management ............................................................................................................................ 44

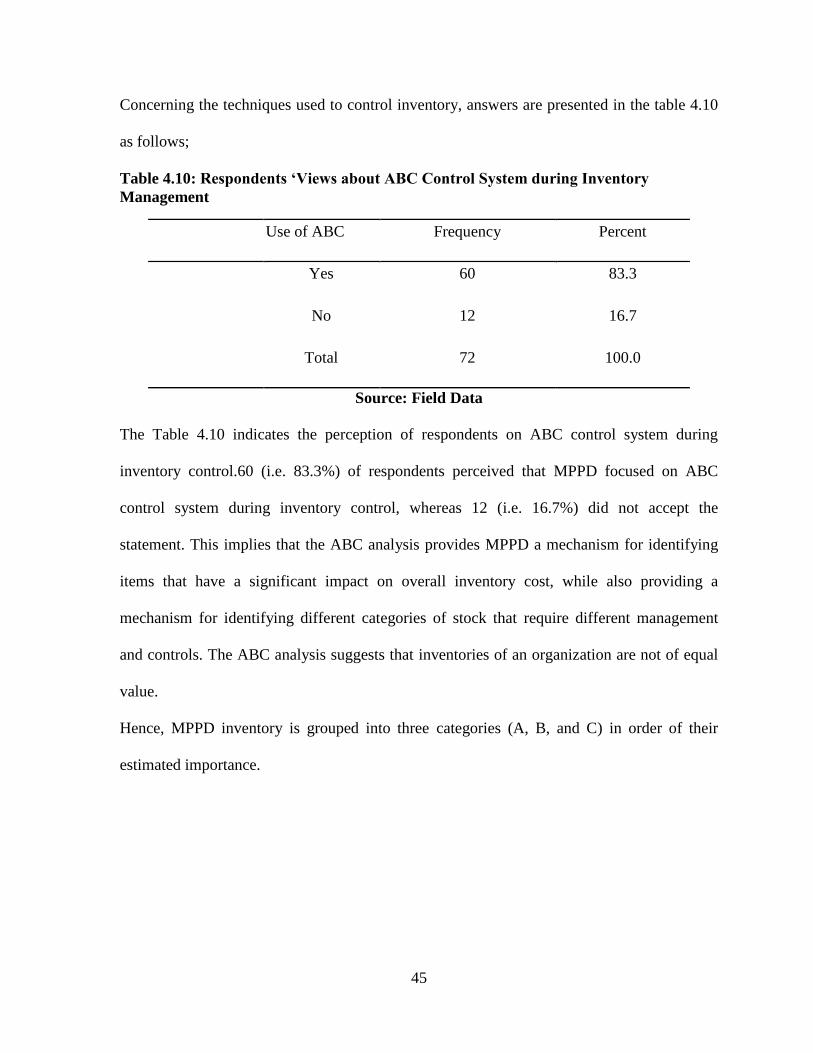

Table 4.10: Respondents „Views about ABC Control System during Inventory Management

................................................................................................................................................. 45

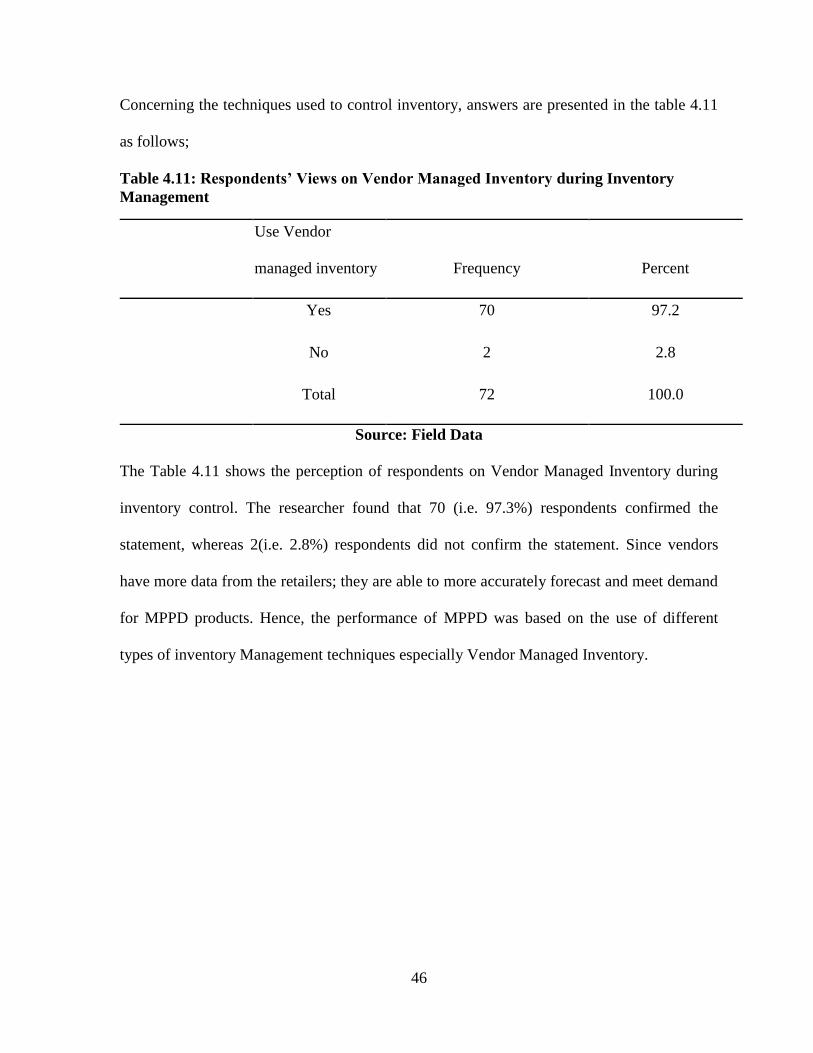

Table 4.11: Respondents‟ Views on Vendor Managed Inventory during Inventory

Management ............................................................................................................................ 46

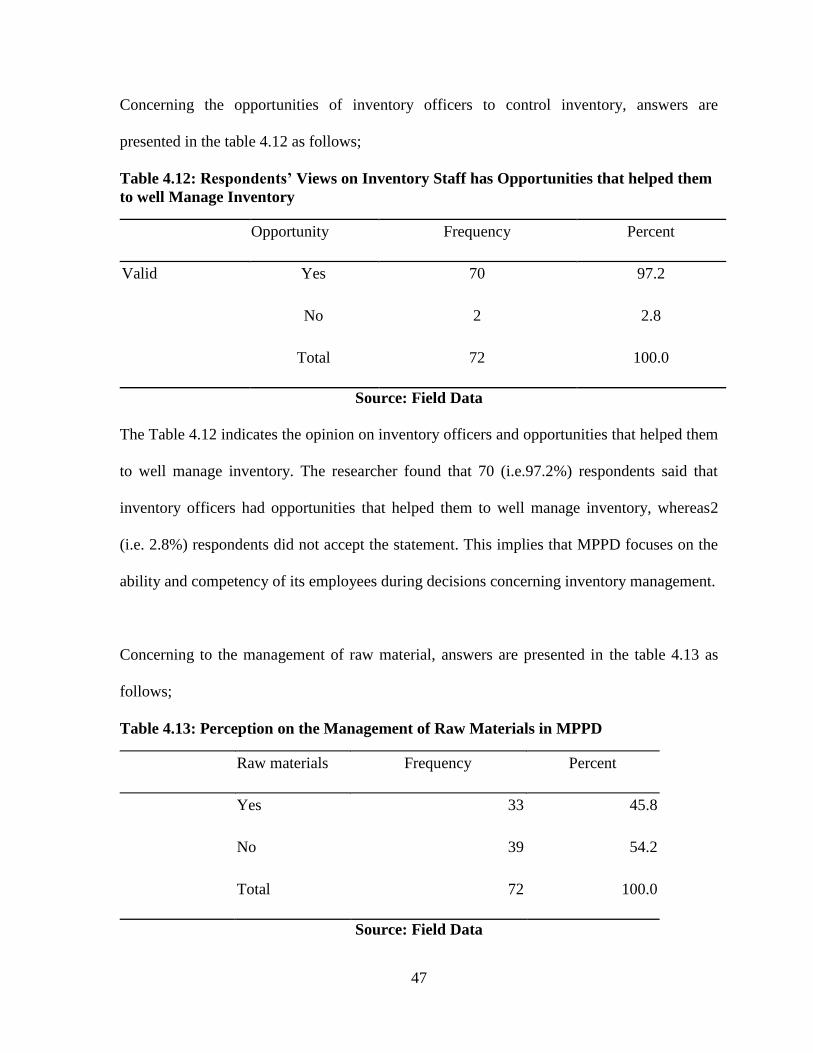

Table 4.12: Respondents‟ Views on Inventory Staff has Opportunities that helped them to

well Manage Inventory ........................................................................................................... 47

Table 4.13: Perception on the Management of Raw Materials in MPPD ............................... 47

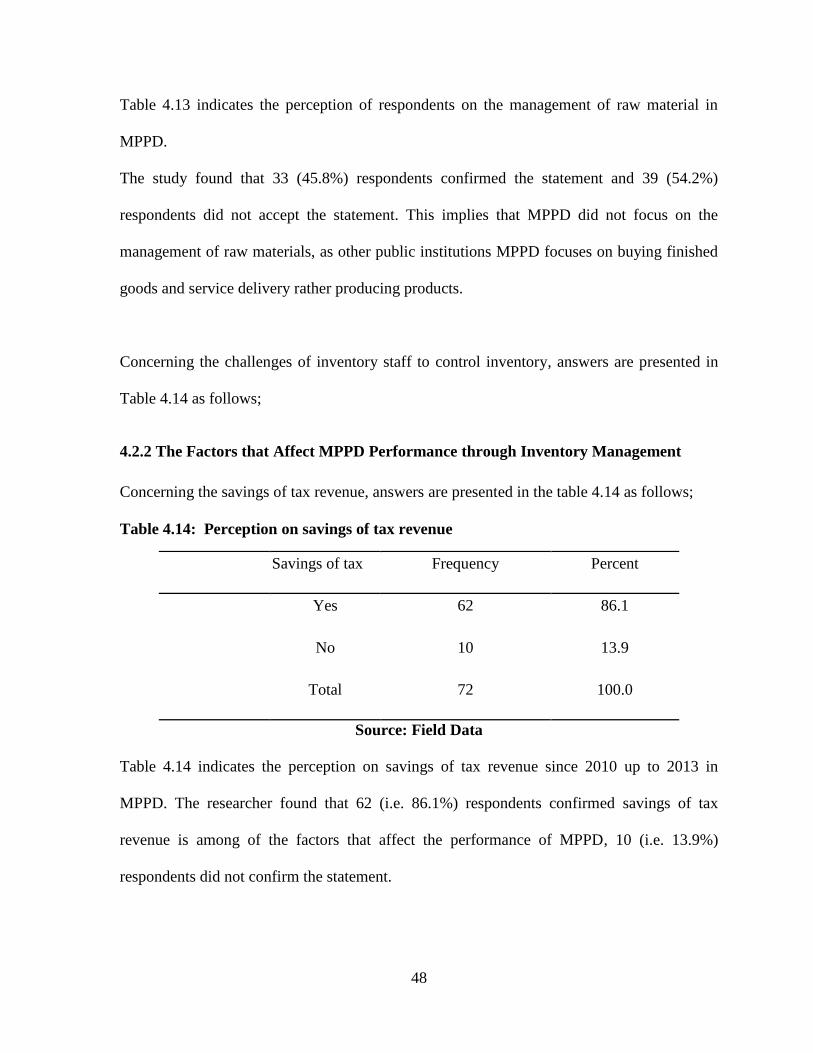

Table 4.14: Perception on savings of tax revenue ................................................................. 48

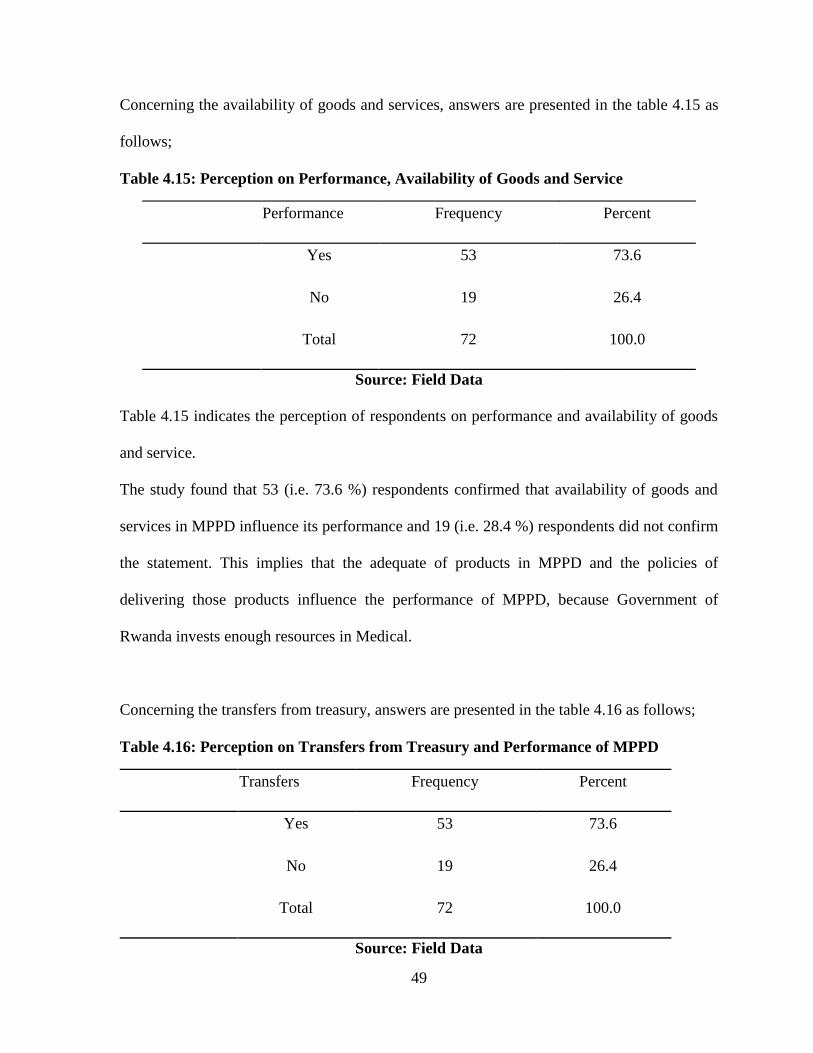

Table 4.15: Perception on Performance, Availability of Goods and Service ......................... 49

Table 4.16: Perception on Transfers from Treasury and Performance of MPPD ................... 49

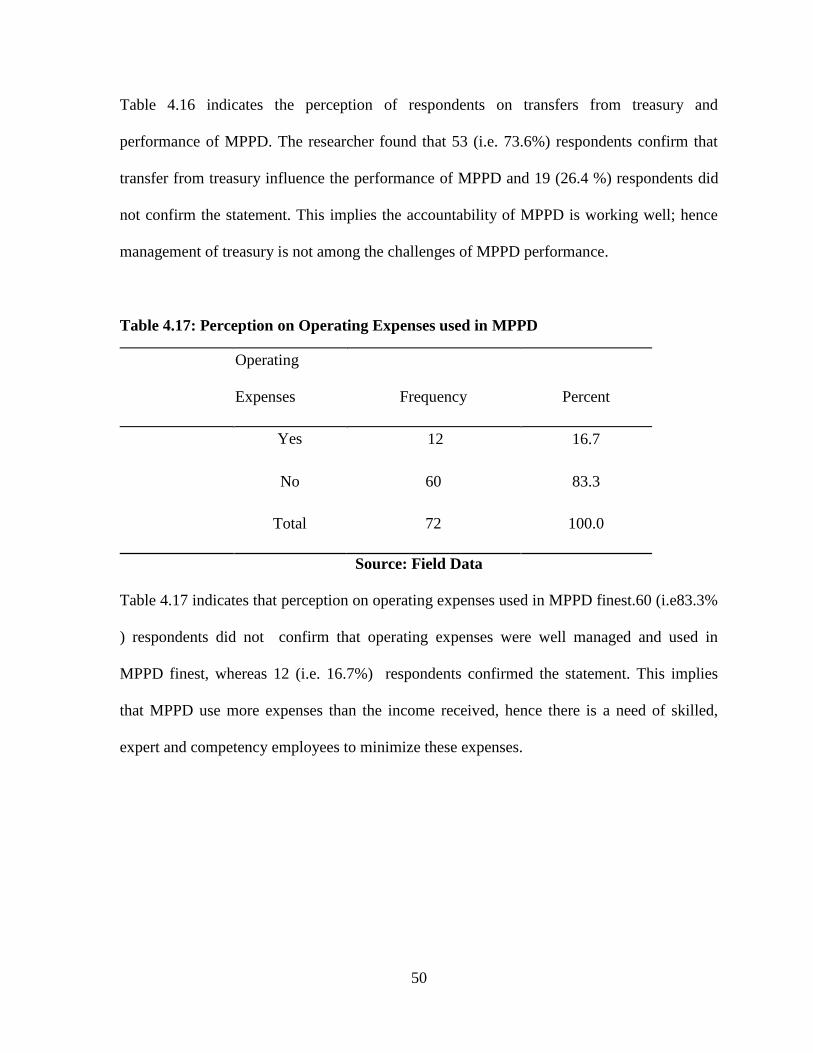

Table 4.17: Perception on Operating Expenses used in MPPD .............................................. 50

xi

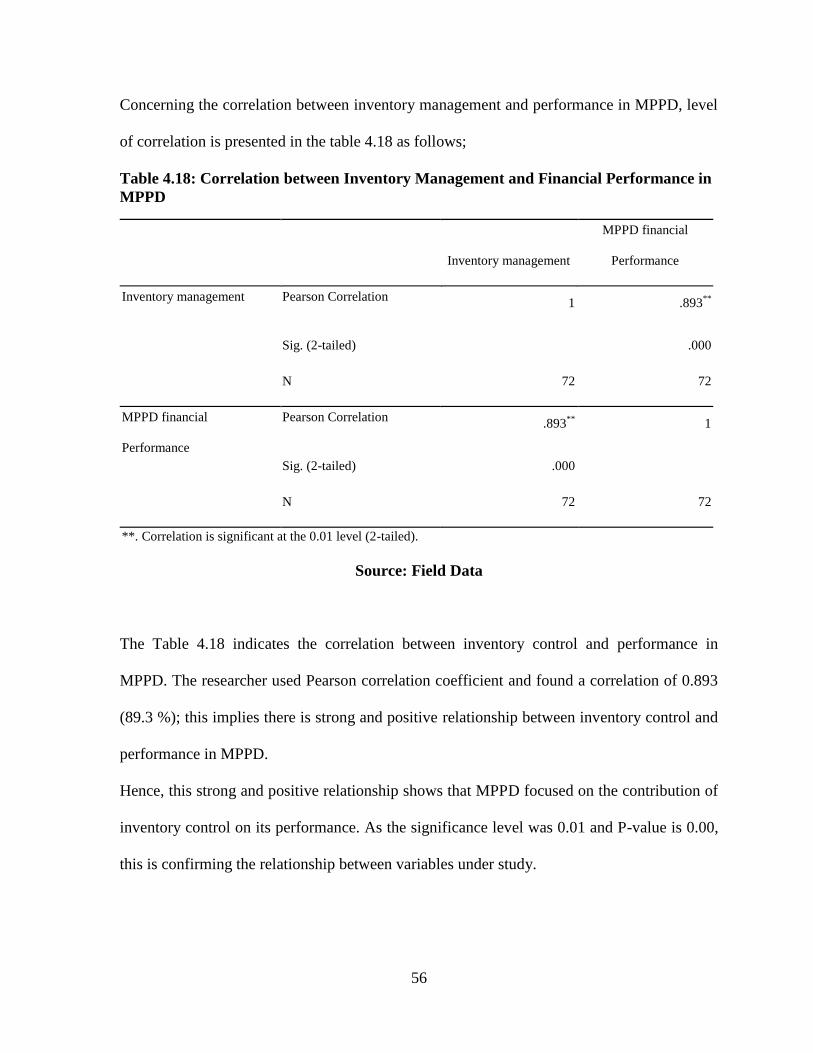

Table 4.18: Correlation between Inventory Management and Financial Performance in

MPPD ...................................................................................................................................... 56

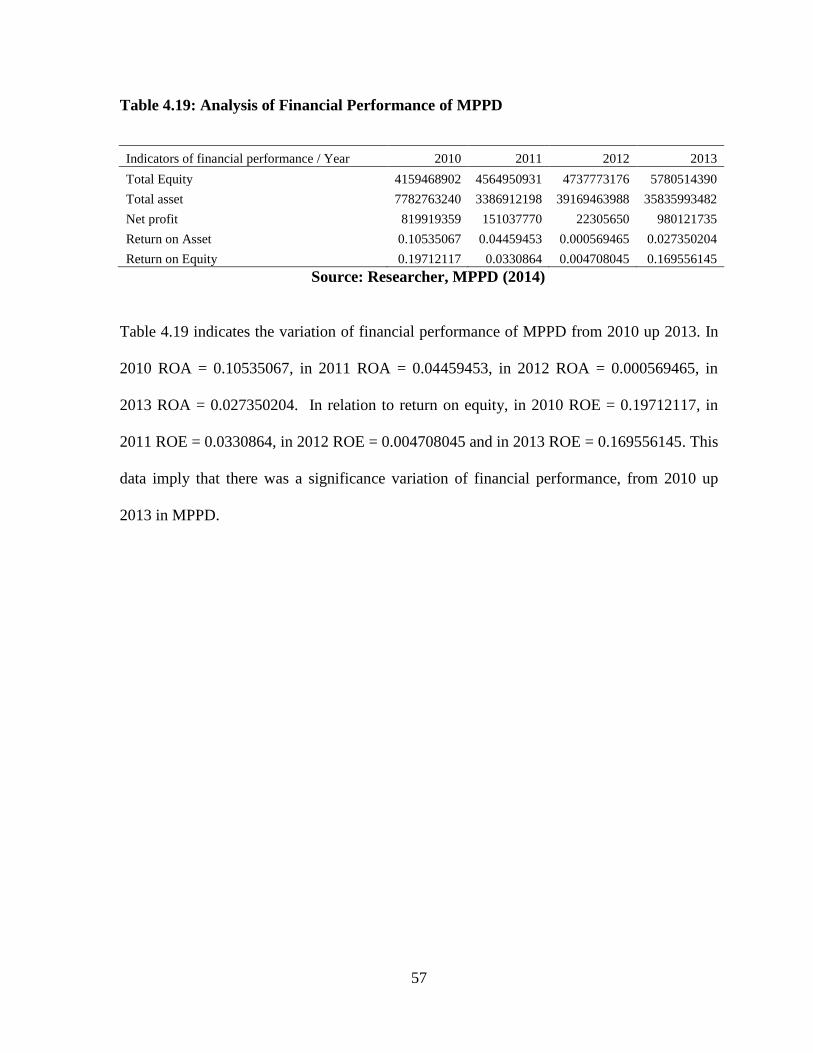

Table 4.19: Analysis of Financial Performance of MPPP ...................................................... 57

xii

LIST OF FIGURES

Figure 2.1: Conceptual framework ......................................................................................... 32

Figure 4.2: Perception on Optimization of the Total Operating and the Needs of MPPD ..... 51

Figure 4.3: Perception on Lead Time and the Productivity of MPPD .................................... 52

Figure 4.4: Perception on Adequate Quantities and the Productivity of MPPD .................... 53

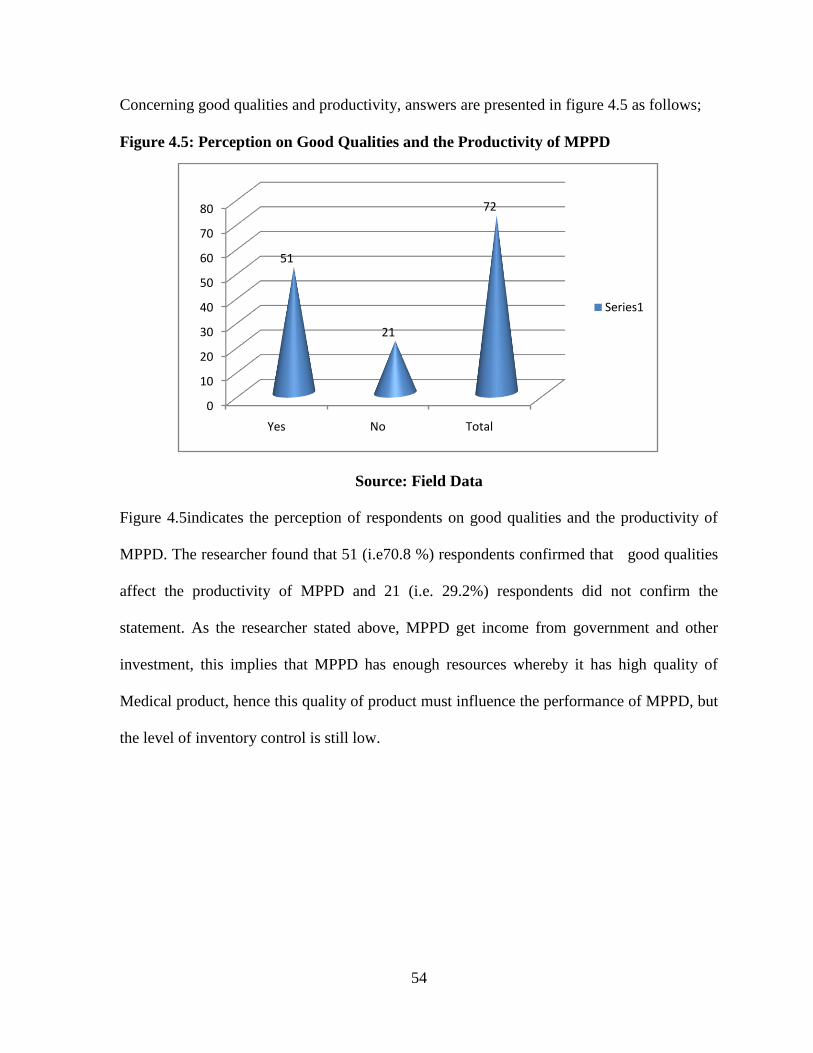

Figure 4.5: Perception on Good Qualities and the Productivity of MPPD ............................. 54

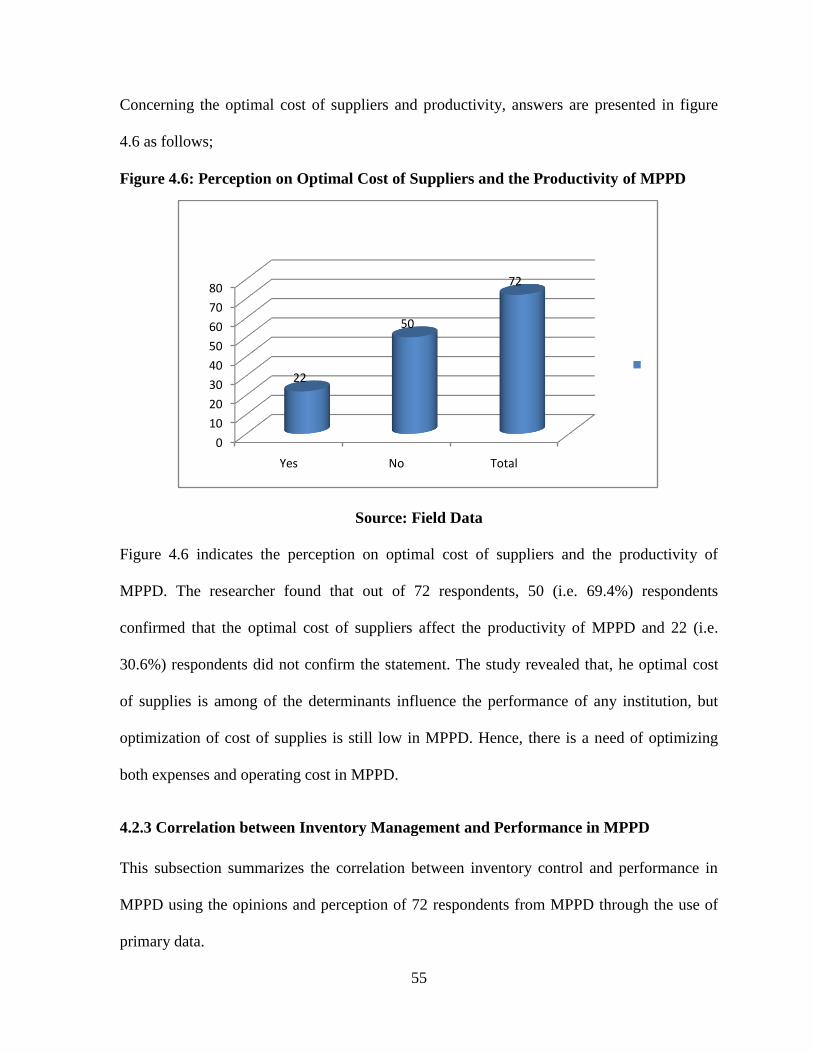

Figure 4.6: Perception on Optimal Cost of Suppliers and the Productivity of MPPD ........... 55

xiii

LIST OF ACRONYMNS AND ABBREVIATIONS

CVP Cost Volume Profit

EOQ: Economic Order Quantity

ICP: Inventory conversion period

JIT: Just In Time

MPPD: Medical Procurement and Production Division

ROA: Return on Assets

ROE: Return on Equity

ROIC: Return on invested capital

VMI: Vendor Management Inventory

VOI: Vendor Owner Inventory

xiv

DEFINITION OF KEY TERMS

Inventory

Inventory is defined as stock of products that a firm is manufacturing for sale, or else the

components that make up the products. Inventory is composed by useful resource that is held

for future use whenever the input or the output of a company is not used as available.

Inventory Management

Inventory management is pivotal in effective and efficient organization. It is also vital in the

control of materials and goods that have to be held for later use in the case of production or

later exchange activities in the case of services. Inventory management is a process of

ensuring adequate quantities, good qualities, at a low cost is procured.

Financial Performance

Financial performance of supply chain institutions is a subjective measure of how well

supply chain institutions use assets from its primary mode of business and generate revenues.

This term is also used as a general measure of a firm's overall financial health over a given

period of time, and can be used to compare similar firms across the same industry or to

compare industries or sectors in aggregation.

Medical Supply

Medical supply is an items deemed necessary for the treatment of an illness or injury,

medical supplies refers to the non-durable disposable health care materials ordered or

prescribed by a physician, which is primarily and customarily used to serve a medical

purpose

1

CHAPTER ONE: INTRODUCTION

1.0 Introduction

This chapter focuses on background of the study, problem statement, objectives of the study,

research questions, significance of the study, limitations, scope of the study and organization

of the study.

1.1 Background of the Study

Inventory management has been of concern for many years to business firms worldwide.

Inventory management systems play a crucial role in enhancing effectiveness and efficiency

in handling inventory of business firms (Imeokparia, 2013). Efficient inventory management

facilitates to invest minimum funds in inventory maintaining continuity in business activity,

increases the size of the business activities by increasing total sales consequently increasing

recycling of funds and generating higher performance (Irungu, & Wanjau, 2011). As against

this, if management proves inefficient in inventory management, it results into higher

inventory conversion period, high costs of inventory, leading to reduced recycling of

funds, ultimately effecting performance and liquidity of the enterprises (Katsiaryna,

2004).

Inventory management is pivotal in effective and efficient organization. It is also vital in the

control of materials and goods that have to be stored for later use in the case of production or

later exchange activities in the caseof services (Anichebe & Agu, 2013).Companies have

been continually in search for sources of sustainable competitive advantage in their

operations.

2

Therefore, there is need for business enterprises to embrace effective Inventory management

practices in order to improve their competitiveness (Rajeev, 2008).Public institutions are

viewed as an essential element of a healthy and vibrant economy in developing countries.

Public institutions are believed to provide a momentum to the economic progress of

developing countries and its importance is gaining widespread recognition. According to

Byoungho (2004), it is neither physically possible nor economically justifiable to wait for the

stock to arrive at the time when they are actually required. Therefore, keeping of inventory is

a must for the efficient working of a business unit. Raw materials represent goods kept by a

manufacturing firm prior to their being utilized in the production process. Supplies generally

include tools and consumables which are consumed in the production of goods and services.

According to Kotabo (2002), inventory costs include: carrying costs such as storage and

insurance; ordering costs like transporting and store placement; and stock out costs like

redundancy and loss of sales. A company cannot achieve an outstanding performance

without proper and efficient control of materials.

Materials are as much as cash itself and any theft, wastage and excessive use of materials are

of immediate financial loss and leads to poor performance of a company. Every company

strives to improve profitability countless hours are spent in meetings devising ways to lower

operating costs while increasing sales and gross margins. In the quest to maximize return on

investment many organizations fail to scrutinize their investment in inventory. This is

unfortunate because improving the way you control and manage your inventory may have the

greatest potential for improving your organization‟s bottom line (Schreibfeder, 2004).

3

Distributors often simultaneously suffer from conflicting complaints concerning their

inventory. They have too much of the wrong products and not enough of the products

necessary to provide a high level of customer service. Furthermore the company‟s

warehouse(s) may not be designed and organized to minimize the cost of filling customer

orders(Brackus, 2000).The success of a firm or company is measured in terms of

performances level; poor inventory management can lead to decrease of performances in

organizations. In spite of Medical Procurement and Production Division (MPPD) elaborate

efforts in inspection, store keeping, coding and stock taking in the procurement department

the company has continued to incur high inventory costs which could be affecting the

performance levels. This research discusses several ideas to help managers to improve the

performance and productivity of their investment in stock inventory.

1.2 Problem Statement

In this fast moving and rapid changing business environment, inventory that keeps in the

warehouse brings significant effect on the daily business operation. Inventory management

involves many levels of the organization, starting from the shop floor workers to the top

management commitment. Therefore, it encounters various problems in the implementation.

Literature on supply chain management and firm‟s operational performance indicate

increased need for improved quality of operations. According to Mogere, Oloko and Okibo

(2013)processing firms face problems of fluctuating inventories, inaccurate forecasts and

low utilization of inventories due to inadequate coordination of operations. Managers do not

focus on Inventory management, whereby inventory is a central process in manufacturing

and merchandized industry.

4

Rwanda Public Institutions is spending much money in medical services; working capital is

very high; in order to achieve the vision of government of Rwanda, which is Vision 2020,

unfortunately the production and performance are still inadequate. Even if government of

Rwanda has that problem; the awareness on Inventory management is still low in Rwanda

public institutions and studies carried out on Inventory management in Rwanda are still few.

Thus, it is against the above problem, the researcher intends to carry out this study on the

case of Medical Procurement and Production Division, in Gasabo District.

1.3 Objectives of the Study

The objectives of this research are divided into two categories, such as the general objective

of the study and three specific objectives of the study.

1.3.1 General Objective

The general objective of this study is to assess the contribution of inventory management on

financial performance of supply chain institutions in Rwanda.

1.3.2 Specific Objectives

i. To assess the techniques used by Medical Procurement and Production Division

during inventory management;

ii. To examine the factors that affect Medical Procurement and Production Division

financial performance through inventory management;

iii. To establish the relationship between inventory management and financial

performance in Medical Procurement and production Division

5

1.4 Research Questions

i. What are the techniques used by Medical Procurement and production Division

during inventory management;

ii. What are the factors that affect Medical Procurement and production Division

performance through inventory management?

iii. Is there any relationship between inventory management and performance in Medical

Procurement and production Division?

1.5 Significance of the Study

The findings of this study should provide literature that is important for the individuals,

public and private institutions.

The study is beneficial to the researcher herself; this is because the researcher will be able to

understand properly, how inventory management can be used to influence public institutions

performance. This study is also beneficial to the researcher because it provides to her with

the knowledge on how to evaluate the performance of public institution.

Regarding individuals, the information collected and analyzed after the study should be

added to the existing literature which should assisted other researchers more specifically

students writing their projects in the same or related area. As far as the public institution is

concerned, the research should be beneficial in that the recommendations and suggestion

given if followed, they would help decision makers to improve their decision making

process. The research could help the public to be aware of the progress of the institution and

its contribution made to the well-being of the society, especially in the field of medical.

6

1.6 Limitations of the Study

This study intends to meet with the limitations of fewer resources like journal, books and

short-time. This research met with the challenges in collecting the data because the public

institutions don‟t like to provide their information. The respondents should quietly refuse to

answer some questions as they think that the weakness was identified.

Despite all of the above problems the researcher developed the strategies to de-limit the

above impediment for the smooth and successful execution of the intended purpose of the

study. This includes the massive and extensive reading in order to be familiarized with the

sites which were convenient to retrieve relevant data without wasting more time. The

researcher presented the cover letter to the governing body under study in order for them to

realize that the purpose of the researcher is purely for academic purpose but not to investigate

their organization.

1.7 Scope of the Study

In order to achieve the research objectives and be more specific to the research area, this

subsection is divided into three scope, such as content scope, geographical scope and time

scope. The research focused on the effect of inventory management on performance of public

institutions. This research focused on this area, because the level of managing inventory in

public institutions is still low. Hence, there is a need to carry out a research in this area.

The research was conducted to the fiscal period of 4 years from 2010 to 2013.The researcher

has chosen this period because, it is in this period where by MPPD faced problems of

fluctuating inventory, inaccurate forecasts and low utilization of inventory.

This research undertook a case study of MPPD that is located in Kigali city, Gasabo District,

near Rwanda National Police Headquarter.

7

The researcher has chosen MPPD as case of study, because is the one of the Rwandan Public

Institutions which uses to distribute products day to day.

1.8 Organization of the Study

The first chapter is composed of introduction to the study, background to the study, problem

statement, objectives of the study, research questions, significance of the study, limitations of

the study, scope of the study and then organization of the study. The second chapter is

composed of introduction to literature review, theoretical literature, empirical literature,

critical review and research gap identification, conceptual framework and then summary of

literature review. The third chapter is composed of introduction to the research methodology,

research design, target population, sample design, sample size, sampling techniques data

collection methods, data analysis procedures and then ethical consideration.

The fourth chapter is composed of the presentation of research findings and discussion,

demographic characteristics of respondents and then presentation of findings.

The fifth chapter is summary of research findings, conclusion, recommendations and

suggestion for further researchers.

8

CHAPTER TWO: REVIEW OF RELATED LITERATURE

2.0 Introduction

This chapter introduces in details the keys concept and is mainly concerned with other

researchers and scholars have said about the key concepts mentioned related to the research

conducted. The purpose of this chapter is to review literature and theoretical framework of

inventory management. The submissions and thoughts of various authors on inventory,

Inventory management, organization performance, and the benefits of inventory management

in organization profitability were reviewed. This study provides clear meaning of terms and

concepts and also reviews the findings of the previous researchers. This helps to clearly

identify the gap and therefore justify the need of doing the study on the role of Inventory

management on organization performance.

2.1 Theoretical Literature

In this sub-section the researcher focuses on different philosophy and techniques regarding

Inventory management and organization profitability. The researcher focuses on past studies,

journals, and books focused on concept of inventory profitability.

2.1.1 Inventory Management Overview

According to Byoungho (2004) inventory management is the process of managing inventory

in order to meet customer demand at the lowest possible cost and with a minimum of

investment.

9

A successfully implemented Inventory management program takes into account such things

as purchasing goods commensurate with demand, seasonal variation, changing usage

patterns, and monitoring for pilferage. A preliminary step in the process of Inventory

management is to determine the approximate costs of carrying inventory. Inventory

management is a vital function to help insure the success of manufacturing and distribution

companies (Langabeer &Stoughton, 2001). The effectiveness of inventory management

systems is directly measurable by how successful a company is in providing high levels of

customer service, low inventory investment, maximum throughput and low costs. The

challenge of productive inventory management is to support an upward trend in sales while

keeping the investment at the lowest level consistent with adequate customer service

(Imeokparia, 2013).

Inventory management involves the coordinating of materials availability, controlling,

utilization and procuring of materials. Inventory management is the direction of activities

with the purpose of getting the right inventory in the right place at the right time and in the

right quantity and it‟s directly linked to production function of any organization which

implies that the inventory management system operated will affect the profitability of an

organization directly and indirectly (Alm, 2000).

According to Kotabo (2002), inventory management refers to all the activities involved in

developing and managing the inventory levels of raw materials, semi-finished materials

(working-progress) and finished good so that adequate supplies are available and the costs of

over or under stocks are low. The nature of inventory depends upon the type of activity

carried on.

10

In the case of a manufacturing unit, inventory will generally include all types of

inventories mentioned above, while in the case of a trading concern, it will comprise

only finished goods or stock -in-trade owned by it for sale to customers in the normal course

of business. Inventory needs proper control as it is one of the largest assets of a business

(Deloof, 2003).

Inventories should neither be excessive nor inadequate. If inventories are kept at a high level,

higher interest and storage costs would be incurred; on the other hand, a low level of

inventories may result in frequent interruption in the production schedule resulting in under-

utilization of capacity and lower sales (Falope & Ajilore, 2009). The objective of inventory

management is therefore to determine and maintain the optimum level of investment in

inventories which help in achieving the required objective.

Inventories are the stock of raw materials, work in progress, finished goods and supplies held

by a business organization to facilitate operations in the production process (Pandey,

1995).Also if the company fails to manage its inventory efficiently, it is likely to face

profitability problems (Block &Hirt, 1987).The goal of inventory management therefore is to

provide the inventories required to sustain operations at minimum costs (Brackus, 2000).

According to Krishna and Yew (2010), inventory is the stock stored that has a resale value in

order to gain profit. It represents the largest cost of the company especially for the trading

firms, wholesalers and retailers. It is mentioned as “piles of money” on the shelf.

Therefore, the inventory should be properly managed in order to facilitate the company

operation. Inventory control is primarily about specifying the shape and percentage of

stocked goods.

11

It is required at different locations within a facility or within many locations of a supply

network to precede the regular and planned course of production, trading and stock of

materials. Inventory conversion period is the average amount of time that a business

holds its inventory (Shin & Soenen,1998). It is the time required to obtain materials for a

product, manufacture it and sell it. The inventory conversion period is essentially the time

period during which a business must invest cash while it converts materials into a sale

(Kotabo, 2002).

2.1.2 Types of Inventory

According Swanson to (2008), there are two basic types of inventory such as merchandising

and manufacturing. Manufacturing is further divided into three more components: raw

material, work in process and finished goods.

If you buy items from other producers to sell in your own gallery or shop, you'll have a

merchandise inventory. A merchandising business is one that buys and sells goods in order to

make a profit. The goods that a company buys in order to resell are known as merchandise.

Merchandise may be accounted for under one of two inventory methods; perpetual inventory

and periodic inventory. Merchandise inventory is an inventory of retailers or wholesalers

(Swanson, 2008).

According to inventory management is pivotal in effective and efficient organization. It is

also vital in the control of materials and goods that have to be held (or stored) for later use in

the case of production or later exchange activities in the case of services. The principal goal

of inventory management involves having to balance the conflicting economics of not

wanting to hold too much stock.

12

If you make your own arts and crafts, you'll have a manufacturing inventory. The term

manufacturing might not seem to fit a hand crafted type of business, but a quick review of the

classifications within the term, will make the relationship clearer (Adeniyi, 2004).

The raw material inventory only includes items that have not yet been put into the production

process. Raw material is very important in various aspects. It is one of the most decisive

factors for the quality of a product (Lange, 2004). Roughly speaking, half of the quality of a

product is determined by the characteristics of raw materials in the current production

technology. Use of proper raw material is critical for producing product of high quality at a

minimal cost. Technologically, the raw material sets a fair starting point for industries. Raw

materials of high quality are in the market, and are equally available for all users for their

disposal. Proper selection of raw powders and their post-treatment is critical for successful

competition in the market. A variety of factors affects the characteristics of raw powders

(Brackus, 2000).

Information on the product specification as well as their production method is very important

in the proper selection of raw materials. Post-treatments such as grinding, mixing and

classification also have critical effects on the characteristics (Alm, 2000). In addition to the

raw materials, the work in process inventory includes the cost of the labor directly doing the

work and manufacturing overhead. Finished goods; the finished goods inventory also

consists of the cost of raw materials, labor and manufacturing overhead, now for the entire

product. Inventory is probably one of the largest costs for merchandising and manufacturing

businesses. Find out how to account for inventory regardless if you are a retailer or

manufacturer (Lange, 2004). When the good is completed as to manufacturing but not yet

sold or distributed to the end-user, it is called a "finished good”.

13

Finished goods are goods that have completed required manufacturing process and are

waiting to be fitted/mixed/processed with final product or final product itself could also be

called finished goods (Deloof, 2003).

2.1.3 Inventory Management Approaches

There are different types of systems that are used in inventory management, companies need

to control the type of materials they purchase, plan which products are to be produced and in

what quantities and ensure that they are able to meet current and future customer demand, all

at the lowest cost possible. Thus a good inventory management system is vital in the

operations of a firm. Graman and Magazine (2006), argued that today, the cost of holding

inventory, extensive product proliferation and the risk of obsolescence, especially in rapidly

changing markets, make the expense of holding large inventories of finished goods excessive

and that high demand items naturally have safety stock assigned to them, But in many

organizations there are so many very-low-demand items that keeping any stock of these

items is unreasonably expensive, so they argue that companies must now provide good

service while maintaining minimal inventories. Therefore, inventory management approaches

are essential aspects of any organization.

2.2.3.1 The Economic Order Quantity (EOQ)

The EOQ has been previously defined by Dervitsiotis (1981), Monks (1996), Lucey (1992),

and Schroeder (2000) as the ordering quantity which minimizes the balance of cost between

inventory holding cost and re-order costs. EOQ technique assumes constant demand and that

inventory is depleted at affixed rate until it reaches a specific level where the inventory is

refilled to bring it to its beginning level, the model assumes instantaneous replacement.

14

Basing on the above, EOQ has been criticized, to some extent is not applicable to developing

countries in the following ways (Lyson, 2006). The demand for a product cannot be known

with certainty, demands of products keep changing depending on the number of factors for

instance price of the product, quality and others.

This method entails a complex analysis and attempts to determine the minimum amount of

products needed to do the job and still keep the cost of inventory as low as possible. Order

quantity is at the point where ordering cost is equal to holdings cost at the minimum level of

total cost (Kakuru, 2000). Economic order quantity is the number of units that a company

should add to inventory with each order to minimize the total cost of inventory, such as

holding costs, ordering costs and stock out costs (Imeokparia, 2013).

EOQ model is a formula to determine the ordering quantity that will minimize total inventory

costs that is ordering and carrying costs. He continues to say that carrying cost rises with

large orders because the more inventories that are ordered the larger the amount of inventory

held by the company. Ordering costs on the other hand decline with large orders.

2.2.3.2 Vendor Managed Inventory

This approach presupposes transfer of responsibility of managing and controlling inventory

from the purchasing organization to the supplier upon agreed terms ( Adeyemi & Salami,

2010). The purchasing organization has legal ownership of the goods, but the goods after

purchase keep with the supplier and delivered at the buyer‟s premises on basis of ordered

quantity.

15

On the other hand modern development have seen the emergence of (VOI) vendor owned

inventory where the inventory is kept in the buyers premises and the buyer pays for what has

been used (Asheroft, 2005).

Vendor Managed Inventory (VMI) is where the manufacturer is given responsibility for

manufacturing and controlling inventory level at the retailer‟s distribution centre and in some

instances at the retail store level as well (Baily, Farmer, Barry, Jessop& David, 2008). VMI

is a process that falls under the „push‟ stock management processes. These are processes that

can be triggered by a tea processing firm‟s interpretation of an expected demand in inventory

and supply is scheduled to meet this demand (Irungu& Wanjau, 2011).

A well designed and developed approach to VMI can lead not only to reductions in inventory

level in the supply chain, but also to secondary savings arising from simplification of systems

and procedures (Rushton, Croucher, & Baker, 2011).

Failure to achieve supply on time may slow down the cash to cash cycle, thus reducing the

organization‟s efficiency or profitability .VMI provides the opportunity to develop a much

close relationship and binding relationship among the retailers and the manufacturers as well

as giving a much better visibility of the real demand. The supplier takes the responsibility for

operational management of the inventory within a mutually agreed framework of

performance targets which are constantly monitored and updated to create an environment of

continuous improvement. Users receive improved service levels, and cash flows, and vendors

enjoy better visibility of changing demand and greater customer loyalty (Emmett &

Granville, 2007). Reduced administrative costs due to elimination of the need to monitor

levels, paper to computer entries and reduced re-ordering costs (Farrington & Lysons, 2006).

16

2.2.2.3 Just In Time (JIT)

This is defined as an Inventory management philosophy whose goal is to maintain just

enough material in just the right time to make just enough amount of product. It‟s the exact

adjustment of production of quantity and time held. JIT is a demand pull system where the

demand for the product dictates the production requirement. It looks at inventory as a waste

and should be eliminated as much as possible. JIT has a benefit on reduction of inventories,

lead time reduction, and costs savings. Adoption of JIT has led to reduced inventory costs

and firms have experienced a high turnover rates (Biggart, 2002).

The philosophy of just in time refers to inventory as waste, it exposes hidden cost of holding

inventory, just in time system focuses on having the right materials at the right time at the

right place and in the exact amount. Liker, (2003) criticizes just in time operations and he

says it‟s risky because it leaves suppliers and downstream consumers open to supply shock

due to large demand changes. He uses an analogy of lowering the water in the river to expose

the rocks to explain how removing inventory from a firm interrupted the production flow.

Just in time policy is very unrealistic, customers demand constantly changes and shortages

due to stock out cost can cause huge losses on profits.

On addition just in time is criticized because it does not embrace the quantity discount model

which provide the lowest total cost for the firm, this means that when inventory is bought in

large quantities there is a discount and this reduces the total cost of inventory, therefore just

in time exposes the business to these dangers and its highly criticized.

17

Two things must happen for JIT to work. All parts must arrive where they are needed, when

they are needed and in the exact quantity needed (Eroglu & Hofe, 2011).

2.2.2.4 ABC Inventory Management Model

Inventory management usually involves a large number of items ranging in price from

relatively expensive, possibly very expensive units. Since inventory itself represent idle

capital, it‟s natural that Inventory management can be exercised on items that are

significantly responsible for the increase in capital cost (Farrington & Lysons, 2006).

ABC is a model that items are classified. Group A normally constitute of all the items that

are expensive and most valued in the organization and sometimes the items with high usage

rate, so if they ran out of stock the customers will be so disappointed. These items are

normally few but high impact. Group B items are those with moderate impact to the company

most of the items fall under this category moderate control is employed.

The remaining items constitute of class C which is low value goods and less concerns and

emphasis are taken. Class A represents small quantities of expensive value and must be

subject to tight Inventory management. Class B is next in order where a moderate form of

inventory can be applied. Class C items should be given the lowest priority. ABC analysis is

usually the first step that must be applied in an Inventory management to be able to decide on

the ideal on the way of controlling inventory (Eroglu & Hofer, 2011).

18

2.2.2.5 Fixed Order Point System or Two Bin System

In this method, inventory is tracked until it reaches a pre-determined point, when its low the

company makes an order to push the stock back to the desirable level the same amount is

ordered in each occasion therefore it is fit to be called continuous review system (Howard J

wells).

This is a system that is designed to track the remaining of an item each time a withdrawal is

made to determine whether its time to reorder, in this system demand is random and fixed

lead time costs which is involved. In this method the stock is segregated into two bins, stock

is first taken from the first bin; the requisition is placed when the stock in the first bin is over.

(Madaba,2005).Gerson, (1998), continue to explain about the periodic review system and he

says that in this method the inventory level is checked at fixed intervals this could be done

weekly or monthly it is known as time triggered system or fixed order. The periodic review

could be weekly, monthly, or any other specific time established by the firm, this method is

also known as economic order internal systems. He says that this is a system for placing

orders of inventories regular intervals and inventory is replenished up to as specified

inventory level.

2.1.4 Factors Influencing Inventory Management

There is several factors influence Inventory management but; because of limited time; the

researcher focuses on product type, product cost, lead time, cost of goods sold, stock level

and technological change. The type of product greatly influences the Inventory management

policies assigned to manage the product. For example, products with short shelf lives, such as

perishable foods, require a different policy.

19

Short shelf life products must rotate based on expiration date (Lucey , 2002). A major factor

that affects Inventory management policies is product lead time; the time from receipt of an

order to the time of delivery. Some industries and products have extraordinarily long lead

times .The increased amount of inventory also increases the workload associated with

managing the inventory, such as cycle counting, yearly physical inventory and general

warehouse maintenance (Irungu &Wanjau, 2011).

Many companies employ additional Inventory management policies for high-value products.

For example, many warehouses that inventory expensive audio-video equipment keep some

of the most expensive equipment; only a few of the warehouse personnel have access to this

equipment. Along with having the products caged, most companies require a signature from

authorized personnel before high-value products move from one location within a facility to

another (Gupta & Boyd, 2008). Companies cost is determined by adding up all the money

spent to buy the materials needed to produce the products this may be simply the money used

to purchase the wholesale products that are put on shelves and sold as stock.

A company‟s cost of goods directly affect the profits since the money used to produce the

products is ultimately deducted from the money taken from the sales , therefore it‟s important

for a firm to shop around for the best deal on products in order to reduce the cost of goods

and increase on the profits (Mutikani,2010). Another aspect of profitability is the degree of

cost, increase in costs will decrease the level of profits, this could include labor, raw

materials costs and rent.

20

On the other hand devaluation of the exchange rate would increase cost and imports and

therefore importing companies would face increase in costs which leads to decrease in

profits. Alternatively a firm with high fixed costs will need to produce a lot of benefits from

economies in order to maintain their profits levels (Kumar).

Maintaining stock levels affect the profits of a firm indirectly in many businesses. If a

company if a company stocks too much of a product, selling a small percentage of the total

products purchased in a given period of time the cost of goods may outweigh the total sales.

On the other hand ordering too few of an item could mean that the cost is reduced of a

product and it‟s easy to miss out sales that could have been made. This also will reduce the

level of profits (Benetts, 1990). Firms that hold high levels of inventory, this affect their level

of profits because stock is idle resources, the more stock a firm holds the more resources is

spend on this stock (Lysons, 2006).

Cost per unit of stock increases this reduces the level of profits due to this, many firms strive

to reduce their inventory costs, during times of price increase, this allows them to maintain

their current pricing levels. When inventory level rises it reduces the level of profits, but

firms try to reduce the cost by taking advantage of the supplier‟s discounts and negotiating

lower prices with their vendors in order to maintain the high level of profitability of a firm

(Lysons, 2005).

Changes in the technological sector have affected the way many firms carryout their

businesses this changes include, e-commerce, smart phones transactions, these technologies

trend enables customers to access goods and services faster. This ability to tap into customers

and the improvement in technology trends means possibly improvement in profits.

21

Technological knowhow and education level of people are so significant and this factor

affects business. Changes in technology has affected the level of profits, due to illiteracy

levels of workers in a firm and the rigidity level of workers in most firms, when the

technology improves this improves the profit level because there is efficiency in production

compared to poor technology where production is low and inefficient (Renuka,2001).

2.1.5 Overview of Organizational Performance

According to Main, (2000), the word profitability is composed of two words, namely; profit

and ability. The term profit has already been discussed at length in detail. The term ability

indicates the power of a firm to earn profits. The ability of an enterprise also denotes its

earning power or operating performance. Financial performance is the ability to earn profit

from all the activities of an enterprise. Business is conducted primarily to earn profits. The

amount of profit earned measures the efficiency of a business. The greater the volume of

profit, the higher is the efficiency of the concern.

The profit of a business may be measured and analyzed by studying the profitability of

investments attained by the business (Newbery & Mayer, 2007).

It indicates how well management of an enterprise generates earnings by using the resources

at its disposal (Storey, Emberson, Godsell & Harrison, 2006). In the other words the ability

to earn profit e.g. profitability, it is composed of two words profit and ability. The word

profit represents the absolute figure of profit but an absolute figure alone does not give an

exact ideas of the adequacy or otherwise of increase or change in performance as shown in

the financial statement of the enterprise (Deloof, 2003).

22

The word „ability‟ reflects the power of an enterprise to earn profits, it is called earning

performance. Earnings are an essential requirement to continue the business. Profitability is a

measure of evaluating the overall efficiency of the business (Main, 2000). The best possible

course for evaluation of business efficiency may be input-output analysis. Profitability can be

measured by relating output as a proportion of input or matching it with the results of other

firms of the same industry or results attained in the different periods of operations.

Profitability of a firm can be evaluated by comparing the amount of capital employed i.e. the

input with income earned i.e. the output (Rajeev, 2008).

This is popularly known as return on investment or return on capital employed. Along with

the economic objective of earning profits, a business is also required to perform a large

number of social objectives. Besides providing better quality of goods and services, it

provides big employment opportunities to the people, better condition of work, fulfill

community needs, conserves resources (Deloof, 2003).

2.1.6 Techniques of Organizational Performance Analysis

A financial analyst can adopt one or more of the following techniques or tools of profitability

analysis. Comparative Financial Statements, Cost volume Profit Analysis and ratio analysis

etc; because of limited time, the researcher is going to focus on ration analysis methods

especially profitability ratio only. According to Friends Consult Ltd (2012), Profitability

ratios are financial performance indicators that indicate how well an institution‟s

resources have been utilized to generate returns. The ratios indicate an institution‟s ability to

generate profits. Under this study, the researcher focuses on: Return on Assets (ROA),

Return on Equity (ROE), and return on invested capital (net profit ratio & turnover ratio).

Gross profit margin is found by subtracting the cost of goods sold from, net sales and then

dividing this amount (gross margin) by net sales.

23

The gross profit margin is an important operating ratio. A small change in the gross margin

has a tremendous impact on local savings. It indicates the cooperative‟s pricing policy and

cost of goods offered for sale (Katsiaryna, 2004)

2.1.7 Measurements of Organizational Performance

Adjusted margin is similar to gross margin in that annual profit dollars are divided by annual

sales dollars.

But to attain a more meaningful and comprehensive profitability measurement, the adjusted

margin calculation subtracts the annual cost of carrying the average inventory investment

from the gross profit dollars. The general formula is Adjusted Margin = [Annual Gross

Margin Dollars – (Annual Carrying Cost % x Average Inventory Investment)] ÷ Annual

Sales Dollars.

The ROA figure gives investors an idea of how effectively the company is converting the

money it has to invest into net income.

The higher the ROA number, the better, because the company is earning more money on less

investment (Damodaran, 2007). An indicator of how profitable a company is relative to its

total assets. ROA gives an idea as to how efficient management is at using its assets to

generate earnings. Calculated by dividing a company's annual earnings by its total assets,

ROA is displayed as a percentage (Mark & Ilse , 2008). The formula for return on assets is:

ROA =

Annual Net Income After Tax

Total asset

ROA for public companies can vary substantially and will be highly dependent on the

industry. This is why when using ROA as a comparative measure, it is best to compare it

against a company's previous ROA numbers or the ROA of a similar company.

24

Investors should compare the ROE of different companies and also check the trend in ROE

over time. However, relying solely on ROE for investment decisions is not safe. It can be

artificially influenced by the management, for example, when debt financing is used to

reduce share capital there will be an increase in ROE even if income remains constant(Mark

& Ilse, 2008).

The formula of return on equity is :

ROE =

Annual Net Income

Average Stockholders' Equity

Where, Net income is the after tax income whereas average shareholders' equity is calculated

by dividing the sum of shareholders' equity at the beginning and at the end of the year by 2.

The net income figure is obtained from income statement and the shareholders' equity is

found on balance sheet. Many distributors are surprised to learn that inventory turnover is as

important to overall corporate profitability as gross margins. Inventory turnover measures the

number of times you sell your average inventory investment each year and is calculated with

the equation: Cost of goods sold over the previous 12 Months /Average inventory investment

over the previous 12 Months (Emmett & Granville, 2007).

For the purpose of this ratio, net profit is equal to gross profit minus operating expenses and

income tax. All non-operating revenues and expenses are not taken into account because the

purpose of this ratio is to evaluate the profitability of the business from its primary

operations. The relationship between net profit and net sales may also be expressed in

percentage form. When it is shown in percentage form, it is known as net profit margin.

25

Turnover ratio showing how many times a company's inventory is sold and replaced over a

period. The days in the period can then be divided by the inventory turnover formula to

calculate the days it takes to sell the inventory on hand or inventory turnover days. Inventory

turnover ratio measures company's efficiency in turning its inventory into sales (Byoungho,

2004). Average inventory should be used for inventory level to minimize the effect of

seasonality. This ratio should be compared against industry averages.

A low turnover rate can indicate poor liquidity, possible overstocking, and obsolescence, but

it may also reflect a planned inventory buildup in the case of material shortages or in

anticipation of rapidly rising prices (Eroglu & Hofer, 2011). Return on invested capital

(ROIC) is always calculated as a percentage. Invested capital can be in buildings, projects,

machinery, other companies etc. One downside of return on capital is that it tells nothing

about where the return is being generated. For example, it does not specify whether it is from

continuing operations or from a one-time event, such as a gain from foreign currency

transactions (Mark & Ilse, 2008).

2.1.8 Inventory Management and Organizational Performance

Inventory management helps organization to establish the proper inventory levels through the

economic order quantity; and to keep track of this level through Inventory management

system which may be manual such as two bin method and red line method, or computerized

Inventory management systems. Proper Inventory managements also require an organization

to undertake stocking and use appropriate method to value stock so as not to under or over

state profits (Kotabo, 2002). Inventory management can be done through introduction of

different measures so as to prevent the company from incurring unnecessary losses made by

different departments (Namusoke, 2011).

26

Capital and operating costs usually are reduced as a distributor‟s investment in inventory

decreases. After all, not as much money is tied up in stock, there isn‟t as much inventory to

keep track of, and less material is subject to shrinkage and obsolescence. Adjusted margin is

similar to gross margin in that annual profit dollars are divided by annual sales dollars

(Schreibfeder, 2004).

Inventory is stored in a warehouse or other storage facility before it is used to fill customer

orders. The efficiency with which this inventory is stored directly affects corporate

profitability, because receiving material as well as processing and filling customer orders are

costs of doing business. While a single warehouse cost factor might not have a significant

effect on corporate profitability, the total extra cost a firm incurs from having inefficient

warehouse operations can have a significant effect on overall corporate profitability

(Schreibfeder, 2004).

Inventory problems of too great or too small quantities on hand can cause business failures. If

a manufacturer experiences stock-out of a critical inventory item, production halts could

result. Moreover, a shopper expects the retailer to carry the item wanted. If an item is not

stocked when the customer thinks it should be, the retailer loses a customer not only on that

item but also on many other items in the future (Adeyemi & Salami, 2010). The conclusion

one might draw is that effective inventory management can make a significant contribution

to company‟s profit as well as increase its return on total assets.

2.2 Empirical Literature

Imeokparia (2013) analyzed Inventory Management System and Performance of Food and

Beverages Companies in Nigeria”, he explored the relationship between inventory

management and control and performance and Food and Beverages companies in Nigeria.

27

Secondary data were obtained from annual financial reports and accounts of Food and

Beverages companies listed on the Nigerian Stock Exchange. The data obtained were

analyzed using simple and multiple regression models. The results show that there significant

relationship between inventory management and control and the performance of Food and

Beverages companies in Nigeria.

The multiple regression correlation coefficient (R) =0.996, R2=0.990 and p-value

=0;00<0.05 The results also show the relative importance of the inventory management

decisions made by the organization, and the implications these decisions have on the

consumer. The findings show that the three key qualities that are essential in inventory

management decisions for manufacturing organization from the perspective of the third party

logistics provider are customer satisfaction, on time delivery and order fulfillment.

Anichebe and Agu (2013) investigated the effect of Inventory Management on

Organisational Effectiveness. The objectives of the study were to analyze the effects of

inventory management on Organizational Effectiveness in selected organizations in

Enugu, and to asses the impact of proper inventory management on organizational

performances in Emenite.Descriptive research method, especially survey and case study were

employed in carrying out the study. The population of the study is six hundred and fifty eight

(658). A sample size of two hundred and fouthy eight (248), was derived using the Taro

Yamene formula for sample size determination from a finite population. Data were generated

using questionnaire, oral interviews, observations.The Findings indicate that there is

significant relationship between good inventory management and organizational

effectiveness. Inventory management has a significant effect on organizational productivity.

28

There is highly positive correlation between good inventory management and organizational

profitability. The study concluded that Inventory Management is very vital to the success and

growth of organizations.

Kennedy, Margaret and Walter (2013), tea processing firms face problems of fluctuating

inventories, inaccurate forecasts and low utilization of inventories due to inadequate

coordination of operations, They indicated that not all Inventory management systems were

necessarily best for application in given firms. The purpose of this study was to assess the

effect of Inventory management systems on operational performance of tea processing firms

with a focus on Gianchore tea factory. Objectives of the study were to: Determine the effect

of material requirement planning on operational performance, establish the influence of

continuous replenishment on operational performance, and establish the extent to which

distribution resource planning influence operational performance and the effect of vendor

managed inventory on operational performance of Gianchore Tea Factory. The study target

population was 119 respondents consisting of one (1) factory manager, sixteen (16) middle

level managers, thirty six(36) factory supervisors and sixty six (66) employees working at

Gianchore tea factory. Purposive sampling and stratified random sampling techniques were

applied to select a sample of fifty five (55) respondents for this study. The main data

collection instrument was a structured questionnaire. Quantitative data was analyzed using

descriptive and inferential statistics, and regression analysis to assess the association between

the variables in the study.

29

2.3 Critical Review and Research Gap Identification

Imeokparia (2013) carrid entitled “Inventory Management System and Performance of Food

and Beverages Companies in Nigeria”, he explored the relationship between inventory

management and control and performance and Food and Beverages companies in Nigeria.

Secondary data were obtained from annual financial reports and accounts of Food and

Beverages companies listed on the Nigerian Stock Exchange.

The data obtained were analyzed using simple and multiple regression models. The results

show that there significant relationship between inventory management and control and the

performance of Food and Beverages companies in Nigeria.

Even if Imeokparia (2013) carried out his research on inventory management, he focused on

Food and Beverages Companies rather medical supply. Kennedy, Margaret and Walter

(2013), tea processing firms face problems of fluctuating inventories, inaccurate forecasts

and low utilization of inventories due to inadequate coordination of operations, they

indicated that not all Inventory management systems were necessarily best for application in

given firms. The purpose of this study was to assess the effect of Inventory management

systems on operational performance; Quantitative data was analyzed using descriptive and

inferential statistics, and regression analysis to assess the association between the variables in

the study. Although Kennedy, Margaret and Walter (2013) carried out their research related

to inventory management, they focused on tea processing firms face problems of fluctuating

inventories and inadequate coordination of operations, they did not focus on the failed of

medical supply during their research process.

30

Hence, from the above critics this research found a gap whereby, the above studies did not

focus on the field of medical supply by assessing the techniques used by organization during

inventory management; the factors that affect organization performance through inventory

management; the level of performance effectiveness in organization and the relationship

between inventory management and performance of organization using profitability ratios,

descriptive and correlation statistics.

2.4 Theoretical Framework

2.4.1 Theory of Constraints

This study will be guided by the theory of constraints is a management idea that needs to

increase performance of companies throughput efficiency or system performance measured

by sales through the identification of those processes that are constraining the production

system. Theory of constraints is based on the principle that a chain is only as strong as the

weakest link or constraint and to elevate and manage the constraint as necessary. The

difficulties in the theory of constraints are: very long lead times, large number of unfulfilled

orders or they are executed with much extra effort (overtimes), high level of unnecessary

inventories or lack of relevant inventories, wrong materials order, large number of

emergency orders and expedition levels, high levels of devolution, lack of key customers

engagement, frequent changes or absence of control related to priority orders, which implies

on schedule conflicts of the resources. These are the bottlenecks tea factories are likely to

face warranting their application of inventory control systems in order to enhance their

operations to meet the projected operational performance.

31

The theory is founded on the belief that an organization that maximizes the output of every

machine will not perform as well as one that ensures optimization of the flow of materials

and value created through its operational performance (Kennedy,Margaret & Walter, 2013).

Therefore, the theory of constraint facilitated the study to link inventory management and

financial performance of supply chain institutions.

2.4.2 Learning Curve Theory

This study will rely on learning curve theory; according to Adeniyi (2004), the origin of the

learning curve theory was developed in 1920; learning is the process by which an individual

acquires skill, knowledge and ability. When a new product or process is started, performance

of worker is not at its best and learning phenomenon takes place. As the experience is gained,

the performance of worker improves, time taken per unit reduces and thus his productivity

goes up. This improvement in productivity of workers is due to learning effect. Cost

predictions especially those relating to direct labor must allow for the effect of learning

process. This technique is a mathematical technique. It is a graphical technique used widely

to predict cost. Learning curve is a geometrical progression, which reveals that there is

steadily decreasing cost for the accomplishment of a given repetitive operation, as the

identical operation is increasingly repeated. The amount of decrease will be less and less with

each successive unit produced. The slope of the decision curve is expressed as a percentage.

This implies that, as long as the inventory management experience improved the cost of

managing inventory reduced.

32

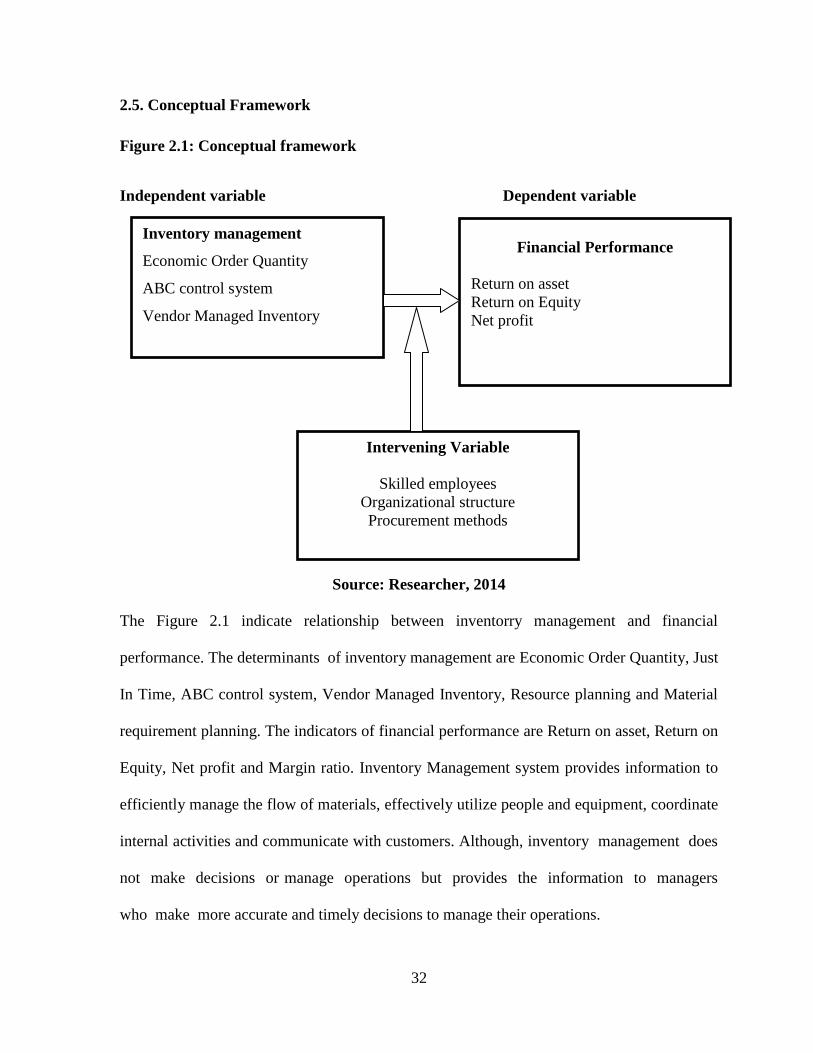

2.5. Conceptual Framework

Figure 2.1: Conceptual framework

Independent variable Dependent variable

Source: Researcher, 2014

The Figure 2.1 indicate relationship between inventorry management and financial

performance. The determinants of inventory management are Economic Order Quantity, Just

In Time, ABC control system, Vendor Managed Inventory, Resource planning and Material

requirement planning. The indicators of financial performance are Return on asset, Return on

Equity, Net profit and Margin ratio. Inventory Management system provides information to

efficiently manage the flow of materials, effectively utilize people and equipment, coordinate

internal activities and communicate with customers. Although, inventory management does

not make decisions or manage operations but provides the information to managers

who make more accurate and timely decisions to manage their operations.

Inventory management

Economic Order Quantity

ABC control system

Vendor Managed Inventory

Financial Performance

Return on asset

Return on Equity

Net profit

Intervening Variable

Skilled employees

Organizational structure

Procurement methods

33

CHAPTER THREE: RESEARCH METHODOLOGY

3.0 Introduction

This chapter sets out and describes the methodology that was used to investigate and

determine the contribution of Inventory management to organizational performance. It

includes the design of the study, the target population, sample design, data collection

procedures and instruments, data processing procedures and data analysis.

3.1 Research Design

This research was designed under case study using both descriptive and correlation research

with the aim of getting all the required qualitative and quantitative information. This design

helped to describe the relationship between the Inventory management and organizational

performance.

3.2 Target Population

The target population of this study was 128 employees of Medical Procurement and

production Division [MPPP, 2014]. The population under study is summarized into Table 3.1

according to the department.

3.3 Sample Design

A sample is a subset or portion of the total population under study. This part concerns the

sample size and sampling procedures used to come up with the sample size.

34

3.3.1 Sample Size Determination

According to our research purpose, we need data from 7 departments such as; 5 employees

from finance and accounting, 6 employees from quality assurance and control, 7 employees

procurement, 4employees from quantification, 9 employees from administrative, 25

employees from warehousing and distribution and then 23 employees from production

department, thus the targeted population used is 128 employees, according to Yamane (1967)

Sampling formula: n=2(e)*N1

NWhere:

𝑁

1+𝑁𝑒2 = 128

1+128∗ 0.072 = 79 People, Therefore sample size was 79 people.

3.3.2 Sampling Techniques