international property handbook h1 2015 - deloitte

TRANSCRIPT

International property handbookH1 2015Confidential – key clients only

International property handbook H1 2015 II

Welcome to the first edition of the International Property Handbook, our semi-annual review of real estate investment in 20 countries and over 50 cities. Drawing on expertise from across Deloitte’s global real estate network, the Handbook tracks the flows of real estate capital and acts as a useful guide to investment trends and key deals in the most active markets.

And there is certainly no shortage of activity: 2014 investment levels exceed those recorded in 2013 in almost every country covered, and in many cases the impact of this demand has pushed down yields, boosting pricing of directly- and indirectly-held real estate alike. What’s more, the share of cross border transactions continues to rise. Nevertheless, just as economic prospects continue to vary markedly from country to country, so too does the outlook for real estate investment and performance, with some locations slowing as others gain momentum.

We hope you find this report useful, and would encourage you to get in touch with your local market contact with any questions.

Robert O’Brien Global Real Estate Leader

Introduction Contents

International economic III overview

International investment V activity

Cross-border investment VI

Pricing and performance VII

Listed property performance X

Private fundraising XI

Data summary XII

International tax rates XIII

Key contacts by market XV

Australia 1

Belgium 9

Canada 14

China 22

France 28

Germany 33

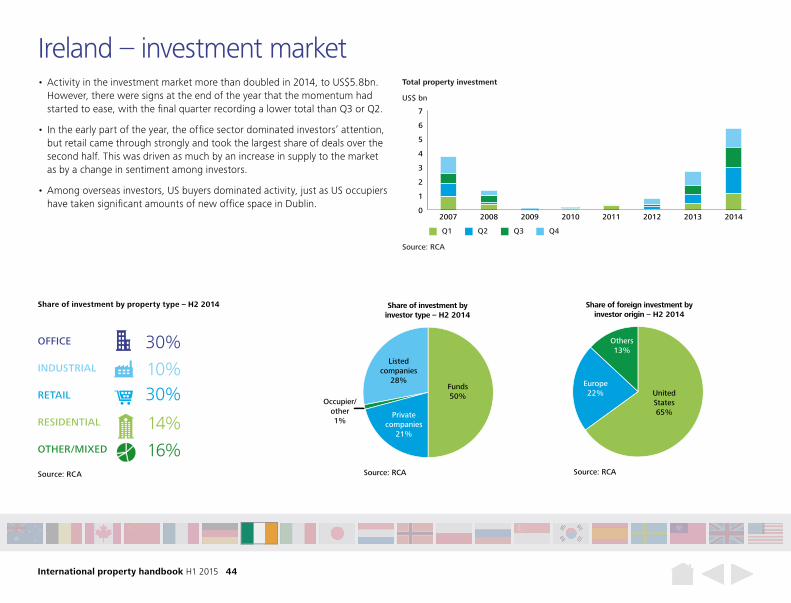

Ireland 41

Italy 46

Japan 51

Netherlands 57

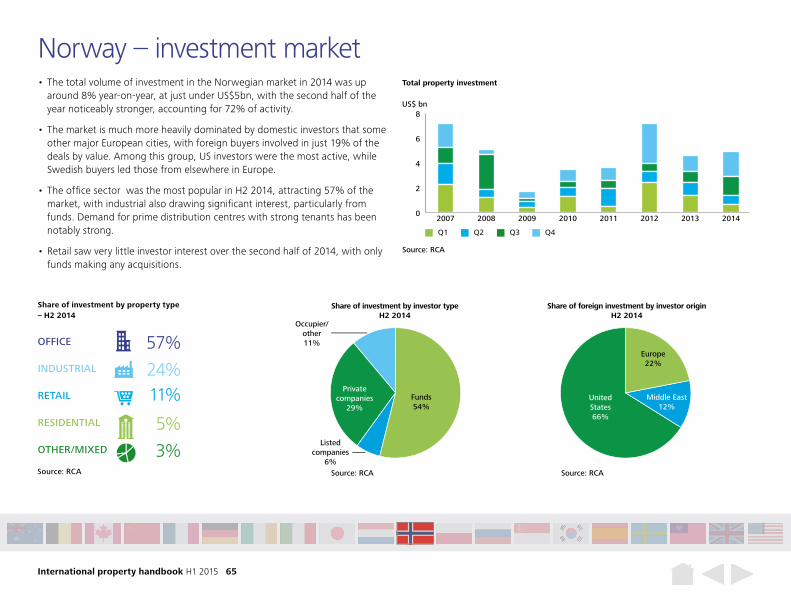

Norway 62

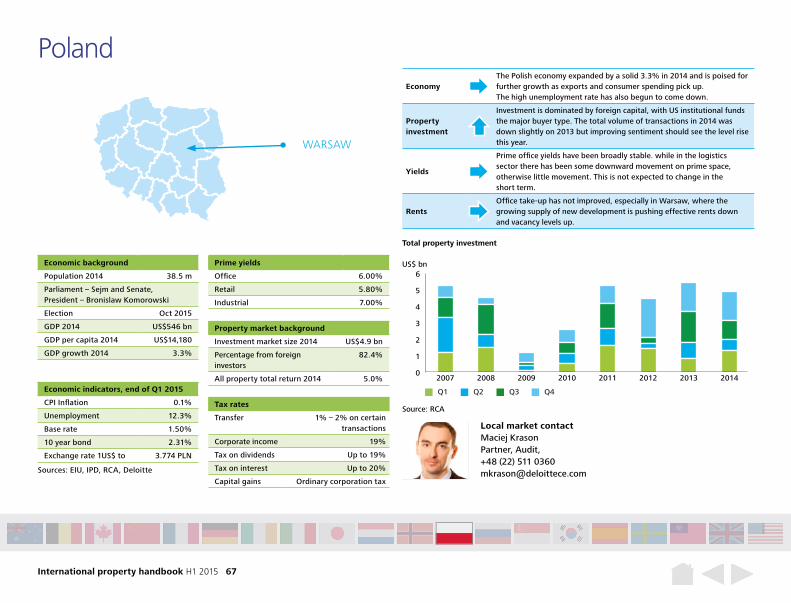

Poland 67

Russia 72

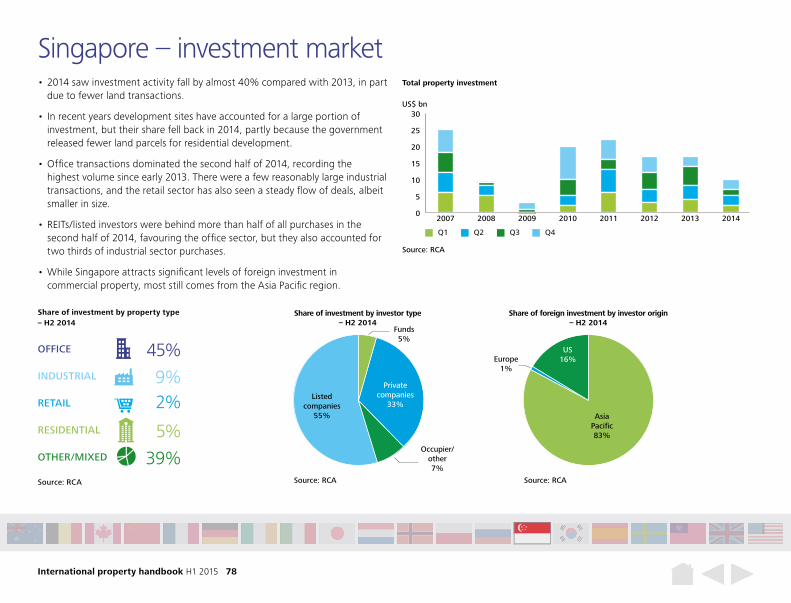

Singapore 76

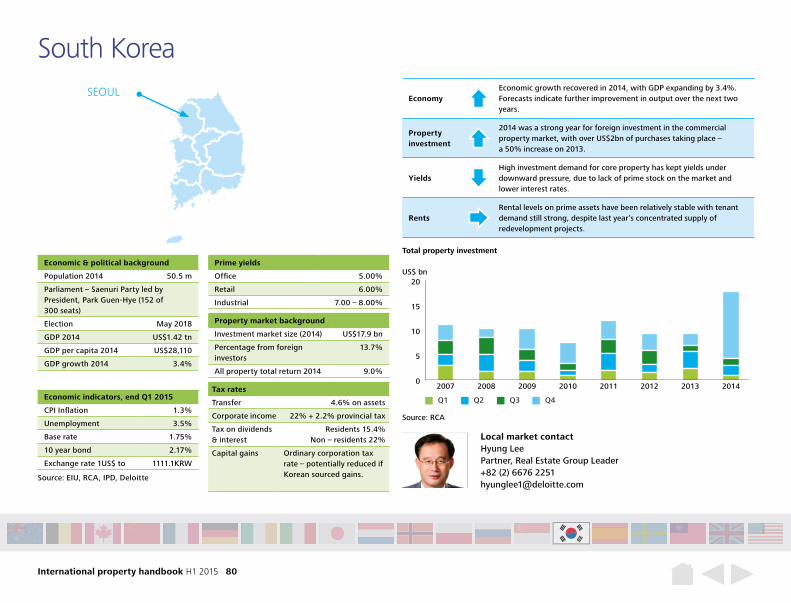

South Korea 80

Spain 85

Sweden 91

Taiwan 96

United Kingdom 100

United States 106

Recent global research 120

International property handbook H1 2015 III

International economic overview

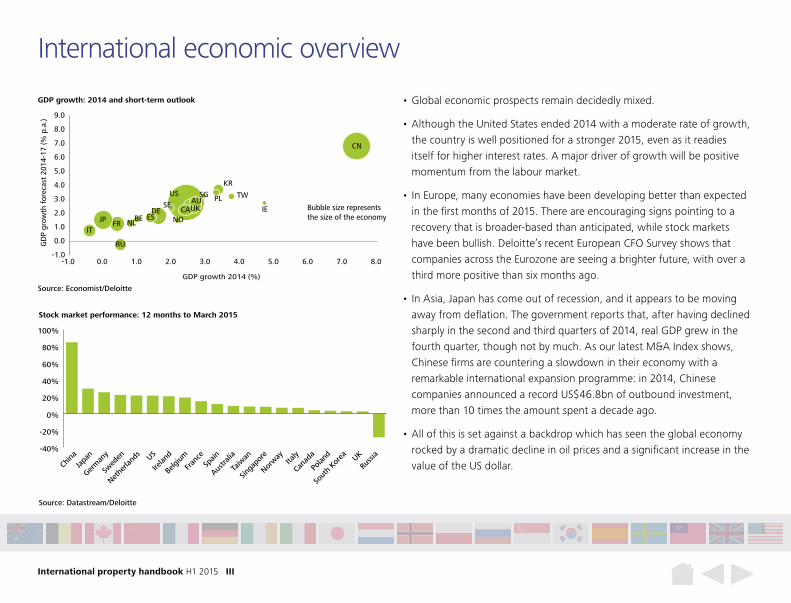

• Global economic prospects remain decidedly mixed.

• Although the United States ended 2014 with a moderate rate of growth, the country is well positioned for a stronger 2015, even as it readies itself for higher interest rates. A major driver of growth will be positive momentum from the labour market.

• In Europe, many economies have been developing better than expected in the first months of 2015. There are encouraging signs pointing to a recovery that is broader-based than anticipated, while stock markets have been bullish. Deloitte’s recent European CFO Survey shows that companies across the Eurozone are seeing a brighter future, with over a third more positive than six months ago.

• In Asia, Japan has come out of recession, and it appears to be moving away from deflation. The government reports that, after having declined sharply in the second and third quarters of 2014, real GDP grew in the fourth quarter, though not by much. As our latest M&A Index shows, Chinese firms are countering a slowdown in their economy with a remarkable international expansion programme: in 2014, Chinese companies announced a record US$46.8bn of outbound investment, more than 10 times the amount spent a decade ago.

• All of this is set against a backdrop which has seen the global economy rocked by a dramatic decline in oil prices and a significant increase in the value of the US dollar.

-40%

-20%

0%

20%

40%

60%

80%

100%

Source: Datastream/Deloitte

Stock market performance: 12 months to March 2015

China

Japa

n

Germ

any

Swed

en

Nethe

rland

s US

Irelan

d

Belgi

um

Fran

ceSp

ain

Austra

lia

Taiw

an

Singa

pore

Norway

Italy

Cana

da

Polan

d

Sout

h Ko

rea UK

Russ

ia

Source: Economist/Deloitte

GDP growth: 2014 and short-term outlook

US

UK

KR

AU

BE CA

CN

FR

DE IE

IT JP NL NO

PL

RU

SG

ES

SE TW

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

-1.0 0.0 1.0 2.0 3.0 4.0 5.0 6.0 7.0 8.0

GDP growth 2014 (%)

GD

P gr

owth

for

ecas

t 20

14-1

7 (%

p.a

.)

Bubble size represents the size of the economy

International property handbook H1 2015 IV

International economic overview

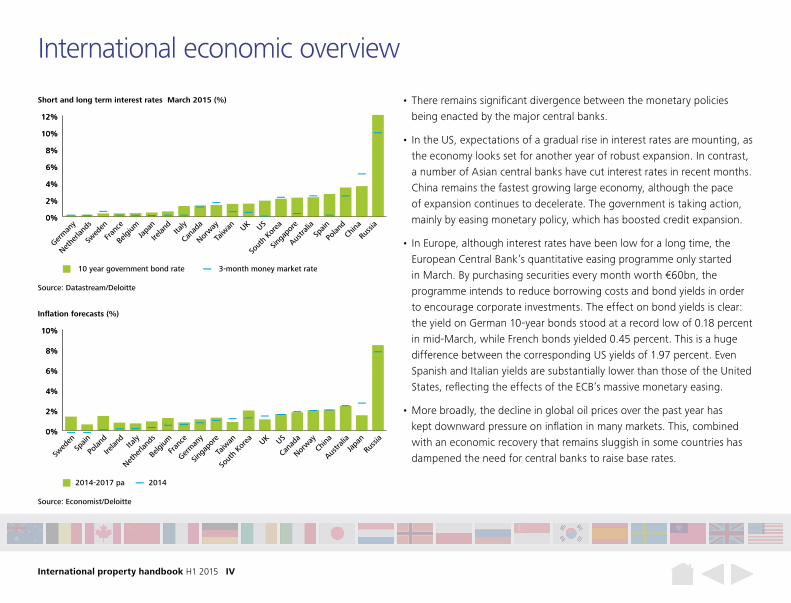

• There remains significant divergence between the monetary policies being enacted by the major central banks.

• In the US, expectations of a gradual rise in interest rates are mounting, as the economy looks set for another year of robust expansion. In contrast, a number of Asian central banks have cut interest rates in recent months. China remains the fastest growing large economy, although the pace of expansion continues to decelerate. The government is taking action, mainly by easing monetary policy, which has boosted credit expansion.

• In Europe, although interest rates have been low for a long time, the European Central Bank’s quantitative easing programme only started in March. By purchasing securities every month worth €60bn, the programme intends to reduce borrowing costs and bond yields in order to encourage corporate investments. The effect on bond yields is clear: the yield on German 10-year bonds stood at a record low of 0.18 percent in mid-March, while French bonds yielded 0.45 percent. This is a huge difference between the corresponding US yields of 1.97 percent. Even Spanish and Italian yields are substantially lower than those of the United States, reflecting the effects of the ECB’s massive monetary easing.

• More broadly, the decline in global oil prices over the past year has kept downward pressure on inflation in many markets. This, combined with an economic recovery that remains sluggish in some countries has dampened the need for central banks to raise base rates.

0%

2%

4%

6%

8%

10%

12%

0%

2%

4%

6%

8%

10%

12%

Source: Datastream/Deloitte

10 year government bond rate 3-month money market rate

Short and long term interest rates March 2015 (%)

Germ

any

Nethe

rland

s

Swed

en

Fran

ce

Belgi

umJa

pan

Irelan

dIta

ly

Cana

da

Norway

Taiw

an UK US

Sout

h Ko

rea

Singa

pore

Austra

liaSp

ain

Polan

dCh

ina

Russ

ia

0%

2%

4%

6%

8%

10%

0%

2%

4%

6%

8%

10%

Source: Economist/Deloitte

2014-2017 pa 2014

Inflation forecasts (%)

Germ

any

Nethe

rland

s

Swed

en

Fran

ce

Belgi

umJa

pan

Irelan

dIta

ly

Cana

da

Norway

Taiw

an UK US

Sout

h Ko

rea

Singa

pore

Austra

liaSp

ain

Polan

dCh

ina

Russ

ia

International property handbook H1 2015 V

International investment activity

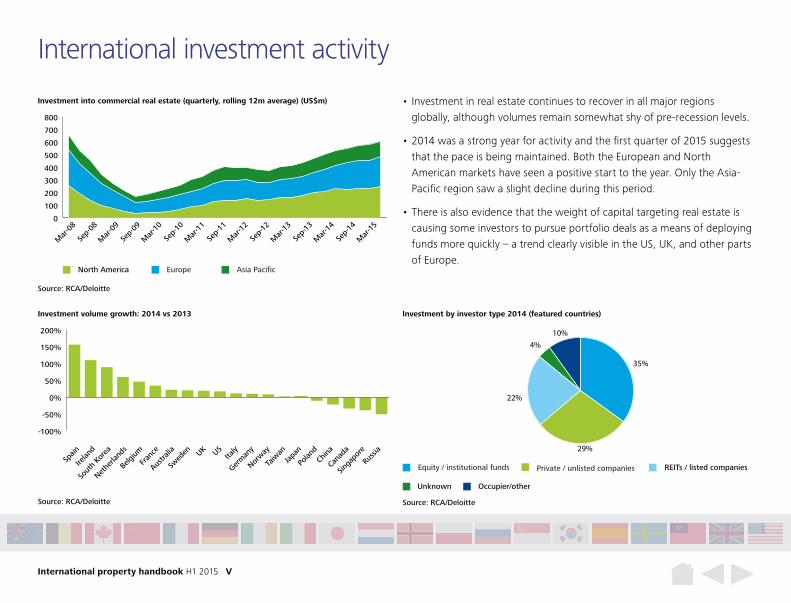

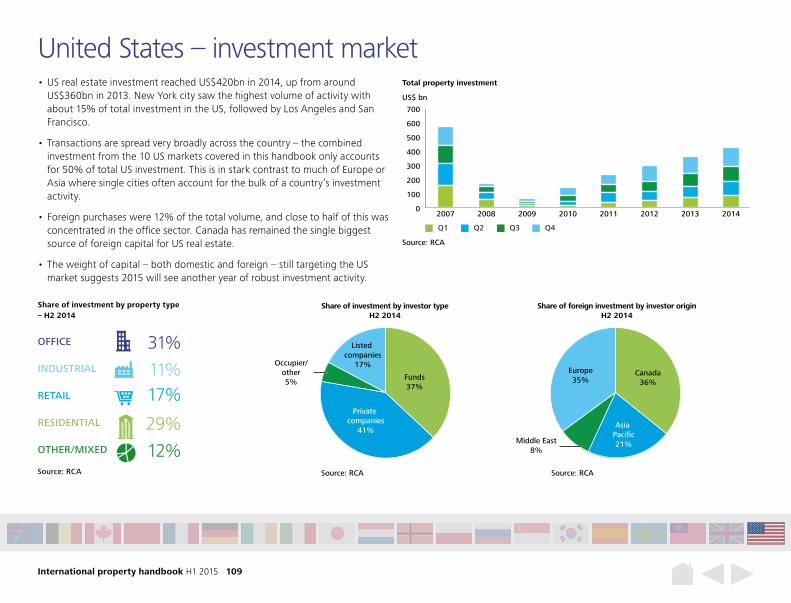

• Investment in real estate continues to recover in all major regions globally, although volumes remain somewhat shy of pre-recession levels.

• 2014 was a strong year for activity and the first quarter of 2015 suggests that the pace is being maintained. Both the European and North American markets have seen a positive start to the year. Only the Asia-Pacific region saw a slight decline during this period.

• There is also evidence that the weight of capital targeting real estate is causing some investors to pursue portfolio deals as a means of deploying funds more quickly – a trend clearly visible in the US, UK, and other parts of Europe.

0

100

200

300

400

500

600

700

800

Source: RCA/Deloitte

Investment into commercial real estate (quarterly, rolling 12m average) (US$m)

Mar

-08

Sep-

08

Mar

-09

Sep-

09

Mar

-10

Sep-

10

Mar

-11

Sep-

11

Mar

-12

Sep-

12

Mar

-13

Sep-

13

Mar

-14

Sep-

14

Mar

-15

North America Europe Asia Pacific

-100%

-50%

0%

50%

100%

150%

200%

Source: RCA/Deloitte

Investment volume growth: 2014 vs 2013

Spain

Irelan

d

Sout

h Ko

rea

Nethe

rland

s

Belgi

um

Fran

ce

Austra

lia

Swed

en UK USIta

ly

Germ

any

Norway

Taiw

anJa

pan

Polan

dCh

ina

Cana

da

Singa

pore

Russ

ia

Source: RCA/Deloitte

Investment by investor type 2014 (featured countries)

35%

10%

22%

29%

4%

Equity / institutional funds Private / unlisted companies

Occupier/otherUnknown

REITs / listed companies

International property handbook H1 2015 VI

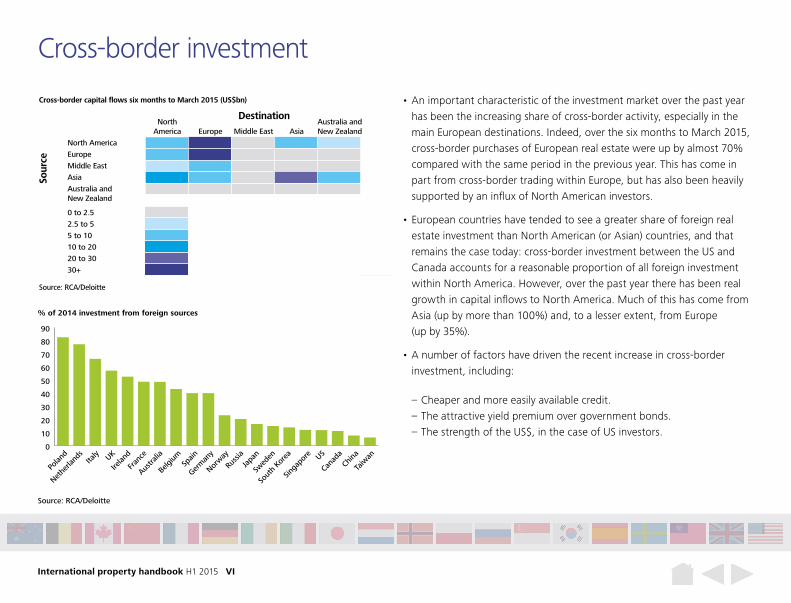

Cross-border investment

• An important characteristic of the investment market over the past year has been the increasing share of cross-border activity, especially in the main European destinations. Indeed, over the six months to March 2015, cross-border purchases of European real estate were up by almost 70% compared with the same period in the previous year. This has come in part from cross-border trading within Europe, but has also been heavily supported by an influx of North American investors.

• European countries have tended to see a greater share of foreign real estate investment than North American (or Asian) countries, and that remains the case today: cross-border investment between the US and Canada accounts for a reasonable proportion of all foreign investment within North America. However, over the past year there has been real growth in capital inflows to North America. Much of this has come from Asia (up by more than 100%) and, to a lesser extent, from Europe (up by 35%).

• A number of factors have driven the recent increase in cross-border investment, including:

– Cheaper and more easily available credit. – The attractive yield premium over government bonds. – The strength of the US$, in the case of US investors.

NorthAmerica Europe Middle East Asia

Australia andNew Zealand

North America

Europe

Middle East

Asia

Australia and New Zealand

0 to 2.5

2.5 to 5

5 to 10

10 to 20

20 to 30

30+

Sour

ce

Destination

Source: RCA/Deloitte

Cross-border capital flows six months to March 2015 (US$bn)

0

10

20

30

40

50

60

70

80

90

Taiw

anCh

ina

Cana

daUS

Singa

pore

Sout

h Ko

rea

Swed

enJa

pan

Russ

ia

Norway

Germ

any

Belgi

um

Austra

lia

Fran

ceSp

ain

Irelan

dUK

Nethe

rland

sIta

ly

Polan

d

Source: RCA/Deloitte

% of 2014 investment from foreign sources

International property handbook H1 2015 VII

Pricing and performance

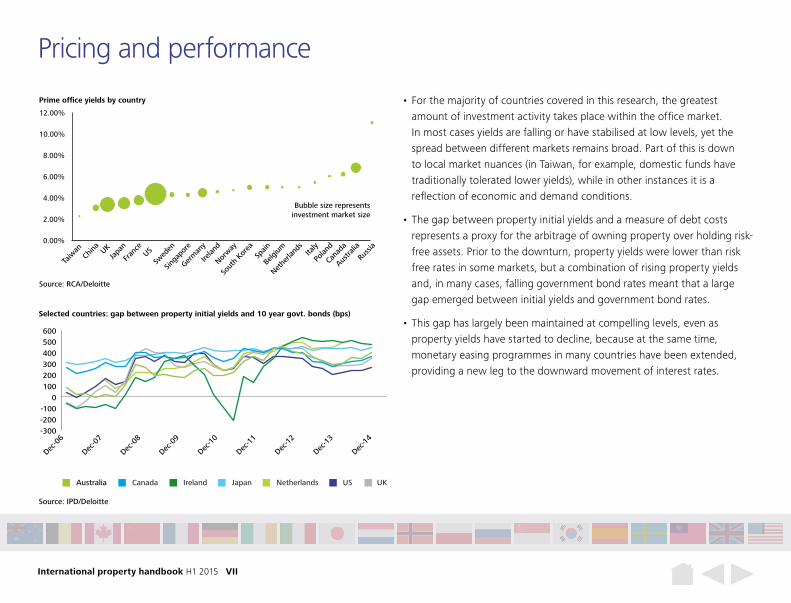

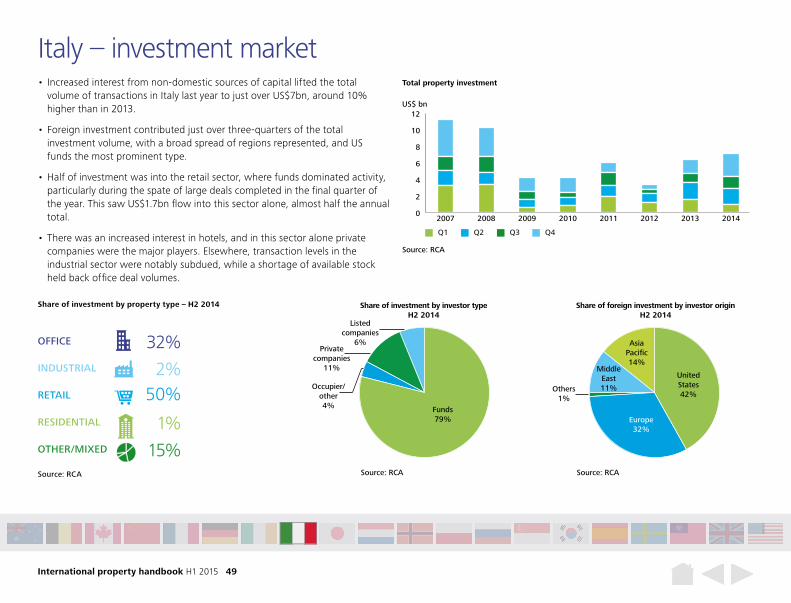

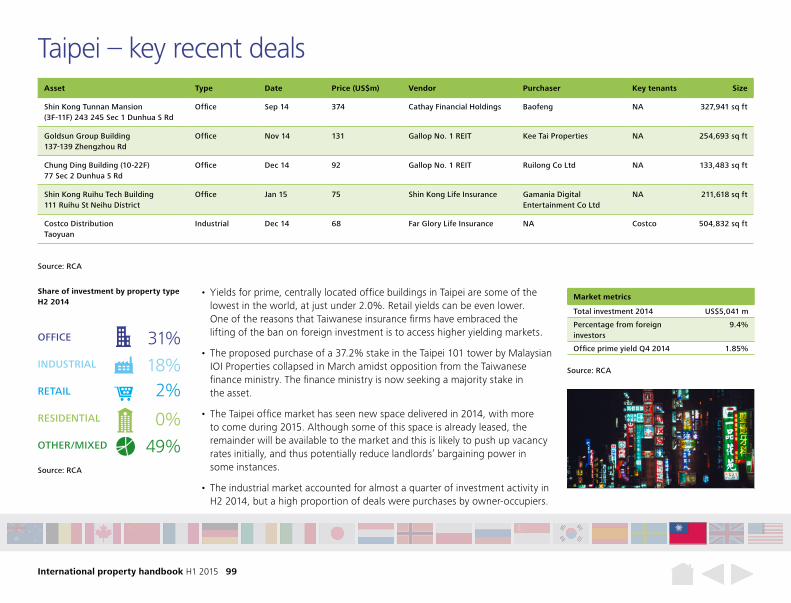

• For the majority of countries covered in this research, the greatest amount of investment activity takes place within the office market. In most cases yields are falling or have stabilised at low levels, yet the spread between different markets remains broad. Part of this is down to local market nuances (in Taiwan, for example, domestic funds have traditionally tolerated lower yields), while in other instances it is a reflection of economic and demand conditions.

• The gap between property initial yields and a measure of debt costs represents a proxy for the arbitrage of owning property over holding risk-free assets. Prior to the downturn, property yields were lower than risk free rates in some markets, but a combination of rising property yields and, in many cases, falling government bond rates meant that a large gap emerged between initial yields and government bond rates.

• This gap has largely been maintained at compelling levels, even as property yields have started to decline, because at the same time, monetary easing programmes in many countries have been extended, providing a new leg to the downward movement of interest rates.

Source: RCA/Deloitte

Bubble size representsinvestment market size

Prime office yields by country

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

Taiw

anCh

ina UK

Fran

ce

Swed

enSin

gapo

reGer

man

yIre

land

Japa

n

Norway

Sout

h Ko

rea

Spain

Belgi

um Italy

Nethe

rland

s

Polan

dCa

nada

US

Austra

liaRu

ssia

-300-200-100

0100200300400500600

Dec-0

6

Dec-0

7

Dec-0

8

Dec-0

9

Dec-1

0

Dec-1

1

Dec-1

2

Dec-1

3

Dec-1

4

Australia Canada Ireland UKUSJapan Netherlands

Source: IPD/Deloitte

Selected countries: gap between property initial yields and 10 year govt. bonds (bps)

International property handbook H1 2015 VIII

Pricing and performance

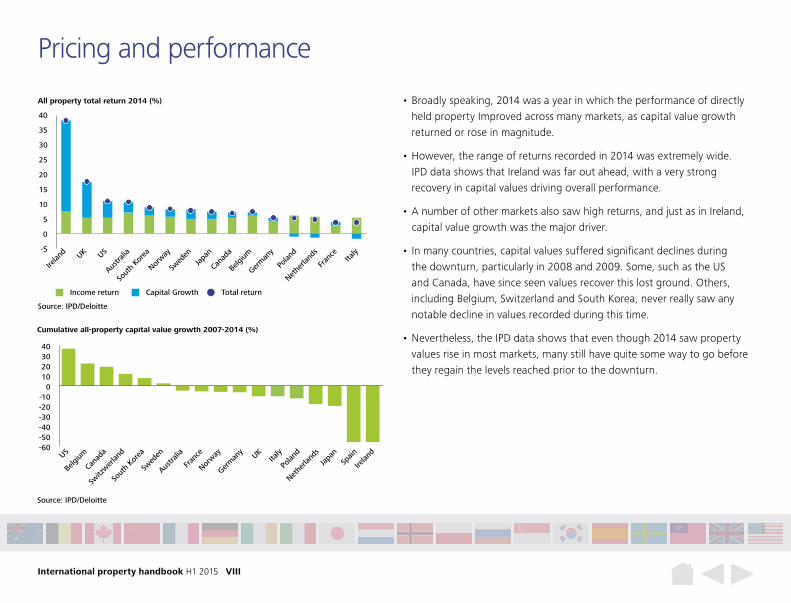

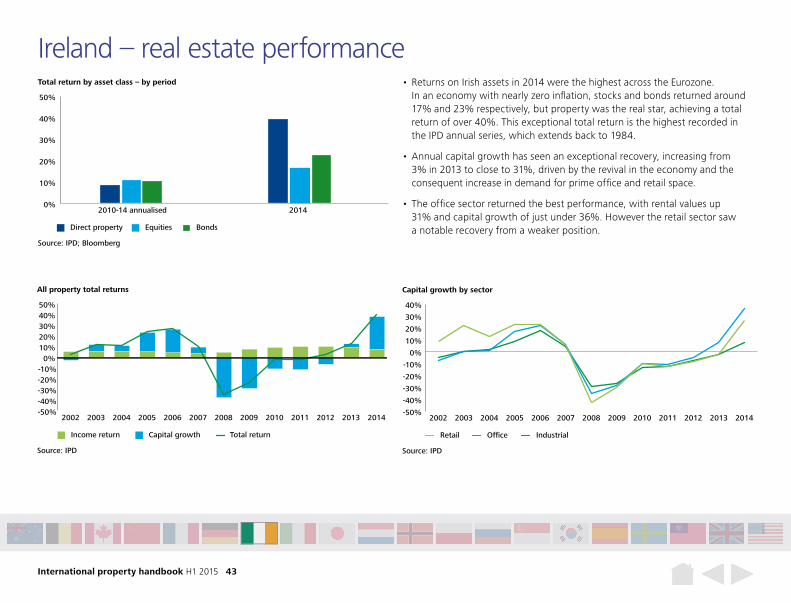

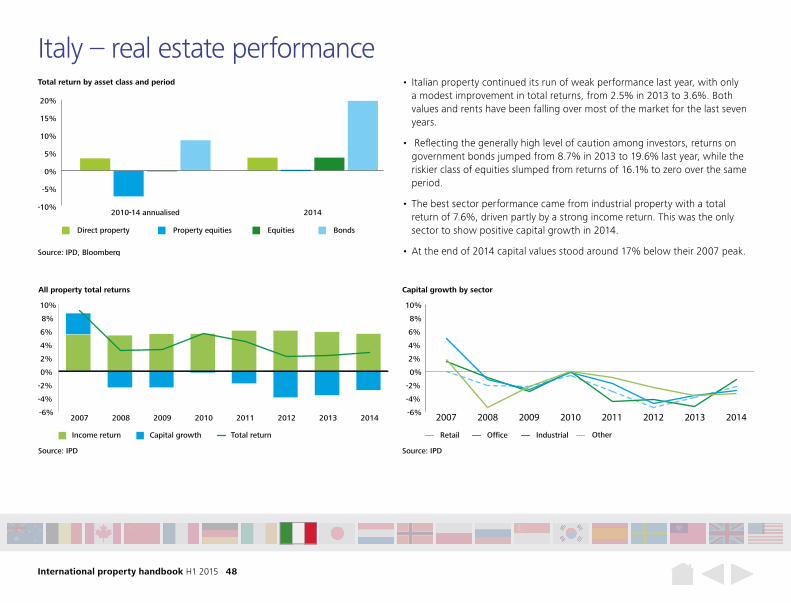

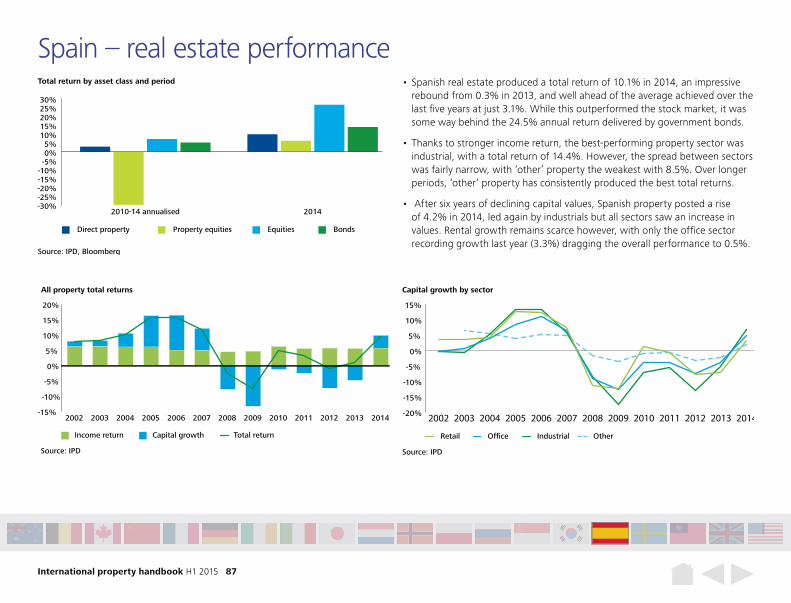

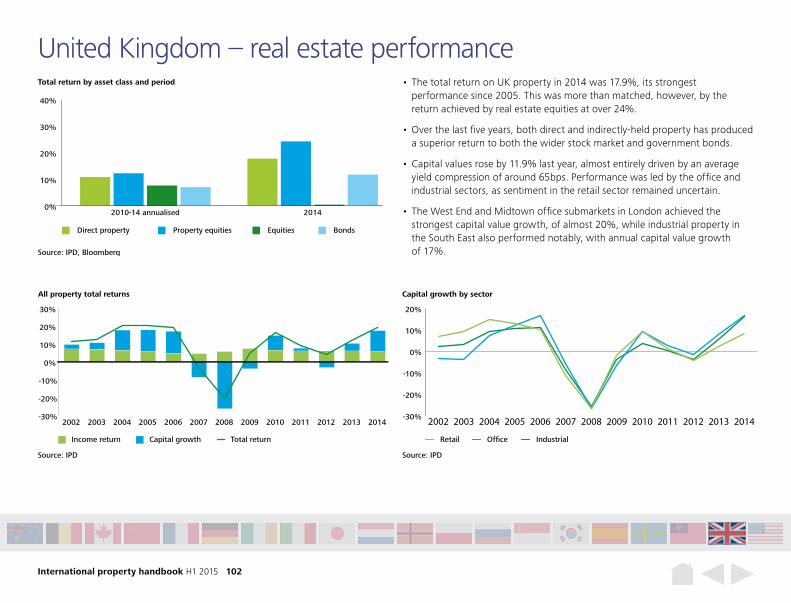

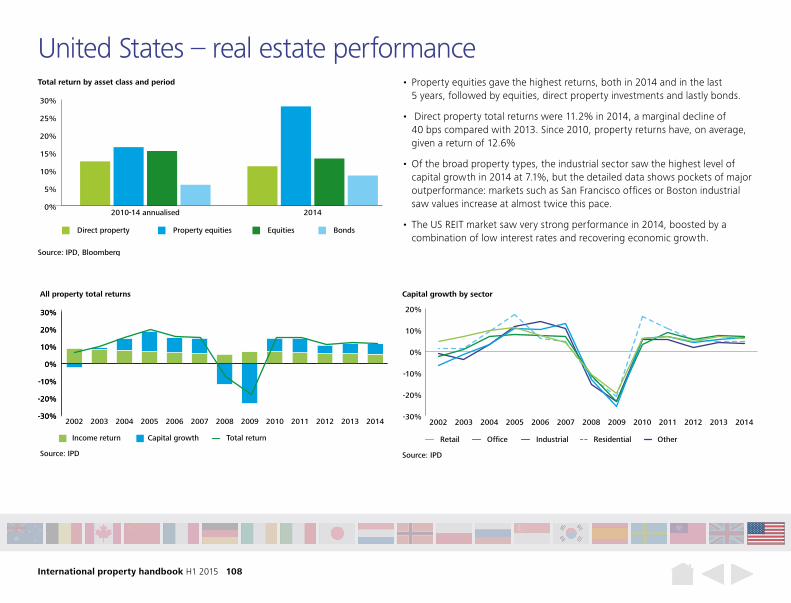

• Broadly speaking, 2014 was a year in which the performance of directly held property Improved across many markets, as capital value growth returned or rose in magnitude.

• However, the range of returns recorded in 2014 was extremely wide. IPD data shows that Ireland was far out ahead, with a very strong recovery in capital values driving overall performance.

• A number of other markets also saw high returns, and just as in Ireland, capital value growth was the major driver.

• In many countries, capital values suffered significant declines during the downturn, particularly in 2008 and 2009. Some, such as the US and Canada, have since seen values recover this lost ground. Others, including Belgium, Switzerland and South Korea, never really saw any notable decline in values recorded during this time.

• Nevertheless, the IPD data shows that even though 2014 saw property values rise in most markets, many still have quite some way to go before they regain the levels reached prior to the downturn.

All property total return 2014 (%)

40

Income return

Source: IPD/Deloitte

Capital Growth Total return

-5

0

5

10

15

20

25

30

35

Cana

daUS

Sout

h Ko

rea

Swed

enJa

pan

Norway

Germ

any

Belgi

um

Austra

lia

Fran

ce

Irelan

d UK

Nethe

rland

sIta

ly

Polan

d

-60-50-40-30-20-10

010203040

Source: IPD/Deloitte

Cumulative all-property capital value growth 2007-2014 (%)

Spain

Irelan

d

Sout

h Ko

rea

Switz

werlan

d

Nethe

rland

s

Belgi

um

Fran

ce

Austra

lia

Swed

en UKUSIta

ly

Germ

any

Norway

Japa

n

Polan

d

Cana

da

International property handbook H1 2015 IX

Pricing and performance

• Over the last two years, the range of yields available to global investors searching for prime assets has begun to narrow, as the highest yields have fallen. In the period before the downturn the range was much wider, with some 650bps separating the highest and lowest yields among the top 20 countries. Last year this spread was at its smallest since 2001, suggesting that market cycles are becoming more closely alligned.

• The range of IPD total return performances tracked over the last ten years across these same countries shows that 2013 was the first year since 2006 that produced positive returns across the board. 2014 saw a further improvement as Ireland dragged the top of the range sharply up.

• This ten years of data clearly show that investors willing to consider purchases around the globe could have found markets producing positive returns in all years, including 2008 and 2009.

0%

2%

4%

6%

8%

10%

12%

All-property yield spread among the countries covered

Source: IPD/Deloitte

2005 2006 2007 2008 2009 2010 2012 2013 2014

-40%-30%-20%-10%

0%10%20%30%40%50%

All-property total return spread among countries covered

Source: IPD/Deloitte

2005 2006 2007 2008 2009 2010 2012 2013 2014

International property handbook H1 2015 X

Listed property performance

• The listed real estate sector has seen strong performance in a number of the countries covered, in many cases outperforming the stock market overall.

• The listed sector has been an active participant in the real estate investment markets of the majority of countries covered. However, in some markets, such as the UK, REITs and other listed vehicles’ share of net purchases has declined, because as yields have continued to decline, some have taken the opportunity to sell down assets.

• There has been a spate of corporate activity in the listed sector over the past year, with significant transactions taking place within the US, Europe, and Asia.

Source: RCA/Deloitte

Share of investment by REITs/listed sector

0%

10%

20%

30%

40%

50%

60%

70%

Germ

any

Spain

Swed

en

Switz

erlan

d

Fran

ce

Belgi

umJa

pan

Italy

Cana

da

Polan

d

Norway

Taiw

an

Irelan

d UKUS

Sout

h Ko

rea

Nethe

rland

s

Hong

Kong

Singa

pore

Austra

liaCh

ina

Russ

ia

Source: EPRA/Deloitte

EPRA listed real estate performance, year to March 2015

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

Germ

any

Nethe

rland

s

Swed

en

Fran

ce

Belgi

umJa

pan

Italy

Cana

da

Norway

Taiw

anUKUS

Singa

pore

Austra

liaSp

ainCh

ina

Russ

ia

International property handbook H1 2015 XI

Private fundraising

• The volume of capital raised each quarter by private real estate funds has been rising since mid-2014.

• 2014 was a very strong year for capital raised to target Europe, although funds raised in the first quarter of 2015 continue to show a greater focus on North America, reflecting interest from institutional investors.

• Nevertheless, both the European and Asian markets have seen an uplift in interest from institutions compared with a year ago.

• Although those with opportunistic strategies account for less than half of the number of funds raised in Q1, in terms of capital, opportunistic funds still dominate.

Source: Preqin/Deloitte

Aggregate capital raised (US$bn)

0

10

20

30

40

Dec-11

Mar

-12

Jun-1

2

Sep-1

2

Dec-12

Mar

-13

Jun-1

3

Sep-1

3

Dec-13

Mar

-14

Mar

-15

Jun-1

4

Sep-1

4

Dec-14

Sep-1

0

Mar

-10

Jun-1

0

Jun-1

1

Mar

-10

Sep-1

1

Dec10

Source: Preqin/Deloitte

Primary focus of capital raised – Q1 2015

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Rest of World EuropeAsiaNorth America

Geography Strategy

DebtCoreDistressedValue AddedOpportunistic

International property handbook H1 2015 XII

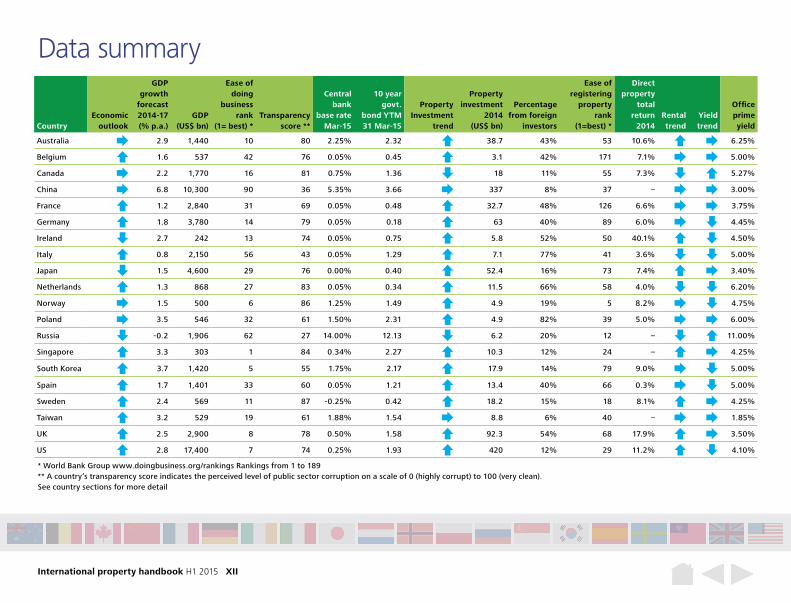

CountryEconomic

outlook

GDP growth

forecast 2014-17 (% p.a.)

GDP (US$ bn)

Ease of doing

business rank

(1= best) *Transparency

score **

Central bank

base rate Mar-15

10 year govt.

bond YTM 31 Mar-15

Property Investment

trend

Property investment

2014 (US$ bn)

Percentage from foreign

investors

Ease of registering

property rank

(1=best) *

Direct property

total return

2014Rental trend

Yield trend

Office prime yield

Australia 2.9 1,440 10 80 2.25% 2.32 38.7 43% 53 10.6% 6.25%

Belgium 1.6 537 42 76 0.05% 0.45 3.1 42% 171 7.1% 5.00%

Canada 2.2 1,770 16 81 0.75% 1.36 18 11% 55 7.3% 5.27%

China 6.8 10,300 90 36 5.35% 3.66 337 8% 37 – 3.00%

France 1.2 2,840 31 69 0.05% 0.48 32.7 48% 126 6.6% 3.75%

Germany 1.8 3,780 14 79 0.05% 0.18 63 40% 89 6.0% 4.45%

Ireland 2.7 242 13 74 0.05% 0.75 5.8 52% 50 40.1% 4.50%

Italy 0.8 2,150 56 43 0.05% 1.29 7.1 77% 41 3.6% 5.00%

Japan 1.5 4,600 29 76 0.00% 0.40 52.4 16% 73 7.4% 3.40%

Netherlands 1.3 868 27 83 0.05% 0.34 11.5 66% 58 4.0% 6.20%

Norway 1.5 500 6 86 1.25% 1.49 4.9 19% 5 8.2% 4.75%

Poland 3.5 546 32 61 1.50% 2.31 4.9 82% 39 5.0% 6.00%

Russia -0.2 1,906 62 27 14.00% 12.13 6.2 20% 12 – 11.00%

Singapore 3.3 303 1 84 0.34% 2.27 10.3 12% 24 – 4.25%

South Korea 3.7 1,420 5 55 1.75% 2.17 17.9 14% 79 9.0% 5.00%

Spain 1.7 1,401 33 60 0.05% 1.21 13.4 40% 66 0.3% 5.00%

Sweden 2.4 569 11 87 -0.25% 0.42 18.2 15% 18 8.1% 4.25%

Taiwan 3.2 529 19 61 1.88% 1.54 8.8 6% 40 – 1.85%

UK 2.5 2,900 8 78 0.50% 1.58 92.3 54% 68 17.9% 3.50%

US 2.8 17,400 7 74 0.25% 1.93 420 12% 29 11.2% 4.10%

Data summary

* World Bank Group www.doingbusiness.org/rankings Rankings from 1 to 189** A country’s transparency score indicates the perceived level of public sector corruption on a scale of 0 (highly corrupt) to 100 (very clean).See country sections for more detail

International property handbook H1 2015 XIII

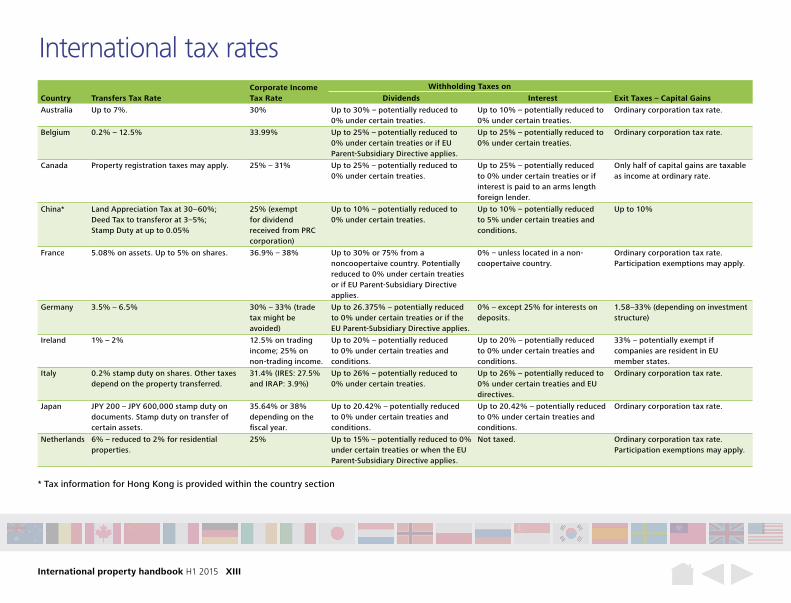

International tax rates

Country Transfers Tax RateCorporate Income Tax Rate

Withholding Taxes on

Exit Taxes – Capital GainsDividends Interest

Australia Up to 7%. 30% Up to 30% – potentially reduced to 0% under certain treaties.

Up to 10% – potentially reduced to 0% under certain treaties.

Ordinary corporation tax rate.

Belgium 0.2% – 12.5% 33.99% Up to 25% – potentially reduced to 0% under certain treaties or if EU Parent-Subsidiary Directive applies.

Up to 25% – potentially reduced to 0% under certain treaties.

Ordinary corporation tax rate.

Canada Property registration taxes may apply. 25% – 31% Up to 25% – potentially reduced to 0% under certain treaties.

Up to 25% – potentially reduced to 0% under certain treaties or if interest is paid to an arms length foreign lender.

Only half of capital gains are taxable as income at ordinary rate.

China* Land Appreciation Tax at 30–60%;Deed Tax to transferor at 3–5%;Stamp Duty at up to 0.05%

25% (exempt for dividend received from PRC corporation)

Up to 10% – potentially reduced to 0% under certain treaties.

Up to 10% – potentially reduced to 5% under certain treaties and conditions.

Up to 10%

France 5.08% on assets. Up to 5% on shares. 36.9% – 38% Up to 30% or 75% from a noncoopertaive country. Potentially reduced to 0% under certain treaties or if EU Parent-Subsidiary Directive applies.

0% – unless located in a non-coopertaive country.

Ordinary corporation tax rate. Participation exemptions may apply.

Germany 3.5% – 6.5% 30% – 33% (trade tax might be avoided)

Up to 26.375% – potentially reduced to 0% under certain treaties or if the EU Parent-Subsidiary Directive applies.

0% – except 25% for interests on deposits.

1.58–33% (depending on investment structure)

Ireland 1% – 2% 12.5% on trading income; 25% on non-trading income.

Up to 20% – potentially reduced to 0% under certain treaties and conditions.

Up to 20% – potentially reduced to 0% under certain treaties and conditions.

33% – potentially exempt if companies are resident in EU member states.

Italy 0.2% stamp duty on shares. Other taxes depend on the property transferred.

31.4% (IRES: 27.5% and IRAP: 3.9%)

Up to 26% – potentially reduced to 0% under certain treaties.

Up to 26% – potentially reduced to 0% under certain treaties and EU directives.

Ordinary corporation tax rate.

Japan JPY 200 – JPY 600,000 stamp duty on documents. Stamp duty on transfer of certain assets.

35.64% or 38% depending on the fiscal year.

Up to 20.42% – potentially reduced to 0% under certain treaties and conditions.

Up to 20.42% – potentially reduced to 0% under certain treaties and conditions.

Ordinary corporation tax rate.

Netherlands 6% – reduced to 2% for residential properties.

25% Up to 15% – potentially reduced to 0% under certain treaties or when the EU Parent-Subsidiary Directive applies.

Not taxed. Ordinary corporation tax rate. Participation exemptions may apply.

* Tax information for Hong Kong is provided within the country section

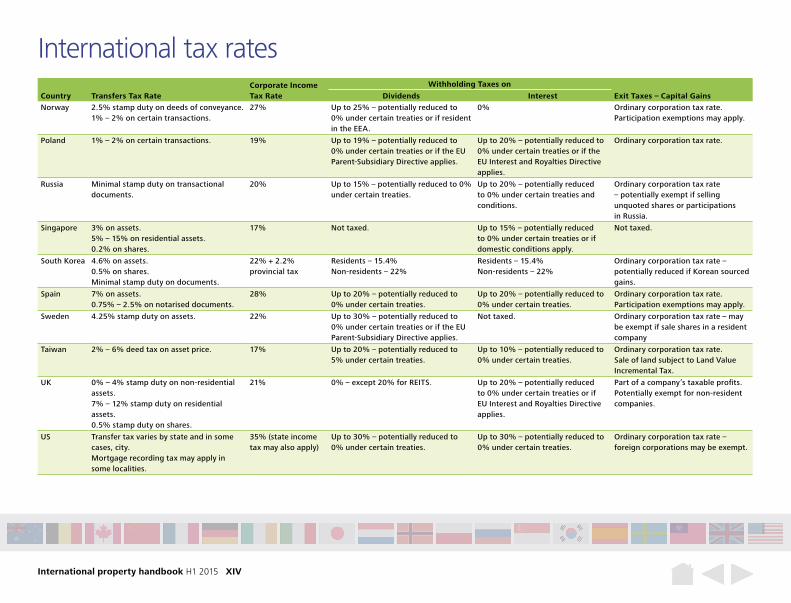

International property handbook H1 2015 XIV

International tax ratesCountry Transfers Tax Rate

Corporate Income Tax Rate

Withholding Taxes on

Exit Taxes – Capital GainsDividends Interest

Norway 2.5% stamp duty on deeds of conveyance. 1% – 2% on certain transactions.

27% Up to 25% – potentially reduced to 0% under certain treaties or if resident in the EEA.

0% Ordinary corporation tax rate. Participation exemptions may apply.

Poland 1% – 2% on certain transactions. 19% Up to 19% – potentially reduced to 0% under certain treaties or if the EU Parent-Subsidiary Directive applies.

Up to 20% – potentially reduced to 0% under certain treaties or if the EU Interest and Royalties Directive applies.

Ordinary corporation tax rate.

Russia Minimal stamp duty on transactional documents.

20% Up to 15% – potentially reduced to 0% under certain treaties.

Up to 20% – potentially reduced to 0% under certain treaties and conditions.

Ordinary corporation tax rate – potentially exempt if selling unquoted shares or participations in Russia.

Singapore 3% on assets.5% – 15% on residential assets.0.2% on shares.

17% Not taxed. Up to 15% – potentially reduced to 0% under certain treaties or if domestic conditions apply.

Not taxed.

South Korea 4.6% on assets.0.5% on shares.Minimal stamp duty on documents.

22% + 2.2% provincial tax

Residents – 15.4%Non-residents – 22%

Residents – 15.4%Non-residents – 22%

Ordinary corporation tax rate – potentially reduced if Korean sourced gains.

Spain 7% on assets.0.75% – 2.5% on notarised documents.

28% Up to 20% – potentially reduced to 0% under certain treaties.

Up to 20% – potentially reduced to 0% under certain treaties.

Ordinary corporation tax rate.Participation exemptions may apply.

Sweden 4.25% stamp duty on assets. 22% Up to 30% – potentially reduced to 0% under certain treaties or if the EU Parent-Subsidiary Directive applies.

Not taxed. Ordinary corporation tax rate – may be exempt if sale shares in a resident company

Taiwan 2% – 6% deed tax on asset price. 17% Up to 20% – potentially reduced to 5% under certain treaties.

Up to 10% – potentially reduced to 0% under certain treaties.

Ordinary corporation tax rate. Sale of land subject to Land Value Incremental Tax.

UK 0% – 4% stamp duty on non-residential assets.7% – 12% stamp duty on residential assets.0.5% stamp duty on shares.

21% 0% – except 20% for REITS. Up to 20% – potentially reduced to 0% under certain treaties or if EU Interest and Royalties Directive applies.

Part of a company’s taxable profits.Potentially exempt for non-resident companies.

US Transfer tax varies by state and in some cases, city. Mortgage recording tax may apply in some localities.

35% (state income tax may also apply)

Up to 30% – potentially reduced to 0% under certain treaties.

Up to 30% – potentially reduced to 0% under certain treaties.

Ordinary corporation tax rate –foreign corporations may be exempt.

International property handbook H1 2015 XV

Key contacts by market

AustraliaJohn LeottaPartner, Assurance & Advisory+61 (2) 9322 [email protected]

BelgiumJean-Paul LoozenPartner, Real Estate+32 2 639 49 [email protected]

CanadaSheila BottingPartner, Canadian Real Estate Leader+1 416 601 [email protected]

ChinaRichard HoManaging Partner,Real Estate Industry+ 852 2852 [email protected]

FranceChristian GilletPrincipal, Real Estate Advisory+33 (1) 4088 [email protected]

GermanyMichael MuellerPartner, Real Estate Industry Leader+49 89290 [email protected]

IrelandPadraic WhelanPartner, TaxHead of Real Estate & Infrastructure Group+353 (1) 417 [email protected]

ItalyElena VistariniPartner, Financial Advisory, National Real Estate & Construction Leader+39 02 833 [email protected]

JapanHiroki KitagataPartner, Tokyo Region Audit Services+81 (0) 906 [email protected]

NetherlandsPaul MeulenbergPartner, Financial Advisory+31 (0) 6533 [email protected]

NorwayThorvald NyquistPartner, Tax & Legal+47 95 75 31 [email protected]

PolandMaciej KrasonPartner, Audit+48 (22) 511 [email protected]

RussiaSteve OpenshawPartner, Audit Real Estate Leader +7 (495) 787 0600 [email protected]

SingaporeWong Siew EngPartner, Assurance & Advisory Services+65 6216 [email protected]

South KoreaHyung LeePartner, Real Estate Group Leader +82 (2) 6676 [email protected]

SpainJavier ParadaPartner, Audit+34 6291 [email protected]

SwedenLars FranckPartner, Corporate Tax+46 75 246 [email protected]

TaiwanChing Cheng YangPartner, Audit+886 (2) 2545 [email protected]

United KingdomNigel ShiltonPartner, Deloitte Real Estate+44 20 7007 [email protected]

United StatesRobert O’BrienPartner, Real Estate Services+1 312 486 [email protected]

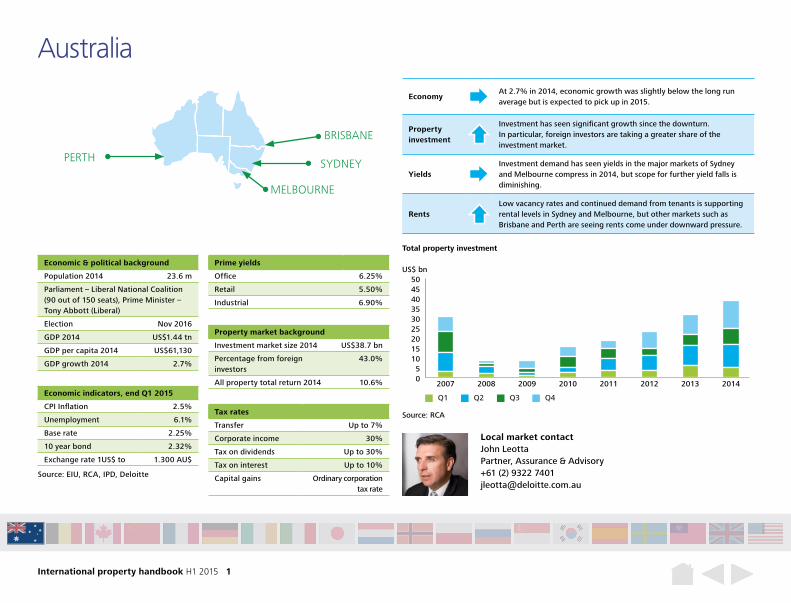

International property handbook H1 2015 1

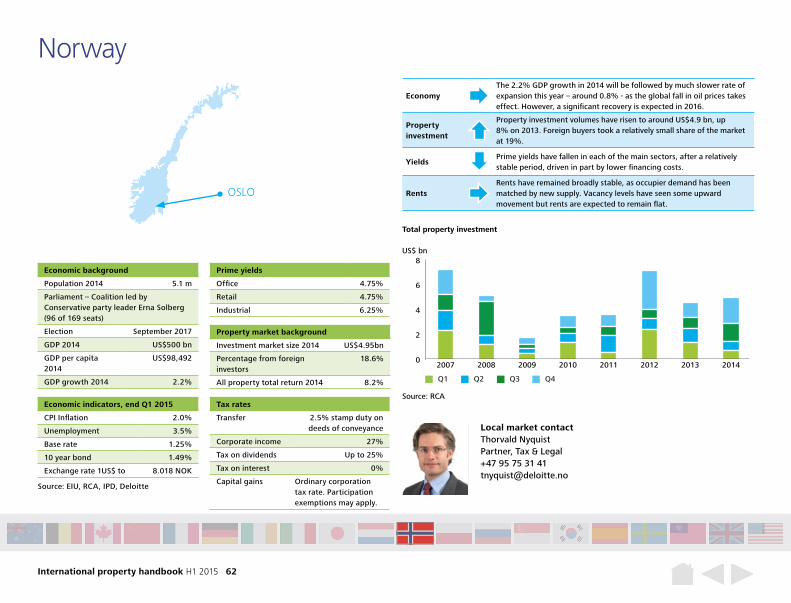

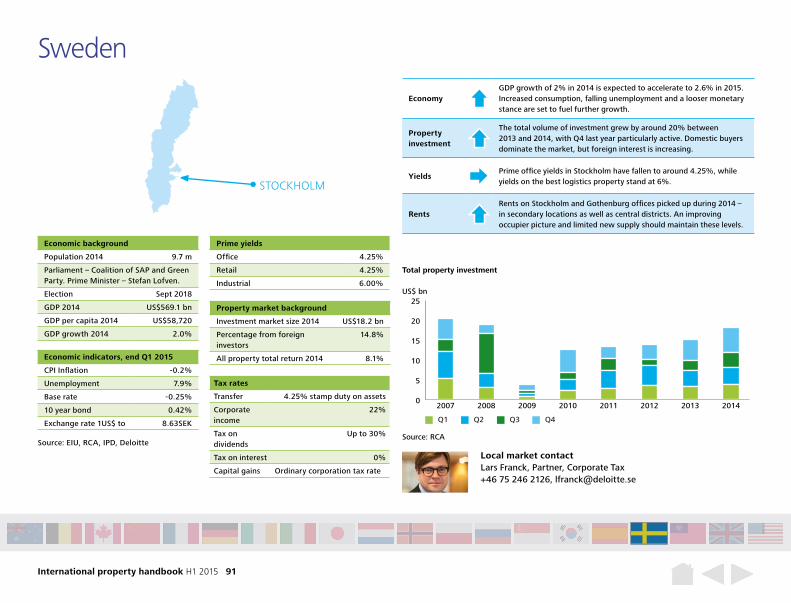

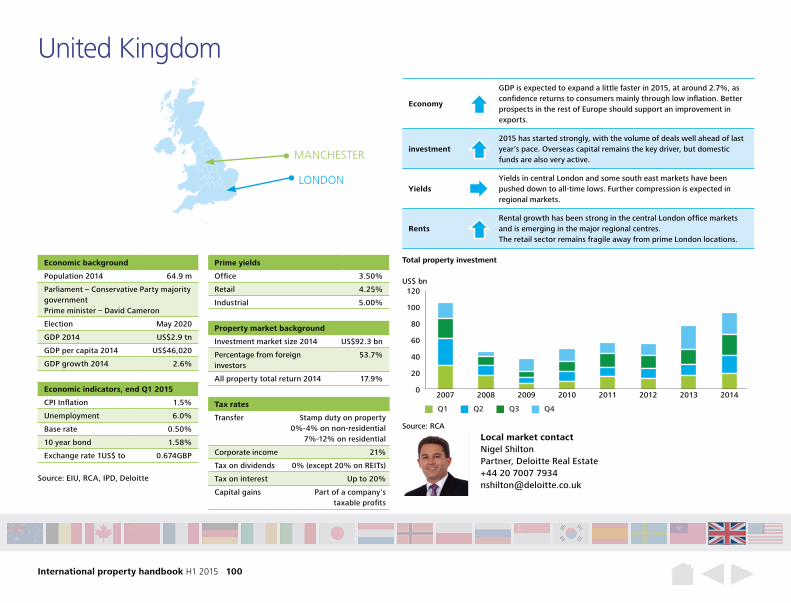

EconomyAt 2.7% in 2014, economic growth was slightly below the long run average but is expected to pick up in 2015.

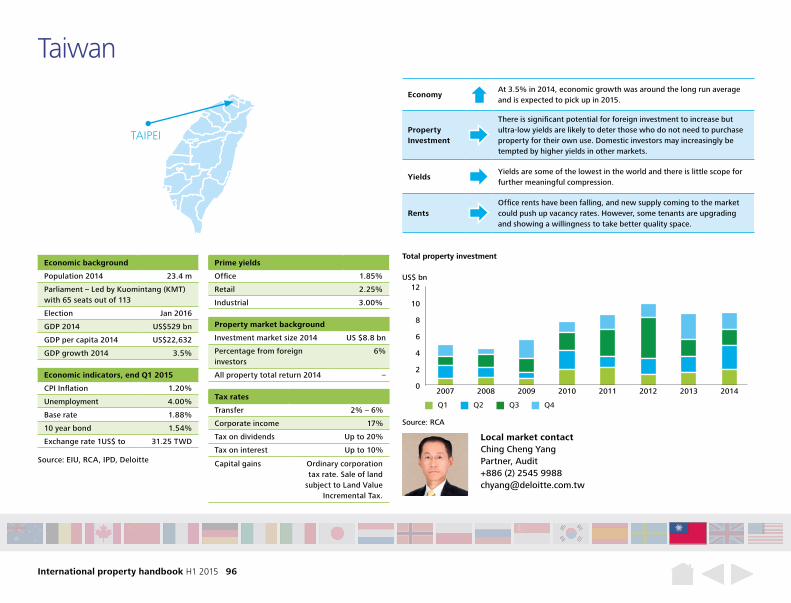

Property investment

Investment has seen significant growth since the downturn.In particular, foreign investors are taking a greater share of the investment market.

YieldsInvestment demand has seen yields in the major markets of Sydney and Melbourne compress in 2014, but scope for further yield falls is diminishing.

RentsLow vacancy rates and continued demand from tenants is supporting rental levels in Sydney and Melbourne, but other markets such as Brisbane and Perth are seeing rents come under downward pressure.

Australia

Economic & political background

Population 2014 23.6 m

Parliament – Liberal National Coalition (90 out of 150 seats), Prime Minister – Tony Abbott (Liberal)

Election Nov 2016

GDP 2014 US$1.44 tn

GDP per capita 2014 US$61,130

GDP growth 2014 2.7%

Prime yields

Office 6.25%

Retail 5.50%

Industrial 6.90%

Property market background

Investment market size 2014 US$38.7 bn

Percentage from foreign investors

43.0%

All property total return 2014 10.6%Economic indicators, end Q1 2015

CPI Inflation 2.5%

Unemployment 6.1%

Base rate 2.25%

10 year bond 2.32%

Exchange rate 1US$ to 1.300 AU$

Local market contactJohn Leotta Partner, Assurance & Advisory +61 (2) 9322 7401 [email protected]

05

101520253035404550

20142013201220112010200920082007

Source: RCA

Total property investment

US$ bn

Q1 Q2 Q3 Q4

Tax rates

Transfer Up to 7%

Corporate income 30%

Tax on dividends Up to 30%

Tax on interest Up to 10%

Capital gains Ordinary corporation tax rate

Source: EIU, RCA, IPD, Deloitte

PERTH

MELBOURNE

BRISBANE

SYDNEY

International property handbook H1 2015 2

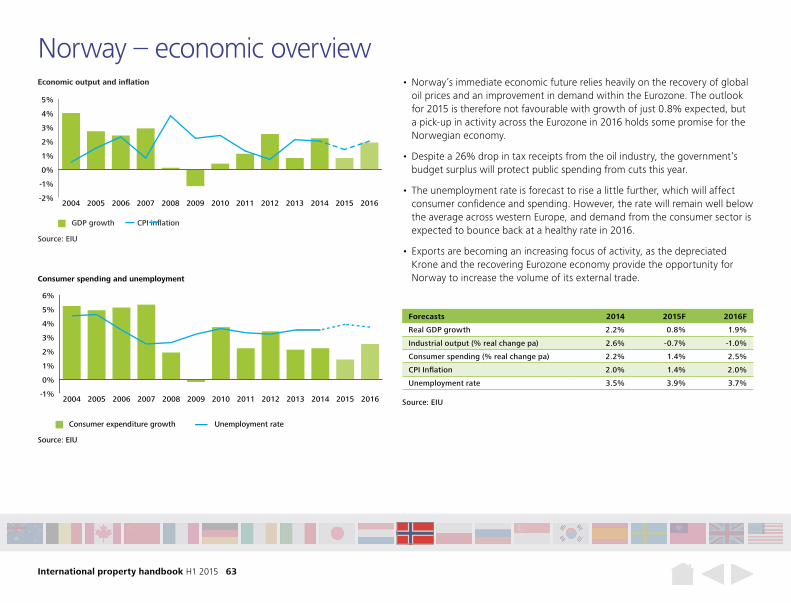

Source: EIU

GDP growth CPI inflation

Economic output and inflation

0%

1%

2%

3%

4%

5%

2016201520142013201220112010200920082007200620052004

0%

1%

2%

3%

4%

5%

6%

7%

2016201520142013201220112010200920082007200620052004

Source: EIU

Consumer expenditure growth

Consumer spending and unemployment

Unemployment rate

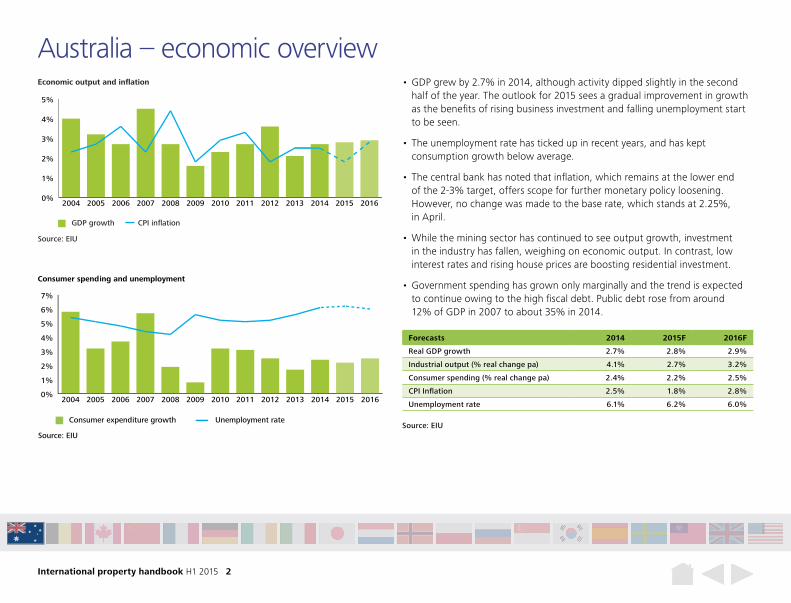

Forecasts 2014 2015F 2016F

Real GDP growth 2.7% 2.8% 2.9%

Industrial output (% real change pa) 4.1% 2.7% 3.2%

Consumer spending (% real change pa) 2.4% 2.2% 2.5%

CPI Inflation 2.5% 1.8% 2.8%

Unemployment rate 6.1% 6.2% 6.0%

Source: EIU

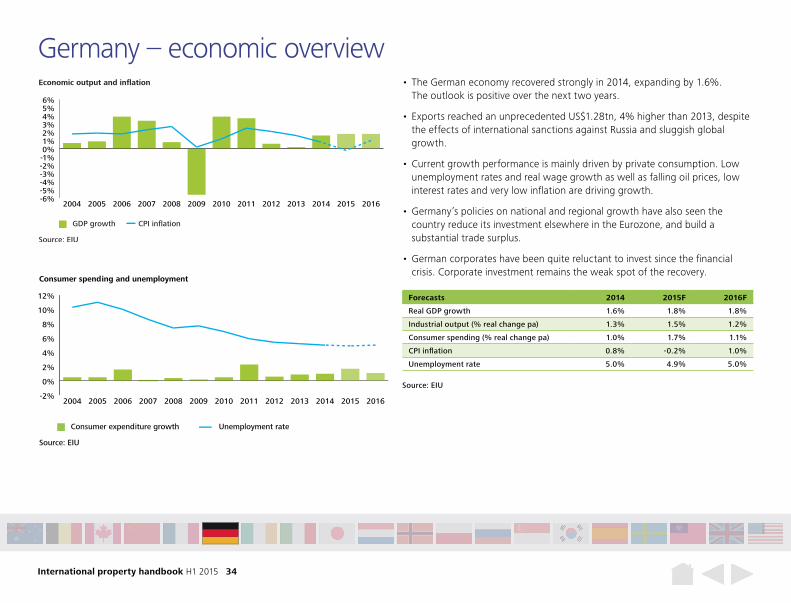

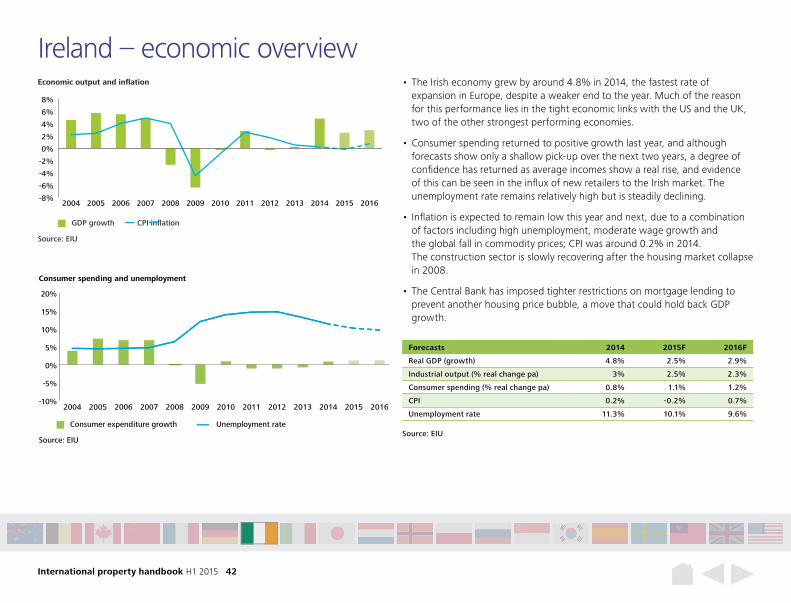

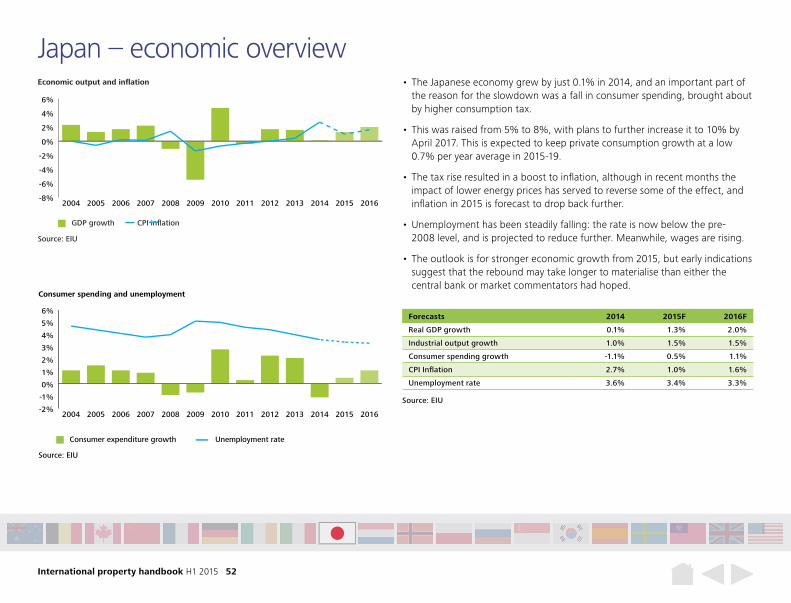

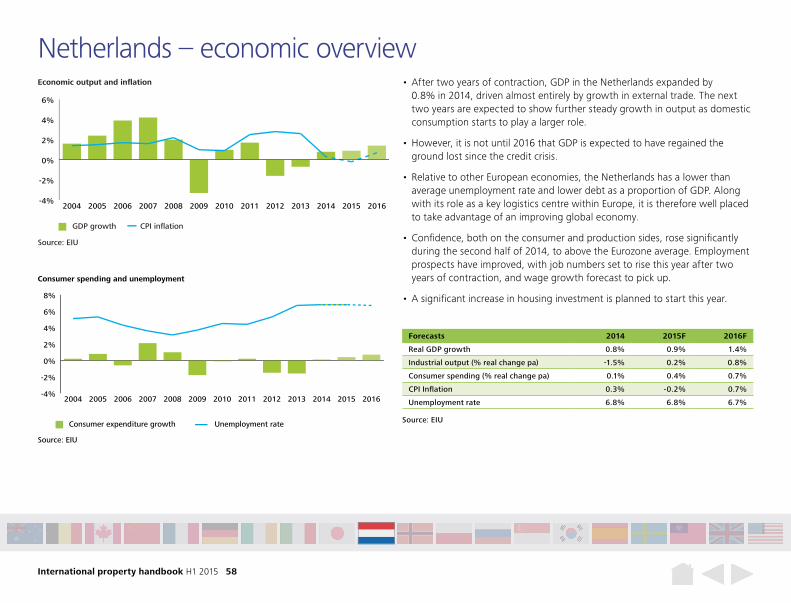

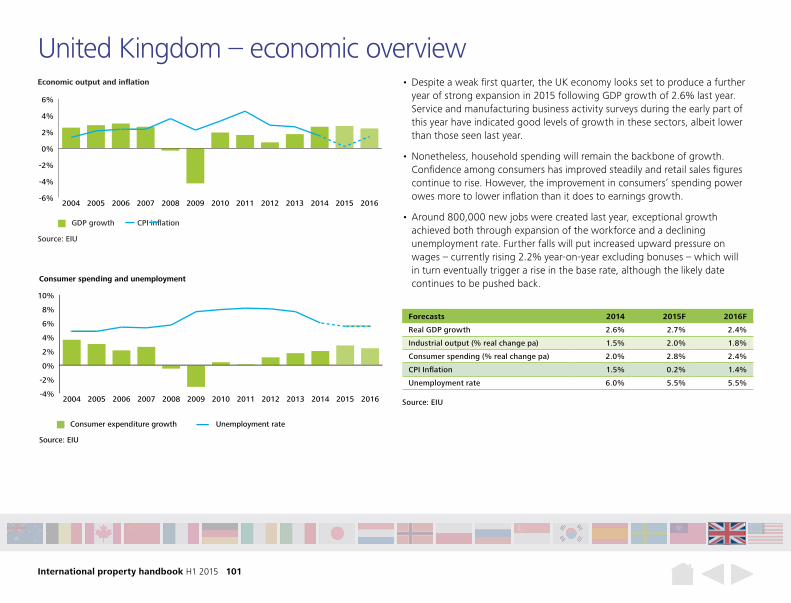

• GDP grew by 2.7% in 2014, although activity dipped slightly in the second half of the year. The outlook for 2015 sees a gradual improvement in growth as the benefits of rising business investment and falling unemployment start to be seen.

• The unemployment rate has ticked up in recent years, and has kept consumption growth below average.

• The central bank has noted that inflation, which remains at the lower end of the 2-3% target, offers scope for further monetary policy loosening. However, no change was made to the base rate, which stands at 2.25%, in April.

• While the mining sector has continued to see output growth, investment in the industry has fallen, weighing on economic output. In contrast, low interest rates and rising house prices are boosting residential investment.

• Government spending has grown only marginally and the trend is expected to continue owing to the high fiscal debt. Public debt rose from around 12% of GDP in 2007 to about 35% in 2014.

Australia – economic overview

International property handbook H1 2015 3

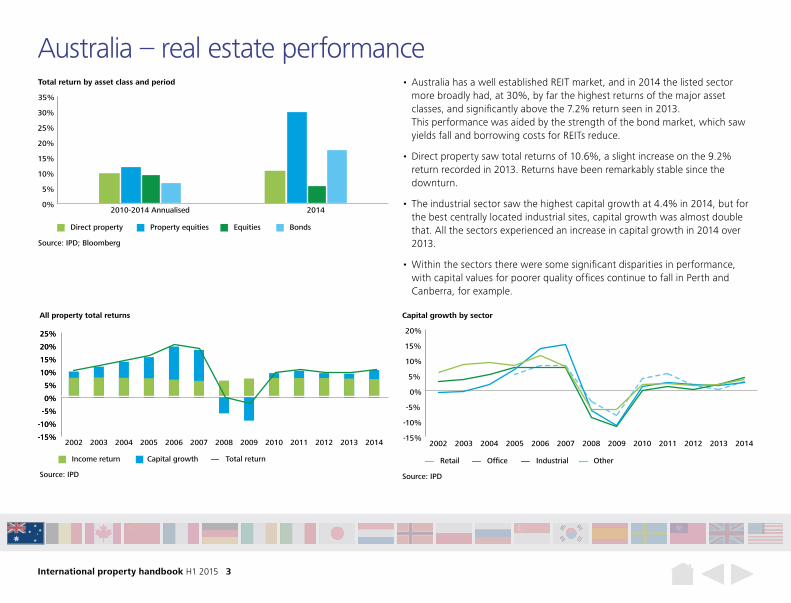

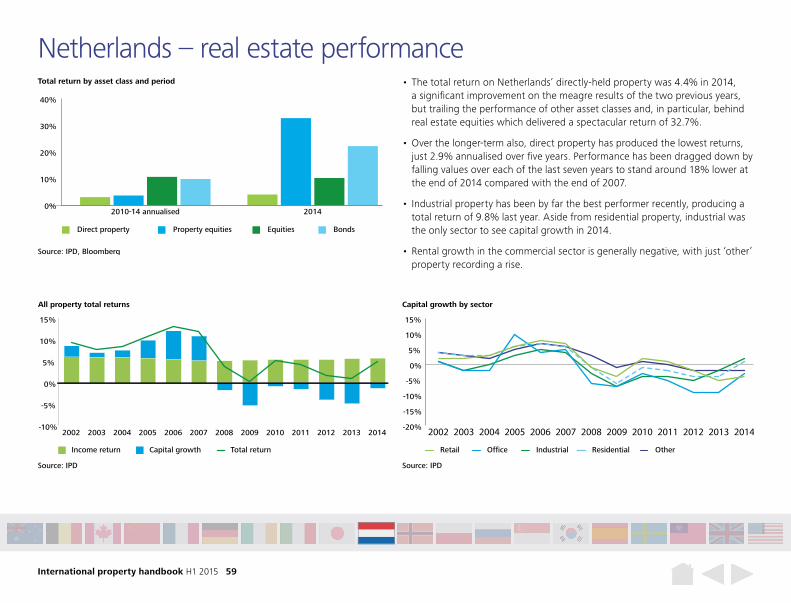

Australia – real estate performance • Australia has a well established REIT market, and in 2014 the listed sector

more broadly had, at 30%, by far the highest returns of the major asset classes, and significantly above the 7.2% return seen in 2013. This performance was aided by the strength of the bond market, which saw yields fall and borrowing costs for REITs reduce.

• Direct property saw total returns of 10.6%, a slight increase on the 9.2% return recorded in 2013. Returns have been remarkably stable since the downturn.

• The industrial sector saw the highest capital growth at 4.4% in 2014, but for the best centrally located industrial sites, capital growth was almost double that. All the sectors experienced an increase in capital growth in 2014 over 2013.

• Within the sectors there were some significant disparities in performance, with capital values for poorer quality offices continue to fall in Perth and Canberra, for example.

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

2014201320122011201020092008200720062005200420032002

All property total returns

Source: IPD

Income return Capital growth Total return

-15%

-10%

-5%

0%

5%

10%

15%

20%

2014201320122011201020092008200720062005200420032002

Source: IPD

OfficeRetail Industrial Other

Capital growth by sector

0%

5%

10%

15%

20%

25%

30%

35%

20142010-2014 Annualised

Source: IPD; Bloomberg

Total return by asset class and period

Direct property Property equities Equities Bonds

International property handbook H1 2015 4

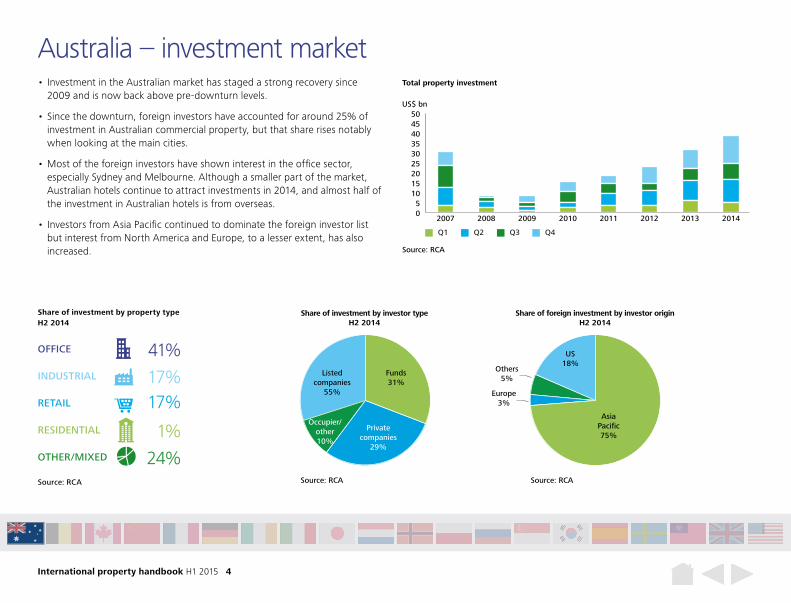

• Investment in the Australian market has staged a strong recovery since 2009 and is now back above pre-downturn levels.

• Since the downturn, foreign investors have accounted for around 25% of investment in Australian commercial property, but that share rises notably when looking at the main cities.

• Most of the foreign investors have shown interest in the office sector, especially Sydney and Melbourne. Although a smaller part of the market, Australian hotels continue to attract investments in 2014, and almost half of the investment in Australian hotels is from overseas.

• Investors from Asia Pacific continued to dominate the foreign investor list but interest from North America and Europe, to a lesser extent, has also increased.

Australia – investment market

Private companies

29%

Share of investment by investor type H2 2014

Source: RCA

Listed companies

55%

Occupier/other10%

Funds31%

Share of foreign investment by investor origin H2 2014

Source: RCA

US18%

Others5%

Asia Pacific75%

Europe3%

Share of investment by property type H2 2014

Source: RCA

OFFICE 41%INDUSTRIAL 17%RETAIL 17%RESIDENTIAL 1%OTHER/MIXED 24%

05

101520253035404550

20142013201220112010200920082007

Source: RCA

Total property investment

US$ bn

Q1 Q2 Q3 Q4

International property handbook H1 2015 5

Sydney – key recent deals

• Sydney is Australia’s largest investment market by some margin, and accounted for around 43% of Australia’s total commercial property investment in 2014 – and attracted more than half of the overseas investments.

• Strong demand for prime office space from both domestic and foreign investors has seen prime office yields compress. The market fundamentals are slowly improving with economic growth pointing to a stronger outlook for occupier demand. However, a significant amount of new space will be delivered in this cycle, with the potential to raise the vacancy rate.

• The hotel sector is another part of the market seeing growth, boosted by the signing of the free trade agreement with China, a more agreeable Australian dollar for inbound visitors and current high occupancy levels. China’s Sunshine Insurance Group’s purchase of the Sheraton at Elizabeth Street was one of Australia’s largest single asset deals of 2014.

• Retail is a smaller part of the investment market. Occupational demand is improving, in part due to foreign retail entrants.

Source: RCA

45%

17%9%

0%

29%

Source: RCA; IPD

Market metrics

Total investment 2014 US$16,815 m

Percentage from foreign investors

52.2%

All property total return 2008-13 (p.a.)

6.4%

All property income return 2008-13 (p.a.)

7.1%

All property capital growth 2008-13 (p.a.)

-0.6%

Office prime yield Q4 2014 6.25%

Asset Type Date Price (US$m) Vendor Purchaser Key tenants Size

Sheraton on the Park 161 Elizabeth St

Hotel Nov 14 407 Starwood Sunshine Insurance Group

NA 557 rooms

175 Liverpool St Office Nov 14 345 GIC Shimao property Hyde Park Medical Centre; Grain Corp; Telstra

514,971 sq ft

Gold Fields House 1 Alfred St

Office Mar 15 324 Blackstone Dalian Wanda Group Aquent; Comensura; CVC; Energeia

260,648 sq ft

Birkenhead Point Shopping Centre, Roseby St

Retail Oct 14 269 Abacus Property Group; Kirsh Group

Mirvac Group French Connection; Gaz Man; Van Heusen

342,510 sq ft

ANZ Tower 163 Castlereagh St

Office Feb 15 186 LaSalle Investment Blackstone ANZ Bank; Herbert Smith Boston Consulting Group

622,159 sq ft

Share of investment by property typeH2 2014

Source: RCA

OFFICE

INDUSTRIAL

RETAIL

RESIDENTIAL

OTHER/MIXED

International property handbook H1 2015 6

Melbourne – key recent deals

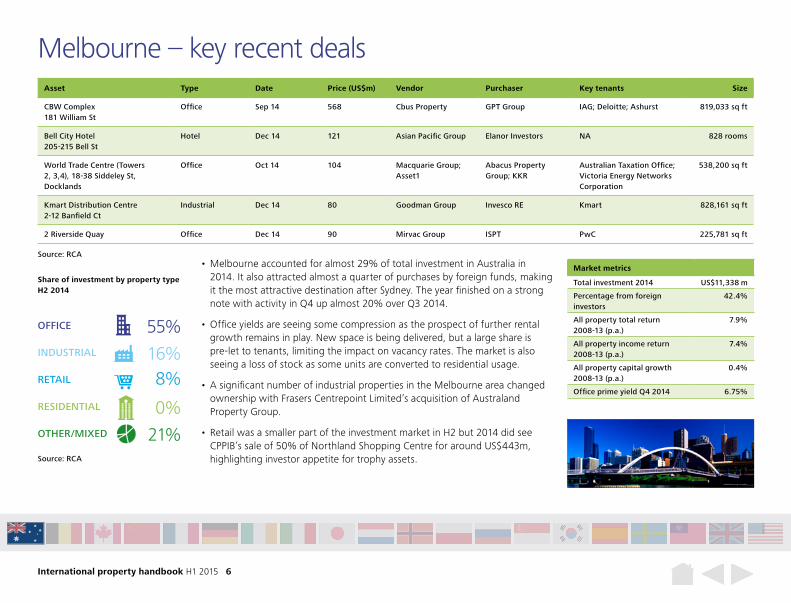

• Melbourne accounted for almost 29% of total investment in Australia in 2014. It also attracted almost a quarter of purchases by foreign funds, making it the most attractive destination after Sydney. The year finished on a strong note with activity in Q4 up almost 20% over Q3 2014.

• Office yields are seeing some compression as the prospect of further rental growth remains in play. New space is being delivered, but a large share is pre-let to tenants, limiting the impact on vacancy rates. The market is also seeing a loss of stock as some units are converted to residential usage.

• A significant number of industrial properties in the Melbourne area changed ownership with Frasers Centrepoint Limited’s acquisition of Australand Property Group.

• Retail was a smaller part of the investment market in H2 but 2014 did see CPPIB’s sale of 50% of Northland Shopping Centre for around US$443m, highlighting investor appetite for trophy assets.

Source: RCA

55%

16%8%

0%

21%Source: RCA; IPD

Market metrics

Total investment 2014 US$11,338 m

Percentage from foreign investors

42.4%

All property total return 2008-13 (p.a.)

7.9%

All property income return 2008-13 (p.a.)

7.4%

All property capital growth 2008-13 (p.a.)

0.4%

Office prime yield Q4 2014 6.75%

Asset Type Date Price (US$m) Vendor Purchaser Key tenants Size

CBW Complex 181 William St

Office Sep 14 568 Cbus Property GPT Group IAG; Deloitte; Ashurst 819,033 sq ft

Bell City Hotel 205-215 Bell St

Hotel Dec 14 121 Asian Pacific Group Elanor Investors NA 828 rooms

World Trade Centre (Towers 2, 3,4), 18-38 Siddeley St, Docklands

Office Oct 14 104 Macquarie Group; Asset1

Abacus Property Group; KKR

Australian Taxation Office; Victoria Energy Networks Corporation

538,200 sq ft

Kmart Distribution Centre 2-12 Banfield Ct

Industrial Dec 14 80 Goodman Group Invesco RE Kmart 828,161 sq ft

2 Riverside Quay Office Dec 14 90 Mirvac Group ISPT PwC 225,781 sq ft

Share of investment by property typeH2 2014

Source: RCA

OFFICE

INDUSTRIAL

RETAIL

RESIDENTIAL

OTHER/MIXED

International property handbook H1 2015 7

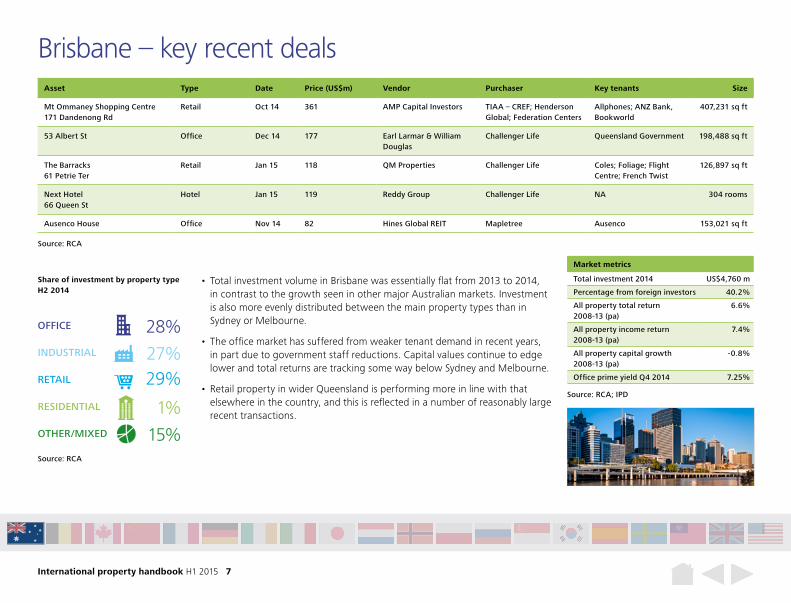

Brisbane – key recent deals

• Total investment volume in Brisbane was essentially flat from 2013 to 2014, in contrast to the growth seen in other major Australian markets. Investment is also more evenly distributed between the main property types than in Sydney or Melbourne.

• The office market has suffered from weaker tenant demand in recent years, in part due to government staff reductions. Capital values continue to edge lower and total returns are tracking some way below Sydney and Melbourne.

• Retail property in wider Queensland is performing more in line with that elsewhere in the country, and this is reflected in a number of reasonably large recent transactions.

Source: RCA

28%

27%29%

1%

15%

Source: RCA; IPD

Market metrics

Total investment 2014 US$4,760 m

Percentage from foreign investors 40.2%

All property total return 2008-13 (pa)

6.6%

All property income return 2008-13 (pa)

7.4%

All property capital growth 2008-13 (pa)

-0.8%

Office prime yield Q4 2014 7.25%

Asset Type Date Price (US$m) Vendor Purchaser Key tenants Size

Mt Ommaney Shopping Centre171 Dandenong Rd

Retail Oct 14 361 AMP Capital Investors TIAA – CREF; Henderson Global; Federation Centers

Allphones; ANZ Bank, Bookworld

407,231 sq ft

53 Albert St Office Dec 14 177 Earl Larmar & William Douglas

Challenger Life Queensland Government 198,488 sq ft

The Barracks 61 Petrie Ter

Retail Jan 15 118 QM Properties Challenger Life Coles; Foliage; Flight Centre; French Twist

126,897 sq ft

Next Hotel 66 Queen St

Hotel Jan 15 119 Reddy Group Challenger Life NA 304 rooms

Ausenco House Office Nov 14 82 Hines Global REIT Mapletree Ausenco 153,021 sq ft

Share of investment by property typeH2 2014

Source: RCA

OFFICE

INDUSTRIAL

RETAIL

RESIDENTIAL

OTHER/MIXED

International property handbook H1 2015 8

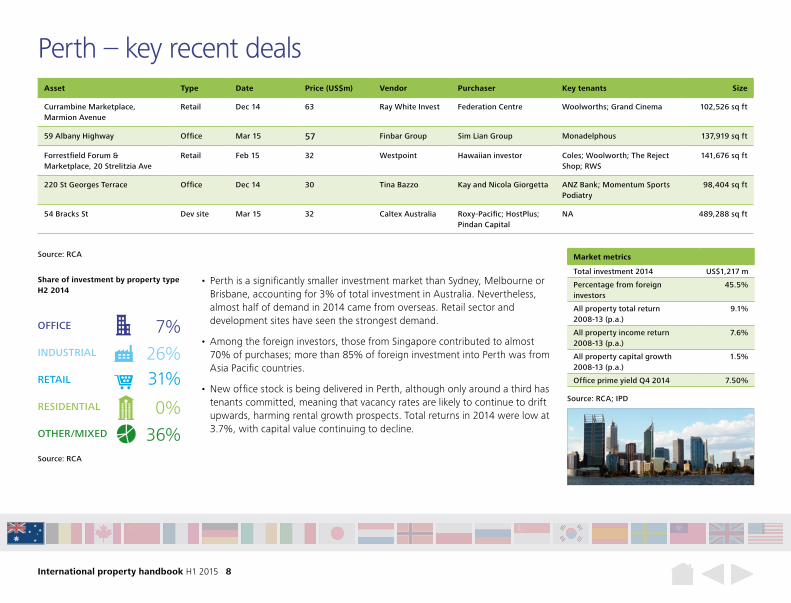

Perth – key recent deals

• Perth is a significantly smaller investment market than Sydney, Melbourne or Brisbane, accounting for 3% of total investment in Australia. Nevertheless, almost half of demand in 2014 came from overseas. Retail sector and development sites have seen the strongest demand.

• Among the foreign investors, those from Singapore contributed to almost 70% of purchases; more than 85% of foreign investment into Perth was from Asia Pacific countries.

• New office stock is being delivered in Perth, although only around a third has tenants committed, meaning that vacancy rates are likely to continue to drift upwards, harming rental growth prospects. Total returns in 2014 were low at 3.7%, with capital value continuing to decline.

Source: RCA

7%

26%31%

0%

36%

Source: RCA; IPD

Market metrics

Total investment 2014 US$1,217 m

Percentage from foreign investors

45.5%

All property total return 2008-13 (p.a.)

9.1%

All property income return 2008-13 (p.a.)

7.6%

All property capital growth 2008-13 (p.a.)

1.5%

Office prime yield Q4 2014 7.50%

Asset Type Date Price (US$m) Vendor Purchaser Key tenants Size

Currambine Marketplace, Marmion Avenue

Retail Dec 14 63 Ray White Invest Federation Centre Woolworths; Grand Cinema 102,526 sq ft

59 Albany Highway Office Mar 15 57 Finbar Group Sim Lian Group Monadelphous 137,919 sq ft

Forrestfield Forum & Marketplace, 20 Strelitzia Ave

Retail Feb 15 32 Westpoint Hawaiian investor Coles; Woolworth; The Reject Shop; RWS

141,676 sq ft

220 St Georges Terrace Office Dec 14 30 Tina Bazzo Kay and Nicola Giorgetta ANZ Bank; Momentum Sports Podiatry

98,404 sq ft

54 Bracks St Dev site Mar 15 32 Caltex Australia Roxy-Pacific; HostPlus; Pindan Capital

NA 489,288 sq ft

Share of investment by property typeH2 2014

Source: RCA

OFFICE

INDUSTRIAL

RETAIL

RESIDENTIAL

OTHER/MIXED

International property handbook H1 2015 9

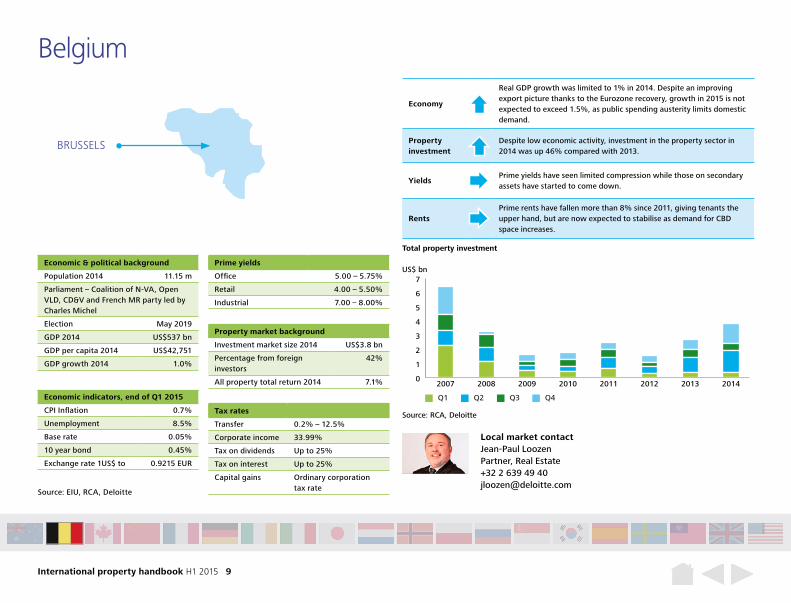

Economy

Real GDP growth was limited to 1% in 2014. Despite an improving export picture thanks to the Eurozone recovery, growth in 2015 is not expected to exceed 1.5%, as public spending austerity limits domestic demand.

Property investment

Despite low economic activity, investment in the property sector in 2014 was up 46% compared with 2013.

YieldsPrime yields have seen limited compression while those on secondary assets have started to come down.

RentsPrime rents have fallen more than 8% since 2011, giving tenants the upper hand, but are now expected to stabilise as demand for CBD space increases.

Belgium

Economic & political background

Population 2014 11.15 m

Parliament – Coalition of N-VA, Open VLD, CD&V and French MR party led by Charles Michel

Election May 2019

GDP 2014 US$537 bn

GDP per capita 2014 US$42,751

GDP growth 2014 1.0%

Prime yields

Office 5.00 – 5.75%

Retail 4.00 – 5.50%

Industrial 7.00 – 8.00%

Property market background

Investment market size 2014 US$3.8 bn

Percentage from foreign investors

42%

All property total return 2014 7.1%

Tax rates

Transfer 0.2% – 12.5%

Corporate income 33.99%

Tax on dividends Up to 25%

Tax on interest Up to 25%

Capital gains Ordinary corporation tax rate

Economic indicators, end of Q1 2015

CPI Inflation 0.7%

Unemployment 8.5%

Base rate 0.05%

10 year bond 0.45%

Exchange rate 1US$ to 0.9215 EUR

Local market contactJean-Paul Loozen Partner, Real Estate +32 2 639 49 40 [email protected]

0

1

2

3

4

5

6

7

20142013201220112010200920082007

Source: RCA, Deloitte

Total property investment

US$ bn

Q1 Q2 Q3 Q4

Source: EIU, RCA, Deloitte

BRUSSELS

International property handbook H1 2015 10

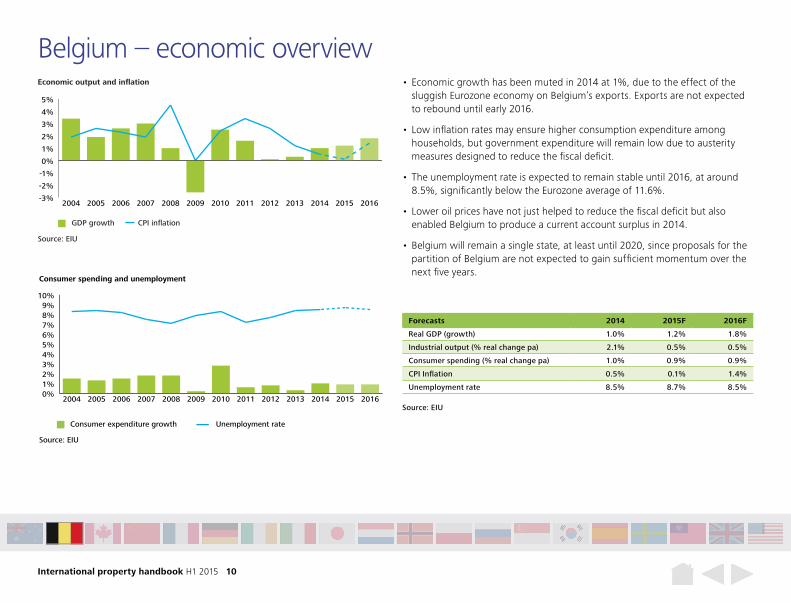

Source: EIU

GDP growth CPI inflation

Economic output and inflation

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

2016201520142013201220112010200920082007200620052004

0%1%2%3%4%5%6%7%8%9%

10%

2016201520142013201220112010200920082007200620052004

Source: EIU

Consumer expenditure growth

Consumer spending and unemployment

Unemployment rate

Forecasts 2014 2015F 2016F

Real GDP (growth) 1.0% 1.2% 1.8%

Industrial output (% real change pa) 2.1% 0.5% 0.5%

Consumer spending (% real change pa) 1.0% 0.9% 0.9%

CPI Inflation 0.5% 0.1% 1.4%

Unemployment rate 8.5% 8.7% 8.5%

Source: EIU

• Economic growth has been muted in 2014 at 1%, due to the effect of the sluggish Eurozone economy on Belgium’s exports. Exports are not expected to rebound until early 2016.

• Low inflation rates may ensure higher consumption expenditure among households, but government expenditure will remain low due to austerity measures designed to reduce the fiscal deficit.

• The unemployment rate is expected to remain stable until 2016, at around 8.5%, significantly below the Eurozone average of 11.6%.

• Lower oil prices have not just helped to reduce the fiscal deficit but also enabled Belgium to produce a current account surplus in 2014.

• Belgium will remain a single state, at least until 2020, since proposals for the partition of Belgium are not expected to gain sufficient momentum over the next five years.

Belgium – economic overview

International property handbook H1 2015 11

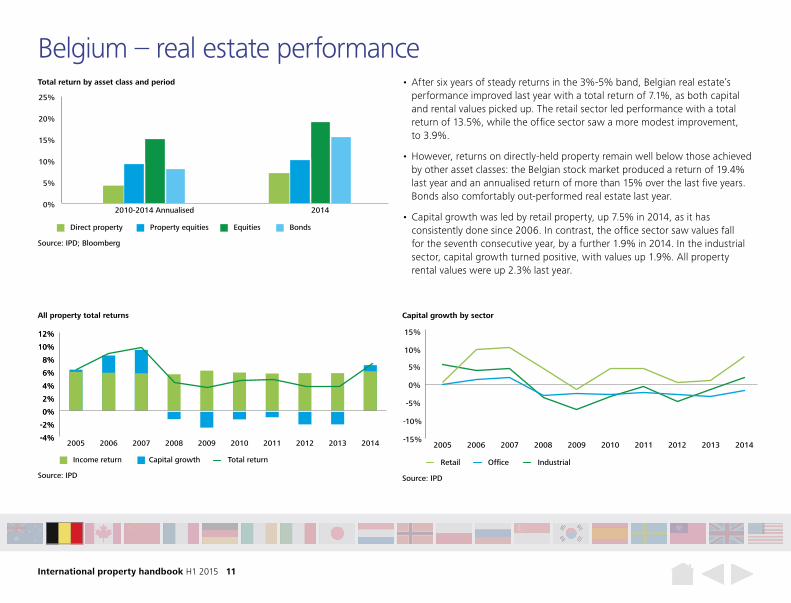

Belgium – real estate performance• After six years of steady returns in the 3%-5% band, Belgian real estate’s

performance improved last year with a total return of 7.1%, as both capital and rental values picked up. The retail sector led performance with a total return of 13.5%, while the office sector saw a more modest improvement, to 3.9%.

• However, returns on directly-held property remain well below those achieved by other asset classes: the Belgian stock market produced a return of 19.4% last year and an annualised return of more than 15% over the last five years. Bonds also comfortably out-performed real estate last year.

• Capital growth was led by retail property, up 7.5% in 2014, as it has consistently done since 2006. In contrast, the office sector saw values fall for the seventh consecutive year, by a further 1.9% in 2014. In the industrial sector, capital growth turned positive, with values up 1.9%. All property rental values were up 2.3% last year.

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

2014201320122011201020092008200720062005

Source: IPD

Income return Capital growth Total return

All property total returns

-15%

-10%

-5%

0%

5%

10%

15%

2014201320122011201020092008200720062005

Source: IPD

OfficeRetail Industrial

Capital growth by sector

0%

5%

10%

15%

20%

25%

20142010-2014 Annualised

Source: IPD; Bloomberg

Total return by asset class and period

Direct property Property equities Equities Bonds

International property handbook H1 2015 12

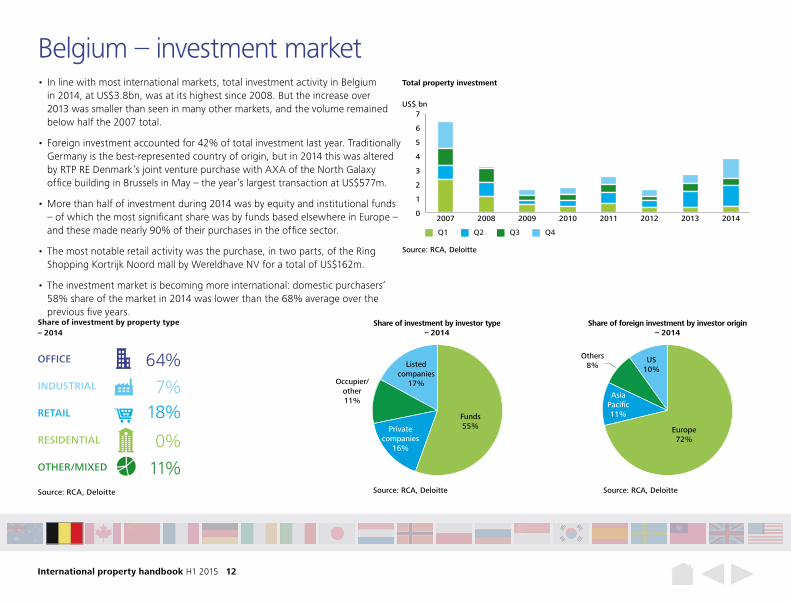

• In line with most international markets, total investment activity in Belgium in 2014, at US$3.8bn, was at its highest since 2008. But the increase over 2013 was smaller than seen in many other markets, and the volume remained below half the 2007 total.

• Foreign investment accounted for 42% of total investment last year. Traditionally Germany is the best-represented country of origin, but in 2014 this was altered by RTP RE Denmark’s joint venture purchase with AXA of the North Galaxy office building in Brussels in May – the year’s largest transaction at US$577m.

• More than half of investment during 2014 was by equity and institutional funds – of which the most significant share was by funds based elsewhere in Europe – and these made nearly 90% of their purchases in the office sector.

• The most notable retail activity was the purchase, in two parts, of the Ring Shopping Kortrijk Noord mall by Wereldhave NV for a total of US$162m.

• The investment market is becoming more international: domestic purchasers’ 58% share of the market in 2014 was lower than the 68% average over the previous five years.

Belgium – investment market

Private companies

16%

Share of investment by investor type – 2014

Source: RCA, Deloitte

Listed companies

17%Occupier/other11%

Funds55%

Share of foreign investment by investor origin – 2014

Source: RCA, Deloitte

US10%

Europe72%

Asia Pacific11%

Others8%

Share of investment by property type – 2014

Source: RCA, Deloitte

OFFICE 64%INDUSTRIAL 7%RETAIL 18%RESIDENTIAL 0%OTHER/MIXED 11%

0

1

2

3

4

5

6

7

20142013201220112010200920082007

Source: RCA, Deloitte

Total property investment

US$ bn

Q1 Q2 Q3 Q4

International property handbook H1 2015 13

Brussels – key recent deals

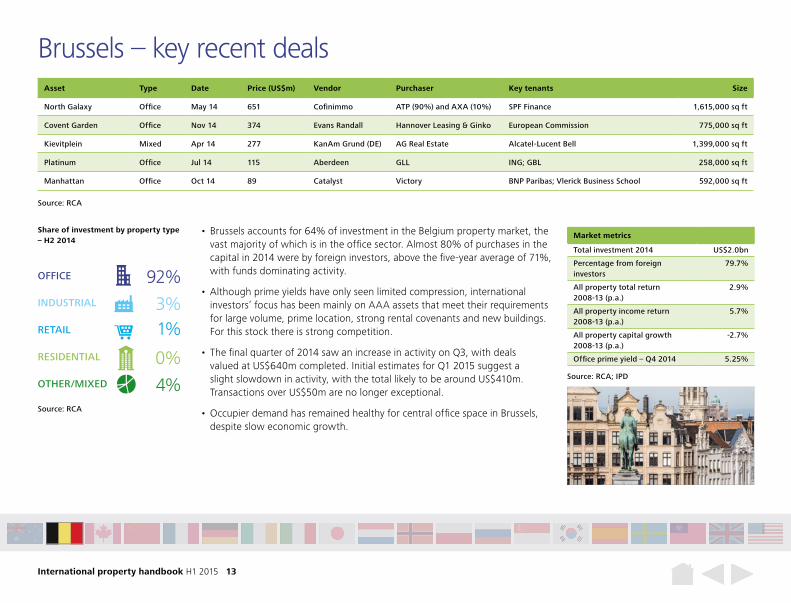

• Brussels accounts for 64% of investment in the Belgium property market, the vast majority of which is in the office sector. Almost 80% of purchases in the capital in 2014 were by foreign investors, above the five-year average of 71%, with funds dominating activity.

• Although prime yields have only seen limited compression, international investors’ focus has been mainly on AAA assets that meet their requirements for large volume, prime location, strong rental covenants and new buildings. For this stock there is strong competition.

• The final quarter of 2014 saw an increase in activity on Q3, with deals valued at US$640m completed. Initial estimates for Q1 2015 suggest a slight slowdown in activity, with the total likely to be around US$410m. Transactions over US$50m are no longer exceptional.

• Occupier demand has remained healthy for central office space in Brussels, despite slow economic growth.

Source: RCA

92%

3%1%

0%

4%Source: RCA; IPD

Market metrics

Total investment 2014 US$2.0bn

Percentage from foreign investors

79.7%

All property total return 2008-13 (p.a.)

2.9%

All property income return 2008-13 (p.a.)

5.7%

All property capital growth 2008-13 (p.a.)

-2.7%

Office prime yield – Q4 2014 5.25%

Asset Type Date Price (US$m) Vendor Purchaser Key tenants Size

North Galaxy Office May 14 651 Cofinimmo ATP (90%) and AXA (10%) SPF Finance 1,615,000 sq ft

Covent Garden Office Nov 14 374 Evans Randall Hannover Leasing & Ginko European Commission 775,000 sq ft

Kievitplein Mixed Apr 14 277 KanAm Grund (DE) AG Real Estate Alcatel-Lucent Bell 1,399,000 sq ft

Platinum Office Jul 14 115 Aberdeen GLL ING; GBL 258,000 sq ft

Manhattan Office Oct 14 89 Catalyst Victory BNP Paribas; Vlerick Business School 592,000 sq ft

Share of investment by property type– H2 2014

Source: RCA

OFFICE

INDUSTRIAL

RETAIL

RESIDENTIAL

OTHER/MIXED

International property handbook H1 2015 14

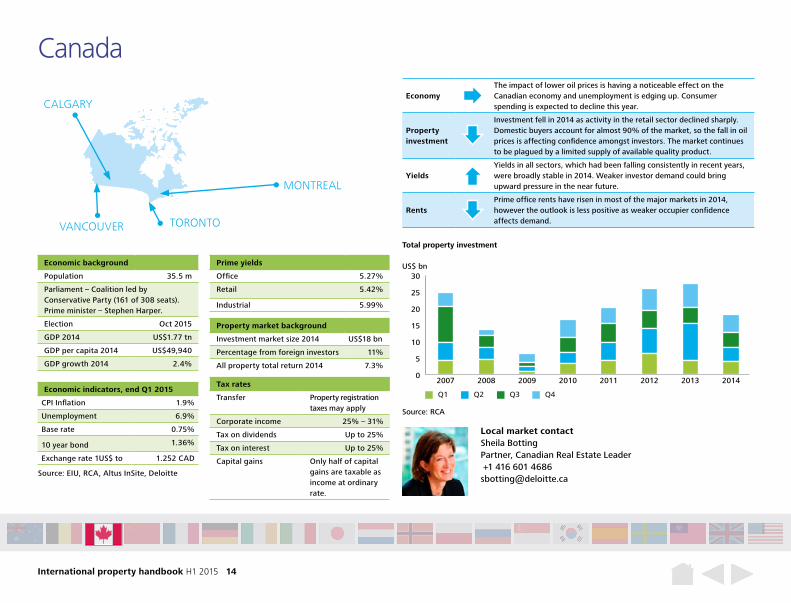

EconomyThe impact of lower oil prices is having a noticeable effect on the Canadian economy and unemployment is edging up. Consumer spending is expected to decline this year.

Property investment

Investment fell in 2014 as activity in the retail sector declined sharply. Domestic buyers account for almost 90% of the market, so the fall in oil prices is affecting confidence amongst investors. The market continues to be plagued by a limited supply of available quality product.

YieldsYields in all sectors, which had been falling consistently in recent years, were broadly stable in 2014. Weaker investor demand could bring upward pressure in the near future.

RentsPrime office rents have risen in most of the major markets in 2014, however the outlook is less positive as weaker occupier confidence affects demand.

Canada

Economic background

Population 35.5 m

Parliament – Coalition led by Conservative Party (161 of 308 seats). Prime minister – Stephen Harper.

Election Oct 2015

GDP 2014 US$1.77 tn

GDP per capita 2014 US$49,940

GDP growth 2014 2.4%

Prime yields

Office 5.27%

Retail 5.42%

Industrial 5.99%

Tax rates

Transfer Property registration taxes may apply

Corporate income 25% – 31%

Tax on dividends Up to 25%

Tax on interest Up to 25%

Capital gains Only half of capital gains are taxable as income at ordinary rate.

Property market background

Investment market size 2014 US$18 bn

Percentage from foreign investors 11%

All property total return 2014 7.3%

Economic indicators, end Q1 2015

CPI Inflation 1.9%

Unemployment 6.9%

Base rate 0.75%

10 year bond 1.36%

Exchange rate 1US$ to 1.252 CAD

Local market contactSheila Botting Partner, Canadian Real Estate Leader +1 416 601 4686 [email protected]

0

5

10

15

20

25

30

20142013201220112010200920082007

Source: RCA

Total property investment

US$ bn

Q1 Q2 Q3 Q4

Source: EIU, RCA, Altus InSite, Deloitte

TORONTO

CALGARY

MONTREAL

VANCOUVER

International property handbook H1 2015 15

Source: EIU

GDP growth CPI inflation

Economic output and inflation

-4%

-3%

-2%

-1%

0%

1%

2%

3%

4%

2016201520142013201220112010200920082007200620052004

0%

2%

4%

6%

8%

10%

2016201520142013201220112010200920082007200620052004

Source: EIU

Consumer expenditure growth

Consumer spending and unemployment

Unemployment rate

Forecasts 2014 2015F 2016F

Real GDP (growth) 2.4% 2.0% 2.3%

Industrial output (% real change pa) 2.0% -1.0% 1.7%

Consumer spending (% real change pa) 2.9% 1.8% 1.8%

CPI Inflation 1.9% 0.7% 2.3%

Unemployment rate 6.9% 6.8% 6.6 %

Source: EIU

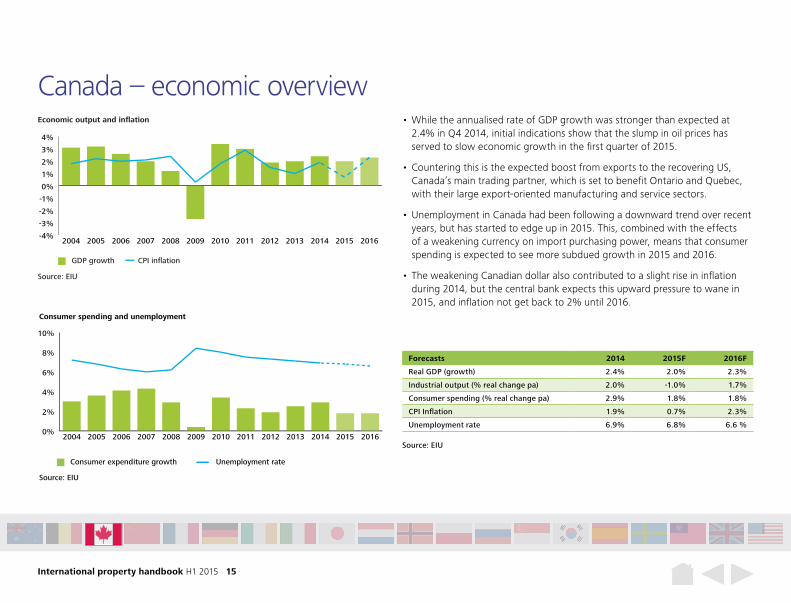

Canada – economic overview • While the annualised rate of GDP growth was stronger than expected at

2.4% in Q4 2014, initial indications show that the slump in oil prices has served to slow economic growth in the first quarter of 2015.

• Countering this is the expected boost from exports to the recovering US, Canada’s main trading partner, which is set to benefit Ontario and Quebec, with their large export-oriented manufacturing and service sectors.

• Unemployment in Canada had been following a downward trend over recent years, but has started to edge up in 2015. This, combined with the effects of a weakening currency on import purchasing power, means that consumer spending is expected to see more subdued growth in 2015 and 2016.

• The weakening Canadian dollar also contributed to a slight rise in inflation during 2014, but the central bank expects this upward pressure to wane in 2015, and inflation not get back to 2% until 2016.

International property handbook H1 2015 16

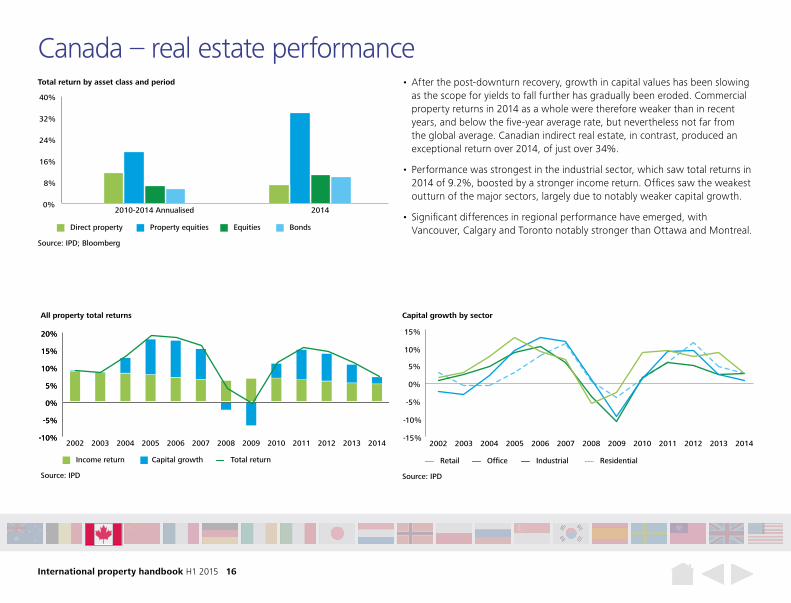

Canada – real estate performance• After the post-downturn recovery, growth in capital values has been slowing

as the scope for yields to fall further has gradually been eroded. Commercial property returns in 2014 as a whole were therefore weaker than in recent years, and below the five-year average rate, but nevertheless not far from the global average. Canadian indirect real estate, in contrast, produced an exceptional return over 2014, of just over 34%.

• Performance was strongest in the industrial sector, which saw total returns in 2014 of 9.2%, boosted by a stronger income return. Offices saw the weakest outturn of the major sectors, largely due to notably weaker capital growth.

• Significant differences in regional performance have emerged, with Vancouver, Calgary and Toronto notably stronger than Ottawa and Montreal.

-10%

-5%

0%

5%

10%

15%

20%

-10%

-5%

0%

5%

10%

15%

20%

2014201320122011201020092008200720062005200420032002

Source: IPD

Income return Capital growth Total return

All property total returns

-15%

-10%

-5%

0%

5%

10%

15%

2014201320122011201020092008200720062005200420032002

Source: IPD

OfficeRetail Industrial Residential

Capital growth by sector

0%

8%

16%

24%

32%

40%

20142010-2014 Annualised

Source: IPD; Bloomberg

Total return by asset class and period

Direct property Property equities Equities Bonds

International property handbook H1 2015 17

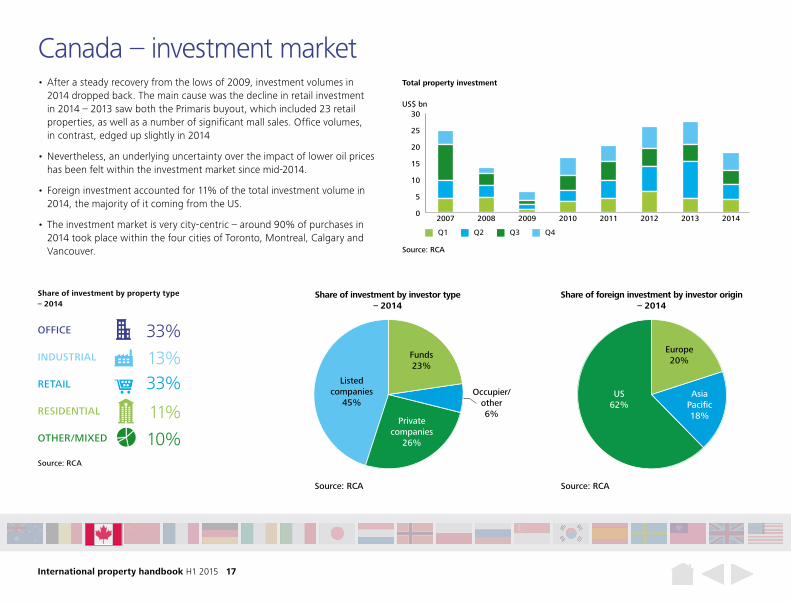

• After a steady recovery from the lows of 2009, investment volumes in 2014 dropped back. The main cause was the decline in retail investment in 2014 – 2013 saw both the Primaris buyout, which included 23 retail properties, as well as a number of significant mall sales. Office volumes, in contrast, edged up slightly in 2014

• Nevertheless, an underlying uncertainty over the impact of lower oil prices has been felt within the investment market since mid-2014.

• Foreign investment accounted for 11% of the total investment volume in 2014, the majority of it coming from the US.

• The investment market is very city-centric – around 90% of purchases in 2014 took place within the four cities of Toronto, Montreal, Calgary and Vancouver.

Canada – investment market

Private companies

26%

Share of investment by investor type – 2014

Source: RCA

Listed companies

45%Occupier/

other6%

Funds23%

Share of foreign investment by investor origin – 2014

Source: RCA

US62%

Europe20%

Asia Pacific18%

Share of investment by property type – 2014

Source: RCA

OFFICE 33%INDUSTRIAL 13%RETAIL 33%RESIDENTIAL 11%OTHER/MIXED 10%

0

5

10

15

20

25

30

20142013201220112010200920082007

Source: RCA

Total property investment

US$ bn

Q1 Q2 Q3 Q4

International property handbook H1 2015 18

Name Type Date Price ($m) Vendor Purchaser Key tenants Size

The One, 1 Bloor St W Retail Oct 14 267 NA Mizrahi Developments Stollerys NA

Renaissance Plaza, 150 Bloor St W

Office Sep 14 234 Kevric, PSP Investments, Cadim Inc

Ponte Gadea Louis Vuitton, Tiffany, HSBC

269,205 sq ft

55 University, 55 University Ave

Office Sep 14 102 Ivanhoe Cambridge Cominar REIT Concert Properties, Canadian Chamber of Commerce

264,328 sq ft

180 Wellington Street West Office Nov 14 101 RBC Capital Manulife Financial RBC 208,000 sq ft

Herons Hill 2001-2005, Sheppard Ave E

Office Dec14 57 LaSalle Investment RedBourne Group Frost & Sullivan, Great West Life Assurance

290,000 sq ft

Toronto – key recent deals

Source: RCA

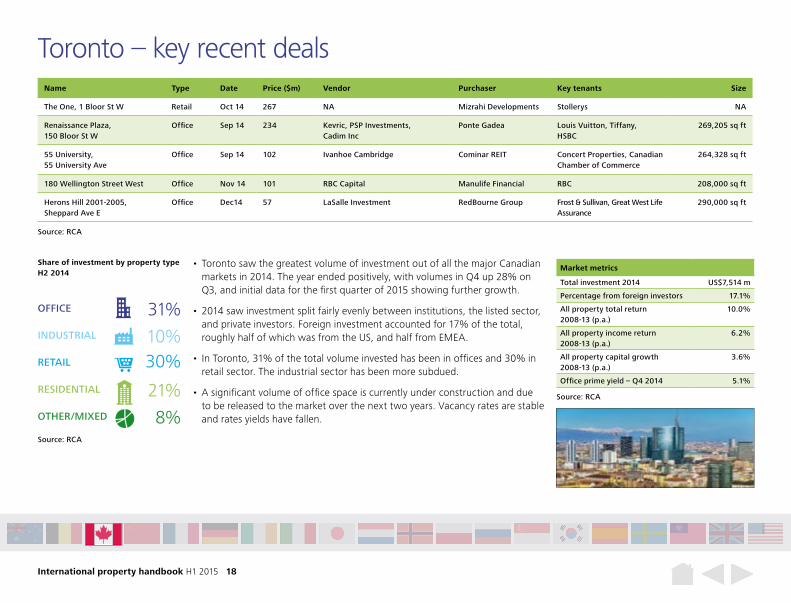

• Toronto saw the greatest volume of investment out of all the major Canadian markets in 2014. The year ended positively, with volumes in Q4 up 28% on Q3, and initial data for the first quarter of 2015 showing further growth.

• 2014 saw investment split fairly evenly between institutions, the listed sector, and private investors. Foreign investment accounted for 17% of the total, roughly half of which was from the US, and half from EMEA.

• In Toronto, 31% of the total volume invested has been in offices and 30% in retail sector. The industrial sector has been more subdued.

• A significant volume of office space is currently under construction and due to be released to the market over the next two years. Vacancy rates are stable and rates yields have fallen.

Source: RCA

Market metrics

Total investment 2014 US$7,514 m

Percentage from foreign investors 17.1%

All property total return 2008-13 (p.a.)

10.0%

All property income return 2008-13 (p.a.)

6.2%

All property capital growth 2008-13 (p.a.)

3.6%

Office prime yield – Q4 2014 5.1%

Share of investment by property type H2 2014

Source: RCA

OFFICE 31%INDUSTRIAL 10%RETAIL 30%RESIDENTIAL 21%OTHER/MIXED 8%

International property handbook H1 2015 19

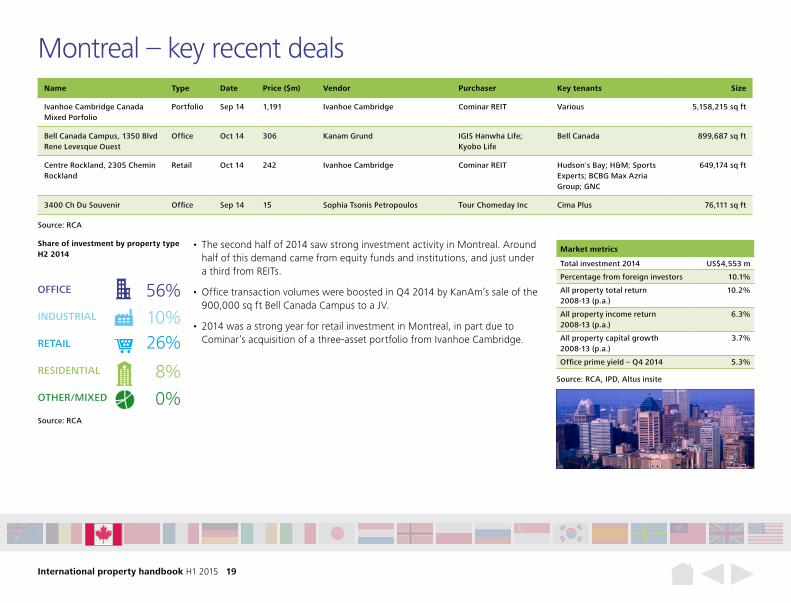

Name Type Date Price ($m) Vendor Purchaser Key tenants Size

Ivanhoe Cambridge Canada Mixed Porfolio

Portfolio Sep 14 1,191 Ivanhoe Cambridge Cominar REIT Various 5,158,215 sq ft

Bell Canada Campus, 1350 Blvd Rene Levesque Ouest

Office Oct 14 306 Kanam Grund IGIS Hanwha Life; Kyobo Life

Bell Canada 899,687 sq ft

Centre Rockland, 2305 Chemin Rockland

Retail Oct 14 242 Ivanhoe Cambridge Cominar REIT Hudson's Bay; H&M; Sports Experts; BCBG Max Azria Group; GNC

649,174 sq ft

3400 Ch Du Souvenir Office Sep 14 15 Sophia Tsonis Petropoulos Tour Chomeday Inc Cima Plus 76,111 sq ft

Montreal – key recent deals

Source: RCA

• The second half of 2014 saw strong investment activity in Montreal. Around half of this demand came from equity funds and institutions, and just under a third from REITs.

• Office transaction volumes were boosted in Q4 2014 by KanAm’s sale of the 900,000 sq ft Bell Canada Campus to a JV.

• 2014 was a strong year for retail investment in Montreal, in part due to Cominar’s acquisition of a three-asset portfolio from Ivanhoe Cambridge.

Market metrics

Total investment 2014 US$4,553 m

Percentage from foreign investors 10.1%

All property total return 2008-13 (p.a.)

10.2%

All property income return 2008-13 (p.a.)

6.3%

All property capital growth 2008-13 (p.a.)

3.7%

Office prime yield – Q4 2014 5.3%

Share of investment by property type H2 2014

Source: RCA

OFFICE 56%INDUSTRIAL 10%RETAIL 26%RESIDENTIAL 8%OTHER/MIXED 0%

Source: RCA, IPD, Altus insite

International property handbook H1 2015 20

Name Type Date Price ($m) Vendor Purchaser Key tenants Size

Brookfield Place Calgary, East 225 6th Ave SW

Office Oct 14 914 Brookfield Property Partners

Brookfield Canada Office Properties

Cenovus 1,400,000 sq ft

Brentwood Village, Brentwood Road

Retail Mar 15 109 Kimco RioCan REIT Safeway; London Drugs; Sears

294,000 sq ft

Grid 5 Apartments 618 5th Ave SW

Residential Dec 14 88 Kingsett Capital AIMCo

Killam Properties Inc NA 307 units

Beverly Centre Lake, 500 Midpark Way SE

Residential Dec 14 63 HealthLease REIT Health Care REIT NA 270 units

1 Executive Place, 1816 Crowchild Trail NW

Office Oct 14 41 GWL Realty Industrial Alliance Insurance & Financial Services Inc

Alberta Human Services 118,644 sq ft

Calgary – key recent deals

Source: RCA

• Investment saw significant growth in the last quarter of 2014, particularly within the office sector, although a major part of this was due to Brookfield Canada Office Properties’ purchase of the Brookfield Place development site from its parent company. A 1.4m sq ft office tower is now under construction.

• The fluctuations in oil prices have raised concerns over the stability of the tenant base, given that a sizeable share of Calgary’s businesses operate within the energy sector.

• Retail investment slowed during the second half of 2014 but picked up in Q1 2015 with RioCan REIT’s purchase of Brentwood Village, a grocery-anchored shopping centre.

• Foreign investment was modest in 2014, and focused on the industial sector.

Source: RCA, IPD, Altus inSite

Market metrics

Total investment 2014 US$2,228 m

Percentage from foreign investors 8.9%

All property total return 2008-13 (p.a.)

10.4%

All property income return 2008-13 (p.a.)

6.6%

All property capital growth 2008-13 (p.a.)

3.6%

Office prime yield – Q4 2014 4.9%

Share of investment by property type H2 2014

Source: RCA

OFFICE 64%INDUSTRIAL 9%RETAIL 5%RESIDENTIAL 16%OTHER/MIXED 7%

International property handbook H1 2015 21

Name Type Date Price ($m) Vendor Purchaser Key tenants Size

Langara Gardens, 501 W 57th Ave

Apartment Sep 14 188 Peterson InvestmentGroup Inc

Concert Properties NA 621 units

Hyatt Regency Vancouver, 655 Burrard St

Hotel Nov 14 124 Hyatt Hotels Innvest REIT Hyatt Hotels 644 rooms

Neelu Bachra Centre 550 W Broadway

Office Dec 14 40 NA Orca West Developments Ltd NA 52,036 sq ft

Real Canadian Super Store, 2855 Gladwin Rd

Retail Oct 14 35 Loblaw Cos Choice Properties Real Canadian Super Store 141,487 sq ft

411 Dunsmuir St Office Sep 14 32 CRS Group; Omincron 411 Dunsmuir Inc; MJD Holdings Inc NA 55,414 sq ft

Vancouver – key recent deals

Source: RCA

• The Vancouver market is almost entirely driven by domestic demand. In 2014, private funds accounted for over half of all transactions by volume, with institutions and listed investors combined taking just one third.

• In H2 2014, the office sector attracted the highest share of investment, although the deals during this period were all of relatively small value at less than US$50m.

• Leasing activity has increased steadily in recent years and although a number of new office developments will be completed in 2015 and 2016, a sizeable proportion of this space has already been let.

• The industrial sector remains a relatively small share of the investment market, but with strong competition from owner-occupiers prices are being pushed up. In addition, recent changes to zoning in the Mount Pleasant industrial district have offered the possibility of adding residential usage to some sites, further increasing their value.

Source: RCA, IPD, Altus insite

Market metrics

Total investment 2014 US$2.20 bn

Percentage from foreign investors 4.6%

All property total return 2008-13 (p.a.)

10.0%

All property income return 2008-13 (p.a.)

5.9%

All property capital growth 2008-13 (p.a.)

3.9%

Office prime yield Q4 2014 %

Share of investment by property type H2 2014

Source: RCA

OFFICE 29%INDUSTRIAL 15%RETAIL 9%RESIDENTIAL 19%OTHER/MIXED 28%

International property handbook H1 2015 22

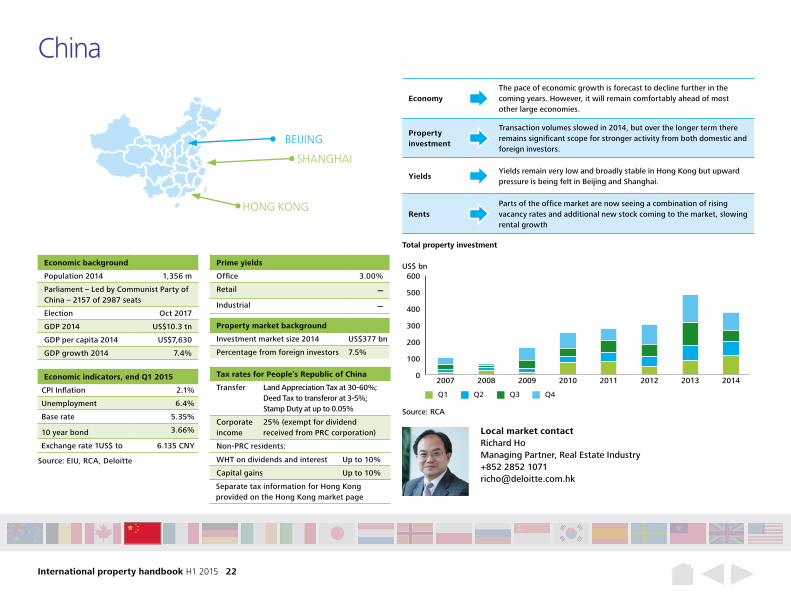

EconomyThe pace of economic growth is forecast to decline further in the coming years. However, it will remain comfortably ahead of most other large economies.

Property investment

Transaction volumes slowed in 2014, but over the longer term there remains significant scope for stronger activity from both domestic and foreign investors.

YieldsYields remain very low and broadly stable in Hong Kong but upward pressure is being felt in Beijing and Shanghai.

RentsParts of the office market are now seeing a combination of rising vacancy rates and additional new stock coming to the market, slowing rental growth

China

Economic background

Population 2014 1,356 m

Parliament – Led by Communist Party of China – 2157 of 2987 seats

Election Oct 2017

GDP 2014 US$10.3 tn

GDP per capita 2014 US$7,630

GDP growth 2014 7.4%

Prime yields

Office 3.00%

Retail –Industrial –

Tax rates for People’s Republic of China

Transfer Land Appreciation Tax at 30-60%; Deed Tax to transferor at 3-5%; Stamp Duty at up to 0.05%

Corporate income

25% (exempt for dividend received from PRC corporation)

Non-PRC residents:

Property market background

Investment market size 2014 US$377 bn

Percentage from foreign investors 7.5%

Economic indicators, end Q1 2015

CPI Inflation 2.1%

Unemployment 6.4%

Base rate 5.35%

10 year bond 3.66%

Exchange rate 1US$ to 6.135 CNY

Local market contactRichard Ho Managing Partner, Real Estate Industry +852 2852 1071 [email protected]

0

100

200

300

400

500

600

20142013201220112010200920082007

Source: RCA

Total property investment

US$ bn

Q1 Q2 Q3 Q4

Source: EIU, RCA, Deloitte

BEIJING

SHANGHAI

HONG KONG

Separate tax information for Hong Kong provided on the Hong Kong market page

WHT on dividends and interest Up to 10%

Capital gains Up to 10%

International property handbook H1 2015 23

Source: EIU

GDP growth CPI inflation

Economic output and inflation

-2%0%2%4%6%8%

10%12%14%16%

2016201520142013201220112010200920082007200620052004

0%

2%

4%

6%

8%

10%

12%

2016201520142013201220112010200920082007200620052004

Source: EIU

Consumer expenditure growth

Consumer spending and unemployment

Unemployment rate

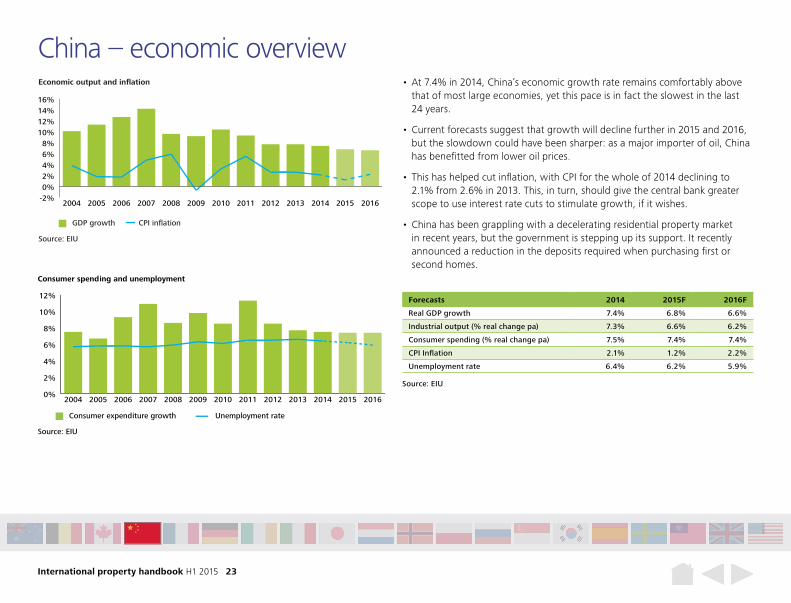

Forecasts 2014 2015F 2016F

Real GDP growth 7.4% 6.8% 6.6%

Industrial output (% real change pa) 7.3% 6.6% 6.2%

Consumer spending (% real change pa) 7.5% 7.4% 7.4%

CPI Inflation 2.1% 1.2% 2.2%

Unemployment rate 6.4% 6.2% 5.9%

Source: EIU

• At 7.4% in 2014, China’s economic growth rate remains comfortably above that of most large economies, yet this pace is in fact the slowest in the last 24 years.

• Current forecasts suggest that growth will decline further in 2015 and 2016, but the slowdown could have been sharper: as a major importer of oil, China has benefitted from lower oil prices.

• This has helped cut inflation, with CPI for the whole of 2014 declining to 2.1% from 2.6% in 2013. This, in turn, should give the central bank greater scope to use interest rate cuts to stimulate growth, if it wishes.

• China has been grappling with a decelerating residential property market in recent years, but the government is stepping up its support. It recently announced a reduction in the deposits required when purchasing first or second homes.

China – economic overview

International property handbook H1 2015 24

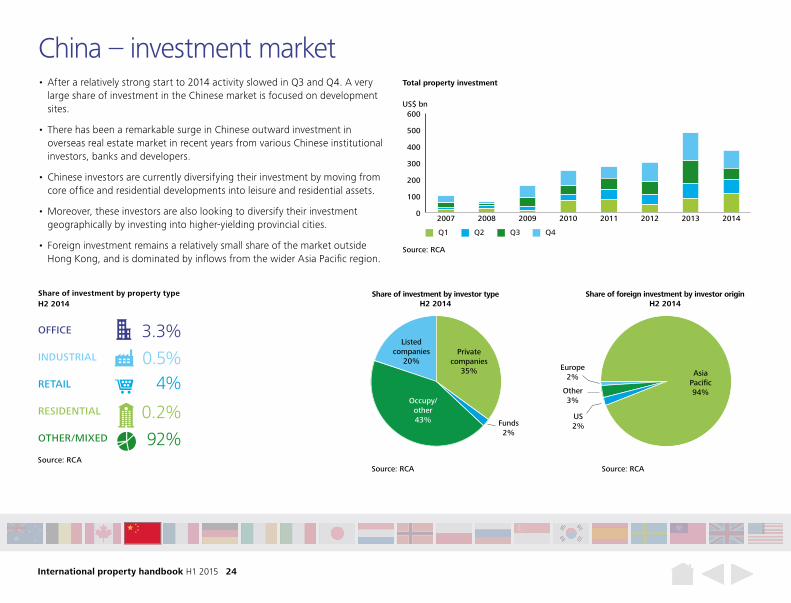

Funds2%

Europe2%

Other3%

US2%

Share of investment by investor type H2 2014

Source: RCA

Listed companies

20%Private

companies 35%

Occupy/other43%

Share of foreign investment by investor originH2 2014

Source: RCA

US31%

Asia Pacific94%

• After a relatively strong start to 2014 activity slowed in Q3 and Q4. A very large share of investment in the Chinese market is focused on development sites.

• There has been a remarkable surge in Chinese outward investment in overseas real estate market in recent years from various Chinese institutional investors, banks and developers.

• Chinese investors are currently diversifying their investment by moving from core office and residential developments into leisure and residential assets.

• Moreover, these investors are also looking to diversify their investment geographically by investing into higher-yielding provincial cities.

• Foreign investment remains a relatively small share of the market outside Hong Kong, and is dominated by inflows from the wider Asia Pacific region.

China – investment market

Share of investment by property type H2 2014

Source: RCA

OFFICE 3.3%INDUSTRIAL 0.5%RETAIL 4%RESIDENTIAL 0.2%OTHER/MIXED 92%

0

100

200

300

400

500

600

20142013201220112010200920082007

Source: RCA

Total property investment

US$ bn

Q1 Q2 Q3 Q4

International property handbook H1 2015 25

Hong Kong – key recent deals

Source: RCA

Asset Type Date Price (US$m) Vendor Purchaser Key tenants Size

Wu Chung House (7-16F) 213 Queens Rd E, Fairmont House 8 Cotton Tree Dr

Office portfolio

Sep 14 1,003 Financial Secretary Inc. HKMA Social Welfare Department; Education Bureau; Communications Authority

NA

41 Heung Yip Rd Office Dec 14 423 Cheung Kong Holdings Leong On-Kei NA 323,984 sq ft

633 King Road Office Mar 15 260 Magnificent Estates Shun Ho Technology P&T Architect and Engineers Limited; LG Electronics

258,384 sq ft

Laguna Plaza 88 Cha Kwo Ling Rd

Retail Dec 14 247 CLSA Capital Fortune REIT McDonald’s; KFC; Ajisen Ramen; Pacific Coffee; 7-11

163,600 sq ft

Grand Central Plaza Tower (01) Office Dec 14 83 JP Morgan Hang Seng Bank Bought for occupancy 88,325 sq ft

• Investment picked up in the second half of 2014, with two strong quarters of activity recorded. Private investors accounted for around a third of purchases over this time, followed by listed vehicles and REITs, which were responsible for a further 31% of purchases.

• The office sector has seen particular interest, with the sale of the Financial Secretary Office portfolio and 41 Heung Yip Road in September followed by further significant purchases in December.

• Physical/land constraints have served to keep office development relatively low in recent years. Vacancy remains tight and Hong Kong is regularly ranked as one of the most expensive office markets in the world.

• February’s budget included the announcement that the government will release four development sites for commercial use, and one for hotel use. Development land accounts for a large share of investment activity in Hong Kong, but less so than in the mainland markets.