hong kong’s monetary handover: hsbc and hkma, 1983 -1996

TRANSCRIPT

HONG KONG’S MONETARY HANDOVER: HSBC AND HKMA, 1983 -1996

David Abraham

The University of Chicago

Abstract: This paper seeks to explain the transition of private to public management of

the value of the Hong Kong dollar (HKD) during the specified time period. Initially, the

1983 currency board system, instituted by the Office of the Exchange Fund (EF), retained

the Hongkong and Shanghai Banking Corporation (HSBC) clearinghouse role, and with it

the power to control the local money market. After five years the 1988 Accounting

Arrangement (AA) compelled HSBC to keep an account with the EF to enable the

monetary authorities to directly influence the exchange rate. However, HSBC continued

to have access to confidential information about competing finance firms and government

decisions until the Hong Kong Monetary Authority (HKMA) instituted the 1996

Aggregate Balance reform (AB) that required all banks to maintain an account with the

EF. In 1988 the EF had a choice between the AA and AB, and they selected the former

for its expediency during Basic Law negotiations, but the secondary literature does not

describe why the HKMA decided revision was necessary in 1996. The argument

presented herein suggests that HSBC’s alleged speculation against the HKD peg in

January 1995 encouraged the authorities to reign in the bank’s influence and, more than

any other factor, compelled the creation of the AB before the 1997 handover to China.

Keywords: Hong Kong, monetary policy, Hong Kong dollar, HSBC, central bank

1

Introduction and Roadmap

Ranked as the third largest global financial center in the world,1 Hong Kong (HK)

Special Administrative Region (SAR) of the People’s Republic of China (‘China’)

embodies the free market. The HK government operates under a framework of “one

country, two systems” that also extends to its administration of a local currency, the Hong

Kong dollar (HKD).2 Developed in 1863, the British colonial government operated the

HKD on the silver standard in parallel with the imperial and the Chinese economies

before the 1935 silver crisis, after which the Currency Ordinance of 1935 linked3 the

HKD to the British Pound Sterling (GBP) and delegated note-issue to commercial banks.

This regime continued up to 1972 when the British government floated the GBP, and

after a brief linkage with the United States dollar (USD) the HKD began trading in the

currency markets4 until a speculative crisis in 1983 forced the creation of a managed

currency board system5 with a peg of 7.80 HKD to 1 USD, which remains to this day.6

As evident in 1997 during the transfer of HK sovereignty from the United

Kingdom (‘the handover’) negotiations, HK considers its currency an important aspect of

its urban identity as a financial center within communist China. While many experts have

predicted the peg’s demise it persists, even withstanding intense speculation during the

1998 Asian Financial Crisis. However, the Hong Kong Monetary Authority (HKMA), the

quasi-central bank for the territory created in 1993, and its predecessor, the Office of the

Exchange Fund (EF), have not always directly controlled the exchange rate. That power

was only acquired in 1988 and expanded in 1996 by the creation of commercial bank

clearing accounts with the EF. During that period only the Hongkong and Shanghai

Banking Corporation (HSBC) held such an account and ‘the Balance’7 dictated the

2

supply of HKD. This paper contends allegations that HSBC speculated against the peg to

the USD in early 1995 compelled the HKMA to assume direct responsibility for

managing the local currency by creating the Aggregate Balance in 1996.

An outline for the presentation of the aforementioned argument includes a

chronological overview, reform comparison, explanation of the thesis, assessment of

alternative causalities, and conclusion to round out the historical narrative. Specifically, it

starts with a review of the changes in the HK monetary system from 1983 through 1996

with portions dedicated to the 1988 Accounting Arrangement (AA), 1993 creation of the

HKMA, and 1996 Aggregate Balance (AB). Next, comparing the reasons behind the

implementation of those two reforms yields the driving question answered by the thesis.

After the statement of inquiry a complete recounting of the January 1995 speculative

crisis will show how HSBC’s alleged involvement compelled the HKMA to create the

AB. Subsequently, analyzing three alternative reasons for the 1996 reform will reveal

their limited explanatory power. The conclusion summarizes the Seven Technical

Measures instituted after the 1998 Asian Financial Crisis, the overall argument, and its

implications for HK’s future monetary considerations.

Evidence and Secondary Literature

Prior to delving into the narrative, this paper will introduce the evidence

employed to support the thesis. Richard Roberts and David Kynaston’s The Lion Wakes:

A Modern History of HSBC provided the inspiration for this specific inquiry by including

the firm’s view of January 1995 crisis8 as part of their commissioned work. Daily

accounts from the time period come from the South China Morning Post (SCMP)

archives, the largest English language newspaper in HK with an extensive financial

3

reporting section. Secondary literature mostly came from Hong Kong SAR's Monetary

and Exchange Rate Challenges: Historical Perspectives, while Y.C. Jao’s "The Working

of the Currency Board: The Experience of Hong Kong 1935-1997" provided additional

analysis. In his chapter in Challenges, Tony Latter barely even mentions the AB despite

being the primary proposer of the AA.9 Both John Greenwood and Joseph Yam consider

the development of a real-time gross settlement (RTGS) system as the driving force

behind the AB, though Yam’s discussion of the AA decision in 1988 includes the AB and

will be discussed critically later on. Y.C. Jao mentions that resentment of HSBC played a

role in the AB’s creation but focuses extensively on 1983 while offering only cursory,

supportive remarks on 1988 and 1996. In contrast, this paper relies on the analysis in

these accounts and period reporting to develop a unique causal story.10 Identifying

HSBC’s alleged actions as the catalyst for banking reform fills a void in the secondary

literature while also contributing to the history of HK regulation. Even in a free-market

zone financial institutions require monetary oversight to preserve the economic system,

and its return in 1983 is where the historical narrative of this paper begins.

Review of Hong Kong’s Monetary History

As previously stated, the HKD floated on international markets for ten years after

delinking from the USD in 1972, but its “continued weakness [during that period]

reflected mounting anxieties about the territory’s [handover] in 1997 [and in the] summer

1982 when … the political uncertainty [evident in the negotiations] compounded the

economic fallout from ending the long boom,”11 causing the HKD to USD exchange rate

to depreciate to 9.50.12 HK’s policymakers concluded that the speculation could only be

stopped with decisive monetary action that reassured the market.13 Multiple mechanisms

4

were proposed14 but the one chosen was a managed currency board system that “would

operate by restoring a fixed rate against the [USD] for the issue and redemption of

[Certificates of Indebtedness (CoIs) with the EF], equivalent to [HKD] banknotes, at

[HKD] 7.80 per [USD]. This meant that the [longstanding] two note-issuing banks

[HSBC and Standard Chartered] would … pay the [EF] for additional CoIs, which they

were required to hold as backing [for the newly issued currency, while] … notes were to

be withdrawn from circulation by the note-issuing banks [by] surrendering CoIs.”15 Very

importantly, the entrenched “note-issuing banks agreed with the other banks that the

former would supply [notes to] the latter also only in exchange for [USD] at the rate of

7.80”16 for the sake of currency stability, thereby forgoing profitable arbitrage. According

to the secondary literature, the “general consensus in [HK was] that the main objective of

monetary policy should be exchange rate stability”17 at the level set in 1983.

However, the EF lacked direct control over the money supply. The amount of

HKD was largely managed by HSBC, “a commercial bank [tasked with balancing its]

private interests … with the public interest of monetary and currency stability.”18 In

addition to raising questions of fiduciary responsibility and corporate ethics, there were

also concerns “that as manager of the clearing system, HSBC had the power to create

credit for other banks … [and] could at times negate any intervention by the authorities”19

through its manipulation and knowledge of other banks’ HKD checking accounts. When

HSBC intervened in the mortgage market on October 13th, 1984 to push the overnight

lending rate below 12 percent20 it prompted an expert to publically encourage “the

government [to] take a 20 to 40 percent stake in [HSBC].”21 These unilateral adjustments

demonstrate the sweeping power afforded to HSBC by the 1983 mechanism. Moreover,

5

HSBC also issued over two thirds of the HKD notes in circulation, and in a 1988 study

described “the present note-issuing system as ‘unhealthy,’ … ‘under which certain profit-

making commercial banks are given quasi central bank status’.”22 Thus, in multiple ways,

HSBC appears overtly influential in the HKD market before 1988.

Over the course of five years the government “made a determined effort to

conceal how extensively [it] had to intervene in financial markets,”23 either indirectly

through HSBC or directly with using currency reserves. While the index for the HK stock

exchange increased after the peg was reinstated “it would [have been] naïve to infer from

the buoyancy of the equity and money markets that [HK] has finally come to terms with

its political fate,”24 according to a 1985 SCMP article. In addition to the discontent with

HSBC, “one of the architects of the linked rate system, said … there were … defects

[such as] the limited convertibility to the banks, which means the [EF would have] buy or

sell [CoIs] corresponding to the note issue of the note-issuing banks”25 instead of just

issuing more currency to increase the money supply. Without the power to control the

monetary base the EF operated at the pleasure of HSBC, making the HKD a ‘privately-

managed’ currency board regime. Policymakers eventually decided to change the system

with what became known as the Accounting Arrangement in 1988.

During the deliberations in 1983 multiple potential mechanisms were considered,

and one “proposed by Tony Latter … argued that the existing scheme was not working

‘because its operation [was] not wholly under government control.’ His [plan] ‘intended

to overcome this deficiency by putting government firmly in the driving seat’.”26 While

this idea only became law in 1988 it received “a mixed response from the financial

community [that suggested] the action [was] effectively chipping away at the position of

6

[HSBC, which was] regarded as a quasi central bank.”27 Latter’s scheme, later named the

AA, “required HSBC to maintain an Account with the [EF], with the level of the balance

in the Account to be set by the monetary authorities”28 and “enabled the authorities for

the first time to influence bank liquidity through their own operations in the foreign

exchange or money markets.”29 Previously, conducting successful open market operations

through HSBC had required the bank to fully acquiesce to the adjustment. But under the

AA the EF could manipulate the Balance and force the bank to issue more, or less, HKD.

This radically increased the authority’s monetary responsibilities.30

Unfortunately, the reform did not operate entirely as designed because “HSBC

was the sole settlement counterparty for official operations [and its] actions in response to

official intervention were key to determining the overall impact of such intervention on

the banking sector.”31 At the time the authorities intended for “[HK]’s new stock clearing

and depository system [to] be run by a procession team unrelated to … [HSBC], which

had expressed interest in the management contract,”32 “but the fact that [HK]’s banks had

maintained a private clearing and settlement system had obscured the fact that the

ultimate settlement bank (HSBC) [had] the power to operate like a central bank in the

sense of granting credit to any bank”33 that cleared HKD checks. Although the EF could

conduct market intervention through other banks,34 “its first disclosed intervention since

assuming control of interbank liquidity … [tightened] the money supply by $150 million

to $1.1 billion [by] reducing the balance of [HSBC]’s account with the [EF] by $150

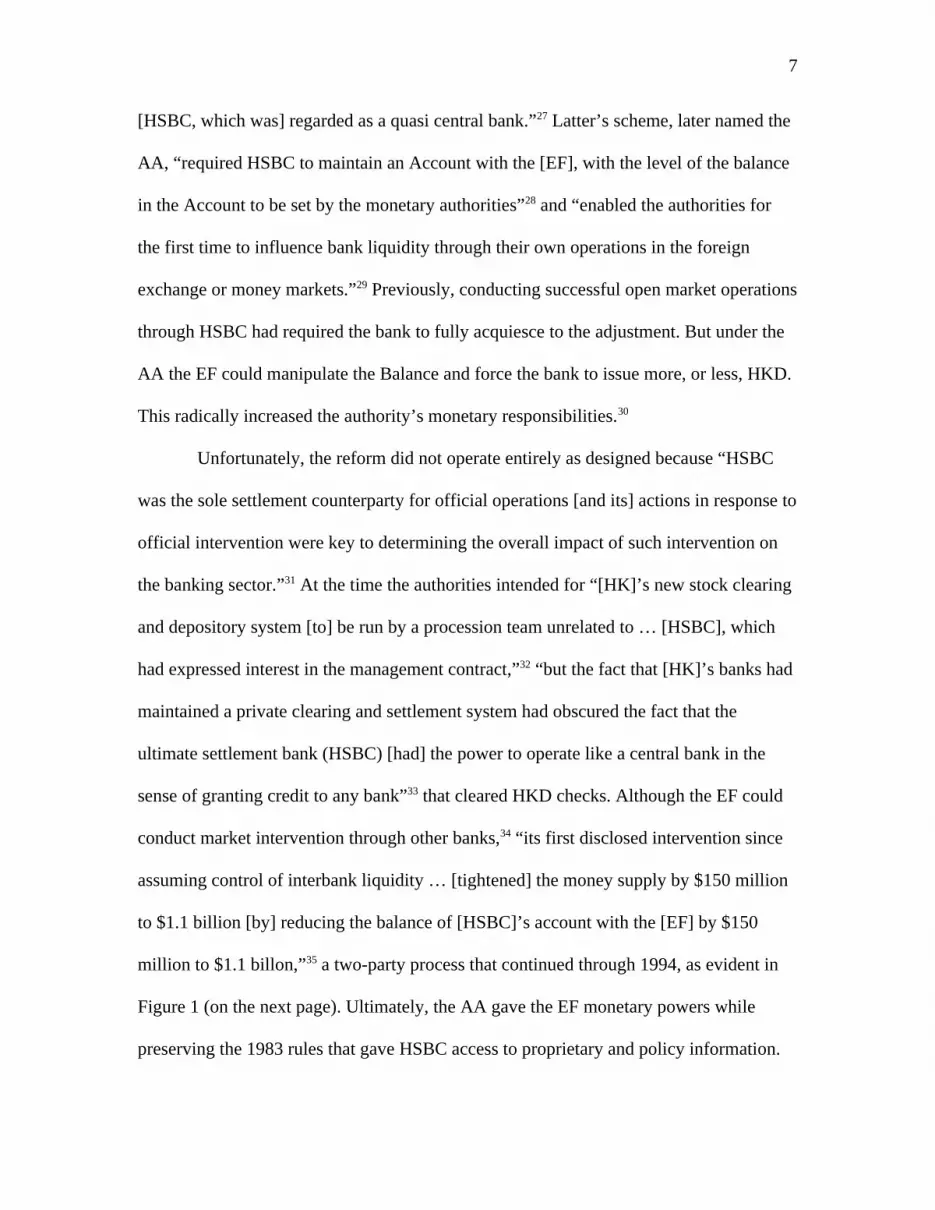

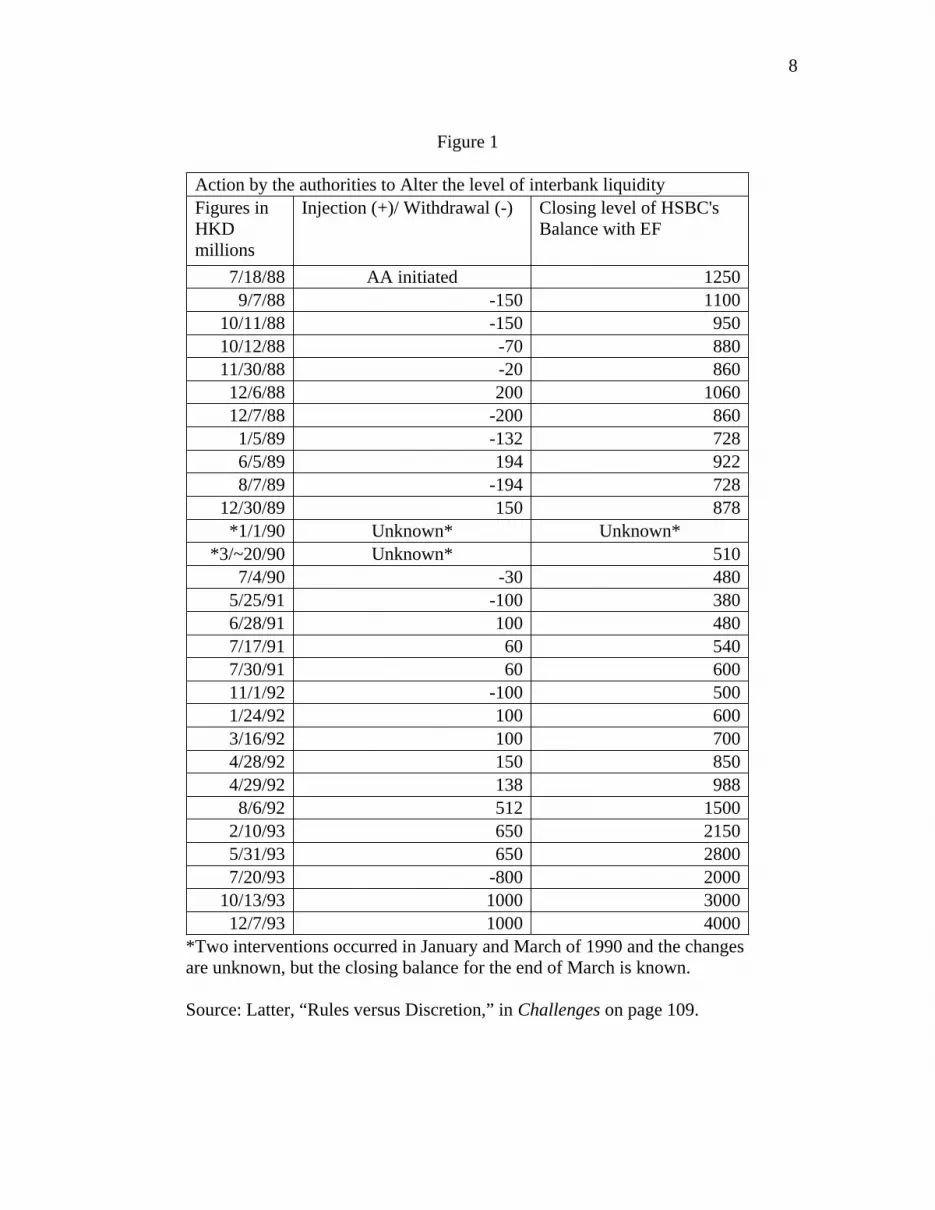

million to $1.1 billon,”35 a two-party process that continued through 1994, as evident in

Figure 1 (on the next page). Ultimately, the AA gave the EF monetary powers while

preserving the 1983 rules that gave HSBC access to proprietary and policy information.

7

Figure 1

Action by the authorities to Alter the level of interbank liquidityFigures in HKD millions

Injection (+)/ Withdrawal (-) Closing level of HSBC's Balance with EF

7/18/88 AA initiated 12509/7/88 -150 1100

10/11/88 -150 95010/12/88 -70 88011/30/88 -20 86012/6/88 200 106012/7/88 -200 8601/5/89 -132 7286/5/89 194 9228/7/89 -194 728

12/30/89 150 878*1/1/90 Unknown* Unknown*

*3/~20/90 Unknown* 5107/4/90 -30 480

5/25/91 -100 3806/28/91 100 4807/17/91 60 5407/30/91 60 60011/1/92 -100 5001/24/92 100 6003/16/92 100 7004/28/92 150 8504/29/92 138 9888/6/92 512 1500

2/10/93 650 21505/31/93 650 28007/20/93 -800 2000

10/13/93 1000 300012/7/93 1000 4000

*Two interventions occurred in January and March of 1990 and the changes are unknown, but the closing balance for the end of March is known.

Source: Latter, “Rules versus Discretion,” in Challenges on page 109.

8

For another five years the 1988 system remained in effect, unchanged, until the

EF merged with the Office of the Commissioner of Banking in April 1993 to form the

HKMA. 36 Back in March of 1992 the SCMP published an article titled “Government

moves closer to central bank,” in which it explained, “the Government [had] previously

vehemently denied any interest in strengthening its central banking functions [until it

learned of HSBC]’s plan to acquire Midland Bank [in the UK, thereby] greatly loosening

its ties to [HK].”37 During 1993 HSBC reincorporated as a holding company in the UK

and the HKMA was developed, but another very significant change occurred in June

1992 when the EF created a Liquidity Adjustment Facility (LAF),38 which operated as a

discount window for institutions looking for capital advances. But apparently HSBC’s

dictation of “market conditions ... was the principle consideration behind the creation of a

deposit facility for banks under the LAF, [which explains how and] why the authorities

[wanted] to monitor [the money market more] closely[:]”39 through a mechanism beyond

the control of the bank. Furthermore, the HKMA in March 1994 “began to allow banks to

submit certain [HK] debt securities other than [EF] paper as collateral for borrowing

under the LAF”40 to diversify its monetary base holdings away complete reliance on the

Balance despite the risk to the peg. However, even with these internal alterations the

main monetary mechanism continued to operate in coordination with HSBC until 1996.

Finally, after thirteen years of quasi-central banking, “HSBC’s pivotal role ended

… when the requirement for all banks to maintain an account at the [EF] was

implemented [to create] a competitive set of counterparties”41 that gave “the HKMA …

direct control over interbank liquidity … in the form of the sum of balances in those

clearing accounts – the so called Aggregate Balance.”42 The new clearing and settlement

9

institution would be jointly operated by the HKMA and the Hongkong Association of

Banks (HKAB), according to the SCMP43 in an article published in April 1995. However,

“[the AA] remained the core of the system … until December 1996 when [the] new

clearing system [using RTGS] was introduced”44 that reduced transfer waiting time from

overnight to milliseconds. This meant that “by the time of [the handover, HSBC had]

only one quasi-central bank role left: the issuing of banknotes,”45 which now shares with

two other banks, Standard Chartered and Bank of China. Thus, monetary authority

successfully transferred from a private to a public institution in a free-market zone in the

years between 1983 and 1996.

Contrasting 1988 and 1996

Unfortunately, the above story lacks an essential causal element for why the 1996

reforms were instituted on top of the 1988 measures. Tony Latter argues, “in terms of the

debate on discretion, it is the 1988 move which is important. The 1996 reform is best

regarded as an operation refinement.”46 But coming from the principle proposer of the

AA that view sounds dismissive, and his article’s section on 1996 only mentions RTGS,

not the AB. While he does “note that the market was dominated by a single commercial

bank, HSBC, and there was always a suspicion that HSBC dictated market conditions to

its own advantage, even after the [AA was] put in place,”47 a reason for the refinement of

his 1983 proposal does not appear.

Although Latter provides no answers an analysis of relevant sentences in Joseph

Yam’s contribution to Challenges reveals key decision in the reform process. As the first

Chief Executive of the HKMA and former deputy secretary at the EF at the time of the

AA, he states that in 1988 “the key change ... was official, indirect control of the clearing

10

balance used to settle interbank transactions … two options were, in fact, discussed ...

The first, which was adopted ... was for HSBC to operate an account with the [EF] ... the

second option was for all banks to open and operate clearing accounts with the [EF].”48

Therefore, on the table as possible revisions to the 1983 system were the 1988 AA as

option one and the 1996 AB as option two. Acknowledging the benefits of hindsight, this

paper asks why the AA was chosen over the AB in 1988 and why further reform was

deemed necessary by the HKMA in 1996?

Answering the first part of the above question requires further analysis of Yam’s

article. On pages 152 and 153 of Challenges, Yam recalls that:

During the five years to 1987, it felt very much as if the financial authorities were fire-fighting one crisis after another … the real turning point came in May 1987 [when] pressures for reform culminated in high-level talks between the Financial Secretary … and Beijing … to address the issue of whether or not the administration was [able] to maintain monetary … stability during a period of political transition … [which] marked a turning point in attempts to reform monetary arrangements.49

Due to the ongoing handover negotiations with China, efficacy and expediency were

paramount in 1987.50 Therefore, the first option was chosen to justify the autonomy of

HK through the strength of the EF because the AB “would have necessitated a more

fundamental overhaul of the clearing system”51 and have taken too much time. According

to Yam, “it proved hard enough to reach agreement between the parties involved … [and]

once Beijing and Whitehall [UK] had agreed there were lengthy negotiations with the

chairman of HSBC”52 that culminated in the July 1988 announcement of the AA. Overall,

the process took fourteen months but was not made public until the reform’s initiation.

Moreover, to answer the second part of the driving question this paper would

perform a similar inquiry for 1996. Unfortunately, none of the secondary literature

11

provides any comparable assessment. Y.C. Jao’s paper identifies the resentment of HSBC

among other HKAB members as a driving factor for the AB,53 along with corroborating

the other authors’ assertion that RTGS compelled the change. In fact, the HKAB

publically commissioned54 and released a study55 that called for the end of HSBC’s

clearing role. But the HKAB put out their findings in December 1994 while the HKMA

announced an end to the AA and the start of the AB in April 1995, an impossible window

for completion given the difficult ascribed in 1988. Furthermore, the system was not fully

implemented until December 1996, or twenty months after the SCMP first publicized the

reform. While in that timeframe the mechanism materialized it does not follow the public

announcement timeline from 1988 when the AA was explained to the press as it went

into effect. Either the HKMA decided to operate on a long-run expectations framework,

not unheard of for central banks but new for HK, or an exogenous event compelled the

systemic change of the AB. This paper argues the latter, specifically that allegations

HSBC speculated against the HKD’s peg to the USD in January 1995 forced the HKMA

to assume direct responsibility for managing the local currency in 1996.

HSBC’s Alleged Speculation in January 1995

Although the January 1995 speculative crisis lasted only a week its intensity and

implications drastically affected the HK monetary system. According to HSBC’s

commissioned history in The Lion Wakes, a bank official “in November … publically

dismissed predictions that the peg would be dismantled after 1997.”56 But during that

press conference he also warned “the peg might face a moment of truth near to 1997.”57

Only two months later the SCMP reported that an “assault on the [HKD] was beaten off

yesterday … after strong intervention by the [HKMA, the currency] recovered ground

12

lost in Thursday’s heavy selling [that left] speculators with burned fingers.”58 Similarly,

Tony Latter recalls that “when the rate momentarily weakened quite sharply in January

1995 – albeit only to 7.7725 – the HKMA intervened significantly in the foreign

exchange market to arrest the decline,”59 demonstrating the resolve of the monetary

authorities. However, while the crisis lasted only a few trading days, the fallout for

HSBC continued into the weekend.

The Lion Wakes’ authors, relying on internal bank documents, recount that after

“the financial authorities managed to fend [off speculators] one of [HK]’s Chinese-

language papers, Ta Kung Pa, was soon running stories critical of [HSBC] for having

failed to shoulder its ‘moral responsibility’,”60 supposedly referring to its role as the

clearing and settlement house for the HKD. It was also reported in the SCMP that

“[HSBC] was the ‘black hand’ behind the scathing attack on the dollar … not only in

terms of carrying through orders … but also through its own proprietary trading,”61

implying that HSBC had internally bet against the HKD. This allegation is especially

serious because as the clearinghouse HSBC had access to confidential HKD and bank

proprietary information that may have directed internal trading desks to bet against the

peg in contradiction with its role as a money market maker.62 In fact, when “[HSBC]

countered rampant rumours that it was speculating against the dollar peg [it] admitted

that senior treasury staff have been moved after losses were incurred in the controversial

trading.”63 While “many market practitioners interpreted this move as a desperate attempt

by the bank to raise funds to cover its speculative positions,”64 the important takeaway is

the exposure of HSBC’s control over the financial system. As “the main source of

liquidity in the HKD market [HSBC could refuse] to accept orders [and] would

13

effectively be imposing foreign exchange control over the HKD,”65 which had compelled

the HKAB to conduct the 1994 study. But in the wake of the crisis the risk of not

reforming the system appeared significantly more serious post-January 1995.

According to Roberts and Kyanston, HSBC officials “had a [private] meeting in

Beijing with the New China News Agency to reiterate that the bank had not speculated

on the [HKD and claimed it was company policy not to bet] against the [HK]

Government position’.”66 But interestingly the authors imply that “the bank [seemed] to

have believed that it was the HKMA which had leaked the story to Ta Kung Pao about

[HSBC]’s reputed speculation against the peg [despite HKMA Chairman Yam assurance]

that the note-issuing banks had ‘co-operated fully in the whole exercise’.”67 Three months

later it was announced that a new clearing house would be managed jointly by the

HKMA and HKAB to eliminate next-day settlement managed by HSBC and replace it

with an RTGS to rationalize HK’s financial system (removing anachronistic powers), as

recommended by the HKAB study.68 Another intriguing article came out a month later

when the SCMP publically revealed on May 7th that “in recent months the relationship

between [HSBC] and the HKMA [had] been strained, reaching a head with alleged short-

selling by traders on the bank’s capital market’s desk, [and while in] the past this kind of

spat would have been handled in private, but the very public nature of the short-selling”69

forced policymakers to announce their intentions to form an AB over a year before it

could even come into effect.

Alternative Explanations for Creating the AB

In order to verify the above thesis, this paper considers three alternative reasons

for the 1996 reform: other speculative events, handover fears, and RTGS implementation.

14

Another issue raised by Jao is resentment of HSBC by HKAB members, but the analysis

of timing of announcements shows that it could not have been the ultimate reason for

instituted the AB, and therefore is not included as its own part of this section.

First, an assessment of comparable crises requires counter examples. The HSBC

official in November 1994 alluded to the more serious European speculative crisis of

1992, during which the British government withdrew from the European Exchange Rate

Mechanism.70 But in January 1995 the SCMP interviewed an HSBC banker who said

during “the monetary crisis in Europe when speculators … savaged the pound [they]

knew the [HKMA] would back [HKD] with [USD], and did not bet against it,”71 which

held true until the bank engaged in speculation. Furthermore, the only relevant US

recession occurred between July 1990 and March 1991,72 just two months after the EF

had issued the first bills in its creation of an HK debt market,73 yet the authorities

indicated no sign of trouble during that period. Since other, more serious currency crises

and trading partner economic disturbances did not approach the same level of exchange

rate destabilization it is reasonable to conclude that January 1995 was unique.

Second, concerns regarding the handover stemmed mostly from negotiations over

the Basic Law, the SAR’s constitution. Exchange rates were discussed in 1987 and

eventually “the supervision and regulation of the post-1997 [HK] financial markets

[were] left to the future [SAR] government instead of being stipulated in detail in the

Basic Law,”74 which became official in 1990 when the National People’s Congress of

China approved the draft.75 The final version states that “the [HKD], as the legal tender in

the [HK SAR], shall continue to circulate [and that the] authority to issue … currency

shall be vested in the Government of the [HK SAR, which may] may authorize

15

designated banks to issue or continue to issue [HKD],”76 thereby neutralizing concerns

that the HKD would disappear after the handover. In fact, the January crisis compelled

the HKMA and the People’s Bank of China (PBOC) to sign a bilateral purchase

agreement77 that later sparked monetary autonomy concerns78 after the AB had already

been announced and the Basic Law signed. Therefore, speculation about the handover’s

effect on the HKD could not have contributed significantly to the January 1995 crisis.

Third, the main reason put forward in the secondary literature is the need for

RTGS to modernize the payment system of HK. While the April 1995 article also

indicates this, and reiterates claims of resentment of HSBC’s anachronistic powers from

the HKAB, another timing issue arises. The US deployed the first large-scale RTGS

system in 1970 and they operated in other highly developed economies by the mid-

1980s.79 An HKAB study only raised the RTGS issue in 1994, and nowhere in Yam’s

article does it mention that in 1988 the EF considered an RTGS system. While the HKAB

may have determined RTGS implementation the best way to remove HSBC’s clearing

role that only explains their waiting, not the HKMA’s. The authority’s decision to

announce the AB in April 1995, despite the belated initiation of the Clearing House

Automated Transfer System (CHATS) in December 1996,80 indicates that technical

concerns could not have compelled such an aggressive, instantaneous overhaul. Even if

resentment within HKAB and its 1994 study encouraged reform before January 1995 the

speculative crisis catalyzed policymakers to publicize their intentions of creating the AB.

Discrediting the explanations in the secondary literature raises the level of validity

ascribable to the alternative presented in this paper by showing the importance of

HSBC’s alleged actions in the causal story and overarching historical narrative.

16

Conclusion: Hong Kong after 1996

In conclusion, the reforms of 1988 and 1996 were necessary to modernize the HK

monetary system before the handover in 1997. One year later the Asian Financial Crisis

caused “several waves of speculative attacks on [HK]’s currency and stock market[, to

which] the government responded … with the intervention in the stock market [and

resolved other] problems of the currency board [by enhancing] the transparency of

currency board operations[. Later that year] the HKMA announced a package of

measures designed to strengthen the mechanism”81 by “[committing] the HKMA to

purchase [HKD] in exchange for [USD] at a predetermined rate.”82 Enhanced operations,

openness, and commitment could not have occurred under the 1983 system and the

creation of the AB gave the HKMA sufficient authority to influence market expectations

for the HKD. The preceding reforms laid the groundwork for the monetary authority’s

response to the 1998 crisis and subsequent policy revisions after the handover. In 1988

the AA reassured Beijing that the EF could manage the HKD, and in 1996 the AB

removed the odious influence of HSBC on the currency before 1997. Moreover,

allegations of HSBC’s speculation against the HKD in January 1995 encouraged the

HKMA to assume responsibility for managing the currency directly, thereby creating an

effective central banking mechanism for HK as a counterpart to the PBOC. Empowering

the HKMA prior to the handover ensured the HK SAR’s ability to negotiate with the

mainland on monetary issues and preserves urban center’s status as a free-market zone

with its own currency. HK’s status as an SAR ends in 2047, and the negotiations

concerning that transition will certainly include the HKD, which continues to play a

significant role in the city’s financial and political identity.

17

Footnotes1. Long Finance. The Global Financial Center’s Index. Qatar Financial Center, 2015.

Accessed December 10, 2015. http://www.longfinance.net/images/GFCI18_23Sep2015.pdf

2. The “one country, two currencies” was a philosophy espoused by Deng Xiaopeng during the 1980s that would allow HK and Macau to exist as SARs while the rest of China used the socialist system.

3. Linked simply means a currency board system was instituted that set the exchange rate at a certain level. There are many names such as peg, fixed rate, etc. but this paper chooses to generally refer to the HK system as a ‘peg.’

4. Hong Kong Monetary Authority, “A brief history of Hong Kong dollar exchange rate arrangements” in Money in Hong Kong: A Brief Introduction. 2000. Accessed December 10, 2015. http://www.hkma.gov.hk/media/eng/publication-and-research/background-briefs/hkmalin/04.pdf

5. Typically currency boards were used for colonial economies with the rate set by the imperial monetary authority, but due to HK’s unique autonomy and the pressing circumstances the policymakers decided to put the EF in charge of maintaining the exchange rate at a predetermined level. The mechanisms by which the EF attempted to fulfill that role are discussed later on.

6. Y.C. Jao, "The Working of the Currency Board: The Experience of Hong Kong 1935-1997." Published in Pacific Economic Rev Pacific Economic Review (3, no. 3, 1998), 219-41.

7. “HSBC’s balance at the [EF] is referred to as the Balance” in Tony Latter, "Rules Versus Discretion in Managing the Hong Kong Dollar, 1983-2007." In Hong Kong SAR's Monetary and Exchange Rate Challenges: Historical Perspectives, ed. Catherine R. Schenk (Basingstoke: HKIMR/Palgrave Macmillan, 2009), 107.

8. Richard Roberts and David Kynaston, The Lion Wakes: A Modern History of HSBC (London: Profile Books, 2015) 91, 281-3.

9. On page 131 of John Greenwood, "The Origin and the Evolution of Hong Kong’s Currency Board I." In Hong Kong SAR's Monetary and Exchange Rate Challenges: Historical Perspectives, ed. Catherine R. Schenk (Basingstoke: HKIMR/Palgrave Macmillan, 2009) the author describes Tony Latter as the original proposer of the 1988 system during the 1983 deliberations.

10. The alternative proposed is entirely the author’s own assessment of the information available and acknowledges that the authorities, historians and actual policymakers, do not explicitly suggest this possibility. While the author believes that is out of political considerations it does not preclude the independent publication of this work.

11. Roberts, Richard, and David Kynaston. The Lion Wakes, 91.12. Michael Blendell, “No relief as dollar dives.” SCMP, September 25, 1983, accessed

November 28, 2015.

18

13. Previous monetary policy was practically nonexistent since “financial secretaries made virtually no use of these two monetary levers [government reserves and checks on bank lending], however, and they consistently argued that formal monetary policies had little or no part to play in [HK]” in Leo Goodstadt, "Laissez-faire’s Limitations: The Evolution of Monetary Policy in Hong Kong, 1935-80." In Hong Kong SAR's Monetary and Exchange Rate Challenges: Historical Perspectives, ed. Catherine R. Schenk (Basingstoke: HKIMR/Palgrave Macmillan, 2009). 79.

14. Greenwood discusses many proposals on page 131 in “Origin and Evolution I.”15. Greenwood, “Origin and Evolution I,” 135.16. Latter, “Rules versus Discretion,” 103.17. Joseph Yam. "The Origin and the Evolution of Hong Kong’s Currency Board II." In

Hong Kong SAR's Monetary and Exchange Rate Challenges: Historical Perspectives, ed. Catherine R. Schenk (Basingstoke: HKIMR/Palgrave Macmillan, 2009), 145.

18. Ibid., 146.19. Greenwood, “Origin and Evolution I,” 136.20. “Bank intervention threat keeps dealer wary.” SCMP, October 13, 1984, Business

News sec, accessed November 28, 2015.21. "Au Urges Public Stake in Hongkong Bank." SCMP, October 17, 1984, Business

News sec, accessed November 28, 2015.22. Eva To, "Study Wants Note Issuing Revamped." SCMP, July 7, 1988, Business Post

sec, accessed November 28, 2015.23. Goodstadt, “Laissez-faire’s Limitations,” 88 that internally cites Latter, “Rules versus

discretion.”24. "Cut the Link and Weaken the Chain." SCMP, July 17, 1985, Business News sec,

accessed November 28, 2015.25. John Mulcahy, "Renewed Support for HK Dollar Peg." SCMP, January 16, 1986,

Business Post sec, accessed November 28, 2015. The expert referenced is Greenwood.

26. Greenwood, “Origin and Evolution I,” 131 citing a memo written by Latter.27. William Barnes, “Opinion split on change in money control system.” SCMP, July 17,

1988, Sunday Money sec, accessed November 28, 2015.28. Greenwood, “Origin and Evolution I,” 136.29. Latter, “Rules versus Discretion,” 100.30. Instead of leaving the monetary levers to the private sector, “the fact that the onus

[now] rested on the authorities to initiate any intervention implied a continuation of a significant element of discretion.” Latter, “Rules versus Discretion,” 107.

31. Latter, “Rules versus Discretion,” 100.32. Chan Chi-Keung, “Clearing body to be independent.” SCMP, July 29, 1988, Business

Post sec, accessed November 28, 2015.33. Greenwood, “Origins and Evolutions I,” 137.

19

34. At the end of 1988 “the [EF had] not yet decided on which banks, apart from [HSBC], through which it would conduct market intervention in the future. Under the previous arrangement, the Exchange Fund conducted market intervention through [HSBC] as well as certain other banks [such as Standard Chartered Bank, the other note-issuing institution at the time].” Eva To, “Exchange fund in interbank scheme.” SCMP, October 3, 1988, Business Post sec, accessed November 28, 2015.

35. Eva To, “Move to tighten money supply.” SCMP, September 8, 1988, Business Post sec, accessed November 28, 2015.

36. Greenwood, “Origins and Evolutions I,” 137.37. Eva To, “Government moves closer to central bank.” SCMP, March 29, 1992,

Sunday Money sec, accessed November 21, 2015.38. Yam, “Origins and Evolutions II,” 154.39. Latter, “Rules and Discretion,” 111.40. Ibid., 114.41. Ibid., 100.42. Yam, “Origins and Evolutions II,” 154.43. Simon Pritchard, “Hongkong Bank to lose clearing role.” SCMP, April 2, 1995,

Sunday Money sec, accessed November 21, 2015.44. Greenwood, “Origins and Evolutions I,” 137.45. Roberts, Richard, and David Kynaston. The Lion Wakes, 283.46. Latter, “Rules versus Discretion,” 107.47. Ibid., 111.48. Yam, “Origins and Evolutions II,” 153.49. Ibid., 152-3.50. Stanley Leung, “SAR to tackle exchanges.” SCMP, October 30, 1987, accessed

November 28, 2015.51. Yam, “Origins and Evolutions II,” 153.52. Ibid., 153.53. Jao, “Working of the Currency Board,” 236.54. Noel Fung, “Bank settlement switch ‘to level playing field’.” SCMP, July 15, 1994,

Business Post sec, accessed November 21, 2015.55. Noel Fung, “Clearing house should be jointly owned: study.” SCMP, December 6,

1994, Business Post sec, accessed November 21, 2015.56. Roberts, Richard, and David Kynaston. The Lion Wakes, 281.57. Sean Kennedy, “Bankers expect HKD link to remain.” SCMP, January 11, 1995,

Business Post sec, accessed November 28, 2015.58. Ray Heath and Noel Fung, "Assault on Dollar Fought off." SCMP, January 14, 1995,

accessed November 28, 2015.59. Latter, “Rules versus Discretion,” 114.60. Roberts, Richard, and David Kynaston. The Lion Wakes, 281-2.

20

61. Noel Fung and Sheel Kohli, “Bank’s hand in the fall of the dollar suspected.” SCMP, January 19, 1995, Business Post sec, accessed November 21, 2015.

62. Ibid.63. Noel Fung, “Bank denies dollar attack.” SCMP, January 19, 1995, accessed

November 21, 2015.64. Ibid.65. Ibid.66. Roberts, Richard, and David Kynaston. The Lion Wakes, 282.67. Ibid., 283.68. Simon Pritchard, “Hongkong Bank to lose clearing role.” SCMP, April 2, 1995.69. Simon Pritchard, “Standing up for the HK dollar.” SCMP, May 7, 1995, Sunday

Money sec, accessed November 21, 2015.70. Litterick, David. “Billionaire who broke the Bank of England.” The Telegraph,

September 13, 2002.71. Sean Kennedy, “Bankers expect HKD link to remain.” SCMP, January 11, 1995.72. NBER Business Cycle Dating Committee - March 1991. "NBER Business Cycle

Dating Committee Determines That Recession Ended in March 1991." NBER Business Cycle Dating Committee, December 2, 1992. Accessed December 8, 2015. http://www.nber.org/March91.html.

73. Latter, “Rules versus Discretion,” 107.74. Stanley Leung, “SAR to tackle exchanges.” SCMP, October 30, 1987.75. Chris Yeung, “NPC puts seal on Basic Law.” SCMP, April 5, 1990, accessed

November 21, 2015.76. Hong Kong Special Administrative Region Government. THE BASIC LAWOF THE

HONG KONG SPECIAL ADMINISTRATIVE REGION OF THE PEOPLE’S REPUBLIC OF CHINA, 35.

77. Josephine Ma, “PBOC, HK seal currency pact.” SCMP, Febuary 2, 1996, accessed November 21, 2015.

78. Renee Lai and Ren Kan, “PBOC seeks to ease monetary fears.” SCMP, November 14, 1996, accessed November 21, 2015.

79. Committee on Payment and Settlement Systems, REAL-TIME GROSS SETTLEMENT SYSTEMS. Bank of International Settlements, 1997. Accessed December 5, 2015. http://www.bis.org/cpmi/publ/d22.pdf

80. Hong Kong Interbank Clearing Limited "Our Services - Real Time Gross Settlement System." 2003. Accessed December 8, 2015. http://www.hkicl.com.hk/clientbrowse.do?docID=102&lang=en.

81. Greenwood, “Origins and Evolutions I,” 140.82. Yam, “Origins and Evolutions II,” 155.

21

Acronyms Index

AA - 1988 Accounting ArrangementAB -1996 Aggregate Balance

EF - Exchange FundCoIs - Certificates of Indebtedness

GBP - British Pound SterlingHK - Hong Kong

HKAB - Hongkong Association of Banks HKD - Hong Kong Dollar

HKMA - Hong Kong Monetary AuthorityHSBC* - Hongkong and Shanghai Banking Corporation

LAF - Liquidity Adjustment FacilityPBOC - People’s Bank of China

RTGS - real-time gross settlement SAR - Special Administrative RegionSCMP - South China Morning Post

USD - United States Dollar

*In multiple sources the authors refer to the local Hong Kong presence of the Hongkong and Shanghai Banking Corporation as simply ‘Hongkong Bank,’ but for the purpose of clarity through consistency it will be written as HSBC where [HSBC] within double quotations denotes a time when the quote read ‘Hongkong Bank’. There are also many divisions within HSBC that are referred to by their corporate roles such as HSBC Holdings, HSBC Markets, HSBC Board, etc. when it is appropriate and/or necessary.

Bibliography

Barnes, William. “Opinion split on change in money control system.” South China Morning Post, July 17, 1988, Sunday Money sec. Accessed November 28, 2015.

Blendell, Michael. “No relief as dollar dives.” South China Morning Post, September 25, 1983. Accessed November 28, 2015.

Chi-Keung, Chan. “Clearing body to be independent.” South China Morning Post, July 29, 1988, Business Post sec. Accessed November 28, 2015.

Committee on Payment and Settlement Systems, REAL-TIME GROSS SETTLEMENT SYSTEMS. Bank of International Settlements, 1997. Accessed December 5, 2015. http://www.bis.org/cpmi/publ/d22.pdf

Fung, Noel. “Bank denies dollar attack.” South China Morning Post, January 19, 1995. Accessed November 21, 2015.

22

Fung, Noel. “Bank settlement switch ‘to level playing field’.” South China Morning Post, July 15, 1994, Business Post sec. Accessed November 21, 2015.

Fung, Noel and Sheel Kohli. “Bank’s hand in the fall of the dollar suspected.” South China Morning Post, January 19, 1995, Business Post sec. Accessed November 21, 2015.

Fung, Noel. “Clearing house should be jointly owned: study.” South China Morning Post, December 6, 1994, Business Post sec. Accessed November 21, 2015.

Goodstadt, Leo. "Laissez-faire’s Limitations: The Evolution of Monetary Policy in Hong Kong, 1935-80." In Hong Kong SAR's Monetary and Exchange Rate Challenges: Historical Perspectives, edited by Catherine R. Schenk, 75-94. Basingstoke: HKIMR/Palgrave Macmillan, 2009.

Greenwood, John. "The Origin and the Evolution of Hong Kong’s Currency Board I." In Hong Kong SAR's Monetary and Exchange Rate Challenges: Historical Perspectives, edited by Catherine R. Schenk, 125-144. Basingstoke: HKIMR/Palgrave Macmillan, 2009.

Heath, Ray, and Noel Fung. "Assault on Dollar Fought off." South China Morning Post, January 14, 1995. Accessed November 21, 2015.

Hong Kong Interbank Clearing Limited "Our Services - Real Time Gross Settlement System." 2003. Accessed December 8, 2015. http://www.hkicl.com.hk/clientbrowse.do?docID=102&lang=en.

Hong Kong Monetary Authority. “A brief history of Hong Kong dollar exchange rate arrangements.” In Money in Hong Kong: A Brief Introduction, 2000. Accessed December 10, 2015. http://www.hkma.gov.hk/media/eng/publication-and-research/background-briefs/hkmalin/04.pdf

Hong Kong Special Administrative Region Government. THE BASIC LAWOF THE HONG KONG SPECIAL ADMINISTRATIVE REGION OF THE PEOPLE’S REPUBLIC OF CHINA. 35.

Jao, Y. C. "The Working of the Currency Board: The Experience of Hong Kong 1935-1997." Pacific Economic Rev Pacific Economic Review 3, no. 3 (1998): 219-41.

Kennedy, Sean. “Bankers expect HKD link to remain.” South China Morning Post, January 11, 1995, Business Post sec. Accessed November 21, 2015.

Lai, Renee and Ren Kan. “PBOC seeks to ease monetary fears.” South China Morning Post, November 14, 1996. Accessed November 21, 2015.

23

Latter, Tony. "Rules Versus Discretion in Managing the Hong Kong Dollar, 1983-2007." In Hong Kong SAR's Monetary and Exchange Rate Challenges: Historical Perspectives, edited by Catherine R. Schenk, 95-124. Basingstoke: HKIMR/Palgrave Macmillan, 2009.

Leung, Stanley. “SAR to tackle exchanges.” South China Morning Post, October 30, 1987. Accessed November 28, 2015.

Litterick, David. “Billionaire who broke the Bank of England.” The Telegraph, September 13, 2002. Accessed December 8, 2015.

Long Finance. The Global Financial Center’s Index. Qatar Financial Center, 2015. Accessed December 10, 2015.

Ma, Josephine. “PBOC, HK seal currency pact.” South China Morning Post, Febuary 2, 1996. Accessed November 21, 2015.

Mulcahy, John. "Renewed Support for HK Dollar Peg." South China Morning Post, January 16, 1986, Business Post sec. Accessed November 28, 2015.

NBER Business Cycle Dating Committee - March 1991. "NBER Business Cycle Dating Committee Determines That Recession Ended in March 1991." NBER Business Cycle Dating Committee - March 1991. December 2, 1992. Accessed December 8, 2015. http://www.nber.org/March91.html.

Pritchard, Simon. “Hongkong Bank to lose clearing role.” South China Morning Post, April 2, 1995, Sunday Money sec. Accessed November 21, 2015.

Pritchard, Simon. “Standing up for the HK dollar.” South China Morning Post, May 7, 1995, Sunday Money sec. Accessed November 21, 2015.

Roberts, Richard, and David Kynaston. The Lion Wakes: A Modern History of HSBC. London: Profile Books, 2015. 91, 281-3.

"Au Urges Public Stake in Hongkong Bank." South China Morning Post, October 17, 1984, Business News sec. Accessed November 28, 2015.

“Bank intervention threat keeps dealer wary.” South China Morning Post, October 13, 1984, Business News sec. Accessed November 28, 2015.

"Cut the Link and Weaken the Chain." South China Morning Post, July 17, 1985, Business News sec. Accessed November 28, 2015.

To, Eva. “Exchange fund in interbank scheme.” South China Morning Post, October 3, 1988, Business Post sec. Accessed November 28, 2015.

24

To, Eva. “Government moves closer to central bank.” South China Morning Post, March 29, 1992, Sunday Money sec. Accessed November 21, 2015.

To, Eva. “Move to tighten money supply.” South China Morning Post, September 8, 1988, Business Post sec. Accessed November 28, 2015.

To, Eva. "Study Wants Note Issuing Revamped." South China Morning Post, July 7, 1988, Business Post sec. Accessed November 28, 2015.

Yam, Joseph. "The Origin and the Evolution of Hong Kong’s Currency Board II." In Hong Kong SAR's Monetary and Exchange Rate Challenges: Historical Perspectives, edited by Catherine R. Schenk, 145-158. Basingstoke: HKIMR/Palgrave Macmillan, 2009.

Yeung, Chris. “NPC puts seal on Basic Law.” South China Morning Post, April 5, 1990. Accessed November 28, 2015.

25