fringe benefits for employees of farm and ranch corporations

TRANSCRIPT

The Texas A&MUniversity System

TexasAgriculturalExtensionService

DirectorDaniel C. PfannstielCollege Station, Texas 77843

8·1334

Fringe Benefits forEmployees of Farm andRanch Corporations

Farm and RanchBusiness Organization in Texas

PREFACEThis publication is one of a series on the incorporation of farms and ranches and is

intended for laymen who want to develop an understanding of the basic tax issuesencountered by,incorporated businesses. The authors have attempted to interpret ourcomplex and technical tax law into understandable language and concepts. However,any dilution of the complexities of the law will necessarily involve omission of somedetails and exceptions to general rules. This publication is intended to convey the typeof information useful to businessmen who are considering the organization of acorporation or who currently are operating a corporation. It is not intended as legaladvice nor should it be construed as an exhaustive treatment of tax implications.

While the authors have written in a manner that should be understandable by mostpersons who are concerned with the incorporation of a business, certain terminologythat is common in tax matters is used. These terms may not be used often in theeveryday conversations of farmers and ranchers. However, as businessmen, farmersand ranchers should develop a basic understanding of this terminology so they caneffectively communicate with their professional advisors. For those not intimatelyfamiliar with such terms, this publication may not be easy to read. Even so, thetechnical nature of the subjects treated herein require some of them, and the benefitsthat the readers can acquire through development of the ability to use these termsoutweigh the initial detriment.

Fringe Benefits forEmployees of Farm andRanch Corporations

Marvin Sartin and Norman Brints*

The organization of a farm business as a corpo-ration provides employee-shareholders with ex-panded opportunities to receive fringe benefits.Generally, fringe benefits include all benefits pro-vided to employees in addition to wages andsalaries. Specifically, corporations can providelarger pension plans, health and accident plans,group life insurance and, in some cases, corporateownership of residences and automobiles.

A proprietor or partner must purchase his owninsurance with after-tax income and is limited in taxsheltered retirement plans to HR-10 plans, Sim-plified Employee Pension Plans (SEPP) or Individu-al Retirement Accounts (IRA's). A corporation canprovide benefit~ to employees, treat the costs asordinary business expenses and not create taxableincome to the recipient. Thus, these benefits in-crease the employees' real income at less cost thanincreasing salaries to that level.

For example, assume a corporation with a 40percent marginal tax rate provides non-pensionfringe benefits costing $2,000 per year to an em-ployee with 50 percent personal tax rate. The after-

*Area Extension economist - management and CPA and areaExtension economist - management, The Texas A&M Universi-ty System.

3

tax cost to the corporation of providing these bene-fits is $1,200. Assuming that none of these benefitswould be tax deductible for the individual, his salarywould have to be increased by $4,000 to provide anafter-tax increase of $2,000. The after-tax cost tothe corporation of the increased salary is $2,400. Anet savings of $1,200 ($2,400 - $1,200) isachieved by having the corporation provide thebenefits.

Realistically, incorporation of a business in-cludes both advantages and disadvantages. Eachindividual must weigh the relative importance ofthese to determine if the action is warranted. Thediscussion which follows will explain specific typesof fringe benefits that have general application inagricultural corporations and some of the rulesgoverning their availability.

LIFE INSURANCELife insurance coverage is one of the most com-

mon and valuable benefits that employers provideemployees. Insurance proceeds received by theinsured's beneficiaries at his death are exempt fromincome taxes and can be excluded from the dece-

dent's estate if all incidents of ownership of thepolicy are vested in someone other than the in-sured.

Group term life insuranee usually is selectedbecause the corporation can deduct costs of up to$50,000 coverage per employee without creatingtaxable income to the individual. The cost of cover-age exceeding $50,000 per employee is taxableincome to the employee. However, a tax benefitmay exist because the taxable "cost" is determinedfrom IRS tables of insurance costs and may be lessthan the premiums paid for the coverage. Groupterm coverage in excess of $50,000 is tax free toformer employees if they are disabled or havereached the company's normal retirement age.

Group term coverage of the spouse and depen-dents of corporate employees is tax free up to$2,000 per individual. The entire cost of coverageexceeding $2,000 for each individual is taxable tothe employee.

Some limitations may be encountered in theamount of coverage under group policies. If morethan 10 employees are covered, the tax law doesnot require that this benefit be provided to all em-ployees. The covered employees must constitute agroup whose members are selected solely on thebasis of age, marital status or "factors related toemployment." Thus, the group cannot be based onthe employee's status as a stockholder or familymember, but it can be based on employment-related duties or compensation received.

If a group has fewer than 10 members, all em-ployees must be covered except those employedfull time for less than 6 months, part-time employ-ees working 20 hours or less per week and notmore than 5 months in any calendar year, thoseelecting not to be covered and those over age 65.The only evidence of insurability that can be re-quired is a medical questionaire to be completedby the employee. Also, the amount of insurancecoverage must be either a uniform percentage ofsalary or on the basis of coverage brackets estab-lished by the insurance company. No bracket mayexceed two and one-half times the next lower bracketand the lowest bracket must be at least 10 percentof the highest bracket.

There usually is no tax advantage in having thecorporation provide ordinary life insurance to itsemployees. The corporation can deduct the pre-miums, but that amount is taxable income to theemployees. If ordinary life policies are preferable toterm insurance, "split dollar" insurance may pro-vide benefits. Split dollar insurance requires thatthe corporation pay the portion of the premiumequal to the increase in cash surrender value in thatyear. The remainder of the premium is paid by theindividual. The employee must pay a substantialpart of the premium in the first year or two, but hisshare will decrease rapidly.

4

The employee will be taxed on an amount equalto the 1-year premium of a declining term life insur-ance policy, less the portion of the premium paid byhim. The corporation cannot deduct any portion ofits payments. However, it is entitled to the cashsurrender value of the policy upon the death of theemployee. The employee's beneficiaries are enti-tled to the excess. Both portions are non-taxable lifeinsurance proceeds.

VOLUNTARY DEATH BENEFITSA corporation can pay death benefits to a de-

ceased employe~'s spouse, children or estate.Payment for past services is deductible by thecorporation as compensation. A payment that doesnot exceed $5,000 can be tax free to the recipientsunder a special death benefits exclusion.

Voluntary payments exceeding $5,000 by thecorporation to the beneficiaries of a deceased em-ployee usually will be regarded by the IRS astaxable compensation or as a dividend. In mostfamily corporations, it is difficult to document thatthe excess payment to the widow of an employee-shareholder was a gift made from "detached anddisinterested generosity."

The death benefits will not be included in theemployee's estate for estate tax purposes if thepayment is wholly voluntary. If the corporation hada contractual obligation to pay the benefit, the valuewould be included in the estate.

MEDICAL AND DISABILITY BENEFITSMedical benefits for employees and their

families can be paid by the corporation and be taxfree to employees if they are made under a healthand accident plan. Plans may be insured or non-insured, and different types of plans can be adopt-ed for various classes of employees. Coveragescan be determined to include only work-relatedillness and injury or can be comprehensive enoughto cover all medical and dental expenses. Suchpayments are usually tax deductible expenses ofthe corporation.

Insured plans can be set up to cover onlyselected employees. The corporation is not limitedto group policies or ordinary health insurance con-tracts. Individual policies can be tailored to providecoverage to fit specific needs. An insured medicalaccident and health plan can cover a few or onlyone employee of a closely held corporation.

Uninsured or self-insured plans provide for thecorporation to reimburse the employee for certain

medical expenditures. If a self-insured medicalreimbursement plan discriminates in favor of cer-tain employees, some or all of the reimbursementwill be taxable to the employee. If the shareholder-employee chooses to purchase medical insurancehimself, the corporation's reimbursement of his pre-miums will be subject to the anti-discriminationrules applicable to self-insured plans.

Corporate payments for periodic medical check-ups will qualify as tax-exempt medical care for keyemployees and is deductible by the corporation.This fringe benefit can be advantageous to both thecorporation and the employee by discovering ill-nesses in their early stages.

Disability insurance provides for payments toemployees unable to work because of illness orinjury. Premiums on disability policies paid by thecorporation are deductible expenses and are notincome to the employee. Disability coverage maybe' provided only to selected employees if such isdesired. Any proceeds received by the employeefrom the disability policy will be taxable income tohim if the corporation paid the insurance premiums.

RETIREMENT BENEFITSThe primary advantages of retirement plans for

employees of a farm corporation are in qualifiedplans that allow greater annual contributions thanHR-10 plans and/or are more flexible concerningthe coverages of various employees. The followingdiscussion focuses on the types of plans that pro-duce current tax deductions for the corporation anddo not produce taxable benefits to the employeeuntil the proceeds are actually received.

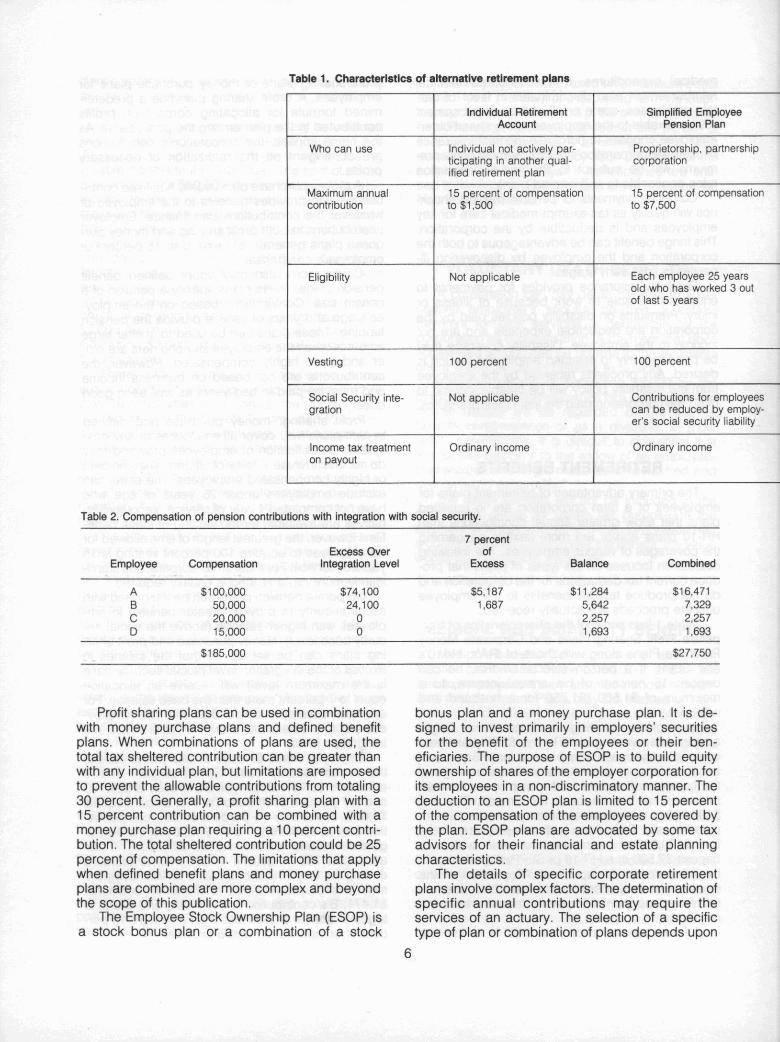

Table 1 lists some of the characteristics of Cor-porate Profit Sharing Plans and Corporate MoneyPurchase Plans along with those of IRA's, Hr-10'sand SEPP. If a person selects an IRA, he candeposit 15 percent of his annual income, to amaximum of $1,500 ($1,750 for a husband andwife) per year.An employer wanting to tax shelter a larger

amount and selecting an HR-10 or SEPP plan, mustcover all employees who have at least 3 years ofservice. He must deposit the same percentage ofthe compensation paid to the employees for theirretirement as he deposits for himself. The first$100,000 of business income may be used to com-pute the rate. Thus, if the business produced morethan $100,000 of income and the owner wished todeposit $7,500 in a HR-10 or SEPP, the rate wouldbe 7.5 percent. A deposit of 7.5 percent of theemployee's compensation also must be made intoretirement accounts for them, and it vests im-mediately.

A farm corporation can use SEPP's, or institute

5

profit sharing plans or money purchase plans foremployees. A profit sharing plan has a predeter-mined formula for allocating corporation profitscontributed to the plan among the participants. Asthe name implies, the corporation's contributionsare contingent on the realization of necessaryprofits.

A money purchase plan usually has fixed contri-butions and provides benefits to the employee ofwhatever the contributions can finance. Employercontributions to both profit sharing and money pur-chase plans generally are limited to 15 percent ofemployee's compensation.

Corporations also may adopt defined benefitpension plans. These plans specify a pension of acertain size. Contributions based on the employ-ee's age and years of service provide the pensionfunding. These plans can be used to shelter largeamounts when the employee shareholders are old-er and more highly compensated. However, thecontributions are not based on business incomeand must be paid in bad years as well as in goodones.

Profit sharing, money purchase and definedbenefit plans may cover all employees or any des-ignated classification of employees provided theydo not discriminate in favor of officers, shareholdersor highly compensated employees. The plans canexclude employees under 25 years of age whohave not completed 1 year of service. Various alter-natives are available for the vesting of these bene-fits. However, the greatest length of time allowed forthe employee to acquire 100 percent vesting is 15years of service. For most small corporations signif-icantly more rapid vesting is usually required.

Corporate pension plans can be integrated withsocial security to provide greater benefits to em-ployees with higher salaries (above the social se-curity base level). Money purchase and profit shar-ing plans can be set up so that the salaries inexcess of the integration level (social security baseis the maximum level) will receive an allocationequal to 7 percent more than the base salaries. Forexample, assume a corporation with four employ-ees and total salaries as shown in Table 2 ($25,900integration level).

Employee A has $74,100 of salary in excess ofthe social security base. Seven percent of thisamount is $5,187. Employee S's excess is $24,100and a 7 percent contribution of that amount equals$1,687. Since only 15 percent of total compensa-tion can be sheltered (.15 x $185,000), the aggre-gate contribution cannot exceed $27,750. The bal-ance ($27,750 - $6,874 = $20,876) is proratedamong the four employees based on total compen-sation. Employee A is able to shelter an additional$1,471, S's contribution is $171 less, and C and Dtogether shelter $1,300 less than a straight 15 per-cent of compensation would provide.

Table 1. Characteristics of alternative retirement plans

Individual Retirement Simplified EmployeeAccount Pension Plan

Who can use Individual not actively par- Proprietorship, partnershipticipating in another qual- corporationified retirement plan

Maximum annual 15 percent of compensation 15 percent of compensationcontribution to $1,500 to $7,500

Eligibility Not applicable Each employee 25 yearsold who has worked 3 outof last 5 years

Vesting 100 percent 100 percent

Social Security inte- Not applicable Contributions for employeesgration can be reduced by employ-

er's social security liability

Income tax treatment Ordinary income Ordinary incomeon payout

Table 2. Compensation of pension contributions with integration with social security.

7 percentExcess Over of

Employee Compensation Integration Level Excess Balance Combined

A $100,000 $74,100 $5,187 $11,284 $16,471B 50,000 24,100 1,687 5,642 7,329C 20,000 0 2,257 2,2570 15,000 0 1,693 1,693

$185.000 $27,750

Profit sharing plans can be used in combinationwith money purchase plans and defined benefitplans. When combinations of plans are used, thetotal tax sheltered contribution can be greater thanwith any individual plan, but limitations are imposedto prevent the allowable contributions from totaling30 percent. Generally, a profit sharing plan with a15 percent contribution can be combined with amoney purchase plan requiring a 10 percent contri-bution. The total sheltered contribution could be 25percent of compensation. The limitations that applywhen defined benefit plans and money purch.aseplans are combined are more complex and beyondthe scope of this publication.

The Employee Stock Ownership Plan (ESOP) isa stock bonus plan or a combination of a stock

bonus plan and a money purchase plan. It is de-signed to invest primarily in employers' securitiesfor the benefit of the employees or their ben-eficiaries. The purpose of ESOP is to build equityownership of shares of the employer corporation forits employees in a non-discriminatory manner. Thededuction to an ESOP plan is limited to 15 percentof the compensation of the employees covered bythe plan. ESOP plans are advocated by some taxadvisors for their financial and estate planningcharacteristics.

The details of specific corporate retirementplans involve complex factors. The determination ofspecific annual contributions may require theservices of an actuary. The selection of a specifictype of plan or combination of plans depends upon

6

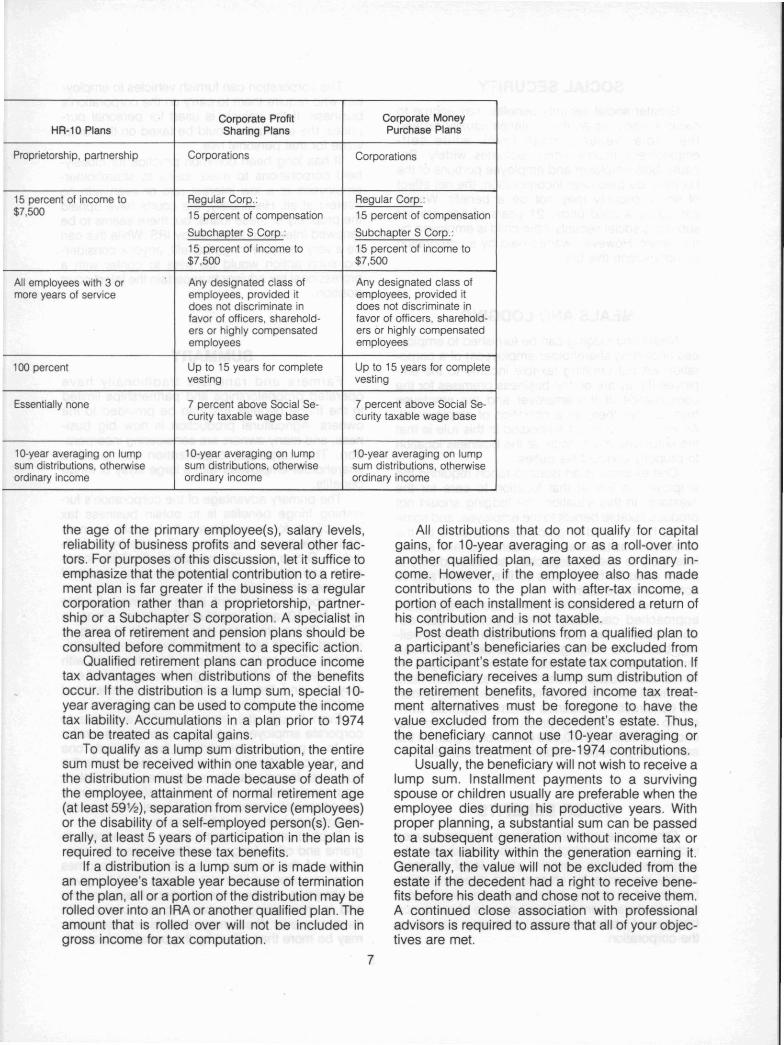

Corporate Profit Corporate MoneyHR-10 Plans Sharing Plans Purchase Plans

Proprietorship, partnership Corporations Corporations

15 percent of income to Regular Corp.: Regular Corp.:$7,500 15 percent of compensation 15 percent of compensation

Subchapter S Corp.: Subchapter S Corp.:15 percent of income to 15 percent of income to$7,500 $7,500

All employees with 3 or Any designated class of Any designated class ofmore years of service employees. provided it employees, provided it

does not discriminate in does not discriminate infavor of officers, sharehold- favor of officers, sharehold-ers or highly compensated ers or highly compensatedemployees employees

100 percent Up to 15 years for complete Up to 15 years for completevesting vesting

Essentially none 7 percent above Social Se- 7 percent above Social Se-curity taxable wage base curity taxable wage base

10-year averaging on lump 10-year averaging on lump 10-year averaging on lumpsum distributions, otherwise sum distributions, otherwise sum distributions, otherwiseordinary income ordinary income ordinary income

the age of the primary employee(s), salary levels,reliability of business profits and several other fac-tors. For purposes of this discussion, let it suffice toemphasize that the potential contribution to a retire-ment plan is far greater if the business is a regularcorporation rather than a proprietorship, partner-ship or a Subchapter S corporation. A specialist inthe area of retirement and pension plans should beconsulted before commitment to a specific action.

Qualified retirement plans can produce incometax advantages when distributions of the benefitsoccur. If the distribution is a lump sum, special 10-year averaging can be used to compute the incometax liability. Accumulations in a plan prior to 1974can be treated as capital gains.

To qualify as a lump sum distribution, the entiresum must be received within one taxable year, andthe distribution must be made because of death ofthe employee, attainment of normal retirement age(at least 591/2), separation from service (employees)or the disability of a self-employed person(s). Gen-erally, at least 5 years of participation in the plan isrequired to receive these tax benefits.

If a distribution is a lump sum or is made withinan employee's taxable year because of terminationof the plan, all or a portion of the distribution may berolled over into an IRA or another qualified plan. Theamount that is rolled over will not be included ingross income for tax computation.

7

All distributions that do not qualify for capitalgains, for 10-year averaging or as a roll-over intoanother qualified plan, are taxed as ordinary in-come. However, if the employee also has madecontributions to the plan with after-tax income, aportion of each installment is considered a return ofhis contribution and is not taxable.

Post death distributions from a qualified plan toa participant's beneficiaries can be excluded fromthe participant's estate for estate tax computation. Ifthe beneficiary receives a lump sum distribution ofthe retirement benefits, favored income tax treat-ment alternatives must be foregone to have thevalue excluded from the decedent's estate. Thus,the beneficiary cannot use 10-year averaging orcapital gains treatment of pre-1974 contributions.

Usually, the beneficiary will not wish to receive alump sum. Installment payments to a survivingspouse or children usually are preferable when theemployee dies during his productive years. Withproper planning, a substantial sum can be passedto a subsequent generation without income tax orestate tax liability within the generation earning it.Generally, the value will not be excluded from theestate if the decedent had a right to receive bene-fits before his death and chose not to receive them.A continued close association with professionaladvisors is required to assure that all of your objec-tives are met.

SOCIAL SECURITYGreater social security benefits may accrue to

owner-employees as their salaries usually exceedthe social security base level, while self-employment income often fluctuates widely. Be-cause both employer and employee portions of thetax must be paid after incorporation, the net effectof social security may not be a benefit. Wagesearned by a child under 21 years of age are notsubject to social security if the child is employed byhis parent. However, wages paid by a corporationdo not escape this tax.

MEALS AND LODGINGMeals and lodging can be furnished to employ-

ees (including shareholder-employees) of a corpo-ration without creating taxable income to the em-ployee if they are on the business premises for theconvenience of the employer and the employeemust accept them as a condition of employment.An important concept embodied in this rule is thatthe employee must reside at the business locationto properly conduct his duties.

One example is an isolated ranch requiring theemployee to live at that location to care for thelivestock. In this situation, the lodging should notproduce taxable benefit to the employee, and somecourts have included groceries purchased by thecorporation as tax exempt. A cash crop farm seemsless likely to qualify, especially as the tendency inmany areas is for farmers to live in town and tocommute to the farm.

Corporate ownership of a residence should beapproached cautiously. The corporation can de-duct depreciation and maintenance on the dwell-ing, but, if the lodging is not tax-exempt, the fairrental value will be taxable to the employee. Afarmer also must consider the future. At retirement,continued use of the corporate property may gener-ate constructive dividends to him. Corporate own-ership of the dwelling precludes the use of theonce-in-a-Iifetime $100,000 exclusion of gain on thesale of the principal residence by an individual.

OTHER BENEFITSOther fringe benefits to shareholder-employees

include company vehicles, membership dues, sub-scriptions to trade journals, group legal services,liability insurance for officers and directors, reim-bursement of moving expenses to a new job loca-tion, reimbursement for "loss" on sale of residencebecause of job transfer, and low interest loans fromthe corporation.

The corporation can furnish vehicles to employ-ees who require them to carry on the corporation'sbusiness. If the vehicle is used for personal pur-poses, the employee would be taxed on the rentalvalue for that personal use.

It has long been common practice for closely-held corporations to make loans to shareholder-employees at a low interest rate or even with nointerest at all. Historically, the courts have upheldthe propriety of these loans, but there seems to berenewed interest in this area by IRS. While this canbe a very valuable fringe benefit, anyone consider-ing such action would be wise to confer with aprofessional tax advisor to ascertain the latest courtposition.

SUMMARYFarmers and ranchers traditionally have

operated proprietorships and partnerships limitedin the fringe benefits that can be provided to theowners. Agricultural production is now big busi-ness, and many owners are considering incorpora-tion. The corporate organization can provideshareholder-employees with a large array of fringebenefits.

The primary advantage of the corporation's fur-nishing fringe benefits is to obtain business taxdeductions for expenditures that would be non-deductible personal expenses if made by an indi-vidual. Group term life insurance, disability insur-ance and medical plans are the most importantnon-pension benefits.

Corporate retirement plans are more flexiblethan HR-10 and Simplified Employee PensionPlans. Corporate plans can be profit sharing ordefined benefit which requires fixed annual contri-butions. Corporate plans can be integrated withsocial security to benefit higher compensated em-ployees, and the allowable annual tax-shelteredcontribution is higher under a corporate plan.

Even though the fringe benefits available tocorporate employees greatly exceed those availa-ble to a proprietor or partner, they are only onefactor to consider in the decision to incorporate thebusiness. Income tax consequences, estate plan-ning considerations, required formalities of corpo-rate organization and additional legal and account-ing expenses also must be considered.

Sophisticated retirement plans, insurance pro-grams and other fringe benefits increase the com-plexity of the business. As a business becomesmore complex, additional emphasis must be givento obtaining the services of specialized advisorsand to maintaining a continuing relationship withthem. However, these requirements and expensesmay be more than offset by the benefits obtained.

8

Educational programs conducted by the Texas Agricultural Extension Service serve people of all ages regardless of socio-economiclevel, race, color, sex, religion or national origin.

Cooperative Extension Work in Agriculture and Home Economics, The Texas A&M University System and the United States Departmentof Agriculture cooperating. Distributed in furtherance of the Acts of Congress of May 8, 1914, as amended, and June 30, 1914.5M - 3-81, New ECO 7-2