fertik chess feb. 2014

TRANSCRIPT

Globalizing Knowledge in a Deglobalizing World

Financial and Technological Expertise in the Global Steel Industry, 1925-1941

Paper presented at the “Knowledge Economies” Graduate Student Conference of

the Center for Historical Enquiry and the Social Sciences (CHESS)

Ted Fertik

Ph.D. Candidate

History Department

Yale University

February 14, 2013

1

Within economic history, an overwhelming consensus exists that across the long 19th

century the world economy became more integrated. “Globalization” was probably just as

pronounced in the years prior to 1914 as it was up until incredibly recently. The most powerful

evidence for this conclusion is shrinking price differentials between competing goods in distant

markets, and factor price convergence – that is, the observed tendency of the ratio of wages to

land prices to rise in countries that exported large quantities of labor power, and the inverse in

countries that imported it.1 Economic historians are unanimous that the interwar period and

especially the Great Depression represented a reversal of this trajectory, that it was a period of

“deglobalization.”2 This is a cautionary history. A nationalist and protectionist backlash against

globalization and in favor of “autarky” was in large part responsible for the economic

imperialism of the Third Reich and Imperial Japan. In a latter-day, backdoor resurrection of

classical liberal visions of commercial cosmopolitanism, economic history has demonstrated the

virtues of “openness” and the delusions of economic self-sufficiency.

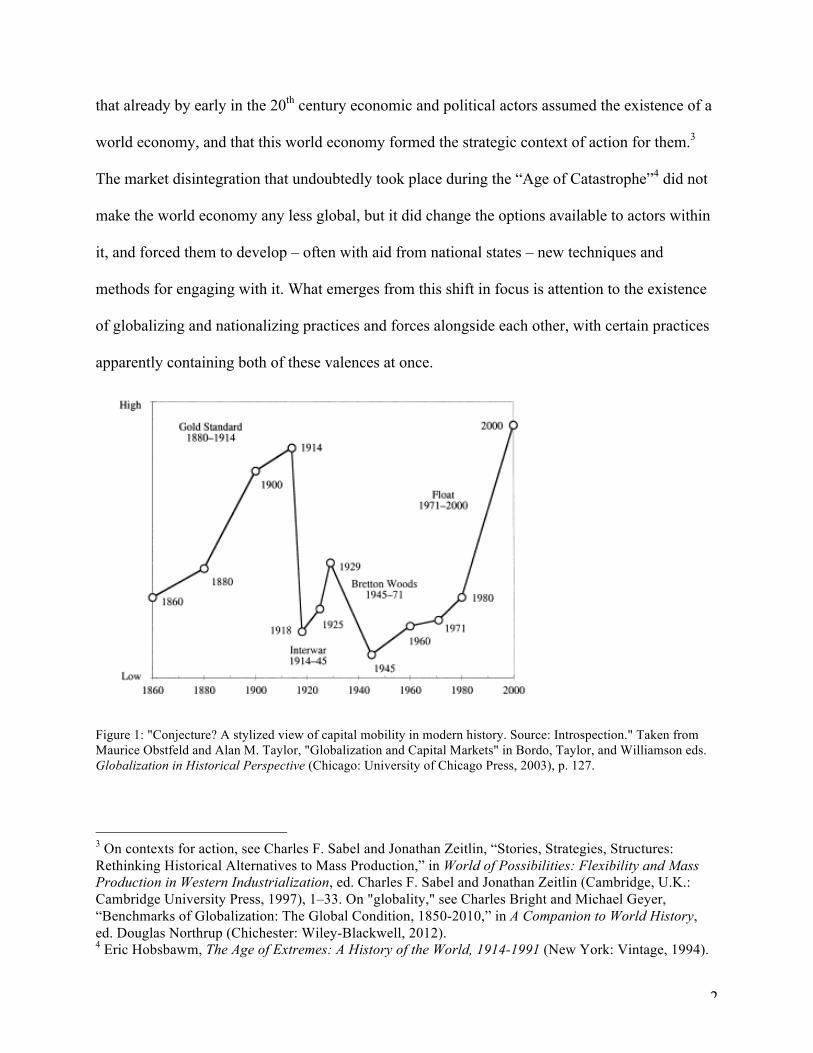

My research uses the history of the world’s steel industries between 1890 and 1950 to

deconstruct the economic history of globalization in the twentieth century, and put it back

together on grounds that are both empirically rich, and theoretically suppler. It moves away from

a simple “up-down-up” (see Figure 1) history of globalization, to one that identifies shifting and

overlapping modalities of globalization and charts their development. My major premises are

Thanks to Mara Caden and Kristin Plys for organizing the conference at which this paper was presented. Thanks to Naomi Lamoreaux and Adam Tooze for helping to steer the research to this point, and to Jeremy Kessler for comments of previous formulations of some of the ideas presented here. Thanks to Stefan Eich for help with German translations. 1 This is the test of the neoclassical Heckscher-Ohlin Theorem proposed and tested in Kevin H O’Rourke and Jeffrey G Williamson, Globalization and History: The Evolution of a Nineteenth-Century Atlantic Economy (Cambridge, Mass: MIT Press, 1999). 2 For a recent survey which expresses the current consensus, see Ronald Findlay and Kevin H. O’Rourke, Power and Plenty: Trade, War, and the World Economy in the Second Millennium, Princeton Economic History of the Western World (Princeton, N.J.: Princeton University Press, 2007).

2

that already by early in the 20th century economic and political actors assumed the existence of a

world economy, and that this world economy formed the strategic context of action for them.3

The market disintegration that undoubtedly took place during the “Age of Catastrophe”4 did not

make the world economy any less global, but it did change the options available to actors within

it, and forced them to develop – often with aid from national states – new techniques and

methods for engaging with it. What emerges from this shift in focus is attention to the existence

of globalizing and nationalizing practices and forces alongside each other, with certain practices

apparently containing both of these valences at once.

Figure 1: "Conjecture? A stylized view of capital mobility in modern history. Source: Introspection." Taken from Maurice Obstfeld and Alan M. Taylor, "Globalization and Capital Markets" in Bordo, Taylor, and Williamson eds. Globalization in Historical Perspective (Chicago: University of Chicago Press, 2003), p. 127.

3 On contexts for action, see Charles F. Sabel and Jonathan Zeitlin, “Stories, Strategies, Structures: Rethinking Historical Alternatives to Mass Production,” in World of Possibilities: Flexibility and Mass Production in Western Industrialization, ed. Charles F. Sabel and Jonathan Zeitlin (Cambridge, U.K.: Cambridge University Press, 1997), 1–33. On "globality," see Charles Bright and Michael Geyer, “Benchmarks of Globalization: The Global Condition, 1850-2010,” in A Companion to World History, ed. Douglas Northrup (Chichester: Wiley-Blackwell, 2012). 4 Eric Hobsbawm, The Age of Extremes: A History of the World, 1914-1991 (New York: Vintage, 1994).

3

This paper takes up two such practices in the interwar period. The first centers on the

great boom in international capital flows of the second half of the 1920s. What at first blush

looks like a classic globalizing practice – the floating of medium- and long-term securities on

foreign markets for productive purposes – emerges through the diaries of the American

investment banker Ferdinand Eberstadt as one existing in uncomfortably close proximity with

nationalist or even imperialist projects. The second practice considered is the planned

rationalization or construction of steel mills across the world between the 1920s and early 1940s,

all of which counted active state involvement. What at first blush looks like a classic

nationalizing practice – state-supported investment in an import-competing strategic industry –

emerges through the career of the American engineer Hermann Brassert, who was implicated in

each of these projects, as part of a dramatic globalization of technical knowledge and of

industrialization itself. In the cases of both Eberstadt and Brassert, specialized knowledge –

expertise – was an important factor in why these men occupied strategic positions in specific

global networks of finance and engineering, as their expertise was necessary to facilitate global

flows of capital and technical knowledge. In both cases, they considered themselves innocent of

attachment to any overtly political project in the countries in which they worked. But both found

themselves entangled in politically charged contestations over what the relationships between

national power and economic life should be.

I proceed in four parts. The first provides historical and institutional context for the spree

of American lending to foreigners in the 1920s, and of trends in the steel industry in the 20s and

30s. The second surveys both men’s careers and demonstrates the ways in which their particular

forms of expertise facilitated transnational flows of capital and technical knowledge. The third

takes up specific projects in which these two men were implicated – separately and together –

4

and the complex political struggles in which they became inadvertently (and sometimes

unknowingly) entangled. The fourth section concludes.

I.

American financiers bounded onto the world stage after World War I. American

financing of the European belligerents had radically reversed the country’s traditional position as

an importer of European capital. The war also accelerated the country’s transition from a net

importer of foreign goods to a net exporter. American financiers had already begun to undertake

portfolio investments in foreign governments and enterprises before World War I, but on a small

scale. The U.S. Treasury’s Liberty Bond program had acclimatized many American households

to investing their savings in securities. After the war, American bankers began looking for

foreign clients. Foreign governments and firms, meanwhile, finding European financiers in no

position to offer long-term loans on anything but wretched terms, also began looking to the

American capital market for support. With the yields on foreign bonds consistently higher than

their domestic counterparts, foreign bonds became an attractive investment vehicle for

prosperous American households. The market grew slowly until the 1923-1924 stabilizations of

Central Europe currencies and economies following the hyperinflations, and then surged once

the Dawes Loan convinced market watchers that Europe was on a path to reconstruction and

reintegration into the global circuits of trade and investment. With some ebbing and flowing, the

boom continued until a worldwide decline in agricultural prices combined with the beginnings of

the industrial depression in 1928 and 1929 caused a collapse in many countries’ foreign

exchange position and thus to a wave of defaults, especially in Latin America.5

5 Barry Eichengreen, “The U.S. Capital Market and Foreign Lending, 1920 – 1955” in Jeffrey D. Sachs ed. Developing Country Debt and Economic Performance, Volume 1: The International Financial System

5

The practices of the sales organizations and securities affiliates of commercial banks

came in for significant scrutiny after millions of Americans lost their savings to foreign defaults.

But the real action in the capital markets was then, as it is now, with the investment banks, who

functioned as financial intermediaries between borrowers and investors. Following Marc

Flandreau and his co-authors, it is possible to think about investment banks as offering their

clients a “structured product,” which included planning, placement, and post-issue support and

performance.6 Investment banks competed with each other to underwrite issues for prestigious

clients on the basis of the overall package of services they provided, which included the fees they

would charge and the price at which the bonds would sell, the length of the maturity, and the

value of the post-issue support that they provided. Potential clients carefully considered firm

reputations when deciding which banks to choose from, and were often willing to pay a premium

price to work with a more prestigious bank, on the grounds that this would ensure the successful

marketing of the bond issue, with insurance in case something went wrong. In an era when

ratings agencies had a purely private role, and the U.S. government exercised almost no

regulation over securities issues, the space occupied by investment banks in the issuance of

securities was largely than it is today.

Investment banks made their money by charging commissions on bond issues. Their goal

was to bring to market as many bond issues for which they could reliably hope to find buyers.

Since the money was in the underwriting, and demand among American investors for foreign

(Chicago: University of Chicago Press, 1989), pp. 107-156; Albert Fishlow, “Lessons from the Past: Capital Markets During the 19th Century and the Interwar Period,” International Organization 39, no. 3 (July 1, 1985): 383–439; Cleona Lewis, America’s Stake in International Investments (Washington, D.C: The Brookings Institution, 1938). 6 Marc Flandreau, Juan H. Flores, Nobert Gaillard and Sebastián Nieto-Parra, “The Changing Role of Global Financial Brands in the Underwriting of Foreign Government Debt (1815-2010).” Graduate Institute of International and Development Studies Working Paper No: 15-2011 (2011). See also Flandreau, Gaillard, and Ugo Panizza, “Conflicts of Interest, Reputation, and the Interwar Debt Crisis: Banksters or Bad Luck?” SSRN Scholarly Paper, No. 1588031 (2010).

6

bonds was strong, there was substantial competition among investment banks for foreign clients,

whether municipal, state and national governments, or business corporations. In this context, the

investment banks had to have agents – either direct employees, or commission brokers of some

sort – present overseas in order to identify business opportunities, develop the relationships

necessary to win the business, and, assuming that any given borrower is likely to go to the trough

more than once, maintain those relationships over time.7 This is the role Ferdinand Eberstadt

played for the investment house of Dillon, Read & Co. between 1925 and 1928.

The innovators whose names we associate with the arrival of modern metallurgy –

Bessemer, Thomas-Gilchrist, Siemens – made their mark in the 1860s and 1870s. By the 1920s

and 1930s iron and steel was considered an “old” industry as compared to chemicals and

electrical engineering. And yet there was significant innovation during the interwar period. In the

1920s total factor productivity in U.S. primary metals increased by 5.5% annually, beating the

spectacular manufacturing-wide average of 5.3%.8 The 1920s saw the introduction of the

continuous rolling mill for wide strip, which one author has called “without doubt the most

important advance[] in rolling-mill technology in the first half of the twentieth century.”

Techniques for substituting scrap metal for pig iron in steelmaking were becoming widespread.

Engineers were rapidly improving their ability to capture and utilize byproducts gasses from

blast furnaces and coke ovens, all of which improved fuel efficiency. Numerous varieties of alloy

steels requiring metals like tungsten, nickel and manganese were finding commercial uses.9 Iron

and steel manufacturing was among the largest users of labor and capital in all of the major 7 George W. Edwards, Investing in Foreign Securities (New York: The Ronald Press Company, 1926), 74–75. 8 John W. Kendrick, Productivity Trends in the United States (Princeton, N.J.: Princeton University Press/NBER, 1961), 136. 9 Tyler Priest, Global Gambits: Big Steel and the U.S. Quest for Manganese (Praeger, 2003).

7

industrialized countries, and steel corporations – most famously the United States Steel

Corporation – ranked as the largest corporate agglomerations in the world.

In the 1920s and 1930s the trend in steelmaking was, as it had been for several previous

decades, towards vertical integration, and to a certain extent towards horizontal integration as

well, although by this time the industry had generally settled into an oligopolistic pattern, with

the fear of an outright U.S. Steel monopoly largely dissipated. Steel in the U.S. in particular was

adapting to new market conditions, with automobiles surpassing railroads and construction as the

major final consumers of finished steel.10 Even if the most exciting technological advances were

happening elsewhere, still steel was practically synecdoche for industrial modernity in much of

the world.11 It had perhaps not yet even reached its summit in terms of the connections it

established between a productive regime and forms of social organization: as Charles Maier has

evocatively suggested, as late as the 1950s, “the integrated wide-band steel mill, in which coal

and ore arrived at one end and wire, plate, and castings emerged at the other . . . [were like]

Etnas of industry that symbolized modernity.”12 And after the experience of industrial warfare

during the Great War it became a crucial factor in calculations of national security in old and

new countries alike. This increase in steel’s importance coincided with technological

10 Thomas J. Misa, A Nation of Steel: The Making of Modern America, 1865-1925 (Johns Hopkins University Press, 1995). The relatively slower growth of the automobile industry in Germany and especially Britain is a large part of the explanation for the slower rates of innovation in the British steel industry relative to the U.S. Steven Tolliday, Business, Banking, and Politics: The Case of British Steel, 1918-1939 (Cambridge, MA: Harvard University Press, 1987). 11 Stephen Kotkin, Magnetic Mountain: Stalinism as a Civilization (Berkeley: University of California Press, 1997), 31–33. 12 Charles S Maier, Among Empires: American Ascendancy and Its Predecessors (Cambridge, Mass: Harvard University Press, 2006), 197. See also Charles S. Maier, “Consigning the Twentieth Century to History: Alternative Narratives for the Modern Era,” The American Historical Review 105, no. 3 (Jun., 2000), pp. 821–822., doi:10.2307/2651811. For Maier, steelmaking is the supreme expression of the “territories of production” which dominated political and economic life from the 1860s through to the 1970s. For Maier’s attempt to incorporate this concept into a long-run history of the nation state, see “Leviathan 2.0: Inventing Modern Statehood,” in A World Connecting: 1870-1945, ed. Emily S. Rosenberg (Harvard University Press, 2012), pp. 29–282.

8

developments – including those mentioned above – which lessened the extent to which large

domestic deposits of coal and iron ore were necessary to erect a cost-effective steelmaking

industry.13 As a result governments and private entrepreneurs in many parts of the world began

to devote significant energy to developing a modern steelmaking industry within their borders.

Lastly, in an era before the widespread use of national income accounting, the health of the steel

industry was often used as shorthand for the health of the economy as a whole.

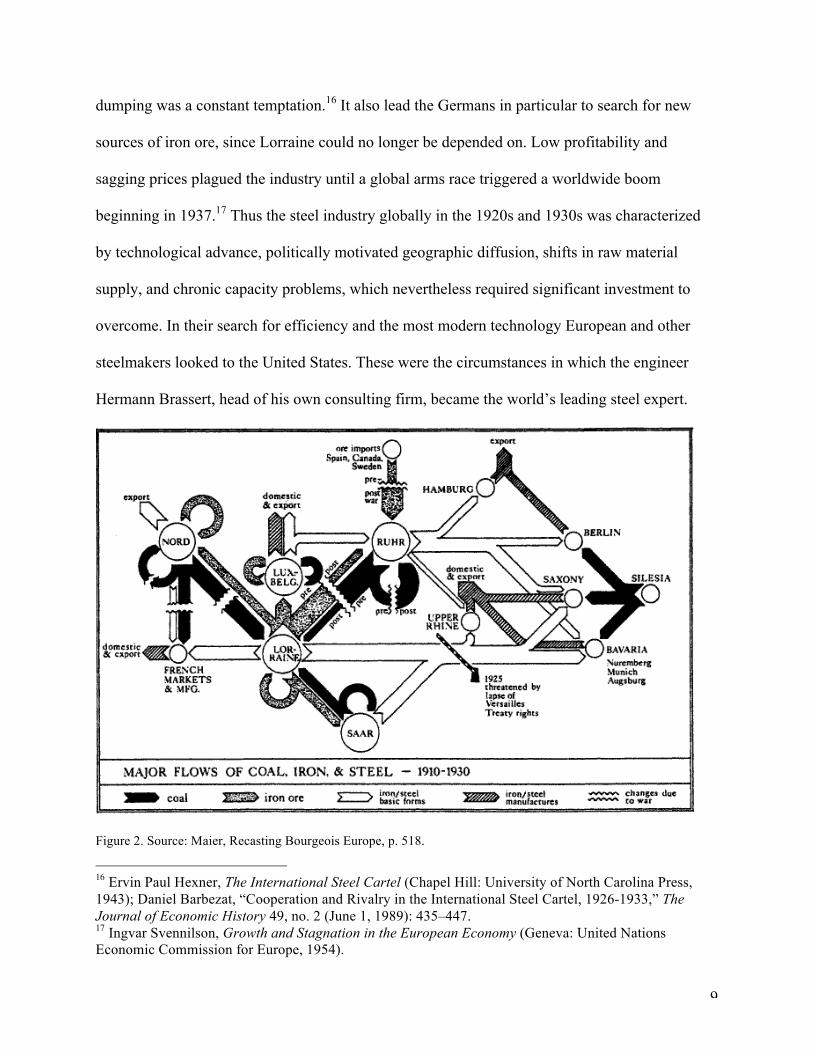

The iron and steel industries of Europe had suffered significant dislocation as a result of

the Versailles treaty, in particular the ceding of Lorraine to France and the division of Upper

Silesia between Germany and the new Polish Republic. (See Figure 2) During the inflation

period German industrialists, with Hugo Stinnes in the lead, had built up vast conglomerates and

also undertaken significant investments in new plant, in order to make up for capacity lost to

France. When stabilization came in 1924, the industry found itself saddled with excess capacity,

which put significant downward pressure on world prices.14 “Rationalization” – short for

capacity reduction under Malthusian conditions – quickly became the order of the day, in

Germany and in Britain.15 For all of the European producers, steel exports were a crucial

component of the balance of payments and a vital support of the restored gold standard. Thus

finding ways to prevent export prices from dropping became a cross-national concern. This

problem was made all the more exigent by the large war debt and reparations overhang weighing

down European economies, especially Germany. In 1926 this led to the formation of the

International Steel Cartel, whose purpose was to keep export prices high in a context where

13 Wilhelm Röpke, International Economic Disintegration (W. Hodge and Company, Limited, 1942). 14 Alfred Reckendrees, “From Cartel Regulation to Monopolistic Control? The Founding of the German ‘Steel Trust’ in 1926 and Its Effect on Market Regulation,” Business History 45, no. 3 (Sept., 2003), pp. 22–51, doi:10.1080/713999324. 15 Charles S Maier, “Between Taylorism and Technocracy: European Ideologies and the Vision of Industrial Productivity in the 1920s,” in In Search of Stability: Explorations in Historical Political Economy (New York: Cambridge University Press, 1987).

9

dumping was a constant temptation.16 It also lead the Germans in particular to search for new

sources of iron ore, since Lorraine could no longer be depended on. Low profitability and

sagging prices plagued the industry until a global arms race triggered a worldwide boom

beginning in 1937.17 Thus the steel industry globally in the 1920s and 1930s was characterized

by technological advance, politically motivated geographic diffusion, shifts in raw material

supply, and chronic capacity problems, which nevertheless required significant investment to

overcome. In their search for efficiency and the most modern technology European and other

steelmakers looked to the United States. These were the circumstances in which the engineer

Hermann Brassert, head of his own consulting firm, became the world’s leading steel expert.

Figure 2. Source: Maier, Recasting Bourgeois Europe, p. 518.

16 Ervin Paul Hexner, The International Steel Cartel (Chapel Hill: University of North Carolina Press, 1943); Daniel Barbezat, “Cooperation and Rivalry in the International Steel Cartel, 1926-1933,” The Journal of Economic History 49, no. 2 (June 1, 1989): 435–447. 17 Ingvar Svennilson, Growth and Stagnation in the European Economy (Geneva: United Nations Economic Commission for Europe, 1954).

10

II.

The new conditions on the American capital market created an opening for upstart

bankers. In the go-go years of the New Era, no financial star shined brighter than Clarence

Dillon. The son of Polish Jews, born in Texas but educated at Harvard, a banker “by accident,”

and then even more accidentally an assistant to Bernard Baruch at the Paris negotiations, Dillon

was a brilliant and enigmatic man. He had been brought in as a partner at the old but not

especially important Wall Street house of William A. Read & Co., and then, after Read’s death,

was rapidly chosen by the firm’s partners to lead it himself. As early as 1921 he was making

major moves on foreign markets, as he elbowed his way into the senior position into a loan to the

Brazilian government jointly underwritten by Dillon, Read and the Rothschilds of London. The

Rothschilds had been the exclusive international bankers of Brazil since the 1870s, but they

accommodated themselves to the new realities.18

Dillon, Read undertook massive investments in Latin America. But the biggest prize of

the 1920s was undoubtedly Germany. Traditionally an importer exporter of capital, and saddling

a massive reparations burden that might have been a deterrent to would-be creditors, Germany

between 1924 and 1929 became the world’s international debtor, with American capital the

source close to 50% of the roughly $4 billion in purely private capital inflows (that is, exluding

the Dawes and Young loans),19 of which $1,239,031,500 were publicly offered bonds.20 Had

they wanted to, leading bankers J. P. Morgan & Co. likely could have occupied the premier

18 See the 1921 correspondence regarding Dillon, Read’s impressive rise between the London Rothschilds and Kuhn, Loeb in the Rothschild and Brazil Online Archive, XI/111/409, http://www.rothschildarchive.org/research/letters/brazil. 19 Charles H. Feinstein and Katherine Watson, “Private International Capital Flows in Europe in the Inter-War Period,” in Banking, Currency, and Finance in Europe Between the Wars, ed. Charles H. Feinstein (Oxford: Oxford University Press, 1995), p. 117. 20 Robert R. Kuczynski, Bankers’ Profits from German Loans (Washington, D.C: The Brookings institution, 1932), 6.

11

position in German financing. But Morgans had lead the mobilization of American finance

behind the Entente war effort, and so counted few German friends. Jack Morgan himself made

no secret of his dislike for the German people. Dillon, Read stepped onto this open field, and

quickly established itself as the leading international bankers doing business in the Weimar

Republic. By 1930 the firm had underwritten some $252 million in German bond issues, more

than any other American investment bank.21

One of the key elements of Dillon’s European and especially his German strategy was the

young lawyer Ferdinand Eberstadt. A 1913 graduate of Princeton, where he was a classmate of

later Dillon, Read president James Forrestal, Eberstadt was an up-and-comer in the Wall St. law

firm of McAdoo, Cotton & Franklin. He was the descendent of German Jews, the first cousin of

Kuhn, Loeb chief Otto Kahn, fluent in German and French, and exceptionally ambitious. Dillon,

Read became one of his major clients, and he advised the firm on some of its most important

domestic deals of the early 1920s, including the financing of the Goodyear Tire company. As a

brilliant young lawyer who had studied in Germany and spoke German, Dillon employed

Eberstadt as his adviser in negotiations over the loan that decisively cleared the path for

American capital to invest in German private industry – the famous $12,000,000 August Thyssen

Iron and Steel Works bond issue of 1925. Accepting Dillon’s offer to move from law to

investment banking, Eberstadt officially joined the firm in late 1925 and took over direct

responsibility for the its European business. In taking on this role, he situated himself in a

strategic position within an exceedingly complex set of political, economic, social, and technical

21 Sale of Foreign Bonds or Securities in the United States (Washington, D.C: GPO, 1932), 501.

12

networks that together would determine the fate of German democracy and the world economic

system.22

The role of financial intermediary that Dillon, Read and especially Eberstadt played was

one that depended on the production of specific forms of knowledge and information. On the one

hand, what the banks offered to their clients was their ability to market bond issues in a foreign

capital market about which the clients knew very little but the bankers knew a great deal. The

bankers’ leverage in negotiations was thus their ability to say what investors would and would

not buy in the U.S. Such knowledge was often proprietary since it was the result of private

conversations that the investment banks had with their customers and co-underwriters. On the

other hand, what the banks offered to the American buying public was their conviction – on

which their reputation stood – that the bonds were good securities worthy of being purchased,

and to do this the investment banks, and Dillon, Read in particular, invested substantial funds in

collecting various kinds of information that would ultimately be brought together in the bond

prospectus. As Clarence Dillon summarized to the Senate Finance Committee:

economic condition is inquired into quite carefully, the history of the company is gone into from its inception. Their accounts, by their own accountants, are examined for years back. Then . . . firms in America . . . are put on the books by us, and check their audits, and make their own independent audits . . . We go further into the question of where their products are sold, particularly with the idea of their being able to pay in foreign exchange, in dollars. We check up the company and see what proportion of its product is sold abroad for which they are paid in foreign currency . . .; the debts, if any, of the company, the record of dividends, and a complete and most thorough investigation is made from the inception of the company.23

Dillon did not mention that the firm also hired technical experts such as Brassert to conduct

details studies not just of exports but of plant facilities and operations, raw materials supplies, 22 Robert Sobel, The Life and Times of Dillon Read (New York: Truman Talley Books/Dutton, 1991); Robert C. Perez, The Will to Win: A Biography of Ferdinand Eberstadt (Westport, Conn: Greenwood Press, 1989); Jeffery M. Dorwart, Eberstadt and Forrestal: A National Security Partnership, 1909-1949 (College Station: Texas A&M University Press, 1991). 23 Sale of Foreign Bonds or Securities in the United States, 456–457.

13

and management culture. As one can easily imagine, investments in systems for collecting

knowledge help give an element of path dependency to institutional relationships. Once Dillon,

Read had successfully brought out issues for German industrial securities in 1925 and 1926, its

reputation in this line of work grew, as American investors considered Dillon, Read a

knowledgeable source on German affairs, and German businessmen and government officials

considered Dillon, Read a knowledgeable source on American markets. Success enhanced the

firm’s reputation, and an enhanced reputation lead to more business.

Eberstadt was a crucial link in this network, and his daily activities give an indication of

how he made it work. His diaries from 1926 and 1927 show him moving constantly between

meetings of industrialists, German and foreign bankers, and government officials in both

Germany and France. These meetings ranged from direct negotiations over the terms of a loan, to

more open-ended discussions about the possibilities of future business, to intelligence gathering

about political conditions in Europe and their bearing on economic prospects. It was Eberstadt’s

ability to navigate these choppy economic and political waters that enabled him to be successful

in making Dillon, Read the most important American investment bank in Germany in the 1920s.

When prominent foreigners – like German Chancellor Gustav Stresemann – questioned whether

such a young firm was fit to compete with the likes of Morgan, Eberstadt proudly bragged of the

firm’s leadership in German financing.24 In this Eberstadt’s most important relationships were

with several of the dominant figures in the German steel industry, especially Fritz Thyssen,

Alfred Vögler, Otto Wolff, and Friedrich Flick of the Vereinigte Stahlwerke. What the history of

these relationships show is that, when politics and economics are intertwined in certain ways,

international capital movements even between purely private actors can have far-reaching 24 Eberstadt to Clarence Dillon, Nov. 20 1926. “Dillon, Clarence”, Box 47, Ferdinand Eberstadt Papers, Department of Rare Books and Special Collections, Princeton University Library; Sobel, The Life and Times of Dillon Read, 106–110.

14

political consequences. Dillon, Read entered the European fold in the wake of the Dawes Plan

and in the “spirit of Locarno.”25 It left having helped strengthen reactionary nationalist forces

within Germany, although this had never been the firm’s purpose in European business.26

Born in Britain and trained at a technical institute in Germany, Hermann Alexander

Brassert chose to make his career in the U.S., where he worked first as an assistant to the world-

famous Julian Kennedy at the Edgar Thomson works of Carnegie Steel before becoming the

head of the blast furnace department at the Chicago South Works of the Illinois Steel Co., one of

the largest subsidiaries of the United States Steel Corporation. By 1914 he was recognized as one

of the country’s leading authorities on blast furnaces. His Germanic name and German

connections led many contemporary and subsequent authors to confuse him for a German

national. Nevertheless he was indeed “one of the most important figures in German-American

steel relations.”27 Steel manufacture is first and foremost a chemical process, and the blast

furnace is where the most basic, but most important chemical reaction – the smelting of iron ores

into solid or “pig” iron – takes place. Success in blast furnaces is a question of consistency and

economy: one wants a metallic product that is reliably the same each time. The key to this

success is for the construction and operation of the furnace to be tailored to the specific inputs

that enter into it. Coal, iron ore, and limestone, the basic inputs of the smelting process, are found

in nature in widely varying forms, with all manner of impurities. Sometimes fuels and ores are

25 Patrick O. Cohrs, The Unfinished Peace after World War I: America, Britain and the Stabilisation of Europe, 1919-1932 (Cambridge, UK: Cambridge University Press, 2006). 26 For a trenchant critique of the ultimately destructive consequences of American loans to Germany, see Stephen A. Schuker, American “Reparations” to Germany, 1919-33: Implications for the Third-World Debt Crisis (Princeton, N.J: International Finance Section, Dept. of Economics, Princeton University, 1988). 27 Jeffrey R. Fear, Organizing Control: August Thyssen and the Construction of German Corporate Management (Harvard University Press, 2005), 504. Fear is one of those who mistake Brassert for a German.

15

naturally well adapted to human demands on them; more often they are not, and much of the real

technical skill that goes into steelmaking is adjusting the basic processes to the peculiarities of

the raw materials on offer. Hermann Brassert’s career was made by the fact that many people

wished to make finished steel on the basis of iron ores that were suboptimal in one way or

another. He made himself an expert in designing blast furnaces that could accommodate these

otherwise unaccommodating materials. As he put it in an important 1914 paper, “Our problem . .

. is to reclaim and put to use those vast bodies of ore and coal which, owing to their adverse

character, have in the past not been available for the manufacture of iron.”28 Whether or not a

country could successfully produce steel depended on whether the raw materials available to it

could be economically combined, a question which only a handful of individuals in the world

were expert to answer. Over the next 25 years, Brassert would deploy this very special expertise

to nationalist steel projects all across the globe.

The demand for Brassert’s services demonstrates some of the ways in which

globalization and national power intersected in the 1920s and 1930s. In the first place, blast

furnace practice was a domain of technical knowledge in which innovations were rarely

proprietary.29 Engineers frequently participated in formal discussions within professional

organizations that published and distributed their papers, for example the American Society of

Mechanical Engineers. It was, nevertheless, a remarkably site-specific process, conforming very

much to the picture painted by Richard Nelson and Gavin Wright of a knowledge that was “local

and incremental, building from and improving on prevailing practice.”30 Thus the accounts of

28 Hermann A. Brassert. Modern American Blast Furnace Practice (New York, 1914), p. 56. 29 Robet C. Allen, “Collective Invention,” Journal of Economic Behavior and Organization 4 (1983): 1–24. 30 Richard R. Nelson and Gavin Wright, “The Rise and Fall of American Technological Leadership: The Postwar Era in Historical Perspective,” Journal of Economic Literature 30, no. 4 (Dec., 1992): p. 1935. Nelson and Wright offer the only account with which I am familiar that attempts to explain why it is

16

their practice that engineers like Brassert published were anything but manuals. Instead they

were narrative, descriptive, and gave evidence of extraordinary amounts of trial and error,

especially in adapting to new raw material sources. The international economic conditions of the

1920s and 1930s, combined with technological changes in steelmaking, meant on the one hand

that many existing producers were increasingly interested in using materials close at hand,

whereas they might previously have been content to import the highest quality materials

available on international markets; and that many countries which previously had had at most

tiny or backward steel industries were looking to create new, modern ones on the basis of

whatever raw materials they happened to possess, at whatever quality. The expertise that these

producers were seeking, then, was the ability to draw up plans for how to manufacture finished

steel out of whatever raw materials those producers wished to utilize. Brassert was given credit

for adapting American blast furnaces to the iron ores of the Mesabi range around Lake Superior,

an innovation which catapulted the U.S. ahead of Britain and Germany in blast furnace

productivity.31 In the 20s, 30s and early 40s he was called on to use these abilities in Britain,

Germany, Russia, Turkey, Manchuria, South Africa, Argentina, Brazil, Peru, and Ecuador, and

possibly more.

III.

As Steven Tolliday’s exceptional 1987 study demonstrated, there was very little in the

nature of product markets, raw material supplies, inter-firm competitive conditions, or labor

supply that would have conduced to prosperity for the British steel industry in the interwar

logical that technological communities should have been primarily national in the late-19th and early-20th centuries. But it is not altogether convincing. 31 Robert C. Allen, “International Competition in Iron and Steel, 1850-1913,” The Journal of Economic History 39, no. 4 (December 1, 1979): 911–937.

17

period. But considering the amount of capital invested in the industry, the amount of labor it

employed, and its close connections to higher value-added sectors like engineering and

shipbuilding, from the late 1920s the British government and the Bank of England devoted

considerable attention to the industry’s health, championing rationalization as a catchall solution

to the industry’s ills. To translate “rationalization” into actual schemes for the industry’s

renewal, Bank of England officials and the executives of a number of British steel firms turned

to Brassert. Tolliday and others have covered Brassert’s myriad proposals in detail, so I will just

briefly summarize. Brassert was brought in to propose plans for the rationalization of the

Scottish steel industry; a “regionalization” scheme that would have reorganized all of British

steelmaking into a set of six discrete regional units each with its own specialization; and by

individual firms (Stewart & Lloyds, Richard Thomas, United Steel, and by a syndicate of

financiers interested in redeveloping a part of the north Midlands steel industry) to design

proposals for future investment. Several things stand out about these proposals. First, Brassert

always proposed something more ambitious than his clients had thought they wanted. Second,

his proposals recommended the use of the most modern technologies for processing difficult raw

materials, most of which had never been attempted in Britain. And third, he insisted again and

again “that the best-practice modern plant had to be a fully integrated chain of processes running

from ore docks to finished products.”32

Most of Brassert’s British proposals came to nothing. But one of them was a triumph. In

1932 Stewarts & Lloyds, Britain’s leading tube steel manufacturers, hired Brassert to investigate

whether the firm could profitably make steel from the large ironstone deposits it owned in

Northhamptonshire. [duplex process] From the firm’s London office, Brassert’s engineers

supervised construction of the new integrated best-practice plant. It was built at breakneck speed, 32 Tolliday, Business, Banking, and Politics, 103.

18

and its successful operation was celebrated in the British press. Corby demonstrated that modern

scientific experience created the possibility of erecting plants ex novo. In a context in which

foreign raw material supplies seemed less reliable and export markets were under threat, and

British firms felt an increasing need to utilize domestic resources and produce for a domestic

market, Corby demonstrated a case of international technology transfer in the service of domestic

competitiveness.

Brassert’s success at Corby created an even greater demand for his services. In 1936

Turkey’s semi-official industrial development bank contracted a deal with the British Export

Credit Guarantee Department to develop an integrated steel mill at Karabük, and Brassert’s firm

was brought in to design and oversea construction of the plant, with the ECGD providing £3

million in financing.33 Japanese businessmen looking to develop the mineral resources of their

economic colony in Manchuria and interested in enlisting American capital in the effort brought

Brassert to Manchuria in 1938 to study their iron ore deposits and propose plans for enlarging the

Showa steel mill in Anshan.34 Both of these projects were central to visions of the planned

industrialization of what were thought to be economically backward countries, and both

associated steel closely with sovereignty. The fact that one (Turkey) was conceived explicitly as

a defense against future domination by outsiders, and the other (Manchuria) was the expression

of one of the purest forms of economic imperialism in the 20th century demonstrates the close

link between steel, territoriality, and sovereignty in the 20th century, at the same time as it

demonstrates the indeterminateness with respect to politics of such a logic of territoriality.

33 “Draft Agreement and draft letter regarding Iron and Steel for Turkey. H. A. Brassert & Co. Ltd.” BT 103 (Export Credit Guarantee Department)/183, UK National Archives, Kew; Yücel Güçlü, “Turco-British Relations on the Eve of the Second World War,” Middle Eastern Studies 39, no. 4 (Oct., 2003), p. 173. 34 Haruo Iguchi, Unfinished Business: Ayukawa Yoshisuke and U.S.-Japan Relations, 1937-1953 (Cambridge, MA: Harvard University Press, 2003), 67. United States Foreign Economic Administration, Far East Enemy Division, Iron Ore: Manchuria (Washington, DC: GPO, 1944).

19

Most importantly, and most controversially, Brassert’s Berlin office was hired to develop

plans for one of the centerpieces of the Third Reich’s Four Year Plan autarky drive, the

establishment of a new iron and steel complex based on low-grade iron ores around Salzgitter in

Saxony. German steelmakers were well acquainted with Brassert, and with the Corby works.

There does not appear to have been any question that Brassert would be hired to design the

massive works at Salzgitter, and in particular the blast furnaces in which the low-iron, high-

sulfur ores would be smelted.35 Brassert could not have been unaware of the connection between

the construction of the Reichswerke “Hermann Göring” and Hitler’s rearmament drive: in

February and March of 1939 he published an extensive two-part summary on American and

European experiences using difficult ores (in which he figures as a central character) in the

official journal of the Four Year Plan, with frontispiece inscriptions from Hitler and Göring on

the need to maximize the utilization of the domestic Lebensraum and for high production to

defend the German people.36 Nevertheless Brassert studiously avoided the appearance of any

political dimension to his work. Instead he held out his career as evidence of the ability of

science, ingenuity, and practical experience to surmount practical problems in industry:

The proper management of a blast furnace operation, especially with difficult fine ores, lies principally in immediately recognizing production opportunities and sustaining them with ironclad energy, irrevocably and with great regularity. This is only possible when similar raw materials are provided in the greatest uniformity through appropriate mixtures and other means. The decision for a particular coke quality, burden, charge, slag operation, blast temperature, blast volume, and correctly timed intervention in the operation, all of this depends not only on experience but also on the correct feeling for the processes in the blast furnace itself, and will always remain as much an art as an exact science.37

35 Adam Tooze, The Wages of Destruction: The Making and Breaking of the Nazi Economy (New York: Penguin, 2006), 235–239; August Meyer, Hitlers Holding.: Die Reichswerke “Hermann Göring”. (Europa Verlag GmbH, 1999), 85–110. 36 H. A. Brassert, “Erfahrungen in amerikanischen und europäischen Hüttenwerken. Mit besonderer Berücksichtigung der Verhüttung von Feinerzen,” Der Vierjahresplan 3 no. 4 (20 Feb. 1939), pp. 370-375; id., 3 no. 6 (23 Mar. 1939), pp. 472-476. 37 Ibid., p. 476.

20

Although the circumstances of the decision are obscure, at some point Brassert

terminated his flirtation with Nazism and departed for the U.K., a move that significantly

compromised the construction schedule of the Salzgitter plant. He now turned his attention to

South America, where many countries continued to operate under exchange restrictions, and

where the effects of war mobilization were being in part in surging prices for steel imports. In

1940 Brassert reinserted himself into the effort to develop a Brazilian steel industry, traveling to

Brazil to advise the Brazilian government on the ideal siting and design for their long-sought

steel plant, and hoping to win the business of constructing the plant for his firm. On the same

South American trip he traveled to Columbia, Peru, Bolivia, and Argentina.38 The Peruvian

government in cooperation with the U.S. government hired Brassert to prepare a report that

formed the basis of a Peruvian steel industry which was established in the 1950s.39 In Argentina,

he told officials who were worried that the quality of their domestic supplies of iron ore was too

low that the processes he had employed at Corby and Salzgitter could solve their problem.40

Although he met with State Department and Export-Import Bank officials on several occasions,

ultimately his connections to the Nazi regime appear to have soured the American government

on him, and he did not win the contract to design or construct any of the South American plants

that sprang up in the 1940s with funding from the American government. Although considerably 38 866.1 No. 655. Brazil, Rio de Janeiro Embassy: "Classified & Unclassified" General Records, 1936-58, Box 84. RG 84, USNA. 39 H. A. Brassert, Report on the Establishment of a Coal, Iron and Steel Industry in Peru (New York: H. A. Brassert & Co., 1941); C. Langdon White and Gary Chenkin, “Peru Moves onto the Iron and Steel Map of the Western Hemisphere,” Journal of Inter-American Studies 1, no. 3 (July 1, 1959): 377–386, doi:10.2307/164902; Jon V. Kofas, Foreign Debt and Underdevelopment: U.S.-Peru Economic Relations, 1930-1970 (University Press of America, 1996), 90. 40 “Argentine Steel Plan Investigation of H. A. Brassert,” Jun. 25, 1940. Brazil, Rio de Janeiro Embassy: "Classified & Unclassified" General Records, 1936-58, Box 84. RG 84, USNA. In Argentina Brassert almost got mixed up with Nazi businessman Fritz Mandl. See Ronald C. Newton, “The Neutralization of Fritz Mandl: Notes on Wartime Journalism, the Arms Trade, and Anglo-American Rivalry in Argentina during World War II,” The Hispanic American Historical Review 66, no. 3 (1986): 541–579, doi:10.2307/2515462.

21

less menacing than the Hermann Göring-Werke, the South American steel developments were

nevertheless versions of the same political-economic-technical logic. In an uncertain world, true

sovereignty depended on the ability to manufacture steel domestically utilizing to the greatest

extent possible raw material sources available within the country’s borders. If not the only

possible version of economic nationalism, this surely is an important manifestation of it. And

although Brassert did not win these particular contracts, other American firms did. Their

expertise was globalized in the service of economically nationalist projects.

In the 1920s Brassert’s path intersected with Ferdinand Eberstadt on at least three

occasions, and these convergences again demonstrate the complex ways in which the

globalization of American capital and technical expertise intersected with politics and a

territorial logic of the post-Versailles world that made the world look significantly less like the

cosmopolitan commercial society of the liberal imagination and more like the hell of ethnically

and ideologically charged industrial war.

The first project appeared then and to most observers since as a far more narrowly

economic proposition. After the stabilization of the German currency and economy in 1924 and

the success of the Dawes loan, German industrialists found themselves with a severe shortage of

working capital. The logical place to turn was to the United States, where investors seemed eager

for foreign investment opportunities. As discussed earlier, Eberstadt, acting as Dillon, Read’s

German expert, had successfully negotiated a $12,000,000, five year bond issue for the venerable

August Thyssen AG in the Ruhr, Germany’s largest pig iron producer. In fact Brassert had a

crucial role is this deal. Dillon, Read commissioned him in early 1925 to make a study of the

Thyssen works to determine the feasibility of the bond issue. The report, in which Brassert

22

praised the Thyssen Concern as having “as modern a type of plant as can be found anywhere”

and “the most efficient steel manufacturers of Europe” was given credit for convincing Dillon,

Read to press ahead with the deal despite their doubts about the American market’s readiness for

German industrial issues.41 Dillon, Read in turn made Brassert’s report the key selling point in its

public advertisements for the bonds.42 Brassert was conscious of the significance of his role, and

he demanded certain actions from Thyssen managers on account of the fact that it was his

reputation that was on the line.43

The loan, however, did not perform as well as Dillon, Read had hoped, and the bank

ended up having to buy up a significant amount of the issue. But this did not scare the firm away

from the German steel industry. After making a $4 million equity investment in Deutsch-Lux, the

center of the Stinnes holdings44, DR moved on to play an active role in the consolidation of the

industry. Eberstadt made clear to the German industrialists that DR would use the need to retire

the Thyssen bonds to prevent the Vestag directors from going to any other American bank for

financing.45 Apparently resentful, the Germans nevertheless acquiesced.46 Brassert was again

crucial in the negotiations. His report on the “Big Three” (Gelsenkirchener, Deutsh-Lux, and

Bochumer Verein), which together formed the Rhein-Elbe-Union, complemented his report on

the Thyssen works and formed the basis for the consolidation those two firms, along with the

41 Fear, Organizing Control, 504–506. 42 “$12,000,000 August Thyssen Iron and Steel Works,” New York Times Jan. 10, 1925, p. 5. 43 Brassert to Carl Rabes, Thyssen’s lead negotiator for the American loan, Feb. 4, 1925. A/830/1 “Amerika Anleihe”. ThyssenKrupp KonzernArchiv, Duisberg, Germany. 44 “Stinnes Stock is Sold to U.S. Banking Group”, Washington Post Jul. 27, 1925, p. 1; Edwards, Investing in Foreign Securities, 221. 45 Eberstadt Diary, Feb. 26, 1926. “Re: European Business Conditions: Information Prepared for Dillon, Read and Company,” Box 172. Ferdinand Eberstadt Papers. 46 Clemens Verenkotte, Das Brüchige Bündnis: Amerikanische Anleihen Und Deutsche Industrie, 1924-1934 ([Germany: C. Vernenkotte, 1991), 208; Alfred Reckendrees, Das “Stahltrust”-Projekt: Die Gründung der Vereinigte Stahlwerke A.G. Und ihre Unternehmensentwicklung 1926-1933/34 (C.H.Beck, 2000), 255–256.

23

Otto Wolff-controlled Phönix and Rheinische Stahlwerke concerns into the new German steel

trust modeled on U.S. Steel, the Vereinigte Stahlwerke AG, or Vestag.47 Dillon, Read first

brought out a $25,000,000 issue for the Rheinelbe Union on Jan. 1, 1926, with Brassert’s

valuation of the trust’s properties standing as the evidence that the company would have no

trouble meeting its obligations.48 Then on June 1, it brought out the wildly successful

$30,000,000, 25-year, 6½ % bond issue for the Vestag itself.49 A further $30,000,000, 20-year 6

½% issue followed in July, 1927.50

For Dillon, Read the Vestag financing had been purely a business proposition. When

combined with the $35,000,000 in long-term issues it underwrote for the electrical giant Siemens

& Halske, the steel financing made DR by far the dominant American bank in German industry.

But for the Vestag’s directors, which included the arch-nationalists Fritz Thyssen and Albert

Vögler, as well as the opportunistic Otto Wolff and the spectacularly unscrupulous Friedrich

Flick, the Vestag was something more. In addition to aiding in the tight cartelization of the

German steel industry and the organization of a Franco-German steel “entente” to divide up

export markets, the Vestag also functioned as a holding company through which to purchase

interests in industrial enterprises throughout Europe, in order to limit international competition

and protect the German firms’ ability to generate export revenues. Because the reparations

burden placed immense pressure on Germany to keep up its export earnings, the German

government was willing to cooperate with German industry in acts of economic imperialism.

47 H. A. Brassert, Report on Gelsenkirchener Bergwerks Aktien Geselleschaft, Deutsch-Luxemburgische Bergwerks Und Hütten Aktien Gesellschaft, Bochumer Verein Für Bergbau Und Gussstahlfabrikation, for Dillon, Read & Co. (Chicago: H.A. Brassert & Co., 1925). Said Vestag directors Fritz Thyssen and Albert Vögler, “Our model was the glistening example of America.” Alfred Reckendrees, “Die Vereinigte Stahlwerke A. G. 1926-1933 Und 'das Glänzende Beispiel Amerika',” Zeitschrift Für Unternehmensgeschichte / Journal of Business History 41, no. 2 (Jan., 1996), pp. 159–186. 48 “$25,000,000 Rheinelbe Union” New York Times Jan. 26, 1926, p. 31. 49 “$30,000,000 United Steel Works Corporation” New York Times Jun. 28, 1926, p. 9. 50 Sale of Foreign Bonds or Securities in the United States, 505.

24

The most egregious of these involved the heavy industrial region of Polish Upper Silesia.

After World War I Upper Silesia had been divided between Germany and the reconstituted

Polish Republic. Developed entirely by German capital, and with much of its production

destined for German markets, Upper Silesia became something of an industrial orphan within

Poland. The initial terms of settlement imposed by the League of Nations had prevented

Germany from imposing tariffs on Polish Upper Silesian producers through 1925, but as soon as

the treaty lapsed Germany inaugurated a tariff war. Denied their “natural” markets, and

uncompetitive on international markets, Polish producers struggled to adapt to producing strictly

for Poland’s limited consumption. Beginning shortly after the border settlement in 1922,

Friedrich Flick, an upstart in German industry who had grown spectacularly rich during World

War I, quietly began buying up control over the formerly German iron and steel companies now

located in the Polish part of Upper Silesia. Flick’s ownership of these properties was apparently

unknown to the Polish authorities, who were increasingly pressing for a “Polonization” of

German firms in the region. Meanwhile Flick wished to effect a consolidation of four of the

largest coal, iron and steel producers into a miniature Polish Vestag – under the control of the

actual German Vestag. In order to disguise this reality, which would have been anathema to the

Poles, he was proposing the creation of American holding company, which would officially own

the firms. Flick brought this proposal directly to Eberstadt in November, 1927.51 Eberstadt seems

to have been favorable towards the deal, although ultimately Dillon, Read did not actually take

the business, perhaps because the firm had underwritten the major loan for Polish stabilization in

1925, and to have been exposed aiding a German scheme to subordinate the Polish economy to

Germany might have been embarrassing, to say the least. Another American, Averell Harriman,

did take the deal, and Harriman hired Brassert to undertake the necessary survey of the 51 Eberstadt Diary, Nov. 3, 1927.

25

properties. Brassert’s proposal for the consolidation of the Polish firms would have had them

redesigned to focus almost exclusively on sales to the Polish market. Whether or not this

reflected the influence of Vestag directors is unclear.52 Nevertheless, as Alfred Reckendrees has

recently documented, Flick’s control of the Polish properties was secretly but actively

encouraged by the Weimar government, which considered German control of Polish industry a

crucial precondition for an ultimate revision of the German-Polish border and the reincorporation

of the Upper Silesian irredenta into an integral Germany.53 The Poles, for their part, found the

new American directors insufficiently energetic in eliminating nationalist Germans from

managerial positions. In this way American capital was mobilized such as to exacerbate

escalating tensions in Central Europe.54

One last project helps to illustrate the entanglements that financial and technological

globalization could lead to. One of the provisions of the Dawes Plan was that Germany would be

given an Agent General for Reparations, whose assignment was to receive reparations payments

from the German government, and then effect their transfer to Germany’s former adversaries.

One of the complications of the flow of foreign loans into Germany in the 1920s was their

relationship to Germany’s reparations obligations. It was not automatic that reparations would be

senior to commercial and other government loans. And although Germany was happy to meet

52 H. A. Brassert & Co., “Report on the Königs-Laura Company, Bismark Company, Kattowitzer Company and Silesia Company in Polish Upper Silesia for W. A. Harriman, Inc.” Jul. 5, 1928. Container 690, W. Averell Harriman Papers, Manuscript Division, Library of Congress, Washington, D.C. 53 Alfred Reckendrees, “Business as a Means of Foreign Policy or Politics as a Means of Production? The German Government and the Creation of Friedrich Flick’s Upper Silesian Industrial Empire (1921–1935),” Enterprise and Society 14, no. 1 (Mar., 2013): 99–143, doi:10.1093/es/khs035. See also Kim Christian Priemel, Flick: Eine Konzerngeschichte Vom Kaiserreich Bis Zur Bundesrepublik (Göttingen: Wallstein Verlag, 2007), pp. 161-175. 54 Stetson (U.S. Envoy to Poland) to Kelley (Chief of the Division of Eastern European Affairs), Aug. 13, 1929. RG 59, 860c.6463 Harriman & Co./10; Stetson to the Secretary of State, Aug. 26, 1929. RG 59, 860c.4016/273.

26

obligations to creditors that it considered fairly incurred, reparations remained illegitimate in the

eyes of many Germans, which gave many quarters of German state and society an active interest

in demonstrating that Germany did not in fact have the ability to make its reparations payments.

In this context the Agent General – a young American named S. Parker Gilbert – began an

increasingly public campaign against German overseas borrowing, arguing that the inflow of

foreign credits was preventing Germany from undertaking the difficult and politically unpopular

task of running a balanced budget, since this would necessarily depress domestic consumption

and leave more of the national product available for reparations payments and other existing

obligations, as well as create a pool of domestic savings for necessary productive investment. A

significant international debate ensued as to the benefits of foreign loans and the meaning of

“productive” vs. “unproductive” investment. It was a debate with a pronounced class valence:

among the most criticized of all German borrowing were the foreign loans of German

municipalities, many of which were applied to various forms of social overhead spending

(electrification and housing, e.g.) whose most enthusiastic advocates were socialist deputies

representing a socialist working class. Although they had earlier criticized the Agent General for

his denunciations of German overseas borrowing, in November, 1927, Germany’s major

industrialists openly expressed their support for Gilbert’s sharp criticism of Germany’s public

finances. There was no small irony, as William McNeill observed, in their reversal, since in

effect it signified that the arch-nationalist, anti-reparations German steel barons had now come to

support a fiscal policy whose principal justification was Germany’s need to meet its reparations

obligations. Yet apparently German industrialists were more determined to prevail in their battle

with the social-democratic Weimar Republic than they were to re-litigate the Versailles treaty.

27

As their principal conduit to the American capital market, to which those selfsame

industrialists desired continued access, Eberstadt found himself a key adviser to his clients in

their political role as spokesmen for German heavy industry. At the same moment as he was

discussing with Flick possible arrangements for the setup of a holding company for the Upper

Silesian firms, Eberstadt was explaining to the Vestag officials Sempell and Freundt how they

should word a Vestag response to Gilbert’s memo. There was “danger [in] a lengthy German

answer: if it were optimistic it would be a boomerang in reparation discussions; if pessimistic, it

would injure their credit.”55 Although I have not yet located the text of this memo, the thrust of it

is clear. Borrowing by German industry was perforce productive and would contribute to

increasing national income; borrowing by German municipalities threatened the solvency, the

stability of the German currency, and therefore the credit of the German Reich. German industry

was healthy and therefore could make good use of foreign capital. Only a government operating

without fiscal restraint could threaten Germany’s overall recovery. All of this needed to be said

with some caution – Eberstadt said of the final version that “the figures are favorable but the

sentiments unfavorable but for public consumption, in order to relieve the company of excessive

burdens now being threatened” – so that the health of German industry and the German economy

not be misinterpreted as a signal that reparations ultimately did not need to be revised down.56

What was not said was that German heavy industry was fighting an all-out war against its own

workers’ demands for higher wages and a shorter working day. A deficitary budget threatened

inflation, which would only further the workers’ wage demands. An overall deflationary policy

was necessary to keep Germany competitive on international markets.57 Thyssen’s party, the

55 Eberstadt Diary, Nov. 5, 1927. 56 Ibid. 57 Bernd Weisbrod, Schwerindustrie in Der Weimarer Republik: Interessenpolitik Zwischen Stabilisierung Und Krise (Wuppertal: P. Hammer, 1978), 282.

28

arch-nationalist German National People’s Party, had issued a strong endorsement of Gilbert’s

memo.58 For Dillon, Read’s representative in Germany, this was a strange position to be in. If

American capital was aiding in the reconstruction of Germany and its reintegration into the

circuits of international commerce, why was the largest American underwriter of German

corporate issues helping German industry pursue a policy supported by a largely agrarian party

hungry for agricultural protection and the return of the German monarchy? The only reasonable

explanation is that the Dillon, Read partner thought that the policy advocated by Gilbert would in

fact contribute to greater economic stability in Germany, which would mean both future

business, and the better performance of existing bonds. But for such a policy to have required an

alliance with the nationalist right-wing is ironic, to say the least.

IV.

For very legitimate reasons, economists are more interested in things that are subject to

the law of large numbers. Generally, this excludes specific actors and their motivations from

serious study. But what a study of globalization organized around actors shows is that who the

actors are mattered, as did their understandings of themselves in relation to their surroundings.

Eberstadt and Brassert are two of many individuals in the interwar period whose careers were

genuinely global, but whose work was intentionally or unintentionally furthering nationalist

ambitions in countries that weren’t their own. In that sense, indirectly, globalization was one

contributor to the increase in tensions in the international system beginning the late-1920s, and

not just as “backlash” against it, as mainstream economic history would suggest. In the struggle

to “sustain[] the capacity to produce autonomous histories,” American capital and technical

58 Eberstadt Diary, Nov. 10, 1927.

29

expertise had an ambiguous role. Both were potentially available to be mobilized by different

states which were potentially in conflict with each other or with the U.S.; both could conceivably

exacerbate domestic political differences in the recipient country. As Bright and Geyer have

insisted, “it is necessary to analyze the structured networks and webs through which

interconnections are made and maintained – as well as contested and renegotiated – if we are

going to attempt . . . to narrate the directions of development that these [global] interactions have

taken over time. For it is precisely the patterning and structuring of these interactions that can

give definition to a history of globalization as something other than a top-down or outward-

thrusting exercise in superior power"59, or, from the other pole, simply the play of market forces.

In a different register, it is necessary for us to get as close as we can to the total set of

determinations – including the actors’ own understanding of what they are doing, and the ways

that their understandings might not accord with those in the recipient countries – that structure

both the interactions between agents of globalization and their “hosts” and that give rise to their

specific effects. Included in that abstract description must be knowledge, since knowledge,

including what we usually think of as skill, is a crucial determinant on both the supply and the

demand sides of globalization. This is true of periods in world history where international

markets worked well, and periods in which they worked less well, too.

59 Charles Bright and Michael Geyer, “Regimes of World Order: Global Integration and the Production of Difference in Twentieth Century World History,” in Interactions: Transregional Perspectives on World History, ed. Jerry H. Bentley, Renate Bridenthal, and Anand A. Yang (Honolulu: University of Hawai’i Press, 2005), 207, 204.