executive summary of the project - environmental clearance

TRANSCRIPT

SNN INFRA POWER PROJECTS PRIVATE LIMITED 1

Executive summary of the project

SNN infra power projects private limited, is a SPV set up under the companies act 1956 in

March 2012 by SNN infra a local construction company in Visakhapatnam who are the project

developers along with Korean South Eastern Power company KOSEP to develop a 1320 MW

supercritical thermal power plant in Andhra Pradesh. The latter is a government owned

subsidiary of KEPCO which is the chief generator, transmission and distributing arm of Korean

power sector.

The proposed project would be located in VEMAVARAM village of THONDANGI mandal of East

Godavari district of Andhra Pradesh. A total of 700 acres of land has been identified for the

proposed project and the land is a mix of single crop and dry scrub land.

The proposed project would be based on super critical technology with a capacity of 2*660MW

capacity each. The technology improves the turbine cycle heat rate significantly than sub critical

technology which is prevalent in the country thus increasing savings on the fuel to an extent of

5% and overall plant efficiency using this technology will be 42%.

The project would be based on 70:30 ratio of domestic and imported coal in case of fuel

availability from CIL. However in the event of non availability of domestic coal the project

would be based on 100% imported coal. The total coal quantity required would be around 6

million tones approximately. The ration of domestic and imported coal or solely imported coal

would be decided at a later stage.

Source of water would be sea water and providence of a de-salination plant is proposed to

convert sea water. Mode of fuel transport would be through sea and rail depending on the

logistic advantage.

PRIYA ENERGY CONSULTANTS, a Bangalore based consulting group has done the pre feasibility

study of the proposed site as well as alternative sites for the project.

SNN INFRA POWER PROJECTS PRIVATE LIMITED 2

Promoters and investor background

LOCAL DEVELOPERS:

SNN INFRA POWER PROJECTS PRIVATE LIMITED, a company registered under the INDIAN

COMPA NIES ACT 1956 and having its registered office in Visakhapatnam, Andhra Pradesh is a

SPV set up in March 2011 intending to set up a 1320 MW super critical thermal power project

in VEMAVARAM village and THONDANGI mandal of Andhra Pradesh.

In January 2011 KOREAN SOUTH EASTERN POWER (KOSEP), one of the ten subsidiaries of

Korean Power visited India to explore the possibility of setting up a super critical thermal power

project in India. KOSEP had then initiated extensive discussions with its local partner DUCKJIN

GLOBAL INVESTMENT in Korea along with SNN INFRA of India for a proposed plant of 1320 MW

capacity in Andhra Pradesh.

Some of the key milestones over the course of last 16 months among the developers of the

project and KOSEP& SI involve

MOU and CA among SNN INFRA POWER PROJECTS PVT LIMITED, DUCKJIN GLOBAL

INVESTMENT KOREA and KOSEP KOREA – April 2011

MOU among KOSEP & KEPCO KPS – October 2011

MOU among KOSEP, PTC INDIA & KEPCO KPS- January 2012

Term sheet & binding agreement among SNN INFRA POWER PROJECTS, KOSEP,

KEPCOKPS, PTC & DUCKJIN GLOBAL INVESTMENT – JUNE 2013 (proposed date)

In accordance with the discussions SNN INFRA POWER PROJECTS PRIVATE LTD was established

in March 2011 as per the Indian companies’ act of 1956 as an SPC for the project development

by SNN INFRA, Visakhapatnam.

The SPC would do all the local development works including finalizing the land acquisition for

the project and obtaining all the necessary permits for the project. After all the approvals for

the project are obtained KOSEP would take over the control holding of the project along with its

consortium members of the project.

SNN INFRA POWER PROJECTS PRIVATE LIMITED 3

The main role of the SPC along with DUCKJIN GLOBAL INVESTMENT is to

Identify land for the project

Identify Indian partners for the project

Obtaining MOEF clearance for the project

Clearances for the project

Consultations with the state government of Andhra Pradesh for providing the necessary

infrastructure facilities for the project.

The strategic investor group led by KOSEP, KEPCO KPS & PTC India would take over the project

once all the permitting is done and complete the financial closure.

SNN INFRA is the local developer for this project while DUCKJIN GLOBAL INVESTMENT is the

developer based in South Korea. SNN INFRA is a partnership firm based in Visakhapatnam

primarily into infrastructure and real estate sectors. SNN INFRA is currently involved in a 400

million INR mining contract for DALMIA CEMENTS plant in CUDDAPH district of Andhra Pradesh

and also constructing nearly 50000 SQ.FT of real estate development in Visakhapatnam district

of Andhra Pradesh.

Mr. K.SURENDRANATH is a young entrepreneur with an MBA.MS degree from who is the main

promoter of the company as well as the SPV is currently involved in infrastructure projects as

well as energy project including fossil fuel and renewable projects in India.

The local developers are mainly responsible for land acquisition and obtaining the necessary

permits for power projects. SNN INFRA is currently pursuing development activities for two

projects in Karnataka and one in Andhra Pradesh and also does financing arrangements both

equity and debt depending on the requirements.

SNN INFRA POWER PROJECTS PRIVATE LIMITED 4

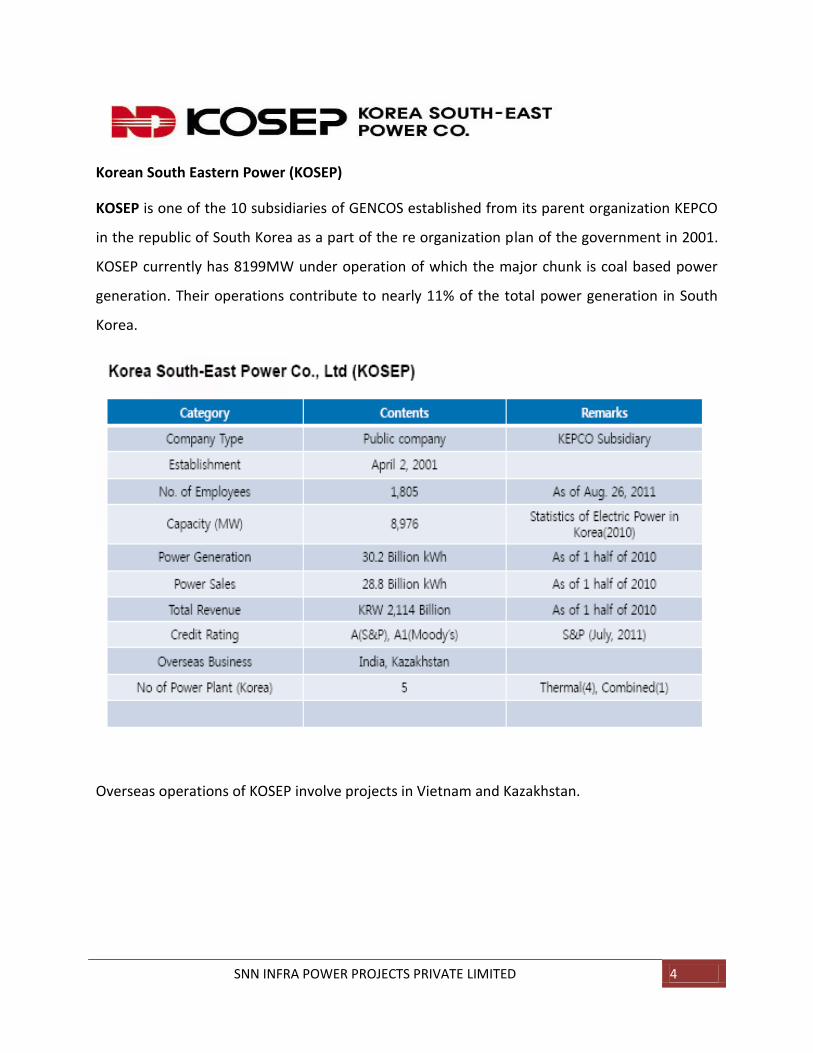

Korean South Eastern Power (KOSEP)

KOSEP is one of the 10 subsidiaries of GENCOS established from its parent organization KEPCO

in the republic of South Korea as a part of the re organization plan of the government in 2001.

KOSEP currently has 8199MW under operation of which the major chunk is coal based power

generation. Their operations contribute to nearly 11% of the total power generation in South

Korea.

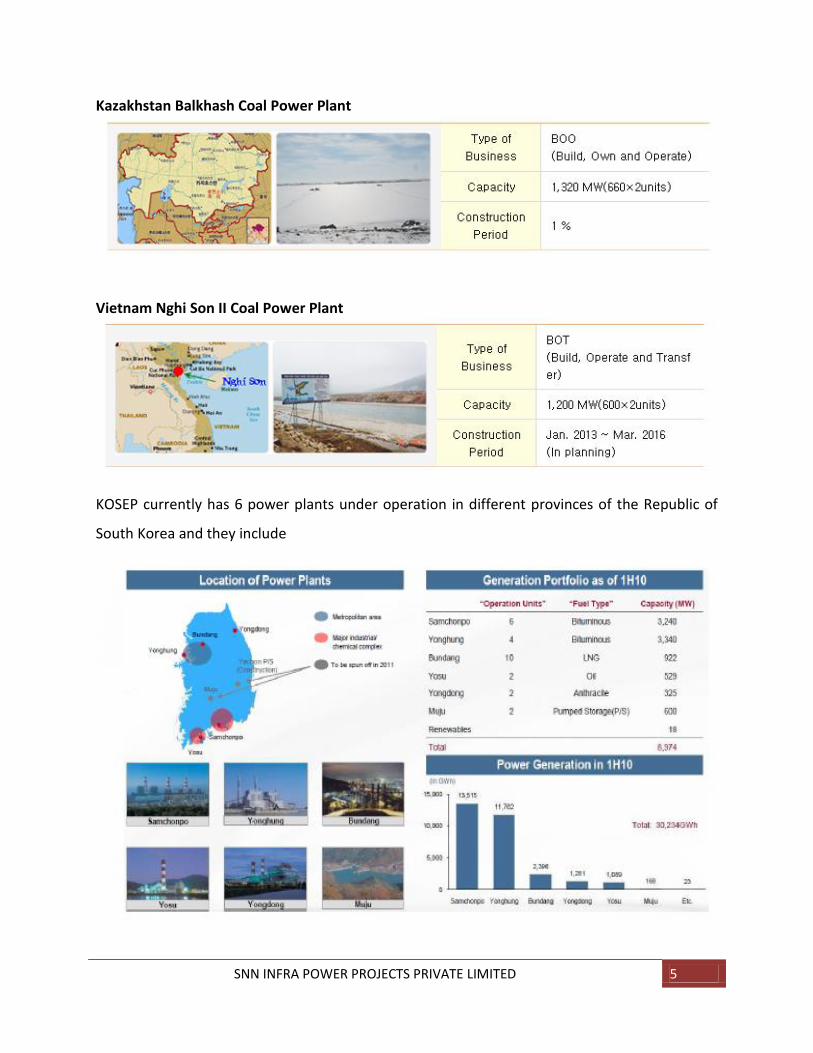

Overseas operations of KOSEP involve projects in Vietnam and Kazakhstan.

SNN INFRA POWER PROJECTS PRIVATE LIMITED 5

Kazakhstan Balkhash Coal Power Plant

Vietnam Nghi Son II Coal Power Plant

KOSEP currently has 6 power plants under operation in different provinces of the Republic of

South Korea and they include

SNN INFRA POWER PROJECTS PRIVATE LIMITED 6

KOSEP has excellent track record of construction and operation of thermal power plants in

Korea with high PLF and some of the key figures explaining their capabilities include

Lowest fuel cost rates among all the generating companies in Korea

Highest PLF at an average 77% annually

Superior operating efficiency and market share of 14% with facility share of 12.1%

KEPCO KPS

KEPCO PLANT AND ENGINEERING SERVICES KEPCO KPS is an electric power facility management

company carrying out high quality maintenance works on power generation and transmission

facilities in Korea and various other countries including India. It was established in 1974. SINCE

ITS ESTABLISHMENT the company managed to maintain the best electric power and industrial

facilities both in South Korea as well as abroad in the countries of their operations.

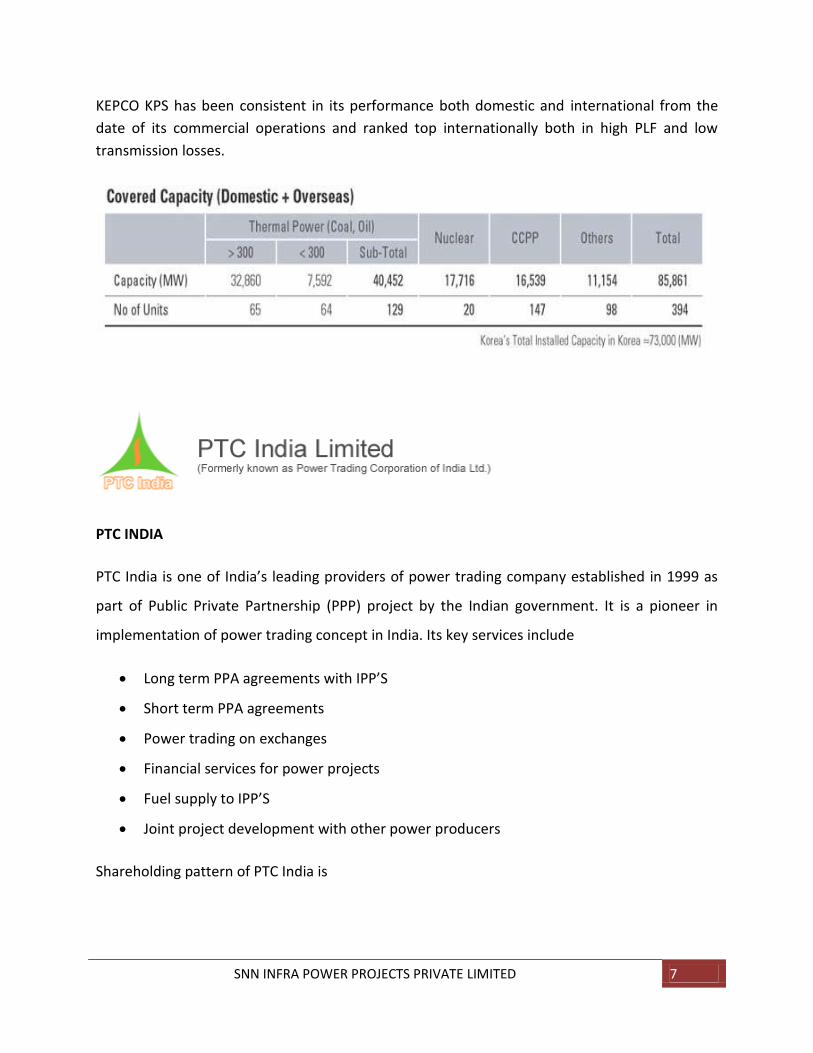

SNN INFRA POWER PROJECTS PRIVATE LIMITED 7

KEPCO KPS has been consistent in its performance both domestic and international from the

date of its commercial operations and ranked top internationally both in high PLF and low

transmission losses.

PTC INDIA

PTC India is one of India’s leading providers of power trading company established in 1999 as

part of Public Private Partnership (PPP) project by the Indian government. It is a pioneer in

implementation of power trading concept in India. Its key services include

Long term PPA agreements with IPP’S

Short term PPA agreements

Power trading on exchanges

Financial services for power projects

Fuel supply to IPP’S

Joint project development with other power producers

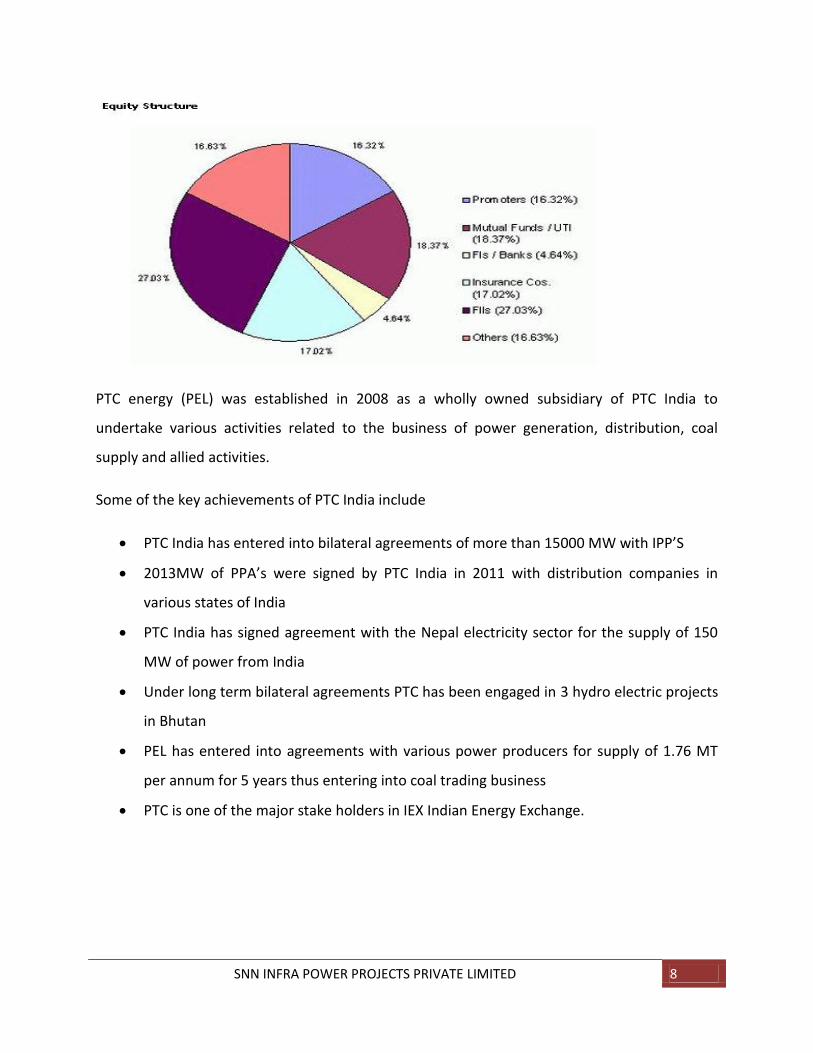

Shareholding pattern of PTC India is

SNN INFRA POWER PROJECTS PRIVATE LIMITED 8

PTC energy (PEL) was established in 2008 as a wholly owned subsidiary of PTC India to

undertake various activities related to the business of power generation, distribution, coal

supply and allied activities.

Some of the key achievements of PTC India include

PTC India has entered into bilateral agreements of more than 15000 MW with IPP’S

2013MW of PPA’s were signed by PTC India in 2011 with distribution companies in

various states of India

PTC India has signed agreement with the Nepal electricity sector for the supply of 150

MW of power from India

Under long term bilateral agreements PTC has been engaged in 3 hydro electric projects

in Bhutan

PEL has entered into agreements with various power producers for supply of 1.76 MT

per annum for 5 years thus entering into coal trading business

PTC is one of the major stake holders in IEX Indian Energy Exchange.

SNN INFRA POWER PROJECTS PRIVATE LIMITED 9

Some of the conventional investments from PTC include

26% equity in 189 MW imported coal based power project in Tamil Nadu - The project is

a merchant power plant and has three units of 63 MW each. The first unit was

commissioned in August 2009. The other units are expected to be commissioned by Mar

2010.

26% equity in the first phase of 270 MW imported coal based power project in Andhra

Pradesh. This is the first of its kind of tolling project in the country in which PTC India Ltd

will be supplying coal to the project and will purchase the power by paying conversion

charges. Financial closure has been achieved. The project is expected to be

commissioned by 2011.

Equity in stage I of 2*660 MW thermal power project in Andhra Pradesh. 70% of coal

required for the project has got the linkage by Ministry of Coal, GOI. Required land for

the project has been already acquired. Financial closure is expected to achieve by Jan

2010. The project is expected to be commissioned by 2012.

Equity in 2*350 MW thermal power project in Orissa. It is a domestic pit-head coal

project, for which the coal linkage has already been obtained. The first unit of IBEUL has

already achieved the financial closure and financial closure for the second unit is in

advanced stages. The first unit of the project is expected to be commissioned by

December 2011 and second unit by March 2012.

SNN INFRA POWER PROJECTS PRIVATE LIMITED 10

Current Indian power sector snapshot

INTRODUCTION

The Indian economy has experienced unprecedented economic growth over the last decade.

Today, India is the ninth largest economy in the world, driven by a real GDP growth of 8.7% in

the last 5 years (7.5% over the last 10 years). In 2010, the real GDP growth of India was 5th

highest in the world, next only to Qatar, Paraguay, Singapore and Taiwan.

Sustained growth in economy comes with growth from all sectors, among which growth in

infrastructure sector is a key requirement for growth in sectors within manufacturing and

services. With in infrastructure, growth in power sector is one of the most important

requirements for sustained growth of a developing economy like India.

“Indian Economy has witnessed rapid growth in the past decade and to sustain a similar growth

trajectory of 9%, power sector needs to grow at-least 8.1 % per annum” - Planning commission.

The present installed power generation capacity in the country as on October 31, 2011 was

182689.62 MW. Thermal power projects of 78545 MW and hydropower projects of 15707 MW

are under construction in the country for likely commissioning during 11th and 12th Plan.

India’s power requirement over the years has largely been dominated by coal based

generation, with close to 55% of the 182 GW of installed capacity being coal based power

plants, accounting for over 80% of the total units generated in the country.

CURRENT MARKET SCENARIO OF THE INDIAN POWER SECTOR

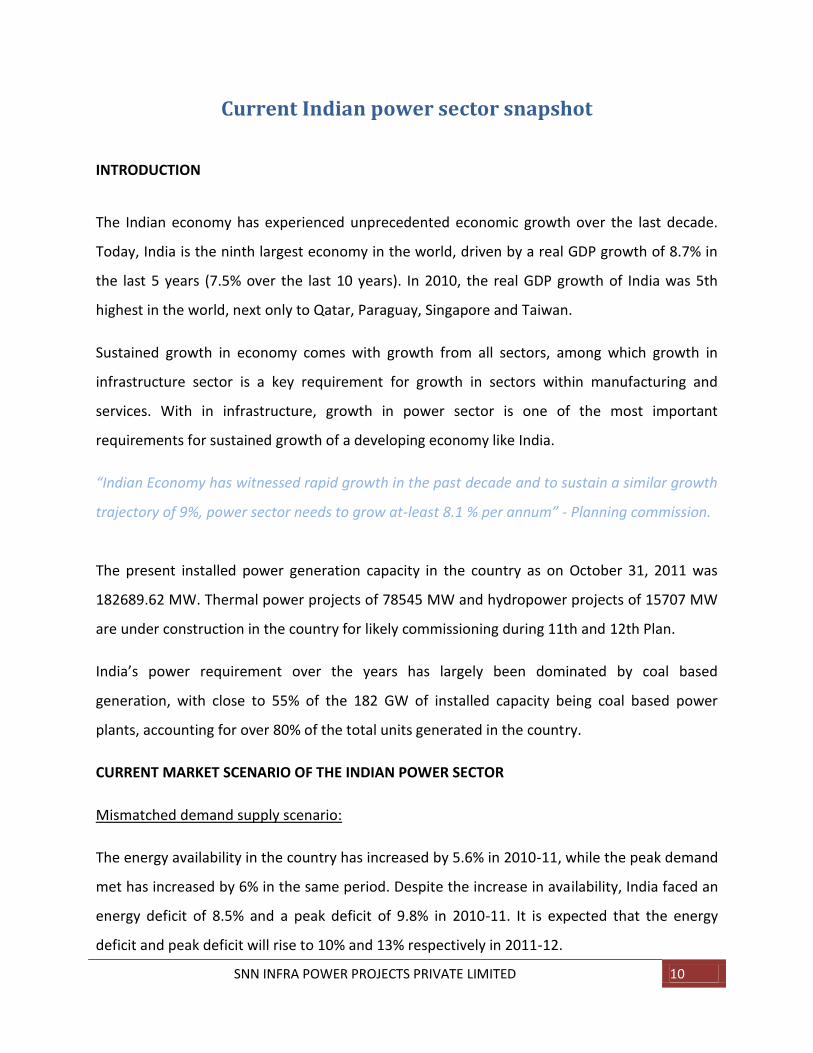

Mismatched demand supply scenario:

The energy availability in the country has increased by 5.6% in 2010-11, while the peak demand

met has increased by 6% in the same period. Despite the increase in availability, India faced an

energy deficit of 8.5% and a peak deficit of 9.8% in 2010-11. It is expected that the energy

deficit and peak deficit will rise to 10% and 13% respectively in 2011-12.

SNN INFRA POWER PROJECTS PRIVATE LIMITED 11

Low Per capita consumption of electricity:

The average per capita consumption of electricity in India is a mere 478 kWh2 (2010),

compared to the world average of 2,300 kWh. This is as per the CIA fact book of 2011-2012.

However according to the UN report on per capita consumption Indian consumption is 770 kWh

in 2010. The other comparable countries, like the other BRIC nations, have significantly higher

per capita consumption compared to India.

The average per-capita consumption has grown steadily at 1.3% CAGR annually over the last 10

years.

The Government of India targets a per capita consumption of 1,000 kWh by 2011-12.

Encouraging policy measures

The policy landscape in India has progressively evolved since Independence and has led to

radical changes in the power sector, especially in terms of competition, private sector

involvement and focus on green energy over the last decade, commencing with the passing of

the Electricity Act 2003.

SNN INFRA POWER PROJECTS PRIVATE LIMITED 12

Till early 1990s’, the power sector was shielded from any private sector involvement; however,

the mounting pressure on Government resources to support capacity additions, repeated

delays encountered by state utilities and the growing demand-supply gap urged the

Government of India to open the power generation sector to private participation along with

country’s globalization policy.

The amendment of Supply Act (1948) in 1991, followed by the enactment of Electricity

Act(2003) and notification of Mega Power Policy(1995), National Tariff Policy (2005), National

Electricity Policy and Integrated Energy Policy have all led to a much liberal power sector, which

then saw active investments from private sector across the value chain.

However, most of the participation by private investors has happened in generation sector,

driven by de-licensing of generation, fiscal incentives for large scale capacity additions and

competitive procurement of power.

The Indian power sector has achieved a lot over the last decade in the areas of policy reforms,

private sector participation in generation and transmission, new manufacturing technology and

capabilities, but there is still much to achieve and a number of challenges to overcome before

the opportunities can be leveraged.

Indian market has evolved over the years as expressed below

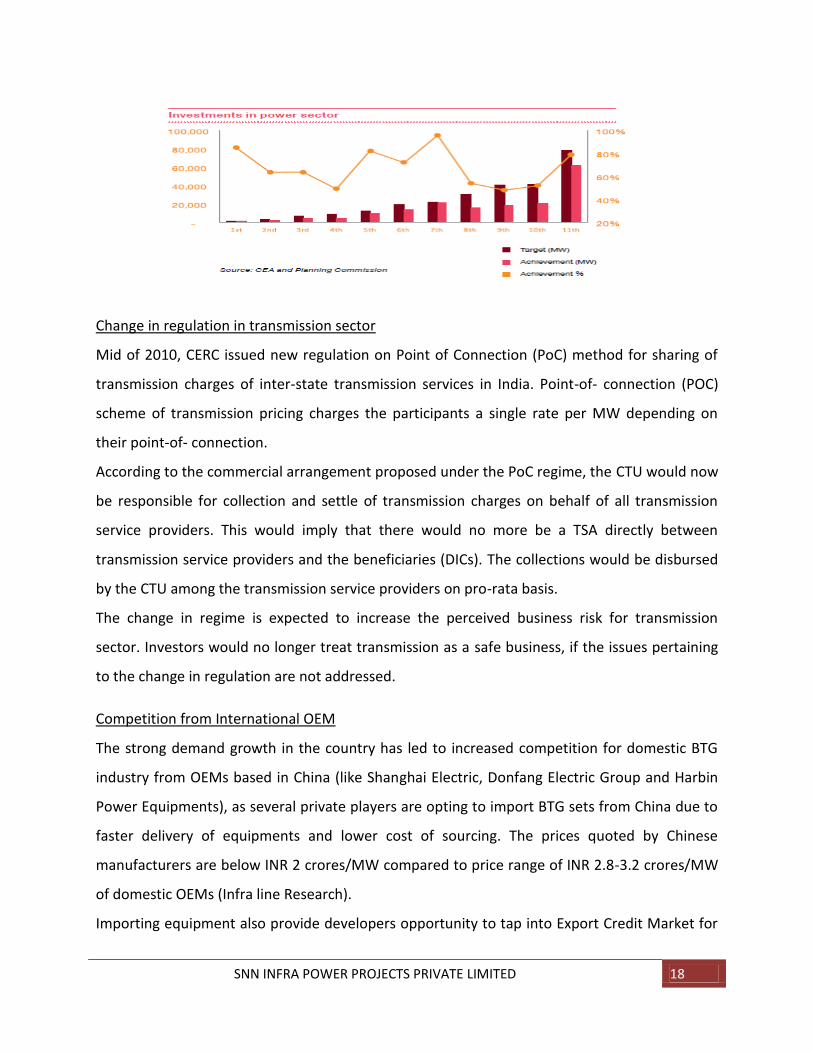

Investment in the power sector

SNN INFRA POWER PROJECTS PRIVATE LIMITED 13

The power sector ranked sixth among the leading sectors of the Indian economy, attracted US$

4.6 billion in Foreign Direct Investment (FDI) since 2000, according to the Ministry of Commerce

and Industry’s Department of Industrial Policy & Promotion (DIPP). FDI in petroleum and

natural gas totaled US$ 2.7 billion for the period, ranking the sector ninth in foreign investment.

The investment climate is very positive in the power sector. Due to the surge in the sector, the

power sector has witnessed higher investment flows than envisaged. The Ministry of Power is

believed to have sent its proposal for addition of 76,000 MW of power capacity in the 12th five-

year plan to the planning commission. The power ministry has set a target for adding 76,000

MW of electricity capacity in the 12th Plan (2012-17) and 93,000 MW in the 13th Five-Year Plan

(2017-2022).

The Working Group on Power for formulation of the 12th Five Year Plan has estimated total

fund requirement of INR 13,72,580 crore for the power sector. During the Twelfth Five Year

Plan, the main sources of financing are commercial banks, public financial institutions,

dedicated infrastructure/power finance institutions, insurance companies, overseas markets,

bilateral/multilateral credit, bond markets and equity markets. In addition, steps have been

taken by Government to make available funds through Credit Enhancement Schemes and

Infrastructure Debt Fund etc.

In order to attract foreign investments in the power sector, Foreign Direct Investment (FDI) up

to 100 per cent is permitted under automatic route for projects of electricity generation (except

atomic energy), transmission, distribution and power trading. Major contributing countries to

the FDI equity inflows during this period are France, Mauritius, Singapore, UAE, United

Kingdom, USA and Morocco. US$ 330.99 million of FDI equity has been received from USA in

the power sector during April 2008 to September, 2011.

SNN INFRA POWER PROJECTS PRIVATE LIMITED 14

KEY CHALLENGES FACING INDIAN POWER SECTOR

Securing fuel:

India’s power requirement over the years has largely been dominated by coal based

generation, with close to 55% of the 182 GW of installed capacity being coal based power

plants, accounting for over 80% of the total units generated in the country.

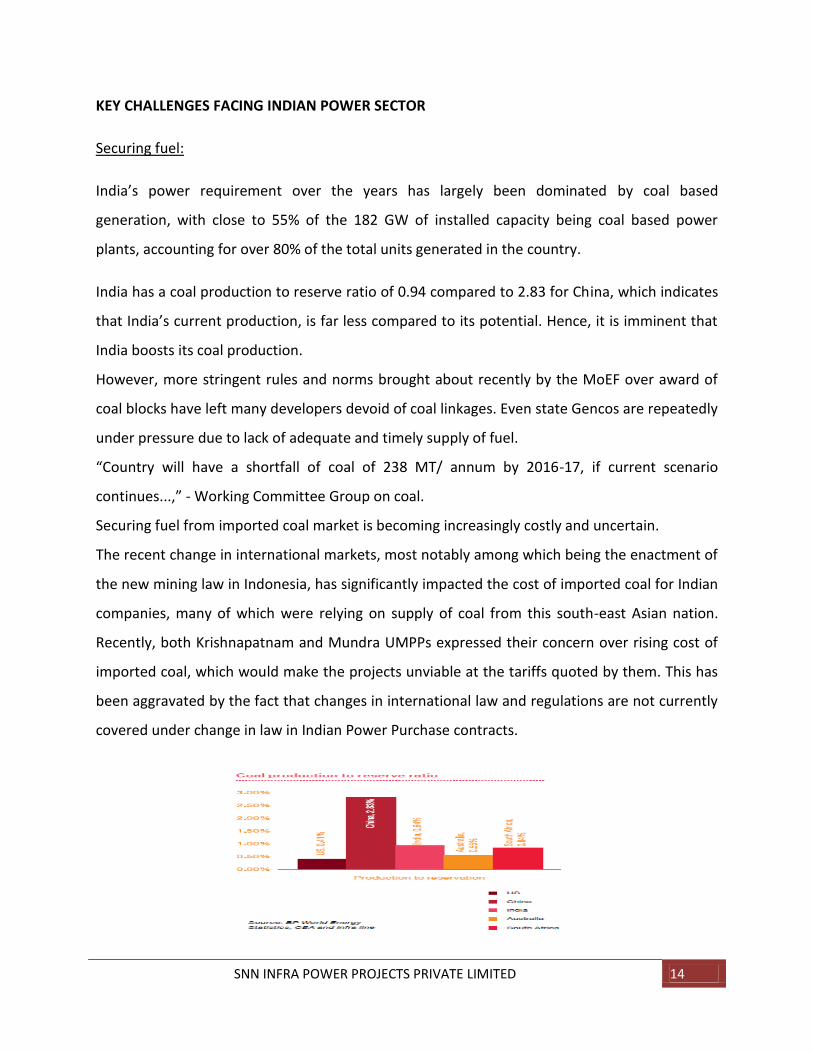

India has a coal production to reserve ratio of 0.94 compared to 2.83 for China, which indicates

that India’s current production, is far less compared to its potential. Hence, it is imminent that

India boosts its coal production.

However, more stringent rules and norms brought about recently by the MoEF over award of

coal blocks have left many developers devoid of coal linkages. Even state Gencos are repeatedly

under pressure due to lack of adequate and timely supply of fuel.

“Country will have a shortfall of coal of 238 MT/ annum by 2016-17, if current scenario

continues...,” - Working Committee Group on coal.

Securing fuel from imported coal market is becoming increasingly costly and uncertain.

The recent change in international markets, most notably among which being the enactment of

the new mining law in Indonesia, has significantly impacted the cost of imported coal for Indian

companies, many of which were relying on supply of coal from this south-east Asian nation.

Recently, both Krishnapatnam and Mundra UMPPs expressed their concern over rising cost of

imported coal, which would make the projects unviable at the tariffs quoted by them. This has

been aggravated by the fact that changes in international law and regulations are not currently

covered under change in law in Indian Power Purchase contracts.

SNN INFRA POWER PROJECTS PRIVATE LIMITED 15

Erratic gas supply for gas based power projects:

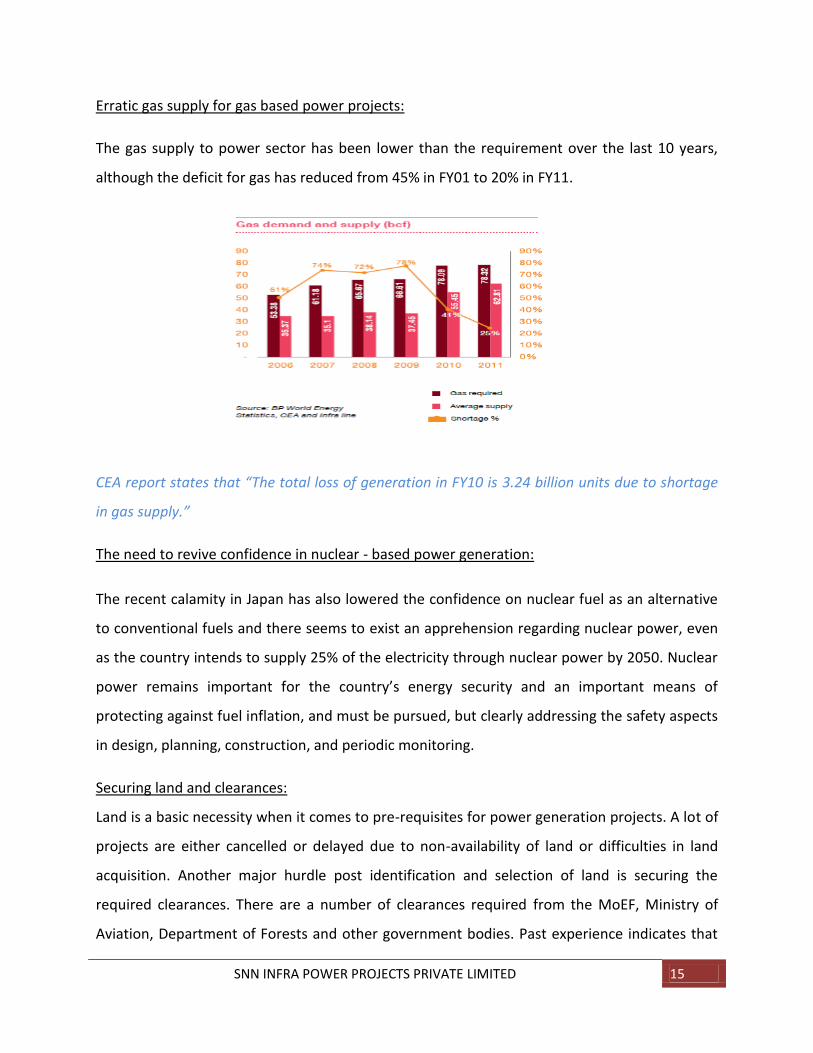

The gas supply to power sector has been lower than the requirement over the last 10 years,

although the deficit for gas has reduced from 45% in FY01 to 20% in FY11.

CEA report states that “The total loss of generation in FY10 is 3.24 billion units due to shortage

in gas supply.”

The need to revive confidence in nuclear - based power generation:

The recent calamity in Japan has also lowered the confidence on nuclear fuel as an alternative

to conventional fuels and there seems to exist an apprehension regarding nuclear power, even

as the country intends to supply 25% of the electricity through nuclear power by 2050. Nuclear

power remains important for the country’s energy security and an important means of

protecting against fuel inflation, and must be pursued, but clearly addressing the safety aspects

in design, planning, construction, and periodic monitoring.

Securing land and clearances:

Land is a basic necessity when it comes to pre-requisites for power generation projects. A lot of

projects are either cancelled or delayed due to non-availability of land or difficulties in land

acquisition. Another major hurdle post identification and selection of land is securing the

required clearances. There are a number of clearances required from the MoEF, Ministry of

Aviation, Department of Forests and other government bodies. Past experience indicates that

SNN INFRA POWER PROJECTS PRIVATE LIMITED 16

there are major hurdles for land acquisition and securing clearances which include the

following:

a. Social reasons like opposition from nearby residents due to concerns over loss of

land, water and pollution;

b. Resettlement and rehabilitation issues;

c. Regulatory delays;

d. Environmental issues like afforestation;

e. State specific issues like unavailability of supporting infrastructure;

f. Financial reasons resulting from rising costs of land.

Issues pertaining to competitive bidding:

Competitive bidding in power generation and transmission is viewed as a major fundamental

change – a move towards a competitive market, which would attract private sector

participation and also help in discovering competitive prices in a largely regulated market. The

typical duration for which companies quote their tariffs in competitive bidding scenario, is 25

years and 35 years for generation and transmission, respectively. The duration is fixed

considering the life of assets and the period within which companies would be able to recover

their costs at reasonable tariffs. The results in competitive bids in the recent past in India

indicate that the tariffs discovered have been in most cases significantly lower than regulated

tariffs.

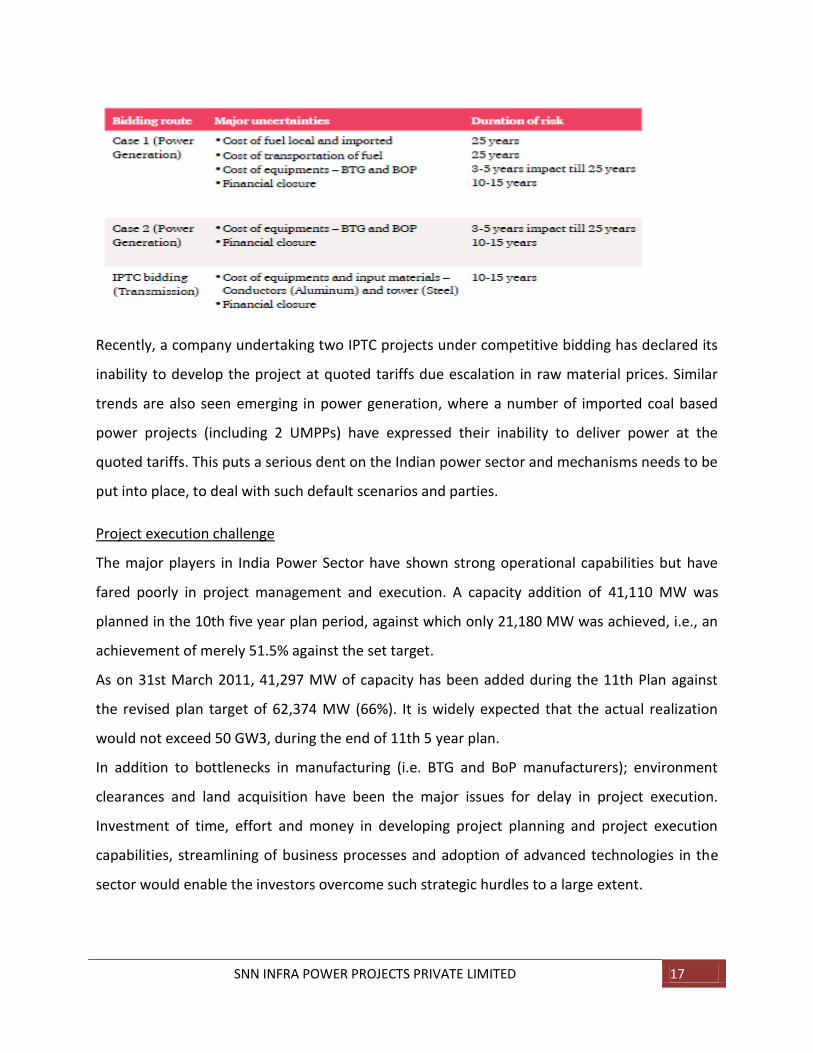

There are risks associated with projects that, if the bidder does not cover/hedge, would expose

the bidder to a potential downside over a 25/35 year period. The table below is a macro level

risk matrix for generation and transmission:

SNN INFRA POWER PROJECTS PRIVATE LIMITED 17

Recently, a company undertaking two IPTC projects under competitive bidding has declared its

inability to develop the project at quoted tariffs due escalation in raw material prices. Similar

trends are also seen emerging in power generation, where a number of imported coal based

power projects (including 2 UMPPs) have expressed their inability to deliver power at the

quoted tariffs. This puts a serious dent on the Indian power sector and mechanisms needs to be

put into place, to deal with such default scenarios and parties.

Project execution challenge

The major players in India Power Sector have shown strong operational capabilities but have

fared poorly in project management and execution. A capacity addition of 41,110 MW was

planned in the 10th five year plan period, against which only 21,180 MW was achieved, i.e., an

achievement of merely 51.5% against the set target.

As on 31st March 2011, 41,297 MW of capacity has been added during the 11th Plan against

the revised plan target of 62,374 MW (66%). It is widely expected that the actual realization

would not exceed 50 GW3, during the end of 11th 5 year plan.

In addition to bottlenecks in manufacturing (i.e. BTG and BoP manufacturers); environment

clearances and land acquisition have been the major issues for delay in project execution.

Investment of time, effort and money in developing project planning and project execution

capabilities, streamlining of business processes and adoption of advanced technologies in the

sector would enable the investors overcome such strategic hurdles to a large extent.

SNN INFRA POWER PROJECTS PRIVATE LIMITED 18

Change in regulation in transmission sector

Mid of 2010, CERC issued new regulation on Point of Connection (PoC) method for sharing of

transmission charges of inter-state transmission services in India. Point-of- connection (POC)

scheme of transmission pricing charges the participants a single rate per MW depending on

their point-of- connection.

According to the commercial arrangement proposed under the PoC regime, the CTU would now

be responsible for collection and settle of transmission charges on behalf of all transmission

service providers. This would imply that there would no more be a TSA directly between

transmission service providers and the beneficiaries (DICs). The collections would be disbursed

by the CTU among the transmission service providers on pro-rata basis.

The change in regime is expected to increase the perceived business risk for transmission

sector. Investors would no longer treat transmission as a safe business, if the issues pertaining

to the change in regulation are not addressed.

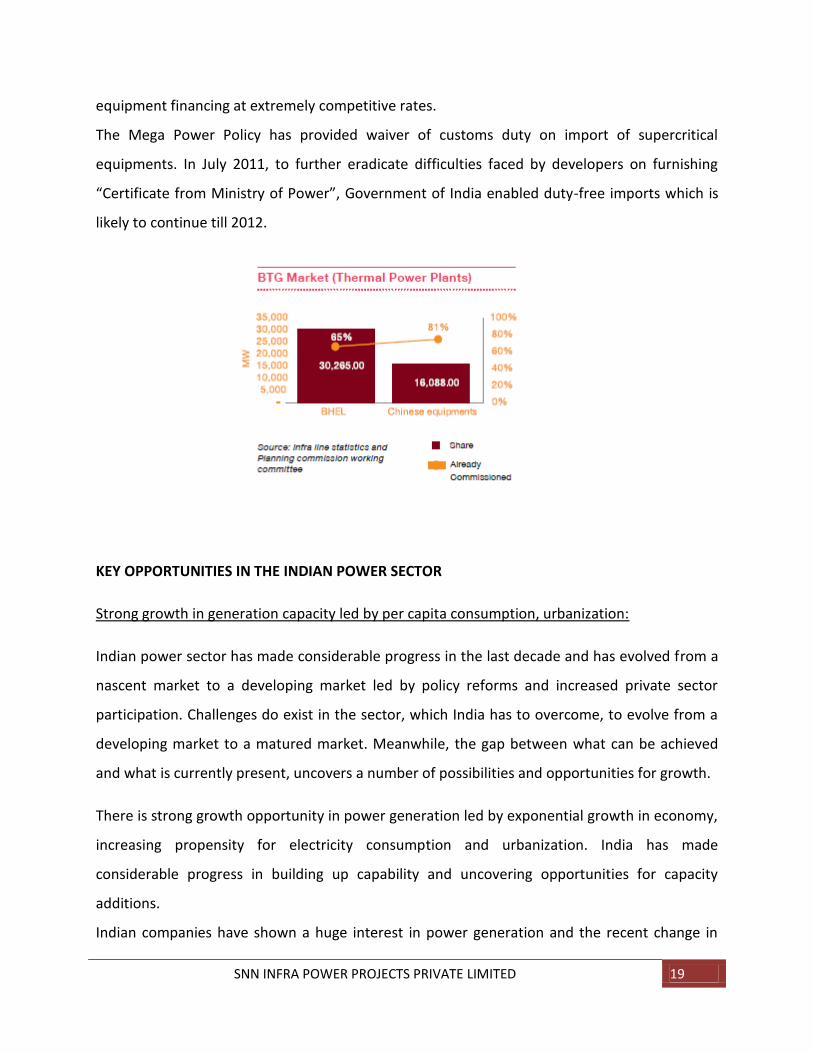

Competition from International OEM

The strong demand growth in the country has led to increased competition for domestic BTG

industry from OEMs based in China (like Shanghai Electric, Donfang Electric Group and Harbin

Power Equipments), as several private players are opting to import BTG sets from China due to

faster delivery of equipments and lower cost of sourcing. The prices quoted by Chinese

manufacturers are below INR 2 crores/MW compared to price range of INR 2.8-3.2 crores/MW

of domestic OEMs (Infra line Research).

Importing equipment also provide developers opportunity to tap into Export Credit Market for

SNN INFRA POWER PROJECTS PRIVATE LIMITED 19

equipment financing at extremely competitive rates.

The Mega Power Policy has provided waiver of customs duty on import of supercritical

equipments. In July 2011, to further eradicate difficulties faced by developers on furnishing

“Certificate from Ministry of Power”, Government of India enabled duty-free imports which is

likely to continue till 2012.

KEY OPPORTUNITIES IN THE INDIAN POWER SECTOR

Strong growth in generation capacity led by per capita consumption, urbanization:

Indian power sector has made considerable progress in the last decade and has evolved from a

nascent market to a developing market led by policy reforms and increased private sector

participation. Challenges do exist in the sector, which India has to overcome, to evolve from a

developing market to a matured market. Meanwhile, the gap between what can be achieved

and what is currently present, uncovers a number of possibilities and opportunities for growth.

There is strong growth opportunity in power generation led by exponential growth in economy,

increasing propensity for electricity consumption and urbanization. India has made

considerable progress in building up capability and uncovering opportunities for capacity

additions.

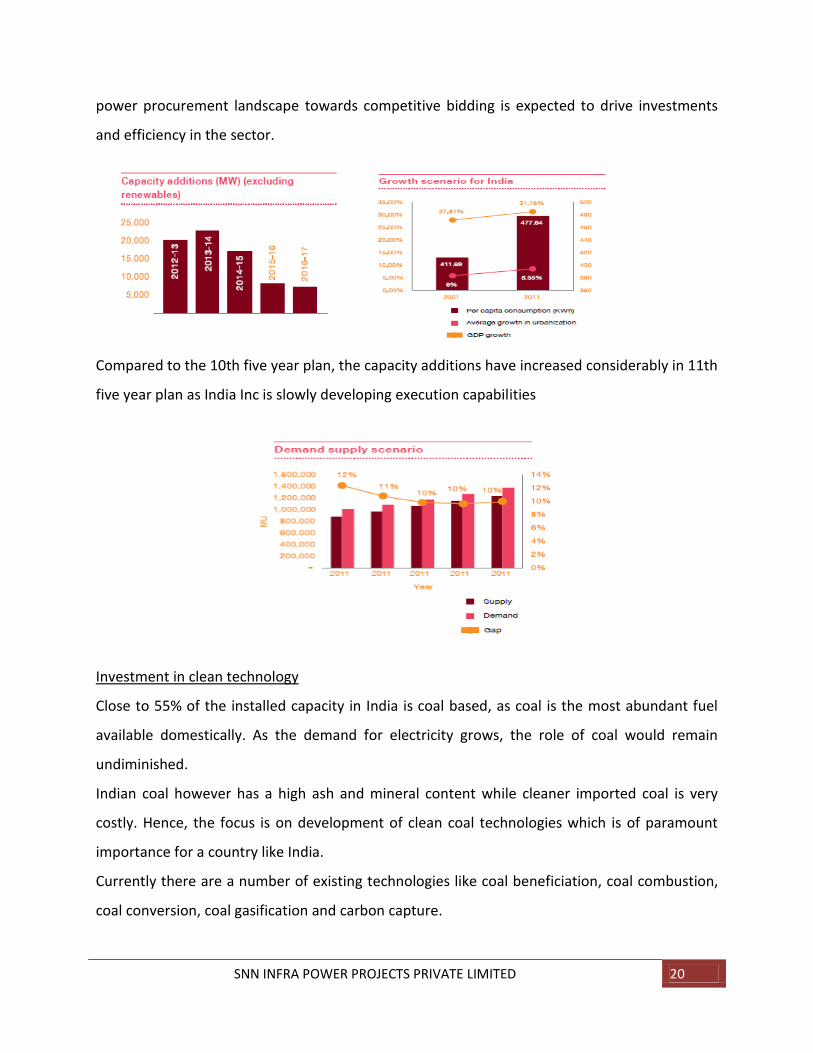

Indian companies have shown a huge interest in power generation and the recent change in

SNN INFRA POWER PROJECTS PRIVATE LIMITED 20

power procurement landscape towards competitive bidding is expected to drive investments

and efficiency in the sector.

Compared to the 10th five year plan, the capacity additions have increased considerably in 11th

five year plan as India Inc is slowly developing execution capabilities

Investment in clean technology

Close to 55% of the installed capacity in India is coal based, as coal is the most abundant fuel

available domestically. As the demand for electricity grows, the role of coal would remain

undiminished.

Indian coal however has a high ash and mineral content while cleaner imported coal is very

costly. Hence, the focus is on development of clean coal technologies which is of paramount

importance for a country like India.

Currently there are a number of existing technologies like coal beneficiation, coal combustion,

coal conversion, coal gasification and carbon capture.

SNN INFRA POWER PROJECTS PRIVATE LIMITED 21

India has made some progress in implementing super critical, pulverized coal combustion, coal

gasification technologies. Such technology choices would have a long term impact (life of the

plant) and needs to be chosen carefully. More favourable policy initiatives would help

overcome any economic hurdles towards which investors might face.

CONCLUSION

The last decade has seen a sea change in India’s electricity sector, from being 10th largest in the

world to 5th largest now. The industry is moving away from negotiated & guaranteed

arrangements of the past era, to more open market and performance based competition. The

approach now is more pro-investment, although the legacy problems of cross-subsidies, losses,

and rural access remain a challenge. The private sector has emerged as a key player in both

conventional and renewable power, and increasingly in other parts of the business. There is still

a long way to go.

The significant achievements of the power sector all sit atop a distribution business that

depends on subsidies and carries growing uncovered financial losses. The losses are said to

have ballooned to over Rs 1 lakhs crores and could get worse as we import higher proportion of

coal and as global commodity prices rise. The resulting uncovered losses will impact the

consumers and investors unless vigorous distribution reforms are pursued.

An encouraging development is the larger number of private bidders showing interest in

distribution. The recent DF (Distribution Franchisee) tenders have attracted 20 to 30 bidders,

and many bring experience from other industries such as power equipment, construction, and

SNN INFRA POWER PROJECTS PRIVATE LIMITED 22

telecoms and IT. This helps seed in new technologies and strategies, such as the use of smart

meters, targeting tools and CRM (Customer Relationship Management), shared services,

standardization, multi-skilling, and other techniques that can upgrade management of

distribution businesses. The size of the distribution opportunity is very large; India could easily

have over 50-60 specialist DF companies even at an enhanced size, that will attract more

investment and innovation.

It is important to get back to basics, namely tariff reforms, private participation, and

competition to make the sector attractive to capital flow. In last one decade, bank credit

doubled in share from about 6% to 12% , and many private and state-owned power companies

accessed capital markets. But it is hard to see the investors and lender return in strength

without an improvement in overall credit standing of the power sector. Addressing sector

viability is a must to avoid risk of non-performing assets cascading upstream. The Discoms must

aggressively pursue performance improvement as the new generation capacity coming from

large UMPPs to smaller solar power plants, can be both a boon (with improved supply and

additional revenue) and a bane (worsening financial losses leading into a liquidity crunch)

depending on how effectively the losses on every kWh sold are reduced.

The spotlight is as much on sector regulation as financial viability of licensees. The sector is

impacted with several years of not revising tariffs, even to cover genuine and reasonable cost

increases. To avoid lumpy hikes and inter-generational conflicts, there is a need to significantly

improve the multi-year tariff methodology to incorporate costs in time, say on quarterly and

annual basis.

Given our energy mix, and fast growing demand, we need to equally pay attention to the

challenges of climate change. The energy efficiency initiatives introduced by the BEE (Bureau of

Energy Efficiency) and others are necessary to reduce our energy intensity, but for them to bear

fruit, we also need to redesign tariff structures to be cost reflective. The REC mechanism is a

major step forward to bring renewable energy into market pricing, in a way that helps move

away from administrative feed-in tariffs, but the REC market cannot form if the RPO (renewable

procurement obligation) is not mandatory.

A closure can now be drawn on industry restructuring with unbundling nearly concluded.

SNN INFRA POWER PROJECTS PRIVATE LIMITED 23

However, there remains considerable work in enhancing the capabilities and systems of these

new companies and in preparing the STUs (State Transmission Unit) to act independently. The

regulatory process for open access approvals also needs streamlining and made more

transparent to promote competition. There is a good case for pursuing open access and

competition for the long-term economic gain in investment, employment, better supply and

lower tariffs.

Energy security is a significant challenge for future as coal based power plants fuel about

80% of power generation today and increasingly coal is imported. The regional electricity

market integration initiated with Nepal, Bangladesh, and Sri Lanka and the strengthening of

Bhutan relationship through the umbrella agreement are important for regional energy

security. Hybrid technologies can also help such as use of concentrated solar power to pre-heat

at power plants to save on coal and transport costs, which will only become costlier over time.

The interest in power sector has spurred a rush for resources viz. wind zones, coal blocks and

hydro sites; and those owning these resources discovered tendering them a good way to raise

funds, in form of upfront premium, in-kind royalty payments over the term, etc. The challenge

is to ensure that these do not end up in a race to corner scarce resources but translate into

producing assets.

The power sector plays a key role in industrialization and urbanization of India and faces

challenges in absorbing high cost of inputs. It plays a socially responsible role in bridging rural-

urban disparities by improving provision of affordable commercial energy access. These are

important goals, and will help improve living standards of a billion people directly and

indirectly, but will clearly need support and collaborative working of all the stakeholders.

SNN INFRA POWER PROJECTS PRIVATE LIMITED 24

Andhra Pradesh electricity scenario

In 1999, the first phases of electricity reforms were initiated in Andhra Pradesh, with

unbundling of the erstwhile AP State Electricity Board (APSEB) into APTRANSCO and APGENCO

in Feb1999. APTRANSCO was further restructured into APTRANSCO managing the transmission

system, and four distribution companies.

Current market scenario of Andhra Pradesh electricity market are highlighted below

Andhra Pradesh has a total thermal installed capacity of 10,797 MW, out of which state

generation utility AP Genco owns over 3,800 MW.

Majority of the 3,734 MW hydro capacity is owned by AP Genco.

Total renewable capacity for the state stands at 870.5 MW.

The CAGR of Domestic & Non-Domestic Consumer has increased by 10.9% & 30.4%

respectively (FY08-10).

The CAGR of agricultural consumer has increased by 9.8% (FY08-10).

The CAGR of industrial HT & LT consumer has increased by 6.7% and 0.2% respectively

Andhra Pradesh had peak and energy deficits of 12.5% and 6.4% in FY12 (till Dec).

Peak and Energy deficits in Andhra Pradesh were at their highest in FY07 and FY09 at

15.4% and 6.8% respectively

Peak and energy deficits for FY11 stood at 6.3% and 3.2% respectively

SNN INFRA POWER PROJECTS PRIVATE LIMITED 25

Need for the project

POWER CRISIS IN ANDHRA PRADESH:

Andhra Pradesh is facing sever power crisis over the last year and half due to increased demand

as also various other reasons. Some of the key findings with regards to the worsening electricity

situation in Andhra Pradesh are explained below

According to APTRANSCO the total demand in the first quarter of 2012 was 261MU per

day while the DISCOMS were able to supply only 245MU per day.

The total demand from April 2011 to February 2012 was 81,320 MU as against 71,301

MU registering a 14% rise in demand.

The average deficit of power this year has been 6.2% in spite of addition of 5311MW

over the last seven years.

Of the nine gas based projects in the state with a combined capacity of 2772 MW only

1272 MW is in generation due to lack of availability of gas.

The Singereni strike last year also added to the woes of the power crisis in the state.

The hydel generation in the state also has decreased from 7048MU to 5837 MU. Severe

transmission corridor constraints also lead to lesser availability of power from the NE

grid.

In the industrial sector 12 days in a month have been declared as power holidays for

SME as well as large scale industries in the state thereby explaining the deteriorating

situation.

Andhra Pradesh state government has recently hiked charges of power to consumers to

overcome financial burdens of the DISCOMS. The state government has recently proposed to

increase tariffs by a minimum of 20% starting April 2013 to overcome the financial burden.

According to recent estimates the state government would need 49,189 INR crores to supply 1

trillion unites of power in the current year but the current recoveries using the DISCOMS is only

around 31,000 INR crores. Of the state deficit around 6000 INR crores would be given to

DISCOMS by the state government and the balance would be through increase in power tariffs.

SNN INFRA POWER PROJECTS PRIVATE LIMITED 26

Over the last year the hikes in power tariffs have been more than thrice in the state.

ADVANTAGES OF THE PROJECT PROPONENTS AND INVESTORS

Operational capabilities of the SI group: The strategic investor group led by KOSEP has

exceptional operational capabilities in the thermal power sector. KOSEP has two major

plants with each operating capacity of over 3000MW capacity and their PLF on average

is more than 90% in the last few years. KEPCO KPS has immense experience in O&M of

virtually every type of fuel in the power sector while PTC India is India’s first company

completely concentrating on power sale. Thus all the three factors together give

exceptional advantage to the project over the others for successful running.

Experience of the group: KOSEP, KEPC KPS and PTC have immense capacity and

experience of successfully managing thermal power plants. Unlike even big Indian firms

like RELIANCE POWER or LANCO INFRA or JSPL which are either in the starting stage or

have minimal capacity running till now KOSEP and the SI group have vast experience like

NTPC and with its vast experience, technology and financial capabilities could prove

more successful in operating projects in India.Though the market has many players in

the sector very few of them actually have the capacity to materialize the projects

planned like KOSEP, KPS & PTC.

Excellent opportunity in the sector: Indian economy is growing at a pace which is second

only to China and thus any company in any sector would see India as a boon for their

project because of huge scope of development. Indian infrastructure requires a lot of

investment and expertise from foreign participants like KOSEP with technical knowhow

knowledge. A large deficiency of power in India and lack of meeting targets over the last

few plans provide the project and its SI’s a valuable opportunity to make its footprint

into Indian power sector.

Availability of coal at competitive prices: Over the last few Indian power sector has been

facing extreme hardships for running due to high cost of imported coal and non

availability of domestic coal. KOSEP has long term relationship with SAMTAN mining

corporation of Korea which has 49% stake in one of the largest mines in Indonesia

SNN INFRA POWER PROJECTS PRIVATE LIMITED 27

KIDECO MINES. KOSEP imports coal from the mines at approximately 10% cheaper price

than others thus becoming more competitive in the Indian power sector.

Availability of the land: The land for the project has no rehabilitation issues and also not

environmental sensitive thus making the project more realistic of coming to production.

The toughest part in starting a power project is land and the land identified for the

project would be ideal due to its coastal region, lack of forest, human inhabitance in the

site and also supportive villagers for industrial development.

SNN INFRA POWER PROJECTS PRIVATE LIMITED 28

General features of the project

Location: Vemavaram village, Thondangi Mandal, East Godavari district, Andhra Pradesh

Extent of land: 700 acres

Land classification: 500 acres single crop land and 200 dry scrub land

Seismic zone of the site: Zone number 2 as per IS 1983

Wildlife sanctuaries and reserve areas in the surrounding areas: none

Rehabilitation issues for the project: none

Land ownership: private lands held by large families

HTL: As per the CRZ coastal regulatory zone rules of coastline the land does not come

under the 500 meters of the High tide line.

Price of the land: Ranging from 600000-1300000 per acre

Surrounding villages: Pydikonda, Vemavaram

Fishing village: None

Interstate borders: none

Railway station: 7 km from the site

Jetty construction feasibility: yes, sea draft I around 15 mts which is ideal for

construction of jetty

Defense areas: None

Archeological important areas: None

Estuaries, water bodies and ecological sensitive areas: None

SNN INFRA POWER PROJECTS PRIVATE LIMITED 29

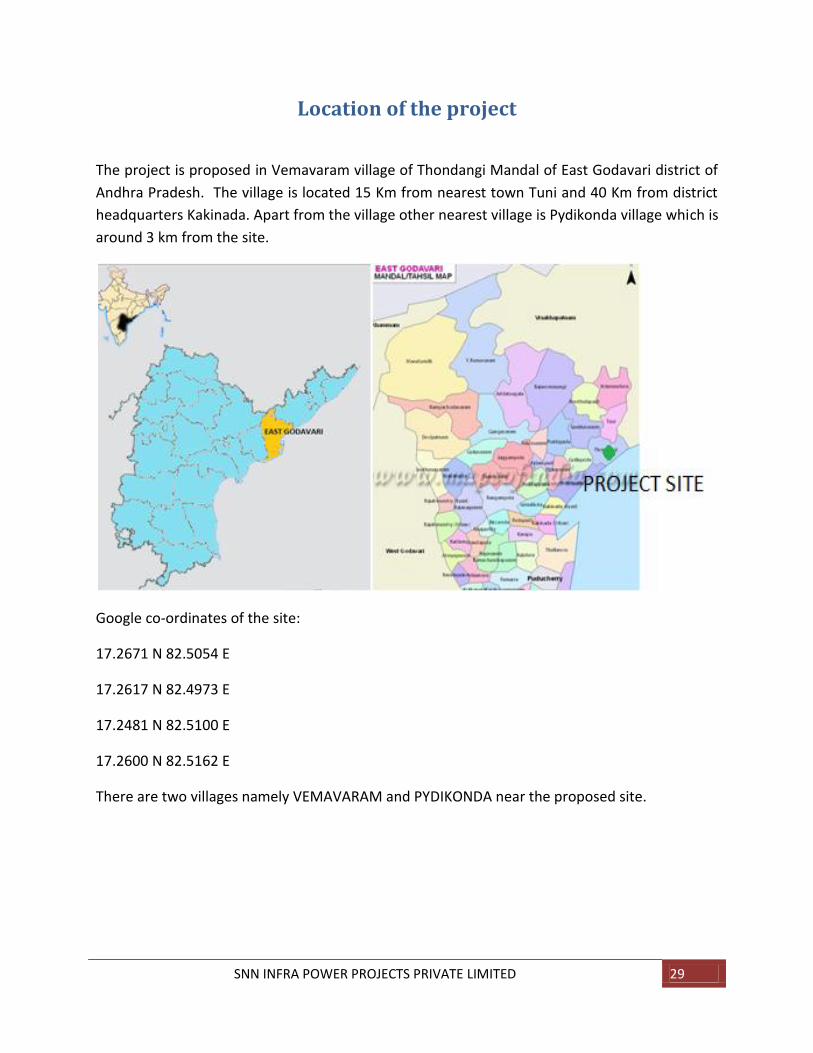

Location of the project

The project is proposed in Vemavaram village of Thondangi Mandal of East Godavari district of

Andhra Pradesh. The village is located 15 Km from nearest town Tuni and 40 Km from district

headquarters Kakinada. Apart from the village other nearest village is Pydikonda village which is

around 3 km from the site.

Google co-ordinates of the site:

17.2671 N 82.5054 E

17.2617 N 82.4973 E

17.2481 N 82.5100 E

17.2600 N 82.5162 E

There are two villages namely VEMAVARAM and PYDIKONDA near the proposed site.

SNN INFRA POWER PROJECTS PRIVATE LIMITED 30

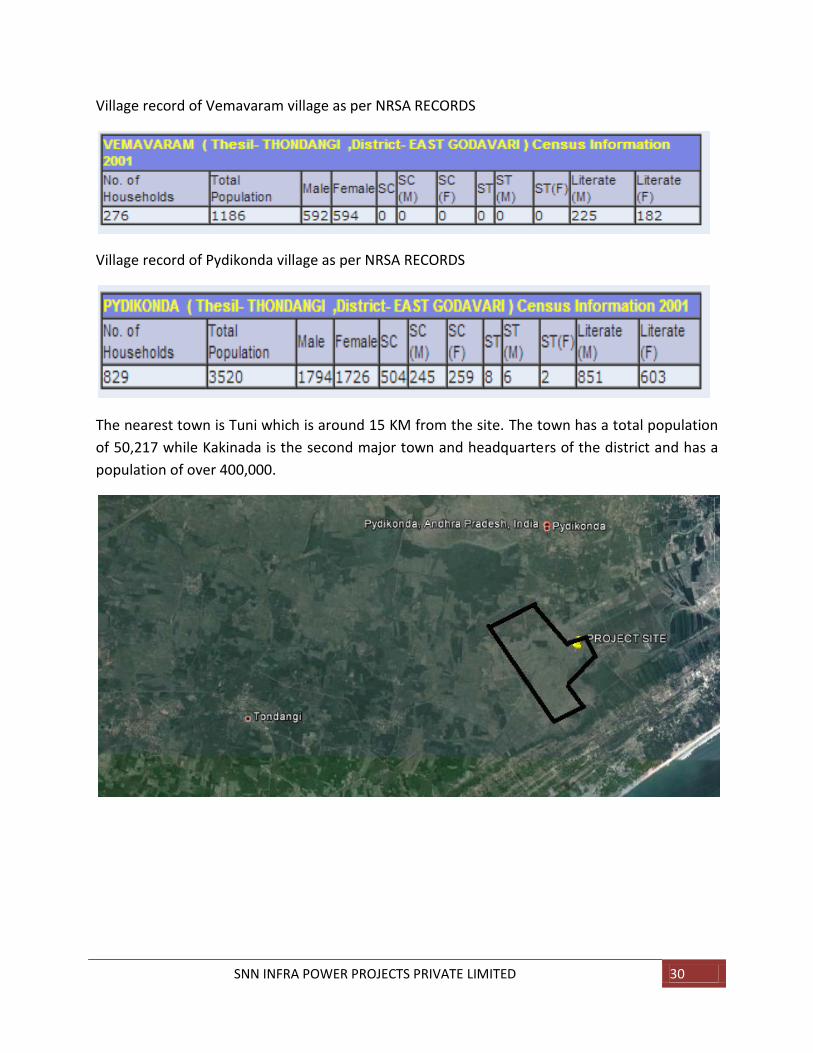

Village record of Vemavaram village as per NRSA RECORDS

Village record of Pydikonda village as per NRSA RECORDS

The nearest town is Tuni which is around 15 KM from the site. The town has a total population

of 50,217 while Kakinada is the second major town and headquarters of the district and has a

population of over 400,000.

SNN INFRA POWER PROJECTS PRIVATE LIMITED 31

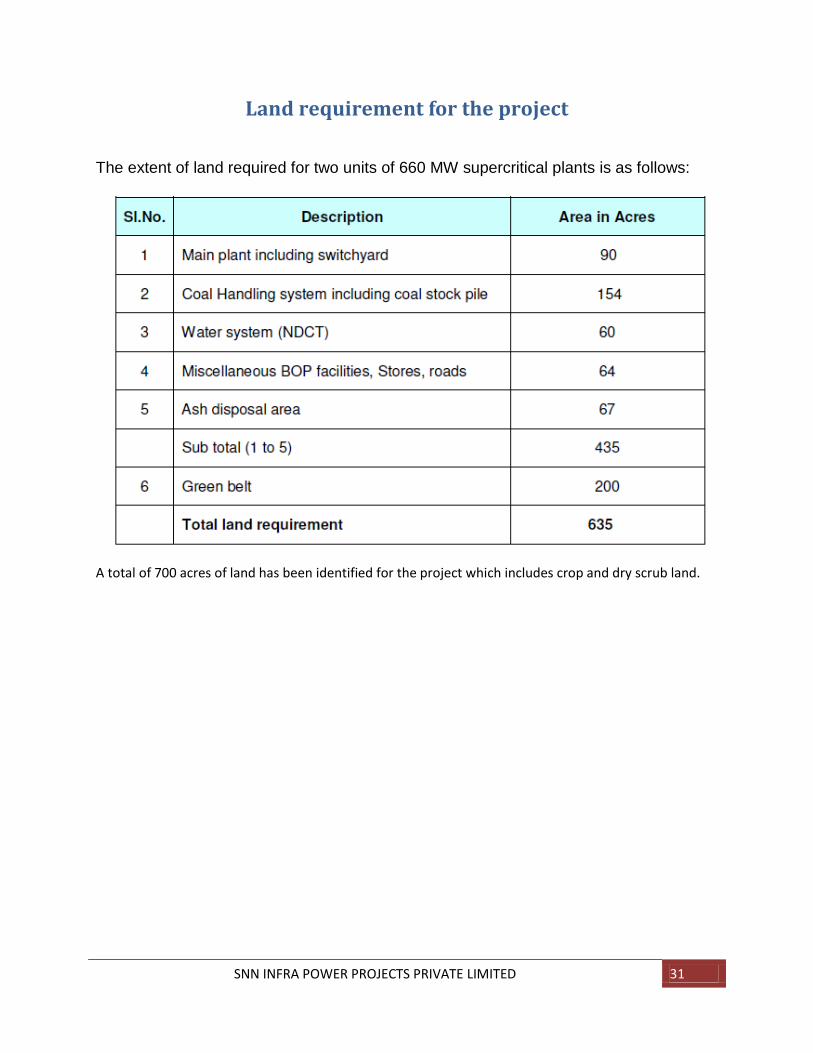

Land requirement for the project

The extent of land required for two units of 660 MW supercritical plants is as follows:

A total of 700 acres of land has been identified for the project which includes crop and dry scrub land.

SNN INFRA POWER PROJECTS PRIVATE LIMITED 32

Ecological aspects of the proposed project

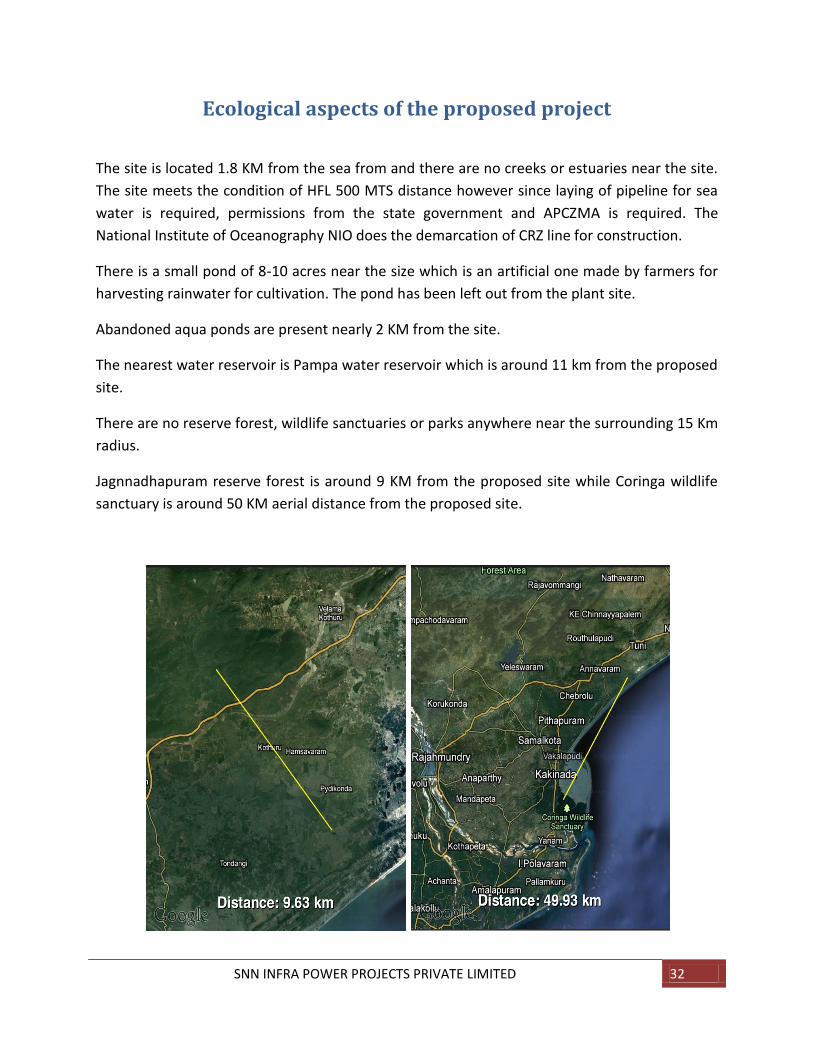

The site is located 1.8 KM from the sea from and there are no creeks or estuaries near the site.

The site meets the condition of HFL 500 MTS distance however since laying of pipeline for sea

water is required, permissions from the state government and APCZMA is required. The

National Institute of Oceanography NIO does the demarcation of CRZ line for construction.

There is a small pond of 8-10 acres near the size which is an artificial one made by farmers for

harvesting rainwater for cultivation. The pond has been left out from the plant site.

Abandoned aqua ponds are present nearly 2 KM from the site.

The nearest water reservoir is Pampa water reservoir which is around 11 km from the proposed

site.

There are no reserve forest, wildlife sanctuaries or parks anywhere near the surrounding 15 Km

radius.

Jagnnadhapuram reserve forest is around 9 KM from the proposed site while Coringa wildlife

sanctuary is around 50 KM aerial distance from the proposed site.

SNN INFRA POWER PROJECTS PRIVATE LIMITED 33

Accessibility to the site

Accessibility of the site:

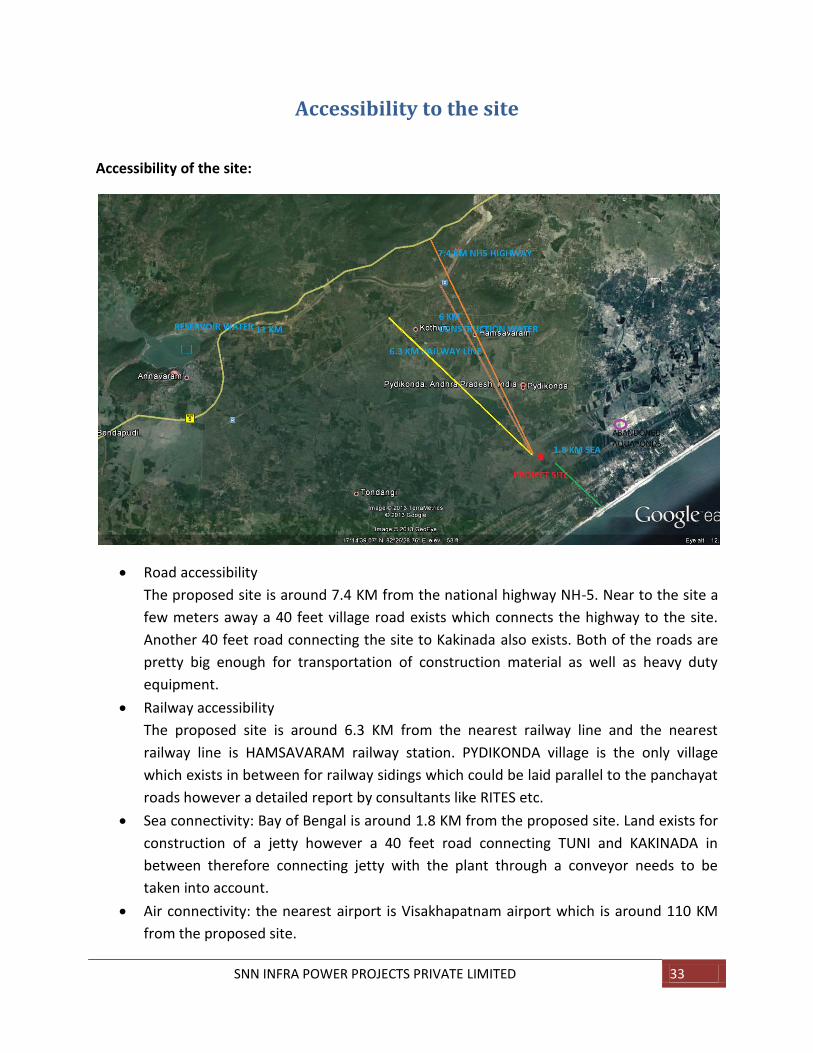

Road accessibility

The proposed site is around 7.4 KM from the national highway NH-5. Near to the site a

few meters away a 40 feet village road exists which connects the highway to the site.

Another 40 feet road connecting the site to Kakinada also exists. Both of the roads are

pretty big enough for transportation of construction material as well as heavy duty

equipment.

Railway accessibility

The proposed site is around 6.3 KM from the nearest railway line and the nearest

railway line is HAMSAVARAM railway station. PYDIKONDA village is the only village

which exists in between for railway sidings which could be laid parallel to the panchayat

roads however a detailed report by consultants like RITES etc.

Sea connectivity: Bay of Bengal is around 1.8 KM from the proposed site. Land exists for

construction of a jetty however a 40 feet road connecting TUNI and KAKINADA in

between therefore connecting jetty with the plant through a conveyor needs to be

taken into account.

Air connectivity: the nearest airport is Visakhapatnam airport which is around 110 KM

from the proposed site.

SNN INFRA POWER PROJECTS PRIVATE LIMITED 34

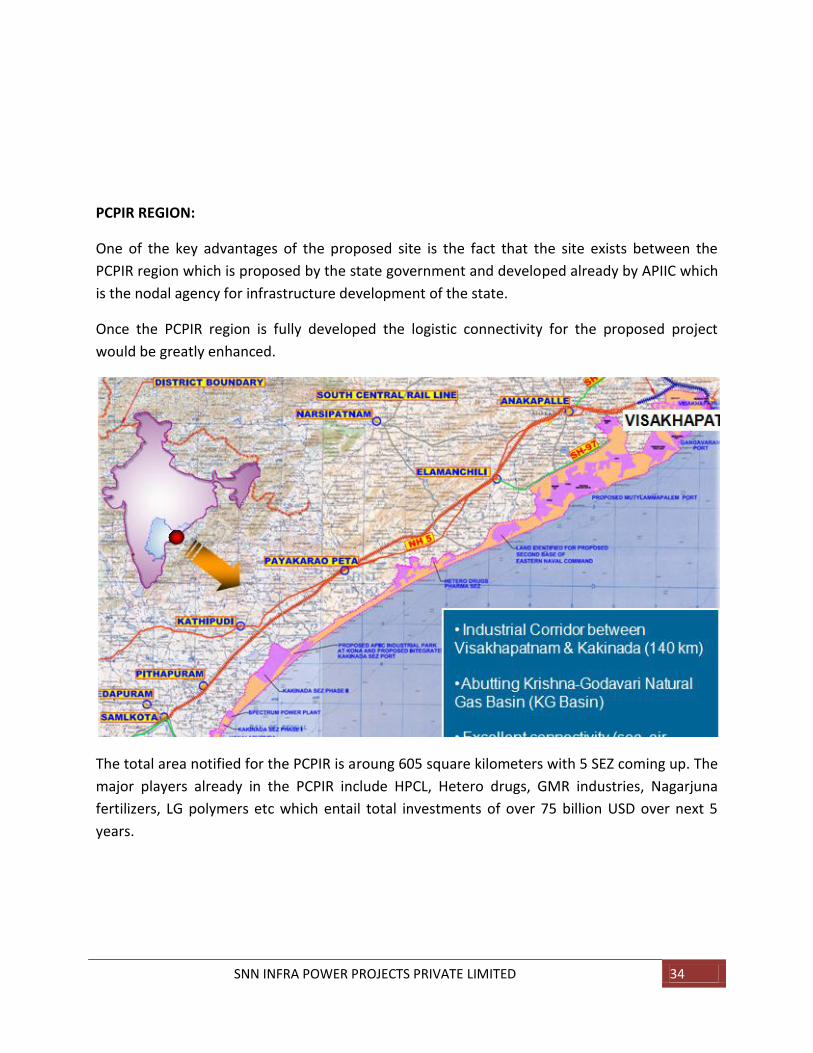

PCPIR REGION:

One of the key advantages of the proposed site is the fact that the site exists between the

PCPIR region which is proposed by the state government and developed already by APIIC which

is the nodal agency for infrastructure development of the state.

Once the PCPIR region is fully developed the logistic connectivity for the proposed project

would be greatly enhanced.

The total area notified for the PCPIR is aroung 605 square kilometers with 5 SEZ coming up. The

major players already in the PCPIR include HPCL, Hetero drugs, GMR industries, Nagarjuna

fertilizers, LG polymers etc which entail total investments of over 75 billion USD over next 5

years.

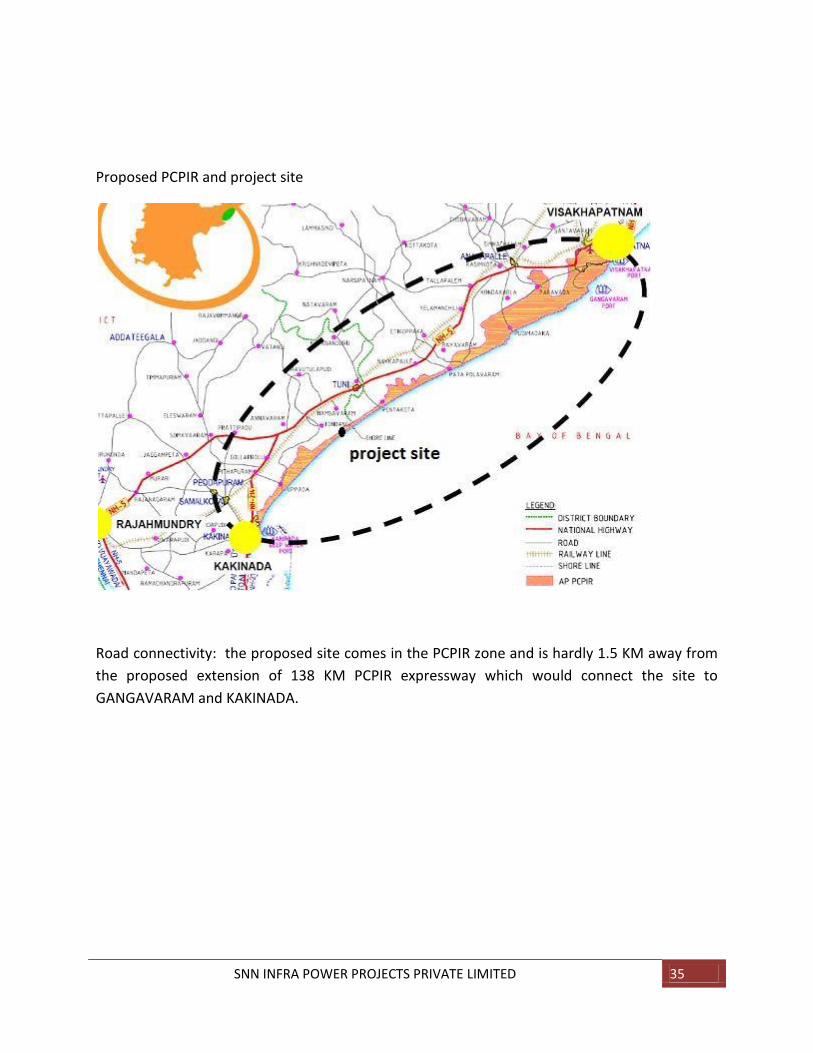

SNN INFRA POWER PROJECTS PRIVATE LIMITED 35

Proposed PCPIR and project site

Road connectivity: the proposed site comes in the PCPIR zone and is hardly 1.5 KM away from

the proposed extension of 138 KM PCPIR expressway which would connect the site to

GANGAVARAM and KAKINADA.

SNN INFRA POWER PROJECTS PRIVATE LIMITED 36

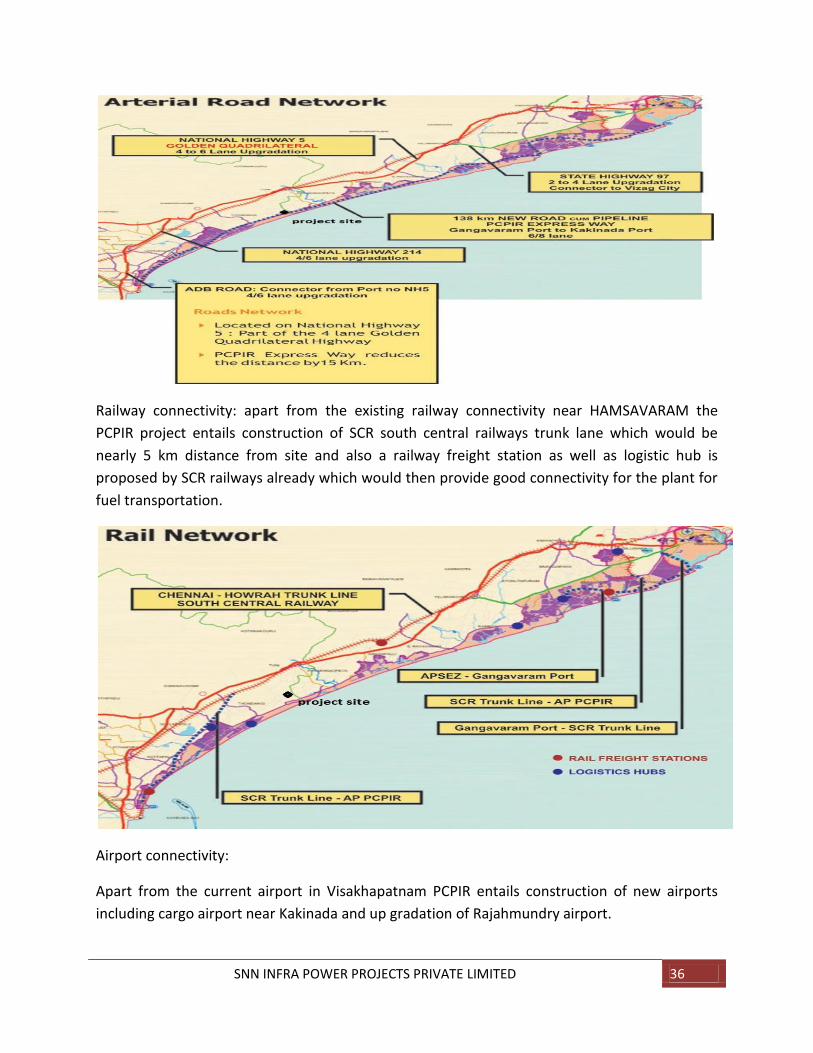

Railway connectivity: apart from the existing railway connectivity near HAMSAVARAM the

PCPIR project entails construction of SCR south central railways trunk lane which would be

nearly 5 km distance from site and also a railway freight station as well as logistic hub is

proposed by SCR railways already which would then provide good connectivity for the plant for

fuel transportation.

Airport connectivity:

Apart from the current airport in Visakhapatnam PCPIR entails construction of new airports

including cargo airport near Kakinada and up gradation of Rajahmundry airport.

SNN INFRA POWER PROJECTS PRIVATE LIMITED 37

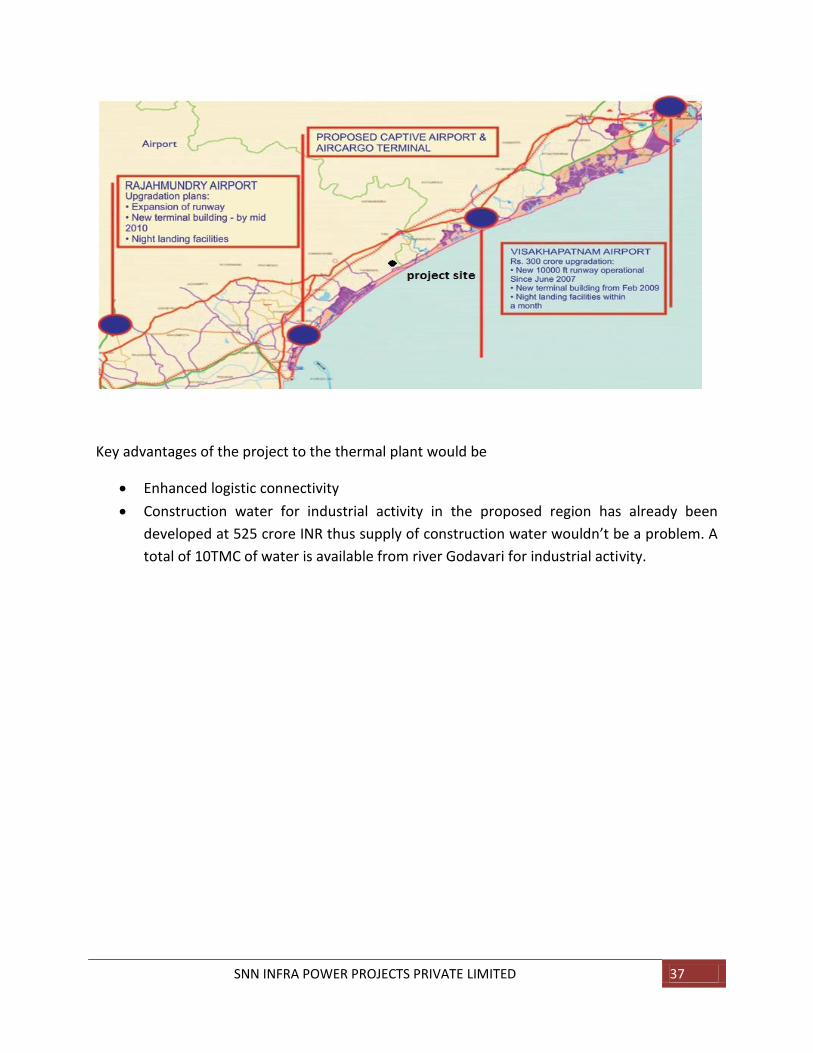

Key advantages of the project to the thermal plant would be

Enhanced logistic connectivity

Construction water for industrial activity in the proposed region has already been

developed at 525 crore INR thus supply of construction water wouldn’t be a problem. A

total of 10TMC of water is available from river Godavari for industrial activity.

SNN INFRA POWER PROJECTS PRIVATE LIMITED 38

Technical issues of the project

Fuel

The proposed project would use steam coal as fuel for the project. The project is proposed to

use either 70:30 domestic to imported coal or 100% imported coal from Indonesia incase of

lack of availability of coal in India. Typically the Indian coal allocated for the power plant has

less calorific value and high ash content when compared to imported coal which has

comparatively higher GCV and less ash content. CEA have stipulated that all coastal power

projects will be allocated upto a maximum of only 70%. In the present scenario, obtaining coal

allocation from the Ministry of Coal is very difficult considering the coal shortage in the country

and the maximum allocation that can be expected could be only 30%. Therefore the major coal

source for the propose project could be only Imported coal. Therefore Imported coal is

considered for computing the area requirement for the proposed plant. The area requirement

for ash pond will be comparatively less with Imported coal and the report considers 100% ash

utilization from the 4th year of operation in line with MoEF regulations. The coal that is

considered is a typical sub-bituminous Indonesian coal that is presently adopted for many

projects considering the cost effectiveness. The GCV and ash content considered for computing

are 4200 Kcal/kg and 12% respectively.

Fuel transportation;

Coal will be received either in the nearest Port or in a captive jetty constructed for the project.

The available transportation modes for the site are by Railways and by Conveyors from coal

receiving point. The nearest Port being Kakinada port at about 30 km from the project site,

establishment of a coal conveyor system from the Port to plant site will not feasible. However

coal can bev conveyed by rail from the Port to the nearest Railway station Hamsavaram which

are at about 6.5 kms from the site area. From the station to the site area, a new railway line has

to be laid out for about 9 km to the site area and this requires a separate study by a railway

consultant for exploring the possibility of providing new line/ railway siding considering the

availability of corridor, traffic density etc. Another aspect to be considered in case of utilization

SNN INFRA POWER PROJECTS PRIVATE LIMITED 39

of existing Ports is that the capacity of the existing ports for the proposed additional capacity

and their willingness to include additional traffic and the commercial terms associated with it.

This needs discussions with the respective Ports for a complete assessment and finalization.

Coal handling system:

In crusher house the coal will be screened and crushed. Crushed coal will be conveyed to the

Steam Generator (SG) bunkers / stored in stockpile. Crushed coal from the stockyard will be

reclaimed and conveyed, to the SG bunkers through belt conveyors as when required.

The system will comprise the following:

a. Unloading System, Crushing and Bunker Feeding System

b. Stacking, Reclaiming and Bunker Feeding System

Water requirement for the project:

Water requirement for the proposed 1320 MW power plant will be in the order of about 12500

m³/h with natural draft cooling tower (NDCT). The required water will be drawn from the Bay of

Bengal near the coal jetty. The intake pipe line can be routed along the conveyor system. Water

for ash slurry / bottom ash system has to be utilized from CT Blow down system. Plant water

requirements can be met by dedicated desalination system. Construction water requirement

for the plant will be about 750 m3 per day during peak construction period. The same can be

met from ground water / local water authorities.

Power evacuation:

Technical requirements of power evacuation from the proposed power plant will be decided by

the grid authority. The power delivery point will be firmed up based on the transmission study

by grid authority. The total power generated by the power plant will be 1320MW. After

meeting the auxiliary power consumption of 6% which is 79.2 MW, 1240.8 MW will be available

for export. Generated power will be stepped up to 400kV level by using step up generator

transformers. To enable power evacuation, a 400kV outdoor air insulated switchyard with one

and half breaker arrangement will be provided.

SNN INFRA POWER PROJECTS PRIVATE LIMITED 40

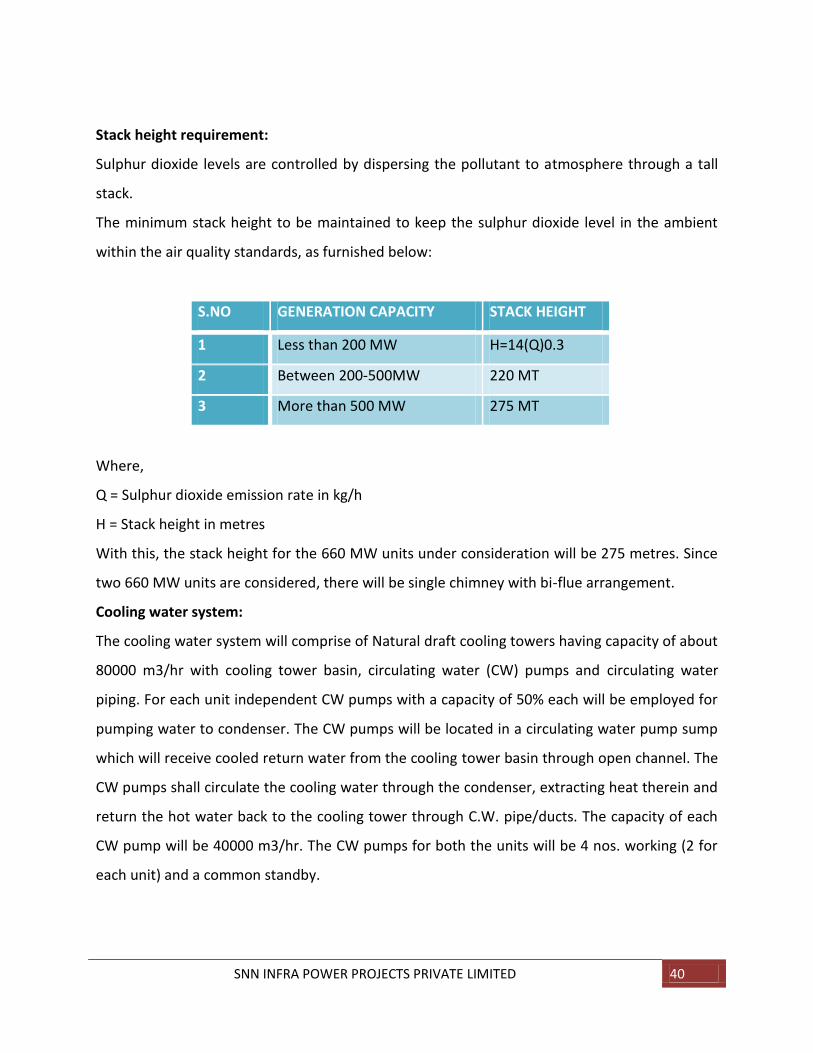

Stack height requirement:

Sulphur dioxide levels are controlled by dispersing the pollutant to atmosphere through a tall

stack.

The minimum stack height to be maintained to keep the sulphur dioxide level in the ambient

within the air quality standards, as furnished below:

S.NO GENERATION CAPACITY STACK HEIGHT

1 Less than 200 MW H=14(Q)0.3

2 Between 200-500MW 220 MT

3 More than 500 MW 275 MT

Where,

Q = Sulphur dioxide emission rate in kg/h

H = Stack height in metres

With this, the stack height for the 660 MW units under consideration will be 275 metres. Since

two 660 MW units are considered, there will be single chimney with bi-flue arrangement.

Cooling water system:

The cooling water system will comprise of Natural draft cooling towers having capacity of about

80000 m3/hr with cooling tower basin, circulating water (CW) pumps and circulating water

piping. For each unit independent CW pumps with a capacity of 50% each will be employed for

pumping water to condenser. The CW pumps will be located in a circulating water pump sump

which will receive cooled return water from the cooling tower basin through open channel. The

CW pumps shall circulate the cooling water through the condenser, extracting heat therein and

return the hot water back to the cooling tower through C.W. pipe/ducts. The capacity of each

CW pump will be 40000 m3/hr. The CW pumps for both the units will be 4 nos. working (2 for

each unit) and a common standby.

SNN INFRA POWER PROJECTS PRIVATE LIMITED 41

Ash handling system:

a. Bottom Ash Removal System will consist of a refractory lined W-shaped, water

impounded, storage type, water-cooled bottom ash hopper located directly below the

bottom water wall header of boiler. Bottom ash (BA) will be collected continuously. BA

hopper will be provided with clinker grinders to limit the size of clinkers. Bottom ash and

economiser ash slurry will be collected in the hydrobin and further disposed by the

trucks. In emergency case, i.e. non-availability of ash utilization, bottom ash slurry will

be diverted ash slurry sump and further to ash pond.

b. Fly ash collected in Air pre-heater hoppers and ESP hoppers will be evacuated by

vacuum cum pressure conveying system. Fly ash can be disposed off in dry mode

through buffer hopper. The dry fly ash collected in fly ash silos will be transported using

trucks. In case of emergency, during non-availability of fly ash utilization, fly ash will be

disposed in wet mode through collector tank and disposed to ash pond through slurry

pump.

c. Ash pond: For estimating the area required for ash pond, fly ash utilization and bottom

ash utilization are considered as per MoEF regulations. For ash handling system, blow

down water from Cooling Tower will be utilized. Dry ash from the silos will be loaded to

trucks for utilization purpose.

Switchyard:

Land requirement for switchyard depends on type of scheme, voltage level and number of bays.

The area requirement varies for 1-½ breaker scheme (D-type), 1-½ breaker scheme (Itype) and

2 main & transfer bus. Land requirement further gets reduced if Gas Insulated Switchgear

Switchyard (GIS) is used over Air Insulated Switchgear Switchyard. GIS option is generally

adopted in coastal areas or in areas where there is acute shortage of land. However a 400kV

outdoor air insulated substation is assumed for the current land requirement study although

GIS may also be selected for the 400 kV level.

SNN INFRA POWER PROJECTS PRIVATE LIMITED 42

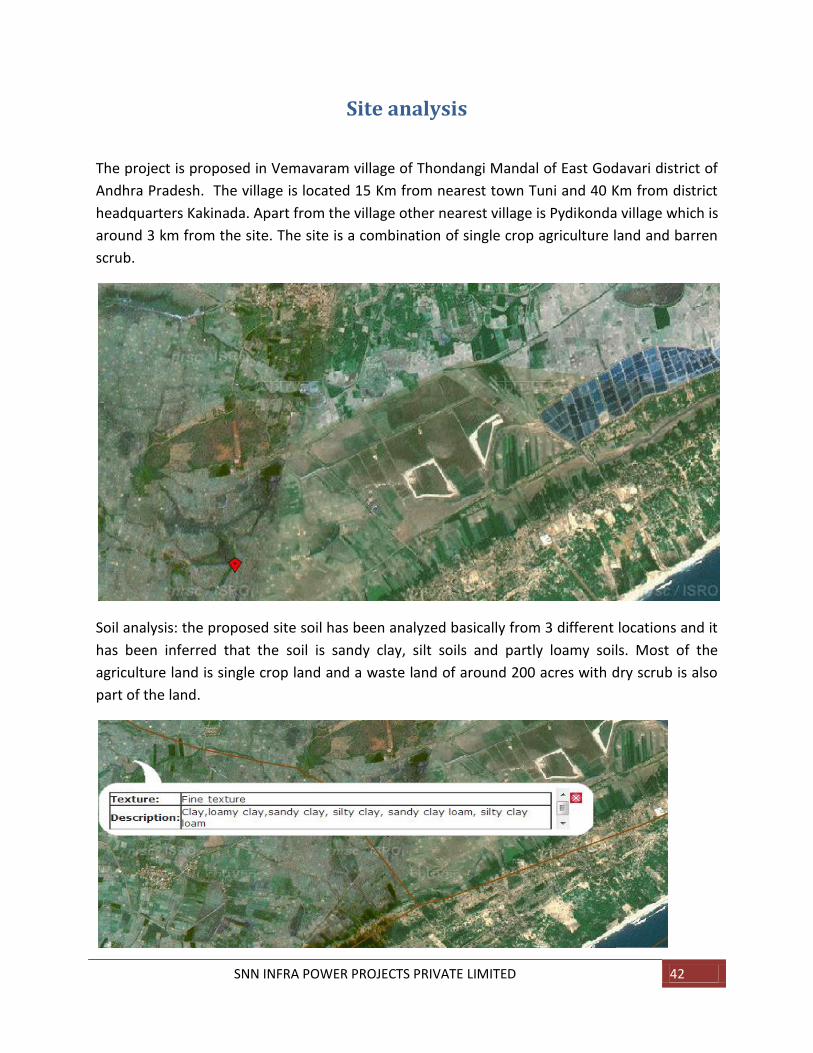

Site analysis

The project is proposed in Vemavaram village of Thondangi Mandal of East Godavari district of

Andhra Pradesh. The village is located 15 Km from nearest town Tuni and 40 Km from district

headquarters Kakinada. Apart from the village other nearest village is Pydikonda village which is

around 3 km from the site. The site is a combination of single crop agriculture land and barren

scrub.

Soil analysis: the proposed site soil has been analyzed basically from 3 different locations and it

has been inferred that the soil is sandy clay, silt soils and partly loamy soils. Most of the

agriculture land is single crop land and a waste land of around 200 acres with dry scrub is also

part of the land.

SNN INFRA POWER PROJECTS PRIVATE LIMITED 43

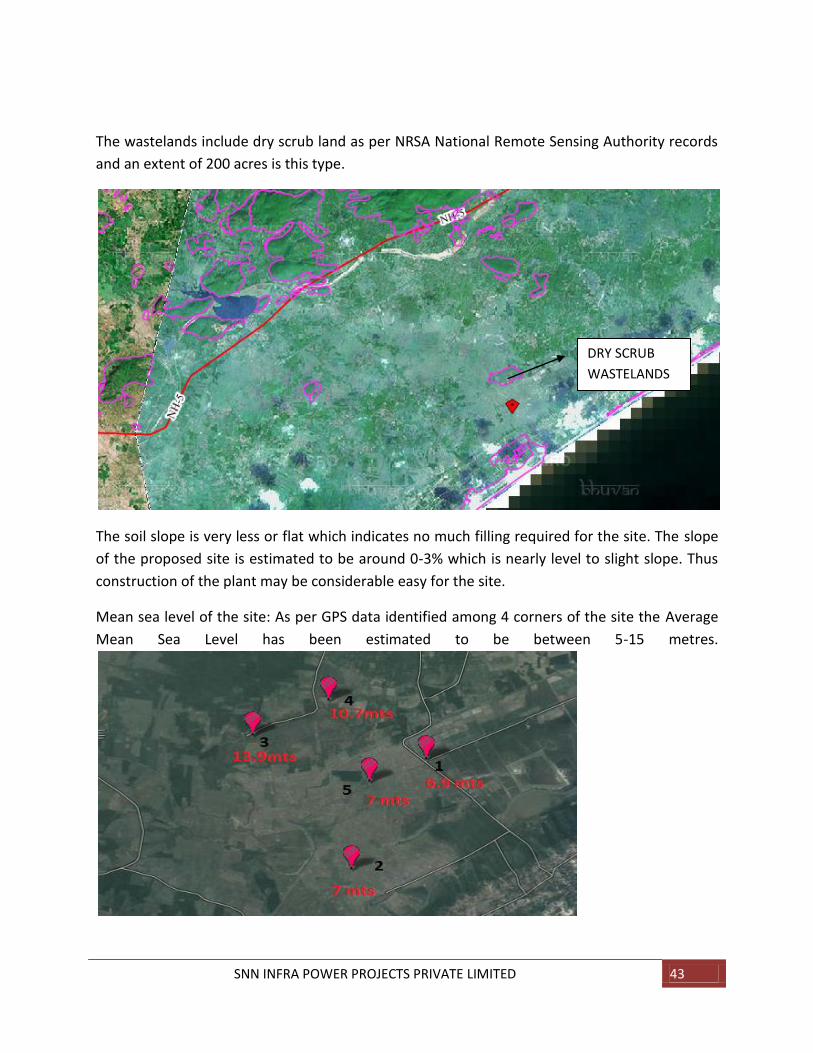

The wastelands include dry scrub land as per NRSA National Remote Sensing Authority records

and an extent of 200 acres is this type.

The soil slope is very less or flat which indicates no much filling required for the site. The slope

of the proposed site is estimated to be around 0-3% which is nearly level to slight slope. Thus

construction of the plant may be considerable easy for the site.

Mean sea level of the site: As per GPS data identified among 4 corners of the site the Average

Mean Sea Level has been estimated to be between 5-15 metres.

DRY SCRUB

WASTELANDS

SNN INFRA POWER PROJECTS PRIVATE LIMITED 44

Toposheet as per Survey of India records:

SNN INFRA POWER PROJECTS PRIVATE LIMITED 45

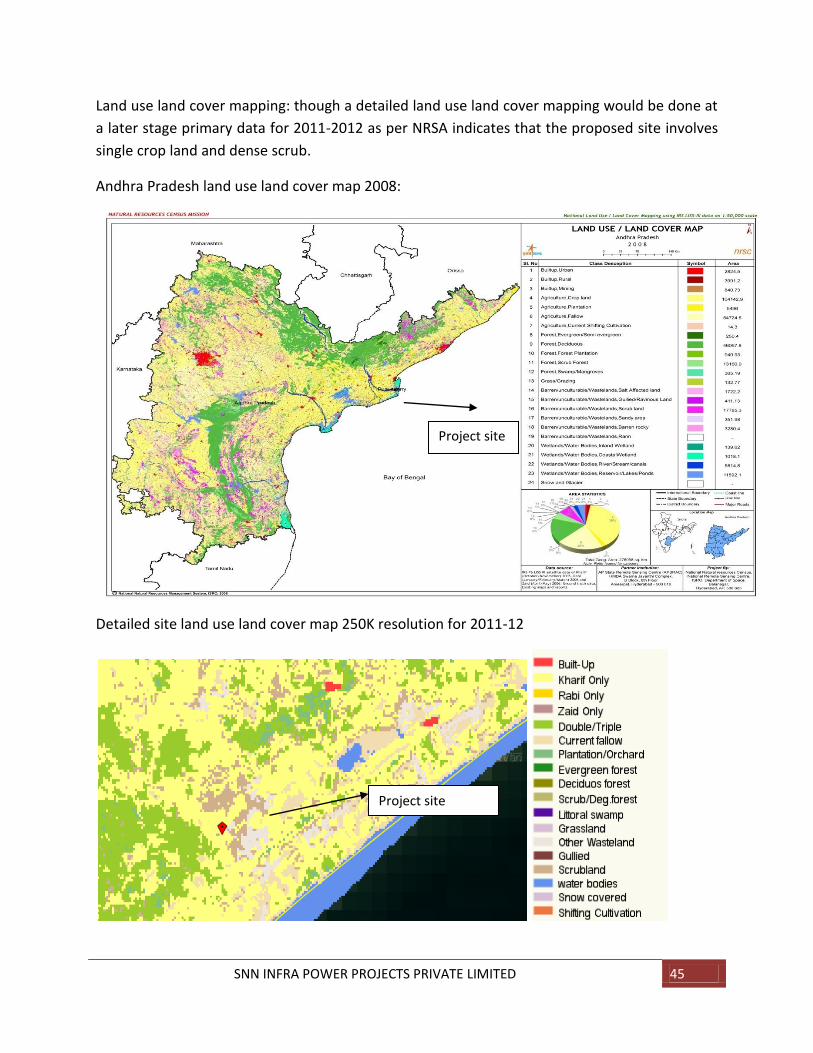

Land use land cover mapping: though a detailed land use land cover mapping would be done at

a later stage primary data for 2011-2012 as per NRSA indicates that the proposed site involves

single crop land and dense scrub.

Andhra Pradesh land use land cover map 2008:

Detailed site land use land cover map 250K resolution for 2011-12

Project site

Project site

SNN INFRA POWER PROJECTS PRIVATE LIMITED 46

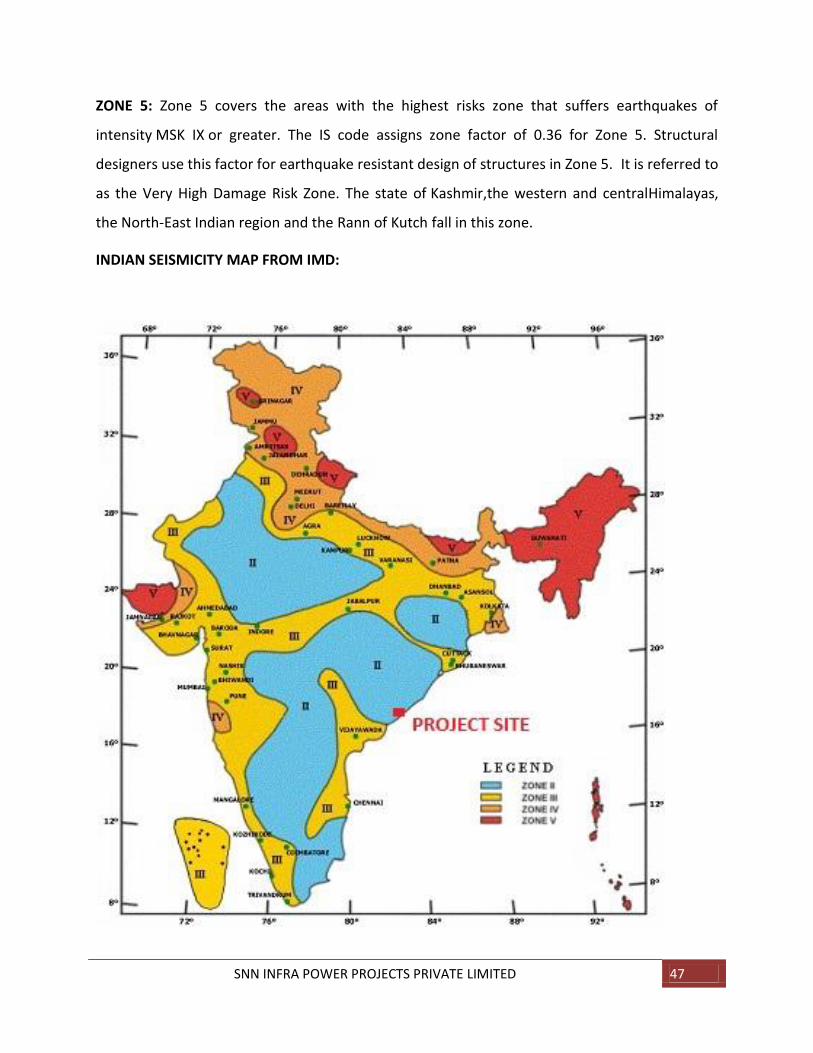

Seismicity and meteorology of the site

CLASSIFICATION OF INDIAN EARTHQUAKE REGIONS

The Indian subcontinent has a history of devastating earthquakes. The major reason for the

high frequency and intensity of the earthquakes is that the Indian plate is driving into Asia at a

rate of approximately 47 mm/year. Geographical statistics of India show that almost 54% of the

land is vulnerable to earthquakes.

The latest version of seismic zoning map of India given in the earthquake resistant design code

of India [IS 1893 (Part 1) 2002] assigns four levels of seismicity for India in terms of zone factors.

In other words, the earthquake zoning map of India divides India into 4 seismic zones (Zone 2,

3, 4 and 5) unlike its previous version which consisted of five or six zones for the country.

According to the present zoning map, Zone 5 expects the highest level of seismicity whereas

Zone 2 is associated with the lowest level of seismicity.

The MSK (Medvedev-Sponheuer-Karnik) intensity broadly associated with the various seismic

zones is VI (or less), VII, VIII and IX (and above) for Zones 2, 3, 4 and 5, respectively,

corresponding to Maximum Considered Earthquake(MCE).

ZONE 2: This region is liable to MSK VI or less and is classified as the Low Damage Risk Zone.

The IS code assigns zone factor of 0.10 (maximum horizontal acceleration that can be

experienced by a structure in this zone is 10% of gravitational acceleration) for Zone 2.

ZONE 3: The Andaman and Nicobar Islands, parts of Kashmir, Western Himalayas fall under this

zone. This zone is classified as Moderate Damage Risk Zone which is liable to MSK VII. The IS

code assigns zone factor of 0.16 for Zone 3.

ZONE 4: This zone is called the High Damage Risk Zone and covers areas liable to MSK VIII. The

IS code assigns zone factor of 0.24 for Zone 4. The Indo-Gangetic basin and the capital of the

country (Delhi), Jammu and Kashmir fall in Zone 4. In Maharashtra Patan area(Koyananager)

also in zone 4. but East Delhi is an earthquake prone area.

SNN INFRA POWER PROJECTS PRIVATE LIMITED 47

ZONE 5: Zone 5 covers the areas with the highest risks zone that suffers earthquakes of

intensity MSK IX or greater. The IS code assigns zone factor of 0.36 for Zone 5. Structural

designers use this factor for earthquake resistant design of structures in Zone 5. It is referred to

as the Very High Damage Risk Zone. The state of Kashmir,the western and centralHimalayas,

the North-East Indian region and the Rann of Kutch fall in this zone.

INDIAN SEISMICITY MAP FROM IMD:

SNN INFRA POWER PROJECTS PRIVATE LIMITED 48

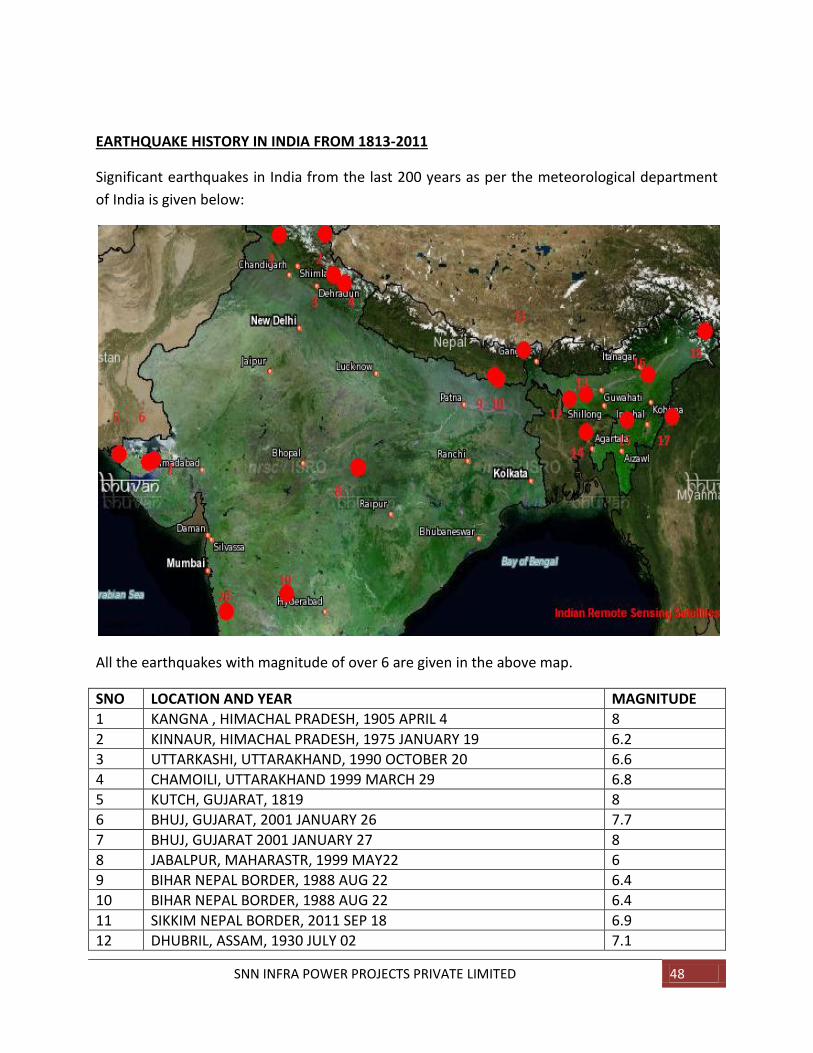

EARTHQUAKE HISTORY IN INDIA FROM 1813-2011

Significant earthquakes in India from the last 200 years as per the meteorological department

of India is given below:

All the earthquakes with magnitude of over 6 are given in the above map.

SNO LOCATION AND YEAR MAGNITUDE

1 KANGNA , HIMACHAL PRADESH, 1905 APRIL 4 8

2 KINNAUR, HIMACHAL PRADESH, 1975 JANUARY 19 6.2

3 UTTARKASHI, UTTARAKHAND, 1990 OCTOBER 20 6.6

4 CHAMOILI, UTTARAKHAND 1999 MARCH 29 6.8

5 KUTCH, GUJARAT, 1819 8

6 BHUJ, GUJARAT, 2001 JANUARY 26 7.7

7 BHUJ, GUJARAT 2001 JANUARY 27 8

8 JABALPUR, MAHARASTR, 1999 MAY22 6

9 BIHAR NEPAL BORDER, 1988 AUG 22 6.4

10 BIHAR NEPAL BORDER, 1988 AUG 22 6.4

11 SIKKIM NEPAL BORDER, 2011 SEP 18 6.9

12 DHUBRIL, ASSAM, 1930 JULY 02 7.1

SNN INFRA POWER PROJECTS PRIVATE LIMITED 49

13 SHILLONG PLATEAU, 1897 JUNE 12 8.7

14 SRIMANGAL, ASSAM 1918 JULY 8 7.6

15 CACHAR, ASSAM, 1869 JANUARY 10 7.5

16 ASSAM, 1943 OCTOBER 23 7.2

17 ARUNACHAL PRADESH CHINA BORDER, 1915 AUG 15 8.5

18 MANIPUR CAMBODIA BORDER, 1988 AUG 6 6.6

19 KOYNA, MAHARASTRA, 1967 DEC10 6.5

20 LATHUR, MAHARASTRA, 1993 SEPT 30 6.3

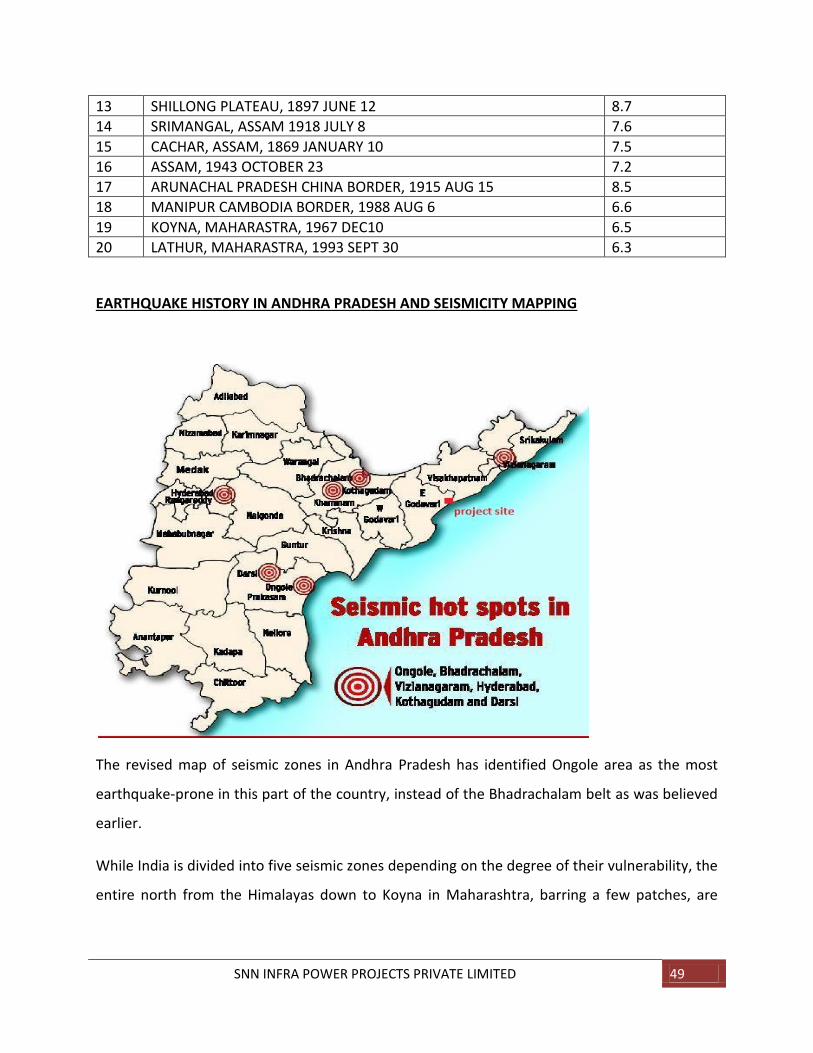

EARTHQUAKE HISTORY IN ANDHRA PRADESH AND SEISMICITY MAPPING

The revised map of seismic zones in Andhra Pradesh has identified Ongole area as the most

earthquake-prone in this part of the country, instead of the Bhadrachalam belt as was believed

earlier.

While India is divided into five seismic zones depending on the degree of their vulnerability, the

entire north from the Himalayas down to Koyna in Maharashtra, barring a few patches, are

SNN INFRA POWER PROJECTS PRIVATE LIMITED 50

rated as susceptible to quakes with a very high damage risk and accordingly listed in Zone V and

IV.

Andhra Pradesh lies on the Peninsular Indian Shield (PSI) long considered as stable and not

vulnerable. The earthquakes of Koyna (1967), Latur (1993) and Jabalpur (1997), however,

demolished this theory, according to the report. Subsequently, a few zones of faults in the

crystal layers of the Peninsular region causing quakes, had been identified, it said.

Many northeast-southwest trending fault-bound basement ridges and depressions traversed by

transverse features like cross-trends have been found, especially in Ongole, Vizianagaram and

other areas. These are likely to cause reactivation with a progressive build up of stress.

The geographical areas of AP fall in Zone I and II where both vulnerability and damage risk is

held low. Ongole area spread over as many as 30 mandals which faced 12 earthquakes in the

past 30 years, including two big ones in 1967 and 1959 with magnitude of 5.4 and 5 on Richter

scale, is held as the most active zone in the State.

Earthquakes in the recent past have occurred along and off the Andhra Pradesh coast and in

regions in the Godavari river valley. Mild tremors have also hit the capital city of Hyderabad

such as in September 2000. In the north, faults associated with the Godavari Graben show

movement during the Holocene epoch. Another NW-SE trending active fault called the Kaddam

Fault runs in a section of the northern Andhra Pradesh and continues in the same direction

towards Bhusawal in north Maharashtra. The other prominent active fault is the Gundlakamma

Fault which trends in a NW-SE direction from near Ongole on the coast running inland in the

same direction for about 100 kilometres. Several smaller faults have been found in the delta

region and along the coast near Vishakhapatnam. However, it must be stated that proximity to

faults does not necessarily translate into a higher hazard as compared to areas located further

away, as damage from earthquakes depends on numerous factors such as subsurface geology

as well as adherence to the building codes.

SNN INFRA POWER PROJECTS PRIVATE LIMITED 51

TECTONICALLY ACTIVE

Eastern Ghats belt and Godavari Valley are found to be tectonically active. A reference is made

to the State's biggest earthquake (5.7) that occurred in Bhadrachalam area of the Godavari

Valley in 1969 when the nearby Kinnerasani reservoir was disturbed. Vizianagaram area of the

Eastern Ghat belt experienced a series of quakes, including one with an intensity of 5.5 in 1917.

SEISMICALLY ACTIVE AREAS

Pinapaka, Gundala, Kothagudem, Manuguru, Yellandu and six other mandals in Khammam

district where Bhadrachalam lies, and 10 mandals in Vizianagaram district, including Garividi

and Nellimerla, are listed as seismically very active.

In Hyderabad, Jubilee Hills and Banjara Hills are included in this category along with the

neighbouring areas of Medchal, Shamirpet, Shankarpalli, Serilingampalli, Rajendernagar and

Moinabad.

CONCLUSION:

The proposed project site comes in the border of Visakhapatnam and East godavari districts and

as per the Indian earthquake zone it is under zone 2 which implies the probability of an

earthquake in the surrounding regions are least thereby concluding the safety of the project.

SNN INFRA POWER PROJECTS PRIVATE LIMITED 52

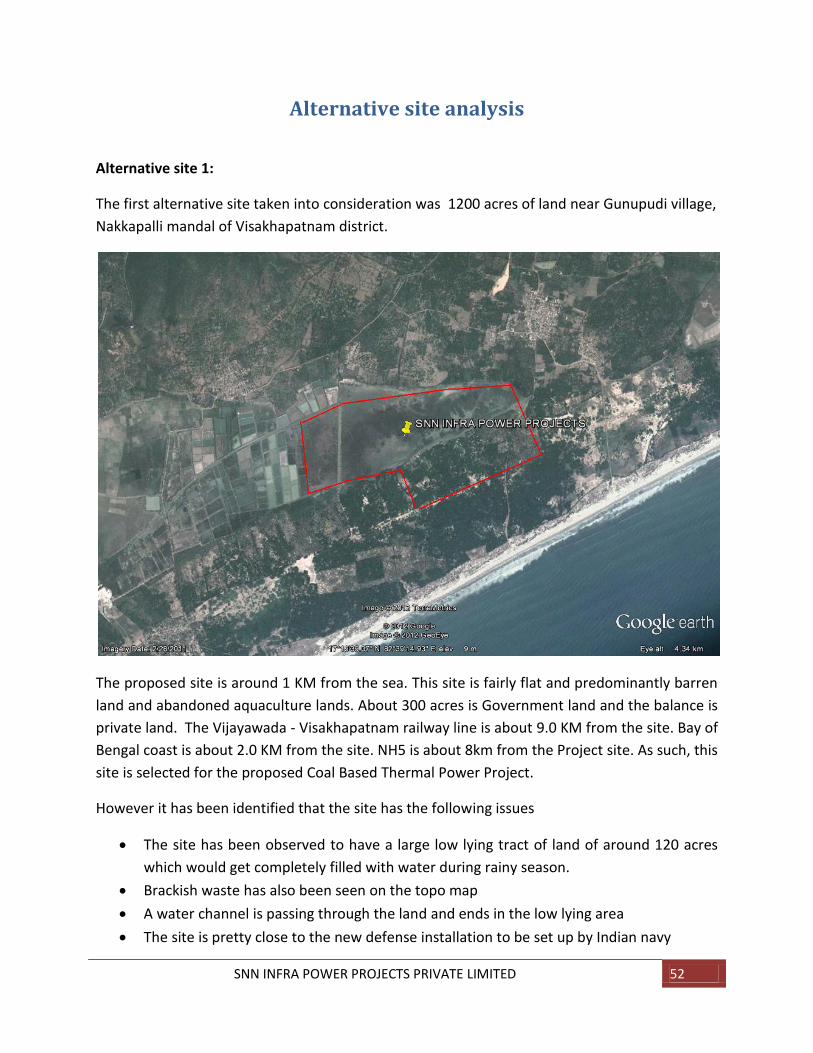

Alternative site analysis

Alternative site 1:

The first alternative site taken into consideration was 1200 acres of land near Gunupudi village,

Nakkapalli mandal of Visakhapatnam district.

The proposed site is around 1 KM from the sea. This site is fairly flat and predominantly barren

land and abandoned aquaculture lands. About 300 acres is Government land and the balance is

private land. The Vijayawada - Visakhapatnam railway line is about 9.0 KM from the site. Bay of

Bengal coast is about 2.0 KM from the site. NH5 is about 8km from the Project site. As such, this

site is selected for the proposed Coal Based Thermal Power Project.

However it has been identified that the site has the following issues

The site has been observed to have a large low lying tract of land of around 120 acres

which would get completely filled with water during rainy season.

Brackish waste has also been seen on the topo map

A water channel is passing through the land and ends in the low lying area

The site is pretty close to the new defense installation to be set up by Indian navy

SNN INFRA POWER PROJECTS PRIVATE LIMITED 53

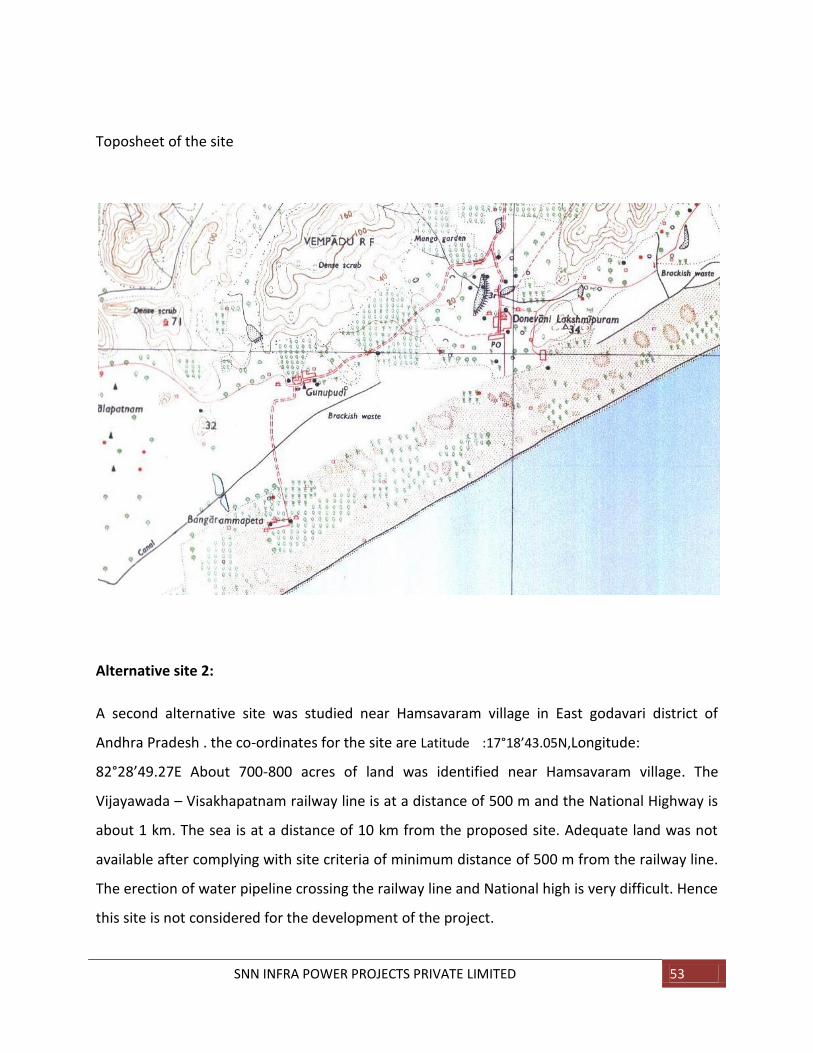

Toposheet of the site

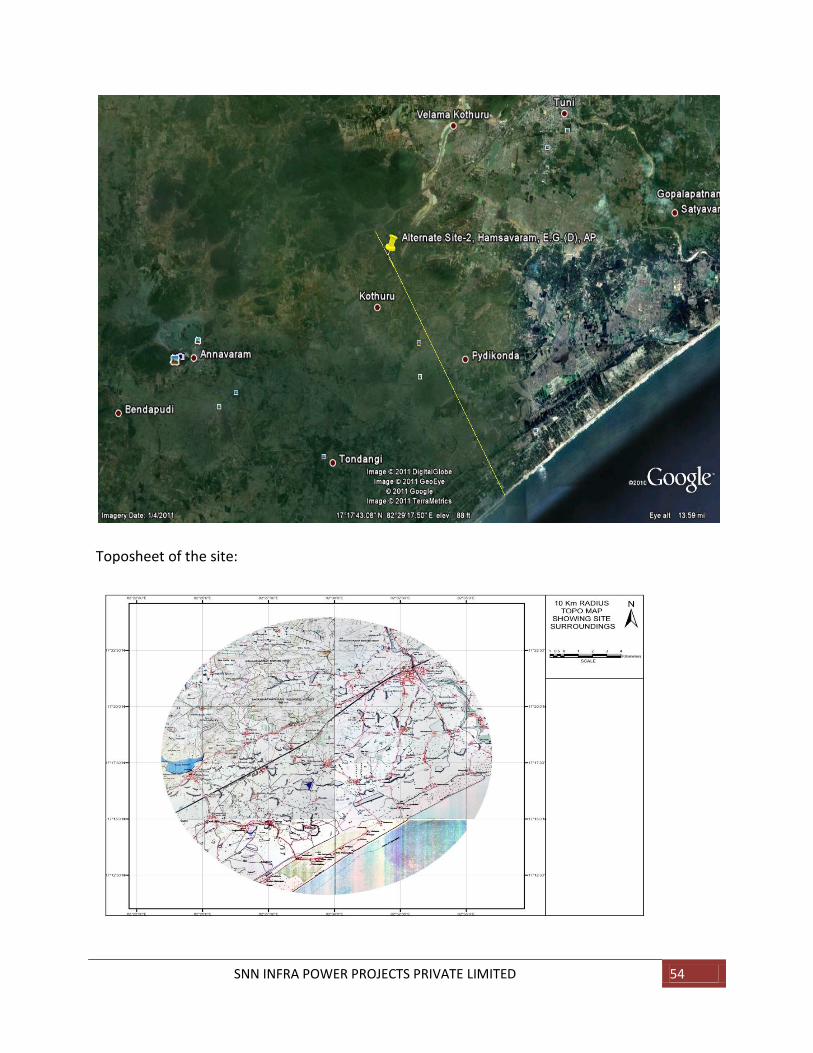

Alternative site 2:

A second alternative site was studied near Hamsavaram village in East godavari district of

Andhra Pradesh . the co-ordinates for the site are Latitude :17°18’43.05N,Longitude:

82°28’49.27E About 700-800 acres of land was identified near Hamsavaram village. The

Vijayawada – Visakhapatnam railway line is at a distance of 500 m and the National Highway is

about 1 km. The sea is at a distance of 10 km from the proposed site. Adequate land was not

available after complying with site criteria of minimum distance of 500 m from the railway line.

The erection of water pipeline crossing the railway line and National high is very difficult. Hence

this site is not considered for the development of the project.

SNN INFRA POWER PROJECTS PRIVATE LIMITED 54

Toposheet of the site:

SNN INFRA POWER PROJECTS PRIVATE LIMITED 55

Rehabilitation and resettlement R&R issues, Employment

generation

The project does not involve any resettlement and rehabilitation issues. A small temple exists in

the site which would not be disturbed. The industrial activity of the proposed project coupled

with the ancillary facilities /industries, would contribute to the overall socio-economic

development of the region.

Some of the direct benefits to the state and national exchequer include

Power Tariff

• Excise Duty

• State Sales Tax or VAT

• Income by way of registration of trucks, payment of road tax and payment of tax

for interstate movements.

• Income by way of transporting clinker /coal / cement / fly ash for railways.

• Income Tax from individual as well as corporate taxes by the Cement Company and Ancillary

units.

• Benefit to local community

Though power projects are highly capital intensive the employment generation would not be in

the proportion to the investment size.

Skilled/Unskilled/semi-skilled manpower related to industrial activities will be drawn locally or

from nearby places. Preference during recruitment will be given to the people of surrounding

areas according to their qualification and experience.