effect of enterprise resource planning systems on the financial performance of sugar companies in...

TRANSCRIPT

EFFECT OF ENTERPRISE RESOURCE PLANNING SYSTEMS ON THE FINANCIAL

PERFORMANCE OF SUGAR COMPANIES IN KENYA.

DAVID SIKUKU

A Thesis Submitted in Partial Fulfillment of the Requirements for the Award of the Degree

of Master of Business Administration (Finance Option) of Masinde Muliro University of

Science and Technology

JUNE, 2014

i

DECLARATION DECLARATION BY THE CANDIDATE

This thesis is my original work prepared with no other than the indicated sources and support and

has not been presented elsewhere for a degree or any other award.

……………………… …………….........................

Sikuku David Date

MBA/G/81/08

DECLARATION BY THE SUPERVISOR

The undersigned certify that they have read and hereby recommend for acceptance of Masinde

Muliro University of Science and Technology a thesis/dissertation entitled “Effect of Enterprise

Resource Planning Systems on the Financial Performance of Sugar Companies in Kenya”.

1. Sign ………………………. ……………………...................

Mr. F.N. Kiongera Date

Department of Business Management

Masinde Muliro University of Science and Technology

2. Sign………………................. ………………………..........

Dr. N.C.O. Keya Date

Department of Sugar Technology

Masinde Muliro University of Science and Technology

ii

COPYRIGHT This thesis is copyright material protected under the Berne Convection, the Copyright Act 1999

and other international and national enactments in that behalf, on intellectual property. It may

not be reproduced by any means in full or in part except for short extracts in fair dealing so for

research or private study, critical scholarly review or discourse with acknowledgment, with

written permission of the Dean School of Graduate Studies on behalf of both the author and

Masinde Muliro University of Science and Technology.

iii

DEDICATION I dedicate this study work to the Sikuku’s that is , Gertrude, Amos, Grace, Eric, Lawrence,

Garret, Elizabeth, Oliver, Nourine, Eunice and Emmanuel who always encouraged and

motivated me to carry on. Through their un-wavering love and enormous support I was able to

successfully complete this study.

iv

ACKNOWLEDGEMENT My deepest appreciation and thanks go to my supervisors, Mr. Kiongera and Dr. Keya, for their

constructive suggestions, right criticisms and guidance that helped me stay on course and to

finish this scholarly work and the entire department business administration, MMUST.

I am also deeply indebted to my friends and course colleagues for their contributions in various

ways towards the completion of this work.

I extend my deepest gratitude to the management and staff of the sugar companies who helped

me to administer questionnaires, and to all the business system users who patiently bore the

displeasures of completing the questionnaires.

The moral support offered by family members who went a long way in sustaining my enthusiasm

in this work.

I finally give thanks to the almighty God for granting me great guidance, energy, wisdom and

academic intellect which enabled me to accomplish this work.

v

ABSTRACT Enterprise Resource Planning (ERP) system is most commonly referenced in the context of commercially available software systems. Although the term ERP system generally refers to a software system, it also encompasses the business processes that drive system requirements and capabilities. ERP Systems have transformed the way organizations go about the process of priority information system. The purpose of this study was to establish the effect of ERP systems on the financial performance of sugar companies in Kenya. Further the study sought to establish the effect of organizational factors on the financial performance of sugar companies in Kenya, and examined organizational factors affecting the relationship between ERP systems and financial performance of sugar companies in Kenya. The major components of ERP systems are; transactional systems, advanced applications systems and management decision support systems. Many entities in the world over are implementing ERP systems, however little research exists in this field. The study adopted a descriptive research and was carried out among three selected sugar millers. The following companies were selected for the study; Mumias Sugar Company Ltd, Nzoia Sugar Company Ltd and West Kenya Sugar Company Ltd since the researcher intended to collect cross-sectional data for sugar companies in Kenya. The target population included 152 licensed business system users of ERP systems in the sugar companies, and the study sample consisted of 48 business system users, a total of 32 of the 48 licensed business system users responded to the survey. However, 27 respondents were usable for the study. Information was obtained from respondents through stratified sampling. Besides reviewing literature on pertinent issues, the information was sourced through questionnaires administered to the respondents and also through content analysis of the financial statements of the selected companies for the period 2007 to 2010. This period was considered ideal as it is during this period the Kenyan economy was reorganizing in response to post election violence that was witnessed in late 2007 and early 2008 because of disputed presidential general election of 2007. Reliability and validity of the data collection tools was established through cronbach alpha test. The data was analyzed using SPSS version 20. Descriptive and inferential statistical tools including mean, one way Analysis of Variance (ANOVA) of 95% confidence, Karl Pearson’s zero order coefficient of correlation (Pearson Product Moment Correlation or simple correlation) was used to determine the direction and strength of the relationship between ERP and performance of the selected sugar firms. Further, Karl Pearson’s first order partial correlation coefficient (rxy.z) was used to ascertain the effect of moderating variables on the relationship between ERP systems and financial performance of sugar companies in Kenya. Simple regression analysis was used to model the relationship between ERP system and financial performance of sugar companies in Kenya. The relationship between ERP systems and the financial performance of sugar firms followed a regression model of the nature FP= α + β1 ERP+ e while the relationship between organizational factors and performance of sugar firms was of the nature FP= α + β2 OF + e. The outcome was statistically significant with a positive linear relationship between ERP and financial performance of sugar firms. On the other hand, organizational factors were found to be having a moderating effect on the relationship between ERP systems and financial performance of sugar firms. The findings are of importance to the Government of Kenya, shareholders, and stakeholders of sugar industry. Further, the findings form a basis of future research by other scholars.

vi

Table of Contents DECLARATION............................................................................................................................ I

COPYRIGHT ............................................................................................................................... II

DEDICATION............................................................................................................................. III

ACKNOWLEDGEMENT .......................................................................................................... IV

ABSTRACT .................................................................................................................................. V

LIST OF TABLES ................................................................................................................... VIII

LIST OF FIGURES .................................................................................................................... IX

LIST OF ABBREVIATIONS AND ACRONYMS ................................................................... X

OPERATIONAL DEFINITION OF KEY TERMS ................................................................ XI

CHAPTER ONE ........................................................................................................................... 1 INTRODUCTION ....................................................................................................................... 1

1.1 Background to the Study ................................................................................................... 1 1.2 Statement of the Research Problem ................................................................................... 5 1.3 Purpose of the Study .......................................................................................................... 6 1.4 Specific Objectives ............................................................................................................ 6 1.5 Hypotheses......................................................................................................................... 6 1.6 The Scope and Limitations of the Study ........................................................................... 7 1.7 Significance of the Study ................................................................................................... 7 1.8 Conceptual Framework...................................................................................................... 8

CHAPTER TWO .......................................................................................................................... 9 LITERATURE REVIEW ............................................................................................................ 9

2.1 Introduction ....................................................................................................................... 9 2.2 Moderating Variables. ..................................................................................................... 15 2.3 Empirical Literature Review. .......................................................................................... 18 2.4 Research Gaps ................................................................................................................. 21

CHAPTER THREE .................................................................................................................... 22 RESEARCH METHODOLOGY .............................................................................................. 22

3.1 Research Design .............................................................................................................. 22 3.2 Study Area ....................................................................................................................... 22 3.3 Study Population.............................................................................................................. 22 3.4 Sampling Techniques and Sample Size ........................................................................... 23 3.5 Data Collection Procedures. ............................................................................................ 23 3.6 Validity and Reliability of Research Instruments. ........................................................... 24 3.7 Data Analysis and Presentation Techniques. ................................................................... 25

vii

3.8 Ethical consideration ....................................................................................................... 26

CHAPTER FOUR ....................................................................................................................... 28 DATA ANALYSIS AND DISCUSSION ................................................................................. 28

4.1 Study Response Rate ....................................................................................................... 28 4.2 Demographic Factors. ...................................................................................................... 29 4.3 ERP Systems ................................................................................................................... 34 4.4 Inferential Statistics of ERP Dimensions ........................................................................ 41 4.5 Inferential Statistics of Moderating Variables. ................................................................ 42 4.6 Hypothesis testing and discussion ................................................................................... 43 4.7 Moderating effect of organizational factors on the relationship between ERP and the financial performance of sugar firms ..................................................................................... 48

CHAPTER FIVE ........................................................................................................................ 51 SUMMARY, CONCLUSIONS AND RECOMMENDATIONS ............................................. 51

5.1 Introduction ..................................................................................................................... 51 5.2 Summary of Findings ...................................................................................................... 51 5.3 Conclusions ..................................................................................................................... 51 5.4 Recommendations ........................................................................................................... 55 5.5 Areas of Further Research .............................................................................................. 55

REFERENCES ............................................................................................................................ 57

APPENDIX .................................................................................................................................. 61

viii

LIST OF TABLES Table 1. 1 ERP Installation in the Kenyan Market ......................................................................... 4

Table 3. 1 Sample Distribution ..................................................................................................... 23

Table 3.2 Reliability Test .............................................................................................................. 24

Table 3. 3 Hypothesis Testing Framework and Analytical Model ............................................... 26

Table 4.1 Breakdown of the Questionnaire Survey ...................................................................... 28

Table 4.2 Respondents Department .............................................................................................. 29

Table 4.3 Gender Distribution ...................................................................................................... 30

Table 4.4 Respondents Duration of Service in the Current Position ............................................ 30

Table 4.5 Respondents Duration of Service in the Current Organization .................................... 31

Table 4.6 Respondents Employement Position during the ERP Implementation ........................ 32

Table 4.7 Descriptive Statistics of the Independent variable ........................................................ 32

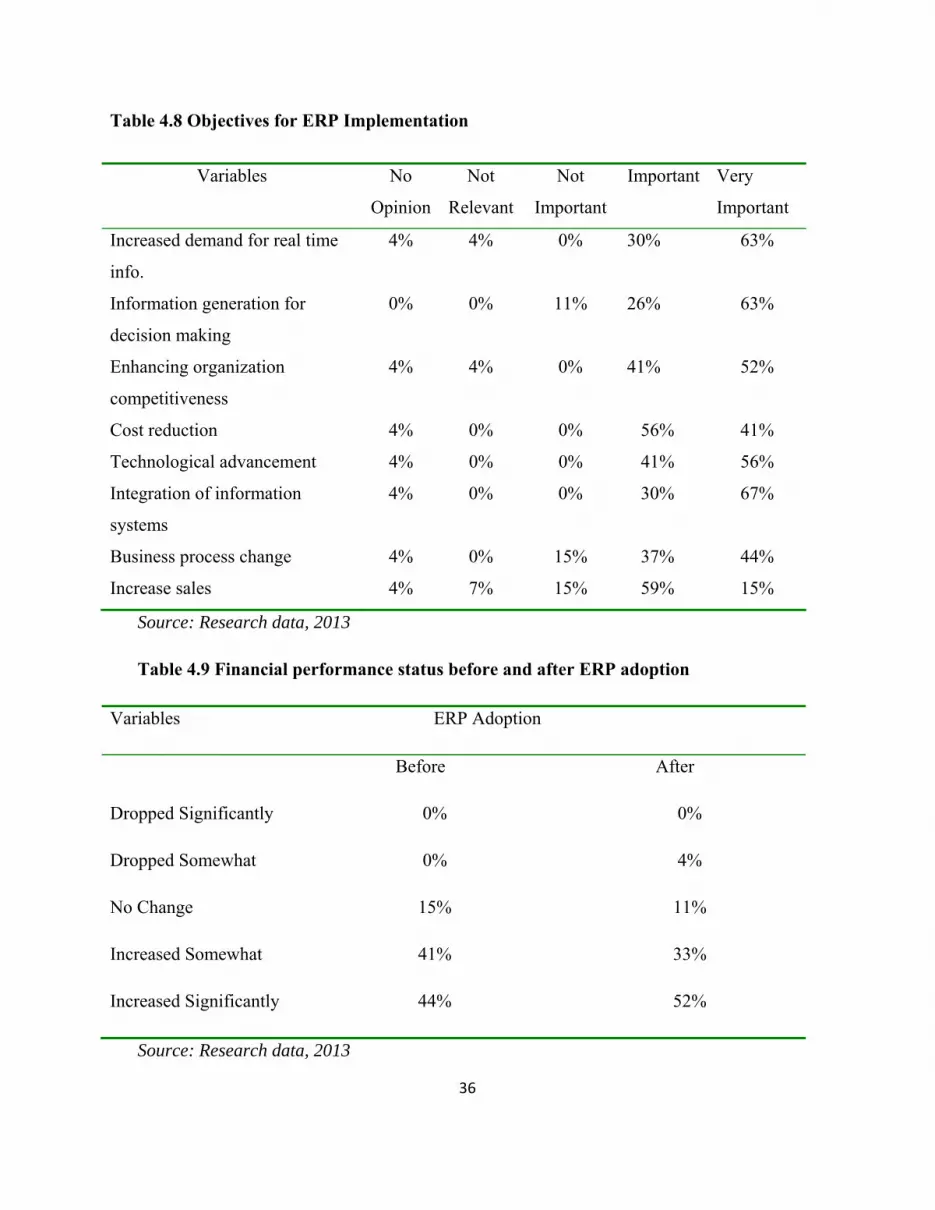

Table 4.8 Objectives of ERP Implementation .............................................................................. 36

Table 4. 9 Financial Performance Status before and after ERP Adoption .................................... 36

Table 4.10 ERP Systems Benefits ................................................................................................ 38

Table 4.11 Challenges of Adopting ERP systems ........................................................................ 39

Table 4.12 Organizational Factors affecting ERP systems ........................................................... 40

Table 4.13 Company Products Targets ......................................................................................... 40

Table 4.14 Correlation results for ERP dimensions...................................................................... 41

Table 4.15 Correlation of Organizational Factors ........................................................................ 43

Table 4.16 Correlation Results of ERP against financial peformance .......................................... 45

Table 4.17 Correlation results of organization factors on financial performance ....................... 47

Table 4.18 Results of the regression of modearting effect ........................................................... 48

Table 4.19 Correlation results when financial performance is held constant ...............................49

Table 4.20 Hypothesis testing framework and analytical model .................................................. 50

ix

LIST OF FIGURES Figure 1. 1 Conceptual Framework ................................................................................................ 8

Figure 2. 1 Enterprise Resource Planning:An integrative review ................................................. 10

Figure 4.1 Four Year Summary Review ....................................................................................... 34

x

LIST OF ABBREVIATIONS AND ACRONYMS ERP Enterprise Resource Planning

ROA Return on Assets

ROE Return on Equity

TCD Tones Crushed Per Day

ICT Information Communication technology

NSE Nairobi Securities Exchange

FP Financial performance

SPSS Statistical Package for Social Sciences

OF Organizational factors

MRP Manufacturing Resource Planning

MRPII Manufacturing Resource Planning II

SAP Systems Application Products

GDP Gross Domestic product

EABL East African Breweries Limited

KWAL Kenya Wines Agency ltd

KPLC Kenya Power & Lighting Company

KPA Kenya Ports Authority

PLM Product Lifecycle Management

CRM Customer Relationship Management

SKU Stock Keeping Unit

COMESA Common Markets of East & Southern Africa

COGS Cost of Goods Sold

xi

OPERATIONAL DEFINITION OF KEY TERMS ERP

Is a set of packaged application software modules, with an integrated architecture,

that can be used by organizations as their primary engine for integrating data,

processes and information technology, in real time, across internal and external

value chains.

Shakedown phase

Is a period attributed to employee learning resulting into more usage and

experience with the ERP system.

Performance

Is a method of measuring the success of the organization to ensure that it achieves

its goals. The success of an organization is gauged from several indicators both

qualitative and quantitative. These include financial and non financial

performance.

Return on Assets

Is a financial ratio that shows the percentage of profit that a company earns in

relation to its overall resources (Total Assets)

ROA=Net Income after tax/Total Assets

Return on Equity

Is the amount of net income returned as a percentage of shareholders equity. It is

often said to be the ultimate ratio or the “mother of all ratios” that can be obtained

from a company’s financial statement.

ROE=Net Income after Tax/Shareholders Equity

1

CHAPTER ONE

INTRODUCTION

1.1 Background to the Study

The adoption of ICT for business goes beyond simply buying an office computer and connecting

it to the internet. It is made more beneficial if it is set up with integrated information systems to

support the functional areas of the business. These areas include operations and management of

accounting, finances, manufacturing, production, transportation, sales and distribution, human

resource, supply chain, customer relationship and e-business. An example of such a system is the

Enterprise Resource Planning (ERP) Software (Torach, 2011).

Enterprise Resource Planning (ERP) is a generic term used to refer to management software that

includes modules such as production, finance, marketing and human resource and allows

companies to plan their goods and services (Stevenson, 2007). This software, used by many

enterprises, particularly by multinational corporations, has a critical role in increasing company

efficiency. ERP systems have their roots in the Manufacturing Resource Planning (MRP) system,

which later developed into Manufacturing Resource Planning II (MRPII) system. MRP system

was used to provide support for the production function. With the intervention of web-enabled

and open source technologies, the function of ERP has today assured added utility and

prominence to companies. The latest advancement in ERP software has been termed as ERP II

that is fully “internet-enabled” to facilitate access from remote locations (Lawton, 2000).

ERP systems help the different parts of an organization to share data and knowledge, reduce

costs and improve management of business processes (Stephen 2000, Buchhout and Nemec

1999). They also hope to provide increased flexibility to organizations in serving its customers.

The most commonly implemented ERP products are; BaaN, BPCS, IFS Applications, JD

Edwards, JBA Systems 21, mfg/pro, Movex, Navision (Microsoft), Oracle applications,

PeopleSoft, SAGE and SAP. With technological advancement, the main motivation of most

companies choosing ERP systems is to achieve an improvement in the management of the

financial aspect of their operations. The financial management module in ERP software is the

core module around which the other modules of the system revolve. The key elements of the

2

finance module of an ERP system include; general ledger controlling, accounts receivable,

accounts payable, cash management, fixed assets, budgeting and financial reporting and

analytics.

Kegode (2005), notes that sugarcane was first introduced in Kenya in 1902 by Asians

constructing the Mombasa-Uganda railway line. Today, the sugar sub-sector plays an important

role in the country’s economy. This sub-sector generates an estimated Kshs.12 billion annually,

provides approximately 500,000 jobs and supports livelihoods of about six million people. There

are, currently approximately 300,000 farmers involved in cane farming in the country. The

subsector accounts for about 15% of the agricultural GDP. The first sugar factory in Kenya was

set up at Miwani in 1922. Currently, the major millers are Miwani Sugar Company Ltd (1922),

Muhoroni Sugar Company Ltd (1966), Chemilil Sugar Company Ltd (1968), Mumias Sugar

Company Ltd (1973), Nzoia Sugar Company Ltd (1978), South Nyanza (SONY) Sugar

Company Ltd (1979), West Kenya Sugar Company Ltd (1981), Soin Sugar Company (2006),

Kibos Sugar and Allied Industries Ltd (2007) and Butali Sugar Company Ltd (2011). The two

older factories ceased operations: Ramisi sugar factory collapsed in 1988 and Miwani sugar

factory was put under receivership. Apart from the regular sugar mills, there are four licensed

and operational jaggery millers, namely; Lubao, Shajanand, Farm Industries and Homa Lime

jaggeries, who have a combined capacity of about 300 TCD. There are also in excess of nine

hundred informal and mostly mobile jaggeries, each which crushes between 3-35 tonnes of

sugarcane per day. The industry is facing pressures that include; globalization and the trend

towards mergers and alliances which requires financial stability and effective management of the

risks.

There is a continuing decline in productivity of the industry because the production technology

used is becoming increasingly obsolete. At the mill level, crushing of cane into sugar is

inefficient due to out of date technology and frequent breakdowns. At the farm level, cane yields

are low because smallholder farmers have little incentive to increase their output (such as by

using faster ripening seed varieties) as it would require higher maintenance, and they would not

be able to sell their extra produce in any case, due to limited milling capacity. In addition, mills

often owe money to farmers, who cannot be sure if or when they will receive payment. As a

3

result, farmers often fail to repay loans made to them by their out-grower associations.

Furthermore, farmers are generally paid for the amount of sugarcane they deliver to the mills in

terms of weight, rather than sucrose content. This does not incentivize farmers to improve the

quality of the cane they produce, which in turn reduces the efficiency of the mills (Ellis, Singh

and Ong’olo, 2010). Kegode (2010) points out that the Kenyan sugar industry has been revolving

around shortages, inefficiencies, inability to compete with imported sugar, perennial losses and

political interferences which cumulatively have a negative bearing on industry’s financial

performance. Despite huge stakeholder investments, self sufficiency in sugar has remained

elusive over the years as consumption continues to outstrip supply (Kegode, 2010).

Initially, implementation of an ERP package was possible only for very large multinationals and

infrastructure companies due to the high costs involved. However, today, many companies

around the globe have implemented ERP software and it is expected that in the near future an

even greater percentage of others will do the same (Mapara, 2005). Numerous researches have

been conducted on ERP implementation challenges. A significantly fewer number of research

has been performed on the realized ERP benefits. This is primarily due to the fact that it may

require up to five years before any benefits are realized (Poston and Grabski, 2001). Since ERP

systems are new, this type of data is seemingly not available as yet. Poston and Grabski (2001)

analyzed four financial performance measures before and after implementing ERP systems using

univariate tests and their results show that adoption of ERP leads to efficiency.

Hunton et al. (2003) also researched on the impact of ERP systems adoption and overall

organizational performance using financial ratios. However, their results fail to indicate a

performance improvement for ERP adopters. In Kenya, little has been done on the ERP system

usage. Majority of researches have focused on success factors and the key challenges to ERP

system implementation. Koske (2005) for example, analyses the impact of the use of ERP in

manufacturing companies in Kenya based on a survey of 16 companies. His results show that at

the organizational level, ERP has a very positive impact on the performance of companies.

Examples of companies that have adopted ERP systems in Kenya include Bamburi Cement,

Chevron Kenya Limited, Kenya Pipeline Company, Safaricom Ltd, Mumias Sugar Company,

Kenya Airways, East Africa Breweries Limited (EABL), Kenya Ports Authority, Nation Media

4

Group, Government of Kenya, Deacons (K) and Uchumi Group of Supermarkets. There is no

clear data on installed base but the table below shows the market domination.

Table1.1 ERP Installations in the Kenyan Market

ERP TARGET COMMENTS/CURRENT INSTALLATIONS

SAP Large enterprises and government KPLC, KENGEN, KPA, Kenya

Pipeline, Caltex

Oracle Financials Large enterprises and government Government of Kenya, Treasury

Baan Large enterprises Bidco, Firestone, Unga Ltd

Sage Line Small and Medium Sized enterprises KWAL, General Motors

Ebizframe Small and Medium Sized enterprises ACFC, Kenya Tea Development

Authority

ACCPAC Small and Medium Sized enterprises James Finlay, BASFEA

Sun Systems Small and Medium Sized enterprises Unilever Kenya, EABL

JD Edwards Large/Medium enterprises Shell & BP

(Source: Symphony Consulting)

5

1.2 Statement of the Research Problem

Enterprise Resource Planning systems or enterprise systems are software systems for business

management, integrating modules that support functional areas such as planning, manufacturing,

sales, marketing, distribution, accounting, financial, human resource management, project

management, inventory management, service and maintenance, transportation and e-business.

The challenge most entities encounter is in consolidating these heterogeneous systems within the

organization. Many companies prefer a system platform that would provide integration for

processes throughout the organization’s divisional systems to replace the previous transactional

systems. To handle challenges encountered by various transactional systems within an entity, a

common course of action has been the adoption of Enterprise Resource Planning (ERP) system.

“ERP systems are configurable information systems packages that integrate information and

information-based processes within and across functional areas in an organization” (Kumar &

Van Hillsgersberg, 2000).

Numerous researches have been conducted on ERP implementation challenges. A significantly

fewer amount of research have been performed on the realized ERP benefits. This is primarily

due to the fact that it may require up to five years before the benefits are realized (Poston and

Grabski, 2001). As these systems are new, this type of data is not seemingly available yet. Poston

and Grabski (2001) analyses four financial performance measures before and after implementing

ERP systems using univariate tests and their results show that adoption of ERP leads to

efficiency. Hunton et al (2003) also researched on the impact of ERP systems adoption and

overall organizational performance using financial ratios and their results fail to indicate a

performance improvement for ERP adopters.

In Kenya little has been done on the ERP system usage but majority of researches have focused

on success factors and the key challenges to its implementation. Koske (2005) for example

analyses the impact of use of ERP in manufacturing companies in Kenya using a survey of 16

companies and his results show that at the organizational level, ERP has very positive impact on

the performance of companies. In his work Koske (2005) did not demonstrate the nature of

organizational performance thus necessitated the need to research further in this under –

6

researched topic but narrowing down to financial performance of the sugar industry since

generalizing the entire manufacturing industry will not cater for the many sub sectors in it.

Therefore the study sought to find out the effect of enterprise resource planning systems on the

financial performance of sugar companies in Kenya.

1.3 Purpose of the Study

The general objective of this study was to assess the effect of Enterprise Resource Planning

systems on the financial performance of sugar companies in Kenya.

1.4 Specific Objectives

Specifically the study sought to:

i. To determine whether ERP systems have an impact on financial performance of sugar

companies in Kenya.

ii. To examine the effect of organizational factors on the financial performance of sugar

companies in Kenya.

iii. To establish the effect of organizational factors on the relationship between ERP systems

and financial performance in sugar companies in Kenya

1.5 Hypotheses

H01: ERP systems have no relationship with financial performance of sugar companies.

H02: Organizational factors do not affect the financial performance of sugar companies.

H03: Organizational factors do not affect the relationship between ERP system and

financial performance of sugar companies.

7

1.6 The Scope and Limitations of the Study

The researcher was interested specifically in exploring the effects of ERP systems on the

financial performance of sugar companies. The sugar industry was selected because of the many

challenges facing the sub-sector. It focused on the benefits of ERP systems, the organizational

factors affecting the adoption of ERP systems, and how they impact the financial performance of

sugar companies. The study was necessitated by the need for the sugar industry in Kenya to cut

production costs and increase efficiency so as to complete with cheap sugar imports from

COMESA.

The study focused on sugar companies that had implemented an ERP system by 31st December,

2010. Generally, the study was conducted in Mumias Sugar Company (listed on NSE), Nzoia

Sugar Company (state-controlled), and West Kenya Sugar Company Ltd (privately owned) but

specifically covering the finance and IT departments. However, Agriculture, Factory,

Commercial, Human Resources and Marketing were not considered in the study. By virtue of

the nature of their ownership, the three sugar companies were selected to represent the entire

population. The employees using ERP systems in the selected sugar companies were targeted as

the respondents. It was assumed in data analysis that the results obtained were representative of

the general population.

1.7 Significance of the Study

This study sought to investigate how ERP systems contribute to the financial performance of

sugar companies in Kenya. Based on the findings of this study, it is hoped that there will be a

theoretical and empirical improvement of ERP adoption, implementation and usage. The senior

managers who are charged with policy implementation will also find the study useful in terms of

handling the highlighted organizational factors during the implementation of ERP systems. The

government will also find this study meaningful since majority of sugar companies are state

controlled. Students pursuing business related courses at different levels would also find this

study useful. Finally, it is also hoped that this study will contribute to extant literature on ERP

systems and its influence of financial performance.

8

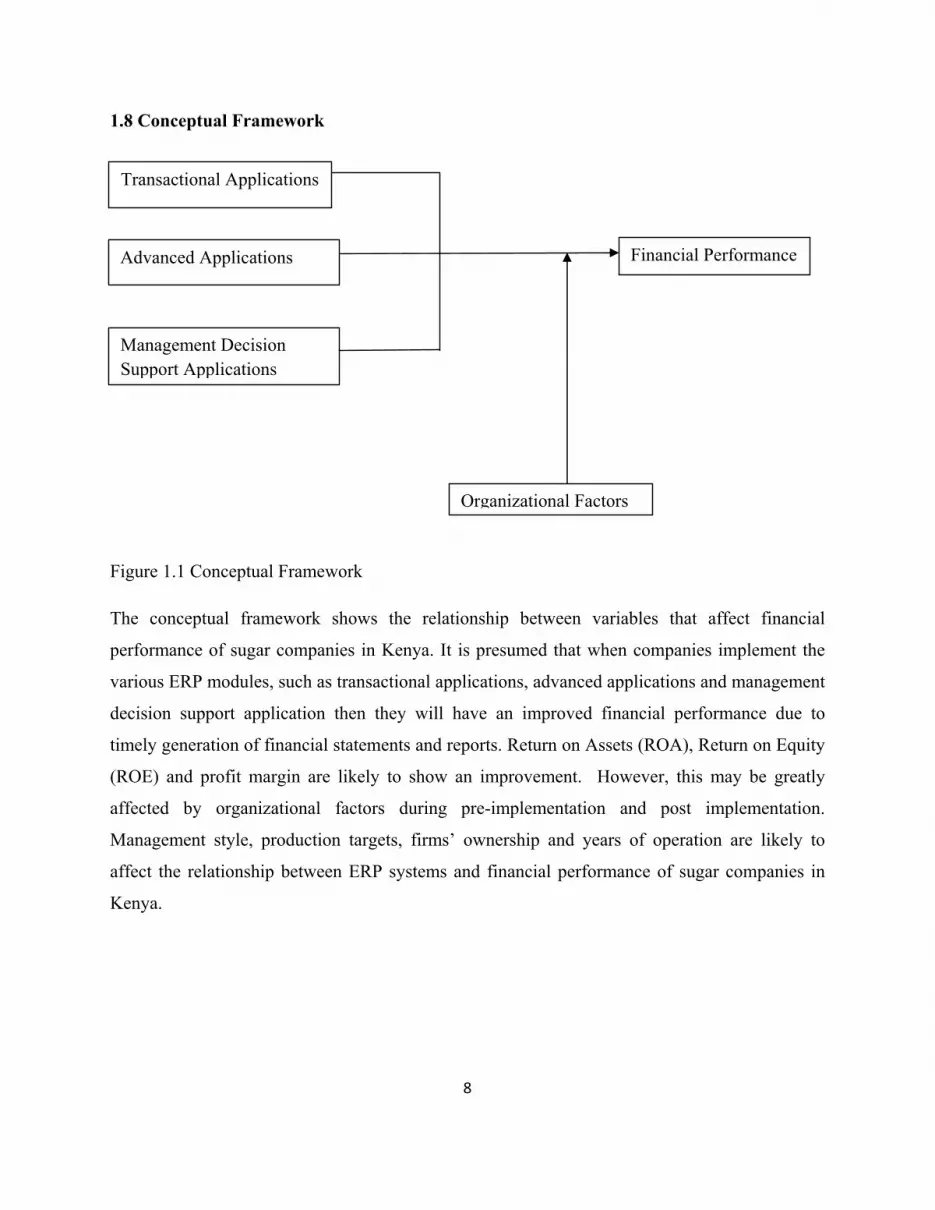

1.8 Conceptual Framework

Figure 1.1 Conceptual Framework

The conceptual framework shows the relationship between variables that affect financial

performance of sugar companies in Kenya. It is presumed that when companies implement the

various ERP modules, such as transactional applications, advanced applications and management

decision support application then they will have an improved financial performance due to

timely generation of financial statements and reports. Return on Assets (ROA), Return on Equity

(ROE) and profit margin are likely to show an improvement. However, this may be greatly

affected by organizational factors during pre-implementation and post implementation.

Management style, production targets, firms’ ownership and years of operation are likely to

affect the relationship between ERP systems and financial performance of sugar companies in

Kenya.

Transactional Applications

Advanced Applications

Management Decision Support Applications

Financial Performance

Organizational Factors

9

CHAPTER TWO

LITERATURE REVIEW

2.1 Introduction

This chapter will present an introduction of Enterprise Resource Planning (ERP) systems,

components as well as the life cycle. The relationship between ERP systems and financial

performance will also be presented.

2.1.1 ERP Systems Drury, (2004), observes that Enterprise Resource Planning (ERP) is a system that has enabled

organizations to exploit better their business information. ERP systems are significantly

distinguished from previous generations of information systems since they permit organizations

to integrate business processes and optimize the available resources (Stephen 2000). According

to Buckhout and Nemec, 1999 ERP is an information system that integrates an enterprise’

internal function working processes, standardizes internal data processing procedures and

combines the operational data generated by different functions. Davenport, 1998 describes ERP

systems as comprising of a commercial software package that promises the seamless integration

of all the information flowing through the company–financial, accounting, human resources,

supply chain and customer information”. A sentiment shared by O’Leary, 2001 who states, “ERP

systems are computer-based systems designed to process an organization’s transactions and

facilitate integrated and real-time planning, production, and customer response”.

Tadjer, (1998), emphasizes that ERP systems are one database, one application and a unified

interface across the entire enterprise”. ERP systems offer unique benefits to the organizations

implementing them. This they do by improving the decision making process of the organizations

through the provision of appropriate and timely information (Hunton et al. 2004). Globalization

has necessitated most companies to standardize processes and learn the best practices embedded

in ERP systems, which ensure quality and predictability in their global business interests by

reducing cycle time from order to delivery (Ross J. W, 1999). With the evolvement of ERP

systems, the interest in the impact that these systems have on organizational performance has

10

risen. Billions of dollars have been spent on these systems worldwide (Kalling, 2003). Yet,

conclusive results on the true benefits are still to be proven.

2.1.2 Components of ERP System The components of an ERP system are subdivided into modules as shown in the figure below.

Figure 2.1 Enterprise Resource Planning: An integrative review (Shehab E.M et al 2004 pg 363)

Gelinas et al, (2005) identified the following core modules of ERP systems. Supply chain

management (SCM) is one of the most important software modules for manufacturers. SCM

provides visibility into the entire supply chain, from start to finish. ERP SM modules typically

include components for forecasting, demand management, procurement and planning; delivery

modules such as logistics; and components for after-market issues like returns, installations and

11

contracts. Manufacturers can use customer relationship management (CRM) software to organize

and view data on individual customer transactions in one accessible place. ERP CRM modules

provide customer data integration, or master data management (MDM), which keeps track of

customers across all the sales channels from in-person (field sales) to phone (including

telemarketing) to online (teleservice and support)

With product lifecycle management (PLM) software, manufacturers can track the design and

attributes of a product throughout its lifecycle, from concept to end-of-life. The components that

make up ERP PLM modules include product data management (PDM), product design, portfolio

management, direct materials sourcing and customer needs management. Human capital

management is another one of the common ERP modules. ERP HCM modules function as the

core employee record, which details personnel actions, benefits administration and payroll,

position management and compliance with government regulations. ERP HCM covers three

areas of employee management: transactional, talent management and extended management.

Warehouse management systems (WMS) software is a must-have for manufacturers. ERP WMS

modules follow the distribution process involved with finished goods or materials from delivery

into the warehouse for storage through replenishment and picking for shipment to fulfill orders.

WMS modules also help synchronize and control stock on the shop floor. Manufacturers can

track physical manufacturing assets involved in production using ERP asset management

modules. Some of the daily functions that ERP asset management handles are maintenance

schedules, equipment uptime and downtime, inventory and warranty management and

compliance with hazardous materials and waste tracking regulations.

Financial management is a critical business function for manufacturers. ERP financial

management modules include functionality for general ledger, which is the core of ERP financial

management. These modules also handle functions for accounts payable and receivable, fixed

assets, financial reporting and treasury management. Order management systems take in data

from orders on the front end and make sure that orders get filled on the back end. Manufacturers

use ERP order management modules to fill product orders at the lowest possible cost. These

modules are equipped to handle functions such as automated order entry, viewing and tracking;

12

order status; cancelled transactions; order and credit limit validation and checking for duplicate

orders.

With project management software, manufacturers can organize and review the data around

project timelines and costs. These software systems are geared toward organizations that bill

clients based on their employees spend working on individual projects. ERP project management

modules handles: project definition, project costing & accounting, project portfolio management,

resource management and project billing. ERP inventory management modules move finished

goods through the production cycle. They are often tied into other functions, including shipping,

logistics, orders, and billing, on a broader scale, warehouse management. ERP order

management software includes functionality for inventory control, serial number tracking, bar

code printing, build materials and kitting, inventory valuation and SKU management.

2.1.3 ERP system life cycle. Markus and Tanis (1999) identify three phases in the lifecycle of an ERP system; the pre-

implementation phase, the implementation phase and the post implementation phase.

a) Pre-implementation phase

According to Ross (1999), the objective of the pre-implementation phase is to identify the ERP

package most appropriate for the organization and the technological infrastructure needed for it.

Usually, a committee is set up to conduct a feasibility study, to identify and select the ERP

solution, streamline the integration framework and access the cost implication of such a project.

b) Implementation phase

This is the main phase of the life cycle of the ERP project. During this phase, organizational

processes are re-designed to work with the ERP system (Vemuri and Palvia 2006). In many

cases, the implementation is done in parallel with the existing system in order to minimize any

interruption with ongoing operations. The ERP system is implemented, end users trained and

acceptance testing conducted (Ross, 1999).

13

c) Post implementation phase

The post implementation phase is normally the longest phase of the ERP life cycle and can last

several years. It consists of the period after ERP implementation. This phase is characterized

with reviews, support and system modifications and/or extensions. Usually a post-

implementation analysis is performed to measure the effectiveness of the ERP solution in

meeting its goals and objectives (Ross, 1999).

2.1.4 Reasons for implementing ERP Systems

Why do firms invest in ERP given the different alternatives for Information integration in a

business? The answer for this question lies between either technical gains e.g. replacing legacy

systems, or for business reasons e.g. improving operational performance and efficiency

(Nicolaou, 2004). Many technical reasons exist including the replacement of disparate systems

into a single integrated system (Hitt et al., 2002). The replacement of legacy of legacy systems

was very important for the boom of ERP during the late 1990s when companies wanted to

replace their legacy systems during the year 2000 (Y2K) with a more Y2K compliant solution so

they have invested into ERP systems (Anderson et al., 2003) ERP also provides a tested system

security basis which promises to keep the organization up to security standards and for providing

data security (FuB et al.,, 2007)

Business reasons also exist. This includes automation and reengineering of business processes

(Hitt et al., 2002). Other business reasons provided by Federici (2009) are better management,

better operations, better information availability and reengineering procedures, which are all

reasons for acquiring ERP. Other business reasons include enhancing cooperation and teamwork

between employees in the company. In addition, benefits expected from implementation of ERP

systems include tangible benefits like reducing costs, reducing operations time, and a lean

organization, while intangible benefits like information integration, better information quality,

and increase in customer satisfaction also exist (Loh et al., 2006;Nicolau, 2004). Such perceived

benefits are expected because ERP help make production inside manufacturing companies more

efficient by integrating information from other departments like sales and procurement into the

14

production system, which as a result helps eliminate costs and improve production schedules

(Matolcsy et al., 2005)

Firms may have several reasons for deciding to adopt ERP Systems depending on for example

industry and size. According to a survey regarding R/3 cited in Al-Mashari (2001), the most

common reason for implementing ERP, as well as its most achieved benefit, is standardization of

processes and systems. Another much cited reason for implementing ERP is the integration

benefits of the system. Other reasons for implementing ERP is problems of fragmentation due to

legacy systems and to solve the year 2000 problem. The year 2000 problem is a term for the

problems that could occur at the turn of the millennium. This meant that when the clocks struck

midnight on Jan. 1 2000, many computers would produce wrong answers or fail to operate

properly unless the computers’ software was repaired or replaced before that date. O’Leary

(2000) states that “one of the primary reasons for movement toward ERP is that the competition

has it [and that] a lot of ERP purchases are premised on the need just to stay in business”. Thus,

the implementation of an ERP System can be seen as a competitive necessity.

According to Hedman, 2002, to make the right business decisions, you need access to the right

information at the right time. With an ERP solution configured to your specific needs, you can

rest assured that you are receiving accurate data to make smart decisions. Even if you already

have an ERP solution in place, years of minor tweaking and connecting with disparate systems

may have turned it into a convoluted mess of obscure information. With a new ERP solution,

your business can put its trust in an up to date and reliable system.

Although the implementation of an ERP system brings many advantages, it may also bring

disadvantages. One of the main disadvantages is the lack of feature-function fit between

available packages and company needs (Markus & Tanis 1999). Al-Mashari (2001) states that

even the best product available can only fit 70% of all company processes. Further reasons for

not adopting ERP are the high costs of the infrastructure and the implementation. This reason is

most commonly stated regarding small firms. The implementation is not only costly but also

requires much time and patience. It also disturbs the routine work within an organization and

many hours of education is needed (Yen et al, 2002). Davenport (1998) argues that the

15

implementation of an ERP may result in the weakening of important sources of competitive

advantage, because it pushes a company towards generic processes, even if the company’s

competitiveness lies in its unique, customized processes. An implementation that has not been

carefully considered may therefore bring disaster rather than the much-sought benefits.

2.1.5 ERP Adoption in Kenya In the past years, a number of companies in Kenya have implemented ERP systems in their

organizations. Since Kenya Power & Lighting Company (KPLC) implemented the SAP system

in 1997, a number of other companies have also implemented similar products. In 2002, Kenya

Ports Authority (KPA), Telkom Kenya Limited and Kenya Pipeline Limited embarked on ERP

implementation. There are many others that also may be planning to implement these systems for

their operations. The major focus is on large ERP and inventory system. JD Edwards has carried

out a few ERP implementations in Kenyan Companies, primarily in the petroleum, soft drinks

and manufacturing sectors. SAP has been implemented in a large number of companies in the

power, transport and petroleum sector. The smaller ERP systems include; Navision, AccPac,

Great Plans and SUN Accounts system. There is no clear data on the total installed but the Table

1.1 is an indication of the market.

2.2 Moderating Variables. The organizational factors are assumed to moderate the relationship between ERP systems and

financial performance of sugar companies in Kenya.

2.2.1 Management Style According to Kegode 2005, the Sugar Industry in Kenya is in chaos, the current state of sugar

industry is primarily as a result of destructive political economy that has seen corruption,

mismanagement, lack of political goodwill, ruin the sector. The result has been a systematic

increase in poverty amongst farmers and subsequent decline in the sustainability and efficient

growth of the sub-sector. The situation has been exacerbated more by non-sequenced trade

liberalization trade policies, leading to unchecked entry of imported (often dumped) sugar into

the local market. The sector is currently operating under COMESA safeguard measures. The

Kenya Sugar sector is expected to have undertaken key reforms in various areas to build

competitiveness and introduce efficient management in the sugar supply chain. Consequently,

16

the institutional and legislative framework governing the sugar sub-sector must be urgently

overhauled in order to respond to an imminent threat that will affect the sector. The sector has

suffered greatly from factors such as external sugar market competition, combined with serious

internal inefficiencies and grandiose corruption that was coordinated by the policy maker’s

bureaucrats and key agents in the industry.

According to Wanyande (2001), poor management, corruption and vested political interests

have made Kenya's sugar industry so inefficient that the country's goal of attaining self-

sufficiency in sugar production will remain unattainable for a long time. The government has

contributed to the current inefficiency in several ways. The government formed the habit of

bailing out sugar companies from collapse by injecting huge amounts of money whenever the

companies were in the red. The companies were therefore assured of returns to their investment

and did not therefore find it necessary to be innovative and competitive. The government has

also been very lenient with those who illegally import sugar into the country, a factor that has

contributed to problems in the industry in that it has led to dumping. Many powerful people are

said to import sugar duty free and sell it at a much cheaper price than the locally produced sugar

and thus making it hard for the local companies to sell their stock. This problem has been

compounded by gross misappropriation of funds meant for improving operations in the industry.

There were also complaints of massive tax evasion in the sugar industry with the culprits going

scot-free. This is done by politically powerful individuals. We are here talking about corruption,

a vice that has become pervasive in the country. Another problem that has made the companies

difficult to manage is the practice in which the government provided loans to the companies and

did nothing to recover such loans. This means that a manager coming to the company finds the

company in such a huge debt that it cannot pay. This simply discourages the manager from even

starting to repay the loans.

The other problem that creates inefficiency in the sugar industry is the appointment of managers

on the basis of political considerations rather than merit. All the chairpersons of the government-

dominated sugar companies are political appointees. In some cases, they are people who failed to

get elective positions but were in good books with the powers that be. Their appointment is,

therefore, more of a political reward than merit that would aim at improving the management of

17

the companies. The same applies to the few local managers of these companies. Many of them

lack the requisite technical qualifications and knowledge, let alone interest, in the sugar industry.

One of the consequences of this is that the managers feel that their duty is to serve the interest of

the state and not necessarily the farmer. (Wanyande, 2001)

Secondly, such employees are uncertain of whether they will retain their jobs should there be a

change of government. Therefore, they resort to taking as much as possible from the companies

before being replaced. They thus turn and treat the companies as mere sources of personal capital

accumulation. There are several other dimensions to the problems in the sugar industry apart

from those caused directly by the state. Among these is the problem of management. According

to a number of farmers, sugar factories appear to lack capacity to collect cane from them. The

farmers observed that many times their cane dries up on the farms simply because the factories

do not collect it in time. The farmers also pointed out that even if they wanted to use their own

transport to take cane to the factories they could not do so since they have to get the okay from

the factory. This implies that either the factories do not have the capacity to receive a certain

amount or quantity of cane at any given time or that they simply are not sensitive to the interests

of the farmers. This is why farmers and politicians from the sugar belt often interpret this as a

deliberate act of sabotage to frustrate the community of sugar cane farmers. They often see the

hand of the state and therefore politics in all this. As a result many farmers become frustrated and

opt not to plant sugar cane and this, too, reduces the amount of cane available (Wanyande, 2001)

2.2.2 Production Targets Consequently, the production targets are not met. The high cost of processing sugar undoubtedly

has implications on the financial performance of the factories and eventually their capability to

pay farmers. Most factories are often unable to realize enough money to pay farmers at the

industry set prices. Indeed, late payment of farmers for cane delivered to the factories is a

common problem in the industry. From the foregoing, it is clear that the problems in the sugar

industry are mainly due to government policies and interference, which does not favor efficient

performance. Although, the government espouses privatization of the industry, it is dragging its

feet and seems not ready to release control over the milling companies. This has led to

18

management inefficiencies of the factories with the belief that the government will always bail

them out of their financial difficulties (Wanyande, 2001)

Every sugar company in the sugar belt area has a nucleus estate and an out growers' scheme. The

nucleus estates belong to the sugar company while the out growers' schemes cover the individual

or private sugar cane farmers. The idea behind the nucleus estates is simply to ensure a constant

supply of cane to the factories. They are some kind of safety valve or insurance just in case

farmers fail to deliver cane to the factories. It is, however, also a source of income for the factory

owners and a chance for them to participate in sugarcane farming. It is interesting to note that

despite the existence of nucleus estates, sugar factories have not been able to meet production

targets. Efficient management of the sugar factories is the key to the success of the sugar

industry (Wanyande, 2001). For a business that handles lots of transactions as a daily basis,

software is more than a necessity. In current competitive scenario, the best option is for

businesses to adopt effective enterprise software (Rai, 2010).

2.3 Empirical Literature Review.

The relation between ERP systems and organizational performance has evoked much interest

among researchers in the whole world. Good examples of ERP financial impact researches have

been conducted by Poston and Grabski (2001) and Hunton et al. (2003). Poston and Grabski

(2001) investigated the impact of ERP system implementation on an organization’s performance.

They examined 50 companies adopting ERP systems over a three-year post-implementation

phase. They concentrated on three major areas, which they presumed would illustrate ERP

system effects on economical performance. These were internal coordination costs, decision

information costs and external coordination costs. All of them are included with more detailed

cost categories. The results demonstrate a limited and insignificant positive correlation between

ERP and firm performance. However, they reported a significant decrease in the ratio of

employees to revenue in each of the 3 years and a significant improvement in the ratio of cost of

goods sold to revenue in year three. Overall, they noted that ERP firms exhibited efficiency gains

in some areas, but increased costs elsewhere seemed to offset such gains. These results are to say

the least wanting.

19

Companies are investing millions of dollars on ERP systems, which consequently fail to deliver

any financial benefits. Poston and Grabski (2001) identify a few reasons for the outcome of their

research. Firstly, as mentioned before, the ERP benefits on an organization may be realized only

after four to five years after the implementation phase. As the time frame in this research was

only three years, it might not have been sufficient. Secondly, Poston and Grabski (2001) suggest

that the true value of ERP systems is realized only after add-on packages such as Customer

Relationship Management (CRM) systems are utilized. Apparently the research did not include

examination of the impact of such features.

Thirdly, it is established that many companies reengineer their business processes while

implementing ERP thus making it difficult to compare previous performance with ERP post-

implementation performance. Therefore, referring to the first limitation, a longer time frame

might be sufficient in ERP financial impact research. Fourthly, macroeconomic or contextual

factors were not considered in this study. Thus, companies of a similar size and industry, which

have not implemented ERP, should have been included. Finally, organizational control or initial

objectives were not managed. Factors affecting organizational change should be distinguished

and measured in order to identify the true success of the ERP implementation. It could be that all

of the 50 companies failed in ERP implementation with little financial impacts. However, it

cannot be proven as the organizational factors are unknown.

Hunton et al. (2003), recognize a sixth reason for the results acquired by Poston and Grabski

(2001). During their research, they established that an earlier research carried out in 1996

discovered that financial gains encountered with the adoption of ERP are passed over to

customers who are charged lower prices. This notion is supported by various other researches

that Hunton et al. (2003) had examined. Hunton et al. wanted to extend the study done by Poston

and Grabski by examining ERP benefits from a wider and different perspective. The objective of

the study was to demonstrate whether or not the financial performance of a non-ERP adopter is

significantly lower than that of an ERP adopter. Their study used four different measures of

financial performance. The first one is the Return on Assets (ROA), which is a common measure

of performance and widely used in research. The two second measures are parts of ROA. These

20

are Return on Sales (ROS) and Asset Turnover (ATO). The last performance indicator is Return

on Investment (ROI).

The study by Hunton et al. (2003) examined 60 companies from which it was possible to acquire

performance information before and after ERP implementation for a sufficient number of years.

The sample included in addition, companies that had not implemented ERP in order to compare

and contrast results. The results by Hunton et al. (2003) indicate similar results as with the

Poston and Grabski (2001) study. No significant difference in ROA is recognized between pre-

and post-implementation performance of ERP companies. The difference among the two studies

is illustrated in that non-ERP adopting companies show a great decline in ROA. Similar results

were acquired with the other financial performance indicators (ROI, ROS, and ATO). However,

it is noted that the decline in financial performance figures for non-ERP adopting companies is

significant only for ROA and ROI.

Evidently, the study by Hunton et al. (2003) does not shed light to the ERP paradox and their

impact on organizational financial performance. Thus, it could be possible that these complex

systems that companies spend millions of dollars on are implemented only to sustain an already

acquired market position and not improve overall financial performance. The research

contributions by Poston and Grabski (2001) and Hunton et al. (2003) seem to reflect upon this

theme. However, various other researchers have identified other types of ERP benefits

(Laughlin, 1999; Plotkin, 1999; Mabert et al., 2001), but recognized that these benefits do not

occur until ERP systems have been successfully implemented and integrated into business

processes (Markus et al., 2001).

Closer home, Koske (2005) performed a study using a survey of 16 manufacturing companies in

Kenya to establish the impact of ERP use. The research findings showed that at organizational

level, ERP had a very positive impact on the performance of manufacturing companies in Kenya.

From this perspective ERP usage would not expect to see post implementation financial gains.

Such inconclusiveness creates room for further study.

21

2.4 Research Gaps

Many studies have been carried out on ERP activities in Kenya and other countries. There exists

a wealth of literature on ERP systems but only few studies have been carried out in Kenya, a lot

of research has been carried out focusing on the relationship between ERP systems and

organizational performance. Positive relations between ERP systems and performance have been

reported in some of the studies (Poston, 2001 and Koske 2005). Other studies like Hunton et al

(2003) do not shed light to the ERP paradox and their impact on organizational financial

performance. Empirical evidence reveals that little research attention has been devoted to

measuring the impact of ERP in sugar subsector in Kenya which forms part of the entire

Agricultural activities that is a dominant sector and accounts for approximately 24% of the

country’s GDP. It is against this background that the purpose of this study will be to determine

the effect of ERP systems on financial performance by assessing the effect of ERP systems on

financial performance of sugar companies in Kenya.

22

CHAPTER THREE

RESEARCH METHODOLOGY

3.1 Research Design

This study adopted a descriptive survey. The choice of this design was preferred because (Oso &

Owen, 2005) agreed that a survey is an excellent tool for it considers issues such as economy of

the design, rapid data collection and ability to understand a population from a part of it.The

researcher was interested in describing the relationship between ERP systems and financial

performance of sugar companies.

3.2 Study Area

Three sugar companies in Kenya, Mumias Sugar Company, Nzoia Sugar Company and West

Kenya Sugar Company were selected for this study. The study area was preferred because

Western Kenya by design is where the bulk of the sugar companies are located and

owned/controlled differently. In addition, all the firms have over 20 years experience in

manufacturing sugar in Kenya. Mumias Sugar Company, Nzoia Sugar and West Kenya represent

the interest of privatized, government owned and private sugar companies respectively. The

industry is controlled by the Kenya Sugar Board, KSB

3.3 Study Population

In the Kenyan business sector, most organizations still continue to use traditional accounting

software. However, a number of them are gradually upgrading to entry level ERP systems

supplied by major ERP vendors such as SAP, Syspro, Microsoft Navision and EbizFrame. The

study population was 152 system end users in Finance and ICT departments of the selected sugar

companies during the study period.

23

3.4 Sampling Techniques and Sample Size

Stratified sampling technique was used to categorize business system users in their strata i.e.

according to their division/function/departments. The sample was drawn from finance and ICT

departments within each selected company. The system administrators generated a supporting

listing of all system end users specified and thereafter the researcher randomized the list of every

section to reduce unfairness. The sample comprised 7 ICT users and 41 finance end users. A total

of 48 respondents were used for this study. Sample distribution is shown in Table 3.1.

Table 3.1 Sample Distribution

POPULATION SAMPLE 30%

ICT FINANCE TOTAL ICT FINANCE TOTAL %

END USERS END USERS USERS END USERS END USERS USERS

MUMIAS SUGAR 8 84 92 3 26 29 31.52%

WEST KENYA 3 12 15 1 4 5 30.00%

NZOIA SUGAR 9 36 45 3 11 14 31.11%

GRAND TOTAL 20 132 152 7 41 48 31.58%

Source; System Administrators (Selected Sugar Companies)

The sampling frame of this study was generated after consultation with the system administrators

of the selected sugar companies, who provided the system end users list. Kerlinger (1993) asserts

that a sample is representative if it is between 10% -30%. Out of 152 system end users, a sample

size of 48 respondents representing 31.58% was used to gather the findings.

3.5 Data Collection Procedures.

Primary and secondary data was used in the study after seeking permission from School of

Graduate studies and National Commission for Science Technology and Innovation (NACOSTI)

see attached research permit appendix 7.To generate primary data, a structured questionnaire was

administered to 48 respondents. The questionnaire included both open-ended and closed

questions which were administered to system end users of the selected divisions through drop

and pick. Structured questions were used because they offered an increased response rate and

were easily coded and analyzed while unstructured questions were used because they provide

24

more information as the respondents express their thoughts freely and spontaneously. In case of

the close ended questions, a Likert-type scale was used for the entire construct.Secondary data

came from annual financial statements & reports.

3.6 Validity and Reliability of Research Instruments.

The questionnaire was the main data collection instrument and hence to ensure that it is reliable

and valid; test-retest was done. To ensure content validity and relevance, the questionnaire was

pretested on a pilot set of respondents who did not form part of the study’s respondents but were

knowledgeable in the study aspects. This enabled the researcher to revise the questionnaire based

on the pilot feedback. On the other hand, to ensure face and construct validity, the questionnaire

was guided researchers conceptual framework. Piloting was carried out in Carried out in Mumias

Sugar Company production section whose findings were used in the final analysis aimed at

establishing the clarity.

The data was then analyzes and the results were correlated to determine their reliability

coefficients. The dependent and independent variables were found to be more reliable with alpha

coefficients of more than 0.70, which is acceptable in the non clinical research work as shown in

Table 3.2 below.

Table 3.2 Reliability Test

Reliability Statistics

Cronbach's Alpha Number of items

0.833 50

Source: Research data 2013

25

3.7 Data Analysis and Presentation Techniques.

Quantitative data collected from respondents was coded and analyzed using Statistical Package

for Social Sciences (SPSS V20). The data was first fed into a computer and analyzed using SPSS.

The study used both descriptive and inferential statistics during data analysis. Opened ended

questions were qualitatively analyzed using the basis of the frequency of responses while

numerical scores were awarded to closed ended questions. Descriptive statistics employed the

use of means, frequencies and percentages and for inferential statistics One-Way Analysis of

Variance (ANOVA) was applied to determine whether there are any significant differences

between ERP and financial performance of sugar companies in Kenya.

Karl Pearson’s zero order coefficient of correlation (Pearson Product Moment Correlation or

simple correlation) was used to determine the direction and strength of the relationship between

ERP and financial performance of sugar companies in Kenya. Further, Karl Pearson’s first order

partial correlation coefficient (rxy.z) was used to ascertain the moderating effect of factors

organizational factors on the relationship between ERP and financial performance. The

relationship between ERP and performance of sugar firms was expected to follow a regression

model of the nature FP= α + β1 ERP + e while the relationship between organizational factors

and financial performance was expected to follow a regression model of the nature FP= α + β2

OF + e where,

FP= Financial performance, α = intercept term, β1 and β2 = Beta coefficients,

ERP= Enterprise Resource Planning

OF= Organizational factors and

e= constant term

Karl Pearson’s zero and first order partial correlation coefficient test will be used to test

hypothesis as shown in the table 3.3.

26

Table 3.3 Hypothesis testing framework and analytical model

Hypothesis Hypothesis test Regression model

H01: ERP systems have no

relationship with financial

performance in sugar companies.

Karl Pearson’s zero

order coefficient of

correlation (Beta test)

Reject H01 if β1≠ O

FP = α + β1 ERP+ e

H02: Organizational factors do not

affect the financial performance of

sugar companies.

Karl Pearson’s zero

order coefficient of

correlation (Beta test)

Reject H02 if β2≠ 0

FP= α + β2 OF + e

H03: Organizational factors do not

affect the relationship between

ERP system usage and financial

performance of sugar companies.

First order partial

correlation coefficient

(rxy.z)

Reject H03 if

rxy.z1 ≠ rxyz2…≠ rxy.zn

≠ rxy.

FP= α + β3 OF + e

Source: Researcher 2013

3.8 Ethical consideration

Ethical considerations protect the rights of participants by ensuring confidentiality. It is unethical

for the researcher to share identifying information regarding the study with anyone not

associated with this study. This ethical consideration is necessary to maintain the integrity of the

study as well as the integrity of the researcher (Creswell, 2002).The respondents were assured of

the confidentiality of information given and were informed that their views were to be used for

the purpose of research only. All information used to fulfill the research objectives of this

research was gained from publicly accessible sources or directly from the companies being

researched. Furthermore, the researcher acquired relevant research permit authorizing him to

carry out research in the field of study. The first ethical consideration that the researcher will

consider in conducting the research is to obey the cardinal rule of voluntary participation

27

amongst participants. This ethical issue is supported by Curry (2006) who affirmed that when

doing a research, participants should not be coerced into taking part in the study. The researcher

considered cardinal rule of voluntary participation amongst participants.

28

CHAPTER FOUR

DATA ANALYSIS AND DISCUSSION

4.1 Study Response Rate

The survey questionnaire was sent to 48 business system users during the first week of May

2013. 20 questionnaires were picked immediately, after 2 weeks 12 more questionnaires were

collected. In total, 32 responses were received by end of May 2013 of which 27 were usable for

the study. The response rate was 67% while the response rate usable for the study was 56%. 10%

of the respondents failed to respond to the entire question asked in the questionnaire.

Table 4.1 Breakdown of the Questionnaire Survey

QUESTIONNAIRE NUMBER PERCENTAGE

Total number of questionnaires sent 48 100.00%

Total number of questionnaires completed by

respondents

32 66.67%

Total number of responses usable for the study. 27 56.25%

Source: Research data, 2013

Of the three companies surveyed, the superior ERP system used was found to be SAP; other

sugar millers were using other systems that were ERP solutions such as Ebizframe, Syspro &

Microsoft Navision. High level of information integration was the major benefit of ERP systems

usage. It was observed that the entire industry was switching over to SAP.

29

4.2 Demographic Factors.

The survey presents scanty information about the background information of the respondents

because the study targeted business system users and thus their personal characteristics were

considered inappropriate, the divisions they belonged whether ICT or Finance, the number of

modules used and duration of use. The key factor was to reach ERP business system users,

however, it should be noted that a large number of the finance and ICT personnel were not ERP

users because of the costly tag of licensing and as a result they import the information from the

ERP systems then later on convert it into spreadsheets for generation of various reports required.

Table 4.2 Respondents Department

Department Frequency Percentage Valid Percentage Cumulative Percentage

Finance 22 81.48 81.48 81.48

ICT 5 18.52 18.52 100.00

Total 27 100.00 100.00

Source: Research data, 2013

The findings in Table 4.2 reveal that 22 (81.48%) of the ERP system are Finance staff and 5

(18.52%) were from ICT. This means that the study population was well presented and majority

users are in Finance Department who were better placed to provide informed responses to the

range of issues covered in the study.

30

Table 4.3 Gender Distribution

Gender Frequency Percentage Valid Percentage Cumulative Percentage

Female 6 22.22 22.22 22.22

Male 21 77.78 77.78 100.00

Total 27 100.00 100.00

Source: Research data, 2013

The findings in Table 4.3 reveal that the majority (77.78%) were male while the female were

22.22%. The study reveals that both Finance and ICT divisions were male dominated. The

gender imbalance did not affect the study as the nature of the research and questions asked were

not gender sensitive and any unlikely error as a result of the gender imbalance may be tolerated.

Table 4.4 Respondents Duration of Service in the Current Position

Period Frequency Percentage Valid Percentage Cumulative Percentage

0-1 Year 6 22.22 22.22 22.22

1-2 Years 3 11.11 11.11 33.33

2-5 Years 5 18.52 18.52 51.85

5-10 Years 1 3.70 3.70 55.56

Over 10 Years 12 44.44 44.44 100.00

Total 27 100.00 100.00

Source: Research data, 2013

31

The study sought to know the duration of respondents in their current positions. The findings in

Table 4.4 indicates that 22.22% of the respondents had been in their current position for less than

one year, 11.11% of the respondent had been in their current position between one and two

years, 18.52 % of the respondents had been in their current position between two and five years,