download - cvc finance limited

TRANSCRIPT

2

3

4

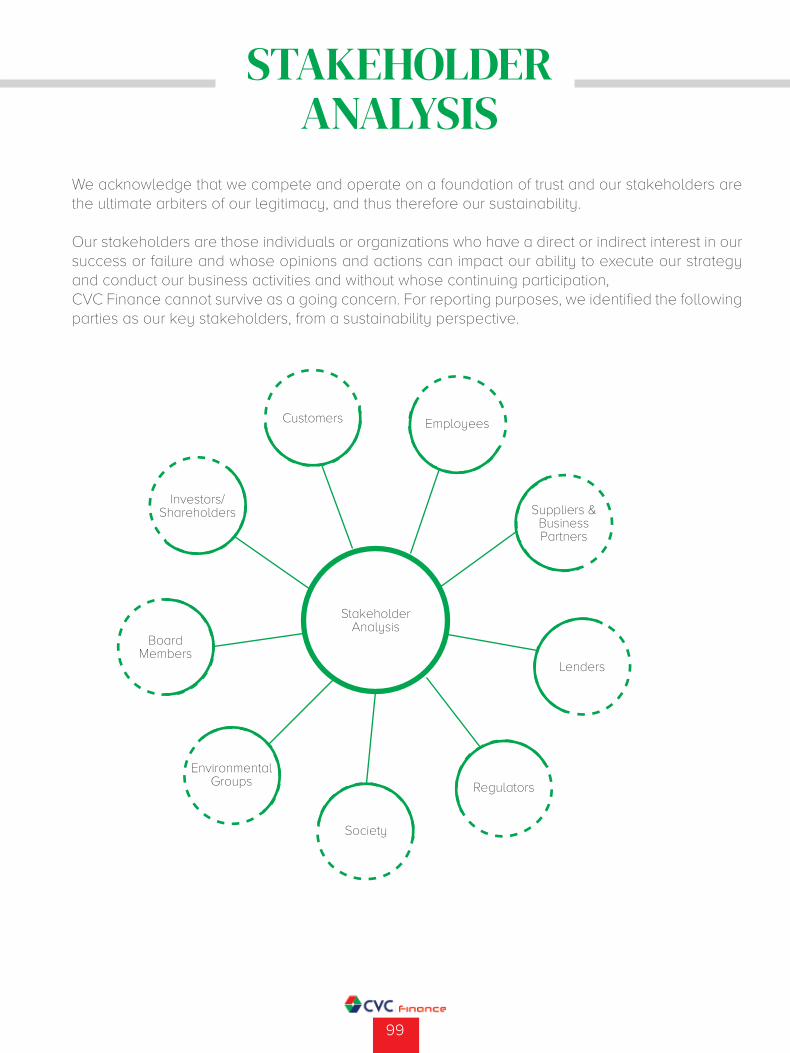

TABLE OF CONTENT01 OVERVIEW 6-32This is CVC 7Historical Snapshots of CVC Finance 9Our Philosophies 12Key Milestones 13Code of Conduct and Ethical Practices 16Our Corporate Values 18What We Do 19Shareholding Structure 24Major Achievements of CVC Finance Limited 26Event Highlights 28

02 STEWARDSHIP 34-75Charter of the Board and its Committees 35Board of Directors 38Committees of the Board 50Message from the Chairman 51Management Committee 54Senior Executives of CVC Finance Limited 63Message from the Managing Director 65Organogram of the Company 71Departments of CVC Finance Limited 72

03 MANAGEMENT DISCUSSION AND PERFORMANCE ANALYSIS 78-137Strategy And Resource Allocation 79Key Operating and Financial Performance Analysis 82Horizontal and Vertical Analysis 91Highlights as required by Bangladesh Bank 98Stakeholder Analysis 99Value Added Statement 115Govt Ex-Chequer Statement 117Economic Outlook 118General Review of the Future Prospect 124Business Segment Review 126Subsidiaries Business Review 137

04 OPERATING ENVIRONMENT AND RISK MANAGEMENT 140-182Macroeconomic Environmental Analysis 143Market Forces and Competitive Landscape Porters 5 Forces 146SWOT Analysis 149

5

Statement of Risk Management 152Report of Risk Management 155Risk Management Framework 158Principle risks in FY 2021 and actions undertaken to mitigate 163Business Continuity Plan at CVC Finance 171Performance Matrices 173Strategy on NPL Management 176Report On Going Concern 180

05 SUSTAINABILITY REPORTING 184-195Environmental Initiative 186Social Responsibility Initiative 187Green Banking Disclosure 189Human Resources and Management 190Information Technology 192Sustainable Development Goals 194

06 CORPORATE GOVERNANCE 198-226Corporate Governance Statement 199Corporate Governance Framework and value Creation 200Board Leadership and Effectiveness 202Roles and Responsibilities of the bored 203Compositions of bored and committee’s 204Statement of Directors’ 206Key Activities of the Board During 2021 207Management Committee 210Internal Control and Risk Management 211Disclosure Under Capital Adequacy and Market Discipline 213Report of the Audit Committee 222Directors Report 2021 224

07 AUDITED FINANCIAL STATEMENTS OF CVC FINANCE & IT’S SUBSIDIARY 228-305

08 CVC IN MEDIA 306-310

09 CVC FINANCE AT A GLANCE 311-314

10 NOTICE OF THE 7TH ANNUAL GENERAL MEETING 315

11 PROXY FORM 316

12 CORPORATE PROFILE 317

6

OVERVIEW

7

CVC Finance Limited, incorporated in 2015 and licensed by Bangladesh Bank, is a fast-growing financial institution. Since its inception, it has consistently contributed to the development of the country. The world is rapidly changing, and we are reinventing our service to meet market demands, CVC Finance Limited aspires to be the country’s most technologically advanced and service-oriented financial institution. CVC Finance Limited has a diverse product portfolio that includes traditional lending and deposit products. Along with the traditional products, it has focused on creating alternate delivery channels leveraging technology. By implementing new technologies, finest corporate practices, and quality service, we aspire to provide innovative financial solutions. We provide value to our consumers by delivering a wide choice of deposit and loan products. Our diversified deposit products assist people in saving and making investments. Their funds eventually contribute to the country’s overall growth. CVC Finance Limited offers a wide range of loan products to help customers meet their personal and business needs. These tailored financial solutions assist businesses in expanding their operations.

The Board of Directors of CVC Finance Limited is made up of professional experts and businessmen from various backgrounds, ensuring strategic decision-making harmony. CVC Finance Limited’s chairman is Mr. Mahmud Hussain. Mr. Hussain has over two decades of diverse local and global financial services market experience with organizations such as the World Bank, Deutsche Bank, and Citigroup UK with a strong a strong educational background in the three broad areas of finance. Our Executive Committee chairman, Mr. Anwar Kamal Pasha is the Managing Director of Moon Readywears Limited. A successful businessman, Mr. Pasha started his career with different types of business organizations. He is the director of Setara Garments Ltd. and Sun Moon Apparels Ltd. He is the Chairman of Kamal Textile Mills Ltd. and Sark Knit Wear Ltd. He holds the position of Managing Director in Pasha Denims Ltd. and is also the owner of Setara Embroidery Services & Design Centre. Our Audit Committee chairman, Mr. Syed Al Farooque is a Sponsor Director and

Chairman of Express Insurance Limited. He started his business career in 1980 and set up a number of Industrial units in the RMG Sector. He was also involved in the real estate sector with a good reputation. He is the Managing Director of WILLS GROUP. He had an active role in BGMEA. He is a member of India-Bangladesh Chamber of Commerce and Industry (IBCCI), Dutch-Bangla Chamber of Commerce and Industry (DBCCI), and Bangladesh German Chamber of Commerce & Industry (BGCCI). He was a member of the Executive Committee of Bangladesh Insurance Association (BIA) and played a vital role in developing the Insurance Industry in the country.

CVC Finance received “A+” in Long Term and “ST-2” in Short Term Credit Rating by Alpha Credit Rating Limited.

THISIS CVC

8

Loan portfolio (as on December 31, 2021) – BDT 412,93,76,833 (BDT 4129 million)

Paid Up capital is BDT 118,96,50,000

CVC Finance Limited has been recognized for its innovative products and services and also for its effort to provide financial services to the rural unbanked community.

- CVC Finance Limited is awarded Women Enterprise Recovery Fund award by UNCDF among 11 Asia Pacific countries.

- CVC Finance Limited is one of the winners of the BFP-B, Challenge Fund Round – 3 partnered with DFID, UKAID

- In partnership with OXFAM, provided access to finance for the rural based MSME’s to benefit marginalized farmers and women.

CAPM ADVISORY

CVC BROKERAGE LIMITED

CVC Finance Limited, a Bangladesh Bank-licensed financial institution that focuses on providing the highest benefit to its clients, purchased 60 percent shares of CAPM Advisory Limited, a private limited company. CAPM Advisory Limited was incorporated as a limited company in November 2011 under the Companies Act, 1994, and was licensed as a full-fledged Merchant Banker and Portfolio Manager in April 2012 under the Bangladesh Securities and Exchanges Commission (Merchant Banker & Portfolio Manager) Rules, 1996.

The Merchant Banking subsidiary will enable CVC Finance Limited to generate non-funded and fee-based revenue in the areas of portfolio management, equity and debt issue management, corporate advisory services, and other allied businesses. CAPM Advisory Limited creates synergy for both companies’ corporate and individual clients, therefore increasing both companies’ profitability. The addition of a merchant banker and portfolio manager subsidiary allows CVC Finance Limited to diversify its operations, offer fee-based financial advisory services, and lower its dependence on traditional lending business.

CVC Brokerage Limited is a fully owned subsidiary of CVC Finance Limited. CVC Brokerage Limited will be engaged in shares, stocks, bonds & other financial instrument, trading and brokerage business under the license issued by SEC and DSE. By trading shares and stocks and assisting a company in registering and issuing stocks to be traded on the primary and secondary markets, CVC Finance Limited will receive commission income and underwriting income. Underwriting fees will be one of the major sources of revenue for brokerage houses. The inauguration of CVC Brokerage will further diversify the revenue streams of CVC Finance Limited.

9

HISTORICAL SNAPSHOTSOF CVC FINANCE

Initial meeting before the formation of the company.

First Annual General Meeting of CVC Finance Limited.

10

Second Annual General Meeting of CVC Finance Limited.

Third Annual General Meeting of CVC Finance Limited.

11

Fourth Annual General Meeting of CVC Finance Limited.

Fifth Annual General Meeting of CVC Finance Limited.

12

OUR VISION

OUR MISSION

To be the innovative & most professional Financial Institution to cater to the need of the market.

Maximize values for both external and internal stakeholders through innovation, skill and professionalism.

Offer comprehensive, professional and innovative financial solutions and services.

Establish an ethical, professional corporate governance and management structure.

Facilitate FDI & optimize the use of capital to spur sustainable economic green growth.

OUR PHILOSOPHIES

13

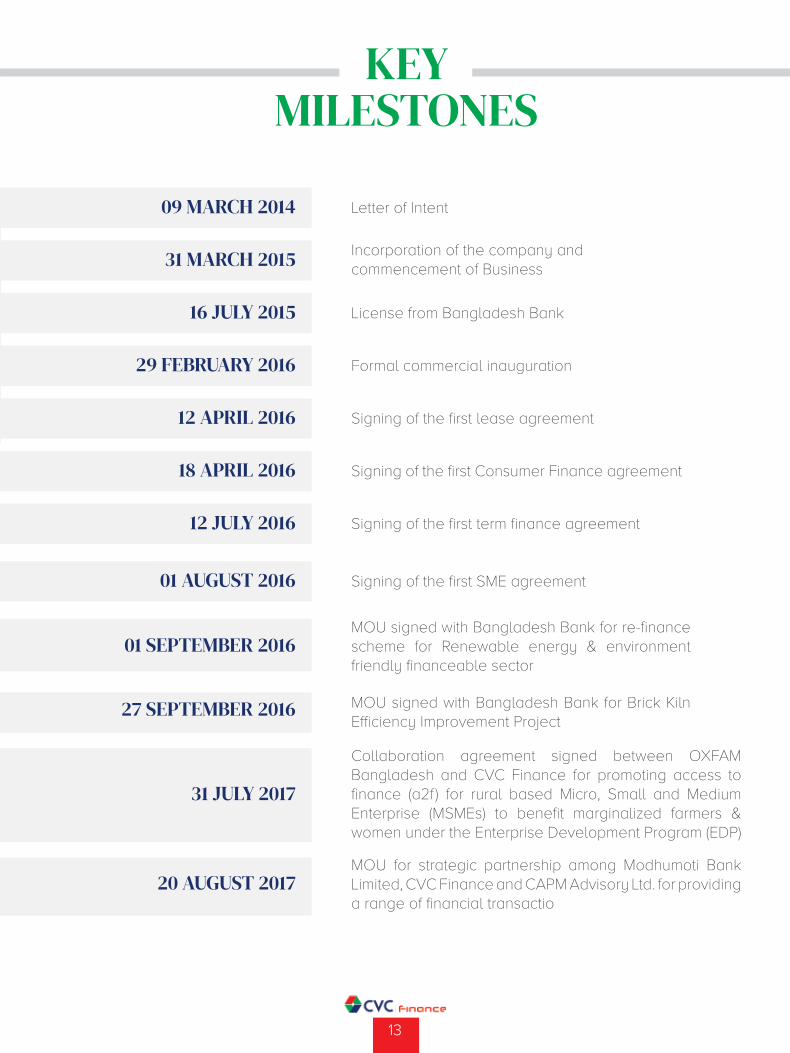

09 MARCH 2014

16 JULY 2015

29 FEBRUARY 2016

12 APRIL 2016

18 APRIL 2016

12 JULY 2016

01 AUGUST 2016

31 MARCH 2015

01 SEPTEMBER 2016

31 JULY 2017

20 AUGUST 2017

27 SEPTEMBER 2016

Letter of Intent

License from Bangladesh Bank

Formal commercial inauguration

Signing of the first lease agreement

Signing of the first Consumer Finance agreement

Signing of the first term finance agreement

Signing of the first SME agreement

Incorporation of the company andcommencement of Business

MOU signed with Bangladesh Bank for re-finance scheme for Renewable energy & environment friendly financeable sector

Collaboration agreement signed between OXFAM Bangladesh and CVC Finance for promoting access to finance (a2f) for rural based Micro, Small and Medium Enterprise (MSMEs) to benefit marginalized farmers & women under the Enterprise Development Program (EDP)

MOU for strategic partnership among Modhumoti Bank Limited, CVC Finance and CAPM Advisory Ltd. for providing a range of financial transactio

MOU signed with Bangladesh Bank for Brick Kiln Efficiency Improvement Project

KEY MILESTONES

14

19 DECEMBER 2017

22 MAY 2018

25 SEPTEMBER 2018

25 JULY 2019

02 FEBRUARY 2021

23 MARCH 2021

13 APRIL 2021

06 JUNE 2021

22 FEBRUARY 2021

01 JUNE 2021

19 AUGUST 2021

Collaboration agreement signing ceremony between CVC Finance Limited and Agromach and Farming Service (AFS).

Contract signing ceremony with Nathan Associates London Ltd and Oxford Policy Management Ltd. in Business Finance for 2018 the Poor in Bangladesh (BFP-B) Program.

Collaboration agreement signing ceremony promoting access to finance for micro, small and medium enterprises (MSMEs) between CVC Finance and Enterprise Café Limited.

Collaboration agreement signing ceremony with Enterprise Café Limited to promote access to finance (A2F) to rural based Micro, Small & Medium Enterprises (MSME) in the Mymensingh Kurigram, Gaibandha.

MoU with Dotlines to create alternate delivery channels.

Signed MoU with Cateina Technologies to enhance Digital Reach.

Signed an NDA with DANA .

Acquired 60% shares of a private limited company, CAPM Advisory Limited.

signed an MoU with OpenArc to develop FinTech products for the digital transformation of CVC Finance Limited’s businesses.

Signed an agreement with Cye Retail Tech Limited to roll out the “Digital Un-Divide” pilot project.

Signed an NDA with OpenArc Bangladesh to create a mobile app for CVC Finance Limited.

31 MARCH 2015 CVC Finance Limited has been renamed from CAPM Venture Capital & Finance Limited.

15

20 AUGUST 2021

31 AUGUST 2021

15 SEPTEMBER 2021

30 SEPTEMBER 2021

01 DECEMBER 2021

31 DECEMBER 2021

28 DECEMBER 2021

Wins a top international award – Women Enterprise Recovery Fund by UNCDF among 11 Asia Pacific countries.

Signed an MoU with BANCAT to collaborate with them in their ‘patient adoption program’ to financially assist three of their cancer patient.

Signed an Agreement with IOTA for the ISO 27001:2013 certification by Bureau Veritas - UK, an international agency.

Signed an Agreement with REVE Chat for creating a chatbot for the CVC Finance website.

Established connection with the EDS money platform and started live money market transaction.

Implemented and launched e-KYC and went live.

Joined hands with JAAGO Foundation to sponsor JAAGO’s furniture and fixtures for the new classrooms.

16

CODE OF CONDUCT AND ETHICAL PRACTICES

Code of conduct is a set of rules outlining the norms, rules and responsibilities of or proper practices for any organization. CVC Finance is a value driven organization with strict adherence to principles even if the situation sometimes provides temporary benefit to the Company. It is the principles, values standards or rules of behavior that guide the decisions, procedures and systems of an organization in a way that contributes to the welfare of its key stakeholders and respects the rights of all constituents affected by its operations.In line with that, the service rule approved by the Board of Directors of CVC Finance, all employees shall require observing and complying with the norms of conduct, manner, behavior and ethical practices stated hereunder in activities they perform in the company. Conduct in such a manner that will enrich the image, dignity and reputation of the company.

Shall carry out his responsibilities with honesty, faithfulness, diligence, and efficiency to the best of his abilities.

Shall attend to his duty punctually and regularly.

Shall not conduct in such a manner as is likely to bring his private interest to conflict with his official duties.

Shall maintain secrecy regarding the affairs of the company and also of its clients.

Shall prevent and avoid potential conflict of interest that may arise and influence whilst he/she performs.

Shall not commit insubordination or non-

compliance with any legitimate, lawful or reasonable order or instruction of a superior.

Environmental and climatic protections should be taken into account in all areas of lending/financing.

Shall not accept directly or indirectly any gift, gratuity or reward or any offer of a gift on his behalf or on behalf of any other person from anyone, which is likely to have a negative effect on the interest of the company.

Shall consider the risks and implications of their actions and in principle, should feel accountable for them and for the potential adverse impacts.

Shall not engage in or participate in any business

dealings for personal gain, such as shareholding, profit sharing, or a partnership of any business company, manufacturing industry, or servicing center.

17

Must give proper attention to the clients and make utmost efforts to render improved customer service at the quickest possible time.

To act and encourage others to behave in a professional way and ethical manner.

Shall not bring or attempt to bring any form of outside influence or pressure.

Shall not take up additional job or employment with another organization or involve in any trade or business without the prior written approval of the management.

Use reasonable care and exercise independent professional judgment.

Shall comply with all applicable laws, rules and regulations, company policies and professional standards.

Shall comply with all current regulatory and legal requirements and endeavor to follow best industry practices.

ETHICAL PRACTICES:

18

OURCORPORATE VALUES

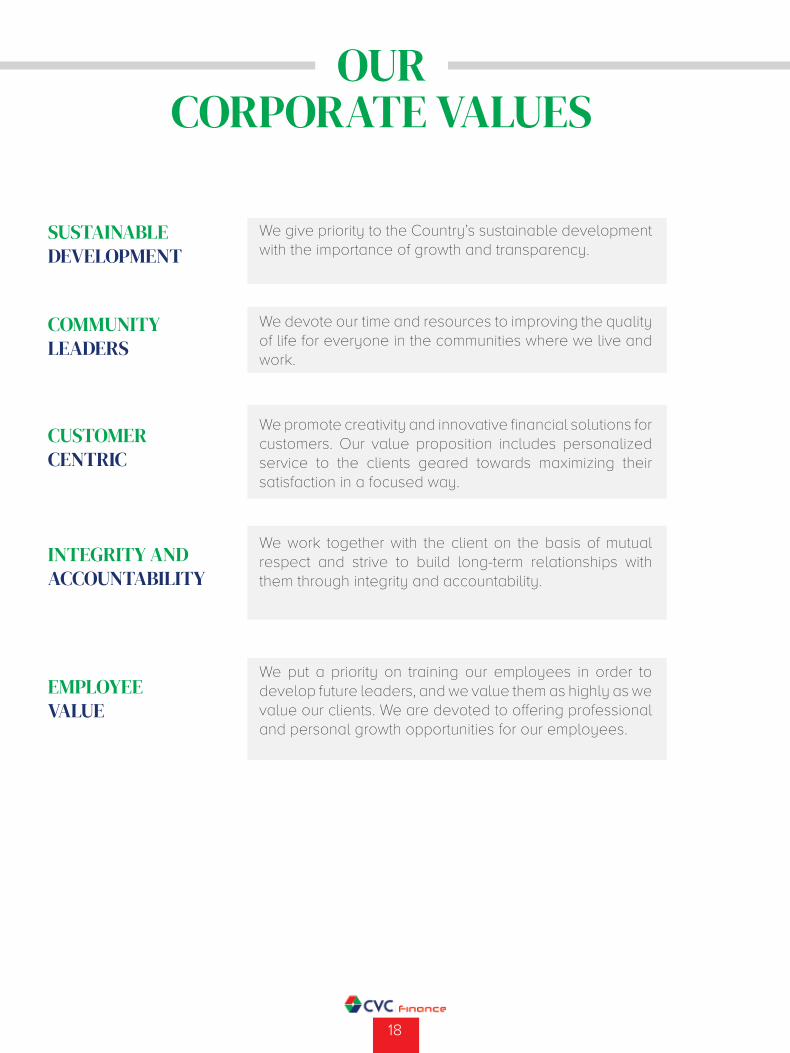

SUSTAINABLE DEVELOPMENT

COMMUNITYLEADERS

CUSTOMERCENTRIC

INTEGRITY AND ACCOUNTABILITY

EMPLOYEEVALUE

We give priority to the Country’s sustainable development with the importance of growth and transparency.

We devote our time and resources to improving the quality of life for everyone in the communities where we live and work.

We promote creativity and innovative financial solutions for customers. Our value proposition includes personalized service to the clients geared towards maximizing their satisfaction in a focused way.

We work together with the client on the basis of mutual respect and strive to build long-term relationships with them through integrity and accountability.

We put a priority on training our employees in order to develop future leaders, and we value them as highly as we value our clients. We are devoted to offering professional and personal growth opportunities for our employees.

19

WHATWE DO

CVC Finance is open to new ideas, perspectives, and nontraditional innovative financing. For faster growth and wealth maximization, customers can get assistance from the company through the following fund and fee-based debt products and services. Through categorizing the products and services by the aforesaid broad generic names, CVC Finance offers different products and services under the following broadheads. In

all cases, management must adhere to the key aspects of the above products as mentioned by Bangladesh Bank in their “Products and Services Guidelines”. CVC Finance has a wide range of conventional and non-conventional financing products for its corporate and individual clients.

LOAN PRODUCTS

SUBSIDIARY PRODUCTS AND SERVICESDEPOSIT PRODUCTS

Corporate Loan

SME Loan

Consumer Loan

Primary Market Services

Secondary Market Services

Investment Banking Services

Research & Investment Advisory

Regular Term Deposit

Income Scheme

Cumulative Term Deposit Scheme

Professional Deposit Scheme

Provident/Gratuity Fund Deposit

Double Money

Triple Money

Monthly Savings Plan

Insured DPS

20

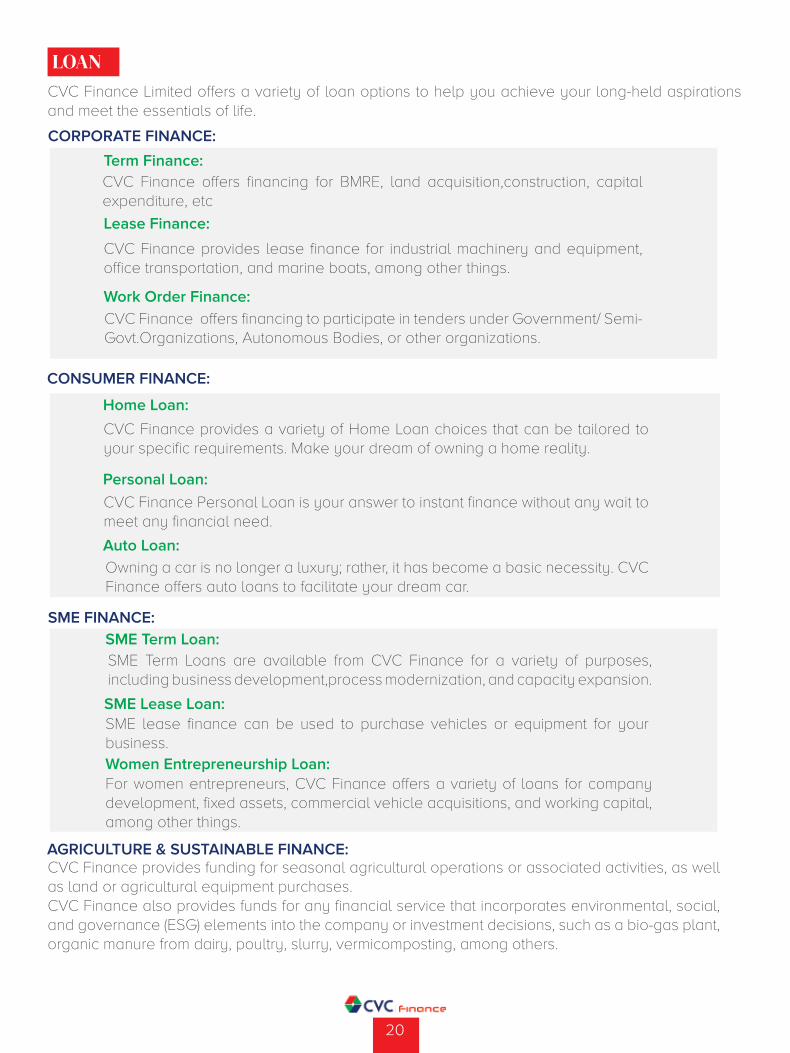

CVC Finance Limited offers a variety of loan options to help you achieve your long-held aspirations and meet the essentials of life.

CVC Finance Personal Loan is your answer to instant finance without any wait to meet any financial need.

CVC Finance offers financing for BMRE, land acquisition,construction, capital expenditure, etc

SME Term Loans are available from CVC Finance for a variety of purposes, including business development,process modernization, and capacity expansion.

CVC Finance provides funding for seasonal agricultural operations or associated activities, as well as land or agricultural equipment purchases. CVC Finance also provides funds for any financial service that incorporates environmental, social, and governance (ESG) elements into the company or investment decisions, such as a bio-gas plant, organic manure from dairy, poultry, slurry, vermicomposting, among others.

CVC Finance provides a variety of Home Loan choices that can be tailored to your specific requirements. Make your dream of owning a home reality.

CVC Finance provides lease finance for industrial machinery and equipment, office transportation, and marine boats, among other things.

SME lease finance can be used to purchase vehicles or equipment for your business.

Owning a car is no longer a luxury; rather, it has become a basic necessity. CVC Finance offers auto loans to facilitate your dream car.

CVC Finance offers financing to participate in tenders under Government/ Semi-Govt.Organizations, Autonomous Bodies, or other organizations.

For women entrepreneurs, CVC Finance offers a variety of loans for company development, fixed assets, commercial vehicle acquisitions, and working capital, among other things.

LOAN

CONSUMER FINANCE:

CORPORATE FINANCE:

SME FINANCE:

Personal Loan:

Term Finance:

SME Term Loan:

AGRICULTURE & SUSTAINABLE FINANCE:

Home Loan:

Lease Finance:

SME Lease Loan:

Auto Loan:

Work Order Finance:

Women Entrepreneurship Loan:

21

CVC Finance provides precision while building a strategy for your ambitions by allowing you to construct your own tenor. Together, we’ll pave the way for a brighter future.

Regular Term Deposits are available to individuals, institutions, or both, and have a variable duration of 3, 6, 9, or 12 months. A minimum deposit of BDT 50,000 is required.

The Professional Deposit Scheme is suitable for self-employed professionals with a flexible tenure from 24 months to 60 months with a lucrative return at maturity.

The minimum deposit for the Double Money Scheme is BDT 100,000, which will be doubled after a fixed tenure.

The minimum deposit for the Triple Money Scheme is BDT 100,000, which will be tripled after a fixed tenure.

The Monthly Savings Plan is a monthly installment-based long-term savings plan with a flexible tenure ranging from 36 months to 120 months and a minimum monthly deposit amount of BDT 1,000.

Here, depositors will have three types of health insurance coverage against their deposit which is BDT 100,000 life insurance coverage at maximum and maximum BDT 30,000 in-patient. Hospitalization and diagnostic charges coverage is up to BDT 4,000 each year against monthly deposit amount of BDT 2,000 to 10,000. A customer can claim online insurance using Carnival-assure-platform (a tech-oriented initiatives by Dotlines Bangladesh) in a hassle-free manner.

Income scheme is suitable for pensioners who prefer interest income on a monthly, quarterly & half yearly basis. The Income Scheme requires a minimum deposit of BDT 100,000 and has a variable tenor ranging from 12 to 60 months.

Provident Fund or Gratuity Fund Deposit Scheme is available for self-employed professionals and organizations with a flexible tenure from 24 months to 60 months.

Individuals and institutions with flexible tenures of two to four years or more are eligible to participate in the Cumulative Term Deposit Scheme. A cumulative term deposit requires a minimum deposit of BDT 50,000.

DEPOSIT PRODUCTS

DEPOSIT SCHEMES:

Regular Term Deposit:Professional Deposit Scheme:

Double Money:

Triple Money:

Monthly Savings Plan:

Insured Deposit Scheme:

Income Scheme:

Provident/GratuityFund Deposit:

CumulativeTerm Deposit Scheme:

22

CVC Finance holds 60% share in CAPM Advisory Limited. CAPM Advisory Limited is a full-fledged Merchant Bank, incorporated as a private limited company under Companies Act, 1994 in November 2011 and licensed as a full-fledged Merchant Bank under Bangladesh Securities and Exchanges Commission (Merchant Banker & Portfolio Manager) Rules, 1996 in April 2012.

It is when a company first offers shares of stock to the public through an exchange, as the name implies. It’s also known as “Going public”

We offer a range of corporate advisory services including the followings:

Capital Restructuring

Financial Consultancy

Feasibility for going public

Structured Solutions

Post issue management

Corporate Governance

Debt issue through private placement.

Our portfolio management service is designed to provide personalized, secure, and simple financial solutions for a wide range of investors who wish to enhance their opportunities while minimizing their administrative burden.

This account is managed by the account holder through CAPM Advisory Limited. The investor bears the risk of

This account is managed by CAPM Advisory Limited on behalf of the client.

investment and also its gain or loss.

Corporate Finance

Foreign Finance

Local Finance

Mergers and Acquisitions

Structured Solutions

Debt Restructuring

Investor Relations Advisory

Structural Asset Finance

Distribution and syndications

Infrastructure & Project Finance

Business Feasibility

Placement Sale

This means further public offering for the issuance of additional security by an issuer that is listed with stock exchanges.

Rights offering (issue) is an issue of rights to a company’s existing shareholders that entitles them to subscribe to additional shares directly from the company in proportion to their existing holdings, within a fixed time period.

Underwriting is the process by which investment bankers raise investment capital from investors on behalf of the corporate issuers who are issuing either equity or debt securities.

SUBSIDIARY SERVICES

PRODUCTS AND SERVICES:

CAPM ADVISORY LIMITED:

A) Primary Market Services:

B) Secondary Market Services:

C) InvestmentBanking Services

i) Equity Capital Management:

Portfolio Management:

ii) Equity Capital Management:

Initial Public Offering (IPO)

Corporate Advisory

Investor DiscretionaryAccount (IDA):

Portfolio Managers Discretionary Account (PMDA)

Repeat Public Offering (RPO)

Right Issue

Underwriting

23

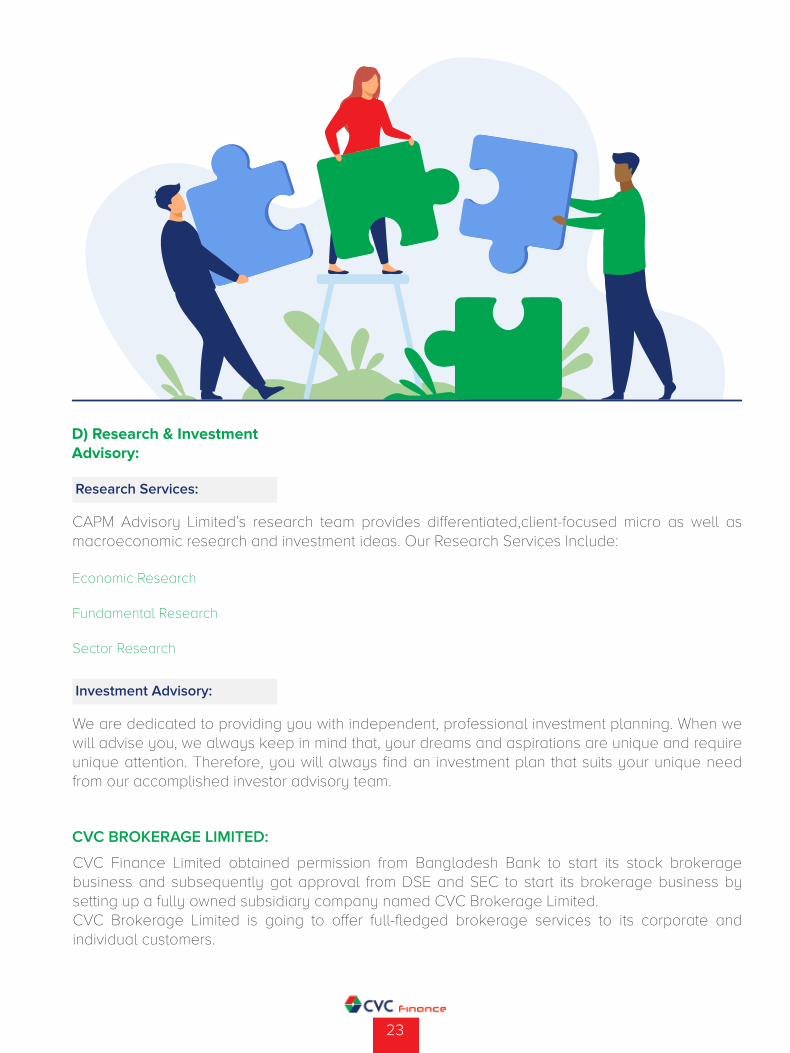

CVC Finance Limited obtained permission from Bangladesh Bank to start its stock brokerage business and subsequently got approval from DSE and SEC to start its brokerage business by setting up a fully owned subsidiary company named CVC Brokerage Limited.CVC Brokerage Limited is going to offer full-fledged brokerage services to its corporate and individual customers.

CVC BROKERAGE LIMITED:

CAPM Advisory Limited’s research team provides differentiated,client-focused micro as well as macroeconomic research and investment ideas. Our Research Services Include:

Economic Research

Fundamental Research

Sector Research

We are dedicated to providing you with independent, professional investment planning. When we will advise you, we always keep in mind that, your dreams and aspirations are unique and require unique attention. Therefore, you will always find an investment plan that suits your unique need from our accomplished investor advisory team.

D) Research & InvestmentAdvisory:

Research Services:

Investment Advisory:

24

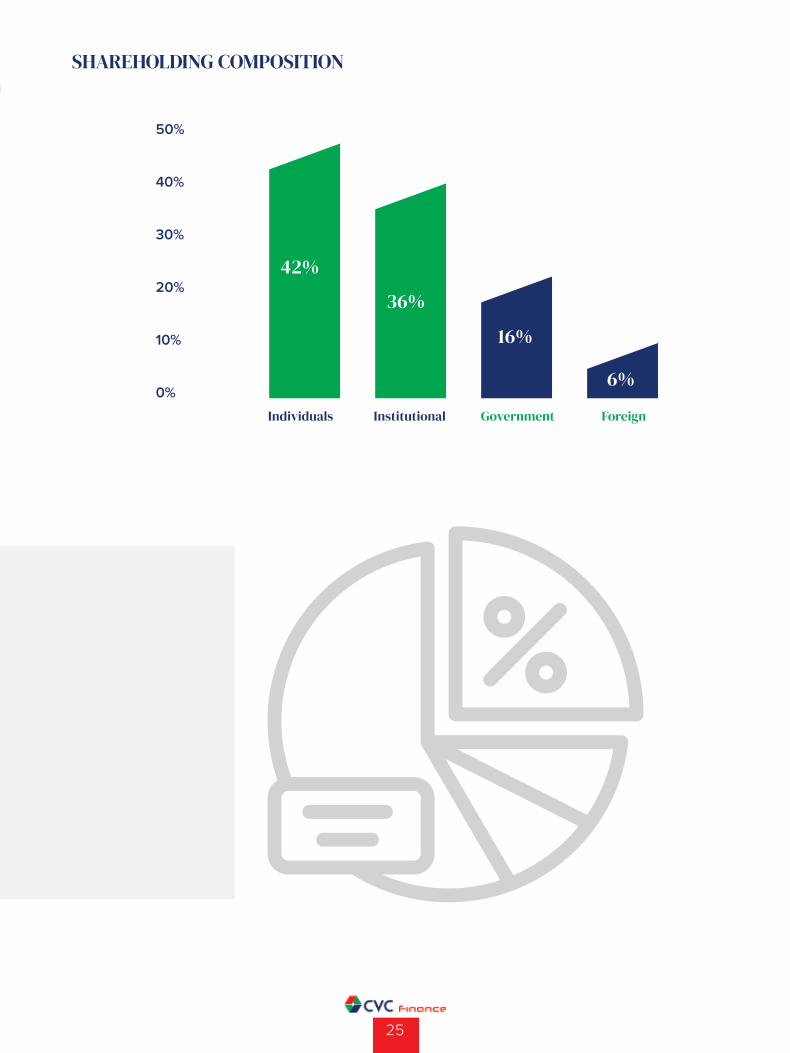

SHAREHOLDING STRUCTURE

Name of the Shareholders Share Percantage Number of shares held

A. INDIVIDUALS 42.00% 49,965,300

Mr. Mahmud Hussain 3.00% 3,568,950

Mr. Syed Al Farooque 2.50% 2,974,125

Ms. Taslima Islam 6.00% 7,137,900

Mr. Naim Hossain 10.00% 11,896,500

Mr. Syed Badrul Alam 6.50% 7,732,725

Ms. Sarwat Khaled Simin 7.50% 8,922,375

Ms. Sabiha Khaleque 2.50% 2,974,125

Mr. Md. Nazrul Islam 2.00% 2,379,300

Mr. Rezaul Karim 2.00% 2,379,300

B. INSTITUTIONAL 36.00% 42,827,400

Khan Brothers Ship Building Ltd. 9.00% 10,706,850

Amanat Shah Weaving Processing Ltd. 8.00% 9,517,200

Moon Readywears Ltd. 10.00% 11,896,500

Padma Glass Ltd. 7.00% 8,327,550

Apsara Holding Limited 2.00% 2,379,300

C. GOVERNMENT 16.00% 19,034,400

Investment Corporation of Bangladesh 10.00% 11,896,500

Sadharan Bima Corporation 6.00% 7,137,900

D. FOREIGN 6.00% 7,137,900

Kowloon Capital Limited 6.00% 7,137,900

TOTAL 11,89,65,000

25

SHAREHOLDING COMPOSITION

50%

40%

30%

20%

10%

0%

Individuals

42%

36%

16%

6%

Institutional Government Foreign

26

UNCDF’S “WOMEN ENTERPRISE RECOVERY FUND”

MAJOR ACHIEVEMENTS OF CVC FINANCE

As a strategic initiative, with partnership with CYE (technological partner), CVC Finance is working for achieving the goal of empowering the women led SME’s through digitizing their operations by offering digital payments, alternative credit scoring, book-keeping, inventory management, business registry thus creating a rural e-commerce market place.

In the thematic area of Women’s Economic Empowerment, UNCDF is leveraging several programs to support women entrepreneur and women-led SMEs - a model that not only focuses on driving local economic development through mobilizing local institutions, but also focuses on closing the digital finance and digital literacy gap, particularly for SMEs.

“Women Enterprise Recovery Fund” is one of the several programs to achieve the Goal. Among the 10 winning Financial Institutions of Asia Pacific countries, CVC Finance proudly represented Bangladesh as one of them.

27

OXFAM

As part of the wider strategy to achieve the Oxfam’s core objectives: Gender and Women’s Leadership and Economic Justice & Resilience, OXFAM in Bangladesh implements the “Enterprise Development program (EDP)” since 2015. The goal of the EDP is to develop sustainable enterprises that will create positive social and environmental impact promoting economic & employment opportunities for marginalized farmers, women and youth. Based on this fact, Oxfam in Bangladesh and CVC Finance has collaborated with each other in 2017 to Promote Access to Finance (A2F) for Rural based Micro, Small and Medium Enterprise (MSMEs) to benefit Marginalized Farmers & Women through collaboration. According to this program CVC Finance has successfully initiated Access to Finance (A2F) program towards Rural based Micro, Small and Medium Enterprise (MSMEs) to benefit Marginalized Farmers.

With funding support from UK Government, the Business Finance for the Poor in Bangladesh (BFP-B) is a program funded by DFID. Its overall objective is to increase Access to Finance (A2F) for Micro and Small Enterprises in Bangladesh (MSEs), with a particular focus on rural and women-led enterprises. Business Finance for Poor – Bangladesh launched its Challenge Fund Round - 3 program on 2017. Among the 10 partners, CVC Finance is one of the winner of Challenge Fund Round – 3. Through this fund CVC Finance has initiated couple of products namely Motsho Chas and Krishir Chaka at rural area of Naogaon District of Bangladesh. These loans were processed through a mobile application and repayments were structured based on farmer’s cash-flow.

https://www.bfp-b.org/news/2018/5/22/7fvk9rn252kkxsfehso0lku9ejp2lq?rq=CVCFL

DFID

28

EVENT HIGHLIGHTS

MoU signing with Bangladesh Cancer Aid Trust (BANCAT) to participatein BANCAT’s Patient Adoption Program

Collaboration agreement signing to roll out the “Digital Un-Divide” pilot project with tech startup Cye Retail Tech Ltd for digitalizing Small and Medium Enterprises (SMEs).

29

Deal signing ceremony with Brilliant Cloud to provide cloudcomputing services to its customers.

Friendly football match amongst the employees of CVC Finance Limited.

Ceremony for winning a top internationalaward – Women Enterprise Recovery Fund by UNCDF

among 11 Asia Pacific countries

Handing over the cheque of sponsorship the furniture and fixtures of the new classrooms of JAAGO Foundation.

30

A daylong session for the employees in order to improve the overall brand value and the organization’s visibility.

The 10th Annual General Meeting of CVC Finance’s subsidiary, CAPM Advisory Limited.

Participated in the SME Fair organized under the collaboration of Bangladesh Bank Training Academy &

SME Foundation

CVC Finance’s strategy session with its core managementcommittee and other senior executives.

31

Celebrating International Women’s Day with the strong, intelligent, talented, and simply wonderful women of CVC Finance Limited.

Friendly cricket match amongst the employeesof CVC Finance Limited.

Welcoming 2021 with all the employeesof CVC Finance.

Agreement signing with Potato Digital – an advertising agency as CVC Finance’s digital

marketing agency to handle the digital activities related to the advertising and communication

32

Collaboration signing agreement with OpenArc Bangladesh (Pvt) Limited to develop a personalized fintech financial solution for our current and potential clients.

Ceremony of acquiring 60% shares of CAPM Advisory Limited.

Celebrating 2 years of the Managing Director of CVC Finance Limited

33

AMENA & MORIYAM STORE

Since 2007, Amena & Moriyam Store has been a sole proprietorship dealing a variety of groceries items. Mr. Md. Abbas Uddin Khan, the owner of Amena and Moriyam Store in Kathalbagan, Dhaka, is a well-known retailer in that area.He was involved in retail sales at the start of the company. In addition to retail sales, he began a wholesale business in 2016. He was unable to expand his business as planned due to a lack of sufficient finance. As a result, he attempted to obtain financial assistance from relatives or other sources, but faced issues regarding assistance. Finally, on the advice of a well-wisher, he went to CVC Finance Limited. He discussed the state of his firm and desired CVC Finance Limited as a financial partner to help him grow it. CVC Finance Limited has always been a name associated with small but promising sectors of the country’s small business. Mr. Md. Abbas Uddin Khan was no exception, and he quickly sought for a loan, as is required by law. CVC Finance, after analysis, financed him for the first time in his life in a short period of time in the amount of Tk. 10,00,000 (10 lac) in easy terms with no difficulty.

Everything was in order, but his company wasn’t ready to deal with the effects of the Covid-19 pandemic. As a result of the government’s lockdown in the event of

a pandemic, the shop remained closed for several months. As a result, the proprietor may be unable to appropriately manage operational costs. Md. Abbas Uddin Khan was clueless yet again as he faced a new challenge. CVC Finance Limited believes in long-term partnerships and does not want to see a good dream come to an end. Thinking that every small business, such as Amena & Morium Store, may thrive if given adequate leadership and sufficient funding. Then, to help him control his operational costs, CVC Finance Limited took the initiative to supply him with Working Capital Finance at a very low interest rate.His shop currently employs five people, which has helped to increase employment. Mr. Abdul Mannan believes CVC Finance Limited has assisted him in his journey and has been a source of support in difficult times. Mr. Abdul Mannan stated, “Achieving success is not tough when CVC Finance Limited is by your side.” We are ecstatic to see him achieve the success he envisioned at the start of his company. As always, CVC Finance Limited attempts to assist aspiring business owners.

34

STEWARDSHIP

35

Charter of the Board and its committees refer to the respective roles, responsibilities and authorities of the Board of Directors and its committees in setting the direction, the management and the control of the company’s overall business. Board charters have become an accepted part of the governance landscape. Many major inquiries, reports and leading practice recommendations refer to the need for board charters in delivering effective governance. The purpose of the charter is to clearly outline the structure of the Board and its committees to define the role of the Board and the committees as a whole through the identification of a schedule of powers reserved solely for the Directors and committee members.

The charter further defines the specific responsibilities of the Board of Directors and committees, in order to enhance coordination and communication between the Chief Executive and the Board and committee members more specifically, to clarify the accountability of all parties for the benefit of the company.

The charter of the Board of Directors and its committees set out in line with Bangladesh Bank guidelines are as follows:

CHARTER OF THE BOARDAND ITS COMMITTEES

BOARD OF DIRECTORS

FORMATION OF SUB-COMMITTEE

FINANCIAL MANAGEMENT

LOAN/LEASE/INVESTMENT APPROVAL

RISK MANAGEMENT

To form sub committees for facilitating company’s operation.

Approve budget, review financial statements and others, set procurement policy and approval of opening of company’s bank account.

Oversight of approval of syndicate loans, leases, investments and large loans.

Approve and implement Core Risk Management Guidelines, delegate power to the management and non-interference in decisions regarding loan processing.

Work-planning and strategic management Setting Vision/Mission, formulating strategic policy, directions, plans and implementation of company’s goal.

Analytical review of success/failure in achieving the target and key performance indicators for the executives.

36

INTERNAL CONTROL AND COMPLIANCE

EXECUTIVE COMMITTEE

BOARD AUDIT COMMITTEE

INTERNAL CONTROL

Effective implementation of an integrated internal control system through the Audit Committee.

Review of Internal Control & Compliance Department’s report by the Board Audit Committee.

The committee will be responsible for proper scrutiny and evaluation of the proposals for facilities to be considered by CVC Finance Limited through an in-depth focus on terms of the financial viability of the credit proposals.

The committee will recommend the proposals to the Board. If the committee thinks proper, they may take any other decision regarding the proposal.

If the committee does not recommend any proposal to the Board, the proposal will be treated as cancelled.

The report of the committee should be attached to the proposal memo to be placed before the Board.

To run the business smoothly and to have a proper focus on financing the Board of Directors formulated the following charters for the Executive Committee:

To ensure the participation of Directors in company affairs through policy framing, proper directive to the management, to operate the different functions of the company properly and in line with the Bangladesh Bank Circular #13 dated 26 October 2011 the Board of Directors formulated the following duties and responsibilities for the Board Audit Committee.

Board Audit Committee will examine the existence of culture for internal control and risk management; executive’s responsibilities and functions and control of their jobs.

Board Audit Committee will examine management initiatives regarding Computerization and MIS management of the Company.

Board Audit Committee will examine the management consideration of various recommendations provided by the Internal/External Auditor for developing internal control procedure/structure.

Board Audit Committee will examine the Risk Management procedure for implementation of work and control.

Board Audit Committee will examine the forgery, weakness of internal control, etc. found by internal or external auditors or regulatory authorities along with their recommendation to eliminate them and accordingly inform the Board regularly.

37

PUBLICATION OF THE FINANCIAL STATEMENTS

INTERNAL AUDIT

IMPLEMENTATION/EXISTENCE OFPRACTICE OF ACTS, RULES AND REGULATIONS

Board Audit Committee will verify that all the information is correctly and properly disclosed in the annual financial statements of the company and the financial statements are prepared on the basis of guidelines issued by Bangladesh Bank and other guidelines relating to the preparation of the financial statements.

Board Audit Committee will discuss with the management and the external auditor before finalization of the financial statements of the company.

The Chairman of the Board Audit Committee will be present before the shareholders in the annual general meeting for answering the questions regarding the financial statements and audit of the financial statements.

Board Audit Committee will examine the audit report and audit procedure of the External Auditor of the company.

Board Audit Committee will examine the implementation/elimination of the recommendation/observation/irregularities as provided by the external auditor in their report by the management properly.

Board Audit Committee will submit their recommend to the Board of Directors regarding appointment of external auditor of the company.

Board Audit Committee will examine the implementation/existence of practice of the acts, rules and regulations enforced by the Regulatory Authority like Bangladesh Bank and other organizations and also adopted by the Board of Directors of the company on regular basis.

38

39

40

Work Experience:Mr. Mahmud Hussain is the Lead Promoter and founding Chairman of CVC Finance Limited. Mr. Hussain has more than two decades of wide ranging local and global experiences (including Tokyo, NY & London) in financial services’ markets with world recognized organizations including World Bank, Deutsche Bank, Salomon Smith Barney and Citigroup UK. Mr. Hussain worked for Citigroup UK as Director of Capital markets & Banking. He possesses an advanced level of understanding and knowledge of financial products and markets, capital market operations, financial management techniques, financial derivatives, asset management and fund management practices. Mr. Hussain has a broad educational background covering different areas of finance and economics. He is a CFA charter holder, and has MBA in Development Management from IBA, Dhaka University as well as an MBA in Finance from International University of Japan. He also holds a Master’s degree in Mathematical Finance from Oxford University and a post-graduate Certificate in International Finance from Stern Business School of New York University.

He is the founder as well as Managing Director & CEO of CAPM (Capital & Asset Portfolio Management) Company Limited. He also provides selective independent consultancy services internationally in the areas of strategic, financial, climate financing & development management. He also occasionally teaches advanced financial topics as Guest faculty. In the recent past, Mr. Hussain was also the Chairman of Bangladesh Government owned Sonali Bank (UK) Ltd and Bank of England (PRA) approved Independent NED (SMF9).

Mr. Mahmud Hussain, CFAChairmanEducation: CFA, MBA

41

Ms. Nasmin Anwar DirectorNominee Director by Investment Corporation of Bangladesh (ICB)

Education: Master’s in Economics

Work Experience:Ms. Nasmin Anwar Joined ICB in 1987 as Senior Officer. She obtained her graduation and post-graduation degree in Economics from Jahangirnagar University. She has been working in different divisions/departments including Central Accounts Department, Fund management Department and Establishment Division of ICB in various capacities for the last 34 years. She also served as the Additional Chief Executive Officer of ICB Securities Trading Company Limited (ISTCL). She has participated in different training courses on various subjects at home and abroad. Currently, she is working as the General Manager of the Operations Wing of ICB. She joined as nominated Director of ICB in the Board of CVC Finance Limited on July 25, 2020. She is also serving as the Director of Golden Son Limited, a public limited company.

42

Mr. Bibekananda SahaDirectorNominee Director by Sadharan Bima Corporation

Education: Master’s in Statistics

Work Experience:Mr. Bibekananda Saha has a wide breadth of knowledge and experience in the financial sector (Non-Life Insurance) who obtained a Diploma degree from Malaysian Insurance Institute and an Associateship from Chartered Insurance Institute (CII), London, United Kingdom. He is the Nominee Director by Sadharan Bima Corporation on the Board of CVC Finance Ltd. He has completed his Master’s in Statistics and currently holds the position of General Manager in the Division of Finance and Claims in Sadharan Bima Corporation.

43

Mr. Tofayel Kabir KhanDirectorRepresentative of Khan Brothers Ship Building Limited

Education: B.Com (Hons), M.com (marketing), Dhaka University, MBA

Work Experience:Mr. Tofayel Kabir Khan has significant business leadership experience as well as first-hand experience in operating across our markets. He is a renowned businessman who is now the Managing Director of Khan Brothers Group. Mr. Khan has completed B.Com (Hons) and M.Com in Marketing from Dhaka University and also has an MBA. After graduation, he gained experience by working in the marketing sector for 5 years in different companies and then joined his own business. Along with Khan Brothers Shipbuilding Ltd., he has also beneficial interests in companies like Khan Brothers PP Woven Bag Ind. Ltd, Khan Brothers PP Bag Ind. Ltd, Khan Brothers Slipways & Engr. Works Ltd. & Khan Brothers Shipping Lines Ltd. Khan Brothers Marble & Granite Ltd., Khan Brothers Equi-Builders Ltd., Khan Brothers Knitwear Industries Limited, Khan Brothers Bag Industries Limited, Khan Brothers Knit Composite Limited and Khan Brothers International and currently holding the position of director in these companies. He is also a Director of CAPM Advisory Limited (A Subsidiary of CVC Finance Limited). He has also a beneficial interest in the private health sector of Bangladesh.

Mr. Tofayel Kabir Khan’s views of business as a means to the material and social wellbeing of the investors, employees and the society at large, led to the accretion of wealth through financial and moral gains as a part of the process of the human civilization. He also is an honorary lecturer in Marketing Department of Dhaka University and National University as a leading Marketing Expert. Mr. Khan is the vice president of Bangladesh Manob Kallyan Society, Dhaka. Member of Federation of Bangladesh Chamber of Commerce and Industry (FBCCI) and Treasurer of Bangladesh Petroleum Tanker Owners Association (BPTOA).

44

Mr. Rezaul KarimDirectorRepresentative of Amanat Shah Weaving Processing Ltd.Education: BBA

Work Experience: Mr. Rezaul Karim has a deep understanding and knowledge of the financial sector. He is a young and dynamic entrepreneur & businessman who is actively involved in the financial market of Bangladesh. He has completed his Bachelor of Business Administration in Finance & Accounting and International Business and currently is associated with organizations like Hazrat Amanat Shah Spinning Mills Ltd., Amanat Shah Weaving Processing Ltd., M. Helal & Brothers Textile Mills Ltd., Standard Composite (Pvt.) Ltd., Standard Company Ltd. and Amanat Shah Fabrics, (Pvt.) Ltd. as Director.

45

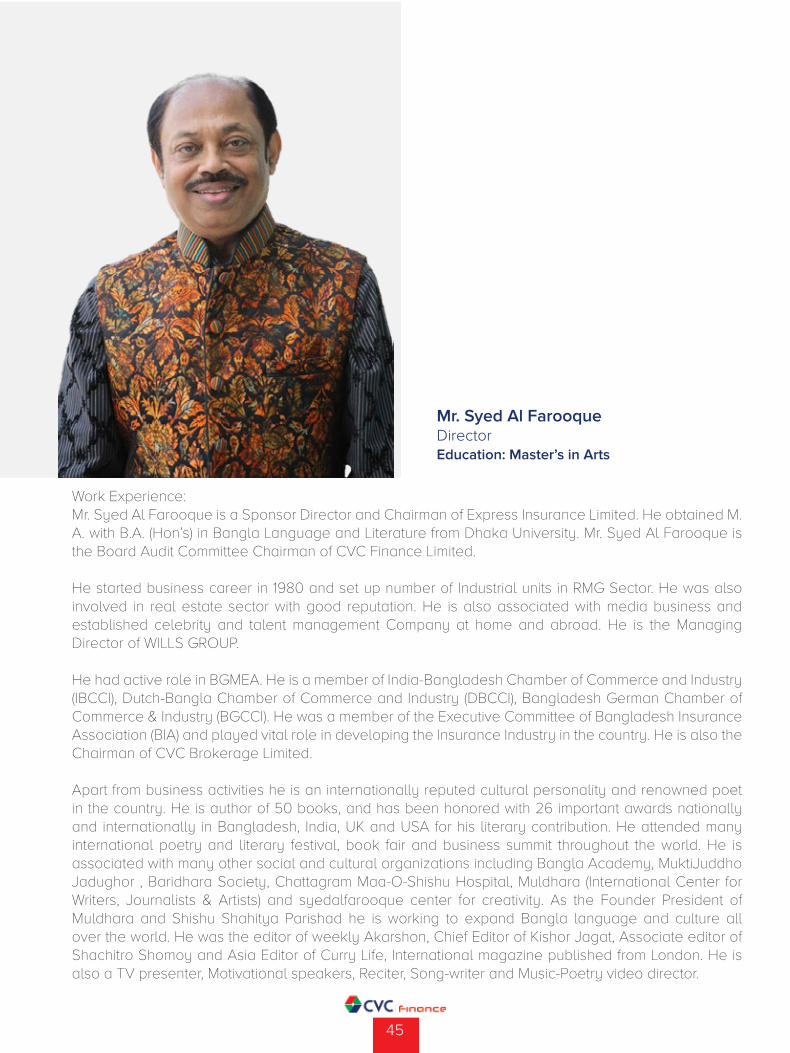

Mr. Syed Al FarooqueDirectorEducation: Master’s in Arts

Work Experience: Mr. Syed Al Farooque is a Sponsor Director and Chairman of Express Insurance Limited. He obtained M. A. with B.A. (Hon’s) in Bangla Language and Literature from Dhaka University. Mr. Syed Al Farooque is the Board Audit Committee Chairman of CVC Finance Limited.

He started business career in 1980 and set up number of Industrial units in RMG Sector. He was also involved in real estate sector with good reputation. He is also associated with media business and established celebrity and talent management Company at home and abroad. He is the Managing Director of WILLS GROUP.

He had active role in BGMEA. He is a member of India-Bangladesh Chamber of Commerce and Industry (IBCCI), Dutch-Bangla Chamber of Commerce and Industry (DBCCI), Bangladesh German Chamber of Commerce & Industry (BGCCI). He was a member of the Executive Committee of Bangladesh Insurance Association (BIA) and played vital role in developing the Insurance Industry in the country. He is also the Chairman of CVC Brokerage Limited.

Apart from business activities he is an internationally reputed cultural personality and renowned poet in the country. He is author of 50 books, and has been honored with 26 important awards nationally and internationally in Bangladesh, India, UK and USA for his literary contribution. He attended many international poetry and literary festival, book fair and business summit throughout the world. He is associated with many other social and cultural organizations including Bangla Academy, MuktiJuddho Jadughor , Baridhara Society, Chattagram Maa-O-Shishu Hospital, Muldhara (International Center for Writers, Journalists & Artists) and syedalfarooque center for creativity. As the Founder President of Muldhara and Shishu Shahitya Parishad he is working to expand Bangla language and culture all over the world. He was the editor of weekly Akarshon, Chief Editor of Kishor Jagat, Associate editor of Shachitro Shomoy and Asia Editor of Curry Life, International magazine published from London. He is also a TV presenter, Motivational speakers, Reciter, Song-writer and Music-Poetry video director.

46

Mr. Anwar Kamal PashaDirectorRepresentative of Moon Readywears Ltd.

Education: B.Com (Honors)

Work Experience:Mr. Pasha has deep experience of managing complex international businesses across dynamic and changing markets. Anwar Kamal Pasha is the Nominated Director by Moon Ready wears Limited on the Board of CVC Finance Limited. A successful businessman, Mr. Anwar Kamal Pasha, runs the business of Moon Ready wears Limited as the Director and also serves Setara Garments Ltd. and Sun Moon Apparels Ltd as Director. Mr. Pasha is the Chairman of Kamal Textile Mills Ltd. & Sark Knit Wear Ltd. and the Managing Director of Pasha Denims Ltd. Mr. Pasha also owns Setara Embroidery Services & Design Centre. He is also a member of Governing Committee of Prime University. He is the Chairman of A & A International Overseas Limited and Recruiting Agent of Zirabo Overseas Limited. Mr. Pasha is the Chairman of S.K Valley Limited. He has also a beneficial interest in Daniel Shipping Lines and he is the owner of Lubna Properties Limited, UK. He is also a Director of Lubna Fashiontex UK Limited. He is currently the Chairman of the Executive Committee of CVC Finance Limited.

47

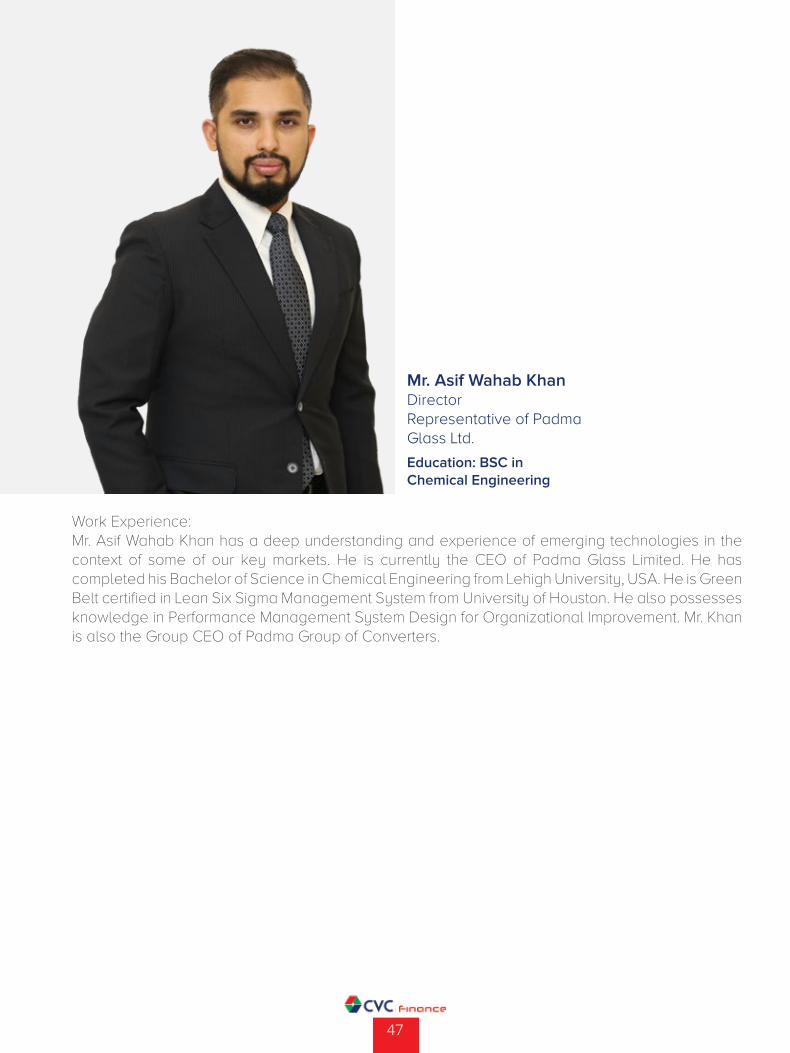

Work Experience:Mr. Asif Wahab Khan has a deep understanding and experience of emerging technologies in the context of some of our key markets. He is currently the CEO of Padma Glass Limited. He has completed his Bachelor of Science in Chemical Engineering from Lehigh University, USA. He is Green Belt certified in Lean Six Sigma Management System from University of Houston. He also possesses knowledge in Performance Management System Design for Organizational Improvement. Mr. Khan is also the Group CEO of Padma Group of Converters.

Mr. Asif Wahab KhanDirectorRepresentative of Padma Glass Ltd.

Education: BSC in Chemical Engineering

48

Mr. Naim HossainDirectorEducation: MBA

Work Experience:Mr. Naim Hossain obtained his Bachelor of Business Administration from Florida Career College, Florida, USA and Master of Business Administration from South University Florida, USA. Presently he is Chairmen of O.N Spinning Mills Limited, Abir Poultry Hatchery & Process Limited, Managing Director of Panama Composite Textile Mills Limited, Continental Spinning Mills Limited, Abir IT Limited, Director of Fareast Islami Securities Limited and also the Proprietor of M/S Millennium Enterprise, M/S Sonali Enterprise. Being determined to make a difference in the society through his work, Naim Hossain is also associated with various social work.

A staunch advocate of professional management and strict adherence to the highest quality standards, Naim Hossain’s leadership qualities have been instrumental in making the company successful in a highly competitive industry. During his short tenure of business carrier he visited many countries for business purposes like USA, Canada, UK, Italy, Switzerland, Spain, Japan, UAE, Australia, China, Singapore, Malaysia, Thailand, India, etc. which enriched his knowledge of the industry and latest technologies. He also participated in seminars and workshops on the textile and spinning industry in China and India.

As a young and dynamic entrepreneur, industrialist and social worker, Naim Hossain has been serving the nation for more than 10 (Ten) years in the field of industrial development, international trade and commerce, setting up and managing industry, business venture and social work. He is used to handling important policies with the assistance of highly experienced and senior personnel of different business organs and looking after the policy decision with regard to business, administration, finance and also day to day activities of the organization.

49

Mr. AKM Monirul IslamDirector

Representative of Apsara Holding Limited Education: Master’s in Political Science

Work Experience:Mr. AKM Monirul Islam has over 20 years of significant investment experience, strong risk management credentials, and in-depth knowledge of the domestic market of Bangladesh. He is the Representative of Apsara Holding Ltd. on the Board of CVC Finance. Along with this, Mr. Islam is also a nominated Director of Prime Insurance Company Limited, representing Ramisha BD Limited. He has done his graduation from a reputed public university in Bangladesh. He is the proprietor of M/S Mollah Traders. Mr. Monirul Islam is the Chairman of Khokon Foundation (A non-profit organization). He is also a member of the Board Audit Committee of CVC Finance Limited.

50

COMMITTEES OF THE BOARD

EXECUTIVE COMMITTEE

AUDIT COMMITTEE

NAME STATUS WITH COMMITTEE

Mr. Anwar Kamal Pasha Chairman Mr. Bibekananda Saha Member

Mr. Tofayel Kabir Khan Member

Mr. Asif Wahab Khan Member

Mr. Naim Hossain Member

NAME STATUS WITH COMMITTEE

Mr. Syed Al Farooque Chairman Ms. Nasmin Anwar Member

Mr. Rezaul Karim Member

Mr. AKM Monirul Islam Member

51

MESSAGE FROM THE CHAIRMAN

52

Dear Stakeholders,

On behalf of Board of Directors of CVC Finance Limited, I am delighted to welcome you all to CVC Finance Limited’s 7th Annual General Meeting. It gives us immense pleasure to present the Company’s Annual Report and Audited Financial Statements for the year ended December 31, 2021.

ECONOMY AFTER THE PANDEMIC The COVID-19 outbreak struck Bangladesh in the middle of 2020, having a negative effect on the country’s economy. COVID 19 was quickly spread, so the government took the required precautions. As a result, the government issued a stringent formal warning to the lockdown and shutdown procedure for the safety of people of Bangladesh. Many business operations were affected, with consequences for employees and their families. The year 2021 was likewise not particularly pleasant. The COVID pandemic’s impact still prevailed. Lockdowns and shutdowns dominated the first part of the year. Due to the uncertain situation, banks and NBFIs focused more on collection and took a cautious approach to lending. Nonetheless, Financial Institutions used to have a negative impact on their reputation. Following the epidemic’s impact, the central bank decided to stop classifying loans in 2020 and 2021 through several circulars in order to assist investors. Despite the pandemic’s unusual disruptions, we were able to have a positive contribution for our clients, employees, and investors by delivering a better financial performance in 2021.

FINANCIAL PERFORMANCE OF THE COMPANYThe formal financial sector faces a major threat in 2021, as the rate of non-performing loans (NPLs) continues to rise at an alarming rate, owing to loan borrowers’ inability to repay their loans due to the loss of their bread and butter at that time. I’m glad to share that, despite the challenging business environment, the company performance stood reasonably to a better place than the previous year. The total credit portfolio of the company stood at BDT 4,129.38 million at the end of 2021, a 3.83% increase in the credit portfolio from previous year. On the other hand, the total deposit was at BDT 1770.55 million witnessed a growth of 15.95% than a year earlier. Net Profit after Tax stood at BDT 47.58 million during 2021 compared to 29.705 million in 2020. The company’s NPL ratio also suffered during 2021. However, we were able to restrict this at 11.61% at the end of 2021, reasonably below the industry average. The company’s goal is always to improve profitability and growth after a reasonably better performance than the previous year. We made it a top priority to strengthen receivables recovery. We’re concentrating on getting the defaulted clients back on track, and we’ve chosen to be even more cautious in the future when it comes to single-party exposure limitations.

DIGITALIZATION IS THE NEW WAYWe are always developing ourselves in order to deliver more consistent high-quality service to our valued clients and to ensure their well-being. We differentiate ourselves apart from other financial institutions by consistently offering high-quality services although remaining under Bangladesh Bank’s regulation. We are working to establish a digital platform for providing better services to customers to meet their financial needs from anywhere in the country and encouraging clients to enjoy any financial service from a formal financial institution at home, as stated by medical science. The Customer Management System and Task Management System were introduced by management in 2021 so that all workers could work in a methodical manner and their work could be tracked. E-KYC, EDS Money, and ISO 27001:2013 certification, were also among the accomplishments. To provide clients with 24-hour customer assistance, the management is also developing an e-wallet platform, a CVC Finance mobile app, and a Chatbot. CVC Finance has strategic partnerships with local stakeholders and international organizations such as OXFAM, , DFID, and the UN Capital Development Fund (UNCDF).

53

The company is collaborating with these global partners to deliver financial services to the bottom of the pyramid.

SUBSIDIARIES OF CVC FINANCEIn 2021, CVC Finance Limited acquired 60% shares of the private limited company, CAPM Advisory Limited. The Merchant Banking subsidiary will allow CVC finance to engage in non-funded and fee-based income in the areas of portfolio management, equity & debt issue management, corporate advisory services, bringing in FDI and other associated businesses. CVC Finance also got approval for another subsidiary which is CVC Finance’s wholly owned brokerage firm.

YOUR WELLBEING IS OUR PRIMARY CONCERNCVC Finance Limited considers human resources to be one of our most important assets. To keep our employees safe and lessen the rate of COVID 19 infection, we created a digital platform and encouraged them to work from home, as well as taking other measures to ensure their safety throughout the pandemic. We have implemented mandatory safety measures for our employees and consumers, including pregnant women and the elderly.In 2021, we have inked an agreement with Bangladesh Cancer Aid Trust so that we can financially support three of their cancer patients on a monthly basis. Keeping the educational sector in mind, we have donated the furniture and fixtures required for JAAGO Foundation’s new classrooms.

GOING FORWARD2021 was a notable year for us. Because of the pandemic’s reduced impact, we were only able to run part of our operations this year. Under these circumstances, we could make few substantial investments in 2021 for future return. We anticipate that the operating environment will continue to improve in 2022, allowing us to operate at full capacity in order to meet our annual targets and contribute to the country’s overall development.As we approach 2022, we start addressing the pandemic’s economic consequences. We are encouraged, though, because the COVID 19 virus vaccine is now more widely available, particularly in our country. Economic activity has restarted, demonstrating a desire to return to pre-pandemic levels. Undoubtedly 2022 would also be a challenging year in terms of sustainability. Our management team, with the help of the Board, has adopted a well-diversified strategy based on diversified products and services to face all challenges companies must focus on. Quality loan portfolio, technological innovation, process improvement, exceptional customer service, deposit portfolio, and other relevant elements would be our primary priority areas. In these changing times, we will continue to strengthen our policies and maintain strong risk management while remaining committed to the highest level of governance.

APPRECIATION I want to express my gratitude to all of our valued clients, shareholders, business partners, and Board of Directors for their guidance and support in growing CVC Finance Limited. I’d also like to thank CVC Finance Limited’s management and employees for their dedication and hard work under the Managing Director’s leadership. I’d like to express my appreciation for the Bangladesh Bank’s cooperation. We are eager to start taking advantage of the opportunities and addressing the issues that may arise in the days ahead.

Mr. Mahmud HussainChairman

54

55

Mr. Syed Minhaj AhmedManaging Director

Mr. Syed Minhaj Ahmed has more than 21 years of experience in the financial sector working in different joint venture financial institutions and multinational banks, such as ANZ Grindlays Bank, Vanik Bangladesh Limited, GSP Finance Company (Bangladesh) Limited, Prime Finance & Investment Limited, National Finance Ltd and Standard Chartered Bank.

He worked in Lankan Alliance Finance Limited as Chief Operating Officer for a period of almost 3 years before joining CVC Finance Ltd and played a major role in setting up, recruitment, policy formulation and business generation of the company.

Mr. Ahmed represents CVC Finance as a Board Director of its investment banking subsidiary company, CAPM Advisory Limited. He is also a key member of BLFCA (Bangladesh Leasing and Finance Companies Association) and works closely with the Executive Committee of the organization.

Mr. Ahmed has completed his M.B.A (Finance) from IBA (Institute of Business Administration), University of Dhaka, Bangladesh, and M. Com (Finance) from University of Dhaka, Bangladesh.

56

Mr. Shah Wareef Hossain is the Deputy Managing Director & Company Secretary of CVC Finance Limited. Mr. Wareef has more than 22 years of experience in the financial sector. Prior to joining CVC Finance Limited, he was the Chief Operating Officer of IPDC Bangladesh. He previously served HSBC Bangladesh, Citibank, Dhaka, Bangladesh; Citibank, Berherd, KL, Malaysia; and American Express Bank Ltd, Dhaka, and has experience in Financial Sector Operations (across Cash Management, Branch Operations, Treasury Operations, and Islamic Banking Operations and Re-Engineering), as well as Management, with exposure to Bangladeshi and ASEAN Markets. Administrative management, risk management, organizational restructuring, project management, and information technology are among his areas of specialization.

Mr. Wareef is on the Board of Directors of CVC Finance’s wholly owned subsidiary, CVC Brokerage Limited.

Mr. Wareef holds a Master of Applied Finance from Monash University in Melbourne, Australia, a Master of Business Administration (Marketing) from the IBA (Institute of Business Administration) at the University of Dhaka in Bangladesh, and a Bachelor of Technology in Civil Engineering from IIT Delhi in India.

Mr. Shah Wareef Hossain Deputy Managing Director & Company Secretary

57

Mr. Mohammad Nejam Uddin is the Head of Corporate Finance at CVC Finance Limited. Mr. Nejam has more than 17 years of extensive experience in five Financial Institutions. He started his career with Prime Finance & Investment Ltd. as Management Trainee in 2004. He worked in International Leasing & Financial Services Ltd., National Finance Ltd., GSP Finance Company (Bangladesh) Limited, Uttara Finance and Investments Limited under different capacities. He attended various training/workshops at Bangladesh Bank, BIBM and different training organizations of Bangladesh.

Mr. Nejam is a Board Director of CVC Finance’s fully owned subsidiary, CVC Brokerage Limited. He has completed his BBA and MBA (major in Finance) from the Department of Finance, University of Dhaka, Bangladesh.

Mr. Mohammad Nejam UddinVP, Head of Corporate Finance

58

Mr. Faisal Amin SAVP, Head of Operations

Mr. Faisal Amin is the Head of Operations at CVC Finance Limited. Mr. Amin has more than 15 years of experience in the financial sector. Mr. Amin worked in International Leasing & Financial Services Limited for a period of almost 10 years before joining CVC Finance Ltd and served in different departments, such as Credit Administration, Special Asset Management, Branch Operation & Risk Management of the company.

Mr. Amin has completed his BBA. (Major in Management), and MBA. (Major in Management Information Systems) from the Faculty of Business Studies, University of Dhaka

59

Mr. Ariful Islam Chowdhury ACAAVP, Head of Internal Control and Compliance

Mr. Ariful Islam Chowdhury is the Head of Internal Control and Compliance at CVC Finance Limited. He is an Associate Member of the Institute of Chartered Accountants of Bangladesh (ICAB). Prior to joining CVC finance Ltd. Mr. Chowdhury has served Khulna Power Company Ltd. as the Company Secretary. Mr. Chowdhury did his article ship in 2016 from Hoda Vasi Chowdhury & Co., a renowned Chartered Accountancy Firm affiliated with the globally reputed Chartered Accountancy Firm named Deloitte Touché Tohmatsu and qualified as Chartered Accountant in December, 2019. He has completed his Masters of Business Administration (MBA) and Bachelor of Business Administration (BBA) from International Islamic University Chittagong. He obtained vice chancellors gold medal award for his academic results in his bachelor’s program.

He has attended various training courses, seminars and workshops arranged by Bangladesh Securities and Exchange Commission, Dhaka Chamber of Commerce & Industry (DCCI), Dhaka & Chittagong Stock Exchange Ltd. and The Institute of Chartered Accountants of Bangladesh (ICAB).

60

Mr. Shakhawat Hossain is the Head of Accounts at CVC Finance Limited. Mr. Hossain has more than 17 years of experience in the field of Finance, Accounts, Internal Audit and Control related jobs in the world’s number one NGO (BRAC), Fine Arts Press Limited and Financial Institutions named Islamic Finance and Investment Limited.

Mr. Hossain has completed his M.Com, MBA (Finance), Banking Diploma (Part-I), CA (Professional Level) & Income Tax Practitioner (ITP).

Mr. Shakhawat HossainHead of Accounts

61

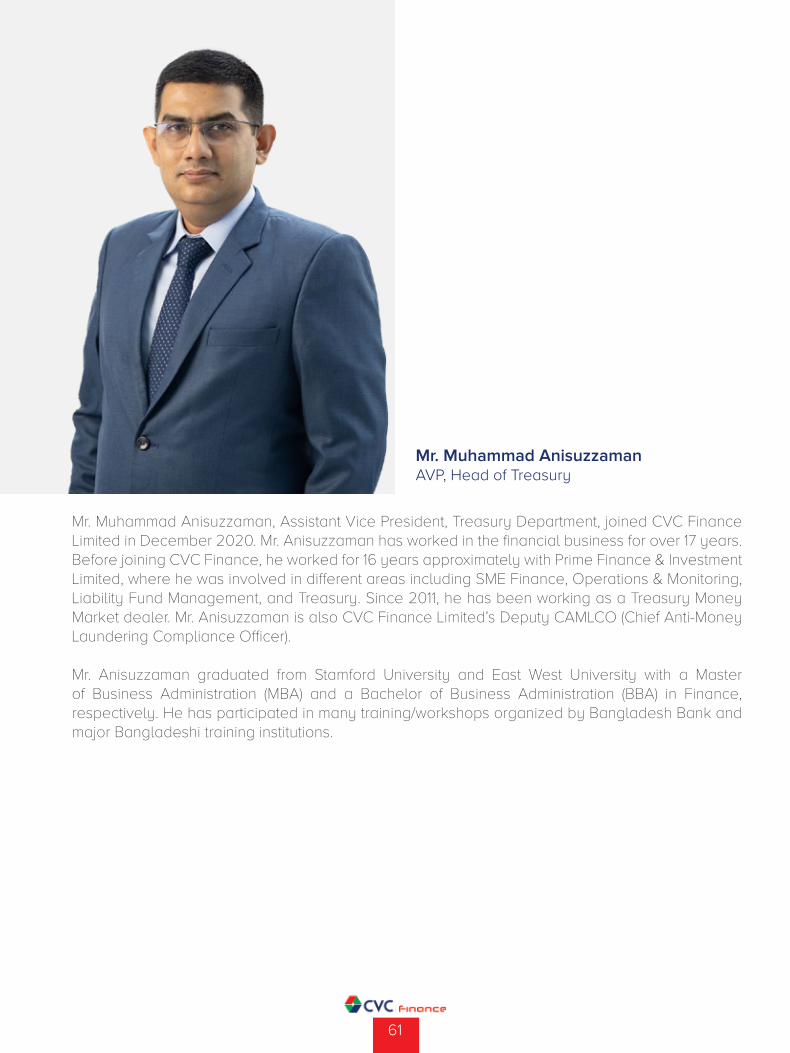

Mr. Muhammad AnisuzzamanAVP, Head of Treasury

Mr. Muhammad Anisuzzaman, Assistant Vice President, Treasury Department, joined CVC Finance Limited in December 2020. Mr. Anisuzzaman has worked in the financial business for over 17 years. Before joining CVC Finance, he worked for 16 years approximately with Prime Finance & Investment Limited, where he was involved in different areas including SME Finance, Operations & Monitoring, Liability Fund Management, and Treasury. Since 2011, he has been working as a Treasury Money Market dealer. Mr. Anisuzzaman is also CVC Finance Limited’s Deputy CAMLCO (Chief Anti-Money Laundering Compliance Officer).

Mr. Anisuzzaman graduated from Stamford University and East West University with a Master of Business Administration (MBA) and a Bachelor of Business Administration (BBA) in Finance, respectively. He has participated in many training/workshops organized by Bangladesh Bank and major Bangladeshi training institutions.

62

Ms. Asma is the member secretary of CVC Finance Limited’s Management Committee. She is responsible for the company’s business strategy and development, branding, corporate communication, public relations, corporate social responsibility, and other associated tasks. Along with that, her responsibility is to assist the management and provide all the required information about the company’s performance to the monthly meetings of the Board and Board Committee’s.

She joined CVC Finance Limited in January 2021 and previously served in the asset operations department before moving to the strategic planning and branding department. Ms. Asma has completed her B.B.A. (major in Finance and Banking) from Bangladesh University of Professionals.

Ms. Asma SadiaSenior Executive, Strategic Planning and Branding

63

Md. Anwar Hossain ChowdhuryAVP & Head of IT

Md. MahamudunnabiHead of Consumer Finance

Md. MainuddinAVP & Head of SAM

Md. Monjur RashidHead of Legal Affairs

SENIOR EXECUTIVES OF CVC FINANCE

64

Mr. Shouman Sinha Head of Liability Unit-1

Md. Shamim AktarHead of Liability Unit-2

65

MESSAGE FROM MANAGING DIRECTOR

66

Dear ShareholdersThe year 2021 marked the beginning of our recovery from the pandemic’s consequences. The years of hard effort we put in to become the country’s one of the most passionate financial brands put us in a good position to meet the unprecedented crisis, allowing us to prosper even in the face of a global epidemic. CVC Finance had a great year. At the end of 2021, the credit portfolio had grown by 3.83% year-over-year (YoY), in a very difficult year. Customer deposits increased by 15.96% YoY to BDT 1,770.55 million in 2021.The company increased total operating income by 44.1% year over year to BDT 281.89 million, owing to maintaining a healthy spread, portfolio growth, and return from stock market investment. Operating expenses increased by 12.81% YoY, resulting in a stunning 82.75% YoY increase in operating profit. After preserving surplus provisioning to cover bad loans, net profit after tax increased by 60.18% to BDT 47.58 million in 2021 from BDT 29.71 million in 2020.

YEAR-END HIGHLIGHTSThis section is about the Covid19 Pandemic, its impact on the economy, governmental and private sector responses to the crisis, government stimulus initiatives, regulatory disturbances, and bulls and bears’ attitudes in the financial market.

COLLECTION AND PORTFOLIO QUALITYWe have focused our business resources on collections in 2021. To ensure efficient monitoring of irregular loan accounts, a separate SAM department was established in 2020. Due to COVID, recovery was seriously affected and getting steady inflow was very difficult. Debt moratorium circulars on the other hand, had a significant impact on loan recovery and collections. Due to COVID, government supported businesses by allowing them minimum payment to Banks and FI’s for a period of two years. Once this facility was lifted many business concerns failed to make regular payments. This is one of the major reasons of increase in NPL percentage. At the same time, some corporate businesses were in a vulnerable position before COVID that has worsened as an impact of the pandemic. As a result, CVC Finance’s NPL increased to 11.61% at the end of 2021, way below the industry average of 19.33% (as quoted in national dailies), thanks to collections from regular and overdue accounts, as well as recovery from loan restructuring under Bangladesh Bank circular letter no. 05 & 06/2020. As needed, adequate loan loss provisions have been established.Until the third quarter of 2021, the lending possibility was rather limited. We have disbursed a total of BDT 542 million in 2021. We had a loan book of BDT 4,129.38 million at the end of the year.

FINANCIAL HIGHLIGHTSAfter the pandemic crisis, our stakeholders, particularly depositors and lending partners, had faith in our commitment, which is commendable given our balance sheet and profitability. Pre- and post-lockdown economic conditions put our prudence and tactical agility to the test, as we had to deal with dry and liquid industries, be tactical in bearish and bullish capital markets, compete with banks and NBFIs for asset spread, and be persistent to keep collection pace, asset quality, and regulatory compliance. Our standalone net profit climbed to BDT 47.58 million in 2021, up by BDT 17.87 million from the previous year’s net profit, contributing to BDT 0.40 standalone EPS, up from BDT 0.25 in 2020, which is 60% higher than previous year. In 2021, the standalone Return on Assets and Return on Equity were 0.83% and 3.70%, compared to 0.54% and 2.35% in 2020.

67

LIQUIDITY MANAGEMENTDuring the first half of 2021, the financial sector faced unstable liquidity situation. Our deposit operations remained fully operational to serve our deposit clients. Despite the fact that loan recovery and collections were substantially hampered by debt moratorium circulars, we prioritized serving our deposit clients during this difficult time. With a commendable performance from Team CVC, we have been able to attract good number of retail and corporate deposits as well as retained most of our existing customers. Our concrete efforts to increase deposit mobilization and improve liquidity enabled us to retain a deposit portfolio of BDT 1,770.55 million at the end of 2021. Regularizing bank payments was another primary aim, in addition to satisfying deposit clients.

REVENUEAs the number of transactions increased in the last two months of 2021, the capital market turned optimistic. Low loan appetite, however, reduced asset volume, which, along with a pric-ing war among competitors, resulted in a slight 4.05% rise in interest income, which was BDT 523.13 million in 2021 compared to BDT 502.76 million in 2020. Furthermore, 72.16% of revenue came from interest income, 21.06% from other operating income, 1.09% from commission bro-kerage, and 5.68% from investment. At the same time, outstanding portfolio rose 3.83% to BDT 4,129.37 million, compared to BDT 3,977.21 mil-lion in the last year.

PROFITABILITYAfter being hammered by the epidemic, the cen-tral bank has given flexibility of repayment to borrowers to help all type of business concerns. The capital market turned positive in the latter several months of 2021, lowering the provision charge for investment depreciation by 530.70% compared to 2020. In 2021, we will have a slight rise standalone in operating expenses by 12.81% when compared to 2020. CVC Finance man-aged the existing portfolio as well as added earning asset. On the other hand, we managed to get good return against the primary and sec-ondary market investment in stock market. At

the same time, we have managed operational costs efficiently. All of these resulted in better profitability for the company. Net Profit after tax is 47.58 million which is 17.87 million (60%) higher than previous year.

ROA AND ROEReturn on Asset and Return on Equity both showed a positive trend in 2021. Our Return on Assets (ROA) for the year 2021 was 0.83%, up from 0.54% in 2020, indicating increased profit-ability throughout the asset base. The return on equity was 3.70% in 2021, up from 2.35% in 2020, indicating increased profitability over the equity basis.As a result, we have maintained an upward trend in recent years. This has been possible as a reflection of visionary leadership from the top management and tireless effort of the entire team.

EPSIn 2021, earnings per share (EPS) were BDT 0.40, up from BDT 0.25 in 2020. Our dedication to in-creasing shareholder wealth is demonstrated by 60% growth in EPS in the year 2021.

TECHNOLOGY ADVANCEMENTThe Company’s initial approach to the Pandem-ic was to give life-saving actions top priority. It modified its business model and moved to re-mote working. During 2021, a large number of CVC Finance personnel worked remotely during various time of the year depending on the severity of COVID situation, resulting in var-ious adjustments to their procedures and con-trol environment, indicating the strength of our IT infrastructure. In addition to leveraging VPN technology to operate remotely and a Remote Attendance System, the company has also digitalized the procedure as much as possible. It’s worth noting that in 2022, we have gained ISO27001:2013 certification at the beginning of 2022. This certification indicates that the organi-zation has met all the requirements for informa-tion security management with high confidence.

68

HUMAN RESOURCES Human resources, according to CVC Finance Limited, are the foundation upon which the company’s success and productivity are built. CVC Finance continues its policy of recruiting the best and implementing continual programs to develop, motivate, and retain its brilliant and capable human resources since human resources are one of the company’s critical success elements. CVC Finance’s commitment to a fair and healthy working environment obligates it to maintain an unbiased/impartial approach in all aspects of its operations, which means it is free of all forms of discrimination based on gender, age, race, national origin, religion, marital status, or any other basis not prohibited by law. This increases task efficiency and aids. Thus, employees are able to realize their full potential.

INTERNAL CONTROL SYSTEMCVC Finance has a good internal control system in place. In terms of operations, business processes, financial reporting, fraud prevention, adherence to relevant rules and regulations, and so forth. Internal controls and systems are designed as part of good governance principles and are applied within the context of suitable checks and balances. Our Company ensures that a reasonably effective internal control framework operates throughout the organization, providing assurance in terms of asset protection, financial and operational data reliability, compliance with applicable statutes, transaction execution as authorized, and adherence to the Company’s internal policies.

STRATEGYIn the shifting economic landscape, CVC Finance has a variety of issues, including sustaining margin, dealing in a competitive market, maintaining asset quality, ensuring collection, dealing with volatile interest rates, and fee income, and optimizing operating capacity.To meet long-term lending requirements, we are focusing on secure funding arrangements such as bonds, foreign funding, and term deposits for more than 12 months. We place a premium on a rigorous collection and monitoring approach, focus on asset quality and cash flow generating