do green banking activities improve the banks ... - mdpi

TRANSCRIPT

�����������������

Citation: Zhang, X.; Wang, Z.; Zhong,

X.; Yang, S.; Siddik, A.B. Do Green

Banking Activities Improve the

Banks’ Environmental Performance?

The Mediating Effect of Green

Financing. Sustainability 2022, 14, 989.

https://doi.org/10.3390/su14020989

Academic Editor: Jean-Pierre Gueyie

Received: 18 December 2021

Accepted: 12 January 2022

Published: 17 January 2022

Publisher’s Note: MDPI stays neutral

with regard to jurisdictional claims in

published maps and institutional affil-

iations.

Copyright: © 2022 by the authors.

Licensee MDPI, Basel, Switzerland.

This article is an open access article

distributed under the terms and

conditions of the Creative Commons

Attribution (CC BY) license (https://

creativecommons.org/licenses/by/

4.0/).

sustainability

Article

Do Green Banking Activities Improve the Banks’Environmental Performance? The Mediating Effect ofGreen FinancingXin Zhang 1, Zhihui Wang 1,*, Xiaobing Zhong 1, Shouzhi Yang 2 and Abu Bakkar Siddik 3,*

1 School of Humanity & Social Science and Law, Harbin Institute of Technology, Harbin 150000, China;[email protected] (X.Z.); [email protected] (X.Z.)

2 School of Economics and Management, Northeast Agricultural University, Harbin 150000, China;[email protected]

3 School of Economics and Management, Shaanxi University of Science and Technology (SUST),Xi’an 710021, China

* Correspondence: [email protected] (Z.W.); [email protected] (A.B.S.)

Abstract: The main purpose of this study is to identify the impact of green banking activities ongreen financing and banks’ environmental performance. It also identifies the mediating effect ofgreen financing on the relationship between green banking activities and environmental performanceof private commercial banks (PCBs) in Bangladesh. Besides, this study also examines the majorchallenges and benefits of green banking development in an emerging economy like Bangladesh.The convenience sampling technique was used to collect primary data from bankers of PCBs inBangladesh, and a final sample size of 352 was recorded. To assess the relationship among the studyvariables, the Structural Equation Modelling (SEM) approach was employed. The empirical resultsrevealed that green banking activities exhibit a significantly positive effect on banks’ environmen-tal performance and sources of green financing, and that sources of green financing significantlyinfluence banks’ environmental performance. Additionally, it was observed that green financingmediates the association between green banking activities and banks’ environmental performance.Furthermore, the study identified customers’ insufficient awareness towards green banking, highinvestment costs, technical obstacles, lack of capable and competent staff in appraising green cred-its/loans, and difficulties and complexity in assessing green projects as major challenges affecting thedevelopment of green banking in Bangladesh. Moreover, the study also discovered that increasingbanks’ competitiveness, reducing long-term costs and expenses, providing online banking facilities,improving customers’ goodwill, and reducing carbon footprints are the key benefits of green bankingdevelopment, as it helps in the achievement of the sustainable economic development of the country.Therefore, major theoretical and managerial policy implications are further discussed with studylimitations and future research directions.

Keywords: green banking activities; green financing; banks’ environmental performance; SEM;Bangladesh

1. Introduction

The planet suffers from climate crises such as droughts, storms, coastal flooding, risingsea level, and tsunamis. These climate changes endanger the sustainable lifestyle on thisglobe, prompting developed and developing countries, particularly Bangladesh, to acturgently and collectively [1]. Bangladesh is perceived as one of the world’s next growingeconomies, as it is characterized by enormous investments, development, and economicpotential to become a prominent market in the 21st century [2,3]. Nevertheless, emergingcountries such as Bangladesh experience challenges of climate change and its associatedimplications on the environment [1,4]. Evidently, Bangladesh is regarded as one of the

Sustainability 2022, 14, 989. https://doi.org/10.3390/su14020989 https://www.mdpi.com/journal/sustainability

Sustainability 2022, 14, 989 2 of 18

most affected nations by climate change due to increasing global sea temperatures, whichharm natural ecosystems and result in economic instability [5–7]. From that point of view,appropriate long-term initiatives must be undertaken to sustain future growth throughthe execution of green strategies and frameworks. As a result, Bangladesh has adaptedthe design of green structures to its wide scope of sustainable development through thebroad implementation of green banking. In addition, banking and financial institutionsspecially influence an economy through their financing roles in various operations, whichwill affect the overall economy and ultimately the mitigation of environmental risks inthe real world [5,7]. These organizations may greatly promote the campaign for a cleanerenvironment, introduce a ‘green’ policy, and facilitate clean technology for customer busi-nesses. Therefore, all financial institutions must pursue a long-term plan to monitor theenvironmental impact of their clients or projects to ensure overall sustainability, as it tendsto decrease costs and contribute to the growth of new businesses [1,8].

Green banking (GB), also known as socially responsible banking, sustainable banking,and ethical banking, is widely used in academic and business settings and has a varietyof meanings [3–5,9,10]. GB is a form of banking with an ultimate goal of preserving theenvironment and protecting natural resources, while taking all social and environmentalfactors into consideration (Bangladesh Bank, 2020). On the one hand, the banking sectoris regarded as one of the key sources of funding for industrial projects that generatesmaximum carbon dioxide emissions via steel, paper, cement, pesticides, fertilizer, electricity,and textiles. Consequently, the banking sector may act as an intermediary between socialand economic growth, and environmental conservation, thus fostering environmentally andsocially responsible investments [1,4]. Therefore, it can be concluded that the GB is a typeof banking established in green and environmentally friendly areas, aimed at reducing theoverall internal and external carbon emissions and improving environmental performance.

Moreover, the banking sectors in Bangladesh are faced with challenges, which forestallthe development of GB in their daily operations, thus hindering their achievement ofsustainable economic growth [1,5,7,8,11]. In addition, Islam [11] studied the challenges andopportunities of GB development in Bangladesh and discovered that high operating costs,diversification issues, start-up, reputational risk, and credit risks were the major challengesof GB development in Bangladesh. More recently, Qureshi & Hussain [12] studied thechallenges and issues of GB products development among Islamic and traditional banksin Pakistan. The study identified lack of knowledge and skills, identification of targetmarket, lack of funding, and customer persuasion as the key barriers to the developmentand implementation of GB products in Pakistan. Furthermore, Sharma & Choubey [13]studied GB initiatives in the Indian banking sector from a qualitative approach. The studyidentified the challenges preventing the Indian banking sector from “going green” as: lowercustomer trust in green goods and services, customers’ reluctance to adopt new tools andtechnologies, lack of customers’ awareness on GB products and technology, lack of educa-tion, lack of knowledge of GB activities among banking staff, high implementation costs inthe short-run, and technical obstacles. Therefore, it can be concluded that high operationcosts, diversification issues, start-up, reputational risks, credit risks, insufficient awarenessof customers about green banking products and technology, lack of education, and igno-rance of banking staffs regarding the green banking activities hinder the development ofGB in developing nations such as Bangladesh.

Recently, various studies have been undertaken in the area of GB development, green fi-nancing, and also the various challenges and benefits associated with GB globally [1,3,6,9,12–21].However, these studies are mainly focused on the adoption of GB [9,22,23]; GB activities and itsdevelopment in the Bangladeshi economy [3,7,19]; challenges and benefits of GB [11–13,24];performance and environmental sustainability of GB [4,6,14,19]; and sustainable financ-ing [1,5,25]. Besides, a couple of studies have examined the impact of GB practices on banks’environmental performance in Pakistan [9], Nepal [26], India [20], and Sri Lanka [27]. InBangladesh, few studies have measured the relationship between GB activities and GBperformance based on secondary data [6,14,19]. However, there are very few documented

Sustainability 2022, 14, 989 3 of 18

studies in the current literature that highlight the influence of GB activities on banks’ envi-ronmental performance via the mediating effect of green financing in emerging countriessuch as Bangladesh. Therefore, a thorough investigation and exploration of the issue inBangladesh is necessary.

This study attempts to bridge the research gap in the following ways: First, it identifiesthe relationship between GB activities, sources of green financing, and banks’ environmen-tal performance based on primary data. Second, the study analyzes the mediating effectof green financing in assessing the relationship between GB activities and banks’ environ-mental performance. Third, this research identifies the major challenges and benefits ofGB development by private commercial banks (PCBs) in Bangladesh. Therefore, the mainpurpose of this study is to investigate the impact of GB activities on green financing andbanks’ environmental performance, and also examine the mediating role of green financingon the relationship between GB activities and banks’ environmental performance in thecontext of PCBs in Bangladesh. This study also identifies the major challenges and benefitsof GB development in an emerging economy like Bangladesh. In order to achieve theaforementioned objectives, this study attempts to answer two questions: (i) “What arethe impacts of GB activities on PCB’s green financing and environmental performance inBangladesh?” and (ii) “What are the major challenges and benefits of GB developmentexperienced by PCBs in Bangladesh?”.

The remainder of the article is structured as follows: Section 2 presents recent litera-ture on GB, GB initiatives in Bangladesh, theoretical background and research hypotheses,and the challenges and benefits of GB development. Section 3 covers sampling, data col-lection, survey instruments, and data analysis techniques. Section 4 provides empiricalfindings and discussions, followed by the conclusion of the study, major policy implica-tions, and study limitations and directions for future studies in Section 5, Section 6, andSection 7, respectively.

2. Literature Review and Hypotheses Development2.1. Green Banking

Green banking is a developing idea that plays a critical role in the domains of climateissues, capital market operations, and sustainable economic development of a country [3].GB was first introduced by the Dutch bank, Triodos Bank, in 1980 [28], and later imple-mented in 2009 by the State of Florida [13]. GB is a type of banking system wherebybanks take the initiative to act as a conscientious institution in the society to achieve envi-ronmental sustainability internally and externally [13]. Banks engaging in such bankingoperations are referred to as green banks, socially responsible and sustainable banks, andethical banks [4,10,29]. Furthermore, a Green Bank indulges in banking activities thatsupport and implement eco-friendly technologies to decrease carbon emissions and en-hance environmental management in bank transactions internally and externally [18]. GBis advantageous, as it helps to promote the goodwill and brand image of banks, whichdemonstrates their dedication in environmental protection [6,30]. Therefore, it can besaid that GB contributes towards the development of sustainable business practices andalleviation of the negative effects of banking activities on the environment through thesupply of loans for environmentally favorable initiatives.

2.2. Green Banking Initiatives in Bangladesh

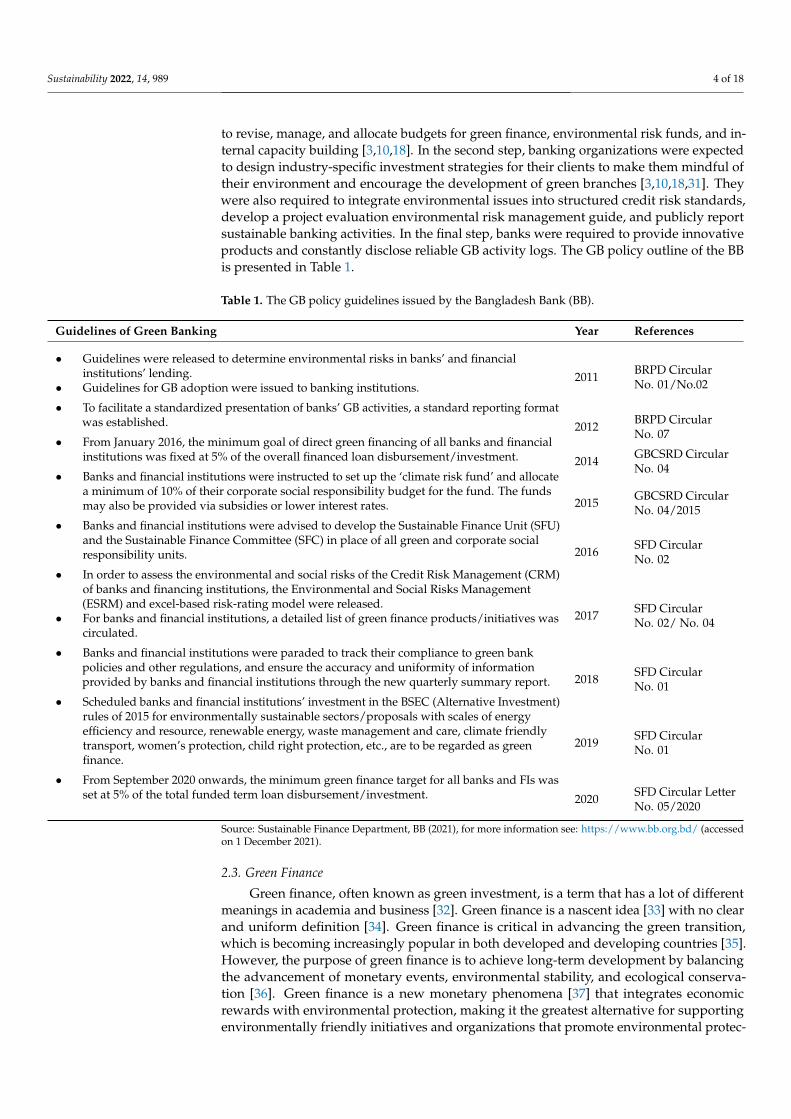

Bangladesh Bank (BB), the country’s central bank, is regarded as the world’s first cen-tral bank to promote GB activities through the issuance of clear GB guidelines for banks andnon-bank financial institutions to protect the environment from adverse weather conditions,greenhouse gas emissions, and decreasing air quality [1,4,5]. Additionally, in 2011, the BBissued GB guidelines instructing banks to implement and enforce extensive GB principlesin three dimensions. In the first part, banks were required to formulate an environmentalstrategy, implement it in their internal operations and lending strategy, and establish aseparate GB unit. Furthermore, banks were required to establish top-level regulatory bodies

Sustainability 2022, 14, 989 4 of 18

to revise, manage, and allocate budgets for green finance, environmental risk funds, and in-ternal capacity building [3,10,18]. In the second step, banking organizations were expectedto design industry-specific investment strategies for their clients to make them mindful oftheir environment and encourage the development of green branches [3,10,18,31]. Theywere also required to integrate environmental issues into structured credit risk standards,develop a project evaluation environmental risk management guide, and publicly reportsustainable banking activities. In the final step, banks were required to provide innovativeproducts and constantly disclose reliable GB activity logs. The GB policy outline of the BBis presented in Table 1.

Table 1. The GB policy guidelines issued by the Bangladesh Bank (BB).

Guidelines of Green Banking Year References

• Guidelines were released to determine environmental risks in banks’ and financialinstitutions’ lending.

• Guidelines for GB adoption were issued to banking institutions.2011 BRPD Circular

No. 01/No.02

• To facilitate a standardized presentation of banks’ GB activities, a standard reporting formatwas established. 2012 BRPD Circular

No. 07• From January 2016, the minimum goal of direct green financing of all banks and financialinstitutions was fixed at 5% of the overall financed loan disbursement/investment. 2014 GBCSRD Circular

No. 04• Banks and financial institutions were instructed to set up the ‘climate risk fund’ and allocatea minimum of 10% of their corporate social responsibility budget for the fund. The fundsmay also be provided via subsidies or lower interest rates. 2015 GBCSRD Circular

No. 04/2015• Banks and financial institutions were advised to develop the Sustainable Finance Unit (SFU)

and the Sustainable Finance Committee (SFC) in place of all green and corporate socialresponsibility units. 2016 SFD Circular

No. 02• In order to assess the environmental and social risks of the Credit Risk Management (CRM)

of banks and financing institutions, the Environmental and Social Risks Management(ESRM) and excel-based risk-rating model were released.

• For banks and financial institutions, a detailed list of green finance products/initiatives wascirculated.

2017 SFD CircularNo. 02/ No. 04

• Banks and financial institutions were paraded to track their compliance to green bankpolicies and other regulations, and ensure the accuracy and uniformity of informationprovided by banks and financial institutions through the new quarterly summary report. 2018 SFD Circular

No. 01• Scheduled banks and financial institutions’ investment in the BSEC (Alternative Investment)

rules of 2015 for environmentally sustainable sectors/proposals with scales of energyefficiency and resource, renewable energy, waste management and care, climate friendlytransport, women’s protection, child right protection, etc., are to be regarded as greenfinance.

2019 SFD CircularNo. 01

• From September 2020 onwards, the minimum green finance target for all banks and FIs wasset at 5% of the total funded term loan disbursement/investment. 2020 SFD Circular Letter

No. 05/2020

Source: Sustainable Finance Department, BB (2021), for more information see: https://www.bb.org.bd/ (accessedon 1 December 2021).

2.3. Green Finance

Green finance, often known as green investment, is a term that has a lot of differentmeanings in academia and business [32]. Green finance is a nascent idea [33] with no clearand uniform definition [34]. Green finance is critical in advancing the green transition,which is becoming increasingly popular in both developed and developing countries [35].However, the purpose of green finance is to achieve long-term development by balancingthe advancement of monetary events, environmental stability, and ecological conserva-tion [36]. Green finance is a new monetary phenomena [37] that integrates economicrewards with environmental protection, making it the greatest alternative for supportingenvironmentally friendly initiatives and organizations that promote environmental protec-

Sustainability 2022, 14, 989 5 of 18

tion [1]. According to the European Commission, green finance in financial services entailsinvestment decisions that incorporate environmental, social, and governance aspects toensure customer and societal satisfaction [38]. As a result, in this study, green finance isdefined as the financing of various environmentally friendly projects such as renewableenergy, alternative energy, energy efficiency, recycling and recyclable products, wastemanagement, and green industry development projects in order to achieve organizationalsustainability [38].

2.4. Environmental Performance

Environmental performance is described as “the influence of a business’s actions on thenatural environment” [39]. Environmental performance includes the use of environmentallyfriendly elements in products, reduced pollution, reduced carbon emissions and waste atthe source, improvements in energy-savings, resource efficiency, and the use of ecologicallyhazardous elements, among other things [40]. On the other hand, carbon and emissiontaxes both have the effect of reducing energy inputs, outputs, profits, and emissions ofan organization [41]. Although the environmental performance of a company can bemeasured through its activities and products [39], the best way to assess the environmentalefficiency of businesses remains the effective use of the material, as stated by Tung et al. [42].It is noteworthy that environmental performance is not organizational protection of theenvironment; rather, it involves constructive and consistent administration of activities toachieve well-defined and long-term goals of natural resources conservation and businessproductivity [27]. As a result, environmental performance can be characterized in thisstudy by giving green training to employees on energy and paper conservation, as well asreducing energy consumption and carbon emissions from banking activities, all of whichcontribute to the country’s long-term development [38].

2.5. Research Hypotheses

Green banking activities are supported not only at firm level but also at policy levelthrough the financing of green projects to ensure environmental sustainability [9]. Thus,GB practices contribute to banks’ environmental performance by cutting down on activitieswith negative impacts on the environment (e.g., reduction of paper use, fuel consumption,and carbon emissions) and promoting environmental benefits (e.g., improvement of em-ployee environmental training and understanding, green infrastructure, and the use of solarand wind power) [5–7]. On the other hand, green finance can be characterized as a modernfinancial event, which considers environmental improvement for social and economicrewards [37]. Similarly, green finance provides a new engine for sustainable economicdevelopment, with a focus on social responsibility and environmental conservation [43]. Inaddition, banks’ overall internal carbon footprint and external carbon production can bereduced via the green financing of GB activities [1]. Thus, the purpose of green finance is toharmonize monetary progress, environmental stability, ecological security, and sustainableeconomic development of a country [36]. Although the environmental performance of acompany can be measured through its activities and products [39], the best way to assessthe environmental efficiency of businesses remains the effective use of the material, asstated by Tung et al. [42]. It is noteworthy that environmental performance is not orga-nizational protection of the environment; rather, it involves constructive and consistentadministration of activities to achieve well-defined and long-term goals of natural resourcesconservation and business productivity [27]. Furthermore, the emission intensity was ap-plied to estimate the environmental performance of the firm [44], and the study stated thatthe firm’s environmental impact can be calculated by using different indexes, rankings, orenvironmental scores. Therefore, it can be concluded that the activities of GB are essentialto the improvement of banks’ green financing and environmental performance, towardsthe attainment of a sustainable economic development.

More recently, Zheng et al. [1] studied the role of PCBs in the development of greenfinance in Bangladesh and identified the four major sources of green financing based on

Sustainability 2022, 14, 989 6 of 18

the bankers’ perception. The sources include investment in waste management, greenestablishment, green brick manufacturing recycling, and recyclable products, all of whichare instrumental to the environmental improvement of banks and the sustainable economicdevelopment of a country. In another study, Rehman et al. [9] highlighted a positiverelationship between GB practices (operations and policy-related practices) and banks’green financing. Furthermore, the GB activities in banks resulted in the improvement oftheir environmental performance by minimizing daily activities with negative environmen-tal impact, such as cutting down on paper use, reducing energy conservation, financingecofriendly projects, lowering fuel consumption, and minimizing carbon emissions [27].Banks also exert a positive effect on the environment through the promotion of proper GBactivities via the enhancement of environmental training and staff awareness, developmentof green buildings, provision of loans for green projects, and the use of solar and windenergy [1,5,27]. Miah et al. [14] studied the factors influencing the environmental perfor-mance of the banking sector in Bangladesh using a multiple regression analysis based onsecondary information. They observed that the credit-rating score had a positive effect onbanks’ environmental performance, as opposed to bank’s longevity in service.

More recently, Rehman et al. [9] studied the association between GB activities and itsimpact on banks’ environmental performance based on the Socially Responsible Invest-ment (SRI) theory. The findings indicate that a strong positive relationship exists amongpolicy-related practices, daily operations practice, and green financing activities of GB inPakistan. Similarly, Shaumya & Arulrajah [27], studied the impact of GB practices on banks’environmental performance in Sri Lanka. The study discovered that GB practices had a pos-itive and significant effect on the banks’ environmental performance. In addition, the studyalso revealed that staff, day-to-day activities, and policy-related practices had a positiveeffect on banks’ overall environmental performance change, while banks’ customer-relatedpractices of GB were statistically insignificant on their environmental performance. Anotherstudy conducted by Kala [20] identified the various green initiatives integrated by bankinginstitutions to improve their environmental performance. The GB activities include envi-ronmental training of employees, energy-efficient practices, green financing, green projects,and green policies. The study further revealed that GB activities positively influencedbanks’ environmental performance in Coimbatore city of India. Similarly, Risal & Joshi [26]studied the impact of GB activities on banks’ environmental performance in Nepal usinga multiple regression analysis. The study concluded that environmental training, banks’green policies, and the availability of energy-efficient equipment significantly affectedthe environmental performance of banks, contrary to customer-related practices (greenfinancing and green projects) whose effects were discovered to be statistically insignif-icant. Therefore, it can be said that the involvement of businesses in GB activities andbanks’ financing of eco-friendly projects are means by which banks can reduce carbonemissions, improve their environmental performance, enhance their business reputation,and ultimately achieve sustainable economic development.

Based on the above discussion, two key research variables and one mediating variablewere identified and include green banking practices as independent variables, sourcesof green financing as a mediating variable, and banks’ environmental performance as adependent variable. As a result, the current study adds to the existing literature on theGB and green funding, as well as organizational environmental management. Besides,this is recognized as one of the earliest studies to investigate the role of green financing inmediating the relationship between GB activities and bank environmental performance inemerging economies such as Bangladesh. Therefore, the following research hypotheses areprovided in view of the theoretical background and review of the previous literature:

Hypothesis 1 (H1). GB activities significantly influence banks’ environmental performance.

Hypothesis 2 (H2). GB activities significantly impact the sources of green financing.

Sustainability 2022, 14, 989 7 of 18

Hypothesis 3 (H3). Sources of green financing significantly affect banks’ environmental perfor-mance.

Hypothesis 4 (H4). The relationship between GB activities and banks’ environmental performanceis significantly mediated by the sources of green financing.

2.6. Challenges and Benefits of Green Banking Development

The banking sector in Bangladesh is faced with numerous challenges pertaining tothe development of GB in its daily operations, which is expected to help in the achieve-ment of the country’s sustainable economic growth [1,5,7,8,11]. In addition, Islam [11]studied the challenges and opportunities of GB development in Bangladesh and discov-ered that high operating cost, diversification issues, start-up, reputational risks, and creditrisks were the major challenges affecting GB development in Bangladesh. More recently,Qureshi & Hussain [12] studied the challenges affecting the development of GB productsamong Islamic and traditional banks in Pakistan. The study revealed that the key barriers inGB product design and execution in Pakistan were lack of skills, awareness, identificationof a target market with suitable sources of funding, and persuasion of the people. In addi-tion, [13] studied the GB initiatives in the Indian banking sector based on the qualitativeapproach and identified the various challenges of “going green’”, with major challengesbeing a lower customer trust issue with green goods and services, customers’ reluctanceto adopt new tools and technology, insufficient customer awareness towards GB productsand technology, lack of education, lack of knowledge among banking staffs regarding theGB activities, high implementation costs in the short-run, and technical obstacles.

In another study by Jayadatta & Nitin [45], it was discovered that the majority ofbanking personnel believed that GB is a proactive strategy to ensure future sustainability.However, Indian banks significantly lag behind their counterparts in industrialized nationsdue to the lack of education, knowledge, and preparedness to implement green projects.In the same year, Tu & Dung [23] identified the numerous challenges of green bankingdevelopment in the Vietnamese banking sector, and the challenges include high costs, longpay-back duration, difficulties and complexity in assessing green projects, lack of well-trained staff, and insufficient customer awareness on the importance of GB services. Besidesthese disadvantages, the study also identified the various benefits of adopting GB in thebanking sector. The major advantages of GB include an increase in bank competitivenessand reputation, achievement of sustainable economic development and green growth, envi-ronmental benefits, higher profits, and increased customer goodwill. Moreover, in anotherstudy conducted by Srivastava [24], it was discovered that various benefits of GB includethe conservation of energy, provision of eco-friendly projects, provision of online bankingfacilities, reduction of long-term costs and expenses, tax advantages, improved businessimage, and reduction in paper consumption. Therefore, it can be concluded that GB con-tributes to the environmental, social, and sustainable economic development of a country.However, the insufficient awareness of customers towards green banking, high investmentcosts, technical obstacles, lack of capable and well-trained staff in appraising green credits,difficulties and complexity in assessing green projects, and issues relating to diversificationmake the development of GB inadequate in an emerging economy like Bangladesh.

3. Research Methods3.1. Study Sample and Data Collection

Private commercial banks, amongst other banks and non-bank financial institutions,were selected due to their significant contributions to GB development in Bangladesh [1,7].Therefore, the primary purpose of this study is to determine the impact of GB activities onbanks’ environmental performance and the mediating effect of green financing on the asso-ciation between GB activities and banks’ environmental performance. Furthermore, thisstudy identifies the major challenges of the implementation of GB by PCBs in Bangladesh

Sustainability 2022, 14, 989 8 of 18

and also shows the significant benefits of GB. To attain the aforementioned research objec-tives, we employed a structured questionnaire and convenience sampling method to obtainprimary data from the bankers of selected PCBs in Bangladesh from May to July 2019.Convenience sampling is a sort of non-probabilistic or non-random sampling in whichparticipants are selected who meet the specified requirements, such as ease of access, geo-graphic closeness, availability at a specific time, or desire to participate, and are includedin the study [46]. As a result, the convenience sampling strategy was a viable alternativedue to the lower costs and ease of obtaining the requisite responses [47,48]. The study’ssample size was calculated using criteria of Barclay et al. [49], which developed a tenfoldsampling rule in which the maximum number of indicators used in the SEM technique wasmultiplied by 10. Based on these criteria, the survey required 140 (10 × 14) respondents. Atotal of 405 inquiries were delivered, of which 352 were retrieved, indicating a responserate of 86.91%. However, in order to reduce the possibility of difficulties stemming fromthe small sample size, 352 respondents were reached using non-probability conveniencesampling approaches. The demographic information of the surveyed bankers are presentedin Table 2. The output revealed that approximately 80% of the respondents were males,while 20% were females. With regards to age, the majority (52.56%) of the respondentswere aged between 26 and 35 years, 22.73% between 36 and 45 years, 14% between 18 to25 years, and the remainder of the respondents were aged 46 years and above. Among therespondents, 68.18% had a master’s degree, 27% had a bachelor’s degree, and only 5% hada PhD qualification. In addition, 52.56% had a working experience of 3–5 years; 38.35%,less than 2 years; and 09.90%, over 5 years.

Table 2. Demographic information of the respondents.

Variable Items Frequency (N) Percentage (%)

GenderMale 282 80.12Female 70 19.88

Age (years)

18–25 50 14.2026–35 185 52.5636–45 80 22.7346 and Above 37 10.52

Educational qualificationBachelor 94 26.71Masters 240 68.18PhD 18 05.11

Working experienceLess than 2 years 135 38.353 to 5 years 185 52.56Above 5 years 32 09.09

Note: N = 352. Source: Authors’ calculations.

3.2. Survey Instrument

The GB activities were formulated based on the study of existing GB literature, whichidentifies the factors influencing the sources of green financing (mediating variable) andbanks’ environmental performance (BEP). To calculate these two study variables (GBand BEP) and one mediating variable (SGF), the initial survey comprised 16 items: Theeight items for GB activities, five for sources of green financing (SGF), and four for banks’environmental performance (BEP). Therefore, Table 3 presents all the questionnaire itemsthat were developed based on the existing literature on GB and green financing. As aninstance, seven items were applied in the assessment of GB activities based on the extantstudies of [5,9,26,27]. Four items were adopted in the assessment of the major sources ofgreen financing according to the studies of [1,5,8], and three items were adopted in assessingbanks’ environmental performance [20,26,27]. Furthermore, the bankers were requested toassess the major challenges hindering the development of PCBs’ GB in Bangladesh. Elevenitems were extracted in the identification of major challenges affecting GB [11,12,23,50].The respondents were also questioned to identify the major benefits of GB, with 13 itemsbeing adopted based on the previously conducted studies [23,24]. The questionnaire was

Sustainability 2022, 14, 989 9 of 18

based on a five-point Likert scale (ranging from one = strongly disagree to five = stronglyagree) for all the study instruments.

Table 3. Questionnaire items.

Item Description References

Green banking activities (GBA).

GBA1 Introducing energy efficient systems, solutions and practices.

[5,9,26,27]

GBA2 Introducing online banking facilities.GBA3 Providing loans for ecofriendly projects.

GBA4 Organizing seminars and symposiums to promoteecofriendly practices.

GBA5 Establishment of more green branches.GBA6 Reduction in paper consumption.

GBA7Encouragement of customers to indulge in ecofriendly-banking

activities such as online bill payment, remote deposit, ande-statements.

Sources of green financing (SGF).

SGF1 My bank has invested more on renewable energy sectors.

[1,5,8,38]SGF2 My bank has invested more on energy efficiency projects.SGF3 My bank has invested more on recycling and recyclable products.

SGF4 My bank has invested more on waste management and otherecofriendly projects.

Bank’s environmental performance (BEP).

BEP1 Reducing energy consumptions.[20,26,27]BEP2 Reducing carbon emissions.

BEP3 Providing green training to staff on energy and paper savings.Note: Deleted measurement items from the final analysis were not included here.

3.3. Data Analysis Technique

The multivariate statistical analysis is a widely used technique, owing to its productionof an accurate and realistic result [51]. The structural equation modeling (SEM) is regardedas a multivariate statistical method often used to verify the relationship among latentvariables. The collected primary data were analyzed in four steps using the SPSS 22.0(Statistical Package for the Social Sciences) and AMOS 23.0 (Analysis of Moment Structures).Descriptive statistics such as the mean and standard deviation were applied in ranking themajor challenges and benefits of GB in the context of PCBs in Bangladesh. To further assessthe accuracy and validity of the measurement models, the study employed the exploratoryfactor analysis (EFA) and confirmatory factor analysis (CFA). After the validation of themeasurement models, the SEM technique was applied to test the research hypothesesused in this study, in accordance with [52]. In addition, the Cronbach’s alpha scoreswere employed to examine the internal reliability of the research constructs. In orderto determine the convergent validity of the study, the average variance extracted (AVE),standardized factor loading values, composite reliability (CR), and various model fit indiceswere used. The model fit was assessed by employing the goodness-of-fit indices, inaccordance with [53].

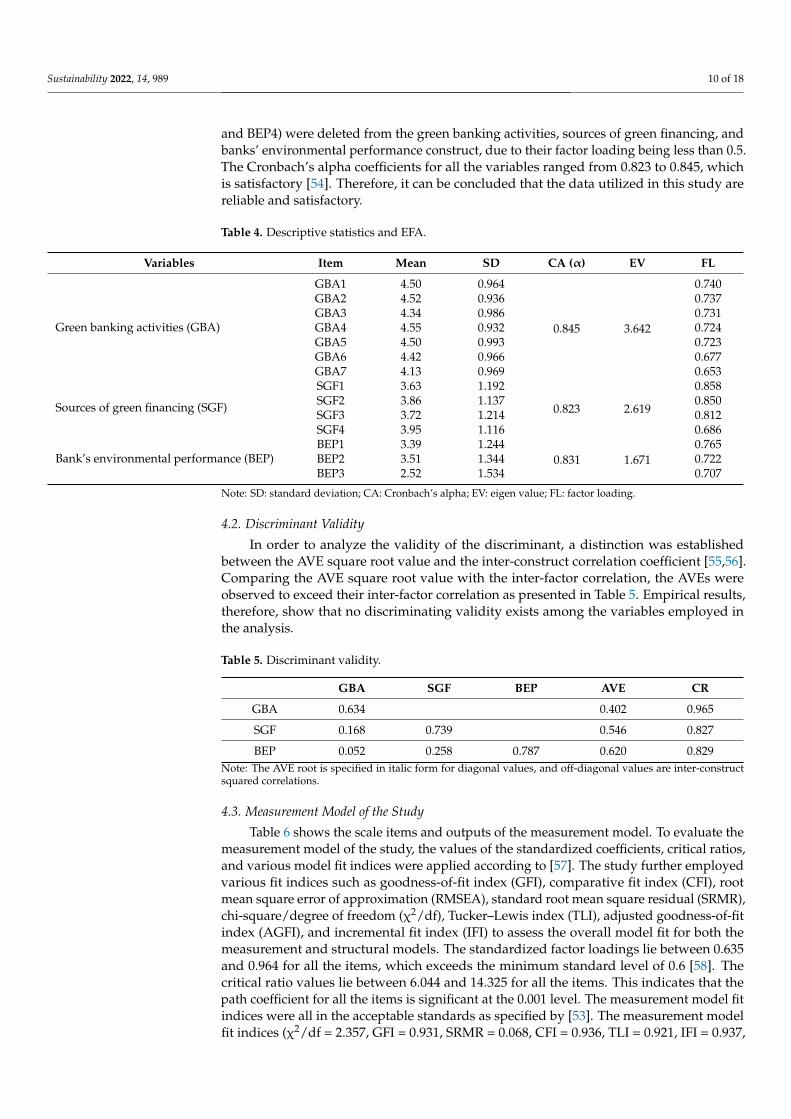

4. Results and Findings4.1. Descriptive Statistics

Table 4 presents the outcomes of descriptive statistics, EFA via a principal componentanalysis (PCA), and the reliability of the study variables. We applied the EFA to calculatethe factor weights of the different variables in the present study. The number of variablesto be processed was determined by applying the Eigenvalue criteria, according to Cattell(1996). Furthermore, the Cronbach’s α values were employed to determine the reliabilityand validity of the research data. Based on the EFA results, four items (GBA8, SGF5, SGF6,

Sustainability 2022, 14, 989 10 of 18

and BEP4) were deleted from the green banking activities, sources of green financing, andbanks’ environmental performance construct, due to their factor loading being less than 0.5.The Cronbach’s alpha coefficients for all the variables ranged from 0.823 to 0.845, whichis satisfactory [54]. Therefore, it can be concluded that the data utilized in this study arereliable and satisfactory.

Table 4. Descriptive statistics and EFA.

Variables Item Mean SD CA (α) EV FL

Green banking activities (GBA)

GBA1 4.50 0.964

0.845 3.642

0.740GBA2 4.52 0.936 0.737GBA3 4.34 0.986 0.731GBA4 4.55 0.932 0.724GBA5 4.50 0.993 0.723GBA6 4.42 0.966 0.677GBA7 4.13 0.969 0.653

Sources of green financing (SGF)

SGF1 3.63 1.192

0.823 2.619

0.858SGF2 3.86 1.137 0.850SGF3 3.72 1.214 0.812SGF4 3.95 1.116 0.686

Bank’s environmental performance (BEP)BEP1 3.39 1.244

0.831 1.6710.765

BEP2 3.51 1.344 0.722BEP3 2.52 1.534 0.707

Note: SD: standard deviation; CA: Cronbach’s alpha; EV: eigen value; FL: factor loading.

4.2. Discriminant Validity

In order to analyze the validity of the discriminant, a distinction was establishedbetween the AVE square root value and the inter-construct correlation coefficient [55,56].Comparing the AVE square root value with the inter-factor correlation, the AVEs wereobserved to exceed their inter-factor correlation as presented in Table 5. Empirical results,therefore, show that no discriminating validity exists among the variables employed inthe analysis.

Table 5. Discriminant validity.

GBA SGF BEP AVE CR

GBA 0.634 0.402 0.965

SGF 0.168 0.739 0.546 0.827

BEP 0.052 0.258 0.787 0.620 0.829Note: The AVE root is specified in italic form for diagonal values, and off-diagonal values are inter-constructsquared correlations.

4.3. Measurement Model of the Study

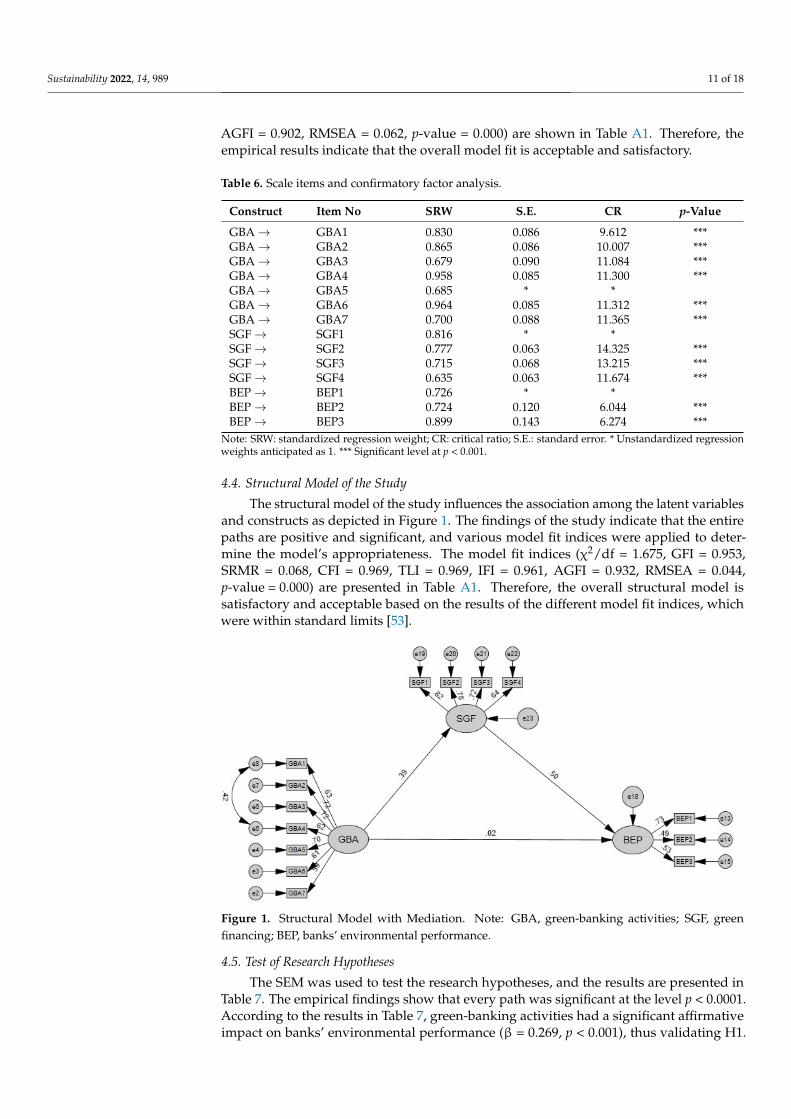

Table 6 shows the scale items and outputs of the measurement model. To evaluate themeasurement model of the study, the values of the standardized coefficients, critical ratios,and various model fit indices were applied according to [57]. The study further employedvarious fit indices such as goodness-of-fit index (GFI), comparative fit index (CFI), rootmean square error of approximation (RMSEA), standard root mean square residual (SRMR),chi-square/degree of freedom (χ2/df), Tucker–Lewis index (TLI), adjusted goodness-of-fitindex (AGFI), and incremental fit index (IFI) to assess the overall model fit for both themeasurement and structural models. The standardized factor loadings lie between 0.635and 0.964 for all the items, which exceeds the minimum standard level of 0.6 [58]. Thecritical ratio values lie between 6.044 and 14.325 for all the items. This indicates that thepath coefficient for all the items is significant at the 0.001 level. The measurement model fitindices were all in the acceptable standards as specified by [53]. The measurement modelfit indices (χ2/df = 2.357, GFI = 0.931, SRMR = 0.068, CFI = 0.936, TLI = 0.921, IFI = 0.937,

Sustainability 2022, 14, 989 11 of 18

AGFI = 0.902, RMSEA = 0.062, p-value = 0.000) are shown in Table A1. Therefore, theempirical results indicate that the overall model fit is acceptable and satisfactory.

Table 6. Scale items and confirmatory factor analysis.

Construct Item No SRW S.E. CR p-Value

GBA→ GBA1 0.830 0.086 9.612 ***GBA→ GBA2 0.865 0.086 10.007 ***GBA→ GBA3 0.679 0.090 11.084 ***GBA→ GBA4 0.958 0.085 11.300 ***GBA→ GBA5 0.685 * *GBA→ GBA6 0.964 0.085 11.312 ***GBA→ GBA7 0.700 0.088 11.365 ***SGF→ SGF1 0.816 * *SGF→ SGF2 0.777 0.063 14.325 ***SGF→ SGF3 0.715 0.068 13.215 ***SGF→ SGF4 0.635 0.063 11.674 ***BEP→ BEP1 0.726 * *BEP→ BEP2 0.724 0.120 6.044 ***BEP→ BEP3 0.899 0.143 6.274 ***

Note: SRW: standardized regression weight; CR: critical ratio; S.E.: standard error. * Unstandardized regressionweights anticipated as 1. *** Significant level at p < 0.001.

4.4. Structural Model of the Study

The structural model of the study influences the association among the latent variablesand constructs as depicted in Figure 1. The findings of the study indicate that the entirepaths are positive and significant, and various model fit indices were applied to deter-mine the model’s appropriateness. The model fit indices (χ2/df = 1.675, GFI = 0.953,SRMR = 0.068, CFI = 0.969, TLI = 0.969, IFI = 0.961, AGFI = 0.932, RMSEA = 0.044,p-value = 0.000) are presented in Table A1. Therefore, the overall structural model issatisfactory and acceptable based on the results of the different model fit indices, whichwere within standard limits [53].

Sustainability 2022, 14, x FOR PEER REVIEW 12 of 19

Figure 1. Structural Model with Mediation. Note: GBA, green-banking activities; SGF, green financ-ing; BEP, banks’ environmental performance.

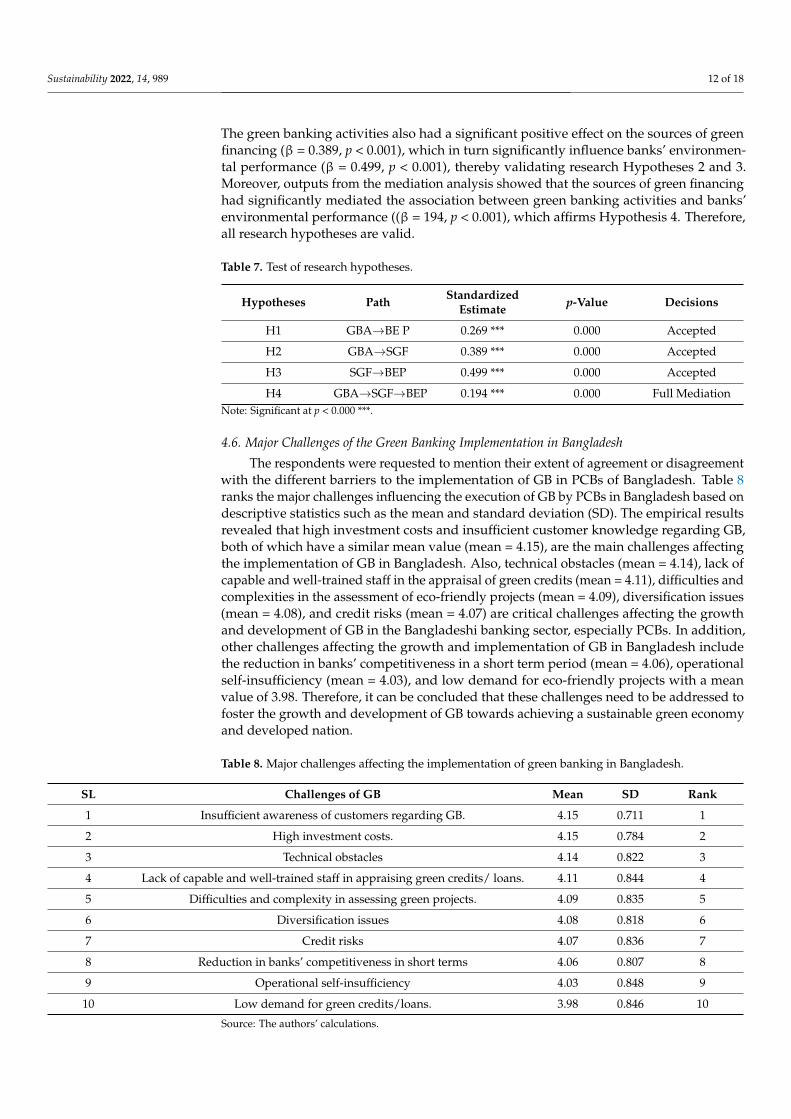

4.5. Test of Research Hypotheses The SEM was used to test the research hypotheses, and the results are presented in

Table 7. The empirical findings show that every path was significant at the level p < 0.0001. According to the results in Table 7, green-banking activities had a significant affirmative impact on banks’ environmental performance (β = 0.269, p < 0.001), thus validating H1. The green banking activities also had a significant positive effect on the sources of green financing (β = 0.389, p < 0.001), which in turn significantly influence banks’ environmental performance (β = 0.499, p < 0.001), thereby validating research hypotheses 2 and 3. More-over, outputs from the mediation analysis showed that the sources of green financing had significantly mediated the association between green banking activities and banks’ envi-ronmental performance ((β = 194, p < 0.001), which affirms hypothesis 4. Therefore, all research hypotheses are valid.

Table 7. Test of research hypotheses.

Hypotheses Path Standardized Estimate p-Value Decisions H1 GBA→BE P 0.269 *** 0.000 Accepted H2 GBA→SGF 0.389 *** 0.000 Accepted H3 SGF→BEP 0.499 *** 0.000 Accepted H4 GBA→SGF→BEP 0.194 *** 0.000 Full Mediation

Note: Significant at p < 0.000 ***.

4.6. Major Challenges of the Green Banking Implementation in Bangladesh The respondents were requested to mention their extent of agreement or disagree-

ment with the different barriers to the implementation of GB in PCBs of Bangladesh. Table 8 ranks the major challenges influencing the execution of GB by PCBs in Bangladesh based on descriptive statistics such as the mean and standard deviation (SD). The empirical re-sults revealed that high investment costs and insufficient customer knowledge regarding GB, both of which have a similar mean value (mean = 4.15), are the main challenges af-fecting the implementation of GB in Bangladesh. Also, technical obstacles (mean = 4.14), lack of capable and well-trained staff in the appraisal of green credits (mean = 4.11), diffi-culties and complexities in the assessment of eco-friendly projects (mean = 4.09), diversi-fication issues (mean = 4.08), and credit risks (mean = 4.07) are critical challenges affecting the growth and development of GB in the Bangladeshi banking sector, especially PCBs.

Figure 1. Structural Model with Mediation. Note: GBA, green-banking activities; SGF, greenfinancing; BEP, banks’ environmental performance.

4.5. Test of Research Hypotheses

The SEM was used to test the research hypotheses, and the results are presented inTable 7. The empirical findings show that every path was significant at the level p < 0.0001.According to the results in Table 7, green-banking activities had a significant affirmativeimpact on banks’ environmental performance (β = 0.269, p < 0.001), thus validating H1.

Sustainability 2022, 14, 989 12 of 18

The green banking activities also had a significant positive effect on the sources of greenfinancing (β = 0.389, p < 0.001), which in turn significantly influence banks’ environmen-tal performance (β = 0.499, p < 0.001), thereby validating research Hypotheses 2 and 3.Moreover, outputs from the mediation analysis showed that the sources of green financinghad significantly mediated the association between green banking activities and banks’environmental performance ((β = 194, p < 0.001), which affirms Hypothesis 4. Therefore,all research hypotheses are valid.

Table 7. Test of research hypotheses.

Hypotheses Path StandardizedEstimate p-Value Decisions

H1 GBA→BE P 0.269 *** 0.000 Accepted

H2 GBA→SGF 0.389 *** 0.000 Accepted

H3 SGF→BEP 0.499 *** 0.000 Accepted

H4 GBA→SGF→BEP 0.194 *** 0.000 Full MediationNote: Significant at p < 0.000 ***.

4.6. Major Challenges of the Green Banking Implementation in Bangladesh

The respondents were requested to mention their extent of agreement or disagreementwith the different barriers to the implementation of GB in PCBs of Bangladesh. Table 8ranks the major challenges influencing the execution of GB by PCBs in Bangladesh based ondescriptive statistics such as the mean and standard deviation (SD). The empirical resultsrevealed that high investment costs and insufficient customer knowledge regarding GB,both of which have a similar mean value (mean = 4.15), are the main challenges affectingthe implementation of GB in Bangladesh. Also, technical obstacles (mean = 4.14), lack ofcapable and well-trained staff in the appraisal of green credits (mean = 4.11), difficulties andcomplexities in the assessment of eco-friendly projects (mean = 4.09), diversification issues(mean = 4.08), and credit risks (mean = 4.07) are critical challenges affecting the growthand development of GB in the Bangladeshi banking sector, especially PCBs. In addition,other challenges affecting the growth and implementation of GB in Bangladesh includethe reduction in banks’ competitiveness in a short term period (mean = 4.06), operationalself-insufficiency (mean = 4.03), and low demand for eco-friendly projects with a meanvalue of 3.98. Therefore, it can be concluded that these challenges need to be addressed tofoster the growth and development of GB towards achieving a sustainable green economyand developed nation.

Table 8. Major challenges affecting the implementation of green banking in Bangladesh.

SL Challenges of GB Mean SD Rank

1 Insufficient awareness of customers regarding GB. 4.15 0.711 1

2 High investment costs. 4.15 0.784 2

3 Technical obstacles 4.14 0.822 3

4 Lack of capable and well-trained staff in appraising green credits/ loans. 4.11 0.844 4

5 Difficulties and complexity in assessing green projects. 4.09 0.835 5

6 Diversification issues 4.08 0.818 6

7 Credit risks 4.07 0.836 7

8 Reduction in banks’ competitiveness in short terms 4.06 0.807 8

9 Operational self-insufficiency 4.03 0.848 9

10 Low demand for green credits/loans. 3.98 0.846 10

Source: The authors’ calculations.

Sustainability 2022, 14, 989 13 of 18

4.7. Major Benefits of Green Banking

Again, respondents were requested to check whether they were in agreement or dis-agreement with the various advantages of GB to assess the major benefits to be derivedfrom the implementation of GB by PCBs in Bangladesh. Table 9 presents the major ben-efits of GB. The findings from the descriptive statistics show that an increase in banks’competitiveness (mean = 4.18, SD = 0.687), reduction in long term costs and expenses(mean = 4.16, SD = 0.854), provision of online banking facilities (mean = 4.15, SD = 0.711),improvement in customer goodwill (mean = 4.12, SD = 0.747), and reduction in the carbonfootprint from banking activities (mean = 4.08, SD = 0.857) are the major benefits of GB.Interestingly, the results indicate that environmental-related benefits of GB include conser-vation of energy and provision of ecofriendly projects, both of which exhibit the same meanvalue of 4.07. Furthermore, achievement of a sustainable economic development by thecountry (mean = 4.06, SD = 0.852), increased profits for banks in the long term (mean = 4.03,SD = 0.716), tax advantages (mean = 4.01, SD = 0.801), economy in paper consumption(mean = 3.99, SD = 0.846), and promotion of banks’ image (mean = 3.98, SD = 0.846) wereidentified as other significant benefits of GB. Therefore, to derive the full benefits of GB, it issuggested that banking authorities take appropriate measures to combat the climate changeissues and achieve the sustainable development goals (SDGs) through the implementationof GB in their daily operations.

Table 9. Major benefits of green banking.

SL Benefits of GB Mean SD Rank

1 Increase in bank competitiveness. 4.18 0.687 1

2 Reduction in long term costs and expenses. 4.16 0.854 2

3 Provision of online banking facilities. 4.15 0.711 3

4 Improvement of customers’ goodwill. 4.12 0.747 4

5 Reduction in the carbon footprint. 4.08 0.857 5

6 Provision of environmental related benefits. 4.07 0.789 6

7 Conservation of energy. 4.07 0.836 7

8 Provision of ecofriendly products. 4.07 0.849 8

9 Contribution towards the attainment of a sustainable economic development of the country. 4.06 0.852 9

10 Higher profits for banks in long terms. 4.03 0.716 10

11 Tax advantages. 4.01 0.801 11

12 Economy in paper consumption. 3.99 0.846 12

13 Promotion of reputation. 3.98 0.846 13

Source: The authors’ calculations.

5. Discussion and Conclusions

During the last two decades, researchers, academics, and experts have become muchmore interested in the subject of GB and green financing in developed and developingcountries. Therefore, the objective of this study was to examine the impact of GB activitieson banks’ environmental performance, and the mediating effect of green financing onthe association between GB activities and banks’ environmental performance. The studyfurther identifies the major challenges encountered in the implementation of GB by PCBsin Bangladesh and presents the significant benefits of GB. Primary data were used in thisstudy to achieve the above research objectives, and data were collected from bankers of theselected PCBs in Bangladesh through structured questionnaires. The SEM technique wasapplied to assess the research model of the study. The empirical outcomes of different modelfit indices revealed that the overall research model was valid and appropriate. The outcomeindicates that Hypothesis 1 is supported, highlighting a significant positive relationship

Sustainability 2022, 14, 989 14 of 18

between GB activities and banks’ environmental performance. This result is supported byprevious studies [20,26,27]. Therefore, it can be concluded that GB activities have a positiveimpact on the improvement of PCBs’ environmental performance in Bangladesh.

Empirical findings revealed that GB activities have a substantial positive impact ongreen financing of PCBs in Bangladesh, validating Hypothesis 2. This implies that GB ac-tivities play a crucial role in the growth and development of green financing in Bangladesh,as it helps to reduce environmental pollution and achieve sustainable development inthe country. This finding is supported by the study conducted by Rehman et al. [9], whodiscovered that GB activities have a positive effect on green investments of Pakistani bank-ing institutions. As per the results, Hypothesis 3 is validated, implying a strong positiverelationship between green financing and banks’ environmental performance. This findingis consistent with the study conducted by [20], but inconsistent with the study conductedby Risal & Joshi [26]. According to the study by Risal & Joshi [26], it was discovered thatgreen loan and green projects have a negative impact on banks’ environmental performancein the Nepalese banking sector. Therefore, it can be concluded that green financing helpsto improve the environmental performance of banks through the investment in variousecofriendly projects such as renewable energy, energy efficiency, recycling and recyclable,waste management, and other ecofriendly projects.

This is the first study to examine the mediating effect of green financing on theassociation between GB activities and banks’ environmental performance in the contextof commercial banks in Bangladesh. The empirical findings suggest that green financinghad significantly mediated the association between GB activities and banks’ environmentalperformance, thus validating Hypothesis 4. The mediating role of green financing on therelationship between GB activities and banks’ environmental performance is yet to be givendue academic attention. As a result, the findings of this study considerably contribute tothe current literature in its claim that green financing mediates the association between GBactivities and banks’ environmental performance.

The current study also revealed the significant barriers to GB development in Bangladesh,and the empirical results showed that high costs and long payback periods with ecofriendlyprojects, and customers’ insufficient knowledge regarding GB, technical obstacles, lackof capable and well-trained staff in appraising green credits, difficulties and complexityin assessing ecofriendly projects, diversification issues, and credit risks are critical chal-lenges affecting the growth and development of GB in the Bangladeshi banking sector.Similar findings were cited by the previously conducted studies [11,12,23,50]. In addition,other challenges affecting the growth and implementation of GB in Bangladesh includethe reduction in banks’ competitiveness in the short term, operational self-insufficiency,and low demand for ecofriendly projects. These results are consistent with the earlierstudies [11,12,23], which identified similar challenges of GB development in developingcountries such as Pakistan, Vietnam, and Bangladesh. Therefore, it is suggested that thesechallenges should be addressed to facilitate the growth and development of GB towardsthe achievement of a sustainable green economy and development of the nation.

Moreover, the findings from the descriptive statistics showed that an increase in bankcompetitiveness, reduction in long-term costs and expenses, provision of online bankingfacilities, improvement in customers’ goodwill, and reduction in carbon footprints frombanking activities are regarded as the major benefits of GB. Interestingly, the results indicatethat benefits of GB also include environmental benefits, such as the conservation of energyand provision of ecofriendly projects, both of which have a similar mean value of 4.07. Inaddition, facilitating the attainment of sustainable economic development, higher profitsfor banks in the long term, tax advantages, economy in paper consumption, and promotionof banks’ reputation are highlighted as other benefits of green banking. These results aresupported by previously conducted studies [23,24]. Therefore, to derive the full benefits ofGB, it is suggested that banking authorities take appropriate measures to combat climatechange issues and achieve the SDGs.

Sustainability 2022, 14, 989 15 of 18

6. Managerial Implications of the Study

The findings of the study provide some valuable implications to researchers, aca-demics, managers, bankers, government authorities, banking institutions, and investors inBangladesh to stimulate green banking through the financing of eco-friendly projects toimprove banks’ environmental performance. First, the empirical findings reveal that GBactivities positively influence banks’ environmental performance. As such, banking authori-ties should be more focused on the development of GB activities in their daily operations byproviding online banking facilities, online bill payments facilities, remote deposits, mobilebanking, green debit and credit cards, etc., to improve banks’ environmental performance,as well as their profitability. In addition, the government of Bangladesh should providetax-free incentives for banks and non-bank financial institutions to promote GB, as it wouldhelp to attain a sustainable development of the country. Second, the empirical findingsindicate that green financing had significantly mediated the association between GB activi-ties and banks’ environmental performance. Therefore, to improve banks’ environmentalperformance, banking institutions should increase their budget for ecofriendly projectssuch as renewable energy, alternative energy, waste management, green industry develop-ment, and energy efficiency projects. It is suggested that BB should strongly monitor thefinancing activities of PCBs, as this will help the country in the attainment of a sustainableeconomic development and SDGs. Third, the study identified various challenges suchas high investment costs, lack of knowledge of customers about green banking, technicalobstacles, lack of capable and well-trained staff in appraising green credits, difficultiesand complexity in assessing ecofriendly projects, diversification issues, and credit riskstowards the development of GB in the Bangladeshi banking sectors. In order to minimizehigh investment costs in the implementation of GB activities by the banking institutionsin Bangladesh, the BB should provide a cooperative loan scheme to enable banks andnon-bank financial institutions to work together in the development of GB in their dailyoperations. In addition, to increase awareness among customers and employees of banksabout GB activities, banking authorities should organize educational training, seminars,and symposiums on GB. Therefore, the present study proposes the need for a collaborationamong nations, banks and non-bank financial institutions, international organizations, andbusinesses to mitigate the problems of GB. In this respect, the BB could play a major rolein monitoring, stimulating, and organizing activities relating to GB. Finally, based on thisstudy, researchers, academics, analysts, and investors will have a better understandingof the adoption of green banking and the manner in which these activities affect banks’environmental performance in general.

7. Study Limitations and Future Directions

Given the considerable contributions offered by this study, several drawbacks thatshould be noted for future studies exist. First, the present study was chosen for convenience,it was restricted to bankers of PCBs, which limits the generalization of the outcomes to anextent. Therefore, the outcomes of the study could be enhanced in terms of generalizationthrough the examination of various stakeholders including customers and clients of allstate-owned commercial banks (SOCBs), foreign-owned commercial banks (FCBs), IslamicBanks (IBs), and non-bank financial institutions (NBFIs). Second, this study only employedan independent variable (GB activities) in the determination of the effect of GB activities onbanks’ environmental performance. Thus, future studies may include more independentvariables such as employee, operation, policy, and customer-related GB practices to assessbanks’ environmental performance. Third, the study variables of this paper are basedon the primary data obtained from the employees of PCBs. As such, future studies maycombine both primary and secondary data in assessing the status of GB and green financingby banking institutions in Bangladesh, thereby enriching the study with a greater substanceand an in-depth comprehension of the subject by allowing for a more communicative visionof customers.

Sustainability 2022, 14, 989 16 of 18

Author Contributions: Conceptualization, X.Z. (Xin Zhang) and A.B.S.; Data curation, Z.W. and S.Y.;Formal analysis, Z.W., X.Z. (Xiaobing Zhong) and A.B.S.; Funding acquisition, X.Z. (Xin Zhang); In-vestigation, X.Z. (Xiaobing Zhong) and A.B.S.; Methodology, Z.W. and A.B.S.; Project administration,X.Z. (Xin Zhang) and X.Z. (Xiaobing Zhong); Resources, X.Z. (Xiaobing Zhong) and S.Y.; Software, S.Y.and A.B.S.; Supervision, X.Z. (Xin Zhang) and X.Z. (Xiaobing Zhong); Validation, S.Y.; Visualization,X.Z. (Xin Zhang), Z.W. and S.Y.; Writing—original draft, A.B.S.; Writing—review & editing, X.Z.(Xin Zhang) and X.Z. (Xiaobing Zhong). All authors have read and agreed to the published versionof the manuscript.

Funding: This research was funded by the Ministry of industry and Information Technology of PRC:(NO. GXZY2115), and Heilongjiang Philosophy and Social Science Research Planning Annual Project(21JYB144). APC was funded by the same grant.

Institutional Review Board Statement: Not applicable.

Informed Consent Statement: Not applicable.

Data Availability Statement: The data that support the findings of this study are available from thecorresponding authors upon reasonable request.

Acknowledgments: The researchers would like to express their gratitude to the anonymous re-viewers for their efforts to improve the quality of this paper.

Conflicts of Interest: The authors declare no conflict of interest.

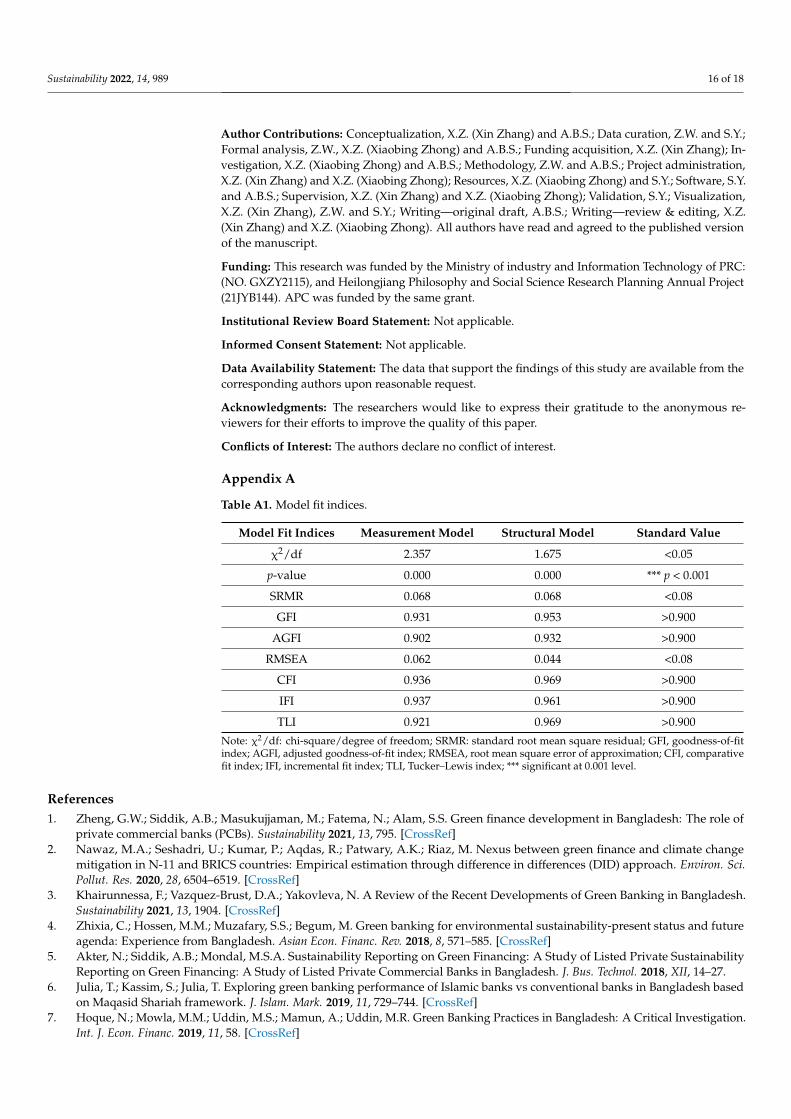

Appendix A

Table A1. Model fit indices.

Model Fit Indices Measurement Model Structural Model Standard Value

χ2/df 2.357 1.675 <0.05

p-value 0.000 0.000 *** p < 0.001

SRMR 0.068 0.068 <0.08

GFI 0.931 0.953 >0.900

AGFI 0.902 0.932 >0.900

RMSEA 0.062 0.044 <0.08

CFI 0.936 0.969 >0.900

IFI 0.937 0.961 >0.900

TLI 0.921 0.969 >0.900

Note: χ2/df: chi-square/degree of freedom; SRMR: standard root mean square residual; GFI, goodness-of-fitindex; AGFI, adjusted goodness-of-fit index; RMSEA, root mean square error of approximation; CFI, comparativefit index; IFI, incremental fit index; TLI, Tucker–Lewis index; *** significant at 0.001 level.

References1. Zheng, G.W.; Siddik, A.B.; Masukujjaman, M.; Fatema, N.; Alam, S.S. Green finance development in Bangladesh: The role of

private commercial banks (PCBs). Sustainability 2021, 13, 795. [CrossRef]2. Nawaz, M.A.; Seshadri, U.; Kumar, P.; Aqdas, R.; Patwary, A.K.; Riaz, M. Nexus between green finance and climate change

mitigation in N-11 and BRICS countries: Empirical estimation through difference in differences (DID) approach. Environ. Sci.Pollut. Res. 2020, 28, 6504–6519. [CrossRef]

3. Khairunnessa, F.; Vazquez-Brust, D.A.; Yakovleva, N. A Review of the Recent Developments of Green Banking in Bangladesh.Sustainability 2021, 13, 1904. [CrossRef]

4. Zhixia, C.; Hossen, M.M.; Muzafary, S.S.; Begum, M. Green banking for environmental sustainability-present status and futureagenda: Experience from Bangladesh. Asian Econ. Financ. Rev. 2018, 8, 571–585. [CrossRef]

5. Akter, N.; Siddik, A.B.; Mondal, M.S.A. Sustainability Reporting on Green Financing: A Study of Listed Private SustainabilityReporting on Green Financing: A Study of Listed Private Commercial Banks in Bangladesh. J. Bus. Technol. 2018, XII, 14–27.

6. Julia, T.; Kassim, S.; Julia, T. Exploring green banking performance of Islamic banks vs conventional banks in Bangladesh basedon Maqasid Shariah framework. J. Islam. Mark. 2019, 11, 729–744. [CrossRef]

7. Hoque, N.; Mowla, M.M.; Uddin, M.S.; Mamun, A.; Uddin, M.R. Green Banking Practices in Bangladesh: A Critical Investigation.Int. J. Econ. Financ. 2019, 11, 58. [CrossRef]

Sustainability 2022, 14, 989 17 of 18

8. Hossain, M. Green Finance in Bangladesh Barriers and Solutions. In Handbook of Green Finance, Sustainable Development; Springer:Berlin/Heidelberg, Germany, 2019; pp. 1–26.

9. Rehman, A.; Ullah, I.; Afridi, F.-A.; Ullah, Z.; Zeeshan, M.; Hussain, A.; Rahman, H.U. Adoption of green banking practicesand environmental performance in Pakistan: A demonstration of structural equation modelling. Environ. Dev. Sustain. 2021,23, 13200–13220. [CrossRef]

10. Masukujjaman, M.; Aktar, S. Green Banking in Bangladesh: A Commitment towards the Global Initiatives. J. Bus. Technol. 2014,8, 17–40. [CrossRef]

11. Islam, M.A. Green Banking and Its Potentiality & Practice in Bangladesh. Int. J. Sci. Res. Methodol. 2018, 10, 17–27. [CrossRef]12. Qureshi, H.; Hussain, T. Green Banking Products: Challenges and Issues in Islamic and Traditional Banks of Pakistan. J. Account.

Financ. Emerg. Econ. 2020, 6, 703–712.13. Sharma, M.; Choubey, A. Green banking initiatives: A qualitative study on Indian banking sector. Environ. Dev. Sustain. 2021,

24, 293–319. [CrossRef] [PubMed]14. Miah, M.D.; Rahman, S.M.; Haque, M. Factors affecting environmental performance: Evidence from banking sector in Bangladesh.

Int. J. Financ. Serv. Manag. 2018, 9, 22–38. [CrossRef]15. Ngwenya, N.; Simatele, M.D. The emergence of green bonds as an integral component of climate finance in South Africa. S. Afr. J.

Sci. 2020, 116, 10–12. [CrossRef]16. Sarma, P.; Roy, A. A Scientometric analysis of literature on Green Banking (1995-March 2019). J. Sustain. Financ. Invest. 2020,

11, 142–162. [CrossRef]17. Sharmeen, K.; Hasan, R.; Miah, M.D. Underpinning the benefits of green banking: A comparative study between Islamic and

conventional banks in Bangladesh. Thunderbird Int. Bus. Rev. 2019, 61, 735–744. [CrossRef]18. Bose, S.; Khan, H.Z.; Rashid, A.; Islam, S. What drives green banking disclosure? An institutional and corporate governance

perspective. Asia Pac. J. Manag. 2018, 35, 501–527. [CrossRef]19. Bose, S.; Khan, H.Z.; Monem, R.M. Does green banking performance pay off? Evidence from a unique regulatory setting in

Bangladesh. Corp. Gov. Int. Rev. 2020, 29, 162–187. [CrossRef]20. Kala, K.N.; Vidyakala, K. A Study on The Impact of Green Banking Practices on Bank ’ s Environmental Performance With Special

Reference To Coimbatore City. Afr. J. Bus. Econ. Res. 2020, 15, 1–6. [CrossRef]21. Malsha, K.P.P.H.G.N.; Arulrajah, A.A.; Senthilnathan, S. Mediating role of employee green behaviour towards sustainability

performance of banks. J. Gov. Regul. 2020, 9, 92–102. [CrossRef]22. Rifat, A.; Nisha, N.; Iqbal, M.; Suviitawat, A. The role of commercial banks in green banking adoption: A Bangladesh perspective.

Int. J. Green Econ. 2016, 10, 226–251. [CrossRef]23. Tu, T.T.T.; Dung, N.T.P. Factors affecting green banking practices: Exploratory factor analysis on Vietnamese banks. J. Econ. Dev.

2017, 24, 4–30. [CrossRef]24. Srivastava, A. Green Banking: Support and Challenges. Int. Adv. Res. J. Sci. Eng. Technol. 2016, 3, 135–137. [CrossRef]25. Raihan, M.Z.; Khan, M.S.U. Sustainable Finance—A Prerequisite for Growth & Development of Banking Industry in Bangladesh.

In Proceedings of the Finance for Sustainable Growth and Development; Department of Finance, Faculty of Business Administra-tion, University of Chittagong: Chittagong, Bangladesh, 2018; pp. 29–49. Available online: https://mijst.mist.ac.bd/mijst/index.php/mijst/article/view/135 (accessed on 1 December 2021).

26. Risal, N.; Joshi, S.K. Measuring Green Banking Practices on Bank’s Environmental Performance: Empirical Evidence fromKathmandu valley. J. Bus. Soc. Sci. 2018, 2, 44–56. [CrossRef]

27. Shaumya, S.; Arulrajah, A. The Impact of Green Banking Practices on Bank’s Environmental Performance: Evidence from SriLanka. J. Financ. Bank Manag. 2017, 5, 77–90. [CrossRef]

28. Yadav, R.; Pathak, G.S. Environmental Sustainability through Green Banking: A Study on Private and Public Sector Banks inIndia. OIDA Int. J. Sustain. Dev. 2013, 6, 37–48.

29. Hossain, M.A.; Rahman, M.M.; Hossain, M.S.; Karim, M.R. The Effects of Green Banking Practices on Financial Performance ofListed Banking Companies in Bangladesh. Can. J. Bus. Inf. Stud. 2020, 2, 120–128. [CrossRef]

30. Shakil, M.H.; Azam, M.K.G.; Tasnia, M.; Munim, Z.H. An Evaluation of Green Banking Practices in Bangladesh. IOSR J. Bus.Manag. 2014, 16, 67–73. [CrossRef]

31. Rahman, M.M.; Ahsan, M.A.; Hossain, M.M.; Hoq, M.R. Green Banking Prospects in Bangladesh. Asian Bus. Rev. 2015, 2, 59.[CrossRef]

32. Dörry, S.; Schulz, C. Green financing, interrupted. Potential directions for sustainable finance in Luxembourg. Local Environ. 2018,23, 717–733. [CrossRef]

33. Liu, N.; Liu, C.; Xia, Y.; Ren, Y.; Liang, J. Examining the coordination between green finance and green economy aiming forsustainable development: A case study of China. Sustainability 2020, 12, 3717. [CrossRef]

34. Rawat, S.K. Recent Advances in Green Finance. Int. J. Recent Technol. Eng. 2020, 8, 5528–5533. [CrossRef]35. Wang, C.; Li, X.; Wen, H.; Nie, P. Order financing for promoting green transition. J. Clean. Prod. 2021, 283, 125415. [CrossRef]36. Zhou, X.; Tang, X.; Zhang, R. Impact of green finance on economic development and environmental quality: A study based on

provincial panel data from China. Environ. Sci. Pollut. Res. 2020, 27, 19915–19932. [CrossRef] [PubMed]37. Wang, Y.; Zhi, Q. The Role of Green Finance in Environmental Protection: Two Aspects of Market Mechanism and Policies. Energy

Procedia 2016, 104, 311–316. [CrossRef]

Sustainability 2022, 14, 989 18 of 18

38. Zheng, G.; Siddik, A.B.; Masukujjaman, M.; Fatema, N. Factors Affecting the Sustainability Performance of Financial Institutionsin Bangladesh: The Role of Green Finance. Sustainability 2021, 13, 10165. [CrossRef]

39. Klassen, R.D.; Whybark, D.C. The Impact of Environmental Technologies on Manufacturing Performance. Acad. Manag. J. 1999,42, 599–615. [CrossRef]

40. Zhu, Q.; Geng, Y.; Fujita, T.; Hashimoto, S. Green supply chain management in leading manufacturers. Manag. Res. Rev. 2010,33, 380–392. [CrossRef]

41. Nie, P.-Y.; Wang, C.; Wen, H.-X. Optimal tax selection under monopoly: Emission tax vs carbon tax. Environ. Sci. Pollut. Res. 2021.[CrossRef] [PubMed]

42. Tung, A.; Baird, K.; Schoch, H. The relationship between organisational factors and the effectiveness of environmental manage-ment. J. Environ. Manag. 2014, 144, 186–196. [CrossRef]

43. Li, S.; Liu, X.; Wang, C. The influence of internet finance on the sustainable development of the financial ecosystem in China.Sustainability 2020, 12, 2365. [CrossRef]

44. Qi, G.Y.; Zeng, S.X.; Shi, J.J.; Meng, X.H.; Lin, H.; Yang, Q.X. Revisiting the relationship between environmental and financialperformance in Chinese industry. J. Environ. Manag. 2014, 145, 349–356. [CrossRef]

45. Jayadatta, S.; Nitin, S.N. Opportunities, Challenges, Initiatives and Avenues for Green Banking in India. Int. J. Bus. Manag. Invent.2017, 6, 10–15.

46. Dörnyei, Z. Research Methods in Applied Linguistics; Oxford University Press: New York, NY, USA, 2007.47. Zheng, G.W.; Siddik, A.B.; Masukujjaman, M.; Alam, S.S.; Akter, A. Perceived environmental responsibilities and green buying

behavior: The mediating effect of attitude. Sustainability 2021, 13, 35. [CrossRef]48. Yan, C.; Siddik, A.B.; Akter, N.; Dong, Q. Factors influencing the adoption intention of using mobile financial service during the

COVID-19 pandemic: The role of FinTech. Environ. Sci. Pollut. Res. 2021. [CrossRef]49. Barclay, M.J. The Determinants of Corporate Leverage and Dividend Policies. J. Appl. Corp. Financ. 1995, 7, 4–19. [CrossRef]50. Rahman, F.; Perves, M.M. Green Banking Activities in Bangladesh: An Analysis and Summary of Initiatives of Bangladesh Bank.

Res. J. Financ. Account. 2016, 25, 1–9.51. Hair, J.F.; Black, W.C.; Babin, B.J.; Anderson, R.E. Multivariate Data Analysis, 4th ed.; Prentice Hall: Hoboken, NJ, USA, 2010.52. Gerbing, D.W.; Anderson, J.C. An updated paradigm for scale development incorporating unidimensionality and its assessment.

J. Mark. Res. 1988, 25, 186–192. [CrossRef]53. Hu, L.T.; Bentler, P.M. Cutoff criteria for fit indexes in covariance structure analysis: Conventional criteria versus new alternatives.

Struct. Equ. Model. 1999, 6, 1–55. [CrossRef]54. Nunnally, J.; Bernstein, I. Psychometric Theory, 3rd ed.; McGraw-Hill: New York, NY, USA, 1994.55. Fornell, C.; Larcker, D.F. Evaluating Structural Equation Models with Unobservable Variables and Measurement Error. J. Mark.

Res. 1981, 18, 39. [CrossRef]56. Chin, W. The Partial Least Squares Approach to SEM chapter. Mod. Methods Bus. Res. 1998, 295, 295–336.57. Anderson, J.C.; Gerbing, D.W. Structural Equation Modeling in Practice: A Review and Recommended Two-Step Approach.

Psychol. Bull. 1988, 103, 411–423. [CrossRef]58. Cortina, J.M. What is coefficient alpha? An examination of theory and applications. J. Appl. Psychol. 1993, 98, 98–104. [CrossRef]