developing a model of measuring islamic relationship marketing practice among takaful agents

TRANSCRIPT

ISRA International Colloquium for Islamic Finance (IICIF 2014)

Developing a Model of Measuring Islamic Relationship Marketing

Practice among Takaful Agents

Marhanum Che Mohd Salleh

1

Nurdianawati Irwani Abdullah2

Abstract.

Purpose - The main objective of this research is to develop a model of

measuring Islamic relationship marketing (IRM) among Takaful agents. This

research basically explores the underlying dimensions of Islamic relationship

marketing practice in the Takaful industry. The other objective is to investigate

the effect of IRM practice towards customers’ satisfaction and retention.

Design/methodology/approach - Few approaches were performed to explore

the dimensions and measures of relationship marketing to the context of

Takaful industry. The first approach was done by reviewing the previous

marketing literatures, second approach took place when three focus group

discussions were held with industry experts, and the final approach is

conducted on the empirical survey of 755 Family Takaful customers.

Findings - Based on structural equation modeling (SEM), the results indicate

that the proposed constructs is significantly measured the practice of Islamic

relationship marketing in the Takaful industry. They are Islamic ethical

behavior, social, structural, and financial bonds. In addition, the practice of

IRM is found significant to influence customers’ satisfaction and future

retention.

Research limitations: This research lacks specific literatures in the context of

Takaful to support its conceptual framework. This limitation however, was

resolved by adopting and adapting from literatures of related academic fields

to the context of the Malaysian Takaful industry.

Practical implications: The results of this research imply that some marketing

aspects should be given priority by marketers in the Takaful industry. Their

responsibility is not limited to offering Takaful products. They should also be

encouraged to build strong relational bonds with their customers, and in doing

so, act in accordance to Islamic ethics.

Originality: The theoretical framework of this research is built on the basis of

Islamic norms; in addition to suggestions from previous marketing researches.

All measurement items were confirmed by industry experts and the overall

1 Assistant Professor, Department of Finance, Kulliyyah of Economics & Management Sciences

International Islamic University Malaysia, P.O.Box 10, 50728 Kuala Lumpur

Email address: [email protected], Tel: 03-61964638, Fax: 03-61964850 2 Associate Professor, Department of Finance, Kulliyyah of Economics & Management Sciences

International Islamic University Malaysia, P.O.Box 10, 50728 Kuala Lumpur

Email address: [email protected], Tel: 03-61964633, Fax: 03-61964850

ISRA International Colloquium for Islamic Finance (IICIF 2014)

framework were tested using primary data obtained from a survey on the

Family Takaful customers.

Keywords: Islamic relationship marketing, Takaful industry, Takaful agent,

structural equation modelling

1. Introduction

Due to its perceived novelty, relationship marketing (RM) has continued to be a

popular academic topic in marketing studies for the past three decades (Palmatier et al.,

2006; Takala & Uusitalo, 1996). Its popularity has attracted not only academicians, but

also industry players (Berry, 1995). In general, RM was advocated in the formulation

stage of marketing theory even though its importance was not previously acknowledged

(Aijo, 1996; Takala & Uusitalo, 1996).

In the 1980s, relationship marketing strategy was widely accepted as a new

marketing paradigm as many companies began to shift their marketing strategy to one

that is focussed on maintaining existing customers (customer retention) rather than on

acquiring new ones (Sheth J. N., 2002). This strategy remains popular today as more

companies continue to plan and organise marketing campaigns that are geared towards

establishing strong relationships with customers (Shamsudin et al., 2010).

In recent times, the ability to maintain good and quality relationships with

customers has become a competitive advantage for a company. Thus, it is necessary

for a company to practice strong RM in order to achieve customer retention (Shammout

et al., 2006). In this context, a few marketing scholars have suggested that retaining

customers is much more profitable than acquiring new ones (Reichheld & Kenny, 1990

and Boone & Kurtz, 2004). Furthermore, it has been proven that a 5 percent increase in

customer retention can generate 80 percent of a company’s profit (Boone & Kurtz,

2004). Given this fact, RM has been implemented in various markets including in

consumer goods, services, industries, as well as in the insurance market (Murphy et al.,

2007).

The RM concept is also important in the context of the Islamic insurance or Takaful

industry as it promotes quality relationships among industry players, which consist of

both buyers and sellers/marketers. The insurance industry is an industry that provides

intangible services, complicated products, and long-term contracts. And among the

ISRA International Colloquium for Islamic Finance (IICIF 2014)

objectives of Takaful is it helps to strengthen relationship among members of the

society. This is consistent with the objectives of Islamic law or maqāsid al-ShariCah,

which aims to promote a sense of brotherhood or strong relationships in a society. From

this perspective, RM is one of the most suitable marketing techniques to be practiced in

the industry. Given limited literatures on RM from the Islamic perspective, this

research investigates and confirms the measurement of Islamic relationship marketing

(IRM) particularly from the perspective of Islamic insurance industry. In details, some

literatures review is conducted on the proposed measure of IRM and it is followed by

methodology adopted in the current research. Besides that, data analysis were

conducted to confirm the proposed measurements of IRM and also to investigate its

influence towards customer satisfaction and retention. Finally, research findings is

disclosed and the paper ends with conclusion and discussion on future research.

2. Literature Review

The research proposes a measurement of IRM using four constructs: Islamic

ethical behaviour, social, structural, and financial bond. Next section will explain

details on these constructs.

2.1 Islamic ethical behavior

Given today’s challenging market environment and customer demands for quality

services, marketers not only have to be customer-focused but also need to be perceived

as Islamic by their customers (Hassan et. al, 2008). A review of past literature has

revealed a large volume of research in marketing that indicate ethics as among the main

issues in marketing and sales (Wotruba, 1990; Piercy & Lane, 2006). However, only a

few of these researches have included religious elements in their domain (Nazlida &

Mizerski, 2010). On that note, Arham (2010) suggests that Islamic teachings could be

implemented in the current marketing conjecture. According to Wotruba (1990) and Fu,

Richards, Hughes, and Jones (2010), the reason why sales persons need to observe

proper ethical behaviour is because it may affect their sales performance. In this

context, Fu et al. (2010) have proven that self efficacy and positive attitude have

influenced the sales persons’ selling intention and this have directly affected their sales

ISRA International Colloquium for Islamic Finance (IICIF 2014)

performance. They must be sincere in addressing their customers’ needs and exert a

spirit of brotherhood in dealing with their customers (HR & Ratnasari, 2012).

From another perspective, religious aspect is found to be an important factor in

acquiring customers’ willingness to deal with the sales person (Nazlida & Mizerski,

2010). Basically, this relates to religious aspects that promote affiliation, commitment,

motivation, knowledge, and social consequences, and is believed to influence

customers’ confidence with the sales person (Nazlida & Mizerski, 2010). In addition,

Hassan et al. (2008) have advocated that Islamic ethical behaviours play a significant

role in the development and maintenance of the buyer-seller relationship. This is further

supported by a more recent study by Shamsudin et al. (2010), in which the authors

claim that Islamic ethical behaviour has promoted a positive environment in

relationship marketing practice, and this naturally would lead to customer satisfaction.

The first proposed construct to measure Islamic relationship marketing is Islamic

ethical behaviour. Ethics is described as ‘the set of moral principles that distinguish

what is right from what is wrong’ (Beekun, 2003: p. 3). Meanwhile, according to Rizk

(2008), ethics is related to the establishment of general guidance for human action or

conduct. In general, the aim of Islamic ethical behaviour is the practice of good

behaviour and the elimination of questionable actions in all aspects of human life

(Shamsudin et al., 2010). In business specifically, Islam views ethical behaviour as an

important requirement in building relationships either with Allah (S.W.T) as the

Creator, and among human beings who are Allah’s trustee in this world. In this regards,

Allah mentions in the Qurʾān in verse 72 of Surah Al-Aḥzāb:

We offered the trust to the heavens, the earth, and the mountains; but

they refused to undertake it, being afraid thereof. But man undertook it

(Qurʾān, Al-Aḥzāb: 72)

Accordingly, in the Takaful industry, the responsibility of a Takaful agent is

similar to that of a financial consultant or an advisor. In practice, they are

responsible for informing and advising customers about their future financial

preparation by proposing Takaful products that suits their backgrounds and

needs. This responsibility, if executed based on Islamic ethics, will inadvertently

ISRA International Colloquium for Islamic Finance (IICIF 2014)

strengthen their relationship with their customers. In this regards, the nature of

the relationship depends much on the Takaful agent because he/she is the one

who is offering the products and providing services to the customer.

2.2 Relational Bonds

The remaining constructs adopted in this research to measure Islamic relationship

marketing are social, structural, and financial bonds.

2.2.1 Concept of Relational Bonds

A bond, as a marketing concept, has been described differently by different

researchers (Wendelin, 2007). Some researchers described it as a tie or a link.

Researchers like Turner (1970) and Wilkinson and Young (1994) have illustrated bond

as ties between different parties. Meanwhile, other researchers including Wilson and

Mummalaneni (1986) and Thorelli (1986) referred to bonds as links. In general, the

distinction between bonds, ties and links remains uncertain in marketing literature. It

has also been regarded as an exit barrier that ties a customer to a supplier to ensure that

the relationship remains in existant (Liljander & Strandvik 1995).

In Western academic literature, the first reseacher who described extensively the

concept of bonds was Albion W. Small, who explained it from a sociological

perspective in his article published in the American Journal of Sociology in 1915

(Wendelin, 2007). Small (1915) applied two concepts in sociology; ‘social structure’

and ‘social achievement’, the former interpreted as ‘social bond’, while the later was

described in relation to efforts in providing for human needs. These two concepts are

mutually connected in the sense that a bond would, in many instances, lead to

achievement in a business relationship (Smalls, 1915). In this regard, it is

acknowledged that the ultimate objective of any party or organization to be involved in

business relationships or bonding is to fulfill their needs and achieve their objectives.

Another contribution in this domain was made by Mark S. Granovetter in 1973

via his article entitled: “The strength of weak ties”. The author basically focussed on

assessing the social network that contains macro and micro elements of an individual

group. In this regards, macro elements is described as external factors that might

ISRA International Colloquium for Islamic Finance (IICIF 2014)

influence the network or interaction in a group, while micro factors are considered as

internal or behavioral elements that differ among individuals.

From the perspective of sociology, McCall’s (1970) have viewed that in essence,

humans are bonded together in a relationship by psychological, emotional, economic or

physical attachments. This is parallel with the views of Butz and Goodstreins (1996)

who stated that customer bonding is basically related to their behaviour or action as a

consequence from the positive interaction with service providers. It depends on the

service providers or marketers who are responsible for building and tightening strong

relationships with their customer (Linjander & Strandvik, 1995).

Overall, there are two research groups that have established various types of

bonds. They are the Industrial Marketing and Purchasing (IMP) group, and the service

marketing group. The IMP group, for example, has introduced six bonds, which are the

technical, economic, time, legal, social, and knowledge bonds (Johanson & Mattsson

1987; Holmlund & Kock 1995). The basis of the concept of bond from this group

comes from the work of Homans (1958) through the social exchange theory, where the

bond concept is presented based on the interaction approach (Johansson & Mattsson

1987). Hence, bonds between business parties would exist once there is some kind of

interaction or communication between them.

Service marketing researchers, on the other hand, have presented various types

of bonds such as the social, financial, economic, and structural bonds (Berry &

Parasuraman, 1991; Sin et al., 2002; Chiu, Lee, Hsieh, & Chen, 2007). This present

research adopts the three types of bonds as proposed by the services marketing

researchers, which is considered to be more in harmony with the context of the Takaful

industry. These three types of bonds are social, structural, and financial bonds.

2.2.2 Social, Structural, and Financial Bonds

As discussed earlier, the three types of bonds; social, structural, and financial

bonds, adopted in this research are based on service marketing literatures (Berry &

Parasuraman, 1991; Lin et al., 2003). These types of bonds are very important for a

marketer who is attempting to fulfill his customer’s needs (Berry, 1995; Peltier &

Westfall, 2000; Williams et al., 1998). In general, social bond measures the strength of

ISRA International Colloquium for Islamic Finance (IICIF 2014)

a personal relationship; structural bond presents the infrastructure that is offered to the

customer, while financial bonds are related to price, incentives, and monetary benefit

given to customers (Rodriguez & Wilson, 1999; Chiu, Lee, Hsieh, & Chen, 2007).

Social bonds are described as ‘the degree of mutual personal friendship and

liking shared by the buyer and seller’ (Wilson, 1995: p. 339). It has a number of

dimensions including social interaction, closeness, friendship, and performance

satisfaction. In relationship marketing, the basis of this type of bond is from a business-

to-business perspective, where it represents strong connections among business

organisations (Smith, 1998; Williams, Han, & Qualls, 1998). Meanwhile, from a

customer’s point-of-view, social bonding emerges as a result of the benefits received

from the relationship with the company (Beautty et al., 1996; Gwinner et al., 1998;

Reynolds & Beatty, 1999).

Accordingly, social bond is built through interpersonal exchanges that can be

measured by the strength of the personal relationship between a buyer and a seller

(Rodriguez & Wilson, 1999; Williams et al., 1998). It also represents a form of non-

economic satisfaction for both parties in a relationship with an enduring social

exchange (Dwyer et al., 1987). Hence, it would be necessary for those in the Takaful

industry to establish social bonds since the role of Takaful agent goes beyond the

selling of Takaful products. This is so because a Takaful agent plays the role of a

trustee who is responsible for advising others in the society about their future financial

preparations, and along the way instil a spirit of brotherhood among them, especially

among the Muslims.

Compare to social bonds, structural bonds are present when a business enhances its

relationship with customers by facilitating them to fulfill their needs through a service-

delivery system (Lin et al., 2003). Based marketing literature, Wilson (1995: p. 339)

describes a structural bond as ‘a vector of forces that create an impediment to

termination of the relationship’. It basically consists of economic, strategic, and

technical factors that are developed in relationships that offer benefits to all contractual

parties (Rodriguez & Wilson, 1999: p. 6). In this case, a company might insert some

value-added incentives to the product infrastructure that might not available elsewhere

ISRA International Colloquium for Islamic Finance (IICIF 2014)

to the customer (Berry, 1995). This research perceives structural bonds as of equal

importance with other types of bonds that share the goal of enhancing relationship with

existing customers in the Takaful industry.

The final type of bond is financial bonds. Researchers in the past have argued

that one of the motivations for engaging in relational exchanges is to save money

(Berry, 1995; Gwinner et al., 1998; Peterson, 1995; Peltier & Westfall, 2000). In this

respect, some researchers agree that this type of bond is at the lowest level of the

relationship hierarchy because in business, pricing is the most easily imitated marketing

element (Chiu et al., 2007). Hence, service providers may reward loyal customers with

special prices (Lin et al., 2003). Accordingly, in the Takaful industry, financial bonds

can be regarded as any economics or material benefits offered to customers by Takaful

operators. Examples of such benefit are free gifts for participation, cash payments for

hospital admission, promotional packages, end-of-the-year bonuses, and other financial

benefits. This present research has investigated whether financial bonds can

significantly impact future customer retention in the Takaful industry.

2.3 Customer Satisfaction

Marketing researchers share the opinion that customer satisfaction has become a

fundamental element in contemporary marketing research (Luo & Homburg, 2007);

whereas among marketing practitioners, they agree that it is the main outcome of

marketing practices (Jamal & Naser, 2002). A large degree of research on customer

satisfaction is based on the work of Oliver (1980, 1981). He initially defines customer

satisfaction as ‘an evaluation of the surprise inherent in a product acquisition and/or

consumption experience’ (Oliver, 1981, p. 27). The other definition is;

In brief, customer satisfaction is a summary of cognitive and affective reaction

to a service incident (or sometimes to a long term service relationship).

Satisfaction or dissatisfaction results from experiencing a service quality

encounter and comparing that encounter with what was expected (Rust & Oliver, 1994,

p. 2)

ISRA International Colloquium for Islamic Finance (IICIF 2014)

There are various opinions on how to describe customer satisfaction. Some

scholars believe that it reflects an emotional response towards products and services

(Swan & Oliver, 1989; Crosby et al., 1990; Olsen, 2002; Jamal & Naser, 2003; Bejou

et al., 1998). On the other hand, other scholars suggest it represents not only the

emotional aspect, but indicates a customer’s evaluation of the sales person, which in the

end will produce either positive or negative feedback (Oliver, 1981; Cronin et al.,

2000). Similarly, Gandhi and Kang (2011) have posited that some comparisons will be

made by customers in terms of expected services and experiences received from sellers

or service providers.

In addition, as argued by Gronroos (2004), modern customers require more than

products or services offered by suppliers. They expect a set of benefits to be delivered

effectively through various instruments like relationship marketing (Chopra, 2009).

They demand all information about a product, which must be delivered within a

pleasant, responsible, and timely manner. Reasons for dissatisfaction tend to come

more from external factors of the product or service offered such as time constraint and

the sales persons’ attitude (Gronroos, 2004). Bejou et al. (1998) suggests that there is a

critical need for financial services company to ensure customer satisfaction on their

relationship-based marketing because of the nature of the industry; an industry that

involves intangible services, complex products, long duration of services, and certainly,

high degree of risk. According to Gustafsson et al. (2005), overall customer

satisfaction may be perceived as overall customer evaluation on service quality, which

at the end may influence their behaviour towards the company.

However, in today’s environment, customer satisfaction cannot merely rely on

the quality of services, but is also reflected by the quality of relationship that exists

between the customer and service provider (Roberts et al., 2003). Therefore,

corresponding with the context of this research and parallel with the findings of

previous researchers, customer satisfaction in this research is referred to as customer

evaluation on the quality of relationship that a customer experiences with the service

provider (Crosby & Stephens, 1987; Rust & Oliver, 1994; Garbarino & Johnson, 1999;

Croni et al., 2000; Roberts et al., 2003). Specifically, service providers in this research

are the Takaful agents.

ISRA International Colloquium for Islamic Finance (IICIF 2014)

2.4 Customer Retention

Studies on customer retention have escalated since the 1990s until recently.

Among the marketing scholars who have conducted studies on customer retention are

Reichheld and Sasser, (1990), Anderson and Sullivan (1993), Hennig-Thurau and Klee

(1997), Ennew & Binks (1996), and many others. Customer retention has been

thoroughly studied in various industries; in insurance, banking, online business, hair

styling, telecommunication and travel, and both in European and Asian countries

including in Malaysia. Basically, customer retention emerged from three managerial

perspectives: service marketing, industrial marketing, and general management.

Accordingly, from the service marketing perspective, customer retention or

customers’ repeat purchase intention represents “the customer’s self reported likelihood

of engaging in further repurchasing behaviour” (Ha, Janda, & Muthaly, 2010, p. 999).

Hennig-Thurau and Klee (1997, p. 741) asserts that “customer retention focuses on the

repeated patronage of a marketer or supplier”. In this regard, Reichheld and Kenny

(1990) have highlighted six advantages of maintaining long-term customers than

attracting new ones. First, it may reduce costs to obtain new customers. Second, long-

term contract with customers will generate more profit. Third, existing customers

better understand company products, thus, it is easier to deal with them in case new

products are offered. Fourth, long-term customers may provide new customers or

referrals to a company. Fifth, they would be more tolerant if there are increases in

product prices. And finally, the probability of leaving the company is less for long-term

customers.

Reflecting on the context of relationship marketing, Barnes (1994) describes

relationship marketing based on three criteria. They are as customer retention, as

locking-in the customer, and as database marketing. In addition, previous scholars

including Menon and O’Connor (2007), Fullerton (2005), Aurier and N’Goala (2010),

and Kamsol et al. (2009) have stressed that effective relationship marketing may ensure

future customer retention to the company. They acknowledge that the main target of

relationship marketing is to ensure customer retention (Hennig-Thurau & Klee, 1997;

Thomas, Blattberg, & Fox, 2004; So, 2007; Shamsudin et al., 2010). This is because

customer retention has become a fundamental ingredient for the financial endurance of

ISRA International Colloquium for Islamic Finance (IICIF 2014)

the service industry in order for it to remain competitive in the business world (Hennig-

Thurau, 2004).

It is harder to maintain existing customers rather than getting new ones

(Hennig-Thurau, Gwinner, & Gremler, 2002). This is because existing customers

would always demand for better services or better products from the company. It

become harder in an industry that offers intangible products such as insurance, in which

customer retention depends mostly on the services offered and the relationship built

between the customer and the provider. Therefore, in addition to offering various types

of products, an insurance company needs to train its employees or sales agents to

provide excellent services and build strong relationship with their customers.

Apparently, many researchers are involved in examining the direct link between

customer satisfaction and retention either from the perspective of business-to-business

(B2B) or business-to-consumer (B2C). Among them are Hennig-Thurau and Klee

(1997), Beatson, Lings, and Gudergan (2008), and Abdul-Muhmin (2011). Meanwhile,

several prior studies have determined factors such as service quality, relationship

quality, and the theory of trust-commitment as affecting customer retention (Ranaweera

& Neely, 2003; Chen, Chen, & Yeah, 2003; Huang (2008); Beatson, Lings, &

Gudergan, 2008). There are however, a limited number of studies on customer retention

in the context of Islamic insurance or Takaful. Given the complexity of the industry in

terms of products and services offered, research on customer retention is of critical

importance. This is because the nature of the industry and its products involve long-

term contract with customers. Ensuring customer retention therefore, is crucial for

future sustainability. It is further important for the Malaysian Takaful industry because

it is the role model for the Islamic financial industries in other Muslim and non-Muslim

countries. Ensuring future Takaful customer retention means guaranteeing the future of

the Takaful industry.

3. Methodology

This present research is designed quantitatively where the data for the study is

collected through a survey based on self-administered questionnaires. Three series of

focus group discussions were conducted with academicians and industry players before

ISRA International Colloquium for Islamic Finance (IICIF 2014)

the final questionnaires were finalized and distributed. It was done to ensure the right

and proper questionnaire is constructed in the context of the Takaful industry. Based on

the feedback and suggestion from focus group members, the final set of questionnaires

was distributed to a small sample of Takaful customers as a pilot study. The pilot study

was conducted to test the questionnaires and measurement items for clarity and

understanding. It is a necessary step in the data collection process to identify any

problems with the research instrument, and to determine the content and face validity

of the measures used in the questionnaires. In this process, a few marketing and

Shariah scholars were involved, as well as 189 Family Takaful customers.

Upon the successful completion the pilot test, the final survey was conducted. The

respondents are Family Takaful customers of eleven Takaful operators in various

locations in the Klang Valley. Data collected were analyzed using two statistical

analyses software (Statistical Package for Social Sciences (SPSS) version 19 and

Analysis of Moment Structures (AMOS) version 16). Accordingly, the measure of

Islamic ethical behaviour are newly built in this research and basically relied on the

Qur’anic verses and reviewed by the industry experts during the focus group discussion.

On the other hand, the measure of relationship bonds are basically adopted from the

past researchers including Crosby et al. (1990), Berry (1995), Lin et al. (2003), and

others. Five-point Likert scales is used to measure all the answers given in the survey.

Out of 1100, 865 questionnaires were returned; which gives it a response rate of 79

percent. However, due to incomplete answers, 65 questionnaires were rejected at the

first screening stage. The remaining 800 questionnaires were brought forward for

normality check. In total, after going through all the screening process, 755

questionnaires were selected for final data analysis, which means the actual response

rate was 69 percent. For a social science research, this response rate is considered high,

and the number in fact exceeded the response rate of 56.7 percent recorded in a

previous study on the same domain by Kamsol et al. (2009).

ISRA International Colloquium for Islamic Finance (IICIF 2014)

4. Data Analysis & Findings

4.1 Background of Respondents

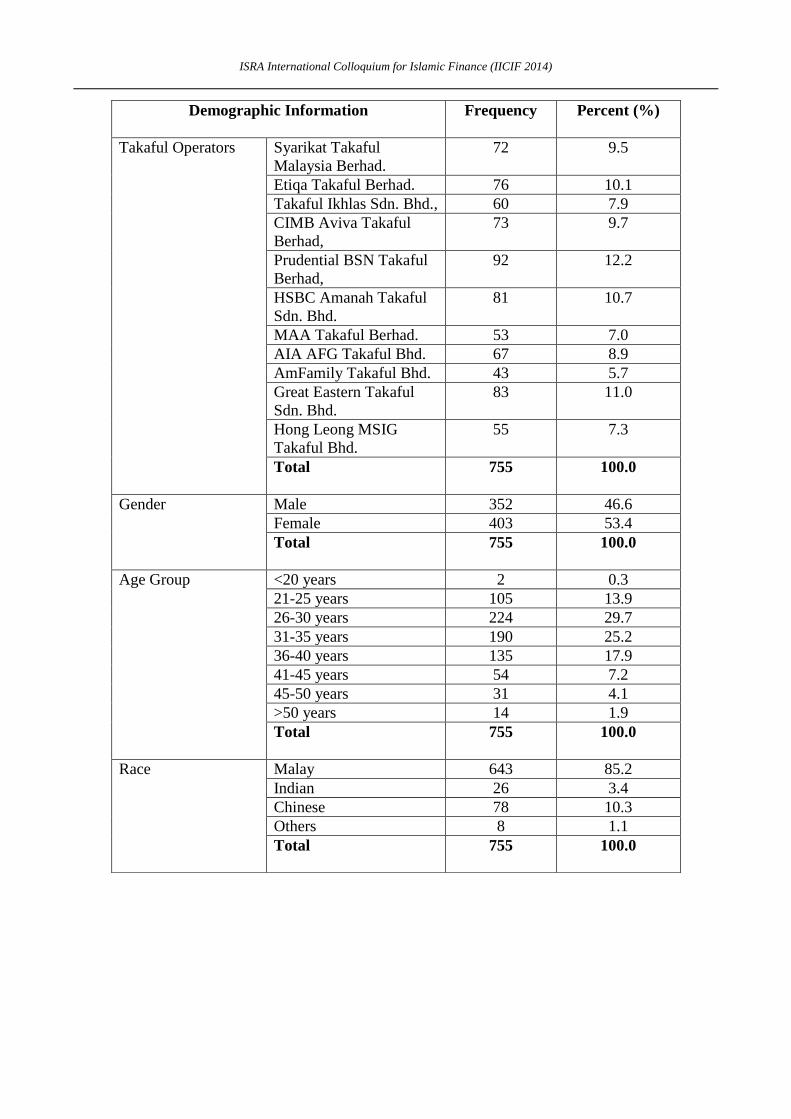

As explained before, a total of 755 cases (Family Takaful customers) successfully

passed the entire data screening process (section 6.3.2). Out of the number of customers

who participated in this research, the highest response was recorded from Prudential-

BSN Takaful Bhd. with 92 responses, which equals to 12 percent of total respondents.

This is followed by Great Eastern Takaful Bhd. (83 responses), Etiqa Takaful Bhd. (76

responses), and others. Meanwhile, the lowest response recorded was from AmFamily

Takaful Bhd. where the response rate was less than 50 percent of questionnaires

distributed (43 responses).

It is observed that respondents in this research are quite balanced between males

(47 percent) and females (53 percent). This balance would eliminate any suspicion of

response bias in terms of gender. In terms of age, most of the respondents were from

the middle group age, which is the age group between 26 and 30 years-old (30 percent),

and between 31 and 35 years-old (25 percent). The rest belong to the age groups 36-40

years (18 percent), 21-25 years (14 percent), 41-45 years (7 percent), and 46-50 years

(4 percent). Only a few of the respondents were from the youngest group (below 20

years = 0.3 percent), and the oldest group (above 50 years = 2 percent).

Nevertheless, consistent with an earlier prediction for the context of this research

(Takaful industry), the majority of the respondents are Muslims (86 percent) and

Malays (85 percent). Only a small number of non-Muslims participated in this research.

For example, 6 percent of the customers are Buddhists (48 respondents), 4 percent are

Christians (30 respondents), 3 percent are Hindus (21 respondents), and the remaining

five customers are from other religions (0.7 percent). In addition, more than half of the

respondents were married (60 percent), and worked in the private sector (66 percent).

Please refer to Appendix 2 for details on these results.

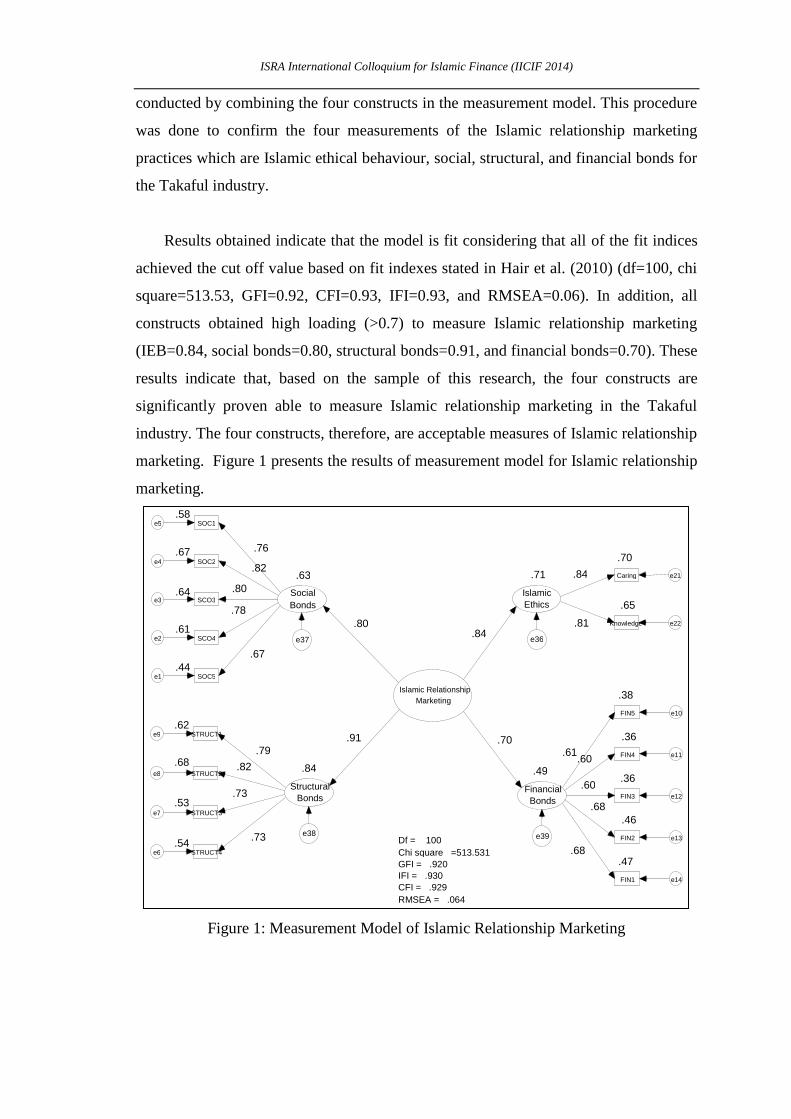

4.2 Measurement Model of Islamic Relationship Marketing

Once the four proposed constructs of Islamic relationship marketing (Islamic

ethical behaviour, social, structural, and financial bonds) were confirmed with their

measurement items, measurement model of Islamic relationship marketing was

ISRA International Colloquium for Islamic Finance (IICIF 2014)

conducted by combining the four constructs in the measurement model. This procedure

was done to confirm the four measurements of the Islamic relationship marketing

practices which are Islamic ethical behaviour, social, structural, and financial bonds for

the Takaful industry.

Results obtained indicate that the model is fit considering that all of the fit indices

achieved the cut off value based on fit indexes stated in Hair et al. (2010) (df=100, chi

square=513.53, GFI=0.92, CFI=0.93, IFI=0.93, and RMSEA=0.06). In addition, all

constructs obtained high loading (>0.7) to measure Islamic relationship marketing

(IEB=0.84, social bonds=0.80, structural bonds=0.91, and financial bonds=0.70). These

results indicate that, based on the sample of this research, the four constructs are

significantly proven able to measure Islamic relationship marketing in the Takaful

industry. The four constructs, therefore, are acceptable measures of Islamic relationship

marketing. Figure 1 presents the results of measurement model for Islamic relationship

marketing.

Figure 1: Measurement Model of Islamic Relationship Marketing

.63

Social Bonds

.44 SOC5 e1

.67

.61 SCO4 e2

.78

.64 SCO3 e3

.80

.67 SOC2 e4

.82

.58 SOC1 e5

.76

.84

Structural Bonds

.54 STRUCT4 e6

.73

.53 STRUCT3 e7

.73

.68 STRUCT2 e8 .82

.62 STRUCT1 e9

.79

.49

Financial Bonds

.38

FIN5 e10

.61

.36

FIN4 e11 .60

.36

FIN3 e12 .60

.46

FIN2 e13

.68

.47

FIN1 e14

.68

.71

Islamic Ethics

.70

Caring e21 .84

.65

Knowledge e22 .81

Islamic Relationship Marketing

.80

.91 .70

e36 e37

e38 e39

.84

Df = 100 Chi square =513.531 GFI = .920 IFI = .930 CFI = .929 RMSEA = .064

ISRA International Colloquium for Islamic Finance (IICIF 2014)

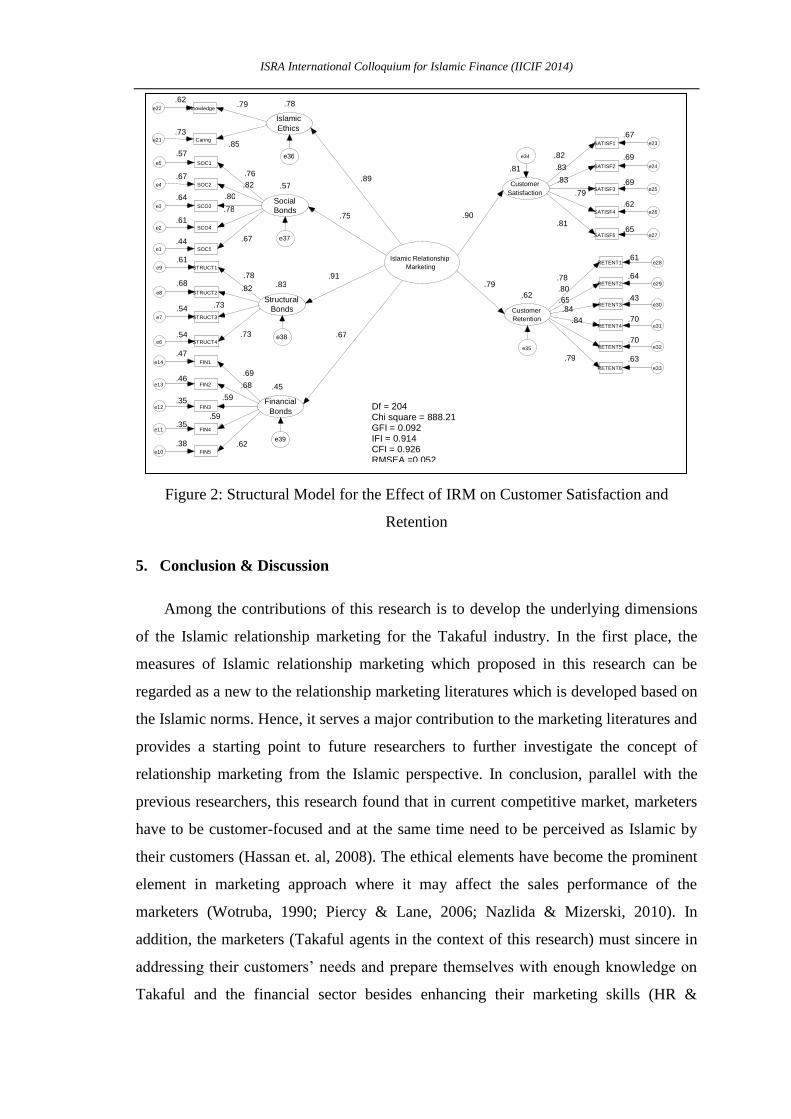

4.3 The Effect of Islamic Relationship Marketing Practice towards Customer

Satisfaction and Retention

As to achieve the second research objectives, structural model is developed to

test the effect of IRM practice towards customer satisfaction and retention. As

illustrates in Figure 2 in the next page, results of SEM shown that the model have

achieved all the fit indices where GFI = 0.902, IFI = 0.914, CFI = 0.926, and RMSEA

= 0.052 given the df = 204, and chi square (CMIN) = 888.211. Accordingly, all the

measures support the model fit assumption, thus the model is proceed to the next level

which is the interpreting of the parameter estimated by SEM. Based upon the value of

regression weights, it is confirmed that the regression model of Islamic relationship

marketing in the customer satisfaction and retention prediction is significantly different

from zero at the 0.001 level. In details, when the Islamic relationship marketing goes up

by 1 standard deviation, it will influence the increase of customer satisfaction and

retention by 0.90 and 0.79 standard deviations respectively.

Other interpretation is made on the squared multiple correlation (R2) value for

the dependent construct of this research which has arrow coming into it, which is

customer satisfaction and retention. From the SEM results, R2 customer satisfaction is

0.81 which means 81 percent of customer satisfaction can be explained by the IRM

practices as a whole. Meanwhile, R2 for customer retention is 0.62 which means 62

percent of customer retention can be explained by the practice of IRM. In conclusion,

the Takaful agents’ Islamic relationship marketing which measured by their Islamic

ethical behavior, social, structural, and financial bonds have significantly proven to

affect the future customer retention. This result provides a clear picture to the industry

on the significance of the practice relationship marketing in accordance with the

Islamic norms.

ISRA International Colloquium for Islamic Finance (IICIF 2014)

Figure 2: Structural Model for the Effect of IRM on Customer Satisfaction and

Retention

5. Conclusion & Discussion

Among the contributions of this research is to develop the underlying dimensions

of the Islamic relationship marketing for the Takaful industry. In the first place, the

measures of Islamic relationship marketing which proposed in this research can be

regarded as a new to the relationship marketing literatures which is developed based on

the Islamic norms. Hence, it serves a major contribution to the marketing literatures and

provides a starting point to future researchers to further investigate the concept of

relationship marketing from the Islamic perspective. In conclusion, parallel with the

previous researchers, this research found that in current competitive market, marketers

have to be customer-focused and at the same time need to be perceived as Islamic by

their customers (Hassan et. al, 2008). The ethical elements have become the prominent

element in marketing approach where it may affect the sales performance of the

marketers (Wotruba, 1990; Piercy & Lane, 2006; Nazlida & Mizerski, 2010). In

addition, the marketers (Takaful agents in the context of this research) must sincere in

addressing their customers’ needs and prepare themselves with enough knowledge on

Takaful and the financial sector besides enhancing their marketing skills (HR &

.57

Social Bonds

.44 SOC5 e1

.67

.61 SCO4 e2

.78 .64

SCO3 e3 .80

.67 SOC2 e4 .82

.57 SOC1 e5

.76

.83

Structural Bonds

.54 STRUCT4 e6

.73

.54 STRUCT3 e7

.73

.68 STRUCT2 e8 .82

.61 STRUCT1 e9

.78

.45 Financial

Bonds

.38 FIN5 e10

.62

.35 FIN4 e11

.59

.35 FIN3 e12

.59

.46 FIN2 e13 .68

.47 FIN1 e14

.69

.78 Islamic Ethics .73

Caring e21 .85

.62 Knowledge e22 .79

.81 Customer

Satisfaction

.67 SATISF1 e23

.82 .69 SATISF2 e24 .83

.69 SATISF3 e25

.83

.62 SATISF4 e26

.79

.65 SATISF5 e27

.81

.62 Customer Retention

.61 RETENT1 e28

.78 .64 RETENT2 e29

.80 .43

RETENT3 e30 .65

.70 RETENT4 e31

.84

.70 RETENT5 e32

.84

.63 RETENT6 e33

.79

e34

e35

Islamic Relationship Marketing

.89

.75

.91

.67

.90

.79

e36

e37

e38

e39

Df = 204 Chi square = 888.21 GFI = 0.092 IFI = 0.914 CFI = 0.926 RMSEA =0.052

ISRA International Colloquium for Islamic Finance (IICIF 2014)

Ratnasari, 2012). Furthermore, the three aspects of relational bonds which are social,

structural, and financial bonds were deemed important in the practicing the Islamic

relationship marketing which at the end may affect customer satisfaction and retention

(found in this research). Therefore, the agents were advised to take care of personal

relationship with their customers and at the same time provide their customer with good

facilities, efficient services, and enough financial benefits.

Finally, the results of this research are empirically significant in the context of the

Malaysian Takaful industry as it has confirmed the four measures of Islamic

relationship marketing that can be applied in services industry. These constructs are

Islamic ethical behaviour, social, structural, and financial bonds. Hence, once the agent

slightly enhances their Islamic relationship marketing practices, it would give big

influence on customer satisfaction and future customer retention.

Since this research is among the earliest studies that scrutinize the practice of

Islamic relationship marketing in the Malaysian Takaful industry, future researchers

may possibly enhance the framework of this research or test it to other countries that

offer Islamic insurance products. The results then can be compared with the findings of

this research as to reach the best approach to market the Takaful products.

6. References

Aijo, T. S. (1996), The theoretical and philosophical underpinnings of relationship

marketing: environmental factors behind the changing paradigm. European

Journal of Marketing, 30(2), pp. 8-18.

Anabila, P., Narteh, B., & Tweneboah-Koduah, E. Y. (2012), Relationship Marketing

Practices and Customer Loyalty: Evidence from the Baking Industry in Ghana.

European Journal of Business and Management, 4(13), pp. 51-61.

Arantola, H. (2002), Consumer bonding - a conceptual exploration. Journal of

Relationship Marketing, 1(1), pp. 93-107.

Beekun, R. (2003), Islamic Business Ethics. New Delhi: Goodword Books.

Berry, L. (1995), Relationship marketing orservices-growing interest, emerging

perspectives. Journal of the Academy of Marketing Sciences, 23(4), pp. pp. 236-

245.

Boone, L., & Kurtz, D. (2004), Contemporary Marketing (Vol. 7th edition). New York:

The Dyrden Press.

Cannon, J. P., & Perreault, W. D. (1999), Buyer-seller relationships in business markets.

Journal of Marketing Research, 36(4), pp. 439-460.

ISRA International Colloquium for Islamic Finance (IICIF 2014)

Crosby, L. A., Evans, K. R., & Cowles, D. (1990), Relationship quality in services

selling: An interpersonal influence perspective. Journal of Marketing, pp. 68-81.

Dwyer, F., Schurr, P., & Oh, S. (1987), Developing buyer-seller relationship. Journal

of Marketing, 51, pp. 11-27.

Hassan, A., Chachi, A., & Salma, A. L. (2008), Islamic marketing ethics and its impact

on customer satisfaction in the Islamic Banking industry. Journal of King Abdul

Aziz, pp. 27-46.

Kamsol, M. K., Anuar, B., Norizah, K., Nik Ramli, N. A., & Kamaruzaman, J. (2009),

Retaining customers through relationship marketing in an Islamic financial

instution in Malaysia. International Journal of Marketing Studies, 1(1), pp. 66-

71.

Murphy, P. E., Lazniak, G. R., & Wood, G. (2007), An ethical basis for relationship

marketing: A virtue ethics perspective. European Journal of Marketing, pp. 37-

57.

Nazlida, M., & Mizerski, D. (2010). The constructs mediating religions' influence on

buyers and consumers. Journal of Islamic Marketing, 1(2), pp. 124-135.

Palmatier, R. W., Rajiv, P. D., Druv, G., & Kenneth, R. E. (2006), Factors influencing

the effectiveness of relationship marketing: A meta-analysis. Journal of

Marketing, 70(October), pp. 136-153.

Piercy, N. F., & Lane, N. (2007), Ethical and moral dilemmas associated with strategic

relationships between business-to-business buyers and sellers. Journal of

Business Ethics, 72, pp. 87-102.

Reichheld, F. F., & Kenny, D. W. (1990), The hidden advantages of customer retention.

Journal of Retail Banking, 12(4), pp. 19-23.

Rizk, R. R. (2008), Back to basic: an Islamic perspective on business and work ethics.

Social Responsibility Journal, 4(1/2), pp. 246-254.

Roberts, K., Varki, S., & Brodie, R. (2003), Measuring the quality of relationships in

consumer services: an empirical study. European Journal of Marketing, 37(1/2),

pp. 169-196.

Rodriquez, C., & Wilson, D. (1999), Relationship bonding and trust as foundation for

commitment in International Strategi Alliances, USA-Mexico: A latent variable

strucral modeling approach. Philadelphia: ISM Report 21: Institute for the

Study of Business Markets.

Shammout, A. B., Zeidan, S., & Polonsky, M. J. (2006), Exploring the links between

relational bonds and customer loyalty: The case of loyal Arabic guest at five

start hotels. Conference proceedings of the Australian and New Zealand

Marketing Academy Conference. Brisbance, Australia: Queensland University

of Technology.

Shamsudin, A. S., Kassim, A. W., Hassan, M. G., & Johari, N. A. (2010), Preliminary

insights on the effect of Islamic work ethics on relationship marketing and

customer satisfaction. The Journal of Human Resource and Adult Learning,

6(1), pp. 106-114.

Sheth, J. N. (2002), The future of relationship marketing. Journal of Services

Marketing, 16(7), pp. 590-592.

Takala, T., & Uusitalo, O. (1996), An alternative view of relationship marketing: a

framework for ethical analysis. European Journal of Marketing, 30(2), pp. 45-

60.

Wendelin, R. (2007), Development of the concept of bonds. Relationship Marketing

Summit (pp. 1-12). Argentina: Universidad Torcuato Di Tella.

ISRA International Colloquium for Islamic Finance (IICIF 2014)

Williams, K. (2012), Core qualities of successful marketing relationship. Journal of

Management and Marketing Research, 10, pp. 1-29.

Wilson, D. T. (1995), An integrated model of buyer-seller relationship. Journal of the

Academy of Marketing Science, Vol. 23, No. 4, pp. 335-345.

Wilson, D. T., & Mummalaneni, V. (1986), Bonding and commitment in buyer-seller

relationships: a preliminary conceptualisation. Industrial Marketing &

Purchasing, 1(8), pp. 44-58.

Wotruba, T. R. (1900), A comprehensive framework for the analysis of ethical

behaviour, with a focus on sales organizations. Journal of Personal Selling &

Sales Management, x(spring), pp. 29-42.

Appendix1

Measurement Items for Social Bonds Sources

Original Items In this research

1. Keeps in touch with me

My Takaful representative

contacts me to keep in

touch.

Crosby et al. (1990),

Berry (1995), Lin et

al. (2003, p. 112)

2. Collects my opinion about

services

He/she asks my feedback

about his/her services.

Lin et al. (2003, p.

112)

3. I can receive greeting cards or

gifts on special days

I receive greeting cards or

gifts from him/her on any

of my special occasion.

Crosby et al. (1990),

Berry (1995)

4. He/she would call or meet me whenever I encounter any

problem.

Develop for this

research from focus

group discussion

5. He/she provides services after I participate in the Takaful

scheme.

ISRA International Colloquium for Islamic Finance (IICIF 2014)

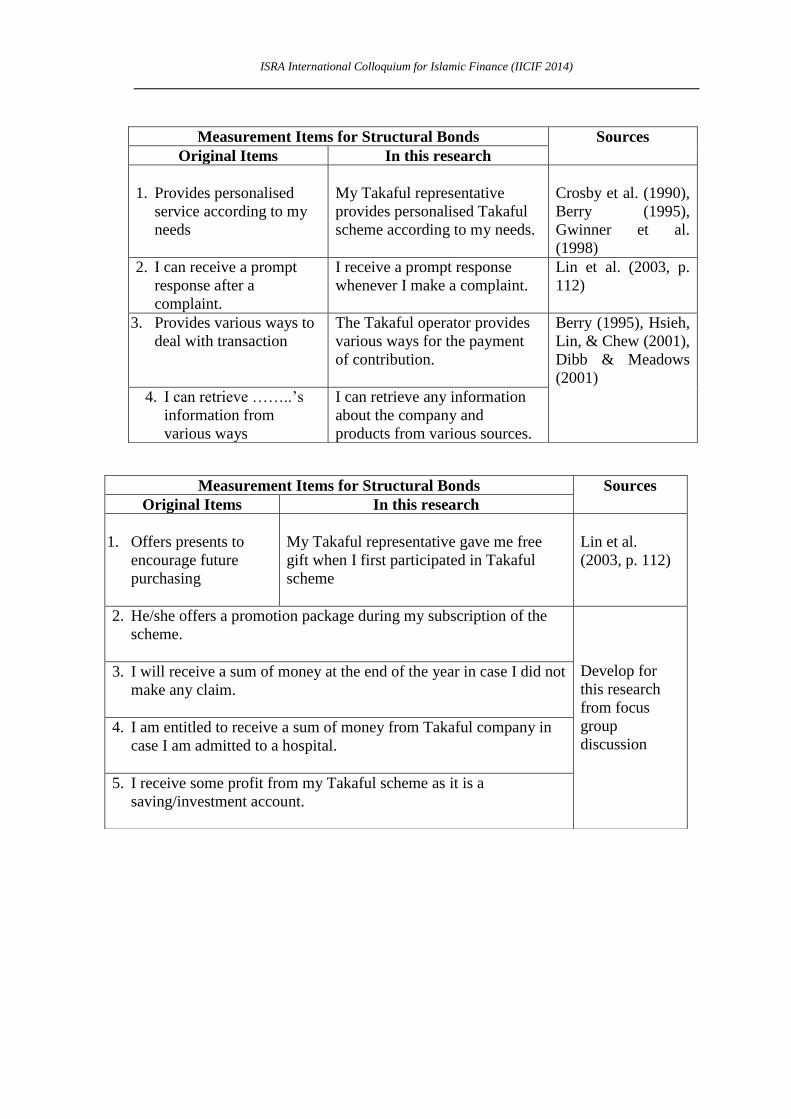

Measurement Items for Structural Bonds Sources

Original Items In this research

1. Provides personalised

service according to my

needs

My Takaful representative

provides personalised Takaful

scheme according to my needs.

Crosby et al. (1990),

Berry (1995),

Gwinner et al.

(1998)

2. I can receive a prompt

response after a

complaint.

I receive a prompt response

whenever I make a complaint.

Lin et al. (2003, p.

112)

3. Provides various ways to

deal with transaction

The Takaful operator provides

various ways for the payment

of contribution.

Berry (1995), Hsieh,

Lin, & Chew (2001),

Dibb & Meadows

(2001)

4. I can retrieve ……..’s

information from

various ways

I can retrieve any information

about the company and

products from various sources.

Measurement Items for Structural Bonds Sources

Original Items In this research

1. Offers presents to

encourage future

purchasing

My Takaful representative gave me free

gift when I first participated in Takaful

scheme

Lin et al.

(2003, p. 112)

2. He/she offers a promotion package during my subscription of the

scheme.

Develop for

this research

from focus

group

discussion

3. I will receive a sum of money at the end of the year in case I did not

make any claim.

4. I am entitled to receive a sum of money from Takaful company in

case I am admitted to a hospital.

5. I receive some profit from my Takaful scheme as it is a

saving/investment account.

ISRA International Colloquium for Islamic Finance (IICIF 2014)

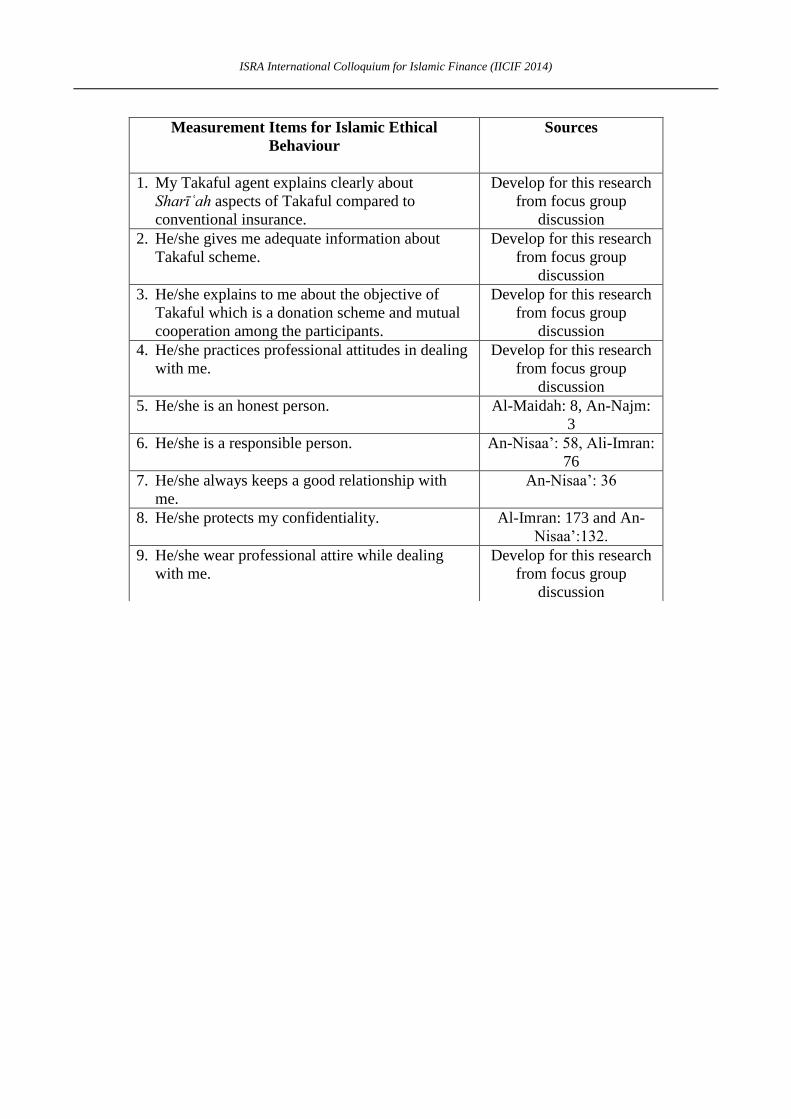

Measurement Items for Islamic Ethical

Behaviour

Sources

1. My Takaful agent explains clearly about

Sharīʿah aspects of Takaful compared to

conventional insurance.

Develop for this research

from focus group

discussion

2. He/she gives me adequate information about

Takaful scheme.

Develop for this research

from focus group

discussion

3. He/she explains to me about the objective of

Takaful which is a donation scheme and mutual

cooperation among the participants.

Develop for this research

from focus group

discussion

4. He/she practices professional attitudes in dealing

with me.

Develop for this research

from focus group

discussion

5. He/she is an honest person. Al-Maidah: 8, An-Najm:

3

6. He/she is a responsible person. An-Nisaa’: 58, Ali-Imran:

76

7. He/she always keeps a good relationship with

me.

An-Nisaa’: 36

8. He/she protects my confidentiality. Al-Imran: 173 and An-

Nisaa’:132.

9. He/she wear professional attire while dealing

with me.

Develop for this research

from focus group

discussion

ISRA International Colloquium for Islamic Finance (IICIF 2014)

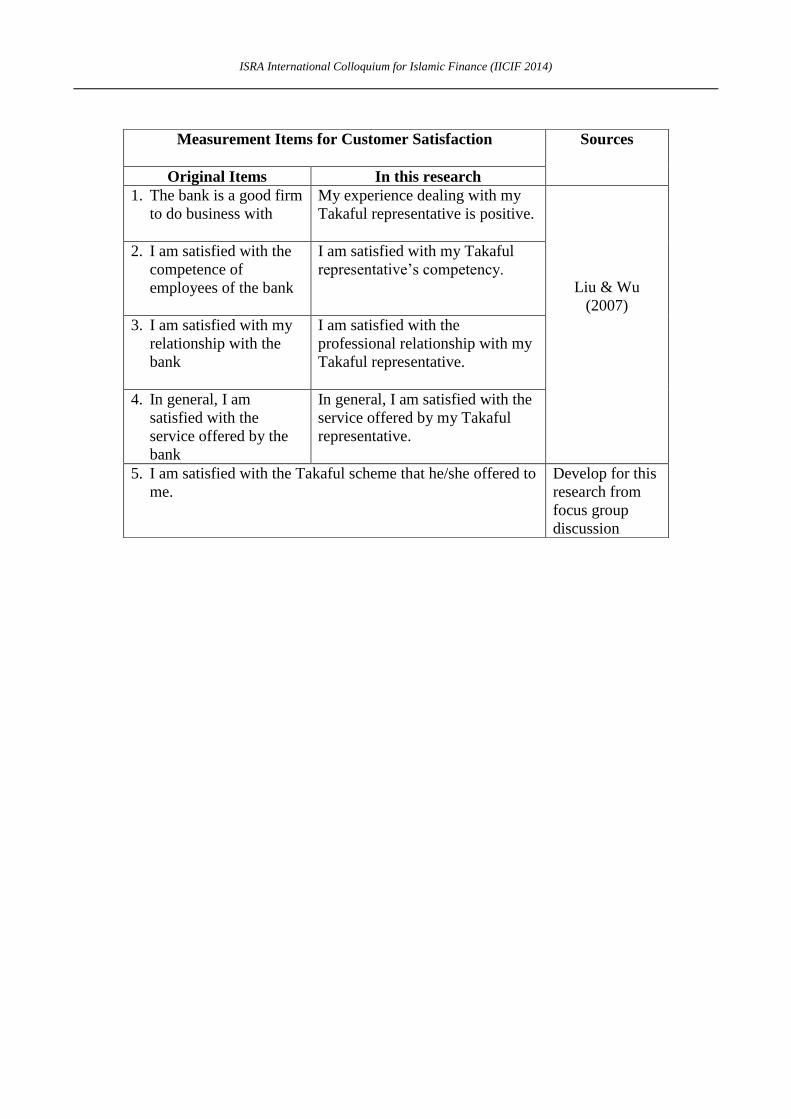

Measurement Items for Customer Satisfaction

Sources

Original Items In this research

1. The bank is a good firm

to do business with

My experience dealing with my

Takaful representative is positive.

Liu & Wu

(2007)

2. I am satisfied with the

competence of

employees of the bank

I am satisfied with my Takaful

representative’s competency.

3. I am satisfied with my

relationship with the

bank

I am satisfied with the

professional relationship with my

Takaful representative.

4. In general, I am

satisfied with the

service offered by the

bank

In general, I am satisfied with the

service offered by my Takaful

representative.

5. I am satisfied with the Takaful scheme that he/she offered to

me.

Develop for this

research from

focus group

discussion

ISRA International Colloquium for Islamic Finance (IICIF 2014)

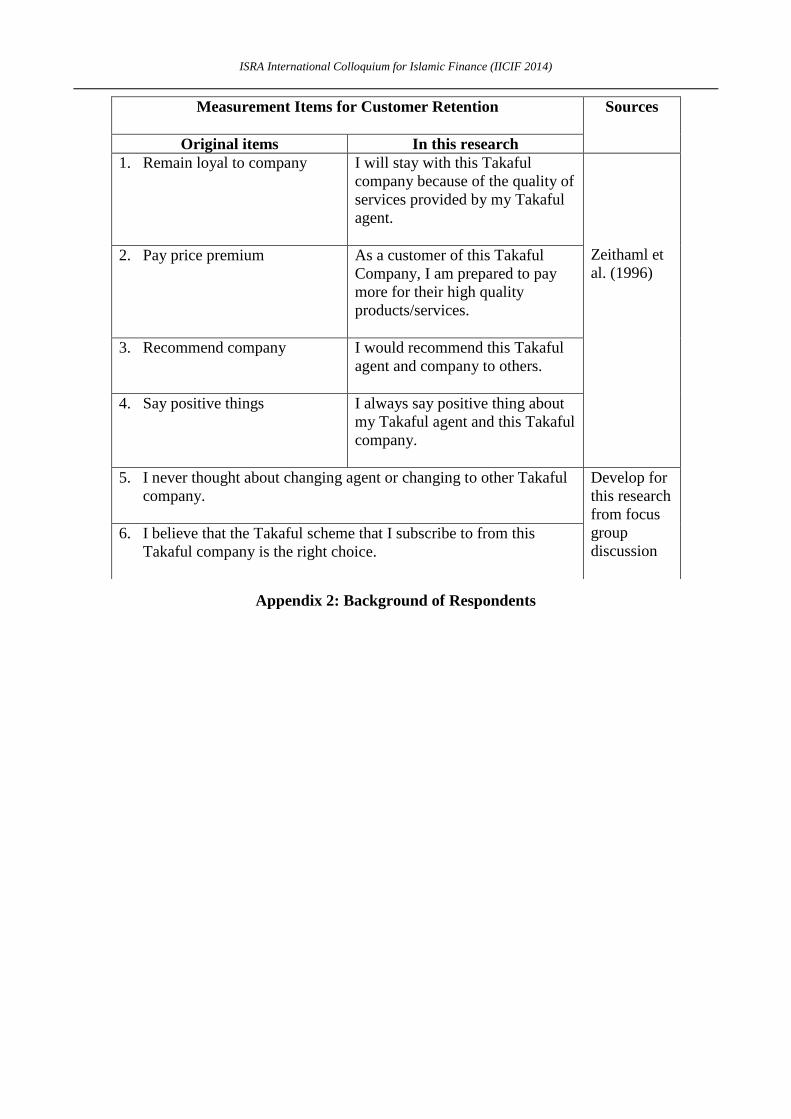

Appendix 2: Background of Respondents

Measurement Items for Customer Retention

Sources

Original items In this research

1. Remain loyal to company I will stay with this Takaful

company because of the quality of

services provided by my Takaful

agent.

Zeithaml et

al. (1996)

2. Pay price premium As a customer of this Takaful

Company, I am prepared to pay

more for their high quality

products/services.

3. Recommend company I would recommend this Takaful

agent and company to others.

4. Say positive things I always say positive thing about

my Takaful agent and this Takaful

company.

5. I never thought about changing agent or changing to other Takaful

company.

Develop for

this research

from focus

group

discussion 6. I believe that the Takaful scheme that I subscribe to from this

Takaful company is the right choice.

ISRA International Colloquium for Islamic Finance (IICIF 2014)

Demographic Information Frequency Percent (%)

Takaful Operators Syarikat Takaful

Malaysia Berhad.

72 9.5

Etiqa Takaful Berhad. 76 10.1

Takaful Ikhlas Sdn. Bhd., 60 7.9

CIMB Aviva Takaful

Berhad,

73 9.7

Prudential BSN Takaful

Berhad,

92 12.2

HSBC Amanah Takaful

Sdn. Bhd.

81 10.7

MAA Takaful Berhad. 53 7.0

AIA AFG Takaful Bhd. 67 8.9

AmFamily Takaful Bhd. 43 5.7

Great Eastern Takaful

Sdn. Bhd.

83 11.0

Hong Leong MSIG

Takaful Bhd.

55 7.3

Total

755 100.0

Gender Male 352 46.6

Female 403 53.4

Total 755 100.0

Age Group <20 years 2 0.3

21-25 years 105 13.9

26-30 years 224 29.7

31-35 years 190 25.2

36-40 years 135 17.9

41-45 years 54 7.2

45-50 years 31 4.1

>50 years 14 1.9

Total

755 100.0

Race Malay 643 85.2

Indian 26 3.4

Chinese 78 10.3

Others 8 1.1

Total

755 100.0

ISRA International Colloquium for Islamic Finance (IICIF 2014)

Religion Islam 651 86.2

Hindu 21 2.8

Buddhist 48 6.4

Christian 30 4.0

Others 5 0.7

Total

755 100.0

Marital Status Single 286 37.9

Married 449 59.5

Divorced 17 2.3

Others 3 0.4

Total

755 100.0

Level of Education SPM 124 16.4

Diploma 221 29.3

Degree 337 44.6

Masters 48 6.4

Phd 4 0.5

Others 21 2.8

Total

755 100.0

Sector of Occupation Government 100 13.2

Semi-Government 50 6.6

Private 500 66.2

Self-employed 101 13.4

Others 4 0.5

Total

755 100.0

Group Income <1000 30 4.0

1001-2000 105 13.9

2001-3000 197 26.1

3001-4000 162 21.5

4001-5000 89 11.8

5001-6000 62 8.2

6001-7000 25 3.3

7001-8000 20 2.6

8001-9000 14 1.9

9001-10000 18 2.4

>10000 33 4.4

Total 755 100.0