council committees and boards the institute of bankers

TRANSCRIPT

Council

Dr. Shamshad Akhtar ChairpersonMr. Zakir Mahmood MemberMr. Atif R. Bokhari MemberMr. S. Ali Raza MemberMr. Mohammad Aftab Manzoor MemberMr. Khalid A. Sherwani MemberMr. Badar Kazmi MemberMr. Aftab Ahmad Khan MemberMs. Zarine Aziz MemberMr. Zaigham Mahmood Rizvi MemberMr. Shaharyar Ahmad MemberMr. Abbas D. Habib MemberMr. Muhammad Saleem Umer Chief Executive

Committees and Boards

Academic BoardMr. Badar Kazmi ChairmanMs. Zarine Aziz MemberMr. Ozair A. Hanafi MemberMr. A.B. Shahid MemberMr. Tahir Ali Tayebi MemberMr. M. Naveed Masud MemberDr. Mirza Abrar Baig MemberDr. Khawaja Amjad Saeed MemberMr. Abdul Ghafoor Member

Finance CommitteeMr. Inam Elahi ChairmanMr. Khalid A. Sherwani MemberMr. Azizullah Memon MemberMr. Safar Ali K. Lakhani MemberMr. A. Saeed Siddiqui Member

Audit CommitteeMr. Aftab Ahmad Khan ChairmanMr. Abbas D. Habib MemberMr. Masood Karim Shaikh Member

H.R. Committee Mr. S. Ali Raza ChairmanMr. Aftab Ahmad Khan MemberMr. A. Saeed Siddiqui Member

Building CommitteeMr. M. Shafi Arshad ChairmanMr. Shameem Ahmed MemberMr. Mohammad Bilal Sheikh MemberMr. Kamran Rasool MemberMr. Tasadduq Hussain Awan MemberMr. Khalid Niaz Khawaja MemberMr. Barbruce Ishaq Member

Editorial BoardMr. Aftab Ahmad Khan ChairmanMr. M. Ashraf Janjua MemberDr. Shahid Hasan Siddiqui MemberMr. Jalees Ahmed Faruqui MemberMr. A.B. Shahid MemberProf. S. Sabir Ali Jaffery Member

Board of Turstees of Staff Provident FundMr. Inam Elahi ChairmanMr. M. Hanif Akhai MemberMr. Muhammad Saleem Umer MemberMr. S. M. Ashique Member

AuditorsMessrs Taseer Hadi Khalid & Co.Chartered Accountants

Registered OfficeThe Institute of Bankers PakistanMoulvi Tamizuddin Khan RoadKarachi — 74200 Pakistan.UAN : 111-111-564 Fax : 5683805Phones: 5680783-5689718-5686955

5684575-5687515-5689364Website : www.ibp.org.pk E-mail : [email protected]

The Institute of Bankers Pakistan

Published by: Mr. Muhammad Saleem Umer for the Institute of Bankers Pakistan, Moulvi Tamizuddin Khan Road, Karachi.The Journal of the Institute of Bankers Pakistan is published quarterly and is provided free to members. Non-members may obtain copies of the Journal from the Institute and/or IBP Local Centres on payment.

Printed at: The Times Press (Pvt) Ltd., C-18, Al-Hilal Society, Off. University Road, Karachi, Pakistan.

Copyright by: The Institute of Bankers PakistanAll rights reserved.The material appearing in this journal may not be reproduced in any form without prior permission of the Institute of Bankers Pakistan.

January - March 2007 Issue

IBP – the knowledge institute

IBP – the knowledge institute

Journal of the Institute of Bankers Pakistan

Volume 74 - Issue No. 1 January – March 2007

ContentsEditorial:Approach To Economic Development:Emerging Consensus 1

SBP First Quarterly Report:Overview and Executive Summary 5

IBP Knowledge Endeavours 13

ISQ Examination (Winter) 2006 Result 19

Research Paper Competition(Summer) 2006 Result 22

Basel II Framework:The IRB Use Test Implementation 23

Collateralization, Risk Management and SME Financing 27

Use of Derivatives inTreasury Management 39

Opportunities and Challengesof Electronic Banking 47

Highlights of Economic Events(October - December, 2006) 69

Legal Decisions Affecting Bankers:I. Attachment of Shares of a CompanyII. Attachment of Debt:

i. before the debt is due.ii. when the debt is in joint names. 73

Questions and Answers onPractice & Law of Banking 75

Collection of Cheques - II (Article in Urdu)

IBP – the knowledge institute

Editorial

Approach To EconomicDevelopment: EmergingConsensus

At the beginning of the current century, after

more than five decades of development

experience, there appears to be more widespread

agreement on policies needed to foster growth in

the developing world than at any time during the

post-World War II period.

Policies recommended by international

financial institutions as well as by leading

development economists in this behalf emphasise

an appropriate macro-economic framework, a

realistic exchange rate which is competitive and

stable, the right set of sectoral policies and

investments, appropriate role of the state in the

economy, integration of the domestic economy

into the world economy, poverty alleviation,

recognition of environmental issues, clear

identification of priorities and peaceful resolution

of conflicts.

Macro-economic development

Sustained economic development is only

possible in a stable macro-economic environment

wherein large fiscal deficits are avoided, inflation

remains low, exchange rate is competitive and

stable and foreign exchange and debt crises are

eschewed.

Fiscal policy has a key role in successful

macro-economic management. It is concerned

with government’s programmes for public

spending and its resource mobilisation strategy.

One important objective of fiscal policy is the need

to abjure unsustainable fiscal deficits in view of

their inflationary and balance of payments

consequences. Fiscal policy has also an important

role in promoting savings not only in the

household and corporate sectors through

modulated tax policies but also as an instrument

for enhanced public savings through a well

designed tax policy and through obtaining

adequate resources from the operation of public

enterprises by levying appropriate user charges.

Public policies on the spending side can determine

the investment pattern and can thus play an

important role in the development of human

resources. The allocation of public funds is no less

important than mobilising them.

Experience in several developing countries

indicates that large fiscal deficits have led to

excessive claims on the government sector, thereby

crowding out the private sector and leading to an

unplanned and excessive monetary expansion.

Most of the major inflations of post-World War

II period have had their roots in excessive fiscal

deficits, which the governments could only finance

by resort to the printing press.

Inflation undermines growth in two ways. First,

it disturbs the most basic process whereby prices

guide resources from lower valued to higher

valued uses. The key to the process of growth is

clear signals about relative prices. Inflation,

especially when it is unanticipated, disturbs those

signals by obscuring the differences between

relative and absolute prices.

Second, inflation tends to generate capricious

transfers of income and wealth among economic

sectors and groups. This breaks the link between

earnings and efforts, and has been known to cause

political upheavals sparked by embittered losers.

A particularly pernicious aspect of inflation is

discrimination against public services who are its

most unrelieved victims apart from those living on

pensions and other fixed provisions for personal

economic security. Social imbalance is also a

natural offspring of inflation. In the words of Prof.

J.K. Galbraith: “In a free market in an age of

endemic inflation, it is unquestionably rewarding

in purely pecuniary terms to be a speculator or a

prostitute rather than a teacher, preacher or

policeman”.

January - March 2007 Issue 1

The exchange rate

Exchange rate plays a crucial role in

establishing market incentives for exports and for

regulating imports. Again, the stability of the

exchange rate is a potential monetary anchor and

an important anti-inflationary factor.

Often governments afraid of unleashing

uncomfortable inflationary pressures in the

economy hold the nominal exchange rate constant

or devalue it too slowly with the result that the

domestic currency appreciates and the pressures

on the balance of payments assume disconcerting

proportions. When the inflation control and export

incentive roles of the exchange rate conflict,

attention should turn to the underlying source of

inflationary pressure, often the budget.

Intermediate steps such as crawling peg in

conjunction with appropriate fiscal policy can

provide some monetary stability without tending to

produce an over-valued currency.

Sectoral Policies and investments

Sectoral policies include investment decisions,

pricing and regulatory policies and institutional

development.

Investments in agriculture, manufacturing,

infrastructure and human resources development

have long formed the core of development efforts.

The traditional approach was to prepare and

implement projects in sectors with the aid of cost-

benefit analysis. It is now generally appreciated

that aside from sound project formulation and

implementation, the effectiveness of projects

depends on the policy environment affecting the

sector and the degree of institutional development.

Measures to bring domestic relative prices closer to

international levels and to establish a relatively

neutral framework that does not favour particular

industries, regions or factors of production are

often necessary for improving sectoral

performance. In agriculture, for example, incentives

were historically suppressed by low agricultural

procurement prices. Perhaps, more important, in

many countries, over-valued exchange rates have

often resulted (frequently unintended) in taxation

of this sector. Adjustment programmes of the

World Bank and regional development banks have

therefore, focused on both macro-economic

policies and sectoral pricing policies (eliminating

price controls on agricultural output, for example).

It is also now universally recognised that

human resource development is both an

independent goal of development and an essential

instrument of economic progress.

High rates of population growth in the post-

World War II era have contributed to low per

capita income growth in many countries in Asia

and Africa. As such reducing the rate of population

growth remains a priority area in development

policy in many low income countries.

Integration with the world economy

Many of the star development performers in

recent decades have been newly industrialising

economies (South Korea, Taiwan, Hong Kong,

Singapore, Malaysia and Thailand), characterised

by relative openness and links with the world

economy. To strengthen these links, they have had

to remain competitive in a rapidly changing world

environment. Common to successful competition

strategies is the reduction or elimination of

discrimination against tradeables-permitting

exports and import substitutes to be produced on

a similar footing with non-tradeables.

Interventions to encourage new technologies

and to industrialise have also paid off in many

countries.

Developing countries with more open and

efficient trade regimes have generally won long

term economic gains. Openness to trade, investment

and ideas has been critical in encouraging

domestic producers to cut costs by introducing

new technologies and to develop new and better

products in East Asian miracle economies.

Role of the state

A major lesson which emerges from the rich

mosaic of successes and failures on the

development front, is about the role of the state.

This role is crucial, but it must be kept within the

January - March 2007 Issue2

IBP – the knowledge institute

limits of the scarcest resource in the developing

world, that is the supply of competent and honest

administrative talent. A large public sector

especially exhausts this with strongly negative

consequences.

The dominant development paradigm in the

quarter century after World War II assigned a

major role to the state in the poor lands by

assuming the state to have certain characteristics

which it turned out not to have. In the name of

planning, a regulatory framework and mechanism

for allocating resources were created to control

private decisions. In exercising such control,

quantitative restrictions rather than price based

measures mediated through the market were most

often used. A chaotic incentive structure and an

unleashing of rapacious rent seeking were the

outcomes.

It is now quite clear that incentive system

matters and competition, domestic and

international, is the most effective way for ensuring

efficient resource allocation.

At present there is a broad consensus that the

state’s emphasis should not be on the production

of commodities and services which the private

sector can provide efficiently. It should rather be

on education, health, protection of the poor,

infrastructure and providing the right environment

for entrepreneurial activity to flourish.

State interventions in the economy, where

necessary, should be market friendly in that these

work with the market and do not become

entitlements of particular groups that cannot be

withdrawn once the need for intervention

disappears. Interventions should be transparent,

rule based rather than discretionary, price based

rather than through quantitative restrictions.

Poverty alleviation

Poverty has now become the hot favourite of

development economists and considerable

research inputs are being made into the

investigation of this theme. These endeavours

have thrown up some useful insights, but much of

the tangled skein of poverty remains unravelled.

This is not only a subject of endless research–

it also calls for action. On the economic side the

problem is now beyond charity and state

welfarism. The productivity of the poor has to be

raised and a more equitable distribution of

incomes brought about. This will have socially

wholesome and economically beneficial results.

Productivity and development will pick-up if

poverty is eradicated.

Recognition of environmental issues

The recognition of environmental issues in

developing countries is an aspect of the widening

of development concept. It is a part of a more

unified or integrated approach to development.

Which developing countries have to

industrialise and grow they also, at the same time,

need to be aware of the ecological limits to growth

and conserve the environment and control

environmental hazards through appropriate

domestic legislation which should be adequately

enforced. Adequate attention to environmental

concerns would obviously facilitate high growth by

sustaining the resource base of the biosphere.

Careful identification of priorities

Most developing countries are resource

constrained and some things are more important

than others. It is the planner’s first task to identify

them and devise an appropriate strategy to achieve

the priority goals in the most cost effective manner.

In this behalf, it is essential to concentrate resources

on priority tasks and not to diffuse them by spreading

these thinly over a broad spectrum of activities.

Peaceful resolution of conflicts

In many countries of the Third World,

development progress has been seriously retarded

by internal as well as international conflicts.

Millions have been killed or impoverished in the

developing world on account of national, ethnic or

religious conflicts. Peace and tolerance must be a

prime goal for the people of the Third World.

Conflicts must be resolved through negotiations,

mediation and, if necessary, through international

arbitration.

January - March 2007 Issue 3

IBP – the knowledge institute

IBP – the knowledge institute

SBP First Quarterly Report:Overview and Executive Summary

The State Bank of Pakistan issued First

Quarterly Report for FY07. Following is an

overview and executive summary of the report:

Overview

Likelihood of achieving 7 percent growth

target for FY07 remains strong despite visible

challenges in meeting growth target of industry

and agriculture. While an anticipated recovery in

large scale manufacturing is likely to be realized, it

seems that achieving the 13 percent growth target

may prove difficult. Similarly, the weak

performance by the three major kharif crops

(cotton, rice and maize) had reduced the

probability of a sharp rebound by agriculture,

though even here, the value-addition is likely to be

an improvement over the preceding year if the

contribution from livestock and the wheat crop

remains strong. This suggests that achievement of

the annual growth target will require the services

sector to turn in an above-target growth.

Encouragingly, although real growth remained

strong and seems likely to exceed the FY06 levels,

inflationary pressures eased somewhat during

FY07, suggesting that tight monetary policy is

striking an appropriate balance, i.e., gradually

removing excess stimulus from the economy,

without dampening the growth momentum.

However, this should not lead to complacency; on

the one hand, the downtrend in the inflation over

the past 12 months clearly shows a degree of

instability, and on the other, reducing domestic

inflation further is essential to improving the

competitiveness of Pakistan's exports, and

ensuring a better return to domestic savers.

It is also important to note that not all of the

instability in inflation can be addressed through

monetary policy. Core inflation has already dipped

significantly and the present high levels of inflation

and its greater variability are both principally

driven by food inflation, which is largely

determined by factors other than monetary policy.

This does not imply that monetary policy cannot

play any role in containing food inflation, but

rather that the cost of monetary policy actions to

contain it should be weighed cautiously. The food

inflation pressures in Pakistan could be better

controlled through by (1) improvement in supply

of key staples, and (2) administrative measures as

were taken in the month of Ramadan.

Another challenge to containing inflationary

pressures is from the divergence between the

expansionary fiscal policy and tight monetary

policy, and the volatility in the government

borrowings from the banking system (and

particularly from SBP). The need to catalyze

improvements in infrastructure and boost

development (and particularly to reconstruct areas

devasted by the October 2005 earthquake) means

that it will be difficult to substantially reduce the

fiscal stimulus in the near term. Unfortunately, the

resulting added burden on monetary policy means

that the offsetting monetary tightening will need to

continue for a longer period.

Fiscal pressures have primarily originated from

higher growth in development expenditure,

although slowdown in revenue growth has also

added to the stress. While weakness in non-tax

receipts is not unexpected (and could potentially

be reversed in H2-FY07), the slowdown in key

CBR taxes is more of a concern. Specifically, the

sharp deceleration in imports during FY07 appears

to have impacted indirect tax collections, which

have remained below target through the initial

months of FY07.

It is noteworthy that aggregate collections have

nonetheless been strong due to a welcome, but

unexpected surge in direct tax receipts. It is hoped

that CBR will be able to recoup the shortfall in

indirect taxes from this recovery in direct taxes.

January - March 2007 Issue 5

However, if any revenue shortfalls do emerge, the

impact on fiscal accounts should be sterilized

through curtailing expenditure (particularly

discretionary non-development spending). Such a

clear demonstration of commitment to fiscal

discipline would likely be crucial in reassuring

international investors, thereby supporting a

further improvement in the country's credit ratings,

and helping domestic companies access

international capital markets on more favorable

terms.

Moreover, in order to reduce the impact of

fiscal developments on monetary policy, it is

important that government reduce the uncertainty

associated with its borrowings (e.g., a start could

be made by publishing its quarterly borrowing

targets at the beginning of the period) and reduce

its dependence on borrowings from the central

bank. The government has indeed sought to do

the latter by reversing its ban on institutional

investments in NSS, but this mode of increasing

non-bank borrowings has significant drawbacks,

and it is important that the government focus

instead on raising funds through issuance of

tradable long-term paper, i.e., PIBs.

Finally, while import growth has decelerated

sharply in recent months, this has not relieved

pressures on monetary policy given the puzzling

decline also visible in export growth that has led to

a further widening of the trade deficit. While some

weakness in exports was not surprising given the

increasingly competitive international markets, the

reported slowdown was quite unexpected.

Moreover, it is not entirely consistent with trends in

associated variables, such as the US and EU

statistics on textile imports from Pakistan, as well as

the exchange record data of SBP (all of which

show stronger export growth than given by FBS

data). This raises hopes that at least a part of the

strong deceleration in exports growth may be a

statistical artifact due to unusual leads and lags in

reporting (this view seems to be supported by the

exceptional 23.9 percent YoY rise in November

2006 exports).

However, even if a part of deceleration is a

statistical phenomenon, there is no denying that

exports growth has been adversely impacted by

competitive pressures, which, in turn, is a major

contributor to the widening of the current account

deficit in FY07. This is in sharp contrast to the

import-led deterioration in the deficit over the

preceding two years. It is in this context that the

SBP seeks to support the government and

exporters by focusing on reducing domestic

inflation in order to help curtail increases in the

cost of business and to reduce any appreciation of

the rupee's real effective exchange rate.

In the meantime, while persistent large current

account deficits are clearly undesirable in the

medium term, Pakistan's current account deficit is

not yet a serious problem, as (1) the current

account deficit is forecast at 4.5 percent of GDP,

which is not unmanageable; (2) the country is in a

position to comfortably finance the deficit through

strong non-debt flows as well as by taking on debt

at relatively favorable terms; (3) and given that this

is without significantly increasing country risk, as

the external debt to GDP ratio will continue to

decline despite the rise in absolute debt levels. The

latter view is supported by the continuing upgrades

to Pakistan's sovereign credit rating by leading

international credit rating agencies.

Looking Ahead

SBP forecasts based on initial data indicate

that the FY07 annual growth target remains

achievable, although risks to the downside have

increased following the below target harvests of

key kharif crops (cotton, rice and maize), and the

possibility of growth in large-scale manufacturing

slowing a little in the months ahead as a result of

power shortages, capacity issues (e.g., fertilizer

production may drop as major units close

temporarily to implement expansions), and a

relative easing of demand due to the tight

monetary policy, etc.

However, M2 growth is forecast to be stronger

than estimated earlier as the contractionary impact

of net foreign assets of the banking system during

Jul-Nov FY07 has been lower than anticipated,

due to the unexpectedly robust net receipts in the

external account. The latter is likely to overshadow

the impact of the deceleration in private sector

credit. The continued strength of aggregate

January - March 2007 Issue6

IBP – the knowledge institute

demand, the unexpected strength in broad money

and, most importantly, the recent uptrend in food

prices reinforces the view that the inflation

outcome for FY07 is likely to be higher than the

annual target.

It is in this context that the SBP continues to

stress the importance of retaining a tight monetary

posture, in order to reduce the excessive monetary

stimulus in the economy. The direction of

monetary policy will need to be supported by the

fiscal policy by avoiding any expansion in the

targeted fiscal deficit (the target looks achievable;

however some risks have emerged as a result of

the slowdown in import-based taxes), improving

predictability in borrowings from banking system

and raising non-bank borrowings through PIBs

rather than NSS. The greater liquidity in larger

market-based issues would also improve price

discovery leading to improved long-term debt

benchmarks, helping develop domestic debt

markets. It should be kept in mind that healthy,

liquid domestic debt markets are not only essential

to long-term international investment in

infrastructure projects etc, but can lead to an

improvement in the balance of payments. To put

this in perspective, it is important to realize that in

order to remain competitive in the international

markets and sustain economic growth, the country

desperately needs to considerably augment and

improve its infrastructure. This will only be possible

by attracting significant private sector participation

in these projects. This will be difficult without long-

term debt markets.

Executive Summary

Agriculture

Hopes of a strong recovery in agricultural

growth during FY07 on the back of improved

water availability, continued access to credit, and

ease in the prices of fertilizers have decreased

following the lackluster performance of key major

kharif crops. The initial production estimates of

cotton, rice and maize posted a weak growth,

which overshadowed the impact of the strong

growth in sugarcane production during FY07

relative to the preceding year. As a result,

realisation of the FY07 agricultural growth target

will be possible if the livestock sub-sector

performance is well above target.

Large Scale Manufacturing

Growth in large scale manufacturing (LSM)

accelerated in Q1-FY07, rising to 9.7 percent as

compared with the 8.8 percent growth seen in Q1-

FY06. This was primarily due to acceleration in the

production in the textile, electronics, chemicals

and metal industries. However, LSM growth

acceleration is not broad-based.

The electronics sub-sector recorded an

extraordinary 41.6 percent YoY growth during Q1-

FY07 as against 9.2 percent YoY growth in the

same period of previous year. Strong income

growth, better access to credit, and the efforts of

power utilities to modernize and extension in their

distribution networks are the main factors behind

the extraordinary performance of the electronics

sub-sector.

As with electronics, the growth in the textiles

sub-group also rose to 12.4 percent during Q1-

FY07 as against a decline of 0.9 percent in the

same period last year. This growth is the second

highest for any first quarter during the last six

years. The growth recorded in textile production

appears to be supported by the acceleration in the

growth of the chemicals sub-sector to 10.1 percent

during Q1-FY07 as compared with 8.2 percent

growth during Q1-FY06.

Metals sub-sector also grew by 14.5 percent

during Q1-FY07 against the decline in the

production by 4.1 percent during the same period

last year. The improvement can be attributed to

the streamlining of production by Pakistan Steel

after completion of repairs of its coke oven

batteries in the last quarter of FY06.

The automobiles sector registered a growth of

only 11.1 percent during Q1-FY07, which is not

only lower than the strong growth of 33.1 percent

in the same period of the preceding year but also

the lowest during the last six years.

The production of fertilizer also fell in Jul-Oct

FY07, dropping by 1.7 percent as against a rise of

January - March 2007 Issue 7

IBP – the knowledge institute

3.7 percent growth during the same period of the

preceding year. This decline was mainly due to

capacity constraints as well as lower demand on

the back of untimely rain and an anticipated

subsidy announcement by the government.

Prices

Although, on average, inflationary pressures

appear to be weakening in the economy, the

downtrend is unstable. This is evident in the

benchmark Consumer Price Index (CPI) inflation,

which jumped to 8.9 percent in August 2006

before dipping to 8.1 percent YoY during October

2006 and remained at the same level in November

2006, slightly higher than the 7.9 percent YoY in

November 2005. The instability emerged

essentially due to the volatility in food prices,

particularly stemming from (1) supply-side

disturbances on account of rains and floods, and

(2) the impact of increases in international prices of

some key food items.

A welcome development, from the monetary

policy perspective, however, is that non-food

inflation now appears to be trending downwards.

This deceleration in non-food inflation is clearly

mirrored in the easing of core inflation. The non-

food non-energy (NFNE) measure of core inflation

dipped to 5.6 percent YoY in November 2006

compared with 7.6 percent YoY for the

corresponding month of 2005, suggesting that

demand pressures in the economy are being

reined-in by the continued tight monetary policy.

As with the core inflation, the Wholesale Price

Index (WPI) inflation exhibited a steady

downtrend, with the overall WPI inflation coming

down to 7.5 percent YoY in November 2006

compared with 10.9 percent in November 2005.

The major contribution to the decline in WPI is

from the non-food group, which outweighed the

acceleration in the food group prices.

Unfortunately, despite the moderation in

inflationary pressures, CPI inflation is still close to

the 8 percent levels by November 2006, which is

significantly higher than the annual average

inflation target of 6.5 percent for FY07. Given that

core inflation is likely to remain contained through

the remaining months of FY07 as a result of a tight

monetary policy, it is important that its impact is

supplemented by measures to address food

inflation and high energy prices. Volatile, double-

digit food inflation is particularly undesirable in

view of its greater adverse impact on low-income

groups. Moreover, it is a source of disquiet for

monetary policy as well since inflationary

expectations are based on overall inflationary

trend. There is a need for effective administrative

measures (as exercised in the month of Ramadan)

to discourage profiteering on food items.

Money and Banking

The impact of monetary tightening pursued in

FY06 as well as the policy signals through the

FY07 changes, is already evident in the slowdown

in private sector credit growth, which has dropped

to 5.9 percent during Jul-Nov FY07 against the

10.9 percent growth witnessed in the

corresponding period of FY06. Moreover, core

inflation, as measured by non-food non energy

inflation has slowed to 5.6 percent (YoY) in

November 2006 from 7.6 percent (YoY) in

November 2005.

However, the growth in monetary aggregates

during Jul-Nov FY07 remained strong. This is

because: (1) the deceleration in private sector

credit has not been matched by an equally strong

decline in government borrowings, which have

remained significant; and (2) the contraction in

NFA during Jul-Nov FY07 has been much lower

than that in FY06.

The impact of continuing pressures on the

external account was evident on the NFA of the

banking system that showed a contraction of

Rs41.1 billion during Jul-Nov FY07, almost

equally distributed between SBP and all

commercial banks. However, it is important to

note that the contraction in the NFA of the banking

system during Jul-Nov FY07 was considerably

lower than the sizeable reduction of Rs90.5 billion

witnessed during Jul-Nov FY06. This is largely

because the NFA of commercial banks did not

decline as sharply as in FY06.

The government borrowings from the banking

January - March 2007 Issue8

IBP – the knowledge institute

system are higher and volatile. Although the

government may be able to remain within the

budgetary borrowing target of Rs120 billion from

the banking system for FY07, excessive borrowing

during the course of the year is a source of concern

for monetary policy, particularly because the

government borrowing is entirely from the central

bank, which is the most inflationary in nature as it

contributes to reserve money growth.

The high government borrowings and the

resulting rise in reserve money, has the potential of

re-igniting inflationary pressures in the economy. If

this happens, the time path for achieving a stable

low inflation could be extended, as in the absence

of low stable inflation, the central bank would have

to keep interest rates high for a longer duration.

The government has however sought to

increase its non-bank borrowings. Unfortunately,

instead of raising these incremental funds entirely

through PIB issues, the government has also re-

allowed institutional investment in NSS. While the

latter decision would, in theory, allow institutional

investors to rollover large NSS maturities, this

major policy reversal is likely to have significant

negative implications for the development of the

domestic debt market, and raise interest rate risk

for the government.

In contrast to government borrowings, the

private sector credit seems to be responding to

interest rate signals from the central bank.

Specifically, the growth in private sector credit

during Jul-Nov FY07 has slowed down to 5.9

percent compared to 10.9 percent rise witnessed

during the corresponding period of the previous

year. However, so far, this slowdown in private

sector credit growth is not a source of disquiet for

SBP for the following reasons:

* The YoY growth in private sector credit

remains very strong at 18.0 percent by 25th

Nov 2006, although down from 31.9 percent

last year.

* A review of monthly trends in private sector

credit shows that the slowdown is largely

concentrated in the month of September 2006.

In fact, trends during October and November

2006 indicate presence of strong demand for

private sector credit in the economy.

* The available evidence suggests that the

slowdown in private sector credit is not broad-

based as (1) the increased net retirement,

particularly by the sugar manufacturers during

Jul-Nov FY07 contained the growth in private

sector credit; and (2) deceleration in bank

credit against equities.

* More importantly, while the nominal lending

rates are rising, the real lending rates are still

very low. The real lending rates under export

finance facility are even negative.

In sum, though the overall demand for credit

by the private sector has decelerated, the

slowdown is not broad-based. This suggests that

monetary policy needs to remain tight.

However, while the transmission of the

monetary policy on lending rates has improved

over the last year, the impact on deposit rates has

been less than desired, contributing to an

unhealthy high banking spread. The available

evidence shows that banks are mobilising deposits

at higher returns and the share of such deposits

has been rising. Since the long-term deposits lower

the maturity mismatch for banks and reduce

liquidity risks, it was expected that the banking

spread would decline. But in the meanwhile,

lending rates have also risen thereby leading to a

sharp rise in the banking spread (calculated on the

basis of incremental loans and deposits) in recent

months. Such a large spread can have a

dampening effect on economic growth by

discouraging savings.

Fiscal Developments

Developments in public finance during Q1-

FY07 present a deterioration in the fiscal accounts.

Fiscal deficit widened by 0.5 percent of GDP to 1.0

percent of GDP in Q1-FY07. The Q1-FY07 fiscal

deficit (as percent of GDP) is not yet inconsistent

with meeting the annual target of 4.2 percent of

GDP. For example, the Q1-FY03 fiscal deficit had

been 0.8 percent of GDP, but full year outcome

was 3.7 percent of GDP. However, in that year the

January - March 2007 Issue 9

IBP – the knowledge institute

growth in CBR taxes had been exceptionally

strong at 9.6 percent of GDP (a level achieved in

FY97 but never since). The FY07 tax target is close

to this level, at 9.5 percent of GDP, and attaining

it will be important to meeting the overall fiscal

deficit target for the year. Unfortunately, given the

recent moderation in import growth, and the high

dependence of tax receipts on import-based taxes,

achievement of the CBR tax target may prove

challenging.

This fiscal squeeze is attributable to both the

lower revenue growth, as the total revenue to GDP

fell from 3.1 percent in Q1-FY06 to 2.9 percent in

Q1-FY07 and the rising expenditure. It is note

worthy that the rise in expenditure to GDP ratio is

only due to the unidentified expenditure that rose

from 0.1 percent of GDP in Q1-FY06 to 0.4

percent of GDP in Q1-FY07. CBR though met its

revenue target of Rs236.2 billion with an actual

collection of Rs237.3 billion during Jul-Oct FY07

yet all the indirect taxes could not meet their

respective targets. A moderate growth in imports

and the large-scale manufacturing resulting in

lower growth in tax collection by the CBR during

first quarter, may keep the growth in indirect tax

revenues relatively weak during FY07. Provincial

governments, however, improved their position

during first quarter. This better fiscal position

stemmed from new formula of revenue sharing

from federal divisible pool of tax revenue, except

Balochistan, all the other provinces seem to be in

a comfortable position.

Balance of Payments

Pakistan's overall external account position

improved during Jul-Nov FY07 compared to the

same period last year despite a worsening of the

current account deficit. Specifically, while the

current account deficit increased from US$3.1

billion to US$4 billion, an increase of 29.1 percent,

the overall external account deficit shrank to US$

0.73 billion in Jul-Nov FY07 compared to US$

0.88 billion in Jul-Nov FY06.

As in the previous year, it was the surpluses in

the capital and financial accounts that offset most

of the deficit in the current account. The bulk of the

35.4 percent YoY increase in the aggregate surplus

in the capital and financial accounts during Jul-

Nov FY07 was contributed by foreign investment.

Although Pakistan was able to finance the Jul-

Nov FY07 current account deficit relatively easily,

the rise in the deficit nonetheless remains a source

of some concern, particularly because unlike the

previous years, it owed more to a substantial

slowdown in the countryís exports rather than an

extraordinary rise in imports. Specifically, while the

imports growth during Jul-Nov FY07 slowed

substantially to 13.9 percent compared to 33.2

percent in the corresponding period last year, it

was the unusual decline in the exports growth (that

dropped to a mere 7.3 percent compared to 13.8

percent in the corresponding period last year), that

drove the trade deficit up by 25.5 percent to US$

4.5 billion.

In addition, the current account deficit was also

adversely affected by an unusual rise in the income

account deficit arising from a higher direct

investment income outflows. The rise in the trade,

services, and income account deficit was, however,

mitigated to an extent by the increase in the

current transfers, which increased by 13.4 percent

during Jul-Nov FY07.

Due to substantial inflows, both on account of

current transfers and foreign investment during

Jul-Nov FY07, the impact of the widening current

account on the country's reserves was relatively

low. Pakistan's overall foreign exchange reserve

declined by US$ 799.4 million during Jul-Nov

FY07 compared to decline of US$ 1,321.6 million

in the same period last year. Nevertheless, a result

of the continuous pressures on the external sector,

Pakistanís currency vis-a-vis US Dollar,

depreciated by 1.1 percent during Jul-Nov FY07

as compared to the 0.1 percent in the

corresponding period last year.

Foreign Trade

The trade deficit continued to rise during Jul-

Nov FY07, although the growth slowed

substantially to 17.8 percent from the 147.5

percent YoY increase recorded during the

corresponding period last year. This welcome

deceleration in the growth of the trade deficit

January - March 2007 Issue10

IBP – the knowledge institute

during Jul-Nov FY07 is principally due to the

slowdown in the import growth.

Specifically, the moderation in import growth,

which has been apparent since H2-FY06 further

strengthened during Jul-Nov FY07 as all major

imports categories other than petroleum,

machinery and other products, recorded negative

growth rates. As a result, the overall growth in

imports fell to 10.4 percent during Jul-Nov FY07

against 54.3 percent rise in the corresponding

period last year. Indeed, the trade deficit would

have been even lower, had it not been for the

unexpected sharp deceleration in export growth to

5.2 percent YoY during Jul-Nov FY07 compared

to 22.3 percent YoY in Jul-Nov FY06.

A part of the decline in the exports growth is

understandable given the more challenging

economic environment as compared to a year

earlier, both domestically and externally.

Nevertheless, the magnitude of the slowdown in

exports is still puzzling.

Specifically, while the FBS data shows a 3.3

percent decline in the textiles exports during Jul-

Nov FY07, exchange records depict a growth of

11.0 percent. Furthermore, EU textiles and

clothing imports from Pakistan also show a rise of

3.2 percent during Jul-Sep FY07,2 and similarly,

the US imports data show a rise of 8.8 percent in

textile and clothing imports from Pakistan.3

However, the November trade figures are some

consolation; although detailed data is not yet

available, the increase of 23.9 percent YoY in

overall exports is nevertheless quite encouraging.

The analysis is based on the provisional data

provided by Federal Bureau of Statistics, which is

subject to revisions. This data may not tally with

the exchange record numbers reported in the

section on Balance of Payments.

January - March 2007 Issue 11

IBP – the knowledge institute

IBP – the knowledge institute

IBP Knowledge Endeavours(October-December 2006)

Training and Development of Human

Resources

During the quarter October - December

2006, IBP continued to follow its critical role

of training and professional development of

human resource of banks and financial

services sector. Overall, the Institute held 23

courses -, 13 in Karachi, 8 at its local centers

and 2 at small centres under mobile training

program. Over 500 participants from banks

and financial institutions received training

under these programs. Details of the courses

held at Karachi and other centres are given

below:

EVENTS AT KARACHI

S. No. Courses Title Speaker

1. KYC & Anti-Money Laundering Mr. Muhammad Ilyas

2. Working Capital Financing Mr. Murtaza Y. Rizvi

3. Basel - II Accord Mr. Jameel Ahmad

4. Customer Relationship Management Mr. Murtaza Y. Rizvi

5. Cash Flow Based Lending Mr. Murtaza Y. Rizvi

6. Branch Banking Operations Mr. Razi Mujtaba

Mr. Muhammad Ilyas

7. Demystifying UCP - 600 (2 courses) Mr. Abid Aziz Merchant

8. SBP Export Refinance - A Detailed Workshop Mr. Ishtiaq Ali

9. Prudential Regulations for Corporate

& Commercial Banking Mr. Muhammad Ilyas

10. The Art of Negotiation for

Achieving Positive Results Mr. M. Afzal Janjua

11. Fraud & Forgery: How to Detect and

Protect the Banks Mr. Muhammad Ilyas

12. Banker-Customer Relationship:

Laws Impacting Banks Operations Mr. Muhammad Ilyas

January - March 2007 Issue 13

January - March 2007 Issue14

IBP – the knowledge institute

EVENTS AT LOCAL CENTRES

The Institute has 11 Local Centres in different

parts of the country. They also hold courses on

topical subjects. During October - December 2006,

following programs were held by the Local

Centres:

EVENTS AT LOCAL CENTRE

S. No. Courses Title Resource Persons

Lahore.

1. Assets & Liability Management Mr. Kh. Waheed Raza

Rawalpindi

1. Cash Flow Based Lending Mr. Malik Dilawar

2. UCP - 600 Mr. Mudassar Hussain

Islamabad

1. How to Spot and Encounter Counterfeit

Bank Notes and Tampered Prize Bonds Mr. Muhammad Arif Azam

2. Time & Stress Management Prof. Dr. Rafiq Ahmed Ghuncha

Quetta

1. Export Refinance Scheme Mr. Ishtiaq Ali

Hyderabad

1. Branch Banking Operations Mr. Muhammad Ilyas

Multan

1. Know Your Customer & AML Mr. Kh. Waheed Raza

MOBILE COURSE

Mirpur A.K.

1. Auditing Financing Operations:

Onsite Inspection by SBP Audit Team Mr. Taslim Kazi

Sargodha

1. Auditing Financing Operations:

Onsite Inspection by SBP Audit Team Mr. Taslim Kazi

January - March 2007 Issue 15

IBP – the knowledge institute

Besides the courses mentioned above, the

following knowledge events were also held during

the quarter under report:

1. Effective Branch Management

The fourth of the series of 120-hours high-

value certificate course on "Effective Branch

Management" is in progress w.e.f. November

21, 2006 at Karachi, Lahore, Rawalpindi and

Peshawar. The program covers core banking

as well as soft skills needed by the Branch

Managers. 93 Managers - , 24 at Karachi, 20 at

Lahore, 29 at Rawalpindi and 20 at Peshawar

are attending this program.

2. Effective Credit Management

Effective Credit Management (ECM) is one of

the critical factors of a bank's overall

management strategy and is vital to the long

term success of a banking organization.

Considering the fact that banks' loan portfolio

is rising and consequently the quantum of risk,

the Institute held a week long workshop on

"Effective Credit Management" from December

4 - 9, 2006. The workshop targeted at middle

management executives who have basic

understanding of credit functions. 28

executives and officers attended the workshop.

Ms. Tahira Raza, EVP/Head of Loan Examiner

Wing, NBP, Mr. Altaf Hussain Saqib, AVP,

Risk Management Division, NBP, Mr.

Azizuddin Khan, Advocate, Mr. Asadullah

Saleem, SVP & Head of Risk Management

Division, PICIC, and Mr. Anjum Noaman

Mirza, Branch Manager, Bank Alfalah Limited

shared their rich knowledge and experience at

the above workshop.

3. Customized Courses

Besides regular programs, IBP also holds

customized training courses tailored to meet

specific needs of banks. During October -

December 2006, the Institute held courses for

the following banks:

a) Arif Habib Rupali Bank Ltd.

6-week course on "Branch Banking

Operations" for the Trainee Officers from

October 2 - November 21, 2006 at

Karachi. 20 Officers attended the program.

b) Emirates Global Islamic Bank

5-day course on "Islamic Banking:

Principles & Products" from October 30-

November 03, 2006 at Karachi. 20 officers

attended the course.

c) First Women Bank Limited

5-day course on "Basel-II, Treasury &

Foreign Exchange" from October 30-

November 03, 2006 at Karachi. 10

executives/ officers attended the course.

d) Crescent Commercial Bank Ltd.

5-week course on "Commercial Banking"

for Operations Management Trainees

from November 06 - December 14, 2006

at Karachi & Lahore. 24 trainees - , 14 at

Karachi and 10 at Lahore attended the

program

e) National Bank of Pakistan

6-week course on "Commercial Banking"

for HR Management Trainees from

November 21 - December 30, 2006 at

Karachi. 19 Management Trainees

attended the program.

f) Habib Bank Limited

1-day course on "SBP Prudential

Regulations for Consumer & SME

Financing" on December 28, 2006 at

Karachi. 22 officers attended the program.

4. Talks/Events by Foreign Speakers

From time to time the Institute invites eminent

personalities from within the country and

abroad for sharing of knowledge and

experience with executives and officers of

banks and financial institutions in Pakistan.

During the quarter under reference, following

knowledge sharing events were held:

a) Basel - II: Issues & Challenges

Considering heavy operational duties of

the bank executives, IBP arranged a

Business Breakfast meeting with Mr.

Bambang Moerwanto, a senior specialist of

SAP Malaysia on the subject of "BASEL -II:

ISSUES & CHALLENGES" on November

23, 2006. Over 70 senior executives and

January - March 2007 Issue16

IBP – the knowledge institute

officers from banks, financial institutions

and the corporates attended the forum.

b) Powerful Presentation Skills

It was an interactive learning session on

November 06, 2006 steered by Dr. Aamir

Shamim, Senior Consultant, Life Skills

Studio, which is a public speaking and

presentation skills consultancy with its

head office in Vancouver, Canada. A

good number of account managers, sales

and marketing professionals, financial

experts, public relations executives,

instructors, trainers and others who deliver

business presentations attended this

session.

c) IBP - MIGA Knowledge Sharing Event

In association with MIGA - Multilateral

Investment Guarantee Agency of World

Bank, IBP organized a high value

knowledge sharing event on "Political Risk

Insurance Coverage" on November 11,

2006. Mr. Azhar Kureshi, Advisor to

Governor on Development Finance, State

Bank of Pakistan was the key-note

speaker. Mr. Arif Elahi, Director General,

Board of Investment who represented

Government of Pakistan. MIGA's team

comprising Mr. Srilal M. Perera, Chief

Counsel, and Mr. Hal G. Bosher,

Investment Officer, Small Investment

Program, MIGA gave presentations at the

program. The presentations were made

covering the following topics:

1. The role of MIGA's political risk

instruments to manage non-commercial

risk and facilitate project financing;

2. Case studies to show how MIGA's risk

mitigation tools have played an important

role in securing foreign direct investment in

Pakistan and other countries;

3. MIGA's new Small Investment Program

targeting smaller investors and businesses;

4. How Pakistani investors can protect

investments in Afghanistan with MIGA's

risk mitigation tools.

This was a senior level forum for

understanding the risk mitigation tools in

promoting foreign direct investment in

Pakistan and other countries as also to

explore the opportunities for taping on the

MIGA's resource. Senior level executives

from SBP and other banks attended the

event.

d) Visit of foreign delegates

During the quarter, Mr. Hans-Joachim

Kiderlen, Consul General, Consulate of the

Federal Republic of Germany visited IBP

on November 28, 2006 and had

discussions on different knowledge

endeavors. He appreciated the role of IBP

in dissemination of knowledge and

expressed the hope that partnership

between IBP and its counterpart

organizations in Germany would

materialize to serve the cause of

knowledge and friendship.

He also delivered an enlightening lecture

to the young bankers who were under

6-week training at the IBP.

5. Recruitment & Selection Process

To meet their continuous need for qualified

professionals in the fast changing and

expanding financial sector, growing number of

banks and DFI's are outsourcing their

recruitment and selection assignments to IBP

for accuracy, impartiality and swiftness of

results. IBP is presently an active partner in the

recruitment and selection of 16 banks and

other financial institutions. During the quarter

under review, recruitment tests and interviews

were conducted for the following banks:

6. IBP Website

Ever since IBP website was given a new look in

July 2006, it is becoming increasing popular

among the users worldwide. During October -

December 2006, it surpassed all time high

record of close to 9.5 million hits. Those who

visited IBP website during the quarter under

report include US Commercial, UAE, Canada,

U.K., Saudi Arabia, France, Ireland,

January - March 2007 Issue 17

IBP – the knowledge institute

Singapore, Egypt, Switzerland, Italy, Jordan,

Netherlands, Sri Lanka, Norway, Thailand,

Belgium, Russian Federation, Japan, Sweden,

Denmark, Australia and India besides the users

in Pakistan. The Institute updates information

on its website continuously on day-to-day

basis. Stakeholders are invited to visit our

website and favor us with their valuable

suggestions for further improvements.

7. Research & Publications

Besides its quarterly Journal and weekly

Economic Letter, IBP published the following

books during the quarter under report:

IBP is committed to improve its services which

meet the human resource and training needs of its

stakeholders. Comments and suggestions from the

stakeholders would be welcome with gratitude.

No. of Total

S. No. Banks Centers Enrolled

1. National Bank of Pakistan -

HR Management Trainees (Interviews) 1 53

2. National Bank of Pakistan -

Management Trainees(Recruitment) 5 2977

3. National Bank of Pakistan -

Management Trainees (Group Discussions) 3 309

4. National Bank of Pakistan -

Operations Management Trainees (Interviews) 3 103

5. State Bank of Pakistan - Economic Analyst (Test) 6 366

Bank-wise, qualification-wise and distinction-wise results are given below:

Bank Wise Position of Successful Candidates

Junior Associateship of IBP (JAIBP)

IBP – the knowledge institute

ISQ Examination (Winter) 2006 Result

Alhamdolilah, the second IBP Superior

Qualification (ISQ) examinations were held

from November 13 to 18, 2006 at 23 different

centres in Pakistan and abroad. The registration

received for ISQ was encouraging, both in terms

of number and qualifications. Most of the

participants were either MBAs, M. Coms, MAs,

CAs, ICMAs, or even B.E.s. Thus ISQ has been

professed as a professional qualification

equivalent to or even to some extent above the

Masters degree.

Since its launching in January 2006, IBP

Superior Qualification (ISQ) has received

greater acceptability among the professionals

from banks, financial institutions and the

corporates. Based on ideally designed syllabi,

the qualification is being recognized and

appreciated and rightly termed as a true value-

based knowledge endeavor.

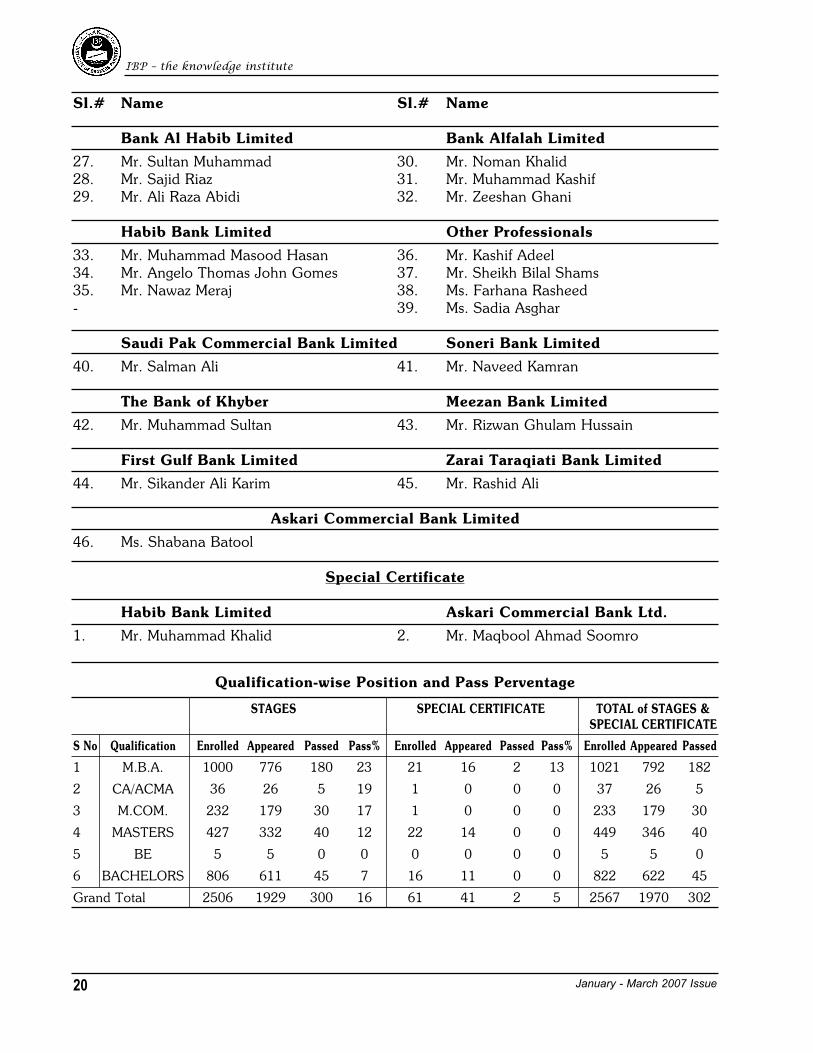

Over 2566 candidates were listed in fifteen

subjects of Junior Associateship of IBP (JAIBP)

and five subjects of Special Certificate. The

aggregate pass percentage was 16%. Forty-

Sixty professionals completed all the requisite

subjects of JAIBP and are eligible to join the

celebrated family of JAIBP/DAIBP.

Sl.# Name Sl.# Name

State Bank of Pakistan

1. Ms. Quratul Ain Javid 2. Mr. Sher Afgan Malik

3. Mr. Shaukat Ali -

National Bank of Pakistan

4. Mr. Imtiaz Ahmed Shaikh 5. Mr. Farhan Abbas Zaidi

6. Mr. Wasim Ahmad 7. Ms. Fareeha Khalil

8. Mr. Shahzad Iqbal 9. Ms. Razia Nazir

10. Mr. Rana Masood Ahmed 11. Mr. Muhammad Ali Qamar

12. Mr. Rashid Ata 13. Mr. Adnan Manzoor

14. Mr. Nadeem Rashid 15. Mr. Jawaid Ahmed Shaikh

16. Mr. Salman Rafiq 17. Ms. Iram Saeed

18. Mr. Muhammad Iqbal 19. Mr. Abid Umar Farooq

MCB Bank Limited

20. Mr. Javeed Ahmed 21. Mr. Najabat Ali

22. Mr. Talat Ejaz 23. Mr. Syed Zafar Hasan Naqvi

24. Mr. Abdul Hafeez 25. Ms. Hira Rasheed

26. Mr. Adil Waheed

January - March 2007 Issue 19

January - March 2007 Issue20

IBP – the knowledge institute

Sl.# Name Sl.# Name

Bank Al Habib Limited Bank Alfalah Limited

27. Mr. Sultan Muhammad 30. Mr. Noman Khalid

28. Mr. Sajid Riaz 31. Mr. Muhammad Kashif

29. Mr. Ali Raza Abidi 32. Mr. Zeeshan Ghani

Habib Bank Limited Other Professionals

33. Mr. Muhammad Masood Hasan 36. Mr. Kashif Adeel

34. Mr. Angelo Thomas John Gomes 37. Mr. Sheikh Bilal Shams

35. Mr. Nawaz Meraj 38. Ms. Farhana Rasheed

- 39. Ms. Sadia Asghar

Saudi Pak Commercial Bank Limited Soneri Bank Limited

40. Mr. Salman Ali 41. Mr. Naveed Kamran

The Bank of Khyber Meezan Bank Limited

42. Mr. Muhammad Sultan 43. Mr. Rizwan Ghulam Hussain

First Gulf Bank Limited Zarai Taraqiati Bank Limited

44. Mr. Sikander Ali Karim 45. Mr. Rashid Ali

Askari Commercial Bank Limited

46. Ms. Shabana Batool

Special Certificate

Habib Bank Limited Askari Commercial Bank Ltd.

1. Mr. Muhammad Khalid 2. Mr. Maqbool Ahmad Soomro

Qualification-wise Position and Pass Perventage

STAGES SPECIAL CERTIFICATE TOTAL of STAGES &

SPECIAL CERTIFICATE

S No Qualification Enrolled Appeared Passed Pass% Enrolled Appeared Passed Pass% Enrolled Appeared Passed

1 M.B.A. 1000 776 180 23 21 16 2 13 1021 792 182

2 CA/ACMA 36 26 5 19 1 0 0 0 37 26 5

3 M.COM. 232 179 30 17 1 0 0 0 233 179 30

4 MASTERS 427 332 40 12 22 14 0 0 449 346 40

5 BE 5 5 0 0 0 0 0 0 5 5 0

6 BACHELORS 806 611 45 7 16 11 0 0 822 622 45

Grand Total 2506 1929 300 16 61 41 2 5 2567 1970 302

January - March 2007 Issue 21

IBP – the knowledge institute

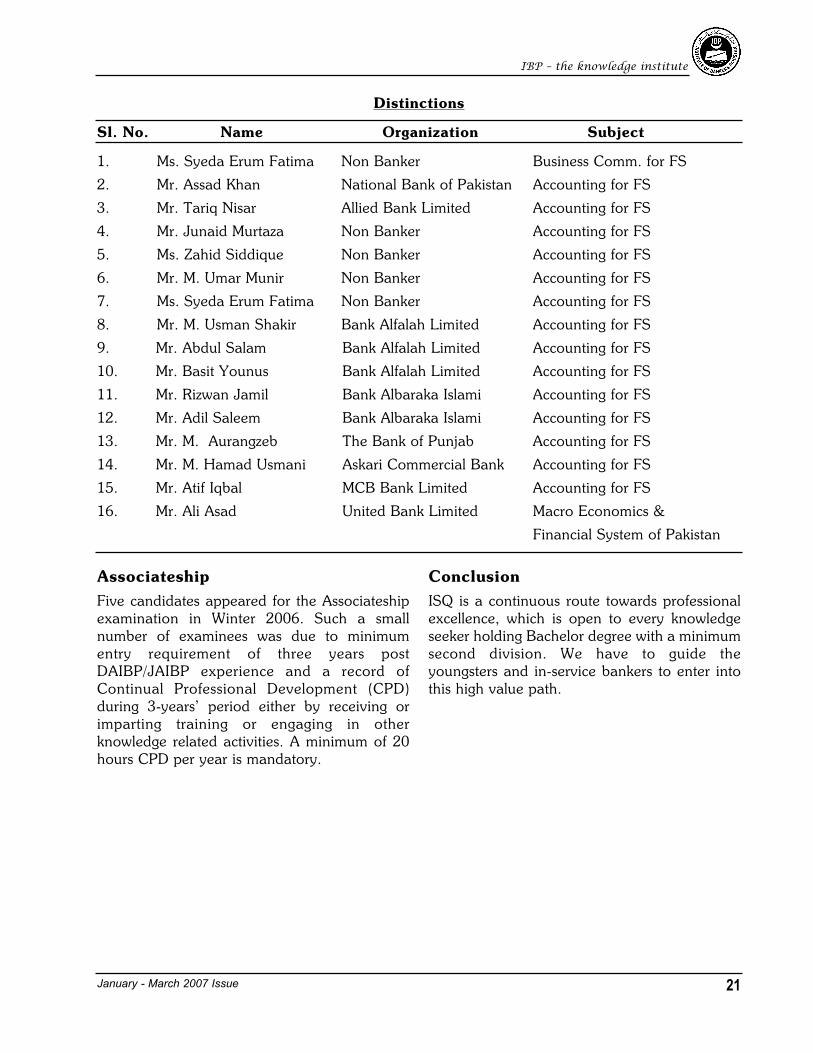

Distinctions

Sl. No. Name Organization Subject

1. Ms. Syeda Erum Fatima Non Banker Business Comm. for FS

2. Mr. Assad Khan National Bank of Pakistan Accounting for FS

3. Mr. Tariq Nisar Allied Bank Limited Accounting for FS

4. Mr. Junaid Murtaza Non Banker Accounting for FS

5. Ms. Zahid Siddique Non Banker Accounting for FS

6. Mr. M. Umar Munir Non Banker Accounting for FS

7. Ms. Syeda Erum Fatima Non Banker Accounting for FS

8. Mr. M. Usman Shakir Bank Alfalah Limited Accounting for FS

9. Mr. Abdul Salam Bank Alfalah Limited Accounting for FS

10. Mr. Basit Younus Bank Alfalah Limited Accounting for FS

11. Mr. Rizwan Jamil Bank Albaraka Islami Accounting for FS

12. Mr. Adil Saleem Bank Albaraka Islami Accounting for FS

13. Mr. M. Aurangzeb The Bank of Punjab Accounting for FS

14. Mr. M. Hamad Usmani Askari Commercial Bank Accounting for FS

15. Mr. Atif Iqbal MCB Bank Limited Accounting for FS

16. Mr. Ali Asad United Bank Limited Macro Economics &

Financial System of Pakistan

Associateship

Five candidates appeared for the Associateship

examination in Winter 2006. Such a small

number of examinees was due to minimum

entry requirement of three years post

DAIBP/JAIBP experience and a record of

Continual Professional Development (CPD)

during 3-years' period either by receiving or

imparting training or engaging in other

knowledge related activities. A minimum of 20

hours CPD per year is mandatory.

Conclusion

ISQ is a continuous route towards professional

excellence, which is open to every knowledge

seeker holding Bachelor degree with a minimum

second division. We have to guide the

youngsters and in-service bankers to enter into

this high value path.

S.No. TITLE

01 Fundamentals of Financial Management

by Chandra Prasanna.

02 Futures & Options Introduction to Equity

Derivatives by Mahajan .R.

03 Human Resource Development in

Financial Sector by Gupta K.C.

04 Investment Analysis and Portfolio

Management by Chandra Prasanna.

05 State Bank Probationary Officer's Guide

by Chopra Ravi.

06 Treasury Risk Management by Bagchi S.K.

07 An Introduction To Islamic Finance by

Usmani Muhammad Taqi.

08 Pakistan the Economy of an Elitist State by

Dr. Ishrat Hussain.

09 Issues in Pakistan's Economy by Zaidi

Akbar .S.

10 Money and Banking in Pakistan by S.A.

Meenai.

11 The Financial Services Marketing

Handbook by Ehrlich Evelyn.

12 Credit Risk Management in Banks By Jain

Arvind.

13 Practice and Law of Banking in Pakistan

by Siddiqui Asrar .H.

14 Accounting and Finance for Banks by N.P.

Agarwal.

15 Introduction to Computer by Peter Norton.

16 Services Marketing by Zeithaml .A. Valarie.

17 Interest Free Banking by Dr. Uzair

Muhammad.

18 Business Data Communication by Stallings

William.

19 Management Information Systems by

Laudon .C. Kenneth.

20 Computer Networks by Tanenbaum.

S.No. TITLE

21 Managing Human Resources by Cascio .F.

Wayne.

22 Macro Economics 9th ed by Dornbusch

Rudiger.

23 Bank Marketing by Patnaik.

24 Banking Sector Efficiency in Globalised

Economy by Kumar Parmod.

25 Credit Risk Management by Bagchi S.K.

26 Microfinance Challenges and

Opportunities by Rajagopalan .S.

27 U$ Banking Strategic Issues by Rao

Nageswara.

28 Agricultural Economics 2nd ed by

Drummond.

29 Business Communication Concepts and

Cases by Chaturvedi.

30 Marketing Management A South Asian

Perspective by Kotler Philip.

31 Total Quality Management by

Charantimath.

32 The Financial Services Marketing

Handbook by Ehrlich Evelyn.

33 Management Information Systems 2nd ed

by Davis .B. Gordon.

34 Introduction to Computers by Norton

Peter.

35 The Financial Services Marketing

Handbook by Ehrlich Evelyn.

36 Model Business Letters E-mails & Other

Business Documents by Taylor Shirley.

37 Principles of Marketing by Kotler Philip.

38 Accounting & Finance for Bankers by

Indian Institute of Banking & Finance.

39 Principles of Bankingby Indian Institute of

Banking & Finance.

40 Treasury Risk Management by Bagchi S.K.

IBP Publications - New Arrivals

January - March 2007 Issue22

IBP – the knowledge institute

IBP – the knowledge institute

Basel II Framework:The IRB Use TestImplementation

Shakil Akhtar QureshiProject ManagerFaysal Bank Ltd.

The new capital adequacy framework

commonly known as “Basel II” was finalized by

Basel Committee on Banking Supervision on June

26, 2004. The new capital allocation framework is

more risk sensitive as compared to Basel I. The

banks are required to establish a strong and

comprehensive risk management framework.

Basel II has also prescribed a strong and vigilant

role of the regulatory authorities. Further, the

accord envisages a detailed disclosure requirement

depending upon the specific approach adopted by

the institution for capital allocation to enhance

transparency and market discipline. This new

capital adequacy regime has been adopted by

State Bank of Pakistan and is applicable to all

banks and Development Financial Institutions

(DFIs) that fall under its regulatory purview.

The new framework offers Standardized

Approach (SA) and Internal Ratings Based (IRB)

Approach for assessment of capital requirements

for credit risk. The timeframe for adoption of IRB

approach is 1st January 2010 with parallel run of

two years starting from 1st January 2008. Banks /

DFIs are required to submit a quarterly statement

on the calculation of their capital adequacy ratio

based on revised regulatory capital framework

under Basel II within 30 days of the end of each

calendar quarter. During the parallel run period

banks will also calculate their Capital Adequacy

Ratio (CAR) on the basis of guidelines issued vide

BSD Circular No. 12 dated 25th August, 2004 and

submit the results of both the calculations on

quarterly basis.

Basel II Framework emphasizes that “Internal

ratings and default and loss estimates must play an

essential role in the credit approval, risk

management, internal capital allocation and

corporate governance functions of banks using the

IRB approach. Rating systems and estimates

designed and implemented exclusively for the

purpose of qualifying for the IRB approach and

used only to provide IRB inputs are not

acceptable. It is recognized that banks will not

necessarily be using exactly the same estimates for

both IRB and all internal purposes. For example,

pricing models are likely to use PDs and LGDs

relevant to the life of the asset. Where there are

such differences, a bank must document them and

demonstrate their reasonableness to their

regulator.”

This paper attempts to clarify expectations for

the use of IRB components and risk estimates for

internal purposes. It expounds a number of

principles that are anticipated to support banks

and regulators in interpreting the key use test

provisions of the Basel II Framework.

Background of the Use Test

The use test pertains to the internal

employment by a bank of the borrower and/or

facility ratings, retail segmentation and estimates of

PD, EAD and LGD that the Basel II Framework

expects banks to use for the calculation of

regulatory capital, hereinafter collectively referred

to as “IRB components”. While the second

consultative paper on the new framework

contained detailed and prescriptive language on

the internal use of IRB components, the Basel II

text (paragraph 444) is more principle based.

The IRB use test is based on the perception

that regulators can take additional comfort in the

IRB components where such components “play a

vital role” in how banks measure and manage risk

in their businesses. If the IRB components are

exclusively used for regulatory capital purposes,

there could be incentives to minimize capital

requirements rather than generate accurate

measurement of the IRB components and the

January - March 2007 Issue 23

resultant capital requirement. Moreover, if IRB

components were used for regulatory purposes

only, banks would have fewer internal incentives

to keep them accurate and up-to-date, whereas the

employment of IRB components in internal

decision-making creates an automatic incentive to

ensure sufficient quality and adequate robustness

of the systems that produce such data.

Use of IRB Components

In general, there are three main areas where

the use of IRB components for internal risk

management purposes should be observable:

strategy and planning processes, credit exposure

management, and reporting. Uses in any of these

areas provide evidence of internal use of IRB

components. If IRB components are not used in

any of these areas, the regulator may require an

explanation for such non-use, or may raise

concerns about the quality of the IRB components.

In many instances, regulators will need to exercise

considerable judgment in assessing the use of IRB

components.

Strategy and planning processes cover all

activities related to a bank specifying its objectives;

developing its policies and the plans to achieve

these objectives; and allocating resources to

implement these plans. IRB components may be

used in assessment and allocation of economic

capital; credit risk strategy; and decisions about

acquisitions, new business lines/products, capacity

and expansions.

Credit exposure measurement and

management covers all activities related to

management and control of the credit risk that a

bank takes as a consequence of implementing its

strategies. IRB components may be used in credit

portfolio management; credit approval, review and

monitoring; performance assessment /

remuneration; pricing; individual / portfolio limit

setting; provisioning; and retail segmentation.

Reporting refers to the information flow from

credit exposure measurement and management to

other functions of the organization. Reporting is a

necessary component of defining a bank's strategic

goals. IRB components may be used in credit

portfolio reporting; credit portfolio analysis; and

other credit risk information.

Principles

The following principles are designed with the

objective of supporting banks and regulators in

interpreting stipulations of the Basel II Framework.

1. Banks are responsible for demonstrating

their compliance with the use test

AIG validation principle 2, as set forth in

“Update on work of the Accord Implementation

Group (AIG) related to validation under the Basel

II Framework”, emphasizes that banks have the

responsibility for validating their rating system and

associated IRB parameter estimates. The use test is

no exception to this principle. Banks are

responsible for complying with the use test

requirement and for demonstrating compliance by

providing relevant documentation and evidence of

use of IRB components.

Banks should demonstrate to their regulators

the processes where IRB components play an

essential role and provide the relevant supporting

evidence for compliance with the use test. Banks

should illustrate how these internal uses confirm

management's belief in the validity of the IRB

components and contribute towards meeting the

use test objectives. Banks should clarify whether

the IRB components are used directly in risk

management processes, or whether they are used

in a derived form or in a partial way. Banks should

also demonstrate how risk management processes

support the accuracy, robustness and timeliness of

the IRB components.

Banks and regulators may rely on existing

internal documentation for the purpose of

demonstrating use test compliance. To a large

extent, the obligations implied by this principle will

be met through normal documentation of the

banks' overall validation and governance

frameworks and internal operating processes.

January - March 2007 Issue24

IBP – the knowledge institute

2. Internal use of IRB components should

be sufficiently material to result in

continuous pressure on the quality of

IRB components.

To make the use of the IRB approach credible,

IRB components should be entrenched in the

bank's internal risk management processes. While

IRB components should play an essential role in

risk management and decision-making, this does

not necessarily mean an exclusive or primary role

in all relevant processes. In addition, as elaborated

upon in principle 3, there may be differences

between the internal risk measures used for risk

management and the IRB components.

One of the aims of the use test is to promote

adequate and appropriate incentives internal to

banks so that the banks have a strong belief and

interest in the accuracy of their IRB components

and the quality of the processes that generate

those components. The following are examples of

situations where a lack of quality in the IRB

components or their underlying processes may

give rise to regulatory concern:

* the IRB components are calculated solely for

regulatory purposes with little or no internal

incentives for ensuring the quality of those

components;

* a deterioration in the accuracy, robustness,

and timeliness of the IRB components is

unlikely to be picked up by the bank's internal

processes;

* the IRB components are based on insufficient

or lower quality data relative to what is used to

estimate internal parameters;

* the bank lacks a process for continuous

improvement of the IRB components; and

* the bank has used the Framework's flexibility

for designing an IRB rating system in a way

that produces artificially low capital

requirements inconsistent with their internal

approach to measuring credit risk.

In a bank that meets the use test, regulators

would expect to see evidence of the occurrence of

internal challenges to the accuracy, robustness,

and timeliness of IRB components resulting from

any direct or indirect employment of IRB

components along the lines stated earlier, i.e.

strategy and planning processes, credit exposure

management, and reporting.

Thus as a quality check of IRB components

and underlying processes, the use test is a

necessary supplement to the overall validation

process. It represents a very important regulatory

tool and a fundamental component of the case

that banks must put to their regulators to

demonstrate that they initially meet the IRB

minimum requirements and will continue to do so,

on an ongoing basis.

As such, the use test plays a key role in

ensuring and encouraging the accuracy,

robustness, and timeliness of a bank's IRB

components, confirms the bank's trust in those

components and allows regulators to place more

reliance on their robustness and thus on the

adequacy of regulatory capital. The evaluation of

the use test in banks' risk management processes