control-ijv (international joint venture)-performance

TRANSCRIPT

86 Nitin Pangarkar and Saul Klein

ABSTRACT

Submitted September 2003Accepted March 2004

© Journal of International MarketingVol. 12, No. 3, 2004, pp. 86–107

ISSN 1069-031X

The authors hypothesize that the exercise of control increasesthe performance of international joint ventures only whentransaction costs are high and when there are large differencesbetween partners and no prior business relationships. Usingsurvey responses and secondary data, the authors find partialsupport for a contingent control–performance relationship.

International joint ventures (IJVs) frequently entail one part-ner performing marketing functions for the other, such asproviding access to distribution channels or evaluating con-sumer needs. In so doing, IJVs raise difficult questions ofhow much control to maintain or relinquish over such activ-ities. However, the relationship between IJV performanceand the extent of control exerted by a parent remains poorlyunderstood (Geringer and Hebert 1989; Yan and Gray 2001).We shed light on this problem by investigating the relation-ship between overall decision-making control exercised by amultinational corporation (MNC) parent and IJV perform-ance from the parent’s perspective. In so doing, we drawheavily on literature from multiple disciplines, includinginternational business and strategic management.

The issue of control has been an important subject in the IJVliterature (Calantone and Zhao 2000; Lee and Beamish 1995;Parkhe 1993; Yan and Gray 2001), but studies on its impacthave been conflicting and inconclusive (Chalos and O’Con-nor 1998; Lecraw 1984; Yan and Gray 2001). We argue thatthe relationship between control and performance is contin-gent; that is, control has a positive impact on performanceonly under particular circumstances, not otherwise (Pan andChi 1999). This study is firmly grounded in transaction cost(TC) economics, in sharp contrast to the “lack of theoreticalrigor” found elsewhere (Mjoen and Tallman 1997; Yan andGray 2001).

Our focus on MNCs from Singapore, which is a newly indus-trialized country (NIC), compared with the prior literature’sfocus on MNCs from developed countries, is a differentiatingfeature of this article. There is a paucity of studies aboutMNCs from NICs, which may adopt different strategies fromthose of their counterparts in developed countries, and thestrategy–performance relationship may vary.

The Impact of Control on InternationalJoint Venture Performance: AContingency Approach

Nitin Pangarkar andSaul Klein

87International Joint Venture Performance

The literature regarding international strategies of firms thatoriginate in developing countries is rather limited (Lee andBeamish 1995; Mjoen and Tallman 1997). Several studiessuggest that strategies and styles of firms that originate inNICs may be distinct from those of firms in developed coun-tries (Calantone and Zhao 2000). For example, Korean firmsrarely have monopolistic advantages to compensate for theinherent disadvantage of their foreignness (Lee and Beamish1995). Furthermore, among joint ventures in China, overseasChinese ventures (including ones in Hong Kong, Taiwan, andSingapore) are the weakest in terms of technology (Li, Lam,and Qian 2001). Lacking a strong technological or managerialknowledge base, MNCs that originate in NICs may exertlower control over their foreign ventures (Luo 2001).

Less competent partners (e.g., MNCs from NICs) exhibit aweaker relationship between control and performance thando more competent partners (Luo, Shenkar, and Nyaw 2001).Lee and Beamish (1995) conclude that the strong ownership–control relationship observed in IJVs in developed countriesis absent in destination developing countries. They also con-clude that whereas dominant-control IJVs perform well indeveloped country contexts, shared management IJVs exhibitbetter performance in developing countries.

In the international business literature, control is considered“the process by which one entity influences, to varyingdegrees, the behavior and output of another entity throughthe use of power, authority, and a range of bureaucratic, cul-tural, and informal mechanisms (Geringer and Hebert 1989,p. 236) or “the efficient and effective management of the rela-tionship between the parent and entry entity that enables theparent to best meet [its] overall goals and objectives” (Wood-cock, Beamish, and Makino 1994, p. 262). A parent uses con-trol to ensure that the IJV’s strategies conform to its interests(Ding 1997).

It has long been recognized that a parent’s control has severalmotivations, including to align the strategy between the IJVand an organization and to manage interdependence (e.g., inthe exchange of components and finished products, inbranding and distribution channel decisions) on an ongoingbasis. Parents also use control to transfer norms, manage-ment practices, and critical knowledge effectively (Beamish1993; Ding 1997) and to influence the strategic direction ofthe IJV, such as resolving any disputes that may arise in orderto maximize return on investment (Yan and Gray 2001).Finally, parents use control to prevent possible opportunisticbehavior and expropriation of assets by a partner (Yan andGray 2001). In the case of IJVs, because the assets are locatedin a foreign country, the possibilities of a local partner’sopportunism and expropriation are greater than in a domes-

LITERATURE REVIEW

Control: Definitions andMotivations

88 Nitin Pangarkar and Saul Klein

tic context. In some emerging economies, such as China, theneed for control may be even stronger, because control might“serve as a substitute for reliable government and an estab-lished law” (Calantone and Zhao 2000, p. 4).

Early literature predicted a positive relationship between for-eign parent control and IJV performance (Franko 1971; Tom-linson 1970). Because high control reduces the possibility ofexpropriation of assets and allows for an IJV’s integrationinto overall strategy, a parent may be willing to contributecritical skills and assets (e.g., technology, management prac-tices) (Mjoen and Tallman 1997), which enhance the IJV’scompetitive position and performance (Fagre and Wells1982; Isobe, Makino, and Montgomery 2000). When host-government intervention is expected to be high (Calantoneand Zhao 2000), high control might mitigate the threat that aforeign government poses to the MNC parent’s assets (Luo,Shenkar, and Nyaw 2001).

Although some control by an MNC parent may enhance IJVperformance, too much control may be detrimental becauseit comes with additional bureaucracy, and it may deny theIJV necessary autonomy and flexibility. In the case of anMNC, excessive control may be particularly problematicbecause the MNC may not be fully aware of the nuances ofoperating in the local environment (Osland 1994). Too muchcontrol may also result in a lack of cooperation from the localpartner (Isobe, Makino, and Montgomery 2000), which iscritical when an IJV sells its output locally, particularly togovernment entities, for which the role of government offi-cials looms larger, and an understanding of the local circum-stances, culture, and politics is essential (Beamish 1985,1993).

Empirical studies of the impact of control on IJV perform-ance have reported inconsistent results (Calantone and Zhao2000). Several studies have found a positive relationship(Ding 1997; Killing 1983; Lee and Beamish 1995; Luo,Shenkar, and Nyaw 2001), and others have found no rela-tionship (Calantone and Zhao 2000 [for their Japanese sub-sample]; Kogut 1988). We believe that TC economics, whichimplies a contingent relationship, may help resolve suchinconsistencies.

As a well-established theoretical base for marketers to applywhen considering interfirm vertical relationships (Klein,Frazier, and Roth 1990), TC economics represents the theo-retical foundation of this study and our examination of hori-zontal relationships. Opportunism and bounded rationalityrepresent two key behavioral assumptions that underlie theTC perspective (Williamson 1975). Bounded rationalitymeans that all possible future contingencies cannot be fore-

The Relationship BetweenControl and Performance

THEORY AND HYPOTHESESDEVELOPMENT

89International Joint Venture Performance

seen, and contracts essentially remain incomplete. Thisproblem is further compounded by uncertainty and assetspecificity. In turn, incomplete contracts create the possibil-ity of opportunism. According to this perspective, firmschoose appropriate organizational structures to economizeon their transaction costs. When transaction costs are high,an appropriate response is to internalize transactions (makerather than buy). Although the initial focus of the TC per-spective was to explain the choice between markets andhierarchies, the focus has been extended to hybrid organiza-tional forms such as joint ventures, which fall between mar-kets and hierarchies on a continuum (Buckley and Casson1996).

The pooling of complementary skills (e.g., marketing skills,research and development expertise) is a key motivation forIJVs. However, IJVs remain mixed-motive games with simul-taneous competitive and cooperative dynamics (Hamel, Doz,and Prahalad 1989); thus, the TC perspective is highlyappropriate for analysis of IJVs. Mutual commitment ofresources in an IJV (equity and other resources) results incoalignment of incentives, thus reducing the tendency forindividual partners to engage in opportunistic behaviorbecause it would negatively affect the value of their owninvestments in the venture. The coalignment of incentivesalso makes IJVs highly adaptable, which may be especiallyuseful in uncertain environments.

Although the ex ante choice of appropriate IJV structure(e.g., distribution of equity stakes) is important, partnersmust ensure, even during the operation of the IJV, that thevalue-creation potential of the IJV is not threatened and thatthe capture of value across partners remains equitable (Tsang2000). This concern may be especially salient for MNCs,compared with local partners, because of the location of IJVsin host countries, resultant uncertainties due to physical andcultural distance, and changes in host-government policies,among other factors. To achieve their objectives, partnersneed to exert control on an ongoing basis.

In summary, firms should choose to exercise more control insituations in which they face higher transaction costs andless control in situations in which they face low transactioncosts. We now turn to contingent factors that reflect differen-tial TC situations.

In IJVs, partner differences manifest in several forms, includ-ing differences in goals (Hennart, Kim, and Zeng 1998), size(Daniels 1971), alliance experience, and management style.Partner differences are believed to influence IJV perform-ance, but previous research is inconsistent as to the form ofthis influence. Some studies have posited that joint ventures

Partner Differences as aContingency Factor

90 Nitin Pangarkar and Saul Klein

are likely to be successful when parents are comparable insophistication and size (Daniels 1971; Geringer 1988).Similar-sized partners might have similar values and controlsystems as well as similar tolerance for losses and risk(Geringer 1988). Similar size also implies that commitmentlevels may not differ across partners because the IJV is ofroughly equal importance to both (Davidson 1982). Finally,there is a possibility of exploitation and opportunism (hightransaction costs) when sizes are asymmetrical. For example,in technology exchange relationships, “partnerships arealmost always competitive in nature” (covert or otherwise)(Doz 1986, p. 32), and the larger firm, whose skills (e.g., dis-tribution networks) are less appropriable than the smallerfirm’s technology, often tries to take control of thepartnership.

Although asymmetry in parent firm sizes could undermineIJV performance because of a mismatch of strategic prioritiesand influence as well as a higher propensity toward oppor-tunistic behavior, some studies have noted that partnershipsbetween different-sized firms are increasingly prevalent(Geringer 1988; Harrigan 1988) and may be synergistic.Potential synergies arise when a local firm’s capabilities indistribution channels, promotional skills, knowledge aboutlocal business practices, and relationships (e.g., with majorbuyers, wholesalers, relevant governmental authorities) arefundamentally important for foreign companies that seekmarket position and power (Calantone and Zhao 2000;Osland 1994).

The impact of asymmetry in alliance experience across part-ners has not been widely studied. High asymmetry maydestabilize an alliance as a result of high transaction costs.The partner that has greater experience and has gone downthe learning curve and benefited from other alliance relation-ships may be able to achieve its objectives more quickly thanits partner, and the alliance may fall apart because of anextreme case of opportunism.

Partner differences in management styles, particularly withrespect to conflict and incompatible goals (Ding 1997; Hen-nart, Kim, and Zeng 1998; Yan and Gray 2001), may lead tobargaining and negotiating between partners, which slowsdown the decision-making process and adds to bureaucraticcosts (Balakrishnan and Koza 1993; Ding 1997). Partner dif-ferences in routines (Hennart, Kim, and Zeng 1998) and con-flicts over issues of product quality, exports, employeewages, or labor policy may similarly result in higher bureau-cratic costs and opportunism (Ding 1997).

In summary, partner differences may increase transactionscosts. They lead to greater uncertainty, the possibility of

91International Joint Venture Performance

opportunism, and higher bureaucratic costs as a result ofgreater bargaining and negotiating between partners. Whenan IJV is in an emerging market, the uncertainties may bemagnified by volatile environments (e.g., frequent andunpredictable changes in government policy; Child andMarkoczy 1993) and by the possibility of collusion betweenthe local partner and local government (especially when thelocal partner is a state-owned enterprise).

Most of the prior literature examines partner differences ashaving a direct effect on performance, as we have discussedpreviously. We believe that it is more appropriate to examinepartner differences as a contingency variable between con-trol and performance, where control can mitigate high trans-action costs. Such a theoretically based approach enables usto resolve the inconsistent findings in prior research. Inresolving similar contradictory findings on the impact of cul-tural distance on vertical integration, Klein and Roth (1990)find support for a contingency model based on TC econom-ics. In conditions that approach market failure (high uncer-tainty and high asset specificity), cultural distance was asso-ciated with greater integration, but this effect was absentwhen uncertainty and asset specificity were low.

A similar case can be made that control has a beneficial effecton performance only when transaction costs are high (i.e.,when partner differences are high). Thus, partner differencesact as a contingency factor that increases the complexity ofmanagement tasks and the potential for an IJV partner’sopportunistic behavior. To prevent this scenario, the exertionof greater decision-making control when partner differencesare large is an efficient response that is likely to have a posi-tive impact on IJV performance. Thus:

H1: Ceteris paribus, control has a positive effect on IJVperformance when differences between the IJV part-ners are large, but not otherwise.

Partners’ opportunistic behavior is an important source ofrisk in IJVs. Repeated ties between the same partners tend toreduce the possibility of opportunism because such behaviormay jeopardize present and future relationships (Parkhe1993). Moreover, a repeated relationship is evidence of somedegree of satisfaction with a partner. Partners that engage inrepeated alliances incur lower transaction costs and thusmay be able to avail themselves of a broader array of cooper-ative arrangements (Gulati 1995). They may also developspecific routines for cooperating with each other, therebyreducing the need to go down the learning curve in each caseand enhancing the benefits accruable to the relationship(Gulati 1995).

Prior Business RelationshipBetween Partners as aContingency Factor

92 Nitin Pangarkar and Saul Klein

In contrast, when IJV partners are new to each other, theMNC parent may be unsure of the local partner’s capability.The risks of opportunism may be significant in terms of leak-age of proprietary technology (a frequent contribution by theMNC parent), and there may be free riding on the generalreputation of the MNC or its brands (Tsang 2000). When theIJV partners have not had a prior relationship, the MNC par-ent may be better off if it exercises greater control over theIJV’s decision making in order to safeguard its interests andenhance the IJV’s performance. Thus:

H2: Ceteris paribus, control has a positive effect on IJVperformance for partners that have no prior relation-ship, but not otherwise.

The phrasing of H1 and H2 follows the traditional TCapproach in which low control reflects the default scenario.We attempt to explain why MNCs incur the costs of exercis-ing greater control by positing the existence of high transac-tion costs in the absence of such control.

We supplemented primary data collected from surveys withsecondary data on country attractiveness and risk from theGlobal Competitiveness Report (World Economic Forum2000) and the country risk service (Business EnvironmentRisk Intelligence 2000). We pretested the survey withevening MBA students (typically middle managers) in Singa-pore. The perceptions of MNC parents on IJV performanceare strongly correlated with those of the other parents(Geringer and Hebert 1991). This approach avoids manylogistical and cost barriers (Geringer and Hebert 1991) andhas been adopted widely (Calantone and Zhao 2000; Glaisterand Buckley 1998).

Dependent Variable: Performance. Different objective meas-ures have been used to assess IJV performance, includingprofitability and costs (Tomlinson 1970), survival (Franko1971; Killing 1983), and duration (Kogut 1988). Recently, ithas been recognized that objective measures of IJV perform-ance may not fully capture the complex goals that parents setfor IJVs, and several studies have introduced perceptualmeasures, such as a partner’s goal achievement (Hatfield etal. 1998) or overall satisfaction with the IJV (Beamish 1985;Killing 1983).

In the context of NIC-originated MNCs that invest in devel-oping countries, perceptual measures of performance may beadvocated. In many developing markets, MNC affiliates maybe used to source low-cost components or finished products,and purely objective measures, such as profitability (Ding1997), may be inadequate. In many emerging markets, profit,market share, and growth by themselves may also be quite

RESEARCH METHODOLOGY

Measures of Key Variables

93International Joint Venture Performance

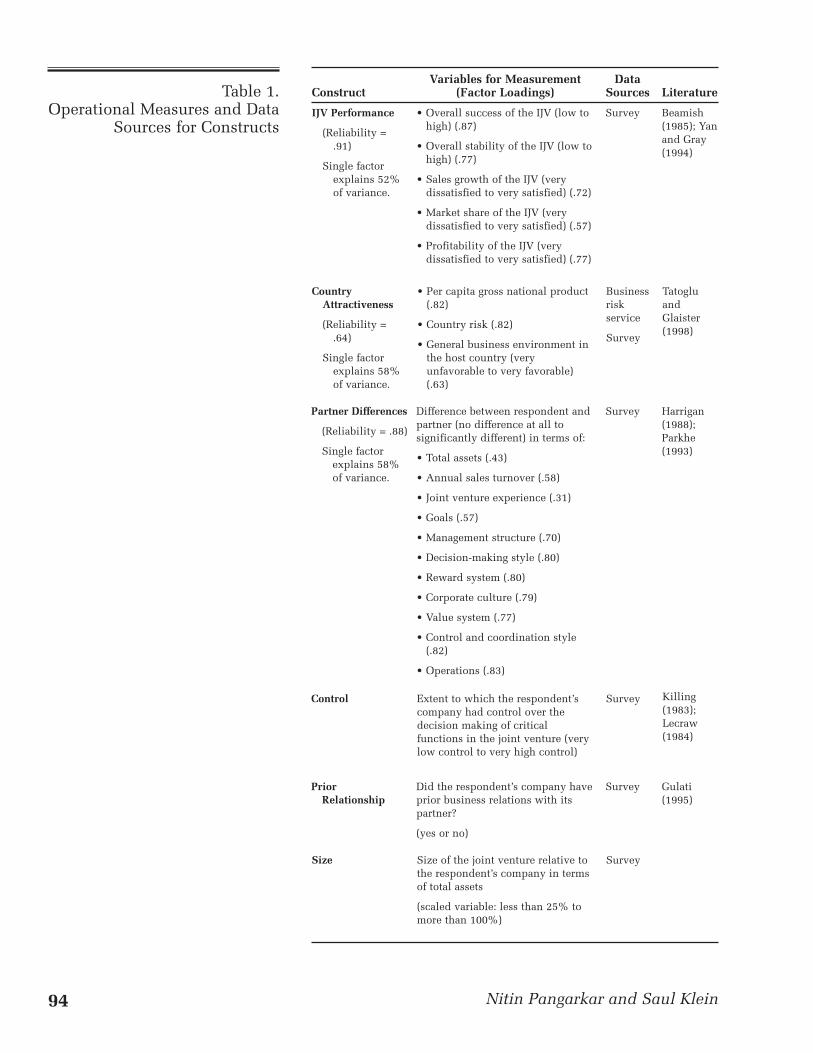

meaningless as measures of performance, at least in the shortrun (Ding 1997; Osland and Cavusgil 1996; Yan and Gray2001). Instead, we use overall satisfaction with IJV perform-ance as the key metric, with component satisfaction meas-ures that evaluate market share, sales growth, profitability,and stability of the IJV. On the basis of these items, we cre-ated a multi-item measure of performance. Table 1 identifiesthe major constructs, their operationalization, and key datasources.

Independent Variable: Control. We focus on decision-makingcontrol because it has been acknowledged as important toforeign investors that want to influence the strategic direc-tion of the IJV (Geringer and Hebert 1989). We examine theextent of such control, because it has the most direct influ-ence on IJV performance. We are not concerned with thefocus of control (particular aspects of the IJV’s operations) orthe mechanisms of control (output versus behavior), whichare likely to have an indirect (if any) impact on performance.For IJVs in emerging markets, specific outcome and behav-ioral control mechanisms may not be well developed oradvanced (Chalos and O’Connor 1998), which makes ourfocus on overall control quite appropriate. Our approach alsodiffers from those of studies that have used the percentage ofownership as a proxy, which reflects the belief that owner-ship is among the most important mechanisms of control(Killing 1983; Makino and Beamish 1999).

Parsimonious measures have often been used to identify theextent of control. For example, Yan and Gray (2001) use 1item each to assess strategic and operational control. Lecraw(1984) finds that the MNC’s percentage of equity ownershipin its subsidiary is highly correlated with effective control (acomprehensive measure that consists of 18 items) over itssubsidiary, which suggests that parsimonious measures arevalid.

Our study includes two measures of control. We used asingle-item measure of the control exerted by the MNC par-ent over strategic decisions of the IJV, which is similar to themeasures used by Luo, Shenkar, and Nyaw (2001) and Yanand Gray (2001). We also obtained information from respon-dents on their equity ownership in the venture to use as acovariate in our estimation model. In many emergingeconomies that serve as destinations for Singaporean foreigndirect investment, equity stakes may not be valid proxies forthe degree of control because local governments placerestrictions on foreign ownership (Lee and Beamish 1995;Luo 2001). Furthermore, potential partners in developingeconomies (e.g., China) view the split of ownership stakes asa signal to proceed with negotiations rather than as an endresult of negotiations (Yan and Gray 1994). An additional

94 Nitin Pangarkar and Saul Klein

Table 1.Operational Measures and Data

Sources for Constructs

Construct

IJV Performance

(Reliability =.91)

Single factorexplains 52%of variance.

Variables for Measurement(Factor Loadings)

• Overall success of the IJV (low tohigh) (.87)

• Overall stability of the IJV (low tohigh) (.77)

• Sales growth of the IJV (verydissatisfied to very satisfied) (.72)

• Market share of the IJV (verydissatisfied to very satisfied) (.57)

• Profitability of the IJV (verydissatisfied to very satisfied) (.77)

DataSources

Survey

Literature

Beamish(1985); Yanand Gray(1994)

CountryAttractiveness

(Reliability =.64)

Single factorexplains 58%of variance.

• Per capita gross national product(.82)

• Country risk (.82)

• General business environment inthe host country (veryunfavorable to very favorable)(.63)

Difference between respondent andpartner (no difference at all tosignificantly different) in terms of:

• Total assets (.43)

• Annual sales turnover (.58)

• Joint venture experience (.31)

• Goals (.57)

• Management structure (.70)

• Decision-making style (.80)

• Reward system (.80)

• Corporate culture (.79)

• Value system (.77)

• Control and coordination style(.82)

• Operations (.83)

Extent to which the respondent’scompany had control over thedecision making of criticalfunctions in the joint venture (verylow control to very high control)

Did the respondent’s company haveprior business relations with itspartner?

(yes or no)

Size of the joint venture relative tothe respondent’s company in termsof total assets

(scaled variable: less than 25% tomore than 100%)

Control

PriorRelationship

Size

Businessriskservice

Survey

Survey

Survey

Survey

Survey

Harrigan(1988);Parkhe(1993)

Killing(1983);Lecraw(1984)

Gulati(1995)

TatogluandGlaister(1998)

Partner Differences

(Reliability = .88)

Single factorexplains 58%of variance.

95International Joint Venture Performance

benefit of our including this variable as a covariate is that itis often highly correlated with the proportion of seats on anIJV’s board of directors, which is another measure for control(Chalos and O’Connor 1998).

Contingent Factors: Partner Differences and Prior Relation-ship. We measure partner differences on 11 dimensions: totalassets, annual sales turnover, joint venture experience (num-ber formed and duration), goals (mission, vision, and objec-tives), top management structure, decision-making style(participatory versus otherwise), reward system (team- ver-sus individual-based), corporate culture (bureaucratic versusflexible), value system, control and coordination style (cen-tralized versus decentralized), and operating procedures(reporting procedures, documentation, and formal planning).We asked respondents, “How different are your companyand your partner on each of the following criteria?” We alsoasked respondents whether they had a prior business rela-tionship with their partner.

We included several covariates in our analysis. We expectedeach covariate to affect IJV performance beyond and inde-pendent of the hypothesized variables.

Cultural Differences. We measured cultural differences bothas a scaled item from respondents and on the basis of Hofst-ede’s (1980) indexes of individualism/collectivism, uncer-tainty avoidance, power distance, and masculinity/feminin-ity. Cultural distance is believed to increase difficulties inmanaging IJVs (Franko 1971; Li and Guisinger 1991) becauseof higher uncertainty (Gulati 1995), different norms of behav-ior and productivity that exacerbate the difficulty of measur-ing and monitoring performance of partners as well as com-municating with them (Lane and Beamish 1990), and agreater possibility of opportunism (Gulati 1995). However,complementary approaches based on cultural differencesmay lead to greater opportunities to achieve synergies (Glais-ter and Buckley 1999). Cultural similarity is believed to bebeneficial because it facilitates knowledge sharing, which iscrucial to a successful IJV (Buckley and Casson 1996). How-ever, empirical results on the impact of cultural differenceshave been inconclusive; some studies have observed a nega-tive impact (Li and Guisinger 1991) and others a positive one(Park and Ungson 1997).

Size of the IJV. We measured size of the IJV as a scaled vari-able. The greater an IJV’s size, the greater is the likelihoodthat it will be able to attain economies of scale (Yan and Gray1994) and consequently cost reductions, which lead to betterperformance. Typically, MNC parents are more committed tolarger ventures because the expected gains are likely to be

Covariates and TheirMeasures

96 Nitin Pangarkar and Saul Klein

substantial (Luo 2001). This commitment may be reflected ingreater contributions, thus leading to better performance.

Host-Country Attractiveness. We included three differentmeasures of host-country attractiveness: per capita grossnational product, country risk, and a scaled item that meas-ures the respondent’s perception of the general businessenvironment in the host country. We drew the data for thefirst two factors from secondary sources (Business Environ-ment Risk Intelligence 2000; World Economic Forum 2000).We extracted the data for the last item from the questionnaire.

A highly attractive environment, as that in Singapore (high-quality infrastructure and business-friendly government)and China (large local market with low-factor costs), helpsforeign firms do business and earn profits. In environmentswith low political risk, firms need to expend fewer resourcesto counter government-induced discontinuities and thusachieve better performance (Child and Markoczy 1993).

In contrast, location factors, such as political instability orexchange rate volatility, negatively affect the performance ofventures. Lack of infrastructure creates uncertainties withregard to cross-border technology transfer, which in turnmay reduce resources that the foreign parent has committed(Isobe, Makino, and Montgomery 2000), thus leading tolower performance, especially if the resources from the for-eign parent (e.g., superior technology) are critical for IJV suc-cess. Prior research has found that IJV performance is lowerin high-uncertainty environments (Beamish 1985).

In all, using various directories, we identified 430 Singapore-based companies that had formed at least one equity jointventure in another country (details are available on request).Surveys were sent in late 1999, and a second mailing wassent to nonrespondents in early 2000. We sought responsesfrom firms whose IJVs were at least three years old (i.e., jointventures formed during or before 1996). We believed that itwould take approximately three years for both partners toreach a comprehensive plan for the IJV and before the IJV’sperformance could be assessed (Pan and Chi 1999; Wood-cock, Beamish, and Makino 1994).

In modeling contingent relationships, a simple multiplica-tive interaction term between control and the contingencyvariables is unsuitable. Such a term confounds some situa-tions of fit with other situations in which fit is lacking. Amoderate value of the interaction variable may result frommoderate values of control and partner differences (situationof fit) and from low control and high partner differences, orvice versa (a situation of misfit). We expect the IJV to exhibithigh performance in the first situation but not in the second.

Population and Sample

Data Handling and AnalysisTechniques

97International Joint Venture Performance

We adopted the “fit-as-matching” approach (Venkatraman1989), which involves calculating a deviation score by sub-tracting one variable from the other and then taking theabsolute value of the difference. Calculation of the fitbetween degree of control and partner differences was rela-tively straightforward because the scales for the two vari-ables are identical. For the prior relationship variable, weconverted the control variable to an equivalent scale beforewe calculated the absolute difference as an index of fit.

Two special cases required additional data handling. First,for the country attractiveness variable, we standardized allcomponent variables (mean = 0, standard deviation = 1) toaddress the issue of different scales. Second, we calculatedcultural distance on the basis of Hofstede’s (1980) scores andKogut and Singh’s (1988) formula.

For data analysis, we used a combination of factor analysis,reliability assessment, and ordinary least squares regression.We also examined collinearity diagnostics to rule out thepossibility of coefficients being affected by correlationsbetween independent variables.

Of the 430 companies in the population, we dropped 42 as aresult of liquidation, wrong contact details, or an erroneouslisting in one or more of the source directories. Of theremaining 388 companies, we received 76 valid responses(20%). This response rate is slightly better than that in otherstudies of emerging markets (e.g., Ding 1997; Isobe, Makino,and Montgomery 2000). Many companies in Singapore aresmall and medium-sized and are rather secretive about theirstrategies. Several are also privately held and thus reluctantto provide information.

However, source directories did not include any detailsabout company sales or number of employees. To address theissue of nonresponse bias, we assumed that the companies inthe sampling frame were roughly similar to the (451) compa-nies in the Singapore 1000 listing for 1999–2000 (DP Infor-mation Network 1999/2000), which is a reasonable assump-tion because larger companies are most likely to form IJVs.1Our comparison of distribution of firms by size led to aninsignificant (5%) statistic, which implies a low likelihoodof nonresponse bias.

The median parent employed between 51 and 199 employ-ees and had sales of S$10 to S$50 million (US$5.9 million toUS$24 million, at a rate of S$1.7 = US$1). A slightly largerproportion of parents (55%) were involved in services thanin manufacturing. The service MNCs operated in sectorssuch as transportation, communications, property develop-ment, and construction. Most of the manufacturing firms

RESULTS AND DISCUSSION

98 Nitin Pangarkar and Saul Klein

were involved in low-technology sectors (e.g., paper andprinting, plastic products), and only a few were involved inhigh-technology products (e.g., electrical and electronicproducts).

The most common destination among the 76 companies wasChina (35 IJVs = 46% of the sample). Singaporean MNCs maybe attracted to China because of its large market size and lowfactor costs and because of cultural affinity. The next mostfrequent destination was Malaysia, which had 10 IJVs (13%).Twelve other countries were represented in the sample, andeach had at least 1 IJV. Only 5 of the IJVs in our sample werelocated in developed countries (1 each in the United Statesand the Netherlands and 3 in Australia). In developing coun-tries, Singaporean MNCs may be more confident about com-peting with other firms. Their relative comfort in handlingan uncertain environmental context (Lee and Beamish 1995)might be the equalizer in overcoming their relative weaknessin technology or management skills.

The most frequent IJV structure (33%) involved a Singa-porean company taking an equity stake of between 60% and79.9%, and 59% of the IJVs were majority owned. In con-trast, Killing (1983) finds that equal ownership is most com-mon in IJVs in developed countries, and Reynolds (1979)finds that most foreign firms have a minority equity positionin IJVs in developing countries. The timing of data collectionmay be an important factor in explaining the uniqueness ofour results. By the time we collected the data, most develop-ing countries (e.g., Vietnam, China) had become more opento foreign investments and foreign ownership of IJVs. Therelative inexperience of Singaporean MNCs may be anotherfactor that causes them to seek higher-equity ownership.

The bivariate correlation coefficient between equity ownedby the MNC parent and the overall control it exerted is .174(p > .10), in support of the arguments we advanced previ-ously that equity ownership is a poor proxy for the extent ofcontrol that the MNC parent exerts. Several prior studieshave observed similar results (e.g., Beamish 1985). However,Lee and Beamish (1995) find a strong, positive correlationbetween ownership and control for their sample of IJVsformed by Korean firms.

All five performance items loaded heavily on a single factor,which accounts for 52% of the variance. A simple additivemeasure has a high reliability coefficient (Cronbach’s alpha =.91) (see Table 1). On a seven-point scale, the composite vari-able has an average value of 4.2, which suggests that IJVs aremoderately successful. Prior literature has observed thatmany IJVs in developing countries suffer from unsatisfactoryperformance (e.g., Andersen Consulting 1995; Beamish

Performance of IJVs

99International Joint Venture Performance

1985). Despite locating most of their IJVs in developingcountries, Singaporean MNCs do not appear to suffer thisfate.

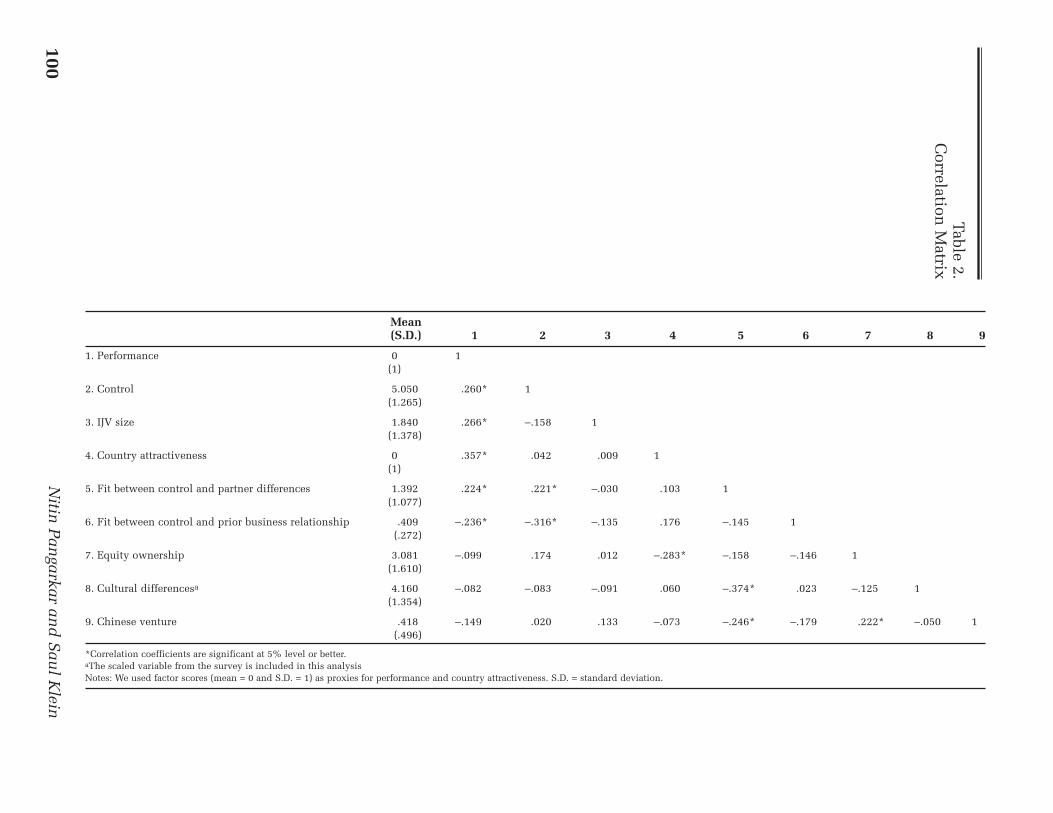

All partner differences items also loaded on a single factor,which explains 58% of the variance (Cronbach’s alpha = .88).The three items for host-country attractiveness loaded on asingle factor, which explains 58% of the variance. The com-posite variable has a reliability of .64, which we judged to beadequate for a covariate. Table 2 shows the correlation matrixfor all variables we included in the analysis and indicates nosignificant problems of multicollinearity.

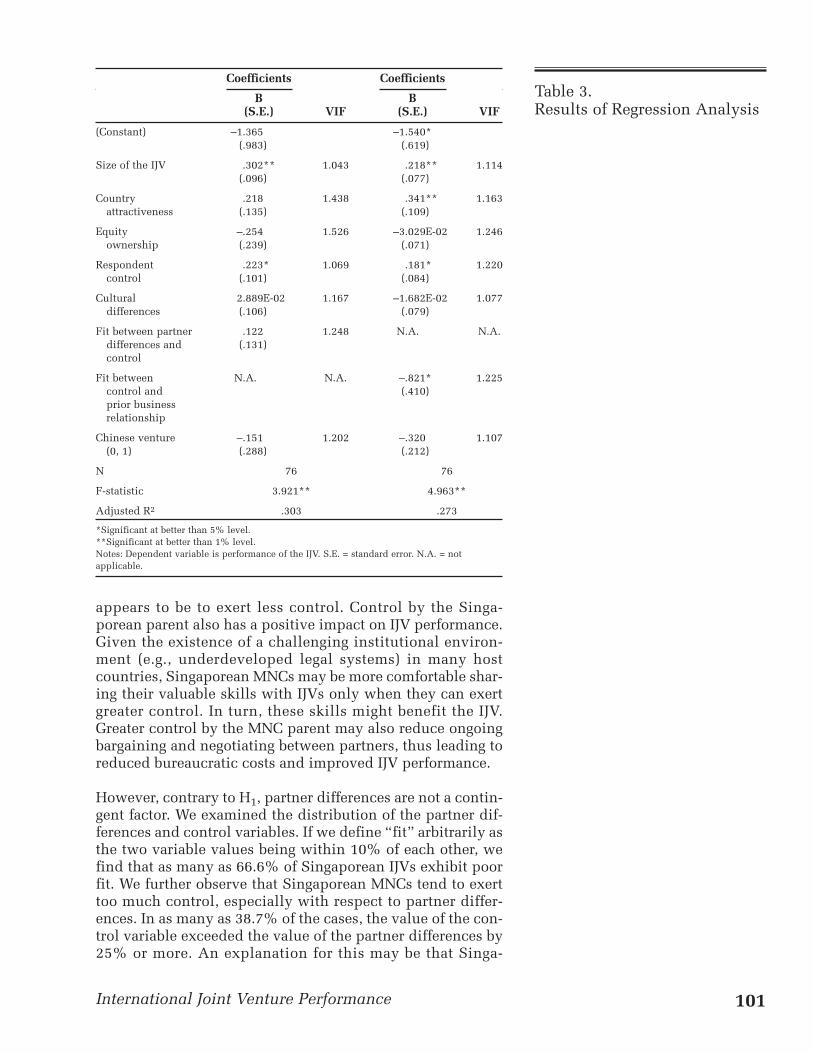

The regression analyses (see Table 3) provide tests of H1 andH2. Despite their parsimony, our models performed quitewell. The F-statistics are highly significant, with adjusted R2

values in the range of 27.3% to 30.3%. We consider none ofthe variance inflation factors (VIFs) large enough to raiseconcerns about collinearity.

The coefficient for the fit between partner differences andMNC control is insignificant, which indicates no support forH1. However, the fit between prior business relationship andthe control variable has a significant coefficient, which indi-cates strong support for H2 and validates the notion of a con-tingent control–performance relationship.

The coefficients for MNC parent control are significant andpositive in both regressions, which suggests that controlindeed has a positive relationship to IJV performance. Thisfinding is similar to that of Lee and Beamish (1995), whoconclude that control is an important factor in determiningthe performance of IJVs formed by Korean MNCs. Severalother studies have found a significant and positive relation-ship (Ding 1997; Killing 1983; Lecraw 1984; Lee andBeamish 1995; Luo, Shenkar, and Nyaw 2001), and ourresults add to this literature.

In terms of covariates, we found country attractiveness tohave a strong, positive impact on IJV performance in oneregression equation, and it approached the 10% level of sig-nificance in the other regression. We found IJV size to have astrong, positive impact in both regression equations. Neithermeasure of cultural distance (scaled or distance) emerged assignificant in the regression analysis, which is consistentwith prior studies (e.g., Glaister and Buckley 1999). Equityownership also was not significant.

Consistent with H2, greater control by the MNC parent has abeneficial impact on IJV performance only when the partnershave no prior business relationship. When partners have hada prior relationship, the appropriate strategy for the MNC

100N

itin P

angarkar an

d S

aul K

lein

Mean(S.D.) 1 2 3 4 5 6 7 8 9

1. Performance 0 1(1)

2. Control 5.050 .260* 1(1.265)

3. IJV size 1.840 .266* –.158 1(1.378)

4. Country attractiveness 0 .357* .042 .009 1(1)

5. Fit between control and partner differences 1.392 .224* .221* –.030 .103 1(1.077)

6. Fit between control and prior business relationship .409 –.236* –.316* –.135 .176 –.145 1(.272)

7. Equity ownership 3.081 –.099 .174 .012 –.283* –.158 –.146 1(1.610)

8. Cultural differencesa 4.160 –.082 –.083 –.091 .060 –.374* .023 –.125 1(1.354)

9. Chinese venture .418 –.149 .020 .133 –.073 –.246* –.179 .222* –.050 1(.496)

*Correlation coefficients are significant at 5% level or better.aThe scaled variable from the survey is included in this analysisNotes: We used factor scores (mean = 0 and S.D. = 1) as proxies for performance and country attractiveness. S.D. = standard deviation.

Table 2.C

orrelation M

atrix

101International Joint Venture Performance

appears to be to exert less control. Control by the Singa-porean parent also has a positive impact on IJV performance.Given the existence of a challenging institutional environ-ment (e.g., underdeveloped legal systems) in many hostcountries, Singaporean MNCs may be more comfortable shar-ing their valuable skills with IJVs only when they can exertgreater control. In turn, these skills might benefit the IJV.Greater control by the MNC parent may also reduce ongoingbargaining and negotiating between partners, thus leading toreduced bureaucratic costs and improved IJV performance.

However, contrary to H1, partner differences are not a contin-gent factor. We examined the distribution of the partner dif-ferences and control variables. If we define “fit” arbitrarily asthe two variable values being within 10% of each other, wefind that as many as 66.6% of Singaporean IJVs exhibit poorfit. We further observe that Singaporean MNCs tend to exerttoo much control, especially with respect to partner differ-ences. In as many as 38.7% of the cases, the value of the con-trol variable exceeded the value of the partner differences by25% or more. An explanation for this may be that Singa-

Coefficients Coefficients

B B(S.E.) VIF (S.E.) VIF

(Constant) –1.365 –1.540*(.983) (.619)

Size of the IJV .302** 1.043 .218** 1.114(.096) (.077)

Country .218 1.438 .341** 1.163attractiveness (.135) (.109)

Equity –.254 1.526 –3.029E-02 1.246ownership (.239) (.071)

Respondent .223* 1.069 .181* 1.220control (.101) (.084)

Cultural 2.889E-02 1.167 –1.682E-02 1.077differences (.106) (.079)

Fit between partner .122 1.248 N.A. N.A.differences and (.131)control

Fit between N.A. N.A. –.821* 1.225control and (.410)prior business relationship

Chinese venture –.151 1.202 –.320 1.107(0, 1) (.288) (.212)

N 76 76

F-statistic 3.921** 4.963**

Adjusted R2 .303 .273

*Significant at better than 5% level.**Significant at better than 1% level.Notes: Dependent variable is performance of the IJV. S.E. = standard error. N.A. = notapplicable.

Table 3.Results of Regression Analysis

102 Nitin Pangarkar and Saul Klein

porean firms are novices at foreign investment (Pangarkarand Lim 2003). Much of Singapore’s foreign investment hasoccurred since 1994, when the government exhorted localcompanies to develop an external wing to the economy. Asnewcomers to foreign investment and to IJVs, SingaporeanMNCs may tend to exert too much control over their IJVs,even when partner differences are low, thus confounding theexpected relationship.

We also speculate on why there is a contingent relationshipfor prior relationships but not for partner differences. Theformer might increase comfort levels significantly, even fornovice foreign investors, thus leading to less control of theIJV. In contrast, low partner differences probably do notincrease the comfort level of Singaporean MNCs sufficientlyfor them to exert lower control.

We believe that the contingency approach adopted in thisstudy holds promise for further research on the relationshipbetween international strategies and performance, such asbetween global integration of an IJV and its performance. Ahigh degree of global integration could help an IJV in onlyparticular conditions, such as in a stable local environmentor when there is trust between the partners. With a fewexceptions, the prior literature has ignored contingent factorsand arrived at inconclusive results.

Some scholars have argued that opportunism, which is a keyassumption in TC theory, may be mitigated by trust, which isa key trait of many cultures, including those of Japan andChina (Ouchi 1980). It has been argued that in such cultures,firms may not resort to hierarchy-like structures even in thepresence of high transaction costs. In contrast, our study sug-gests that the TC perspective may be equally applicable indeveloping countries. Luo (2001) also provides some evi-dence on the applicability of the TC framework by examin-ing organizational choices in China. However, Luo’s studyfocuses on the choices made by developed country MNCsthat operate in a high-trust emerging market (China). We gofurther by examining the choices of firms based in a high-trust society (Singapore) that invest in destinations also char-acterized by high trust.

As a key decision, MNC managers must judiciously choosethe level of control that they exert on an IJV. Contrary to thedesires of many managers, control is not always beneficial,and it requires sound judgment to know when to back off.Because control has costs associated with it, control shouldbe exercised only when the benefits that accrue from itexceed the inherent costs. When transaction costs are low,managers may be better off by allowing their foreign venturesmore autonomy.

IMPLICATIONS, LIMITATIONS,AND DIRECTIONS FORFURTHER RESEARCH

103International Joint Venture Performance

Our analysis also suggests that it is possible to attain goodperformance even in emerging economies. Managers neednot be disheartened by prior reports of lack of profitabilityfor IJVs formed in emerging countries (Andersen Consulting1995), which may be attributable to long learning periods.However, they may need to define performance on a broaderbasis than stand-alone profitability. The size of IJVs is a criti-cal determinant of their performance, possibly because ofscale economies, and greater commitment and/or contribu-tions from the MNC parent. Thus, MNCs should focus onforming fewer, larger subsidiaries in the most attractive loca-tions rather than spreading their resources over a wide rangeof markets.

In terms of limitations, we were constrained by a relativelysmall sample, which limited the type of analysis that wecould undertake. As is true for most survey research, there isalso a possible problem of survival bias in our sample and apossible distortion of descriptive results. However, weremain confident of the validity of our findings on the con-tingent nature of the control–performance relationship. Ourresults may also be specific to their context, because givenSingapore’s limitations regarding landmass, population, andindigenous technology base, it is a somewhat unique homeground for MNCs. We did not have data on all contextual andstrategy aspects (e.g., experience of the MNC, overall globalstrategy of the MNC parent), which also might have shedadditional light on the core phenomenon of interest.

Further empirical research is needed on determinants of IJVperformance, especially for those that originate in NICs.Larger samples would allow for performance comparisonsacross industries and destination countries. Further researchcould examine whether integration into a parent’s overallglobal strategy has a significant impact on performance.Finally, the impact of partner characteristics could beexplored in greater depth by incorporating factors such asthe foreign parent’s prior experience at being a multinationalor experience in the host country and the local parent’s priorexperience with IJVs.

1. The Singapore 1000 listing is published by DP InformationNetwork (1999/2000) and has been published since 1990.It covers the Singapore operations of foreign firms.

Andersen Consulting (1995), Moving China Ventures out of the Redinto the Black: Insights from Best and Worst Performers. London:The Economist Intelligence Unit.

Balakrishnan, Srinivasan and Mitchell P. Koza (1993), “Informa-tion Asymmetry, Adverse Selection, and Joint Ventures,” Journalof Economic Behavior and Organization, 20 (1), 99–117.

NOTE

REFERENCES

104 Nitin Pangarkar and Saul Klein

Beamish, Paul W. (1985), “The Characteristics of Joint Ventures inDeveloped and Developing Countries,” Columbia Journal ofWorld Business, 29 (Winter), 13–19.

——— (1993), “Characteristics of Joint Ventures in the People’sRepublic of China,” Journal of International Marketing, 1 (1), 29–48.

Buckley, Peter J. and Mark C. Casson (1996), “An Economic Modelof International Joint Venture Development,” Journal of Interna-tional Business Studies, 27 (5), 849–76.

Business Environment Risk Intelligence (2000), (accessed October2000), [available at http://www.beri.com].

Calantone, Roger J. and Yushan Sam Zhao (2000), “Joint Venturesin China: A Comparative Study of Japanese, Korean, and U.S.Partners,” Journal of International Marketing, 10 (4), 53–77.

Chalos, Peter and Neal G. O’Connor (1998), “Management Controlsin Sino-American Joint Ventures: A Comparative Case Study,”Managerial Finance, 24 (5), 53–72.

Child, John and L. Markoczy (1993), “Host-Country ManagerialBehavior and Learning in Chinese and Hungarian Joint Ven-tures,” Journal of Management Studies, 30 (4), 611–31.

Daniels, J.D. (1971), Recent Foreign Direct Manufacturing Invest-ment in the United States. New York: Praeger.

Davidson, William H. (1982), Global Strategic Management. NewYork: John Wiley & Sons.

Ding, Daniel Z. (1997), “Control, Conflict, and Performance: AStudy of U.S.–Chinese Joint Ventures,” Journal of InternationalMarketing, 5 (3), 31–45.

Doz, Yves (1986), “Technology Partnerships Between Larger andSmaller Firms: Some Critical Issues,” International Studies ofManagement and Organization, 17 (4), 31–57.

DP Information Network (1999/2000), “Singapore 1000.” CD-ROM.

Fagre, Nathan and Louis T. Wells (1982), “Bargaining Power ofMultinationals,” Journal of International Business Studies, 13(3), 9–24.

Franko, L.G. (1971), Joint Venture Survival in Multinational Corpo-rations. New York: Praeger.

Geringer, J.M. (1988), Joint Venture Partner Selection: Strategies forDeveloped Countries. Westport, CT: Quorum Books.

——— and L. Hebert (1989), “Control and Performance of Interna-tional Joint Ventures,” Journal of International Business Studies,20 (2), 235–54.

——— and ——— (1991), “Measuring Performance of InternationalJoint Ventures,” Journal of International Business Studies, 22 (2),249–63.

Glaister Keith W. and Peter J. Buckley (1998), “Measures of Perfor-mance in U.K. International Alliances,” Organization Studies, 19(1), 89–118.

——— and ——— (1999), “Performance Relationships in U.K.International Alliances,” Management International Review, 39(2), 1223–47.

THE AUTHORS

Nitin Pangarkar is AssociateProfessor of Corporate Strategy,

School of Business, NationalUniversity of Singapore (e-mail:

Saul Klein is LansdowneProfessor of International

Business, Faculty of Business,University of Victoria (e-mail:

ACKNOWLEDGMENTSThe authors thank the three

anonymous JIM reviewers for theirinsightful comments and

constructive reviews of previousdrafts of this article.

105International Joint Venture Performance

Gulati, R. (1995), “Does Familiarity Breed Trust? The Implicationsof Repeated Ties for Contractual Choice in Alliances,” Academyof Management Journal, 38 (1), 85–112.

Hamel, Gary, Yves Doz, and C.K. Prahalad (1989), “Collaboratewith Your Competitors and Win,” Harvard Business Review, 67(1), 133–39.

Harrigan, Katherine R. (1988), “Joint Ventures and CompetitiveStrategy,” Strategic Management Journal, 9 (2), 141–58.

Hatfield, Louise, John A. Pearce III, Randall G. Sleeth, and MichaelW. Pitts (1998), “Toward Validation of Partner Goal Achievementas a Measure of Joint Venture Performance,” Journal of Manager-ial Issues, 10 (3), 355–72.

Hennart, J.F., D.J. Kim, and M. Zeng (1998), “The Impact of JointVenture Status on the Longevity of Japanese Stakes in US Manu-facturing Alliances,” Organization Science, 9 (3), 382–95.

Hofstede, Geert (1980), Culture’s Consequences: International Dif-ferences in Work-Related Values. Thousand Oaks, CA: SagePublications.

Isobe, Takehiko, Shige Makino, and David B. Montgomery (2000),“Resource Commitment, Entry Timing, and Market Performanceof Foreign Direct Investments in Emerging Economies: The Caseof Japanese International Joint Ventures in China,” Academy ofManagement Journal, 43 (3), 468–84.

Killing, J.P. (1983), Strategies for Joint Venture Success. New York:Praeger.

Klein, Saul, Gary Frazier, and Victor J. Roth (1990), “A TransactionCost Analysis Model of Channel Integration in International Mar-kets,” Journal of Marketing Research, 27 (May), 196–208.

——— and Victor J. Roth (1990), “Determinants of Export ChannelStructure: The Effects of Experience and Psychic DistanceReconsidered,” International Marketing Review, 7 (5), 27–39.

Kogut, Bruce (1988), “A Study of the Life Cycle of Joint Ventures,”in Cooperative Strategies in International Business, F.J. Contrac-tor and P. Lorange, eds. Lexington, MA: Lexington Books, 169–86.

——— and H. Singh (1988), “The Effect of National Culture on theChoice of Entry Mode,” Journal of International Business Stud-ies, 19 (Fall), 411–32.

Lane H.W. and Paul W. Beamish (1990), “Cross-Cultural Coopera-tive Behavior in Joint Ventures in LDCs,” Management Interna-tional Review, 30 (Special Issue), 87–102.

Lecraw, Donald J. (1984), “Bargaining Power, Ownership, and Prof-itability of Transnational Corporations in Developing Countries,”Journal of International Business Studies, 16 (3), 37–43.

Lee, Chol and Paul W. Beamish (1995), “The Characteristics andPerformance of Korean Joint Ventures in LDCs,” Journal of Inter-national Business Studies, 26 (3), 637–54.

Li, Jiatao and Steven Guisinger (1991), “Comparative BusinessFailures of Foreign-Controlled Firms in the United States,” Jour-nal of International Business Studies, 22 (2), 209–224.

106 Nitin Pangarkar and Saul Klein

———, Kevin Lam, and Gongming Qian (2001), “Does CultureAffect Behavior and the Performance of Firms? The Case of JointVentures in China,” Journal of International Business Studies, 32(1), 115–31.

Luo, Yadong (2001), “Determinants of Entry in an Emerging Econ-omy: A Multilevel Approach,” Journal of International BusinessStudies, 38 (3), 443–73.

———, Oded Shenkar, and Mee-Kau Nyaw (2001), “A Dual ParentPerspective on Control and Performance in International JointVentures: Lessons from a Developing Economy,” Journal of Inter-national Business Studies, 32 (1), 41–58.

Makino, Shige and Paul W. Beamish (1999), “Matching Strategywith Ownership Structure: Japanese Joint Ventures in Asia,”Academy of Management Executive, 13 (4), 17–26.

Mjoen H. and S. Tallman (1997), “Control and Performance inInternational Joint Ventures,” Organization Science, 8 (3), 257–74.

Osland, Gregory E. (1994), “Successful Operating Strategies in thePerformance of U.S.–China Joint Ventures,” Journal of Interna-tional Marketing, 2 (4), 53–78.

——— and S. Tamer Cavusgil (1996), “Performance Issues in U.S.-China Joint Ventures,” California Management Review, 38 (2),106–30.

Ouchi, William G. (1980), “Markets, Bureaucracies, and Clans,”Administrative Science Quarterly, 25 (1), 129–42.

Pan, Yigang and Peter S.K. Chi (1999), “Financial Performance andSurvival of Multinational Corporations in China,” Strategic Man-agement Journal, 20 (4), 359–74.

Pangarkar, Nitin and Hendry Lim (2003), “Performance of ForeignDirect Investment from Singapore,” International BusinessReview, 12 (5), 601–624.

Park, H.S. and G.R. Ungson (1997), “The Effect of OrganizationalComplementarity and Economic Motivation on Joint VentureDissolution,” Academy of Management Journal, 40 (2), 279–307.

Parkhe, Arvind (1993), “Strategic Alliance Structuring: A GameTheoretic and Transaction Cost Examination of Inter-Firm Coop-eration,” Academy of Management Journal, 36 (4), 794–829.

Reynolds, John I. (1979), Indian-American Joint Ventures: BusinessPolicy Relationships. Washington, DC: University Press ofAmerica.

Tatoglu, Ekrem and Keith W. Glaister (1998), “Western MNCs’ FDIin Turkey: An Analysis of Location Specific Factors,” Manage-ment International Review, 38 (2), 133–59.

Tomlinson, J.W.C. (1970), The Joint Venture Process in Interna-tional Business: India and Pakistan. Cambridge: MassachusettsInstitute of Technology Press.

Tsang, Eric W. (2000), “Transaction Cost and Resource-BasedExplanations of Joint Ventures: A Comparison and Synthesis,”Organization Studies, 21 (1), 215–42.

107International Joint Venture Performance

Venkatraman, N. (1989), “The Concept of Fit in StatisticalResearch: Toward Verbal and Statistical Correspondence,” Acad-emy of Management Review, 14 (3), 423–44.

Williamson, O.E. (1975), Markets and Hierarchies: Analysis andAntitrust Implications. New York: The Free Press.

Woodcock, C. Patrick, Paul W. Beamish, and Shige Makino (1994),“Ownership-Based Entry Mode Strategies and International Per-formance,” Journal of International Business Studies, 25 (2),253–73.

World Economic Forum (2000), Global Competitiveness Report,1996–2000. Geneva: World Economic Forum.

Yan, A. and B. Gray (1994), “Bargaining Power, Management Con-trol, and Performance in the United States–China Joint Ventures:A Comparative Case Study,” Academy of Management Journal,37 (6), 1478–1517.

——— and ——— (2001), “Antecedents and Effects of Parent Con-trol in International Joint Ventures,” Journal of ManagementStudies, 38 (3), 393–416.