bypl-order1.pdf - delhi electricity regulatory commission

TRANSCRIPT

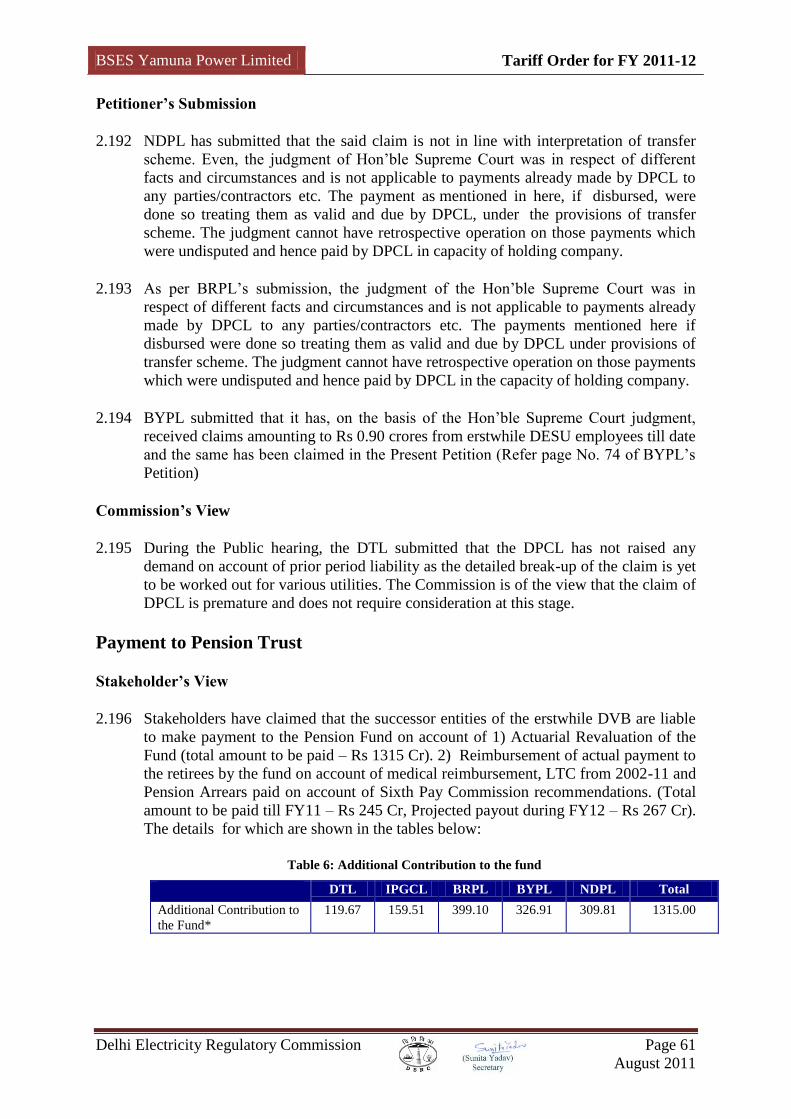

ORDER

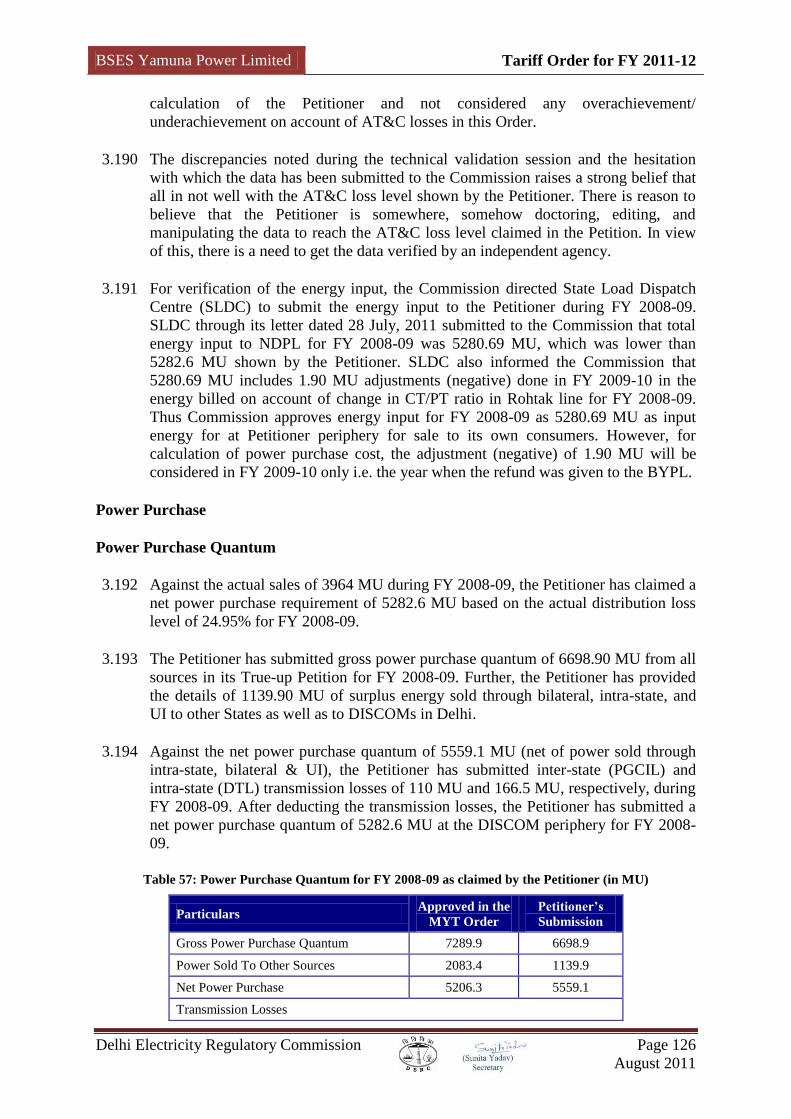

on

TRUE UP

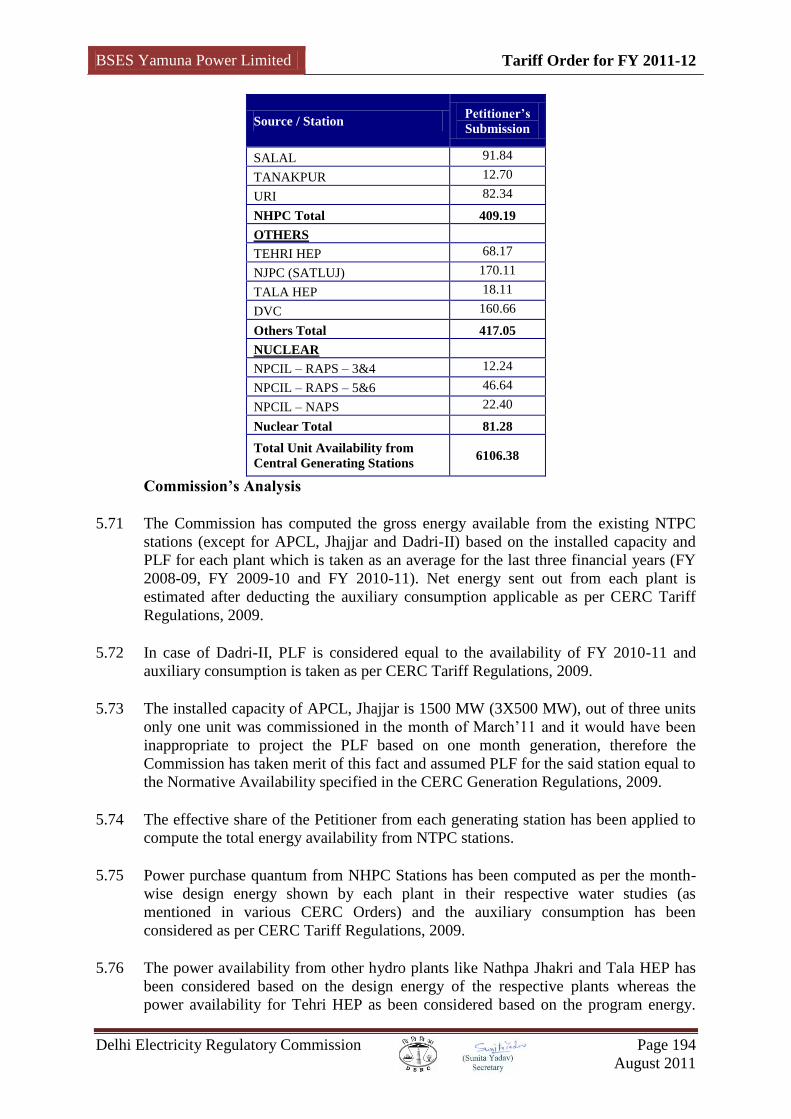

for

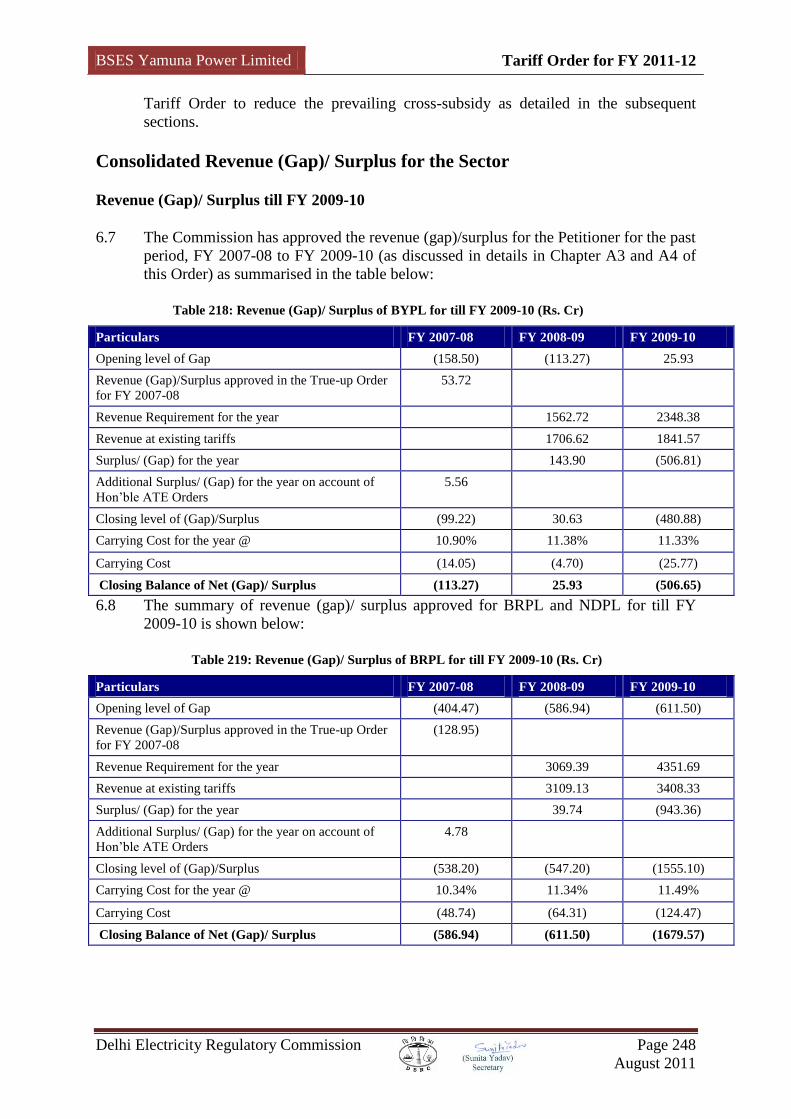

FY 2008-09 & FY 2009-10

and

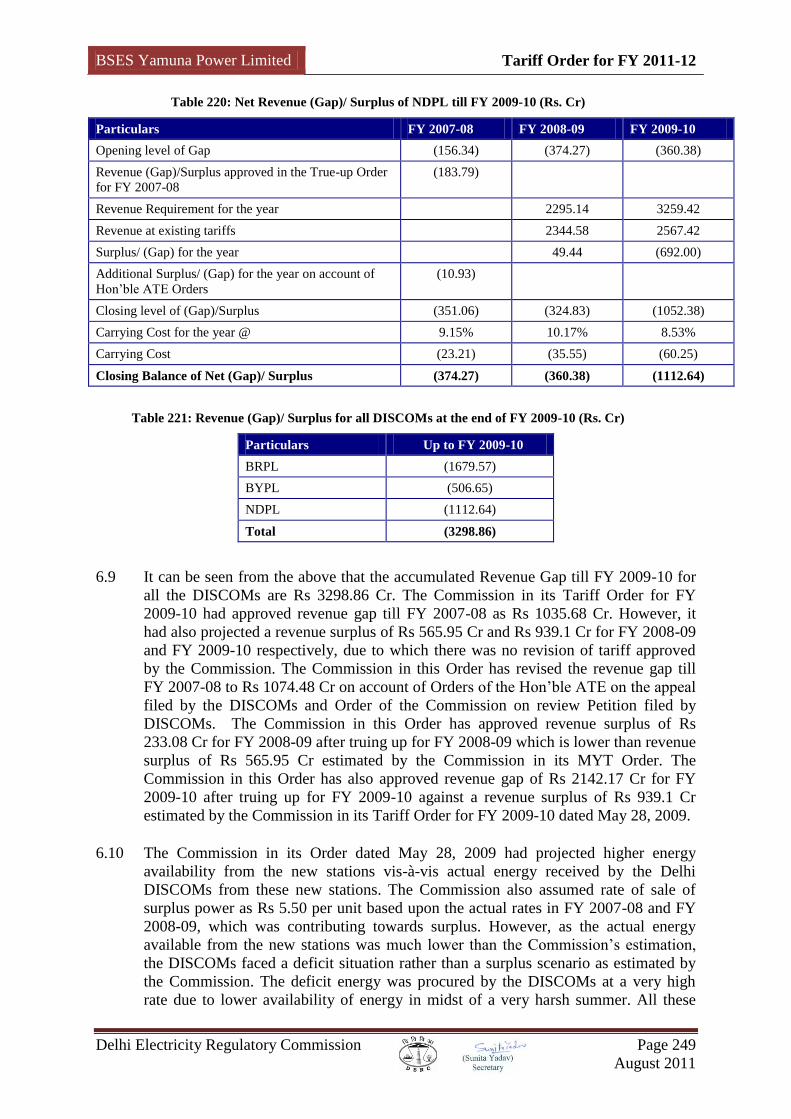

AGGREGATE REVENUE REQUIREMENT

for

FY 2011-12

for

BSES YAMUNA POWER LIMITED

DELHI ELECTRICITY REGULATORY COMMISSION

AUGUST, 2011

BSES Yamuna Power Limited Tariff Order for FY 2011-12

Delhi Electricity Regulatory Commission Page 1

August 2011

A1: INTRODUCTION ................................................................................................................................ 15

TRANSFER SCHEME .......................................................................................................................................... 15 BSES YAMUNA POWER LIMITED (BYPL) ........................................................................................................ 15 DELHI ELECTRICITY REGULATORY COMMISSION (DERC) ............................................................................... 16

Functions of the Commission ...................................................................................................................... 17 THE COORDINATION FORUM ............................................................................................................................ 19 MULTI YEAR TARIFF REGULATIONS AND EXTENSION OF THE CONTROL PERIOD ............................................. 20 FILING OF TARIFF PETITION FOR TRUE UP OF EXPENSES FOR FY 2008-09 ........................................................ 20

Filing of Petition ......................................................................................................................................... 20 Acceptance of Petition................................................................................................................................. 21

FILING OF PETITION FOR TRUE UP OF EXPENSES FOR FY 2009-10 AND APPROVAL OF ARR FOR FY 2011-12 .. 21 Filing of Petition ......................................................................................................................................... 21 Acceptance of Petition................................................................................................................................. 21

INTERACTION WITH THE PETITIONER ................................................................................................................ 21 PUBLIC HEARING .............................................................................................................................................. 23 LAYOUT OF THE ORDER .................................................................................................................................... 26 PERFORMANCE REVIEW .................................................................................................................................... 27 APPROACH OF THE ORDER ................................................................................................................................ 29

Approach for True Up ................................................................................................................................. 29 Approach for FY 2010-11 ........................................................................................................................... 30 Approach for FY 2011-12 ........................................................................................................................... 30

A2: RESPONSE FROM STAKEHOLDERS ............................................................................................ 32

INTRODUCTION ................................................................................................................................................. 32 RATIONALIZATION OF FIXED CHARGES ............................................................................................................ 32

Stakeholder‟s View ...................................................................................................................................... 32 Petitioner‟s Submission ............................................................................................................................... 32 Commission‟s View ..................................................................................................................................... 33

METERING AND METER TESTING ...................................................................................................................... 34 Stakeholder‟s View ...................................................................................................................................... 34 Petitioner‟s Submission ............................................................................................................................... 35 Commission‟s View ..................................................................................................................................... 35

AT&C LOSS REDUCTION ................................................................................................................................. 36 Stakeholder‟s View ...................................................................................................................................... 36 Petitioner‟s Submission ............................................................................................................................... 37 Commission‟s View ..................................................................................................................................... 37

LOAD SHEDDING .............................................................................................................................................. 39 Stakeholder‟s View ...................................................................................................................................... 39 Petitioner‟s Submission ............................................................................................................................... 39 Commission‟s View ..................................................................................................................................... 40

TRANSPARENCY IN DISCOM‟S ACCOUNTS...................................................................................................... 40 Stakeholder‟s View ...................................................................................................................................... 40 Petitioner‟s Submission ............................................................................................................................... 41 Commission‟s View ..................................................................................................................................... 41

USE OF ELECTRICITY POLES FOR OTHER BUSINESS ............................................................................................ 42 Stakeholder‟s View ...................................................................................................................................... 42 Petitioner‟s Submission ............................................................................................................................... 42 Commission‟s View ..................................................................................................................................... 42

PHYSICAL VERIFICATION OF ASSETS ................................................................................................................ 43 Stakeholder‟s View ...................................................................................................................................... 43 Petitioner‟s Submission ............................................................................................................................... 43 Commission‟s View ..................................................................................................................................... 43

POWER PURCHASE COST ADJUSTMENT MECHANISM ....................................................................................... 44 Stakeholder‟s View ...................................................................................................................................... 44 Petitioner‟s Views ....................................................................................................................................... 44 Commission‟s View ..................................................................................................................................... 45

TIME OF DAY METERING .................................................................................................................................. 46 Stakeholder‟s View ...................................................................................................................................... 46 Petitioner‟s Submission ............................................................................................................................... 46 Commission‟s View ..................................................................................................................................... 46

BSES Yamuna Power Limited Tariff Order for FY 2011-12

Delhi Electricity Regulatory Commission Page 2

August 2011

CROSS - SUBSIDY .............................................................................................................................................. 47 Stakeholder‟s View ...................................................................................................................................... 47 Petitioner‟s Submission ............................................................................................................................... 47 Commission‟s View ..................................................................................................................................... 48

BILLING BASED ON KVAH FOR INDUSTRIAL AND NON DOMESTIC CONSUMERS WITH MDI GREATER THAN 10

KW ................................................................................................................................................................... 49 Stakeholder‟s View ...................................................................................................................................... 49 Petitioner‟s Submission ............................................................................................................................... 49 Commission‟s View ..................................................................................................................................... 50

METERING OF DISTRIBUTION LICENSEES‟ PREMISES AND SUB-STATIONS.......................................................... 51 Stakeholder‟s View ...................................................................................................................................... 51 Petitioner‟s Submission ............................................................................................................................... 51 Commission‟s View ..................................................................................................................................... 51

THEFT OF ELECTRICITY .................................................................................................................................... 51 Stakeholder‟s View ...................................................................................................................................... 51 Petitioner‟s Submission ............................................................................................................................... 52 Commission‟s View ..................................................................................................................................... 52

STREET LIGHTING ............................................................................................................................................. 53 Stakeholder‟s View ...................................................................................................................................... 53 Petitioner‟s Submission ............................................................................................................................... 53 Commission‟s View ..................................................................................................................................... 53

COMPETITION IN POWER DISTRIBUTION BUSINESS ........................................................................................... 54 Stakeholder‟s View ...................................................................................................................................... 54 Petitioner‟s Submission ............................................................................................................................... 54 Commission‟s View ..................................................................................................................................... 54

PREVENTION OF FAULTS ................................................................................................................................... 55 Stakeholder‟s View ...................................................................................................................................... 55 Petitioner‟s Submission ............................................................................................................................... 55 Commission‟s View ..................................................................................................................................... 55

CHEAP POWER TO NDMC AND RESULTANT LOWER TARIFF .............................................................................. 55 Stakeholder‟s View ...................................................................................................................................... 55 Petitioner‟s Submission ............................................................................................................................... 55 Commission‟s View ..................................................................................................................................... 55

PAYMENT OF BILLS THROUGH CASH ................................................................................................................ 56 Stakeholder‟s View ...................................................................................................................................... 56 Petitioner‟s Submission ............................................................................................................................... 56 Commission‟s View ..................................................................................................................................... 56

UNIFORM FIXED CHARGES UPTO SANCTIONED LOAD OF 5 KW .......................................................................... 56 Stakeholder‟s View ...................................................................................................................................... 56 Petitioner‟s Submission ............................................................................................................................... 56 Commission‟s View ..................................................................................................................................... 57

APPLICABILITY OF TARIFF WITH LOAD >100 KW FOR RESIDENTIAL USERS ....................................................... 58 Stakeholder‟s View ...................................................................................................................................... 58 Petitioner‟s Submission ............................................................................................................................... 58 Commission‟s view ...................................................................................................................................... 58

SPECIAL TREATMENT FOR GOVT. AIDED SCHOOLS/INSTITUTIONS .................................................................... 58 Stakeholder‟s View ...................................................................................................................................... 58 Petitioner‟s Submission ............................................................................................................................... 58 Commission‟s view ...................................................................................................................................... 59

REDUCTION IN NUMBER OF SLABS FOR DOMESTIC CATEGORY .......................................................................... 59 Stakeholder‟s View ...................................................................................................................................... 59 Petitioner‟s Submission ............................................................................................................................... 59 Commission‟s view ...................................................................................................................................... 59

RESPONSE OF DTL ON ARR PETITION FILED BY DISTRIBUTION LICENSEES ..................................................... 60 Stakeholder‟s View ...................................................................................................................................... 60 Petitioner‟s Submission ............................................................................................................................... 60 Commission‟s View ..................................................................................................................................... 60

PAYMENT TO DPCL ON ACCOUNT OF PRIOR PERIOD LIABILITY ........................................................................ 60 Stakeholder‟s View ...................................................................................................................................... 60 Petitioner‟s Submission ............................................................................................................................... 61

BSES Yamuna Power Limited Tariff Order for FY 2011-12

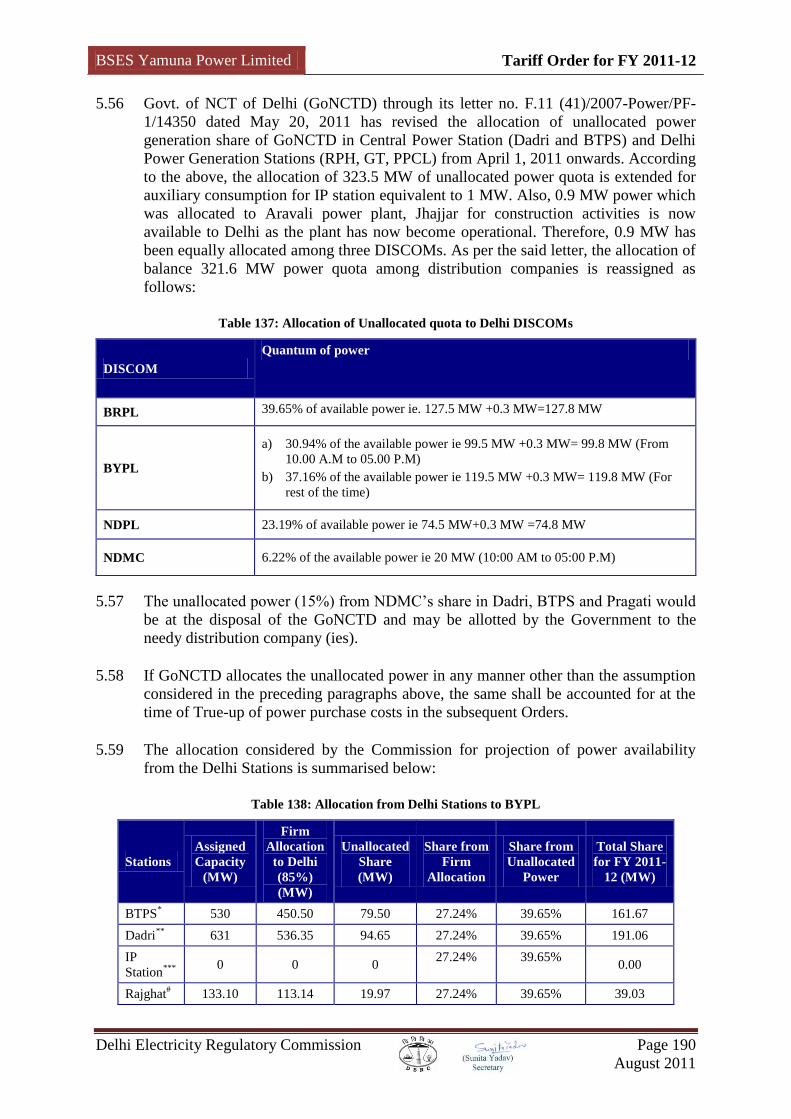

Delhi Electricity Regulatory Commission Page 3

August 2011

Commission‟s View ..................................................................................................................................... 61 PAYMENT TO PENSION TRUST .......................................................................................................................... 61

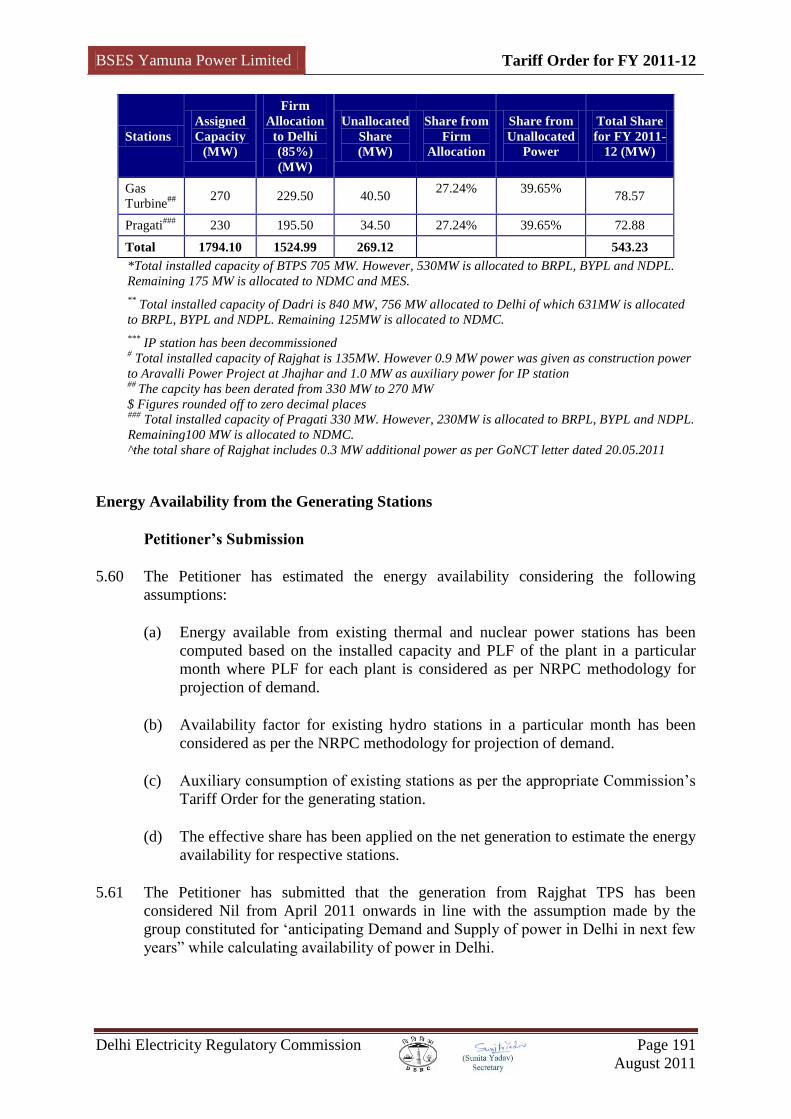

Stakeholder‟s View ...................................................................................................................................... 61 Petitioner‟s Submission ............................................................................................................................... 62 Commission‟s View ..................................................................................................................................... 63

COOPERATIVE GROUP HOUSING SOCIETIES (CGHS) ........................................................................................ 63 Stakeholder‟s View ...................................................................................................................................... 63 Petitioner‟s Submission ............................................................................................................................... 64 Commission‟s View ..................................................................................................................................... 64

DELHI METRO RAIL CORPORATION (DMRC) ................................................................................................... 64 Stakeholder‟s View ...................................................................................................................................... 64 Petitioner‟s Submission ............................................................................................................................... 65 Commission‟s View ..................................................................................................................................... 65

RAILWAYS TRACTION TARIFF .......................................................................................................................... 65 Stakeholder‟s View ...................................................................................................................................... 65 Petitioner‟s Submission ............................................................................................................................... 66 Commission‟s View ..................................................................................................................................... 67

SEPARATE TARIFF FOR DELHI INTERNATIONAL AIRPORT LIMITED (DIAL) ...................................................... 68 Stakeholder‟s View ...................................................................................................................................... 68 Petitioner‟s Submission ............................................................................................................................... 68 Commission‟s View ..................................................................................................................................... 68

MERGER OF MLHT AND NDLT II (NON DOMESTIC) CONSUMER CATEGORIES ............................................... 69 Stakeholder‟s View ...................................................................................................................................... 69 Petitioner‟s Submission ............................................................................................................................... 69 Commission‟s View ..................................................................................................................................... 69

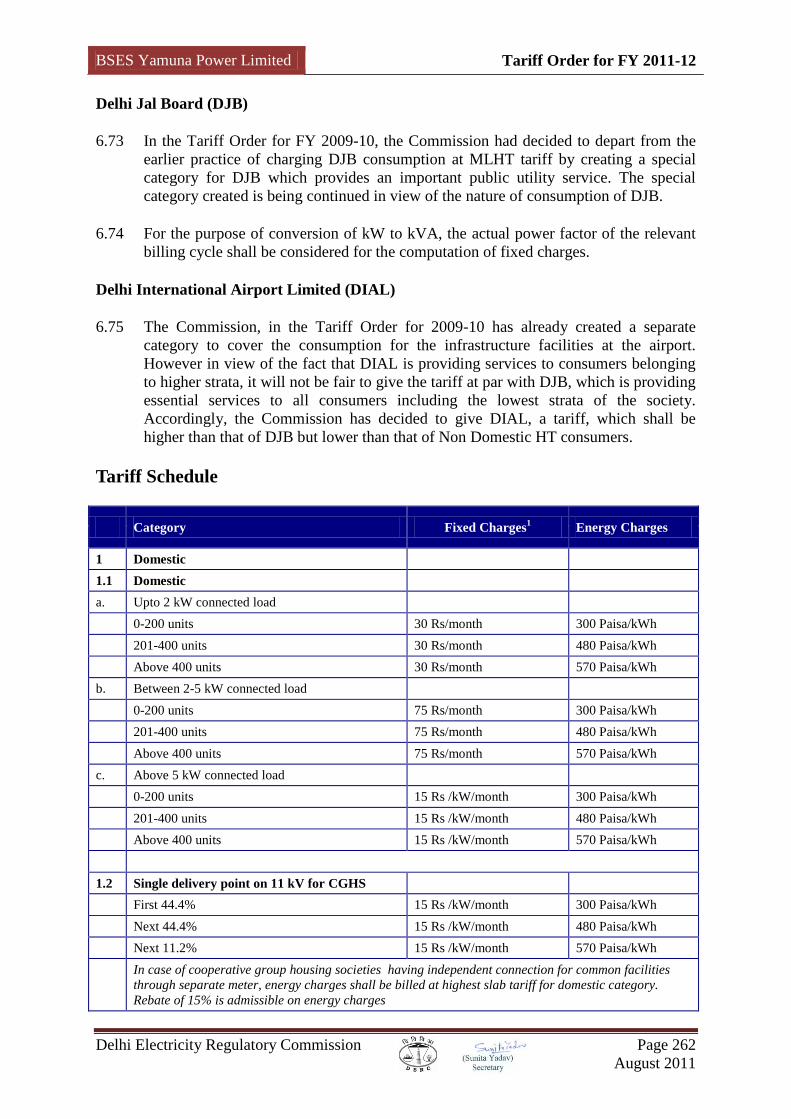

DELHI JAL BOARD (DJB) .................................................................................................................................. 69 Stakeholder‟s View ...................................................................................................................................... 69 Petitioner‟s Submission ............................................................................................................................... 70 Commission‟s View ..................................................................................................................................... 71

ENFORCEMENT PRACTICES ADOPTED BY THE PETITIONER ............................................................................... 71 Stakeholder‟s View ...................................................................................................................................... 71 Petitioner‟s Submission ............................................................................................................................... 71 Commission‟s View ..................................................................................................................................... 72

GENERAL COMPLAINTS .................................................................................................................................... 72 Petitioner‟s Submission ............................................................................................................................... 73 Commissions‟ Views ................................................................................................................................... 75

A3: TRUE UP FOR FY 2008-09 ................................................................................................................ 79

BACKGROUND .................................................................................................................................................. 79 POLICY DIRECTION PERIOD ............................................................................................................................... 79

Reactive Energy Charges ............................................................................................................................ 79 R&M and A&G Expenses............................................................................................................................ 80

MYT PERIOD .................................................................................................................................................... 86 Depreciation ............................................................................................................................................... 86 Advance Against Depreciation (AAD) ........................................................................................................ 90 Regulatory Rate Base .................................................................................................................................. 92 Return on Capital Employed and Supply Margin for the MYT Period ....................................................... 93 Employee Expenses ................................................................................................................................... 101 Payment to SVRS Optees ........................................................................................................................... 102 Business Growth ....................................................................................................................................... 102 Sixth Pay Commission for employees other than DVB employees ............................................................ 103 Impact of Recommendations of 6

th Pay Commission ................................................................................ 107

Capitalisation of Expenses ........................................................................................................................ 110 Capitalisation of Interest........................................................................................................................... 110 Consumers‟ Security Deposits .................................................................................................................. 112 Carrying Cost ............................................................................................................................................ 113 Net Impact of True Up for Past Period ..................................................................................................... 114

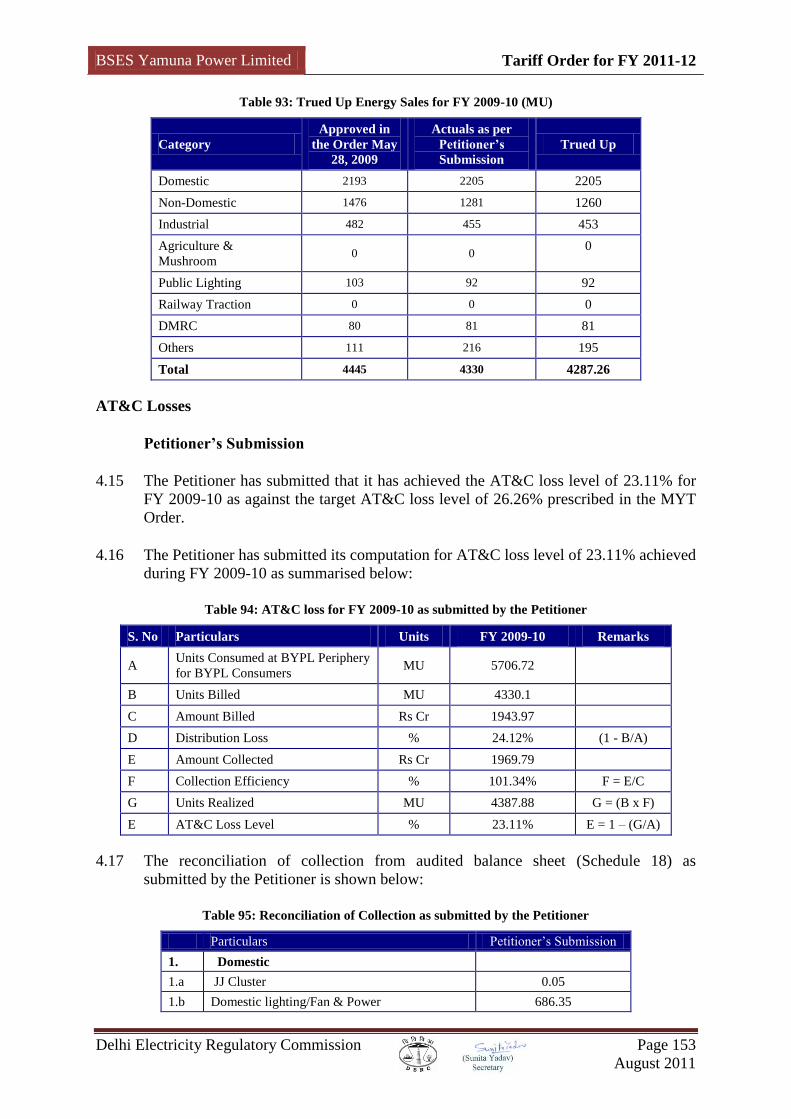

TRUE UP FOR FY 2008-09 .............................................................................................................................. 115 Energy Sales .............................................................................................................................................. 115 AT&C Losses ............................................................................................................................................ 116

BSES Yamuna Power Limited Tariff Order for FY 2011-12

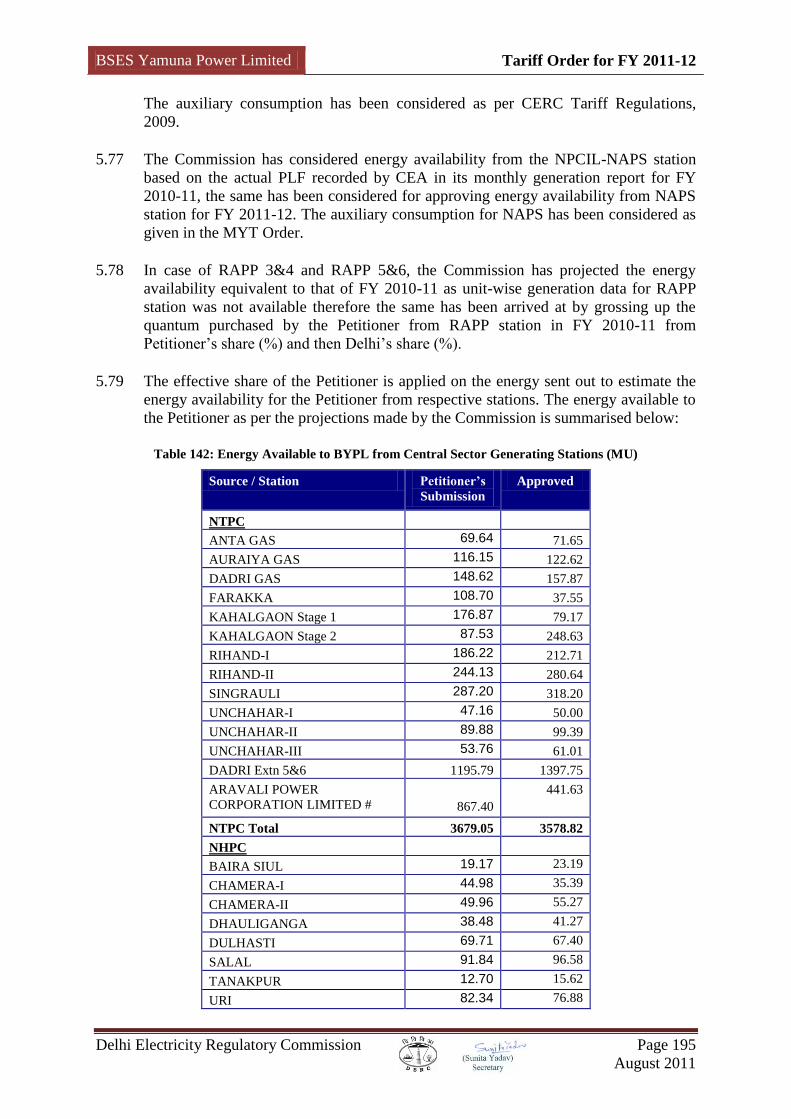

Delhi Electricity Regulatory Commission Page 4

August 2011

Power Purchase ........................................................................................................................................ 126 Power Purchase Quantum ........................................................................................................................ 126 Power Purchase Cost ................................................................................................................................ 127 Review of Controllable Parameters .......................................................................................................... 129 Employee Expenses ................................................................................................................................... 129 Administration & General (A&G) Expenses ............................................................................................. 132 Repairs & Maintenance (R&M) Expenses ................................................................................................ 133 Operation & Maintenance Expense .......................................................................................................... 134 Review of Capital Expenditure & Capitalisation ...................................................................................... 134 Review of Depreciation ............................................................................................................................. 137 Review of Return on Capital Employed .................................................................................................... 137 Income Tax ................................................................................................................................................ 139 Other Expenses ......................................................................................................................................... 140 Non Tariff Income (NTI) ........................................................................................................................... 144

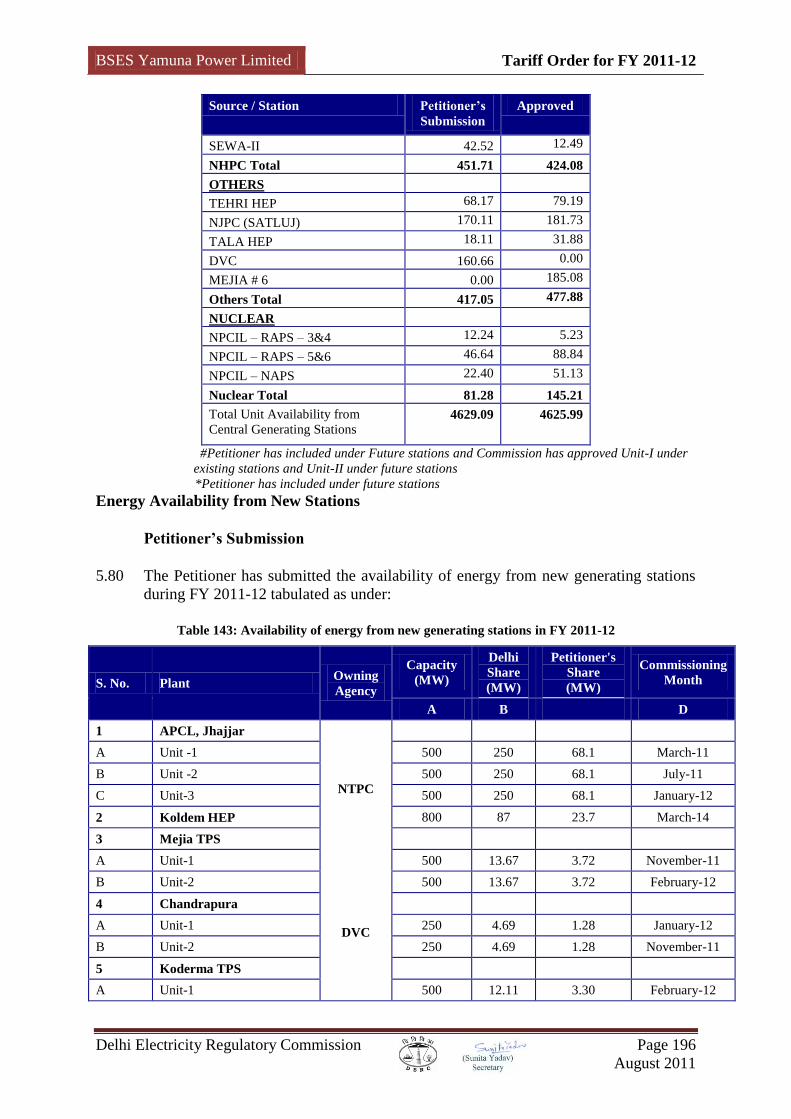

ANNUAL REVENUE REQUIREMENT FOR FY 2008-09 ...................................................................................... 146 REVENUE AVAILABLE TOWARDS ARR ........................................................................................................... 147

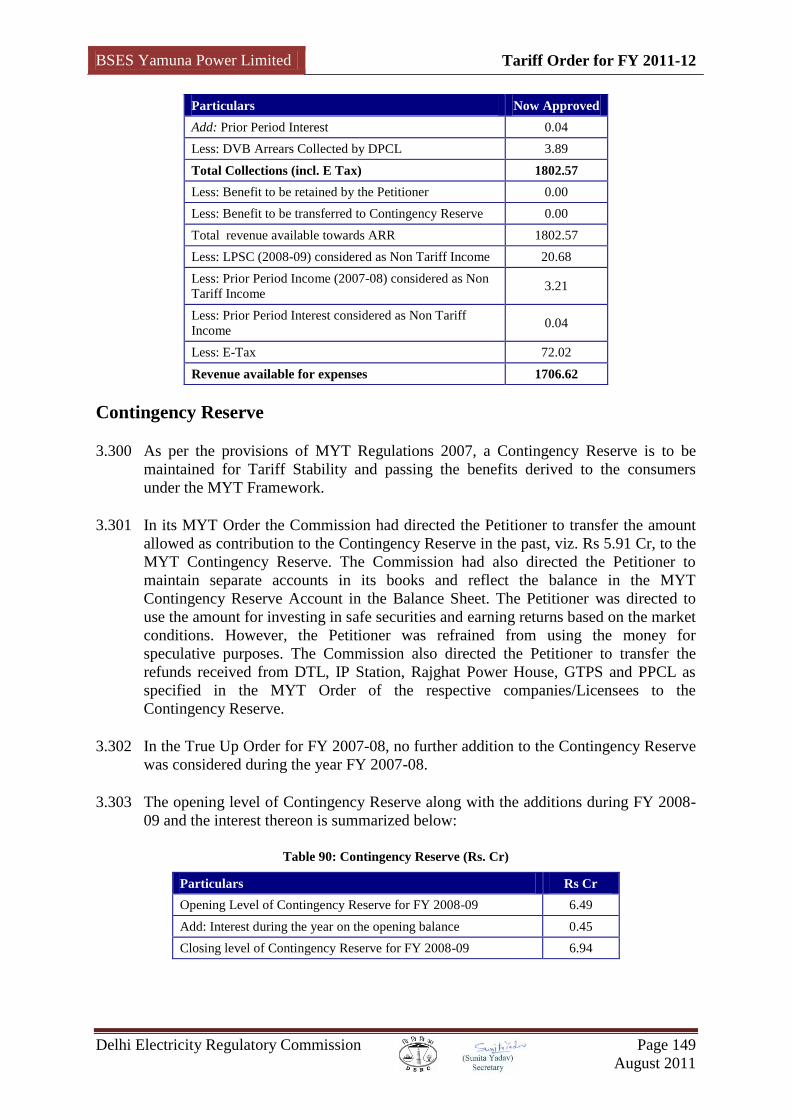

Petitioner‟s Submission ............................................................................................................................. 147 Commission‟s Analysis ............................................................................................................................. 147

CONTINGENCY RESERVE ................................................................................................................................ 149 REVENUE SURPLUS / GAP FOR FY 2008-09 .................................................................................................... 150

Petitioner‟s Submission ............................................................................................................................. 150 Commission‟s Analysis ............................................................................................................................. 150

A4: TRUE UP FOR FY 2009-10 .............................................................................................................. 151

BACKGROUND ................................................................................................................................................ 151 Energy Sales .............................................................................................................................................. 151 AT&C Losses ............................................................................................................................................ 153 Power Purchase Quantum ........................................................................................................................ 160 Power Purchase Cost ................................................................................................................................ 161 Review of Controllable Parameters .......................................................................................................... 163 Employee Expenses ................................................................................................................................... 163 Petitioner‟s Submission ............................................................................................................................. 163 Administration & General (A&G) Expenses ............................................................................................. 164 Repairs & Maintenance (R&M) Expenses ................................................................................................ 165 Operation & Maintenance Expense .......................................................................................................... 165 Review of Capital Expenditure & Capitalisation ...................................................................................... 166 Review of Depreciation ............................................................................................................................. 167 Review of Return on Capital Employed (RoCE) and Supply Margin ........................................................ 168 Consumers‟ Security Deposits .................................................................................................................. 168 Income Tax ................................................................................................................................................ 169 Other Expenses ......................................................................................................................................... 170 Non Tariff Income (NTI) ........................................................................................................................... 172

DTL CLAIM .................................................................................................................................................... 175 ANNUAL REVENUE REQUIREMENT FOR FY 2009-10 ...................................................................................... 176 REVENUE AVAILABLE TOWARDS ARR ........................................................................................................... 176

Petitioner‟s Submission ............................................................................................................................. 176 Commission‟s Analysis ............................................................................................................................. 177

CONTINGENCY RESERVE ................................................................................................................................ 177 REVENUE (GAP)/ SURPLUS ............................................................................................................................. 178

A5: ARR FOR FY 2011-12 ....................................................................................................................... 179

ENERGY SALES ............................................................................................................................................... 179 Petitioner‟s Submission ............................................................................................................................. 179 Commission‟s Analysis ............................................................................................................................. 180

REVENUE IN FY 2011-12 AT EXISTING TARIFF ............................................................................................... 185 AT&C LOSSES ............................................................................................................................................... 186

Petitioner‟s Submission ............................................................................................................................. 186 Commission‟s Analysis ............................................................................................................................. 187

ENERGY REQUIREMENT .................................................................................................................................. 187 Petitioner‟s Submission ............................................................................................................................. 187

BSES Yamuna Power Limited Tariff Order for FY 2011-12

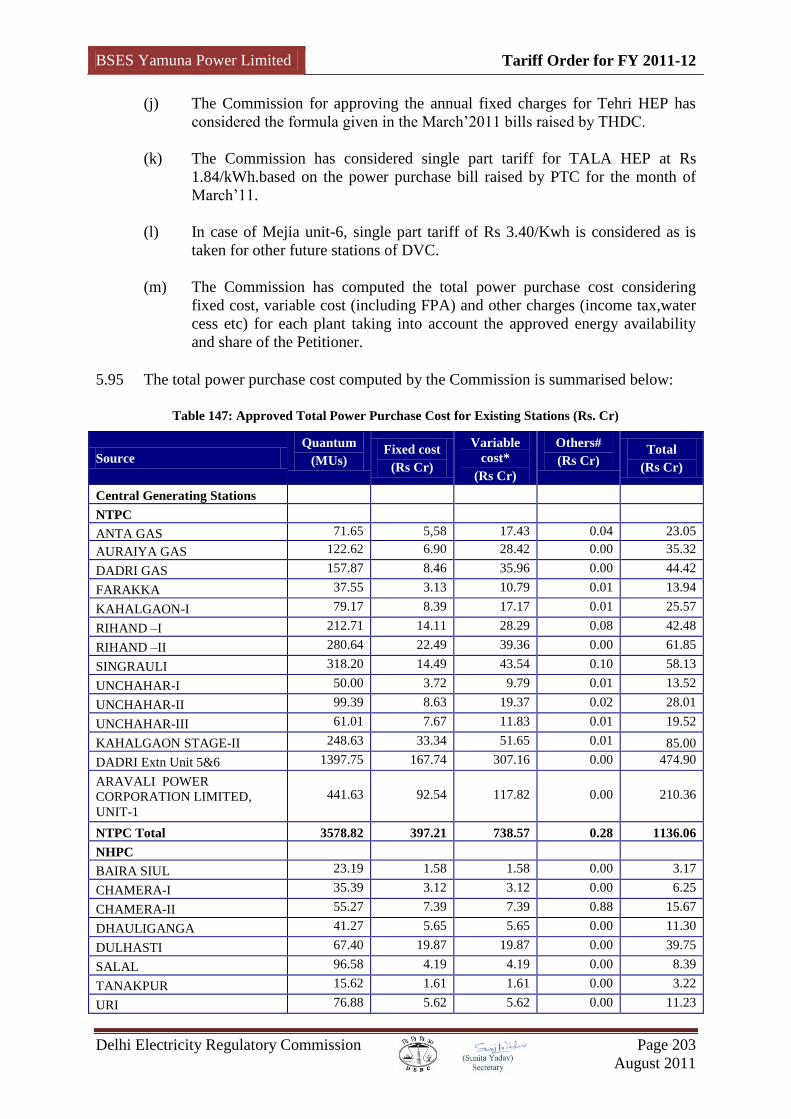

Delhi Electricity Regulatory Commission Page 5

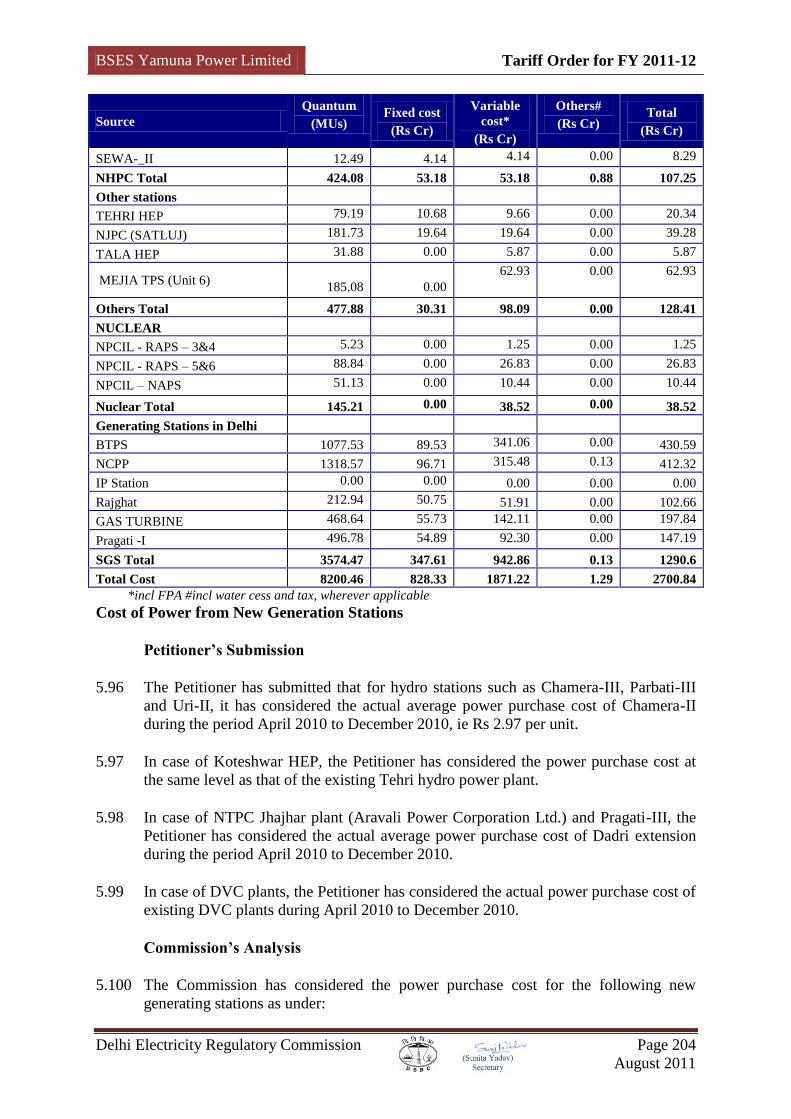

August 2011

Commission‟s Analysis ............................................................................................................................. 187 POWER PURCHASE .......................................................................................................................................... 188

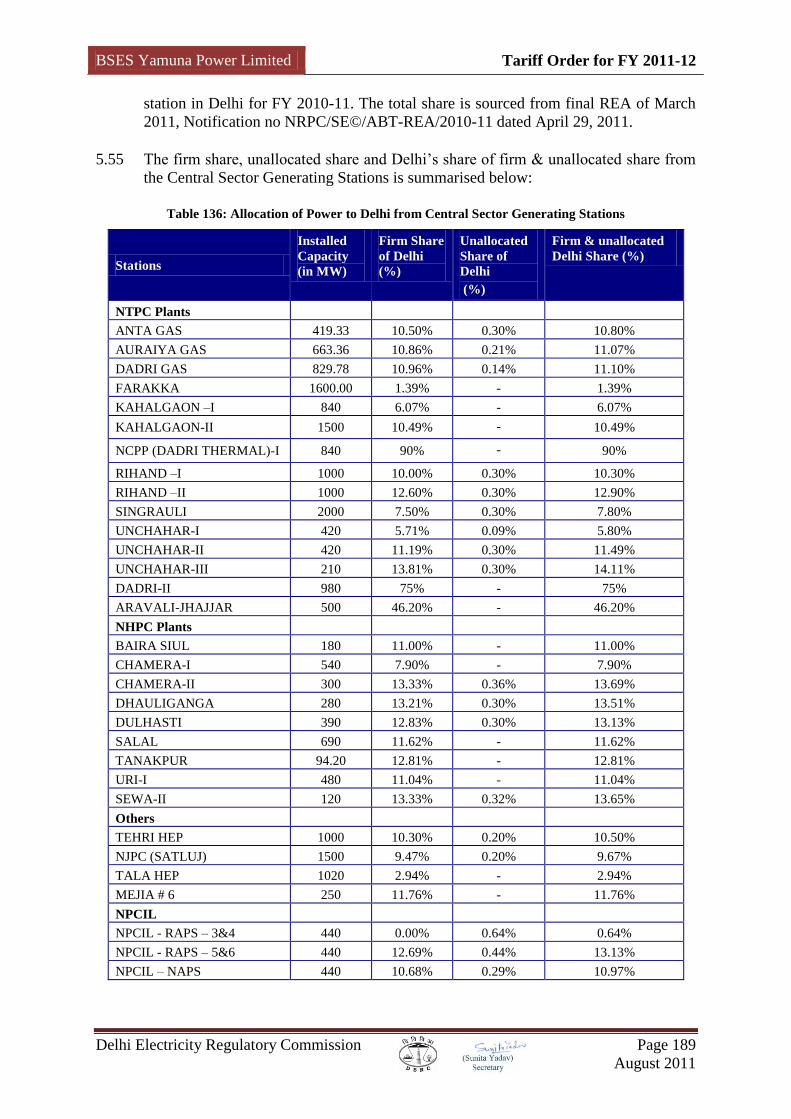

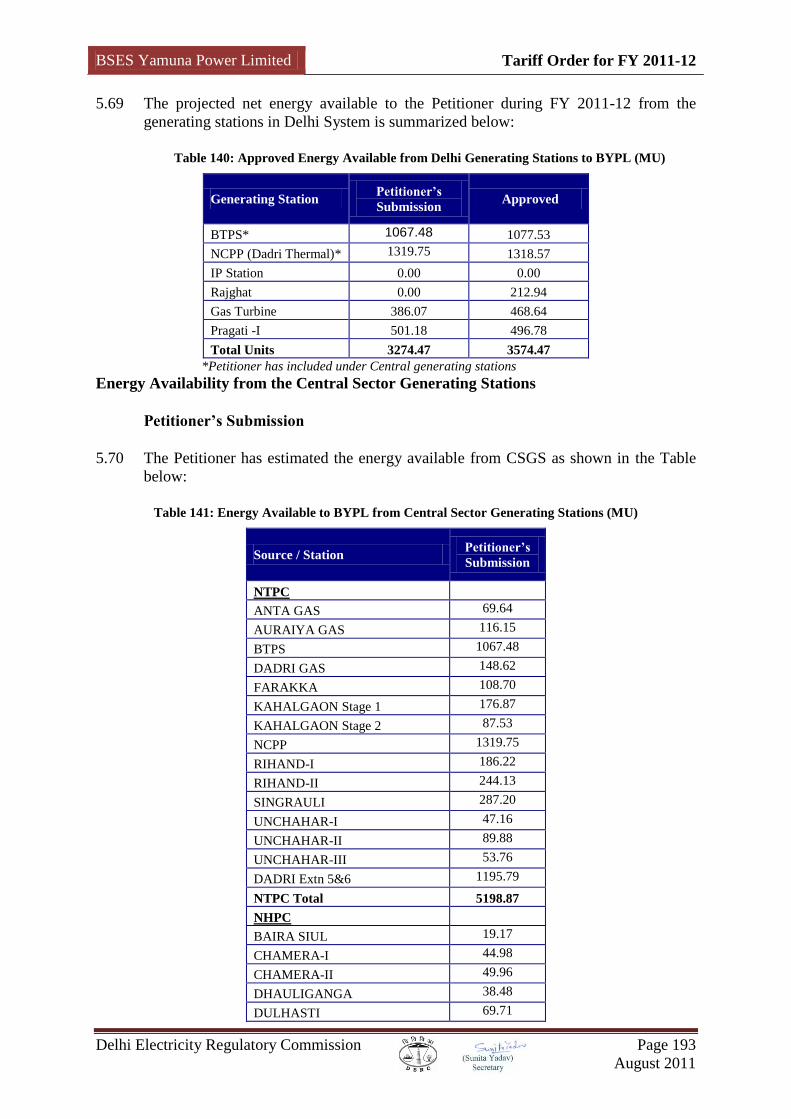

Allocation of Power from Central and State Generating Stations ............................................................ 188 Energy Availability from the Generating Stations .................................................................................... 191 Energy Availability from the Generating Stations in Delhi system ........................................................... 192 Energy Availability from the Central Sector Generating Stations ............................................................ 193 Energy Availability from New Stations ..................................................................................................... 196 Power Purchase Quantum from Other Sources: Intra-State, Bilateral & Banking .................................. 199

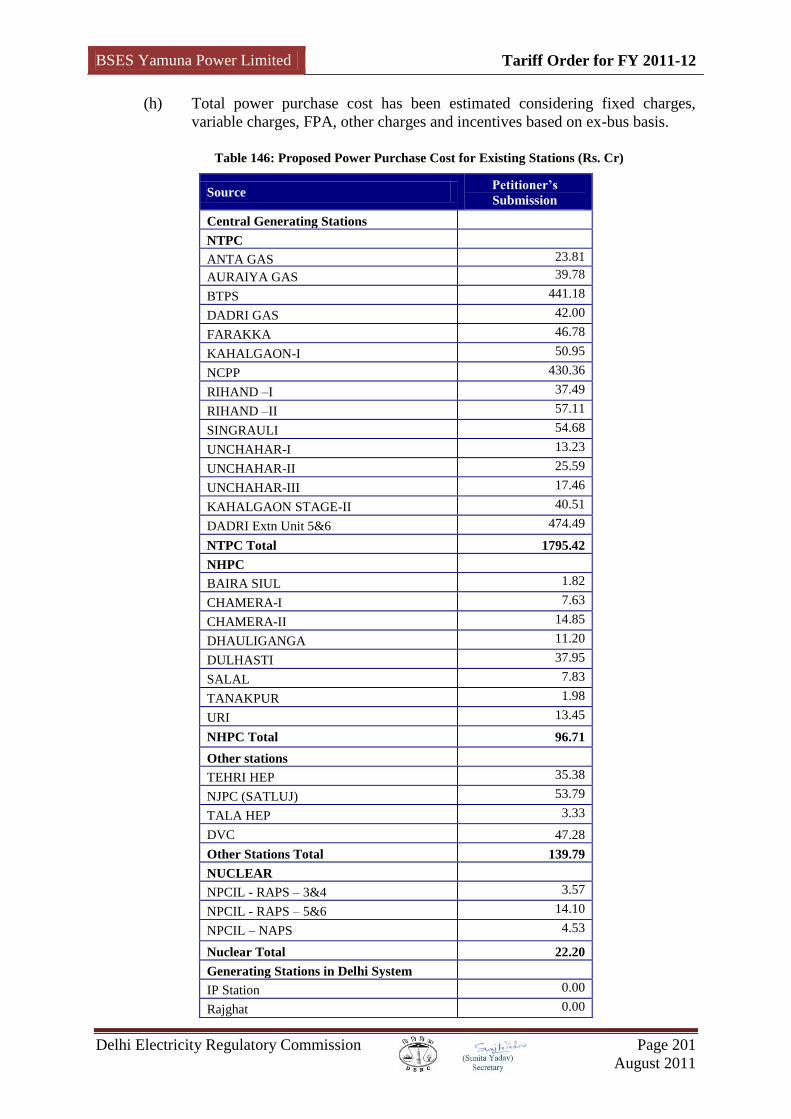

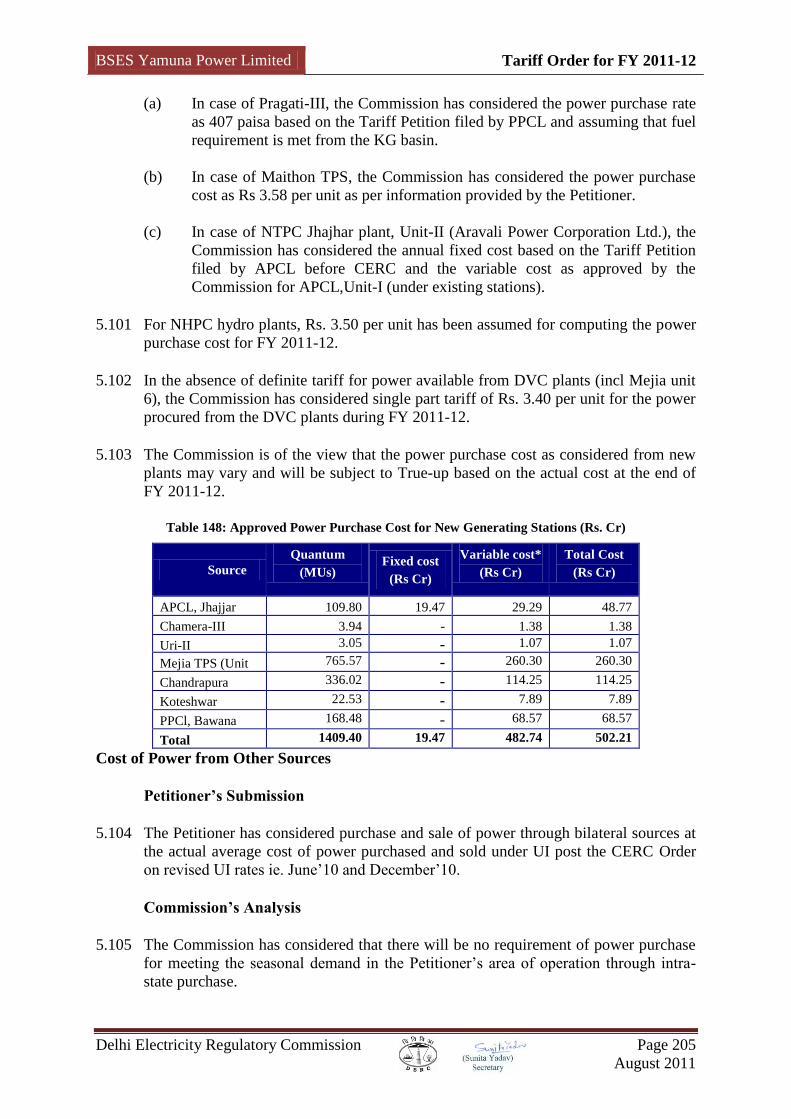

POWER PURCHASE COST ................................................................................................................................ 200 Cost of Power Purchase from Existing Stations ....................................................................................... 200 Cost of Power from New Generation Stations .......................................................................................... 204 Cost of Power from Other Sources ........................................................................................................... 205 Transmission Losses and Charges ............................................................................................................ 206

ENERGY BALANCE.......................................................................................................................................... 208 FUEL PRICE ADJUSTMENT SURCHARGE .......................................................................................................... 208 CONTROLLABLE PARAMETERS ....................................................................................................................... 211 OPERATION & MAINTENANCE EXPENSES ....................................................................................................... 212 EMPLOYEE EXPENSES ..................................................................................................................................... 212 ADMINISTRATIVE & GENERAL EXPENSES ...................................................................................................... 215 REPAIRS AND MAINTENANCE (R&M) EXPENSES ........................................................................................... 217

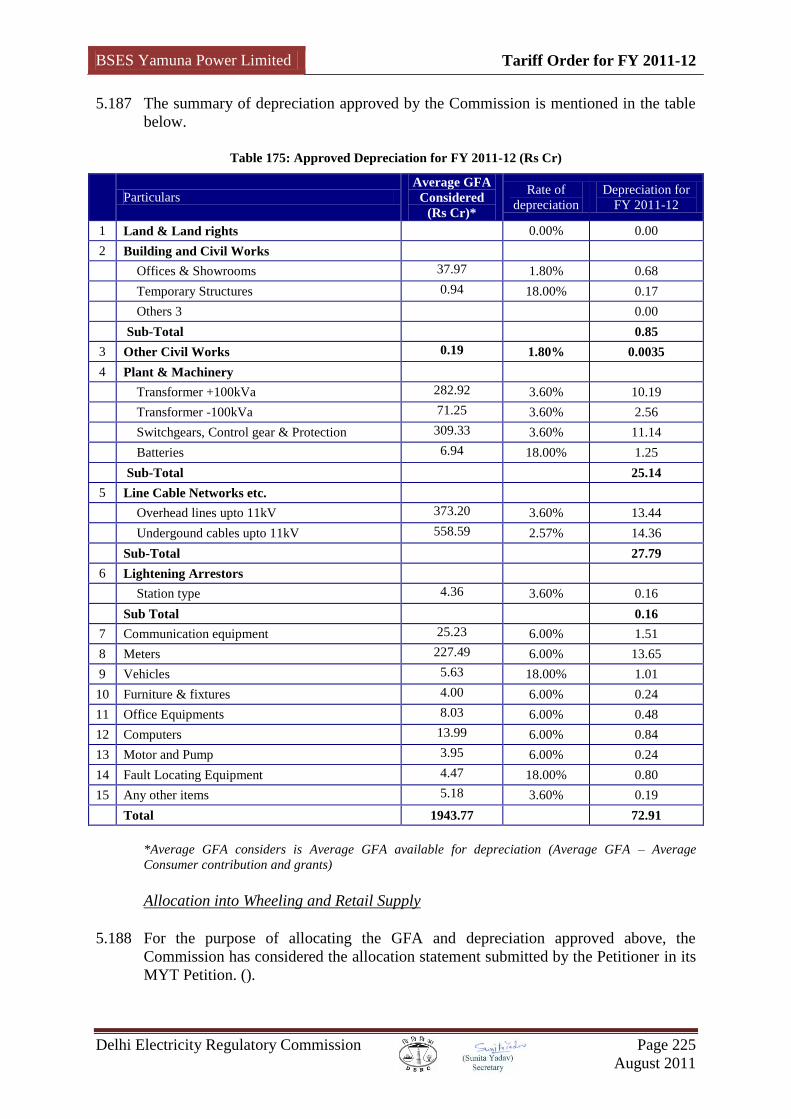

Efficiency Factor ....................................................................................................................................... 220 CAPITAL INVESTMENT .................................................................................................................................... 221 ASSETS CAPITALISATION ................................................................................................................................ 222 DEPRECIATION................................................................................................................................................ 223

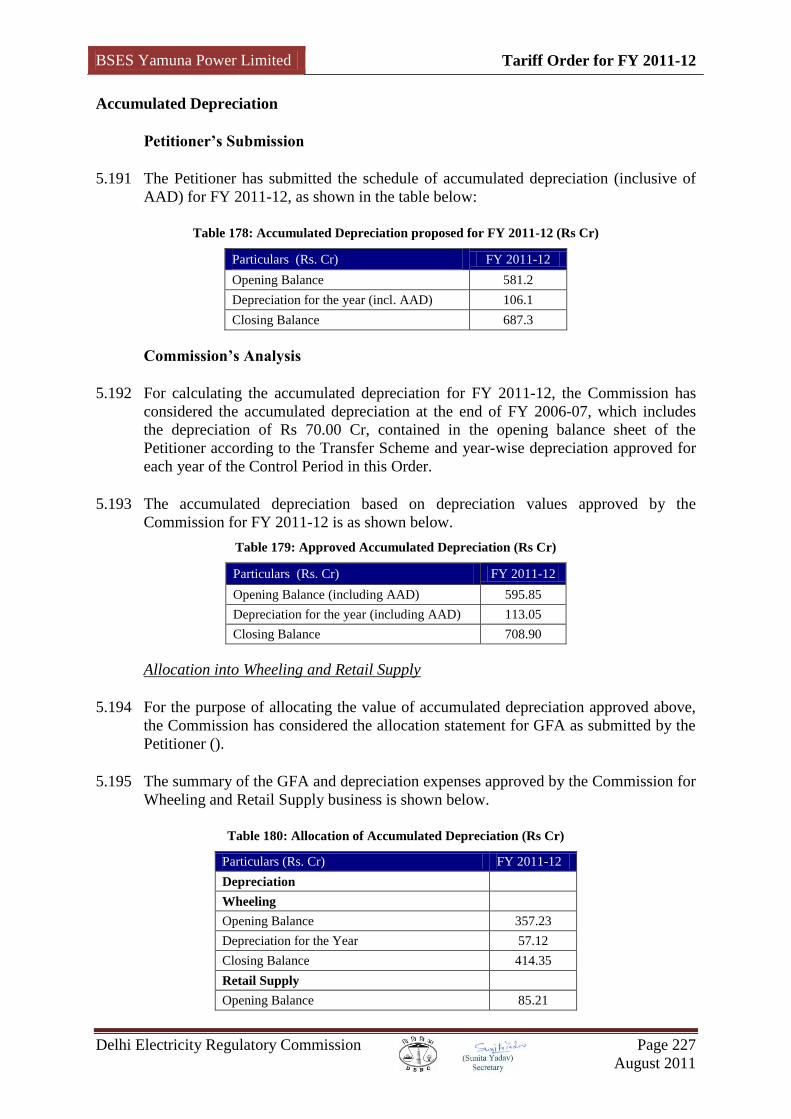

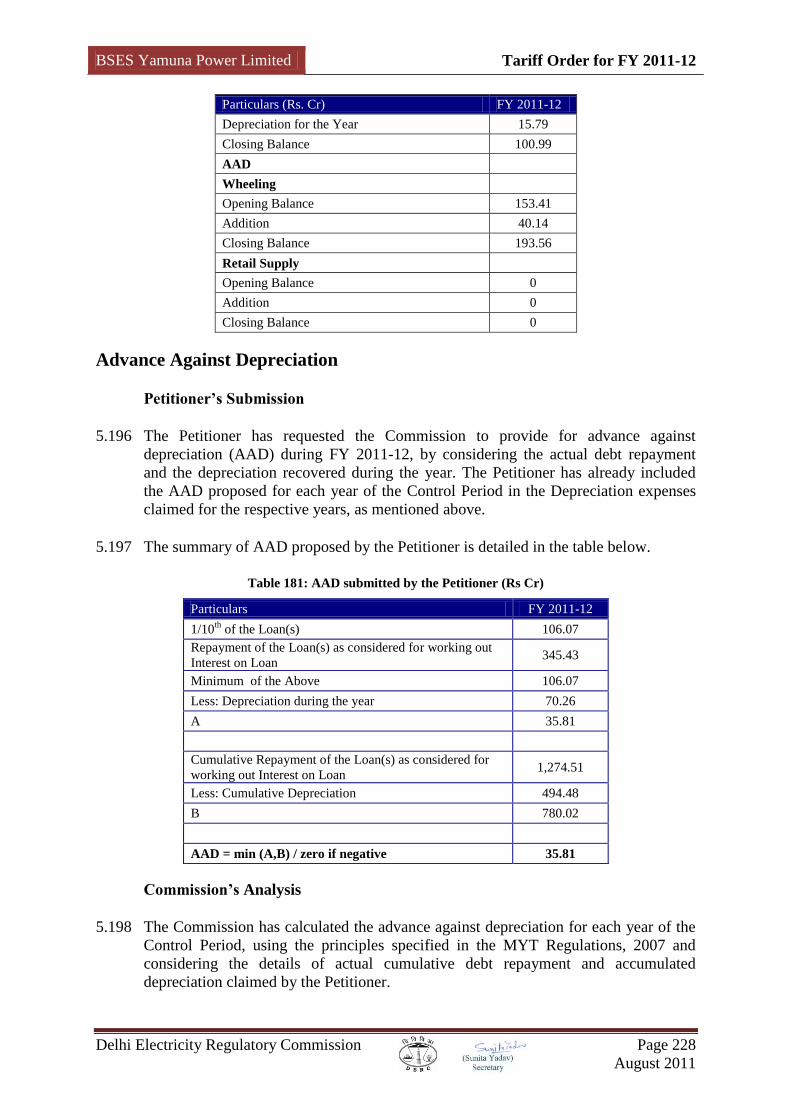

Accumulated Depreciation ........................................................................................................................ 227 ADVANCE AGAINST DEPRECIATION ............................................................................................................... 228 RETURN ON CAPITAL EMPLOYED ................................................................................................................... 229

Regulated Rate Base ................................................................................................................................. 229 Working Capital Requirement ................................................................................................................... 232 Means of Finance ...................................................................................................................................... 233 Determination of WACC and RoCE .......................................................................................................... 235

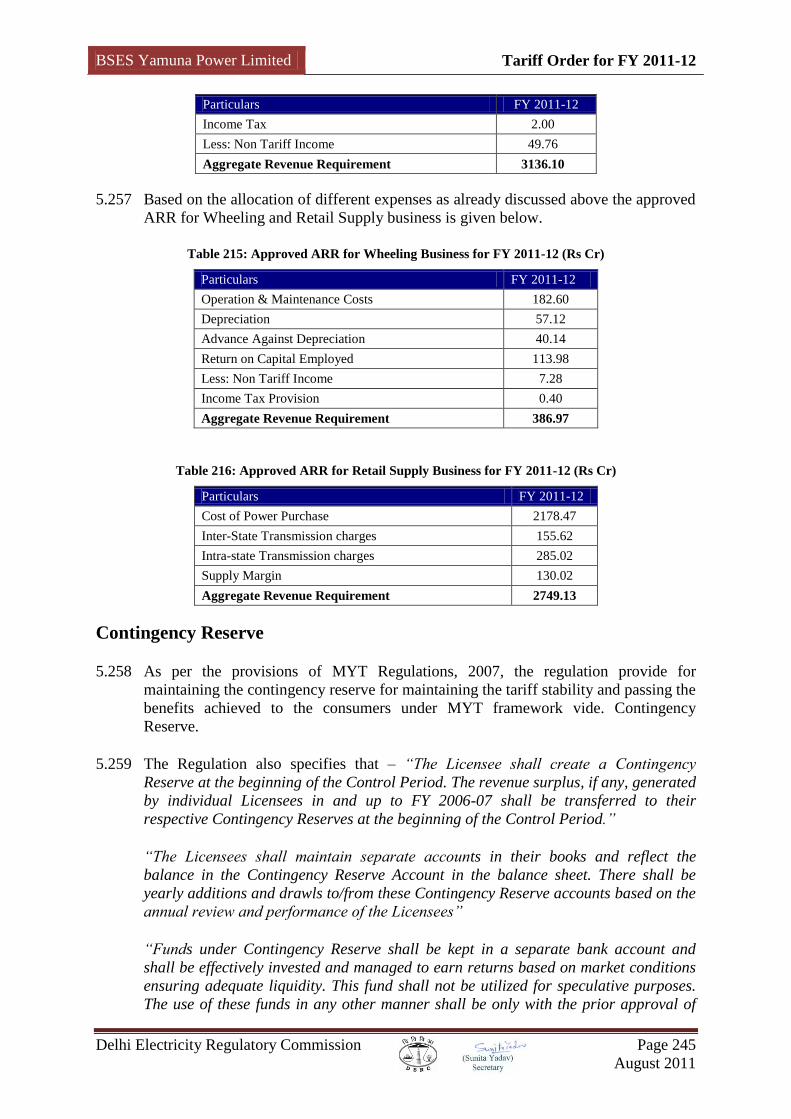

CAPITALISATION OF EXPENSES ....................................................................................................................... 237 TAX EXPENSES ............................................................................................................................................... 238 NON TARIFF INCOME ...................................................................................................................................... 238 OTHER MISCELLANEOUS EXPENSES ............................................................................................................... 240 CLAIM OF POWER PURCHASE REBATE PAID TO DTL ...................................................................................... 241 SUPPLY MARGIN ............................................................................................................................................. 242 AGGREGATE REVENUE REQUIREMENT ........................................................................................................... 243 CONTINGENCY RESERVE ................................................................................................................................ 245

A6: TARIFF DESIGN ............................................................................................................................... 247

COMPONENTS OF TARIFF DESIGN ................................................................................................................... 247 CROSS-SUBSIDISATION IN TARIFF STRUCTURE ............................................................................................... 247 CONSOLIDATED REVENUE (GAP)/ SURPLUS FOR THE SECTOR ........................................................................ 248 REVENUE (GAP)/ SURPLUS FOR FY 2011-12 AT EXISTING TARIFFS ............................................................... 250 TREATMENT OF REVENUE (GAP)/SURPLUS ..................................................................................................... 250

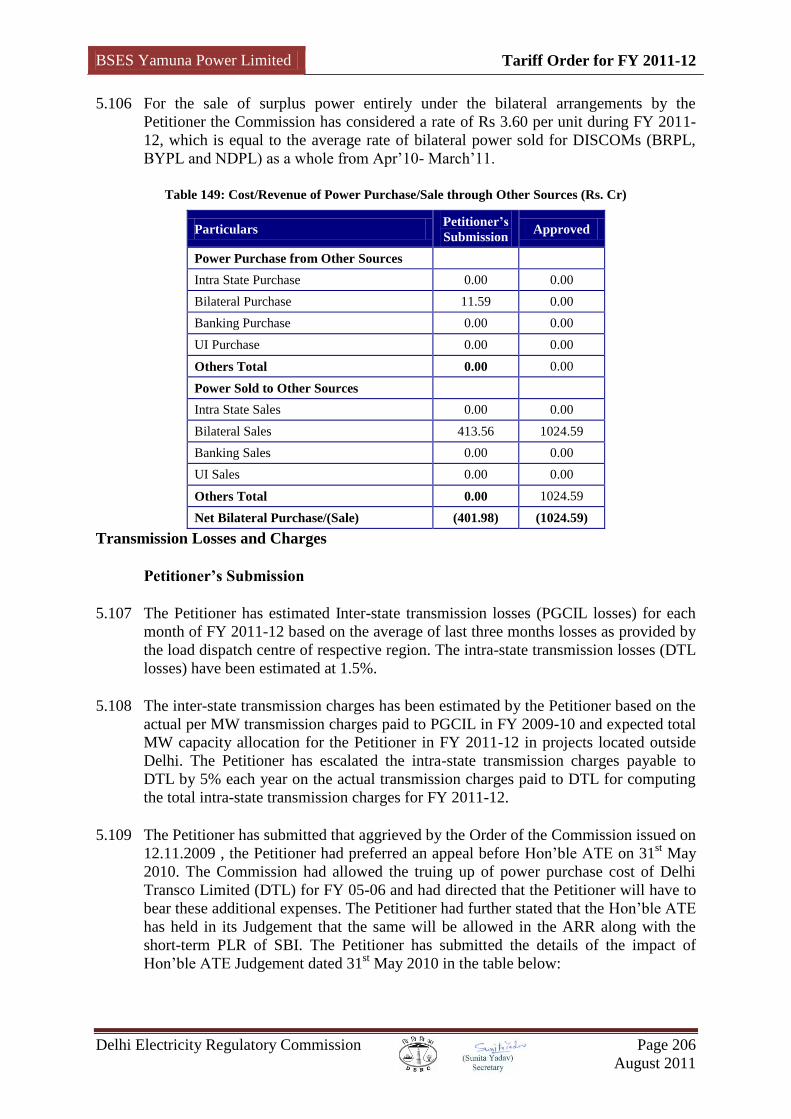

Petitioner‟s Submission ............................................................................................................................. 250 Commission‟s Analysis ............................................................................................................................. 251

REVENUE (GAP)/SURPLUS AT APPROVED TARIFFS ......................................................................................... 251 COST OF SERVICE MODEL .............................................................................................................................. 253

Allocation of Wheeling ARR ...................................................................................................................... 254 Allocation of Supply Margin and balance of Retail Supply ARR .............................................................. 256

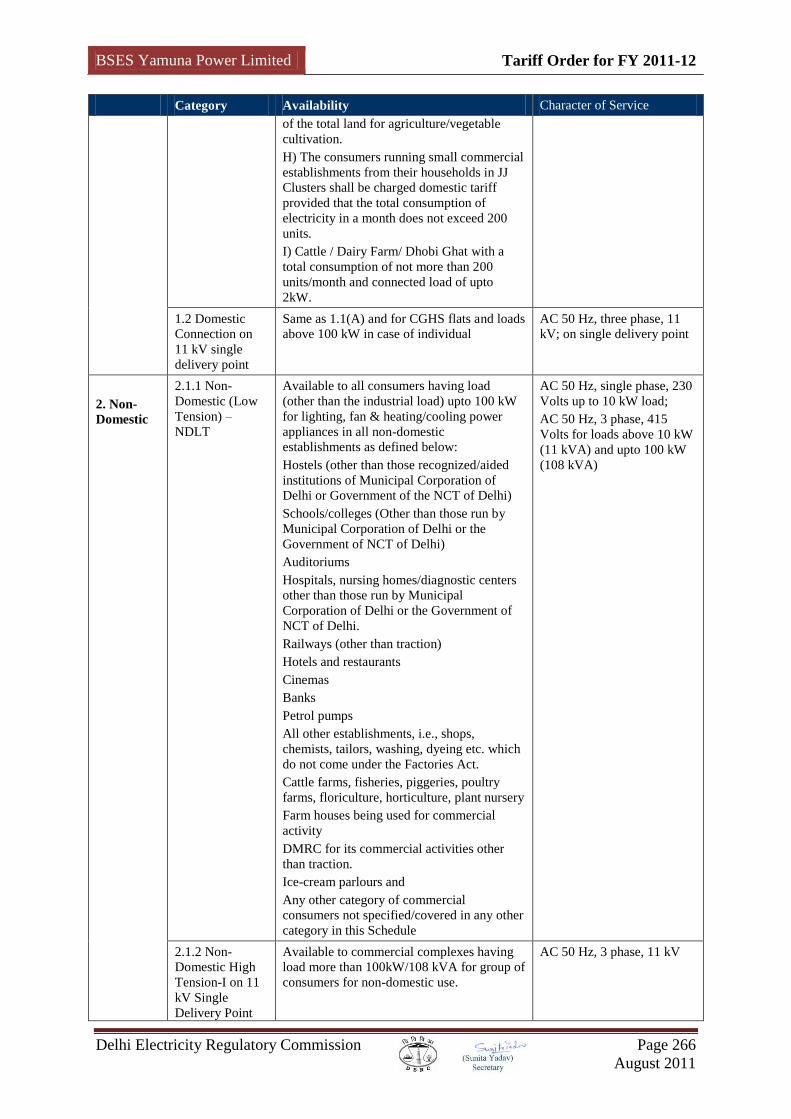

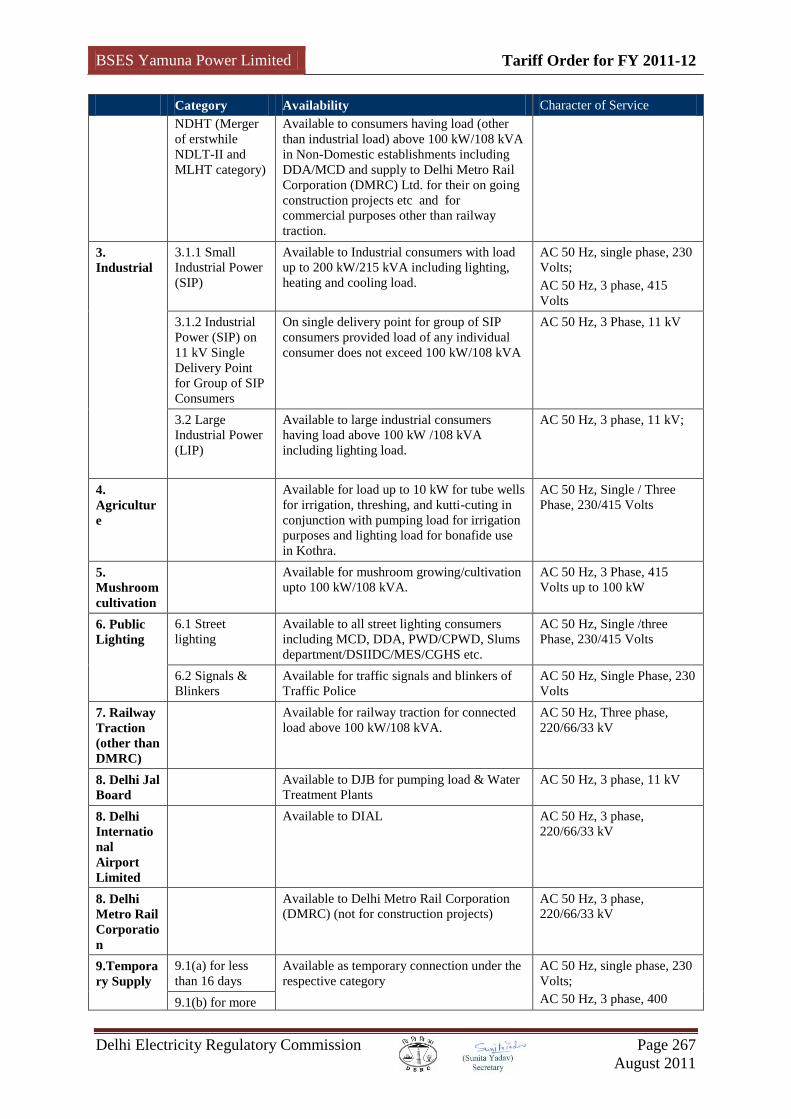

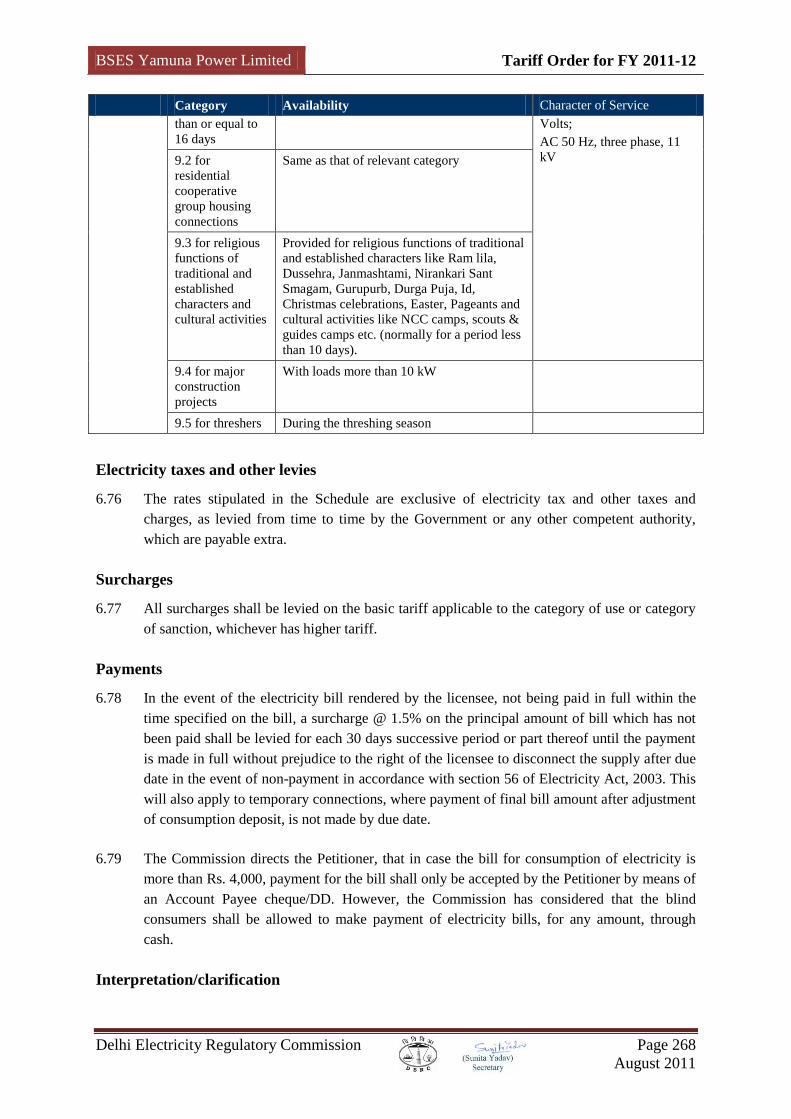

TARIFF STRUCTURE ........................................................................................................................................ 257 Domestic Tariff ......................................................................................................................................... 257 Non-Domestic Tariff ................................................................................................................................. 259 Industrial Tariff ......................................................................................................................................... 260 Agriculture ................................................................................................................................................ 261 Mushroom Cultivation .............................................................................................................................. 261 Public Lighting .......................................................................................................................................... 261 Railway Traction ....................................................................................................................................... 261

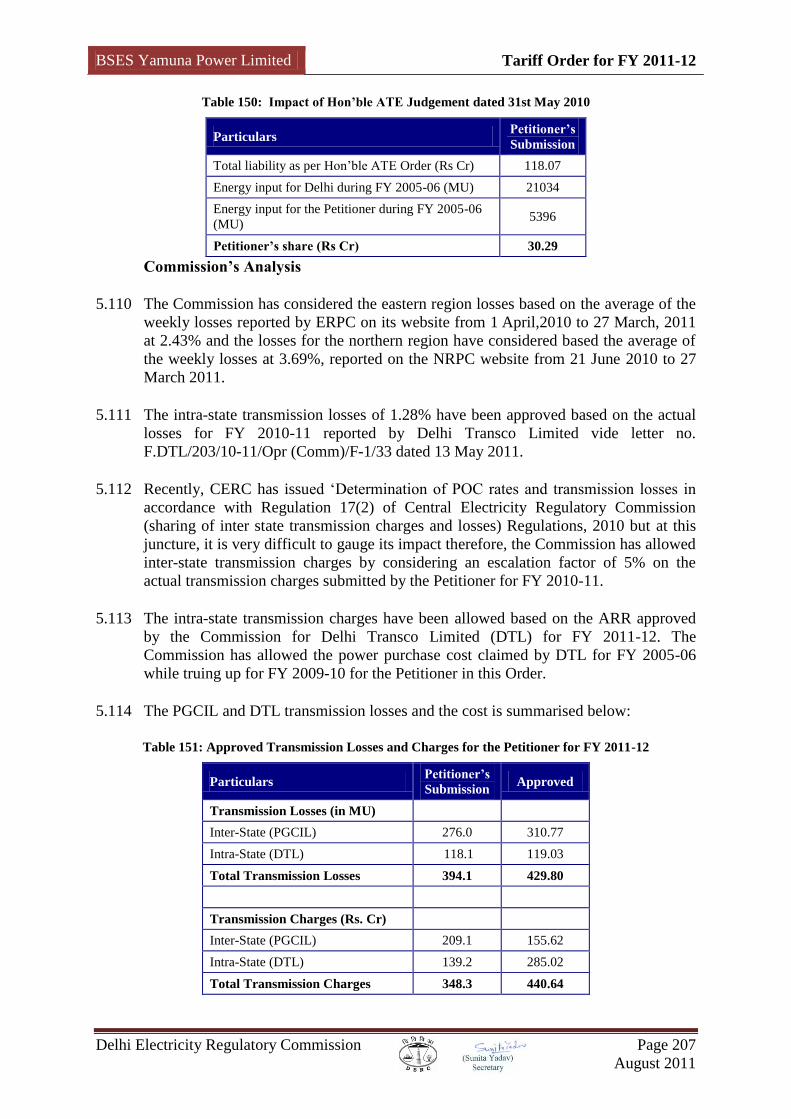

BSES Yamuna Power Limited Tariff Order for FY 2011-12

Delhi Electricity Regulatory Commission Page 6

August 2011

DMRC ....................................................................................................................................................... 261 Temporary Supply ..................................................................................................................................... 261 Delhi Jal Board (DJB) .............................................................................................................................. 262 Delhi International Airport Limited (DIAL) ............................................................................................. 262

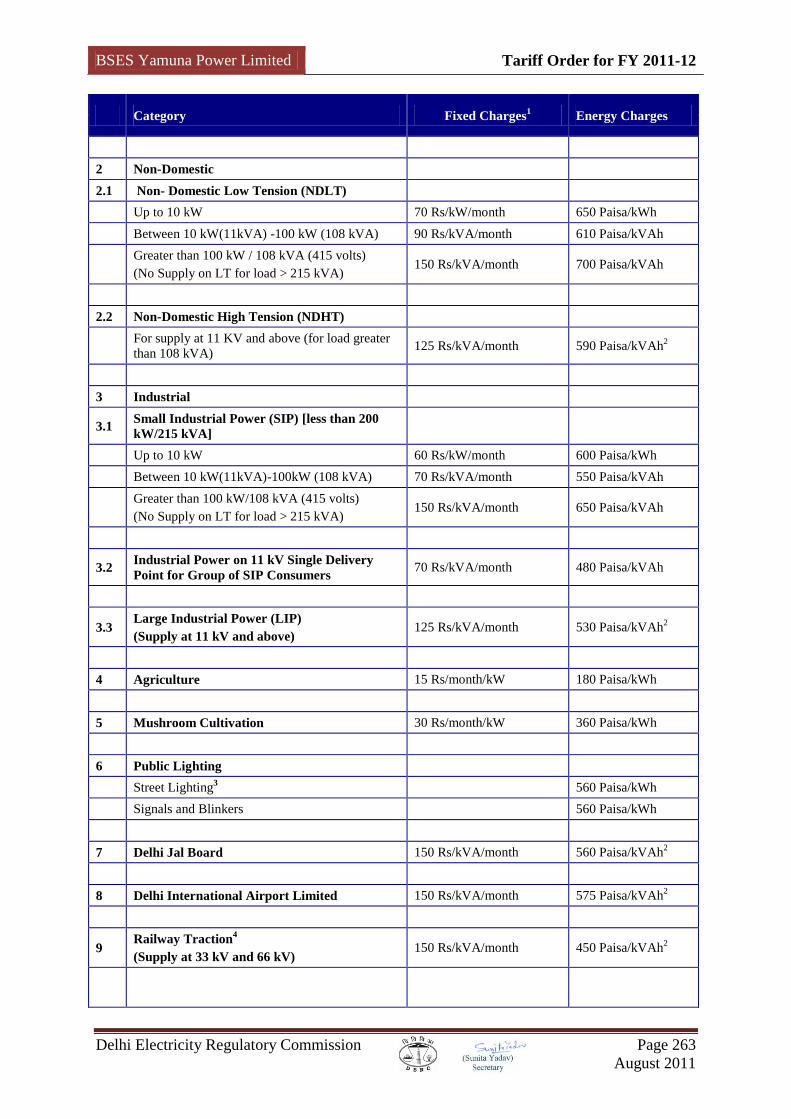

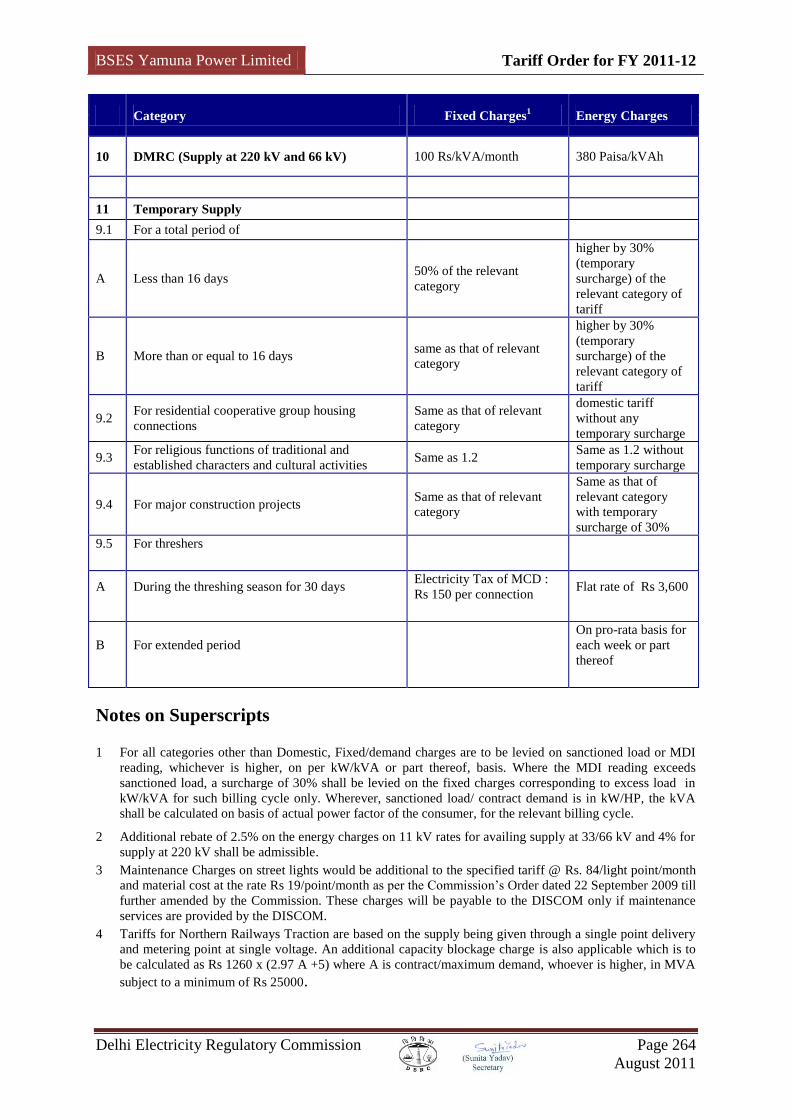

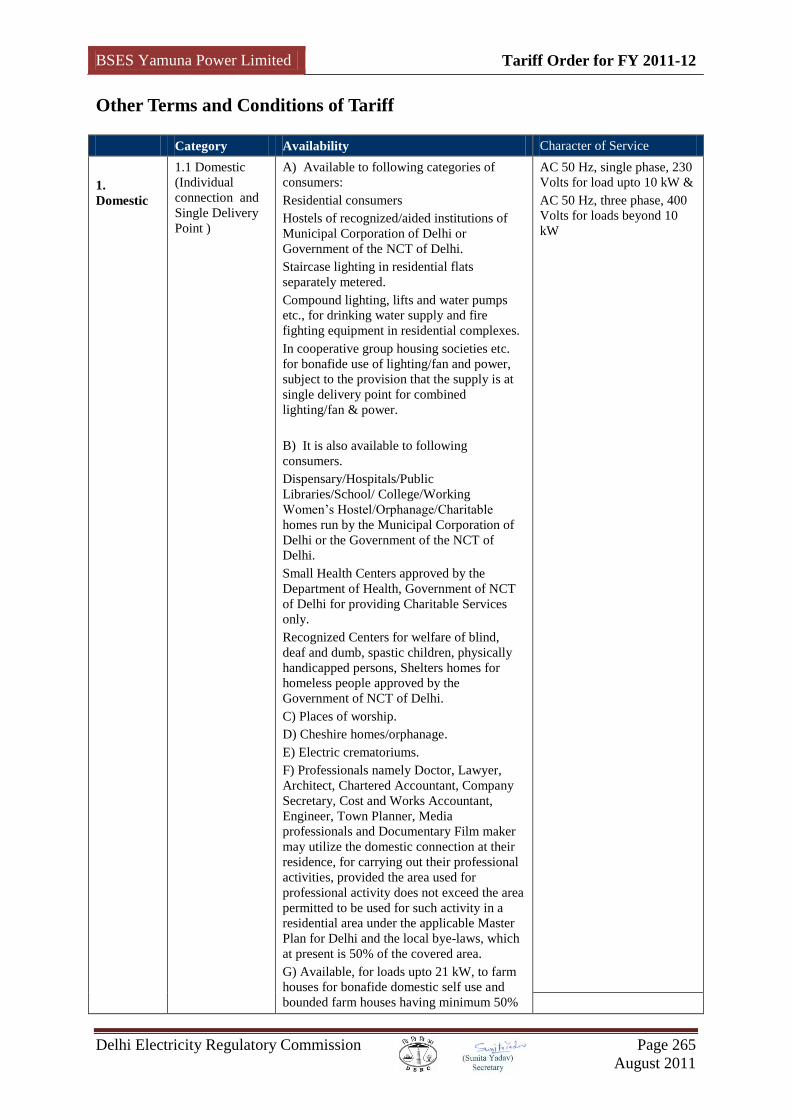

TARIFF SCHEDULE .......................................................................................................................................... 262 NOTES ON SUPERSCRIPTS ............................................................................................................................... 264 OTHER TERMS AND CONDITIONS OF TARIFF ................................................................................................... 265

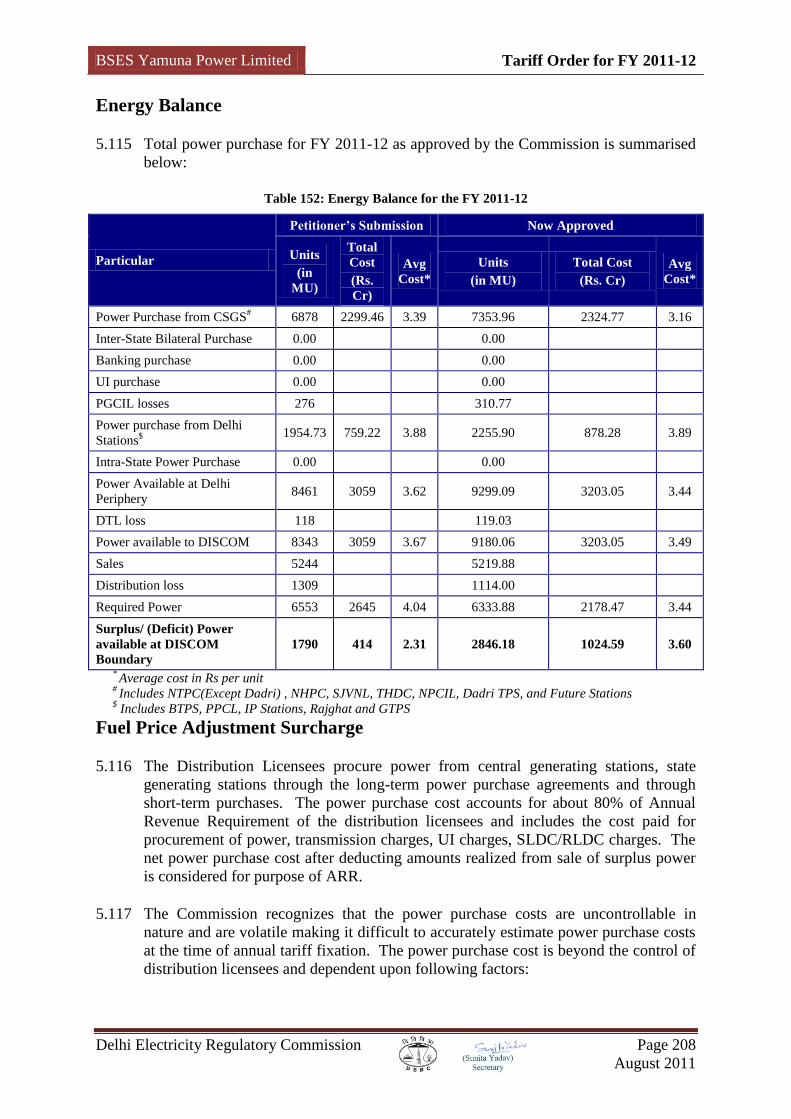

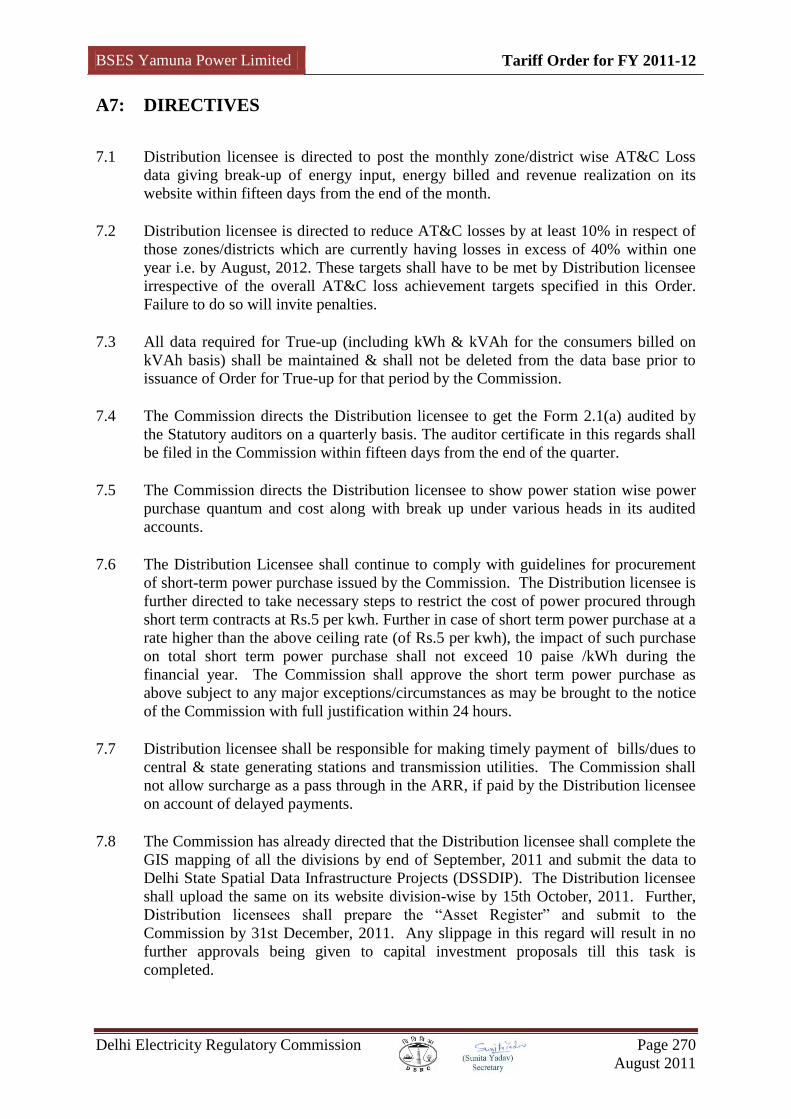

A7: DIRECTIVES ..................................................................................................................................... 270

BSES Yamuna Power Limited Tariff Order for FY 2011-12

Delhi Electricity Regulatory Commission Page 7

August 2011

TABLE 1: MEETINGS OF COORDINATION FORUM 19 TABLE 2: LIST OF CORRESPONDENCE WITH BYPL 22 TABLE 3: SCHEDULE FOR PUBLIC HEARING 25 TABLE 4: OVERALL STANDARDS OF PERFORMANCE FOR APRIL 2009 – MARCH 2010 27 TABLE 5: OVERALL STANDARDS OF PERFORMANCE FOR APRIL 2008 – MARCH 2009 28 TABLE 6: ADDITIONAL CONTRIBUTION TO THE FUND 61 TABLE 7: TERMINAL BENEFITS AS ON 28.02.2011 62 TABLE 8: R&M EXPENSES APPROVED BY COMMISSION IN PREVIOUS TARIFF ORDERS (RS CR) 81 TABLE 9: APPROVED A&G EXPENSES FOR FY 2004-05 IN PREVIOUS TARIFF ORDERS (RS CR) 82 TABLE 10: APPROVED A&G EXPENSES FOR FY 2005-06 IN PREVIOUS TARIFF ORDERS (RS CR) 86 TABLE 11: GFA APPROVED BY THE COMMISSION IN MYT ORDER (RS CR) 86 TABLE 12: OPENING GFA FOR FY 2007-08 (RS CR) 86 TABLE 13: DEPRECIATION APPROVED FOR THE CONTROL PERIOD IN MYT ORDER (RS CR.) 87 TABLE 14: FRESH CONSUMER CONTRIBUTION RECEIVED AND CAPITALISED FOR MYT PERIOD (RS CR.) 89 TABLE 15: CONSUMER CONTRIBUTION CAPITALISED AND GRANTS FOR MYT PERIOD (RS CR.) 89 TABLE 16: GFA CONSIDERED BY THE COMMISSION FOR DEPRECIATION (RS CR) 89 TABLE 17: DEPRECIATION NOW APPROVED FOR THE CONTROL PERIOD (RS CR) 90 TABLE 18: AAD APPROVED BY COMMISSION IN THE MYT ORDER (RS CR) 91 TABLE 19: AAD NOW APPROVED BY COMMISSION (RS CR) 91 TABLE 20: APPROVED RRB FOR THE CONTROL PERIOD IN THE MYT ORDER (RS CR) 92 TABLE 21: REVISED APPROVED RRB FOR THE CONTROL PERIOD (RS CR) 93 TABLE 22: WACC / ROCE / SUPPLY MARGIN COMPUTED IN THE MYT TARIFF ORDER 94 TABLE 23: LOAN & EQUITY APPROVED IN MYT ORDER FOR CAPITAL EXPENDITURE (FY 2002-03-FY 2006-07) 95 TABLE 24: LOAN & EQUITY APPROVED IN MYT ORDER FOR CAPITAL EXPENDITURE (FY 2007-08-FY 2010-11) 95 TABLE 25: WORKING CAPITAL AND FUNDING APPROVED IN THE MYT ORDER (RS. CR) 96 TABLE 26: EQUITY AND FREE RESERVE 96 TABLE 27: LOAN (INCLUDING WORKING CAPITAL LOAN) 96 TABLE 28: WACC / ROCE / SUPPLY MARGIN NOW APPROVED 97 TABLE 29: FUNDING OF LPSC (RS CR) 99 TABLE 30: AT&C LOSS FOR FY 2007-08 99 TABLE 31: REVISED INCENTIVE ON ACCOUNT OF AT&C LOSS OVERACHIEVEMENT FOR FY 2007-08 99 TABLE 32: ACTUAL CPI AND WPI 106 TABLE 33: PROJECTED CPI AND WPI DURING THE CONTROL PERIOD 106 TABLE 34: REVISED ESCALATION FACTOR FOR THE CONTROL PERIOD 106 TABLE 35: REVISED A&G EXPENSES (RS CR) 107 TABLE 36: REVISED EMPLOYEE EXPENSES (RS CR) 107 TABLE 37: IMPACT OF WAGE REVISION AS SUBMITTED BY THE PETITIONER (RS CR) 107 TABLE 38: REVISED EMPLOYEE EXPENSES FOR FY 2005-06 AND FY 2006-07 (RS CR) 108 TABLE 39: IMPACT OF WAGE REVISION ON EMPLOYEE COST APPROVED BY THE COMMISSION (RS CR) 108 TABLE 40: APPROVED ARREAR FOR FY 2007-08 - FY 2010-11 DUE TO REVISION OF BASE YEAR SALARY (RS CR)

109 TABLE 41: ADDITIONAL AMOUNT ALLOWED ON WAGE REVISION (RS CR) 109 TABLE 42: TOTAL ARREARS APPROVED FOR FY 2007-08 TO FY 2010-11 (RS CR) 109 TABLE 43: APPROVED ARREARS PAY OUT FOR FY 2007-08-FY 2009-10 & SALARY HIKE IN FY 2010-11(RS CR) 110 TABLE 44: REVISED EMPLOYEE EXPENSES (RS CR) 110 TABLE 45: INTEREST CAPITALISATION APPROVED IN MYT ORDER (RS CR) 110 TABLE 46: EMPLOYEE EXPENSE CAPITALISATION (RS CR) 111 TABLE 47: CONSUMER SECURITY DEPOSIT (RS. CR) 112 TABLE 48: CONSUMER SECURITY DEPOSIT (RS. CR) 112 TABLE 49: INTEREST RATE (RS CR) 113 TABLE 50 YEAR WISE CARRYING COST CONSIDERED BY THE COMMISSION (RS. CR) 114 TABLE 51: NET IMPACT OF PAST TRUE UP APPROVED BY THE COMMISSION (RS CR) 114 TABLE 52: TRUED UP ENERGY SALES FOR FY 2008-09 (MU) 115 TABLE 53: AT&C LOSS FOR FY 2008-09 AS SUBMITTED BY THE PETITIONER 116 TABLE 54: AT&C LOSS FOR FY 2008-09 AS SUBMITTED BY THE PETITIONER 117 TABLE 55: COMPUTATION OF OVERACHIEVEMENT INCENTIVE AS SUBMITTED BY THE PETITIONER 118 TABLE 56: ACTUAL AT&C LOSS FOR FY 2008-09 AS SUBMITTED BY THE PETITIONER 120

BSES Yamuna Power Limited Tariff Order for FY 2011-12

Delhi Electricity Regulatory Commission Page 8

August 2011

TABLE 57: POWER PURCHASE QUANTUM FOR FY 2008-09 AS CLAIMED BY THE PETITIONER (IN MU) 126 TABLE 58: TRUED-UP POWER PURCHASE QUANTUM FOR FY 2008-09 (IN MU) 127 TABLE 59: POWER PURCHASE COST FOR FY 2008-09 CLAIMED BY THE PETITIONER (IN RS CR) 128 TABLE 60: TRUED-UP POWER PURCHASE COST FOR FY 2008-09 (IN RS CR) 128 TABLE 61: EMPLOYEE EXPENSES PROPOSED FOR FY 2008-09 (RS. CR) 131 TABLE 62: ACTUAL EMPLOYEE EXPENSES FOR FY 2008-09 (RS. CR) 131 TABLE 63: EMPLOYEE EXPENSES APPROVED BY THE COMMISSION FOR FY 2008-09 (RS. CR) 132 TABLE 64: A&G EXPENSES PROPOSED FOR FY 2008-09 (RS. CR) 133 TABLE 65: A&G EXPENSES APPROVED FOR FY 2008-09 (RS. CR) 133 TABLE 66: R&M EXPENSES PROPOSED FOR FY 2008-09 (RS. CR) 133 TABLE 67: R&M EXPENSES APPROVED FOR FY 2008-09 (RS. CR) 134 TABLE 68: O&M EXPENSES APPROVED BY THE COMMISSION FOR FY 2008-09 (RS. CR) 134 TABLE 69: CAPITAL EXPENDITURE (CAPEX) PROPOSED BY THE PETITIONER (RS. CR) 135 TABLE 70: REVISED CAPEX PROPOSED BY THE PETITIONER (RS. CR) 135 TABLE 71: CAPITAL EXPENDITURE IN FY 2008-09 AS SUBMITTED BY THE PETITIONER (RS CR) 135 TABLE 72: CAPITALISATION CLAIMED BY THE PETITIONER (RS CR) 136 TABLE 73: DEPRECIATION AND AAD APPROVED FOR FY 2008-09 (RS. CR) 137 TABLE 74: NOW APPROVED ROCE FOR FY 2008-09 (RS. CR) 138 TABLE 75: CONSUMER SECURITY DEPOSIT (RS. CR) 138 TABLE 76: CONSUMER SECURITY DEPOSIT (RS. CR) 139 TABLE 77: INCOME TAX EXPENSE CLAIMED BY THE PETITIONER (RS. CR) 139 TABLE 78: INCOME TAX EXPENSE APPROVED FOR FY 2008-09 (RS. CR) 140 TABLE 79: INCREASE IN LICENSE FEE SUBMITTED BY THE PETITIONER (RS. CR) 141 TABLE 80: INCREMENTAL AUDIT FEES CLAIMED BY THE PETITIONER (RS. CR) 141 TABLE 81: OTHER EXPENSES CLAIMED BY THE PETITIONER (RS CR) 142 TABLE 82: OTHER EXPENSES APPROVED FOR FY 2008-09 (RS CR) 143 TABLE 83: NON TARIFF INCOME PROPOSED BY THE PETITIONER (RS. CR) 144 TABLE 84: FUNDING OF LPSC (RS CR) 145 TABLE 85: TRUED-UP NON TARIFF INCOME APPROVED (RS. CR) 146 TABLE 86: NON TARIFF INCOME APPROVED FOR FY 2008-09 (RS. CR) 146 TABLE 87: ARR FOR FY 2008-09 APPROVED IN THIS ORDER 146 TABLE 88: REVENUE AVAILABLE TOWARDS ARR IN FY 2008-09 PROPOSED BY THE PETITIONER (RS. CR) 147 TABLE 89: REVENUE AVAILABLE TOWARDS ARR APPROVED FOR FY 2008-09 148 TABLE 90: CONTINGENCY RESERVE (RS. CR) 149 TABLE 91: REVENUE (GAP) / SURPLUS PROPOSED FOR FY 2008-09 (RS. CR) 150 TABLE 92: REVENUE (GAP) / SURPLUS FOR FY 2008-09 (RS. CR) 150 TABLE 93: TRUED UP ENERGY SALES FOR FY 2009-10 (MU) 153 TABLE 94: AT&C LOSS FOR FY 2009-10 AS SUBMITTED BY THE PETITIONER 153 TABLE 95: RECONCILIATION OF COLLECTION AS SUBMITTED BY THE PETITIONER 153 TABLE 96: COMPUTATION OF OVERACHIEVEMENT INCENTIVE AS SUBMITTED BY THE PETITIONER 154 TABLE 97: AT&C LOSS FOR FY 2009-10 AS SUBMITTED BY THE PETITIONER 156 TABLE 98: AT&C LOSS FOR FY 2009-10 AS APPROVED BY THE COMMISSION 158 TABLE 99: AT&C LOSS FOR FY 2009-10 159 TABLE 100: COMPUTATION OF OVERACHIEVEMENT INCENTIVE APPROVED BY THE COMMISSION 159 TABLE 101: POWER PURCHASE QUANTUM FOR FY 2009-10 AS CLAIMED BY THE PETITIONER (IN MU) 160 TABLE 102: POWER PURCHASE COST FOR FY 2009-10 AS CLAIMED BY THE PETITIONER (IN RS CR) 162 TABLE 103: TRUED-UP POWER PURCHASE COST FOR FY 2009-10 (IN RS CR) 162 TABLE 104: EMPLOYEE EXPENSES APPROVED BY THE COMMISSION FOR FY 2009-10 (RS. CR) 164 TABLE 105: A&G EXPENSES APPROVED FOR FY 2009-10 (RS. CR) 164 TABLE 106: R&M EXPENSES PROPOSED FOR FY 2009-10 (RS. CR) 165 TABLE 107: APPROVED R&M EXPENSES (RS. CR) 165 TABLE 108: O&M EXPENSES APPROVED BY THE COMMISSION FOR FY 2009-10 (RS. CR) 166 TABLE 109: CAPITAL EXPENDITURE (CAPEX) PROPOSED BY THE PETITIONER (RS. CR) 166 TABLE 110: REVISED CAPEX PROPOSED BY THE PETITIONER (RS. CR) 166 TABLE 111: CAPITALISATION CLAIMED BY THE PETITIONER (RS CR) 167 TABLE 112: DEPRECIATION INCLUDING AAD SUBMITTED BY PETITIONER FOR FY 2009-10 (RS. CR) 167 TABLE 113: DEPRECIATION AND AAD APPROVED FOR FY 2009-10 (RS. CR) 167

BSES Yamuna Power Limited Tariff Order for FY 2011-12

Delhi Electricity Regulatory Commission Page 9

August 2011

TABLE 114: NOW APPROVED ROCE FOR FY 2009-10 (RS. CR) 168 TABLE 115: CONSUMER SECURITY DEPOSIT (RS. CR) 169 TABLE 116: INTEREST ON CONSUMER SECURITY DEPOSIT (RS. CR) 169 TABLE 117: INCOME TAX EXPENSE CLAIMED BY THE PETITIONER 170 TABLE 118: INCOME TAX EXPENSE APPROVED 170 TABLE 119: ADDITIONAL EXPENSES CLAIMED FOR FY 2009-10 (RS CR) 171 TABLE 120: OTHER EXPENSES APPROVED FOR FY 2009-10 (RS CR) 172 TABLE 121: NON TARIFF INCOME FOR FY 2009-10 (RS CR) 173 TABLE 122: FUNDING OF LPSC (RS CR) 174 TABLE 123: TRUED-UP NON TARIFF INCOME APPROVED (RS. CR) 175 TABLE 124: NON TARIFF INCOME (RS. CR) 175 TABLE 125: AGGREGATE REVENUE REQUIREMENT (RS CR) 176 TABLE 126: REVENUE DETAILS SUBMITTED BY THE PETITIONER 177 TABLE 127: REVENUE AVAILABLE TOWARDS ARR APPROVED FOR FY 2009-10 177 TABLE 128: CONTINGENCY RESERVE (RS. CR) 178 TABLE 129: REVENUE (GAP)/ SURPLUS FOR FY 2009-10 (RS CR) 178 TABLE 130: PETITIONER’S SUBMISSION OF ENERGY SALES FOR FY 2011-12 (MU) 179 TABLE 131: APPROVED SALES FOR FY 2011-12 (MU) 185 TABLE 132: POWER FACTOR CONSIDERED BY THE COMMISSION 186 TABLE 133: REVENUE PROJECTED FOR FY 2011-12 186 TABLE 134: AT&C LOSS TARGETS FOR FY 2011-12 (%) 187 TABLE 135: APPROVED ENERGY REQUIREMENT FOR FY 2011-12 187 TABLE 136: ALLOCATION OF POWER TO DELHI FROM CENTRAL SECTOR GENERATING STATIONS 189 TABLE 137: ALLOCATION OF UNALLOCATED QUOTA TO DELHI DISCOMS 190 TABLE 138: ALLOCATION FROM DELHI STATIONS TO BYPL 190 TABLE 139: ENERGY AVAILABLE TO BYPL AS PER THE PETITIONER (MU) 192 TABLE 140: APPROVED ENERGY AVAILABLE FROM DELHI GENERATING STATIONS TO BYPL (MU) 193 TABLE 141: ENERGY AVAILABLE TO BYPL FROM CENTRAL SECTOR GENERATING STATIONS (MU) 193 TABLE 142: ENERGY AVAILABLE TO BYPL FROM CENTRAL SECTOR GENERATING STATIONS (MU) 195 TABLE 143: AVAILABILITY OF ENERGY FROM NEW GENERATING STATIONS IN FY 2011-12 196 TABLE 144: ENERGY AVAILABLE FROM FUTURE STATIONS AS APPROVED BY THE COMMISSION (MU) 198 TABLE 145: ENERGY PURCHASE /SALES THROUGH OTHER SOURCES FOR FY 2011-12 (MU) 199 TABLE 146: PROPOSED POWER PURCHASE COST FOR EXISTING STATIONS (RS. CR) 201 TABLE 147: APPROVED TOTAL POWER PURCHASE COST FOR EXISTING STATIONS (RS. CR) 203 TABLE 148: APPROVED POWER PURCHASE COST FOR NEW GENERATING STATIONS (RS. CR) 205 TABLE 149: COST/REVENUE OF POWER PURCHASE/SALE THROUGH OTHER SOURCES (RS. CR) 206 TABLE 150: IMPACT OF HON’BLE ATE JUDGEMENT DATED 31ST MAY 2010 207 TABLE 151: APPROVED TRANSMISSION LOSSES AND CHARGES FOR THE PETITIONER FOR FY 2011-12 207 TABLE 152: ENERGY BALANCE FOR THE FY 2011-12 208 TABLE 153: SCHEDULE – BASE VARIABLE COST FY 2011-12 210 TABLE 154: APPROVED SVRS PENSION EXPENSES (RS CR) 213 TABLE 155: EMPLOYEE COST APPROVED FOR FY 2011-12 (RS CR) 214 TABLE 156: NUMBER OF EMPLOYEES 214 TABLE 157: STATEMENT OF ALLOCATION OF EMPLOYEE COST BETWEEN WHEELING AND RETAIL SUPPLY 214 TABLE 158: APPROVED ALLOCATION OF EMPLOYEE COST (RS. CR) 215 TABLE 159: APPROVED A&G EXPENSES FOR THE CONTROL PERIOD (RS CR) 216 TABLE 160: ALLOCATION OF A&G EXPENSES BETWEEN WHEELING & RETAIL SUPPLY BUSINESS 216 TABLE 161: APPROVED ALLOCATION OF A&G EXPENSES (RS CR) 217 TABLE 162 PROPOSED K FACTOR 217 TABLE 163 PROPOSED R&M EXPENSES 218 TABLE 164: DETERMINATION OF ‘K’ 218 TABLE 165: APPROVED R&M EXPENSES FOR FY 2011-12 (RS CR) 219 TABLE 166: ALLOCATION OF R&M EXPENSES BETWEEN WHEELING & RETAIL SUPPLY BUSINESS 219 TABLE 167: APPROVED ALLOCATION OF R&M EXPENSES (RS CR) 220 TABLE 168: APPROVED O&M EXPENSES FOR FY 2011-12 (RS CR) 220 TABLE 169: PROPOSED CAPITAL INVESTMENT DURING THE CONTROL PERIOD (RS CR) 221 TABLE 170 PROPOSED CAPITALIZATION AND CWIP FOR FY 2011-12 222

BSES Yamuna Power Limited Tariff Order for FY 2011-12

Delhi Electricity Regulatory Commission Page 10

August 2011

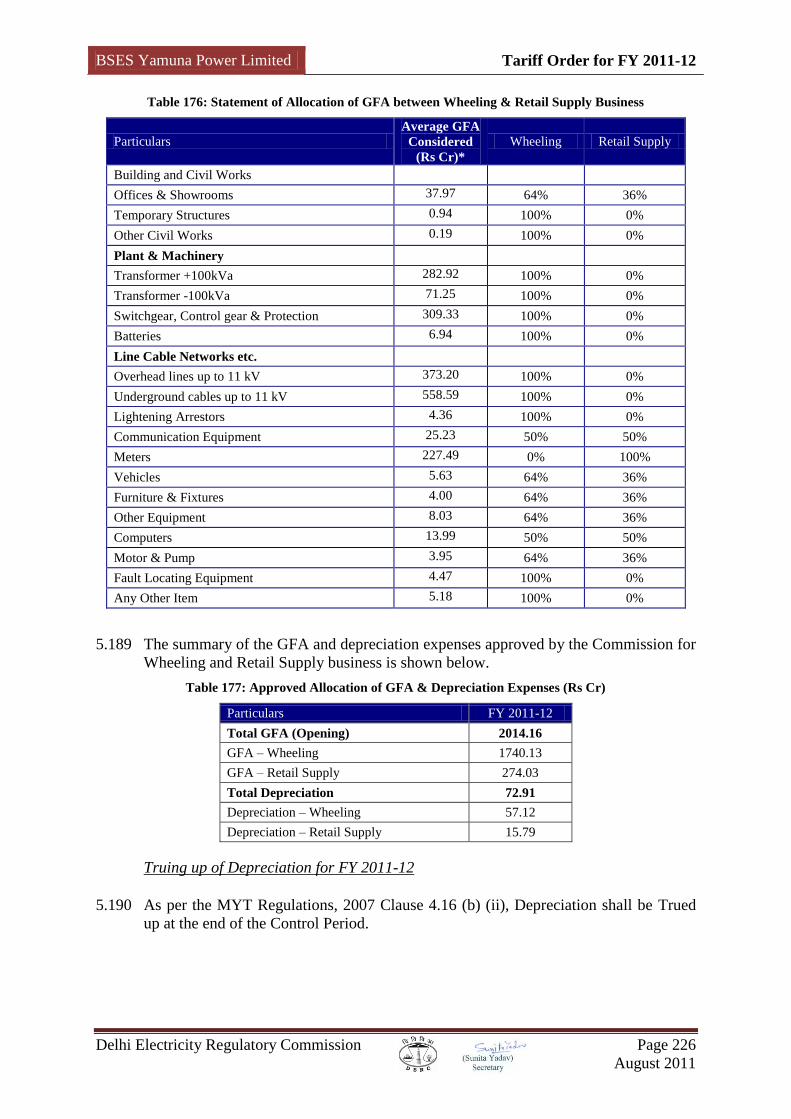

TABLE 171: APPROVED CWIP FOR FY 2011-12 (RS CR) 223 TABLE 172: PROPOSED GROSS FIXED ASSETS AND DEPRECIATION (RS CR) 223 TABLE 173: GROSS FIXED ASSETS FOR FY 2011-12 (RS CR) 224 TABLE 174: CONSUMER CONTRIBUTION AND GRANTS FOR FY 2011-12 (RS CR) 224 TABLE 175: APPROVED DEPRECIATION FOR FY 2011-12 (RS CR) 225 TABLE 176: STATEMENT OF ALLOCATION OF GFA BETWEEN WHEELING & RETAIL SUPPLY BUSINESS 226 TABLE 177: APPROVED ALLOCATION OF GFA & DEPRECIATION EXPENSES (RS CR) 226 TABLE 178: ACCUMULATED DEPRECIATION PROPOSED FOR FY 2011-12 (RS CR) 227 TABLE 179: APPROVED ACCUMULATED DEPRECIATION (RS CR) 227 TABLE 180: ALLOCATION OF ACCUMULATED DEPRECIATION (RS CR) 227 TABLE 181: AAD SUBMITTED BY THE PETITIONER (RS CR) 228 TABLE 182: AAD APPROVED BY COMMISSION (RS CR) 229 TABLE 183 ALLOCATION OF AAD INTO WHEELING AND RETAIL SUPPLY (RS. CR) 229 TABLE 184: PROPOSED RRB FOR FY 2011-12 (RS CR) 230 TABLE 185: CAPITALISED CONSUMER CONTRIBUTION FOR FY 2011-12 (RS CR) 230 TABLE 186: APPROVED RRB FOR THE CONTROL PERIOD (RS CR) 231 TABLE 187: ALLOCATION OF RRB FOR THE CONTROL PERIOD (RS CR) 231 TABLE 188: PROPOSED WORKING CAPITAL FOR THE CONTROL PERIOD (RS CR) 232 TABLE 189: APPROVED WORKING CAPITAL FOR FY 2011-12 (RS CR) 232 TABLE 190: ALLOCATION OF WORKING CAPITAL FOR THE CONTROL PERIOD (RS CR) 233 TABLE 191: PROPOSED MEANS OF FINANCE FOR FY 2011-12 (RS CR) 234 TABLE 192: APPROVED MEANS OF FINANCE FOR FY 2011-12 (RS CR) 234 TABLE 193: LOAN DETAILS 234 TABLE 194: APPROVED ADDITION IN EQUITY AND FREE RESERVES (RS CR) 235 TABLE 195: APPROVED DEBT (RS CR) 235 TABLE 196: PROPOSED ROCE FOR FY 2011-12 (RS CR) 235 TABLE 197: APPROVED ROCE FOR FY 2011-12 (RS CR) 236 TABLE 198: ALLOCATION OF ROCE FOR FY 2011-12 (RS CR) 236 TABLE 199: PROPOSED CAPITALISATION OF INTEREST AND OTHER EXPENSES (RS CR) 237 TABLE 200: APPROVED EXPENSE CAPITALISATION FOR FY 2011-12 (RS CR) 237 TABLE 201 ALLOCATION OF APPROVED EXPENSE CAPITALIZATION (RS. CR) 238 TABLE 202: PROPOSED TAX EXPENSES FOR FY 2011-12 (RS CR) 238 TABLE 203 APPROVED TAX EXPENSES FOR FY 2011-12 238 TABLE 204: PROPOSED NON-TARIFF INCOME FOR FY 2011-12 (RS CR) 238 TABLE 205: APPROVED NON-TARIFF INCOME FOR FY 2011-12 (RS CR) 239 TABLE 206: ALLOCATION OF NTI EXPENSES BETWEEN WHEELING & RETAIL SUPPLY BUSINESS 239 TABLE 207: APPROVED ALLOCATION OF NTI FOR FY 2011-12 (RS CR) 239 TABLE 208: ADDITIONAL RETURN PROPOSED BY THE PETITIONER (RS. CR) 242 TABLE 209: ADDITIONAL RETURN APPROVED BY THE COMMISSION (RS. CR) 242 TABLE 210: APPROVED SUPPLY MARGIN FOR FY 2011-12 (RS. CR) 243 TABLE 211: PROPOSED ARR FOR FY 2011-12 (RS CR) 243 TABLE 212: ARR FOR WHEELING BUSINESS FOR FY 2011-12 (RS CR) 244 TABLE 213: ARR FOR RETAIL SUPPLY BUSINESS FOR FY 2011-12 (RS CR) 244 TABLE 214: APPROVED ARR FOR FY 2011-12 (RS CR) 244 TABLE 215: APPROVED ARR FOR WHEELING BUSINESS FOR FY 2011-12 (RS CR) 245 TABLE 216: APPROVED ARR FOR RETAIL SUPPLY BUSINESS FOR FY 2011-12 (RS CR) 245 TABLE 217: APPROVED CONTINGENCY RESERVE AT THE END OF FY 2009-10 (RS CR) 246 TABLE 218: REVENUE (GAP)/ SURPLUS OF BYPL FOR TILL FY 2009-10 (RS. CR) 248 TABLE 219: REVENUE (GAP)/ SURPLUS OF BRPL FOR TILL FY 2009-10 (RS. CR) 248 TABLE 220: NET REVENUE (GAP)/ SURPLUS OF NDPL TILL FY 2009-10 (RS. CR) 249 TABLE 221: REVENUE (GAP)/ SURPLUS FOR ALL DISCOMS AT THE END OF FY 2009-10 (RS. CR) 249 TABLE 222: REVENUE (GAP)/ SURPLUS OF BYPL AT EXISTING TARIFFS FOR FY 2011-12 (RS. CR) 250 TABLE 223: REVENUE (GAP)/ SURPLUS OF NDPL AT EXISTING TARIFFS FOR FY 2011-12 (RS. CR) 250 TABLE 224: REVENUE (GAP)/ SURPLUS OF BRPL AT EXISTING TARIFFS FOR FY 2011-12 (RS. CR) 250 TABLE 225 REVENUE (GAP)/ SURPLUS FOR ALL DISCOMS FOR FY 2011-12 (RS. CR) 250 TABLE 226: REVENUE AT EXISTING TARIFFS (RS. CR) 252 TABLE 227: REVENUE AT REVISED TARIFFS (RS. CR) 252

BSES Yamuna Power Limited Tariff Order for FY 2011-12

Delhi Electricity Regulatory Commission Page 11

August 2011

TABLE 228: NET REVENUE (GAP)/ SURPLUS OF BYPL AT REVISED TARIFFS (RS. CR) 253 TABLE 229: APPROVED ENERGY SALES (MU) 254 TABLE 230: DISTRIBUTION LOSS (%) 254 TABLE 231: APPROVED ENERGY INPUT (MU) 255 TABLE 232: WHEELING COST ALLOCATION ASSET WISE (RS CR) 255 TABLE 233: WHEELING COST ALLOCATED TO DIFFERENT VOLTAGES (RS CR) 255 TABLE 234: WHEELING CHARGE (PAISA PER UNIT) 256 TABLE 235: RETAIL SUPPLY CHARGE (PAISA PER UNIT) 256 TABLE 236: SUPPLY MARGIN CHARGE (PAISA PER UNIT) 256 TABLE 237: COST OF SUPPLY FOR NDPL (PAISA PER UNIT) 257 TABLE 238: COST OF SUPPLY FOR BRPL (PAISA PER UNIT) 257 TABLE 239: COST OF SUPPLY FOR BYPL (PAISA PER UNIT) 257

BSES Yamuna Power Limited Tariff Order for FY 2011-12

Delhi Electricity Regulatory Commission Page 12

August 2011

List of Abbreviations

ARR Aggregate Revenue Requirement

A&G Administrative and General

AAD Advance Against Depreciation

ABT Availability Based Tariff

ACD Advance Consumption Deposit

AMR Automated Meter Reading

APDRP Accelerated Power Development and Reforms Program

AT&C Aggregate Technical and Commercial

ATE Appellate Tribunal for Electricity

BEST Birhanmumbai Electric Supply Test

BHEL Bharat Heavy Electrical Limited

BIS Bureau of Indian Standards

BPTA Bulk Power Transmission Agreement

BRPL BSES Rajdhani Power Limited

BST Bulk Supply Tariff

BTPS Badarpur Thermal Power Station

BYPL BSES Yamuna Power Limited

CAGR Compounded Annual Growth Rate

CCGT Combined Cycle Gas Turbine

CEA Central Electricity Authority

CERC Central Electricity Regulatory Commission

CFL Compact Fluorescent Lamp

CGHS Cooperative Group Housing Societies

CGS Central Generating Stations

CIC Central Information Commission

CISF Central Industrial Security Force

CoS Cost of Supply

CPI Consumer Price Index

CPRI Central Power Research Institute

CPSUs Central Power Sector Utilities

CSGS Central Sector Generating Stations

CWIP Capital Work in Progress

DA Dearness Allowance

DA Distribution Automation

DDA Delhi Development Authority

DERA Delhi Electricity Reform Act

DERC Delhi Electricity Regulatory Commission

DIAL Delhi International Airport Limited

DISCOMs Distribution Companies (BRPL, BYPL & NDPL)

DMRC Delhi Metro Rail Corporation

DPCL Delhi Power Corporation Limited

BSES Yamuna Power Limited Tariff Order for FY 2011-12

Delhi Electricity Regulatory Commission Page 13

August 2011

DTL Delhi Transco Limited

DVB Delhi Vidyut Board

DVC Damodar Valley Corporation

EHV Extra High Voltage

EPS Electric Power Survey

FBT Fringe Benefit Tax

FPA Fuel Price Adjustment

GFA Gross Fixed Assets

GIS Geographical Information System

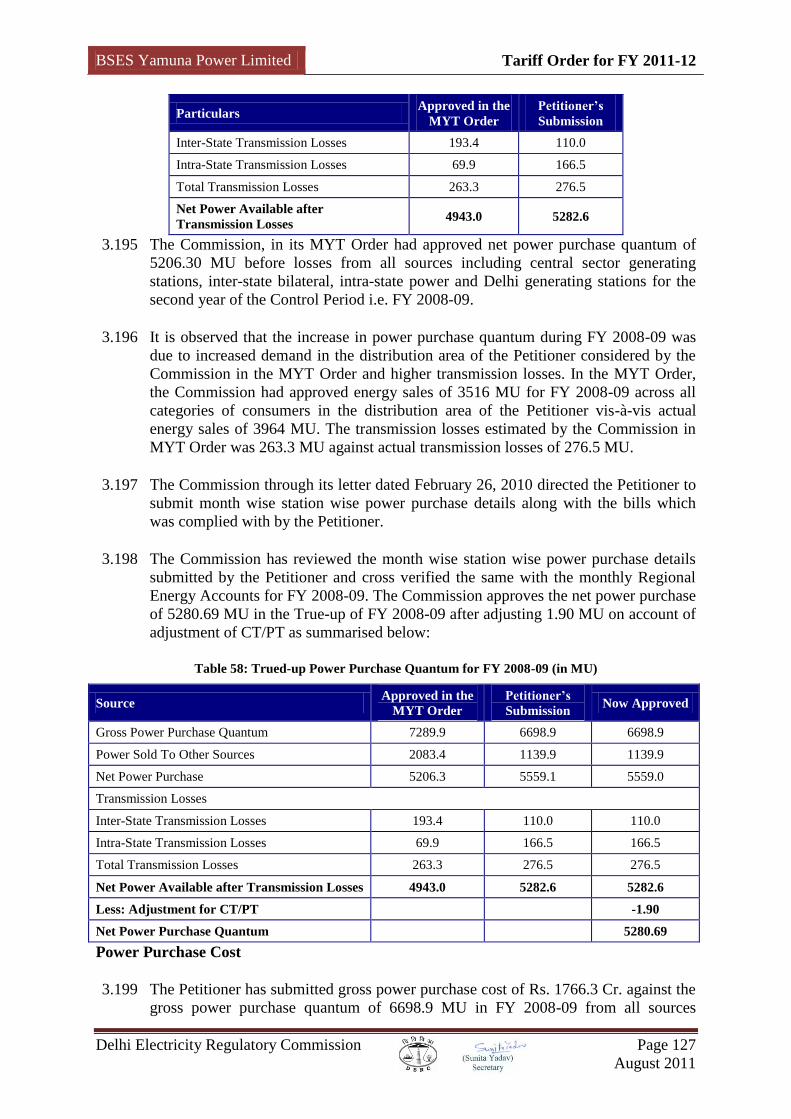

GoNCTD Government of National Capital Territory of Delhi

GTPS Gas Turbine Power Station

HEP Hydro Electric Power

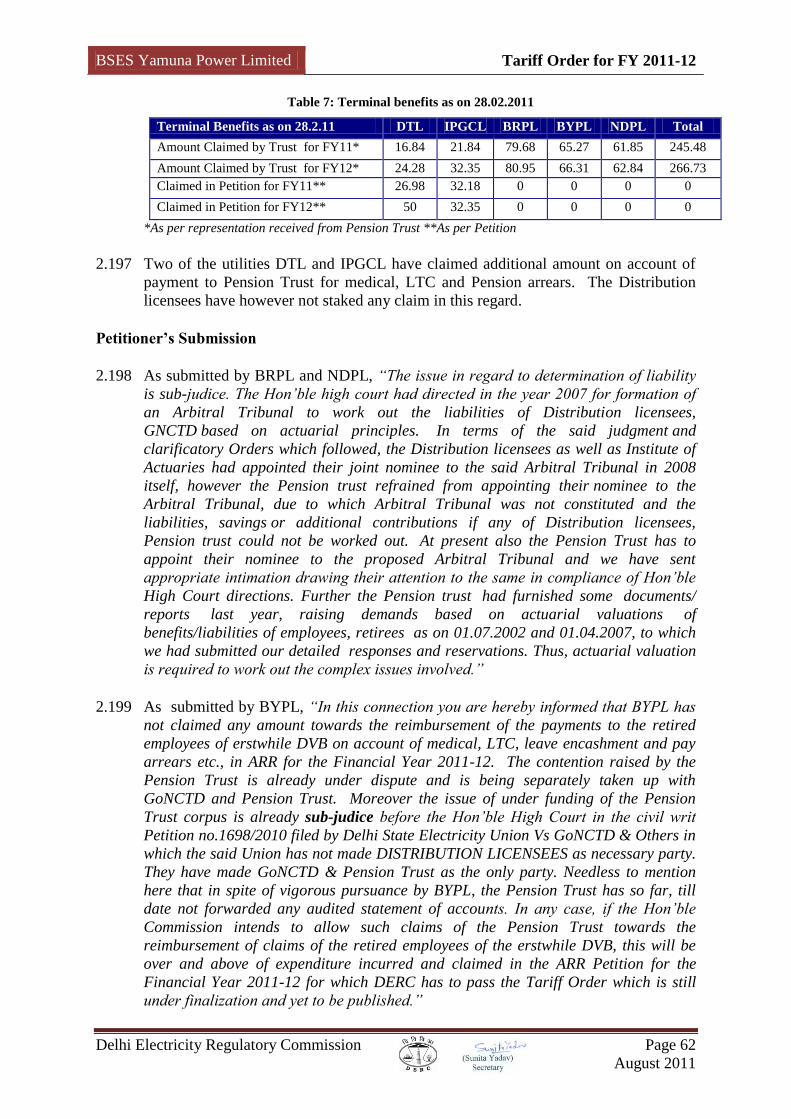

HPSEB Himachal Pradesh State Electricity Board

HRA House Rent Allowance

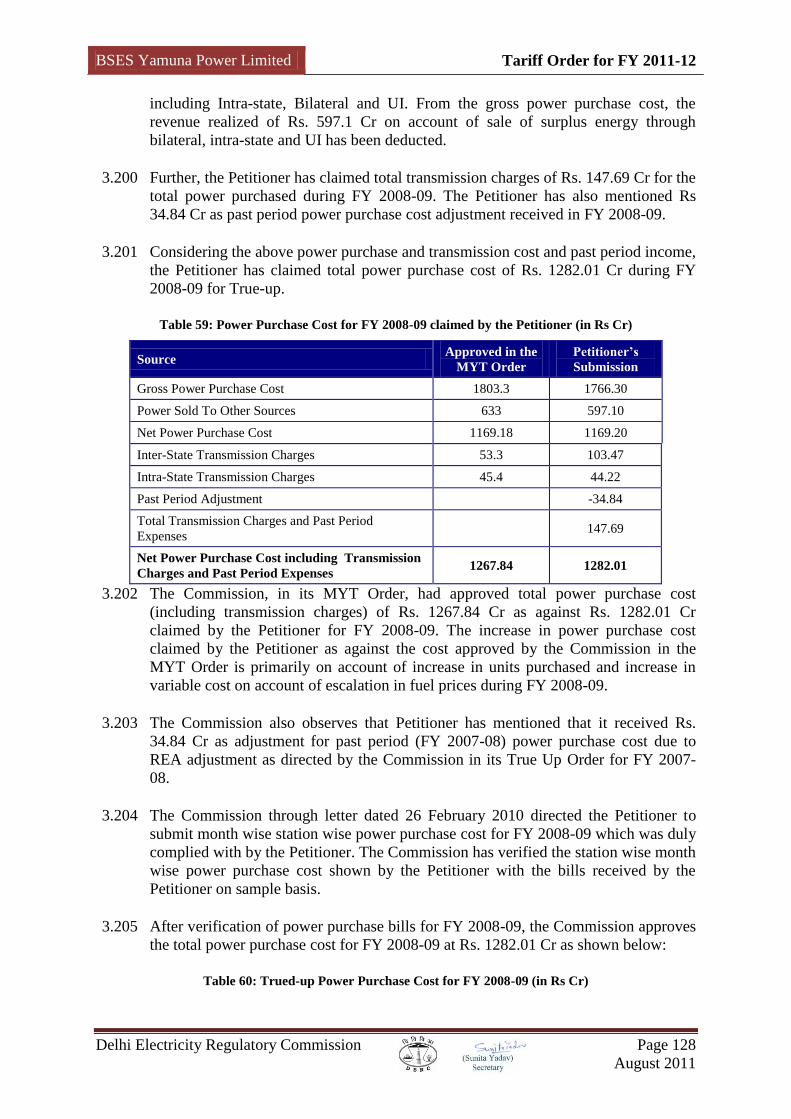

HT High Tension

HVDS High Voltage Distribution System

IDC Interest During Construction

IGI Airport Indira Gandhi International Airport

IPGCL Indraprastha Power Generation Company Limited

JJ Cluster Jhugghi Jhopadi Cluster

KSEB Kerala State Electricity Board

LED Light Emitting Diode

LIP Large Industrial Power

LT Low Tension

LVDS Low Voltage Distribution System

MCD Municipal Corporation of Delhi

MES Military Engineering Service

MLHT Mixed Load High Tension

MMC Monthly Minimum Charge

MoP Ministry of Power

MTNL Mahanagar Telephone Nigam Limited

MU Million Units

MYT Multi Year Tariff

NABL National Accreditation Board for Testing and Calibration of

Laboratories

NAPS Narora Atomic Power Station

NCT National Capital Territory

NDLT Non Domestic Lowe Tension

NDMC New Delhi Municipal Corporation

NDPL North Delhi Power Limited

NEP National Electricity Policy

NGO Non Government Organisation

NHPC National Hydroelectric Power Corporation

BSES Yamuna Power Limited Tariff Order for FY 2011-12

Delhi Electricity Regulatory Commission Page 14

August 2011

NPCIL Nuclear Power Corporation of India Limited

NRPC Northern Regional Power Committee

NTI Non Tariff Income

NTP National Tariff Policy

O&M Operations and Maintenance

OCFA Opening Cost of Fixed Assets

PGCIL Power Grid Corporation of India

PLF Plant Load Factor

PLR Prime Lending Rate

PPA Power Purchase Agreement

PPCL Pragati Power Corporation Limited

PTC Power Trading Corporation

PWD Public Works Department

R&M Repair and Maintenance

RAPS Rajasthan Atomic Power Station

REA Regional Energy Account

RoCE Return on Capital Employed

ROE Return on Equity

RRB Regulated Rate Base

RTI Right to Information

RWA Resident Welfare Associations

SBI State Bank of India

SERC State Electricity Regulatory Commission

SIP Small Industrial Power

SJVNL Satluj Jal Vidyut Nigam Limited

SLDC State Load Despatch Center

SPD Single Point Delivery

SPUs State Power Utilities

SVRS Special Voluntary Retirement Scheme

THDC Tehri Hydro Development Corporation

ToD Time of Day

TPS Thermal Power Station

UI Unscheduled Interchange

WACC Weighted Average Cost of Capital

WC Working Capital

WPI Wholesale Price Index

BSES Yamuna Power Limited Tariff Order for FY 2011-12

Delhi Electricity Regulatory Commission Page 15

August 2011

A1: INTRODUCTION

1.1 This Order relates to the Petition filed by BSES Yamuna Power Limited (hereinafter

referred to as „BYPL‟ or the „Petitioner‟) for True Up of uncontrollable expenses for

FY 2009-10 and approval of Aggregate Revenue Requirement (ARR) and Wheeling

and Retail Supply Tariffs for all consumer categories for FY 2011-12 using Multi

Year Tariff Principles specified in the Delhi Electricity Regulatory Commission

(Terms and Conditions for Determination of Wheeling Tariff and Retail Supply

Tariff) Regulations, 2007 (hereinafter referred to as the „MYT Regulations‟).

Transfer Scheme

1.2 Prior to the year 2001, Delhi Vidyut Board (hereinafter referred to as „DVB‟) was the

sole entity handling all functions of generation, transmission and distribution of

electricity in the National Capital Territory of Delhi (hereinafter referred to as

„Delhi‟). The Government of National Capital Territory of Delhi (hereinafter referred

to as „GoNCTD‟), however, notified the Delhi Electricity Reform (Transfer Scheme)

Rules, 2001 (hereinafter referred to as „Transfer Scheme‟) on November 20, 2001 and

provided for unbundling of DVB into different entities handling generation,

transmission and distribution of electricity.

1.3 The Transfer Scheme provided for unbundling of DVB and the transfer of existing

distribution assets of DVB in the areas of Central East and East of Delhi to BYPL

(formerly known as Central East Delhi Distribution Company Limited) and transfer of

the distribution assets in other areas of Delhi were transferred to two other distribution

companies. All the three distribution companies shall hereinafter be collectively

referred to as „DISCOMs‟.

BSES Yamuna Power Limited (BYPL)

1.4 BYPL is a company incorporated under the Companies Act, 1956 and is entrusted

with the business of distribution and retail supply of electricity in the specified area of

Central East and East of Delhi in the NCT of Delhi (as specified in the Transfer

Scheme).

1.5 Till March 31, 2007, Delhi Transco Limited (DTL) was the sole entity responsible for

the bulk procurement and bulk supply of power in Delhi. All the DISCOMs in Delhi

had to purchase power from DTL at an approved Bulk Supply Tariff (BST) based on

their capacity to pay. On June 28, 2006, GoNCTD issued a set of Policy Directions

for making power supply arrangements in Delhi from April 1, 2007. These Policy

Directions were issued under Section 108 of the Electricity Act 2003 (hereinafter

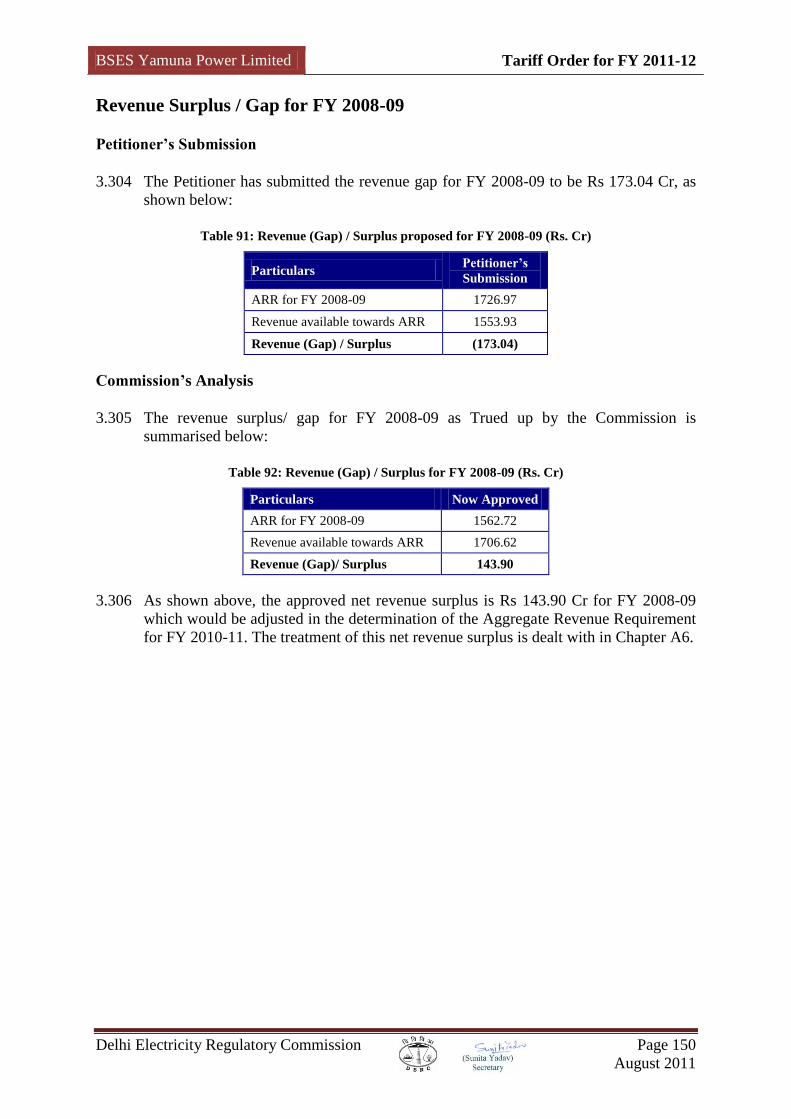

referred to as the „Act‟) and stated the following:

(a) With effect from April 1, 2007, the responsibility for arranging supply of

power in Delhi shall rest with the Distribution Companies in accordance with

the provisions of the Electricity Act 2003 and also the National Electricity

Policy. The DERC may initiate all measures well in advance so that necessary

arrangements are put in place.

BSES Yamuna Power Limited Tariff Order for FY 2011-12

Delhi Electricity Regulatory Commission Page 16

August 2011

(b) With effect from April 1, 2007, the Delhi Transco Limited will be a Company

engaged in only wheeling of power and also operate the State Load Dispatch

Centre (SLDC) in accordance with the mandate of the GoNCTD.

(c) The DERC would have to make arrangements on the various existing Power

Purchase Agreements (PPAs) between the present Distribution Companies in a

manner to take care of different load profiles of the three DISCOMs, the New

Delhi Municipal Council (NDMC) and also the Military Engineering Services

(MES).

(d) While addressing the issue of transition to new arrangements in which the

Distribution Companies would trade in power, specific Orders may be issued

by DERC for ensuring that there is no disruption in the transmission network.

1.6 The business of Bulk Supply of electricity is no longer a part of the business of DTL,

and the same is vested with the distribution licensees (DISCOMs) of the State, w.e.f.

April 1, 2007.

1.7 The PPAs of the existing and upcoming projects were assigned to the DISCOMs; vide

the Commission‟s Order dated March 31, 2007. In the same Order, the Commission

Ordered for introduction of Intra state ABT in Delhi w.e.f April 1, 2007 with the

following conditions:

(a) The UI rate should be the same as prescribed by CERC as on March 31, 2007.

All the five Distribution Companies/ Agencies as well as DTL shall comply

with the various provisions of the IEGC/ Regulations issued by CERC in this

regard.

(b) The SLDC shall act as the nodal agency for the collection and distribution of

UI charges as far as ABT is concerned.

(c) Scheduling be followed as is being practiced which is also generally in

conformity with the procedure followed by NRLDC.

(d) STU/SLDC shall exercise necessary control in transmission/ load dispatch,

system protection as specified in the Act, IEGC, Regulations of CERC, CEA,

Rules etc.

(e) Any Violations of the Act, Rules, Regulations, IEGC etc. shall be brought to

the notice of the Commission by STU/SLDC.

Delhi Electricity Regulatory Commission (DERC)

1.8 The Delhi Electricity Regulatory Commission (hereinafter referred to as „DERC or

the „Commission‟) was constituted by the GoNCTD on March 3, 1999 and it became

operational from December 10, 1999.

1.9 The Commission‟s approach to regulation is driven by the Electricity Act 2003, the

National Electricity Plan, the National Tariff Policy and the Delhi Electricity Reform

BSES Yamuna Power Limited Tariff Order for FY 2011-12

Delhi Electricity Regulatory Commission Page 17

August 2011

Act 2000 (hereinafter referred to as „DERA‟). The Act mandates the Commission to

take measures conducive to the development and management of the electricity

industry in an efficient, economic and competitive manner.

Functions of the Commission

1.10 The Commission derives its powers from DERA as well as from the Act. The major

functions assigned to the Commission under the DERA are as follows:

(a) to determine the tariff for electricity, wholesale, bulk, grid or retail and for the

use of the transmission facilities;

(b) to regulate power purchase, transmission, distribution, sale and supply;

(c) to promote competition, efficiency and economy in the activities of the

electricity industry in the National Capital Territory of Delhi;

(d) to aid and advise the Government on power policy;

(e) to collect and publish data and forecasts;

(f) to regulate the assets, properties and interest in properties concerned or related

to the electricity industry in the National Capital Territory of Delhi including

the conditions governing entry into, and exit from the electricity industry in

such manner as to safeguard the public interest;

(g) to issue licenses for transmission, bulk supply, distribution or supply of

electricity;

(h) to regulate the working of the licensees; and

(i) to adjudicate upon the disputes and differences between licensees.

1.11 The functions assigned to the Commission under the Act are as follows:

“Section 86 (1) The State Commission shall discharge the following functions,

namely: -

(a) determine the tariff for generation, supply, transmission and wheeling of

electricity, wholesale, bulk or retail, as the case may be, within the State:

Provided that where open access has been permitted to a category of

consumers under Section 42, the State Commission shall determine only the

wheeling charges and surcharge thereon, if any, for the said category of

consumers;

(b) regulate electricity purchase and procurement process of distribution licensees

including the price at which electricity shall be procured from the generating

companies or licensees or from other sources through agreements for purchase

of power for distribution and supply within the State;

BSES Yamuna Power Limited Tariff Order for FY 2011-12

Delhi Electricity Regulatory Commission Page 18

August 2011

(c) facilitate intra-state transmission and wheeling of electricity;

(d) issue licences to persons seeking to act as transmission licensees, distribution

licensees and electricity traders with respect to their operations within the

State;

(e) promote cogeneration and generation of electricity from renewable sources of

energy by providing suitable measures for connectivity with the grid and sale

of electricity to any person, and also specify, for purchase of electricity from

such sources, a percentage of the total consumption of electricity in the area of

a distribution licensee;

(f) adjudicate upon the disputes between the licensees and generating companies

and to refer any dispute for arbitration;

(g) levy fee for the purposes of this Act;

(h) specify State Grid Code consistent with the Grid Code specified under Clause

(h) of sub-section (1) of Section 79;

(i) specify or enforce standards with respect to quality, continuity and reliability

of service by licensees;

(j) fix the trading margin in the intra-state trading of electricity, if considered,

necessary;

(k) discharge such other functions as may be assigned to it under this Act.

(2) The State Commission shall advise the State Government on all or any of the

following matters, namely: -.

(i) promotion of competition, efficiency and economy in activities of the

electricity industry;

(ii) promotion of investment in electricity industry;

(iii) reorganisation and restructuring of electricity industry in the State;

(iv) matters concerning generation, transmission, distribution and trading of

electricity or any other matter referred to the State Commission by that

Government.”

1.12 As part of the tariff related provisions of the Act, the State Electricity Regulatory

Commission (SERC) has to be guided by the National Electricity Policy, National

Tariff Policy and the National Electricity Plan.

BSES Yamuna Power Limited Tariff Order for FY 2011-12

Delhi Electricity Regulatory Commission Page 19

August 2011

The Coordination Forum

1.13 The Commission wrote to Government of NCT of Delhi (GoNCTD) on 1st April,

2005 to constitute the Coordination Forum consisting of the Chairperson of the State

Commission and the Members thereof, representatives of the generating companies,

transmission licensees, and distribution licensees engaged in generation, transmission

and distribution etc. in accordance with section 166(4) of the Electricity Act, 2003.

1.14 Accordingly, the GoNCTD vide Notification No. F.11/36/2005/Power/1789 dated

16.06.2005 constituted the Coordination Forum, comprising of Chairperson and

Members of DERC, CMD of DTL, Managing Director of IPGCL/PPCL, CEOs of

NDPL, BYPL and BRPL with Secretary, DERC as the Member Secretary. Since the

Committee constituted did not include NDMC and MES, who also distribute power in

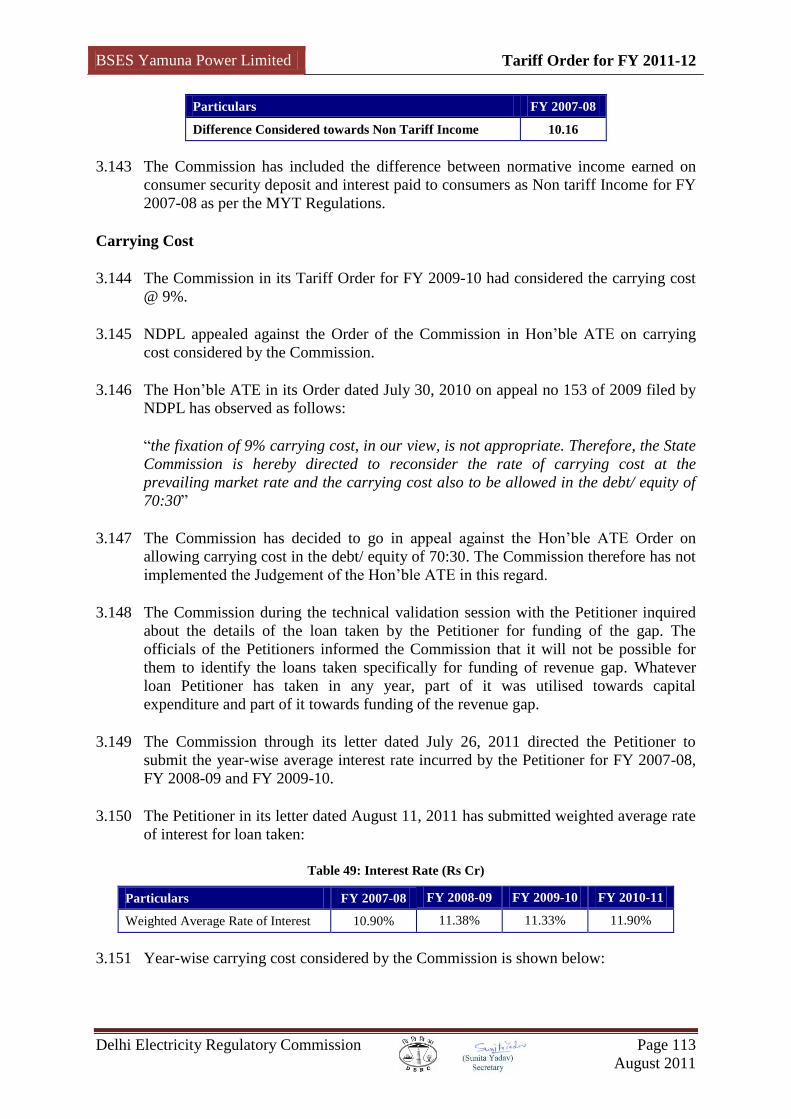

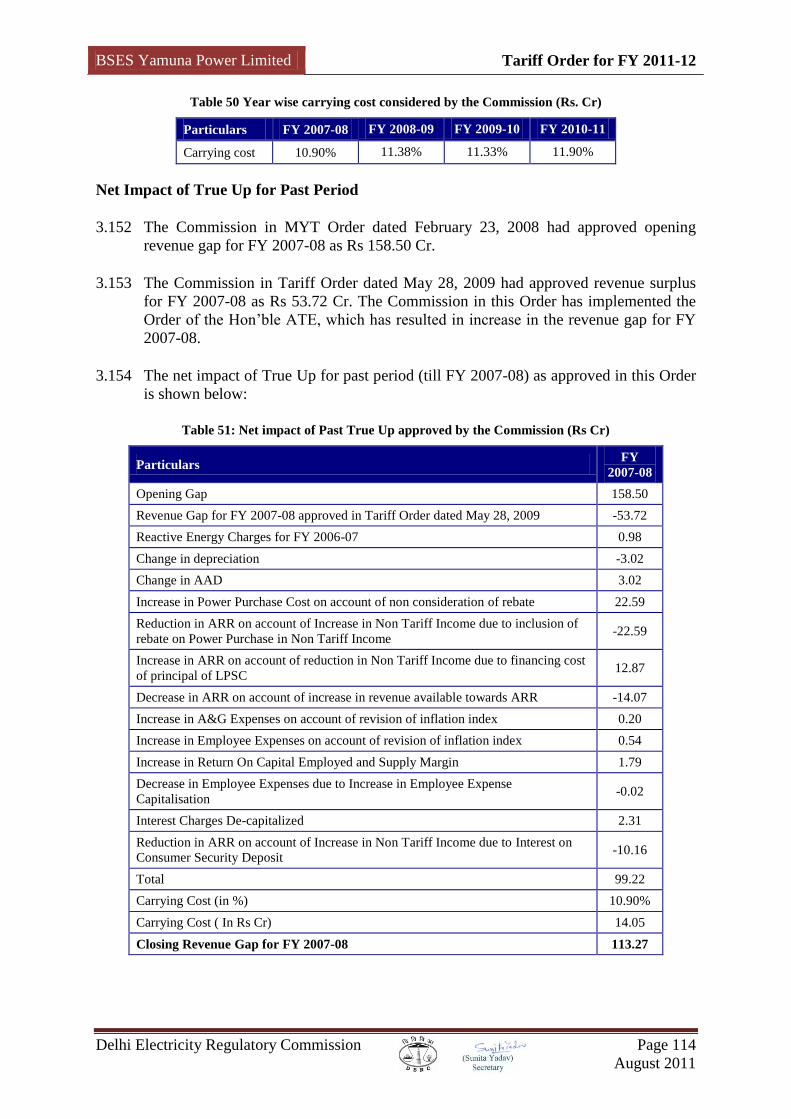

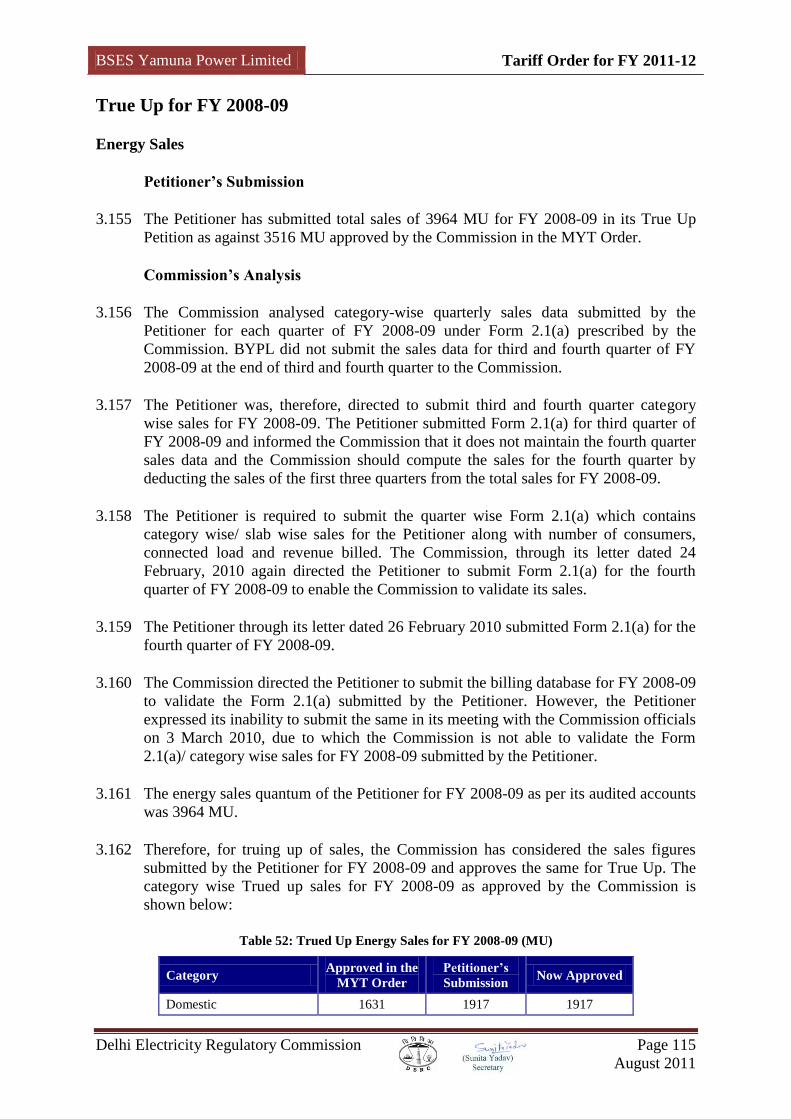

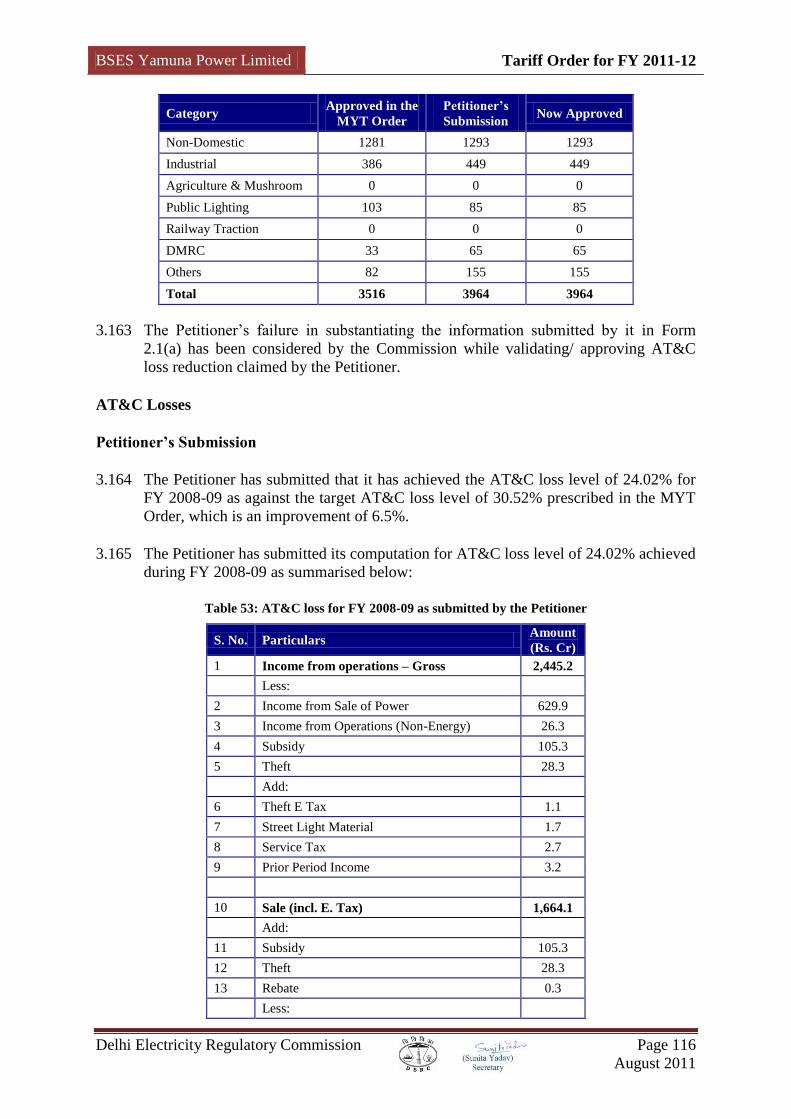

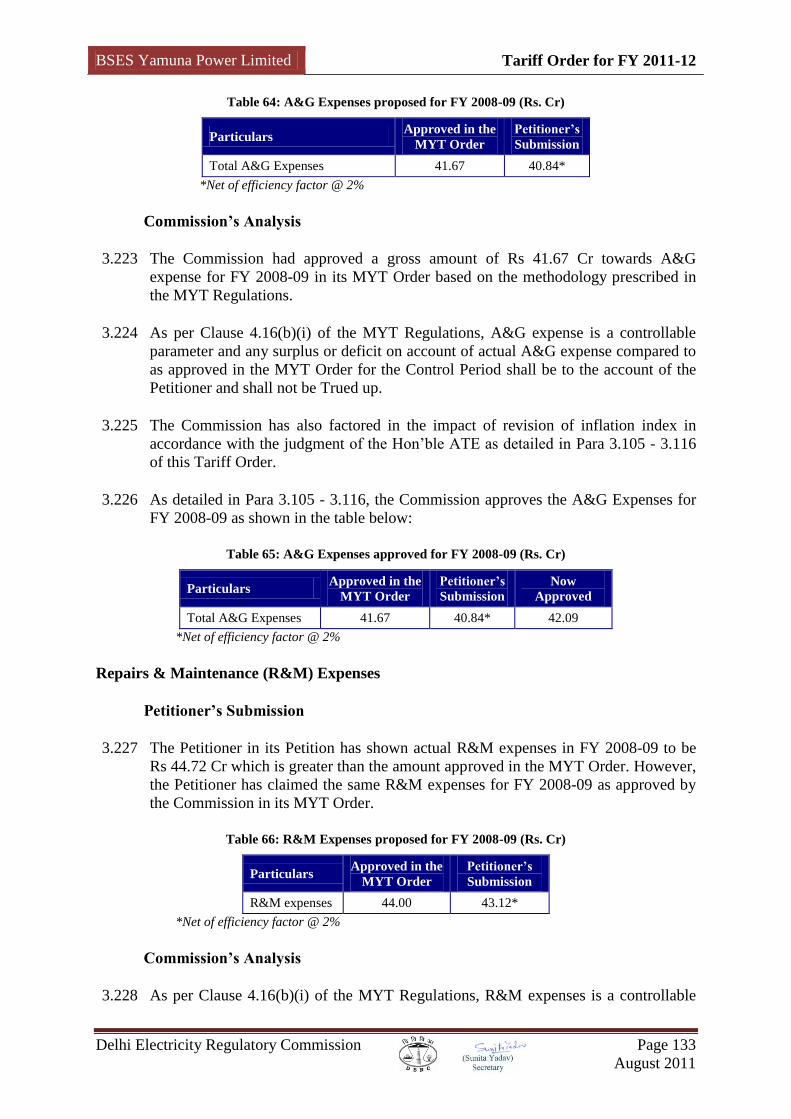

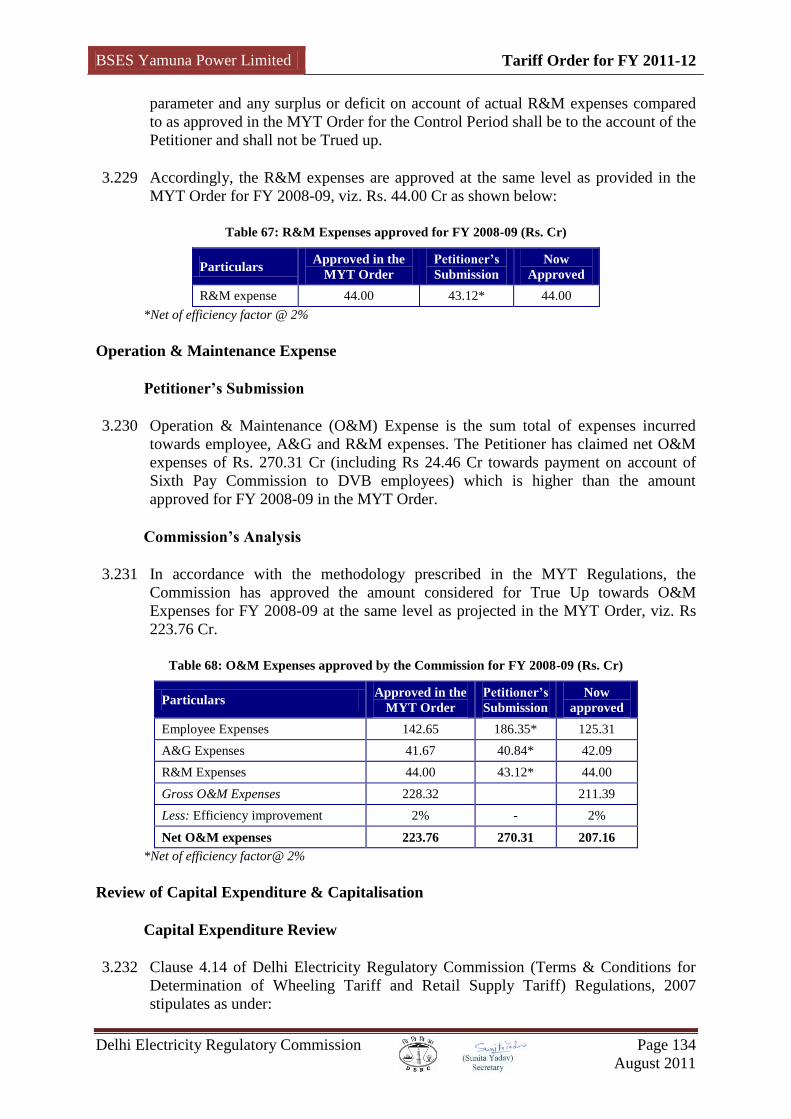

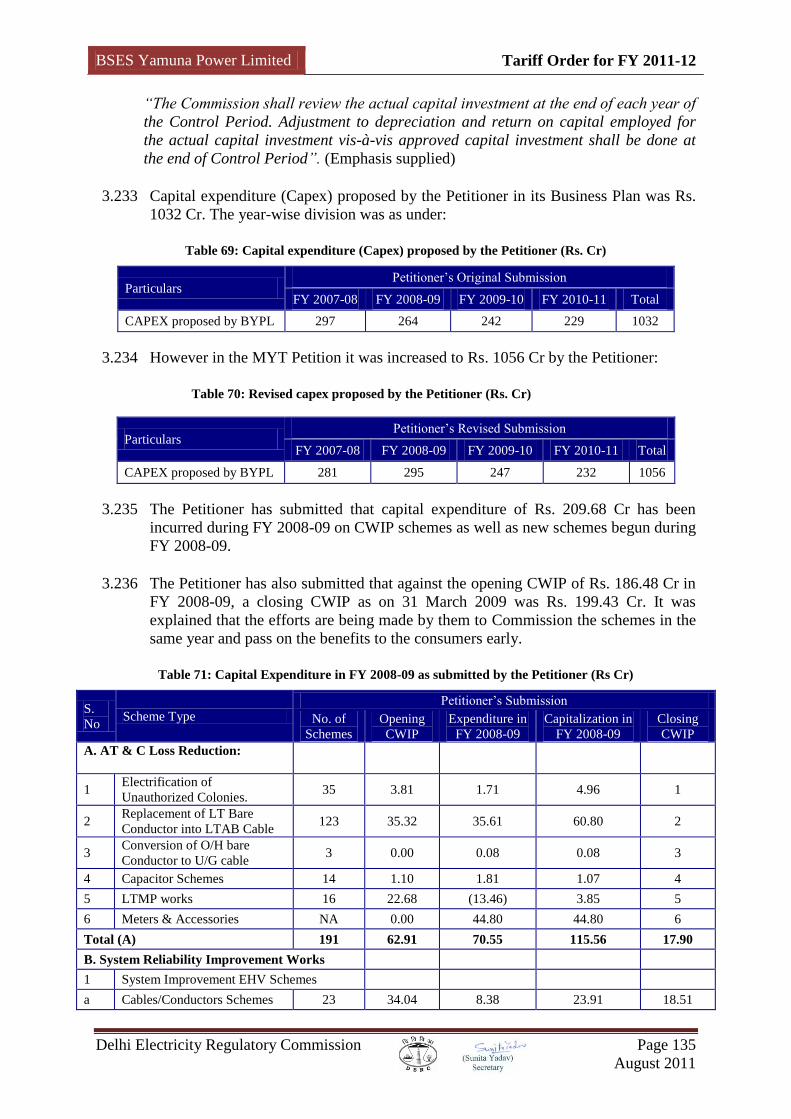

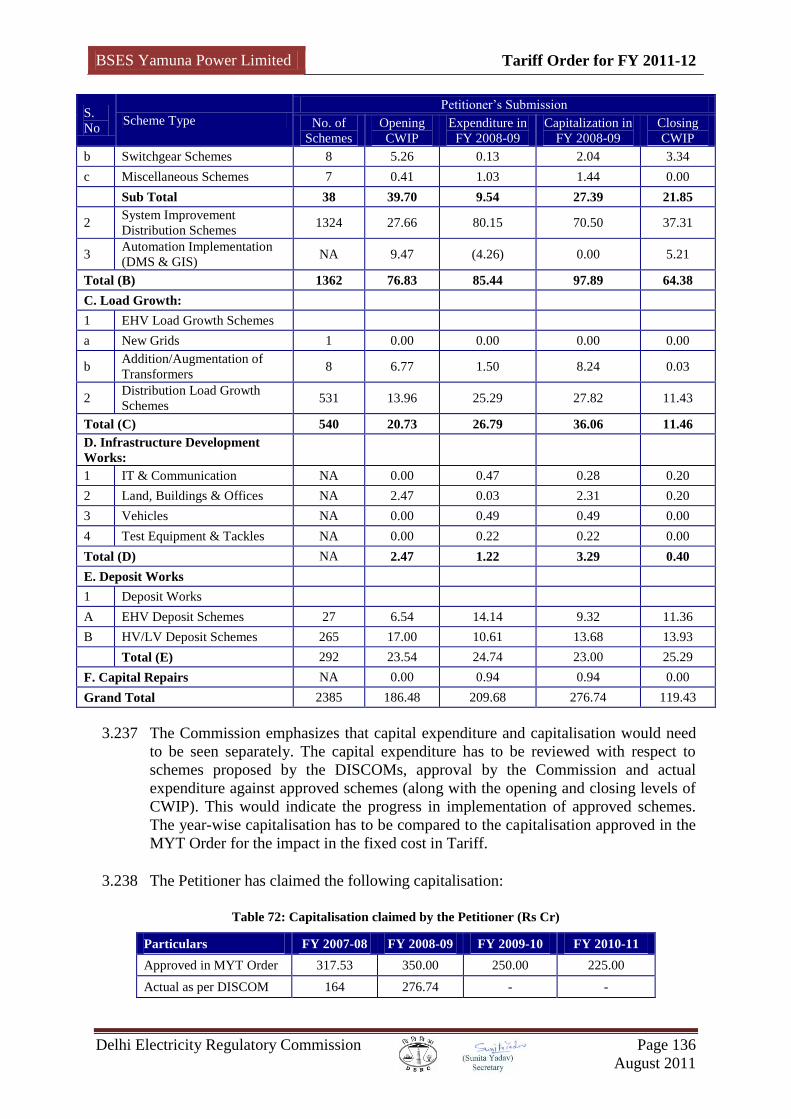

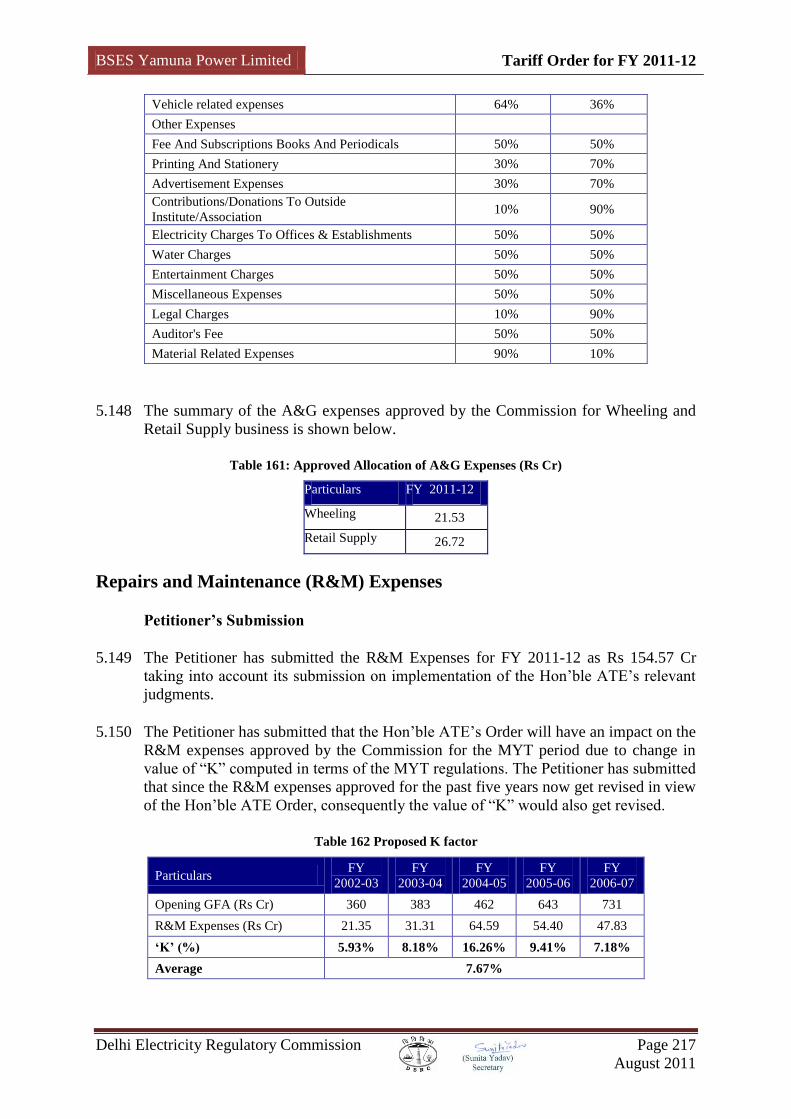

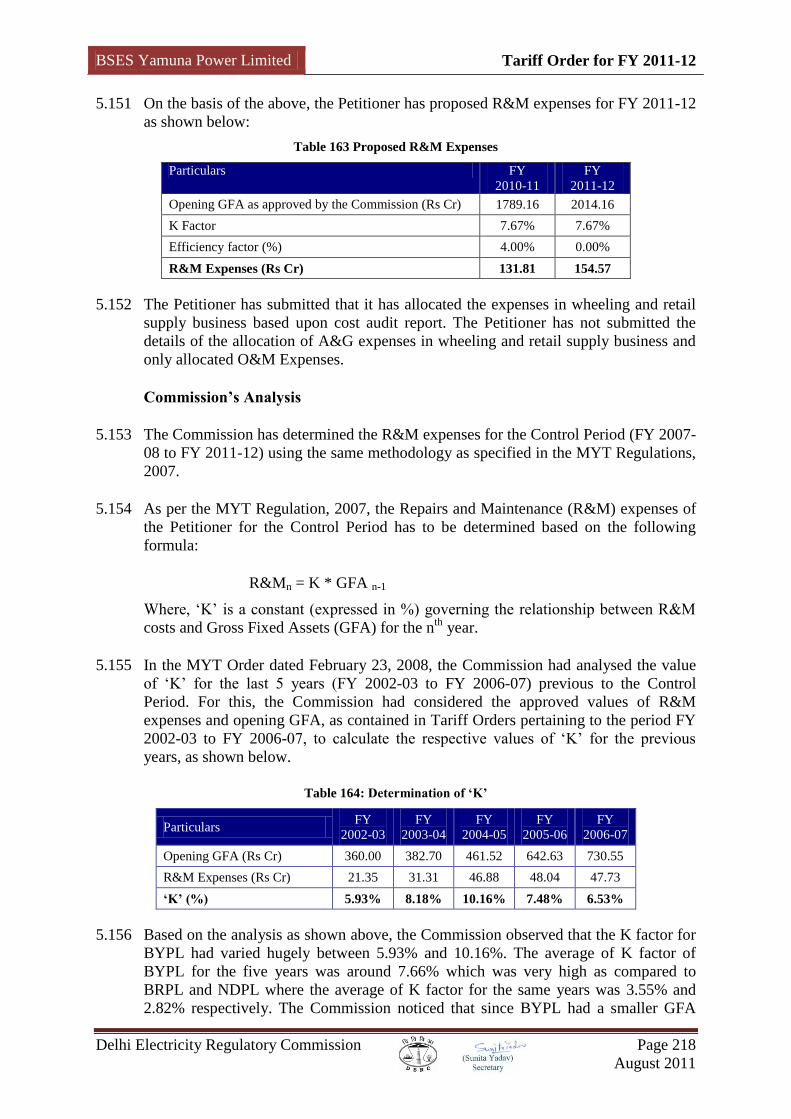

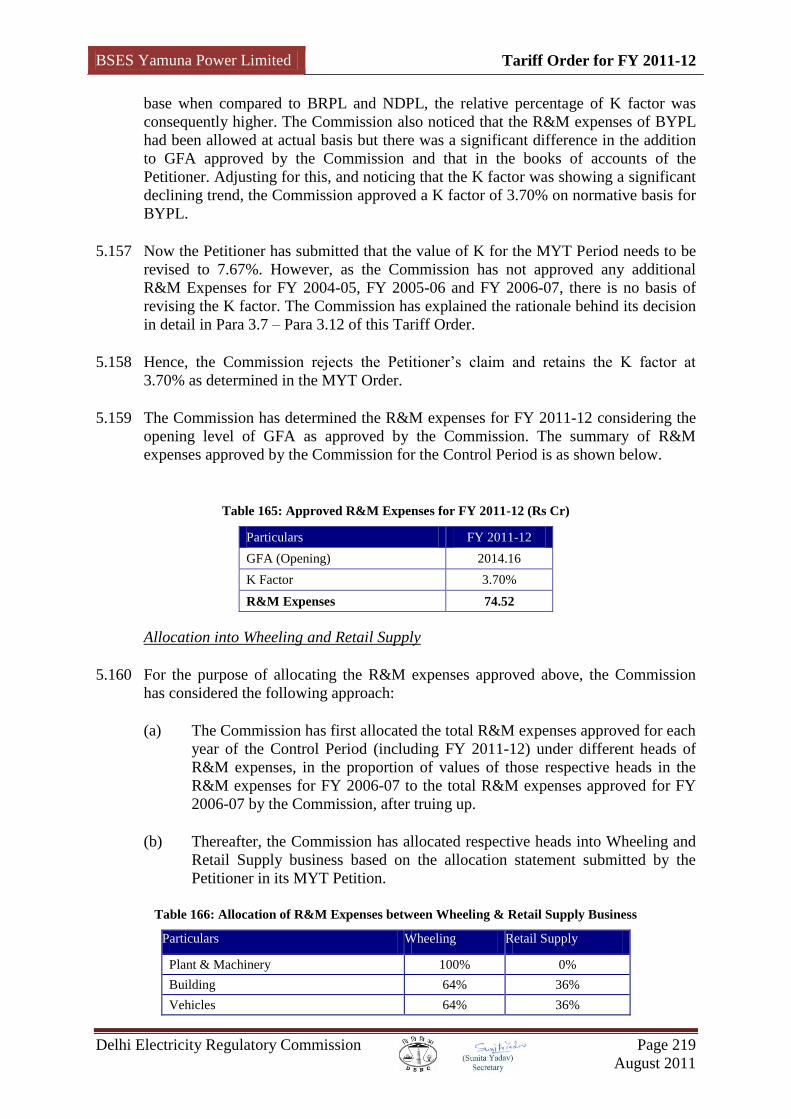

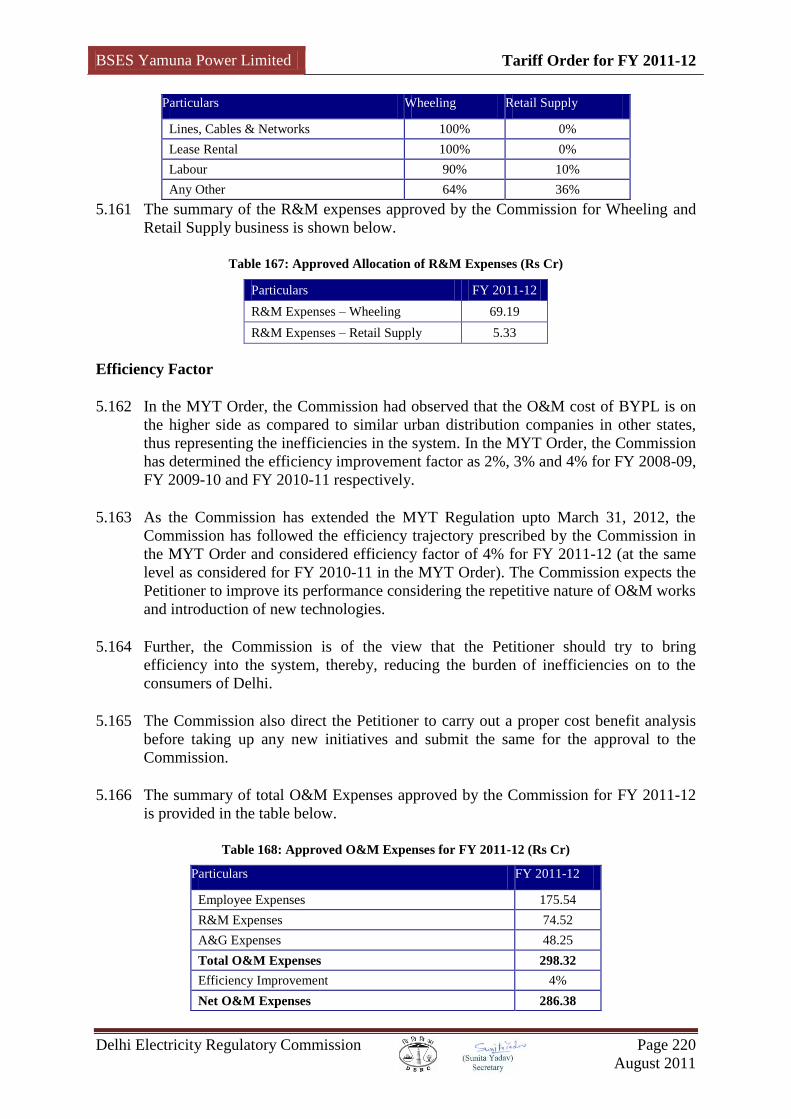

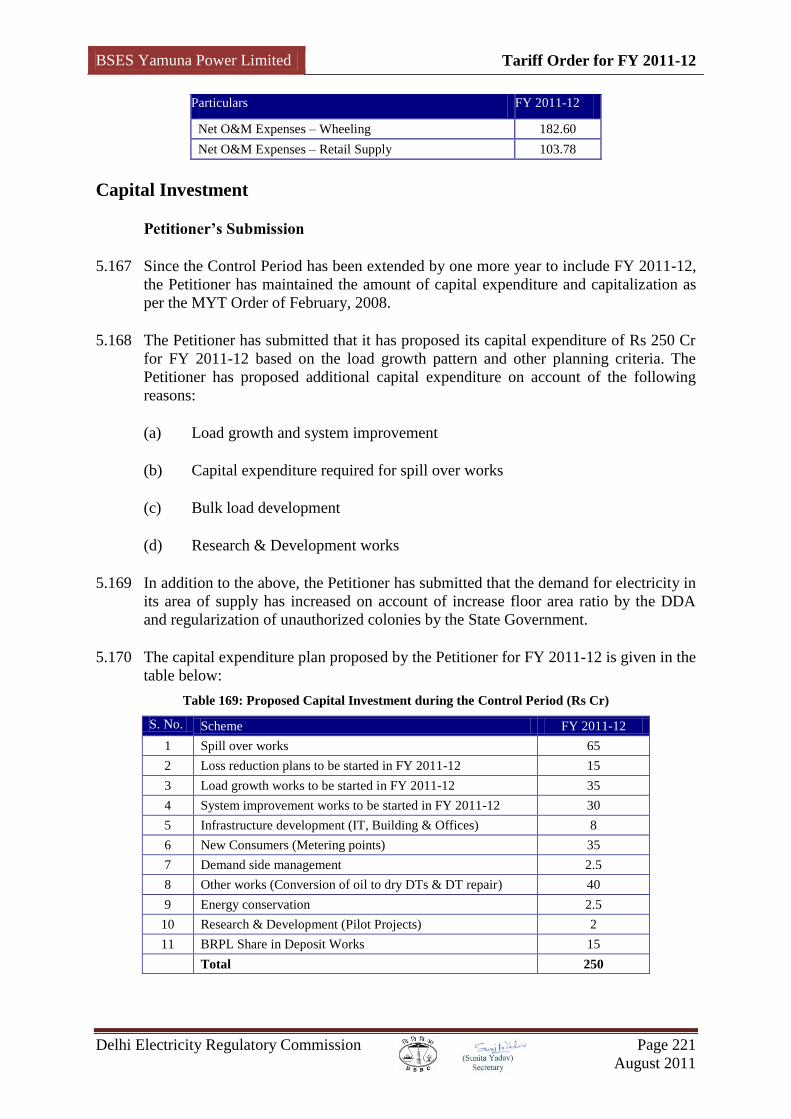

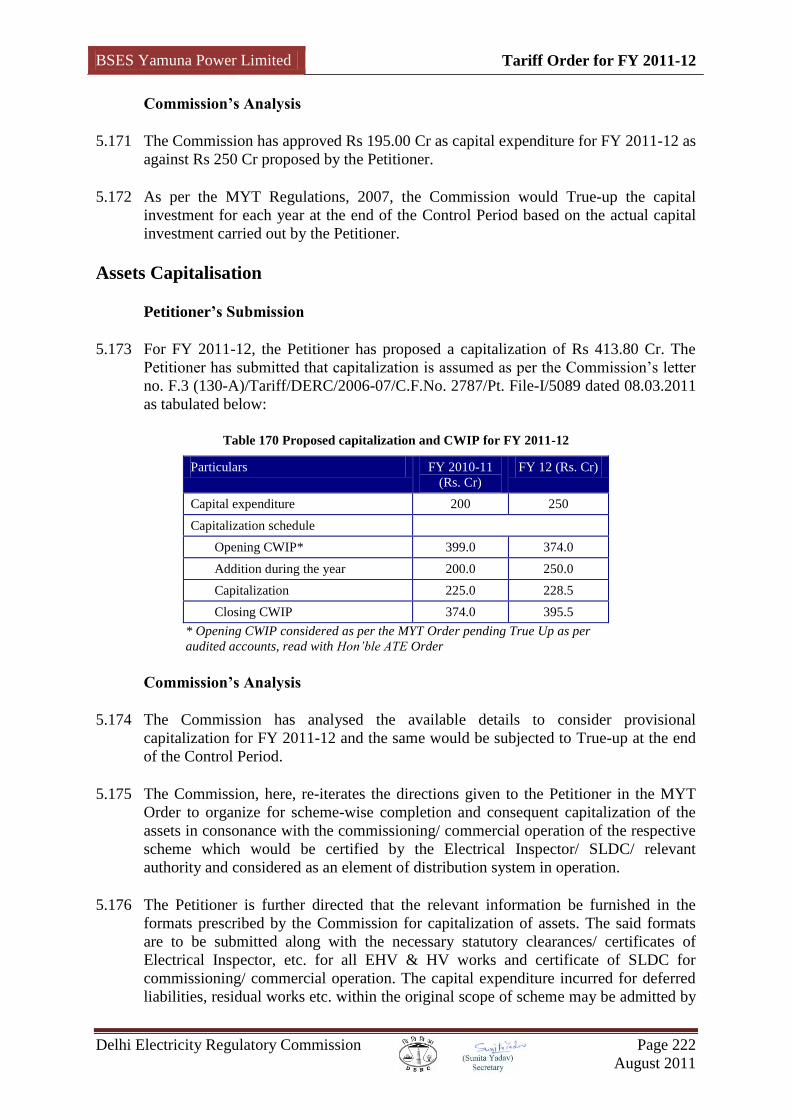

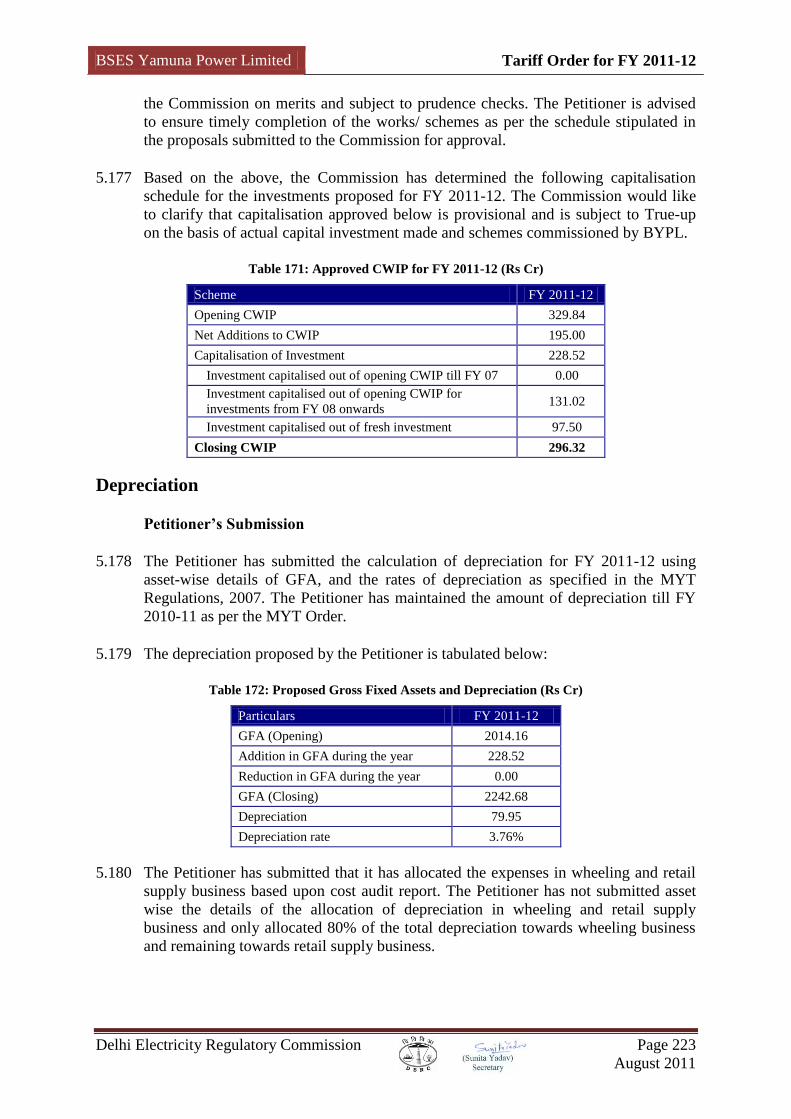

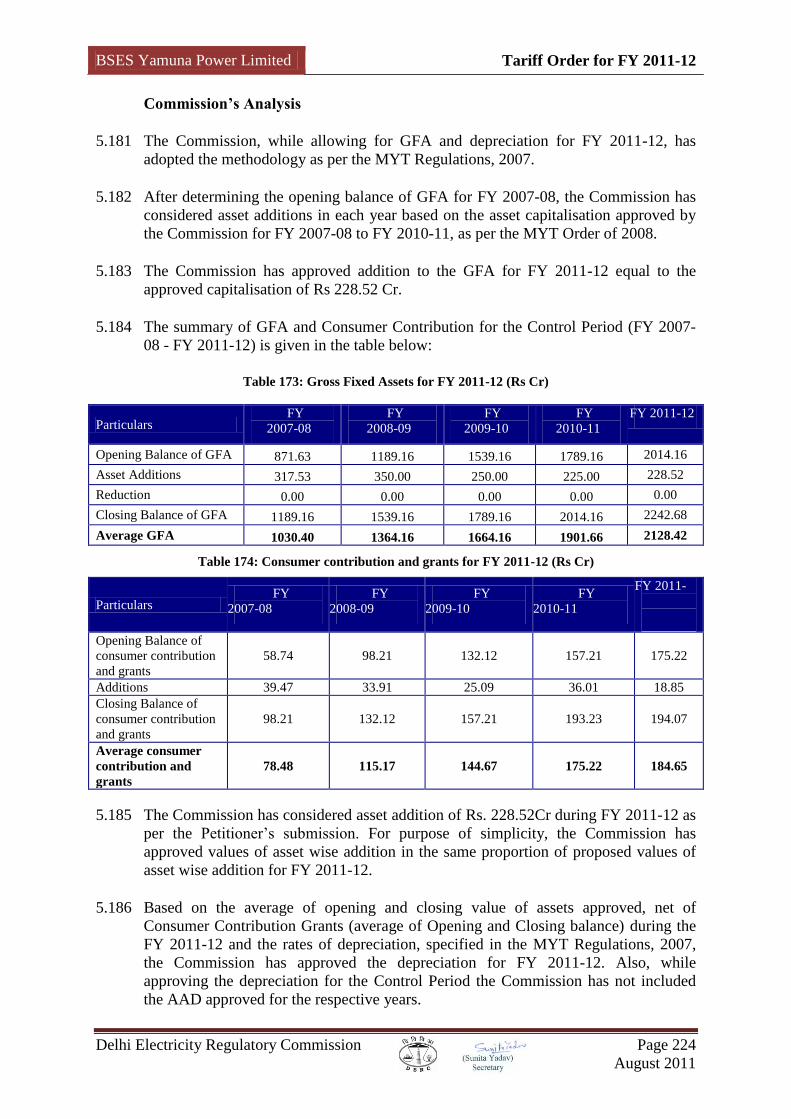

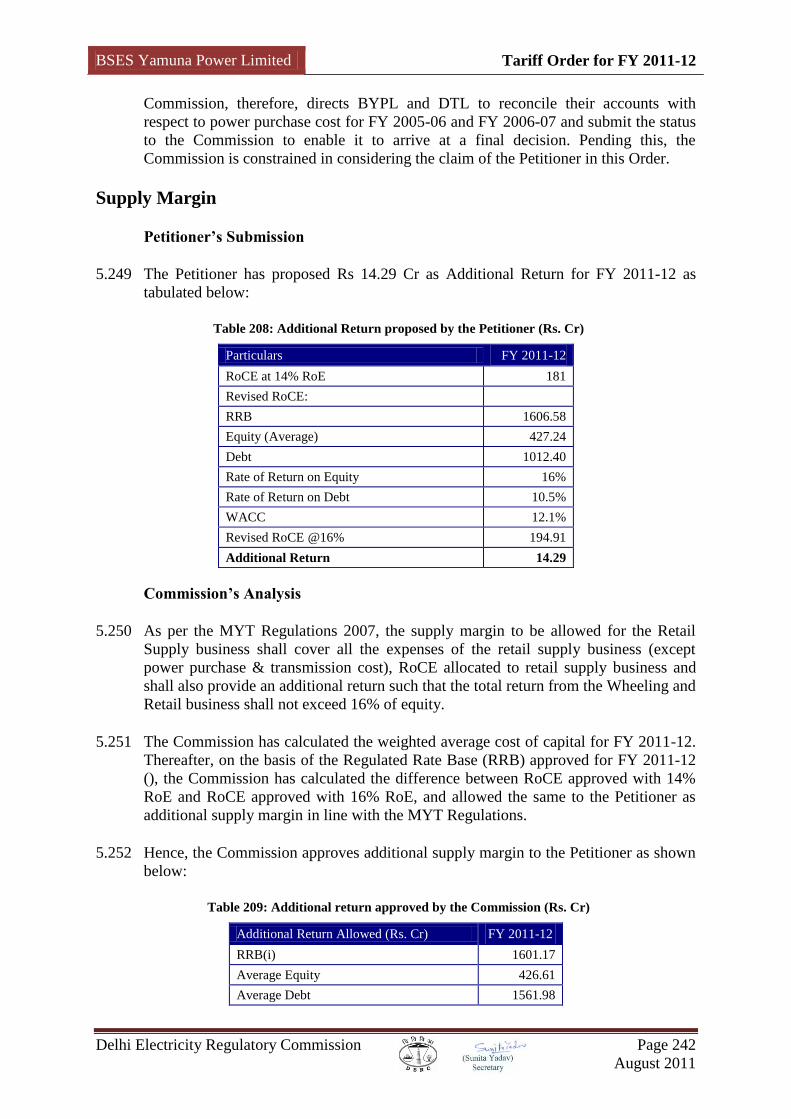

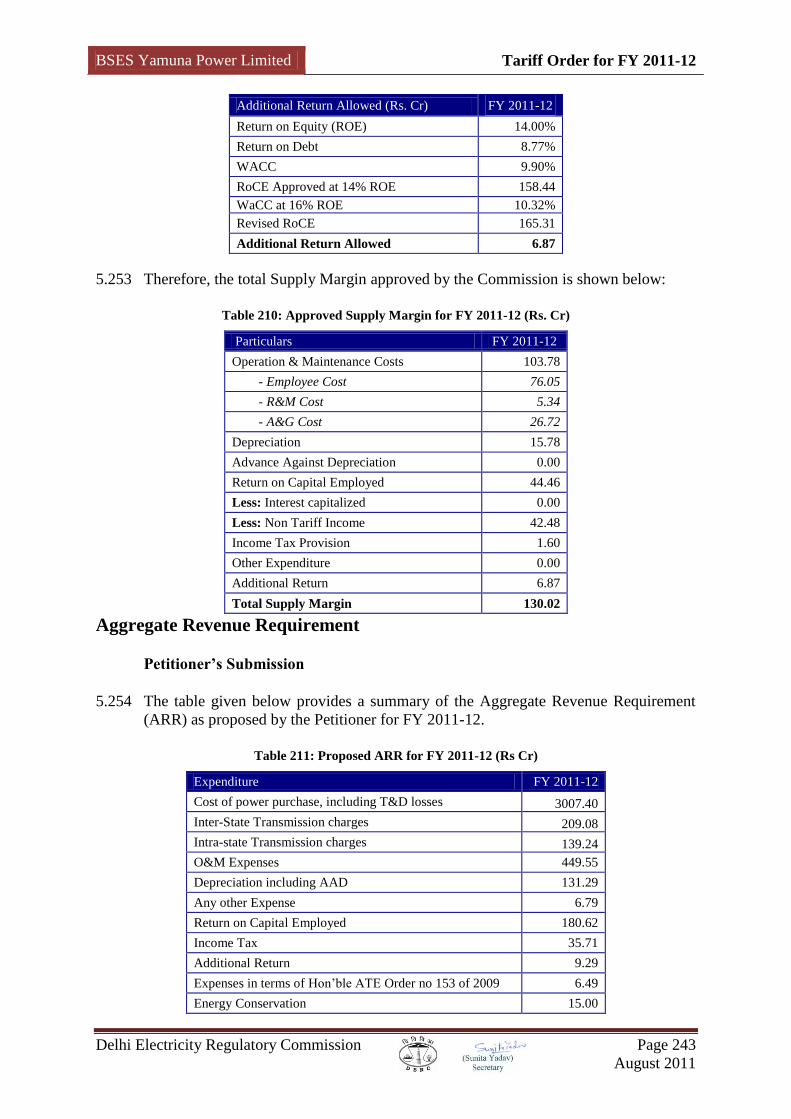

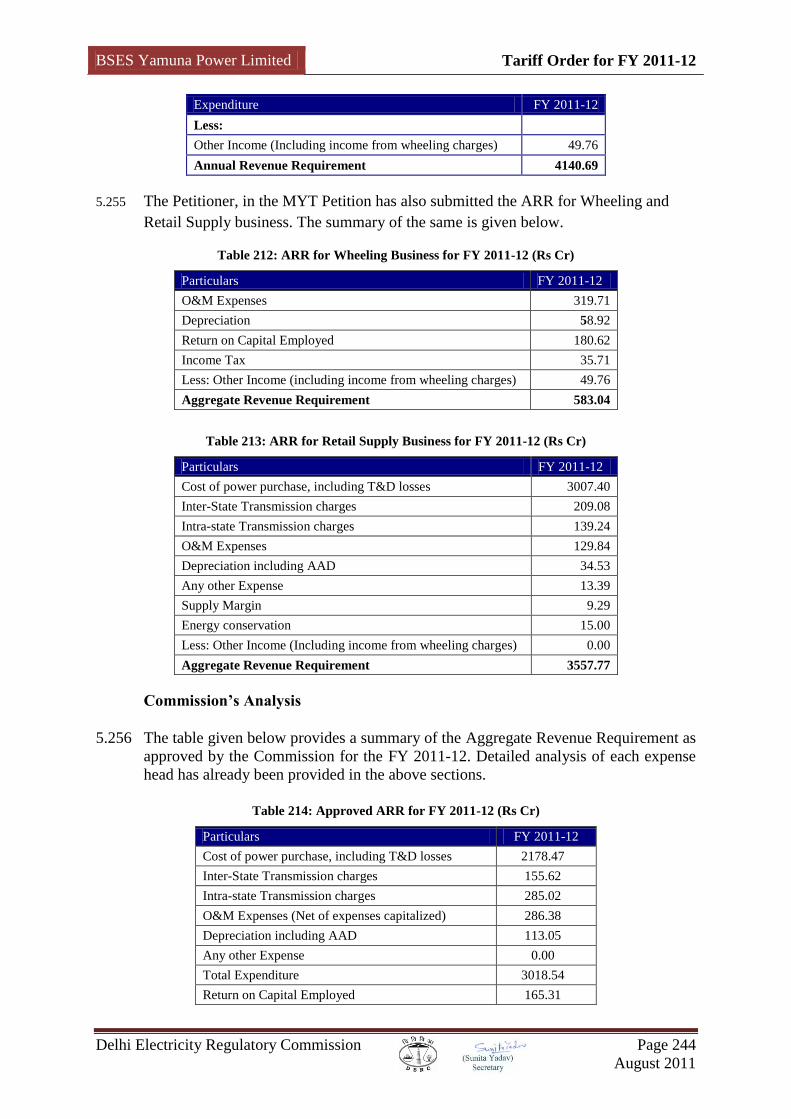

Delhi, the Commission had decided to invite them for all the meetings. The