blank proforma limited - partial text - read only

TRANSCRIPT

�

�

�

�����������

����������� ��� � ����� �� � ����������

��������������������������

�!����"������#�

��"������#����

���������������������� ������������������������ �������

�

�

�

Valtech SE

P a g e 2 | 12

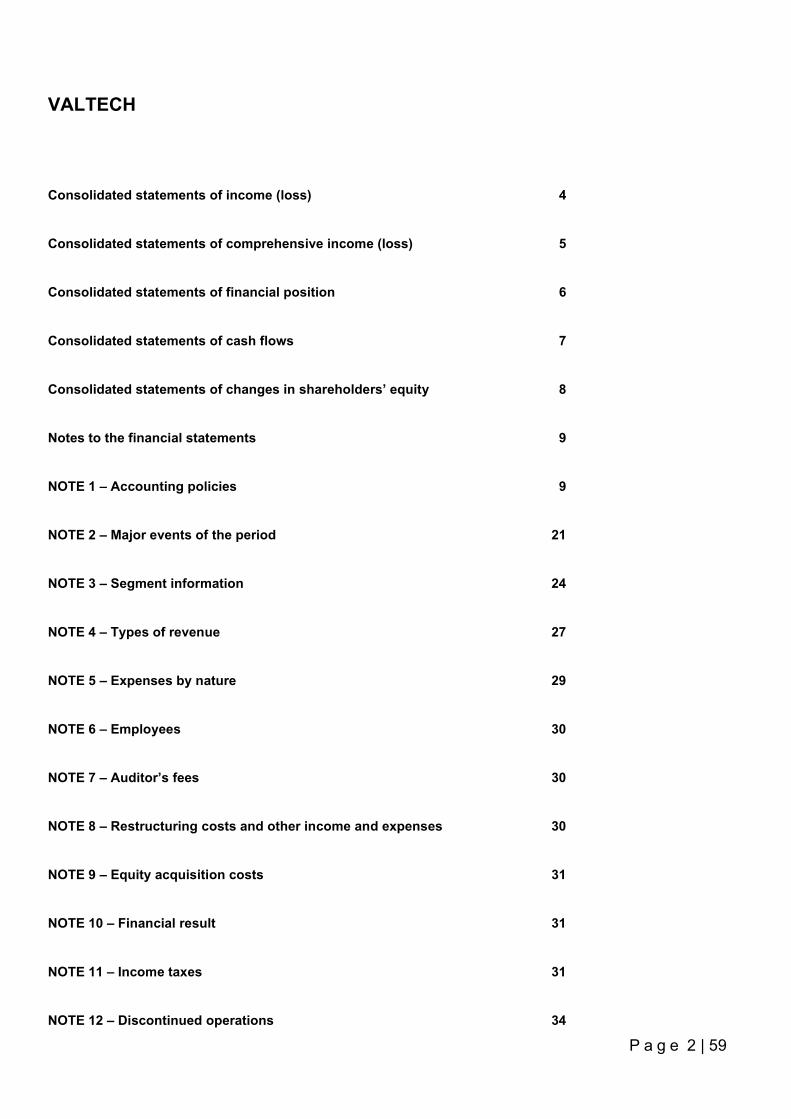

Consolidated statements of income (loss) 3

Consolidated statements of financial position 4

Principal activities 5

Review and development of the Company’s business and financial position 5

Major events of the year 6

Likely future developments 8

By back of own shares 8

Environment 8

Employees 9

Research and development activities 9

Branches 9

Principal risk and uncertainties 9

Major events after the closing date 11

Valtech SE

P a g e 3 | 12

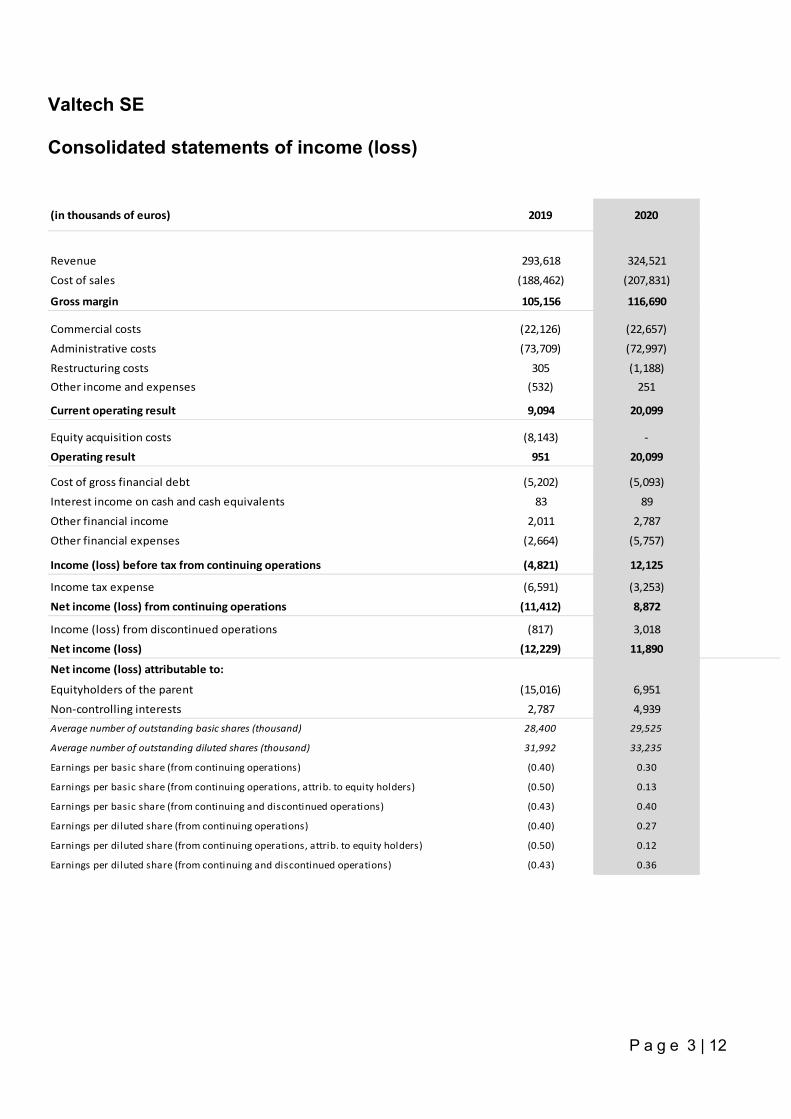

Consolidated statements of income (loss)

(in thousands of euros) 2019 2020

Revenue 293,618 324,521

Cost of sales (188,462) (207,831)

Gross margin 105,156 116,690

Commercial costs (22,126) (22,657)

Administrative costs (73,709) (72,997)

Restructuring costs 305 (1,188)Other income and expenses (532) 251

Current operating result 9,094 20,099

Equity acquisition costs (8,143) -

Operating result 951 20,099

Cost of gross financial debt (5,202) (5,093)

Interest income on cash and cash equivalents 83 89

Other financial income 2,011 2,787

Other financial expenses (2,664) (5,757)

Income (loss) before tax from continuing operations (4,821) 12,125

Income tax expense (6,591) (3,253)

Net income (loss) from continuing operations (11,412) 8,872

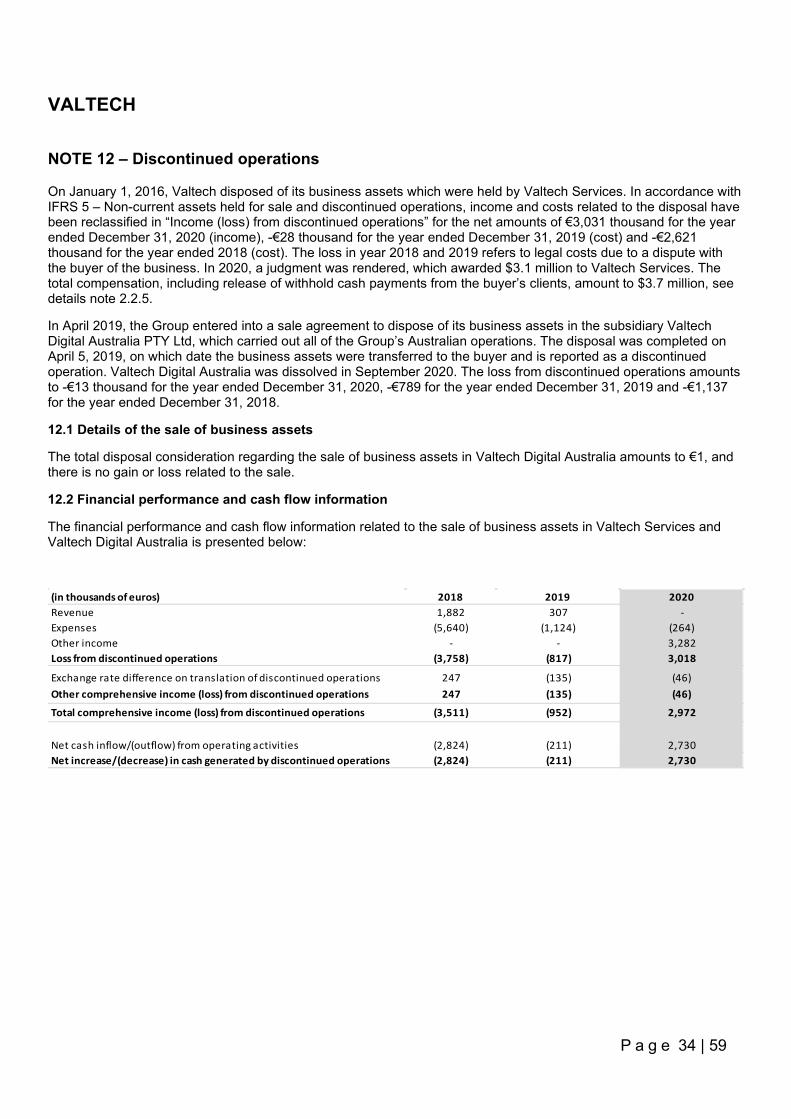

Income (loss) from discontinued operations (817) 3,018

Net income (loss) (12,229) 11,890

Net income (loss) attributable to:

Equityholders of the parent (15,016) 6,951

Non-controlling interests 2,787 4,939Average number of outstanding basic shares (thousand) 28,400 29,525

Average number of outstanding diluted shares (thousand) 31,992 33,235

Earnings per basic share (from continuing operations) (0.40) 0.30

Earnings per basic share (from continuing operations, attrib. to equity holders) (0.50) 0.13

Earnings per basic share (from continuing and discontinued operations) (0.43) 0.40

Earnings per diluted share (from continuing operations) (0.40) 0.27

Earnings per diluted share (from continuing operations, attrib. to equity holders) (0.50) 0.12

Earnings per diluted share (from continuing and discontinued operations) (0.43) 0.36

Valtech SE

P a g e 4 | 12

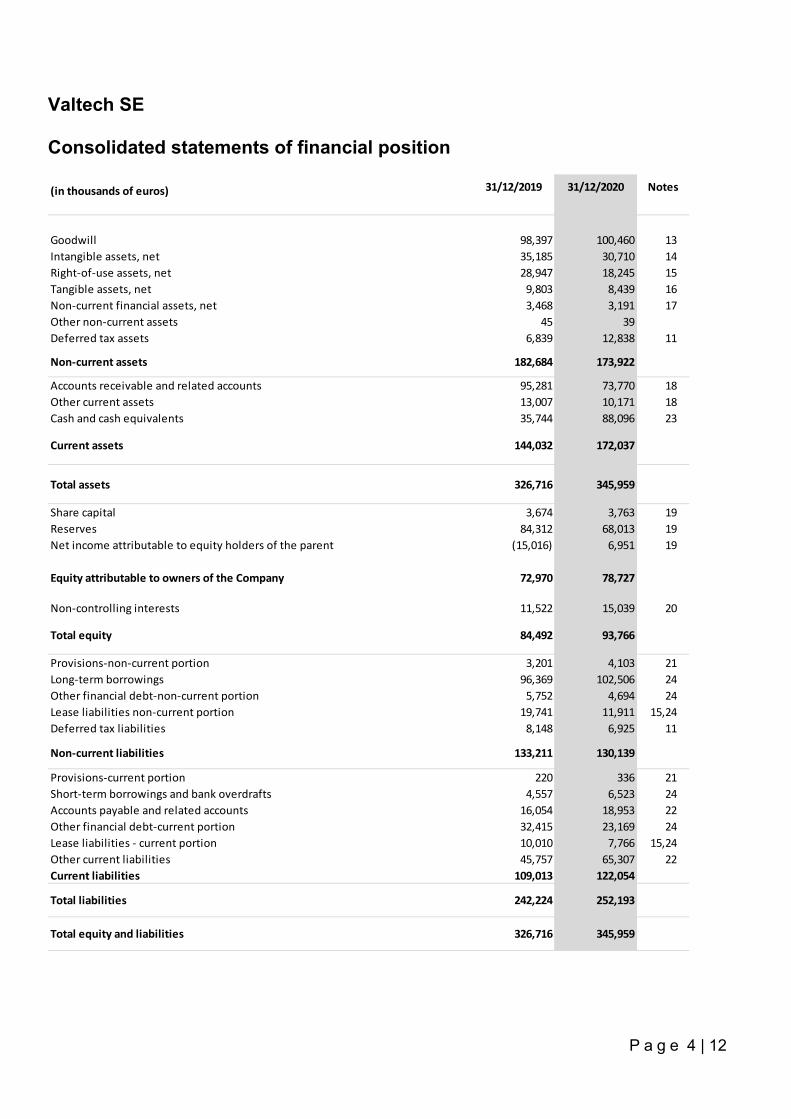

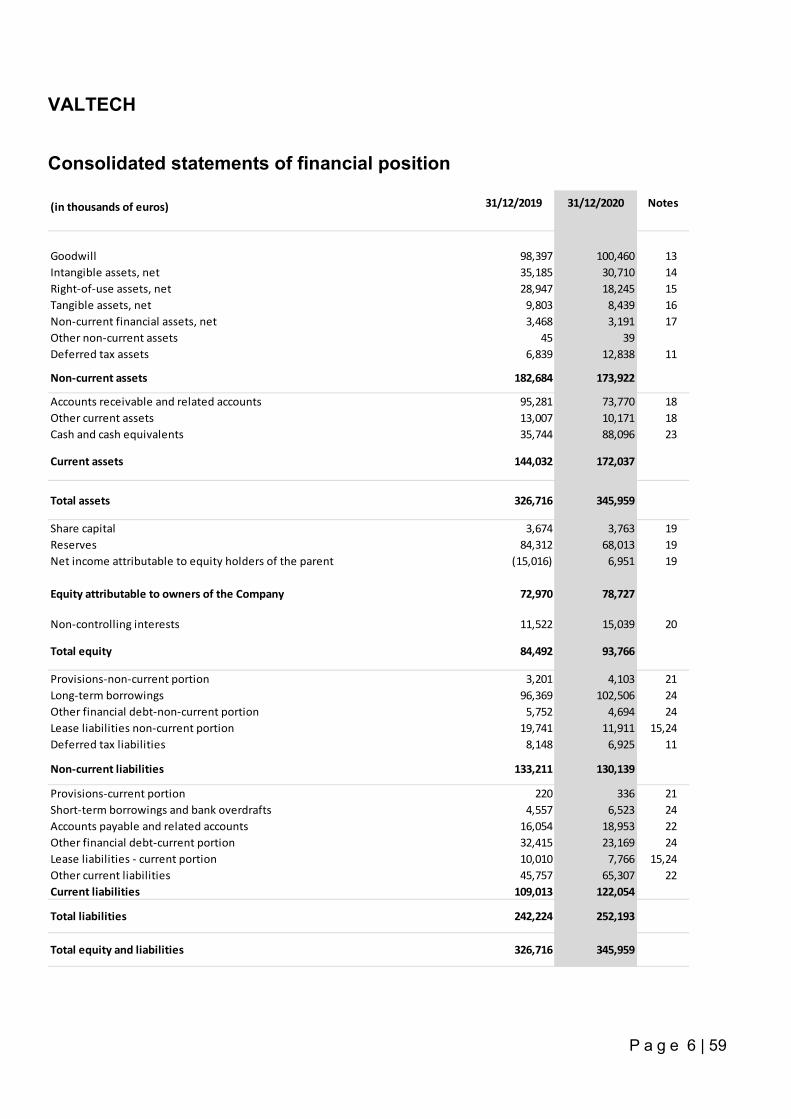

Consolidated statements of financial position

(in thousands of euros) 31/12/2019 31/12/2020 Notes

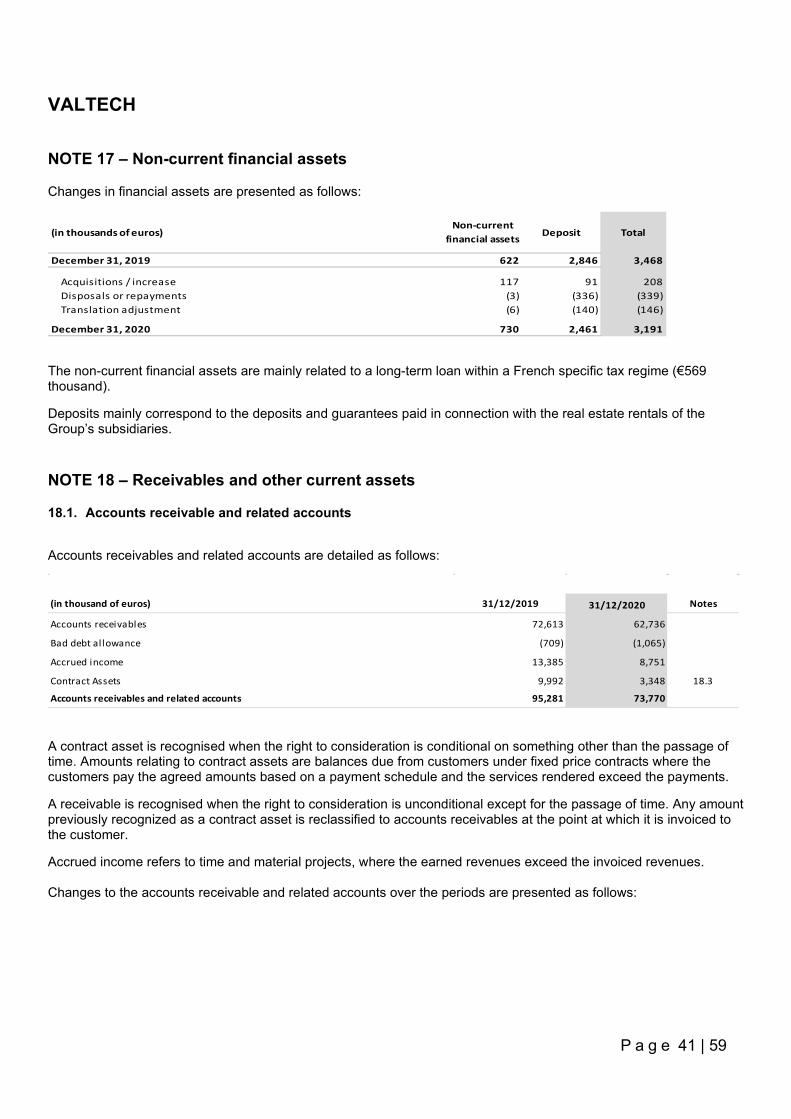

Goodwill 98,397 100,460 13Intangible assets, net 35,185 30,710 14Right-of-use assets, net 28,947 18,245 15Tangible assets, net 9,803 8,439 16Non-current financial assets, net 3,468 3,191 17Other non-current assets 45 39Deferred tax assets 6,839 12,838 11

Non-current assets 182,684 173,922

Accounts receivable and related accounts 95,281 73,770 18Other current assets 13,007 10,171 18Cash and cash equivalents 35,744 88,096 23

Current assets 144,032 172,037

Total assets 326,716 345,959

Share capital 3,674 3,763 19Reserves 84,312 68,013 19Net income attributable to equity holders of the parent (15,016) 6,951 19

Equity attributable to owners of the Company 72,970 78,727

Non-controlling interests 11,522 15,039 20

Total equity 84,492 93,766

Provisions-non-current portion 3,201 4,103 21Long-term borrowings 96,369 102,506 24Other financial debt-non-current portion 5,752 4,694 24Lease liabilities non-current portion 19,741 11,911 15,24Deferred tax liabilities 8,148 6,925 11

Non-current liabilities 133,211 130,139

Provisions-current portion 220 336 21Short-term borrowings and bank overdrafts 4,557 6,523 24Accounts payable and related accounts 16,054 18,953 22Other financial debt-current portion 32,415 23,169 24Lease liabilities - current portion 10,010 7,766 15,24Other current liabilities 45,757 65,307 22Current liabilities 109,013 122,054

Total liabilities 242,224 252,193

Total equity and liabilities 326,716 345,959

Valtech SE

P a g e 5 | 12

Principal activities

Valtech is a next-generation digital transformation services provider focused on helping medium and large organizations as they embrace the digital age. Valtech provides a streamlined portfolio of integrated offerings, encompassing strategy, design, technology integration and data analytics through which it builds and operates its clients’ critical customer engagement and e-commerce platforms, while maintaining brand consistency. Valtech defines “digital transformation” as a new approach for envisioning, creating, selling, delivering, servicing, and consuming products and services with increased agility, time-to-market, reliability and scalability. This new approach impacts many aspects of clients’ operating models, from the way investment decisions are made, measured and managed to the sales experience and engagement offered to the customers.

Valtech’s clients primarily consist of medium and large corporations located across Europe, North America, South America, and Asia. 72% of 2020 revenues were generated from our operations in Europe, 18% from operations located in North America and 10% from operations located in the rest of the world.

Valtech has become one of the leading independent digital transformation services providers in the world, with 3,167 employees as of December 31, 2020, and with broad geographic and industry diversification. Revenues have grown from €293.6 million in 2019 to €324.5 million in 2020, representing a growth rate of 10%.

Review and development of the Group’s business and financial position

Profit and loss

Revenue grew from €293.6 million in 2019 to €324.5 million in 2020, representing an increase of €30.9 million, or 10.5%. The net increase was primarily attributable to increase of revenues in Switzerland (+€34.8 million), Germany (+€5.9 million) and decrease of revenues in United Kingdom (-€11.1 million). Increase of revenues in Switzerland is mainly attributable to the acquisition of Infocentric Research AG in December 2019, with full impact on revenues in year 2020.

Cost of sales increased from €188.5 million in 2019 to €207.8 million in 2020, representing an increase of €19.4 million, or 10.3%. The increase was primarily attributable to an increase in staff costs, which grew €8.9 million, or 6.0%, from €148.3 million in 2019 to €157.2 million (net of received government grants €3.2 million) in 2020, mainly due to an increase in our average headcount of IT professionals from 2,312 for the year 2019 to 2,533 for the year 2020, and an increase in subcontractor costs, which increased by €9.9 million, or 28.2%, from 2019 to 2020. Gross margin grew from €105.1 million in 2019 to €116.7 million in 2020, representing an increase of €11.5 million, or 11.0%. Gross margin % increased with 0.2%, from 35.8% in 2019 to 36.0% in 2020.

Commercial costs increased from €22.2 million in 2019 to €22.7 million in 2020, representing an increase of €0.5 million, or 2.0%. The increase mainly refers to increase in sales- and marketing salary costs (+€0.6 million compared to 2019), increase in cost for amortization of intangible assets identified in purchase price allocations (+€1.3 million compared to 2019) and decreased cost for marketing (-€1.1 million compared to 2019).

Administrative costs decreased from €73.7 million in 2019 to €73.0 million in 2020, representing a decrease of €0.7 million, or 1.0%. The decrease mainly refers to cost related to share based payments (-€3.6 million compared to 2019), off-set by increase in management- and administration salary costs (+€1.8 million compared to 2019) and increase in costs related to bad debts and provision for risks (+€1.4 million compared to 2019).

Restructuring costs increased from +€0.3 million in 2019 (income) to a loss of €1.2 million in 2020, representing an increase of €1.5 million, which is primarily attributable to severance costs in the United States and the United Kingdom.

Other income and expenses increased from a loss of €0.5 million in 2019 to an income of €0.3 million in 2020, mainly referring to adjustment of earn-out related to the acquisitions of MJD and Infocentric.

Equity acquisition costs decreased from €8.1 million in 2019 to €0.0 million in 2020. Equity acquisition cost in 2019 was attributable to reversal of deferred offering costs as a consequence of the postponement of the initial public offering.

Valtech SE

P a g e 6 | 12

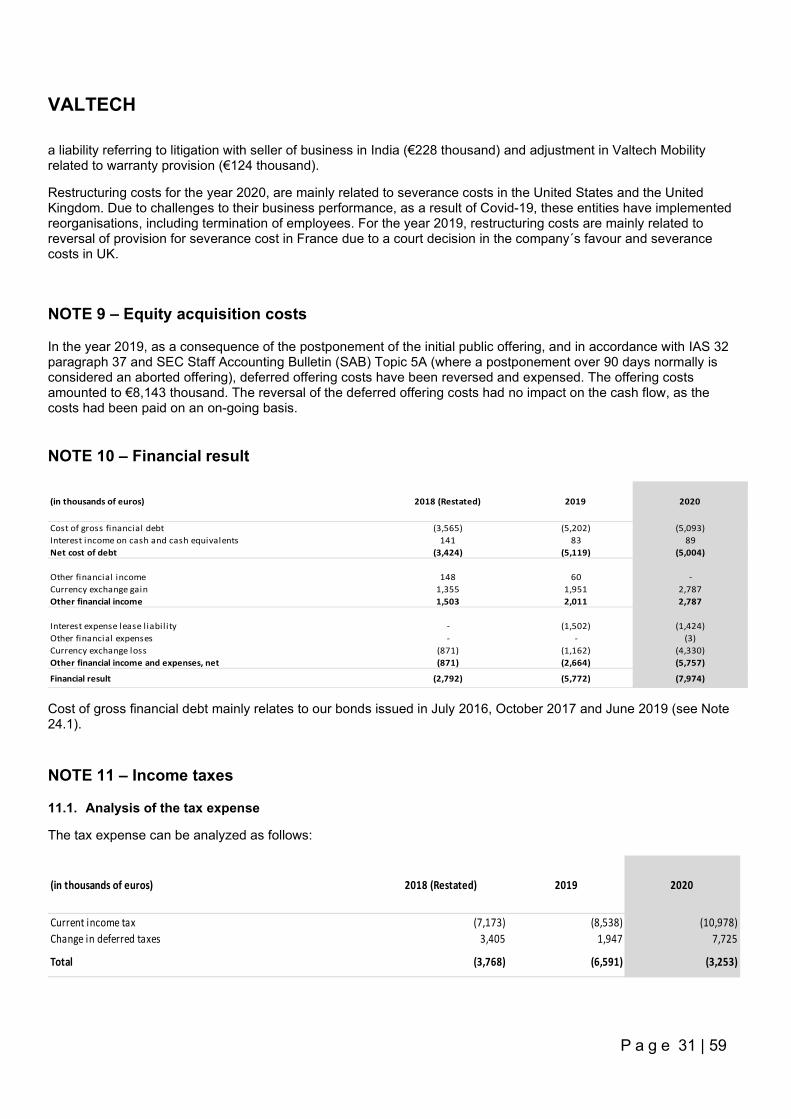

Financial income and expenses increased from €5.8 million in 2019 to €8.0 million in 2020, an increase with €2.2 million. The increase was primarily attributable to the increase in net currency loss for an amount of €2.3 million.

Income tax expense decreased from €6.6 million in 2019 to €3.3 million in 2020, a decrease of €3.3 million. In 2020, a deferred tax asset for an amount of €6.1 million for a portion of the available unused tax losses in France and for the full amount of unused tax losses in USA was recognized. In 2019, an increase of the deferred tax asset for an amount of €0.6 million regarding unused tax losses in USA was recognized.

Income (loss) from discontinued operations refers to disposed businesses in USA and Australia and have changed from a loss of €0.8 million in 2019 to an income of €3.0 million in 2020, an increase with €3.8 million. In 2020, a judgment was rendered in a dispute with the buyer or the business in US, which awarded $3.1 million to Valtech.

Non-controlling interests were €2.8 million in 2019 and €4.9 million in 2020. Non-controlling interest represent the portion of the net income of our joint-venture with Audi that is attributable to our venture partner.

As a result of the foregoing, we had a net loss of €12.2 million in 2019 and a net income of €11.9 million in 2020, representing an increase of €24.1 million.

Balance sheet

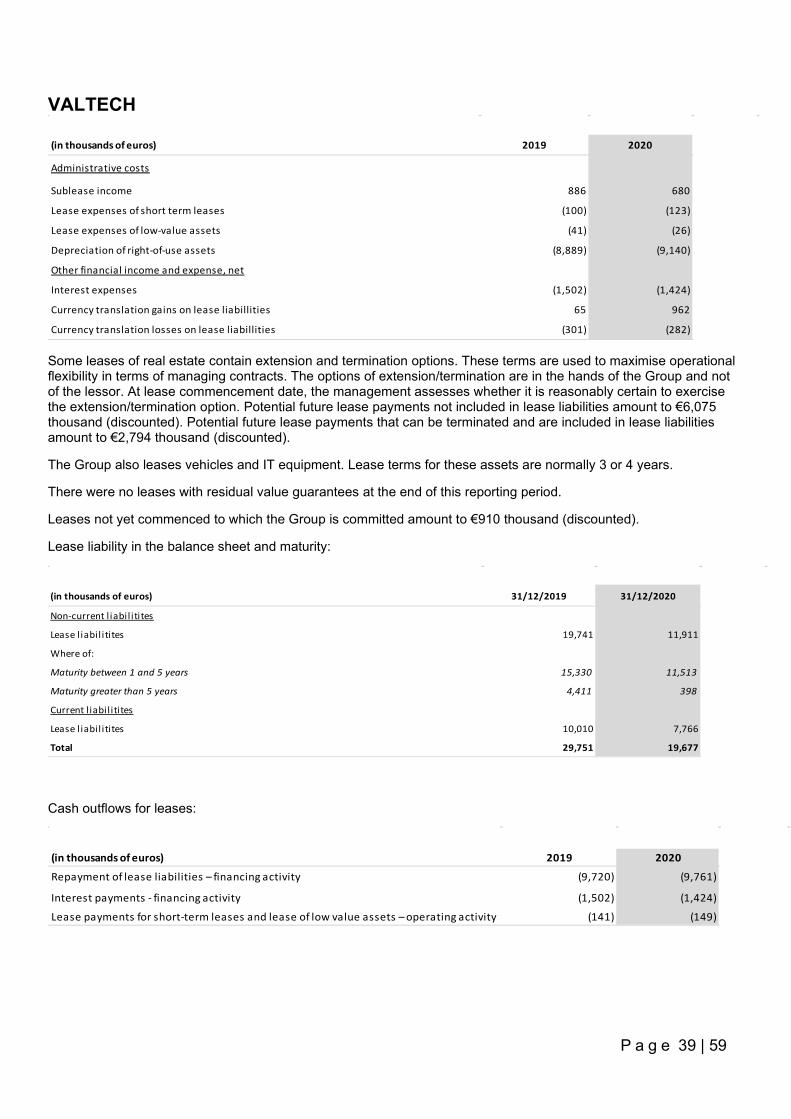

Total assets increased by 5.9% compared with previous year to €346.0 million as of 31 December 2020 (2019: €326.7 million). The net increase of €19.3 million mainly refers to increase in cash (+€52.4 million), mainly attributable to operating activities, decrease in right-of-use assets (-€10.7 million), mainly attributable to depreciations, and decrease in accounts receivables and related accounts (-€21.5 million).

Total liabilities increased by 4.1% compared with previous year to €252.2 million as of 31 December 2020 (2019: €242.2 million). The increase of €10.0 million mainly refers to increase in other current liabilities (+€19.6 million), which mainly refers to deferred tax and social security payments, offered by governments in some countries due to Covid-19, and net decrease in financial liability (-€12.3 million), mainly attributable to decrease in debt related to acquisitions (-€14.8 million), decrease of lease liability (-€10.0 million), attributable to payments and increase of long term borrowings (+€6.1 million), attributable to rent-free loans in France guaranteed by the French Government, to support the business in the light of the Covid-19 pandemic.

As of December 31, 2020, our primary sources of liquidity were €87.7 million of cash and cash equivalents net of bank overdrafts and factoring with recourse (€0.4 million).

Major events of the year

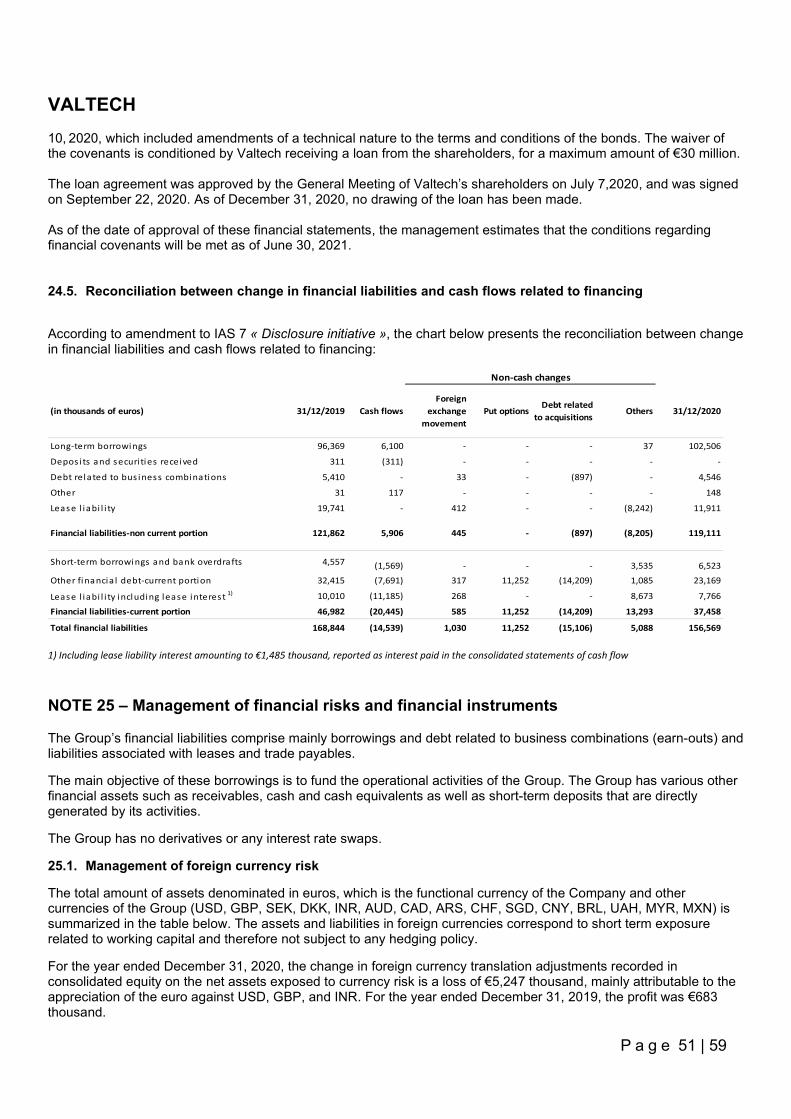

Increase in capital On March 6, 2020, the Board of Valtech, on behalf of the shareholders, decided to issue 264,209 new shares at €17.5 per share as payment for the acquisition of MJD Interactive, leading to a capital increase of €4,624 thousand (out of which €33 thousand in share capital). On March 6, 2020, the Board of Valtech, on behalf of the shareholders, decided to issue 453,348 new shares at €17.5 per share as payment for the acquisition of Infocentric Research AG, leading to a capital increase of €7,934 thousand (out of which €57 thousand in share capital). Total capital increase regarding issue of new shares amounts to €12,557 thousand, of which €89 thousand has increased the capital and €12,468 thousand increased additional paid in capital. Net increase in capital amounts to €0 thousand and corresponds to €12,557 thousand minus the put options given in 2020 to the sellers of MJD Interactive and Infocentric at €12,557 thousand.

Valtech SE

P a g e 7 | 12

Hyperinflation in Argentina

Entities with a functional currency of the Argentine peso are required to apply IAS 29 in accounting periods ending on or after 1 July 2018. Valtech’s Argentinian business represented 1.2% of the total revenue for the year 2020. Adoption of IAS 29 requires the non-monetary assets and liabilities and the income statement to be restated to reflect the changes in the general pricing power of its functional currency, leading to a gain or loss on the net monetary position included in the net income. Gain in net monetary position due to restatement amounts to less than €100 thousand as per December 31, 2020 and is deemed as immaterial.

Waiver of financial covenants

As a result of the impact of the Covid-19 outbreak on our financial performance and financial position, we assessed the situation in March 2020 and anticipated then that the Group would not comply with the financial covenants of its bonds, as of June 30 and December 31, 2020. We entered into discussions with the holders of the bonds, who in May 2020 agreed in writing to waive those covenants for June 30 and December 31, 2020, subject to a minimum amount of cash of €25 million to be available in the Group by June 30 and December 31, 2020. The written agreement to waive those covenants was reaffirmed in the resolutions passed by the general assembly of the bond holders on July 10, 2020, which included amendments of a technical nature to the terms and conditions of the bonds. The waiver of the covenants was conditioned by Valtech receiving a loan from the shareholders, for a maximum amount of €30 million. The loan agreement was approved by the General Meeting of Valtech’s shareholders on July 7, 2020 and was signed on September 22, 2020. Loan from shareholders

To secure the Group’s financial position and to cover possible shortfall of cash caused by the Covid-19 pandemic, we have agreed with the shareholders on a loan of maximum €30 million on September 22, 2020. The loan can be drawn in one, two or three drawing(s), for an amount of €10 million each, between the effective date and at the latest on December 10, 2020. No drawing of the loan has been made in year 2020, and the opportunity to borrow has expired without being used.

Dispute with buyer of business in USA

Valtech Services (USA) sold its business assets on January 1, 2016. In August 2018, Valtech Services introduced claims against the buyer to recover payments due under the sale contract, plus legal expenses. In October 2020 the Appeal Court rendered a judgment, which awarded $3.1 million to Valtech Services in payment for the assets sold, plus interest, sanctions and legal fee and costs. In December 2020, the full amount was paid by the buyer to an escrow account, and in January 2021, Valtech received the full amount in cash. The total compensation, including release of withhold cash payments from the buyer’s clients, amount to $3.7 million. Received compensation and legal fees related to the litigation is recorded under discontinued operations. Acquisition of the companies Headways Digital Strategy S.A. de C.V. and Branteza S. de R.L de C.V. (Mexico)

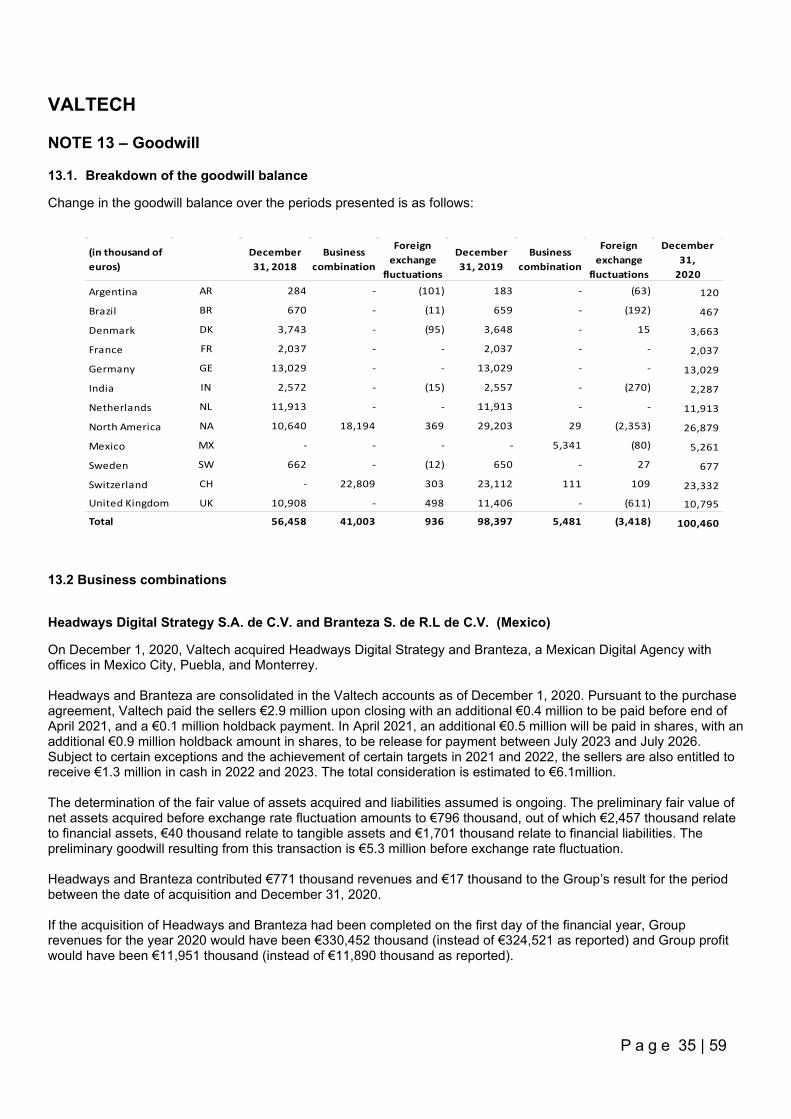

On December 1, 2020, Valtech acquired Headways Digital Strategy and Branteza, a Mexican Digital Agency with offices in Mexico City. Headways and Branteza are consolidated in the Valtech accounts as of December 1, 2020. Pursuant to the purchase agreement, Valtech paid the sellers €2.9 million upon closing with an additional €0.4 million to be paid before end of April 2021, and a €0.1 million holdback payment. In April 2021, an additional €0.5 million will be paid in shares, with an additional €0.9 million holdback amount in shares, to be released for payment between July 2023 and July 2026. Subject to certain exceptions and the achievement of certain targets in 2021 and 2022, the sellers are also entitled to receive €1.3 million in cash in 2022 and 2023. The total consideration is estimated at €6.1million. The determination of the fair value of assets acquired and liabilities assumed is ongoing. The preliminary fair value of net assets acquired before exchange rate fluctuation amounts to €796 thousand, out of which €2,457 thousand relate to financial assets, €40 thousand relate to tangible assets and €1,701 thousand relate to financial liabilities. The preliminary goodwill resulting from this transaction is €5.3 million before exchange rate fluctuation.

Valtech SE

P a g e 8 | 12

Headways and Branteza contributed €771 thousand revenues and €17 thousand to the Group’s result for the period between the date of acquisition and December 31, 2020. If the acquisition of Headways and Branteza had been completed on the first day of the financial year, Group revenues for the year 2020 would have been €330,452 thousand (instead of €324,521 as reported) and Group profit would have been €11,951 thousand (instead of €11,890 thousand as reported).

Likely future developments Valtech will continue to develop its client and activity portfolio in the countries where the group has a presence. Valtech will also explore opportunities to acquire new businesses if and when opportunities arise to expand its activities in geographies, technologies and know-how that can contribute to its growth.

Buy-back of own shares During the year 2020, the Company purchased 566,595 own shares, amounting to €8,777 thousand (purchased from the sellers of People Interactive, El Chalten, Non Linear and Codehouse). 53,000 of the shares bought back was used for exercise of warrants, leading to an outstanding number of 513,595 treasury shares at a value of €7,982 thousand as per December 31, 2020.

Environment Valtech is a s professional service company and has no production of its own. This means that we have relatively small material flows and waste disposal. We strive to reduce our negative environmental impact and increase our positive social imprint.

We work continuously with environmental and sustainability issues, social responsibility, gender equality and diversity. We are committed to these issues because we believe that it contributes to a positive, attractive and evolving working climate and we believe in the power of individuals and businesses to positively influence the development of society.

Here’s some examples of our environment work:

• We have a careful attitude to how we use the earth's resources. We consider environmental aspects, sustainability and social responsibility in decisions made, both large and small

• Environmental issues should be taken into account when choosing new premises, whether it concerns (i) their energy consumption and (ii) their location and thus their ease of access by public transportation.

• We work to minimize our environmental impact and choose the alternatives that are most environmentally friendly. We make relevant environmental requirements when purchasing goods and services.

• We strive to reduce our waste and to have a responsible and efficient waste disposal • We recycle consumed materials and products to the highest extent possible • Through innovation, design and technology, we strive to help our customers choose more sustainable

solutions and approaches that promote sustainable societal development. • We take advantage of employees' interest and commitment in environmental and sustainability issues

Given the very light environmental impact of its business, Valtech does not yet have a definitive responsibility for the responsibility for the coordination of environmental management. A reflection is under way which could lead to a connection with the Group's General Secretariat.

Valtech SE

P a g e 9 | 12

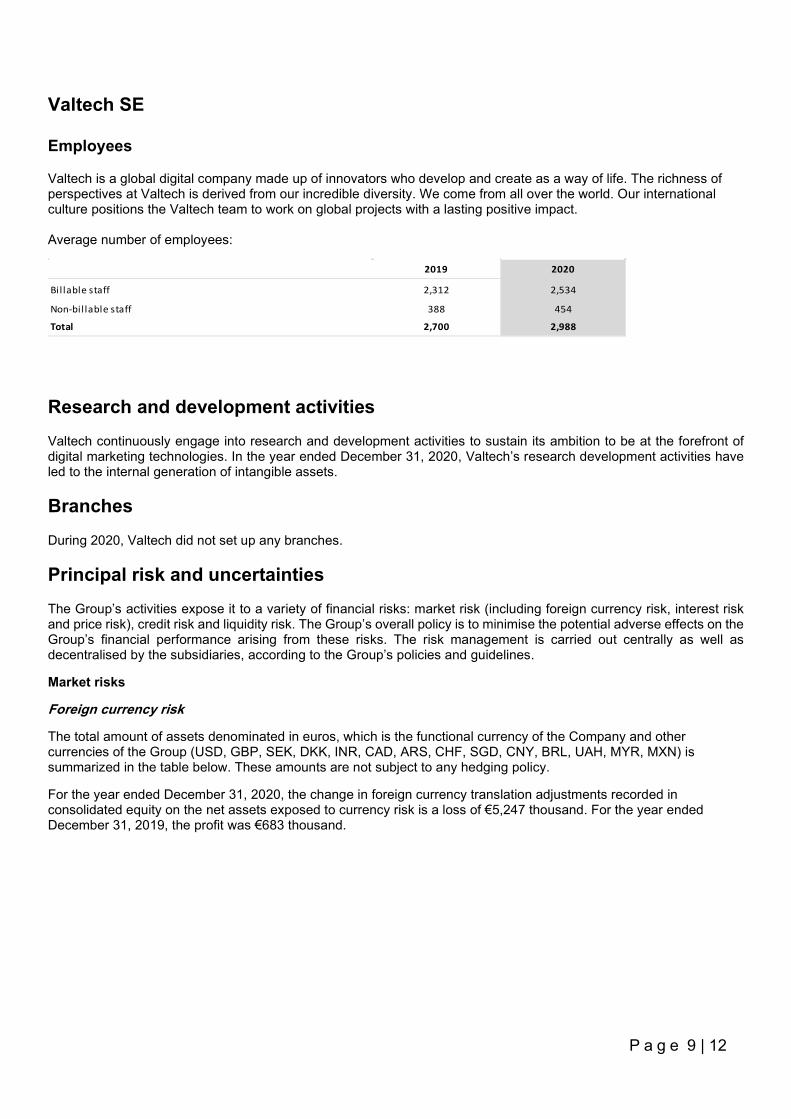

Employees

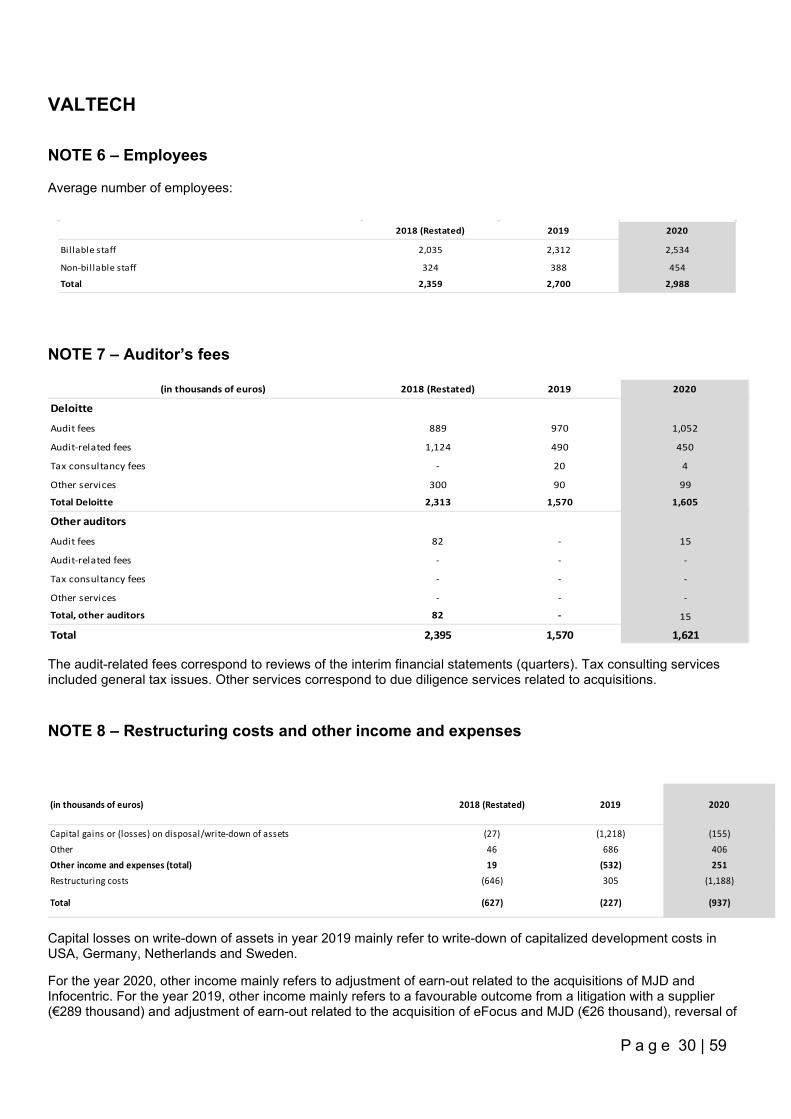

Valtech is a global digital company made up of innovators who develop and create as a way of life. The richness of perspectives at Valtech is derived from our incredible diversity. We come from all over the world. Our international culture positions the Valtech team to work on global projects with a lasting positive impact. Average number of employees:

2019 2020

Billable staff 2,312 2,534

Non-bil lable staff 388 454

Total 2,700 2,988

Research and development activities Valtech continuously engage into research and development activities to sustain its ambition to be at the forefront of digital marketing technologies. In the year ended December 31, 2020, Valtech’s research development activities have led to the internal generation of intangible assets.

Branches During 2020, Valtech did not set up any branches.

Principal risk and uncertainties The Group’s activities expose it to a variety of financial risks: market risk (including foreign currency risk, interest risk and price risk), credit risk and liquidity risk. The Group’s overall policy is to minimise the potential adverse effects on the Group’s financial performance arising from these risks. The risk management is carried out centrally as well as decentralised by the subsidiaries, according to the Group’s policies and guidelines.

Market risks

Foreign currency risk

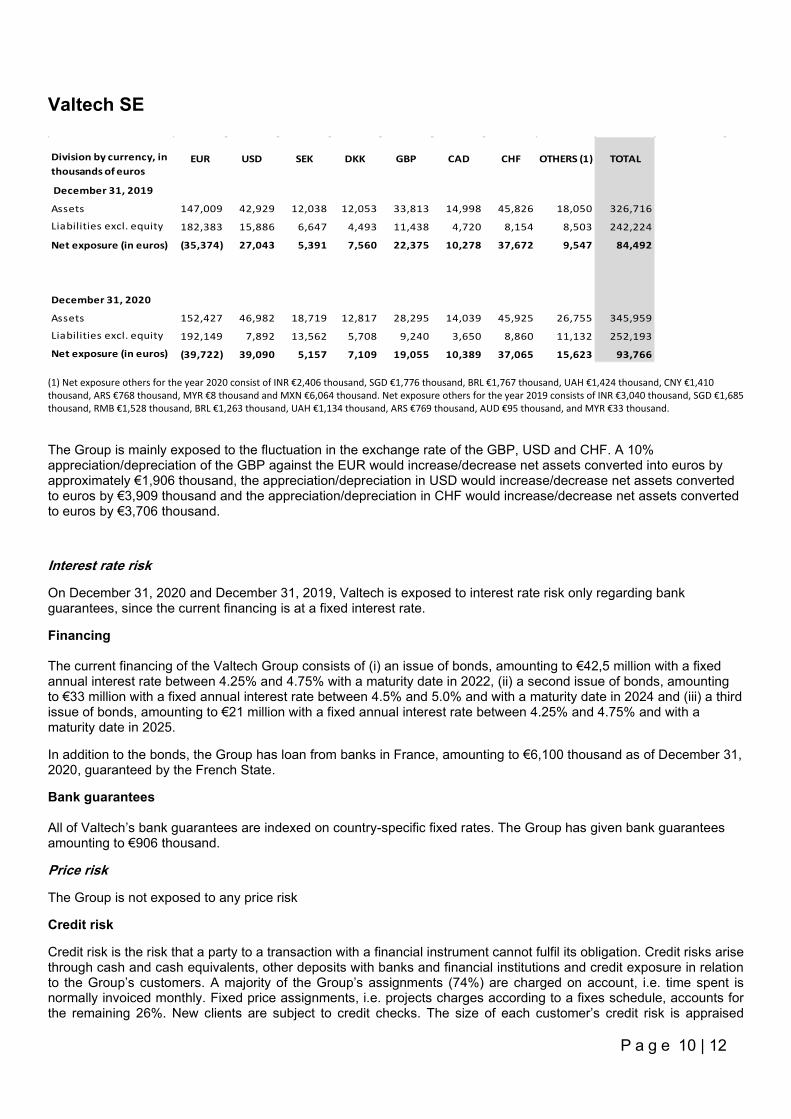

The total amount of assets denominated in euros, which is the functional currency of the Company and other currencies of the Group (USD, GBP, SEK, DKK, INR, CAD, ARS, CHF, SGD, CNY, BRL, UAH, MYR, MXN) is summarized in the table below. These amounts are not subject to any hedging policy.

For the year ended December 31, 2020, the change in foreign currency translation adjustments recorded in consolidated equity on the net assets exposed to currency risk is a loss of €5,247 thousand. For the year ended December 31, 2019, the profit was €683 thousand.

Valtech SE

P a g e 10 | 12

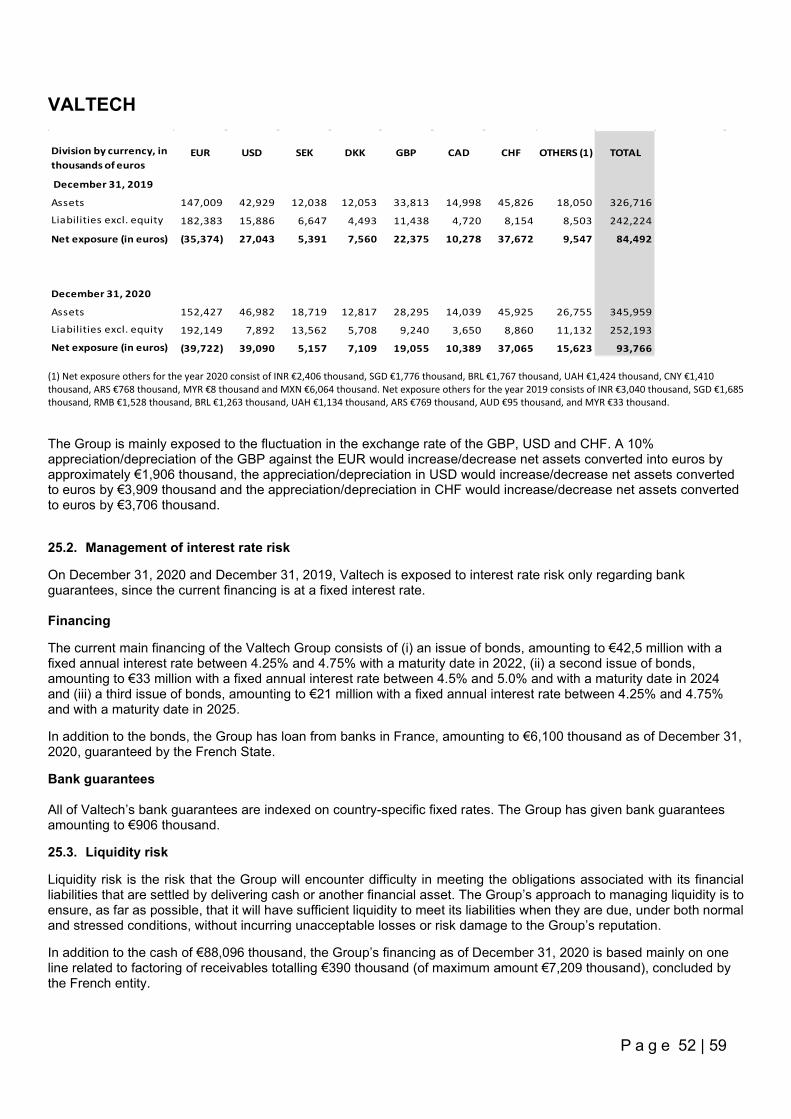

Division by currency, in thousands of euros

EUR USD SEK DKK GBP CAD CHF OTHERS (1) TOTAL

December 31, 2019

Assets 147,009 42,929 12,038 12,053 33,813 14,998 45,826 18,050 326,716

Liabilities excl. equity 182,383 15,886 6,647 4,493 11,438 4,720 8,154 8,503 242,224

Net exposure (in euros) (35,374) 27,043 5,391 7,560 22,375 10,278 37,672 9,547 84,492

December 31, 2020

Assets 152,427 46,982 18,719 12,817 28,295 14,039 45,925 26,755 345,959

Liabilities excl. equity 192,149 7,892 13,562 5,708 9,240 3,650 8,860 11,132 252,193

Net exposure (in euros) (39,722) 39,090 5,157 7,109 19,055 10,389 37,065 15,623 93,766 (1) Net exposure others for the year 2020 consist of INR €2,406 thousand, SGD €1,776 thousand, BRL €1,767 thousand, UAH €1,424 thousand, CNY €1,410 thousand, ARS €768 thousand, MYR €8 thousand and MXN €6,064 thousand. Net exposure others for the year 2019 consists of INR €3,040 thousand, SGD €1,685 thousand, RMB €1,528 thousand, BRL €1,263 thousand, UAH €1,134 thousand, ARS €769 thousand, AUD €95 thousand, and MYR €33 thousand.

The Group is mainly exposed to the fluctuation in the exchange rate of the GBP, USD and CHF. A 10% appreciation/depreciation of the GBP against the EUR would increase/decrease net assets converted into euros by approximately €1,906 thousand, the appreciation/depreciation in USD would increase/decrease net assets converted to euros by €3,909 thousand and the appreciation/depreciation in CHF would increase/decrease net assets converted to euros by €3,706 thousand.

Interest rate risk

On December 31, 2020 and December 31, 2019, Valtech is exposed to interest rate risk only regarding bank guarantees, since the current financing is at a fixed interest rate.

Financing The current financing of the Valtech Group consists of (i) an issue of bonds, amounting to €42,5 million with a fixed annual interest rate between 4.25% and 4.75% with a maturity date in 2022, (ii) a second issue of bonds, amounting to €33 million with a fixed annual interest rate between 4.5% and 5.0% and with a maturity date in 2024 and (iii) a third issue of bonds, amounting to €21 million with a fixed annual interest rate between 4.25% and 4.75% and with a maturity date in 2025.

In addition to the bonds, the Group has loan from banks in France, amounting to €6,100 thousand as of December 31, 2020, guaranteed by the French State.

Bank guarantees All of Valtech’s bank guarantees are indexed on country-specific fixed rates. The Group has given bank guarantees amounting to €906 thousand.

Price risk

The Group is not exposed to any price risk

Credit risk

Credit risk is the risk that a party to a transaction with a financial instrument cannot fulfil its obligation. Credit risks arise through cash and cash equivalents, other deposits with banks and financial institutions and credit exposure in relation to the Group’s customers. A majority of the Group’s assignments (74%) are charged on account, i.e. time spent is normally invoiced monthly. Fixed price assignments, i.e. projects charges according to a fixes schedule, accounts for the remaining 26%. New clients are subject to credit checks. The size of each customer’s credit risk is appraised

Valtech SE

P a g e 11 | 12

individually. A monthly review of the aging of balances is conducted, and each customer and its associated credit limit is closely monitored.

Liquidity risk

Liquidity risk is the risk that the Group will encounter difficulty in meeting the obligations associated with its financial liabilities that are settled by delivering cash or another financial asset. The Group’s approach to managing liquidity is to ensure, as far as possible, that it will have sufficient liquidity to meet its liabilities when they are due, under both normal and stressed conditions, without incurring unacceptable losses or risk damage to the Group’s reputation.

In addition to the cash of €88,096 thousand, the Group’s financing as of December 31, 2020 is based mainly on one line related to factoring of receivables totalling €390 thousand (of maximum amount €7,209 thousand), concluded by the French entity.

As of December 31, 2020, the cash and cash equivalents has increased by €53.9 million compared to December 31, 2019. Increase in cash related to Covid-19 government supports amounts to €22.2 million, and refer to delayed payments of taxes €9.2 million, received loans granted by governments €8.2 million and received government grants related to salary costs €4.8 million.

Risk on shares and other financial investments

Valtech does not hold any marketable securities, and the Group is not exposed to the risk of share price fluctuation.

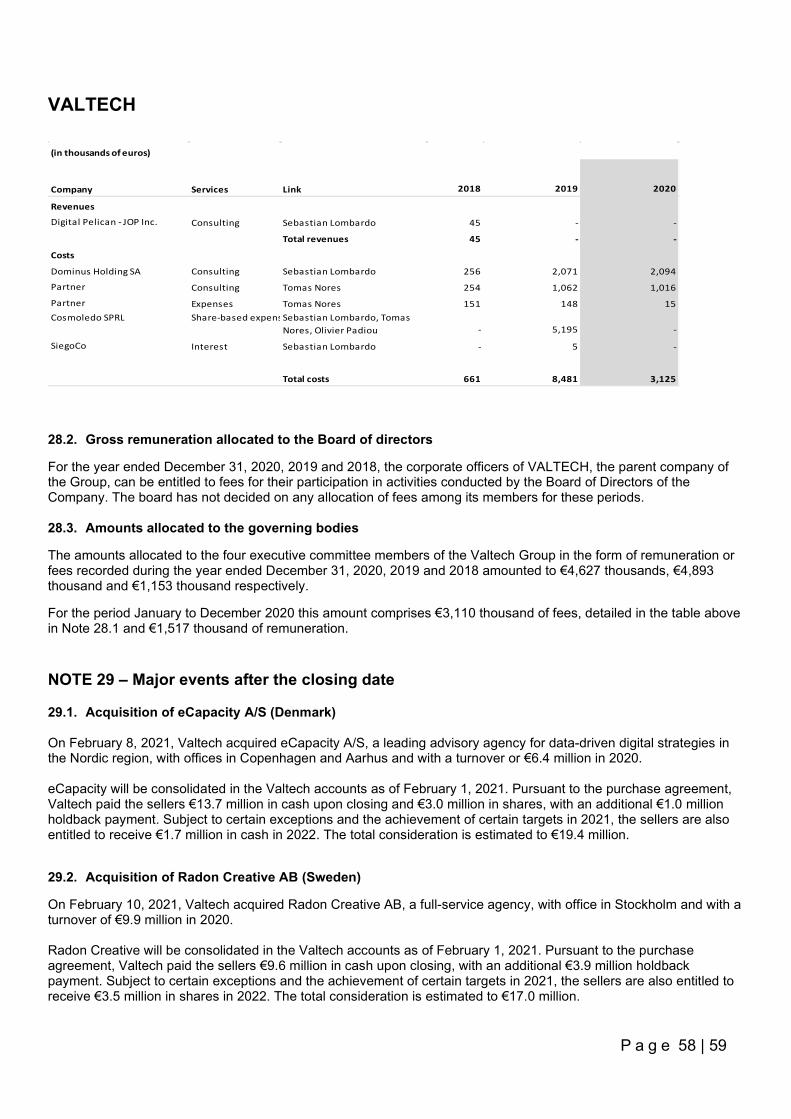

Major events after the closing date Acquisition of eCapacity A/S (Denmark) On February 8, 2021, Valtech acquired eCapacity A/S, a leading advisory agency for data-driven digital strategies in the Nordic region, with offices in Copenhagen and Aarhus and with a turnover or €6.4 million in 2020. eCapacity will be consolidated in the Valtech accounts as of February 1, 2021. Pursuant to the purchase agreement, Valtech paid the sellers €13.7 million in cash upon closing and €3.0 million in shares, with an additional €1.0 million holdback payment. Subject to certain exceptions and the achievement of certain targets in 2021, the sellers are also entitled to receive €1.7 million in cash in 2022. The total consideration is estimated to €19.4 million.

Acquisition of Radon Creative AB (Sweden)

On February 10, 2021, Valtech acquired Radon Creative AB, a full-service agency, with office in Stockholm and with a turnover of €9.9 million in 2020. Radon Creative will be consolidated in the Valtech accounts as of February 1, 2021. Pursuant to the purchase agreement, Valtech paid the sellers €9.6 million in cash upon closing, with an additional €3.9 million holdback payment. Subject to certain exceptions and the achievement of certain targets in 2021, the sellers are also entitled to receive €3.5 million in shares in 2022. The total consideration is estimated to €17.0 million.

Acquisition of Codeflair Group (Switzerland and North Macedonia)

On March 30, 2021, Valtech acquired Codeflair Group, a Swiss company with a subsidiary in North Macedonia and with a turnover of €1.9 million in 2020. Codeflair will be consolidated in the Valtech accounts as of April 1, 2021. Pursuant to the purchase agreement, Valtech paid the sellers €2.2 million in cash upon closing, with an additional €0.8 million payment in shares to be paid in April 2021.

Valtech SE

P a g e 12 | 12

Approval of restricted share unit plan

On March 25, 2021, the Board of Valtech, on behalf on the shareholders, approved a restricted share unit (RSU) plan, issued to key employees. Total number of issued RSUs amount to 268.334, divided between 7 beneficiaries. The restricted share units give the employees the right to receive shares on the vesting dates. The plan vests between June 30, 2021 and June 30, 2022.

Société à responsabilité limitée au capital de 360.000 € RCS Luxembourg B 67.895 Autorisation d’établissement 10022179 © Deloitte Audit, SARL 13

Deloitte Audit Société à responsabilité limitée 20 Boulevard de Kockelscheuer L-1821 Luxembourg Tel: +352 451 451 www.deloitte.lu

To the Shareholders of

Valtech S.E.

European Public Limited Liability Company

28/30 Boulevard Joseph II

1840 Luxembourg

Luxembourg

REPORT OF THE REVISEUR D’ENTREPRISES AGREE

Report on the Audit of the Consolidated Financial Statements

Opinion

We have audited the consolidated financial statements of Valtech S.E and its subsidiaries (the “Group”), which

comprise the consolidated statement of financial position as at December 31, 2020, and the consolidated statement

of comprehensive income, consolidated statement of changes in equity and consolidated statement of cash flows for

the year then ended, and notes to the consolidated financial statements, including a summary of significant

accounting policies.

In our opinion, the accompanying consolidated financial statements present fairly, in all material respects, the

consolidated financial position of the Group as at December 31, 2020, and of its consolidated financial performance

and of its consolidated cash flows for the year then ended in accordance with International Financial Reporting

Standards (IFRSs) as adopted by the European Union.

Basis for Opinion

We conducted our audit in accordance with the Law of July 23, 2016 on the audit profession (Law of July 23, 2016) and

with International Standards on Auditing (ISAs) as adopted for Luxembourg by the “Commission de Surveillance du

Secteur Financier” (CSSF). Our responsibilities under the Law of July 23, 2016 and ISAs as adopted for Luxembourg by

the CSSF are further described in the “Responsibilities of the “réviseur d’entreprises agréé” for the Audit of the

Consolidated Financial Statements” section of our report. We are also independent of the Group in accordance with

the International Code of Ethics for Professional Accountants, including International Independence Standards, issued

by the International Ethics Standards Board for Accountants (IESBA Code) as adopted for Luxembourg by the CSSF

together with the ethical requirements that are relevant to our audit of the consolidated financial statements, and

have fulfilled our other ethical responsibilities under those ethical requirements. We believe that the audit evidence

we have obtained is sufficient and appropriate to provide a basis for our opinion.

14

Other information

The Board of Directors is responsible for the other information. The other information comprises the information

stated in the consolidated management report but does not include the consolidated financial statements and our

report of the “réviseur d’entreprises agréé” thereon.

Our opinion on the consolidated financial statements does not cover the other information and we do not express any

form of assurance conclusion thereon.

In connection with our audit of the consolidated financial statements, our responsibility is to read the other

information and, in doing so, consider whether the other information is materially inconsistent with the consolidated

financial statements or our knowledge obtained in the audit or otherwise appears to be materially misstated. If, based

on the work we have performed, we conclude that there is a material misstatement of this other information, we are

required to report this fact. We have nothing to report in this regard.

Responsibilities of the Board of Directors and Those Charged with Governance for the Consolidated Financial

Statements

The Board of Directors is responsible for the preparation and fair presentation of these consolidated financial

statements in accordance with IFRSs as adopted by the European Union, and for such internal control as the Board of

Directors determines is necessary to enable the preparation of consolidated financial statements that are free from

material misstatement, whether due to fraud or error.

In preparing the consolidated financial statements, the Board of Directors is responsible for assessing the Group’s

ability to continue as a going concern, disclosing, as applicable, matters related to going concern and using the going

concern basis of accounting unless the Board of Directors either intends to liquidate the Group or to cease operations,

or has no realistic alternative but to do so.

Responsibilities of the “réviseur d’entreprises agréé” for the Audit of the Consolidated Financial Statements

Our objectives are to obtain reasonable assurance about whether the consolidated financial statements as a whole

are free from material misstatement, whether due to fraud or error, and to issue a report of the “réviseur

d’entreprises agréé” that includes our opinion. Reasonable assurance is a high level of assurance, but is not a

guarantee that an audit conducted in accordance with the Law of July 23, 2016 and with ISAs as adopted for

Luxembourg by the CSSF will always detect a material misstatement when it exists. Misstatements can arise from

fraud or error and are considered material if, individually or in the aggregate, they could reasonably be expected to

influence the economic decisions of users taken on the basis of these consolidated financial statements.

15

As part of an audit in accordance with the Law of July 23, 2016 and with ISAs as adopted for Luxembourg by the CSSF,

we exercise professional judgment and maintain professional skepticism throughout the audit. We also:

• Identify and assess the risks of material misstatement of the consolidated financial statements, whether due to

fraud or error, design and perform audit procedures responsive to those risks, and obtain audit evidence that is

sufficient and appropriate to provide a basis for our opinion. The risk of not detecting a material misstatement

resulting from fraud is higher than for one resulting from error, as fraud may involve collusion, forgery,

intentional omissions, misrepresentations, or the override of internal control.

• Obtain an understanding of internal control relevant to the audit in order to design audit procedures that are

appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the

Group’s internal control.

• Evaluate the appropriateness of accounting policies used and the reasonableness of accounting estimates and

related disclosures made by the Board of Directors.

• Conclude on the appropriateness of Board of Directors’ use of the going concern basis of accounting and, based

on the audit evidence obtained, whether a material uncertainty exists related to events or conditions that may

cast significant doubt on the Group’s ability to continue as a going concern. If we conclude that a material

uncertainty exists, we are required to draw attention in our report of the “réviseur d’entreprises agréé” to the

related disclosures in the consolidated financial statements or, if such disclosures are inadequate, to modify

our opinion. Our conclusions are based on the audit evidence obtained up to the date of our report of the

“réviseur d’entreprises agréé”. However, future events or conditions may cause the Group to cease to continue

as a going concern.

• Evaluate the overall presentation, structure and content of the consolidated financial statements, including the

disclosures, and whether the consolidated financial statements represent the underlying transactions and

events in a manner that achieves fair presentation.

• Obtain sufficient appropriate audit evidence regarding the financial information of the entities and business

activities within the Group to express an opinion on the consolidated financial statements. We are responsible

for the direction, supervision and performance of the Group audit. We remain solely responsible for our audit

opinion.

We communicate with those charged with governance regarding, among other matters, the planned scope and timing

of the audit and significant audit findings, including any significant deficiencies in internal control that we identify

during our audit.

16

Report on Other Legal and Regulatory Requirements

The consolidated management report is consistent with the consolidated financial statements and has been prepared

in accordance with applicable legal requirements.

For Deloitte Audit, Cabinet de révision agréé

Marco Crosetto, Réviseur d’entreprises agréé Partner

May 6, 2021

VALTECH

P a g e 1 | 59

VALTECH Consolidated financial statements

Years ended December 31 2020, December 31 2019 and December 31 2018

VALTECH

P a g e 2 | 59

Consolidated statements of income (loss) 4

Consolidated statements of comprehensive income (loss) 5

Consolidated statements of financial position 6

Consolidated statements of cash flows 7

Consolidated statements of changes in shareholders’ equity 8

Notes to the financial statements 9

NOTE 1 – Accounting policies 9

NOTE 2 – Major events of the period 21

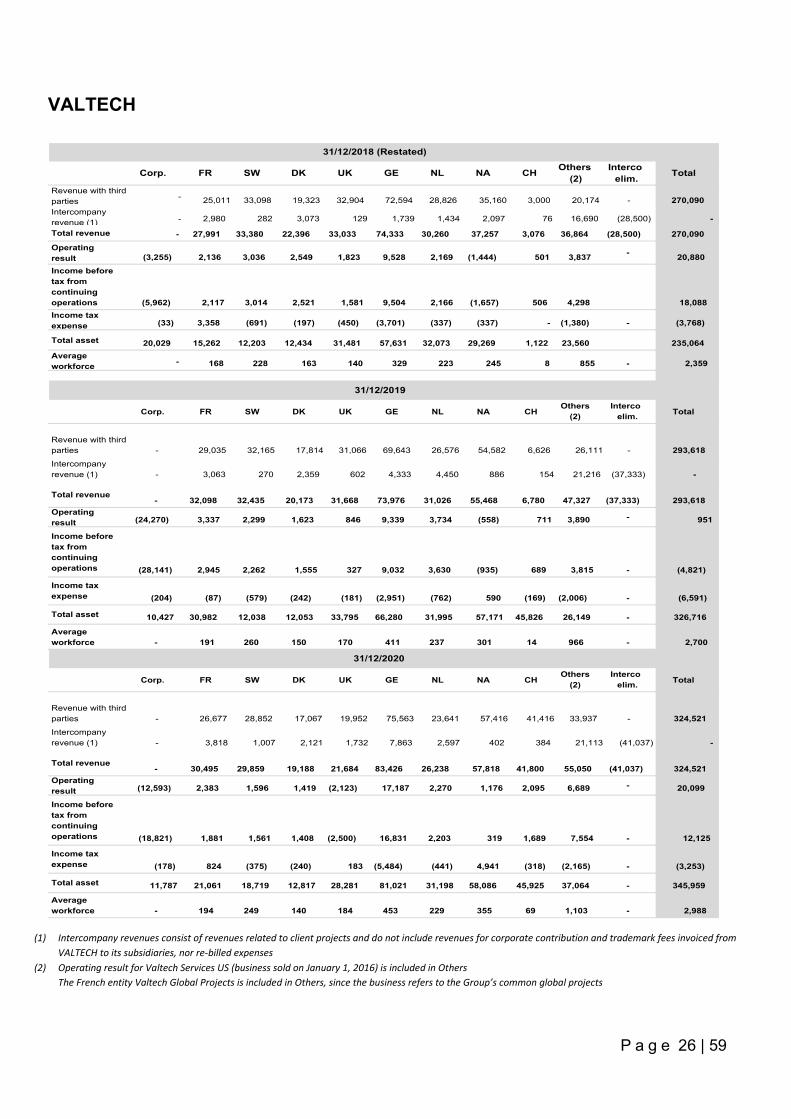

NOTE 3 – Segment information 24

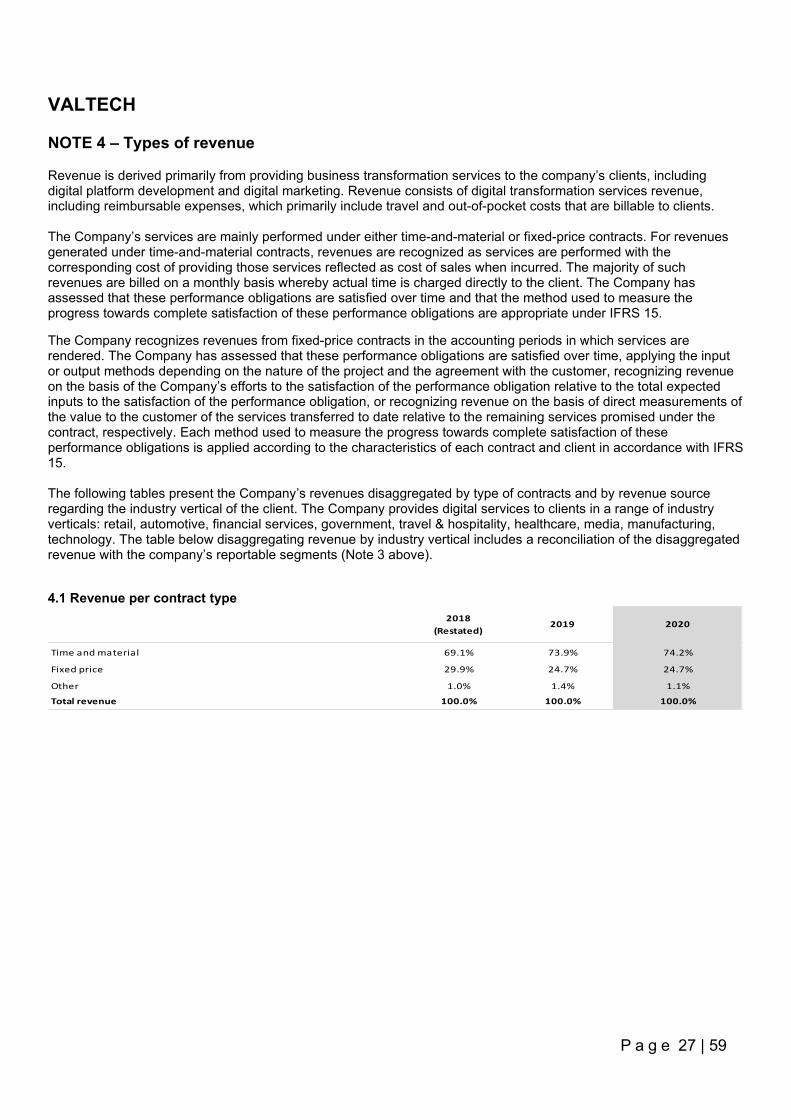

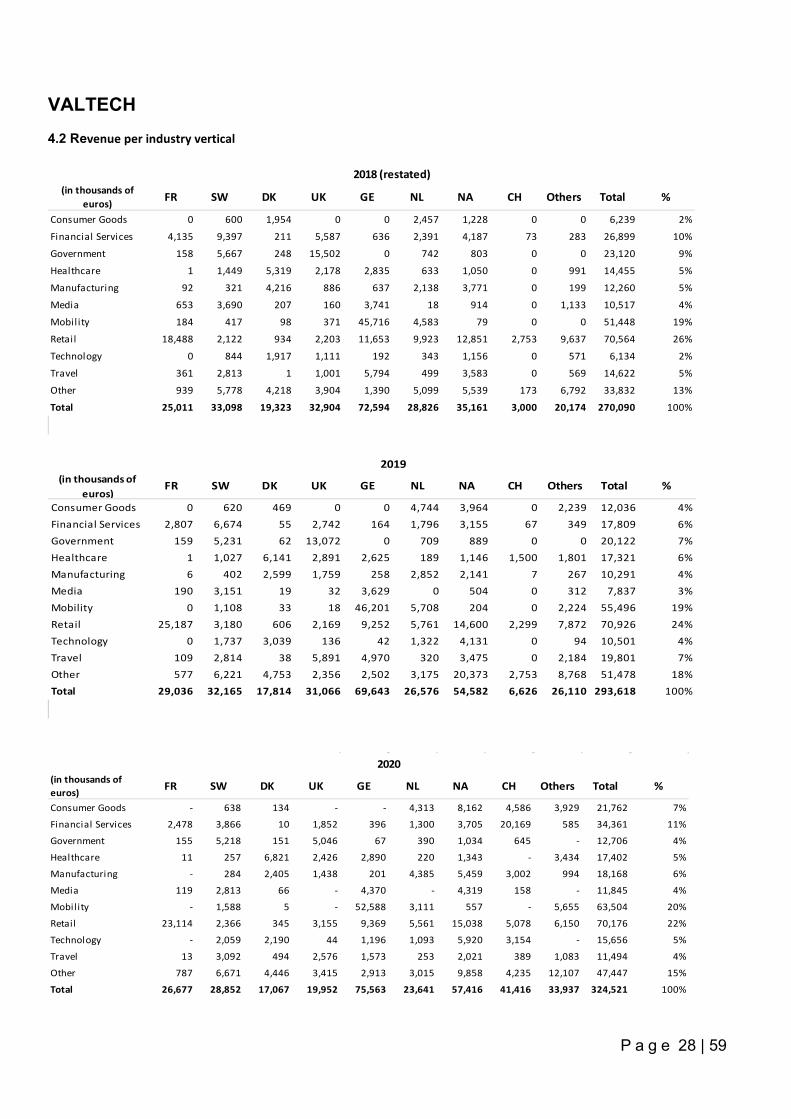

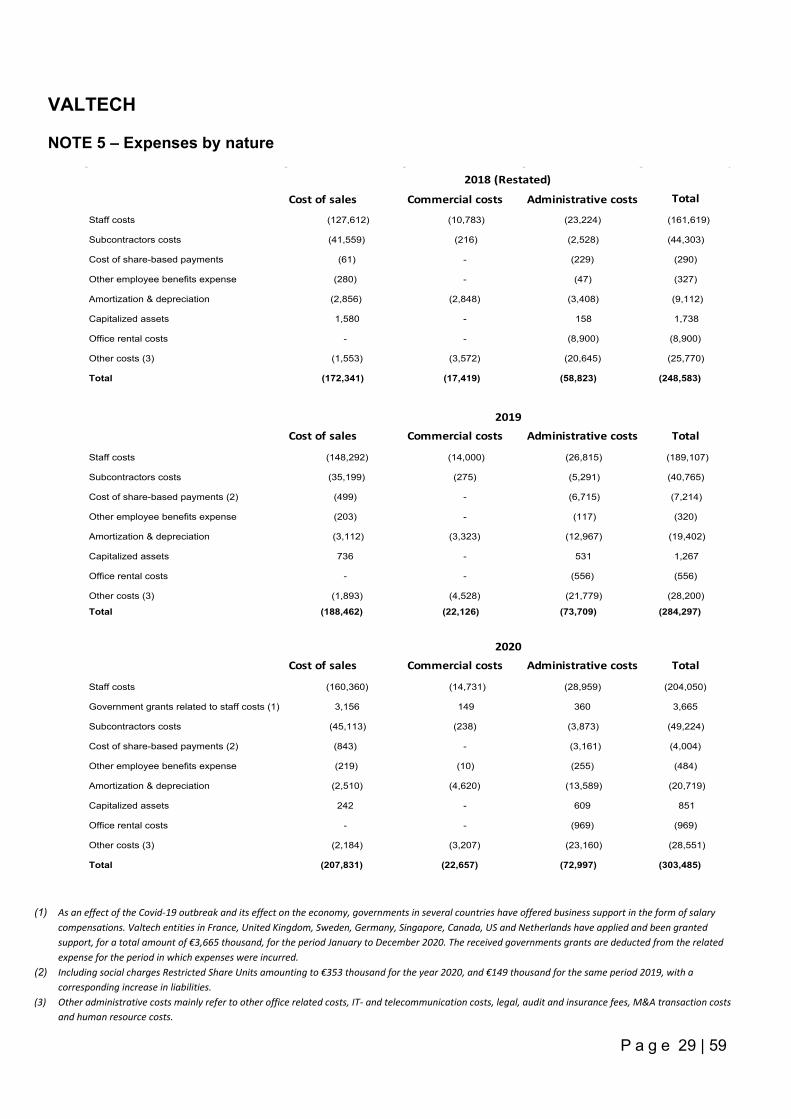

NOTE 4 – Types of revenue 27

NOTE 5 – Expenses by nature 29

NOTE 6 – Employees 30

NOTE 7 – Auditor’s fees 30

NOTE 8 – Restructuring costs and other income and expenses 30

NOTE 9 – Equity acquisition costs 31

NOTE 10 – Financial result 31

NOTE 11 – Income taxes 31

NOTE 12 – Discontinued operations 34

VALTECH

P a g e 3 | 59

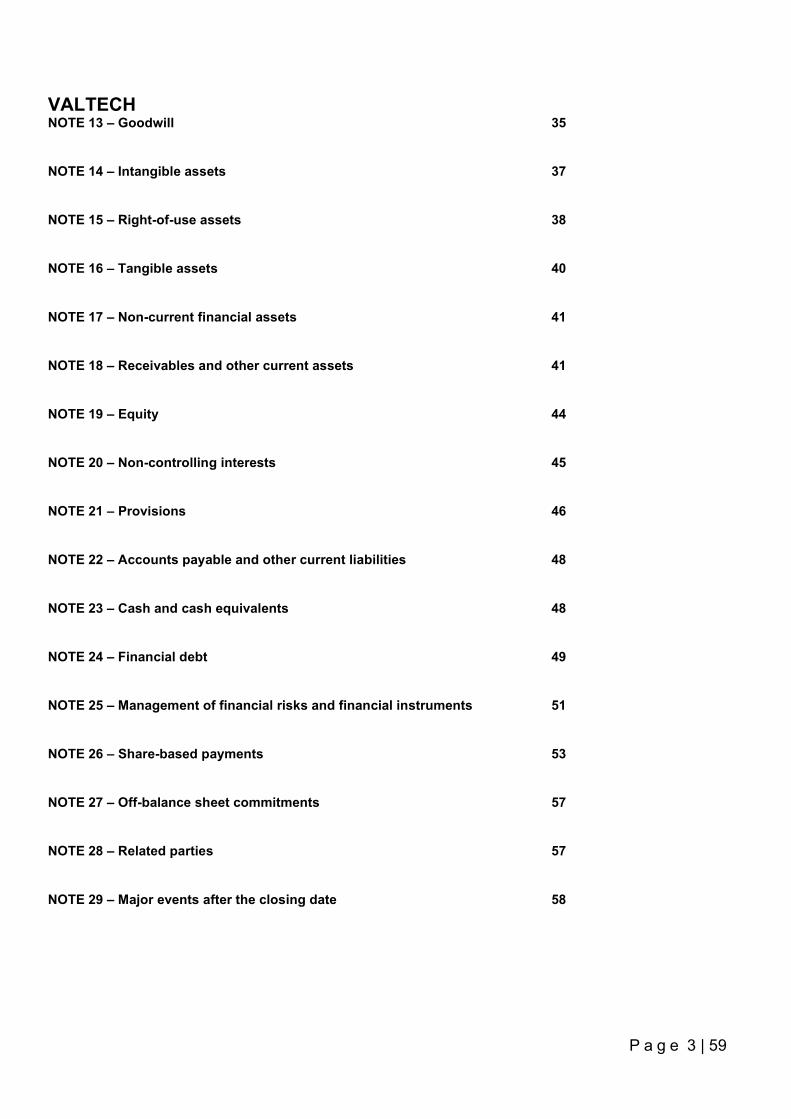

NOTE 13 – Goodwill 35

NOTE 14 – Intangible assets 37

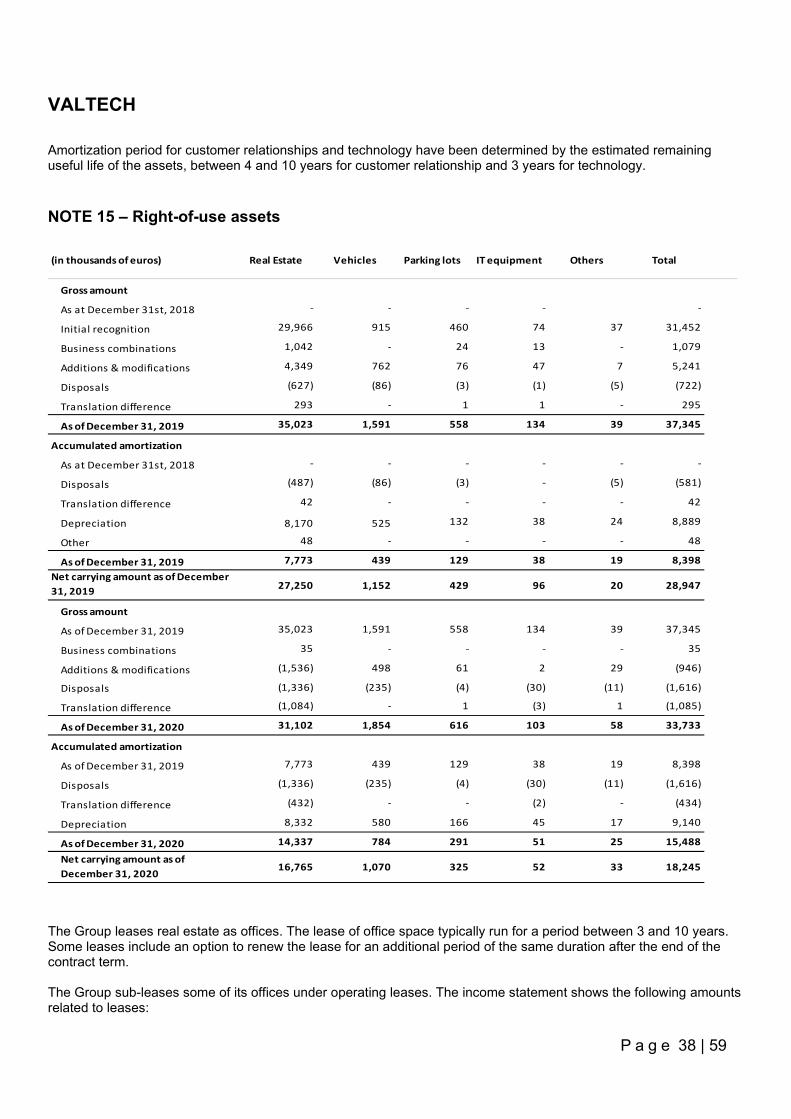

NOTE 15 – Right-of-use assets 38

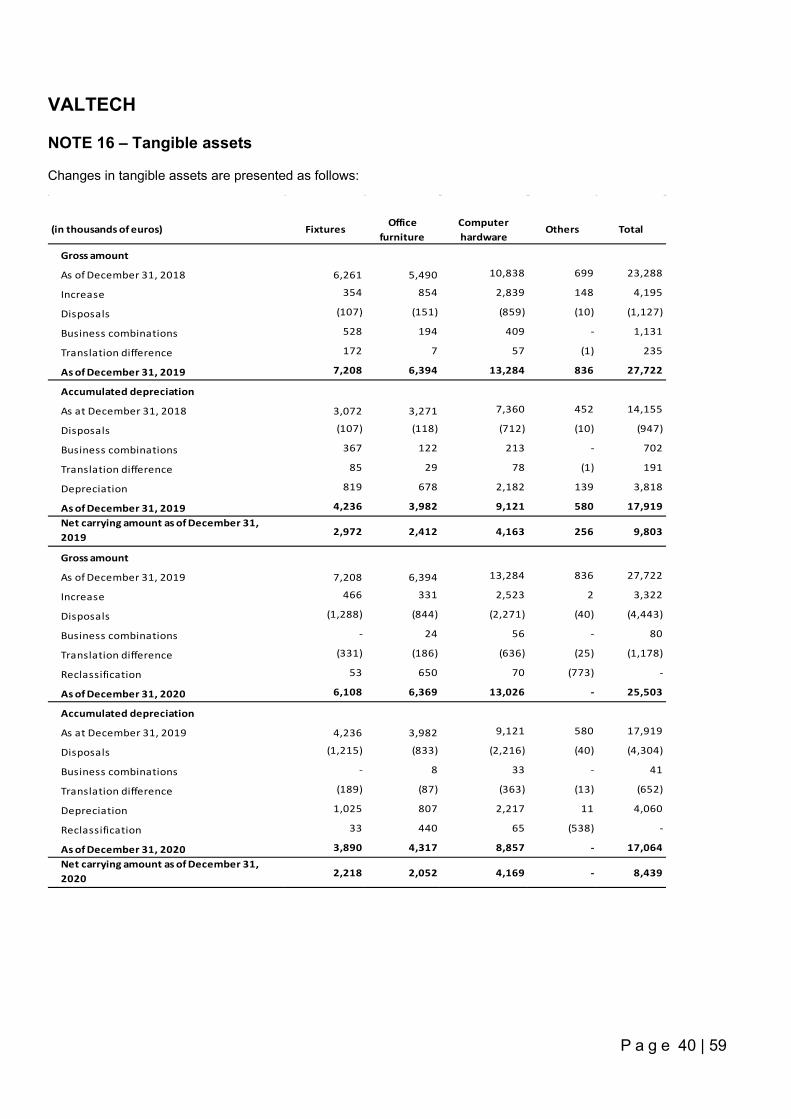

NOTE 16 – Tangible assets 40

NOTE 17 – Non-current financial assets 41

NOTE 18 – Receivables and other current assets 41

NOTE 19 – Equity 44

NOTE 20 – Non-controlling interests 45

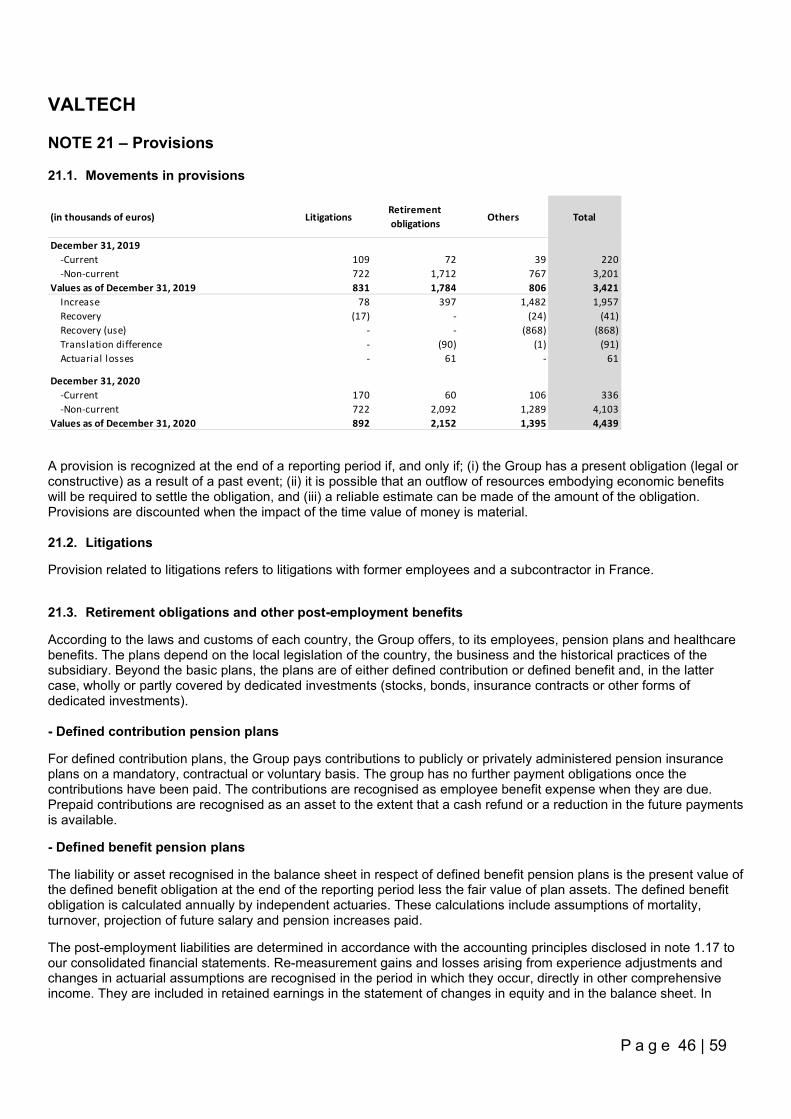

NOTE 21 – Provisions 46

NOTE 22 – Accounts payable and other current liabilities 48

NOTE 23 – Cash and cash equivalents 48

NOTE 24 – Financial debt 49

NOTE 25 – Management of financial risks and financial instruments 51

NOTE 26 – Share-based payments 53

NOTE 27 – Off-balance sheet commitments 57

NOTE 28 – Related parties 57

NOTE 29 – Major events after the closing date 58

VALTECH

P a g e 4 | 59

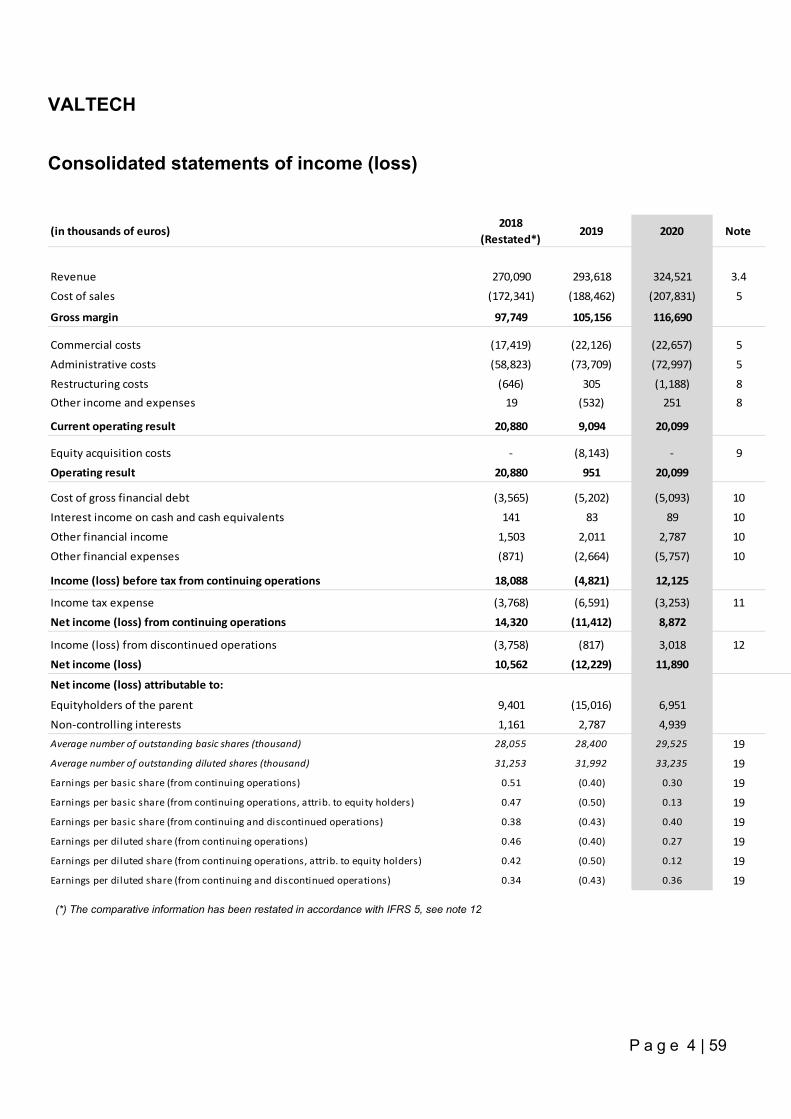

Consolidated statements of income (loss)

(in thousands of euros)2018

(Restated*)2019 2020 Note

Revenue 270,090 293,618 324,521 3.4

Cost of sales (172,341) (188,462) (207,831) 5

Gross margin 97,749 105,156 116,690

Commercial costs (17,419) (22,126) (22,657) 5

Administrative costs (58,823) (73,709) (72,997) 5

Restructuring costs (646) 305 (1,188) 8Other income and expenses 19 (532) 251 8

Current operating result 20,880 9,094 20,099

Equity acquisition costs - (8,143) - 9

Operating result 20,880 951 20,099

Cost of gross financial debt (3,565) (5,202) (5,093) 10

Interest income on cash and cash equivalents 141 83 89 10

Other financial income 1,503 2,011 2,787 10

Other financial expenses (871) (2,664) (5,757) 10

Income (loss) before tax from continuing operations 18,088 (4,821) 12,125

Income tax expense (3,768) (6,591) (3,253) 11

Net income (loss) from continuing operations 14,320 (11,412) 8,872

Income (loss) from discontinued operations (3,758) (817) 3,018 12

Net income (loss) 10,562 (12,229) 11,890

Net income (loss) attributable to:

Equityholders of the parent 9,401 (15,016) 6,951

Non-controlling interests 1,161 2,787 4,939Average number of outstanding basic shares (thousand) 28,055 28,400 29,525 19Average number of outstanding diluted shares (thousand) 31,253 31,992 33,235 19Earnings per basic share (from continuing operations) 0.51 (0.40) 0.30 19Earnings per basic share (from continuing operations, attrib. to equity holders) 0.47 (0.50) 0.13 19Earnings per basic share (from continuing and discontinued operations) 0.38 (0.43) 0.40 19Earnings per diluted share (from continuing operations) 0.46 (0.40) 0.27 19Earnings per diluted share (from continuing operations, attrib. to equity holders) 0.42 (0.50) 0.12 19Earnings per diluted share (from continuing and discontinued operations) 0.34 (0.43) 0.36 19

(*) The comparative information has been restated in accordance with IFRS 5, see note 12

VALTECH

P a g e 5 | 59

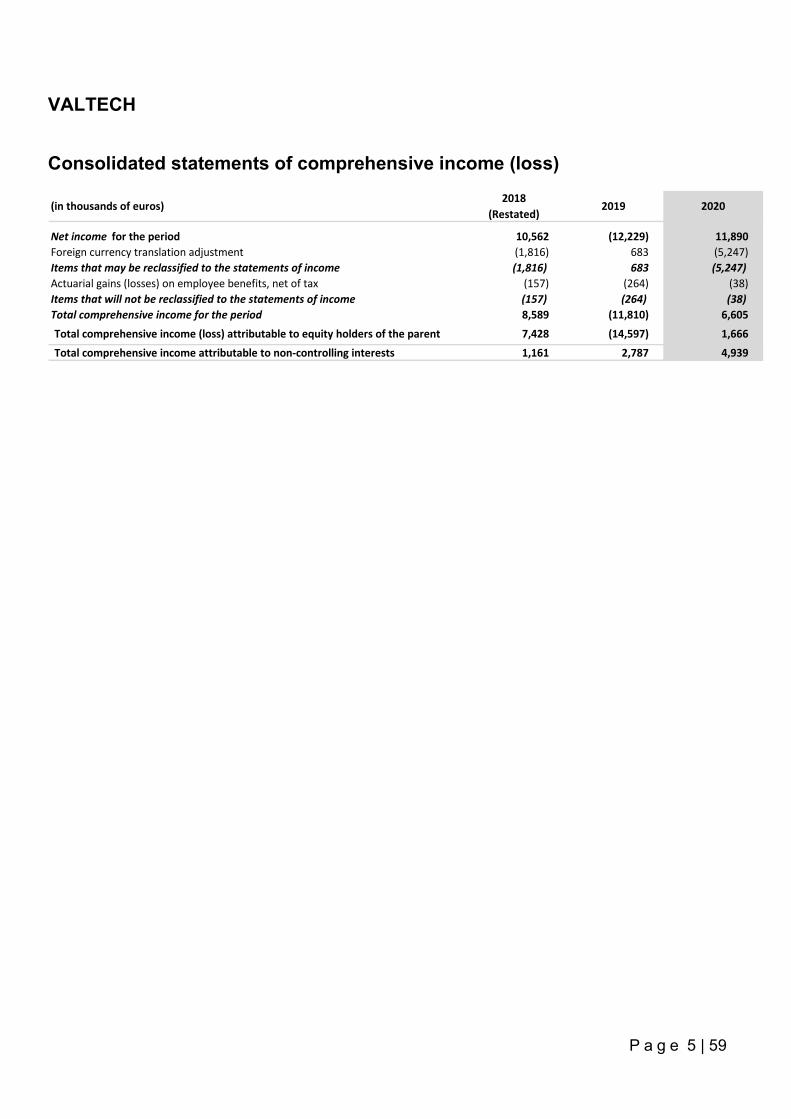

Consolidated statements of comprehensive income (loss)

(in thousands of euros)2018

(Restated)2019 2020

Net income for the period 10,562 (12,229) 11,890 Foreign currency translation adjustment (1,816) 683 (5,247) Items that may be reclassified to the statements of income (1,816) 683 (5,247) Actuarial gains (losses) on employee benefits, net of tax (157) (264) (38) Items that will not be reclassified to the statements of income (157) (264) (38) Total comprehensive income for the period 8,589 (11,810) 6,605 Total comprehensive income (loss) attributable to equity holders of the parent 7,428 (14,597) 1,666 Total comprehensive income attributable to non-controlling interests 1,161 2,787 4,939

VALTECH

P a g e 6 | 59

Consolidated statements of financial position

(in thousands of euros) 31/12/2019 31/12/2020 Notes

Goodwill 98,397 100,460 13Intangible assets, net 35,185 30,710 14Right-of-use assets, net 28,947 18,245 15Tangible assets, net 9,803 8,439 16Non-current financial assets, net 3,468 3,191 17Other non-current assets 45 39Deferred tax assets 6,839 12,838 11

Non-current assets 182,684 173,922

Accounts receivable and related accounts 95,281 73,770 18Other current assets 13,007 10,171 18Cash and cash equivalents 35,744 88,096 23

Current assets 144,032 172,037

Total assets 326,716 345,959

Share capital 3,674 3,763 19Reserves 84,312 68,013 19Net income attributable to equity holders of the parent (15,016) 6,951 19

Equity attributable to owners of the Company 72,970 78,727

Non-controlling interests 11,522 15,039 20

Total equity 84,492 93,766

Provisions-non-current portion 3,201 4,103 21Long-term borrowings 96,369 102,506 24Other financial debt-non-current portion 5,752 4,694 24Lease liabilities non-current portion 19,741 11,911 15,24Deferred tax liabilities 8,148 6,925 11

Non-current liabilities 133,211 130,139

Provisions-current portion 220 336 21Short-term borrowings and bank overdrafts 4,557 6,523 24Accounts payable and related accounts 16,054 18,953 22Other financial debt-current portion 32,415 23,169 24Lease liabilities - current portion 10,010 7,766 15,24Other current liabilities 45,757 65,307 22Current liabilities 109,013 122,054

Total liabilities 242,224 252,193

Total equity and liabilities 326,716 345,959

VALTECH

P a g e 7 | 59

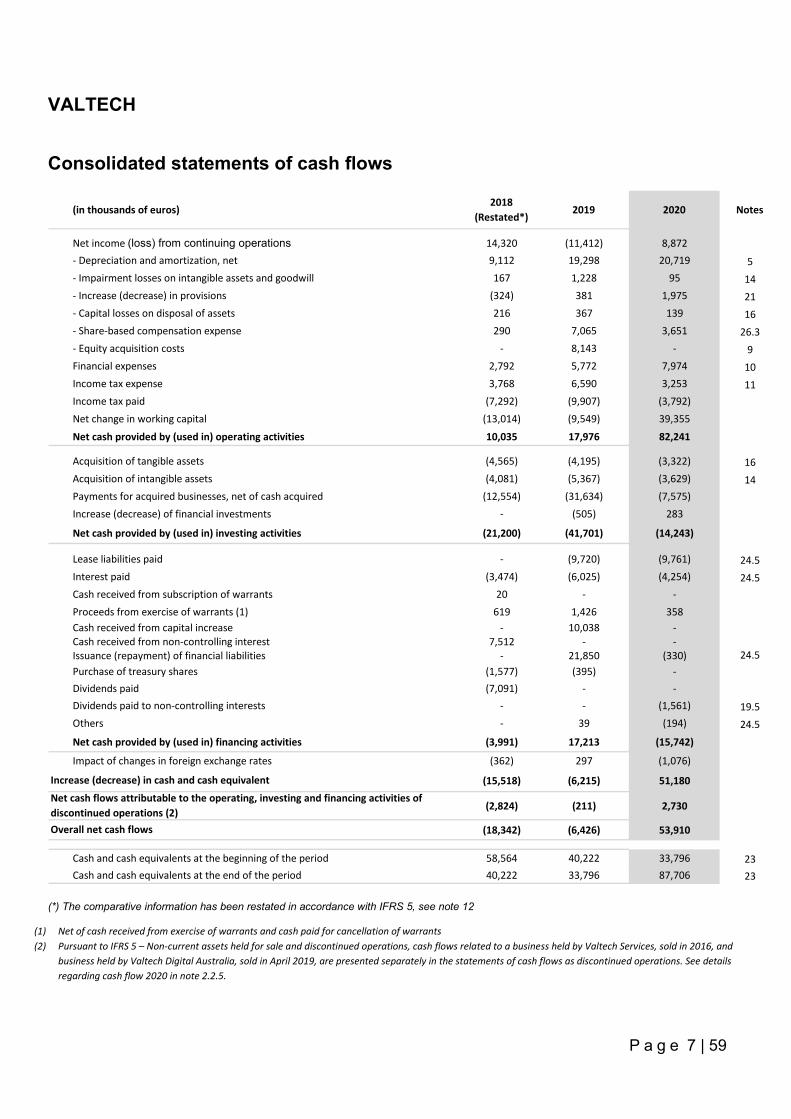

Consolidated statements of cash flows

(in thousands of euros)2018

(Restated*)2019 2020 Notes

Net income (loss) from continuing operations 14,320 (11,412) 8,872- Depreciation and amortization, net 9,112 19,298 20,719 5- Impairment losses on intangible assets and goodwill 167 1,228 95 14- Increase (decrease) in provisions (324) 381 1,975 21- Capital losses on disposal of assets 216 367 139 16- Share-based compensation expense 290 7,065 3,651 26.3- Equity acquisition costs - 8,143 - 9Financial expenses 2,792 5,772 7,974 10Income tax expense 3,768 6,590 3,253 11Income tax paid (7,292) (9,907) (3,792)Net change in working capital (13,014) (9,549) 39,355

Net cash provided by (used in) operating activities 10,035 17,976 82,241

Acquisition of tangible assets (4,565) (4,195) (3,322) 16Acquisition of intangible assets (4,081) (5,367) (3,629) 14Payments for acquired businesses, net of cash acquired (12,554) (31,634) (7,575)Increase (decrease) of financial investments - (505) 283

Net cash provided by (used in) investing activities (21,200) (41,701) (14,243)

Lease liabilities paid - (9,720) (9,761) 24.5Interest paid (3,474) (6,025) (4,254) 24.5Cash received from subscription of warrants 20 - -Proceeds from exercise of warrants (1) 619 1,426 358Cash received from capital increase - 10,038 -Cash received from non-controlling interest 7,512 - -Issuance (repayment) of financial liabilities - 21,850 (330) 24.5Purchase of treasury shares (1,577) (395) -Dividends paid (7,091) - -Dividends paid to non-controlling interests - - (1,561) 19.5Others - 39 (194) 24.5Net cash provided by (used in) financing activities (3,991) 17,213 (15,742)

Impact of changes in foreign exchange rates (362) 297 (1,076)

(15,518) (6,215) 51,180

(2,824) (211) 2,730

(18,342) (6,426) 53,910

Cash and cash equivalents at the beginning of the period 58,564 40,222 33,796 23Cash and cash equivalents at the end of the period 40,222 33,796 87,706 23

Net cash flows attributable to the operating, investing and financing activities of discontinued operations (2)Overall net cash flows

Increase (decrease) in cash and cash equivalent

(*) The comparative information has been restated in accordance with IFRS 5, see note 12

(1) Net of cash received from exercise of warrants and cash paid for cancellation of warrants (2) Pursuant to IFRS 5 – Non-current assets held for sale and discontinued operations, cash flows related to a business held by Valtech Services, sold in 2016, and

business held by Valtech Digital Australia, sold in April 2019, are presented separately in the statements of cash flows as discontinued operations. See details regarding cash flow 2020 in note 2.2.5.

VALTECH

P a g e 8 | 59

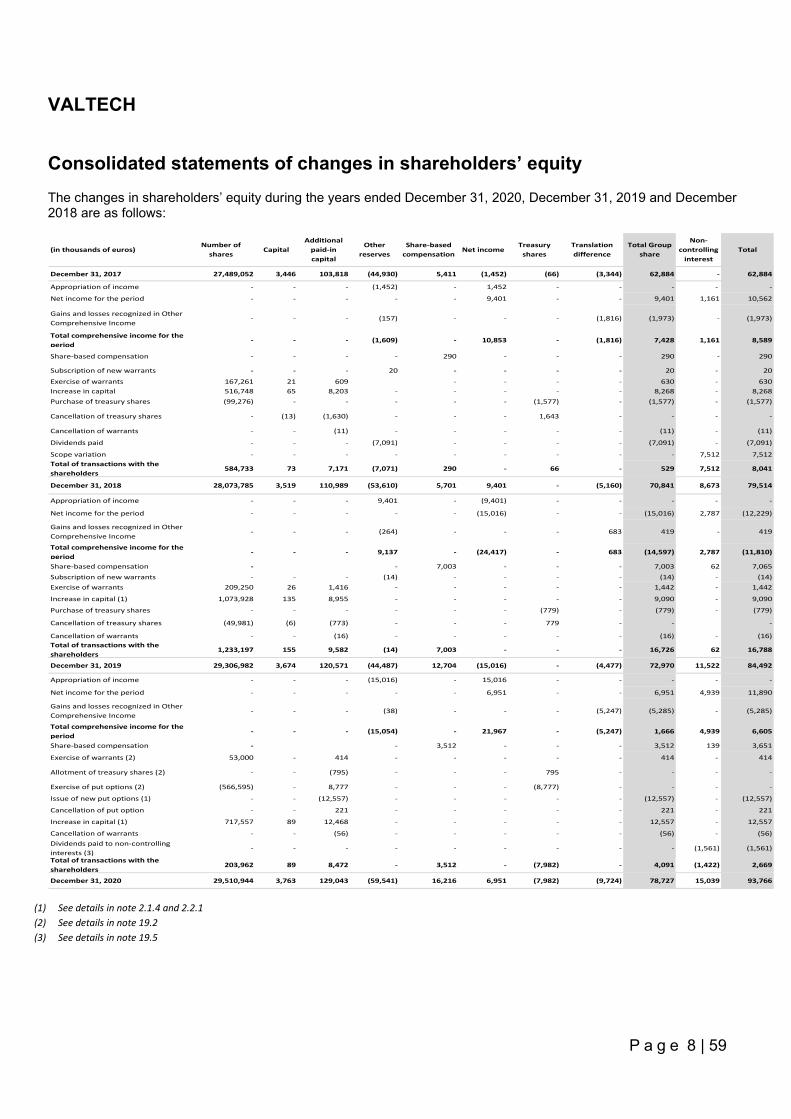

Consolidated statements of changes in shareholders’ equity The changes in shareholders’ equity during the years ended December 31, 2020, December 31, 2019 and December 2018 are as follows:

(in thousands of euros)Number of

sharesCapital

Additional paid-in capital

Other reserves

Share-based compensation

Net incomeTreasury

sharesTranslation difference

Total Group share

Non-controlling

interestTotal

Total of transactions with the 723 1 129 - (6 167) - (4 315) - (4 315)December 31, 2017 27,489,052 3,446 103,818 (44,930) 5,411 (1,452) (66) (3,344) 62,884 - 62,884

Appropriation of income - - - (1,452) - 1,452 - - - - -

Net income for the period - - - - - 9,401 - - 9,401 1,161 10,562

Gains and losses recognized in Other Comprehensive Income

- - - (157) - - - (1,816) (1,973) - (1,973)

Total comprehensive income for the period

- - - (1,609) - 10,853 - (1,816) 7,428 1,161 8,589

Share-based compensation - - - - 290 - - - 290 - 290

Subscription of new warrants - - - 20 - - - - 20 - 20

Exercise of warrants 167,261 21 609 - - - - 630 - 630Increase in capital 516,748 65 8,203 - - - - - 8,268 - 8,268Purchase of treasury shares (99,276) - - - - - (1,577) - (1,577) - (1,577)

Cancellation of treasury shares - (13) (1,630) - - - 1,643 - - - -

Cancellation of warrants - - (11) - - - - - (11) - (11)

Dividends paid - - - (7,091) - - - - (7,091) - (7,091)

Scope variation - - - - - - - - - 7,512 7,512Total of transactions with the shareholders

584,733 73 7,171 (7,071) 290 - 66 - 529 7,512 8,041

December 31, 2018 28,073,785 3,519 110,989 (53,610) 5,701 9,401 - (5,160) 70,841 8,673 79,514

Appropriation of income - - - 9,401 - (9,401) - - - - -

Net income for the period - - - - - (15,016) - - (15,016) 2,787 (12,229)

Gains and losses recognized in Other Comprehensive Income

- - - (264) - - - 683 419 - 419

Total comprehensive income for the period

- - - 9,137 - (24,417) - 683 (14,597) 2,787 (11,810)

Share-based compensation - - 7,003 - - - 7,003 62 7,065Subscription of new warrants - - - (14) - - - - (14) - (14)Exercise of warrants 209,250 26 1,416 - - - - - 1,442 - 1,442

Increase in capital (1) 1,073,928 135 8,955 - - - - - 9,090 - 9,090

Purchase of treasury shares - - - - - - (779) - (779) - (779)

Cancellation of treasury shares (49,981) (6) (773) - - - 779 - - -

Cancellation of warrants - - (16) - - - - - (16) - (16)Total of transactions with the shareholders

1,233,197 155 9,582 (14) 7,003 - - - 16,726 62 16,788

December 31, 2019 29,306,982 3,674 120,571 (44,487) 12,704 (15,016) - (4,477) 72,970 11,522 84,492

Appropriation of income - - - (15,016) - 15,016 - - - - -

Net income for the period - - - - - 6,951 - - 6,951 4,939 11,890

Gains and losses recognized in Other Comprehensive Income

- - - (38) - - - (5,247) (5,285) - (5,285)

Total comprehensive income for the period

- - - (15,054) - 21,967 - (5,247) 1,666 4,939 6,605

Share-based compensation - - 3,512 - - - 3,512 139 3,651

Exercise of warrants (2) 53,000 - 414 - - - - - 414 - 414

Allotment of treasury shares (2) - - (795) - - - 795 - - - -

Exercise of put options (2) (566,595) - 8,777 - - - (8,777) - - - -

Issue of new put options (1) - - (12,557) - - - - - (12,557) - (12,557)

Cancellation of put option - - 221 - - - - - 221 - 221

Increase in capital (1) 717,557 89 12,468 - - - - - 12,557 - 12,557

Cancellation of warrants - - (56) - - - - - (56) - (56)Dividends paid to non-controlling interests (3)

- - - - - - - - - (1,561) (1,561)

Total of transactions with the shareholders

203,962 89 8,472 - 3,512 - (7,982) - 4,091 (1,422) 2,669

December 31, 2020 29,510,944 3,763 129,043 (59,541) 16,216 6,951 (7,982) (9,724) 78,727 15,039 93,766 (1) See details in note 2.1.4 and 2.2.1 (2) See details in note 19.2 (3) See details in note 19.5

VALTECH

P a g e 9 | 59

Notes to the financial statements

The accompanying notes to the consolidated financial statements form an integral part of such consolidated financial statements (notes 3 to 12 primarily relate to the statements of income and notes 13 to 29 primarily relate to the consolidated statements of financial position).

NOTE 1 – Accounting policies

1.1. Basis of preparation

Incorporated in November 2016, VALTECH (hereinafter referred to as “Valtech”, or the “Company” as the parent company or, together with its consolidated subsidiaries, the “Group”) is a Societas Europea (“SE”) incorporated and registered in Luxembourg. The registered office of the company is located at 28/30 Boulevard Joseph II, 1840 Luxembourg, Luxembourg.

Valtech is a global business transformation agency, who enable clients to anticipate tomorrow’s trends and connect more directly with consumers across their digital and physical touch points while optimizing time-to-market and ROI. The company consists of a network of more than 3,000 innovators, design thinkers, marketers, creatives and developers spanning 4 continents with offices in 17 countries. The expertise is experience design, technology and marketing, and delivered services includes strategy consulting, service design, technology services, and optimization of business-critical digital platforms for multichannel commerce and marketing.

The Company prepared its consolidated financial statements for the year ended December 31, 2020 in accordance with International Financial Reporting Standards (“IFRS”) as adopted by the European Union, and IFRS as issued by the International Accounting Standards Board (“IASB”). The term “IFRS” refers collectively to international accounting and financial reporting standards (IASs and IFRSs) and to interpretations of the interpretations committees (IFRIC and SIC), whose application is mandatory for the period ended December 31, 2020. Comparative figures are presented for the year ended December 31, 2019 and December 31, 2018 for consolidated statements of income (loss), consolidated statements of comprehensive income (loss), consolidated statements of cash flows, and consolidated statement of changes in shareholders´ equity and for December 31, 2019 for consolidated statements of financial position.

The Consolidated Financial Statements are presented in thousands of euros unless stated otherwise (functional currency of the parent company and of most of the geographies the Group is operating in). Some amounts may be rounded for the calculation of financial information contained in the Consolidated Financial Statements. Accordingly, the totals in some tables may not be the exact sum of the preceding figures.

The Consolidated Financial Statements have been prepared on a historical cost basis, except for certain items such as financial assets and liabilities measured at fair value.

The Societas Europea is a form of European company with a board of directors, subject to the provisions of Luxembourg law. The consolidated financial statements have been approved and authorized for issuance by the board of directors of Valtech (the “Board of Directors” or the “Board”) on May 6, 2021.

1.2. New standards, amendments and interpretations

1.2.1 New standards, amendments and interpretation implemented in the financial statements of the Group for the year ended December 31, 2020

A number of new standards, amendments and interpretations are effective from periods beginning after 1 January 2020. The IASB has published the following new or amended standards that are assessed to have no significant impact on Valtech´s Financial Statement:

- Amendments to IAS39 and IFRS7: IBOR Reform - Amendments to IFRS3: Definition of a Business - Amendments to IAS1 and IAS8: Definition of Material - Amendments to References to the Conceptual Framework in IFRS Standards - Amendments to IFRS 16: Covid-19 related rent concessions

VALTECH

P a g e 10 | 59

1.2.2 New standards, amendments and interpretations not adopted early (or “not yet effective”)

New IFRS standards and Interpretations that have not yet been applied: the IASB has published the following new or amended standards that are assessed to have no significant impact on Valtech´s Financial Statement in the period of initial applications:

- Amendments to IAS 1: Classification of Liabilities as Current or Non-Current - - Amendments to IFRS 3: Reference to the Conceptual Framework - Amendments to IAS 16: Property, Plant and Equipment - Proceeds before Intended Use - - Amendments to IAS 37: Onerous Contracts - Cost of fulfilling a Contract - - Amendments to IFRS 1, IFRS 9, IFRS 16 and IAS 41: Annual Improvements to IFRS 2018-2020 - - Amendments to IFRS 9, IAS 39, IFRS 7, IFRS 4 and IFRS 16: Interest Rate Benchmark Reform - Phase 2

1.3 Presentation of the statements

The Group presents one income statement by function, highlighting the following:

- cost of sales (direct expenses necessary for project implementation), - commercial costs, and - administrative costs.

In addition, in accordance with IAS 1, expenses are provided by nature in Note 5. 1.4 Scope and methods of consolidation

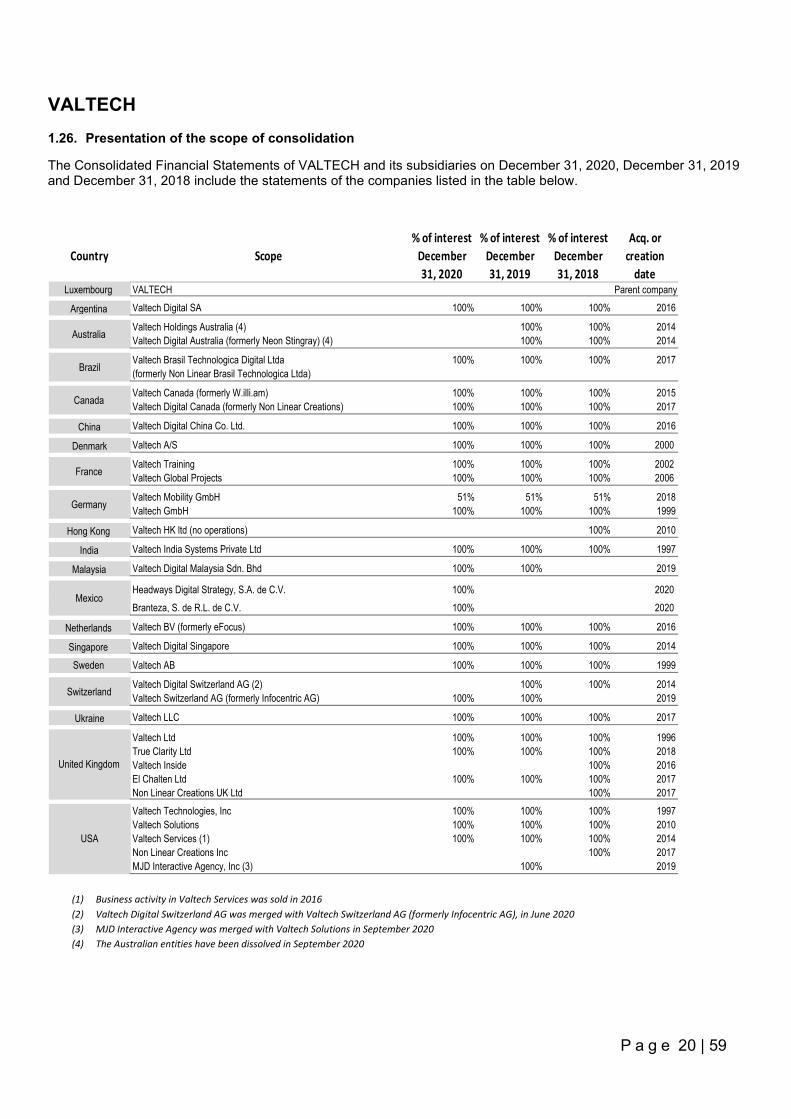

The Consolidated Financial Statements include the statements of the parent company VALTECH and all its subsidiaries, controlled under IFRS 10 Consolidated Financial Statements. The income (loss) of subsidiaries acquired or sold during the year is included in the consolidated net income of the Group from the date the control is obtained or lost. The scope of consolidation is detailed in Note 1.26 to our consolidated financial statements.

Pursuant to IFRS 10 Consolidated Financial Statements, three criteria are assessed in order to determine the exercise of control by the parent company over its subsidiaries. An investor controls an investee if and only if the investor has the following elements:

- power over the investee, i.e. the investor has existing rights that give the ability to direct the relevant activities (the activities that significantly affect the investee’s returns);

- exposure, or rights, to variable returns from its involvement with the investee; and - the ability to use its power to affects the amount of the investor’s returns.

The Company reassesses whether or not it controls an investee if facts and circumstances indicate that there are changes to one or more of the three elements of control listed above.

Based on the above mentioned criteria, the Company controls Valtech Mobility GmbH which is owned 51% by Valtech GmbH and 49% by Audi Electronics Venture GmbH (AEV).

Profit or loss and each component of other comprehensive income are attributed to the owners of the Company and to the non‑controlling interests. Total comprehensive income (loss) of the subsidiaries is attributed to the owners of the Company and to the non‑controlling interests.

1.5 Critical accounting judgements and key sources of estimation uncertainty

In the application of the Company's accounting policies, the Company's management is required to make judgments, estimates and assumptions about the carrying amounts of assets and liabilities that are not readily apparent from

VALTECH

P a g e 11 | 59

other sources. The estimates and associated assumptions are based on historical experience and other factors that are considered to be relevant. Actual results may differ from these estimates.

The estimates and underlying assumptions are reviewed on an ongoing basis. Revisions to accounting estimates are recognized in the year in which the estimate is revised if the revision affects only that year or in the year of the revision and future years if the revision affects both current and future years.

The critical accounting estimates concerning the future and other key sources of estimation uncertainty at the end of the reporting year that have a significant risk of causing a material adjustment to the carrying amounts of assets and liabilities within the next year are the following:

- recognition of revenue regarding fixed price projects: see Notes 1.20 and 4, - goodwill, subject to impairment testing: see Notes 1.6, 1.7 and 13.3, - share-based payment: see Notes 1.18 and 26, - recognition of deferred tax assets related to tax loss carry forwards: see Notes 1.23 and 11

The Consolidated Financial Statements reflect the best estimates based on information available on the date such statements are issued. 1.6 Business combinations and accounting for goodwill

Business combinations

Business combinations are accounted for using the acquisition method when the acquired set of activities and assets meets the definition of a business and control is transferred to the Group. In determining whether a particular set of activities and assets is a business, the Group assesses whether the set of assets and activities acquired includes, at a minimum, an input and substantive process and whether the acquired set has the ability to produce outputs.

The assets acquired and the liabilities and contingent liabilities assumed are measured at their fair value on the acquisition date in accordance with the requirements of IFRS 3: “Business combination”.

The evaluation of the purchase price, including, where appropriate, the estimated fair value of contingent considerations, and the identifiable assets acquired and liabilities assumed are completed within twelve months following the acquisition. In accordance with IFRS 3, any adjustment of the purchase price and/or any adjustment of the acquired assets/liabilities beyond the twelve-months period are recognized in the consolidated statements of income (loss).

Contingent consideration or earn-outs are recorded in equity if the contingent payment is settled by delivery of a fixed number of the acquirer’s equity instruments (according to IAS 32). In all other cases, they are recognized in liabilities related to business combinations. Contingent consideration or earn-outs are measured at fair value at acquisition date. This initial measurement is subsequently adjusted through goodwill only when additional information is obtained after the acquisition date about facts and circumstances existing on that date. Such adjustments are made only during the 12-months measurement period that follows the acquisition date. Any other subsequent adjustments are recorded through the consolidated statement of income (loss).

On the acquisition date, the goodwill corresponds to the aggregate of the consideration transferred and the amount of any non-controlling interest in the acquired company, minus the net amounts (generally at fair value) of the identifiable assets acquired and the liabilities assumed at the acquisition date. Goodwill is subject to annual impairment tests or more frequently if events or changes in circumstances indicate that goodwill might be impaired.

Transaction costs directly attributable to an acquisition are recorded as expenses in the period during which the costs are incurred.

Accounting for goodwill

Goodwill is allocated and then monitored at the level of the cash generating unit "CGU” or group of cash generating units "CGUs”. These units correspond to entities whose economic activity generates cash flows that are largely independent of each other. These are primarily geographical areas.

Goodwill is recognized in the currency of the acquired company in accordance with IFRS 3.

VALTECH

P a g e 12 | 59

Goodwill is not amortized, but is subject to impairment testing whenever there is any indication that an asset may be impaired, and at least once a year in accordance with the methods and assumptions described in Note 1.7 to our consolidated financial statements.

1.7 Impairment tests (IAS 36)

The Group conducts regular impairment testing of assets (tangible assets, goodwill and other intangible assets). These tests consist in comparing the carrying value of assets to their recoverable amount, which is defined as the greater of the asset’s fair value less costs of disposal, and its value in use, estimated by the net present value of the future cash flows generated by the asset. The carrying amount of assets is compared with the recoverable amount, which most of the times corresponds to net present value of future cash flows excluding financial expenses.

For tangible and intangible assets with finite lives, this impairment test is performed whenever indicators of impairment are observable.

The method projects to perpetuity a normative amount with a perpetual growth rate. The discount rate applied to those cash flows corresponds to the average cost of capital of each CGU or group of CGUs.

In case the annual impairment test reveals a recoverable amount lower than the carrying amount, an impairment is recognized to reduce the book value of the asset or of the goodwill to its recoverable amount. If the recoverable amount of an intangible (excluding goodwill) or tangible asset appreciates in subsequent years and the recoverable amount exceeds the carrying amount, any impairment losses recognized during prior years is reversed in the consolidated statement of income (loss).

An impairment loss recognised for goodwill is not reversed in a subsequent period. 1.8 Intercompany transactions All intragroup assets and liabilities, equity, income, expenses and cash flows relating to transactions between the members of the Group are eliminated at consolidation level. 1.9 Transactions in foreign currencies Transactions concluded in currencies other than the functional currency of any Group’s entity are recorded based on the exchange rate on the date of the transaction. Assets and liabilities in foreign currencies are converted at the closing rate and the exchange differences resulting from this conversion are recognized in the consolidated statement of income. 1.10 Conversion of financial statements of foreign subsidiaries

The functional currency of the parent company is the euro.

Assets and liabilities of foreign subsidiaries are converted at the exchange rate at the closing date of each reporting period. The statement of income is converted at the average exchange rate for the period. The resulting conversion difference is recorded in the comprehensive income under ‘Foreign currency translation adjustment’. This difference impacts the consolidated statement of income if there is a subsequent sale of the entity. At such point in time, the related foreign currency translation adjustment is recycled through the statement of income (loss).

1.11 Other intangible assets

Software and user rights acquired under full ownership, software developed for internal use, as well as developments of new or enhanced services, which are expected to generate future cash flows, are capitalized and amortized on a straight line basis over their estimated lifetime (generally between 3 and 5 years).

Internally-generated intangible assets

The capitalized development costs of either a software developed for internal use or an internal project are those directly associated with their production, which primarily consists of expenses related to salary costs of personnel who developed the software or the internal project.

VALTECH

P a g e 13 | 59

An intangible asset that results from the development of an internal project is recorded if the Group can demonstrate that all of the following conditions have been met:

- The technical feasibility of completing the intangible asset so that it will be available for use or sale; - Its intention of completing the intangible asset to use or sell it; - Its ability to use or sell the intangible asset; - The capacity of the intangible asset to generate probable future economic benefits; - Among other things, the Group may demonstrate the existence of a market for the output of the intangible

asset or the intangible asset itself or, if it is to be used internally, its usefulness; - The availability of adequate technical, financial and other resources to complete the development, and to use

or sell the intangible asset; Its ability to reliably measure the expenditures attributable to the intangible asset during its development.

The amount initially recognised for internally‑generated intangible assets is the sum of the expenditure incurred from the date when the intangible asset first meets the recognition criteria listed above. Where no internally‑generated intangible asset can be recognised, development expenditure is recognised in profit or loss in the period in which it is incurred. Intangible assets acquired in a business combination Intangible assets acquired in a business combination and recognised separately from goodwill at their fair value at the acquisition date (which is regarded as their cost).

Subsequent to initial recognition, these assets are reported at cost less accumulated amortization and accumulated impairment losses, on the same basis as intangible assets that are acquired separately.

1.12 Tangible assets

The tangible assets are recorded under assets in the statement of financial position at historical amortized cost, minus any impairment. They are not subsequently revalued.

Depreciation is calculated using the straight line method over the estimated useful lives of the different assets. It is calculated on the basis of the purchase price. The assets are depreciated over their expected life, as follows:

- Fixtures, fitting, technical facilities which cannot be removed depend on the useful life or the term of the real estate lease agreement if shorter

- Hardware 3-5 years - Furniture 5-7 years

1.13 Leases

At inception of a contract, the Group assesses whether a contract contains a lease. A contract contains a lease if the contract conveys the right to control the use of an identified asset for a period of time in exchange for consideration. To assess whether a contract conveys the right to control the use of an identified asset, the Group assesses whether:

- the contract involves the use of an identified asset that is physically distinct, with no right of substitution by the

lessor - the Group has the right to obtain substantially all of the economic benefits from the asset during the period of

use - the Group has the right to direct the use of the asset (decision-making rights to changing how and for what

purpose the asset is used)

The Group recognises a right-of-use asset and a lease liability at the lease commencement date. The right-of-use asset is initially measured at the amount of the lease liability, adjusted for any lease prepayments made at or before the commencement date, plus any initial direct costs incurred and an estimate of costs to dismantle, remove or restore the underlying asset, less any lease incentive received.

VALTECH

P a g e 14 | 59

The right-of-use assets is depreciated using the straight-line method from the commencement date to the earlier of the end of the useful life or the end of the lease term.

The lease liability is initially measured at the present value of the lease payments that are not paid at the commencement date, discounted using the interest rate implicit in the lease or, if that rate cannot be readily determined, the Group’s incremental borrowing rates. Generally, the group uses the incremental borrowing rate as the discount rate.

The incremental borrowing rate is defined as the rate of interest that the lessee would have to pay to borrow a similar term and with a similar security of funds necessary to obtain an asset of a similar value to the right of use asset in a similar economic environment.

The lease liability is re-measured when there is a change in future lease payments arising from a change in an index or rate, change in the amount expected to be payable under a residual value guarantee or changes in extension or termination options. When the lease liability is re-measured, a corresponding adjustment is made to the carrying amount of the right-of-use asset. Rent concessions as a result of Covid-19 are treated in accordance with IASB’s “Covid-19-Related Rent Concessions (Amendment to IFRS 16)”, and instead of re-measuring the lease liability, the full effect of the rent concessions are recognized in the statements of income at the date of the change of consideration. Short-term leases and leases of low value assets

The Group has elected not to recognise right-of-use assets and lease liabilities for short-term leases with a lease term of 12 months or less and lease of low-value assets, including IT equipment. Lease payments associated with these leases are recognized as an expense on a straight-line basis over the lease term.

1.14. Investments and other financial assets The recognition and measurement of financial assets and liabilities is governed by IFRS 9—Financial Instruments. The Group classifies its financial assets in the following measurement categories:

- those to be measured subsequently at fair value (either through other comprehensive income (OCI), or through profit or loss), and

- those to be measured at amortized cost. The classification depends on the entity’s business model for managing the financial assets and the contractual terms of the cash flows. For assets measured at fair value, gains and losses will either be recorded in OCI or profit or loss. For investments in equity instruments that are not held for trading, the classification will depend on whether the Group has made an irrevocable election at the time of initial recognition to account for the equity investment at fair value through other comprehensive income (FVOCI). The Group did not hold any derivatives or employed any form of currency hedging during the periods ended December 31, 2020 and December 31, 2019. The Group determines the classification of its financial assets. In the consolidated statements of financial position, financial assets are primarily comprised of accounts receivable and related accounts, other current assets and cash and cash equivalents. These financial assets are carried at amortized cost if the business model involves holding the instrument in order to collect contractual cash flows which consist entirely of principal and interests. Measurement On initial recognition, a financial asset is classified as measured at: amortized cost, FVOCI (fair value with any changes in fair value reported in other comprehensive income) or FVTPL (fair value with all changes in fair value reported in consolidated statements of income). At initial recognition, the Group measures a financial asset at its fair value plus, in the case of a financial asset not at

VALTECH

P a g e 15 | 59

fair value through profit or loss (FVPL), transaction costs that are directly attributable to the acquisition of the financial asset. Transaction costs of financial assets carried at FVPL are expensed in the consolidated statements of income. A financial asset is measured at amortized cost if it meets both of the following conditions and is not designated as a FVTPL:

- it is held within a business model whose objective is to hold assets to correct contractual cash flows; and - its contractual terms give rise on specified dates to cash flows that are solely payments of principal and

interest on principal amount outstanding.

The Group’s financial assets (non-current financial assets (deposits and loans), accounts receivable and related accounts, other current assets and cash and cash equivalents) are measured at amortised cost, using the effective interest method. The amortised cost is reduced by impairment losses. Interest income, foreign exchange gains and losses and impairment are recognised in the profit or loss. Any gain or loss on derecognition is recognized in the consolidated statements of income.

Impairment

The Group assesses on a forward-looking basis for the expected credit losses associated with its debt instruments carried at amortized cost. The impairment methodology applied depends on whether there has been a significant increase in credit risk. For trade receivables, the Group applies the simplified approach permitted by IFRS 9, which requires expected lifetime losses to be recognized from initial recognition of the receivables. 1.15. Accounts receivable and de-recognition of financial assets

Accounts receivable are recorded at nominal value, which generally approximates their fair value.

The Company always recognizes lifetime expected credit losses ("ECL") for trade receivables, using a simplified approach. The expected credit losses on these financial assets are estimated based on the Company’s historical credit loss experience, adjusted for factors that are specific to debtors, general economic conditions and an assessment of both the current as well as the forecast direction of conditions at the reporting date. The amount of expected credit losses is updated at each reporting date to reflect changes in credit risk since initial recognition.

The Group enters into agreements to assign, sell or transfer receivables in certain countries:

- When the risks associated with trade receivables are not transferred in substance to third parties such as financing institutions, the trade receivables are retained on the consolidated statements of financial position under receivables, and a financial liability is recorded as short-term financial liability.

- When the risks associated with trade receivables are transferred to third parties such as financing institutions, cash received is recognized as cash and cash equivalents and the receivables assigned, sold or transferred are derecognized in the consolidated statements of financial position.

As of December 31, 2020, the Group’s only subsidiary with factoring is in France, where the sale of accounts receivable is with recourse. Valtech France has transferred the relevant receivables to the factor in exchange for cash and is prevented from selling or pledging the receivables. However, Valtech France has retained the credit risk, and the transferred assets are therefore recognized entirely in the balance sheet. The amount repayable under the factoring agreement is presented as short-term borrowing.

1.16. Cash and cash equivalents

In accordance with IAS 7 - Cash Flow Statements, cash and cash equivalents presented in the consolidated statements of cash flows include cash (cash on hand and demand deposits) and cash equivalents (short-term, highly liquid investments that are readily convertible to cash and which are subject to an insignificant risk of change in value).

Investments with initial maturity over three months without possibility of early termination as well as bank accounts subject to restrictions (escrow accounts) other than those related to regulations specific to individual countries or sectors (exchange controls, etc.) are excluded from cash and cash equivalents in the statements of cash flows.

VALTECH

P a g e 16 | 59

1.17. Retirement and termination benefit costs

Pension obligations

For defined contribution plans, the group pays contributions to publicly or privately administered pension insurance plans on a mandatory, contractual or voluntary basis. The group has no further payment obligations once the contributions have been paid. The contributions are recognised as employee benefit expense when they are due.