beyond agency conceptions of the work of the non-executive director: creating accountability in the...

TRANSCRIPT

Beyond Agency Conceptions of the Work ofthe Non-Executive Director: Creating

Accountability in the Boardroom

John Roberts, Terry McNulty* and Philip StilesThe Judge Institute of Management, University of Cambridge, Trumpington Street, Cambridge, CB2 1AG,

UK, and *Leeds University Business School, Maurice Keyworth Building, University of Leeds, Leeds, LS2 9JT, UK

Corresponding author email: [email protected]

This paper examines board effectiveness through an examination of the work andrelationships of non-executive directors. It is based on 40 in-depth interviews with

company directors, commissioned for the Higgs Review. The paper observes that

research on corporate governance lacks understanding of the behavioural processes and

effects of boards of directors. Whilst board structure, composition and independencecondition board effectiveness it is the actual conduct of the non-executive vis-a-vis the

executive that determines board effectiveness. Data about behaviour and relationships

on boards suggest that traditional theoretical divisions between agency and stewardship

theory, and control versus collaboration models of the board do not adequately reflectthe lived experience of non-executive directors and other directors on the board.

Developing accountability as a central concept in the explanation of how boards operate

effectively enables the paper to both challenge the dominant grip of agency theory on

governance research and support the search for theoretical pluralism and greaterunderstanding of board processes and dynamics. Practically, the work suggests that

corporate governance reform will be undermined by prescription that supports distant

perceptions of board effectiveness but not the actual effectiveness of boards.

Introduction

This paper addresses the effectiveness of boardsthrough an examination of the work andrelationships of non-executive directors. Recentreviews of corporate governance in the economicand management literatures conclude that despiteconsiderable empirical work there remains verylimited understanding of the working processesand effects of boards of directors (Daily, Daltonand Cannella, Jr, 2003; Hermalin and Weisbach,2003). Many researchers and those in the policydomains continue to focus on issues of boardstructure and composition, particularly non-exe-cutive independence, as proxies for understand-ing board effectiveness. Better understanding ofthe inner workings of boards is necessary both toadvance management research and to promote its

relevance to corporate governance practice andreform.The field research reported here was conducted

for an independent review of the role and effec-tiveness of non-executives led by Derek Higgs, atthe behest of the UK government in 2002. Whileother countries such as the USA responded torecent governance scandals and shocks by intro-ducing legislation (Sarbanes-Oxley Act, 2002)and new listing rules – the UK’s response wasto conduct a review to explore, what, if anythingcould be done to strengthen to the CombinedCode on Corporate Governance (Financial Report-ing Council, 2003) in relation to the role andeffectiveness of non-executive directors. Havingcontributed to the process of governance reformin the UK (Higgs, 2003; McNulty, Roberts andStiles, 2003), we seek in this paper to locate our

British Journal of Management, Vol. 16, S5–S26 (2005)DOI: 10.1111/j.1467-8551.2005.00444.x

r 2005 British Academy of Management

findings within the wider theoretical debatesabout corporate governance, and enhance knowl-edge about the work of non-executives and theconditions under which they contribute to boardeffectiveness.The paper begins with a review of the treat-

ment of the non-executive within the existingliterature on governance and boards. We arguethat this literature has been dominated by theassumptions of agency theory, and that thesecontinue to have a profound influence ongovernance reform and practice. It is a literature,however, increasingly subjected to criticism, byboth economists and management scholars, forequivocal empirical findings, doubtful theoreticalassumptions and a methodology that remains toodistant from governance phenomena. There arecalls for greater theoretical pluralism and moredetailed attention to board processes anddynamics. Whilst we support these moves, weargue that purely theoretical models of boarddynamics that typically retain a polarized view ofthe non-executive role and remain at an empiricaldistance from board conduct and director beha-viour are inadequate. Instead, we suggest that amore appropriate conceptual focus is to be foundin attention to dynamic processes of account-ability within boards, albeit in a way that goesbeyond the narrow view of accountability impliedby the emphasis within agency theory on non-executive monitoring and control.The empirical part of the paper explores this

fuller concept of accountability and how it isenacted in practice through presenting some ofour primary research data. We suggest that thework of the non-executive director is indeed vital,both for enhancing the actual effectiveness ofboards and as a source of confidence to distantinvestors as to the effectiveness of what goes on inboards. Whilst board structure, composition andindependence condition board effectiveness, weargue that it is the actual conduct of the non-executive vis-a-vis the executive that determinesboard effectiveness. Non-executives can bothsupport the executives in their leadership of thebusiness and monitor and control executiveconduct. Rather than discover an inherent ten-sion in these two aspects of the role, our researchsuggested that the key to board effectiveness liesin the degree to which non-executives actingindividually and collectively are able to createaccountability within the board in relation to

both strategy and performance. Such account-ability is in practice achieved through a widevariety of behaviours – challenging, questioning,probing, discussing, testing, informing, debating,exploring, encouraging – that are at the veryheart of how non-executives seek to be effective.We present the section of our report that exploressuch accountability in terms of three linked setsof behaviours that suggest the non-executiveshould be ‘engaged but non-executive’, ‘challeng-ing but supportive’ and ‘independent butinvolved’.In the concluding part of the paper we reflect

on the methodological, theoretical and policycontributions and implications of our work. Weargue that both governance theory and govern-ance reform need to be informed by primaryqualitative research on key governance relation-ships. We question both the theoretical utilityand empirical robustness of established distinc-tions in the literature about the service, controland resourcing roles of boards and the adequacyof theoretically derived models of boarddynamics in the literature. We also observe someof the present dangers in the tendency for agencyassumptions to dominate corporate governancedebate and reform. Instead, we suggest the meritsof a focus, both theoretical and empirical, on thepractical challenges that non-executives andboards face in creating and sustaining account-ability. We also explore the potential of such afocus on accountability for our understanding ofgovernance relationships beyond the board, inparticular relationships between boards andinvestors. Lastly, we offer some reflections onthe process of governance reform as illuminatedin the response of some to the draft recommen-dation of the Higgs Review. Rather than conceiveof governance reform as a struggle over thedivided loyalties of the non-executive – aconception encouraged by agency theory – wepropose a different conception. Governance re-form, we suggest, should have two different butrelated objectives – to enhance actual boardeffectiveness and to enhance the confidence ofdistant investors and others as to the effectivenessof what goes on in boards. The response to theHiggs Review suggests that at times theseobjectives conflict with each other, and we pointto the dangers within reform of undermining theconditions for actual effectiveness for the sake ofdistant perceptions of effectiveness.

S6 J. Roberts, T. McNulty and P. Stiles

Literature review

Corporate governance: an agency view and itscritics

Since Berle and Means (1932) identified aseparation of corporate ownership from opera-tional control, the issue of how the diversifiedorganization can be governed has been central togovernance studies (Fama, 1980; Fama andJensen, 1983). The dominant theoretical lens forexamining corporate governance is agency theo-ry. Agency theory provides a rationale for howthe modern organization can be governed,primarily though the provision of two broad setsof controls: an external mechanism, the marketfor corporate control, and internal mechanisms,primary among them the board of directors.Decision-making responsibility is delegated byshareholders to executives within an organiza-tion, but potential agency costs are then reducedby boards exercising decision control, whichinvolves monitoring managerial decision-makingand performance (particularly through indepen-dent non-executive directors or outside directorsas they are variously called in the UK and USArespectively).Agency assumptions have had an important

influence on the process of governance reformas directed at boards and non-executive directors.Effectiveness is assumed to be a function of boardindependence from management, trust relationsare formally discounted and the ‘control’ role ofthe independent non-executive is emphasized.Through successive rounds of governance failure,the non-executive has been the target of bothblame and reform. As a target of blame, agencytheory assumptions suggest the dangers of tooclose a relationship between executive and non-executive directors and the capture and collusionthat this might imply. As a target of reform, theseconcerns have led to the splitting of the rolesof chairman and chief executive, a progressiveincrease in the prescribed number of ‘indepen-dent’ non-executives, and an insistence that theyshould dominate on audit, remuneration andaudit committees, where conflict of interestare most likely (Financial Reporting Council2003; Sarbanes Oxley Act, 2002). The rise ofshareholder activism has also shown shareholdersdisciplining executives and calling for greaterdirector independence and enhanced boardscrutiny.

Despite its dominance, several recent reviewsof a growing literature about boards anddirectors cast doubt on the efficacy of agencytheory and its associated prescriptions (Daily,Dalton and Cannella, Jr, 2003; Hermalin andWeisbach, 2003; Johnson, Daily and Ellstrand,1996). The empirical testing of agency theoryassumptions has in the main focused on thestructural characteristics of boards, and theirrelationship to outcomes such as firm perfor-mance (Hermalin and Weisbach, 1991), absenceof shareholder suits (Kesner, 1990), adoption ofpoison pills (G. F. Davis, 1991; Mallette andFowler 1992) and the commission of illegal acts(Kesner, Victor and Lamont, 1986). In theirreview of the economic literature on boards,Hermalin and Weisbach (2003) conclude thatthere are few definitive and striking findings tolink structural characteristics of boards (some ofwhich are used as proxies for board indepen-dence), to board outcomes, evolution and firmperformance. Similarly, Daily, Dalton and Can-nella (2003) observe the absence of clear empiri-cal support for a monitoring and oversightapproach to governance from a shareholder-value perspective. It seems that our knowledgebase, both economic and managerial, is beset byproblems not only of sampling and specification,but also of inadequate attention to the potentiallylarge number of intervening variables betweenthe board and firm-level outcomes.Alongside observations of equivocal empirical

results are criticisms of the fundamental assump-tions of agency theory. Critiques have focusedvariously on: the optimistic assumptions oftheory Y as a basis for managerial motivationrather than theory X proposed by agency theory(Davis, Schoorman and Donaldson, 1997; Do-naldson and Davis, 1991); the cooperativepotentials of agency (Perrow, 1986; Westphal,1999); and the frequent isomorphism betweenmanagers and shareholders interests (Donaldson,1995). Most recently, the pessimistic assumptionsof agency theory – the self-serving nature ofmanagers and their opportunism – have beenargued to constitute a simplistic view of humannature (Daily, Dalton and Cannella, 2003).Against this background, a turn is observablewithin the literature about corporate governanceand boards of directors that is characterized byattention to alternative theories and methods forresearching boards and corporate governance.

Creating Accountability in the Boardroom S7

Corporate governance: towards theoretical andmethodological pluralism

In the context of these critiques of agency theory,alternative theories of governance have emerged,notably stewardship theory (Davis, Schoormanand Donaldson, 1997) and resource dependencytheory (Pfeffer, 1972; Pfeffer and Salancik, 1978).Also advanced are methodologies that involvestudying the operation of the board itself, thelived experience of directors and the potentialeffects on board performance of the quality anddynamic of board relationships (Daily, Daltonand Cannella, 2003; Hermalin and Weisbach,2003; Pettigrew, 1992).Theoretical pluralism rather than the substitu-

tion of one dominant theory by another is arguedto be critical to the progress of governanceresearch. Eisenhardt (1989) argued for additionalperspectives to overcome the partiality of agencytheory and capture the complexity of phenom-ena. Stewardship theory rejects agency assump-tions, and argues that managers perceive thatserving shareholders’ interests is also in their owninterests, whilst resource dependency theoryfocuses on the boundary spanning role ofdirectors and the access they provide to scarceresources. But Donaldson and Davis (1991)argue, in relation to stewardship theory andagency theory, that the key issue is not whetherone is more valid than the other, for ‘each may bevalid for some phenomena but not for others’(1991, p. 61). Most recently, Hillman and Dalziel(2003) have argued for linking agency andresource dependence theories, whilst Daily, Dal-ton and Cannella (2003, p. 372) conclude that ‘amulti-theoretic approach to corporate govern-ance is essential for recognizing the manymechanisms and structures that might reasonablyenhance organizational functioning’. In our view,whilst these calls for theoretical integration areimportant responses to the limitations of agencytheory as applied to boards, they still rest onrather abstract theorizing, and what empiricalsupport there is for stewardship or resourcedependence theories continues to rely uponlarge-scale archival data gathering techniques.Seemingly, a point of agreement in the

literature is that theoretical progress will dependupon greater attention to the ‘inner workings ofboards’ (Hermalin and Weisbach, 2003; Petti-grew, 1992). Problems of access to boards and

directors are well recognized (Daily, Dalton andCannella, 2003) but are not insurmountable, andthere is already a considerable body of empiricalprimary board research. Such research has had anumber of strong advocates and exponents(Demb and Neubauer, 1992; Hill, 1995; Lorschand MacIver, 1989; Mace, 1971; O’Neal andThomas, 1995; Pahl and Winkler, 1974; Petti-grew, 1992; Pettigrew and McNulty, 1995; Pye,2001). This work has sought to open-up the‘black box’ of the boardroom by examiningperceptions of roles and tasks and exploring thedynamics of power and influence, collaborationand control.In contrast to the agency model of the board as

a control mechanism, empirical data suggest thatboards have a broader, more inclusive role, withnon-executive directors involved in giving adviceand enhancing strategy discussions. Lorsch andMacIver (1989, p. 64) stated that many directorsbelieve the giving of advice and counsel ‘to be theboard’s key normal duty’. Demb and Neubauer(1992, p. 82) claimed that non-executive directors‘need to be invited into the decision-makingprocess’. Hill’s (1995) study of UK boards foundnon-executives involved in reviewing and refiningthe strategic decisions of their organizations, andconcludes that evidence for the divergencebetween the interests of shareholders and man-agers was scant, with managers wanting to beseen as good professionals running the company.Pye’s (2002) analysis of sense-making amongdirectors also points to the importance of non-executives in ‘corporate directing’ activity thatinvolves strategizing, governing and leading.These studies also show that even in the absenceof overt interventions, the expectation of non-executive scrutiny has an important disciplinaryeffect on executives raising the standard ofproposals that come before the board (Lorschand MacIver, 1989; Mace, 1971). The develop-ment of closer social ties between the CEO andthe board has also been argued to provide strongbenefits, including the enhancement of mutualtrust, allowing space for advice-seeking on thepart of the executives, a reduction in defensiveand political behaviour within the board and theopportunity for enhanced learning (Westphal,1998).The dynamics of board behaviour have been

explored in some of our own work. Pettigrew andMcNulty (1995, p. 857) distinguished minimalist

S8 J. Roberts, T. McNulty and P. Stiles

and maximalist boards. Minimalist board cul-tures are those in which a set of conditionsseverely limit the involvement and influence ofthe board and its incumbent non-executivedirectors on the affairs of the firm. By contrast,a maximalist culture is one where the board andnon-executives actively contribute to dialoguewithin the board and build their organizationalawareness and influence through contacts withexecutive directors, managers and other non-executives beyond the boardroom. The differen-tiation in levels of board involvement, it isargued, stems from the effects of size andcomposition, the attitudes of a powerful chair-man or chief executive, the nature of the boardprocess, and the will and skill of the non-executive directors themselves. Variation in theprocesses and effects of boards was furtherexplored by McNulty and Pettigrew (1999) intheir differentiation of three modes of behaviouron boards in respect of strategy: ‘taking strategicdecisions’, ‘shaping strategic decisions’ and‘shaping the content, context and conduct ofstrategy’. In a further exploration of the non-executives’ role in strategy, Stiles (2001) high-lighted the perception of non-executives that thereview of strategic initiatives was a central featureof their contribution, and that their presence inthe minds of the executive helped to ‘raise thebar’ in terms of the quality of strategic proposalsand the effectiveness of decision-making.In a study of the relationship between chairmen

and chief executives in the UK (Roberts andStiles, 1999) two broad types of relationship –competitive and complementary – were identified,with very different consequences for board effec-tiveness. The separation of the roles of chairmanand chief executives has been justified in terms oflimiting executive power and enhancing non-executive independence (Cadbury, 1992), but thisstudy points to the dangers of competition andconflict between individuals, as well as the positivepotential of a ‘deepening reciprocal sense of bothpersonal and professional trust, confidence andrespect’ (Roberts and Stiles, 1999, p. 46). Such acomplementary relationship, it is argued, serves asan invaluable source of advice and counsel for thechief executive and, given the pivotal character ofthis relationship, is a key determinant of thedegree to which the chairman can then help tocreate the conditions under which non-executivescan be effective (Roberts, 2002).

These studies suggest that the work andfunctioning of boards are empirically variable,and that the involvement and influence of boardswithin the host firm will be mediated not only byexternal conditions and the structural features ofboards, but also by board processes and themotivation and skill of individual directors actingas members of a functioning group (Pettigrew andMcNulty, 1998). Contrary to agency theoryassumptions, this work also suggests that non-executives place a high premium on the closenessand openness of their relationships with executives.In addition to such empirical board research,

there have also been some recent attempts tomodel board dynamics theoretically (Forbes andMilliken, 1999; Sundaramurthy and Lewis, 2003).Forbes and Milliken argue that the effectivenessof boards depends on social-psychological pro-cesses, related to group participation and inter-action, the exchange of information and criticaldiscussion. They define an effective board as onethat can perform distinctive service and controlactivities successfully (task effectiveness) and yetcontinue working together (cohesiveness). Thesetwo outcome criteria are distinct, but bothcontribute to firm performance. The relationshipbetween board task performance and cohesive-ness is theorized as curvilinear. Task performanceby boards requires ‘extensive communication anddeliberation, and board members must have acertain minimum level of interpersonal attractionin order to engage in these things . . . [they] musttrust in each others judgement and expertise’(Forbes and Milliken, 1999, p. 495). Curvilinear-ity however, recognizes that within decision-making entities, high levels of cohesiveness canbe dysfunctional and result in a reduction inindependent critical thinking, an absence ofcognitive conflict and the phenomenon knownas ‘group-think’ (Janis, 1983). Forbes and Milli-ken propose that the most effective boards will becharacterized by high levels of interpersonalattraction (cohesiveness) and task-oriented dis-agreement (cognitive conflict).Sundaramurthy and Lewis (2003) propose a

‘simultaneous need for control and collaboration’in the working style and dynamic of boards.Agency theory approaches, they suggest, assertthe need for control, whilst stewardship theoryasserts the need for collaboration. Their inno-vation is to suggest that an either/or approachto these may produce counter-productive

Creating Accountability in the Boardroom S9

reinforcing cycles. They seek to model such‘dysfunctional dynamics’ by looking at thereinforcing cycles of collaboration and controlin relation to both high and low performance.Collaboration and past success, they suggest, cansow the seeds of complacency, group-think andfaulty attribution that may lead to inappropriatestrategic persistence. Similarly, they suggest thatan over-emphasis on control may be counter-productive. Control may be read as distrust, andset up a self-fulfilling cycle that produces the verybehaviours it is designed to prevent. Executivefrustration may rise, motivation may be damagedand information flows may become restricted,thereby feeding mutual distrust and providing therationale for a further increase in controls. Thealternative to such negative self-reinforcing cycles,they suggest, requires the paradoxical combina-tion of control and collaboration, conflict andtrust, to create self-correcting cycles. Sundara-murthy and Lewis propose a future researchagenda that might get closer to understandingsuch processual dynamics, but surprisingly, thisdoes not include qualitative primary research.These conceptual analyses are important in

suggesting how an over-emphasis on either trustor distrust may result in negative self-fulfillingand self-reinforcing consequences for boardrelationships. However, in our view, talk ofcontrol and collaboration does not really takeus near to the behaviour and conduct involved.Instead, the terms seem only to define a broadorientation in conduct – the non-executivesshould be wary and alert to potential perfor-mance problems in the executive, or they shouldbe supportive of the work of executives. To definethe purpose of non-executives in this way stillpreserves the sense that the non-executives arecaught between two masters – investors andexecutives – and somehow have to ‘switch’between roles in order to perform their taskseffectively. In our view, there is a need totranscend the traditional bi-polar thinking thatconceives of non-executives as either monitors orcollaborators. In this respect we believe that ourown focus on processes of accountability withinthe board has considerable potential.

Corporate governance: boards and accountability

Accountability is ‘a central concept in under-standing social action’ (Czarniawska-Joerges,

1996) and has been called a foundation stone ofmodern institutions (Douglas, 1986). Accordingto Giddens, ‘to be ‘‘accountable’’ for one’sactivities is to explicate the reasons for themand to supply the normative grounds wherebythey may be justified’ (1984, p. 30).Superficially, the importance of effective ac-

countability in corporate governance has longbeen recognized (Cadbury 1992; Monks andMinow, 1991). The board of directors is the keymeans for ensuring both the accountability ofdirectors to shareholders and the accountabilityof corporate employees to the corporation(Sternberg, 2004). Accountability has, in somecases, been equated with monitoring and controls(Garratt, 1996; Tricker, 1984) and, as such, isheld to be conceptually distinct from a ‘perfor-mance’ or ‘enterprise’ role (Keasey and Wright,1993; Short et al., 1998). This approach en-courages the view that accountability is con-cerned with ensuring compliance with specifiedprocesses and outcomes (sometimes pejorativelyreferred to as ‘box ticking’ (Hampel, 1998)). Italso places an emphasis on the need for explicitcontracting between principal and agent, detail-ing clear expectations and stressing a hierarchicalrelationship in which conformance or deviationfrom expectations brings clearly specified rewardsor sanctions. Some commentators, indeed, haveargued that only where accountability is con-tractually bound does accountability exist (Trick-er, 1984).In our view, however, setting up accountability

and performance as distinct and contrastingobjectives within corporate governance can be-come problematic. The emphasis on narrow,formal accountability within governance researchpresents an impoverished view of the differentforms that accountability can take and the verydifferent effects, both subjective and objective,that such accountability generates (Roberts,2001). In particular, we want to draw attentionto the very different potentials of remoteaccountability to investors and face-to-face ac-countability within the board between executiveand non-executive directors. Remote mechanismsof (board) accountability include the routinereporting of performance, with associated meet-ings with analysts and fund managers, thepotential threat of takeover and the labourmarket for senior executives. Within theassumptions of agency theory, the presence of

S10 J. Roberts, T. McNulty and P. Stiles

independent non-executives within the board canthen sharpen the effectiveness of these mechan-isms through direct monitoring and the appro-priate manipulation of rewards (remuneration)and sanctions (executive dismissal). Such me-chanisms deliberately target executive’s calcula-tion of self-interest – both positive and negative.They can be seen not merely to constrain, but toactually promote and encourage the very self-interested opportunism that they are seeking toalign. But the regular presence of non-executivesat board-related meetings has other, very differ-ent, potentials for accountability.In her recent Reith lectures, O’Neill (2002, p. 7)

observes the paradoxical effects of ‘transparency’,suggesting that it can encourage people to be lesshonest, increase deception and displace trust withwhat she calls a ‘culture of suspicion’. In contrastto transparency, which involves one-way com-munication, she suggests the need for what shecalls ‘intelligent’ or ‘real’ accountability based on‘substantive and knowledgeable independentjudgement of an institutions or professionalswork’. ‘Well placed trust’, she suggests, growsout of active enquiry rather than blind accep-tance. ‘In traditional relations of trust, activeinquiry was usually extended over time by talkingand asking questions, by listening and seeing howwell claims to know and undertakings to act heldup’ (O’Neill, 2002, p. 7). When applied specifi-cally to corporate governance, these ideas suggestthat we should be alert not only to the limitationsof remote transparency and the deception it mayunintentionally promote, for example, share-price management at Enron, but also to thepositive potentials for non-executives to create‘intelligent accountability’ within the board. Theunique potential of face-to-face board account-ability is that it offers an opportunity for activeinquiry extended over time, for talking andasking questions, for listening and seeing whetherwhat is said and promised is actually delivered.The non-executive in this respect is not merely thelocal representative of distant investor interests(or fears) but rather has the potential capabilityto do something qualitatively different.Our interview-based research pointed to both

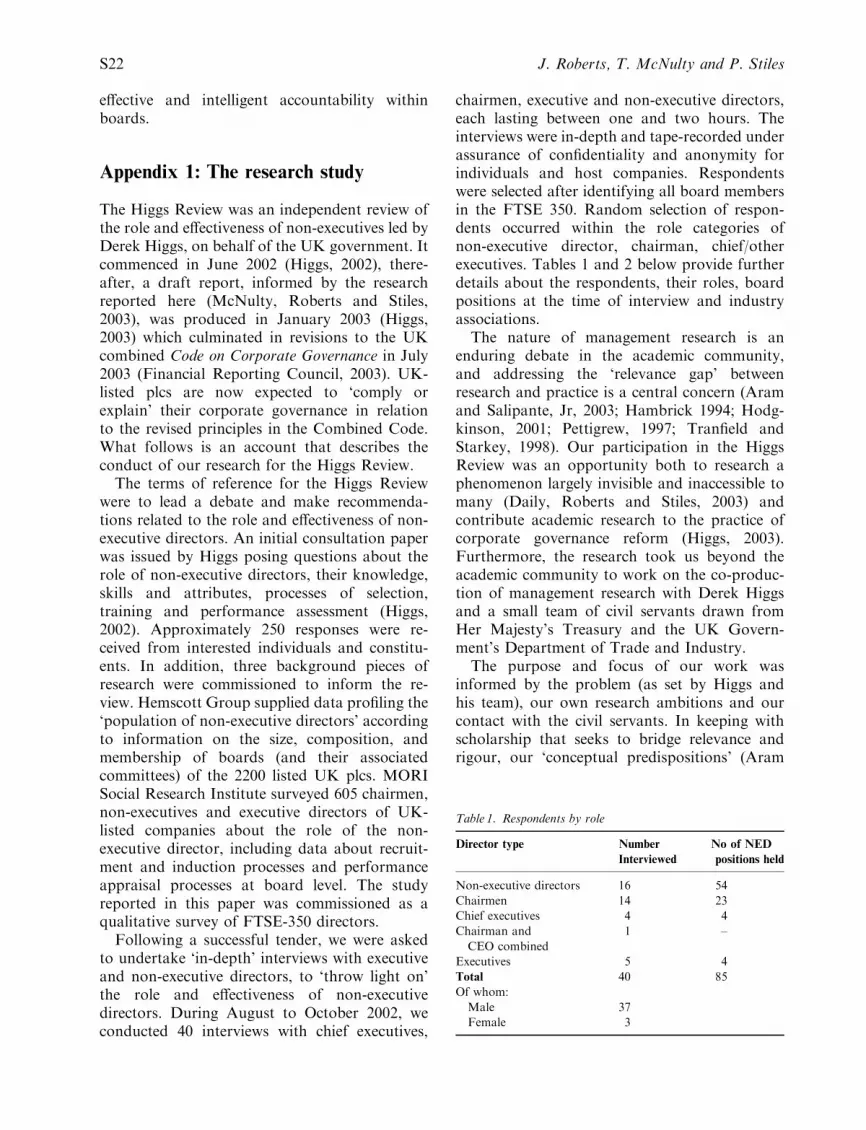

the conditions that allow non-executives to createaccountability, and some of the key attitudes andskills that this involved. Appendix 1 provides afull account of the purpose and conduct of thisresearch. Briefly, the study was commissioned by

Derek Higgs as a qualitative survey of directorsof FTSE 350 companies. We conducted a total of40 interviews with chief executives, chairmen,executive and non-executive directors, with eachinterview lasting between one and two hours. Theinterviews were in-depth and taped under assur-ance of confidentiality and anonymity for in-dividuals and host companies.

Creating accountability in theboardroom

In framing our report to Derek Higgs, we arguedthat the tension between control and collabora-tion in the academic governance literature isanalogous to a perceived tension within boardsbetween the ‘control’ role of the non-executiveand their ‘strategic’ role. Since governance re-form has typically followed governance failure,much of the focus of reform has been ondeveloping the control role of the non-executives.In the UK, both Cadbury (1992) and laterHampel (1998) warned against the dangers ofover-emphasizing the control role of non-execu-tive directors at the expense of their strategic role.Cadbury describes the latter as the ‘primary andpositive’ contribution that non-executives canmake to ‘the leadership of a company’. However,investors, working at a distance, have typicallyemphasized the control role, treating codecompliance on issues of board structure andcomposition, particularly non-executive indepen-dence, as appropriate and adequate proxies forboard effectiveness. What was immediately evi-dent in our research was that the work of thenon-executive is almost completely invisible to allbut fellow board members and as a result poorlyunderstood. Our own qualitative research was anopportunity to explore this invisible labour, andthe conditions that support its effectiveness.In our research report to Higgs we argued that,

whilst board structure and composition arevisible from a distance, in our view, at best thesecondition, rather than determine, effectiveness.Actual board effectiveness, we suggested, de-pends upon the behavioural dynamics of a board,and how the web of interpersonal and grouprelationships between executive and non-execu-tives is developed in a particular companycontext. Within these relationships we arguedthat the role of the non-executive is to both

Creating Accountability in the Boardroom S11

support executives in their leadership of thebusiness and to monitor and control theirconduct. But we then suggested that both aspectsof the role can only be achieved through strongand rigorous processes of accountability withinthe board. Drawing from our research we arguedthat, in practice, such accountability is realizedthrough a wide range of behaviours – challen-ging, questioning, probing, discussing, testing,informing, debating and exploring – that drawsupon non-executive experience in support ofexecutive performance. Through such conduct,non-executives are constantly seeking to establishand maintain their own confidence in the conductof the company: that is the performance andbehaviour of the executives; the development ofstrategy; the adequacy of financial reporting andrisk assessment; the appropriateness of remu-neration and the appointment and replacement ofkey personnel.Our research interviews pointed to the potential,

within the UK unitary board for a positive dynamicof relationships between executives and non-execu-tives based on executive perceptions of therelevance and value of non-executive contributions.This encourages executives into a greater opennessand trust, which in turn builds non-executiveknowledge and confidence. By contrast, a negativedynamic is possible, in which executives come toresent or be frustrated by non-executive contribu-tions that they perceive to be either ill-informed orinappropriate. This in turn can contribute to adynamic of deteriorating board relationships,characterized by withholding of information andmistrust. As one executive described it:

‘When a non-executive director displays insight and

real knowledge and undertakes a role in a very

serious fashion, asks brave questions, takes an

interest in issues the directors know that they are

going to be kept on their toes in relation to these

issues, and the respect level rises. Then that person

becomes an approachable person . . . it is actually

cumulative in terms of the benefits that can come

from that . . . it can go completely the other way

because it is just, ‘‘well, they don’t know anything

about the business, they had to ask the obligatory

three questions’’ and then the respect gets lost

between the parties and you do not have a

relationship that is built. It gets back down to what

is the ability of the person and what is driving them

to become engaged . . . When that engagement

actually adds value and can be seen to add value,

then very quickly you get a dynamic where you

improve the situation.’

In what follows, we want to offer an elaboratedview of how the attitudes, experience and conductof the non-executive can contribute to suchpositive and negative board dynamics. We willseek to do this by presenting just one section ofour report to the Higgs Review; the section thatdealt directly with the work of the non-executive.In the report itself this was preceded by anexploration of the different roles within theunitary board, and in particular of the role ofthe chairman, and followed by sections thatexplored the non-executives work in relation tostrategy and the audit, remuneration and nomi-nations committees.In looking at the vital work of the chairman,

we argued that a complementary relationshipwith the chief executive was at the heart ofeffective board relationships (Pettigrew andMcNulty, 1995; Roberts, 2002; Roberts andStiles, 1999). Such a relationship not onlycontributes directly to the performance of thechief executive through providing informedcounsel and advice, but also gives the chairmanthe knowledge and understanding of the com-pany that then allows him or her to create theconditions under which the non-executives can beeffective. We argued that the chairman’s work inmanaging the board, in building non-executiveknowledge through induction, strategy eventsand various off-board meetings, in structuringthe board agenda and ensuring the quality andtimeliness of board papers and in chairing themeetings themselves, was ‘pivotal’ in creating theconditions for non-executives to be effective. Wethen went on to discuss the work of the non-executive in some detail, and it is this part of ourwork that we will present here.

The work of the non-executive director

We structured our treatment of the attitudes,behaviours and skills of non-executive directorsin terms of three couplets each designed tosuggest an aspect of how, in creating account-ability, non-executive conduct combines elementsof control and collaboration. In relation to eachcouplet we sought then to differentiate betweeneffective and ineffective non-executive conductand briefly suggest how the chairman canintervene to support such effectiveness.

S12 J. Roberts, T. McNulty and P. Stiles

Engaged but non-executive

Non-executive directors will always be lessknowledgeable about a business than theirexecutive colleagues, but this disparity in knowl-edge will be particularly strong when an indivi-dual first joins a board, and when they are likelyto be preoccupied with establishing their owncredibility as a new non-executive. In part a non-executive’s credibility will depend on the skillsand experience that they bring with them to aboard, but this will then have to be demonstratedthrough the way that an individual seeks tooperate within the board.

‘I found it just terribly important to watch what

was going on quite a bit actually and not allow

myself to get too agitated that I was not instanta-

neously making a contribution. If you don’t do

that, then I don’t think you can know what is going

on. I think it takes several months to get to the

point where you have enough understanding of the

particular circumstances of that company, the

markets it is working in and all the other things,

to be able to make a meaningful contribution. I

think there is a great danger if you try and

contribute instantly because everyone will know

that you cannot really understand the thing, so why

are you so opinionated on things?’

Many non-executives felt that such learningabout the people and the company could not bedone simply within the confines of the board-room. Instead, building one’s knowledge of thecompany requires that the non-executives get tovisit the plants, go to company events, havedinner with the executives or travel with them.Such informal contact with the executives bothsignals a non-executive’s commitment and buildstheir knowledge in a way that is likely to increasethe perceived credibility of their boardroomcontributions.

‘I think the concept of a non-executive sitting

outside, knowing nothing about the business, acting

as a policeman is completely wrong. They would

not even know what to police. It seems to me

important that non-executives do get involved in

understanding the business as much as possible. I

see directors, executive or non-executive, as equal –

under the law they are all equal. How can non-

executives be remotely equal if they are sitting out

here somewhere, without knowledge, sort of criti-

quing what is happening. Without knowledge

critique is impossible.’

As this non-executive perceptively points out,building a good knowledge of the business is acondition not only of their credibility withexecutives, but also the only possible basis uponwhich they can feel able to critique whatexecutives are doing.Whilst the credibility of a non-executive de-

pends in part on the knowledge they bring to andthen acquire about a particular company, it alsodepends crucially on how they then use thatknowledge. The value of past or current executiveexperience elsewhere will be almost entirelynegated if, as a non-executive, an individual seeksto play an executive role. Our research offerednumerous examples of non-executives failing tounderstand their essentially non-executive role.

‘It is one thing to challenge; it’s another thing to be

a bloody nuisance. We’ve had a series of difficulties

with people who’ve come from executive roles

straight into being a non-executive. It actually

takes time for people to realise they’re not in charge

of making the decisions.’

One of the major challenges of the non-executiverole is that executives prefer non-executives withpast or current executive experience, but theythen need them to be able to draw upon thatexperience without seeking, as a non-executive, toassume an executive role. ‘Second-guessing’ orover-involvement in executive decisions creates adestructive friction between executives and non-executives. Some suggested that non-executivesshould ideally be people who are ‘alreadysatisfied with what they have done’, because thenthey find it easier to be a ‘contributor’ rather thanan ‘active player’.The chairman is vital to such non-executive

engagement in a variety of ways. Who is selectedand, in particular, an appraisal of their attitudesand commitment to the role, is obviously vital. Itis the chairman and company secretary who thenfacilitate a non-executive’s exposure to andknowledge of the business. The chairman alsoestablishes the expectations he or she has of non-executives. It may be that problem non-execu-tives have to be replaced. However, it is alsopossible for the chairman to intervene to fore-close destructive boardroom behaviour from oneof the non-executives.

‘When I was an executive director we had a pretty

powerful set of non-executives. One was terribly

Creating Accountability in the Boardroom S13

hands on . . . The chairman told me that he’d taken

him aside and said ‘‘look, you’re a non-executive. If

you want to run the business, do the job, but don’t

sit outside and try to do it, just ask them.’’’

Challenging but supportive

Whilst strong non-executive engagement in acompany serves to build an individual’s cred-ibility both with executives, and in their ownmind, as a non-executive your knowledge of acompany will never match that of your executivecolleagues. However, what a non-executive canbring to the relationship is the objectivity thattheir relative distance from day-to day mattersallows, along with the experience and knowledgeacquired elsewhere. The key non-executive skill isto draw upon this objectivity and experience asthe basis for questioning and challenging theexecutive. Such questioning from a position ofwhat will always be relative ignorance requiresthe courage to ‘speak out or make an issue ofsomething’.

‘Whilst you need to understand and learn the

business, actually there is an awful lot of sticking

to your last. It is asking the questions and feeling

stupid at times asking the questions . . . as you go

into a business, you are not going to know every-

thing, you can never learn everything, but don’t sit

there dumb. If you think there is something that just

does not sound right, try and open it up. You have

to be brave and wilful enough to do it . . .’

In practice, such experienced ignorance can be avery valuable resource for a board, but only if anon-executive risks speaking out; as one non-executive put it ‘just by asking the idiot-boyquestions you can really add value’. Only withsuch active questioning does the non-executivebring his or her experience to bear on the conductof a company. The question then elicits aresponse in the executive.

‘The first question I asked was to challenge the

executive of a particular business because I did not

think it was performing very well. A simple

question I asked was ‘‘why aren’t you being

reviewed and why aren’t you performing’’. That

basically meant that he came to the board meeting

and presented his company and his performance

and track record. We then had site visits to inspect

what he was doing and why, and he is here

tomorrow afternoon to go through his next year’s

plan and why he thinks that this will actually

achieve and rectify what I believe is a very poor

performance. So he has taken the issue very

seriously, he is trying to convince me, and I am

very willing to listen, as to why what was a very

poor performance will get better and how it will. I

take that as a serious response to a couple of

questions at a board.’

The above offers a very direct example of theeffectiveness of board accountability; of askingquestions and the actions that can follow directlyfrom this. The response to a question can itself bevery informative for all the non-executives.Questioning can not only address specific con-cerns about executive performance, and revealmuch more than is perhaps intended aboutexecutive attitudes, it can also begin to set newnorms and standards for executive conduct.Reflecting on the non-executive involvement ina spectacular fall in the fortunes of a company,one director lamented that:

‘We under-estimated the severity of the problems,

frankly . . . One generic point is being much tougher

in getting precise information at the board which

indicated that you really knew what was going on in

the business, and not merely accepting as a non-

executive that this pile of paper that came every

month was good enough.’

Without appropriate information it is impossiblefor non-executives to develop a confidence thatmanagement are focused on the most appropriateindicators of business conduct and performance.When compared with attempts to ‘second-guess’the executive, the skilful questioning of theexecutive can be seen to be both far morepenetrating and demanding. Questioning acceptsexecutive authority, but then insists upon theresponsibility that goes with this by asking whatis being done and why, and how performance willbe measured. The response can both reassure thenon-executives as to the competence and probityof the executive and stimulate both reflection andactions that contribute to more effective executiveperformance.What is possibly the most important aspect of

the skill of such questioning is the ability to do itin a manner that is felt by the executives tobe both helpful and supportive. Our researchinterviews suggest that it is this combination ofinformed challenge and support that executivesmost desire and value in the contribution of non-executives.

S14 J. Roberts, T. McNulty and P. Stiles

‘My starting point was with a chap who was a non-

exec director of [company], we would put up

papers, whether it was an acquisition or an

investment or whatever, and he was incisive in

quizzing us and picking holes in it. You had the

position where you really could not be woolly with

what you presented. He would go for it. Yet having

answered the questions satisfactorily, he was as

supportive as hell in getting to the next stage of

helping you in any way.’

The corollary of the positive effects of this skilfulcombination of challenge and support is thenegative impact of the ill-prepared non-executive.

‘It is extremely frustrating when you are an

executive and you are presenting something. You

get asked all these questions that, if they had read

the report and board papers, they would have

known the answers to.’

Similar negative effects in the minds of theexecutive can be created by questions that maybe informed but are posed in an unskilledmanner. Likewise non-executive credibility cansuffer if questions are unbalanced.

‘I have found that the least successful people on

boards are those who come with too narrow

experience. The marketing expert, the people who

are great experts at PR, some peculiarly narrow

retailer of property, they cannot get out of their

own box and therefore all their questions reveal

their lack of context for the wider issues.’

Such ineffective questioning by non-executivescan then begin to feed what we earlier describedas a ‘negative’ dynamic of board accountabilityin which executives become frustrated, and inresponse, seek to minimize the role of the non-executives by hiding or withholding information.

‘It meant that inevitably the board meetings were

not open; people would hold things back and be

defensive.’

Again the chairman is vital in supporting suchnon-executive challenge in support of executiveperformance. Their own conduct does much toset the culture of the board. Beyond this, thentheir greater involvement and exposure to thechief executive and executive directors mean thatthey can play a vital role in identifying and

focusing issues that require non-executive atten-tion.

‘This is something that, until you start being on

boards, you don’t really appreciate. The chairman

is in a completely different position from other

independent directors and it is his job to make sure

that issues that are important are brought to his

attention and from his attention to that of the

whole board.’

Both the quality and timing of board papers andthe organization of the agenda create the spacefor effective challenge. The chairman can alsoensure that a non-executive challenge is followed-up by executives rather than ignored. Periodicappraisals of board performance allow the chair-man to get feedback on his or her ownperformance as well as provide an opportunityfor the chairman to discuss the contribution ofindividual non-executives.

Independent but involved

‘I think there is a skill in having a relationship

where you are independent of the executives and

have to be, but not so detached that they see you as

somebody who is there, distrustful. It would be

different if something goes materially wrong. You

then have to change your view, you have to be

willing to wade in, and sometimes you have to wade

in very quickly. But to get the right quality of

information, which is not always the figures and

things, but really a sense of, what is building up,

you need to get people to open out, ‘‘what problems

do you foresee’’ without being jumped on. That is

quite good, to be able to draw people out without

getting cosy to them or sacrificing your indepen-

dence.’

Where non-executives are felt to be engaged butclear about their non-executive role, and canactively challenge, but in a way that is felt to besupportive of executive performance, then overtime there is likely to be a change in the culture ofthe board such that the independence of non-executives is viewed not as a threat or criticism,but as a positive resource that executives candraw upon to support their performance.Whilst for distant investors, ‘independence’ is

seen primarily as a protection against the potentialfor executive ‘capture’ of non-executives, withinthe context of processes of accountability within aboard, independence has a variety of other mean-

Creating Accountability in the Boardroom S15

ings. In part, independence is about the ability, asan outside director, to see things differently.

‘I think you do have the advantage of seeing things

instantly as a non-executive. It is a little bit like the

ageing process. You look at yourself every day in

the mirror and you never get older but, if you only

see yourself once every ten years, you have

definitely changed. I think the executive who lives

day by day sometimes cannot see the problem in the

same way that you cannot see that your house has

not been redecorated for a long time. But the non-

executives quite often have that vision of being able

to see something in a flash rather than be involved

in bits, seeing the wood and not the trees. As a non-

exec, you can discern whether there is a proper

succession plan, things like that. The way people

present themselves and speak, the quality of the

papers that are presented to non-execs, all those

things are key component parts of assessing what

kind of an outfit you have joined.’

The experience that a non-executive brings, bornof extensive past experience elsewhere, along withtheir distance from the day-to-day affairs of thecompany, allows him or her to offer a differentperspective from executives on what they aredoing, or planning to do. Over time, a non-executive also begins to acquire a deeper familiaritywith a company and its executives, and their waysof working, which can then be usefully comparedwith their experiences elsewhere. Within boardprocesses of accountability non-executive indepen-dence is, then, typically understood in terms ofretaining an ‘independence of mind’ and theconfidence to exercise it in boardroom discussions.

‘Perspective, questioning, testing . . . the usefulness

of the board forum to me in terms of how I do my

job is to get perspectives from these guys who have

between them a very wide range of experience, to

subject my thinking to test by them.’

Whilst from a distance ‘independence’ can beimagined as requiring that a non-executiveremain aloof and suspicious of the executives,in practice it can come to be seen as a valuableresource for executives, and provide them withclear incentives to make as full a use as possibleof the different views and experiences that non-executive independence allows. This in turnencourages the executive into being entirely openwith the non-executives in order to maximize the

potential value of their input, and this opennessitself builds non-executive confidence.

‘Openness is a major league issue. Do you feel you

are being offered what they think you would like to

have rather than what you are looking for? You

have a feeling that you ought to be asking some-

thing around a subject. The good guy will answer

your question and say ‘‘but actually what you need

to know is’’ and ‘‘you should have asked that’’. The

chief executive I worry about is the one who just

answers the question, because he has probably

managed to avoid something a little nasty.’

For those we interviewed, the level of opennesswas one of the key determinants of the quality,perceived value and indeed enjoyment of board-room debate. Rather than a stiff and formalappraisal of executive proposals by non-execu-tives, people described ‘debate’ and ‘dialogue’motivated by a shared concern to make the bestpossible decisions for the company.

‘The way we work when we reach conclusions at the

board is that we don’t distinguish between ‘‘there is

the camp of non-executives and there is the camp of

executives’’ and actually they are somehow con-

frontational by which one is trying to supervise or

control the other. It is a real collective debate

whereby you have both executive and non-executive

directors expressing their opinion or asking ques-

tions about a certain concern. I think this is where I

see the biggest contribution of a non-executive

director. You could not possibly get that from

within the company.’

Part of the quality of such debate is that theinterplay of different skills and perspectivesamongst different members of the board canitself produce new perspectives that offer creativesolutions to particular dilemmas.

‘The best views often come out of dialogue. Maybe

you have something latent within you. You talk

about it and then suddenly you see a different part

of it.’

Such collective and creative thinking on a boardis perhaps rare, but is one of the potentials of thewilling subjection of executive thinking to thechallenging scrutiny of independent non-execu-tives. Independence under such circumstances isnot an independence from executives, but ratherexercising an independence of mind in support of

S16 J. Roberts, T. McNulty and P. Stiles

executive and company success. In bad times,non-executives can support executives with sug-gestions and advice about how to weather astorm. In good times, they can act as a guardianagainst executive exuberance.

‘Non-executives should be supporting the chief

executive. They are part of the team. They should

feel a corporate pride in the success of the business.

They should feel part of a business that is operating

to the highest standards and has a good place in its

industry and, if it does not, they should be helping

to make sure that it does improve itself as it goes

forward and is successful.’

Enacted in the form of suspicion, ‘independence’emphasizes the division between executive andnon-executive directors, and possibly heightensthis. Enacted as a resource for the success of thecompany, ‘independence’ merely strengthens thecapabilities of the unitary board in dealing withthe challenges and risks that are always asso-ciated with decision-making. Through such dia-logue executive thoughts, aspirations and actionsare tested and refined, and more fully informed.Management can then be pursued by executiveswith a clearer understanding of the risks and withan increased confidence.The paradox of this close involvement and

engagement of non-executives is that they canboth contribute directly to the quality of execu-tive decision-making, but can also ensure thatany weakness in the executive will quicklybecome visible to the non-executives. Far frombeing an impediment to non-executive indepen-dence, involvement and engagement inform itsexercise. At any point in the process, active non-executive engagement, challenge and involve-ment, through the response it elicits from theexecutives, can begin to sow the seeds of doubt innon-executive minds as to the capabilities ofexecutives. Over time, doubts can either besatisfied or instead begin to crystallize into aconviction that something needs to be addressed.Here, informal meetings with other non-execu-tives and the chairman and, if appropriate, thechief executive, can be used to check outperceptions and begin to plan a course of action.

‘When something starts to break, then you have to

decide where you are going. I identified a like-

minded non-executive. I think this is what you have

to do. You have to develop a group, a team, a gang,

whatever you call it, because you cannot raise these

things out cold in the open. I think non-executives

have to be prepared to devote a huge amount of

time when a problem comes along.’

The difficulties associated with such non-execu-tives moves will vary depending on the situationand the particular individual who has become theobject of their concerns. Given the pivotal role ofthe chairman, forcing change in this area mayrequire the careful construction of an alliancebetween the executives and non-executives. Mov-ing against an executive director will be easierthan addressing concerns about the performanceof a chief executive. However, there are occasionswhen the concerns of a particular non-executivefind no resonance in the minds of the other non-executives and the chairman. An individual canthen be faced with a much more difficult decisionof whether or not to resign.What we have sought to describe in the above

is how engagement and the exercise of construc-tive independence can serve to forestall manyissues that, if left unchallenged, would otherwisehave led to such a point.Within the boardroom the chairman can be

alert for signs of non-executive disquiet, and domuch to encourage or insist that such concernsare aired. Less formal off-board meetings withnon-executives also serve as a vital space wherebackground concerns can begin to be shared anddiscussed amongst the non-executives, and ifappropriate, the chief executive. Where thechairman seeks to dominate discussions, orallows the executive to determine the agenda,much of the potential for the exercise of non-executive independence is inevitably foreclosed.

Governance research and reform: theimplications of our study

Governance research

Forbes and Milliken (1999, p. 502) state that‘understanding the nature of effective boardfunctioning is among the most important areasof management research’. In this paper, we havepresented some of the interview data throughwhich we came to understand the role andeffectiveness of the non-executive director interms of the conditions and conduct that supporttheir ability to create accountability within aboard. In what follows, we want to reflect on

Creating Accountability in the Boardroom S17

some of the key theoretical, methodological andpolicy implications of this work.Relative to the assumptions of both agency and

stewardship theory, we believe that there are anumber of merits to our empirical and theoreticalfocus on the conditions and consequences ofprocesses of board accountability. We believethat describing the work of the non-executive interms of creating accountability brings us muchcloser to the conduct and practices – questioning,probing, challenging, inter alia through whichthey can be effective. Rather than an awkwardswitching between control and collaboration,skilful accountability combines elements of both.At least in the minds of those we interviewed, itwas impossible to exercise effective control with-out a concomitant understanding of the businessand its strategy. Furthermore, this suggests thatthe practical challenges associated with creatingand sustaining accountability within the boardare not well served by conceptual distinctionsbetween the ‘control’, ‘service’ and ‘resourcing’roles of the board.Where agency theory assumes self-interested

opportunism as a given of human nature, andfrom this reads the necessity for monitoring andcontrol, a focus on accountability points to amore complex view of causality, in whichexecutive motives are themselves conditioned bygovernance processes. From this perspective,share-options and threats to executive tenure,for example, feed the very self-interested oppor-tunism that they assume, and an over-emphasison the control role of non-executive directorsmay promote the very self-defensiveness anddeceit, the consequences of which it is apparentlyseeking to prevent. But as Sundaramurthy andLewis (2003) usefully suggest, such self-reinfor-cing processes are not to be avoided by simplyreversing assumptions, by swapping agencyassumptions with those of stewardship theory.Where stewardship theory predicts the benefits

of CEO/chair duality for the clarity and authorityof executive leadership, our research suggests thataccountability within a complementary relation-ship between a separate chief executive andchairman can support executive leadership – butonly if the chairman has the discipline to remainnon-executive, and the knowledge to be of valueto the chief executive. Separating the roles canalso mean that the chairman has both the timeand inclination to create the conditions for other

non-executives to be effective. Our researchsuggests that executive openness was a source ofconfidence and trust for non-executives, and thatthese were in turn encouraged by executiveperceptions of non-executive engagement andinvolvement in support of executive and com-pany performance. But such a collaborativeclimate does not imply a passive or automatictrust. Rather, it is the product of a certain style ofinformed ‘intelligent’ accountability created bythe non-executive. Given the powerful incentivesthat promote executive self-interest, non-execu-tive involvement – their identification with thesuccess of the company – and the accountabilitythat flows from this, can be seen to be an essentialsupport to the ‘pro-organizational’ motivation ofdirectors.In our view, distrust or trust in executives is not

to be assumed ex ante, but is rather to beunderstood as the condition and consequence ofcontinuous processes of accountability. At anymoment in time there is likely to be both trustand distrust in different aspects of executivefunctioning, which is precisely what then focusesthe attention and action of non-executives. Wesupport the view that the concepts of trust anddistrust are not bipolar constructs (Lewicki,McAllister and Bies, 1998); in other words, theopposite of trust is not distrust, and vice versa.The implication of this separation is that thepossibility exists for the coexistence of trust anddistrust: ‘social structures appear most stablewhere there is a healthy dose of both trust anddistrust, a productive tension of confidencesexists’ (Lewicki, McAllister and Bies, 1998,p. 450). Framing the non-executive director’swork in terms of accountability respects thecomplexity of relationships within groups andthe multifaceted nature and demands of boardwork, which are often characterized by uncer-tainty, incomplete information and interdepen-dency, and where patterns of trust and distrustare often shifting.Our research also extends discussion of

accountability per se within governance research.Accountability within this tradition has normallybeen used synonymously with monitoring or, insome cases, compliance. This narrow approachsuggests a hierarchical view of relationships, withexecutives scrutinized by the non-executives whodetermine and decide appropriate categories ofconformance. Our use of the term ‘accountabil-

S18 J. Roberts, T. McNulty and P. Stiles

ity’ has a wider scope, and is intended to signalthe potential for lateral processes of learning(Roberts, 1996), whereby instead of the defensiveroutines frequently provoked by traditionalapproaches to being ‘called to account’, opendialogue can promote reciprocal understandingand creative thought. Accountability here is notconcerned solely with logics of appropriateness(MacIntyre, 1980) or justification (Rorty, 1980)but also with creating the conditions for dialoguethrough which the often tacit assumptions thatinform plans and proposals are challenged,developed and refined (Bohm and Peat, 1989;Senge 1990).Our work responds to recent calls for a better

understanding of the inner workings of boardsand the potential value of opening up the ‘black-box’ of board relationships and dynamics (Daily,Dalton and Cannella, 2003; Hermalin andWeisbach, 2003). Pettigrew and McNulty (1995,1998) previously argued that non-executives needto mobilize power and influence in order torealize intended effects. In line with this, we haveargued that independence is only significantwithin a board in the form of a willingness toexercise independence of mind in relation toexecutive strategy and performance. Mere num-bers of independent non-executives achievesnothing; the non-executives must be ‘active’ inorder to be effective (Keasey and Hudson, 2002;Millstein and MacAvoy, 1998). A strong norma-tive implication of this is that the advocacy byinstitutional investors, policy advisors and thebusiness media of greater non-executive indepen-dence may be too crude or even counter-productive. Our findings suggest that it is anon-executive’s skill in exercising ‘independenceof mind’ that is the key to effective boardbehaviour.Where Forbes and Milliken (1999) model

board dynamics in terms of the relation betweentask effectiveness and cohesiveness, and Sundar-amurthy and Lewis (2003) model the self-reinforcing and self-correcting tensions in controland collaboration, our research points to moremundane drivers of positive and negative boarddynamics. Both executive perceptions of therelevance and value of non-executive interven-tions, and indeed the non-executives’ confidencein intervening, depend upon their perceivedknowledge and understanding of a company. Inother words, the exercise of power and influence

that comes with the position of non-executive iscritically conditioned by their knowledge of thecompany. Effectiveness also depends upon howsuch power is mobilized. Here we have suggestedthat, except in circumstances where confidence inthe executive has been lost, challenge andquestioning – getting the executive to accountfor their conduct – is the most effective means ofintervention and influence. Such challenges ac-knowledge executive authority and responsibilitywhilst subjecting executive thinking and perfor-mance to test and scrutiny. Here, a culture ofopenness ensures that the fullest possible use ismade of the non-executive in support of executiveperformance. It also ensures that, should trust inthe executive be lost in the course of such activeinquiry, the non-executive is sufficiently engagedand involved to be willing to confront this.Our focus on processes of accountability also

has the potential to offer a different under-standing of the dynamics of other governance-related relationships. The challenge that agencytheory sets for governance mechanisms is to findways to align executive self-interest with those ofowner ‘principals’. Within this theorization, thelarge institutional investors are treated as theprincipals. But, of course, in practice they arethemselves agents of the ultimate beneficiaries –in the case of Enron this included the employees’pension scheme. Seeking to align executiveself-interest with investor interests throughstock options risks too close an alignmentbetween the interests of executives and fundmanagers as agents in share-price management(Kennedy, 2000; Useem, 1996). This coincidenceof executive and fund manager self-interest wasarguably an important part of the Enron collapse(Bratton, 2002). Such potentials suggest thatthe interests of the principal in long-run wealthgeneration may be much more dependent uponthe role of the non-executive than we imagine.The involved non-executive who identifieswith the long-term success of the company maybe vital as a check and balance to the self-interestof both executives and fund managers – andindeed in our research interviews some chair-men and non-executives seemed to conceive ofthe value and importance of their work in thisway. Understanding the proper relationshipbetween board and investor accountability is anobvious and vital focus for future qualitativeresearch.

Creating Accountability in the Boardroom S19

Whilst our research is clearly focused on theUK governance context, given the almost uni-versal use of board structures as a centralmechanism of governance our research poten-tially has a much wider relevance. Predictably,there was strong support from those we inter-viewed for the UK model of the unitary board,when compared to boards in the USA or Europe.The separation of the chairman’s role from thatof the CEO and the importance of the separatenon-executive chairman in creating the condi-tions for non-executive effectiveness were seen asparticular strengths of the UK relative to theUSA. That UK boards have an equal balance ofexecutive and non-executive directors was alsoseen positively, since this was held to give thenon-executives greater exposure to the executivesand the business strategy, and to make it lesspossible for executives to hide or withholdinformation from the board. The dominanceand number of non-executives on USA boards,and the separation of management and super-visory functions in German two-tier boards wereboth seen as potential obstacles to what we haveargued is an essential need for non-executives tohave a strong involvement in strategy, if they areto be sufficiently knowledgeable about a businessto be able to fulfil their control role.Methodologically, the key implication of our

research concerns the value and indeed necessityfor qualitative primary research on the dynamicsof governance relationships. Whilst researchersremain wedded to the testing of theoreticalmodels and assumptions against large quantita-tive data sets, they remain at a considerabledistance from the object of their inquiry and, as aresult, are inevitably obliged, as Pettigrew (1992)asserts, to make huge inferential leaps. In ourview, for theory to ‘go behind the backs’ ofpractitioners (Giddens, 1984) is to risk irrele-vance or worse. This is particularly the case inrelation to corporate governance, where agencytheory has been highly influential in guidinggovernance reform, most notably in relation tothe role of the independent non-executive. Thattheir work within boards is completely invisiblemakes it all too easy for theory to impose its ownassumptions in a way that is practically counter-productive or indeed destructive. Notwithstand-ing the partial and interested nature of therationalizations offered by directors of theirexperiences and conduct within boards, it seems

foolish for theory to refuse to be informed bytheir experience and understanding.

Governance reform

We want now to look at how our research cameto be embedded in the final Higgs Review, and onthe basis of this, offer some reflections on thenature of governance reform.As might be expected, having submitted our

report to Derek Higgs we were then veryinterested to see how our research wouldinfluence his final report. Judging by initial pressreports of the key recommendations, our researchappeared to have had little impact. What thepress picked up on were the key structuralrecommendations; the proposed increase in thenumber of independent non-executives to 50%excluding the chairman, an absolute separationof the role of chairman and chief executive, theenhanced role for the senior independent directorboth within the board and in relation to share-holders and the specification of a normal term ofsix years for non-executive directors. Superficiallyat least, these could all be read in terms of afurther strengthening of the traditional ‘control’role of the board. However, a close reading of thetext of the report – something that Derek Higgsrecommended to his critics on a number ofsubsequent occasions – suggested that the im-plications of our own process-oriented view ofboard effectiveness had indeed been recognized inthe report, and were evidenced by its innovativefocus on board relationships and behaviours.Numerous new proposed provisions in the

code seek to maximize the potential for the sortof positive dynamic of accountability that wehave described above. Evaluating the balance ofskills, knowledge and experience on the board, inadvance of making new appointments, is anobvious but frequently neglected part of ensuringthat the right people are appointed as non-executives. Similarly, provisions that encourageclarity about the nature of likely time commit-ments, and an individual’s ability to meet these,get at one of the key conditions under which achairman, or non-executive is, in practice, able tocontribute to a board. Lastly, recommendationsabout induction and professional developmentare directed at ensuring that non-executives are,and remain, sufficiently knowledgeable about thecompany on whose board they serve.

S20 J. Roberts, T. McNulty and P. Stiles

However, even with careful selection, inductionand development, relative to the executive, thenon-executive will always be at a disadvantage.Here the Higgs Review emphasizes the ‘pivotalrole’ of the chairman in creating the conditionsfor non-executive effectiveness. The chairman’s‘much greater degree of involvement’ with thechief executive and executive team, and theknowledge and understanding that comes withthis, is precisely what allows them to focus theefforts, energies and attention of the non-execu-tive. The proposed role for the chairman inarranging a regular board evaluation, and actingupon it, ensures that there is an opportunity forboard members constantly to seek to refine theeffectiveness of both their individual behaviourand their reciprocal relationships.In seeking to more closely define the work of

the non-executive, the Higgs Report followed ourresearch in emphasizing their role in ‘questioningand challenging’ the executive; that the non-executive should ‘inquire and probe’ and can onlydo so on the basis of an adequate knowledge ofthe company and its markets. Again followingour report, it suggests the dangers of ‘over-emphasizing’ either their control role or their rolein strategy. However, what Higgs did not do wasto follow our singular definition of the role of thenon-executive in terms of ‘creating accountabil-ity’ in the board; informal discussions suggestedthat the word accountability was felt to have toomany associations with the control role. Instead,Higgs followed his predecessors, Cadbury (1992)and Hampel (1998), in suggesting only that therole of the non-executive is ‘both to supportexecutives in their leadership of the business andto monitor and supervise their conduct’.The response of directors and investors to the

draft review of the Higgs Report (Higgs, 2003)was decidedly mixed. Debate about boards was,and remains, prone to a polarized definition ofthe role of the non-executive in terms of, on theone hand, control and monitoring on behalf ofinvestors, and, on the other hand, of support forthe executives in the strategy process. Framed inthese terms, governance reform will almostinevitably produce a clash between the perceivedinterests of executives and investors, and theclash itself is then taken as evidence of the realityof the assumed conflict. But, as we have sought todescribe above, non-executive effectiveness de-pends upon the ability to create strong and

rigorous accountability in relation to both boardperformance and strategy. Close involvement instrategy is precisely what gives non-executives theknowledge upon which they can then critiqueexecutive performance.Rather than frame governance reform in terms

of an assumed fight over the (divided) loyalties ofthe non-executive, we believe that it is betterunderstood in terms of two distinct but relatedobjectives. First, reform must seek to enhance theeffectiveness of the direction and control ofcompanies. Second, it must seek to createconfidence, particularly in investors who operateat a distance from the boardroom, as to theeffectiveness of what goes on in boards. Much ofthe controversy around the Higgs Review, andindeed earlier reforms, we suggest, arises notfrom an inherent conflict of interest betweeninvestors and executives, but rather from atension between what serves actual effectivenessand what supports distant perceptions of effec-tiveness. Distant investors draw confidence fromchanges to the structure and composition ofboards that are visible from a distance and can betreated as proxies for board effectiveness, forexample, increased numbers of formally indepen-dent non-executives. However, actual effective-ness, as Higgs suggests (2003, p. 33), requires ‘aculture of openness and constructive dialogue inan environment of trust and mutual respect’ as a‘prerequisite for an effective board’.This research for us has highlighted a generic