beware the reformers: a machiavellian view of the accounting profession and public sector reform in...

TRANSCRIPT

1

Chau, Ching and Cooper, Kathie and Irvine, Helen J. (2007) Beware the reformers: a Machiavellian view of the accounting profession and public sector reform in Australia. In Proceedings Asia Pacific Interdisciplinary perspectives on Accounting Conference (APIRA), pages pp. 1-29, Auckland, New Zealand.

Copyright 2007 (please consult author)

BEWARE THE REFORMERS: A MACHIAVELLIAN VIEW OF THE ACCOUNTING PROFESSION AND PUBLIC SECTOR REFORM IN

AUSTRALIA.

Ching Chau

Kathie Cooper

Helen Irvine

University of Wollongong, Australia

2

BEWARE THE REFORMERS: A MACHIAVELLIAN VIEW OF THE ACCOUNTING PROFESSION AND PUBLIC SECTOR REFORM IN

AUSTRALIA.

ABSTRACT During the last two decades of New Public Management (NPM), reformist governments have transformed the principle underlying Australia’s government accountability from compliance to performance evaluation. This change has been instituted in three phases, against a backdrop of uncertainty, complexity, and the diverse interests of pressure groups. A Machiavellian interpretation of reform, focusing on resistance and power, proposes that the development of public sector accounting in Australia has been highly politicized and characterized by power battles between the accounting profession and government departments. This is illustrated by analyzing the process by which a policy for the valuation of public sector assets in Australia was developed. The result is that control over accounting standard setting has been wrested from the accounting profession by the government, using the adoption of international financial reporting standards as a catalyst for change, at the expense of professional and governmental accountability.

Keywords. Public sector Accounting standard setting Valuation of assets Machiavelli

3

INTRODUCTION Principles of responsible government at the heart of Australia’s Westminster system have transformed progressively in the past two decades from compliance to performance evaluation. The origin of this transformation was the shift of public administrative reform towards commercialization and New Public Management (NPM) throughout OECD (Organization for Economic Co-operation and Development) countries. These reforms have been both a response to rapidly expanding demands for public sector accountability and a consequence of initiatives by reformist governments to achieve a performance culture within the public sector. Central to NPM was the reform of governmental accounting from a fund system to the adoption of a commercially-orientated accrual accounting system. This paper reviews and evaluates the accounting and accountability reforms of NPM, the ascendancy of the accounting profession as part of the reform process and the decline of accounting profession dominance in the standard setting process following the adoption of international accounting standards in both the public and private sector.

Political participation in the policy reform process will be specifically addressed including the role of the accounting profession and the adoption of accrual accounting in the public sector. The political dynamics of reform and the motivation of participants in the decision making process will be analysed from the perspective of the sixteenth century political scientist, Niccolò Machiavelli. For this purpose, reference is made to The Prince and The Discourses in which Machiavelli (1970, 1988) provides political leaders with guidelines about strategic action for seizing and maintaining power. On the basis of this analysis, the paper will argue that the doctrine of responsible government has had little involvement in the development of policies governing public sector financial reporting and accountability. Contrary to the principles of the Westminster system, policy formulation is not a politically neutral process. The bureaucracy and the governing parties capture each other in order to progress their own interests.

The paper will take the following format. Australia’s system of government and the power structure of the bureaucracy will be outlined first. Following this, issues of accountability and financial reporting will be introduced, and will then be highlighted further in discussion about th eprocess by which government accounting systems have been devloped. The notion of public sector reform will then be considered from the viewpoint of Machiavelli’s political insights, and applied to the Australian context. Three phases of this reform will be identified, and the role of the accounting profession in this process analysed. Conclusions will be drawn about the Australian government’s political behaviour in overcoming reform resistance.

AUSTRALIA’S SYSTEM OF GOVERNMENT: THE POWER STRUCTURE OF AUSTRALIAN BUREAUCRACY The Commonwealth of Australia was established in 1901. The name refers to the federation of the six former self-governing British colonies, now six states: New South Wales (NSW), Queensland, Victoria, Tasmania, South Australia and Western Australia. The system of government is based on a constitutional monarchy

4

combined with representative or parliamentary democracy (The Constitution, 2003). This means the Australian government is ruled under its constitutional system, acknowledging Queen Elizabeth II, who as the monarch, is the formal head of state. The Queen is a figurehead, and performs ceremonial functions only without exercising political power. The Australian Constitution places the power in the hands of the people who elect representatives to act on their behalf. These representatives form parliaments and compose governments to make legislation and policies.

Government in Australia includes the Commonwealth or Federal Government, the six State governments, the two Territory governments and local governments. Under the Australian Constitution, each State is authorized to preserve its own constitution and parliament, exercising legislative powers (The Constitution, 2003, s.106 & 107). Although the power of making laws in relation to the Territories is vested in the Commonwealth Parliament, they have been conferred a large measure of self-government and are treated like states (The Constitution, 2003, s.122). Political power is distributed between the Commonwealth and six states and exercised by their parliaments, but if there is conflict between Commonwealth and State powers, Commonwealth law may override State law (The Constitution, 2003, s.199).

The constitutional power of the people is organized through the power structure of Australian bureaucracy. The Australian Government is chosen by the democratically elected parliament. Parliaments, Federal and State, as the legislature, are composed of chambers or houses. A parliament which consists of a single house, is called a unicameral legislature. In Australia, apart from Queensland and the two Territories, all State Parliaments are bicameral, with two chambers: the upper and lower houses. In the Commonwealth, the name of the upper house is the Senate, and the name of the lower house is the House of Representatives. The party which has a majority of seats in the House of Representatives becomes the executive government, with the leader of the party commanding a majority becoming the prime minister. The same system applies throughout all eight states and territories. After forming the government, the elected parliament exercises its legislative power to make laws. The power of implementing these laws rests in the executive government, and judicial power rests in the courts to enforce laws. The Parliament, the Executive Government and the Judiciary are known as the three “arms” of Australian Government (Australian Public Service Commission, 2003, p22).

Although the executive government is chosen through elections, the leader who retains the majority support of the House of Representatives, needs to be appointed by the Governor-General, who represents Queen Elizabeth II (The Constitution, 2003, s.64). The powers of the Governor-General are known as “reserve powers”. They refer to the power to appoint and dismiss a Prime Minister, and the power to force the dissolution of the Parliament or to refuse to dissolve the Parliament (The Constitution, 2003, s.2). In exercising a reserve power, the Governor-General ordinarily acts on the advice of government Ministers, except in exceptional circumstances, for example, in 1975, when the Governor-General, Sir John Kerr dismissed the Prime Minister, Mr. E.G. Whitlam.

5

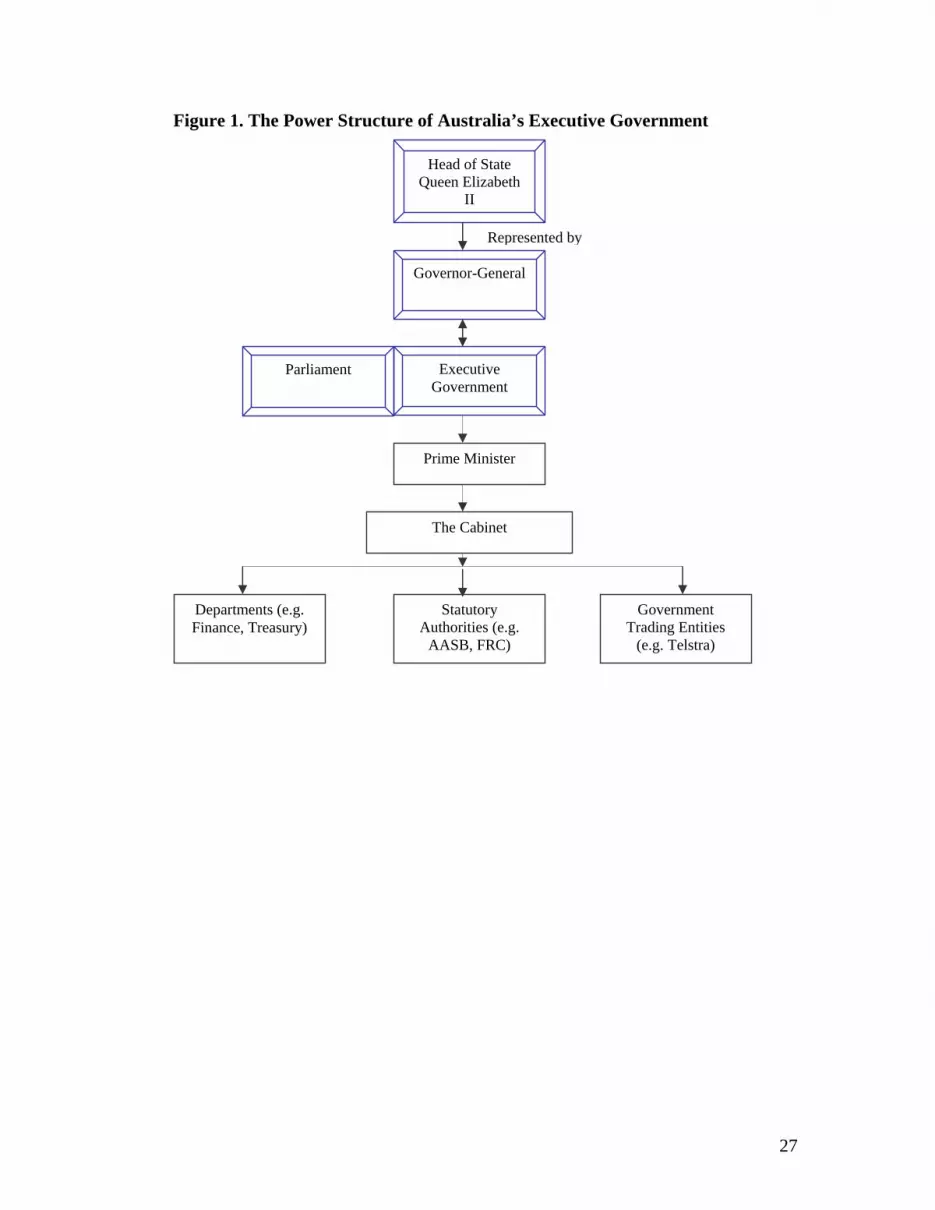

The power structure of the Executive Government of the Commonwealth is illustrated in Figure 1. The appointed Prime Minister and the senior executive officers form the Cabinet. The Cabinet, with the assistance of its government agencies, exercises authorized powers and governs the country by making, enforcing and delivering laws and policies.

Take in Figure 1 This Westminister system is also commonly known as responsible government. The term “responsible” describes the system of executive government accountability, first to the parliament and ultimately to the people (Fuller & Roffey, 1993). According to Parkin (2006, pp.3-5), this involves two main sets of ideas: the democratic and the liberal. Democratic ideas promote the notion that government is ultimately accountable to its citizens. They are elected by a majority of citizens in a free vote, and the country is governed in the interests of the community. Liberal ideas promote the notion that although governments are chosen by a majority of citizens, they are constrained in their capacity to override the interests of minorities or individuals. Thus, the accountability of a democratic government like Australia is not only manifest in democratic elections, but is also evident in public policy, which should be community-oriented.

ACCOUNTABILITY, FINANCIAL REPORTING AND POLICY FORMATION It is clear that accountability is at the heart of the Australian Government system, although there is no certain agreement on the definition of public accountability or accountability itself. In general terms, Funnell and Cooper (1998, p30) perceived that to be accountable meant “an obligation to answer for one’s actions and decisions which arises when authority to act on behalf of an individual or body (the principal) is transferred to another (the agent)”. Fuller and Roffey (1993, p151) protrayed accountability as fundamental to Australia’s system of government so that “those to whom such power and responsibilities are given are required to exercise them in the public interest”. The Royal Commission on Australian Government Administration (RCAGA) raised issues of accountable management in the public sector and saw responsibility and accountability as closely related concepts. Thus, in broad concept, accountability could be referred to as the responsibility that government institutions or individuals are required to take for their discretions, vested by law, in the public interest.

In a more specific sense, accountability has been defined often as the applied outcome of an accounting reporting function or an explanation or justification of actions (Patton, 1992). In this respect, accounting has been viewed as a system of techniques providing evidence of government’s performance and accountability. The former NSW Premier Nick Greiner (1990, p31) said of public sector accountability that “it involves the fundamentals of honesty, openness, adequate disclosure and careful, effective application of resources”. He added that:

[b]y increasing community knowledge of the government’s financial affairs, the financial statements are further evidence of the government’s determination to improve its accountability. It is through knowing the

6

facts that the community and government can make rational decisions about spending, staffing, investment, taxation, pricing, borrowing and debt. Improved public accountability is the best way of ensuring both economic efficiency and, just as importantly, social sensitivity (Greiner, 1990, p33).

Government performance and accountability is assessed through financial reporting information in relation to the traditional role of government in performing public duties. This includes the provision of public goods, efficient and effective management of government resources so as to minimize the cost of providing public services, social justice programs to bring about a more equitable distribution of income and wealth, and macroeconomic management of the economy (Parker & Gould, 1999). The traditional role of government reflects the government’s multi-dimensional responsibilities involving issues of the economy, social welfare, equity and ethics.

Historically, information on the financial operations and performance of government were provided through a cash-based Fund accounting system under the Westminster system of government. The significant shortcoming of Fund Accounting is its over-emphasis on the accurate recording of cash receipts and cash payments, with little concern about resource management by the government. Under the Fund system, only cash transactions are recorded and cash spent on a non-current asset is treated in the same way as cash spent on wages. The system does not produce any records of assets. For example, in the 1989-90 Annual Report of the National Museum of Australia, although there was a significant cost incurred in acquiring museum collections, the items were not capitalized and recorded as assets (see National Museum of Australia Annual Report, 1989-90).

As argued by Funnell & Cooper (1998), the failure to record and recognize an asset and its related consumption and maintenance means that the full cost of government activities or service delivery cannot be calculated accurately. In such a situation, there would be no liabilities for governments in discharge of their resources management and allocation; hence, the government would not be fully accountable.

The inadequacy of Fund accounting resulted in the adoption of the private sector’s accrual financial reporting system during the NPM reform of the 1990s. Accrual accounting enables a distinction between capital and operating expenditure and takes into account non-cash transactions such as asset depreciation. This is deemed important in terms of the assessment of government’s financial performance and resource allocation.

The concept of commercially-oriented accrual accounting emphasizes economic rationalism, where resource allocation decisions are predominantly made on the basis of financial cost and benefit analysis. The notions of economy, efficiency and effectiveness have permeated new public sector accountability during the NPM reform. Proponents argued that improved accountability would result as accrual accounting introduced the ability to measure performance and to assist in overall economic management and the formulation of policies of service delivery (Funnell & Cooper, 1998).

7

However, the major argument for the use of accrual accounting in the public sector is the model’s neoclassical economic philosophy, which is based on the assumption of a free market and individual self-interest. This may result in a diminished role of government in providing public goods, and its public accountability. McCrae and Aiken (1994) pointed out that the greater economic orientation of accrual accounting may trivialize many of the fundamental dimensions of accountability and responsibility inherent in the Westminster model of government.

Funnell and Cooper (1998, p296) argued that the new accountability applied to the public sector has enabled central government to shift responsibility and blame to the private sector in the event of problems. This has been reflected in the fact that the government successfully took control over accounting standard setting from the accounting profession after the corporate collapses of the late 1990s. Earlier, Hopwood (1985) had suggested that accounting may provide freedom and opportunity for an organization to be unaccountable through appealing to legitimate action. This was apparent when the Australian Accounting Research Foundation (AARF), a private sector accounting standard setter, merged with the Australian Accounting Standard Board (a government body) through accounting reform in 1991.

POLICY PROCESS AND GOVERNMENT ACCOUNTING REGULATION As mentioned earlier, under the principles of responsible government, policy orientation is shaped by broad community-oriented notions of governmental accountability:

[t]he main concern in deciding policy should be to act for the common good … while the interests and claims of individuals and groups are ingredients to be added to the cauldron of policy making, the final decision should reach beyond particular concerns to a broader sense of the interests of all (Galligan 1996, p455).

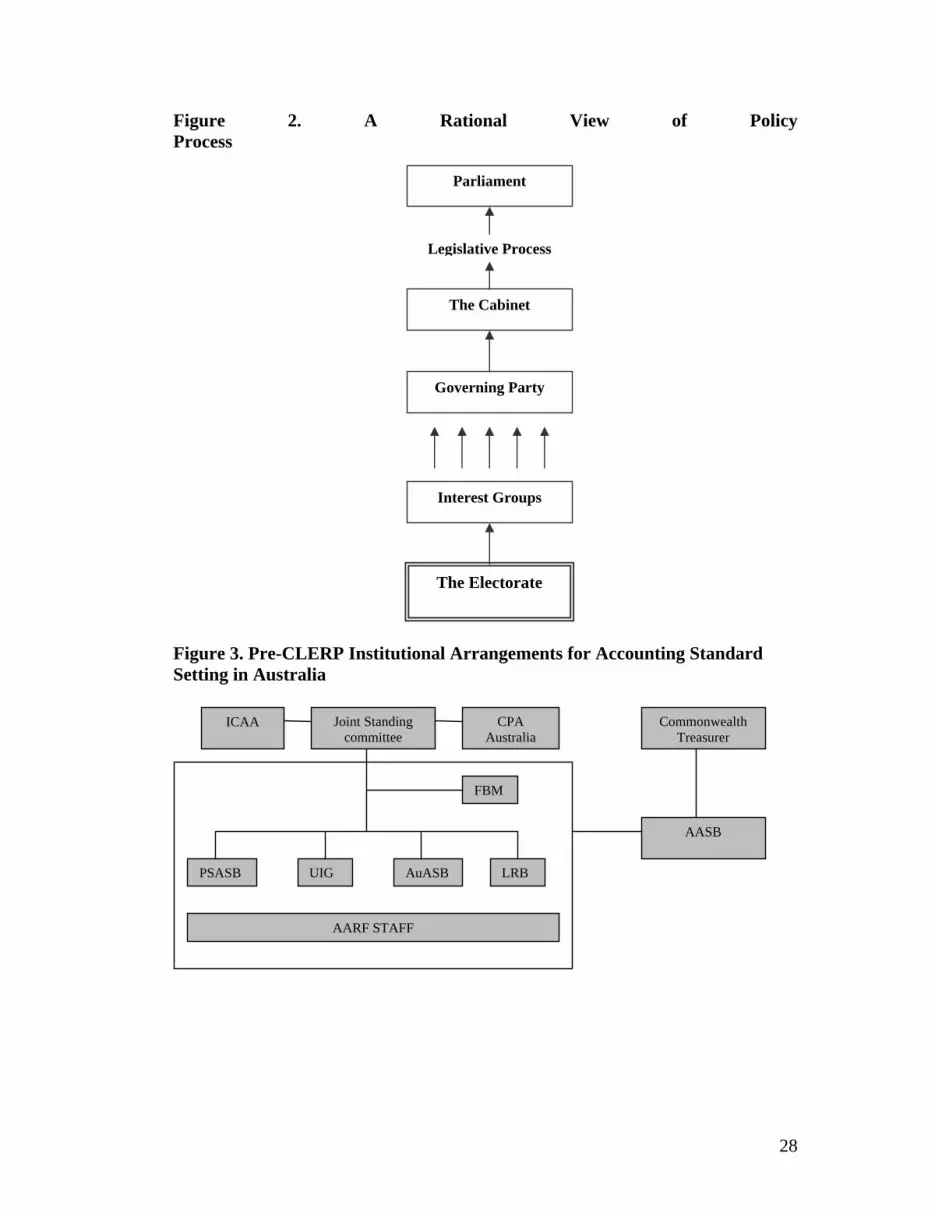

This implies that the objective of policy making is to achieve the desired outcome, which is in response to the community in general. Under the notions of democratic participation, policy is formulated by political parties in the best interest of the people, while the bureaucracy is perceived as a politically neutral instrument of implementing policy, and not a powerful governmental institution in its own right (Hawker et al, 1979). This rational approach of policy process is illustrated in Figure 2. Theoretically, policy demands emerge from the electorate or the community and are articulated through interest groups. They are then aggregated by governing parties. The Cabinet makes the choice between proposals and introduces the policy proposal to the Parliament. After parliamentary debates, if the proposal is passed by both Houses, the proposed policy is legitimized and then implemented by public servants. The legitimized policy becomes an Act of Parliament or a Legislative Instrument such as Finance Minister’s Orders (accounting policy guidelines issued by Department of Finance and Administration).

Take in Figure 2 In the Australian governmental accounting policy domain, regulating the reporting activities of departments and statutory authorities is determined by the central

8

agencies of Treasury and the Department of Finance (now the Department of Finance and Administration). For example, the traditional Commonwealth fund accounts were prepared in accordance with accounting guidelines issued by Department of Finance pursuant to the Audit Act 1901 (Department of Finance, 1990) and the later Financial Management and Accountability Act 1997 (Department of Finance and Administration, 2003). In the NSW government, governmental financial reporting was prepared according to Treasury’s Directions under the Public Finance and Audit Act 1983 (NSW Treasury, 1990).

Since 1993, with the adoption of accrual accounting at all levels of government, accounting guidelines issued by the Department of Finance and NSW Treasury started requiring their departments and authorities to prepare their financial statements in accordance with Australian Accounting Standards and other relevant mandatory professional reporting requirement (Department of Finance, 1993). From reporting periods beginning on or after 1 January 2005, in Australia all reporting entities, including both private and public sector entities, have been required to adopt financial reporting standards issued by the International Accounting Standards Board (IASB). The responsibility for developing Australian equivalent international accounting standards is undertaken by the Australian Accounting Standard Board (AASB). Accounting guidelines now issued by Department of Finance and Administration and NSW Treasury are generally based on the AASB standards. However, if there are inconsistencies between the requirements of the AASB standards and legislation, the legislative provisions prevail.

The procedures of AASB standard setting follow a due process. The concept of due process originated in English law, based on the theory of natural justice which entails democratic participation (Galligan, 1996). Due process in accounting standard setting refers to the process of allowing public participation in standard setting, for example, making comment (e.g. Exposure Drafts) on proposed standards, so as to ensure that those standards are framed with reference to the common good (AARF, 1993). Thus, it is obvious that the principle of due process of setting accounting standards is consistent with the objectives of policy making under the notion of governmental accountability, in response to general community interests and needs. This would have directed the development of governmental financial reporting policy from its fund system to the final adoption of the international accounting standards.

However, Hawker et al (1979, p22) suggested that policy process does not follow any neat rational model. Instead, he argued that the policy process is pluralistic. It consists of “continuing patterns of political and administrative activity that are shaped both by deliberate decisions and by the interplay of political and environmental forces”. Lucy (1985) stated that the bureaucracy is not a neutral governmental mechanism. He referenced a statement by the Liberal Party’s Committee of Review, which stated that:

The bureaucracy is no longer mere adjuncts to government, public services departments have become powerful organizations in their own right, and like all other institutions, they tend to view the world through the filter of their own institutional interests (cited in Lucy, 1985, p275).

9

Emy and Hughes (1988) confirmed conflicting objectives between departments in making policies. They stated that clashes between the government agencies are not uncommon, for example, the Treasury, in its advice always places the problems of the economy in front by understating the effects of the political issues, in order to achieve its own departmental objectives (Wilenski, 1986).

In fact, as will be shown, the policy development of governmental accounting deviates from the theories of responsible government. The policy process is shaped by complex interactions and conflicts between interest groups. Wilenski (1986, p173) asserted that this power struggle among interest groups is often disguised by the conception of governmental administration as a value-neutral activity:

[t]hose who stand to lose consider that they have been performing their duties responsibly; they may think that proposals for change imply unjustified criticism … and will certainly see very clearly all the risks involved in such proposals. They will not regard their opposition as being self-interested and are likely to express their resistance in terms of national interest. They fight reform, and being power-holders are in a strong position to do so.

Thus, the policy process involves the uncertainty and complexity of policy discretion, and the diversity of influences from pressure groups. Accounting regulation was seized upon by both the accounting profession and the central government agencies (e.g. the Treasury) to establish their own power and interests instead of discharging professional or governmental accountability. Thus the development of public sector accounting in Australia has been highly politicized and characterized by power battles between the accounting profession and government departments.

THEORY AND GENERAL PRINCIPLES OF REFORM APPLIED TO AUSTRALIA Australia’s earlier experience of public sector reform can be traced to the case of reform failure by the Whitlam Labor Government during its short life from 1972 to 1975. According to Peter Wilenski (1986), the former Chair of the Australian Public Service Board, one of the most significant problems was the Whitlam Government’s lack of a majority in the Senate. This resulted in its inability to legislate reform programs. Under the unfavorable economic conditions of the time, the extensive reform programs were considered undesirable. They resulted in increased public expenditure and an expanded public sector, and consequently the government was unable to convince the electorate (Wilenski, 1986). Many reform programs were hence greeted with hostility by privileged groups, allowing a broad opposition of special interests to develop. As a result, Whitlam’s reform programs were rejected by the Senate. His government was dismissed by the Governor-General John Kerr and the Liberal Fraser Government was appointed on 11 November 1975. The reform experience of the Whitlam Government reveals the most important feature of reform, that it always takes place against resistance. Without the ability to achieve and keep power in the face of reform resistance, a reforming government will always result in failure because of the assaults on it by its opponents.

10

In general terms, the impetus for reform may vary with the context and with the values and purposes of the reformers or of the reforming government. In Self’s (1978) framework for the analysis of the forces for change in public administration, reform is seen as the product of an interaction between three overlapping arenas of behaviour and beliefs: the social, the political and the bureaucratic:

The social arena is the widest, and refers to the accumulated sets of beliefs, expectations and grievances which the members of a society hold about its government and bureaucracy. The political and bureaucratic arenas refer in the first place to the attitude sets held by politicians about public servants and to public servants about themselves (Self, 1978, p313).

Each of these three arenas generates its own agenda. The social agenda results from the interaction between bureaucracy and society, covering “not only service delivery, and the ‘responsiveness’ and ‘openness’ of government to the wants, complaints and grievances of clientele groups and of the public generally; but also the adoption of the rules, practices and norms of bureaucracy to social pressures and changes” (Self, 1978, p313). The political agenda focuses on relationships between bureaucracy and political institutions. It covers issues including the relationship between ministers and officials, the responsiveness of departmental administration to political will, and the accountability of discretionary policy-makers to Parliament (Self, 1978). The bureaucratic agenda concerns the effective and efficient organization of government, emphasizing organizational structure, public management and other issues related to the performance of government (Self, 1978).

These three agendas of reform share some aspects with Wilenski’s (1986) three categorization of the aims of reform. There are the searches for more efficient administration, for more democratic administration and for more equitable administration. According to Wilenski (1986), the social, bureaucratic and political agendas in public administration parallel the issues of equity, efficiency, and democracy respectively, because the demands for greater equity, efficiency and for democratic accountability have been the leading items on social, bureaucratic and political agendas. Thus, reform is usually considered to aim at improving the efficiency and effectiveness of governmental operations and promoting the accountability of government.

However, Wilenski (1986) further argued that as reform implied a change in the decision-making processes, there would be a redistribution of power and benefits among individuals or groups who are affected. This shift in power inevitably would result in resistance to reform. This view was also reflected in Caiden’s (1969, p1) definition of reform as "the artificial inducement of administrative transformation against resistance". He added that reform

… is power politics in action; it contains ideological rationalisations, fights for control of areas, services and people, political participants, power drives, campaign strategies and obstructive tactics, compromises and concessions (Caiden, 1969, p9).

11

Thus, despite the fact that reform varies in its initiatives and aims, it almost always takes place against a backdrop of resistance. Failure to recognize the various sources of opposition may result in a failure of reform efforts. This dynamic situation of reform resistance, in particular the power relationship between reformer and resisters, and its role of power in reform can be addressed by adopting Machiavelli’s political theory.

MACHIAVELLI’S REFORM AND RESISTANCE Machiavelli is the author of arguably the two greatest works in political philosophy, The Prince and The Discourses, written in 1513 and 1518 respectively. For Machiavelli, reform was a political process, where politics was no more than one thing, acquiring and maintaining power. He believed that for a reformer or a political leader, success was dependent only on ability or skills to stay in power and enable change regardless of strength or deception. Anything else such as moral judgment should be secondary to getting, increasing and maintaining power (Machiavelli, 1988). Machiavelli’s view of the nature of political rule was shaped by his pessimistic conception of human nature. He believed that most men had lost goodness, and that power and glory were the motivating forces of their action (Machiavelli, 1988). An extension of this perception was Machiavelli’s view on the best way to achieve a stable regime through a balance of power (Machiavelli, 1970).

Machiavelli believed that liberty was fundamental to regime stability. This could be achieved by reforming a society dominated by a popular republic. He suggested that the best form of government was a mixed government embodying the characteristics of three forms of regime: principality, aristocracy, and democracy:

All the forms of government are far from satisfactory … Hence, prudent legislators, aware of their defects, refrained from adopting as such any one of these forms, and chose instead one that shared in them all, since they thought such a government would be stronger and more stable, for it in one and the same state there was principality, aristocracy and democracy each would keep watch over the other (Machiavelli, 1970, p109).

This theory of mixed government shares some features with Australian government under the form of constitutional monarchy, in which the Australian constitution with its separation of power from the legislature, executive and judiciary is based on the idea of balance and the checking of power.

Machiavelli’s reflections and the political proposals in his works refer directly to events in his life. The Prince contains advice to a new prince (intended to represent Lorenzo de' Medici, the new ruler of Florence), who tried to reform or make a number of changes, in the early years of forming a new republic, or acquiring power in new territories. The recurring theme in Machiavelli’s works was that power should be with the people rather than the elite, the nobles:

A man who becomes ruler through the help of the nobles will find it harder to maintain his power than one who becomes ruler through the help of the people, because he is surrounded by many men who consider

12

that they are equals, and therefore he cannot give them orders or deals with them as he would wish (Machiavelli, 1988, p34).

Differing from The Prince, citizen liberty in a republic is the primary concern in The Discourses. This is because the book was a response to the Medici’s rule in Florence, which tried to impose a tyrannical regime and deprive citizens of the liberties they had enjoyed under a previous republic government.

Overall, both The Prince and The Discourses provided strategies for a reformer on how to seize and maintain his power, when he wants to introduce new regulations to establish his position securely. This fundamental view about the political process and the nature of political rule can be applied in identifying two major elements of reform: resistance and the role of power.

REFORM AND RESISTANCE According to Machiavelli, a new prince who tried to reform or make a number of changes would create many enemies among those indebted to the older order:

There is nothing more difficult and dangerous, or more doubtful of success, than an attempt to introduce a new order of things in any state. For the reformer has for enemies all those who derived advantages from the old order of things, whilst those who expect to be benefited by the new institutions will be but lukewarm defenders. This indifference arises in part from fear of their adversaries who were favored by the existing laws, and partly from the incredulity of men who have no faith in anything new that is not the result of well-established experience (Machiavelli, 1988, p 20).

Machiavelli’s argument involved two causes of opposition to reform: fear of change and the reluctance to relinquish power. The fear of change referred to the fear of uncertainty regarding the redistribution of gains and losses in new systems. As argued by Wilenski (1986), the existing system may be unsatisfactory, but at least the status, power and position of each individual within the bureaucracy is known and predictable. Reform implies changes in the decision-making process. Losers and winners cannot be identified beforehand. This results in reform resistance that is defensive of the status quo, combined with an attack on the initiatives by the reformer.

In the case of Australian public sector reform, the fear of change is reflected in the differences about the desirability and acceptability of particular reform programs, including goals and the means employed to pursue them (Wilenski, 1986). This is evident in resistance on the part of the Australian State governments to adoption of accounting standards promulgated by the accounting profession during the period of NPM reform.

The dynamics of the difficult position facing the reformer also reflect the second cause of resistance, the reluctance to relinquish power or advantage. According to Wilenski (1986), it is rare for power holders ever to surrender power and position voluntarily. However, reform, which is perceived by Machiavelli as a political process, involves a substantial shift in the power structure among groups within the

13

bureaucracy (Machiavelli, 1988). This will consequently bring about resistance, as existing power holders do not want to give up their advantages or power.

For such opposition, Machiavelli emphasized the need to impress the elites (powerful groups) with displays of strong leadership and control. In Machiavelli’s analysis, a reformer needed to manage to distribute power between the people and the elites in a manner that controlled the latter. For Machiavelli, the people were better than the elites at distributing power, as he believed that elites were motivated by an insatiable will to dominate a position, whereas the people only wanted not to be oppressed. They would support the prince as long as he protected them from the elites. Machiavelli advised a reformer that

a wise man will not ignore public opinion in regard to particular matters, such as the distribution of offices and preferments; for here the populace, when left to itself, does not make mistakes, or, if sometimes it does, its mistakes are rare in comparison with those that would occur if the few had to make such as distribution (Machiavelli, 1970, p228).

From this, it can be argued that under contemporary democratic theory, for a reformer, controlling the powerful groups to make them accountable to the people is considered the most important strategy in enforcing reform and enabling change. The adoption of accrual accounting and commercial concepts of measurement and valuation in the public sector can be viewed as part of a strategy to facilitate change under the guise of making government more accountable or responsible to the electorate.

REFORM AND POWER IN PUBLIC SECTOR ACCOUNTING The historical antecedents of the reform of accounting in the public sector in Australia featured three distinct phases during which the accounting profession sought to establish itself in an area hitherto outside its sphere of influence. The first phase (1970s) featured reform initiatives resulting from social, political and bureaucratic pressures. The second phase (1980-1983) saw the entry of the accounting profession into the public sector accounting domain by the introduction of accrual accounting into the public sector. In the final phase (1984-1988), the accounting profession reinterpreted the definition of assets so as to push commercial accounting principles into the public sector reporting environment.

Phase 1 (1970s): The Social, Political And Bureaucratic Agendas Preceding The Reform

During a period of economic depression in the 1970s, there was widespread questioning of the functions, responsibilities and effectiveness of the federal and state public service in Australia. This broad questioning was reflected in the establishment of a wave of public service inquiries. These inquiries included reports of the Whitlam years: the 1973-1975 Report of the Committee of Inquiry into the Public Service of South Australia (1974), the 1974-1975 Board of Inquiry in the Victorian Public Service (1975), and at the federal level, the 1974-1976 Royal Commission on Australian Government Administration (RCAGA) (1976). After Fraser became Prime Minister in 1975, there was the conduct of the Wilenski

14

Inquiry, the Review of N.S.W. Government Administration (1977) and other state inquiries:

[t]ogether these reports came to a near identical definition of the problem with the Australian public sector – it had become too big, complex, unaccountable and was difficult to control using traditional centralized management strategies (Chua and Sinclair, 1994, p677).

The RCAGA together with the RNSWGA were considered as “highly influential in thinking about public sector reform in Australia” (Halligan & Power, 1992, p120). The RCAGA commission’s recommendations ranged widely over efficiency, democracy and accountability issues. It expressed concern about the “excessively centralized, hierarchical, rigid and inflexible” government structure, and the resultant inadequacy and inconsistency of public sector financial reporting and their standards of accountability (RCAGA, 1976, p18). The Commission specifically recommended that

the Treasury, the Auditor-General and suitable representatives from departments and the Public Service Board review the range of financial information available, and its content, and prepare alternative methods of publication which will reduce the amount of overlap between different reports (RCAGA, 1976, pp75-76).

The introduction of efficiency reviews by the Auditor-General was seen as the most visible success (Wilenski, 1986, p185). The Commission also recognized the lack of expertise and knowledge within the public service in facing economic globalization, and suggested structuring the bureaucracy towards professionalism (RCAGA, 1976).

The RNSWGA was subsequently launched and drew much of its inspiration from the RCAGA. The Review provided the more investigative view into the issues of governmental accountability, and reflected its belief in a “more efficient” business sector and the motivation of many critics of government administration, who compared its performance with the private sector as “insufficient” and “unaccountable” (Chua & Sinclair, 1994). Moreover, Wilenski (1986) indicated that the newly elected Fraser Government, and its younger breed of politicians, with great interest in managerial matters, provided a favorable environment for change.

Thus, in Self’s (1978) words, these three overlapping agendas of reform, the social, the political and the bureaucratic, finally resulted in the NPM reforms in Australia for the purpose of improving the efficiency and effectiveness of public administration and promoting governmental accountability.

Phase 2 (1980-1983): The Entry Of The Accounting Profession Into The Public Sector Accounting Policy Domain Chua & Sinclair (1994) argued the broad findings of inquiries and the public belief in the ‘more efficient’ practice in business sector created the opportunities for the accounting profession to enter into the public sector accounting policy domain. Historically, Australian corporate financial reporting was largely regulated by the accounting professional bodies, the Institute of Chartered Accountants in Australia (ICAA) and the Australian Society of Accountants (ASA, now CPA Australia), and

15

the Australian Accounting Research Foundation (AARF). On the other hand, the accounts of public sector entities were regulated by governments themselves. Government accounts were kept on a cash basis, and the work of government accounts was confined to bookkeeping, with very little involvement in public managerial skills and expertise. The ASA’s submission to the RCAGA pointed out that many accounting jobs in the public services were filled by persons who were not professionally credentialed by either the ASA or the ICAA (Chua and Sinclair, 1994).

This lack of managerial skills and expertise of many public servants and the increased social and bureaucratic demands for a ‘more efficient’ and ‘accountable’ public sector, provided opportunities for the Australian accounting profession to establish a substantial demand for professional accounting services in the public sector.

Machiavelli saw an opportunity as the favorable time or set of circumstances, which provided permission for success. He believed that men are successful when their ways are suited to the times and circumstances, and unsuccessful when they are not. He argued that

[o]pportunities then permitted these men to be successful, and their surpassing abilities enabled them to recognize and grasp these opportunities (Machiavelli, 1988, p20) .

He illustrated the ancient example of Cyrus The Great, founder of the Achaemenid Persian Empire. He attributed Cyrus’s remarkable success to both his ability and opportunities. He argued of people like Cyrus that if “they had lacked opportunity, the strength of their spirit would have been sapped; if they had lacked ability, the opportunity would have been wasted” (Machiavelli, 1988, p20).

In facing the demands of professional services in the public sector, the accounting profession demonstrated successfully its ability to grasp the opportunity, which finally resulted in its entry into public sector accounting standard setting. The profession seized the perceived limitations of the cash-based fund system and lack of managerial skills and expertise in the public sector as an opportunity to demonstrate the need for it to play a dominant role in both the public sector accounting standard setting process and public sector financial reporting policy. Specifically, through its financial reporting conceptual framework, the profession established a link between accrual accounting and public sector accountability.

Support for accrual accounting as a means to enhance public sector accountability came from a number of Commonwealth and State parliamentary committees such as the Commonwealth Senate Standing Committee on Finance and Governance Operations (SSCFGO), Commonwealth Joint Committee of Public Accounts (JCPA) and the Victorian Parliamentary Economic and Budget Review Committee (EBRC) (Ryan, 1998) and from Commonwealth and State Auditors-General (Wanna et al, 2001). The legitimacy of the accounting profession’s role in public sector financial reporting was confirmed with the establishment in 1983 of the Public Sector Accounting Standards Board (PSASB) under the auspices of the Australian Accounting Research Foundation (AARF) (Sutcliffe, 1985). This victory for the

16

profession was all the more significant given the view expressed in Report 199 of the JCPA that public sector accounting standard setting should be located within the authority of the Department of Finance rather than controlled by the accounting profession (JCPA, 1982).

Phase 3 (1984-1988): The Reinterpretation Of The Definition Of Public Sector Assets The government’s commitment to accrual accounting enabled the accounting profession to establish a central role in the public sector policy domain. However, debates about the appropriateness of commercial accounting concepts in the public sector environment persisted. A prime focus of these debates was accounting for assets. The source of contention revolved around differences in the reasons for acquiring and holding assets in the private sector as opposed to the public sector.

Under the Westminster system of government, there is a traditional notion underlying public sector accounting that the ownership of all public assets resides in society, not in executive government. The role of the government is more like a trustee of the public resources, with ongoing accountability to society for its policy and for its use of resources (Barton, 1999). In terms of public-sector asset valuation, the aim would be to produce non-financial and qualitative information, which would enhance the success of public sector asset management and accountability processes (Carnegie and Wolnizer 1995). On the other hand, the commercial concept of an asset is characterized by aspects of service potential or future economic benefits, control and a past transaction as the three main elements of the definition. The future economic benefits and the control aspect are considered to be the most important components, which warrant the examination of an asset (Barton, 1999). A detailed discussion of the differences between assets in the public sector and assets in the private sector, is beyond the scope of this paper. However, the public sector concept of heritage assets will be used to highlight these differences.

Public sector heritage assets comprise a class of physical assets as defined by NSW Treasury (1989, p6):

… those non-current assets that a government intends to preserve indefinitely because of their unique historical, cultural or environmental attributes. A common feature of heritage assets is that they cannot be replaced (e.g. monuments, historical museum collections, wilderness preserves and historic buildings).

Heritage assets include art, museum and library collections, memorials, historical buildings, national parks and places of historical significance. They are maintained by the government for cultural, heritage, recreation and other community purposes rather than for the purposes of government administration or income generation.

Some accounting writers such as Pallot (1990, p84) have classified those assets under a separate category of “community assets”. It is perceived that they play an important role in the development of a nation’s culture. They raise and enhance the quality of life of a nation. Consequently, it has been argued that these unique features of public heritage assets should orient its definition and valuation. Burritt et

17

al (1996) claimed that public sector assets represent bundles of resources, contributed by the public to entities under the trusteeship of parliament and the management of successive governments. As indicated by Rowles (1992), reporting of heritage assets is essential from the perspective of improved resource management, performance and accountability. Communities and members of parliaments would also be interested to know the information about the stock of assets and the consumption of service potential.

Public sector reform and the transition from a Fund System to accrual accounting saw the adoption of a policy consistent with the views expressed by Rowles (1992) whereby all public heritage facilities would be recognized as government assets and recorded in the financial statements. This can be seen in various public policy documents including SAC 4 (1992) Definition and Recognition of the Elements of Financial Statements, AAS 27 (1993) Financial Reporting by Local Government, AAS 29 (1993), Financial Reporting by Government Departments, AAS 31 (1996) Financial Reporting by Governments, and the Commonwealth and states’ own accounting guidelines for adoption by departments and statutory authorities (e.g. NSW Treasury 1989, Department of Finance 1995). These various policies, however, led to diversity in the definitions and valuation requirements of heritage assets. Until 2003, with the uniform adoption of the fair value approach, there were different methods required by different government authorities or departments including not reporting them, reporting them at $1, and reporting them by applying methods used in the commercial sector, such as current replacement cost, deprival value and fair value.

Even within the PSASB, there was doubt about the appropriateness of applying a commercial definition to public sector assets (Sutcliff, 1985). This represented a challenge to the successful implementation of full accrual accounting. In confronting challenges or difficulties, Machiavelli argued that a successful innovator can change events if he is able to persuade or force others to believe his schemes. He explained that

[t]he people are fickle; it is easy to persuade them about something, but difficult to keep them persuaded. Hence, when they no longer believe in you and your schemes, you must be able to force them to believe (Machiavelli, 1988, p21).

From this perspective, the accounting profession successfully resolved the difficulties in the definition of public sector assets, by reinterpreting rhetorically asset definition and recognition criteria that were sufficiently broad to encompass items held in the public domain. This is reflected in the “answer” produced in 1987, a series of Exposure Drafts (ED) issued by the PSASB, to form the basis of the Conceptual Framework for financial reporting in the public and private sectors (PSASB, 1987). ED 42A (1987), Objective of Financial Reporting, justified the application of private sector standards to the public sector. It stated that the objectives of financial reporting were fundamentally similar between business entities and non-business entities, because

18

while business entities seek to maximize profits or earn desired rates of return and non-business entities typically pursue service-related objectives, both types of entities provide goods and services to the community and use scarce resources in the process; both control stocks of resources; both incur obligations; and both must be financially viable to meet their operating objectives (ED 42A, 1987 para.13).

Consequently, consistent with the above stated objective of financial reporting, the ED 42C (1987, para.7), Definition and Recognition of Assets reinforced the notion of future economic benefit as “service potential or future economic benefits controlled by the reporting entity as a result of past transactions or other past events”. ED 42C further argued that this definition could be readily applied to all public assets, because future economic benefit could be substituted by service potential to beneficiaries provided by public assets. This was based on the reason that the purpose of goods or services provided by business or non-business, was to satisfy human wants and needs. Thus,

[i]n non-business entities, including both government non-business entities and not-for-profit entities in the private sector, the service potential or future economic benefit is also used to provide goods and services in accordance with the entities’ objectives (ED 42C, 1987, para.13);

As for the control aspect, ED 42C identified that items are required to be recognized as assets, depending upon the ability of the entity to benefit from the asset:

[t]he capacity of an entity to control the service potential or future economic benefits would normally stem from legal rights and may be evidenced by title deeds, possession or other sanctions and devices that protect the entity’s interests. However, legal enforceability of a right is not a prerequisite to the establishment of control over service potential or future economic benefit (ED 42C, 1987, para.18).

This interpretation successfully supplemented the view from Canning (1929) that possession or ownership of an object or right is not essential, and an entity could have an enforceable right to an asset without having ownership.

The definition and interpretation of public assets in ED 42C effectively divorced the notion of future economic benefit from cash flows, and excluded “ownership” from asset definition. This meant that the concern identified in Monograph 5 about the inappropriateness of commercial accounting concepts in the public sector environment, had been addressed. Many items in the public domain, such as cultural, heritage and scientific collections and other community resources, would then be able to be recognized as assets in accrual-based financial reports.

The hurdle to the successful carrying out of accounting reform in the public sector had been overcome and commercial accounting standards seemed to be ready for application to the public sector. The extended definition of assets was embraced in subsequent policy papers such as Accounting Theory Monograph 7 Definition and Recognition of Assets (Miller & Islam, 1988). Walker (1989) argued that these

19

documents provided the rationale for common standards and the impetus required for the accounting profession to successfully convince the government to proceed with the implementation of those proposals in 1989.

IMPLEMENTATION OF ACCRUAL ACCOUNTING IN THE PUBLIC SECTOR IN AUSTRALIA The government of the state of New South Wales (NSW) was the first to implement the adoption of accrual accounting in the public sector in Australia. According to Ryan (1998), the NSW Government’s decision to adopt accrual accounting was shaped by two contemporary forces, political commitment by the newly elected Greiner Government and pressure from the NSW Commission of Audit.

The Greiner election platform included public sector reform through an emphasis on improved management techniques, operating efficiency and financial results. Achievement of these goals turned on making government more business-like (Ryan, 1998). This was a significant period in the history of the implementation of accrual accounting in the public sector in Australia. In initiating the reform of financial reporting and accountability in the NSW public sector, the Greiner Government formed alliances with influential members of the accounting profession including a senior US partner of Arthur Andersen & Co, the Australian Society of Accountants (now CPA Australia) and the then NSW Auditor-General, Mr Ken Robson, who coincidentally was a prominent member of the Australian accounting profession. In 1988, the report of the Commission of Audit, staffed by accountants from the large accountancy firms and units from Treasury and the Department of Finance (Groom, 1990) advocated the adoption of accrual accounting in the NSW public administration (Christensen, 2003). On successful election, the Greiner Government formally implemented accrual accounting in 1989.

In accordance with Machiavelli’s political theory, both the accounting profession and Greiner’s Government identified and seized an opportunity to further their own respective ambitions and goals. Both demonstrated leadership and control in the drive to improve public sector accountability but the underlying motive was not altruistic but self-centred. In the final analysis, Greiner and his party won government while the accounting profession gained an opportunity to control not only the standard setting process in the private sector but also the public sector.

In 1991, the accounting profession’s dominance of the standard setting process in Australia received a welcome boost with the passing of legislation to give the force of law to Australian accounting standards. Under the Corporations Act 1991, 2M.3, failure to comply with an AASB standard constituted a breach of the legislation. In addition, the legislation replaced the Australian Standards Review Board (ASRB) with the newly established Australian Accounting Standards Board (AASB). However, as will be discussed below, the establishment of the AASB with enhanced political power represented a threat to the power of the accounting profession and its domination of the accounting standard setting process.

Nonetheless, throughout the decade of the 1990s, the profession strengthened its power over financial reporting in the public sector. In 1991, full accrual accounting was extended to local government in Australia by the promulgation of Australian

20

Accounting Standard AAS 27 Accounting for Local Government. In 1993, AAS 29 Financial Reporting by Government Departments effectively brought accrual accounting to State and Commonwealth government entities. Both standards required the application of accrual-accounting and the conceptual framework to government financial statements. During this time, accounting guidelines issued by the Department of Finance (Commonwealth) and State Treasuries were amend to incorporate the concepts of financial reporting outlined in the conceptual framework (Department of Finance, 1993). According to Ryan (1998), endorsement of the accounting profession dominated conceptual framework constituted the realization of a long-standing goal of the profession in general and the PSASB in particular. By 1996, the profession’s domination of accounting in the public sector was complete with the promulgation by the PSASB of AAS 31 Financial Reporting by Government applying to all Commonwealth, State and Territory governments. However, the following year so a reversal of government support for accounting profession domination of the accounting standard setting process.

MACHIAVELLI AND THE SIDE-LINING OF THE ACCOUNTANCY PROFESSION The establishment of the PSASB and the advent of statutory backing for Australian accounting standards conferred upon the accounting profession significant influence in the formulation of public sector accounting policy, and in the setting of accounting standards to be applied in the public and private sectors. As already noted, however, the establishment of the AASB in 1991, with enhanced authority from Corporations Law, constituted a threat to the accounting profession’s position of power. In 1997 the threat was realized with the establishment of the Corporate Law Economic Reform Program (CLERP) by the Howard Liberal Government. The Program reconstituted the AASB as a government body in the name of the public interest, and imposed accountability on the accounting profession to perform the government’s political objective of the adoption of the International Accounting Standards Board (IASB) standards. The genesis of the government’s desire to adopt international accounting standards can be traced to the Whitlam Government.

Halligan & Power (1992) have argued that during the Whitlam years, governments exposed public policy to the influence of the international economy. This was evident when the International Accounting Standards Committee (IASC, now the IASB) was established and Australia, under the Whitlam Government, became a member country. However, due to the significant influence of the accounting profession on the direction of policy formulation, this political will was not fulfilled until 1997, when the Howard Government announced CLERP. Consequently, CLERP saw control over accounting standard setting in both the private and public sector completely transmitted to the Commonwealth government. Once again, this turn of events can be analysed within Machiavelli’s political framework.

According to Machiavelli (1988), the increased power of elite groups, in this case the accounting profession, is a barrier to a reforming government in pursuit of its own political will. Thus, Machiavelli further advised a prince who came to power through the influence of the nobles, to turn his allegiance to the people and dispose of the nobles by hacking them all to pieces, once he succeeded in stabilizing his

21

power (Machiavelli, 1970). The establishment of CLERP reflected the effective utilization of this strategy by the Howard Government.

CLERP, as a form of corporate regulation, built its argument on protecting public interest against corporate failure (Clarke et al, 2003), and successfully shifted the power over accounting standard setting from the accounting profession to the government. Moreover, it was claimed that it would “ensure that business regulation is consistent with promoting a strong and vibrant economy and provide a framework that helps business adapt to global change” (Department of the Treasury, 1997).

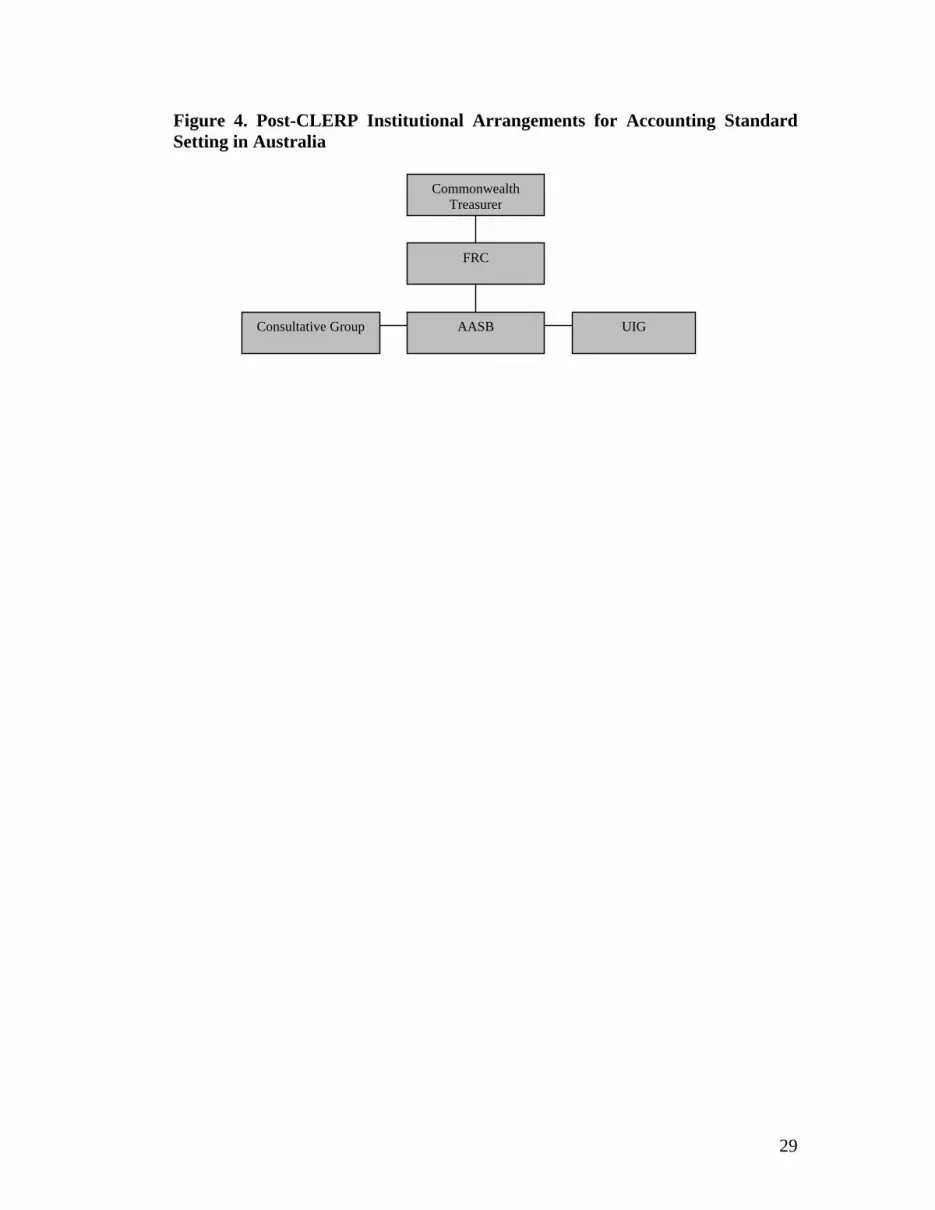

Under the new arrangement of CLERP 11, the structure of accounting standard setting was used to legitimize the government’s political will, seeking to increase the influence of the international marketplace on the Australian economy. The role of the AARF was hence reduced, and the PSASB was disbanded, with all the responsibilities of these two bodies for developing accounting standards for both the public and private sector being transferred to the restructured AASB. The Financial Reporting Council (FRC), as an overseer, was established under the control of Commonwealth Treasury, aiming at ensuring that the AASB standard setting process be committed to the adoption of International Accounting Standards Board (IASB) standards. This, it was argued, would help Australian corporations to raise capital in international capital market. This change in the power structure of accounting standard setting can be viewed in Figures 3 and 4, which adopt diagrams from Henderson et al (2006, p11 & 14).

Take in Figure 3

Take in Figure 4 Obviously, under the post-CLERP structure, the power of the accounting profession in setting accounting standards has been greatly reduced. Australian accounting standard setting is now controlled by the Commonwealth Treasurer, whereas the accounting profession’s influence is only exercised through consultative groups.

Applying Machiavelli’s perspective to this case reveals that the government’s ambition to become powerful over the accounting standards setting process has been achieved. The accounting profession no longer participates in policy formulation. In other words, the profession was an instrument of the Commonwealth and State governments in public sector reform. Briefly, the profession was rewarded with a dominant position in the standard setting process. However, once the profession had outlived its usefulness, the Commonwealth Government relegated it to a subordinate position in order to pursue the Government’s own agenda to facilitate the access of Australian companies to global capital markets.

In achieving its purpose, the government focused attention away from public sector accountability to the role of accountants in the unexpectedness of corporate failures. In particular, the accounting profession was blamed by the government for its inadequate and unenforceable accounting standards. The validity of this stance is debatable. Cooper (1997, p3), for example, argued that corporate collapse was [1] The first paper of the CLERP, Accounting Standards: Building International Opportunities for Australian Business.

22

“characterized by a recurring cycle of regulatory failure, regulatory reform”, where regulatory failure was not restricted to the accounting standards promulgated by the accounting profession. Deficiencies in government regulatory bodies were also evident in corporate failures. Similarly, Funnell and Cooper (1998) pointed out that reforming public sector accounting to a commercial model enabled the central government to shift responsibility and blame to the accounting profession in the event of financial reporting failures by public sector entities.

SUMMARY AND CONCLUSIONS The system of accountability inherent in the Westminster mode of government is at the heart of Australia’s system of government. It has been traditionally understood that government institutions or individual public servants are required to be accountable for their decisions in the public interest. Under this doctrine, policy process is orientated to broad societal notions of governmental accountability. The bureaucracy, as a policy implementing mechanism, is supposed to operate in response to political demands, which are transmitted from social needs.

Australia’s experience of public sector accounting reform and the adoption of accrual-accounting in order to make public sector entities more business-like demonstrates the validity of Machiavelli’s political philosophy. Reform, as a political process, involves a substantial shift in the power structure among powerful groups within the bureaucracy. The progression of reforming public sector accountability through the adoption of private sector bench marks and accounting standards set solely by the accounting profession demonstrates Machiavelli’s political theory in action.

The reformer, the Commonwealth and State governments, sought the support of an elite, in this case, the accounting profession, successfully to institute reform that was premised on serving the public interest. While the reformer espoused altruistic reasons for the new order, the reality is that the reformer’s motives were self-centered. When the reformer’s aspirations were realized, the facilitating elite were eliminated so that the reformer could implement further self-serving reforms. In other words, the claim of enhancing public accountability and improving the efficiency and effectiveness of public administration was secondary to obtaining and maintaining power. Once this was achieved, the Australian accounting profession was sacrificed in order to achieve the political goal of a smooth entry of Australian business to global capital markets through the adoption of international accounting standards. However, if the outcome of the government’s activities follows Machiavelli’s theory to the next stage, the profession may well have the last laugh.

From a Machiavellian perspective, IASB standards can be viewed as a “foreign troop”. By using this foreign troop instead of local or domestic accounting standard setters, the diminished role of Australian accounting setters will lead to a decline in Australian accounting research and development. This, in turn, could lead to an erosion of Australia’s standing in the global business community and thwart government efforts to boost the image of Australian companies and thereby provide access to global capital markets. As explained by Machiavelli:

23

[e]xperience has shown that only rulers and republics that possess their own armies are very successful, whereas mercenary armies never achieve anything, and cause only harm. And it is more difficult for a citizen to seize power in a republic that possesses its own troops than in one that relies upon foreign troops (Machiavelli, 1988, p44).

BIBLIOGRAPHY AARF (1993), The Development of Statements of Accounting Concepts and

Accounting Standards (Policy Statement 1), Australian Accounting Research Foundation, Melbourne.

AAS 27 (1993), Financial Reporting by Local Government, Australian Accounting Standard Board.

AAS 29 (1993), Financial Reporting by Government Departments, Australian Accounting Standard Board.

AAS 31 (1996), Financial Reporting by Governments, Australian Accounting Standard Board.

Australian Public Service Commission (2003), Australia Experience of Public Sector Reform, Commonwealth of Australia.

Barton, A.D. (1999), ‘Accounting for public heritage facilities – assets or liabilities of the government?’, Accounting, Auditing & Accountability Journal, Vol.13, No.2, pp. 219-235.

Board of Inquiry in the Victorian Public Service (1975), Government Printer, Melbourne.

Burritt, R. L., McGrae, M. & Benjamin, C. (1996), ‘What is Public-Sector Asset?’, Australian Accounting Review, Vol.6, No.1, pp.23-28.

Caiden, G.E. (1969), Administrative Reform, Aldine Publishing Co, Chicago

Canning, J. B. (1929), The Economics of Accountancy, Ronald Press Co, New York.

Carnegie, G.D. and Wolnizer, P.W. (1995), ‘The financial value of cultural heritage and scientific collections: an accounting fiction’, Australian Accounting Review, Vol 5, No.1, pp.31-47.

Christensen, M. (2003), ‘Without ‘Reinventing The Wheel’: Business Accounting Applied to the Public Sector’, Australian Accounting Review, Vol.13, No.2, pp. 22-27.

Chua, W.F. & Sinclair, A. (1994), ‘Interests and the Profession-State Dynamic: Explaining the Emergence of the Australian Public Sector Accounting Standard Board’, Journal of Business Finance and Accounting, Vol. 21, No. 5, pp669-705.

Clarke, F., Dean, G. & Oliver, K. (2003), Corporate Collapse: Accounting, Regulatory and Ethical Failure, Cambridge University Press, UK.

Cooper, K. (1997), ‘Corporate Regulation in Australia: Fact or Fiction’, Working Paper Series, University of Wollongong.

24

Department of Finance (1990), Guidelines for Financial Statements of Commonwealth Entities.

Department of Finance (1993), Annual Report 1992-1993.

Department of Finance (1995), Commonwealth of Australia, Guidelines for Financial Statements of Public Authorities and Commercial Activities, Canberra.

Department of Finance (1997), Financial Statements of Commonwealth Department, Guidelines issued by the honourable John Fahey Mister for Finance, Canberra.

Department of Finance and Administration (2003), Requirement and Guidance for the Preparation of Financial Statements of Commonwealth Agencies and Authorities, Commonwealth of Australia.

Department of the Treasury (1997), Corporate Law Economic Reform Program – Policy Framework.

ED 42A (1987), Objective of Financial Reporting, Australian Accounting Research Foundation.

ED 42C (1987), Definition and Recognition of Assets, Australian Accounting Research Foundation.

Emy, H.V. & Hughes, O.E. (1988), Australian Politics: Realities in Conflict, The Macmillian Company of Australia Pty Ltd, Australia.

Fuller, D. & Roffey, B. (1993), ‘Improving Public Sector Accountability and Strategic Decision-Making’, Australian Journal of Public Administration, Vol.52, No.2, pp14-163.

Funnell, W. & Cooper, K. (1998), Public Sector Accounting and Accountability in Australia, UNSW Press, Australia.

Galligan, D.J. (1996), Due Process and Fair Procedures: A Study of Administrative Procedures, Oxford University Press, New York.

Greiner, N. (1990), ‘Accountability in government organizations’, in The Public Sector: Contemporary Readings in Accounting and Auditing, eds. J. Guthrie, L. Parker & D Shand (1990)., HBJ, Sydney.

Groom, E. (1990), The Curran Report and the Role of the State, Australian Journal of Public Administration, Vol.49, No.2, pp144-154.

Halligan, J. & Power, J. (1992), Political Management in the 1990s, Oxford University Press, Melbourne.

Hawker, G. Smith, R.F.I. and Weller, P. (1979), Politics and Policy in Australia, University of Queensland Press, Australia.

Henderson, S. Peirson, G. & Herbohn, K. (2006), Issues in Financial Accounting, Perason, Australia.

25

Hopwood, A.G. (1985), ‘Accounting and the domain of the public – some observations on current development’, in The Public Sector: Contemporary Readings in Accounting and Auditing, eds. J. Guthrie, L. Parker & D. Shand (1990), HBJ, Sydney.

JCPA (1982), 199th Report The Form and Standard of Financial Statements of Commonwealth Undertakings A Discussion Paper, Australian Government Publishing Service, Canberra.

Lucy, R. (1985), The Australian Form of Government, Macmillan, Melbourne.

Machiavelli, Niccolò (1970), The Discourses, trans. L.J. Walker, ed. B. Crick, Penguin Books, Great Britain.

Machiavelli, Niccolò (1988), The Prince, eds. Q. Skinner & R. Price, Cambridge University Press, New York.

McCrae, M., Aiken, M. (1994), ‘AAS 29 and public sector reporting: unresolved issues’, Australian Accounting Review, Vol. 4 No.2, pp.65-72.

Miller, M.C. and M. Islam, A. (1988), The Definition and Recognition of Assets (Accounting Theory Monograph 7), PSASB. Mellor, T. (1996), ‘The Treasury View’, in Public Accounts Committee Assets Valuation Seminar (Chaired Terry Rumble).

National Museum of Australia (1990), Annual Report 1989-90.

NSW Treasury (1989), Accounting Guidelines for Reporting Physical Assets in the Budget Sector, NSW Treasury.

NSW Treasury (1990), Treasury’s Directions Public Finance and Audit Act, 1983, New South Wales.

Pallot, J. (1990), The Nature of Public Assets: A Response to Mautz, Accounting Horizons, Vol.4, No.2, pp.79-85.

Parker, L. & Gould, G. (1999), ‘Changing public sector accountability: critiquing new directions’, Accounting Forum, Vol.23, No.2, pp.109-135.

Parkin, A. (2006), ‘Understanding liberal-democratic politics’, in Government, Politics, Power and Policy in Australia, ed. A. Parkin, J. Summers & D. Woodward, Pearson, Australia.

Patton, J.M. (1992), ‘Accountability and Governmental Financial Reporting’, Financial Accountability and Management, Vol.8, No.3, pp.165-180.

PSASB (1987), Proposed Statements of Accounting Concepts, Series No. 1, Australian Accounting Research Foundation.

Report of the Committee of Inquiry into the Public Service of South Australia (1974), Government Printer, Adelaide.

Review of N.S.W. Government Administration: Directions for change (1977), Government Printer, NSW.

26

RCAGA (1976), Royal Commission on Australian Government Administration Report A.G.P.S., Canberra

Rowles, T.R. (1992), Financial Reporting of Infrastructure and Heritage Assets by Public Sector Entities, Discussion Paper No.17, AARF.

Ryan, C. (1998), ‘The introduction of accrual reporting policy in the Australian public sector: An agenda setting explanation’, Accounting, Auditing & Accountability Journal, Vol. 11, No.5, pp. 518-539.

SAC 4 (1992), Definition and Recognition of the Elements of Financial Statement, AARF.

Self, P. (1978), ‘The Coombs Commission: An Overview’, in R.F.I. Smith & P. Weller (eds.), Public Service Inquires in Australia, University of Queensland Press, Australia.

Sutcliffe, P. (1985), Financial Reporting in the Public Sector – A Framework for Analysis and Identification of Issues (Accounting Theory Monograph 5), Australian Accounting Research Foundation, Melbourne.

The Constitution (2003), Commonwealth of Australia

The Corporations Act (1991), Leo Cussen Institute, Melbourne.

Walker, R.G. (1989), ‘Should there be common standards for the public and private sector’, in The Public Sector Contemporary Readings in Accounting and Auditing, eds. J. Guthrie, L. Parker and D. Shard (1990), HBJ, Sydney.

Wanna, J., Ryan, C. & Ng, C. (2001), From Accounting to Accountability: A Centenary History of the Australian National Audit Office, Allen & Unwin, Victoria.

Wilenski, P. (1986), Public Power and Public Administration, Hale & Iremonger, NSW.

27

Figure 1. The Power Structure of Australia’s Executive Government

Prime Minister

Departments (e.g. Finance, Treasury)

Statutory Authorities (e.g.

AASB, FRC)

Government Trading Entities

(e.g. Telstra)

The Cabinet

Executive Government

Parliament

Governor-General

Head of State Queen Elizabeth

II

Represented by

28

Figure 2. A Rational View of Policy Process

Figure 3. Pre-CLERP Institutional Arrangements for Accounting Standard Setting in Australia

Joint Standing committee

CPA Australia

ICAA Commonwealth Treasurer

FBM

PSASB AuASBUIG LRB

AARF STAFF

AASB

The Electorate

Governing Party

Interest Groups

The Cabinet

Legislative Process

Parliament

29

Figure 4. Post-CLERP Institutional Arrangements for Accounting Standard Setting in Australia

Commonwealth Treasurer

FRC

Consultative Group AASB UIG