barring bank

TRANSCRIPT

CASE STUDY NICK LEESON 1

Reflection

Georgia Stein

MGT 619 Z1 Strategic Management

April 23, 2014

Dr. Herbert Rau

CASE STUDY NICK LEESON 2

Barings Bank, the oldest merchant bank in England was

founded in 1762 by Sir Francis Baring. The history of the bank is

one that is long and well connected to the world's leading

financiers. Baring's history was the high-risk bank

extraordinaire. The Louisiana Purchase, the first of many

historical transactions, was financed by the Barings brothers,

who in 1802 assisted the United States with the purchase from

Napoleon. The transaction though successful would be followed by

the banks first debacle caused by poor management oversight.

To recover the bank became involved in financially

facilitating high-risk ventures and the trading of U.S.

securities throughout Europe, Canada, Argentina, and Uruguay.

With the increasing number of countries the bank had built

relationships with commercial credit became the banks leading

strategy, and core competence. In the 1890s, the bank became

overexposed to risky debt and that combined with their

CASE STUDY NICK LEESON 3

involvement of buying stock to hold for future settlement caused

the banks second major banking debacle of its time.

The Bank of England kept Barings from insolvency; however,

for a time, the bank lost their prominent position. Recovery from

the Panic of 1890 was slow and methodical. Risk taking became

marginally subdued and by catering to only the most affluent,

publically invisible. The more conservative the bank became in

image the more it resembled what was dubbed the epitome of the

British monarchy; and, a long-established relationship as the

Queen’s blue blood bank ensued.

In 1995, Barings faced its third and final financial debacle

due largely to a lack of managerial oversight, and poorly managed

internal controls. It has been said that a young man who had been

hired as the rising star would save the bank and that he alone

was solely responsible for the banks untimely death. However,

there is much more to the story, then the hiring of Nicolas

Leeson, who it is said brought the bank down.

Barings office in Singapore, it would seem, was predestined

to be a repeat of the now long forgotten panic of 1890. The

primary focus of the Singapore office was equities. The trading

CASE STUDY NICK LEESON 4

of futures was increasing and the commissions being paid by the

bank were based on each and every transaction. (Holton, 2014).

Hence, the banks' objective was to gain a seat on the Simex

exchange. The bank's key participant’s objective may have been

entirely different.

In 1989, Nick Leeson with a checkered history of various

clerk positions at several local banks, and a limited education

was hired by Barings Bank London office. Born in 1967, to a

plasterer from Watford, Herefordshire England, Leeson was

educated at the voluntary aided grammar and upper school,

Parmiter. The school completed student’s education in the upper

sixth, or the 13th year of education. Leeson completed the

equivalency of a high school education in 1985. In his last year

of school, Leeson failed math.

Leeson, the son of a plasterer in Watford, Herefordshire

England did not do well in his last year of school as a student,

he did not have family ties to nobility, did not attend the

privileged and elite schools at Eton, and had not served in the

Coldstream guards, the sum of which make him a highly unlikely

candidate to serve in any meaningful way at Baring Bank. (AW-BC,

CASE STUDY NICK LEESON 5

2003). The area in which Leeson grew up in was one that was built

by breweries and housed by narrow alleys and slums that were

close in proximity and unsanitary. He had large aspirations, but

below average qualifications. Prior to being hired by Barings

Bank Leeson had spent two years as a clerk in operations at

Morgan Stanley.

After four years at Barings Bank, Leeson applied for a

securities license. Reporting from Singapore, the Seattle Times

stated the industry group that issues securities licenses in

Britain denied Leeson a trader’s license for having lied on his

application. The group said that Barings knew this and

“transferred Leeson to Singapore where he did not need a British

license to trade at the Singapore International Monetary

Exchange” (Seattle Times, 1995, para 3). Further, the information

“should have been disclosed to SIMEX because it would have been

essential in assessing his application to become a trader in

Singapore," said the authority of the exchange (Seattle Times,

1995, para 4). Hence, there is false representation, material

fact, scienter, and justifiable reliance present in this act of

omission.

CASE STUDY NICK LEESON 6

Meanwhile, Leeson was gaining experience and knowledge while

working in a back office in Jakarta. His task was to clear the

100MM in stock certificates and bearer bonds. Because of a

declining market clients were avoiding delivery by complaining

that the certificates were in the wrong denomination or were

otherwise in "physically unacceptable condition” (Holton, 2014,

para 2). For 10 months Leeson worked in a back office on the

problems and made delivery of the certificates. (Holton, 2014).

In this time it would seem nobody knew of Nicholas Leeson’s

existence, let alone his potential to become the star trader for

one of the most prestigious investment banks in the world. He

had potentially been given the necessary skills, the opportunity,

and a non-shareable problem that would undoubtedly arise. (Hall,

n.d. p 4).

None the less, Barings management was so impressed by

Leeson’s abilities that they made him a general manager, and head

of derivatives at Barings Securities Singapore. Included in his

responsibilities was the authority to hire and fire traders and

back office staff. Leeson having no experience in managing a

team, or in trading was not qualified for the position. The

CASE STUDY NICK LEESON 7

promotion of Nicholas Leeson was not only a questionable choice,

but an inappropriate one. It doesn’t take a leap of faith to

realize that before even having started his position in Singapore

that Leeson was in over his head.

In 1992, Leeson began his position with Barings Futures

Singapore, later known as Barings Securities Singapore. In his

position as Head of Derivatives he was immediately given

authority to trade futures and options for Barings clients and

other companies within Barings organization. The Barings group

consisted of Barings Plc, led by Ron Baker, and its Baring

Securities Limited (BSL), Baring Securities Limited London

(BSLL), Baring Securities Limited Japan (BSJ) managed and led by

Mike Killian, and Baring Securities Singapore (BSS). (Holton,

2014). The funding for Baring Singapore came mostly from BSL,

BSLL, and BSJ. (Holton, 2014).

Leeson was responsible for reporting to four different

people; his direct supervisor in Singapore, Simon Jones, whose

interests were more in football than in the options pit, Mike

Killian, head of Global Equity Futures and Options Sales in

Tokyo, who sought ways to gain by Leeson's trades, and Mary Walz,

CASE STUDY NICK LEESON 8

and her boss Ron Baker in the London office Financial Products

Group. Ron Baker, who saw the profit side of things took direct

responsibility over Leeson. Of this matrix, Leeson had to say,

“My reporting lines were as hazy and inbred as the Baring family

tree itself" (Independent, 1996, para 7). In addition, Leeson

worked with Brenda Granger who was in charge of the transfers of

cash. (Independent, 1996). It would later be reported that Jones,

and Walz denied having operational responsibility for any of

Leeson’s activities, and Baker denied having any responsibility

for Leeson prior to January 1, 1995. (Brown, 2007).

Leeson also had a reporting responsibility to the “senior

directors of the Barings Group who sat on the Management

Committee (MANCO), Executive Committee (EXCO), and Barings' Asset

and Liability Committee (ALCO)” (Brown, 2007, p 1587). "The fact

that Leeson's fraudulent activities resulted in both him and his

bosses receiving substantial bonuses, and thus that they had a

financial interest in ignoring his misdemeanors, is noted but

not commented on by the Baring Report of the incident” which

would be later released (Brown, 2007, p 1587).

CASE STUDY NICK LEESON 9

In 1992, Leeson began the hiring of a local staff. Leeson’s

trading activities started soon thereafter, and he proceeded to

lose in excess of 2 million pounds. To hide the losses Leeson

claimed to have been made by his traders, he opened and used a

replica of the internally bank established error account 88888

(used while in Indonesia), to which he had noted, nobody in

London took notice (AW-BC, 2003).

The symbolic meaning of the number 8, a lucky number to

those who know the Chinese culture, and 5 eights to maximize luck

suggests first the speculative nature of Leeson’s personality,

and secondly that he was not in this trading debacle alone. Now

in charge of both the front and back offices, and with the

support of his staff and seemingly unlimited lack of

accountability, Leeson began trading in a maniacal, purportedly

unauthorized way. His failure to hedge the portfolio and his

inability in the use of pricing models and calculating risk were

becoming more apparent each day. (Brown, 2007). By July 1993 the

losses incurred exceeded six million pounds, or an approximated

12 million US dollars.

CASE STUDY NICK LEESON 10

By summer 1993, Leeson had the opportunity to recover the

losses made in 1992 when the Simex market had a very significant

rally. But, true to his nature, was back in debt by the following

week. Once again the losses were posted to the luck of the draw

88888 account. Masking the losses, Leeson continued arbitraging

and trading the “Nikkei 225 index, ten year Japanese government

bonds, and euro yen deposits while trading simultaneously on the

Osaka Securities Exchange and the Singapore International

Monetary Exchange” (AW-BC, 2003, p 214). The perceived profits

were so large that his reputation as a star performer gave him

unlimited access to the Baring capital. (AW-BC, 2003). Hence,

there was situational pressure, availability of opportunity, and

personal characteristics present.

At this point even by casual observation, the narcissi

personality disorder that Leeson most assuredly developed while

growing up in a less than perceived self-image of himself had

taken root. The denial of a top tier education, and mediocrity of

the circumstances Leeson had lived with captured the rage from

within, alienated him from reality, and furthered his grandiose

ideas. (Maccoby, 2000). The sudden rise in status had taken hold

CASE STUDY NICK LEESON 11

of his senses and there would be no turning back. Even under the

mounting pressure of having to hide more losses than profit,

Leeson continued to exhibit the farthest reach of hubris.

(Goldman, 2009).

Remarkably, the more than substantial losses continued to go

undetected. In reporting earnings in February of 1994, Peter

Baring boldly announced, "1993 was a good year for the investment

banking, Barings made profits before tax of 200 m pounds and

deducted 100m for staff bonuses, which gave a net pretax profit of 100m

pounds" (Independent, 1996, para 9). The actual amount attributed

to BSS was not disclosed; however, it had been reported that

Leeson brought in 20% of Barings worldwide profit, and in the

early part of 1994 50% of its earnings. (AW-BC, 2003). "By year

end 1994, Leeson’s reported profits were 500% of the banks

budgeted estimate" (AW-BC, 2003, p 214). However, losses

sustained and hidden in 88888 were by 1994 more than 50 million

pounds and escalating. Ron Baker, seeing now nothing but profits

coming from Singapore secured his position as the person solely

in charge of Nicholas Leeson.

CASE STUDY NICK LEESON 12

In the meantime, 1993, BB&Co. and Barings Securities limited

(BSL) merged. Later, 1994, BB&Co. and BSL merged with the

Investment Bank (BIB). The combination of the two mergers

presented an extreme clash of cultures, causing confusion between

the loosely managed business of Baring Securitas Limited and the

more blue blood conservative business of BB&Co. and Barings

Investment Bank. “It was a distraction right in the middle of

Leeson’s tenure at BSL” (Holton, 2014, para 14). To further

complicate matters, there was no risk controller in Singapore,

and there was no independent verification of information being

sent from Singapore to London. Essentially, this gave Leeson

access to better than 300 million unchecked pounds. This is

extraordinary in light of the fact that the bank only had 31

million pounds in client funds. To confound the situation even

more Baker had little understanding of derivatives or the trading

floor, the new Credit Committee was led by a man with no

experience in credit, and the 88888 account being sent to London

was not being managed because nobody was assigned the task.

(Brown, 2007).

CASE STUDY NICK LEESON 13

Early one morning, Nov. 1994, Baker now looking forward to

year end bonuses, called Leeson and pressed him for another 2

million pounds of profit while also mentioning that London was

expressing growing concerns. Whether or not Baker had any insight

as to the deception behind the scenes is not discernable;

however, the message to Leeson was clear. Although the profits

recorded Leeson as having “produced for Barings some 28.5 million

pounds in revenue, or the equivalent to 77% of the total net

profit of the Barings Bank Group” the London office was beginning

to question the funding requirements that were keeping Leeson's

trades afloat. (Millar, 2009, para 7). The bank may not have

fully realized it, but they were considerably over leveraged and

Leeson was scared. (Leeson, 2006).

During the years 1993 and 1994, the directors of Baring Bank

had on several occasions approached the Bank of England to seek

informal approval for the allowance of more than the legal amount

of 25% of its capital to be transferred out of England to

operations in Singapore, and Tokyo. Barings Bank had exceeded its

legal limits of its share of capital in overseas trading

operations. By the third quarter of 1994, George Maclean, who

CASE STUDY NICK LEESON 14

served as the head of banking in Barings London office, contacted

Christopher Thompson, who was the Bank of England's senior

supervising agent in charge of merchant banks, to confirm by

necessary protocol that the legal limits had been exceeded. In a

cat and mouse exchange, it can be surmised that the Bank of

England had turned the other cheek with a blind eye to the excess

capital leaving London. (Independent, 1996).

Juxtaposing the events in London, and the causal oversight

of the law the continuing requests and payment of funds kept

Leeson from being exposed. By November of 1994 Leeson’s doubling

of bets in a frantic attempt to profit began to slide into the

abyss and loss accumulation now at 208 million pounds, which was

“more than the reported profit of 205 million pounds” and “more

than double the 102 million pounds paid out in bonus,” presented

an obvious outcome. (Primia, 2005, p 1). The illusion of

Leeson’s brilliant trading strategies was permanently shattered

when the long and the short positions he held had to be sold

disproportionately to meet the margin calls of the exchanges. The

end was near.

CASE STUDY NICK LEESON 15

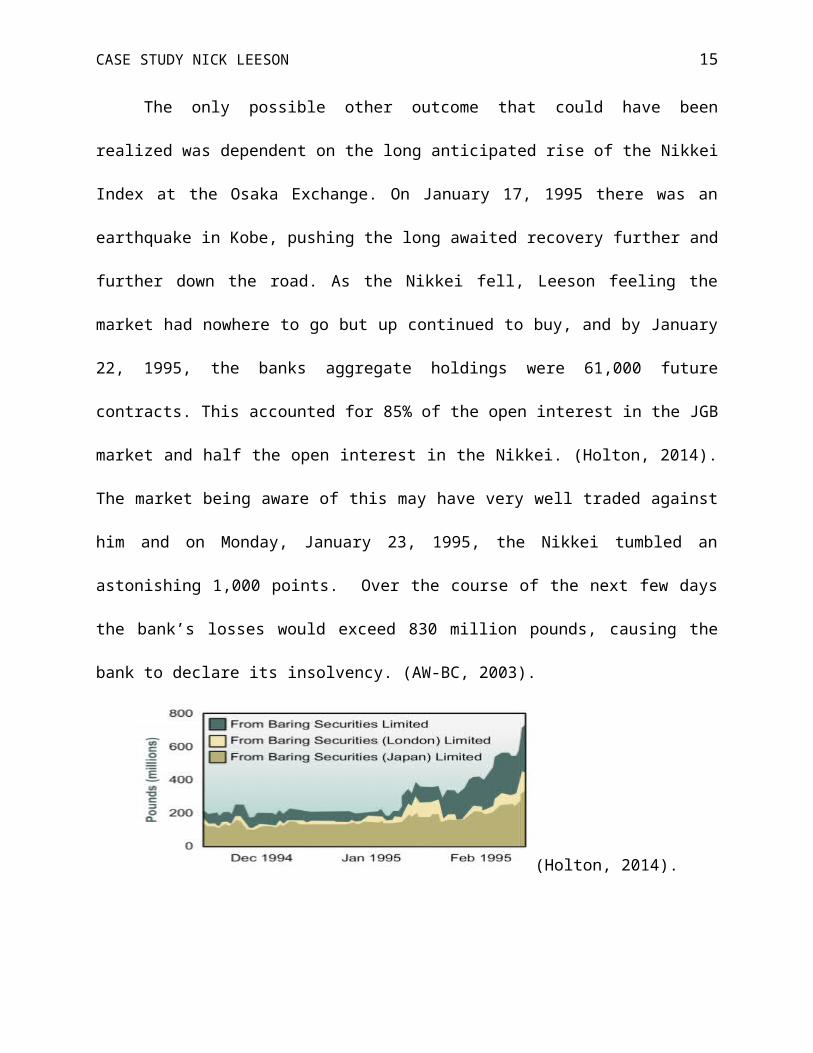

The only possible other outcome that could have been

realized was dependent on the long anticipated rise of the Nikkei

Index at the Osaka Exchange. On January 17, 1995 there was an

earthquake in Kobe, pushing the long awaited recovery further and

further down the road. As the Nikkei fell, Leeson feeling the

market had nowhere to go but up continued to buy, and by January

22, 1995, the banks aggregate holdings were 61,000 future

contracts. This accounted for 85% of the open interest in the JGB

market and half the open interest in the Nikkei. (Holton, 2014).

The market being aware of this may have very well traded against

him and on Monday, January 23, 1995, the Nikkei tumbled an

astonishing 1,000 points. Over the course of the next few days

the bank’s losses would exceed 830 million pounds, causing the

bank to declare its insolvency. (AW-BC, 2003).

(Holton, 2014).

CASE STUDY NICK LEESON 16

Two days after the failure of the bank was announced, the

“London High Court named a panel to manage Barings” (Lugtu, 2006,

p 1). And, Leeson took an unannounced vacation to which he hoped

none would be the wiser.

The lessons from this case are more than obvious, it’s the

number of lessons learned that is so astounding. The first of the

events occurred when Leeson opened a replicate of the 88888

account he had used while working in Jakarta. The account was

used to house imbalances and Leeson soon discovered the account

was never reconciled. When he got into a position where he felt

pressured to show profits he hid his unauthorized trading losses

in this account, which he thought symbolized luck. Management for

whatever the reasons paid no heed to the 88888 account showing

the failure of separation, internal controls and potential

ethical issues with respect to the exercise of corporate power.

To compound the problems identified in this case the external

auditors, supervisors and regulators failed to act when the

impending doom became obvious. Instead both senior management,

and the Bank of England who was charged with maintaining the

appropriate limits to funds leaving England turned a blind eye.

CASE STUDY NICK LEESON 17

Within two months of having done so the bank became insolvent.

Had they acted sooner the catastrophe would have been avoided.

The risks that were exposed show a lack of managerial

control. When Leeson was promoted to General Manager, and given

the position to head the derivatives he was also given the

authority to manage both the front and back office of the

Singapore operation. The lack of segregation enabled Leeson to

manipulate the staff and the organizational operations he sought

funds from. The operational risk and the implied lack of

understanding of the activities on the trading floor, the lack of

oversight and reconciliation of the 88888 accounts, the failure

to verify the information being provided to obtain funds, and the

blind eye from the Bank of England led to the complete failure of

the check and balance system and enabled fraud to occur. The

failures were observed at numerous levels of the organization,

and in numerous locations, and the ultimate cost due to the lack

of managerial controls to the organization were its own demise.

The government of Singapore through an investigation

conducted by their auditors conclude, "The fall of Baring Futures

Singapore was caused by institutional incompetence, lack of

CASE STUDY NICK LEESON 18

understanding of futures business among senior executives, and a

total failure of internal controls. The report also claimed that

Barings CEO Peter Norris and other top officers not only tried to

conceal Leeson's unauthorized dealings but also played down their

significance" (Lugtu, 2006, p 1).

There are two types of fraud that have occurred. The first

being management fraud, and the second employee fraud. For fraud

to have occurred there are five conditions that must be met.

False representation occurred when London omitted the fact that

Leeson had failed his trading exam due to his dishonesty on the

application. There was material fact, in that it did matter in

the decision being made to license Leeson in Singapore. Scienter

was present because there was intent to deceive, and it did

indeed affect the licensing board’s decision in Singapore. Injury

and loss did occur. The five conditions that must be met for the

acts of both management and employee malfeasance to be considered

fraud were present as evidenced by: false representation,

material fact, scienter, justifiable reliance and injury or loss.

For employee fraud to be present it involves the theft of

assets and involves three steps. The steps include “take, sell,

CASE STUDY NICK LEESON 19

and hide" (Hall, 2004, p. 3-3). For management fraud to occur

there are several factors. It happens at levels that are above

the internal control systems. There is an intent that is usually

meant to deceive, and if assets are manipulated the plan is

intentionally misleading and underhanded. (Hall, 2004).

The factors that contribute to fraud as presented by the

Certified Fraud Examiners, includes the "types of forces which

can interact to inspire an otherwise responsible person to commit

fraud such as situational pressure, availability of opportunity,

personal characteristics." (Hall, 2004, p 3-4). When interacted

with having the necessary skills, opportunity and a condition

where there is a non-shareable problem there must be suspicion of

complicity.

Leeson was inspired by the advantages of a more than

idealistic situation. Leeson had a recognizable personality

disorder. For a young man having grown up in an underprivileged

class, the rise to fame, which when coupled by having been given

the necessary skills, and the opportunity to use them and then to

later commit fraud is unparalleled by the unbridled enthusiasm he

received from those he sought to be like and the situational

CASE STUDY NICK LEESON 20

pressures to perform and deliver disproportionate profits to

those who enabled him to do so. In having been given complete

control of the trading floor, and unlimited access to company

funds, he was compromised in such a way that he unwittingly

bargained for a non-shareable problem in which he did first

provide the necessary documentation of profit that would be used

to substantiate bonuses being paid to Peter Barings, Ron Baker,

himself, and others. And, though nobody came out of this

discursive narrative unscathed, it was he who would necessarily

take blame for an internally created non-shareable problem and

the failing of Barings Bank.

In conclusion, it was the flaws of the organizational

structure itself and the lack of adherence to an otherwise

generally acceptable practice of internal controls as specified

by the Foreign Corrupt Practices act of 1977 that were the

primary reasons for the banks' failure. This is not to suggest

that the role Nicolas Leeson played in the failure of the bank

was not a genuine cause for its failure, it is to redirect the

focus to the breakdown in the organizational structure of the

CASE STUDY NICK LEESON 21

bank and the otherwise status quo belief of the banking

institutions' overall legitimacy.

Had the management teams fully understood the businesses

they managed, and had they taken full responsibility for each

business activity with a clear segregation of duties, relevant

internal controls, including appropriate independent risk

management for all business activities, there would not have been

the possibility to commit such egregious fraud. Had top

management and Audit committees taken the precautions and met the

mandate of the Foreign Corrupt Practices Act of 1977 by

safeguarding the firm’s assets, and ensuring the accuracy and

reliability of accounting records and information, promoted

efficiency in the firm's operation, by measuring their compliance

efforts with management's prescribed policies and procedures, and

management responsibility, there would have been reasonable

assurance that exposure to such risk as seen in the Leeson

debacle could not have occurred.

It is the opinion of the Singapore Minister of Finance that

the Barings Group sought to legitimize their lack of oversight,

and internal controls as being the failures of particular

CASE STUDY NICK LEESON 22

individuals who did not perform their duties with efficiency. It

is also of the same opinion that the "key individuals of the

Baring Groups management were wilfully blind and reckless to the

truth” (Brown, 2007, p 1587). The Singapore Report admonishes the

claim that the Baring Group Management was unaware of the 88888

account and states "In our view, the Baring Group's management

either knew or should have known about the existence of account

88888” (Brown, 2007, p 1589).

In what seems a collaborative effort between the regulators,

the Bank of England and Barings Bank, the Group slants the truth

to make it look as though all acted legitimately in a time of

crisis. However, in respect to the explanations Norris had given

about other Baring Group management members as to why they

believed that “Leeson could make such large profits from such a

perceived low risk activity,” the Singapore Report states this

“it is implausible in our view, and it demonstrates a degree of

ignorance of market reality that totally lacks credibility”

(Brown, 2007, p 1587). In conclusion, the Singapore Report notes:

“For three years, account 88888 purportedly escaped the notice of

the entire Baring Group management. Yet within hours after the

CASE STUDY NICK LEESON 23

Baring Group senior management concluded that Mr. Leeson had

fled, BSL personnel working in London and Singapore with

incomplete documentation uncovered account 88888 and identified

it as the immediate cause of collapse” to which I concur, lacks

credibility (Brown, 2007, p 1588). The banks first, and second

crisis situations were the cause of poor management oversight;

but, the third debacle caused by poor management oversight was to

be its end. The oldest bank in England, Baring Bank could not be

saved by the Bank of England this time.

Barriers to Critical Thinking

The barriers to critical thinking are probably as obvious as

the lack of internal controls, and the poor demonstration of

ignorance of market reality. The protagonist’s barriers to

critical thinking include a complex pluralist system of

methodology, with a wild mess dynamic, created by a distorted

mental model of a complicated personality that used a selective

process to substantiate an illusion of control based on

distortions of reality, and wishful thinking. The self-deception

was caused by intensified feelings of invulnerability.

CASE STUDY NICK LEESON 24

The structural complexity caused a distortion by personal

interests because of a false sense of confidence. Trapped by the

myth of the management team Leeson became a boiling frog with no

choice but to jump. To successfully counter the barriers Leeson

will need to learn to be aware of the barriers he encounters, and

practice recognizing patterns, ask disconfirming questions, and

keep track of information that is counter to his future position

in life.

Being a narcissist Leeson will need to learn to provide

ranges and multiple anchor points, and learn to reevaluate how he

engages in effective group dynamics and communication with

others. Had he framed his situation as to what it was, he would

have seen the potential threats to what he was doing, and rather

than seizing an ill opportunity, collapsed it. Learning to

clearly identify what is known, and what is not, and what cannot

be known will further his abilities if he learns to practice

mindfulness of what he and others around him are doing. Another

words Leeson has much to learn. "Learning takes place over time

and involves movement from thought to action and back and forth”

(Rau, 2014, slide 11).

CASE STUDY NICK LEESON 25

Based on his experiences with the Barings Group he should be

able to develop concrete theories, and conceptualize future

events by reflection, avoidance, and new experiments. His new

system will improve by initiating a self-stabilizing thermostat

which is purposeful in the goals he is trying to attain. To

accomplish change the realization that there is no free lunch

will be the hardest of all for him to master because he has a

sense of entitlement which finds no easy solution. And, if by

chance he has learned that good intentions are not enough, he has

learned. (Rau, 2014).

CASE STUDY NICK LEESON 26

References

AW-BC. (2003). 7 Barings Bank PLC: Lesson's Lessons. Retrieved

from

http://www.aw-bc.com/scp/0321197488/assets/downloads/ch7.pdf

Brown, A. (2005). Making Sense of the Collapse of Barings Bank.

Retrieved from

http://www.uk.sagepub.com/managingandorganizations/downloads

/Online%20articles/ch05/3%20-%20Brown.pdf

Goldman, A. (2009). Destructive Leaders and Dysfunctional

Organizations. Cambridge, MA: Cambridge University Press.

Hall, J.A. (2004). Accounting Information Systems, 4th. ED.

Ethics, Fraud and Internal Control. Retrieved April 12, 2014

from

http://www.swlearning.com/accounting/hall/ais_4e/study_notes

/ch03.pdf

Holton, G. (2014). Barings Debacle. Retrieved April 15, 2014 from

http://riskencyclopedia.com/articles/barings_debacle/

CASE STUDY NICK LEESON 27

Independent. (1996), How account 88888 sank Britain’s oldest

bank. Retrieved April 22, 2014 from

http://www.independent.co.uk/news/business/how-account-

88888-sank-britains-oldest-bank-1319275.html

Leeson, N. (1996). The Rogue Trader.

Lugtu, R. (2006). Who Killed Barings Bank? Retrieved April 14,

2014 from

http://r.search.yahoo.com/_ylt=A0LEVzS951dTmmEAG9VXNyoA;_ylu

=X3oDMTEzdjBsOGpxBHNlYwNzcgRwb3MDMQRjb2xvA2JmMQR2dGlkA1NNRTM

5OF8x/RV=2/RE=1398298686/RO=10/RU=http%3a%2f%2fdlsps-

online.com%2ffile.php%2f1%2fWho_Killed_Barings_Bank2.doc/

RK=0/RS=1Um8LGkQZT1KOmTR63XuFqGRPvc-

Maccoby, M. (2000). Narcissistic Leaders: The Incredible Pros,

the Inevitable Cons. Retrieved April 22, 2014 from

http://hbswk.hbs.edu/archive/1565.html

Millar, D. (2009).The Professional Risk Manager International

Association. Barings Brothers & Co. LTD. Retrieved from

http://www.prmia.org/sites/default/files/references/Baring_B

rothers_Short_version_April_2009.pdf

CASE STUDY NICK LEESON 28

The Seattle Times. (1985). Barings trader Leeson was denied

license in Britain. Retrieved April 17, 2014 from

http://community.seattletimes.nwsource.com/archive/?

date=19950315&slug=2110250

Walsh, C. (2005). The Guardian. Few Escaped unscathed from

glittering class of 1995). Retrieved April 22, 2014 from

http://www.theguardian.com/money/2005/feb/20/accounts.busine

ss1#

http://icongfesr2011.tolgaerdogan.net/documents/

internatonal_presantations/KIN17.pdf