avt natural products ltd. - hdfc securities

TRANSCRIPT

1

AVT Natural Products Ltd.

Initiating Coverage

AVT Natural Products Ltd.

March 14, 2022

Initiating Coverage

2

AVT Natural Products Ltd.

Our Take: AVT Natural Products Ltd (AVT) was incorporated in 1994 by the AV Thomas Group to diversify itself from the traditional plantation business. AVT is a leading manufacturer of plant-based extracts and natural ingredients solutions for the food, beverage, animal nutrition and nutraceutical industries of the world. Founded in 1925 as a plantation company, AVT (A. V. Thomas Group) is a family owned, professionally managed group of companies with its headquarters in Chennai, India. The group’s business interests include Plantations (tea, rubber, coffee and spice plantations), Consumer Products (tea, coffee and spices), Leather Goods, Medical Appliances (manufactures and markets Rusch Foley Catheters and distributes several other products in India), Biotechnology (plant tissue culture), Commodity Exports (spices, natural rubber, coir products and food items), Logistics (licensed custom agents, air & sea cargo agents and warehousing), Trading & Agencies (building materials, rubber chemicals etc) and Food & Feed Ingredients (via AVT Natural Products Ltd, AVT Integrated Spice Project and AVT McCormick Ingredients Pvt Ltd). The group’s products have a fair brand value in South India and the family is respected for its business acumen. AVT has good credibility due to its long presence in the region and industry. Valuation & Recommendation: AVT is a leading manufacturer of plant-based extracts and natural ingredients solutions. At its core, the company is focused on replacing

synthetic additives, colours and flavourings with natural alternatives. In the past, products AVT produced answered customers’ requests

for specific ingredients. However, going ahead, with focus on R&D, the company looks to transform itself from product to solution based

offerings provider. This should aid the profitability expansion whilst reducing the exposure to exposure to individual clients with widening

of product basket.

Besides food ingredients, the company is the largest player in specialty teas (decaffeinated and instant) and is poised to capitalize on

benefits of capacity expansions and increasing market share of instant tea products leading to better margin realization.

AVT has reported a mixed financial performance over past decade. In FY10-14, the company witnessed revenue growth at ~35% CAGR,

however, the growth plunged to 3.2% CAGR over FY14-18. Reporting a turnaround, the company grew at 20% CAGR over FY19-21. Going

ahead, we expect the company to report ~15% CAGR growth over FY21-24E largely driven by instant tea and animal nutrition business.

Industry LTP Recommendation Base Case Fair Value Bull Case Fair Value Time Horizon

Solvent Extraction Rs. 99.6 Buy in Rs 97-102 band and add more on dips in Rs. 87-91 band Rs. 112 Rs. 124 2 quarters

HDFC Scrip Code AVTNATEQNR

BSE Code 519105

NSE Code AVTNPL

Bloomberg AVTH IN

CMP (Mar 11, 2022) 99.6

Equity Capital (RsCr) 15.2

Face Value (Rs) 1

Equity Share O/S (Cr) 15.2

Market Cap (RsCr) 1521

Book Value (Rs) 21

Avg. 52 Wk Volumes 425464

52 Week High 110

52 Week Low 41.6

Share holding Pattern % (Dec, 2021)

Promoters 75.0

Institutions 0

Non Institutions 25.0

Total 100.0

* Refer at the end for explanation on Risk Ratings

Fundamental Research Analyst Harsh Sheth

3

AVT Natural Products Ltd.

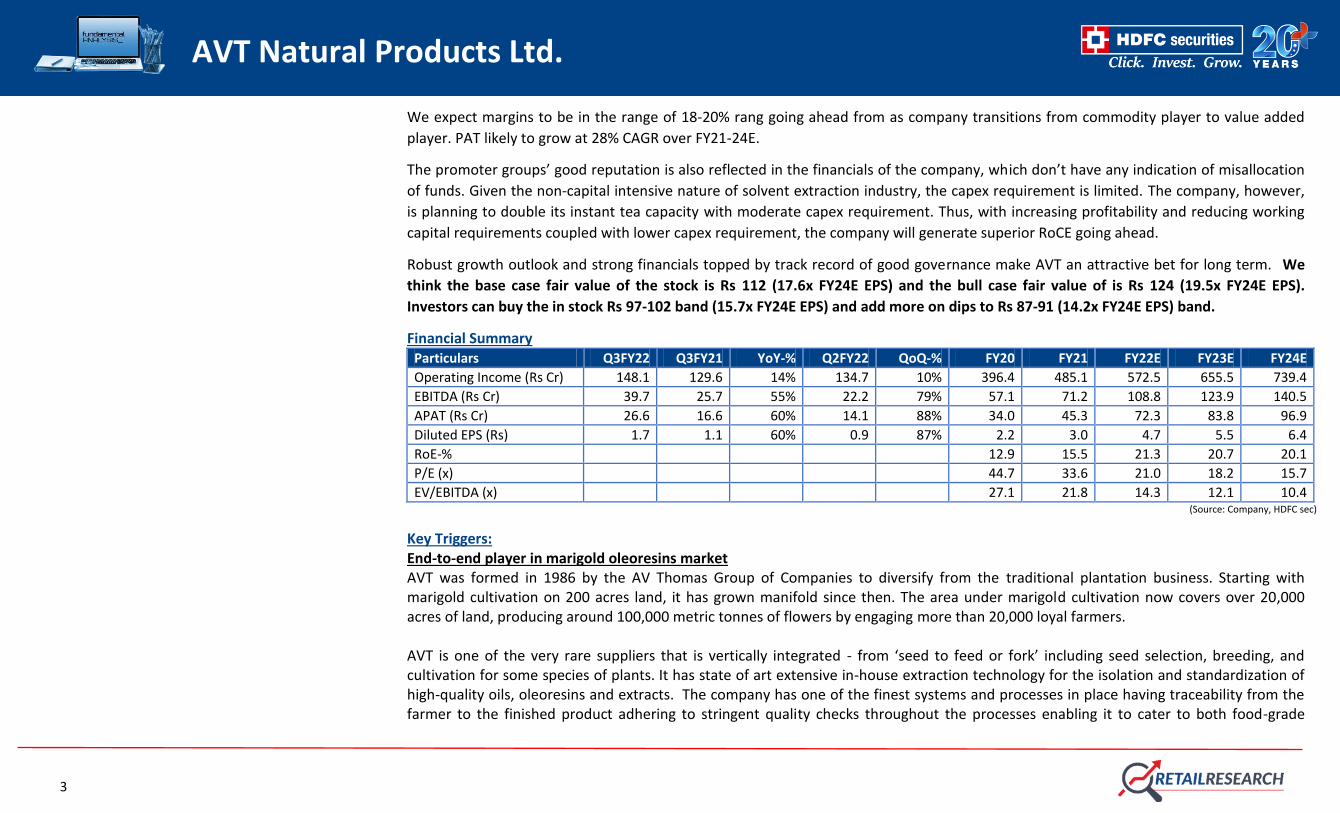

We expect margins to be in the range of 18-20% rang going ahead from as company transitions from commodity player to value added

player. PAT likely to grow at 28% CAGR over FY21-24E.

The promoter groups’ good reputation is also reflected in the financials of the company, which don’t have any indication of misallocation

of funds. Given the non-capital intensive nature of solvent extraction industry, the capex requirement is limited. The company, however,

is planning to double its instant tea capacity with moderate capex requirement. Thus, with increasing profitability and reducing working

capital requirements coupled with lower capex requirement, the company will generate superior RoCE going ahead.

Robust growth outlook and strong financials topped by track record of good governance make AVT an attractive bet for long term. We

think the base case fair value of the stock is Rs 112 (17.6x FY24E EPS) and the bull case fair value of is Rs 124 (19.5x FY24E EPS).

Investors can buy the in stock Rs 97-102 band (15.7x FY24E EPS) and add more on dips to Rs 87-91 (14.2x FY24E EPS) band.

Financial Summary Particulars Q3FY22 Q3FY21 YoY-% Q2FY22 QoQ-% FY20 FY21 FY22E FY23E FY24E

Operating Income (Rs Cr) 148.1 129.6 14% 134.7 10% 396.4 485.1 572.5 655.5 739.4

EBITDA (Rs Cr) 39.7 25.7 55% 22.2 79% 57.1 71.2 108.8 123.9 140.5

APAT (Rs Cr) 26.6 16.6 60% 14.1 88% 34.0 45.3 72.3 83.8 96.9

Diluted EPS (Rs) 1.7 1.1 60% 0.9 87% 2.2 3.0 4.7 5.5 6.4

RoE-% 12.9 15.5 21.3 20.7 20.1

P/E (x) 44.7 33.6 21.0 18.2 15.7

EV/EBITDA (x) 27.1 21.8 14.3 12.1 10.4 (Source: Company, HDFC sec)

Key Triggers: End-to-end player in marigold oleoresins market AVT was formed in 1986 by the AV Thomas Group of Companies to diversify from the traditional plantation business. Starting with marigold cultivation on 200 acres land, it has grown manifold since then. The area under marigold cultivation now covers over 20,000 acres of land, producing around 100,000 metric tonnes of flowers by engaging more than 20,000 loyal farmers. AVT is one of the very rare suppliers that is vertically integrated - from ‘seed to feed or fork’ including seed selection, breeding, and cultivation for some species of plants. It has state of art extensive in-house extraction technology for the isolation and standardization of high-quality oils, oleoresins and extracts. The company has one of the finest systems and processes in place having traceability from the farmer to the finished product adhering to stringent quality checks throughout the processes enabling it to cater to both food-grade

4

AVT Natural Products Ltd.

(human consumption) and feed-grade (animal consumption) oleoresins markets. Its dedicated R&D and Extraction facilities have the capabilities to offer customised solutions to clients. Applications of marigold - Marigold flowers are rich source of carotenoids and being grown on commercial scale for extracting these carotenoids. These carotenoids are rich source of Lutein, Zeaxanthin, and other products. Food grade lutein has applications across numerous industries; as a colorant in foods & beverages, in high-grade perfumes and cosmetics/anti-septics due to anti-inflammatory, antifungal & antibacterial compounds, and crop protection due to its insect repellent activities. Besides, marigold oleoresin is widely used in the pharma industry because of its medicinal attributes, particularly in eye-care industry. Lutein is beneficial for treating AMD i.e. Age-related Macular Degeneration, cataract-related risks & improving eye health. It is also well known for its antioxidant & anti-cancer activities. Feed-grade lutein is used in animal feed particularly in poultry i.e. for imparting colour to the egg-yolks. (Oleoresins are a naturally occurring combination of oil and resin that can be extracted from plant, and are highly concentrated in nature. Marigold Oleoresin is a dark brown viscous liquid extracted from marigold flower having characteristic herbal note.) Contract farming ensures quality and steady supply – AVT has cordial relations with farmers built over time and has gained enough goodwill. The company engages in contract farming to ensure a continuous supply of high quality raw material. The farmers are provided with superior high yielding seeds and free agro services such as fertilizers and knowledge on good agricultural practices and in return they supply the marigold produced to the company. Moreover, the farmers need not transport their produce to domestic markets as AVT bears the cost of transportation. Price for the marigold supplied by the farmer to AVT is fixed at the beginning of the season while quantity cannot be fixed, as the produce is dependent on several factors such as weather, pests, quality of seeds and farming techniques. The farmer is not bound to sell his produce to AVT, which could be a concern. However, since AVT maintains a good relationship with the farmers, gives them good quality seeds and fertilizers and pays them a fair price, they are unlikely to sell their flowers elsewhere. Exclusive supplier to Kemin Industries AVT has long term "Critical Global Strategic Partnership Agreement" with USA based Kemin Industries Inc. (Kemin). AVT has a mutually exclusive supply agreement with Kemin for food-grade marigold oleoresins specifically used for eye-care products. As discussed above, Lutein and Zeaxanthin derived from marigold oleoresins are widely used in eye-health segment. Kemin through its flagship ‘FloraGLO® Lutein’ brand dominates this market while AVT is the exclusive supplier of marigold oleoresins to them. Both Kemin and AVT enjoyed exponential growth in profitability over 2011-14 phase (aided by shortage of marigold) until the expiry of Kemin’s lutein patent. While the growth rationalised in subsequent years, the FloraGLO still enjoys superior brand equity and given the growing eye-related health issues across the globe, the management expects 6-8% organic growth in volumes, going ahead.

5

AVT Natural Products Ltd.

Key player in feed-grade marigold oleoresins market Apart from food-grade marigold oleoresins, AVT also supplies feed-grade (for animal consumption) marigold oleoresins to Kemin, however, there’s no exclusivity clause and AVT exports this product to various markets. The feed-grade marigold oleoresins market is largely dominated by Chinese players as they account for ~85% of the global supply. It is widely used in poultry industry as a feed additive which intensifies the colour of yolk and boiler skin. The golden yolks are largely preferred by consumers as it represents good health. Lutein is a key pigment responsible for the yolk colour. Given this is highly commoditised market, AVT has moved up the value chain in the poultry pigment market with unique finished product offerings to become an end-to-end solutions provider. Introduction of Rosemary extract In its continued bid to diversify away from marigold and develop new ingredients, AVT in FY21 started processing Rosemary. Similar to food-grade marigold oleoresins, the company has signed a strategic supply agreement with Kemin Industries for Rosemary extract. Rosemary is widely used in Food & Beverage industry as a preservative due to its antioxidant and antimicrobial activities. Several studies demonstrate that the antioxidant capacity of rosemary extracts is more effective than that of other conventional antioxidants used in the food industry. In its first year of supply, Rosemary accounted for ~Rs 34 Cr (~7%) of FY21 sales. Kemin which currently sources part of its requirement of Rosemary from China will increasingly source from AVT going ahead with it becoming the exclusive supplier in future, as was the case for food-grade marigold oleoresins. This assures a robust volume growth for near term. Focus on value added spice oleoresins AVT offers a very exhaustive range of oleoresins, essential oils, and spice extracts to service its customers across various industries and applications. The company through its R&D is focused on developing highly value added and specialty products as it looks to cater to customized needs clients across F&B and pharmaceutical industries. General spice oleoresins is purely commoditized business with higher working capital requirements and intense competition. AVT here is rather focused on high margin niche products rather than chasing the volume game. Thus, the sales contribution of this segment is likely come down in favour of other growing segments. Spice Oleoresins Industry - Spice oleoresins are the concentrated liquid from the spices that reproduce the character of the respective spice fully without compromising aroma, flavour or texture. They are easy to store and transport because concentrated forms reduce space and bulk. Besides, they have longer shelf life due to lower moisture content.

6

AVT Natural Products Ltd.

Being the world’s largest producer of spices, India also controls ~60% of global spice oleoresins market with over 90% of the produce being exported. The biggest consumers of oleoresins is the processed food sector in developed countries and include flavour and fragrances makers, seasoning companies, spice blenders, meat processors, and organic retail chains in cosmetics and fragrances. While the demand from HoReCa channel was impacted post outbreak of Covid-19, the growth for ready-to-products across the world has more than compensated for shortfall in demand. Synthite Industries is the largest exporter of Spice Oils and Oleoresins followed by Plant Lipids and AVT in the market which otherwise is largely fragmented. Increasing contribution of Value Added Teas To diversify away from spice oleoresins, the company ventured into speciality tea business. Besides having its own plantations, AVT Group is one of the largest player in branded teas in India, however, it operates in specialty teas (decaffeinated tea and instant tea) under AVT Natural Products Ltd. It was the first Indian company to venture into decaffeinated tea space. Decaffeinated tea refers to a specialized tea variety that has low levels of caffeine. It is derived from black or green teas. The demand for decaffeinated tea is particularly higher in developed countries and specifically in Europe due to health conscious consumers. The market for decaffeinated teas is a niche market and AVT is the largest player with ~50% global market share. Most of the other beverage companies around the world outsource their decaffeination requirement via what is called as toll arrangement wherein they provide tea or coffee to de-caffeinators (like AVT) and pay a fix processing fee. This is because, to set-up and maintain a decaffeination plant, it requires higher level of skill and so not many companies venture into this business. AVT has a long term marketing association with some of the largest tea players in the world including the likes of Harris Freeman. Instant Tea – The company leveraged its success in de-caffeinated teas to venture into instant tea business. Instant tea is a powder that can be mixed with water to form a tea beverage. It’s made by extracting the solids from tea leaves (not all that different from brewing tea at home) and then removing the water, usually by a technique called spray drying. The actual process is much more complicated, sometimes involving solvents other than water and/or gases to isolate tea components and steps needed to make the ultimately reconstituted beverage clear as consumers prefer. AVT offers a wide and customized range of soluble (hot water and cold water) - instant and green tea powders for the international markets. With strong technical know-how and product development capabilities, the company remains a preferred supplier to some of

7

AVT Natural Products Ltd.

the most prominent customers in the industry, such as Unilever, Nestle, Tata Consumer, Coca-Cola, etc. While China is a strong competitor in green tea, AVT is the biggest in black tea. Instant Tea segment has been recognized as a major growth area for the company as it continues to expand the customer base. The company also has planned an expansion here as it looks to double the sales of instant tea in near term. The company’s focused approach on winning key customer accounts, newer additions to its customer base, garnering greater share of clients by servicing newer geographies, increased production efficiencies and strategic raw material purchases has helped AVT to consolidate its position in speciality tea market. Foray into animal nutrition can be a potential game changer: While the company was already catering to animal nutrition market indirectly through supply of feed-grade oleoresins, as discussed above, it wanted to move up the value chain. With strong research and technical capabilities, the company has the infrastructure to provide end-to-end solutions where it can partner with clients (livestock provider/feed manufacturer) to select ingredients, formulate, and develop solutions to tackle specific problem/s. For instance, the company has launched a product, an alternative for antibiotics, designed to promote performance and productivity across animal species. There has been growing restraint globally against use of antibiotics/synthetics to fast track the growth in animals. Given the rising consumer awareness, global food companies such as McDonald’s are working on sustainable procurement where they source chicken raised without using antibiotic. In certain markets such as LATAM, AVT is looking to directly reach the consumer by building its own distribution network while in others it is looking to tie-up with feed manufacturers. In Canada, for instance, it has signed an exclusive agreement with Trouw Nutrition. Trouw Nutrition (a part of Nutreco Company with revs of Euro 9 bn) is a global leader in innovative feed specialities, premixes and nutritional services for the animal nutrition industry. It is the #2 premix producer globally, with a #1 position in Europe and Canada. AVT is looking to extend this relationship beyond Canada, in other markets. AVT ventured into animal nutrition space in early-2020, however, the onset of Covid-19 delayed the ramp up. As guided by the management, lot of prospective consumers are at final stages of clinical trials. While lead time for customer acquisition here is long due to numerous trials and the cost involved, once successful it’s a sticky business.

8

AVT Natural Products Ltd.

The company setup a dedicated subsidiary in Mexico as it sees LATAM to be its one of the biggest markets going ahead. FY22 and H1FY23 is likely to be a breakthrough for the company in this segment and given higher margins here, this segment is expected to contribute to the business significantly to company’s bottomline over the medium term and grow as a key pillar going forward. Renewed strategy to make it the company of the future: Mr Rahul Thomas (son of Mr Ajit Thomas, Promoter & Chairman) has envisioned to transform AVT from mere solvent extractor to ingredient solutions provider backed by higher investments in Research and Development. The company has knowledge of working with lot of ingredients and has now plans to move up the value chain as it looks to develop formulations to tackle wide array of problems. Also, rather than working on individual ingredient basis, the company has now formed 4 business division with each business acting as separate business unit: 1) Food & Beverage 2) Animal Health & Nutrition 3) Cosmetics & Personal Care 4) Crop Protection

Food & Beverage division includes company’s traditional oleoresins and tea businesses while animal nutrition business, as discussed above, is at nascent stage but will be key growth driver going ahead. In cosmetics & personal care products, demand for “cleaner” alternatives in cosmetics and personal care products is increasing, resulting in a growing number of companies giving greater emphasis to the concept of “clean beauty.” AVT here offers products that replace synthetic ingredients with natural and sustainable alternatives. The company here is in talks with leading cosmetic companies across the world including the likes of L’Oreal. Under crop protection, AVT’s vertically integrated facilities provides individual actives and formulated solution for crop protection needs. Greater awareness regarding the use of environment-friendly products has led to an increased demand for sustainable crop protection solutions. This decreased use of synthetic products is backed by an increasing trend in the number of natural product offerings. While prima facie it may look like AVT is spreading itself too thin by venturing into multiple categories, it’s primarily into solvent extraction business and the products here have applications across multiple categories. Additionally, the new businesses like animal nutrition, crop science, cosmetics, etc. require minimum capital investment. R&D is the only major cost as the company looks to move from products to solution based selling.

9

AVT Natural Products Ltd.

Expect revenue to grow at ~15% CAGR over FY21-24E AVT has reported a mixed performance over past decade. In FY10-14, the company witnessed it revenue growth at ~35% CAGR aided by Kemin’s patent and AVT’s exclusive supply agreement with them coupled with consecutive seasons of poor crop in China which further pushed up the marigold prices. However, post the expiry of patent, the growth plunged to 3.2% CAGR over FY14-18. Reporting a turnaround, the company grew at 20% CAGR over FY19-21 driven by robust growth in instant tea business and launch of rosemary extract. Going ahead, we expect the company to report ~15% CAGR growth over FY21-24E largely driven by instant tea and animal nutrition business. The increasing adoption of ‘China Plus One Strategy’ augurs well for the company as China is one of the biggest suppliers of marigold oleoresins, certain spice extracts and green tea. We expect margins to be in the range of 18-20% going ahead from as company transitions from commodity player to value added player. Notably, the company has able to grow profitability in FY21 post withdrawal of MEIS incentives which stood at Rs 17 Cr/15 Cr/ 14 Cr in FY20/19/18 respectively. PAT likely to grow at 28% CAGR over FY21-24E. Improving profitability, limited capex requirements to aid superior cash flow generation - The Solvent Extraction industry, specifically the marigold oleoresin and spice oleoresin segments, does not require significant capital expenditure and does not demand significant capital to operate a plant. The same plant can be used for marigold oleoresin and spice oleoresin with minor part changes. The company, however, is planning to double its instant tea capacity with moderate capex requirement. AVT has to maintain certain level of inventory, specifically of marigold oleoresins due to inherent seasonal nature of business and with bumper output over past two seasons, there has been further spike in inventories. Going ahead, with increasing contribution from other businesses, working capital as a proportion of sales is likely to come down. Going ahead as the volumes increase, AVT can procure the base material from outside while focusing on R&D, blending and encapsulation. This will help the company to generate even higher margins while bringing down the working capital requirements driving superior incremental RoCEs. Key Risks: High working capital intensity: AVT’s working capital intensity remains high, primarily because of the seasonal availability of raw

materials, necessitating higher stock levels at the end of the procurement season for marigold and spices. Despite the high stock levels,

demand and price risks are limited to an extent because of order-backed procurement of marigold and few spices.

10

AVT Natural Products Ltd.

Low barriers to entry: The solvent extraction industry, specifically the marigold and spice extraction segments, has a low barrier to entry.

Setting up a plant does not require significant capital and the process is relatively simple and does not require much expertise. However,

product, process and plant approval are required from the food association of the countries in which the product is to be sold. Building

credibility with customers can take time. Also, AVT is increasingly focused on value added products backed by superior R&D capabilities

and protected by patents in some case.

Forex risk: AVT primarily being export oriented company, foreign exchange income accounts for over 80% of company’s revenues and is

exposed to currency volatility. AVT takes forward contracts for 60-71% of net exposure build systematically to hedge its forex risk.

High volatility in raw material and finished good prices: Being an agriculture dependent industry, prices of raw materials and finished goods are very volatile. China accounts for >70% of world’s marigold oleoresin production. A bumper crop in China can lead to reduced finished good prices and vice versa. Moreover, a failure in the Indian crop could make procuring raw material difficult and expensive. High dependence on Kemin: Kemin is the largest customer of AVT, accounting for a quarter of their total sales. If Kemin discontinues or reduces business with AVT, the company could face a setback. However, AVT has been dealing with Kemin for over 16 years and has established its reputation as a reliable supplier which is reflected from the fact that they have extended their relationship beyond Marigold to Rosemary where Kemin is looking to make AVT exclusive supplier. Additionally, Kemin is also bound by contract to purchase marigold oleoresin from AVT till 2028.

11

AVT Natural Products Ltd.

Financials: Income Statement

Balance Sheet

Particulars (Rs Cr) FY19 FY20 FY21 FY22E FY23E FY24E

Particulars (Rs Cr)As at March FY19 FY20 FY21 FY22E FY23E FY24E

Net Revenues 339 396 485 572 655 739

SOURCE OF FUNDS

Growth (%) 3.4 16.9 22.4 18.0 14.5 12.8

Share Capital 15 15 15 15 15 15

Operating Expenses 297 339 414 464 532 599

Reserves 236 260 295 355 425 507

EBITDA 42 57 71 109 124 140

Shareholders' Funds 252 275 310 370 441 522

Growth (%) 27.9 36.9 24.8 52.7 13.9 13.4

Minority Interest 0 0 0 0 0 0

EBITDA Margin (%) 12.3 14.4 14.7 19.0 18.9 19.0

Total Debt 81 42 50 68 46 26

Depreciation 11 14 15 15 16 18

Net Deferred Taxes 7 3 3 3 3 3

Other Income 4 7 9 8 9 10

Total Sources of Funds 340 320 363 441 489 551

EBIT 35 50 65 102 117 133

APPLICATION OF FUNDS

Interest expenses 5 6 4 5 5 3

Net Block & Goodwill 98 99 89 79 85 82

PBT 30 45 61 97 112 130

CWIP 0 0 0 0 0 0

Tax 9 11 15 24 28 33

Investments 7 0 0 0 0 0

PAT 21 34 45 72 84 97

Other Non-Curr. Assets 7 6 4 9 8 9

Share of Asso./Minority Int. 0.0 0.0 0.0 0.0 0.0 0.0

Total Non-Current Assets 112 105 93 88 93 91

Adj. PAT 7 34 45 72 84 97

Inventories 144 123 164 204 207 239

Growth (%) -75.5 414.4 33.2 59.7 15.9 15.6

Debtors 82 75 102 123 134 150

EPS 0.4 2.2 3.0 4.7 5.5 6.4

Cash & Equivalents 12 19 16 37 66 86

Other Current Assets 39 56 50 69 79 85

Total Current Assets 276 272 333 433 486 560

Creditors 35 23 38 45 47 56

Other Current Liab & Provisions 14 35 25 35 44 44

Total Current Liabilities 49 58 63 80 91 100

Net Current Assets 227 214 270 353 396 460

Total Application of Funds 340 320 363 440 489 551

12

AVT Natural Products Ltd.

Cash Flow Statement Key Ratios

Particulars (Rs Cr) FY19 FY20 FY21 FY22E FY23E FY24E

Particulars FY19 FY20 FY21 FY22E FY23E FY24E

Reported PBT 29.9 44.8 60.6 96.7 112.1 129.6

Profitability Ratios (%)

Non-operating & EO items 0.1 -3.0 -1.7 -4.6 1.7 -0.3

EBITDA Margin 12.3 14.4 14.7 19.0 18.9 19.0

Interest Expenses 5.0 5.2 3.5 5.3 4.8 3.1

EBIT Margin 10.3 12.7 13.3 17.8 17.8 17.9

Depreciation 10.9 13.7 15.2 14.8 16.2 18.1

APAT Margin 1.9 8.6 9.3 12.6 12.8 13.1

Working Capital Change -66.9 23.3 -54.5 -61.3 -15.8 -44.0

RoE 2.7 12.9 15.5 21.3 20.7 20.1

Tax Paid -8.6 -13.5 -15.3 -24.4 -28.2 -32.7

RoCE 11.5 15.5 19.1 25.6 25.3 25.7

OPERATING CASH FLOW ( a ) -29.6 70.6 7.6 26.4 90.7 73.9

Solvency Ratio (x)

Capex -20.4 -14.5 -5.0 -5.0 -22.0 -15.0

Net Debt/EBITDA 1.7 0.4 0.5 0.3 -0.2 -0.4

Free Cash Flow -50.0 56.1 2.6 21.4 68.7 58.9

Net D/E 0.3 0.1 0.1 0.1 0.0 -0.1

Investments 23.6 0.0 0.0 0.0 0.0 0.0

PER SHARE DATA (Rs)

Non-operating income 0.5 0.3 0.6 0.0 0.0 0.0

EPS 0.4 2.2 3.0 4.7 5.5 6.4

INVESTING CASH FLOW ( b ) 3.7 -14.2 -4.4 -5.0 -22.0 -15.0

CEPS 1.1 3.1 4.0 5.7 6.6 7.6

Debt Issuance / (Repaid) 41.1 -35.4 8.2 17.5 -21.4 -20.4

BV 16.5 18.0 20.4 24.3 28.9 34.3

Interest Expenses -5.1 -5.3 -3.8 -5.3 -4.8 -3.1

Dividend 0.4 0.6 0.7 0.8 0.9 1.0

FCFE 10.1 15.7 7.7 33.6 42.5 35.4

Turnover Ratios (days)

Share Capital Issuance 0.0 0.0 0.0 0.0 0.0 0.0

Debtor days 78 72 67 72 72 70

Dividend -7.3 -8.3 -9.9 -12.2 -13.7 -15.2

Inventory days 128 123 108 118 114 110

FINANCING CASH FLOW ( c ) 28.7 -49.0 -5.4 0.0 -39.9 -38.7

Creditors days 37 26 23 26 26 25

NET CASH FLOW (a+b+c) 2.8 7.4 -2.2 21.5 28.8 20.1

VALUATION

Opening balance of cash 11.8 14.6 22.0 19.8 41.3 70.1

P/E 230.2 44.7 33.6 21.0 18.2 15.7

Closing balance of cash 14.6 22.0 19.8 41.3 70.1 90.2

P/BV 6.0 5.5 4.9 4.1 3.5 2.9

EV/EBITDA 38.0 27.1 21.8 14.3 12.1 10.4

EV / Revenues 4.7 3.9 3.2 2.7 2.3 2.0

(Source: Company, HDFC sec)

One-year Share Price Movement:

020406080

100120

Mar

-21

Ap

r-2

1

Ap

r-2

1

May

-21

Jun

-21

Jun

-21

Jul-

21

Au

g-2

1

Au

g-2

1

Sep

-21

Oct

-21

Oct

-21

No

v-2

1

Dec

-21

Dec

-21

Jan

-22

Feb

-22

Mar

-22

13

AVT Natural Products Ltd.

HDFC Sec Retail Research Rating description Green Rating stocks This rating is given to stocks that represent large and established business having track record of decades and good reputation in the industry. They are industry leaders or have significant market share. They have multiple streams of cash flows and/or strong balance sheet to withstand downturn in

economic cycle. These stocks offer moderate returns and at the same time are unlikely to suffer severe drawdown in their stock prices. These stocks can be kept as a part of long term portfolio holding, if so desired. This stocks offer low risk and lower reward and are suitable for beginners. They offer

stability to the portfolio.

Yellow Rating stocks This rating is given to stocks that have strong balance sheet and are from relatively stable industries which are likely to remain relevant for long time and unlikely to be affected much by economic or technological disruptions. These stocks have emerged stronger over time but are yet to reach the

level of green rating stocks. They offer medium risk, medium return opportunities. Some of these have the potential to attain green rating over time.

Red Rating stocks This rating is given to emerging companies which are riskier than their established peers. Their share price tends to be volatile though they offer high growth potential. They are susceptible to severe downturn in their industry or in overall economy. Management of these companies need to prove

their mettle in handling cyclicality of their business. If they are successful in navigating challenges, the market rewards their shareholders with handsome gains; otherwise their stock prices can take a severe beating. Overall these stocks offer high risk high return opportunities. Disclosure: I, Harsh Sheth, MCom, authors and the names subscribed to this report, hereby certify that all of the views expressed in this research report accurately reflect our views about the subject issuer(s) or securities. HSL has no material adverse disciplinary history as on the date of publication of this report. We also certify that no part of our

compensation was, is, or will be directly or indirectly related to the specific recommendation(s) or view(s) in this report.

Research Analyst or her relative or HDFC Securities Ltd. does not have any financial interest in the subject company. Also Research Analyst or his relative or HDFC Securities Ltd. or its Associate may have beneficial ownership of 1% or more in the subject company at the end of the month immediately preceding the date of publication of the

Research Report. Further Research Analyst or her relative or HDFC Securities Ltd. or its associate

does not have any material conflict of interest.

Any holding in stock – No

HDFC Securities Limited (HSL) is a SEBI Registered Research Analyst having registration no. INH000002475.

Disclaimer:

This report has been prepared by HDFC Securities Ltd and is meant for sole use by the recipient and not for circulation. The information and opinions contained herein have been compiled or arrived at, based upon information obtained in good faith from sources believed to be reliable. Such information has not been independently verified and

no guaranty, representation of warranty, express or implied, is made as to its accuracy, completeness or correctness. All such information and opinions are subject to change without notice. This document is for information purposes only. Descriptions of any company or companies or their securities mentioned herein are not intended to be

complete and this document is not, and should not be construed as an offer or solicitation of an offer, to buy or sell any securities or other financial instruments.

This report is not directed to, or intended for display, downloading, printing, reproducing or for distribution to or use by, any person or entity who is a citizen or resident or located in any locality, state, country or other jurisdiction where such distribution, publication, reproduction, availability or use would be contrary to law or regulation or

what would subject HSL or its affiliates to any registration or licensing requirement within such jurisdiction.

If this report is inadvertently sent or has reached any person in such country, especially, United States of America, the same should be ignored and brought to the attention of the sender. This document may not be reproduced, distributed or published in whole or in part, directly or indirectly, for any purposes or in any manner.

Foreign currencies denominated securities, wherever mentioned, are subject to exchange rate fluctuations, which could have an adverse effect on their value or price, or the income derived from them. In addition, investors in securities such as ADRs, the values of which are influenced by foreign currencies effectively assume currency risk.

It should not be considered to be taken as an offer to sell or a solicitation to buy any security. HSL may from time to time solicit from, or perform broking, or other services for, any company mentioned in this mail and/or its attachments.

HSL and its affiliated company(ies), their directors and employees may; (a) from time to time, have a long or short position in, and buy or sell the securities of the company(ies) mentioned herein or (b) be engaged in any other transaction involving such securities and earn brokerage or other compensation or act as a market maker in the

financial instruments of the company(ies) discussed herein or act as an advisor or lender/borrower to such company(ies) or may have any other potential conflict of interests with respect to any recommendation and other related information and opinions.

HSL, its directors, analysts or employees do not take any responsibility, financial or otherwise, of the losses or the damages sustained due to the investments made or any action taken on basis of this report, including but not restricted to, fluctuation in the prices of shares and bonds, changes in the currency rates, diminution in the NAVs,

reduction in the dividend or income, etc.

HSL and other group companies, its directors, associates, employees may have various positions in any of the stocks, securities and financial instruments dealt in the report, or may make sell or purchase or other deals in these securities from time to time or may deal in other securities of the companies / organizations described in this report.

HSL or its associates might have managed or co-managed public offering of securities for the subject company or might have been mandated by the subject company for any other assignment in the past twelve months.

HSL or its associates might have received any compensation from the companies mentioned in the report during the period preceding twelve months from t date of this report for services in respect of managing or co-managing public offerings, corporate finance, investment banking or merchant banking, brokerage services or other advisory

service in a merger or specific transaction in the normal course of business.

HSL or its analysts did not receive any compensation or other benefits from the companies mentioned in the report or third party in connection with preparation of the research report. Accordingly, neither HSL nor Research Analysts have any material conflict of interest at the time of publication of this report. Compensation of our Research

Analysts is not based on any specific merchant banking, investment banking or brokerage service transactions. HSL may have issued other reports that are inconsistent with and reach different conclusion from the information presented in this report.

Research entity has not been engaged in market making activity for the subject company. Research analyst has not served as an officer, director or employee of the subject company. We have not received any compensation/benefits from the subject company or third party in connection with the Research Report.

HDFC securities Limited, I Think Techno Campus, Building - B, "Alpha", Office Floor 8, Near Kanjurmarg Station, Opp. Crompton Greaves, Kanjurmarg (East), Mumbai 400 042 Phone: (022) 3075 3400 Fax: (022) 2496 5066

Compliance Officer: Binkle R. Oza Email: [email protected] Phone: (022) 3045 3600

HDFC Securities Limited, SEBI Reg. No.: NSE, BSE, MSEI, MCX: INZ000186937; AMFI Reg. No. ARN: 13549; PFRDA Reg. No. POP: 11092018; IRDA Corporate Agent License No.: CA0062; SEBI Research Analyst Reg. No.: INH000002475; SEBI Investment Adviser Reg. No.: INA000011538; CIN - U67120MH2000PLC152193

Mutual Funds Investments are subject to market risk. Please read the offer and scheme related documents carefully before investing.