annual report 2002 - 2003 - international training centre

TRANSCRIPT

A N N U A L R E P O R T 2 0 0 2 - 2 0 0 3

Even as it provides wheelsto a sub-continent, India’sroad transport sector hasbeen a lively engine ofgrowth, powered by theboundless energy of humanenterprise. It is repletewith stories – of its unsungheroes, their struggles andsuccesses. Of courageousmen who overcame themany roadblocks in lifewith drive, grit, hard workand self-belief. Thegeographies vary, so do thecircumstances. Yet theessential plot has anunmistakable sameness,including the ride on AshokLeyland vehicles that theytook at some crucial phase

in their life, to reachdestinations set byambition. Through their single-minded pursuit, theyhave actualized thepromise inherent in"Engineering yourTomorrows." Not justthat: they have, inturn, been catalysts-touching andchanging livesaround them,spreading further theripples of prosperity.In the process,partnering AshokLeyland in“Engineering yourTomorrows”.

Poverty thwarted Kisanrao Dalvi’s academic life at 17, in a night

school. Eldest among six brothers and a sister, he started selling

tea from a cart outside the sales office of Rajesh Motors, Kolhapur.

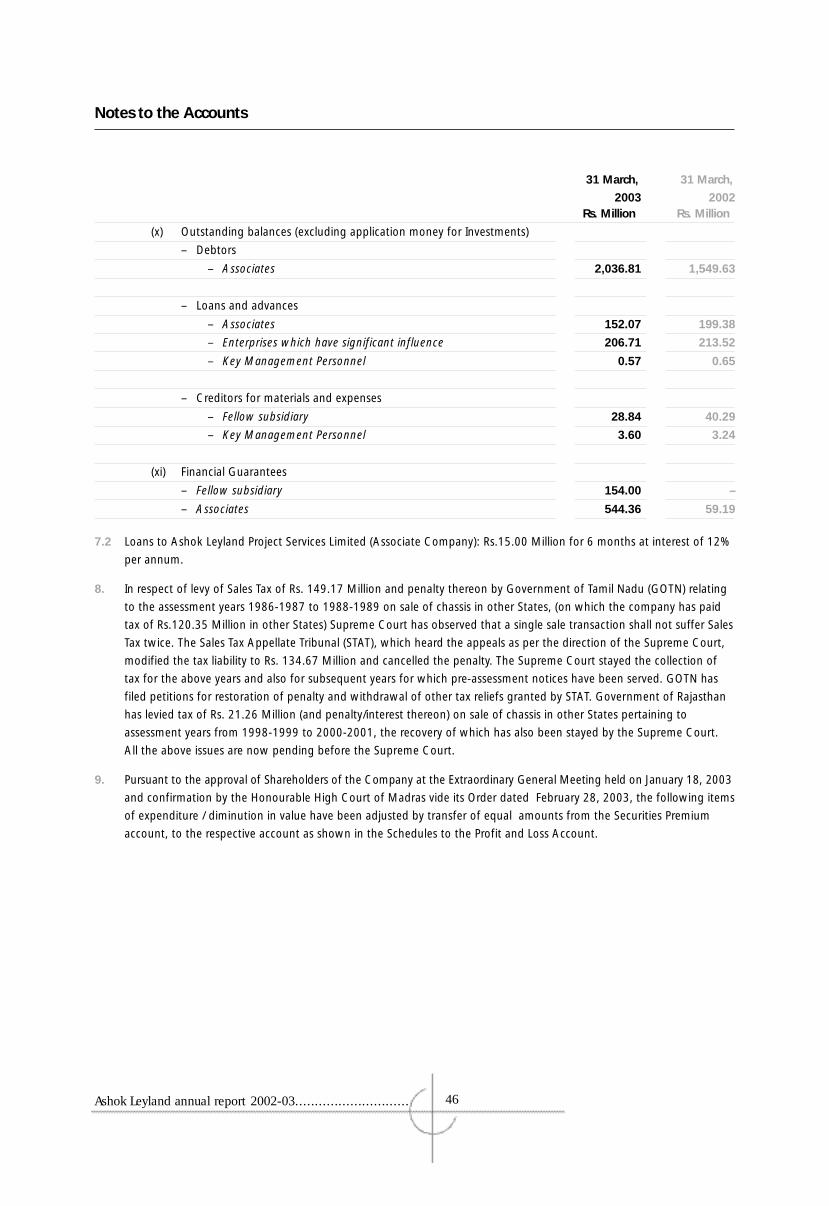

His clientele was the convoy drivers who brought Ashok Leyland

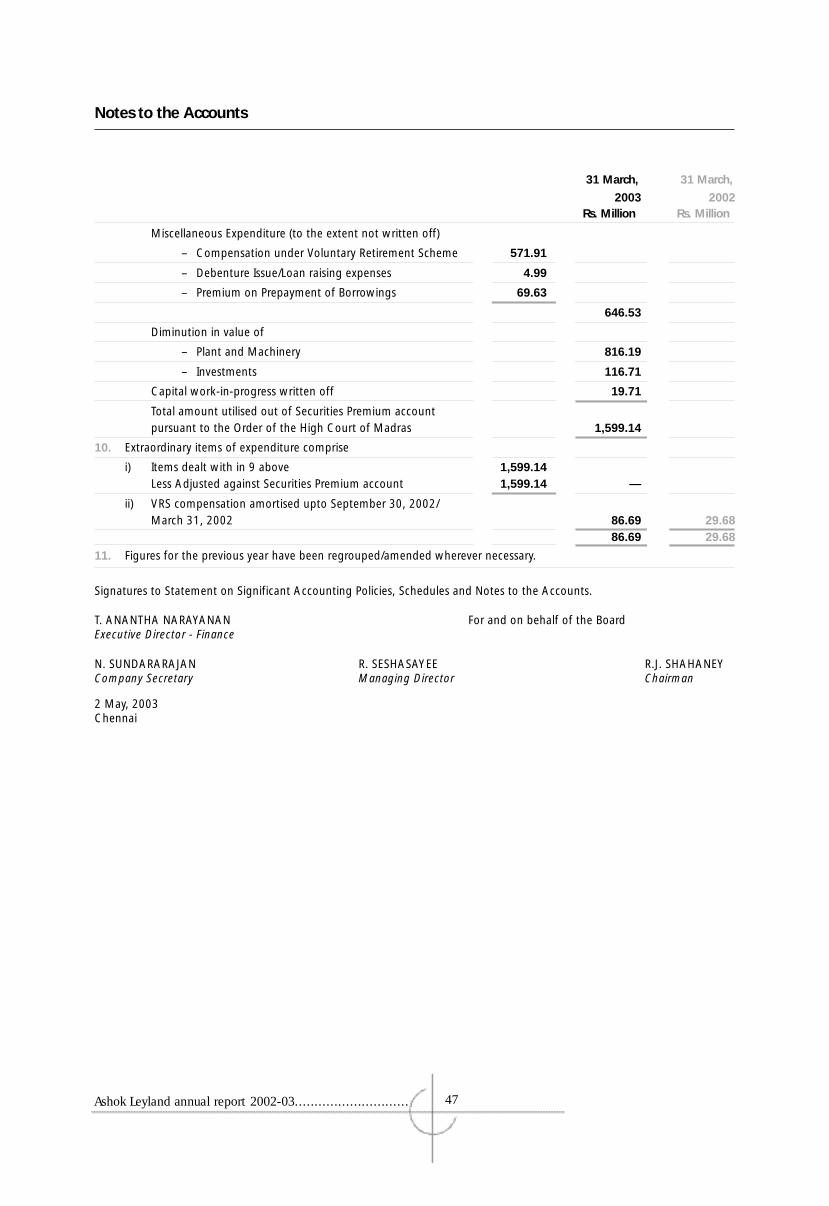

chassis from the Ennore plant. Throughout the day, the teenager

would watch the powerful machines being driven in and will sit

behind the wheels when the drivers were in a good mood. The

youngster dreamt of owning a truck one day. Trucks fascinated him

and became his passion. And the sales yard, his classroom.

Passing on the tea cart to a younger brother, Dalvi joined Ghadge

Patil as a cleaner. That was in 1976. A monthly salary of Rs 45 came

with a perk: a sleeping place at the garage. For a while he drove

a businessman’s car. Till his grandfather told him : "do you want to

end up in life washing someone else’s vehicle? Why can’t you get

one for yourself? " Dignity and dream hardened the family’s will to

find a way forward. In 1978, Dalvi took his first step in the

transport trade by mortgaging the family’s modest house for margin

money to buy a Matador. ("100% finance 25 years back!", he

beams). Slowly but steadily things started looking up. The family

diversified into businesses, including hotels.

A breakthrough for Dalvi came when he got a construction contract

for Indal’s mining operations "in the middle of the jungle, where no

vehicle can reach, no electricity nor water." The last three

kilometers could be crossed only by foot. Employing the tribals, he

built a road of sorts. This was a testing time. Unanticipated

problems created self-doubt. But then, having dared, there was no

turning back. What Dalvi lacked in experience was made up by his

“Education isnot a must,but there isno substitutefor enterprise”“Education is not amust, but there isno substitute forenterprise”

FROM

TEA

CAR

T TO

TRUC

K FL

EET

Mr. Dalvi in his self designed mansion

grit. When the mines became

operational in 1994, Indal offered him

a contract for transporting bauxite from

the mines to their factory – the

established contractors were not

interested, so bad were the roads.

Dalvi bought six Ashok Leyland Comet

Supers - one for each brother. Six more

were bought in 1995 and another six

the next year.

Dalvi is almost offended when asked

why he chose Ashok Leyland trucks.

"I grew up dreaming about them sitting

outside the Company gates, I owed it to

the Company and the dealership", he

says. "And market reports were good

and I liked them." With expansion in

the mining operation, Dalvi roped in

acquaintances by arranging for truck

finance and built a reputation for

reliable leadership in co-operative

trucking business. The group that Dalvi

built around him has a total fleet of 40

vehicles. "If the members are good and

the leadership reliable, groups can last

and flourish", explains Dalvi. "When

money starts coming in, some get

tempted to divert it for life’s comforts.

If you do it too early, you can fold up",

says Dalvi, based on the few failures in

his own group.

Success succeeded success. In 1997,

came a contract from Narmada Cement

for 25 trucks. Dalvi passed the acid test

of acquiring and offering 19 trucks in

under three months – by now he had

built a reputation with the truckers, the

financiers and the dealership. In no

time, Dalvi had built a group of truckers

with a total fleet strength of 90.

Dalvi does not recommend formalized co-

operative societies – "Leadership can

make or mar them. All members have to

be good alike. Also, different members

will have their ups and downs which can

affect the Society". Dalvi finds his style

of federal group structure advantageous

to all – the end-customer who does not

have to deal with individual truckers; the

truckers who get the trucks, finance and

business more easily. As for himself, his

leadership helps him make a mark in the

trade. "I have made a name for myself. I

have helped people find a livelihood and

build their lives. And they give me

respect".

At 47, Dalvi looks back at his past 30

years of struggles and success with

contentment. Today, all the brothers live

in palatial bungalows. Dalvi’s two sons

went to the best school where they

made no secret of their admiration for

their dad who made it from nowhere.

Dalvi summarises the moral of his story

as "education is not a must, but there is

no substitute for enterprise". That will

not stop him from shortly adopting a

couple of under-privileged children and

taking care of their education "as long

as they want to study".

Modesty must have stopped him from

describing his brand of enterprise as the

uncanny knack of spotting opportunities

in the midst of adversities. His latest

move is yet another example:

Two years back, Dalvi’s pet dog fell ill.

His sick dog in hand, Dalvi set out

looking for medicines. To his

disappointment and shock, he could not

find a pharmacist for miles and his dog

died. In this unhappy situation, Dalvi

spots an opportunity. The incident

becomes a trigger for opening

a pharmacy specializing in veterinary

medicines. In a matter of two years,

Dalvi has a thriving business. He is now

mulling over taking up wholesale agency

for medicines. And his next move?

To start a factory for basic drugs. The

CEO is in the making: his first son Sagar,

who has joined B. Pharm.

Mr. Kisanrao Dalvi can be contacted at +91 231 5682556 / 2691803

Ashok Leyland annual report 2002-03............................. III

Every day, more people in the State of Karnataka wake up to the

headlines in Vijay Karnataka than any other newspaper. And to

remember that, till three years ago, it was only an idea in one

man’s mind, is to recognize an unparalleled success story in the

world of Indian publishing where well-established leaders do not

yield ground easily. A newspaper is, after all, a habit. And habits

are often for a lifetime.

For a newcomer in the field, its founder Vijay Sankeshwar’s product

positioning is so rational, one wonders how come no one before him

noticed the so very obvious void. By focusing on the felt needs of

rural regions through content mix and reach, Sankeshwar has

expanded the market. In effect, Vijay Karnataka has spread the

reading habit to distant villages. New readers, according to him,

make up half the 500,000 plus circulation of this Kannada daily.

Vijay Karnataka’s newsgathering network spreads wide and far with

over 500 stringers. Its nine editions published from as many centers

give it the statewide stature – a conscious break from the city-

centricity prevalent among newspapers.

An equally powerful USP is time. "We deliver copies even in the

remote villages before six in the morning," explains Sankeshwar.

This is a new experience for far-flung villages. In distribution,

Sankeshwar has an unmatched competitive advantage: the statewide

network of offices that supports the operations of Vijayanand

Roadlines with a fleet strength of 1,200 trucks and 170 buses, with

Ashok Leyland models dominating.

Product and distribution taken care of, Vijay Karnataka, clearly

gunning for leadership position, dropped price to Rs 1.50 for a copy

"We delivercopies even inthe remotevillages beforesix.00 in themorning”"We deliver copieseven in the remotevillages before six in the morning”

VIJA

Y SA

NKES

HWAR

’SSU

CCES

S FO

RMUL

A

Thanks to the logistics backbone of VijayanandRoadlines, Vijay Karnataka can keep its earlymorning tryst with its readers

– "less than the cost of a cigarette."

Competition had to match price and,

in the process, bleed: bleed more on

their larger circulation base. The pricing

action worked: it expanded the market.

Through the resultant penetration and

conversion, circulation boomed.

Advertisers could no more ignore Vijay

Karnataka.

Not content with this success,

Sankeshwar was quick to exploit the

obvious synergy in newsgathering and

distribution by starting Vijay Times,

an English daily.

Publishing is in Sankeshwar’s genes.

In 1920, Basavannappa, his father,

migrated from Sankeshwar village to

settle down near Hubli where he set up

a successful business in printing and

publishing educational literature.

Sankeshwar’s entrepreneurial abilities

surfaced in his teens. As a 16-year-old,

he took charge of the family printing

press and modernized it. Yet, the

distribution end of his business left him

unhappy what with its dependence on

a monopolistic transport agency who,

Sankeshwar felt, ignored the customer

and his needs.

In this unpleasantness, Sankeshwar

detected an opportunity and despite

the family’s dissuasion, entered the

trucking trade with a single truck in

1976. He was quick to realize that in

this trade, big was beautiful. When

Vijayanand Roadlines was born three

years later, it had just two trucks. He

rapidly expanded operations by opening

booking offices and acquiring trucks to

support parcel services.

In his own unhappy experience as a

customer, Sankeshwar found the

ingredients of his customer-centric

mission statement. Size and

geographical coverage apart, he knew

how customers could benefit from

specialized services and set a trend by

offering courier, express cargo and parcel

services. He was a trendsetter also in

offering time-bound, assured deliveries

with compensation in the event of

failures. As a leader, he set values and

ensured their practise. Anyone who

reports an unauthorized person travelling

in the driver’s cabin in any of his

vehicles, is rewarded and the cost

debited to the driver. Old timers also

remember the time Sankeshwar received

the "Udyog Ratna" award in 1994. The

first thing he did was to raise

employees’ salaries by 25% because "it

was they who are responsible for the

spectacular growth of the Company".

By 1990, Vijaynand Roadlines had 125

branches in 12 States and a fleet of 100

vehicles. It only took him another 10

years to cross 1,000 vehicles and 600

branches. In 1996, Vijayanand Roadlines

diversified into passenger transportation,

with emphasis on connecting neglected

interiors. The diversification had obvious

synergies with the parcel services.

A public limited company since 1996,

Vijayanand Roadline’s 2002-03 turnover

was Rs 3 billion. Today, the

breadwinners of over 10,000 families

work directly or otherwise for Vijayanand

Roadlines.

1996 marked Sankeshwar’s jumpstart in

politics when he won from the Dharwad

(North) parliamentary constituency.

Re-elected in 1998 and a third time in

1999, he is a sitting MP. Sankeshwar

ensures that his political convictions do

not colour the pages of his newspaper.

Vijay, in most Indian languages, means

success. In Vijay Karnataka and

Vijayanand Roalines, even in politics,

Sankeshwar’s common success formula

stems from a grassroot level

understanding of the market.

"I dip into my own experience as a

customer", he says with more sincerity

than bitterness.

Mr. Vijay Sankeshwar can be contacted at +91 836 237511e-mail : [email protected] (or) [email protected]

Ashok Leyland annual report 2002-03............................. V

Constantly updated through incessant incoming calls, he carries it

all in his head: the departure/arrival details of 104 trucks ever

on the move across the country with tight delivery deadlines. "What

else is my work?", asks Raj Singh Narwal of Ahmedabad Bengal

Roadways, sitting in his functional office-cum-workshop near the

Delhi-Gurgaon border. The largest truck contractor for the fast-

growing SafExpress and Om Carrying Corporation, Raj Singh’s self-

confessed single obsession in life is Ahmedabad Bengal Roadways.

And make no mistakes, his mind is ever ticking on how to drive

down costs and turnaround time, how to fight the squeeze on

margins.

But for the brick kilns in his native village named Rithal, in Rohtak

district in the North Indian State of Haryana, Raj Singh, in all

probability, would have become a farmer like his father. But the

brick kilns – rather, the trucks that frequented the kilns – became

persuasive direction boards that changed his life’s course. His

earliest childhood memories revolve around those powerful trucks

that cast a spell on the youngster.

Chasing his dream, Raj Singh left his 9th standard studies in 1975

and went through the typical learning and start-up process of an

Indian trucker. An apprenticeship with a mechanic followed a

helper’s job with a trucker and acquisition of the all-important

driving license. He turned down a secure Government job – greatly

coveted by village lads – and instead chose to drive trucks. By

1978, he had saved enough to part-own and self-drive a second-

hand truck. All the earnings went into buying trucks for the four

brothers who followed Raj Singh’s example. 1982 and an Ashok

"I have survivedon Rs. 250 amonth. God hasraised me to thislevel. Beinghumane mattersnot money”

"I have survived on Rs. 250 a month. Godhas raised me to thislevel. Being humanematters, not money”

WIT

H FO

CUS,

IT

‘SSI

MPL

E

Leyland Tusker joined Raj Singh’s stable.

Thus began a tryst leading to a strong

association and loyalty.

Raj Singh’s truck fleet kept growing but

the five brothers continued to drive

trucks, maximizing revenue and they

loved driving, anyway. The 44-year-old

recalls a round trip he did in the early

90s. His truck loaded with high-density

(but compact) metal springs, Raj Singh

drove from Chennai to Bangalore where

he topped it with tyres. Enroute Delhi,

outside Bijapur he came across a loaded

truck, its cabin badly damaged in an

accident. Its front tyres removed and

the front mounted on his Delhi-bound

truck, Raj Singh drove the makeshift

"trailer", earning Rs 28,000 as against a

normal Rs 9,000 for that trip. "Those

days, we had easy delivery deadlines

and could wait for market loads",

remembers Raj Singh.

Today, delivery schedules have become

tighter and meeting them without fail is

pivotal to the success of Ahmedabad

Bengal Roadways. "We manage 98%

compliance", says Raj Singh, who has

won awards from SafExpress for

exemplary delivery record. Raj Singh’s

crew routinely covers the Delhi –

Mumbai route in 45 hours and Delhi –

Ahmedabad in 24 hours. From October

2002, he has been able to slash running

time for all routes by around 10%. How

he manages such efficiency

improvements is simple – befitting the

simple man that he is. "We brothers (the

five are equal partners in the Company)

drive the trucks with our drivers by our

side, see the time it takes, the fuel

consumption and expect them to match

it. We don’t put pressure. It is no miracle

either – after all, the roads are

improving and so are the vehicles". Over

80% of his fleet are Ashok Leyland

vehicles – their "reliability, lower

maintenance cost and better fuel

average help us maintain delivery

schedules and operate them in these

times of thin margins". His mind is

already at work to further cut running

time to command more remunerative

rates from the customer – and more

trips.

For someone who cannot stand waste,

his closed fists loosen for essentials.

Without batting an eyelid, he flies down

drivers as replacement for their

indisposed colleagues. A heart ailment

or losing eyesight, his drivers can count

on Raj Singh’s benevolence. Raj Singh

dismisses his acts of kindness by saying:

"I have survived on Rs 250 a month.

God has raised me to this level. Being

humane matters, not money".

Raj Singh’s only other obsession is the

satsangh (a prayer group, literally

meaning, group of the good) held every

Saturday in his native village which none

of the 38-member joint family will miss.

His is a family of teetotalers. Raj Singh

believes his simple ways have helped in

his success and is fiercely proud that

success has not spoilt him: he has not

changed even his dress style, he has no

fancy for flashy cars. Distinctly hands-

on, Raj Singh is at his desk, day or

night, whenever business demands.

"Timely service is not easy", he explains,

even as answering into his mobile – his

only personal concession to modernity.

Mr. Raj Singh Narwal can be contacted at +91 11 5062377

Ashok Leyland annual report 2002-03............................. VII

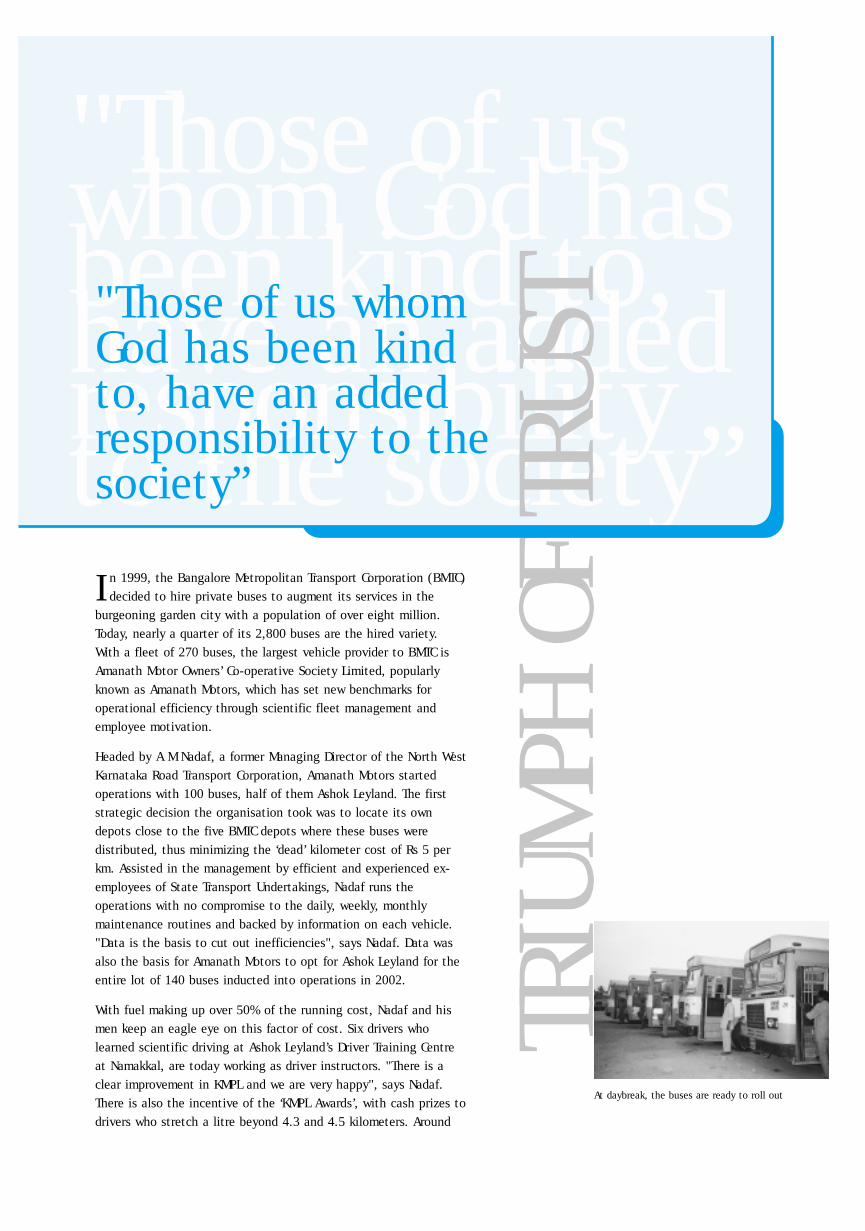

In 1999, the Bangalore Metropolitan Transport Corporation (BMTC)decided to hire private buses to augment its services in the

burgeoning garden city with a population of over eight million.Today, nearly a quarter of its 2,800 buses are the hired variety. With a fleet of 270 buses, the largest vehicle provider to BMTC isAmanath Motor Owners’ Co-operative Society Limited, popularlyknown as Amanath Motors, which has set new benchmarks foroperational efficiency through scientific fleet management andemployee motivation.

Headed by A M Nadaf, a former Managing Director of the North WestKarnataka Road Transport Corporation, Amanath Motors startedoperations with 100 buses, half of them Ashok Leyland. The firststrategic decision the organisation took was to locate its owndepots close to the five BMTC depots where these buses weredistributed, thus minimizing the ‘dead’ kilometer cost of Rs 5 perkm. Assisted in the management by efficient and experienced ex-employees of State Transport Undertakings, Nadaf runs theoperations with no compromise to the daily, weekly, monthlymaintenance routines and backed by information on each vehicle."Data is the basis to cut out inefficiencies", says Nadaf. Data wasalso the basis for Amanath Motors to opt for Ashok Leyland for theentire lot of 140 buses inducted into operations in 2002.

With fuel making up over 50% of the running cost, Nadaf and hismen keep an eagle eye on this factor of cost. Six drivers wholearned scientific driving at Ashok Leyland’s Driver Training Centreat Namakkal, are today working as driver instructors. "There is aclear improvement in KMPL and we are very happy", says Nadaf.There is also the incentive of the ‘KMPL Awards’, with cash prizes todrivers who stretch a litre beyond 4.3 and 4.5 kilometers. Around

"Those of uswhom God hasbeen kind to,have an addedresponsibilityto the society”TR

IUM

PH O

F TR

UST"Those of us whom

God has been kindto, have an addedresponsibility to thesociety”

At daybreak, the buses are ready to roll out

10% of the drivers qualify for theseawards every month. In the offing is anannual awards scheme for consistentfuel efficiency.

Even with all costs under reins, Nadaf isconscious that if the employees do notbuy into the efficiency mission, therecan be no results. "Our employees hadto realize that a cancellation of a tripmeans a loss to the organisation. Justkeeping 2.5% spare bus capacity is notenough; human response is thedeterminant", says Nadaf. A cancellations rate of under 0.5% forAmanath Motors is a new benchmarkwhere the industry average is 3~4%.This maximizes revenues from the BMTC.

Amanath Motors was born out of twochance happenings in the mind of

K Rahman Khan, a Bangalore-basedChartered Accountant. Khan’s majorinfluence in life has been his father, a principled man, who used to tell hisson: "Those of us whom God has beenkind to, have an added responsibility tothe society". Even while practisingAccountancy, Khan entered politics ashe found it "a powerful instrument forsocial change". In 1978, Khan became a member of the Karnataka LegislativeCouncil and was Chairman of theLegislative Council from 1982 to 1984.Since 1994, he has been a member ofthe Rajya Sabha.

In his close interactions with themasses, Khan realized how "lack ofaccess to funds and education were

blocking growth opportunities to under-privileged sections of the community". This prompted him to promote a bank inthe co-operative sector. Appropriately,he named it "Amanath Co-operativeBank". Amanath, meaning "trust", wasideal branding in the financial sector;soon it was to become Khan’s own brandvalue. What was started with a capital of Rs 300,000 has grown to become thelargest urban bank in the State with 15 branches, 500 employees anddeposits and reserves together exceedingRs 5 billion. Khan rationalizes theunexpected success of the bank bypointing out that the bank became analternative to moneylenders whoexploited sections of society notoriented towards banking.

Khan also has three decades ofassociation with the Al-AmeenEducational Society and had been itsChairman during 1985-2000. The 100plus educational institutions fromnurseries to professional colleges provideeducation to 40,000 students, with a fees structure that underscores theobjective: provide a window ofopportunities to growth. The KKEducational Trust, which commemoratesKhan’s father, runs two popular schoolsin Bangalore under the franchise of theDelhi Public School.

The two chance happenings thatprompted the birth of Amanath

Motors date back to 1999. One was anapplication the co-operative bank

received for a vehicle loan. Scrutinyconfirmed Khan’s suspicion: the loanamount was hugely inflated. He alsolearned that this prevalent practice wasthe cause of many entrepreneurs failing,unable to repay the equally inflatedmonthly installments. Around the sametime, while visiting Gujarat, Khan saw a successful trucker co-operative whichhad the financial strength to disbursemuch-needed funds to its members whena calamity struck, without waiting forGovernment help to arrive. An idea tookshape in his mind.

The trigger that actualized the idea asAmanath Motors was the BMTC move tohire buses. Khan sought 100 membersbut had 300 registrations, thanks to hisreputation. The terms: make a deposit ofRs 275,000 for six years for a monthlyreturn of Rs 4,500. The membership hassince grown to 215 with over 100applicants in the waiting list.

Amanath works. Every time.

Mr. K Rahman Khan can be contacted at +91 80 6539168 / 6539183

Ashok Leyland annual report 2002-03............................. IX

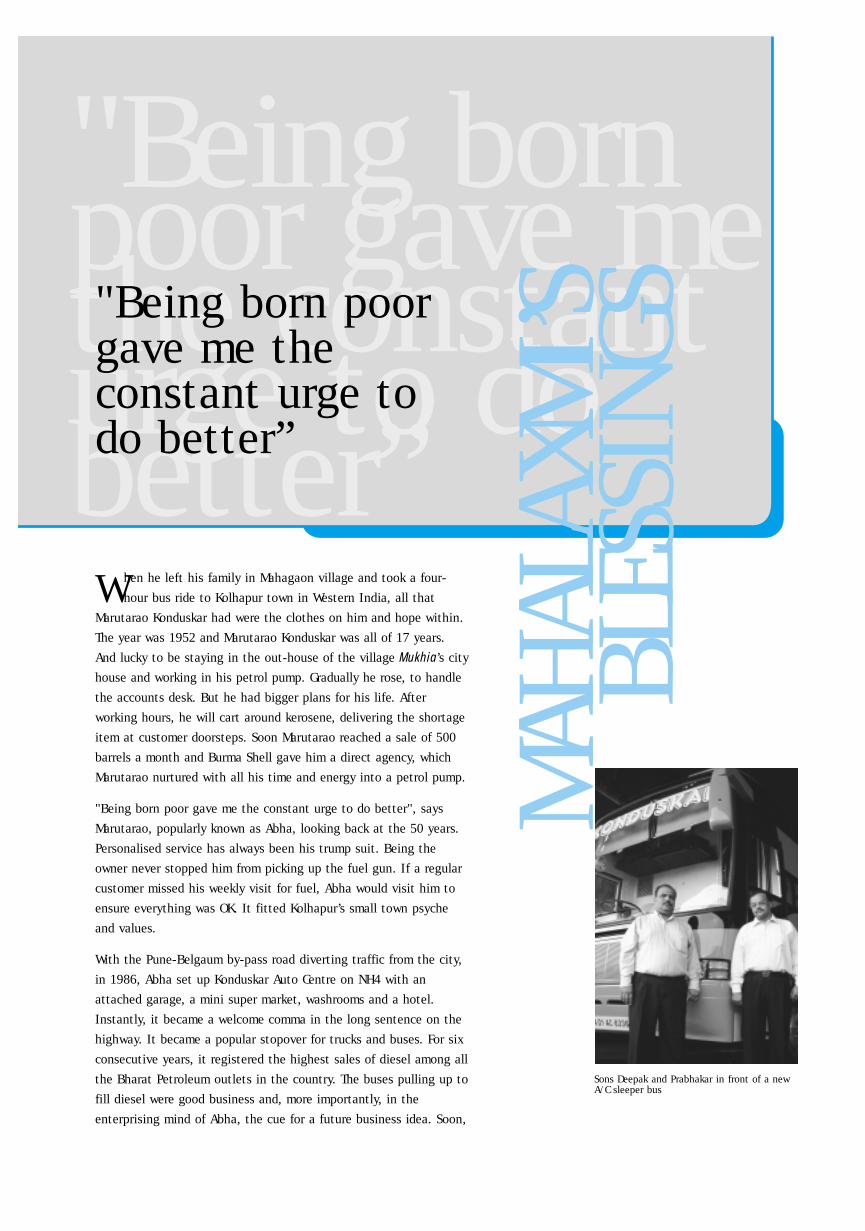

When he left his family in Mahagaon village and took a four-

hour bus ride to Kolhapur town in Western India, all that

Marutarao Konduskar had were the clothes on him and hope within.

The year was 1952 and Marutarao Konduskar was all of 17 years.

And lucky to be staying in the out-house of the village Mukhia’s city

house and working in his petrol pump. Gradually he rose, to handle

the accounts desk. But he had bigger plans for his life. After

working hours, he will cart around kerosene, delivering the shortage

item at customer doorsteps. Soon Marutarao reached a sale of 500

barrels a month and Burma Shell gave him a direct agency, which

Marutarao nurtured with all his time and energy into a petrol pump.

"Being born poor gave me the constant urge to do better", says

Marutarao, popularly known as Abha, looking back at the 50 years.

Personalised service has always been his trump suit. Being the

owner never stopped him from picking up the fuel gun. If a regular

customer missed his weekly visit for fuel, Abha would visit him to

ensure everything was OK. It fitted Kolhapur’s small town psyche

and values.

With the Pune-Belgaum by-pass road diverting traffic from the city,

in 1986, Abha set up Konduskar Auto Centre on NH4 with an

attached garage, a mini super market, washrooms and a hotel.

Instantly, it became a welcome comma in the long sentence on the

highway. It became a popular stopover for trucks and buses. For six

consecutive years, it registered the highest sales of diesel among all

the Bharat Petroleum outlets in the country. The buses pulling up to

fill diesel were good business and, more importantly, in the

enterprising mind of Abha, the cue for a future business idea. Soon,

"Being bornpoor gave methe constanturge to dobetter”

MAH

ALAX

MI’S

BLES

SING

S "Being born poorgave me theconstant urge todo better”

Sons Deepak and Prabhakar in front of a newA/C sleeper bus

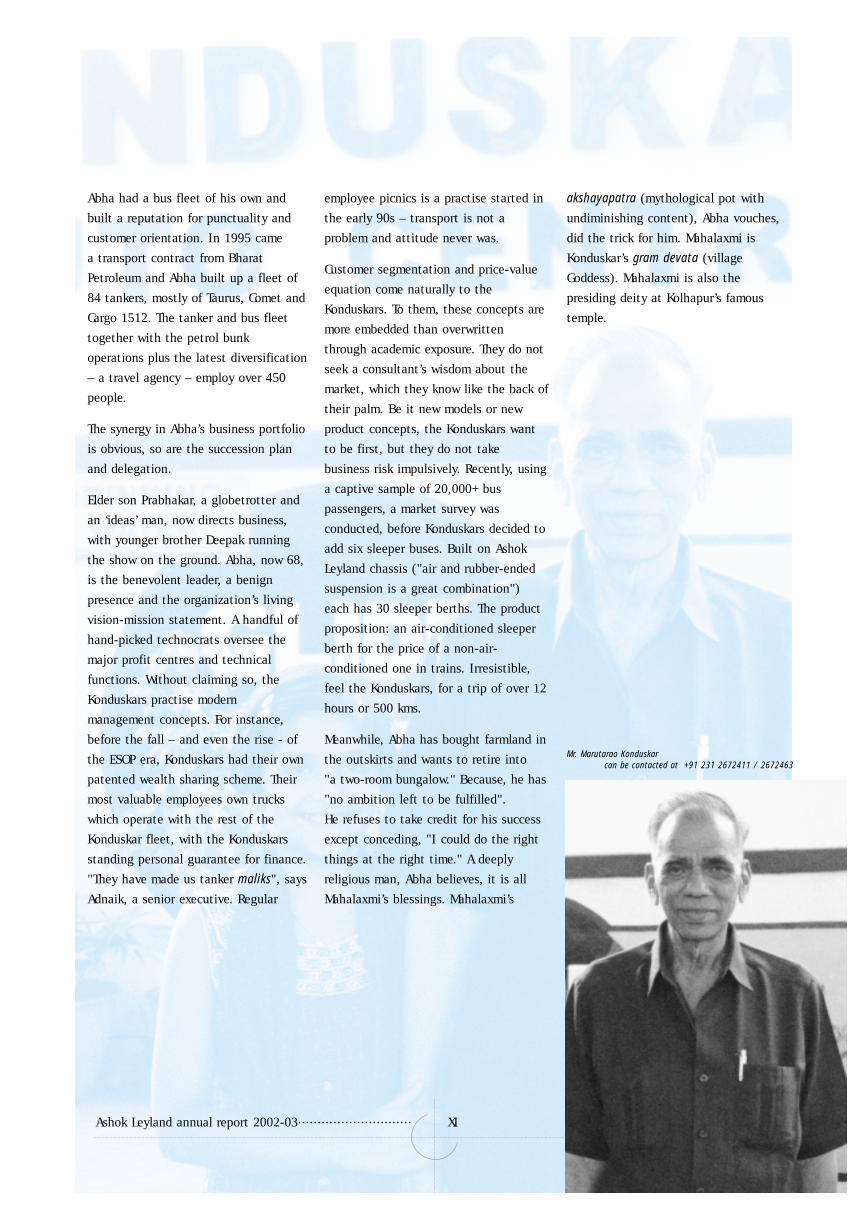

Abha had a bus fleet of his own and

built a reputation for punctuality and

customer orientation. In 1995 came

a transport contract from Bharat

Petroleum and Abha built up a fleet of

84 tankers, mostly of Taurus, Comet and

Cargo 1512. The tanker and bus fleet

together with the petrol bunk

operations plus the latest diversification

– a travel agency – employ over 450

people.

The synergy in Abha’s business portfolio

is obvious, so are the succession plan

and delegation.

Elder son Prabhakar, a globetrotter and

an ‘ideas’ man, now directs business,

with younger brother Deepak running

the show on the ground. Abha, now 68,

is the benevolent leader, a benign

presence and the organization’s living

vision-mission statement. A handful of

hand-picked technocrats oversee the

major profit centres and technical

functions. Without claiming so, the

Konduskars practise modern

management concepts. For instance,

before the fall – and even the rise - of

the ESOP era, Konduskars had their own

patented wealth sharing scheme. Their

most valuable employees own trucks

which operate with the rest of the

Konduskar fleet, with the Konduskars

standing personal guarantee for finance.

"They have made us tanker maliks", says

Adnaik, a senior executive. Regular

employee picnics is a practise started in

the early 90s – transport is not a

problem and attitude never was.

Customer segmentation and price-value

equation come naturally to the

Konduskars. To them, these concepts are

more embedded than overwritten

through academic exposure. They do not

seek a consultant’s wisdom about the

market, which they know like the back of

their palm. Be it new models or new

product concepts, the Konduskars want

to be first, but they do not take

business risk impulsively. Recently, using

a captive sample of 20,000+ bus

passengers, a market survey was

conducted, before Konduskars decided to

add six sleeper buses. Built on Ashok

Leyland chassis ("air and rubber-ended

suspension is a great combination")

each has 30 sleeper berths. The product

proposition: an air-conditioned sleeper

berth for the price of a non-air-

conditioned one in trains. Irresistible,

feel the Konduskars, for a trip of over 12

hours or 500 kms.

Meanwhile, Abha has bought farmland in

the outskirts and wants to retire into

"a two-room bungalow." Because, he has

"no ambition left to be fulfilled".

He refuses to take credit for his success

except conceding, "I could do the right

things at the right time." A deeply

religious man, Abha believes, it is all

Mahalaxmi’s blessings. Mahalaxmi’s

akshayapatra (mythological pot with

undiminishing content), Abha vouches,

did the trick for him. Mahalaxmi is

Konduskar’s gram devata (village

Goddess). Mahalaxmi is also the

presiding deity at Kolhapur’s famous

temple.

Mr. Marutarao Konduskar can be contacted at +91 231 2672411 / 2672463

Ashok Leyland annual report 2002-03............................. XI

Reams of black and grey ribbons are rolling out rapidly acrossIndia’s remote countryside, connecting cities and villages,

shortening distances, slashing transit time and transportation costs.B Seenaiah, President, National Highways Builders Federation,estimates that 6,000 commercial vehicles – of which, 60~70% AshokLeyland vehicles – are engaged in the mammoth task of buildingover 13,000 kms of modern roads under the Golden Quadrilateraland the North South East West corridor projects.

Seenaiah is also Managing Director of M/s B Seenaiah & Company(Projects) Limited (BSCPL), one of the largest road constructioncompanies in the country. The Hyderabad-based BSCPL is in thethick of action, with two projects, together worth over Rs 4.8billion, under execution. BSCPL also partners GVK Group and L&T inthe Rs 6 billion Jaipur-Kishangarh BOT project.

Hailing from Mamuduru village, 35 kms off Nellore in AndhraPradesh, Seenaiah gives all the credit for the joint family’s fortunes,to the education he and his two brothers received. ("Father ran up adebt of Rs one lakh in the process, though," reminiscences 51-yearold Seenaiah). After his post-graduation in Agricultural Science, the23-year old entered road construction field via the partnership firmelder brother Krishnaiah, an M.Tech, had just set up. With fiveAshok Leyland Comet tippers, the partnership firm started small, butgrew. After ten years, in 1983, the two brothers set up BSCPL. Thefirst breakthrough for the fledgling firm came when an initiallyskeptical district administration realized the virtue of hot mixconcreting that the two technocrats insisted on and demonstratedin a small job. As years passed, the project sizes kept growing.BSCPL has done many prestigious mega projects, some of themfunded by the World Bank and Asian Development Bank, in theprocess, partnering some big international players. For BSCPL’s scale

"I insistedthat everyfamilycontributes, ifnothing else,with labour"

"I insisted that everyfamily contributes, ifnothing else, withlabour"

THE

BUIL

DER

OFRO

ADS

But for the school built by Seenaiah’s family,many of these students might have been farmhands

of operations, sample this : thecommercial vehicle fleet is 120 strongwith 90% Ashok Leyland vehicles; theCompany’s operations consume 70,000litres of diesel as also 12,000 tonnes ofblue metal produced by Seenaiah’snetwork of crushing units, everyday.Seenaiah expects his turnover to triple,to over Rs 4.5 billion, in the currentyear.

Mamuduru village owes its refreshinggreenery and widely shared

prosperity, to the adjacent river Pennar.Yet, till not so long ago, the land wasbarren. And during the rainy months theriver swelled, the village would beflooded. What has brought about thedramatic change are rural roads,irrigation and grassroots participation."The village’s first bore well was put upby my family in 1964. Today, the villagehas 400 bore wells and 23 transformers"to take care of the months when theriver shrinks, points out Seenaiah, theprincipal change agent.

Seenaiah’s frequent visits to his nativevillage kindled an urge to help in itsdevelopment. From the mid 90s, hestarted spending more time in thevillage addressing local issues andresolving community problems to familydisputes. He quickly envisioned what adeep road network and watermanagement, together, can achieve.Diverting his construction machineryfrom his work site, Seenaiah firstaddressed total road connectivity for hisvillage under the Janmabhoomi schemeof the State Government. "I insisted

that every family contributes, if nothingelse, with labour". He matched it byexecuting the Rs 20 million project,"without a profit, with contribution incash and kind worth Rs 1.4 million". Inthe next one month, some 40 cycleswere bought in the village. Land pricesbegan to rise. Seenaiah estimates theroad access has benefited over 1,000acres of agricultural land. "Before theroads came, transportation ofagricultural produce used to cost Rs 5,000 per acre", he explains.

Seenaiah stationed two excavatorspermanently in the village, to handleany community work that benefits all -activities like desilting of irrigationcanals and mass house construction. By channelising government grants andhis own resources and organizing ability,Seenaiah could complete 54 houses inMamuduru’s harijan (one-timeuntouchable “lower” caste) colony. Eachhouse has tap water.

In deference to the wishes of his father,Seenaiah and brothers built classroomsin a seven-acre plot and handed over tothe district administration to run aschool. Today, the place teems with 300children who, otherwise, would havebeen free farm-hands. The adjacenthostel houses 100 students, spreadingthe benefits of education to surroundingvillages without schools.

The 150-bed, Bollineni Super SpecialtyHospital is proving to be a boon to theneighbouring Nellore town andsurroundings. Bollineni is the family

surname and heading the institution isDr B Bhaskar Rao, heart surgeon and theyoungest brother in the joint family.

Another instance of how this roadbuilder connects needs to createopportunities is his latest project: a sixmegawatt biomass power plant that willconsume 200 tonnes of fuel wood andagricultural waste everyday. While thepower is enough to light up over 32,000homes, the plant will pay out Rs 140,000 to the villagers for theorganic fuel everyday.

So seamlessly does Seenaiah manage hisbusinesses and social work, inevitablyhis family was drawn into politics, withelder brother Krishnaiah winning hismaiden election to become a Member ofthe State Legislative Assembly in 1999.

As he juggles his multi-locationalconstruction work and the demands ofthe villages, with the help of an ever-active mobile phone and trustedsupervisors at each work spot, it is clearthat Seenaiah likes what he is doing.Rather, he is doing what is to his liking.

Mr. B Seenaiah can be contacted at +91 40 23307831 / 23307704email : [email protected]

Ashok Leyland annual report 2002-03............................. XIII

Virtually orphaned with the death of his mother when seven

months old and then at the age of eight, the loss of his

grandmother, rest of childhood under the care of an uncle, and, at

13, a shed cleaner for a coal-fired truck – what psychologists will

describe as a troubled and deprived childhood was, to K Rengarajan,

his baptism by fire that steeled his will to secure his own place

under the sun.

In 1949, the 15-year-old earned his independence by moving to the

South Indian town of Trichy. There he realized his childhood

ambition of "learning something in the mechanical line" by landing

a fitter’s job. Followed seven years of grime, grease, learning and

saving. Then, in 1959, Rengarajan applied for a truck permit.

Rengarajan traded his savings for a condemned truck, assembled

separately procured grill, chassis and truck body. A few months of

long days and hard work, and Rengarajan became the owner of MDU

3368. It did not matter that the engine would stop without the

weight of his foot on the accelerated pedal, it did not matter the

only way to start the truck was a specially fitted cranker, because

he had enough technical expertise to make the junk work – and the

work ethic to earn the goodwill of construction contractors which

ensured regular business. A new brand was born: K R T, for

K Rengarajan Transport.

Looking back, the septuagenarian recalls: "I don’t know how this

sounds to you. Whenever the shift driver failed to turn up, I had to

work on continuous shifts, driving long distances. Sometimes it was

too tiring… I felt too sleepy. For such times, I used to keep a ready

stock of chillies in a small hole near the windshield wiper. To keep

"I was thefirst tointroduceAshokLeyland busesin Trichy”

"I was the first tointroduce AshokLeyland buses inTrichy”

DHAR

MA

INBU

SINE

SS

Sons Venkatesh and Suresh Kumar are bothpart of the Internet generation

myself awake, I would squeeze some

chilly juice into my eyes…

it would burn for a while… but it

definitely kept me awake".

"In my 10 years of work I have taken,

maybe, 20 days leave – and no tea or

coffee", Rengarajan reminiscences.

Slowly but surely, a decade of hard work

started paying. More route permits,

more second-hand buses done up and

readied – till he bought his first Ashok

Leyland bus – a Viking – in 1976.

Since then, it has only been Ashok

Leyland, over 150 of them, bought and

sold off at regular intervals. There is a

special twinkle in his eyes when he

talks about the Viking he assembled

with separately bought spares and

aggregates, in the 80s when Vikings

were in short supply. "I was the first to

introduce Ashok Leyland buses in

Trichy", says this longstanding

customer, his voice choked with

emotions, and points out that today

Ashok Leyland’s market share in the

Trichy passenger market is 90 plus.

The Indian concept of dharma is lot

more than just "duty". Rengarajan

has always treated his hard-earned

prosperity as an instrument to fulfill his

dharma. He married the daughter of an

acquaintance who showed compassion

in his childhood. Against the Indian

custom, he bore the entire marriage

expenses because his father-in-law

could not afford it. Taking under his

wings his extended family, Rengarajan

took care of 18 marriages (read finding

alliances, matching horoscopes, and

funding). Peeved by admission denied to

a deserving student, Rengarajan

galvanized his community to start the

Cauveri Women’s College, of which he is

the President and the Cauveri

Matriculation School. As for his business,

retaining two buses for himself, in 1990

Rengarajan divided the remaining buses

between his two sons, then in their mid

20s.

K R Venkatesh and K R Suresh Kumar are

both part of the Internet generation.

Venkatesh has diversified into vehicle

finance besides taking up a two-wheeler

dealership. Internet is his telescope as

he scans the horizon for new business

ideas. Venkatesh is determined to make

a comeback in trucking, undeterred by

his unhappy experience and exit once –

it has made him wiser, he feels. Suresh

Kumar’s 12-hour day is not complete

without Internet surfing. His 30-strong

fleet transporting LPG bullets covers

entire India. Leyparts.com (the website

for Ashok Leyland genuine spares) comes

in handy to direct his drivers in case of

a vehicle breakdown. He maintains an

all-Ashok Leyland fleet of 3516s and CO

1611s – and a complete fleet logbook in

his IBM Thinkpad supported by a

custom-built software.

Both sons retain the KRT brand in all

their operations – and the business

ethics of their father. Neither will

compromise on KRT’s reputation which is

an extension of Rengarajan’s dharma

principle. To the customer, it translates

as punctuality; to the supplier, dues paid

on time; and to all associates, a fair

deal. "We are enjoying the fruits of our

father’s ethics", says Venkatesh.

Mr. K Rengarajan can be contacted at +91 431 2410877

Ashok Leyland annual report 2002-03............................. XV

Ashok Leyland annual report 2002-03............................. xvi

Contents Board of Directors 2

Highlights of Performance 3

Directors’ Report 4

Report on Corporate Governance 7

Management Discussion and Analysis Report 17

Directors’ Responsibility Statement 23

Auditors’ Report to the Members 24

Balance Sheet 26

Profit and Loss Account 27

Cash Flow Statement 28

Statement on Significant Accounting Policies 30

Schedules to Balance Sheet 32

Schedules to Profit and Loss Account 38

Notes to the Accounts 41

Balance Sheet Abstract and Company’s General Business Profile 48

Annexure to Directors’ Report - Particulars of Employees 49

Annual Report 2002 - 2003

Ashok Leyland annual report 2002-03............................. 2

Board of Directors R J Shahaney, Chairman

D J Balaji Rao

M Bianchi (Alternate : G Sagone)

P K Choksey

A K Das (Alternate : I N Chatterjee)

D G Hinduja (Alternate : Y M Kale)

H Klingele

S R Krishnaswamy (Nominee of LIC)

E A Kshirsagar

F Sahami (Alternate : B D Punjabi)

R Seshasayee, Managing Director

R Jagannath, Dy. Managing Director

(upto 31/3/03)

Executive Directors J N Amrolia

T Anantha Narayanan

K K S Bhalla

A S Mundkur

S Nagarajan

M Natraj

Secretary N Sundararajan

Auditors M S Krishnaswami & Rajan

Price Waterhouse

Cost Auditor Geeyes & Co.

Bankers Bank of America

Bank of Baroda

Bank of India

Canara Bank

Central Bank of India

Citibank N.A.

ICICI Bank Limited

Punjab National Bank

Standard Chartered Bank

State Bank of India

The Hongkong and Shanghai Banking

Corporation Limited

Registered Office 19, Rajaji Salai

Chennai 600 001

Plants Ennore and Ambattur, Chennai

Hosur, Tamil Nadu

Bhandara, Maharashtra

Alwar, Rajasthan

Uppal, Hyderabad

Ashok Leyland annual report 2002-03............................. 3

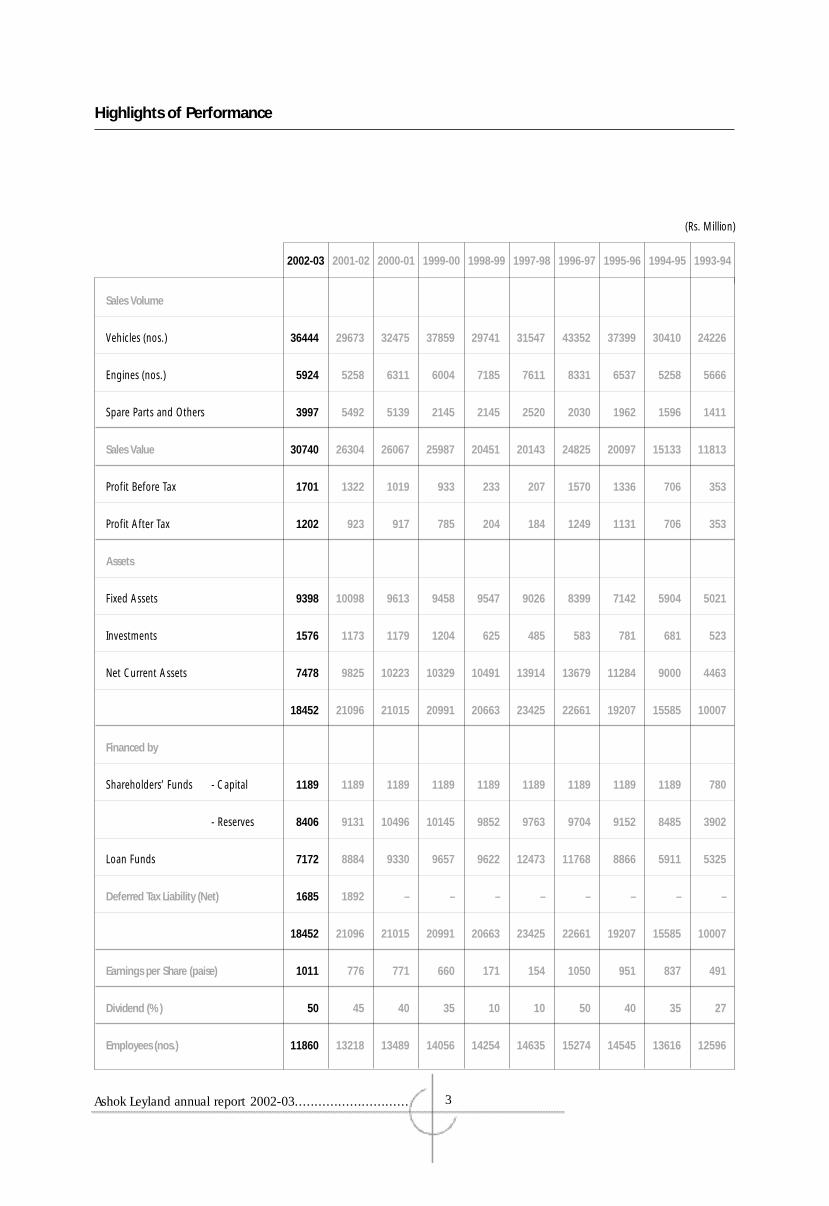

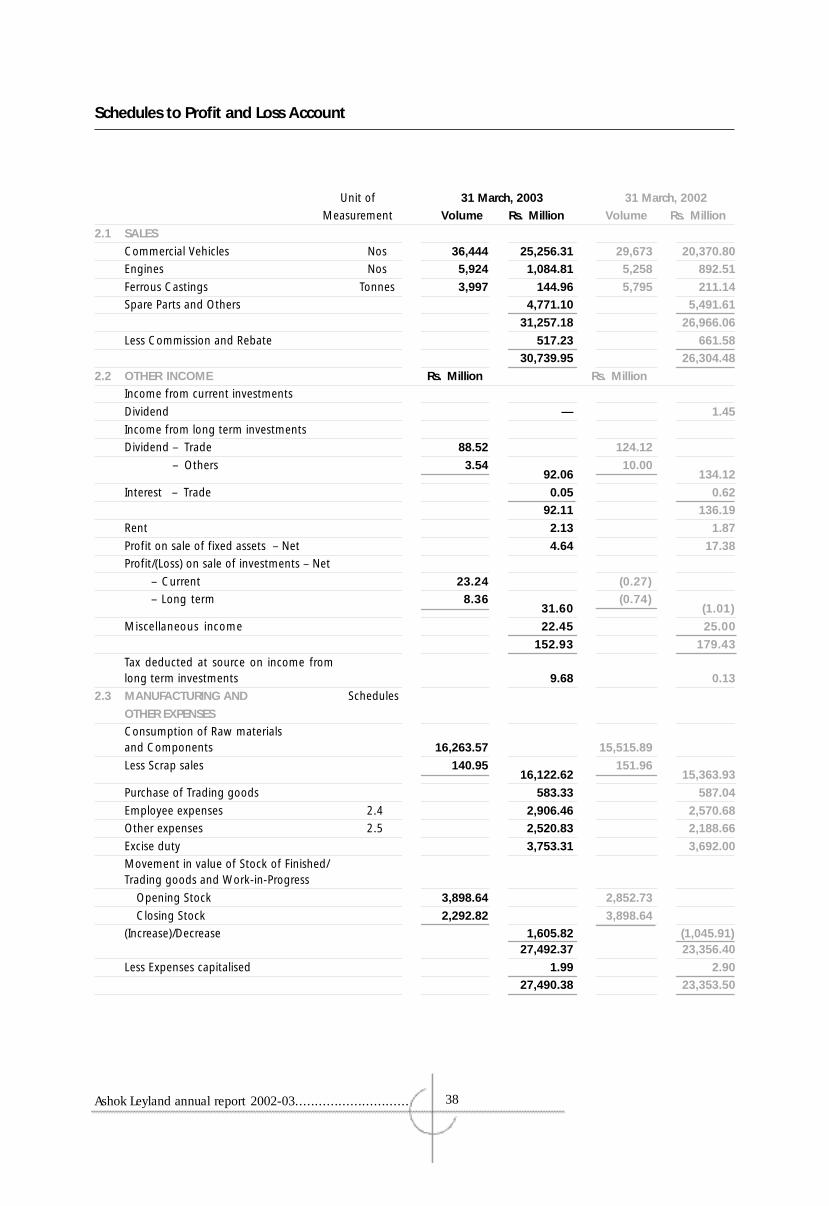

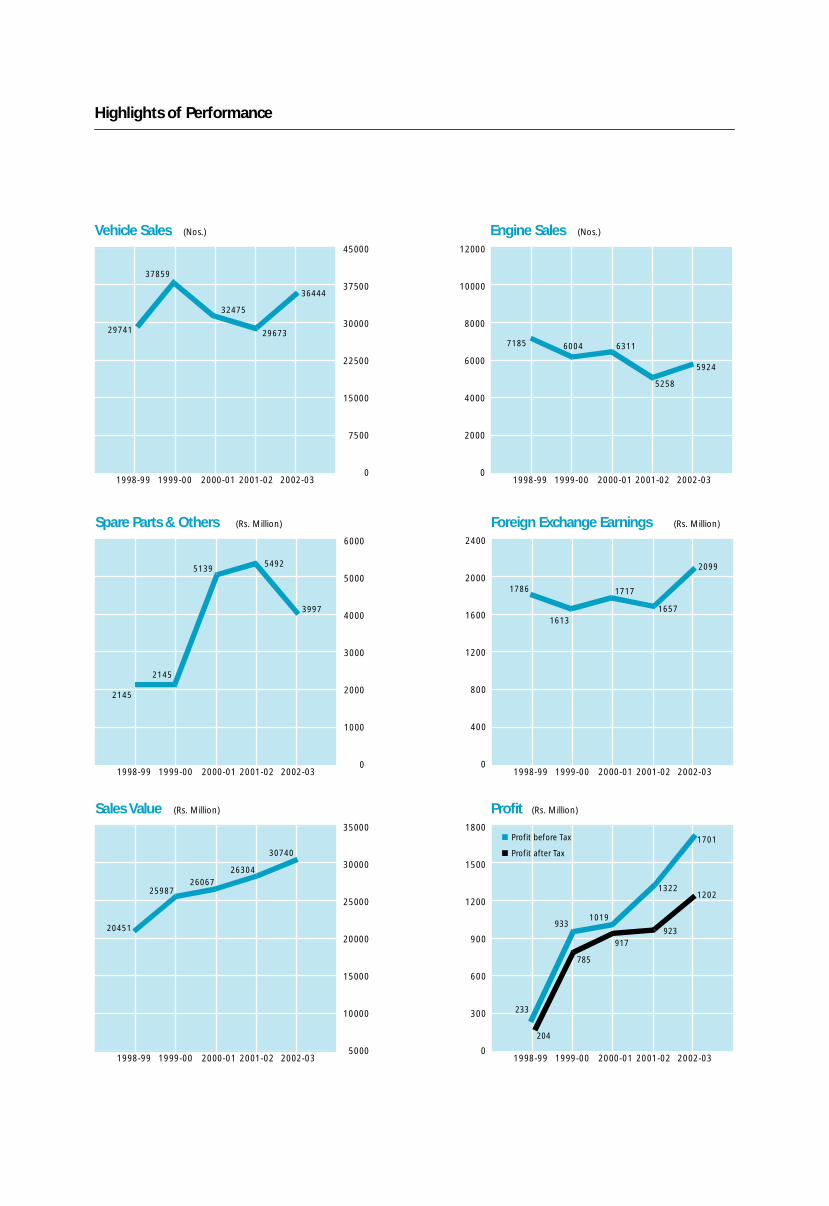

2002-03 2001-02 2000-01 1999-00 1998-99 1997-98 1996-97 1995-96 1994-95 1993-94

Sales Volume

Vehicles (nos.) 36444 29673 32475 37859 29741 31547 43352 37399 30410 24226

Engines (nos.) 5924 5258 6311 6004 7185 7611 8331 6537 5258 5666

Spare Parts and Others 3997 5492 5139 2145 2145 2520 2030 1962 1596 1411

Sales Value 30740 26304 26067 25987 20451 20143 24825 20097 15133 11813

Profit Before Tax 1701 1322 1019 933 233 207 1570 1336 706 353

Profit After Tax 1202 923 917 785 204 184 1249 1131 706 353

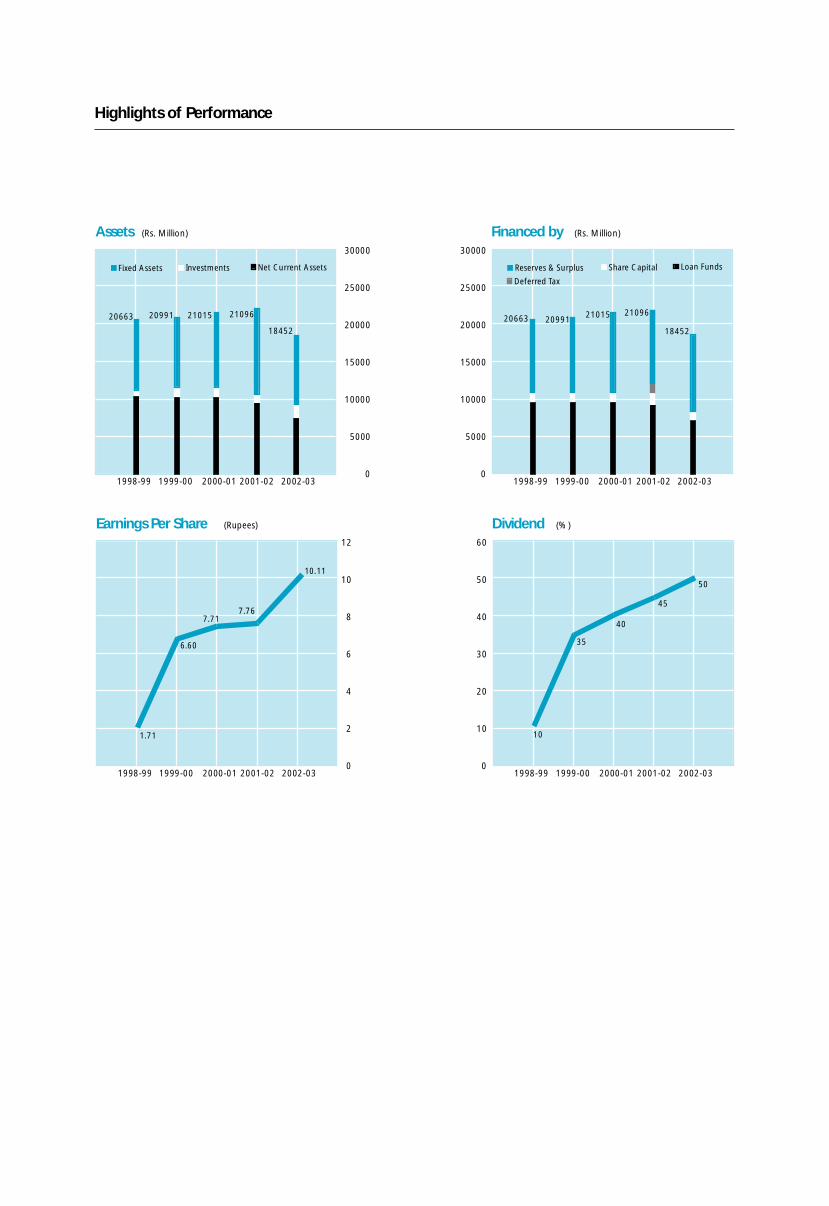

Assets

Fixed Assets 9398 10098 9613 9458 9547 9026 8399 7142 5904 5021

Investments 1576 1173 1179 1204 625 485 583 781 681 523

Net Current Assets 7478 9825 10223 10329 10491 13914 13679 11284 9000 4463

18452 21096 21015 20991 20663 23425 22661 19207 15585 10007

Financed by

Shareholders’ Funds - Capital 1189 1189 1189 1189 1189 1189 1189 1189 1189 780

- Reserves 8406 9131 10496 10145 9852 9763 9704 9152 8485 3902

Loan Funds 7172 8884 9330 9657 9622 12473 11768 8866 5911 5325

Deferred Tax Liability (Net) 1685 1892 – – – – – – – –

18452 21096 21015 20991 20663 23425 22661 19207 15585 10007

Earnings per Share (paise) 1011 776 771 660 171 154 1050 951 837 491

Dividend (%) 50 45 40 35 10 10 50 40 35 27

Employees (nos.) 11860 13218 13489 14056 14254 14635 15274 14545 13616 12596

Highlights of Performance

(Rs. Million)

Ashok Leyland annual report 2002-03............................. 4

Dividend

The Directors recommend a dividend of50% (Rs.5/- per equity share of Rs.10/-)

for the year ended March 31, 2003.

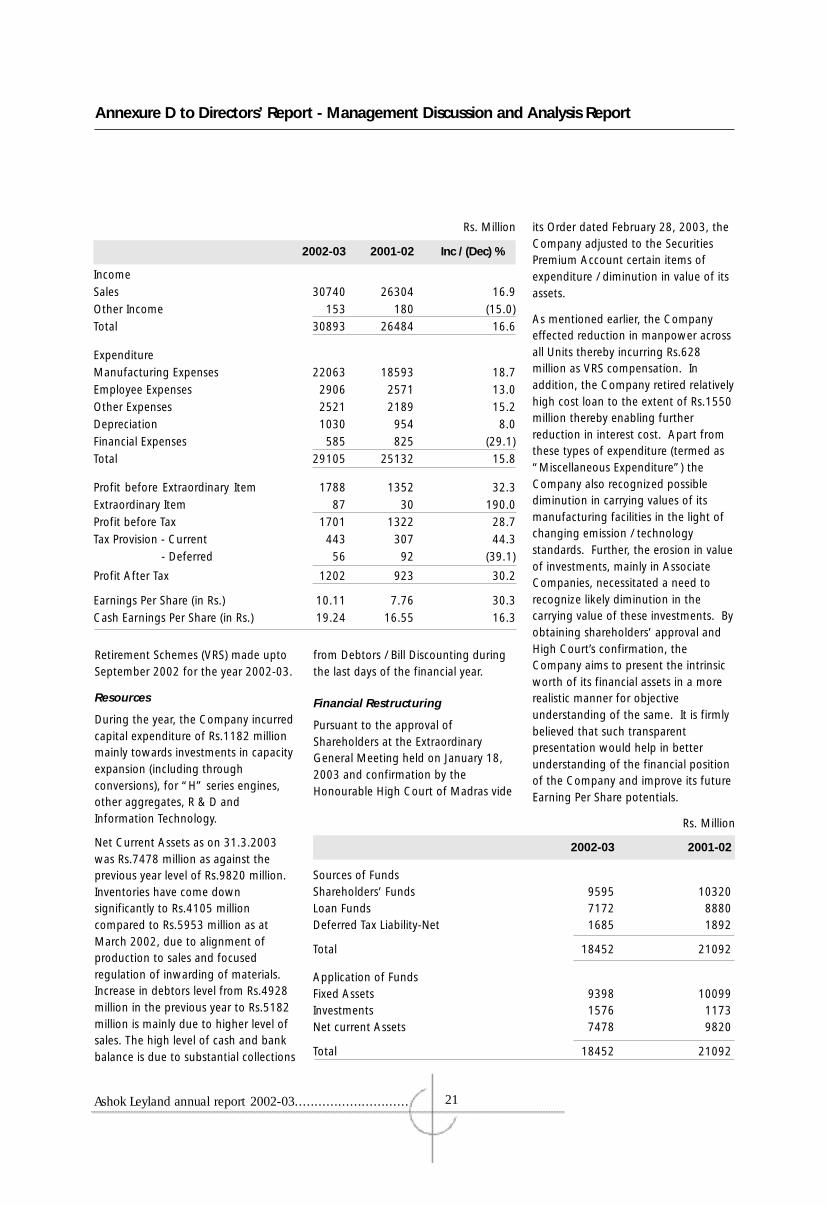

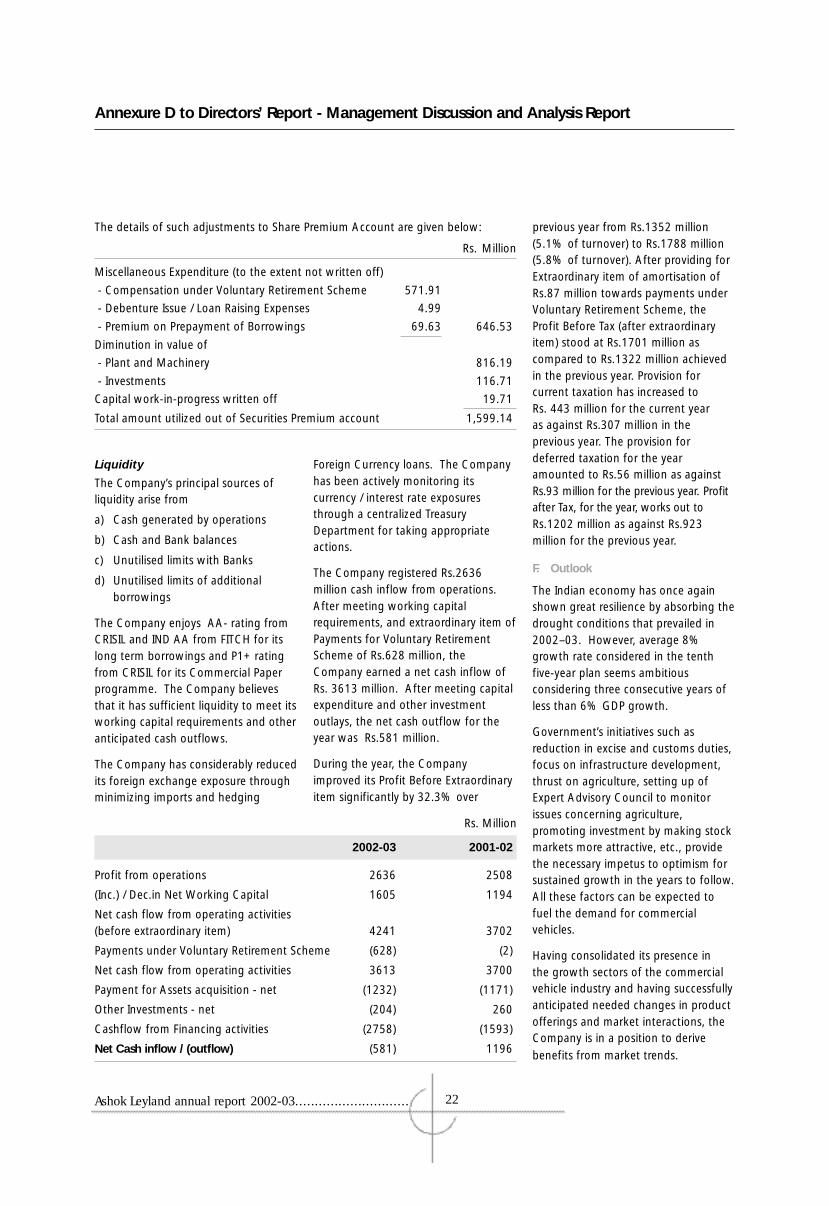

Sales

After a prolonged period of recession /reduced demand, there was asignificant improvement in the marketconditions during 2002-03. The overallimprovement in economic activity, theconsiderable investments made ininfrastructure activities, including theGolden Quadrilateral Highway projectsand increase in the cyclical replacementdemand of vehicles, all contributed tothe growth. However, for a major partof the year, distribution of thepattern within the country was notuniform, with a much higher growth inthe Northern markets (where yourCompany’s market share is lower), anda lower growth in the Southernmarkets, where your Company has a

larger market share.

Directors’ Report

Part - I Performance/Operations

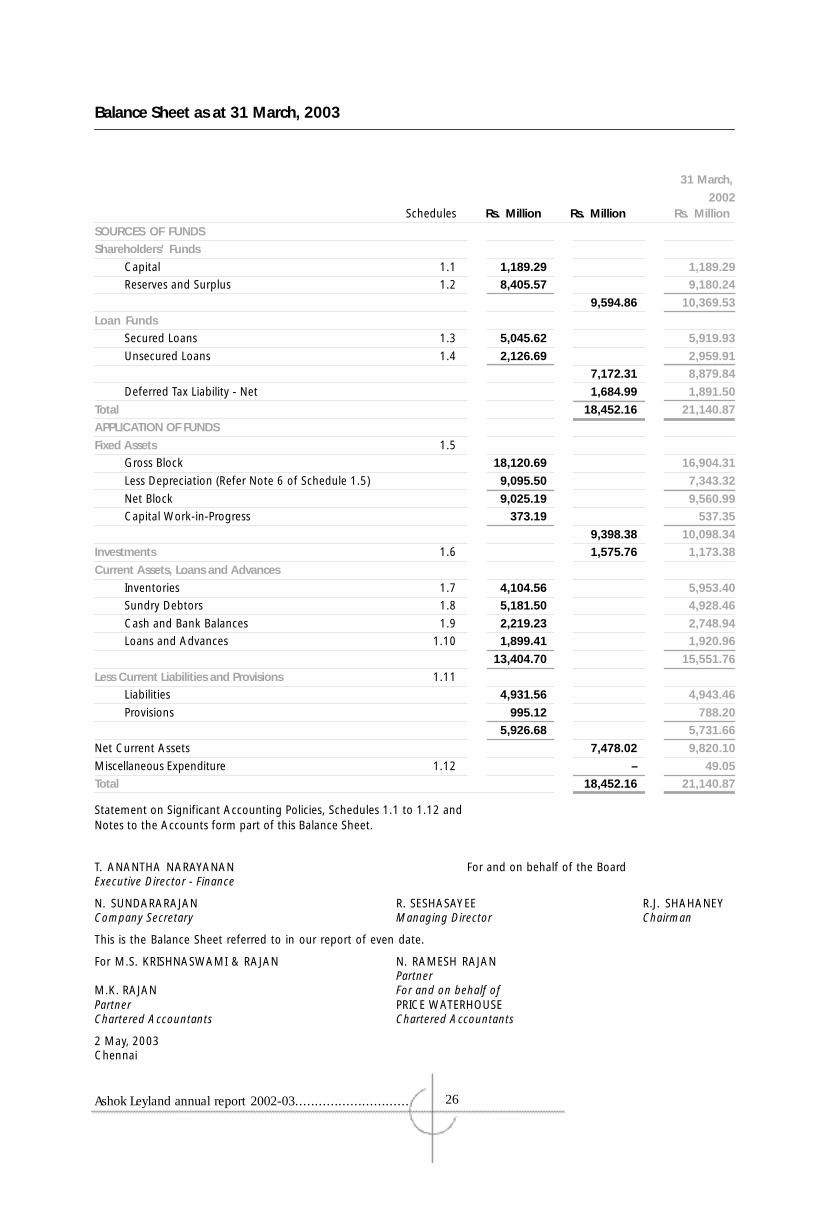

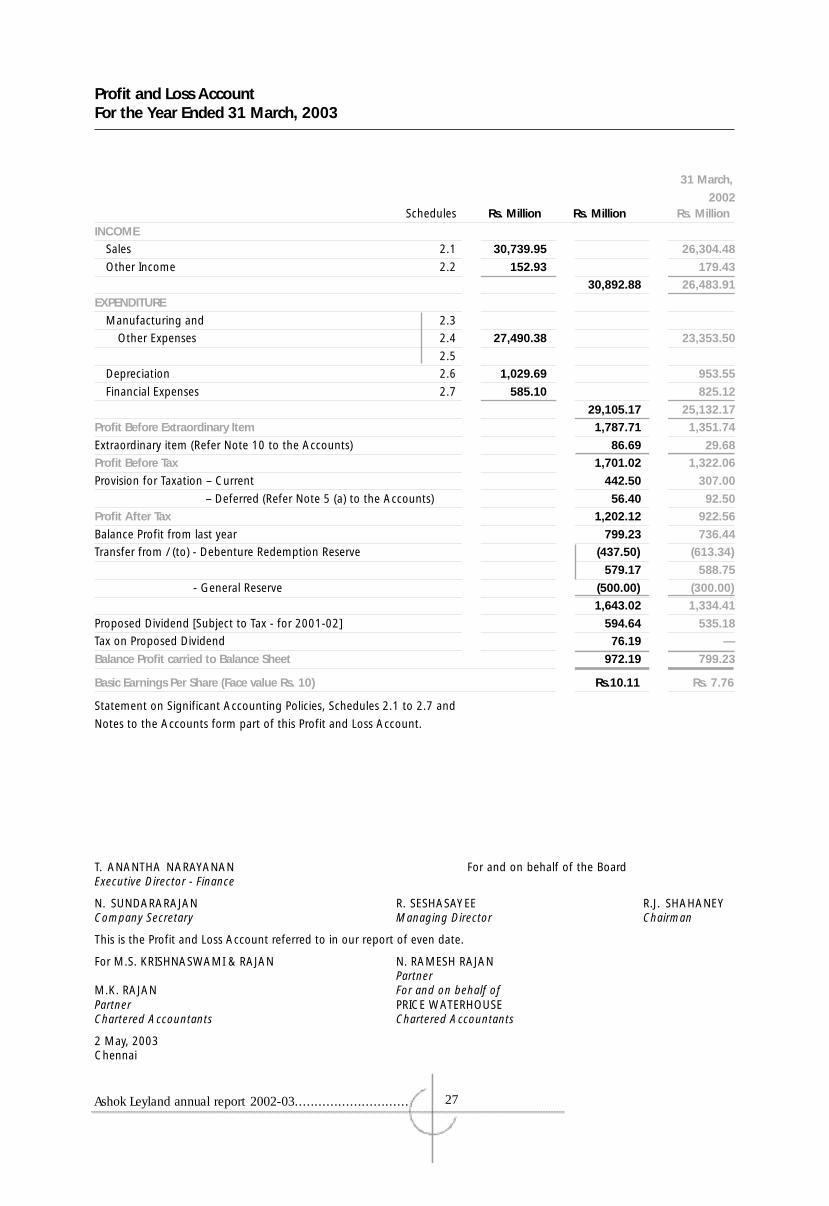

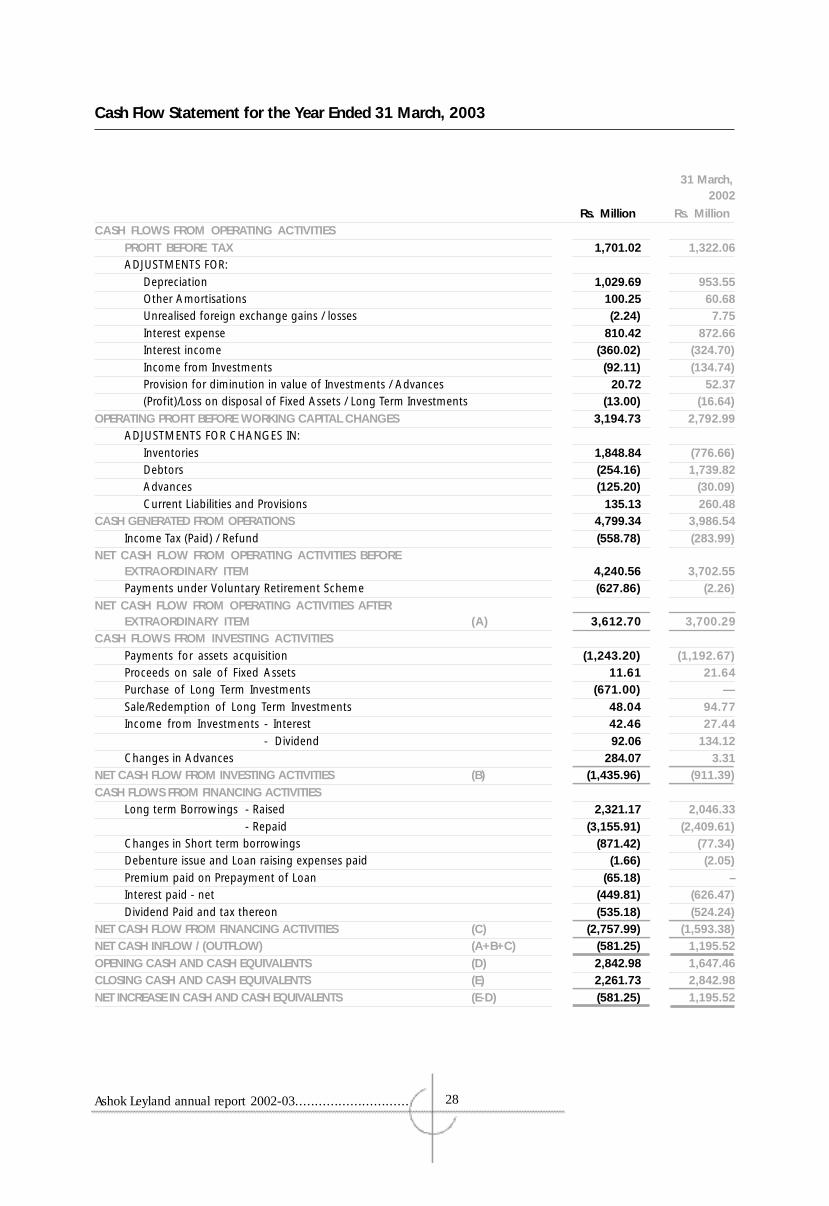

The Directors are happy to present the Annual Report of the Company togetherwith the audited Accounts for the year ended March 31, 2003.

Financial Results

2002-2003 2001-2002

(Rs. Million) (Rs. Million)

Profit Before Tax 1,701.02 1,322.06

Less : Provision for Taxation 498.90 399.50

1,202.12 922.56

Add : Transfer from/(to):

Debenture Redemption Reserve 141.67 (24.59)

Balance in Profit and Loss Account

Brought forward from previous year 799.23 736.44

General Reserve (500.00) (300.00)

Profit available for appropriation 1,643.02 1,334.41

Appropriation :

Proposed Dividend 594.64 535.18

Tax on Dividend 76.19 —

Surplus - Balance in Profit and Loss Account

Carried forward to next year..... 972.19 799.23

Basic Earnings Per Share (Face Value Rs.10) Rs. 10.11 Rs. 7.76

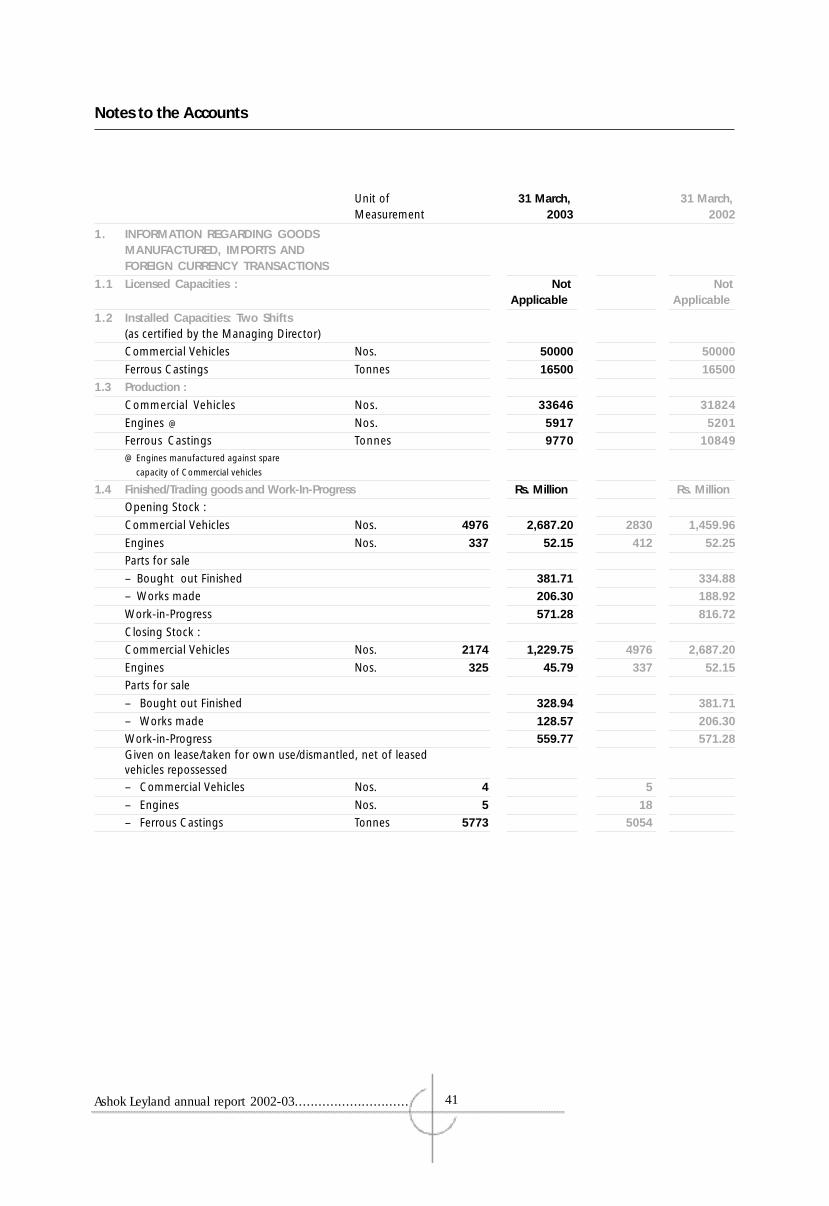

The Company achieved total sales of36444 vehicles (including for export).The improvement came mostly fromthe goods segment; with off-take fromthe State Transport Undertakings beinglower than anticipated. The Company’ssales to Defence segment (includingsales to Vehicles Factory, Jabalpur in kit

form) continued to be satisfactory.

Exports

Your Company’s export during 2002-2003 was 2550 vehicles, compared to2170 in the previous year. YourCompany has been able to also export

to new markets during the year.

Production

The various initiatives to alignproduction with market requirementwere further strengthened during theyear. Employee productivity improveddue to sizeable reduction in workforcethrough Voluntary Retirement

Schemes.

Profitability

Your Directors are happy to reportsatisfactory profits achieved during theyear 2002-03. While improvement insales was the major factor, significantcontributions to profitability camethrough continued emphasis on costcontrol, better treasury managementetc.

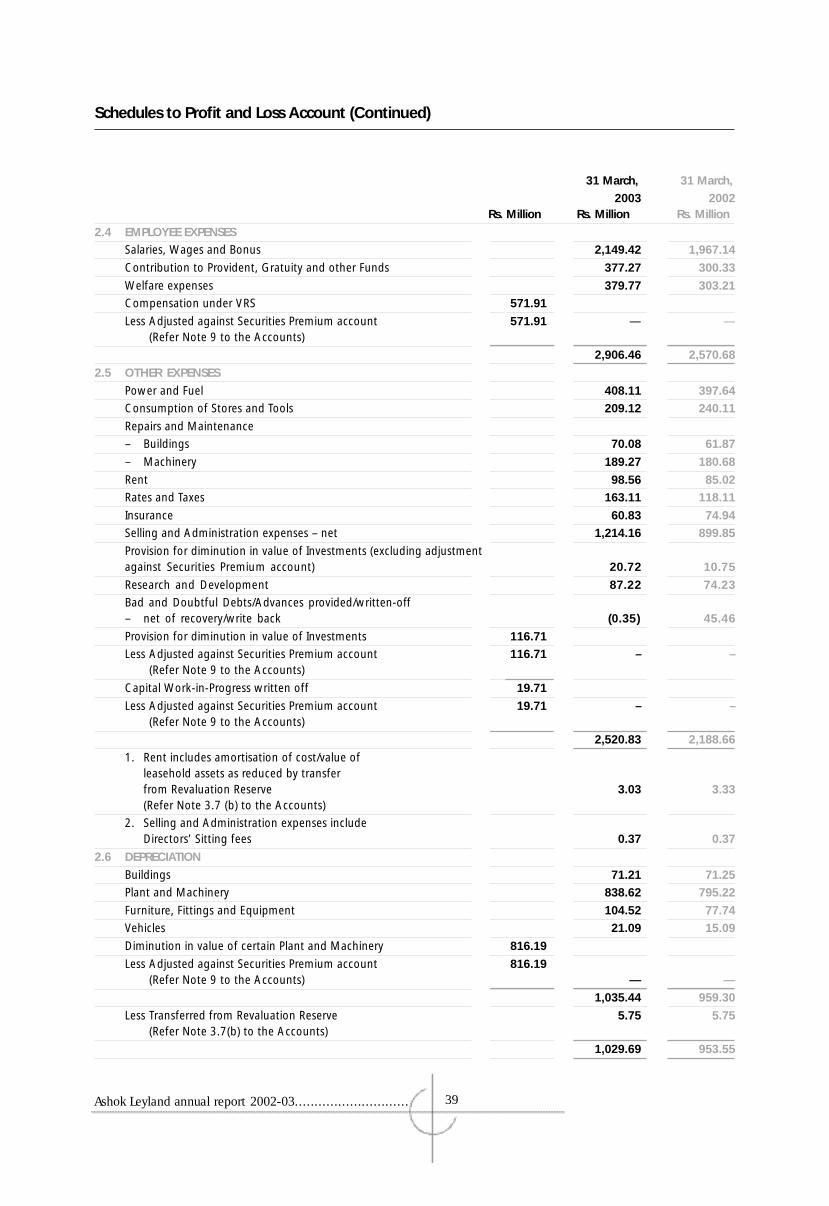

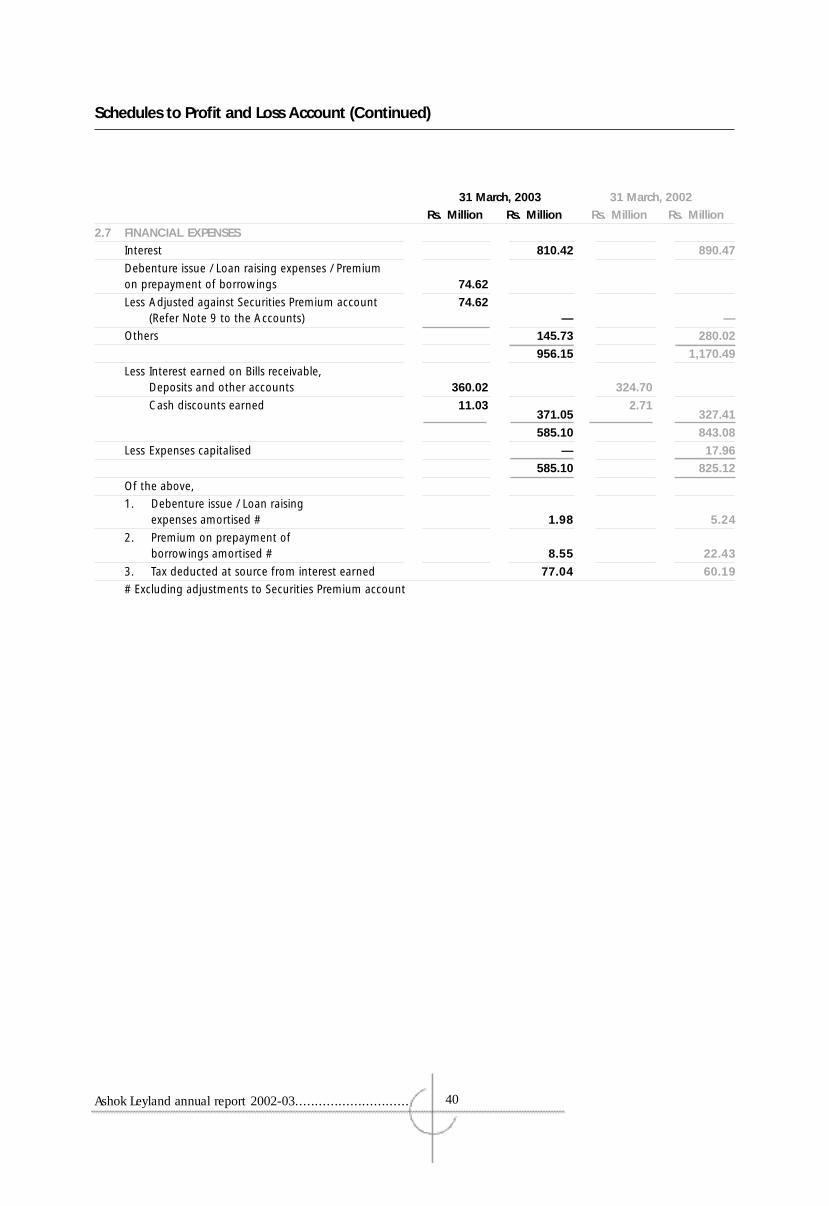

Adjustment against Securities

(Share) Premium Account

Shareholders, at the ExtraordinaryGeneral Meeting held on January 18,2003, had approved the Board’sproposal to adjust against theCompany’s Securities (Share) PremiumAccount, a sum not exceeding Rs.160crores representing MiscellaneousExpenditure not written off, theestimated future diminution in thevalue of certain investments, andestimated future diminution in value ofcertain fixed assets and capital work-in-progress. This proposal was confirmedby the Hon’ble Madras High Court, andthe other procedures have been fullycompleted. The necessary adjustmentshave been incorporated in the accounts

for the year ended March 31,2003.

Dispute Regarding Central Sales Tax

The Company’s appeal against thedisputed levy of Central Sales Tax bythe Government of Tamilnadu ispending before the Supreme Court.Meanwhile, the Stay granted by itcontinues to be in force. The CentralGovernment proposal to establish aCentral Adjudicatory Mechansim andother related aspects of the disputehave been challenged on various

grounds.

Industrial Relations

The year under review registeredfurther improvements in industrialrelations and there was commendablecooperation between Management and

the Unions.

Ashok Leyland annual report 2002-03............................. 5

Research and Development,

Technology Absorption, Energy

Conservation etc.

The particulars prescribed by theCompanies (Disclosure of Particulars inthe Report of Board of Directors)Rules,1988 relating to Conservationof Energy, Technology Absorption,Foreign Exchange are furnished in

Annexure - A to this Report.

Part - II Corporate Matters

Corporate Governance

Your Directors are happy to report thatfrom 2001, your Company has beenfully compliant with the SEBI Guidelineson Corporate Governance, which havebeen incorporated in Clause 49 of theListing Agreement with the StockExchanges. In many areas, the Boardand Management practices exceed SEBIstipulations.

A detailed report on this subject formsAnnexure-B to this Report.

The Statutory Auditors of the Companyhave examined the Company’scompliance, and have certified thesame, as required under SEBIGuidelines. Such certificate isreproduced as Annexure - C to thisReport.

A Management Discussion and AnalysisReport covering a wide range of issuesrelating to performance, outlook etc., isgiven as Annexure - D to this Report.

The Directors’ Responsibility Statementas required under Section 217 (2AA) ofthe Companies Act,1956 is furnishedas Annexure - E to this Report.

The particulars of employees asprescribed by the Companies(Particulars of Employees) Rules,1975are furnished in Annexure - F to this

Report.

Directors

Mr R Jagannath, Deputy ManagingDirector, ceased to be a Director on the

Directors’ Report

expiry of his term of office on March31, 2003. Having joined the Companyas a Graduate Engineer, he handledvarious roles in Product Development,Marketing, Exports, Manufacturingetc., before he became WholetimeDirector and then Deputy ManagingDirector. Your Directors wish to placeon record the deep appreciation ofMr Jagannath’s dedicated service andvaluable contribution during his longtenure of 38 years with the Company.It is not proposed to fill this vacancy forthe time being.

Mr P A Balasubramanian, whorepresented LIC of India as a largeshareholder, stepped down from theBoard on July 26,2002 consequent tohis appointment as a Member of theInsurance Regulatory DevelopmentAuthority (IRDA). Your Directors wish tothank Mr Balasubramanian for hisadvice and guidance during hisassociation with the Board.

Mr S R Krishnaswamy, ExecutiveDirector (P&GS) joined the Board as aDirector from July 26, 2002 as aNominee of LIC, in place of Mr P ABalasubramanian.

Mr R Sorce ceased to be a Director ofthe Board effective from October 25,2002. In his place, Mr M Bianchi,General Legal Counsel of IVECO SpA,Italy was nominated to the Board bythe major shareholder M/s LRLIHLimited. The Board wishes to record itsappreciation of Mr Sorce’s services.

Mr D G Hinduja, Mr S R Krishnaswamy,Mr E A Kshirsagar and Mr M Bianchiretire by rotation at the forthcomingAnnual General Meeting, and areeligible for re-appointment. Thenecessary resolutions are being placed

before the members for approval.

Cost Auditor

The Government has stipulated CostAudit of the Company’s records in

respect of commercial vehicles as wellas engines. M/s GEEYES & Co., CostAuditors have carried out theseassignments. Their findings have beenvery satisfactory.

Secretarial Audit

As directed by Securities and ExchangeBoard of India (SEBI), Secretarial Auditis being carried out at the specifiedperiodicity by a Practising CompanySecretary. The findings of theSecretarial Audit were entirely

satisfactory.

Auditors

M/s M S Krishnaswami & Rajan andM/s Price Waterhouse retire at theensuing Annual General Meeting andare eligible for re-appointment. TheAudit Committee of the Board hasrecommended their re-appointment.The necessary resolution is being placedbefore the shareholders for approval.

The Company has receivedconfirmation that their appointmentwill be within the limits prescribedunder Section 224(1B) of the

Companies Act, 1956.

Acknowledgement

The Directors wish to express theirappreciation of the continuedco-operation of the Central and StateGovernments, Bankers, FinancialInstitutions, Customers, Dealers andSuppliers and also the valuableassistance and advice received frommajor shareholders LRLIH Ltd., theHinduja Group and IVECO. TheDirectors also wish to thank all theemployees for their contribution,support and continued co-operation

through the year.

On behalf of the Board of Directors

Chennai R J SHAHANEY

May 2, 2003 Chairman

Ashok Leyland annual report 2002-03............................. 6

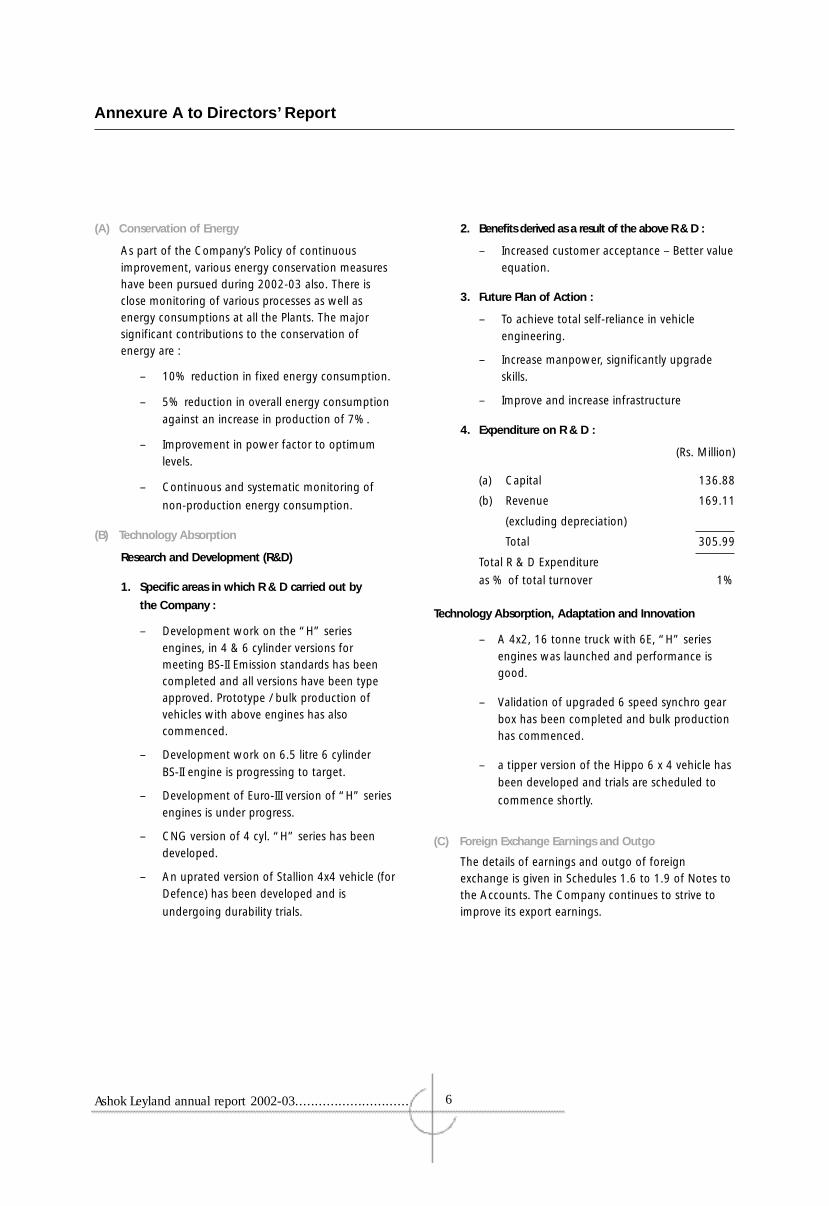

Annexure A to Directors’ Report

2. Benefits derived as a result of the above R & D :

– Increased customer acceptance – Better value

equation.

3. Future Plan of Action :

– To achieve total self-reliance in vehicle

engineering.

– Increase manpower, significantly upgrade

skills.

– Improve and increase infrastructure

4. Expenditure on R & D :

(Rs. Million)

(a) Capital 136.88

(b) Revenue 169.11

(excluding depreciation)

Total 305.99

Total R & D Expenditure

as % of total turnover 1%

Technology Absorption, Adaptation and Innovation

– A 4x2, 16 tonne truck with 6E, “H” series

engines was launched and performance isgood.

– Validation of upgraded 6 speed synchro gear

box has been completed and bulk productionhas commenced.

– a tipper version of the Hippo 6 x 4 vehicle has

been developed and trials are scheduled to

commence shortly.

(C) Foreign Exchange Earnings and Outgo

The details of earnings and outgo of foreignexchange is given in Schedules 1.6 to 1.9 of Notes tothe Accounts. The Company continues to strive toimprove its export earnings.

(A) Conservation of Energy

As part of the Company’s Policy of continuous

improvement, various energy conservation measureshave been pursued during 2002-03 also. There isclose monitoring of various processes as well asenergy consumptions at all the Plants. The majorsignificant contributions to the conservation ofenergy are :

– 10% reduction in fixed energy consumption.

– 5% reduction in overall energy consumption

against an increase in production of 7%.

– Improvement in power factor to optimum

levels.

– Continuous and systematic monitoring of

non-production energy consumption.

(B) Technology Absorption

Research and Development (R&D)

1. Specific areas in which R & D carried out by

the Company :

– Development work on the “H” series

engines, in 4 & 6 cylinder versions formeeting BS-II Emission standards has beencompleted and all versions have been typeapproved. Prototype / bulk production ofvehicles with above engines has alsocommenced.

– Development work on 6.5 litre 6 cylinder

BS-II engine is progressing to target.

– Development of Euro-III version of “H” series

engines is under progress.

– CNG version of 4 cyl. “H” series has been

developed.

– An uprated version of Stallion 4x4 vehicle (for

Defence) has been developed and is

undergoing durability trials.

Ashok Leyland annual report 2002-03............................. 7

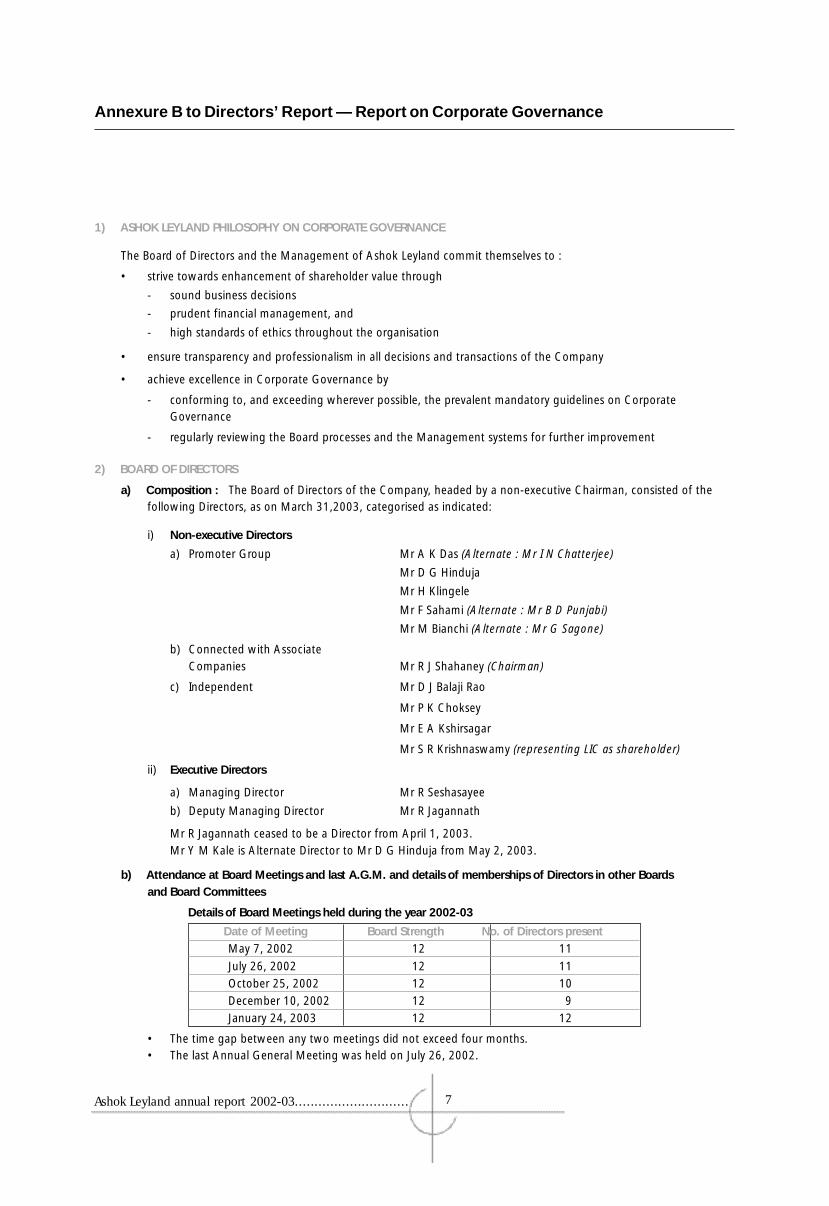

Annexure B to Directors’ Report — Report on Corporate Governance

1) ASHOK LEYLAND PHILOSOPHY ON CORPORATE GOVERNANCE

The Board of Directors and the Management of Ashok Leyland commit themselves to :

• strive towards enhancement of shareholder value through

- sound business decisions

- prudent financial management, and

- high standards of ethics throughout the organisation

• ensure transparency and professionalism in all decisions and transactions of the Company

• achieve excellence in Corporate Governance by

- conforming to, and exceeding wherever possible, the prevalent mandatory guidelines on CorporateGovernance

- regularly reviewing the Board processes and the Management systems for further improvement

2) BOARD OF DIRECTORS

a) Composition : The Board of Directors of the Company, headed by a non-executive Chairman, consisted of thefollowing Directors, as on March 31,2003, categorised as indicated:

i) Non-executive Directors

a) Promoter Group Mr A K Das (Alternate : Mr I N Chatterjee)

Mr D G Hinduja

Mr H Klingele

Mr F Sahami (Alternate : Mr B D Punjabi)

Mr M Bianchi (Alternate : Mr G Sagone)

b) Connected with Associate

Companies Mr R J Shahaney (Chairman)

c) Independent Mr D J Balaji Rao

Mr P K Choksey

Mr E A Kshirsagar

Mr S R Krishnaswamy (representing LIC as shareholder)

ii) Executive Directors

a) Managing Director Mr R Seshasayee

b) Deputy Managing Director Mr R Jagannath

Mr R Jagannath ceased to be a Director from April 1, 2003.

Mr Y M Kale is Alternate Director to Mr D G Hinduja from May 2, 2003.

b) Attendance at Board Meetings and last A.G.M. and details of memberships of Directors in other Boards

and Board Committees

Details of Board Meetings held during the year 2002-03

• The time gap between any two meetings did not exceed four months.• The last Annual General Meeting was held on July 26, 2002.

Date of Meeting Board Strength No. of Directors present

May 7, 2002 12 11

July 26, 2002 12 11

October 25, 2002 12 10

December 10, 2002 12 9

January 24, 2003 12 12

Ashok Leyland annual report 2002-03............................. 8

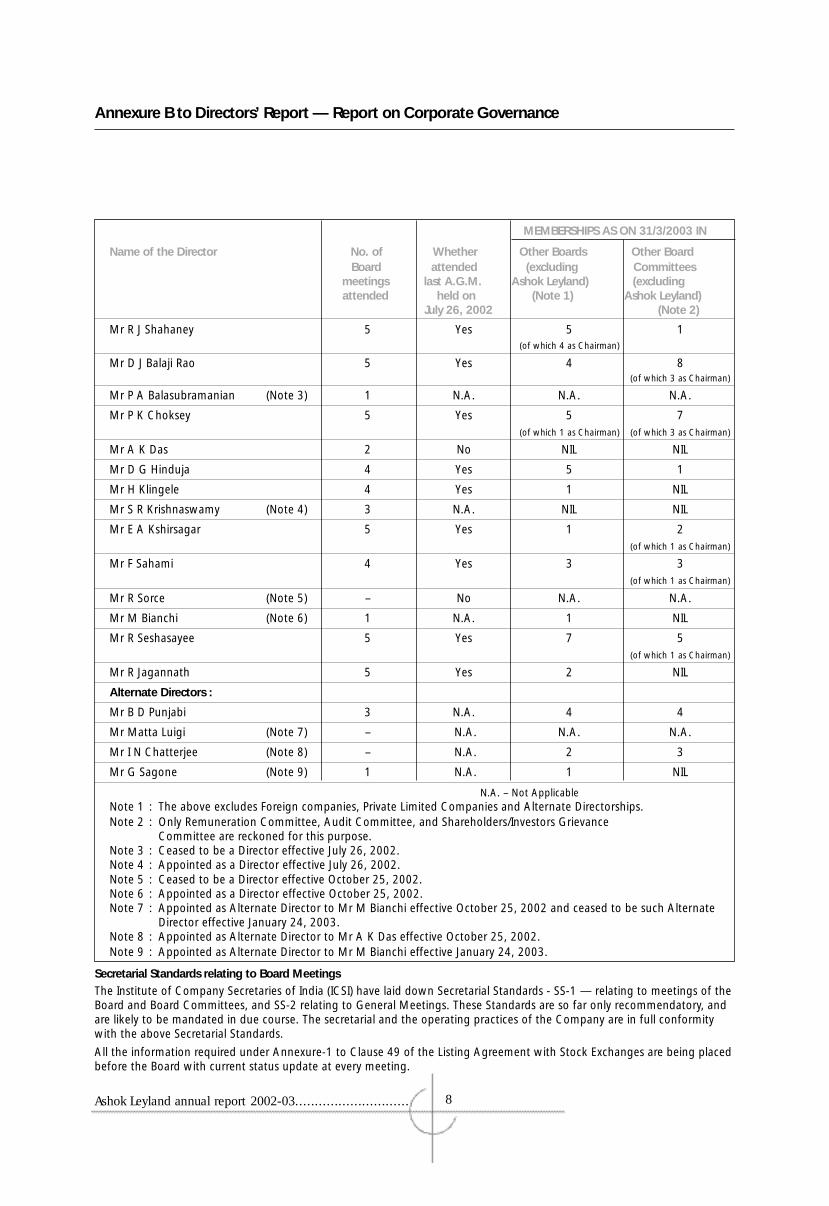

Name of the Director No. of Whether Other Boards Other BoardBoard attended (excluding Committees

meetings last A.G.M. Ashok Leyland) (excludingattended held on (Note 1) Ashok Leyland)

July 26, 2002 (Note 2)

Mr R J Shahaney 5 Yes 5 1(of which 4 as Chairman)

Mr D J Balaji Rao 5 Yes 4 8(of which 3 as Chairman)

Mr P A Balasubramanian (Note 3) 1 N.A. N.A. N.A.

Mr P K Choksey 5 Yes 5 7(of which 1 as Chairman) (of which 3 as Chairman)

Mr A K Das 2 No NIL NIL

Mr D G Hinduja 4 Yes 5 1

Mr H Klingele 4 Yes 1 NIL

Mr S R Krishnaswamy (Note 4) 3 N.A. NIL NIL

Mr E A Kshirsagar 5 Yes 1 2(of which 1 as Chairman)

Mr F Sahami 4 Yes 3 3(of which 1 as Chairman)

Mr R Sorce (Note 5) – No N.A. N.A.

Mr M Bianchi (Note 6) 1 N.A. 1 NIL

Mr R Seshasayee 5 Yes 7 5(of which 1 as Chairman)

Mr R Jagannath 5 Yes 2 NIL

Alternate Directors :

Mr B D Punjabi 3 N.A. 4 4

Mr Matta Luigi (Note 7) – N.A. N.A. N.A.

Mr I N Chatterjee (Note 8) – N.A. 2 3

Mr G Sagone (Note 9) 1 N.A. 1 NIL

Note 1 : The above excludes Foreign companies, Private Limited Companies and Alternate Directorships.Note 2 : Only Remuneration Committee, Audit Committee, and Shareholders/Investors Grievance

Committee are reckoned for this purpose.Note 3 : Ceased to be a Director effective July 26, 2002.Note 4 : Appointed as a Director effective July 26, 2002.Note 5 : Ceased to be a Director effective October 25, 2002.Note 6 : Appointed as a Director effective October 25, 2002.Note 7 : Appointed as Alternate Director to Mr M Bianchi effective October 25, 2002 and ceased to be such Alternate

Director effective January 24, 2003.Note 8 : Appointed as Alternate Director to Mr A K Das effective October 25, 2002.Note 9 : Appointed as Alternate Director to Mr M Bianchi effective January 24, 2003.

MEMBERSHIPS AS ON 31/3/2003 IN

Annexure B to Directors’ Report — Report on Corporate Governance

Secretarial Standards relating to Board Meetings

The Institute of Company Secretaries of India (ICSI) have laid down Secretarial Standards - SS-1 — relating to meetings of theBoard and Board Committees, and SS-2 relating to General Meetings. These Standards are so far only recommendatory, andare likely to be mandated in due course. The secretarial and the operating practices of the Company are in full conformitywith the above Secretarial Standards.

All the information required under Annexure-1 to Clause 49 of the Listing Agreement with Stock Exchanges are being placedbefore the Board with current status update at every meeting.

N.A. – Not Applicable

Ashok Leyland annual report 2002-03............................. 9

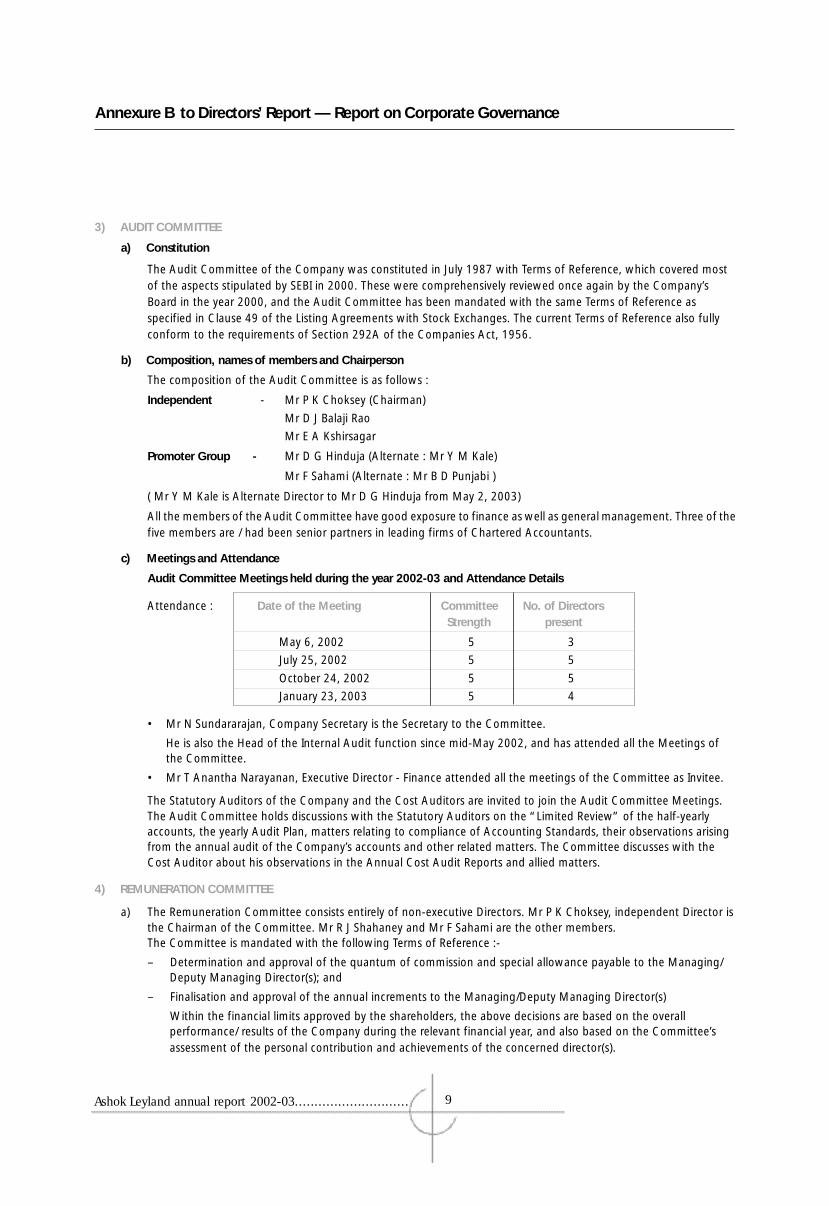

3) AUDIT COMMITTEE

a) Constitution

The Audit Committee of the Company was constituted in July 1987 with Terms of Reference, which covered mostof the aspects stipulated by SEBI in 2000. These were comprehensively reviewed once again by the Company’sBoard in the year 2000, and the Audit Committee has been mandated with the same Terms of Reference asspecified in Clause 49 of the Listing Agreements with Stock Exchanges. The current Terms of Reference also fullyconform to the requirements of Section 292A of the Companies Act, 1956.

b) Composition, names of members and Chairperson

The composition of the Audit Committee is as follows :

Independent - Mr P K Choksey (Chairman)

Mr D J Balaji Rao

Mr E A Kshirsagar

Promoter Group - Mr D G Hinduja (Alternate : Mr Y M Kale)

Mr F Sahami (Alternate : Mr B D Punjabi )

( Mr Y M Kale is Alternate Director to Mr D G Hinduja from May 2, 2003)

All the members of the Audit Committee have good exposure to finance as well as general management. Three of thefive members are / had been senior partners in leading firms of Chartered Accountants.

c) Meetings and Attendance

Audit Committee Meetings held during the year 2002-03 and Attendance Details

Attendance : Date of the Meeting Committee No. of DirectorsStrength present

May 6, 2002 5 3

July 25, 2002 5 5

October 24, 2002 5 5

January 23, 2003 5 4

• Mr N Sundararajan, Company Secretary is the Secretary to the Committee.

He is also the Head of the Internal Audit function since mid-May 2002, and has attended all the Meetings ofthe Committee.

• Mr T Anantha Narayanan, Executive Director - Finance attended all the meetings of the Committee as Invitee.

The Statutory Auditors of the Company and the Cost Auditors are invited to join the Audit Committee Meetings.The Audit Committee holds discussions with the Statutory Auditors on the “Limited Review” of the half-yearlyaccounts, the yearly Audit Plan, matters relating to compliance of Accounting Standards, their observations arisingfrom the annual audit of the Company’s accounts and other related matters. The Committee discusses with theCost Auditor about his observations in the Annual Cost Audit Reports and allied matters.

4) REMUNERATION COMMITTEE

a) The Remuneration Committee consists entirely of non-executive Directors. Mr P K Choksey, independent Director isthe Chairman of the Committee. Mr R J Shahaney and Mr F Sahami are the other members.The Committee is mandated with the following Terms of Reference :-

– Determination and approval of the quantum of commission and special allowance payable to the Managing/Deputy Managing Director(s); and

– Finalisation and approval of the annual increments to the Managing/Deputy Managing Director(s)

Within the financial limits approved by the shareholders, the above decisions are based on the overallperformance/ results of the Company during the relevant financial year, and also based on the Committee’sassessment of the personal contribution and achievements of the concerned director(s).

Annexure B to Directors’ Report — Report on Corporate Governance

Ashok Leyland annual report 2002-03............................. 10

Annexure B to Directors’ Report — Report on Corporate Governance

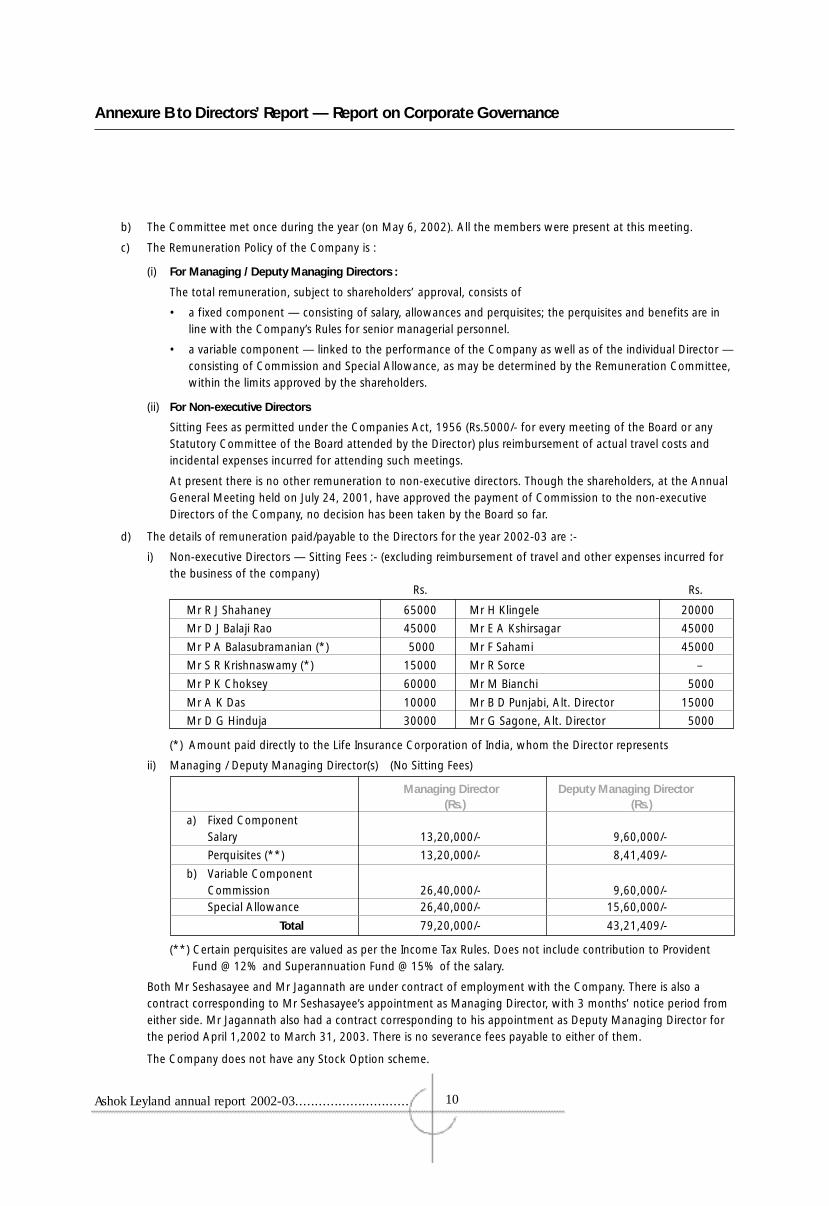

b) The Committee met once during the year (on May 6, 2002). All the members were present at this meeting.

c) The Remuneration Policy of the Company is :

(i) For Managing / Deputy Managing Directors :

The total remuneration, subject to shareholders’ approval, consists of

• a fixed component — consisting of salary, allowances and perquisites; the perquisites and benefits are inline with the Company’s Rules for senior managerial personnel.

• a variable component — linked to the performance of the Company as well as of the individual Director —consisting of Commission and Special Allowance, as may be determined by the Remuneration Committee,within the limits approved by the shareholders.

(ii) For Non-executive Directors

Sitting Fees as permitted under the Companies Act, 1956 (Rs.5000/- for every meeting of the Board or anyStatutory Committee of the Board attended by the Director) plus reimbursement of actual travel costs andincidental expenses incurred for attending such meetings.

At present there is no other remuneration to non-executive directors. Though the shareholders, at the AnnualGeneral Meeting held on July 24, 2001, have approved the payment of Commission to the non-executiveDirectors of the Company, no decision has been taken by the Board so far.

d) The details of remuneration paid/payable to the Directors for the year 2002-03 are :-

i) Non-executive Directors — Sitting Fees :- (excluding reimbursement of travel and other expenses incurred forthe business of the company)

Rs. Rs.

Mr R J Shahaney 65000 Mr H Klingele 20000

Mr D J Balaji Rao 45000 Mr E A Kshirsagar 45000

Mr P A Balasubramanian (*) 5000 Mr F Sahami 45000

Mr S R Krishnaswamy (*) 15000 Mr R Sorce –

Mr P K Choksey 60000 Mr M Bianchi 5000

Mr A K Das 10000 Mr B D Punjabi, Alt. Director 15000

Mr D G Hinduja 30000 Mr G Sagone, Alt. Director 5000

(*) Amount paid directly to the Life Insurance Corporation of India, whom the Director represents

ii) Managing / Deputy Managing Director(s) (No Sitting Fees)

Managing Director Deputy Managing Director(Rs.) (Rs.)

a) Fixed ComponentSalary 13,20,000/- 9,60,000/-

Perquisites (**) 13,20,000/- 8,41,409/-

b) Variable ComponentCommission 26,40,000/- 9,60,000/-Special Allowance 26,40,000/- 15,60,000/-

Total 79,20,000/- 43,21,409/-

(**) Certain perquisites are valued as per the Income Tax Rules. Does not include contribution to ProvidentFund @ 12% and Superannuation Fund @ 15% of the salary.

Both Mr Seshasayee and Mr Jagannath are under contract of employment with the Company. There is also acontract corresponding to Mr Seshasayee’s appointment as Managing Director, with 3 months’ notice period fromeither side. Mr Jagannath also had a contract corresponding to his appointment as Deputy Managing Director forthe period April 1,2002 to March 31, 2003. There is no severance fees payable to either of them.

The Company does not have any Stock Option scheme.

Ashok Leyland annual report 2002-03............................. 11

Annexure B to Directors’ Report — Report on Corporate Governance

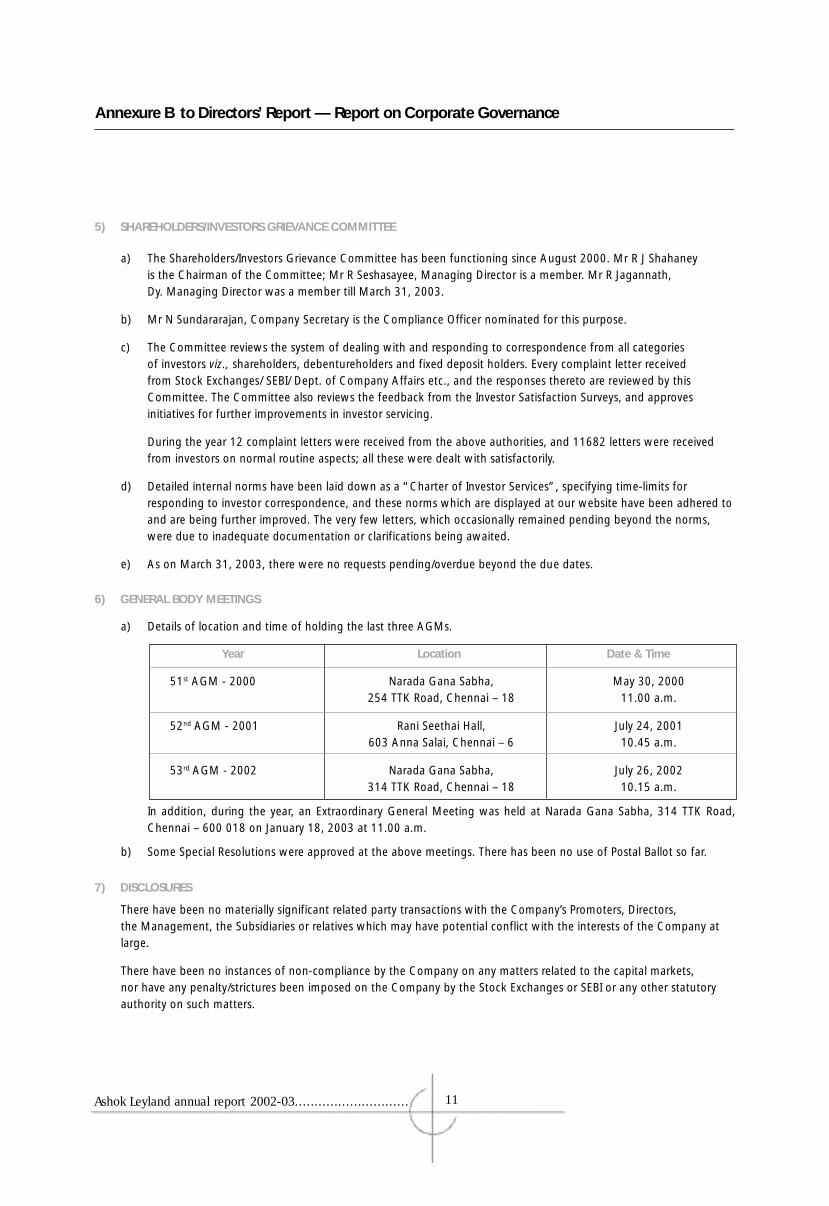

5) SHAREHOLDERS/INVESTORS GRIEVANCE COMMITTEE

a) The Shareholders/Investors Grievance Committee has been functioning since August 2000. Mr R J Shahaneyis the Chairman of the Committee; Mr R Seshasayee, Managing Director is a member. Mr R Jagannath,Dy. Managing Director was a member till March 31, 2003.

b) Mr N Sundararajan, Company Secretary is the Compliance Officer nominated for this purpose.

c) The Committee reviews the system of dealing with and responding to correspondence from all categoriesof investors viz., shareholders, debentureholders and fixed deposit holders. Every complaint letter receivedfrom Stock Exchanges/ SEBI/ Dept. of Company Affairs etc., and the responses thereto are reviewed by thisCommittee. The Committee also reviews the feedback from the Investor Satisfaction Surveys, and approvesinitiatives for further improvements in investor servicing.

During the year 12 complaint letters were received from the above authorities, and 11682 letters were receivedfrom investors on normal routine aspects; all these were dealt with satisfactorily.

d) Detailed internal norms have been laid down as a “Charter of Investor Services”, specifying time-limits forresponding to investor correspondence, and these norms which are displayed at our website have been adhered toand are being further improved. The very few letters, which occasionally remained pending beyond the norms,were due to inadequate documentation or clarifications being awaited.

e) As on March 31, 2003, there were no requests pending/overdue beyond the due dates.

6) GENERAL BODY MEETINGS

a) Details of location and time of holding the last three AGMs.

Year Location Date & Time

51st AGM - 2000 Narada Gana Sabha, May 30, 2000254 TTK Road, Chennai – 18 11.00 a.m.

52nd AGM - 2001 Rani Seethai Hall, July 24, 2001603 Anna Salai, Chennai – 6 10.45 a.m.

53rd AGM - 2002 Narada Gana Sabha, July 26, 2002314 TTK Road, Chennai – 18 10.15 a.m.

In addition, during the year, an Extraordinary General Meeting was held at Narada Gana Sabha, 314 TTK Road,Chennai – 600 018 on January 18, 2003 at 11.00 a.m.

b) Some Special Resolutions were approved at the above meetings. There has been no use of Postal Ballot so far.

7) DISCLOSURES

There have been no materially significant related party transactions with the Company’s Promoters, Directors,the Management, the Subsidiaries or relatives which may have potential conflict with the interests of the Company atlarge.

There have been no instances of non-compliance by the Company on any matters related to the capital markets,nor have any penalty/strictures been imposed on the Company by the Stock Exchanges or SEBI or any other statutoryauthority on such matters.

Ashok Leyland annual report 2002-03............................. 12

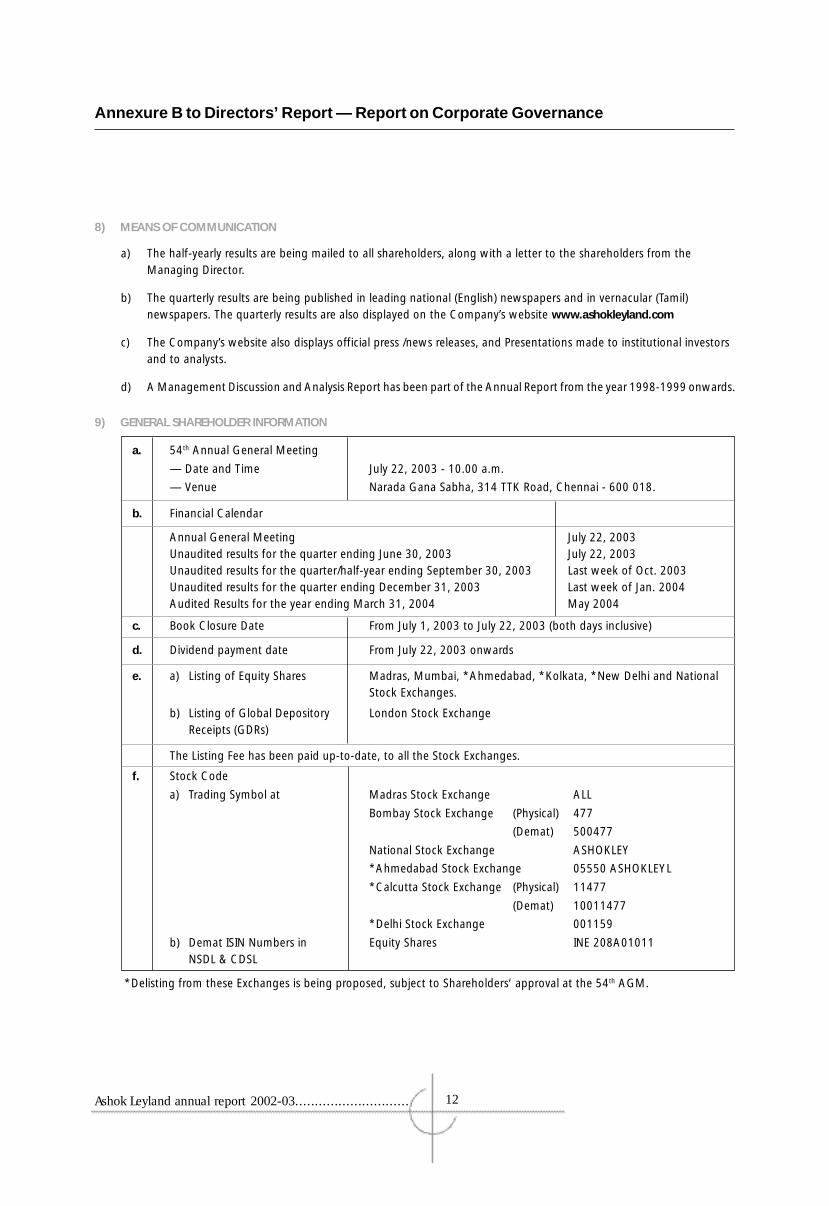

8) MEANS OF COMMUNICATION

a) The half-yearly results are being mailed to all shareholders, along with a letter to the shareholders from theManaging Director.

b) The quarterly results are being published in leading national (English) newspapers and in vernacular (Tamil)newspapers. The quarterly results are also displayed on the Company’s website www.ashokleyland.com

c) The Company’s website also displays official press /news releases, and Presentations made to institutional investorsand to analysts.

d) A Management Discussion and Analysis Report has been part of the Annual Report from the year 1998-1999 onwards.

9) GENERAL SHAREHOLDER INFORMATION

a. 54th Annual General Meeting

— Date and Time July 22, 2003 - 10.00 a.m.

— Venue Narada Gana Sabha, 314 TTK Road, Chennai - 600 018.

b. Financial Calendar

Annual General Meeting July 22, 2003Unaudited results for the quarter ending June 30, 2003 July 22, 2003Unaudited results for the quarter/half-year ending September 30, 2003 Last week of Oct. 2003Unaudited results for the quarter ending December 31, 2003 Last week of Jan. 2004Audited Results for the year ending March 31, 2004 May 2004

c. Book Closure Date From July 1, 2003 to July 22, 2003 (both days inclusive)

d. Dividend payment date From July 22, 2003 onwards

e. a) Listing of Equity Shares Madras, Mumbai, *Ahmedabad, *Kolkata, *New Delhi and NationalStock Exchanges.

b) Listing of Global Depository London Stock ExchangeReceipts (GDRs)

The Listing Fee has been paid up-to-date, to all the Stock Exchanges.

f. Stock Code

a) Trading Symbol at Madras Stock Exchange ALL

Bombay Stock Exchange (Physical) 477

(Demat) 500477

National Stock Exchange ASHOKLEY

*Ahmedabad Stock Exchange 05550 ASHOKLEYL

*Calcutta Stock Exchange (Physical) 11477

(Demat) 10011477

*Delhi Stock Exchange 001159

b) Demat ISIN Numbers in Equity Shares INE 208A01011NSDL & CDSL

*Delisting from these Exchanges is being proposed, subject to Shareholders‘ approval at the 54th AGM.

Annexure B to Directors’ Report — Report on Corporate Governance

Ashok Leyland annual report 2002-03............................. 13

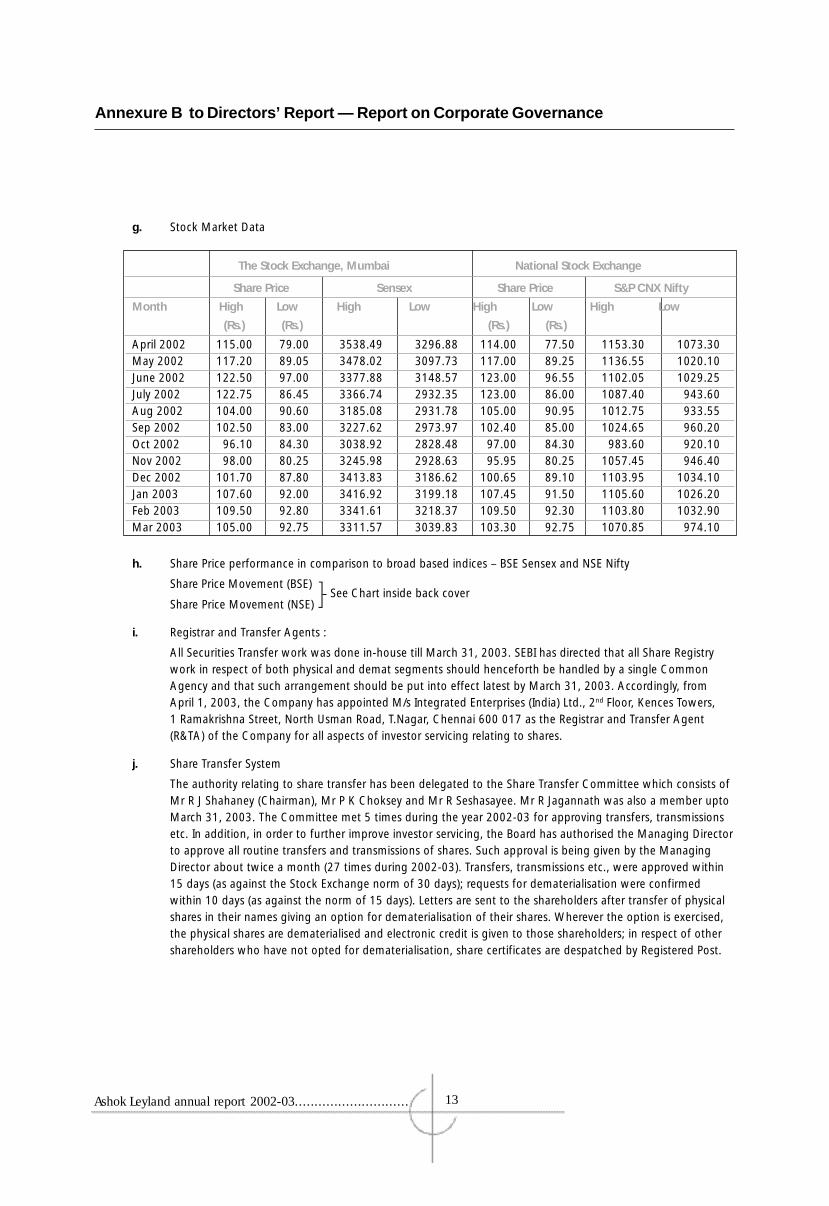

h. Share Price performance in comparison to broad based indices – BSE Sensex and NSE Nifty

Share Price Movement (BSE) See Chart inside back cover

Share Price Movement (NSE)

i. Registrar and Transfer Agents :

All Securities Transfer work was done in-house till March 31, 2003. SEBI has directed that all Share Registrywork in respect of both physical and demat segments should henceforth be handled by a single CommonAgency and that such arrangement should be put into effect latest by March 31, 2003. Accordingly, fromApril 1, 2003, the Company has appointed M/s Integrated Enterprises (India) Ltd., 2nd Floor, Kences Towers,1 Ramakrishna Street, North Usman Road, T.Nagar, Chennai 600 017 as the Registrar and Transfer Agent(R&TA) of the Company for all aspects of investor servicing relating to shares.

j. Share Transfer System

The authority relating to share transfer has been delegated to the Share Transfer Committee which consists ofMr R J Shahaney (Chairman), Mr P K Choksey and Mr R Seshasayee. Mr R Jagannath was also a member uptoMarch 31, 2003. The Committee met 5 times during the year 2002-03 for approving transfers, transmissionsetc. In addition, in order to further improve investor servicing, the Board has authorised the Managing Directorto approve all routine transfers and transmissions of shares. Such approval is being given by the ManagingDirector about twice a month (27 times during 2002-03). Transfers, transmissions etc., were approved within15 days (as against the Stock Exchange norm of 30 days); requests for dematerialisation were confirmedwithin 10 days (as against the norm of 15 days). Letters are sent to the shareholders after transfer of physicalshares in their names giving an option for dematerialisation of their shares. Wherever the option is exercised,the physical shares are dematerialised and electronic credit is given to those shareholders; in respect of othershareholders who have not opted for dematerialisation, share certificates are despatched by Registered Post.

Annexure B to Directors’ Report — Report on Corporate Governance

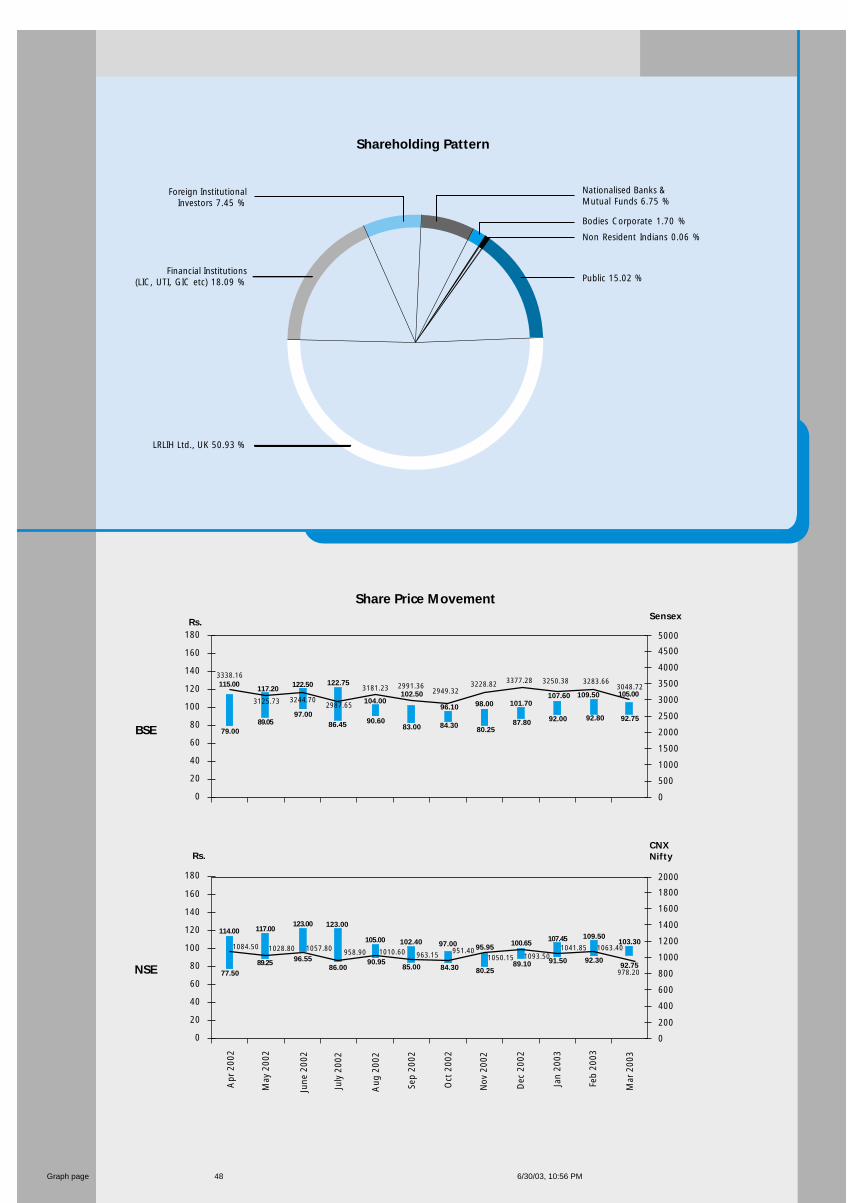

g. Stock Market Data

The Stock Exchange, Mumbai National Stock Exchange

Share Price Sensex Share Price S&P CNX Nifty

Month High Low High Low High Low High Low

(Rs.) (Rs.) (Rs.) (Rs.)

April 2002 115.00 79.00 3538.49 3296.88 114.00 77.50 1153.30 1073.30May 2002 117.20 89.05 3478.02 3097.73 117.00 89.25 1136.55 1020.10June 2002 122.50 97.00 3377.88 3148.57 123.00 96.55 1102.05 1029.25July 2002 122.75 86.45 3366.74 2932.35 123.00 86.00 1087.40 943.60Aug 2002 104.00 90.60 3185.08 2931.78 105.00 90.95 1012.75 933.55Sep 2002 102.50 83.00 3227.62 2973.97 102.40 85.00 1024.65 960.20Oct 2002 96.10 84.30 3038.92 2828.48 97.00 84.30 983.60 920.10Nov 2002 98.00 80.25 3245.98 2928.63 95.95 80.25 1057.45 946.40Dec 2002 101.70 87.80 3413.83 3186.62 100.65 89.10 1103.95 1034.10Jan 2003 107.60 92.00 3416.92 3199.18 107.45 91.50 1105.60 1026.20Feb 2003 109.50 92.80 3341.61 3218.37 109.50 92.30 1103.80 1032.90Mar 2003 105.00 92.75 3311.57 3039.83 103.30 92.75 1070.85 974.10

Ashok Leyland annual report 2002-03............................. 14

Annexure B to Directors’ Report — Report on Corporate Governance

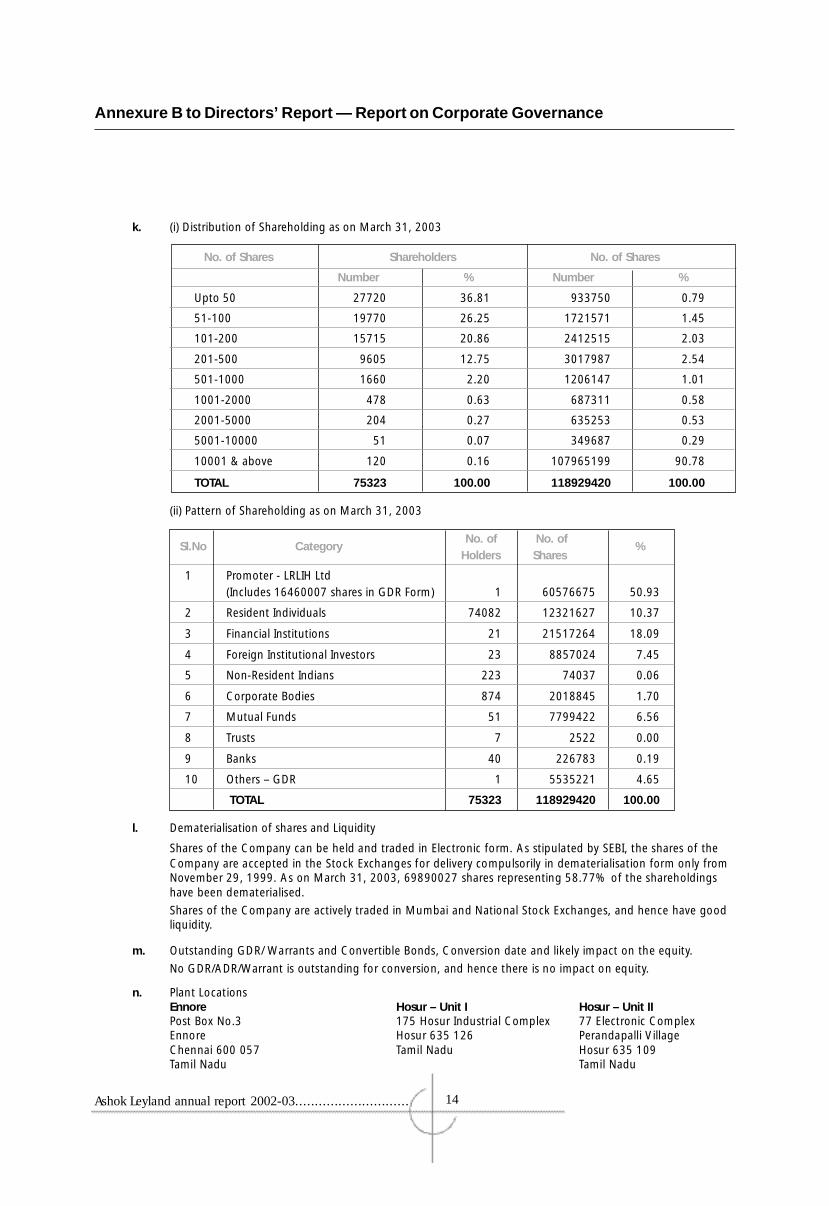

k. (i) Distribution of Shareholding as on March 31, 2003

No. of Shares Shareholders No. of Shares

Number % Number %

Upto 50 27720 36.81 933750 0.79

51-100 19770 26.25 1721571 1.45

101-200 15715 20.86 2412515 2.03

201-500 9605 12.75 3017987 2.54

501-1000 1660 2.20 1206147 1.01

1001-2000 478 0.63 687311 0.58

2001-5000 204 0.27 635253 0.53

5001-10000 51 0.07 349687 0.29

10001 & above 120 0.16 107965199 90.78

TOTAL 75323 100.00 118929420 100.00

(ii) Pattern of Shareholding as on March 31, 2003

Sl.No CategoryNo. of No. of

%Holders Shares

1 Promoter - LRLIH Ltd(Includes 16460007 shares in GDR Form) 1 60576675 50.93

2 Resident Individuals 74082 12321627 10.37

3 Financial Institutions 21 21517264 18.09

4 Foreign Institutional Investors 23 8857024 7.45

5 Non-Resident Indians 223 74037 0.06

6 Corporate Bodies 874 2018845 1.70

7 Mutual Funds 51 7799422 6.56

8 Trusts 7 2522 0.00

9 Banks 40 226783 0.19

10 Others – GDR 1 5535221 4.65

TOTAL 75323 118929420 100.00

l. Dematerialisation of shares and Liquidity

Shares of the Company can be held and traded in Electronic form. As stipulated by SEBI, the shares of theCompany are accepted in the Stock Exchanges for delivery compulsorily in dematerialisation form only fromNovember 29, 1999. As on March 31, 2003, 69890027 shares representing 58.77% of the shareholdingshave been dematerialised.

Shares of the Company are actively traded in Mumbai and National Stock Exchanges, and hence have goodliquidity.

m. Outstanding GDR/ Warrants and Convertible Bonds, Conversion date and likely impact on the equity.

No GDR/ADR/Warrant is outstanding for conversion, and hence there is no impact on equity.

n. Plant LocationsEnnore Hosur – Unit I Hosur – Unit IIPost Box No.3 175 Hosur Industrial Complex 77 Electronic ComplexEnnore Hosur 635 126 Perandapalli VillageChennai 600 057 Tamil Nadu Hosur 635 109Tamil Nadu Tamil Nadu

Ashok Leyland annual report 2002-03............................. 15

Annexure B to Directors’ Report — Report on Corporate Governance