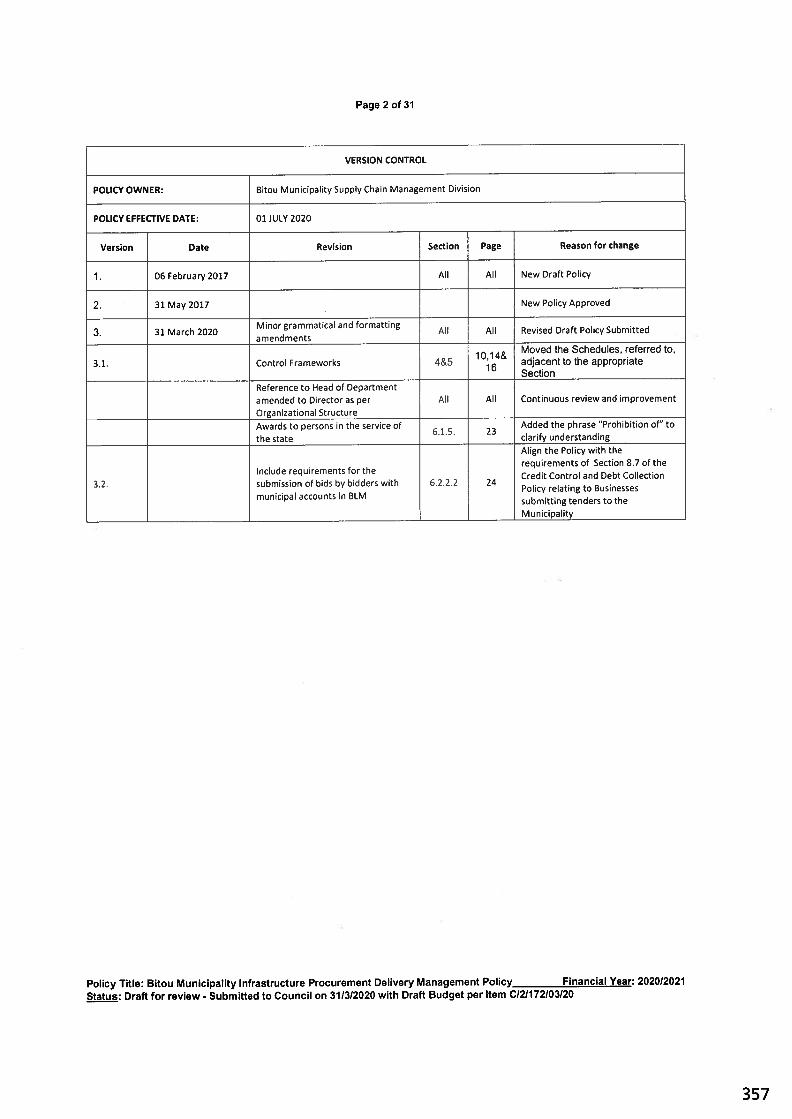

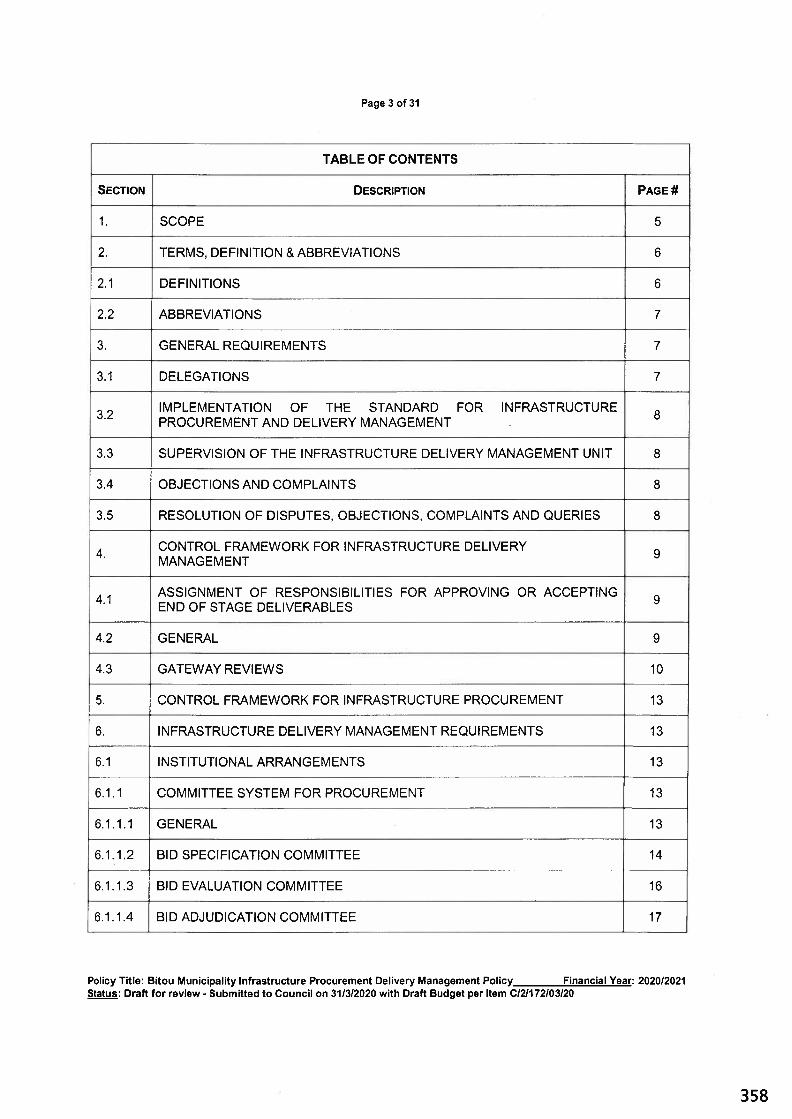

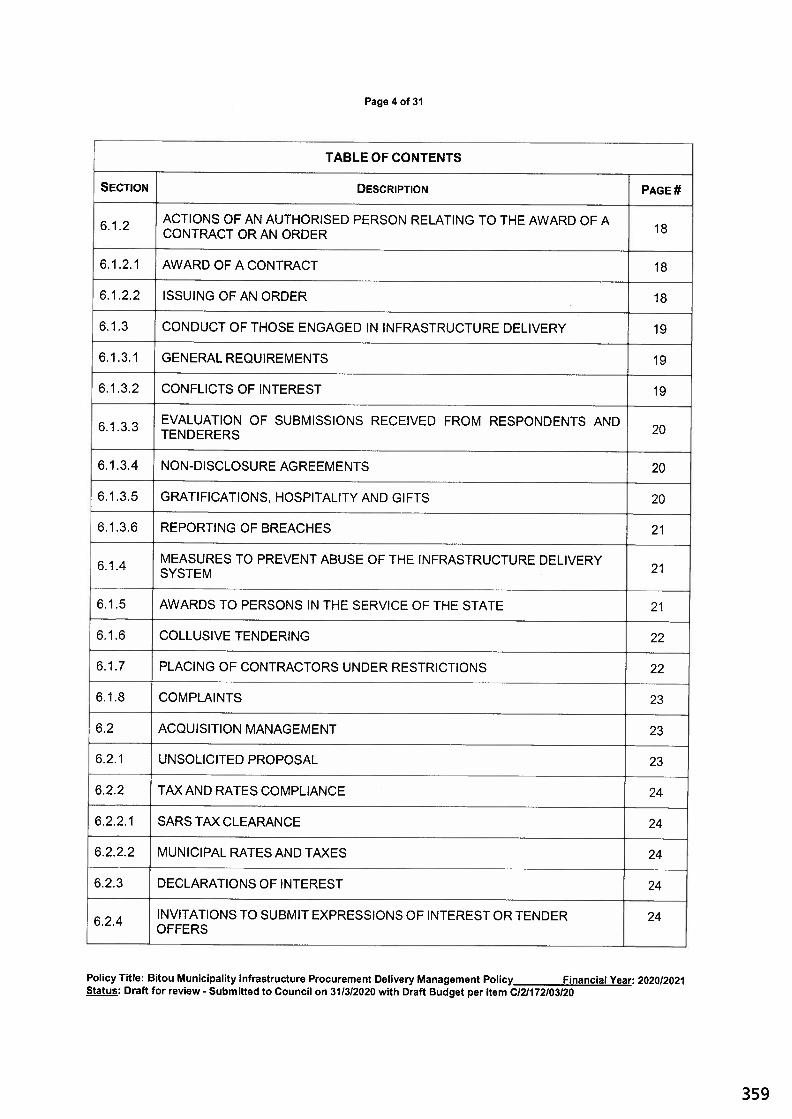

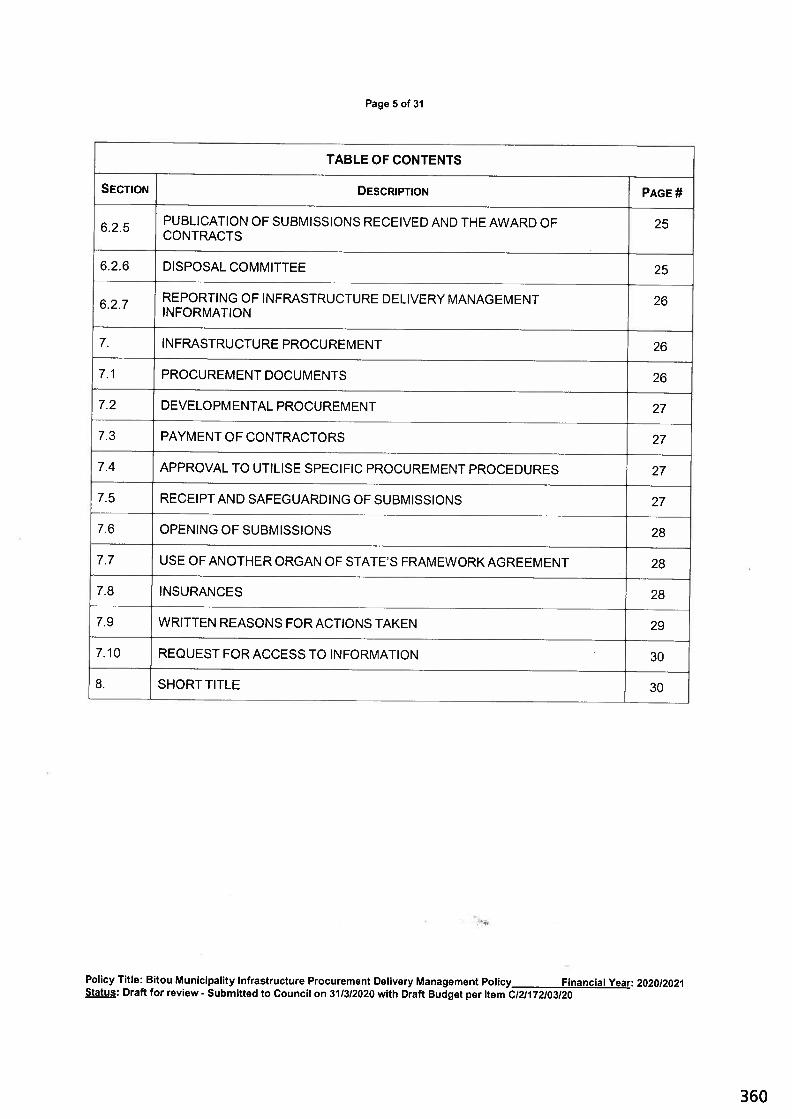

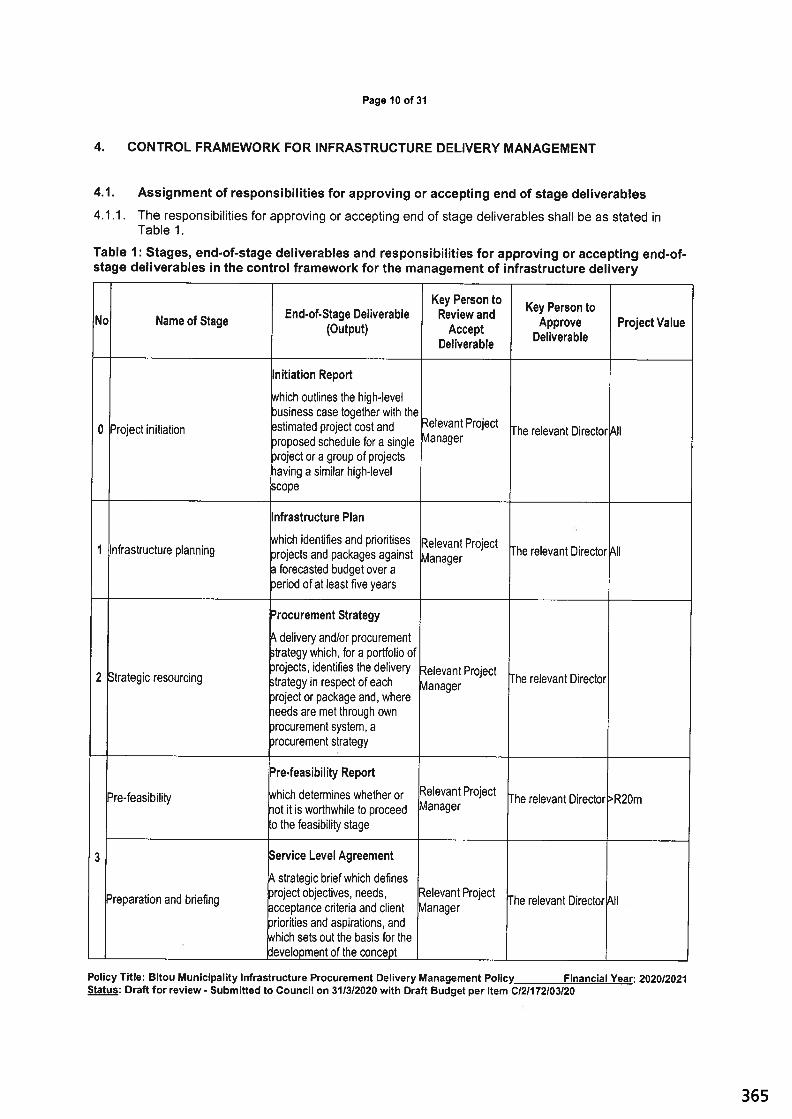

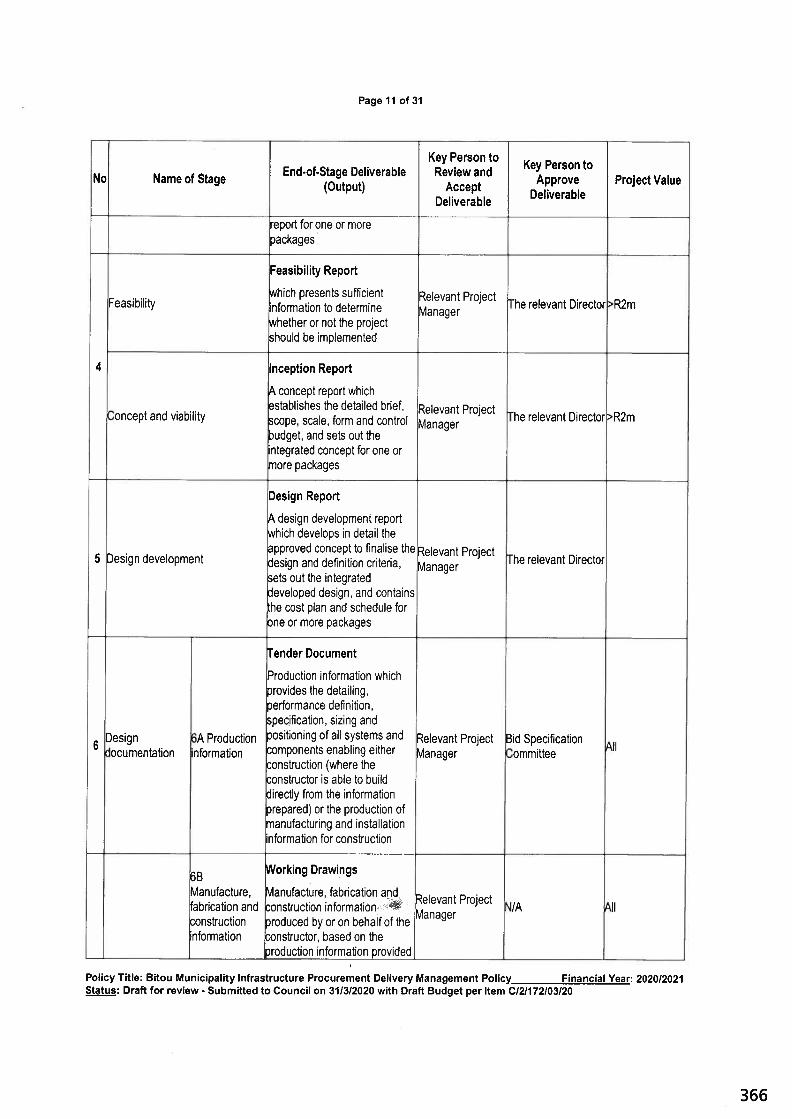

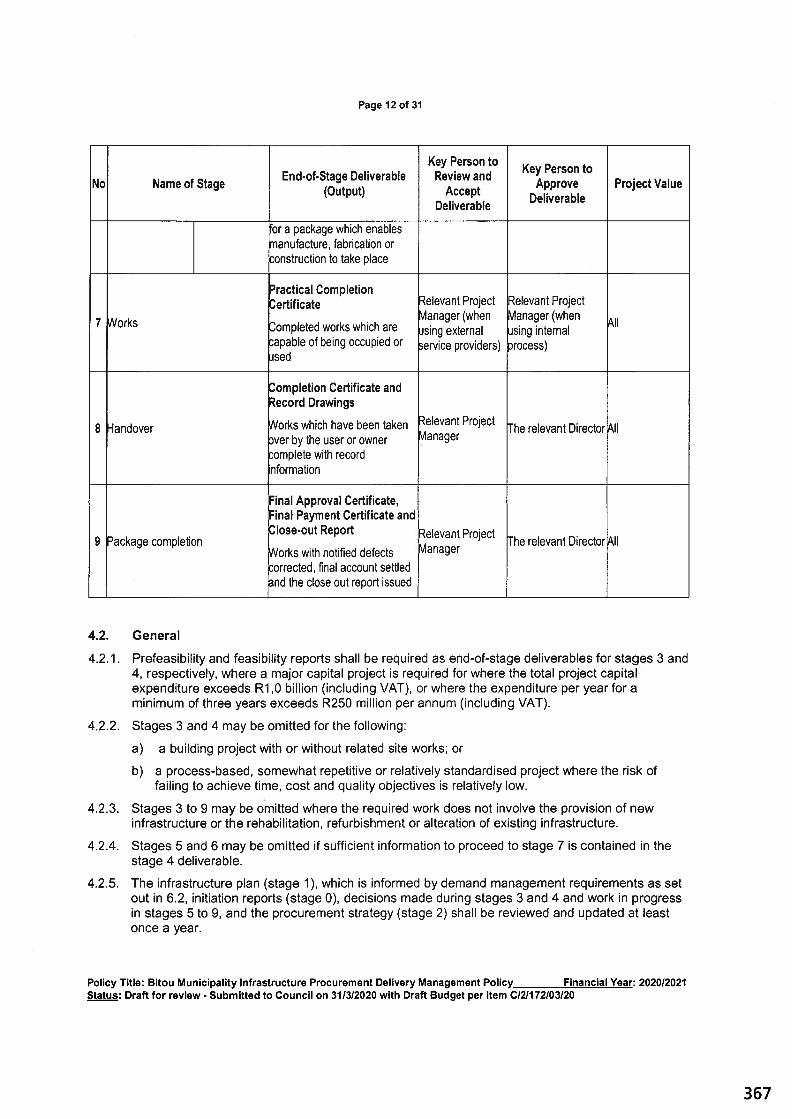

annexure d - bitou municipality

TRANSCRIPT

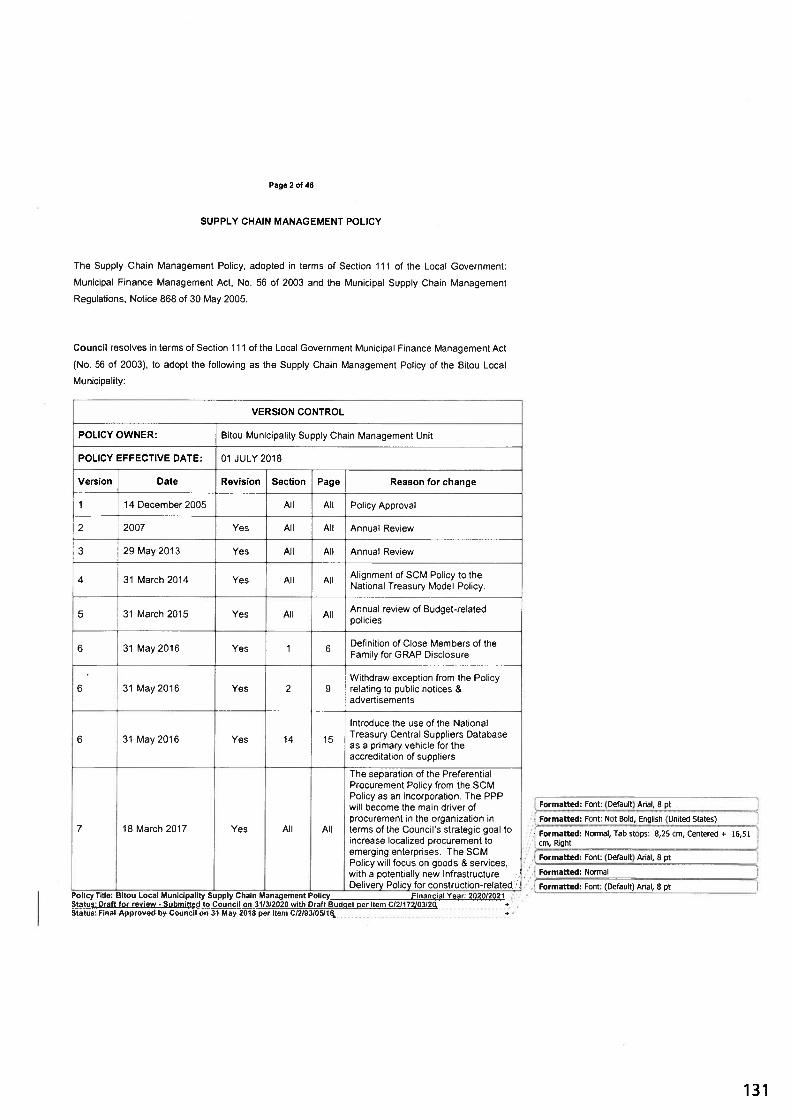

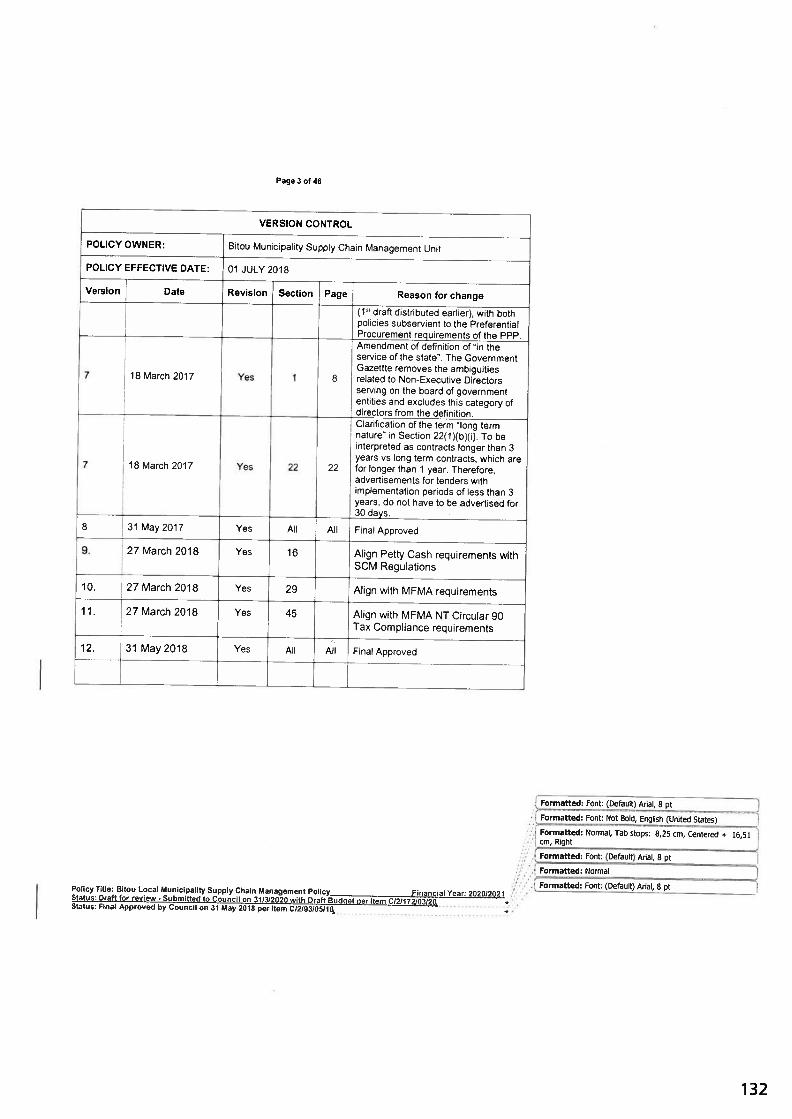

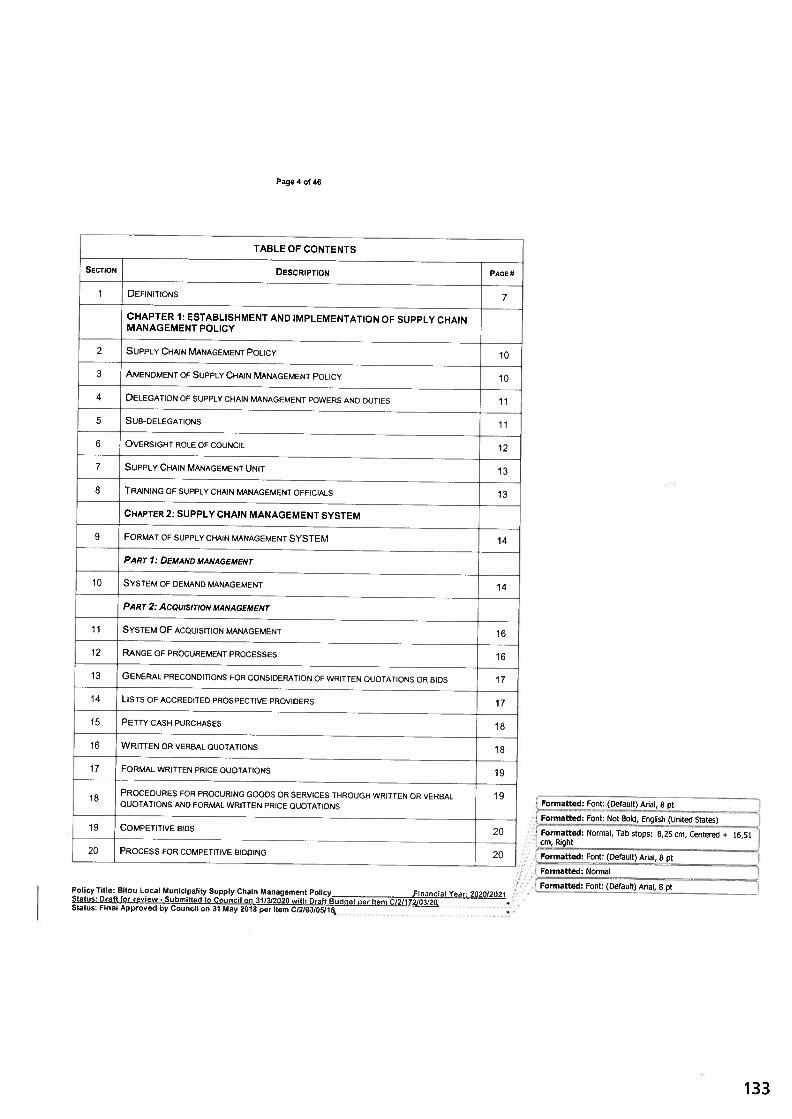

Budget Policy Documents

Annexure DItem C/2/172/03/20:

Draft Annual Budget: 2020/2021 to 2022/2023 MTREF

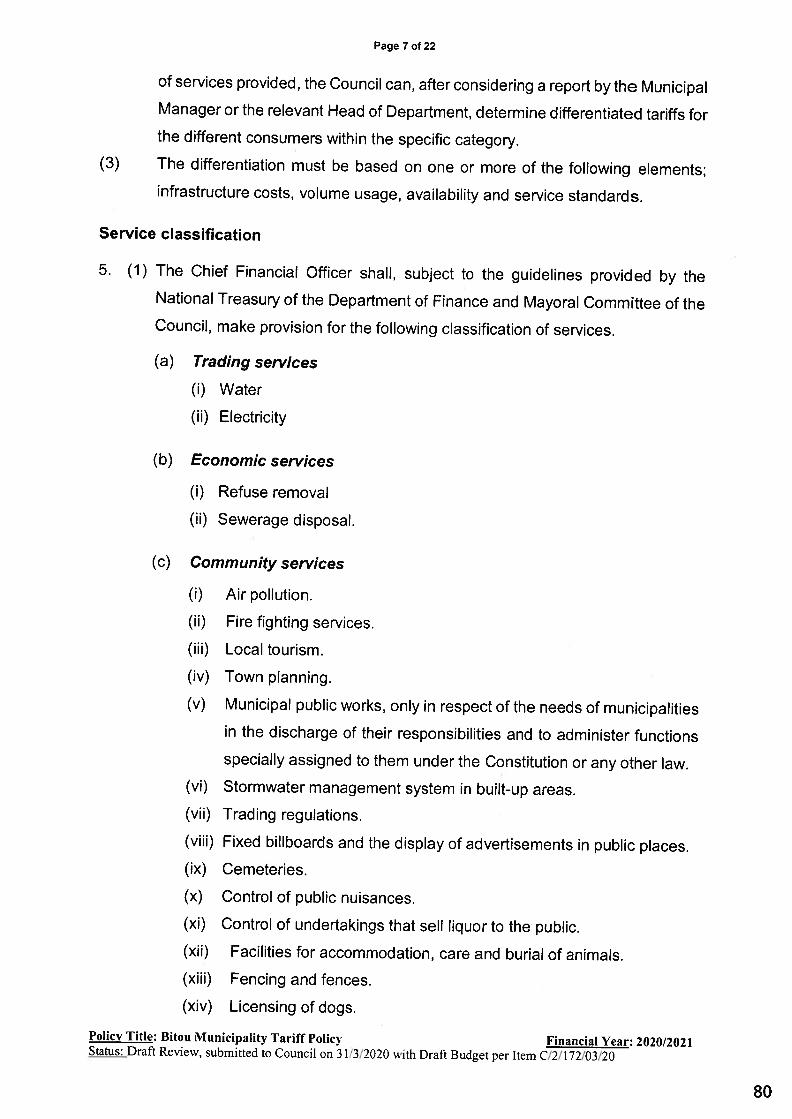

Please read this document as an annexure to the above item

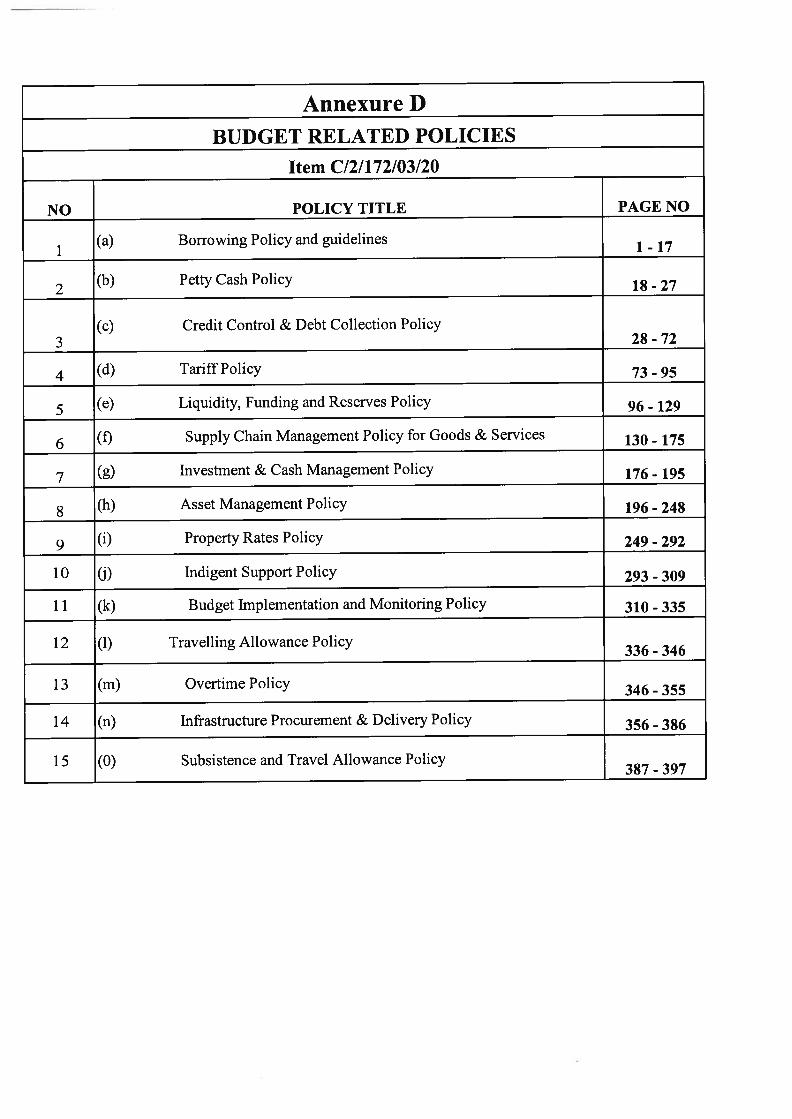

Annexure D

BUDGET RELATED POLICIES

Item C!2/172/03/20

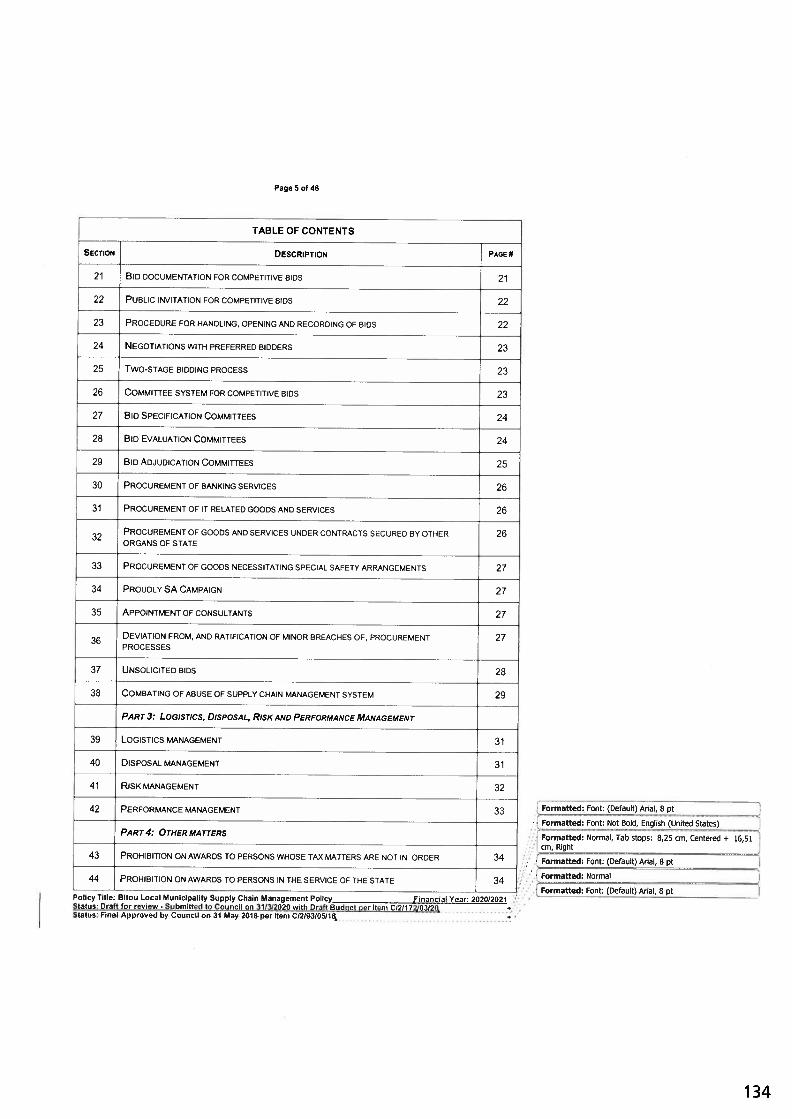

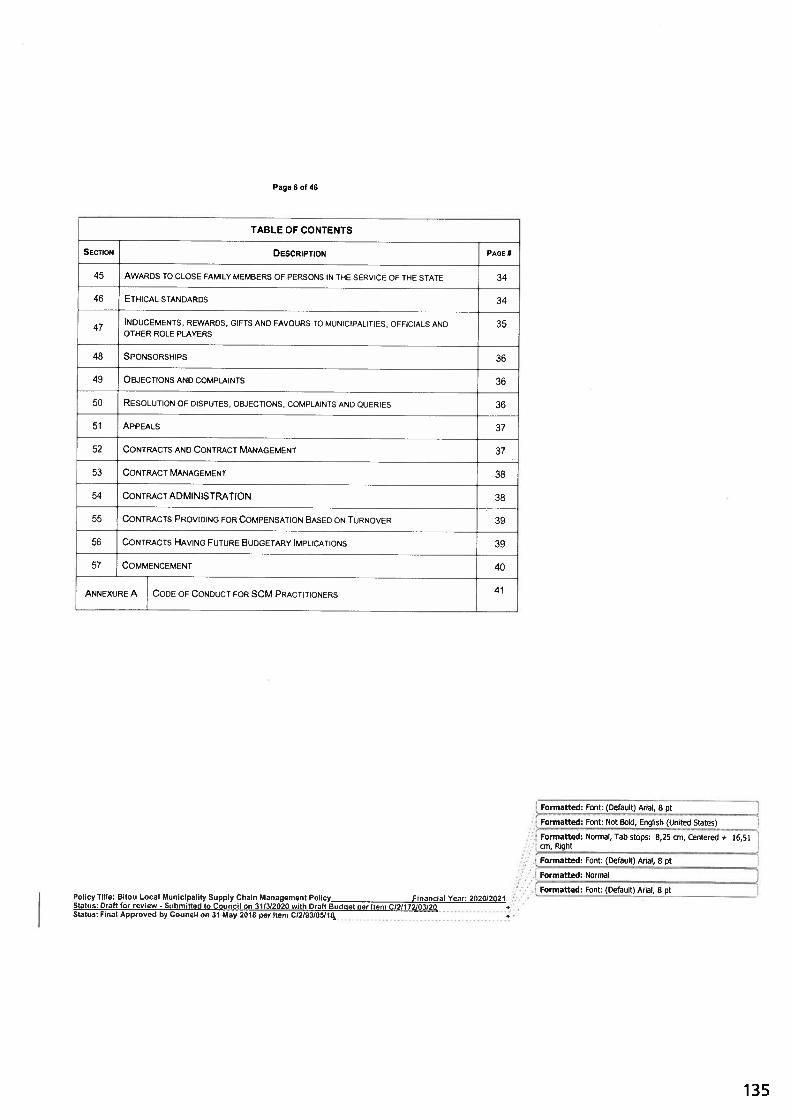

NO POLICY TITLE PAGE NO

1(a) Borrowing Policy and guidelines 1 - 17

2(b) Petty Cash Policy 18 - 27

(c) Credit Control & Debt Collection Policy3 28-72

(d) Tariff Policy 73 - 95

(e) Liquidity, Funding and Reserves Policy 96 - 129

6 (f) Supply Chain Management Policy for Goods & Services 130 - 175

(g) Investment & Cash Management Policy 176 - 195

8 (h) Asset Management Policy 196 - 248

(i) Property Rates Policy 249 - 292

10 (j) Indigent Support Policy 293 - 309

1 1 (k) Budget Implementation and Monitoring Policy 310 - 335

12 (1) Travelling Allowance Policy336 - 346

13 (m) Overtime Policy 346 - 355

14 (n) Infrastructure Procurement & Delivery Policy 356 - 386

15 (0) Subsistence and Travel Allowance Policy387 - 397

Page 1 of 17

rexu1e,

Draft BorrowingPolicy2020/2021

No Amendment to the Policy

I

I

4.I1t

Policy Title: Borrowing Policy Financial Year: 2020/202 1Status: Draft for Review - Submitted to Council on 3 1/03/2020 with Draft Budget per Item C/2/172/03120

1

Page 2 of 17

1. Purpose

1.1. The purpose of this policy is to establish a borrowing framework for the

Municipality and to set out the objectives, policies, statutory requirements and

guidelines for the borrowing of funds, in order to:

• Manage interest rate and credit risk exposure:

• Maintain debt within specified limits and ensure adequate provision

for the repayment of debt:

• Ensure compliance with all Legislation and Council policy governing

borrowing of funds.

1.2 This Policy should be implemented in conjunction with the approved Liquidity,

Funding and Reserves Policy.

1.3 This policy is implemented to provide guidance on the appropriation of capital

funding resources on a sustainable basis in the longer term.

1.4 Although legislation provides guidance as to the broader framework to ensure

financial management of resources to ensure the Council meets all of its

obligations timeously, it is not prescriptive with regards to quantifying not only the

prudent level of Borrowing but more so the optimal level hereof.

1.5 Therefore in this Policy cognisance has been taken of the legislative guidelines

whilst more prescriptive guidelines are set for the optimal management and

monitoring of external funding sources to the Municipality’s avail based on sound

financial practices.

Policy Title: Borrowing Policy Financial Year: 2020/2021Status: Draft for Review - Submitted to Council on 3 1/03/2020 with Draft Budget per Item C/2/172/03/20

2

Page 3 of 17

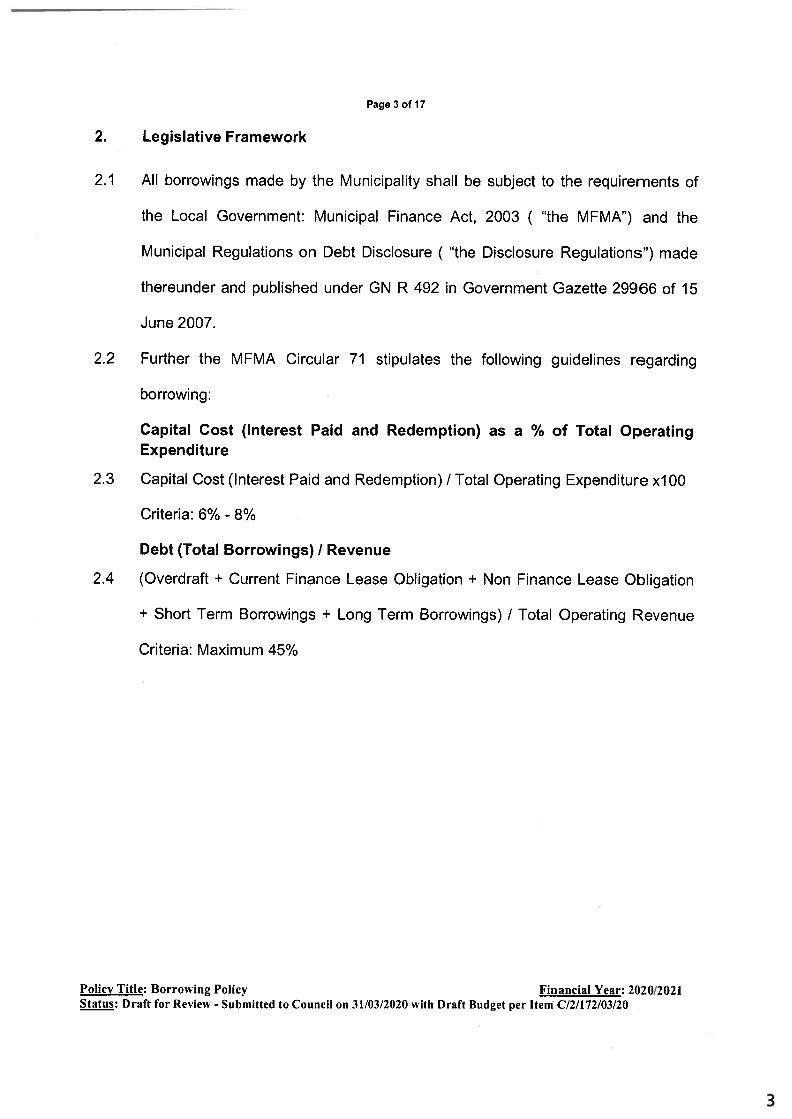

2. Legislative Framework

2.1 All borrowings made by the Municipality shall be subject to the requirements of

the Local Government: Municipal Finance Act, 2003 ( “the MFMA’) and the

Municipal Regulations on Debt Disclosure ( “the Disclosure Regulations’) made

thereunder and published under GN R 492 in Government Gazette 29966 of 15

June 2007.

2.2 Further the MFMA Circular 71 stipulates the following guidelines regarding

borrowing:

Capital Cost (Interest Paid and Redemption) as a % of Total OperatingExpenditure

2.3 Capital Cost (Interest Paid and Redemption)! Total Operating Expenditure xlOO

Criteria: 6% - 8%

Debt (Total Borrowings) I Revenue

2.4 (Overdraft + Current Finance Lease Obligation + Non Finance Lease Obligation

+ Short Term Borrowings + Long Term Borrowings)! Total Operating Revenue

Criteria: Maximum 45%

Policy Title: Borrowing Policy Financial Year: 2020/2021Status: Draft for Review - Submitted to Council on 3 1/03/2020 with Draft Budget per Item C/2/172/03/20

3

Page 4 of 17

3. Definitions

Any word or expression used in this policy shall, unless the context clearly

requires a different interpretation, bear the same meaning attached to it in the

MFMA or the Disclosure Regulations, as the case may be; provided that if there

is any conflict between a definition contained in the MFMA and a definition

contained in the Disclosure Regulations, then the definition contained in the

MFMA shall prevail.

4. Types of Debt

4.1 This policy applies to the debt incurred by the Municipality through the issue of

municipal debt instruments or in any other way.

4.2 Without derogating from the generality of the preceding subparagraph, this policy

will apply:

4.2.1

4.2.2

To any debt, whether short -term or long term;

To any debt incurred pursuant to any financing agreement, which includes

any of the following agreements under which the Municipality undertakes

to repay a long-term debt over a period of time:

4.2.2.1 Loan agreements;

4.2.2.2Leases;

Instalment purchase contracts;

Hire purchase arrangements;

4.2.3

4.2.4

Policy Title: Borrowing Policy Financial Year: 2020/2021Status: Draft for Review - Submitted to Council on 31/03/2020 with Draft Budget per Item C121172/03/20

4

Page 5 of 17

4.2.5 To any debt created by the issuance of municipal debt instruments,

including:

4.2.5.lAny note;

4.2.5.2Bond; or

4.2.5.3Debenture; and

4.2.6 To any contingent liability such as that created by guaranteeing a

monetary liability or obligation of another.

4.3 Types of loan financing

4.3.1 Annuity Loans enable the Municipality to provide for the redemption of

loans on an amortising basis which is generally the most cost effective

method of financing often referred to as vanilla funding;

4.3.2 Bullet Redemption Loans are attractive as interest on the loan is serviced

with the capital redemption only taking place at the end of the tenure of the

loan. However, this method is more costly as interest is paid on the full

debt throughout the term as the Capital does not reduce. This type of loan

also requires an annual contribution to a sinking fund, which in essence

then mimics the traits of an annuity loan although at a higher cost. The use

of such structure warrants a detailed motivation based on the benefits to

the implementation of the capital project;

Policy Title: Borrowing Policy Financial Year: 2020/2021Status: Draft for Review - Submitted to Council on 31/03/2020 with Draft Budget per Item C12/172/03/20

5

Page 6 of 17

4.3.3 Sculpted Repayment Loans offer a combination of the above two types, as

loans are sculpted according to the potential cash flows to be generated

from the capital project in future. For example the following can be included

in a sculpted loan:

4.3.3.1 A capital grace period in the first years of the development of

the capital project;

4.3.3.2 An incremental annual increase in the repayment in relation

to the projected growth in revenue from the project.

5. Principles Guiding Borrowing Practices

The following principle shall guide the borrowing practices of the Municipality,

namely:

5.1 Risk Management: The need to manage interest rate risk, credit risk exposure

and to maintain debt within specified limits is the foremost objective of the

borrowing policy. To attain this objective, diversification is required to ensure that

the Chief Financial Officer prudently manages interest rate and credit risk

exposure;

5.2 Cost of Borrowings : The borrowings should be structured to obtain the lowest

possible interest rate, on the most advantageous terms and conditions, taking

cognisance of borrowing risk constraints, infrastructure needs and the borrowing

limits determined by Legislation;

Policy Title: Borrowing Policy Financial \7car: 2020/2021

Status: Draft for Review - Submitted to Council on 3 1/03/2020 ith Draft Budget per Item C/2/172/03/20

6

Page 7 of 17

5.3 Prudence: Borrowings shall be made with care, skill, prudence and diligence. To

this end, officials of the Municipality are required to:

5.3.1 adhere to this policy, and other procedures and guidelines;

53.2 exercise due diligence;

5.3.3 prepare all reports in a timely fashion;

5.3.4 ensure strict compliance with all Legislation and Council policy.

6. Factors to be taken into account when borrowing

6.1 The Municipality shall take into account the following factors when deciding

whether to incur debt:

6.1.1 the type and extent of benefits to be obtained from the borrowing;

6.1 .2 the length of time the benefits will be received;

6.1.3 beneficiaries of the acquisition or development financed by the debt;

6.1.4 the impact of interest and redemption payments on both current and

forecast income;

6.1.5 the current and future capacity of the Municipality’s revenue base to pay

for borrowings;

6.1 .6 other current and projected sources of funds;

6.1.7 likely movements in interest rates for variable rate borrowings;

6.1.8 competing demands for funds;

6.1.9 timing of money market interest rate movements and the long term rates

on the interest rate curve.

Policy Title: Borrowing Policy Financial Year: 2020/2021

Status: Draft for Review - Submitted to Council on 3 1/03/2020 with Draft Budget per Item C12/172/03120

7

Page 8 of 17

6.1.lOThe Borrowing and other financial ratios norms, standards and

benchmarks applicable to comparable municipalities

6.2 The Municipality will, in general, seek to minimize its dependence on borrowings

in order to limit future revenue committed to debt servicing and redemption

charges.

7. Sources of Borrowings

7.1 Subject to any particular determination of the Council of the Municipality, the

Municipality may enter into financing agreements with:

7.1.1 Registered South African Banks;

7.1.2 The Development Bank of Southern Africa;

7.1.3 Vendors or suppliers of goods acquired under leases, installment

purchase contracts or hire purchase arrangements;

7.1 .4 Any other institution approved by the Council from time to time.

7.2 Unless the Council of the Municipality specifically determines otherwise, the

Municipality shall not incur any debt by the issuance of any municipal debt

instruments.

8. Short-term Debt

8.1 The Municipality may incur short —term debt only in accordance with and in

the circumstances contemplated in Section 45 of the MFMA.

Policy Title: Borrowing Policy Financial Year: 2020/2021Status: Draft for Revie - Submitted to Council on 3 1/03/2020 with Draft Budget per Item C/21172/03/20

8

Page 9 of 17

8.2 In particular, the provisions of section 45 (1) of the MFMA must be noted,

these requiring that the Municipality may incur short —term debt only when

necessary to bridge:

82.1 Shortfalls within a financial year during which the debt is incurred, in

expectation of specific and realistic anticipated income to be received

within that financial year; or

8.2.2 Capital needs within a financial year, to be repaid from specific funds

to be received from enforceable allocations or long-term debt

commitments.

8.3 Furthermore, as required by section 45 (4) of the MFMA, the Municipality

must pay off short term debt within the financial year.

9. Overdraft Facility

9.1 Overdraft facilities are regulated by Section 45(3) of the MFMA.

9.2 The current policy of the Council of the Municipality is that the Municipality

shall not have an overdraft facility.

10. LongTerm Debt

10.1 The Municipality may incur long-term debt only in accordance with and in the

circumstances contemplated in Section 46 of the MFMA.

10.2Long-term debt may be incurred only for the purposes contemplated in

Section 46(1) of the MFMA, namely:

10.2.1 Capital expenditure on property, plant or equipment to be used for the

purpose of achieving the objects ofIøcal government, as set out in

Section 152 of the Constitution; or

Policy Title: Borrowing Policy Financial Year: 2020/2021Status: Draft for Review - Submitted to Council on 3 1/03/2020 with Draft Budget per Iteni C/2/172103/20 21

9

Page 10 of 17

10.2.2 Re-financing existing long term debt, subject to section 46(5).

11. Council approval

Sections 45(2) and 46(2) require that sort-term debt and long-term debt respectively

may be incurred only if:

11.1A resolution of the Council, signed by the Mayor, has approved the debt

agreement;

11 .2The accounting officer has signed the agreement or other document whichcreates or acknowledges the debt.

12. Refinancing

12.1 Short-term debt may not be renewed or refinanced where that would have

the effect of extending the short-term debt into a new financial year.

12.2The Municipality may borrow in order to refinance long-term debt subject to

the conditions contained in Section 46(5) of the MFMA.

13. Early repayment of loans

13.1 No loans will be repaid before due date unless there is a financial benefit to

the Municipality.

13.2The Municipality shall therefore assess the nature and extent of any benefits

of early repayment before it makes any such early repayment.

13.3Cognisance must be taken of any early repayment penalty clauses in the

initial loan agreement, as part of the assessment.

14. Debt Repayment Period

14.lAs far as is practical, cognisance must be taken of the useful lives of the

underlying assets to be financed by the debt for purposes of determining the

duration of the debt.

Policy Title: Borrowing Policy Financial Year: 2020/202 1Status: Draft for Review - Submitted to Council on 31/03/2020 sith Draft Budget per Item C/21172/03/20 21

10

Page 11 of 17

14.2Should it be established that it is cost effective to borrow the funds for a

duration shorter than that of the life of the asset, the Municipality should

endeavour to negotiate terms for the loan agreement on a shorter duration.

15. Provision for Redemption of Loans

15.lThe Municipality may set up sinking funds to facilitate loan repayments,

especially when the repayment is to be met by a bullet payment on the

maturity date of the loan.

15.2Such sinking funds may be invested directly with the Lender’s Bank.

15.3The maturity date and accumulated value of such investment must coincide

with the maturity date and amount of the intended loan that is to be repaid.

16. Non-Repayment or Non-Servicing of Loan

16.1 The Municipality must honour all its loan obligations.

16.2Failure to effect prompt payment may jeopardise the Municipality’s credit

rating and adversely affect the ability of the Municipality to raise loans in the

future at favourable interest rates.

16.3ln addition to ensuring the timely payment of the loans, the Municipality

must adhere to the covenants stipulated in the loan agreements, including, in

particular, the following where applicable:

16.3.1 furnishing audited annual financial statements;

16.3.2 maintaining long-term credit rating;

16.3.3 reporting of material changes in financial position of the Municipality.

17. Borrowing for Investment Prohibited

The Municipality shall not under any circumstances borrow funds for the purposes of

Policy Title: Borrowing Policy Financial Year: 2020/2021Status: Draft for Review - Submitted to Council 01131/03/2020 ith Draft Budget per Item C/2/172/03/20 21

Page 12 of 17

investing them.

18. Interest Rate Risk Management

18.1 The impact of interest and capital redemption payments on both the current

and forecasted property rates and service charges through tariffs taking into

consideration the current and future capacity of the consumer to pay

therefore;

18.2 Likely movement in interest rates for variable rate borrowings. There are

benefits to be yielded from borrowing on a variable rate if rates are projected

to decrease in future, however it is prudent for the municipality to enter into

fixed interest rate loans to accurately budget for expenses incurred.

19. Loan Covenants

19.lThe municipality is to maintain a Loan Covenants Register detailing the

covenants entered into with each active loan agreement until date of maturity

thereof;

19.2Compliance with all loan covenants are to be monitored and reported on

semi-annually to ensure that the municipality does not breach any covenants;

19.3 Should a default be triggered based on non-compliance with loan covenants,

the municipality is to alert Council and send the related Financial Institutions

a written commitment to address the matter within a reasonable timeframe.

20. Level of gearing

20.1 Gearing is not only limited by the level of debt against the Total Operating

Income (excluding conditional grants) but also limited by other operational

Policy Title: Borrowing Policy Financial Year: 2020/2021Status: Draft for Review - Submitted to Council on 3 1/03/2020 with Draft Budget per Item C/2/172103/20 21

1)

Page 13 of 17

factors including compliance with the stipulations of the approved Liquidity,

Funding and Reserves Policy.

20.2 Should the municipality not be in contravention with any stipulations n the

Liquidity Policy or any other approved financial policy, then it is

recommended that the municipality maintain external gearing at levels not

lower than 25% but not higher than 35%.

20.3The ratios to be considered to take up additional borrowings are as follows,

unless in contravention with any loan covenants:

20.3.1 Estimated long-term credit rating of BBB and higher;

20.3.2 Interest Paid to Total Expenditure not to exceed 5%;

20.3.3 Total Long-term Debt to Total Operating Revenue (excluding

conditional grants and transfers) not to exceed 35%;

20.3.4 Operating Cash Surplus generated before loan repayments are made

covers the Total Annual Repayment at least I time;

20.3.5 Percentages of Total Annual Repayment (Capital and Interest) to

Operating Expenditure to be less than 10%.

21. Security

21 .1 Section 48 of the MFMA provides that the Municipality may provide security

for any of its debt obligations in any of the forms referred to in Section 48(2).

21.2Such security shall be given only pursuant to a resolution of the Council,

which resolution must comply with the provisions of Section 48(3), (4) and (5)

of the MFMA.

21.3Unless sufficient motivation is provided and other than for the provision of a

sinking fund for the redemption of a bullet loan, the provision of any security

Policy Title: Borrowing Policy Financial Year: 2020/2021Status: Draft for Review - Subniitted to Council on 31/03/2020 with Draft Budget per Item C/2/172/03/20 21

Page 14 of 17

against external borrowings, should be specifically motivated by the CFO for

approval.

22. Disclosure

22.1 Section 49 of the MFMA requires that any person involved in the borrowing

of money by a municipality must, when interfacing with a prospective lender

or when preparing documentation for consideration by a prospective investor,

disclose all relevant information in that persons possession or within that

person’s knowledge that may be material to the decision of that lender or

investor, and take reasonable care to ensure the accuracy of any information

disclosed.

22.2 In addition the Disclosure Regulations establish detailed requirements for the

disclosure of information to prospective lenders and investors. Regulations

2, 3, 4, 5, 15, 16 and 17 are of particular importance to the Municipality, given

the nature of the borrowings which it intends to make.

23. Guarantees

The Municipality may issue guarantees only in accordance with the provisions of

Section 50 of the MFMA.

24. Internal Control

The accounting officer shall ensure that mechanisms, procedures and systems are

put in place to ensure that:

24.1 Duties are separated in order to prevent fraud, collusion and other

misconduct;

24.2 loan agreements and contracts are kept in proper safe custody;Policy Title: Borrowing Policy Financial Year: 2020/2021Status: Draft for Review - Submitted to Council on 3 1/03/2020 with Draft Budget per keni C/2/172/03/20 21

IL’

Page 15 of 17

24.3 there is a clear delegation of duties relating to the borrowing process;

24.4 senior officials check and verify all transactions;

24.5 transactions and repayments are properly documented;

24.6 Code of ethics and standards is established and adhered to;

24.7 procedures relating to the borrowing process are established.

25. National Treasury Reporting and Monitoring Requirements

The Municipality shall promptly submit all returns and reports relating to borrowings

as required by National Treasury, including reports on the Municipality’s external

interest paid each month, and the quarterly itemization of all of its external

borrowings.

26. Other Reporting and Monitoring Requirements

26.lThe Municipality shall on a monthly basis perform the following control and

reporting functions relevant to borrowings:

26.1.1 Reconciliation of bank accounts;

26.1 .2 Payment requisition verification and authorization;

26.1.3 Completion of South African Reserve Bank returns;

26.1.4 Maintain schedule of payment dates and amounts;

26.1.5 Complete National Treasury Cash Flow returns;

26.1.6 Submission of particulars of borrowings as required by Section 71 of

MFMA;

26.1.7 Perform analysis of ratios;

26.1.8 Scrutinise loan agreements to ensure compliance with loan covenants.

Policy Title: Borrowing Policy Financial Year: 2020/2021Status: Draft for Review’ - Submitted to Council on 3 1/03/2020 with Draft Budget per Item C12/172/03/20 21

15

Page 16 of 17

26.2The Municipality shall on a quarterly basis perform the following control and

reporting functions relevant to borrowings:

26.2.1 Submit National Treasury Borrowings return

26.2.2 Prepare debt schedules for reporting to the Executive Committee.

27. Corporate Governance (Oversight)

Compliance with the various stipulations as documented in this Borrowing Policy need

to be monitored by the Chief Financial Officer and reported on to the Municipal Manager

on a monthly basis and to the Executive Mayor on a quarterly basis.

Where compliance has been breached the Chief Financial Officer must present an

action plan to correct the non-compliance. The Executive Mayor must monitor the

successful implementation of the corrective action plans and report progress to Council.

28. Transitional Arrangement

Upon adoption of this policy by the Council, the Municipal Manager in conjunction with

the Chief Financial Officer must determine the current performance levels of the

municipality against this Policy and present a plan of action towards achieving and

maintaining the stipulation as set out in this policy thereby utilising a more blended

funding mix for capital infrastructure investment.

The Council must approve an appropriate timeframe within which the municipality must

achieve the approved stipulations as set out in this Policy. The period between the date

of the policy adoption by Council and the target date for compliance shall be known as

the Transitional Period.

The Executive Mayor must report progress during the approved Transitional Period to

the Council.

29. Policy Management

Policy Title: Borrowing Policy Financial Year: 2020/2021Status: Draft for Review - Submitted to Council on 3 1/03/2020 with Draft Budget per Item C/2/172/03/20 21

Page 17 of 17

The Borrowing Policy forms part of the municipality overall financial objectives and

therefore forms part of approved Budget Policies. The policy must be reviewed at least

annually during the budget revision and presented to Council for approval.

30. Related Policies

This policy must be read in conjunction with the following other policies of the

Municipality:

30.1 Budget Process Policy;

30.2 Cash Management and Investment Policy;

30.3 Virement Policy

30.4 Liquidity, Funds and Reserves Policy.

30.5 Long term financial planning policy

31. Municipal Manager to Implement Policy

The Municipal Manager, as accounting officer of the Municipality, shall be

responsible for implementing this policy, provided that he or she may delegate in

writing any of his or her powers under this policy to any senior finance official of the

Municipality.

32. Commencement

This policy shall come into force on a date to be determined by Council of the

Municipality.

Policy Title: Borrowing Policy Financial Year: 2020/2021Status: Draft for Review - Submitted to Council on 3 1/03/2020 with Draft Budget per Item C/2/172/03/20 21

17

/\rneUfti I

BITOU MUNICIPALITY

(J

kt

DRAFT PETTY CASH POLICY

2020/21

POLICY TITLE: PETTY CASH POLICY FINANCIAL YEAR: 2020/21

Draft Review, submitted to Council on 31/03/2020 with Draft Budget per Item C/2/172/03/30

18

Table of Contents1. INTRODUCTION .3

2. OBJECTIVES OF POLICY 3

3. LEGISLATIVE FRAMEWORK 3

4. AUTHORISED LIMIT FOR PETTY CASH 3

5. PETTY CASH PURCHASES 4

6. APPROVED LIST OF PETTY CASH PURCHASES 5

7. SAFEGUARDING 6

8. TRANSFER OF PETTY CASH BOX AND KEYS 6

9. OTHER 7

10. PETTY CASH REPLENISHMENT 7

11. DISBURSEMENT OF PETTY CASH 8

12. SHORTAGES AND LOSSES 9

13. INTERNAL CONTROLS 9

14. REPORTING 9

15. GENERALADMINISTRATION 10

16. REVIEW 10

17. SHORT TITLE 10

POLICY TITLE: PETTY CASH POLICY FINANCIAL YEAR: 2020/21

Draft Review, submitted to Council on 31/03/2020 with Draft Budget per Item C/2/172/03/30

19

1. INTRODUCTION

1.1. Petty cash is small amount of discretionary funds in the form of cash used for

expenditure where it is impractical to follow the official procurement processes

due to the nature of the goods and/or services required.

2. OBJECTIVES OF POLICY

2.1. The objectives of the policy are to:

2.1 .1. Ensure goods and services are procured by the municipality in accordance

with authorized processes only,

2.1.2. Ensure that the municipality has and maintains an effective petty cash

system for expenditure control,

2.1 .3. Ensure that sufficient petty cash is available when required,

2.1.4. Ensure that the items required to be procured are approved petty cash

items.

3. LEGISLATIVE FRAMEWORK

3.1. The legislative framework governing petty cash are:

3.1.1. The Local Government Municipal Finance Management Act, Act 56 of 2003,

3.1.2. The Municipal Supply Chain Management Regulations, Regulation 868,

published under Government Gazette 27636, 30 May 2005,

3.1.3. The municipal supply chain management policy.

4. AUTHORISED LIMIT FOR PETTY CASH

4.1 The Petty Cash float will be maintained at RiO 000.00 per month.

4.2 The requisitioned amount must not exceed a maximum amount of R2 000.00 per

transaction as outlined in the Municipal Supply Chain Management Policy unlessPOLICY TITLE: PETTY CASH POLICY FINANCIAL YEAR: 2020/21

Draft Review, submitted to CounCil on 31/03/2020 with Draft Budget per Item C/2/172/03/30

2fl

otherwise motivated and approved by the Chief Financial Officer with theprovision that the amount my not exceed the limits as determined in accordancewith the Municipal Supply chain regulations applicable to petty cash purchases.

Section 55. PETTY CASH PURCHASES 4 amended

4.1 The Chief Financial Officer must delegate personnel from the ExpenditureManagement Division to keep petty cash registers and make petty cashpayments up to the maximum amount as allowed per transaction.

4.2 Petty cash is restricted to cash purchases up to a transaction value of R500,00VAT included.

4.3 Petty cash purchases may not deliberately be broken up over two (2) or moretransaction claims or be split over more than one (1) day for the same items inorder to fall within the determined threshold of R500,00 VAT included.

4.4 To limit the risk of cash handling and misuse of petty cash, purchases from theminimum amount of R501 ,00 up to the maximum amount of R2 000,00 will bepaid through a SCM Petty Cash Order System subject to the following conditions:

4.4.1 The originator of the SCM order obtains a quotation from the supplier orservice provider,

4.4.2 The Director and/or delegated signs the quotation, reflects a U-Key andwrites: “Request for Petty Cash Order” as an approval for petty cashprocurement,

4.4.3 The originator submits the quotation to Creditors Section for processing,4.4.4 The Creditors Clerk completes an SCM Petty Cash Order and records the

transaction in the SCM PCO Register,

4.4.5 The Creditors Clerk will issue an SCM Petty Cash Order Number (as perregister),

4.4.6 The SCM PCO voucher will then be submitted to the Manager: Expenditure

and/or delegated official for approval,

POLICY TITLE: PETTY CASH POLICY FINANCIAL YEAR: 2020/21

Draft Review, submitted to Council on 31/03/2020 with Draft Budget per Item C/2/172/03/30

21

4.4.7 On receipt of the P00 voucher, the originator would then collect the goods

and be issued with an invoice which he/she will submit to Creditors Section

for payment,

4.4.8 The Creditors Clerk will then process a direct payment to the supplier.

4.5 The SCM Petty Cash Order Register will be submitted to the Manager:

Expenditure as part of monthly reporting.

Section 66. APPROVED LISTOF PETTYCASH PURCHASES amended

6.1. Approved items for petty cash purchases, but not limited:

6.1 .1 Refreshments and catering/entertainment for official meetings and events,

6.1 .2. Pay-as-you-go cellular airtime,

6.1.3. Purchases of an urgent nature where it is impractical to follow the official

procurement process, and/or

6.2. Approved items for petty cash reimbursements through direct payment method:

6.2.1. Materials for urgent repair work not kept or not available at the municipal

stores;

6.2.2. Ad hoc stationery items;

6.2.3. Refreshments and catering/entertainment for official meetings and events,

6.2.4. Materials of special nature only available at specific suppliers; and

6.2.5. Purchases of an urgent nature where it is impractical to follow the official

procurement processes.

6.3. Departments may not utilize the petty cash for the following items:

6.3.1. Approved store items which are kept at the municipal stores,

6.3.2. Any items which can be classified as assets,

6.3.3. Subsistence and travel claims;

6.3.4. Safety equipment and clothing such as clothes, ear protectors, safety

glasses, etc.,

6.3.5. Wages for contract work performed which may or may not include material,

6.3.6. Fuel purchases,

POLICY TITLE: PETTY CASH POLICY FINANCIAL YEAR: 2020/21

Draft Review, submitted to Council on 31/03/2020 with Draft Budget per tern C/2/172/03/30

22

6.4. Petty cash specified in 6.2 above must be approved by the Chief Financial Officeror Manager: SCM and/or any delegated senior official prior to the transactionbeing processed.

7. SAFEGUARDING

6.1 The petty cash box is to be safeguarded in a lockable safe and locked away whennot in use during normal business hours.

6.2 The keys of the petty cash box must be safeguarded by the petty cash official.6.3 After normal business hours, the responsible petty cash official must lock away

the petty cash box in a fire and theft resistant safe as identified.

6.4 The petty cash officia’ is responsible to keep the keys of the cash box, whereasthe Assistant Accountant: Creditors is responsible to keep the keys of the safe.

8. TRANSFER OF PETTY CASH BOX AND KEYS

8.1. When the petty cash box is transferred to another delegated official, petty cashmust first be reconciled and be verified by the Asst. Accountant: Creditors beforebeing officially handed over. The new incumbent must sign for the petty cash boxas well as for the keys to the box.

8.2. The Asst. Accountant: Creditors will be responsible to record the transfer of thebox as well as the transfer of the keys in the appropriate register and also ensure

that the officials sign the register.

8.3. The Asst. Accountant: Creditors must ensure that the new holder of the pettycash box is aware of his/her responsibilities relating to the petty cash transactionsas well as the contents of this policy.

8.4. For proper segregation of duties, the following should apply: -

8.4.1. only the official delegated official may have the key to the petty cash box,8.4.2. the Asst. Accountant: Creditors must ensure that the petty cash box in the

lockable safe,POLICY TITLE: PETIY CASH POLICY FINANCIAL YEAR: 2020/21

Draft Review, submitted to CounCil on 31/03/2020 with Draft Budget per Item C/2/172/03/30

23

8.5. The spare keys of the petty cash box must be in the possession Manager:Expenditure and the spare key of the safe must be in the possession of the ChiefFinancial Officer.

9. OTHER

9.1. The maximum amount allocated in a petty cash box will be determined from timeto time by the Chief Financial Officer, based on the operational requirements ofthe municipality and the risk of safeguarding petty cash box.

9.2. When the amount in petty cash box is increased, the Accountant: Creditors mustdraw a cheque and for encashment with the municipal banker.

9.3. The responsible petty cash official must sign for the acceptance of the increasedcash amount together with the Asst. Accountant: Creditors and verified by theAccountant: Creditors.

10. PETTY CASH REPLENISHMENT

10.1.Petty cash replenishments will only be done after having fully exhausted theavailable cash in the box.

10.2. A proper petty cash register must be kept where each disbursement of petty cashtransactions are recorded.

10.3. The minimum detail to be recorded in the petty cash register is:10.3.1. department name,

10.3.2. U-Key to allocate petty cash transaction,10.3.3. name of vendor,

10.3.4. date,

10.3.5. amount issued, and

10.3.6. name of person.

10.4. The petty cash register with all petty cash vouchers, receipts or slips must beattached to the cheque and/or request for payment voucher.

POLICY TITLE: PETTY CASH POLICYFINANCIAL YEAR: 2020/21

Draft Review, submitted to Council on 31/03/2020 with Draft Budget per Item C/2/172/03/30

24

10.5. The Asst. Accountant: Creditors must check the petty cash float against the pettycash payment vouchers.

10.6. The amount must be the difference between the petty cash float and themaximum allowable amount allocated to the petty cash box.

11. DISBURSEMENT OF PETTY CASH

11.1.All petty cash disbursements must be completed on the prescribed petty cashvoucher, authorized by the delegated official of each department as approved byCouncil in terms of the delegation of authorities.

11 .2. The authorized official must ensure that funds are available in the budget priorthe submission of claims. The Budget Office must also provide with confirmationto the U-Key utilized and the availability of funds.

11.3.An invoice or an original receipt, clearly indicating the description of itemspurchased must support the petty cash voucher.

11 .4. The authorized official or delegated person must sign for the acceptance of thepetty cash monies and ensure that the monies are correct. Once paid out, theExpenditure Management will take no responsibility if the money is not receivedby the originator of the transaction.

11 .5. In the case where a petty cash advance has been granted: the recipient of theadvance must submit an invoice and/or original receipt within five (5) workingdays from receipt of the advance to the petty cash official from when he/shereceived the cash advance.

11 .6. Where proof of expenditure could not be provided on petty cash advances withinthe prescribed period, the advance will automatically be deducted from therespective employee’s salary.

POLICY TITLE: PETTY CASH POLICY FINANCIAL YEAR: 2020/21

Draft Review, submitted to Council on 31/03/2020 with Draft Budget per Item C/2/172/03/30

12. SHORTAGES AND LOSSES

12.1. The holder of the petty cash box will be held accountable for losses and shortagesunless there is physical evidence of breaking-in and no act or omission on thepart of the relevant official contributed to the loss.

12.2. All the identified shortages and/or losses must immediately be reported to theChief Financial Officer and paid in by the holder of the petty cash box.

13. INTERNAL CONTROLS

13.1.Surprise petty cash audits must be concluded on random basis throughout thefinancial year.

13.2. Petty cash reconciliations with the general ledger must be reconciled before 30June of each year and the petty cash replenished to the maximum amountallowed.

13.3. The petty cash reconciliations must be verified by the Accountant: Creditors andapproved by the Manager: Expenditure. A copy of the register must be submittedto the Manager: Annual Financial Statements for audit purposes.

14. REPORTING

14.1. A monthly reconciliation report, including the total amount of petty cashpurchases for that month, must be prepared by the petty cash holder.

14.2. The monthly reconciliation report of petty cash must be reviewed by theAccountant: Creditors or delegate and verified by Manager: Expenditure.

POLICY TITLE: PETTY CASH POLICYFINANCIAL YEAR: 2020/21

Draft Review, submitted to Counci’ On 31/03/2020 with Draft Budget per Item C/2/172/o3/30

26

15. GENERAL ADMINISTRATION

15.1 Petty cash will be reimbursed from Monday to Thursday between 14h00 until16h00.

16. REVIEW

16.1.This policy will be reviewed annually to be in line with municipal practices andlegislation.

17. SHORT TITLE

17.1. This policy shall be called the Petty Cash Policy of the Bitou Municipality.

POLICY TITLE: PETTY CASH POLICY FINANCIAL YEAR: 2020/21

Draft Review, submitted to Council on 31/03/2020 with Draft Budget per Item C/2/172/03/30

27

I

Page 0 of 44

CREDIT CONTROL ANDDEBT COLLECTIONPOLICY2020/202 1

Draft Review: MARCH

rexufe 0 (p)

2O2O!2Q24.

Policy Title: Credit Control and Debt Collection PoIic Financial ear: 2020-2021DrlHRc,IthrL[ J t Cu ljnI )nB L (

Dft—1yiew----Miur-e4i-34)-24J

Formatted: Fout: 10 pt

Formatted: Font: 9 pt

28

Page I of 44

Whereas section 96 of the Local Government: Municipal Systems Act No. 32 of

2000 (hereinafter referred to as the Systems Act) stipulates that a municipality

must adopt, maintain and implement a credit control and debt collection policy;

And whereas section 97 of the Systems Act stipulates what must be provided for

in the policy;

Now therefore the Municipal Council of Bitou Local Municipality accepts the

following Credit Control and Debt Collection Policy:

Formatted: Font: 10 pt

Formatted: Font: 9 pt

Policy Title: Credit Control and Debt Collection Policy Financial Year: 2020-2021jju Dritt Rc.\ (.0 I’m 1 (1k ( tm. n ii ) II B I.u It m ( I i

29

Page 2 of 44

TABLE OF CONTENTS

1. DEFINITIONS 4

2. OBJECTS OF POLICY 8

3. PRINCIPLES OF POLICY 9

4. DUTIES AND FUNCTIONS 11

5. PERFORMANCE MEASUREMENT 15

6. REPORTING 17

7. CUSTOMER CARE POLICY 18

8. CREDIT CONTROL POLICY 31

9. DEBT COLLECTION POLICY 37

10. SHORT TITLE 42

ANNEXURE A - PERFORMANCE MEASUREMENT 43

ANN EXURE B — CUSTOMER CARE AND DEBT COLLECTION 45

ANNEXURE C - ARRANGEMENT FOR PAYMENT 48

P01kv Title: Credit Control and Debt Collection Policy Financial \ear: 2020-2021jj F)rT R \L UI’flI ( t) (. mcii n iih F) It I ctJLji)i._..j

_Formatted: Font: 10 pt

,

30

Page 3 of 44

BITOU LOCAL MUNICIPALITY

CREDIT CONTROL AND DEBT COLLECTION POLICY

- Formatted: Left

DEFINITIONS

For the purposes of this policy the wording or any expression will have the

same meaning as contained in the Act, accept where it is explicitly

indicated otherwise and means:

1.1 “occupant” — any person that occupies any property or portion thereof,

without taking cognisance of the capacity in which he/she occupies the

property;

1.2 “property” — any portion of land, of which the boundary has been

determined, within the jurisdiction of the municipality;

1.3 “owner”

(a) the person in whose name the title of the property is rightfully

vested;

(b) in the case where the person in whose name the property is

rightfully vested becomes insolvent or deceased, that person under

who the administration or control of such a property is vested as

curator, trustee, executor, rightful manager, liquidator, or any other

legal representative;

(c) in any event where the municipal council cannot determine the

identity of such person, any person who may rightfully benefit from

such stand or any building thereon;

(d) in the case of a stand for which a rental agreement of 30 years or

longer have been adopted, the hirer thereof;

(ei with regard to:-

Formatted: Numbered ÷ Level: 1 + Numbering Style: a, b,c,+ Start at: 1 + Alignment: Left + Aligned at: 1,27cm +

(i) a portion of land demarcated on a sectional title plan which is Tabafter: 1,9cm+tndentat: 1,9cm

registered in terms of the Sectional Titles Act No. 95 of 1986, ormatted: Font: 10 p1

Formatted: Font: 9 pt

Policy Title: Credit Control and Debt Collection Polic Financial \ ear: 2020-2021tlus: F)r::t R,\ IC\V. suhniHct to C ‘ccci] ‘n ‘ it]’ Dr,t ]tu,Lct o,.-r tOm (2] 2

-

Status: Draft Re; jew ‘sTarch 2021)

31

Page 4 of 4-4

and without limiting the aforementioned stipulations, the

developer or governing body with regard to the common

property; or

(ii) a portion as defined in the Sectional Titles Act, the person in

whose name that portion is registered in terms of a sectional

title deed, including the legally appointed representative of

such a person;

(f) Any corporate body, including but not limited to:

(i) A company registered in terms of the Companies Act No. 61

of 1973, a trust inter vivos, trust mod/s causa, a close

corporation registered in terms of the Close Corporations Act

No. 69 of 1984, and a Voluntary Association;

(ii) Any local-, provincial-, or national authority;

(iii) any council or governing body instituted in terms of any

legislation enforceable in the Republic of South Africa; and

(iv) any embassy or other international entity;

1.4 “rightful representative” — the person or organisation legally appointed

by the municipal council to act on behalf of the municipal council or to

perform a duty on behalf of the municipal council;

1.5 “Chief Financial Officer” the person, appointed by the municipal

council, in control of the finances regardless of the title attached to the

post;

1.6 “client” any occupant of a property where to the municipality agreed to

deliver services or already delivers, or if the occupant is not responsible,

the owner of the property;

1.7 “Engineer” — the person in charge of the civil and electrical sections of

the municipality;

1.8 “Municipal Manager” — the person appointed in terms of section 82 of the

Local Government: Municipal Structures Act No. 117 of 1998, including any

Formatted: Font: 10 pt

Formatted: Font: 9 pt

Policy Title: Credit Control and Debt Collection Polk Financial Year: 2020-2021Stalus: raft Rovew. rhmtttod to CuItc1 ‘n 31:3 3fl.: ‘sit!’ Dr-it DiI-ct ocr ltnt C2H73O5:2i), - -

i-e-,: Dr,,f[ Review !areh 2l24l

32

Page 5 of 44

person acting in the position or to whom the authority have been

delegated;

1.9 “municipal services” — the services provided by the municipality, such

as the provision of water and electricity, refuse removal, and sewerage

removal, where service charges are levied;

1.10 “municipal account” an account reflecting the costs for services

rendered by the municipality or any authorised or contracted services

provider and/or property tax in the form of, but not limited to:-

(a) “yearly account” delivered yearly and in the levies indicate property tax

and/or building clause, availability fees, sewerage removal and refuse

removal; and

(b) “monthly account” delivered monthly and indicates electricity,

water, sundry levies, housing rental fees and instalments, as well as

the monthly instalment of yearly services paid on in monthly

instalments;

1.11 “municipality” — the organisation responsible for the collection of funds

and provision of services to clients of Bitou Local Municipality;

1.12 “council” —the municipal council of Bitou Local Municipality;

1.13 “interest” — a cost levied with the same legal preference as service tariffs

and calculated against an interest rate determined by the council from time

to time;

1.14 “equipment” a building or other structure, pipe, pump, wiring, cable,

meter, machine or any fittings;

1.15 “defaulter” — a person owing money to the municipality after the due date

has lapsed; and

1.16 “Act” — the Local Government: Municipal Systems Act No. 32 of 2000, as

amended from time to time.

Policy Title: Credit Control and Debt Collection Polic Financial ear: 2020-2021aWs: Drab R,s c’ hm!t.d 0 (0uncI 031 3:32 1)-o I ocr Itcin (-21Stotu: l)-,-aft—R-e4ew \larch40-2-4}

Formatted: Font: 10 pt

Formatted: Font: Opt

33

Page 6 of 44

2. OBJECTS OF THE POLICY

The objects of the policy are to:

2.1 provide a framework within which the municipal council can exercise itsexecutive and legal authority with regard to credit control and debtcollection;

2.2 ensure that all funds owed and due to the municipality are collected in afinancially sustainable manner, and utilised in the best interest of thecommunity, residents and taxpayers;

2.3 establish a framework for customer care and support to indigenthouseholds;

2.4 establish credit control measures and to describe the sequence of steps;2.5 draft procedures and mechanisms with regard to credit control and debt

collection; and

2.6 Establish realistic objectives with regard to credit control and debt collection.3. PRINCIPLES OF THE POLICY

3.1 The administrative integrity of the municipality must be maintained at all

times. The democratically elected councillors are responsible for policy

making, whilst it is the responsibility of the Municipal Manager to executesuch policies;

3.2 Consumers must complete an official application form wherein they requestthe municipality to connect them to service connection points. Owners must

in writing take responsibility for the debt as debtor of last resort and liablefor payment of any outstanding balance due and owing to the municipality.Existing consumers may be requested from time to time, as determined by

the Municipal Manager, to complete new application forms;

3.3 Copies of the application form, preconditions for service delivery andextracts from the credit control and debt collection policy and regulations

Policy Title: Credit Control and Debt Collection PoIic Financial Year: 2020-2021stihm:itod to C,’uncil n 31

Formatted: Font: lOpt

, Formatted: Font: 9 pt

34

Page 7 of 44

of the council must on request by consumers be provided at costs

determined by the council, if applicable;

3.4 Accounts must be distributed timeously and must be accurate and easily

understandable;

3.5 The consumer is entitled to access to pay points and to a selection of

reliable payment methods;

3.6 The consumer is entitled to a good, effective and reasonable answer to

enquiries I appeals, and may suffer no disadvantage during the

processing of a reasonable enquiry I appeal;

3.7 Measures to enforce payments must be applied consistently and

effectively;

3 8 Unauthorised usage, connection and cutoffs, fiddling with or theft of meters,

service provision equipment and the reticular network, and any fraudulent /

illegal conduct with regard to the provision of municipal services will lead to

termination of service delivery, the imposition of heavy fines, forfeiting of

rights and I or public prosecution;

3.9 Both incentives and discouragement can be used in collection procedures;

3.10 The collection procedures must be cost effective;

3.11 Results will be reported and monitored regularly and effectively;

3.12 Application forms will be used to, amongst others, categorise consumers on

the basis of credit risk and to determine service levels and deposits for

services;

3.13 Goals / objectives for performance in both customer care and debt collection

must be established and pursued and corrective measures for under

performance must be instituted;

3.14 Where practically feasible, the customer care and debt collection policies

will be handled separately and will the organisational structure reflect it as

separate sections; and

3 15 The support of the principle to provide services in exchange for the payment

of overdue debts.

Policy Title: Credit Control and Debt Collection Polic Financial ear: 2020-2021Dra Re\ icr . rrbrn iiicd to ( uncii ‘n 3 /3 2Q20 woir Drr i F3::ri/er cr Item ( 2 I 2 322t)

Status: Draft-Res-lew March 2024

Formatted: Font: 10 p1

‘ Formatted: Font: 9 p1

35

Page 8 of 44

4. DUTIES AND FUNCTIONS

4.1 Duties and functions of the Municipal Council:

(a) To approve a budget in line with the council’s IntegratedDevelopment Plan;

(b) To institute taxes and tariffs and to determine service costs, fees andfines in order to finance the budget;

(c) To provide sufficient funds to provide access to basic services for thepoor;

(d) To make provision for bad debts, corresponding with the paymentrecord of the community, ratepayers and residents as reflected in thefinancial statements of the municipality;

(e) To establish a goal / objective for improving debt collection,

corresponding with acceptable accounting relationships and thecapacity of the Municipal Manager;

(f) To approve a reporting framework with regard to customer care,credit control and debt collection;

(g) To consider and approve regulations that will give effect to theexecution of the council’s policy;

(h) To monitor the performance of the Municipal Manager in the areasof customer care, credit control and debt collection through theExecutive Mayoral Committee;

(i) To adjust the budget if the council’s goal / objective for customercare, credit control and debt collection is not attained;

(j) To institute disciplinary steps and/or legal action against councillors,

officials and agents who do not execute the council’s policy andregulations or act improperly in terms thereof;

(k) To note a list of attorneys who will represent the council in all legal

matters relating to debt collection;

(I) To delegate adequate powers to the Executive Mayoral Committee,Municipal Manager and service providers to execute and monitor thecustomer care-, credit control- and debt collection policy; Formatted: Foot: 10 pt

Formatted: FOnt: 9 pt

Policy Title: Credit Control and Debt Collection Polic Financial \ear: 2020-2021LItu i)rt Rc.\ s inu d tc C i,nc 01 \Inl)lBli _ I m C

36

Page 9 of 44

(m) To adequately capacitate the municipality’s finance department toexecute credit control and debt collection, or to alternatively appoint

debt collection agents;

(n) To support the Municipal Manager in the execution of his/her duties;

(o) To provide funds for the training of personnel; and

(p) To annually review the Credit Control and Debt Collection Policy.

4.2 Duties and functions of the Executive Mayor:

(a) to ensure that the council’s budget, cash flow and goals / objectives

with regard to debt collection are executed in terms of official policy

and regulations;

(b) To monitor the performance of the Municipal Manager in the

implementation of policy and regulations;

(c) to revise and evaluate policy and regulations to improve the

effectiveness of procedures, mechanisms and processes with

regard to customer care, credit control and debt collection, and

(d) To report to the council.

4.3 Duties and functions of the Municipal Manager:

(a) to implement good customer care;

(b) to implement the council’s policy with regard to customer care, credit

control and debt collection;

(c) to institute and maintain an appropriate accounting system;

(d) to distribute accounts to clients;

(e) to claim payments on due dates;

(f) to impose fines with regard to non-payment;

(g) to utilise payments received;

(h) to collect outstanding debts;

(i) to implement “Best Practices”;

(j) to provide a variety of payment methods; Formatted: Font: 10 p1

Formatted: Font: 9 p1

Pollcv Title: Credit Control and Debt Collection Policy Financial Year: 2020-2021alu l)rit Rc.\ c hnii (I t ( n I F) itt _Lt I nt ( I

37

Page 10 of 44

(k) to determine customer care-, credit control- and debt collection

measures;

(I) to determine work procedures for the following: public relations,

arrangements, disconnection of services, summonses, attachment

of property, sales in execution, debt write-offs, sundry debtors and

legal processes;

(m) To appoint a firm of attorneys to execute legal proceedings (e.g.

attachment of and sale in execution of property, attachment order in

terms of compensation, etc.);

(n) to determine performance targets for staff;

(o) to appoint staff in terms of the council’s recruitment and selection

policy to execute the council’s policy and regulations;

(p) to delegate appropriate functions to Heads of Department;

(q) to determine control procedures; and

(r) To monitor contracts with service providers with regard to credit

control and debt collection.

4.4 Duties and functions of communities, taxpayers and residents:

(a) To fulfil certain responsibilities based on privilege and/or the right to

use and enjoy public amenities and municipal services;

(b) to pay on due dates all service fees, property tax and other taxes,

levies and tariffs as determined by the municipality;

(C) To obtain a duplicate account at the municipal help desk in instances

where the account is not delivered within the normal account cycle;

(d) To inform the municipality when services are no longer needed at a

specific service point, and of any change in address;

(e) To respect the mechanisms and processes of the municipality when

exercising their rights;

(f) To provide reasonable access to their property to allow municipal

officials to execute their functions;

Formatted: Font: 10 pt

Formatted: Font: 9 pt

Pokey Title: Credit Control and Debt Collection Policy Financial Year: 2020-2021Stdi1J: l)ri Rc ic. .t:bmiicd t’ C,iicil n 2 i!32fl2: \v{i;’ i)rii B.iet ir lwm C 21

38

Page 11 of 44

(g) To adhere to the regulations and other legislation of the municipality;and

(h) To refrain from fiddling with municipal property and services.

4.5 Duties and functions of councillors:

(a) to hold regular ward meetings (Ward Councillors),(b) to adhere to municipal policy and regulations and to convey this

information to residents and ratepayers;

(c) to adhere to the Code of Conduct for Councillors;(d) to provide input with regard to applications for indigent households

as and when requested and

(e) to, as policy-makers, refrain from interfering with the administrativeprocess.

5. PERFORMANCE MEASUREMENT (Appendix A)

The council must institute the necessary mechanisms to set and measureperformance against targets with regard to debt collection, customer careand administrative performance, and take corrective steps in order topromote credit control and debt collection.

5.1 Income Collection Targets:-

The council must set targets that include the following:(a) The council wants to collect all monies owed to the municipality. The

council is aiming to achieve a 95% collection in the

2O2O2O211&:2O1financialyear.

5.2 Customer Care Targets:

The council must set targets that include the following:

(a) response times with regard to enquiries by clients;(b) the date on which the first account must be rendered to customers;(c) the time frame for the reconnection of services; and Formatted: Font: 10 pt

_______________________I

‘Formatted: Font: 9 Pt

P00ev Title: Credit Control and Debt Collection Polic Financial \ear: 2020-2021,S1JIU Dri

I I m C

39

Page 12 of 44

(ci) The meter reading cycle.

5.3 Administrative Performance:

The council must set targets that include the following:

(a) cost effectiveness of debt collection;

(b) enquiry and appeal procedures; and

(c) Implementation mechanism relationships.

6. REPORTING

6.1 The Chief Financial Officer must report on a monthly basis andappropriate format to the Municipal Manager in order to allow the latter toreport to the Executive Mayor in terms of section 99 of the Act, read withsection 100 (c). This report must include:

6.1 .1 Statistics with regard to high-level debt collection (number of clients,enquiries, default arrangements, increase or decline in outstandingdebtors). Where possible the statistics must be divided according to wards,businesses (trade and industry), household, government, institutional andany other divisions; and

6.1.2 Performance in all areas against the targets / goals agreed upon in terms ofparagraph 5 of this document.

6.2 Should the council in the opinion of the Chief Financial Officer not receiveincome equivalent to the income projected in the annual budget asapproved by the council, the Chief Financial Officer will report this withmotivation to the Municipal Manager in terms of section 28(2)(a) of theMunicipal Finance Management Act as amended. The Municipal Managerwill concur with the Chief Financial Officer and immediately request that thebudget be adjusted to realistically attainable income levels (realisticanticipated revenue).

6.3 The Executive Mayor must report to the council on a quarterly basis asstipulated in section 99(c) of the Act.

Formatted: Font: 10 pt

Formatted: Font: 9 p1

Policy Title: Credit Control and Debt Collection Policy Financial Year: 2020-2021Sub [)rb RL\IL\ pm d ( un n I ii T)

40

Page 13 of 44

7. CUSTOMER CARE POLICY

7.1 Aim

To focus on the needs of the consumer in an accountable and pro-activemanner, to improve the payment of service fees and to establish a positiveand cooperative relationship between the persons responsible forpayment for services and the municipality and, where applicable, theservice provider.

7.2 Communication and feedback

7.2.1 The municipality must, within its financial and administrative capacity,undertake a process to compile a budget, which include the targets forcredit control and debt collection and communicate these targets to thebroader community;

7.2.2 The council’s policy with regard to Customer Care, Credit Control andDebt Collection, or appropriate extracts thereof, must be available inEnglish, Afrikaans and Xhosa, must be available via general publicationand on specific request, and must be kept at municipal offices forinspection;

7.2.3 The council must endeavour to release a regular newsletter focusing oncustomer care and debt collection matters;

7.2.4 The Ward Councillors must hold regular ward meetings during whichemphasis must be placed on customer care and debt collection matters;and

7.2.5 The press must be motivated to provide prominent coverage of councilmatters with regard to customer care, credit control and debt collection,and must be invited to attend council and committee meetings where suchmatters are discussed.

Policy Title: Credit Control and Debt Collection Policy Financial Year: 2020-2021lus: F)r.iII Re’, e. suhmicd (,‘unc’I n il [ct-,.: I:.n_cJZi..u

Formatted: Font: 10 pt

Formatted: Font: 9 pt

41

Page 14 of 44

7.3 Metering system

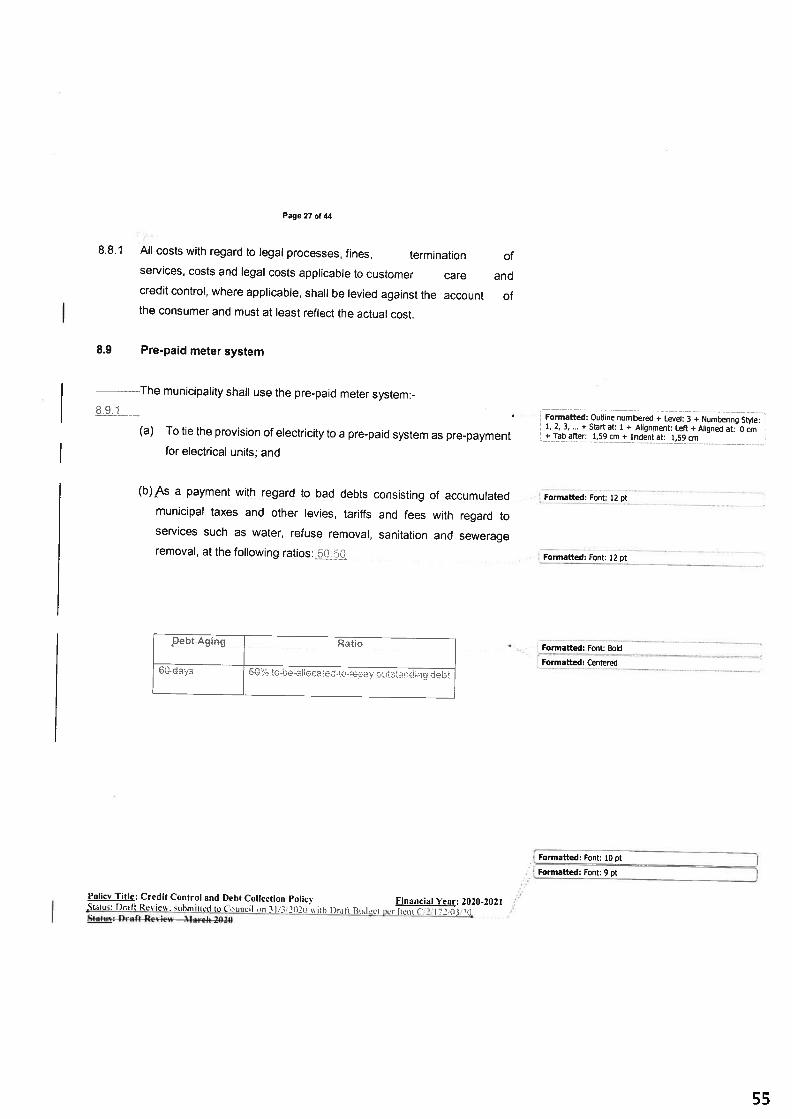

73.1 The municipality must endeavour to, within practical and financial limits

provide meters for all measurable services to each paying consumer;

7.3.2 If possible, all meters must be read on a monthly basis in cuce5 ofnnoraima:ev 35 days. Should the meter -—----not be read on a monthly

basis,

_____the

council may estimate consumption.

c-tecms-of tine eoLi -oeeiet,oeai pc°o’

7.3.3 Consumers are entitled to submit enquiries with regard to the confirmationof meter readings and are entitled to meter readings which is as accurate

as can reasonably be expected, but can be held liable for the costs thereof;7.3.4 Consumers will be informed of the replacement of meters; and

7 3 Where a meter has been installed for a service, but cannot be read due to

financial or manpower limitations, or due to circumstances outsidethe

--- control of the municipality or its legal agent, and the consumer’saccount is calculated on average consumption, the account that followson the —-——reading of metered consumption must reflect the differencebetween actual consumption and average consumption, and theresulting credit-or debit adjustments.

715

7.4 Accounts and invoices

7.4.1 Consumers will receive from the municipality an understandable and

accurate account that consolidates all service fees for the property;

7.4.2 Accounts will be drawn up in accordance with the meter reading cycle,and payment dates will be matched with the date of the invoice;

7.4.3 Accounts will be sent monthly in cycles of approximately 35 days to the

most recent address recorded at the municipality or its legal agent;

7.4.4 It is the responsibility of the consumer to ensure that his/her postal

address and other contact details are correct;

7.4.5 In cases where accounts are not received, the responsibility to pay the

account timeously resides with the consumer;

• .. Formatted: Font: (Default) Aria)

Formatted: Outline numbered + Level: 3 + Numbering Style:1, 2, 3, ... + Start at: 4 + Aligement: Left + Aligeed at: 0 cm+ Tab after: 1,27 cm + Indent at: 1,27cm

Formatted: Font: 10 pt

Formatted: Font: 9 pt

Policy Title: Credit Control and Debt Collection Policy Financial Year: 2O2O2O2l5ilus: Drall R\ ic. uhm:iid [ (,unc5 ‘n 3 i32ii7i lb i)r,ii I la-ri,,.’: lrcn3[7J53ji3:7ii,tafuc: Dralt tc icv ---\larch.2020

42

Page 15 of 44

74.6 The payment date is reflected on the account and under normalcircumstances is as follows:

(a) monthly accounts are payable before or on the /5th day, or the firstsubsequent work day should it fall on a weekend or public holiday, ofthe month that follows on the month in terms of which the account isrendered;

(b) Yearly accounts are payable within a time frame of three (3) monthsfrom the date on which such fees became due and payable; and

(c) Accounts of councillors and employees are deducted from theirsalaries / allowances.

7.4.7 Should an account not be paid in full, no smaller payment offered andaccepted will be regarded as the final payment of the applicable account;

7.4.8 Where any payment to the municipality or its legal agent by means oftransferable instrument is rejected by the bank:

(a) The municipality or its legal agent may recuperate the average bankcosts incurred with regard to the rejected transferable instrumentfrom the account of the consumer;

(b) the municipality or its legal agent must regard it as non-payment andservices will only be reconnected upon receipt of cash or a bankguaranteed cheque; and

(c) The municipality or its legal agent may insist on cash payment withregard to all future accounts.

7.4.9 The municipality or its legal agent must, where requested andadministratively possible, issue the consumer with a duplicate account orany acceptable alternative at costs determined by the council from time totime.

7.4,10 If an account is not paid by the due date interest will be charged one month’ Formatted: lnden Left: 0cm Hrst hne: 0cm

.._from Billing date. Interest will be equivalent to a full month from this date foreach month, or part thereof that the account is overdue.

Polkv Title: Credit Control and Debt Collection Policy Financial Year: 2020-20211)rrt R I (U ( I— 0

Formatted: Font: 10 p1

Formatted: Font: 9 p1

43

Page 16of44

7.4.11 The municipality supports the principle of a consolidated account and

reserve the right to disconnect/restrict/block any service with regards to

non-payment of the consolidated account.

7.5 Payment facilities and methods

7.5.1 The municipality must administer and maintain appropriate bank-and cash

facilities that must be accessible to clients;

7.5.2 The municipality must at its discretion allocate a payment between service

debts — a debtor in arrears may not specify that the payment must be used

for a specific part of his/her account;

7.5.3 The municipality may, in terms of Section 103 of the Act, with the

permission of the consumer, approach an employer to implement a debit-

or stop order arrangement; and

7.5.4 The consumer must acknowledge in all consumer agreements that the

use of consumer agents in the transfer of payments to the municipality will

occur at the risk of the consumer. This is applicable also to the time of

transfer of payment.

7.5.5 Debtors who pay the account by means of a credit card transaction, and

where the value of the payment is R 5 000 or more, or an amount as

determined by council when determining tariffs may be liable for the cost of

the transaction as passed on to the Municipality by the Financial Institution.

7.6 Enquiries, appeals and service complaints

7.6.1 The council will provide the following within its financial and administrative

capacity:

(a) a centralised complaints-/feedback office;

(b) a centralised database for complaints, that will make it easier to

coordinate and solve complaints, and to communicate more

effectively with clients;

(c) appropriate training for officials that deals directly with the public in

order to improve communication and service delivery; and Formatted: Font: 10 p1

I Formaed: Font: 9 pt

Policy Title: Credit Control and Debt Collection Polic Financial Year: 2020-2021Sub F)rit RL\ \ HiHI (1t. ( un..I n I \ib 1) 1 11 Ljj I IStatus: Draft Rc jew March 2020

44

Page 17 of 44

(d) a communication mechanism to inform the council with regard to theimplementation of the Policy with regard to Customer Care, Credit

Control and Debt Collection, as well as other matters.

7.6.2 If a consumer is convinced that his/her account is not accurate, he/she canrequest that the applicable account be investigated (dispute as per 7.7.4)and, where applicable, the necessary corrections be made;

7.6.3 The debtor must in the meantime pay an average based on the previous 3month’s consumption if the history of the account is available. Should thishistory not be available, the debtor must pay, without infringinghis/her rights, an estimated amount provided by the municipalitybefore the payment date until the case is resolved;

7,6.4 Customers can dispute the municipal account. In order for a dispute to beregistered with the Municipality, the following procedures must be followed

— by the debtor:

(a) The dispute must be submitted in writingDisuuhe Form, or dictated to the official who will record it in writing and

have it signed as correct. The document must then immediately belodged with the relevant authorised official;

(b) No dispute will be registered verbally whether in person or over thetelephone;

(c) The debtor must furnish full personal particulars including all theiraccount numbers held with the Municipality, direct contact telephone

numbers, fax numbers, postal and e-mail addresses and any otherrelevant particulars required by the Municipality;

(d) The full nature of the dispute must be described in the correspondence

referred to the above; and

(e) The onus will be on the debtor to ensure that he receives a writtenacknowledgement of the dispute.

In order for a dispute to be registered with the Municipality, the municipality must .——•-——-—

______________

Formatted: Font: 10 Pt

____________________________

follow the following procedures —:,. lormattei: Font: 9 Pt

______________________

Polkv Title: Credit Control and Debt Collection Policy Financial Year: 2020-2021

45

Page 18 of 44

(a) All disputes received are to be recorded in a register kept for thatpurpose. The following information should be entered into this register,namely debtors account number; debtors name; debtors address; full

particulars of the dispute; name of the official to whom the dispute is

given to investigate and resolve; actions that have, or were, taken to

resolve the dispute; signature of the controlling official;

(b) An authorised controlling official will keep custody of the register andconduct a daily or weekly check or follow-up on all disputes as yet

unresolved; and

(c) A written acknowledgement of receipt of the dispute must be provided

to the debtor.

The following provisions apply to the consideration of disputes:

(a) All disputes must be concluded by the Chief Finance Officer;

(b) The Chief Finance Officer’s decision is final and will result in the

immediate implementation of any debt collection and credit controlmeasures provided after the debtor is provided with the outcome of the

dispute; and

(c) The same debt will not again be defined as a dispute and will not bereconsidered as the subject of a dispute.

7.6.5 Lessors that fail to pay such agreed upon interim payments will be

subject and part of the normal credit control and debt collectionprocedures;

7.6.6 A consumer may appeal against the finding of the municipality or its legalagent in terms of sub-paragraph 7.7.4; and

7.6.7 An appeal and request in terms of sub-paragraph 7.7.6 must within twentyone (21) days after notification of the findings mentioned in sub-paragraph7.6.4 be addressed to and submitted at the municipality and must:

(a) set out the grounds for the appeal; and

Policy Title: Credit Control and Debt Collection Policy Financial Year: 2020-202 I‘n

rmafted:_FOnt: 10 p1

Formatted: Font: 9 p1

46

Page 19 of 44

Be accompanied of any security determined for the testing of the ‘Formatted: Numbered -+- Level: 1 + Numbering Style: a, b, C,+ Start at: 1 + Alignment: Left + Aligned at: 1,27cm +

metering device, if applicable. Tab after: 2,54cm + Indent at: 2,54 cm, Tab stops: Not at1,25 cm

Formatted: Indent: Left: 2,54 cm, No bullets or numberinp

Formatted: Tab stops: Not at 1,25cm

7.7 Customer support programmes

7.7.1 Water leakages:

(a) If the leakage is at the consumer’s side of the meter, the consumer

will be responsible for payment of the full account;

(b) Upon submission of sufficient proof of repair costs or sworn written

affidavit regarding the repair! repair cost the municipality may, at its

own discretion, provide relief; and

(c) It is the responsibility of the client to control and monitor his/her

consumption.

7.7.2 Tax rebates:

(a) The municipal council may grant on an annual basis rebates to

categories of rate payers in accordance with the tax policy and

regulations of the municipality; and

(b) Tax rebates will be subject to criteria as determined by the council

from time to time.

7.7.3 Arrangements for payment (Annexure C)

(a) If required, consumers in arrears must agree to change to pre-paid

meters. Subsequent to installation, the amount in arrears and the Formatted: Font: 10 pt .1Formatted: Font: 9 pt

Pelicy Title: Credit Control and Debt Collection Polic Financial \ear: 2020-2021Ste Dril Rt IL\ hmtii tc C 1_nC I n I ii F) I IC L_ F It it C I 1Status.: Draft Rcs icw March 2020

47

Page 20 of 44

cost of the pre-paid meter will be payable on one of the followingmethods:

(i) The total in arrears are added to the account and anagreement is arranged;

(b) The council reserves the right to increase the required deposit /security of debtors that opt to make arrangements with themunicipality.

7.7.4 Property Rates and Services in instalments:-

(a) Property Rates and services must be paid in twelve (12) eveninstalments, with no interest charges thereon, with the understandingthat no tax pertaining to the previous period is outstanding and thatall payments be fully paid at the date that precedes the following tax

cycle-bird

7.8 Subsidies for indigent consumers (should be read in conjunction withthe Indigent Policy- (Annexure B)

7.8.1 A basic level of services will be provided to qualifying households with atotal bruto income which is less than a predetermined amount and meet

specificcriteria determined by the council from time to time;

7.8.2 Subsidies to indigent consumers will be financed from the equitable sharecontribution from National Government and for which provision is made inthe municipal budget;

7.8.3 The subsidised services are electricity, sewerage removal, refuse removaland water;

7.8.4 If a consumer’s consumption or use of a municipal service is less than thesubsidised service, may the unused portion not be accrued to the consumer

Formatted: Font: 10 p1

Formatted: Font: 9 pt

Policy Title: Credit Control and Debt Collection Polic’, Financial Year: 2020-2021t)nIt t. ( ç1 n

48

Page 21 of44

and will it not entitle the consumer to cash or a rebate with regard to the

unused portion;

78.5 If a consumer’s consumption or use of a municipal service exceeds the

subsidised service, the consumer will be liable to pay for the amount in

excess at an appropriate rate;

Formatted: Left, Indent: Left: 0cm, Hanging: 1cm, Tabstops: 1,25 cm, Left

7.8.6 The consumption of all consumers who qualify for an indigent subsidy will

be limited to prevent further escalation of debt;

7.8.7 If applicable, indigent households will be exempted of a portion of their

debts;

78 8 Where the account of a consumer that qualifies for an indigent subsidy is

paid in full or pays the account in full on a regular basis at the time of

application, the limitation on consumption may be lifted;

78.8 Formatted: Indent: Left: 1,25 cm, No bullets or numbering

7.9 Additional subsidy categories

7.9.1 The council may provide certain portions of basic consumption of electricity

and water free of charge to a consumer (including indigent- and sub-

economic users), as determined from time to time;

Formatted: Indent: Left: 0cm, Hanging: 1,25cm

7.9.2 The council may grant donations to alleviate the tax burden on specific

categories of consumers, as determined from time to time;

7.9.3 Rebates may be granted to sports organisations, but services fees must at

least cover the cost of the service; and

7.9.4 Rebates may be granted to large scale consumers to encourage them to

reside in Plettenberg Bay, where it will be to the benefit of the

community.

7.10 Consumer categories

Policy Title: Credit Control and Debt Collection Policy Financial Year: 2020-2021Drift Ru\ ici hiniii d tot. jn l_ I ..iii t):lj7.jjt.t. I ii: (j77

rmatted: Font: 10 pt

Formatted: Font: 9_Pt

49

Page 22 of 44

710.1 Consumers will be categorised in terms of special classifications thatprovides for, amongst others, the type of business, appropriate tariffsand the risk attached to service delivery. Credit control procedures, debtcollection and customer care may differ from category to category asdetermined by the Municipal Manager from time to time.

7.11 Preferential customer management

7.1 1 .1 Certain consumers can be classified as preferential consumers by theMunicipal Manager according to certain criteria, such as the number ofproperties and volume of consumption: and

7.11.2 A specific municipal official will be tasked to deal with the interestsof preferential consumers, and will execute such tasks as the checkaccounts for accuracy, monitoring timeous payments, and answeringenquiries.