analysis of the grocery industry coles supermarkets

TRANSCRIPT

Analysis of the grocery industry Coles Supermarkets Australia

October 2012

Analysis of the grocery industry

Liability limited by a scheme approved under Professional Standards Legislation. Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee, and its network of member firms, each of which is a legally separate and independent entity. Please see www.deloitte.com/au/about for a detailed description of the legal structure of Deloitte Touche Tohmatsu Limited and its member firms. © 2012 Deloitte Access Economics Pty Ltd

Contents Glossary ..................................................................................................................................... i

Executive Summary .................................................................................................................. iii

1 Introduction .................................................................................................................... 1

1.1 Project approach and objectives........................................................................................ 1

1.2 Report structure ............................................................................................................... 2

2 Coles – an overview ........................................................................................................ 3

3 Economic contribution of Coles ....................................................................................... 5

3.1 Modelling approach .......................................................................................................... 5

3.2 Direct economic contribution ............................................................................................ 6

3.3 Indirect economic contribution ......................................................................................... 6

3.4 Total economic contribution ............................................................................................. 7

3.5 Regional economic contribution ........................................................................................ 8

3.6 Indirect contribution – Facilitated ..................................................................................... 8

3.7 Economic contribution comparison ................................................................................... 9

4 Price and productivity ................................................................................................... 10

4.1 Context: Analysing ‘Down Down’ ..................................................................................... 10

4.2 ‘Down Down’: A whole of company perspective .............................................................. 11

4.3 ‘Down Down’: product prices under the microscope ....................................................... 14

4.4 The volume impact of ‘down down’ ................................................................................ 20

4.5 Explaining ‘Down Down’: the benefits of scale ................................................................. 21

4.6 Private labels .................................................................................................................. 22

5 Consumer benefits ........................................................................................................ 24

5.1 Consumer welfare benefits of ‘down down’ .................................................................... 24

5.2 Consumer welfare benefits of retail grocery prices .......................................................... 25

5.3 Variety and choice at the supermarket ............................................................................ 27

5.4 Supermarket convenience: benefits for consumers ......................................................... 29

5.5 Supermarket quality: benefits for consumers .................................................................. 31

6 Competition in the grocery industry .............................................................................. 32

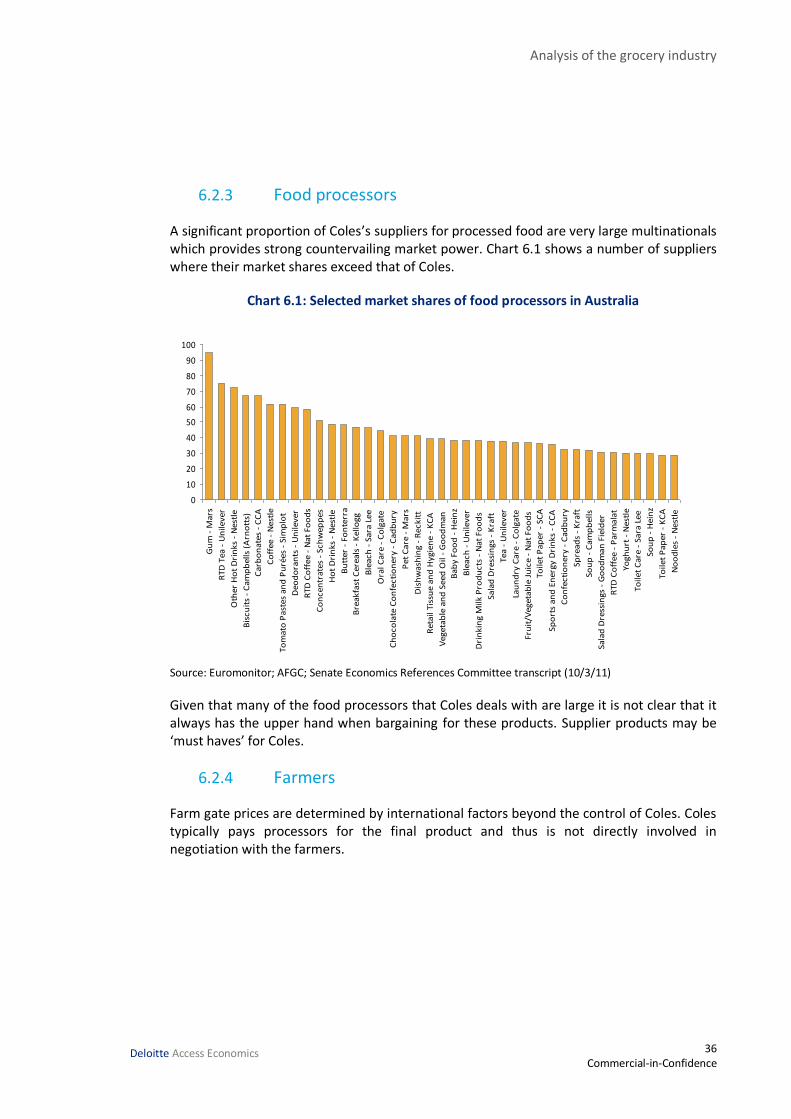

6.1 Key concepts and background ......................................................................................... 32

6.2 The grocery industry ....................................................................................................... 34

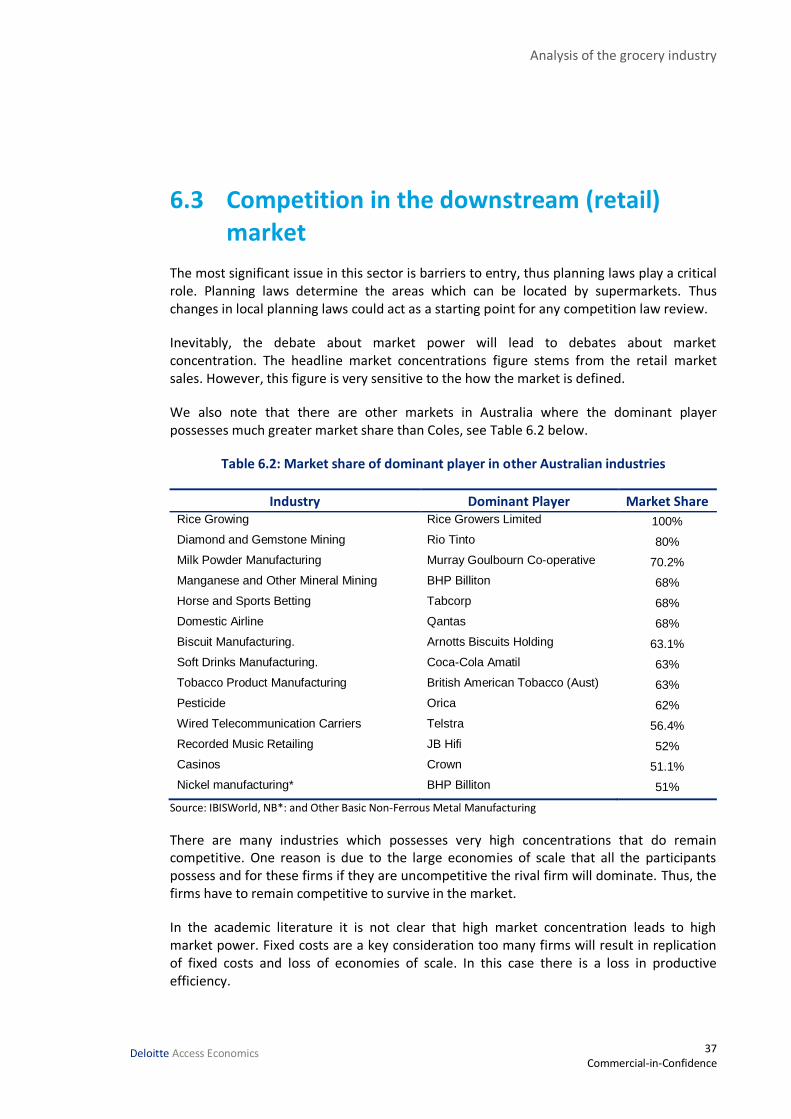

6.3 Competition in the downstream (retail) market ............................................................... 37

6.4 Competition in the upstream market .............................................................................. 38

6.5 Review of arguments ...................................................................................................... 39

7 Impact of proposed policies .......................................................................................... 41

7.1 Competition policy in Australia ........................................................................................ 41

7.2 Government policy directions ......................................................................................... 42

Deloitte Access Economics Commercial-in-confidence

7.3 Competition law review .................................................................................................. 44

7.4 Market share cap and forced divestiture ......................................................................... 45

References .............................................................................................................................. 48

Limitation of our work ............................................................................................................... 50

Charts Chart 3.1 : Value added: Coles and selected industries .............................................................. 9

Chart 4.1 : 2L Coles milk price composition ............................................................................ 16

Chart 4.2 : Milk production figures .......................................................................................... 17

Chart 4.3 : Milk sales figures ................................................................................................... 18

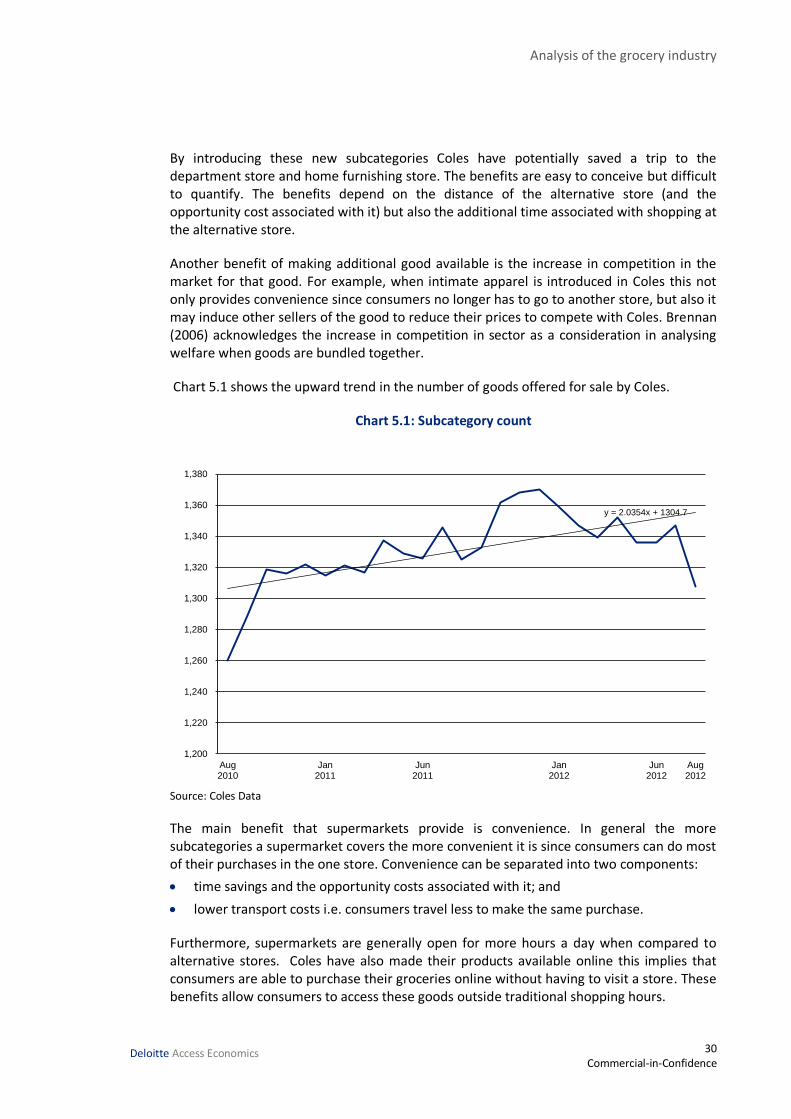

Chart 5.1 : Subcategory count ................................................................................................. 30

Chart 6.1 : Selected market shares of food processors in Australia .......................................... 36

Tables Table 3.1 : Direct contribution, 2011-12 .................................................................................... 6

Table 3.2 : Indirect economic contribution – Intermediate Inputs 2011-12 ................................ 7

Table 3.3 : Total economic contribution 2011-12 ...................................................................... 7

Table 3.4 : Direct regional employment contribution 2011-12 ................................................... 8

Table 3.5 : Regional value added 2011-12 ................................................................................. 8

Table 3.6 : Economic contribution – Facilitated 2011-12............................................................ 8

Table 3.7 : Economic contribution: direct, indirect and facilitated 2011-12................................ 9

Table 4.1 : Coles Income Statement ........................................................................................ 11

Table 4.2 : Change in key aggregates for the 'Down Down' products (Jan 2011 to mid-2012) .. 14

Table 4.3 : Coles milk 2L .......................................................................................................... 15

Table 4.4 : Coles Smart Buy white bread 650g ......................................................................... 18

Table 4.5 : Coles chicken roast family ...................................................................................... 19

Table 4.6 : Coles 2 ply paper towel white 2 pack ..................................................................... 19

Table 4.7 : Colgate regular toothpaste 120g ............................................................................ 20

Table 4.8 : Coles volume of selected goods ............................................................................. 21

Table 4.9 : White bread 650g .................................................................................................. 23

Table 4.10 : Eggs 12 pack 700g ................................................................................................ 23

Table 4.11 : Soft drinks ............................................................................................................ 23

Table 5.1 : Price changes at Coles, by product category ........................................................... 24

Deloitte Access Economics Commercial-in-confidence

Table 5.2 : Sales revenue and savings (all figures in $m) .......................................................... 25

Table 5.3 : Food and beverage price inflation 1980-2012 ........................................................ 26

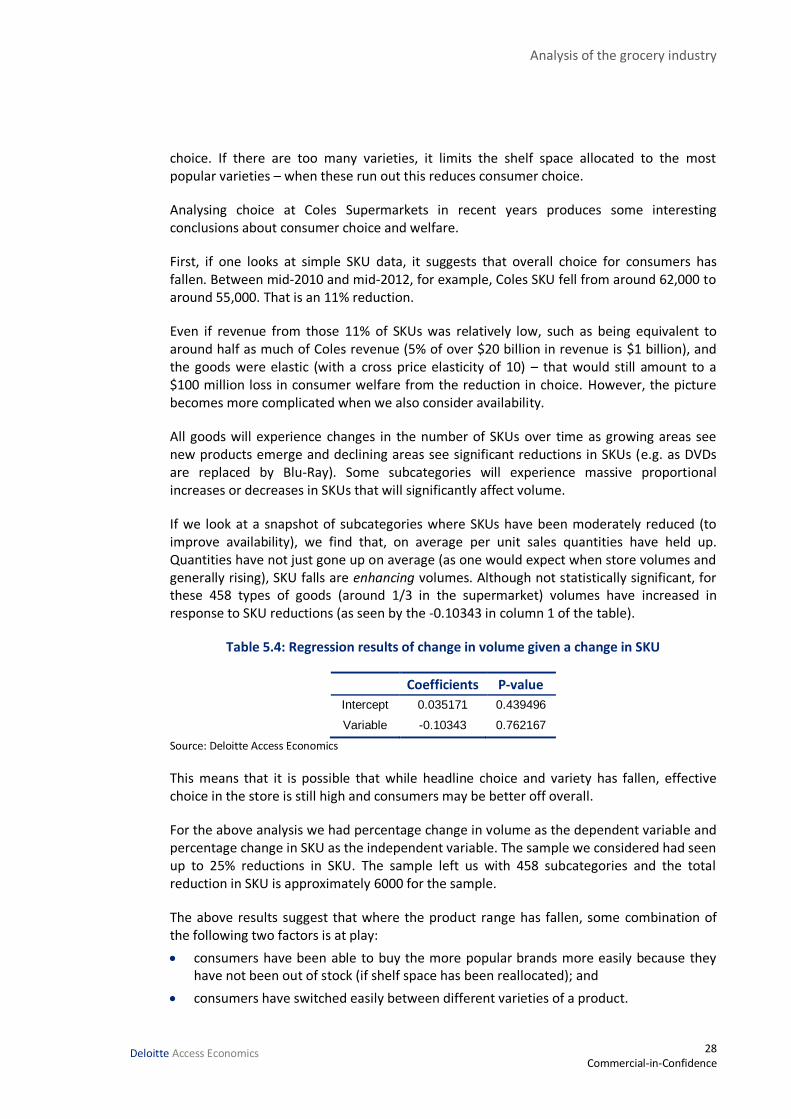

Table 5.4 : Regression results of change in volume given a change in SKU ............................... 28

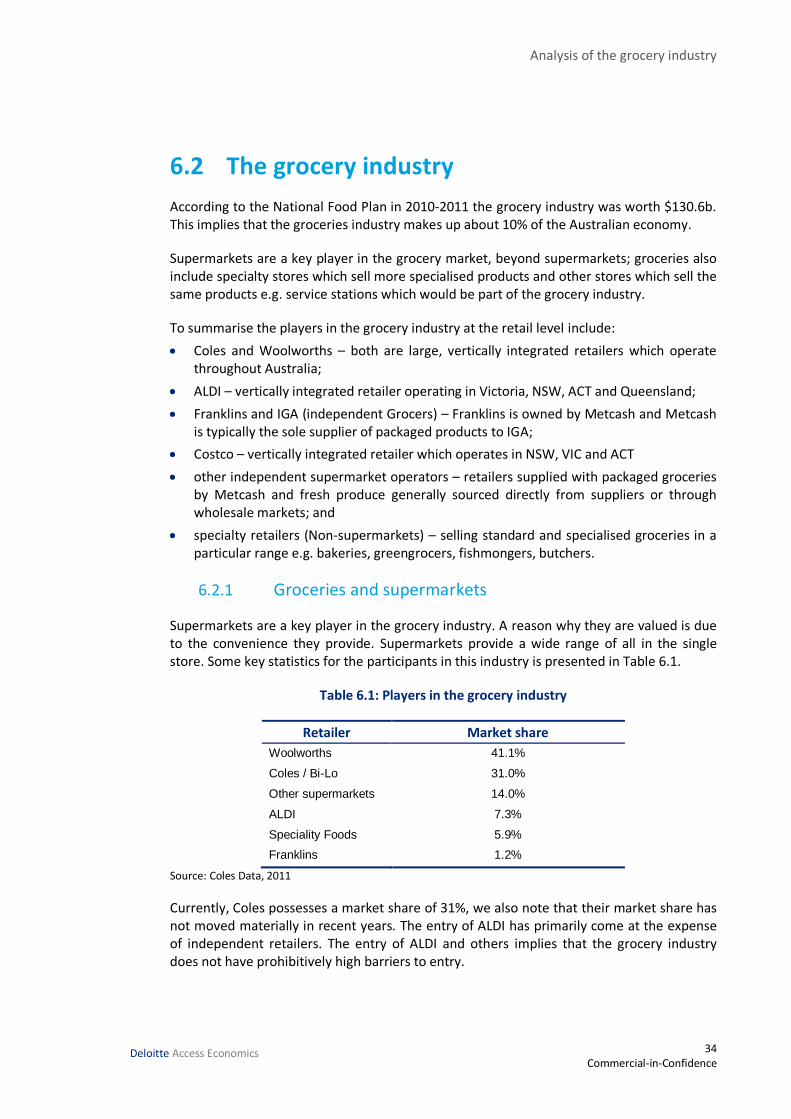

Table 6.1 : Players in the grocery industry ............................................................................... 34

Table 6.2 : Market share of dominant player in other Australian industries ............................. 37

Figures Figure 1.1 : Framework for the analysis ..................................................................................... 2

Figure 2.1 : Coles supply chain .................................................................................................. 4

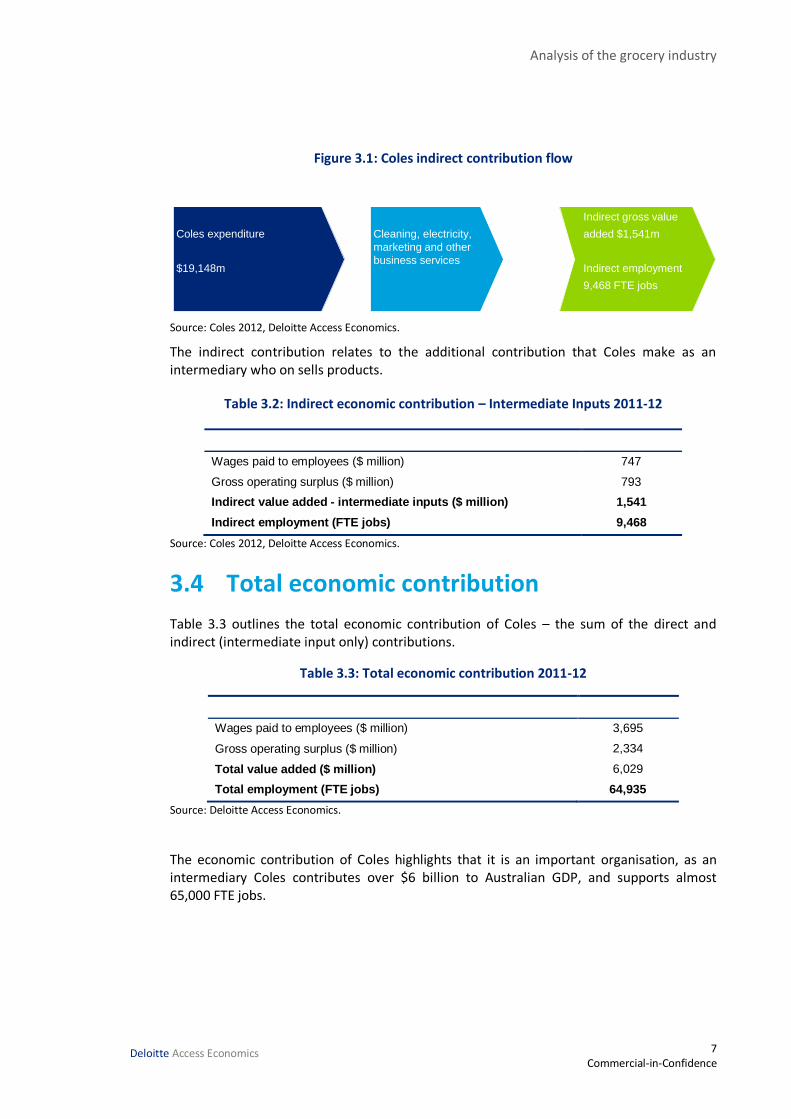

Figure 3.1 : Coles indirect contribution flow .............................................................................. 7

Figure 4.1 : Direct to store logistics network ........................................................................... 13

Figure 4.2 : Distribution centre to store logistics network........................................................ 13

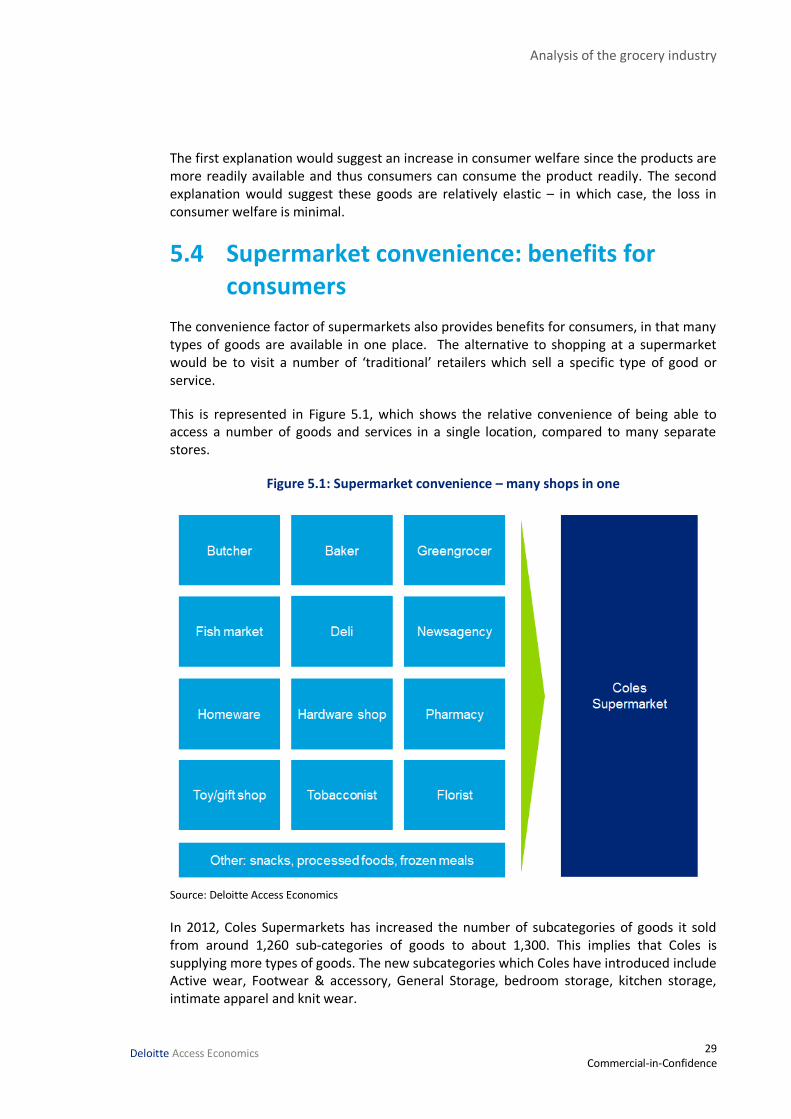

Figure 5.1 : Supermarket convenience – many shops in one .................................................... 29

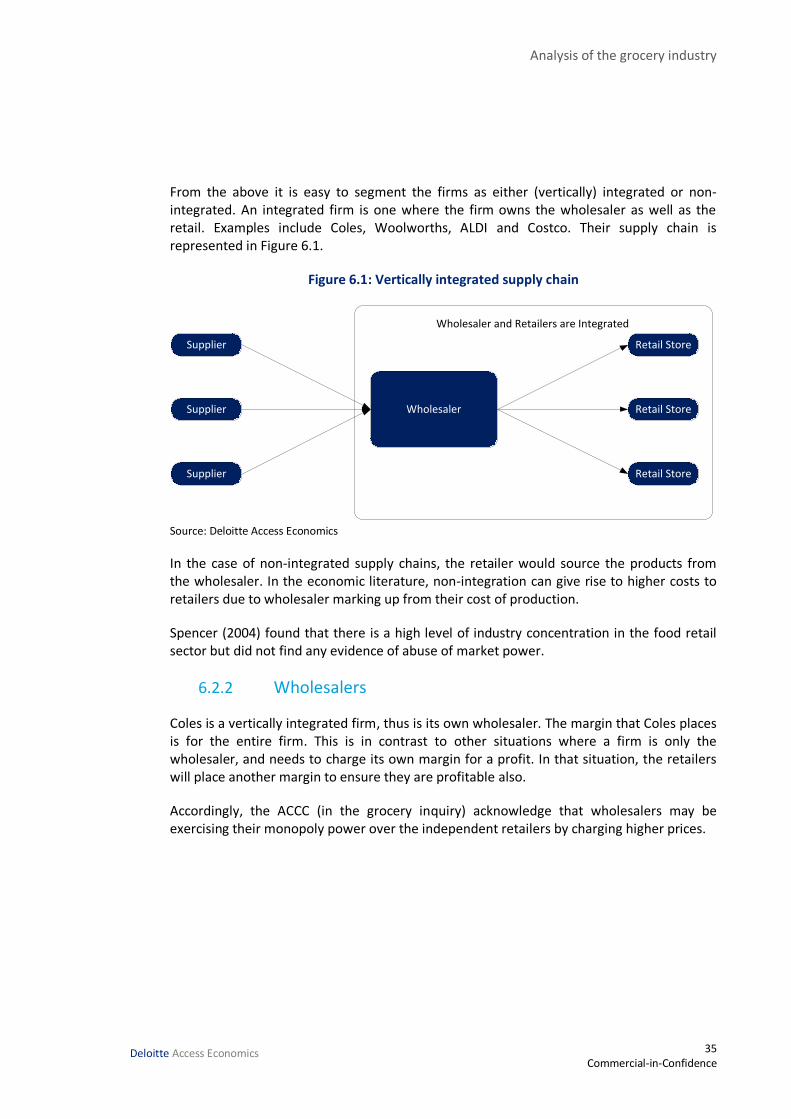

Figure 6.1 : Vertically integrated supply chain ......................................................................... 35

i Commercial-in-Confidence

Deloitte Access Economics

Glossary

ABARES Australian Bureau of Agricultural and Resource Economics and Sciences

ABS Australian Bureau of Statistics

ACCC Australian Competition and Consumer Commission

AFCG Australia Food and Grocery Council

ASX Australian Stock Exchange

AVE Average

CCA Competition and Consumer Act (2010)

COAG Council of Australian Governments

CODB Cost of doing business

COGS Cost of goods sold

CPI Consumer Price Index

DAE Deloitte Access Economics

DAFF Australian Department of Agriculture, Fisheries and Forestry

EBIT Earnings Before Interest and Tax

EBITDA Earnings Before Interest, Tax, Depreciation and Amortisation

FMCG Fast Moving Consumer Goods

FTE Full-time equivalent

FY Financial Year

GDP Gross Domestic Product

GFC Global Financial Crisis (2008)

GLA Gross Leasable Area

IGA Independent Grocers Alliance

IT Information Technology

ii Commercial-in-Confidence

Deloitte Access Economics

KAP Katter’s Australian Party

RBA Reserve Bank of Australia

SKU Stock Keeping Units

SSNIP Small but Significant Non-transitory Increase in Prices

TLS Tobacco, Liquor and Services

iii Commercial-in-Confidence

Deloitte Access Economics

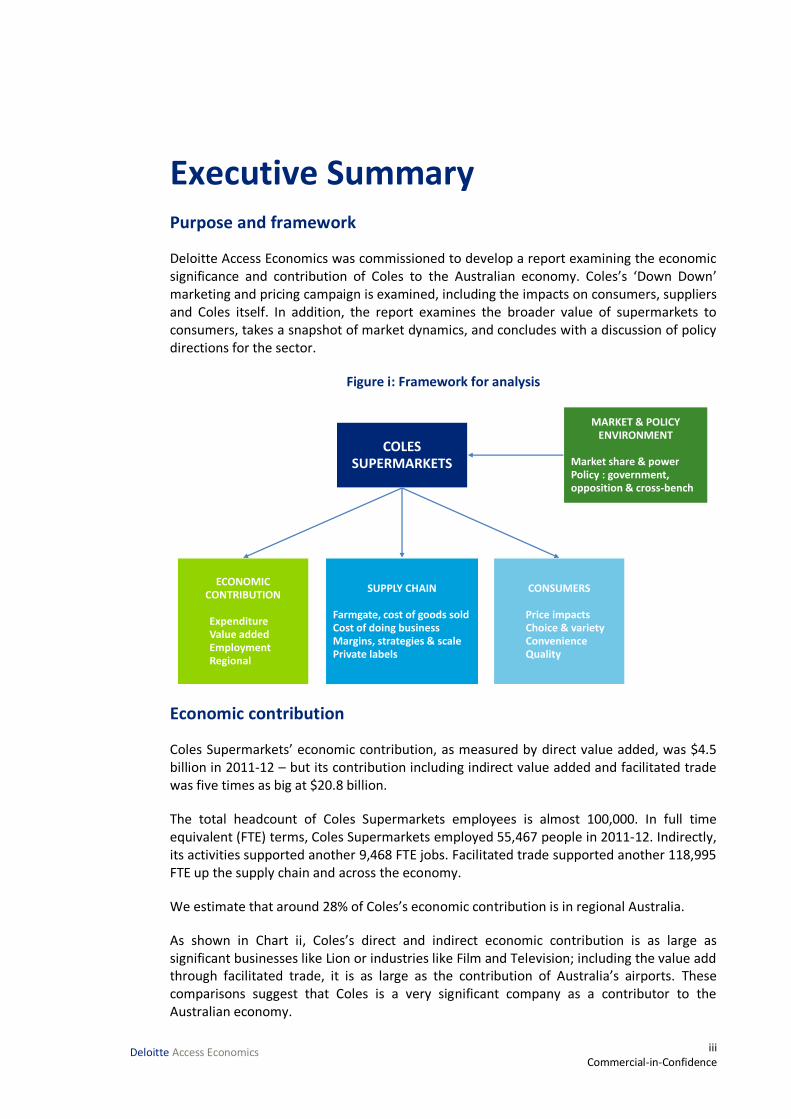

Executive Summary Purpose and framework

Deloitte Access Economics was commissioned to develop a report examining the economic significance and contribution of Coles to the Australian economy. Coles’s ‘Down Down’ marketing and pricing campaign is examined, including the impacts on consumers, suppliers and Coles itself. In addition, the report examines the broader value of supermarkets to consumers, takes a snapshot of market dynamics, and concludes with a discussion of policy directions for the sector.

Figure i: Framework for analysis

Economic contribution

Coles Supermarkets’ economic contribution, as measured by direct value added, was $4.5 billion in 2011-12 – but its contribution including indirect value added and facilitated trade was five times as big at $20.8 billion.

The total headcount of Coles Supermarkets employees is almost 100,000. In full time equivalent (FTE) terms, Coles Supermarkets employed 55,467 people in 2011-12. Indirectly, its activities supported another 9,468 FTE jobs. Facilitated trade supported another 118,995 FTE up the supply chain and across the economy.

We estimate that around 28% of Coles’s economic contribution is in regional Australia.

As shown in Chart ii, Coles’s direct and indirect economic contribution is as large as significant businesses like Lion or industries like Film and Television; including the value add through facilitated trade, it is as large as the contribution of Australia’s airports. These comparisons suggest that Coles is a very significant company as a contributor to the Australian economy.

COLES SUPERMARKETS

ECONOMIC CONTRIBUTION

ExpenditureValue addedEmploymentRegional

SUPPLY CHAIN

Farmgate, cost of goods soldCost of doing businessMargins, strategies & scalePrivate labels

CONSUMERS

Price impactsChoice & varietyConvenienceQuality

MARKET & POLICY ENVIRONMENT

Market share & powerPolicy : government,opposition & cross-bench

iv Commercial-in-Confidence

Deloitte Access Economics

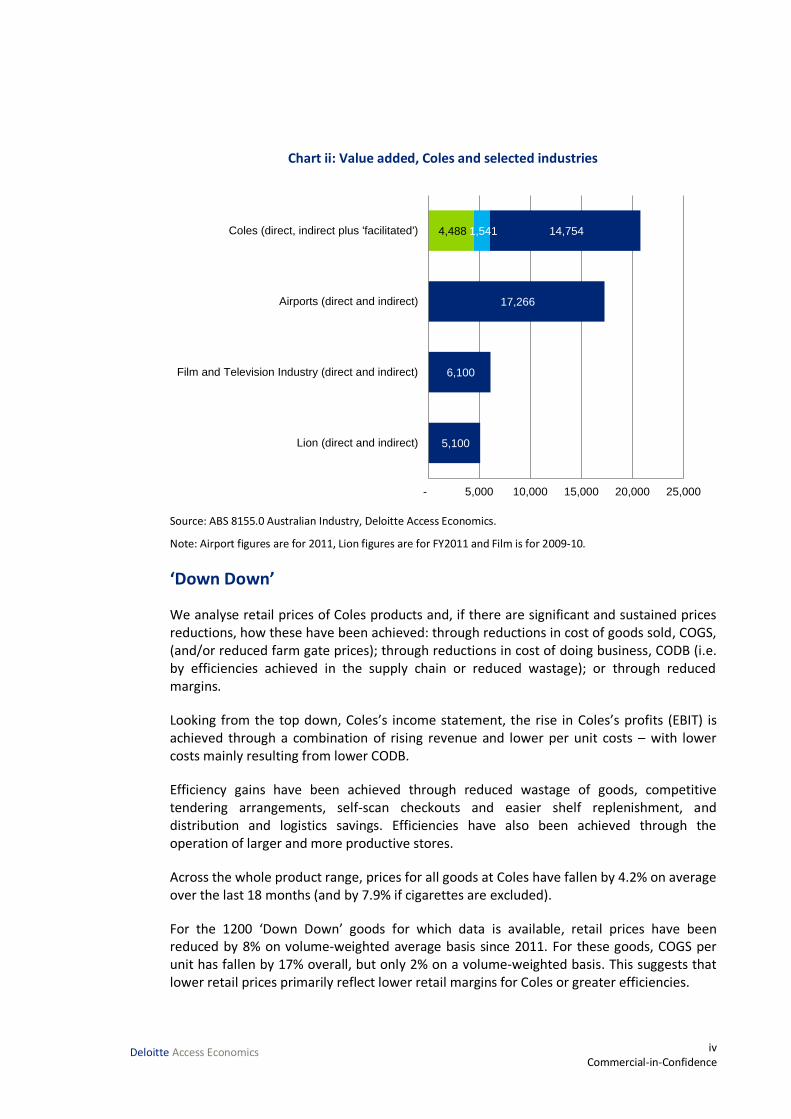

Chart ii: Value added, Coles and selected industries

Source: ABS 8155.0 Australian Industry, Deloitte Access Economics.

Note: Airport figures are for 2011, Lion figures are for FY2011 and Film is for 2009-10.

‘Down Down’

We analyse retail prices of Coles products and, if there are significant and sustained prices reductions, how these have been achieved: through reductions in cost of goods sold, COGS, (and/or reduced farm gate prices); through reductions in cost of doing business, CODB (i.e. by efficiencies achieved in the supply chain or reduced wastage); or through reduced margins.

Looking from the top down, Coles’s income statement, the rise in Coles’s profits (EBIT) is achieved through a combination of rising revenue and lower per unit costs – with lower costs mainly resulting from lower CODB.

Efficiency gains have been achieved through reduced wastage of goods, competitive tendering arrangements, self-scan checkouts and easier shelf replenishment, and distribution and logistics savings. Efficiencies have also been achieved through the operation of larger and more productive stores.

Across the whole product range, prices for all goods at Coles have fallen by 4.2% on average over the last 18 months (and by 7.9% if cigarettes are excluded).

For the 1200 ‘Down Down’ goods for which data is available, retail prices have been reduced by 8% on volume-weighted average basis since 2011. For these goods, COGS per unit has fallen by 17% overall, but only 2% on a volume-weighted basis. This suggests that lower retail prices primarily reflect lower retail margins for Coles or greater efficiencies.

4,488 1,541

5,100

6,100

17,266

14,754

- 5,000 10,000 15,000 20,000 25,000

Lion (direct and indirect)

Film and Television Industry (direct and indirect)

Airports (direct and indirect)

Coles (direct, indirect plus 'facilitated')

v Commercial-in-Confidence

Deloitte Access Economics

Individual goods

We apply our analysis of retail prices, margins, efficiencies (cost of doing business) and suppliers (farm gate prices and cost of goods sold) to individual products included in the ‘Down Down’ campaign – for a more forensic look at pricing dynamics.

We find a number of different scenarios regarding the relationship between retail prices, supplier income, efficiencies, Coles’s margin and volume. Sometimes, Coles pays the same or more per unit to suppliers and reduces prices by reducing its margins or achieving efficiencies. On the other hand, sometimes Coles may pay suppliers less in headline income but provide more favourable contract terms (or assists in achieving efficiencies). Lower supplier income could also reflect an agreement between Coles and the supplier to reduce retail prices to drive volume. Of course, there will also be situations where Coles reduces prices paid to suppliers who then experience lower margins and profits.

Consumer benefits of ‘Down Down’

Over an 18 month period retail prices for most categories of goods have come down. On a weighted average basis, prices have fallen by 4.1%. The main exception is cigarette prices, which have increase because of changes in excise arrangements.

To obtain an overall picture of the savings to consumers we aggregate the price movement during this period and calculate a savings figure – based on both old volumes and current volumes. We find that in 2011-12, the one-year savings of the price reductions during the ‘Down Down’ campaign (i.e. over the 18 months from January 2011) is between $1.05 billion and $1.19 billion. The midpoint is $1.12 billion.

Benefits of lower retail grocery prices overall

It is important to recognise that ‘Down Down’ is not just an individual company strategy – it is also reflective of overall market conditions. ‘Down Down’ is one company’s strategy in a competitive market. Other companies also use pricing strategies to increase their market share. Some of these are a competitive response to Coles. Price reductions across the sector are of significant benefit to consumers.

CPI for food and beverage from March 2011 to June 2012 was -1.85%. Based on a $78.4 billion industry this implies a saving of $1.45 billion across food and beverages. If we also take account of substitution bias, because CPI overstates inflation, price reductions could be worth $2 billion to consumers in 2011-12. It is not possible to precisely estimate Coles’s contribution to overall savings from food price reductions. However, the figures referred to in the report strongly suggest that Coles’s contribution to industry-wide savings is higher than its market share (of around 31%).

Variety, convenience and quality

It is important to recognise that beyond the price benefits to consumers, supermarkets, like any store, provide other benefits through variety of products and convenience of services.

vi Commercial-in-Confidence

Deloitte Access Economics

In the supermarket, we can measure variety by the total number of products offered – the number of stock keeping units (SKUs). A greater number of SKUs means consumers have more products, varieties, brands and sizes to choose from.

Our analysis is that while SKU data shows declining variety at Coles Supermarkets in recent years, moderately lower SKUs are associated with higher sales volumes. This means there is either greater in store availability of goods because it is easier to keep fewer brands in stock, or that consumer demand for these goods is relatively ‘elastic’ - i.e. consumers switch between options relatively easily.

Private labels

The growing role of private labels has been controversial, with claims they are part of a long term strategy to increase market power and increase retail prices.

Analysis of some examples suggests that it is unlikely that Coles systematically achieves higher margins on its own products and directly encourages consumers not to buy branded products.

While it is difficult to speculate on the long term effects of private labels – so far the federal Department of Agriculture says they reflect consumer preferences and increase competitive pressures.

Snapshot of market dynamics

At one level, the grocery industry in Australia may appear highly concentrated, dominated by the major supermarket chains, Coles and Woolworths. However, a more sophisticated analysis reveals a complex picture which is heavily dependent on how the markets are defined and what methodologies are used to segment markets.

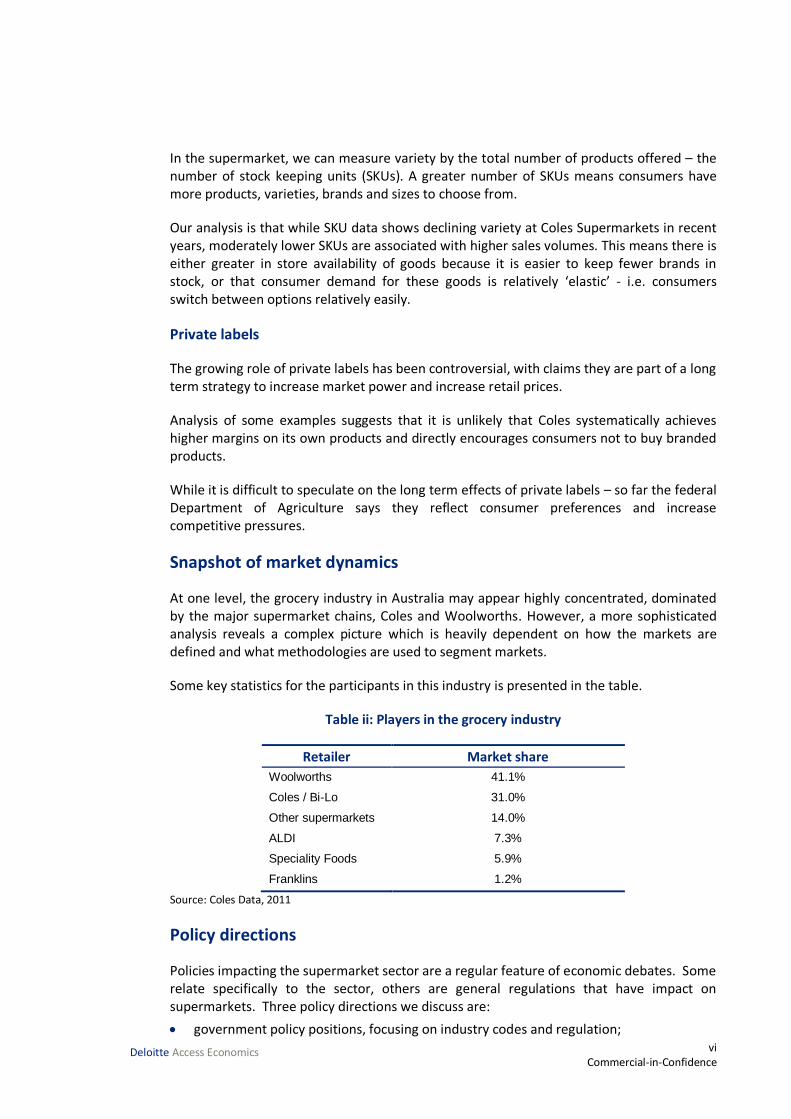

Some key statistics for the participants in this industry is presented in the table.

Table ii: Players in the grocery industry

Retailer Market share

Woolworths 41.1%

Coles / Bi-Lo 31.0%

Other supermarkets 14.0%

ALDI 7.3%

Speciality Foods 5.9%

Franklins 1.2%

Source: Coles Data, 2011

Policy directions

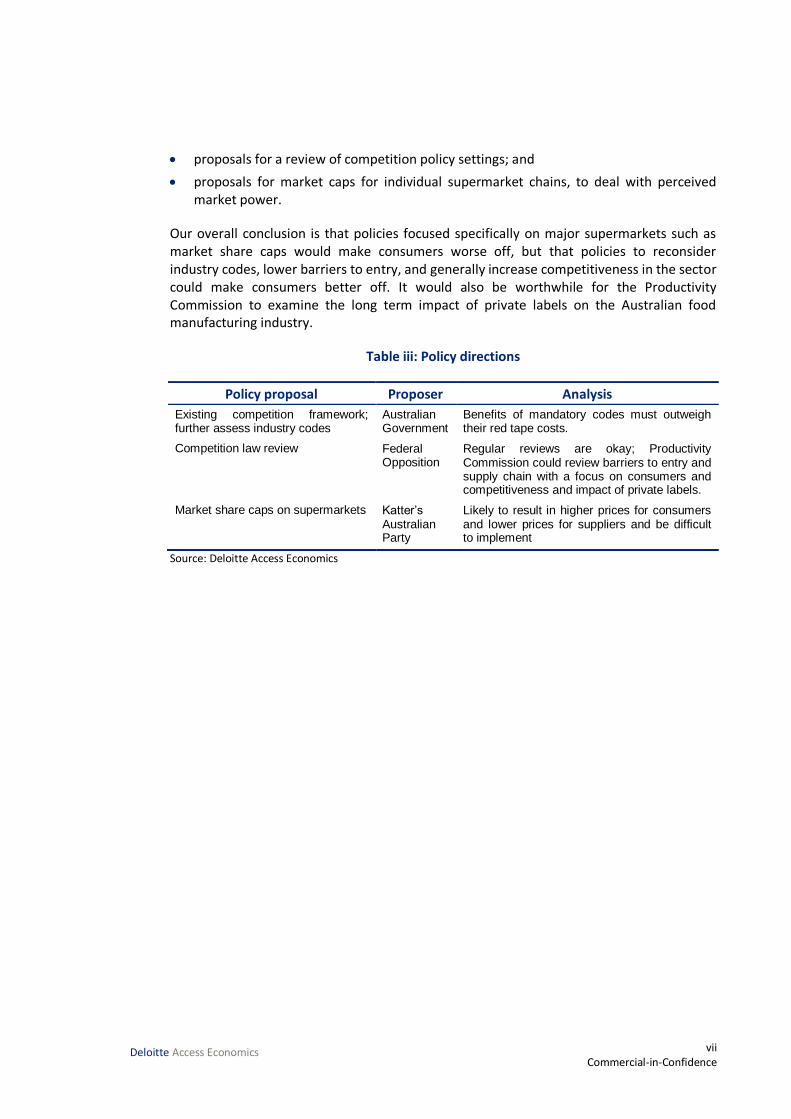

Policies impacting the supermarket sector are a regular feature of economic debates. Some relate specifically to the sector, others are general regulations that have impact on supermarkets. Three policy directions we discuss are:

government policy positions, focusing on industry codes and regulation;

vii Commercial-in-Confidence

Deloitte Access Economics

proposals for a review of competition policy settings; and

proposals for market caps for individual supermarket chains, to deal with perceived market power.

Our overall conclusion is that policies focused specifically on major supermarkets such as market share caps would make consumers worse off, but that policies to reconsider industry codes, lower barriers to entry, and generally increase competitiveness in the sector could make consumers better off. It would also be worthwhile for the Productivity Commission to examine the long term impact of private labels on the Australian food manufacturing industry.

Table iii: Policy directions

Policy proposal Proposer Analysis

Existing competition framework; further assess industry codes

Australian Government

Benefits of mandatory codes must outweigh their red tape costs.

Competition law review Federal Opposition

Regular reviews are okay; Productivity Commission could review barriers to entry and supply chain with a focus on consumers and competitiveness and impact of private labels.

Market share caps on supermarkets Katter’s Australian Party

Likely to result in higher prices for consumers and lower prices for suppliers and be difficult to implement

Source: Deloitte Access Economics

Analysis of the grocery industry

1 Commercial-in-Confidence

Deloitte Access Economics

1 Introduction The grocery industry is one of the most important industries in the Australian economy. The price of food and other staples has a day to day impact on the lives of consumers. The industry employs a significant proportion of the workforce and has links to many other industries in the Australian economy, including agriculture, manufacturing and transport. Accordingly, it is an area of interest to policy makers and government. In Australia, supermarkets are one of the key players in the grocery industry providing around 70% of the value of the retail market for food and groceries.

Over the past five years, there have been some significant developments in the supermarket sector. New players like Costco have entered the market, while ALDI has expanded since its entry in 2001. The links between supermarket and fuel industries have been normalised. In response to concerns that cost of living pressures were affecting families, in 2008, the Australian Government commissioned the Australian Competition and Consumer Commission to review of the industry. In 2010, the Trade Practices Act was recast as the Competition and Consumer Act, with several competition policy amendments in recent years. Supermarkets themselves have developed new pricing and marketing strategies.

‘Down Down’ is Coles’s pricing and marketing campaign. This has been a high profile campaign from its commencement in early 2010. Other supermarkets have their own pricing strategies to compete, including IGA’s with “Locked Down Low Prices” from July 2012 and Woolworths’s “everyday low prices”.

It is against this background that the Coles Supermarkets commissioned Deloitte Access Economics to report on the economic significance and contribution of Coles in the grocery industry. Coles’s ‘Down Down’ strategy is examined in detail – drawing out the impacts on consumers, suppliers and other stakeholders. In addition to this, we examine the value of supermarkets to consumers and the take a snapshot of market dynamics. We conclude with a discussion of policy directions for the sector.

1.1 Project approach and objectives

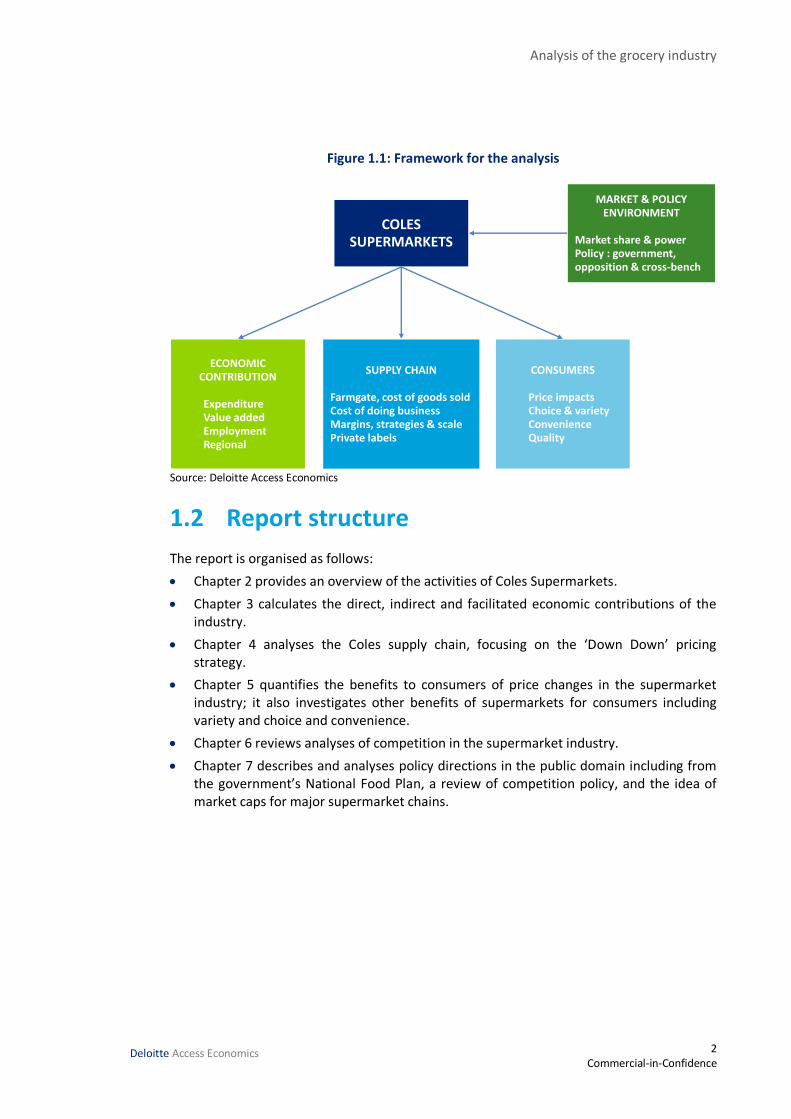

The purpose of this study is to develop a comprehensive report to examine the impact of Coles’s pricing strategy and analyse relevant issues that the policy makers currently face. As outlined in Figure 1.1, we look at Coles Supermarkets’ economic contribution, the supply chain, impacts on consumers, and how the market and policy environment affects Coles.

Analysis of the grocery industry

2 Commercial-in-Confidence

Deloitte Access Economics

Figure 1.1: Framework for the analysis

Source: Deloitte Access Economics

1.2 Report structure

The report is organised as follows:

Chapter 2 provides an overview of the activities of Coles Supermarkets.

Chapter 3 calculates the direct, indirect and facilitated economic contributions of the industry.

Chapter 4 analyses the Coles supply chain, focusing on the ‘Down Down’ pricing strategy.

Chapter 5 quantifies the benefits to consumers of price changes in the supermarket industry; it also investigates other benefits of supermarkets for consumers including variety and choice and convenience.

Chapter 6 reviews analyses of competition in the supermarket industry.

Chapter 7 describes and analyses policy directions in the public domain including from the government’s National Food Plan, a review of competition policy, and the idea of market caps for major supermarket chains.

COLES SUPERMARKETS

ECONOMIC CONTRIBUTION

ExpenditureValue addedEmploymentRegional

SUPPLY CHAIN

Farmgate, cost of goods soldCost of doing businessMargins, strategies & scalePrivate labels

CONSUMERS

Price impactsChoice & varietyConvenienceQuality

MARKET & POLICY ENVIRONMENT

Market share & powerPolicy : government,opposition & cross-bench

Analysis of the grocery industry

3 Commercial-in-Confidence

Deloitte Access Economics

2 Coles – an overview In 19th century the Australian groceries market was very fragmented and typically operated by sole operators. Typically, they were called ‘corner stores’ and were very region specific and served a small community. Moreover, the range of products they stocked was somewhat limited as the purpose was to meet the needs of that small community. Given the limited range, this allowed other specialty stores to spawn such as bakers and delicatessens. The 20th century, saw the development of the ‘supermarket’ as we know today. Specifically, supermarkets provided a one stop shop for its consumers for their weekly grocery needs. Gradually over time, these supermarkets expanded their product range which furthers the convenience of the store. Coles was amongst the first supermarkets in Australia.

Coles was founded by George Coles in 1914, he opened the first Coles Variety store in Collingwood as a variety store. In 1921, Coles became a propriety company and in 1927 the company was floated on the Melbourne Stock exchange. In 1985, Coles Myer Ltd. was established, after a merger with Myer Emporium Ltd. (Myer). Myer was acquired through total cash offer of $918 million. In July 2007, Wesfarmers purchased Coles Group Limited for $22 billion. Myer was demerged from the Coles Group in 2005 to private equity interests in 2005 and floated as a listed entity in 2009. It has therefore not been part of the Coles Group since 2005. Wesfarmers was founded in 1914 as a farmers' co-operative in Western Australia, in 1985 it was restructured to a public company and was listed on the ASX.

Today, Coles Supermarkets is one of two major supermarkets operating in Australia. There are also several other supermarkets as well as numerous speciality retailers that comprise the grocery industry in Australia.

Coles Supermarkets is part of the Coles Group owned by Wesfarmers. The Coles Group comprises:

national full service supermarket retailer operating 749 stores (Wesfarmers 2012);

liquor retailer operating three brands through 792 liquor outlets and 92 hotels (Wesfarmers 2012); and

national fuel and convenience operator managing 627 sites (Wesfarmers, 2012).

Between the different parts of the Coles Group, there were approximately 18 million customer transactions each week in 2011-12, and over 100,000 employees. In 2011-12, the Coles earned $23.6 billion in revenue from their supermarkets.

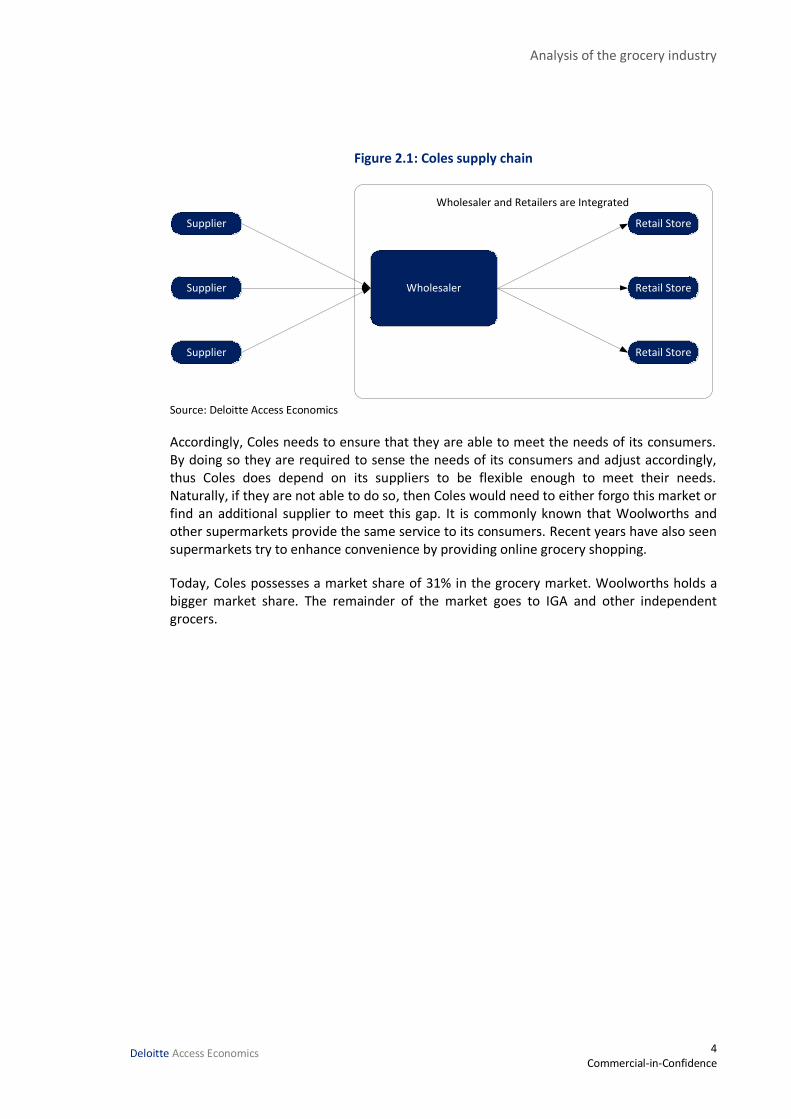

Currently, Coles Supermarkets is represented in all states and territories in Australia. Coles can be characterized as a bundling service where all suppliers meet in Coles and consumers go to Coles to purchase the product. Thus, the product which Coles provides is convenience to its consumers. Accordingly, it is the supplier which provides the input for Coles to supply to the final consumers of the product. Thus, without the suppliers Coles cannot provide a service. A diagram of Coles Supply Chain is provided below:

Analysis of the grocery industry

4 Commercial-in-Confidence

Deloitte Access Economics

Figure 2.1: Coles supply chain

Supplier

Supplier

Supplier

Wholesaler

Retail Store

Retail Store

Retail Store

Wholesaler and Retailers are Integrated

Source: Deloitte Access Economics

Accordingly, Coles needs to ensure that they are able to meet the needs of its consumers. By doing so they are required to sense the needs of its consumers and adjust accordingly, thus Coles does depend on its suppliers to be flexible enough to meet their needs. Naturally, if they are not able to do so, then Coles would need to either forgo this market or find an additional supplier to meet this gap. It is commonly known that Woolworths and other supermarkets provide the same service to its consumers. Recent years have also seen supermarkets try to enhance convenience by providing online grocery shopping.

Today, Coles possesses a market share of 31% in the grocery market. Woolworths holds a bigger market share. The remainder of the market goes to IGA and other independent grocers.

Analysis of the grocery industry

5 Commercial-in-Confidence

Deloitte Access Economics

Value added is a measure of how much economic activity directly happens inside an organisation and how much it generates elsewhere in the economy

Coles Supermarkets’ direct ‘value added’ was $4.5 billion in 2011-12 – but its contribution including indirect value added and facilitated trade was five times as big at $20.8 billion.

Coles Supermarkets contributed 55,467 FTE jobs in 2011-12, but including indirect and facilitated trade, it was 183,930 FTE jobs up the supply chain and across the economy

3 Economic contribution of Coles The economic contribution of Coles Supermarkets to the Australian economy is measured in terms of:

value added which is the contribution to GDP, and includes wages paid to employees and the gross operating surplus generated (including taxes); and

employment which is measured by full-time equivalent (FTE) jobs.

The economic contribution is the sum of the direct and indirect value added by the economic activity undertaken by Coles Supermarkets. In addition, there is trade ‘facilitated’ by Coles.

3.1 Modelling approach

The basis for estimating the economic contribution is the direct value added and employment contributed by capital and labour inputs employed directly by Coles Supermarkets in the provision of its goods and services. These outputs are the retail services offered in the sale of various goods including grocery, frozen, meat, dairy deli, fresh produce, bakery, general merchandise and apparel, tobacco, liquor and services. The value added is the most appropriate measure of the economic contribution to GDP. It is the sum of the returns to the primary factors of production – labour and capital – and can be calculated by adding the gross operating surplus1 and wages paid to employees. This is then combined with a selection of input-output economic multipliers to determine the indirect or flow-on contribution to the economy. The indirect contribution is a

1 Gross operating surplus represents the value of income generated by the entity’s direct capital inputs, generally measured as the earnings before interest, tax, depreciation and amortisation (EBITDA).

Analysis of the grocery industry

6 Commercial-in-Confidence

Deloitte Access Economics

measure of the demand for goods and services produced in other sectors of the economy as a result of the direct economic activity of Coles Supermarkets. The size of the flow-on activity is determined by the extent of the linkages with other sectors of the economy.

Given that Coles is in the retailing sector, beyond indirect we also look at the impacts arising from Coles as an intermediary for the suppliers – i.e. the trade ‘facilitated’ by Coles. According to the ABS:

“Although retailers actually buy and sell goods, the goods purchased are not treated as part of their intermediate consumption when they are resold with only minimal processing such as grading, cleaning, packaging, etc. Wholesalers and retailers are treated as supplying services rather than goods to their customers by storing and displaying a selection of goods in convenient locations and making them easily available for customers to buy. Their output is measured by the total value of the trade margins realised on the goods they purchase for resale.”

This effect is called, “Indirect Contribution – Intermediate Inputs”.

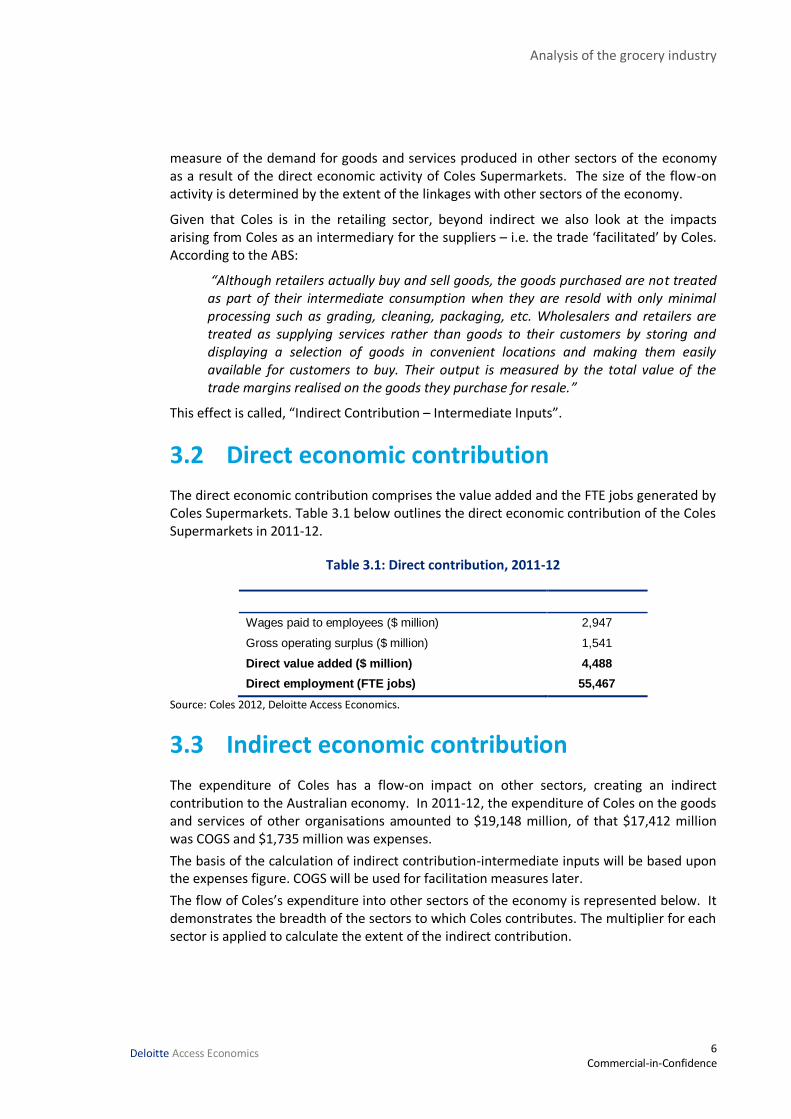

3.2 Direct economic contribution

The direct economic contribution comprises the value added and the FTE jobs generated by Coles Supermarkets. Table 3.1 below outlines the direct economic contribution of the Coles Supermarkets in 2011-12.

Table 3.1: Direct contribution, 2011-12

Wages paid to employees ($ million) 2,947

Gross operating surplus ($ million) 1,541

Direct value added ($ million) 4,488

Direct employment (FTE jobs) 55,467

Source: Coles 2012, Deloitte Access Economics.

3.3 Indirect economic contribution

The expenditure of Coles has a flow-on impact on other sectors, creating an indirect contribution to the Australian economy. In 2011-12, the expenditure of Coles on the goods and services of other organisations amounted to $19,148 million, of that $17,412 million was COGS and $1,735 million was expenses.

The basis of the calculation of indirect contribution-intermediate inputs will be based upon the expenses figure. COGS will be used for facilitation measures later.

The flow of Coles’s expenditure into other sectors of the economy is represented below. It demonstrates the breadth of the sectors to which Coles contributes. The multiplier for each sector is applied to calculate the extent of the indirect contribution.

Analysis of the grocery industry

7 Commercial-in-Confidence

Deloitte Access Economics

Figure 3.1: Coles indirect contribution flow

Source: Coles 2012, Deloitte Access Economics.

The indirect contribution relates to the additional contribution that Coles make as an intermediary who on sells products.

Table 3.2: Indirect economic contribution – Intermediate Inputs 2011-12

Wages paid to employees ($ million) 747

Gross operating surplus ($ million) 793

Indirect value added - intermediate inputs ($ million) 1,541

Indirect employment (FTE jobs) 9,468

Source: Coles 2012, Deloitte Access Economics.

3.4 Total economic contribution

Table 3.3 outlines the total economic contribution of Coles – the sum of the direct and indirect (intermediate input only) contributions.

Table 3.3: Total economic contribution 2011-12

Wages paid to employees ($ million) 3,695

Gross operating surplus ($ million) 2,334

Total value added ($ million) 6,029

Total employment (FTE jobs) 64,935

Source: Deloitte Access Economics.

The economic contribution of Coles highlights that it is an important organisation, as an intermediary Coles contributes over $6 billion to Australian GDP, and supports almost 65,000 FTE jobs.

Indirect gross value

added $1,541m

Indirect employment

9,468 FTE jobs

Cleaning, electricity,

marketing and other

business services

Coles expenditure

$19,148m

Analysis of the grocery industry

8 Commercial-in-Confidence

Deloitte Access Economics

3.5 Regional economic contribution

Table 3.4 outlines the direct regional employment economic contribution of Coles. Of the 77,827 (total) employees employed in Coles supermarkets in CBD, metro and country areas, (not including Bi-Lo) 22,503 are employed in country supermarkets. That is, almost 30%:

Table 3.4: Direct regional employment contribution 2011-12

Total employees, Coles country supermarkets 22,503

Total employees, Coles supermarkets 77,827

Country proportion of Coles direct regional employment 29%

Source: Deloitte Access Economics. Note: does not include BiLo or Store Support Centres

Note that these figures are for supermarkets only and do not include distribution centres. We assume that distribution centre activity is also divided between regional and non-regional areas in the same proportion.

Assuming that regional/non-regional breakdown of direct activity is same as store sales figure that have been provided by Coles we have a regional contribution of direct activity of 30%. Further, our analysis of the industries and regions of Coles’s indirect activities, suggests a regional proportion of 23%. The proportion of total activity in regional areas is 28%.

Table 3.5: Regional value added 2011-12

Value Added Proportion of Total

Direct value added 1,330 30%

Indirect economic contribution – intermediate input 351 23%

Total Value added 1,681 28%

Source: Deloitte Access Economics. Note: does not include BiLo or Store Support Centres

3.6 Indirect contribution – Facilitated

Coles purchases products which in turn generate business for the suppliers and thus contributes to the economy. The figures presented reflect the contribution of Coles when it is facilitating trade for the suppliers.

Table 3.6: Economic contribution – Facilitated 2011-12

Total Regional

Wages paid to employees ($ million) 6,997 1,952

Gross operating surplus ($ million) 7,757 3,216

Indirect value added - Facilitated ($ million) 14,754 5,167

Indirect employment (FTE jobs) 118,995 n/a

Source: Coles 2012, Deloitte Access Economics.

Analysis of the grocery industry

9 Commercial-in-Confidence

Deloitte Access Economics

If the figures are included as part of Coles’s economic contribution we find its contribution to be:

Table 3.7: Economic contribution: direct, indirect and facilitated 2011-12

Total value added ($ million) 20,783

Total employment (FTE jobs) 183,930

Source: Deloitte Access Economics.

If we consider Coles as a facilitator as well, this would imply Coles’s economic contribution to more than $20 billion which supports more than 180,000 jobs.

3.7 Economic contribution comparison

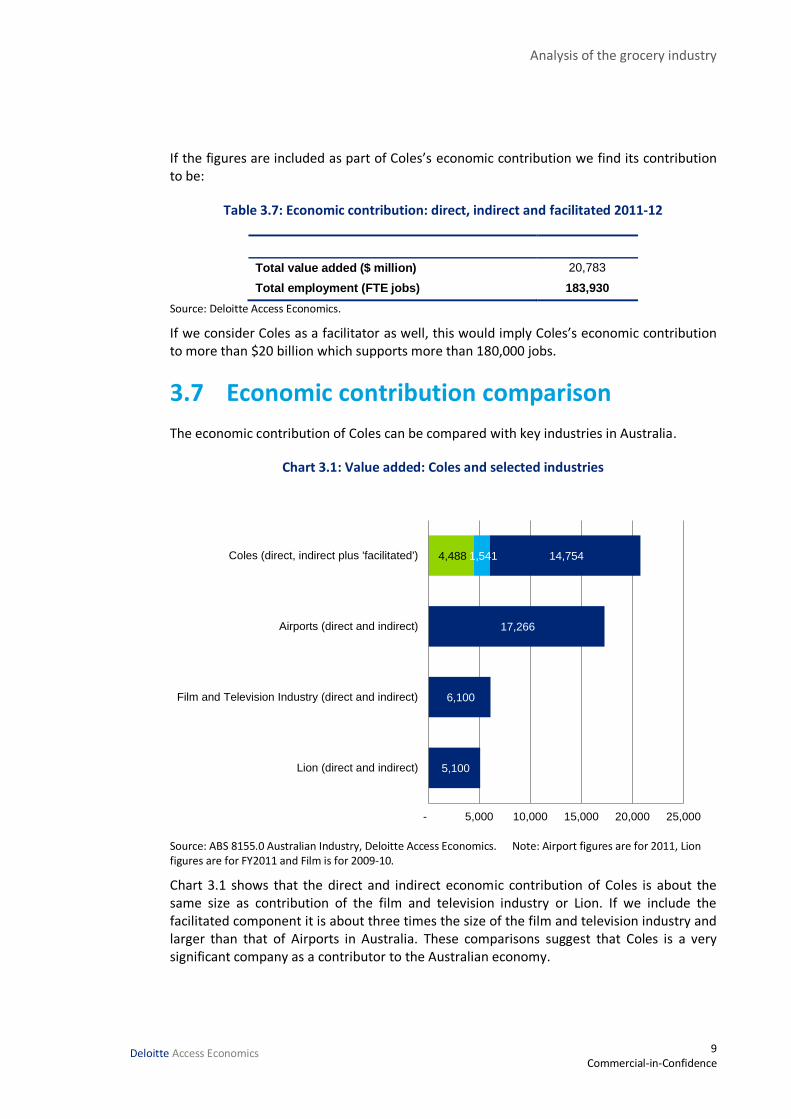

The economic contribution of Coles can be compared with key industries in Australia.

Chart 3.1: Value added: Coles and selected industries

Source: ABS 8155.0 Australian Industry, Deloitte Access Economics. Note: Airport figures are for 2011, Lion figures are for FY2011 and Film is for 2009-10.

Chart 3.1 shows that the direct and indirect economic contribution of Coles is about the same size as contribution of the film and television industry or Lion. If we include the facilitated component it is about three times the size of the film and television industry and larger than that of Airports in Australia. These comparisons suggest that Coles is a very significant company as a contributor to the Australian economy.

4,488 1,541

5,100

6,100

17,266

14,754

- 5,000 10,000 15,000 20,000 25,000

Lion (direct and indirect)

Film and Television Industry (direct and indirect)

Airports (direct and indirect)

Coles (direct, indirect plus 'facilitated')

Analysis of the grocery industry

10 Commercial-in-Confidence

Deloitte Access Economics

4 Price and productivity

4.1 Context: Analysing ‘Down Down’

The ‘Down Down’ pricing strategy of Coles Supermarkets has occurred within a dynamic supermarket industry. Just the last few years have seen significant developments, including the shift of Coles Supermarkets from Coles Group to Wesfarmers, the takeover of Franklins by Metcash, and the entry and expansion of new competitors ALDI and Costco.

All these developments have occurred since the ACCC’s 2008 grocery inquiry, which took place in response to perceived rising prices of groceries. It found that important factors included drought and supply disruptions, quarantine restrictions, and world commodity prices. By contrast, it found that ‘the potential contribution of any weakening of price competition in grocery retailing/wholesaling to food price inflation is limited.’ It found that a very small proportion of increases in food prices over the previous five years could be directly attributable to the increase in the gross margins achieved by major grocery players.

Over the last four years, Coles sales have increased by $4.8 billion to around $24 billion. Coles have out-performed the supermarket sector overall over the last four years, market share has gone up slightly. Growth in revenue reflects changes in prices and volumes. On the face of it, a campaign like ‘Down Down’ should have the effect of lowering prices and increasing volumes.

As might be expected with any increase in market share, Coles have been criticised for being too big and abusing its market power by squeezing the suppliers. Furthermore, there has been public debate about the current competition policy framework.

What is ‘Down Down’?

‘Down Down’ is a pricing and marketing strategy adopted by Coles from 2010 designed to increase its company performance. Part of the strategy is that prices for selected goods stay down rather than experience a short term price reduction as during a normal sale.

The purpose of this Chapter is to analyse consumer retail prices of Coles products and, if there are significant and sustained prices reductions, how these have been achieved: through reductions in cost of goods sold (and/or reduced farm gate prices); through reductions in cost of doing business (i.e. by efficiencies achieved in the supply chain or reduced wastage); or through reduced margins.

Specifically, we analyse food prices and the role of Coles’s ‘Down Down’ pricing strategy:

What has happened to Coles prices and profits over time?

Where have ‘Down Down’ savings come from?

What has been the role of private labels?

In presenting this analysis we recognise that there can be changes in impacts over time.

Analysis of the grocery industry

11 Commercial-in-Confidence

Deloitte Access Economics

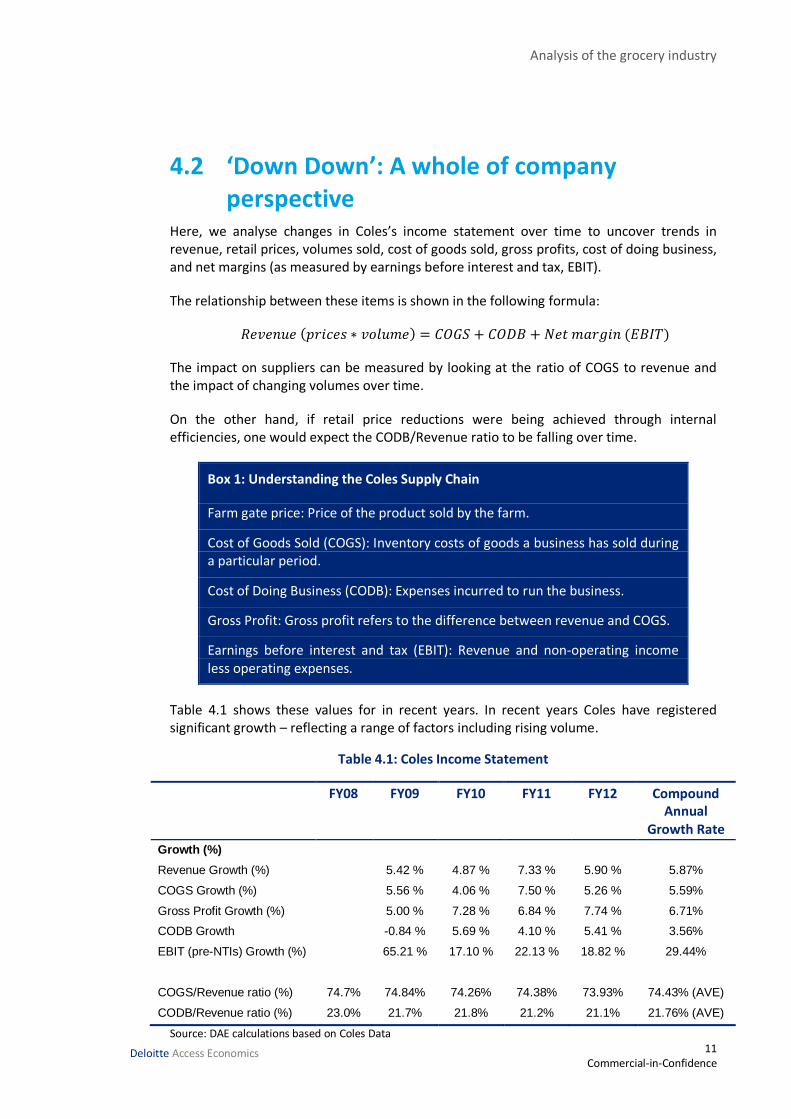

4.2 ‘Down Down’: A whole of company perspective

Here, we analyse changes in Coles’s income statement over time to uncover trends in revenue, retail prices, volumes sold, cost of goods sold, gross profits, cost of doing business, and net margins (as measured by earnings before interest and tax, EBIT).

The relationship between these items is shown in the following formula:

( ) ( )

The impact on suppliers can be measured by looking at the ratio of COGS to revenue and the impact of changing volumes over time.

On the other hand, if retail price reductions were being achieved through internal efficiencies, one would expect the CODB/Revenue ratio to be falling over time.

Box 1: Understanding the Coles Supply Chain

Farm gate price: Price of the product sold by the farm.

Cost of Goods Sold (COGS): Inventory costs of goods a business has sold during a particular period.

Cost of Doing Business (CODB): Expenses incurred to run the business.

Gross Profit: Gross profit refers to the difference between revenue and COGS.

Earnings before interest and tax (EBIT): Revenue and non-operating income less operating expenses.

Table 4.1 shows these values for in recent years. In recent years Coles have registered significant growth – reflecting a range of factors including rising volume.

Table 4.1: Coles Income Statement

FY08 FY09 FY10 FY11 FY12 Compound Annual

Growth Rate

Growth (%)

Revenue Growth (%) 5.42 % 4.87 % 7.33 % 5.90 % 5.87%

COGS Growth (%) 5.56 % 4.06 % 7.50 % 5.26 % 5.59%

Gross Profit Growth (%) 5.00 % 7.28 % 6.84 % 7.74 % 6.71%

CODB Growth -0.84 % 5.69 % 4.10 % 5.41 % 3.56%

EBIT (pre-NTIs) Growth (%) 65.21 % 17.10 % 22.13 % 18.82 % 29.44%

COGS/Revenue ratio (%) 74.7% 74.84% 74.26% 74.38% 73.93% 74.43% (AVE)

CODB/Revenue ratio (%) 23.0% 21.7% 21.8% 21.2% 21.1% 21.76% (AVE)

Source: DAE calculations based on Coles Data

Analysis of the grocery industry

12 Commercial-in-Confidence

Deloitte Access Economics

From the above, the following observations can be made:

EBIT has seen significant growth, recording a compound annual growth rate of 24.44% (or 19.4% over the last three years);

compound average annual growth of revenue was 5.87% and 5.59 for COGS – but for CODB was only 3.56%;

COGS/Revenue has been relatively constant in recent years; and

CODB/Revenue has fallen marginally in recent years.

Overall, we observe that the rise in profits is achieved through a combination of rising revenue and lower per unit costs – with lower costs mainly resulting from lower CODB.

4.2.1 Suppliers and efficiency

The figures above suggest that lower CODB has played a role in rising profits.

Partly, this has been achieved through savings through reduced waste (worth more than $400 million a year in FY12):

Changing fresh produce sourcing strategy from 100% spot purchases to 90% planned purchases.

Increasing the proportion of fresh produce purchased directly from farmers from 54% to 67%, which has enabled a shorter field to shelf lead time (and greater shelf life).

Coles claims distribution and transportation improvements have increased the speed of stocks through the supply chain and increased the shelf life of goods in-store. By moving to a system where the goods are collated in a distribution centre, Coles has been able to increase their capacity utilisation by 2.9%, cartons packed by 8.9% and their on-time deliveries by 2.4%. This reduces the cost by about 10%.

Grocery and dairy products are now ordered into store via an automated sales-based system known as Easy Ordering. This systems forecasts demand for a particular store and makes orders based on a just-in-time approach.

Secondly, Coles claims savings through competitive tendering, centralising procurement and improvement specification of requirements of goods (worth more than $200 million a year in FY12).

Thirdly, savings of almost $100 million have been achieved through self-scan checkouts and changes to shelf replenishment.

Finally, there have been efficiencies by increasing sales per square metre of selling floor area by almost 20%. These changes are discussed in more detail in 4.5.

The savings generated for the above initiatives contributes to the savings pool which can then be utilised to fund price reductions in the store.

One of the key changes in Coles’s supply change is in logistics. In the past, many of Coles products were delivered direct to store i.e. the supplier/Coles pays for a truck to deliver their goods to the store.

Analysis of the grocery industry

13 Commercial-in-Confidence

Deloitte Access Economics

Figure 4.1: Direct to store logistics network

Supplier

Supplier

Supplier

Retail Store

Retail Store

Retail Store

Source: Deloitte Access Economics.

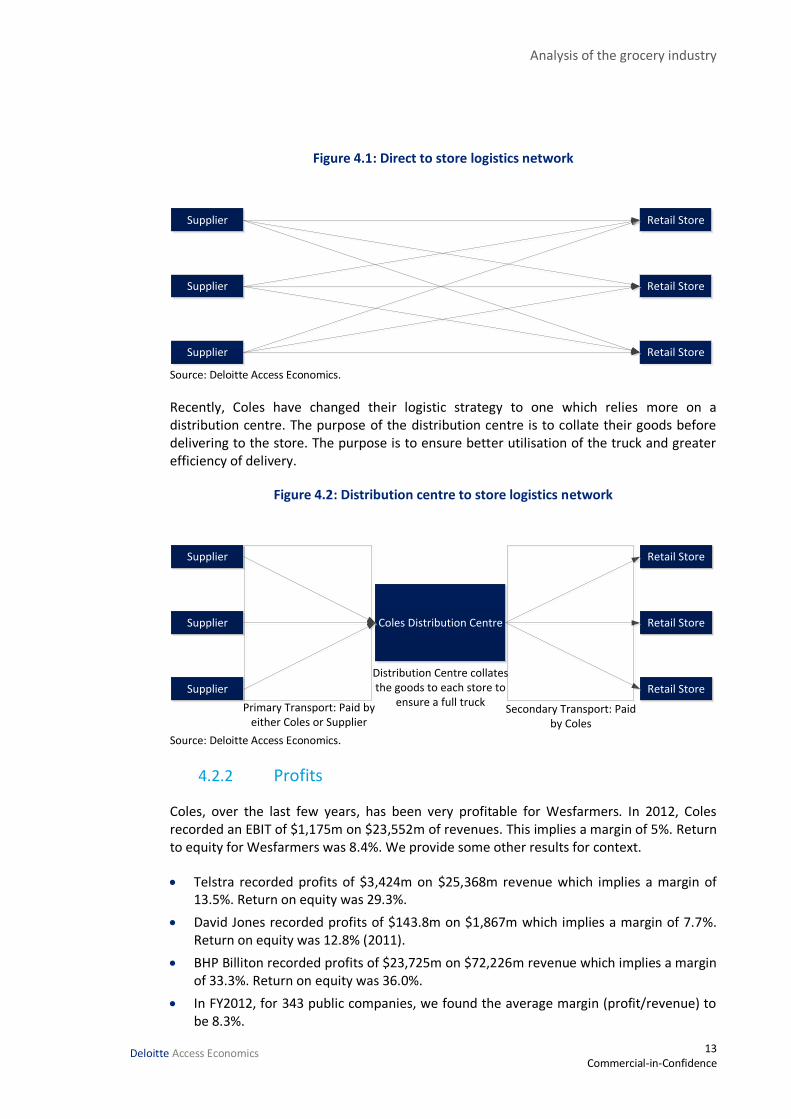

Recently, Coles have changed their logistic strategy to one which relies more on a distribution centre. The purpose of the distribution centre is to collate their goods before delivering to the store. The purpose is to ensure better utilisation of the truck and greater efficiency of delivery.

Figure 4.2: Distribution centre to store logistics network

Supplier

Supplier

Supplier

Coles Distribution Centre

Retail Store

Retail Store

Retail Store

Primary Transport: Paid by either Coles or Supplier

Secondary Transport: Paid by Coles

Distribution Centre collates the goods to each store to

ensure a full truck

Source: Deloitte Access Economics.

4.2.2 Profits

Coles, over the last few years, has been very profitable for Wesfarmers. In 2012, Coles recorded an EBIT of $1,175m on $23,552m of revenues. This implies a margin of 5%. Return to equity for Wesfarmers was 8.4%. We provide some other results for context.

Telstra recorded profits of $3,424m on $25,368m revenue which implies a margin of 13.5%. Return on equity was 29.3%.

David Jones recorded profits of $143.8m on $1,867m which implies a margin of 7.7%. Return on equity was 12.8% (2011).

BHP Billiton recorded profits of $23,725m on $72,226m revenue which implies a margin of 33.3%. Return on equity was 36.0%.

In FY2012, for 343 public companies, we found the average margin (profit/revenue) to be 8.3%.

Analysis of the grocery industry

14 Commercial-in-Confidence

Deloitte Access Economics

This suggests that while Coles returns have increased in recent years, there are other profitable listed companies as well.

4.2.3 Overall prices all goods

Before we look specifically at the prices of goods in the ‘Down Down’ strategy it is important to mention overall trends in a basket of goods.

If non-‘Down Down’ goods experienced an increase in prices to offset ‘Down Down’ reductions consumers would be worse off overall by buying at Coles (assuming that they do not substitute between goods).

Overall, we find that all goods prices have fallen by 4.2% on average over the last 18 months (and by 7.9% if cigarettes are excluded). This is discussed in more detail in chapter 5. While many goods prices increase over time, this suggests that on average prices have come down.

4.2.4 Overall prices ‘Down Down’ goods

For the 1200 ‘Down Down’ goods for which data is available, retail prices have fall by 8% on average, on a volume-weighted basis since 2011. For these goods, COGS per unit has fallen by 17% overall, but only 2% on a volume-weighted basis.

It is difficult to come to one broad conclusion about the impacts of these changes on suppliers because there will be many individual experiences. But overall, while supplier volume has increased faster (50%) than income (30%), reducing per unit margins, it is likely that this will be significantly offset by rising volumes itself, contributing to profit.

From another perspective, with retail prices falling faster (8%) than COGS per unit (2%), it suggests that most of the savings to drive volumes has come from Coles (either as reduced per unit margins or internal efficiencies).

Table 4.2: Change in key aggregates for the 'Down Down' products (Jan 2011 to mid-2012)

Volume of goods

Supplier Income ($)

COGS per unit (unweighted)

COGS per unit (volume weighted)

Retail prices ($)

+49.63% +30.45% -17.02% -2.00% -8.00%

Source: Coles Data

4.3 ‘Down Down’: product prices under the microscope

We now apply our analysis of retail prices, margins, efficiencies (cost of doing business) and suppliers (farm gate prices and cost of goods sold) to individual products included in the ‘Down Down’ campaign – for a more forensic look at pricing dynamics.

Though the overall result for suppliers is higher income and margins, there are different dynamics for different goods.

Analysis of the grocery industry

15 Commercial-in-Confidence

Deloitte Access Economics

We find a number of different scenarios regarding the relationship between retail prices, supplier income, efficiencies, Coles’s margin and volume. Lower retail prices can reflect:

Coles pays the same or more per unit to suppliers and reduces prices by reducing its margins or achieving efficiencies;

Coles pays suppliers less in headline income but provides more favourable contract terms (or assists in achieving efficiencies) and covers own costs by achieving efficiencies elsewhere; and

Coles and a supplier may together agree to reduce supplier and retail prices to drive volume to mutual benefit.

Of course, there will also be situations where Coles reduces prices paid to suppliers who then experience lower margins and profits.

4.3.1 Milk

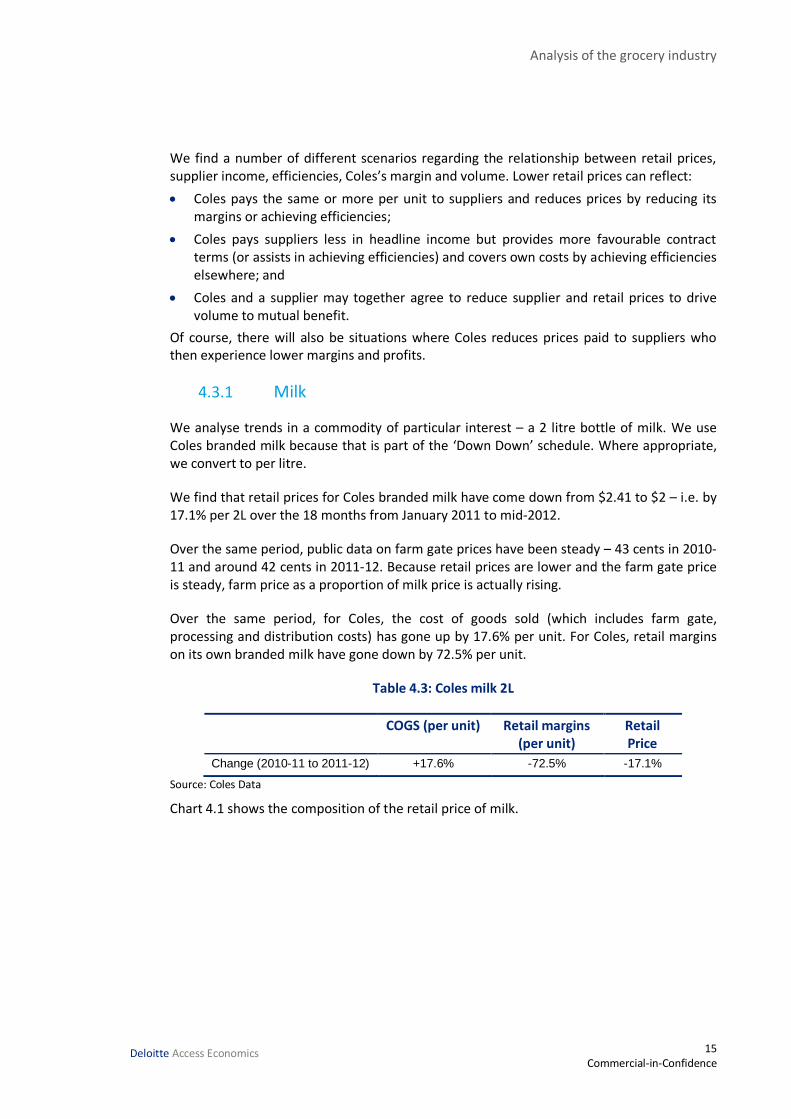

We analyse trends in a commodity of particular interest – a 2 litre bottle of milk. We use Coles branded milk because that is part of the ‘Down Down’ schedule. Where appropriate, we convert to per litre.

We find that retail prices for Coles branded milk have come down from $2.41 to $2 – i.e. by 17.1% per 2L over the 18 months from January 2011 to mid-2012.

Over the same period, public data on farm gate prices have been steady – 43 cents in 2010-11 and around 42 cents in 2011-12. Because retail prices are lower and the farm gate price is steady, farm price as a proportion of milk price is actually rising.

Over the same period, for Coles, the cost of goods sold (which includes farm gate, processing and distribution costs) has gone up by 17.6% per unit. For Coles, retail margins on its own branded milk have gone down by 72.5% per unit.

Table 4.3: Coles milk 2L

COGS (per unit) Retail margins (per unit)

Retail Price

Change (2010-11 to 2011-12) +17.6% -72.5% -17.1%

Source: Coles Data

Chart 4.1 shows the composition of the retail price of milk.

Analysis of the grocery industry

16 Commercial-in-Confidence

Deloitte Access Economics

Chart 4.1: 2L Coles milk price composition

Source: ABARES 2012, Coles data

Coles purchases their milk from the milk processors and not the farmers. As a result, farm gate prices are not directly influenced by Coles’s purchase decisions. In fact, about 47% of milk products are actually exported and drinking Milk makes up about 25% of all dairy products.

ABARES predicts that for 2012-13, that farm gate prices will come down from 84 cents to 78 cents. However, we note that the farm gate price is not primarily driven by Coles, but rather through international factors and the Australian Dollar.

We also note that during this period that Coles have made a number of changes in their logistics network to improve their efficiency. For milk ,Coles changed from a direct-to-store delivery system to a system where the suppliers deliver to a distribution centre then delivers to the store.

Therefore, we conclude that over this period, the reduction in retail prices is not accounted for by a reduction in farm gate prices but rather through some combination of lower retail margins (and most probably internal efficiencies). Volume has increased and supplier payments have increased.

We note that while these are current trends in the market, they can change over time. It is possible that changes to any part of the milk supply chain – farmers, processors, transport operators, retailers – could see the effects of competition play out differently over time.

$0.86 (36%) $0.84 (45%)

$1.54 (64%)

$1.16 (55%)

$0.00

$0.20

$0.40

$0.60

$0.80

$1.00

$1.20

$1.40

$1.60

$1.80

$2.00

$2.20

$2.40

$2.60

2010-2011 2011-2012

Farmgate price Processing, Distribution retail activity and margins

Retail Price = $2.41 Retail Price = $2.00

Analysis of the grocery industry

17 Commercial-in-Confidence

Deloitte Access Economics

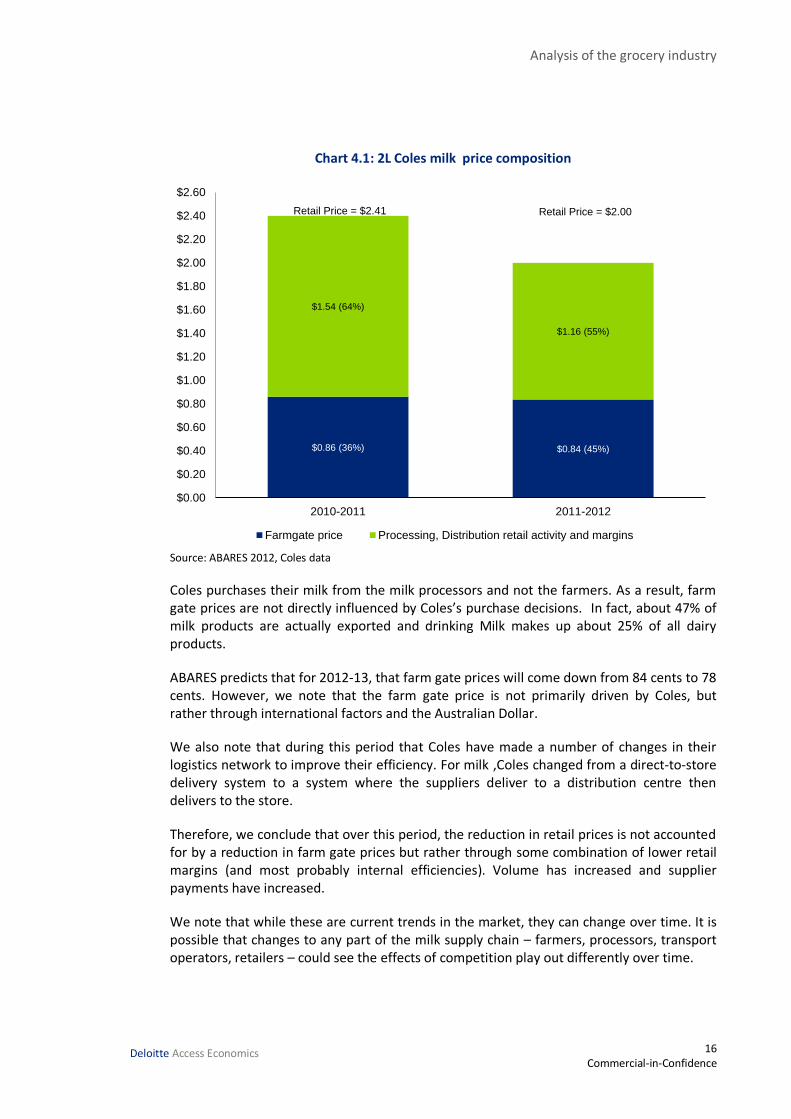

We conclude with a few observations about milk volumes. In the 1980s and 1990s, the production of milk trended up. Since 2002, production has come down due to the drought and deregulation of the milk industry. In the last two years production and sales has picked up. Chart 4.2 shows milk production figures for the last 25 years.

Chart 4.2: Milk production figures

Source: Dairy Australia

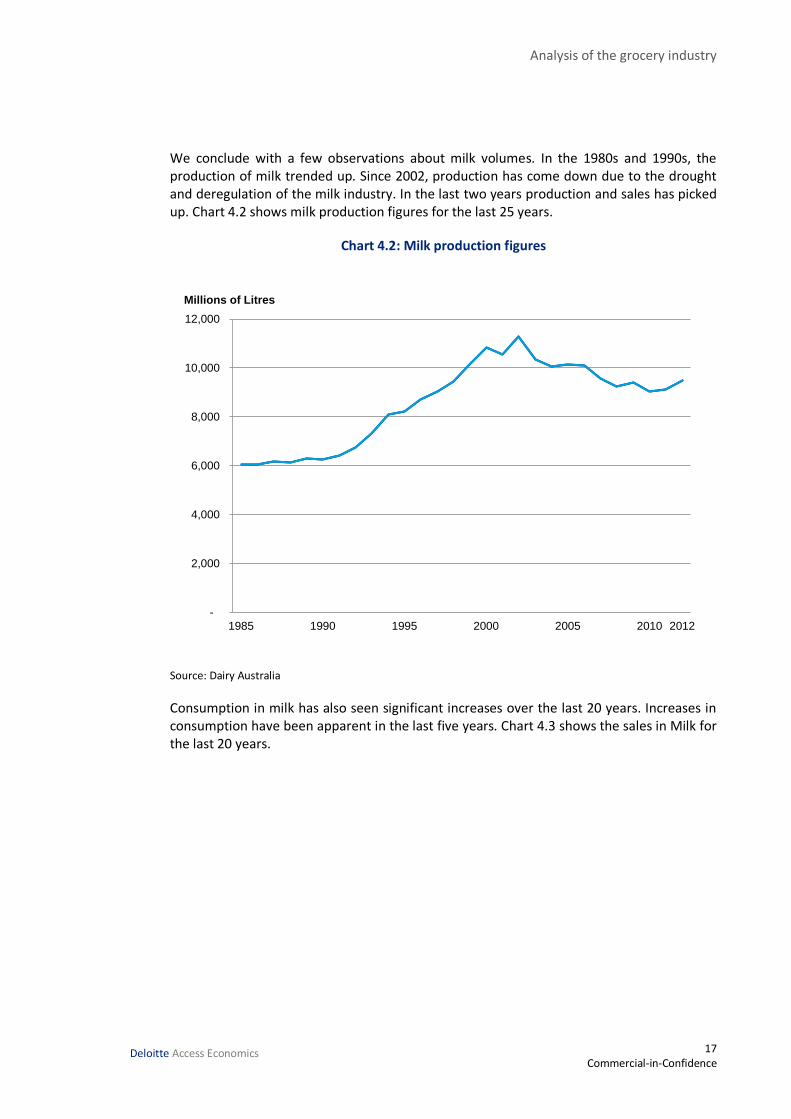

Consumption in milk has also seen significant increases over the last 20 years. Increases in consumption have been apparent in the last five years. Chart 4.3 shows the sales in Milk for the last 20 years.

-

2,000

4,000

6,000

8,000

10,000

12,000

1985 1990 1995 2000 2005 2010 2012

Millions of Litres

Analysis of the grocery industry

18 Commercial-in-Confidence

Deloitte Access Economics

Chart 4.3: Milk sales figures

Source: Dairy Australia

Rising production and consumption suggest that conditions in the retail market are favourable for the milk industry.

4.3.2 Bread

Retail prices of a loaf of white bread have come down from $1.15 to $1.00 per loaf over the 12 months from July 2011 to mid-2012 which implies a reduction of 13.04%.

Over the same period, the cost of goods sold has decreased by 16.1%.

Table 4.4: Coles Smart Buy white bread 650g

COGS (per unit) Retail Prices

Change -16.10% -13.04%

In the same period wheat has reduced from $274.11 to $253.46 per metric ton. This implies a reduction of 7.53%. According to the suppliers of bread, they have been undergoing fundamental restructuring to improve efficiencies. Publicly available information suggests some suppliers are planning to reduce costs significantly in coming years. Accordingly, the supplier is able to reduce the price of the goods they sell, which Coles is then able to pass onto consumers.

Another factor changes in bread is a change in the contractual change in the management of wastage. Whereas normal bread supply contracts see the supplier paying for unsold bread, for Coles Smart Buy bread sold through the ‘Down Down’ programme, Coles pays for

-

500

1,000

1,500

2,000

2,500

3,000

1990 1995 2000 2005 2010 2012

Analysis of the grocery industry

19 Commercial-in-Confidence

Deloitte Access Economics

unsold bread. Therefore, while suppliers receive a lower headline price, this will be offset by this.

Therefore, we conclude that over this period, the reduction in retail prices reflects lower COGS, but there could also be internal efficiencies. Lower COGS represents a combination of lower prices to suppliers, offset by some efficiencies and changes in contract terms.

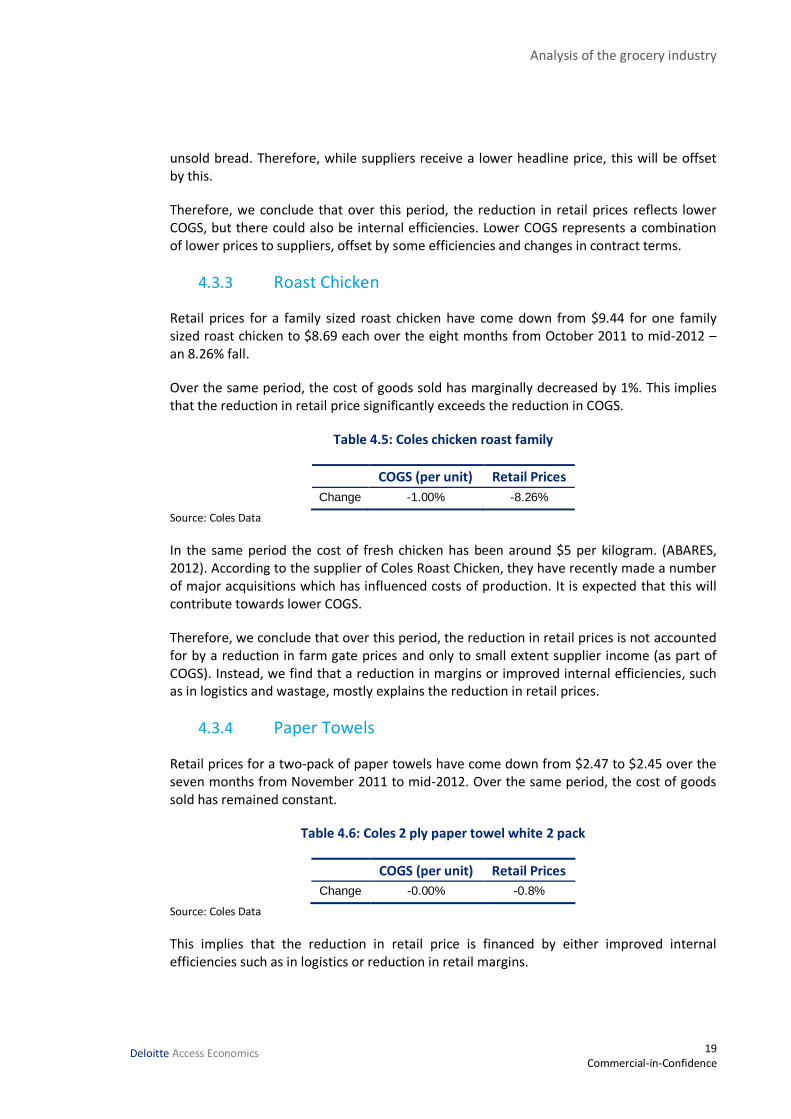

4.3.3 Roast Chicken

Retail prices for a family sized roast chicken have come down from $9.44 for one family sized roast chicken to $8.69 each over the eight months from October 2011 to mid-2012 – an 8.26% fall.

Over the same period, the cost of goods sold has marginally decreased by 1%. This implies that the reduction in retail price significantly exceeds the reduction in COGS.

Table 4.5: Coles chicken roast family

COGS (per unit) Retail Prices

Change -1.00% -8.26%

Source: Coles Data

In the same period the cost of fresh chicken has been around $5 per kilogram. (ABARES, 2012). According to the supplier of Coles Roast Chicken, they have recently made a number of major acquisitions which has influenced costs of production. It is expected that this will contribute towards lower COGS.

Therefore, we conclude that over this period, the reduction in retail prices is not accounted for by a reduction in farm gate prices and only to small extent supplier income (as part of COGS). Instead, we find that a reduction in margins or improved internal efficiencies, such as in logistics and wastage, mostly explains the reduction in retail prices.

4.3.4 Paper Towels

Retail prices for a two-pack of paper towels have come down from $2.47 to $2.45 over the seven months from November 2011 to mid-2012. Over the same period, the cost of goods sold has remained constant.

Table 4.6: Coles 2 ply paper towel white 2 pack

COGS (per unit) Retail Prices

Change -0.00% -0.8%

Source: Coles Data

This implies that the reduction in retail price is financed by either improved internal efficiencies such as in logistics or reduction in retail margins.

Analysis of the grocery industry

20 Commercial-in-Confidence

Deloitte Access Economics

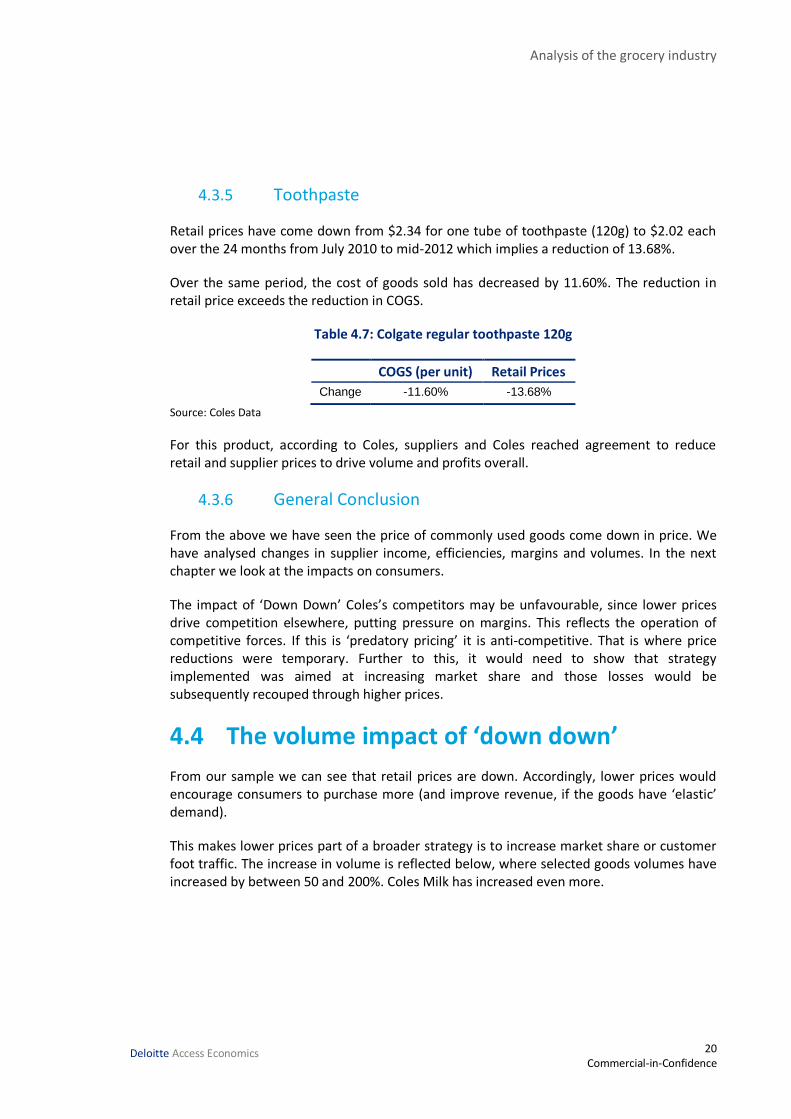

4.3.5 Toothpaste

Retail prices have come down from $2.34 for one tube of toothpaste (120g) to $2.02 each over the 24 months from July 2010 to mid-2012 which implies a reduction of 13.68%.

Over the same period, the cost of goods sold has decreased by 11.60%. The reduction in retail price exceeds the reduction in COGS.

Table 4.7: Colgate regular toothpaste 120g

COGS (per unit) Retail Prices

Change -11.60% -13.68%

Source: Coles Data

For this product, according to Coles, suppliers and Coles reached agreement to reduce retail and supplier prices to drive volume and profits overall.

4.3.6 General Conclusion

From the above we have seen the price of commonly used goods come down in price. We have analysed changes in supplier income, efficiencies, margins and volumes. In the next chapter we look at the impacts on consumers.

The impact of ‘Down Down’ Coles’s competitors may be unfavourable, since lower prices drive competition elsewhere, putting pressure on margins. This reflects the operation of competitive forces. If this is ‘predatory pricing’ it is anti-competitive. That is where price reductions were temporary. Further to this, it would need to show that strategy implemented was aimed at increasing market share and those losses would be subsequently recouped through higher prices.

4.4 The volume impact of ‘down down’

From our sample we can see that retail prices are down. Accordingly, lower prices would encourage consumers to purchase more (and improve revenue, if the goods have ‘elastic’ demand).

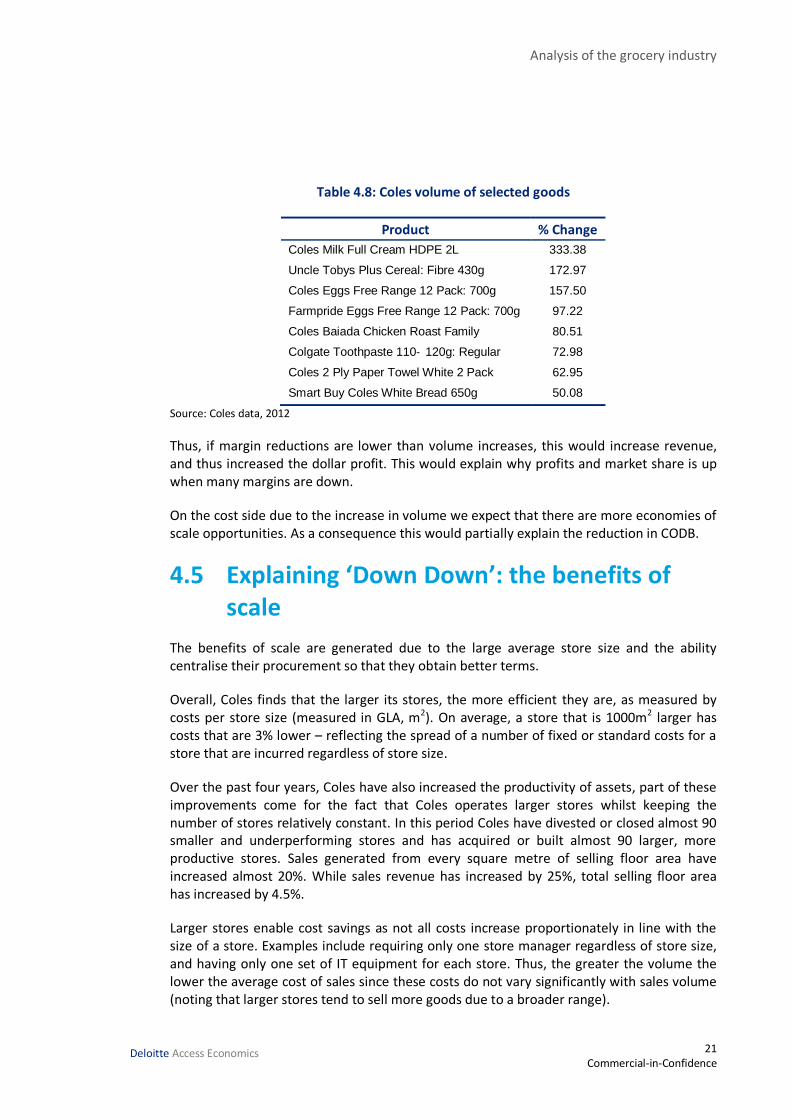

This makes lower prices part of a broader strategy is to increase market share or customer foot traffic. The increase in volume is reflected below, where selected goods volumes have increased by between 50 and 200%. Coles Milk has increased even more.

Analysis of the grocery industry

21 Commercial-in-Confidence

Deloitte Access Economics

Table 4.8: Coles volume of selected goods

Product % Change

Coles Milk Full Cream HDPE 2L 333.38

Uncle Tobys Plus Cereal: Fibre 430g 172.97

Coles Eggs Free Range 12 Pack: 700g 157.50

Farmpride Eggs Free Range 12 Pack: 700g 97.22

Coles Baiada Chicken Roast Family 80.51

Colgate Toothpaste 110‐ 120g: Regular 72.98

Coles 2 Ply Paper Towel White 2 Pack 62.95

Smart Buy Coles White Bread 650g 50.08

Source: Coles data, 2012

Thus, if margin reductions are lower than volume increases, this would increase revenue, and thus increased the dollar profit. This would explain why profits and market share is up when many margins are down.

On the cost side due to the increase in volume we expect that there are more economies of scale opportunities. As a consequence this would partially explain the reduction in CODB.

4.5 Explaining ‘Down Down’: the benefits of scale

The benefits of scale are generated due to the large average store size and the ability centralise their procurement so that they obtain better terms.

Overall, Coles finds that the larger its stores, the more efficient they are, as measured by costs per store size (measured in GLA, m2). On average, a store that is 1000m2 larger has costs that are 3% lower – reflecting the spread of a number of fixed or standard costs for a store that are incurred regardless of store size.

Over the past four years, Coles have also increased the productivity of assets, part of these improvements come for the fact that Coles operates larger stores whilst keeping the number of stores relatively constant. In this period Coles have divested or closed almost 90 smaller and underperforming stores and has acquired or built almost 90 larger, more productive stores. Sales generated from every square metre of selling floor area have increased almost 20%. While sales revenue has increased by 25%, total selling floor area has increased by 4.5%.

Larger stores enable cost savings as not all costs increase proportionately in line with the size of a store. Examples include requiring only one store manager regardless of store size, and having only one set of IT equipment for each store. Thus, the greater the volume the lower the average cost of sales since these costs do not vary significantly with sales volume (noting that larger stores tend to sell more goods due to a broader range).

Analysis of the grocery industry

22 Commercial-in-Confidence

Deloitte Access Economics

It is apparent that a lot of the savings mentioned in this section are generated through the significant size of Coles and the fact that they are integrated. If Coles was non-integrated this would make the savings (mentioned above) difficult to realise.

4.6 Private labels

Private labels are unbranded products purchased by supermarkets and then sold as their own products. Typically, these products are cheaper than branded products because of limited marketing activities. Historically, private brands had an image of being ‘no-frills’, targeting the most price-sensitive consumer; these days they are increasing thought of as an equal-quality, lower-price alternative.

Private labels in Australia are not produced by the Supermarkets. They are sourced from a major supplier of the product which is then labelled as a Coles product.

In Australia, private labels make up about 23% (Oct 2011) of fast moving consumer goods (FMCG). This is relatively small when compared to the UK where private labels represent a market share of 49.2% (2011). Compared with the US where private labels represent 18.5%, private labels in Australia are marginally more prevalent.

Private labels have been a matter of policy discussion: critics have asserted that they are part of a strategy to dominate the supply chain, thus reducing the viability of branded products. The claim is that the volume sold gives supermarkets more bargaining power which enables them to achieve lower COGS and thus higher margins. In the short run the supermarkets gain is at the expense of the suppliers.

In the long run it is claimed that it could be part of a predatory pricing strategy. That is, eventually prices will rise and this will enhance margins. Consequently, there will be less choice for consumers.

Another contention is shelving preference: where the supermarket deliberately places preferred products (in this case private labels products) so that it is readily visible to the consumer. Thus, consumers are more likely to choose that product over another given the convenience of the location.

According to Coles’s data on ranging and space allocation decisions, Coles brand products are treated in the same manner as proprietary brand products. In many cases Coles brand products are located together with similar brands and less shelf space than proprietary brands. Coles periodically reviews if their brand is over/under represented by examining the quantity they sell relative to the space on the shelves. If a good is underrepresented i.e. Coles Brand items have less proportion of the space than their sales, an independent review will be undertaken that may lead to more shelf space. If the opposite occurs, the Items will likely be reworked / deleted at next review.

According to Coles’s data, shelving decisions are driven by the demands of consumers. If a product is popular, then potentially more shelf space will allocated. Accordingly, if a product is underperforming then it may be removed from their product range.

Analysis of the grocery industry

23 Commercial-in-Confidence

Deloitte Access Economics

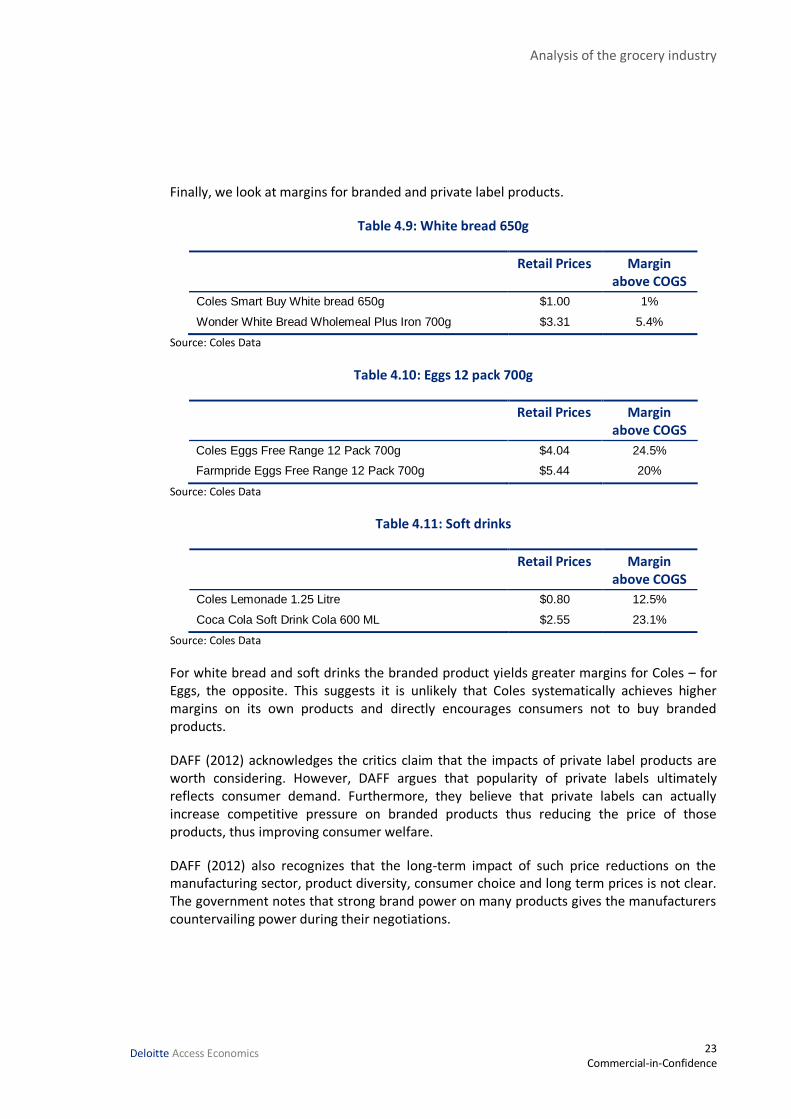

Finally, we look at margins for branded and private label products.

Table 4.9: White bread 650g

Retail Prices Margin above COGS

Coles Smart Buy White bread 650g $1.00 1%

Wonder White Bread Wholemeal Plus Iron 700g $3.31 5.4%

Source: Coles Data

Table 4.10: Eggs 12 pack 700g

Retail Prices Margin above COGS

Coles Eggs Free Range 12 Pack 700g $4.04 24.5%

Farmpride Eggs Free Range 12 Pack 700g $5.44 20%

Source: Coles Data

Table 4.11: Soft drinks

Retail Prices Margin above COGS

Coles Lemonade 1.25 Litre $0.80 12.5%

Coca Cola Soft Drink Cola 600 ML $2.55 23.1%

Source: Coles Data

For white bread and soft drinks the branded product yields greater margins for Coles – for Eggs, the opposite. This suggests it is unlikely that Coles systematically achieves higher margins on its own products and directly encourages consumers not to buy branded products.

DAFF (2012) acknowledges the critics claim that the impacts of private label products are worth considering. However, DAFF argues that popularity of private labels ultimately reflects consumer demand. Furthermore, they believe that private labels can actually increase competitive pressure on branded products thus reducing the price of those products, thus improving consumer welfare.

DAFF (2012) also recognizes that the long-term impact of such price reductions on the manufacturing sector, product diversity, consumer choice and long term prices is not clear. The government notes that strong brand power on many products gives the manufacturers countervailing power during their negotiations.

Analysis of the grocery industry

24 Commercial-in-Confidence

Deloitte Access Economics

5 Consumer benefits In this chapter we analyse the consumer impacts price changes at Coles and other supermarkets. We also look at some of the broader benefits offered by supermarkets in terms of choice and convenience.

5.1 Consumer welfare benefits of ‘down down’

Consumers face a choice about how they allocate their income to spending and saving decisions. How much they decide to spend and on what will be determined by incomes and prices. If prices rise, this reduces the purchasing power of income. Conversely, lower prices are the equivalent of an increase in the purchasing power of income.

Consumers can decide what to do with such additional income: whether to save it, or spend it on goods whose prices have come down, or spend it on other goods. (If it is a ‘normal good’, spending on the cheaper good should increase). However, they use it, lower prices and increased purchasing power is an unambiguous improvement in consumer welfare (provided consumers are rational, in the economic sense). For further background, see Mas-Colell, Whinston and Green’s “Microeconomic Theory”.

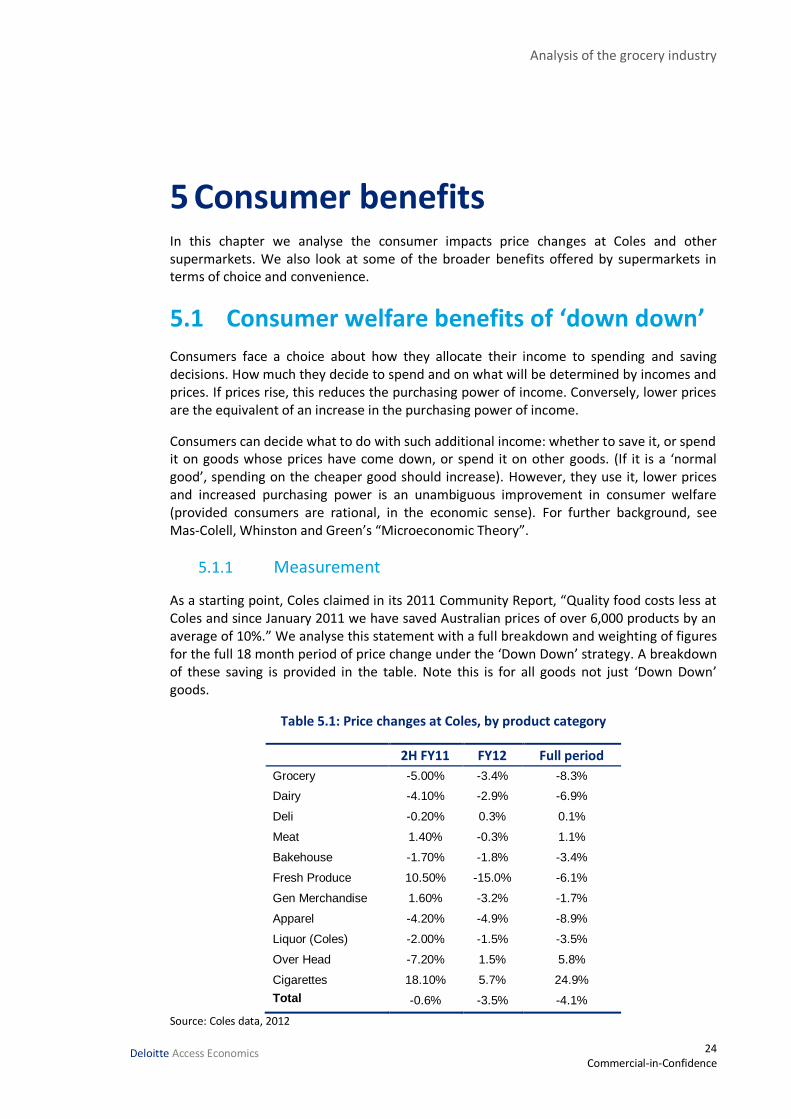

5.1.1 Measurement

As a starting point, Coles claimed in its 2011 Community Report, “Quality food costs less at Coles and since January 2011 we have saved Australian prices of over 6,000 products by an average of 10%.” We analyse this statement with a full breakdown and weighting of figures for the full 18 month period of price change under the ‘Down Down’ strategy. A breakdown of these saving is provided in the table. Note this is for all goods not just ‘Down Down’ goods.

Table 5.1: Price changes at Coles, by product category

2H FY11 FY12 Full period

Grocery -5.00% -3.4% -8.3%

Dairy -4.10% -2.9% -6.9%

Deli -0.20% 0.3% 0.1%

Meat 1.40% -0.3% 1.1%

Bakehouse -1.70% -1.8% -3.4%

Fresh Produce 10.50% -15.0% -6.1%

Gen Merchandise 1.60% -3.2% -1.7%

Apparel -4.20% -4.9% -8.9%

Liquor (Coles) -2.00% -1.5% -3.5%

Over Head -7.20% 1.5% 5.8%

Cigarettes 18.10% 5.7% 24.9%

Total -0.6% -3.5% -4.1%

Source: Coles data, 2012

Analysis of the grocery industry

25 Commercial-in-Confidence

Deloitte Access Economics

The table above describes the movement of Coles’s inflation figures over an 18 month period. FY2012 refers to financial Year 2012 and is an annual figure; 2H 2011 reflects the inflation for the second half of 2011.

Over an 18 month period prices for most categories have come down. On a weighted average basis, prices have fallen by 4.1%.

The main exception is cigarette prices, which have increase dramatically because of changes in excise arrangements.

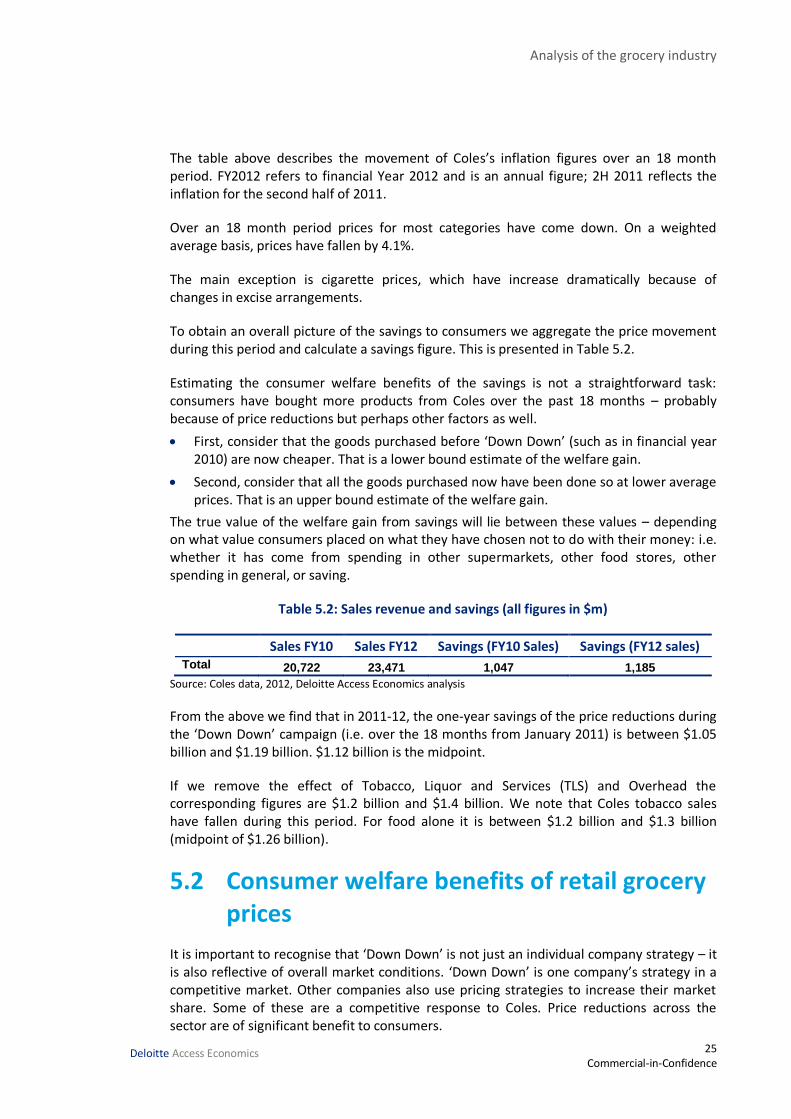

To obtain an overall picture of the savings to consumers we aggregate the price movement during this period and calculate a savings figure. This is presented in Table 5.2.

Estimating the consumer welfare benefits of the savings is not a straightforward task: consumers have bought more products from Coles over the past 18 months – probably because of price reductions but perhaps other factors as well.

First, consider that the goods purchased before ‘Down Down’ (such as in financial year 2010) are now cheaper. That is a lower bound estimate of the welfare gain.

Second, consider that all the goods purchased now have been done so at lower average prices. That is an upper bound estimate of the welfare gain.

The true value of the welfare gain from savings will lie between these values – depending on what value consumers placed on what they have chosen not to do with their money: i.e. whether it has come from spending in other supermarkets, other food stores, other spending in general, or saving.

Table 5.2: Sales revenue and savings (all figures in $m)

Sales FY10 Sales FY12 Savings (FY10 Sales) Savings (FY12 sales) Total 20,722 23,471 1,047 1,185

Source: Coles data, 2012, Deloitte Access Economics analysis

From the above we find that in 2011-12, the one-year savings of the price reductions during the ‘Down Down’ campaign (i.e. over the 18 months from January 2011) is between $1.05 billion and $1.19 billion. $1.12 billion is the midpoint.

If we remove the effect of Tobacco, Liquor and Services (TLS) and Overhead the corresponding figures are $1.2 billion and $1.4 billion. We note that Coles tobacco sales have fallen during this period. For food alone it is between $1.2 billion and $1.3 billion (midpoint of $1.26 billion).

5.2 Consumer welfare benefits of retail grocery prices

It is important to recognise that ‘Down Down’ is not just an individual company strategy – it is also reflective of overall market conditions. ‘Down Down’ is one company’s strategy in a competitive market. Other companies also use pricing strategies to increase their market share. Some of these are a competitive response to Coles. Price reductions across the sector are of significant benefit to consumers.

Analysis of the grocery industry

26 Commercial-in-Confidence

Deloitte Access Economics

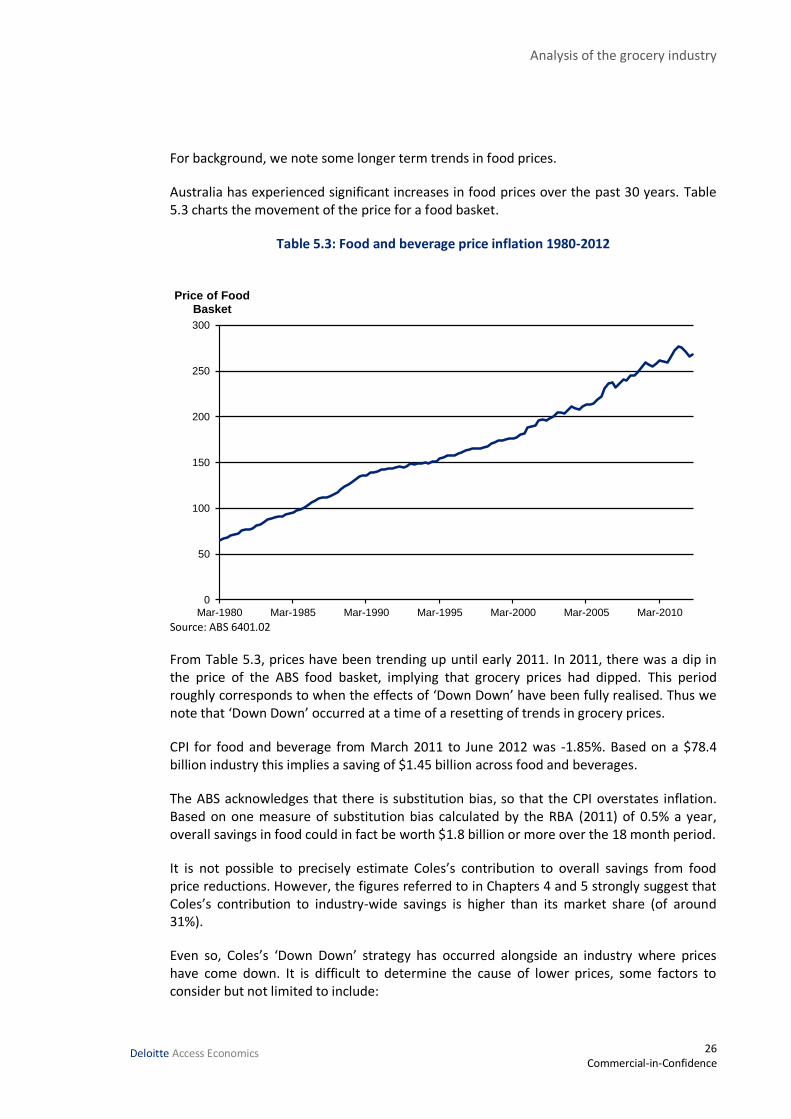

For background, we note some longer term trends in food prices.

Australia has experienced significant increases in food prices over the past 30 years. Table 5.3 charts the movement of the price for a food basket.

Table 5.3: Food and beverage price inflation 1980-2012

Source: ABS 6401.02

From Table 5.3, prices have been trending up until early 2011. In 2011, there was a dip in the price of the ABS food basket, implying that grocery prices had dipped. This period roughly corresponds to when the effects of ‘Down Down’ have been fully realised. Thus we note that ‘Down Down’ occurred at a time of a resetting of trends in grocery prices.

CPI for food and beverage from March 2011 to June 2012 was -1.85%. Based on a $78.4 billion industry this implies a saving of $1.45 billion across food and beverages.

The ABS acknowledges that there is substitution bias, so that the CPI overstates inflation. Based on one measure of substitution bias calculated by the RBA (2011) of 0.5% a year, overall savings in food could in fact be worth $1.8 billion or more over the 18 month period.

It is not possible to precisely estimate Coles’s contribution to overall savings from food price reductions. However, the figures referred to in Chapters 4 and 5 strongly suggest that Coles’s contribution to industry-wide savings is higher than its market share (of around 31%).

Even so, Coles’s ‘Down Down’ strategy has occurred alongside an industry where prices have come down. It is difficult to determine the cause of lower prices, some factors to consider but not limited to include:

0

50

100

150

200

250

300

Mar-1980 Mar-1985 Mar-1990 Mar-1995 Mar-2000 Mar-2005 Mar-2010

Price of Food Basket

Analysis of the grocery industry

27 Commercial-in-Confidence

Deloitte Access Economics

entry of new supermarkets including ALDI and Costco;

Coles’s ‘Down Down’ strategy itself: to focus more on volume and lower prices (i.e. improve market share and profits);

competitive responses to ‘Down Down’ from other major supermarket chains and speciality retailers;

other market dynamics such as changes in consumer spending pattern consumers are more cautionary in their spending post GFC;

changes in competition policy and other regulatory measures; and

strong Australian dollar (for imported or import-competing food items).

5.3 Variety and choice at the supermarket

Recently, choice in the supermarkets has come under scrutiny. The argument is that by restricting choice, the supermarkets are able to increase their bargaining power with the suppliers whilst reducing their overheads. Further to this the reduction in choice is also damaging to welfare since consumers have less choice and are unable to purchase goods they desire.

The economic value of choice for a large supermarket is difficult to measure. In the supermarket, choice is measured by the number of stock keeping units (SKUs) – the most granular measure of items offered for sale. For example, each different brand, variety and size of a product has its own SKU.