alternative revenue generation in vermont public schools: raising funds outside the tax base to...

TRANSCRIPT

Alternative Revenue Generation in Vermont Public Schools:

Raising funds outside the tax base to support public education

Thomas Downes Department of Economics

Tufts University e-mail: [email protected]

Jason Steinman

Division of Monetary Affairs Board of Governors of the Federal Reserve System

e-mail: [email protected]

March 2007

Abstract: Nationwide, public school districts are increasingly seeking revenue from non-tax sources, through a variety of direct fund-raising strategies and through affiliated fund-raising organizations (local education foundations, parent teacher associations, parent teacher organizations and booster clubs). The growing importance of private funds in public schools raises a number of questions. This paper uses the intriguing case of Vermont to shed light on two of them: How sensitive is school district fund-raising to policy changes that create incentives for the generation of private revenue? Why do some school districts and supporting organizations raise private funds more effectively than others? We find compelling evidence that the extent to which districts substitute nontraditional revenues for property tax revenues depends on the local tax price. We also document links between variation in the use of nontraditional revenues and variation in factors that are likely to be correlated with the median voter’s tax price. Finally, we find that the success of local education foundations depends both on the environment in which they operate, particularly the wealth of the community, and on the scope of their solicitation activities. Thanks to Eric Brunner, Bill Mathis, Bill Hoyt, Gib Metcalf, Steve Cohen, Lori Taylor, participants at the annual meetings of the National Tax Association and the American Education Finance Association for their helpful suggestions. All remaining errors are attributable to the authors.

1

Introduction

Concerns of educational equity have motivated a series of education finance reforms at

the state level, often dramatically altering the funding streams available to schools. In the past 30

years, states including California, Vermont and Michigan have passed legislation linking

education reform and tax relief, weakening the autonomous capacity of municipalities to raise

revenue through property taxes to support education. School district adaptation to altered policy

incentives and the general fiscal strain of state financial crises, escalating special education costs

and No Child Left Behind compliance, juxtaposed against rising enrollments and rising

expectations for academic success and accountability, demands capitalizing on new opportunities

for revenue creation. Fiscal shortfalls present a noxious alternative, imperiling art and music

instruction, non-fee athletic participation and extracurricular programs, obstructing purchases of

new technology, depressing teacher and administrator salaries and placing upward pressure on

class sizes.

Nationwide, public school districts are increasingly seeking revenue from non-tax

sources, through a variety of direct fundraising strategies and through affiliated fundraising

organizations (local education foundations (LEFs), parent teacher associations (PTAs), parent

teacher organizations (PTOs) and booster clubs). The growing importance of private funds in

public schools raises a number of questions. This paper uses the intriguing case of Vermont to

shed light on two of them: How sensitive is school district fundraising to policy changes that

create incentives for the generation of private revenue? Why do some school districts and

supporting organizations raise private funds more effectively than others?

The existing literature on the questions of interest is relatively sparse. The only study

explicitly linking policy incentives to increased private revenue generation in public schools is

2

Brunner and Sonstelie’s (1996) analysis of the California case. The only academic investigation

of fundraising performed directly by schools and districts appears to be Zimmer, Krop and

Brewer’s (2003) investigation of 6 Southern California districts. The literature on supporting

fundraising organizations – local education foundations, parent teacher

associations/organizations and booster clubs is somewhat broader. Generally, however, these

studies leverage only a single source of information: quantitative IRS data, quantitative school

district data, or survey data. In addition, none of these studies have shed light on the relative

efficacy of specific fundraising strategies.

A dramatic policy change and stable demographic conditions in Vermont provide an

excellent opportunity to study the sensitivity of public school alternative revenue generation to

policy incentives and determinants of its success. The Equal Educational Opportunity Act (Act

60) of 1997 dramatically changed the school finance landscape in Vermont. Act 60, incremental

implementation of which began in fiscal year 1999 with full implementation in fiscal year 2001,

created tax prices of more than $1 for education in 125 of Vermont’s 253 towns and tax prices of

$2 or more in 37 towns. (Schmidt and Scott, 2004). For Stratton, the most extreme case,

taxpayers were required to contribute more than $30 in local taxes for every $1 increase in local

education spending above the foundation amount (Schmidt and Scott, 2004). Since Act 60 did

not regulate the generation of non-tax revenue, (every dollar of non-tax revenue generated

directly increased local education spending by $1), towns with a tax price of more than one

dollar faced an incentive to generate all local revenue for education above foundation outside of

the tax system.

Community members in many towns with high tax prices (gold towns) formed LEFs,

501(c)3 non profit organizations with the express purpose of raising resources for the public

3

schools. These LEFs served as the primary conduit for generation of sharing pool exempt non-

tax revenue in the gold towns. Foundations in towns with as few as 1000 residents raised more

than one million dollars in annual revenue, with some towns disdaining to use property taxes to

fund education beyond the base level of spending that was financed through state aid. Incentives

for private fundraising were strong enough that some towns used strong arm tactics, such as

publishing names of non-contributors or boycotting non-contributing businesses.

Nevertheless, local education foundations were not successfully established in all

Vermont towns where there was a financial incentive for their operation. Among foundations

successfully launched, some raised per pupil more revenue than others. Some easily cleared

fundraising goals, while others struggled, and still others failed.

This paper seeks to explain the response of the Vermont gold towns to Act 60 and the

varying success of their private fundraising efforts. In particular, the empirical analysis

investigates the rapidity and extent of the gold towns’ responses, and the role demographics,

district characteristics, selection of fundraising strategy, and foundation governance and

operation played in the fundraising disparities between districts.

The study encompasses fiscal years 1996 through 2004, covering the pre-Act 60 period

(1996-1998) in which a traditional foundation formula allocated state aid, the incremental

implementation of Act 60 (1999-2000) and the full implementation of Act 60 (2001-2004).

Detailed quantitative IRS data on affiliated fundraising organizations, school district financial

and administrative data, Census data, survey data and personal interviews provide a rich basis of

information.

The first section reviews the existing literature. The next section describes the data

sources analyzed. The third section describes the methods used for analysis. Results appear in the

4

fourth section. We find compelling evidence that the extent to which districts substitute

nontraditional revenues for property tax revenues depends on the local tax price. We also

document links between variation in the use of nontraditional revenues and variation in factors

that are likely to be correlated with the median voter’s tax price. Finally, we find that the success

of local education foundations depends both on the environment in which they operate,

particularly the wealth of the community, and on the scope of their solicitation activities. The

fifth section concludes.

Context

In 1997 the Supreme Court of the State of Vermont invalidated the existing system of

education financing in the state, concluding that the system deprived “children of an equal

educational opportunity in violation of the Vermont Constitution” (Brigham v. State (96-502);

166 Vt. 246). While the court decision focused on inequities in spending, the support in the state

for the suit grew out of widespread dissatisfaction with inequalities in educational spending and

disparities in property tax burdens resulting from the existing foundation system of education

financing and the existing system of property taxation.

The discontent with the system of education finance which resulted in the suit also

influenced the dynamics of the 1996 legislative elections. The state senate that was elected in

1996 was committed to property tax reform (Mathis, 2001). The result was a state legislature

that was ready to move on legislation that would comply with the Brigham decision and reduce

the property tax burdens of poor individuals.

Given the political dynamic in Vermont, the speed with which Act 60, the legislation

designed to comply with Brigham and to provide property tax relief, was passed surprised no

one. Signed into law on June 26, 1997, Act 60 created a system of school financing that

5

combined elements of foundation and power equalization plans. A statewide property tax was

established, with revenues from the tax being used to finance a portion of foundation aid.1 If in a

locality property tax revenues generated by levying the statewide rate exceed the amount needed

to finance the foundation level of spending, the excess property tax revenues are recaptured by

the state.

Under Act 60, localities were allowed to choose spending levels in excess of the

foundation level. To weaken the link between property wealth and spending in excess of the

foundation level, the act established a power equalization scheme that insured that localities with

the same nominal tax rates would have the same levels of education spending. As other district

power equalization reforms, Act 60 sought to equalize tax bases and per pupil tax yields for

education across the state. Act 60 importantly diverged from traditional district power

equalization in the financing of the system. In most district power equalization systems, aid

drawn from state funds supplements the tax yields of the low property wealth towns. Act 60

deviated from this norm, creating a sharing pool that directly tapped local property tax revenues

from property-rich towns to supply the aid to property-poor towns. Because the sharing pool’s

redistribution mechanism utilized property tax revenues from gold towns to finance the power

equalizing aid to property-poor towns, the marginal tax price of education increased in some

towns, and the tax rate required for a given level of additional education spending fell in others.

Schmidt and Scott (2004) document the dramatic impact of the reforms on the tax prices for

education faced by Vermont towns.

While the Brigham decision forced state policy makers to implement finance reforms, the

reality was that Act 60 was as much about property tax relief as it was about school finance

reform. For taxpayers in many communities, the finance reforms by themselves would have

1In the 2000-2001 school year, the nominal property tax rate was 1.1 percent, and the foundation level was $5200.

6

dramatically reduced tax burdens by allowing localities to maintain or even increase education

spending with substantially lower tax rates. At the same time, taxpayers in high-wealth

communities, which have been labeled “gold towns,” necessarily faced increases in their

property tax payments.2 To lessen the burden on low-income residents of the “gold towns,” the

drafters of Act 60 included in the legislation a provision that granted tax adjustments to certain

homestead owners. These tax adjustments were explicitly linked to the taxpayer’s income; the

original legislation specified that all owners with incomes at or below $75,000 were eligible for

adjustments.

All residents of “gold towns” had access to a second avenue for limiting their tax

liability, private contributions. Act 60 did not regulate the generation of non-tax revenue; every

dollar of non-tax revenue generated directly increased local education spending by $1. As a

result, towns with a tax price of more than one dollar faced an incentive to generate all local

revenue for education above foundation outside of the tax system. Yet not all towns with tax

prices in excess of $1 made equal use of this option. Understanding why this was so is the main

goal of this paper.

Not surprisingly, Act 60 generated significant unhappiness and strong criticism from the

property rich towns3 and was repealed by the Vermont legislature in 2004 by the passage of Act

68. Act 68 eliminated the sharing pool and reduced the marginal tax rates for education to below

$1 in the gold towns. Implemented in fiscal year 2005, Act 68 entirely removed Act 60’s

incentives for financing public education through non-tax revenue.

2In the 1994-95 school year, 69 of the 248 towns in Vermont for which data were available had effective education property tax rates below $1.10 per $100 in assessed value. While the percentage of towns with effective education rates below $1.10 had undoubtedly declined by the 1997-98 school year, the last year before the phasing in of Act 60 began, the reality was still that Act 60 forced a sizeable fraction of the towns in Vermont to increase property tax rates. 3 A lawsuit filed by the towns of Wilmington and Whitingham challenging the legality of Act 60, and the town of Killington’s threat of secession from the state provide the most extreme examples of the disapproval of the property-rich towns.

7

The short period in which Act 60 was fully operative provides us with a stark natural

experiment that allows us to quantify the extent to which generation of nontraditional revenues

responds to the incentives created by the financing system. In addition, the Vermont context

gives us a unique opportunity to document the degree to which nontraditional revenues limit the

extent to which finance reform has produced equalization.

Literature Review

Exploring the extent to which residents of school districts in Vermont responded to the

incentives implicit in Act 60 will be at the core of the empirical work that follows. As a result.,

this paper builds most directly off of the work of Brunner and Sonstelie (1996). In 1978,

California’s Proposition 13 limited local property taxes to 1% of assessed value, severely

inhibiting the ability of municipalities to raise revenue to supplement state foundation aid.

Brunner and Sonstelie chart the explosive growth of local education foundations in California,

from 22 in 1978, to more than 500 by the mid-90s. By 1992, LEFs, PTAs, PTOs, booster clubs

and urban foundations contributed more than $100 million in total to support public education.

Brunner and Sonstelie demonstrate that districts whose revenue generating capacity was most

severely constrained by Proposition 13 generated much more average private revenue per pupil

than less constrained districts.

In a follow-up paper, Brunner and Sonstelie (2003) describe the fallout from Proposition

13 as a government failure to provide a level of service (education) for which taxpayers were

willing to pay, equating private support of public schools to a type of voluntary fiscal federalism.

Collective action filled the taxation void, generating new fundraising organizations and strategies

to privately supplement public schooling.

8

Devoid of the legally binding authority to compel cooperation, collective action is

perpetually haunted by the specter of free riding. In the case of local education foundations, as

in other efforts to provide privately public goods, a variety of strategies and circumstances

ameliorate and intensify the free rider problem. As a result, in addition to exploring the link

between the incentives implicit in Act 60 and the extent to which nontraditional revenues were

part of a school district’s total revenues, we will also draw on the growing literature that has

examined the determinants of private fundraising success. It is to that literature that we now

turn.

Brunner and Sonstelie posit that social interaction, through the creation of a group

identity among families, enhances individual generosity4. The depressing effect of face to face

encounters on free riding may explain the greater success of foundations in Vermont towns with

a defined town center as compared to Vermont towns with no defined center (Fischel, 2003).

Fundraising organizations set annual fundraising goals, institutionalizing the collective

philanthropic decision-making process (Brunner and Sonstelie, 1996). To promote a sense of

sustainability and collective responsibility, many Vermont LEFs set a minimum monetary goal

and a minimum contribution rate for the initiation of a fund.

Social norms condemning free riding on the contributions of others encourage successful

collective generosity (Fehr and Gachter, 2000), while individual differences in demand for

school quality, income level and attitudes toward free riding discourage equal contributions.

Brunner and Sonstelie (2003) hypothesize that individuals contribute up to where the price of

cooperation equals the cost of free-riding. In Vermont, foundations attempted to enhance

contributions by raising the cost of free-riding. The Manchester School Fund publicized names

4 The authors explicitly reject Sugden’s (1985) theory that social interactions reduce generosity through fear of one individual’s contributions encouraging others to free ride.

9

of non contributors, and some residents refused to patronize businesses which were not

scholastic benefactors (Fischel, 2003).

The surrounding socioeconomic and community context also influence the fundraising

dynamic, as the success of various strategies and the generosity of different types of donors vary

by community type. In Zimmer, Krop and Brewer (2003), parental support was strongest in the

communities on the highest end of the socioeconomic scale. Wealthier schools relied more on

parents for in-kind as well as monetary contributions, while poorer schools, which did not have

strong parent associations, received more in-kind donations from local businesses and

community organizations. Poorer districts reached out to more donors than wealthier districts,

and enjoyed greater access to corporations, philanthropic foundations and community-based

organizations than wealthier schools.

In Zimmer, Krop and Brewer (2003), wealthier schools, despite relying on relatively

fewer donors, employed more mechanisms to attract their support. Wealthier schools and

districts strongly focused on securing monetary donations, while poorer schools and districts

focused relatively more on in-kind contributions.

The inconstancy of fundraising across community types raises equity concerns. If

wealthier schools and districts can more successfully attract private resources than poorer

schools and districts, private fundraising threatens to undo state resource equalizing mechanisms.

Thus far, private fundraising has been sufficiently small in relative terms so as to not severely

alter the distributions of resources, but relative advantages in fundraising in wealthy

communities pose long-term concerns if a scholastic reliance on private funds continues to

increase. In Zimmer, Krop and Brewer (2003), wealthier districts attracted more monetary

10

support than poorer districts5, and, as district wealth increased, so did the number of programs,

services and materials purchased with private monetary donations. However, middle and lower

income schools attracted at least as much in-kind support as the wealthier schools and, even for

the wealthiest schools, private monetary contributions accounted for less than 5% of the school

budget.

Of the various public school fundraising strategies, one of the most intriguing, most

studied, and perhaps the most relevant to the Vermont context is the creation of local education

foundations. Nationwide, most local education foundations came in existence after 1989 (Merz

and Frankel, 1995). Most were formed with specific goals in mind and a majority in

Massachusetts (Medina, 1988), California6, Illinois, Oregon, and Washington were formed

because of declining public school revenue. In Vermont, the passage of Act 60 in 1997 provided

the impetus for the state’s LEF boom.

Research on LEF formation has established that, while the district administration most

often initiated LEFs, broad community support tended to be crucial for their survival (Merz and

Frankel, 1995). Foundations tended to develop faster in cohesive communities, as compared to

large districts or multiple districts (McCormick, Bauer, and Ferguson, 2001).

Few foundations pay employees (Merz and Frankel, 1995), but those with paid

fundraisers and/or paid staff raise significantly more revenue7 (Merz and Frankel, 1995, Muro,

1995) more quickly (Muro, 1995) than LEFs entirely reliant on volunteers. Most staff positions

5 This was partly attributed to increased revenue generation through LEFs. 6 Brunner and Sonstelie (1996) found that school fundraising organizations in districts whose revenue generating capacity was most negatively impacted by reform generated the most revenue per pupil. However, the high correlation between statutory impact and district wealth muddies this conclusion. 7 Merz and Frankel acknowledge that LEFs which employ paid fundraisers and staff tend to be larger and older. At least some of their increased revenue generating potential, then, is likely explained by reach and experience as opposed to hired staff.

11

were found to be part-time and very low paying. In addition to staff support,8 a paid executive

director facilitates fundraising (McCormick, Bauer, and Ferguson, 2001, Muro, 1995), because

of the director’s broad responsibilities - brokering relations, implementing programs, raising

organizational visibility - and the dramatic increase in volunteer time necessary to compensate

for the absence of a paid director (Muro, 1995).

Foundations which directly solicited contributions raised on average more than one and a

half times as much as those which did not (Merz and Frankel, 1995). Most foundations used mail

or phone solicitations and asked for annual contributions. Direct mail solicitation is costly, but

builds a donor list (McCormick, Bauer, and Ferguson, 2001).

Elementary and K-12 foundations raised more than high school foundations (averages of

$41,267 and $37,817 as compared to an average of $12,950) (Merz and Frankel, 1995).9

Brunner and Sonstelie (1996) discovered that California education fundraising organizations

associated with elementary schools raised more revenue per pupil than organizations associated

with other grade levels. Brunner and Sonstelie (2003) found that parental philanthropic

collaboration deteriorated, albeit slowly, as schools increased in size.

LEFs have generally enjoyed greater success in wealthier communities, but in neither

California nor Michigan have LEFs have not have raised sufficient revenue to affect significantly

state efforts to equalize the distribution of revenue. Merz and Frankel (1995) discovered

foundations to be more successful, but not more prevalent, in high-income communities, and

noted that successful LEFs have been formed in communities of all income levels. Addonizio

(1998) found Michigan foundations to be more prevalent in districts with higher average

8 In the first two years, generally 6 hours a week of secretarial support is sufficient for foundations, which, in many cases, can be provided by the school district (McCormick, Bauer, and Ferguson, 2001). 9 Personal interviews attributed this to lesser parent involvement in the education of high school children, a shorter time frame (4 years) for developing a relationship with parents and parental focus on saving for college.

12

incomes, smaller fractions minority, larger enrollments, higher spending, and higher levels of

scholastic achievement. In progressively wealthier districts in California, there were more non-

profits reporting more than $25,000 in revenues, and a better chance that an LEF would be found

in the district (Brunner and Sonstelie, 1996). These progressively wealthier districts also raised

increasing amounts of revenue per pupil. In Zimmer, Krop, and Brewer, (2003) LEFs were found

at districts of all income levels, but were particularly active in the two wealthiest districts.

McCormick, Bauer, and Ferguson (2001) argued that a large corporate base, a large base of

individual wealth, and a high percentage of professionals facilitate a foundation’s success.

Surprisingly, the existence of many retired people or many families without children in

foundation districts did not affect fundraising success (Merz and Frankel, 1995). Case study

analysis of foundation success in Vermont has tended to confirm this observation, with

nonresidential property owners the least likely to free ride and owners of vacation homes in ski

resorts contributing reliably (Fischel, 2003). In Killington, where most of the condominiums are

managed by full time employees, the managers collectively convinced the owners’ associations

to bill members for LEF contributions. Because of the tax prebates awarded to families with less

than $75,000 in adjusted gross income, successfully organizing a foundation was more difficult

for property-rich towns with many low-income families (Fischel, 2003).

Addonizio (1998) concluded that LEFs did not “measurably negate” Michigan’s

education equalization efforts. Analyzing private contribution levels by district type and linking

contribution levels to school inputs and resource levels in California, Brunner and Imazeki

(2003) concluded that more than 99% of elementary school students attended schools where

private contributions “have almost no effect on inputs.” A few schools, small in number and

generally small in size, raised large amounts of private funds (more than $500 per pupil) which

13

were used to purchase more computers and teacher aides and reduce class-sizes and teacher-

pupil ratios, but these were isolated instances and appeared to offset lower levels of government

revenue that the higher income districts receive. Merz and Frankel also found LEF funds to be

decidedly supplemental, with foundations raising an average of 0.3% of the district budget.

Data

The data analyzed in this research are comprised of financial data on Vermont non-profit

organizations acquired through the purchase of data sets from the Urban Institute’s National

Center for Charitable Statistics (NCCS), school district data available through the Common Core

of Data maintained by the National Center for Education Statistics, town level school

expenditure and administrative data obtained from the Vermont School Report, publications of

the Vermont Tax Department, and the Vermont Department of Education, and migration and age

demographic data from the Census.

The NCCS data contain detailed financial information gleaned from the form 990 that all

501(c)3 non-profit organizations generating more than $25,000 in annual revenue must file with

the Internal Revenue Service. Included among these organizations are the local education

foundations, parent teacher organizations and booster clubs which this paper substantially

investigates. Nineteen NCCS data sets of three different types were acquired. Core data sets for

Vermont public charities for the years 1995-2002 contain data on from 73 (1995) to 124 (2002)

variables from the Form 990 including classification and identifying information, revenue,

expenses and net income, balance sheet and net assets information, and organizational activities.

Core data sets for Vermont private foundations for the years 1995-2002 contain data on from 60

(1995) to 154 (2002) variables from the Form 990 including classification and identifying

information, revenue, expenses and net income, balance sheet and net assets information, and

14

foundation activities. Digitized data sets include 178 variables from the functional expenses

portion of the 990 form, 121 variables from the balance sheet portion of the 990 form and 52

variables from the other information portion of the 990 form for public charities for the years

1998-2001.

The subset of nonprofits wholly or substantially supporting local public schools was

drawn in an iterative manner. Searches were performed on Guidestar, an online national database

of nonprofits. For public charities, searches were performed for Vermont nonprofits for the

following key words in field “non-profit name”: “school and foundation,” “education and

foundation,” “education and fund,” “school and fund,” “educational and foundation,” “friends

of,” “parent and teacher,” “parents and teacher,” and “PTO.” Keyword searches for “school” and

“public education” were also performed.

The general National Taxonomy of Exempt Entities major group codes for education (B)

and Philanthropy, Voluntarism and Grantmaking Foundations as well as the NTEE core codes of

each organization in the subset were searched in the Core 2002, Core 2000, Core 1998 and Core

1996 data sets. Since the core data sets contain the most recent return year for each organization

that filed in the last three calendar years and cover one of the last three fiscal years (the core

2001 data sets cover fiscal years 1999 through 2002, for example), this search encompassed all

organizations filing within the time period.

For the private foundations, a search was performed for all Vermont private operating

and non-operating foundations in the category of education and as well as for public, society

benefit. Name and keyword searches for “school” and “education” were also performed. The

NTEE major group codes for education (B) and Philanthropy, Voluntarism, and Grantmaking

15

Foundations (T), as well as the Z99 NTEE Core code (unknown) were searched in the Core

2002, Core 2000, Core 1998 and Core 1996 data sets.

The profiles of the organizations were in most cases sufficient to determine the primary

purpose of the organization, but when profiles did not contain sufficient information, PDF

versions of the 990 forms were examined10 and Google searches were used to find out more

about the organizations. Those organizations with a primary purpose of providing support to

local public schools were included in the local education foundation subset. These organizations

were then compared against a spreadsheet of private contributions reported from each town in

Vermont compiled by the Vermont Department of Education. In cases where towns reported

receiving significant (greater than $10,000) private donations and the public contribution figures

from education foundations located in the town did not closely match, or no local education

foundations with the same zip code as the town were represented in the local education

foundation subset, city and county searches were then performed on Guidestar to identify any

organizations missed by the initial search.

The Common Core data provide information on school district revenues and expenses,

including data on tax revenue and non-tax income sources such as user fees, capital gains,

tuition, and miscellaneous alternative revenue as well as enrollment figures, per pupil expenses

and test score information. The Vermont Education Report, Vermont Tax Department

publications, and Vermont Department of Education data provide measures of school district

characteristics, including property wealth, income, school inputs, and salaries.

There are several important limitations to the data. The affiliated organizations data

exclude organizations raising less than $25,000 in annual revenue. Some organizations raising

more than $25,000 in annual revenue are also excluded from the analysis either due to a lack of

10 For the private foundations, the “direct charitable activities” section was particularly useful in this regard.

16

enrollment information for the school district (Craftsbury School Corporation) or due to their

absence in the underlying data (the North Hero Education Fund). Additionally, the Freeman

Foundation provided more than $14 million in grants to these organizations between 1999 and

2001 to facilitate start-up and to match taxpayer donations. These contributions represent a

potentially significant confounding factor. As Freeman grants were awarded to virtually every

major local education foundation, with most receiving matching grants, their effect is mostly one

of magnitude, not distribution. In the empirical models below, we use time dummies to account

for the impact of Freeman Foundation grants and other effects that tended to be common across

foundations.

The membership figures from the Common Core of Data do not include students that are

tuitioned out of a district to attend public school in a neighboring district. These data provide an

accurate picture of the number of students educated in a district in a given year, but may not

accurately indicate the number of pupils for whose schooling a district is required to pay. For

that reason, average daily membership figures from the Vermont Department of Education were

used to calculate all per pupil revenue and expenditure amounts.

In the limited literature that has examined the determinants of nontraditional revenue,

schools or districts have always been the unit of analysis. When contributions have been the

component of nontraditional revenues analyzed, the $25,000 minimum required for reporting has

created a censoring problem. Our data allow us to avoid that problem in two ways. First, when

school districts are the unit of analysis, we use as our dependent variables the various measures

of nontraditional revenue available from the Common Core of Data. Since most districts

generate some of these revenues, particularly in times of fiscal stress, censoring is not a problem.

17

In addition, we are able to look more completely at the nature of district responses to fiscal

stress.

What the Common Core data do not allow us to do is separately analyze districts and

schools. Therefore, we cannot, as Brunner and Sonstelie could, determine if there were

differences between districts and schools in the impact of certain determinants of contributions.

This inability is less problematic in the Vermont context than it was in the California context

considered by Brunner and Sonstelie, since the norm in Vermont is that districts include a single

school.

While our data on nonprofits supporting public schools are similar to the data analyzed

by Brunner and Sonstelie (1997, 2003) and Brunner and Imazeki (2005), we have chosen to

analyze these data by treating the nonprofits themselves as the unit of analysis, rather than

creating district- and school-level measures of voluntary contributions. This decision was driven

partly by our concern that the $25,000 reporting threshold could create substantial selection

problems. But the main motivation for treating the nonprofits as the unit of analysis was our

desire to understand better the factors that contribute to foundation success. Thus, while we

mirror the work of Brunner and Sonstelie (2003) and examine the link between the attributes of

the district(s) served by a foundation and its contributions, we also take advantage of the richness

of our data to consider other attributes of foundations that could contribute to their success.

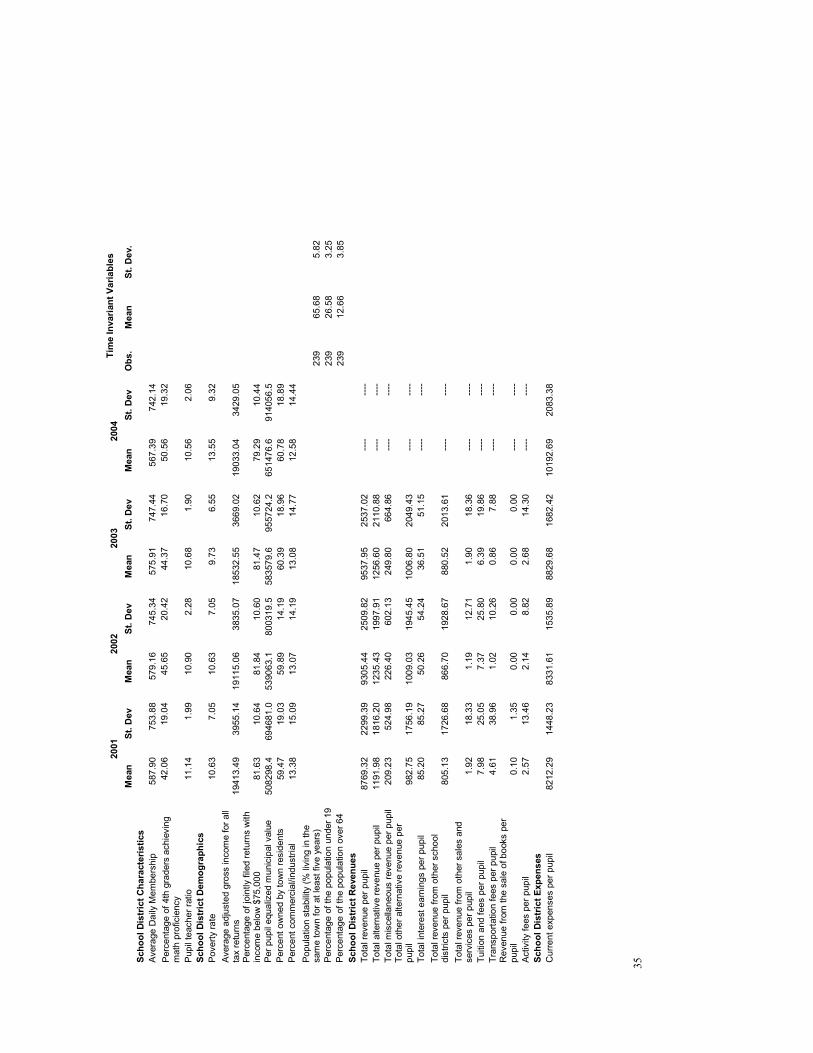

Table 1 includes summary measures for the school district data. Student enrollment in

Vermont declined for each post-Act 60 year. School achievement, as measured by fourth grade

test scores, was on the rise, and the pupil-teacher ratio was consistently declining. Total school

district revenue consistently increased, and per pupil expenditures did the same after the passage

of Act 60. Most relevant to this study, alternative revenue, composed of interest earnings,

18

revenue from other school districts, revenue from other sales and services, tuition and fees,

transportation fees, revenue from book sales, activity fees, federal math, science and professional

development grants, and miscellaneous revenues, increased constantly, registering dramatic

increases in 2000 and 2001. The mean per pupil level of alternative revenue increased almost

25% between fiscal years 1999 and 2001.

The bulk of this increase is derived from two sources: miscellaneous revenues and

revenues from other school districts. Miscellaneous revenues, a catch-all alternative revenue

category including contributions from the local education foundations, increased the most

dramatically. After an unexplained decline to about $60 per pupil in fiscal year 1999,

miscellaneous revenues more than doubled, in real terms, by fiscal year 2001. Revenues from

other school districts, comprised most significantly of tuition monies received to educate

students from other towns, jumped from $795.73 per pupil in fiscal year 2000 to $865.19 in

fiscal year 2001 and $957.83 by fiscal year 2003.

The numbers in Table 1 provide an incomplete picture of the import of nontraditional

revenues for some districts. Examining the evolution of the distribution of miscellaneous

revenues as a share of total revenues provides a much clear indication of how important for some

districts contributions became in the post-Act 60 period. In the period we consider, the median

of miscellaneous revenues as a fraction of total revenues reached its maximum of 0.00934 in

fiscal year 1997. In the fiscal years from 1999 to 2003, this median moved up and down, never

exceeding 0.00425. The evolution of the upper percentiles of this fraction was very different.

For example, the 95th percentile of miscellaneous revenues as a fraction of total revenues drifted

upward to 0.03547 in fiscal 1998, and then declined to 0.02492 in fiscal year 1999. In every

fiscal year after 1999, the 95th percentile increased, rising to 0.07833 in 2000, 0.1637 in 2001,

19

0.2067 in 2002, and 0.2194 in 2003. For a subset of districts, miscellaneous revenues had gone

from being inconsequential to comprising over a fifth of revenues.

The effect of this growth in nontraditional revenues on inequality is difficult to quantify,

since we can never know what would have happened to revenues if districts with dramatic

growth of nontraditional revenues had been forced to participate in the sharing pool. If,

however, we assume that miscellaneous revenues remained at their pre-Act 60 levels and that

districts opting out of the sharing pool post-Act 60 would have done so even if they did not have

access to contributions and other nontraditional revenues, we can provide an upper bound on the

extent to which access to nontraditional revenues limited inequality reductions after Act 60.

To execute this thought exercise, we set per pupil miscellaneous revenues in each fiscal

year from 1999 to 2003 equal to the real value of the average of per pupil miscellaneous

revenues in fiscal years 1996, 1997, and 1998. We then computed pupil-weighted inequality

measures using actual revenues and this alternative revenue measure. For Vermont districts

serving elementary students, the Gini coefficient for actual revenues was 0.1026 in 1998. For

these districts for the fiscal years from 1999 to 2003, the actual values of the Gini coefficients

were 0.1007, 0.0869, 0.0986, 0.1008, and 0.0965. For these districts for fiscal years 1999 to

2003, the Gini coefficients for the alternative revenue measure were 0.1003, 0.0887, 0.0935,

0.0958, and 0.0903. The implication is that, while nontraditional revenues had little impact on

inequality in the transition years of 1999 and 2000, the effects of these revenues had potentially

become large by fiscal year 2003. And while the actual Gini likely would not have fallen to

0.0903 in 2003 if access to nontraditional revenues had been constrained, the difference between

the actual Gini of 0.0965 and this alternative Gini of 0.0903 may give a rough indication of the

extent to which redistribution of economic resources was undone by access to nontraditional

20

revenues, since the economic burden of financing the local schools on property owners in gold

towns would have been larger if those towns had not been able to opt out of the sharing pool.

Further trends present themselves in the affiliated fundraising organizations data,

summarized in Table 2. The number of affiliated organization dramatically increases from 10 in

fiscal year 1998 to 29 in fiscal year 1999, the first year of Act 60’s implementation. By the full

implementation of Act 60, the number of organizations had increased to 40. Beginning in 1998,

the organizations generated much greater per pupil contribution levels and much more total

revenue. Mean real per pupil contributions increased from $57.78 in 1997 to $343.67 in 1998 to

$996.20 in 1999. After 1999, contributions declined and flattened out at between $889 and $982

per pupil11. Beginning in 1998, contributions accounted for virtually all revenues received by the

organizations.

Solicitation expenses and compensation do not significantly detract from overall

affiliated organizations revenue, with solicitation expenses never exceeding 1.5% of mean total

revenue and total compensation never exceeding 2% of mean total revenue. No organization

reported any rental expenses and the $100 in lobbying expenses by the Edmunds Elementary

School Parent Teacher Organization was the only reported political expenditure. This largely

corroborates Merz and Frankel (1995), who also found that, for local education foundations,

there was very little leakage of revenue targeted for schools.

Beginning in 1998, solicitation expenses and their component parts followed no time

trend. The presence of paid staff hovered between 26% and 40% between 1998 and 2003, with

the exception of 1999 where this percentage fell to 13.8%. The concurrence of a decline in paid

11 The decline of contributions in 2002 is attributable, at least in part, to the cessation of Freeman Foundation grants. Data from the Vermont Department of Education indicate that these foundation contributions virtually disappeared after the passage of Act 68. Donated dollars reported by the schools dropped from more than $11million in fiscal year 2004 to less than $80,000 in fiscal year 2005.

21

staff and the initial filings of a majority of the Act 60 local education foundations likely indicates

a lag between organization start-up and hiring staff. Other compensation increased dramatically

from 1999 to 2003, rising in real dollars per pupil every year, with particularly large increases

between 2000 and 2001 and between 2002 and 2003.

Empirical Models

In developing our empirical models of alternative revenue generation, we have built on

two literatures that have modeled the determination of school district expenditures and revenues.

In part, we draw on such papers as Hoxby (2001) and Schmidt and Scott (2004), which use the

basic model of local demand for public services developed by Borcherding and Deacon (1972)

and Bergstrom and Goodman (1973). Papers in this tradition emphasize the importance of the

local tax price, local taxable resources, and local demographics in modeling the determination of

local expenditures. While in the empirical analysis that follows we consider sub-components of

total revenue, the balanced budget requirement facing all districts in Vermont insures that the

determinants of total expenditures will tend to be the determinants of total revenues and of the

subcomponents of revenue.

At the same time, the extent to which districts utilize the various subcomponents of

revenue depends on the extent to which districts have access to the nondiscretionary components

of revenue and on the relative attractiveness of the discretionary components of revenue. Both

before and after Act 60, commonly noted determinants of donations, such as the size of the

district (Brunner and Sonstelie, 2003) and the presence of a large commercial base (McCormick,

Bauer, and Ferguson, 2001), should be strongly related to the extent to which districts utilize

nontraditional revenues.

22

We expect, however, that the nature of the relationship between nontraditional revenues

and other determinants of these revenues will change after Act 60 becomes operative. Prior to

Act 60, one dollar in local resources cost local residents a dollar in local resources, as did a dollar

in local property taxes. After Act 60, the marginal cost in property tax revenues of an additional

dollar of spending depended on the property wealth of the locality. As Schmidt and Scott (2004)

note, tax prices in fiscal year 2004 ranged widely, with 21 towns with tax prices below $0.60 and

9 towns with tax prices in excess of $5. Donations continued to cost localities one dollar in local

resources for each dollar of additional spending. Thus, for high wealth communities an

additional dollar of spending could require fewer local resources if financed out of donations

rather than out of property taxes.

A simple illustrative model helps clarify how Act 60 changed the relationship between

nontraditional revenues and the factors that determine the extent to which districts utilize these

revenues.12

This change in the relative attractiveness of nontraditional revenues post-Act 60 means

our basic empirical strategy is simple. In the pre-Act 60 era, the attractiveness of donations

relative to property taxes would depend on their relative cost to the median voter. As Downes

and Pogue (1994) observe, the cost to the median voter of an increase in property taxes is

proportional to the ratio of the median voter’s property wealth and the total property wealth in

the community. We do not have a measure of the median voter’s property wealth. We would

expect, however, that once we have accounted for community size, the median voter’s property

wealth would be positively correlated with both total property wealth and the fraction of property

wealth owned by town residents. As a result, we do not have a clear prediction of the

relationship between total property wealth and the use of nontraditional revenues in the pre-Act

12 Many thanks to Eric Brunner for this illustrative model.

Deleted: eextent

23

60 period. Prior to Act 60, we do expect relatively more use of nontraditional revenues in

communities with higher shares of property owned by town residents, since the median voter’s

tax price will tend to be higher in such communities.

After Act 60, nontraditional revenues become substantially more attractive to

communities with higher levels of total property wealth, since a community’s tax price and its

total wealth are positively correlated. Thus, we expect a positive relationship between property

wealth and nontraditional revenues in the post-Act 60 period.

In the post-Act 60 period, modeling the determination of contributions and, thus,

nontraditional revenues is complicated by the fact that the extent to which the median voter,

versus the town as a whole, preferred donations to property taxes depended critically on whether

the median voter was eligible for the tax adjustments provided to taxpayers with incomes below

$75,000. For that reason, we control for the fraction of joint filers in each community with

incomes below $75,000. We would not expect this fraction to be related to nontraditional

revenue generation prior to Act 60, since the differential treatment post-dated Act 60. After Act

60, in communities with higher fractions of voters eligible for the prebate, generating widespread

support for replacing property taxes with nontraditional revenues should have been harder, since

the income sensitivity provisions of Act 60 limited the tax liability of taxpayers with incomes

below $75,000. As a result, such taxpayers might have favored increased use of the property tax

since, on the margin, the burden of property tax increases tended to be shifted to high income

residents, nonresidents, and owners of commercial and industrial properties.

Most of the results presented below were generated using fixed effects regressions

performed on our two longitudinal data sets. By using both data sets, we could examine both the

sensitivity of school districts to policy changes creating incentives for the generation of non-tax

24

revenue and the efficacy of the response of the non-profit organizations raising non-tax revenue

for the schools. The fixed effects models allowed us to control for temporally stable, unobserved

factors that might have influenced use of nontraditional revenues or foundation success.

For the regressions in which a measure of nontraditional revenue was the dependent

variable, the most inclusive specification took the form:

Yit = αi + τt + Xitβ + Wi,t-1γ + Act60tDitζ + Act60tZiη + εit .13

In these regressions the dependent variable Yit was the log of one of the measures of real non-tax

per pupil revenue raised by school district i in year t. The vector Xit included contemporaneous

school district characteristics including income, poverty and enrollment levels, while the vector

Wi,t-1 included school district characteristics, such as per pupil expenditures, 4th grade test scores

and pupil teacher ratios, lagged one year. Act60 was a dummy variable indicating the presence of

Act 60’s alternative revenue generation incentives. It was equal to one for the fiscal years 2000-

2003 and equal to zero otherwise.14 The vector Dit included several time-varying factors which,

in light of the discussion above, could have a different relationship with nontraditional revenues

in the post-Act 60 period. Among these variables were per pupil equalized municipal property

wealth, the fraction of joint filers with incomes less than $75,000, the fraction of property wealth

judged by assessors to be residential, and the fraction of property wealth judged to be

commercial or industrial. The vector Zi included demographic variables, such as the stability of

the local population, that are observed only at the time of the 2000 Census and that may have

influenced the ease with which communities raised contributions. The district-specific fixed

13 In this specification, the impact of Act 60 on the level of each nontraditional revenue source was absorbed into the year dummies. 14 The choice of 2000 as the starting year was driven by the incomplete implementation of the sharing pool in fiscal year 1999. We experimented with both 1999 and 2001 as the starting year. Results generated using these alternative definitions of the Act 60 dummy variable are qualitatively the same as those presented below and are available from the authors upon request.

25

effect is denoted by αi, while the τt denote year effects for all years except 1995, 1996 and 2003,

which were dropped to avoid perfect multicollinearity. All financial variables as well as school

district enrollment are measured in logs.

The affiliated organizations regressions took a similar form

Yit = αi + τt + Xitβ + Wi,t-1γ + Vitς + Ditζ + εit .

The dependent variable Yit was the real per pupil contributions received by the organization and

most of the remaining variables were defined as above. In addition, we included in this

specification Vit, a vector of foundation attributes. The existence of a significant number of zero

values for the independent variables necessitated a level-level model. Further, because most

affiliated organization activity post-dated Act 60, we could not estimate variants of this model

that included interactions with the Act 60 dummy.

All district variables for foundations which covered multiple districts were enrollment-

weighted sums.

Results

As is apparent from Tables 3, 4, and 5, all school district regression results indicated that

towns did respond to the policy incentives of Act 60 to increasingly finance K-12 education

through nontraditional revenue. While the coefficient on per pupil equalized municipal property

wealth is insignificant in most of the specifications, the coefficient on the interaction of this

variable with the Act60 dummy is positive and significant in all models. Thus, as expected, in

high wealth communities, after Act 60 the extent to which nontraditional revenues were used

increased significantly. For example, the results in the third column of Table 3 indicate that,

when the dependent variable is the log of the most inclusive measure of alternative revenue

available in the Common Core of data, a 1% increase in a school district’s per pupil real

26

equalized property wealth increased the district’s Act 60 response by about 0.24%. This

elasticity fluctuates between .24 and .37 for the specifications in Table 3.

Income levels of a school districts residents and variation in these income levels do not

appear to have a consistently significant impact on the alternative revenue response. While in a

few specifications, the coefficient on the poverty rate is significant and negative, this expected

effect is not evident in all specifications. And in no specification is the coefficient on average

adjusted gross income significant. Since the results in Table 4 indicate that prior to Act 60 there

was a negative relationship between property wealth and the amount of miscellaneous revenue in

a district, we find no evidence that school districts with higher incomes and higher wealth more

successfully generated alternative revenue in the pre-Act 60 period.

What we do find, however, is evidence of a link between alternative revenue generation

and those factors that correlate with the attractiveness to the median voter of replacing property

tax revenues with contributions and other alternative revenues. As was noted above, residents

earning less than $75,000 in annual income were essentially exempt from the incentives of the

sharing pool. While high income residents of gold towns enjoyed tax savings in excess of fair

share contributions15 if a town were to generate above-foundation education revenue using non-

property tax sources of revenue, low income residents did not. Anecdotal evidence that gold

towns with higher proportions of low-income residents had more difficulty generating non-tax

revenue in response to Act 60 is supported by these data. As expected, an interaction term

between the percent of school district residents earning less than $75,000 in annual income as

measured by joint/ head of household returns and the Act 60 dummy was significant at the 10

percent level in all specifications.

15 Fair share contributions were the contributions requested by local education foundations of Vermont taxpayers based on property values.

27

The negative coefficient on the interaction between the Act 60 dummy and the share of

property owned by town residents also provides evidence that, in communities in which larger

percentages of taxpayers were eligible for tax breaks, raising contributions was more difficult.

Due to a real estate boom, the proportion of out of state residents of many gold towns increased

during the period. The exclusion of out-of-state residents from the low-income prebate implies

that all else equal, out-of-state residents enjoyed greater economic benefit from successful school

district alternative revenue generation than in-state residents.

In contrast to what some in the literature have argued, we find no consistent evidence that

generating alternative revenue was easier in communities with a larger corporate presence. Our

estimates also indicate that Act 60 had no impact on the link between alternative revenue and the

share of property the assessor estimated to be commercial or industrial.

The coefficient on enrollment is consistently negative and highly significant. Increases in

district enrollment implied increasing difficulty or decreasing willingness to generate alterative

revenue. In the second regression, a 1% decline in membership implies a 1.7% increase in

alternative revenue generation. This result concurs with the hypothesis, first posited by Brunner

and Sonstelie (2003), that smaller community size mitigates the free rider problem inherent in

alternative revenue generation efforts.

In Table 3 we observe a positive, significant coefficient on the interaction between the

Act 60 dummy variable and the fraction of a district’s population over the age of 64 indicates

that the presence of many senior citizens enhanced a town’s Act 60 response. A potential

explanation involves the surplus of volunteer hours implied by a large elderly population. The

Vermont foundations relied heavily on volunteers, and anecdotal evidence indicated that many

older, retired residents were particularly active on foundation boards. But given the absence of a

28

significant coefficient on similar interaction terms in Tables 4 and 5, what seems more likely is

that communities with larger shares elderly were able to tap into non-contribution sources of

revenue.

The absence of a significant coefficient on the interaction between the Act 60 dummy and

the proxy for population stability indicates that these results provide little support for a

hypothesis that with towns more stable populations would be more cohesive, contain more

school alumni and therefore be able to generate alternative revenue more effectively.

Since alternative revenue includes all nontraditional revenue, we also estimated

specifications using as our dependent variable the log of miscellaneous revenues. As can be seen

in Table 1, miscellaneous revenue increased dramatically after Act 60. This jump in

miscellaneous revenue is largely due to school district receipt of contributions by local education

foundations.

As is apparent from Table 4, in the all of the specifications of the model with

miscellaneous revenue as the dependent variable, the coefficient on the interaction between

property wealth and the Act 60 dummy is highly significant. In the richest specification, the

coefficient on the interaction implies a .9% increase in miscellaneous revenue raised for every

1% increase in per pupil equalized property wealth during the Act 60 period. The coefficient on

enrollment is negative, significant and quantitatively large, implying a positive relationship

between smaller enrollments and increased generation of miscellaneous revenue. A 1% decrease

in enrollment implies a nearly 2.8% increase in the generation of miscellaneous revenue,

corroborating Fischel (2003) that smaller community size reduces free-riding. The interaction

between the Act 60 dummy and the percent of joint/head of household returns reporting less than

$75,000 continues to provide evidence that towns with a higher percentage of residents with less

29

than $75,000 in annual income had greater difficulty generating miscellaneous revenue during

Act 60. We do not continue to see any evidence that miscellaneous revenues grew more in

districts with older populations. Thus, as was noted above, we do not have a clear indication that

the presence of relatively more senior citizens facilitated fundraising.

Because of the lag in availability of Common Core data, we also constructed a measure if

non-tax, non-tuition revenue using administrative data from Vermont. By using this measure as

our dependent variable, we were able to add to our analysis fiscal year 2004. The results with

this dependent variable,16 which are presented in Table 5, closely parallel those generated when

the dependent variable was constructed from miscellaneous revenue. Incentives continue to

matter, as does the size of the school district.

The regressions using contributions to affiliated organizations regressions, which are

presented in Table 6, tell, in many important dimensions, the same story as do the regressions in

which nontraditional revenue measures are the dependent variable. For example, we find that

contributions were higher in communities with more property wealth, and we see no link

between contributions and average income in a community. We do see some evidence that

affiliated organizations are less successful in communities with higher levels of poverty, since

the coefficient on the poverty rate is negative and significant in specifications 2 and 3.

Two differences between these results and those for the measures of nontraditional

revenues are also worth noting. First, we see no evidence that organizations in larger school

districts were less successful at generating contributions. Second, we find that more

contributions were generated in communities in which larger fractions of students had in the past

shown evidence of math proficiency. This result would certainly be consistent with

16 Because the data on state and federal aid were drawn from the Common Core, these variables were omitted from the specifications given in Table 5. Adding these variables to the specification and dropping fiscal year 2004 resulted in no qualitative changes in the results.

30

organizations using past schooling success as a selling point for contributions. We found,

however, when we included test score measures in specifications with a nontraditional revenue

measure as the dependent variable, no similar evidence of success breeding success.

In specification 2, real solicitation expenses were consistently positive and significant,

with a consistently quantitatively large coefficient. A one dollar increase in solicitation expenses

implied at least a $10.70 increase in contributions. That a greater foundation fundraising effort

would generate a greater level of contributions, particularly at a sufficiently low level of

fundraising expenses to mitigate concerns of contributions funding solicitation rather than the

organization’s charitable purpose is a logical result. The magnitude of the impact of additional

solicitation expenses is impressive.

We find no evidence that compensation of officers and executive directors increases

contributions. We do, however, find some support for the argument that paid staff matters; the

relationship between compensation to the support staff and contributions is consistently positive

and significant.

As can be seen from Table 7, specifications run solely on local education foundations

(about three quarters of the affiliated organizations subset) yielded similar results.

Conclusion

Act 60 provided powerful incentives to generate revenue outside of the tax base to fund

public education, and Vermont taxpayers responded, forming local education foundations to

circumvent unusually high tax prices for education. A strong, consistent relationship between the

non-tax revenue raised and the incentives facing the taxpayers to raise it clearly demarcates the

impact of a sharp change in education finance policy on taxation and supplementary financial

activity.

31

The data also reveal certain district characteristics dampen or magnify the alternative

revenue generation response. In particular, higher property values (a stronger Act 60 incentive),

lower district memberships, and a smaller percentage of residents eligible for property tax

reductions, and a larger percentage of property owned by town residents facilitated raising

alternative revenue during Act 60. These results indicate that the incentives implicit in Act 60

influenced the extent to which supplemental funding was provided by contributions. These

estimates also confirm Brunner and Sonstelie’s main conclusion; size matters because size helps

determine the sense of community in a school district.

For the Vermont affiliated organizations, solicitation expenses enhanced real

contributions received. The Act 60 incentive, measured by property wealth, and the poverty rate

also appeared to significantly impact contributions. The data did not reveal other school district

characteristics and other foundation activities to significantly impact revenue generating efforts.

More detailed data on the composition and operation of the foundations, as well as other

analytical models, may yield further conclusions in this regard.

The policy incentive of Act 60 was unequivocally unique, but the issues of alternative

revenue generation in public schools and education finance reform are broadly relevant. Several

of the lessons learned from Vermont should be applicable to school districts and local education

foundations in other states facing similar demands for non tax funds to support K-12 education.

A crucial direction of future study is to determine the applicability of these lessons.

32

References

Addonizio, M.F. (1998). New revenues for public schools: Alternatives to broad based taxes. In W. J. Fowler, (Ed.), Selected Papers in School Finance, 1997–99. Washington, D.C.: National Center for Education Statistics 1999-334, 89–110.

Addonizio, M. F. (2000). Private funds for public schools. The Clearing House, (74)2.

Addonizio, M. F. (1998). Private funding of public schools: local education foundations. Nonprofit Sector Research Fund Working Paper Series.

Bergstrom, T. C. and Goodman, R. P. (1973). Private Demands for Public Goods. American

Economic Review, 63(3), 280-96.

Borcherding, T. E. and Deacon, R. T. (1972). The Demand for the Services of Non-Federal Governments. American Economic Review, 62(5), 891-901

Brunner, E. J., & Imazeki. J. (2003). Private Contributions and Public School Resources. Center

for Public Economics Discussion Paper 07-03. San Diego, CA: San Diego State University.

Brunner, E., & Sonstelie, J. (2003). School finance reform and voluntary fiscal federalism. Journal of Public Economics, 87(9-10), 2157-2185.

Brunner, E., & Sonstelie, J. (1997). Coping with serrano: Voluntary contributions to California's local public schools. In National Tax Association-Tax Institute of America (Ed.), 1996

proceedings of the eighty-ninth annual conference on taxation held under the auspices of the

national tax association at Boston, Massachusetts, November 10-12, 1996 and minutes of

the annual meeting Held sunday, November 10, 1996 (pp. 372-381). Columbus: Author.

Downes, T. (2004). School finance reform and school quality: Lessons from Vermont. In William C. Fowler, (Ed.), Developments in School Finance: 2003. Washington, D.C.: National Center for Education Statistics.

Downes, Thomas A. and Pogue, Thomas F. (1994). "Accounting for Fiscal Capacity and Need in the Design of School Aid Formulas." In Anderson, John E., ed., Fiscal Equalization for

State and Local Government Finance. New York: Praeger Publishers.

Fischel, W. (2003). Notes on the voluntary payment of taxes: How Vermont towns avoid the Act 60’s penalties for local school spending. Unpublished manuscript.

Fehr, E., & Gachter, S. (2000). Cooperation and punishment in public goods experiments. American Economic Review, 90(4), 980-994.

Hoxby, C. M. (2001). All school finance equalizations are not created equal. Quarterly Journal

of Economics, 116(4), 1189-1231.

33

Huntsinger, J. (1989). Fund raising letters : A comprehensive study guide to raising money by

direct response marketing (3rd ed.). Richmond, Va: Emerson Publishers.

Lampkin, L. & Stern, D. (2003). Who helps public schools: A portrait of local education funds, 1991-2001. Distributed by the Public Education Network and the Urban Institute.

Mathis, W. J. (2001). “Vermont.” In Catherine C. Sielke , John Dayton, C. Thomas Holmes, and Anne L. Jefferson, editors, Public School Finance Programs of the U.S. and Canada:

1998-99. Washington, DC: National Center for Education Statistics.

McCormick, D. H., Bauer, D. G., & Ferguson, D. E. (2001). Creating foundations for American

schools. Gaithersburg, Md: Aspen Publishers.

Medina, N. J., Education Policy Research, Massachusetts, Dept. of Education, & Community Education Office. (1988). Private support for public schools : A description of local

education funds in Massachusetts. Quincy, Mass.: Office of Community Education, Massachusetts Dept. of Education.

Merz, C., & Frankel, S. S. (1995). Private funds for public schools : A study of school

foundations. Tacoma, Wash: distributed by the School of Education, Univ. of Puget Sound.

Muro, J. J. (1995). Creating and funding educational foundations : A guide for local school

districts. Boston: Allyn and Bacon.

Raphael, J. & Anderson, A. (2002). PEN Leading Ways: Preliminary research on LEF leadership for the Public Education Network. Distributed by the Public Education Network and the Urban Institute.

Schmidt, S.J. and Scott, K. (2004). Reforming reforms: Incentive effects in education finance in Vermont. Renssselaer Working Papers in Economics, Number 0425.

Sugden, R. (1985). Consistent conjectures and voluntary contributions to public goods: Why the conventional theory does not work. Journal of Public Economics, 27(1), 117-124.

Zimmer, R.W., Krop, C. & Brewer, D. J. (2003) Private resources in public schools: Evidence from a pilot study. Journal of Education Finance 28(Spring), 485-522.

34

Table 1: School District Summary Statistics

1996

1997

1998

1999

2000

Mean

Standard

Deviation

Mean

Standard

Deviation

Mean

Standard

Deviation

Mean

Standard

Deviation

Mean

Standard

Deviation

School District Characteristics

Average Daily Membership

591.217

758.26

591.36

756.47

594.09

758.92

589.34

759.47

588.97

760.39

17.97

16.54

----

----

32.66

19.24

37.94

17.88

38.14

18.85

Percentage of 4th graders achieving

math proficiency

Pupil teacher ratio

21.49

61.27

12.98

2.13

12.75

2.32

12.30

2.29

12.15

2.25

School District Demographics

Poverty rate

12.28

7.74

12.46

7.89

11.55

7.41

10.71

7.52

11.81

7.70

16377.64

3221.10

16599.11

3293.60

17316.98

3513.02

18337.46

3695.69

18993.97

3747.93

Average adjusted gross income for all

tax returns

Percentage of jointly filed returns with

income below $75,000

----

----

89.30

7.50

87.04

8.40

85.34

9.20

83.58

9.58

Per pupil equalized m

unicipal value

551877.5

896217.2

494406.2

676312.9

480944.6

611934.9

484676.4

600454.8

496968.4

661983.0

Percent owned by town residents

57.22

19.45

57.91

19.78

58.15

19.56

58.67

19.41

58.95

19.20

Percent commercial/industrial

14.25

17.07

14.13

17.07

14.09

17.00

13.42

15.86

13.40

15.68

School District Revenues

Total revenue per pupil

7496.59

2114.42

7520.72

2061.63

7735.20

2214.63

8230.90

2386.36

8383.15

2150.16

Total alternative revenue per pupil

923.99

1597.56

905.39

1531.47

930.33

1591.96

954.32

1614.04

1076.45

1679.17

Total miscellaneous revenue per pupil

88.94

223.37

107.46

158.55

98.09

134.19

63.99

168.12

182.15

542.19

Total other alternative revenue per

pupil

835.04

1549.72

797.92

1489.93

832.24

1539.96

890.33

1568.63

894.30

1603.31

Total interest earnings per pupil

74.98

75.27

67.85

64.46

66.45

61.41

68.22

68.23

71.91

77.85

Total revenue from other school

districts per pupil

654.52

1469.49

645.24

1460.13

684.49

1513.93

732.69

1550.12

741.37

1583.67

Total revenue from other sales and

services per pupil

0.36

4.18

1.28

9.20

0.40

5.17

0.87

7.56

0.02

0.29

Tuition and fees per pupil

33.51

243.33

12.89

93.52

12.55

93.75

15.01

95.89

7.34

28.18

Transportation fees per pupil

3.35

29.87

3.49

31.77

2.00

18.46

1.45

18.70

0.59

5.37

Revenue from the sale of books per

pupil

0.76

12.26

0.00

0.00

0.00

0.00

0.00

0.00

0.08

1.25

Activity fees per pupil

4.16

17.81

3.74

15.88

3.17

16.07

3.06

13.31

1.72

7.33

School District Expenditures

Current expenditures per pupil

6626.30

1614.59

6622.75

1130.02

6753.76

1207.02

7217.65

1403.97

8142.53

1425.03

35

2001

2002

2003

2004

Tim

e Invariant Variables

Mean

St. Dev

Mean

St. Dev

Mean

St. Dev

Mean

St. Dev

Obs.

Mean

St. Dev.

School District Characteristics

Average Daily Membership

587.90

753.88

579.16

745.34

575.91

747.44

567.39

742.14

42.06

19.04

45.65

20.42

44.37

16.70

50.56

19.32

Percentage of 4th graders achieving

math proficiency

Pupil teacher ratio

11.14

1.99

10.90

2.28

10.68

1.90

10.56

2.06

School District Demographics

Poverty rate

10.63

7.05

10.63

7.05

9.73

6.55

13.55

9.32

Average adjusted gross income for all

tax returns

19413.49

3955.14

19115.06

3835.07

18532.55

3669.02

19033.04

3429.05

Percentage of jointly filed returns with

income below $75,000

81.63

10.64

81.84

10.60

81.47

10.62

79.29

10.44

Per pupil equalized m

unicipal value

508298.4

694681.0

539063.1

800319.5

583579.6

955724.2

651476.6

914056.5

Percent owned by town residents

59.47

19.03

59.89

14.19

60.39

18.96

60.78

18.89

Percent commercial/industrial

13.38

15.09

13.07

14.19

13.08

14.77

12.58

14.44

Population stability (% living in the

same town for at least five years)

239

65.68

5.82