agri inputs and specialty chemicals

TRANSCRIPT

April 08, 2022 2

Agri Inputs and Specialty ChemicalsPrice hike to support growth

Q4FY2022 Results Preview

Sector: Agri Inputs and Specialty Chemicals

Sector View: Positive

Se

cto

r U

pd

ate

Companies CMP (Rs)

Reco/View

PT (Rs)

Agri Inputs

Coromandel International

834 Buy 1,070

Insecticides (India)

638 Buy 855

PI Industries 2,921 Buy 3,500

UPL 810 Buy 930

Sumitomo Chemical India

426 Buy 500

Speciality Chemicals

Aarti Industries 970 Buy 1,155

Atul Limited 9,965 Buy 11,000

NOCIL 242 Buy 348

SRF 2,748 Buy 2,800

Sudarshan Chemical

539 Buy 760

Vinati Organics 1,986 Buy 2,350

Source: Sharekhan Research

Our coverage universe

Price chart

For Q4FY2022, we expect agri-input and specialty chemical companies in our coverage universe to report strong revenue growth, led by price hikes and decent demand environment. However, we expect margin contraction due to elevated input cost. Exports-oriented and MNC-backed agro-chemical players such as UPL, PI Industries, and Sumitomo Chemical India are well placed to ride on higher crop prices and are expected to deliver strong earnings growth in Q4FY2022. Among specialty chemical players, SRF Limited is expected to outperform as all of its business segments are likely to witness margin improvement, led by better price realisation. Overall, we expect agro-chemical/specialty chemical companies under our coverage universe to report 16.8%/21% y-o-y PAT growth in Q4FY2022.

� Agri inputs – Export-oriented/MNC-backed players to perform well: We expect high global crop price to help price hikes as well as drive volume growth for export-oriented and MNC-backed companies. However, domestic-focused, agro-chemical players would see moderate growth as Rabi accounts for a small percentage of overall revenue. Higher subsidy support would lead to revenue growth for fertiliser companies. Margin performance is also expected to be mixed, with large players expected to witness stable-to-improving margin on price hike and because of benefit of operating leverage; but small agro-chemical/fetilisers companies would witness margin contraction, given the steep increase in input cost. Overall, we expect our agro-chemical coverage companies to post revenue growth of 19.8% y-o-y, margin contraction of 105 bps y-o-y, and consequently PAT growth of 16.8% y-o-y. UPL, PI Industries, and Sumitomo Chemical are expected to perform well in Q4FY2022.

� Specialty chemicals – Strong demand and price hike to offset margin pressure: We expect specialty chemical companies under our coverage to post strong 32% y-o-y revenue growth, led by price hikes and decent volume growth. Most companies would witness y-o-y margin contraction due to elevated input cost (sharp rally in oil price and its derivate products), energy cost, and freight cost. However, SRF Limited is likely to witness expansion and we expect its margin to increase by 233 bps y-o-y/31 bps q-o-q, led by strong pricing led margin for its specialty chemical, re-gas and packaging film business segments. Overall, we expect 21% y-o-y PAT growth for specialty chemical companies under our coverage.

� Outlook – High crop price bodes well for the agri-input space; Specialty chemical players well placed to gain global market share: High global crop prices, government support to produce farm produce at minimum support price (MSP), and expectation of another year of normal monsoons bode well for volume growth for agri-input companies. Strong demand environment, potential global market share gain, and capex plan (to expand capacities) provide confidence on medium to long-term growth prospects for the Indian specialty chemical sector despite near-term challenges on elevated input/logistics/energy costs.

Valuation:The Indian specialty chemicals sector is well poised to capitalise on global tailwinds and expand its global market share to 7-8% in the next few years from 4% currently supported by structural drivers, including China Plus One strategy, import substitution, and opportunities emerging from the recent supply chain disruption in China. Agri-input companies are also well poised to reap benefits of high global crop price as the same would aid demand and support realisations. Thus, the recent correction in broader markets due to global geopolitical tensions provides good opportunity to invest in quality stocks as we see structural tailwinds for sustained double-digit earnings growth going forward.

Key Risks: � Higher raw-material cost for agri and speciality chemical companies might affect

margins if they are unable to pass it on to customers.

� Lower demand offtake for products of specialty chemicals players owing to slowdown in economic activity may also affect earnings.

Leaders for Q4FY2022: UPL, PI Industries, Sumitomo Chemical India, and SRF Limited

Laggards for Q4FY2022: Coromandel, Atul Limited, NOCIL, and Sudarshan Chemical.

Preferred Picks: Coromandel International, PI Industries, Sumitomo Chemical India, SRF, Aarti Industries, NOCIL, and Vinati Organics.

Source: BSE; Sharekhan Research

Summary

� For Q4FY2022, we expect export-oriented agri-input companies to perform well, given benefit of high global crop price, while domestic/fertiliser players are likely to witness margin pressure due to elevated cost. Overall, we expect agro-chemical companies under our coverage to post 17% y-o-y PAT growth in Q4FY2022.

� We expect specialty chemical companies to sustain strong revenue growth, led by price hikes and decent volume growth; however, crude-linked input cost surge would mean margin contraction. SRF Limited is best placed with likely strong growth across segments.

� A potential normalisation of input cost is expected to bring back focus on structural earnings growth drivers (global market share gain) for quality agri-input and specialty chemical stocks.

� Preferred Picks: Coromandel International, PI Industries, Sumitomo Chemical India, SRF Limited, Aarti Industries, NOCIL, and Vinati Organics.

80 90

100 110 120 130 140

Apr-

21M

ay-2

1Ju

n-21

Jul-2

1Ju

l-21

Aug-

21Se

p-21

Oct

-21

Nov

-21

Dec-

21Ja

n-22

Feb-

22M

ar-2

2Ap

r-22

BSE MidCap Index Sensex

April 08, 2022 3

Sect

or U

pdat

e

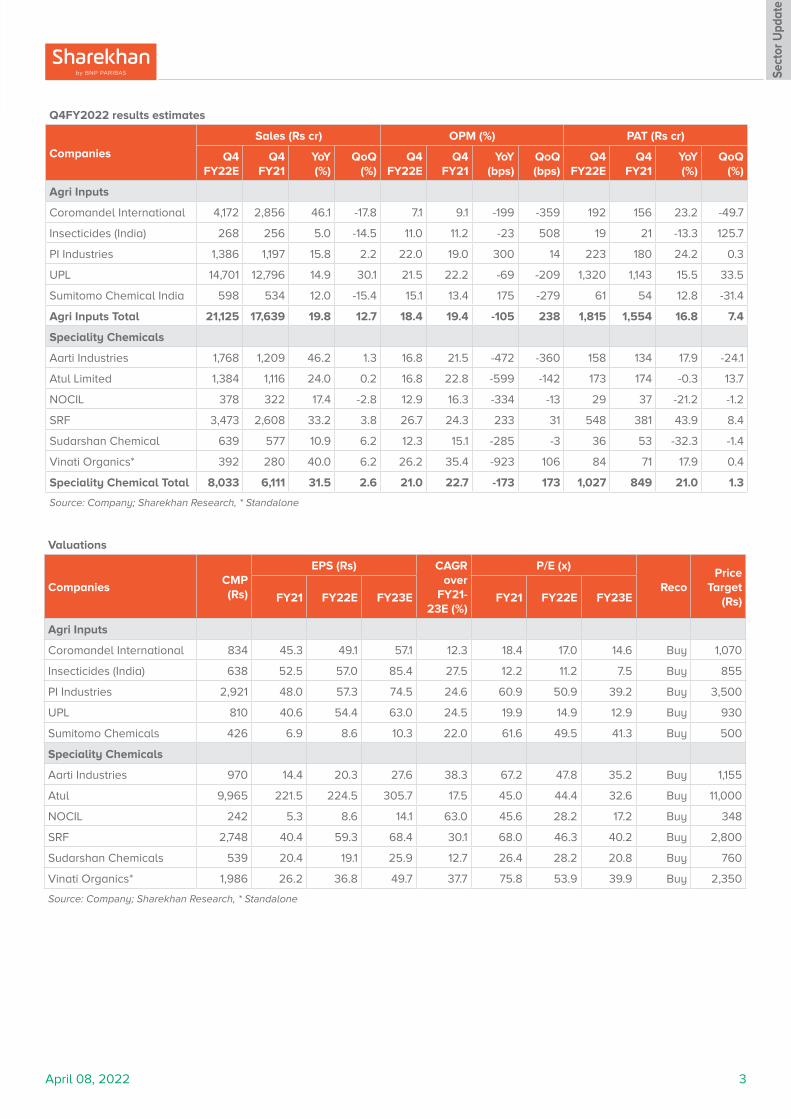

Q4FY2022 results estimates

Companies

Sales (Rs cr) OPM (%) PAT (Rs cr)

Q4 FY22E

Q4 FY21

YoY (%)

QoQ (%)

Q4 FY22E

Q4 FY21

YoY (bps)

QoQ (bps)

Q4 FY22E

Q4 FY21

YoY (%)

QoQ (%)

Agri Inputs

Coromandel International 4,172 2,856 46.1 -17.8 7.1 9.1 -199 -359 192 156 23.2 -49.7

Insecticides (India) 268 256 5.0 -14.5 11.0 11.2 -23 508 19 21 -13.3 125.7

PI Industries 1,386 1,197 15.8 2.2 22.0 19.0 300 14 223 180 24.2 0.3

UPL 14,701 12,796 14.9 30.1 21.5 22.2 -69 -209 1,320 1,143 15.5 33.5

Sumitomo Chemical India 598 534 12.0 -15.4 15.1 13.4 175 -279 61 54 12.8 -31.4

Agri Inputs Total 21,125 17,639 19.8 12.7 18.4 19.4 -105 238 1,815 1,554 16.8 7.4

Speciality Chemicals

Aarti Industries 1,768 1,209 46.2 1.3 16.8 21.5 -472 -360 158 134 17.9 -24.1

Atul Limited 1,384 1,116 24.0 0.2 16.8 22.8 -599 -142 173 174 -0.3 13.7

NOCIL 378 322 17.4 -2.8 12.9 16.3 -334 -13 29 37 -21.2 -1.2

SRF 3,473 2,608 33.2 3.8 26.7 24.3 233 31 548 381 43.9 8.4

Sudarshan Chemical 639 577 10.9 6.2 12.3 15.1 -285 -3 36 53 -32.3 -1.4

Vinati Organics* 392 280 40.0 6.2 26.2 35.4 -923 106 84 71 17.9 0.4

Speciality Chemical Total 8,033 6,111 31.5 2.6 21.0 22.7 -173 173 1,027 849 21.0 1.3

Source: Company; Sharekhan Research, * Standalone

Valuations

CompaniesCMP (Rs)

EPS (Rs) CAGR over

FY21-23E (%)

P/E (x)

RecoPrice

Target (Rs)FY21 FY22E FY23E FY21 FY22E FY23E

Agri Inputs

Coromandel International 834 45.3 49.1 57.1 12.3 18.4 17.0 14.6 Buy 1,070

Insecticides (India) 638 52.5 57.0 85.4 27.5 12.2 11.2 7.5 Buy 855

PI Industries 2,921 48.0 57.3 74.5 24.6 60.9 50.9 39.2 Buy 3,500

UPL 810 40.6 54.4 63.0 24.5 19.9 14.9 12.9 Buy 930

Sumitomo Chemicals 426 6.9 8.6 10.3 22.0 61.6 49.5 41.3 Buy 500

Speciality Chemicals

Aarti Industries 970 14.4 20.3 27.6 38.3 67.2 47.8 35.2 Buy 1,155

Atul 9,965 221.5 224.5 305.7 17.5 45.0 44.4 32.6 Buy 11,000

NOCIL 242 5.3 8.6 14.1 63.0 45.6 28.2 17.2 Buy 348

SRF 2,748 40.4 59.3 68.4 30.1 68.0 46.3 40.2 Buy 2,800

Sudarshan Chemicals 539 20.4 19.1 25.9 12.7 26.4 28.2 20.8 Buy 760

Vinati Organics* 1,986 26.2 36.8 49.7 37.7 75.8 53.9 39.9 Buy 2,350

Source: Company; Sharekhan Research, * Standalone

April 08, 2022 4

Sect

or U

pdat

e

Q4FY2022E results: Company-wise key comments

Company Comments

Agri-inputs

Coromandel International Subsidy support and better realisation to drive strong 46% y-o-y revenue growth, but high input cost (phos acid) to result in 199 bps y-o-y margin contraction. We expect PAT to grow by 23% y-o-y in Q4FY2022.

PI Industries We expect robust growth in the CSM business and moderate domestic business to result in strong 16% y-o-y revenue growth and margin to improve by 300 bps y-o-y, led by price hike to pass on high raw-material cost.

UPL We expect 15% y-o-y revenue growth, led by better pricing/volume growth in Latin America, North America, and Europe. Price hike and advantage of backward integration to cushion margins against elevated input cost.

Insecticides (India) We expect moderate revenue growth of 5% y-o-y, while EBITDA is expected to decline marginally as price hike would provide cushion against input cost pressure.

Sumitomo Chemical India We expect 12% y-o-y topline growth, given decent growth in domestic market and high growth in the exports business. OPM is expected to improve by 175 bps y-o-y on proactive pricing.

Specialty Chemicals

Aarti Industries We expect strong revenue growth of 46% y-o-y on price hike in the domestic market and low base of last year; however, we expect muted growth on a q-o-q basis, given absence of contract cancellation fee. Margin is expected to decline by 472 bps y-o-y due to time lag to pass on input cost rise for the export business and higher energy cost.

Atul Industries We expect strong revenue growth of 24% y-o-y due to improved pricing of key products. However, margin is likely to decline by 599 bps y-o-y due to high input, power, and logistic costs.

NOCIL Limited We expect revenue growth of 17% q-o-q due to higher volume and realisation but decline on a q-o-q basis. Margin is expected to decline by 334 bps y-o-y, as we expect raw-material cost to be much higher than price hikes.

SRF Limited High growth in speciality chemicals and refrigerants and recovery in packaging films business on improved pricing would drive strong 33% y-o-y revenue growth. Margin is expected to improve by 233 bps, as higher price is expected to drive up margin for chemical, while spreads in the packing film business are expected to see improvement.

Sudarshan Chemical We expect revenue to witness 11% y-o-y growth and margins to contract by 285 bps y-o-y due to higher input, power, and logistics costs.

Vinati Organics We expect strong 40% y-o-y revenue growth led by robust recovery in the ATBS business and ramp-up of butyl phenol capacity. Although margin would decline on a y-o-y basis, it is expected to post strong recovery of 106 bps q-o-q on benefit of operating leverage.

Source: Sharekhan Research

Sharekhan Limited, its analyst or dependant(s) of the analyst might be holding or having a position in the companies mentioned in the article.

April 08, 2022 5

Summary

� High global crop prices would help Sumitomo Chemical India Ltd (SCIL) to hike prices continuously to pass on elevated input costs. Moreover, the focus on high-margin PGRs/Herbicides and further synergies from Excel Crop Care to drive 411bps margin expansion over FY21-24E.

� SCIL reported a robust 44% y-o-y growth in its export revenue in 9MFY22. We are optimistic that high growth in this segment to sustain given the CRAMs opportunity from parent and high growth in Latin America.

� We expect SCIL’s revenue, EBITDA and PAT to clock a 13%/21%/21% CAGR over FY21-24E led by robust rise in in exports (revenue share to reach 28-30% by FY24E) and above-industry growth in Indian markets.

� We maintain a Buy rating on SCIL with an unchanged PT of Rs. 500 as a massive contract manufacturing opportunity from parent provides superior growth prospects and continue enjoying premium valuation over domestic peers. SCIL is our preferred pick in the agri-input space.

Powered by the Sharekhan 3R Research Philosophy

+ Positive = Neutral – Negative

3R MATRIX + = -

Right Sector (RS) ü

Right Quality (RQ) ü

Right Valuation (RV) ü

What has changed in 3R MATRIX

Old New

RS

RQ

RV

Shareholding (%)

Promoters 75.0

FII 1.4

DII 6.2

Others 17.5

Price performance

(%) 1m 3m 6m 12m

Absolute 10 8 3 45

Relative to Sensex

1 10 4 25

Sharekhan Research, Bloomberg

Price chart

Company details

Market cap: Rs. 21,264 cr

52-week high/low: Rs. 460/278

NSE volume: (No of shares)

3.7 lakh

BSE code: 542920

NSE code: SUMICHEM

Free float: (No of shares)

12.5 cr

Valuation (Consolidated) Rs cr

Particulars FY21 FY22E FY23E FY24E

Revenue 2,645 2,995 3,357 3,801

OPM (%) 18.4 20.4 21.7 22.5

Adjusted PAT 345 429 514 605

% YoY growth 46.6 24.3 19.8 17.7

Adjusted EPS (Rs.) 6.9 8.6 10.3 12.1

P/E (x) 61.6 49.5 41.3 35.1

P/B (x) 13.8 11.2 9.2 7.6

EV/EBITDA (x) 43.2 33.8 27.8 23.1

RoNW (%) 25.0 25.0 24.4 23.6

RoCE (%) 32.7 33.1 32.4 31.4

Source: Company; Sharekhan estimates

Source: Morningstar

ESG Disclosure Score ESG RISK RATING 39.58 Updated Jan 08, 2022

High Risk

NEGL LOW MED HIGH SEVERE

0-10 10-20 20-30 30-40 40+

NEWThe recent surge in international crop prices would support price hikes and improve margin for Sumitomo Chemical India Limited (SCIL) despite the elevated input and logistics costs. Moreover, the massive CRAMS opportunity, leveraging of parent’s global distribution network and above industry growth in India market is likely to sustain mid-double digit revenue growth. We expect a strong 21% PAT CAGR over FY21-24E along with high RoE of ~24%. We maintain a Buy on SCIL with an unchanged PT of Rs. 500.

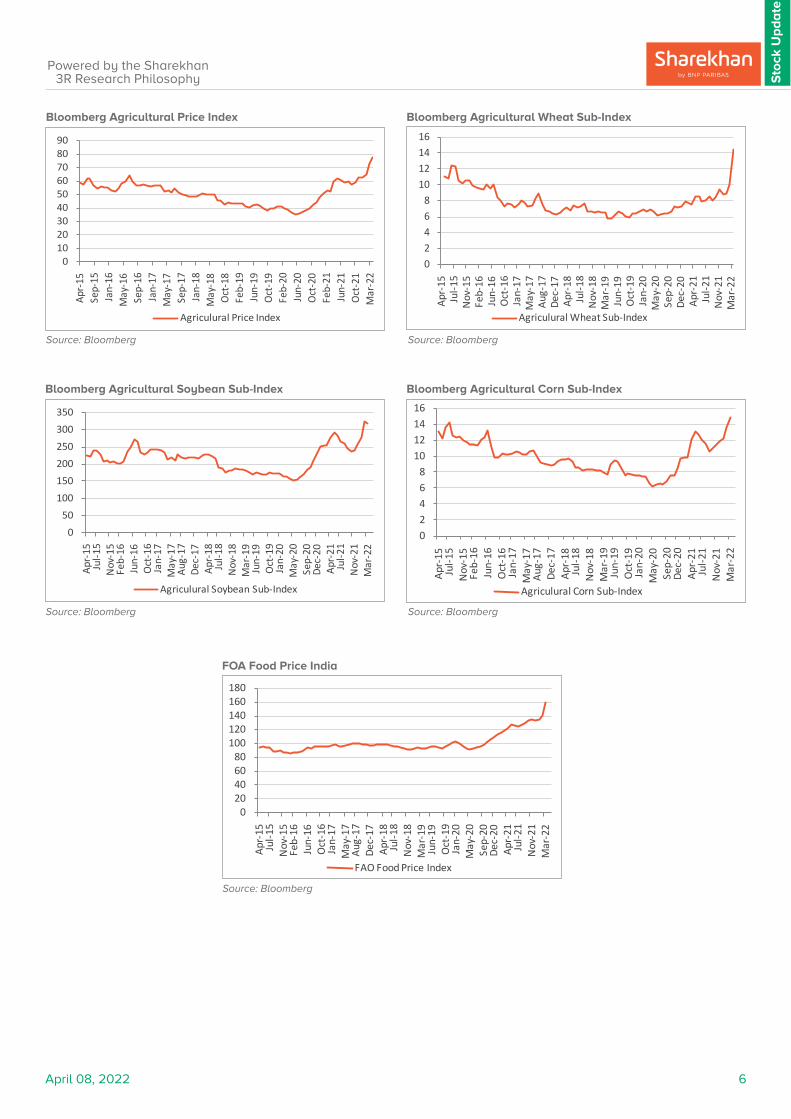

� Favourable global agro-chemical cycle bodes well for price hikes and margin improvement: The recent surge in global crop prices (of wheat/soybean/corn indices rose 63%/25%/27% over December-2021 to March 2022) is expected to improve pricing environment and also aid volumes for agro-chemical companies as farmers likely to increase usage of crop protection products. We believe that this would help MNC-backed companies like SCIL to implement product price hikes which would offset raw material cost pressure. This coupled with focus on high margin PGRs/Herbicides and further synergies from Excel Crop Care would drive411 bps improvement in EBITDA margin to 22.5% over FY21-24E.

� Exports at inflection point; sustained high-growth phase ahead: SCIL’s export revenues grew phenomenally, by 44% y-o-y to Rs456 crore in 9MFY22 primarily led by strong growth from Latin America. We expect strong exports growth to sustain supported by 1) ramp-up of new product registration in Latin America (SCIL can supply 8-10 technicals with overall opportunity size of $1 billion) and strong demand for generic products and 2) massive contract manufacturing (CRAMS) opportunity – SCIL has received approval for manufacturing and exporting five proprietary molecules of the parent company with revenue potential of Rs200-250 crore (asset turnover of 2-2.5x). We thus expect share of exports in overall revenues to 28-30% by FY2024E.

� Expect robust PAT CAGR of 21% over FY21-24: Strong CRAMS opportunity from parent and dominant position in India market makes SCIL well positioned to grow its revenues/EBITDA/PAT at 13%/21%/21% CAGR over FY2021-FY2024E along high RoE of 23-24%.

Our Call

Maintain Buy on SCIL with an unchanged PT of Rs. 500: We believe SCIL would continue to enjoy premium valuation versus domestic peers given its superior earnings growth outlook (growth could accelerate future given massive revenue opportunity from contract manufacturing), its strong parental advantage (robust R&D capabilities, global distribution, and financial strength) and a robust balance sheet (Rs. 664 crore of cash & cash equivalents as of December 2021). Hence, we maintain a Buy rating on SCIL with an unchanged PT of Rs. 500. At CMP, SCIL is trading at 41.5x its FY2023E EPS and 35.3x its FY2024E EPS.

Key Risks

Ban on products such as Glyphosate (that fetch 15% of revenue) could impact earnings outlook. Delay in supply of raw material from China could affect margins. Adverse weather conditions could affect demand for agri inputs and affect earnings outlook.

Sumitomo Chemical India LtdPrice hikes, robust exports to drive growth

Agri Chem Sharekhan code: SUMICHEM

Reco/View: Buy CMP: Rs. 426 Price Target: Rs. 500 á Upgrade Maintain â Downgrade

Sto

ck U

pd

ate

Co

mp

an

y U

pd

ate

200250300350400450500

Apr-2

1

Aug-

21

Dec-

21

Apr-2

2

April 08, 2022 6

Sto

ck U

pd

ate

Powered by the Sharekhan3R Research Philosophy

Source: Bloomberg

Source: Bloomberg

Bloomberg Agricultural Soybean Sub-Index

FOA Food Price India

Source: Bloomberg

Bloomberg Agricultural Wheat Sub-Index

Bloomberg Agricultural Corn Sub-Index

Source: Bloomberg

Bloomberg Agricultural Price Index

Source: Bloomberg

0102030405060708090

Apr-

15Se

p-15

Jan-

16M

ay-1

6Se

p-16

Jan-

17M

ay-1

7Se

p-17

Jan-

18M

ay-1

8O

ct-1

8Fe

b-19

Jun-

19O

ct-1

9Fe

b-20

Jun-

20O

ct-2

0Fe

b-21

Jun-

21O

ct-2

1M

ar-2

2

Agriculural Price Index

02468

10121416

Apr-

15Ju

l-15

Nov

-15

Feb-

16Ju

n-16

Oct

-16

Jan-

17M

ay-1

7Au

g-17

Dec-

17Ap

r-18

Jul-1

8N

ov-1

8M

ar-1

9Ju

n-19

Oct

-19

Jan-

20M

ay-2

0Se

p-20

Dec-

20Ap

r-21

Jul-2

1N

ov-2

1M

ar-2

2

Agriculural Wheat Sub-Index

050

100150200250300350

Apr-

15Ju

l-15

Nov

-15

Feb-

16Ju

n-16

Oct

-16

Jan-

17M

ay-1

7Au

g-17

Dec-

17Ap

r-18

Jul-1

8N

ov-1

8M

ar-1

9Ju

n-19

Oct

-19

Jan-

20M

ay-2

0Se

p-20

Dec-

20Ap

r-21

Jul-2

1N

ov-2

1M

ar-2

2

Agriculural Soybean Sub-Index

02468

10121416

Apr-

15Ju

l-15

Nov

-15

Feb-

16Ju

n-16

Oct

-16

Jan-

17M

ay-1

7Au

g-17

Dec-

17Ap

r-18

Jul-1

8N

ov-1

8M

ar-1

9Ju

n-19

Oct

-19

Jan-

20M

ay-2

0Se

p-20

Dec-

20Ap

r-21

Jul-2

1N

ov-2

1M

ar-2

2

Agriculural Corn Sub-Index

020406080

100120140160180

Apr-

15Ju

l-15

Nov

-15

Feb-

16Ju

n-16

Oct

-16

Jan-

17M

ay-1

7Au

g-17

Dec-

17Ap

r-18

Jul-1

8N

ov-1

8M

ar-1

9Ju

n-19

Oct

-19

Jan-

20M

ay-2

0Se

p-20

Dec-

20Ap

r-21

Jul-2

1N

ov-2

1M

ar-2

2

FAO Food Price Index

April 08, 2022 7

Sto

ck U

pd

ate

Powered by the Sharekhan3R Research Philosophy

Source: Company, Sharekhan Research

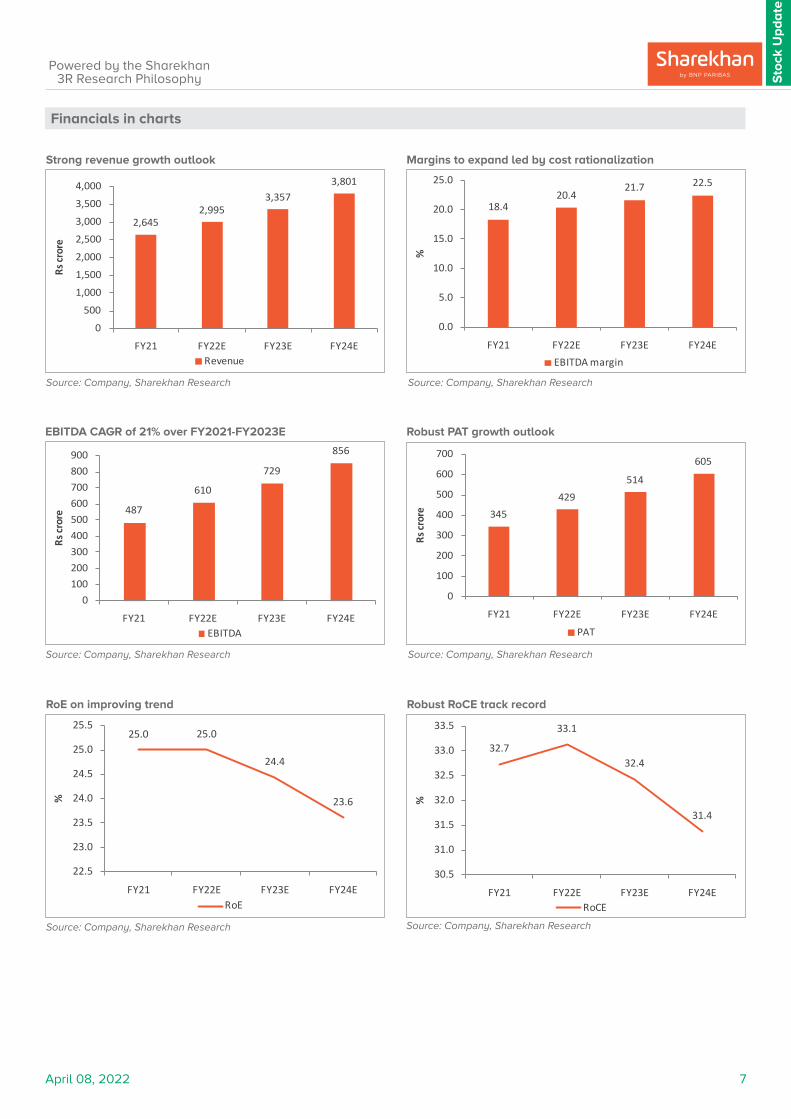

EBITDA CAGR of 21% over FY2021-FY2023E

Source: Company, Sharekhan Research

Margins to expand led by cost rationalization

Robust PAT growth outlook

Source: Company, Sharekhan Research

Financials in charts

Strong revenue growth outlook

Source: Company, Sharekhan Research

RoE on improving trend

Source: Company, Sharekhan Research

Robust RoCE track record

Source: Company, Sharekhan Research

2,6452,995

3,3573,801

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

FY21 FY22E FY23E FY24E

Rs cr

ore

Revenue

18.420.4

21.7 22.5

0.0

5.0

10.0

15.0

20.0

25.0

FY21 FY22E FY23E FY24E

%

EBITDA margin

487

610

729

856

0100200300400500600700800900

FY21 FY22E FY23E FY24E

Rs cr

ore

EBITDA

345429

514

605

0

100

200

300

400

500

600

700

FY21 FY22E FY23E FY24E

Rs cr

ore

PAT

25.0 25.0

24.4

23.6

22.5

23.0

23.5

24.0

24.5

25.0

25.5

FY21 FY22E FY23E FY24E

%

RoE

32.7

33.1

32.4

31.4

30.5

31.0

31.5

32.0

32.5

33.0

33.5

FY21 FY22E FY23E FY24E

%

RoCE

April 08, 2022 8

Sto

ck U

pd

ate

Powered by the Sharekhan3R Research Philosophy

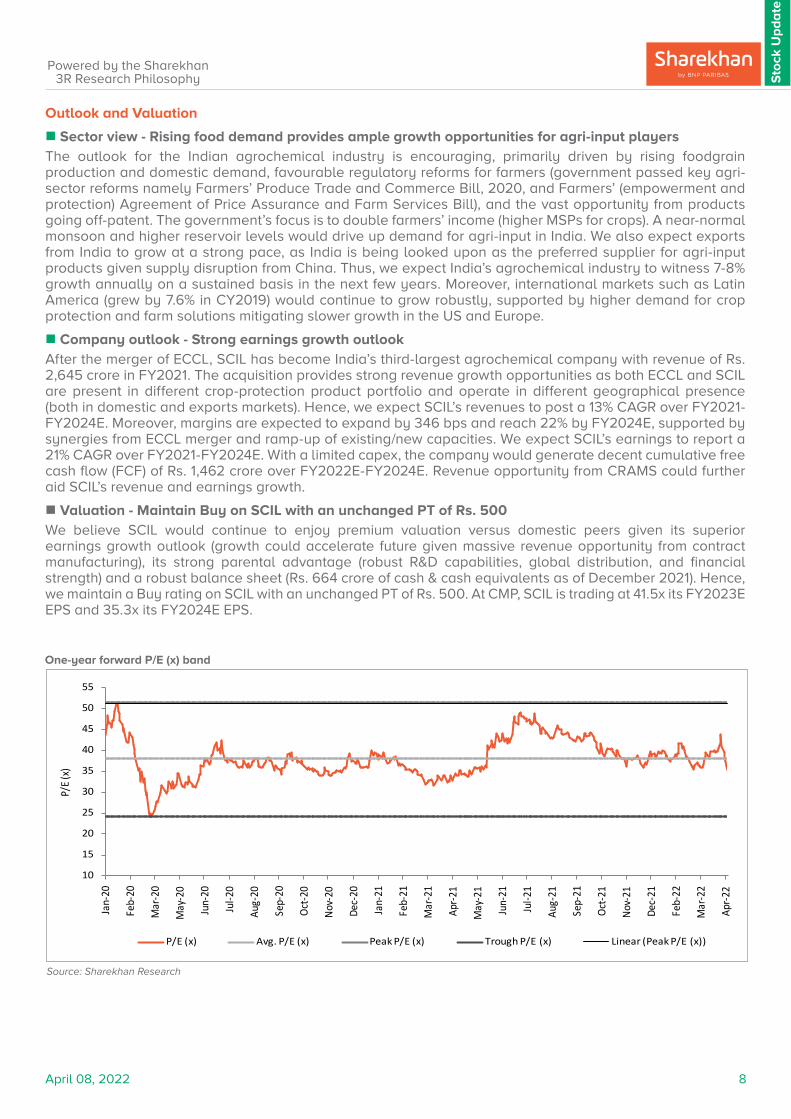

One-year forward P/E (x) band

Source: Sharekhan Research

Outlook and Valuation

n Sector view - Rising food demand provides ample growth opportunities for agri-input playersThe outlook for the Indian agrochemical industry is encouraging, primarily driven by rising foodgrain production and domestic demand, favourable regulatory reforms for farmers (government passed key agri-sector reforms namely Farmers’ Produce Trade and Commerce Bill, 2020, and Farmers’ (empowerment and protection) Agreement of Price Assurance and Farm Services Bill), and the vast opportunity from products going off-patent. The government’s focus is to double farmers’ income (higher MSPs for crops). A near-normal monsoon and higher reservoir levels would drive up demand for agri-input in India. We also expect exports from India to grow at a strong pace, as India is being looked upon as the preferred supplier for agri-input products given supply disruption from China. Thus, we expect India’s agrochemical industry to witness 7-8% growth annually on a sustained basis in the next few years. Moreover, international markets such as Latin America (grew by 7.6% in CY2019) would continue to grow robustly, supported by higher demand for crop protection and farm solutions mitigating slower growth in the US and Europe.

n Company outlook - Strong earnings growth outlookAfter the merger of ECCL, SCIL has become India’s third-largest agrochemical company with revenue of Rs. 2,645 crore in FY2021. The acquisition provides strong revenue growth opportunities as both ECCL and SCIL are present in different crop-protection product portfolio and operate in different geographical presence (both in domestic and exports markets). Hence, we expect SCIL’s revenues to post a 13% CAGR over FY2021-FY2024E. Moreover, margins are expected to expand by 346 bps and reach 22% by FY2024E, supported by synergies from ECCL merger and ramp-up of existing/new capacities. We expect SCIL’s earnings to report a 21% CAGR over FY2021-FY2024E. With a limited capex, the company would generate decent cumulative free cash flow (FCF) of Rs. 1,462 crore over FY2022E-FY2024E. Revenue opportunity from CRAMS could further aid SCIL’s revenue and earnings growth.

n Valuation - Maintain Buy on SCIL with an unchanged PT of Rs. 500We believe SCIL would continue to enjoy premium valuation versus domestic peers given its superior earnings growth outlook (growth could accelerate future given massive revenue opportunity from contract manufacturing), its strong parental advantage (robust R&D capabilities, global distribution, and financial strength) and a robust balance sheet (Rs. 664 crore of cash & cash equivalents as of December 2021). Hence, we maintain a Buy rating on SCIL with an unchanged PT of Rs. 500. At CMP, SCIL is trading at 41.5x its FY2023E EPS and 35.3x its FY2024E EPS.

10

15

20

25

30

35

40

45

50

55

Jan-

20

Feb-

20

Mar

-20

May

-20

Jun-

20

Jul-2

0

Aug-

20

Sep-

20

Oct-2

0

Nov-

20

Dec-

20

Jan-

21

Feb-

21

Mar

-21

Apr-2

1

May

-21

Jun-

21

Jul-2

1

Aug-

21

Sep-

21

Oct-2

1

Nov-

21

Dec-

21

Feb-

22

Mar

-22

Apr-2

2

P/E (

x)

P/E (x) Avg. P/E (x) Peak P/E (x) Trough P/E (x) Linear (Peak P/E (x))

April 08, 2022 9

Sto

ck U

pd

ate

Powered by the Sharekhan3R Research Philosophy

About company

SCIL manufactures, imports and markets products for crop protection, grain fumigation, rodent control, bio pesticides, environmental health, professional pest control and feed additives for use in India. SCIL has also marked its presence in Africa and several other geographies of the world. The company’s product range comprises conventional chemistry sourced from its parent company, Sumitomo Chemical Company, and biological products sourced from US-based subsidiary, Valent Biosciences LLC, a leader in producing a range of naturally occurring, environmentally compatible pesticides, and plant growth regulators for over 40 years. The company also produces many technical grade pesticides at its state-of-the-art manufacturing units with indigenous R&D facility.

Investment theme

Few crop protection chemicals are expected to be off patent in years, thus genetic crop-protection chemicals should grow in double digits. Hence, the merger of ECCL (has 100% generic portfolio in crop protection market along with backward integration of a few technical) bodes well for industry leading revenue growth of SCIL. Cost synergies in terms of reduction in imported of raw material (post ECCL merger) would drive strong margin expansion. Additionally, SCIL derives multiple benefits from its parent’s R&D capabilities and global presence. Key Risks

� Ban on products such as Glyphosate (15% of revenues) could impact earnings outlook.

� Delay in supply of raw material from China could impact margins lower.

� Adverse weather conditions could affect demand of agri inputs and impact earnings outlook.

Additional Data

Key management personnel

Mukul Govindji Asher Chairman & Independent Director

Chetan Shantilal Shah Managing Director

Sushil Champaklal Marfatia Executive Director

Hiroyoshi Mukai Non-executive DirectorSource: Bloomberg

Top 10 shareholders

Sr. No. Holder Name Holding (%)

1 Life Insurance Corporation of India 3.6

2 Axis Asset Management Company Ltd 0.9

3 Vanguard Group Inc 0.7

4 L&T Mutual Fund Trustee Ltd 0.4

5 Invesco Asset Management India Private Limited 0.3

6 Union Mutual Fund 0.2

7 Norges Bank 0.2

8 BlackRock Inc 0.1

9 Quant Money Managers 0.04

10 Exide Life Insurance 0.04Source: Bloomberg (old data)

Sharekhan Limited, its analyst or dependant(s) of the analyst might be holding or having a position in the companies mentioned in the article.

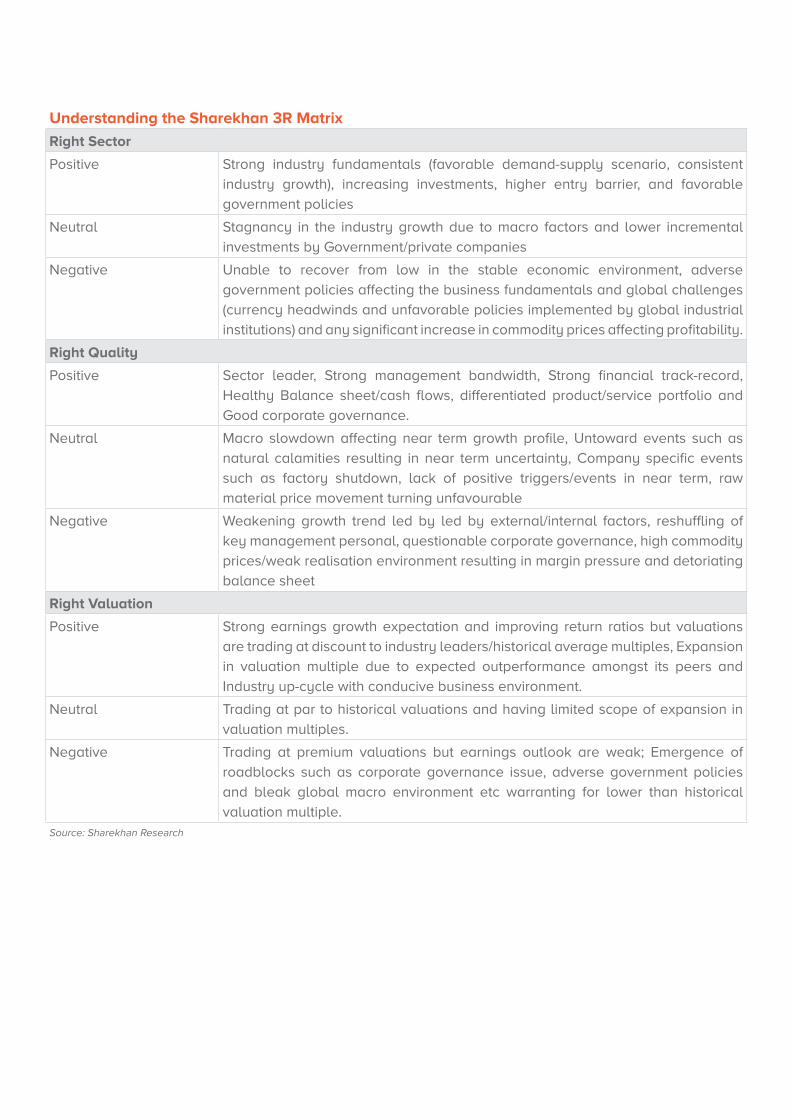

Understanding the Sharekhan 3R Matrix

Right Sector

Positive Strong industry fundamentals (favorable demand-supply scenario, consistent

industry growth), increasing investments, higher entry barrier, and favorable

government policies

Neutral Stagnancy in the industry growth due to macro factors and lower incremental

investments by Government/private companies

Negative Unable to recover from low in the stable economic environment, adverse

government policies affecting the business fundamentals and global challenges

(currency headwinds and unfavorable policies implemented by global industrial

institutions) and any significant increase in commodity prices affecting profitability.

Right Quality

Positive Sector leader, Strong management bandwidth, Strong financial track-record,

Healthy Balance sheet/cash flows, differentiated product/service portfolio and

Good corporate governance.

Neutral Macro slowdown affecting near term growth profile, Untoward events such as

natural calamities resulting in near term uncertainty, Company specific events

such as factory shutdown, lack of positive triggers/events in near term, raw

material price movement turning unfavourable

Negative Weakening growth trend led by led by external/internal factors, reshuffling of

key management personal, questionable corporate governance, high commodity

prices/weak realisation environment resulting in margin pressure and detoriating

balance sheet

Right Valuation

Positive Strong earnings growth expectation and improving return ratios but valuations

are trading at discount to industry leaders/historical average multiples, Expansion

in valuation multiple due to expected outperformance amongst its peers and

Industry up-cycle with conducive business environment.

Neutral Trading at par to historical valuations and having limited scope of expansion in

valuation multiples.

Negative Trading at premium valuations but earnings outlook are weak; Emergence of

roadblocks such as corporate governance issue, adverse government policies

and bleak global macro environment etc warranting for lower than historical

valuation multiple.Source: Sharekhan Research

Disclaimer: This document has been prepared by Sharekhan Ltd. (SHAREKHAN) and is intended for use only by the person or entity to which it is addressed to. This Document may contain confidential and/or privileged material and is not for any type of circulation and any review, retransmission, or any other use is strictly prohibited. This Document is subject to changes without prior notice. This document does not constitute an offer to sell or solicitation for the purchase or sale of any financial instrument or as an official confirmation of any transaction. Though disseminated to all customers who are due to receive the same, not all customers may receive this report at the same time. SHAREKHAN will not treat recipients as customers by virtue of their receiving this report.

The information contained herein is obtained from publicly available data or other sources believed to be reliable and SHAREKHAN has not independently verified the accuracy and completeness of the said data and hence it should not be relied upon as such. While we would endeavour to update the information herein on reasonable basis, SHAREKHAN, its subsidiaries and associated companies, their directors and employees (“SHAREKHAN and affiliates”) are under no obligation to update or keep the information current. Also, there may be regulatory, compliance, or other reasons that may prevent SHAREKHAN and affiliates from doing so. This document is prepared for assistance only and is not intended to be and must not alone be taken as the basis for an investment decision. Recipients of this report should also be aware that past performance is not necessarily a guide to future performance and value of investments can go down as well. The user assumes the entire risk of any use made of this information. Each recipient of this document should make such investigations as it deems necessary to arrive at an independent evaluation of an investment in the securities of companies referred to in this document (including the merits and risks involved), and should consult its own advisors to determine the merits and risks of such an investment. The investment discussed or views expressed may not be suitable for all investors. We do not undertake to advise you as to any change of our views. Affiliates of Sharekhan may have issued other reports that are inconsistent with and reach different conclusions from the information presented in this report.

This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution, publication, availability or use would be contrary to law, regulation or which would subject SHAREKHAN and affiliates to any registration or licensing requirement within such jurisdiction. The securities described herein may or may not be eligible for sale in all jurisdictions or to certain category of investors. Persons in whose possession this document may come are required to inform themselves of and to observe such restriction.

The analyst certifies that the analyst has not dealt or traded directly or indirectly in securities of the company and that all of the views expressed in this document accurately reflect his or her personal views about the subject company or companies and its or their securities and do not necessarily reflect those of SHAREKHAN. The analyst and SHAREKHAN further certifies that neither he or his relatives or Sharekhan associates has any direct or indirect financial interest nor have actual or beneficial ownership of 1% or more in the securities of the company at the end of the month immediately preceding the date of publication of the research report nor have any material conflict of interest nor has served as officer, director or employee or engaged in market making activity of the company. Further, the analyst has also not been a part of the team which has managed or co-managed the public offerings of the company and no part of the analyst’s compensation was, is or will be, directly or indirectly related to specific recommendations or views expressed in this document. Sharekhan Limited or its associates or analysts have not received any compensation for investment banking, merchant banking, brokerage services or any compensation or other benefits from the subject company or from third party in the past twelve months in connection with the research report.

Either, SHAREKHAN or its affiliates or its directors or employees / representatives / clients or their relatives may have position(s), make market, act as principal or engage in transactions of purchase or sell of securities, from time to time or may be materially interested in any of the securities or related securities referred to in this report and they may have used the information set forth herein before publication. SHAREKHAN may from time to time solicit from, or perform investment banking, or other services for, any company mentioned herein. Without limiting any of the foregoing, in no event shall SHAREKHAN, any of its affiliates or any third party involved in, or related to, computing or compiling the information have any liability for any damages of any kind.

Compliance Officer: Mr. Joby John Meledan; Tel: 022-61150000; email id: [email protected];

For any queries or grievances kindly email [email protected] or contact: [email protected]

Registered Office: Sharekhan Limited, 10th Floor, Beta Building, Lodha iThink Techno Campus, Off. JVLR, Opp. Kanjurmarg Railway Station, Kanjurmarg (East), Mumbai – 400042, Maharashtra. Tel: 022 - 61150000. Sharekhan Ltd.: SEBI Regn. Nos.: BSE / NSE / MSEI (CASH / F&O / CD) / MCX - Commodity: INZ000171337; DP: NSDL/CDSL-IN-DP-365-2018; PMS: INP000005786; Mutual Fund: ARN 20669; Research Analyst: INH000006183;

Disclaimer: Client should read the Risk Disclosure Document issued by SEBI & relevant exchanges and the T&C on www.sharekhan.com; Investment in securities market are subject to market risks, read all the related documents carefully before investing.

Know more about our products and services

For Private Circulation only