a184720-eng_pinganora_investorday_eng.pdf - irasia

TRANSCRIPT

Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this announcement, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this announcement.

OVERSEAS REGULATORY ANNOUNCEMENT

This announcement is made pursuant to Rule 13.10B of the Rules Governing the Listing of Securities on the Stock Exchange of Hong Kong Limited. “The Announcement of Ping An Insurance (Group) Company of China, Ltd. regarding the Disclosure of Relevant Reports on 2017 Investor Day”, which is published by Ping An Insurance (Group) Company of China, Ltd. on the website of Shanghai Stock Exchange, is reproduced herein for your reference.

By order of the Board Yao Jun

Company Secretary Shenzhen, PRC, November 19, 2017 As at the date of this announcement, the Executive Directors of the Company are Ma Mingzhe, Sun Jianyi, Ren Huichuan, Yao Jason Bo, Lee Yuansiong and Cai Fangfang; the Non-executive Directors are Lin Lijun, Soopakij Chearavanont, Yang Xiaoping, Xiong Peijin and Liu Chong; the Independent Non-executive Directors are Stephen Thomas Meldrum, Yip Dicky Peter, Wong Oscar Sai Hung, Sun Dongdong, Ge Ming and Ouyang Hui.

Stock Code: 601318 Stock Short Name: Ping An of China Serial No.: Lin 2017-044

THE ANNOUNCEMENT OF

PING AN INSURANCE (GROUP) COMPANY OF CHINA, LTD.

REGARDING THE DISCLOSURE OF RELEVANT REPORTS ON

2017 INVESTOR DAY

The board of directors and all directors of Ping An Insurance (Group) Company of China, Ltd. (hereinafter referred to as the "Company") confirm that there are no false representations and misleading statements contained in, or material omissions in this announcement, and severally and jointly accept the responsibility for the truthfulness, accuracy and completeness of the contents of this announcement.

The Company will hold the 2017 Investor Day on Monday, November 20, 2017, in which The "Financial Service + Technology" Strategy of Ping An, Ping An Life's Value Inside Out (II), Boost Value of Traditional Financial Businesses with Technologies and From Ping An to Platform: Technology Innovation for Growth will be reported.

Please refer to the attachments of this announcement as disclosed by the Company on the

website of Shanghai Stock Exchange (www.sse.com.cn) on the same day for the details of the above reports.

Attachments of this announcement on the website: 1. The “Financial Service + Technology” Strategy of Ping An 2. Ping An Life's Value Inside Out (II) 3. Boost Value of Traditional Financial Businesses with Technologies 4. From Ping An to Platform: Technology Innovation for Growth

The Board of Directors Ping An Insurance (Group) Company of China, Ltd.

November 19, 2017

The “Financial Service + Technology”

Strategy of Ping An

2017.11

Shenzhen

Jason Yao

Important Notes Cautionary Statements Regarding Forward-Looking Statement To the extent any statements made in this presentation containing information that is not historical are essentially forward-looking. These forward-looking statements include but are not limited to projections, targets, estimates and business plans that the Company expects or anticipates will or may occur in the future. These forward-looking statements are subject to known and unknown risks and uncertainties that may be general or specific. Certain statements, such as those including the words or phrases "potential", "estimates", "expects", "anticipates", "objective", "intends", "plans", "believes", "will", "may", "should", and similar expressions or variations on such expressions may be considered forward-looking statements. Readers should be cautioned that a variety of factors, many of which may be beyond the Company's control, affect the performance, operations, and results of the Company, and could cause actual results to differ materially from the expectations expressed in any of the Company's forward-looking statements. These factors include but are not limited to exchange rate fluctuations, market shares, competition, environmental risks, changes in legal, financial and regulatory frameworks, international economic and financial market conditions, and other risks and factors beyond our control. These and other factors should be considered carefully, and readers should not place undue reliance on the Company's forward-looking statements. In addition, the Company undertakes no obligation to publicly update or revise any forward-looking statement that is contained in this presentation as a result of new information, future events, or otherwise. None of the Company, or any of its employees or affiliates is responsible for, or is making, any representation concerning the future performance of the Company.

01

Ping An’s Performance on Value

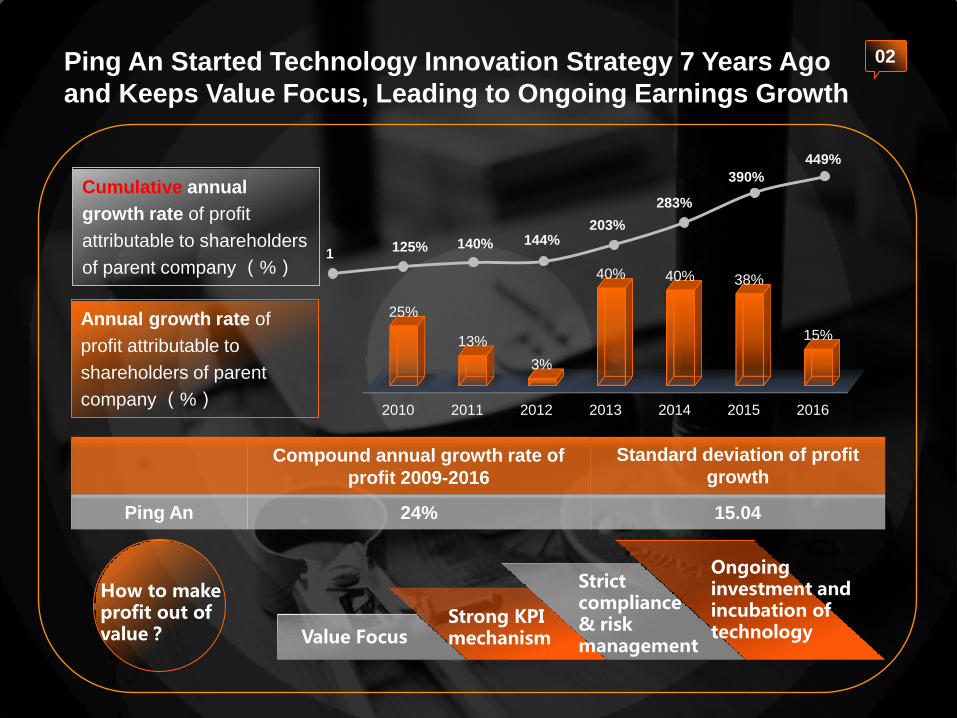

Ping An Started Technology Innovation Strategy 7 Years Ago

and Keeps Value Focus, Leading to Ongoing Earnings Growth

02

Compound annual growth rate of

profit 2009-2016

Standard deviation of profit

growth

Ping An 24% 15.04

Cumulative annual

growth rate of profit

attributable to shareholders

of parent company (%) 1

125% 140% 144% 203%

283%

390%

449%

Annual growth rate of

profit attributable to

shareholders of parent

company (%) 2010 2011 2012 2013 2014 2015 2016

25%

13%

3%

40% 40% 38%

15%

Value Focus Strong KPI mechanism

Strict compliance & risk management

Ongoing investment and incubation of technology

How to make profit out of value?

03

The Strategy of

“Financial Service + Technology”

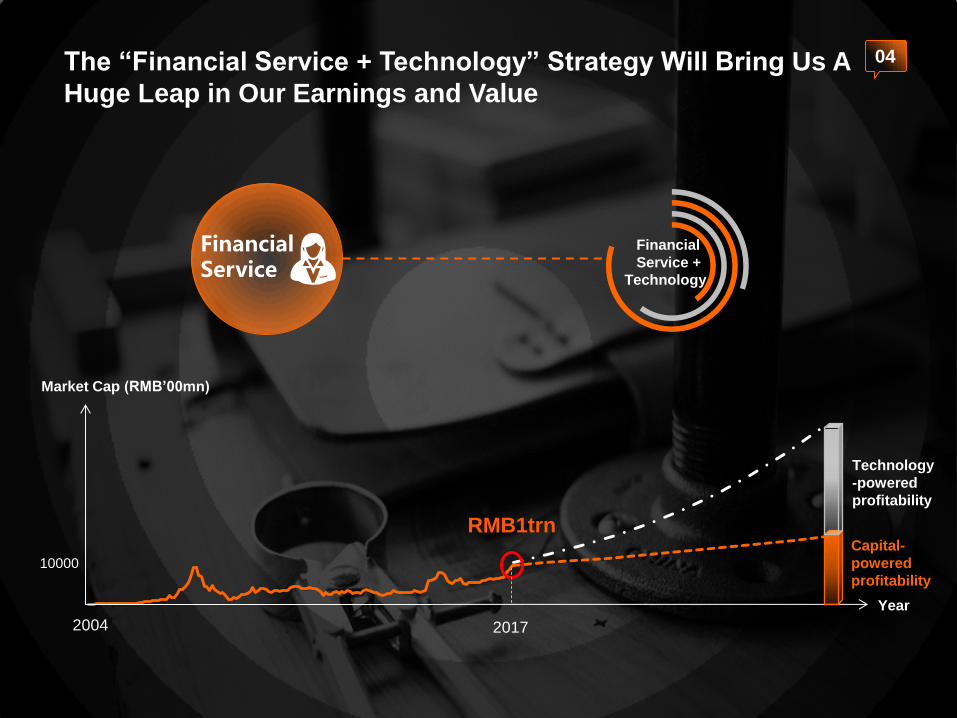

04 The “Financial Service + Technology” Strategy Will Bring Us A

Huge Leap in Our Earnings and Value

Financial

Service +

Technology

Financial Service

RMB1trn

2004 2017

10000

Market Cap (RMB’00mn)

Year

Capital-

powered

profitability

Technology

-powered

profitability

05

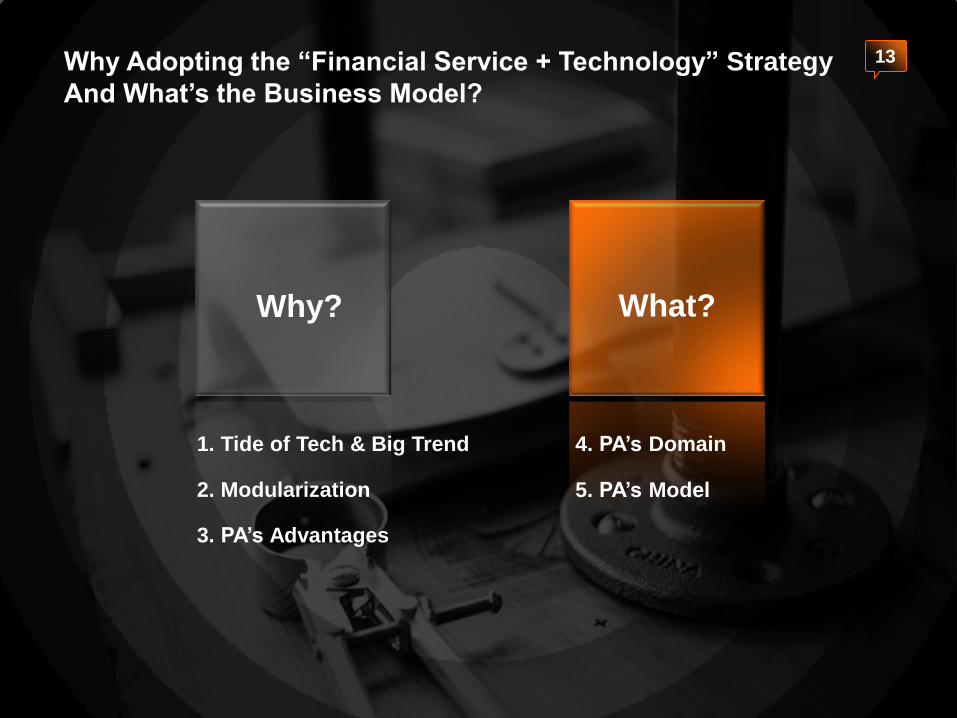

Why? What?

2. Modularization

1. Tide of Tech & Big Trend

3. PA’s Advantages

5. PA’s Model

4. PA’s Domain

Why Adopting the “Financial Service + Technology” Strategy

And What’s the Business Model?

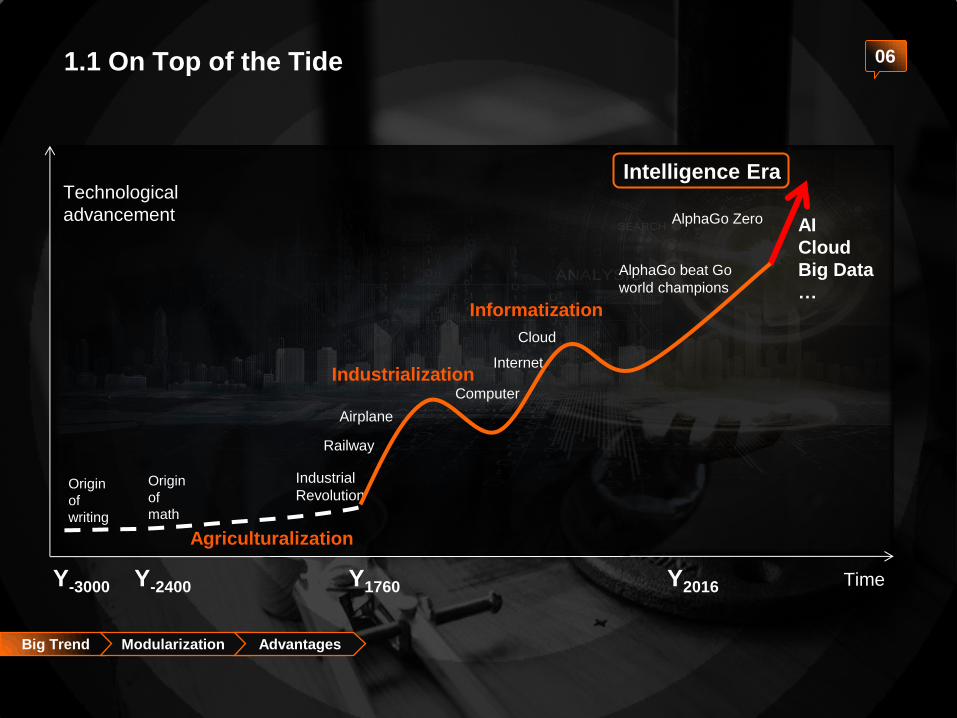

1.1 On Top of the Tide 06

Y-3000 Y-2400 Y1760

Origin

of

writing

Origin

of

math

Industrial

Revolution

Railway

Airplane

Internet

Computer

Technological

advancement

Time Y2016

Intelligence Era

Informatization

Industrialization

Agriculturalization

AlphaGo beat Go

world champions

Cloud

AlphaGo Zero

Big Trend Modularization Advantages

AI

Cloud

Big Data

…

07

Big Trend Modularization Advantages

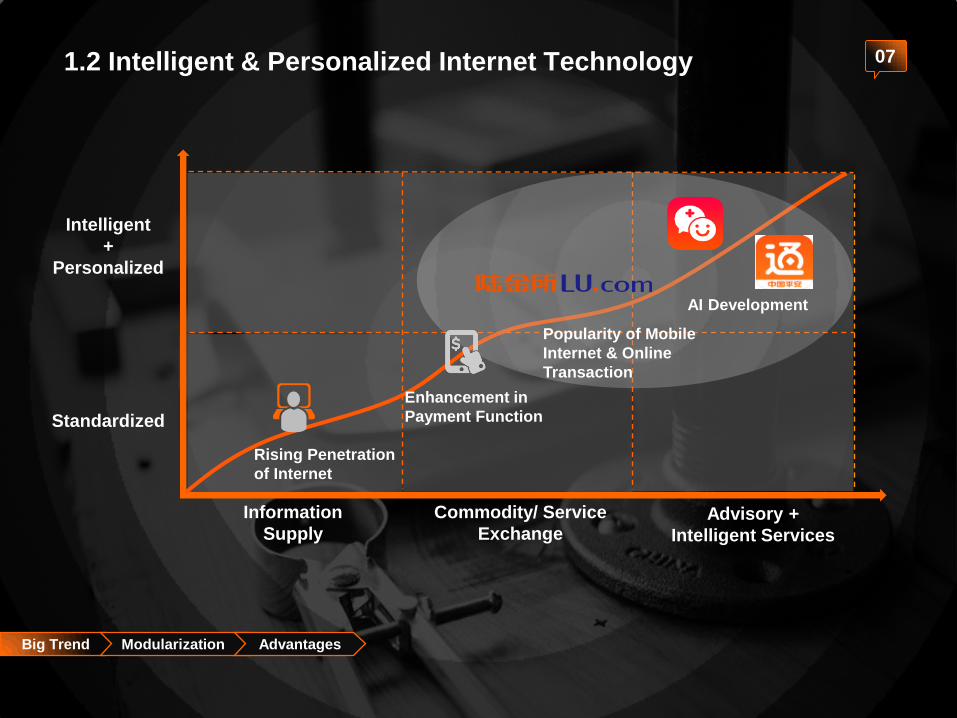

1.2 Intelligent & Personalized Internet Technology

Rising Penetration

of Internet

Enhancement in

Payment Function

Popularity of Mobile

Internet & Online

Transaction

AI Development

Intelligent

+

Personalized

Standardized

Information

Supply

Commodity/ Service

Exchange Advisory +

Intelligent Services

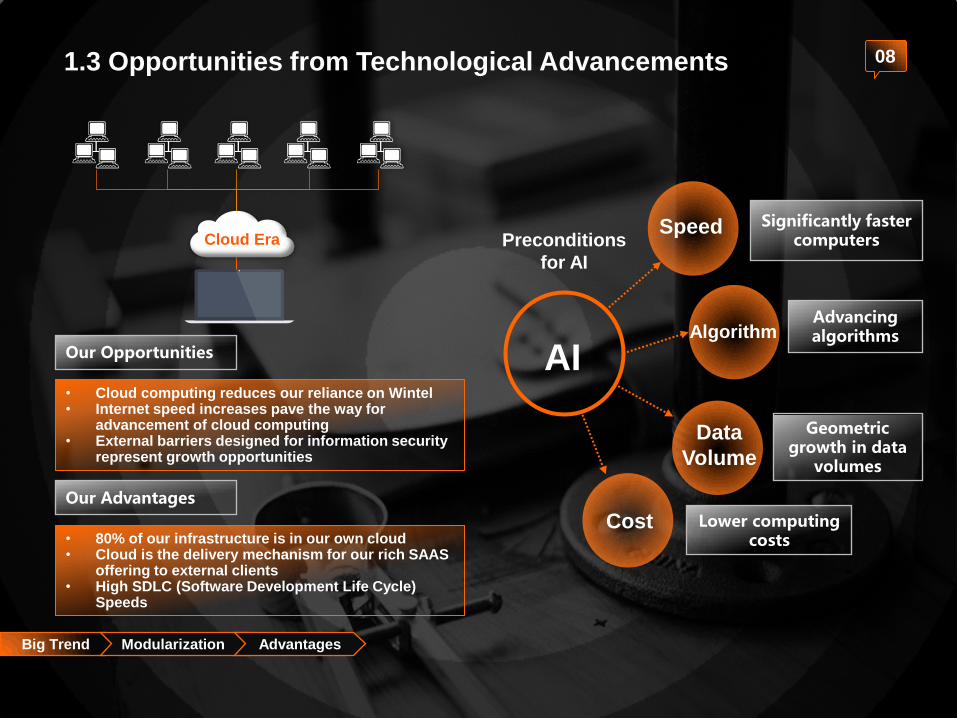

1.3 Opportunities from Technological Advancements 08

Cloud Era

• Cloud computing reduces our reliance on Wintel • Internet speed increases pave the way for

advancement of cloud computing • External barriers designed for information security

represent growth opportunities

AI Algorithm

Speed

Cost

Data

Volume

Significantly faster computers

Lower computing costs

Geometric growth in data

volumes

Advancing algorithms

Preconditions

for AI

Big Trend Modularization Advantages

Our Opportunities

• 80% of our infrastructure is in our own cloud • Cloud is the delivery mechanism for our rich SAAS

offering to external clients • High SDLC (Software Development Life Cycle)

Speeds

Our Advantages

Big Trend

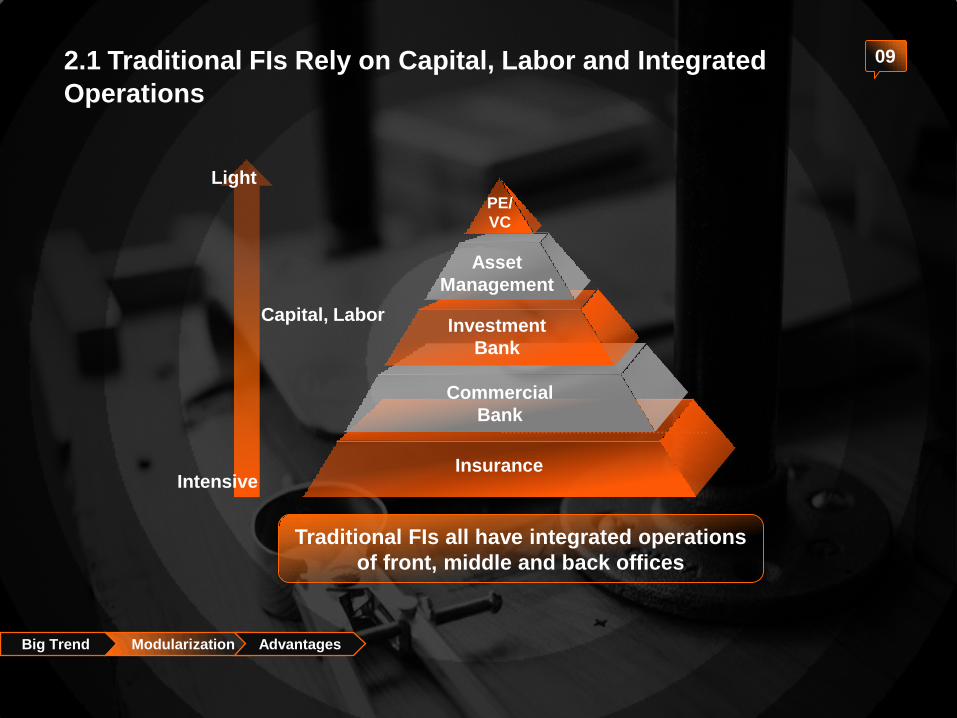

2.1 Traditional FIs Rely on Capital, Labor and Integrated

Operations

09

PE/

VC

Asset

Management

Investment

Bank

Commercial

Bank

Insurance

Light

Intensive

Capital, Labor

Traditional FIs all have integrated operations

of front, middle and back offices

Modularization Advantages

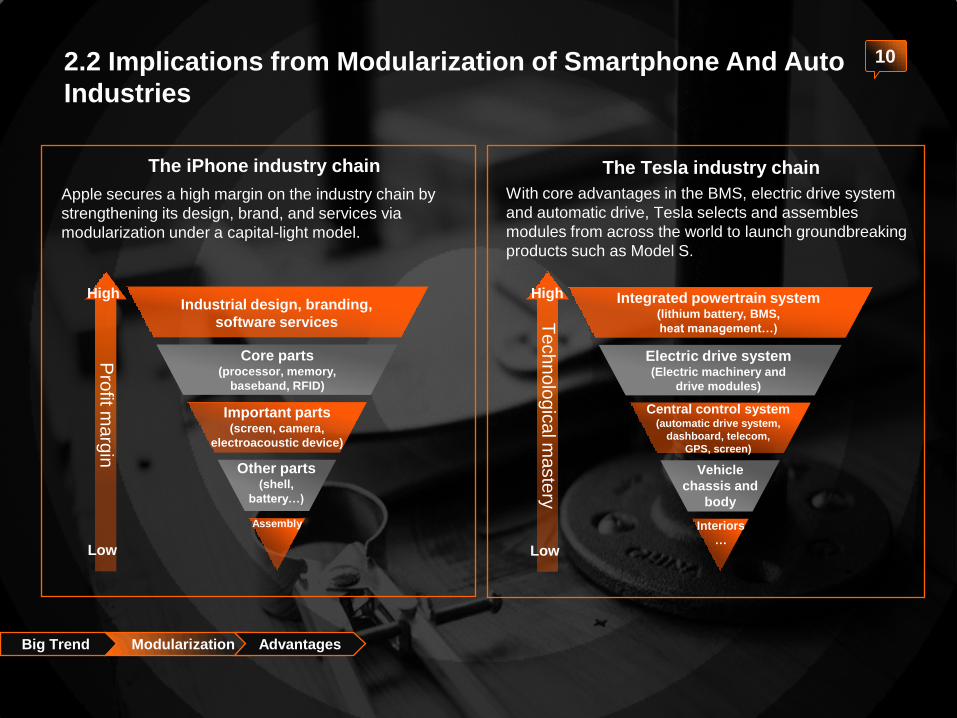

2.2 Implications from Modularization of Smartphone And Auto

Industries

10

Big Trend Modularization Advantages

The iPhone industry chain

Apple secures a high margin on the industry chain by

strengthening its design, brand, and services via

modularization under a capital-light model.

The Tesla industry chain

With core advantages in the BMS, electric drive system

and automatic drive, Tesla selects and assembles

modules from across the world to launch groundbreaking

products such as Model S.

Pro

fit marg

in

Low

High

Te

ch

no

log

ica

l ma

ste

ry

High

Low

Industrial design, branding,

software services

Assembly

Core parts (processor, memory,

baseband, RFID)

Important parts (screen, camera,

electroacoustic device)

Other parts (shell,

battery…)

Integrated powertrain system (lithium battery, BMS,

heat management…)

Interiors

…

Electric drive system (Electric machinery and

drive modules)

Central control system (automatic drive system,

dashboard, telecom,

GPS, screen)

Vehicle

chassis and

body

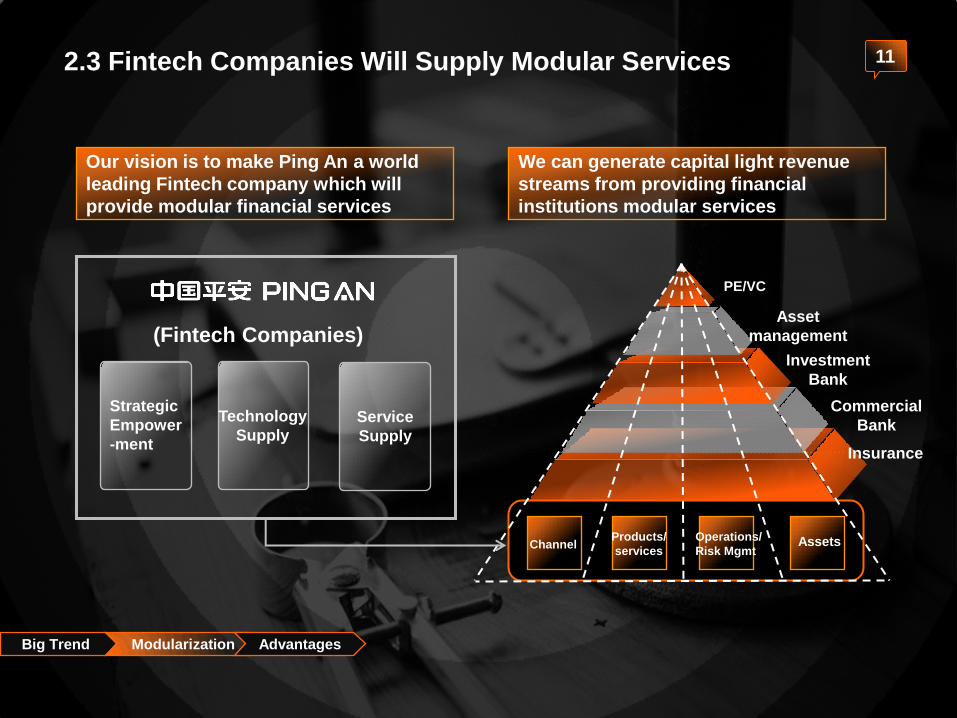

11 2.3 Fintech Companies Will Supply Modular Services

PE/VC

Asset

management

Investment

Bank

Commercial

Bank

Insurance

Channel Products/

services

Operations/

Risk Mgmt Assets

We can generate capital light revenue

streams from providing financial

institutions modular services

Our vision is to make Ping An a world

leading Fintech company which will

provide modular financial services

(Fintech Companies)

Technology

Supply Service

Supply

Strategic

Empower

-ment

Big Trend Modularization Advantages

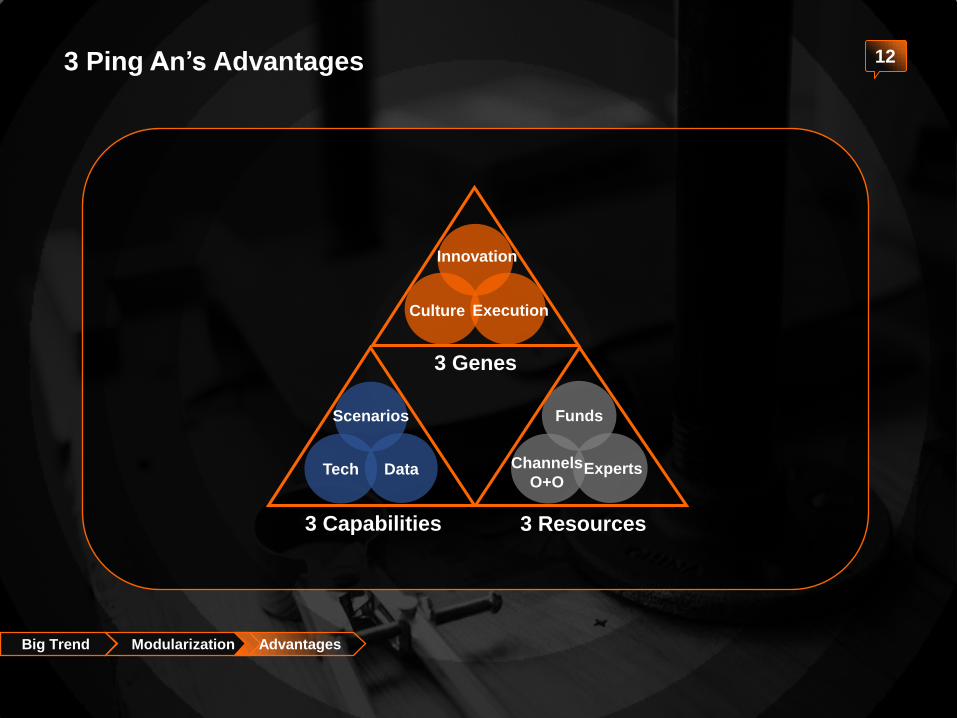

3 Ping An’s Advantages 12

3 Capabilities 3 Resources

3 Genes

Big Trend Modularization Advantages

Innovation

Culture Execution

Scenarios

Tech Data

Funds

Channels

O+O Experts

13

Why? What?

2. Modularization

1. Tide of Tech & Big Trend

3. PA’s Advantages

5. PA’s Model

4. PA’s Domain

Why Adopting the “Financial Service + Technology” Strategy

And What’s the Business Model?

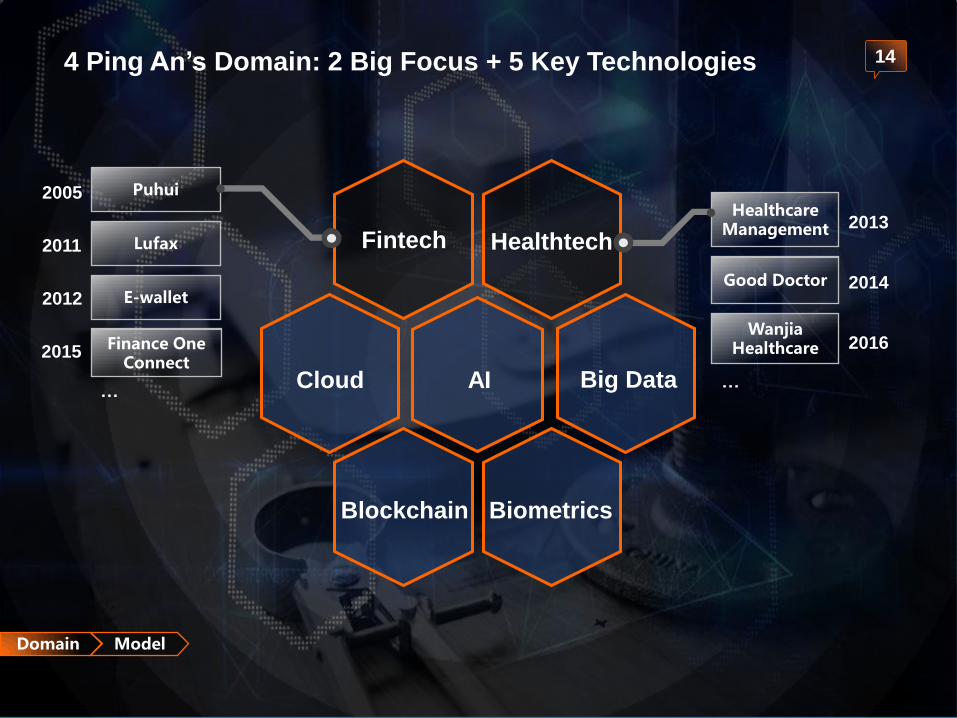

4 Ping An’s Domain: 2 Big Focus + 5 Key Technologies 14

Fintech

Domain Model

Healthtech

Cloud AI Big Data

Blockchain Biometrics

Lufax

Finance One Connect

…

2011

2015

Healthcare Management

…

2013

Good Doctor

Wanjia Healthcare

2014

2016

Puhui 2005

E-wallet 2012

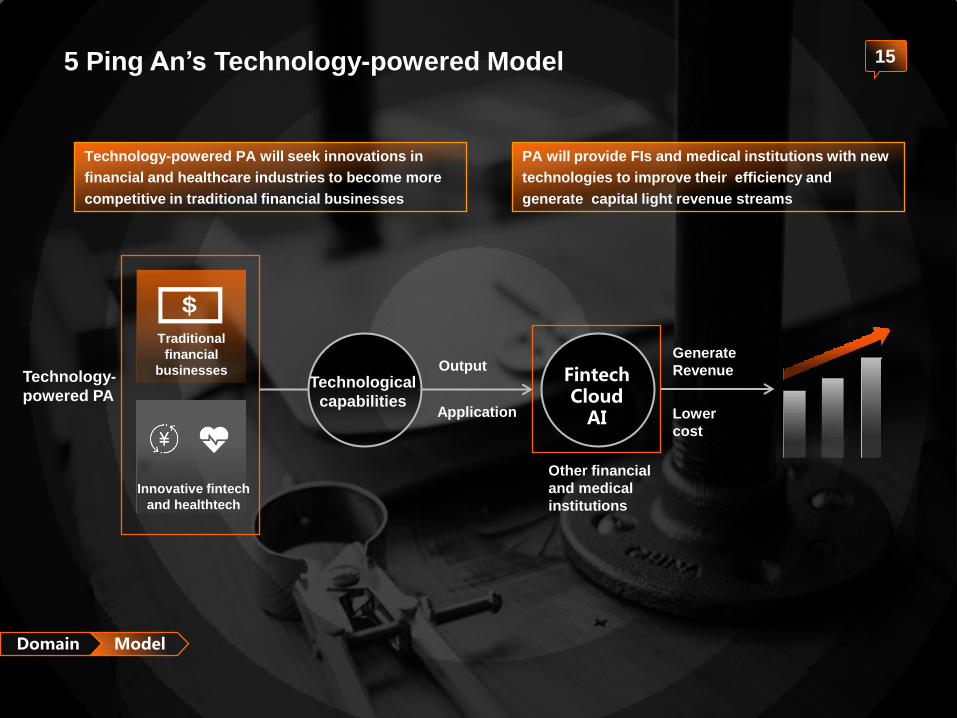

5 Ping An’s Technology-powered Model 15

Technology-powered PA will seek innovations in

financial and healthcare industries to become more

competitive in traditional financial businesses

PA will provide FIs and medical institutions with new

technologies to improve their efficiency and

generate capital light revenue streams

Fintech Cloud

AI

Domain Model

Technology-

powered PA

Traditional

financial

businesses

Innovative fintech

and healthtech

Technological

capabilities

Output

Application

Generate

Revenue

Lower

cost

Other financial

and medical

institutions

“Financial Service + Technology”, An Ongoing Value

Generating Strategy

Invest and develop world-leading technologies; incubate new business models

Keep the advantages in traditional financial businesses and focus on value

Traditional finance

Technological innovation “Financial Service +

Technology” Strategy

Elevate the efficiency of capital, continue rewarding shareholders

Provide the society, government and other businesses with technologies to

boost efficiency, cut costs, and reduce risks

16

Thank you

17

Ping An Life’s Value

Inside Out (II) Jason Yao

November, 2017

Important Notes Cautionary Statements Regarding Forward-Looking Statement

To the extent any statements made in this presentation containing information that is not historical are

essentially forward-looking. These forward-looking statements include but are not limited to projections,

targets, estimates and business plans that the Company expects or anticipates will or may occur in the

future. These forward-looking statements are subject to known and unknown risks and uncertainties

that may be general or specific. Certain statements, such as those including the words or phrases

"potential", "estimates", "expects", "anticipates", "objective", "intends", "plans", "believes", "will", "may",

"should", and similar expressions or variations on such expressions may be considered forward-looking

statements.

Readers should be cautioned that a variety of factors, many of which may be beyond the Company's

control, affect the performance, operations, and results of the Company, and could cause actual results

to differ materially from the expectations expressed in any of the Company's forward-looking

statements. These factors include but are not limited to exchange rate fluctuations, market shares,

competition, environmental risks, changes in legal, financial and regulatory frameworks, international

economic and financial market conditions, and other risks and factors beyond our control. These and

other factors should be considered carefully, and readers should not place undue reliance on the

Company's forward-looking statements. In addition, the Company undertakes no obligation to publicly

update or revise any forward-looking statement that is contained in this presentation as a result of new

information, future events, or otherwise. None of the Company, or any of its employees or affiliates is

responsible for, or is making, any representation concerning the future performance of the Company.

Specification of Disclosure

Value of new business stated in this presentation is of life and health insurance business unless

otherwise specified, which is comprised of insurance business from Ping An Life, Ping An Annuity and

Ping An Health. Embedded value stated in this presentation is at group level.

Growth rates disclosed in the charts and tables of this presentation are annual compound growth rates

unless otherwise specified.

2

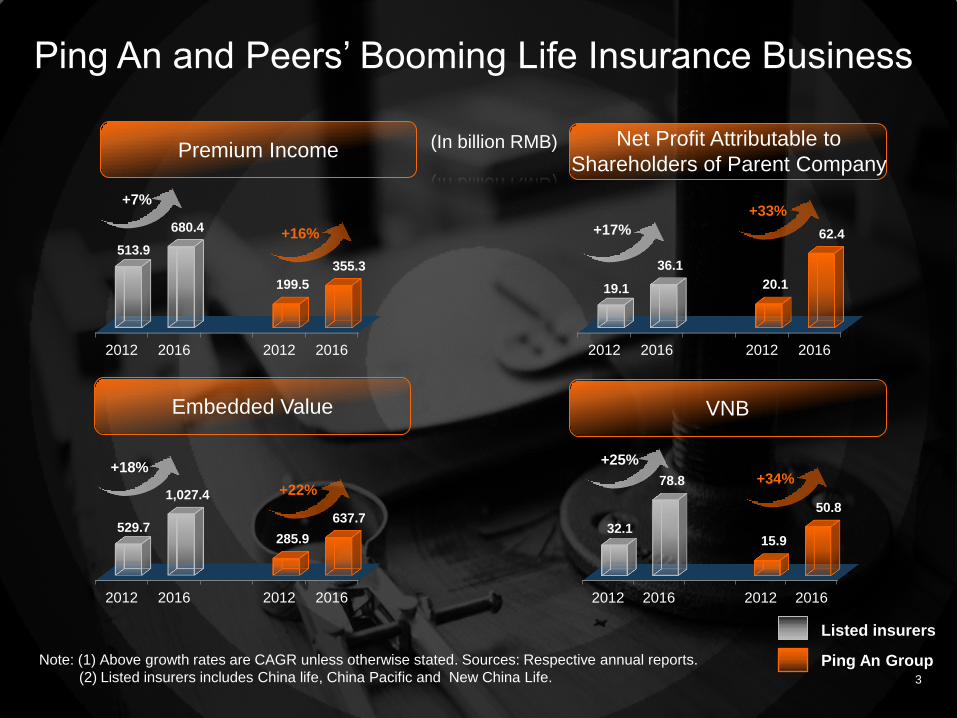

Net Profit Attributable to

Shareholders of Parent Company

2012 2016 2012 2016

529.7

1,027.4

285.9

637.7

2012 2016 2012 2016

32.1

78.8

15.9

50.8

2012 2016 2012 2016

513.9

680.4

199.5

355.3

Ping An and Peers’ Booming Life Insurance Business

Embedded Value

Premium Income

Note: (1) Above growth rates are CAGR unless otherwise stated. Sources: Respective annual reports.

(2) Listed insurers includes China life, China Pacific and New China Life.

(In billion RMB)

Listed insurers

Ping An Group 3

+7%

+16%

2012 2016 2012 2016

19.1

36.1

20.1

62.4

+18%

+22%

+25%

+34%

+17%

+33%

VNB

Main Market Concerns from Last Year

Will lasting low interest rate environment significantly impair its profitability?

Are EV assumptions prudent and reasonable?

How does C-ROSS affect the company's solvency and EV?

Is Ping An Life steady growth sustainable during the economic downturn?

Answer

4

• Long-term protection products

are the main contributor of NBEV

• Long-term protection products

depend less on interest margin

Less Affected

by Low

Interest

• Prudent actuarial assumptions

with low deviation

• On-going review of assumptions

and adjustments

Prudent

Assumptions

• NBEV improved due to sound

product mix

• Solvency improved steadily

Positive

Impact of

C-ROSS

• Residual margin release sustains

high growth

• Large residual margin supports

sustainable future profit

Sustainable

Future Profit

Th

e M

ain

4

Co

nce

rns

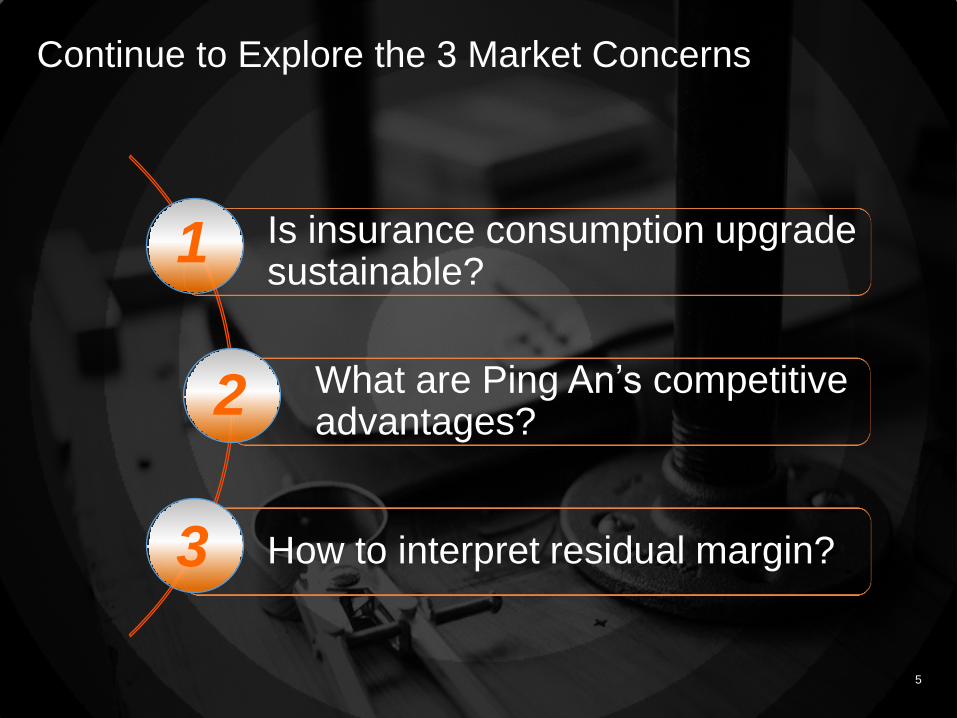

Continue to Explore the 3 Market Concerns

Is insurance consumption upgrade sustainable?

What are Ping An’s competitive advantages?

How to interpret residual margin?

1

2

3

5

Contents

1. Is insurance consumption upgrade sustainable?

2. What are Ping An’s competitive advantages?

3. How to interpret residual margin?

6

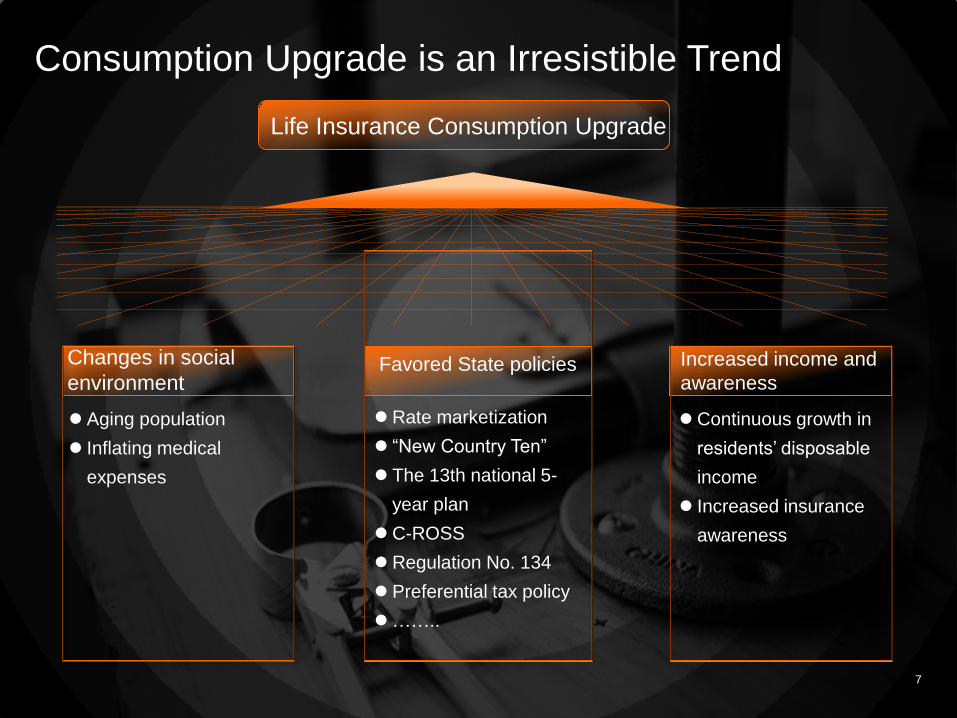

Changes in social

environment Favored State policies Increased income and

awareness

Aging population

Inflating medical

expenses

Continuous growth in

residents’ disposable

income

Increased insurance

awareness

Consumption Upgrade is an Irresistible Trend

Rate marketization

“New Country Ten”

The 13th national 5-

year plan

C-ROSS

Regulation No. 134

Preferential tax policy

……..

Life Insurance Consumption Upgrade

7

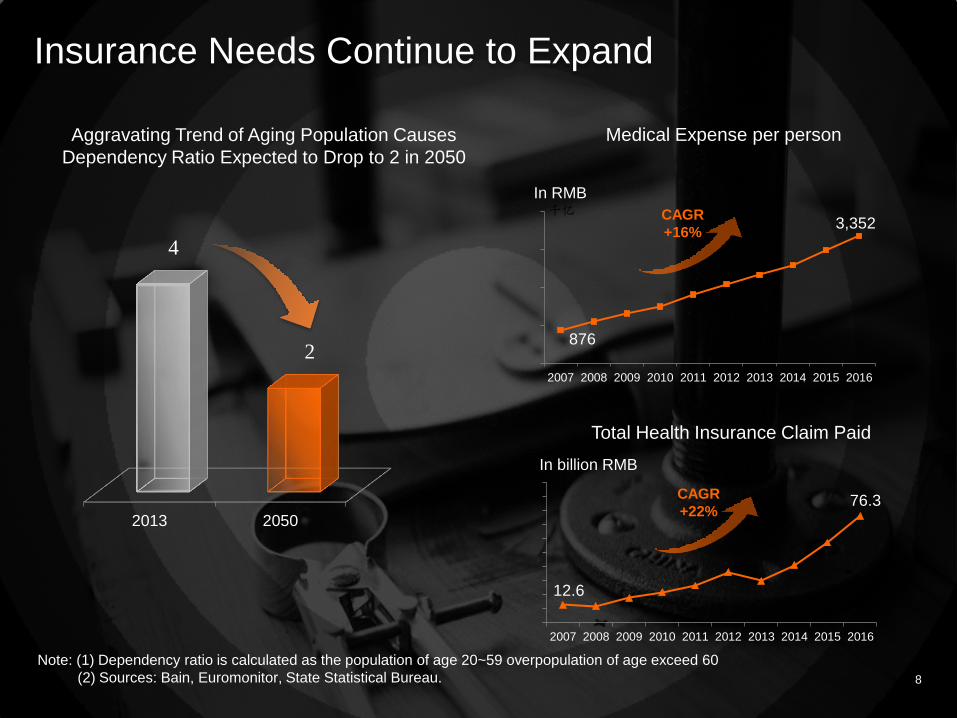

Insurance Needs Continue to Expand

Note: (1) Dependency ratio is calculated as the population of age 20~59 overpopulation of age exceed 60

(2) Sources: Bain, Euromonitor, State Statistical Bureau.

Aggravating Trend of Aging Population Causes

Dependency Ratio Expected to Drop to 2 in 2050

8

876

3,352

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

千亿

Medical Expense per person

12.6

76.3

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

亿

Total Health Insurance Claim Paid

2013 2050

4

2

In RMB

In billion RMB

CAGR

+16%

CAGR

+22%

2012 2013 2014 2015 2016

1,015.7 1,101.0 1,303.1

1,628.8

2,223.5

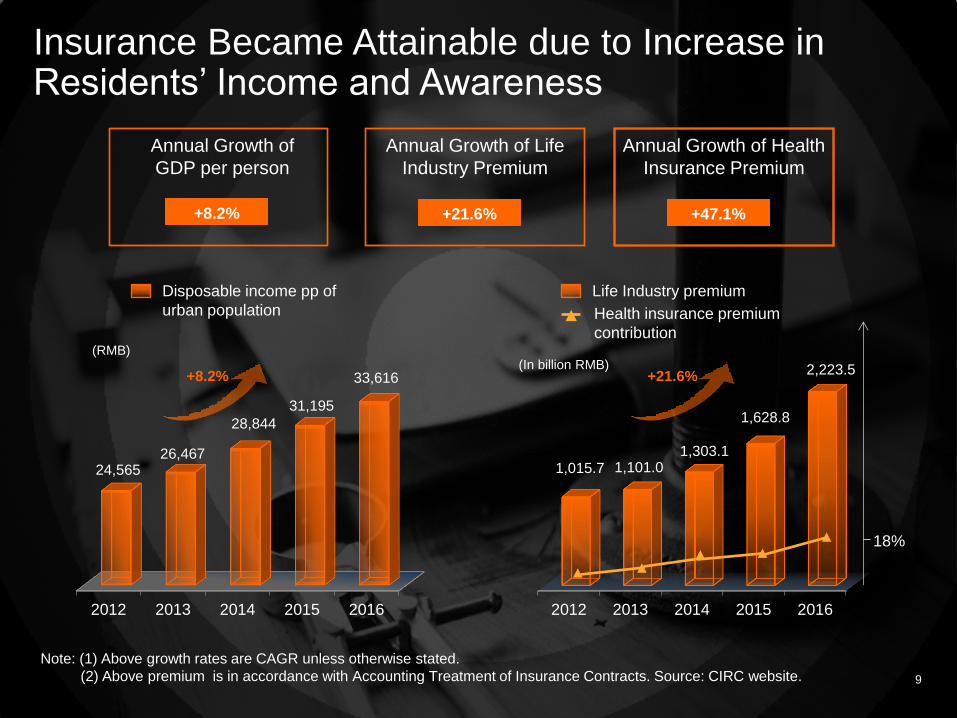

Insurance Became Attainable due to Increase in Residents’ Income and Awareness

2012 2013 2014 2015 2016

24,565 26,467

28,844

31,195

33,616

Note: (1) Above growth rates are CAGR unless otherwise stated.

(2) Above premium is in accordance with Accounting Treatment of Insurance Contracts. Source: CIRC website.

+8.2%

Annual Growth of

GDP per person

+21.6%

Annual Growth of Life

Industry Premium

+47.1%

Annual Growth of Health

Insurance Premium

(RMB)

9

+8.2% +21.6% Life Industry premium Disposable income pp of

urban population Health insurance premium

contribution

18%

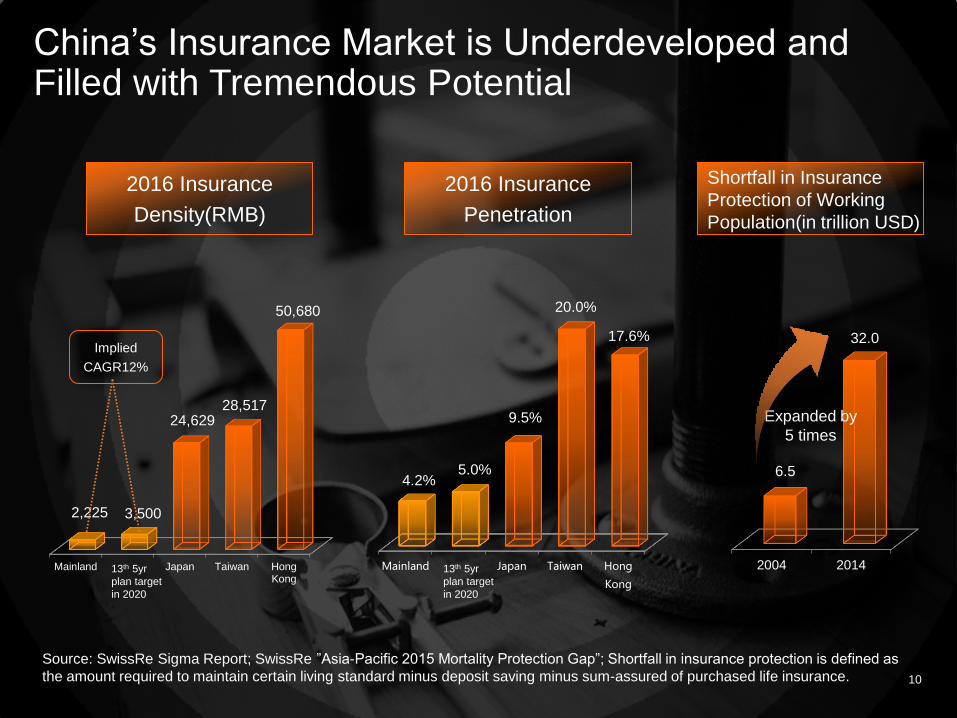

(In billion RMB)

Shortfall in Insurance

Protection of Working

Population(in trillion USD)

China’s Insurance Market is Underdeveloped and Filled with Tremendous Potential

2004 2014

Source: SwissRe Sigma Report; SwissRe ”Asia-Pacific 2015 Mortality Protection Gap”; Shortfall in insurance protection is defined as

the amount required to maintain certain living standard minus deposit saving minus sum-assured of purchased life insurance.

Mainland Japan Taiwan HongKong

2,225 3,500

24,629 28,517

50,680

Mainland Japan Taiwan Hong

Kong

4.2% 5.0%

9.5%

20.0%

17.6%

6.5

32.0

Expanded by

5 times

10

2016 Insurance

Penetration

2016 Insurance

Density(RMB)

Implied

CAGR12%

13th 5yr

plan target

in 2020

13th 5yr

plan target

in 2020

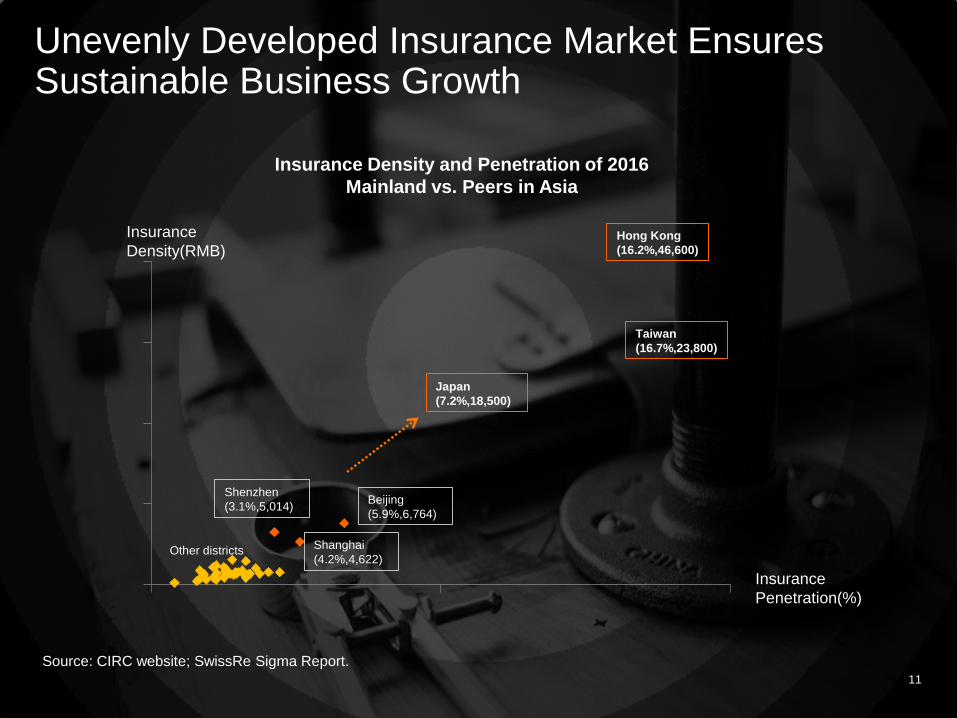

Unevenly Developed Insurance Market Ensures Sustainable Business Growth

Hong Kong

(16.2%,46,600)

Taiwan

(16.7%,23,800)

Source: CIRC website; SwissRe Sigma Report.

Insurance Density and Penetration of 2016

Mainland vs. Peers in Asia

Insurance

Density(RMB)

Japan

(7.2%,18,500)

Insurance

Penetration(%)

Beijing

(5.9%,6,764)

Shenzhen

(3.1%,5,014)

Shanghai

(4.2%,4,622)

11

Other districts

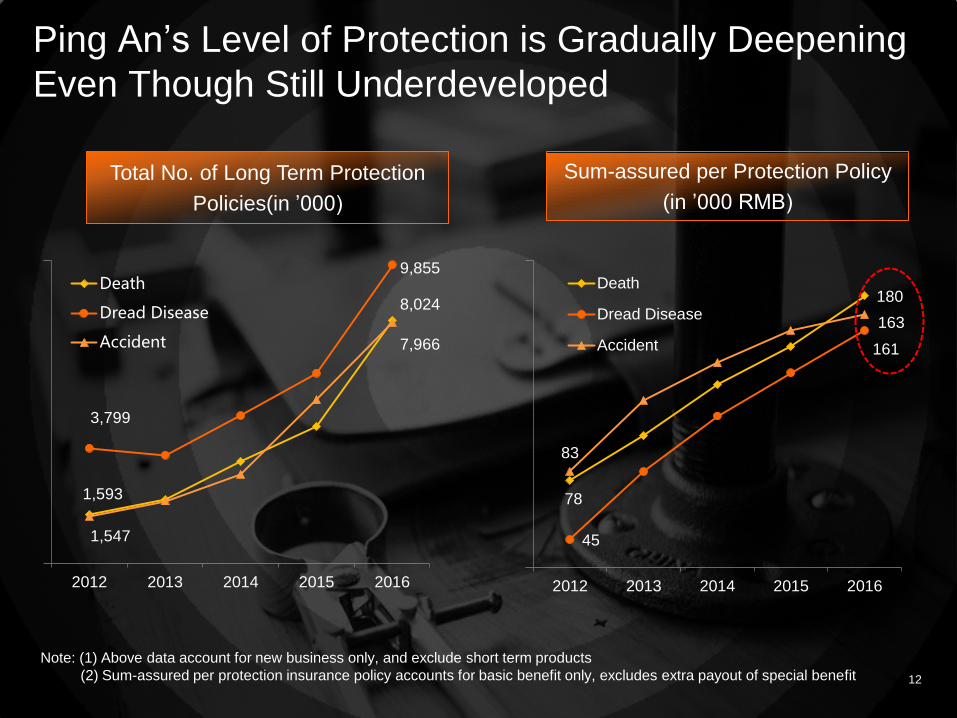

Total No. of Long Term Protection

Policies(in ’000)

Note: (1) Above data account for new business only, and exclude short term products

(2) Sum-assured per protection insurance policy accounts for basic benefit only, excludes extra payout of special benefit

78

180

45

161

83

163

2012 2013 2014 2015 2016

Death

Dread Disease

Accident

Ping An’s Level of Protection is Gradually Deepening

Even Though Still Underdeveloped

12

Sum-assured per Protection Policy

(in ’000 RMB)

1,593

8,024

3,799

9,855

1,547

7,966

2012 2013 2014 2015 2016

Death

Dread Disease

Accident

13

Contents

1. Is insurance consumption upgrade sustainable?

2. What are Ping An’s competitive advantages?

3. How to interpret residual margin?

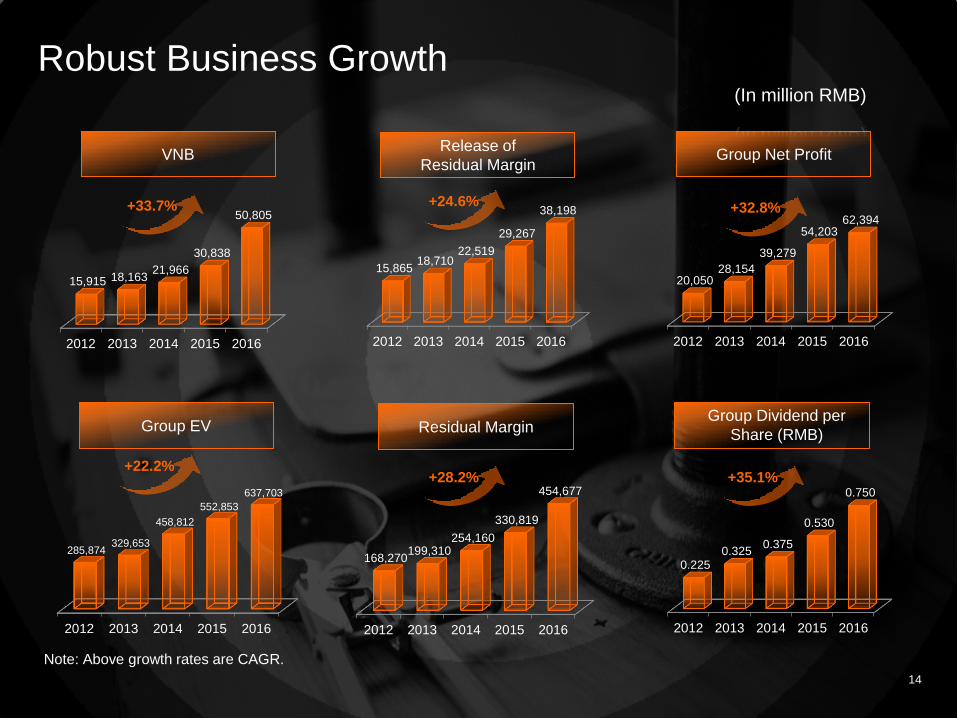

2012 2013 2014 2015 2016

285,874 329,653

458,812

552,853

637,703

Robust Business Growth

2012 2013 2014 2015 2016

168,270 199,310

254,160

330,819

454,677

2012 2013 2014 2015 2016

15,865 18,710

22,519

29,267

38,198

2012 2013 2014 2015 2016

20,050 28,154

39,279

54,203 62,394

2012 2013 2014 2015 2016

0.225 0.325

0.375

0.530

0.750

2012 2013 2014 2015 2016

15,915 18,163 21,966

30,838

50,805

14

VNB Group Net Profit

Group EV Residual Margin

+33.7%

+28.2% +22.2%

+32.8% +24.6%

+35.1%

(In million RMB)

Release of

Residual Margin

Group Dividend per

Share (RMB)

Note: Above growth rates are CAGR.

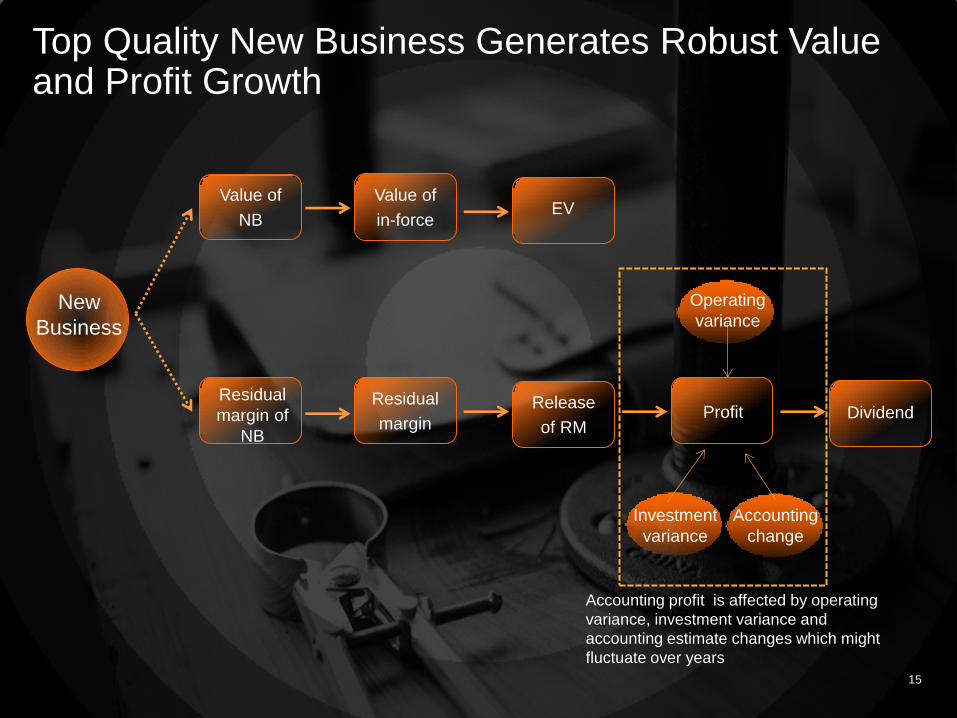

Top Quality New Business Generates Robust Value and Profit Growth

Value of

NB

Residual

margin

Accounting profit is affected by operating

variance, investment variance and

accounting estimate changes which might

fluctuate over years

Value of

in-force

Release

of RM

Operating

variance

Investment

variance

Accounting

change

15

New

Business

Residual

margin of

NB

EV

Profit Dividend

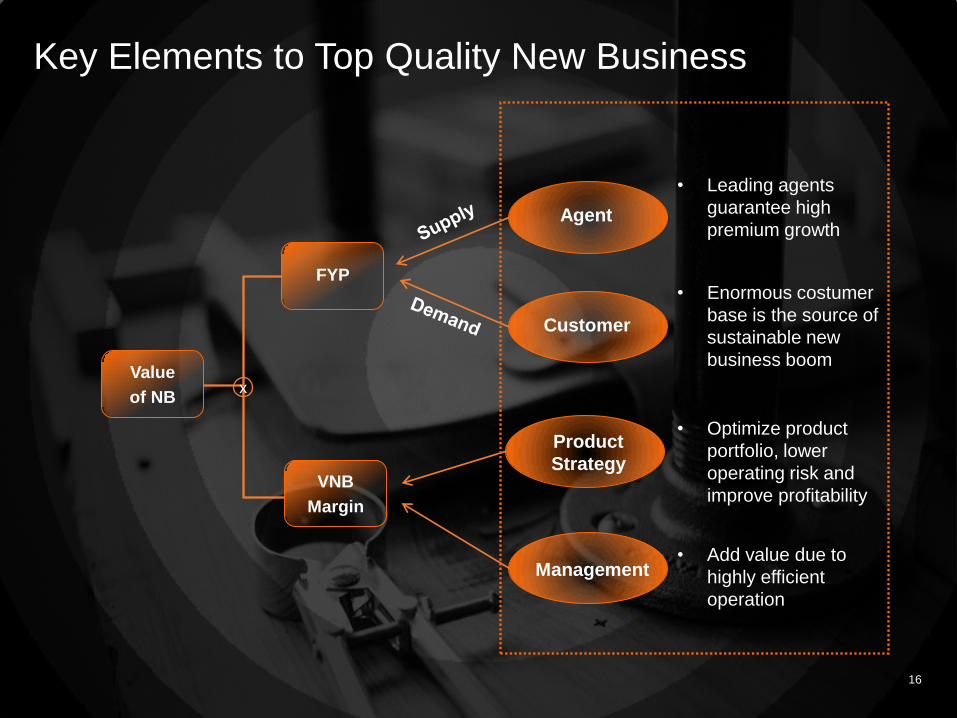

Key Elements to Top Quality New Business

Value

of NB

x

VNB

Margin

Agent

Customer

Product

Strategy

Management

• Leading agents

guarantee high

premium growth

• Optimize product

portfolio, lower

operating risk and

improve profitability

• Add value due to

highly efficient

operation

• Enormous costumer

base is the source of

sustainable new

business boom

16

FYP

Contents

1. Is insurance consumption upgrade sustainable?

2. What are Ping An’s competitive advantages?

2.1 Leading Agency Workforce

2.2 Enormous Group Customer Base

2.3 The Right Product Strategy

2.4 Excellent Management

3. How to interpret residual margin?

17

The Key Factors to Leading Agency Workforce

High

Standard

Strict

Appraisal

Integrated

Financial

Platform

“Tech+”

Boost

Productivity

• Requirement to retention

and promotion higher than

peers

• Strict dismissal policy

• Provide enormous

customer base

• Cross-selling increases

agents’ income which

attract new recruit and

enhance retention

• Over 120 million “Jin Guan

Jia” APP registered users

• Online training with no time

and space constraint

18

Agents Fully Equipped Through “Tech+”

Recruitment

Training Sale

Management

Retention

Tech+

Apply AI to analyze agents’

character, habit and

background to provide tailored-

made training and coaching

Current and previously

employed agents conduct sales

on “Jin Guan Jia” APP

Zhiniao and live training, with no time

and space constraint

338 thousand live sessions took place

during March to October Over 120 million “Jin Guan Jia”

APP registered users, world

most used insurance APP

Ad. forwarded 220 million times

on WeChat, resulted in 3.6

million sales

Big data applied to analyze

preference and behavioral

pattern of existing and potential

costumers to increase

successful sales

Online training improve agents’ ability

“Jin Guan Jia” APP + Integrated Finance

Model increase sales, agents’ income, and

retention rate

“Onsite and offsite” team

management model

Apply AI to optimize agents’

development, enhance performance

19

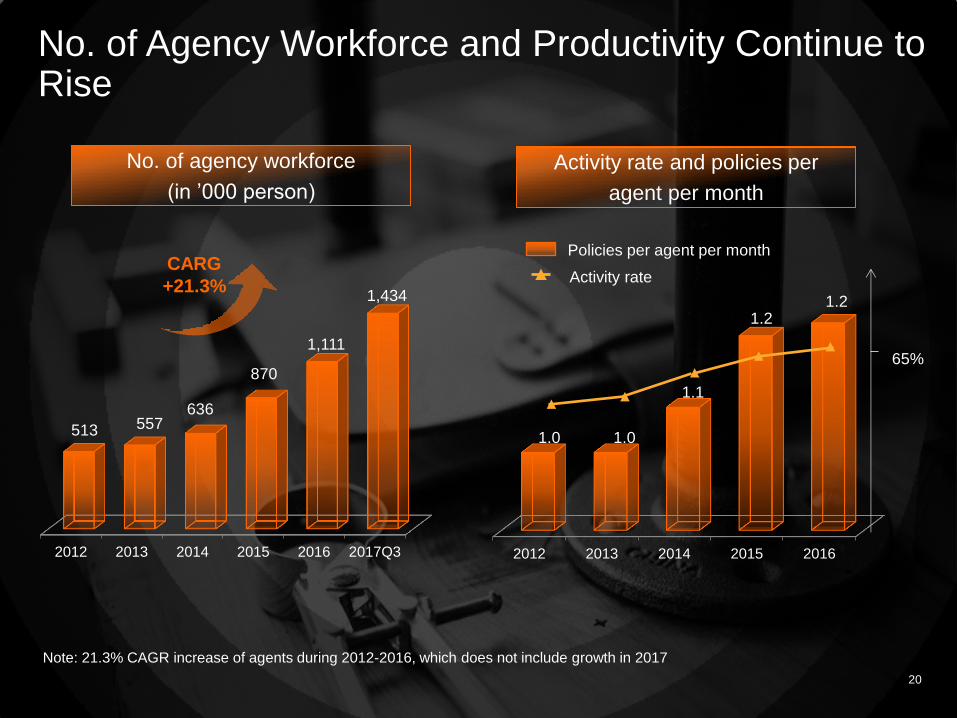

2012 2013 2014 2015 2016

1.0 1.0

1.1

1.2 1.2

No. of Agency Workforce and Productivity Continue to Rise

2012 2013 2014 2015 2016 2017Q3

513 557 636

870

1,111

1,434

Note: 21.3% CAGR increase of agents during 2012-2016, which does not include growth in 2017

20

CARG

+21.3%

Policies per agent per month

Activity rate

No. of agency workforce

(in ’000 person)

Activity rate and policies per

agent per month

65%

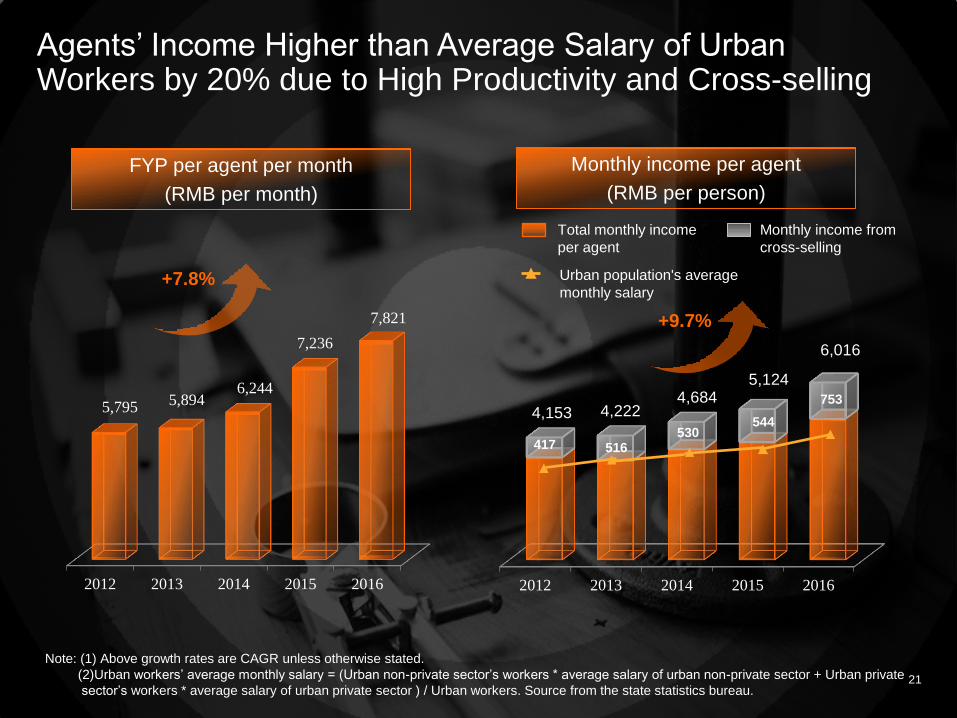

Agents’ Income Higher than Average Salary of Urban Workers by 20% due to High Productivity and Cross-selling

Note: (1) Above growth rates are CAGR unless otherwise stated.

(2)Urban workers’ average monthly salary = (Urban non-private sector’s workers * average salary of urban non-private sector + Urban private

sector’s workers * average salary of urban private sector ) / Urban workers. Source from the state statistics bureau.

2012 2013 2014 2015 2016

417 516 530

544

753 4,153 4,222

4,684 5,124

6,016

2012 2013 2014 2015 2016

5,795 5,894 6,244

7,236

7,821

21

FYP per agent per month

(RMB per month)

Monthly income per agent

(RMB per person)

+7.8%

+9.7%

Total monthly income

per agent

Urban population's average

monthly salary

Monthly income from

cross-selling

22

Contents

1. Is insurance consumption upgrade sustainable?

2. What are Ping An’s competitive advantages?

2.1 Leading Agency Workforce

2.2 Enormous Group Customer Base

2.3 The Right Product Strategy

2.4 Excellent Management

3. How to interpret residual margin?

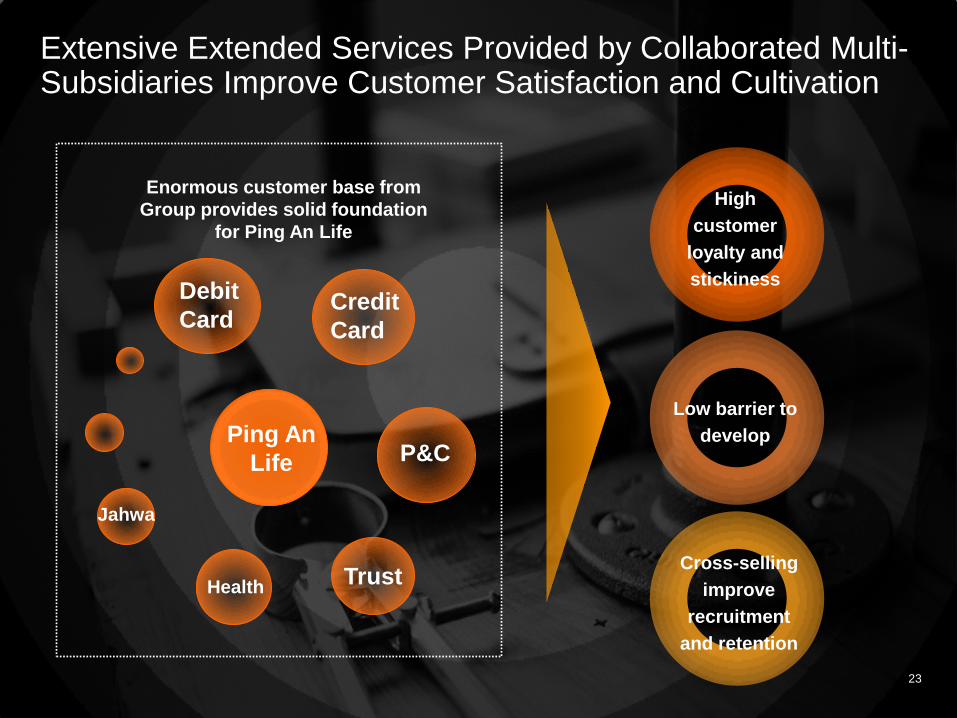

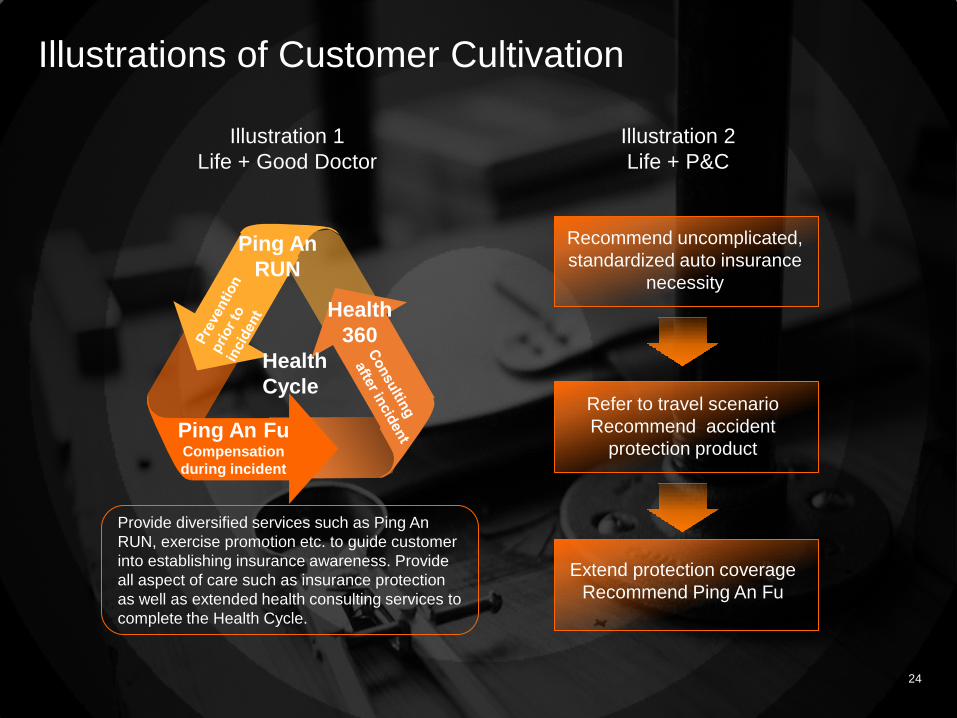

Extensive Extended Services Provided by Collaborated Multi-Subsidiaries Improve Customer Satisfaction and Cultivation

Health

Enormous customer base from

Group provides solid foundation

for Ping An Life

Jahwa

23

Debit

Card Credit

Card

Ping An

Life P&C

Trust

High

customer

loyalty and

stickiness

Low barrier to

develop

Cross-selling

improve

recruitment

and retention

Extend protection coverage

Recommend Ping An Fu

Refer to travel scenario

Recommend accident

protection product

Recommend uncomplicated,

standardized auto insurance

necessity

Illustrations of Customer Cultivation

Health

Cycle

Illustration 1

Life + Good Doctor

Illustration 2

Life + P&C

Provide diversified services such as Ping An

RUN, exercise promotion etc. to guide customer

into establishing insurance awareness. Provide

all aspect of care such as insurance protection

as well as extended health consulting services to

complete the Health Cycle.

24

Ping An

RUN

Ping An Fu Compensation

during incident

Health

360

25

Contents

1. Is insurance consumption upgrade sustainable?

2. What are Ping An’s competitive advantages?

2.1 Leading Agency Workforce

2.2 Enormous Group Customer Base

2.3 The Right Product Strategy

2.4 Excellent Management

3. How to interpret residual margin?

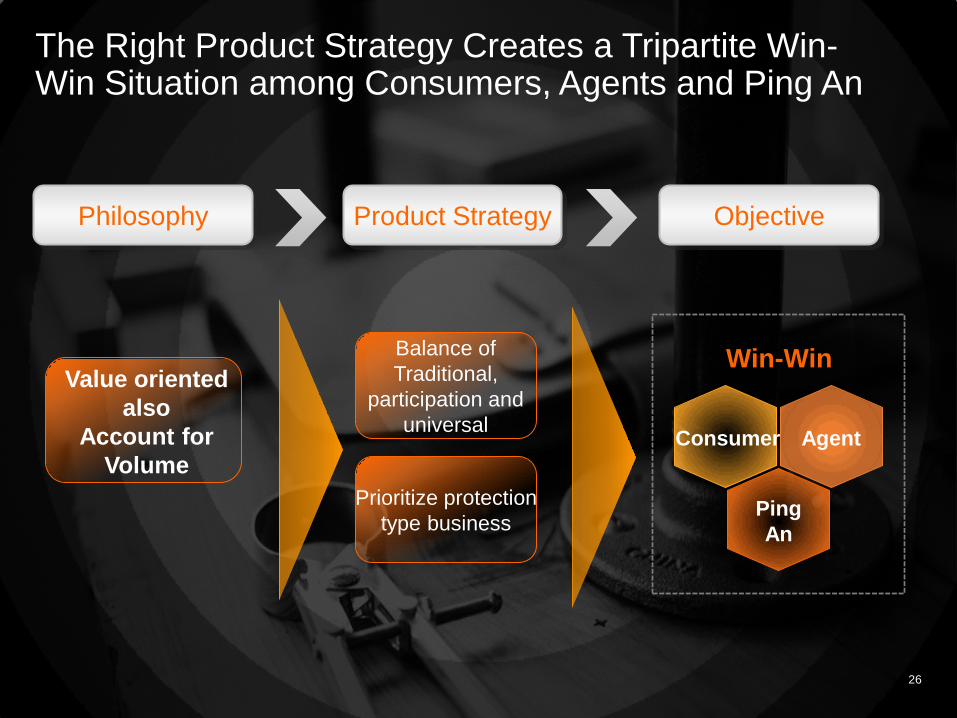

Balance of

Traditional,

participation and

universal

The Right Product Strategy Creates a Tripartite Win-Win Situation among Consumers, Agents and Ping An

Philosophy Product Strategy Objective

Win-Win

Consumer Agent

26

Ping

An

Value oriented

also

Account for

Volume

Prioritize protection

type business

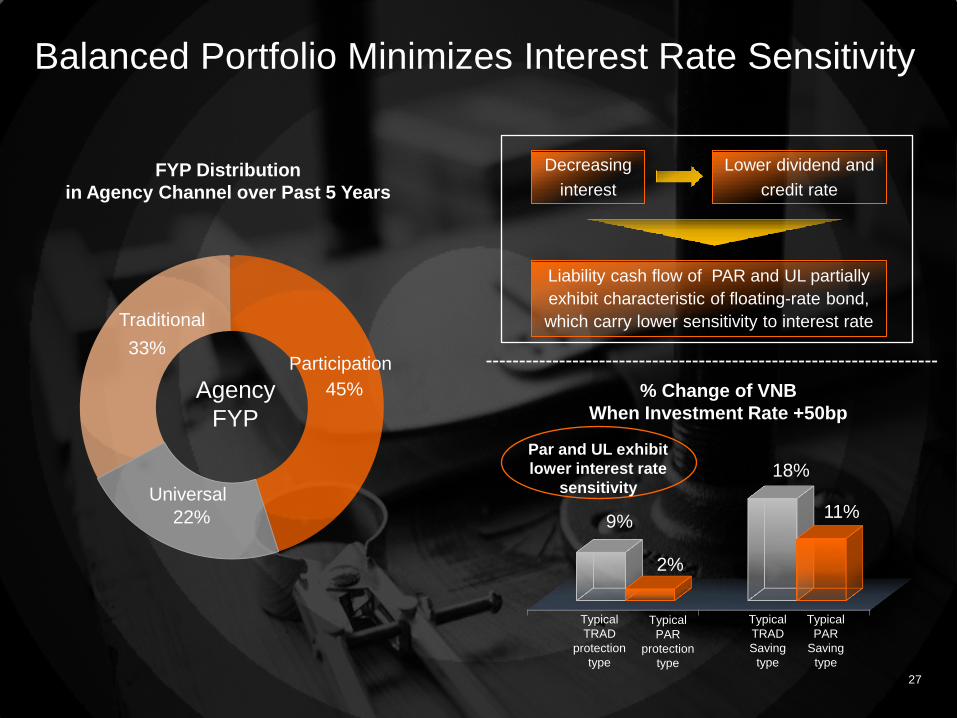

Balanced Portfolio Minimizes Interest Rate Sensitivity

FYP Distribution

in Agency Channel over Past 5 Years

% Change of VNB

When Investment Rate +50bp

Par and UL exhibit

lower interest rate

sensitivity

Decreasing

interest

Lower dividend and

credit rate

Liability cash flow of PAR and UL partially

exhibit characteristic of floating-rate bond,

which carry lower sensitivity to interest rate

27

Agency

FYP

Typical

TRAD

protection

type

Typical

PAR

protection

type

Typical

TRAD

Saving

type

Typical

PAR

Saving

type

33%

45%

22%

Traditional

Universal

Participation

9%

18%

2%

11%

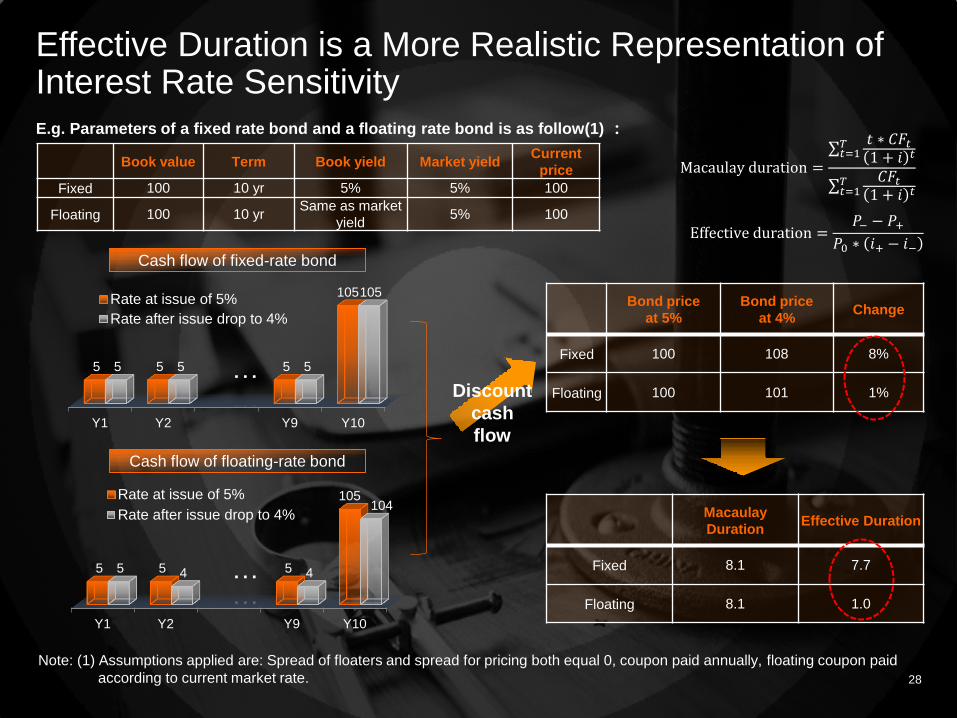

Effective Duration is a More Realistic Representation of Interest Rate Sensitivity

Book value Term Book yield Market yield Current

price

Fixed 100 10 yr 5% 5% 100

Floating 100 10 yr Same as market

yield 5% 100

… …

Bond price

at 5%

Bond price

at 4% Change

Fixed 100 108 8%

Floating 100 101 1%

E.g. Parameters of a fixed rate bond and a floating rate bond is as follow(1) :

… …

Macaulay

Duration Effective Duration

Fixed 8.1 7.7

Floating 8.1 1.0

Note: (1) Assumptions applied are: Spread of floaters and spread for pricing both equal 0, coupon paid annually, floating coupon paid

according to current market rate. 28

Discount

cash

flow

Macaulay duration =

𝑡 ∗ 𝐶𝐹𝑡1 + 𝑖 𝑡

𝑇𝑡=1

𝐶𝐹𝑡1 + 𝑖 𝑡

𝑇𝑡=1

Effective duration =𝑃− − 𝑃+

𝑃0 ∗ 𝑖+ − 𝑖−

Y1 Y2 Y9 Y10

5 5 5

105

5 5 5

105 Rate at issue of 5%

Rate after issue drop to 4%

Cash flow of fixed-rate bond

Y1 Y2 Y9 Y10

5 5 5

105

5 4 4

104 Rate at issue of 5%

Rate after issue drop to 4%

Cash flow of floating-rate bond

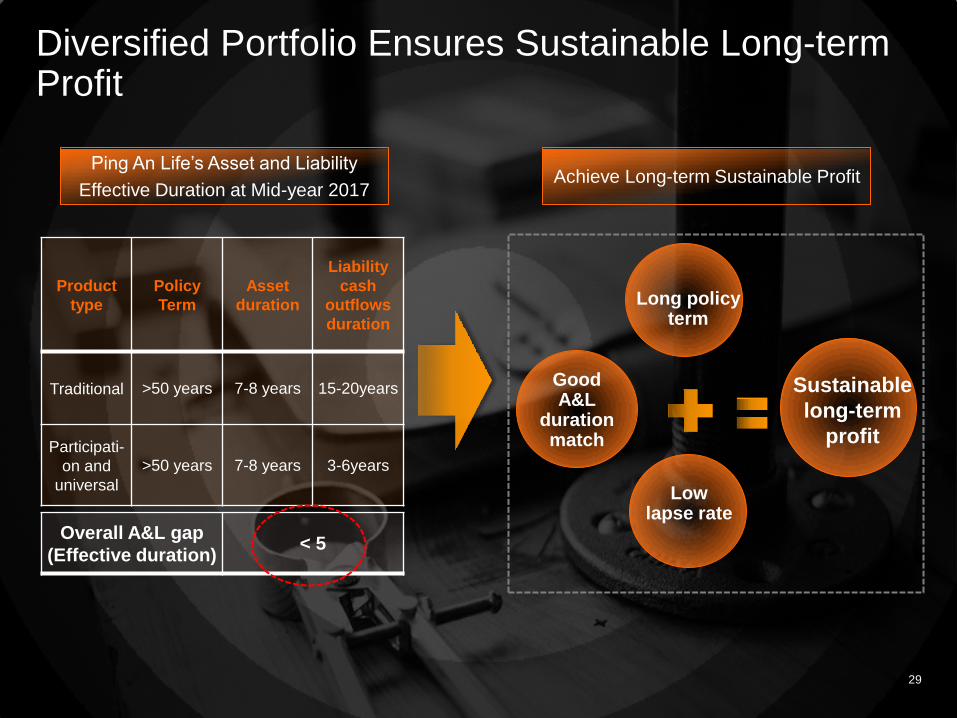

Diversified Portfolio Ensures Sustainable Long-term Profit

Product

type

Policy

Term

Asset

duration

Liability

cash

outflows

duration

Traditional >50 years 7-8 years 15-20years

Participati-

on and

universal

>50 years 7-8 years 3-6years

Ping An Life’s Asset and Liability

Effective Duration at Mid-year 2017

Overall A&L gap

(Effective duration) < 5

29

Long policy term

Good A&L

duration match

Low lapse rate

Sustainable

long-term

profit

Achieve Long-term Sustainable Profit

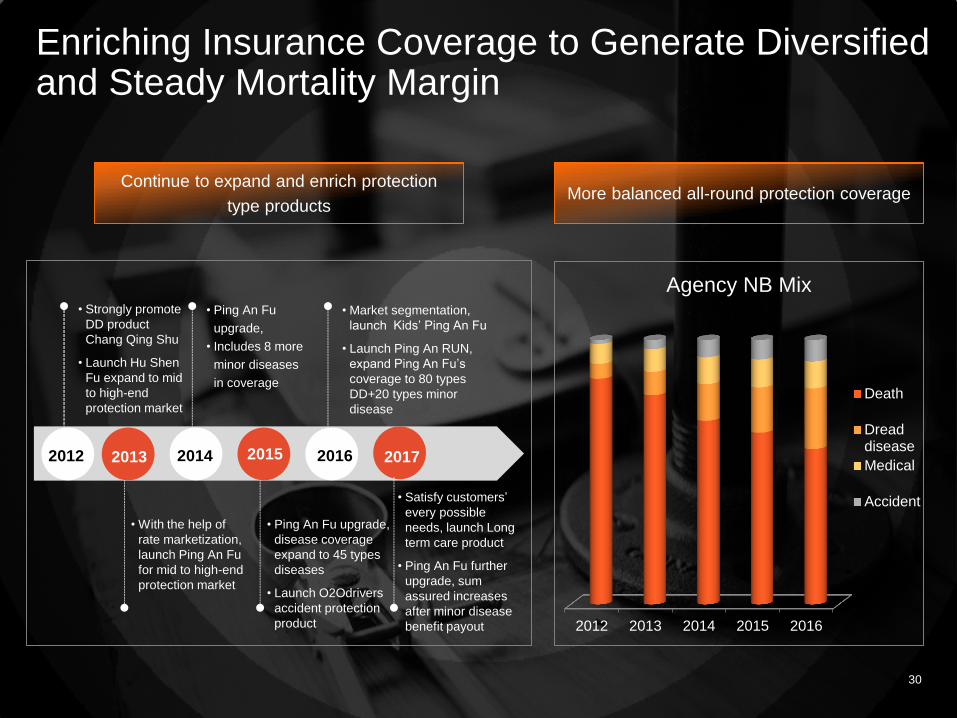

Enriching Insurance Coverage to Generate Diversified and Steady Mortality Margin

• With the help of

rate marketization,

launch Ping An Fu

for mid to high-end

protection market

• Ping An Fu

upgrade,

• Includes 8 more

minor diseases

in coverage

• Ping An Fu upgrade,

disease coverage

expand to 45 types

diseases

• Launch O2Odrivers

accident protection

product

• Market segmentation,

launch Kids’ Ping An Fu

• Launch Ping An RUN,

expand Ping An Fu’s

coverage to 80 types

DD+20 types minor

disease

2012 2013 2014 2015 2016

Continue to expand and enrich protection

type products

2012 2013 2014 2015 2016

Agency NB Mix

Death

Dreaddisease

Medical

Accident

More balanced all-round protection coverage

• Strongly promote

DD product

Chang Qing Shu

• Launch Hu Shen

Fu expand to mid

to high-end

protection market

2017

• Satisfy customers’

every possible

needs, launch Long

term care product

• Ping An Fu further

upgrade, sum

assured increases

after minor disease

benefit payout

30

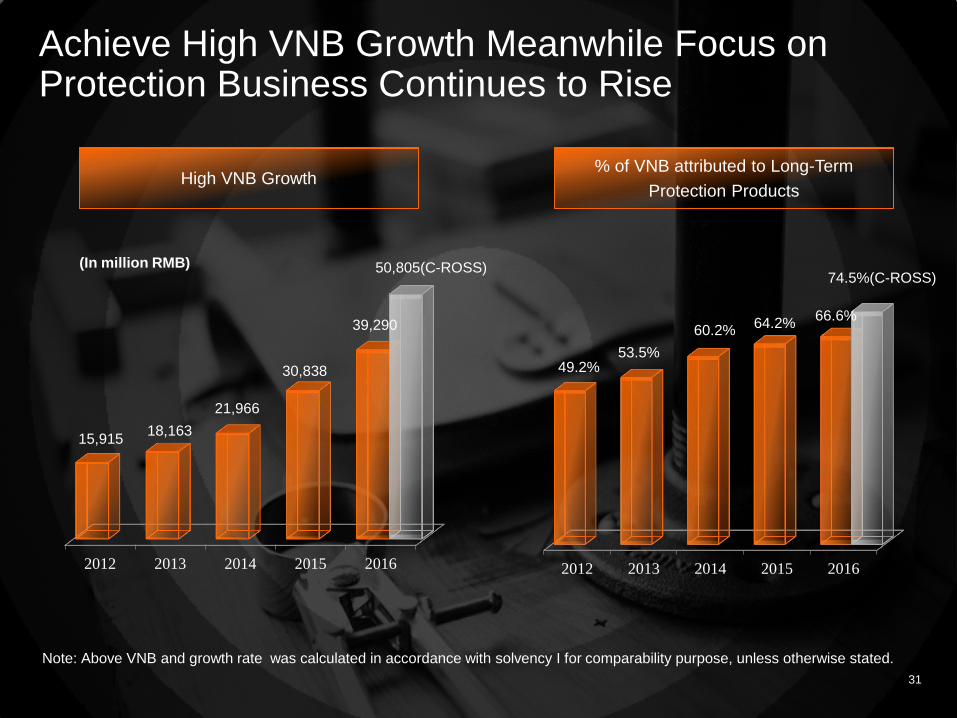

2012 2013 2014 2015 2016

15,915 18,163

21,966

30,838

39,290

Achieve High VNB Growth Meanwhile Focus on Protection Business Continues to Rise

2012 2013 2014 2015 2016

49.2% 53.5%

60.2% 64.2%

66.6%

Note: Above VNB and growth rate was calculated in accordance with solvency I for comparability purpose, unless otherwise stated.

50,805(C-ROSS)

74.5%(C-ROSS)

31

High VNB Growth % of VNB attributed to Long-Term

Protection Products

(In million RMB)

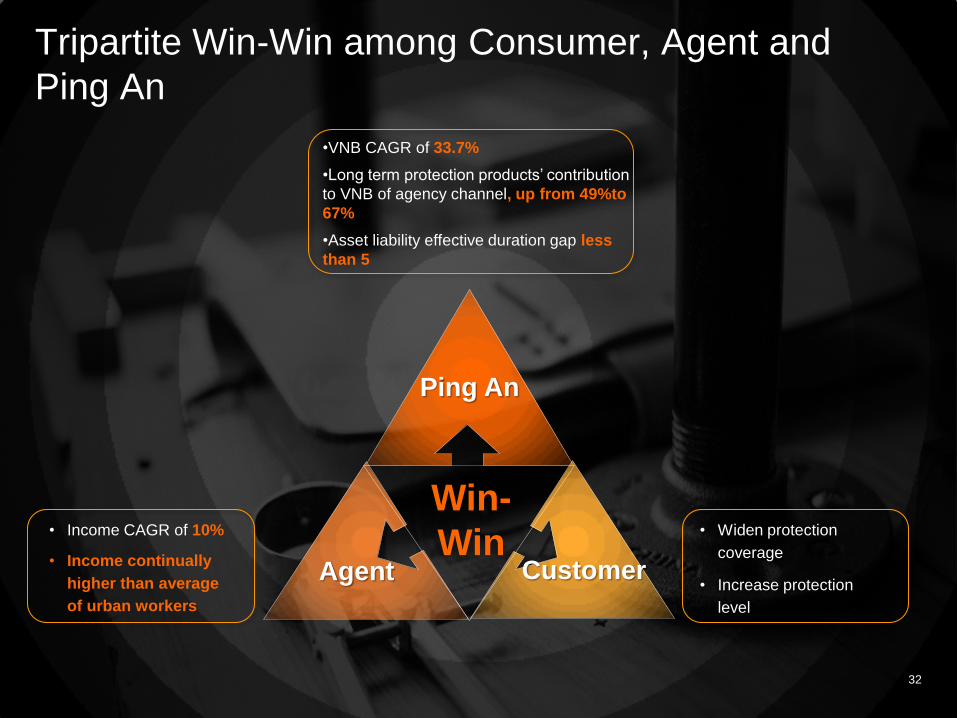

Win-

Win

Tripartite Win-Win among Consumer, Agent and

Ping An

32

•VNB CAGR of 33.7%

•Long term protection products’ contribution

to VNB of agency channel, up from 49%to

67%

•Asset liability effective duration gap less

than 5

• Income CAGR of 10%

• Income continually

higher than average

of urban workers

• Widen protection

coverage

• Increase protection

level

Ping An

Customer Agent

33

Contents

1. Is insurance consumption upgrade sustainable?

2. What are Ping An’s competitive advantages?

2.1 Leading Agency Workforce

2.2 Enormous Group Customer Base

2.3 The Right Product Strategy

2.4 Excellent Management

3. How to interpret residual margin?

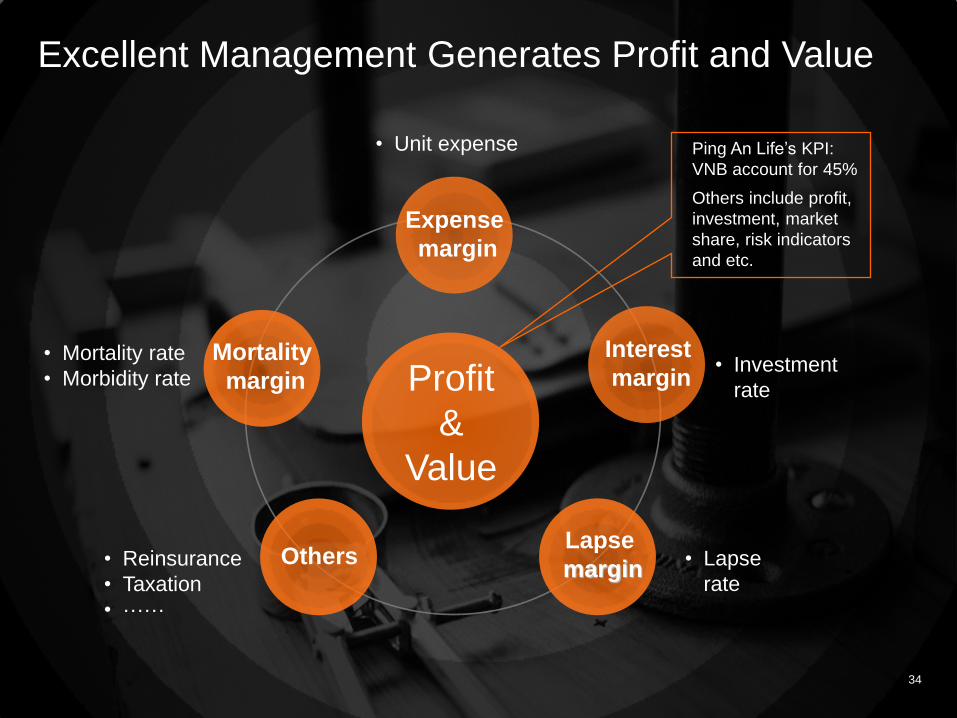

Excellent Management Generates Profit and Value

• Mortality rate

• Morbidity rate

• Unit expense

• Investment

rate

• Reinsurance

• Taxation

• ······

• Lapse

rate

34

Profit

&

Value

Mortality

margin

Others Lapse

margin

Expense

margin

Interest

margin

Ping An Life’s KPI:

VNB account for 45%

Others include profit,

investment, market

share, risk indicators

and etc.

Prior to

Policy

Issuance

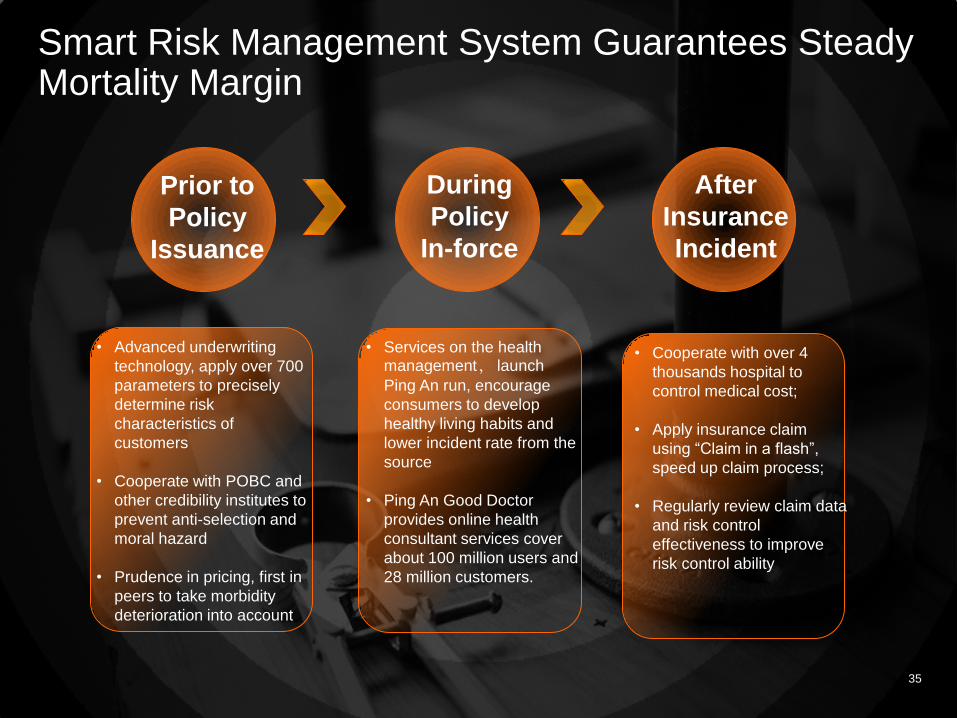

Smart Risk Management System Guarantees Steady Mortality Margin

During

Policy

In-force

After

Insurance

Incident

• Advanced underwriting

technology, apply over 700

parameters to precisely

determine risk

characteristics of

customers

• Cooperate with POBC and

other credibility institutes to

prevent anti-selection and

moral hazard

• Prudence in pricing, first in

peers to take morbidity

deterioration into account

• Services on the health management, launch

Ping An run, encourage

consumers to develop

healthy living habits and

lower incident rate from the

source

• Ping An Good Doctor

provides online health

consultant services cover

about 100 million users and

28 million customers.

35

• Cooperate with over 4

thousands hospital to

control medical cost;

• Apply insurance claim

using “Claim in a flash”,

speed up claim process;

• Regularly review claim data

and risk control

effectiveness to improve

risk control ability

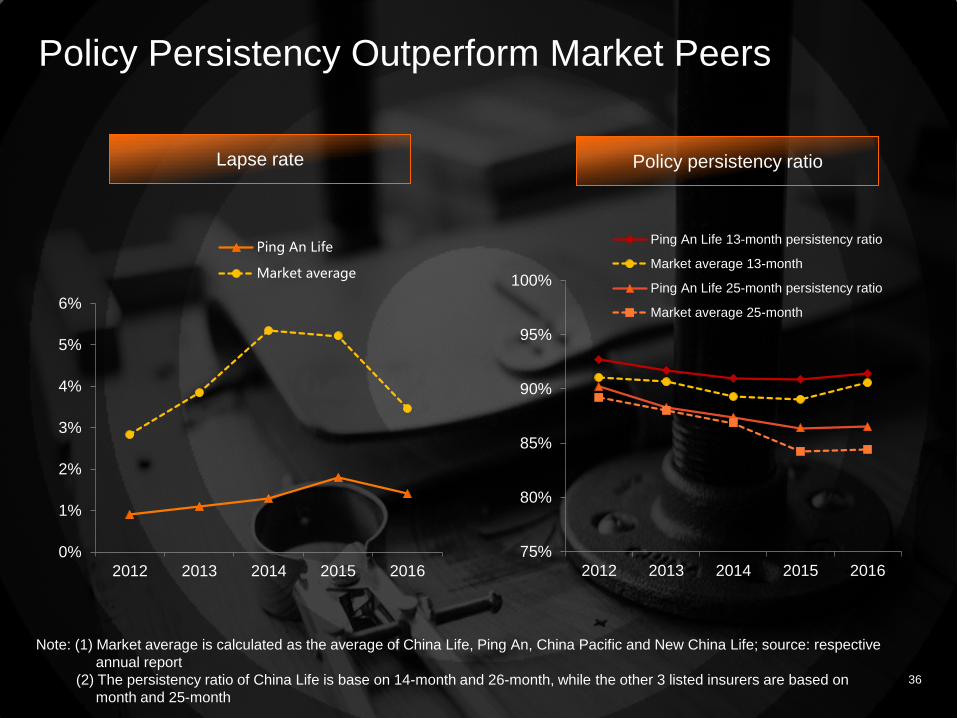

0%

1%

2%

3%

4%

5%

6%

2012 2013 2014 2015 2016

Ping An Life

Market average

Policy Persistency Outperform Market Peers

75%

80%

85%

90%

95%

100%

2012 2013 2014 2015 2016

Ping An Life 13-month persistency ratio

Market average 13-month

Ping An Life 25-month persistency ratio

Market average 25-month

Policy persistency ratio Lapse rate

Note: (1) Market average is calculated as the average of China Life, Ping An, China Pacific and New China Life; source: respective

annual report

(2) The persistency ratio of China Life is base on 14-month and 26-month, while the other 3 listed insurers are based on

month and 25-month

36

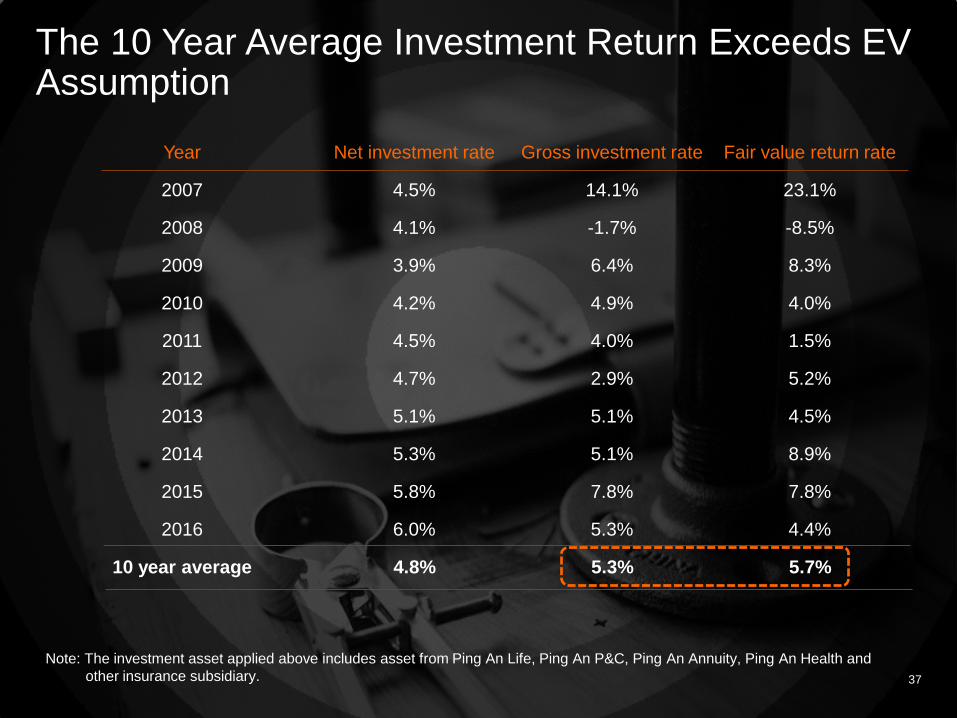

The 10 Year Average Investment Return Exceeds EV Assumption

Note: The investment asset applied above includes asset from Ping An Life, Ping An P&C, Ping An Annuity, Ping An Health and

other insurance subsidiary.

37

Year Net investment rate Gross investment rate Fair value return rate

2007 4.5% 14.1% 23.1%

2008 4.1% -1.7% -8.5%

2009 3.9% 6.4% 8.3%

2010 4.2% 4.9% 4.0%

2011 4.5% 4.0% 1.5%

2012 4.7% 2.9% 5.2%

2013 5.1% 5.1% 4.5%

2014 5.3% 5.1% 8.9%

2015 5.8% 7.8% 7.8%

2016 6.0% 5.3% 4.4%

10 year average 4.8% 5.3% 5.7%

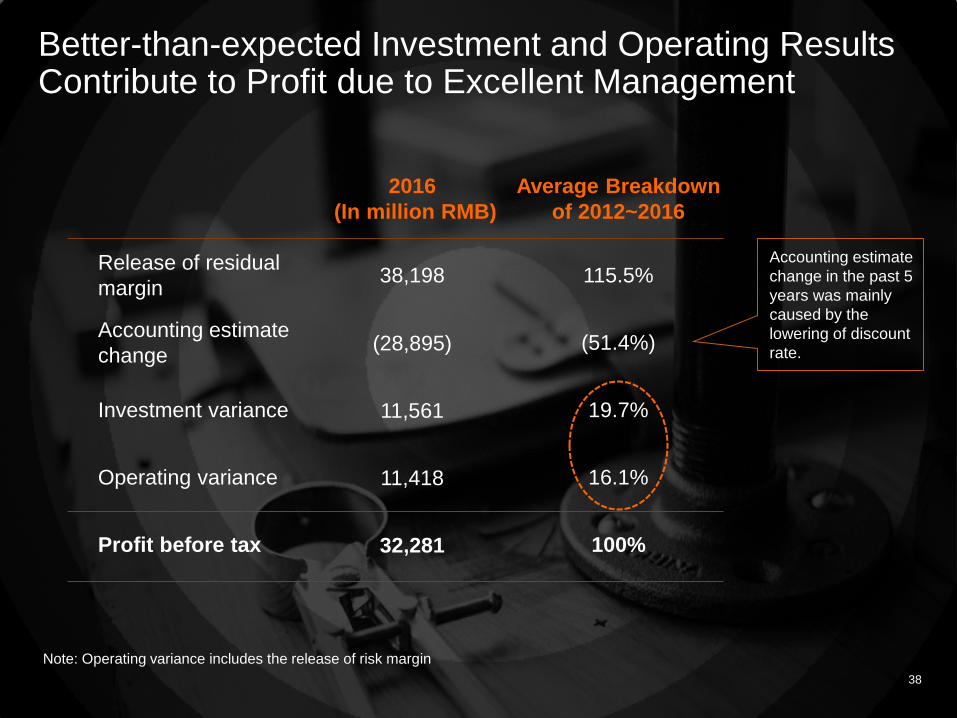

Better-than-expected Investment and Operating Results Contribute to Profit due to Excellent Management

Note: Operating variance includes the release of risk margin

38

2016

(In million RMB)

Average Breakdown

of 2012~2016

Release of residual

margin 38,198 115.5%

Accounting estimate

change (28,895) (51.4%)

Investment variance 11,561 19.7%

Operating variance 11,418 16.1%

Profit before tax 32,281 100%

Accounting estimate

change in the past 5

years was mainly

caused by the

lowering of discount

rate.

39

Contents

1. Is insurance consumption upgrade sustainable?

2. What are Ping An’s competitive advantages?

3. How to interpret residual margin?

Residual margin

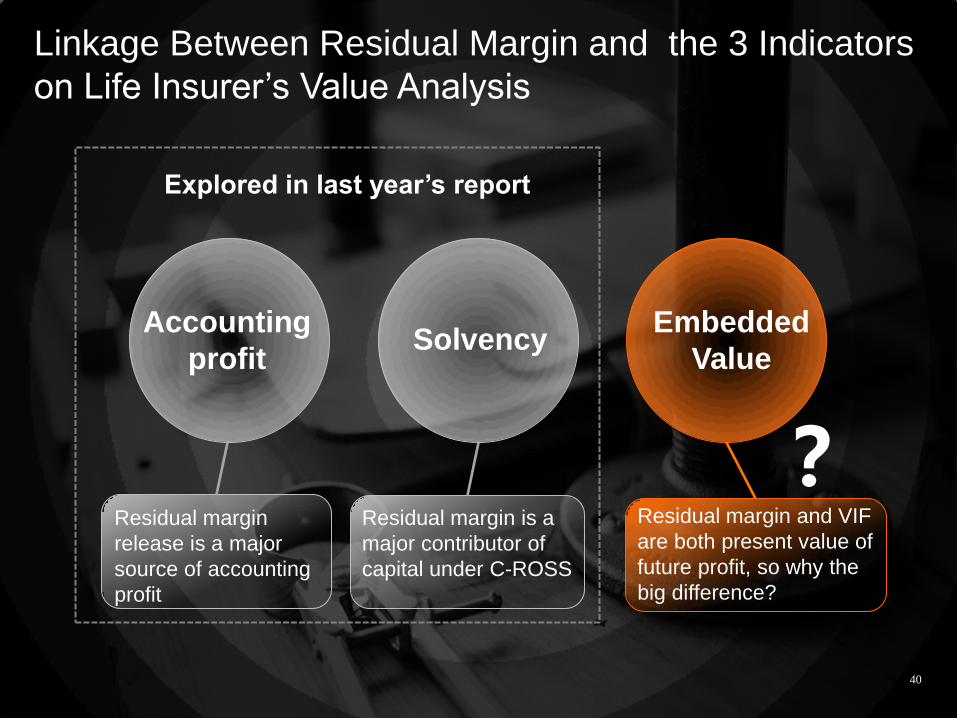

release is a major

source of accounting

profit

Residual margin is a

major contributor of

capital under C-ROSS

Linkage Between Residual Margin and the 3 Indicators

on Life Insurer’s Value Analysis

Explored in last year’s report

?

40

Accounting

profit Solvency

Embedded

Value

Residual margin and VIF

are both present value of

future profit, so why the

big difference?

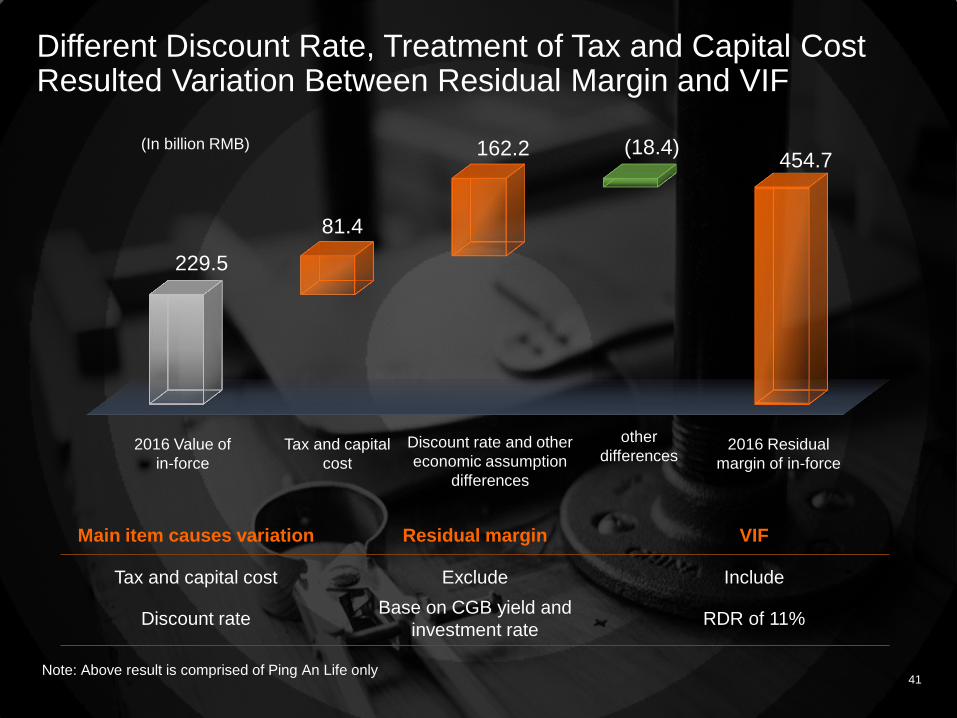

Different Discount Rate, Treatment of Tax and Capital Cost Resulted Variation Between Residual Margin and VIF

229.5

81.4

162.2 (18.4) 454.7

(In billion RMB)

Note: Above result is comprised of Ping An Life only

Main item causes variation Residual margin VIF

Tax and capital cost Exclude Include

Discount rate Base on CGB yield and

investment rate RDR of 11%

41

2016 Value of

in-force

Tax and capital

cost

Discount rate and other

economic assumption

differences

other

differences 2016 Residual

margin of in-force

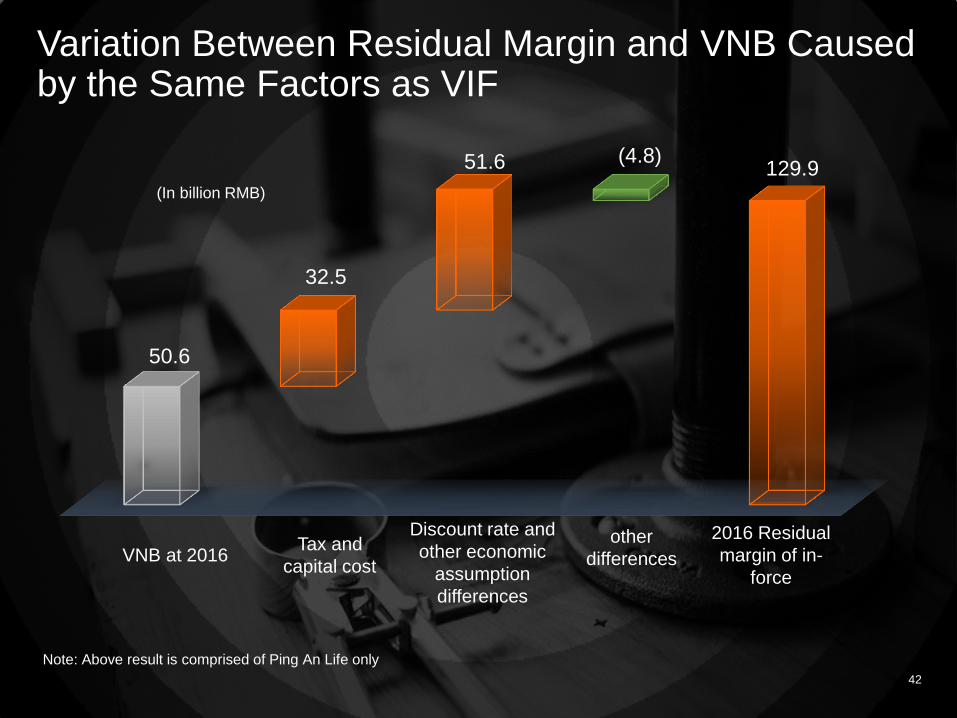

Variation Between Residual Margin and VNB Caused by the Same Factors as VIF

50.6

32.5

51.6 (4.8) 129.9

Note: Above result is comprised of Ping An Life only

42

(In billion RMB)

VNB at 2016 Tax and

capital cost

Discount rate and

other economic

assumption

differences

other

differences

2016 Residual

margin of in-

force

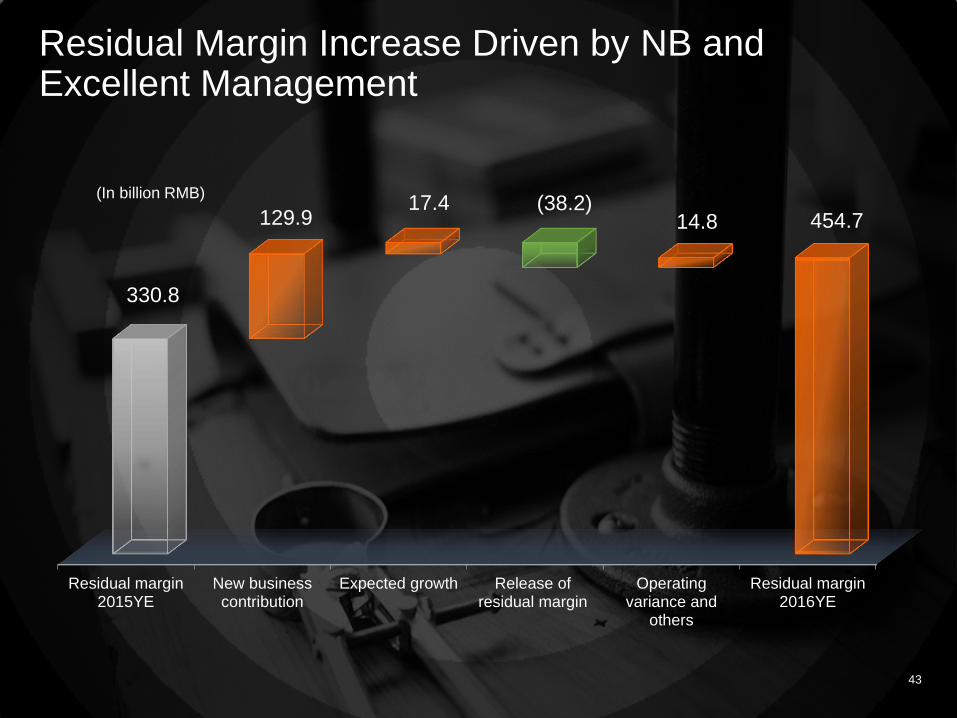

Residual Margin Increase Driven by NB and Excellent Management

Residual margin2015YE

New businesscontribution

Expected growth Release ofresidual margin

Operatingvariance and

others

Residual margin2016YE

330.8

129.9 17.4 (38.2)

14.8 454.7

43

(In billion RMB)

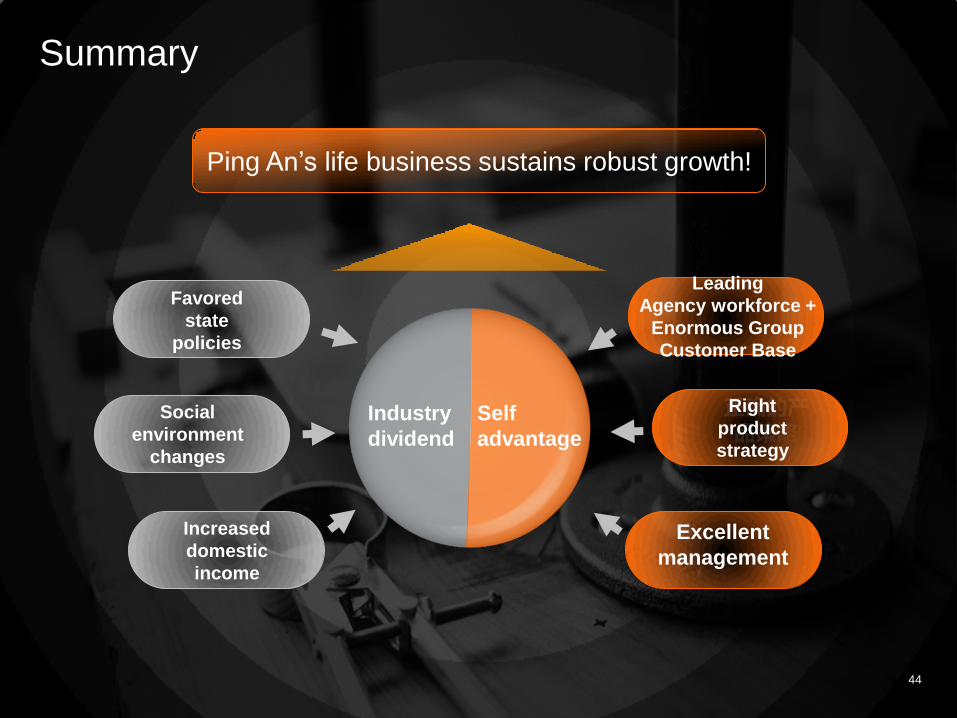

Summary

44

正确的产品策略

Ping An’s life business sustains robust growth!

Industry

dividend

Self

advantage

Favored

state

policies

Social

environment

changes

Increased

domestic

income

Leading

Agency workforce +

Enormous Group

Customer Base

Right

product

strategy

Excellent

management

Thank you!

Boost Value of Traditional Financial

Businesses with Technologies

Shenzhen Nov 2017

Yuansiong Lee Group Deputy CEO & Chief Insurance Business Officer

2

Important Notes

Cautionary Statements Regarding Forward-Looking Statement To the extent any statements made in this presentation containing information that is not historical

are essentially forward-looking. These forward-looking statements include but are not limited to projections, targets, estimates and business plans that the Company expects or anticipates will or may occur in the future. These forward-looking statements are subject to known and unknown risks

and uncertainties that may be general or specific. Certain statements, such as those including the words or phrases "potential", "estimates", "expects", "anticipates", "objective", "intends", "plans",

"believes", "will", "may", "should", and similar expressions or variations on such expressions may be considered forward-looking statements. Readers should be cautioned that a variety of factors, many of which may be beyond the Company's

control, affect the performance, operations, and results of the Company, and could cause actual results to differ materially from the expectations expressed in any of the Company's forward-looking

statements. These factors include but are not limited to exchange rate fluctuations, market shares, competition, environmental risks, changes in legal, financial and regulatory frameworks, international economic and financial market conditions, and other risks and factors beyond our control. These and

other factors should be considered carefully, and readers should not place undue reliance on the Company's forward-looking statements. In addition, the Company undertakes no obligation to publicly

update or revise any forward-looking statement that is contained in this presentation as a result of new information, future events, or otherwise. None of the Company, or any of its employees or affiliates is responsible for, or is making, any representation concerning the future performance of the

Company.

Increase

efficiency

Cut costs

Enhance risk

management

Improve

experience

Extensive

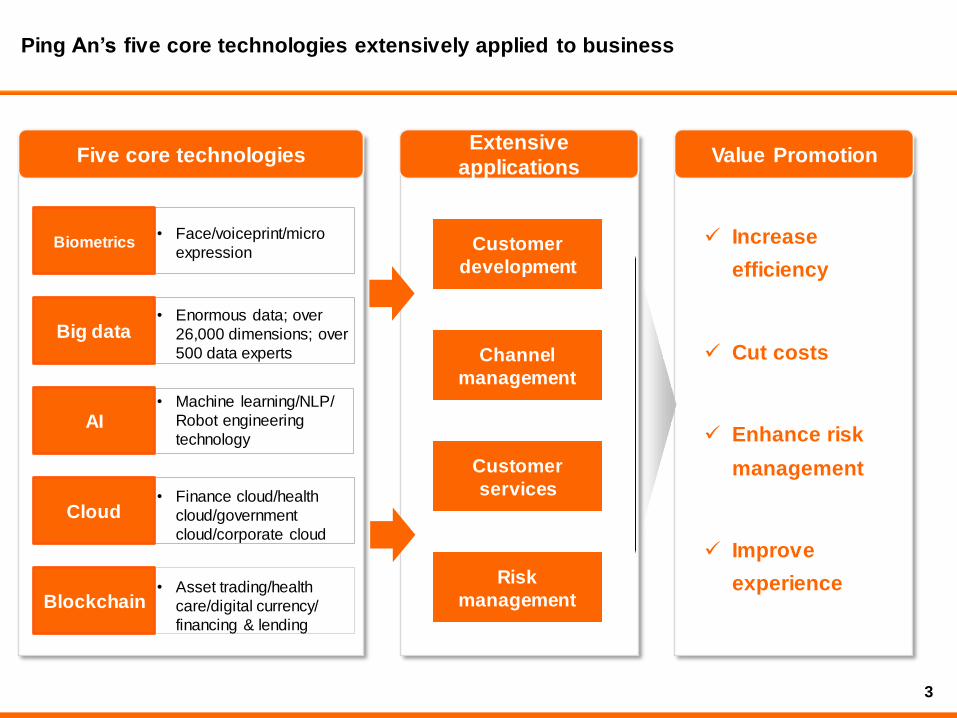

applications Five core technologies

Biometrics • Face/voiceprint/micro

expression

Big data • Enormous data; over

26,000 dimensions; over

500 data experts

AI • Machine learning/NLP/

Robot engineering

technology

Cloud • Finance cloud/health

cloud/government

cloud/corporate cloud

Customer

development

Channel

management

Customer

services

Risk

management Blockchain • Asset trading/health

care/digital currency/

financing & lending

Value Promotion

Ping An’s five core technologies extensively applied to business

3

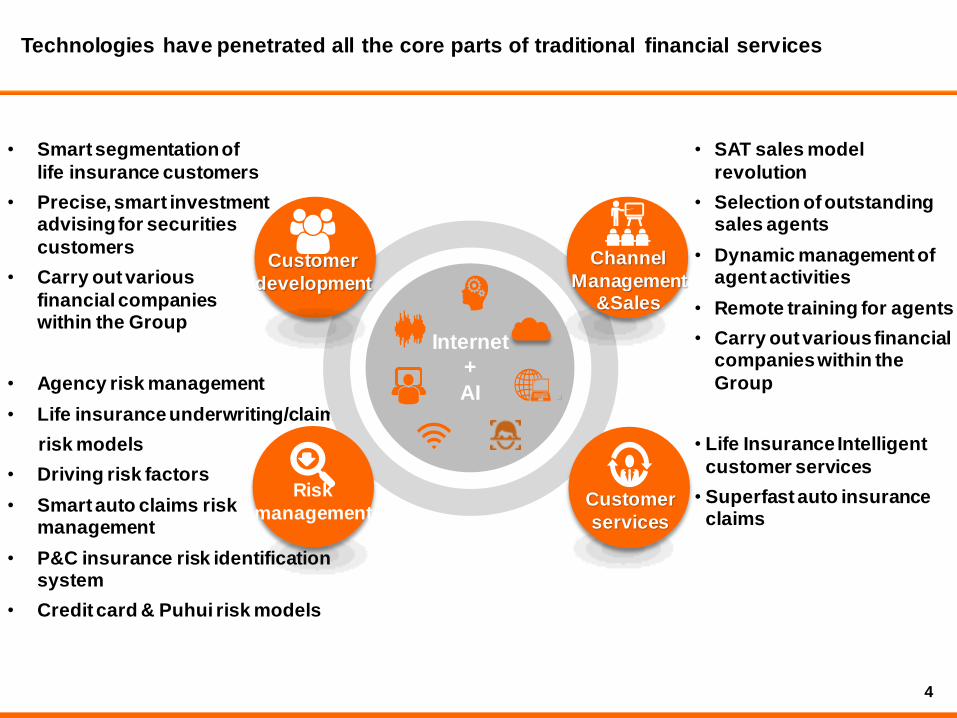

• Smart segmentation of

life insurance customers

• Precise, smart investment advising for securities

customers

• Carry out various

financial companies within the Group

• SAT sales model

revolution

• Selection of outstanding sales agents

• Dynamic management of agent activities

• Remote training for agents

• Carry out various financial companies within the

Group

• Life Insurance Intelligent

customer services

• Superfast auto insurance claims

• Agency risk management

• Life insurance underwriting/claim

risk models

• Driving risk factors

• Smart auto claims risk management

• P&C insurance risk identification system

• Credit card & Puhui risk models

Internet

+

AI

Customer

development

Technologies have penetrated all the core parts of traditional financial services

Risk

management

Channel

Management &Sales

Customer

services

4

5

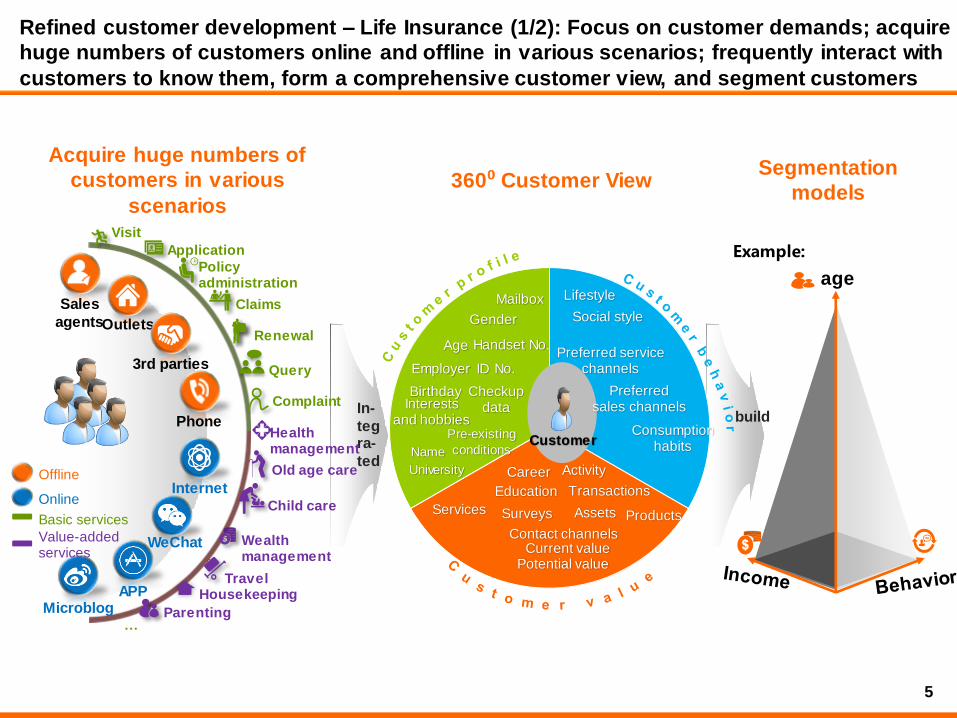

In-

tegra-

ted

360⁰ Customer View

消费习惯偏好

Segmentation

models

Acquire huge numbers of

customers in various

scenarios

build

age

Example:

Refined customer development – Life Insurance (1/2): Focus on customer demands; acquire

huge numbers of customers online and offline in various scenarios; frequently interact with

customers to know them, form a comprehensive customer view, and segment customers

Customer

Career

Education

Age

Gender

Handset No.

Mailbox

Employer

University

Interests and hobbies

Birthday

ID No.

Pre-existing

conditions

Checkup data

Name

Services

Activity

Surveys

Contact channels

Products Assets

Transactions

Current value Potential value

Lifestyle

Social style

Preferred sales channels

Preferred service channels

Consumption habits

Visit

Application

Policy administration

Claims

Renewal

Query

Complaint

Health management

Old age care

Child care

Wealth management

Travel

Parenting

Housekeeping

…

Sales

agents Outlets

3rd parties

Phone

Internet

APP

Microblog

Basic services

Offline

Online

Value-added services

6

Services (300+)

Opportunities (full policy

cycle)

Products (600+)

Channels (online+offline)

Smart generation of

products/services/

channels/opportunities

12-month lead

conversion rate

>20%

Note: 12-month lead conversion rate = converted leads provided in past 12 months/converted or still useful leads

Proportion of

repeat buyers

67%

Differential customer

development

Directly contact

customers

Send leads to

sales agents

Products/s

ervices

meeting

customer

demands

Effects

Refined customer development - Life Insurance (2/2): Segment customers on the basis of

the customer view; generate products, services, channels, and contact opportunities

smartly; directly contact customers or send leads to sales agents

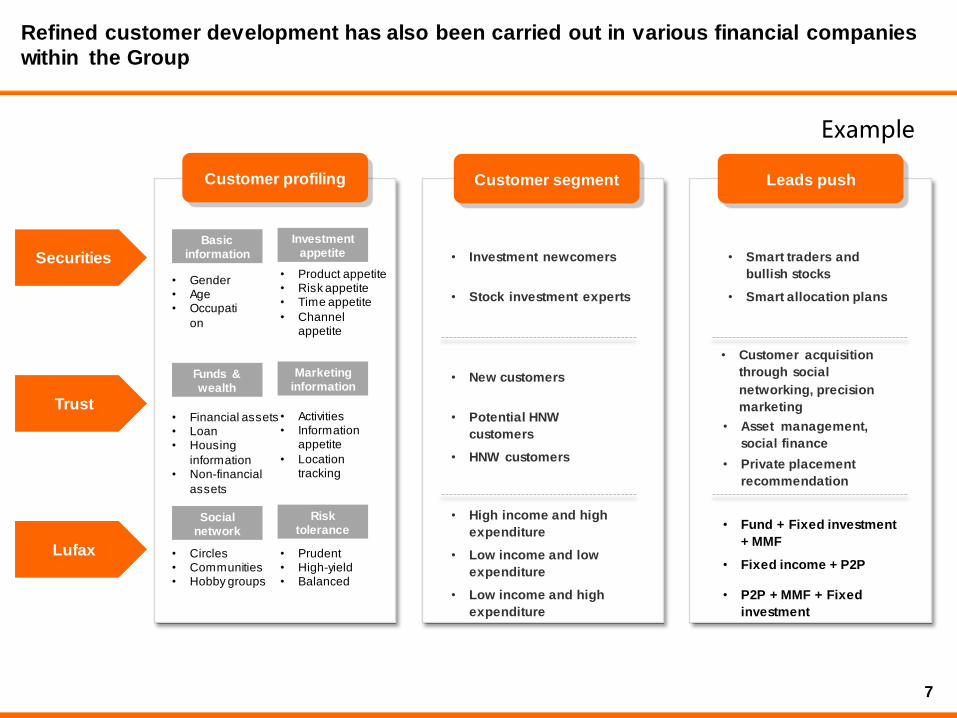

Securities

Trust

Lufax

Customer profiling Customer segment Leads push

• New customers

• HNW customers

• Potential HNW

customers

• High income and high

expenditure

• Low income and high

expenditure

• Low income and low

expenditure

• Fund + Fixed investment

+ MMF

• P2P + MMF + Fixed

investment

• Fixed income + P2P

• Customer acquisition

through social

networking, precision

marketing

• Private placement

recommendation

• Asset management,

social finance

• Investment newcomers

• Stock investment experts

• Smart traders and

bullish stocks

• Smart allocation plans

Basic information

Investment appetite

Funds & wealth

Marketing information

Social network

Risk tolerance

Refined customer development has also been carried out in various financial companies

within the Group

• Gender • Age • Occupati

on

• Prudent • High-yield • Balanced

• Financial assets • Loan • Housing

information • Non-financial

assets

• Circles • Communities • Hobby groups

• Activities • Information

appetite

• Location tracking

• Product appetite • Risk appetite • Time appetite

• Channel appetite

7

Example

8

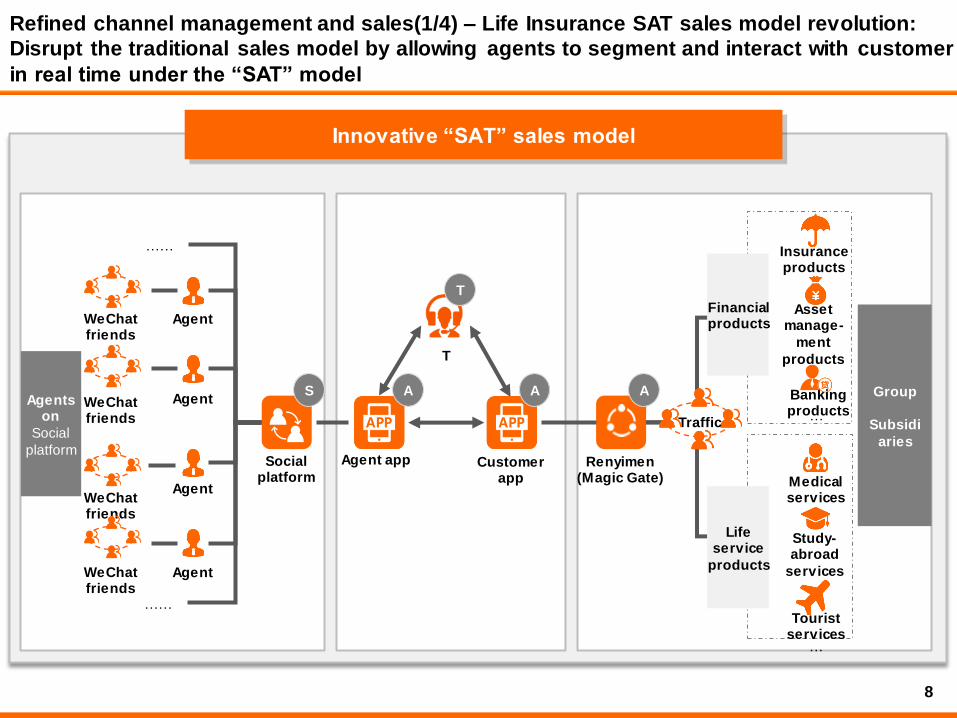

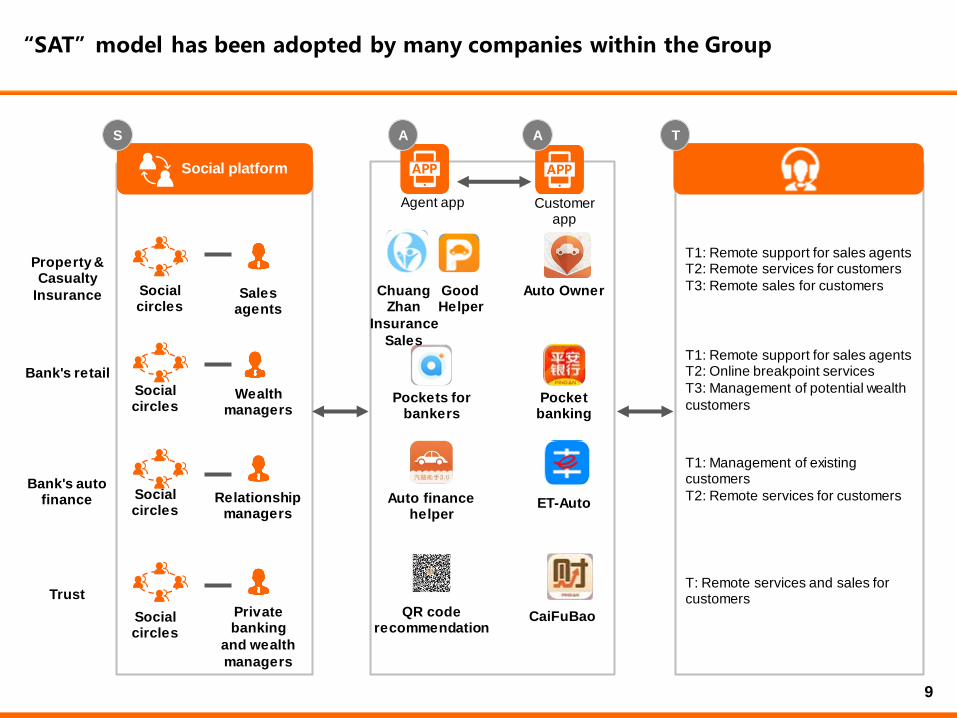

Refined channel management and sales(1/4) – Life Insurance SAT sales model revolution:

Disrupt the traditional sales model by allowing agents to segment and interact with customer

in real time under the “SAT” model

Customer app

Social platform

Agent

Agent

Agent

Agent

……

Agents on

Social

platform

Insurance products

Asset manage-

ment

products

Banking products

Medical services

…

Study-abroad

services

Tourist services

…

Financial products

Life service

products

WeChat friends

WeChat friends

WeChat friends

WeChat friends

T

Renyimen (Magic Gate)

T

A A Group

Subsidi

aries

S

Traffic

……

Innovative “SAT” sales model

Agent app

A

“SAT”model has been adopted by many companies within the Group

Agent app

T S

Bank's retail

T1: Remote support for sales agents T2: Remote services for customers

T3: Remote sales for customers

T1: Remote support for sales agents T2: Online breakpoint services

T3: Management of potential wealth

customers

T1: Management of existing customers

T2: Remote services for customers

Customer app

Wealth managers

Property & Casualty

Insurance Sales agents

Social circles

Pockets for bankers

Pocket banking

Bank's auto finance Relationship

managers Auto finance

helper ET-Auto

Trust

Private banking

and wealth

managers

CaiFuBao QR code recommendation

Chuang Zhan

Insurance

Sales

Auto Owner Good Helper

T: Remote services and sales for customers

Social platform

A A

9

Social circles

Social circles

Social circles

10

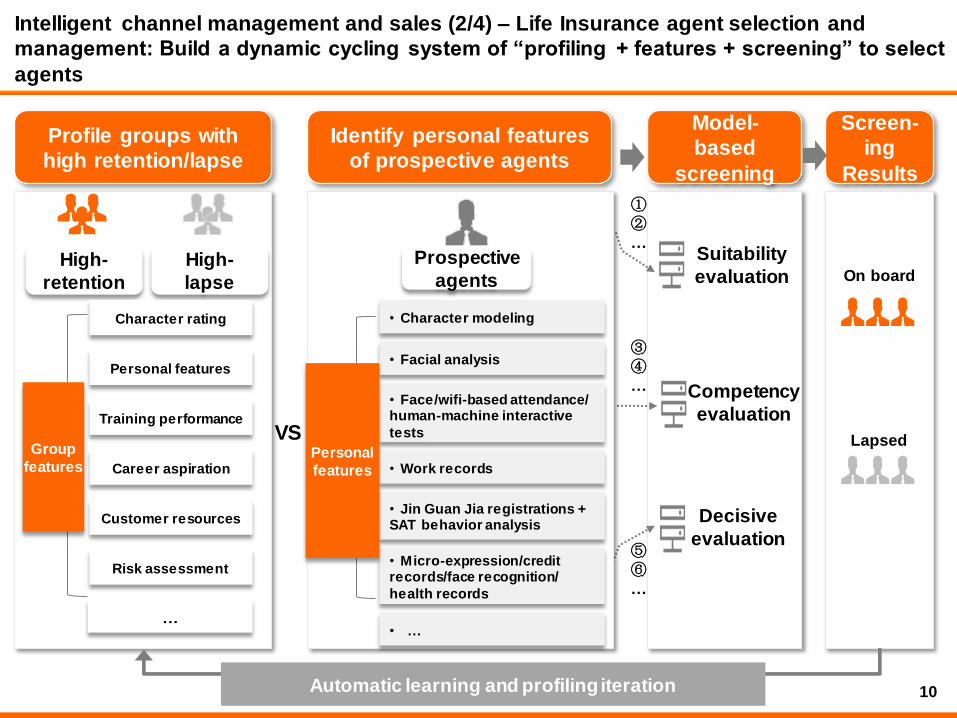

Intelligent channel management and sales (2/4) – Life Insurance agent selection and

management: Build a dynamic cycling system of “profiling + features + screening” to select

agents

Profile groups with

high retention/lapse

High-

retention

High-

lapse

Model-

based

screening

On board

Screen-

ing

Results

Lapsed

Suitability

evaluation

Competency

evaluation

Decisive

evaluation

①

②

…

③

④

…

⑤

⑥

…

Automatic learning and profiling iteration

Personal features

VS

Character rating

Training performance

Career aspiration

Customer resources

Risk assessment

…

• Micro-expression/credit records/face recognition/

health records

• Jin Guan Jia registrations + SAT behavior analysis

• Work records

Identify personal features

of prospective agents

• Character modeling

• Facial analysis

• Face/wifi-based attendance/ human-machine interactive

tests

• …

Personal

features

Prospective

agents

Group

features

Goals

20%

30%

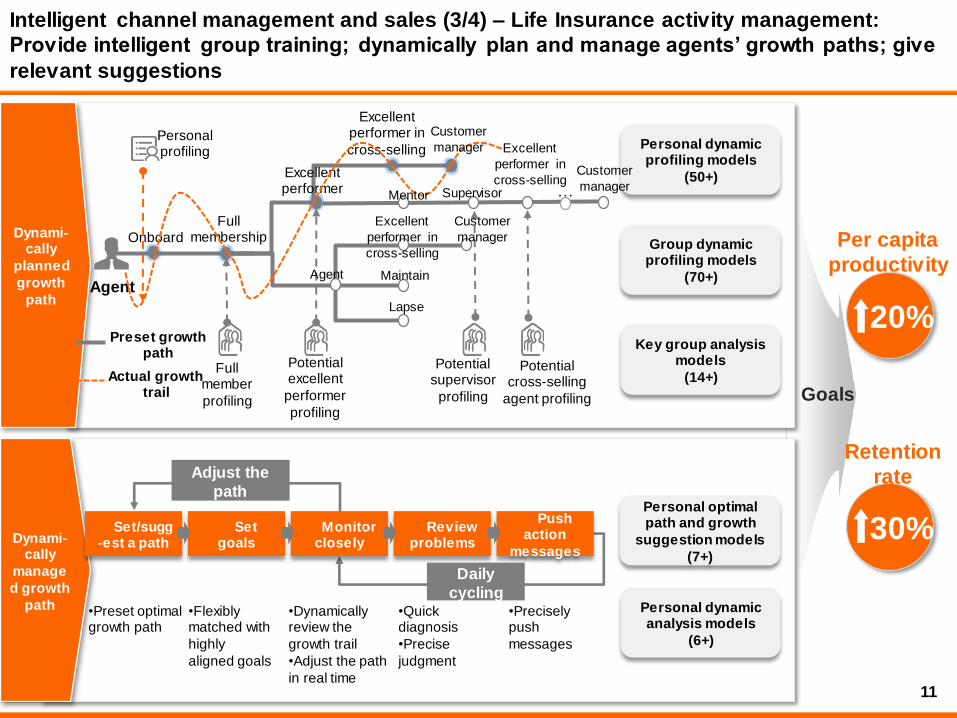

Intelligent channel management and sales (3/4) – Life Insurance activity management:

Provide intelligent group training; dynamically plan and manage agents’ growth paths; give

relevant suggestions

Personal optimal path and growth

suggestion models

(7+)

Personal dynamic analysis models

(6+)

Personal dynamic profiling models

(50+)

Key group analysis models

(14+)

Group dynamic profiling models

(70+)

Dynami-cally

planned

growth

path

Dynami-cally

manage

d growth

path

Excellent performer in

cross-selling

Agent

Preset growth path

Onboard Full

membership

Excellent performer …

Actual growth trail

Personal profiling

Full member

profiling

Potential excellent

performer

profiling

Potential cross-selling

agent profiling

•Dynamically review the

growth trail

•Adjust the path

in real time

•Quick diagnosis

•Precise

judgment

•Precisely push

messages

•Preset optimal growth path

•Flexibly matched with

highly

aligned goals

Set/sugg-est a path

Set goals

Review problems

Monitor closely

Push action

messages

Adjust the

path

Daily

cycling

Customer

manager

Customer

manager

Mentor Supervisor

Excellent

performer in

cross-selling

Agent

Excellent

performer in

cross-selling

Maintain

Lapse

Customer

manager

Potential supervisor

profiling

Per capita

productivity

Retention

rate

11

Human-machine

interaction

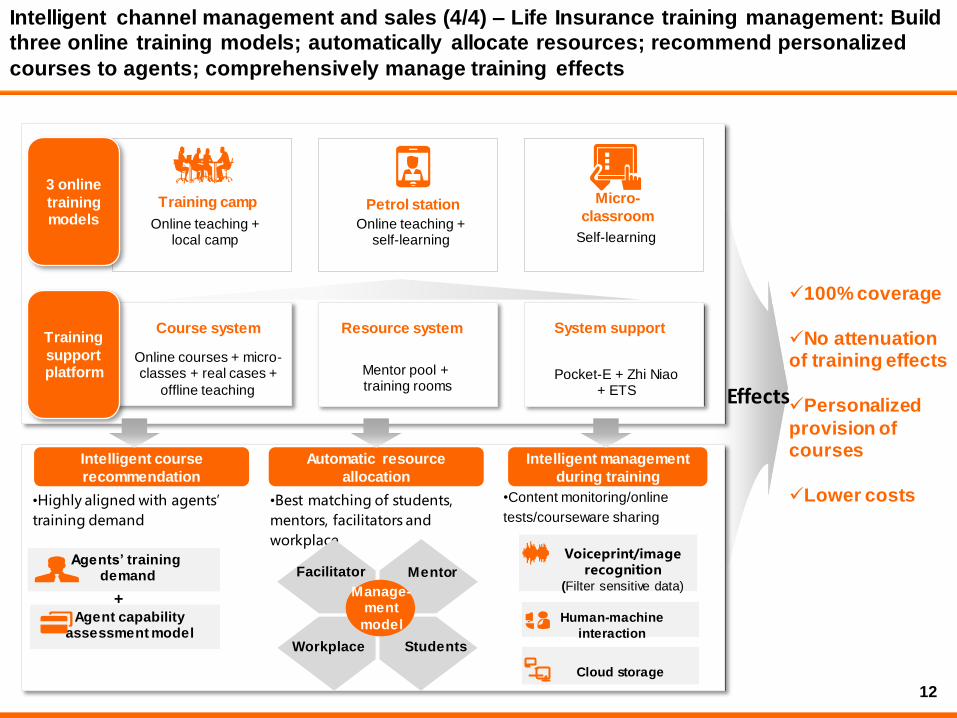

Cloud storage

Online courses + micro-classes + real cases +

offline teaching

Course system System support Training

support platform

Resource system

Mentor pool + training rooms

Pocket-E + Zhi Niao + ETS

Intelligent course

recommendation

Agents’ training demand

Agent capability assessment model

+

Automatic resource

allocation

Intelligent management

during training

•Best matching of students,

mentors, facilitators and

workplace

•Highly aligned with agents’

training demand

Voiceprint/image recognition

(Filter sensitive data)

Training camp Petrol station

Online teaching + local camp

Online teaching + self-learning

Micro-

classroom

Self-learning

•Content monitoring/online

tests/courseware sharing

Intelligent channel management and sales (4/4) – Life Insurance training management: Build

three online training models; automatically allocate resources; recommend personalized

courses to agents; comprehensively manage training effects

3 online

training models

Manage- ment

model

Facilitator Mentor

Workplace Students

Effects

100% coverage

No attenuation of training effects

Personalized

provision of courses

Lower costs

12

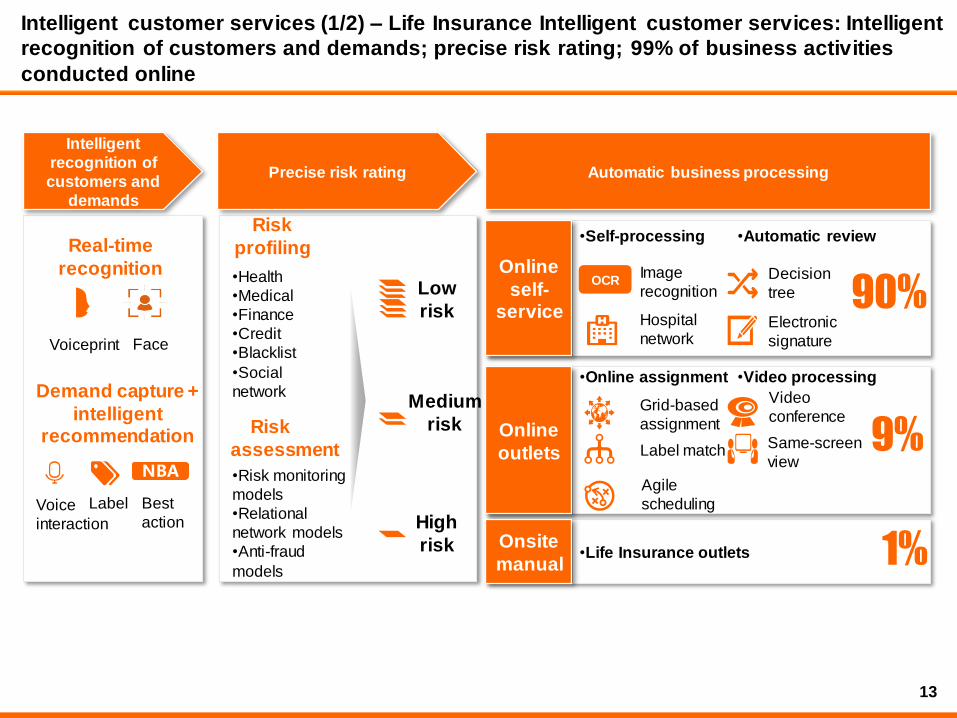

Intelligent customer services (1/2) – Life Insurance Intelligent customer services: Intelligent

recognition of customers and demands; precise risk rating; 99% of business activities

conducted online

Precise risk rating Automatic business processing

Intelligent

recognition of

customers and

demands

Real-time

recognition

NBA

Online

self-service

Online

outlets

Onsite

manual

90%

9%

1%

OCR

Voiceprint Face

Demand capture +

intelligent recommendation

Voice

interaction

Label Best

action

Risk

profiling

Risk

assessment

•Health

•Medical

•Finance

•Credit

•Blacklist

•Social

network

•Risk monitoring

models

•Relational

network models

•Anti-fraud

models

Low

risk

Medium

risk

High

risk

•Self-processing •Automatic review

•Online assignment •Video processing

•Life Insurance outlets

Image

recognition

Hospital

network

Decision

tree

Electronic

signature

Grid-based

assignment

Label match

Agile

scheduling

Video

conference

Same-screen

view

13

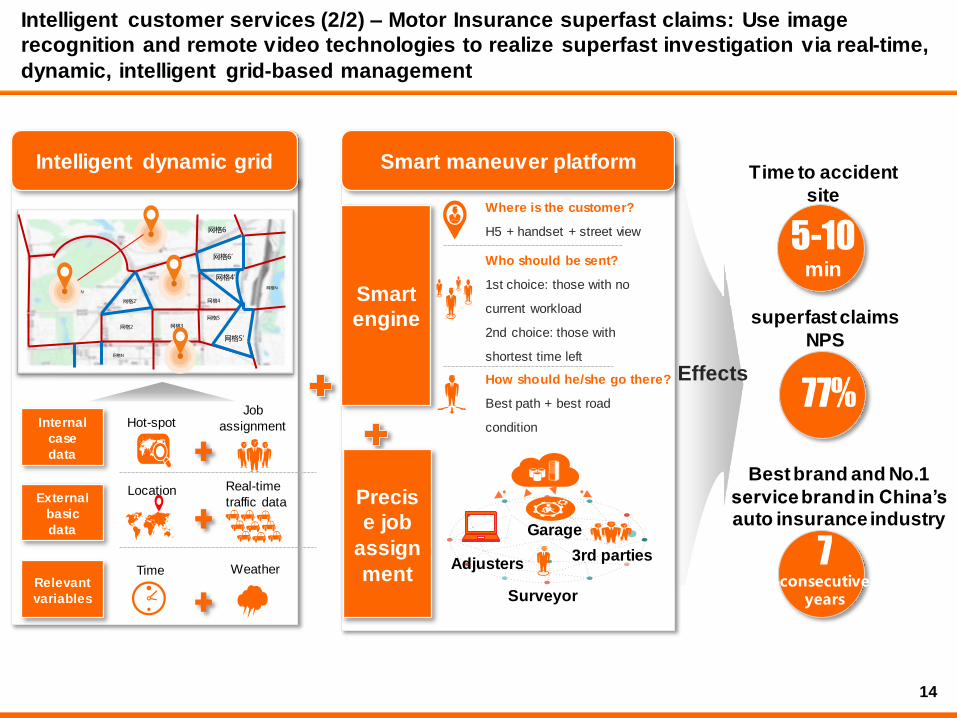

Intelligent customer services (2/2) – Motor Insurance superfast claims: Use image

recognition and remote video technologies to realize superfast investigation via real-time,

dynamic, intelligent grid-based management

Effects

Time to accident

site

Intelligent dynamic grid

External

basic

data

Internal

case

data

Relevant

variables

Hot-spot Job

assignment

Smart maneuver platform

Where is the customer?

H5 + handset + street view

How should he/she go there?

Best path + best road

condition

Smart

engine

Who should be sent?

1st choice: those with no

current workload

2nd choice: those with

shortest time left

14

网格N

网格N

网格2’

网格1

网格3

网格4

网格5

网格6

网格N

网格4’

网格6’

网格5’

网格2

5-10 min

superfast claims

NPS

77%

Best brand and No.1

service brand in China’s auto insurance industry

7 consecutive

years

Location Real-time

traffic data

Time Weather

Precis

e job

assign

ment Adjusters

Garage

3rd parties

Surveyor

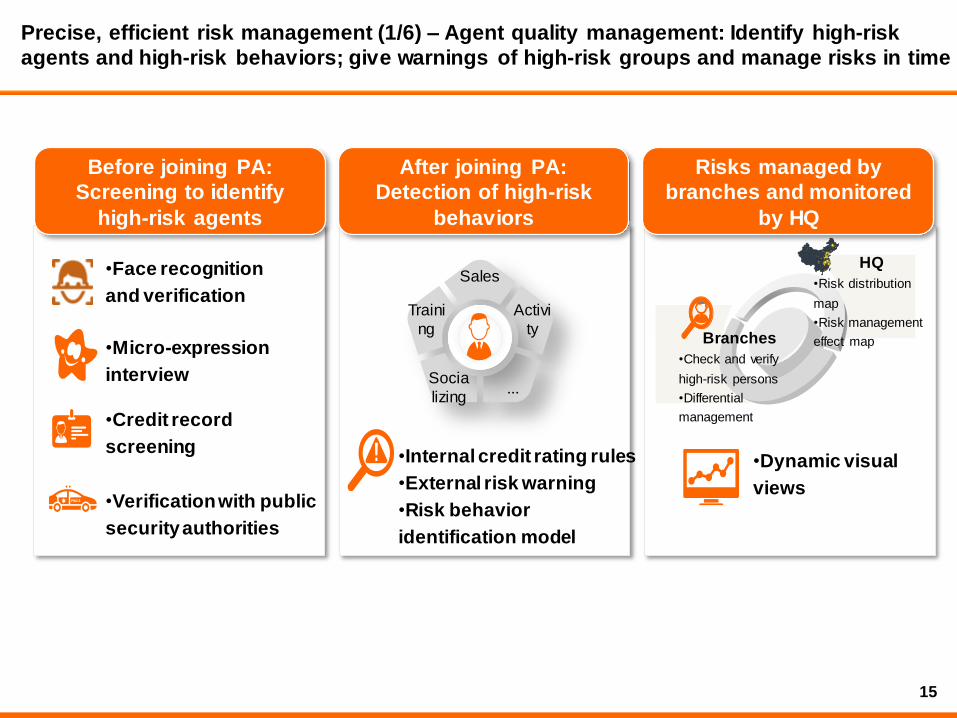

Precise, efficient risk management (1/6) – Agent quality management: Identify high-risk

agents and high-risk behaviors; give warnings of high-risk groups and manage risks in time

15

Before joining PA:

Screening to identify

high-risk agents

After joining PA:

Detection of high-risk

behaviors

•Credit record

screening

•Verification with public

security authorities

•Micro-expression

interview …

Risks managed by

branches and monitored

by HQ

•Face recognition

and verification

•Internal credit rating rules

•External risk warning

•Risk behavior

identification model

Sales

Activi

ty

Traini

ng

Socia

lizing

•Dynamic visual

views

Branches

•Check and verify

high-risk persons

•Differential

management

HQ

•Risk distribution

map

•Risk management

effect map

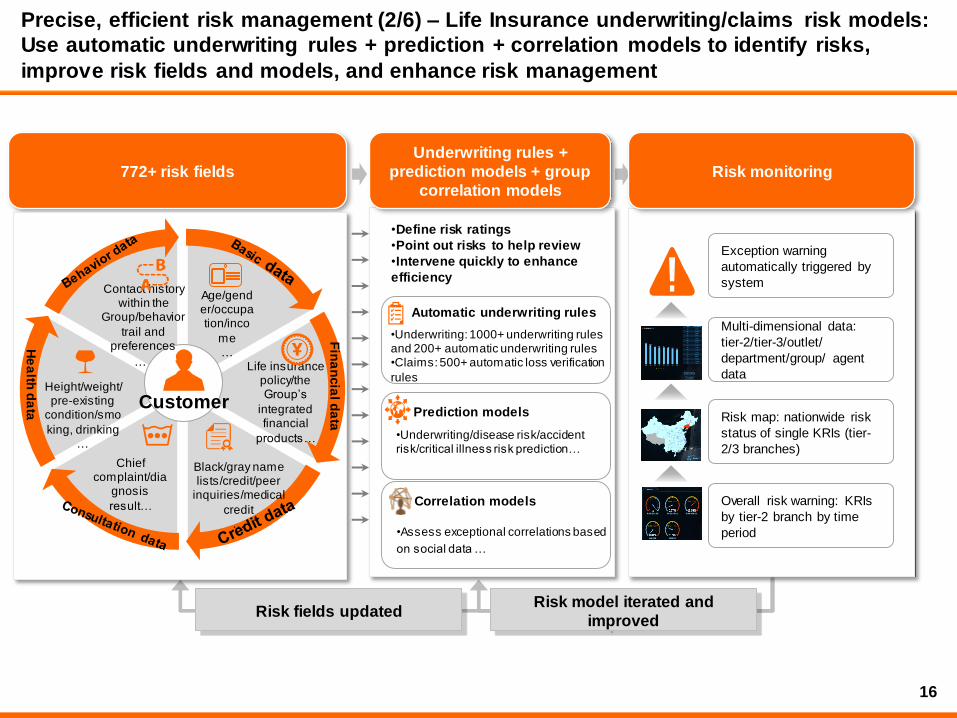

Precise, efficient risk management (2/6) – Life Insurance underwriting/claims risk models:

Use automatic underwriting rules + prediction + correlation models to identify risks,

improve risk fields and models, and enhance risk management

16

772+ risk fields

Risk fields updated Risk model iterated and

improved

Underwriting rules +

prediction models + group

correlation models

•Define risk ratings

•Point out risks to help review

•Intervene quickly to enhance

efficiency

Automatic underwriting rules

Risk monitoring

Overall risk warning: KRIs

by tier-2 branch by time

period

Risk map: nationwide risk

status of single KRIs (tier-

2/3 branches)

Multi-dimensional data:

tier-2/tier-3/outlet/

department/group/ agent

data

Exception warning

automatically triggered by

system

… 信用信息

Height/weight/pre-existing

condition/smo

king, drinking …

Life insurance policy/the Group’s

integrated financial

products…

Black/gray name lists/credit/peer

inquiries/medical

credit …

Customer

Age/gender/occupation/inco

me …

Contact history within the

Group/behavior

trail and preferences

…

Fin

an

cia

l da

ta

He

alth

da

ta

Chief complaint/dia

gnosis

result…

•Underwriting: 1000+ underwriting rules and 200+ automatic underwriting rules •Claims: 500+ automatic loss verification

rules

Prediction models

•Underwriting/disease risk/accident risk/critical illness risk prediction…

Correlation models

•Assess exceptional correlations based

on social data …

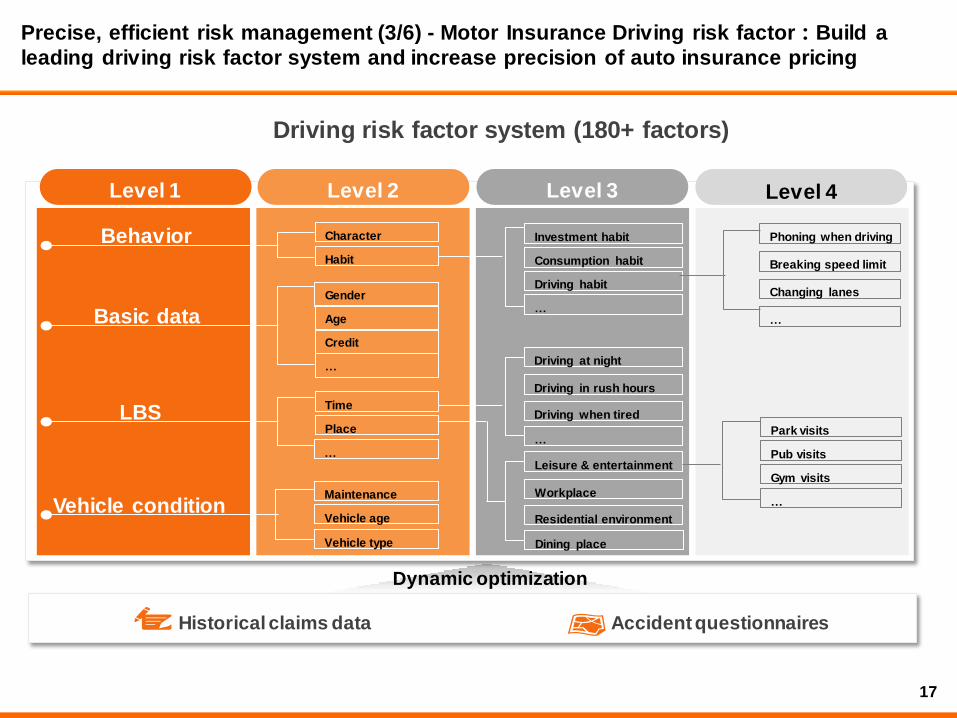

Precise, efficient risk management (3/6) - Motor Insurance Driving risk factor:Build a

leading driving risk factor system and increase precision of auto insurance pricing

17

Level 1 Level 2 Level 3 Level 4

Dynamic optimization

Driving risk factor system (180+ factors)

Behavior

Basic data

LBS

Vehicle condition

Character

Habit

Gender

Age

Credit

…

Time

Place

Maintenance

Vehicle age

Investment habit

Consumption habit

Driving habit

…

Driving at night

Driving in rush hours

Driving when tired

…

Vehicle type

…

Leisure & entertainment

Workplace

Residential environment

Dining place

Park visits

Pub visits

Gym visits

…

Phoning when driving

Breaking speed limit

Changing lanes

…

Historical claims data Accident questionnaires

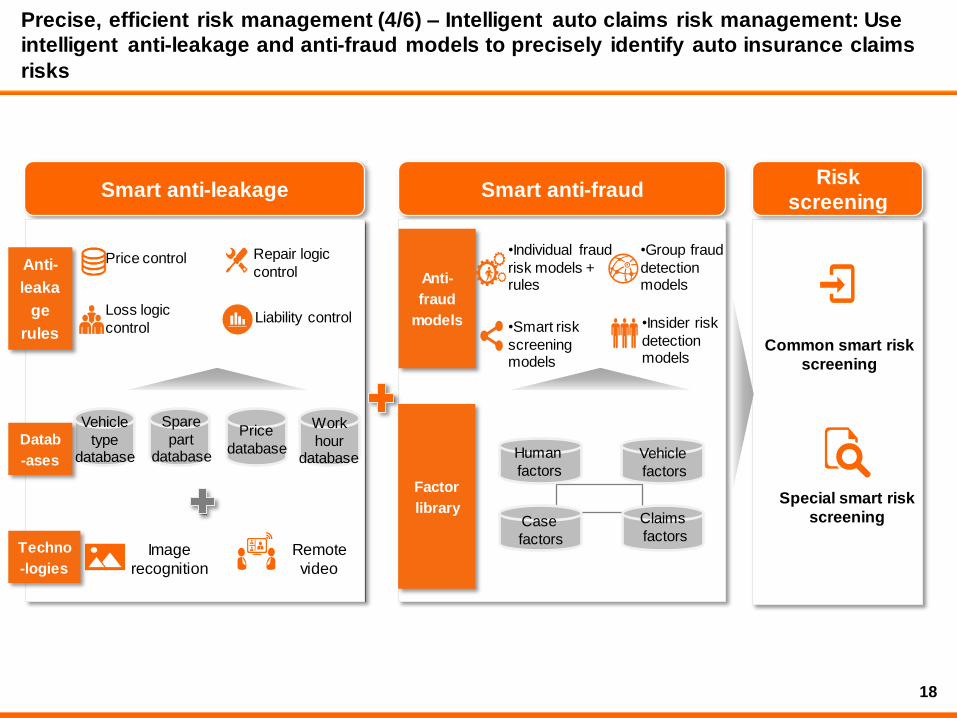

Precise, efficient risk management (4/6) – Intelligent auto claims risk management: Use

intelligent anti-leakage and anti-fraud models to precisely identify auto insurance claims

risks

Smart anti-leakage Smart anti-fraud

Image

recognition

Vehicle

type database

Spare

part database

Price

database

Work

hour database

Datab

-ases

Techno

-logies

Anti-

leaka

ge

rules Liability control

Price control Repair logic

control

Loss logic

control

Remote

video

Factor

library

Anti-

fraud

models

•Individual fraud

risk models + rules

•Group fraud

detection models

•Insider risk

detection models

•Smart risk

screening models

Risk

screening

Common smart risk

screening

Special smart risk

screening

Human

factors Vehicle

factors

Case

factors

Claims

factors

18

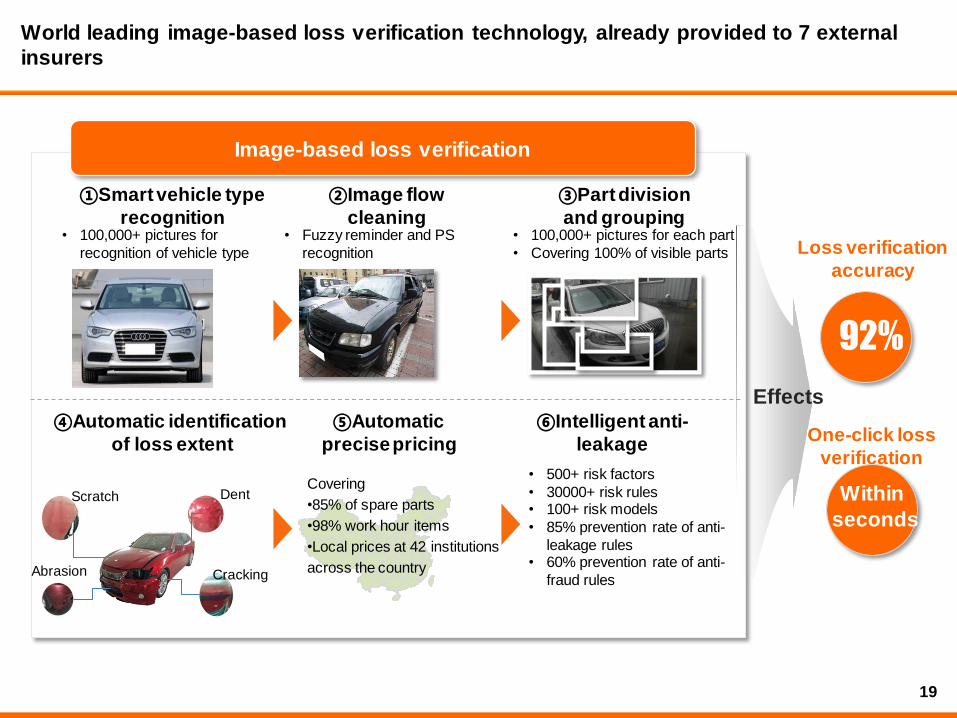

World leading image-based loss verification technology, already provided to 7 external

insurers

19

③Part division

and grouping

①Smart vehicle type

recognition

②Image flow

cleaning

④Automatic identification

of loss extent

⑤Automatic

precise pricing

⑥Intelligent anti-

leakage

Image-based loss verification

• 100,000+ pictures for

recognition of vehicle type

• Fuzzy reminder and PS

recognition

• 100,000+ pictures for each part

• Covering 100% of visible parts

Covering

•85% of spare parts

•98% work hour items

•Local prices at 42 institutions

across the country

• 500+ risk factors

• 30000+ risk rules • 100+ risk models

• 85% prevention rate of anti-

leakage rules • 60% prevention rate of anti-

fraud rules

Effects

Loss verification

accuracy

92%

One-click loss

verification Within

seconds

Scratch

Abrasion

Dent

Cracking

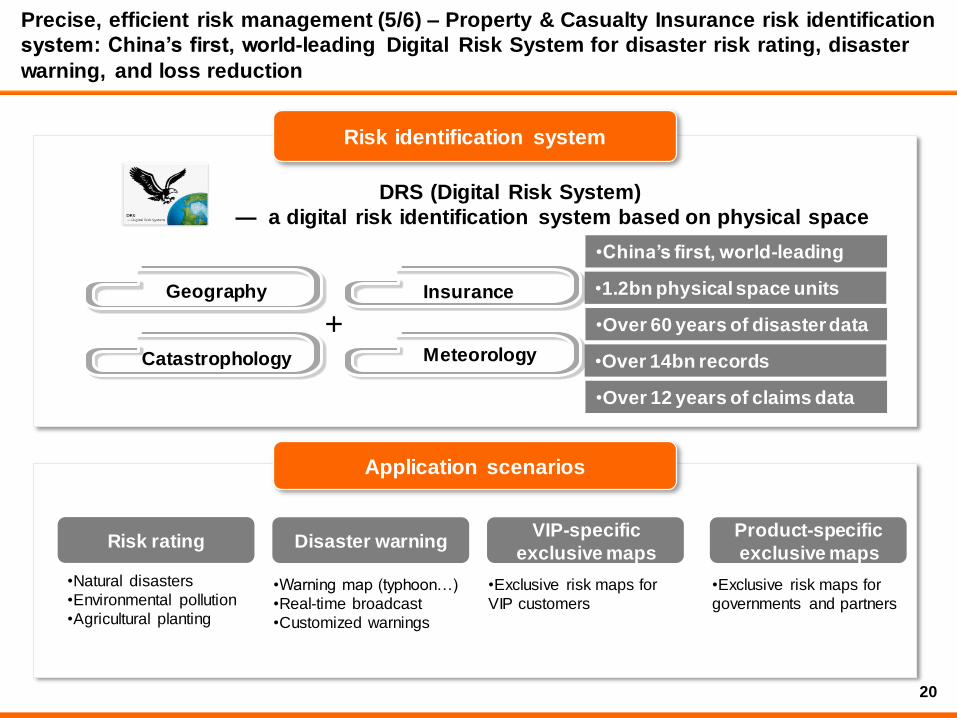

Precise, efficient risk management (5/6) – Property & Casualty Insurance risk identification

system: China’s first, world-leading Digital Risk System for disaster risk rating, disaster

warning, and loss reduction

20

Risk identification system

Application scenarios

DRS (Digital Risk System)

— a digital risk identification system based on physical space

+ Geography

Catastrophology Meteorology

Insurance

•China’s first, world-leading

•Over 12 years of claims data

•1.2bn physical space units

•Over 60 years of disaster data

•Over 14bn records

Risk rating Disaster warning VIP-specific

exclusive maps

Product-specific

exclusive maps

•Natural disasters

•Environmental pollution

•Agricultural planting

•Warning map (typhoon…)

•Real-time broadcast

•Customized warnings

•Exclusive risk maps for

VIP customers

•Exclusive risk maps for

governments and partners

Precise, efficient risk management (6/6) – Credit Card & PuHui's smart risk management:

Build a risk management model to improve the risk identification capability

Credit Card NPL Ratio

Top 3 in terms of the lowest

NPL ratio in the industry

Use big data to build a risk management model

Smart

review

models of

PuHui

Multi-dimensional: Phone, IP,

GPS

Multi-layer: customer and

social networks

Big data factors Smart models

Big data Transaction

behavior

Assets &

wealth

Geographic location

Credit rating

Other data

Basic information

Anti-fraud

models of

Credit

Card

Risk identification

ratio of PuHui

Effects

Chain-type clustering model

Data verification model

Income calculation

model

Limit calculation model

PBoC rating model

Customer data anti-fraud model

Micro-expression lie detection model

Group anti-fraud model

Relational network model

Device anti-fraud model

1.18%

Better than industry

performance

21

Thanks

From Ping An to Platform:

Technology Innovation for Growth

Jessica Tan

Ping An Group

Group Deputy CEO

Group COO & CIO

2017.11.20

Important Notes Cautionary Statements Regarding Forward-Looking Statement To the extent any statements made in this presentation containing information that is not historical are essentially forward-looking. These forward-looking statements include but are not limited to projections, targets, estimates and business plans that the Company expects or anticipates will or may occur in the future. These forward-looking statements are subject to known and unknown risks and uncertainties that may be general or specific. Certain statements, such as those including the words or phrases "potential", "estimates", "expects", "anticipates", "objective", "intends", "plans", "believes", "will", "may", "should", and similar expressions or variations on such expressions may be considered forward-looking statements. Readers should be cautioned that a variety of factors, many of which may be beyond the Company's control, affect the performance, operations, and results of the Company, and could cause actual results to differ materially from the expectations expressed in any of the Company's forward-looking statements. These factors include but are not limited to exchange rate fluctuations, market shares, competition, environmental risks, changes in legal, financial and regulatory frameworks, international economic and financial market conditions, and other risks and factors beyond our control. These and other factors should be considered carefully, and readers should not place undue reliance on the Company's forward-looking statements. In addition, the Company undertakes no obligation to publicly update or revise any forward-looking statement that is contained in this presentation as a result of new information, future events, or otherwise. None of the Company, or any of its employees or affiliates is responsible for, or is making, any representation concerning the future performance of the Company.

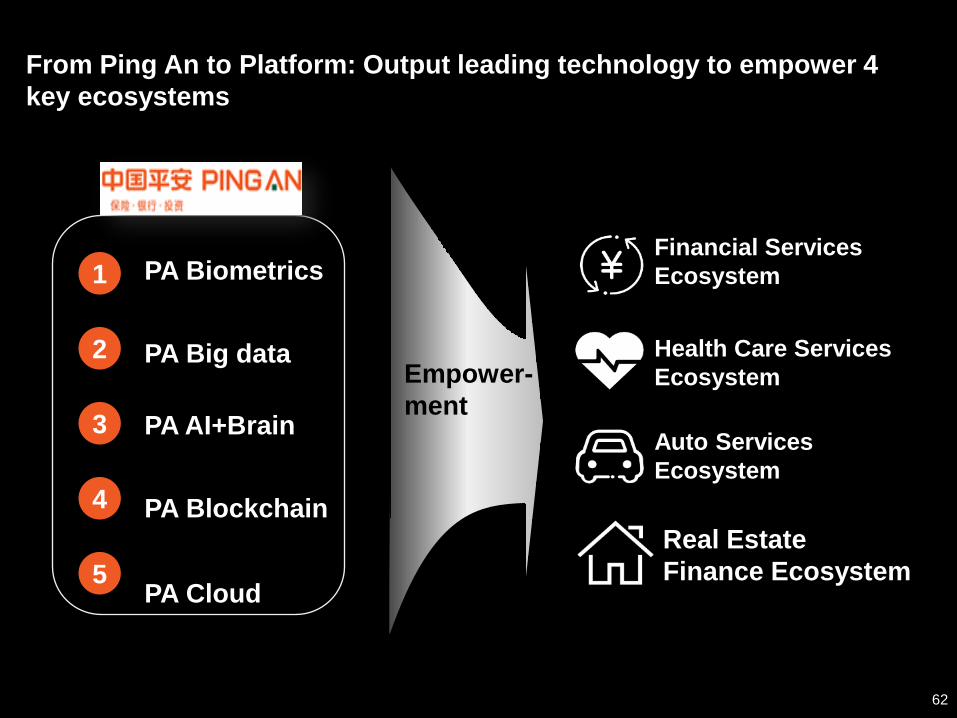

1. Ping An Group: 5 Core Technologies

2. From Ping An to platform: Output

services to 4 ecosystems a. Financial Services Ecosystem

b. Health Care Services Ecosystem

c. Auto Services Ecosystem

d. Real Estate Finance Ecosystem

Agenda

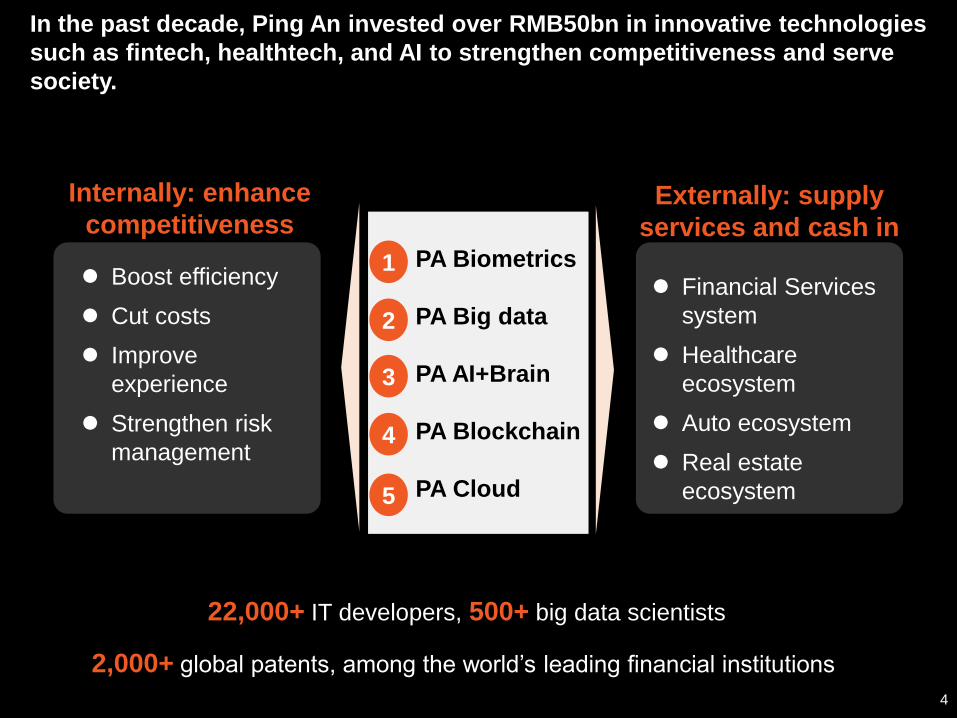

Internally: enhance

competitiveness Externally: supply

services and cash in

2,000+ global patents, among the world’s leading financial institutions

Boost efficiency

Cut costs

Improve

experience

Strengthen risk

management

In the past decade, Ping An invested over RMB50bn in innovative technologies

such as fintech, healthtech, and AI to strengthen competitiveness and serve

society.

Financial Services

system

Healthcare

ecosystem

Auto ecosystem

Real estate

ecosystem

4

22,000+ IT developers, 500+ big data scientists

PA Biometrics

PA Big data

PA AI+Brain

PA Blockchain

PA Cloud

1

2

3

4

5

PA Facial

recognition

PA voiceprint

recognition PA Big Data

+ +

PA Micro-

expression

+

5

PA Biometrics:World-leading technologies

1

• 99.8% accuracy,

the world’s No.1

• 800mn+ usages

• 200+ scenarios

• 100+ clients

• 99+% accuracy

• 50mn+ voiceprint

records

• 10+ scenarios

• 880mn people

• 26K data fields

• 3,300+ data fields per

person overage

• 730mn credit inquiries

• 54 complex

micro-expressions

• 1-second recognition

• 300k+ loan approvals

6

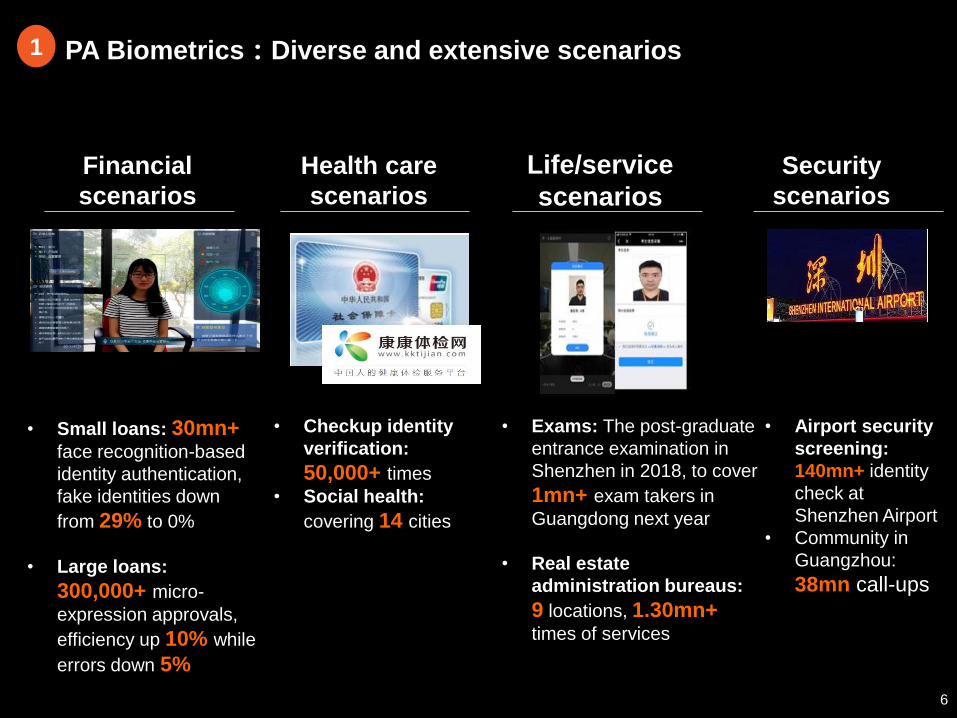

PA Biometrics:Diverse and extensive scenarios

1

Financial

scenarios

Health care

scenarios

Life/service

scenarios

Security

scenarios

• Small loans: 30mn+

face recognition-based

identity authentication,

fake identities down

from 29% to 0%

• Large loans:

300,000+ micro-

expression approvals,

efficiency up 10% while

errors down 5%

• Checkup identity

verification:

50,000+ times

• Social health:

covering 14 cities

• Exams: The post-graduate

entrance examination in

Shenzhen in 2018, to cover

1mn+ exam takers in

Guangdong next year

• Real estate

administration bureaus:

9 locations, 1.30mn+ times of services

• Airport security

screening:

140mn+ identity

check at

Shenzhen Airport

• Community in

Guangzhou:

38mn call-ups

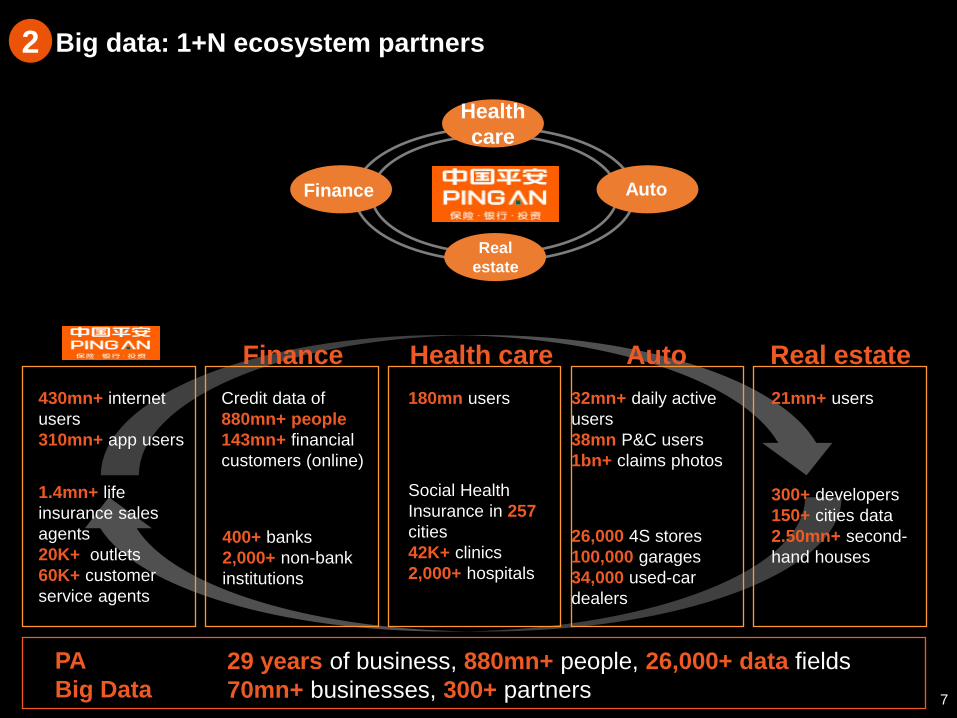

Big data: 1+N ecosystem partners 2

Finance

Health

care

Auto

Real

estate

7

PA

Big Data

Finance Health care Auto Real estate

430mn+ internet

users

310mn+ app users

1.4mn+ life

insurance sales

agents

20K+ outlets

60K+ customer

service agents

400+ banks

2,000+ non-bank

institutions

Credit data of

880mn+ people

143mn+ financial

customers (online)

Social Health

Insurance in 257

cities

42K+ clinics

2,000+ hospitals

180mn users

26,000 4S stores

100,000 garages

34,000 used-car

dealers

32mn+ daily active

users

38mn P&C users

1bn+ claims photos

300+ developers

150+ cities data

2.50mn+ second-

hand houses

21mn+ users

29 years of business, 880mn+ people, 26,000+ data fields

70mn+ businesses, 300+ partners

I

H

G

F

D

C

B

A

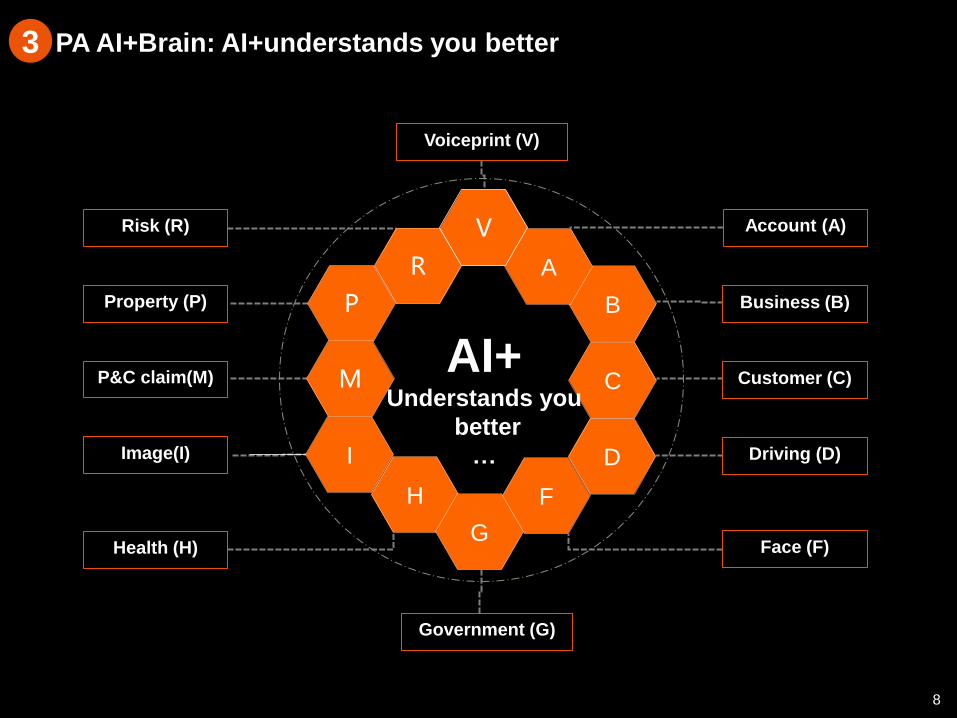

Government (G)

AI+ Understands you

better

…

PA AI+Brain: AI+understands you better 3

8

Business (B)

Customer (C)

Driving (D)

Face (F)

Account (A)

Voiceprint (V)

Property (P)

Health (H)

P&C claim(M)

Risk (R)

Image(I)

R

P

M

V

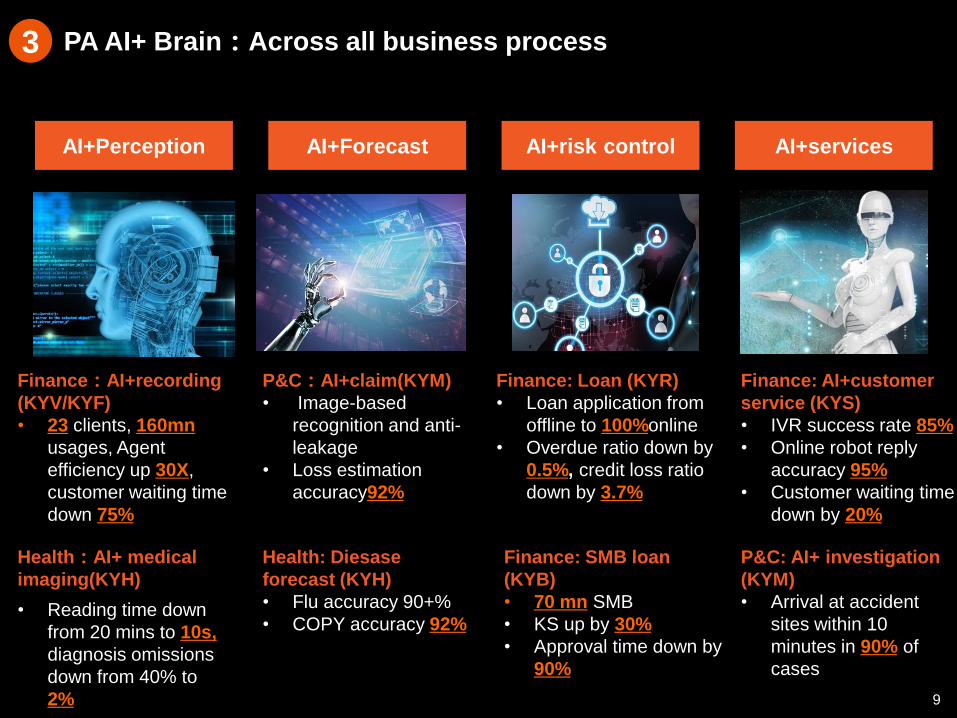

PA AI+ Brain:Across all business process

AI+Perception AI+Forecast AI+risk control AI+services

3

9

P&C:AI+claim(KYM)

• Image-based

recognition and anti-

leakage

• Loss estimation

accuracy92%

Health: Diesase

forecast (KYH)

• Flu accuracy 90+%

• COPY accuracy 92%

Health:AI+ medical

imaging(KYH)

• Reading time down

from 20 mins to 10s,

diagnosis omissions

down from 40% to

2%

Finance: Loan (KYR)

• Loan application from

offline to 100%online

• Overdue ratio down by

0.5%, credit loss ratio

down by 3.7%

Finance: AI+customer

service (KYS)

• IVR success rate 85%

• Online robot reply

accuracy 95%

• Customer waiting time

down by 20%内

Finance:AI+recording

(KYV/KYF)

• 23 clients, 160mn

usages, Agent

efficiency up 30X,

customer waiting time

down 75%

Finance: SMB loan

(KYB)

• 70 mn SMB

• KS up by 30%

• Approval time down by

90%

P&C: AI+ investigation

(KYM)

• Arrival at accident

sites within 10

minutes in 90% of

cases

10 1. 2020 forecast 2. Impact comparison based on 2015 vs 2017 Jan to Oct

10

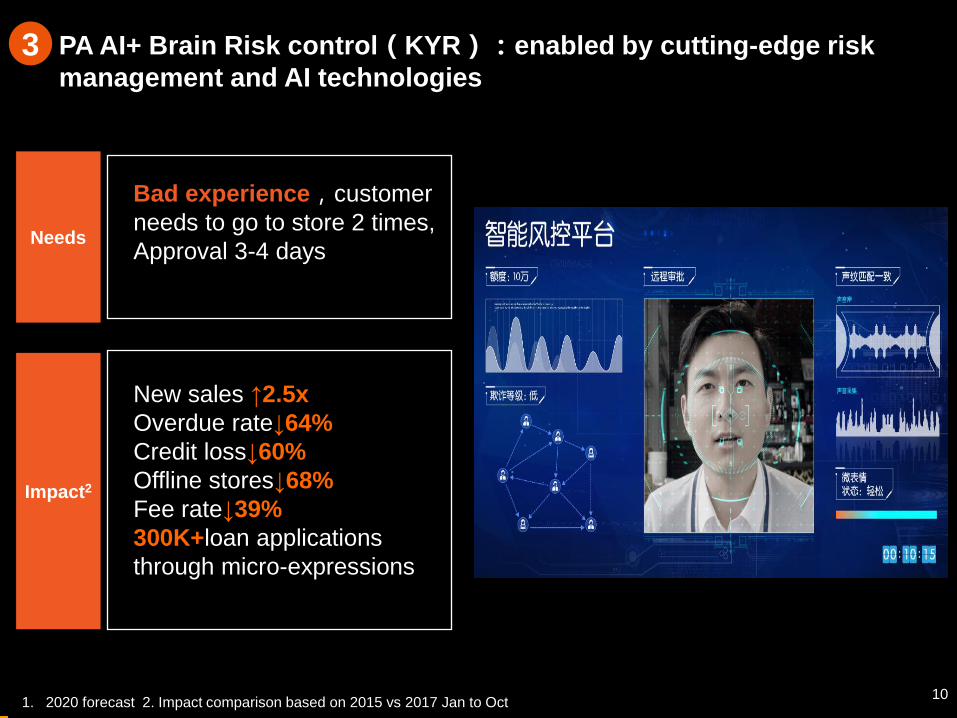

3 PA AI+ Brain Risk control(KYR):enabled by cutting-edge risk

management and AI technologies

New sales ↑2.5x

Overdue rate↓64%

Credit loss↓60%

Offline stores↓68%

Fee rate↓39%

300K+loan applications

through micro-expressions

Bad experience,customer

needs to go to store 2 times,

Approval 3-4 days

Needs

Impact2

11

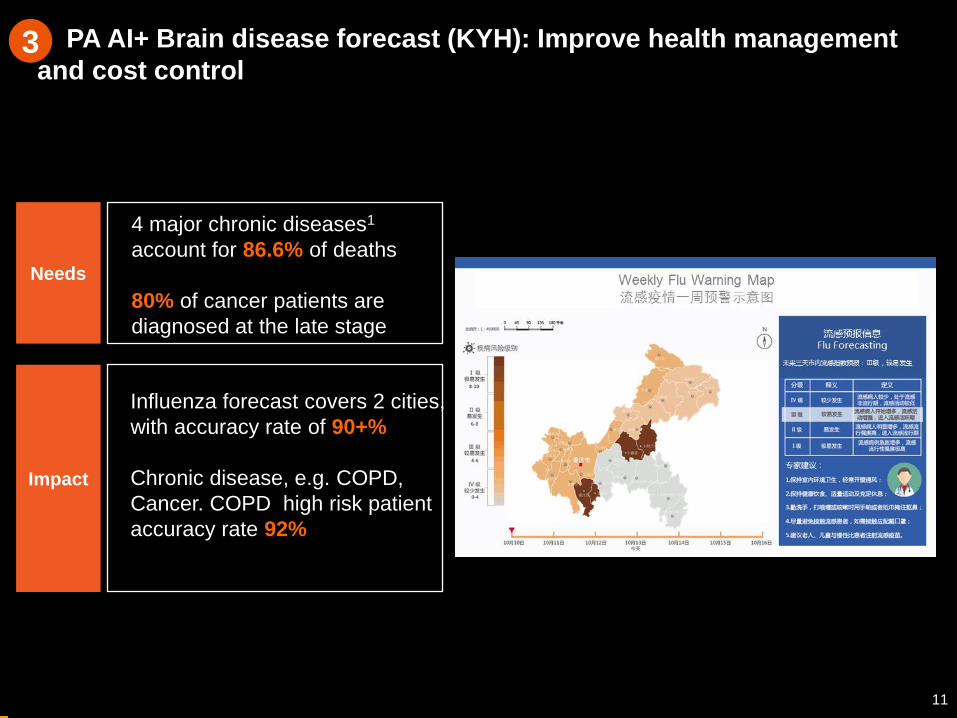

Influenza forecast covers 2 cities,

with accuracy rate of 90+%

Chronic disease, e.g. COPD,

Cancer. COPD high risk patient

accuracy rate 92%

Needs

Impact

PA AI+ Brain disease forecast (KYH): Improve health management

and cost control 3

11

4 major chronic diseases1

account for 86.6% of deaths

80% of cancer patients are

diagnosed at the late stage

PA Onechain:provide safe, traceable and effective transaction

recording

PA

Advantage

4

12

Highest performance • Exceeding open source

version by 50-100%

• 100,000 transactions/second

Leading encryption • Meet Chinese standards

• 100x speed of other apps

Convenient supervision • Super key can decrypt any ZKP

encryption

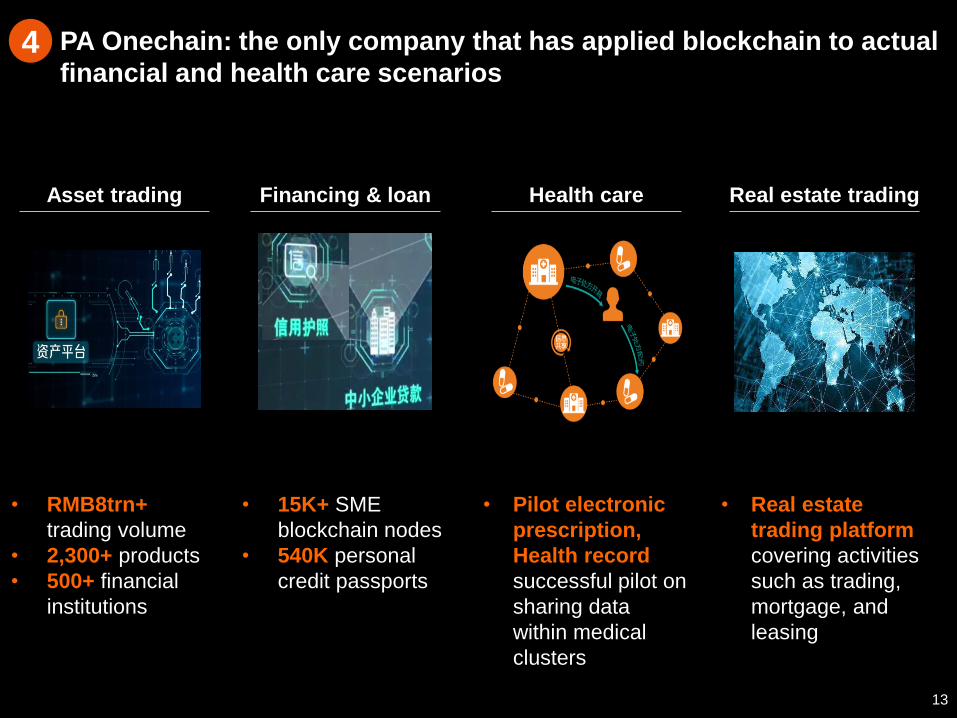

PA Onechain: the only company that has applied blockchain to actual

financial and health care scenarios 4

13

Asset trading Financing & loan Health care Real estate trading

• RMB8trn+

trading volume

• 2,300+ products

• 500+ financial

institutions

• 15K+ SME

blockchain nodes

• 540K personal

credit passports

• Pilot electronic

prescription,

Health record

successful pilot on

sharing data

within medical

clusters

• Real estate

trading platform

covering activities

such as trading,

mortgage, and

leasing

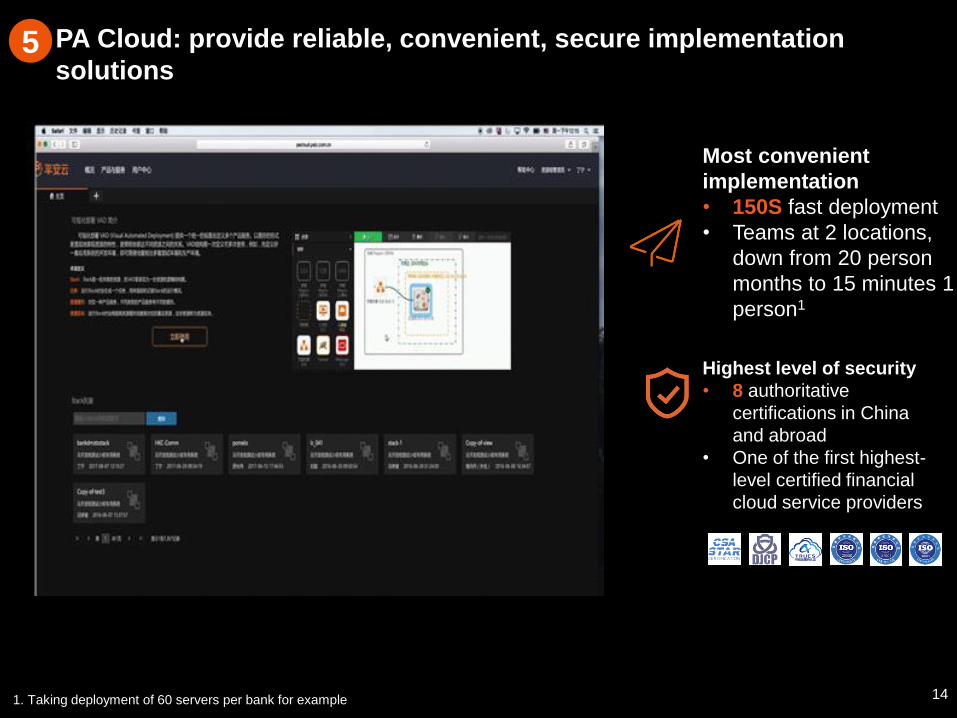

Most convenient

implementation

• 150S fast deployment

• Teams at 2 locations,

down from 20 person

months to 15 minutes 1

person1

14

PA Cloud: provide reliable, convenient, secure implementation

solutions 5

1. Taking deployment of 60 servers per bank for example

Highest level of security

• 8 authoritative

certifications in China

and abroad

• One of the first highest-

level certified financial

cloud service providers

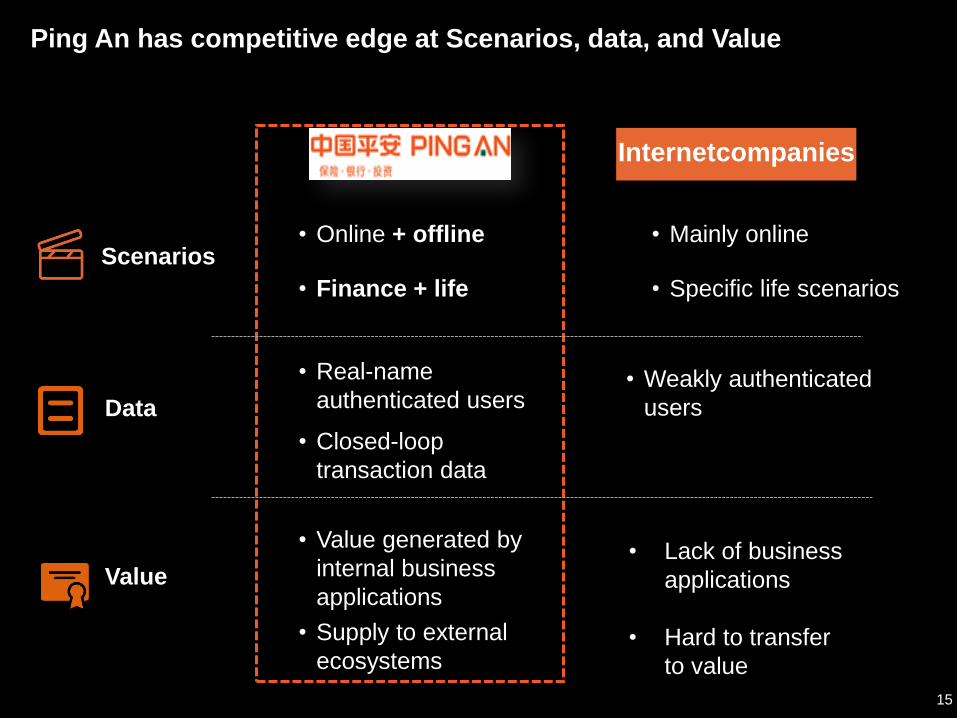

Internetcompanies

• Lack of business

applications

• Hard to transfer

to value

Ping An has competitive edge at Scenarios, data, and Value

• Weakly authenticated

users

15

• Online + offline

• Finance + life

• Mainly online

• Specific life scenarios

• Real-name

authenticated users

• Closed-loop

transaction data

• Value generated by

internal business

applications

• Supply to external

ecosystems

Scenarios

Data

Value

1. Ping An Group: 5 Core Technologies

2. From Ping An to platform: Output

services to 4 ecosystems a. Financial Services Ecosystem

b. Health Care Services Ecosystem

c. Auto Services Ecosystem

d. Real Estate Finance Ecosystem

Agenda

Financial

Services

Ecosystem

Health Care

Services

Ecosystem

Auto

Services

Ecosystem

Real Estate

Finance

Ecosystem

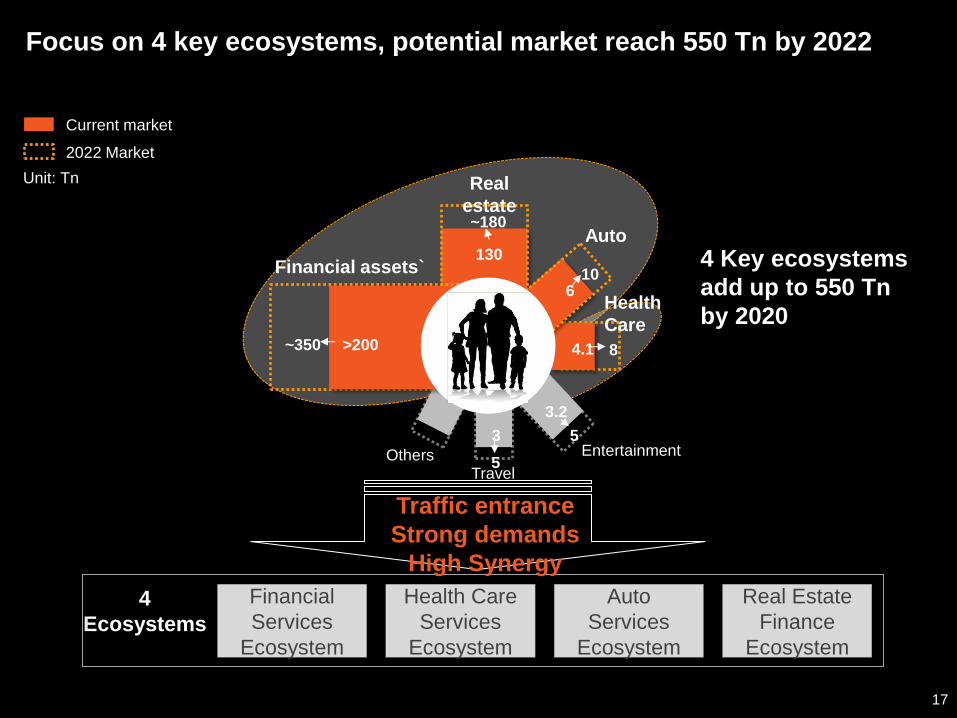

130

~180

>200 ~350

6 10

4.1 8

3.2

5 3

5

4

Ecosystems

Current market

2022 Market

Unit: Tn

Financial assets`

Real

estate

Health

Care

Auto

Entertainment

Travel Others

Focus on 4 key ecosystems, potential market reach 550 Tn by 2022

17

Traffic entrance

Strong demands

High Synergy

4 Key ecosystems

add up to 550 Tn

by 2020

Financial

Services

Ecosystem

金融服务生态圈

Health Care

Services

Ecosystem

医疗健康生态圈

Auto Services

Ecosystem

汽车服务生态圈

Real Estate

Finance

Ecosystem

房产金融生态圈

18

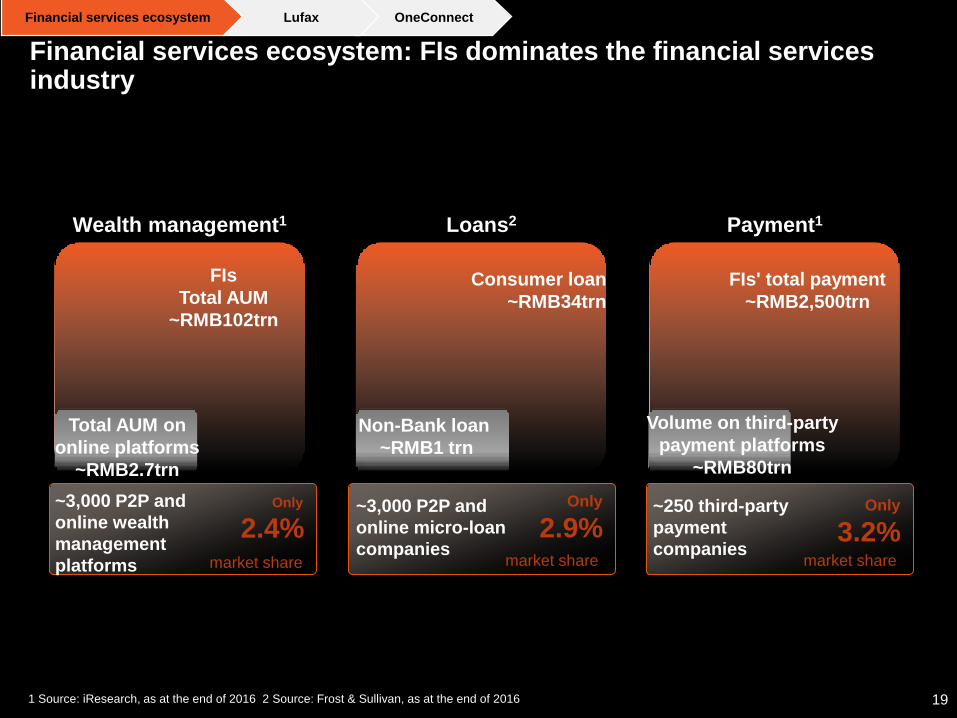

Financial services ecosystem: FIs dominates the financial services industry

~3,000 P2P and