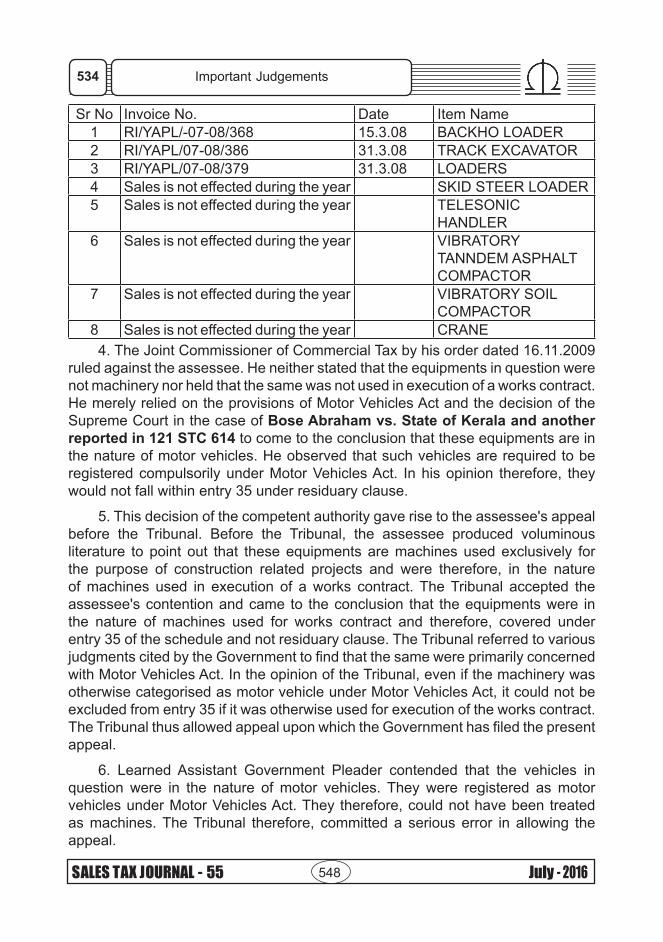

3 +ÉyÉÖÊ{Éh +nÉl«É{ÉÉ ¶É¥qÉà{ÉÒ »É©Éw 6 ÊwÅqnÉÒ

TRANSCRIPT

457

July - 2016 SALES TAX JOURNAL - 55

Volume : 55 Part - 4 JULY - 2016

EDITORS : N. N. PATEL - KUNTAL A. PARIKH

The G.S.T.B. Association 4th Floor, “C” Block, Multi Storyed Building, Lal Darwaja, Ahmedabad. Phone : 25506305 Fax : 25501731 Email : [email protected]

471

No. Particulars By Page No.

1 Editorial N. N. Patel & Kuntal A. Parikh

463

2 President’s Desk Rupesh S. Shah 461

3 +ÉyÉÖÊ{ÉH +NÉl«É{ÉÉ ¶É¥qÉà{ÉÒ »É©ÉW Harish N. Shah 462

4 Fraternal Twins – Central Indirect Taxes and VAT

Uchit N. Sheth 477

5 3D - No Service Tax if Composite Works Contracts includes Land

CA Abhay Desai 480

6 ÊWÅqNÉÒ - +àH HàʱÉeÉà»HÉà~É Sunil Sagar 483

7 swËe swËe yËk÷íkkuLkk yøkíÞLkk [qfkËk J.S.Amin & M.J. Amin 486

8 Gist of Judgments Reported in June, 2016 Lalit M. Leuva 492

9 Gist of the Judgements G. D. Jain 511

10 Advance Note Bhavin Vakil 513

11 Tribunal Judgements N. N. Patel - Ashok J. Patel 515

12 {ÉÉ.´ÉÉÊiÉÎV«ÉH ´ÉàùÉ ~ÉÅSÉ{ÉÉ 2015{ÉÉ +NÉl«É{ÉÉ SÉÚHÉqÉ+Éà{ÉÒ NÉÖWùÉlÉÒ©ÉÉÅ ÷ÚÅHÒ {ÉÉáyÉ

Sachin R. Nakar 520

13 Important Judgements 530

14 Notifications 538

15 Association News Anand S. Jambuwala Shantilal C. Thakkar

539

Continuous Page No. of this issue is 469 to 556 including title.

458

SALES TAX JOURNAL - 55 July - 2016

Thought of the Month : Anywhere you go liking everyone, everyone will be likeable.

Notes:

1. Cheques/DD or Postal Orders should be drawn in favour of the “The Gujarat Sales Tax Bar Association”, payable at Ahmedabad. Outstation Cheques shall not be accepted.

2. Non-receipt of any part of The Sales Tax Journal should be intimated in writing to the Office of the Gujarat Sales Tax Bar Association or through e-mail on [email protected] within fifteen days of the following month to which the journal relates.

3. Total number of pages in any part of The Sales Tax Journal includes its Title page also.

4. Annual Subscription for The Sales Tax Journal is Rs. 1,500/- for the Financial Year from April to March.

5. Publisher: The Gujarat Sales Tax Bar Association.

6. Printed by: Shri V. G. Thakor

7. Printed at: Navprabhat Printing Press, Ahmedabad.

Disclaimer:

All data, information and views published in the articles, columns or in any other format in this Sales Tax Journal, is only for general information. No responsibility or liability is taken by The Gujarat Sales Tax Bar Association or editors or any copyright holders for any injury or damage to any person or property as a consequence of the reading, use or interpretation of its published content. Whilst every effort is made to ensure accuracy, The Gujarat Sales Tax Bar Association, the authors, editors and copyright holders cannot be held responsible for any omissions or errors. The views or opinions expressed are of the writer/s and do not necessarily reflect the views of The Gujarat Sales Tax Bar Association.

472

459

July - 2016 SALES TAX JOURNAL - 55

EDITORIAL

N. N. Patel - Kuntal A. Parikh

Read, Writ and Share

Dear Members,

New Committee has taken a charge and Showers have blessed the wonderland!

Monsoon is seasonal reversal wind. South-West monsoon winds bless us with showers. Similarly we, the tax practitioners wish, Reversal Winds blow from Delhi, bless us not only with GST Law but with rights to do Audit also. Whether wind blows as we wish or not, since we are experienced practitioners in the field, ‘Right to do Audit’ under GST Law cannot only be a reason to survive. We would say that if rights of Audit are granted, it would be surplus.

Be that as it may, we do invite members of our association to give their contribution in Journal by expressing their views by writing articles and columns. We do expect our members to express their views not only about VAT laws but also to writ columns and / or articles about other indirect tax laws because under GST regime adjudication procedure, valuation principles, etc. are taken from Excise and Service Tax laws. Therefore, it is pertinent to know about other tax laws also. We do believe that if members would share their knowledge in other than VAT laws also, it would be benefited to all readers.

To enrich our Journal and to make it remarkable, it would be our kind request to all members to Read, Writ and Share.

EDITORIAL

473

460

SALES TAX JOURNAL - 55 July - 2016

CONGRATULATION & BEST WISHES

Dr. HIRAL PARIKHThe daughter of Shri Mahendrabhai C. Parikh – A member of our Association and wife of late Shri Malav Pravinbhai Soni (Ex-Committee Member of GSTBA) has been awarded degree of Doctorate in Philosophy by the Gujarat University. The thesis written by her on the subject accountancy / commerce has been accepted for the degree of Doctorate in Philosophy. She is also a member of our Bar Association. We wish her heartiest congratulations for successfully completing her Doctorate (PhD) in the said subject. We wish more success may come in her life.

Meet Desai Devam Sheth Aneri Sheth son of Hetal R. Desai son of Sanjay R. Sheth Daughter of Sanjay R. Sheth

Hirak Shah Viraj Gopani Shraddha Thacker Parthiv Thakkar son of son of (Gopani) son of Rajesh J.Shah Vaikkuth R.Gopani Daughter in Law of Dilipbhai B. Thakkar Vaikkuth R.GopaniThe Brilliant and Shining Sons and/or Daughters of Members of our

Bar Association who have passed their C. A. final examination. We wish them success in their life.

474

461

July - 2016 SALES TAX JOURNAL - 55

President’s Desk

RUPESH S. SHAH [email protected]

´ÉeÒ±ÉÉà +{Éà Ê©ÉmÉÉà,OÉÒº©É{ÉÒ NÉù©ÉÒ +{Éà ¥É£ÉùÉ{ÉÉ ©ÉɾÉà±É ´ÉSSÉà ]ù©Éù ]ù©Éù ´Éù»ÉÉqà +É{ÉÅq{ÉÉà ©ÉɾÉà±É »ÉWâ±É Uà. ¾WÖ

~ÉiÉ OÉÒ{É NÉÖWùÉlÉ ©ÉÉ÷à ´Éù»ÉÉq{ÉÒ »ÉLlÉ W°Êù«ÉÉlÉ Uà.»É{É 2014-15©ÉÉÅ ÷Äà]ùù{ÉÒ W´ÉÉ¥ÉqÉùÒ ©É{Éà »ÉÉá~É´ÉÉ©ÉÉÅ +É´Éà±É. »É{É 2015-16©ÉÉÅ »ÉàJà÷ùÒ lÉùÒHà{ÉÒ

W´ÉÉ¥ÉqÉùÒ »ÉÉá~É´ÉÉ©ÉÉÅ +É´ÉÒ ¾lÉÒ +{Éà ¾´Éà ´ÉºÉÇ 2016-17 ©ÉÉ÷à ¡É©ÉÖLÉ lÉùÒHà{ÉÒ W´ÉÉ¥ÉqÉùÒ ©É{Éà »ÉÉá~É´ÉÉ©ÉÉÅ +É´ÉÒ Uà. +É ¾lÉÖÅ ~ÉÊù´ÉlÉÇ{É +{Éà Y+à»É÷Ò¥ÉÒ+à©ÉÉÅ oÉ«Éà±É HÉ«ÉÉâ Wà ¥É{ÉÒ ùÂÖÅ Uà lÉà©ÉÉÅ HÅ<H {É´ÉÖÅ Hù´ÉÉ{ÉÉ, ©ÉÚ±«É-´ÉÊyÉÇlÉ Hù´ÉÉ{ÉÉ +ʧÉNÉ©É{ÉÒ Ê{ɶÉÉ{ÉÒ Uà.

¥ÉÉù +à»ÉÉà»ÉÒ+à¶É{É{ÉÉ ©ÉɳLÉÉ{ÉÒ »ÉùLÉÉ©ÉiÉÒ ¾ÖÅ +àH »ÉÖ»ÉÅSÉÉʱÉlÉ «ÉÅmÉ »ÉÉoÉà HùÖÅ UÖÅ. ¡É©ÉÖLÉ{ÉÒ »ÉÉoÉà LÉÚ¥É W +{É֧ɴÉÒ ¾ÉàtàqÉùÉà »ÉlÉlÉ HÉ«ÉÇùlÉ ¾Éà«É Uà. Y+à»É÷Ò¥ÉÒ+à{ÉÉ HÉ«ÉÇKÉ©É HÉà-+Éà~÷ »É§«ÉÉà, +àeÒ÷ùÉà, »É¥É-HÊ©É÷Ò{ÉÉ H{´ÉÒ{ÉùÉà +{Éà »É§«ÉÉà +{Éà ~ÉÚ́ ÉÇ-¡É©ÉÖLɸÉÒ+Éà{ÉÉà ±ÉÉ§É ©É³lÉÉà ù¾àlÉÉà ¾Éà«É Uà +{Éà +É~ÉiÉÉ ¥ÉÉù +à»ÉÉà»ÉÒ+à¶É{É{ÉÒ ¡ÉÊlɧÉÉ lÉoÉÉ NÉÊù©ÉÉ{Éà »É¾àW ~ÉiÉ +ÉÅSÉ {É +É´Éà lÉà ©ÉÉ÷à ¡É©ÉÖLÉ lÉoÉÉ lÉà+Éà{ÉÒ ÷Ò©É{Éà +à©~ÉÉ´ÉeÇ HÊ©ÉÊ÷{ÉÉ H{´ÉÒ{Éù +{Éà »É§«É¸ÉÒ+Éà{ÉÖÅ ©ÉÉNÉÇq¶ÉÇ{É ©É³lÉÖÅ ù¾àlÉÖÅ ¾Éà«É Uà. +É ¥ÉyÉÉ{ÉÉ ~ÉÒc¥É³ lÉùÒHà +à»ÉÉà»ÉÒ+à¶É{É{ÉÉ »÷É£ Ê©ÉmÉÉà +©ÉÉùÒ ~ÉÉ»Éà HùÉàeùVWÖ »É©ÉÉ{É »ÉÉÊ¥ÉlÉ oɶÉà. +É ¥ÉyÉÉ oÉHÒ +©ÉÉùÉà “Roadmap” LÉÚ¥É W »ÉÖÊ{ÉÊýÉlÉ Hù´ÉÉ{ÉÉà Uà. ´ÉºÉÇ qùÊ©É«ÉÉ{É{ÉÉ HÉ«ÉÇJ©ÉÉà{ÉÒ ©ÉÉʾlÉÒ qù ©ÉÉ»Éà ©ÉÉùÉ “¡É©ÉÖLɸÉÒ{ÉÒ H±É©Éà“ lÉoÉÉ “+à»ÉÉà»ÉÒ+à¶É{É {«ÉÖ]“ wÉùÉ +É~É »ÉÉä »É§«ÉÉà{Éà ©É³lÉÉ ù¾à¶Éà.

©Éà{ÉàYÅNÉ HÊ©É÷Ò{ÉÒ »É¾É«É +oÉâ +±ÉNÉ +±ÉNÉ ~Éà÷É-HÊ©É÷Ò+Éà{ÉÒ ùSÉ{ÉÉ oÉ< NÉ«Éà±É Uà. Wà{ÉÖÅ ~Éà÷É-HÊ©É÷Ò´ÉÉù ±ÉÒ»÷ +É +ÅH©ÉÉÅ +à»ÉÉà»ÉÒ+à¶É{É {«ÉÖ]©ÉÉÅ +É~Éà±É Uà. +±ÉNÉ +±ÉNÉ HÊ©É÷Ò+Éà{ÉÒ +´ÉÉù{É´ÉÉù Ê©É÷ÓNÉÉà Hù´ÉÉ{ÉÖÅ +É«ÉÉàW{É {ÉIÒ Hùà±É Uà. WàoÉÒ Ê´ÉSÉÉùÉà{ÉÖÅ +ÉqÉ{É-¡ÉqÉ{É oÉHÒ ´ÉºÉÇ qùÊ©É«ÉÉ{É{ÉÉ HÉ«ÉÇJ©ÉÉà{ÉÖÅ ´«É´ÉλoÉlÉ +{Éà ~ÉÊùiÉɩɱÉKÉÒ +É«ÉÉàW{É oÉ< ¶ÉHà.

¥É¾Éà³É ¡É©ÉÉiÉ©ÉÉÅ {É´ÉÉ «ÉÖ´ÉÉ{É »É§«ÉÉà oÉÉ«É Uà Wà +É{ÉÅq{ÉÒ ´ÉÉlÉ Uà. +É~ÉiÉÒ »ÉÅ»oÉÉ{ÉÉà +àH {É´ÉÒ Êq¶ÉÉ©ÉÉÅ Ê´ÉHÉ»É oÉÉ«É lÉà ©ÉÉ÷à{ÉÉ »ÉÚSÉ{ÉÉà +©ÉÉà{Éà SÉÉàI»É WiÉɴɶÉÉà. +É~É{ÉÉ ¡ÉüÉÉà{ÉÒ XiÉ »ÉÅ»oÉÉ{Éà ±ÉàÊLÉlÉ©ÉÉÅ Hù´ÉÉ©ÉÉÅ +É´Éà lÉà <SU{ÉÒ«É Uà WàoÉÒ lÉà ¥ÉÉ¥ÉlÉà +©ÉÉà ~ÉÊùiÉɩɱÉKÉÒ HÉ«ÉÇ »ÉÉoÉà ©É³Ò HùÒ ¶ÉHÒ+à. ùÒ¤à¶Éù HÉà»ÉÇ{ÉÉ »É§«ÉÉà ©ÉÉ÷à{ÉÒ ¡ÉoÉ©É Ê©É÷ÓNÉ »É~÷à©¥Éù ©ÉɻɩÉÉÅ oɶÉà. Wà{ÉÒ +±ÉNÉoÉÒ ùÒ¤à¶Éù HÉà»ÉÇ{ÉÉ »É§«ÉÉà{Éà XiÉ Hù´ÉÉ©ÉÉÅ +ɴɶÉà.

¥Éà{ÉÒ´ÉÉà±É{÷ »HÒ©É{ÉÉ »É§«ÉÉà{Éà +àe´ÉÉ{»É £à÷ù{ÉÒ÷Ò{ÉÉ ¾~lÉÉ ©ÉÉ÷à{ÉÉà ~ÉÊù~ÉmÉ ÷ÚÅH »É©É«É©ÉÉÅ ©ÉÉàH±ÉÒ ùÂÉ Uà.+É~É{ÉÉ +Ê´ÉùlÉ »ÉÉoÉ +{Éà »É¾HÉù »ÉÉoÉ+à ©ÉÉNÉÇq¶ÉÇ{É{ÉÉà +ʧɱÉɺÉÒ.

°~Éà¶É +à»É. ¶Éɾ ¡É©ÉÖLÉ

yÉÒ NÉÖWùÉlÉ »Éà±»É÷àKÉ ¥ÉÉù +à»ÉÉà»ÉÒ+à¶É{É

President’s Desk

475

462

SALES TAX JOURNAL - 55 July - 2016

+…y…÷�{…HÌ +N…l´…{……

∂…•qÌ…‡{…“ ª…©…WHarish N. Shah - Vat Consultant

+…‡+‡©…+…‡ +‡`±…‡ ∂…÷≈ ?

+…‡+‡©…+…‡ +‡ +…‡~…{… ©……HÌ‚` +…‡~…2‡∂…{ª…{……‡ `⁄≈HÌ…K…2“ ∂…•qÌ U‡. Ê2]¥…« •…‡{HÌ +…‡£Ì >Œ{e´…… ª…2HÌ…2“ •……‡{e{……≈ ¥…‡S……i… Ḣ L…2“qÌ“ w…2… +o…«l…≈m…©……≈ {……i……≈ °…¥……ÊæÌl……{…÷≈ Ê{…´…©…{… HÌ2‡ U‡. W‡{…‡ +…‡+‡©…+…‡ HÌæ̇ U‡.

+…‡+‡©…+…‡ A~…2…≈l… Ê2]¥…« •…‡{HÌ ~……ª…‡ {……i……≈ °…¥……ÊæÌl……{…… Ê{…´…©…{… ©……`‡ Ḣ∂… Ê2]¥…« 2‡Ê∂…´……‡ (ª…“+…2+…2), ª`‡S´…÷`2“ ʱ…ŒG¥…Êe`“ 2‡Ê∂…´……‡ (+‡ª…+‡±…+…2) W‡¥…… æÌÊo…´……2…‡ ~…i… U‡.

Ê2]¥…« •…‡À{HÌN… +o…«l…≈m…©……≈ {……i……≈ °…¥……ÊæÌl…… +…‡U“ HÌ2¥…“ æÌ…‡´… l……‡ l…‡ ª…2HÌ…2“ •……‡{e{…÷≈ ¥…‡S……i… HÌ2‡ U‡. •……‡{HÌ L…2“qÌ{……2…{……≈ {……i……≈ +… 2“l…‡ +…2•…“+…> ~……ª…‡ +…¥…l…… °…¥……ÊæÌl……{…÷≈ qÌ•……i… +…‡U÷≈ o……´… U‡. l…‡ 2“l…‡ l…‡{…“ °…¥……ÊæÌl…… ¥…y……2¥…“ æÌ…‡´… l……‡ l…‡ ~……‡l……{…… W •……‡{e L…2“q̇ U‡.

Ê2]¥…« •…‡{HÌ S……2 ©…÷qÌl…{…… •……‡e« •…æÌ…2 ~……e‡ U‡. q̪… ¥…∫…«{…… •……‡{e •…‡{S…©……HÌ« U‡. +… A~…2…≈l… l…‡ 91 ÊqÌ¥…ª…, 182 ÊqÌ¥…ª… +{…‡ 364 ÊqÌ¥…ª…{…… `ƒ…‡¥…2“ Ê•…±ª… •…æÌ…2 ~……e‡ U‡. °…l´…‡HÌ{…… ¥´……WqÌ2 W÷qÌ… æÌ…‡´… U‡. Ê2]¥…« •…‡{HÌ `⁄≈HÌ…, ©…y´…©… l…o…… ±……≈•…… N……≥…{…… {……i……≈ °…¥……ÊæÌl……{…… Ê{…´…©…{… ©……`‡ +… •……‡{e{…÷≈ L…2“qÌ - ¥…‡S……i… HÌ2‡ U‡. ©…÷L´…l¥…‡ •…‡{HÌ…‡ +… •……‡{e©……≈ ª…æÌß……N…“ •…{…‡ U‡. Ê2]¥…« •…‡{HÌ{…… 2‡~……‡qÌ2 HÌ2l……≈ l…‡©…{…‡ +… •……‡{e©……≈ ¥…y…÷ ¥…≥l…2 U⁄`l…÷≈ æÌ…‡¥……o…“ l…‡+…‡ ª…2HÌ…2“ •……‡{e©……≈ 2…‡HÌ…i… HÌ2¥…… °…‡2…´… U‡.

Ê2]¥…« •…‡{HÌ{…… +…‡+‡©…+…‡{…“ l…lHÌ…≥ +ª…2 {……i……≈ •…X2 A~…2 +{…‡ ©…y´…©… ±……≈•…… N……≥‡ •…‡{HÌ…‡{…… Êe~……‡Ê]` Êy…2…i…{…… ¥´……WqÌ2 A~…2 ~…e‡ U‡.

+‡ª…e•±´…÷~…“ +‡`±…‡ ∂…÷≈ ?

+‡ª…e•±´…÷~…“ +‡ ʪ…ª`©…‡Ê`HÌ Ê¥…eƒ…‡+±… ~±……{…{……‡ `⁄≈HÌ…K…2“ ∂…•qÌ U‡. W‡©… 2…‡HÌ…i…HÌ…2 l…‡{……≈ {……i……≈ ©´…÷S´…÷+±… £Ì≈e{…… +‡ª…+…>~…“ (ʪ…ª`©…‡Ê`HÌ >{¥…‡ª`©…‡{` ~±……{…) w…2… 2…‡HÌ…i… HÌ2‡ U‡ l…‡{……o…“ C±`÷≈ +‡ª…e•±´…÷~…“ 2…‡HÌ…i…HÌ…2{…‡ l…‡{…… 2…‡HÌ…i…©……≈o…“ Ê{…´…Ê©…l… A~……e{…“ ª…÷Ê¥…y…… °…qÌ…{… HÌ2‡ U‡.

+‡ª…+…>~…“{…‡ ©…≥l…“ +…¥…‡ l…‡¥…“ ´……‡W{……+…‡ U‡ ~……‡ª` +…‡Ê£Ìª…{…“ +‡©…+…>~…“ (©…≈o…±…“ >{HÌ©… ~±……{…) +{…‡ ʪ…Ê{…´…2 ʪ…Ê`]{ª… ª…‡À¥…N… ªHÌ“©…. +…¥…“ ªHÌ“©……‡©……≈ 2…‡HÌ…i…{…… A~……e A~…2 HÌ…‡> ¥…y……2…{……‡ S……W« ±…‡¥……l……‡ {…o…“, ~…2≈l…÷ P…i……≈ ©´…÷S´…÷+±… £Ì≈e√ª… l…‡{…… +‡ª…e•±´…÷~…“©……≈ A~……e A~…2 +‡ŒG]` ±……‡e {……L…‡ U‡, W‡ 2…‡HÌ…i…HÌ…2…‡ A~…2 ¥…y……2…{……‡ L…S…« U‡. Ê{…¥…fin… ¥´…ŒGl…+…‡ ©……`‡ +‡ª…e•±´…÷~…“ •…æÌ÷ A~…´……‡N…“ U‡. l…‡+…‡ l…‡©…{…“ +‡+‡©…ª…“ (+‡ª…‡` ©…‡{…‡W©…‡{` HÌ≈~…{…“) {…‡ +‡HÌ +… A~……e ©……`‡{…“ m…i… - U ©…ÊæÌ{……{…“ æÌ…‡´… +o…¥…… 2…‡HÌ…i…HÌ…2{…“ ~…ª…≈qÌN…“{…“ æÌ…‡´… U‡. +… ~…⁄¥…«Ê{…y……«Ê2l… l……2“L…‡ +‡+‡©…ª…“ 2…‡HÌ…i…HÌ…2{…… ´…÷Ê{…` ~…÷{…: L…2“qÌ“{…‡ +o…¥…… ¥…‡S…“{…‡ l…‡ {……i……≈ 2…‡HÌ…i…HÌ…2{…… •…‡{HÌ L……l……©……≈ W©…… HÌ2‡ U‡.

+ÉyÉÖÊ{ÉH +NÉl«É{ÉÉ ¶É¥qÉà{ÉÒ »É©ÉW

476

463

July - 2016 SALES TAX JOURNAL - 55

+‡ª…e•±´…÷~…“©……≈ A~……e{…… ÊqÌ¥…ª…‡ ́ …÷Ê{…`{…“ W‡ {…‡` +‡ª…‡` ¥…‡±´…÷ (+‡{…+‡¥…“) æÌ…‡´… l…‡{…… +…y……2‡ l…‡{……≈ ́ …÷Ê{…`{…÷≈ +{…÷∞~… ¥…‡S……i… - ~…÷{…«L…2“qÌ“ o……´… U‡. +‡{…+‡¥…“©……≈ o…l…… £Ì‡2£Ì…2{…‡ +{…÷∞~… ´…÷Ê{…`{…÷≈ ¥…‡S……i… - ~…÷{…«L…2“qÌ“ +‡ °…©……i…©……≈ o……´… U‡, W‡o…“ 2…‡HÌ…i…HÌ…2‡ l…‡i…‡ {…I“ HÌ2‡±…“ 2HÌ©… l…‡{…… •…‡{HÌ L……l……©……≈ W©…… o…l…“ 2æ̇.

`…‡~… +~… ~±……{… +‡`±…‡ ∂…÷≈ ?

`…‡~… +~… ~±……{… +‡`±…‡ W‡ ¥…y……2…{…… ©…´……«ÊqÌl… L…S…«©……≈ ¥…y……2…{…÷≈ ¥…“©…… HÌ¥…S… ~…⁄2÷≈ ~……e‡.

HÌ≈~…{…“+…‡ W‡ ª……qÌ“ +…2…‡N´… ¥…“©…… +…‡£Ì2 HÌ2‡ l…‡©……≈ æÌ…‡Œª~…`±…{…… L…S…«{…‡ ©…´……«ÊqÌl… L…S…«©……≈ +…¥…2‡ U‡. +…©……≈ P…i…“¥……2 +‡¥…÷≈ •…{…‡ Ḣ •…“©……2“ N…≈ß…“2 æÌ…‡´… +{…‡ ±……≈•……‡ ª…©…´… æÌ…‡Œª~…`±… ª……2¥……2{…“ W∞2 ~…e‡ l……‡ +… ¥…“©…… HÌ¥…S…{……‡ 5{……‡ `⁄≈HÌ…‡ ~…e‡ U‡. +‡`±…‡ `…‡~… +~… ~±……{… ±…“y……‡ æÌ…‡´… l……‡ o……‡e÷≈ ¥…y…÷ °…“Ê©…´…©… S…⁄HÌ¥…“{…‡ +…2…‡N´…{…… ¥…y…÷ X‡L…©… ª……©…‡ ¥…“©…… HÌ¥…S… ©…‡≥¥…“ ∂…HÌ…´… U‡.

ª……qÌ… >{e‡Œ©{…`“ ~±……{…©……≈ +©…÷HÌ 2HÌ©… ª…÷y…“ HÌ¥…S… ©…≥‡ U‡, ~…i… +… 2HÌ©…o…“ ¥…y…÷ W‡ L…S…« +…¥…‡ l…‡ ~……‡Ê±…ª…“y……2Ḣ ß……‡N…¥…¥……‡ ~…e‡ U‡. +… ¥…y……2…{…… L…S…«{…‡ ÊeeHÌ`“•…±… HÌæ̇ U‡. `…‡~… +~… ~±……{…{……‡ qÌ…¥……‡ HÌ2l…… O……æÌHÌ{…‡ l…‡{…… ©…⁄≥ 2HÌ©…{…“ S…÷HÌ¥…i…“ o…´…… ~…U“ ¥…y……2…{……‡ W‡ L…S…« o…´……‡ æÌ…‡´… l…‡ `…‡~… +~… ~±……{…{…“ ©…´……«qÌ… ~…⁄2l……‡ ©…≥‡ U‡. qÌ….l…. ~……≈S… ±……L… ∞Ê~…´……{…… `…‡~… +~… ~±……{…©……≈ ÊeeHÌ`“•…±… ∞…. 3 ±……L…{…÷≈ æÌ…‡´… +{…‡ qÌ…¥……‡ S……2 ±……L… ∞Ê~…´……{……‡ HÌ´……‚ æÌ…‡´… l……‡ ©…⁄≥ m…i… ±……L… ∞Ê~…´……{…… ~……‡Ê±…ª…“ HÌ¥…S…{…“ ~…⁄2“ S…÷HÌ¥…i…“ HÌ2¥……{…“ ª……o…‡ +‡HÌ ±……L… ∞Ê~…´……{…“ S…÷HÌ¥…i…“ `…‡~… +~… ~±……{…©……≈o…“ HÌ2¥……©……≈ +…¥…∂…‡.

`…‡~… +~… ~±……{…©……≈ ~…i… ¥´…ŒGl…N…l… +{…‡ £Ì±……‡`2 ~±……{… æÌ…‡´… U‡. £Ì±……‡`2©……≈ ~…Ê2¥……2{…“ +‡HÌo…“ ¥…y…÷ ¥´…ŒGl…{…‡ +…¥…2“ ±…‡¥……´… U‡. Àª…N…±… >Œ{ª…e{ª… ̀ …‡~… +~… ~±……{…©……≈ æÌ…‡Œª~…`±… •…“±… +‡HÌ W •…“©……2“©……≈ ÊeeG`“•…±…o…“ ¥…y…÷ +…¥…‡ l´……2‡ ©…≥‡ U‡. •…“X °…HÌ…2{…… æÌ…‡Œª~…`±…©……≈ 2æ̇¥……{…… +‡HÌo…“ ¥…y…÷ ÊH̪ª……{…… qÌ…¥……{…‡ N…i…l…2“©……≈ ±…> ÊeeHÌ`“•…±… {…HÌHÌ“ o……´… U‡.

°……‡©…{……e (PROMENADE)

∂…æ̇2…‡©……≈ P…i…… +‡¥…… L…÷±±…… Xæ̇2 ©……N…« æÌ…‡´… U‡, V´……≈ ª…¥……2‡ {…‡ ª……≈W‡ ±……‡HÌ…‡ S……±…¥…… W> ∂…Ḣ. §‡{S… ∂…•qÌ PROMENADE {……‡ +o…« U‡ +…2…©…o…“ S……±…¥…÷≈ Ḣ ª…æ̇±… HÌ2¥…“, W‡{…… ~…2o…“ +… +≈O…‡Y ∂…•qÌ Aq√ß…¥´……‡ U‡. +‡HÌ ª…©…´…‡ P……·e‡ª…¥……2“ HÌ2¥……{…“ Xæ̇2 WN´…… ~…i… +… {……©…o…“ +…‡≥L……l…“ æÌl…“. V´……2‡ qÌÊ2´……> ª…£Ì2{……≈ ¥…æÌ…i……‡ ±……‡HÌÊ°…´… æÌl……≈ l´……2‡ °…¥……ª…“+…‡{…“ ª…æ̇±… ©……`‡ +‡HÌ L……ª… e‡HÌ 2L……l……‡ æÌl……‡, W‡ °……‡©…{……e e‡HÌ {……©…o…“ +…‡≥L……l……‡ æÌl……‡. HÌ´……2‡HÌ L…÷±±…… ©…‡qÌ…{…©……≈ ª…≈N…“l…{…… +‡¥…… W±…ª…… ´……‡X´… U‡, W‡©……≈ •…‡ª…¥……{…“ ¥´…¥…ªo…… {… æÌ…‡´… +{…‡ ∏……‡l……+…‡ æÌ2“£Ì2“ ∂…Ḣ +…¥……‡ W±…ª……‡ °……‡©…{……e HÌ…‡{ª…`« HÌæ̇¥……´… U‡. +… ∂…•qÌ{…÷≈ +‡HÌ +‡¥…÷≈ ~…i… +o…«P…`{… HÌ2¥……©……≈ +…¥…‡ U‡ Ḣ ©……m… qÌÊ2´……ÊHÌ{……2‡ S……±…¥……{……‡ ©……N…« +‡{…“ ¥´……L´……©……≈ +…¥…‡. +… xŒ∫`+‡ ©…÷≈•…>{……‡ ©…2“{… eƒ…>¥… L…2…‡ °……‡©…{……e U‡.

�2y…©…Ì (RHYTHM)

HÌ…‡> ~…i… Œªo…Êl…©……≈ l……±…©…‡±… +o…¥…… y¥…Ê{…{…“ ª…©……{…l…… ©……`‡ +…W‡ +… ∂…•qÌ{……‡ °…´……‡N… HÌ2¥……©……≈ +…¥…‡ U‡. HÌÊ¥…l……©……≈ °……ª… ©…‡≥¥…¥…… ª…2L…… y¥…Ê{…{…… W‡ ∂…•qÌ…‡ ¥…~…2…´… U‡ +‡©…{…… ©……`‡ RHYTHM ª…≈•……‡y…{… °…S…ʱ…l… U‡. +… •…{{…‡ ∂…•qÌ…‡{…÷≈ ©…⁄≥ O…“HÌ ß……∫……{…… RHUTHMOS ©……≈ U‡, W‡{……‡ +o…« U‡ ¥……2≈¥……2 •…{…l…“ P…`{……. 2…>©…

+ÉyÉÖÊ{ÉH +NÉl«É{ÉÉ ¶É¥qÉà{ÉÒ »É©ÉW

477

464

SALES TAX JOURNAL - 55 July - 2016

∂…•qÌ©……≈ ~…i… �2y…©… æÌ…‡¥…÷≈ W∞2“ U‡ ©……`‡ W +‡ ∂…•qÌ{……‡ °…´……‡N… X‡eHÌi…… W‡¥…“ •……≥HÌÊ¥…l……+…‡ ©……`‡ o……´… U‡ +{…‡ +‡ {…ª…«2“ 2…>©… HÌæ̇¥……´… U‡. W‡©……≈ l……±…©…‡±… {… æÌ…‡´… +‡¥…“ ¥…l…«i…⁄HÌ ©……`‡ ß……∫……©……≈ +‡HÌ AŒGl… A©…‡2…> U‡ - Ê¥…y……A` 2…>©… +…‡2 Ê2]{… (h≈N…P…e… ¥…N…2{…÷≈). ª…≥≈N…l…… X≥¥…“ 2…L…¥…… Ê2y…©… W∞2“ U‡, ~…i… +…W‡ ª…≈N…“l…{…… K…‡m…‡ l……±…•…ul…… ©……`‡ +… ∂…•qÌ ¥…y……2‡ ¥…~…2…´… U‡.

2‡{ª…©… Ì(RANSOM)

HÌ…‡> ¥´…ŒGl…{…÷≈ +~…æÌ2i… o…´…… •……qÌ +‡{…‡ ©…÷Gl… HÌ2¥…… ©……`‡ W‡ 2HÌ©…{…“ ©……N…i…“ HÌ2¥……©……≈ +…¥…‡ U‡ +‡{…… ©……`‡ +… ∂…•qÌ{……‡ °…´……‡N… o…l……‡ æÌ…‡´… U‡. +‡HÌ ª…©…´…‡ e…HÌ÷+…‡ w…2… +~…æÌ2i… HÌ2¥……©……≈ +…¥…l……≈ æÌl……≈, ~…i… +…W‡ ©……‡`…≈ ∂…æ̇2…‡©……≈ ©……m… ~…‰ª…… HÌ©……¥……{…… >2…qÌ…o…“ ª…©……WÊ¥…2…‡y…“ l…n¥……‡ +…¥…“ °…¥…fiŒn… HÌ2l……≈ æÌ…‡´… U‡. ©…⁄≥ §‡{S… ∂…•qÌ RANSOM {……‡ +o…« U‡ ~…‰ª…… +…~…“{…‡ U÷`HÌ…2…‡ ©…‡≥¥…¥……‡, W‡{…‡ +≈O…‡Y©……≈ +…~…{……¥…¥……©……≈ +…¥´……‡ U‡. +≈O…‡Y©……≈ ¥…~…2…l…… +‡HÌ •…“X ∂…•qÌ Ê2e“©…{……‡ ~…i… ª…2L……‡ W +o…« o……´… U‡. +… ∂…•qÌ W~l… HÌ2‡±……≈ ©……±… Ḣ Ê©…±…HÌl…{…‡ U…‡e…¥…¥…… ©……`‡ ¥…~…2…´… U‡. +…¥……‡ ©……±… U…‡e…¥…l…“ ¥…L…l…‡ W‡ qÌ≈e ß…2¥……‡ ~…e‡ U‡ +‡ ~…i… Ê2e‡©~…∂…{… £Ì…>{… l…2“Ḣ +…‡≥L……´… U‡, V´……2‡ 2‡{ª…©… ∂…•qÌ ¥´…ŒGl…{…‡ ©…÷Gl… HÌ2¥…… ~…⁄2l……‡ W ©…´……«ÊqÌl… U‡.

2…>`Ì (WRITE)

±…L…¥……{…“ ∂…∞+…l…{…… ÊqÌ¥…ª……‡©……≈ HÌ…‡> y……2qÌ…2 ¥…ªl…÷ w…2… HÌ…∫c +o…¥…… ~…oo…2 ~…2 ∂…•qÌ…‡ HÌ≈e…2¥……©……≈ +…¥…l…… æÌl……. °……S…“{… ª…©…´…{……≈ ¥……ª…i……‡ ~…2 ~…i… +… °…HÌ…2{……≈ ±…L……i… X‡¥…… ©…≥‡ U‡. W⁄{…… +≈O…‡Y©……≈ +…¥…… ±…L……i… ©……`‡ WRITAN ∂…•qÌ °…´……‡N…©……≈ +…¥´……‡ æÌl……‡, W‡{……‡ +o…« æÌl……‡ ʱ…ª……‡`…‡ ~…‡Œ{ª…±… +{…‡ ~…‡{…{…“ ∂……‡y… ~…U“ W⁄{……≈ A~…HÌ2i……‡ ß…÷±……> N…´……≈ +{…‡ +…W‡ `…>~… HÌ2‡±…÷≈ ±…L……i… ~…i… +… ∂…•qÌ{…“ ¥´……L´……©……≈ +…¥…“ N…´…÷≈ U‡. ±…‡ÊL…l… ß……∫…… Ê¥…S……2…‡ ¥´…Gl… HÌ2¥……{…÷≈ ©…÷L´… ©……y´…©… •…{…“ N…> U‡ +{…‡ +…¥…÷≈ ±…L…{……2“ ¥´…ŒGl…{…‡ 2…>`2 HÌæ̇¥……©……≈ +…¥…“. HÌ…´…qÌ…{…“ ß……∫……©……≈ ±…‡ÊL…l… +…q̇∂… ©……`‡ WRITE ∂…•qÌ{……‡ °…´……‡N… o…l……‡ æÌ…‡´… U‡. HÌ…‡> Ê¥…∫…´… ~…2 ©……ÊæÌl…“ +…~…l…÷≈ ±…L……i… 2…>`-+~… HÌæ̇¥……´… U‡ +{…‡ X‡ ¥…ªl…÷+…‡{…“ ª…⁄ÊS…©……≈o…“ HÌ≈> •……qÌ HÌ2“ q̇¥……©……≈ +…¥…‡ l……‡ 2…>`-+…‡£Ì ∂…•qÌ°…´……‡N… HÌ2¥……©……≈ +…¥…‡ U‡.

`ƒ…{ª…£Ì2 (TRANSFER)

{……‡HÌ2“©……≈ o…l…“ •…q̱…“ ©……`‡ +… ∂…•qÌ{……‡ °…´……‡N… ¥…y……2‡ X‡¥…… ©…≥‡ U‡. ª¥…‡SU…+‡ HÌ2¥……©……≈ +…¥…l…÷≈ ªo…≥…≈l…2 ©……>O…‡∂…{… U‡, V´……2‡ HÌ…‡>{…… +…q̇∂…o…“ ªo……{… •…q̱…¥…… ©……`‡ `ƒ…{£Ìª…2 ∂…•qÌ ¥…~…2…´… U‡. •…‡ §‡{S… ∂…•qÌ TRANS (ª……©…‡ ~……2) +{…‡ FERER (±…> W¥…÷≈) {…‡ ß…‡N…… HÌ2¥……o…“ +… ∂…•qÌ •…{´……‡ U‡. +… `ƒ…{ª… ∂…•qÌ ~…2o…“ +≈O…‡Y ß……∫……©……≈ P…i…… ∂…•qÌ A©…‡2…´…… U‡. +‡HÌ ß……∫……{…… ª……ÊæÌl´…{…‡ +{´… ß……∫……©……≈ ±…> W¥…÷≈ +‡`±…‡ +{…÷¥……qÌ HÌ2¥……‡. +…¥…“ °…¥…fiŒn… `ƒ…{ª…±…‡∂…{… {……©…o…“ +…‡≥L……´… U‡. ±……≈•…… +≈l…2{……≈ •…‡ ªo…≥{…‡ X‡el…… °…¥……ª… ©……`‡ ~…i… `ƒ…{ª… ∂…•qÌ ¥…~…2…´… U‡, W‡©… Ḣ 2…Ê∂…´……{…“ ±……≈•…“ `ƒ‡{…ª…‡¥…… `ƒ…{ª… ª……>•…‡Ê2´…{… 2‡±…¥…‡. V´……2‡ HÌ…‡> Ê©…±…HÌl…{…÷≈ ¥…‡S……i… o……´… U‡ l´……2‡ HÌ…´…qÌ…{…“ ß……∫……©……≈ +…¥…… ¥´…¥…æÌ…2 ©……`‡ `ƒ…{ª…£Ì2 +…‡£Ì °……‡~…`‘ ∂…•qÌ…‡{……‡ °…´……‡N… HÌ2¥……©……≈ +…¥…‡ U‡.

¥…Ã∂…~…Ì (WORSHIP)

+…W‡ >π…2{…“ °……o…«{…… Ḣ ~…⁄X ©……`‡ +… ∂…•qÌ ¥…~…2…´… U‡. W⁄{…… +≈O…‡Y©……≈ WORSHIP ∂…•qÌ{……‡ ´……‡N´…l…… ©……`‡ °…´……‡N… HÌ2¥……©……≈ +…¥…l……‡ æÌl……‡ +‡©……≈ SCIPE (Œªo…Êl…) A©…‡2¥……o…“ ¥…Ã∂…~… ∂…•qÌ •…{´……‡ U‡, W‡

+ÉyÉÖÊ{ÉH +NÉl«É{ÉÉ ¶É¥qÉà{ÉÒ »É©ÉW

478

465

July - 2016 SALES TAX JOURNAL - 55

´……‡N´… ¥´…ŒGl… °…l´…‡ +…qÌ2 ¥´…Gl… HÌ2¥…… ©……`‡ ¥…~…2…¥…… ±……N´……‡. +…2≈ß…©……≈ +… ∂…•qÌ HÌ…‡> HÌ…•…‡±… ¥´…ŒGl… ©……`‡ ß…ŒGl…ß……¥… qÌ∂……«¥…¥…… ~…⁄2l……‡ W ©…´……«ÊqÌl… æÌl……‡. ß……∫……©……≈ ¥…o…« +{…‡ ¥…Ã∂…~… ∂…•qÌ…‡ +‡HÌ•…“X{…… ~…⁄2HÌ U‡ +‡©… HÌæÌ“ ∂…HÌ…´…, HÌ…2i… Ḣ W‡ ´……‡N´… U‡ +‡{…“ W ß…ŒGl… o…l…“ æÌ…‡´… U‡. HÌ´……2‡HÌ {´……´……y…“∂… ©……`‡ ~…i… ª…©©……{…ª…⁄S…HÌ ª…≈•……‡y…{… ´……‡2 ¥…Ã∂…~… °…S…ʱ…l… æÌl…÷≈. ª…©…´… Wl……≈ ¥…Ã∂…~… ∂…•qÌ{……‡ °…´……‡N… y……é…HÌ Ê¥…Êy…+…‡©……≈ ¥…y……2‡ X‡¥…… ©…≥‡ U‡ +{…‡ +…W‡ +‡ ~…⁄X - ~……c ~…⁄2l……‡ W ©…´……«ÊqÌl… 2æÌ“ N…´……‡ U‡.

O…÷~… (GROUP)

+…W‡ HÌ…‡> ~…i… °…HÌ…2{…… ª…©…⁄æÌ Ḣ W⁄o… ©……`‡ +… ∂…•qÌ{……‡ °…´……‡N… HÌ2¥……©……≈ +…¥…‡ U‡. ª…n…2©…“ ª…qÌ“©……≈ V´……2‡ +… ∂…•qÌ §‡{S… ß……∫……{…… GROUPE ~…2o…“ +~…{……¥…¥……©……≈ +…¥´……‡ l´……2‡ +‡ ÊS…m…HÌ≥… ~…⁄2l……‡ W ©…´……«ÊÊqÌl… æÌl……‡. W‡ ÊS…m……‡©……≈ +‡HÌo…“ ¥…y……2‡ ¥…ªl…÷ qÌ∂……«¥…¥……©……≈ +…¥…“ æÌ…‡´… +‡ +… {……©…o…“ +…‡≥L……l…“ æÌl…“. l´……2 •……qÌ ¥´…ŒGl… +o…¥…… ¥…ªl…÷{…… ª…©…⁄æÌ ©……`‡ +‡ ¥…~…2…¥…… ±……N´……‡, W‡ +…W‡ ~…i… HÌ…´…©… U‡. ©…{……‡Ê¥…[……{…©……≈ O…÷~…o…‡2…~…“ +‡HÌ +‡¥…“ ª……2¥……2 U‡, W‡ ª…2L…“ ª…©…ª´……{……‡ ª……©…{……‡ HÌ2l…… ±……‡HÌ…‡{…‡ +…~…¥……©……≈ +…¥…‡ U‡. ª……©……{´… 2“l…‡ +…¥…“ o…‡2…~…“{……‡ °…´……‡N… °……HÌfiÊl…HÌ æÌ…‡{……2l…{…… +…P……l… •……qÌ HÌ2¥……©……≈ +…¥…l……‡ æÌ…‡´… U‡. +…W‡ ¥…N…‘HÌ2i… ©……`‡ ~…i… +… ∂…•qÌ ¥…~…2…´… U‡, W‡©… Ḣ O…÷~… >{ª´……‡2{ª…, ª…≈N…Êcl… ª…≈N…“l…HÌ…2…‡ ~…i… HÌ´……2‡HÌ +… {……©…o…“ +…‡≥L……´… U‡. ÊS…m…HÌ≥…o…“ +…2≈ß… o…´…‡±……‡ +… ∂…•qÌ +…W‡ +{´… K…‡m…©……≈ ª……©……{´… •…{…“ N…´……‡ U‡.

+‡Gª…`‡©~……‡2 (EXTEMPORE)P…i…… ¥…Gl…… ±…L…‡±…÷≈ ß……∫…i… ¥……≈S…l…… æÌ…‡´… U‡ +o…¥…… ©…÷L´… ©…÷t…{…“ ±…‡ÊL…l… {……·y… 2…L…l…… æÌ…‡´… U‡. +©…÷HÌ

+‡¥…… ¥…Gl…… U‡, W‡ HÌ…‡> ~…i… °…HÌ…2{…“ ~…⁄¥…«l…‰´……2“ Ê¥…{…… ~……‡l……{…… Ê¥…S……2…‡ ¥´…Gl… HÌ2“ ∂…Ḣ U‡. ©……m… ¥…HÌl…… W {…æÌ”, X‡ HÌ…‡> H̱……HÌ…2 ~…i… +… 2“l…‡ 2W⁄+…l… HÌ2‡ l……‡ +… ∂…•qÌ{…“ ¥´……L´……©……≈ +…¥…“ X´… U‡. •…‡ ±…‡Ê`{… ∂…•qÌ EX (Ê¥…{……) +{…‡ TEMPORE (ª…©…´…) ß…‡N…… HÌ2“ +… ∂…•qÌ •…{´……‡ U‡. +‡{……‡ +o…« U‡ ª…©…´…{…“ ©…´……«qÌ… {…æÌ”, ~…2≈l…÷ +‡{…“ ©……N… °…©……i…‡ •……‡±…¥…÷≈. HÌ´……2‡HÌ +…¥…÷≈ ¥…Gl…¥´… °…Êl…ÊJ´…… l…2“Ḣ ~…i… +…~…¥……©……≈ +…¥…l…÷≈ æÌ…‡´… U‡. Ê¥…S……2…‡ +…¥…‡ l…‡ °…©……i…‡ ¥´…Gl… HÌ2¥……{…“ +…¥…el… y…2…¥…l…… ¥…Gl…… ∏……‡l……+…‡{…‡ ¥…y……2‡ °…ß……Ê¥…l… HÌ2“ ∂…Ḣ U‡. X‡ Ḣ +…‰~…S……Ê2HÌ ß……∫…i……‡ ±…‡ÊL…l… æÌ…‡´… U‡.

§‡X>±… (FRAGILE)+‡¥…“ ¥…ªl…÷, W‡ ª…æ̇±……>o…“ l…⁄`“ X´… +‡ +… ∂…•qÌ{…“ ¥´……L´……©……≈ +…¥…“ X´… U‡. +…¥…“ ¥…ªl…÷, W‡©… Ḣ

HÌ…S…{……‡ ª……©……{…, W‡{…‡ +{´… ªo…≥‡ ©……‡H̱…l…“ ¥…L…l…‡ +‡{…… ~…‡ÀHÌN… ~…2 L……ª… ª…⁄S…{…… ±…L…¥……©……≈ +…¥…‡ U‡ - §‡X>±…, æ̇{e±… Ê¥…o… Ḣ2. •…æÌ…2 ©……‡H̱…¥…… A~…2…≈l… P…2©……≈ ~…i… +…¥…“ ¥…ªl…÷+…‡{…‡ ¥……~…2l…“Ì ¥…L…l…‡ HÌ…≥Y 2…L…¥…“ ~…e‡ U‡. ±…‡Ê`{… ∂…•qÌ FRAGILIS {……‡ +o…« U‡ l…H̱……qÌ“ +o…¥…… {……W÷HÌ, +…{…… ~…2o…“ +≈O…‡Y ß……∫……©……≈ ©……m… +… ∂…•qÌ W {…æÌ”, +{´… ∂…•qÌ…‡ ~…i… •…{´…… U‡, W‡©… Ḣ §‡>±… (+∂…Gl…), §‡N…©…‡{` (L…≈Êel… ß……N…), ¥…N…‡2‡. ¥…ªl…÷{…“ {……W÷HÌl…… ©……`‡ §‡X>±… ¥…~…2…´… U‡, V´……2‡ ©……i…ª…{…“ ∂……2“Ê2HÌ {…•…≥…> ©……`‡ §‡>±…{……‡ °…´……‡N… HÌ2¥……©……≈ +…¥…‡ U‡. +… ∂…•qÌ…‡ +‡HÌ•…“Xo…“ ª…≈HÌ≥…´…‡±…… U‡. HÌ…‡> §‡X>±… ¥…ªl…÷ l…⁄`‡ l´……2‡ +‡{…… §‡N…©…‡{` •…{…“ X´… U‡.

¥…‡>` +‡`±…‡ ∂…÷≈ ?

¥…‡>` +‡`±…‡ ª`‡Ê`Œª`Gª…{…“ ~…Ê2ß……∫……©……≈ ~…Ê2•…≥{…‡ +…~…¥……©……≈ +…¥…l…÷≈ ©…æÌn¥…. Ê¥…Ê¥…y… ~…Ê2•…≥…‡{…÷≈ ~……2ª~……Ê2HÌ ©…æÌn¥… °…ªl……Ê~…l… HÌ2¥…… ©……`‡ °…l´…‡HÌ ~…Ê2•…≥{…‡ +…≈HÌe…HÌ“´… ¥…‡>`‡W `HÌ…©……≈ +‡ 2“l…‡ +…~…¥……©……≈ +…¥…‡ U‡, W‡{……‡ HÌ÷±… ª…2¥……≥…‡ 100 `HÌ… o……´….

+ÉyÉÖÊ{ÉH +NÉl«É{ÉÉ ¶É¥qÉà{ÉÒ »É©ÉW

479

466

SALES TAX JOURNAL - 55 July - 2016

£Ì÷N……¥……{…… ÊH̪ª……©……≈ ~…i… S…“W¥…ªl…÷+…‡{…… ª…©…⁄æÌ - W⁄o…{…‡ ¥…‡>`‡W +…~…¥……©……≈ +…¥…‡ U‡. O……æÌHÌ ß……¥……≈HÌ (HÌ{]´…÷©…2 °……>ª… >{e‡Gª… - ª…“~…“+…>) +{…‡ Woo……•…≈y… ß……¥……≈HÌ (æÌ…‡±…ª…‡±… °……>ª… >{e‡Gª… - e•…±´…÷~…“+…>) ª…“~…“+…>©……≈ HÌ÷±… 399 +…>`©… U‡, W‡©……≈ +{{… +{…‡ c≈e…≈ ~…“i……≈{…… ª…©…⁄æÌ{……‡ 127 +…>`©… ª……o…‡ 45.86 `HÌ… Êæ̪ª……‡ U‡. +… 127 +…>`©…{…… ß……¥…©……≈ W‡ £Ì‡2£Ì…2 o……´… l…‡{…“ ~…æ̇±…“ +ª…2 ª…“~…“+…>©……≈ {……·y……´… U‡, HÌ…2i… Ḣ l…‡©……≈ ª……‰o…“ ¥…y…÷ ¥…‡>`‡W +{{… +{…‡ c≈e…≈ ~…“i……≈{……‡ Êæ̪ª……‡ U‡. Woo……•…≈y… ß……¥……≈HÌ©……≈ +{{… ~…qÌ…o……‚{…÷≈ ¥…‡>`‡W 14.33 `HÌ…{…÷≈ +{…‡ Al~……ÊqÌl… S…“X‡{…÷≈ 65 `HÌ… U‡.

ª…“~…“+…>©……≈ ~…2S…÷2i… +…>`©……‡ 28.32 `HÌ… ª……o…‡ •…“X J©…‡ U‡. l´……2 •……qÌ 10.07 `HÌ… ª……o…‡ æÌ…AÀª…N…, •…≥l…i… +{…‡ ¥…“W≥“ L…S…« 6.84 `HÌ…, HÌ~…e…≈ +{…‡ ~…N…2L……≈ 6.53 `HÌ… +{…‡ ~……{…, l…©……HÌ÷ W‡¥…… ©……qÌHÌ ~…qÌ…o……‚{……‡ 2.38 `HÌ… Êæ̪ª……‡ U‡.

+… A~…2…≈l…, ª…2HÌ…2 w…2… 2…V´……‡{…‡ ~…i… Ê¥…Ê¥…y… ~…Ê2•…≥…‡{…‡ +…y……2‡ ¥…‡>`‡W +…~…¥……©……≈ +…¥…‡ U‡. ©…æÌ…2…∫`ƒ{…‡ 13.18 `HÌ… ª……o…‡ ª……‰o…“ ¥…y…÷ +{…‡ qÌ©…i… - qÌ“¥…{…‡ 0.02 `HÌ… ª……o…‡ ª……‰o…“ ¥…y…÷ ¥…‡>`‡W +…~…¥……©……≈ +…¥´…÷≈ U‡. °…l´…‡HÌ 2…V´……‡©……≈ O……æÌHÌ ß……¥……≈HÌ (ª…“~…“+…>) {…“ L…2‡L…2“ +ª…2 Xi…¥…… ©……`‡ ª…“~…“+…>{…“ l…÷±…{…… W‡ l…‡ 2…V´…{…… ¥…‡>`‡W{…“ ª……o…‡ HÌ2¥……©……≈ +…¥…‡ U‡.

ʪ…©… HÌ…e« H̱……‡À{…N… +‡`±…‡ ∂…÷≈ ?

ʪ…©… HÌ…e« H̱……‡À{…N… +‡`±…‡ +‡HÌ Êª…©… HÌ…e«{…… e‡`…{…“ HÌ…‡~…“ •…“X HÌ…‡2… ʪ…©… HÌ…e« A~…2 `ƒ…{ª…£Ì2 HÌ2“ q̇¥…“. ©…÷L´…l¥…‡ æ̇H̪…« +{…‡ N…÷{…‡N……2…‡ w…2… +… HÌ…©… o……´… U‡. +… ©……`‡ l…‡+…‡ ʪ…©… HÌ…e« 2“e2 +{…‡ Ê¥…∂…‡∫… ª……‡£Ì`¥…‡2{……‡ A~…´……‡N… o……´… U‡.

H̱……‡À{…N… ©……`‡ +‡HÌ e‡`…¥……≥÷≈ ʪ…©… HÌ…e« æÌ…‡´… l……‡ °…l´…K… +o…¥…… qÌ⁄2o…“ •…“X HÌ…‡2… ʪ…©… HÌ…e« A~…2 H̱……‡À{…N… o…> ∂…Ḣ U‡. ʪ…©… HÌ…e«{…… qÌ⁄2 •…‡c… H̱……‡À{…N… ©……`‡ +…‡¥…2 - y… - +‡2 (+…‡`“+‡) HÌ©……{e{…“ W∞2 ~…e‡ U‡. +… HÌ©……{e +‡ª…+‡©…+‡ª… ¥…e‡ ©……‡H̱…¥……©……≈ +…¥…‡ U‡. l…©…‡ ʪ…©… HÌ…e«{…÷≈ H̱……‡À{…N…{……‡ Ê∂…HÌ…2 •…{…“ 2¬… æÌ…‡´… l……‡ l…‡ Xi…¥…… ©……`‡ HÌ…‡> `‡ŒG{…H̱… ©……ÊæÌl…“ y…2…¥…¥……{…“ +…¥…∂´…HÌl…… {…o…“. Ḣ`±…“HÌ ª……qÌ“ ©……ÊæÌl…“ æÌ…‡´… l…‡ ~…i… ~…⁄2l…÷≈ U‡.

ʪ…©… HÌ…e«©……≈ ¥……2≈¥……2 2…·N… {…≈•…2 +…¥…l…… æÌ…‡´… +o…¥…… ©……‡•……>±…©……≈ •…“X HÌ…‡>{……‡ HÌ…‡±… X‡e…> Wl……‡ æÌ…‡´… +o…¥…… l……‡ l…©……2…‡ ©……‡•……>±… Ê•…±…©……≈ +Xi´…… {…≈•…2 ¥…y…÷ æÌ…‡´… +o…¥…… l…©…‡ ¥……l… HÌ2l…… {… æÌ…‡¥… Ul……≈ ©……‡•……>±… £Ì…‡{… Ê•…]“ +…¥…‡ +o…¥…… ©……‡•……>±… •…‡À{HÌN… HÌ2l…“ ¥…‡≥… ª…≈~…HÌ« o…¥……{…“ °…ÊJ´…… y…“©…“ æÌ…‡´… l´……2‡ y……2¥…÷≈ Ḣ HÌ≈>HÌ N…2•…e S……‡HÌH̪… o…> 2æÌ“ U‡. +…¥…“ ∂…≈HÌ… ~…e‡ l´……2‡ •…“X HÌ…‡> £Ì…‡{…o…“ l…©……2…‡ ©……‡•……>±… £Ì…‡{… {…≈•…2 X‡e¥……‡. À2N… ¥……N…‡ {…æÌ” +o…¥…… •…“Y HÌ…‡> ¥´…ŒGl… £Ì…‡{… A~……e‡ l……‡ Xi…¥…÷≈ Ḣ l…©…‡ H̱……‡À{…N…{…… Ê∂…HÌ…2 •…{…“ 2¬… U‡ +{…‡ ©……‡`“ {…÷HÌ∂……{…“ o…¥……{…“ ∂…HÌ´…l…… U‡. W∞2 ~…e‡ U‡. +… HÌ©……{e +‡ª…+‡©…+‡ª… ¥…e‡ ©……‡H̱…¥……©……≈ +…¥…‡ U‡.

l…©…‡ ʪ…©… HÌ…e«{…÷≈ H̱……‡À{…N…{……‡ Ê∂…HÌ…2 •…{…“ 2¬… æÌ…‡¥… l……‡ l…‡ Xi…¥…… ©……`‡ HÌ…‡> `‡ŒG{…H̱… ©……ÊæÌl…“ y…2…¥…¥……{…“ +…¥…∂HÌ´…l…… {…o…“. Ḣ`±…“HÌ ª……qÌ“ ©……ÊæÌl…“ æÌ…‡´… l……‡ ~…i… ~…⁄2l…÷≈ U‡.

ʪ…©… HÌ…e«©……≈ ¥……2≈¥……2 {…≈N… {…≈•…2 +…¥…l…… æÌ…‡´… +o…¥…… ©……‡•……>±…©……≈ •…“X HÌ…‡>{……‡ HÌ…‡±… X‡e…> Wl……‡ æÌ…‡´… +o…¥…… l……‡ l…©……2…‡ ©……‡•……>±… Ê•…±…©……≈ +Xi´…… {…≈•…2 ¥…y…÷ æÌ…‡´… +o…¥…… l…©…‡ ¥……l… HÌ2l…… {… æÌ…‡¥… Ul……≈ ©……‡•……>±… £Ì…‡{… Ê•…]“ +…¥…‡ +o…¥…… ©……‡•……>±… •…‡À{HÌN… HÌ2l…“ ¥…‡≥… ª…≈~…HÌ« o…¥……{…“ °…ÊJ´…… y…“©…“ æÌ…‡´… l´……2‡ y……2¥…÷≈ Ḣ HÌ≈>HÌ N…2•…e S……‡HÌH̪… o…> 2æÌ“ U‡.

+ÉyÉÖÊ{ÉH +NÉl«É{ÉÉ ¶É¥qÉà{ÉÒ »É©ÉW

480

467

July - 2016 SALES TAX JOURNAL - 55

+…¥…“ ∂…≈HÌ… ~…e‡ l´……2‡ •…“X HÌ…‡> £Ì…‡{…o…“ l…©……2…‡ ©……‡•……>±… £Ì…‡{… {…≈•…2 X‡e¥……‡. Ê2N… ¥……N…‡ {…æÌ” +o…¥…… •…“Y HÌ…‡> ¥´…ŒGl… £Ì…‡{… A~……e‡ l……‡ Xi…¥…÷≈ Ḣ l…©…‡ H̱……‡Ê{…N…{…… Ê∂…HÌ…2 •…{…“ 2¬… U‡ +{…‡ ©……‡`“ {…÷HÌ∂……{…“ o…¥……{…“ ∂…HÌ´…l…… U‡.

~…2~…‡S´…÷+±… •……‡{e +‡`±…‡ ∂…÷≈ ?

~…2~…‡S´…÷+±… •……‡{e +‡`±…‡ l…‡{……‡ ∂…•qÌ…o…« W‡©… ª…⁄S…¥…‡ U‡, l…‡¥…… HÌ…´…©…“ ©…÷tl…{…… •……‡{e W‡{…“ ~……HÌl…“ ©…÷tl… {…æÌ” æÌ…‡¥……o…“ l…‡{……≈ {……i……≈ ~…2l… HÌ2¥……{……≈ æÌ…‡l……≈ {…o…“.

+… °…HÌ…2{…… •……‡{e ©……‡`… ß……N…‡ ª…2HÌ…2 +{…‡ ª…2HÌ…2“ +‡W{ª…“+…‡ +{…‡ Ḣ`±…“HÌ °…Êl…Œ∫cl… L……{…N…“ HÌ≈~…{…“+…‡ w…2… l…‡©…{…“ ±……≈•……N……≥…{…“ {……i……≈HÌ“´… W∞Ê2´……l… ©……`‡ •…æÌ…2 ~……e¥……©……≈ +…¥…‡ U‡. +… •……‡{e A~…2 ©……m… ¥´……W{…“ S…÷HÌ¥…i…“ HÌ2¥……©……≈ +…¥…‡ U‡. l…‡{…“ ©…÷t±… 2HÌ©…{…“ S…÷HÌ¥…i…“ HÌ2¥……{…“ {…æÌ” æÌ…‡¥……o…“ +…¥…… •……‡{e •…æÌ÷ ±……‡HÌÊ°…´… •…{…“ ∂…HÌ´…… {…o…“. •…“W÷≈, +…¥…… °…l´…‡HÌ •……‡{e{…“ ©…⁄≥ ÀHÌ©…l… ±……L……‡ ∞Ê~…´……{…“ æÌ…‡¥……o…“ l…‡©……≈ {……{…… 2…‡HÌ…i…HÌ…2…‡ +…¥…l…… {…o…“. ©……m… ©……‡`… +{…‡ ª…≈ªo……HÌ“´… 2…‡HÌ…i…HÌ…2…‡ l…‡©……≈ 2…‡HÌ…i… HÌ2‡ U‡.

~…2~…‡S´…÷+±… •……‡{e{…‡ >ŒG¥…`“ ∂…‡2{…“ ª……o…‡ ª…2L……¥…“ ∂…HÌ…´…. W‡©… HÌ≈~…{…“ HÌ…´…©…“ ©…÷tl…{……‡ >ŒG¥…`“ ∂…‡2 •…æÌ…2 ~……e‡, l…‡©… +… •……‡{e{……≈ {……i……≈ HÌ…´…©…“ ©…÷tl… ©……`‡ HÌ≈~…{…“ ©…‡≥¥…‡ U‡. +…©… Ul……≈ ª…≈ªo……+…‡ +{…‡ HÌ≈~…{…“+…‡ HÌ…‡±… +…‡~∂…{…¥……≥… •……‡{e +…~…‡ U‡. HÌ≈~…{…“ {……i……≈ S…⁄HÌ¥…“{…‡ +…¥…… •……‡{e ~……U… L…·S…“ ±…‡¥……{……‡ Ê¥…H̱~… 2…L…‡ U‡. HÌ≈~…{…“ l…‡{…… ©…⁄e“ ©……≥L……{…÷≈ ~…÷{…«N…c{… HÌ2¥…÷≈ æÌ…‡´… +o…¥…… •…X2©……≈ ¥´……WqÌ2 P…`“ 2¬… æÌ…‡´… l´……2‡ l…‡{…… ¥´……WqÌ2 BS…… ±……N…l…… æÌ…‡¥……o…“ l´……2‡ +… Ê¥…H̱~… +W©……¥…‡ U‡. +… ª……o…‡ •…X2©……≈ ¥´……WqÌ2 P…`“ 2¬… æÌ…‡´… l´……2‡ BS…… ¥´……WqÌ2{…… ~…2~…‡S´…÷+±… •……‡{e{…“ ©……N… ¥…y…‡ U‡.

•…‡À{HÌN… ª`‡Ê•…ʱ…`“ >{e‡K… +‡`±…‡ ∂…÷≈ ?

•…‡À{HÌN… ª`‡Ê•…ʱ…`“ >{e‡K… (•…“+‡ª…+…>) +‡`±…‡ •…‡{HÌ{…“ {……i……HÌ“´… Œªo…Êl…{…÷≈ +…H̱…{… HÌ2l……‡ +…≈HÌ, Ê2]¥…« •…‡{HÌ +…‡£Ì >Œ{e´……+‡ •…“+‡ª…+…>{…“ ¥´……L´…… +… +…~…“ U‡ : +…‡U…©……≈ +…‡U“ +‡HÌ •…‡{HÌ ({……i……≈HÌ“´…) l……i…´…÷Gl… æÌ…‡´… l…‡¥…“ y……2i……{…… +…y……2‡ •…“Y •…‡{Gª…{…“ l……i…©…÷Gl… æÌ…‡¥……{…“ ∂…HÌ´…l…… ª…⁄S…¥…l……‡ +…≈HÌ.

Ê2]¥…« •…‡{Ḣ 2013 ©……≈ £Ì…>{……Œ{ª…´…±… ª`‡Ê•…ʱ…`“ Ê2~……‡`« (+‡£Ì+‡ª…+…>) 2W⁄ HÌ2l……≈ H̬÷≈ æÌl…÷≈ Ḣ +…‡N…ª`, 2013 ~…U“ •…“+‡ª…+…> ¥…y´……‡ U‡. +…{……‡ +o…« Ḣ +…‡U…©……≈ +…‡U“ +‡HÌ •…‡{HÌ {……i……HÌ“´… l……i…©…÷Gl… æÌ…‡¥……o…“ ¥…y…÷ •…‡{HÌ…‡ l……i…©…÷Gl… æÌ…‡¥……{…“ ∂…HÌ´…l…… U‡. •…“Y •……W÷, •…‡{HÌ…‡{…“ ±…‡i…“ 2HÌ©… ∂…≈HÌ…ª~…qÌ (+‡{…~…“+‡) +o…¥…… l…‡ e⁄•…¥……{…÷≈ (•…‡e e‡•`√ª…) °…©……i… ¥…y…÷ æÌ…‡´… l……‡ l…‡{……‡ ¥…±{…2‡Ê•…ʱ…`“ +…≈HÌ DS……‡ X´… U‡. +…¥…“ •…‡{HÌ…‡{…… ª…©…⁄æÌ{…… +…≈HÌ{…‡ •…“+‡ª…+…>{…“ ª……o…‡ ª…2L……©…i…“ HÌ2¥……©……≈ +…¥…‡ U‡. •…“+‡ª…+…>{…‡ ¥…y…÷ S……‡H̪……>o…“ ©……~…¥…… ©……`‡ l…‡{…“ ¥…±{…2‡Ê•…ʱ…`“ >{e‡K…{…“ ª……o…‡ l…÷±…{…… HÌ2¥……©……≈ +…¥…‡ U‡. •…‡{HÌ…‡{…“ ¥…±{…2‡Ê•…ʱ…`“ >{e‡K… ¥…y…‡ l……‡ X‡L…©…{…÷≈ °…©……i… ¥…y…÷ æÌ…‡¥……{…÷≈ ª…⁄S…¥…‡ U‡. Ê2]¥…« •…‡{HÌ{…… 2016 {…… +‡£Ì+‡ª…+…2©……≈ Wi……¥´…÷≈ æÌl…÷≈ Ḣ 2010 {…… ª…~`‡©•…2 ~…U“ •…“+‡ª…+…> ¥…y´……‡ +{…‡ 2013 {…… ~…⁄¥……«y…«©……≈ l…‡ P…`´……‡ æÌl……‡. l´……2 •……qÌ £Ì2“o…“ l…‡ ¥…y…¥…… ±……N´……‡ æÌl……‡, W‡ •…‡{HÌ…‡{…“ {……i……HÌ“´… Œªo…Êl…©……≈ ª…÷y……2…‡ ª…⁄S…¥…l……‡ æÌl……‡.

¥…“HÌ (WEAK)

+∂…HÌl… Ḣ +ª…©…o…« ¥´…ŒGl… ©……`‡ +… ª…≈•……‡y…{… ¥…~…2…´… U‡. W©…«{… ∂…•qÌ WEICH +≈O…‡Y©……≈ +~…{……¥…¥……©……≈

+ÉyÉÖÊ{ÉH +NÉl«É{ÉÉ ¶É¥qÉà{ÉÒ »É©ÉW

481

468

SALES TAX JOURNAL - 55 July - 2016

+…¥´……‡ l´……2‡ +‡{……‡ °…´……‡N… +‡{…… ©…⁄≥ +o…« °…©……i…‡ ¥´…ŒGl… {…æÌ”, ~…i… °…HÌfiÊl…{…… ª…≈qÌß…«©……≈ W o…l……‡ æÌl……‡. ¥…fiK…{…“ +‡¥…“ e…≥“, W‡{…‡ ª…æ̇±……>o…“ ¥……≥“ ∂…HÌ…´… +‡ ¥…“HÌ HÌæ̇¥……l…“. ª…©…´… Wl……≈ +… ∂…•qÌ +‡¥…“ ¥´…ŒGl… ©……`‡ ¥…~…2…¥…… ±……N´……‡, W‡{…… Ê¥…S……2…‡{…‡ ª…æ̇±……>o…“ +…~…i…“ l…2£Ì ¥……≥“ ∂…HÌ…´…. ©……{…ʪ…HÌ {…•…≥…> ©……`‡ ¥…~…2…l……‡ +… ∂…•qÌ +…W‡ ∂……2“Ê2HÌ HÌ©…X‡2“{……‡ ~…´……«´… •…{…“ N…´……‡ U‡. {…•…≥…‡ °…Êl…ª~…y…‘ ~…i… ¥…“HÌ HÌæ̇¥……´… U‡. HÌ…‡>{…… °…ß……¥…©……≈ +…¥…“{…‡ X‡ {……{…“ - ©……‡`“ ß…⁄±… HÌ2“ •…‡ª……´… l……‡ +‡¥…“ K…i… ©……`‡ ~…i… ¥…“HÌ ©……‡©…‡{` W‡¥…… ∂…•qÌ…‡ ¥…~…2…´… U‡. °……HÌfiÊl…HÌ P…`{……o…“ +…2≈ß… o…´…‡±…… +… ∂…•qÌ{……‡ +…W‡ ©……i…ª…{…“ °…¥…fiŒn… ©……`‡ °…´……‡N… HÌ2¥……©……≈ +…¥…‡ U‡.

Ê`ƒ~… (TRIP)

•……‡±…S……±…{…“ ß……∫……©……≈ +… ∂…•qÌ HÌ…‡> ~…i… °…HÌ…2{…… °…¥……ª… ©……`‡ ¥…~…2…l……‡ X‡¥…… ©…≥‡ U‡. L…2… +o…«©……≈ ±……≈•…… N……≥…{……‡ °…¥……ª… `ƒ…¥…‡±… U‡, V´……2‡ `⁄≈HÌ… N……≥…{……‡ Ê`ƒ~… U‡. +…W‡ +… ª…≈qÌß…« ß…÷±……> N…´……‡ U‡ +{…‡ ±……≈•…“ ©…÷ª……£Ì2“ ©……`‡ Wl…“ ¥´…ŒGl…{…‡ ~…i… +‡{X‡´… ´……‡2 Ê`ƒ~… HÌæ̇¥……l…÷≈ æÌ…‡´… U‡. eS… ß……∫……©……≈ TRIPPEN ∂…•qÌ{……‡ c‡HÌe…‡ ©……2¥……‡. ¥…æÌ…i…¥…`…©……≈ +… ∂…•qÌ `⁄≈HÌ… +≈l…2{…“ ©…÷ª……£Ì2“ ©……`‡ ¥…~…2…¥……{……‡ +…2≈ß… o…´……‡ +{…‡ ~…U“ qÌ2‡HÌ {……{…… °…¥……ª… ©……`‡ +‡{……‡ °…´……‡N… o…¥…… ±……N´……‡. ß……∫……©……≈ +… ∂…•qÌ{……‡ +‡HÌ •…“X‡ ~…i… +o…« o……´… U‡. c…‡HÌ2 ¥……N…¥…“. o……‡e… ª…©…´… ©……`‡ X‡ ¥…“W≥“{……‡ ~…÷2¥…c…‡ +`HÌ“ X´… l……‡ +‡{…… ©……`‡ ~…i… Ê`ƒ~… ª…≈•……‡y…{… ¥…~…2…´… U‡. +…W‡ +… ∂…•qÌ +‡{…… •…{{…‡ +o…«©……≈ ¥…~…2…´… U‡.

>{ª´…÷ʱ…{… (INSULIN)

e…´……Ê•…`“ª…{…“ •…“©……2“{…… A~…S……2©……≈ ¥…~…2…l…“ +… +‡HÌ Xi…“l…“ qÌ¥…… U‡. +…~…i…… ∂…2“2©……≈ ~…‡Ê{J´……ª… (ª¥……qÌ÷À~…e) +‡HÌ +‡¥…“ O…≈Êo… U‡, W‡ ~……≈S…{…©……≈ ©…qÌqÌ∞~… o……´… U‡. +æÌ” Al~…{{… o…l…÷≈ >{ª´…÷ʱ…{… ±……‡æÌ“©……≈o…“ ©…“c…∂…{…÷≈ °…©……i… P…`…e‡ U‡, V´……2‡ +‡{…… Al~……qÌ{…©……≈ P…`…e…‡ o……´… +{…‡ ±……‡æÌ“©……≈ ©…“c…∂…{…“ ©……m…… ¥…y…“ X´… +‡¥…“ Œªo…Êl…{…‡ e…´……Ê•…`“ª… +o…¥…… ©…y…÷°…©…‡æÌ HÌæ̇¥……´… U‡. >{ª´…÷ʱ…{…{…÷≈ ©…‡ÊeH̱… {……©… U‡ +…>±…‡`√ª… +…‡£Ì ±…·N…2æÌ…{…, W‡ W©…«{… ~…‡o……‡±……‡ÊWª` ~……‡±… ±…·N…2æÌ…{…{…… {……©… ª……o…‡ X‡e…´…‡±…÷≈ U‡. 1921 ©……≈ •…‡ ʶ…Ê`∂… Ê¥…[……{…“ •…‡À{`N… +{…‡ •…‡ª` w…2… +… æÌ…‡©……‚{…{…‡ W÷qÌ… ~……e“ >{ª´…÷ʱ…{… {……©… +…~…¥……©……≈ +…¥´…÷≈ æÌl…÷≈, W‡ ±…‡Ê`{… ∂…•qÌ INSULA ~…2 +…y……Ê2l… æÌl…÷≈. +… ∂…•qÌ{……‡ +o…« U‡ `…~…÷ +o…¥…… W÷qÌ÷≈ ~……e‡±…÷≈. l…•…“•…“ K…‡m…‡ >{ª´…÷ʱ…{… +‡HÌ qÌ¥…… U‡, V´……2‡ ª……©……{´… ß……∫……©……≈ +‡ W ©…⁄≥{…… >{ª´…÷±…‡` ∂…•qÌ{……‡ +o…« U‡ +‡H̱…… ~……e“ q̇¥…÷≈.

~……‡+‡©… (POEM)

+… ∂…•qÌ{……‡ +o…« U‡ HÌ…¥´… +{…‡ HÌÊ¥… ~……‡+‡` HÌæ̇¥……´… U‡. P…i…“ ß……∫……©……≈ °……S…“{… ª…©…´…o…“ ª……ÊæÌl´…ª…W«{… HÌÊ¥…l……{…… ©……y´…©… w…2… o…l…÷≈ +…¥´…÷≈ U‡. O…“HÌ ∂…•qÌ POEMA {……‡ +o…« U‡ HÌ≈>HÌ {…¥…÷≈ HÌ2¥…÷≈, W‡ ª…W«{…{……‡ ~…´……«´… •…{…“ +≈O…‡Y©……≈ +~…{……¥…¥……©……≈ +…¥…“ N…´……‡. +…W‡ ~…÷∞∫… +{…‡ ªm…“ •…{{…‡ ©……`‡ ~……‡+‡` ª…≈•……‡y…{… °…S…ʱ…l… U‡. +‡HÌ ª…©…´…‡ ªm…“ ©……`‡ ~……‡+‡`‡ª… ∂…•qÌ ¥…~…2…l……‡ æÌl……‡. @N±…‡{e©……≈ 2…X w…2… Ê{…´…÷Gl… HÌ2¥……©……≈ +…¥…‡±…… qÌ2•……2“ 2…WHÌÊ¥…{…‡ ~……‡+‡` ±……‡Ê2´…‡`{…“ ~…qÌ¥…“ +…~…¥……{…“ °…o…… +…W‡ ~…i… S……±…÷ U‡. 1668 ©……≈ WæÌ…‡{… eƒ…´…e{…{…‡ °…o…©… 2…WHÌÊ¥… Xæ̇2 HÌ2¥……©……≈ +…¥´…… æÌl……. +…¥…… HÌÊ¥… w…2… 2…V´…©……≈ AX¥…¥……©……≈ +…¥…l…… ©…æÌn¥…{…… °…ª…≈N…‡ L……ª… 2S…{…… °…ªl…÷l… HÌ2¥……©……≈ +…¥…‡ U‡. @N±…‡{e©……≈ °…©…÷L… HÌÊ¥…+…‡{…‡ +‡`±…÷≈ ©…æÌn¥… +…~…¥……©……≈ +…¥…‡ U‡ Ḣ ±…≈e{…{…“ ¥…‡ª` Ê©…{ª`2 +‡•…“©……≈ +‡HÌ ~……‡+‡`√ª… HÌ…‡{…«2 U‡, V´……≈ +¥…ª……{… •……qÌ +‡©…{…“ qÌ£Ì{…Ê¥…Êy… HÌ2¥……©……≈ +…¥…‡ U‡.

+ÉyÉÖÊ{ÉH +NÉl«É{ÉÉ ¶É¥qÉà{ÉÒ »É©ÉW

482

469

July - 2016 SALES TAX JOURNAL - 55

>{ª`◊©…‡{` (INSTRUMENT)

HÌ…‡> ~…i… ¥…ªl…÷{…÷≈ Ê{…©……«i… HÌ2¥…… ©……`‡ +‡{…‡ A~…´…÷«Gl… +…‡X2…‡ æÌ…‡´… +‡ W∞2“ U‡. +…¥……≈ +…‡X2…‡ Ḣ ª……y…{……‡ ©……`‡ +… ∂…•qÌ{……‡ °…´……‡N… ∂…∞ o…´……‡ æÌl……‡. ±…‡Ê`{… ∂…•qÌ INSTRUERE, W‡{……‡ +o…« U‡ HÌ≈>HÌ Ê{…©……«i… HÌ2¥…÷≈ +o…¥…… +‡{…“ l…‰´……2“ HÌ2¥…“..... +‡{…… ~…2o…“ +… +≈O…‡Y ∂…•qÌ Aq√ß…¥´……‡ U‡. +… ©…⁄≥ +o…« æÌl……‡, ~…i… ª…©…´… Wl……≈ +‡{…… ª…≈qÌß……‚ •…q̱……l…… N…´…… U‡. ª…≈N…“l…{…… K…‡m…‡ A~…´……‡N… HÌ2¥……©……≈ +…¥…l……≈ ¥……v…‡ ©……`‡ +… ª…≈•……‡y…{… ¥…~…2…¥…… ±……N´…÷≈. +…W‡ ¥……vª…≈N…“l… ~…i… >{ª`◊©…‡{` ©´…÷Ê]HÌ HÌæ̇¥……´… U‡. ª…©…´… Wl……≈ +… ∂…•qÌ{……‡ ¥´……~… ¥…y…l……‡ N…´……‡ U‡. HÌ…´…qÌ…{…“ ß……∫……©……≈ ©…æÌn¥…{…… +…‰~…S……Ê2HÌ q̪l……¥…‡W ©……`‡ ~…i… +… ∂…•qÌ{……‡ °…´……‡N… HÌ2¥……©……≈ +…¥…‡ U‡. +…W‡ HÌ≈> ~…i… Ê{…©……«i… HÌ2¥……{…… ©……y´…©… l…2“Ḣ +… ∂…•qÌ ¥……~…2“ ∂…HÌ…´… U‡.

N……e« (GUARD)

ª……©……{´… 2“l…‡ ª…÷2K…… °…qÌ…{… HÌ2{……2“ ¥´…ŒGl… ©……`‡ +… ª…≈•……‡y…{… ¥…~…2…l…÷≈ æÌ…‡´… U‡. +…{…… ~…2o…“ W Ê¥…v…o…‘{…“ W¥……•…qÌ…2“ ±…‡{……2… ¥……±…“ ©……`‡ N……Ãe´…{… ∂…•qÌ Aq√ß…¥´……‡ U‡. §‡{S… ß……∫……©……≈ ª…÷2K…… ©……`‡ GARDER ¥…~…2…´… U‡, W‡ +… +≈O…‡Y ∂…•qÌ{…÷≈ ©…⁄≥ U‡. Ê¥…Ê¥…y… K…‡m……‡©……≈ W¥……•…qÌ…2“ Ê{…ß……¥…{……2“ ¥´…ŒGl…{…… æÌ…‡t… ©……`‡ ~…i… +… ∂…•qÌ{……‡ °…´……‡N… X‡¥…… ©…≥‡ U‡. qÌ…L…±…… l…2“Ḣ, 2‡±…¥…‡©……≈ `ƒ‡{……‡{…“ W¥……•…qÌ…2“ ±…‡{……2“ ¥´…ŒGl… ©……`‡ N……e« +{…‡ +≈N…2K…HÌ{…“ HÌ…©…N…“2“ HÌ2{……2 ©……`‡ ʪ…G´……‡Ê2`“ N……e« W‡¥……≈ ª…≈•……‡y…{……‡ °…S…ʱ…l… U‡. ª……¥…S…‡l…“ ß…2‡±…“ ß……∫…… •……‡±…¥…… ©……`‡ ~…i… N……e‚ ±…‡{N¥…‡W W‡¥…÷≈ ª…≈•……‡y…{… ¥…~…2…´… U‡. +‡HÌ l…t{… W÷qÌ… W K…‡m…‡©……≈, W´……2‡ HÌ…‡> q̇∂…{…… ¥…e…{…‡ +‡©…{…… æÌ…‡t…{…‡ +{…÷∞~… ª…‰{´…{…“ `÷HÌe“ w…2… ª…±……©…“ +…~…¥……©……≈ +…¥…‡ U‡ +‡ ~…i… N……e« +…‡£Ì +…‡{…2 {……©…o…“ +…‡≥L……´… U‡.

~……‡©~…ª… (POMPOUS)

+…W‡ Xæ̇2©……≈ HÌ…‡> ~…i… °…HÌ…2{……‡ ß…ß…HÌ…qÌ…2 q̇L……¥… HÌ2¥……©……≈ +…¥…‡ l´……2‡ +… ∂…•qÌ ¥…~…2…l……‡ æÌ…‡´… U‡. +…¥…÷≈ L…S……«≥ °…qÌ∂…«{… Xæ̇2 ª…≈ªo……+…‡ ª…÷y…“ ª…“Ê©…l… {…o…“ 2¬÷≈, ~…i… ¥´…ŒGl…N…l… Y¥…{…©……≈ +~…{……¥……> N…´…÷≈ U‡. ±…N{…°…ª…≈N…, Aq√P……`{… ª…©……2≈ß…, ¥…N…‡2‡©……≈ HÌ´……2‡HÌ ~……‡l……{…“ ª…©…fiŒu{…÷≈ +…¥…÷≈ °…qÌ∂…«{… HÌ2¥……©……≈ +…¥…l…÷≈ æÌ…‡´… U‡. ©…⁄≥ ±…‡Ê`{… ∂…•qÌ U‡ POMPA, W‡{……‡ +o…« U‡ ª…2P…ª… +o…¥…… ~…2‡e. l…‡ ª…©…´…‡ Ê¥…W´…HÌ⁄S… l…2“Ḣ ª…‰{´…{…“ ~…2‡e ©……‡`… ~……´…‡ ´……‡W¥……©……≈ +…¥…l…“ æÌl…“, W‡{…… ©……`‡ ~……‡©~… +‡{e N±……‡2“ W‡¥…“ AŒGl… ¥…~…2…¥…… ±……N…“. +…W‡ L……‡`… q̇L……¥… Ḣ +…e≈•…2 ©……`‡ +… ∂…•qÌ{……‡ °…´……‡N… HÌ2¥……©……≈ +…¥…‡ U‡. ß……∫……©……≈ +…{……‡ +‡HÌ •…“X‡ °…´……‡N… ~…i… o…l……‡ æÌ…‡´… U‡, V´……2‡ HÌ…‡> ¥´…ŒGl… +±…≈HÌ…2´…÷Gl… ß……∫…… ¥……~…2‡ l´……2‡ +‡{…‡ ~……‡©~…ª… HÌæ̇¥……©……≈ +…¥…‡ U‡.

Œ¥æÌ~… (WHIP)

+…W‡ +… ∂…•qÌ S……•…÷HÌ +o…¥…… æÌ÷HÌ©… ©……`‡ ¥…~…2…´… U‡. ©…⁄≥ W©…«{… ∂…•qÌ WIPPEN +‡H ÊJ´……~…qÌ l…2“Ḣ ¥…~…2…l……‡ æÌl……‡, W‡{……‡ +o…« æÌl……‡ HÌ…©…©……≈ ]e~… ±……¥…¥…“, P……‡e… ~…2 S……•…÷HÌ AN……©…¥……{……‡ y´…‡´… ~…i… +‡ W æÌl……‡ Ḣ +‡ ]e~…o…“ qÌ…‡e‡ ©……`‡ +… ∂…•qÌ +≈O…‡Y©……≈ +~…{……¥…¥……©……≈ +…¥´……‡. +©…÷HÌ q̇∂…©……≈ HÌ⁄l…2…≈{…“ 2‡ª…©……≈ L……ª… XÊl…{…… π……{… ß……N… ±…‡l…… +‡ ~…i… +… ∂…•qÌ ~…2o…“ WHIPPET HÌæ̇¥……©……≈ +…¥´……. ª…©…´… Wl……≈ ß……∫……©……≈ +… ∂…•qÌ{……‡ +‡HÌ •…“X‡ ª…≈qÌß…« Aq√ß…¥´……‡ U‡. ʶ…Ê`∂… ~……±……«©…‡{`©……≈ 2…WHÌ“´… ~……`‘{…… {…‡l…… w…2… ~……‡l……{…… ª……≈ª…qÌ…‡{…‡ æÌ…W2 2æÌ“ HÌ…‡> +N…l´…{…“ •……•…l…©……≈ ¥……‡` HÌ2¥……{…… +…q̇∂… ©……`‡ ~…i… Œ¥æÌ~… ∂…•qÌ{……‡ °…´……‡N… o…¥…… ±……N´……‡. HÌ…‡>+‡ HÌ2‡±…“ ß…⁄±…{……‡ qÌ…‡∫… X‡ +{´… ~…2 h…‡≥“ q̇¥……´… l´……2‡ Œ¥æÌÀ~…N… •……Ë´… W‡¥…“ AŒGl… ~…i… ¥…~…2…´… U‡.

+ÉyÉÖÊ{ÉH +NÉl«É{ÉÉ ¶É¥qÉà{ÉÒ »É©ÉW

483

470

SALES TAX JOURNAL - 55 July - 2016

�∂…¥…±2“ (CHIVALRY)

©…y´…´…÷N…{…… ´…÷2…‡~…©……≈ ~…2…J©…“ ´……‡u…+…‡{…‡ {……>` HÌæ̇¥……©……≈ +…¥…l…… +{…‡ qÌ2‡HÌ 2…X{…… qÌ2•……2©……≈ +… °…HÌ…2{…… ∂…⁄2¥…“2…‡ æÌl……. +‡©…{…“ ∂……‰´…«N……o……+…‡{…“ ª……o…‡ +‡©…{……‡ ª……‰W{´…~…⁄i…« ¥´…¥…æÌ…2 ~…i… Xi…“l……‡ æÌl……‡. +…¥…… ´……‡u…+…‡ ªm…“+…‡, •……≥HÌ…‡ +{…‡ ª…©……W{…… {…•…≥… ¥…N……‚ ©……`‡ +…qÌ2 2…L…l…… +{…‡ ª…≈HÌ`©……≈ ©…qÌqÌ∞~… o…l…… æÌl……. +…¥…… {……>` P……‡e‡ª…¥……2“ HÌ2l…… +{…‡ ©…÷ª…“•…l…©……≈ £Ìª……´…‡±…“ ªm…“{…‡ •…S……¥…“ ±…‡¥…… ©……`‡ ¥…L…i……l…… æÌl……. +…¥…… +π……2…‡æÌ“ ´……‡u…+…‡ ©……`‡ §‡{S… ß……∫……©……≈ CHEVALIER ∂…•qÌ æÌl……‡, W‡{…… ~…2o…“ +…¥…“ ¥…l…«i…⁄≈HÌ ©……`‡ +… ∂…•qÌ +≈O…‡Y©……≈ +~…{……¥…¥……©……≈ +…¥´……‡ U‡. ©…y´…´…÷N…{…… ´…÷2…‡~…©……≈ +‡©…{…“ ∂……‰´…«N……o……+…‡ ±……‡H̪…≈N…“l…©……≈ ¥…i……> o…> æÌl…“. N……©…‡N……©… £Ì2l…“ ª…≈N…“l…©…≈e≥“+…‡, W‡ m…÷•……qÌ…‡2 HÌæ̇¥……l…“ +‡©…{…“ •…æÌ…qÌ÷2“{……≈ N…“l……‡ N……l…“ æÌl…“. +…¥…… ∂…⁄2¥…“2…‡ æÌ¥…‡ +‰Êl…æ̅ʪ…HÌ •…{…“ S…⁄HÌ´…… U‡, ~…i… +…W‡ ªm…“qÌ…ŒK…i´… ©……`‡ ß……∫……©……≈ Ê∂…¥…±2“ ∂…•qÌ{……‡ °…´……‡N… HÌ2¥……©……≈ +…¥…‡ U‡.

�•…`HÌ…‡>{… +‡`±…‡ ∂…÷≈ ?

©…y´…ªo… •…‡{HÌ…‡ w…2… {……i……•…X2©……≈ ©……‡`… ~……´…‡ qÌ2Ê©…´……{…N…“2“ o……´… l´……2‡ l…‡©…{…… ª…≈•…≈Êy…l… 2…∫`ƒ{…÷≈ S…±…i… {…•…≥÷≈ ~…e‡ U‡ +{…‡ •…S…l… HÌ2{……2…{…‡ l…‡{…“ Ê¥…~…2“l… +ª…2 o……´… U‡. +… ʪ…ª`©…o…“ {……i……~…÷2¥…c…‡ ¥…y…‡ +‡`±…‡ £Ì÷N……¥……‡ ¥…y…‡ +{…‡ L…2“qÌ∂…ŒGl… P…`‡ U‡. +… ª…©…ª´……©……≈o…“ Ḣ`±……HÌ ±……‡HÌ…‡+‡ +‡HÌ ©……N…« ∂……‡y´……‡ U‡, +‡ ©……N…« U‡ - Ê•…`HÌ…‡>{….

Ê•…`HÌ…‡>{… {……©…‡ +…‡≥L……l…… ª…©……≈l…2 S…±…i…{…÷≈ ©…æÌn¥… ¥…y…“ N…´…÷≈ U‡. +… S…±…i… HÌ…‡©~´…÷`2{…“ æÌ…e« eƒ…>¥…©……≈ 2æ̇ U‡ +{…‡ l…‡{…‡ ©……©…⁄±…“ L…S…‚ •…“X{…‡ `ƒ…{ª…£Ì2 HÌ2“ ∂…HÌ…´… U‡. +… ª…©……≈l…2 S…±…i… Ḣ`±…“HÌ ¥…‡•…ª……>`…‡ ~…2 Ê¥…Ê{…©…´…{…… ©……y´…©… l…2“Ḣ •…{´…÷≈ U‡.

X‡Ḣ, +… S…±…i…{…‡ HÌ…‡> ª…2HÌ…2 Ḣ ©…y´…ªo… •…‡{HÌ{……‡ `‡HÌ…‡ {…o…“. l…‡{…÷≈ ª…W«{… Ḣ`±……HÌ °……‡O……©…ª…«{……‡ +Xi´…… O…÷~…‡ HÌ´…÷» U‡. X‡Ḣ, Ê•…`HÌ…‡>{…{…“ ±…‡¥…e - q̇¥…e ©……`‡ +©…‡Ê2HÌ…{…… ª……{…§…Œ{ª…ªHÌ…‡©……≈ +‡HÌ +‡GªS…‡{W ∂…∞ HÌ´…÷» U‡.

+… S…±…i…{…÷≈ ª…W«{… HÌ…‡©~´…÷`2 °……‡O……©… w…2… o……´… U‡. +… °……‡O……©… +‡¥……‡ U‡ Ḣ W‡©… ¥…y…÷ ʪ…HÌHÌ…{…÷≈ ª…≈S……±…{… o……´… l…‡©… S…±…i…{…÷≈ ª…W«{… ¥…y…÷ ©…÷∂Ḣ±… •…{…‡ U‡.

l…‡o…“ +… S…±…i… L…2“qÌ¥…… W‡ +…¥…‡ l…‡{…‡ ~…÷∫HÌ≥ {……i……≈ ©…≥‡ U‡, HÌ…2i… Ḣ Ê•…`HÌ…‡>{…{…“ ©……N… ¥…y…“ 2æÌ“ U‡. +l´……2 ª…÷y…“ +©…‡Ê2HÌ… +o…¥…… +{´… HÌ…‡> q̇∂…{…… Ê{…´……©…Ḣ +… ª…©……≈l…2 S…±…i…{…“ ª……©…‡ HÌ…‡> °…Êl…ß……¥… +…~´……‡ {…o…“, ~…2≈l…÷ +… S…±…i…{……‡ +©…±… ±……≈•…… ª…©…´… ª…÷y…“ S……±…∂…‡ l……‡ Ê{…´……©…HÌ…‡ HÌeHÌ ¥…±…i… ±…‡ l…‡¥…“ ∂…HÌ´…l…… U‡.

Ḣ`±……HÌ Ê¥…ªl……2©……≈ Ê•…`HÌ…‡>{…‡ ©…æÌn¥… ©…‡≥¥´…÷≈ U‡ L…∞≈, ~…i… ©…W•…⁄l… 2“l…‡ l…‡©……≈ P…i…“ ©…÷∂Ḣ±…“ U‡. ª……‰o…“ ~…æ̇±…“ •……•…l… +‡ U‡ Ḣ Ê•…`HÌ…‡>{…{…‡ HÌ…‡> +…y……2 {…o…“. +… ~…÷2¥…c…‡ HÌ…‡i… Ê{…´…≈Êm…l… HÌ2‡ U‡ l…‡ ª~…∫` {…o…“. ¥…y…÷©……≈ HÌ`…‡HÌ`“{…… ª…©…´…©……≈ •…S…l… HÌ2{……2… +{…‡ 2…‡HÌ…i…HÌ…2…‡ Ê¥…π……ª… ¥…y……2‡ l…‡¥…“ +ªHÌ´……©…l… ~…ª…≈qÌ HÌ2‡ U‡. {……i……HÌ“´… ʪ…ª`©…©……≈ X‡L…©… ¥…y…‡ l´……2‡ e…‡±…2 Ḣ ª……‡{……©……≈ 2…‡HÌ…i… ¥…y……2“ ∂…HÌ…´…, V´……2‡ Ê•…`HÌ…‡>{… W‡¥…… ª©……`« ©…{…“©……≈ l…‡ ª…≈ß…¥… {…o…“.

HÌ2{ª…“ ª¥……Ë~… +‡`±…‡ ∂…÷≈ ?

W∞Ê2´……l… +‡ ∂……‡y…{…“ W{…‡l…… U‡, +‡¥…“ °…L´……l… HÌæ̇¥…l… U‡. l…‡ 2“l…‡ HÌ2{ª…“ ª¥……Ë~…{…“ ∂……‡y… ʪ…n…‡2{……

+ÉyÉÖÊ{ÉH +NÉl«É{ÉÉ ¶É¥qÉà{ÉÒ »É©ÉW

484

471

July - 2016 SALES TAX JOURNAL - 55

qÌ…´…HÌ…©……≈ Ê¥…Ê¥…y… q̇∂……‡©……≈ °…¥…l…«©……{… ḢÊ~…`±… HÌ{`ƒ…‡±… (Ê¥…q̇∂…“ ©…⁄e“{…… °…¥……æÌ A~…2 Ê{…´…≈m…i……‡) ©……≈o…“ 2ªl……‡ ∂……‡y…l…… o…> æÌl…“.

©…y´…ªo… •…‡{HÌ…‡ ¥…SS…‡ ª……©……{´… 2“l…‡ HÌ2{ª…“ ª¥……Ë~… HÌ2…2 o…l…… æÌ…‡´… U‡. HÌ…‡> +‡HÌ q̇∂…{…‡ •…“X q̇∂…{…… S…±…i… ~…÷2¥…c…{…“ L…·S… ~…e‡ l´……2‡ l…‡{…… HÌ…©…S…±……A A~……´… l…2“Ḣ +…¥…… HÌ2…2 o……´… U‡. ©…y´…ªo… •…‡{HÌ…‡ ¥…SS…‡ o…l…… HÌ2{ª…“ ª¥……Ë~… HÌ2…2 Ê{…Œ∑S…l… ª¥……Ë~… HÌ2…2 Ê{…Œ∑S…l… ª…©…´… ©……`‡{…… æÌ…‡´… U‡. ©……‡`… ß……N…{……‡ Ê¥…π… ¥…‡~……2 ´…÷+‡ª… e…‡±…2©……≈ o……´… U‡, l…‡o…“ £Ì‡e2±… Ê2]¥…«+‡ •…“X q̇∂……‡{…“ ©…y´…ªo… •…‡{HÌ…‡ ª……o…‡ e…‡±…2 +…~…¥…… ª……©…‡ W‡ l…‡ q̇∂……‡{…“ HÌ2{ª…“ Ê{…Œ∑S…l… Ê¥…Ê{…©…©… qÌ2‡ L…2“qÌ¥……{…“ ¥´…¥…ªo…… HÌ2“ U‡ (+…{…‡ “e…‡±…2 ʱ…ŒG¥…Êe`“ ª¥……Ë~… ±……>{…’ HÌæ̇ U‡). +…©……≈ ∂…2l… +‡ U‡ Ḣ Ê¥…q̇∂…“ ©…y´…ªo… •…‡{HÌ V´……2‡ ~……‡l……{…÷≈ S…±…i… Ê{…Œ∑S…l… l……2“L…‡ ~……U÷≈ L…2“q̇ l´……2‡ +N……A{……‡ Ê¥…Ê{…©…´… qÌ2 W ±……N…÷ ~…e‡ U‡.

X‡Ḣ ¥´……~……2 - Av…‡N… K…‡m…‡ ~…i… +…¥…… HÌ2…2 o…l……≈ æÌ…‡´… U‡. qÌ….l…. +‡HÌ ß……2l…“´… HÌ≈~…{…“{…‡ ´…÷+‡ª… e…‡±…2©……≈ Êy…2…i… X‡>+‡ U‡, ~…2≈l…÷ q̇∂…©……≈ ©…⁄e“ +≈HÌ÷∂……‡{…‡ HÌ…2i…‡ l…‡ ∂…HÌ´… {…o…“. •…“Y •……W÷, +©…‡Ê2HÌ{… HÌ≈~…{…“{…‡ ß……2l…©……≈ ¥…y…÷ 2…‡HÌ…i… HÌ2¥…÷≈ U‡. +… Œªo…Êl…©……≈ •…≈{{…‡ HÌ≈~…{…“ ¥´…¥…æÌ…∞ 2ªl……‡ ∂……‡y…∂…‡. ß……2l…“´… HÌ≈~…{…“ ∞Ê~…´……©……≈ Êy…2…i… ±…>{…‡ l…‡{…“ ß……2l…©……≈ HÌ…©… HÌ2l…“ +©…‡Ê2HÌ{… HÌ≈~…{…“{…‡ ±……‡{… +…~…∂…‡, V´……2‡ +©…‡Ê2HÌ{… HÌ≈~…{…“ ´…÷+‡ª… e…‡±…2©……≈ Êy…2…i… ±…>{…‡ l…‡ ß……2l…“´… HÌ≈~…{…“{…‡ ±……‡{… +…~…∂…‡.

X‡Ḣ, æÌ¥…‡ l……‡ P…i…“ HÌ≈~…{…“+…‡ l…‡©…{…… Ê¥…q̇∂…“ S…±…i…©……≈ +…¥…{……2… HÌË∂… £Ì±……‡{…÷≈ æ̇ÀWN… HÌ2¥…… ©……`‡ HÌ2{ª…“ ª¥……Ë~… HÌ2…2 HÌ2l…“ æÌ…‡´… U‡. +… HÌ2…2 E i… +{…‡ ¥´……W{…“ S…÷HÌ¥…i…“ ©……`‡ ~…i… o…> ∂…Ḣ U‡.

•…‡{J~ª…“ HÌ…Ëe +‡`±…‡ ∂…÷≈ ?

•…‡{J~ª…“ HÌ…‡e +‡`±…‡ {……qÌ…2“{…‡ ±…N…l……‡ HÌ…´…qÌ…‡. V´……2‡ HÌ…‡> ¥´…ŒGl… Ḣ HÌ≈~…{…“ l…‡{…÷≈ q̇¥…÷≈ S…⁄HÌ¥…¥……©……≈ Ê{…∫£Ì≥ X´… l´……2‡ +qÌ…±…l… l…‡{…‡ •…‡{J2~` +o…¥…… {……qÌ…2 Xæ̇2 HÌ2‡ U‡. ª…⁄ÊS…l… •…‡{HÌ2~ª…“ HÌ…‡e©……≈ >{ª……‡±¥…{ª…“ Ê2]…‡±´…÷∂…{… °……‡ª…‡ª… (+…>+…2~…“) {…“ X‡N…¥……> U‡. +… X‡N…¥……> +{¥…´…‡ ¥´…ŒGl… +o…¥…… HÌ≈~…{…“ l…‡{…… ~…÷{…∞u…2 ©……`‡ Ê¥…H̱~……‡ ª…⁄S…¥…‡ +o…¥…… l…‡{…‡ £ÌeS……©……≈ ¥…æ̇±…“ l…Ḣ ±…> W¥…… ©……`‡{…“ +2Y HÌ2“ ∂…Ḣ. +…>+…2~…“ ©……`‡{…“ HÌ…´…«¥……æÌ“ q̇¥……≈qÌ…2 +o…¥…… ±…‡i…qÌ…2 - •…‡©……≈o…“ HÌ…‡> ~…i… HÌ2“ ∂…Ḣ l…‡¥…“ X‡N…¥……> °…ªl…÷l… y……2…©……≈ U‡. ±…‡i…qÌ…2©……≈ ʪ…HÌ´……‡e« +{…‡ +{…ʪ…G´……‡e« •…{{…‡ °…HÌ…2{……≈ ±…‡i……≈ +…¥…“ X´… U‡.

+…>+…2~…“ ±……N…÷ o…´…… ~…U“ ±…‡i…qÌ…2…‡{…… qÌ…¥…… 180 ÊqÌ¥…ª… ª…÷y…“ ªo…ÊN…l… HÌ2“ q̇¥……{…“ X‡N…¥……> U‡. +… ÊqÌ¥…ª……‡©……≈ ¥´…ŒGl…{…‡ q̇¥…÷≈ S…⁄HÌ¥…¥……≈ ª…K…©… •…{……¥…¥…… +o…¥…… HÌ≈~…{…“{…‡ ~…N…ß…2 HÌ2¥……{…… Ê¥…H̱~……‡{…“ Ê¥…S……2i…… HÌ2¥……©……≈ +…¥…‡ U‡. +… Ê¥…H̱~……‡{…‡ 75 `HÌ… ±…‡i…qÌ…2…‡{…“ ª…≈©…Êl… ©…≥¥…“ W∞2“ U‡. X‡ +…`±…“ ©…‡≥¥…“ {… ∂…HÌ…´… l……‡ HÌ≈~…{…“ +…~……‡+…~… £ÌeS……©……≈ W∂…‡.

~…2≈l…÷ X‡ 75 `HÌ… ±…‡i…qÌ…2…‡ +‡¥…… °…ªl……¥… l…‰´……2 HÌ2‡ Ḣ HÌ≈~…{…“{…“ ~…÷{…N…«c{… ´……‡W{…… {…HÌHÌ“ HÌ2¥……{…÷≈ 180 ÊqÌ¥…ª…©……≈ ∂…HÌ´… {…o…“, l……‡ l…‡+…‡ ±…¥……qÌ{…‡ +… ª…©…´… ±…≈•……¥…“ +…~…¥……{…“ +2Y HÌ2“ ∂…HÌ∂…‡. ±…¥……qÌ ¥…y…÷©……≈ ¥…y…÷ +‡HÌ W ¥……2{…“ 90 ÊqÌ¥…ª…{…“ ©…÷qÌl… +…~…“ ∂…HÌ∂…‡.

+…Ë~……‡S´…÷«Ê{…`“ H̅˪` +‡`±…‡ ∂…÷≈

+…Ë~……‡S´…÷«Ê{…`“ H̅˪` +‡`±…‡ 2…‡HÌ…i…{…… Ê¥…H̱~…©……≈o…“ ~…ª…≈qÌN…“ HÌ2¥…… ©……`‡ +‡HÌ 2…‡HÌ…i…©……≈ °……~l… o…{……2…‡

+ÉyÉÖÊ{ÉH +NÉl«É{ÉÉ ¶É¥qÉà{ÉÒ »É©ÉW

485

472

SALES TAX JOURNAL - 55 July - 2016

±……ß… U…‡e“ q̇¥……‡. 2…‡HÌ…i… ©……`‡{…… ª…¥…«©……{´… Ê¥…H̱~… U‡ - ∂…‡2, Ê£ÌH̪e Êe~……‡Ê]` +{…‡ W©…“{… - °……‡~…`‘ ∂…‡2©……≈ 2…‡HÌ…i… ª…“y…“ L…2“qÌ“ w…2… +o…¥…… ©´…÷S´…÷+±… £Ì≈e√ª… ©……2£Ìl…‡ HÌ2“ ∂…HÌ…´… U‡.

2…‡HÌ…i…HÌ…2 +… •…{{…‡ ©……N…‚ 2…‡HÌ…i… HÌ2“ ∂…Ḣ, ~…i… ∂…‡©……≈ 2…‡HÌ…i… HÌ2¥…÷≈ l…‡{……‡ +…L…2“ Ê{…i…«´… •…{{…‡©……≈ ©…≥{……2… £Ì…´…qÌ… - N…‡2£Ì…´…qÌ…{…“ l…÷±…{……l©…HÌ N…i…l…2“ ©……≈e“{…‡ ±…‡ U‡. ∂…‡2{…“ ª…“y…“ L…2“qÌ“ HÌ2‡ l……‡ l…‡{…… ß……¥…{…“ q̉Ê{…HÌ ¥…y…P…` A~…2 {…W2 2…L…“{…‡ ±…‡-¥…‡S… HÌ2l……≈ 2æ̇¥…÷≈ ~…e‡. +…©……≈ l…‡{…‡ {…£Ì…‡ Ḣ {…÷HÌ∂……{… o……´… U‡. ∂…‡2{…÷≈ ©…⁄±´… +…L…2‡ l……‡ l…‡{…… +…≈l…Ê2HÌ ~…Ê2•…≥…‡{…… +…y……2‡ {…I“ o……´… U‡. l…‡o…“ ª…“y…“ L…2“qÌ“ w…2… 2…‡HÌ…i…{…… ¥…≥l…2 •……•…l… +Ê{…Œ∑S…l…l…… 2æ̇ U‡. +… ¥…≥l…2 £Ì÷N……¥……{…… ±……≈•……N……≥…{…… qÌ2 HÌ2l……≈ ¥…y…÷ æÌ…‡´… l……‡ W l…‡{…‡ ß……¥…{…“ q̉Ê{…HÌ ¥…y…P…`{…… W‡¥…… `⁄≈HÌ… N……≥…{…… w…2… ©…≥{……2… ª…≈ß…Ê¥…l… ¥…≥l…2{…“ +¥…N…i…{…… HÌ2“ ∂…Ḣ U‡.

©´…÷S´…÷+±… £Ì≈e√ª…{…“ {…‡` +‡ª…‡` ¥…‡±´…⁄ (+‡{…+‡¥…“) ©……≈ q̉Ê{…HÌ £Ì‡2£Ì…2 o…l……≈ 2æ̇ U‡, ~…2≈l…÷ l…‡{……o…“ ±……≈•……N……≥…{…… ¥…≥l…2©……≈ •…æÌ÷ £Ì2HÌ ~…el……‡ {…o…“.

Ê£ÌH̪e Êe~……‡Ê]` +{…‡ °……‡Ê¥…e{` £Ì≈e©……≈ 2…‡HÌ…i… A~…2{…÷≈ ¥…≥l…2 +N……Ao…“ Xi…“ ∂…HÌ…´… U‡, ~…2≈l…÷ l…‡ £Ì÷N……¥……{…… ±……≈•……N……≥…{…… qÌ2 HÌ2l……≈ +…‡U÷≈ æÌ…‡´… l…‡ ∂…HÌ´… U‡. +‡`±…‡ 2…‡HÌ…i…HÌ…2‡ ~……‡l……{……‡ Ê{…i…«´… +…~……‡S´…÷«Ê{…`“ HÌ…‡ª`{…… +…y……2‡ ±…‡¥……{……‡ æÌ…‡´… U‡ Ḣ HÌ´…… ª……y…{…©……≈ 2…‡HÌ…i… HÌ2¥…÷≈ U‡.

•…‡{`©… ¥…‡>` (BANTAM WEIGHT)

•……‡ÀGª…N… Ḣ HÌ÷ªl…“©……≈ L…‡±……e“+…‡{…÷≈ ¥…N…‘HÌ2i… +‡©…{…… ¥…W{… °…©……i…‡ HÌ2¥……©……≈ +…¥…‡ U‡, W‡o…“ +‡©…{…“ ª~…y……« ª…2L…÷≈ ¥…W{… y…2…¥…l…… ¥…SS…‡ o…> ∂…Ḣ. •…‡{`©… ¥…‡>`{……‡ +o…« U‡ 51 o…“ 54 ÊH̱……‡ ¥…W{… y…2…¥…l…… L…‡±……e“+…‡, W‡{…‡ æÌ≥¥…÷≈ ¥…W{… N…i…¥……©……≈ +…¥…‡ U‡. +…¥…… L…‡±……e“+…‡ ß…±…‡ HÌqÌ©……≈ {……{…… æÌ…‡´…, ~…i… +‡©…{…“ +…J©…HÌl…… Ḣ ±…e¥……{…“ ∂…ŒGl… W2… ~…i… +…‡U“ {…o…“ æÌ…‡l…“. +‡Ê∂…´……{…… q̇∂……‡{…… ª~…y…«HÌ…‡ +… ∏…‡i…“©……≈ ¥…y……2‡ X‡¥…… ©…≥‡ U‡. +… {……©… +‡HÌ ª…©…´…‡ ±……‡HÌÊ°…´… HÌ⁄HÌe…+…‡{…“ ±…e…> ~…2o…“ ±…‡¥……©……≈ +…¥´…÷≈ U‡. X¥…… `…~…÷{…… +‡HÌ °…q̇∂… BANTAM ©……≈ +‡…¥… {……{…… HÌqÌ{…… HÌ⁄HÌe… o…l…… æÌl……, W‡ +‡©…{…… HÌqÌ{…“ ª…2L……©…i…“©……≈ P…i…… W +…J©…HÌ N…i……l…… æÌl……. +‡©…{…“ +… L……ʪ…´…l… ~…2o…“ •……‡ÀGª…N… Ḣ HÌ÷ªl…“©……≈ +… {……©… +~…{……¥…¥……©……≈ +…¥´…÷≈ æÌ…‡¥……{…÷≈ ©……{…¥……©……≈ +…¥…‡ U‡.

+…2.+‡S…. £Ì‡HÌ`2 (RH FACTOR)

HÌ…‡> qÌ2qÌ“{…‡ V´……2‡ ±……‡æÌ“ S…e…¥…¥……{…“ W∞2l… ~…e‡ U‡ l´……2‡ ª……‰°…o…©… +‡{……≈ ±……‡æÌ“{…÷≈ RH £Ì‡HÌ`2 {…HÌHÌ“ HÌ2¥……©……≈ +…¥…‡ U‡. ±……‡æÌ“ S…e…¥…l……≈ ~…æ̇±……≈ +… ¥…N…‘HÌ2i… Xi…¥…÷≈ W∞2“ U‡. +‡ ~……‡Ê]Ê`¥… +o…¥…… {…‡N…‡Ê`¥… æÌ…‡> ∂…Ḣ U‡. X‡ qÌ2qÌ“{…‡ L……‡`÷≈ ±……‡æÌ“ +~……> X´… l……‡ +{…‡HÌ N…≈ß…“2 ©…÷ª…“•…l……‡{……‡ ª……©…{……‡ HÌ2¥……‡ ~…e‡. qÌŒK…i… +‡Ê∂…´……©……≈ +‡HÌ XÊl…{…… ¥……≈qÌ2… o……´… U‡, W‡©…{…‡ RHESUS HÌæ̇¥……´… U‡. ~…Œ∑S…©…{…… q̇∂……‡©……≈ ¥……{…2…‡ ~…2 °…´……‡N… HÌ2“ l…•…“•…“ K…‡m…‡ ª…≈∂……‡y…{… HÌ2¥……©……≈ +…¥…‡ U‡. +…¥…… ¥……{…2…‡{…÷≈ ±……‡æÌ“ ©…≥l…÷≈ +…¥…l…÷≈ æÌ…‡¥……o…“ +‡©…{…‡ +…¥…… °…´……‡N… ©……`‡ A~…´…÷«Gl… ©……{…¥……©……≈ +…¥´…… æÌl……. +…{…… ±…“y…‡ +…~…i…… ±……‡æÌ“{…… ¥…N…‘HÌ2i…{…‡ +‡©…{…… {……©… ~…2o…“ 2“ª…ª… £Ì‡HÌ`2 HÌæ̇ U‡. +… ∂…•qÌ{…÷≈ `⁄≈HÌ÷≈ ∞~… U‡ RH £Ì‡HÌ`2, W‡{…÷≈ •±…e •…‡{HÌ +{…‡ +…‡~…2‡∂…{… Êo…´…‡`2©……≈ L……ª… ©…æÌn¥… U‡.

2…‡•…ª` (ROBUST)

+…W‡ +… ∂…•qÌ HÌ…‡> ~…i… {…“2…‡N…“ +{…‡ ∂…ŒGl…∂……≥“ ¥´…ŒGl… ©……`‡ ¥……~…2“ ∂…HÌ…´… U‡. +… ∂…•qÌ{…… ©…⁄≥{…‡

+ÉyÉÖÊ{ÉH +NÉl«É{ÉÉ ¶É¥qÉà{ÉÒ »É©ÉW

486

473

July - 2016 SALES TAX JOURNAL - 55

¥´…ŒGl… ª……o…‡ HÌ…‡> W ª…≈•…≈y… {…æÌ…‡l……‡. ´…÷2…‡~…©……≈ +…‡HÌ {……©…{…÷≈ ¥…fiK… o……´… U‡, W‡{…÷≈ +…U… ±……±… 2≈N…{…÷≈ ±……HÌe÷≈ P…i…÷≈ ©…W•…⁄l… +{…‡ `HÌ…A æÌ…‡´… U‡. +… HÌqÌ…¥…2 ¥…fiK…{…÷≈ o…e >©……2l……‡ +{…‡ ¥…æÌ…i……‡{……≈ •……≈y…HÌ…©…©……≈, +‡{…“ ©…W•…⁄l…“{…… ±…“y…‡ ~…ª…≈qÌ HÌ2¥……©……≈ +…¥…l…÷≈. ±…‡Ê`{… ß……∫……©……≈ +… ¥…fiK… ©……`‡ ROBUS ∂…•qÌ ¥…~…2…´… U‡. +‡{…… ~…2o…“ +… +≈O…‡Y ∂…•qÌ •…{´……‡ U‡, W‡{……‡ ª…“y……‡ +o…« U‡ - +…‡HÌ ¥…fiK… W‡{…“ ∂…ŒGl… y…2…¥…{……2. L……ª… °…HÌ…2{…“ HÌeHÌ H̅ˣ̓ ©……`‡ ~…i… H̅ˣ̓ 2…‡•…ª`… W‡¥…÷≈ ª…≈•……‡y…{… ¥…~…2…´… U‡. +…W‡ +… ∂…•qÌ ©…W•…⁄l…“ ©……`‡{……‡ ~…´……«´… •…{…“ N…´……‡ U‡ +{…‡ l…≈qÌ÷2ªl…“{…… ª…≈qÌß…«©……≈ ¥…y……2‡ ¥…~…2…l……‡ X‡¥…… ©…≥‡ U‡.

©…‡] (MAZE)

HÌ…‡> ~…i… °…HÌ…2{…“ N…⁄≈S…¥…i… ß…2‡±…“ Œªo…Êl… ©……`‡ +… ∂…•qÌ{……‡ °…´……‡N… o…> ∂…Ḣ U‡. +…¥…“ 2S…{……{……‡ ©…⁄≥ æ̇l…÷ U‡ HÌ…‡> ¥´…ŒGl…{…‡ ®…©…©……≈ 2…L…¥…“. +©…÷HÌ +‰Êl…æ̅ʪ…HÌ 2…W©…æ̇±……‡©……≈ ©…{……‡2≈W{… ©……`‡ +…≈`“P…⁄≈`“¥……≥… 2ªl……+…‡{…÷≈ •……≈y…HÌ…©… HÌ2¥……©……≈ +…¥…l…÷≈ æÌl…÷≈. ±…≈e{… {…YHÌ +…¥…‡±…… æ̇©~…`{… HÌ…‡`«{…… ©…æ̇±…{…“ ©…‡] °…¥……ª…“+…‡{…÷≈ L……ª… +…HÌ∫…«i… U‡. +…~…i…‡ l´……≈ ~…i… £Ìl…‡æÌ~…÷2 ʪ…J“©……≈ ß…÷±…ß…÷±…‰´…… U‡, W‡ ~…i… +‡HÌ °…HÌ…2{…“ ©…‡] U‡. +‡¥……‡ HÌ…‡´…e…‡, W‡{…÷≈ +o…«P…`{… ª…2≥ {… æÌ…‡´… +{…‡ ©…{…©……≈ ®…©… ~…‡qÌ… HÌ2‡ +‡ +… ∂…•qÌ{…“ ¥´……L´……©……≈ +…¥…“ X´… U‡. +≈O…‡Y ∂…•qÌ AMAZE {…÷≈ +… `÷≈HÌ÷≈ ∞~… U‡. +…W‡ X‡ Ḣ ß……∫……©……≈ +… °…´……‡N… ©……m… >©……2l……‡ Ḣ •……≈y…HÌ…©… ª…÷y…“ ©…´……«ÊqÌl… {…o…“ 2¬…‡ +{…‡ Xi…“ X‡>{…‡ Aß…“ HÌ2‡±…“ ©…⁄≈]¥…i… ©……`‡ ¥……~…2“ ∂…HÌ…´… U‡.

`ƒ‡�e∂…{… (TRADITION)

ª…©…´… °…©……i…‡ Y¥…{… ~…uÊl… •…q̱……l…“ X´… U‡ l…‡©… Ul……≈ +©…÷HÌ 2“l… - Ê2¥……X‡ ~…2≈~…2…N…l… 2“l…‡ S……±…÷ 2æ̇ U‡. +…~…i…“ ©……{´…l……+…‡ +{…‡ Ê2¥……X‡ ª……©……{´… 2“l…‡ ©……‰ÊL…HÌ ~…2≈~…2… w…2… ~…‡h“ - qÌ2 - ~…‡h“ ¥……2ª……©……≈ +~……l…… 2æ̇l…… æÌ…‡´… U‡. ±…‡Ê`{… ∂…•qÌ TRADITION {……‡ +o…« U‡ HÌ…‡>{…‡ HÌ≈>HÌ +…~…¥…÷≈. +…~…i…… 2“l…‡ - Ê2¥……X‡ ~…i… +‡HÌ ~…‡h“ w…2… •…“Y ~…‡h“{…‡ +…~…¥……©……≈ +…¥…l…… æÌ…‡¥……o…“ +‡©…{…‡ `ƒ‡Êe∂…{… {……©… +…~…¥………≈ +…¥´…÷≈. ~…2q̇∂…©……≈ ¥…ª…l…… ±……‡HÌ…‡ ~…i… ~……‡l……{…… ¥…l…{…{…… l…æ̇¥……2…‡ ~……2≈~…Ê2HÌ 2“l…‡ CW¥…‡ U‡ +{…‡ +‡ ~…i… +… ª…≈•……‡y…{…o…“ W +…‡≥L……´… U‡. +©…÷HÌ °…HÌ…2{……≈ ¥…ªm……‡ +…¥…… °…ª…≈N…‡ ~…æ̇2…l……≈ æÌ…‡´… U‡ +{…‡ +‡©…{…… ©……`‡ ~…i… `ƒ‡Êe∂…{…±… eƒ‡Êª…ª… ∂…•qÌ°…´……‡N… o……´… U‡. HÌ´……2‡HÌ +©…÷HÌ ±……‡HÌ…‡ +…¥…“ ¥……2ª……N…l… ~…2≈~…2…{…‡ +‡`±…“ æÌqÌ ª…÷y…“ ¥…≥N…“ 2æ̇ U‡ Ḣ +‡©…{…… ©……`‡ ∞ÊhS…÷ªl… ª…≈•……‡y…{… ¥……~…2¥……©……≈ +…¥…‡ U‡. qÌ2‡HÌ q̇∂…{…‡ ~……‡l……{…“ W÷qÌ“ ª……≈ªHÌfiÊl…HÌ ~…2≈~…2… æÌ…‡> ∂…Ḣ U‡.

¥……‡±… (WALL)

+…W‡ qÌ“¥……±… Ḣ ß…”l… ©……`‡ +… ∂…•qÌ{……‡ °…´……‡N… HÌ2¥……©……≈ +…¥…‡ U‡. +‡HÌ ª…©…´…‡ ª…≈2K…i… ©……`‡ qÌ2‡HÌ ∂…æ̇2{…‡ £Ì2l……‡ HÌ…‡` •……≈y…¥……©……≈ +…¥…l……‡ æÌl……‡. +…¥…… HÌ…‡`{…“ qÌ“¥……±… +‡¥…“ ©…W•…⁄l… •…{……¥…¥……©……≈ +…¥…l…“ æÌl…“ Ḣ ª…æ̇±……>o…“ l…⁄`“ {… ∂…Ḣ. ±…‡Ê`{… ß……∫……©……≈ +‡ VALLUM HÌæ̇¥……o…“, W‡{……‡ +o…« æÌl……‡ ÊH̱±……{…“ qÌ“¥……±…. +…{…… ~…2o…“ +… +≈O…‡Y ∂…•qÌ Aq√ß…¥´……‡ U‡. Ê¥…π…ß…2©……≈ ª……‰o…“ ±……≈•…“ S…“{…{…“ +‰Êl…æ̅ʪ…HÌ qÌ“¥……±… ©……{…¥……©……≈ +…¥…‡ U‡, W‡{…… +¥…∂…‡∫……‡ +…W‡ ~…i… X‡> ∂…HÌ…´… U‡. •…ñ…{… ∂…æ̇2{…‡ +‡HÌ ª…©…´…‡ qÌ“¥……±… w…2… •…‡ ß……N…©……≈ ¥…æÌ·S…¥……©……≈ +…¥´…÷≈ æÌl…÷≈ +{…‡ +‡ y… ¥……‡±… {……©…o…“ +…‡≥L……l…“ æÌl…“. ª…≈2K…i… A~…2…≈l… HÌ´……2‡HÌ ß……N…±…… ~……e¥…… ©……`‡ ~…i… qÌ“¥……±… S…i…¥……©……≈ +…¥…l…“ æÌl…“.

+ÉyÉÖÊ{ÉH +NÉl«É{ÉÉ ¶É¥qÉà{ÉÒ »É©ÉW

487

474

SALES TAX JOURNAL - 55 July - 2016

~±…‡�`{…©… (PLATINUM)

+… ß…⁄2… 2≈N…{…“ +‡HÌ +‡¥…“ HÌ“©…l…“ y……l…÷ U‡, W‡ ª……‡{…… +{…‡ S……≈qÌ“{…“ W‡©… W +‡HÌ L…Ê{…W ~…qÌ…o…« U‡. Ê{…H̱… y……l…÷{…“ L……i…{…÷≈ W +… +‡HÌ Al~……qÌ{… U‡, W‡{…‡ ª……‡{……{…“ W‡©… Ê¥…Ê¥…y… +…HÌ…2©……≈ ¥……≥“ ∂…HÌ…´… U‡. +… L……ʪ…´…l…{…… ±…“y…‡ +… HÌ“©…l…“ y……l…÷ HÌ´……2‡HÌ qÌ…N…“{……©……≈ ~…i… ¥…~…2…l…“ æÌ…‡´… U‡ +{…‡ +‡©……≈´… æÌ“2…WÊel… P…2‡i……©……≈ +‡{……‡ °…´……‡N… ¥…y……2‡ o…l……‡ æÌ…‡´… U‡. ª~…‡Ê{…∂… ß……∫……{…… PLATINA ∂…•qÌ ~…2 +… {……©… +…y……Ê2l… U‡, W‡{……‡ +o…« U‡ q̇L……¥…©……≈ S……≈qÌ“ W‡¥…÷≈, W‡ +‡{…… ∞~…‡2“ 2≈N…{…… ±…“y…‡ ~…e¨÷≈ U‡. £Ì‡∂…{… ©……`‡ +…¥…… 2≈N…{…… ¥……≥ 2…L…¥……©……≈ +…¥…‡ l……‡ +‡{…‡ ~±…‡Ê`{…©… •±……‡{e HÌæ̇¥……©……≈ +…¥…‡ U‡. HÌ…‡> N…“l…{…“ ª…“e“{…“ X‡ q̪… ±……L… HÌ…‡~…“ ¥…‡S……´… l……‡ +{…‡ ~±…‡Ê`{…©… ÊeªHÌ{……‡ qÌ2VX‡ +…~…¥……©……≈ +…¥…‡ U‡.

>{… y… ª…‡©… •……‡` (IN THE SAME BOAT)

+≈O…‡Y ß……∫……©……≈ ¥…~…2…l…“ +… AŒGl…{……‡ ª…≈qÌß…« qÌÊ2´……> ª…£Ì≥ ª……o…‡ U‡. +‡HÌ ª…©…´…‡ ±……≈•…… +≈l…2{…“ ´……m…… qÌÊ2´……> ©……N…‚ W o…l…“ æÌl…“. l´……2‡ qÌÊ2´……> ´……m…… +…W‡ U‡ +‡¥…“ ª…÷2ŒK…l… {…æÌ…‡l…“ +{…‡ P…i…“ ¥……2 ´……m…… qÌ2Ê©…´……{… ¥…æÌ…i… e⁄•…“ Wl……≈ æÌl……≈. +…¥…… ª…©…´…‡ •…S……¥…HÌ…´…« ©……`‡ æÌ…‡e“{……‡ A~…´……‡N… HÌ2¥……©……≈ +…¥…l……‡ æÌl……‡. +…¥…“ •……‡`©……≈ DS… - {…“S…{…… HÌ…‡> ~…i… Xl…{…… ß…‡qÌß……¥… Ê¥…{…… °…¥……ª…“+…‡ Y¥… •…S……¥…¥…… +‡HÌ ª……o…‡ ß…‡N…… o…> Wl…… æÌl……. ¥…æÌ…i…{…… Ḣ~`{… +{…‡ ª……©……{´… L……2¥…… +o…¥…… ASS… ∏…‡i…“{…… °…¥……ª…“+…‡ ¥…SS…‡ HÌ…‡> W l…£Ì…¥…l… 2æ̇l……‡ {…æÌ”, HÌ…2i… Ḣ qÌ2‡HÌ{……‡ æ̇l…÷ Y¥… •…S……¥…¥……{……‡ æÌl……‡. +…W‡ HÌ÷qÌ2l…“ æÌ…‡{……2l…{…… ª…©…´…‡ +…¥…“ Œªo…Êl… X‡¥…… ©…≥‡ U‡. +…W‡ +… AŒGl… HÌ…‡> ~…i… L…2…•… ª…©……{… Œªo…Êl…©……≈ ©…÷HÌ…´…‡±…… ±……‡HÌ…‡{…… ª…≈qÌß…«©……≈ ¥……~…2“ ∂…HÌ…´… U‡. +‡¥…“ Œªo…Êl… W‡©……≈ ¥…N…«ß…‡qÌ {… æÌ…‡´…........

�~…{…±… (PENAL)HÌ…´…qÌ… w…2… +…~…¥……©……≈ +…¥…l…“ ª…X Ḣ qÌ≈e +… ∂…•qÌ{…“ ¥´……L´……©……≈ +…¥…“ X´… U‡. 2…Wr…‡æÌ HÌ2{……2

+o…¥…… °…ªo……Ê~…l… y…©…«{……‡ Xæ̇2©……≈ Ê¥…2…‡y… HÌ2{……2{…‡ ª…X £Ì`HÌ…2¥……{…“ °…o…… ª…qÌ“+…‡ W⁄{…“ U‡. ±…‡Ê`{… ∂…•qÌ POENA {……‡ +o…« U‡ +‡¥…“ ª…X, W‡ ~……~…“+…‡{…‡ +…~…¥……©……≈ +…¥…l…“ æÌl…“. +… ∂…•qÌ ~…2o…“ Ê~…{…±… A~…2…≈l… ~…‡{…±`“ (qÌ≈e) +{…‡ ~…‡{…{ª… (°……´…Œ∑S…l…) •…{´…… U‡. @N±…‡{e©……≈ 2…i…“ +‡Ê±…]…•…‡o… °…o…©…{…… ª…©…´…©……≈ S…S…« +…‡£Ì @N±…‡{e{……‡ L…÷±±……‡ Ê¥…2…‡y… HÌ2{……2… 2…‡©…{… Ḣo…ʱ…HÌ ±……‡HÌ…‡ ©……`‡ +‡HÌ qÌ≈eª…≈ÊæÌl…… (Ê~…{…±… HÌ…‡e) Xæ̇2 HÌ2¥……©……≈ +…¥…“ æÌl…“. ª…©…´… Wl……≈ qÌ2‡HÌ °…HÌ…2{…“ N…÷{……ÊæÌl… °…¥…fiŒn…{…‡ +… Ê~…{…±… HÌ…‡e {…“S…‡ ª…©……¥…“ ±…‡¥……©……≈ +…¥…“ +{…‡ +‡{…… +©…±… ©……`‡ L……ª… £Ì…‡WqÌ…2“ HÌ…‡`«{…“ ªo……~…{…… ~…i… HÌ2¥……©……≈ +…¥…“. HÌ´……2‡HÌ +…¥…“ ª…X ©……m… +…Ão…HÌ qÌ≈e{…… ∞~…©……≈ +…~…¥……©……≈ +…¥…l…“ æÌ…‡´… U‡.

¥…‡±…‡{`…>{ª… e‡ (VALENTINE’S DAY)qÌ2 ¥…∫…«{…“ 14 £Ì‡¶…÷+…2“{…… Êq¥…ª…‡ ~……‡l……{…… Ê°…´… ~……m…{…‡ HÌ…e« +o…¥…… ß…‡` ©……‡H̱…¥……{…“ °…o…… +…W‡

°…S…ʱ…l… o…> S…⁄HÌ“ U‡. +‡HÌ ©……{´…l…… °…©……i…‡ +…{……‡ ª…≈•…≈y… m…“Y ª…qÌ“{…… +‡HÌ 2…‡©…{… ª…≈l… ¥…‡±…‡{`…>{… ª……o…‡ U‡. +‡©…{…“ y……é…HÌ ©……{´…l……+…‡ ©……`‡ +… ª…≈l…{…‡ W‡±… HÌ2¥……©……≈ +…¥…“ æÌl…“. V´……2‡ +‡©…{…‡ £Ì…≈ª…“{…“ ª…X +…~…¥……{…“ æÌl…“ l´……2‡ +‡©…i…‡ ~……‡l……{…“ °…‡´…ª…“{…‡ +‡HÌ ÊS…d“ ©……‡H̱…“ æÌl…“. Ê¥…o… ±…¥… §…‡©… ´……‡2 ¥…‡±…‡{`…>{…. •…“Y ©……{´…l…… +‡ ~…i… U‡ Ḣ @N±…‡{e©……≈ +… ª…©…´…‡ ~…K…“+…‡{…… E l…÷HÌ…≥{……‡ +…2≈ß… o…l……‡ æÌ…‡´… U‡ +{…‡ +‡ ©……≥…‡ •……≈y…¥……{…“ l…‰´……2 HÌ2‡ U‡. ©……{´…l…… W‡ ~…i… æÌ…‡´…, +…W‡ Ê°…´… ~……m…{…‡ ~……‡l……{…“ °…‡©… ß……¥…{…… ¥´…Gl… HÌ2¥……{…… ÊqÌ¥…ª… l…2“Ḣ ¥…‡±…‡{`…>{ª… e‡ {…“ AW¥…i…“ HÌ2¥……©……≈ +…¥…‡ U‡ +{…‡ +‡ Ê¥…π…ß…2©……≈ ±……‡HÌÊ°…´… o…> S…⁄HÌ´……‡ U‡.

+ÉyÉÖÊ{ÉH +NÉl«É{ÉÉ ¶É¥qÉà{ÉÒ »É©ÉW

488

475

July - 2016 SALES TAX JOURNAL - 55

±…“~… >´…2 (LEAP YEAR)

qÌ2 S……2 ¥…∫…‚ £Ì‡¶…÷+…2“ ©…ÊæÌ{……©……≈ 29 ÊqÌ¥…ª… æÌ…‡´… U‡. +… +‡¥…÷≈ ¥…∫…« U‡, W‡{…‡ S……2o…“ ß……N…“ ∂…HÌ…´… +{…‡ +‡ ¥…∫…«{…‡ ±…“~…´…2 HÌæ̇¥……©……≈ +…¥…‡ U‡. 2016 {…÷≈ ¥…∫…« ~…i… ±…“~… ´…2 U‡. ª……‡≥©…“ ª…qÌ“o…“ V´……‡ÃW´…{… HÌ˱…‡{e2 °…´……‡N…©……≈ +…¥´…÷≈Ì. W‡©……≈ ¥…∫…«{…‡ 365.25 ÊqÌ¥…ª…{…÷≈ ©……{…¥……©……≈ +…¥…‡ U‡. +…{…… ±…“y…‡ qÌ2 S……2 ¥…∫…‚ +‡HÌ ÊqÌ¥…ª…{……‡ A©…‡2…‡ o……´… U‡. W©…«{… ∂…•qÌ LAUFEN ~…2o…“ ±…“~… ∂…•qÌ Aq√ß…¥´……‡ U‡, W‡{……‡ +o…« U‡ HÌ⁄qÌHÌ…‡ +o…¥…… U±……≈N…. X‡ HÌ…‡> {…HÌHÌ“ l……2“L…¥……≥…‡ Alª…¥…, W‡©… Ḣ ÊJª…©…ª… +… ¥…∫…‚ ª……‡©…¥……2‡ +…¥…l……‡ æÌ…‡´… l……‡ +…¥…l…… ¥…∫…‚ ©…≈N…≥ +{…‡ +‡{…… ~…U“ •…÷y…¥……2‡ +…¥…∂…‡. S……‡o…… ¥…∫…‚ +‡ N…÷∞{…“ WN´……+‡ ∂…÷J¥……2‡ +…¥…∂…‡. +… +‡HÌ ÊqÌ¥…ª…{…“ U±……≈N…{…… ±…“y…‡ +…¥…÷≈ ¥…∫…« ±…“~…´…2 {……©…o…“ +…‡≥L……´… U‡, W‡©……≈ +‡HÌ +Êy…HÌ ÊqÌ¥…ª… æÌ…‡´… U‡.

�O…e±……‡HÌ (GRIDLOCK)

©……‡`…≈ ∂…æ̇2…‡©……≈ ¥…y……2‡ 2ªl…… ©…≥l…… æÌ…‡´… l´……≈ +©…÷HÌ ª…©…´…‡ o…l…… ª…≈~…⁄i…« `ƒ…Ê£ÌHÌX©… ©……`‡ +… ∂…•qÌ ¥……~…2¥……©……≈ +…¥…‡ U‡. +… +‡ °…HÌ…2{……‡ `ƒ…Ê£ÌHÌX©… U‡, W‡©……≈ ¥……æÌ{……‡{…“ ±……≈•…“ HÌl……2 ±……N…“ X´… +{…‡ +…N…≥ Ḣ ~……U≥ W¥……{……‡ HÌ…‡> W Ê¥…H̱~… {… 2æ̇. X≥“ ©……`‡ ¥…~…2…l…… GRIDLOCK ∂…•qÌ ~…2 +… +…y……Ê2l… U‡. ¥…“W≥“o…“ S……±…l……≈ A~…HÌ2i……‡{…“ +≈qÌ2 l……2{…÷≈ W‡ N…⁄≈S…≥÷≈ æÌ…‡´… U‡ +‡{…… ©……`‡ ÊO…e ∂…•qÌ{……‡ °…´……‡N… o…l……‡ æÌ…‡´… U‡. +…¥……≈ N…⁄≈S…≥…≈ ª……o…‡ ª…2L……©…i…“ o…> ∂…Ḣ +‡¥…… ª…≈~…⁄i…« `ƒ…Ê£ÌHÌX©…{…“ Œªo…Êl… ©……`‡ +… ∂…•qÌ ¥…“ª…©…“ ª…qÌ“o…“ ß……∫……©……≈ A©…‡2…´……‡ U‡. HÌ…‡> +‡¥…“ Œªo…Êl… W‡©……≈ £Ìª……> W¥……´… +{…‡ HÌ…‡> A~……´… {… We‡ +‡{…… ©……`‡ ~…i… HÌ´……2‡HÌ +… ∂…•qÌ{……‡ °…´……‡N… HÌ2¥……©……≈ +…¥…‡ U‡.

�¥…ª…±…•±……‡+2 (WHISTLE BLOWER)ª…2HÌ…2“ +o…¥…… HÌ…‡> Xæ̇2 ª…≈ªo……©……≈ N…‡2HÌ…{…⁄{…“ °…¥…fiŒn… o…> 2æÌ“ æÌ…‡´… l´……2‡ +‡{…“ ©……ÊæÌl…“ •…æÌ…2

~……e{……2… ©……`‡ +… ª…≈•……‡y…{… ¥…~…2…´… U‡. Ê¥…ª…±… +‡`±…‡ ª…“`“ +{…‡ •±……‡{……‡ +o…« U‡ ¥…N……e¥…“. ª…“`“ ¥…N……e“{…‡ W‡ +{´…{…‡ S…‡l…¥…“ q̇ +‡ �¥…ª…±…•±……‡+2 U‡. P…i…“ ¥……2 +…¥…“ ª…≈ªo……{……‡ W HÌ…‡> HÌ©…«S……2“ +… ß…⁄Ê©…HÌ… ß…W¥…l……‡ æÌ…‡´… U‡, W‡{…… ±…“y…‡ HÌ…‰ß……≈e…‡ •…æÌ…2 +…¥…l……≈ æÌ…‡´… U‡. +…W‡ ©……ÊæÌl…“ +Êy…HÌ…2{…… HÌ…´…qÌ…{…… ±…“y…‡ HÌ…‡> ~…i… {……N…Ê2HÌ ª…2HÌ…2“ Ê¥…ß……N……‡ ~……ª…‡o…“ Xæ̇2 ÊæÌl…{…“ ©……ÊæÌl…“ ©…‡≥¥…“ ∂…Ḣ U‡. +…{…… ±…“y…‡ ª…2HÌ…2“ HÌS…‡2“+…‡©……≈ S……±…l…“ N…‡2“Êl…+…‡{…‡ •…æÌ…2 ~……e“ ∂…HÌ…´… U‡ +{…‡ HÌ…‡> ~…i… ¥´…ŒGl… Ê¥…ª…±…•±……‡+2 •…{…“ ∂…Ḣ U‡. Ê¥…ª…±…•±……‡+2{…… ª…≈2K…i… ©……`‡ HÌ…´…qÌ…©……≈ ~…i… L……ª… X‡N…¥……> 2…L…¥……©……≈ +…¥…l…“ æÌ…‡´… U‡. P…i…… q̇∂…©……≈ +… °…o…©… ª¥…“HÌ…2¥……©……≈ +…¥…“ U‡.

�ª…{o…‡ª……>]2 (SYNTHESIZER)+…W‡ P…i…“ ¥……2 ª…≈N…“l…{…… W±…ª……©……≈ ß……N… ±…‡l…… +…‡2Ḣª`ƒ…©……≈ +… {……©…{…÷≈ +‡HÌ >±…‡G`ƒ…‡Ê{…HÌ A~…HÌ2i…

X‡¥…… ©…≥‡ U‡. HÌ“-•……‡e« y…2…¥…l…… +… ª……y…{… w…2… ±…N…ß…N… •…y……≈ W ~……2≈~…Ê2HÌ ¥……v…‡ W‡¥…÷≈ ª…≈N…“l… ¥…N……e“ ∂…HÌ…´… U‡. +‡ A~…2…≈l…, +{´… °…HÌ…2{…… ª¥…2 ~…i… 2W⁄ HÌ2“ ∂…HÌ…´… U‡. +… >±…‡G`ƒ…‡Ê{…HÌ ¥……v{…“ ∂……‡y… ~…U“ +‡{…÷≈ {……©… O…“HÌ ß……∫……{…… ∂…•qÌ SYNTHESIS ~…2o…“ ~……e¥……©……≈ +…¥´…÷≈ U‡, W‡{……‡ +o…« U‡ Ê¥…Ê¥…y… ¥…ªl…÷+…‡{…‡ +‡HÌ W ªo…≥‡ ß…‡N…“ HÌ2“ HÌ≈>HÌ {…¥…÷≈ •…{……¥…¥…÷≈. ʪ…{o…‡ª……>]2 ~…i… +‡¥…÷≈ ´…≈m… U‡, W‡©……≈ Ê¥…Ê¥…y… °…HÌ…2{……≈ ¥……v…‡{…… ª¥…2…‡ +‡HÌÊm…l… HÌ2¥……©……≈ +…¥´…… U‡. +… ´…≈m…{…“ ∂……‡y… +‡HÌ +©…‡Ê2HÌ{… >W{…‡2 +…2. +‡. ©…⁄N…‡ HÌ2“ æÌ…‡¥……{…÷≈ ©……{…¥……©……≈ +…¥…‡ U‡. +…‡2Ḣª`ƒ…©……≈ +…{…“ æÌ…W2“ æÌ…‡´… l……‡ HÌ…‡> ¥……v{…“ L……‡` Wi……l…“ {…o…“, HÌ…2i… Ḣ +‡ ¥……v{……‡ ª¥…2 ~…⁄2…‡ ~……e“ ∂…HÌ…´… U‡.

+ÉyÉÖÊ{ÉH +NÉl«É{ÉÉ ¶É¥qÉà{ÉÒ »É©ÉW

489

476

SALES TAX JOURNAL - 55 July - 2016

©……‡{…‡`2“ ~……‡�±…ª…“ HÌ�©…`“ +‡`±…‡ ∂…÷≈ ?

©……‡{…‡`2“ ~……‡Ê±…ª…“ HÌÊ©…`“ +‡`±…‡ ª…2HÌ…2 w…2… Ê{…´…÷Gl… o…{……2“ HÌÊ©…`“, W‡ £Ì÷N……¥……{…… ±…K´……≈HÌ{…‡ ʪ…u HÌ2l…“ {……i……{…“Êl… •…{……¥…∂…‡. U ª…ß´…{…“ +… ª…Ê©…Êl…©……≈ m…i… ª…ß´… Ê2]¥…« •…‡{HÌ +…‡£Ì >Œ{e´……{…… +{…‡ m…i… ª…2HÌ…2‡ Ê{…´…÷Gl… HÌ2‡±…… °…Êl…Ê{…Êy… æÌ∂…‡. +… ª…Ê©…Êl…{…“ Xæ̇2…l… 9 +…‡N…ª` ~…æ̇±……≈ o…> W¥……{…“ ∂…HÌ´…l…… U‡.

ª…2HÌ…2 +{…‡ Ê2]¥…« •…‡{HÌ ¥…SS…‡ {……i……≈{…“Êl…{…÷≈ ©……≥L…÷≈ P…e¥……{…‡ ±…N…l…… HÌ2…2 2015 {…… ©……S…«©……≈ o…´…… æÌl……. +… {……i……{…“Êl… +≈l…N…«l… O……æÌHÌ ªl…2‡ £Ì÷N……¥……‡ 2017 {…… ©……S…« ª…÷y…“©……≈ 4 `HÌ…+‡ ±……¥…¥……{…÷≈ ±…K´… {…HÌHÌ“ HÌ2¥……©……≈ +…¥´…÷≈ æÌl…÷≈. +±…•…n… +… ±…K´… •…‡ `HÌ… A~…2 {…“S…‡ o…> ∂…Ḣ l…‡¥…“ X‡N…¥……> æÌl…“. £Ì÷N……¥……{…… +… ±…K´…{…‡ ʪ…u HÌ2l…“ ¥´……WqÌ2{…“ {…“Êl… •…{……¥…¥……©……≈ +…¥…∂…‡. ª…2HÌ…2 qÌ2 ~……≈S… ¥…∫…«{…… £Ì÷N……¥……{……‡ ±…K´……≈HÌ Ê2]¥…« •…‡{HÌ{…… ª……o…‡{…“ S…S……« - Ê¥…S……2i…… •……qÌ {…HÌHÌ“ HÌ2∂…‡ +{…‡ ¥…∫……«{…÷ ¥…∫…« O……æÌHÌ ß……¥……≈HÌ (ª…“~…“+…>) {…… ª…≈qÌß…«©……≈ l…‡{…“ ª…©…“K…… o…∂…‡.

ª…2HÌ…2‡ 27©…“ W⁄{…, 2016 {…… 2…‡W °…N…` HÌ2‡±…… {……‡Ê`Ê£ÌḢ∂…{…©……≈ ©……‡{…‡`2“ ~……‡Ê±…ª…“ HÌÊ©…`“©……≈ ª…ß´……‡{…“ Ê{…©…i…⁄≈HÌ l…o…… l…‡{…“ ∂…2l……‡{…“ Ê¥…N…l……‡ °…N…` HÌ2¥……©……≈ +…¥…“ æÌl…“.

+… HÌÊ©…`“{……‡ ©…÷L´… y´…‡´… “ß……¥…©……≈ Œªo…2l…… X≥¥…“ 2…L…“{…‡ +…Ão…HÌ Ê¥…HÌ…ª…{…‡ ʪ…u HÌ2¥……{……‡” U‡.

ª…Ê©…Êl…©……≈ ª…2HÌ…2{…… °…Êl…Ê{…Êy…+…‡{…“ ~…ª…≈qÌN…“ HÌ2¥…… ©……`‡ +‡HÌ ª…Ê©…Êl… {…“©…¥……©……≈ +…¥…“ U‡. +… ª…Ê©…Êl…©……≈ °…y……{…©…≈e≥{…… ª…ÊS…¥…, +…2•…“+…> N…¥…{…«2 +{…‡ +…Ão…HÌ •……•…l……‡{…… ª…ÊS…¥…{……‡ ª…©……¥…‡∂… HÌ2…´……‡ U‡.

MEHSANA SALES TAX BAR ASSOCIATION

Managing Committee for the year 2016-17

Shri Kaushik N. Chhabda Shri Arpan A. Yagnik President Hon. Secretary

Shri Janak J. Bhavsar Shri Harshadkumar V. Oza Joint Secretary I. T. Cell

+ÉyÉÖÊ{ÉH +NÉl«É{ÉÉ ¶É¥qÉà{ÉÒ »É©ÉW

490

477

July - 2016 SALES TAX JOURNAL - 55

FRATERNAL TWINS – CENTRAL INDIRECT TAXES AND

VAT

Fraternal twins are siblings who are not completely identical but nonetheless they are twins. Similarly, while Central Excise, Customs, Service Tax and Value Added Tax may have their own peculiarities, they are species of the same genus. Therefore the law decided in the context of one is likely to be relevant even in the context of another. The objective of this column is to highlight decisions rendered in the context of Central Indirect Taxes which are relevant to the provisions of the Gujarat Value Added Tax Act, 2003.

Exemption was available to lenses which were required to be customized before being fitted for a particular customer. Customs tariff changed from 6 digit entries to 8 digit entries. Thereafter exemption denied.

Held that the change in tariff was only as part of the numbering scheme and could not lead to denial of exemption to lenses without any change in language of notification

Many classification issues raised under the GVat Act on the ground of subsequent events even though there is no change in the language of the relevant entry.

Essilor India Pvt. Ltd. v/s Commissioner of Customs 2016 (335) ELT 584 (SC)

The assessee was importing spectacle lenses and he was claiming exemption under the Customs Act, 1962. Earlier the Customs Tariff itself provided for Nil rate of duty in respect of the spectacle lenses. Thereafter from the year 2004 the tariff entry for spectacle lenses, intra-ocular lenses and contact lenses contained rate of 8%. Simultaneously the spectacle lenses, intra-ocular lenses and contact lenses were given exemption from payment of duty. From 28.2.2005 8 digit headings were introduced in respect of tariff entries. The classification of the spectacle lenses was thereafter changed to the entry for “semi-finished spectacle lenses” and the benefit of exemption was denied on the ground that the exemption was admissible only in respect of finished spectacle lenses. The Customs Excise and Service Tax Tribunal confirmed such view of the Customs department. The assessee filed appeal against such order before Hon. Supreme Court.

Uchit N. Sheth - Advocate - [email protected]

Fraternal Twins – Central Indirect Taxes and VAT

491

478

SALES TAX JOURNAL - 55 July - 2016

View of Hon. Supreme CourtHon. Supreme Court observed that the change in the tariff structure from 6

digit entries to 8 digit entries was only with a view to facilitating information about state wise revenues and there was no change in the tariff regime. A paragraph of the notification was referred to wherein it was clearly observed that the amendment did not involve any substantive change in the existing notification. Hon. Supreme Court observed that there was no change in the nomenclature of the exemption notification on the basis of which the spectacle lenses of the assessee were granted exemption. On such basis it was held by Hon. Supreme Court that the assessee would continue to get the exemption which was earlier granted to the assessee by the department itself and that the change in tariff entries would not have any bearing on the issue.

Applicability of the judgement to the GVat ActThere are many instances under the Gujarat Sales Tax Act, 1969 (herein after

referred to as “the Sales Tax Act”) as well as under the Gujarat Value Added Tax Act, 2003 (herein after referred to as “the Vat Act”) and the Gujarat Tax on Entry of Specified Goods into Local Areas Act, 2001 (herein after referred to as “the Entry Tax Act”) wherein the department has changed its stand on a particular issue on the basis of an event or amendment which as such should not have been treated as relevant. Examples are as under:

(1) Classification of patasha, sakaria, harda, alchidana, etc

Hon. Supreme Court had held in the case of The State of Gujarat V/S Sakarwala Brothers 19 S.T.C. 24 (S.C.) that patasa, harda and alchidana are covered by entry relating to sugar since the term “sugar” had been defined with reference to the entry under the Excise law. Thereafter there were certain changes in the Excise tariff which were not at all relevant in so far as the Sales Tax Act was concerned. Even then the sales tax department took a view that after the changes in the excise law patasha, harda and alchidana would not remain exempt under the Sales Tax Act. Hon. Gujarat High Court in the case of State of Gujarat v/s Virumal Santumal 72 VST 403 (Guj.) analyzed the legislative history relating to the entry of “sugar” and came to the conclusion that all forms of sugar continued to remain exempt. It was noted in the judgement that even the Sales tax department had expressed such view by way of public circular and even then different view was being taken in assessments.

(2) Entry tax on tractors

Entry tax was expressly introduced to protect the interest of local dealers in cases where rate of sales tax in other States was lower than the rate of sales tax in Gujarat. It has time and again been clarified that the rate of entry tax has a direct linkage to the rate of sales tax/value added tax. Tractors attracted 4% sales

Fraternal Twins – Central Indirect Taxes and VAT

492

479

July - 2016 SALES TAX JOURNAL - 55

tax under the Sales Tax Act. Even after the introduction of the Vat Act tractors continued to be governed by a separate entry for which rate of tax prescribed was 4%. As against this the rate of entry tax on motor vehicles was 12% which was ultimately increased to 15%. Thus it was never the intention of the legislature of the government to treat tractors as motor vehicles. However huge demand has been raised on tractor manufacturers by treating tractors as motor vehicles for the purpose of entry tax on the basis of a judgement of Hon. Gujarat High Court rendered in the context of Motor Vehicles Act. Thereafter on the basis of representations made from the trade, levy of entry tax on tractors in excess of 5% has been exempted. However this has been done prospectively and hence the issue as to whether entry tax can be levied on tractors in respect of past period survives and it would require decision by Hon. High Court where matters in this regard are pending.

(3) Prawn feed

A determination order was passed under Section 62 of the Sales Tax Act in the case of West Coast Water base Pvt. Ltd. wherein prawn feed was held to be classifiable under the Entry for “Cattle feed” and therefore exempt from sales tax. Thereafter even under the Vat Act the Schedule entry for “Cattle feed” was materially kept the same and hence prawn feed continued to be treated as exempt. On 1.4.2012 a separate entry “Aquatic feed” was introduced in the exemption notification issued under Section 5(2) of the Vat Act. On this basis view has now been taken in a number of cases that aquatic feed was taxable for the period prior to 1.4.2012 even though there was a determination order holding that it was exempt from tax.

ConclusionThus the Government / department has been known to change its stand on

several issues even though express intention to the contrary was conveyed on earlier occasions. In an ideal scenario if once a conscious decision is taken to exempt or not levy tax on particular commodities by accepting a particular interpretation then it is expected from the Government / department that it sticks to such stand. Dealers arrange their business on the basis of assurances/views expressed by the Government. Even if there is a different judicial interpretation by some Court, the Government / department should be firm enough in sticking to its policy decision which was admittedly in favour of the dealers earlier. However if the department indeed changes its stand then the dealer is left with no option but to litigate on the issue. In litigation the legislative history and departmental pronouncements such as determination order or public circular need to be relied upon. The judgement of Hon. Supreme Court in the case of Essilor India Ltd. (supra) wherein it has been held that the assessee continued to be eligible for exemption as was held earlier by the Customs department itself since there was no change in the language of the exemption notification can be helpful in such cases.

Fraternal Twins – Central Indirect Taxes and VAT

493

480

SALES TAX JOURNAL - 55 July - 2016

CA Abhay Desai - [email protected]

3DNO SERVICE TAX IF COMPOSITE WORKS CONTRACTS INCLUDES LAND

Lao Tzu said “The key to growth is the introduction of higher dimensions of consciousness into our awareness”. Thinking about an issue only from one-dimension may result in faulty action. This is also true for indirect taxes. One has to think from all points of view to get the best answer. This column attempts to discuss various issues pertaining to indirect taxes from all the three dimensions i.e. Central Excise, Service Tax & VAT.

INTRODCUTIONHon. Delhi High Court in the case of Suresh Kumar Bansal v. Union of

India [2016] 70 taxmann.com 55 (Delhi) dated 03.06.2016 has held that Rule 2A of Service Tax (Determination of Value) Rules, 2006 shall not apply when the consideration for a composite works contract includes the value of land and hence such contracts shall not be liable to service tax. Let us understand the said decision and its implications.

FACTS OF THE CASEPetitioners had entered into a composite contract with the builders to buy

flats in a multi-storey group housing project named ―Sethi Group - Max Royal being developed by the builder in Sector 76, Noida, Uttar Pradesh. The builder had in addition to the consideration for the flats also recovered service tax from the Petitioners, which is payable by him for services in relation to construction of complex and on preferential location charges. Petitioner challenged the levy of service tax both on the construction service as well as preferential location charges.

ISSUES BEFORE THE COURTMoot question before the Hon. Delhi High Court was whether the option under

Rule 2A (ii) of Service Tax (Determination of Value) Rules, 2006 shall apply to a composite works contract when the value of contract includes the value of land. Another question before the Hon. Court was whether charges collected for giving a preferential location can be considered as a service.

DECISION OF THE COURT & REASONINGHon. Delhi High Court held that Rule 2A (ii) shall not apply to composite works

contract when the value of contract includes the value of land. Let us understand the reasoning for said decision.

3D - No Service Tax if Composite Works Contracts includes Land

494

481

July - 2016 SALES TAX JOURNAL - 55

Under Rule 2A of Service Tax (Determination of Value) Rules, 2006 value of service involved in the composite works contract can be determined as follows:

1) Splitting the contract (when land is not part of contract value): Under this method as per Rule 2A (i), value of service shall be total value of contract less the value of transfer of property in goods involved in the execution of the said works contract. As per explanation (c) value adopted for the purposes of payment of value added tax, shall be taken as the value of transfer of property in goods involved in the execution of the said works contract for determining the value of works contract service Under this method there is no controversy about the inclusion of value of land as a part of taxable service. Moreover Hon. Punjab and Haryana High Court in the case of CHD Developers Ltd. v. State of Haryana [2015] 57 taxmann.com 315 (Punjab & Haryana) has held that value of land must be allowed as a deduction in such circumstances when the contract is bifurcated into individual components. Practically this method is not preferred by the service providers as the amount to be claimed as deduction towards value of material and land involved is not easily ascertainable.

2) Composition scheme: If the consideration for composite works contract cannot be bifurcated into service and goods portion, service provider can choose to pay tax as per Rule 2A (ii) by arriving at the value of service which is 40% of total amount charged in case of original works or 70% of total amount charged in case of other works contracts.

In the present case, issue is with regard to option under Rule 2A (ii). Hon. Delhi High Court held that as Rule 2A (ii) does not provide for the deduction of value of land, the mechanism to tax such contracts fail as the Act provides for levy of service tax only on the service component involved in the composite works contract. Reliance was placed on following decisions:

a) In Mathuram Agrawal v. State of M.P. (1999) 8 SCC 667, the Supreme Court held that in a taxing Act it is not possible to assume any intention or governing purpose of the statute more than what is stated in the plain language. It is not the economic results sought to be obtained by making the provision which is relevant in interpreting a fiscal statute. Equally impermissible is an interpretation which does not follow from the plain, unambiguous language of the statute. Words cannot be added to or substituted so as to give a meaning to the statute which will serve the spirit and intention of the legislature. The statute should clearly and unambiguously convey the three components of the tax law i.e. the subject of the tax, the person who is liable to pay the tax and the rate at which the tax is to be paid. If there is any ambiguity regarding any of these ingredients in a taxation statute then there is no tax in law. Then it is for the legislature to do the needful in the matter.‖

b) Supreme Court in Govind Saran Ganga Saran v. CST: (1985) 155 ITR 144 (SC) wherein the Court held that the components which enter into the concept of a tax are well known. The first is the character of the imposition known by its nature which prescribes the taxable event attracting the levy, the second is a clear

3D - No Service Tax if Composite Works Contracts includes Land

495

482

SALES TAX JOURNAL - 55 July - 2016

indication of the person on whom the levy is imposed and who is obliged to pay the tax, the third is the rate at which the tax is imposed, and the fourth is the measure or value to which the rate will be applied for computing the tax liability. If those components are not clearly and definitely ascertainable, it is difficult to say that the levy exists in point of law. Any uncertainty or vagueness ill the legislative scheme defining any of those components of the levy will be fatal to its validity.‖

c) In Commissioner Central Excise and Customs, Kerala v. Larsen & Toubro Ltd. (2016) 1 SCC 170 the Supreme Court held that since neither the Act nor Rules provided for any machinery provisions to exclude the non-service element from a composite contract, the taxable services referred in clauses (g), (zzd), (zzh), (zzq) and (zzzh) of sub-section 105 of Section 65 of the Act could only refer to services in relation to a service contract simplicitor and not to composite contracts.

d) In CIT v. B. C. Srinivasa Shetty (1981) 2 SCC 460, the Supreme Court held that the charging Sections and the computation provisions together constitute an integrated code and the transaction to which the computation provisions cannot be applied must be regarded as never intended to be subjected to charge of tax.

Hence it held that neither the Act nor the Rules framed therein provide for a machinery provision for excluding the value of land and hence no service tax can be imposed on composite works contract which includes the value of land. Hon. Court however upheld the stand of the department that consideration received for preferential location amounts to a service.

CONCLUSIONIt must be noted that Punjab and Haryana High Court in the case of CHD

Developers Ltd. v. State of Haryana [2015] 57 taxmann.com 315 (Punjab & Haryana) had held that as the composition method is optional in nature, once a dealer opts for composition scheme, he gets various advantages and privileges which otherwise are not available to ordinary VAT dealers. As the composition provisions are not charging provisions, composition tax is to be paid on the total consideration and this could not be challenged. Hence value of land cannot be excluded under the composition method. In our article dated 25.06.2015 we had opined that the said view is incorrect and value of land cannot be a part of taxable turnover in VAT under the composition scheme. Hon. Delhi High Court (supra) has not discussed the decision of CHD Developers Ltd. but has implicitly differed with the view expressed by Hon. Punjab and Haryana High Court. One more point to consider in this judgment is that the challenge to levy of service tax was not made by the service provider but by the service receiver. It must also be noted that attention of Hon. High Court was not drawn to Notification no. 26/2012 – ST which clearly stipulates that value of land shall be part of the consideration to claim abetment. The said decision however shall be very helpful under GVAT Act as Notification No. (GHN-88)VAT-2006-S.14A(4)-TH does not expressly distinguish between works contract with land and without land.

3D - No Service Tax if Composite Works Contracts includes Land

496

483

July - 2016 SALES TAX JOURNAL - 55

Sunil Sagar - Advocate - [email protected]

hkÞ ËuLkk ÷urfLk shk Mkku[fu, shk Mkt¼÷fu..!!!

yuf fkÕÃkrLkf ½xLkk ÷Eyu...ík{u ÃkhMkuðu huçkÍuçk Aku, ¾qçk íkhMk ÷køke Au, Ãký fÞktÞ Ãkkýe {¤u yu{ LkÚke, yu Mktòuøkku{kt ík{u yuf

ÍkzLkk AktÞzk{kt Úkkf ¾kðk Q¼k hnku Aku !!!íÞkt s Mkk{uÚke {fkLkLkk Ãknu÷k {k¤Lke çkkhe ¾w÷u Au. yLku ík{khe yLku íku ÔÞrfíkLke ykt¾ku {¤u Au.

ík{khe nk÷ík òuELku íku ÔÞrfík ík{Lku Ãkkýe òuEyu Au íkuðku Eþkhku fhu Au íku ð¾íku ík{Lku yu ÔÞÂõík fuðe ÷køku? yk ík{khku Ãknu÷ku yr¼«kÞ Au.

íku ÔÞrfík Lke[u ykððkLkku Eþkhku fheLku çkkhe çktÄ fhu Au. 15 r{rLkx Úkðk AíkktÞ Lke[uLkku Ëhðkòu LkÚke ¾w÷íkku nðu íku ÔÞrfík «íÞu ík{khku yr¼«kÞ þwt nþu?

- yk ík{khku çkeòu yr¼«kÞ Au.Úkkuzeðkh ÃkAe Ëhðkòu ¾w÷u yLku íku ÔÞrfík yu{ fnu fu “{Lku rð÷tçk Úkðk {kxu {kV fhòu, Ãký ík{khe

nk÷ík òuELku {Lku Ãkkýe fhíkkt ÷ªçkLkwt þhçkík ykÃkðwt ÞkuøÞ ÷køÞwt {kxu Úkkuze ðkh ÷køke.”nðu íku ÔÞrfík rð»ku ík{khku yr¼«kÞ fuðku nþu?- ÞkË hk¾òu fu, nsw íkku Ãkkýe fu þhçkík {éÞwt LkÚke íkku ík{khku ºkeòu yr¼«kÞ {Lk{kt s hk¾ku.nðu suðwt ík{u þhçkík S¼Lku ÷økkðku Aku íÞkts ík{Lku ÏÞk÷ ykðu fu íku{kt ¾ktz shk Ãký LkÚke!! nðu íku ÔÞrfík ík{Lku fuðe ÷køke ?yuf Mkk{kLÞ «Mktøk{kt Ãký òu ykÃkýku yr¼«kÞ ykx÷ku ¾ku¾÷ku yLku Mkíkík çkË÷kíkku nkuÞ íkku

ykÃkýu fkuELkku Ãký yr¼«kÞ ykÃkðkLku ÷kÞf Mk{sðk òuEyu fu Lkrn?nfefíku ËwrLkÞk{kt yux÷wt íkku Mk{òÞwt fu, òu ík{khe yÃkuûkkLkk [ku¾Xk{kt çktÄçkuMkíkwt ðíkoLk Mkk{uLke

ÔÞrfík fhu íkku íku Mkkhe Lkrn íkku íku ¾hkçk.hksfkhýLke íkksuíkhLke ½xLkk Ãký ynª çktÄçkuMkíke ÷køku Au...h½whk{Lk heÍðo çkUfLkk økðLkoh. çkUfhkuLke yk÷{{kt yu Mxkh økýkÞ Au. yu{Lkk «þtMkíkeÞ Ãkøk÷ktÚke

ykÃkýLku yuðku ynku¼kð òøku yu Mðk¼krðf Au, íÞkt þhkhíke Mkwçkú{ÛÞ{ Mðk{e fqËe ÃkzÞk, “h½whk{Lk

ÊWÅqNÉÒ - +àH HàʱÉeÉà»HÉà~É

497

ÊWÅqNÉÒ - +àH HàʱÉeÉà»HÉà~É

484

SALES TAX JOURNAL - 55 July - 2016

yMk÷ ¼khíkeÞ LkÚke. y{urhfk íkhVe ykŠÚkf ð÷ý Ähkðu Au.” h½whk{ rð»ku ykÃkýku yr¼«kÞ çkË÷kþu. yuf yr¼«kÞ yuðku Ãký çktÄkþu fu {kLkLkeÞ ðzk«ÄkLk fu{ [qÃk Au? ðzk«ÄkLkLke yk rð»kÞLke [qÃkfeËe ykÃkýLku ðzk«ÄkLk «íÞu Lkfkhkí{f yr¼«kÞ íkhV ÷E sþu Ãký íÞkts ÃkkAtwt r[ºk çkË÷kÞ Au. yýoð økkuMðk{eLkk ELxhÔÞw{kt ðzk«ÄkLk çkhkçkh ¾eÕÞk Au yLku h½whk{LkLke {kUVkx «þtMkk fhu Au yLku ykzfíkhku Eþkhku fhu Au {kºk MkMíke ÷kufr«Þíkk ¾kíkh øk{u íkuðkt rLkðuËLkku Lk fhðkt òuEyu. nðu ykÃkýku yr¼«kÞ Mðk{e rðþu Ãký çkË÷kÞkuLku?

{kýMk ÃkkuíkkLku {kxu su yr¼«kÞ çkktÄu íku fhíkkt (íkuLkku) þºkw (íkuLku {kxu) çkktÄu íku{kt MkíÞLke {kºkk ðÄw nkuÞ Au. øk¼hw ÔÞrfík yr¼«kÞ Mkk{u zøkzøke òÞ Au. {q¾koyku íkuLkku «ríkfkh fhu Au, þkýkyku íkuLkku íkku÷ fhu Au yLku fkçku÷ {kýMkku íkuLku Ëkuhðu Au. {qh¾kE¼Þkou yr¼«kÞ yu {qh¾ yr¼«kÞ s Au - ¼÷u Lku íku ÷k¾ku ÷kufkuLkku nkuÞ ! (ynª EM÷kr{f hksðx ÞkË ykðu AuLku?)

fkuE ÔÞÂõík ík{khku yr¼«kÞ ÷uðk ykðu íÞkhu nfefík{kt AwÃkkÞu÷wt fkhý íkku yu nkuÞ Au fu, íku ÔÞrfík ÃkkuíkkLkk yr¼«kÞLku Ãkw»x fhðk MkkÁt ykðu Au, íku{kt MkwÄkhk fhðk {kxu Lkrn. ík{khu yufË{ ¼zfku WíÃkÒk fhðku nkuÞ íkku, Mkk{Mkk{k yr¼«kÞku Ähkðíke çku ÔÞrfíkykuLku ¼uøke fhe Ëku. xe.ðe. WÃkh rðrðÄ ÃkûkLkk «ríkrLkrÄykuLke [[koyku fux÷e hMk«Ë, çkq{çkhkzkÞwõík Ãký rLkhÚkof nkuÞ Au Lku? rLkhÚkof yr¼«kÞkuLkk ÞwØ{ktÚke Ãký ykÃkýLku ykLktË {¤íkku nkuÞ Au. nk, yYý sux÷e - frÃk÷ rMkççk÷, yku{Ãkwhe - LkMkYËTeLk þknLke [[koyku, yr¼«kÞku òuðk - Mkkt¼¤ðk sÕMkku Ãkze òÞ Au - fkhý fu yu{Lke ô[e çkkirØf «rík¼k, ÃkhMÃkh MkL{kLk, íkfoþwØ Ë÷e÷kuLkk {nkMkkøkh{kt ykÃkýu {òLke Ak÷fku {kýeyu Aeyu.

MkqVe MkkrníÞLkwt yuf {ÍkLkwt Ãkkºk yux÷u {wÕ÷k LkMkeYrÆLk. yu{Lkk SðLk{kt çkLku÷e ½xLkkykuÚke yu{Lke ÃkíLkeLkku {wÕ÷k rðþu ({wÕ÷k ÃkíLkerLk»X nkuðk AíkktÞ) yr¼«kÞ çkË÷kíkku LkÚke yuLke hrMkf fnkýe yk hne...

yuf ðkh {wÕ÷k ykurVMkÚke ½hu ykðu Au, íÞkhu yu{Lkkt ÃkíLkeLku fkux WÃkh yuf ÷ktçkku ðk¤ {¤u Au. yLku yu frsÞkÚke ½hLku ºkkrn{k{ fhe {qfu Au. yu {wÕ÷kLku Ä{fkðíkkt fnu Au, “ík{u sYh fkuE ÞwðkLk AkufheLkk «u{{kt ÷køkku Aku!” Äehs yLku þktríkÚke {wÕ÷k Mk{òðu Au fu, “òu nwt çkòhLke røkhËe{ktÚke ÃkMkkh ÚkELku ½hu ykðíkku níkku. {khk{kt rðïkMk hk¾... yu ¼ez{kt yLkkÞkMku fkuELkku ðk¤ {khk fkux Ãkh Ãkze økÞku nþu.” (ÃkíLkeLkku yr¼«kÞ nS çkË÷kÞku LkÚke) Ãký ÃkíLkeLku {wÕ÷k Ãkh hrík¼kh ¼hkuMkku Lkrn. yu {wÕ÷kLku Ä{fkððkLkwt [k÷ws hk¾u Au.

çkeò rËðMku ßÞkhu {wÕ÷k ½hu ykðu Au íÞkhu ÃkíLke yu{Lkk fkux Ãkh MkVuË ðk¤ swyu Au, “fk÷u íkku ík{u ÞwðkLk AkufheLkk [¬h{kt níkk yLku yksu yuf ½hzeLkk †eLkk MktçktÄ{k? yhhh... ík{u fuðk ÷tÃkx Aku ? ík{u {kÁt SðLk çkhçkkË fhe LkkÏÞwt...”

íÞkh ÃkAeLkk rËðMku, ½hu ykðíkkt Ãknu÷kt {wÕ÷kLku yu{Lke ÃkíLkeLkku frsÞku, ff¤kx çkhkçkh ÞkË níkkt. yLku íkuÚke íku{ýu ½h{kt Ëk¾÷ Úkíkk Ãknu÷kt s ÃkkuíkkLkku fkux çkhkçkh MkkV fhe ËeÄku. ½h{kt ykðíkkt s ÃkíLkeyu WÄzku ÷uíkkt fkux çkhkçkh íkÃkkMke òuÞku Ãký yuLku yuf Ãký ðk¤ Lk Ëu¾kÞku. {wÕ÷kLku ÚkÞwt fu nkþ nðu AqxÞk Ãký ÃkíLkeíkku yk¾hu ÃkíLke Au yLku yu Ãký {wÕ÷kt LkMkeYËTeLkLke. yuýu ºkkz ÃkkzeLku fÌkwt, “ík{u fux÷k çkË{kþ Aku! yksu íkku ík{u yx÷e nðu ÃknkU[e økÞk fu xk÷ðk¤e MºkeLku Ãký Akuzíkk LkÚke.” yk{ fnuíkkt

ÊWÅqNÉÒ - +àH HàʱÉeÉà»HÉà~É

498

485

July - 2016 SALES TAX JOURNAL - 55