1 abstract 2 preface - uis brage - unit

TRANSCRIPT

1 Abstract The purpose of this thesis is to estimate the intrinsic value of Siem Offshore. The main

method is the discounted cash flows approach (DCF). This is complemented by a ratio

analysis. The present value calculation gives at target share price of NOK 7.72.1 The latest

closing price was NOK 8.3.2 The relative valuation based on peers on the Oslo Stock

Exchange came up with a price of NOK 6.43. Siem Offshore is still struggling for profitability

after the slump that hit the OSV business in 2008. The conclusion and recommendation in this

thesis is to sell SIOFF.

2 Preface The most important reason for writing a valuation as a final thesis – is to learn and get close to

the real life of economics. Valuation has not been part of my curriculum, but I have followed

the lectures in valuation at UiS. Valuation is a core discipline in my major field of study in

graduate school – applied finance. It sums up and brings together several skills from the

business education. Valuation is a complex and diverse economic exercise.

Like many other fields in economics, it is not an exact science, but it is nevertheless a

necessary task to perform valuations to form a basis for informed economic decisions.

The goal was to take a stand and end up with a single number, and translate that into an

unequivocally recommendation. In hindsight this has of course proven difficult.

One of the challenges in valuation is to find updated, unbiased information. In this respect I

had hopes for more exact information from SIOFF, but it turned out that the restrictions on

listed firms would not allow them do disclose information beyond annual reports, stock

exchange releases and the likes.

The reason for choosing to write about a company in the offshore supply business is personal

interest in shipping, the importance of shipping in Norway, and more recently the importance

of energy for the increased wealth in my nation.

1 NOK/USD 13 June 2014 is 6.0038 http://www.norges-bank.no/no/prisstabilitet/valutakurser/usd/ 2 http://www.oslobors.no/markedsaktivitet/stockOverview?newt__ticker=SIOFF

1

The reason for selecting Siem Offshore in particular among all the OSV players is that

Kristoffer Stensrud, one of the founders and the manager of the mutual fund Skagen Kon-

Tiki has expressed that SIOFF will be part of his portfolio at least to the end of 2014. As

Skagenfondene are a value based mutual fund, I was hoping to find the stock to be

undervalued.

I would like to extend my gratitude to those parties taking their time to supply me with

information, data and guidance. This includes IHS, RS Platou, SR Bank and Mads Holm

representing UiS. The list is not exhaustive.

I have tried, to the best of my ability to give appropriate credit to my sources. If there are any

discrepancies, the bibliography should be exhaustive.

Table of Contents 1 Abstract ........................................................................................................................................... 1

2 Preface ............................................................................................................................................. 1

3 Siem Offshore - a company overview ............................................................................................. 4

4 The OSV Industry ............................................................................................................................. 7

4.1 Vessels and segments .............................................................................................................. 8

4.2 Drilling rigs ............................................................................................................................... 9

4.3 Demand drivers ..................................................................................................................... 10

4.4 Deeper water ......................................................................................................................... 15

4.5 Arctic ...................................................................................................................................... 16

4.6 Wind ...................................................................................................................................... 17

4.7 Regional markets ................................................................................................................... 17

4.8 Macro drivers prompting OSV demand................................................................................. 18

4.9 Struggle .................................................................................................................................. 19

4.10 Challenges ............................................................................................................................. 19

4.11 Expectations and Outlook.................................................................................................... 20

4.11.1 IHS Petrodata– Former ODS Petrodata ......................................................................... 21

4.12 Prices historic ........................................................................................................................ 25

4.13 Fleet ....................................................................................................................................... 26

4.13.1 AHTS a closer look ......................................................................................................... 30

2

4.13.2 PSV a closer look ............................................................................................................ 31

4.14 Subsea ................................................................................................................................... 33

4.15 Risks ....................................................................................................................................... 34

4.16 Possible ups and downs by Swedbank First Securities .......................................................... 36

4.17 Energy in the future ............................................................................................................... 37

4.18 Macro and Energy ................................................................................................................. 38

4.19 Conclusion ............................................................................................................................. 49

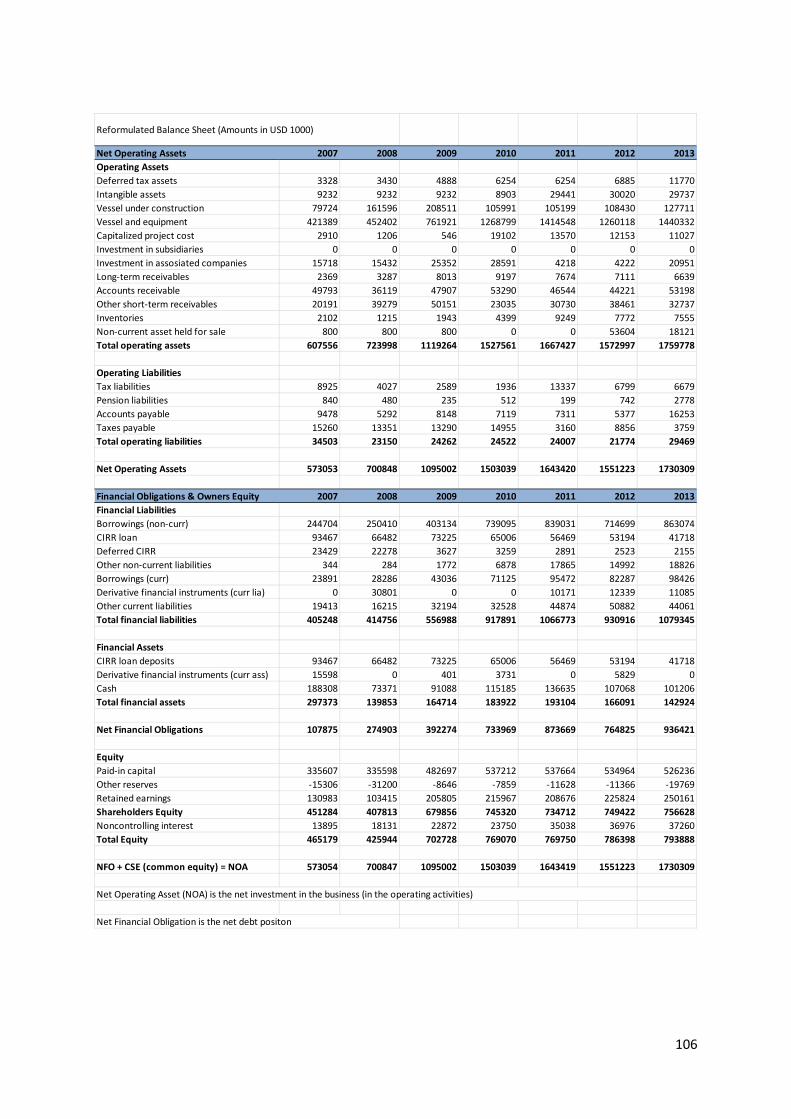

5 Financial Statement – Reformulated balance sheet and P&L ....................................................... 50

5.1 Income statement ................................................................................................................. 50

5.2 Extraordinary items and Recurring vs. Non-recurring bookings ........................................... 50

5.3 Balance sheet ........................................................................................................................ 51

5.4 Accounting Measures of Risk ................................................................................................ 51

5.4.1 Financial ratios ............................................................................................................... 51

5.5 Credit rating ........................................................................................................................... 56

5.6 Depreciation .......................................................................................................................... 56

5.7 Tax rate and tax regime ......................................................................................................... 56

6 Valuation and Valuation Models ................................................................................................... 60

7 Cost of Capital ............................................................................................................................... 63

7.1 Risk ........................................................................................................................................ 63

7.2 Cost of Capital ....................................................................................................................... 63

7.3 Cost of equity ........................................................................................................................ 64

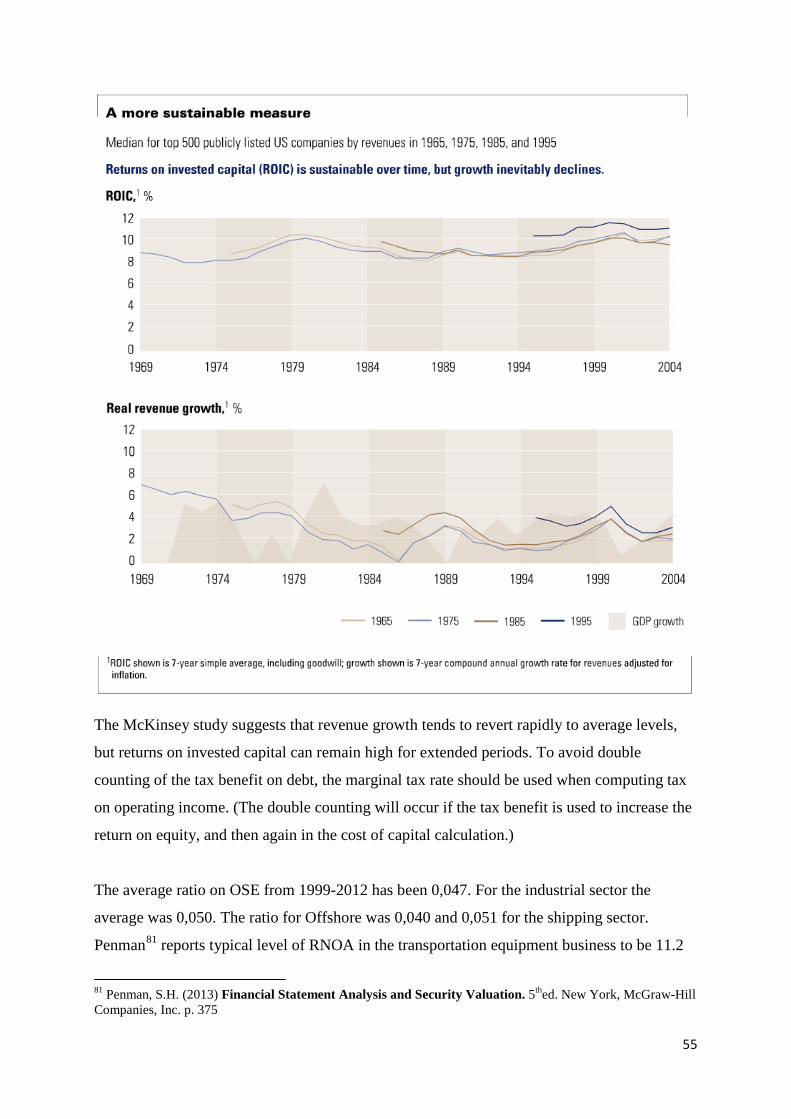

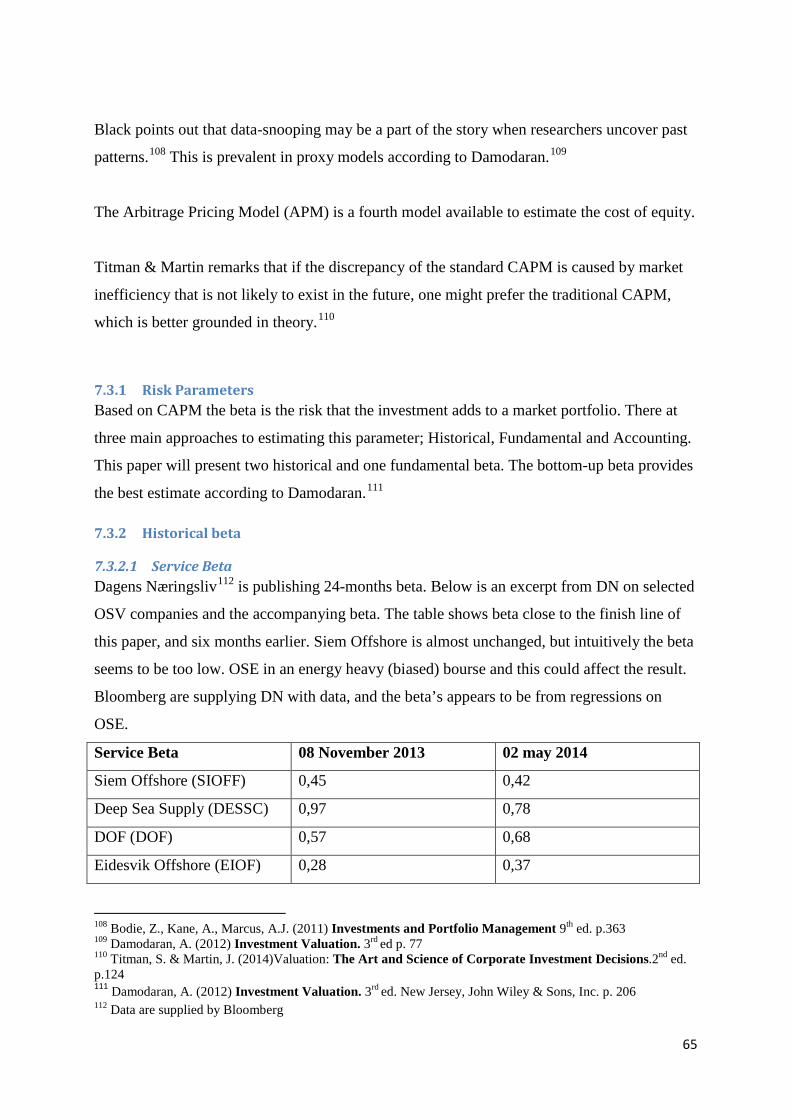

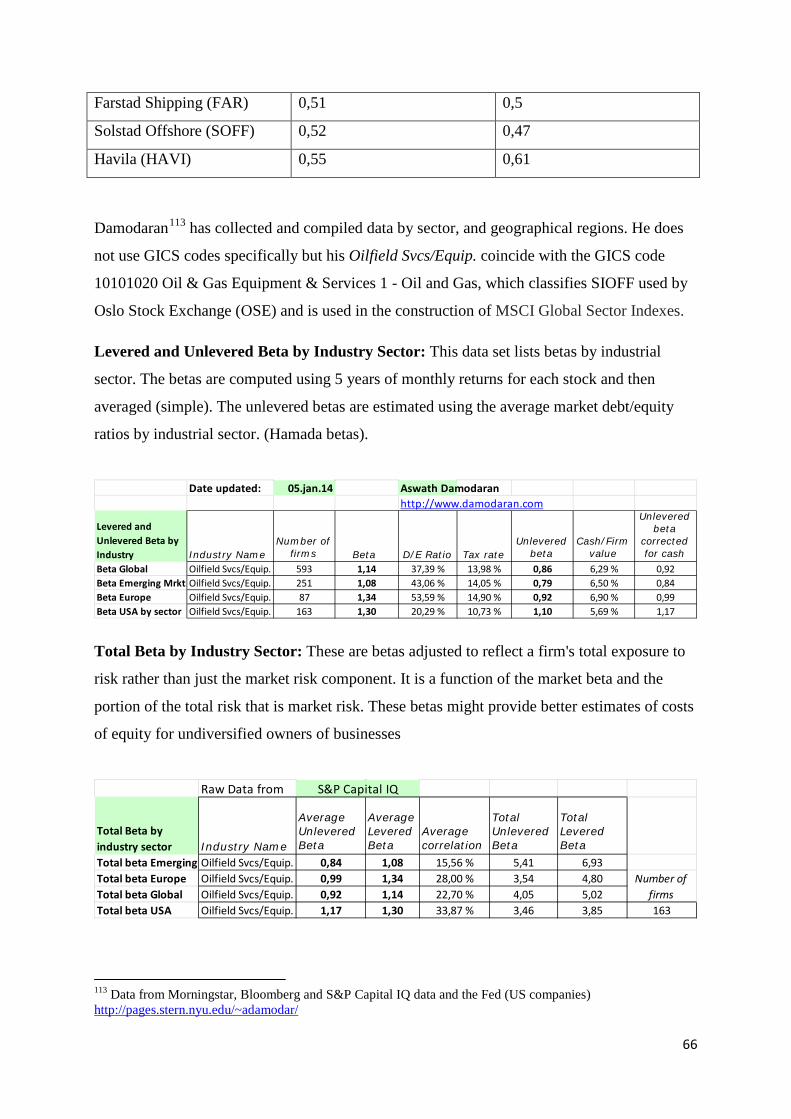

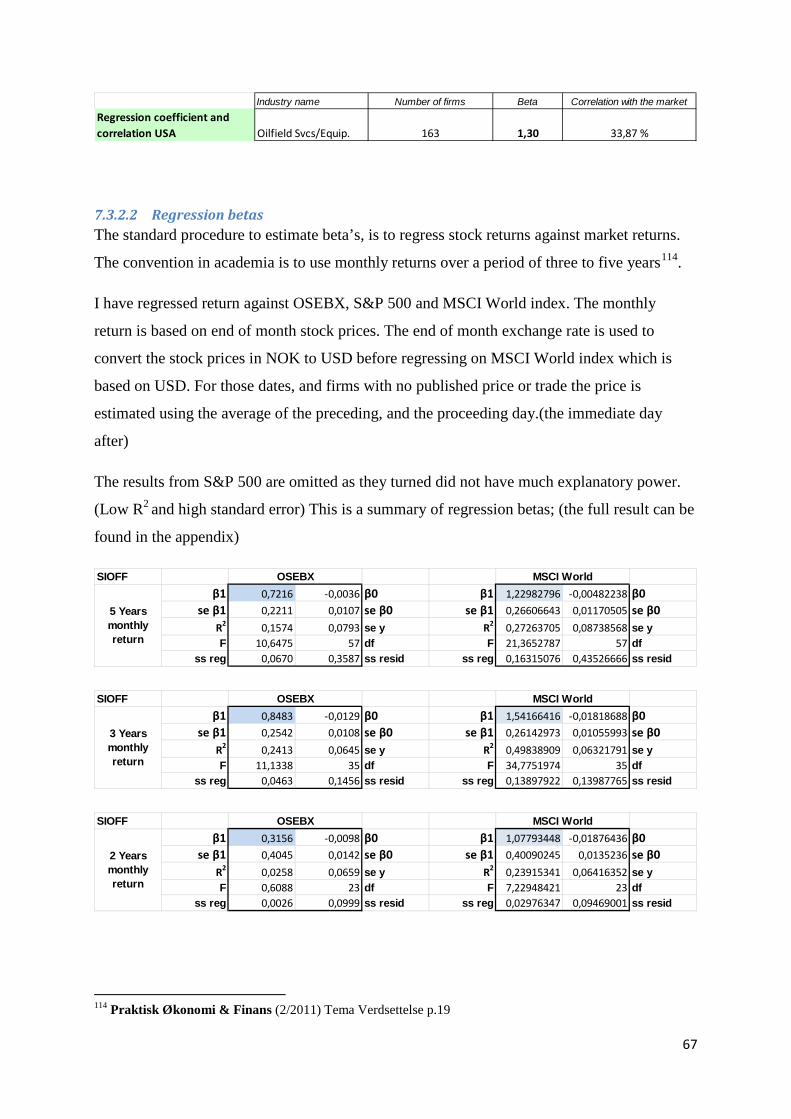

7.3.1 Risk Parameters ............................................................................................................. 65

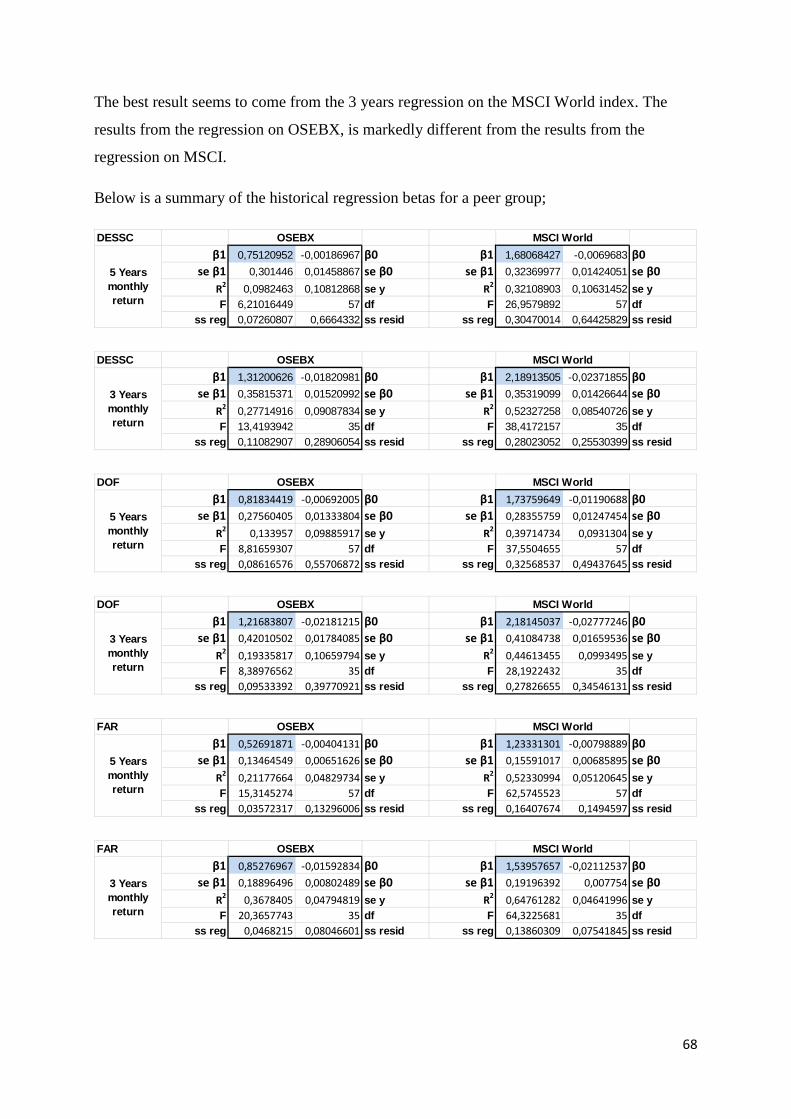

7.3.2 Historical beta................................................................................................................ 65

7.3.3 Fundamental betas ........................................................................................................ 69

7.3.4 Market risk premium ..................................................................................................... 72

7.3.5 The riskless rate ............................................................................................................. 74

7.3.6 CAPM ............................................................................................................................. 75

7.4 Cost of debt ........................................................................................................................... 75

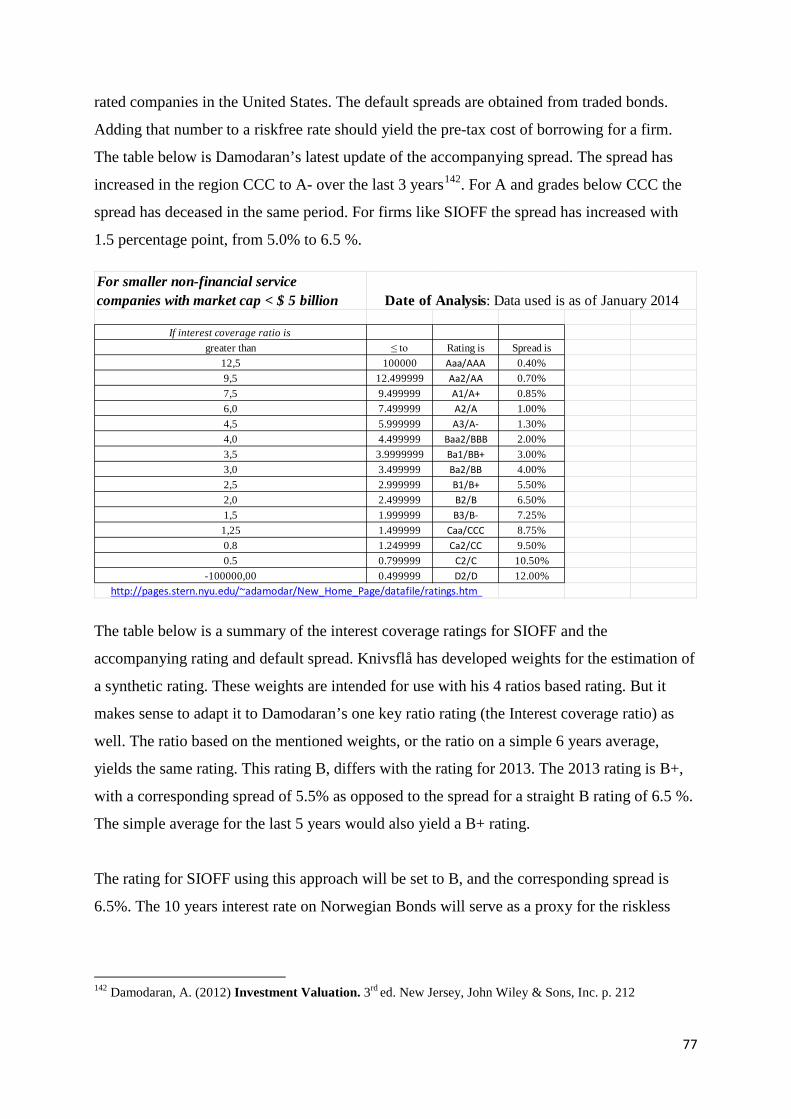

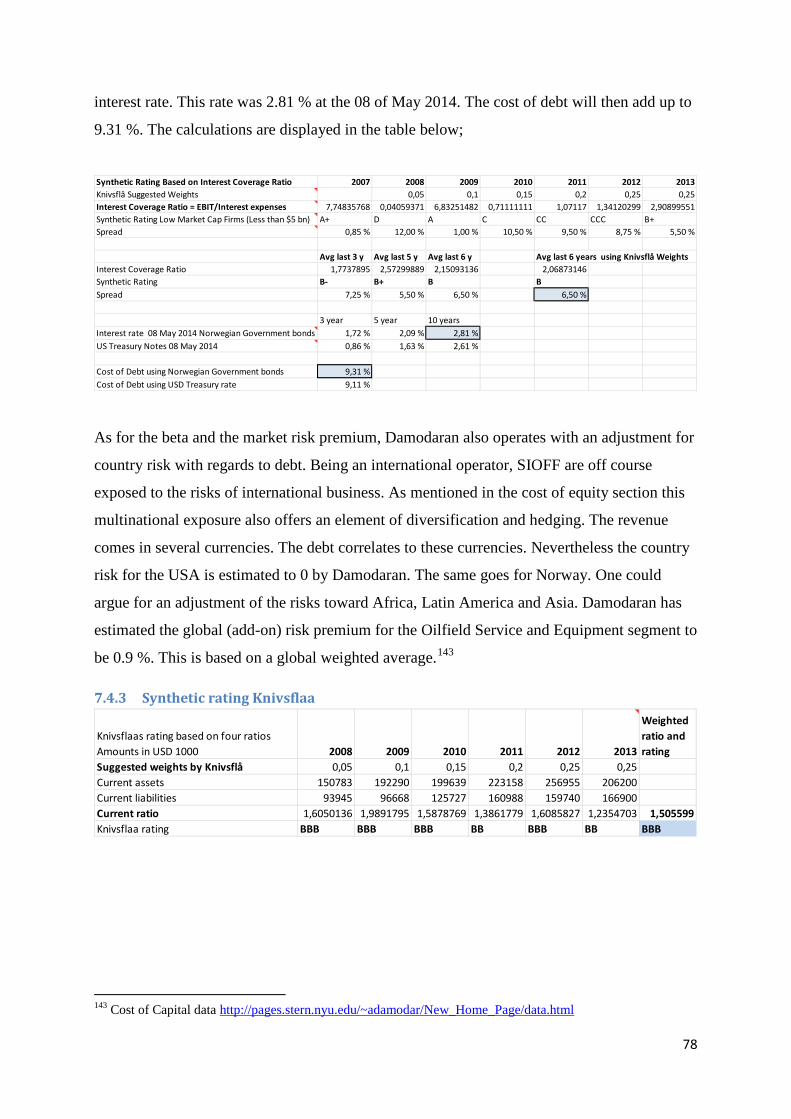

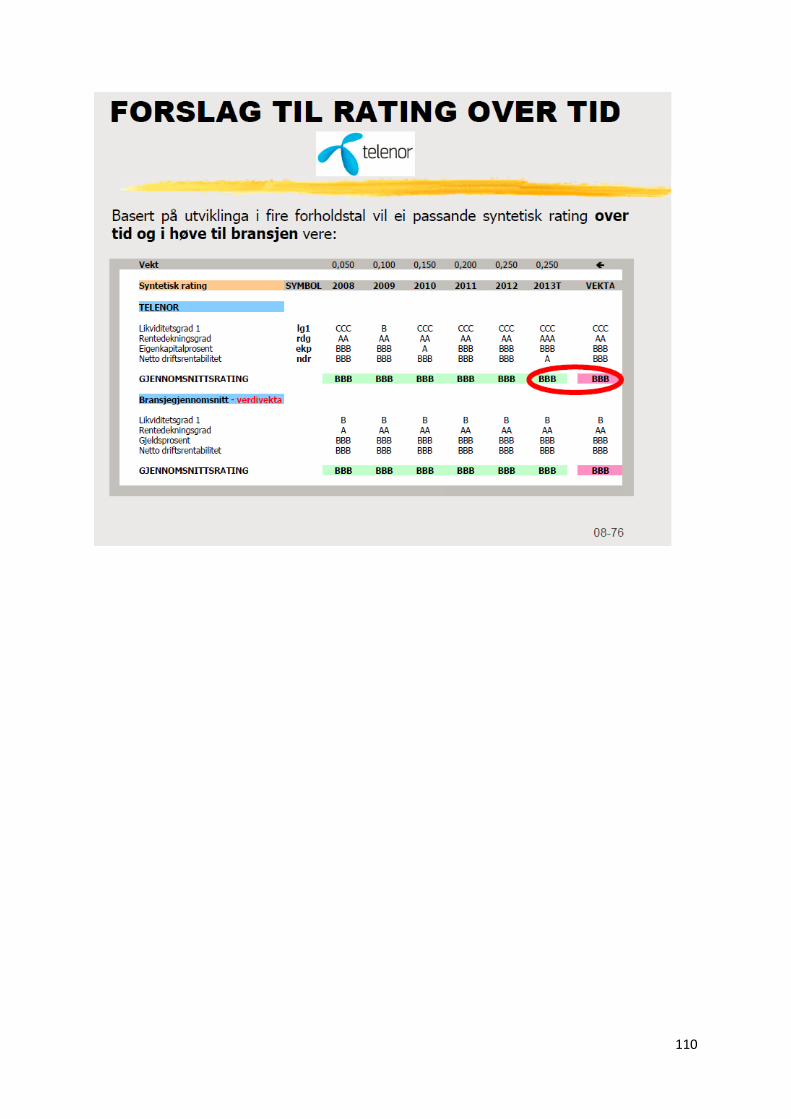

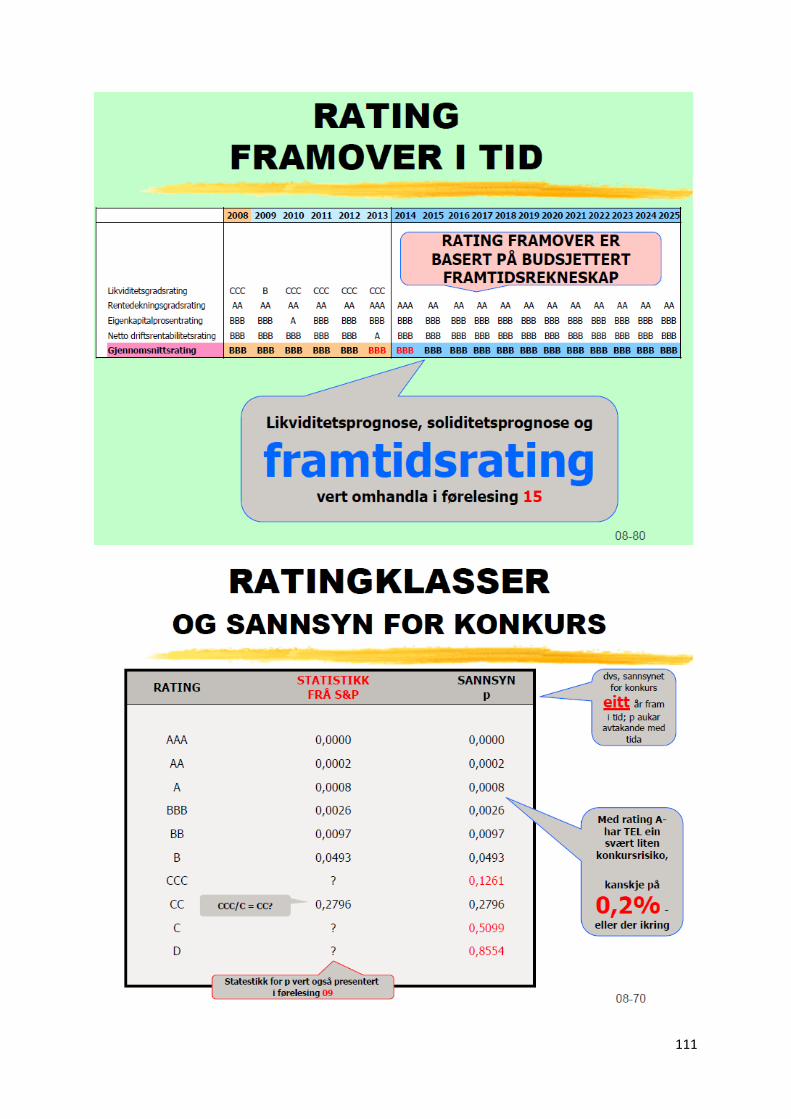

7.4.1 Traded Loans ................................................................................................................. 76

7.4.2 Synthetic rating Damodaran.......................................................................................... 76

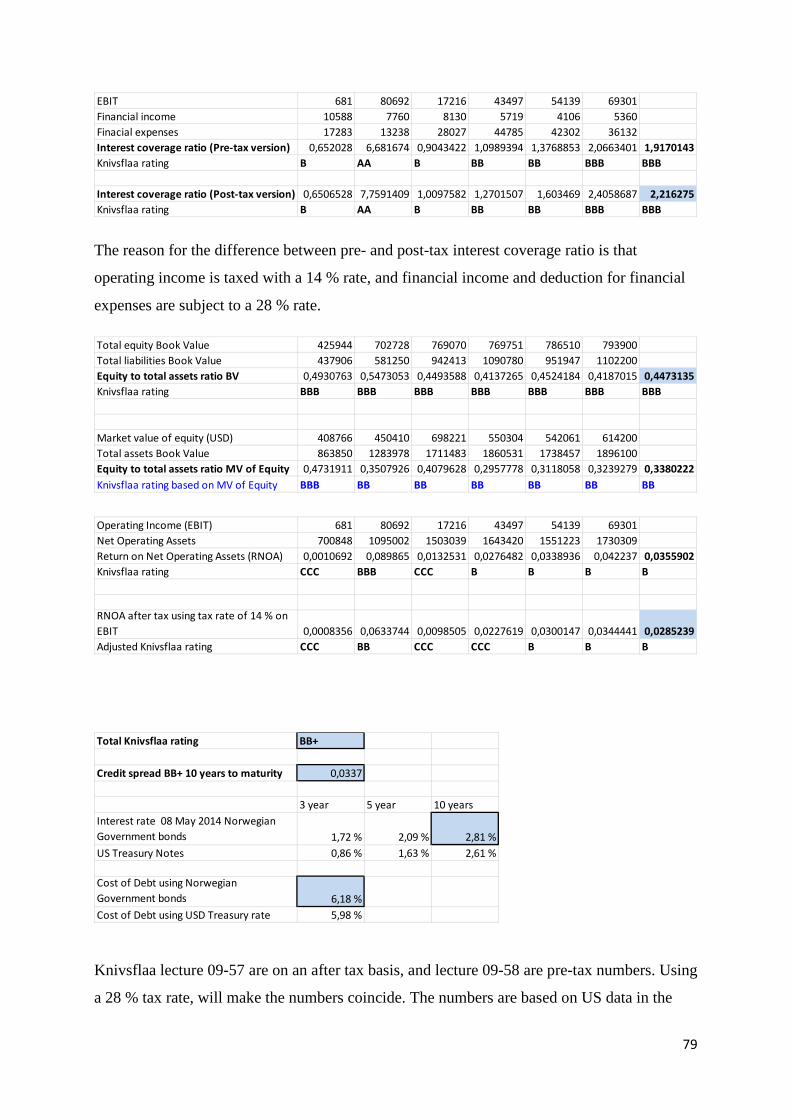

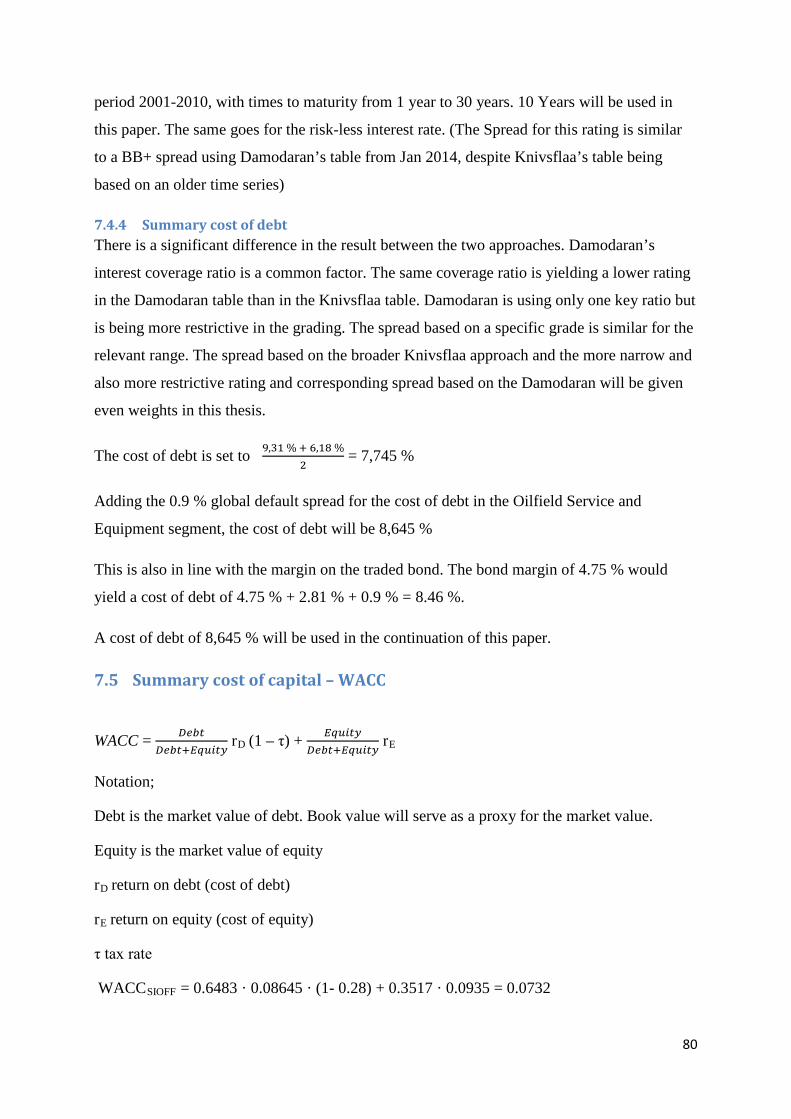

7.4.3 Synthetic rating Knivsflaa .............................................................................................. 78

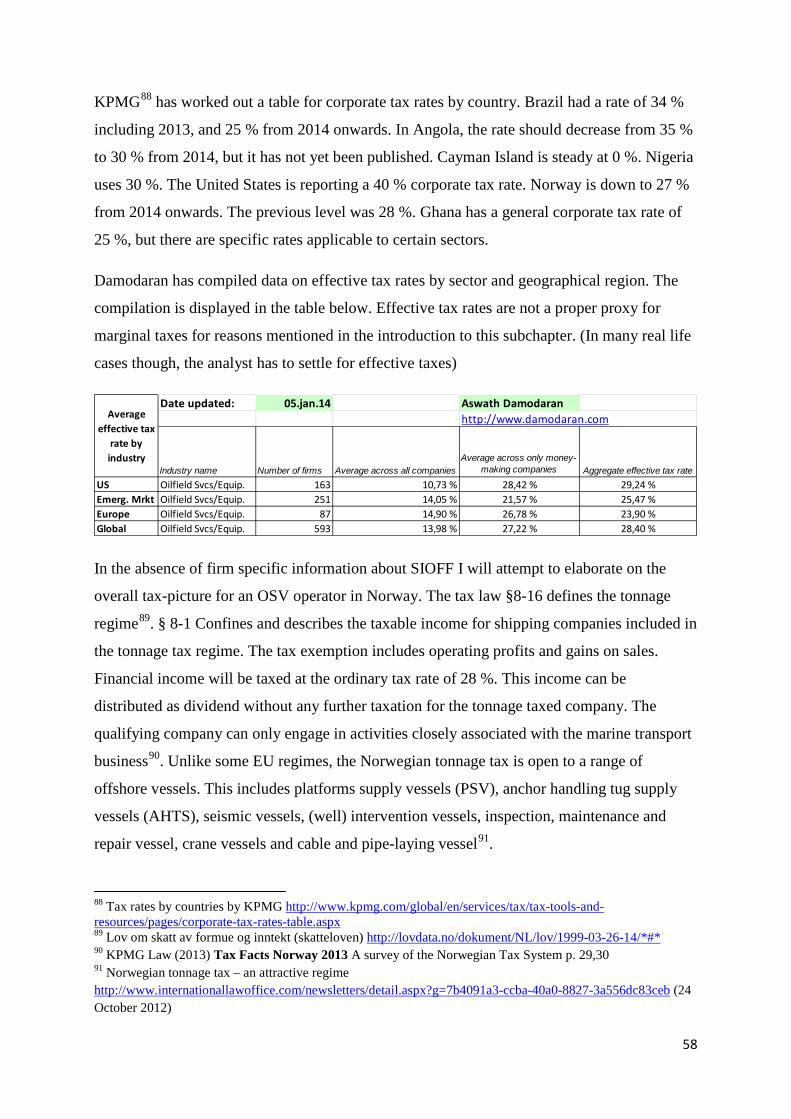

7.4.4 Summary cost of debt ................................................................................................... 80

7.5 Summary cost of capital – WACC .......................................................................................... 80

8 Growth ........................................................................................................................................... 82

3

8.1 Growth in SIOFF ..................................................................................................................... 84

8.2 The historical growth in revenue for SIOFF ........................................................................... 85

8.3 Analyst estimates of growth .................................................................................................. 85

8.4 Fundamental determinants in SIOFF ..................................................................................... 86

8.5 Steely business ...................................................................................................................... 87

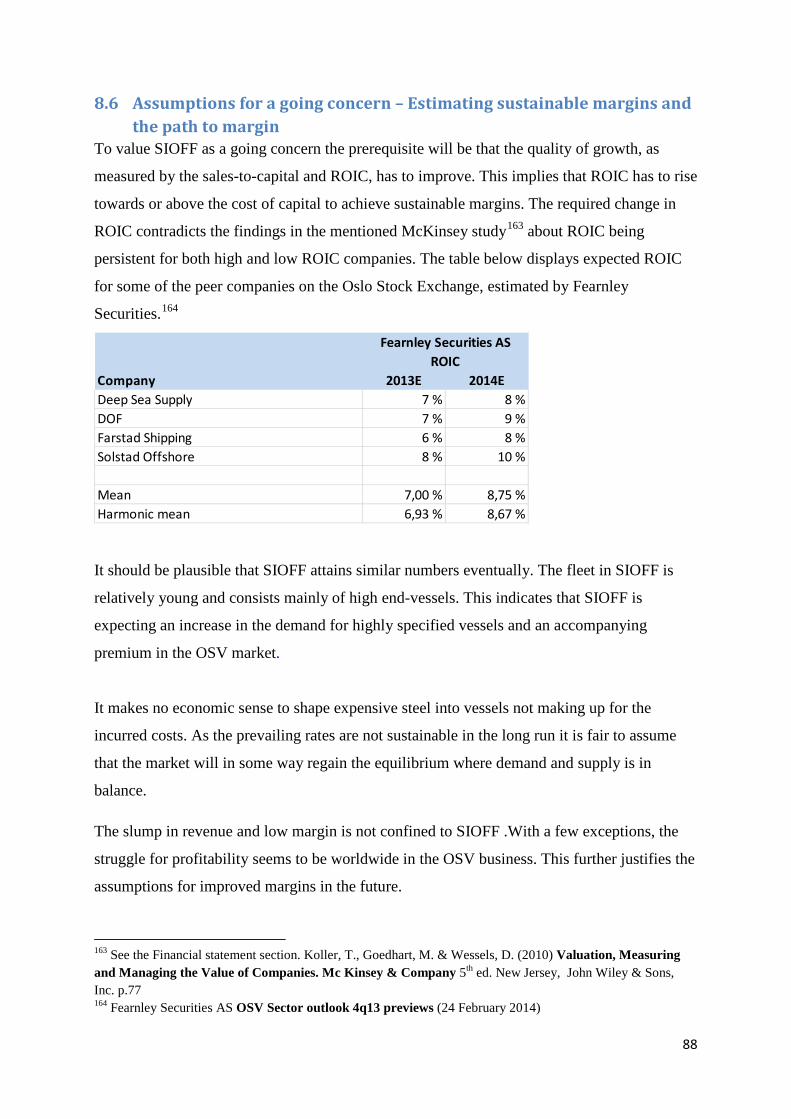

8.6 Assumptions for a going concern – Estimating sustainable margins and the path to margin 88

9 Forecasting Pro Forma financial statement, P&L (Measuring FCFF) ............................................. 89

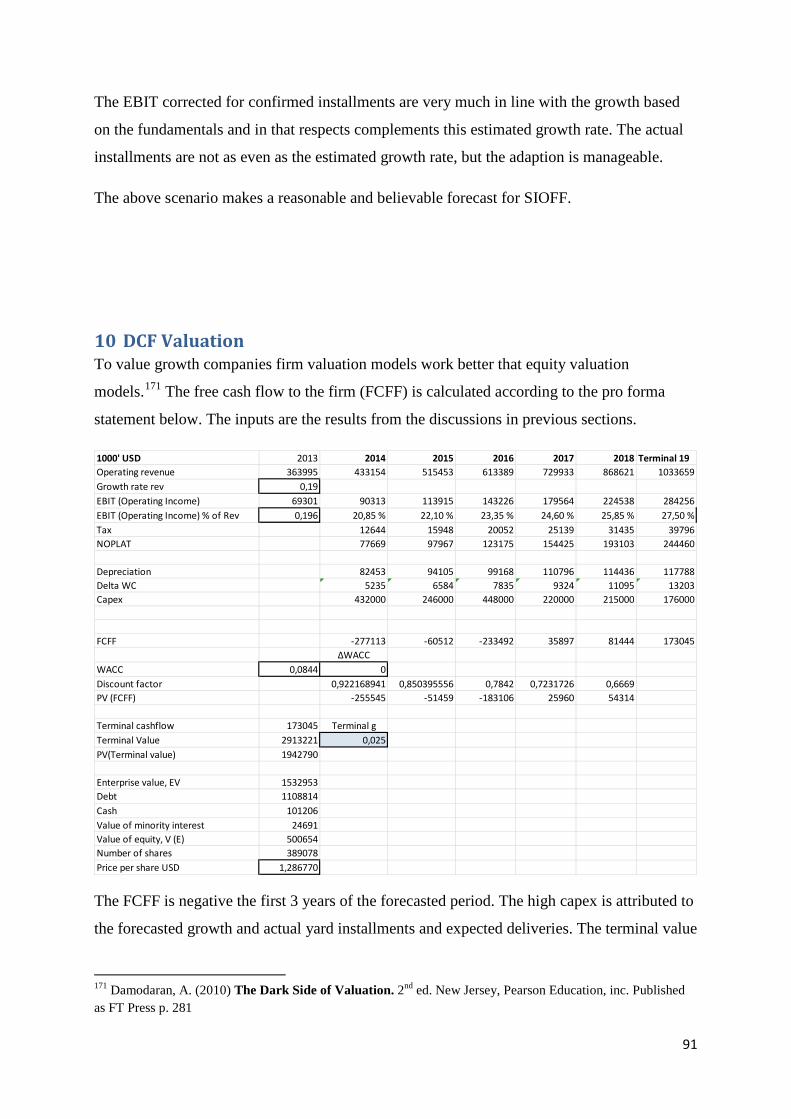

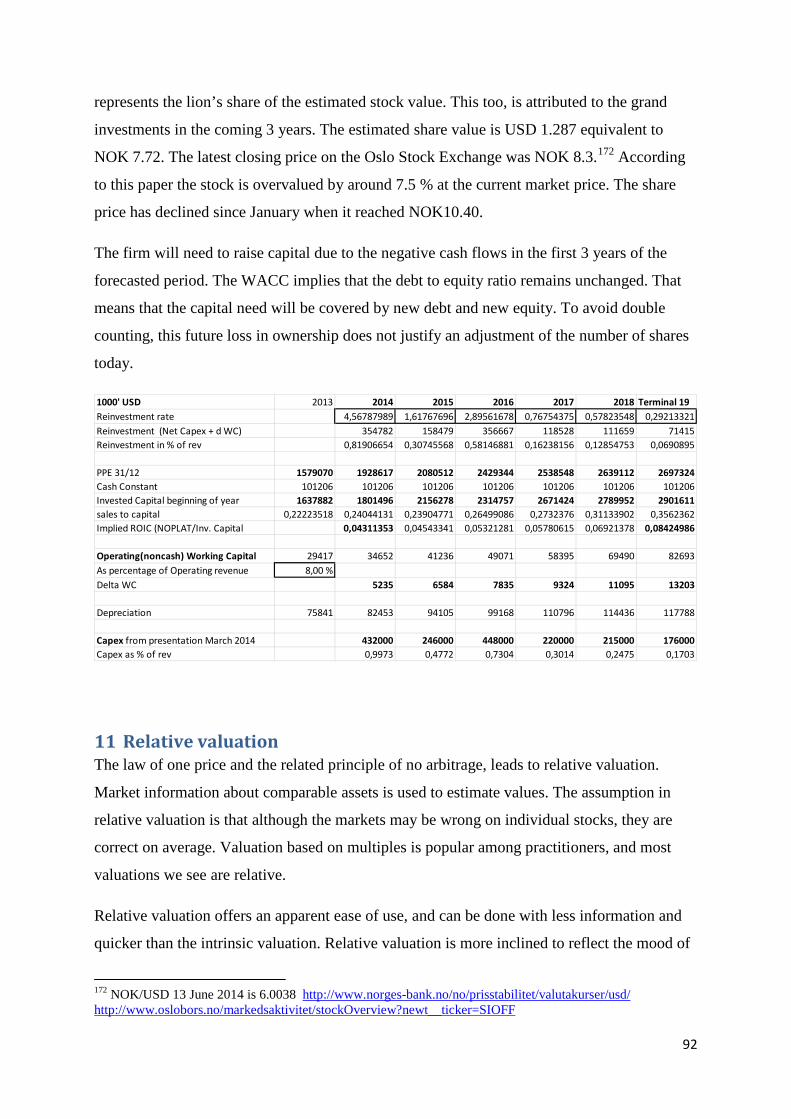

10 DCF Valuation ............................................................................................................................ 91

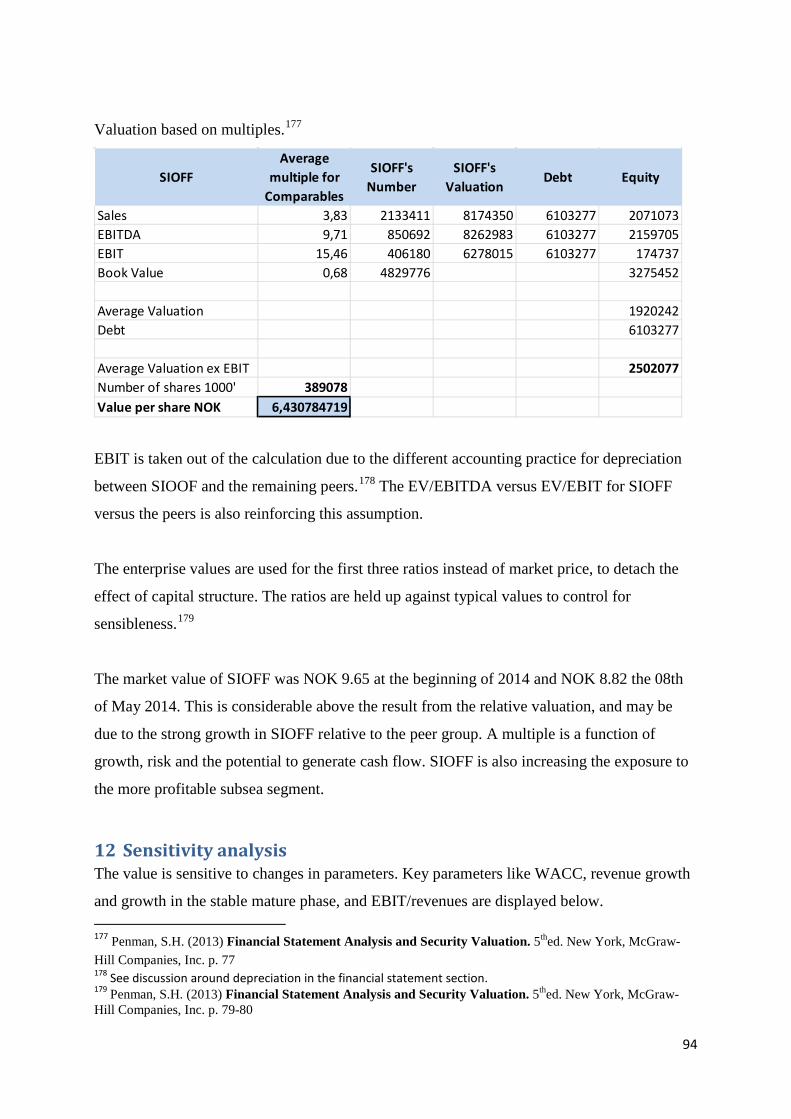

11 Relative valuation ...................................................................................................................... 92

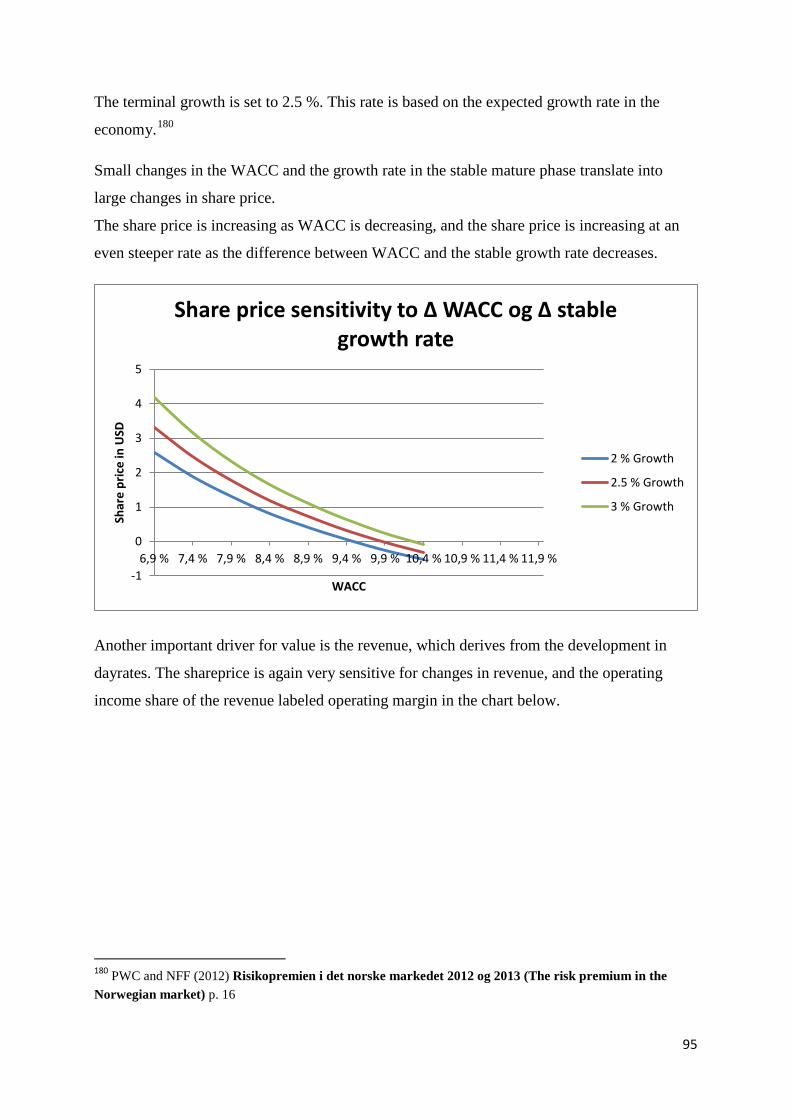

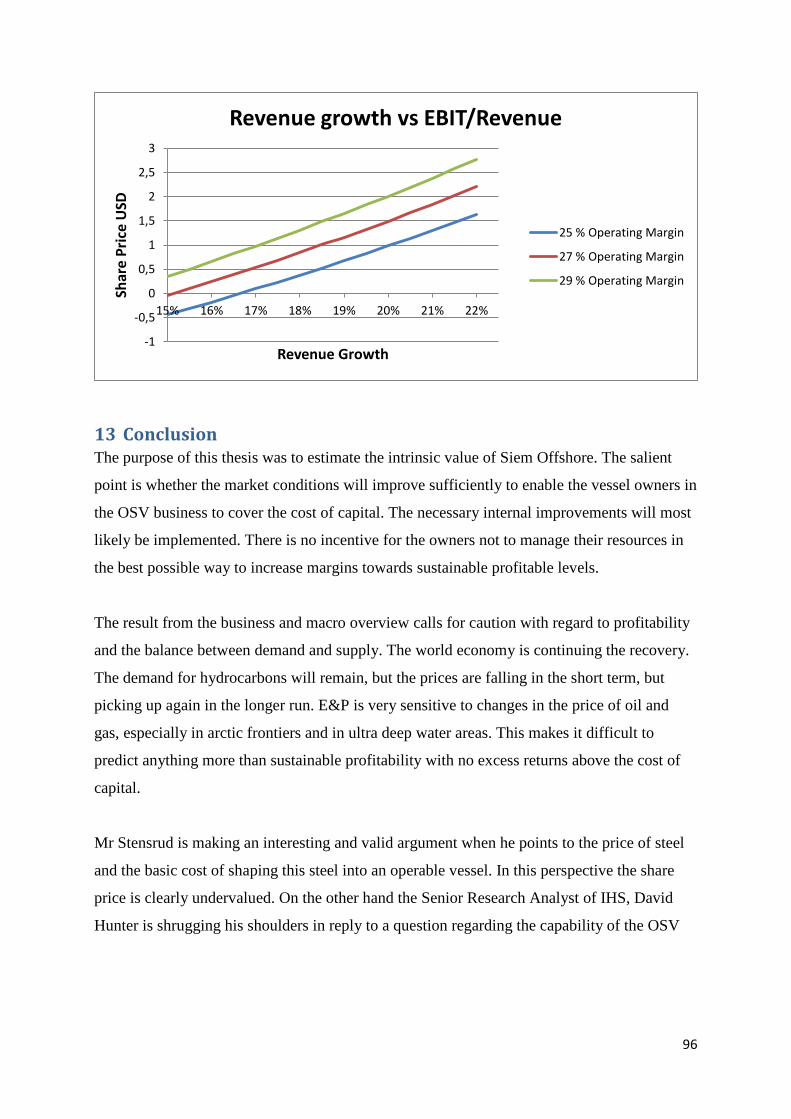

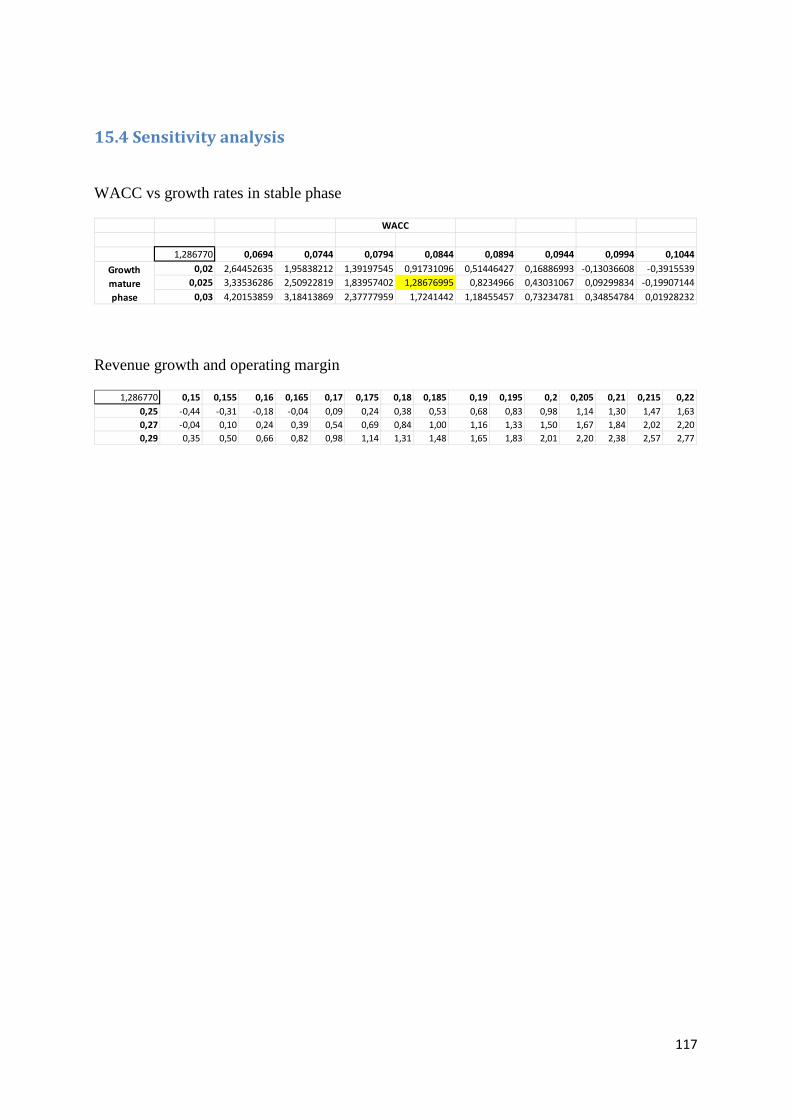

12 Sensitivity analysis ..................................................................................................................... 94

13 Conclusion ................................................................................................................................. 96

14 Bibliography ............................................................................................................................... 98

14.1 Books ..................................................................................................................................... 98

14.2 Lecture and lecture notes...................................................................................................... 98

14.3 Research reports and papers ................................................................................................ 99

14.4 Articles, surveys and publications ....................................................................................... 100

14.5 Analytical reports ................................................................................................................ 101

14.6 Annual and Quarterly reports ............................................................................................. 102

14.7 Personal Communication .................................................................................................... 102

14.8 Web ..................................................................................................................................... 102

15 Appendix .................................................................................................................................. 104

15.1 Financial Statement Appendix............................................................................................. 104

15.2 Cost of Capital Appendix ..................................................................................................... 107

15.3 Growth Appendix ................................................................................................................ 113

15.4 Sensitivity analysis ............................................................................................................... 117

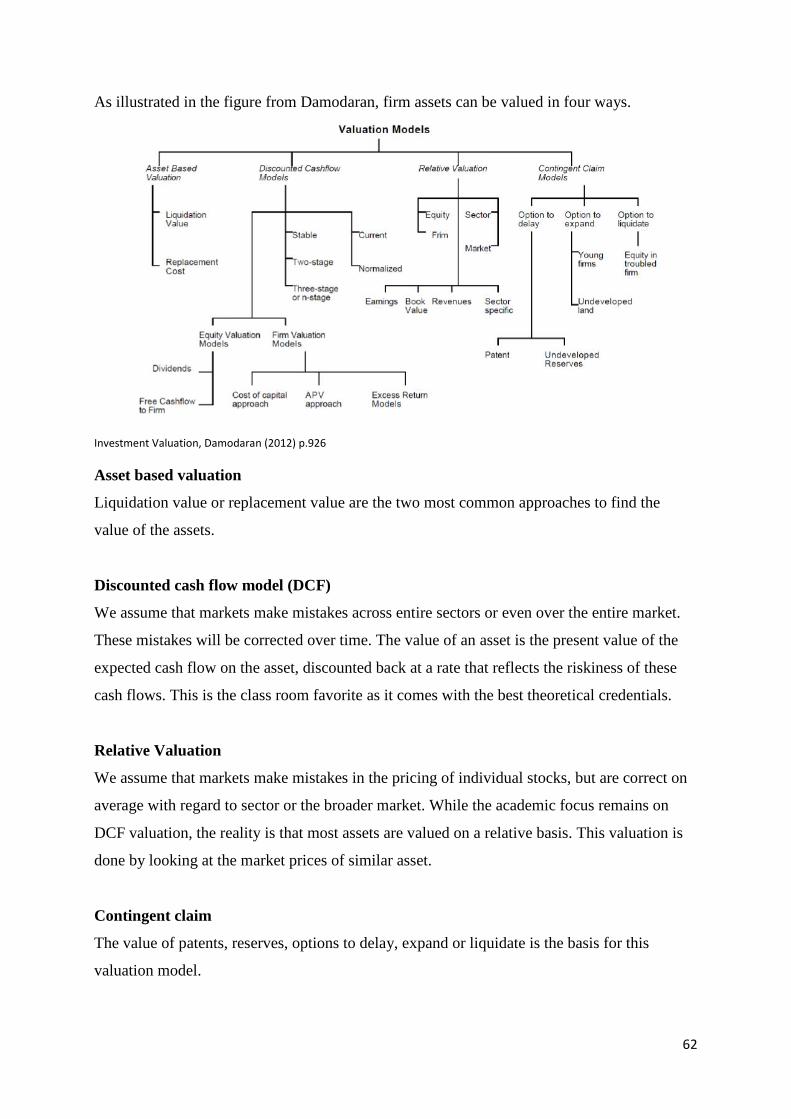

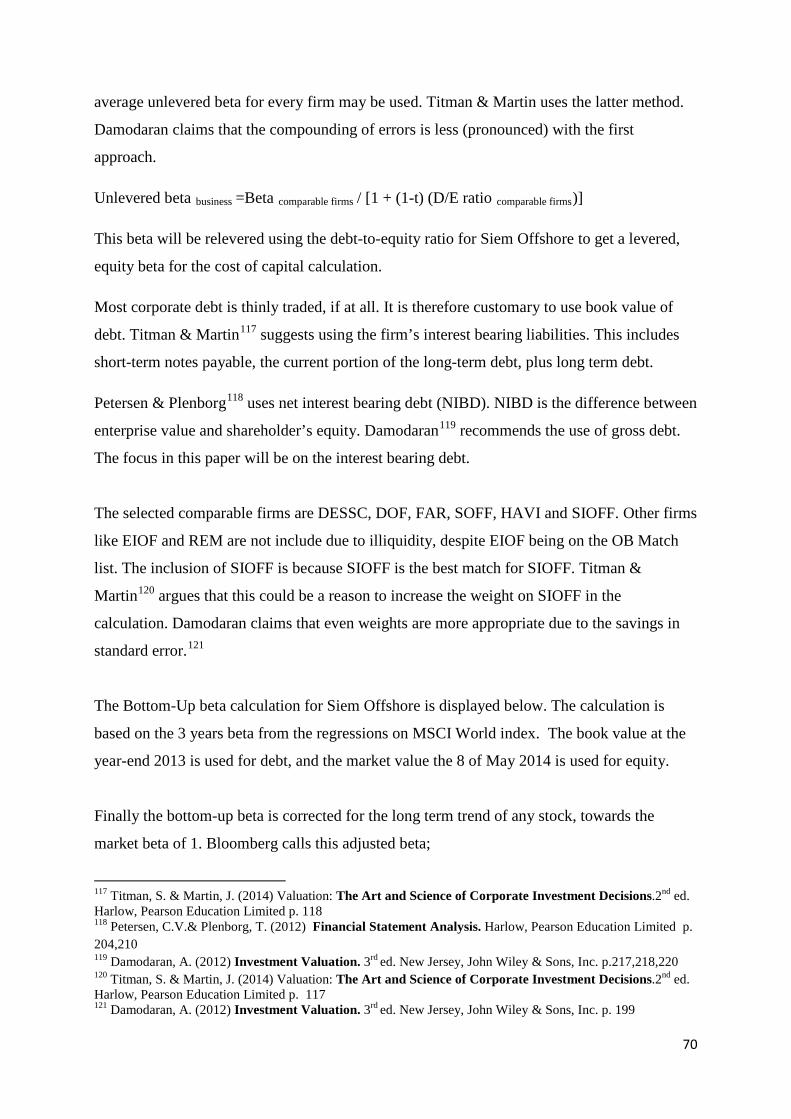

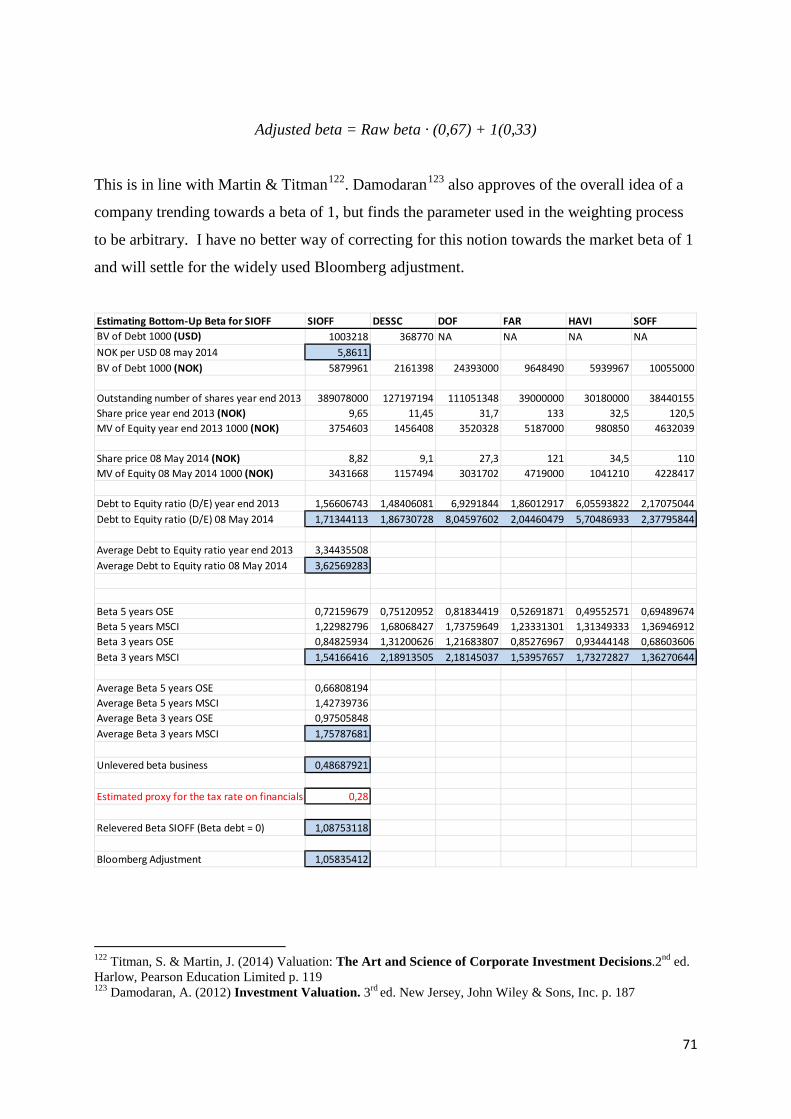

3 Siem Offshore - a company overview Siem Offshore was established as a stand-alone company in July 2005 following a spin-off

from the company Subsea 7 Inc.

Siem Offshore is a Cayman Island-based (registered) shipping company engaged in marine

services for the offshore oil and gas industry. Siem Offshore is organized as at parent

4

company with several subsidiaries and associates. The company is listed on the Oslo Stock

Exchange, with the ticker SIOFF. The GICS3 code is 10101020 Oil & Gas Equipment &

Services 1 - Oil and Gas. The headquarter is located in Kristiansand, Norway with subsidiary

offices located in Brazil, Germany, the Netherlands, Ghana, USA, India, Canada, Poland and

Australia.

The fleet operates in the North Sea, West Africa, the Middle East, the United States, India

and Nigeria.

The company’s primary activity is to own and operate offshore support vessels (OSV).

According to the annual report 2013, Siem operated 42 vessels, with an additional 13 vessels

under construction. The fleet comprised of 18 Platform Supply Vessels (PSV), 6 Offshore

Subsea Construction Vessels (OSCV) and Multipurpose Field & ROV Support Vessels

(MRSV), 10 Anchor Handling Tug Supply Vessels (AHTS). The AHTS vessels are operated

in a pool, and 2 of the vessels are operated on behalf of a pool partner. The company has also

entered the submarine power cable installation, repair and maintenance business aimed at the

offshore wind farm market. Siem also operates a Scientific Drilling Vessel (SCDV) and part

of a Well Stimulation Vessel (WSV).The Brazilian subsidiary operates smaller Fast Supply

Vessels (FSV), Fast Crew Vessels (FSV) and Oil Spill Recovery Vessels (OSRV). In addition

they provide combat management systems for vessels in the Brazilian navy. Siem WIS has

designed and developed a pressure control device to improve managed pressure drilling

operations. Siem expect a rising demand for this technology as demand for increased oil

recovery and the increased number of deep sea and high pressure, high temperature reservoirs.

Siem WIS has recently landed a contract for Statoil on the Gullfaks, Valemon and Gudrun

fields and the prospects Romeo and Julius in the North Sea.4

The vessels under construction will expand the existing fleet type, in addition to Well

Intervention Vessels (WIV) and Oil Spill Recovery Vessels (OSRV).

3 The MSCI Global Sector Indexes are constructed using the Global Industry Classification Standard (GICS®), a widely accepted industry analysis framework for investment research, portfolio management and asset allocation jointly developed and maintained by MSCI and Standard & Poor's. The MSCI Global Sector Indexs comprise regional and country sector, industry group and industry indexes based on the MSCI Global Investable Market Indexes. 10101020 Oil & Gas Equipment & Services; Manufacturers of equipment, including drilling rigs and equipment, and providers of supplies and services to companies involved in the drilling, evaluation and completion of oil and gas wells. http://www.msci.com/products/indexes/sector/gics/

4 Siem WIS MPD http://www.offshore.no/sak/61261_gjennombrudd_for_boreteknologi (09 May 2014)

5

Siem acquired 50% ownership in Secunda Canada LP in the third quarter 2013. Sucunda

operates six offshore support vessels.

Siem classifies their own fleet of PSV’s and AHTS’s as “high end”. They also use the

terminology “large” PSV and OSCV. The term “high end” for PSV’s is based on usable cargo

deck area measured in square meters. For AHTS’s the pulling power is included measured by

brake horse power (BHP) or pulling power in water measured as Bollard Pull. The distinction

between high end and low end is not a universal measure. The vessels are divided in several

steps depending on the above mentioned capabilities in addition to age, class of dynamic

position systems (DP)5 and the level of technological specifications.

The majority of the fleet is on long-term contract. Even half the vessels under construction

have long term contracts.

Siem Industries Inc. is the largest owner with 34.23 % of the shares. Siem Industries inc. is

controlled by a trust whose beneficiaries include Kristian Siem’s immediate family. Kristian

Siem is a director of Siem Offshore and chairman for Siem Industries Inc. The second largest

owner is the Hong Kong based Ace Crown International Ltd. with at 19.72 % share.6 Ace

Crown is recorded as a “Local Company” in Hong Kong. Ace Crown keeps a low profile with

no more information easily available.

Total employees are 1110 by year end 2013. CEO Terje Sørensen is explaining to

Sunnmørsposten that Siem is planning to lay off 60 Scandinavian seamen. This is due to the

competitive international market, but the opposite argument of increasing protectionism is

another reason mentioned for the layoffs. The increasing protectionism in the global market is

giving demand to a so called “Local Content”.7

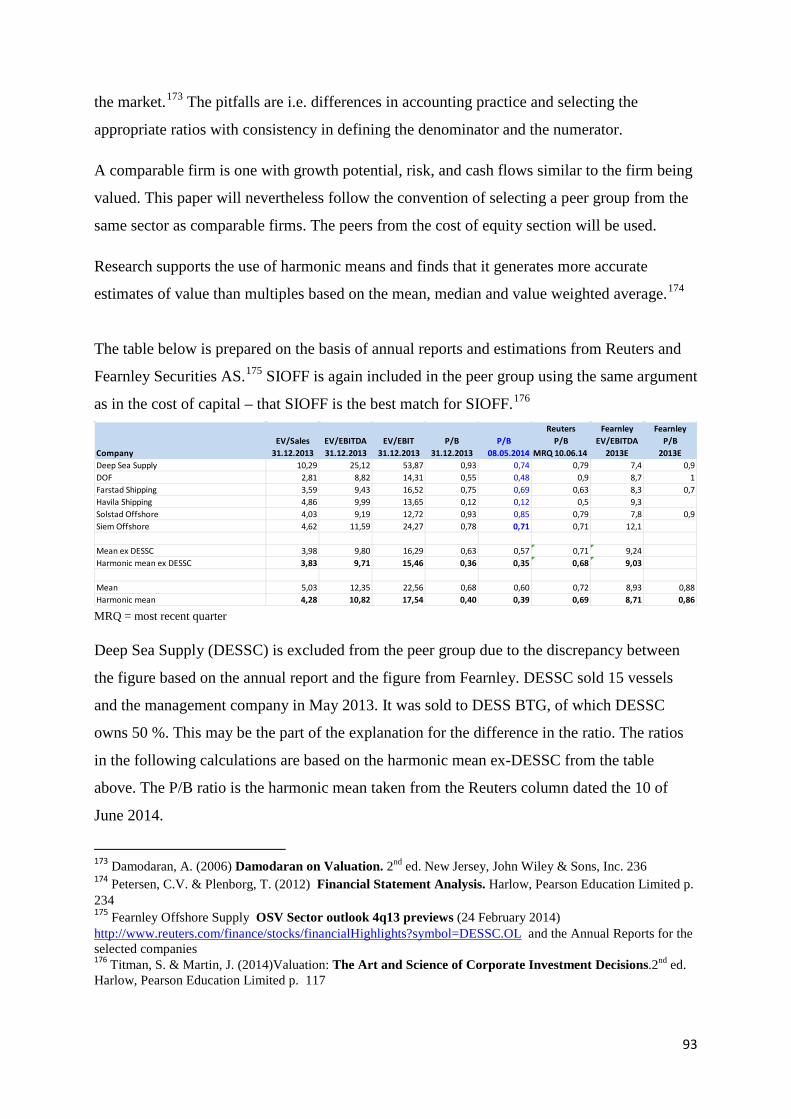

The peers used in this thesis on the Oslo Stock Exchange are Deep Sea Supply (DESSC),

DOF (DOF), Farstad Shipping (FAR), Solstad Offshore (SOFF), Havila Supply (HAVI),

Eidesvik Offshore (EIOF), REM (REM). The tickers for the peers and Siem Offshore

(SIOFF) will for convenience be used interchangeably throughout this paper.

5 DP will be explained in the next chapter. 6 Annual report 2013 7 Sunnmørsposten http://www.smp.no/nyheter/article7704395.ece (07 June 2013)

6

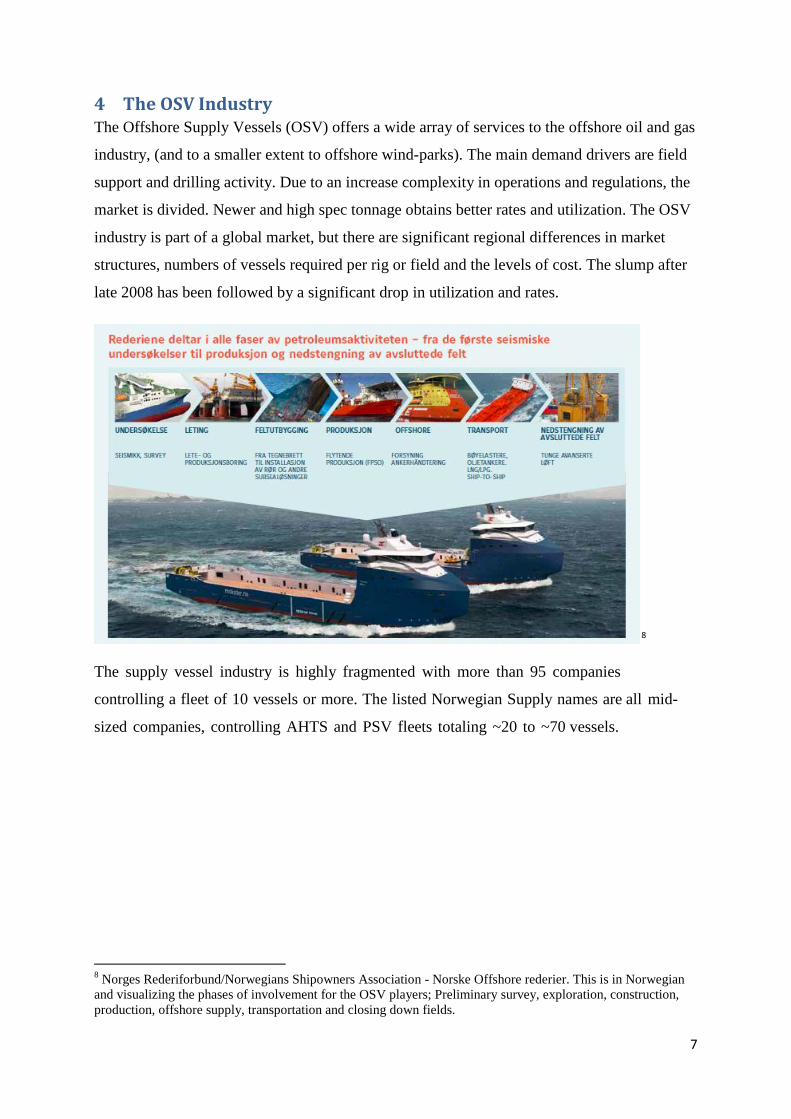

4 The OSV Industry The Offshore Supply Vessels (OSV) offers a wide array of services to the offshore oil and gas

industry, (and to a smaller extent to offshore wind-parks). The main demand drivers are field

support and drilling activity. Due to an increase complexity in operations and regulations, the

market is divided. Newer and high spec tonnage obtains better rates and utilization. The OSV

industry is part of a global market, but there are significant regional differences in market

structures, numbers of vessels required per rig or field and the levels of cost. The slump after

late 2008 has been followed by a significant drop in utilization and rates.

8

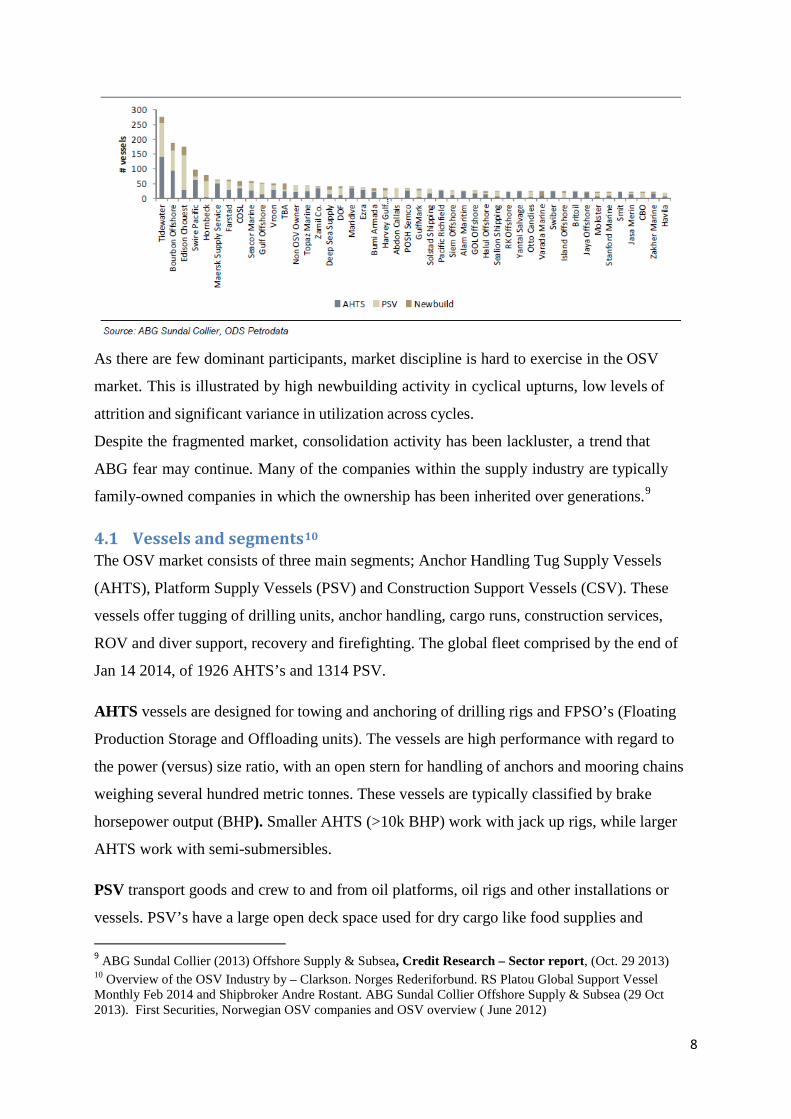

The supply vessel industry is highly fragmented with more than 95 companies

controlling a fleet of 10 vessels or more. The listed Norwegian Supply names are all mid-

sized companies, controlling AHTS and PSV fleets totaling ~20 to ~70 vessels.

8 Norges Rederiforbund/Norwegians Shipowners Association - Norske Offshore rederier. This is in Norwegian and visualizing the phases of involvement for the OSV players; Preliminary survey, exploration, construction, production, offshore supply, transportation and closing down fields.

7

As there are few dominant participants, market discipline is hard to exercise in the OSV

market. This is illustrated by high newbuilding activity in cyclical upturns, low levels of

attrition and significant variance in utilization across cycles.

Despite the fragmented market, consolidation activity has been lackluster, a trend that

ABG fear may continue. Many of the companies within the supply industry are typically

family-owned companies in which the ownership has been inherited over generations.9

4.1 Vessels and segments10 The OSV market consists of three main segments; Anchor Handling Tug Supply Vessels

(AHTS), Platform Supply Vessels (PSV) and Construction Support Vessels (CSV). These

vessels offer tugging of drilling units, anchor handling, cargo runs, construction services,

ROV and diver support, recovery and firefighting. The global fleet comprised by the end of

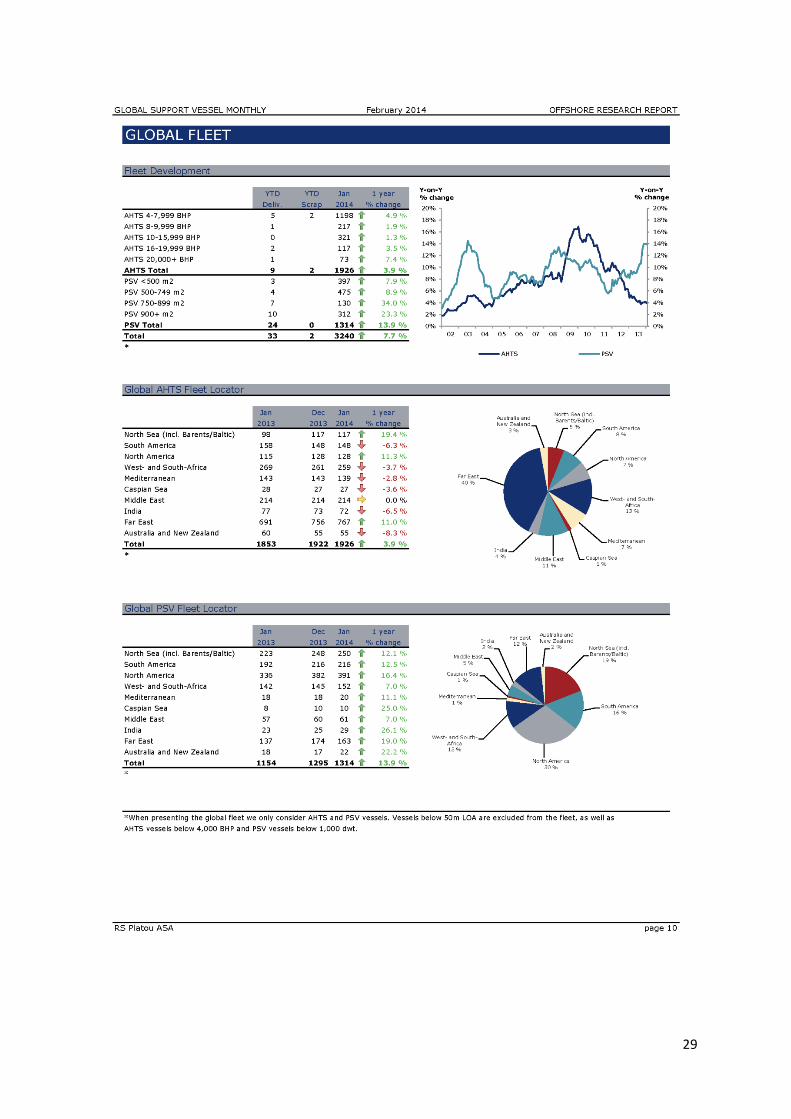

Jan 14 2014, of 1926 AHTS’s and 1314 PSV.

AHTS vessels are designed for towing and anchoring of drilling rigs and FPSO’s (Floating

Production Storage and Offloading units). The vessels are high performance with regard to

the power (versus) size ratio, with an open stern for handling of anchors and mooring chains

weighing several hundred metric tonnes. These vessels are typically classified by brake

horsepower output (BHP). Smaller AHTS (>10k BHP) work with jack up rigs, while larger

AHTS work with semi-submersibles.

PSV transport goods and crew to and from oil platforms, oil rigs and other installations or

vessels. PSV’s have a large open deck space used for dry cargo like food supplies and

9 ABG Sundal Collier (2013) Offshore Supply & Subsea, Credit Research – Sector report, (Oct. 29 2013) 10 Overview of the OSV Industry by – Clarkson. Norges Rederiforbund. RS Platou Global Support Vessel Monthly Feb 2014 and Shipbroker Andre Rostant. ABG Sundal Collier Offshore Supply & Subsea (29 Oct 2013). First Securities, Norwegian OSV companies and OSV overview ( June 2012)

8

equipment, and several different cargo tanks used for the transportation of fluids like fuel,

water, drilling mud, chemicals and cement, drill-pipe, casing etc. These vessels are also used

as standby vessels and are often equipped with firefighting and oil recovery capabilities.

PSV’s are typically classified by deadweight tonnage (dwt) and/or total deck space (square

meters) and are relatively uncomplicated vessels compared to other OSVs

Large PSV’s have more than 900 m2 available deck area. Medium size PSV’s have 700-800

m2. (“High end” is also common terminology about modern tonnage, maybe built or outfitted

in Norway.)

CSV’s perform tasks related to subsea activities and general field construction operations.

This includes pipe laying, well stimulation, diving, ROV (remotely operated vehicle), IMR

(inspection, maintenance and repair) and seabed mapping and surveying. The CSV are

significantly more diversified than the PSV and AHTS segment. Vessels are typically

classified according to length, although this does not fully explain the capability of a specific

vessel within this highly diversified segment.

4.2 Drilling rigs11 Mobile offshore drilling units (MODU’s) consist of Jackups and floaters.

Jackups stand on the ocean floor with their hull and drilling equipment elevated above water

on connected leg supports. A jack-up rig is a self-elevating unit with a buoyant hull, capable

of raising its hull over the surface of the sea. The buoyant hull enables transportation of the

unit and all attached machinery to a desired location.

Jackup rigs are generally preferred over other rig types in water depths of 400 feet or less,

primarily because jackup rigs provide a more stable drilling platform with above water

blowout prevention (BOP) equipment.

Jack up platforms are used as exploratory drilling platforms and offshore wind farm service

platforms.

11 http://www.enscoplc.com/Rig-Fleet/Definitions/default.aspx and RS Platou Rig Montly jan 2013

9

Floaters comprise of semi-submersible rigs and drillship’s.

Semisubmersible rigs are floating offshore drilling units supported by pontoon type columns

that can be partially submerged to a predetermined depth. While in transit semis can float on

top of the water making tugging of these rigs from location to location easier. Semis are

capable of drilling in water depths up to 8,000 feet. Semisubmersibles are chosen for their

stability, but drillship’s are capable of holding more equipment.

Drillship rigs are maritime vessels that have been outfitted with drilling apparatus. Most often

used for exploratory drilling of new oil and gas wells in deep water. Drillships may also be

used as platforms to carry out well maintenance or completion work such as casing and tubing

installation or subsea tree installations. Drillship rigs are capable of ultra-deepwater drilling in

depths of up to 10,000 feet with a total vertical drilling depth of 40,000 feet

Both Semis and drillships can be conventionally moored (CM) or dynamically positioned

(DP). Dynamically-positioned floaters are held in a fixed location over the ocean floor by

computer-controlled propellers or "thrusters."

4.3 Demand drivers The main drivers for the PSV, AHTS and CSV segments are field activity as in

developments, new fields coming on stream and development drilling and offshore

construction.12 The demand for these ships, are closely linked to exploration and production

(E&P). The numbers of rigs, determine the demand for OSV’s. 4 AHTS are required to move

1 rig in Norway, and 3 vessels are required in the UK. For PSV’s the number is 2.5-3 per rig.

Exploration is a driver as the drilling period for one well is +/- 30 days. There is high boat

12 ABG Sundal Collier (2013) Offshore Supply & Subsea, Credit Research – Sector report, (Oct. 29 2013)

10

intensity during rig moves and for PSV’s during the drilling period. Production (drilling)

mostly involves PSV’s.

Future OSV demand driven by an expanding MODU fleet

Both shallow and Deepwater offshore activity is likely to propel PSV demand further in the

period 2014 and 2015. Discoveries of oil and gas in deep-water (>3000ft) have been

bountiful. As a result, significant investments in mobile offshore drilling units (MODUs) to

help explore and develop deep-water oil and gas resources have been made. In total, more

than 100 units have been delivered in the last five years and the order books are currently

indicating that 35 and 27 units will be delivered in 2014 and 2015, respectively. Having said

this, the floater market is facing some headwinds, but the large contract backlog of rig owners

should keep floater utilization at a high level. In shallow water RS Platou also expect

increases in demand, with the redevelopment of older fields being the main driver.13

The world fleet development of AHTS and PSV has a CAGR of 9 %. The OSV to Rig ratio is

expected to fall below 3.9 by 2014 from 4.1 as of March 2012, reflecting a tilt in market

balance in favor of vessel owners. 14

The OSV demand per rig/field (what ABG denote as the “demand multiplier”) also differs

between geographical regions. Demand tends to be highest on a per rig/field basis in

immature areas, where a large proportion of the total demand stems from (exploration)

drilling activity. The demand also increases with distance to shore, poor onshore

infrastructure and a high degree of government regulation. As ABG have defined the

supply as the mid- to high-end of the OSV fleet, the multiplier also accounts for

crowding out of low-end capacity. Relatively new oil and gas regions such as Brazil and

West Africa fit the “high demand” description well.15

For the AHTS segment, the number of prelays16, have increased over the past years. This

reduces time for anchoring, optimizing rig and vessel time. Reduced weather window reduces

13 RS Platou ASA Global Support Vessel Monthly (January & February 2014) RS Platou Montly (February 2014) The North Sea OSV Market (January 2014) The Platou Report (2014) 14 Clarkson Capital Markets (2012) Overview of the OSV Industry, International Monetary Fund (IMF), World Economic Outlook (April 2012) 15 ABG Sundal Collier (2013) Offshore Supply & Subsea, Credit Research – Sector report, (Oct. 29 2013) 16 Prelaying means that a significant part of the mooring work can be conducted weeks in advance and at the optimal time with respect to weather conditions and vessel availability or prices.

11

weather risk. Prelaying is safer for the oil company. Maersk FPSO17 Gryphon18 sustained

damage in a storm in 2011, when four anchor chains broke and the vessel moved off station,

causing considerable damage to the vessel and the subsea architecture. The number of Heading

Control fixtures, have been increasing since. Demand for larger AHTS vessels are likely to

come from Brazil. It is increasingly difficult to attain term charter contract in order to finance

due to the banks being more focused on the Subsea sector. Many owners are uncertain about

mooring vs DP in the future. Limited order-book is combined with a lower vessel to rig ratio.19

Clarkson Capital claims that oil consumption seems to be strongly correlated with GDP

Growth. High energy demand and high oil prices leads to high exploration & production

(E&P), which again leads to an increase in offshore activity as onshore fields mature. The

OSV demand is robust. The global offshore CAPEX is expected to increase by CAGR20

12%.21

17 Floating Production Storage and Offloading system is used extensively by oil companies for the purpose of storing oil from the oil rigs in the middle of the ocean and in the high seas. 18 http://www.maerskoil.com/media/newsroom/pages/maerskoiluk%E2%80%99sgryphonfpsobackinproduction.aspx 19 Westshore Shipbrokers AS (2013) Market Presentation 20 Compound Annual Growth Rate 21 Clarkson Capital Markets (2012) Overview of the OSV Industry, International Monetary Fund (IMF), World Economic Outlook (April 2012)

12

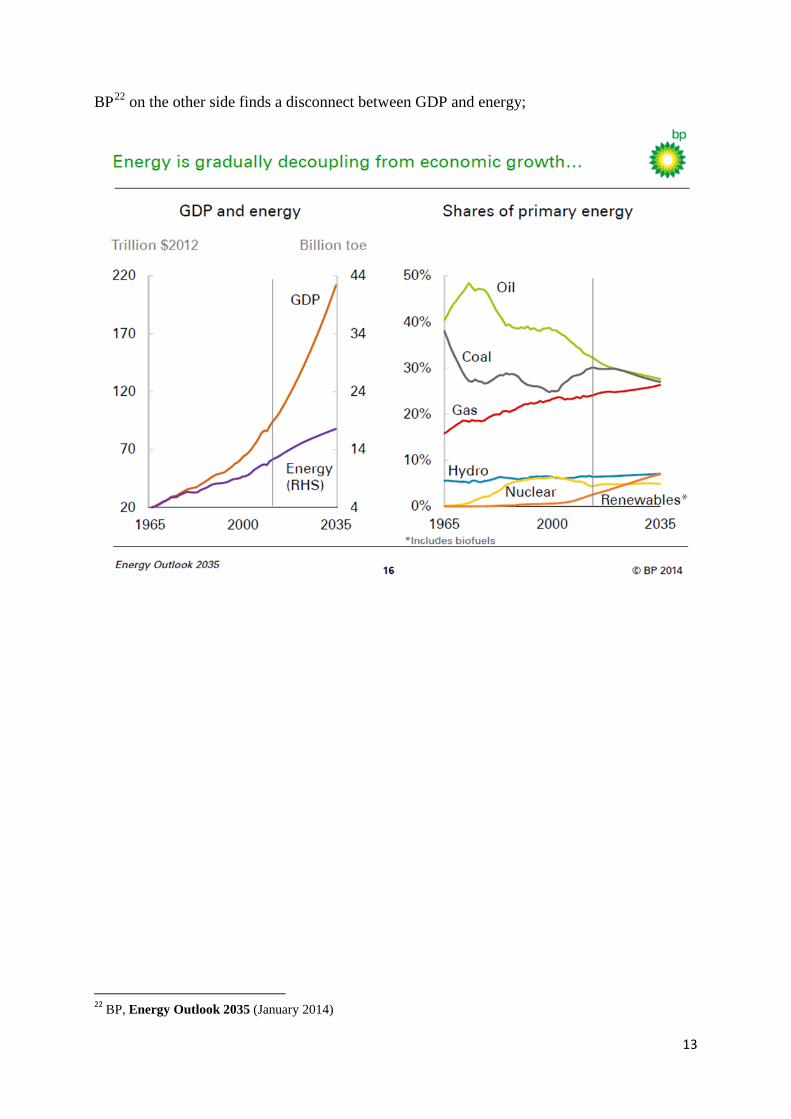

BP22 on the other side finds a disconnect between GDP and energy;

22 BP, Energy Outlook 2035 (January 2014)

13

14

4.4 Deeper water Offshore oil production contribution is expected to increase its share on behalf of onshore

fields. Deepwater (water depths > 600 feet) CAPEX is expected to increase its share of the

offshore production, with at CAGR of 23 %. The Golden Triangle of Latin America, The Gulf

of Mexico and West Africa are expected to dominate deepwater expenditure over the next

four to five years according to Douglas-Westwood23. The exploration trend goes deeper and

deeper, concentrated in the deep-water regions such as; Angola, USA, Brazil, Nigeria,

Malaysia and Norway. There are significant Hydrocarbon discoveries in these deep-water

regions24.

Frontier operations absorb more supply capacity. Newer and larger vessels should intuitively

bring efficiency gains to the industry, but the “real” world (count) confirms theory of 3-4

supply vessels per rig. Large PSV’s are taking a larger portion of the PSV segment in all

offshore basins. The PSV platform is versatile and will also be used for subsea support, well

intervention, renewables offshore and possibly seismic operations. Limited growth should be

expected from current balance sheets due to low equity ratio.25

As oil exploration and development become increasingly complex, moving into deep sea

and harsh water acreages, the demands of the offshore supply vessel industry also

increase. On top of this, stricter government regulations also support a trend for increasingly

complex vessels, typically by adding requirements such as firefighting and oil recovery

capabilities. This effect is expected to increase in the wake of the Macondo oil spill (BP

Deepwater Horizon in 2010) and with oil and gas activity moving into more

environmentally sensitive areas.26

Increased operations in remote areas are fantastic for the industry, but are also dependent on

the oil prices hovering at “healthy levels”. Fearnley comments that they have seen it before and

23 http://www.offshoreenergytoday.com/douglas-westwood-golden-triangle-to-dominate-deepwater-expenditure-over-5-years/ 24 Clarkson Capital Markets (2012) Overview of the OSV Industry, International Monetary Fund (IMF), World Economic Outlook (April 2012) 25 Swedbank First Securities (2012) Offshore Supply Vessels 26 ABG Sundal Collier (2013) Offshore Supply & Subsea, Credit Research – Sector report, (Oct. 29 2013)

15

will see it again – if or when the oil price takes a sharp dip and remains low for a period,

such projects together with deep water drilling are the first ones to be put on the shelves.27

4.5 Arctic The Arctic frontiers are seeing more activity. The Barents and Kara seas, Sakhalin,

Canada and Greenland should all create demand for high end tonnage inclusive of

ice management services.

Drilling in Arctic areas, with tough weather conditions, large distances and poor infrastructure

does create a much higher relative demand for larger and more sophisticated Offshore Support

Vessels (OSV). During 2014 there will be an increase of about 250 percent in deliveries of

Deepwater rigs (34 in 2014 versus 13 in 2013), and this should drive demand for high-end

OSVs. Over the next 12-24 month’s we could see a somewhat challenging market for offshore

drilling rigs, but longer-term this segment still looks firm. Fearnley expect the oil price will

continue to perform better than current analyst consensus expects. Geopolitical risks are likely

to continue to affect the supply side, and Fearnley expect to see oil demand surprise on the

upside as the global economy, hopefully gathers long-sought after momentum.

AHTS demand (but also PSV demand) is expected to receive a significant boost from

increasing offshore activity in the oil and gas basins of the Arctic, as the vessel intensity per

rig is much higher than in other regions. Past experience from the Cairn Greenland campaigns

indicates that each rig operating in Greenland will require three suitably sized and specified

AHTS ‘vessels for ice management. Due to the challenges in the Arctic, charterers will

generally require top-end tonnage, which will, in most cases, be sourced from the North Sea

market.

Although the timing of offshore activity in Arctic basins can be challenging to estimate, some

Arctic campaigns for 2014 and 2015 have been booked already. AHTS vessels representing

nearly 15 percent of the North Sea fleet are already booked for Arctic activity in 2014.

Excessive supply growth, especially of the PSV fleet, has been the concern of many OSV

owners and investors. These concerns are based on the considerable PSV order book. Last

year (2013), for example, 229 PSVs of various sizes were scheduled for delivery. Vessel

27 Fearnley Offshore Supply The Offshore Report No.1&2 Offshore Support and Specialized Vessels

16

deliveries from yards were, however, extensively delayed. Inexperience, especially at new

Asian yards and especially in the final construction stages, is cited as the main reason for

delays. Furthermore, anecdotal evidence suggests that labor rotation at yards is high, thus

preventing many yards from progressing along the ‘learning curve’ at the desired rate. The

latest quarter is, however, showing a rise in deliveries. If this is an actual lift in productivity,

then PSV fleet growth could be accelerating further.28

4.6 Wind29 The offshore wind market has been extremely active in 2013 in terms of construction activity,

but this will change for the worse in 2015 and 2016. The UK dominance in the offshore wind

market is now being, and will continue to be, challenged by Germany in 2014 and 2015.

Germany saw a tremendous level of construction activity during 2013, with most of the

projects set to be finalized in 2014 and 2015. New megawatts are being lined up in Europe,

Asia and North America, but a significant proportion of the megawatts added are pilot

projects and not commercial wind farms. Delays in current and future projects continue to be

due to cabling issues, but in addition to that there have been several delays due to fabrication

and installation problems.

The prevalent market driver in the offshore wind sector is, and will continue to be,

government subsidies. In order to reach grid parity, technological progress, which is driven by

large-scale government support, is essential.

4.7 Regional markets US Gulf of Mexico (US GoM) is the most actively explored and drilled offshore basin.

Deepwater activity remains near historically high. The E&P companies prefer to contract new

DP drillships, with increased capabilities such as dual activity derrick and dual BOP’s.

Deepwater PSV’s are on the orderbook to meet the increased demand from these vessels.

Latin America is one of the important OSV markets given its huge growth potential over the

next decade. Petrobras indicated that the seventh OSV newbuilding tender, will be the last out

of a 146 vessel renewal program. The tender calls for vessel constructed in Brazil with

28 RS Platou ASA Global Support Vessel Monthly (January & February 2014) The North Sea OSV Market (January 2014) The Platou Report (2014) 29 RS Platou ASA Global Support Vessel Monthly (January & February 2014) The North Sea OSV Market (January 2014) The Platou Report (2014)

17

contract duration of 4, 6 and 8 years with an option to extend with the same number of years.

It is expected that Petrobras will come to the market for foreign PSV’s again.

West African region is both a shallow and deepwater play. The additional demand is likely to

come from deepwater projects in Angola, Nigeria and Ghana.

Middle East region is primarily a shallow water play. The Jackup count is an important

driver for OSV activity and demand. The dayrates in the region are among the lowest in the

world due to shallow waters and Saudi Aramco’s ability to dictate prices.

The North Sea is one of the oldest and most explored oil and gas basins. It is the only

established spot market in the supply industry. This is as close as it gets towards a perfect

market as it is 100 % driven by supply and demand. The North Sea is the only market in

shipping where the rates can surge 400 % in 4 hours.

In Norway, the tonnage is mostly high end. The tonnage in Aberdeen, are mixed bags as the

requirements/specifications are lower. (The operators are holding a high standard though)

The Barents Sea has increased drilling activity. Boats for this spotmarket are based or on

standby in Bergen and Stavanger. Ad hoc rig moves and supply in this area occupies 10 days

just in sailing time up and down. This affects the availability in the spot market. The

importance of arctic regions is growing. The Kara Sea is also attracting available tonnage.

The Asia Pacific region has witnessed rapid growth in production.

4.8 Macro drivers prompting OSV demand Damodaran30 warns against bringing macro into the valuation. Macroeconomic changes will

affect value, but building the macroeconomic view into the valuation model will make it

…”impossible to separate how much of the result is attributed to views about the firm, and

how much to the macroeconomic judgment”. Hirt and Block31, on the other hand brings in a

Top-Down, and Bottom-Up approach into the valuation. In this thesis the company was

chosen before analyzing the macroeconomic picture and consequently it will be closer to the

bottom-up methodology. Another challenge is to quantify subjective factors. Qualitative

views have to be translated into quantitative elements of growth32.

30 Damodaran, A. (2006) Damodaran on Valuation 2nd ed. pp. 5-7 and 663 and Damodaran, A. (2012) Investment Valuation 3rd ed. p. 622 31 Hirt, G.A. & Block, S.B. (2012) Fundamentals of Investment Management 10th ed. ch. 5 and 6 32 Damodaran, A. (2012) Investment Valuation 3rd ed. pp. 301-302

18

4.9 Struggle Many of the participants in the industry are still struggling to deliver decent returns, with

high financial gearing due to extensive investments in recent years. So far, the companies

have been able to generate sufficient cash flows to service interest and debt amortization.

However, some companies appear to be in sight of harvesting the fruit of the high

investments made.33

4.10 Challenges The industry has several challenges such as: Tremendous yard capacity - it is estimated that

approximately 50% of the yard capacity in China is being utilized, hence we have seen in

2013 that many private shipyards have gone bankrupt and closed up. China is not the only

challenge. In many other countries there is just too much capacity which is also fuelled by

the fact that due to lack of orders for conventional ships many shipyards have switched to

building offshore vessels.

Turkish shipyards are now offering prices which are very competitive compared to Norwegian

and European yards, in fact prices have been close to Chinese prices which makes some of

them very attractive alternatives. Rising costs - in areas such as Norway and Brazil we have

reached level’s which by many is considered “too much”. Statoil has officially said that they

are having difficulties in making a profit with oil prices around USD 100 per barrel and they

have started a cost cutting process. Crew and operating costs have also reached level’s, which

seems to be (almost) too high and many owners have miscalculated totally the cost of

operating in Brazil and to a certain extent regrets going in there. A few years ago it was

unheard of for a Norwegian supply vessel owner to have any other crew than full Norwegian

speaking crew. Today the situation has changed totally and most of these owners have today a

large amount of Non Norwegian crew onboard.

Commercial life time for offshore support vessels - during 2013 we saw several vessels built

in the early 80´s being removed from the market and went into scrapping and the last two

years have shown that the commercial life time for a supply vessel has been quite reduced.34

Financing - or rather lack of financing will continue to be a big challenge during 2014 and we

will see a large amount of sale/ leaseback which was also the case for 2013. Many of them

might go into KS or DIS companies (or other limited liability companies) with bareboat

charter back to the sellers. Secured or unsecured bonds will also be much in demand. From a

33 ABG Sundal Collier (2013) Offshore Supply & Subsea, Credit Research – Sector report 34 IHS does not agree. Ref IHS subchapter.

19

market prospective and in theory, it is quite good that financing is tight as it is supposed to

reduce the speculative new buildings or make life to speculative projects. As certain yards are

offering extremely attractive payment terms and no take out guarantee, the speculative new

building will still carry on.

The OSV owners have two years behind them with “expectations not quite fulfilled”.

It seems as if the expected activity wave has been pushed in front of them - the high

activity peak with high rates being pushed to the right.35

4.11 Expectations and Outlook ABG expect a healthy CSV market, improved rates in the AHTS market and continued

oversupply putting pressure on the PSV segment. Due to the opening up of new oil and gas

regions such as Brazil and West Africa, mature regions such as the NWECS36 being

given a second life through new discoveries and increased exploration efforts in frontier

arctic regions, ABG believe the underlying demand fundamentals in the OSV industry are

strong.

Looking at E&P spending levels over the next few years, ABG still expect this to grow,

albeit at a slower pace than in recent years. ABG forecast 3% growth in offshore

spending in ’14e and no growth in ’15e.

The outlook for the mid- and high-end AHTS (> 10k BHP) market is slightly positive for

2014e. A 9% year-on-year increase in demand and a 5% forecast increase in supply should

translate to a slight increase in utilization from 2013. For the PSV segment, the outlook is

worse, as a 10% growth in demand stemming from growth in offshore fields and drilling

units should be insufficient compared to a forecast of 15% growth in supply. 37

Fearnley generally have a positive outlook for the industry. Utilization has been picking up,

but the rates have been lagging behind. Term rates for certain types of vessels will most likely

pick up during 2014.38

35 Fearnley Offshore Supply The Offshore Report No.1&2 Offshore Support and Specialized Vessels 36 North West Europe Continental Shelf 37 ABG Sundal Collier (2013) Offshore Supply & Subsea, Credit Research – Sector report 38 Fearnley Securities AS OSV Sector outlook 4q13 previews (24 February 2014)

20

E&P Spending 2013 to 2017 in the Norwegian Continental Shelf (NCS) is expected to be 7.7

% CAGR. The UK Continental Shelf (UKCS) is benefitting from record investment in new

development. Exploration and Appraisal wells are up from previous years and possibly facing

the most active drilling period in the last 15 years. Westshore sees a global potential of 950

offshore rigs by the end of 2015. Smaller operators are entering the NCS and the UKCS

leading to more activity on the shelf.39

RS Platou expects escalating costs and flat oil prices. Public oil companies face the challenge

of maintaining dividend payments to their shareholders, while continuing to increase their

E&P budgets. Global E&P is still expected to grow by approximately 6 percent to 700—750

bill USD, but growth in real oil service purchasing power will be relatively modest.40

4.11.1 IHS Petrodata41– Former ODS Petrodata IHS is a leading supplier of data to, among else, the shipping and offshore industry, and to

those who follow these markets and make forecasts etc. As this is based on a breakfast

briefing, and not written reports, their view will be hurdled up in this separate subchapter. IHS

is tracking every vessel and rig individually. They are basing their prognosis and forecasts

mainly on regression. The rigmarket is in a cyclical pause with signs of slowdown for 2014.

South East Asia is primarily a midwater region, with increased deepwater development.

Mediterranean with Israel, Cyprus and the Black Sea have promising discoveries. West Africa

is the best UDW area with high rates and high utility. The bureaucracies are time consuming.

The US Gulf of Mexico has DW discoveries, and Mexico is opening up exploration. East

Africa has major discoveries and large future DW developments. The demand in North West

Europe appears to be weak through 2014-2015. The Falkland Islands have promising first

development. Brazil looks good for long term development, with new exploration. It’s a

regulated market, but it seems the authorities are easing on requirements like local content.

The harsh environment areas of the Kara Sea, and Greenland does not look promising for the

next few years, but maybe on a longer term.

Contractors prefer drillship’s. IHS predicts that the fleet of drillship’s will grow till 170 by

2020. 71 of 75 of the new ships will be capable of UDW drilling. Semisubmersibles are less

attractive. The market for floaters is softening. The dayrates for UDW capability are expected

39 Westshore Shipbrokers AS (2013) Market Presentation 40 RS Platou ASA Global Support Vessel Monthly (January & February 2014) RS Platou Montly (February 2014) The North Sea OSV Market (January 2014) The Platou Report (2014) 41 IHS Petrodata Breakfast Briefing: Offshore Rig Market, Supply Vessel Trends (March 26, 2014)

21

to fall from 630 000 USD to 450-500 000 USD. Few UDW rigs are drilling in UDW. This is

pushing down the rates of lesser specified rigs. Latin America and Africa dominates

discoveries. Chinese yards only require 10 % down payment for ship orders. They may get

order for 3 vessels but builds 5 with hope to sell the last 2 later. The global PSV rates are on a

slide 2009-2014. In many markets the Rig/OSV ratio is 90 % correlated, but there are regional

differences. Examples of segmentation in the regional markets are; local content requirement

in Brasil, Jones act in USGoM, high Norwegian requirement relative to lower requirements in

the UK and the Aramco monopoly in the Mideast.

There is almost no attrition as OSV don’t get scapped but cold stacked, and used in market

with lower specification requirement .This observation contradicts Fearnley in the challenges

chapter.

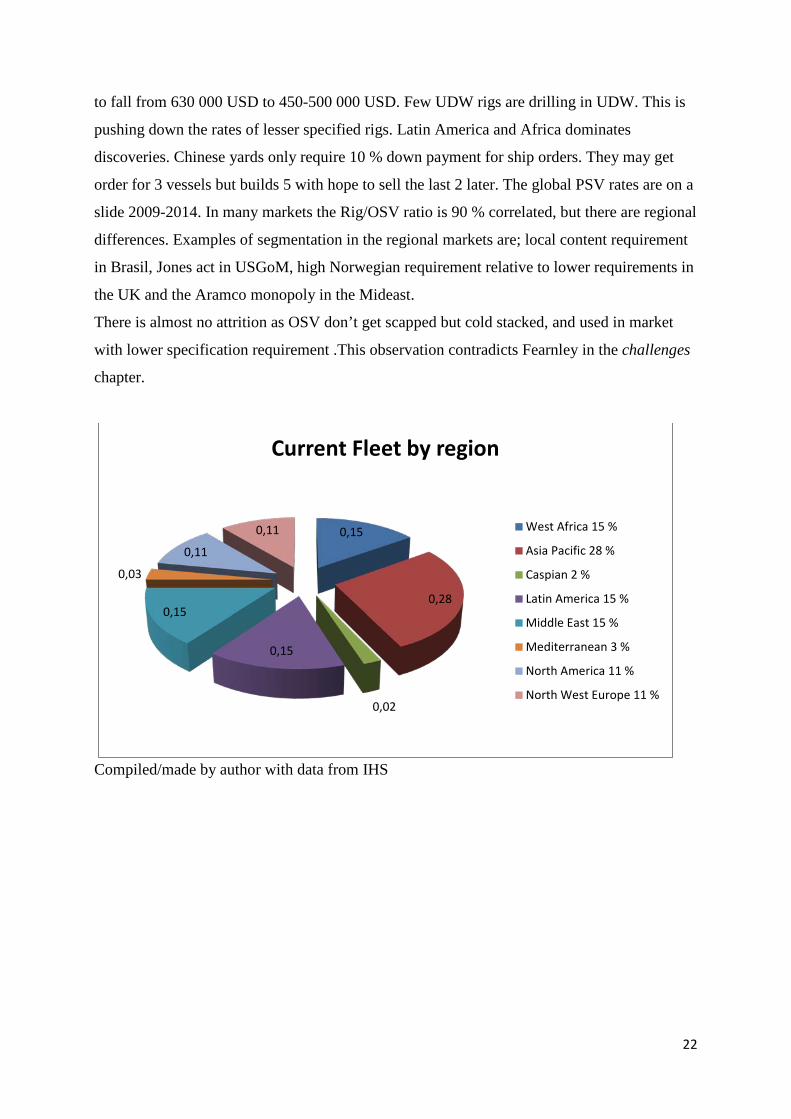

Compiled/made by author with data from IHS

0,15

0,28

0,02

0,15

0,15

0,03

0,11

0,11

Current Fleet by region

West Africa 15 %

Asia Pacific 28 %

Caspian 2 %

Latin America 15 %

Middle East 15 %

Mediterranean 3 %

North America 11 %

North West Europe 11 %

22

Compiled/made by author with data from IHS

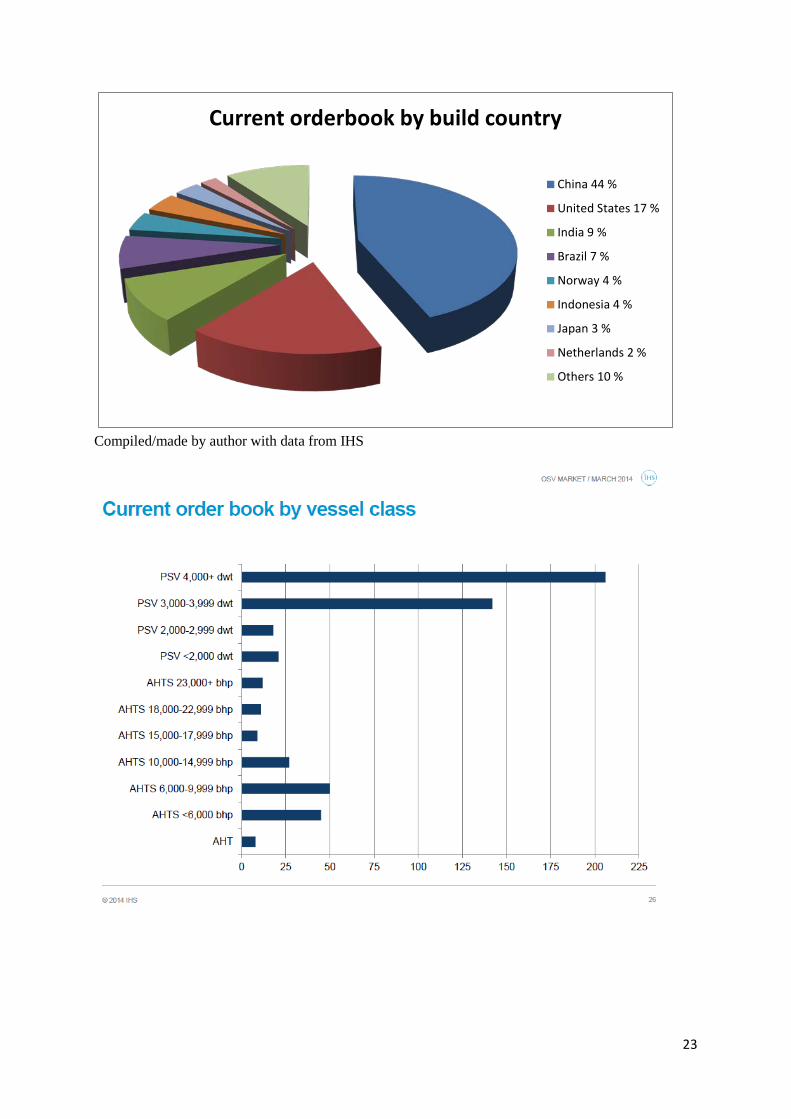

Current orderbook by build country

China 44 %

United States 17 %

India 9 %

Brazil 7 %

Norway 4 %

Indonesia 4 %

Japan 3 %

Netherlands 2 %

Others 10 %

23

24

4.12 Prices historic

25

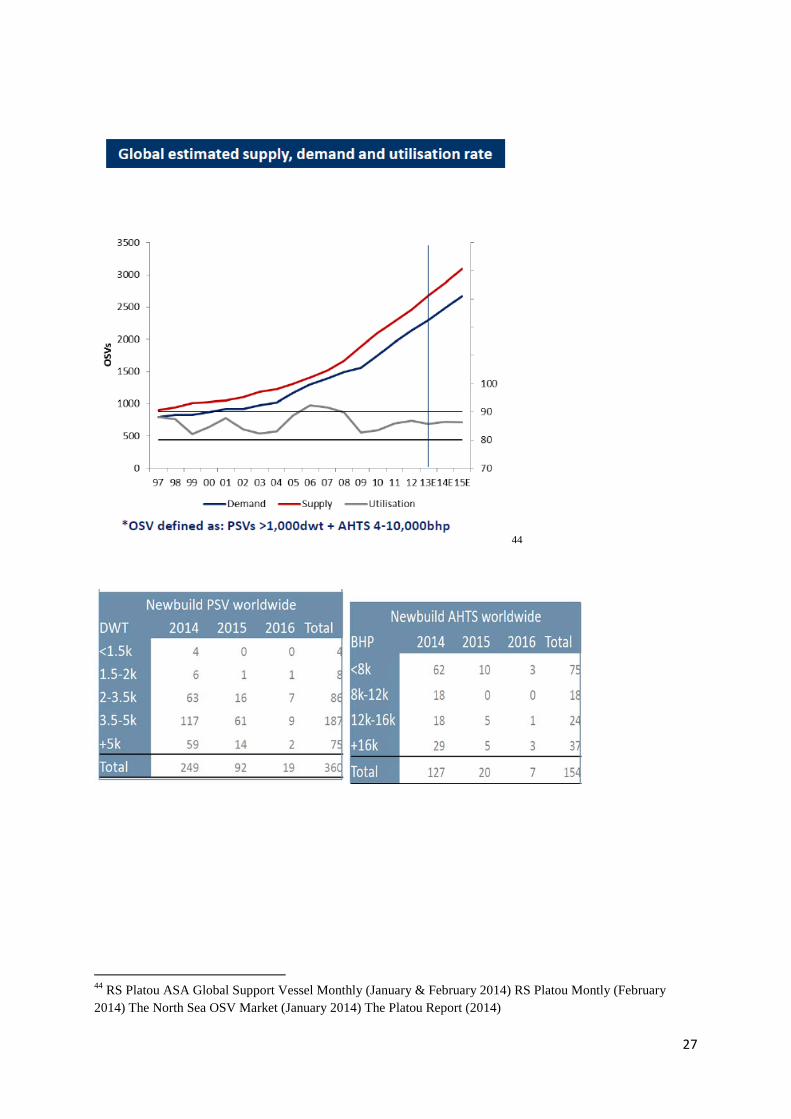

4.13 Fleet The global OSV market balance is expected to remain stable through 2014 and 2015.

However, some regional variations are expected, due to local regulations and content

requirements. The main driver of demand will still be the large number of new UDW floaters

entering service through 2014 and 2015. The new UDW drillship’s, are likely to be serviced

by larger sized DP II42 PSV’s. Oil and gas companies’ safety concerns are also driving

demand for high specialization modern units. Such vessels are likely to command a premium

in contract terms.

The prospects for medium-sized AHTS vessels seem very good, as the renewal of the jackup

fleet will continue in the period 2014-15, and further floating production units will enter

service. At the same time the number of vessels on order for this asset class is relatively low

and RS Platou therefore expects utilization to keep rising in the period 2014-15. However, the

larger AHTS vessels, which are mostly in service with conventionally moored floaters, may

face some headwind due to a softer floater market. This may lead to increased substitution

through the asset classes and a more modest increase in day rates for the mid-size AHTS

vessels.43

42 Dynamic Positioning; DP2 involves increased level of system redundancy compared to DP1. DP3 is the most advanced class defined by the International Maritime Organization (IMO). DP3 enables the ship to maintain position during fire and flooding. 43RS Platou ASA Global Support Vessel Monthly (January & February 2014) RS Platou Montly (February 2014) The North Sea OSV Market (January 2014) The Platou Report (2014)

26

44

44 RS Platou ASA Global Support Vessel Monthly (January & February 2014) RS Platou Montly (February 2014) The North Sea OSV Market (January 2014) The Platou Report (2014)

27

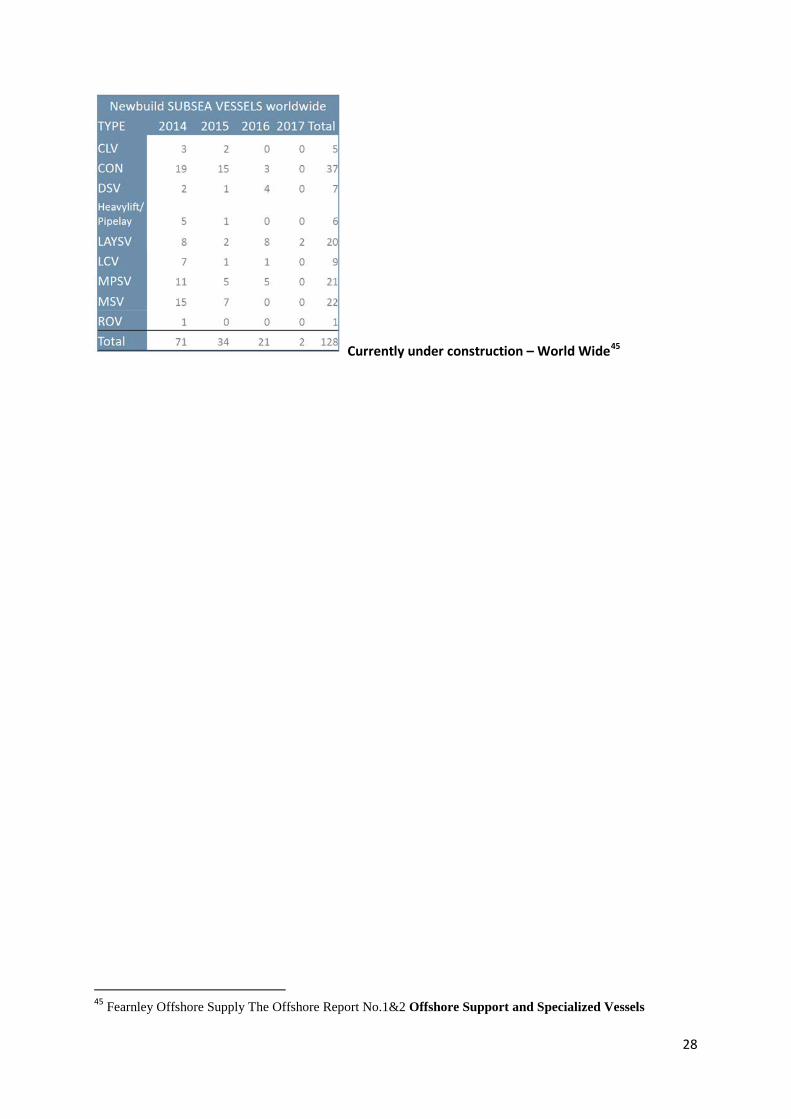

Currently under construction – World Wide45

45 Fearnley Offshore Supply The Offshore Report No.1&2 Offshore Support and Specialized Vessels

28

29

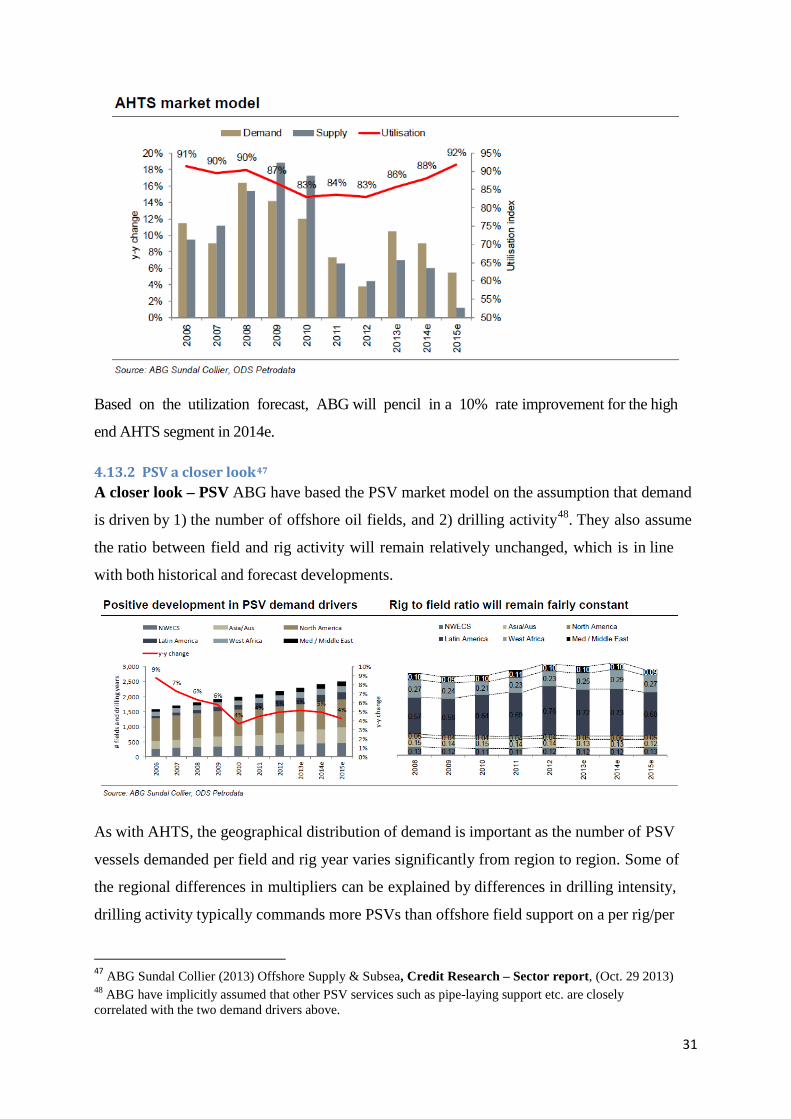

4.13.1 AHTS a closer look46 A closer look – AHTS The underlying assumption behind the ABG AHTS market

model is that demand is mainly driven by drilling activity. The following graphs

illustrate the forecast drilling demand stemming from exploration and development

drilling, as well as the geographical split.

The geographical distribution of drilling activity is important, as the demand for AHTS vessels

per rig year varies significantly from region to region. This is due to factors such as the water

depth in the oil and gas basins, government regulations, distance to shore, existing onshore

infrastructure etc.

In summary, ABG find that the AHTS market should remain fairly unchanged going into

2014e, while ABG forecast utilization (term+spot demand vs. supply) to increase

marginally.

46 ABG Sundal Collier (2013) Offshore Supply & Subsea, Credit Research – Sector report, (Oct. 29 2013)

30

Based on the utilization forecast, ABG will pencil in a 10% rate improvement for the high

end AHTS segment in 2014e.

4.13.2 PSV a closer look47 A closer look – PSV ABG have based the PSV market model on the assumption that demand

is driven by 1) the number of offshore oil fields, and 2) drilling activity48. They also assume

the ratio between field and rig activity will remain relatively unchanged, which is in line

with both historical and forecast developments.

As with AHTS, the geographical distribution of demand is important as the number of PSV

vessels demanded per field and rig year varies significantly from region to region. Some of

the regional differences in multipliers can be explained by differences in drilling intensity,

drilling activity typically commands more PSVs than offshore field support on a per rig/per

47 ABG Sundal Collier (2013) Offshore Supply & Subsea, Credit Research – Sector report, (Oct. 29 2013) 48 ABG have implicitly assumed that other PSV services such as pipe-laying support etc. are closely correlated with the two demand drivers above.

31

field basis.49

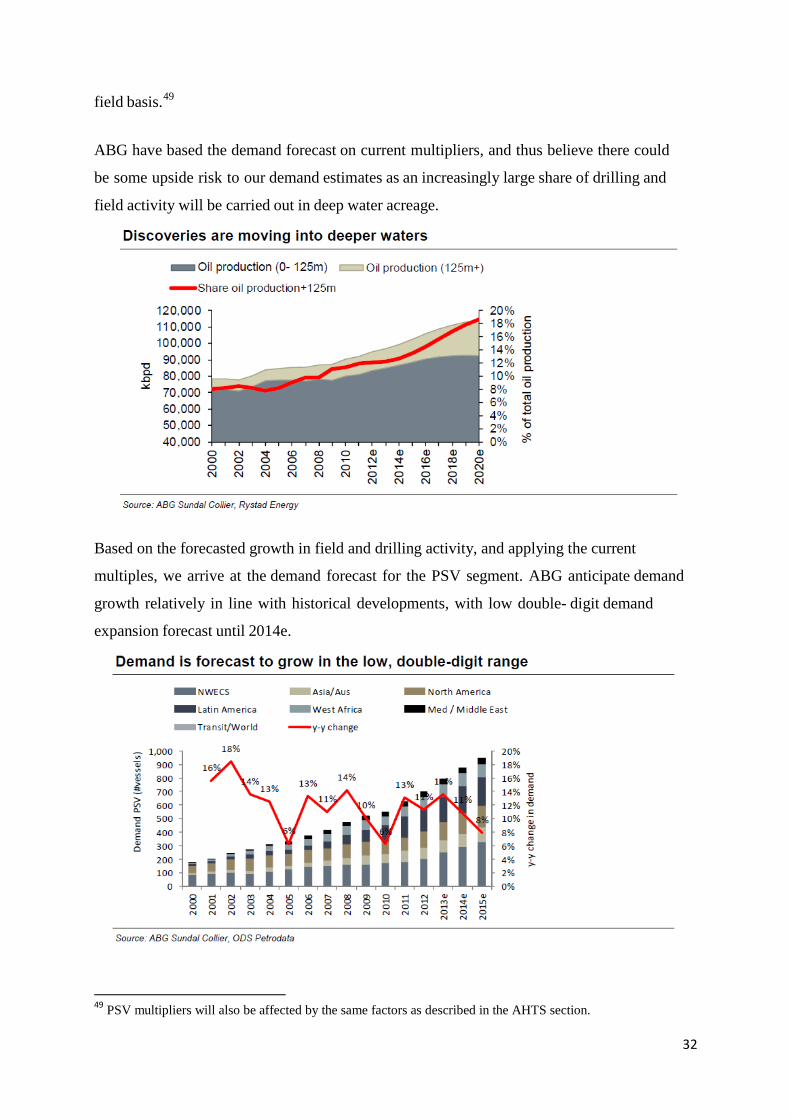

ABG have based the demand forecast on current multipliers, and thus believe there could

be some upside risk to our demand estimates as an increasingly large share of drilling and

field activity will be carried out in deep water acreage.

Based on the forecasted growth in field and drilling activity, and applying the current

multiples, we arrive at the demand forecast for the PSV segment. ABG anticipate demand

growth relatively in line with historical developments, with low double- digit demand

expansion forecast until 2014e.

49 PSV multipliers will also be affected by the same factors as described in the AHTS section.

32

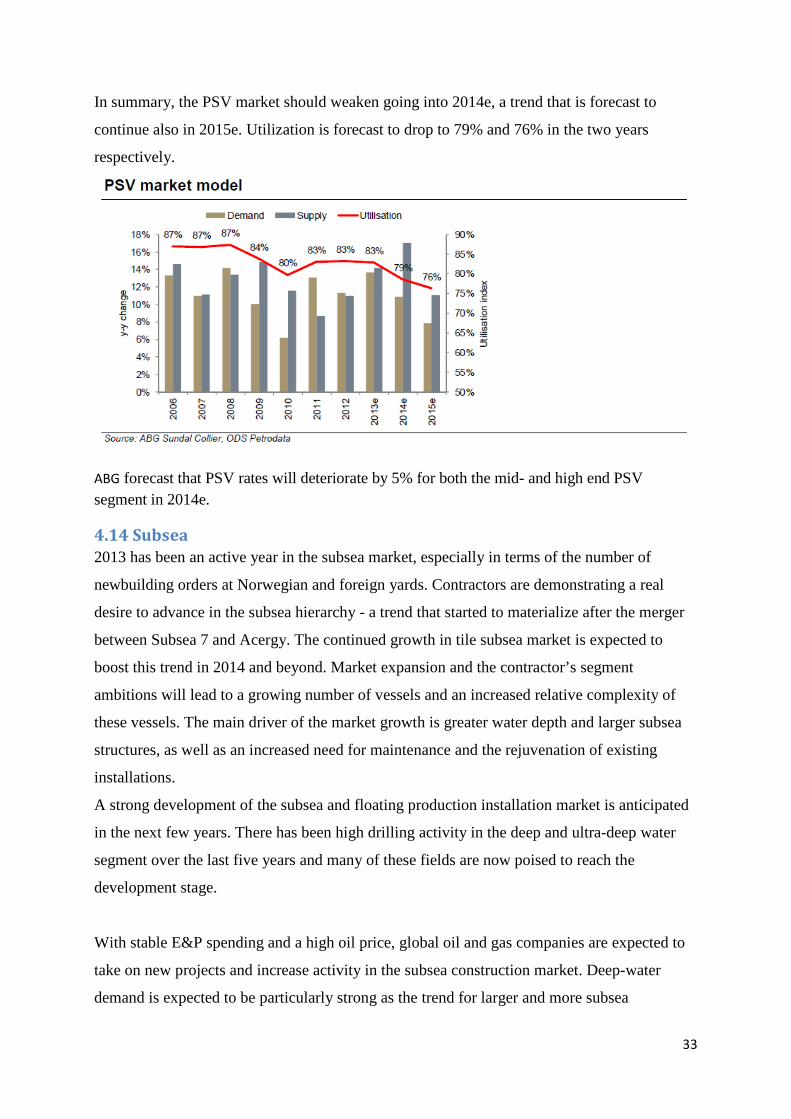

In summary, the PSV market should weaken going into 2014e, a trend that is forecast to

continue also in 2015e. Utilization is forecast to drop to 79% and 76% in the two years

respectively.

ABG forecast that PSV rates will deteriorate by 5% for both the mid- and high end PSV segment in 2014e.

4.14 Subsea 2013 has been an active year in the subsea market, especially in terms of the number of

newbuilding orders at Norwegian and foreign yards. Contractors are demonstrating a real

desire to advance in the subsea hierarchy - a trend that started to materialize after the merger

between Subsea 7 and Acergy. The continued growth in tile subsea market is expected to

boost this trend in 2014 and beyond. Market expansion and the contractor’s segment

ambitions will lead to a growing number of vessels and an increased relative complexity of

these vessels. The main driver of the market growth is greater water depth and larger subsea

structures, as well as an increased need for maintenance and the rejuvenation of existing

installations.

A strong development of the subsea and floating production installation market is anticipated

in the next few years. There has been high drilling activity in the deep and ultra-deep water

segment over the last five years and many of these fields are now poised to reach the

development stage.

With stable E&P spending and a high oil price, global oil and gas companies are expected to

take on new projects and increase activity in the subsea construction market. Deep-water

demand is expected to be particularly strong as the trend for larger and more subsea

33

equipment being put on the seabed will continue. Offshore wind farms are being placed

further offshore and thus will demand more subsea vessels in the years to come. Several

vessels were absorbed during 2013. In 2014 and 2015 several tidal projects are reaching the

start of the construction stage and this will require subsea tonnage. In recent times, many oil

companies have turned their focus on the escalation of costs, which is seen as a major threat

for several projects. However, the field economics are still sufficient to continue developing

deep-water subsea fields, where oil companies have reported higher return on the employed

capital than in the shallow and medium water segments. Healthy growth across the coming

years is expected in the subsea vessel market, but timing will still be crucial in this relatively

young market.50

The subsea market has been solid for PSV’s. Owners are likely to upgrade those vessel’s that

have the ability to be upgraded to work in the subsea market. Medium to long term

fundamentals for the subsea construction market is strong. Deepwater drilling activity, and

subsea tree awards indicates significant growth. The market has absorbed new tonnage well,

but there is an oversupply of PSV’s. Banks favor subsea or specialized offshore areas. Larger

PSV sector will be tight going forward, while mid sector is swamped. 51

The Subsea Vessel segment was undoubtedly the hottest sector in 2013 according to

Fearnley. There are few OSV owners left who have not bought a ticket in this demanding

niche, and several large speculative investments were made both by existing players and by

newcomers to the subsea industry. 2014 may prove to be the “acid test” to the sustainability

of the fleet growth we have seen in 2013. Needless to say, all the planned deepwater

developments will require a growing fleet of installation- and maintenance vessels with larger

cranes and ROV’s for depth in excess of 1500 meters.52

4.15 Risks53 ABG Sundal Collier offers this perspective on the risks in OSV business:

1. Business risks

50 RS Platou ASA Global Support Vessel Monthly (January & February 2014) RS Platou Montly (February 2014) The North Sea OSV Market (January 2014) The Platou Report (2014) 51 Westshore Shipbrokers AS (2013) Market Presentation 52 Fearnley Offshore Supply The Offshore Report No.1&2 Offshore Support and Specialized Vessels 53 ABG Sundal Collier (2013) Offshore Supply & Subsea, Credit Research – Sector report, (Oct. 29 2013)

34

Commodity price risks

We identify the oil price as the most important risk factor affecting growth in oil

services. A sudden and unexpected long-term drop in the oil price would have a negative

impact on demand for oil services and equipment. Activity within the supply segment,

especially for AHTS vessels, is driven by rig activity. Rig activity depends on the oil

companies’ E&P spend, which in turn depends on the oil price.

Market supply

Besides the oil price and the implicit demand for supply services, supply growth is a key

risk for the offshore supply names. The big increase in orders for newbuilds in recent

years could potentially lead to massive supply growth over the next few years, thus

putting further downward pressure on day rates and profitability within the supply industry.

Operational risk

The offshore supply companies have several vessels operating globally in challenging

environments. This represents risk relating to damage and erosion to vessels, which could

lead to significant cost and reduced utilization.

Construction risk

The companies currently have several vessels under construction at different ship yards.

This represents risks related to prepayments that have been paid. Also, it’s prudent to

assume a delay in the delivery schedule, which in turn would impact the company’s cash

flow.

Counterparty risk

Many of the companies in the industry have contracts with major E&P counterparties like

Statoil, Petrobas, and Total, mitigating the counterparty risk. The offshore supply

companies are exposed to the volatility in the oil price through their counterparties.

2. Financial risk

35

Financial gearing

Several companies in the offshore industry tend to have high financial gearing due to

large capex from extensive newbuild activity. The level of indebtedness depends

predominantly on the pattern of vessel investments. For many companies in this industry,

deleveraging is highly important in order to achieve a more prudent credit profile.

Cash flow position

The debt characteristics, i.e. the pattern of debt issuance, amortizations and redemption,

will have a major impact on the total cash flow position in the capital intensive offshore

supply industry. Capex related to new vessel programs will in some companies be partly

funded by internally generated cash, which will have a negative effect on the total cash flows.

Currency risk

There is also risk related to currency exposure, as the local currency acts as the functional

currency in several countries in which it operates, whereas the liabilities are predominantly

denominated in NOK. The actual currency risk depends on the degree to which any

currency mismatches are hedged.

4.16 Possible ups and downs by Swedbank First Securities54 Possible positive surprises: Brazil sourcing more capacity, at higher rates - Greenland

shows real impact in frontier operations - An increased activity in Canada and Alaska -

Subsea segment increased appetite for large AHTS units, for ploughing and installation -

Rigs being reactivated - Accidents with more widespread impact on demand than expected -

High end vessels are preferred in emerging markets like West Africa.

Possible negative impact: Significant drop in oil price - Financing once again becomes

cheap - Large scale accidents occur - An increased in local content, that induces less

business and growth - Significant efficiency gains in operations and yards.

At the event “Aksjeåret 2014”55 Chief Strategist Peter Hermanrud at Swedbank First

54 Swedbank First Securities Offshore Supply Vessels (June 2012) 55 Madsen, A. (2014) Gullalderen kan være over. Offshore.no (07 January 2014) http://www.offshore.no/sak/60484_gullalderen_kan_vaere_over_#

36

Securities gave his view of the future. Shale gas will possibly sail up as the most important

source of energy. Shale gas is less expensive than oil, and therefore a treat in the long term

perspective. The oil companies are making a profit, but the cost of E&P is rising. The

offshore market will stagnate. The rig rates will fall as the number of rigs will increase by 30

% over the next 3 years. He is expecting a drop in E&P during 2014. Up until now there has

been a lack of capacity, and suddenly this has turned around to a lack of capital. The oil

service profitability is disappointing, but the stock prices are increasing (rising) due to the

markets expectations for 2015-16. The price of oil will average around 115 USD and end

over 120 USD.

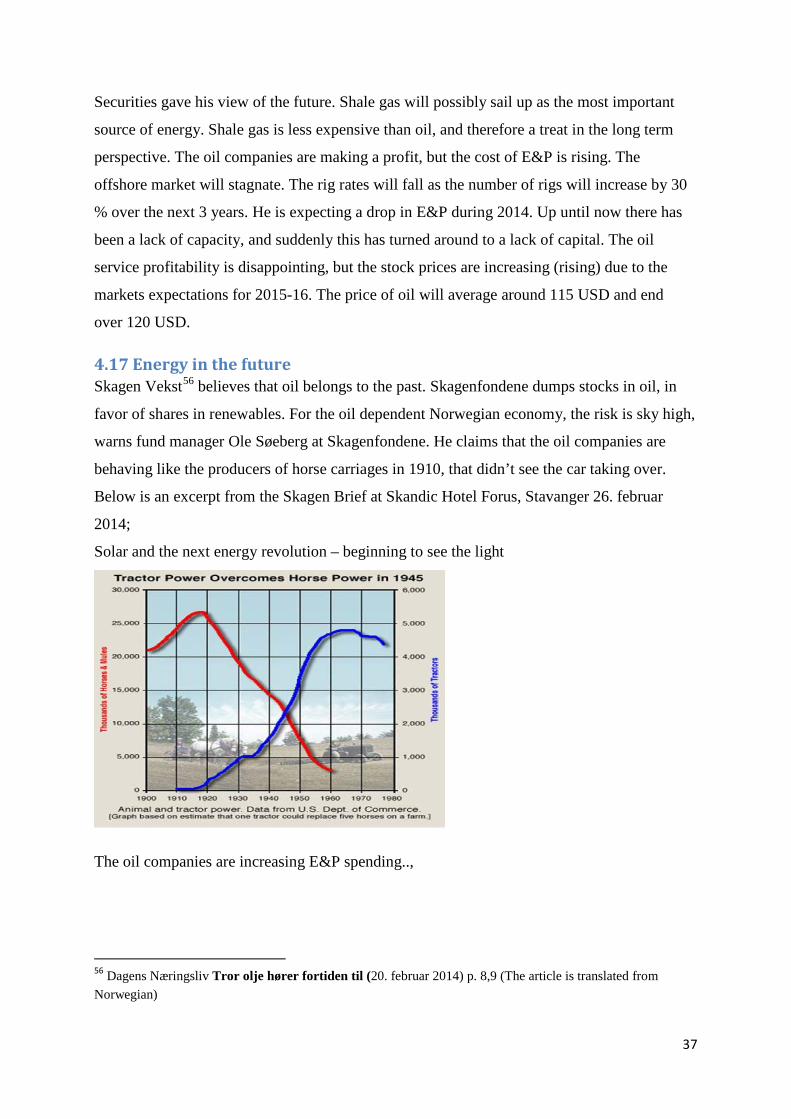

4.17 Energy in the future Skagen Vekst56 believes that oil belongs to the past. Skagenfondene dumps stocks in oil, in

favor of shares in renewables. For the oil dependent Norwegian economy, the risk is sky high,

warns fund manager Ole Søeberg at Skagenfondene. He claims that the oil companies are

behaving like the producers of horse carriages in 1910, that didn’t see the car taking over.

Below is an excerpt from the Skagen Brief at Skandic Hotel Forus, Stavanger 26. februar

2014;

Solar and the next energy revolution – beginning to see the light

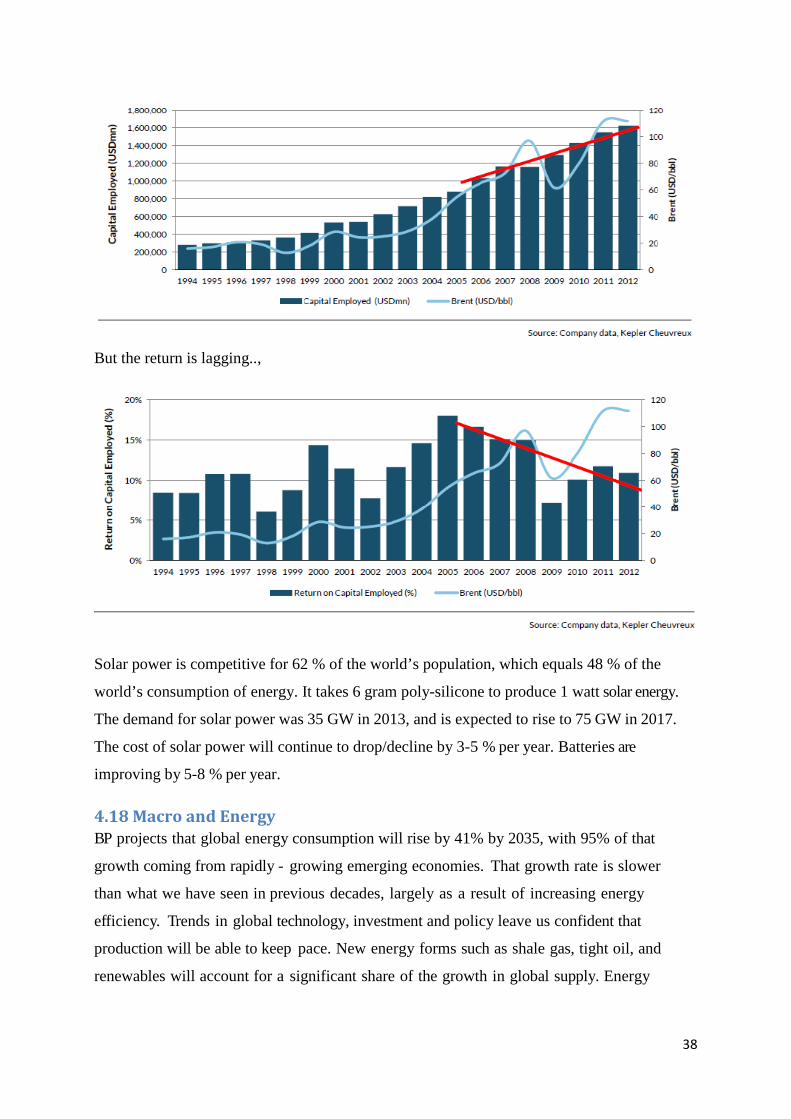

The oil companies are increasing E&P spending..,

56 Dagens Næringsliv Tror olje hører fortiden til (20. februar 2014) p. 8,9 (The article is translated from Norwegian)

37

But the return is lagging..,

Solar power is competitive for 62 % of the world’s population, which equals 48 % of the

world’s consumption of energy. It takes 6 gram poly-silicone to produce 1 watt solar energy.

The demand for solar power was 35 GW in 2013, and is expected to rise to 75 GW in 2017.

The cost of solar power will continue to drop/decline by 3-5 % per year. Batteries are

improving by 5-8 % per year.

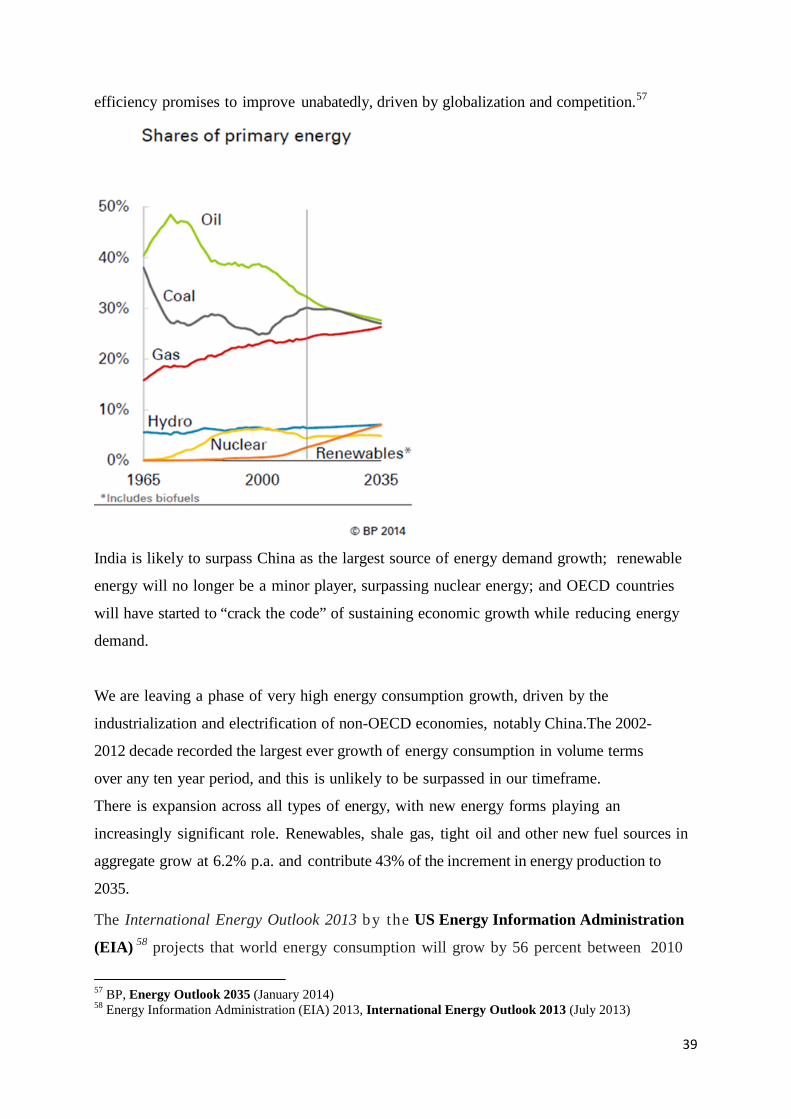

4.18 Macro and Energy BP projects that global energy consumption will rise by 41% by 2035, with 95% of that

growth coming from rapidly - growing emerging economies. That growth rate is slower

than what we have seen in previous decades, largely as a result of increasing energy

efficiency. Trends in global technology, investment and policy leave us confident that

production will be able to keep pace. New energy forms such as shale gas, tight oil, and

renewables will account for a significant share of the growth in global supply. Energy

38

efficiency promises to improve unabatedly, driven by globalization and competition.57

India is likely to surpass China as the largest source of energy demand growth; renewable

energy will no longer be a minor player, surpassing nuclear energy; and OECD countries

will have started to “crack the code” of sustaining economic growth while reducing energy

demand.

We are leaving a phase of very high energy consumption growth, driven by the

industrialization and electrification of non-OECD economies, notably China. The 2002-

2012 decade recorded the largest ever growth of energy consumption in volume terms

over any ten year period, and this is unlikely to be surpassed in our timeframe.

There is expansion across all types of energy, with new energy forms playing an

increasingly significant role. Renewables, shale gas, tight oil and other new fuel sources in

aggregate grow at 6.2% p.a. and contribute 43% of the increment in energy production to

2035.

The International Energy Outlook 2013 by the US Energy Information Administration

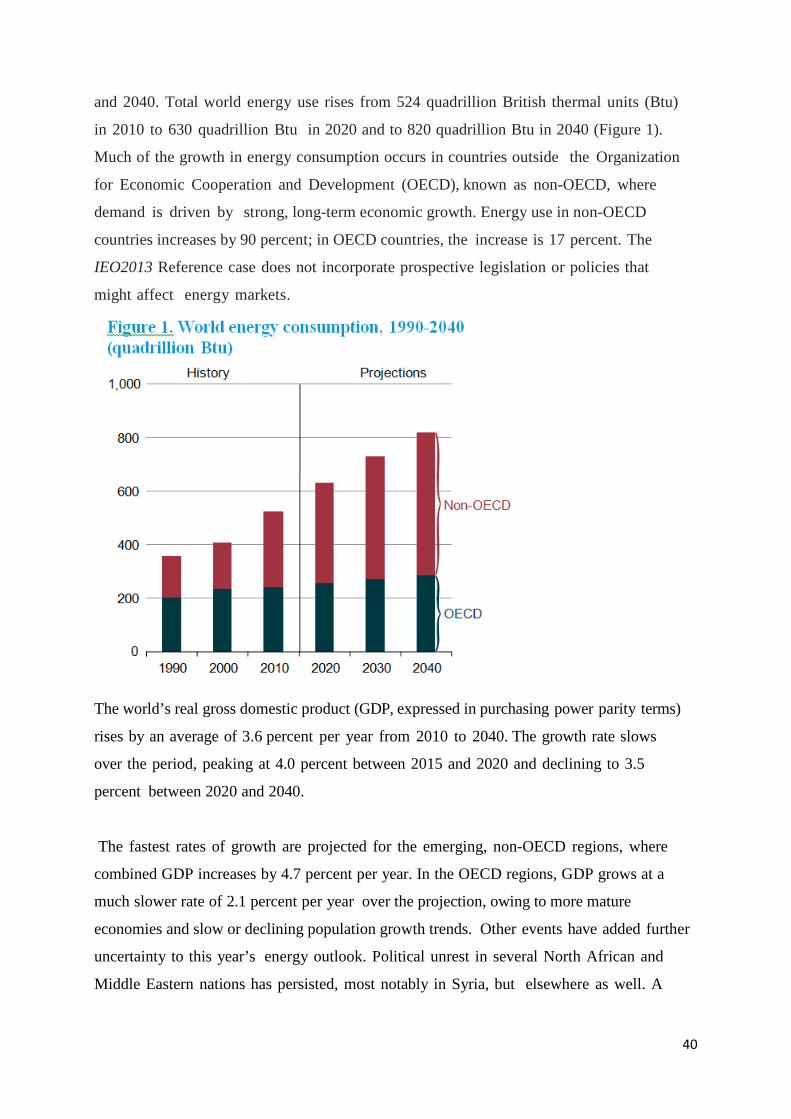

(EIA) 58 projects that world energy consumption will grow by 56 percent between 2010

57 BP, Energy Outlook 2035 (January 2014) 58 Energy Information Administration (EIA) 2013, International Energy Outlook 2013 (July 2013)

39

and 2040. Total world energy use rises from 524 quadrillion British thermal units (Btu)

in 2010 to 630 quadrillion Btu in 2020 and to 820 quadrillion Btu in 2040 (Figure 1).

Much of the growth in energy consumption occurs in countries outside the Organization

for Economic Cooperation and Development (OECD), known as non-OECD, where

demand is driven by strong, long-term economic growth. Energy use in non-OECD

countries increases by 90 percent; in OECD countries, the increase is 17 percent. The

IEO2013 Reference case does not incorporate prospective legislation or policies that

might affect energy markets.

The world’s real gross domestic product (GDP, expressed in purchasing power parity terms)

rises by an average of 3.6 percent per year from 2010 to 2040. The growth rate slows

over the period, peaking at 4.0 percent between 2015 and 2020 and declining to 3.5

percent between 2020 and 2040.

The fastest rates of growth are projected for the emerging, non-OECD regions, where

combined GDP increases by 4.7 percent per year. In the OECD regions, GDP grows at a

much slower rate of 2.1 percent per year over the projection, owing to more mature

economies and slow or declining population growth trends. Other events have added further

uncertainty to this year’s energy outlook. Political unrest in several North African and

Middle Eastern nations has persisted, most notably in Syria, but elsewhere as well. A

40

number of the countries that experienced political transition as a result of the Arab Spring

revolutions, including Egypt, Tunisia, and Yemen, have struggled to establish stability. In

addition, the sanctions imposed on Iran as a result of its nuclear program have dampened the

country’s growth outlook.

Economic growth is among the most important factors to be considered in projecting

changes in world energy consumption.

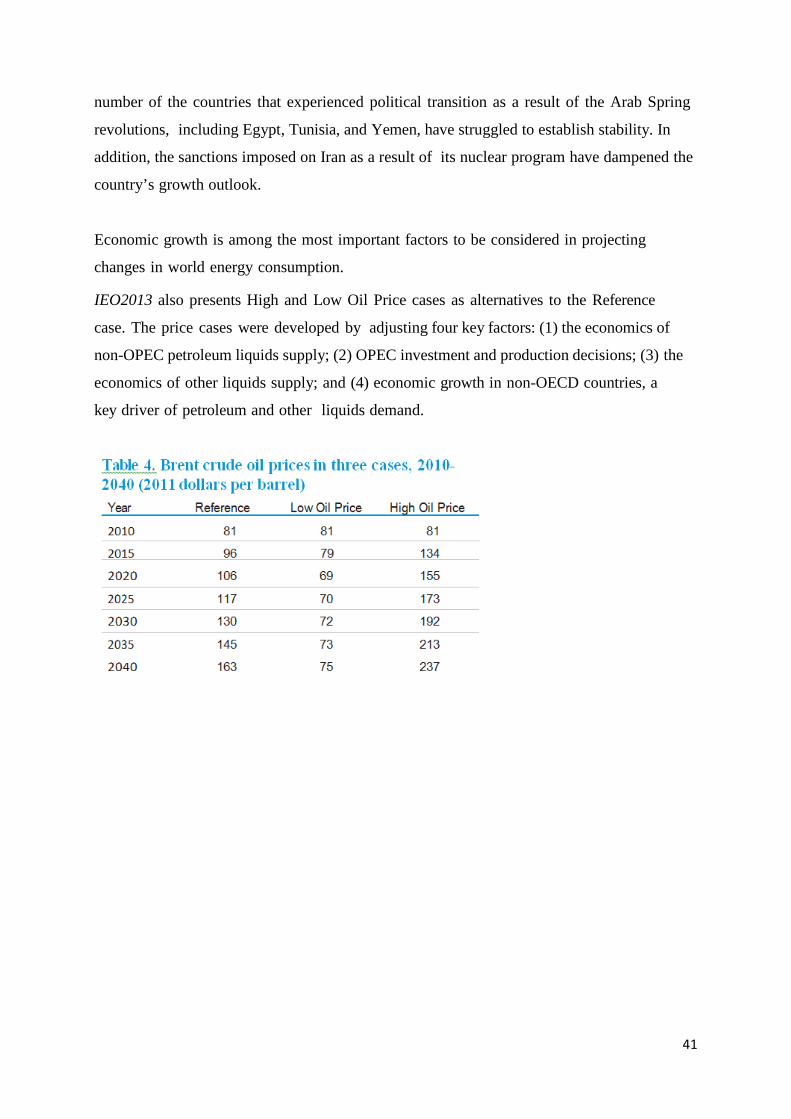

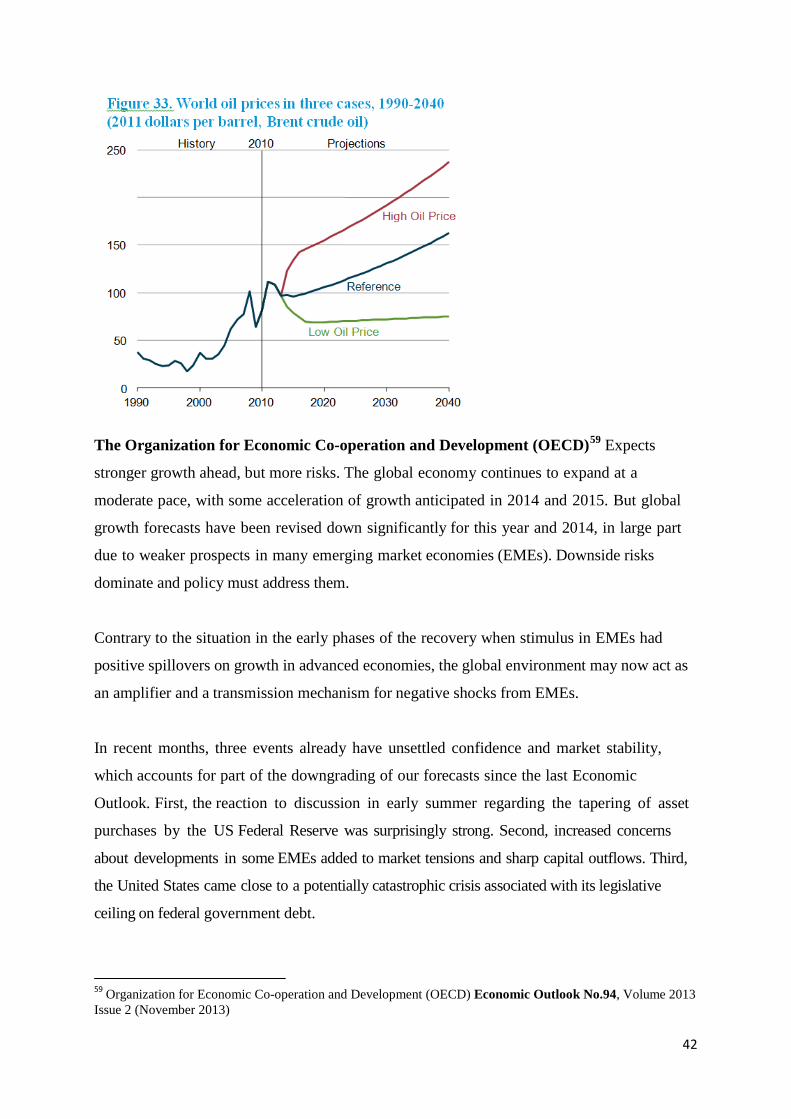

IEO2013 also presents High and Low Oil Price cases as alternatives to the Reference

case. The price cases were developed by adjusting four key factors: (1) the economics of

non-OPEC petroleum liquids supply; (2) OPEC investment and production decisions; (3) the

economics of other liquids supply; and (4) economic growth in non-OECD countries, a

key driver of petroleum and other liquids demand.

41

The Organization for Economic Co-operation and Development (OECD)59 Expects

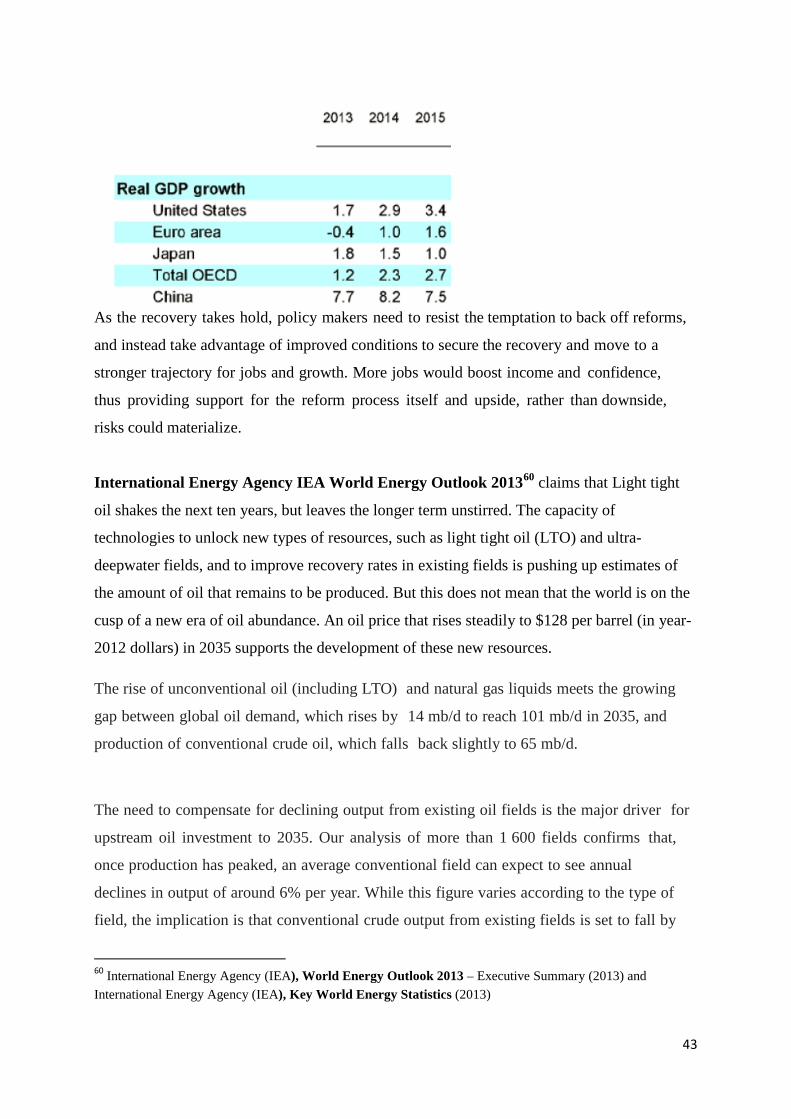

stronger growth ahead, but more risks. The global economy continues to expand at a

moderate pace, with some acceleration of growth anticipated in 2014 and 2015. But global

growth forecasts have been revised down significantly for this year and 2014, in large part

due to weaker prospects in many emerging market economies (EMEs). Downside risks

dominate and policy must address them.

Contrary to the situation in the early phases of the recovery when stimulus in EMEs had

positive spillovers on growth in advanced economies, the global environment may now act as

an amplifier and a transmission mechanism for negative shocks from EMEs.

In recent months, three events already have unsettled confidence and market stability,

which accounts for part of the downgrading of our forecasts since the last Economic

Outlook. First, the reaction to discussion in early summer regarding the tapering of asset

purchases by the US Federal Reserve was surprisingly strong. Second, increased concerns

about developments in some EMEs added to market tensions and sharp capital outflows. Third,

the United States came close to a potentially catastrophic crisis associated with its legislative

ceiling on federal government debt.

59 Organization for Economic Co-operation and Development (OECD) Economic Outlook No.94, Volume 2013 Issue 2 (November 2013)

42

As the recovery takes hold, policy makers need to resist the temptation to back off reforms,

and instead take advantage of improved conditions to secure the recovery and move to a

stronger trajectory for jobs and growth. More jobs would boost income and confidence,

thus providing support for the reform process itself and upside, rather than downside,

risks could materialize.

International Energy Agency IEA World Energy Outlook 201360 claims that Light tight

oil shakes the next ten years, but leaves the longer term unstirred. The capacity of

technologies to unlock new types of resources, such as light tight oil (LTO) and ultra-

deepwater fields, and to improve recovery rates in existing fields is pushing up estimates of

the amount of oil that remains to be produced. But this does not mean that the world is on the

cusp of a new era of oil abundance. An oil price that rises steadily to $128 per barrel (in year-

2012 dollars) in 2035 supports the development of these new resources.

The rise of unconventional oil (including LTO) and natural gas liquids meets the growing

gap between global oil demand, which rises by 14 mb/d to reach 101 mb/d in 2035, and

production of conventional crude oil, which falls back slightly to 65 mb/d.

The need to compensate for declining output from existing oil fields is the major driver for

upstream oil investment to 2035. Our analysis of more than 1 600 fields confirms that,

once production has peaked, an average conventional field can expect to see annual

declines in output of around 6% per year. While this figure varies according to the type of

field, the implication is that conventional crude output from existing fields is set to fall by

60 International Energy Agency (IEA), World Energy Outlook 2013 – Executive Summary (2013) and International Energy Agency (IEA), Key World Energy Statistics (2013)

43

more than 40 mb/d by 2035. Among the other sources of oil, most unconventional plays

are heavily dependent on continuous drilling to prevent rapid field-level declines. Of the

790 billion barrels of total production required to meet our projections for demand to

2035, more than half is needed just to offset declining production.

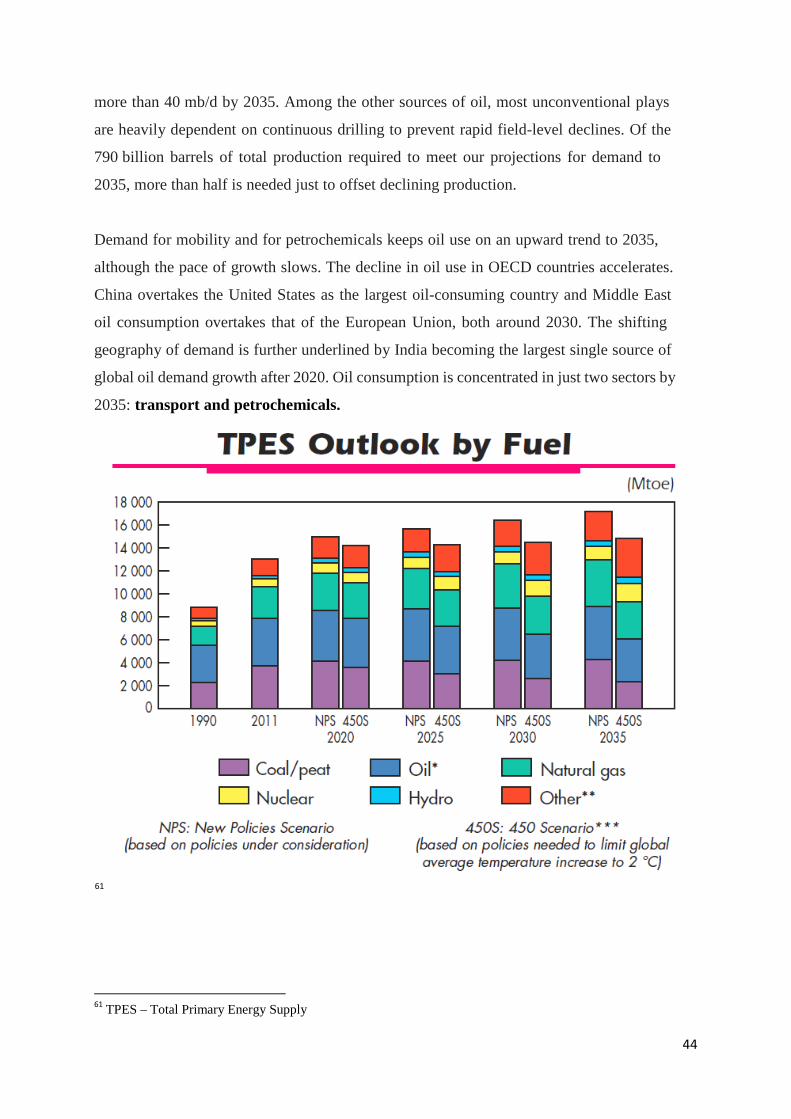

Demand for mobility and for petrochemicals keeps oil use on an upward trend to 2035,

although the pace of growth slows. The decline in oil use in OECD countries accelerates.

China overtakes the United States as the largest oil-consuming country and Middle East

oil consumption overtakes that of the European Union, both around 2030. The shifting

geography of demand is further underlined by India becoming the largest single source of

global oil demand growth after 2020. Oil consumption is concentrated in just two sectors by

2035: transport and petrochemicals.

61

61 TPES – Total Primary Energy Supply

44

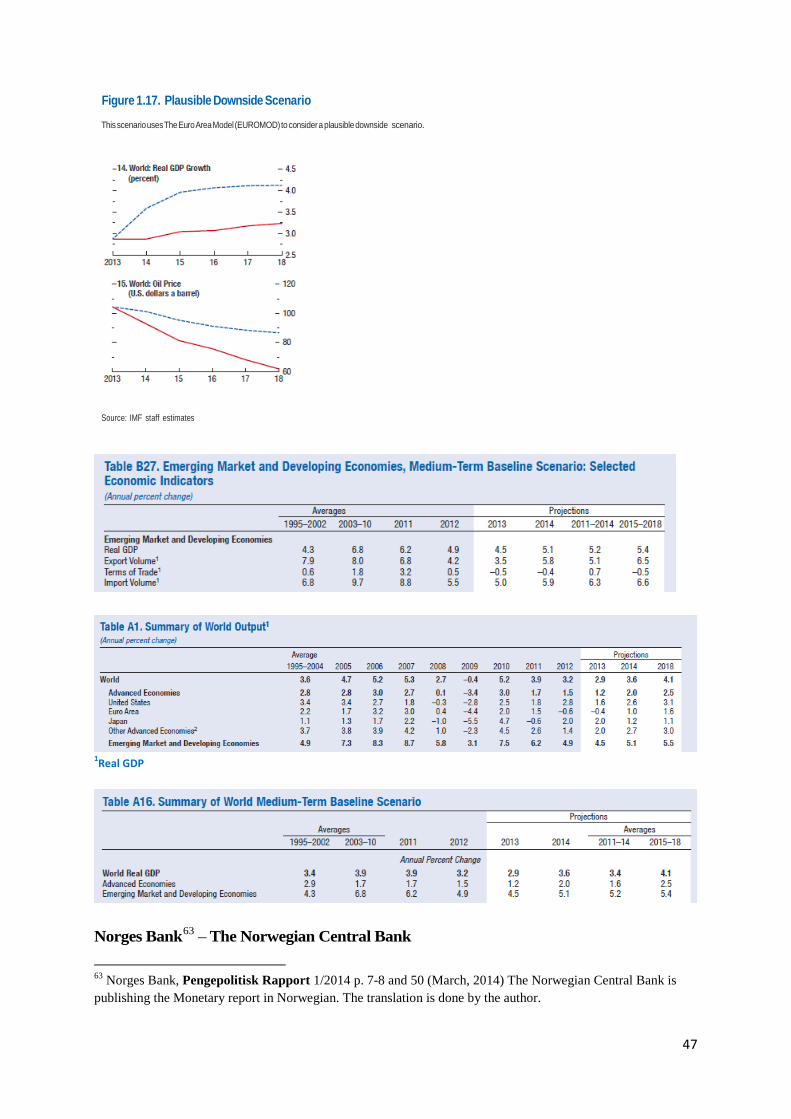

International Monetary Fund (IMF) 62 The global activity strengthened during the second

half of 2013, as anticipated in the October 2013 World Economic Outlook (WEO). Activity is

expected to improve further in 2014–15, largely on account of recovery in the advanced

economies. Global growth is now projected to be slightly higher in 2014, at around 3.7

percent, rising to 3.9 percent in 2015, a broadly unchanged outlook from the October 2013

WEO. But downward revisions to growth forecasts in some economies highlight continued

fragilities, and downside risks remain. In advanced economies, output gaps generally remain

large and, given the risks, the monetary policy stance should stay accommodative while fiscal

consolidation continues. In many emerging market and developing economies, stronger

external demand from advanced economies will lift growth, although domestic weaknesses

remain a concern. Some economies may have room for monetary policy support. In many

others, output is close to potential, suggesting that growth declines partly reflect structural

factors or a cyclical cooling and that the main policy approach for raising growth must be to

push ahead with structural reform. In some economies, there is a need to manage

vulnerabilities associated with weakening credit quality and larger capital outflows.

Risks to activity associated with very low inflation in advanced economies, especially

the euro area, have come to the fore. With inflation likely to remain below target for

some time, longer-term inflation expectations might drift down. This raises the risks of

lower-than-expected inflation, which increases real debt burdens, and of premature real

interest rate increases, as monetary policy is constrained in lowering nominal interest

rates. It also raises the likelihood of deflation in the event of adverse shocks to activity.

In emerging market economies, increased financial market and capital flow volatility remain

a concern given that the Fed will start tapering in early 2014.Portfolio shifts and some capital

outflows are likely with Fed tapering. When combined with domestic weaknesses, the result

could be sharper capital outflows and exchange rate adjustments.

In advanced economies, it will be critical to avoid a premature withdrawal of monetary policy

accommodation, including in the United States, as output gaps are still large while inflation is

low and fiscal consolidation continues. Stronger growth is needed to complete balance sheet

1.1.1 62 International Monetary Fund (IMF), World Economic Outlook (October 2013) p. xv, 12, 17, 42, 153 & 180 and International Monetary Fund (IMF), World Economic Outlook - Update (January 21, 2014)

45

repair after the crisis and to lower related legacy risks.

European Central Bank (ECB) will need to consider additional measures, such as longer-

term liquidity provision, including targeted lending, would strengthen demand and reduce

financial market fragmentation. Repairing bank balance sheets through the Balance Sheet

Assessment exercise and recapitalizing weak banks and completing the Banking Union.

In emerging market and developing economies, recent developments highlight the need

to manage the risks of potential capital flow reversals. Economies with domestic

weaknesses and partly related external current account deficits appear particularly exposed.