document of the world bank · document of the world bank. ... (exchange rate effective april 30,...

TRANSCRIPT

Document of The World Bank

Report No: ICR00003137

IMPLEMENTATION COMPLETION AND RESULTS REPORT (IBRD-75650 IDA-44630 IDA-44640)

ON A

LOAN

IN THE AMOUNT OF US$ 135.85 MILLION AND

CREDITS

IN THE AMOUNT OF SDR 9.5 and 25.6 MILLION (US$ 58.95 MILLION EQUIVALENT)

TO THE

ISLAMIC REPUBLIC OF PAKISTAN

FOR AN

ELECTRICITY DISTRIBUTION AND TRANSMISSION IMPROVEMENT PROJECT

September 23, 2014

Energy & Extractives Global Practice South Asia Region

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

ii

CURRENCY EQUIVALENTS (Exchange Rate Effective April 30, 2014)

Currency Unit = Pakistan Rupees (PKR)

PKR 1.00 = US$ 0.01 US$ 1.00 = PKR 100

FISCAL YEAR July 1 – June 30

ABBREVIATIONS AND ACRONYMS

ABC Aerial Bundled Conductor ADB Asian Development Bank APL Adaptable Program Loan BER Bid Evaluation Report BOD Board of Directors CCP Competition Commission of Pakistan CPPA Central Power Purchasing Agency CPS Country Partnership Strategy DISCOs Distribution Companies DLI Disbursement Linked Indicator DM Distribution Margin DPC Development Policy Credit DSCR Debt Service Coverage Ratio DTrs Distribution Transformers EDTIP Electricity Distribution And Transmission Improvement Project ELR Energy Loss Reduction EPAs Environmental Protection Agencies ERP Enterprise Resource Planning ERR Economic Rate of Return ESA Environmental and Social Assessment ESMP Environmental and Social Management Plan FRR Financial Rate of Return FY Fiscal Year GDP Gross Domestic Product GIS Gas Insulated Substation GOP Government of Pakistan GWh Gigawatt hours HESCO Hyderabad Electric Supply Company IBRD International Bank for Reconstruction and Development ICB International Competitive Bidding ICR Implementation Completion and Results Report IDA International Development Association IEC International Electro-technical Commission IEs Implementing Entities IESCO Islamabad Electric Supply Company Limited IP Implementation Progress IPA International Procurement Advisor IPP Independent Power Producers IPR Independent Procurement Review

iii

IRR Internal Rate of Return ISR Implementation Status Report JICA Km

Japan International Cooperation Agency Kilometre

kV Kilo Volt kWh Kilowatt Hour LERB Lowest Evaluated Responsive Bidder LESCO Lahore Electric Supply Company M MEPCO

Million Multan Electric Power Company

MOWP Ministry of Water and Power MTR Mid Term Review MW Megawatt NCB National Competitive Bidding NEPRA National Electric Power Regulatory Authority NPV Net Present Value NTDC National Transmission and Despatch Company O&M Operations and Maintenance OLTC On Load Tap Changer PAD Project Appraisal Document PAP Procurement Action Plan PCD Project Closing Date of February 28, 2014 PD Project Director PDO Project Development Objective PEPCO Pakistan Electric Power Company PKR Pakistan Rupee PPAs Power Purchase Agreements PTrs Power Transformers QPR Quarterly Progress Report RAP Resettlement Action Plan SDR Special Drawing Right SECP Securities & Exchange Commission of Pakistan ST Secondary Transmission STG Secondary Transmission and Grid T&D Transmission and Distribution TA Technical Assistance TDS Tariff Differential Subsidies USAID United States Agency for International Development USD United States Dollars WAPDA Water and Power Development Authority

Vice President: Philippe H. Le Houerou

Country Director: Rachid Benmessaoud Senior Director: Anita Marangoly George

Practice Director: Charles Feinstein Practice Manager: Julia Bucknall

Project Team Leader: Mohammad Saqib ICR Team Leader: Mohammad Saqib

iv

PAKISTAN Electricity Distribution and Transmission Improvement Project

CONTENTS

Data Sheet A. Basic Information B. Key Dates C. Ratings Summary D. Sector and Theme Codes E. Bank Staff F. Results Framework Analysis G. Ratings of Project Performance in ISRs H. Restructuring I. Disbursement Graph

1. Project Context, Development Objectives and Design ............................................... 1 2. Key Factors Affecting Implementation and Outcomes .............................................. 4 3. Assessment of Outcomes .......................................................................................... 15 4. Assessment of Risk to Development Outcome ......................................................... 22 5. Assessment of Bank and Borrower Performance ..................................................... 22 6. Lessons Learned ....................................................................................................... 27 7. Comments on Issues Raised by Borrower/Implementing Agencies/Partners .......... 30 Annex 1. Project Costs and Financing .......................................................................... 31 Annex 2. Outputs by Component ................................................................................. 32 Annex 3. Economic and Financial Analysis ................................................................. 38 Annex 4. Bank Lending and Implementation Support/Supervision Processes ............ 46 Annex 5. Beneficiary Survey Results ........................................................................... 48 Annex 6. Stakeholder Workshop Report and Results ................................................... 49 Annex 7. Summary of Borrower's ICR and/or Comments on Draft ICR ..................... 50 Annex 8. Comments of Cofinanciers and Other Partners/Stakeholders ....................... 54 Annex 9. List of Supporting Documents ...................................................................... 55 Annex 10. Review of procurment and technical aspects ............................................. 56 Map of Pakistan ........................................................................................................... 60

v

A. Basic Information

Country: Pakistan Project Name: Electricity Distribution and Transmission Improvement Project

Project ID: P095982 L/C/TF Number(s): IBRD-75650,IDA-44630,IDA-44640

ICR Date: 09/22/2014 ICR Type: Core ICR

Lending Instrument: APL Borrower: GOVERNMENT OF PAKISTAN

Original Total Commitment:

USD 256.70M Disbursed Amount: USD 141.82M

Revised Amount: USD 194.80M Environmental Category: B Implementing Agencies: Islamabad Electric Supply Company (IESCO) Lahore Electric Supply Company (LESCO) Multan Electric Power Company (MEPCO) National Transmission and Despatch Company (NTDC) Pakistan Electric Power Company (PEPCO) Hyderabad Electric Supply Company (HESCO) Cofinanciers and Other External Partners: B. Key Dates

Process Date Process Original Date Revised / Actual Date(s)

Concept Review: 09/01/2005 Effectiveness: 12/05/2008 12/05/2008

Appraisal: 08/27/2007 Restructuring(s): 10/05/2012 02/28/2014

Approval: 06/17/2008 Mid-term Review: 12/31/2010 04/30/2011 Closing: 06/30/2012 02/28/2014 C. Ratings Summary C.1 Performance Rating by ICR Outcomes: Moderately Unsatisfactory Risk to Development Outcome: Substantial Bank Performance: Unsatisfactory Borrower Performance: Unsatisfactory

vi

C.2 Detailed Ratings of Bank and Borrower Performance (by ICR) Bank Ratings Borrower Ratings

Quality at Entry: Unsatisfactory Government: Unsatisfactory

Quality of Supervision: Unsatisfactory Implementing Agency/Agencies: Unsatisfactory

Overall Bank Performance: Unsatisfactory Overall Borrower

Performance: Unsatisfactory

C.3 Quality at Entry and Implementation Performance Indicators

Implementation Performance Indicators QAG Assessments

(if any) Rating

Potential Problem Project at any time (Yes/No):

Yes Quality at Entry (QEA):

None

Problem Project at any time (Yes/No):

Yes Quality of Supervision (QSA):

None

DO rating before Closing/Inactive status:

Moderately Unsatisfactory

D. Sector and Theme Codes

Original Actual Sector Code (as % of total Bank financing) Central government administration 2 2 Energy efficiency in Heat and Power 6 6 Transmission and Distribution of Electricity 92 92

Theme Code (as % of total Bank financing) Infrastructure services for private sector development 100 100 E. Bank Staff

Positions At ICR At Approval Vice President: Philippe H. Le Houerou Praful C. Patel Country Director: Rachid Benmessaoud Yusupha B. Crookes Practice Manager/Manager:

Julia Bucknall Salman Zaheer

Project Team Leader: Mohammad Saqib Vladislav Vucetic / Rashid Aziz ICR Team Leader: Mohammad Saqib ICR Primary Author: Mohammad Saqib Abdul Rahim Khan

vii

F. Results Framework Analysis Project Development Objectives (from Project Appraisal Document) The objectives of the APL1 project are to: (i) strengthen the capacity of the distribution and transmission networks to meet increasing electricity demand in the selected areas more efficiently and with better reliability and quality; and (ii) strengthen institutional capacity of the selected distribution companies and support other priority areas of the power sector reform. Revised Project Development Objectives (as approved by original approving authority) PDOs remained the same. (a) PDO Indicator(s)

Indicator Baseline Value

Original Target Values (from

approval documents)

Formally Revised Target Values

Actual Value Achieved at

Completion or Target Years

Indicator 1 : NTDC - Loading on Yousufwala Grid Station, percentage Value quantitative or Qualitative)

98 77 77 100

Date achieved 06/30/2007 06/30/2012 06/30/2013 02/28/2014 Comments (incl. % achievement)

Target was not met because Kassowal grid station (financed under the project) could not be completed by the project closing date. Loading will reduce after the commissioning of the Kassowal grid station.

Indicator 2 : NTDC - Loading on Vehari Grid Station, percentage Value quantitative or Qualitative)

92 74 74 100

Date achieved 06/30/2007 06/30/2012 06/30/2013 02/28/2014 Comments (incl. % achievement)

Grid station was changed from Piranghaib to Vehari through amendment to the legal documents. Baseline and target values remained the same. Target was not met because Kassowal grid station could not be completed by the PCD.

Indicator 3 : IESCO - Electricity Handled by the Network - Gigawatt-hours per year Value quantitative or Qualitative)

7,065 11,640 8,784 8,830

Date achieved 06/30/2007 06/30/2012 06/30/2013 02/28/2014 Comments (incl. % achievement)

The revised reduced target was met with a delay because in FY2013 corresponding to the target period only 8,561 GWh were procured.

Indicator 4 : IESCO - Annual T&D Losses, percentage Value quantitative or Qualitative)

12.2 11.4 9.55 8.6

Date achieved 06/30/2007 06/30/2012 06/30/2013 02/28/2014 Comments IESCO successfully met the original and revised target. 9.4% T&D losses for

viii

(incl. % achievement)

FY2013 were also less than the target.

Indicator 5 : IESCO - Collection as percentage of billing Value quantitative or Qualitative)

98.1 98.6 95.9 90.0

Date achieved 06/30/2007 06/30/2012 06/30/2013 02/28/2014

Comments (incl. % achievement)

Target was not achieved. Collection in FY13 was 94.4% and declined further mainly because of non-payment by public sector consumers; collection from private consumers was almost 100%. Indicator, however, is not related to the project intervention.

Indicator 6 : IESCO - TA: Completion of local and foreign training (cumulative total is in parenthesis)

Value quantitative or Qualitative)

20 186 120 272 (936)

Date achieved 06/30/2007 06/30/2012 06/30/2013 06/30/2013 Comments (incl. % achievement)

The figures present number of participants of various training courses during the year. The target was met on a cumulative basis as about 936 staff attended these courses between June 30, 2007 and June 30, 2013.

Indicator 7 : HESCO - Electricity handled by the network - Gigawatt-hours per year Value quantitative or Qualitative)

7,681 9,807 9,683 9,356

Date achieved 06/30/2007 06/30/2012 06/30/2013 06/30/2013

Comments (incl. % achievement)

Even the revised reduced target was not achieved because of the prevailing supply shortfall. Data for last 12 months before project closing was not provided. In FY2014, about 9,420 GWh were procured which was also less than the FY2013 target.

Indicator 8 : HESCO - Annual T&D Losses, percentage Value quantitative or Qualitative)

36.9 29.4 32.2 33.2

Date achieved 06/30/2007 06/30/2012 06/30/2013 06/30/2013 Comments (incl. % achievement)

There is some reduction in losses but neither the revised nor the actual target was met. In FY2014, losses declined to 32.2% but were still quite high than the NEPRA target of 24.9%.

Indicator 9 : HESCO - Collection as percentage of billing Value quantitative or Qualitative)

86 90 73.5 67.6

Date achieved 06/30/2007 06/30/2012 06/30/2013 06/30/2013 Comments (incl. % achievement)

Collection rate has deteriorated quite sharply in HESCO and even the revised target which was set significantly below the baseline was not met.

Indicator 10 : HESCO - TA: Completion of local and foreign training (cumulative total is in parenthesis)

Value 20 148 148 3 (320)

ix

quantitative or Qualitative) Date achieved 06/30/2007 06/30/2012 06/30/2013 06/30/2013 Comments (incl. % achievement)

The figures present number of participants of various training courses during the year. The target was met on a cumulative basis as about 320 staff attended these courses between June 30, 2007 and June 30, 2013.

Indicator 11 : LESCO - Electricity handled by the network - Gigawatt-hours per year Value quantitative or Qualitative)

15,999 22,153 18,126 16,458

Date achieved 06/30/2007 06/30/2012 06/30/2013 06/30/2013 Comments (incl. % achievement)

LESCO did not provide last 12 months data and therefore FY2013 figures are presented. Even the target which was revised downwards could not be achieved mainly because of the prevailing supply shortfall in the country.

Indicator 12 : LESCO - Annual T&D Losses, percentage Value quantitative or Qualitative)

12.8 11.7 12.1 13.2

Date achieved 06/30/2007 06/30/2012 06/30/2013 06/30/2013 Comments (incl. % achievement)

T&D losses in LESCO have increased compared to the baseline. The target was revised upwards but even that could not be met.

Indicator 13 : LESCO - Collection as percentage of billing Value quantitative or Qualitative)

99 99 97.5 97.9

Date achieved 06/30/2007 06/30/2012 06/30/2013 06/30/2013 Comments (incl. % achievement)

Met the revised target but performance has declined from base year. This indicator, however, is not directly related to project intervention.

Indicator 14 : LESCO - TA: Completion of local and foreign training (cumulative total is in parenthesis)

Value quantitative or Qualitative)

55 77 440 0 (667)

Date achieved 06/30/2007 06/30/2012 06/30/2013 06/30/2013 Comments (incl. % achievement)

The figures present number of participants of various training courses during the year. The target was met on a cumulative basis as about 667 trainees attended these courses between June 30, 2007 and June 30, 2013.

Indicator 15 : MEPCO - Electricity handled by the network - Gigawatt-hours per year Value quantitative or Qualitative)

11,767 14,398 12,830 13,274

Date achieved 06/30/2007 06/30/2012 06/30/2013 02/28/2014 Comments (incl. % achievement)

The revised reduced target was met by the project closing date but with a delay because in FY2013 corresponding to the target period only 11,951 GWh were procured compared to a revised target of 12,830 GWh.

Indicator 16 : MEPCO - Annual T&D Losses, percentage

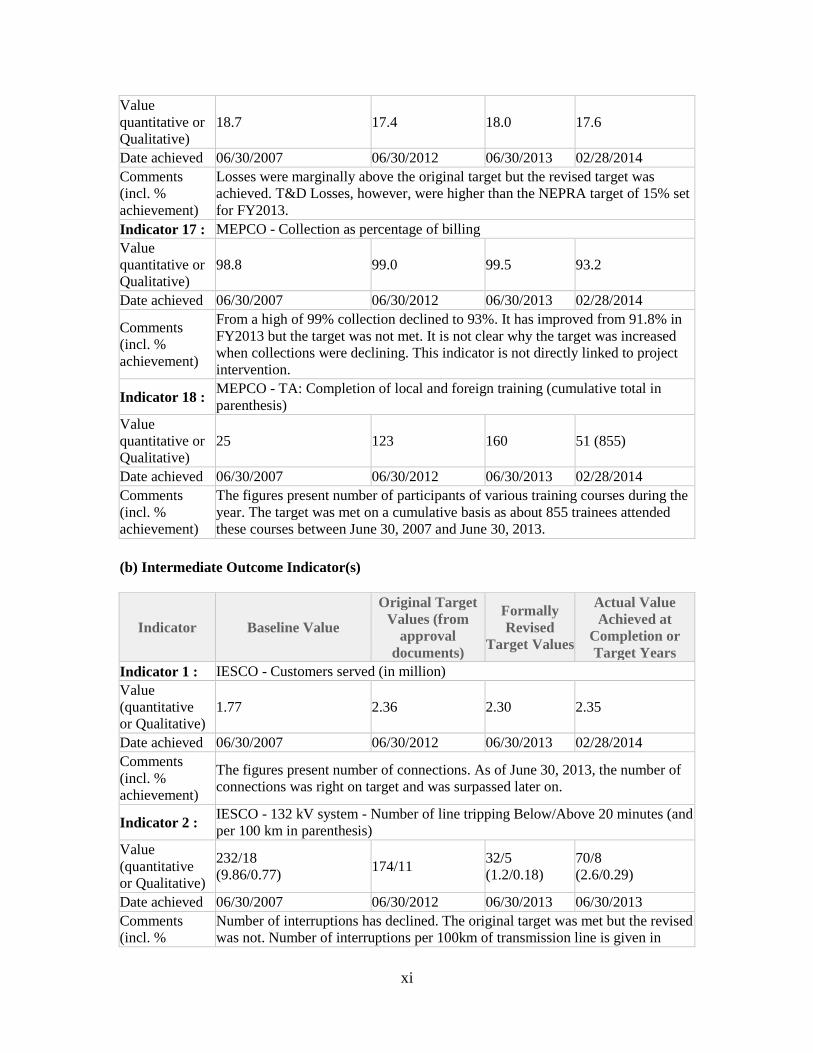

x

Value quantitative or Qualitative)

18.7 17.4 18.0 17.6

Date achieved 06/30/2007 06/30/2012 06/30/2013 02/28/2014 Comments (incl. % achievement)

Losses were marginally above the original target but the revised target was achieved. T&D Losses, however, were higher than the NEPRA target of 15% set for FY2013.

Indicator 17 : MEPCO - Collection as percentage of billing Value quantitative or Qualitative)

98.8 99.0 99.5 93.2

Date achieved 06/30/2007 06/30/2012 06/30/2013 02/28/2014

Comments (incl. % achievement)

From a high of 99% collection declined to 93%. It has improved from 91.8% in FY2013 but the target was not met. It is not clear why the target was increased when collections were declining. This indicator is not directly linked to project intervention.

Indicator 18 : MEPCO - TA: Completion of local and foreign training (cumulative total in parenthesis)

Value quantitative or Qualitative)

25 123 160 51 (855)

Date achieved 06/30/2007 06/30/2012 06/30/2013 02/28/2014 Comments (incl. % achievement)

The figures present number of participants of various training courses during the year. The target was met on a cumulative basis as about 855 trainees attended these courses between June 30, 2007 and June 30, 2013.

(b) Intermediate Outcome Indicator(s)

Indicator Baseline Value

Original Target Values (from

approval documents)

Formally Revised

Target Values

Actual Value Achieved at

Completion or Target Years

Indicator 1 : IESCO - Customers served (in million) Value (quantitative or Qualitative)

1.77 2.36 2.30 2.35

Date achieved 06/30/2007 06/30/2012 06/30/2013 02/28/2014 Comments (incl. % achievement)

The figures present number of connections. As of June 30, 2013, the number of connections was right on target and was surpassed later on.

Indicator 2 : IESCO - 132 kV system - Number of line tripping Below/Above 20 minutes (and per 100 km in parenthesis)

Value (quantitative or Qualitative)

232/18 (9.86/0.77) 174/11 32/5

(1.2/0.18) 70/8 (2.6/0.29)

Date achieved 06/30/2007 06/30/2012 06/30/2013 06/30/2013 Comments (incl. %

Number of interruptions has declined. The original target was met but the revised was not. Number of interruptions per 100km of transmission line is given in

xi

achievement) parenthesis for comparison over time and across companies.

Indicator 3 : IESCO - Average Voltage condition for 132 kV System (Max/Min in parenthesis)

Value (quantitative or Qualitative)

130.5 132 133.8 (137.8/129.8) 132.4 (137.5/127.4)

Date achieved 06/30/2007 06/30/2012 06/30/2013 06/30/2013 Comments (incl. % achievement)

The average is close to 132kV and therefore the target was met. Max and Min values are given in parenthesis to show the fluctuation which are also within the revised target limits.

Indicator 4 : IESCO - Cost not covered from consumer revenues, PKR Million Value (quantitative or Qualitative)

881 4,068 6,969 34,207

Date achieved 06/30/2007 06/30/2012 06/30/2013 06/30/2013 Comments (incl. % achievement)

Tariff differential subsidy (TDS) billed is used to measure cost not recovered from consumer revenue. TDS exceeded the target mainly because of rise in power purchase cost and not passing on the burden to end consumers.

Indicator 5 : IESCO - Training plan and effectiveness

Value (quantitative or Qualitative)

No plan Report of the effectiveness of training completed

Report of the effectiveness of training completed

Effectiveness of training is included in the client's completion report.

Date achieved 06/30/2007 06/30/2012 06/30/2013 02/28/2014 Comments (incl. % achievement)

Foreign and local training were held at good reputable institutes for a large number of staff. Training covered technical, financial management, project management, procurement and other relevant subjects.

Indicator 6 : HESCO - Customers served (in million) Value (quantitative or Qualitative)

1.41 1.80 1.61 1.61

Date achieved 06/30/2007 06/30/2012 06/30/2013 06/30/2013 Comments (incl. % achievement)

The figures present number of connections as of the given date. The target was revised downwards and was achieved by June 30, 2013.

Indicator 7 : HESCO - 132 kV system - Number of line tripping Below/Above 20 minutes (and per 100 km in parenthesis)

Value (quantitative or Qualitative)

132/352 (3.621/9.655)

78/208 (not available)

64/103 (1.2/0.18)

91/400 (2.38/10.46)

Date achieved 06/30/2007 06/30/2012 06/30/2013 06/30/2013 Comments (incl. % achievement)

Neither the original nor the revised target was met. Number of interruptions above 20 minutes has increased compared to baseline. Data per 100km is given in parenthesis for comparison over time and across companies.

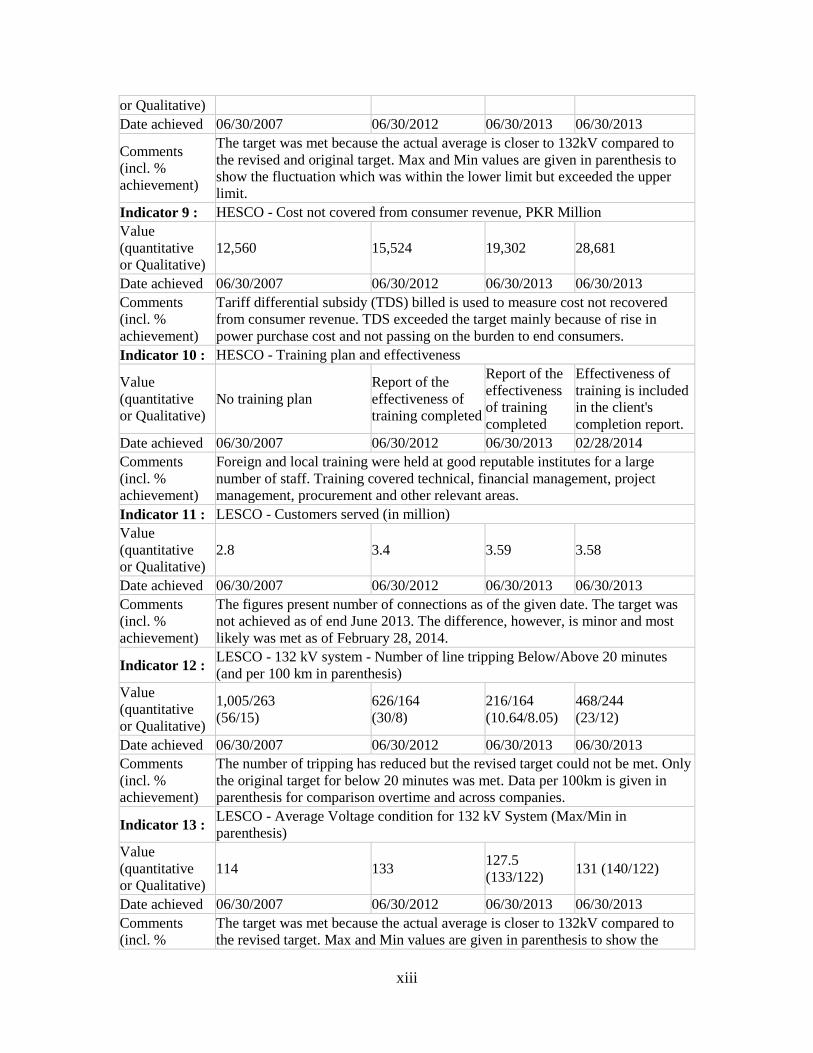

Indicator 8 : HESCO - Average Voltage condition for 132 kV System (Max/Min in parenthesis)

Value (quantitative 100 117 117 (141/93) 120.5 (144/97)

xii

or Qualitative) Date achieved 06/30/2007 06/30/2012 06/30/2013 06/30/2013

Comments (incl. % achievement)

The target was met because the actual average is closer to 132kV compared to the revised and original target. Max and Min values are given in parenthesis to show the fluctuation which was within the lower limit but exceeded the upper limit.

Indicator 9 : HESCO - Cost not covered from consumer revenue, PKR Million Value (quantitative or Qualitative)

12,560 15,524 19,302 28,681

Date achieved 06/30/2007 06/30/2012 06/30/2013 06/30/2013 Comments (incl. % achievement)

Tariff differential subsidy (TDS) billed is used to measure cost not recovered from consumer revenue. TDS exceeded the target mainly because of rise in power purchase cost and not passing on the burden to end consumers.

Indicator 10 : HESCO - Training plan and effectiveness

Value (quantitative or Qualitative)

No training plan Report of the effectiveness of training completed

Report of the effectiveness of training completed

Effectiveness of training is included in the client's completion report.

Date achieved 06/30/2007 06/30/2012 06/30/2013 02/28/2014 Comments (incl. % achievement)

Foreign and local training were held at good reputable institutes for a large number of staff. Training covered technical, financial management, project management, procurement and other relevant areas.

Indicator 11 : LESCO - Customers served (in million) Value (quantitative or Qualitative)

2.8 3.4 3.59 3.58

Date achieved 06/30/2007 06/30/2012 06/30/2013 06/30/2013 Comments (incl. % achievement)

The figures present number of connections as of the given date. The target was not achieved as of end June 2013. The difference, however, is minor and most likely was met as of February 28, 2014.

Indicator 12 : LESCO - 132 kV system - Number of line tripping Below/Above 20 minutes (and per 100 km in parenthesis)

Value (quantitative or Qualitative)

1,005/263 (56/15)

626/164 (30/8)

216/164 (10.64/8.05)

468/244 (23/12)

Date achieved 06/30/2007 06/30/2012 06/30/2013 06/30/2013 Comments (incl. % achievement)

The number of tripping has reduced but the revised target could not be met. Only the original target for below 20 minutes was met. Data per 100km is given in parenthesis for comparison overtime and across companies.

Indicator 13 : LESCO - Average Voltage condition for 132 kV System (Max/Min in parenthesis)

Value (quantitative or Qualitative)

114 133 127.5 (133/122) 131 (140/122)

Date achieved 06/30/2007 06/30/2012 06/30/2013 06/30/2013 Comments (incl. %

The target was met because the actual average is closer to 132kV compared to the revised target. Max and Min values are given in parenthesis to show the

xiii

achievement) fluctuation which was within the lower limit but exceeded the upper revised limit.

Indicator 14 : LESCO - Cost not covered from consumer revenues, PKR Million Value (quantitative or Qualitative)

4,416 5,507 14,177 19,786

Date achieved 06/30/2007 06/30/2012 06/30/2013 06/30/2013 Comments (incl. % achievement)

Tariff differential subsidy (TDS) billed is used to measure cost not recovered from consumer revenue. TDS exceeds the target mainly because of rise in power purchase cost and not passing on the burden to end consumers.

Indicator 15 : LESCO - Training plan and effectiveness

Value (quantitative or Qualitative)

No training plan Report of the effectiveness of training completed

Report of the effectiveness of training completed

Effectiveness of training is included in the client's completion report.

Date achieved 06/30/2007 06/30/2012 06/30/2013 02/28/2014 Comments (incl. % achievement)

Foreign and local training were held at good reputable institutes for a large number of staff. Training covered technical, financial management, project management, procurement and other relevant areas.

Indicator 16 : MEPCO - Customers served (in million) Value (quantitative or Qualitative)

3.37 4.68 4.60 4.67

Date achieved 06/30/2007 06/30/2012 06/30/2013 06/30/2013 Comments (incl. % achievement)

The figures present number of connections as of the given date. The revised target was achieved.

Indicator 17 : MEPCO - 132 kV system - Number of line tripping Below/Above 20 minutes (and per 100 km in parenthesis)

Value (quantitative or Qualitative)

87/123 (2.97/4.2) 73/102 49/94

(1.64/3.14) 133/171 (4.44/5.73)

Date achieved 06/30/2007 06/30/2012 06/30/2013 06/30/2013

Comments (incl. % achievement)

Neither the original nor the revised target was met. Compared to baseline, number of interruptions both for above and below 20 minutes has increased. Data per 100km is given in parenthesis for comparison over time and across companies.

Indicator 18 : MEPCO - Average Voltage condition for 132 kV System (Max/Min in parenthesis)

Value (quantitative or Qualitative)

124 132.5 126 (138/114) 126 (138/114)

Date achieved 06/30/2007 06/30/2012 06/30/2013 06/30/2013 Comments (incl. % achievement)

Revised target was met but there is only marginal improvement compared to baseline.

Indicator 19 : MEPCO - Cost not covered from consumer revenue, PKR Million Value 6,280 5,983 34,952 31,780

xiv

(quantitative or Qualitative) Date achieved 06/30/2007 06/30/2012 06/30/2013 06/30/2013

Comments (incl. % achievement)

TDS billed is used to measure cost not recovered from consumer revenue. The revised target has been met but compared to baseline TDS increased by manifolds mainly because of rise in power purchase cost and not passing on the burden to end consumers.

Indicator 20 : MEPCO - Training plan and effectiveness

Value (quantitative or Qualitative)

No training plan

Report of the effectiveness of training completed.

Report of the effectiveness of training completed.

Effectiveness of training is included in the client's completion report.

Date achieved 06/30/2007 06/30/2012 06/30/2013 02/28/2014 Comments (incl. % achievement)

Foreign and local training were held at good reputable institutes for a large number of staff. Training covered technical, financial management, project management, procurement and other relevant areas.

G. Ratings of Project Performance in ISRs

No. Date ISR Archived DO IP

Actual Disbursements (USD millions)

1 12/17/2008 Satisfactory Satisfactory 0.00 2 05/28/2009 Moderately Satisfactory Satisfactory 3.30 3 11/27/2009 Moderately Satisfactory Moderately Satisfactory 23.95 4 05/28/2010 Moderately Satisfactory Moderately Satisfactory 39.24 5 12/20/2010 Moderately Satisfactory Moderately Satisfactory 54.81

6 06/27/2011 Moderately Unsatisfactory Unsatisfactory 65.05

7 01/12/2012 Moderately Unsatisfactory Unsatisfactory 85.85

8 07/11/2012 Moderately Satisfactory Moderately Satisfactory 96.72 9 01/27/2013 Moderately Satisfactory Moderately Satisfactory 114.03

10 06/18/2013 Moderately Unsatisfactory

Moderately Unsatisfactory 125.53

11 12/15/2013 Moderately Unsatisfactory Unsatisfactory 130.30

H. Restructuring (if any)

Restructuring Date(s)

Board Approved

PDO Change

ISR Ratings at Restructuring

Amount Disbursed at

Restructuring in USD millions

Reason for Restructuring & Key Changes Made DO IP

10/05/2012 MS MS 101.26 US$ 62 million were cancelled

xv

Restructuring Date(s)

Board Approved

PDO Change

ISR Ratings at Restructuring

Amount Disbursed at

Restructuring in USD millions

Reason for Restructuring & Key Changes Made DO IP

and contracts that were at final stage of award and could be completed within the extended time of 20 months were taken forward.

02/28/2014 MU U 134.09

US$ 2 million of unutilized IDA was cancelled so that the amount could be reallocated to the Pakistan program.

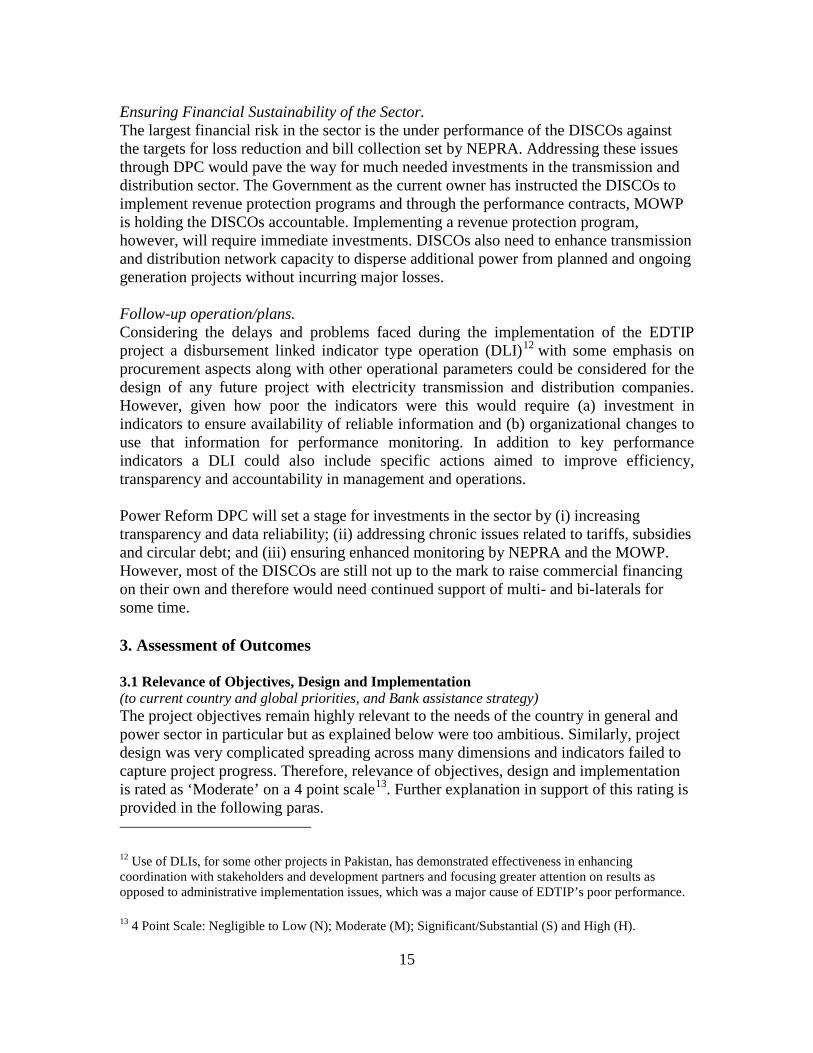

I. Disbursement Profile

xvi

1. Project Context, Development Objectives and Design (this section is descriptive, taken from other documents, e.g., PAD/ISR, not evaluative)

1.1 Context at Appraisal Country Background After a decade of political instability, macroeconomic crisis, and limited economic and social progress in the 1990s, Pakistan emerged as one of the fastest-growing economies in Asia, with rising per capita income and improved social indicators. Successive years of high growth (between FY04 and FY07 real GDP grew at more than 7% average) led to commensurate high growth in electricity demand. During FY08, when financial crisis hit world economies, Pakistan’s macro-economic performance deteriorated significantly with double digit inflation, widening fiscal deficit and falling GDP growth. Nevertheless, the electric utilities continued to experience a sharp increase in electricity demand. Sector Background At the time of appraisal, Pakistan power sector was in crisis because of stalled reforms, energy shortages and financial deficit. Electricity sales rose by 40% in the five years ending on June 30, 2007, period of high economic growth, while generation remained practically stagnant and the system was unable to cover 2,000MW of peak demand with acceptable reliability. With demand expected to grow at 7-8% per year in the medium-term, plans for capacity additions needed to be revised upward to eliminate shortages. The sector also needed significant fiscal support – approx. US$1.7 billion for FY08 (close to 20% of the projected operating revenues and 1% of GDP) – to cover the revenue deficit. Poor electricity service was identified as a major constraint to economic growth. Some of this deterioration in service was a result of Pakistan’s success at adding about one million new (mainly household) connections each year, without a commensurate expansion of generation capacity. Therefore, sector was in dire need of (a) substantial investment in new generation to secure supply of electricity, (b) strengthening of overloaded transmission and distribution system and improvements in energy efficiency, and (c) bringing sector into financial equilibrium through tariff and subsidy reforms. Power Sector Reforms The government’s strategy for the sector, built on the wide-ranging power sector reforms initiated in the early 1990s, aimed at improving sector performance and long term sustainability through institutional, regulatory, and structural reforms. As part of the reform, the Government opened up the sector to private investment, an independent National Electric Power Regulatory Agency (NEPRA) was established in 1998, and WAPDA Power Wing (a vertically integrated power sector utility) was unbundled into four generation, one transmission, and nine distribution companies. After a period of deteriorating financial performance in the late 1990s, the sector made some significant improvements, especially in terms of improved collections of bills. However, there was inadequate investment in low-cost base load generation capacity; from 2000-2008 there was almost no investment in generation and from 2009 to 2013 there was a net increase in capacity of just 3,000 MW. In addition, because of gas shortfall generation started to shift to expensive fuel oil; in FY05 gas accounted for 50% and in FY13 it was only 27%. As a result generation costs became significantly high and are difficult to control by the

1

DISCOs. The objectives of power sector reforms have not been fully achieved, as some important reform measures are yet to be implemented. Rationale for Bank Involvement Sustaining growth and improving competitiveness of the Pakistani economy was an important pillar of the Bank’s Country Partnership Strategy (CPS) FY06-09. Attaining this objective required significant investment in infrastructure, including power sector. The World Bank was engaged in policy advice and backed the power sector reform program through a series of budget-support operations. Improving electricity distribution and transmission services was considered a key element of the overall effort of reforming Pakistan’s power sector and strengthening its operating performance. The new companies established as a result of sector restructuring needed to invest in their physical networks to keep up with increasing demand, reduce losses, and improve services. They also needed to strengthen the capacity in various areas of corporate functions and establish a track record of performance and creditworthiness. Bank involvement in the project helped the companies finance important investments for which there were no alternative financiers. The Project was a first of a series of Adaptable Program Loan (APL). The indicative triggers for APL-2 were: (i) successful progress of APL-1; (ii) corporate autonomy of the DISCOs; and (iii) a fully functional wholesale market.

1.2 Original Project Development Objectives (PDO) and Key Indicators (as approved) The objectives were to: (i) strengthen the capacity of the distribution and transmission networks to meet increasing electricity demand in the selected areas more efficiently and with better reliability and quality; and (ii) strengthen institutional capacity of the selected distribution companies and support other priority areas of the power sector reform. The key performance indicators measured the effect of the project on the capacity of the distribution and transmission networks to deliver the amounts of electricity which consumers demand with improved reliability in terms of the overall annual electricity throughput and the total level of losses (which include both technical and commercial losses) to cover the efficiency aspect of the first objective. Selected intermediate indicators also measured increased access, reliability and quality of supply in terms of number of customers, interruptions and voltage conditions. The collection and number of trainings were used to measure entities financial performance and capacity building efforts and can be attributable to the second objective. While intermediate indicators related to decline in tariff differential subsidies could be linked to progress on reforms.

1.3 Revised PDO (as approved by original approving authority) and Key Indicators, and reasons/justification PDO and key indicators remained the same. However, at the time of restructuring in June 2012 target values were revised to reflect the reduced scope due to cancellation of about US$ 62 million (25% of the original loan amount). The component-wise break-up of cost before and after restructuring is given in Annex 1(a). Original and formally revised indicators are listed in the Data Sheet Section F.

2

1.4 Main Beneficiaries The immediate beneficiaries of the project were the national transmission and four distribution companies as the project would improve their revenues and profitability by reducing system losses, operation and maintenance costs, and the potential of accidents. The consumers in their service area would also benefit through safer, better and more reliable electric supply.

1.5 Original Components (as approved) The project included the following components:

A. physical strengthening of distribution networks (including sub transmission) operated by four distribution companies1;

B. removing some bottlenecks in the transmission grid, operated by NTDC2; C. technical assistance for capacity building, specialized studies, energy efficiency

and sector reform; and D. a pilot energy efficiency program, involving installation of energy saving

equipment at the customer level.

1.6 Revised Components Prior to original closing date the Project was restructured with the approval of the Regional Vice President to simplify the project design to focus on activities that were critical to the achievement of the PDO and could be completed within the extended time frame. As a result the following activities were dropped: (i) project activities under Part A, totaling an estimated US$ 38.28 million, that were not urgently required due to the recent power shortages caused by the lack of generation capacity; (ii) technical assistance activities under Part C, totaling an estimated US$ 8.72 million, that were being financed by other development partners, as well as those that were not ready for immediate financing; and (iii) all activities under Part D (Energy Efficiency Component), totaling an estimated US$ 15 million. In addition, US$ 4 million of the funds under the technical assistance component were reallocated to the Ministry of Water and Power (MOWP) from the four distribution companies to support the sector’s emerging urgent priorities, including power trade with neighboring countries. The Project was again restructured prior to the revised closing date to cancel the available IDA funds (about US$ 2 million) so that those can be reallocated to the Pakistan program.

1.7 Other significant changes (in design, scope and scale, implementation arrangements and schedule, and funding allocations) None

1 It included: (i) a 2 year time slice of the 5 year investment program in secondary transmission grid (STG) of the HESCO, IESCO, LESCO and MEPCO, (ii) a 2 year time slice of the investment in electricity loss reduction (ELR) program of IESCO, MEPCO and a pilot ELR program for HESCO.

2 A substation and transmission line for NTDC to relieve a bottleneck in serving MEPCO.

3

2. Key Factors Affecting Implementation and Outcomes

2.1 Project Preparation, Design and Quality at Entry (including whether lessons of earlier operations were taken into account, risks and their mitigations identified, and adequacy of participatory processes, as applicable)

The overall quality at entry is rated as Unsatisfactory. As discussed below this is based on little attention given to the corporate governance issues and risks were underestimated. In addition, some of the indictors were not directly correlated with this intervention and did not capture project development objectives. Intermediate indicators also failed to measure implementation progress3.

Soundness of Background Analysis.

The project was conceived as one of the investment components underpinning the government’s power sector reforms initiated by power sector restructuring. In addition to strengthening the newly formed entities the project also aimed at addressing broader power sector issues related to governance, regulatory and investments so that the power sector entities can function independently on pure commercial basis. However, these were not supported with a political economy study to provide relevant inputs into project design and to address critical risk factors. Therefore, technical assistance component for capacity building, specialized studies, energy efficiency and sector reforms could not be implemented in a manner envisaged.

At the time of Project inception and appraisal the country was experiencing a growing electricity demand driven by a respectable economic growth in the years 2004 to 2007. The four DISCOs selected for the EDTIP had experienced an average load growth in peak demand (during 2005, 2006 and 2007) of 7.7% for IESCO, 19.3% for LESCO. 12.8 % for MEPCO and 14.7% for HESCO. The peak demand in the overall system was expected to grow to 23,500 MW by 2012, requiring an addition of about 9,000 MW in additional effective generation capability by 2012. The peak demand was already exceeding effective generation capability in FY2006/074, therefore additions of at least 1,600 MW in generation capability were expected to be inducted every year between 2007 and 2017. Commensurate with such increase in peak demand and generation capability the transmission capacity had also to be increased at transmission level by NTDC and the sub-transmission level in DISCOs. Failure to provide such capacity additions would have resulted in forced outages, lower reliability and sub-standard quality of supply to the consumers, leading to an adverse impact on economic growth.

3 Please see Section 2.3 for detailed assessment of the key indicators.

4 During FY 2007 difference between Peak NTDC system demand and effective generation capability was1,846 MW. Source: NEPRA SOI Report 2009.

4

All DISCOs and NTDC had 5 year system expansion plans approved by the Planning Commission of the Government of Pakistan (GOP). The EDTIP project, however, covered only a small portion of the total investment needs of the transmission and distribution companies5. Initial discussions were held with all eight distribution companies but only four6 were selected based on the readiness of their projects, implementation capacity, need and government’s preferences. The selected entities were asked to prepare Project Description Documents focusing on two years of their investment program for possible Bank funding covering Secondary Transmission and Grid (STG) and Energy Loss Reduction (ELR) component which are at the core of the electricity distribution business. Individual project components were selected on the basis of technical and economic analysis of candidate projects in each entity. Several projects were also considered for APL-2. In parallel, some of the investment to implement the 5 year plans was expected from other sources, such as Asian Development Bank (ADB) or by IEs themselves.

Assessment of the project design.

NTDC was expected to cover most of its needs through other investment sources, so only a small unaddressed portion of capacity enhancement (220 kV Grid station at Kassowal and associated transmission line) in NTDC was included to address capacity restraint issues affecting delivery to MEPCO at 220 kV. A substantial portion of the project (more than 60 %) was designed to address the urgent need of DISCOs to satisfy the requirement of capacity enhancement at the sub-transmission level, for efficient delivery of service to consumers. The Project was thus appropriately designed to address the important and urgent need for investment in the transmission and distribution system. The design of the project, however, was overly complex covering both transmission and distribution with too many implementing entities and an energy efficiency pilot program. Therefore, project faced number of implementation challenges. Each of these components could have been a separate project prioritizing the development challenges of each company and appropriately addressing those.

After the unbundling, DISCOs were in the process of re-aligning their structures and processes to function as corporate entities. This is a major change management exercise and requires hand-holding support. Therefore, it would have been better to start with one or two utilities (one DISCO and NTDC), instead of 5 and help the entities develop a Business Plan and build their capacity. This would have helped prepare a robust project design and the project could have been expanded later with additional financing and bringing in more entities.

5 For example, in case of IESCO, the EDTIP STG and ELR component was about one-fourth of US$ 230 million, the total requirement for its five years approved development plan.

6 (1) Hyderabad Electric Supply Company– HESCO, (2) Islamabad Electric Supply Company– IESCO, (3) Lahore Electric Supply Company– LESCO, and (4) Multan Electric Power Company- MEPCO. In 2012, HESCO was bifurcated into two separate companies to form new Sukkur Electric Power Company-SEPCO.

5

Selection of DISCOs. The four DISCOs were identified by the Government and stated to be representative of companies in the sector ranging from top to bottom of the scale. The identification by Government also took into consideration other factors, such as law and order situation, ease of implementation and policy for privatization of some DISCOs. In all the four selected DISCO there was a need for Grid station capacity expansion and even though the Project has been closed, the need of Grid station capacity expansion remains insatiate even in the better performing DISCOs.

Design of sub projects for DISCOs within the categories of ST and 11kV. Within the DISCOs the segregation and ratio of subprojects between Sub-Transmission and Downstream Distribution at 11/0.4 kV (11kV), were based upon the operational demands of DISCOs as identified by them during need assessment, rather than being based on an optimization of benefits approach. For example in the case of LESCO, during FY2007 the ST Losses were less than1.0 % and 11kV losses were 12.7 % as compared to 3.6% and 8.9 % for IESCO, however project design did not include an ELR that LESCO decided to undertake from its own resources. Inclusion of ELR component could have given some flexibility to appropriately reallocate resources as LESCO’s STG component faced many difficulties and several contracts were not awarded. Project restructuring was done too late and left no choice other than cancellation. There was an emphasis on technical loss reduction but as explained below the project was missing a comprehensive revenue protection program including, disconnection of non-paying consumers, consumer classification for billing, computerized metering etc.

Were alternatives considered? ST capacity expansion is an essential need of DISCOs to carry out their business and service obligation and as such had no alternative7. However in the case of 11/0.4 kV distribution system, the alternative or sharing between technical energy loss reduction measures and pilferage reduction measures should have been considered for each DISCO to optimize project benefits8. Since no study was available to identify percentage of area wise pilferage in overall losses, the selection of projects was done under the constraint of assuming that the loading on line was arising out of a legitimate demand on the system. Alternately, it could have been based on a minimum revenue billing and collection requirement from the sub project area. This aspect has been taken into consideration on an overall basis while selecting HESCO for investing in Aerial Bundled conductor (ABC) installation as a measure of addressing the pilferage issue on a pilot basis. Other modes of addressing the pilferage issue could also have been considered in all DISCOs, such as (a) extending 11kV overhead line and installing smaller capacity distribution transformers

7 Although Captive power is stated as an alternative in PAD, but it cannot be made available in the exact same location where ST capacity constraint is being experienced; moreover it involves technical, regulatory and functional issues which restricts its availability as a feasible alternative to capacity expansion.

8 Distribution transformer and line capacity enhancement measures can become counterproductive if carried out in areas where large scale pilferage is evident. Sub-projects, aimed at pilferage reduction could have been included in all DISCOs, on the basis of grading of overall losses at the 11kV feeder level.

6

(Dtrs) to reduce or eliminate 0.4 kV overhead system, in areas where direct hooks are being applied for pilferage; and (b) installation of smart meters having over load circuit breaking and remote disconnection capability.

Overall, the project was missing a comprehensive revenue protection program and therefore the intended targets were not achieved. A component on automated metering and billing system implementation would have helped address this but as argued in this report project design was too complicated and inclusion of another component would have made it even more complex. Alternately, PDO could have been changed to bring it in line with the power sector attributes directly influenced through this intervention. Availability of reliable data is another consideration. The indicators therefore should either be based on the data which can be measured reliably or for which management information systems could be developed as part of the project.

Adequacy of government commitment.

Government commitment/ownership remained high during the preparation and design phase as it continued the power sector reform program articulated in early 1990s to transform the successor generation, transmission and distribution companies created from WAPDA, into commercially oriented and efficiently managed and operated companies. First annual consumer tariff determinations for DISCOs were completed in 2007 (an essential first step towards their financial autonomy) by NEPRA, almost six years after it became fully operational.

Unfortunately, the power sector reforms didn’t continue with the same vigor and the sector plunged deeper into energy and financial crisis and is unable to recover its costs from the current combination of tariffs and subsidies. This gave rise to inter corporate arrears (also referred as circular debt) that amounted to about 4% of GDP in FY2013 and the sector receives subsidies in the range of 1-2% of GDP. This also affected project implementation in several ways because of weak governance structure and governments interference in corporate decisions. The current government is trying to put things back on track. It has cleared the entire stock of circular debt in June/July 2013 and is now addressing underlying issues through policy measures, including the level of tariffs and inadequate management resulting in higher than acceptable level of losses and non-recovery of revenue. As part of government’s reform measures and its vision for the power sector delineated in National Power Policy 2013, the Board of Directors (BODs) of publically owned power sector entities have been strengthened, DISCOs have been put under the Companies Act and new performance contracts are being signed including revenue protection plans.

Assessment of Risks.

The risks were divided into two broad categories – (i) risks to project development objectives that largely dealt with the success of the power sector reforms; and (ii) risks to component results that depended upon selected DISCOs’ capacity to implement the project and administer procurement, environmental and social action plans. Some of

7

these risk factors particularly those related to tariffs and subsidies were translated into legal covenants so that financial viability of the sector and its entities can be ensured and IEs capacity to function independently can be built. These legal covenants were either not met or were met with significant delays.

The issues in the power sector were well laid out in the PAD, but the overall project risk was underestimated and should have been High rather than Substantial because of the issues related to corporate governance, lack of autonomy given to power sector entities and weak accountability structure, government’s unwillingness to implement tariff & subsidy policy and procurement related issues indicating collusion9.

In addition to the risks identified at the design stage, project faced several other risks that caused significant delays. Key ones are: (i) land acquisition became a major problem e.g. a grid station could not be built on already acquired piece of land and an alternate was suggested; (ii) other unforeseen risks such as markets volatility, floods/natural disasters e.g. bids were cancelled after a blip in commodity prices in 2008.

2.2 Implementation (including any project changes/restructuring, mid-term review, Project at Risk status, and actions taken, as applicable) Implementation of the project remained slower than planned since its approval on June 17, 2008 particularly during initial phase of the Project. Project’s effectiveness was unduly delayed because legal opinions and ratifications of the Project Agreement by respective Boards of the DISCOs took 6 months and opening of designated account took another 6 months after effectiveness. There were major delays in procurement cycle due to several iterations to procurement documents, multiple rebidding of activities due to all non-responsive bids or no bids received, and undue time taken from tendering/evaluation to contract award. These issues arose because project was not ready for implementation which points towards its poor quality at entry. The mid-term review was carried out one year before project closing and the ratings were downgraded from Moderately Satisfactory (MS) to Moderately Unsatisfactory (MU) and Unsatisfactory(U) for Development Objective (DO) and Implementation Progress (IP) respectively primarily because of slow pace of contract award, lag in disbursements, delay in implementing the Procurement Action Plan (PAP)10, and weak institutional capacity. Specific actions and timelines were agreed but even those were not adhered to and the project was restructured in June 2012 (few days prior to the original closing date). The project was again

9 INT was involved to address the issues of collusion and several actions were agreed under the procurement action plan including amendment to SRO827(1) (See Section 2.4 Procurement for details).

10 At the start of the project there were some instances of collusion and unethical practices in the sector for which the Bank had proposed a Procurement Action Plan. Despite of repeated efforts there was very little implementation. Lack of ownership and seriousness to implement PAP was a major reason for not meeting this legal covenant.

8

restructured prior to the revised closing date to reallocate the unutilized IDA portion to the Pakistan program. At first restructuring, recognizing the complexities involved in the nature of the project and the delays caused due to factors outside the control of the IEs’ management the project was extended for 20 months and only the contracts which were ongoing or at final stage of award were carried forward. This did not improve the project performance and the ratings for DO and IP in the last Implementation Status and Results Report (ISR) were still MU and U. The implementation performance varies widely among IEs but all have experienced significant delays and have contracts that go beyond the revised Project Closing Date of February 28, 2014 (PCD) or were not awarded. As of PCD only 75 sub-projects (i.e. 65%) were completed and about 72.5% were disbursed. Four large value contracts representing 23 sub-projects (amounting to about US$ 32 million, 16.5% by value) were not awarded even after an extension of 20 months. About 11.0% of the contractual commitment is going beyond the PCD and has to be funded by the IEs themselves. (See Annex 2 for entity-wise details). Based on a sample of 27 contracts from a total of 70 it was observed that procurement cycle took more than 400 days on average for ICB contracts, an estimated delay of more than 100 days on average. The average cycle time for NCB is in the range of 250 – 350 days which is also quite high. Similarly, for a selected sample of 63 contracts more than 75% of the contracts were not completed on time, experienced delays ranging from 1 to 18 months with an average delay of 3 months. Delays occurred almost at every stage of the project cycle. As of project closing only 75 out of 115 subprojects were completed. Majority about 23 were not awarded and 17 went beyond the PCD because of delay in implementation. Following factors contributed to the delay of project implementation: • IEs’ weak capacity in contract management and ineffective use of technical

assistance. The project had six implementing agencies most of which were established in 1998, after unbundling of the integrated utility. Secondly, it was the first Bank investment lending operation in Pakistan’s power sector since 1995. Therefore, the IEs didn’t have much experience in preparing or implementing Bank-funded projects. Also, frequent staff turnover eroded the capacity which was built in the interim. Figure 1 compares procurement cycle for similar NCB contracts funded by Bank versus own resources. For Bank funded projects a major gap was observed in bid evaluation for following reasons: (i) low clearing thresholds for DISCOs required multiple internal approvals, (ii) historical track record to assess quality and bidders’ past experience required for Bank funded activities was missing from the bids as bidders were only used to submit qualifications details as per the activities done through DISCOs own resources which

Figure 1: Procurement Cycle in Days

9

did not require such details. A logical rationale for delay in contract award and signing could not be ascertained. Generally the bid validity requested was 120 days, which is normally an adequate time period for doing evaluations and contract award. But there are instances where bid validity had expired and bidders were not willing to extend due to floating exchange rate and increasing prices of raw materials. Also, the TA funds were not utilized to build the capacity during the early phase of the project. For example:

a. Lack of skill to deal with procurement/contract management relating to the ST portion of the project, particularly turn key projects including entire package of a 132 kV Grid station, was already realized at the Project appraisal stage. When the DISCOs took over the ST part of Transmission from NTDC, the Grid system operation and construction staff was transferred to the respective DISCOs but Procurement and contract management staff with NTDC was not shared with DISCOs. Acquisition of skills in this area was therefore an ongoing process during the implementation of the project involving delays in sending back and forth Bidding Documents and Bid Evaluation reports between WB and the IEs before approvals could be obtained and contracts signed by IEs. Gearing the TA component to building capacity in this context right at the beginning of the Project could have avoided most of the protracted delays.

b. It was agreed that International Procurement Advisor (IPA) would be appointed by no later than December 31, 2008 but the consultant was engaged after the MTR and the procurement manual prepared by the IPA and reviewed by the IEs to strengthen procurement systems was never adopted by the IEs.

• Revision of Technical Specifications during project implementation was time consuming and could have been done at the design stage or immediately afterwards. The government agreed with the Bank in mid-2009 that the IEs and PEPCO will work with the Bank to update the specifications of key equipment and material to be procured under the Project. This was necessitated by a need to ensure that the specifications used by the IEs in the bidding documents are non-restrictive by bringing them in line with the latest international standards and norms and to address collusion but the process was time consuming and about six months were spent to update/revise the technical specifications of main equipment.

• Frequent complaints, contractual disputes and litigation issues held up project progress. Power equipment market was also not quite open, competitive and efficient. Manufacturers of distribution equipment and materials in Pakistan were not used to open and competitive bidding processes, based on WB guidelines and therefore there were several complaints and concerns raised by the potential bidders. Project received more than its share of complaints – 30% of the complaints received over the past 10 years were related to this project. A number of complaints also arose out of local manufacturers and vendors trying to resist competition from international firms. To highlight the issue one ICB can be quoted here which was the cause of substantial underutilization of the loan.

a. WB issued “No objection” for purchase of 27 number 31.5- 40 MVA Power Transformers (PTrs), relating to LESCO ICB 631-01. However, LESCO could

10

not sign the contract with the lowest evaluated bidder as the case remained under consideration of the LESCO Board for an indefinite period due to the issue of equivalency of On Load Tap Changer (OLTC, essentially required to change output voltage according to requirement during operation). The matter regarding OLTC also affected few other DISCOs/contracts not financed by the Bank and was investigated by the Competition Commission of Pakistan (CCP) on the complaint filed by an international manufacturer into the alleged monopoly created by specifying a particular make for OLTC in PTrs. The CCP concluded this to be a violation of the Competition Act 2010 based on imposing restrictive trading conditions. Later, NTDC filed a writ petition against CCP Decision and as a result the matter remained suspended.

• Lack of preparedness to deal with unforeseen risks resulting in ineffective use of project funds. For example:

a. Almost all bidding process in 2008 was cancelled due to sudden spike in commodity prices that didn’t seem like a valid trend and could have made these investments unfeasible. In retrospect, it seemed like a good decision because the spike disappeared within four months.

b. In 2010, floods damaged distribution equipment and assets. Procurement activities in some DISCOs (particularly LESCO) were halted for about 8 months so that the savings can be diverted for the restoration of distribution assets damaged by the floods. However, the government subsequently decided not to utilize the existing funds for such purposes and it appears that this was not communicated to the IEs in time and caused some delays.

2.3 Monitoring and Evaluation (M&E) Design, Implementation and Utilization Design. The PDO of EDTIP was generic, overambitious and mixed investments and reforms. Such wide ranging objectives made it extremely difficult to measure the project achievements. Moreover, the indicators selected for the project represented entity level data and captured the intended outcomes on an overall operational performance of the IEs in terms of units purchased, losses, collection, subsidies, interruptions, voltage profile etc. The indicators were not project specific and therefore performance of one sub-component could not be compared against the other for informed decision making and appropriate reallocation of resources. The indicators also did not capture the effect of similar concurrent activities by other lending agencies such as ADB or IEs’ own development resource. The intermediate indicators also did not capture other actions that had direct effect on IEs financial performance e.g. the timing and adequacy of tariffs adjustment approvals and receipt of subsidies. The lack of reporting on project results, therefore, posed lot of challenges for M&E. The intermediate indicators, therefore, should have included project specific indicators such as 132/11kV capacity added in the ST system and number of ELR projects completed out of total sub projects envisaged in the 11/0.4 kV system to measure project’s progress and benefits directly attributable to this project. Implementation/Utilization. The Quarterly Progress Reports (QPRs) submitted by the IEs included Key Performance Indicators. Most of these key indicators are widely reported and are included in the regulators’ industry reports, tariff petitions/determinations, etc.

11

The losses and collection figures are expected to be reliable as the amounts are audited by independent auditors and units purchased and billed is largely through metering. The data on quality and reliability of supply, however, show such a vast variation in numbers across DISCOs and across time that it cannot be relied upon as a credible indicator to judge progress of implementation or project’s effectiveness. No system was put in place either as part of the project or by utilities themselves to improve data collection for better monitoring and decision making purposes. The Technical Assistance (TA) component was not used effectively to directly support project implementation. An owner’s engineer for example would have helped identify and address the issues leading to significant capacity building on project implementation.

2.4 Safeguard and Fiduciary Compliance (focusing on issues and their resolution, as applicable)

Environmental Safeguards: The project triggered Bank’s safeguard policies OP4.01 and 4.12 and was assessed as Environment Category B based upon the fact that most of the anticipated/potential impacts were mild to moderate in significance and associated with the construction activities and hence temporary in nature. In accordance with the requirements detailed in the ESAs cleared by the Bank, the IAs established safeguard departments to implement ESAs and ESMPs but often faced reluctance and sometimes even resistance from within their respective organizations and from contractors. The key factor affecting the safeguard implementation and outcome included lack of relevant experience and awareness at the IE level. Similarly the contractors and consultants engaged by the IEs were also quite weak in terms of understanding and implementing environmental safeguard requirements. In addition, no monitoring was carried out by the regulatory agencies (EPAs) for the ESA compliance during the project implementation.

Initially during the project implementation, the safeguard compliance was not satisfactory primarily because the IEs and their contractors did not have any previous experience in terms of understanding and implementing environmental safeguard requirements. However the compliance improved gradually as a result of continued support and guidance provided by the task team and the final monitoring conducted at the end of the construction phase revealed that the project did not cause any significant, lasting and or irreversible environmental impacts.

Social Safeguards: The Project used two instruments to address social safeguards issues – Environment and Social Assessments, Resettlement Action Plans and one Abbreviated Resettlement Action Plan. While ESMPs were formed for all IEs (HESCO, IESCO, LESCO, MEPCO and NTDC), the RAPs were prepared and implemented only by entities that undertook land acquisition for grid stations. This included IESCO and MEPCO while LESCO prepared and implemented an Abbreviated Resettlement Action Plan. Mostly, the RAPs were implemented for small number of Project Affected People e.g. in Lahore, LESCO acquired land from 15 affected people. However, the major area of compensation remained that for crop and other losses that were incurred during the implementation of the Transmission Line components. These losses were assessed and addressed under the

12

existing practices used by the IEs. The procedure involves post-assessment of losses through the patwaris/land revenue officers and local staff. In the absence of standardized guidelines and procedures for assessment of losses, the common practice across all DISCOs is to undertake assessment after the damages. Further, there is no clarity on standardization of compensation payments. The result was that compensation payments were severely and consistently delayed in the Project. IESCO, LESCO and MEPCO reported pending/outstanding payments even at the end of the Project. In the case of IESCO, the payments were delayed for a year while MEPCO had only paid 19% of the compensation owed for crop losses by the end of the project.

The Project supported the creation of Social and Environment Cells in each IE to oversee the implementation of social safeguards. Over the life of the Project, these played a significant role in monitoring safeguards implementation in the field, raising awareness both within DISCOs and among contractors/implementing partners and conducting periodic public consultations. A Grievance Redress Mechanism was operational throughout the project. However, it had limited scope to address the major issue related to delays in loss assessment and award of compensation payments for losses due to Transmission Lines.

Financial Management In compliance with Corporate Governance Rules 2013 issued by the Securities & Exchange Commission of Pakistan (SECP), new Boards including independent directors of all DISCOs were appointed in August – October 2013. Oversight committees of the Boards on internal audit and finance have also been made effective to ensure effective controls and financial reporting. The Bank was informed, at the project appraisal stage that Enterprise Resource Planning (ERP)11 is underway in all implementing agencies, except MEPCO, which is expected to be completed during 2008 – only LESCO has successfully implemented accounting module. Further, it was agreed at time of appraisal that the fixed assets physical verification and tagging exercise would be initiated by DISCOs and is yet to be completed. Whereas, internal audit approach, to conduct the audit is based on transaction-audit, a weak audit approach, instead of Risk-Based audit approach as envisaged in the DISCOs Internal Audit Manuals. Implementing agencies arrangements for financial reporting are given in the ensuing paragraphs. Existing financial management arrangements in the six implementing agencies of this project were used. Adequate staffing was maintained during life of the project. Internal audit arrangements were also in place except for PEPCO where no internal audit was conducted despite regular follow up. Despite the above-mentioned drawbacks, the implementing agencies remained compliant with the financial covenants submitting acceptable interim quarterly financial reports and annual audited financial statements except NTDC in which case Bank had to take

11 ERP cover computerization of accounts, human resource, billing, inventory and fixed assets management.

13

remedial measures as audited financial statements were submitted after a delay of over four months after the due date. The delay was attributable to the board of directors not being in place. Auditors’ performance remained satisfactory.

2.5 Post-completion Operation/Next Phase (including transition arrangement to post-completion operation of investments financed by present operation, Operation & Maintenance arrangements, sustaining reforms and institutional capacity, and next phase/follow-up operation, if applicable) Completion of On-going Contracts and Operation & Maintenance (O&M) arrangements. No transition arrangements are required to be made by the Bank as DISCOs are liable for the completion of the on-going activities from their own resources. The annual distribution margins (DM) determined by NEPRA will cover O&M cost and provides return on assets and depreciation to cover the debt servicing. The tariff revenue also ensures that the DISCOs are able to contribute equity for new projects and therefore DISCOs/NTDC can finance the portion of the work (about US$ 20 million) that went beyond PCD from their own resources. Most DISCOs, however, are not meeting the efficiency targets set by NEPRA for system losses and bill collection which affect their cash flows and profitability. Even though these companies are in perpetual loss and require government support to remain financially viable retain their DM in full by delaying the payments to NTDC/CPPA (single buyer and seller) for the power procured. As part of the reform measures and action covered under Power Reform DPC, CPPA would become independent of NTDC and would sign PPAs with the power generators on behalf of DISCOs making them liable for their losses. This may also lead to reduced access to generating capacity if DISCOs are unable to pay for the power procured. Sustaining Reforms and Institutional Capacity. Further strengthening of technical capacity would require an active TA or a lending operation. Though the Bank will continue to remain engaged with the government and other entities as part of its policy dialogue other development partners particularly ADB and USAID are providing more direct support to power sector public entities. As mentioned in Section 1.1, prior conditions including those related to power reforms have not been met even today and APL-2 was never approved. One of those conditions relates to Power Sector Reforms which have been a long drawn process. The Bank, however, has remained engaged with the government in its reforms efforts. The National Power Policy 2013 of the Government of Pakistan (GOP) has given a fresh impetus to these reform efforts to develop an efficient and consumer centric electric power system. The GOP has also developed an implementation plan, which is supported by the development partners. The IMF approved in September 2013 a 36 month Extended Fund Facility in the amount of US$ 6.68 billion, which includes reforms to the power sector. The Bank’s power sector reform DPC series, first of which (US$ 600 million) was approved in May 2014, also supports these reforms and was developed in collaboration with ADB and JICA. These reforms efforts are expected to have positive results on the sector and will improve financial viability of generating companies, NTDC and the DISCOs.

14

Ensuring Financial Sustainability of the Sector. The largest financial risk in the sector is the under performance of the DISCOs against the targets for loss reduction and bill collection set by NEPRA. Addressing these issues through DPC would pave the way for much needed investments in the transmission and distribution sector. The Government as the current owner has instructed the DISCOs to implement revenue protection programs and through the performance contracts, MOWP is holding the DISCOs accountable. Implementing a revenue protection program, however, will require immediate investments. DISCOs also need to enhance transmission and distribution network capacity to disperse additional power from planned and ongoing generation projects without incurring major losses. Follow-up operation/plans. Considering the delays and problems faced during the implementation of the EDTIP project a disbursement linked indicator type operation (DLI)12 with some emphasis on procurement aspects along with other operational parameters could be considered for the design of any future project with electricity transmission and distribution companies. However, given how poor the indicators were this would require (a) investment in indicators to ensure availability of reliable information and (b) organizational changes to use that information for performance monitoring. In addition to key performance indicators a DLI could also include specific actions aimed to improve efficiency, transparency and accountability in management and operations. Power Reform DPC will set a stage for investments in the sector by (i) increasing transparency and data reliability; (ii) addressing chronic issues related to tariffs, subsidies and circular debt; and (iii) ensuring enhanced monitoring by NEPRA and the MOWP. However, most of the DISCOs are still not up to the mark to raise commercial financing on their own and therefore would need continued support of multi- and bi-laterals for some time.

3. Assessment of Outcomes

3.1 Relevance of Objectives, Design and Implementation (to current country and global priorities, and Bank assistance strategy) The project objectives remain highly relevant to the needs of the country in general and power sector in particular but as explained below were too ambitious. Similarly, project design was very complicated spreading across many dimensions and indicators failed to capture project progress. Therefore, relevance of objectives, design and implementation is rated as ‘Moderate’ on a 4 point scale13. Further explanation in support of this rating is provided in the following paras.

12 Use of DLIs, for some other projects in Pakistan, has demonstrated effectiveness in enhancing coordination with stakeholders and development partners and focusing greater attention on results as opposed to administrative implementation issues, which was a major cause of EDTIP’s poor performance.

13 4 Point Scale: Negligible to Low (N); Moderate (M); Significant/Substantial (S) and High (H).

15